UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | | | | | |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended SeptemberJune 30, 20222023

OR | | | | | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-10258

Tredegar Corporation

(Exact Name of Registrant as Specified in Its Charter)

| | | | | | | | |

| Virginia | | 54-1497771 |

(State or Other Jurisdiction of

Incorporation or Organization) | | (I.R.S. Employer

Identification No.) |

| | | | | | | | | | | |

| 1100 Boulders Parkway | | |

| Richmond, | Virginia | | 23225 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: (804) 330-1000

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, no par value | TG | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | ¨ | Accelerated filer | x | Smaller reporting company | | ☐ |

| | | | | |

| Non-accelerated filer | | ¨ | | Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The number of shares of Common Stock, no par value, outstanding as of NovemberAugust 4, 2022: 34,000,6422023: 34,384,677

Tredegar Corporation

Table of Contents

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements.

Tredegar Corporation

Condensed Consolidated Balance Sheets

(In Thousands, Except Share Data)

(Unaudited) | | | September 30, | | December 31, | | June 30, | | December 31, |

| | 2022 | | 2021 | | 2023 | | 2022 |

| Assets | Assets | | Assets | |

| Current assets: | Current assets: | | Current assets: | |

| Cash and cash equivalents | Cash and cash equivalents | $ | 19,250 | | | $ | 30,521 | | Cash and cash equivalents | $ | 21,193 | | | $ | 19,232 | |

| Accounts and other receivables, net | Accounts and other receivables, net | 110,077 | | | 103,312 | | Accounts and other receivables, net | 79,139 | | | 84,544 | |

| Income taxes recoverable | Income taxes recoverable | 1,834 | | | 2,558 | | Income taxes recoverable | 1,216 | | | 733 | |

| Inventories | Inventories | 114,103 | | | 88,569 | | Inventories | 86,692 | | | 127,771 | |

| Prepaid expenses and other | Prepaid expenses and other | 9,601 | | | 11,275 | | Prepaid expenses and other | 10,214 | | | 10,304 | |

| Current assets of discontinued operations | 151 | | | 178 | | |

| Total current assets | Total current assets | 255,016 | | | 236,413 | | Total current assets | 198,454 | | | 242,584 | |

| Property, plant and equipment, at cost | Property, plant and equipment, at cost | 520,371 | | | 498,311 | | Property, plant and equipment, at cost | 545,048 | | | 531,921 | |

| Less: accumulated depreciation | Less: accumulated depreciation | (340,868) | | | (327,930) | | Less: accumulated depreciation | (355,156) | | | (345,510) | |

| Net property, plant and equipment | Net property, plant and equipment | 179,503 | | | 170,381 | | Net property, plant and equipment | 189,892 | | | 186,411 | |

| Right-of-use leased assets | Right-of-use leased assets | 14,356 | | | 13,847 | | Right-of-use leased assets | 12,794 | | | 14,021 | |

| Identifiable intangible assets, net | Identifiable intangible assets, net | 12,200 | | | 14,152 | | Identifiable intangible assets, net | 10,785 | | | 11,690 | |

| Goodwill | Goodwill | 70,608 | | | 70,608 | | Goodwill | 55,195 | | | 70,608 | |

| Deferred income taxes | Deferred income taxes | 11,820 | | | 15,723 | | Deferred income taxes | 14,610 | | | 13,900 | |

| Other assets | Other assets | 3,155 | | | 2,460 | | Other assets | 3,139 | | | 2,879 | |

| Total assets | Total assets | $ | 546,658 | | | $ | 523,584 | | Total assets | $ | 484,869 | | | $ | 542,093 | |

| Liabilities and Shareholders’ Equity | Liabilities and Shareholders’ Equity | | Liabilities and Shareholders’ Equity | |

| Current liabilities: | Current liabilities: | | Current liabilities: | |

| Accounts payable | Accounts payable | $ | 126,848 | | | $ | 123,760 | | Accounts payable | $ | 82,290 | | | $ | 114,938 | |

| Accrued expenses | Accrued expenses | 36,894 | | | 33,104 | | Accrued expenses | 23,501 | | | 31,603 | |

| Lease liability, short-term | Lease liability, short-term | 2,003 | | | 2,158 | | Lease liability, short-term | 2,163 | | | 2,035 | |

| Income taxes payable | Income taxes payable | 1,391 | | | 9,333 | | Income taxes payable | 579 | | | 1,137 | |

| Current liabilities of discontinued operations | 71 | | | 193 | | |

| Total current liabilities | Total current liabilities | 167,207 | | | 168,548 | | Total current liabilities | 108,533 | | | 149,713 | |

| Lease liability, long-term | Lease liability, long-term | 13,160 | | | 12,831 | | Lease liability, long-term | 11,991 | | | 12,738 | |

| Long-term debt | Long-term debt | 124,000 | | | 73,000 | | Long-term debt | 141,000 | | | 137,000 | |

| Pension and other postretirement benefit obligations, net | Pension and other postretirement benefit obligations, net | 28,464 | | | 78,265 | | Pension and other postretirement benefit obligations, net | 35,747 | | | 35,046 | |

| | Other non-current liabilities | Other non-current liabilities | 6,769 | | | 6,218 | | Other non-current liabilities | 4,449 | | | 5,834 | |

| Total liabilities | Total liabilities | 339,600 | | | 338,862 | | Total liabilities | 301,720 | | | 340,331 | |

| Shareholders’ equity: | Shareholders’ equity: | | Shareholders’ equity: | |

| Common stock, no par value (issued and outstanding 33,982,479 shares at September 30, 2022 and 33,736,629 shares at December 31, 2021) | 57,902 | | | 55,174 | | |

| Common stock held in trust for savings restoration plan (111,861 shares at September 30, 2022 and 108,433 shares at December 31, 2021) | (2,174) | | | (2,135) | | |

| Common stock, no par value (authorized shares 150,000,000, issued and outstanding 34,363,845 shares at June 30, 2023 and 34,000,642 shares at December 31, 2022) | | Common stock, no par value (authorized shares 150,000,000, issued and outstanding 34,363,845 shares at June 30, 2023 and 34,000,642 shares at December 31, 2022) | 60,078 | | | 58,824 | |

| Common stock held in trust for savings restoration plan (116,336 shares at June 30, 2023 and 113,316 shares at December 31, 2022) | | Common stock held in trust for savings restoration plan (116,336 shares at June 30, 2023 and 113,316 shares at December 31, 2022) | (2,218) | | | (2,188) | |

| Accumulated other comprehensive income (loss): | Accumulated other comprehensive income (loss): | | Accumulated other comprehensive income (loss): | |

| Foreign currency translation adjustment | Foreign currency translation adjustment | (87,826) | | | (85,792) | | Foreign currency translation adjustment | (83,338) | | | (86,079) | |

| Gain (loss) on derivative financial instruments | Gain (loss) on derivative financial instruments | (4,877) | | | 901 | | Gain (loss) on derivative financial instruments | (843) | | | (2,480) | |

| Pension and other postretirement benefit adjustments | Pension and other postretirement benefit adjustments | (56,963) | | | (64,613) | | Pension and other postretirement benefit adjustments | (54,463) | | | (59,036) | |

| Retained earnings | Retained earnings | 300,996 | | | 281,187 | | Retained earnings | 263,933 | | | 292,721 | |

| Total shareholders’ equity | Total shareholders’ equity | 207,058 | | | 184,722 | | Total shareholders’ equity | 183,149 | | | 201,762 | |

| Total liabilities and shareholders’ equity | Total liabilities and shareholders’ equity | $ | 546,658 | | | $ | 523,584 | | Total liabilities and shareholders’ equity | $ | 484,869 | | | $ | 542,093 | |

See accompanying notes to the condensed consolidated financial statements.

Tredegar Corporation

Condensed Consolidated Statements of Income (Loss)

(In Thousands, Except Per Share Data)

(Unaudited)

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | | Three Months Ended June 30, | | Six Months Ended June 30, |

| | | 2022 | | 2021 | | 2022 | | 2021 | | 2023 | | 2022 | | 2023 | | 2022 |

| Revenues and other items: | Revenues and other items: | | Revenues and other items: | |

| Sales | Sales | $ | 238,486 | | | $ | 209,517 | | | $ | 749,415 | | | $ | 605,468 | | Sales | $ | 178,167 | | | $ | 274,363 | | | $ | 369,289 | | | $ | 510,929 | |

| Other income (expense), net | Other income (expense), net | 119 | | | 391 | | | 1,113 | | | 9,272 | | Other income (expense), net | (20) | | | 1,342 | | | 260 | | | 1,041 | |

| | 238,605 | | | 209,908 | | | 750,528 | | | 614,740 | | | 178,147 | | | 275,705 | | | 369,549 | | | 511,970 | |

| Costs and expenses: | Costs and expenses: | | Costs and expenses: | |

| Cost of goods sold | Cost of goods sold | 200,582 | | | 170,756 | | | 601,930 | | | 470,733 | | Cost of goods sold | 153,267 | | | 218,088 | | | 312,792 | | | 401,348 | |

| Freight | Freight | 9,500 | | | 7,264 | | | 28,619 | | | 20,531 | | Freight | 7,199 | | | 11,036 | | | 13,243 | | | 19,118 | |

| Selling, general and administrative | Selling, general and administrative | 19,018 | | | 16,767 | | | 59,160 | | | 55,422 | | Selling, general and administrative | 16,889 | | | 18,862 | | | 35,894 | | | 40,143 | |

| Research and development | Research and development | 1,576 | | | 1,613 | | | 4,855 | | | 4,770 | | Research and development | 1,376 | | | 1,754 | | | 2,581 | | | 3,278 | |

| Amortization of identifiable intangibles | Amortization of identifiable intangibles | 653 | | | 724 | | | 1,982 | | | 2,170 | | Amortization of identifiable intangibles | 464 | | | 666 | | | 968 | | | 1,329 | |

| Pension and postretirement benefits | Pension and postretirement benefits | 3,506 | | | 3,540 | | | 10,489 | | | 10,622 | | Pension and postretirement benefits | 3,418 | | | 3,506 | | | 6,837 | | | 6,982 | |

| Interest expense | Interest expense | 1,138 | | | 842 | | | 3,158 | | | 2,555 | | Interest expense | 2,374 | | | 1,234 | | | 4,686 | | | 2,020 | |

| Asset impairments and costs associated with exit and disposal activities, net of adjustments | Asset impairments and costs associated with exit and disposal activities, net of adjustments | 495 | | | 265 | | | 621 | | | 633 | | Asset impairments and costs associated with exit and disposal activities, net of adjustments | — | | | 134 | | | 69 | | | 126 | |

| Goodwill impairment | | Goodwill impairment | 15,413 | | | — | | | 15,413 | | | — | |

| Total | Total | 236,468 | | | 201,771 | | | 710,814 | | | 567,436 | | Total | 200,400 | | | 255,280 | | | 392,483 | | | 474,344 | |

| Income (loss) from continuing operations before income taxes | 2,137 | | | 8,137 | | | 39,714 | | | 47,304 | | |

| Income (loss) before income taxes | | Income (loss) before income taxes | (22,253) | | | 20,425 | | | (22,934) | | | 37,626 | |

| Income tax expense (benefit) | Income tax expense (benefit) | 1,125 | | | 1,908 | | | 7,460 | | | 10,728 | | Income tax expense (benefit) | (3,331) | | | 5,556 | | | (3,000) | | | 6,334 | |

| Net income (loss) from continuing operations | 1,012 | | | 6,229 | | | 32,254 | | | 36,576 | | |

| Income (loss) from discontinued operations, net of tax | 21 | | | (26) | | | 68 | | | (104) | | |

| Net income (loss) | Net income (loss) | $ | 1,033 | | | $ | 6,203 | | | $ | 32,322 | | | $ | 36,472 | | Net income (loss) | $ | (18,922) | | | $ | 14,869 | | | $ | (19,934) | | | $ | 31,292 | |

| | Earnings (loss) per share: | Earnings (loss) per share: | | Earnings (loss) per share: | |

| Basic: | | |

| Continuing operations | $ | 0.03 | | | $ | 0.19 | | | $ | 0.96 | | | $ | 1.09 | | |

| Discontinued operations | — | | | — | | | — | | | — | | |

| Basic earnings (loss) per share | $ | 0.03 | | | $ | 0.19 | | | $ | 0.96 | | | $ | 1.09 | | |

| Diluted: | | |

| Continuing operations | $ | 0.03 | | | $ | 0.19 | | | $ | 0.96 | | | $ | 1.09 | | |

| Discontinued operations | — | | | — | | | — | | | — | | |

| Diluted earnings (loss) per share | $ | 0.03 | | | $ | 0.19 | | | $ | 0.96 | | | $ | 1.09 | | |

| Basic | | Basic | $ | (0.56) | | | $ | 0.44 | | | $ | (0.59) | | | $ | 0.93 | |

| Diluted | | Diluted | $ | (0.56) | | | $ | 0.44 | | | $ | (0.59) | | | $ | 0.93 | |

| | Shares used to compute earnings (loss) per share: | Shares used to compute earnings (loss) per share: | | Shares used to compute earnings (loss) per share: | |

| Basic | Basic | 33,870 | | | 33,620 | | | 33,780 | | | 33,541 | | Basic | 34,079 | | | 33,814 | | | 33,988 | | | 33,734 | |

| Diluted | Diluted | 33,871 | | | 33,649 | | | 33,808 | | | 33,678 | | Diluted | 34,079 | | | 33,854 | | | 33,988 | | | 33,776 | |

See accompanying notes to the condensed consolidated financial statements.

Tredegar Corporation

Condensed Consolidated Statements of Comprehensive Income (Loss)

(In Thousands)

(Unaudited)

| | | Three Months Ended September 30, | | Three Months Ended June 30, |

| | | 2022 | | 2021 | | 2023 | | 2022 |

| Net income (loss) | Net income (loss) | $ | 1,033 | | | $ | 6,203 | | Net income (loss) | $ | (18,922) | | | $ | 14,869 | |

| Other comprehensive income (loss): | Other comprehensive income (loss): | | Other comprehensive income (loss): | |

| Unrealized foreign currency translation adjustment (net of tax benefit of $148 in 2022 and net of tax benefit of $294 in 2021) | (2,340) | | | (2,788) | | |

| Derivative financial instruments adjustment (net of tax benefit of $818 in 2022 and net of tax benefit of $174 in 2021) | (2,547) | | | (717) | | |

| Amortization of prior service costs and net gains or losses (net of tax expense of $712 in 2022 and net of tax expense of $927 in 2021) | 2,556 | | | 3,317 | | |

| Unrealized foreign currency translation adjustment (net of tax expense of $179 in 2023 and net of tax benefit of $482 in 2022) | | Unrealized foreign currency translation adjustment (net of tax expense of $179 in 2023 and net of tax benefit of $482 in 2022) | 1,621 | | | (5,230) | |

| Derivative financial instruments adjustment (net of tax expense of $500 in 2023 and net of tax benefit of $3,359 in 2022) | | Derivative financial instruments adjustment (net of tax expense of $500 in 2023 and net of tax benefit of $3,359 in 2022) | 368 | | | (9,161) | |

| Amortization of prior service costs and net gains or losses (net of tax expense of $637 in 2023 and net of tax expense of $712 in 2022) | | Amortization of prior service costs and net gains or losses (net of tax expense of $637 in 2023 and net of tax expense of $712 in 2022) | 2,286 | | | 2,556 | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | (2,331) | | | (188) | | Other comprehensive income (loss) | 4,275 | | | (11,835) | |

| Comprehensive income (loss) | Comprehensive income (loss) | $ | (1,298) | | | $ | 6,015 | | Comprehensive income (loss) | $ | (14,647) | | | $ | 3,034 | |

| | | Nine Months Ended September 30, | | Six Months Ended June 30, |

| | | 2022 | | 2021 | | 2023 | | 2022 |

| Net income (loss) | Net income (loss) | $ | 32,322 | | | $ | 36,472 | | Net income (loss) | $ | (19,934) | | | $ | 31,292 | |

| Other comprehensive income (loss): | Other comprehensive income (loss): | | Other comprehensive income (loss): | |

| Unrealized foreign currency translation adjustment (net of tax expense of $98 in 2022 and net of tax benefit of $103 in 2021) | (2,034) | | | (1,443) | | |

| Derivative financial instruments adjustment (net of tax benefit of $1,261 in 2022 and net of tax expense of $185 in 2021) | (5,778) | | | 515 | | |

| Amortization of prior service costs and net gains or losses (net of tax expense of $2,136 in 2022 and net of tax expense of $2,773 in 2021) | 7,650 | | | 9,954 | | |

| Unrealized foreign currency translation adjustment (net of tax expense of $615 in 2023 and net of tax expense of $246 in 2022) | | Unrealized foreign currency translation adjustment (net of tax expense of $615 in 2023 and net of tax expense of $246 in 2022) | 2,741 | | | 306 | |

| Derivative financial instruments adjustment (net of tax expense of $1,336 in 2023 and net of tax benefit of $443 in 2022) | | Derivative financial instruments adjustment (net of tax expense of $1,336 in 2023 and net of tax benefit of $443 in 2022) | 1,637 | | | (3,231) | |

| Amortization of prior service costs and net gains or losses (net of tax expense of $1,274 in 2023 and net of tax expense of $1,424 in 2022) | | Amortization of prior service costs and net gains or losses (net of tax expense of $1,274 in 2023 and net of tax expense of $1,424 in 2022) | 4,573 | | | 5,094 | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | (162) | | | 9,026 | | Other comprehensive income (loss) | 8,951 | | | 2,169 | |

| Comprehensive income (loss) | Comprehensive income (loss) | $ | 32,160 | | | $ | 45,498 | | Comprehensive income (loss) | $ | (10,983) | | | $ | 33,461 | |

See accompanying notes to the condensed consolidated financial statements.

Tredegar Corporation

Condensed Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited) | | | Nine Months Ended September 30, | | Six Months Ended June 30, |

| | 2022 | | 2021 | | 2023 | | 2022 |

| Cash flows from operating activities: | Cash flows from operating activities: | | Cash flows from operating activities: | |

| Net income (loss) | Net income (loss) | $ | 32,322 | | | $ | 36,472 | | Net income (loss) | $ | (19,934) | | | $ | 31,292 | |

| Adjustments for noncash items: | Adjustments for noncash items: | | Adjustments for noncash items: | |

| Depreciation | Depreciation | 17,538 | | | 16,169 | | Depreciation | 12,387 | | | 11,536 | |

| Amortization of identifiable intangibles | Amortization of identifiable intangibles | 1,982 | | | 2,170 | | Amortization of identifiable intangibles | 968 | | | 1,329 | |

| Reduction of right-of-use lease asset | Reduction of right-of-use lease asset | 1,590 | | | 1,582 | | Reduction of right-of-use lease asset | 1,075 | | | 1,072 | |

| Goodwill impairment | | Goodwill impairment | 15,413 | | | — | |

| Deferred income taxes | Deferred income taxes | 3,078 | | | 4,120 | | Deferred income taxes | (3,731) | | | 2,516 | |

| Accrued pension and post-retirement benefits | Accrued pension and post-retirement benefits | 10,519 | | | 10,622 | | Accrued pension and post-retirement benefits | 6,837 | | | 7,013 | |

| Stock-based compensation expense | Stock-based compensation expense | 2,575 | | | 3,227 | | Stock-based compensation expense | 521 | | | 1,842 | |

| Gain on investment in kaléo | Gain on investment in kaléo | (1,406) | | | (879) | | Gain on investment in kaléo | (262) | | | (1,406) | |

| Changes in assets and liabilities: | Changes in assets and liabilities: | | Changes in assets and liabilities: | |

| Accounts and other receivables | Accounts and other receivables | (7,222) | | | (11,379) | | Accounts and other receivables | 6,190 | | | (24,172) | |

| Inventories | Inventories | (24,855) | | | (19,902) | | Inventories | 43,013 | | | (31,495) | |

| Income taxes recoverable/payable | Income taxes recoverable/payable | (7,227) | | | 111 | | Income taxes recoverable/payable | (1,060) | | | (6,129) | |

| Prepaid expenses and other | Prepaid expenses and other | (5,365) | | | 3,422 | | Prepaid expenses and other | 2,976 | | | (516) | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | 3,624 | | | 12,078 | | Accounts payable and accrued expenses | (39,629) | | | 47,388 | |

| Lease liability | Lease liability | (1,737) | | | (1,566) | | Lease liability | (1,095) | | | (1,166) | |

| Pension and postretirement benefit plan contributions | Pension and postretirement benefit plan contributions | (50,503) | | | (5,510) | | Pension and postretirement benefit plan contributions | (279) | | | (50,314) | |

| Other, net | Other, net | 1,935 | | | 750 | | Other, net | (692) | | | 1,781 | |

| Net cash (used in) provided by operating activities | (23,152) | | | 51,487 | | |

| Net cash provided by (used in) operating activities | | Net cash provided by (used in) operating activities | 22,698 | | | (9,429) | |

| Cash flows from investing activities: | Cash flows from investing activities: | | Cash flows from investing activities: | |

| Capital expenditures | Capital expenditures | (25,527) | | | (19,576) | | Capital expenditures | (15,907) | | | (13,514) | |

| Proceeds from the sale of kaléo | Proceeds from the sale of kaléo | 1,406 | | | — | | Proceeds from the sale of kaléo | 262 | | | 1,406 | |

| Proceeds from the sale of assets | — | | | 4,749 | | |

| Net cash used in investing activities | (24,121) | | | (14,827) | | |

| | Net cash provided by (used in) investing activities | | Net cash provided by (used in) investing activities | (15,645) | | | (12,108) | |

| Cash flows from financing activities: | Cash flows from financing activities: | | Cash flows from financing activities: | |

| Borrowings | Borrowings | 279,250 | | | 69,250 | | Borrowings | 41,250 | | | 221,250 | |

| Debt principal payments | Debt principal payments | (228,250) | | | (76,250) | | Debt principal payments | (37,250) | | | (192,750) | |

| Dividends paid | Dividends paid | (12,552) | | | (12,114) | | Dividends paid | (8,884) | | | (8,135) | |

| Debt financing costs | Debt financing costs | (1,245) | | | — | | Debt financing costs | — | | | (1,245) | |

| Other | Other | (396) | | | 915 | | Other | — | | | (396) | |

| Net cash provided by (used in) financing activities | Net cash provided by (used in) financing activities | 36,807 | | | (18,199) | | Net cash provided by (used in) financing activities | (4,884) | | | 18,724 | |

| Effect of exchange rate changes on cash | Effect of exchange rate changes on cash | (805) | | | (54) | | Effect of exchange rate changes on cash | (208) | | | (246) | |

| Increase (decrease) in cash & cash equivalents | Increase (decrease) in cash & cash equivalents | (11,271) | | | 18,407 | | Increase (decrease) in cash & cash equivalents | 1,961 | | | (3,059) | |

| Cash and cash equivalents at beginning of period | Cash and cash equivalents at beginning of period | 30,521 | | | 11,846 | | Cash and cash equivalents at beginning of period | 19,232 | | | 30,521 | |

| Cash and cash equivalents at end of period | Cash and cash equivalents at end of period | $ | 19,250 | | | $ | 30,253 | | Cash and cash equivalents at end of period | $ | 21,193 | | | $ | 27,462 | |

See accompanying notes to the condensed consolidated financial statements.

Tredegar Corporation

Condensed Consolidated Statements of Shareholders’ Equity

(In Thousands, Except Share and Per Share Data)

(Unaudited)

The following summarizes the changes in shareholders’ equity for the three month period ended SeptemberJune 30, 2022:2023:

| | | Common Stock | | Retained Earnings | | Trust for Savings Restoration Plan | | Accumulated Other Comprehensive Income (Loss) | | Total Shareholders’ Equity | | Common Stock | | Retained Earnings | | Trust for Savings Restoration Plan | | Accumulated Other Comprehensive Income (Loss) | | Total Shareholders’ Equity |

| Balance July 1, 2022 | $ | 56,911 | | | $ | 304,370 | | | $ | (2,161) | | | $ | (147,335) | | | $ | 211,785 | | |

| Balance April 1, 2023 | | Balance April 1, 2023 | $ | 59,423 | | | $ | 287,308 | | | $ | (2,203) | | | $ | (142,919) | | | $ | 201,609 | |

| Net income (loss) | Net income (loss) | — | | | 1,033 | | | — | | | — | | | 1,033 | | Net income (loss) | — | | | (18,922) | | | — | | | — | | | (18,922) | |

| Foreign currency translation adjustment | Foreign currency translation adjustment | — | | | — | | | — | | | (2,340) | | | (2,340) | | Foreign currency translation adjustment | — | | | — | | | — | | | 1,621 | | | 1,621 | |

| Derivative financial instruments adjustment | Derivative financial instruments adjustment | — | | | — | | | — | | | (2,547) | | | (2,547) | | Derivative financial instruments adjustment | — | | | — | | | — | | | 368 | | | 368 | |

| Amortization of prior service costs and net gains or losses | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 2,556 | | | 2,556 | | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 2,286 | | | 2,286 | |

| Cash dividends declared ($0.13 per share) | Cash dividends declared ($0.13 per share) | — | | | (4,420) | | | — | | | — | | | (4,420) | | Cash dividends declared ($0.13 per share) | — | | | (4,468) | | | — | | | — | | | (4,468) | |

| Stock-based compensation expense | Stock-based compensation expense | 991 | | | — | | | — | | | — | | | 991 | | Stock-based compensation expense | 655 | | | — | | | — | | | — | | | 655 | |

| | Tredegar common stock purchased by trust for savings restoration plan | Tredegar common stock purchased by trust for savings restoration plan | — | | | 13 | | | (13) | | | — | | | — | | Tredegar common stock purchased by trust for savings restoration plan | — | | | 15 | | | (15) | | | — | | | — | |

| Balance September 30, 2022 | $ | 57,902 | | | $ | 300,996 | | | $ | (2,174) | | | $ | (149,666) | | | $ | 207,058 | | |

| Balance June 30, 2023 | | Balance June 30, 2023 | $ | 60,078 | | | $ | 263,933 | | | $ | (2,218) | | | $ | (138,644) | | | $ | 183,149 | |

The following summarizes the changes in shareholders’ equity for the ninesix month period ended SeptemberJune 30, 2022:2023:

| | | Common Stock | | Retained Earnings | | Trust for Savings Restoration Plan | | Accumulated Other Comprehensive Income (Loss) | | Total Shareholders’ Equity | | Common Stock | | Retained Earnings | | Trust for Savings Restoration Plan | | Accumulated Other Comprehensive Income (Loss) | | Total Shareholders’ Equity |

| Balance January 1, 2022 | $ | 55,174 | | | $ | 281,187 | | | $ | (2,135) | | | $ | (149,504) | | | $ | 184,722 | | |

| Balance January 1, 2023 | | Balance January 1, 2023 | $ | 58,824 | | | $ | 292,721 | | | $ | (2,188) | | | $ | (147,595) | | | $ | 201,762 | |

| Net income (loss) | Net income (loss) | — | | | 32,322 | | | — | | | — | | | 32,322 | | Net income (loss) | — | | | (19,934) | | | — | | | — | | | (19,934) | |

| Foreign currency translation adjustment | Foreign currency translation adjustment | — | | | — | | | — | | | (2,034) | | | (2,034) | | Foreign currency translation adjustment | — | | | — | | | — | | | 2,741 | | | 2,741 | |

| Derivative financial instruments adjustment | Derivative financial instruments adjustment | — | | | — | | | — | | | (5,778) | | | (5,778) | | Derivative financial instruments adjustment | — | | | — | | | — | | | 1,637 | | | 1,637 | |

| Amortization of prior service costs and net gains or losses | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 7,650 | | | 7,650 | | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 4,573 | | | 4,573 | |

| Cash dividends declared ($0.37 per share) | — | | | (12,552) | | | — | | | — | | | (12,552) | | |

| Cash dividends declared ($0.26 per share) | | Cash dividends declared ($0.26 per share) | — | | | (8,884) | | | — | | | — | | | (8,884) | |

| Stock-based compensation expense | Stock-based compensation expense | 3,124 | | | — | | | — | | | — | | | 3,124 | | Stock-based compensation expense | 1,508 | | | — | | | — | | | — | | | 1,508 | |

Repurchase of employee common stock for tax

withholdings | Repurchase of employee common stock for tax

withholdings | (396) | | | — | | | — | | | — | | | (396) | | Repurchase of employee common stock for tax

withholdings | (254) | | | — | | | — | | | — | | | (254) | |

| Tredegar common stock purchased by trust for savings restoration plan | Tredegar common stock purchased by trust for savings restoration plan | — | | | 39 | | | (39) | | | — | | | — | | Tredegar common stock purchased by trust for savings restoration plan | — | | | 30 | | | (30) | | | — | | | — | |

| Balance September 30, 2022 | $ | 57,902 | | | $ | 300,996 | | | $ | (2,174) | | | $ | (149,666) | | | $ | 207,058 | | |

| Balance June 30, 2023 | | Balance June 30, 2023 | $ | 60,078 | | | $ | 263,933 | | | $ | (2,218) | | | $ | (138,644) | | | $ | 183,149 | |

The following summarizes the changes in shareholders’ equity for the three month period ended SeptemberJune 30, 2021: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | Retained

Earnings | | Trust for

Savings

Restoration

Plan | | Accumulated Other

Comprehensive Income (Loss) | | Total

Shareholders’

Equity |

| Balance at July 1, 2021 | $ | 52,940 | | | $ | 261,699 | | | $ | (2,109) | | | $ | (169,190) | | | $ | 143,340 | |

| Net income (loss) | — | | | 6,203 | | | — | | | — | | | 6,203 | |

| Foreign currency translation adjustment | — | | | — | | | — | | | (2,788) | | | (2,788) | |

| Derivative financial instruments adjustment | — | | | — | | | — | | | (717) | | | (717) | |

| Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 3,317 | | | 3,317 | |

| Cash dividends declared ($0.12 per share) | — | | | (4,042) | | | — | | | — | | | (4,042) | |

| Stock-based compensation expense | 966 | | | — | | | — | | | — | | | 966 | |

| Tredegar common stock purchased by trust for savings restoration plan | — | | | 13 | | | (13) | | | — | | | — | |

| Balance at September 30, 2021 | $ | 53,906 | | | $ | 263,873 | | | $ | (2,122) | | | $ | (169,378) | | | $ | 146,279 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | Retained

Earnings | | Trust for

Savings

Restoration

Plan | | Accumulated Other

Comprehensive Income (Loss) | | Total

Shareholders’

Equity |

| Balance at April 1, 2022 | $ | 55,953 | | | $ | 293,563 | | | $ | (2,148) | | | $ | (135,500) | | | $ | 211,868 | |

| Net income (loss) | — | | | 14,869 | | | — | | | — | | | 14,869 | |

| Foreign currency translation adjustment | — | | | — | | | — | | | (5,230) | | | (5,230) | |

| Derivative financial instruments adjustment | — | | | — | | | — | | | (9,161) | | | (9,161) | |

| Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 2,556 | | | 2,556 | |

| Cash dividends declared ($0.12 per share) | — | | | (4,075) | | | — | | | — | | | (4,075) | |

| Stock-based compensation expense | 958 | | | — | | | — | | | — | | | 958 | |

| Tredegar common stock purchased by trust for savings restoration plan | — | | | 13 | | | (13) | | | — | | | — | |

| Balance at June 30, 2022 | $ | 56,911 | | | $ | 304,370 | | | $ | (2,161) | | | $ | (147,335) | | | $ | 211,785 | |

The following summarizes the changes in shareholders’ equity for the ninesix month period ended SeptemberJune 30, 2021:2022: | | | | Common

Stock | | Retained

Earnings | | Trust for

Savings

Restoration

Plan | | Accumulated Other

Comprehensive Income (Loss) | | Total

Shareholders’

Equity | | Common

Stock | | Retained

Earnings | | Trust for

Savings

Restoration

Plan | | Accumulated Other

Comprehensive Income (Loss) | | Total

Shareholders’

Equity |

| Balance at January 1, 2021 | $ | 50,066 | | | $ | 239,480 | | | $ | (2,087) | | | $ | (178,404) | | | $ | 109,055 | | |

| Balance at January 1, 2022 | | Balance at January 1, 2022 | $ | 55,174 | | | $ | 281,187 | | | $ | (2,135) | | | $ | (149,504) | | | $ | 184,722 | |

| Net income (loss) | Net income (loss) | — | | | 36,472 | | | — | | | — | | | 36,472 | | Net income (loss) | — | | | 31,292 | | | — | | | — | | | 31,292 | |

| Foreign currency translation adjustment | Foreign currency translation adjustment | — | | | — | | | — | | | (1,443) | | | (1,443) | | Foreign currency translation adjustment | — | | | — | | | — | | | 306 | | | 306 | |

| Derivative financial instruments adjustment | Derivative financial instruments adjustment | — | | | — | | | — | | | 515 | | | 515 | | Derivative financial instruments adjustment | — | | | — | | | — | | | (3,231) | | | (3,231) | |

| Amortization of prior service costs and net gains or losses | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 9,954 | | | 9,954 | | Amortization of prior service costs and net gains or losses | — | | | — | | | — | | | 5,094 | | | 5,094 | |

| Cash dividends declared ($0.36 per share) | — | | | (12,114) | | | — | | | — | | | (12,114) | | |

| Cash dividends declared ($0.24 per share) | | Cash dividends declared ($0.24 per share) | — | | | (8,135) | | | — | | | — | | | (8,135) | |

| Stock-based compensation expense | Stock-based compensation expense | 2,925 | | | — | | | — | | | — | | | 2,925 | | Stock-based compensation expense | 2,133 | | | — | | | — | | | — | | | 2,133 | |

| Shares issued upon exercise of stock options | 915 | | | — | | | — | | | — | | | 915 | | |

Repurchase of employee common stock for tax

withholdings | | Repurchase of employee common stock for tax

withholdings | (396) | | | — | | | — | | | — | | | (396) | |

| Tredegar common stock purchased by trust for savings restoration plan | Tredegar common stock purchased by trust for savings restoration plan | — | | | 35 | | | (35) | | | — | | | — | | Tredegar common stock purchased by trust for savings restoration plan | — | | | 26 | | | (26) | | | — | | | — | |

| Balance at September 30, 2021 | $ | 53,906 | | | $ | 263,873 | | | $ | (2,122) | | | $ | (169,378) | | | $ | 146,279 | | |

| Balance at June 30, 2022 | | Balance at June 30, 2022 | $ | 56,911 | | | $ | 304,370 | | | $ | (2,161) | | | $ | (147,335) | | | $ | 211,785 | |

See accompanying notes to the condensed consolidated financial statements.

TREDEGAR CORPORATION

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. BASIS OF PRESENTATION

In the opinion of management, the accompanying condensed consolidated financial statements of Tredegar Corporation and its subsidiaries (“Tredegar,” “the Company,” “we,” “us” or “our”) contain all adjustments necessary to state fairly, in all material respects, Tredegar’s condensed consolidated financial position as of SeptemberJune 30, 2022,2023, the condensed consolidated results of operations for the three and ninesix months ended SeptemberJune 30, 20222023 and 2021,2022, the condensed consolidated cash flows for the ninesix months ended SeptemberJune 30, 20222023 and 2021,2022, and the condensed consolidated changes in shareholders’ equity for the ninesix months ended SeptemberJune 30, 20222023 and 2021,2022, in accordance with U.S. generally accepted accounting principles (“GAAP”). All such adjustments, unless otherwise detailed in the notes to the condensed consolidated financial statements, are deemed to be of a normal, recurring nature.

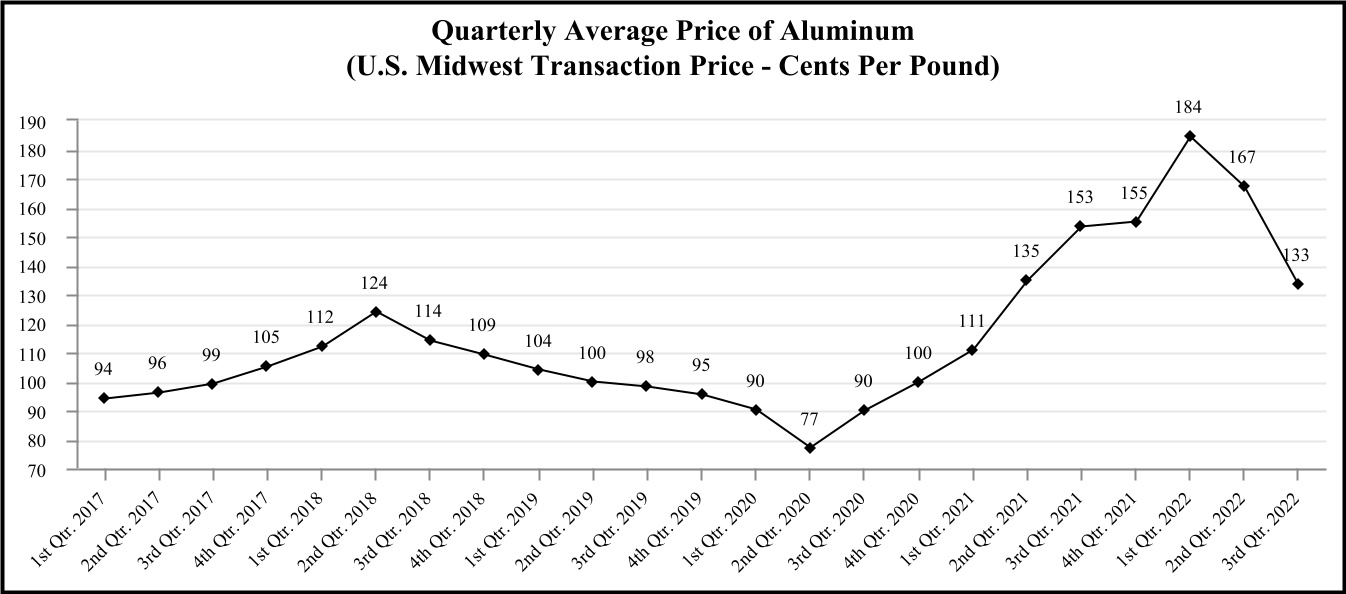

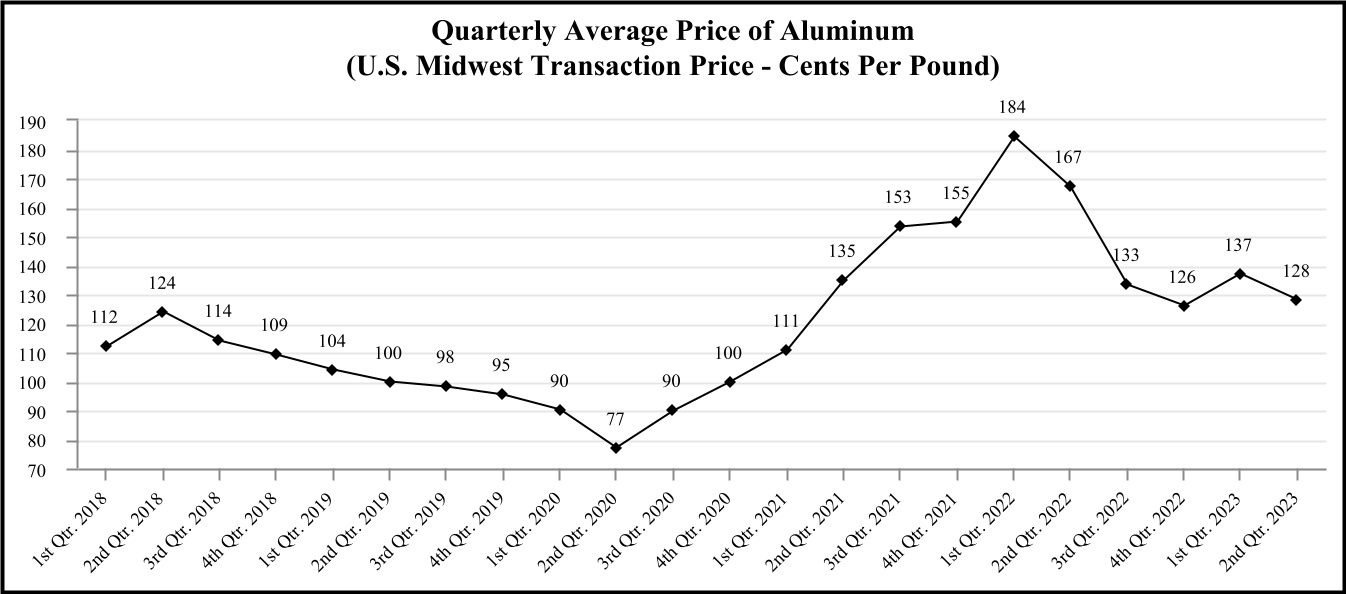

The Company operates on a calendar fiscal year except for the Aluminum Extrusions segment, which operates on a 52/53-week fiscal year basis. As such, the fiscal thirdsecond quarter for 20222023 and 20212022 for this segment references 13-week periods ended SeptemberJune 25, 2023 and June 26, 2022, and September 26, 2021.respectively. The Company does not believe the impact of reporting the results of this segment as stated above is material to the consolidated financial results. The Company may fund or receive cash from the Aluminum Extrusions segment based on Aluminum Extrusion’s cash flows from operations during the intervening period from Aluminum Extrusion’s fiscal quarter end and the Company’s fiscal quarter end. There was no intercompany funding with Aluminum Extrusions between SeptemberJune 25, 20222023 and SeptemberJune 30, 2022.2023.

The condensed consolidated financial position datastatements as of December 31, 20212022 that is included herein was derived from the audited consolidated financial statements provided in the Company’s Annual Report on Form 10-K for the year ended December 31, 20212022 (“20212022 Form 10-K”) but does not include all disclosures required by GAAP. These financial statements should be read in conjunction with the audited consolidated financial statements and related notes included in the 20212022 Form 10-K.

The results of operations for the three and ninesix months ended SeptemberJune 30, 2022,2023, are not necessarily indicative of the results to be expected for the full year.

RisksImpairment of Goodwill

The Company assesses goodwill for impairment when events or circumstances indicate that the carrying value may not be recoverable, or, at a minimum, on an annual basis (December 1st of each year). As of June 30, 2023, the Company’s reporting units with goodwill were Surface Protection in PE Films ("Surface Protection") and UncertaintiesFutura in Aluminum Extrusions (“Futura”). No events or circumstances were identified during the second quarter of 2023 that indicate that Futura’s fair value is more likely than not less than its carrying amount.

DuringHowever, manufacturers in the three months ended September 30, 2022, eventssupply chain for consumer electronics continue to experience reduced capacity utilization and circumstances indicated thatinventory corrections. In light of the continued uncertainty about the timing of a recovery for this market and the expected adverse future impact to the Surface Protection reporting unit ("Surface Protection"), which is alsobusiness, the asset group, might be impaired. The Company performed a Step 1 goodwill and long-lived impairment analysis forof the Surface Protection component of PE Films using projections that contemplate the expected market recovery and determinedbusiness conditions, as these events indicated Surface Protection’s fair value is more likely than not less than its carrying amount.

The Company estimated the fair value of Surface Protection at June 30, 2023 by: (i) computing an estimated enterprise value (“EV”) utilizing the discounted cash flow method (the “DCF Method”), (ii) applying adjustments for any surplus or deficient working capital, (iii) adding cash and cash equivalents, and (iv) subtracting interest-bearing debt. The DCF Method was used since Surface Protection’s projections reflect the expected recovery from the weak market demand, competitive pricing and cash flows associated with new surface protection products, applications, customers, production efficiencies, and cost savings.

The analysis concluded that the fair value of Surface Protection exceededwas less than its carrying value. value, thus a non-cash partial goodwill impairment of $15.4 million ($11.9 million after deferred income tax benefits) was recognized during the second quarter of 2023.

Given the uncertain demand for Surface Protections products, it is reasonably possible that the cash flow estimates used in deriving such fair value measurements may change in the future.

As of September 30, 2022, the The Surface Protection reporting unit had goodwill of $41.9 million and $57.3 million as of June 30, 2023 and long-lived identifiable assets of $29.5 million.December 31, 2022, respectively.

Accounting Standards Adopted

In March 2020,No Accounting Standard Updates issued by the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") 2020-04, which provides optional expedients and exceptions for applying GAAP to contracts, hedging relationships and other transactions affected by the discontinuation of the London Interbank Offered Rate or by another reference rate expected to be discontinued because of reference rate reform. The guidance was effective beginning March 12, 2020 and can be applied prospectively through December 31, 2022. In January 2021, the FASB issued ASU 2021-01, which clarified the scope and application of the original guidance. Inwere adopted during the second quarter of 2022, the Company adopted ASU 2020-04, which did not have a material impact on the Company’s consolidated financial statements.2023.

Accounting Standards Not Yet Adopted

In September 2022, the FASB issued ASU 2022-04, which requires that a buyer in a supplier finance program disclose sufficient information about the program to allow a user of financial statements to understand the program’s nature, activity during the period, changes from period to period, and potential magnitude. The guidance is effective for annual periods beginning after December 15, 2022, with early adoption permitted. The Company is currently evaluating the potential impact of adopting this guidance, but does not expect it to have a material impact on the consolidated financial statements.

2. ACCOUNTS AND OTHER RECEIVABLES

As of SeptemberJune 30, 20222023 and December 31, 2021,2022, accounts receivable and other receivables, net include the following: | | | | | | | | | | | |

| September 30, | | December 31, |

| (In thousands) | 2022 | | 2021 |

| Customer receivables | $ | 108,438 | | | $ | 102,090 | |

| Other receivables | 3,959 | | | 2,958 | |

| Total accounts and other receivables | 112,397 | | | 105,048 | |

| Less: Allowance for bad debts | (2,320) | | | (1,736) | |

| Total accounts and other receivables, net | $ | 110,077 | | | $ | 103,312 | |

| | | | | | | | | | | |

| (In thousands) | June 30, 2023 | | December 31, 2022 |

| Customer receivables | $ | 79,112 | | | $ | 83,667 | |

| Other receivables | 2,233 | | | 3,874 | |

| Total accounts and other receivables | 81,345 | | | 87,541 | |

| Less: Allowance for bad debts | (2,206) | | | (2,997) | |

| Total accounts and other receivables, net | $ | 79,139 | | | $ | 84,544 | |

3. INVENTORIES

The components of inventories are as follows: | | (In thousands) | (In thousands) | September 30, 2022 | | December 31, 2021 | (In thousands) | June 30, 2023 | | December 31, 2022 |

| Finished goods | Finished goods | $ | 30,025 | | | $ | 25,199 | | Finished goods | $ | 29,677 | | | $ | 34,686 | |

| Work-in-process | Work-in-process | 17,201 | | | 11,955 | | Work-in-process | 12,678 | | | 15,604 | |

| Raw materials | Raw materials | 49,212 | | | 32,958 | | Raw materials | 23,897 | | | 58,262 | |

| Stores, supplies and other | Stores, supplies and other | 17,665 | | | 18,457 | | Stores, supplies and other | 20,440 | | | 19,219 | |

| Total | Total | $ | 114,103 | | | $ | 88,569 | | Total | $ | 86,692 | | | $ | 127,771 | |

4. PENSION AND OTHER POSTRETIREMENT BENEFITS

Tredegar sponsors a noncontributory defined benefit (pension) plan covering certain current and former U.S. employees. As of January 31, 2018, the plan no longer accrued benefits associated with crediting employees for service, thereby freezing all future benefits under the plan. On February 10, 2022, Tredegar announced the initiation of a process to terminate and settle its frozen defined benefit pension plan, which could take up to 24 months to complete.plan. In connection therewith, on February 9, 2022, the Company contributed $50 million to the pension plan (the “Special Contribution”). The Company estimates that, with the Special Contribution, there will be no required minimum contributions to the pension plan until final settlement.

Tredegar also has a non-qualified supplemental pension plan covering certain employees. Effective December 31, 2005, further participation in this plan was terminated and benefit accruals for existing participants were frozen. Pension expense recognized for this plan was immaterial in the third quarter of 2022three and 2021, respectively.six months ended June 30, 2023 and 2022. This information has been included in the pension benefit table below.

The components of net periodic benefit cost for the pension and other postretirement benefit programs reflected in the condensed consolidated statements of income for the three and ninesix months ended SeptemberJune 30, 20222023 and 2021,2022, are shown below: | | | Pension Benefits | | Other Post-Retirement Benefits | | Pension Benefits | | Other Post-Retirement Benefits |

| | | Three Months Ended September 30, | | Three Months Ended September 30, | | Three Months Ended June 30, | | Three Months Ended June 30, |

| (In thousands) | (In thousands) | 2022 | | 2021 | | 2022 | | 2021 | (In thousands) | 2023 | | 2022 | | 2023 | | 2022 |

| Service cost | Service cost | $ | — | | | $ | — | | | $ | 5 | | | $ | 9 | | Service cost | $ | — | | | $ | — | | | $ | 3 | | | $ | 5 | |

| Interest cost | Interest cost | 2,226 | | | 2,101 | | | 51 | | | 50 | | Interest cost | 3,028 | | | 2,225 | | | 71 | | | 51 | |

| Expected return on plan assets | Expected return on plan assets | (2,044) | | | (2,862) | | | — | | | — | | Expected return on plan assets | (2,607) | | | (2,043) | | | — | | | — | |

| Amortization of prior service costs, (gains) losses and net transition asset | Amortization of prior service costs, (gains) losses and net transition asset | 3,301 | | | 4,268 | | | (33) | | | (24) | | Amortization of prior service costs, (gains) losses and net transition asset | 2,982 | | | 3,302 | | | (59) | | | (34) | |

| Net periodic benefit cost | Net periodic benefit cost | $ | 3,483 | | | $ | 3,507 | | | $ | 23 | | | $ | 35 | | Net periodic benefit cost | $ | 3,403 | | | $ | 3,484 | | | $ | 15 | | | $ | 22 | |

| | | Pension Benefits | | Other Post-Retirement Benefits | | Pension Benefits | | Other Post-Retirement Benefits |

| | | Nine Months Ended September 30, | | Nine Months Ended September 30, | | Six Months Ended June 30, | | Six Months Ended June 30, |

| (In thousands) | (In thousands) | 2022 | | 2021 | | 2022 | | 2021 | (In thousands) | 2023 | | 2022 | | 2023 | | 2022 |

| Service cost | Service cost | $ | — | | | $ | — | | | $ | 15 | | | $ | 26 | | Service cost | $ | — | | | $ | — | | | $ | 6 | | | $ | 10 | |

| Interest cost | Interest cost | 6,676 | | | 6,305 | | | 153 | | | 151 | | Interest cost | 6,056 | | | 4,450 | | | 142 | | | 102 | |

| Expected return on plan assets | Expected return on plan assets | (6,141) | | | (8,587) | | | — | | | — | | Expected return on plan assets | (5,214) | | | (4,098) | | | — | | | — | |

| Amortization of prior service costs, (gains) losses and net transition asset | Amortization of prior service costs, (gains) losses and net transition asset | 9,887 | | | 12,799 | | | (101) | | | (72) | | Amortization of prior service costs, (gains) losses and net transition asset | 5,965 | | | 6,586 | | | (118) | | | (68) | |

| Net periodic benefit cost | Net periodic benefit cost | $ | 10,422 | | | $ | 10,517 | | | $ | 67 | | | $ | 105 | | Net periodic benefit cost | $ | 6,807 | | | $ | 6,938 | | | $ | 30 | | | $ | 44 | |

Pension and other postretirement liabilities were $29.1$36.4 million and $78.9$35.7 million at SeptemberJune 30, 20222023 and December 31, 2021,2022, respectively ($0.7 million included in “Accrued expenses” at SeptemberJune 30, 20222023 and December 31, 2021,2022, respectively, with the remainder included in “Pension and other postretirement benefit obligations, net” in the condensed consolidated balance sheets).

Tredegar funds its other postretirement benefits on a claims-made basis; for 2022,2023, the Company anticipates the amount will be consistent with amounts paid for the year ended December 31, 2021,2022, or approximately $0.5 million.

5. OTHER INCOME (EXPENSE), NET

Other income (expense), net consists of the following: | | | Three Months Ended September 30, | | Nine Months Ended September 30, | | Three Months Ended June 30, | | Six Months Ended June 30, |

| (In thousands) | (In thousands) | 2022 | | 2021 | | 2022 | | 2021 | (In thousands) | 2023 | | 2022 | | 2023 | | 2022 |

Gain on investment in kaléo(a) | Gain on investment in kaléo(a) | $ | — | | | $ | 279 | | | $ | 1,406 | | | $ | 1,197 | | Gain on investment in kaléo(a) | $ | — | | | $ | 1,406 | | | $ | 262 | | | $ | 1,406 | |

| One-time tax credit in Brazil for unemployment/social security insurance non-income taxes resulting from a favorable decision by Brazil's Supreme Court regarding the calculation of such tax | — | | | — | | | — | | | 8,486 | | |

COVID-19-related expenses, net of relief (b) | | COVID-19-related expenses, net of relief (b) | — | | | (96) | | | — | | | (308) | |

| | Other | Other | 119 | | | 112 | | | (293) | | | (411) | | Other | (20) | | | 32 | | | (2) | | | (57) | |

| Total | Total | $ | 119 | | | $ | 391 | | | $ | 1,113 | | | $ | 9,272 | | Total | $ | (20) | | | $ | 1,342 | | | $ | 260 | | | $ | 1,041 | |

| (a) In May 2022, additional cash consideration of $1.4 million was received related to customary post-closing adjustments. See Note 12 for additional information on the sale of the investment in kaléo. | |

(a) In January 2023, additional cash consideration of $0.3 million was received related to the customary post-closing adjustments on the sale of the investment in kaleo, Inc ("kaléo"), which was sold in December 2021. (b) Costs associated with operating under COVID-19 conditions include employee overtime expenses associated with absenteeism, personal protective equipment supplies and facility maintenance. | | (a) In January 2023, additional cash consideration of $0.3 million was received related to the customary post-closing adjustments on the sale of the investment in kaleo, Inc ("kaléo"), which was sold in December 2021. (b) Costs associated with operating under COVID-19 conditions include employee overtime expenses associated with absenteeism, personal protective equipment supplies and facility maintenance. |

In May 2021, the Brazil Supreme Court ruled in a leading case related to the amount of Brazilian value-added tax to exclude from the calculation of unemployment/social security insurance non-income taxes ("PIS/COFINS"). As a result, in the second quarter of 2021, the Company recorded a pre-tax gain of $8.5 million for certain excess PIS/COFINS paid from 2003 to 2021, plus applicable interest, which the Company applied to required Brazilian federal tax payments during 2021.

6. EARNINGS PER SHARE

Basic earnings per share is computed by dividing net income (loss) from continuing and discontinued operations by the weighted average number of shares of common stock outstanding. Diluted earnings per share is computed by dividing net income (loss) from continuing and discontinued operations by the weighted average common and potentially dilutive common equivalent shares outstanding, determined as follows: | | | Three Months Ended | | Nine Months Ended | | Three Months Ended | | Six Months Ended |

| | | September 30, | | September 30, | | June 30, | | June 30, |

| (In thousands) | (In thousands) | 2022 | | 2021 | | 2022 | | 2021 | (In thousands) | 2023 | | 2022 | | 2023 | | 2022 |

| Weighted average shares outstanding used to compute basic earnings per share | Weighted average shares outstanding used to compute basic earnings per share | 33,870 | | | 33,620 | | | 33,780 | | | 33,541 | | Weighted average shares outstanding used to compute basic earnings per share | 34,079 | | | 33,814 | | | 33,988 | | | 33,734 | |

| Incremental dilutive shares attributable to stock options and restricted stock | Incremental dilutive shares attributable to stock options and restricted stock | 1 | | | 29 | | | 28 | | | 137 | | Incremental dilutive shares attributable to stock options and restricted stock | — | | | 40 | | | — | | | 42 | |

| Shares used to compute diluted earnings per share | Shares used to compute diluted earnings per share | 33,871 | | | 33,649 | | | 33,808 | | | 33,678 | | Shares used to compute diluted earnings per share | 34,079 | | | 33,854 | | | 33,988 | | | 33,776 | |

Incremental shares attributable to stock options and restricted stock are computed under the treasury stock method using the average market price during the related period. The Company had a net loss for the three and six months ended June 30, 2023, so there is no dilutive impact for such shares. If the Company had reported net income for the three and six months ended June 30, 2023, average out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock would have been 3,019,333 and 2,830,849, respectively. The average out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock were 2,932,3782,525,104 and 2,645,0632,501,406 for the three and ninesix months ended SeptemberJune 30, 2022, respectively, and 2,433,213 and 1,280,376 for the three and nine months ended September 30, 2021, respectively.

7. ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS)

The changes in accumulated other comprehensive income (loss) by component for the three months ended SeptemberJune 30, 2022.2023.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at April 1, 2023 | $ | (84,959) | | | $ | (1,211) | | | $ | (56,749) | | | $ | (142,919) | |

| Other comprehensive income (loss) | 1,800 | | | 2,488 | | | — | | | 4,288 | |

| Income tax (expense) benefit | (179) | | | (945) | | | — | | | (1,124) | |

| Other comprehensive income (loss), net of tax | 1,621 | | | 1,543 | | | — | | | 3,164 | |

| Reclassification adjustment to net income (loss) | — | | | (1,621) | | | 2,923 | | | 1,302 | |

| Income tax (expense) benefit | — | | | 446 | | | (637) | | | (191) | |

| Reclassification adjustment to net income (loss), net of tax | — | | | (1,175) | | | 2,286 | | | 1,111 | |

| Other comprehensive income (loss), net of tax | 1,621 | | | 368 | | | 2,286 | | | 4,275 | |

| Balance at June 30, 2023 | $ | (83,338) | | | $ | (843) | | | $ | (54,463) | | | $ | (138,644) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at July 1, 2022 | $ | (85,486) | | | $ | (2,330) | | | $ | (59,519) | | | $ | (147,335) | |

| Other comprehensive income (loss) | (2,488) | | | (2,205) | | | — | | | (4,693) | |

| Income tax (expense) benefit | 148 | | | 522 | | | — | | | 670 | |

| Other comprehensive income (loss), net of tax | (2,340) | | | (1,683) | | | — | | | (4,023) | |

| Reclassification adjustment to net income (loss) | — | | | (1,159) | | | 3,268 | | | 2,109 | |

| Income tax (expense) benefit | — | | | 295 | | | (712) | | | (417) | |

| Reclassification adjustment to net income (loss), net of tax | — | | | (864) | | | 2,556 | | | 1,692 | |

| Other comprehensive income (loss), net of tax | (2,340) | | | (2,547) | | | 2,556 | | | (2,331) | |

| Balance at September 30, 2022 | $ | (87,826) | | | $ | (4,877) | | | $ | (56,963) | | | $ | (149,666) | |

The changes in accumulated other comprehensive income (loss) by component for the ninesix months ended SeptemberJune 30, 2023.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at January 1, 2023 | $ | (86,079) | | | $ | (2,480) | | | $ | (59,036) | | | $ | (147,595) | |

| Other comprehensive income (loss) | 3,356 | | | 5,565 | | | — | | | 8,921 | |

| Income tax (expense) benefit | (615) | | | (2,031) | | | — | | | (2,646) | |

| Other comprehensive income (loss), net of tax | 2,741 | | | 3,534 | | | — | | | 6,275 | |

| Reclassification adjustment to net income (loss) | — | | | (2,594) | | | 5,847 | | | 3,253 | |

| Income tax (expense) benefit | — | | | 697 | | | (1,274) | | | (577) | |

| Reclassification adjustment to net income (loss), net of tax | — | | | (1,897) | | | 4,573 | | | 2,676 | |

| Other comprehensive income (loss), net of tax | 2,741 | | | 1,637 | | | 4,573 | | | 8,951 | |

| Balance at June 30, 2023 | $ | (83,338) | | | $ | (843) | | | $ | (54,463) | | | $ | (138,644) | |

The changes in accumulated other comprehensive income (loss) by component for the three months ended June 30, 2022.

| | (In thousands) | (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) | (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at January 1, 2022 | $ | (85,792) | | | $ | 901 | | | $ | (64,613) | | | $ | (149,504) | | |

| Balance at April 1, 2022 | | Balance at April 1, 2022 | $ | (80,256) | | | $ | 6,831 | | | $ | (62,075) | | | $ | (135,500) | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | (1,936) | | | (3,883) | | | — | | | (5,819) | | Other comprehensive income (loss) | (5,712) | | | (11,681) | | | — | | | (17,393) | |

| Income tax (expense) benefit | Income tax (expense) benefit | (98) | | | 442 | | | — | | | 344 | | Income tax (expense) benefit | 482 | | | 3,110 | | | — | | | 3,592 | |

| Other comprehensive income (loss), net of tax | Other comprehensive income (loss), net of tax | (2,034) | | | (3,441) | | | — | | | (5,475) | | Other comprehensive income (loss), net of tax | (5,230) | | | (8,571) | | | — | | | (13,801) | |

| Reclassification adjustment to net income (loss) | Reclassification adjustment to net income (loss) | — | | | (3,156) | | | 9,786 | | | 6,630 | | Reclassification adjustment to net income (loss) | — | | | (840) | | | 3,268 | | | 2,428 | |

| Income tax (expense) benefit | Income tax (expense) benefit | — | | | 819 | | | (2,136) | | | (1,317) | | Income tax (expense) benefit | — | | | 250 | | | (712) | | | (462) | |

| Reclassification adjustment to net income (loss), net of tax | Reclassification adjustment to net income (loss), net of tax | — | | | (2,337) | | | 7,650 | | | 5,313 | | Reclassification adjustment to net income (loss), net of tax | — | | | (590) | | | 2,556 | | | 1,966 | |

| Other comprehensive income (loss), net of tax | Other comprehensive income (loss), net of tax | (2,034) | | | (5,778) | | | 7,650 | | | (162) | | Other comprehensive income (loss), net of tax | (5,230) | | | (9,161) | | | 2,556 | | | (11,835) | |

| Balance at September 30, 2022 | $ | (87,826) | | | $ | (4,877) | | | $ | (56,963) | | | $ | (149,666) | | |

| Balance at June 30, 2022 | | Balance at June 30, 2022 | $ | (85,486) | | | $ | (2,330) | | | $ | (59,519) | | | $ | (147,335) | |

The changes in accumulated other comprehensive income (loss) by component for the threesix months ended SeptemberJune 30, 2021.2022.

| | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at July 1, 2021 | $ | (82,804) | | | $ | 3,496 | | | $ | (89,882) | | | $ | (169,190) | |

| Other comprehensive income (loss) | (3,082) | | | 1,245 | | | — | | | (1,837) | |

| Income tax (expense) benefit | 294 | | | (297) | | | — | | | (3) | |

| Other comprehensive income (loss), net of tax | (2,788) | | | 948 | | | — | | | (1,840) | |

| Reclassification adjustment to net income (loss) | — | | | (2,141) | | | 4,244 | | | 2,103 | |

| Income tax (expense) benefit | — | | | 476 | | | (927) | | | (451) | |

| Reclassification adjustment to net income (loss), net of tax | — | | | (1,665) | | | 3,317 | | | 1,652 | |

| Other comprehensive income (loss), net of tax | (2,788) | | | (717) | | | 3,317 | | | (188) | |

| Balance at September 30, 2021 | $ | (85,592) | | | $ | 2,779 | | | $ | (86,565) | | | $ | (169,378) | |

The changes in accumulated other comprehensive income (loss) by component for the nine months ended September 30, 2021.

| | (In thousands) | (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) | (In thousands) | Foreign Currency Translation | | Gain (Loss) on Derivative Financial Instruments | | Pension & Other Postretirement Benefit Adjust | | Total Accumulated Other Comprehensive Income (Loss) |

| Balance at January 1, 2021 | $ | (84,149) | | | $ | 2,264 | | | $ | (96,519) | | | $ | (178,404) | | |

| Balance at January 1, 2022 | | Balance at January 1, 2022 | $ | (85,792) | | | $ | 901 | | | $ | (64,613) | | | $ | (149,504) | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | (1,546) | | | 4,736 | | | — | | | 3,190 | | Other comprehensive income (loss) | 552 | | | (1,678) | | | — | | | (1,126) | |

| Income tax (expense) benefit | Income tax (expense) benefit | 103 | | | (1,064) | | | — | | | (961) | | Income tax (expense) benefit | (246) | | | (80) | | | — | | | (326) | |

| Other comprehensive income (loss), net of tax | Other comprehensive income (loss), net of tax | (1,443) | | | 3,672 | | | — | | | 2,229 | | Other comprehensive income (loss), net of tax | 306 | | | (1,758) | | | — | | | (1,452) | |

| Reclassification adjustment to net income (loss) | Reclassification adjustment to net income (loss) | — | | | (4,037) | | | 12,727 | | | 8,690 | | Reclassification adjustment to net income (loss) | — | | | (1,997) | | | 6,518 | | | 4,521 | |

| Income tax (expense) benefit | Income tax (expense) benefit | — | | | 880 | | | (2,773) | | | (1,893) | | Income tax (expense) benefit | — | | | 524 | | | (1,424) | | | (900) | |

| Reclassification adjustment to net income (loss), net of tax | Reclassification adjustment to net income (loss), net of tax | — | | | (3,157) | | | 9,954 | | | 6,797 | | Reclassification adjustment to net income (loss), net of tax | — | | | (1,473) | | | 5,094 | | | 3,621 | |

| Other comprehensive income (loss), net of tax | Other comprehensive income (loss), net of tax | (1,443) | | | 515 | | | 9,954 | | | 9,026 | | Other comprehensive income (loss), net of tax | 306 | | | (3,231) | | | 5,094 | | | 2,169 | |

| Balance at September 30, 2021 | $ | (85,592) | | | $ | 2,779 | | | $ | (86,565) | | | $ | (169,378) | | |

| Balance at June 30, 2022 | | Balance at June 30, 2022 | $ | (85,486) | | | $ | (2,330) | | | $ | (59,519) | | | $ | (147,335) | |

The amounts reclassified out of accumulated other comprehensive income (loss) related to pension and other postretirement benefits is included in the computation of net periodic pension costs, seecosts. See Note 4 for additional details.

8. DERIVATIVES

Tredegar uses derivative financial instruments for the purpose of hedging margin exposure from fixed-price forward sales contracts in Aluminum Extrusions and exposure from currency volatility that exists as part of ongoing business operations in Flexible Packaging Films. These derivative financial instruments are designated as and qualify as cash flow hedges and are recognized in the condensed consolidated balance sheet at fair value. If individual derivative instruments with the same counterparty can be settled on a net basis, the Company records the corresponding derivative fair values as a net asset or net liability.

In the normal course of business, Aluminum Extrusions enters into fixed-price forward sales contracts with certain customers for the future sale of fixed quantities of aluminum extrusions at scheduled intervals. In order to hedge margin exposure created from the fixing of future sales prices relative to volatile raw material (aluminum) costs, Aluminum Extrusions enters into a combination of forward purchase commitments and futures contracts to acquire or hedge aluminum, based on the scheduled purchases for the firm sales commitments. The fixed-price firm sales commitments and related hedging instruments

have durations generally no longer than 2412 months. The notional amount of aluminum futures contracts that hedged future purchases of aluminum to meet fixed-price forward sales contract obligations was $33.7$17.0 million (18.4(11.1 million pounds of aluminum) at SeptemberJune 30, 20222023 and $22.1$30.7 million (14.9(20.3 million pounds of aluminum) at December 31, 2021.2022.

The table below summarizes the location and gross amounts of aluminum futures contract fair values (Level 2) in the condensed consolidated balance sheets as of SeptemberJune 30, 20222023 and December 31, 2021:2022: | | | | September 30, 2022 | | December 31, 2021 | | June 30, 2023 | | December 31, 2022 |

| (In thousands) | (In thousands) | Balance Sheet

Account | | Fair

Value | | Balance Sheet

Account | | Fair

Value | (In thousands) | Balance Sheet

Account | | Fair

Value | | Balance Sheet

Account | | Fair

Value |

| Derivatives Designated as Hedging Instruments | Derivatives Designated as Hedging Instruments | | Derivatives Designated as Hedging Instruments | |

Asset derivatives: Aluminum futures contracts | Asset derivatives: Aluminum futures contracts | Prepaid expenses and other | | $ | 8 | | | Prepaid expenses and other | | $ | 2,085 | | Asset derivatives: Aluminum futures contracts | Prepaid expenses and other | | $ | — | | | Prepaid expenses and other | | $ | 48 | |

| Liability derivatives: Aluminum futures contracts | Liability derivatives: Aluminum futures contracts | Accrued expenses | | (5,016) | | | Accrued expenses | | (119) | | Liability derivatives: Aluminum futures contracts | Accrued expenses | | (3,050) | | | Accrued expenses | | (3,260) | |

| Aluminum futures contracts | Aluminum futures contracts | Other non-current liabilities | | (1,222) | | | Other non-current liabilities | | — | | Aluminum futures contracts | Other non-current liabilities | | (255) | | | Other non-current liabilities | | (369) | |

| Net asset (liability) | Net asset (liability) | | $ | (6,230) | | | $ | 1,966 | | Net asset (liability) | | $ | (3,305) | | | $ | (3,581) | |

In the event that a counterparty to an aluminum fixed-price forward sales contract chooses not to take delivery of its aluminum extrusions, the customer is contractually obligated to compensate Aluminum Extrusions for any losses on the related aluminum futures and/or forward contracts through the date of cancellation.

The Company's earnings are exposed to foreign currency exchange risk primarily through the translation of the financial statements of subsidiaries that have a functional currency other than the U.S. Dollar. The Company estimates that the net mismatch translation exposure for the Flexible Packaging Film's business unit in Brazil (“Terphane Ltda.”) of its sales and raw materials quoted or priced in U.S. Dollars and its variable conversion, fixed conversion and sales, general and administrative costs (before depreciation and amortization) quoted or priced in Brazilian Real ("R$") iswill result in an annual net costscost of R$150177 million for the full year of 2022.

Terphane Ltda. hashad the following outstanding foreign exchange average forward rate contracts to purchase Brazilian Real and sell U.S. Dollars:Dollars as of June 30, 2023: | | USD Notional Amount (000s) | USD Notional Amount (000s) | Average Forward Rate Contracted on USD/BRL | R$ Equivalent Amount (000s) | Applicable Month | Estimated % of Terphane Ltda. R$ Operating Cost Exposure Hedged | USD Notional Amount (000s) | Average Forward Rate Contracted on USD/BRL | R$ Equivalent Amount (000s) | Applicable Month | Estimated % of Terphane Ltda. R$ Operating Cost Exposure Hedged |

| $1,793 | 5.6264 | R$10,088 | Oct-22 | 78% | |

| $1,784 | 5.6597 | R$10,097 | Nov-22 | 78% | |

| $1,659 | 5.6962 | R$9,450 | Dec-22 | 73% | |

| $1,728 | 5.4310 | R$9,385 | Jan-23 | 64% | |

| $1,822 | 5.4657 | R$9,959 | Feb-23 | 68% | |

| $1,921 | 5.4995 | R$10,565 | Mar-23 | 72% | |

| $1,903 | 5.5379 | R$10,539 | Apr-23 | 72% | |

| $1,873 | 5.5753 | R$10,443 | May-23 | 71% | |

| $1,928 | 5.6118 | R$10,820 | Jun-23 | 74% | |

| | $2,154 | $2,154 | 5.6378 | R$12,144 | Jul-23 | 83% | $2,154 | 5.6378 | R$12,144 | Jul-23 | 83% |

| $2,020 | $2,020 | 5.6831 | R$11,480 | Aug-23 | 78% | $2,020 | 5.6831 | R$11,480 | Aug-23 | 78% |

| $2,071 | $2,071 | 5.7174 | R$11,841 | Sep-23 | 80% | $2,071 | 5.7174 | R$11,841 | Sep-23 | 80% |

| $2,013 | $2,013 | 5.7556 | R$11,586 | Oct-23 | 79% | $2,013 | 5.7556 | R$11,586 | Oct-23 | 79% |

| $2,018 | $2,018 | 5.7836 | R$11,671 | Nov-23 | 79% | $2,018 | 5.7836 | R$11,671 | Nov-23 | 79% |

| $1,786 | $1,786 | 5.8312 | R$10,414 | Dec-23 | 71% | $1,786 | 5.8312 | R$10,414 | Dec-23 | 71% |

| $659 | $659 | 5.7360 | R$3,780 | Jan-24 | 23% | $659 | 5.7360 | R$3,780 | Jan-24 | 23% |

| $659 | $659 | 5.7562 | R$3,793 | Feb-24 | 23% | $659 | 5.7562 | R$3,793 | Feb-24 | 23% |

| $659 | $659 | 5.7774 | R$3,807 | Mar-24 | 23% | $659 | 5.7774 | R$3,807 | Mar-24 | 23% |

| $659 | $659 | 5.8000 | R$3,822 | Apr-24 | 23% | $659 | 5.8000 | R$3,822 | Apr-24 | 23% |

| $659 | $659 | 5.8207 | R$3,836 | May-24 | 24% | $659 | 5.8207 | R$3,836 | May-24 | 24% |

| $659 | $659 | 5.8419 | R$3,850 | Jun-24 | 24% | $659 | 5.8419 | R$3,850 | Jun-24 | 24% |

| $659 | $659 | 5.8636 | R$3,864 | Jul-24 | 24% | $659 | 5.8636 | R$3,864 | Jul-24 | 24% |

| $659 | $659 | 5.8872 | R$3,880 | Aug-24 | 24% | $659 | 5.8872 | R$3,880 | Aug-24 | 24% |

| $659 | $659 | 5.9118 | R$3,896 | Sep-24 | 24% | $659 | 5.9118 | R$3,896 | Sep-24 | 24% |

| $659 | $659 | 5.9350 | R$3,911 | Oct-24 | 24% | $659 | 5.9350 | R$3,911 | Oct-24 | 24% |

| $659 | $659 | 5.9581 | R$3,926 | Nov-24 | 24% | $659 | 5.9581 | R$3,926 | Nov-24 | 24% |

| $659 | $659 | 5.9813 | R$3,942 | Dec-24 | 24% | $659 | 5.9813 | R$3,942 | Dec-24 | 24% |

| $36,381 | 5.6840 | R$206,789 | | 50% | |

| $19,970 | | $19,970 | 5.7808 | R$115,443 | | 40% |

These foreign currency exchange contracts have been designated and qualify as cash flow hedges of Terphane Ltda.’s forecasted sales to customers quoted or priced in U.S. Dollars over that period. By changing the currency risk associated with these U.S. Dollar sales, the derivatives have the effect of offsetting operating costs quoted or priced in Brazilian Real and decreasing the net exposure to Brazilian Real in the condensed consolidated statements of income.

The table below summarizes the location and gross amounts of foreign currency forward contract fair values (Level 2) in the condensed consolidated balance sheets as of SeptemberJune 30, 20222023 and December 31, 2021:2022: | | | | September 30, 2022 | | December 31, 2021 | | June 30, 2023 | | December 31, 2022 |

| (In thousands) | (In thousands) | Balance Sheet

Account | | Fair

Value | | Balance Sheet

Account | | | Fair

Value | (In thousands) | Balance Sheet

Account | | Fair

Value | | Balance Sheet

Account | | | Fair

Value |

| Derivatives Designated as Hedging Instruments | Derivatives Designated as Hedging Instruments | | | | Derivatives Designated as Hedging Instruments | | | |

Asset derivatives: Foreign currency forward contracts | Asset derivatives: Foreign currency forward contracts | Prepaid expenses and other | | $ | 397 | | | Prepaid expenses and other | | | $ | — | | Asset derivatives: Foreign currency forward contracts | Prepaid expenses and other | | $ | 2,974 | | | Prepaid expenses and other | | | $ | 781 | |

| Foreign currency forward contracts | Foreign currency forward contracts | Other assets | | 59 | | | Other assets | | | — | | Foreign currency forward contracts | Other assets | | 723 | | | Other assets | | | 33 | |

Liability derivatives: Foreign currency forward contracts | Liability derivatives: Foreign currency forward contracts | Accrued expenses | | (363) | | | Accrued expenses | | | (1,255) | | Liability derivatives: Foreign currency forward contracts | Accrued expenses | | — | | | Other non-current liabilities | | | (3) | |

| Net asset (liability) | Net asset (liability) | | $ | 93 | | | | | $ | (1,255) | | Net asset (liability) | | $ | 3,697 | | | | | $ | 811 | |

These derivative contracts involve elements of market risk that are not reflected on the condensed consolidated balance sheet, including the risk of dealing with counterparties and their ability to meet the terms of the contracts. The counterparties to any forward purchase commitments are major aluminum brokers and suppliers, and the counterparties to any aluminum futures contracts are major financial institutions. Fixed-price forward sales contracts are only made available to the best and most credit-worthy customers. The counterparties to the Company’s foreign currency cash flow hedge contracts are major financial institutions.

The pre-tax effect on net income (loss) and other comprehensive income (loss) of derivative instruments classified as cash flow hedges and described in the previous paragraphs for the three and ninesix month periods ended SeptemberJune 30, 20222023 and 20212022 is summarized in the table below: | | | Cash Flow Derivative Hedges | | Cash Flow Derivative Hedges |

| | | Three Months Ended September 30, | | Three Months Ended June 30, |

| | | Aluminum Futures Contracts | | Foreign Currency Forwards | | Aluminum Futures Contracts | | Foreign Currency Forwards |

| (In thousands) | (In thousands) | 2022 | | 2021 | | 2022 | | 2021 | (In thousands) | 2023 | | 2022 | | 2023 | | 2022 |

| Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | (2,320) | | | $ | 2,919 | | | $ | — | | $ | 115 | | | $ | — | | | $ | (1,670) | | Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | 557 | | | $ | (9,923) | | | $ | — | | $ | 1,931 | | | $ | — | | | $ | (1,758) | |

| Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (effective portion) | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (effective portion) | Cost of goods sold | | Cost of goods sold | | Cost of goods sold | Selling, general & admin | | Cost of goods sold | | Selling, general & admin | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (effective portion) | Cost of goods sold | | Cost of goods sold | | Cost of goods sold | Selling, general & admin | | Cost of goods sold | | Selling, general & admin |

| Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (effective portion) | Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (effective portion) | $ | 837 | | | $ | 2,160 | | | $ | 16 | | $ | 306 | | | $ | 15 | | | $ | (34) | | Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (effective portion) | $ | 885 | | | $ | 293 | | | $ | 15 | | $ | 721 | | | $ | 15 | | | $ | 532 | |

| | | Nine Months Ended September 30, | | Six Months Ended June 30, |

| | | Aluminum Futures Contracts | | Foreign Currency Forwards | | Aluminum Futures Contracts | | Foreign Currency Forwards |

| | | 2022 | | 2021 | | 2022 | | 2021 | | 2023 | | 2022 | | 2023 | | 2022 |

| Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | (6,060) | | | $ | 6,629 | | | $ | — | | $ | 2,177 | | | $ | — | | | $ | (1,892) | | Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | 1,959 | | | $ | (3,741) | | | $ | — | | $ | 3,606 | | | $ | — | | | $ | 2,063 | |