UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

|

| |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2017MARCH 31, 2019 |

| or |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO |

Commission file number 000-19319

Vertex Pharmaceuticals Incorporated

(Exact name of registrant as specified in its charter) |

| |

| Massachusetts | 04-3039129 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

| 50 Northern Avenue, Boston, Massachusetts | 02210 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (617) 341-6100

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | |

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

| | | | |

Emerging growth company o | (Do not check if a smaller reporting company) |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

|

| |

| Common Stock, par value $0.01 per share | 252,902,848256,121,360 |

| Class | Outstanding at October 20, 2017April 24, 2019 |

VERTEX PHARMACEUTICALS INCORPORATED

FORM 10-Q

FOR THE QUARTER ENDED SEPTEMBER 30, 2017MARCH 31, 2019

TABLE OF CONTENTS

|

| | |

| | | Page |

| |

| | |

| | | |

| | Condensed Consolidated Statements of Operations - Three and Nine Months Ended September 30, 2017March 31, 2019 and 20162018 | |

| | Condensed Consolidated Statements of Comprehensive Income (Loss) - Three and Nine Months Ended September 30, 2017March 31, 2019 and 20162018 | |

| | Condensed Consolidated Balance Sheets - September 30, 2017March 31, 2019 and December 31, 20162018 | |

| | Condensed Consolidated Statements of Shareholders' Equity and Noncontrolling Interest - NineThree Months Ended September 30, 2017March 31, 2019 and 20162018 | |

| | Condensed Consolidated Statements of Cash Flows - NineThree Months Ended September 30, 2017March 31, 2019 and 20162018 | |

| | | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | |

| | |

“We,” “us,” “Vertex” and the “Company” as used in this Quarterly Report on Form 10-Q refer to Vertex Pharmaceuticals Incorporated, a Massachusetts corporation, and its subsidiaries.

“Vertex,” “KALYDECO®,” “ORKAMBI®,” “SYMDEKO®” and “ORKAMBI“SYMKEVI®” are registered trademarks of Vertex. Other brands, names and trademarks contained in this Quarterly Report on Form 10-Q are the property of their respective owners.

We use the brand name for our products when we refer to the product that has been approved and with respect to the indications on the approved label. Otherwise, including in discussions of our cystic fibrosis development programs, we refer to our compounds by their scientific (or generic) name or VX developmental designation.

Part I. Financial Information

Item 1. Financial Statements

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Operations

(unaudited)

(in thousands, except per share amounts)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Revenues: | | | | | | | |

| Product revenues, net | $ | 549,642 |

| | $ | 409,689 |

| | $ | 1,544,252 |

| | $ | 1,229,750 |

|

| Royalty revenues | 2,231 |

| | 3,835 |

| | 6,643 |

| | 12,713 |

|

| Collaborative revenues | 26,292 |

| | 259 |

| | 286,123 |

| | 1,008 |

|

| Total revenues | 578,165 |

| | 413,783 |

| | 1,837,018 |

| | 1,243,471 |

|

| Costs and expenses: | | | | | | | |

| Cost of product revenues | 72,186 |

| | 53,222 |

| | 188,963 |

| | 147,165 |

|

| Royalty expenses | 688 |

| | 855 |

| | 2,104 |

| | 2,813 |

|

| Research and development expenses | 454,947 |

| | 272,370 |

| | 1,017,961 |

| | 799,238 |

|

| Sales, general and administrative expenses | 120,710 |

| | 106,055 |

| | 361,285 |

| | 322,921 |

|

| Restructuring expenses, net | 337 |

| | 8 |

| | 13,859 |

| | 1,038 |

|

| Intangible asset impairment charge | 255,340 |

| | — |

| | 255,340 |

| | — |

|

| Total costs and expenses | 904,208 |

| | 432,510 |

| | 1,839,512 |

| | 1,273,175 |

|

| Loss from operations | (326,043 | ) | | (18,727 | ) | | (2,494 | ) | | (29,704 | ) |

| Interest expense, net | (13,574 | ) | | (20,140 | ) | | (45,003 | ) | | (60,993 | ) |

| Other (expenses) income, net | (77,553 | ) | | (167 | ) | | (80,634 | ) | | 3,025 |

|

| Loss before (benefit from) provision for income taxes | (417,170 | ) | | (39,034 | ) | | (128,131 | ) | | (87,672 | ) |

| (Benefit from) provision for income taxes | (125,903 | ) | | 503 |

| | (117,581 | ) | | 24,118 |

|

| Net loss | (291,267 | ) | | (39,537 | ) | | (10,550 | ) | | (111,790 | ) |

| Loss (income) attributable to noncontrolling interest | 188,315 |

| | 696 |

| | 173,350 |

| | (33,207 | ) |

| Net (loss) income attributable to Vertex | $ | (102,952 | ) | | $ | (38,841 | ) | | $ | 162,800 |

| | $ | (144,997 | ) |

| | | | | | | | |

| Amounts per share attributable to Vertex common shareholders: | | | | | | | |

| Net (loss) income: | | | | | | | |

| Basic | $ | (0.41 | ) | | $ | (0.16 | ) | | $ | 0.66 |

| | $ | (0.59 | ) |

| Diluted | $ | (0.41 | ) | | $ | (0.16 | ) | | $ | 0.64 |

| | $ | (0.59 | ) |

| Shares used in per share calculations: | | | | | | | |

| Basic | 250,268 |

| | 244,920 |

| | 247,963 |

| | 244,529 |

|

| Diluted | 250,268 |

| | 244,920 |

| | 252,095 |

| | 244,529 |

|

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2019 | | 2018 |

| Revenues: | | | |

| Product revenues, net | $ | 857,253 |

| | $ | 637,729 |

|

| Collaborative and royalty revenues | 1,182 |

| | 3,070 |

|

| Total revenues | 858,435 |

| | 640,799 |

|

| Costs and expenses: | | | |

| Cost of sales | 95,092 |

| | 71,613 |

|

| Research and development expenses | 339,490 |

| | 310,553 |

|

| Sales, general and administrative expenses | 147,045 |

| | 129,808 |

|

| Restructuring income | — |

| | (76 | ) |

| Total costs and expenses | 581,627 |

| | 511,898 |

|

| Income from operations | 276,808 |

| | 128,901 |

|

| Interest income | 15,615 |

| | 5,789 |

|

| Interest expense | (14,868 | ) | | (16,886 | ) |

| Other income, net | 42,610 |

| | 96,838 |

|

| Income before provision for (benefit from) income taxes | 320,165 |

| | 214,642 |

|

| Provision for (benefit from) income taxes | 51,534 |

| | (12,659 | ) |

| Net income | 268,631 |

| | 227,301 |

|

| Income attributable to noncontrolling interest | — |

| | (17,038 | ) |

| Net income attributable to Vertex | $ | 268,631 |

| | $ | 210,263 |

|

| | | | |

| Amounts per share attributable to Vertex common shareholders: | | | |

| Net income: | | | |

| Basic | $ | 1.05 |

| | $ | 0.83 |

|

| Diluted | $ | 1.03 |

| | $ | 0.81 |

|

| Shares used in per share calculations: | | | |

| Basic | 255,695 |

| | 253,231 |

|

| Diluted | 260,175 |

| | 258,526 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Comprehensive Income (Loss)

(unaudited)

(in thousands)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Net loss | $ | (291,267 | ) | | $ | (39,537 | ) | | $ | (10,550 | ) | | $ | (111,790 | ) |

| Changes in other comprehensive loss: | | | | | | | |

| Unrealized holding gains (losses) on marketable securities, net of tax of zero, respectively | 5,961 |

| | (96 | ) | | (7,786 | ) | | 104 |

|

| Unrealized (losses) gains on foreign currency forward contracts, net of tax of $0.9 million, $0.2 million, $2.9 million and $(0.4) million, respectively | (5,453 | ) | | 2,149 |

| | (27,379 | ) | | 1,936 |

|

| Foreign currency translation adjustment | (3,884 | ) | | (2,508 | ) | | (11,137 | ) | | (7,709 | ) |

| Total changes in other comprehensive loss | (3,376 | ) | | (455 | ) | | (46,302 | ) | | (5,669 | ) |

| Comprehensive loss | (294,643 | ) | | (39,992 | ) | | (56,852 | ) | | (117,459 | ) |

| Comprehensive loss (income) attributable to noncontrolling interest | 188,315 |

| | 696 |

| | 173,350 |

| | (33,207 | ) |

| Comprehensive (loss) income attributable to Vertex | $ | (106,328 | ) | | $ | (39,296 | ) | | $ | 116,498 |

| | $ | (150,666 | ) |

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2019 | | 2018 |

| Net income | $ | 268,631 |

| | $ | 227,301 |

|

| Changes in other comprehensive income (loss): | | | |

| Unrealized holding gains (losses) on marketable securities, net | 596 |

| | (460 | ) |

| Unrealized losses on foreign currency forward contracts, net of tax of $1.5 million and $0.3 million, respectively | (222 | ) | | (862 | ) |

| Foreign currency translation adjustment | 4,967 |

| | (2,729 | ) |

| Total changes in other comprehensive income (loss) | 5,341 |

| | (4,051 | ) |

| Comprehensive income | 273,972 |

| | 223,250 |

|

| Comprehensive income attributable to noncontrolling interest | — |

| | (17,038 | ) |

| Comprehensive income attributable to Vertex | $ | 273,972 |

| | $ | 206,212 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Balance Sheets

(unaudited)

(in thousands, except share and per share amounts)

| | | | September 30, | | December 31, | March 31, | | December 31, |

| | 2017 | | 2016 | 2019 | | 2018 |

| Assets | | | | | | |

| Current assets: | | | | | | |

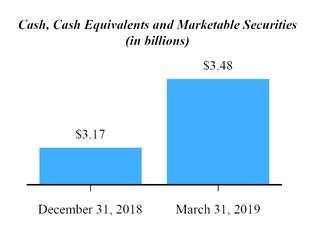

| Cash and cash equivalents | $ | 1,384,966 |

| | $ | 1,183,945 |

| $ | 2,893,885 |

| | $ | 2,650,134 |

|

| Marketable securities, available for sale | 427,282 |

| | 250,612 |

| |

| Restricted cash and cash equivalents (VIE) | 1,803 |

| | 47,762 |

| |

| Marketable securities | | 584,150 |

| | 518,108 |

|

| Accounts receivable, net | 263,493 |

| | 201,083 |

| 438,297 |

| | 409,688 |

|

| Inventories | 98,192 |

| | 77,604 |

| 136,698 |

| | 124,360 |

|

| Prepaid expenses and other current assets | 152,238 |

| | 70,534 |

| 130,009 |

| | 140,819 |

|

| Total current assets | 2,327,974 |

| | 1,831,540 |

| 4,183,039 |

| | 3,843,109 |

|

| Property and equipment, net | 759,978 |

| | 698,362 |

| 742,559 |

| | 812,005 |

|

| Intangible assets | 29,000 |

| | 284,340 |

| |

| Goodwill | 50,384 |

| | 50,384 |

| 50,384 |

| | 50,384 |

|

| Cost method investments | 20,447 |

| | 20,276 |

| |

| Deferred tax assets | | 1,467,518 |

| | 1,499,672 |

|

| Operating lease assets | | 60,573 |

| | — |

|

| Other assets | 10,542 |

| | 11,885 |

| 39,041 |

| | 40,728 |

|

| Total assets | $ | 3,198,325 |

| | $ | 2,896,787 |

| $ | 6,543,114 |

| | $ | 6,245,898 |

|

| Liabilities and Shareholders’ Equity | | | | | | |

| Current liabilities: | | | | | | |

| Accounts payable | $ | 77,138 |

| | $ | 61,451 |

| $ | 82,262 |

| | $ | 110,987 |

|

| Accrued expenses | 378,554 |

| | 315,249 |

| 532,745 |

| | 604,495 |

|

| Deferred revenues, current portion | 13,003 |

| | 6,005 |

| |

| Accrued restructuring expenses, current portion | 4,205 |

| | 6,047 |

| |

| Capital lease obligations, current portion | 19,881 |

| | 19,426 |

| |

| Customer deposits | 190,272 |

| | 73,416 |

| |

| Credit facility | — |

| | 300,000 |

| |

| Other liabilities, current portion | 27,686 |

| | 10,943 |

| |

| Early access sales accrual | | 382,703 |

| | 354,404 |

|

| Other current liabilities | | 108,758 |

| | 50,406 |

|

| Total current liabilities | 710,739 |

| | 792,537 |

| 1,106,468 |

| | 1,120,292 |

|

| Deferred revenues, excluding current portion | 2,917 |

| | 6,632 |

| |

| Accrued restructuring expenses, excluding current portion | 146 |

| | 1,907 |

| |

| Capital lease obligations, excluding current portion | 20,259 |

| | 34,976 |

| |

| Deferred tax liability | 10,682 |

| | 134,063 |

| |

| Construction financing lease obligation, excluding current portion | 547,051 |

| | 486,359 |

| |

| Advance from collaborator | 77,258 |

| | 73,423 |

| |

| Other liabilities, excluding current portion | 26,029 |

| | 28,699 |

| |

| Long-term finance lease liabilities | | 560,381 |

| | 581,550 |

|

| Long-term operating lease liabilities | | 63,484 |

| | — |

|

| Long-term advance from collaborator | | 83,471 |

| | 82,573 |

|

| Other long-term liabilities | | 5,997 |

| | 26,280 |

|

| Total liabilities | 1,395,081 |

| | 1,558,596 |

| 1,819,801 |

| | 1,810,695 |

|

| Commitments and contingencies |

|

| |

|

| — |

| | — |

|

| Shareholders’ equity: | | | | | | |

| Preferred stock, $0.01 par value; 1,000,000 shares authorized; none issued and outstanding | — |

| | — |

| |

| Common stock, $0.01 par value; 500,000,000 shares authorized; 252,683,346 and 248,300,517 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively | 2,500 |

| | 2,450 |

| |

| Preferred stock, $0.01 par value; 1,000 shares authorized; none issued and outstanding | | — |

| | — |

|

| Common stock, $0.01 par value; 500,000 shares authorized, 256,351 and 255,172 shares issued and outstanding, respectively | | 2,561 |

| | 2,546 |

|

| Additional paid-in capital | 7,034,113 |

| | 6,506,795 |

| 7,475,909 |

| | 7,421,476 |

|

| Accumulated other comprehensive (loss) income | (25,129 | ) | | 21,173 |

| |

| Accumulated other comprehensive income | | 6,000 |

| | 659 |

|

| Accumulated deficit | (5,220,407 | ) | | (5,373,836 | ) | (2,761,157 | ) | | (2,989,478 | ) |

| Total Vertex shareholders’ equity | 1,791,077 |

| | 1,156,582 |

| |

| Noncontrolling interest | 12,167 |

| | 181,609 |

| |

| Total shareholders’ equity | 1,803,244 |

| | 1,338,191 |

| 4,723,313 |

| | 4,435,203 |

|

| Total liabilities and shareholders’ equity | $ | 3,198,325 |

| | $ | 2,896,787 |

| $ | 6,543,114 |

| | $ | 6,245,898 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Shareholders’ Equity and Noncontrolling Interest

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional

Paid-in Capital | | Accumulated

Other

Comprehensive (Loss) Income | | Accumulated Deficit | | Total Vertex

Shareholders’ Equity | | Noncontrolling

Interest | | Total

Shareholders’ Equity |

| | Shares | | Amount | | | | | | |

| Balance at December 31, 2015 | 246,307 |

| | $ | 2,427 |

| | $ | 6,197,500 |

| | $ | 1,824 |

| | $ | (5,261,784 | ) | | $ | 939,967 |

| | $ | 153,661 |

| | $ | 1,093,628 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | (5,669 | ) | | — |

| | (5,669 | ) | | — |

| | (5,669 | ) |

| Net (loss) income | — |

| | — |

| | — |

| | — |

| | (144,997 | ) | | (144,997 | ) | | 33,207 |

| | (111,790 | ) |

| Issuance of common stock under benefit plans | 1,722 |

| | 19 |

| | 50,875 |

| | — |

| | — |

| | 50,894 |

| | — |

| | 50,894 |

|

| Stock-based compensation expense | — |

| | — |

| | 181,351 |

| | — |

| | — |

| | 181,351 |

| | (73 | ) | | 181,278 |

|

| Balance at September 30, 2016 | 248,029 |

| | $ | 2,446 |

| | $ | 6,429,726 |

| | $ | (3,845 | ) | | $ | (5,406,781 | ) | | $ | 1,021,546 |

| | $ | 186,795 |

| | $ | 1,208,341 |

|

| | | | | | | | | | | | | | | | |

| Balance at December 31, 2016 | 248,301 |

| | $ | 2,450 |

| | $ | 6,506,795 |

| | $ | 21,173 |

| | $ | (5,373,836 | ) | | $ | 1,156,582 |

| | $ | 181,609 |

| | $ | 1,338,191 |

|

| Cumulative effect adjustment for adoption of new accounting guidance | — |

| | — |

| | 9,371 |

| | | | (9,371 | ) | | — |

| | — |

| | — |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | (46,302 | ) | | — |

| | (46,302 | ) | | — |

| | (46,302 | ) |

| Net income (loss) | — |

| | — |

| | — |

| | — |

| | 162,800 |

| | 162,800 |

| | (173,350 | ) | | (10,550 | ) |

| Issuance of common stock under benefit plans | 4,382 |

| | 50 |

| | 298,956 |

| | — |

| | — |

| | 299,006 |

| | 33 |

| | 299,039 |

|

| Stock-based compensation expense | — |

| | — |

| | 218,991 |

| | — |

| | — |

| | 218,991 |

| | — |

| | 218,991 |

|

| VIE noncontrolling interest upon deconsolidation | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 3,910 |

| | 3,910 |

|

| Other | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (35 | ) | | (35 | ) |

| Balance at September 30, 2017 | 252,683 |

| | $ | 2,500 |

| | $ | 7,034,113 |

| | $ | (25,129 | ) | | $ | (5,220,407 | ) | | $ | 1,791,077 |

| | $ | 12,167 |

| | $ | 1,803,244 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional

Paid-in Capital | | Accumulated

Other

Comprehensive (Loss) Income | | Accumulated Deficit | | Total Vertex

Shareholders’ Equity | | Noncontrolling

Interest | | Total

Shareholders’ Equity |

| | Shares | | Amount | | | | | | |

| Balance at December 31, 2017 | 253,253 |

| | $ | 2,512 |

| | $ | 7,157,362 |

| | $ | (11,572 | ) | | $ | (5,119,723 | ) | | $ | 2,028,579 |

| | $ | 13,727 |

| | $ | 2,042,306 |

|

| Cumulative effect adjustment for adoption of new accounting guidance | — |

| | — |

| | — |

| | (24,120 | ) | | 33,349 |

| | 9,229 |

| | — |

| | 9,229 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | (4,051 | ) | | — |

| | (4,051 | ) | | — |

| | (4,051 | ) |

| Net income | — |

| | — |

| | — |

| | — |

| | 210,263 |

| | 210,263 |

| | 17,038 |

| | 227,301 |

|

| Repurchase of common stock | (67 | ) | | (1 | ) | | (11,250 | ) | | — |

| | — |

| | (11,251 | ) | | — |

| | (11,251 | ) |

| Issuance of common stock under benefit plans | 1,682 |

| | 30 |

| | 89,656 |

| | — |

| | — |

| | 89,686 |

| | — |

| | 89,686 |

|

| Stock-based compensation expense | — |

| | — |

| | 78,601 |

| | — |

| | — |

| | 78,601 |

| | — |

| | 78,601 |

|

| Other VIE activity | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1,000 | ) | | (1,000 | ) |

| Balance at March 31, 2018 | 254,868 |

| | $ | 2,541 |

| | $ | 7,314,369 |

| | $ | (39,743 | ) | | $ | (4,876,111 | ) | | $ | 2,401,056 |

| | $ | 29,765 |

| | $ | 2,430,821 |

|

| | | | | | | | | | | | | | | | |

| Balance at December 31, 2018 | 255,172 |

| | $ | 2,546 |

| | $ | 7,421,476 |

| | $ | 659 |

| | $ | (2,989,478 | ) | | $ | 4,435,203 |

| | $ | — |

| | $ | 4,435,203 |

|

| Cumulative effect adjustment for adoption of new accounting guidance | — |

| | — |

| | — |

| | — |

| | (40,310 | ) | | (40,310 | ) | | — |

| | (40,310 | ) |

| Other comprehensive income, net of tax | — |

| | — |

| | — |

| | 5,341 |

| | — |

| | 5,341 |

| | — |

| | 5,341 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | 268,631 |

| | 268,631 |

| | — |

| | 268,631 |

|

| Repurchases of common stock | (564 | ) | | (6 | ) | | (103,833 | ) | | — |

| | — |

| | (103,839 | ) | | — |

| | (103,839 | ) |

| Issuance of common stock under benefit plans | 1,743 |

| | 21 |

| | 64,023 |

| | — |

| | — |

| | 64,044 |

| | — |

| | 64,044 |

|

| Stock-based compensation expense | — |

| | — |

| | 94,243 |

| | — |

| | — |

| | 94,243 |

| | — |

| | 94,243 |

|

| Balance at March 31, 2019 | 256,351 |

| | $ | 2,561 |

| | $ | 7,475,909 |

| | $ | 6,000 |

| | $ | (2,761,157 | ) | | $ | 4,723,313 |

| | $ | — |

| | $ | 4,723,313 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Cash Flows

(unaudited)

(in thousands)

| | | | Nine Months Ended September 30, | Three Months Ended March 31, |

| | 2017 | | 2016 | 2019 | | 2018 |

| Cash flows from operating activities: | | | | | | |

| Net loss | $ | (10,550 | ) | | $ | (111,790 | ) | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | | |

| Net income | | $ | 268,631 |

| | $ | 227,301 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | |

| Stock-based compensation expense | 215,334 |

| | 178,623 |

| 93,791 |

| | 78,136 |

|

| Depreciation and amortization expense | 44,965 |

| | 45,947 |

| |

| Depreciation expense | | 27,140 |

| | 16,343 |

|

| Write-downs of inventories to net realizable value | 11,138 |

| | — |

| 1,270 |

| | 3,619 |

|

| Deferred income taxes | (113,969 | ) | | 23,544 |

| 43,425 |

| | 3,587 |

|

| Impairment of property and equipment | 1,946 |

| | — |

| |

| Intangible asset impairment charge | 255,340 |

| | — |

| |

| Acquired in-process research & development | 160,000 |

| | — |

| |

| Deconsolidation of VIE | 76,644 |

| | — |

| |

| Unrealized gain on equity securities | | (43,551 | ) | | (95,458 | ) |

| Other non-cash items, net | (4,787 | ) | | (904 | ) | (3,701 | ) | | 5,827 |

|

| Changes in operating assets and liabilities: | | | | | | |

| Accounts receivable, net | (54,455 | ) | | (9,760 | ) | (30,136 | ) | | (13,473 | ) |

| Inventories | (28,570 | ) | | (11,536 | ) | (13,139 | ) | | (8,208 | ) |

| Prepaid expenses and other assets | (90,006 | ) | | (8,979 | ) | 7,941 |

| | 25,482 |

|

| Accounts payable | 6,925 |

| | (21,532 | ) | (24,145 | ) | | 2,154 |

|

| Accrued expenses and other liabilities | 148,102 |

| | 26,121 |

| (38,425 | ) | | (31,469 | ) |

| Accrued restructuring expense | (3,863 | ) | | (8,151 | ) | |

| Deferred revenues | 3,237 |

| | (10,204 | ) | |

| Early access sales accrual | | 35,683 |

| | 38,816 |

|

| Net cash provided by operating activities | 617,431 |

| | 91,379 |

| 324,784 |

| | 252,657 |

|

| Cash flows from investing activities: | | | | | | |

| Purchases of marketable securities | (431,653 | ) | | (616,625 | ) | |

| Maturities of marketable securities | 247,149 |

| | 535,379 |

| |

| Purchases of available-for-sale debt securities | | (128,215 | ) | | (38,653 | ) |

| Maturities of available-for-sale debt securities | | 107,118 |

| | 94,365 |

|

| Expenditures for property and equipment | (56,817 | ) | | (41,775 | ) | (18,041 | ) | | (29,279 | ) |

| Purchase of in-process research & development | (160,000 | ) | | — |

| |

| (Decrease) increase in restricted cash and cash equivalents (VIE) | (15,643 | ) | | 20,490 |

| |

| Investment in equity securities | — |

| | (23,075 | ) | — |

| | (21,500 | ) |

| Decrease (increase) in other assets | 380 |

| | (93 | ) | |

| Net cash used in investing activities | (416,584 | ) | | (125,699 | ) | |

| Net cash (used in) provided by investing activities | | (39,138 | ) | | 4,933 |

|

| Cash flows from financing activities: | | | | | | |

| Issuances of common stock under benefit plans | 298,205 |

| | 51,165 |

| 63,620 |

| | 88,403 |

|

| Payments on revolving credit facility | (300,000 | ) | | — |

| |

| Repurchase of common stock | | (99,839 | ) | | (10,000 | ) |

| Advance from collaborator | 10,000 |

| | — |

| 5,000 |

| | 2,500 |

|

| Payments on capital lease obligations | (14,188 | ) | | (13,330 | ) | |

| Proceeds from capital lease financing | — |

| | 2,030 |

| |

| Payments on construction financing lease obligation | (412 | ) | | (356 | ) | |

| Payments on capital lease and construction financing lease obligations | | — |

| | (9,331 | ) |

| Payments on finance leases | | (9,385 | ) | | — |

|

| Proceeds related to construction financing lease obligation | 4,700 |

|

| — |

| — |

| | 9,566 |

|

| Repayments of advanced funding | (3,132 | ) | | — |

| (1,385 | ) | | (1,182 | ) |

| Other financing activities | | — |

| | (1,000 | ) |

| Net cash (used in) provided by financing activities | (4,827 | ) | | 39,509 |

| (41,989 | ) | | 78,956 |

|

| Effect of changes in exchange rates on cash | 5,001 |

| | (265 | ) | (378 | ) | | 1,656 |

|

| Net increase in cash and cash equivalents | 201,021 |

| | 4,924 |

| 243,279 |

| | 338,202 |

|

| Cash and cash equivalents—beginning of period | 1,183,945 |

| | 714,768 |

| |

| Cash and cash equivalents—end of period | $ | 1,384,966 |

| | $ | 719,692 |

| |

| Cash, cash equivalents and restricted cash—beginning of period | | 2,658,253 |

| | 1,667,526 |

|

| Cash, cash equivalents and restricted cash—end of period | | $ | 2,901,532 |

| | $ | 2,005,728 |

|

| | | | | | | |

| Supplemental disclosure of cash flow information: | | | | | | |

| Cash paid for interest | $ | 51,990 |

| | $ | 64,662 |

| $ | 13,148 |

| | $ | 16,825 |

|

| Cash paid for income taxes | $ | 4,154 |

| | $ | 1,617 |

| $ | 1,835 |

| | $ | 1,897 |

|

| Capitalization of costs related to construction financing lease obligation | $ | 33,827 |

| | $ | 824 |

| $ | — |

| | $ | 3,716 |

|

| Issuances of common stock from employee benefit plans receivable | $ | 868 |

| | $ | 19 |

| $ | 510 |

| | $ | 2,124 |

|

| Accrued share repurchase liability | | $ | 4,000 |

| | $ | — |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

A. Basis of Presentation and Accounting Policies

Basis of Presentation

The accompanying condensed consolidated financial statements are unaudited and have been prepared by Vertex Pharmaceuticals Incorporated (“Vertex” or the “Company”) in accordance with accounting principles generally accepted in the United States of America (“GAAP”).

The condensed consolidated financial statements reflect the operations of (i) the Company (ii)and its wholly-owned subsidiaries and (iii)subsidiaries. The Company's condensed consolidated financial statements for the interim period ended March 31, 2018 also include the financial results of BioAxone Biosciences, Inc. (“BioAxone”), a variable interest entities (VIEs).entity (“VIE”) that the Company consolidated from 2014 through December 31, 2018. All material intercompany balances and transactions have been eliminated. The Company operates in one segment, pharmaceuticals. As of September 30, 2017, the Company deconsolidated Parion Sciences, Inc. (“Parion”), a VIE theThe Company has reclassified certain items from the prior year’s condensed consolidated since 2015. The Company's consolidated balance sheet as of September 30, 2017 excludes Parion. Please referfinancial statements to Note C, “Collaborative Arrangements and Acquisitions” for further information regardingconform to the deconsolidation of Parion.current year’s presentation.

Certain information and footnote disclosures normally included in the Company’s annual financial statements2018 Annual Report on Form 10-K have been condensed or omitted. These interim financial statements, in the opinion of management, reflect all normal recurring adjustments necessary for a fair presentation of the financial position and results of operations for the interim periods ended September 30, 2017March 31, 2019 and 2016.2018.

The results of operations for the interim periods are not necessarily indicative of the results of operations to be expected for the full fiscal year. These interim financial statements should be read in conjunction with the audited financial statements for the year ended December 31, 2016,2018, which are contained in the Company’s2018 Annual Report on Form 10-K for the year ended December 31, 2016 that was filed with the Securities and Exchange Commission (the “SEC”) on February 23, 2017 (the “2016 Annual Report on Form 10-K”).10-K.

Use of Estimates and Summary of Significant Accounting Policies

The preparation of condensed consolidated financial statements in accordance with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements, and the amounts of revenues and expenses during the reported periods. Significant estimates in these condensed consolidated financial statements have been made in connection with the calculation of revenues, inventories, research and development expenses, stock-based compensation expense, restructuring expense, the fair value of intangible assets, goodwill, contingent consideration, noncontrolling interest, the consolidation and deconsolidation of VIEs, leases, the fair value of cash flow hedgesdeferred tax asset valuation allowances and the provision for or benefit from income taxes. The Company bases its estimates on historical experience and various other assumptions, including in certain circumstances future projections that management believes to be reasonable under the circumstances. Actual results could differ from those estimates. Changes in estimates are reflected in reported results in the period in which they become known.

Recently Adopted Accounting Standards

Leases

In 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842) (“ASC 842”), which amends a number of aspects of lease accounting and requires entities to recognize right-of-use assets and liabilities on the balance sheet. ASC 842 became effective on January 1, 2019. The Company’s significantCompany has finalized its review of its portfolio of existing leases and current accounting policies are described in Note A, “Nature of Business and Accounting Policies,”has concluded that the amended guidance results in the 2016 Annual Reportrecognition of additional assets and corresponding liabilities on Form 10-K.its balance sheets. The Company also has finalized changes to its controls to address the adoption and ongoing lease accounting and related disclosure requirements of the new standard.

Recent Accounting Pronouncements

In 2014,Until December 31, 2018, the Financial Accounting Standards Board (“FASB”) issued newCompany applied build-to-suit accounting and was the deemed owner of its leased corporate headquarters in Boston and research site in San Diego, for which it was recognizing depreciation expense over the buildings’ useful lives and imputed interest on the corresponding construction financing lease obligations. Under the amended guidance applicable to revenue recognition that will bebecame effective January 1, 2018. Early adoption was permitted for the year-ending December 31, 2017. The new guidance applies a more principles based approach to recognizing revenue. Under the new guidance, revenue is recognized when a customer obtains control of promised goods or services and is recognized in an amount that reflects the consideration that an entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The new guidance must be adopted using either a modified retrospective approach or a full retrospective approach for all periods presented. Under the modified retrospective method, the cumulative effect of applying the standard would be recognized at the date of initial application within retained earnings. Under the full retrospective approach, the standard would be applied to each prior reporting period presented. Upon adoption,2019, the Company will useaccounts for these buildings as finance leases, resulting in increased depreciation expense over the modified retrospective method.respective lease terms of 15-16 years, which are significantly shorter than the buildings’ useful lives of 40 years. The Company continuesalso expects a reduction in its imputed interest expense in the initial years of each finance lease term. In 2019, the Company expects an increase in operating expenses of approximately $26 million and a decrease in interest expense of approximately $13 million due to evaluate the new guidance and the effect the adoption will have on the condensed consolidated financialthis change.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

statements. The Company’s project team is finalizing its review of existing customer contracts and current accounting policies to identify and assess the potential differences that would result from applying the requirements of the new standard. Based on the Company’s assessment performed to date, the new revenue recognition guidance could impact the Company’s accounting for product shipments to certain countries through early access programs, including the French early access programs, whereby the associated product has received regulatory approval but the price is not fixed or determinable based on the status of ongoing pricing discussions, and could impact the Company’s accounting for certain reimbursement agreements that the Company plans to negotiate in the fourth quarter of 2017. As the Company completes its assessment, it is implementing appropriate changes to its controls to support revenue recognition and additional revenue-related disclosures under the new standard.

In 2016,July 2018, the FASB issued amended guidance applicableASU No. 2018-11, Leases (Topic 842): Targeted Improvements (“ASU 2018-11”), which offered a transition option to share-based compensationentities adopting ASC 842. Under ASU 2018-11, entities could elect to employees that simplifies the accounting for employee share-based payment transactions, including the accounting for income taxes, forfeitures, and statutory tax withholding requirements, as well as classificationapply ASC 842 using a modified-retrospective adoption approach resulting in the statement of cash flows. The amended guidance became effective for the Company during the first quarter of 2017. The amended guidance eliminates the requirement that excess tax benefits be realized as a reduction in current taxes payable before the associated tax benefit can be recognized as an increase in additional paid-in capital. This created approximately $410.8 million of deferred tax asset (“DTA”) relating to federal and state net operating losses (“NOLs”) that are fully reserved by an equal increase in valuation allowance. The Company recorded DTAs of approximately $404.7 million relating to Federal NOLs and approximately $6.1 million relating to State NOLs, both of which are offset by a full valuation allowance. Upon adoption, the Company also elected to change its accounting policy to account for forfeitures of options and awards as they occur. The change was applied on a modified retrospective basis with a cumulative effect adjustment to accumulated deficit at the beginning of the year in which the new lease standard is adopted, rather than adjustments to the earliest comparative period presented in their financial statements. The Company adopted ASC 842 using the modified-retrospective method. As of January 1, 2019, the Company recorded a cumulative effect adjustment to increase its “Accumulated deficit” by $40.3 million related to the adjustments to its build-to-suit leases described in the previous paragraph.

The Company elected the package of transition practical expedients for leases that commenced prior to January 1, 2019, allowing it not to reassess (i) whether any expired or existing contracts contain leases, (ii) the lease classification for any expired or existing leases and (iii) the initial indirect costs for any existing leases.

Additionally, the Company recorded, upon adoption of ASC 842 on January 1, 2019, operating lease assets of $61.7 million and corresponding liabilities of $71.9 million related to its real estate leases that are not treated as finance leases under ASC 842. The difference between these assets and liabilities is primarily attributable to prepaid or accrued lease payments. The Company also reclassified amounts that were recorded as “Capital lease obligations, current portion” and “Capital lease obligations, excluding current portion” as of December 31, 2018 to “Other current liabilities” and “Long-term finance lease liabilities,” respectively, on January 1, 2019. These adjustments had no impact on the Company’s condensed consolidated statement of operations and had no impact on the Company’s accumulated deficitdeficit.

The cumulative effect of $9.4 million, which increasedapplying ASC 842 on the accumulated deficitCompany’s condensed consolidated balance sheet as of January 1, 2017. This change also resulted in an increase2019 was as follows:

|

| | | | | | | | | | | |

| | Balance as of | | | | Balance as of |

| | December 31, 2018 ^ | | Adjustments | | January 1, 2019 |

| Assets | (in thousands) |

| Prepaid expenses and other current assets | $ | 140,819 |

| | $ | (2,930 | ) | | $ | 137,889 |

|

| Property and equipment, net | 812,005 |

| | (53,920 | ) | | 758,085 |

|

| Deferred tax assets | 1,499,672 |

| | 11,236 |

| | 1,510,908 |

|

| Operating lease assets | — |

| | 61,674 |

| | 61,674 |

|

| Total assets | $ | 6,245,898 |

| | $ | 16,060 |

| | $ | 6,261,958 |

|

| Liabilities and Shareholders’ Equity | | | | | |

| Capital lease obligations, current portion | $ | 9,817 |

| | $ | (9,817 | ) | | $ | — |

|

| Other current liabilities | 40,589 |

| | 34,304 |

| | 74,893 |

|

| Capital lease obligations, excluding current portion | 19,658 |

| | (19,658 | ) | | — |

|

| Construction financing lease obligation, excluding current portion | 561,892 |

| | (561,892 | ) | | — |

|

| Long-term finance lease liabilities | — |

| | 569,487 |

| | 569,487 |

|

| Long-term operating lease liabilities | — |

| | 64,849 |

| | 64,849 |

|

| Other long-term liabilities | 26,280 |

| | (20,903 | ) | | 5,377 |

|

| Accumulated deficit | (2,989,478 | ) | | (40,310 | ) | | (3,029,788 | ) |

| Total liabilities and shareholders’ equity | $ | 6,245,898 |

| | $ | 16,060 |

| | $ | 6,261,958 |

|

| ^ As reported in the Company’s 2018 Annual Report on Form 10-K. |

Please refer to Note K, “Leases,” for further information regarding the DTA of $3.4 million, which is offsetCompany’s leases as well as certain disclosures required by a full valuation allowance. As a result, there was no cumulative-effect adjustment to accumulated deficit. The provisions related to the recognition of excess tax benefits in the income statementASC 842.

Derivatives and classification in the statement of cash flows were adopted prospectively, and as such, the prior periods were not retrospectively adjusted.Hedging

In 2016,2017, the FASB issued amended guidance related to the recordingASU 2017-12, Derivatives and Hedging (Topic 815) (“ASU 2017-12”), which helps simplify certain aspects of financial assetshedge accounting and financial liabilities. Under the amended guidance, equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) are to be measured at fair value with changes in fair value recognized in net income. However, an entity has the option to either measure equity investments without readily determinable fair values at fair value or at cost adjusted for changes in observable prices minus impairment. Changes in measurement under either alternative will be recognized in net income. The amended guidance is effective for the year ending December 31, 2018. Early adoption is permitted. The Company expects the implementation of this standard to have an impact on its consolidated financial statements and related disclosures, as the Company held publicly traded equity investments as of September 30, 2017 as well as equity investments accounted for under the cost method. A cumulative-effect adjustment to the balance sheet will be recorded as of the beginning of the fiscal year of adoption. The implementation of this amended guidance is expected to increase volatility in net income as the volatility currently recorded in other comprehensive income related to changes in the fair market value of available-for-sale equity investments will be reflected in net income after adoption.

In 2016, the FASB issued amended guidance applicable to leases that will be effective for the year ending December 31, 2019. Early adoption is permitted. This guidance requiresenables entities to recognize assets and liabilities for leases with lease termsmore accurately present their risk management activities in their financial statements. ASU 2017-12 became effective January 1, 2019. The adoption of more than 12 monthsASU 2017-12 did not have a significant effect on the balance sheet. The Company is in the process of evaluating this guidance and determining the expected effect on itsCompany’s condensed consolidated financial statements.

In 2016, the FASB issued amended guidance related to intra-entity transfers other than inventory. This guidance removes the current exception in GAAP prohibiting entities from recognizing current and deferred income tax expenses or benefits related to transfer of assets, other than inventory, within the consolidated entity. The current exception to defer the recognition of any tax impact on the transfer of inventory within the consolidated entity until it is sold to a third party remains unaffected. The amended guidance is effective for the year ending December 31, 2018. Early adoption is permitted. The Company is in the process of evaluating this guidance and determining the expected effect on its condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Recently Issued Accounting Standards

Internal-Use Software

In 2017,2018, the FASB issued amended guidance related to business combinations. The amended guidanceASU 2018-15, Intangibles—Goodwill and Other—Internal-Use Software (Subtopic 350-40): Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract (“ASU 2018-15”), which clarifies the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accountedaccounting for as acquisitions (or disposals) of assets or businesses. The new accounting guidanceimplementation costs in cloud computing arrangements. ASU 2018-15 is effective for annual periods beginning after December 15, 2017, including interim periods within those periods. Early adoption is permitted. The Company early adopted this new guidance as ofon January 1, 2017 and will apply this new guidance to future acquisitions.

In 2017, the FASB issued amended guidance related to measurements of goodwill. The amended guidance eliminates a step from the goodwill impairment test. Under the amended guidance, an entity should perform its annual or interim goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity would recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. The amended guidance is effective for the year-ending December 31, 2020. Early adoption is permitted. The Company does not expect a significant effectcurrently is evaluating the impact the adoption of ASU 2018-15 may have on its condensed consolidated financial statements upon adoption of this new guidance.statements.

Fair Value Measurement

In 2017,2018, the FASB issued amended guidance relatedASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework-Changes to the scope of stock option modification accounting, to reduce diversity in practice and provide clarity regarding existing guidance. The new accounting guidanceDisclosure Requirements for Fair Value Measurement (“ASU 2018-13”), which modifies the disclosure requirements for fair value measurements. ASU 2018-13 is effective for annual periods beginning after December 15, 2017, including interim periods within those periods.on January 1, 2020. Early adoption is permitted. The Company does not expectcurrently is evaluating the impact the adoption of this guidance toASU 2018-13 may have a material effect on its condensed consolidated financial statements and related disclosures.

In 2017, the FASB issued amended guidance applicable to hedge accounting. The new accounting guidance is effective for annual periods beginning after December 15, 2018, including interim periods within those periods. Early adoption is permitted. The amended guidance helps simplify certain aspects of hedge accounting and enables entities to more accurately present their risk management activities in their financial statements. The Company is in the process of evaluating this guidance and determining the expected effect on its condensed consolidated financial statements.

For a discussion of other recent accounting pronouncements please refer to Note A, “Nature of Business and Accounting Policies—Recent Accounting Pronouncements,” in the 20162018 Annual Report on Form 10-K.

Summary of Significant Accounting Policies

The Company sells its products principally to a limited number of specialty pharmacy providers in North America as well as government-owned and supported customers in international markets (collectively, its “Customers”). The Company’s Customers in North America subsequently resell the products to patients and health care providers. The Company recognizes net revenues from product sales upon delivery to the Customer as long as (i) there is persuasive evidence that an arrangement exists between the Company and the Customer, (ii) collectibility is reasonably assured and (iii) the price is fixed or determinable.

In order to conclude that the price is fixed or determinable, the Company must be able to (i) calculate its gross product revenues from sales to Customers and (ii) reasonably estimate its net product revenues upon delivery to its Customers’ locations. The Company calculates gross product revenues based on the price that the Company charges its Customers. The Company estimates its net product revenues by deducting from its gross product revenues (a) trade allowances, such as invoice discounts for prompt payment and Customer fees, (b) estimated government and private payor rebates, chargebacks and discounts, (c) estimated reserves for expected product returns and (d) estimated costs of co-pay assistance programs for patients, as well as other incentives for certain indirect customers.

The Company makes significant estimates and judgments that materially affect the Company’s recognition of net product revenues. In certain instances, the Company may be unable to reasonably conclude that the price is fixed or determinable at the time of delivery, in which case it defers the recognition of revenues. Once the Company is able to determine that the price is fixed or determinable, it recognizes the net product revenues associated with the units in which revenue recognition was deferred.

Revenue recognition related to the Company’s French early access programs could be impacted by the new revenue recognition guidance that is effective January 1, 2018 andaccounting policies are described in Note A, “Basis“Nature of PresentationBusiness and Accounting Policies,” in its 2018 Annual Report on Form 10-K. The Company is disclosing changes in its accounting policies related to guidance that became effective January 1, 2019 in this Quarterly Report on Form 10-Q. Specifically, the Company has included its policy pursuant to its adoption of ASC 842 below.

Leases

At the inception of an arrangement, the Company determines whether the arrangement contains a lease. If a lease is identified in an arrangement, the Company recognizes a right-of-use asset and liability on its balance sheet and determines whether the lease should be classified as a finance or operating lease. The Company does not recognize assets or liabilities for leases with lease terms of less than 12 months.

A lease qualifies as a finance lease if any of the following criteria are met at the inception of the lease: (i) there is a transfer of ownership of the leased asset to the Company by the end of the lease term, (ii) the Company holds an option to purchase the leased asset that it is reasonably certain to exercise, (iii) the lease term is for a major part of the remaining economic life of the leased asset, (iv) the present value of the sum of lease payments equals or exceeds substantially all of the fair value of the leased asset, or (v) the nature of the leased asset is specialized to the point that it is expected to provide the lessor no alternative use at the end of the lease term. All other leases are recorded as operating leases.

Finance and operating lease assets and liabilities are recognized at the lease commencement date based on the present value of the lease payments over the lease term using the discount rate implicit in the lease. If the rate implicit is not readily determinable, the Company utilizes its incremental borrowing rate at the lease commencement date. Operating lease assets are further adjusted for prepaid or accrued lease payments. Operating lease payments are expensed using the straight-line method as an operating expense over the lease term. Finance lease assets are amortized to depreciation expense using the straight-line method over the shorter of the useful life of the related asset or the lease term. Finance lease payments are bifurcated into (i) a portion that is recorded as imputed interest expense and (ii) a portion that reduces the finance liability associated with the lease.

The Company does not separate lease and non-lease components when determining which lease payments to include in the calculation of its lease assets and liabilities. Variable lease payments are expensed as incurred. If a lease includes an option to extend or terminate the lease, the Company reflects the option in the lease term if it is reasonably certain it will exercise the option.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Policies”. TheFinance leases are recorded in “Property and equipment, net,” “Other current liabilities” and “Long-term finance lease liabilities” on the Company’s ORKAMBIcondensed consolidated balance sheet. Operating leases are recorded in “Operating lease assets,” “Other current liabilities” and “Long-term operating lease liabilities” on the Company’s condensed consolidated balance sheet.

Disaggregation of Revenue

Revenues by Product

Product revenues, net consisted of the following:

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2019 | | 2018 |

| | (in thousands) |

| SYMDEKO/SYMKEVI | $ | 320,275 |

| | $ | 34,124 |

|

| ORKAMBI | 293,007 |

| | 354,066 |

|

| KALYDECO | 243,971 |

| | 249,539 |

|

| Total product revenues, net | $ | 857,253 |

| | $ | 637,729 |

|

Revenues by Geographic Location

Net product revenues are attributed to date do not include anycountries based on the location of the customer. Collaborative and royalty revenues are attributed to countries based on the location of the Company’s subsidiary associated with the collaborative arrangement related to such revenues. Total revenues from product sales in France becauseexternal customers and collaborators by geographic region consisted of the price is not fixed or determinable. Thefollowing:

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2019 | | 2018 |

| | (in thousands) |

| United States | $ | 641,104 |

| | $ | 482,667 |

|

| Outside of the United States | | | |

| Europe | 167,751 |

| | 131,895 |

|

| Other | 49,580 |

| | 26,237 |

|

| Total revenues outside of the United States | 217,331 |

| | 158,132 |

|

| Total revenues | $ | 858,435 |

| | $ | 640,799 |

|

In the three months ended March 31, 2019 and 2018, revenues attributable to Germany contributed the largest amount to the Company’s European revenues.

French Early Access Programs

In 2015, the Company began distributing ORKAMBI through early access programs in France duringand continues to be engaged in ongoing pricing discussions regarding the fourth quarter of 2015. As of September 30, 2017, the Company’s condensed consolidated balance sheet includes $190.3 million collectedfinal price for ORKAMBI in France related to shipments of ORKAMBI under the early access programs that is classified as Customer deposits.France. The Company expects that the difference between the amounts it has collected to date based on the invoiced price and the final negotiated price for ORKAMBI in France will be returned to the French government.

IfPursuant to the Company concludes as ofrevenue recognition accounting guidance that was applicable until December 31, 2017, that the price of theCompany’s ORKAMBI supplied under the early access programs is fixed or determinable based on, among other factors, the status of negotiations in France, it would record net product revenues for all2015, 2016 and 2017 did not include any net product revenues from sales since the inception of the early access programs for ORKAMBI based on the fixed or determinable price in the fourth quarter of 2017.

If the Company concludes thatFrance because the price iswas not fixed orand determinable asat the time of December 31, 2017, these amounts would be subject to the new guidance applicable to revenue recognition effective January 1, 2018 using the modified retrospective adoption approach. Pursuant to the new guidance, the Company would record a cumulative effect adjustment to the Company’s accumulated deficit delivery. Upon adopting ASU 2014-09, Revenues from Contracts with Customers (Topic 606),in the first quarter of 2018. The amount2018, the Company began recognizing net product revenues on a portion of the adjustment to accumulated deficit would be determinedits current period sales based upon (i) the status of pricing discussions in France upon adoption and (ii) the Company’son its estimate of the amount of consideration the Companyit expects to retain related to the French ORKAMBI sales that occurred on or prior to December 31, 2017 that wouldwill not be subject to a significant reversal in amounts recognized. For French ORKAMBI sales after December 31, 2017 under the early access programs, the Company would recognize product revenues based onIf the Company’s estimate of consideration the Company expects to retain for which it is probable that a significant reversal in amounts recognized will not occur. In future periods, if the Company’s estimates regarding the amounts it will receive for ORKAMBI supplied pursuant to these programs change, the effect of the change in estimates would be reflected in net product revenues in the period in which the change in estimate occurred.

The following table summarizes activity in each of the product revenue allowance and reserve categories for the nine months ended September 30, 2017: |

| | | | | | | | | | | | | | | | | | | |

| | Trade

Allowances | | Rebates,

Chargebacks

and Discounts | | Product

Returns | | Other

Incentives | | Total |

| | (in thousands) |

| Balance at December 31, 2016 | $ | 2,568 |

| | $ | 81,927 |

| | $ | 3,492 |

| | $ | 1,214 |

| | $ | 89,201 |

|

| Provision related to current period sales | 18,776 |

| | 118,592 |

| | 3,603 |

| | 12,238 |

| | 153,209 |

|

| Adjustments related to prior period sales | (188 | ) | | (4,327 | ) | | (13 | ) | | (355 | ) | | (4,883 | ) |

| Credits/payments made | (18,409 | ) | | (97,393 | ) | | (1,809 | ) | | (10,021 | ) | | (127,632 | ) |

| Balance at September 30, 2017 | $ | 2,747 |

| | $ | 98,799 |

| | $ | 5,273 |

| | $ | 3,076 |

| | $ | 109,895 |

|

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

ORKAMBI supplied pursuant to these early access programs changes, the Company will reflect the effect of the change in estimate in “Product revenues, net” in the period in which the change in estimate occurs.

As of March 31, 2019 and December 31, 2018, the Company’s condensed consolidated balance sheets included an “Early access sales accrual” of $382.7 million and $354.4 million, respectively, which was primarily related to the amount it may be required to return to the French government related to ORKAMBI early access programs, which is considered to be a refund liability.

Contract Liabilities

The Company recorded contract liabilities of $51.4 million and $24.9 million as of March 31, 2019 and December 31, 2018, respectively, related to annual contracts with government-owned and supported customers in international markets that limit the amount of annual reimbursement the Company can receive. Upon exceeding the annual reimbursement amount, products are provided free of charge, which is a material right. These contracts, which are classified as “Other current liabilities,” include upfront payments and fees. The Company defers a portion of the consideration received for shipments made up to the annual reimbursement limit, and the deferred amount is recognized as revenue when the free products are shipped. The Company’s product revenue contracts include performance obligations that are one year or less.

Several of the Company’s contract liabilities relate to contracts with annual reimbursement limits in international markets in which the annual period associated with the contract is not the same as the Company’s fiscal year. In the majority of international markets in which the Company has a contract with an annual reimbursement limit, the annual period associated with the contract is the same as the Company’s fiscal year, resulting in no contract liability balance at the end of the year and no revenues recognized in the current year related to performance obligations satisfied in previous years. For the international markets in which the periods associated with these annual contracts are not the same as the Company’s fiscal year, the Company recognizes revenues related to performance obligations satisfied in previous years; however, these amounts are not material to the Company’s financial statements and do not relate to any performance obligations that were satisfied more than 12 months prior to the beginning of the current year.

| |

| C. | Collaborative Arrangements and Acquisitions |

The Company has entered into numerous agreements pursuant to which it collaborates with third parties on research, development and commercialization programs, including in-license and out-license agreements and asset acquisitions.

In-license Agreements

The Company has entered into a number of license agreements in order to advance and obtain access to technologies and services related to its research and early-development activities. The Company is generally required to make an upfront payment upon execution of the license agreement; development, regulatory and commercialization milestones payments upon the achievement of certain product research, development and commercialization objectives; and royalty payments on future sales, if any, of commercial products resulting from the collaboration.

Pursuant to the terms of its in-license agreements, the Company’s collaborators lead the discovery efforts and the Company leads all preclinical, development and commercialization activities associated with the advancement of any drug candidates and funds all expenses unless otherwise described below.

The Company typically can terminate its in-license agreements by providing advance notice to its collaborators; the required length of notice is dependent on whether any product developed under the license agreement has received marketing approval. The Company’s license agreements may be terminated by either party for a material breach by the other, subject to notice and cure provisions. Unless earlier terminated, these license agreements generally remain in effect until the date on which the royalty term and all payment obligations with respect to all products in all countries have expired.

CRISPR Therapeutics AG

In 2015, the Company entered into a strategic collaboration, option and license agreement (the “CRISPR Agreement”) with CRISPR Therapeutics AG and its affiliates (“CRISPR”) to collaborate on the discovery and development of potential new treatments aimed at the underlying genetic causes of human diseases using CRISPR-Cas9 gene-editing technology. The

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Company has the exclusive right to license up to six CRISPR-Cas9-based targets, including targets for the potential treatment of sickle cell disease. In connection with the CRISPR Agreement, the Company made an upfront payment to CRISPR of $75.0 million and an investment in CRISPR’s stock. The Company has also made several subsequent investments in CRISPR’s common stock, which has resulted in CRISPR becoming a related party of the Company. Please refer to Note F, “Marketable Securities and Equity Investments,” for further information regarding the Company’s investment in CRISPR’s common stock.

The Company funds all the discovery activities conducted pursuant to the CRISPR Agreement. For targets that the Company elects to license, other than hemoglobinopathy treatments, the Company would lead all development and global commercialization activities. For each target that the Company elects to license, other than hemoglobinopathy targets, CRISPR has the potential to receive up to $420.0 million in development, regulatory and commercial milestones as well as royalties on net product sales. As part of the collaboration, the Company and CRISPR share equally all development costs and potential worldwide revenues related to potential hemoglobinopathy treatments, including treatments for beta thalassemia and sickle cell disease.

In 2017, the Company entered into a co-development and co-commercialization agreement with CRISPR pursuant to the terms of the CRISPR Agreement, under which the Company and CRISPR are co-developing and will co-commercialize CTX001 (the “CTX001 Co-Co Agreement”) for the treatment of hemoglobinopathy, including treatments for sickle cell disease and beta thalassemia. The Company concluded that the CTX001 Co-Co Agreement is a cost-sharing arrangement, which results in the net impact of the arrangement being recorded in “Research and development expenses” in its condensed consolidated statements of operations. During the three months ended March 31, 2019 and 2018, the net expense related to the CTX001 Co-Co Agreement was $7.0 million and $3.6 million, respectively.

Other In-license Agreements

In 2016, the Company entered into a strategic collaboration and licensing agreement with Moderna Therapeutics, Inc. (“Moderna”), pursuant to which the parties are seeking to identify and develop messenger ribonucleic acid, or mRNA, therapeutics for the treatment of CF. The Company made an upfront payment to Moderna of $20.0 million and an investment in Moderna’s preferred stock, which converted to common stock when Moderna became a publicly traded company in December 2018. Moderna has the potential to receive future development and regulatory milestones of up to $275.0 million, as well as royalties on net product sales. Please refer to Note F, “Marketable Securities and Equity Investments,” for further information regarding the Company’s investment in Moderna’s common stock.

In December 2018, the Company entered into a strategic collaboration and licensing agreement (the “Arbor Agreement”) with Arbor Biotechnologies, Inc. (“Arbor”) focused on the discovery of novel proteins, including DNA endonucleases, to advance the development of new gene-editing therapies. Pursuant to the Arbor Agreement, Arbor’s platform technology is being applied in the collaboration activities for up to five Vertex disease areas in exchange for an upfront payment of $30.0 million. In addition, the Company received a convertible promissory note that matures in 2023 for an additional $15.0 million payment. For each product identified by the collaboration, Arbor has the potential to receive up to $337.5 million in development, regulatory and commercial milestones as well as royalties on net product sales.

The Company determined that the fair value of the convertible promissory note approximated its contractual value upon agreement execution and classifies the convertible note in “Other assets” at amortized cost. The Company determined that substantially all of the fair value of the Arbor Agreement was attributable to an in-process research and development asset and no substantive processes were acquired that would constitute a business. The Company concluded that it did not have any alternative future use for the acquired in-process research and development asset and recorded the $30.0 million upfront payment to “Research and development expenses.”

In 2015, the Company entered into a strategic collaboration and license agreement with Parion Sciences, Inc. (“Parion”) focused on the development of investigational epithelial sodium channel (“ENaC”) inhibitors for the potential treatment of CF and all other pulmonary diseases. Parion received a $5.0 million milestone that was recorded as “Research and development expenses” in the three months ended March 31, 2019 and has the potential to receive additional development and regulatory milestones related to the ENaC inhibitors.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Variable Interest Entities (VIEs)

The Company has licensed rights to certain drug candidates from these third-party collaborators, which has resulted in the consolidation of certain third-parties’ financial statements into the Company’s condensed consolidated financial statements as VIEs for certain periods of time. As of December 31, 2018, and continuing through the first quarter of 2019, the Company had no consolidated VIEs reflected in its financial statements.

BioAxone Biosciences, Inc.

In 2014, the Company entered into a license and collaboration agreement (the “BioAxone Agreement”) with BioAxone, which resulted in the consolidation of BioAxone as a VIE beginning in October 2014. The Company made an initial payment to BioAxone of $10.0 million in 2014.

In the three months ended March 31, 2018, the Company recorded net income attributable to noncontrolling interest of $17.0 million, which was primarily related to a $24.0 million increase in the fair value of the contingent payments payable by Vertex to BioAxone due to (i) the expiration of an option held by the Company to purchase BioAxone in the first quarter of 2018 that increased the probability of a $10.0 million license continuation fee for VX-210 (which was ultimately paid in the first quarter of 2018) and (ii) the probability that additional milestone and royalty payments related to the BioAxone Agreement would be paid. Net income attributable to noncontrolling interest also included a $6.4 million benefit from income taxes during the three months ended March 31, 2018 that was primarily related to the increase in the fair value of the contingent payments.

In October 2018, the Company announced it would stop clinical development of VX-210 and terminate the Phase 2b clinical trial of VX-210 based on the recommendation of the clinical trial’s Data Safety Monitoring Board and the Company’s review of interim data from the clinical trial. In December 2018, the Company notified BioAxone of its intent to terminate the BioAxone Agreement and executed a release that immediately allowed BioAxone to control development of its neurological programs other than VX-210 without the Company’s consent. As a result, the Company deconsolidated BioAxone as of December 31, 2018 because it determined that it no longer was the primary beneficiary of BioAxone as it no longer had the power to direct the significant activities of BioAxone. The net impact of the deconsolidation was not material to the Company’s condensed consolidated statement of operations.

Asset Acquisition

Concert Pharmaceuticals

In 2017, the Company acquired certain CF assets including VX-561 (the “Concert Assets”) from Concert Pharmaceuticals Inc. (“Concert”) pursuant to an asset purchase agreement (the “Concert Agreement”). VX-561 is an investigational CFTR potentiator that has the potential to be used as part of combination regimens of CFTR modulators to treat CF. Pursuant to the Concert Agreement, Vertex paid Concert $160.0 million in cash for the Concert Assets, which was recorded to “Research and development expenses” in 2017. If VX-561 is approved as part of a combination regimen to treat CF, Concert could receive up to an additional $90.0 million in milestones based on regulatory approval in the United States and reimbursement in the United Kingdom, Germany or France.

Out-license agreements

The Company has entered into licensing agreements pursuant to which it has out-licensed rights to certain drug candidates to third-party collaborators. Pursuant to these out-license agreements, the Company’s collaborators become responsible for all costs related to the continued development of such drug candidates and obtain development and commercialization rights to these drug candidates. Depending on the terms of the agreements, the Company’s collaborators may be required to make upfront payments, milestone payments upon the achievement of certain product research and development objectives and may also be required to pay royalties on future sales, if any, of commercial products resulting from the collaboration. The termination provisions associated with these collaborations are generally the same as those described above related to the Company’s in-license agreements.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Merck KGaA, Darmstadt, Germany

In January 2017, the Company entered into a strategic collaboration and license agreement (the “Oncology Agreement”) with Merck KGaA, Darmstadt, Germany (the “Licensee”). Pursuant to the Oncology Agreement, the Company granted the Licensee an exclusive worldwide license to research, develop and commercialize four oncology research and development programs including two clinical-stage programs targeting DNA damage repair: its ataxia telangiectasia and Rad3-related protein kinase inhibitor program, or ATR program, including VX-970 and VX-803, and its DNA-dependent protein kinase inhibitor program, or DNA-PK program, including VX-984. In addition, the Company granted the Licensee exclusive, worldwide rights to two pre-clinical programs. The Company recorded the $230.0 million upfront payment related to the Oncology Agreement as “Collaborative and royalty revenues” upon delivery of the license in 2017. The Company’s activities related to the Oncology Agreement were substantially complete in 2017.

In December 2018, the Company entered into an agreement with Merck KGaA, Darmstadt, Germany (the “DNA-PK Agreement”) whereby the Company licensed the two lead Vertex DNA-PK compounds from its DNA-PK program for use in the field of gene integration for six specific indications. In exchange for this exclusive worldwide license to research, develop and commercialize the DNA-PK program for the specified indications within the field of gene integration, the Company made an upfront payment of $65.0 million. Merck KGaA, Darmstadt, Germany has the potential to receive additional milestones, primarily related to approval and reimbursement in various markets, as well as royalties on net product sales.

The Company evaluated the DNA-PK Agreement and concluded it represents a modification of the Oncology Agreement pursuant to ASC 606. As of December 2018, when the Company entered into the DNA-PK Agreement, the Company had completed its obligations under the Oncology Agreement, but the Oncology Agreement was an open contract pursuant to ASC 606 since the Company could receive future royalty payments from the commercialization of the licensed programs under the Oncology Agreement.