UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

|

| |

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2017 |

or |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

|

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2020

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

Commission file number 000-19319

Vertex Pharmaceuticals Incorporated

(Exact name of registrant as specified in its charter)

Massachusetts

(State or other jurisdiction of incorporation or organization)

50 Northern Avenue, Boston, Massachusetts

(Address of principal executive offices)

|

| |

Massachusetts | 04-3039129 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

50 Northern Avenue, Boston, Massachusetts | 02210 |

(Address of principal executive offices) | (Zip Code) |

04-3039129

(I.R.S. Employer Identification No.)

02210

(Zip Code)

Registrant’s telephone number, including area code (617) 341-6100

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, $0.01 Par Value Per Share | | VRTX | | The Nasdaq Global Select Market |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x☒ No o☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x☒ No o☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐ |

| | | |

Large accelerated filer x

| Accelerated filer o

| Non-accelerated filer o

| Smaller reporting company o

|

| | | |

Emerging growth company o

| (Do not check if a smaller reporting company) |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o☐ No x☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

|

| | | | | | | |

| Common Stock, par value $0.01 per share | 252,902,848 |

Class260,467,334 | Outstanding at October 20, 2017July 23, 2020 |

VERTEX PHARMACEUTICALS INCORPORATED

FORM 10-Q

FOR THE QUARTER ENDED SEPTEMBERJune 30, 20172020

TABLE OF CONTENTS

| | | | | | | | |

| | |

| | Page |

| | |

| | |

| | |

| Condensed Consolidated Statements of Operations - Three and NineSix Months Ended SeptemberJune 30, 20172020 and 20162019 | |

| Condensed Consolidated Statements of Comprehensive Income (Loss) - Three and NineSix Months Ended SeptemberJune 30, 20172020 and 20162019 | |

| Condensed Consolidated Balance Sheets - SeptemberJune 30, 20172020 and December 31, 20162019 | |

| Condensed Consolidated Statements of Shareholders' Equity - Three and Noncontrolling Interest - NineSix Months Ended SeptemberJune 30, 20172020 and 20162019 | |

| Condensed Consolidated Statements of Cash Flows - NineThree and Six Months Ended SeptemberJune 30, 20172020 and 20162019 | |

| | |

| | |

| | |

| | |

| | |

| | |

| Item 1A. | | |

| | |

| | |

| | |

| | |

“We,” “us,” “Vertex” and the “Company” as used in this Quarterly Report on Form 10-Q refer to Vertex Pharmaceuticals Incorporated, a Massachusetts corporation, and its subsidiaries.

“Vertex,” “KALYDECO®,” “ORKAMBI®,” “SYMDEKO®,” “SYMKEVI®” and “ORKAMBI“TRIKAFTA®” are registered trademarks of Vertex. The trademark for “KAFTRIOTM” is pending in the United States and registered in the European Union. Other brands, names and trademarks contained in this Quarterly Report on Form 10-Q are the property of their respective owners.

We use the brand name for our products when we refer to the product that has been approved and with respect to the indications on the approved label. Otherwise, including in discussions of our cystic fibrosis development programs, we refer to our compounds by their scientific (or generic) name or VX developmental designation.

Part I. Financial Information

Item 1. Financial Statements

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Operations

(unaudited)

(in thousands, except per share amounts)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Revenues: | | | | | | | |

| Product revenues, net | $ | 549,642 |

| | $ | 409,689 |

| | $ | 1,544,252 |

| | $ | 1,229,750 |

|

| Royalty revenues | 2,231 |

| | 3,835 |

| | 6,643 |

| | 12,713 |

|

| Collaborative revenues | 26,292 |

| | 259 |

| | 286,123 |

| | 1,008 |

|

| Total revenues | 578,165 |

| | 413,783 |

| | 1,837,018 |

| | 1,243,471 |

|

| Costs and expenses: | | | | | | | |

| Cost of product revenues | 72,186 |

| | 53,222 |

| | 188,963 |

| | 147,165 |

|

| Royalty expenses | 688 |

| | 855 |

| | 2,104 |

| | 2,813 |

|

| Research and development expenses | 454,947 |

| | 272,370 |

| | 1,017,961 |

| | 799,238 |

|

| Sales, general and administrative expenses | 120,710 |

| | 106,055 |

| | 361,285 |

| | 322,921 |

|

| Restructuring expenses, net | 337 |

| | 8 |

| | 13,859 |

| | 1,038 |

|

| Intangible asset impairment charge | 255,340 |

| | — |

| | 255,340 |

| | — |

|

| Total costs and expenses | 904,208 |

| | 432,510 |

| | 1,839,512 |

| | 1,273,175 |

|

| Loss from operations | (326,043 | ) | | (18,727 | ) | | (2,494 | ) | | (29,704 | ) |

| Interest expense, net | (13,574 | ) | | (20,140 | ) | | (45,003 | ) | | (60,993 | ) |

| Other (expenses) income, net | (77,553 | ) | | (167 | ) | | (80,634 | ) | | 3,025 |

|

| Loss before (benefit from) provision for income taxes | (417,170 | ) | | (39,034 | ) | | (128,131 | ) | | (87,672 | ) |

| (Benefit from) provision for income taxes | (125,903 | ) | | 503 |

| | (117,581 | ) | | 24,118 |

|

| Net loss | (291,267 | ) | | (39,537 | ) | | (10,550 | ) | | (111,790 | ) |

| Loss (income) attributable to noncontrolling interest | 188,315 |

| | 696 |

| | 173,350 |

| | (33,207 | ) |

| Net (loss) income attributable to Vertex | $ | (102,952 | ) | | $ | (38,841 | ) | | $ | 162,800 |

| | $ | (144,997 | ) |

| | | | | | | | |

| Amounts per share attributable to Vertex common shareholders: | | | | | | | |

| Net (loss) income: | | | | | | | |

| Basic | $ | (0.41 | ) | | $ | (0.16 | ) | | $ | 0.66 |

| | $ | (0.59 | ) |

| Diluted | $ | (0.41 | ) | | $ | (0.16 | ) | | $ | 0.64 |

| | $ | (0.59 | ) |

| Shares used in per share calculations: | | | | | | | |

| Basic | 250,268 |

| | 244,920 |

| | 247,963 |

| | 244,529 |

|

| Diluted | 250,268 |

| | 244,920 |

| | 252,095 |

| | 244,529 |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, | | | | Six Months Ended June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| Revenues: | | | | | | | |

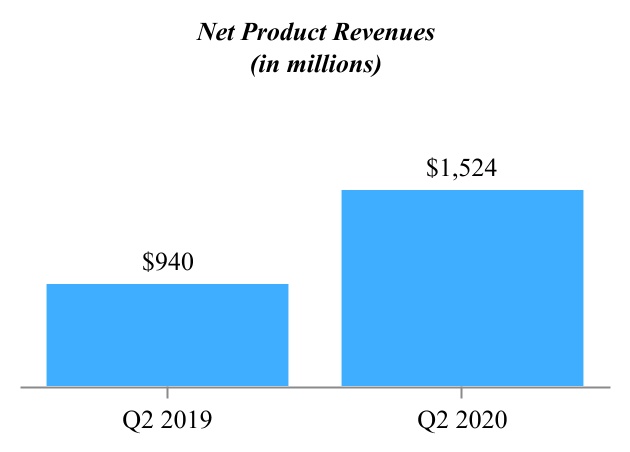

| Product revenues, net | $ | 1,524,485 | | | $ | 940,380 | | | $ | 3,039,592 | | | $ | 1,797,633 | |

| Collaborative and royalty revenues | — | | | 913 | | | — | | | 2,095 | |

| Total revenues | 1,524,485 | | | 941,293 | | | 3,039,592 | | | 1,799,728 | |

| Costs and expenses: | | | | | | | |

| Cost of sales | 184,520 | | | 135,740 | | | 347,017 | | | 230,832 | |

| Research and development expenses | 420,928 | | | 379,091 | | | 869,456 | | | 718,581 | |

| Sales, general and administrative expenses | 191,804 | | | 156,502 | | | 374,062 | | | 303,547 | |

| Change in fair value of contingent consideration | 9,200 | | | — | | | 10,800 | | | — | |

| Total costs and expenses | 806,452 | | | 671,333 | | | 1,601,335 | | | 1,252,960 | |

| Income from operations | 718,033 | | | 269,960 | | | 1,438,257 | | | 546,768 | |

| Interest income | 4,243 | | | 18,076 | | | 16,819 | | | 33,691 | |

| Interest expense | (13,871) | | | (14,837) | | | (28,007) | | | (29,705) | |

| Other income, net | 116,365 | | | 53,939 | | | 55,235 | | | 96,549 | |

| Income before (benefit from) provision for income taxes | 824,770 | | | 327,138 | | | 1,482,304 | | | 647,303 | |

| (Benefit from) provision for income taxes | (12,500) | | | 59,711 | | | 42,281 | | | 111,245 | |

| Net income | $ | 837,270 | | | $ | 267,427 | | | $ | 1,440,023 | | | $ | 536,058 | |

| | | | | | | |

| Net income per common share: | | | | | | | |

| Basic | $ | 3.22 | | | $ | 1.04 | | | $ | 5.54 | | | $ | 2.09 | |

| Diluted | $ | 3.18 | | | $ | 1.03 | | | $ | 5.46 | | | $ | 2.06 | |

| Shares used in per share calculations: | | | | | | | |

| Basic | 259,637 | | | 256,154 | | | 260,013 | | | 255,941 | |

| Diluted | 263,403 | | | 259,822 | | | 263,746 | | | 260,015 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Comprehensive Income (Loss)

(unaudited)

(in thousands)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Net loss | $ | (291,267 | ) | | $ | (39,537 | ) | | $ | (10,550 | ) | | $ | (111,790 | ) |

| Changes in other comprehensive loss: | | | | | | | |

| Unrealized holding gains (losses) on marketable securities, net of tax of zero, respectively | 5,961 |

| | (96 | ) | | (7,786 | ) | | 104 |

|

| Unrealized (losses) gains on foreign currency forward contracts, net of tax of $0.9 million, $0.2 million, $2.9 million and $(0.4) million, respectively | (5,453 | ) | | 2,149 |

| | (27,379 | ) | | 1,936 |

|

| Foreign currency translation adjustment | (3,884 | ) | | (2,508 | ) | | (11,137 | ) | | (7,709 | ) |

| Total changes in other comprehensive loss | (3,376 | ) | | (455 | ) | | (46,302 | ) | | (5,669 | ) |

| Comprehensive loss | (294,643 | ) | | (39,992 | ) | | (56,852 | ) | | (117,459 | ) |

| Comprehensive loss (income) attributable to noncontrolling interest | 188,315 |

| | 696 |

| | 173,350 |

| | (33,207 | ) |

| Comprehensive (loss) income attributable to Vertex | $ | (106,328 | ) | | $ | (39,296 | ) | | $ | 116,498 |

| | $ | (150,666 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, | | | | Six Months Ended June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| Net income | $ | 837,270 | | | $ | 267,427 | | | $ | 1,440,023 | | | $ | 536,058 | |

| Other comprehensive loss: | | | | | | | |

| Unrealized holding gains on marketable securities, net | 2,714 | | | 451 | | | 1,950 | | | 1,047 | |

| Unrealized losses on foreign currency forward contracts, net of tax of $4.7 million, $1.8 million, $(0.3) million and $3.3 million, respectively | (19,680) | | | (5,776) | | | (898) | | | (5,998) | |

| Foreign currency translation adjustment | (10,538) | | | (3,876) | | | (13,200) | | | 1,091 | |

| Total other comprehensive loss | (27,504) | | | (9,201) | | | (12,148) | | | (3,860) | |

| Comprehensive income | $ | 809,766 | | | $ | 258,226 | | | $ | 1,427,875 | | | $ | 532,198 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Balance Sheets

(unaudited)

(in thousands, except share and per share amounts)

| | | | September 30, | | December 31, | | June 30, | | December 31, |

| | 2017 | | 2016 | | 2020 | | 2019 |

| Assets | | | | Assets | | | |

| Current assets: | | | | Current assets: | |

| Cash and cash equivalents | $ | 1,384,966 |

| | $ | 1,183,945 |

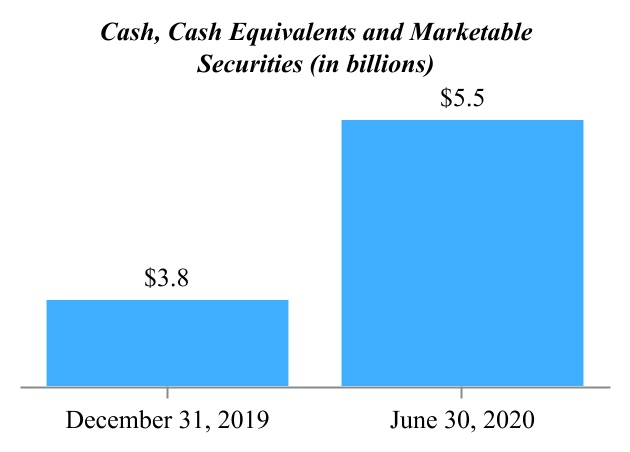

| Cash and cash equivalents | $ | 4,831,332 | | | $ | 3,109,322 | |

| Marketable securities, available for sale | 427,282 |

| | 250,612 |

| |

| Restricted cash and cash equivalents (VIE) | 1,803 |

| | 47,762 |

| |

| Marketable securities | | Marketable securities | 619,437 | | | 698,972 | |

| Accounts receivable, net | 263,493 |

| | 201,083 |

| Accounts receivable, net | 791,768 | | | 633,518 | |

| Inventories | 98,192 |

| | 77,604 |

| Inventories | 219,218 | | | 167,502 | |

| Prepaid expenses and other current assets | 152,238 |

| | 70,534 |

| Prepaid expenses and other current assets | 232,565 | | | 213,515 | |

| Total current assets | 2,327,974 |

| | 1,831,540 |

| Total current assets | 6,694,320 | | | 4,822,829 | |

| Property and equipment, net | 759,978 |

| | 698,362 |

| Property and equipment, net | 728,357 | | | 745,080 | |

| Goodwill | | Goodwill | 1,002,158 | | | 1,002,158 | |

| Intangible assets | 29,000 |

| | 284,340 |

| Intangible assets | 400,000 | | | 400,000 | |

| Goodwill | 50,384 |

| | 50,384 |

| |

| Cost method investments | 20,447 |

| | 20,276 |

| |

| Deferred tax assets | | Deferred tax assets | 1,214,968 | | | 1,190,815 | |

| Other assets | 10,542 |

| | 11,885 |

| Other assets | 176,564 | | | 157,583 | |

| Total assets | $ | 3,198,325 |

| | $ | 2,896,787 |

| Total assets | $ | 10,216,367 | | | $ | 8,318,465 | |

| Liabilities and Shareholders’ Equity | | | | Liabilities and Shareholders’ Equity | | | |

| Current liabilities: | | | | Current liabilities: | |

| Accounts payable | $ | 77,138 |

| | $ | 61,451 |

| Accounts payable | $ | 101,451 | | | $ | 87,610 | |

| Accrued expenses | 378,554 |

| | 315,249 |

| Accrued expenses | 1,545,407 | | | 1,116,912 | |

| Deferred revenues, current portion | 13,003 |

| | 6,005 |

| |

| Accrued restructuring expenses, current portion | 4,205 |

| | 6,047 |

| |

| Capital lease obligations, current portion | 19,881 |

| | 19,426 |

| |

| Customer deposits | 190,272 |

| | 73,416 |

| |

| Credit facility | — |

| | 300,000 |

| |

| Other liabilities, current portion | 27,686 |

| | 10,943 |

| |

| Other current liabilities | | Other current liabilities | 151,782 | | | 130,305 | |

| Total current liabilities | 710,739 |

| | 792,537 |

| Total current liabilities | 1,798,640 | | | 1,334,827 | |

| Deferred revenues, excluding current portion | 2,917 |

| | 6,632 |

| |

| Accrued restructuring expenses, excluding current portion | 146 |

| | 1,907 |

| |

| Capital lease obligations, excluding current portion | 20,259 |

| | 34,976 |

| |

| Deferred tax liability | 10,682 |

| | 134,063 |

| |

| Construction financing lease obligation, excluding current portion | 547,051 |

| | 486,359 |

| |

| Advance from collaborator | 77,258 |

| | 73,423 |

| |

| Other liabilities, excluding current portion | 26,029 |

| | 28,699 |

| |

| Long-term finance lease liabilities | | Long-term finance lease liabilities | 522,067 | | | 538,576 | |

| Long-term contingent consideration | | Long-term contingent consideration | 187,300 | | | 176,500 | |

| Other long-term liabilities | | Other long-term liabilities | 189,118 | | | 183,318 | |

| Total liabilities | 1,395,081 |

| | 1,558,596 |

| Total liabilities | 2,697,125 | | | 2,233,221 | |

| Commitments and contingencies |

|

| |

|

| Commitments and contingencies | — | | | — | |

| Shareholders’ equity: | | | | Shareholders’ equity: | |

| Preferred stock, $0.01 par value; 1,000,000 shares authorized; none issued and outstanding | — |

| | — |

| |

| Common stock, $0.01 par value; 500,000,000 shares authorized; 252,683,346 and 248,300,517 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively | 2,500 |

| | 2,450 |

| |

| Preferred stock, $0.01 par value; 1,000 shares authorized; NaN issued and outstanding | | Preferred stock, $0.01 par value; 1,000 shares authorized; NaN issued and outstanding | — | | | — | |

| Common stock, $0.01 par value; 500,000 shares authorized, 260,124 and 258,993 shares issued and outstanding, respectively | | Common stock, $0.01 par value; 500,000 shares authorized, 260,124 and 258,993 shares issued and outstanding, respectively | 2,601 | | | 2,589 | |

| Additional paid-in capital | 7,034,113 |

| | 6,506,795 |

| Additional paid-in capital | 7,943,717 | | | 7,937,606 | |

| Accumulated other comprehensive (loss) income | (25,129 | ) | | 21,173 |

| |

| Accumulated other comprehensive loss | | Accumulated other comprehensive loss | (14,121) | | | (1,973) | |

| Accumulated deficit | (5,220,407 | ) | | (5,373,836 | ) | Accumulated deficit | (412,955) | | | (1,852,978) | |

| Total Vertex shareholders’ equity | 1,791,077 |

| | 1,156,582 |

| |

| Noncontrolling interest | 12,167 |

| | 181,609 |

| |

| Total shareholders’ equity | 1,803,244 |

| | 1,338,191 |

| Total shareholders’ equity | 7,519,242 | | | 6,085,244 | |

| Total liabilities and shareholders’ equity | $ | 3,198,325 |

| | $ | 2,896,787 |

| Total liabilities and shareholders’ equity | $ | 10,216,367 | | | $ | 8,318,465 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Shareholders’ Equity and Noncontrolling Interest

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional

Paid-in Capital | | Accumulated

Other

Comprehensive (Loss) Income | | Accumulated Deficit | | Total Vertex

Shareholders’ Equity | | Noncontrolling

Interest | | Total

Shareholders’ Equity |

| | Shares | | Amount | | | | | | |

| Balance at December 31, 2015 | 246,307 |

| | $ | 2,427 |

| | $ | 6,197,500 |

| | $ | 1,824 |

| | $ | (5,261,784 | ) | | $ | 939,967 |

| | $ | 153,661 |

| | $ | 1,093,628 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | (5,669 | ) | | — |

| | (5,669 | ) | | — |

| | (5,669 | ) |

| Net (loss) income | — |

| | — |

| | — |

| | — |

| | (144,997 | ) | | (144,997 | ) | | 33,207 |

| | (111,790 | ) |

| Issuance of common stock under benefit plans | 1,722 |

| | 19 |

| | 50,875 |

| | — |

| | — |

| | 50,894 |

| | — |

| | 50,894 |

|

| Stock-based compensation expense | — |

| | — |

| | 181,351 |

| | — |

| | — |

| | 181,351 |

| | (73 | ) | | 181,278 |

|

| Balance at September 30, 2016 | 248,029 |

| | $ | 2,446 |

| | $ | 6,429,726 |

| | $ | (3,845 | ) | | $ | (5,406,781 | ) | | $ | 1,021,546 |

| | $ | 186,795 |

| | $ | 1,208,341 |

|

| | | | | | | | | | | | | | | | |

| Balance at December 31, 2016 | 248,301 |

| | $ | 2,450 |

| | $ | 6,506,795 |

| | $ | 21,173 |

| | $ | (5,373,836 | ) | | $ | 1,156,582 |

| | $ | 181,609 |

| | $ | 1,338,191 |

|

| Cumulative effect adjustment for adoption of new accounting guidance | — |

| | — |

| | 9,371 |

| | | | (9,371 | ) | | — |

| | — |

| | — |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | (46,302 | ) | | — |

| | (46,302 | ) | | — |

| | (46,302 | ) |

| Net income (loss) | — |

| | — |

| | — |

| | — |

| | 162,800 |

| | 162,800 |

| | (173,350 | ) | | (10,550 | ) |

| Issuance of common stock under benefit plans | 4,382 |

| | 50 |

| | 298,956 |

| | — |

| | — |

| | 299,006 |

| | 33 |

| | 299,039 |

|

| Stock-based compensation expense | — |

| | — |

| | 218,991 |

| | — |

| | — |

| | 218,991 |

| | — |

| | 218,991 |

|

| VIE noncontrolling interest upon deconsolidation | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 3,910 |

| | 3,910 |

|

| Other | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (35 | ) | | (35 | ) |

| Balance at September 30, 2017 | 252,683 |

| | $ | 2,500 |

| | $ | 7,034,113 |

| | $ | (25,129 | ) | | $ | (5,220,407 | ) | | $ | 1,791,077 |

| | $ | 12,167 |

| | $ | 1,803,244 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | | | | | | | | | |

| Common Stock | | | | Additional Paid-in Capital | | Accumulated Other Comprehensive Income (Loss) | | Accumulated Deficit | | Total Shareholders’ Equity |

| Shares | | Amount | | | | | | | | |

| Balance at March 31, 2019 | 256,351 | | | $ | 2,561 | | | $ | 7,475,909 | | | $ | 6,000 | | | $ | (2,761,157) | | | $ | 4,723,313 | |

| Other comprehensive loss, net of tax | — | | | — | | | — | | | (9,201) | | | — | | | (9,201) | |

| Net income | — | | | — | | | — | | | — | | | 267,427 | | | 267,427 | |

| Repurchase of common stock | (296) | | | (3) | | | (52,007) | | | — | | | — | | | (52,010) | |

| | | | | | | | | | | |

| Issuance of common stock under benefit plans | 616 | | | 7 | | | 50,494 | | | — | | | — | | | 50,501 | |

| Stock-based compensation expense | — | | | — | | | 89,935 | | | — | | | — | | | 89,935 | |

| Balance at June 30, 2019 | 256,671 | | | $ | 2,565 | | | $ | 7,564,331 | | | $ | (3,201) | | | $ | (2,493,730) | | | $ | 5,069,965 | |

| | | | | | | | | | | |

| Balance at March 31, 2020 | 259,079 | | | $ | 2,591 | | | $ | 7,695,905 | | | $ | 13,383 | | | $ | (1,250,225) | | | $ | 6,461,654 | |

| Other comprehensive loss, net of tax | — | | | — | | | — | | | (27,504) | | | — | | | (27,504) | |

| Net income | — | | | — | | | — | | | — | | | 837,270 | | | 837,270 | |

| | | | | | | | | | | |

| Common stock withheld for employee tax obligations | (11) | | | — | | | (3,080) | | | — | | | — | | | (3,080) | |

| Issuance of common stock under benefit plans | 1,056 | | | 10 | | | 132,771 | | | — | | | — | | | 132,781 | |

| Stock-based compensation expense | — | | | — | | | 118,121 | | | — | | | — | | | 118,121 | |

| Balance at June 30, 2020 | 260,124 | | | $ | 2,601 | | | $ | 7,943,717 | | | $ | (14,121) | | | $ | (412,955) | | | $ | 7,519,242 | |

| | | | | | | | | | | |

| Six Months Ended | | | | | | | | | | |

| Common Stock | | | | Additional

Paid-in Capital | | Accumulated Other Comprehensive Income (Loss) | | Accumulated Deficit | | Total

Shareholders’ Equity |

| Shares | | Amount | | | | | | | | |

| Balance at December 31, 2018 | 255,172 | | | $ | 2,546 | | | $ | 7,421,476 | | | $ | 659 | | | $ | (2,989,478) | | | $ | 4,435,203 | |

| Cumulative effect adjustment for adoption of new accounting guidance | — | | | — | | | — | | | — | | | (40,310) | | | (40,310) | |

| Other comprehensive loss, net of tax | — | | | — | | | — | | | (3,860) | | | — | | | (3,860) | |

| Net income | — | | | — | | | — | | | — | | | 536,058 | | | 536,058 | |

| Repurchase of common stock | (833) | | | (9) | | | (150,008) | | | — | | | — | | | (150,017) | |

| Common stock withheld for employee tax obligations | (27) | | | — | | | (5,832) | | | — | | | — | | | (5,832) | |

| Issuance of common stock under benefit plans | 2,359 | | | 28 | | | 114,517 | | | — | | | — | | | 114,545 | |

| Stock-based compensation expense | — | | | — | | | 184,178 | | | — | | | — | | | 184,178 | |

| Balance at June 30, 2019 | 256,671 | | | $ | 2,565 | | | $ | 7,564,331 | | | $ | (3,201) | | | $ | (2,493,730) | | | $ | 5,069,965 | |

| | | | | | | | | | | |

| Balance at December 31, 2019 | 258,993 | | | $ | 2,589 | | | $ | 7,937,606 | | | $ | (1,973) | | | $ | (1,852,978) | | | $ | 6,085,244 | |

| Other comprehensive loss, net of tax | — | | | — | | | — | | | (12,148) | | | — | | | (12,148) | |

| Net income | — | | | — | | | — | | | — | | | 1,440,023 | | | 1,440,023 | |

| Repurchase of common stock | (1,404) | | | (14) | | | (300,012) | | | — | | | — | | | (300,026) | |

| Common stock withheld for employee tax obligations | (586) | | | (6) | | | (139,241) | | | | | | | (139,247) | |

| Issuance of common stock under benefit plans | 3,121 | | | 32 | | | 210,343 | | | — | | | — | | | 210,375 | |

| Stock-based compensation expense | — | | | — | | | 235,021 | | | — | | | — | | | 235,021 | |

| Balance at June 30, 2020 | 260,124 | | | $ | 2,601 | | | $ | 7,943,717 | | | $ | (14,121) | | | $ | (412,955) | | | $ | 7,519,242 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Condensed Consolidated Statements of Cash Flows

(unaudited)

(in thousands)

|

| | | | | | | |

| | Nine Months Ended September 30, |

| | 2017 | | 2016 |

| Cash flows from operating activities: | | | |

| Net loss | $ | (10,550 | ) | | $ | (111,790 | ) |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

| Stock-based compensation expense | 215,334 |

| | 178,623 |

|

| Depreciation and amortization expense | 44,965 |

| | 45,947 |

|

| Write-downs of inventories to net realizable value | 11,138 |

| | — |

|

| Deferred income taxes | (113,969 | ) | | 23,544 |

|

| Impairment of property and equipment | 1,946 |

| | — |

|

| Intangible asset impairment charge | 255,340 |

| | — |

|

| Acquired in-process research & development | 160,000 |

| | — |

|

| Deconsolidation of VIE | 76,644 |

| | — |

|

| Other non-cash items, net | (4,787 | ) | | (904 | ) |

| Changes in operating assets and liabilities: | | | |

| Accounts receivable, net | (54,455 | ) | | (9,760 | ) |

| Inventories | (28,570 | ) | | (11,536 | ) |

| Prepaid expenses and other assets | (90,006 | ) | | (8,979 | ) |

| Accounts payable | 6,925 |

| | (21,532 | ) |

| Accrued expenses and other liabilities | 148,102 |

| | 26,121 |

|

| Accrued restructuring expense | (3,863 | ) | | (8,151 | ) |

| Deferred revenues | 3,237 |

| | (10,204 | ) |

| Net cash provided by operating activities | 617,431 |

| | 91,379 |

|

| Cash flows from investing activities: | | | |

| Purchases of marketable securities | (431,653 | ) | | (616,625 | ) |

| Maturities of marketable securities | 247,149 |

| | 535,379 |

|

| Expenditures for property and equipment | (56,817 | ) | | (41,775 | ) |

| Purchase of in-process research & development | (160,000 | ) | | — |

|

| (Decrease) increase in restricted cash and cash equivalents (VIE) | (15,643 | ) | | 20,490 |

|

| Investment in equity securities | — |

| | (23,075 | ) |

| Decrease (increase) in other assets | 380 |

| | (93 | ) |

| Net cash used in investing activities | (416,584 | ) | | (125,699 | ) |

| Cash flows from financing activities: | | | |

| Issuances of common stock under benefit plans | 298,205 |

| | 51,165 |

|

| Payments on revolving credit facility | (300,000 | ) | | — |

|

| Advance from collaborator | 10,000 |

| | — |

|

| Payments on capital lease obligations | (14,188 | ) | | (13,330 | ) |

| Proceeds from capital lease financing | — |

| | 2,030 |

|

| Payments on construction financing lease obligation | (412 | ) | | (356 | ) |

| Proceeds related to construction financing lease obligation | 4,700 |

|

| — |

|

| Repayments of advanced funding | (3,132 | ) | | — |

|

| Net cash (used in) provided by financing activities | (4,827 | ) | | 39,509 |

|

| Effect of changes in exchange rates on cash | 5,001 |

| | (265 | ) |

| Net increase in cash and cash equivalents | 201,021 |

| | 4,924 |

|

| Cash and cash equivalents—beginning of period | 1,183,945 |

| | 714,768 |

|

| Cash and cash equivalents—end of period | $ | 1,384,966 |

| | $ | 719,692 |

|

| | | | |

| Supplemental disclosure of cash flow information: | | | |

| Cash paid for interest | $ | 51,990 |

| | $ | 64,662 |

|

| Cash paid for income taxes | $ | 4,154 |

| | $ | 1,617 |

|

| Capitalization of costs related to construction financing lease obligation | $ | 33,827 |

| | $ | 824 |

|

| Issuances of common stock from employee benefit plans receivable | $ | 868 |

| | $ | 19 |

|

| | | | | | | | | | | |

| Six Months Ended June 30, | | |

| 2020 | | 2019 |

| Cash flows from operating activities: | | | |

| Net income | $ | 1,440,023 | | | $ | 536,058 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | |

| Stock-based compensation expense | 232,895 | | | 183,478 | |

| Depreciation expense | 53,518 | | | 54,838 | |

| Increase in fair value of contingent consideration | 10,800 | | | — | |

| Deferred income taxes | 8,963 | | | 87,358 | |

| Gains on equity securities | (65,116) | | | (100,078) | |

| Other non-cash items, net | 16,307 | | | 6,006 | |

| Changes in operating assets and liabilities: | | | |

| Accounts receivable, net | (164,139) | | | (55,870) | |

| Inventories | (64,386) | | | (25,174) | |

| Prepaid expenses and other assets | (28,923) | | | (17,580) | |

| Accounts payable | 14,697 | | | (28,074) | |

| Accrued expenses | 369,851 | | | 113,968 | |

| Other liabilities | 29,735 | | | 33,603 | |

| Net cash provided by operating activities | 1,854,225 | | | 788,533 | |

| Cash flows from investing activities: | | | |

| Purchases of available-for-sale debt securities | (126,577) | | | (263,636) | |

| Maturities of available-for-sale debt securities | 145,395 | | | 228,707 | |

| Sale of equity securities | 127,874 | | | — | |

| Expenditures for property and equipment | (37,314) | | | (34,399) | |

| Investment in equity securities | (5,800) | | | (20,000) | |

| Net cash provided by (used in) investing activities | 103,578 | | | (89,328) | |

| Cash flows from financing activities: | | | |

| Issuances of common stock under benefit plans | 213,058 | | | 114,092 | |

| Repurchases of common stock | (300,026) | | | (150,017) | |

| Payments in connection with common stock withheld for employee tax obligations | (139,247) | | | (5,832) | |

| Payments on finance leases | (20,730) | | | (18,926) | |

| Proceeds related to finance leases | 5,833 | | | 1,002 | |

| Advance from collaborator | 3,500 | | | 7,500 | |

| Repayments of advanced funding | (1,793) | | | (2,823) | |

| Net cash used in financing activities | (239,405) | | | (55,004) | |

| Effect of changes in exchange rates on cash | (3,379) | | | (808) | |

| Net increase in cash and cash equivalents | 1,715,019 | | | 643,393 | |

| Cash, cash equivalents and restricted cash—beginning of period | 3,120,681 | | | 2,658,253 | |

| Cash, cash equivalents and restricted cash—end of period | $ | 4,835,700 | | | $ | 3,301,646 | |

| | | |

| Supplemental disclosure of cash flow information: | | | |

| Cash paid for interest | $ | 27,347 | | | $ | 27,109 | |

| Cash paid for income taxes | $ | 36,813 | | | $ | 10,902 | |

| Issuances of common stock from employee benefit plans receivable | $ | 137 | | | $ | 539 | |

| | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

A.Basis of Presentation and Accounting Policies

Basis of Presentation

The accompanying condensed consolidated financial statements are unaudited and have been prepared by Vertex Pharmaceuticals Incorporated (“Vertex” or the “Company”) in accordance with accounting principles generally accepted in the United States of America (“GAAP”).

The condensed consolidated financial statements reflect the operations of (i) the Company (ii)and its wholly-owned subsidiaries and (iii) consolidated variable interest entities (VIEs).subsidiaries. All material intercompany balances and transactions have been eliminated. The Company operates in one1 segment, pharmaceuticals. As of September 30, 2017, the Company deconsolidated Parion Sciences, Inc. (“Parion”), a VIE theThe Company has reclassified certain items from the prior year’s condensed consolidated since 2015. The Company's consolidated balance sheet as of September 30, 2017 excludes Parion. Please referfinancial statements to Note C, “Collaborative Arrangements and Acquisitions” for further information regardingconform to the deconsolidation of Parion.current year’s presentation.

Certain information and footnote disclosures normally included in the Company’s annual financial statements2019 Annual Report on Form 10-K have been condensed or omitted. These interim financial statements, in the opinion of management, reflect all normal recurring adjustments necessary for a fair presentation of the financial position and results of operations for the interim periods ended SeptemberJune 30, 20172020 and 2016.2019.

The results of operations for the interim periods are not necessarily indicative of the results of operations to be expected for the full fiscal year. These interim financial statements should be read in conjunction with the audited financial statements for the year ended December 31, 2016,2019, which are contained in the Company’s 2019 Annual Report on Form 10-K for the year ended December 31, 2016 that was filed with the Securities and Exchange Commission (the “SEC”) on February 23, 2017 (the “2016 Annual Report on Form 10-K”).10-K.

Use of Estimates and Summary of Significant Accounting Policies

The preparation of condensed consolidated financial statements in accordance with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements, and the amounts of revenues and expenses during the reported periods. Significant estimates in these condensed consolidated financial statements have been made in connection with (i) determining the calculationtransaction price of revenues inventories, research and development expenses, stock-based compensation expense, restructuring expense, the fair value of(ii) accounting for intangible assets goodwill,and contingent consideration, noncontrolling interest, the consolidation and deconsolidation of VIEs, leases, the fair value of cash flow hedges and the provision for or benefit from income taxes.consideration. The Company bases its estimates on historical experience and various other assumptions, including in certain circumstances future projections that management believes to be reasonable under the circumstances. Actual results could differ from those estimates. Changes in estimates are reflected in reported results in the period in which they become known.

The Company’s significantRecently Adopted Accounting Standards

Leases

On January 1, 2019, the Company adopted Accounting Standards Codification (“ASC”) 842, Leases (“ASC 842”) using the modified-retrospective method, which amended a number of aspects of lease accounting policies are described in Note A, “Natureand required the Company to recognize right-of-use assets and liabilities on the balance sheet. As of Business and Accounting Policies,” inJanuary 1, 2019, the 2016 Annual Report on Form 10-K.Company recorded a cumulative effect adjustment to increase its “Accumulated deficit” by $40.3 million, which related to its leases that were accounted for as build-to-suit leases under the previous accounting guidance.

Recent Accounting PronouncementsInternal-Use Software

In 2014,2018, the Financial Accounting Standards Board (“FASB”) issued new guidance applicable to revenue recognition that will beAccounting Standards Update (“ASU”) 2018-15, Intangibles—Goodwill and Other—Internal-Use Software (Subtopic 350-40): Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract (“ASU 2018-15”), which clarifies the accounting for implementation costs in cloud computing arrangements. ASU 2018-15 became effective on January 1, 2018. Early2020. The adoption was permitted for the year-ending December 31, 2017. The new guidance applies a more principles based approach to recognizing revenue. Under the new guidance, revenue is recognized when a customer obtains control of promised goods or services and is recognizedASU 2018-15 resulted in an insignificant amount that reflects the consideration that an entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The new guidance must be adopted using either a modified retrospective approach or a full retrospective approach for all periods presented. Under the modified retrospective method, the cumulative effect of applying the standard would be recognized at the date of initial application within retained earnings. Under the full retrospective approach, the standard would be applied to each prior reporting period presented. Upon adoption, the Company will use the modified retrospective method. The Company continues to evaluate the new guidance and the effect the adoption will haveadditional assets recorded on the Company’s condensed consolidated financial

balance sheet.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Fair Value Measurement

statements.In 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”), which modifies the disclosure requirements for fair value measurements. ASU 2018-13 became effective on January 1, 2020. The Company’s project team is finalizing its reviewadoption of existing customer contracts and current accounting policiesASU 2018-13 resulted in additional disclosures related to identify and assess the potential differences that would result from applying the requirements of the new standard. Based on the Company’s assessment performedLevel 3 inputs. Please refer to date, the new revenue recognition guidance could impact the Company’s accountingNote E, “Fair Value Measurements,” for product shipments to certain countries through early access programs, including the French early access programs, whereby the associated product has received regulatory approval but the price is not fixed or determinable based on the status of ongoing pricing discussions, and could impact the Company’s accounting for certain reimbursement agreements that the Company plans to negotiate in the fourth quarter of 2017. As the Company completes its assessment, it is implementing appropriate changes to its controls to support revenue recognition and additional revenue-related disclosures under the new standard.further information.

Credit Losses

In 2016, the FASB issued amended guidance applicableASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”), which requires entities to share-based compensationrecord expected credit losses for certain financial instruments, including trade receivables, as an allowance that reflects the entity's current estimate of credit losses expected to employees thatbe incurred. For available-for-sale debt securities in unrealized loss positions, ASU 2016-13 requires allowances to be recorded instead of reducing the amortized cost of the investment. ASU 2016-13 became effective on January 1, 2020. The adoption of ASU 2016-13 did not have a significant impact on the Company’s condensed consolidated financial statements.

Recently Issued Accounting Standards

Income Taxes

In 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740) (“ASU 2019-12”), which simplifies the accounting for employee share-based payment transactions, including the accounting for income taxes, forfeitures, and statutory tax withholding requirements, as well as classification in the statement of cash flows. The amended guidance becametaxes. ASU 2019-12 is effective for the Company during the first quarter of 2017. The amended guidance eliminates the requirement that excess tax benefits be realized as a reduction in current taxes payable before the associated tax benefit can be recognized as an increase in additional paid-in capital. This created approximately $410.8 million of deferred tax asset (“DTA”) relating to federal and state net operating losses (“NOLs”) that are fully reserved by an equal increase in valuation allowance. The Company recorded DTAs of approximately $404.7 million relating to Federal NOLs and approximately $6.1 million relating to State NOLs, both of which are offset by a full valuation allowance. Upon adoption, the Company also elected to change its accounting policy to account for forfeitures of options and awards as they occur. The change was applied on a modified retrospective basis with a cumulative effect adjustment to the Company’s accumulated deficit of $9.4 million, which increased the accumulated deficit as of January 1, 2017. This change also resulted in an increase to the DTA of $3.4 million, which is offset by a full valuation allowance. As a result, there was no cumulative-effect adjustment to accumulated deficit. The provisions related to the recognition of excess tax benefits in the income statement and classification in the statement of cash flows were adopted prospectively, and as such, the prior periods were not retrospectively adjusted.

In 2016, the FASB issued amended guidance related to the recording of financial assets and financial liabilities. Under the amended guidance, equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) are to be measured at fair value with changes in fair value recognized in net income. However, an entity has the option to either measure equity investments without readily determinable fair values at fair value or at cost adjusted for changes in observable prices minus impairment. Changes in measurement under either alternative will be recognized in net income. The amended guidance is effective for the year ending December 31, 2018. Early adoption is permitted. The Company expects the implementation of this standard to have an impact on its consolidated financial statements and related disclosures, as the Company held publicly traded equity investments as of September 30, 2017 as well as equity investments accounted for under the cost method. A cumulative-effect adjustment to the balance sheet will be recorded as of the beginning of the fiscal year of adoption. The implementation of this amended guidance is expected to increase volatility in net income as the volatility currently recorded in other comprehensive income related to changes in the fair market value of available-for-sale equity investments will be reflected in net income after adoption.

In 2016, the FASB issued amended guidance applicable to leases that will be effective for the year ending December 31, 2019. Early adoption is permitted. This guidance requires entities to recognize assets and liabilities for leases with lease terms of more than 12 months on the balance sheet.2021. The Company is inevaluating the processimpact the adoption of evaluating this guidance and determining the expected effectASU 2019-12 may have on its condensed consolidated financial statements.

In 2016, the FASB issued amended guidance related to intra-entity transfers other than inventory. This guidance removes the current exception in GAAP prohibiting entities from recognizing current and deferred income tax expenses or benefits related to transfer of assets, other than inventory, within the consolidated entity. The current exception to defer the recognition of any tax impact on the transfer of inventory within the consolidated entity until it is sold to a third party remains unaffected. The amended guidance is effective for the year ending December 31, 2018. Early adoption is permitted. The Company is in the process of evaluating this guidance and determining the expected effect on its condensed consolidated financial statements.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

In 2017, the FASB issued amended guidance related to business combinations. The amended guidance clarifies the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The new accounting guidance is effective for annual periods beginning after December 15, 2017, including interim periods within those periods. Early adoption is permitted. The Company early adopted this new guidance as of January 1, 2017 and will apply this new guidance to future acquisitions.

In 2017, the FASB issued amended guidance related to measurements of goodwill. The amended guidance eliminates a step from the goodwill impairment test. Under the amended guidance, an entity should perform its annual or interim goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity would recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. The amended guidance is effective for the year-ending December 31, 2020. Early adoption is permitted. The Company does not expect a significant effect on its condensed consolidated financial statements upon adoption of this new guidance.

In 2017, the FASB issued amended guidance related to the scope of stock option modification accounting, to reduce diversity in practice and provide clarity regarding existing guidance. The new accounting guidance is effective for annual periods beginning after December 15, 2017, including interim periods within those periods. Early adoption is permitted. The Company does not expect the adoption of this guidance to have a material effect on its condensed consolidated financial statements and related disclosures.

In 2017, the FASB issued amended guidance applicable to hedge accounting. The new accounting guidance is effective for annual periods beginning after December 15, 2018, including interim periods within those periods. Early adoption is permitted. The amended guidance helps simplify certain aspects of hedge accounting and enables entities to more accurately present their risk management activities in their financial statements. The Company is in the process of evaluating this guidance and determining the expected effect on its condensed consolidated financial statements.

For a discussion of other recent accounting pronouncements please refer to Note A, “Nature of Business and Accounting Policies—Recent Accounting Pronouncements,Policies,” in the 2016Company’s 2019 Annual Report on Form 10-K.

Summary of Significant Accounting Policies

The Company sells its products principally to a limited number of specialty pharmacy providers in North America as well as government-owned and supported customers in international markets (collectively, its “Customers”). The Company’s Customers in North America subsequently resell the products to patients and health care providers. The Company recognizes net revenues from product sales upon delivery to the Customer as long as (i) there is persuasive evidence that an arrangement exists between the Company and the Customer, (ii) collectibility is reasonably assured and (iii) the price is fixed or determinable.

In order to conclude that the price is fixed or determinable, the Company must be able to (i) calculate its gross product revenues from sales to Customers and (ii) reasonably estimate its net product revenues upon delivery to its Customers’ locations. The Company calculates gross product revenues based on the price that the Company charges its Customers. The Company estimates its net product revenues by deducting from its gross product revenues (a) trade allowances, such as invoice discounts for prompt payment and Customer fees, (b) estimated government and private payor rebates, chargebacks and discounts, (c) estimated reserves for expected product returns and (d) estimated costs of co-pay assistance programs for patients, as well as other incentives for certain indirect customers.

The Company makes significant estimates and judgments that materially affect the Company’s recognition of net product revenues. In certain instances, the Company may be unable to reasonably conclude that the price is fixed or determinable at the time of delivery, in which case it defers the recognition of revenues. Once the Company is able to determine that the price is fixed or determinable, it recognizes the net product revenues associated with the units in which revenue recognition was deferred.

Revenue recognition related to the Company’s French early access programs could be impacted by the new revenue recognition guidance that is effective January 1, 2018 andaccounting policies are described in Note A, “Basis“Nature of PresentationBusiness and Accounting Policies,” in its 2019 Annual Report on Form 10-K.

B.Revenue Recognition

Disaggregation of Revenue

Revenues by Product

Product revenues, net consisted of the following:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, | | | | Six Months Ended June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (in thousands) | | | | | | |

| TRIKAFTA | $ | 917,715 | | | $ | — | | | $ | 1,812,948 | | | $ | — | |

| SYMDEKO/SYMKEVI | 171,729 | | | 361,832 | | | 344,888 | | | 682,107 | |

| ORKAMBI | 231,981 | | | 316,441 | | | 466,119 | | | 609,448 | |

| KALYDECO | 203,060 | | | 262,107 | | | 415,637 | | | 506,078 | |

Total product revenues, net* | $ | 1,524,485 | | | $ | 940,380 | | | $ | 3,039,592 | | | $ | 1,797,633 | |

* The preceding table does not include collaborative and royalty revenues.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Revenues by Geographic Location

Policies”. The Company’s ORKAMBI netNet product revenues are attributed to date do not include any revenues from product sales in France because the price is not fixed or determinable. The Company began distributing ORKAMBI through early access programs in France during the fourth quarter of 2015. As of September 30, 2017, the Company’s condensed consolidated balance sheet includes $190.3 million collected in France related to shipments of ORKAMBI under the early access programs that is classified as Customer deposits. The Company expects that the difference between the amounts collectedcountries based on the invoiced price and the final price for ORKAMBI in France will be returned to the French government.

If the Company concludes as of December 31, 2017 that the pricelocation of the ORKAMBI supplied under the early access programs is fixed or determinable based on, among other factors, the status of negotiations in France, it would record net productcustomer. Collaborative and royalty revenues for all sales since the inception of the early access programs for ORKAMBIare attributed to countries based on the fixed or determinable pricelocation of the Company’s subsidiary associated with the collaborative arrangement related to such revenues. Total revenues from external customers and collaborators by geographic region consisted of the following:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, | | | | Six Months Ended June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (in thousands) | | | | | | |

| United States | $ | 1,210,314 | | | $ | 700,618 | | | $ | 2,397,902 | | | $ | 1,341,721 | |

| Outside of the United States | | | | | | | |

| Europe | 257,681 | | | 180,196 | | | 515,072 | | | 347,947 | |

| Other | 56,490 | | | 60,479 | | | 126,618 | | | 110,060 | |

| Total revenues outside of the United States | 314,171 | | | 240,675 | | | 641,690 | | | 458,007 | |

| Total revenues | $ | 1,524,485 | | | $ | 941,293 | | | $ | 3,039,592 | | | $ | 1,799,728 | |

Contract Liabilities

The Company recorded contract liabilities of $70.7 million and $62.3 million as of June 30, 2020 and December 31, 2019, respectively, related to annual contracts with government-owned and supported customers in international markets that limit the fourth quarteramount of 2017.

Ifannual reimbursement the Company concludescan receive. Upon exceeding the annual reimbursement amount, products are provided free of charge, which is a material right. These contracts include upfront payments and fees. The Company defers a portion of the consideration received for shipments made up to the annual reimbursement limit as a portion of “Other current liabilities.” The deferred amount is recognized as revenue when the free products are shipped. The Company’s product revenue contracts include performance obligations that are one year or less.

The Company’s contract liabilities at the priceend of each fiscal year relate to contracts with annual reimbursement limits in international markets in which the annual period associated with the contract is not fixed or determinablethe same as of December 31, 2017,the Company’s fiscal year. In these amounts would be subjectmarkets, the Company recognizes revenues related to performance obligations satisfied in previous years; however, these revenues do not relate to any performance obligations that were satisfied more than 12 months prior to the beginning of the current year.

C.Collaborative Arrangements

The Company has entered into numerous agreements pursuant to which it collaborates with third parties on research, development and commercialization programs, including in-license and out-license agreements.

The Company’s in-license and out-license agreements that had a significant impact on its financial statements for the three and six months ended June 30, 2020 and 2019, or were new guidance applicableduring the three and six months ended June 30, 2020, are described below. Additional in-license and out-license agreements were described in Note B, “Collaborative Arrangements,” of the Company’s 2019 Annual Report on Form 10-K.

In-license Agreements

The Company has entered into a number of license agreements in order to revenue recognition effective January 1, 2018 usingadvance and obtain access to technologies and services related to its research and early-development activities. The Company is generally required to make an upfront payment upon execution of the modified retrospective adoption approach. license agreement; development, regulatory and commercialization milestones payments upon the achievement of certain product research, development and commercialization objectives; and royalty payments on future sales, if any, of commercial products resulting from the collaboration.

Pursuant to the new guidance,terms of its in-license agreements, the Company’s collaborators typically lead the discovery efforts and the Company would record a cumulative effect adjustment toleads all preclinical, development and commercialization activities associated with the Company’s accumulated deficit in the first quarteradvancement of 2018. The amount of the adjustment to accumulated deficit would be determined based upon (i) the status of pricing discussions in France upon adoptionany drug candidates and (ii) the Company’s estimate of the amount of consideration the Company expects to retain related to the French ORKAMBI sales that occurred on or prior to December 31, 2017 that would not be subject to a significant reversal in amounts recognized. For French ORKAMBI sales after December 31, 2017 under the early access programs, the Company would recognize product revenues based on the Company’s estimate of consideration the Company expects to retain for which it is probable that a significant reversal in amounts recognized will not occur. In future periods, if the Company’s estimates regarding the amounts it will receive for ORKAMBI supplied pursuant to these programs change, the effect of the change in estimates would be reflected in net product revenues in the period in which the change in estimate occurred.

The following table summarizes activity in each of the product revenue allowance and reserve categories for the nine months ended September 30, 2017: |

| | | | | | | | | | | | | | | | | | | |

| | Trade

Allowances | | Rebates,

Chargebacks

and Discounts | | Product

Returns | | Other

Incentives | | Total |

| | (in thousands) |

| Balance at December 31, 2016 | $ | 2,568 |

| | $ | 81,927 |

| | $ | 3,492 |

| | $ | 1,214 |

| | $ | 89,201 |

|

| Provision related to current period sales | 18,776 |

| | 118,592 |

| | 3,603 |

| | 12,238 |

| | 153,209 |

|

| Adjustments related to prior period sales | (188 | ) | | (4,327 | ) | | (13 | ) | | (355 | ) | | (4,883 | ) |

| Credits/payments made | (18,409 | ) | | (97,393 | ) | | (1,809 | ) | | (10,021 | ) | | (127,632 | ) |

| Balance at September 30, 2017 | $ | 2,747 |

| | $ | 98,799 |

| | $ | 5,273 |

| | $ | 3,076 |

| | $ | 109,895 |

|

funds all expenses.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

| |

C. | Collaborative Arrangements and Acquisitions |

Cystic Fibrosis Foundation Therapeutics Incorporated

The Company typically can terminate its in-license agreements by providing advance notice to its collaborators; the required length of notice is dependent on whether any product developed under the license agreement has received marketing approval. The Company’s license agreements may be terminated by either party for a research, development and commercialization agreement with Cystic Fibrosis Foundation Therapeutics Incorporated (“CFFT”) that was originally entered into in May 2004, and was most recently amended in October 2016 (the “2016 Amendment”). Pursuant to the agreement, as amended, the Company has agreed to pay royalties ranging from low-single digits to mid-single digits on potential sales of certain compounds first synthesized and/or tested between March 1, 2014 and August 31, 2016 and tiered royalties ranging from single digits to sub-teens on any approved drugs first synthesized and/or tested during a research term on or before February 28, 2014, including (i) KALYDECO (ivacaftor) and ORKAMBI (lumacaftor in combination with ivacaftor), which are the Company’s current products and (ii) tezacaftor in combination with ivacaftor. For combination products, such as ORKAMBI, sales will be allocated equally to each of the active pharmaceutical ingredients in the combination product.

In the first quarter of 2016, CFFT earned a commercial milestone payment of $13.9 million from the Company upon achievement of certain sales levels of lumacaftor. There are no additional commercial milestone payments payablematerial breach by the Companyother, subject to CFFT pursuant tonotice and cure provisions. Unless earlier terminated, these license agreements generally remain in effect until the agreement. Pursuant todate on which the 2016 Amendment, the CFFT provided the Company an upfront program award of $75.0 million and agreed to provide development funding to the Company of up to $6.0 million annually. The program award plus any future development funding represent a form of financing pursuant to Accounting Standards Codification (ASC) 730, Research and Development, and thus the amounts are recorded as a liability on the condensed consolidated balance sheet, primarily reflected in Advance from collaborator. The liability is reduced over the estimated royalty term of the agreement. Reductionsand all payment obligations with respect to all products in the liability are reflected as an offset to cost of product revenues and as interest expense.

The Company has royalty obligations to CFFT for ivacaftor, lumacaftor and tezacaftor until the expiration of patents covering those compounds. The Company has patents in the United States and European Union covering the composition-of-matter of ivacaftor that expire in 2027 and 2025, respectively, subject to potential patent extensions. The Company has patents in the United States and European Union covering the composition-of-matter of lumacaftor that expire in 2030 and 2026, respectively, subject to potential extension. The Company has patents in the United States and European Union covering the composition-of-matter of tezacaftor that expire in 2027 and 2028, respectively, subject to potential extension.all countries have expired.

CRISPR Therapeutics AG

In 2015, the Company entered into a strategic collaboration, option and license agreement (the “CRISPR Agreement”) with CRISPR Therapeutics AG and its affiliates (“CRISPR”) to collaborate on the discovery and development of potential new treatments aimed at the underlying genetic causes of human diseases using CRISPR-Cas9 gene editinggene-editing technology. The Company hashad the exclusive right to license upcertain targets. In the fourth quarter of 2019, the Company elected to six CRISPR-Cas9-basedexclusively license 3 targets, including targets for the potential treatment of sickle cell disease. In connection with the CRISPR Agreement, the Company made an upfront payment to CRISPR of $75.0 million and a $30.0 million investment in CRISPR pursuant to a convertible loan agreement that converted into preferred stock in January 2016. The Company expensed $75.0 million to research and development, and the $30.0 million investment was recorded at cost and was classified as a long-term asset on the Company’s condensed consolidated balance sheets. In the second quarter of 2016, the Company made an additional preferred stock investment in CRISPR of approximately $3.1 million. In connection with CRISPR’s initial public offering in October 2016, the Company purchased $10.0 million of common shares at the public offering price and the Company’s preferred stock investments in CRISPR converted into common shares. As of September 30, 2017, the Company recorded the fair value of its investment in CRISPR common shares of $56.9 million in marketable securities and a $13.7 million unrealized gain related to these common shares in accumulated other comprehensive income (loss) on the condensed consolidated balance sheet.

The Company will fund all of the discovery activities conductedcystic fibrosis, pursuant to the CRISPR Agreement. For potential hemoglobinapathy treatments, including treatments for sickle cell disease,each of the Company and CRISPR will share equally all development costs and worldwide revenues. For other3 targets that the Company electselected to license, the Company would lead all development and global commercialization activities. For each of up to six targets that the Company elects to license, other than hemoglobinapathy targets, CRISPR has the potential to receive up to $420.0an additional $410.0 million in development, regulatory and commercial milestones andas well as royalties on net product sales.

In 2017, the Company entered into a co-development and co-commercialization agreement with CRISPR pursuant to the terms of the CRISPR Agreement, under which the Company and CRISPR are co-developing and will co-commercialize CTX001 (the “CTX001 Co-Co Agreement”) for the treatment of hemoglobinopathies, including treatments for sickle cell disease and beta thalassemia. As part of the collaboration, the Company and CRISPR share equally all development costs and potential worldwide revenues related to potential hemoglobinopathy treatments. The Company concluded that the CTX001 Co-Co Agreement is a cost-sharing arrangement, which results in the net impact of the arrangement being recorded in “Research and development expenses” in its condensed consolidated statements of operations. During the three and six months ended June 30, 2020, the net expense related to the CTX001 Co-Co Agreement was $9.8 million and $19.0 million, respectively. During the three and six months ended June 30, 2019, the net expense related to the CTX001 Co-Co Agreement was $7.5 million and $14.6 million, respectively.

In July 2019, the Company entered into a separate strategic collaboration and license agreement (the “CRISPR DMD/DM1 Agreement”) with CRISPR. Pursuant to this agreement, the Company received an exclusive worldwide license to CRISPR’s existing and future intellectual property for Duchenne muscular dystrophy (“DMD”) and myotonic dystrophy type 1 (“DM1”). In the first quarter of 2020, the Company recorded $25.0 million to “Research and development expenses” related to a pre-clinical milestone earned by CRISPR under the CRISPR DMD/DM1 Agreement. CRISPR has the potential to receive up to an additional $800.0 million in research, development, regulatory and commercial milestones for the DMD and DM1 programs as well as royalties on net product sales. CRISPR has the option to co-develop and co-commercialize all DM1 products globally and forego the milestones and royalties associated with the DM1 program. The Company funds all expenses associated with the collaboration except for research costs for specified guide RNA research conducted by CRISPR, which the Company and CRISPR share equally.

Please refer to Note F, “Marketable Securities and Equity Investments,” for further information regarding the Company’s investment in CRISPR’s common stock.

Out-license Agreements

The Company has entered into licensing agreements pursuant to which it has out-licensed rights to certain drug candidates to third-party collaborators. Pursuant to these out-license agreements, the Company’s collaborators become responsible for all costs related to the continued development of such drug candidates and obtain development and commercialization rights to these drug candidates. Depending on the terms of the agreements, the Company’s collaborators may be required to make upfront payments, milestone payments upon the achievement of certain product research and development objectives and may also be required to pay royalties on future sales, if any, of commercial products resulting from the collaboration. The termination provisions associated with these collaborations are generally the same as those described above related to the Company’s in-license agreements. None of the Company’s out-license agreements had a significant impact on the Company’s condensed consolidated statement of operations during the three and six months ended June 30, 2020 and 2019.

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Cystic Fibrosis Foundation

The Company may terminate the CRISPR Agreement upon 90 days’ notice to CRISPR prior to any product receiving marketing approval or upon 270 days’ notice afterhas a product has received marketing approval. The CRISPR Agreement also may be terminated by either party for a material breach by the other, subject to noticeresearch, development and cure provisions. Unless earlier terminated, the CRISPR Agreement will continue in effect until the expiration of the Company’s payment obligations under the CRISPR Agreement.

Merck KGaA

On January 10, 2017, the Companycommercialization agreement that was originally entered into a strategic collaboration and licensein 2004 with the Cystic Fibrosis Foundation (“CFF”), as successor in interest to the Cystic Fibrosis Foundation Therapeutics, Inc. This agreement (the “Merck KGaA Agreement”) with Merck KGaA, Darmstadt, Germany (“Merck KGaA”).was most recently amended in 2016. Pursuant to the Merck KGaA Agreement,agreement, as amended, the Company granted Merck KGaA an exclusive worldwide licenseagreed to research, develop and commercialize four oncology research and development programs. Under the Merck KGaA Agreement, the Company granted Merck KGaA exclusive, worldwide rightspay royalties ranging from low-single digits to two clinical-stage programs targeting DNA damage repair: its ataxia telangiectasia and Rad3-related protein inhibitor program, including VX-970 and VX-803, and its DNA-dependent protein kinase inhibitor program, including VX-984. In addition, the Company granted Merck KGaA exclusive, worldwide rights to two pre-clinical programs.

The Merck KGaA Agreement provided for an upfront payment from Merck KGaA to the Company of $230.0 million. During the first quarter of 2017, the Company received $193.6 million of the upfront payment and the remaining $36.4 million was remitted to the German tax authorities. Pursuant to a tax treaty between the United States and Germany, the Company filed a refund application for the tax withholding and expects to receive the refund in the fourth quarter of 2017. The income tax receivable is included in Prepaid expenses and other current assets at September 30, 2017. In addition to the upfront payment, the Company will receive tiered royaltiesmid-single digits on potential sales of licensed products, calculated as a percentage of net sales, that rangecertain compounds first synthesized and/or tested between March 1, 2014 and August 31, 2016, including elexacaftor, and tiered royalties ranging from (i) mid-singlesingle digits to mid-twenties for clinical-stage programssub-teens on covered compounds first synthesized and/or tested during a research term on or before February 28, 2014, including KALYDECO (ivacaftor), ORKAMBI (lumacaftor in combination with ivacaftor) and (ii) mid-single digitsSYMDEKO/SYMKEVI (tezacaftor in combination with ivacaftor). For combination products, such as ORKAMBI, SYMDEKO/SYMKEVI and TRIKAFTA (elexacaftor/tezacaftor/ivacaftor and ivacaftor), sales are allocated equally to high single digits foreach of the pre-clinical research programs. Merck KGaA has assumed full responsibility for development and commercialization costs for all programs.

The Company evaluated the deliverables, primarily consisting of a license to the four programs and the obligation to complete certain fully-reimbursable research and development and transition activities as directed by Merck KGaA, pursuant to the Merck KGaA Agreement, under the multiple element arrangement accounting guidance. The Company concluded that the license has stand-alone value from the research and development and transition activities based on the resources and know-how possessed by Merck KGaA, and thus concluded that there are two units of accountingactive pharmaceutical ingredients in the arrangement. The Company determined the relative selling price of the units of accounting based on the Company’s best estimate of selling price. The Company utilized key assumptions to determine the best estimate of selling price for the license, which included future potential net sales of licensed products, development timelines, reimbursement rates for personnel costs, discount rates, and estimated third-party development costs. The Company utilized a discounted cash flow model to determine its best estimate of selling price for the license and determined the best estimate of selling price for the research and development and transition activities based on what it would sell the services for separately. Based on this analysis, the Company recognized approximately $231.7 million in collaborative revenues related to the upfront payment upon delivery of the license and to the research and development and transition activities provided during the first quarter of 2017. During the three and nine months ended September 30, 2017, the Company recorded the reimbursement for the research and development and transition activities of $5.2 million and $12.8 million, respectively, as revenue in the Company’s consolidated statements of operations primarily due to the fact that the Company is the primary obligor in the arrangement. The Company is providing research and development and transition activities and will recognize the revenues and associated expenses as the services are provided.combination product.

Merck KGaA may terminate the Merck KGaA Agreement or any individual program by providing 90 days’ notice, or, in the case of termination of a program with a product that has received marketing approval, 180 days’ notice. The Merck KGaA Agreement also may be terminated by either party for a material breach by the other party, subject to notice and cure provisions. Unless earlier terminated, the Merck KGaA Agreement will continue in effect until the date on which the royalty term and all payment obligations with respect to all products in all countries have expired.

D.Earnings Per Share

VERTEX PHARMACEUTICALS INCORPORATED

Notes to Condensed Consolidated Financial Statements

(unaudited)

Variable Interest Entities

The Company has entered into several agreements pursuant to which it has licensed rights to certain drug candidates from third-party collaborators, resulting in the consolidation of the third parties’ financial statements into the Company’s condensed consolidated financial statements as VIEs. In order to account for the fair value of the contingent payments, which consist of milestone, royalty and option payments, related to these collaborations under GAAP, the Company uses present-value models based on assumptions regarding the probability of achieving the relevant milestones, estimates regarding the timing of achieving the milestones, estimates of future product sales and the appropriate discount rates. The Company bases its estimate of the probability of achieving the relevant milestones on industry data for similar assets and its own experience. The discount rates used in the valuation model represent a measure of credit risk and market risk associated with settling the liabilities. Significant judgment is used in determining the appropriateness of these assumptions at each reporting period. Changes in these assumptions could have a material effect on the fair value of the contingent payments. The following collaborations are reflected in the Company’s financial statements as consolidated VIEs for portions or all of the periods presented:

Parion Sciences, Inc.

In June 2015, the Company entered into a strategic collaboration and license agreement (the “Parion Agreement”) with Parion. Pursuant to the agreement, the Company is collaborating with Parion to develop investigational epithelial sodium channel (“ENaC”) inhibitors, including VX-371 (formerly P-1037) and VX-551 (formerly P-1055), for the potential treatment of CF and all other pulmonary diseases. The Company is leading development activities for VX-371 and VX-551 and is responsible for all costs, subject to certain exceptions, related to development and commercialization of the compounds.