UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________

FORM 10-Q

_____________________________

(Mark One)

|

| |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 20182019

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-11356

Radian Group Inc.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 23-2691170 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | |

| 1500 Market Street, Philadelphia, PA | | 19102 |

| (Address of principal executive offices) | | (Zip Code) |

(215) 231-1000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | |

Large accelerated filer x | | Accelerated filer o | | Non-accelerated filer o | | Smaller reporting company o | Emerging growth company o |

| | | | (Do not check if a smaller reporting company) | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.001 par value per share | RDN | New York Stock Exchange |

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 214,621,425208,020,528 shares of common stock, $0.001 par value per share, outstanding on May 4, 2018.6, 2019.

|

| | |

| TABLE OF CONTENTS | |

| | | Page Number |

| |

| |

| |

| Item 1. | | |

| | | |

| | |

| | | |

| | |

| | | |

| | | |

| | |

| | | |

| | |

| | | |

| | | |

| | | |

| | |

| | | |

| | |

| | |

| | |

| | | |

| | | |

| | |

| | |

| | |

| | | |

| | |

| | |

| | |

| | | |

| | |

| | |

| | |

| | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 6. | | |

| | | |

| |

GLOSSARY OF ABBREVIATIONS AND ACRONYMS

The following list defines various abbreviations and acronyms used throughout this report, including the Condensed Consolidated Financial Statements, the Notes to Unaudited Condensed Consolidated Financial Statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

| |

| Term | Definition |

| 2014 Master Policy | Radian Guaranty’s master insurance policy, setting forth the terms and conditions of our mortgage insurance coverage, which became effective October 1, 2014 |

2016 Single Premium QSR TransactionAgreement | Quota share reinsurance agreement entered into with a panel of third-party reinsurance providers in the first quarter of 2016 and subsequently amended in the fourth quarter of 2017 |

2017 Form 10-K | Annual Report on Form 10-K for the year ended December 31, 2017 |

2018 Single Premium QSR TransactionAgreement | Quota share reinsurance agreement entered into with a panel of third-party reinsurance providers in October 2017 to cede a portion of Single Premium NIW beginning January 1, 2018 |

| ABS | Asset-backed securities |

| Alt-A | Alternative-A loans, representing loans for which the underwriting documentation is generally limited as compared to fully documented loans (considered a non-prime loan grade) |

| Available Assets | As defined in the PMIERs, assets primarily including the liquid assets of a mortgage insurer, and reduced by premiums received but not yet earned |

| Back-end | With respect to credit risk transfer programs established by the GSEs, policies written on loans that are already part of an existing GSE portfolio, as contrasted with loans that are to be purchased by the GSEs in the future |

BofA Settlement Agreement | The Confidential Settlement Agreement and Release dated September 16, 2014, by and among Radian Guaranty and Countrywide Home Loans, Inc. and Bank of America, N.A., as a successor to BofA Home Loan Servicing f/k/a Countrywide Home Loan Servicing LP, entered into in order to resolve various actual and potential claims or disputes as to mortgage insurance coverage on the specific population of loans covered by the agreement |

| Borrower | With respect to our securities lending agreements, the third-party institutions to which we loan certain securities in our investment portfolio for short periods of time |

| CCF | Conservatorship Capital Framework |

| Claim Curtailment | Our legal right, under certain conditions, to reduce the amount of a claim, including due to servicer negligence |

| Claim Denial | Our legal right, under certain conditions, to deny a claim |

| Claim Severity | The total claim amount paid divided by the original coverage amount |

| Clayton | Clayton Holdings LLC, a Delaware domiciled indirect non-insurance subsidiary of Radian Group |

| Clayton Intercompany Note | A $300 million note payable from Radian Mortgage Services Inc. (formerly Clayton Group Holdings Inc.) to Radian Group (with terms consistent with the terms of our Senior Notes due 2019 that were used to fund our purchase of Clayton) |

| CMBS | Commercial mortgage-backed securities |

Convertible Senior Notes due 2017 | Our 3.000% convertible unsecured senior notes due November 2017 ($450 million original principal amount) |

Convertible Senior Notes due 2019 | Our 2.250% convertible unsecured senior notes due March 2019 ($400 million original principal amount) |

| Cures | Loans that were in default as of the beginning of a period and are no longer in default because payments were received such that the loan is no longer 60 or more days past due |

| Default to Claim Rate | The percentage of defaulted loans that are assumed to result in a claim |

Deficiency AmountEagle Re 2018-1 | The assessed tax liabilities, penalties and interest associated with a formal Notice of Deficiency from the IRSEagle Re 2018-1 Ltd., an unaffiliated special purpose reinsurer (a VIE) domiciled in Bermuda |

Discrete Item(s)Eagle Re 2019-1 | For tax calculation purposes, certain items that are required to be accounted forEagle Re 2019-1 Ltd., an unaffiliated special purpose reinsurer (a VIE) domiciled in the provision for income taxes as they occur and are not considered a component of the estimated annualized effective tax rate for purposes of reporting interim results. Generally, these are items that are: (i) clearly defined (such as changes in tax rate or tax law); (ii) infrequent or unusual in nature; or (iii) gains or losses that are not a component of continuing operating income, such as income from discontinued operations or losses reflected as a component of other comprehensive income. These items impact the difference between the statutory rate and Radian’s effective tax rate.Bermuda |

| EnTitle Direct | EnTitle Direct Group, Inc., a wholly-owned subsidiary of Radian Group, acquired in March 2018 |

| EnTitle Insurance | EnTitle Insurance Company, a wholly-ownedan Ohio domiciled insurance subsidiary of EnTitle Direct |

|

| Excess-of-Loss Program | |

Term | DefinitionThe credit risk protection obtained by Radian Guaranty in November 2018, including: (i) the excess-of-loss reinsurance agreement with Eagle Re 2018-1, in connection with the issuance by Eagle Re 2018-1 of mortgage insurance-linked notes, and (ii) a separate excess-of-loss reinsurance agreement with a third-party reinsurer. Excess-of-loss reinsurance is a type of reinsurance that indemnifies the ceding company against loss in excess of a specific agreed limit, up to a specified sum. Effective in April 2019, it also includes the new credit risk protection obtained through an excess-of-loss reinsurance agreement with Eagle Re 2019-1. |

| Exchange Act | Securities Exchange Act of 1934, as amended |

Extraordinary DividendDistribution | A dividend or distribution of capital that is required to be approved by an insurance company’s primary regulator that is greater than would be permitted as an ordinary dividend whichdistribution (which does not require regulatory approvalapproval) |

|

| |

| Term | Definition |

| Fannie Mae | Federal National Mortgage Association |

| FASB | Financial Accounting Standards Board |

| FEMA | Federal Emergency Management Agency, an agency of the U.S. Department of Homeland Security |

| FEMA Designated Area | Generally, an area that has been subject to a disaster, designated by FEMA as an individual assistance disaster area for the purpose of determining eligibility for various forms of federal assistance |

| FHA | Federal Housing Administration |

| FHFA | Federal Housing Finance Agency |

| FHLB | Federal Home Loan Bank of Pittsburgh |

| FICO | Fair Isaac Corporation (“FICO”) credit scores, for Radian’s portfolio statistics, represent the borrower’s credit score at origination and, in circumstances where there is more than one borrower,are multiple borrowers, the lowest of the borrowers’ FICO score for the primary borrowerscores is utilized |

Flow BasisFive Bridges | With respect to mortgage insurance, includes mortgage insurance policies that are written on an individual loan basis as each loan is originated or on an aggregated basis (in which each individual loanFive Bridges Advisors, LLC. Radian acquired the assets of Five Bridges in a group of loans is insured in a single transaction, typically shortly after the loans have been originated). Among other items, Flow Basis business excludes Pool Insurance, which we originated prior to 2009.December 2018 |

| Foreclosure Stage Default | The Stage of Default indicating that the foreclosure sale has been scheduled or held |

| Freddie Mac | Federal Home Loan Mortgage Corporation |

| Front-end | With respect to credit risk transfer programs established by the GSEs, policies written on loans that are to be purchased by the GSEs in the future, as contrasted with loans that are already part of an existing GSE portfolio |

| GAAP | AccountingGenerally accepted accounting principles generally accepted in the U.S., as amended from time to time |

| Green River Capital | Green River Capital LLC, a wholly-owned subsidiary of Clayton |

GSEsGSE(s) | Government-Sponsored Enterprises (Fannie Mae and Freddie Mac) |

| HARP | Home Affordable Refinance Program |

| IBNR | Losses incurred but not reported |

| IIF | Insurance in force, equal to the aggregate unpaid principal balances of the underlying loans |

| Independent Settlement Services | Independent Settlement Services, LLC, a subsidiary of Radian Group, acquired in November 2018 |

| IRC | Internal Revenue Code of 1986, as amended |

| IRS | Internal Revenue Service |

| IRS Matter | Our dispute with the IRS that we settled and fully resolved in the second quarter of 2018 that was related to the Deficiency Amountassessed tax liabilities, penalties and interest from the IRS’s examination of our 2000 through 2007 consolidated federal income tax returns. See Note 9 of Notes to Unaudited Condensed Consolidated Financial Statements for more information. |

JCT | Congressional Joint Committee on Taxation |

| LAE | Loss adjustment expenses, which include the cost of investigating and adjusting losses and paying claims |

Legacy Portfolio | Mortgage insurance written during the poor underwriting years of 2005 through 2008, together with business written prior to 2005 |

| Loss Mitigation Activity/Activities | Activities such as Rescissions, Claim Denials, Claim Curtailments and cancellations |

| LTV | Loan-to-value ratio, calculated as the percentage of the original loan amount to the original value of the property |

| Master Policies | The Prior Master Policy and the 2014 Master Policy, collectivelytogether |

| Minimum Required Assets | A risk-based minimum required asset amount, as defined in the PMIERs, calculated based on net RIF (RIF, net of credits permitted for reinsurance) and a variety of measures related to expected credit performance and other factors |

|

| |

Term | Definition |

| Model Act | Mortgage Guaranty InsurersInsurance Model Act, as issued by the NAIC to establish minimum capital and surplus requirements for mortgage insurers |

| Monthly and Other Recurring Premiums (or Recurring Premium Policies) | Insurance premiums or policies, respectively, where premiums are paid on a monthly or other installment basis, in contrast to Single Premium Policies |

|

| |

| Term | Definition |

| Monthly Premium Policies | Insurance policies where premiums are paid on a monthly installment basis |

| Moody’s | Moody’s Investors Service |

| Mortgage Insurance | Radian’s Mortgage Insurancemortgage insurance business segment, which provides credit-related insurance coverage, principally through private mortgage insurance on residential first-lien mortgage loans, as well as other credit risk management solutions to mortgage lending institutions nationwideand mortgage credit investors |

| MPP Requirement | Certain states’ statutory or regulatory risk-based capital requirement that the mortgage insurer must maintain a minimum policyholder position, which is calculated based on both risk and surplus levels |

| NAIC | National Association of Insurance Commissioners |

| NIW | New insurance written |

| NOL | Net operating loss; for tax purposes, accumulated during years a company reported more tax deductions than taxable income. NOLs may be carried back or carried forward a certain number of years, depending on each jurisdiction, thus reducingvarious factors which can reduce a company’s tax liability |

Notices of Deficiency | Formal letters from the IRS informing the taxpayer of an IRS determination of tax deficiency and appeal rights |

OCI | Other comprehensive income (loss)liability. |

| Persistency Rate | The percentage of insurance in forceIIF that remains in force over a period of time |

| PMIERs | Private Mortgage Insurer Eligibility Requirements effective on December 31, 2015, issued by the GSEs under oversight of the FHFA to set forth requirements an approved insurer must meet and maintain to provide mortgage guaranty insurance on loans acquired by the GSEs |

| PMIERs 1.0 | The original PMIERs effective on December 31, 2015 |

| PMIERs 2.0 | The revised PMIERs issued by the GSEs on September 27, 2018, which became effective on March 31, 2019 |

| Pool Insurance | Pool Insurance differs from primary insurance in that our maximum liability is not limited to a specific coverage percentage on an individual mortgage loan. Instead, an aggregate exposure limit, or “stop loss,” is applied to the initial aggregate loan balance on a group or “pool” of mortgages |

Post-legacy | The time period subsequent to 2008 |

Post-legacy Portfolio | Mortgage insurance on loans written subsequent to 2008mortgages. |

| Prior Master Policy | Radian Guaranty’s master insurance policy, setting forth the terms and conditions of our mortgage insurance coverage, which was in effect prior to the effective date of itsthe 2014 Master Policy |

QSR TransactionsProgram | The quota share reinsurance agreements entered into with a third-party reinsurance provider in the second and fourth quarters of 2012, collectively |

| Radian | Radian Group Inc. together with its consolidated subsidiaries |

| Radian Group | Radian Group Inc. |

| Radian Guaranty | Radian Guaranty Inc., a Pennsylvania domiciled insurance subsidiary of Radian Group |

| Radian Reinsurance | Radian Reinsurance Inc., a Pennsylvania domiciled insurance subsidiary of Radian Group |

| Radian Settlement Services | Radian Settlement Services Inc., a subsidiary of Clayton, formerly known as ValuAmerica, Inc. |

| RBC States | Risk-based capital states, which are those states that currently impose a statutory or regulatory risk-based capital requirement |

| Red Bell | Red Bell Real Estate, LLC, a wholly-owned subsidiary of Clayton |

| Reinstatements | Reversals of previous Rescissions, Claim Denials and Claim Curtailments |

| REMIC | Real Estate Mortgage Investment Conduit |

| REO | Real estate owned |

| Rescission | Our legal right, under certain conditions, to unilaterally rescind coverage on our mortgage insurance policies if we determine that a loan did not qualify for insurance |

| RIF | Risk in force; for primary insurance, RIF is equal to the underlying loan unpaid principal balance multiplied by the insurance coverage percentage, whereas for Pool Insurance, it represents the remaining exposure under the agreements |

| Risk-to-capital | Under certain state regulations, a maximum ratio of net RIF calculated relative to the level of statutory capital |

| RMBS | Residential mortgage-backed securities |

|

| |

| Term | Definition |

Risk-to-capital | Under certain state regulations, a minimum ratio of statutory capital calculated relative to the level of net RIF |

RMBS | Residential mortgage-backed securities |

| S&P | Standard & Poor’s Financial Services LLC |

SAB 118 | Staff Accounting Bulletin No. 118, “Income Tax Accounting Implications of the Tax Cuts and Jobs Act,” issued by the SEC staff in December 2017 |

| SAPP | Statutory accounting principles and practices, includeincluding those required or permitted, if applicable, by the insurance departments of the respective states of domicile of our insurance subsidiaries |

| SEC | United States Securities and Exchange Commission |

Senior Notes due 2017 | Our 9.000% unsecured senior notes due June 2017 ($195.5 million original principal amount, of which the remaining outstanding principal was redeemed in August 2016) |

| Senior Notes due 2019 | Our 5.500% unsecured senior notes due June 2019 ($300 million original principal amount) |

| Senior Notes due 2020 | Our 5.250% unsecured senior notes due June 2020 ($350 million original principal amount) |

| Senior Notes due 2021 | Our 7.000% unsecured senior notes due March 2021 ($350 million original principal amount) |

| Senior Notes due 2024 | Our 4.500% unsecured senior notes due October 2024 ($450 million original principal amount) |

| Services | Radian’s Services business segment, which is primarily a fee-for-service business that offers a broad array of both mortgage, and real estate and title services to market participants across the mortgage and real estate value chain |

Single Premium NIW (or IIF)/ RIF / IIF | New insurance writtenNIW, RIF or insurance in force,IIF, respectively, on Single Premium Policies |

Single Premium Policy/Policy / Policies | Insurance policies where premiums are paid in a single payment, andwhich includes policies written on an individual basis (as each loan is originated) and on an aggregated basis (in which each individual loan in a group of loans is insured in a single transaction, typically shortly after the loans have been originated) |

Single Premium QSR TransactionsProgram | The 2016 Single Premium QSR TransactionAgreement and the 2018 Single Premium QSR Transaction, collectivelyAgreement, together |

| Stage of Default | The stage a loan is in relative to the foreclosure process, based on whether a foreclosure sale has been scheduled or held |

| Statutory RBC Requirement | Risk-based capital requirement imposed by the RBC States, requiring a minimum surplus level and, in certain states, a minimum ratio of statutory capital relative to the level of risk |

| Surplus Note | An intercompany 0.000% surplus note issued by Radian Guaranty to Radian Group |

TCJA | H.R. 1, known as the Tax Cuts and Jobs Act, signed into law on December 22, 2017 |

| Time in Default | The time period from the point a loan reaches default status (based on the month the default occurred) to the current reporting date |

| U.S. | The United States of America |

| U.S. Treasury | United States Department of the Treasury |

| VA | U.S. Department of Veterans Affairs |

ValuAmericaVIE | ValuAmerica, Inc., a wholly-owned subsidiary of ClaytonVariable interest entity |

Cautionary Note Regarding Forward-Looking Statements—Safe Harbor Provisions

All statements in this report that address events, developments or results that we expect or anticipate may occur in the future are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Exchange Act and the U.S. Private Securities Litigation Reform Act of 1995. In most cases, forward-looking statements may be identified by words such as “anticipate,” “may,” “will,” “could,” “should,” “would,” “expect,” “intend,” “plan,” “goal,” “contemplate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “seek,” “strategy,” “future,” “likely” or the negative or other variations on these words and other similar expressions. These statements, which may include, without limitation, projections regarding our future performance and financial condition, are made on the basis of management’s current views and assumptions with respect to future events. Any forward-looking statement is not a guarantee of future performance and actual results could differ materially from those contained in the forward-looking statement. These statements speak only as of the date they were made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. We operate in a changing environment where new risks emerge from time to time and it is not possible for us to predict all risks that may affect us. The forward-looking statements, as well as our prospects as a whole, are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in the forward-looking statements. These risks and uncertainties include, without limitation:

changes in economic and political conditions that impact the size of the insurable market, the credit performance of our insured portfolio, and our business prospects;

changes in the way customers, investors, ratings agencies, regulators or legislators perceive our performance, financial strength and future prospects;

Radian Guaranty’s ability to remain eligible under the PMIERs and other applicable requirements imposed by the FHFA and by the GSEs to insure loans purchased by the GSEs;GSEs, including potential future changes to the PMIERs which, among other things, may be impacted by the general economic environment and housing market, as well as the proposed CCF that would establish capital requirements for the GSEs, if the CCF is finalized;

our ability to successfully execute and implement our capital plans, including our risk distribution strategy through the capital markets and reinsurance markets, and to maintain sufficient holding company liquidity to meet our short- and long-term liquidity needs;

our ability to successfully execute and implement our business plans and strategies, including plans and strategies to reposition and grow our Services segment as well as plans and strategies that require GSE and/or regulatory approvals and licenses;

our ability to maintain an adequate level of capital in our insurance subsidiaries to satisfy existing and future state regulatory requirements;

changes in the charters or business practices of, or rules or regulations imposed by or applicable to, the GSEs, including:which may include changes imposed byin the FHFA that impactrequirements to remain an approved insurer to the GSEs’ business prospects;GSEs, the GSEs’ interpretation and application of the PMIERs, as well as changes impacting loans purchased by the GSEs, such as the GSEs’ requirements regarding mortgage credit and the proposed changes to the PMIERs;loan size and the GSEs’ use of alternative forms of credit enhancement;pricing;

changes in the current housing finance system in the U.S., including the role of the FHA, the GSEs and private mortgage insurers in this system;

any disruption in the servicing of mortgages covered by our insurance policies, as well as poor servicer performance;

a significant decrease in the Persistency Rates of our mortgage insurance on monthly premium products;

competition in our mortgage insurance business, including price competition and competition from the FHA and VA as well as from other forms of credit enhancement;enhancement, including GSE sponsored alternatives to traditional mortgage insurance;

the effect of the Dodd-Frank Wall Street Reform and Consumer Protection Act on the financial services industry in general, and on our businesses in particular;particular, including future changes to the Qualified Mortgage (QM) loan requirements;

legislative and regulatory activity (or inactivity), including the adoption of (or failure to adopt) new laws and regulations, or changes in existing laws and regulations, or the way they are interpreted or applied, including interpretations and guidance pertaining to recently enacted tax reform legislation;applied;

legal and regulatory claims, assertions, actions, reviews, audits, inquiries and investigations that could result in adverse judgments, settlements, fines, injunctions, restitutions or other relief that could require significant expenditures, increased reserves or have other effects on our business;

the amount and timing of potential settlements, payments or adjustments associated with federal or other tax examinations, including the IRS matter;

examinations;

the possibility that we may fail to estimate accurately the likelihood, magnitude and timing of losses in establishing loss reserves for our mortgage insurance business or to accurately calculate and/or project our Available Assets and Minimum Required Assets under the PMIERs, which will be impacted by, among other things, the size and mix of our IIF, the level of defaults in assessing our ability to comply withportfolio, the proposed PMIERs when implemented;level of cash flow generated by our insurance operations and our risk distribution strategies;

volatility in our financial results of operations caused by changes in the fair value of our assets and liabilities, including a significant portion of our investment portfolio, and potential volatility in our Available Assets if proposed changes to the PMIERs requiring us to mark certain of our Available Assets to fair value were to become effective;portfolio;

potential future impairment charges related to our goodwill and other acquired intangible assets, and uncertainties regarding our ability to execute our restructuring plans within expected costs;assets;

changes in GAAP or SAPP rules and guidance, or their interpretation;

our ability to attract and retain key employees; and

legal and other limitations on dividends and other amounts we may receive from our subsidiaries.subsidiaries, including dividends or ordinary course distributions under our internal tax- and expense-sharing arrangements.

For more information regarding these risks and uncertainties as well as certain additional risks that we face, you should refer to the Risk Factors detailed in Item 1A of our 2017Annual Report on Form 10-K for the year ended December 31, 2018, and to subsequent reports filed from time to time with the SEC. We caution you not to place undue reliance on these forward-looking statements, which are current only as of the date on which we issued this report. We do not intend to, and we disclaim any duty or obligation to, update or revise any forward-looking statements to reflect new information or future events or for any other reason.

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

Radian Group Inc.

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED) | | | ($ in thousands, except per-share amounts) | March 31,

2018 | | December 31,

2017 | March 31,

2019 | | December 31,

2018 |

| | | | | | | |

| Assets | | | | | | |

| Investments (Note 5) | | | | | | |

| Fixed-maturities available for sale—at fair value (amortized cost $3,594,591 and $3,426,217) | $ | 3,554,734 |

| | $ | 3,458,719 |

| |

| Fixed-maturities available for sale—at fair value (amortized cost $3,875,919 and $4,098,962) | | $ | 3,897,584 |

| | $ | 4,021,575 |

|

| Trading securities—at fair value | 563,377 |

| | 606,401 |

| 383,992 |

| | 469,071 |

|

| Equity securities—at fair value (at December 31, 2017, classified as available for sale with related cost of $163,106) | 111,032 |

| | 162,830 |

| |

| Short-term investments—at fair value (includes $39,077 and $19,357 of reinvested cash collateral held under securities lending agreements) | 435,756 |

| | 415,658 |

| |

| Other invested assets—at fair value (amortized cost at December 31, 2017) | 3,318 |

| | 334 |

| |

| Equity securities—at fair value (cost of $125,153 and $139,377) | | 125,025 |

| | 130,565 |

|

| Short-term investments—at fair value (includes $6,233 and $11,699 of reinvested cash collateral held under securities lending agreements) | | 1,066,110 |

| | 528,403 |

|

| Other invested assets—at fair value | | 3,059 |

| | 3,415 |

|

| Total investments | 4,668,217 |

| | 4,643,942 |

| 5,475,770 |

| | 5,153,029 |

|

| Cash | 122,481 |

| | 80,569 |

| 118,668 |

| | 95,393 |

|

| Restricted cash | 7,623 |

| | 15,675 |

| 9,086 |

| | 11,609 |

|

| Accounts and notes receivable | 80,068 |

| | 72,558 |

| 89,237 |

| | 78,652 |

|

| Deferred income taxes, net (Note 9) | 253,381 |

| | 229,567 |

| 67,697 |

| | 131,643 |

|

| Goodwill and other intangible assets, net (Note 6) | 61,465 |

| | 64,212 |

| |

| Goodwill and other acquired intangible assets, net (Note 6) | | 56,811 |

| | 58,998 |

|

| Prepaid reinsurance premium | 390,241 |

| | 386,509 |

| 408,622 |

| | 417,628 |

|

| Other assets (Note 8) | 426,773 |

| | 407,849 |

| 373,678 |

| | 367,700 |

|

| Total assets | $ | 6,010,249 |

| | $ | 5,900,881 |

| $ | 6,599,569 |

| | $ | 6,314,652 |

|

| | | | | | | |

| Liabilities and Stockholders’ Equity | | | | | | |

| Unearned premiums | $ | 723,100 |

| | $ | 723,938 |

| $ | 720,159 |

| | $ | 739,357 |

|

| Reserve for losses and loss adjustment expense (“LAE”) (Note 10) | 488,656 |

| | 507,588 |

| |

| Reserve for losses and loss adjustment expense (Note 10) | | 388,784 |

| | 401,361 |

|

| Senior notes (Note 11) | 1,027,875 |

| | 1,027,074 |

| 1,031,197 |

| | 1,030,348 |

|

| Reinsurance funds withheld | 305,409 |

| | 288,398 |

| 329,868 |

| | 321,212 |

|

| Other liabilities (Note 12) | 412,793 |

| | 353,845 |

| 419,470 |

| | 333,659 |

|

| Total liabilities | 2,957,833 |

| | 2,900,843 |

| 2,889,478 |

| | 2,825,937 |

|

| Commitments and contingencies (Note 13) |

| |

|

| |

|

| Stockholders’ equity | | | | | | |

| Common stock: par value $0.001 per share; 485,000,000 shares authorized at March 31, 2018 and December 31, 2017; 233,160,146 and 233,416,989 shares issued at March 31, 2018 and December 31, 2017, respectively; 215,542,607 and 215,814,188 shares outstanding at March 31, 2018 and December 31, 2017, respectively | 233 |

| | 233 |

| |

| Treasury stock, at cost: 17,617,539 and 17,602,801 shares at March 31, 2018 and December 31, 2017, respectively | (894,191 | ) | | (893,888 | ) | |

| Common stock: par value $0.001 per share; 485,000 shares authorized at March 31, 2019 and December 31, 2018; 229,817 and 231,132 shares issued at March 31, 2019 and December 31, 2018, respectively; 212,136 and 213,473 shares outstanding at March 31, 2019 and December 31, 2018, respectively | | 230 |

| | 231 |

|

| Treasury stock, at cost: 17,681 and 17,660 shares at March 31, 2019 and December 31, 2018, respectively | | (895,321 | ) | | (894,870 | ) |

| Additional paid-in capital | 2,748,233 |

| | 2,754,275 |

| 2,697,724 |

| | 2,724,733 |

|

| Retained earnings | 1,229,616 |

| | 1,116,333 |

| 1,889,964 |

| | 1,719,541 |

|

| Accumulated other comprehensive income (loss) (Note 15) | (31,475 | ) | | 23,085 |

| 17,494 |

| | (60,920 | ) |

| Total stockholders’ equity | 3,052,416 |

| | 3,000,038 |

| 3,710,091 |

| | 3,488,715 |

|

| Total liabilities and stockholders’ equity | $ | 6,010,249 |

| | $ | 5,900,881 |

| $ | 6,599,569 |

| | $ | 6,314,652 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| | | | Three Months Ended

March 31, | Three Months Ended

March 31, |

| (In thousands, except per-share amounts) | 2018 |

| 2017 | 2019 |

| 2018 |

| Revenues: | | | | | | |

| Net premiums earned—insurance | $ | 242,550 |

|

| $ | 221,800 |

| $ | 263,512 |

|

| $ | 242,550 |

|

| Services revenue | 33,164 |

|

| 38,027 |

| 32,753 |

|

| 33,164 |

|

| Net investment income | 33,956 |

| | 31,032 |

| 43,847 |

| | 33,956 |

|

| Net gains (losses) on investments and other financial instruments | (18,887 | ) | | (2,851 | ) | 21,913 |

| | (18,887 | ) |

| Other income | 807 |

| | 746 |

| 1,604 |

| | 807 |

|

| Total revenues | 291,590 |

| | 288,754 |

| 363,629 |

| | 291,590 |

|

| Expenses: | | | | | | |

| Provision for losses | 37,283 |

| | 46,913 |

| 20,754 |

| | 37,283 |

|

| Policy acquisition costs | 7,117 |

| | 6,729 |

| 5,893 |

| | 7,117 |

|

| Cost of services | 23,126 |

| | 28,375 |

| 24,157 |

| | 23,126 |

|

| Other operating expenses | 63,243 |

| | 68,377 |

| 78,805 |

| | 63,243 |

|

| Restructuring and other exit costs (Note 1) | 551 |

| | — |

| |

| Restructuring and other exit costs | | — |

| | 551 |

|

| Interest expense | 15,080 |

| | 15,938 |

| 15,697 |

| | 15,080 |

|

| Loss on induced conversion and debt extinguishment | — |

| | 4,456 |

| |

| Amortization and impairment of other intangible assets | 2,748 |

|

| 3,296 |

| |

| Amortization and impairment of other acquired intangible assets | | 2,187 |

|

| 2,748 |

|

| Total expenses | 149,148 |

| | 174,084 |

| 147,493 |

| | 149,148 |

|

| Pretax income | 142,442 |

|

| 114,670 |

| 216,136 |

|

| 142,442 |

|

| Income tax provision | 27,956 |

| | 38,198 |

| 45,179 |

| | 27,956 |

|

| Net income | $ | 114,486 |

|

| $ | 76,472 |

| $ | 170,957 |

|

| $ | 114,486 |

|

| | | | | | | |

| Net income per share: | | | | | | |

| Basic | $ | 0.53 |

| | $ | 0.36 |

| $ | 0.80 |

| | $ | 0.53 |

|

| Diluted | $ | 0.52 |

| | $ | 0.34 |

| $ | 0.78 |

| | $ | 0.52 |

|

| | | |

|

| | |

|

|

| Weighted-average number of common shares outstanding—basic | 215,967 |

| | 214,925 |

| 213,537 |

| | 215,967 |

|

| Weighted-average number of common and common equivalent shares outstanding—diluted | 219,883 |

| | 221,497 |

| 218,343 |

| | 219,883 |

|

| | | | | |

| Dividends per share | $ | 0.0025 |

| | $ | 0.0025 |

| |

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

| | | | Three Months Ended

March 31, | Three Months Ended

March 31, |

| (In thousands) | 2018 | | 2017 | 2019 | | 2018 |

| | | | | | | |

| Net income | $ | 114,486 |

| | $ | 76,472 |

| $ | 170,957 |

| | $ | 114,486 |

|

| Other comprehensive income, net of tax (Note 15): | | | | |

| Other comprehensive income (loss), net of tax (Note 15): | | | | |

| Unrealized gains (losses) on investments: | | | | | | |

| Unrealized holding gains (losses) arising during the period | (60,643 | ) | | 7,367 |

| 78,023 |

| | (60,643 | ) |

| Less: Reclassification adjustment for net gains (losses) included in net income | (3,132 | ) | | (1,631 | ) | (391 | ) | | (3,132 | ) |

| Net unrealized gains (losses) on investments | (57,511 | ) | | 8,998 |

| 78,414 |

| | (57,511 | ) |

| Unrealized foreign currency translation adjustments | 3 |

| | 34 |

| — |

| | 3 |

|

| Cumulative effect of adopting the accounting standard update for financial instruments | 224 |

| | — |

| |

| Cumulative effect of adopting the accounting standard update for the reclassification of certain tax effects | 2,724 |

| | — |

| |

| Other comprehensive income (loss), net of tax | (54,560 | ) | | 9,032 |

| 78,414 |

| | (57,508 | ) |

| Comprehensive income | $ | 59,926 |

| | $ | 85,504 |

| $ | 249,371 |

| | $ | 56,978 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN COMMON STOCKHOLDERS’ EQUITY (UNAUDITED)(UNAUDITED)

| | | | Three Months Ended March 31, | Three Months Ended

March 31, |

| (In thousands) | 2018 | | 2017 | 2019 | | 2018 |

| Common Stock | | | | | | |

| Balance, beginning of period | $ | 233 |

| | $ | 232 |

| $ | 231 |

| | $ | 233 |

|

| Issuance of common stock under incentive and benefit plans | — |

| | 1 |

| |

| Shares repurchased under share repurchase program (Note 14) | | (1 | ) | | — |

|

| Balance, end of period | 233 |

| | 233 |

| 230 |

| | 233 |

|

| | | | | | | |

| Treasury Stock | | | | | | |

| Balance, beginning of period | (893,888 | ) | | (893,332 | ) | (894,870 | ) | | (893,888 | ) |

| Repurchases of common stock under incentive plans | (303 | ) | | (40 | ) | (451 | ) | | (303 | ) |

| Balance, end of period | (894,191 | ) | | (893,372 | ) | (895,321 | ) | | (894,191 | ) |

| | | | | | | |

| Additional Paid-in Capital | | | | | | |

| Balance, beginning of period | 2,754,275 |

| | 2,779,891 |

| 2,724,733 |

| | 2,754,275 |

|

| Issuance of common stock under incentive and benefit plans | 1,433 |

| | 3,548 |

| 1,069 |

| | 1,433 |

|

| Share-based compensation | 2,528 |

| | 3,222 |

| 3,695 |

| | 2,528 |

|

| Impact of extinguishment of convertible senior notes | — |

| | (42,940 | ) | |

| Cumulative effect of adopting the accounting standard update for share-based payment transactions | — |

| | 756 |

| |

| Change in equity component of currently redeemable convertible senior notes | — |

| | (883 | ) | |

| Shares repurchased under share repurchase program (Note 14) | (10,003 | ) | | — |

| (31,773 | ) | | (10,003 | ) |

| Balance, end of period | 2,748,233 |

| | 2,743,594 |

| 2,697,724 |

| | 2,748,233 |

|

| | | | | | | |

| Retained Earnings | | | | | | |

| Balance, beginning of period | 1,116,333 |

| | 997,890 |

| 1,719,541 |

| | 1,116,333 |

|

| Net income | 114,486 |

| | 76,472 |

| 170,957 |

| | 114,486 |

|

| Dividends declared | (540 | ) | | (538 | ) | (534 | ) | | (540 | ) |

| Cumulative effect of adopting the accounting standard update for financial instruments | 2,061 |

| | — |

| — |

| | 2,061 |

|

| Cumulative effect of adopting the accounting standard update for the reclassification of certain tax effects from accumulated other comprehensive income | (2,724 | ) | | — |

| — |

| | (2,724 | ) |

| Cumulative effect of adopting the accounting standard update for share-based payment transactions, net of tax | — |

| | (491 | ) | |

| Balance, end of period | 1,229,616 |

| | 1,073,333 |

| 1,889,964 |

| | 1,229,616 |

|

| | | | | | | |

| Accumulated Other Comprehensive Income (Loss) | | | | | | |

| Balance, beginning of period | 23,085 |

| | (12,395 | ) | (60,920 | ) | | 23,085 |

|

| Net foreign currency translation adjustment, net of tax | 3 |

| | 34 |

| |

| Net unrealized gains (losses) on investments, net of tax | (57,511 | ) | | 8,998 |

| |

| Cumulative effect of adopting the accounting standard update for financial instruments | 224 |

| | — |

| — |

| | 224 |

|

| Cumulative effect of adopting the accounting standard update for the reclassification of certain tax effects from accumulated other comprehensive income | 2,724 |

| | — |

| — |

| | 2,724 |

|

| Net unrealized gains (losses) on investments, net of tax | | 78,414 |

| | (57,511 | ) |

| Net foreign currency translation adjustment, net of tax | | — |

| | 3 |

|

| Balance, end of period | (31,475 | ) | | (3,363 | ) | 17,494 |

| | (31,475 | ) |

| | | | | | | |

| Total Stockholders’ Equity | $ | 3,052,416 |

| | $ | 2,920,425 |

| $ | 3,710,091 |

| | $ | 3,052,416 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

| | Radian Group Inc. | CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) | | | | | | | | |

| (In thousands) | Three Months Ended

March 31, | Three Months Ended

March 31, |

| 2018 | | 2017 | 2019 | | 2018 |

| Cash flows from operating activities: | | | | | | |

| Net cash provided by (used in) operating activities | $ | 118,447 |

| | $ | 83,932 |

| $ | 217,778 |

| | $ | 118,447 |

|

| Cash flows from investing activities: | | | | | | |

| Proceeds from sales of: | | | | | | |

| Fixed-maturity investments available for sale | 224,597 |

| | 253,121 |

| 435,709 |

| | 224,597 |

|

| Trading securities | | 70,083 |

| | 11,964 |

|

| Equity securities | 55,795 |

| | — |

| 33,278 |

| | 55,795 |

|

| Trading securities | 11,964 |

| | 46,688 |

| |

| Proceeds from redemptions of: | | | | | | |

| Fixed-maturity investments available for sale | 94,356 |

| | 123,683 |

| 79,915 |

| | 94,356 |

|

| Trading securities | 17,890 |

| | 19,543 |

| 23,293 |

| | 17,890 |

|

| Purchases of: | | | | | | |

| Fixed-maturity investments available for sale | (482,260 | ) | | (444,873 | ) | (275,531 | ) | | (482,260 | ) |

| Equity securities | (19,994 | ) | | — |

| (19,767 | ) | | (19,994 | ) |

| Sales, redemptions and (purchases) of: | | | | | | |

| Short-term investments, net | (17,217 | ) | | 57,923 |

| (526,013 | ) | | (17,217 | ) |

| Other assets and other invested assets, net | 92 |

| | 222 |

| 349 |

| | 92 |

|

| Purchases of property and equipment, net | (4,702 | ) | | (7,687 | ) | (6,659 | ) | | (4,702 | ) |

| Acquisitions, net of cash acquired | (261 | ) | | (86 | ) | — |

| | (261 | ) |

| Net cash provided by (used in) investing activities | (119,740 | ) | | 48,534 |

| (185,343 | ) | | (119,740 | ) |

| Cash flows from financing activities: | | | | | | |

| Dividends paid | (540 | ) | | (538 | ) | (534 | ) | | (540 | ) |

| Purchases and redemptions of senior notes | — |

| | (110,160 | ) | |

| Issuance of common stock | 663 |

| | 2,865 |

| 363 |

| | 663 |

|

| Purchase of common shares | (10,003 | ) | | — |

| (31,774 | ) | | (10,003 | ) |

| Credit facility commitment fees paid | (185 | ) | | — |

| (234 | ) | | (185 | ) |

| Change in secured borrowings (Note 12) | 38,719 |

| | — |

| |

| Change in secured borrowings, net (with terms less than 3 months) | | 21,534 |

| | 38,719 |

|

| Proceeds from secured borrowings (with terms greater than 3 months) | 6,550 |

| | — |

| 6,000 |

| | 6,550 |

|

| Payments of secured borrowings (with terms greater than 3 months) | | (7,000 | ) | | — |

|

| Repayment of other borrowings | (50 | ) | | (81 | ) | (38 | ) | | (50 | ) |

| Net cash provided by (used in) financing activities | 35,154 |

| | (107,914 | ) | (11,683 | ) | | 35,154 |

|

| Effect of exchange rate changes on cash and restricted cash | (1 | ) | | 24 |

| — |

| | (1 | ) |

| Increase (decrease) in cash and restricted cash | 33,860 |

| | 24,576 |

| 20,752 |

| | 33,860 |

|

| Cash and restricted cash, beginning of period | 96,244 |

| | 61,814 |

| 107,002 |

| | 96,244 |

|

| Cash and restricted cash, end of period | $ | 130,104 |

| | $ | 86,390 |

| $ | 127,754 |

| | $ | 130,104 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

1. Condensed Consolidated Financial Statements—Business Overview, Recent Developments and Significant Accounting Policies

Business Overview

We are a diversified mortgage and real estate services business, providing both credit-related insurance coverage and other credit risk management solutions, as well as a broad array of mortgage, and real estate and title services. We have two reportable business segments—Mortgage Insurance and Services.

Mortgage Insurance

Our Mortgage Insurance segment provides credit-related insurance coverage, principally through private mortgage insurance on residential first-lien mortgage loans, as well as other credit risk management solutions, to mortgage lending institutions nationwide.and mortgage credit investors. We provide our mortgage insurance products and services mainly through our wholly-owned subsidiary, Radian Guaranty. Private mortgage insurance plays an important role in the U.S. housing finance system because it promotes affordable home ownership and helps protect mortgage lenders, investors and other beneficiaries by mitigating default-related losses on residential mortgage loans. Generally, these loans are made to home buyers who make down payments of less than 20% of the purchase price for their home or, in the case of refinancings, have less than 20% equity in their homes.home. Private mortgage insurance also facilitates the sale of these low down payment loans in the secondary mortgage market, most of which are currently sold to the GSEs.

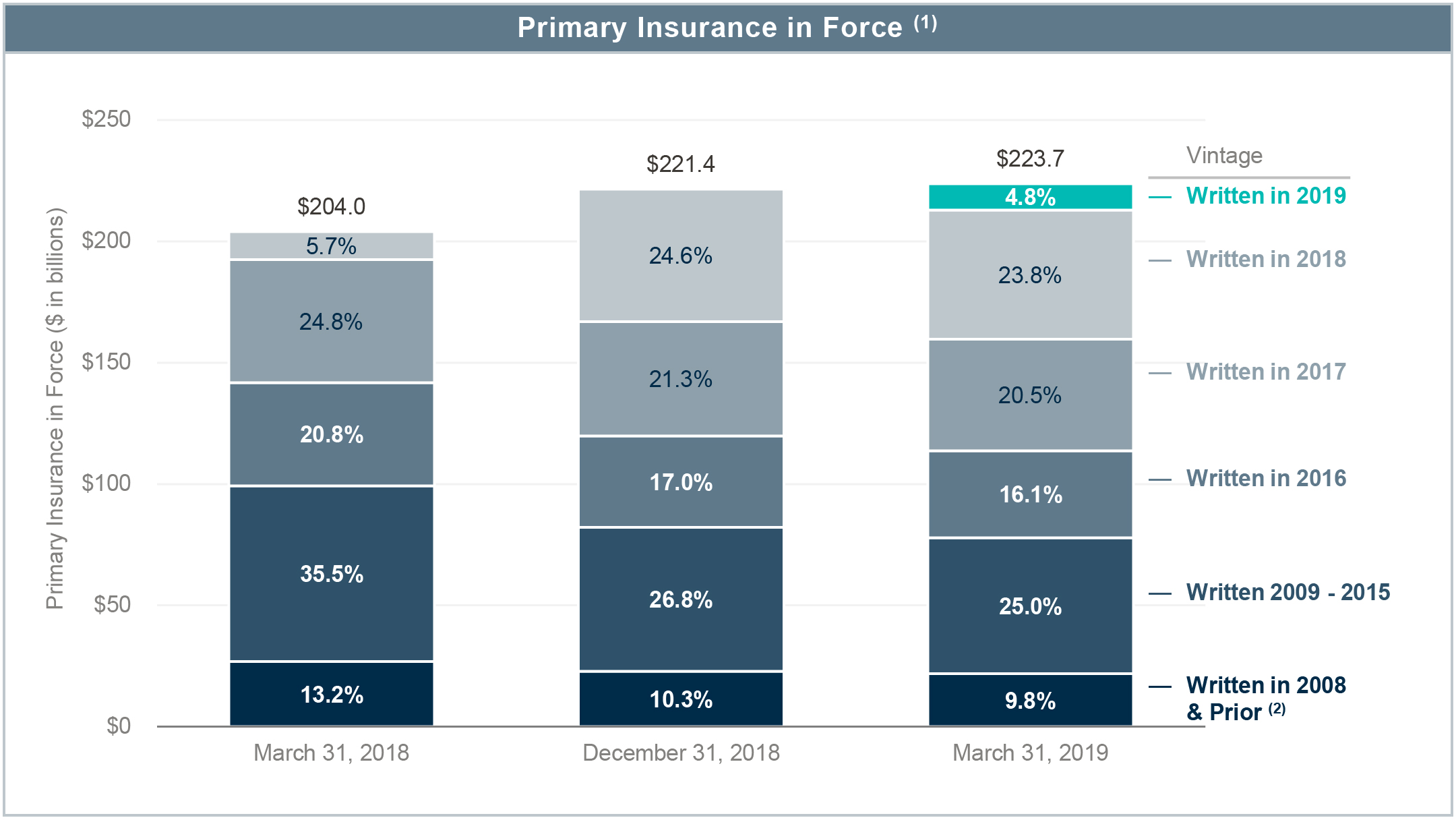

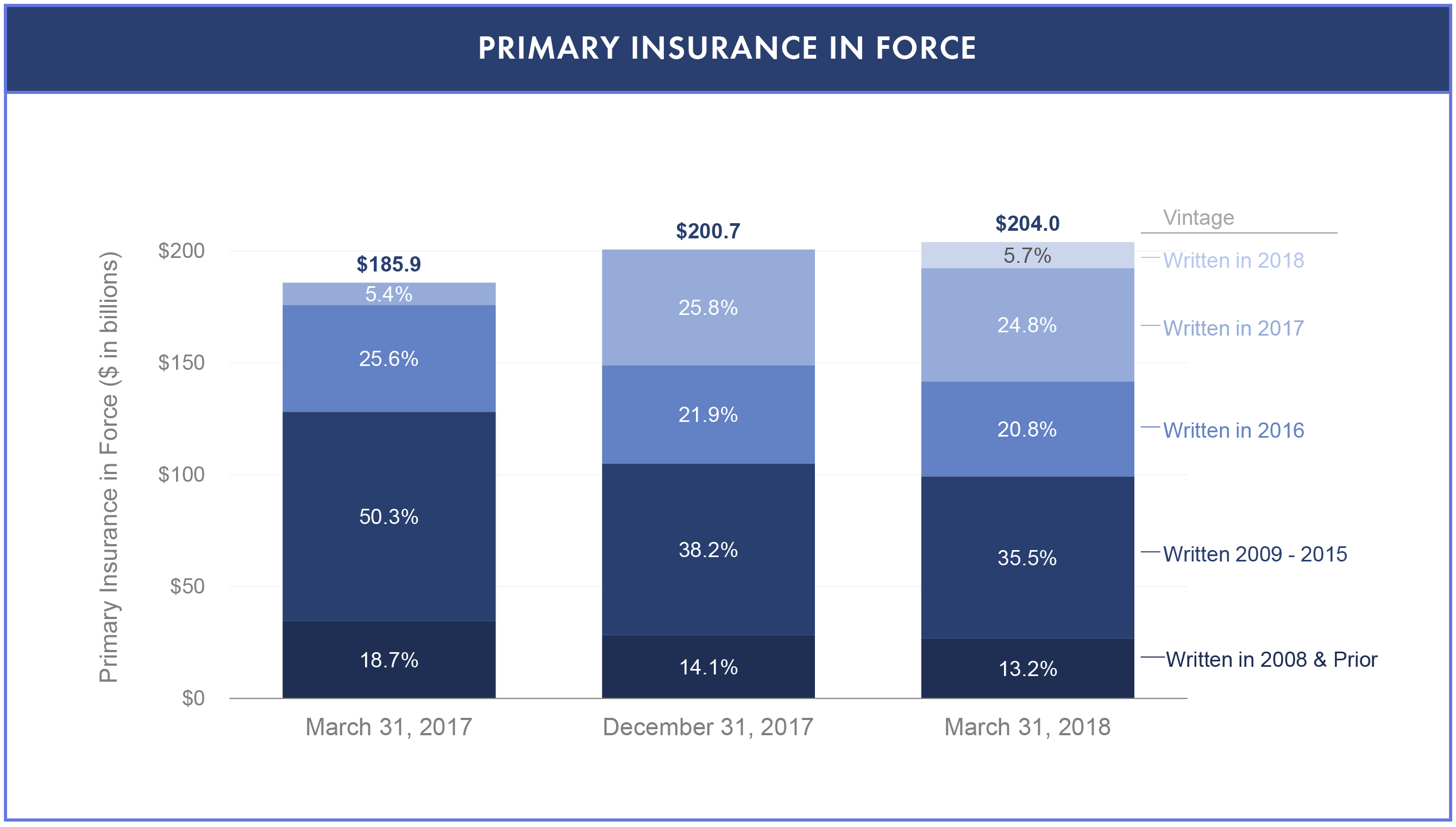

Our Mortgage Insurance segment currently offers primary mortgage insurance coverage on residential first-lien mortgage loans. Our total direct primary mortgage insurance RIF was $52.2$57.4 billion as of March 31, 2018.2019.

The GSEs and state insurance regulators impose various capital and financial requirements on our insurance subsidiaries. These include Risk-to-capital, other risk-based capital measures and surplus requirements, as well as the PMIERs financial requirements discussed below. Failure to comply with these capital and financial requirements may limit the amount of insurance that our mortgage insurance subsidiaries may write or prohibit our mortgage insurance subsidiaries from writing insurance altogether. The GSEs and state insurance regulators also possess significant discretion with respect to our mortgage insurance subsidiaries and all aspects of their business. See Note 16 for additional regulatory information.

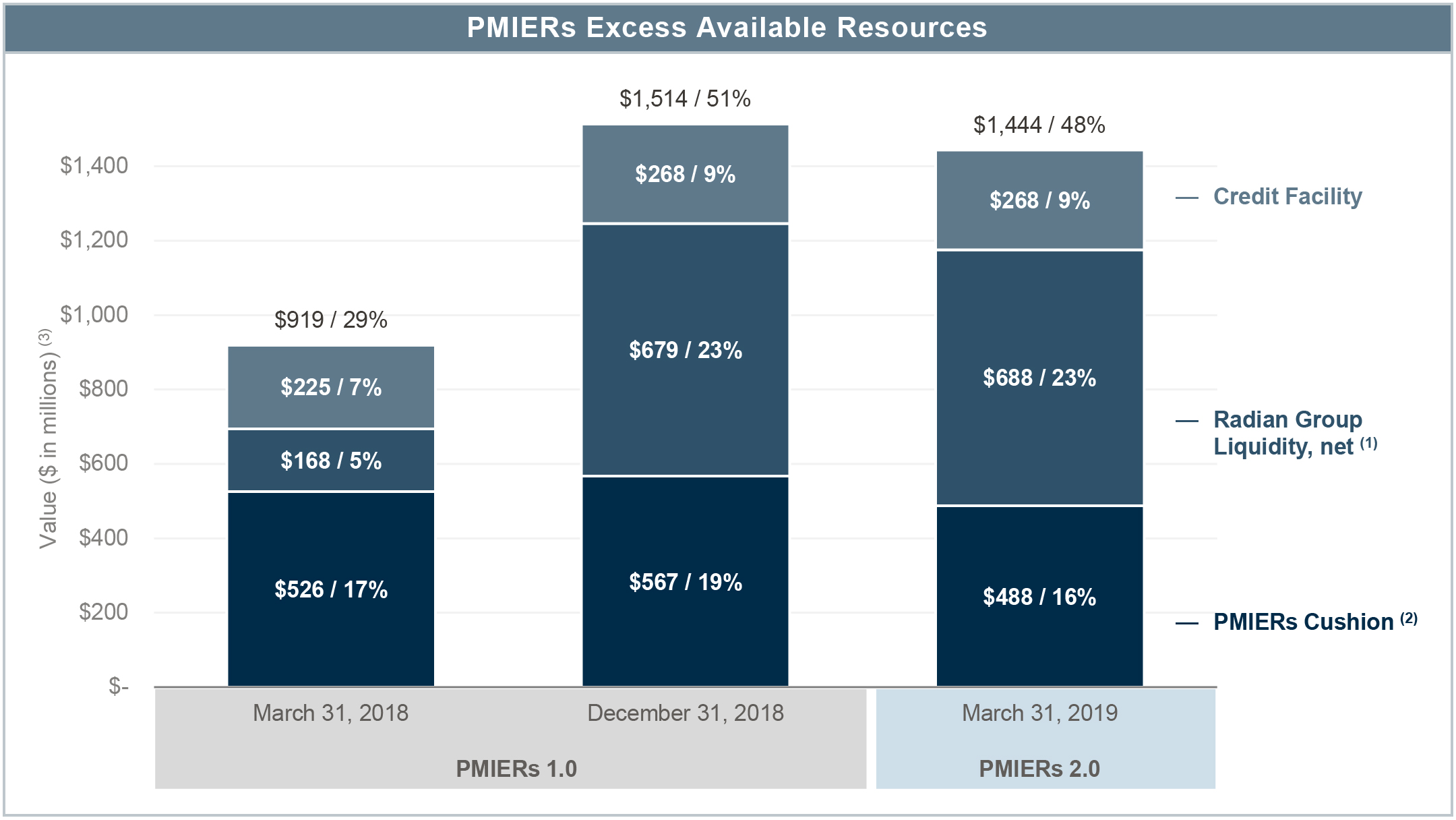

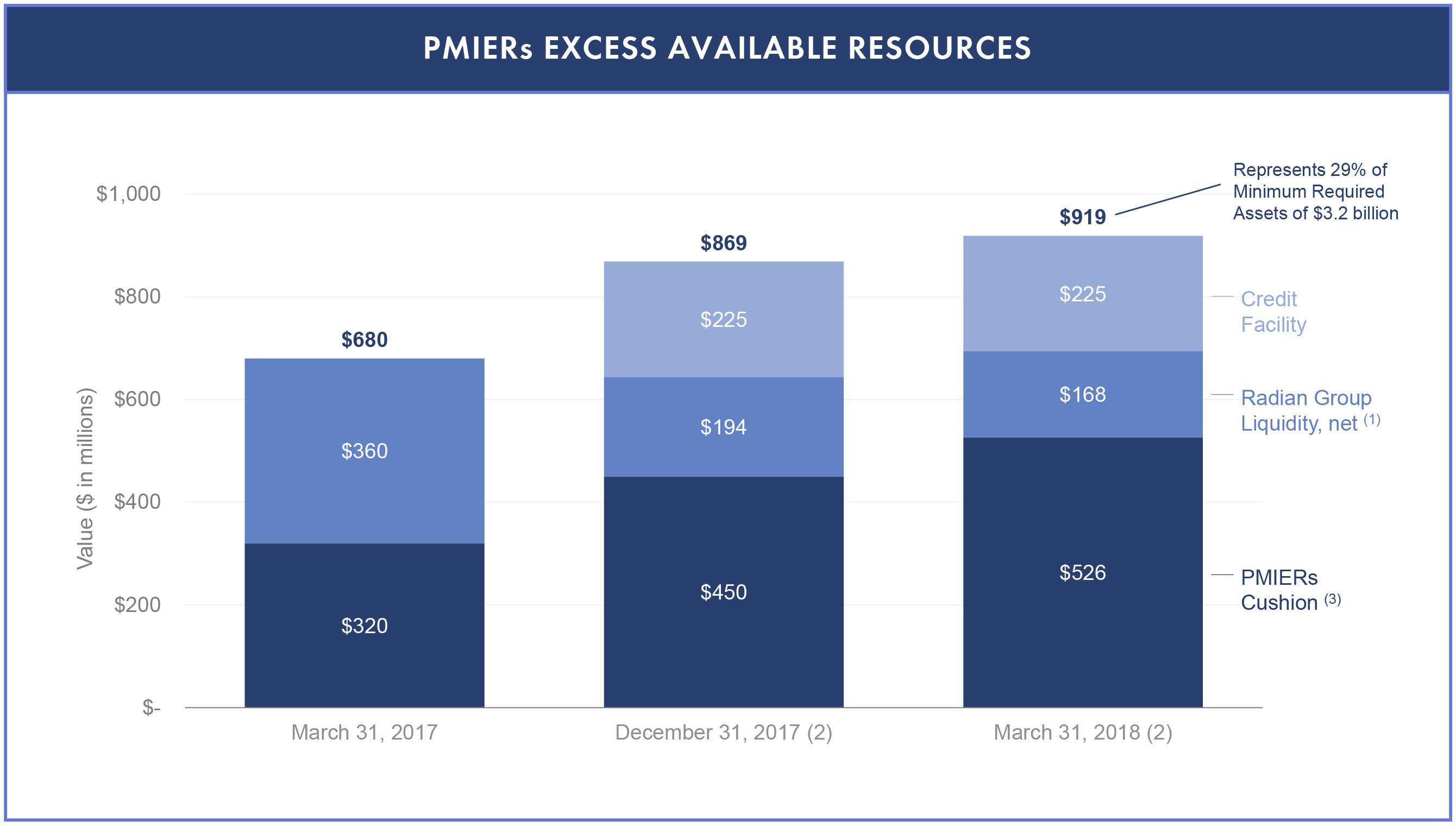

PMIERs. In order to be eligible to insure loans purchased by the GSEs, mortgage insurers such as Radian Guaranty must meet the GSEs’ eligibility requirements, or PMIERs. At March 31, 2018,2019, Radian Guaranty is an approved mortgage insurer under the PMIERs and is in compliance with the current PMIERs financial requirements. The PMIERs financial requirements require that a mortgage insurer’s Available Assets meet or exceed its Minimum Required Assets. The GSEs may amend the PMIERs at any time, and they have broad discretion to interpret the requirements, which could impact the calculation of Radian Guaranty’s Available Assets and/or Minimum Required Assets.

The PMIERs are comprehensive, covering virtually all aspects of the business and operations of a private mortgage insurer, including internal risk management and quality controls, the relationship between the GSEs and the approved insurer, as well as the approved insurer’s financial condition. In addition, the GSEs have a broad range of consent rights under the PMIERs and require private mortgage insurers to obtain the prior consent of the GSEs before taking certain actions, which may include paying dividends, entering into various intercompany agreements and commuting or reinsuring risk, among others. If Radian Guaranty is unable to satisfy the requirements set forth in the PMIERs, the GSEs could restrict it from conducting certain types of business with them or take actions that may include not purchasing loans insured by Radian Guaranty.

The PMIERs financial requirements require that a mortgage insurer’s Available Assets meet or exceed its Minimum Required Assets. The GSEs may amend the PMIERs at any time, and they have broad discretion to interpret the requirements, which could impact the calculation of Radian Guaranty’s Available Assets and/or Minimum Required Assets. Further, the PMIERs specifically provide that the factors applied to determine a mortgage insurer’s Minimum Required Assets may be updated every two years following a minimum of 180 days’ notice, or more frequently, as determined by the GSEs. As previously announced, Radian Guaranty received, on a confidential basis, proposed changes to the PMIERs. Based on this information, which has been subject to comment by the private mortgage insurance industry, Radian expects to be able to fully comply with the proposed PMIERs and to maintain an excess of Available Assets over Minimum Required Assets under the PMIERs as of their effective date, which is expected to be no earlier than the end of 2018.

From time to time, we enter into reinsurance transactions as parta component of our long-term risk distribution strategy to manage our capital position and risk profile, which includes managing Radian Guaranty’s capital position under the PMIERs financial requirements. The credit that we receive under the PMIERs financial requirements for these transactions is subject to the periodicinitial and ongoing review ofby the GSEs.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

Services

Our Services segment is primarily a fee-for-service business that offers a broad array of services to market participants across the mortgage and real estate value chain. These services comprise mortgage services, real estate services and title services, including technology and turn-key solutions, that provide mortgage lenders, financial institutions, mortgage and real estate investors and government entities, among others, with information and other resources and services that are used to originate, evaluate, acquire, securitize, service and monitor residential real estate and loans secured by residential real estate. These services are primarily provided to mortgage lenders, financial institutions, investors and government entities. In addition, we provide title insurance to mortgage lenders as well as directly to borrowers.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements (Continued)

Our mortgage services include transaction managementhelp loan originators and investors evaluate, acquire, surveil and securitize mortgages. These services such asinclude loan review, RMBS securitization and distressed asset reviews, review and valuation services related to single family rental properties, servicer and loan surveillance and underwriting. Our real estate services include:help lenders, investors and real estate agents evaluate, manage, monitor and sell properties. These real estate services include software as a service solutions and platforms, as well as managed services, such as REO asset management; review and valuation services related to single family rental properties;management, real estate valuation services and real estate brokerage services. Our title services include title search,provide a comprehensive suite of title insurance products, title settlement services and both traditional and digital closing services.

20182019 Developments

Capital and Liquidity Actions. On August 9, 2017,March 20, 2019, Radian Group’s board of directors renewedapproved a $150 million increase in authorization for the Company’s existing share repurchase program, authorizingplan, bringing the Companytotal authorization to repurchase shares up to $50$250 million, of its common stock.excluding commissions. During the three months ended March 31, 2018, we2019, the Company purchased 531,0131,546,674 shares at an average price of $18.84$20.54 per share, including commissions. At March 31, 2018,2019, purchase authority of up to $40.0$218.2 million remained available under this program.program, which expires on July 31, 2020. Subsequent to March 31, 2018,2019, we have purchased additional4,131,329 shares of our common stock under this program.program at an average price of $21.94 per share, including commissions. See Note 14 for additional information.details on our share repurchase program.

Restructuring and Other Exit Costs. Pretax restructuring chargesIn April 2019, the Pennsylvania Insurance Department approved a $375 million distribution of $0.6 million were recognizedcapital from Radian Guaranty to Radian Group, which was paid on April 30, 2019 in the first quarterform of cash and marketable securities. See Note 16 for a discussion of this distribution of capital.

Reinsurance. In April 2019, Radian Guaranty entered into a fully collateralized reinsurance agreement with Eagle Re 2019-1. Eagle Re 2019-1 is a VIE and is not a subsidiary or affiliate of Radian Guaranty. This reinsurance agreement provides for up to $562.0 million of aggregate excess-of-loss reinsurance coverage for the mortgage insurance losses on new defaults on an existing portfolio of eligible Recurring Premium Policies issued between January 1, 2018 including $0.5 million in cash expenses. These charges were a result of the Company’s 2017 plan to restructure the Services business. We expect to incur additional pretax charges of approximately $3.1 million under this plan, including approximately $2.5 million in cash payments. These remaining charges are expected to be recognized byand December 31, 2018. The total estimated restructuring charges2018, with an initial RIF of approximately $3.7$10.7 billion. Eagle Re 2019-1 financed its coverage by issuing mortgage insurance-linked notes in an aggregate amount of $562.0 million during 2018 are expected to consist of: (i) asset impairment charges of approximately $0.6 million; (ii) employee severance and benefit costs of approximately $0.9 million; (iii) facility and lease termination costs of approximately $1.6 million; and (iv) contract termination and other restructuring costs of approximately $0.6 million.eligible third-party capital markets investors in an unregistered private offering. See Notes 1 andNote 7 of Notes to Consolidated Financial Statements in our 2017 Form 10-K for additional information, including the events that led to the restructuring decision.

Developments subsequent to March 31, 2018. For informationdetails on events that occurred subsequent to March 31, 2018, including capital actions and the IRS Matter, see Notes 9 and 14, respectively.our reinsurance programs.

Significant Accounting Policies

Basis of Presentation

Our condensed consolidated financial statements are prepared in accordance with GAAP and include the accounts of Radian Group Inc. and its subsidiaries. All intercompany accounts and transactions, and intercompany profits and losses, have been eliminated. We have condensed or omitted certain information and footnote disclosures normally included in consolidated financial statements prepared in accordance with GAAP pursuant to the instructions set forth in Article 10 of Regulation S-X of the SEC.

We refer to Radian Group Inc. together with its consolidated subsidiaries as “Radian,” the “Company,” “we,” “us” or “our,” unless the context requires otherwise. We generally refer to Radian Group Inc. alone, without its consolidated subsidiaries, as “Radian Group.” Unless otherwise defined in this report, certain terms and acronyms used throughout this report are defined in the Glossary of Abbreviations and Acronyms included as part of this report.

The financial information presented for interim periods is unaudited; however, such information reflects all adjustments that are, in the opinion of management, necessary for the fair statement of the financial position, results of operations, comprehensive income and cash flows for the interim periods presented. Such adjustments are of a normal recurring nature. The year-end condensed balance sheet data was derived from our audited financial statements, but does not include all disclosures required by GAAP. These interim financial statements should be read in conjunction with the audited financial statements and notes thereto included in our 20172018 Form 10-K. The results of operations for interim periods are not necessarily indicative of results to be expected for the full year or for any other period. Certain prior period amounts have been reclassified to conform to current period presentation.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

Use of Estimates

The preparation of financial statements in conformity with GAAP requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of our contingent assets and liabilities at the dates of the financial statements, as well as the reported amounts of revenues and expenses during the reporting periods. While the amounts

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements (Continued)

included in our condensed consolidated financial statements include our best estimates and assumptions, actual results may vary materially.

Other Significant Accounting Policies

See Note 2 of Notes to Consolidated Financial Statements in our 20172018 Form 10-K for information regarding other significant accounting policies. There have been no significant changes in our significant accounting policies from those discussed in our 20172018 Form 10-K, other than described below including in “—Revenues“—Leases” and “—“—Recent Accounting Pronouncements—Accounting Standards Adopted during 2018.During 2019.”

Revenue Recognition—ServicesLeases

The FASB issuedWe determine if an updatearrangement includes a lease at inception. A right of use asset and lease liability is recognized for operating leases and is included in other assets and other liabilities, respectively, in our condensed consolidated balance sheet at March 31, 2019. Right-of-use assets represent our right to use an underlying asset for the accounting standard regarding revenue recognition, Revenue from Contracts with Customers, which establishes principles for reporting information about the nature, amount, timinglease term and uncertainty of revenue and cash flowslease liabilities represent our obligation to make lease payments arising from our contracts with customers to provide services. We adopted this update effective January 1, 2018, using the modified retrospective approach. The principle of this update requires an entity to recognize revenue representing the transfer of services to customers in an amount that reflects the consideration that it expects to be entitled to receive in exchange for those services, recognized as the performance obligations are satisfied.

The majority of our revenue-generating transactions are not subject to the new standard as this update did not change revenue recognition principles related to our investmentslease. Operating lease right-of-use assets and insurance products, which together represented the majority of our total revenue for the three months ending March 31, 2018 and are subject to other GAAP guidance discussed elsewhere within our disclosures. This update is primarily applicable to revenues from our Services segment. See “—Business Overview—Services” for information about the services we offer.

The table below represents the disaggregation of Services revenues by revenue type:

|

| | | | | | | |

| | Three Months Ended

March 31, |

| (In thousands) | 2018 | | 2017 |

| Services segment revenue | | | |

Mortgage Services (1) | $ | 13,989 |

| | $ | 18,371 |

|

Real Estate Services (1) | 17,903 |

| | 17,014 |

|

| Title Services | 2,274 |

| | 4,704 |

|

Total (2) | $ | 34,166 |

| | $ | 40,089 |

|

______________________

| |

(1) | 2017 revenues include immaterial amounts of Services revenue related to services that we no longer offer as a result of restructuring our Services business. |

| |

(2) | Includes inter-segment revenues of $1.0 million and $2.1 million for the three months ended March 31, 2018 and 2017, respectively. See Note 3 for segment information. |

Our Services segment revenuesliabilities are recognized over time and measured each periodat the lease commencement date based on the progresspresent value of lease payments over the lease term. Right of use assets are recognized net of any payments made or received from the lessor. In determining the net present value of lease payments, we use our incremental borrowing rate based on the information available at the lease commencement date or as of our date of adoption, January 1, 2019.

Lease expense is recognized on a straight-line basis over the expected lease term. For lease agreements entered into after the adoption of this accounting standard that include lease and non-lease components, such components are generally not accounted for separately. For our building leases, as a result of us having elected to dateadopt the package of practical expedients permitted under the transition guidance, we account for the lease and non-lease components, such as services are performed and made available to customers. Ourcommon area maintenance charges, as a single lease component. We have elected the short-term exemption for contracts with customers, including paymentlease terms are generally short-termof 12 months or less. Prior period amounts continue to be reported in nature; therefore, any impact relatedaccordance with our historic accounting under previous lease guidance.

Our lease agreements primarily relate to timing is immaterial. Revenue recognized related to services made available to customers and billed is reflectedoperating leases for office space we use in accounts receivables. Revenue recognized related to services performed andour operations. Certain of our leases include renewal options and/or termination options that we did not yet billed is recordedconsider in unbilled receivables and reflected in other assets. We have no material bad-debt expense. The following represents balances related to Services contracts asthe determination of the dates indicated:

|

| | | | | | | |

| (In thousands) | March 31, 2018 | | December 31, 2017 |

| Accounts Receivable - Services Contracts | $ | 13,236 |

| | $ | 17,391 |

|

| Unbilled Receivables - Services Contracts | 20,949 |

| | 22,257 |

|

| Deferred Revenues - Services Contracts | 3,481 |

| | 3,235 |

|

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

Revenue expected to be recognized in any future period related to remaining performance obligations,right-of-use asset or the lease liability as we did not consider it reasonably certain that we would exercise such as contracts where revenue is recognized as invoiced and contracts with variable consideration related to undelivered performance obligations, is not material.

Fee-for-Service Contracts

Generally, our contracts with our clientsoptions. Our lease agreements do not include minimum volume commitments and can be terminated atcontain any time by our clients. Although some of our contracts and assignments are recurring in nature, and include repetitive monthly assignments, a significant portion of our engagements are transactional in nature and may be performed in connection with securitizations, loan sales, loan purchasesvariable lease payments, material residual value guarantees or other transactions. Due to the transactional nature of our business, our Services segment revenues may fluctuate from period to period as transactions are commenced or completed.material restrictive covenants. We do not recognize revenue or expense related to amounts advanced by ushave material sublease agreements. As of March 31, 2019, there were no leases which had not yet commenced but that create significant rights and subsequently reimbursed by clientsobligations for maintenance or repairs because we do not take control of the service prior to the client taking control. We record an expense if an advance is made that is not in accordance with a client contract and the client is not obligated to reimburse us.

Due to the nature of the services provided, See Note 12 for more information about our Services arrangements with customers may include any of the following three basic types of contracts:

Fixed-Price Contracts. We use fixed-price contracts in our real estate valuation and component services, our loan review, underwriting and due diligence services as well as our title and closing services. We also use fixed-price contracts in our surveillance business for our servicer oversight services and RMBS surveillance services, and in our asset management business activities. Under fixed-price contracts we agree to perform the specified services and deliverables for a pre-determined per-unit or per-file price or day rate. Each service qualifies as a separate performance obligation and revenue is recognized as the service performed is made available to the client.

Time-and-Expense Contracts. The Services segment also derives a portion of its revenue from professional service activities under time-and-expense contracts. In these types of contracts, we are paid a fixed hourly rate, and we are reimbursed for billable out-of-pocket expenses as work is performed. These contracts are used in our loan review, underwriting and due diligence services. Services revenue consisting of billed time fees and pass-through expenses is recorded over time and based on the progress to date as services are performed and made available to customers. Services revenue may also include expenses billed to clients, which includes travel and other out-of-pocket expenses, and other reimbursable expenses.

Percentage-of-Sale Contracts. Under percentage-of-sale contracts, we are paid a contractual percentage of the sale proceeds upon the sale of each property. These contracts are only used for a portion of our REO management services and our real estate brokerage services. In addition, through the use of our proprietary technology, property leads are sent to select clients. Revenue attributable to services provided under a percentage-of-sale contract is recognized over time and measured based on the progress to date and typically coincides with the client’s successful closing on the property. The revenue recognized for these transactions is based on a percentage of the sale.

In certain instances, fees are received at the time that an asset is assigned to Radian for management. These fees are recorded as deferred revenue and are recognized over time based on progress to date and the availability to customers.lease agreements.

Recent Accounting Pronouncements

Accounting Standards Adopted During 2018. In May 2014, the FASB issued an update to the accounting standard regarding revenue recognition. In July 2015, the FASB delayed the effective date for this updated standard for public companies to interim and annual periods beginning after December 15, 2017, and subsequently issued various clarifying updates. Our adoption of this standard, effective January 1, 2018, had no material impact on our financial statements. The disclosures required by this update are included above in “—Revenue Recognition—Services.”

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

In January 2016, the FASB issued an update that makes certain changes to the standard for the accounting of financial instruments. Among other things, the update requires: (i) equity investments to be measured at fair value with changes in fair value recognized in net income; (ii) the use of the exit price notion when measuring the fair value of financial instruments for disclosure purposes; (iii) separate presentation of financial assets and financial liabilities by measurement category and form of financial asset; and (iv) separate presentation in other comprehensive income of the portion of the total change in the fair value of a liability resulting from a change in the instrument-specific credit risk (also referred to as “own credit”) when the organization has elected to measure the liability at fair value in accordance with the fair value option for financial instruments. The update also eliminates the requirement to disclose the methods and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet. This update is effective for public companies for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. In February 2018, the FASB issued technical corrections related to this update, which addresses common questions regarding the application and adoption of the new guidance and the subsequent amendments. As a result of adopting these updates, equity securities are no longer classified as available for sale securities and changes in fair value are recognized through earnings. Consequently, we recorded a cumulative effect adjustment to retained earnings from accumulated other comprehensive income representing unrealized losses related to equity securities in the amount of $0.2 million, net of tax. In addition, we elected to utilize net asset value as a practical expedient to measure certain other investments, which resulted in an increase to other invested assets with an offset to retained earnings in the amount of $2.3 million, net of tax. Our adoption of both these updates effective January 1, 2018 resulted in a net adjustment to retained earnings of $2.1 million. See Notes 4 and 5 for additional information.

In February 2018, the FASB issued an update to the accounting standard regarding income statement reporting of comprehensive income and reclassification of certain tax effects from accumulated other comprehensive income. The amendments in this update allow a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the TCJA. The provisions of this update are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted, including adoption in an interim period, for reporting periods for which financial statements have not been available for issuance. We elected to early adopt this update effective January 1, 2018. As a result we recorded a reclassification adjustment from other comprehensive income to retained earnings in the amount of $2.7 million. See Note 9 for additional information regarding the TCJA.

Accounting Standards Not Yet Adopted.

2019. In February 2016, the FASB issued an update that replaces the existing accounting and disclosure requirements for leases of property, plant and equipment. The updateequipment, which requires lessees to recognize, as of the lease commencement date, assets and liabilities for all leases with lease terms of more than 12 months, which is a change from the current GAAP requirement to recognize only capital leases on the balance sheet. Pursuant to the new standard, the liability initially recognized for the lease obligation is equal to the present value of the lease payments not yet made, discounted over the lease term at the implicit interest rate of the lease, if available, or otherwise at the lessee’s incremental borrowing rate. The lessee is also required to recognize an asset for its right to use the underlying asset for the lease term, based on the liability subject to certain adjustments, such as for initial direct costs.months. Leases are required to be classified as either operating or finance, with expense on operating leases recorded as a single lease cost on a straight-line basis. For finance leases, interest expense on the lease liability is required to be recognized separately from the straight-line amortization of the right-of-use asset. Quantitative disclosures are required

We elected the optional transition method, which requires the recognition of a cumulative-effect adjustment as of the beginning of the period of adoption, and we also elected the practical expedients for certain items, includingtransitioning existing leases to the costnew standard as of leases, the weighted-average remainingeffective date. As a result of applying the practical expedients: (i) we did not reassess expired or existing contracts to determine if they contain additional leases; (ii) we did not reassess the lease term, the weighted-average discount rateclassification for expired and existing leases; and (iii) we did not reassess initial direct costs for existing leases. Our adoption of this update, effective January 1, 2019, resulted in our recording an increase in other liabilities of $73.5 million, and a maturity analysiscorresponding increase in other assets. The increase to other assets was partially offset by an adjustment for unamortized allowances and incentives of $24.1 million, resulting in a right of use asset of $49.4 million. The increase in other liabilities represents a discounted lease liabilities. Additional qualitativeliability from operating leases, primarily for our various facilities, which represents the present value of these future lease payments discounted at our incremental borrowing rate. Additionally, we expanded our financial statement disclosures are alsoas required by the amendments. Our adoption of this standard did not impact our stockholders’ equity, results of operations or liquidity. See above for a discussion of our accounting policy regarding leases and Note 12.

In March 2017, the natureFASB issued an update to the accounting standard regarding receivables. The new standard requires certain premiums on purchased callable debt securities to be amortized to the earliest call date. The amortization period for callable debt securities purchased at a discount will not be impacted. The provisions of the leases, such as basis, terms and conditions of: (i) variable interest payments; (ii) extension and termination options; and (iii) residual value guarantees. Thisthis update isare effective for public companies for fiscal years

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements (Continued)