UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________

FORM 10-Q

_____________________________

(Mark One)

|

| |

x☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20182019

OR

|

| |

o☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-11356

Radian Group Inc.Inc.

(Exact name of registrant as specified in its charter)

|

| | | | | | |

| Delaware | | 23-2691170 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | | | | | |

| 1500 Market Street | , | Philadelphia | , | PA | | 19102 |

| (Address of principal executive offices) | | (Zip Code) |

(215) (215) 231-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.001 par value per share | RDN | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes xYes☒ No o☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes xYes☒ No o☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | | | | | | |

Large accelerated filer x Accelerated Filer | ☒ | | Accelerated filero | ☐ | | Non-accelerated filero | ☐ | | Smaller reporting companyo | ☐ | | Emerging growth companyo | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o☐ No x☒

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 213,333,428201,149,388 shares of common stock, $0.001 par value per share, outstanding on November 5, 2018.8, 2019.

|

| | |

| TABLE OF CONTENTS | |

| | | Page Number |

| |

| |

| |

| Item 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 6. | | |

| | | |

| |

GLOSSARY OF ABBREVIATIONS AND ACRONYMS

The following list defines various abbreviations and acronyms used throughout this report, including the Condensed Consolidated Financial Statements, the Notes to Unaudited Condensed Consolidated Financial Statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

| |

| Term | Definition |

| 2014 Master Policy | Radian Guaranty’s master insurance policy, setting forth the terms and conditions of our mortgage insurance coverage, which became effective October 1, 2014 |

| 2016 Single Premium QSR Agreement | Quota share reinsurance agreement entered into with a panel of third-party reinsurance providers in the first quarter of 2016 and subsequently amended in the fourth quarter of 2017 |

2017 Form 10-K | Annual Report on Form 10-K for the year ended December 31, 2017 |

| 2018 Single Premium QSR Agreement | Quota share reinsurance agreement entered into with a panel of third-party reinsurance providers in October 2017 to cede a portion of Single Premium NIW beginning January 1, 2018 |

| ABS | Asset-backed securities |

Alt-AASU | Alternative-A loans, representing loans for whichAccounting Standards Update, issued by the underwriting documentation is generally limited as comparedFASB to fully documented loans (considered a non-prime loan grade)communicate changes to GAAP |

| Available Assets | As defined in the PMIERs, assets primarily including the liquid assets of a mortgage insurer, and reduced by premiums received but not yet earned |

Back-endCFPB | With respect to credit risk transfer programs established by the GSEs, policies written on loans that are already part of an existing GSE portfolio, as contrasted with loans that are to be purchased by the GSEs in the future |

Borrower | With respect to our securities lending agreements, the third-party institutions to which we loan certain securities in our investment portfolio for short periods of timeConsumer Financial Protection Bureau |

| Claim Curtailment | Our legal right, under certain conditions, to reduce the amount of a claim, including due to servicer negligence |

| Claim Denial | Our legal right, under certain conditions, to deny a claim |

| Claim Severity | The total claim amount paid divided by the original coverage amount |

| Clayton | Clayton Holdings LLC, a Delaware domiciled indirect non-insurance subsidiary of Radian Group |

| Clayton Intercompany Note | A $300 million note payable from Radian Mortgage Services Inc. (formerly Clayton Group Holdings Inc.) to Radian Group (with terms consistent with the terms of our Senior Notes due 2019 that were used to fund our purchase of Clayton) |

| CMBS | Commercial mortgage-backed securities |

Convertible Senior Notes due 2017 | Our 3.000% convertible unsecured senior notes due November 2017 ($450 million original principal amount) |

Convertible Senior Notes due 2019 | Our 2.250% convertible unsecured senior notes due March 2019 ($400 million original principal amount) |

| Cures | Loans that were in default as of the beginning of a period and are no longer in default because payments were received such that the loan is no longer 60 or more days past due |

| Default to Claim Rate | The percentage of defaulted loans that are assumed to result in a claim |

| Discrete Item(s) | For tax calculation purposes, certain items that are required to be accounted for in the provision for income taxes as they occur and are not considered components of the estimated annualized effective tax rate for purposes of reporting interim results. Generally, these are items that are: (i) clearly defined (such as changes in tax rate or tax law); (ii) infrequent or unusual in nature; or (iii) gains or losses that are not components of continuing operating income, such as income from discontinued operations or losses reflected as components of other comprehensive income. These items impact the difference between the statutory rate and Radian’s effective tax rate. |

EnTitle DirectDodd-Frank Act | EnTitle Direct Group, Inc., a wholly-owned subsidiary of Radian GroupDodd-Frank Wall Street Reform and Consumer Protection Act, as amended |

EnTitle InsuranceEagle Re 2018-1 | EnTitle Insurance Company,Eagle Re 2018-1 Ltd., an unaffiliated special purpose reinsurer (a VIE) domiciled in Bermuda |

| Eagle Re 2019-1 | Eagle Re 2019-1 Ltd., an unaffiliated special purpose reinsurer (a VIE) domiciled in Bermuda |

| Eagle Re Issuer(s) | Eagle Re 2018-1 Ltd. and Eagle Re 2019-1 Ltd. |

| Excess-of-Loss Program | The credit risk protection obtained by Radian Guaranty in the form of excess-of-loss reinsurance, which indemnifies the ceding company against loss in excess of a wholly-owned subsidiaryspecific agreed limit, up to a specified sum. The program includes reinsurance agreements with Eagle Re 2018-1 and Eagle Re 2019-1, in connection with the issuance by the Eagle Re Issuers of EnTitle Directmortgage insurance-linked notes in November 2018 and April 2019, respectively. The program also includes a separate agreement with a third-party reinsurer, representing a pro rata share of the credit risk alongside the risk assumed by Eagle Re 2018-1. |

| Exchange Act | Securities Exchange Act of 1934, as amended |

Extraordinary Dividend | A dividend distribution required to be approved by an insurance company’s primary regulator that is greater than would be permitted as an ordinary dividend which does not require regulatory approval |

Fannie Mae | Federal National Mortgage Association |

FASB | Financial Accounting Standards Board |

|

| |

| Term | Definition |

| Extraordinary Distribution | A dividend or distribution of capital that is required to be approved by an insurance company’s primary regulator that is greater than would be permitted as an ordinary distribution (which does not require regulatory approval) |

| Fannie Mae | Federal National Mortgage Association |

| FASB | Financial Accounting Standards Board |

| FEMA | Federal Emergency Management Agency, an agency of the U.S. Department of Homeland Security |

FEMA Designated Area | Generally, an area that has been subject to a disaster, designated by FEMA as an individual assistance disaster area for the purpose of determining eligibility for various forms of federal assistance |

| FHA | Federal Housing Administration |

| FHFA | Federal Housing Finance Agency |

| FHLB | Federal Home Loan Bank of Pittsburgh |

| FICO | Fair Isaac Corporation (“FICO”) credit scores, for Radian’s portfolio statistics, represent the borrower’s credit score at origination and, in circumstances where there is more than one borrower,are multiple borrowers, the lowest of the borrowers’ FICO score for the primary borrowerscores is utilized |

Flow BasisFive Bridges | With respect to mortgage insurance, includes mortgage insurance policies that are written on an individual loan basis as each loan is originated or on an aggregated basis (in which each individual loanFive Bridges Advisors, LLC. Radian acquired the assets of Five Bridges in a group of loans is insured in a single transaction, typically shortly after the loans have been originated). Among other items, Flow Basis business excludes Pool Insurance, which we originated prior to 2009.December 2018 |

| Foreclosure Stage Default | The Stagestage of Default indicating that thedefault of a loan in which a foreclosure sale has been scheduled or held |

| Freddie Mac | Federal Home Loan Mortgage Corporation |

Freddie Mac Agreement | The Master Transaction Agreement between Radian Guaranty and Freddie Mac entered into in August 2013 |

Front-end | With respect to credit risk transfer programs established by the GSEs, policies written on loans that are to be purchased by the GSEs in the future, as contrasted with loans that are already part of an existing GSE portfolio |

| GAAP | AccountingGenerally accepted accounting principles generally accepted in the U.S., as amended from time to time |

Green River Capital | Green River Capital LLC, a wholly-owned subsidiary of Clayton |

GSEsGSE(s) | Government-Sponsored Enterprises (Fannie Mae and Freddie Mac) |

| HARP | Home Affordable Refinance Program. See “Item 1. Business—Regulation—Federal Regulation—Homeowner Assistance Programs” in our 2017 Form 10-K for more information. Program |

| IBNR | Losses incurred but not reported |

| IIF | Insurance in force, equal to the aggregate unpaid principal balances of the underlying loans |

| IRC | Internal Revenue Code of 1986, as amended |

| IRS | Internal Revenue Service |

| IRS Matter | Our dispute with the IRS that we settled and fully resolved in the second quarter of 2018 that was related to the assessed tax liabilities, penalties and interest from the IRS’s examination of our 2000 through 2007 consolidated federal income tax returns. See Note 9 of Notes to Unaudited Condensed Consolidated Financial Statements for more information. |

| LAE | Loss adjustment expenses, which include the cost of investigating and adjusting losses and paying claims |

| Loss Mitigation Activity/Activities | Activities such as Rescissions, Claim Denials, Claim Curtailments and cancellations |

| LTV | Loan-to-value ratio, calculated as the percentage of the original loan amount to the original value of the property |

| Master Policies | The Prior Master Policy and the 2014 Master Policy, collectivelytogether |

| Minimum Required Assets | A risk-based minimum required asset amount, as defined in the PMIERs, calculated based on net RIF (RIF, net of credits permitted for reinsurance) and a variety of measures related to expected credit performance and other factors |

Model Act | Mortgage Guaranty Insurers Model Act, as issued by the NAIC to establish minimum capital and surplus requirements for mortgage insurers |

| Monthly and Other Recurring Premiums (or Recurring Premium Policies) | Insurance premiums or policies, respectively, where premiums are paid on a monthly or other installment basis, in contrast to Single Premium Policies |

Monthly Premium Policies | Insurance policies where premiums are paid on a monthly installment basis |

| Moody’s | Moody’s Investors Service |

|

| |

Term | Definition |

| Mortgage Insurance | Radian’s Mortgage InsuranceRadian's mortgage insurance and risk services business segment, which provides credit-related insurance coverage, principally through private mortgage insurance on residential first-lien mortgage loans, as well as other credit risk management solutions to mortgage lending institutions and mortgage credit investors |

| MPP Requirement | Certain states’ statutory or regulatory risk-based capital requirement that the mortgage insurer must maintain a minimum policyholder position, which is calculated based on both risk and surplus levels |

NAIC | National Association of Insurance Commissioners |

| NIW | New insurance written |

|

| |

| Term | Definition |

| NOL | Net operating loss; for tax purposes, accumulated during years a company reported more tax deductions than taxable income. NOLs may be carried back or carried forward a certain number of years, depending on each jurisdiction, when the NOL occurs and the type of legal entity, thus reducingvarious factors which can reduce a company’s tax liability |

OCI | Other comprehensive income (loss)liability. |

| Persistency Rate | The percentage of insurance in forceIIF that remains in force over a period of time |

| PMIERs | Private Mortgage Insurer Eligibility Requirements effective on December 31, 2015, issued by the GSEs under oversight of the FHFA to set forth requirements an approved insurer must meet and maintain to provide mortgage guaranty insurance on loans acquired by the GSEs |

| PMIERs 1.0 | The original PMIERs effective on December 31, 2015 |

| PMIERs 2.0 | RevisedThe revised PMIERs issued by the GSEs on September 27, 2018, which will becomebecame effective on March 31, 2019 |

| Pool Insurance | Pool Insurance differs from primary insurance in that our maximum liability is not limited to a specific coverage percentage on an individual mortgage loan. Instead, an aggregate exposure limit, or “stop loss,” is applied to the initial aggregate loan balance on a group or “pool” of mortgagesmortgages. |

| Prior Master Policy | Radian Guaranty’s master insurance policy, setting forth the terms and conditions of our mortgage insurance coverage, which was in effect prior to the effective date of itsthe 2014 Master Policy |

| QM | A mortgage that possesses certain low-risk characteristics that enable it to qualify for lender protection under the ability to repay rule instituted by the Dodd-Frank Act |

| QSR Program | The quota share reinsurance agreements entered into with a third-party reinsurance provider in the second and fourth quarters of 2012, collectively |

| Radian | Radian Group Inc. together with its consolidated subsidiaries |

| Radian Group | Radian Group Inc. |

| Radian Guaranty | Radian Guaranty Inc., a Pennsylvania domiciled insurance subsidiary of Radian Group |

| Radian Reinsurance | Radian Reinsurance Inc., a Pennsylvania domiciled insurance subsidiary of Radian Group |

| Radian Title Insurance | Radian Title Insurance Inc., formerly known as EnTitle Insurance, an Ohio domiciled insurance subsidiary of Radian Group |

| RBC States | Risk-based capital states, which are those states that currently impose a statutory or regulatory risk-based capital requirement |

Red Bell | Red Bell Real Estate, LLC, a wholly-owned subsidiary of Clayton |

| Reinstatements | Reversals of previous Rescissions, Claim Denials and Claim Curtailments |

REMIC | Real Estate Mortgage Investment Conduit |

REO | Real estate owned |

| Rescission | Our legal right, under certain conditions, to unilaterally rescind coverage on our mortgage insurance policies if we determine that a loan did not qualify for insurance |

| RIF | Risk in force; for primary insurance, RIF is equal to the underlying loan unpaid principal balance multiplied by the insurance coverage percentage, whereas for Pool Insurance, it represents the remaining exposure under the agreements |

| Risk-to-capital | Under certain state regulations, a minimummaximum ratio of statutory capitalnet RIF calculated relative to the level of net RIFstatutory capital |

| RMBS | Residential mortgage-backed securities |

| S&P | Standard & Poor’s Financial Services LLC |

| SAPP | Statutory accounting principles and practices, includeincluding those required or permitted, if applicable, by the insurance departments of the respective states of domicile of our insurance subsidiaries |

| SEC | United States Securities and Exchange Commission |

|

| |

Term | Definition |

Senior Notes due 2017 | Our 9.000% unsecured senior notes due June 2017 ($195.5 million original principal amount, of which the remaining outstanding principal was redeemed in August 2016) |

| Senior Notes due 2019 | Our 5.500% unsecured senior notes due June 2019 ($300 million original principal amount) |

| Senior Notes due 2020 | Our 5.250% unsecured senior notes due June 2020 ($350 million original principal amount) |

| Senior Notes due 2021 | Our 7.000% unsecured senior notes due March 2021 ($350 million original principal amount) |

| Senior Notes due 2024 | Our 4.500% unsecured senior notes due October 2024 ($450 million original principal amount) |

|

| |

| Term | Definition |

| Senior Notes due 2027 | Our 4.875% unsecured senior notes due March 2027 ($450 million original principal amount) |

| Services | Radian’s ServicesRadian's mortgage, real estate and title services business segment, which is primarily a fee-for-service business that offers a broad array of both mortgage, and real estate and title services to market participants across the mortgage and real estate value chain |

Single Premium NIW (or IIF) | New insurance written or insurance in force, respectively, on Single Premium Policies |

Single Premium Policy/Policy / Policies | Insurance policies where premiums are paid in a single payment, which includes policies written on an individual basis (as each loan is originated) and on an aggregated basis (in which each individual loan in a group of loans is insured in a single transaction, typically shortly after the loans have been originated) |

| Single Premium QSR Program | The 2016 Single Premium QSR Agreement and the 2018 Single Premium QSR Agreement, collectively |

Stage of Default | The stage a loan is in relative to the foreclosure process, based on whether a foreclosure sale has been scheduled or heldtogether |

| Statutory RBC Requirement | Risk-based capital requirement imposed by the RBC States, requiring a minimum surplus level and, in certain states, a minimum ratio of statutory capital relative to the level of risk |

| Surplus Note | An intercompany 0.000% surplus note issued by Radian Guaranty to Radian Group |

TCJA | H.R. 1, known as the Tax Cuts and Jobs Act, signed into law on December 22, 2017 |

Time in Default | The time period from the point a loan reaches default status (based on the month the default occurred) to the current reporting date |

| U.S. | The United States of America |

| U.S. Treasury | United States Department of the Treasury |

| VA | U.S. Department of Veterans Affairs |

ValuAmericaVIE | ValuAmerica, Inc., a wholly-owned subsidiary of ClaytonVariable interest entity |

Cautionary Note Regarding Forward-Looking Statements—Safe Harbor Provisions

All statements in this report that address events, developments or results that we expect or anticipate may occur in the future are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Exchange Act and the U.S. Private Securities Litigation Reform Act of 1995. In most cases, forward-looking statements may be identified by words such as “anticipate,” “may,” “will,” “could,” “should,” “would,” “expect,” “intend,” “plan,” “goal,” “contemplate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “seek,” “strategy,” “future,” “likely” or the negative or other variations on these words and other similar expressions. These statements, which may include, without limitation, projections regarding our future performance and financial condition, are made on the basis of management’s current views and assumptions with respect to future events. Any forward-looking statement is not a guarantee of future performance and actual results could differ materially from those contained in the forward-looking statement. These statements speak only as of the date they were made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. We operate in a changing environment where new risks emerge from time to time and it is not possible for us to predict all risks that may affect us. The forward-looking statements, as well as our prospects as a whole, are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in the forward-looking statements. These risks and uncertainties include, without limitation:

changes in economic and political conditions that impact the size of the insurable market, the credit performance of our insured portfolio, and our business prospects;

changes in the way customers, investors, ratings agencies, regulators or legislators perceive our performance, financial strength and future prospects;

Radian Guaranty’s ability to remain eligible under the PMIERs and other applicable requirements imposed by the FHFA and by the GSEs to insure loans purchased by the GSEs;GSEs, including potential future changes to the PMIERs which, among other things, may be impacted by the general economic environment and housing market, as well as the proposed Conservatorship Capital Framework (“CCF”) that would establish capital requirements for the GSEs, if the CCF is finalized;

our ability to successfully execute and implement our capital plans, including plans for expanding our risk distribution strategy through the capital markets and reinsurance markets, and to maintain sufficient holding company liquidity to meet our short- and long-term liquidity needs;

our ability to successfully execute and implement our business plans and strategies, including plans and strategies to reposition our Services segment as well as plans and strategies that require GSE and/or regulatory approvals and licenses;

our ability to maintain an adequate level of capital in our insurance subsidiaries to satisfy existing and future state regulatory requirements;

changes in the charters or business practices of, or rules or regulations imposed by or applicable to, the GSEs, which may include changes in the requirements to remain an approved insurer to the GSEs, the GSEs’ interpretation and application of the PMIERs, as well as potential future changes to the PMIERs requirements which, among other things, may be impactedimpacting loans purchased by the general economic environmentGSEs, such as whether GSE eligible loans meet the QM loan requirements under applicable law, requirements regarding mortgage credit and housing market, as well asloan size and the proposed Conservator Capital Framework (“CCF”) that would establish capital requirements for the GSEs, if the CCF is finalized;GSEs’ pricing;

changes in the current housing finance system in the U.S., including the role of the FHA, the GSEs and private mortgage insurers in this system;

any disruption in the servicing of mortgages covered by our insurance policies, as well as poor servicer performance;

a significant decrease in the Persistency Rates of our mortgage insurance on monthly premium products;

competition in our mortgage insurance business, including price competition and competition from the FHA and VA as well as from other forms of credit enhancement;enhancement, including GSE sponsored alternatives to traditional mortgage insurance;

the effect of the Dodd-Frank Wall Street Reform and Consumer Protection Act on the financial services industry in general, and on our businesses in particular;particular, including future changes to the QM loan requirements, which currently are subject to an Advanced Notice of Proposed Rulemaking issued by the CFPB;

legislative and regulatory activity (or inactivity), including the adoption of (or failure to adopt) new laws and regulations, or changes in existing laws and regulations, or the way they are interpreted or applied, including interpretations and guidance pertaining to recently enacted tax reform legislation;applied;

legal and regulatory claims, assertions, actions, reviews, audits, inquiries and investigations that could result in adverse judgments, settlements, fines, injunctions, restitutions or other relief that could require significant expenditures, new or increased reserves or have other effects on our business;

the amount and timing of potential settlements, payments or adjustments associated with federal or other tax examinations;

the amount and timing of potential settlements, payments or adjustments associated with federal or other tax examinations;

the possibility that we may fail to estimate accurately the likelihood, magnitude and timing of losses in establishing loss reserves for our mortgage insurance business or to accurately calculate and/or project our Available Assets and Minimum Required Assets under the PMIERs, including PMIERs 2.0, which will be impacted by, among other things, the size and mix of our IIF, the level of defaults in our portfolio, the level of cash flow generated by our insurance operations and our risk distribution strategies;

volatility in our financial results of operations caused by changes in the fair value of our assets and liabilities, including a significant portion of our investment portfolio;

potential future impairment charges related to our goodwill and other acquired intangible assets, and uncertainties regarding our ability to execute our restructuring plans within expected costs;assets;

changes in GAAP or SAPP rules and guidance, or their interpretation;

our ability to attract and retain key employees; and

legal and other limitations on dividends and other amounts we may receive from our subsidiaries.subsidiaries, including dividends or ordinary course distributions under our internal tax- and expense-sharing arrangements.

For more information regarding these risks and uncertainties as well as certain additional risks that we face, you should refer to the Risk Factors detailed in Item 1A of our 2017Annual Report on Form 10-K for the year ended December 31, 2018, and to subsequent reports and registration statements filed from time to time with the SEC. We caution you not to place undue reliance on these forward-looking statements, which are current only as of the date on which we issued this report. We do not intend to, and we disclaim any duty or obligation to, update or revise any forward-looking statements to reflect new information or future events or for any other reason.

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

Radian Group Inc.

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED) | | | ($ in thousands, except per-share amounts) | September 30,

2018 | | December 31,

2017 | September 30,

2019 | | December 31,

2018 |

| | | | | | | |

| Assets | | | | | | |

| Investments (Note 5) | | | | | | |

| Fixed-maturities available for sale—at fair value (amortized cost $3,838,823 and $3,426,217) | $ | 3,763,710 |

| | $ | 3,458,719 |

| |

| Trading securities—at fair value | 493,956 |

| | 606,401 |

| |

| Equity securities—at fair value (at December 31, 2017, classified as available for sale with related cost of $163,106) | 121,865 |

| | 162,830 |

| |

| Short-term investments—at fair value (includes $31,799 and $19,357 of reinvested cash collateral held under securities lending agreements) | 645,119 |

| | 415,658 |

| |

| Other invested assets—at fair value (amortized cost at December 31, 2017) | 3,585 |

| | 334 |

| |

| Fixed-maturities available for sale—at fair value (amortized cost $4,369,273 and $4,098,962) | | $ | 4,527,223 |

| | $ | 4,021,575 |

|

| Trading securities—at fair value (amortized cost of $307,891 and $468,696) | | 329,935 |

| | 469,071 |

|

| Equity securities—at fair value (cost of $119,408 and $139,377) | | 121,759 |

| | 130,565 |

|

| Short-term investments—at fair value (includes $34,767 and $11,699 of reinvested cash collateral held under securities lending agreements) | | 552,095 |

| | 528,403 |

|

| Other invested assets—at fair value | | 2,712 |

| | 3,415 |

|

| Total investments | 5,028,235 |

| | 4,643,942 |

| 5,533,724 |

| | 5,153,029 |

|

| Cash | 104,413 |

| | 80,569 |

| 49,393 |

| | 95,393 |

|

| Restricted cash | 9,925 |

| | 15,675 |

| 2,853 |

| | 11,609 |

|

| Accounts and notes receivable | 108,003 |

| | 72,558 |

| 144,113 |

| | 78,652 |

|

| Deferred income taxes, net (Note 9) | 134,201 |

| | 229,567 |

| — |

| | 131,643 |

|

| Goodwill and other acquired intangible assets, net (Note 6) | 55,707 |

| | 64,212 |

| 52,533 |

| | 58,998 |

|

| Prepaid reinsurance premium | 413,728 |

| | 386,509 |

| 374,339 |

| | 417,628 |

|

| Other assets (Note 8) | 415,272 |

| | 407,849 |

| 513,647 |

| | 367,700 |

|

| Total assets | $ | 6,269,484 |

| | $ | 5,900,881 |

| $ | 6,670,602 |

| | $ | 6,314,652 |

|

| | | | | | | |

| Liabilities and Stockholders’ Equity | | | | | | |

| Unearned premiums | $ | 747,921 |

| | $ | 723,938 |

| $ | 647,856 |

| | $ | 739,357 |

|

| Reserve for losses and loss adjustment expense (“LAE”) (Note 10) | 412,460 |

| | 507,588 |

| |

| Reserve for losses and loss adjustment expense (Note 10) | | 398,141 |

| | 401,361 |

|

| Senior notes (Note 11) | 1,029,511 |

| | 1,027,074 |

| 886,643 |

| | 1,030,348 |

|

| FHLB advances (Note 11) | | 104,492 |

| | 82,532 |

|

| Reinsurance funds withheld | 352,952 |

| | 288,398 |

| 352,532 |

| | 321,212 |

|

| Other liabilities (Note 12) | 379,362 |

| | 353,845 |

| |

| Other liabilities | | 358,431 |

| | 251,127 |

|

| Total liabilities | 2,922,206 |

| | 2,900,843 |

| 2,748,095 |

| | 2,825,937 |

|

| Commitments and contingencies (Note 13) |

| |

| |

| Commitments and contingencies (Note 12) | |

| |

|

| Stockholders’ equity | | | | | | |

| Common stock: par value $0.001 per share; 485,000,000 shares authorized at September 30, 2018 and December 31, 2017; 230,978,401 and 233,416,989 shares issued at September 30, 2018 and December 31, 2017, respectively; 213,333,428 and 215,814,188 shares outstanding at September 30, 2018 and December 31, 2017, respectively | 231 |

| | 233 |

| |

| Treasury stock, at cost: 17,644,973 and 17,602,801 shares at September 30, 2018 and December 31, 2017, respectively | (894,635 | ) | | (893,888 | ) | |

| Common stock: par value $0.001 per share; 485,000 shares authorized at September 30, 2019 and December 31, 2018; 220,174 and 231,132 shares issued at September 30, 2019 and December 31, 2018, respectively; 202,219 and 213,473 shares outstanding at September 30, 2019 and December 31, 2018, respectively | | 220 |

| | 231 |

|

| Treasury stock, at cost: 17,955 and 17,660 shares at September 30, 2019 and December 31, 2018, respectively | | (901,556 | ) | | (894,870 | ) |

| Additional paid-in capital | 2,720,626 |

| | 2,754,275 |

| 2,469,097 |

| | 2,724,733 |

|

| Retained earnings | 1,580,296 |

| | 1,116,333 |

| 2,229,107 |

| | 1,719,541 |

|

| Accumulated other comprehensive income (loss) (Note 15) | (59,240 | ) | | 23,085 |

| |

| Accumulated other comprehensive income (loss) (Note 14) | | 125,639 |

| | (60,920 | ) |

| Total stockholders’ equity | 3,347,278 |

| | 3,000,038 |

| 3,922,507 |

| | 3,488,715 |

|

| Total liabilities and stockholders’ equity | $ | 6,269,484 |

| | $ | 5,900,881 |

| $ | 6,670,602 |

| | $ | 6,314,652 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| | | | Three Months Ended

September 30, |

| Nine Months Ended

September 30, | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| (In thousands, except per-share amounts) | 2018 |

| 2017 |

| 2018 |

| 2017 | 2019 | | 2018 | | 2019 |

| 2018 |

| Revenues: | | | | | | | | | | | | | | |

| Net premiums earned—insurance | $ | 258,431 |

| | $ | 236,702 |

|

| $ | 752,325 |

|

| $ | 687,598 |

| $ | 281,185 |

| | $ | 258,431 |

| | $ | 843,863 |

|

| $ | 752,325 |

|

| Services revenue | 36,566 |

| | 39,571 |

|

| 106,558 |

|

| 115,400 |

| 42,509 |

| | 36,566 |

| | 114,565 |

|

| 106,558 |

|

| Net investment income | 38,995 |

| | 32,540 |

| | 110,424 |

| | 93,643 |

| 42,756 |

| | 38,995 |

| | 130,364 |

| | 110,424 |

|

| Net gains (losses) on investments and other financial instruments | (4,480 | ) | | 2,480 |

| | (30,771 | ) | | 4,960 |

| 13,009 |

| | (4,480 | ) | | 47,462 |

| | (30,771 | ) |

| Other income | 1,174 |

| | 760 |

| | 2,997 |

| | 2,118 |

| 879 |

| | 1,174 |

| | 2,677 |

| | 2,997 |

|

| Total revenues | 330,686 |

| | 312,053 |

| | 941,533 |

| | 903,719 |

| 380,338 |

| | 330,686 |

| | 1,138,931 |

| | 941,533 |

|

| Expenses: | | | | | | | | | | | | | | |

| Provision for losses | 20,881 |

| | 35,841 |

| | 77,501 |

| | 99,976 |

| 29,231 |

| | 20,881 |

| | 97,412 |

| | 77,501 |

|

| Policy acquisition costs | 5,667 |

| | 5,554 |

| | 18,780 |

| | 18,406 |

| 6,435 |

| | 5,667 |

| | 18,531 |

| | 18,780 |

|

| Cost of services | 25,854 |

| | 27,240 |

| | 73,185 |

| | 81,250 |

| 29,044 |

| | 25,854 |

| | 81,046 |

| | 73,185 |

|

| Other operating expenses | 70,125 |

| | 64,195 |

| | 203,552 |

| | 201,322 |

| 76,384 |

| | 70,125 |

| | 225,235 |

| | 203,552 |

|

| Restructuring and other exit costs (Note 1) | 4,464 |

| | 12,038 |

| | 5,940 |

| | 12,038 |

| |

| Restructuring and other exit costs | | — |

| | 4,464 |

| | — |

| | 5,940 |

|

| Interest expense | 15,535 |

| | 15,715 |

|

| 45,906 |

| | 47,832 |

| 13,492 |

| | 15,535 |

| | 44,150 |

| | 45,906 |

|

| Loss on induced conversion and debt extinguishment | — |

| | 45,766 |

| | — |

| | 51,469 |

| |

| Impairment of goodwill (Note 6) | — |

| | — |

| | — |

| | 184,374 |

| |

| Loss on extinguishment of debt | | 5,940 |

| | — |

| | 22,738 |

| | — |

|

| Amortization and impairment of other acquired intangible assets | 3,472 |

| | 2,890 |

|

| 8,968 |

|

| 25,042 |

| 2,139 |

| | 3,472 |

| | 6,465 |

|

| 8,968 |

|

| Total expenses | 145,998 |

| | 209,239 |

| | 433,832 |

| | 721,709 |

| 162,665 |

| | 145,998 |

| | 495,577 |

| | 433,832 |

|

| Pretax income | 184,688 |

|

| 102,814 |

|

| 507,701 |

|

| 182,010 |

| 217,673 |

| | 184,688 |

| | 643,354 |

|

| 507,701 |

|

| Income tax provision | 41,891 |

| | 37,672 |

|

| 41,469 |

| | 67,738 |

| 44,235 |

| | 41,891 |

| | 132,229 |

| | 41,469 |

|

| Net income | $ | 142,797 |

|

| $ | 65,142 |

|

| $ | 466,232 |

|

| $ | 114,272 |

| $ | 173,438 |

| | $ | 142,797 |

| | $ | 511,125 |

|

| $ | 466,232 |

|

| | | | | | | | | | | | | | | |

| Net income per share: | | | | | | | | | | | | | | |

| Basic | $ | 0.67 |

| | $ | 0.30 |

| | $ | 2.17 |

| | $ | 0.53 |

| $ | 0.85 |

| | $ | 0.67 |

| | $ | 2.45 |

| | $ | 2.17 |

|

| Diluted | $ | 0.66 |

| | $ | 0.30 |

| | $ | 2.13 |

| | $ | 0.52 |

| $ | 0.83 |

| | $ | 0.66 |

| | $ | 2.39 |

| | $ | 2.13 |

|

| | | | | | | |

|

| | | | | | |

|

|

| Weighted-average number of common shares outstanding—basic | 213,309 |

| | 215,279 |

| | 214,499 |

| | 215,194 |

| 203,107 |

| | 213,309 |

| | 208,561 |

| | 214,499 |

|

| Weighted-average number of common and common equivalent shares outstanding—diluted | 217,902 |

| | 219,391 |

| | 218,783 |

| | 220,230 |

| 208,691 |

| | 217,902 |

| | 213,963 |

| | 218,783 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| (In thousands) | 2018 | | 2017 | | 2018 | | 2017 |

| | | | | | | | |

| Net income | $ | 142,797 |

| | $ | 65,142 |

| | $ | 466,232 |

| | $ | 114,272 |

|

| Other comprehensive income, net of tax (Note 15): | | | | | | | |

| Unrealized gains (losses) on investments: | | | | | | | |

| Unrealized holding gains (losses) arising during the period | (5,341 | ) | | 6,239 |

| | (93,788 | ) | | 33,845 |

|

| Less: Reclassification adjustment for net gains (losses) included in net income | (4,044 | ) | | 111 |

| | (8,512 | ) | | (2,687 | ) |

| Net unrealized gains (losses) on investments | (1,297 | ) | | 6,128 |

| | (85,276 | ) | | 36,532 |

|

| Unrealized foreign currency translation adjustments | — |

| | 28 |

| | 3 |

| | 136 |

|

| Other comprehensive income (loss), net of tax | (1,297 | ) | | 6,156 |

| | (85,273 | ) | | 36,668 |

|

| Comprehensive income | $ | 141,500 |

| | $ | 71,298 |

| | $ | 380,959 |

| | $ | 150,940 |

|

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| (In thousands) | 2019 | | 2018 | | 2019 | | 2018 |

| | | | | | | | |

| Net income | $ | 173,438 |

| | $ | 142,797 |

| | $ | 511,125 |

| | $ | 466,232 |

|

| Other comprehensive income (loss), net of tax (Note 14): | | | | | | | |

| Unrealized gains (losses) on investments: | | | | | | | |

| Unrealized holding gains (losses) arising during the period | 40,654 |

| | (5,341 | ) | | 190,677 |

| | (93,788 | ) |

| Less: Reclassification adjustment for net gains (losses) included in net income | 3,477 |

| | (4,044 | ) | | 4,115 |

| | (8,512 | ) |

| Net unrealized gains (losses) on investments | 37,177 |

| | (1,297 | ) | | 186,562 |

| | (85,276 | ) |

| Net foreign currency translation adjustments | — |

| | — |

| | (3 | ) | | 3 |

|

| Other comprehensive income (loss), net of tax | 37,177 |

| | (1,297 | ) | | 186,559 |

| | (85,273 | ) |

| Comprehensive income | $ | 210,615 |

| | $ | 141,500 |

| | $ | 697,684 |

| | $ | 380,959 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN COMMON STOCKHOLDERS’ EQUITY (UNAUDITED)

| | | | Nine Months Ended September 30, | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| (In thousands) | 2018 | | 2017 | 2019 | | 2018 | | 2019 | | 2018 |

| Common Stock | | | | | | | | | | |

| Balance, beginning of period | $ | 233 |

| | $ | 232 |

| $ | 223 |

| | $ | 231 |

| | $ | 231 |

| | $ | 233 |

|

| Issuance of common stock under incentive and benefit plans | 1 |

| | 1 |

| — |

| | — |

| | 1 |

| | 1 |

|

| Shares repurchased under share repurchase program (Note 14) | (3 | ) | | — |

| |

| Shares repurchased under share repurchase program (Note 13) | | (3 | ) | | — |

| | (12 | ) | | (3 | ) |

| Balance, end of period | 231 |

| | 233 |

| 220 |

| | 231 |

| | 220 |

| | 231 |

|

| | | | | | | | | | | |

| Treasury Stock | | | | | | | | | | |

| Balance, beginning of period | (893,888 | ) | | (893,332 | ) | (901,419 | ) | | (894,610 | ) | | (894,870 | ) | | (893,888 | ) |

| Repurchases of common stock under incentive plans | (747 | ) | | (422 | ) | (137 | ) | | (25 | ) | | (6,686 | ) | | (747 | ) |

| Balance, end of period | (894,635 | ) | | (893,754 | ) | (901,556 | ) | | (894,635 | ) | | (901,556 | ) | | (894,635 | ) |

| | | | | | | | | | | |

| Additional Paid-in Capital | | | | | | | | | | |

| Balance, beginning of period | 2,754,275 |

| | 2,779,891 |

| 2,539,803 |

| | 2,715,426 |

| | 2,724,733 |

| | 2,754,275 |

|

| Issuance of common stock under incentive and benefit plans | 2,593 |

| | 4,761 |

| 1,660 |

| | 1,014 |

| | 4,418 |

| | 2,593 |

|

| Share-based compensation | 13,808 |

| | 10,290 |

| 5,169 |

| | 4,186 |

| | 15,119 |

| | 13,808 |

|

| Impact of extinguishment of convertible senior notes | — |

| | (52,408 | ) | |

| Cumulative effect of adopting the accounting standard update for share-based payment transactions | — |

| | 756 |

| |

| Termination of capped calls | — |

| | 4,109 |

| |

| Shares repurchased under share repurchase program (Note 14) | (50,050 | ) | | (6 | ) | |

| Shares repurchased under share repurchase program (Note 13) | | (77,535 | ) | | — |

| | (275,173 | ) | | (50,050 | ) |

| Balance, end of period | 2,720,626 |

| | 2,747,393 |

| 2,469,097 |

| | 2,720,626 |

| | 2,469,097 |

| | 2,720,626 |

|

| | | | | | | | | | | |

| Retained Earnings | | | | | | | | | | |

| Balance, beginning of period | 1,116,333 |

| | 997,890 |

| 2,056,175 |

| | 1,438,032 |

| | 1,719,541 |

| | 1,116,333 |

|

| Cumulative effect of adopting accounting standard updates | | — |

| | — |

| | — |

| | (663 | ) |

| Net income | 466,232 |

| | 114,272 |

| 173,438 |

| | 142,797 |

| | 511,125 |

| | 466,232 |

|

| Dividends declared | (1,606 | ) | | (1,614 | ) | (506 | ) | | (533 | ) | | (1,559 | ) | | (1,606 | ) |

| Cumulative effect of adopting the accounting standard update for financial instruments | 2,061 |

| | — |

| |

| Cumulative effect of adopting the accounting standard update for the reclassification of certain tax effects from accumulated other comprehensive income | (2,724 | ) | | — |

| |

| Cumulative effect of adopting the accounting standard update for share-based payment transactions, net of tax | — |

| | (491 | ) | |

| Balance, end of period | 1,580,296 |

| | 1,110,057 |

| 2,229,107 |

| | 1,580,296 |

| | 2,229,107 |

| | 1,580,296 |

|

| | | | | | | | | | | |

| Accumulated Other Comprehensive Income (Loss) | | | | | | | | | | |

| Balance, beginning of period | 23,085 |

| | (12,395 | ) | 88,462 |

| | (57,943 | ) | | (60,920 | ) | | 23,085 |

|

| Cumulative effect of adopting the accounting standard update for financial instruments | 224 |

| | — |

| |

| Cumulative effect of adopting the accounting standard update for the reclassification of certain tax effects from accumulated other comprehensive income | 2,724 |

| | — |

| |

| Cumulative effect of adopting accounting standard updates | | — |

| | — |

| | — |

| | 2,948 |

|

| Net unrealized gains (losses) on investments, net of tax | (85,276 | ) | | 36,532 |

| 37,177 |

| | (1,297 | ) | | 186,562 |

| | (85,276 | ) |

| Net foreign currency translation adjustment, net of tax | 3 |

| | 136 |

| — |

| | — |

| | (3 | ) | | 3 |

|

| Balance, end of period | (59,240 | ) | | 24,273 |

| 125,639 |

| | (59,240 | ) | | 125,639 |

| | (59,240 | ) |

| | | | | | | | | | | |

| Total Stockholders’ Equity | $ | 3,347,278 |

| | $ | 2,988,202 |

| $ | 3,922,507 |

| | $ | 3,347,278 |

| | $ | 3,922,507 |

| | $ | 3,347,278 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

| | Radian Group Inc. | CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) | | | | | | | | |

| (In thousands) | Nine Months Ended

September 30, | Nine Months Ended

September 30, |

| 2018 | | 2017 | 2019 | | 2018 |

| Cash flows from operating activities: | | | | | | |

| Net cash provided by (used in) operating activities | $ | 491,929 |

| | $ | 218,425 |

| $ | 506,805 |

| | $ | 491,929 |

|

| Cash flows from investing activities: | | | | | | |

| Proceeds from sales of: | | | | | | |

| Fixed-maturity investments available for sale | 577,034 |

| | 737,054 |

| |

| Fixed-maturities available for sale | | 770,393 |

| | 577,034 |

|

| Trading securities | 35,182 |

| | 176,448 |

| 120,875 |

| | 35,182 |

|

| Equity securities | 92,702 |

| | 23,423 |

| 52,295 |

| | 92,702 |

|

| Proceeds from redemptions of: | | | | | | |

| Fixed-maturity investments available for sale | 337,857 |

| | 377,219 |

| |

| Fixed-maturities available for sale | | 287,557 |

| | 337,857 |

|

| Trading securities | 53,437 |

| | 70,161 |

| 36,827 |

| | 53,437 |

|

| Purchases of: | | | | | | |

| Fixed-maturity investments available for sale | (1,307,335 | ) | | (1,491,083 | ) | |

| Fixed-maturities available for sale | | (1,352,883 | ) | | (1,307,335 | ) |

| Equity securities | (59,625 | ) | | (195,297 | ) | (45,748 | ) | | (59,625 | ) |

| Sales, redemptions and (purchases) of: | | | | | | |

| Short-term investments, net | (216,778 | ) | | 251,509 |

| (12,199 | ) | | (216,778 | ) |

| Other assets and other invested assets, net | 2,111 |

| | 596 |

| 687 |

| | 2,111 |

|

| Purchases of property and equipment, net | (20,323 | ) | | (25,173 | ) | (20,707 | ) | | (20,323 | ) |

| Acquisitions, net of cash acquired | (662 | ) | | (86 | ) | — |

| | (662 | ) |

| Net cash provided by (used in) investing activities | (506,400 | ) | | (75,229 | ) | (162,903 | ) | | (506,400 | ) |

| Cash flows from financing activities: | | | | | | |

| Dividends paid | (1,606 | ) | | (1,614 | ) | (1,559 | ) | | (1,606 | ) |

| Issuance of senior notes, net | — |

| | 443,250 |

| 442,498 |

| | — |

|

| Purchases and redemptions of senior notes | — |

| | (591,918 | ) | |

| Proceeds from termination of capped calls | — |

| | 4,109 |

| |

| Repayments and repurchases of senior notes | | (610,739 | ) | | — |

|

| Issuance of common stock | 1,128 |

| | 3,283 |

| 2,126 |

| | 1,128 |

|

| Purchase of common shares | (50,053 | ) | | (6 | ) | |

| Repurchases of common shares | | (275,185 | ) | | (50,053 | ) |

| Credit facility commitment fees paid | (643 | ) | | — |

| (710 | ) | | (643 | ) |

| Change in secured borrowings (Note 12) | 41,414 |

| | 36,782 |

| |

| Change in secured borrowings, net (with terms less than 3 months) | | 9,568 |

| | 41,414 |

|

| Proceeds from secured borrowings (with terms greater than 3 months) | 45,458 |

| | — |

| 73,011 |

| | 45,458 |

|

| Payments of secured borrowings (with terms greater than 3 months) | (3,000 | ) | | — |

| |

| Repayment of other borrowings | (133 | ) | | (207 | ) | |

| Repayments of secured borrowings (with terms greater than 3 months) | | (37,550 | ) | | (3,000 | ) |

| Repayments of other borrowings | | (114 | ) | | (133 | ) |

| Net cash provided by (used in) financing activities | 32,565 |

| | (106,321 | ) | (398,654 | ) | | 32,565 |

|

| Effect of exchange rate changes on cash and restricted cash | — |

| | 116 |

| (4 | ) | | — |

|

| Increase (decrease) in cash and restricted cash | 18,094 |

| | 36,991 |

| (54,756 | ) | | 18,094 |

|

| Cash and restricted cash, beginning of period | 96,244 |

| | 61,814 |

| 107,002 |

| | 96,244 |

|

| Cash and restricted cash, end of period | $ | 114,338 |

| | $ | 98,805 |

| $ | 52,246 |

| | $ | 114,338 |

|

See Notes to Unaudited Condensed Consolidated Financial Statements.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

1. Condensed Consolidated Financial Statements—Business Overview Recent Developments and Significant Accounting Policies

Business Overview

We are a diversified mortgage and real estate services business, providing both credit-related insurance coverage and other credit risk management solutions, as well as a broad array of mortgage, and real estate and title services. We have two2 reportable business segments—Mortgage Insurance and Services.

Mortgage Insurance

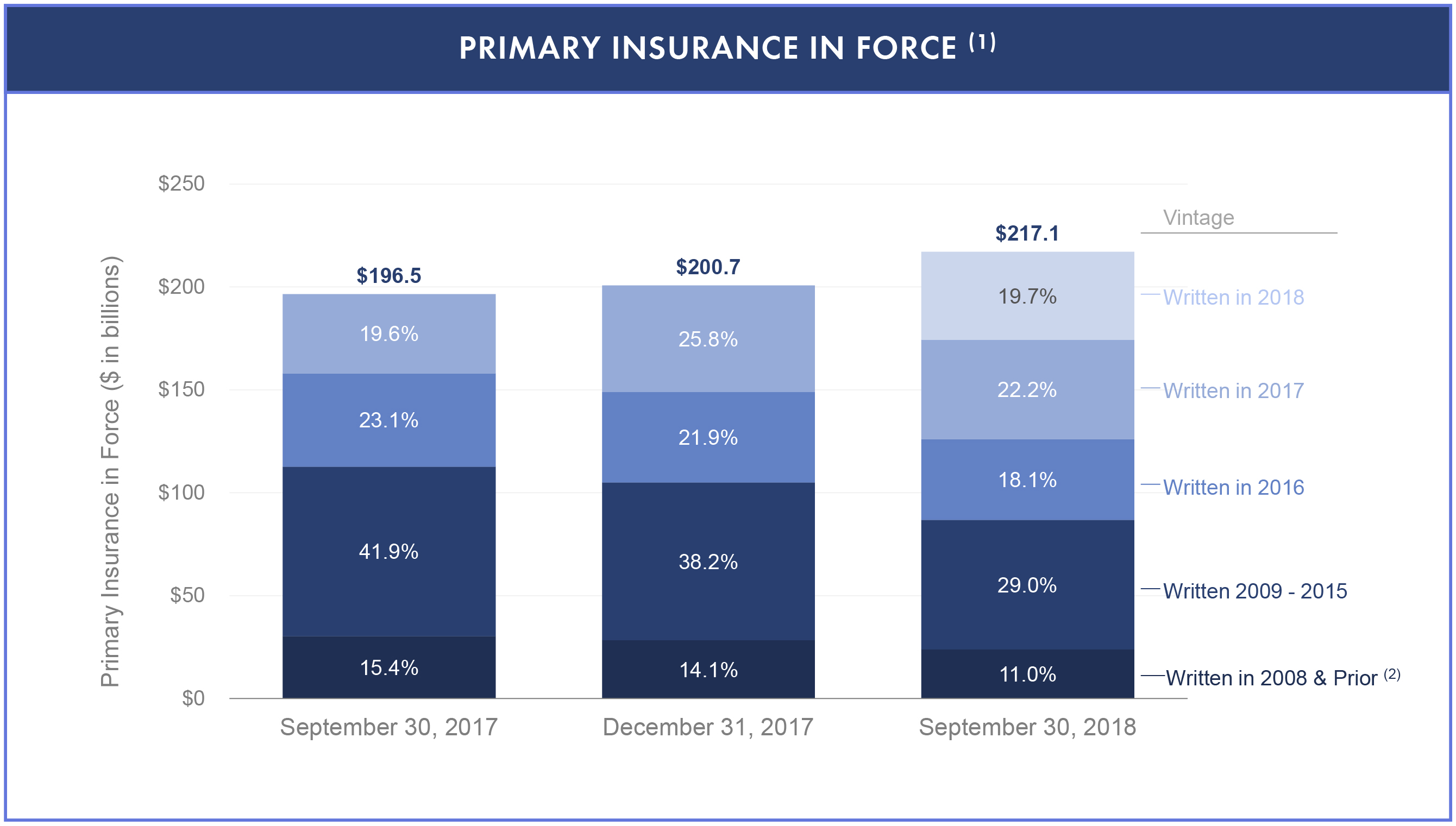

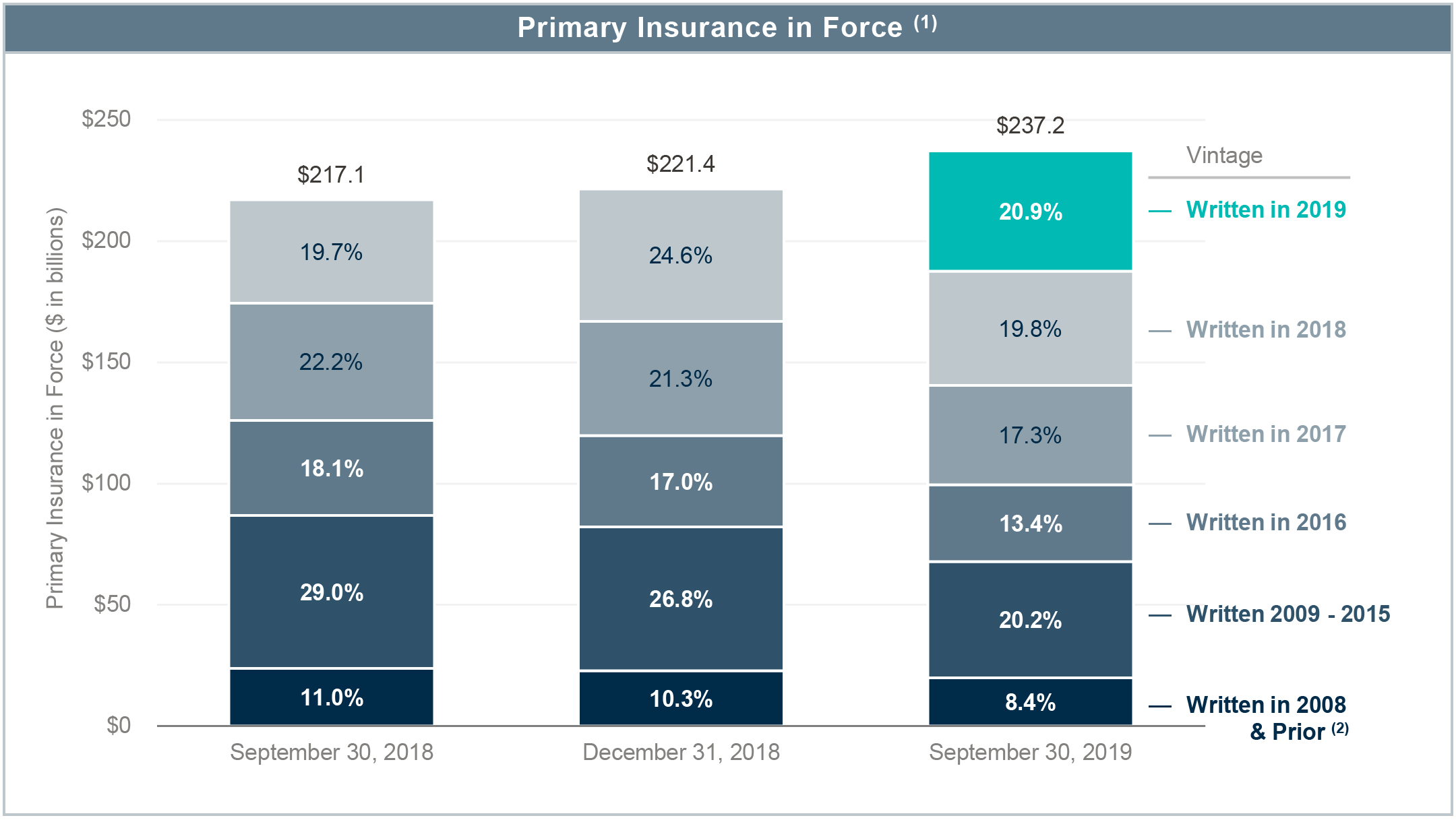

Our Mortgage Insurance segment provides credit-related insurance coverage, principally through private mortgage insurance on residential first-lien mortgage loans, as well as other credit risk management solutions, to mortgage lending institutions and mortgage credit investors. We provide our mortgage insurance products and services mainly through our wholly-owned subsidiary, Radian Guaranty. Private mortgage insurance plays an important role in the U.S. housing finance system because it promotes affordable home ownership and helps protect mortgage lenders, investors and other beneficiaries by mitigating default-related losses on residential mortgage loans. Generally, these loans are made to home buyershomebuyers who make down payments of less than 20% of the purchase price for their home or, in the case of refinancings, have less than 20% equity in their homes.home. Private mortgage insurance also facilitates the sale of these low down payment loans in the secondary mortgage market, most of which are currently sold to the GSEs. Our total direct primary mortgage insuranceIIF and RIF was $55.6were $237.2 billion and $60.4 billion, respectively, as of September 30, 2018.

The GSEs and state insurance regulators impose various capital and financial requirements on our insurance subsidiaries. These include Risk-to-capital, other risk-based capital measures and surplus requirements, as well as the PMIERs financial requirements discussed below. Failure to comply with these capital and financial requirements may limit the amount of insurance that our insurance subsidiaries may write or prohibit our insurance subsidiaries from writing insurance altogether. The GSEs and state insurance regulators also possess significant discretion with respect to our insurance subsidiaries and all aspects of their businesses. See Note 16 for additional regulatory information.

PMIERs. In order to be eligible to insure loans purchased by the GSEs, mortgage insurers such as Radian Guaranty must meet the GSEs’ eligibility requirements, or PMIERs. At September 30, 2018, Radian Guaranty is an approved mortgage insurer under the PMIERs and is in compliance with the PMIERs financial requirements.

The PMIERs are comprehensive, covering virtually all aspects of the business and operations of a private mortgage insurer, including internal risk management and quality controls, the relationship between the GSEs and the approved insurer as well as the approved insurer’s financial condition. In addition, the GSEs have a broad range of consent rights under the PMIERs, and require private mortgage insurers to obtain the prior consent of the GSEs before taking certain actions, which may include paying dividends, entering into various intercompany agreements, and commuting or reinsuring risk, among others. If Radian Guaranty is unable to satisfy the requirements set forth in the PMIERs, the GSEs could restrict it from conducting certain types of business with them or take actions that may include not purchasing loans insured by Radian Guaranty.

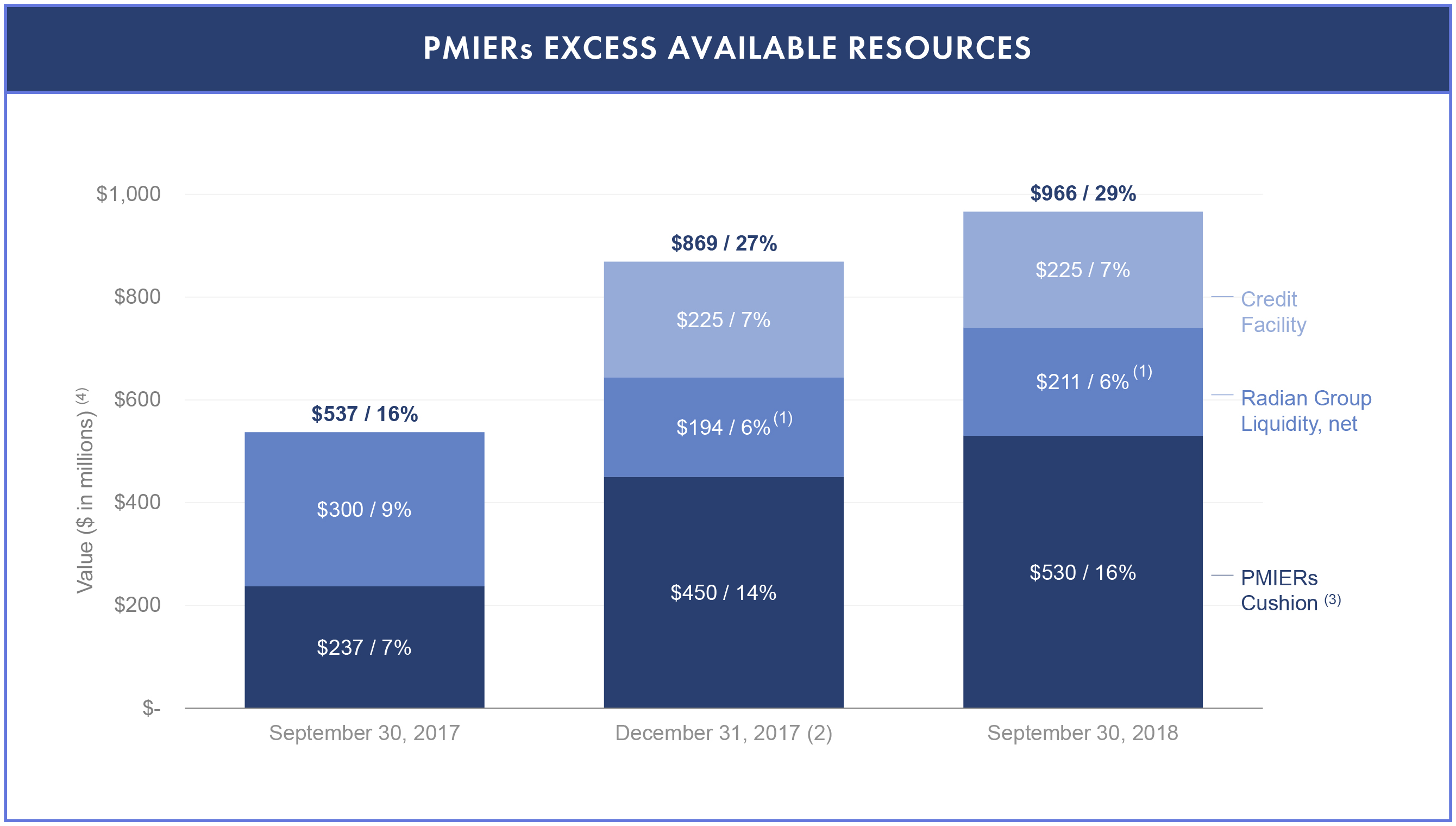

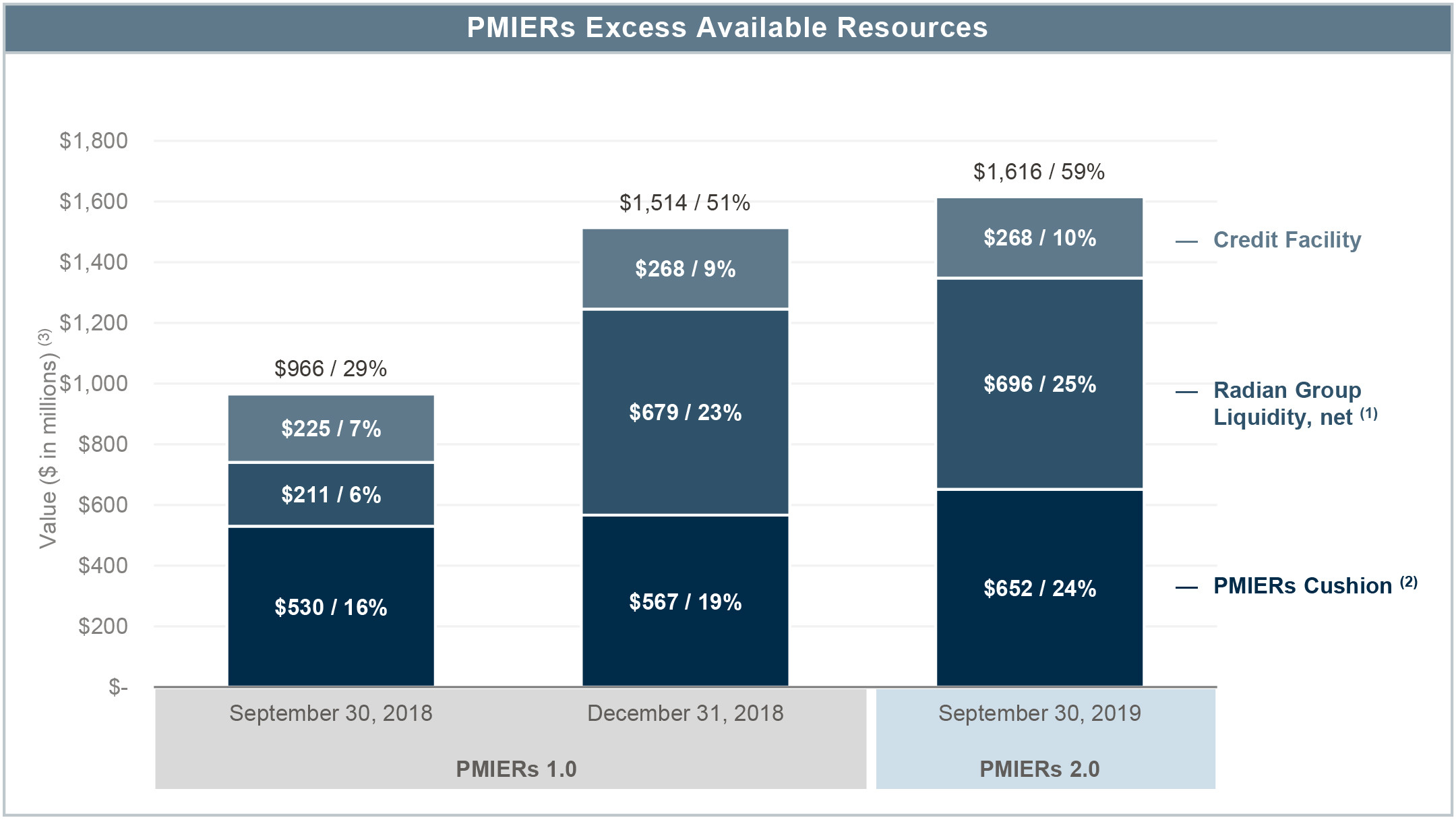

The PMIERs financial requirements require that a mortgage insurer’s Available Assets meet or exceed its Minimum Required Assets. The GSEs may amend the PMIERs at any time, and they have broad discretion to interpret the requirements, which could impact the calculation of Radian Guaranty’s Available Assets and/or Minimum Required Assets. On September 27, 2018, the GSEs issued PMIERs 2.0, which will become effective on March 31, 2019. Radian expects that it will be able to fully comply with PMIERs 2.0 and maintain an excess of Available Assets over Minimum Required Assets as of the effective date.

Services

Our Services segment is primarily a fee-for-service business that offers a broad array of services to market participants across the mortgage and real estate value chain. These services comprise mortgage services, real estate services and title services, including technology-basedtechnology and turn-key solutions, that provide information and other resources and services used to originate, evaluate, acquire, securitize, service and monitor residential real estate and loans secured by residential real estate. We provide theseThese services are primarily provided to among others, mortgage lenders, financial institutions, mortgage and real estate investors and government entities.

Our In addition, we provide title insurance to mortgage services include transaction management services such as loan review, RMBS securitization and distressed asset reviews, servicer and loan surveillance and underwriting. We offer a comprehensive suite of real estate services that includes software solutions and platforms,lenders as well as digitally delivered services, including: REO asset management; review

Radian Group Inc.

Notesdirectly to Unaudited Condensed Consolidated Financial Statements — (Continued)

and valuation services related to single family rental properties; real estate valuation services and real estate brokerage services. Our title services include title search, title insurance, settlement and closing services.

2018 Developments

Capital and Liquidity Actions. On August 9, 2017, Radian Group’s board of directors authorized the Company to repurchase up to $50 million of its common stock. The Company completed this program during the first half of 2018 by purchasing 3,022,856 shares at an average price of $16.56 per share, including commissions.

On August 16, 2018, Radian Group’s board of directors approved a new share repurchase program that authorizes the Company to repurchase up to $100 million of its common stock in the open market or in privately negotiated transactions until expiration of the program on July 31, 2019. As of September 30, 2018, the full purchase authority of up to $100 million remained available under this program. See Note 14 for additional information.

Restructuring and Other Exit Costs. As a result of the Company’s continued implementation of its 2017 plan to restructure the Services business, in the three months ended September 30, 2018, pretax restructuring charges of $0.9 million were recognized, which include: (i) $0.4 million in cash expenses and (ii) $0.5 million of asset impairment charges. For the nine months ended September 30, 2018, pretax restructuring charges of $2.4 million were recognized, including: (i) $1.9 million of cash expenses; (ii) $0.6 million asset impairment charges; and (iii) an adjustment to the previously recognized loss related to the sale of our EuroRisk business. We expect to incur additional pretax charges of approximately $0.2 million under this restructuring plan, all of which represent cash payments. These remaining charges are expected to be recognized by December 31, 2018. Total estimated restructuring charges for 2018 of approximately $2.6 million are expected to consist of: (i) asset impairment charges of approximately $0.5 million; (ii) employee severance and benefit costs of approximately $0.8 million; and (iii) facility and lease termination costs of approximately $1.3 million. See Notes 1 and 7 of Notes to Consolidated Financial Statements in our 2017 Form 10-K for additional information, including the events that led to the restructuring plan.

We review assets for impairment in accordance with the accounting guidance for long-lived assets. As part of this assessment, during the three months ended September 30, 2018, we incurred $3.6 million of other exit costs associated with impairment of internal-use software that was in addition to the asset impairment charges recognized as part of the restructuring charges associated with our services business.

IRS Matter. Radian finalized a settlement with the IRS which resolved the issues and concluded all disputes related to the IRS Matter. In the three-month period ended June 30, 2018, we recorded tax benefits of $73.6 million, which includes both the impact of the settlement with the IRS as well as the reversal of certain previously accrued state and local tax liabilities. Under the terms of the settlement, Radian will submit to the IRS approximately $31 million of its $89 million “qualified deposits” with the U.S. Treasury, and the remaining balance will be returned to Radian. See Note 9 for additional information.borrowers.

Significant Accounting Policies

Basis of Presentation

Our condensed consolidated financial statements are prepared in accordance with GAAP and include the accounts of Radian Group Inc. and its subsidiaries. All intercompany accounts and transactions, and intercompany profits and losses, have been eliminated. We have condensed or omitted certain information and footnote disclosures normally included in consolidated financial statements prepared in accordance with GAAP pursuant to the instructions set forth in Article 10 of Regulation S-X of the SEC.

We refer to Radian Group Inc. together with its consolidated subsidiaries as “Radian,” the “Company,” “we,” “us” or “our,” unless the context requires otherwise. We generally refer to Radian Group Inc. alone, without its consolidated subsidiaries, as “Radian Group.” Unless otherwise defined in this report, certain terms and acronyms used throughout this report are defined in the Glossary of Abbreviations and Acronyms included as part of this report.

The financial information presented for interim periods is unaudited; however, such information reflects all adjustments that are, in the opinion of management, necessary for the fair statement of the financial position, results of operations, comprehensive income and cash flows for the interim periods presented. Such adjustments are of a normal recurring nature. The year-end condensed balance sheet data was derived from our audited financial statements, but does not include all disclosures required by GAAP. These

To fully understand the basis of presentation, these interim financial statements and related notes contained herein should be read in conjunction with the audited financial statements and notes thereto included in our 20172018 Form 10-K. The results of operations for interim periods are not necessarily indicative of results to be expected for the full year or for any other period. Certain prior period amounts have been reclassified to conform to current period presentation.

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

Use of Estimates

The preparation of financial statements in conformity with GAAP requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of our contingent assets and liabilities at the dates of the financial statements, as well as the reported amounts of revenues and expenses during the reporting periods. While the amounts

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements (Continued)

included in our condensed consolidated financial statements include our best estimates and assumptions, actual results may vary materially.

Other Significant Accounting Policies

See Note 2 of Notes to Consolidated Financial Statements in our 20172018 Form 10-K for information regarding other significant accounting policies. There have been no significant changes in our significant accounting policies from those discussed in our 20172018 Form 10-K, other than described below including in ““——Revenue Recognition” and “—Recent Accounting Pronouncements—Accounting Standards Adopted During 2018.2019.”

Revenue Recognition

The FASB issued an update to the accounting standard regarding revenue recognition, Revenue from Contracts with Customers, which establishes principles for reporting information about the nature, amount, timing and uncertainty of revenue and cash flows arising from our contracts with customers to provide services. We adopted this update effective January 1, 2018, using the modified retrospective approach. The principle of this update requires an entity to recognize revenue representing the transfer of services to customers in an amount that reflects the consideration that it expects to be entitled to receive in exchange for those services, recognized as the performance obligations are satisfied.

The majority of our revenue-generating transactions are not subject to the new standard as this update did not change revenue recognition principles related to our investments and insurance products, which together represented the majority of our total revenue for the nine months ending September 30, 2018 and are subject to other GAAP guidance discussed elsewhere within our disclosures. This update is primarily applicable to revenues from our Services segment. See “—Business Overview—Services” for information about the services we offer.

The table below represents the disaggregation of Services revenues by revenue type:

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| (In thousands) | 2018 | | 2017 | | 2018 | | 2017 |

| Services segment revenue | | | | | | | |

| Mortgage Services | $ | 14,663 |

| | $ | 17,005 |

| | $ | 44,998 |

| | $ | 53,158 |

|

| Real Estate Services | 20,920 |

| | 17,386 |

| | 58,124 |

| | 49,863 |

|

| Title Services | 2,198 |

| | 6,671 |

| | 6,933 |

| | 18,105 |

|

Total (1) | $ | 37,781 |

| | $ | 41,062 |

| | $ | 110,055 |

| | $ | 121,126 |

|

______________________

| |

(1) | Includes inter-segment revenues of $0.8 million and $2.7 million for the three and nine months ended September 30, 2018 and $1.5 million and $5.7 million for the three and nine months ended September 30, 2017, respectively. For the three and nine months ended September 30, 2018, amounts exclude $3.1 million and $5.5 million, respectively, of Services segment net premiums earned—insurance and net investment income, as both are excluded from the scope of the revenue recognition standard. See Note 3 for segment information.

|

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

Our Services segment revenues are recognized over time and measured each period based on the progress to date as services are performed and made available to customers. Our contracts with customers, including payment terms, are generally short-term in nature; therefore, any impact related to timing is immaterial. Revenue recognized related to services made available to customers and billed is reflected in accounts receivables. Revenue recognized related to services performed and not yet billed is recorded in unbilled receivables and reflected in other assets. We have no material bad-debt expense. The following represents balances related to Services contracts as of the dates indicated:

|

| | | | | | | |

| (In thousands) | September 30, 2018 | | December 31, 2017 |

| Accounts Receivable - Services Contracts | $ | 12,544 |

| | $ | 17,391 |

|

| Unbilled Receivables - Services Contracts | 19,580 |

| | 22,257 |

|

| Deferred Revenues - Services Contracts | 4,131 |

| | 3,235 |

|

Revenue expected to be recognized in any future period related to remaining performance obligations, such as contracts where revenue is recognized as invoiced and contracts with variable consideration related to undelivered performance obligations, is not material.

Fee-for-Service Contracts

Generally, our contracts with our clients do not include minimum volume commitments and can be terminated at any time by our clients. Although some of our contracts and assignments are recurring in nature, and include repetitive monthly assignments, a significant portion of our engagements are transactional in nature and may be performed in connection with securitizations, loan sales, loan purchases or other transactions. Due to the transactional nature of our business, our Services segment revenues may fluctuate from period to period as transactions are commenced or completed. We do not recognize revenue or expense related to amounts advanced by us and subsequently reimbursed by clients for maintenance or repairs because we do not take control of the service prior to the client taking control. We record an expense if an advance is made that is not in accordance with a client contract and the client is not obligated to reimburse us.

Due to the nature of the services provided, our Services arrangements with customers may include any of the following three basic types of contracts:

Fixed-Price Contracts. We use fixed-price contracts in our real estate valuation and component services, our loan review, underwriting and due diligence services as well as our title and closing services. We also use fixed-price contracts in our surveillance business for our servicer oversight services and RMBS surveillance services, and in our asset management business activities. Under fixed-price contracts we agree to perform the specified services and deliverables for a pre-determined per-unit or per-file price or day rate. Each service qualifies as a separate performance obligation and revenue is recognized as the service performed is made available to the client.

Time-and-Expense Contracts. The Services segment also derives a portion of its revenue from professional service activities under time-and-expense contracts. In these types of contracts, we are paid a fixed hourly rate, and we are reimbursed for billable out-of-pocket expenses as work is performed. These contracts are used in our loan review, underwriting and due diligence services. Services revenue consisting of billed time fees and pass-through expenses is recorded over time and based on the progress to date as services are performed and made available to customers. Services revenue may also include expenses billed to clients, which includes travel and other out-of-pocket expenses, and other reimbursable expenses.

Percentage-of-Sale Contracts. Under percentage-of-sale contracts, we are paid a contractual percentage of the sale proceeds upon the sale of each property. These contracts are only used for a portion of our REO management services and our real estate brokerage services. In addition, through the use of our proprietary technology, property leads are sent to select clients. Revenue attributable to services provided under a percentage-of-sale contract is recognized over time and measured based on the progress to date and typically coincides with the client’s successful closing on the property. The revenue recognized for these transactions is based on a percentage of the sale.

In certain instances, fees are received at the time that an asset is assigned to Radian for management. These fees are recorded as deferred revenue and are recognized over time based on progress to date and the availability to customers.

Recent Accounting Pronouncements

Accounting Standards Adopted During 2018. 2019.In May 2014, the FASB issued an update to the accounting standard regarding revenue recognition. In July 2015, the FASB delayed the effective date for this updated standard for public companies to interim and annual periods beginning after December 15, 2017, and subsequently issued various clarifying updates. Our

Radian Group Inc.

Notes to Unaudited Condensed Consolidated Financial Statements — (Continued)

adoption of this standard, effective We adopted ASU 2016-02, Leases (“ASU 2016-02”), on January 1, 2018, had no impact on our financial statements. The disclosures required by2019. Most significantly, this update are included above in “—Revenue Recognition.”

In January 2016, the FASB issued an update that makes certain changes to the standard for the accounting of financial instruments. Among other things, the update requires: (i) equity investments to be measured at fair value with changes in fair value recognized in net income; (ii) the use of the exit price notion when measuring the fair value of financial instruments for disclosure purposes; (iii) separate presentation of financial assets and financial liabilities by measurement category and form of financial asset; and (iv) separate presentation in other comprehensive income of the portion of the total change in the fair value ofrequires a liability resulting from a change in the instrument-specific credit risk (also referred to as “own credit”) when the organization has elected to measure the liability at fair value in accordance with the fair value option for financial instruments. The update also eliminates the requirement to disclose the methods and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet. This update is effective for public companies for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. In February 2018, the FASB issued technical corrections related to this update, which addresses common questions regarding the application and adoption of the new guidance and the subsequent amendments. As a result of adopting these updates, equity securities are no longer classified as available for sale securities and changes in fair value are recognized through earnings. Consequently, we recorded a cumulative effect adjustment to retained earnings from accumulated other comprehensive income representing unrealized losses related to equity securities in the amount of $0.2 million, net of tax. In addition, we elected to utilize net asset value as a practical expedient to measure certain other investments, which resulted in an increase to other invested assets with an offset to retained earnings in the amount of $2.3 million, net of tax. Our adoption of both these updates effective January 1, 2018 resulted in a net increase to retained earnings of $2.1 million. See Notes 4 and 5 for additional information.

In February 2018, the FASB issued an update to the accounting standard regarding income statement reporting of comprehensive income and reclassification of certain tax effects from accumulated other comprehensive income. The amendments in this update allow a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the TCJA. The provisions of this update are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. Early adoption is permitted, including adoption in an interim period, for reporting periods for which financial statements have not been available for issuance. We elected to early adopt this update effective January 1, 2018. As a result we recorded a reclassification adjustment from other comprehensive income to retained earnings in the amount of $2.7 million. See Note 9 for additional information regarding the TCJA.