UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q10-Q/A

(Amendment No. 1)

(Mark One)

|

| |

x☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended SeptemberJune 29, 2018

2019

or

|

| |

o☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________to _________

Commission File Number: 001-12696

Plantronics, Inc.

(Exact name of registrant as specified in its charter)

|

| |

| Delaware | 77-0207692 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

345 Encinal Street

Santa Cruz, California95060

(Address of principal executive offices)

(Zip Code)

(831) (831) 426-5858

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act

|

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 par value | PLT | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx☒ No o☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesx☒ No o☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | |

Large accelerated filerx | ☒ | Accelerated filero | ☐ |

Non-accelerated filero | ☐ | Smaller reporting companyo | Emerging growth company o

☐ |

| | | (Do not check if a smaller reporting company)Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o ☐No x☒

As of November 2, 2018, 39,803,774July 31, 2019, 39,575,910 shares of the registrant's common stock were outstanding.

EXPLANATORY NOTE

This Amendment No. 1 on Form 10-Q/A (the “Amendment”) of Plantronics, Inc. (the “Company”) amends the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2019, originally filed with the Securities and Exchange Commission on August 6, 2019 (the “Original Report”). The Original Report inadvertently excluded certain XBRL information in portions of the financial statements and accompanying notes to the condensed consolidated financial statements.

This Amendment No. 1 includes the XBRL information and does not reflect events that may have occurred subsequent to the original filing date, and does not modify or update in any way disclosures made in the Original Report. No other changes have been made to the Original Report.

As required by Rule 12b-15 of the Securities Exchange Act of 1934, as amended, this Amendment contains new certifications by the Company’s principal executive officer and principal financial officer, which are being filed as exhibits to the Amendment.

Plantronics, Inc.

FORM 10-Q

TABLE OF CONTENTS

|

| |

| PART I. FINANCIAL INFORMATION | Page No. |

| | |

| |

| | |

| |

| |

| |

| | |

| |

| | |

| |

| |

| |

| | |

| |

| |

| |

| | |

| |

| |

| |

| |

| |

| | |

| |

| |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| |

| |

| | |

| PART II. OTHER INFORMATION | |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

Plantronics® and, Poly®, Simply Smarter Communications® , and the propeller design are trademarks or registered trademarks of Plantronics, Inc. All other trademarks are the property of their respective owners.

DECT™ is a trademark of ETSI registered for the benefit of its members in France and other jurisdictions.

The Bluetooth name and the Bluetooth® trademarks are owned by Bluetooth SIG, Inc. and are used by Plantronics, Inc. under license. All other trademarks are the property of their respective owners.

Part I -- FINANCIAL INFORMATION

Management’s Discussion and Analysis of Financial Condition and Results of Operations

CERTAIN FORWARD-LOOKING INFORMATION:

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 ("Securities Act") and Section 21E of the Securities Exchange Act of 1934 ("Exchange Act"). Forward-looking statements may generally be identified by the use of such words as "anticipate," "believe," “could,” "expect," "intend," “may,” "plan," "potential," "shall," "will," “would,” or variations of such words and similar expressions, or the negative of these terms. Specific forward-looking statements contained within this Form 10-Q include, but are not limited to, statements regarding (i) our beliefs regarding the EnterpriseUC&C market, market dynamics and opportunities, and customer and partner behavior as well as our position in the market, (ii) our expectations for the impact of the Acquisition as it relates to our strategic vision and additional market opportunities for our combined hardware and services offerings, as well as our plans and expectation for the integration of the operations of Polycom, (iii) our beliefs regarding the Consumer market, our new product introductions and the expected effect of such introductions, (iii) our belief that our "as-a-service" offerings will benefit ourfuture enterprise growth long-term but their contribution will not be material in the near term,drivers, (iv) our intention to provide customer data insight through softwareexpectations regarding the impact of UC&C on headset adoption and service solutions,how it may impact our investment and partnering activities, (v) the Unified Communications ("UC") market, including adoption of UC products, our position,expectations for new and timingnext generation product and growth expectations in this market,services offerings, (vi) our plans regarding our "as a service" offerings including sales and marketing efforts, (vii) our intentions regarding investments in long-term growth opportunities and our core research and development efforts, in particular in the UC market, (viii) our intentions regarding the focus of our sales, marketing and customer services and support teams, on UC, (ix) the future of UC technologies, including the transition of businesses to UC-supported systems and the effects on headset adoption and use, enterprises that adopt UC and our revenue opportunity and profit growth, (x)(vii) our expenses, including research, development and engineering expenses and selling, general and administrative expenses, (xi) fluctuations in our cash provided by operating activities as a result of various factors, including fluctuations in revenues and operating expenses, the timing of compensation-related payments including stock based compensation, timing of product shipments, accounts receivable collections, inventory and supply chain management, and the timing and amount of taxes and other payments, (xii) our future tax rate and payments related to unrecognized tax benefits, (xiii) our anticipated range of capital expenditures for the remainder of Fiscal Year 20182020 and the sufficiency of our cash, cash equivalents, and cash from operations to sustain future operations and discretionary cash requirements, (xiv) our ability to pay future stockholder dividends, (xv) our ability to draw funds on our credit facility as needed, (xvi) the sufficiency of our capital resources to fund operations, and other statements regarding our future operations, financial condition and prospects, and business strategies. Such forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties that may cause actual results to differ materially from the forward-looking statements. Factors that could cause actual results and events to differ materially from such forward-looking statements are included, but not limited to, those discussed in this Quarterly Report on Form 10-Q; in Part I, "Item 1A. Risk Factors" of our Annual Report on Form 10-K for the fiscal year ended March 31, 2018,2019, filed with the Securities and Exchange Commission (“SEC”) on May 9, 2018;17, 2019; and other documents we have filed with the SEC. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by applicable law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

OVERVIEW

We are a leading global designer, manufacturer, and marketer of lightweightintegrated communications and collaboration solutions that span headsets, telephone headset systems, otheropen SIP desktop phones, audio and video conferencing, cloud management and analytics software solutions, and services. Our major product categories are Enterprise Headsets, which includes corded and cordless communication headsets; Consumer Headsets, which includes Bluetooth and corded products for mobile device applications, personal computer and gaming; Voice, Video, and Content Sharing Solutions, which includes open SIP desktop phones, conference room phones, and video endpoints, including cameras, speakers and accessories for the worldwide business and consumer markets under the Plantronics brand. After July 2, 2018, we also becamemicrophones. All of our solutions are designed to work in a leading global providerwide range of open, standards-based Unified Communications & Collaboration "UC("UC&C"), Unified Communication as a Service ("UCaaS"), and Video as a Service ("VaaS") environments. Our RealPresence collaboration solutions range from infrastructure to endpoints and allow people to connect and collaborate globally and naturally. In addition, we offer comprehensive support services including support for voice, video and content sharingour solutions and hardware devices, as well as professional, hosted, and managed services. We continue to operate under a comprehensive linesingle operating segment.

We sell our Enterprise products through a high-touch sales team and a well-developed global network of supportdistributors and channel partners including value-added resellers, integrators, direct marketing resellers, service atproviders, and resellers. We sell our Consumer products through both traditional and online consumer electronics retailers, consumer product retailers, office supply distributors, wireless carriers, catalog and mail order companies, and mass merchants. We have well-established distribution channels in the workplace underAmericas, Europe, Middle East, Africa, and Asia Pacific where use of our products is widespread.

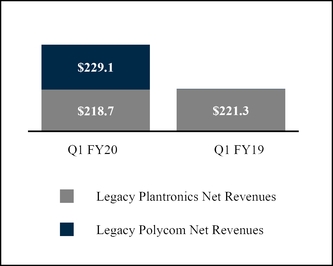

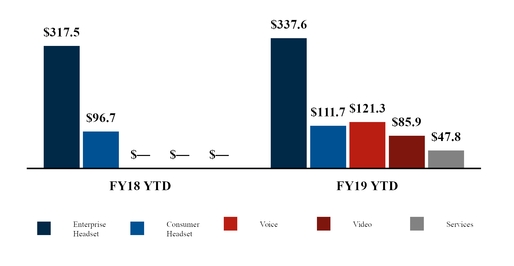

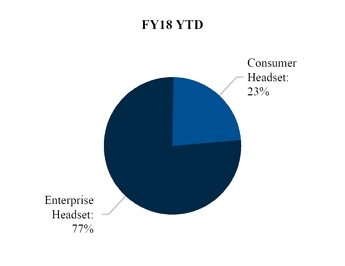

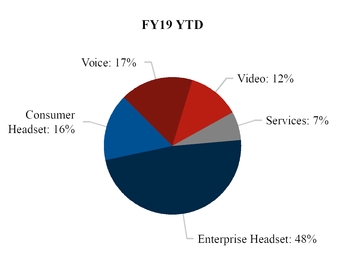

Total Net Revenues (in millions)

Compared to the Polycom brand.

On July 2, 2018, we completedfirst quarter of Fiscal Year 2019 total net revenues increased 102% to $447.8 million; the increase in total net revenues is primarily related to our acquisition (the “Acquisition”) of all of the issued and outstanding shares of capital stock of Polycom, Inc. (“Polycom”("the Acquisition") which was completed on July 2, 2018. As a result of purchase accounting, a total of $12.2 million of deferred revenue that otherwise would have been recognized in the first quarter of Fiscal Year 2020 was excluded from first quarter revenue of $447.8 million.

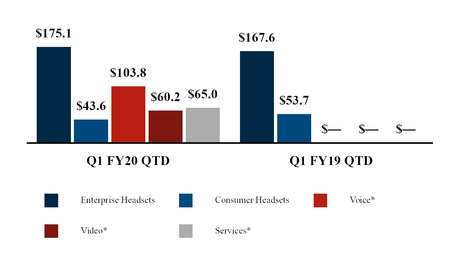

The table below summarizes net revenues for approximately $2.2 billionthe three months ended June 30, 2019 and 2018 by product categories:

|

| | | | | | | | | | | | | | | |

| (in thousands, except percentages) | | Three Months Ended | | | | |

| | June 30, | | Increase |

| | 2019 | | 2018 | | (Decrease) |

| Enterprise Headsets | | $ | 175,084 |

| | $ | 167,642 |

| | $ | 7,442 |

| | 4.4 | % |

| Consumer Headsets | | 43,566 |

| | 53,667 |

| | (10,101 | ) | | (18.8 | )% |

Voice 1 | | 103,847 |

| | — |

| | 103,847 |

| | 100.0 | % |

Video 1 | | 60,248 |

| | — |

| | 60,248 |

| | 100.0 | % |

Services 2 | | 65,022 |

| | — |

| | 65,022 |

| | 100.0 | % |

| Total | | $ | 447,767 |

| | $ | 221,309 |

| | $ | 226,458 |

| | 102.3 | % |

1 Voice and Video product net revenues presented net of fair value adjustments to deferred revenue of $0.6 million.

2 Services net revenues presented net of fair value adjustments to deferred revenue of $11.6 million.

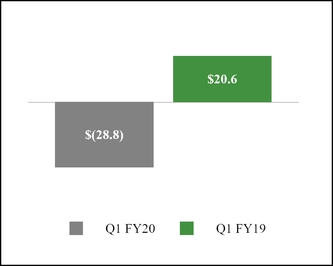

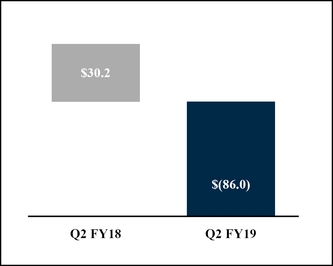

Operating Income (Loss) (in millions)

We reported a net loss of $44.9 million and an operating loss of $28.8 million for the first quarter of Fiscal Year 2020. We reported a net income of $14.5 million and an operating income of $20.6 million for the first quarter of Fiscal Year 2019. The decrease in stockour results from operations is primarily due to $45.3 million of amortization of purchased intangibles and cash.$20.4 million of post-Acquisition integration related expenses incurred during the first quarter of Fiscal Year 2020. We will continue to work on integrating Polycom into our business in order to streamline our operations and realize synergies from the combined companies.

Our strategic initiatives are primarily focused on driving long-term growth through our end-to-end portfolio of audio and video endpoints, including headsets, desktop phones, conference room phones, and video collaboration solutions. The Acquisition was consummated in accordance with the terms and conditions of the Stock Purchase Agreement (the “Purchase Agreement”), dated March 28, 2018, among the Company, Triangle Private Holdings II, LLC (“Triangle”), and Polycom. We believe this acquisition will better position Plantronics with our channel partners, customers, and strategic alliance partners by allowingpositions us to pursue additional opportunities across the UC&C market in both hardware end points and services. The addition of Polycom’s product and services portfolio is expected to enable us to accelerate our strategic vision of becomingas a global leader in communications and collaboration experiences. We believe this acquisition will positionendpoints, target the faster-growing market categories, such as the Huddle Room for video collaboration, allows us to capture additional opportunities through data analytics and insight services across a broad portfoliorange of communications endpoints. We continueendpoints, and better positions us with our channel partners, customers and strategic alliance partners to operate under a single operating segment.

Our major product categories are Enterprise headsets, which includes headsets optimized for UC&C, other corded and cordless communication headsets, audio processors and telephone systems; Consumer headsets, which includes Bluetooth and corded products for mobile device applications, personal computer ("PC"), and gaming headsets; Voice, Video, and content sharing UC&Cpursue comprehensive solutions which includes products designed to work with a wide range of Unified Communication (UC), Unified Communication as a Service (UCaaS), and VaaS environments, including our RealPresence collaboration solutions of infrastructure to endpoints which allows people all over the world to connect and collaborate naturally without beingcommunications challenges in the same physical location; and comprehensive support services including supportmarketplace, each of which we believe will drive long-term revenue growth.

During the quarter we focused on our solutions, hardware devices, professional, hosted, and managed services.

We sell our products through a high touch sales team and well developed global network of distributors and channel partners including Value-added Resellers (VARs), integrators, direct marketing resellers (DMRs), service providers, resellers, and retailers.

Our consolidated financial resultsintegration activities which included various systems integrations for the threecombined company. We also rationalized our sales channel and six months ended September 30, 2018 includesintroduced a new consolidated distribution agreement with our partners globally. These efforts are expected to decrease redundancies and leverage our competitive advantages for the financial resultsbenefit of Polycom from July 2, 2018,our partners and end customers. We believe the date of acquisition. For more information regarding the acquisition, refer to Note 3, Acquisition, Goodwill,changes have resulted in short-term disruptions in our operations which will be resolved as sales and Acquired Intangible Assets, of the accompanying notes to condensed consolidated financial statements.

|

| |

Total Net Revenues (in millions)

| Operating Income (Loss) (in millions)

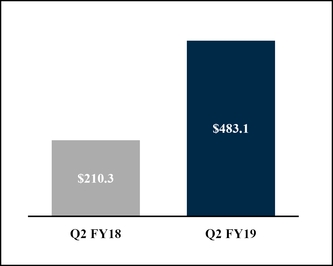

|

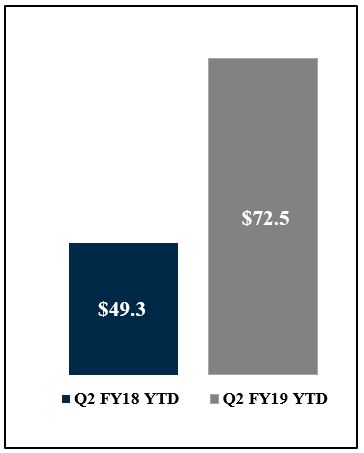

Comparedsupply partners adjust to the second quarter of Fiscal Year 2018 total net revenues increased 130% to $483.1 million; the increase in total net revenues is primarily related to the Acquisition.changes.

Voice and Video product net revenues were $207.2 million, net of fair value adjustments to deferred revenue of $3.4 million; Services net revenues were $47.8 million, net of fair value adjustments to deferred revenue of $33.1 million. Consumer headsets net revenues increased $10.7 million, or 22.5% from the year ago quarter and Enterprise headset net revenues increased $7.1 million, or 4.3%.

We reported a net loss of $(86.7) million and an operating loss of $(86.0) million for the second quarter of Fiscal Year 2019, representing a decrease of (535)% and (385)% respectively. The decrease is primarily due to the Acquisition and the related acquisition and integration costs incurred during the second quarter of Fiscal Year 2019. Refer to Note 3, Acquisition, Goodwill, and Acquired Intangible Assets, in the accompanying footnotes to the condensed consolidated financial statements.

Our primary focus for long-term growth opportunities, strategic initiatives, and the majority of our revenue and profits remains in our Enterprise headset and our new voice, video, and content sharing solution business. As we integrate Polycom, we will focus on accelerating our strategic vision of becoming a global leader in communications and collaboration experiences. Polycom is a leading provider of open, standards-based UC&C solutions for voice, video and content sharing, and has a comprehensive line of support and service solutions. As the market is rapidly changing with increasing adoption of hosted services and more influential players entering the market, users and user groups within customer organizations have more choices than ever before and they are taking advantage of those choices. It is becoming increasingly common place for the same customer organization to use multiple UC&C solutions, creating very diverse and heterogeneous environments. Polycom's approach of designing endpoint solutions that provide the highest flexibility in terms of interworking with these services provides the investment protections that customer organizations are looking for. Polycom solutions are also sold globally through a high-touch sales model that leverages a broad network of channel partners. Therefore, we believe this Acquisition will position us to capture additional opportunities through data analytics and insight services across a broad portfolio of communications endpoints.

Within the market for our Enterprise headset products,Headsets, we anticipate the key driver of growth over the next few years will be the continued adoption of UC&C audio solutions. We believe enterprises are increasing their adoption of UC&C systems to reduce costs, improve collaboration, and migrate technology from obsolete legacy systems.to more capable and flexible technology. We expect the growth of UC&C solutions will increase overall headset adoption in enterprise environments, and we believe most of the growth in our Enterprise Headsets product category over the next three years will come from headsets designed for UC&C. As such, UC&C remains the central focus of our sales, marketing, and support functions, and we will continue investing in key strategic alliances and integrations with major UC&C vendors. We continue to invest in new ideas and technology to create additional growth opportunities, such as Plantronics Manager Pro, our software-as-a-service ("SaaS") data insights offering, and Habitat Soundscaping, our intelligent acoustic management service. While we anticipate these investments will prove beneficial in the long term, we do not expect their contributions to be material in the near term.

Revenues from our Consumer headset products channelHeadsets are seasonal and typically strongest in our third fiscal quarter, which includes the majority of the holiday shopping season. Additionally, otherOther factors that directly impact our Consumerperformance in the product category performance, such asinclude product life cycles (including the introduction and pace of adoption of new technology), the market acceptance of new product introductions, consumer preferences and the competitive retail environment, changes in consumer confidence and other macroeconomic factors. While sales in the mobile headset market continues to decline, we believe future growth opportunities exist in gaming headsets primarily due to growth trends in the console gaming market. In addition, the timing or non-recurrence of retailer product placements can cause volatility in quarter-to-quarter results.

In an effort to align our strategy and focus on our core enterprise markets, we announced on May 7, 2019 that we intend to evaluate strategic alternatives for our Consumer Headset products. We have not yet determined the timing, structure, or financial impact of any potential transaction.

We remain cautious about the macroeconomic environment, based on uncertainty around trade and fiscal policy in the U.S. and internationally and broader economic uncertainty in many parts of Europe and Asia Pacific, which makes it difficult for us to gauge the economic impacts on our future business. We will continue to monitor our expenditures and prioritize expenditures that further our strategic long-term growth opportunities.

RESULTS OF OPERATIONS

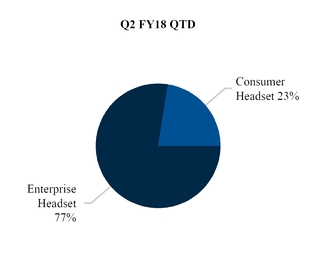

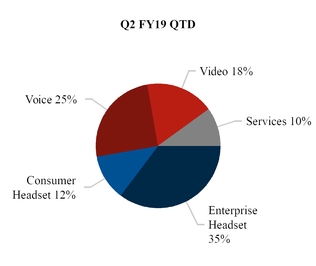

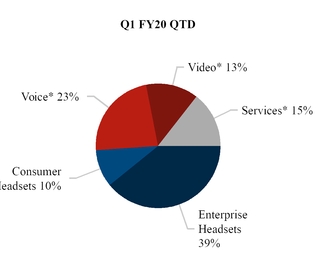

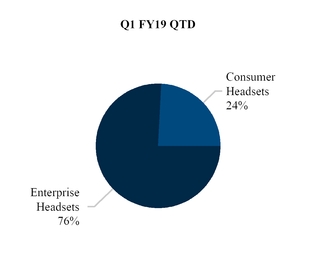

The following graphs display net revenues by product category for the three and six months ended SeptemberJune 30, 20172019 and 2018:

Net Revenues(in millions)

Revenue by Product Category (percent)

* These product categories were created as a result of the Acquisition, SeeNote 3, Acquisition, of the accompanying notes to condensed consolidated financial statements.

Total net revenues increased in the three and six months ended SeptemberJune 30, 20182019 compared to the prior year periods due primarily to the Acquisition as well as higher revenues within bothour Enterprise Headset product category partially offset by declines in our Consumer and Enterprise headsetHeadset product categories.category. The growth in our Consumer category was driven by Gaming product revenues while the growth in our Enterprise Headset category was driven by UC&C product revenues and the decline in our Consumer Headset category was driven by Gaming and Mono product revenues.

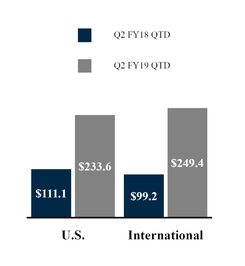

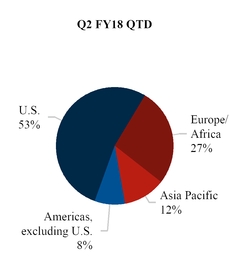

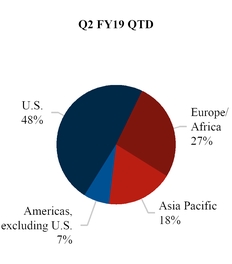

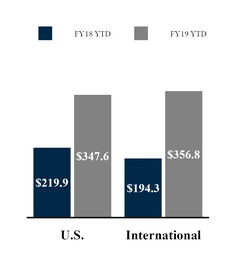

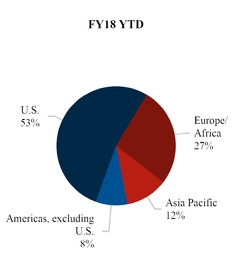

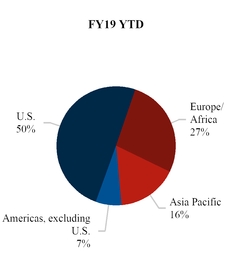

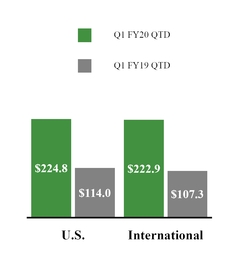

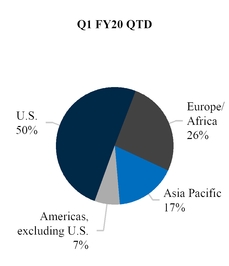

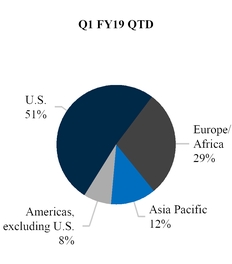

Geographic Information (in millions) Revenue by Region (percent)

Compared to the same prior year period, U.S. net revenues for the three months ended SeptemberJune 30, 20182019 increased due primarily to the Acquisition, as well as higher revenues within our ConsumerEnterprise Headsets product categoriescategory driven by our Gaming products.

Compared to the same prior year period, U.S. net revenues for the six months ended September 30, 2018 increased due primarily to the Acquisition. Consumer product revenues also grew, driven by our Gaming products and partially offset by the divestiture of our Clarity business in June 2017. Enterprise product revenues were up slightly with growth in UC&C revenues partially offset by continued declines in our non-UC&C product revenues. Consumer Headsets product revenues were down, driven by declines in sales of our Gaming products.

International net revenues for the three and six months ended SeptemberJune 30, 20182019 increased from the same prior year period due primarily to the Acquisition;Acquisition as well as growth in our Enterprise Headsets category driven by UC&C product sales. This growth was partially offset by declines in our Consumer Headset product revenues as a result of declines in sales also increased driven byof our Gaming and Mono products.

Changes in foreign exchange rates did not have a material impact on revenues forDuring the three months ended SeptemberJune 30, 2018 or 2017. During the six months ended September 30, 2018,2019, changes in foreign exchange rates positivelynegatively impacted net revenues by $5.6$3.9 million, net of the effects of hedging, compared to a $2.7$6 million favorable impact on revenuenet revenues in the prior year period.

COST OF REVENUES AND GROSS PROFIT

Cost of revenues consists primarily of direct and contract manufacturing costs, warranty, freight, depreciation, duties, charges for excess and obsolete inventory, royalties, and overhead expenses.

| | | | | Three Months Ended | | | | Six Months Ended | | | | Three Months Ended | | |

| | | September 30, | | Increase | | September 30, | | Increase | | June 30, | | Increase |

| (in thousands, except percentages) | | 2017 | | 2018 | | (Decrease) | | 2017 | | 2018 | | (Decrease) | | 2019 | | 2018 | | (Decrease) |

| Total net revenues | | $ | 210,300 |

| | $ | 483,069 |

| | $ | 272,769 |

| | 129.7 | % | | $ | 414,226 |

| | $ | 704,378 |

| | $ | 290,152 |

| | 70.0 | % | | $ | 447,767 |

| | $ | 221,309 |

| | $ | 226,458 |

| | 102.3 | % |

| Cost of revenues | | 102,668 |

| | 330,440 |

| | 227,772 |

| | 221.9 | % | | 203,311 |

| | 441,906 |

| | 238,595 |

| | 117.4 | % | | 235,121 |

| | 111,466 |

| | 123,655 |

| | 110.9 | % |

| Gross profit | | $ | 107,632 |

| | $ | 152,629 |

| | $ | 44,997 |

| | 41.8 | % | | $ | 210,915 |

| | $ | 262,472 |

| | $ | 51,557 |

| | 24.4 | % | | $ | 212,646 |

| | $ | 109,843 |

| | $ | 102,803 |

| | 93.6 | % |

| Gross profit % | | 51.2 | % | | 31.6 | % | |

|

| | | | 50.9 | % | | 37.3 | % | | | | | | 47.5 | % | | 49.6 | % | |

|

| | |

Compared to the same prior year periods,period, gross profit as a percentage of net revenues decreased in the three and six months ended SeptemberJune 30, 2018,2019, due primarily to $30.0 million of amortization of both purchased intangibles and $12.2 million of deferred revenue fair value adjustment, and the inventory step-up associated with the Acquisition; refer torespectively. See Note 3, Acquisition, Goodwill, and Acquired Intangible Assets. Other unfavorable items were cost increases on a commodity component driven by industry capacity shortages and a product mix with higher gaming revenues within our Consumer product category.accompanying notes to condensed consolidated financial statements. These increased costs were partially offset by material cost reductions and favorable currency movements.reductions.

There are significant variances in gross profit percentages between our higher and lower margin products;products including Polycom products acquired through the Acquisition; therefore, small variations in product mix, which can be difficult to predict, can have a significant impact on gross profit as a percentage of net revenues. Gross profit percentages may also vary based on distribution channel,channels, return rates, and other factors.

OPERATING EXPENSES

Operating expenses consists primarily of research, development and engineering; selling, general and administrative; gain, net of litigation settlements and restructuring and other related charges (credits) expenses which are summarized in the table below for the three and six months ended SeptemberJune 30, 20172019 and 2018:

| | | | | Three Months Ended | | | | Six Months Ended | | | | Three Months Ended | | | |

| | | September 30, | | Increase | | September 30, | | Increase | | June 30, | | Increase | |

| (in thousands, except percentages) | | 2017 | | 2018 | | (Decrease) | | 2017 | | 2018 | | (Decrease) | | 2019 | | 2018 | | (Decrease) | |

| Research, development, and engineering | | $ | 19,932 |

| | $ | 57,047 |

| | $ | 37,115 |

| | 186 | % | | $ | 41,145 |

| | $ | 80,748 |

| | $ | 39,603 |

| | 96 | % | | $ | 59,524 |

| | $ | 23,701 |

| | $ | 35,823 |

| | 151 | % | |

| Selling, general and administrative | | $ | 57,696 |

| | $ | 174,297 |

| | $ | 116,601 |

| | 202 | % | | $ | 113,929 |

| | $ | 238,500 |

| | $ | 124,571 |

| | 109 | % | | 163,608 |

| | 64,203 |

| | 99,405 |

| | 155 | % | |

| Gain, net of litigation settlements | | (104 | ) | | $ | — |

| | $ | 104 |

| | (100 | )% | | $ | (280 | ) | | $ | (30 | ) | | $ | 250 |

| | (89 | )% | | (1,162 | ) | | (30 | ) | | (1,132 | ) | | 3,773 | % | |

| Restructuring and other related charges (credits) | | (51 | ) | | $ | 7,261 |

| | $ | 7,312 |

| | (14,337 | )% | | $ | 2,522 |

| | $ | 8,581 |

| | $ | 6,059 |

| | 240 | % | |

| Restructuring and other related charges | | | 19,525 |

| | 1,320 |

| | 18,205 |

| | 1,379 | % | |

| Total Operating Expenses | | $ | 77,473 |

| | $ | 238,605 |

| | $ | 161,132 |

| | 208 | % | | $ | 157,316 |

| | $ | 327,799 |

| | $ | 170,483 |

| | 108 | % | | $ | 241,495 |

| | $ | 89,194 |

| | $ | 152,301 |

| | 171 | % | |

| % of net revenues | | 36.8 | % | | 49.4 | % | |

| | | | 38.0 | % | | 46.5 | % | | | | | | 53.9 | % | | 40.3 | % | |

| | | |

Our Research, development, and engineering expenses and selling, general and administrative expenses increased during the three and six months ended SeptemberJune 30, 2018,2019, primarily due to the impactinclusion of Polycom operating expenses after the Acquisition, and related acquisition andas well as $19.5 million of Acquisition-related integration costs and $15.3 million of amortization of purchased intangibles incurred during the periods; refer to Note 3, Acquisition, Goodwill, and Acquired Intangible Assets, of the accompanying notes to condensed consolidated financial statements. .period.

We recognized immaterial gains from litigation in the three and six months ended September 30, 2017 and 2018.

Compared to the prior year period, restructuring and other related charges (credits) increased in the three and six months ended SeptemberJune 30, 2018,2019, due primarily to restructuring actions initiated during the second quarter of Fiscal Year 2019 as a result ofperiod to streamline the Acquisition.global workforce and achieve planned synergies. For more information regarding restructuring activities, refer toactivities. See Note 9, 10, Restructuring and Other Related Charges, of the accompanying notes to condensed consolidated financial statements.

INTEREST EXPENSE

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | | | |

| | | June 30, | | Increase | |

| (in thousands, except percentages) | | 2019 |

| 2018 | | (Decrease) | |

| Interest expense | | $ | (23,932 | ) | | $ | (7,327 | ) | | $ | 16,605 |

| | 226.6 | % | |

| % of net revenues | | (5.3 | )% | | (1.6 | )% | | | | | |

Interest expense increased for the three and six months ended SeptemberJune 30, 2017 and 2018 was $7.3 million, $14.6 million, $23.9 million, and $31.2 million, respectively and relates2019 primarily due to interest incurred on our 5.50% Senior Notes and the Credit Facility Agreement. Refer toAgreement entered into in connection with the Acquisition. See Note 8, 9, Debt, of the accompanying notes to condensed consolidated financial statementsstatements.

OTHER NON-OPERATING INCOME, NET

| | | | | Three Months Ended | | | | Six Months Ended | | | | Three Months Ended | | | |

| | | September 30, | | Increase | | September 30, | | Increase | | June 30, | | Increase | |

| (in thousands, except percentages) | | 2017 | | 2018 | | (Decrease) | | 2017 | | 2018 | | (Decrease) | | 2019 | | 2018 | | (Decrease) | |

Other non-operating income, net

| | $ | 1,826 |

| | $ | 1,610 |

| | $ | (216 | ) | | (11.8 | )% | | $ | 2,740 |

| | $ | 3,606 |

| | $ | 866 |

| | 31.6 | % | | $ | 333 |

| | $ | 1,996 |

| | $ | (1,663 | ) | | (83.3 | )% | |

| % of net revenues | | 0.9 | % | | 0.3 | % | | | | | | 0.7 | % | | 0.5 | % | | | | | | 0.1 | % | | 0.9 | % | | | | | |

Other non-operating income, net for the three months ended SeptemberJune 30, 20182019 decreased primarily due to lower interest income as theour investment portfolios were liquidated during the First Quarter of Fiscal Year 2019.2019 to facilitate the Acquisition.

Other non-operating income, net for the six months ended September 30, 2018 increased primarily due to immaterial net foreign currency gains compared to immaterial net foreign currency losses in the prior period.

INCOME TAX EXPENSE (BENEFIT)

| | | | | Three Months Ended | | | | | | Six Months Ended | | | | | | Three Months Ended | | | | | |

| | | September 30, | | Increase | | September 30, | | Increase | | June 30, | | Increase | |

| (in thousands except percentages) | | 2017 |

| 2018 | | (Decrease) | | 2017 |

| 2018 | | (Decrease) | | 2019 |

| 2018 | | (Decrease) | |

| Income (Loss) before income taxes | | $ | 24,725 |

| | $ | (108,259 | ) | | $ | (132,984 | ) | | (537.9 | )% | | $ | 41,776 |

| | $ | (92,941 | ) | | $ | (134,717 | ) | | (322.5 | )% | |

| Income (loss) before income taxes | | | $ | (52,448 | ) | | $ | 15,318 |

| | $ | (67,766 | ) | | (442.4 | )% | |

| Income tax expense (benefit) | | 4,772 |

| | (21,550 | ) | | (26,322 | ) | | (551.6 | )% | | 2,995 |

| | (20,703 | ) | | (23,698 | ) | | (791.3 | )% | | (7,577 | ) | | 847 |

| | (8,424 | ) | | (994.6 | )% | |

| Net income (loss) | | $ | 19,953 |

| | $ | (86,709 | ) | | $ | (106,662 | ) | | (534.6 | )% | | $ | 38,781 |

| | $ | (72,238 | ) | | $ | (111,019 | ) | | (286.3 | )% | | $ | (44,871 | ) | | $ | 14,471 |

| | $ | (59,342 | ) | | (410.1 | )% | |

| Effective tax rate | | 19.3 | % | | (19.9 | )% | |

|

| |

| | 7.2 | % | | (22.3 | )% | | | | | | 14.4 | % | | 5.5 | % | |

|

| |

| |

The Company and its subsidiaries are subject to taxation in the U.S. and in various foreign and state jurisdictions. Our tax provision or benefit is determined using an estimate of our annual effective tax rate and adjusted for discrete items that are taken into account in the relevant period. The effective tax rates for the three months ended SeptemberJune 30, 20172019 and 2018 were 19.3%14.4% and 19.9%5.5%, respectively.

The annual effective tax rates for the six months ended Septemberas of June 30, 20172019 and 2018 were 7.2% and 22.3%, respectively. The period over periodvaried from the statutory tax rate has beenof 21% primarily due to our jurisdictional mix of income, state taxes, U.S. taxation of foreign earnings, and may continueR&D credits.

During the quarter ended June 30, 2019, we recognized a discrete $11.6 million tax benefit related to be subjectan intra-entity transfer of an intangible asset that will have a deferred future benefit, for which we established a deferred tax asset.

On June 7, 2019, a Ninth Circuit panel reversed the United States Tax Court’s holding in Altera Corp. v. Commissioner and upheld the portion of the Treasury regulations issued under IRC Section 482 requiring related-party participants in a cost sharing arrangement to variations relatingshare stock-based compensation costs. At this time, the taxpayer is still eligible to several factors including but not limitedprotest the decision. We have considered the issue and have recorded a $8.6 million discrete tax charge resulting from the cost sharing of prior stock-based compensation, partially offset by a reduction to changes from IRS rule making and interpretation of US tax legislation, including the 2017 Tax Cuts and Jobs Act (H.R. 1) (the "Act"), statutory tax rates reduced from 35%toll charge accrued in prior periods. We will continue to 21%, adjustmentsmonitor developments related to foreign tax regimes, interest expense limitations, mix of jurisdictional incomethe case and expense, cost and deductibility of acquisitions expenses (including integration), foreign currency gains (losses) and changes in deferred tax assets and liabilities and their valuation or utilization.the potential impact on its consolidated financial statements.

As a result of a current period loss before income taxes during the three and six months ended September 30, 2018, recurring permanent tax benefits increased the effective tax rate, where discrete prior year benefits reduced the effective tax rate on profits before tax generated during the three and six months ended September 30, 2017. For the three and six months ended September 30, 2018 the effective tax rate changed through a release of a valuation allowance for California R&D credits. Prior to the acquisition of Polycom, the Company had limited utilization over future periods and recognized a valuation allowance. With the acquisition of Polycom the California R&D tax credits will decrease resulting in full utilization. Other increases to the effective tax rate for the six-month period ended September 30, 2018 are attributable to the Act and the new mandatory charge on global intangible low-taxed income on previously unremitted foreign subsidiary earnings.

Due to the timing of the enactment and the complexity involved in applying the provisions of the Act, we made reasonable estimates of the effects and recorded provisional amounts in our financial statements as of December 31, 2017. As we collect and prepare necessary data, and interpret the Act and any additional guidance issued by the U.S. Treasury Department, the Internal Revenue Service (IRS), and other standard-setting bodies, we may make adjustments to the provisional amounts. Those adjustments may materially affect our provision for income taxes and effective tax rate in the period in which the adjustments are made. The adjustments made in the second quarter of 2018 were not significant. The accounting for the tax effects of the Act will be completed in 2018.

Included in long-term income taxes payable in the condensed consolidated balance sheets as of March 31, 2018 and September 30, 2018 were unrecognized tax benefits of $12.6 million and $26.2 million, respectively, which would favorably impact the effective tax rate in future periods if recognized. The increase is predominantly due to acquired uncertain tax benefits of Polycom. The Company’s continuing practice is to recognize interest and/or penalties related to income tax matters in income tax expense in the condensed consolidated statements of operations. The accrued interest related to unrecognized tax benefits was immaterial as of March 31, 2018 and September 30, 2018, respectively. No penalties have been accrued.

The Company believes that an adequate provision has been made for any adjustments that may result from tax examinations; however, the outcome of such examinations cannot be predicted with certainty. If any issues addressed in the tax examinations are resolved in a manner inconsistent with the Company's expectations, the Company could be required to adjust its provision for income tax in the period such resolution occurs. The timing of any resolution and/or closure of tax examinations is not certain.

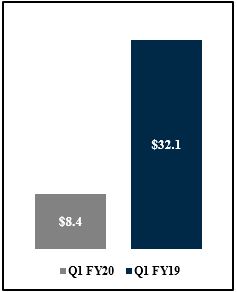

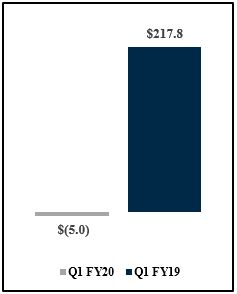

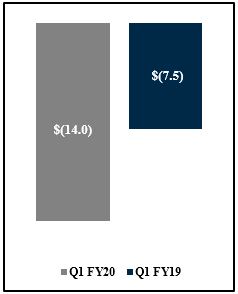

FINANCIAL CONDITION

|

| | |

Operating Cash Flow (in millions) | Investing Cash Flow(in millions) | Financing Cash Flow (in millions) |

| | |

We use cash provided by operating activities as our primary source of liquidity. We expect that cash provided by operating activities will fluctuate in future periods as a result of a number of factors, including fluctuations in our revenues, the timing of compensation-related payments such as our annual bonus/variable compensation plan and Employee Stock Purchase Plan ("ESPP") plan,, integration costs related to the Acquisition, product shipments during the quarter, accounts receivable collections, inventory and supply chain management, and the timing and amount of tax and other payments.

Operating Activities

Compared to the same year ago period, net cash provided by operating activities during the sixthree months ended SeptemberJune 30, 2018 increased2019 decreased primarily due to increased salescash paid for interest payments on long-term debt, integration related expenses, and restructuring activities that did not occur in the comparative period. The decrease was partially offset by higher cash collections from customers as a result of the Acquisition which is partially offset by acquisition and integration related costs.increased revenue.

Investing Activities

Net cash used for investing activities during the sixthree months ended SeptemberJune 30, 20182019 was primarily used for the Acquisition which closed on July 2, 2018, refer to Note 3 Acquisition, Goodwill,purchase of personal property, plant and Acquired Intangible Assets. This decrease was partially offset by the proceeds from the sales of short term investments.equipment.

We estimate total capital expenditures for Fiscal Year 20192020 will be approximately $40 million to $50 million. We expect capital expenditures for the remainder of Fiscal Year 20192020 to consist primarily of ITnew information technology investments, capital investment in our manufacturing capabilities, including tooling for new products, and facilities upgrades.

Financing Activities

Net cash used for financing activities during the sixthree months ended SeptemberJune 30, 2018 increased from the prior year period as a result2019, consisted primarily of taxes paid on behalf of employees related to net share settlements of vested employee equity awards and payment of the proceeds received from the term loan facility which were partially offset by financing costs paid during the quarter.

On November 6, 2018, we announced that the Audit Committee of our Board ("the Audit Committee") had declared a cash dividend of $0.15 per share, payable on December 10, 2018 to stockholders of record at the close of business on November 20, 2018. We expect to continue paying a quarterly dividend of $0.15 per share; however, the actual declaration of dividends and the establishment of record and payment dates are subject to final determination by the Audit Committee each quarter after its review ofon our financial performance and financial position.common stock.

Liquidity and Capital Resources

Our primary discretionarysources of liquidity as of June 30, 2019, consisted of cash, requirements have historically been for repurchases of our common stockcash equivalents, and short-term investments, cash we expect to fund stockholder dividends.generate from operations, and a $100 million revolving credit facility. At SeptemberJune 30, 2018,2019, we had working capital of $316.7$214.2 million, including $305.8$206.1 million of cash, cash equivalents, and short-term investments, compared with working capital of $774.2$252.9 million, including $660.0$215.8 million of cash, cash equivalents, and short-term investments at March 31, 2018.2019. The decrease in working capital at SeptemberJune 30, 20182019 compared to March 31, 20182019 resulted from the impactnet decrease in cash and cash equivalents and a net increase in accounts payable due to payment timing.

Our cash and cash equivalents as of June 30, 2019 consisted of bank deposits with third party financial institutions. We monitor bank balances in our operating accounts and adjust the balances as appropriate. Cash balances are held throughout the world, including substantial amounts held outside of the U.S. As of June 30, 2019, of our $206.1 million of cash, cash equivalents, and short-term investments, $60.6 million was held domestically while $145.5 million was held by foreign subsidiaries, and approximately 61% was based in USD-denominated instruments. During the quarter ended June 30, 2018, we sold most of our short-term investments to generate cash to fund the Acquisition during the quarter.

Onon July 2, 2018, we completed the acquisition2018. As of allJune 30, 2019, our remaining investments were composed of the issued and outstanding shares of capital stock of Polycom. The Acquisition was consummatedMutual Funds.

During Fiscal Year 2019, in accordance with the terms and conditions of the previously announced Purchase Agreement, dated March 28, 2018, among the Company, Triangle and Polycom. At the closing of the Acquisition, Plantronics acquired Polycom for approximately $2.2 billion with the total consideration consisting of (1) 6.4 million shares of our common stock (the "Stock Consideration") and (2) $1.7 billion in cash (the "Cash Consideration"), resulting in Triangle, which was Polycom’s sole shareholder, owning approximately 16.0% of Plantronics following the acquisition. The consideration paid at closing is also subject to a working capital, tax and other adjustments. We financed the Cash Consideration by using available cash-on-hand and funds drawn from our new term loan facility which is described further below. Portions of the Stock Consideration and Cash Considerations were each deposited into separate escrow accounts to secure certain indemnification obligations of Triangle pursuant to the Purchase Agreement.

In connection with the Acquisition, we entered into a Credit Agreement with Wells Fargo Bank, National Association, as administrative agent, and the lenders party thereto (the “Credit Agreement”). The Credit Agreement replaced the Company’sour prior revolving credit facility in its entirety. The Credit Agreement provides for (i) a revolving credit facility with an initial maximum aggregate amount available of $100 million that matures in July 2023 and (ii) a $1.275 billion term loan facility due in quarterly principal installments commencing on December 28, 2018 for the aggregate principal amount funded on the Closing Date multiplied by 0.25% (subject to prepayments outlined in the Credit Agreement) and all remaining outstanding principal due at maturitythat matures in July 2025. The availability under the revolving credit facility is reduced by the amount necessary to meet our obligations under three outstanding letters of credit. We may increase the aggregate principal amount of any outstanding tranche of term loans, add one or more additional tranches of term loans and/or increase the aggregate principal amount of revolving commitments under the Credit Agreement by an aggregate amount of up to the sum of (1) $500 million, (2) an amount such that, after giving effect to the incurrence of such amount, the consolidated secured net leverage ratio (as defined in the Credit Agreement) is equal to or less than 2.75 to 1.00 and (3) the amount of certain prepayments made under the Credit Agreement from time to time. Any such increase would be subject to the satisfaction of certain conditions, including that no default or event of default be continuing under the Credit Agreement at the time of the increase and that we obtain the consent of each lender providing any such additional loans or commitments.

On July 2, 2018, the Company borrowed the full amount available under the term loan facility of $1.245 billion, net of approximately $30 million of discounts and issuance costs. Proceeds from the initial borrowing under the Credit Agreement were used to finance the acquisition of Polycom, to refinance certain debt of Polycom, to pay related fees, commissions and transaction costs. We have additional borrowing capacity under the Credit Agreement through the revolving credit facility which could be used to provide ongoing working capital and capital for other general corporate purposes of us and our subsidiaries. Our obligations under the Credit Agreement are currently guaranteed by Polycom and will from time to time be guaranteed by, subject to certain exceptions, any domestic subsidiaries that may become material in the future. Subject to certain exceptions, the Credit Agreement is secured by first-priority perfected liens and security interests in substantially all of our and each of our subsidiary guarantor personal property and will from time to time also be secured by certain material real property that we or any of our subsidiary guarantor may acquire. Borrowings under the Credit Agreement bear interest due on a monthly basis at a variable rate equal to (i) LIBOR plus a specified margin, or (ii) the base rate (which is the highest of (a) the prime rate publicly announced from time to time by Wells Fargo Bank, National Association, (b) the federal funds rate plus 0.50% or (c) the sum of 1% plus one-month LIBOR) plus a specified margin. We must also pay (i) an unused commitment fee ranging from 0.200% to 0.300% per annum ofSee Note 9, Debt, in the average daily unused portion of the aggregate revolving credit commitments under the Credit Agreement, and (ii) a per annum fee equal to (a) for each performance standby letter of credit outstanding under the Credit Agreement with respect to non-financial contractual obligations, 50% of the applicable margin over LIBOR under the revolving credit facility in effect from time to time multiplied by the daily amount available to be drawn under such letter of credit, and (b) for each other letter of credit outstanding under the Credit Agreement, the applicable margin over LIBOR under the revolving credit facility in effect from time to time multiplied by the daily amount available to be drawn for such letter of credit.

The Credit Agreement contains various restrictions and covenants, including requirements that we maintain certain financial ratios at prescribed levels for the revolving credit facility and restrictions on our ability and certain of our subsidiaries ability to consolidate or merge, create liens, incur additional indebtedness, dispose of assets, consummate acquisitions, make investments and pay dividends and other distributions. The Credit Agreement includes the following financial covenants applicableaccompanying notes to the revolving credit facility only: (i) a maximumcondensed consolidated secured net leverage ratio (defined as, with certain adjustments and exclusions, our ratio of consolidated secured indebtedness as of the end of the relevant fiscal quarter to consolidated net income before interest, taxes, depreciation, amortization, non-cash charges and certain other items (“EBITDA”) for the period of four fiscal quarters then ended) of 3.50 to 1.00 as of the last day of any fiscal quarter ending during the period from December 29, 2018 through June 29, 2019; 3.25 to 1.00 as of the last day of any fiscal quarter ending during the period from June 30, 2019 through March 28, 2020; 3.00 to 1.00 as of the last day of any fiscal quarter ending during the period from March 29, 2020 through April 3, 2021; and 2.75 to 1.00 as of the last day of any fiscal quarter ending on or after April 4, 2021; and (ii) a minimum interest coverage ratio (defined as, with certain adjustments, the ratio of our EBITDA to our consolidated interest expense to the extent paid or payable in cash) of 2.75 to 1.00 as of the last day of any fiscal quarter ending on or after December 29, 2018.The Credit Agreement also contains customary events of default. If an event of default under the Credit Agreement occurs and is continuing, then the lenders may declare any outstanding obligations under the Credit Agreement to be immediately due and payable; provided, however, that the occurrence of an event of default as a result of a breach of a financial covenant under the Credit Agreement does not constitute a default or event of default with respect to any term facility under the Credit Agreement unless and until the required revolving lenders shall have terminated their revolving commitments and declared all amounts outstanding under the revolving credit facility to be due and payable. In addition, if we or any of our subsidiary guarantor or, with certain exceptions, any other subsidiary becomes the subject of voluntary or involuntary proceedings under any bankruptcy, insolvency or similar law, then any outstanding obligations under the Credit Agreement will automatically become immediately due and payable. Loans outstanding under the Credit Agreement will bear interest at a rate of 2.00% per annum in excess of the otherwise applicable rate (i) while a payment or bankruptcy event of default exists or (ii) upon the lenders’ request, during the continuance of any other event of default.statements.

On July 30, 2018, we entered into a 4-year amortizing interest rate swap agreement with Bank of America, NA. The swap has an initial notional amount of $831 million and matures on July 31, 2022. The purpose of this swap is to hedge against changes in cash flows (interest payments) attributable to fluctuations in the contractually specified LIBOR interest rate associated with our new credit facility agreement. The swap involves the receipt of floating-rate amounts for fixed interest rate payments over the life of the agreement. We have designated this interest rate swap as a cash flow hedge. The derivative is valued based on prevailing LIBOR rate curves on the date of measurement. We also evaluate counterparty credit risk when we calculate the fair value of the swap. For additional details, refer tosee Note 13,14, Derivatives, of the accompanying notes to condensed consolidated financial statements.

The enactment of the Tax Cuts and Jobs Act (H.R. 1) (the "Act") in the U.S. on December 22, 2017, introduced, among other things, applying new taxes on certain foreign source earnings and imposed the toll charge. We have a $73.3 million toll charge liability recognized on our condensed consolidated balance sheet as of September 30, 2018, which we intend to pay over a seven-year period as permitted under the Act. With enactment of the Act, the Company is no longer asserting a position that its foreign earnings are indefinitely reinvested. In addition, we recorded a $5 million liability for state income taxes and foreign withholding taxes that will become due from the repatriation of foreign earnings. Polycom recorded a toll charge that was paid in October 2018 with the filing of its 2017 tax return. For additional details, refer to Note 14, Income Taxes, of the accompanying notes to condensed consolidated financial statements.

Our cash and cash equivalents as of September 30, 2018 consisted of bank deposits with third party financial institutions. We monitor bank balances in our operating accounts and adjust the balances as appropriate. Cash balances are held throughout the world, including substantial amounts held outside of the U.S. As of September 30, 2018, of our $305.8 million of cash, cash equivalents, and short-term investments, $138.3 million was held domestically while $167.5 million was held by foreign subsidiaries, approximately 77% of which was based in USD-denominated instruments. During the quarter ended June 30, 2018, we sold most of our short-term investments to generate cash used to fund the Acquisition which was finalized on July 2, 2018. As of September 30, 2018, our remaining investments were composed of Mutual Funds.

From time to time, our Board of Directors ("the Board") authorizes programs under which we may repurchase shares of our common stock in the open market or through privately negotiated transactions, including accelerated stock repurchase agreements. As of September 30, 2018, there remained 730,105 shares authorized for repurchase under the stock repurchase program approved by the Board on July 27, 2017. We have temporarily curtailed open market common stock repurchases to help us manage our liquidity and leverage ratios resulting from the Acquisition. We had no retirements of treasury stock in the first quarter of Fiscal Years 2018 and 2019. Refer to Note 11, Common Stock Repurchases, in the accompanying notes to the condensed consolidated financial statements.

During the year ended March 31,Year 2016, we obtained $488.4 million from debt financing, net of issuance costs. The debt matures on May 31, 2023 and bears interest at a rate of 5.50% per annum, payable semi-annually on May 15 and November 15 of each year. Refer toSee Note 8, 9, Debt, in the accompanying notes to the condensed consolidated financial statements.

From time to time, our Board of Directors ("the Board") authorizes programs under which we may repurchase shares of our common stock in the open market or through privately negotiated transactions, including accelerated stock repurchase agreements. On November 28, 2018, the Board approved a 1 million share repurchase program expanding our capacity to repurchase shares to approximately 1.7 million shares. During the first quarter of Fiscal Year 2020, we did not repurchase any shares of our common stock. As of June 30, 2019, there remained 1,369,014 shares authorized for repurchase under the existing stock repurchase program. See Note 12, Common Stock Repurchases, in the accompanying notes to the condensed consolidated financial statements.

Our liquidity, capital resources, and results of operations in any period could be affected by repurchases of our common stock, the payment of cash dividends, the exercise of outstanding stock options, restricted stock grants under stock plans, and the issuance of common stock under our ESPP. We expect theEmployee Stock Purchase Plan ("ESPP"). The Acquisition to affecthas negatively affected our liquidity and leverage ratios and we plan toratios. To reduce our debt leverage ratios, by prioritizingwe expect to prioritize the repayment of the debt obtained to financeunder the Acquisition andCredit Agreement.

Additionally, the temporary curtailment of open market common stock repurchases. The Acquisition impacted our cash conversion cycle due to Polycom's use of third-party partner financing and early payment discounts to drive down cash collection cycles.

We are still assessing these changes as we integrate Polycom into our business. Wealso receive cash from the exercise of outstanding stock options under our stock plan and the issuance of shares under our ESPP. However, the resulting increase in the number of outstanding shares from these equity grants and issuances could affect our earnings per share. We cannot predict the timing or amount of proceeds from the sale or exercise of these securities or whether they will be exercised, forfeited, canceled, or will expire.

On August 6, 2019, we announced that the Audit Committee of our Board declared a cash dividend of $0.15 per share, payable on September 10, 2019 to stockholders of record at the close of business on August 20, 2019.

We believe that our current cash and cash equivalents, cash provided by operations, and the availability of additional funds under the Credit Agreement will be sufficient to fund operations for at least the next 12 months; however, any projections of future financial needs and sources of working capital are subject to uncertainty. Readers are cautioned to review the risks, uncertainties, and assumptions set forth in this Quarterly Report on Form 10-Q, including the section entitled "Certain"Certain Forward-Looking Information"Information" and the risk factors set forth in our Annual Report on Form 10-K for the fiscal year ended March 31, 2018,2019, filed with the SEC on May 9, 2018,17, 2019, and other periodic filings with the SEC, any of which could affect our estimates for future financial needs and sources of working capital.

OFF BALANCE SHEET ARRANGEMENTS AND CONTRACTUAL OBLIGATIONS

We have not entered into any transactions with unconsolidated entities whereby we have financial guarantees, subordinated retained interests, derivative instruments, or other contingent arrangements that expose us to material continuing risks, contingent liabilities, or any other obligation under a variable interest in an unconsolidated entity that provides us with financing and liquidity support, market risk, or credit risk support.

A substantial portion of the raw materials, components, and subassemblies used in our products are provided by our suppliers on a consignment basis. These consigned inventories are not recorded on our consolidated balance sheet until we take title to the raw materials, components, and subassemblies, which occurs when they are consumed in the production process. Prior to consumption in the production process, our suppliers bear the risk of loss and retain title to the consigned inventory. The terms of the agreements allow the Companyus to return parts in excess of maximum order quantities to the suppliers at the supplier’s expense. Returns for other reasons are negotiated with the suppliers on a case-by-case basis and to date have been immaterial. If our suppliers were to discontinue financing consigned inventory, it would require us to make cash outlays and we could incur expenses which, if material, could negatively affect our business and financial results. As of June 30, 2019, and March 31, 2018 and September 30, 2018,2019, we had off-balance sheet consigned inventories of $48.8$48.2 million and $41.5$47.1 million, respectively.

Unconditional Purchase Obligations

We use several contract manufacturers to manufacture raw materials, components, and subassemblies for our products. We provide these contract manufacturers with demand information that typically covers periods up to 13 weeks, and they use this information to acquire components and build products. We also obtain individual components for our products from a wide variety of individual suppliers. Consistent with industry practice, we acquire components through a combination of purchase orders, supplier contracts, and open orders based on projected demand information. As of SeptemberJune 30, 2018,2019, we had outstanding off-balance sheet third-party manufacturing, component purchase, and other general and administrative commitments of $446.1$406.4 million, including the off-balance sheet consigned inventories of $41.5$48.2 million as discussed above.

Polycom Acquisition

On July 2, 2018,above, of which we completed the acquisition of Polycom, referexpect to Note 3, Acquisition, Goodwill, and Acquired Intangible Assets,consume in the accompanying footnotes to the condensed consolidated financial statements. As a resultnormal course of the Acquisition, in addition to the contractual obligation of Plantronics described in our Annual Report on Form 10-K for the fiscal year ended March 31, 2018, we became subject to the following future contractual obligations as of September 30, 2018:business.

|

| | | | | | | | | | | | | | | | | | | | |

| | | Payments Due by Period |

| (in thousands) | | Total | | Less than 1 year | | 1-3 years | | 4-5 years | | More than 5 years |

Operating leases (1) | | $ | 41,091 |

| | $ | 15,336 |

| | $ | 25,258 |

| | $ | 497 |

| | $ | — |

|

Unconditional purchase obligations (2) | | 252,446 |

| | 245,013 |

| | 7,433 |

| | — |

| | — |

|

Long term debt (Term Loan Facility) (3) | | 1,275,000 |

| | 9,563 |

| | 28,687 |

| | 25,500 |

| | 1,211,250 |

|

| Total contractual cash obligations | | $ | 1,568,537 |

| | $ | 269,912 |

| | $ | 61,378 |

| | $ | 25,997 |

| | $ | 1,211,250 |

|

(1) We acquired Polycom's lease obligations for certain office facilities and equipment under non-cancelable operating leases expiring through our Fiscal Year 2023. In addition to the net minimum lease payments noted above, we are contractually obligated to pay certain operating expenses during the term of the lease such as maintenance, taxes and insurance. Included in the lease obligations acquired are Polycom’s sublease receipts, which have been netted against the gross lease payments above to arrive at our net minimum lease payments.Certain of these leases provide for renewal options and we may exercise the renewal options.

(2) Refer to Unconditional Purchase Obligations note above.

(3) On July 2, 2018, the Company borrowed the full amount available under the term loan facility of $1.245 billion, net of approximately $30 million of discounts and issuance costs. Proceeds from the initial borrowing under the Credit Agreement were used to finance the acquisition of Polycom, to refinance certain debt of Polycom, to pay related fees, commissions and transaction costs. We owe quarterly principal installments commencing on December 28, 2018 for the aggregate principal amount funded on July 2, 2018 multiplied by 0.25% (subject to prepayments outlined in the Credit Agreement) and all remaining outstanding principal due at maturity in July 2025.

Except as described above, there have been no material changes in our contractual obligations as described in our Annual Report on Form 10-K for the fiscal year ended March 31, 2018.2019.

CRITICAL ACCOUNTING ESTIMATES

For a complete description of what we believe to be the critical accounting estimates used in the preparation of our condensed consolidated financial statements, refer to our Annual Report on Form 10-K for the fiscal year ended March 31, 2018,2019, filed with the SEC on May 9, 2018. 17, 2019.

Refer to Note 2, Recent Accounting Pronouncements, of the accompanying notes to the condensed consolidated financial statements for details regarding the adoption of the contracts with customers (Topic 606) accounting guidance in the first quarter of Fiscal Year 2019.

Refer to Note 3, Acquisition, Goodwill, and Acquired Intangible Assets, of the accompanying notes to the condensed consolidated financial statements for critical accounting estimates used in the acquisition of Polycom completed on July 2, 2018.

Income Taxes

Management assesses the available positive and negative evidence to estimate if sufficient future taxable income will be generated to use the existing deferred tax assets. The amount of the deferred tax asset considered realizable, however, could be adjusted if estimates of future taxable income during the carryforward period are reduced or increased.

Under the acquisition method of accounting for business combinations, if we identify changes to acquired deferred tax asset valuation allowances or liabilities related to uncertain tax positions during the measurement period and they relate to new information obtained about facts and circumstances that existed as of the acquisition date, those changes are considered a measurement period adjustment, and we record the offset to goodwill. We record all other changes to deferred tax asset valuation allowances and liabilities related to uncertain tax positions in current period income tax expense.

Except as described above, there have been no changes to our critical accounting estimates during the sixthree months ended SeptemberJune 30, 2018.2019.

Recent Accounting Pronouncements

For more information regarding the Recent Accounting Pronouncements that may impact us, refer tosee Note 2, Recent Accounting Pronouncements, of the accompanying notes to the condensed consolidated financial statements.

Financial Statements (Unaudited)

PLANTRONICS, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands)

| | | | March 31,

2018 | | September 30,

2018 | June 30,

2019 | | March 31,

2019 |

| ASSETS | | | | | | |

| Current assets: | | | | | | |

| Cash and cash equivalents | $ | 390,661 |

| | $ | 291,086 |

| $ | 191,904 |

| | $ | 202,509 |

|

| Short-term investments | 269,313 |

| | 14,705 |

| 14,169 |

| | 13,332 |

|

| Accounts receivable, net | 152,888 |

| | 354,066 |

| 318,235 |

| | 337,671 |

|

| Inventory, net | 68,276 |

| | 156,908 |

| 217,424 |

| | 177,146 |

|

| Other current assets | 18,588 |

| | 57,584 |

| 47,430 |

| | 50,488 |

|

| Total current assets | 899,726 |

| | 874,349 |

| 789,162 |

| | 781,146 |

|

| Property, plant, and equipment, net | 142,129 |

| | 216,802 |

| 196,376 |

| | 204,826 |

|

| Goodwill | 15,498 |

| | 1,334,534 |

| 1,279,897 |

| | 1,278,380 |

|

| Purchased intangibles, net | — |

| | 914,455 |

| 780,348 |

| | 825,675 |

|

| Deferred tax assets | 17,950 |

| | 5,320 |

| 3,182 |

| | 5,567 |

|

| Other assets | 1,584 |

| | 24,647 |

| 73,066 |

| | 20,941 |

|

| Total assets | $ | 1,076,887 |

| | $ | 3,370,107 |

| $ | 3,122,031 |

| | $ | 3,116,535 |

|

| | | | | | | |

| LIABILITIES AND STOCKHOLDERS' EQUITY | |

| | |

| |

| | |

|

| Current liabilities: | |

| | |

| |

| | |

|

| Accounts payable | $ | 45,417 |

| | $ | 149,917 |

| $ | 166,618 |

| | $ | 129,514 |

|

| Accrued liabilities | 80,097 |

| | 407,777 |

| 408,306 |

| | 398,715 |

|

| Total current liabilities | 125,514 |

| | 557,694 |

| 574,924 |

| | 528,229 |

|

| Long term debt, net of issuance costs | 492,509 |

| | 1,726,241 |

| 1,642,163 |

| | 1,640,801 |

|

| Deferred tax liability | 1,976 |

| | 115,887 |

| |

| Long-term income taxes payable | 87,328 |

| | 95,228 |

| 95,573 |

| | 83,121 |

|

| Other long-term liabilities | 16,590 |

| | 84,997 |

| 139,873 |

| | 142,697 |

|

| Total liabilities | 723,917 |

| | 2,580,047 |

| 2,452,533 |

| | 2,394,848 |

|

| Commitments and contingencies (Note 7) |

|

| |

|

| |

| Commitments and contingencies (Note 8) | |

|

| |

|

|

| Stockholders' equity: | |

| | |

| |

| | |

|

| Common stock | 816 |

| | 884 |

| 887 |

| | 884 |

|

| Additional paid-in capital | 876,645 |

| | 1,404,713 |

| 1,445,097 |

| | 1,431,607 |

|

| Accumulated other comprehensive income | 2,870 |

| | 5,667 |

| |

| Accumulated other comprehensive loss | | (6,628 | ) | | (475 | ) |

| Retained earnings | 299,066 |

| | 218,565 |

| 92,437 |

| | 143,344 |

|

| Total stockholders' equity before treasury stock | 1,179,397 |

| | 1,629,829 |

| 1,531,793 |

| | 1,575,360 |

|

| Less: Treasury stock, at cost | (826,427 | ) | | (839,769 | ) | (862,295 | ) | | (853,673 | ) |

| Total stockholders' equity | 352,970 |

| | 790,060 |

| 669,498 |

| | 721,687 |

|

| Total liabilities and stockholders' equity | $ | 1,076,887 |

| | $ | 3,370,107 |

| $ | 3,122,031 |

| | $ | 3,116,535 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

PLANTRONICS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(Unaudited)

| | | | Three Months Ended September 30, | | Six Months Ended September 30, | Three Months Ended June 30, |

| | 2017 | | 2018 | | 2017 | | 2018 | 2019 | | 2018 |

| Net revenues | | | | | | | | | | |

| Net product revenues | $ | 210,300 |

| | $ | 435,262 |

| | $ | 414,226 |

| | $ | 656,571 |

| $ | 382,745 |

| | $ | 221,309 |

|

| Net service revenues | — |

| | 47,807 |

| | — |

| | 47,807 |

| 65,022 |

| | — |

|

| Total net revenues | 210,300 |

| | 483,069 |

| | 414,226 |

| | 704,378 |

| 447,767 |

| | 221,309 |

|

| Cost of revenues | | | | | | | | | | |

| Cost of product revenues | 102,668 |

| | 305,477 |

| | 203,311 |

| | 416,943 |

| 208,616 |

| | 111,466 |

|

| Cost of service revenues | — |

| | 24,963 |

| | — |

| | 24,963 |

| 26,505 |

| | — |

|

| Total cost of revenues | 102,668 |

| | 330,440 |

| | 203,311 |

| | 441,906 |

| 235,121 |

| | 111,466 |

|

| Gross profit | 107,632 |

| | 152,629 |

| | 210,915 |

| | 262,472 |

| 212,646 |

| | 109,843 |

|

| Operating expenses: | | | | | | | | | | |

| Research, development, and engineering | 19,932 |

| | 57,047 |

| | 41,145 |

| | 80,748 |

| 59,524 |

| | 23,701 |

|

| Selling, general, and administrative | 57,696 |

| | 174,297 |

| | 113,929 |

| | 238,500 |

| 163,608 |

| | 64,203 |

|

| Gain, net from litigation settlements | (104 | ) | | — |

| | (280 | ) | | (30 | ) | (1,162 | ) | | (30 | ) |

| Restructuring and other related charges (credits) | (51 | ) | | 7,261 |

| | 2,522 |

| | 8,581 |

| |

| Restructuring and other related charges | | 19,525 |

| | 1,320 |

|

| Total operating expenses | 77,473 |

| | 238,605 |

| | 157,316 |

| | 327,799 |

| 241,495 |

| | 89,194 |

|

| Operating income (loss) | 30,159 |

| | (85,976 | ) | | 53,599 |

| | (65,327 | ) | (28,849 | ) | | 20,649 |

|

| Interest expense | (7,260 | ) | | (23,893 | ) | | (14,563 | ) | | (31,220 | ) | (23,932 | ) | | (7,327 | ) |

| Other non-operating income, net | 1,826 |

| | 1,610 |

| | 2,740 |

| | 3,606 |

| 333 |

| | 1,996 |

|

| Income (Loss) before income taxes | 24,725 |

| | (108,259 | ) | | 41,776 |

| | (92,941 | ) | |

| Income (loss) before income taxes | | (52,448 | ) | | 15,318 |

|

| Income tax expense (benefit) | 4,772 |

| | (21,550 | ) | | 2,995 |

| | (20,703 | ) | (7,577 | ) | | 847 |

|

| Net income (loss) | $ | 19,953 |

| | $ | (86,709 | ) | | $ | 38,781 |

| | $ | (72,238 | ) | $ | (44,871 | ) | | $ | 14,471 |

|

| | | | | | | | | | | |

| Earnings (Loss) per common share: | | | | | | | | |

| Income (loss) per common share: | | | | |

| Basic | $ | 0.59 |

| | $ | (2.21 | ) | | $ | 1.16 |

| | $ | (2.01 | ) | $ | (1.14 | ) | | $ | 0.43 |

|

| Diluted | $ | 0.59 |

| | $ | (2.21 | ) | | $ | 1.14 |

| | $ | (2.01 | ) | $ | (1.14 | ) | | $ | 0.42 |

|

| | | | | | | | | | | |

| Shares used in computing earnings (loss) per common share: | | | | | | | | |

| Shares used in computing loss per common share: | | | | |

| Basic | 32,570 |

| | 39,281 |

| | 32,538 |

| | 35,938 |

| 39,239 |

| | 32,594 |

|

| Diluted | 32,809 |

| | 39,281 |

| | 33,111 |

| | 35,938 |

| 39,239 |

| | 33,534 |

|

| | | | | | | | | | | |

| Cash dividends declared per common share | $ | 0.15 |

| | $ | 0.15 |

| | $ | 0.30 |

| | $ | 0.30 |

| |

The accompanying notes are an integral part of these condensed consolidated financial statements.

PLANTRONICS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(in thousands)

(Unaudited)

| | | | Three Months Ended September 30, | | Six Months Ended September 30, | Three Months Ended June 30, |

| | 2017 | | 2018 | | 2017 | | 2018 | 2019 | | 2018 |

| Net income (loss) | $ | 19,953 |

| | $ | (86,709 | ) | | $ | 38,781 |

| | $ | (72,238 | ) | $ | (44,871 | ) | | $ | 14,471 |

|

| Other comprehensive income (loss): | | | | | | | | | | |

| Foreign currency translation adjustments | 57 |

| | (1,815 | ) | | 257 |

| | (1,815 | ) | (219 | ) | | — |

|

| Unrealized gains (losses) on cash flow hedges: | | | | | | | | | | |

| Unrealized cash flow hedge gains (losses) arising during the period | (2,302 | ) | | 813 |

| | (4,647 | ) | | 4,769 |

| (6,704 | ) | | 3,956 |

|

| Net (gains) losses reclassified into income for revenue hedges | 1,131 |

| | (900 | ) | | 1,149 |

| | (1,149 | ) | (1,359 | ) | | (249 | ) |

| Net (gains) losses reclassified into income for cost of revenue hedges | (174 | ) | | — |

| | (132 | ) | | (79 | ) | (104 | ) | | (79 | ) |

| Net (gains) losses reclassified into income for interest rate swaps | — |

| | 977 |

| | — |

| | 977 |

| 652 |

| | — |

|

| Net unrealized gains (losses) on cash flow hedges | (1,345 | ) | | 890 |

| | (3,630 | ) | | 4,518 |

| (7,515 | ) | | 3,628 |

|

| Unrealized gains (losses) on investments: | | | | | | | | | | |

| Unrealized holding gains (losses) during the period | 133 |

| | — |

| | 209 |

| | 198 |

| — |

| | 198 |

|