UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2017

2018

Commission File Number 1-11921

________________________________

E TRADE Financial Corporation

TRADE Financial Corporation (Exact Name of Registrant as Specified in its Charter)

|

| | |

| Delaware | | 94-2844166 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

11 Times Square, 32nd Floor, New York, New York 10036

(Address of principal executive offices and Zip Code)

(646) 521-4300

(Registrant’s telephone number, including area code)

_____________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act. |

| | | |

Large accelerated filer x | Accelerated filer | | ¨ |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company | | ¨ |

Emerging growth company ¨ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

As of October 31, 2017,30, 2018, there were 269,659,766254,239,061 shares of common stock outstanding.

E*TRADE FINANCIAL CORPORATION

FORM 10-Q QUARTERLY REPORT

For the Quarter Ended September 30, 20172018

TABLE OF CONTENTS |

| | |

| PART I | FINANCIAL INFORMATION | |

| | |

| Item 1. | | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | |

| | |

| | |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Item 2. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

PARTPart II | | |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

Item 5.5 | | |

| Item 6. | | |

| | | |

|

| | |

E*TRADE | Q3 2017 10-Q | | E*TRADE Q3 2018 10-Q | Page i |

Unless otherwise indicated, references to "the Company," "we," "us," "our," "E*TRADE" and "E*TRADE Financial" mean E*TRADE Financial Corporation and its subsidiaries, and references to the parent company mean E*TRADE Financial Corporation but not its subsidiaries.

E*TRADE, E*TRADE Financial, E*TRADE Bank, the Converging Arrows logo, OptionsHouse, Equity Edge Online, Trust Company of America (TCA), and OptionsHouseLibertyTM are trademarks or registered trademarks of E*TRADE Financial Corporation in the United States and in other countries. All other trademarks are the property of their respective owners.

|

| | |

E*TRADE | Q3 2017 10-Q | | E*TRADE Q3 2018 10-Q | Page ii |

PART I

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. These statements discuss, among other things, things:

our future plans, objectives, outlook, strategies, expectations and intentions relating to our business and future financial and operating results and the assumptions that underlie these matters and include statements regarding the Company'sour proposed transaction with Trust Company of America (TCA)Capital One Financial Corporation (Capital One) and its benefits and timing, our business strategy, objectives and vision; our plans and ability to deliver new products and solutions; our ability to improve client acquisition and deepen relationships with existing clients; our ability to effectively monetize brokerage relationships by investing in agency mortgage-backed securities;

our capital plan initiatives,

the expected balance sheet size, any balance sheet growthtiming and the incremental regulatory and reporting requirements that our balance sheet size and growth may require; our plans to run off our legacy mortgage and consumer loan portfolio; repurchases of our common stock, payment of dividends on our capital stock, including our common and preferred stock; our ability to maintain required regulatory capital ratios; our plans for stock,

the payment of dividends from our subsidiaries to our parent company; proposed issuancecompany,

the management of preferred stockour legacy mortgage and the expected financing of the proposed transaction; our target liquidity positions; consumer loan portfolio,

our ability to identifyutilize deferred tax assets, the expected implementation and applicability of government regulation and our ability to comply with these regulations,

our ability to maintain required regulatory capital ratios,

continued repurchases of our common stock,

our ability to meet upcoming debt obligations,

the integration and related restructuring costs of past and any future acquisitions,

the expected outcome of existing or new litigation,

our ability to execute our business plans and manage risks appropriately;risk,

future sources of revenue, expense and liquidity, and

any other statement that is not historical in nature.

These statements may be identified by the use of words such as "assume," "expect," "believe," "may," "will," "should," "anticipate," "intend," "plan," "estimate," "continue" and similar expressions.

We caution that actual results could differ materially from those discussed in these forward-looking statements. Important factors that could contribute to our actual results differing materially from any forward-looking statements include, but are not limited to, to:

the closing of the proposed transaction with TCACapital One may not occur or may be delayed regulatory risks associatedand that the actual aggregate consideration paid in connection with the proposed transaction unanticipated restructuring costs which may be incurred or undisclosed liabilities assumed, attemptsis still subject to retain key TCA personnel may not succeed, expected synergies and other financial benefits may not be realized or integration plans may not be implemented as anticipated; final determination,

changes in business, economic or political condition; conditions,

performance, volume and volatility in the equity and capital markets; fluctuationsmarkets,

changes in interest rates; rates or interest rate volatility,

customer demand for financial products and services; increased competition; services,

our ability to continue to compete effectively and respond to aggressive price competition within our industry,

cyber security threats, potential system disruptions and other security breaches; breaches or incidents,

our ability to participate in consolidation opportunities in our industry; industry, to complete consolidation transactions and to realize synergies or implement integration plans,

our ability to service our corporate debt; debt and, if necessary, to raise additional capital,

changes in government regulation or actions by our regulators; regulators, including those that may result from the implementation and enforcement of regulatory reform legislation,

E*TRADE Q3 2018 10-Q | Page 1

our ability to move capital to our parent company from our subsidiaries; subsidiaries,

adverse developments in litigation, or regulatory matters;

our ability to manage our balance sheet growth,

the timing, duration and durationcosts associated with our stock repurchase program,

our ability to manage credit risk with customers and counterparties, and

the impact of federal tax reform, including as a result of future regulations and the amount of shares repurchased and amount of cash expended in connection with, the share repurchase program; the availability, timing and size of any preferred stock issuance; and other factors discussed under guidance.

Part II. Item 1A. Risk Factors and Part I. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Form 10-Q; and Part I. Item 1A. Risk Factors of our Annual Report on Form 10-K for the year ended December 31, 2016, filed with the Securities and Exchange Commission (SEC), which are incorporated herein by reference. By their nature forward-looking statements are not guarantees of future performance or results and are subject to risks, uncertainties and assumptions that are difficult to predict or quantify. Actual future results may vary materially from expectations expressed or implied in this report or any of our prior communications. Investors should also consider the risks and uncertainties described elsewhere in this report, including under Part I. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Part II. Item 1A. Risk Factors of this Quarterly Report and Part I. Item 1A. Risk Factors of our Annual Report on Form 10-K for the year ended December 31, 2017, filed with the Securities and Exchange Commission (SEC), which are incorporated herein by reference. The forward-looking statements contained in this report reflect our expectations only as of the date of this report. YouInvestors should not place undue reliance on forward-looking statements, as we do not undertake to update or revise forward-looking statements, to reflect the impact of circumstances or events that arise after the date the forward-looking statements were made, except as required by law.

E*TRADE Q3 2018 10-Q | Page 2

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (MD&A)

The following discussion should be read in conjunction with the consolidated financial statements and the related notes that appear elsewhere in this document and with the Annual Report on Form 10-K for the year ended December 31, 2016.2017.

Company Overview

E*TRADE is a financial services company that provides online brokerage and related products and services primarily to individual retail investors. Our mission isFounded on the principle of innovation, we aim to enhance the financial independence of traders and investors through a powerful digital experience that includes tools and educational materials, supported by professional guidance, to help individual investors and traders meet both near- and long-term investing goals. We provide these services to customers through our digital platforms and network of industry-licensed customer service representatives and financial consultants, over the phone, by email and online via two national financial centers and in-person at 30 regional financial centers across the United States. We operate directly and through several subsidiaries, many of which are overseen by governmental and self-regulatory organizations. Our most important subsidiaries are described below:

E*TRADE Securities LLC (E*TRADE Securities) is a registered broker-dealer that clears and settles customer securities transactions.

E*TRADE Bank is a federally chartered savings bank that provides Federal Deposit Insurance Corporation (FDIC) insurance on qualifying amounts of customer deposits and provides other banking and cash management capabilities.

E*TRADE Savings Bank, a subsidiary of E*TRADE Bank, is a federally chartered savings bank that provides FDIC insurance on qualifying amounts of customer deposits and custody solutions for registered investment advisors (RIAs).

E*TRADE Financial Corporate Services is a provider of software and services for managing equity compensation plans to our corporate clients.

E*TRADE Futures LLC (E*TRADE Futures) is a registered non-clearing Futures Commission Merchant (FCM) that provides clearing and settlement services for customer futures transactions.

E*TRADE Capital Management, LLC (E*TRADE Capital Management) is an RIA that provides investment advisory services for our customers.

E*TRADE Q3 2018 10-Q | Page 3

Delivering a powerful digital offering and professional guidance. Our visionfor our customers is to be the #1 digital broker and advisor to traders and investors, known for ease of use and the completenessa core pillar of our offering.business strategy and we believe our focus on being a digital leader in the financial services industry is a competitive advantage. Our hybrid delivery model is available through the following award-winning digital platforms:

|

| |

| Web |

| Our leading-edge sites for customers and our primary channel to interact with prospects |

|

• Access to a broad range of trading solutions • Actionable ideas and information • Research and education for decision making |

|

| Mobile |

| Powerful trading applications for smartphones, tablets and watches |

|

• Award-winning mobile apps • Platforms to manage accounts on the move • Stock and portfolio alerts |

| |

| Active Trading Platforms |

| Powerful software and web-based trading solutions |

|

• Sophisticated trading tools • Idea generation and analysis • Advanced portfolio and market tracking |

Strategy

Our business strategy is centered on two key objectives: accelerating the growth of our core brokerage business to drive organic growth and improve competitive position,market share, and generating robust earnings growth and healthy returns on capital to deliver long-term value for our stakeholders.shareholders.

Accelerate Growth of Core Brokerage Business

Enhance overall customer experience

We are focused on delivering cutting-edge trading solutions while improving our market position in investing products. Through these offerings, we aim to drivecontinue growing our customer acquisitionbase while deepening engagement with our existing customers.

Capitalize on value of corporate services channel

Our corporate services channel is a strategically important driver of brokerage account and asset growth. We leverage our industry-leading position in corporate stock plan administration to improve client acquisition and engage with plan participants to bolster awareness of our full suite of offerings. Our corporate services channel is a strategically important driver

E*TRADE Q3 2018 10-Q | Page 4

Generate Robust Earnings Growth and Healthy Returns on Capital

Utilize balance sheet to enhance returns

We utilize our bank structure to effectively monetize brokerage relationships by investing stable, low-cost deposits primarily in agency mortgage-backed securities. Meanwhile, we continue to manage down the size and risk associated with our legacy mortgage and consumer loan portfolio.

Put capital to work for shareholders

We have put significantAs we continue to deliver on our capital to work through balance sheet growth, share repurchases and acquisition activity. Weplan initiatives, we are focused on generating and effectively deploying and returning excess capital, including through our share repurchase program and common stock dividends, for the benefit of our shareholders.

Products and Services

We offer a broad range of products and services to our customers. Our core brokerage business is organized into four product areas: Trading, Investing, Corporate Services, and Advisor Services. Additionally, we offer banking and cash management capabilities, including deposit accounts insured by the FDIC, which are fully integrated into customer brokerage accounts. Among other features, customers have access to debit cards with ATM fee refunds, online and mobile bill pay, mobile check deposits, and E*TRADE Line of Credit, a program which allows customers to borrow against the market value of securities pledged as collateral.

Trading

The Company delivers automated trade order placement and execution services, offering our customers a full range of investment vehicles, including US equities, exchange-traded funds (ETFs), options, bonds, futures, American depositary receipts and non-proprietary mutual funds. Margin accounts are also available to qualifying customers, enabling them to borrow against their securities. We help customers plan and execute margin trades through robust margin solutions, including calculators and requirement lookup and analysis tools. The Company also offers a fully paid lending program, which allows our customers to be compensated for allowing us to lend certain securities in their account.

The Company markets trading products and services to self-directed investors and active traders. Products and services are delivered through web, desktop and mobile digital channels. Trading and investing tools are supported by guidance, including fixed income, options and futures specialists available on-call for customers. Other tools and resources include independent research and analytics, live and on-demand education, market commentary, and strategies, trading ideas and screeners for major asset classes.

Investing

The Company endeavors to help investors build wealth and address their long-term investing needs. Products and services include individual retirement accounts (IRAs), including Roth IRAs, and a suite of managed products and asset allocation models. These include our Core Portfolios, Blend Portfolios, Dedicated Portfolios, and Fixed Income Portfolios. Investors are provided a full suite of digital tools across the Company's web and mobile channels to address their investing needs. These include planning and allocation tools, education and editorial content.

The Company also offers guidance through a team of licensed financial consultants and Chartered Retirement Planning CounselorsSM at our 30 regional financial centers across the country. Guidance is also accessible through our two national financial centers by phone, email and online channels. Customers can receive complimentary portfolio reviews and personalized investment recommendations.

E*TRADE Q3 2018 10-Q | Page 5

Corporate Services

The Company provides stock plan administration services for both public and private companies. Through our industry-leading platform, Equity Edge OnlineTM, the Company offers management of employee stock option plans, employee stock purchase plans and restricted stock plans with fully-automated stock plan administration. Accounting, reporting and scenario modeling tools are also available. The integrated stock plan solutions include multi-currency settlement and delivery, disbursement in various currencies and streamlined tax calculation. Additionally, corporate clients are offered 10b5-1 plan design and implementation and SEC filing assistance. The Company's digital platforms allow participants in corporate client stock plans to view and manage their holdings. Participants have access to education tools, restricted stock sales support and dedicated stock plan service representatives. Our Corporate Services channel is an important driver of brokerage account and asset growth, serving as an introductory channel to the Company, with over 1.7 million individual stock plan accounts. We serve approximately 20% of S&P 500 companies, including nearly 40% of technology companies and nearly 50% of healthcare companies within the index. In total, we serve over 50% of all publicly traded U.S. technology companies. As of September 30, 2018, approximately 35% of customer cash is related to the Corporate Services channel.

Advisor Services

With the acquisition of TCA, which was completed on April 9, 2018, the Company has expanded its ability to provide technology solutions and custody services to independent RIAs. Liberty, our proprietary technology platform, includes sophisticated modeling, rebalancing, reporting and practice management capabilities that are fully customizable for the RIA. We expect our Advisor Services channel to provide access to a growing segment of our industry and help bolster the Company's ability to attract and retain customers in need of specialized and sophisticated customer service engagement. As of September 30, 2018, the Advisor Services channel had approximately $12 billion in commitments for future assets under custody from RIAs, representing a significant increase from the $17 billion in assets under custody when the Company announced the planned acquisition of TCA in October 2017.

For additional information about our business see Part I. Item 1. Business in the Annual Report on Form 10-K for the year ended December 31, 2017.

Financial Performance

Our net revenue is generated primarily from net interest income, commissions and fees and service charges.

Net interest income is largely impacted by the size of our balance sheet, our balance sheet mix, and average yields on our assets and liabilities. Net interest income is driven primarily from interest earned on investment securities, and margin receivables, and our legacy loan portfolio, less interest paidincurred on interest-bearing liabilities, including deposits, customer

payables, corporate debt and other borrowings. Net interest income is also earned on our legacy mortgage and consumer loan portfolio which we expect to continue to run off in future periods.

Commissions revenue is generated by customer trades and is largely impacted by trade volume, trade type, and commission rates.

Fees and service charges revenue is mainly impacted by order flow revenue, fees earned on off-balance sheet customer cash and other assets, and advisor management and custody fees, and mutual fund service fees.

Our net revenue is offset by non-interest expenses, the largest of which are compensation and benefits and advertising and market development.

E*TRADE Q3 2018 10-Q | Page 6

Significant Events in the Third Quarter of 20172018

Announced Trust CompanyDeclared quarterly dividend on common stock

In October 2018, our Board of America acquisition

On October 19, 2017, we announced an agreement to acquire Trust CompanyDirectors declared a quarterly cash dividend of America, Inc. (TCA), a leading provider$0.14 per share on our outstanding shares of technology solutions and custody services to the registered investment adviser market, for $275 million in cash. We anticipate funding the transaction through the issuance of non-cumulative perpetual preferredcommon stock. The acquisitiondividend is expectedpayable on November 15, 2018, to shareholders of record as of the close inof business on October 30, 2018.

Completed prior $1 billion share repurchase program and approved new $1 billion program

During the secondthird quarter of 2018, subject to customary closing conditions and regulatory approvals.

Completed OptionsHouse integration

In August 2017, we completed the integration of Aperture, LLC (dba OptionsHouse), which was acquired by the Company in 2016. Completion of the integration included the rollout of OptionsHouse features and functionality through E*TRADE.com and the transfer of retail brokerage accounts and customer-related balances of OptionsHouse to E*TRADE Securities LLC (E*TRADE Securities). Futures accounts and balances of E*TRADE Securities were transferred to E*TRADE Futures LLC (formerly known as Aperture, LLC).

Issuedour prior $1 billion of senior notes and redeemed higher cost corporate debt

We issued $600 million of 2.95% Senior Notes and $400 million of 3.80% Senior Notes and usedshare repurchase program with the net proceeds, along with existing corporate cash, to redeem our outstanding $540 million of 5.375% Senior Notes and $460 million of 4.625% Senior Notes, resulting in a $58 million loss on early extinguishment of debt. This transaction reduces our annual corporate debt service costs from $50 million to $33 million.

Repurchased 4.6 million shares of our common stock

We continue to execute on our stock repurchase plan, under which the Board of Directors has authorized a $1 billion repurchase of shares of our common stock. During the three months ended September 30, 2017, the Company repurchased 4.65.3 million shares of common stock at an average price of $40.64 for a total of $187 million.$58.74 per share, or $310 million in the aggregate during the quarter. As of September 30, 2017, $813 million remained available for additional repurchases. As of October 31, 2017,2018, we have subsequently repurchased an additional 1.019.5 million shares of common stock at an average price of $43.53.$51.38 per share since we began repurchasing shares under this authorization in the third quarter of 2017. In October 2018, our Board of Directors authorized a new $1 billion share repurchase program. The timing and exact amount of any common stock repurchases will depend on various factors, including market conditions and our capital position. We have the ability to complete up to half of the authorization during the fourth quarter of 2018 and intend to complete the remainder by the end of 2019. As of October 30, 2018, we have subsequently repurchased an additional 2.5 million shares of common stock at an average price of $47.77 per share.

Redeemed our Trust Preferred Securities (TRUPs)

During the third quarter of 2018, the Company redeemed all $413 million of its outstanding TRUPs. In connection with the redemption, we recognized a loss on early extinguishment of debt of $4 million, consisting of the difference between the carrying value of the TRUPs redeemed, including unamortized debt issuance costs, and the total cash amount paid, including related fees and expenses. Net proceeds from the June 2018 issuance of the 4.50% Senior Notes due 2028 (Senior Notes) were used to redeem the TRUPs. For additional information about the debt issuance, see Note 11—Corporate Debt.

E*TRADE Q3 2018 10-Q | Page 7

Key Performance Metrics

Management monitors a number of customer activity and companycorporate metrics to evaluate the Company’s performance. The most significant of these are displayed below along with the percentage variance for the three months ended September 30, 20172018 from the same period in 2016, where applicable, and includes OptionsHouse2017. These metrics include the impact of the TCA acquisition from the September 12, 2016April 9, 2018 acquisition date.date, as applicable.

Customer Activity Metrics:

E*TRADE Q3 2018 10-Q | Page 8

E*TRADE Q3 2018 10-Q | Page 9

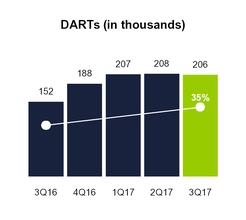

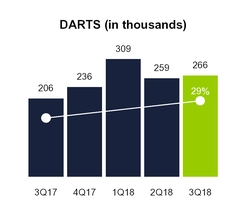

Daily Average Revenue Trades (DARTs) is the predominant driver of commissions revenue from our customers. DARTs were 205,763266,290 and 207,065277,796 for the three and nine months ended September 30, 2017,2018, respectively, compared to 151,905205,763 and 156,368207,065 for the same periods in 2016.2017.

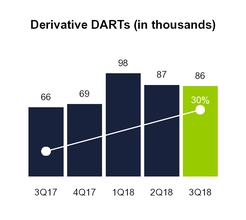

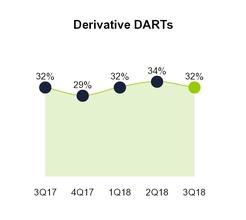

Derivative DARTs, a key driver of commissions revenue, is the daily average number of options and futures trades, and Derivative DARTs percentage is the mix of options and futures as a component of total DARTs and is a key driver of commissions revenue.DARTs. Derivative DARTs represented 32%were 85,977 and 31% of total DARTs90,075 for the three and nine months ended September 30, 2017,2018, respectively, compared to 26%66,122 and 25%63,869 for the same periods in 2016.2017. Derivative DARTs represented 32% of total DARTs for both the three and nine months ended September 30, 2018, compared to 32% and 31% for the same periods in 2017.

E*TRADE Q3 2018 10-Q | Page 10

Average commission per trade is an indicator of changes in our customer mix, product mix and/or product pricing. Average commission per trade was $7.76$7.04 and $8.54$7.21 for the three and nine months ended September 30, 2017,2018, respectively, compared to $10.97$7.76 and $10.81$8.54 for the same periods in 2016.2017. Average commission per trade for the three and nine months ended September 30, 20172018 was impacted by trade mix and the continued migration of customers to lower active trader commission pricing resulting from our reduced commission rates for equity and options trades effective March 13, 2017, which were as follows:

Stock, options and exchange-traded fund (ETF)ETF trade commissions reduced to $6.95 from $9.99

For active traders, commissions reduced to $4.95 from $7.99 and options charges reduced to $0.50 per contract from $0.75; trades required for active trader tier reduced to 30 per quarter from 150150.

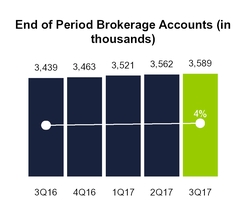

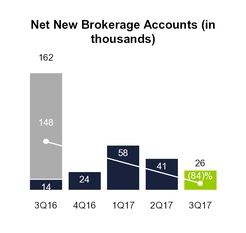

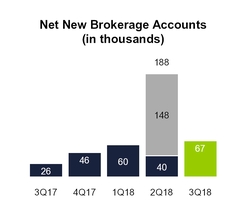

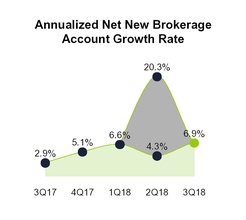

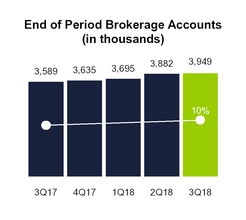

End of period brokerage accounts and net new brokerage accountsare indicators of our ability to attract and retain brokerage customers. End of period brokerage accounts were 3.9 million and 3.6 million at September 30, 2018 and 2017, respectively. Net new brokerage accounts were 67,163 and 314,490 for the three and nine months ended September 30, 2018, respectively, compared to 26,225 and 125,711 for the same periods in 2017. Our annualized net new brokerage account growth rate was 6.9% and 11.5% for the three and nine months ended September 30, 2018, respectively, compared to 2.9% and 4.8% for the same periods in 2017. Excluding the 145,891 accounts acquired on April 9, 2018 as part of the TCA acquisition, the adjusted annualized net new brokerage account growth rate was 6.2% for the nine months ended September 30, 2018.

Customer margin balances represents credit extended to customers to finance their purchases of securities by borrowing against securities they own and is a key driver of net interest income. Customer margin balances were $8.5$11.2 billion and $6.8$8.5 billion at September 30, 2018 and 2017, and 2016, respectively. Customer margin for periods prior to September 30, 2017, includes OptionsHouse balances which were held by a third party clearing firm. In connection with the integration of OptionsHouse, $0.4 billion of customer margin held by the third party clearing firm was transferred to our balance sheet and is reflected as margin receivables at September 30, 2017.

Managed products represents customer assets in our Managed Investment Portfolio, Unified Managed Account, Adaptive Portfolio, and Fixed Income Separately Managed Account products. Managed products are a driver of fees and service charges revenue. Managed products were $4.9 billion and $3.7 billion at September 30, 2017 and 2016, respectively.

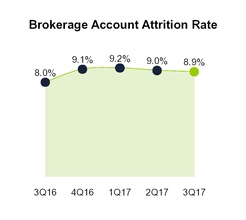

End of period brokerage accounts, net new brokerage accountsandbrokerage account attrition rate are indicators of our ability to attract and retain brokerage customers. End of period brokerage accounts were 3.6 million and 3.4 million at September 30, 2017 and 2016, respectively. Net new brokerage accounts were 26,225 and 125,711 for the three and nine months ended September 30, 2017, respectively, and 161,885 and 225,434 for the same periods in 2016. Our annualized brokerage account attrition rate was 8.9% and 9.1% for the three and nine months ended September 30, 2017, respectively, compared to 8.0% and 8.1% for the same periods in 2016. During the three and nine months ended September 30, 2017, our annualized net new brokerage account growth rate was 2.9% and 4.8% respectively, compared to 1.7% and 3.2% for the same periods in 2016. End of period brokerage accounts and net new brokerage accounts for the three months ended September 30, 2016 include 147,761 accounts from the OptionsHouse acquisition.

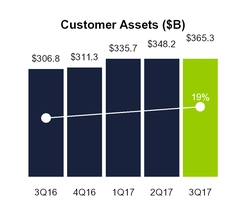

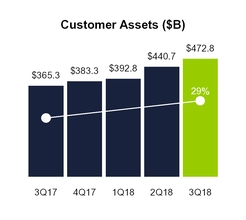

Customer assets is an indicator of the value of our relationship with the customer. An increase generally indicates that the use of our products and services by existingnew and newexisting customers is expanding. Changes in this metric are also driven by changes in the valuations of our customers' underlying securities. Customer assets were $365.3$472.8 billion and $306.8$365.3 billion at September 30, 2018 and 2017, respectively.

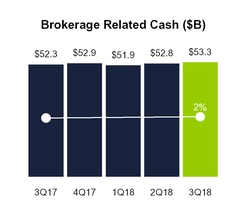

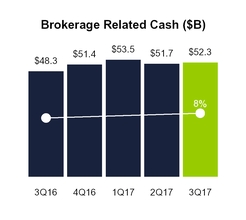

Brokerage related cash is an indicator of the level of engagement with our brokerage customers and 2016,is a key driver of net interest income as well as fees and service charges revenue, which includes fees earned on customer cash held by third parties. Brokerage related cash was $53.3 billion and $52.3 billion at September 30, 2018 and 2017, respectively.

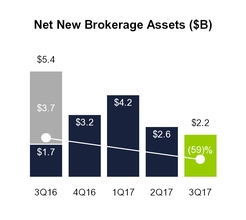

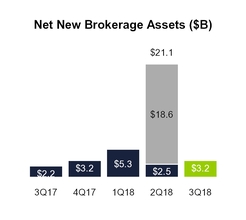

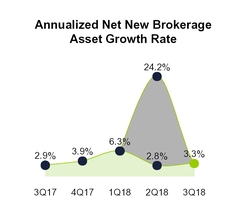

Net new brokerage assets is total inflows to new and existing brokerage accounts less total outflows from closed and existing brokerage accounts. The net new brokerage assets metric is a general indicator of the use of our products and services by new and existing brokerage customers. Net new brokerage assets were $2.2$3.2 billion and $9.0$29.6 billion for the three and nine months ended September 30, 2017,2018, respectively, compared to $5.4$2.2 billion and $9.9$9.0 billion for the same periods in 2016.2017. During the three and nine months ended September 30, 2017,2018, our annualized net new brokerage asset growth rate was 2.9%3.3% and 4.4%11.6%, respectively, compared to 2.7%2.9% and 3.4%4.4% for the same periods in 2016. Net2017. Excluding the $18.4 billion of assets acquired on April 9, 2018 as part of the TCA acquisition, the adjusted annualized net new brokerage assetsasset growth rate was 4.4% for the threenine months ended September 30, 2016 includes $3.72018.

Managed products represents customer assets in our Managed Portfolios which are a driver of fees and service charges revenue. Managed products were $6.2 billion from the OptionsHouse acquisition.and $4.9 billion at September 30, 2018 and 2017, respectively.

E*TRADE Q3 2018 10-Q | Page 11

Brokerage related cash is an indicator of the level of engagement with our brokerage customers and is a key driver of net interest income as well as fees and service charges revenue, which includes fees earned on customer cash held by third parties. Brokerage related cash was $52.3 billion and $48.3 billion at September 30, 2017 and 2016, respectively.

CompanyCorporate Metrics:

E*TRADE Q3 2018 10-Q | Page 12

Operating margin is the percentage of net revenue that results in income before income taxes and is an indicator of the Company's profitability. Operating margin was 37%52% and 44%49% for the three and nine months ended September 30, 2017,2018, respectively, compared to 46%37% and 44% for the same periods in 2016.2017.

Adjusted operating margin is a non-GAAP measure that provides useful information about our ongoing operating performance by excluding the provision (benefit) for loan losses and losses on early extinguishment of debt, which are not viewed as key factors governing our investment in the business and are excluded by management when evaluating operating margin performance. Adjusted operating margin was 42%48% and 39%46% for the three and nine months ended September 30, 2017,2018, respectively, compared to 34%42% and 35%39% for the same periods in 2016.2017. See MD&A—Earnings Overview for a reconciliation of thisadjusted operating margin to operating margin.

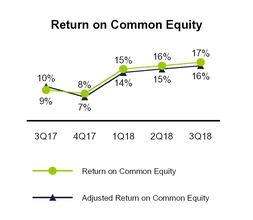

Return on common equity is calculated by dividing annualized net income available to common shareholders by average common shareholders' equity, which excludes preferred stock. Return on common equity was 17% and 16% for the three and nine months ended September 30, 2018, respectively, compared to 9% and 10% for the same periods in 2017.

Adjusted return on common equity is a non-GAAP measure calculated by dividing annualized adjusted net income available to common shareholders, a non-GAAP measure which excludes the most directly comparable GAAP measure.provision (benefit) for loan losses and losses on early extinguishment of debt, which are not viewed as key factors governing our investment in the business and are excluded by management when evaluating return on common equity performance, by average common shareholders' equity, which excludes preferred stock. Adjusted return on common equity was 16% and 15% for the three and nine months ended September 30, 2018, respectively, compared to 10% and 9% for the same periods in 2017. See MD&A—Earnings Overview for a reconciliation of adjusted net income available to common shareholders to net income and adjusted return on common equity to return on common equity.

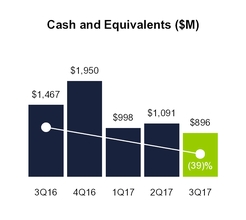

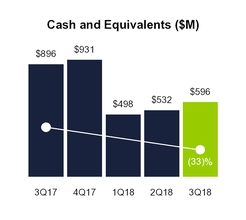

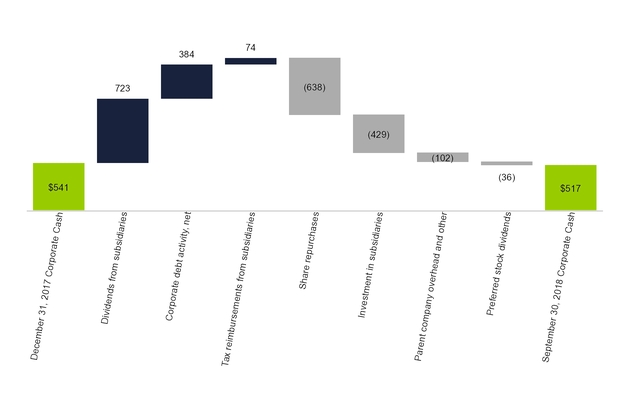

Corporate cash, a non-GAAP measure, is a component of cash and equivalents and represents the primary source of capital above and beyond the capital deployed in our regulated subsidiaries. Corporate cashCash and equivalents was $309$596 million and $306$896 million at September 30, 20172018 and 2016,2017, respectively, while corporate cash and equivalents was $896$517 million and $1.5 billion$309 million for the same periods. See MD&A—Liquidity and Capital Resources for a reconciliation of corporate cash to cash and equivalents.

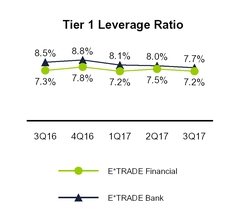

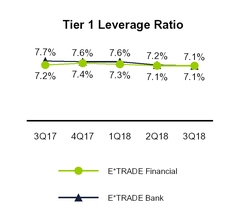

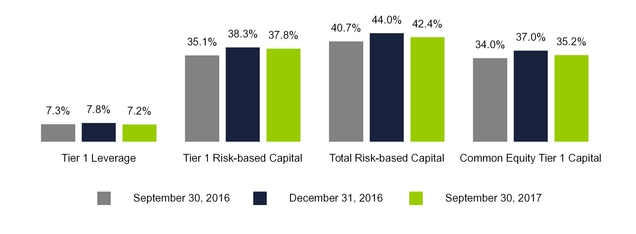

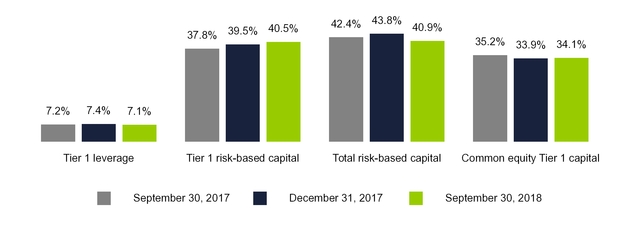

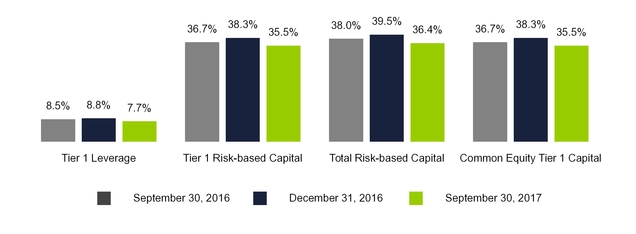

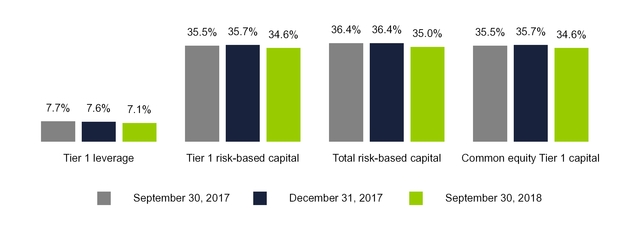

Tier 1 leverage ratio is an indicator of capital adequacy for E*TRADE Financial and E*TRADE Bank. Tier 1 leverage ratio is Tier 1 capital divided by adjusted average assets for leverage capital purposes. E*TRADE Financial's Tier 1 leverage ratio was 7.2%7.1% and 7.3%7.2% at September 30, 20172018 and 2016,2017, respectively. E*TRADE Bank's Tier 1 leverage ratio was 7.7%7.1% and 8.5%7.7% at September 30, 20172018 and 2016,2017, respectively. See MD&A—Liquidity and Capital Resources for additional information, including the calculation of regulatory capital ratios.

Allowance for loan losses is an estimate

E*TRADE Q3 2018 10-Q | Page 13

Interest-earning assets, along with net interest margin, isare an indicator of our ability to generate net interest income. Average interest-earning assets were $54.8$60.1 billion and $51.8$60.0 billion for the three and nine months ended September 30, 2017,2018, respectively, compared to $44.5$54.8 billion and $42.9$51.8 billion for the same periods in 2016.2017.

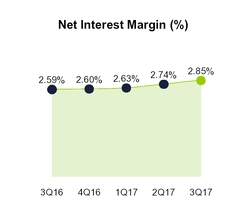

Net interest margin is a measure of the net yield on our average interest-earning assets. Net interest margin is calculated for a given period by dividing the annualized sum of net interest income by average interest-earning assets. Net interest margin was 2.85%3.10% and 2.74%3.03% for the three and nine months ended September 30, 2017,2018, respectively, compared to 2.59%2.85% and 2.67%2.74% for the same periods in 2016.2017.

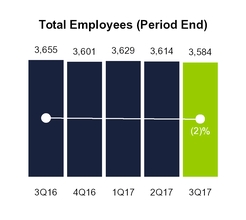

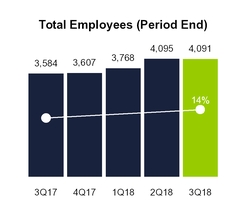

Total employees were 3,5844,091 and 3,6553,584 at September 30, 2018 and 2017, and 2016, respectively.

Regulatory Developments

In April 2016, the U.S.US Department of Labor (DOL) published its final fiduciaryConflicts of Interest Rule—Retirement Investment Advice regulations under the Employee Retirement Income Security Act of 1974 and the Internal Revenue Code of 1986. Certain aspects of these regulations began to take effect in June 2017. These regulations1986 (Fiduciary Rule). The Fiduciary Rule generally subjectsubjects particular persons, such as broker-dealers and other financial advisersadvisors providing investment advice to individual retirement accounts and other qualified retirement plans and accounts, to fiduciary duties and additional regulatory restrictions for a wider range of customer interactions. On March 5, 2018, the Fifth Circuit Court of Appeals issued a decision vacating the Fiduciary Rule in its entirety, and on June 21, 2018, following expiration of the appeals period for the decision and resolution of certain motions for appeal and intervention, issued a mandate making the decision effective.

In May 2018, the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 (EGRRCPA) was passed. The remaining aspects of these regulations are currently scheduled to take effect on January 1, 2018. During this transition period, the Department of Labor indicated in Field Assistance Bulletin 2017-02 issued in May 2017, that it will not take enforcement actions against impacted parties that are in reasonable compliance with the regulations. The Company isEGRRCPA amended provisions in the processDodd-Frank Wall Street Reform and Consumer Protection Act of implementing2010 (Dodd-Frank Act) as well as other statutes administered by the remaining applicable components for compliance.

The Company has historically not been subject to certain regulatory requirements that apply to banking organizations with $50 billion or more in total consolidated assets as defined by each applicable regulation. Total consolidated assets of $50 billion, which is measured in accordance with each applicable regulation, but generally onFederal Reserve Board, the basisOffice of the averageComptroller of the four most recent quarters, isCurrency, and the FDIC (collectively, the “federal banking agencies”). In July 2018, the federal banking agencies issued a meaningful regulatory thresholdjoint release clarifying that as U.S. banking organizations become subject to a numberresult of additionalthe passage of EGRRCPA, certain requirements, including company-run stress testing requirements under the Dodd-Frank Act, would no longer be required for savings and in some cases, more stringent regulatory requirements once they reach that size. The Company surpassed $50loan holding companies and banks with less than $100 billion in total consolidated assets, on a four quarter average in the first quarter of 2017.

The Company expects these regulatory requirements, not all of which have been finalized, to start becoming applicable to it in 2018. The Company has begun implementing policies, procedures, systems and governance structures that are designed to comply with the requirements. Additionally, while savings and loan holding companies are currently excluded from the scope of certain regulations that apply to bank holding companies,such as the Company expectsand E*TRADE Bank. In addition the Federal Reserve Board issued a separate statement clarifying that, pursuant to EGRRCPA, it will ultimately be subjectnot take action to these requirements. For additional information seeenforce certain regulatory and reporting requirements, including the modified liquidity coverage ratio (LCR) for firms, like the Company, with less than $100 billion in total consolidated assets. Part I. Item 1. BusinessSee MD&A—Liquidity and Capital Resources of our Annual Report on Form 10-K for the year ended December 31, 2016.further information.

E*TRADE Q3 2018 10-Q | Page 14

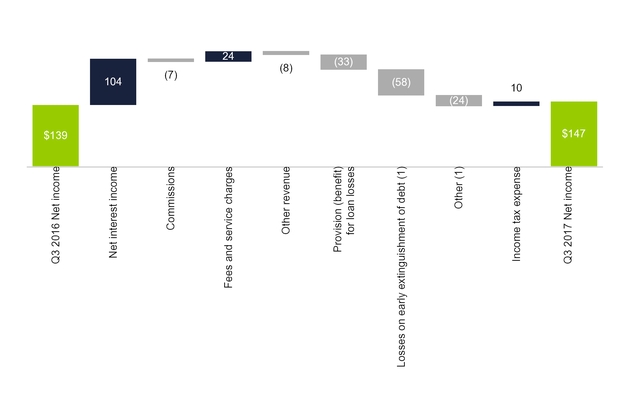

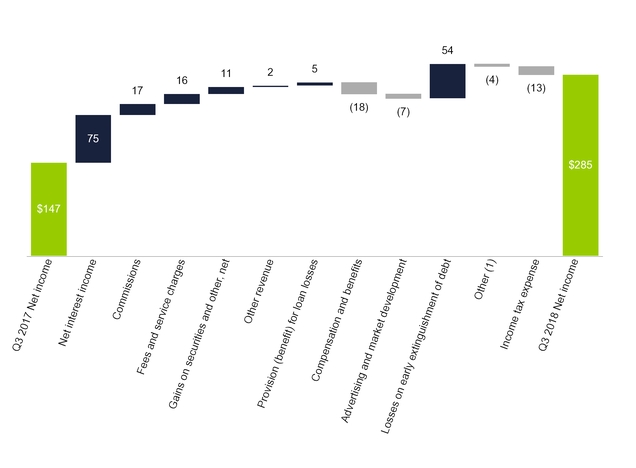

We generated net income of $147$285 million and $485$782 million on total net revenue of $599$720 million and $1.7$2.1 billion for the three and nine months ended September 30, 2017,2018, respectively. The following chart providespresents a reconciliation of net income for the three months ended September 30, 20162017 to net income for the three months ended September 30, 20172018 (dollars in millions):

| |

| (1) | TotalIncludes clearing and servicing, professional services, occupancy and equipment, communications, depreciation and amortization, FDIC insurance premiums, amortization of other intangibles, restructuring and acquisition-related activities and other non-interest expense increased $82 million for the periods presented which includes $58 million of losses on early extinguishment of debt.expenses. |

|

| | |

E*TRADE | Q3 2017 10-Q | | 10 |

E*TRADE Q3 2018 10-Q | Page 15

The following table presents significant components of the consolidated statement of income are as follows (dollars in millions except per share amounts): | | | | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2017 vs. 2016 | | 2017 vs. 2016 | | 2018 vs. 2017 | | 2018 vs. 2017 |

| | 2017 | | 2016 | | Amount | | % | | 2017 | | 2016 | | Amount | | % | 2018 | | 2017 | | Amount | | % | | 2018 | | 2017 | | Amount | | % |

| Net interest income | $ | 391 |

| | $ | 287 |

| | $ | 104 |

| | 36 | % | | $ | 1,066 |

| | $ | 860 |

| | $ | 206 |

| | 24 | % | $ | 466 |

| | $ | 391 |

| | $ | 75 |

| | 19 | % | | $ | 1,364 |

| | $ | 1,066 |

| | $ | 298 |

| | 28 | % |

| Total non-interest income | 208 |

| | 199 |

| | 9 |

| | 5 | % | | 663 |

| | 572 |

| | 91 |

| | 16 | % | 254 |

| | 208 |

| | 46 |

| | 22 | % | | 774 |

| | 663 |

| | 111 |

| | 17 | % |

| Total net revenue | 599 |

| | 486 |

| | 113 |

| | 23 | % | | 1,729 |

| | 1,432 |

| | 297 |

| | 21 | % | 720 |

| | 599 |

| | 121 |

| | 20 | % | | 2,138 |

| | 1,729 |

| | 409 |

| | 24 | % |

| Provision (benefit) for loan losses | (29 | ) | | (62 | ) | | 33 |

| | (53 | )% | | (142 | ) | | (131 | ) | | (11 | ) | | 8 | % | (34 | ) | | (29 | ) | | (5 | ) | | 17 | % | | (74 | ) | | (142 | ) | | 68 |

| | (48 | )% |

| Total non-interest expense | 405 |

| | 323 |

| | 82 |

| | 25 | % | | 1,106 |

| | 930 |

| | 176 |

| | 19 | % | 380 |

| | 405 |

| | (25 | ) | | (6 | )% | | 1,159 |

| | 1,106 |

| | 53 |

| | 5 | % |

| Income before income tax expense | 223 |

| | 225 |

| | (2 | ) | | (1 | )% | | 765 |

| | 633 |

| | 132 |

| | 21 | % | 374 |

| | 223 |

| | 151 |

| | 68 | % | | 1,053 |

| | 765 |

| | 288 |

| | 38 | % |

| Income tax expense | 76 |

| | 86 |

| | (10 | ) | | (12 | )% | | 280 |

| | 208 |

| | 72 |

| | 35 | % | 89 |

| | 76 |

| | 13 |

| | 17 | % | | 271 |

| | 280 |

| | (9 | ) | | (3 | )% |

| Net income | $ | 147 |

| | $ | 139 |

| | $ | 8 |

| | 6 | % | | $ | 485 |

| | $ | 425 |

| | $ | 60 |

| | 14 | % | $ | 285 |

| | $ | 147 |

| | $ | 138 |

| | 94 | % | | $ | 782 |

| | $ | 485 |

| | $ | 297 |

| | 61 | % |

| Preferred stock dividends | 12 |

| | — |

| | 12 |

| | 100 | % | | 25 |

| | — |

| | 25 |

| | 100 | % | 24 |

| | 12 |

| | 12 |

| | 100 | % | | 36 |

| | 25 |

| | 11 |

| | 44 | % |

| Net income available to common shareholders | $ | 135 |

| | $ | 139 |

| | $ | (4 | ) | | (3 | )% | | $ | 460 |

| | $ | 425 |

| | $ | 35 |

| | 8 | % | $ | 261 |

| | $ | 135 |

| | $ | 126 |

| | 93 | % | | $ | 746 |

| | $ | 460 |

| | $ | 286 |

| | 62 | % |

| Diluted earnings per common share | $ | 0.49 |

| | $ | 0.51 |

| | $ | (0.02 | ) | | (4 | )% | | $ | 1.67 |

| | $ | 1.52 |

| | $ | 0.15 |

| | 10 | % | $ | 1.00 |

| | $ | 0.49 |

| | $ | 0.51 |

| | 104 | % | | $ | 2.82 |

| | $ | 1.67 |

| | $ | 1.15 |

|

| 69 | % |

Net income increased 6%94% to $147$285 million and 14%61% to $485$782 million for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. Net income available to common shareholders was $261 million and $746 million for the three and nine months ended September 30, 2018, respectively, which reflects payments of $24 million and $36 million in preferred stock dividends, respectively. This compares to $135 million and $460 million for the three and nine months ended September 30, 2017 respectively, which reflects payments of $12 million and $25 million in preferred stock dividends, respectively, compared to net income available to common shareholders of $139 million and $425 million during the same periods in 2016. respectively.

The increase in net income for both periods in 2017 was driven by higher interest income due to a larger average balance sheet and higheran improvement in net interest rates,margin, as well as higher commissions, fees and service charges revenue. We recognized a benefit for loan losses of $29 million and $142 million for the threenet gains on securities and nine months ended September 30, 2017, respectively, compared to $62 million and $131 million for the same periods in 2016. Net income for the three and nine months ended September 30, 2017 also included $11 million and $27 million, respectively, of pre-tax costs primarily incurred in connection with the OptionsHouse integration and preparation for the incremental regulatory and reporting requirements that our balance sheet growth requires, as well as pre-taxother. Lower losses on early extinguishment of debt of $58 million. Non-interest expensealso contributed to increase net income for the three and nine months ended September 30, 2017 also included higher advertising and market development expenses driven by our new advertising campaign, as well as increased communications expense. These expenses were partially offset by lower restructuring and acquisition-related activities and an income tax benefit related to the revaluation of certain net state deferred tax assets. Net income forboth periods. During the nine months ended September 30, 2016 included an income tax2018, these increases were partially offset by a lower benefit relatedfor loan losses and higher non-interest expense due primarily to increased compensation and benefits and advertising and market development expenses.

Net Revenue

The following table presents the releasesignificant components of a valuation allowance against certain state deferred tax assets.net revenue (dollars in millions): |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2018 vs. 2017 | | | 2018 vs. 2017 |

| | 2018 | | 2017 | | Amount | | % | | 2018 | | 2017 | | Amount | | % |

| Net interest income | $ | 466 |

| | $ | 391 |

| | $ | 75 |

| | 19 | % | | $ | 1,364 |

| | $ | 1,066 |

| | $ | 298 |

| | 28 | % |

| Commissions | 117 |

| | 100 |

| | 17 |

| | 17 | % | | 375 |

| | 332 |

| | 43 |

| | 13 | % |

| Fees and service charges | 108 |

| | 92 |

| | 16 |

| | 17 | % | | 323 |

| | 276 |

| | 47 |

| | 17 | % |

| Gains on securities and other, net | 17 |

| | 6 |

| | 11 |

| | 183 | % | | 42 |

| | 23 |

| | 19 |

| | 83 | % |

| Other revenue | 12 |

| | 10 |

| | 2 |

| | 20 | % | | 34 |

| | 32 |

| | 2 |

| | 6 | % |

| Total non-interest income | 254 |

| | 208 |

| | 46 |

| | 22 | % | | 774 |

| | 663 |

| | 111 |

| | 17 | % |

| Total net revenue | $ | 720 |

| | $ | 599 |

| | $ | 121 |

| | 20 | % | | $ | 2,138 |

| | $ | 1,729 |

| | $ | 409 |

| | 24 | % |

|

| | |

E*TRADE | Q3 2017 10-Q | | 11 |

E*TRADE Q3 2018 10-Q | Page 16

Net Revenue

The components of net revenue and the resulting variances are as follows (dollars in millions): |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2017 vs. 2016 | | | 2017 vs. 2016 |

| | 2017 | | 2016 | | Amount | | % | | 2017 | | 2016 | | Amount | | % |

| Net interest income | $ | 391 |

| | $ | 287 |

| | $ | 104 |

| | 36 | % | | $ | 1,066 |

| | $ | 860 |

| | $ | 206 |

| | 24 | % |

| Commissions | 100 |

| | 107 |

| | (7 | ) | | (7 | )% | | 332 |

| | 320 |

| | 12 |

| | 4 | % |

| Fees and service charges | 92 |

| | 68 |

| | 24 |

| | 35 | % | | 276 |

| | 188 |

| | 88 |

| | 47 | % |

| Gains on securities and other, net | 6 |

| | 14 |

| | (8 | ) | | (57 | )% | | 23 |

| | 34 |

| | (11 | ) | | (32 | )% |

| Other revenue | 10 |

| | 10 |

| | — |

| | — | % | | 32 |

| | 30 |

| | 2 |

| | 7 | % |

| Total non-interest income | 208 |

| | 199 |

| | 9 |

| | 5 | % | | 663 |

| | 572 |

| | 91 |

| | 16 | % |

| Total net revenue | $ | 599 |

| | $ | 486 |

| | $ | 113 |

| | 23 | % | | $ | 1,729 |

| | $ | 1,432 |

| | $ | 297 |

| | 21 | % |

Net Interest Income

Net interest income increased 36%19% to $391$466 million and 24%28% to $1.1$1.4 billion for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. Net interest income is earned primarily through investment securities, margin receivables and our legacy mortgage and consumer loan portfolio, offset by funding costs.

|

| | |

E*TRADE | Q3 2017 10-Q | | 12 |

The following table presents average balance sheet data and interest income and expense data, as well as the related net interest margin, yields and rates prepared on the basis required by the SEC’s Industry Guide 3, "Statistical Disclosure by Bank Holding Companies"(dollars in millions):

| | | | Three Months Ended September 30, | Three Months Ended September 30, |

| | 2017 | | 2016 | 2018 | | 2017 |

| | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost |

| Cash and equivalents | $ | 905 |

| | $ | 2 |

| | 1.06 | % | | $ | 1,989 |

| | $ | 2 |

| | 0.42 | % | $ | 471 |

| | $ | 2 |

| | 1.84 | % | | $ | 905 |

| | $ | 2 |

| | 1.06 | % |

| Cash required to be segregated under federal or other regulations | 759 |

| | 3 |

| | 1.26 | % | | 1,885 |

| | 2 |

| | 0.33 | % | 836 |

| | 4 |

| | 2.15 | % | | 759 |

| | 3 |

| | 1.26 | % |

| Available-for-sale securities | 19,064 |

| | 102 |

| | 2.13 | % | | 13,301 |

| | 66 |

| | 1.99 | % | |

| Held-to-maturity securities | 22,162 |

| | 153 |

| | 2.77 | % | | 15,937 |

| | 109 |

| | 2.73 | % | |

Investment securities(1) | | 44,773 |

| | 315 |

| | 2.82 | % | | 41,226 |

| | 255 |

| | 2.47 | % |

| Margin receivables | 8,096 |

| | 87 |

| | 4.26 | % | | 6,479 |

| | 60 |

| | 3.68 | % | 10,902 |

| | 130 |

| | 4.74 | % | | 8,096 |

| | 87 |

| | 4.26 | % |

Loans (1) | 3,024 |

| | 37 |

| | 4.95 | % | | 4,202 |

| | 46 |

| | 4.44 | % | |

Loans(2) | | 2,332 |

| | 32 |

| | 5.38 | % | | 3,024 |

| | 37 |

| | 4.95 | % |

| Broker-related receivables and other | 829 |

| | 1 |

| | 0.45 | % | | 696 |

| | — |

| | 0.13 | % | 798 |

| | 4 |

| | 2.02 | % | | 829 |

| | 1 |

| | 0.45 | % |

| Subtotal interest-earning assets | 54,839 |

| | 385 |

| | 2.80 | % | | 44,489 |

| | 285 |

| | 2.56 | % | 60,112 |

| | 487 |

| | 3.24 | % | | 54,839 |

| | 385 |

| | 2.80 | % |

Other interest revenue (2) | — |

| | 28 |

| | | | — |

| | 24 |

| | | |

Other interest revenue(3) | | — |

| | 27 |

| | | | — |

| | 28 |

| | |

| Total interest-earning assets | 54,839 |

| | 413 |

| | 3.01 | % | | 44,489 |

| | 309 |

| | 2.77 | % | 60,112 |

| | 514 |

| | 3.41 | % | | 54,839 |

| | 413 |

| | 3.01 | % |

Total non-interest-earning assets (3) | 4,952 |

| | | | | | 4,793 |

| | | | | |

| Total non-interest-earning assets | | 4,291 |

| | | | | | 4,952 |

| | | | |

| Total assets | $ | 59,791 |

| | | | | | $ | 49,282 |

| | | | | $ | 64,403 |

| | | | | | $ | 59,791 |

| | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Deposits | $ | 40,758 |

| | $ | 1 |

| | 0.01 | % | | $ | 32,285 |

| | $ | 1 |

| | 0.01 | % | $ | 42,456 |

| | $ | 16 |

| | 0.15 | % | | $ | 40,758 |

| | $ | 1 |

| | 0.01 | % |

| Customer payables | 8,463 |

| | 1 |

| | 0.06 | % | | 7,592 |

| | 2 |

| | 0.06 | % | 10,352 |

| | 8 |

| | 0.30 | % | | 8,463 |

| | 1 |

| | 0.06 | % |

| Broker-related payables and other | 1,301 |

| | — |

| | 0.00 | % | | 1,258 |

| | — |

| | 0.00 | % | 1,880 |

| | 3 |

| | 0.53 | % | | 1,301 |

| | — |

| | 0.00 | % |

| Other borrowings | 831 |

| | 6 |

| | 2.91 | % | | 409 |

| | 4 |

| | 4.15 | % | 752 |

| | 6 |

| | 2.95 | % | | 831 |

| | 6 |

| | 2.91 | % |

| Corporate debt | 1,002 |

| | 12 |

| | 4.64 | % | | 993 |

| | 13 |

| | 5.40 | % | 1,408 |

| | 13 |

| | 3.90 | % | | 1,002 |

| | 12 |

| | 4.64 | % |

| Subtotal interest-bearing liabilities | 52,355 |

| | 20 |

| | 0.15 | % | | 42,537 |

| | 20 |

| | 0.19 | % | 56,848 |

| | 46 |

| | 0.32 | % | | 52,355 |

| | 20 |

| | 0.15 | % |

Other interest expense (4) | — |

| | 2 |

| | | | — |

| | 2 |

| | | — |

| | 2 |

| | | | — |

| | 2 |

| | |

| Total interest-bearing liabilities | 52,355 |

| | 22 |

| | 0.17 | % | | 42,537 |

| | 22 |

| | 0.20 | % | 56,848 |

| | 48 |

| | 0.33 | % | | 52,355 |

| | 22 |

| | 0.17 | % |

| Total non-interest-bearing liabilities | 820 |

| | | | | | 719 |

| | | | | 859 |

| | | | | | 820 |

| | | | |

| Total liabilities | 53,175 |

| | | | | | 43,256 |

| | | | | 57,707 |

| | | | | | 53,175 |

| | | | |

| Total shareholders' equity | 6,616 |

| | | | | | 6,026 |

| | | | | 6,696 |

| | | | | | 6,616 |

| | | | |

| Total liabilities and shareholders' equity | $ | 59,791 |

| | | | | | $ | 49,282 |

| | | | | $ | 64,403 |

| | | | | | $ | 59,791 |

| | | | |

| Excess interest earning assets over interest bearing liabilities/net interest income/net interest margin | $ | 2,484 |

| | $ | 391 |

| | 2.85 | % | | $ | 1,952 |

| | $ | 287 |

| | 2.59 | % | $ | 3,264 |

| | $ | 466 |

| | 3.10 | % | | $ | 2,484 |

| | $ | 391 |

| | 2.85 | % |

| |

| (1) | For the three months ended September 30, 2018, includes a $5 million net loss related to fair value hedging adjustments, previously referred to as hedge ineffectiveness. Amounts prior to 2018 have not been reclassified to conform to current period presentation and continue to be reflected within the gains on securities and other, net line item. See Note 8—Derivative Instruments and Hedging Activities for additional information. |

| |

| (2) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

| |

(2)(3) | Represents interest income on securities loaned. |

| |

(3) | Non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate interest income. |

| |

| (4) | Represents interest expense on securities borrowed. |

|

| | |

E*TRADE | Q3 2017 10-Q | | 13 |

E*TRADE Q3 2018 10-Q | Page 17

| | | | Nine Months Ended September 30, | Nine Months Ended September 30, |

| | 2017 | | 2016 | 2018 | | 2017 |

| | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost | | Average Balance | | Interest Inc./Exp. | | Average Yield/ Cost |

| Cash and equivalents | $ | 1,045 |

| | $ | 6 |

| | 0.83 | % | | $ | 1,730 |

| | $ | 5 |

| | 0.40 | % | $ | 601 |

| | $ | 7 |

| | 1.60 | % | | $ | 1,045 |

| | $ | 6 |

| | 0.83 | % |

| Cash required to be segregated under federal or other regulations | 1,263 |

| | 9 |

| | 0.90 | % | | 1,540 |

| | 4 |

| | 0.33 | % | 795 |

| | 11 |

| | 1.91 | % | | 1,263 |

| | 9 |

| | 0.90 | % |

| Available-for-sale securities | 17,958 |

| | 282 |

| | 2.09 | % | | 13,149 |

| | 198 |

| | 2.01 | % | |

| Held-to-maturity securities | 19,823 |

| | 410 |

| | 2.76 | % | | 14,993 |

| | 319 |

| | 2.84 | % | |

Investment securities(1) | | 44,979 |

| | 908 |

| | 2.69 | % | | 37,781 |

| | 692 |

| | 2.44 | % |

| Margin receivables | 7,383 |

| | 228 |

| | 4.12 | % | | 6,553 |

| | 185 |

| | 3.77 | % | 10,225 |

| | 351 |

| | 4.59 | % | | 7,383 |

| | 228 |

| | 4.12 | % |

Loans (1) | 3,319 |

| | 121 |

| | 4.86 | % | | 4,505 |

| | 146 |

| | 4.33 | % | |

Loans(2) | | 2,475 |

| | 98 |

| | 5.25 | % | | 3,319 |

| | 121 |

| | 4.86 | % |

| Broker-related receivables and other | 1,029 |

| | 2 |

| | 0.24 | % | | 470 |

| | 1 |

| | 0.21 | % | 898 |

| | 12 |

| | 1.76 | % | | 1,029 |

| | 2 |

| | 0.24 | % |

| Subtotal interest-earning assets | 51,820 |

| | 1,058 |

| | 2.72 | % | | 42,940 |

| | 858 |

| | 2.67 | % | 59,973 |

| | 1,387 |

| | 3.09 | % | | 51,820 |

| | 1,058 |

| | 2.72 | % |

Other interest revenue (2) | — |

| | 74 |

| | | | — |

| | 65 |

| | | |

Other interest revenue(3) | | — |

| | 84 |

| | | | — |

| | 74 |

| | |

| Total interest-earning assets | 51,820 |

| | 1,132 |

| | 2.91 | % | | 42,940 |

| | 923 |

| | 2.87 | % | 59,973 |

| | 1,471 |

| | 3.27 | % | | 51,820 |

| | 1,132 |

| | 2.91 | % |

Total non-interest-earning assets (3) | 5,051 |

| | | | | | 4,882 |

| | | | | |

| Total non-interest-earning assets | | 4,479 |

| | | | | | 5,051 |

| | | | |

| Total assets | $ | 56,871 |

| | | | | | $ | 47,822 |

| | | | | $ | 64,452 |

| | | | | | $ | 56,871 |

| | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Deposits | $ | 37,862 |

| | $ | 3 |

| | 0.01 | % | | $ | 31,243 |

| | $ | 3 |

| | 0.01 | % | $ | 42,877 |

| | $ | 26 |

| | 0.08 | % | | $ | 37,862 |

| | $ | 3 |

| | 0.01 | % |

| Customer payables | 8,611 |

| | 4 |

| | 0.06 | % | | 6,988 |

| | 4 |

| | 0.07 | % | 9,817 |

| | 13 |

| | 0.18 | % | | 8,611 |

| | 4 |

| | 0.06 | % |

| Broker-related payables and other | 1,233 |

| | — |

| | 0.00 | % | | 1,351 |

| | — |

| | 0.00 | % | 1,885 |

| | 7 |

| | 0.49 | % | | 1,233 |

| | — |

| | 0.00 | % |

| Other borrowings | 667 |

| | 16 |

| | 3.23 | % | | 418 |

| | 13 |

| | 4.23 | % | 837 |

| | 21 |

| | 3.28 | % | | 667 |

| | 16 |

| | 3.23 | % |

| Corporate debt | 996 |

| | 39 |

| | 5.14 | % | | 994 |

| | 40 |

| | 5.40 | % | 1,149 |

| | 32 |

| | 3.75 | % | | 996 |

| | 39 |

| | 5.14 | % |

| Subtotal interest-bearing liabilities | 49,369 |

| | 62 |

| | 0.17 | % | | 40,994 |

| | 60 |

| | 0.19 | % | 56,565 |

| | 99 |

| | 0.23 | % | | 49,369 |

| | 62 |

| | 0.17 | % |

Other interest expense (4) | — |

| | 4 |

| | | | — |

| | 3 |

| | | — |

| | 8 |

| | | | — |

| | 4 |

| | |

| Total interest-bearing liabilities | 49,369 |

| | 66 |

| | 0.18 | % | | 40,994 |

| | 63 |

| | 0.20 | % | 56,565 |

| | 107 |

| | 0.25 | % | | 49,369 |

| | 66 |

| | 0.18 | % |

| Total non-interest-bearing liabilities | 1,033 |

| | | | | | 1,010 |

| | | | | 939 |

| | | | | | 1,033 |

| | | | |

| Total liabilities | 50,402 |

| | | | | | 42,004 |

| | | | | 57,504 |

| | | | | | 50,402 |

| | | | |

| Total shareholders' equity | 6,469 |

| | | | | | 5,818 |

| | | | | 6,948 |

| | | | | | 6,469 |

| | | | |

| Total liabilities and shareholders' equity | $ | 56,871 |

| | | | | | $ | 47,822 |

| | | | | $ | 64,452 |

| | | | | | $ | 56,871 |

| | | | |

| Excess interest earning assets over interest bearing liabilities/net interest income/net interest margin | $ | 2,451 |

| | $ | 1,066 |

| | 2.74 | % | | $ | 1,946 |

| | $ | 860 |

| | 2.67 | % | $ | 3,408 |

| | $ | 1,364 |

| | 3.03 | % | | $ | 2,451 |

| | $ | 1,066 |

| | 2.74 | % |

| |

| (1) | For the nine months ended September 30, 2018, includes a $13 million net loss related to fair value hedging adjustments, previously referred to as hedge ineffectiveness. Amounts prior to 2018 have not been reclassified to conform to current period presentation and continue to be reflected within the gains on securities and other, net line item. See Note 8—Derivative Instruments and Hedging Activities for additional information. |

| |

| (2) | Nonaccrual loans are included in the average loan balances. Interest payments received on nonaccrual loans are recognized on a cash basis in interest income until it is doubtful that full payment will be collected, at which point payments are applied to principal. |

| |

(2)(3) | Represents interest income on securities loaned. |

| |

(3) | Non-interest earning assets consist of property and equipment, net, goodwill, other intangibles, net and other assets that do not generate interest income. |

| |

| (4) | Represents interest expense on securities borrowed. |

Average interest-earning assets increased 23%10% to $54.8$60.1 billion and 21%16% to $51.8$60.0 billion for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. The fluctuation in interest-earning assets is generally driven by changes in interest-bearing liabilities, primarily deposits and customer payables. Average interest-bearing liabilities increased 23%9% to $52.4$56.8 billion and 20%15% to $49.4$56.6 billion for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. The increase during the nine months ended September 30, 2018, was primarily due to higher deposits as a result of transferring customer cash held by third parties to our balance sheet. For additional information on our balance sheet growththroughout 2017 and early 2018, partially offset by customer cash held by third parties, see Balance Sheet Overview.net buying of $12.0 billion during the nine months ended September 30, 2018, compared to $6.9 billion during the same period in 2017.

E*TRADE Q3 2018 10-Q | Page 18

Net interest margin increased 2625 basis points to 2.85%3.10% and 729 basis points to 2.74%3.03% for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. Net interest margin is driven by the mix of average asset and liability average balances and the interest rates earned or paid on those balances. The increase during the three and nine months ended September 30, 2017,2018, compared to the same period in 2016,2017 is due to higher interest rates earned on increasedhigher margin receivablereceivables and investment securities balances,

|

| | |

E*TRADE | Q3 2017 10-Q | | 14 |

and higher securities lending activities, partially offset by the continued run-off of our higher yielding legacy mortgage and consumer loan portfolio. Additionally, funding costs increased primarily due to increased rates paid on deposits and customer payables during the three and nine months ended September 30, 2018. These increases were partially offset by lower corporate debt service costs during the nine months ended September 30, 2018.

Commissions

Commissions revenue decreased 7%increased 17% to $100$117 million and increased 4%13% to $332$375 million for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. The mainprimary factors that affect commissions revenue are DARTs, average commission per trade and the number of trading days.

DARTs volume increased 35%29% to 205,763266,290 and 32%34% to 207,065277,796 for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016,2017. The increase during the three and nine months ended September 30, 2018 was mainly driven by continued improved market sentiment along with the inclusion of OptionsHouse accounts and the strengthhigher volatility of the equity markets. Derivative DARTs represented 32%volume increased 30% to 85,977 and 31% of trading volume41% to 90,075 for the three and nine months ended September 30, 2017,2018, respectively, compared to 26% and 25% of trading volume for the same periods in 2016.2017.

Average commission per trade decreased 29%9% to $7.76$7.04 and 21%16% to $8.54$7.21 for the three and nine months ended September 30, 2017,2018, respectively, compared to the same periods in 2016.2017. Average commission per trade is impacted by customertrade mix and differing commission rates on various trade types (e.g. equities, derivatives, stock plan and mutual funds). Average commission per trade for the three and nine months ended September 30, 20172018 was also impacted by reduced commission rates implemented in March 2017 as well as the lower price structure for customer accounts associated with the OptionsHouse acquisition. We have also experienced increased trading activity from certaincontinued migration of customers qualifying them forto lower commission rates due to our new active trader pricing. This increased engagement is a key driver behind the decrease in average commission per trade.pricing.

Fees and Service Charges

The following table presents the significant components of fees and service charges and the resulting variances are as follows (dollars in millions): | | | | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2017 vs. 2016 | | 2017 vs. 2016 | | 2018 vs. 2017 | | 2018 vs. 2017 |

| | 2017 | | 2016 | | Amount | | % | | 2017 | | 2016 | | Amount | | % | 2018 | | 2017 | | Amount | | % | | 2018 | | 2017 | | Amount | | % |

| Order flow revenue | $ | 33 |

| | $ | 24 |

| | $ | 9 |

| | 38 | % | | $ | 98 |

| | $ | 68 |

| | $ | 30 |

| | 44 | % | $ | 40 |

| | $ | 33 |

| | $ | 7 |

| | 21 | % | | $ | 130 |

| | $ | 98 |

| | $ | 32 |

| | 33 | % |

Money market funds and sweep deposits revenue(1) | 23 |

| | 13 |

| | 10 |

| | 77 | % | | 71 |

| | 31 |

| | 40 |

| | 129 | % | 18 |

| | 23 |

| | (5 | ) | | (22 | )% | | 53 |

| | 71 |

| | (18 | ) | | (25 | )% |

| Advisor management and custody fees | | 19 |

| | 9 |

| | 10 |

| | 111 | % | | 46 |

| | 26 |

| | 20 |

| | 77 | % |

| Mutual fund service fees | 10 |

| | 9 |

| | 1 |

| | 11 | % | | 29 |

| | 27 |

| | 2 |

| | 7 | % | 13 |

| | 10 |

| | 3 |

| | 30 | % | | 36 |

| | 29 |

| | 7 |

| | 24 | % |

| Advisor management fees | 9 |

| | 8 |

| | 1 |

| | 13 | % | | 26 |

| | 21 |

| | 5 |

| | 24 | % | |

| Foreign exchange revenue | 6 |

| | 6 |

| | — |

| | — | % | | 20 |

| | 15 |

| | 5 |

| | 33 | % | 7 |

| | 6 |

| | 1 |

| | 17 | % | | 21 |

| | 20 |

| | 1 |

| | 5 | % |

| Reorganization fees | 5 |

| | 4 |

| | 1 |

| | 25 | % | | 13 |

| | 11 |

| | 2 |

| | 18 | % | 3 |

| | 5 |

| | (2 | ) | | (40 | )% | | 10 |

| | 13 |

| | (3 | ) | | (23 | )% |

| Other fees and service charges | 6 |

| | 4 |

| | 2 |

| | 50 | % | | 19 |

| | 15 |

| | 4 |

| | 27 | % | 8 |

| | 6 |

| | 2 |

| | 33 | % | | 27 |

| | 19 |

| | 8 |

| | 42 | % |

| Total fees and service charges | $ | 92 |

| | $ | 68 |

| | $ | 24 |

| | 35 | % | | $ | 276 |

| | $ | 188 |

| | $ | 88 |

| | 47 | % | $ | 108 |

| | $ | 92 |

| | $ | 16 |

| | 17 | % | | $ | 323 |

| | $ | 276 |

| | $ | 47 |

| | 17 | % |

| |

| (1) | Includes revenue earned on average customer cash held by third parties based on the federal funds rate or LIBOR plus a negotiated spread or other contractual arrangements with the third party institutions. |

Fees and service charges increased 35% to $92 million and 47% to $276 million for the three and nine months ended September 30, 2017, respectively, compared to the same periods in 2016. The increase in fees and service charges was largely driven by an increase in revenue earned on customer cash held by third parties, which was impacted by a higher interest rate environment, partially offset by lower average balances. The gross yield on customer cash held by third parties for the three and nine months ended September 30, 2017 of approximately 120 and 85 basis points compares to approximately 45 and 40 basis

|

| | |

E*TRADE | Q3 2017 10-Q | | 15 |

E*TRADE Q3 2018 10-Q | Page 19

Fees and service charges increased 17% for both the three and nine months ended September 30, 2018, to $108 million and $323 million, respectively, compared to the same periods in 2017. These increases were primarily driven by increased order flow revenue due to higher trade volume and improved rates as well as increased advisor management and custody fees as a result of the acquisition of TCA and higher balances held in our managed products. This increase was partially offset by decreased money market funds and sweep deposits revenue driven by lower customer cash balances held by third parties as a result of transferring cash onto our balance sheet. The impact of the lower balances was partially offset by a higher yield of approximately 145 and 140 basis points for the three and nine months ended September 30, 2018, respectively, compared to approximately 120 and 85 basis points for the same periods in 2016. In addition, fees and service charges benefited from increased order flow revenue resulting primarily from higher options trading activity and improved rates.2017.

Gains on Securities and Other, Net

The following table presents the significant components of gains on securities and other, net and the resulting variances are as follows (dollars in millions): |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2017 vs. 2016 | | | 2017 vs. 2016 |

| | 2017 | | 2016 | | Amount | | % | | 2017 | | 2016 | | Amount | | % |

| Gains on available-for-sale securities | $ | 7 |

| | $ | 17 |

| | $ | (10 | ) | | (59 | )% | | $ | 25 |

| | $ | 46 |

| | $ | (21 | ) | | (46 | )% |

| Hedge ineffectiveness | (2 | ) | | (4 | ) | | 2 |

| | (50 | )% | | (5 | ) | | (8 | ) | | 3 |

| | (38 | )% |

| Equity method investment income (loss) and other | 1 |

| | 1 |

| | — |

| | — | % | | 3 |

| | (4 | ) | | 7 |

| | (175 | )% |

| Gains on securities and other, net | $ | 6 |

| | $ | 14 |

| | $ | (8 | ) | | (57 | )% | | $ | 23 |

| | $ | 34 |

| | $ | (11 | ) | | (32 | )% |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Variance | | Nine Months Ended September 30, | | Variance |

| | | 2018 vs. 2017 | | | 2018 vs. 2017 |

| | 2018 | | 2017 | | Amount | | % | | 2018 | | 2017 | | Amount | | % |

Gains on available-for-sale securities, net(1) | 11 |

| | 7 |

| | 4 |

| | 57 | % | | 33 |

| | 25 |

| | 8 |

| | 32 | % |

Equity method investment income (loss) and other(2)(3) | 6 |

| | (1 | ) | | 7 |

| | * |

| | 9 |

| | (2 | ) | | 11 |

| | * |

|

| Gains on securities and other, net | $ | 17 |

| | $ | 6 |

| | $ | 11 |

| | 183 | % | | $ | 42 |

| | $ | 23 |

| | $ | 19 |

| | 83 | % |

| |

| * | Percentage not meaningful. |

| |

| (1) | In August 2018, the Company sold available-for-sale securities and reinvested the sale proceeds in agency-backed securities at current market rates. See Note 6—Available-for-Sale and Held-to-Maturity Securities for additional information. |

| |