| ☒ | |||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. | |||||

| ☐ | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. | |||||

Federally chartered | 52-0904874 | 8200 Jones Branch Drive | 22102-3110 | (703) | 903-2000 | |||||||||||||||||||||||||||||||||||||||||

| corporation | McLean, | Virginia | ||||||||||||||||||||||||||||||||||||||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | (Address of principal executive | (Zip Code) | ( | number, including area code) | |||||||||||||||||||||||||||||||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| None | N/A | N/A | ||||||

Large accelerated filer | ☐ | Accelerated filer | ☒ | |||||||||||||||||

Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||||||||||||||

Emerging growth company | ☐ | |||||||||||||||||||

| Table of Contents | ||

| Page | |||||

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |||||

n Introduction | |||||

n Housing and Mortgage Market Conditions | |||||

n Consolidated Results of Operations | |||||

n Consolidated Balance Sheets Analysis | |||||

n Our Portfolios | |||||

n Our Business Segments | |||||

n Risk Management | |||||

l Credit Risk | |||||

l Market Risk | |||||

n Liquidity and Capital Resources | |||||

n Critical Accounting Estimates | |||||

n Regulation and Supervision | |||||

n Forward-Looking Statements | |||||

| FINANCIAL STATEMENTS | |||||

| OTHER INFORMATION | |||||

| CONTROLS AND PROCEDURES | |||||

| EXHIBIT INDEX | |||||

| SIGNATURES | |||||

| FORM 10-Q INDEX | |||||

| Freddie Mac 1Q 2024 Form 10-Q | i | |||||||

| Table of Contents | ||

| Table | Description | Page | ||||||

| 1 | Summary of Consolidated Statements of Income and Comprehensive Income | |||||||

| 2 | Components of Net Interest Income | |||||||

| 3 | Analysis of Net Interest Yield | |||||||

| 4 | Components of Non-Interest Income | |||||||

| 5 | (Provision) Benefit for Credit Losses | |||||||

| 6 | Components of Non-Interest Expense | |||||||

| 7 | Summarized Condensed Consolidated Balance Sheets | |||||||

| 8 | Mortgage Portfolio | |||||||

| 9 | Mortgage-Related Investments Portfolio | |||||||

| 10 | Other Investments Portfolio | |||||||

| 11 | Single-Family Segment Financial Results | |||||||

| 12 | Multifamily Segment Financial Results | |||||||

| 13 | Allowance for Credit Losses Activity | |||||||

| 14 | Allowance for Credit Losses Ratios | |||||||

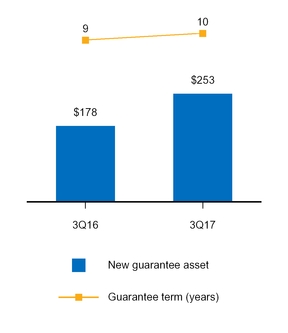

| 15 | Single-Family New Business Activity | |||||||

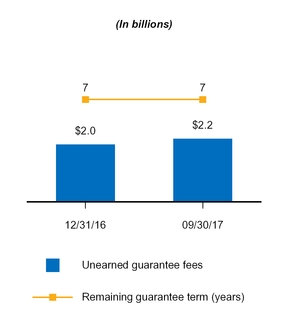

| 16 | Single-Family Mortgage Portfolio Newly Acquired Credit Enhancements | |||||||

| 17 | Single-Family Mortgage Portfolio Credit Enhancement Coverage Outstanding | |||||||

| 18 | Serious Delinquency Rates for Credit-Enhanced and Non-Credit-Enhanced Loans in Our Single-Family Mortgage Portfolio | |||||||

| 19 | Credit Quality Characteristics of Our Single-Family Mortgage Portfolio | |||||||

| 20 | Single-Family Mortgage Portfolio Attribute Combinations | |||||||

| 21 | Single-Family Completed Loan Workout Activity | |||||||

| 22 | Multifamily Mortgage Portfolio CRT Issuance | |||||||

| 23 | Credit-Enhanced and Non-Credit-Enhanced Loans Underlying Our Multifamily Mortgage Portfolio | |||||||

| 24 | Credit Quality of Our Multifamily Mortgage Portfolio Without Credit Enhancement | |||||||

| 25 | PVS-YC and PVS-L Results Assuming Shifts of the Yield Curve | |||||||

| 26 | Duration Gap and PVS Results | |||||||

| 27 | PVS-L Results Before Derivatives and After Derivatives | |||||||

| 28 | Earnings Sensitivity to Changes in Interest Rates | |||||||

| 29 | Liquidity Sources | |||||||

| 30 | Funding Sources | |||||||

| 31 | Debt of Freddie Mac Activity | |||||||

| 32 | Maturity and Redemption Dates | |||||||

| 33 | Debt of Consolidated Trusts Activity | |||||||

| 34 | Net Worth Activity | |||||||

| 35 | Regulatory Capital Components | |||||||

| 36 | Statutory Capital Components | |||||||

| 37 | Capital Metrics Under ERCF | |||||||

| 38 | Forecasted House Price Growth Rates | |||||||

| Freddie Mac 1Q 2024 Form 10-Q | ii | |||||||

| Management's Discussion and Analysis | Introduction | |||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Introduction | |||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | ||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 3 | |||||||

| Management's Discussion and Analysis | Housing and Mortgage Market Conditions | |||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Net interest income | $3,489 | $3,646 | ($157 | ) | (4 | )% | $10,663 | $10,494 | $169 | 2 | % | |||||||||||||||||||

| Benefit (provision) for credit losses | (716 | ) | (113 | ) | (603 | ) | (534 | )% | (178 | ) | 1,129 | (1,307 | ) | (116 | )% | |||||||||||||||

| Net interest income after benefit (provision) for credit losses | 2,773 | 3,533 | (760 | ) | (22 | )% | 10,485 | 11,623 | (1,138 | ) | (10 | )% | ||||||||||||||||||

| Non-interest income (loss): | ||||||||||||||||||||||||||||||

| Gains (losses) on extinguishment of debt | 27 | (92 | ) | 119 | 129 | % | 295 | (266 | ) | 561 | 211 | % | ||||||||||||||||||

| Derivative gains (losses) | (678 | ) | (36 | ) | (642 | ) | (1,783 | )% | (2,076 | ) | (6,655 | ) | 4,579 | 69 | % | |||||||||||||||

| Net impairment of available-for-sale securities recognized in earnings | (1 | ) | (9 | ) | 8 | 89 | % | (17 | ) | (138 | ) | 121 | 88 | % | ||||||||||||||||

| Other gains on investment securities recognized in earnings | 723 | 309 | 414 | 134 | % | 840 | 1,062 | (222 | ) | (21 | )% | |||||||||||||||||||

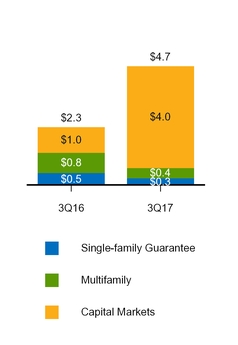

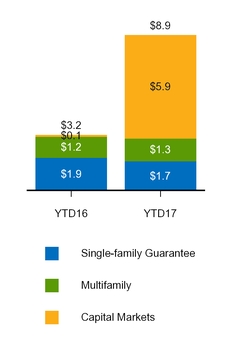

| Other income (loss) | 5,403 | 605 | 4,798 | 793 | % | 6,512 | 1,527 | 4,985 | 326 | % | ||||||||||||||||||||

| Total non-interest income (loss) | 5,474 | 777 | 4,697 | 605 | % | 5,554 | (4,470 | ) | 10,024 | 224 | % | |||||||||||||||||||

| Non-interest expense: | ||||||||||||||||||||||||||||||

| Administrative expense | (524 | ) | (498 | ) | (26 | ) | (5 | )% | (1,548 | ) | (1,421 | ) | (127 | ) | (9 | )% | ||||||||||||||

| REO operations expense | (35 | ) | (56 | ) | 21 | 38 | % | (128 | ) | (169 | ) | 41 | 24 | % | ||||||||||||||||

| Temporary Payroll Tax Cut Continuation Act of 2011 expense | (339 | ) | (293 | ) | (46 | ) | (16 | )% | (990 | ) | (845 | ) | (145 | ) | (17 | )% | ||||||||||||||

| Other expense | (159 | ) | (138 | ) | (21 | ) | (15 | )% | (361 | ) | (442 | ) | 81 | 18 | % | |||||||||||||||

| Total non-interest expense | (1,057 | ) | (985 | ) | (72 | ) | (7 | )% | (3,027 | ) | (2,877 | ) | (150 | ) | (5 | )% | ||||||||||||||

| Income (loss) before income tax (expense) benefit | 7,190 | 3,325 | 3,865 | 116 | % | 13,012 | 4,276 | 8,736 | 204 | % | ||||||||||||||||||||

| Income tax (expense) benefit | (2,519 | ) | (996 | ) | (1,523 | ) | (153 | )% | (4,466 | ) | (1,308 | ) | (3,158 | ) | (241 | )% | ||||||||||||||

| Net income (loss) | 4,671 | 2,329 | 2,342 | 101 | % | 8,546 | 2,968 | 5,578 | 188 | % | ||||||||||||||||||||

| Total other comprehensive income (loss), net of taxes and reclassification adjustments | (21 | ) | (19 | ) | (2 | ) | (11 | )% | 324 | 275 | 49 | 18 | % | |||||||||||||||||

| Comprehensive income (loss) | $4,650 | $2,310 | $2,340 | 101 | % | $8,870 | $3,243 | $5,627 | 174 | % | ||||||||||||||||||||

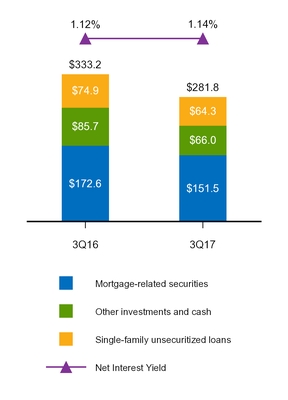

| 3Q 2017 | 3Q 2016 | |||||||||||||||||||||

| (Dollars in millions) | Average Balance | Interest Income (Expense)(1) | Average Rate | Average Balance | Interest Income (Expense)(1) | Average Rate | ||||||||||||||||

| Interest-earning assets: | ||||||||||||||||||||||

| Cash and cash equivalents | $10,064 | $14 | 0.53 | % | $21,664 | $15 | 0.28 | % | ||||||||||||||

| Securities purchased under agreements to resell | 57,107 | 166 | 1.16 | 62,086 | 56 | 0.36 | ||||||||||||||||

| Advances to lenders and other secured lending | 804 | 5 | 2.51 | 649 | 3 | 2.06 | ||||||||||||||||

| Mortgage-related securities: | ||||||||||||||||||||||

| Mortgage-related securities | 159,640 | 1,572 | 3.94 | 185,235 | 1,779 | 3.84 | ||||||||||||||||

| Extinguishment of PCs held by Freddie Mac | (85,198 | ) | (811 | ) | (3.81 | ) | (88,066 | ) | (829 | ) | (3.76 | ) | ||||||||||

| Total mortgage-related securities, net | 74,442 | 761 | 4.09 | 97,169 | 950 | 3.91 | ||||||||||||||||

| Non-mortgage-related securities | 15,127 | 60 | 1.62 | 15,671 | 26 | 0.67 | ||||||||||||||||

Loans held by consolidated trusts(1) | 1,731,577 | 14,617 | 3.38 | 1,654,288 | 13,602 | 3.29 | ||||||||||||||||

Loans held by Freddie Mac(1) | 117,298 | 1,250 | 4.26 | 131,945 | 1,395 | 4.23 | ||||||||||||||||

| Total interest-earning assets | $2,006,419 | $16,873 | 3.37 | $1,983,472 | $16,047 | 3.24 | ||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||||

| Debt securities of consolidated trusts including PCs held by Freddie Mac | $1,755,578 | ($12,663 | ) | (2.89 | ) | $1,680,388 | ($11,716 | ) | (2.79 | ) | ||||||||||||

| Extinguishment of PCs held by Freddie Mac | (85,198 | ) | 811 | 3.81 | (88,066 | ) | 829 | 3.76 | ||||||||||||||

| Total debt securities of consolidated trusts held by third parties | 1,670,380 | (11,852 | ) | (2.84 | ) | 1,592,322 | (10,887 | ) | (2.73 | ) | ||||||||||||

| Other debt: | ||||||||||||||||||||||

| Short-term debt | 68,868 | (173 | ) | (0.99 | ) | 81,057 | (83 | ) | (0.40 | ) | ||||||||||||

| Long-term debt | 259,075 | (1,319 | ) | (2.02 | ) | 302,062 | (1,384 | ) | (1.82 | ) | ||||||||||||

| Total other debt | 327,943 | (1,492 | ) | (1.80 | ) | 383,119 | (1,467 | ) | (1.53 | ) | ||||||||||||

| Total interest-bearing liabilities | 1,998,323 | (13,344 | ) | (2.67 | ) | 1,975,441 | (12,354 | ) | (2.50 | ) | ||||||||||||

| Expense related to derivatives | — | (40 | ) | (0.01 | ) | — | (47 | ) | (0.01 | ) | ||||||||||||

| Impact of net non-interest-bearing funding | 8,096 | — | 0.01 | 8,031 | — | 0.01 | ||||||||||||||||

| Total funding of interest-earning assets | $2,006,419 | ($13,384 | ) | (2.67 | ) | $1,983,472 | ($12,401 | ) | (2.50 | ) | ||||||||||||

| Net interest income/yield | $3,489 | 0.70 | $3,646 | 0.74 | ||||||||||||||||||

(1) Loan fees, primarily consisting of amortization of delivery fees, included in interest income were $634 million and $737 million for loans held by consolidated trusts and $37 million and $53 million for loans held by Freddie Mac during 3Q 2017 and 3Q 2016, respectively. | ||||||||||||||||||||||

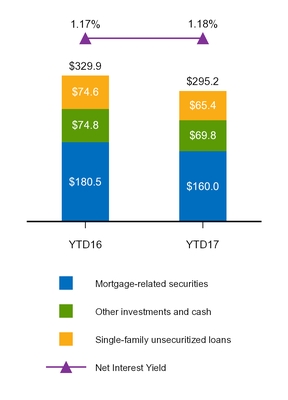

| YTD 2017 | YTD 2016 | ||||||||||||||||||||

| (Dollars in millions) | Average Balance | Interest Income (Expense)(1) | Average Rate | Average Balance | Interest Income (Expense)(1) | Average Rate | |||||||||||||||

| Interest-earning assets: | |||||||||||||||||||||

| Cash and cash equivalents | $11,417 | $38 | 0.44 | % | $16,112 | $31 | 0.26 | % | |||||||||||||

| Securities purchased under agreements to resell | 55,903 | 386 | 0.92 | 57,348 | 149 | 0.35 | |||||||||||||||

| Advances to lenders and other secured lending | 651 | 12 | 2.42 | 419 | 7 | 2.33 | |||||||||||||||

| Mortgage-related securities: | |||||||||||||||||||||

| Mortgage-related securities | 168,819 | 4,886 | 3.86 | 193,492 | 5,546 | 3.82 | |||||||||||||||

| Extinguishment of PCs held by Freddie Mac | (87,883 | ) | (2,456 | ) | (3.73 | ) | (96,388 | ) | (2,679 | ) | (3.71 | ) | |||||||||

| Total mortgage-related securities, net | 80,936 | 2,430 | 4.00 | 97,104 | 2,867 | 3.94 | |||||||||||||||

| Non-mortgage-related securities | 18,049 | 207 | 1.54 | 14,219 | 56 | 0.53 | |||||||||||||||

Loans held by consolidated trusts(1) | 1,720,906 | 43,810 | 3.39 | 1,640,997 | 41,735 | 3.39 | |||||||||||||||

Loans held by Freddie Mac(1) | 119,843 | 3,870 | 4.31 | 138,648 | 4,318 | 4.15 | |||||||||||||||

| Total interest-earning assets | $2,007,705 | $50,753 | 3.37 | $1,964,847 | $49,163 | 3.33 | |||||||||||||||

| Interest-bearing liabilities: | |||||||||||||||||||||

| Debt securities of consolidated trusts including PCs held by Freddie Mac | $1,744,260 | ($38,023 | ) | (2.91 | ) | $1,665,226 | ($36,606 | ) | (2.93 | ) | |||||||||||

| Extinguishment of PCs held by Freddie Mac | (87,883 | ) | 2,456 | 3.73 | (96,388 | ) | 2,679 | 3.71 | |||||||||||||

| Total debt securities of consolidated trusts held by third parties | 1,656,377 | (35,567 | ) | (2.86 | ) | 1,568,838 | (33,927 | ) | (2.88 | ) | |||||||||||

| Other debt: | |||||||||||||||||||||

| Short-term debt | 72,292 | (414 | ) | (0.76 | ) | 85,995 | (258 | ) | (0.39 | ) | |||||||||||

| Long-term debt | 270,251 | (3,984 | ) | (1.96 | ) | 301,791 | (4,338 | ) | (1.91 | ) | |||||||||||

| Total other debt | 342,543 | (4,398 | ) | (1.71 | ) | 387,786 | (4,596 | ) | (1.58 | ) | |||||||||||

| Total interest-bearing liabilities | 1,998,920 | (39,965 | ) | (2.66 | ) | 1,956,624 | (38,523 | ) | (2.62 | ) | |||||||||||

| Expense related to derivatives | — | (125 | ) | (0.01 | ) | — | (146 | ) | (0.01 | ) | |||||||||||

| Impact of net non-interest-bearing funding | 8,785 | — | 0.01 | 8,223 | — | 0.01 | |||||||||||||||

| Total funding of interest-earning assets | $2,007,705 | ($40,090 | ) | (2.66 | ) | $1,964,847 | ($38,669 | ) | (2.62 | ) | |||||||||||

| Net interest income/yield | $10,663 | 0.71 | $10,494 | 0.71 | |||||||||||||||||

(1) Loan fees, primarily consisting of amortization of delivery fees, included in interest income were $1.7 billion and $1.9 billion for loans held by consolidated trusts and $132 million and $184 million for loans held by Freddie Mac during YTD 2017 and YTD 2016, respectively. | |||||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | ||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | |||||||||||||||||||||||||

| Contractual net interest income: | |||||||||||||||||||||||||||||

| Guarantee fee income | $808 | $822 | ($14 | ) | (2 | )% | $2,495 | $2,212 | $283 | 13 | % | ||||||||||||||||||

| Guarantee fee income related to the Temporary Payroll Tax Cut Continuation Act of 2011 | 333 | 292 | 41 | 14 | % | 974 | 838 | 136 | 16 | % | |||||||||||||||||||

| Other contractual net interest income | 1,604 | 1,635 | (31 | ) | (2 | )% | 4,900 | 5,219 | (319 | ) | (6 | )% | |||||||||||||||||

| Total contractual net interest income | 2,745 | 2,749 | (4 | ) | — | % | 8,369 | 8,269 | 100 | 1 | % | ||||||||||||||||||

| Net amortization - loans and debt securities of consolidated trusts | 822 | 884 | (62 | ) | (7 | )% | 2,442 | 2,191 | 251 | 11 | % | ||||||||||||||||||

| Net amortization - other assets and debt | (38 | ) | 60 | (98 | ) | (163 | )% | (23 | ) | 180 | (203 | ) | (113 | )% | |||||||||||||||

| Expense related to derivatives | (40 | ) | (47 | ) | 7 | 15 | % | (125 | ) | (146 | ) | 21 | 14 | % | |||||||||||||||

| Net interest income | $3,489 | $3,646 | ($157 | ) | (4 | )% | $10,663 | $10,494 | $169 | 2 | % | ||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in billions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Benefit (provision) for newly impaired loans | ($0.2 | ) | ($0.2 | ) | $— | — | % | ($0.5 | ) | ($0.6 | ) | $0.1 | 17 | % | ||||||||||||||||

| Amortization of interest rate concessions | 0.1 | 0.2 | (0.1 | ) | (50 | )% | 0.5 | 0.7 | (0.2 | ) | (29 | )% | ||||||||||||||||||

| Reclassifications of held-for-investment loans to held-for-sale loans | — | — | — | N/A | 0.3 | 0.6 | (0.3 | ) | (50 | )% | ||||||||||||||||||||

| Other, including changes in estimated default probability and loss severity | (0.6 | ) | (0.1 | ) | (0.5 | ) | (500 | )% | (0.5 | ) | 0.4 | (0.9 | ) | (225 | )% | |||||||||||||||

| Benefit (provision) for credit losses | ($0.7 | ) | ($0.1 | ) | ($0.6 | ) | (600 | )% | ($0.2 | ) | $1.1 | ($1.3 | ) | (118 | )% | |||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Fair value change in interest-rate swaps | $23 | $541 | ($518 | ) | (96 | )% | $116 | ($7,513 | ) | $7,629 | 102 | % | ||||||||||||||||||

| Fair value change in option-based derivatives | (198 | ) | (235 | ) | 37 | 16 | % | (519 | ) | 2,841 | (3,360 | ) | (118 | )% | ||||||||||||||||

| Fair value change in other derivatives | (105 | ) | 74 | (179 | ) | (242 | )% | (379 | ) | (657 | ) | 278 | 42 | % | ||||||||||||||||

| Accrual of periodic cash settlements | (398 | ) | (416 | ) | 18 | 4 | % | (1,294 | ) | (1,326 | ) | 32 | 2 | % | ||||||||||||||||

| Derivative gains (losses) | ($678 | ) | ($36 | ) | ($642 | ) | (1,783 | )% | ($2,076 | ) | ($6,655 | ) | $4,579 | 69 | % | |||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | ||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | |||||||||||||||||||||||||

| Other income (loss) | |||||||||||||||||||||||||||||

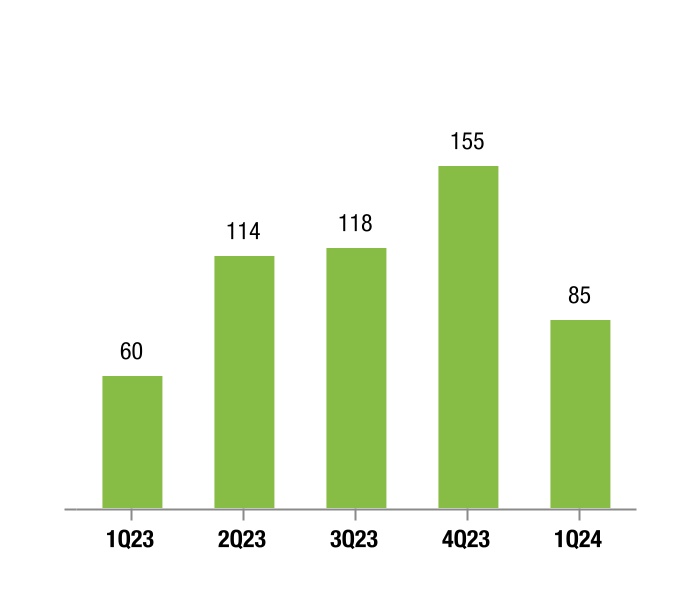

| Non-agency mortgage-related securities settlements | $4,525 | $— | $4,525 | N/A | $4,525 | $— | $4,525 | N/A | |||||||||||||||||||||

| Gains (losses) on loans | 203 | 139 | $64 | 46 | % | 410 | 136 | 274 | 201 | % | |||||||||||||||||||

| Gains (losses) on held-for-sale loan purchase commitments | 271 | 391 | (120 | ) | (31 | )% | 826 | 635 | 191 | 30 | % | ||||||||||||||||||

| (Losses) gains on debt where we elected the fair value option | 62 | (174 | ) | 236 | 136 | % | (129 | ) | (268 | ) | 139 | 52 | % | ||||||||||||||||

| All other | 272 | 249 | 23 | 9 | % | 744 | 1,024 | (280 | ) | (27 | )% | ||||||||||||||||||

| Fair value hedge accounting | |||||||||||||||||||||||||||||

| Change in fair value of derivatives in qualifying hedge relationships | 85 | — | 85 | N/A | (215 | ) | — | (215 | ) | N/A | |||||||||||||||||||

| Change in fair value of hedged items in qualifying hedge relationships | (15 | ) | — | (15 | ) | N/A | 351 | — | 351 | N/A | |||||||||||||||||||

| Ineffectiveness related to fair value hedge accounting | 70 | — | 70 | N/A | 136 | — | 136 | N/A | |||||||||||||||||||||

| Total other income (loss) | $5,403 | $605 | $4,798 | 793 | % | $6,512 | $1,527 | $4,985 | 326 | % | |||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | ||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | |||||||||||||||||||||||||

| Other comprehensive income, excluding certain items | $504 | $336 | $168 | 50 | % | $1,090 | $948 | $142 | 15 | % | |||||||||||||||||||

| Excluded items: | |||||||||||||||||||||||||||||

| Accretion due to significant increases in expected cash flows on previously impaired available-for-sale securities | (34 | ) | (66 | ) | 32 | 48 | % | (137 | ) | (235 | ) | 98 | 42 | % | |||||||||||||||

| Realized (gains) losses reclassified from AOCI | (491 | ) | (289 | ) | (202 | ) | (70 | )% | (629 | ) | (438 | ) | (191 | ) | (44 | )% | |||||||||||||

| Total excluded items | (525 | ) | (355 | ) | (170 | ) | (48 | )% | (766 | ) | (673 | ) | (93 | ) | (14 | )% | |||||||||||||

| Total other comprehensive income (loss) | ($21 | ) | ($19 | ) | ($2 | ) | (11 | )% | $324 | $275 | $49 | 18 | % | ||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Benefit (provision) for credit losses | $52 | $59 | ($7 | ) | (12 | )% | $352 | $632 | ($280 | ) | (44 | )% | ||||||||||||||||||

| Other income (loss) - lower-of-cost-or-fair-value adjustment | — | (65 | ) | 65 | 100 | % | — | (799 | ) | 799 | 100 | % | ||||||||||||||||||

| Other expense - property taxes and insurance associated with these loans | — | (10 | ) | 10 | 100 | % | — | (150 | ) | 150 | 100 | % | ||||||||||||||||||

| Effect on income before income tax (expense) benefit | $52 | ($16 | ) | $68 | 425 | % | $352 | ($317 | ) | $669 | 211 | % | ||||||||||||||||||

| September 30, 2017 | December 31, 2016 | Change | |||||||||||||

| (Dollars in millions) | $ | % | |||||||||||||

| Assets: | |||||||||||||||

| Cash and cash equivalents | $8,183 | $12,369 | ($4,186 | ) | (34 | )% | |||||||||

| Restricted cash and cash equivalents | 7,684 | 9,851 | (2,167 | ) | (22 | )% | |||||||||

| Securities purchased under agreements to resell | 47,202 | 51,548 | (4,346 | ) | (8 | )% | |||||||||

| Subtotal | 63,069 | 73,768 | (10,699 | ) | (15 | )% | |||||||||

| Investments in securities, at fair value | 87,148 | 111,547 | (24,399 | ) | (22 | )% | |||||||||

| Mortgage loans, net | 1,844,892 | 1,803,003 | 41,889 | 2 | % | ||||||||||

| Accrued interest receivable | 6,268 | 6,135 | 133 | 2 | % | ||||||||||

| Derivative assets, net | 705 | 747 | (42 | ) | (6 | )% | |||||||||

| Deferred tax assets, net | 14,576 | 15,818 | (1,242 | ) | (8 | )% | |||||||||

| Other assets | 13,998 | 12,358 | 1,640 | 13 | % | ||||||||||

| Total assets | $2,030,656 | $2,023,376 | $7,280 | — | % | ||||||||||

| Liabilities and Equity: | |||||||||||||||

| Liabilities: | |||||||||||||||

| Accrued interest payable | $5,990 | $6,015 | ($25 | ) | — | % | |||||||||

| Debt, net | 2,009,578 | 2,002,004 | 7,574 | — | % | ||||||||||

| Derivative liabilities, net | 212 | 795 | (583 | ) | (73 | )% | |||||||||

| Other liabilities | 9,626 | 9,487 | 139 | 1 | % | ||||||||||

| Total liabilities | 2,025,406 | 2,018,301 | 7,105 | — | % | ||||||||||

| Total equity | 5,250 | 5,075 | 175 | 3 | % | ||||||||||

| Total liabilities and equity | $2,030,656 | $2,023,376 | $7,280 | — | % | ||||||||||

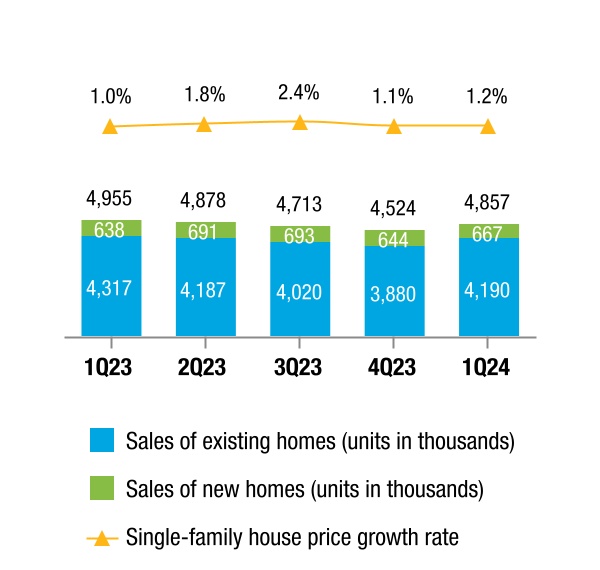

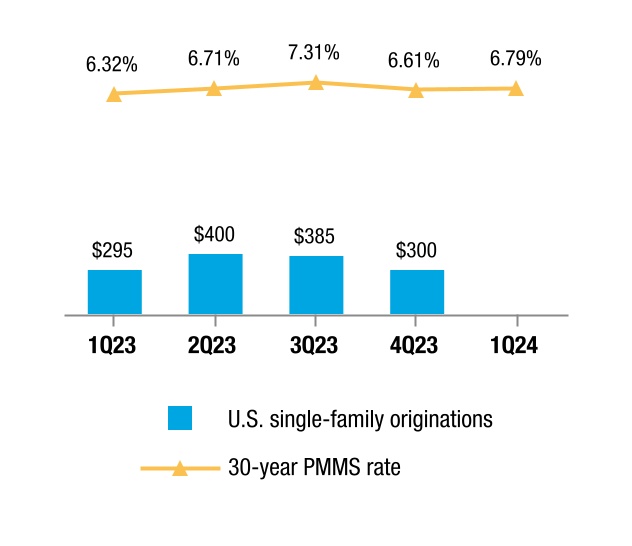

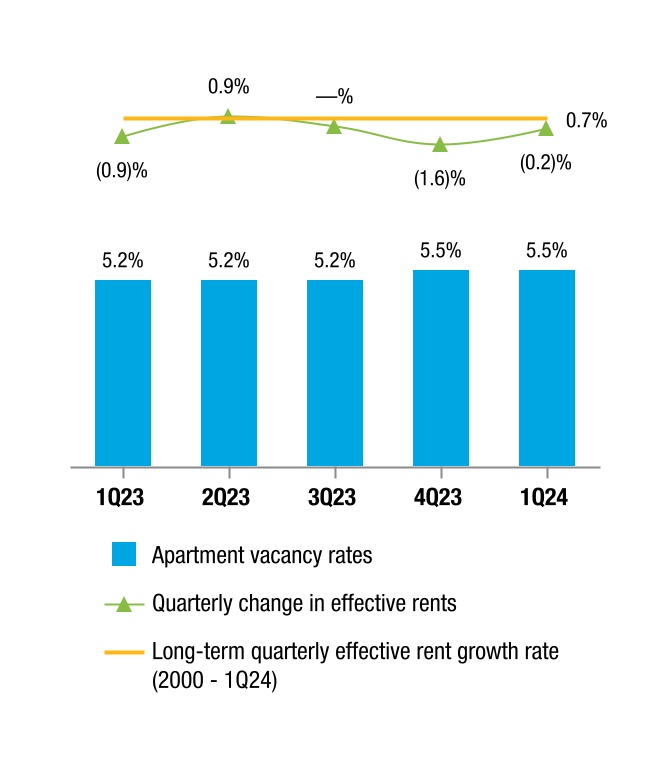

Sources: National Association of Realtors, U.S. Census Bureau, and Freddie Mac House Price Index (seasonally adjusted rate).

Sources: National Association of Realtors, U.S. Census Bureau, and Freddie Mac House Price Index (seasonally adjusted rate).

| Freddie Mac 1Q 2024 Form 10-Q | 4 | |||||||

| Management's Discussion and Analysis | Housing and Mortgage Market Conditions | |||||||

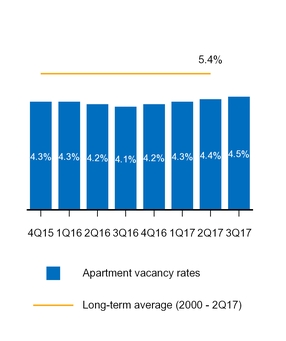

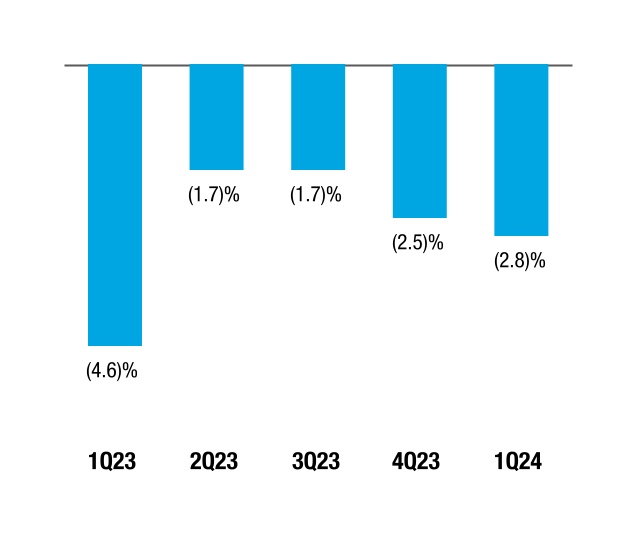

Source: Reis.

Source: Reis.

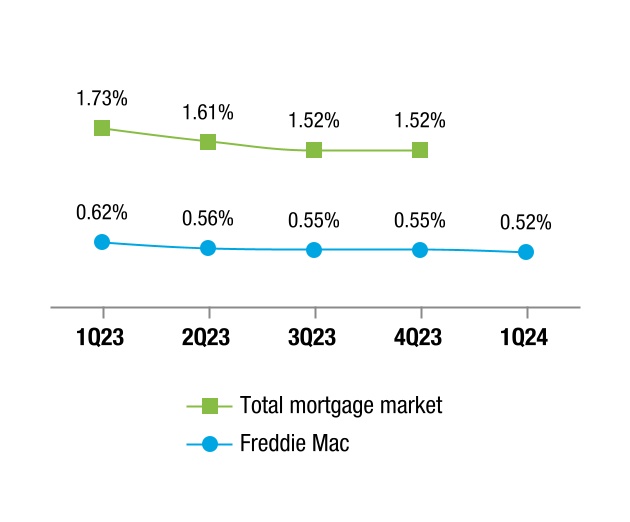

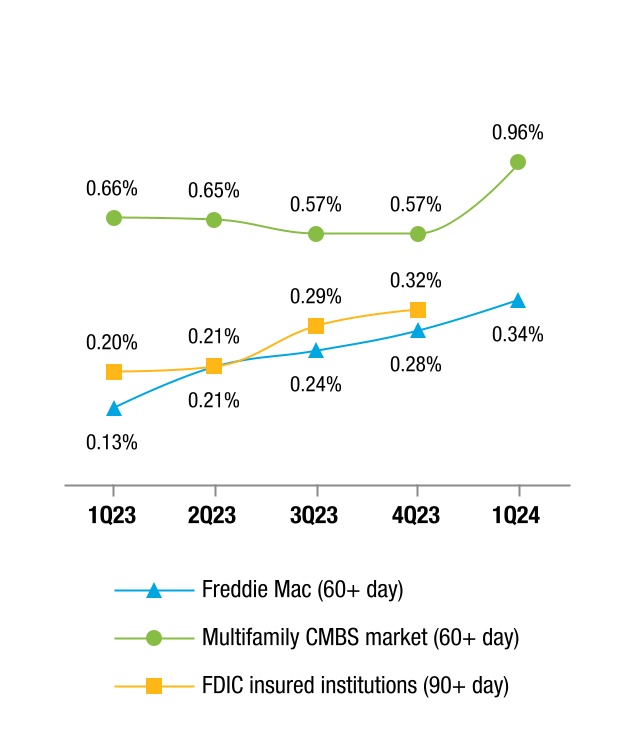

Source: Freddie Mac, FDIC Quarterly Banking Profile, Intex Solutions, Inc., and Wells Fargo Securities (Multifamily CMBS conduit market, excluding REOs). The 1Q 2024 delinquency rate for FDIC insured institutions is not yet available.

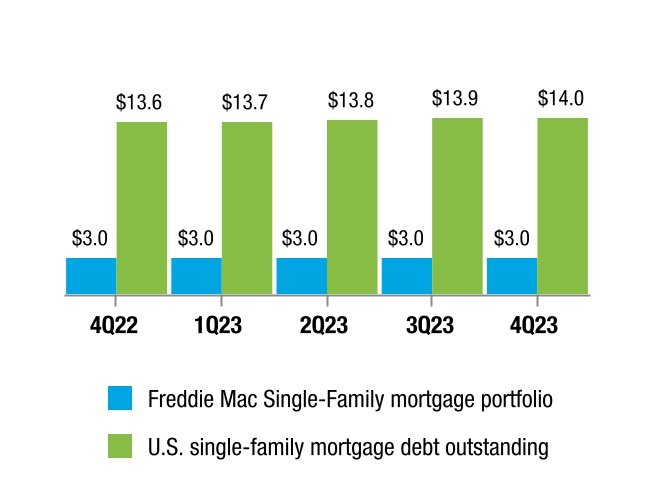

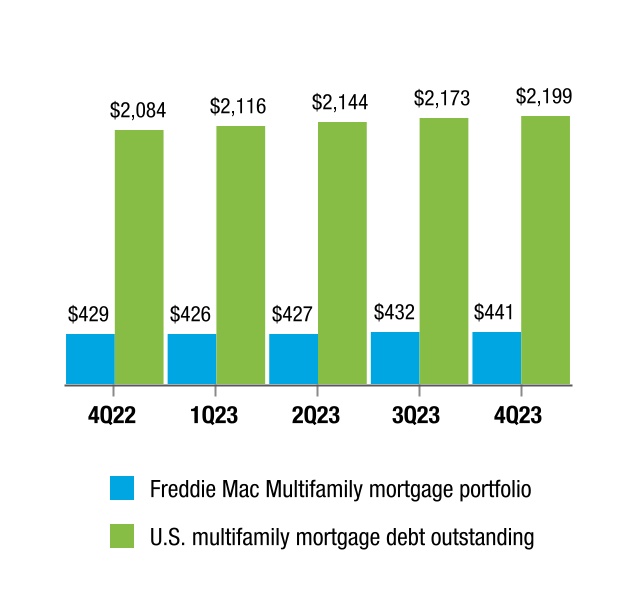

Source: Freddie Mac, FDIC Quarterly Banking Profile, Intex Solutions, Inc., and Wells Fargo Securities (Multifamily CMBS conduit market, excluding REOs). The 1Q 2024 delinquency rate for FDIC insured institutions is not yet available. Source: Freddie Mac and Federal Reserve Financial Accounts of the United States of America. The 1Q 2024 U.S.

Source: Freddie Mac and Federal Reserve Financial Accounts of the United States of America. The 1Q 2024 U.S. | Freddie Mac 1Q 2024 Form 10-Q | 5 | |||||||

| Management's Discussion and Analysis | Consolidated Results of Operations | |||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

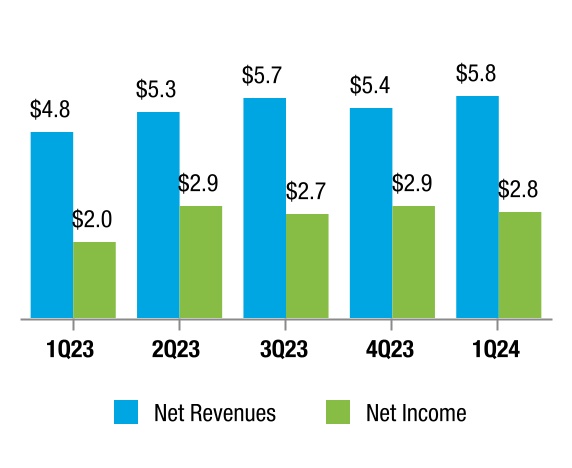

| Net interest income | $4,759 | $4,501 | $258 | 6 | % | |||||||||||||||||||||||||||||||||

| Non-interest income | 998 | 326 | 672 | 206 | ||||||||||||||||||||||||||||||||||

| Net revenues | 5,757 | 4,827 | 930 | 19 | ||||||||||||||||||||||||||||||||||

| (Provision) benefit for credit losses | (181) | (395) | 214 | 54 | ||||||||||||||||||||||||||||||||||

| Non-interest expense | (2,122) | (1,932) | (190) | (10) | ||||||||||||||||||||||||||||||||||

| Income before income tax expense | 3,454 | 2,500 | 954 | 38 | ||||||||||||||||||||||||||||||||||

| Income tax expense | (688) | (505) | (183) | (36) | ||||||||||||||||||||||||||||||||||

| Net income | 2,766 | 1,995 | 771 | 39 | ||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of taxes and reclassification adjustments | (25) | 54 | (79) | (146) | ||||||||||||||||||||||||||||||||||

| Comprehensive income | $2,741 | $2,049 | $692 | 34 | % | |||||||||||||||||||||||||||||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Guarantee net interest income: | ||||||||||||||||||||||||||||||||||||||

| Contractual net interest income | $3,772 | $3,666 | $106 | 3 | % | |||||||||||||||||||||||||||||||||

| Deferred fee income | 166 | 207 | (41) | (20) | ||||||||||||||||||||||||||||||||||

| Total guarantee net interest income | 3,938 | 3,873 | 65 | 2 | ||||||||||||||||||||||||||||||||||

| Investments net interest income | 1,514 | 1,432 | 82 | 6 | ||||||||||||||||||||||||||||||||||

| Impact on net interest income from hedge accounting | (693) | (804) | 111 | 14 | ||||||||||||||||||||||||||||||||||

| Net interest income | $4,759 | $4,501 | $258 | 6 | % | |||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | ||||||||

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | Average Balance | Interest Income (Expense) | Average Rate | Average Balance | Interest Income (Expense) | Average Rate | ||||||||||||||||||||||||||||||||||||||

| Interest-earning assets: | ||||||||||||||||||||||||||||||||||||||||||||

| Cash and cash equivalents | $12,141 | $125 | 4.09 | % | $13,758 | $121 | 3.51 | % | ||||||||||||||||||||||||||||||||||||

| Securities purchased under agreements to resell | 111,796 | 1,532 | 5.48 | 107,516 | 1,220 | 4.54 | ||||||||||||||||||||||||||||||||||||||

| Investment securities | 41,293 | 470 | 4.56 | 38,126 | 316 | 3.31 | ||||||||||||||||||||||||||||||||||||||

Mortgage loans(1) | 3,100,111 | 26,229 | 3.38 | 3,042,128 | 23,304 | 3.06 | ||||||||||||||||||||||||||||||||||||||

| Other assets | 1,784 | 29 | 6.48 | 1,930 | 26 | 5.30 | ||||||||||||||||||||||||||||||||||||||

| Total interest-earning assets | 3,267,125 | 28,385 | 3.47 | 3,203,458 | 24,987 | 3.12 | ||||||||||||||||||||||||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||||||||||||||||||||||||||

| Debt of consolidated trusts | 3,035,073 | (21,122) | (2.78) | 2,975,417 | (18,261) | (2.45) | ||||||||||||||||||||||||||||||||||||||

| Debt of Freddie Mac | 180,850 | (2,504) | (5.53) | 187,599 | (2,225) | (4.74) | ||||||||||||||||||||||||||||||||||||||

| Total interest-bearing liabilities | 3,215,923 | (23,626) | (2.94) | 3,163,016 | (20,486) | (2.59) | ||||||||||||||||||||||||||||||||||||||

| Impact of net non-interest-bearing funding | 51,202 | — | 0.05 | 40,442 | — | 0.03 | ||||||||||||||||||||||||||||||||||||||

| Total funding of interest-earning assets | 3,267,125 | (23,626) | (2.89) | 3,203,458 | (20,486) | (2.56) | ||||||||||||||||||||||||||||||||||||||

| Net interest income/yield | $4,759 | 0.58 | % | $4,501 | 0.56 | % | ||||||||||||||||||||||||||||||||||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Guarantee income | $496 | $466 | $30 | 6 | % | |||||||||||||||||||||||||||||||||

| Investment gains, net | 405 | (225) | 630 | 280 | ||||||||||||||||||||||||||||||||||

| Other income | 97 | 85 | 12 | 14 | ||||||||||||||||||||||||||||||||||

| Non-interest income | $998 | $326 | $672 | 206 | % | |||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Single-Family | ($120) | ($318) | $198 | 62 | % | |||||||||||||||||||||||||||||||||

| Multifamily | (61) | (77) | 16 | 21 | ||||||||||||||||||||||||||||||||||

| (Provision) benefit for credit losses | ($181) | ($395) | $214 | 54 | % | |||||||||||||||||||||||||||||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Salaries and employee benefits | ($421) | ($374) | ($47) | (13) | % | |||||||||||||||||||||||||||||||||

| Credit enhancement expense | (597) | (530) | (67) | (13) | ||||||||||||||||||||||||||||||||||

| Benefit for (decrease in) credit enhancement recoveries | 1 | 49 | (48) | (98) | ||||||||||||||||||||||||||||||||||

| Legislative assessments expense: | ||||||||||||||||||||||||||||||||||||||

| Legislated guarantee fees expense | (724) | (708) | (16) | (2) | ||||||||||||||||||||||||||||||||||

| Affordable housing funds allocation | (30) | (27) | (3) | (11) | ||||||||||||||||||||||||||||||||||

| Total legislative assessments expense | (754) | (735) | (19) | (3) | ||||||||||||||||||||||||||||||||||

| Other expense | (351) | (342) | (9) | (3) | ||||||||||||||||||||||||||||||||||

| Non-interest expense | ($2,122) | ($1,932) | ($190) | (10) | % | |||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 8 | |||||||

| Management's Discussion and Analysis | Consolidated Balance Sheets Analysis | |||||||

| Change | ||||||||||||||||||||

| (Dollars in millions) | March 31, 2024 | December 31, 2023 | $ | % | ||||||||||||||||

| Assets: | ||||||||||||||||||||

| Cash and cash equivalents | $3,531 | $6,019 | ($2,488) | (41) | % | |||||||||||||||

| Securities purchased under agreements to resell | 102,257 | 95,148 | 7,109 | 7 | ||||||||||||||||

| Investment securities, at fair value | 41,400 | 43,275 | (1,875) | (4) | ||||||||||||||||

| Mortgage loans held-for-sale | 12,034 | 12,941 | (907) | (7) | ||||||||||||||||

| Mortgage loans held-for-investment | 3,088,687 | 3,083,665 | 5,022 | — | ||||||||||||||||

| Accrued interest receivable, net | 10,047 | 9,925 | 122 | 1 | ||||||||||||||||

| Deferred tax assets, net | 4,227 | 4,076 | 151 | 4 | ||||||||||||||||

| Other assets | 25,190 | 25,927 | (737) | (3) | ||||||||||||||||

| Total assets | $3,287,373 | $3,280,976 | $6,397 | — | % | |||||||||||||||

| Liabilities and Equity: | ||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||

| Accrued interest payable | $8,712 | $8,812 | ($100) | (1) | % | |||||||||||||||

| Debt | 3,211,742 | 3,208,346 | 3,396 | — | ||||||||||||||||

| Other liabilities | 16,456 | 16,096 | 360 | 2 | ||||||||||||||||

| Total liabilities | 3,236,910 | 3,233,254 | 3,656 | — | ||||||||||||||||

| Total equity | 50,463 | 47,722 | 2,741 | 6 | ||||||||||||||||

| Total liabilities and equity | $3,287,373 | $3,280,976 | $6,397 | — | % | |||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 9 | |||||||

| Management's Discussion and Analysis | Our Portfolios | |||||||

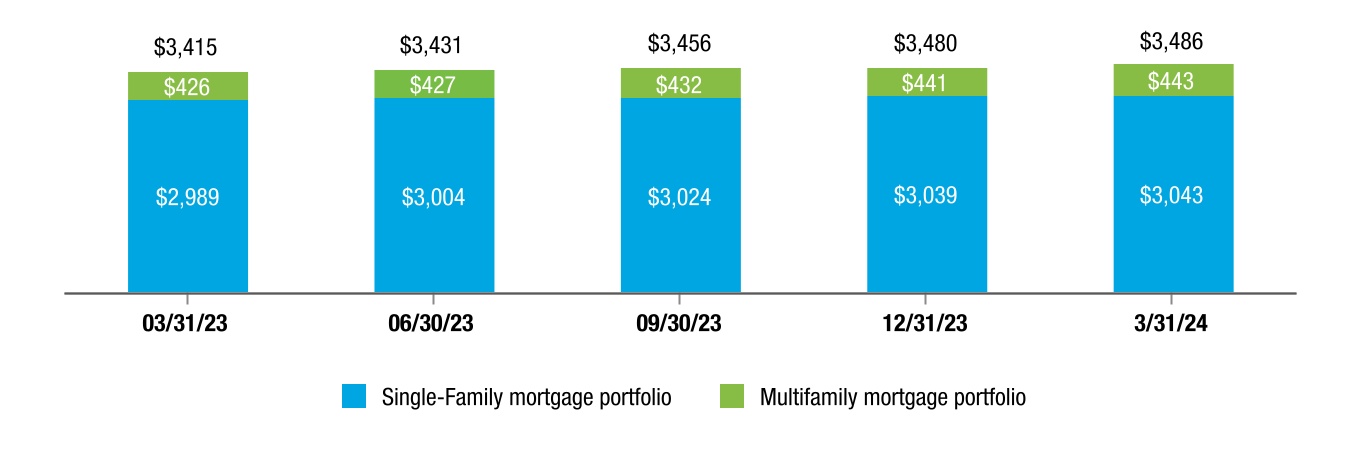

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||

| (In millions) | Single-Family | Multifamily | Total | Single-Family | Multifamily | Total | ||||||||||||||||||||

| Mortgage loans held-for-investment: | ||||||||||||||||||||||||||

| By consolidated trusts | $2,965,370 | $51,757 | $3,017,127 | $2,963,296 | $47,433 | $3,010,729 | ||||||||||||||||||||

| By Freddie Mac | 35,643 | 10,000 | 45,643 | 33,213 | 11,770 | 44,983 | ||||||||||||||||||||

| Total mortgage loans held-for-investment | 3,001,013 | 61,757 | 3,062,770 | 2,996,509 | 59,203 | 3,055,712 | ||||||||||||||||||||

| Mortgage loans held-for-sale | 3,104 | 9,446 | 12,550 | 3,527 | 9,905 | 13,432 | ||||||||||||||||||||

| Total mortgage loans | 3,004,117 | 71,203 | 3,075,320 | 3,000,036 | 69,108 | 3,069,144 | ||||||||||||||||||||

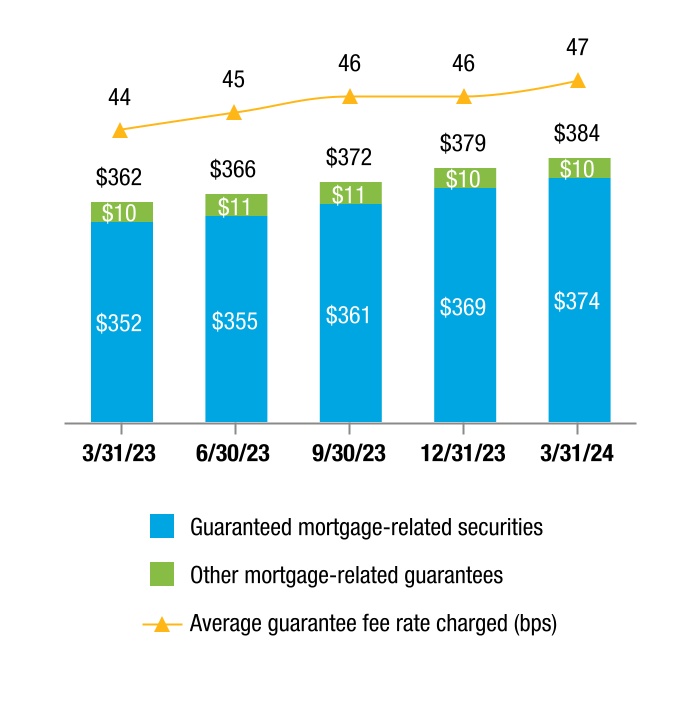

| Mortgage-related guarantees: | ||||||||||||||||||||||||||

| Mortgage loans held by nonconsolidated trusts | 30,324 | 361,164 | 391,488 | 30,182 | 360,928 | 391,110 | ||||||||||||||||||||

| Other mortgage-related guarantees | 8,511 | 10,720 | 19,231 | 8,692 | 10,761 | 19,453 | ||||||||||||||||||||

| Total mortgage-related guarantees | 38,835 | 371,884 | 410,719 | 38,874 | 371,689 | 410,563 | ||||||||||||||||||||

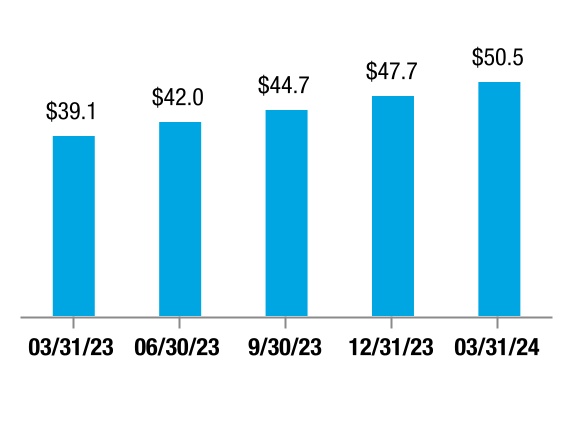

| Total mortgage portfolio | $3,042,952 | $443,087 | $3,486,039 | $3,038,910 | $440,797 | $3,479,707 | ||||||||||||||||||||

| Guaranteed mortgage-related securities: | ||||||||||||||||||||||||||

| Issued by consolidated trusts | $2,975,161 | $51,811 | $3,026,972 | $2,970,707 | $47,436 | $3,018,143 | ||||||||||||||||||||

| Issued by nonconsolidated trusts | 24,762 | 321,905 | 346,667 | 24,600 | 321,262 | 345,862 | ||||||||||||||||||||

| Total guaranteed mortgage-related securities | $2,999,923 | $373,716 | $3,373,639 | $2,995,307 | $368,698 | $3,364,005 | ||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 10 | |||||||

| Management's Discussion and Analysis | Our Portfolios | |||||||

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||

| (In millions) | Single-Family | Multifamily | Total | Single-Family | Multifamily | Total | ||||||||||||||||||||

| Unsecuritized mortgage loans: | ||||||||||||||||||||||||||

Securitization pipeline loans(1) | $9,749 | $13,057 | $22,806 | $8,225 | $15,197 | $23,422 | ||||||||||||||||||||

Other loans(2) | 28,998 | 6,389 | 35,387 | 28,515 | 6,478 | 34,993 | ||||||||||||||||||||

| Total unsecuritized mortgage loans | 38,747 | 19,446 | 58,193 | 36,740 | 21,675 | 58,415 | ||||||||||||||||||||

| Mortgage-related securities: | ||||||||||||||||||||||||||

| Investment securities | 2,916 | 4,486 | 7,402 | 2,667 | 4,613 | 7,280 | ||||||||||||||||||||

| Debt of consolidated trusts | 18,367 | 684 | 19,051 | 18,639 | 660 | 19,299 | ||||||||||||||||||||

| Total mortgage-related securities | 21,283 | 5,170 | 26,453 | 21,306 | 5,273 | 26,579 | ||||||||||||||||||||

| Mortgage-related investments portfolio | $60,030 | $24,616 | $84,646 | $58,046 | $26,948 | $84,994 | ||||||||||||||||||||

| 10% of notional amount of interest-only securities | $23,126 | $22,186 | ||||||||||||||||||||||||

| Mortgage-related investments portfolio for purposes of Purchase Agreement cap | 107,772 | 107,180 | ||||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||||||||

| (In millions) | Liquidity and Contingency Operating Portfolio | Custodial Account | Other | Total Other Investments Portfolio (1) | Liquidity and Contingency Operating Portfolio | Custodial Account | Other | Total Other Investments Portfolio (1) | ||||||||||||||||||||||||

| Cash and cash equivalents | $1,947 | $1,483 | $101 | $3,531 | $5,041 | $890 | $88 | $6,019 | ||||||||||||||||||||||||

Securities purchased under agreements to resell | 104,243 | 10,777 | 1,037 | 116,057 | 94,904 | 9,396 | 1,093 | 105,393 | ||||||||||||||||||||||||

Non-mortgage related securities(2) | 22,960 | — | 5,593 | 28,553 | 24,153 | — | 6,119 | 30,272 | ||||||||||||||||||||||||

| Other assets | — | — | 6,479 | 6,479 | — | — | 5,555 | 5,555 | ||||||||||||||||||||||||

| Other investments portfolio | $129,150 | $12,260 | $13,210 | $154,620 | $124,098 | $10,286 | $12,855 | $147,239 | ||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 11 | |||||||

| Management's Discussion and Analysis | Our Business Segments | |||||||

| Segment | Description | ||||

| Single-Family | Reflects results from our purchase, securitization, and guarantee of single-family loans, our investments in single-family loans and mortgage-related securities, the management of Single-Family mortgage credit risk and market risk, and any results of our treasury function that are not allocated to each segment. | ||||

| Multifamily | Reflects results from our purchase, securitization, and guarantee of multifamily loans, our investments in multifamily loans and mortgage-related securities, and the management of Multifamily mortgage credit risk and market risk. | ||||

| Freddie Mac 1Q 2024 Form 10-Q | 12 | |||||||

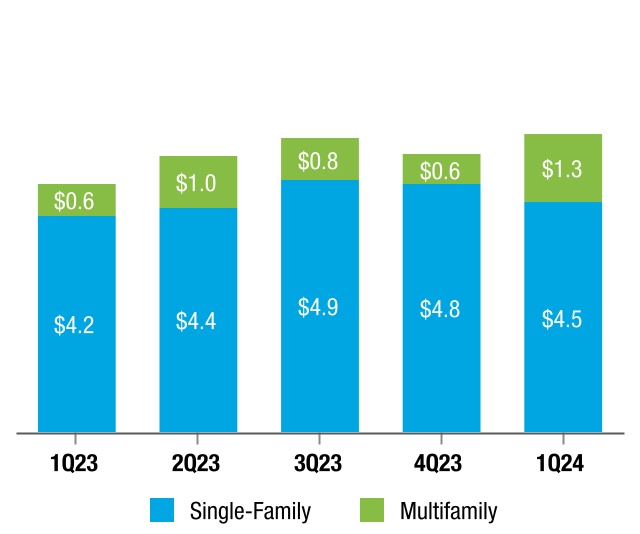

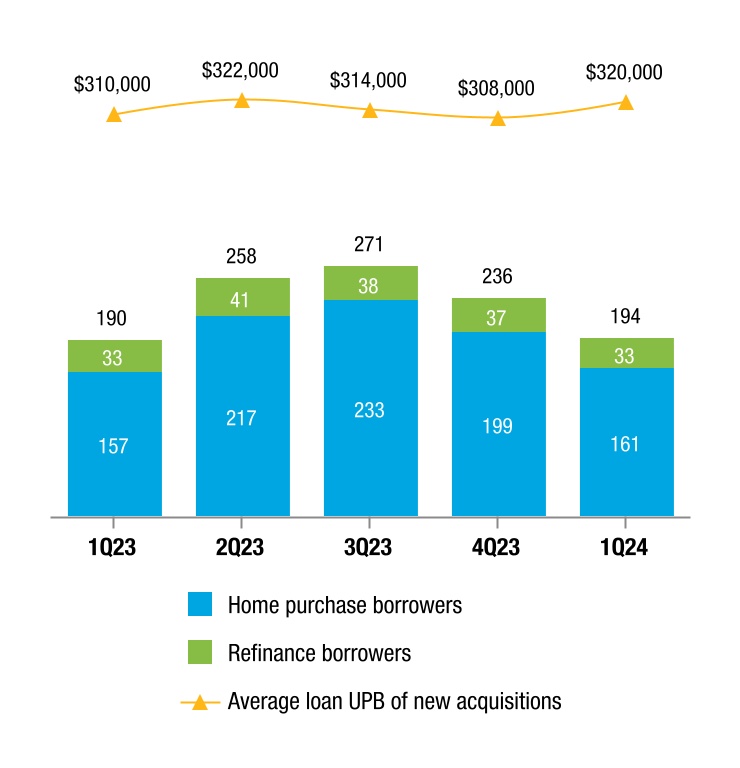

| Management's Discussion and Analysis | Our Business Segments | Single-Family | ||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments | Single-Family | ||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments | Single-Family | ||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments | Single-Family | ||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Net interest income | $4,488 | $4,296 | $192 | 4 | % | |||||||||||||||||||||||||||||||||

| Non-interest income | (14) | (93) | 79 | 85 | ||||||||||||||||||||||||||||||||||

| Net revenues | 4,474 | 4,203 | 271 | 6 | ||||||||||||||||||||||||||||||||||

| (Provision) benefit for credit losses | (120) | (318) | 198 | 62 | ||||||||||||||||||||||||||||||||||

| Non-interest expense | (1,925) | (1,783) | (142) | (8) | ||||||||||||||||||||||||||||||||||

| Income before Income tax expense | 2,429 | 2,102 | 327 | 16 | ||||||||||||||||||||||||||||||||||

| Income tax expense | (484) | (425) | (59) | (14) | ||||||||||||||||||||||||||||||||||

| Net income | 1,945 | 1,677 | 268 | 16 | ||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of taxes and reclassification adjustments | (5) | (1) | (4) | (400) | ||||||||||||||||||||||||||||||||||

| Comprehensive income | $1,940 | $1,676 | $264 | 16 | % | |||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments | | |||||||

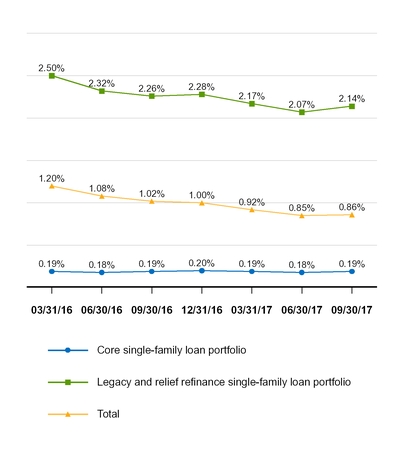

| September 30, 2017 | |||||||||||||||||||||||||||

| CLTV ≤ 80 | CLTV > 80 to 100 | CLTV > 100 | All Loans | ||||||||||||||||||||||||

| (Credit score) | % Portfolio | SDQ Rate(1) | % Portfolio | SDQ Rate(1) | % Portfolio | SDQ Rate(1) | % Portfolio | SDQ Rate(1) | % Modified | ||||||||||||||||||

| Core single-family loan portfolio: | |||||||||||||||||||||||||||

| < 620 | 0.3 | % | 1.89 | % | — | % | NM | — | % | NM | 0.3 | % | 2.11 | % | 3.3 | % | |||||||||||

| 620 to 659 | 1.7 | 0.98 | % | 0.4 | 1.11 | % | — | NM | 2.1 | 1.00 | % | 1.4 | % | ||||||||||||||

| ≥ 660 | 64.8 | 0.15 | % | 9.4 | 0.21 | % | — | NM | 74.2 | 0.16 | % | 0.2 | % | ||||||||||||||

| Not available | — | NM | — | NM | — | NM | — | NM | 3.7 | % | |||||||||||||||||

| Total | 66.8 | % | 0.18 | % | 9.8 | % | 0.25 | % | — | % | NM | 76.6 | % | 0.19 | % | 0.3 | % | ||||||||||

| Legacy and relief refinance single-family loan portfolio: | |||||||||||||||||||||||||||

| < 620 | 1.2 | % | 4.46 | % | 0.3 | % | 8.49 | % | 0.2 | % | 14.35 | % | 1.7 | % | 5.55 | % | 24.2 | % | |||||||||

| 620 to 659 | 2.0 | 3.32 | % | 0.5 | 6.65 | % | 0.2 | 12.07 | % | 2.7 | 4.18 | % | 20.8 | % | |||||||||||||

| ≥ 660 | 15.5 | 1.16 | % | 2.5 | 3.37 | % | 0.9 | 5.87 | % | 18.9 | 1.49 | % | 7.5 | % | |||||||||||||

| Not available | 0.1 | 4.85 | % | — | NM | — | NM | 0.1 | 5.32 | % | 17.5 | % | |||||||||||||||

| Total | 18.8 | % | 1.66 | % | 3.3 | % | 4.42 | % | 1.3 | % | 7.97 | % | 23.4 | % | 2.14 | % | 10.3 | % | |||||||||

| September 30, 2017 | December 31, 2016 | |||||||||||||||||||||||||

| (Dollars in billions) | UPB | CLTV | % Modified | SDQ Rate | UPB | CLTV | % Modified | SDQ Rate | ||||||||||||||||||

| Alt-A | $28.2 | 68 | % | 25.8 | % | 5.00 | % | $32.6 | 72 | % | 25.9 | % | 5.21 | % | ||||||||||||

| (Dollars in millions) | 3Q 2017 | 3Q 2016 | YTD 2017 | YTD 2016 | |||||||||||

Charge-offs, gross(1) | $1,140 | $461 | $4,033 | $1,516 | |||||||||||

| Recoveries | (145 | ) | (115 | ) | (327 | ) | (395 | ) | |||||||

| Charge-offs, net | 995 | 346 | 3,706 | 1,121 | |||||||||||

| REO operations expense | 35 | 56 | 128 | 169 | |||||||||||

| Total credit losses | $1,030 | $402 | $3,834 | $1,290 | |||||||||||

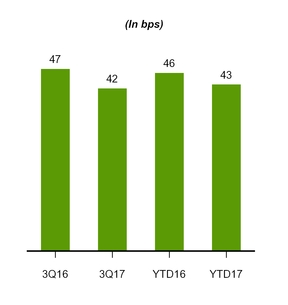

Total credit losses(1) (in bps) | 22.7 | 9.2 | 28.4 | 9.9 | |||||||||||

| September 30, 2017 | September 30, 2016 | |||||||||||||

| (Dollars in millions) | Loan Count | Amount | Loan Count | Amount | ||||||||||

| TDRs, at January 1 | 485,709 | $78,869 | 512,253 | $85,960 | ||||||||||

| New additions | 29,867 | 4,130 | 32,581 | 4,482 | ||||||||||

| Repayments and reclassifications to held-for-sale | (113,933 | ) | (21,828 | ) | (45,334 | ) | (8,863 | ) | ||||||

| Foreclosure transfers and foreclosure alternatives | (8,169 | ) | (1,122 | ) | (8,856 | ) | (1,261 | ) | ||||||

| TDRs, at September 30 | 393,474 | 60,049 | 490,644 | 80,318 | ||||||||||

| Loans impaired upon purchase | 5,782 | 380 | 8,266 | 583 | ||||||||||

| Total impaired loans with specific reserve | 399,256 | 60,429 | 498,910 | 80,901 | ||||||||||

| Allowance for loan losses | (7,706 | ) | (11,910 | ) | ||||||||||

| Net investment, at September 30 | $52,723 | $68,991 | ||||||||||||

| (In millions) | September 30, 2017 | December 31, 2016 | ||||||

| TDRs on accrual status | $58,065 | $77,122 | ||||||

| Non-accrual loans | 13,899 | 16,164 | ||||||

| Total TDRs and non-accrual loans | $71,964 | $93,286 | ||||||

| Loan loss reserves associated with: | ||||||||

| TDRs on accrual status | $6,326 | $10,295 | ||||||

| Non-accrual loans | 1,830 | 2,290 | ||||||

| Total | $8,156 | $12,585 | ||||||

| (In millions) | YTD 2017 | YTD 2016 | ||||||

Foregone interest income on TDRs and non-accrual loans(1) | $1,325 | $1,720 | ||||||

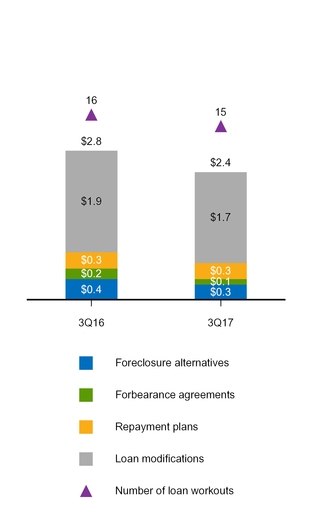

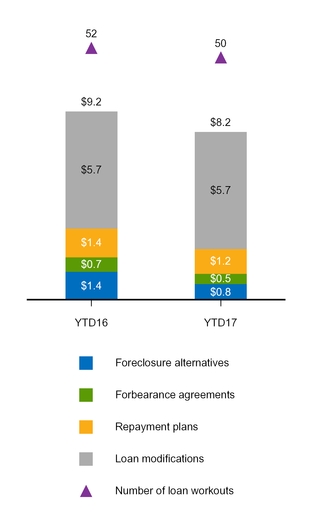

| 3Q 2017 | 3Q 2016 | YTD 2017 | YTD 2016 | |||||||||||||||||||||||||

| (Dollars in millions) | Number of Properties | Amount | Number of Properties | Amount | Number of Properties | Amount | Number of Properties | Amount | ||||||||||||||||||||

| Beginning balance — REO | 9,915 | $1,046 | 13,284 | $1,394 | 11,418 | $1,215 | 17,004 | $1,774 | ||||||||||||||||||||

| Additions | 2,853 | 282 | 3,986 | 397 | 9,697 | 949 | 12,770 | 1,229 | ||||||||||||||||||||

| Dispositions | (3,622 | ) | (348 | ) | (5,085 | ) | (503 | ) | (11,969 | ) | (1,184 | ) | (17,589 | ) | (1,715 | ) | ||||||||||||

| Ending balance — REO | 9,146 | 980 | 12,185 | 1,288 | 9,146 | 980 | 12,185 | 1,288 | ||||||||||||||||||||

| Beginning balance, valuation allowance | (10 | ) | (17 | ) | (17 | ) | (52 | ) | ||||||||||||||||||||

| Change in valuation allowance | (4 | ) | 1 | 3 | 36 | |||||||||||||||||||||||

| Ending balance, valuation allowance | (14 | ) | (16 | ) | (14 | ) | (16 | ) | ||||||||||||||||||||

| Ending balance — REO, net | $966 | $1,272 | $966 | $1,272 | ||||||||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Guarantee fee income | $1,581 | $1,641 | ($60 | ) | (4 | )% | $4,505 | $4,427 | $78 | 2 | % | |||||||||||||||||||

| Benefit (provision) for credit losses | (826 | ) | (297 | ) | (529 | ) | (178 | )% | (775 | ) | 113 | (888 | ) | (786 | )% | |||||||||||||||

| Other non-interest income (loss) | 403 | 6 | 397 | 6,617 | % | 1,081 | 131 | 950 | 725 | % | ||||||||||||||||||||

| Administrative expense | (353 | ) | (330 | ) | (23 | ) | (7 | )% | (1,018 | ) | (939 | ) | (79 | ) | (8 | )% | ||||||||||||||

| REO operations expense | (38 | ) | (59 | ) | 21 | 36 | % | (138 | ) | (177 | ) | 39 | 22 | % | ||||||||||||||||

| Other non-interest expense | (348 | ) | (311 | ) | (37 | ) | (12 | )% | (1,001 | ) | (832 | ) | (169 | ) | (20 | )% | ||||||||||||||

| Segment Earnings before income tax expense | 419 | 650 | (231 | ) | (36 | )% | 2,654 | 2,723 | (69 | ) | (3 | )% | ||||||||||||||||||

| Income tax expense | (164 | ) | (153 | ) | (11 | ) | (7 | )% | (911 | ) | (833 | ) | (78 | ) | (9 | )% | ||||||||||||||

| Segment Earnings, net of taxes | 255 | 497 | (242 | ) | (49 | )% | 1,743 | 1,890 | (147 | ) | (8 | )% | ||||||||||||||||||

| Total other comprehensive income (loss), net of tax | — | (1 | ) | 1 | 100 | % | (2 | ) | (1 | ) | (1 | ) | (100 | )% | ||||||||||||||||

| Total comprehensive income | $255 | $496 | ($241 | ) | (49 | )% | $1,741 | $1,889 | ($148 | ) | (8 | )% | ||||||||||||||||||

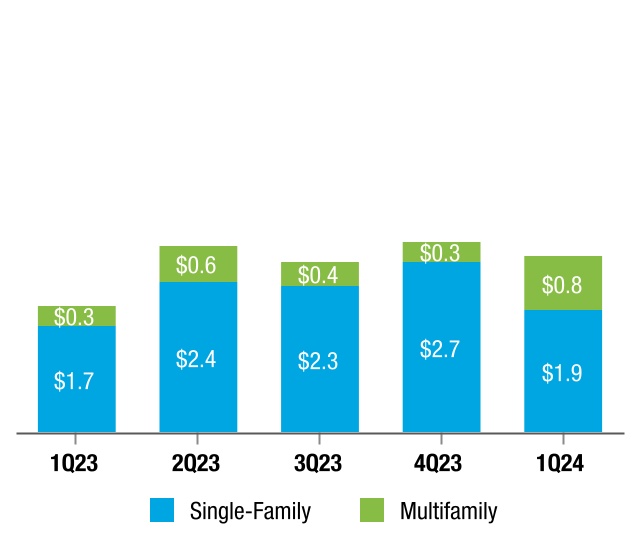

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments |Multifamily | |||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments |Multifamily | |||||||

| (UPB in millions) | September 30, 2017 | December 31, 2016 | |||||

| Unsecuritized mortgage loans held-for-sale | $19,118 | $16,544 | |||||

| Unsecuritized mortgage loans held-for-investment | 20,019 | 25,874 | |||||

| Unsecuritized non-mortgage loans | 303 | — | |||||

| Mortgage-related securities | 9,172 | 12,517 | |||||

| Guarantee portfolio | 184,200 | 157,992 | |||||

| Total multifamily portfolio | 232,812 | 212,927 | |||||

Add: Unguaranteed securities(1) | 28,376 | 24,573 | |||||

Less: Acquired mortgage-related securities(2) | (5,413 | ) | (5,793 | ) | |||

| Total multifamily market support | $255,775 | $231,707 | |||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Our Business Segments |Multifamily | |||||||

| Change | ||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | 1Q 2024 | 1Q 2023 | $ | % | ||||||||||||||||||||||||||||||||||

| Net interest income | $271 | $205 | $66 | 32 | % | |||||||||||||||||||||||||||||||||

| Non-interest income | 1,012 | 419 | 593 | 142 | ||||||||||||||||||||||||||||||||||

| Net revenues | 1,283 | 624 | 659 | 106 | ||||||||||||||||||||||||||||||||||

| (Provision) benefit for credit losses | (61) | (77) | 16 | 21 | ||||||||||||||||||||||||||||||||||

| Non-interest expense | (197) | (149) | (48) | (32) | ||||||||||||||||||||||||||||||||||

| Income before income tax expense | 1,025 | 398 | 627 | 158 | ||||||||||||||||||||||||||||||||||

| Income tax expense | (204) | (80) | (124) | (155) | ||||||||||||||||||||||||||||||||||

| Net income | 821 | 318 | 503 | 158 | ||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of taxes and reclassification adjustments | (20) | 55 | (75) | (136) | ||||||||||||||||||||||||||||||||||

| Comprehensive income | $801 | $373 | $428 | 115 | % | |||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | ||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | |||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | ||||||||||||||||||||||||||

| Net interest income | $342 | $255 | $87 | 34 | % | $905 | $791 | $114 | 14 | % | ||||||||||||||||||||

| Guarantee fee income | 170 | 134 | 36 | 27 | % | 483 | 366 | 117 | 32 | % | ||||||||||||||||||||

| Benefit (provision) for credit losses | (22 | ) | 8 | (30 | ) | (375 | )% | (10 | ) | 19 | (29 | ) | (153 | )% | ||||||||||||||||

| Gains (losses) on loans and other non-interest income | 183 | 551 | (368 | ) | (67 | )% | 831 | 1,666 | (835 | ) | (50 | )% | ||||||||||||||||||

| Derivative gains (losses) | 22 | 205 | (183 | ) | (89 | )% | (31 | ) | (878 | ) | 847 | 96 | % | |||||||||||||||||

| Administrative expense | (98 | ) | (89 | ) | (9 | ) | (10 | )% | (288 | ) | (255 | ) | (33 | ) | (13 | )% | ||||||||||||||

| Other non-interest expense | (11 | ) | (10 | ) | (1 | ) | (10 | )% | (44 | ) | (43 | ) | (1 | ) | (2 | )% | ||||||||||||||

| Segment Earnings before income tax (expense) benefit | 586 | 1,054 | (468 | ) | (44 | )% | 1,846 | 1,666 | 180 | 11 | % | |||||||||||||||||||

| Income tax (expense) benefit | (212 | ) | (310 | ) | 98 | 32 | % | (634 | ) | (510 | ) | (124 | ) | (24 | )% | |||||||||||||||

| Segment Earnings, net of taxes | 374 | 744 | (370 | ) | (50 | )% | 1,212 | 1,156 | 56 | 5 | % | |||||||||||||||||||

| Total other comprehensive income (loss), net of tax | (4 | ) | 46 | (50 | ) | (109 | )% | 65 | 56 | 9 | 16 | % | ||||||||||||||||||

| Total comprehensive income (loss) | $370 | $790 | ($420 | ) | (53 | )% | $1,277 | $1,212 | $65 | 5 | % | |||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | ||||||||||||||||||||||||

| (Dollars in millions) | $ | % | $ | % | |||||||||||||||||||||||||

| Net interest income | $804 | $933 | ($129 | ) | (14 | )% | $2,608 | $2,887 | ($279 | ) | (10 | )% | |||||||||||||||||

| Net impairment of available-for-sale securities recognized in earnings | 50 | 94 | (44 | ) | (47 | )% | 194 | 224 | (30 | ) | (13 | )% | |||||||||||||||||

| Derivative gains (losses) | (324 | ) | 212 | (536 | ) | (253 | )% | (757 | ) | (4,386 | ) | 3,629 | 83 | % | |||||||||||||||

| Gains (losses) on trading securities | (26 | ) | (203 | ) | 177 | 87 | % | (207 | ) | (12 | ) | (195 | ) | (1,625 | )% | ||||||||||||||

| Other non-interest income | 5,754 | 664 | 5,090 | 767 | % | 6,916 | 1,401 | 5,515 | 394 | % | |||||||||||||||||||

| Administrative expense | (73 | ) | (79 | ) | 6 | 8 | % | (242 | ) | (227 | ) | (15 | ) | (7 | )% | ||||||||||||||

| Segment Earnings before income tax (expense) benefit | 6,185 | 1,621 | 4,564 | 282 | % | 8,512 | (113 | ) | 8,625 | 7,633 | % | ||||||||||||||||||

| Income tax (expense) benefit | (2,143 | ) | (533 | ) | (1,610 | ) | (302 | )% | (2,921 | ) | 35 | (2,956 | ) | (8,446 | )% | ||||||||||||||

| Segment Earnings, net of taxes | 4,042 | 1,088 | 2,954 | 272 | % | 5,591 | (78 | ) | 5,669 | 7,268 | % | ||||||||||||||||||

| Total other comprehensive income (loss), net of tax | (17 | ) | (64 | ) | 47 | 73 | % | 261 | 220 | 41 | 19 | % | |||||||||||||||||

| Total comprehensive income (loss) | $4,025 | $1,024 | $3,001 | 293 | % | $5,852 | $142 | $5,710 | 4,021 | % | |||||||||||||||||||

| 3Q 2017 | 3Q 2016 | Change | YTD 2017 | YTD 2016 | Change | ||||||||||||||||||||||||

| (Dollars in billions) | $ | % | $ | % | |||||||||||||||||||||||||

| Interest rate-related | $— | $— | $— | — | % | ($0.1 | ) | ($1.9 | ) | $1.8 | 95 | % | |||||||||||||||||

| Market spread-related | 0.5 | 0.4 | 0.1 | 25 | % | 0.8 | 0.1 | 0.7 | 700 | % | |||||||||||||||||||

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||||||||||||||||||||||||||

| (Dollars in millions) | Single-Family | Multifamily | Total | Single-Family | Multifamily | Total | ||||||||||||||||||||||||||||||||||||||

| Allowance for credit losses: | ||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | $6,402 | $447 | $6,849 | $7,746 | $147 | $7,893 | ||||||||||||||||||||||||||||||||||||||

| Provision (benefit) for credit losses | 120 | 61 | 181 | 318 | 77 | 395 | ||||||||||||||||||||||||||||||||||||||

| Charge-offs | (123) | — | (123) | (90) | — | (90) | ||||||||||||||||||||||||||||||||||||||

| Recoveries collected | 26 | — | 26 | 32 | — | 32 | ||||||||||||||||||||||||||||||||||||||

| Net charge-offs | (97) | — | (97) | (58) | — | (58) | ||||||||||||||||||||||||||||||||||||||

Other(1) | 83 | — | 83 | 91 | — | 91 | ||||||||||||||||||||||||||||||||||||||

| Ending balance | $6,508 | $508 | $7,016 | $8,097 | $224 | $8,321 | ||||||||||||||||||||||||||||||||||||||

Average loans outstanding during the period(2) | $3,030,531 | $58,504 | $3,089,035 | $2,985,726 | $47,748 | $3,033,474 | ||||||||||||||||||||||||||||||||||||||

| Net charge-offs to average loans outstanding | — | % | — | % | — | % | — | % | — | % | — | % | ||||||||||||||||||||||||||||||||

| Components of ending balance of allowance for credit losses: | ||||||||||||||||||||||||||||||||||||||||||||

| Mortgage loans held-for-investment | $6,189 | $381 | $6,570 | $7,675 | $160 | $7,835 | ||||||||||||||||||||||||||||||||||||||

Other(3) | 319 | 127 | 446 | 422 | 64 | 486 | ||||||||||||||||||||||||||||||||||||||

| Total ending balance | $6,508 | $508 | $7,016 | $8,097 | $224 | $8,321 | ||||||||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Risk Management | |||||||

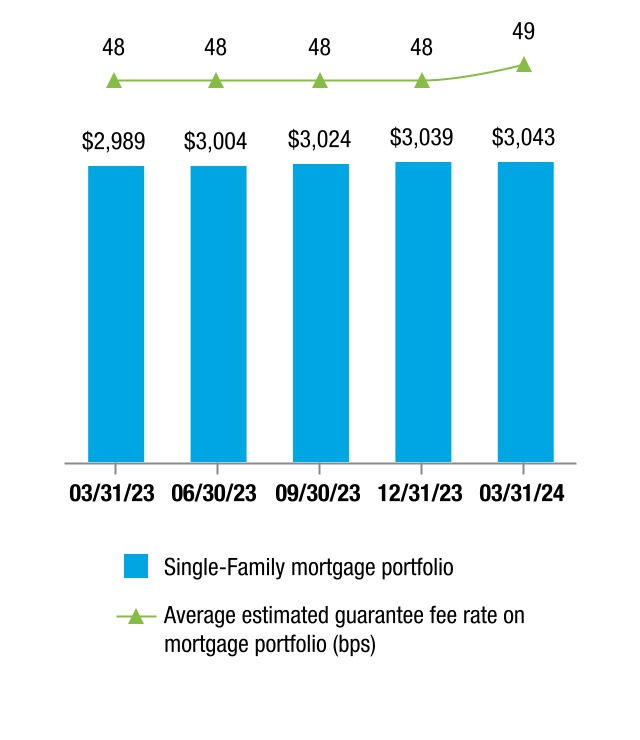

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollars in millions) | Single-Family | Multifamily | Total | Single-Family | Multifamily | Total | |||||||||||||||||

| Allowance for credit losses ratios: | |||||||||||||||||||||||

Allowance for credit losses(1) to total loans outstanding | 0.20 | % | 0.64 | % | 0.21 | % | 0.20 | % | 0.57 | % | 0.21 | % | |||||||||||

| Non-accrual loans to total loans outstanding | 0.43 | 0.17 | 0.42 | 0.44 | 0.11 | 0.44 | |||||||||||||||||

| Allowance for credit losses to non-accrual loans | 47.90 | 369.90 | 50.45 | 45.01 | 509.38 | 47.20 | |||||||||||||||||

| Balances: | |||||||||||||||||||||||

| Allowance for credit losses on mortgage loans held-for-investment | $6,189 | $381 | $6,570 | $6,057 | $326 | $6,383 | |||||||||||||||||

Total loans outstanding(2) | 3,033,817 | 59,509 | 3,093,326 | 3,031,136 | 57,107 | 3,088,243 | |||||||||||||||||

Non-accrual loans(2) | 12,921 | 103 | 13,024 | 13,458 | 64 | 13,522 | |||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Risk Management | |||||||

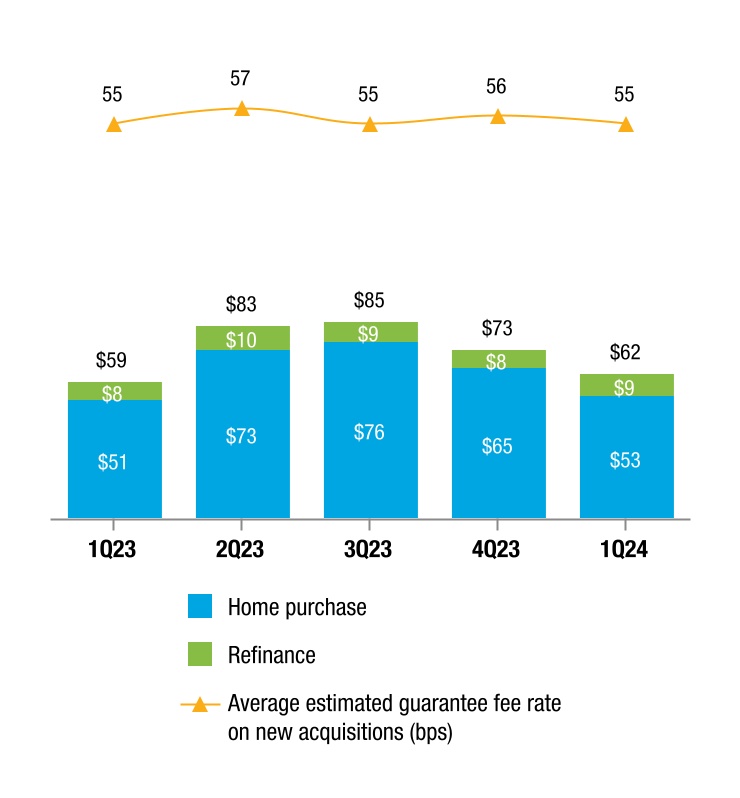

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||||||||||||||

| (Dollars in millions) | Amount | % of Total | Amount | % of Total | ||||||||||||||||||||||||||||

| 20- and 30-year, amortizing fixed-rate | $59,091 | 95 | % | $55,469 | 94 | % | ||||||||||||||||||||||||||

| 15-year or less, amortizing fixed-rate | 2,278 | 4 | 2,214 | 4 | ||||||||||||||||||||||||||||

| Adjustable-rate | 900 | 1 | 1,282 | 2 | ||||||||||||||||||||||||||||

| Total | $62,269 | 100 | % | $58,965 | 100 | % | ||||||||||||||||||||||||||

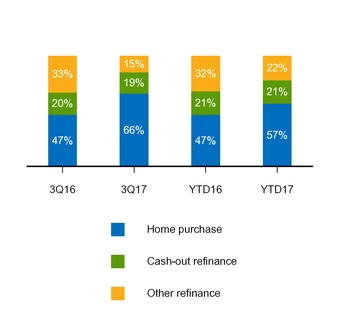

| Percentage of purchases | ||||||||||||||||||||||||||||||||

| DTI ratio > 45% | 28 | % | 23 | % | ||||||||||||||||||||||||||||

| Original LTV ratio > 90% | 25 | 28 | ||||||||||||||||||||||||||||||

| Transaction type: | ||||||||||||||||||||||||||||||||

| Guarantor swap | 66 | 72 | ||||||||||||||||||||||||||||||

| Cash window | 34 | 28 | ||||||||||||||||||||||||||||||

| Property type: | ||||||||||||||||||||||||||||||||

| Detached single-family houses and townhouses | 91 | 91 | ||||||||||||||||||||||||||||||

| Condominium or co-op | 9 | 9 | ||||||||||||||||||||||||||||||

| Occupancy type: | ||||||||||||||||||||||||||||||||

| Primary residence | 93 | 92 | ||||||||||||||||||||||||||||||

| Second home | 2 | 2 | ||||||||||||||||||||||||||||||

| Investment property | 5 | 6 | ||||||||||||||||||||||||||||||

| Loan purpose: | ||||||||||||||||||||||||||||||||

| Purchase | 86 | 86 | ||||||||||||||||||||||||||||||

| Cash-out refinance | 8 | 9 | ||||||||||||||||||||||||||||||

| Other refinance | 6 | 5 | ||||||||||||||||||||||||||||||

| 1Q 2024 | 1Q 2023 | ||||||||||||||||

| (In millions) | UPB(1)(2) | Maximum Coverage(3)(4) | UPB(1)(2) | Maximum Coverage(3)(4) | |||||||||||||

| Primary mortgage insurance | $25,135 | $6,616 | $26,518 | $6,920 | |||||||||||||

| CRT transactions: | |||||||||||||||||

| STACR | 41,402 | 1,284 | 14,887 | 611 | |||||||||||||

| ACIS | 15,523 | 559 | — | — | |||||||||||||

| Other | 692 | 107 | 46 | 46 | |||||||||||||

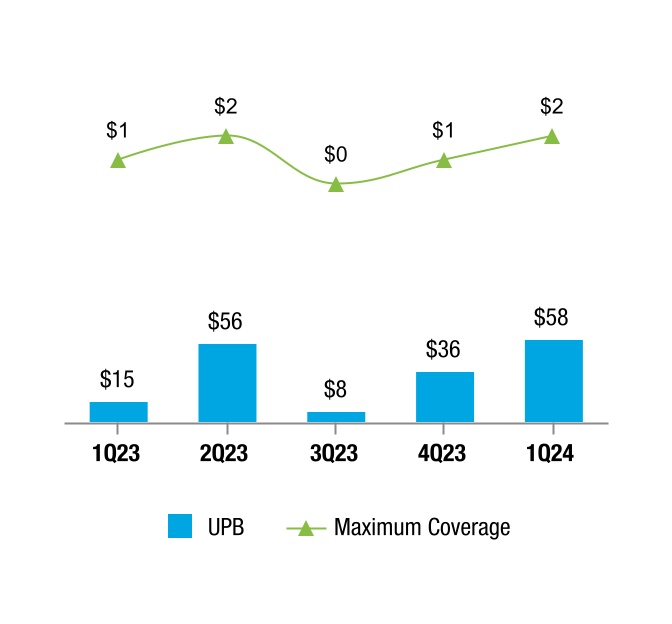

| Total CRT issuance | $57,617 | $1,950 | $14,933 | $657 | |||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 23 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| March 31, 2024 | ||||||||||||||

| (Dollars in millions) | UPB(1) | % of Portfolio | Maximum Coverage(2)(3) | |||||||||||

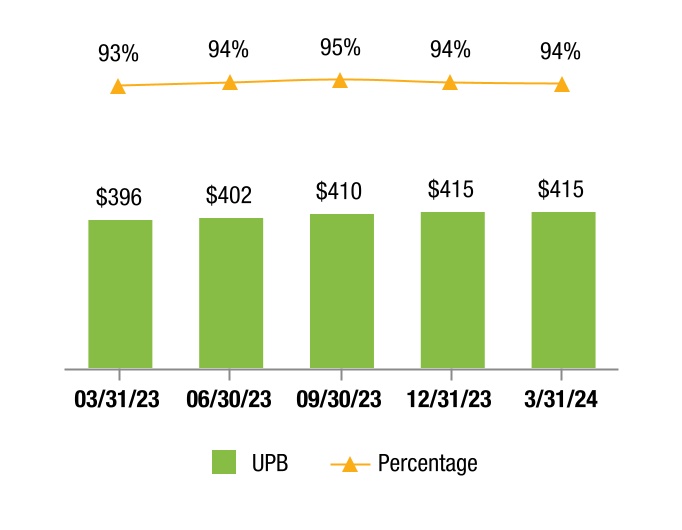

Primary mortgage insurance(4) | $636,735 | 21 | % | $166,486 | ||||||||||

| STACR | 1,187,102 | 39 | 31,085 | |||||||||||

| ACIS | 804,323 | 26 | 17,535 | |||||||||||

| Other | 39,871 | 1 | 10,911 | |||||||||||

Less: UPB with multiple credit enhancements and other reconciling items(5) | (801,385) | (26) | — | |||||||||||

| Single-Family mortgage portfolio - credit-enhanced | 1,866,646 | 61 | 226,017 | |||||||||||

| Single-Family mortgage portfolio - non-credit-enhanced | 1,176,306 | 39 | N/A | |||||||||||

| Total | $3,042,952 | 100 | % | $226,017 | ||||||||||

| December 31, 2023 | ||||||||||||||

| (Dollars in millions) | UPB(1) | % of Portfolio | Maximum Coverage(2)(3) | |||||||||||

Primary mortgage insurance(4) | $637,037 | 21 | % | $165,738 | ||||||||||

| STACR | 1,175,837 | 39 | 31,222 | |||||||||||

| ACIS | 821,048 | 27 | 17,647 | |||||||||||

| Other | 39,901 | 1 | 11,027 | |||||||||||

Less: UPB with multiple credit enhancements and other reconciling items(5) | (813,966) | (27) | — | |||||||||||

| Single-Family mortgage portfolio - credit-enhanced | 1,859,857 | 61 | 225,634 | |||||||||||

| Single-Family mortgage portfolio - non-credit-enhanced | 1,179,053 | 39 | N/A | |||||||||||

| Total | $3,038,910 | 100 | % | $225,634 | ||||||||||

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||

(% of portfolio based on UPB)(1) | % of Portfolio(2) | SDQ Rate | % of Portfolio(2) | SDQ Rate | ||||||||||||||||

| Credit-enhanced: | ||||||||||||||||||||

| Primary mortgage insurance | 21 | % | 0.92 | % | 21 | % | 0.95 | % | ||||||||||||

| CRT and other | 55 | 0.57 | 55 | 0.60 | ||||||||||||||||

| Non-credit-enhanced | 39 | 0.40 | 39 | 0.42 | ||||||||||||||||

| Total | N/A | 0.52 | N/A | 0.55 | ||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 24 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| March 31, 2024 | ||||||||||||||||||||

| (Dollars in millions) | UPB | Original Credit Score(1) | Current Credit Score(1)(2) | Original LTV Ratio | Current LTV Ratio | |||||||||||||||

| Single-Family mortgage portfolio year of origination: | ||||||||||||||||||||

| 2024 | $42,481 | 754 | 754 | 78 | % | 78 | % | |||||||||||||

| 2023 | 278,342 | 751 | 744 | 79 | 75 | |||||||||||||||

| 2022 | 426,234 | 746 | 744 | 76 | 68 | |||||||||||||||

| 2021 | 968,107 | 752 | 755 | 71 | 53 | |||||||||||||||

| 2020 | 707,779 | 761 | 767 | 71 | 46 | |||||||||||||||

| 2019 and prior | 620,009 | 738 | 751 | 75 | 34 | |||||||||||||||

| Total | $3,042,952 | 750 | 754 | 73 | 52 | |||||||||||||||

| December 31, 2023 | ||||||||||||||||||||

| (Dollars in millions) | UPB | Original Credit Score (1) | Current Credit Score(1)(2) | Original LTV Ratio | Current LTV Ratio | |||||||||||||||

| Single-Family mortgage portfolio year of origination: | ||||||||||||||||||||

| 2023 | $265,072 | 751 | 745 | 79 | % | 75 | % | |||||||||||||

| 2022 | 433,252 | 745 | 746 | 76 | 68 | |||||||||||||||

| 2021 | 984,004 | 752 | 756 | 71 | 54 | |||||||||||||||

| 2020 | 719,822 | 761 | 768 | 71 | 46 | |||||||||||||||

| 2019 | 119,557 | 746 | 753 | 76 | 46 | |||||||||||||||

| 2018 and prior | 517,203 | 736 | 751 | 75 | 32 | |||||||||||||||

| Total | $3,038,910 | 750 | 755 | 73 | 52 | |||||||||||||||

| March 31, 2024 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CLTV ≤ 60 | CLTV > 60 to 80 | CLTV > 80 to 90 | CLTV > 90 to 100 | CLTV > 100 | All Loans | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Original credit score | % of Portfolio | SDQ Rate | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate | ||||||||||||||||||||||||||||||||||||||||||||

| 740 and above | 44 | % | 0.15 | % | 15 | % | 0.23 | % | 4 | % | 0.31 | % | 2 | % | 0.29 | % | — | % | NM | 65 | % | 0.17 | % | |||||||||||||||||||||||||||||||||

| 700 to 739 | 12 | 0.49 | 6 | 0.79 | 2 | 0.89 | 1 | 0.73 | — | NM | 21 | 0.58 | ||||||||||||||||||||||||||||||||||||||||||||

| 680 to 699 | 4 | 0.85 | 2 | 1.48 | — | NM | — | NM | — | NM | 6 | 1.00 | ||||||||||||||||||||||||||||||||||||||||||||

| 660 to 679 | 3 | 1.21 | 1 | 2.13 | — | NM | — | NM | — | NM | 4 | 1.40 | ||||||||||||||||||||||||||||||||||||||||||||

| 620 to 659 | 2 | 1.89 | 1 | 3.28 | — | NM | — | NM | — | NM | 3 | 2.10 | ||||||||||||||||||||||||||||||||||||||||||||

| Less than 620 | 1 | 4.30 | — | NM | — | NM | — | NM | — | NM | 1 | 4.63 | ||||||||||||||||||||||||||||||||||||||||||||

| Total | 66 | % | 0.46 | 25 | % | 0.67 | 6 | % | 0.71 | 3 | % | 0.59 | — | % | NM | 100 | % | 0.52 | ||||||||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 25 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CLTV ≤ 60 | CLTV > 60 to 80 | CLTV > 80 to 90 | CLTV > 90 to 100 | CLTV > 100 | All Loans | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Original credit score | % of Portfolio | SDQ Rate | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate(2) | % of Portfolio | SDQ Rate | ||||||||||||||||||||||||||||||||||||||||||||

| 740 and above | 45 | % | 0.16 | % | 15 | % | 0.24 | % | 4 | % | 0.32 | % | 1 | % | 0.27 | % | — | % | NM | 65 | % | 0.18 | % | |||||||||||||||||||||||||||||||||

| 700 to 739 | 13 | 0.53 | 5 | 0.82 | 2 | 0.93 | 1 | 0.59 | — | NM | 21 | 0.61 | ||||||||||||||||||||||||||||||||||||||||||||

| 680 to 699 | 4 | 0.90 | 2 | 1.50 | — | NM | — | NM | — | NM | 6 | 1.05 | ||||||||||||||||||||||||||||||||||||||||||||

| 660 to 679 | 3 | 1.28 | 1 | 2.18 | — | NM | — | NM | — | NM | 4 | 1.45 | ||||||||||||||||||||||||||||||||||||||||||||

| 620 to 659 | 2 | 2.00 | 1 | 3.37 | — | NM | — | NM | — | NM | 3 | 2.21 | ||||||||||||||||||||||||||||||||||||||||||||

| Less than 620 | 1 | 4.41 | — | NM | — | NM | — | NM | — | NM | 1 | 4.74 | ||||||||||||||||||||||||||||||||||||||||||||

| Total | 68 | % | 0.49 | 24 | % | 0.70 | 6 | % | 0.72 | 2 | % | 0.52 | — | % | NM | 100 | % | 0.55 | ||||||||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 26 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| 1Q 2024 | 1Q 2023 | ||||||||||||||||

| (UPB in millions, loan count in thousands) | UPB | Loan Count | UPB | Loan Count | |||||||||||||

| Payment deferral plans | $2,670 | 10 | $2,735 | 11 | |||||||||||||

| Loan modifications | 1,382 | 6 | 1,259 | 6 | |||||||||||||

Forbearance plans and other(1) | 1,180 | 5 | 1,490 | 7 | |||||||||||||

| Total | $5,232 | 21 | $5,484 | 24 | |||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 27 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

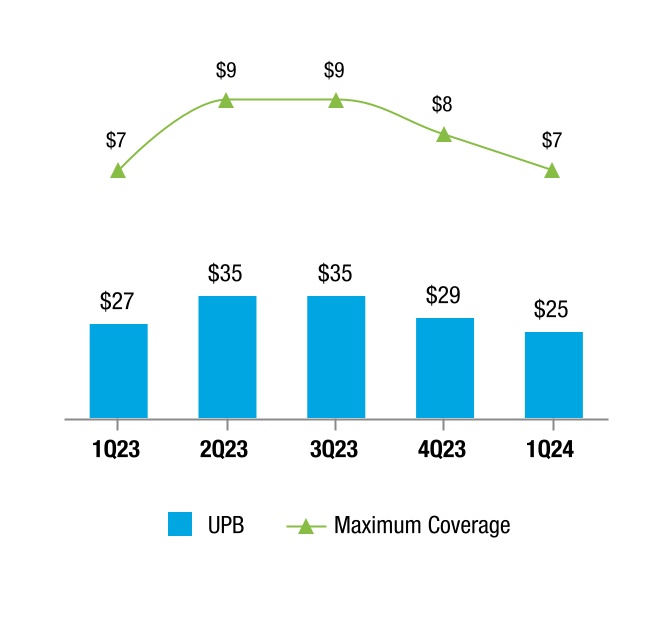

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||||||||||||||||||||

| (In millions) | UPB(1) | Maximum Coverage(2)(3) | UPB(1) | Maximum Coverage(2)(3) | ||||||||||||||||||||||||||||||||||

| Subordination | $6,598 | $399 | $6,149 | $425 | ||||||||||||||||||||||||||||||||||

| SCR | — | — | 1,166 | 105 | ||||||||||||||||||||||||||||||||||

| Lender risk-sharing | — | — | 239 | 48 | ||||||||||||||||||||||||||||||||||

| Total CRT issuance | $6,598 | $399 | $7,554 | $578 | ||||||||||||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 28 | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||

| (Dollars in millions) | UPB | Delinquency Rate | UPB | Delinquency Rate | |||||||||||||||||||||||||||||||

| Credit-enhanced: | |||||||||||||||||||||||||||||||||||

| Subordination | $359,244 | 0.34 | % | $358,944 | 0.26 | % | |||||||||||||||||||||||||||||

| SCR/MCIP | 46,904 | 0.23 | 47,011 | 0.23 | |||||||||||||||||||||||||||||||

| Other | 8,779 | 0.86 | 8,844 | 0.89 | |||||||||||||||||||||||||||||||

| Total credit-enhanced | 414,927 | 0.34 | 414,799 | 0.27 | |||||||||||||||||||||||||||||||

| Non-credit-enhanced | 28,160 | 0.33 | 25,998 | 0.51 | |||||||||||||||||||||||||||||||

| Total | $443,087 | 0.34 | $440,797 | 0.28 | |||||||||||||||||||||||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (Dollars in millions) | UPB | Delinquency Rate | UPB | Delinquency Rate | |||||||||||||||||||

| Mortgage loans held-for-sale | $8,602 | — | % | $8,823 | — | % | |||||||||||||||||

| Mortgage loans held-for-investment: | |||||||||||||||||||||||

| Held by Freddie Mac | 7,980 | 0.99 | 9,941 | 1.21 | |||||||||||||||||||

| Held by consolidated trusts | 9,182 | 0.14 | 4,851 | 0.27 | |||||||||||||||||||

| Other mortgage-related guarantees | 2,396 | — | 2,383 | — | |||||||||||||||||||

| Total | $28,160 | 0.33 | $25,998 | 0.51 | |||||||||||||||||||

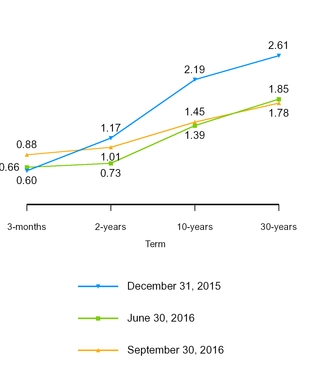

| PMVS-YC | PMVS-L | |||||||||||

| (In millions) | 25 bps | 50 bps | 100 bps | |||||||||

| Assuming shifts of the LIBOR yield curve: | ||||||||||||

| September 30, 2017 | $9 | $6 | $2 | |||||||||

| December 31, 2016 | $7 | $— | $— | |||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Risk Management | |||||||

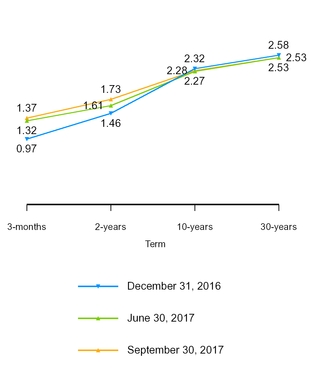

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||||||||

| PVS-YC | PVS-L | PVS-YC | PVS-L | |||||||||||||||||||||||||||||

| (In millions) | 25 bps | 50 bps | 100 bps | 25 bps | 50 bps | 100 bps | ||||||||||||||||||||||||||

Assuming shifts of the yield curve, (gains) losses on:(1) | ||||||||||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||

| Investments | $316 | $3,047 | $6,015 | ($301) | $3,150 | $6,229 | ||||||||||||||||||||||||||

Guarantees(2) | (15) | (314) | (599) | 34 | (369) | (678) | ||||||||||||||||||||||||||

| Total assets | 301 | 2,733 | 5,416 | (267) | 2,781 | 5,551 | ||||||||||||||||||||||||||

| Liabilities | 56 | (1,496) | (3,044) | (52) | (1,519) | (3,073) | ||||||||||||||||||||||||||

| Derivatives | (357) | (1,267) | (2,494) | 322 | (1,274) | (2,547) | ||||||||||||||||||||||||||

| Total | $— | ($30) | ($122) | $3 | ($12) | ($69) | ||||||||||||||||||||||||||

| PVS | $— | $— | $— | $3 | $— | $— | ||||||||||||||||||||||||||

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||||||||

(Duration gap in months, dollars in millions) | Duration Gap | PVS-YC 25 bps | PVS-L 50 bps | Duration Gap | PVS-YC 25 bps | PVS-L 50 bps | ||||||||||||||||||||

| Average | 0.1 | $2 | $— | — | $3 | $3 | ||||||||||||||||||||

| Minimum | (0.1) | — | — | (0.2) | — | — | ||||||||||||||||||||

| Maximum | 0.2 | 5 | 5 | 0.2 | 9 | 24 | ||||||||||||||||||||

| Standard deviation | 0.1 | 1 | 1 | 0.1 | 2 | 6 | ||||||||||||||||||||

| 3Q 2017 | 3Q 2016 | |||||||||||||||||||||

| (Duration gap in months, dollars in millions) | Duration Gap | PMVS-YC 25 bps | PMVS-L 50 bps | Duration Gap | PMVS-YC 25 bps | PMVS-L 50 bps | ||||||||||||||||

| Average | — | $9 | $35 | 0.1 | $6 | $14 | ||||||||||||||||

| Minimum | (0.4 | ) | $— | $— | (0.4 | ) | $— | $— | ||||||||||||||

| Maximum | 0.4 | $26 | $78 | 0.6 | $21 | $68 | ||||||||||||||||

| Standard deviation | 0.2 | $7 | $17 | 0.2 | $4 | $17 | ||||||||||||||||

| YTD 2017 | YTD 2016 | |||||||||||||||||||||

| (Duration gap in months, dollars in millions) | Duration Gap | PMVS-YC 25 bps | PMVS-L 50 bps | Duration Gap | PMVS-YC 25 bps | PMVS-L 50 bps | ||||||||||||||||

| Average | 0.1 | $7 | $16 | 0.1 | $6 | $21 | ||||||||||||||||

| Minimum | (0.4 | ) | $— | $— | (0.4 | ) | $— | $— | ||||||||||||||

| Maximum | 0.8 | $26 | $78 | 0.7 | $31 | $92 | ||||||||||||||||

| Standard deviation | 0.2 | $6 | $20 | 0.2 | $5 | $22 | ||||||||||||||||

| PVS-L (50 bps) | |||||||||||||||||

| (In millions) | Before Derivatives | After Derivatives | Effect of Derivatives | ||||||||||||||

| March 31, 2024 | $1,236 | $— | ($1,236) | ||||||||||||||

| December 31, 2023 | 1,261 | — | (1,261) | ||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | 30 | |||||||

| PMVS-L (50 bps) | |||||||||||

| (In millions) | Before Derivatives | After Derivatives | Effect of Derivatives | ||||||||

| September 30, 2017 | $3,214 | $6 | ($3,208 | ) | |||||||

| December 31, 2016 | $3,651 | $— | ($3,651 | ) | |||||||

| Management's Discussion and Analysis | Risk Management | |||||||

| (In billions) | 3Q 2017 | 3Q 2016 | YTD 2017 | YTD 2016 | |||||||||||

| Interest rate effect on derivative fair values | $— | $0.5 | ($0.6 | ) | ($5.2 | ) | |||||||||

Estimate of offsetting interest rate effect related to financial instruments measured at fair value(1) | — | (0.5 | ) | — | 2.4 | ||||||||||

| Gains (losses) on mortgage loans in fair value hedge relationships | — | — | 0.4 | — | |||||||||||

| Income tax (expense) benefit | — | — | 0.1 | 1.0 | |||||||||||

| Estimated net interest rate effect on comprehensive income (loss) | $— | $— | ($0.1 | ) | ($1.8 | ) | |||||||||

| GAAP Adverse Scenario (Before-Tax) | ||||||||||

| (Dollars in billions) | Before Hedge Accounting | After Hedge Accounting | % Change | |||||||

| September 30, 2017 | ($2.8 | ) | ($1.2 | ) | 58 | % | ||||

| (In millions) | March 31, 2024 | March 31, 2023 | ||||||||||||

Interest Rate Scenarios(1) | ||||||||||||||

| Parallel yield curve shifts: | ||||||||||||||

| +100 bps | $10 | $25 | ||||||||||||

| -100 bps | (10) | (25) | ||||||||||||

| Non-parallel yield curve shifts - long-term interest rates: | ||||||||||||||

| +100 bps | 282 | 118 | ||||||||||||

| -100 bps | (282) | (118) | ||||||||||||

| Non-parallel yield curve shifts - short-term and medium-term interest rates: | ||||||||||||||

| +100 bps | (272) | (92) | ||||||||||||

| -100 bps | 272 | 92 | ||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | ||||||||

| Liquidity and Capital Resources | ||

| 3Q 2017 | |||||||||||||

| (Dollars in millions) | Short-term | Average Rate(1) | Long-term | Average Rate(1) | |||||||||

| Discount notes and Reference Bills: | |||||||||||||

| Beginning balance | $52,354 | 0.91 | % | $— | — | % | |||||||

| Issuances | 89,827 | 0.99 | % | — | — | % | |||||||

| Repurchases | — | — | % | — | — | % | |||||||

| Maturities | (93,716 | ) | 0.92 | % | — | — | % | ||||||

| Ending Balance | 48,465 | 1.05 | % | — | — | % | |||||||

| Securities sold under agreements to repurchase: | |||||||||||||

| Beginning balance | 4,772 | 1.01 | % | — | — | % | |||||||

| Additions | 30,803 | 0.92 | % | — | — | % | |||||||

| Repayments | (27,402 | ) | 0.93 | % | — | — | % | ||||||

| Ending Balance | 8,173 | 0.75 | % | — | — | % | |||||||

| Callable debt: | |||||||||||||

| Beginning balance | — | — | % | 120,450 | 1.53 | % | |||||||

| Issuances | — | — | % | 9,850 | 1.90 | % | |||||||

| Repurchases | — | — | % | (49 | ) | 2.39 | % | ||||||

| Calls | — | — | % | (13,011 | ) | 1.80 | % | ||||||

| Maturities | — | — | % | (3,850 | ) | 0.92 | % | ||||||

| Ending Balance | — | — | % | 113,390 | 1.51 | % | |||||||

Non-callable debt:(2) | |||||||||||||

| Beginning balance | 10,616 | 0.82 | % | 151,279 | 2.38 | % | |||||||

| Issuances | 2,300 | 1.07 | % | 7,555 | 1.51 | % | |||||||

| Repurchases | — | — | % | (167 | ) | 2.54 | % | ||||||

| Maturities | — | — | % | (20,947 | ) | 1.62 | % | ||||||

| Ending Balance | 12,916 | 0.86 | % | 137,720 | 2.47 | % | |||||||

| Total other debt | $69,554 | 0.98 | % | $251,110 | 2.04 | % | |||||||

| YTD 2017 | |||||||||||||

| (Dollars in millions) | Short-term | Average Rate(1) | Long-term | Average Rate(1) | |||||||||

| Discount notes and Reference Bills: | |||||||||||||

| Beginning balance | $61,042 | 0.47 | % | $— | — | % | |||||||

| Issuances | 289,138 | 0.79 | % | — | — | % | |||||||

| Repurchases | (57 | ) | 0.91 | % | — | — | % | ||||||

| Maturities | (301,658 | ) | 0.69 | % | — | — | % | ||||||

| Ending Balance | 48,465 | 1.05 | % | — | — | % | |||||||

| Securities sold under agreements to repurchase: | |||||||||||||

| Beginning balance | 3,040 | 0.42 | % | — | — | % | |||||||

| Additions | 93,948 | 0.61 | % | — | — | % | |||||||

| Repayments | (88,815 | ) | 0.57 | % | — | — | % | ||||||

| Ending Balance | 8,173 | 0.75 | % | — | — | % | |||||||

| Callable debt: | |||||||||||||

| Beginning balance | — | — | % | 98,420 | 1.44 | % | |||||||

| Issuances | — | — | % | 46,979 | 1.90 | % | |||||||

| Repurchases | — | — | % | (49 | ) | 2.39 | % | ||||||

| Calls | — | — | % | (24,227 | ) | 1.76 | % | ||||||

| Maturities | — | — | % | (7,733 | ) | 0.85 | % | ||||||

| Ending Balance | — | — | % | 113,390 | 1.51 | % | |||||||

Non-callable debt:(2) | |||||||||||||

| Beginning balance | 7,435 | 0.41 | % | 186,806 | 2.10 | % | |||||||

| Issuances | 12,866 | 0.87 | % | 18,673 | 1.99 | % | |||||||

| Repurchases | (500 | ) | 0.82 | % | (1,211 | ) | 1.40 | % | |||||

| Maturities | (6,885 | ) | 0.40 | % | (66,548 | ) | 1.46 | % | |||||

| Ending Balance | 12,916 | 0.86 | % | 137,720 | 2.47 | % | |||||||

| Total other debt | $69,554 | 0.98 | % | $251,110 | 2.04 | % | |||||||

| (In millions) | March 31, 2024(1) | December 31, 2023(1) | Description | ||||||||||||||

| Other Investments Portfolio - Liquidity and Contingency Operating Portfolio | $129,150 | $124,098 | The liquidity and contingency operating portfolio, included within our other investments portfolio, is primarily used for short-term liquidity management. | ||||||||||||||

| Mortgage-Related Investments Portfolio | 24,440 | 24,469 | The liquid portion of our mortgage-related investments portfolio can be pledged or sold for liquidity purposes. The amount of cash we may be able to successfully raise may be substantially less than the balance. | ||||||||||||||

| (In millions) | 3Q 2017 | YTD 2017 | |||||

| Beginning balance | $1,625,619 | $1,602,162 | |||||

| Issuances: | |||||||

| New issuances to third parties | 63,552 | 187,273 | |||||

| Additional issuances of securities | 39,425 | 100,507 | |||||

| Total issuances | 102,977 | 287,780 | |||||

| Extinguishments: | |||||||

| Purchases of debt securities from third parties | (7,221 | ) | (27,492 | ) | |||

| Debt securities received in settlement of advances to lenders | (8,630 | ) | (24,341 | ) | |||

| Repayments of debt securities | (68,833 | ) | (194,197 | ) | |||

| Total extinguishments | (84,684 | ) | (246,030 | ) | |||

| Ending balance | $1,643,912 | $1,643,912 | |||||

| Unamortized premiums and discounts | 47,612 | 47,612 | |||||

| Debt securities of consolidated trusts held by third parties | $1,691,524 | $1,691,524 | |||||

| September 30, 2017 | December 31, 2016 | |||||||||||||||||||||||||||||||

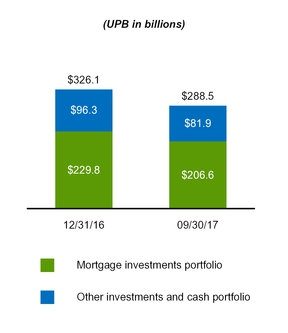

| (In billions) | Liquidity and Contingency Operating Portfolio | Custodial Account | Other(1) | Total Other Investments and Cash Portfolio | Liquidity and Contingency Operating Portfolio | Custodial Account | Other(1) | Total Other Investments and Cash Portfolio | ||||||||||||||||||||||||

| Cash and cash equivalents | $8.2 | $— | $— | $8.2 | $12.4 | $— | $— | $12.4 | ||||||||||||||||||||||||

| Restricted cash and cash equivalents | — | 5.1 | 2.6 | 7.7 | — | 9.5 | 0.4 | 9.9 | ||||||||||||||||||||||||

| Securities purchased under agreements to resell | 34.2 | 12.8 | 0.2 | 47.2 | 37.5 | 13.6 | 0.4 | 51.5 | ||||||||||||||||||||||||

| Non-mortgage-related securities | 16.9 | — | 0.6 | 17.5 | 19.6 | — | 1.5 | 21.1 | ||||||||||||||||||||||||

| Advances to lenders | — | — | 1.3 | 1.3 | — | — | 1.3 | 1.3 | ||||||||||||||||||||||||

| Total | $59.3 | $17.9 | $4.7 | $81.9 | $69.5 | $23.1 | $3.6 | $96.2 | ||||||||||||||||||||||||

| Freddie Mac 1Q 2024 Form 10-Q | ||||||||

| Management's Discussion and Analysis | Liquidity and Capital Resources | |||||||

| (In millions) | March 31, 2024(1) | December 31, 2023(1) | Description | ||||||||

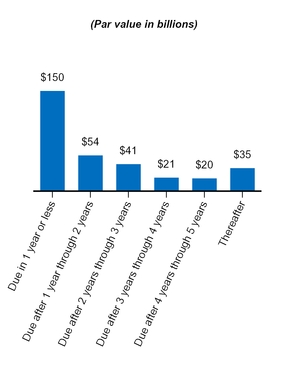

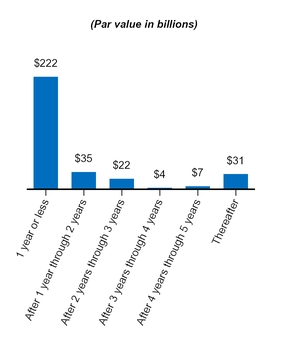

| Debt of Freddie Mac | $161,704 | $166,419 | Debt of Freddie Mac is used to fund our business activities. | ||||||||

| Debt of Consolidated Trusts | 3,050,038 | 3,041,927 | Debt of consolidated trusts is used primarily to fund our Single-Family guarantee activities. This type of debt is principally repaid by the cash flows of the associated mortgage loans. As a result, our repayment obligation is limited to amounts paid pursuant to our guarantee of principal and interest and to purchase modified or seriously delinquent loans from the trusts. | ||||||||

| 1Q 2024 | 1Q 2023 | |||||||||||||||||||

| (Dollars in millions) | Par Value | Average Rate(1) | Par Value | Average Rate(1) | ||||||||||||||||

| Short-term: | ||||||||||||||||||||

| Beginning balance | $6,031 | 5.39 | % | $7,716 | 3.49 | % | ||||||||||||||

| Issuances | 15,943 | 5.29 | 50,739 | 4.18 | ||||||||||||||||

| Repayments | — | — | — | — | ||||||||||||||||

| Maturities | (13,043) | 5.26 | (49,739) | 4.04 | ||||||||||||||||

| Total short-term debt | 8,931 | 5.37 | 8,716 | 4.36 | ||||||||||||||||

| Long-term: | ||||||||||||||||||||

| Beginning balance | 168,009 | 3.31 | 170,363 | 2.22 | ||||||||||||||||

| Issuances | 16,438 | 5.38 | 14,192 | 5.33 | ||||||||||||||||

| Repayments | (20,812) | 5.62 | (2,491) | 5.93 | ||||||||||||||||

| Maturities | (3,164) | 2.62 | (680) | 1.50 | ||||||||||||||||