UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

| | |

| ý | | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended SeptemberJune 30, 20172018 |

| or |

| o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Commission File Number 1-13953 |

W. R. GRACE & CO.

(Exact name of registrant as specified in its charter)

|

| |

Delaware (State or other jurisdiction of incorporation or organization) | 65-0773649 (I.R.S. Employer Identification No.) |

7500 Grace Drive, Columbia, Maryland 21044-4098

(Address of principal executive offices) (Zip Code)code)

(410) 531-4000

(Registrant'sRegistrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large“large accelerated filer," "accelerated” “accelerated filer," "smaller” “smaller reporting company,"” and "emerging“emerging growth company"company” in Rule 12b-2 of the Exchange Act.

|

| | |

Large accelerated filer ý | | Accelerated filer o |

Non-accelerated filer o (Do not check if a smaller reporting company) | | Smaller reporting company o |

Emerging growth company o | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ý No o

Indicate the number of shares outstanding of each of the issuer'sissuer’s classes of common stock, as of the latest practicable date.

|

| | |

| Class | | Outstanding at OctoberJuly 31, 20172018 |

| Common Stock, $0.01 par value per share | | 67,763,20167,238,067 shares |

TABLE OF CONTENTS

GRACE®, the GRACE® logo and, except as otherwise indicated, the other trademarks, service marks or trade names used in the text of this Report are trademarks, service marks, or trade names of operating units of W. R. Grace & Co. or its subsidiaries and/or affiliates. Unless the context indicates otherwise, indicated, in this Report the terms "Grace," "we," "us,"“Grace,” “we,” “us,” or "our"“our” mean W. R. Grace & Co. and/or its consolidated subsidiaries and affiliates, and the term "the Company"the “Company” means W. R. Grace & Co. Unless otherwise indicated, the contents of websites mentioned in this report are not incorporated by reference or otherwise made a part of this Report.

The Financial Accounting Standards Board® is referred to in this Report as the "FASB."“FASB.” The FASB issues, among other things, the FASB Accounting Standards Codifications ("ASC"Codification® (“ASC”) and Accounting Standards Updates ("ASU"(“ASU”).

The U.S. Internal Revenue Service is referred to in this Report as the “IRS.”

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

Review by Independent Registered Public Accounting Firm

With respect to the interim consolidated financial statements included in this Quarterly Report on Form 10-Q for the quarter ended SeptemberJune 30, 20172018, PricewaterhouseCoopers LLP, the Company'sCompany’s independent registered public accounting firm, has applied limited procedures in accordance with professional auditing standards for a review of such information. Their report on the interim consolidated financial statements, which follows, states that they did not audit and they do not express an opinion on the unaudited interim consolidated financial statements. Accordingly, the degree of reliance on their report on the unaudited interim consolidated financial statements should be restricted in light of the limited nature of the review procedures applied. This report is not considered a "report"“report” within the meaning of Sections 7 and 11 of the Securities Act of 1933, and, therefore, the independent accountants'accountants’ liability under Section 11 does not extend to it.

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors of W. R. Grace & Co.:

Results of Review of Financial Statements

We have reviewed the accompanying consolidated balance sheet of W. R. Grace & Co. and its subsidiaries as of SeptemberJune 30, 2017,2018, and the related consolidated statements of operations and comprehensive income (loss) for the three-month and nine-monthsix-month periods ended SeptemberJune 30, 20172018 and 20162017 and the consolidated statements of equity and of cash flows and equity for the nine-monthsix-month periods ended SeptemberJune 30, 2018 and 2017, and 2016. Theseincluding the related notes (collectively referred to as the “interim financial statements”). Based on our reviews, we are not aware of any material modifications that should be made to the accompanying interim financial statements arefor them to be in conformity with accounting principles generally accepted in the responsibilityUnited States of the Company’s management.America.

We conducted our reviewhave previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States)., the consolidated balance sheet of the Company as of December 31, 2017, and the related consolidated statements of operations, of comprehensive income, of equity, and of cash flows for the year then ended (not presented herein), and in our report dated February 22, 2018, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying consolidated balance sheet information as of December 31, 2017, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

Basis for Review Results

These interim financial statements are the responsibility of the Company’s management. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We conducted our review in accordance with the standards of the PCAOB. A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States),PCAOB, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the accompanying consolidated interim financial statements for them to be in conformity with accounting principles generally accepted in the United States of America.

We previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet as of December 31, 2016, and the related consolidated statements of operations, comprehensive income, equity and of cash flows for the year then ended (not presented herein), and in our report dated February 23, 2017, which included a paragraph describing a change in the manner of accounting for debt issuance costs and stock compensation in 2016, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying consolidated balance sheet as of December 31, 2016, is fairly stated in all material respects in relation to the consolidated balance sheet from which it has been derived.

/s/ PricewaterhouseCoopers LLP

Baltimore, Maryland

November 2, 2017August 8, 2018

W. R. Grace & Co. and Subsidiaries

Consolidated Statements of Operations (unaudited)

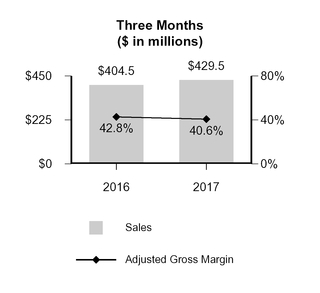

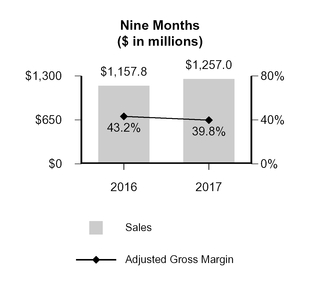

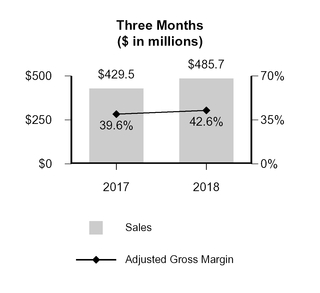

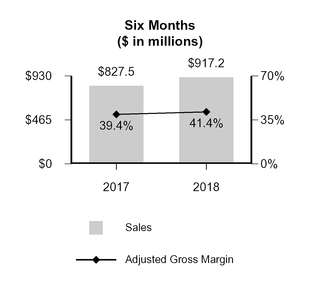

| | | | Three Months Ended September 30, | | Nine Months Ended September 30, | Three Months Ended June 30, | | Six Months Ended June 30, |

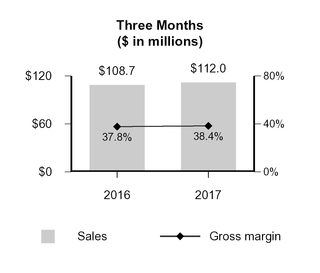

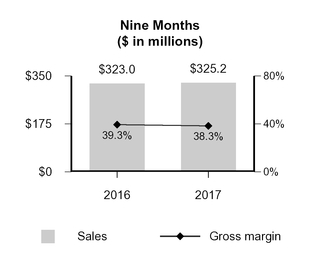

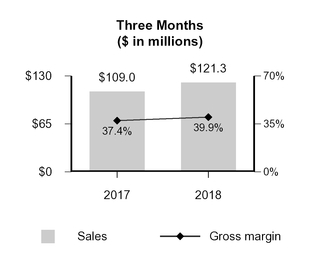

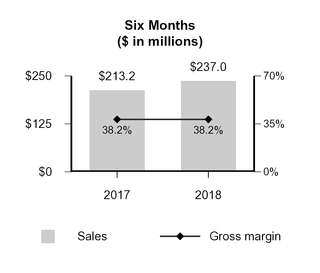

| (In millions, except per share amounts) | 2017 | | 2016 | | 2017 | | 2016 | 2018 | | 2017 | | 2018 | | 2017 |

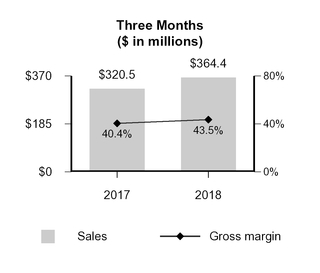

| Net sales | $ | 429.5 |

| | $ | 404.5 |

| | $ | 1,257.0 |

| | $ | 1,157.8 |

| $ | 485.7 |

| | $ | 429.5 |

| | $ | 917.2 |

| | $ | 827.5 |

|

| Cost of goods sold | 256.2 |

| | 236.3 |

| | 761.2 |

| | 663.7 |

| 287.0 |

| | 262.3 |

| | 549.0 |

| | 507.1 |

|

| Gross profit | 173.3 |

| | 168.2 |

| | 495.8 |

| | 494.1 |

| 198.7 |

| | 167.2 |

| | 368.2 |

| | 320.4 |

|

| Selling, general and administrative expenses | 70.5 |

| | 67.1 |

| | 207.3 |

| | 201.5 |

| 82.2 |

| | 69.3 |

| | 151.5 |

| | 134.8 |

|

| Research and development expenses | 13.3 |

| | 12.1 |

| | 39.4 |

| | 36.2 |

| 16.1 |

| | 13.6 |

| | 30.8 |

| | 27.5 |

|

| Provision for environmental remediation, net | 6.4 |

| | 11.9 |

| | 19.6 |

| | 19.4 |

| 0.5 |

| | 13.2 |

| | 0.6 |

| | 13.2 |

|

| Equity in earnings of unconsolidated affiliate | (4.8 | ) | | (8.5 | ) | | (17.9 | ) | | (18.0 | ) | (8.2 | ) | | (6.1 | ) | | (13.6 | ) | | (13.1 | ) |

| Restructuring and repositioning expenses | 9.3 |

| | 5.6 |

| | 17.0 |

| | 28.6 |

| 18.8 |

| | 5.4 |

| | 24.4 |

| | 7.7 |

|

| Interest expense and related financing costs | 20.1 |

| | 19.8 |

| | 59.7 |

| | 61.6 |

| 19.9 |

| | 20.1 |

| | 39.2 |

| | 39.6 |

|

| Other (income) expense, net | (0.2 | ) | | (0.5 | ) | | (12.0 | ) | | 13.3 |

| 5.8 |

| | (11.4 | ) | | 3.5 |

| | (13.3 | ) |

| Total costs and expenses | 114.6 |

| | 107.5 |

| | 313.1 |

| | 342.6 |

| 135.1 |

| | 104.1 |

| | 236.4 |

| | 196.4 |

|

| Income (loss) from continuing operations before income taxes | 58.7 |

| | 60.7 |

| | 182.7 |

| | 151.5 |

| |

| Income (loss) before income taxes | | 63.6 |

| | 63.1 |

| | 131.8 |

| | 124.0 |

|

| (Provision for) benefit from income taxes | (11.6 | ) |

| (19.4 | ) | | (49.2 | ) | | (62.1 | ) | (25.0 | ) |

| (19.6 | ) | | (49.8 | ) | | (37.6 | ) |

| Income (loss) from continuing operations | 47.1 |

|

| 41.3 |

| | 133.5 |

| | 89.4 |

| |

| Income (loss) from discontinued operations, net of income taxes | — |

| | (1.6 | ) | | — |

| | (10.9 | ) | |

| Net income (loss) | 47.1 |

| | 39.7 |

| | 133.5 |

| | 78.5 |

| 38.6 |

| | 43.5 |

| | 82.0 |

| | 86.4 |

|

| Less: Net (income) loss attributable to noncontrolling interests | 0.3 |

| | (0.1 | ) | | 0.7 |

| | 0.3 |

| 0.2 |

| | 0.4 |

| | 0.4 |

| | 0.4 |

|

| Net income (loss) attributable to W. R. Grace & Co. shareholders | $ | 47.4 |

| | $ | 39.6 |

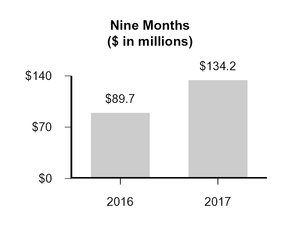

| | $ | 134.2 |

| | $ | 78.8 |

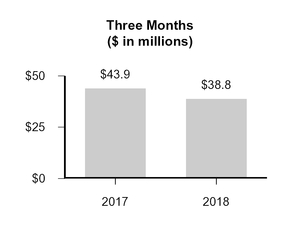

| $ | 38.8 |

| | $ | 43.9 |

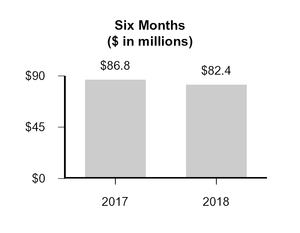

| | $ | 82.4 |

| | $ | 86.8 |

|

| Amounts Attributable to W. R. Grace & Co. Shareholders: | | | | | | | | |

| Income (loss) from continuing operations attributable to W. R. Grace & Co. shareholders | $ | 47.4 |

| | $ | 41.2 |

| | $ | 134.2 |

| | $ | 89.7 |

| |

| Income (loss) from discontinued operations, net of income taxes | — |

| | (1.6 | ) | | — |

| | (10.9 | ) | |

| Net income (loss) attributable to W. R. Grace & Co. shareholders | $ | 47.4 |

| | $ | 39.6 |

| | $ | 134.2 |

| | $ | 78.8 |

| |

| Earnings Per Share Attributable to W. R. Grace & Co. Shareholders | | | | | | | | | | | | | | |

| Basic earnings per share: | | | | | | | | | | | | | | |

| Income (loss) from continuing operations | $ | 0.70 |

| | $ | 0.59 |

| | $ | 1.97 |

| | $ | 1.27 |

| |

| Income (loss) from discontinued operations, net of income taxes | — |

| | (0.03 | ) | | — |

| | (0.15 | ) | |

| Net income (loss) | $ | 0.70 |

| | $ | 0.56 |

| | $ | 1.97 |

| | $ | 1.12 |

| $ | 0.58 |

| | $ | 0.64 |

| | $ | 1.22 |

| | $ | 1.27 |

|

| Weighted average number of basic shares | 67.9 |

|

| 70.3 |

| | 68.2 |

| | 70.5 |

| 67.3 |

|

| 68.3 |

| | 67.4 |

| | 68.3 |

|

| Diluted earnings per share: | | | | | | | | | | | | | | |

| Income (loss) from continuing operations | $ | 0.70 |

| | $ | 0.58 |

| | $ | 1.96 |

| | $ | 1.27 |

| |

| Income (loss) from discontinued operations, net of income taxes | — |

| | (0.02 | ) | | — |

| | (0.16 | ) | |

| Net income (loss) | $ | 0.70 |

| | $ | 0.56 |

| | $ | 1.96 |

| | $ | 1.11 |

| $ | 0.58 |

| | $ | 0.64 |

| | $ | 1.22 |

| | $ | 1.27 |

|

| Weighted average number of diluted shares | 68.0 |

| | 70.7 |

| | 68.3 |

| | 70.9 |

| 67.4 |

| | 68.4 |

| | 67.5 |

| | 68.5 |

|

| Dividends per common share | $ | 0.21 |

| | $ | 0.17 |

| | $ | 0.63 |

| | $ | 0.34 |

| $ | 0.24 |

| | $ | 0.21 |

| | $ | 0.48 |

| | $ | 0.42 |

|

The Notes to Consolidated Financial Statements are an integral part of these statements.

5

W. R. Grace & Co. and Subsidiaries

Consolidated Statements of Comprehensive Income (Loss) (unaudited)

| | | | Three Months Ended September 30, | | Nine Months Ended September 30, | Three Months Ended June 30, | | Six Months Ended June 30, |

| (In millions) | 2017 | | 2016 | | 2017 | | 2016 | 2018 | | 2017 | | 2018 | | 2017 |

| Net income (loss) | $ | 47.1 |

| | $ | 39.7 |

| | $ | 133.5 |

| | $ | 78.5 |

| $ | 38.6 |

| | $ | 43.5 |

| | $ | 82.0 |

| | $ | 86.4 |

|

| Other comprehensive income (loss): | | | | | | | | |

| Defined benefit pension and other postretirement plans, net of income taxes | (0.3 | ) | | (0.3 | ) | | (1.0 | ) | | (1.0 | ) | |

| Currency translation adjustments, net of income taxes | (12.1 | ) | | (2.3 | ) | | (21.8 | ) | | (6.4 | ) | |

| Gain (loss) from hedging activities, net of income taxes | (0.4 | ) | | 0.6 |

| | 0.1 |

| | (2.7 | ) | |

| Total other comprehensive income (loss) attributable to noncontrolling interests | — |

| | — |

| | — |

| | 2.6 |

| |

| Other comprehensive income (loss), net of income taxes: | | | | | | | | |

| Defined benefit pension and other postretirement plans | | (0.2 | ) | | (0.4 | ) | | (0.4 | ) | | (0.7 | ) |

| Currency translation adjustments | | 37.9 |

| | (8.3 | ) | | 19.7 |

| | (9.7 | ) |

| Gain (loss) from hedging activities | | (5.2 | ) | | (0.2 | ) | | (3.4 | ) | | 0.5 |

|

| Total other comprehensive income (loss) | (12.8 | ) | | (2.0 | ) | | (22.7 | ) | | (7.5 | ) | 32.5 |

| | (8.9 | ) | | 15.9 |

| | (9.9 | ) |

| Comprehensive income (loss) | 34.3 |

| | 37.7 |

| | 110.8 |

| | 71.0 |

| 71.1 |

| | 34.6 |

| | 97.9 |

| | 76.5 |

|

| Less: comprehensive (income) loss attributable to noncontrolling interests | 0.3 |

| | (0.1 | ) | | 0.7 |

| | (2.3 | ) | 0.2 |

| | 0.4 |

| | 0.4 |

| | 0.4 |

|

| Comprehensive income (loss) attributable to W. R. Grace & Co. shareholders | $ | 34.6 |

| | $ | 37.6 |

| | $ | 111.5 |

| | $ | 68.7 |

| $ | 71.3 |

| | $ | 35.0 |

| | $ | 98.3 |

| | $ | 76.9 |

|

The Notes to Consolidated Financial Statements are an integral part of these statements.

6

W. R. Grace & Co. and Subsidiaries

Consolidated Statements of Cash Flows (unaudited)

| | | | Nine Months Ended September 30, | Six Months Ended June 30, |

| (In millions) | 2017 | | 2016 | 2018 | | 2017 |

| OPERATING ACTIVITIES | | | | | | |

| Net income (loss) | $ | 133.5 |

| | $ | 78.5 |

| $ | 82.0 |

| | $ | 86.4 |

|

| Less: loss (income) from discontinued operations | — |

| | 10.9 |

| |

| Income from continuing operations | 133.5 |

| | 89.4 |

| |

| Reconciliation to net cash provided by (used for) operating activities from continuing operations: | | | | |

| Reconciliation to net cash provided by (used for) operating activities: | | | | |

| Depreciation and amortization | 82.6 |

| | 73.8 |

| 50.9 |

| | 54.2 |

|

| Equity in earnings of unconsolidated affiliate | (17.9 | ) | | (18.0 | ) | (13.6 | ) | | (13.1 | ) |

| Dividends received from unconsolidated affiliate | 19.0 |

| | 24.8 |

| |

| Costs related to legacy product, environmental and other claims | 25.5 |

|

| 24.2 |

| 4.3 |

|

| 17.0 |

|

| Cash paid for legacy product, environmental and other claims | (50.1 | ) | | (17.3 | ) | (12.6 | ) | | (44.2 | ) |

| Provision for (benefit from) income taxes | 49.2 |

| | 62.1 |

| 49.8 |

| | 37.6 |

|

| Cash paid for income taxes | (44.1 | ) | | (42.4 | ) | (16.7 | ) | | (31.3 | ) |

| Income tax refunds received | 30.2 |

| | 2.3 |

| 0.1 |

| | 29.7 |

|

| Loss on early extinguishment of debt | — |

| | 11.1 |

| 4.8 |

| | — |

|

| Interest expense and related financing costs | 59.7 |

|

| 61.6 |

| 39.2 |

|

| 39.6 |

|

| Cash paid for interest | (40.1 | ) | | (45.5 | ) | (39.6 | ) | | (34.3 | ) |

| Defined benefit pension expense | 11.6 |

| | 8.2 |

| 7.8 |

| | 8.2 |

|

| Cash paid under defined benefit pension arrangements | (12.2 | ) | | (12.1 | ) | (57.9 | ) | | (7.8 | ) |

| Accounts receivable reserve—Venezuela | 10.0 |

| | — |

| |

| Changes in assets and liabilities, excluding effect of currency translation and acquisitions: | | | | | | |

| Trade accounts receivable | 20.7 |

| | 9.7 |

| 14.8 |

| | 4.3 |

|

| Inventories | (4.5 | ) | | (5.8 | ) | (50.8 | ) | | (3.9 | ) |

| Accounts payable | 3.0 |

| | 11.0 |

| 34.0 |

| | 7.4 |

|

| All other items, net | (8.6 | ) | | (29.5 | ) | 22.5 |

| | (9.3 | ) |

| Net cash provided by (used for) operating activities from continuing operations | 267.5 |

| | 207.6 |

| |

| Net cash provided by (used for) operating activities | | 119.0 |

| | 140.5 |

|

| INVESTING ACTIVITIES | | | | | | |

| Capital expenditures | (85.6 | ) | | (89.4 | ) | (90.8 | ) | | (59.1 | ) |

| Business acquired | (3.5 | ) | | (245.1 | ) | |

| Proceeds from sale of assets | 0.6 |

| | 11.3 |

| |

| Business acquired, net of cash acquired | | (420.9 | ) | | — |

|

| Other investing activities | (1.5 | ) | | (1.4 | ) | 12.7 |

| | 0.3 |

|

| Net cash provided by (used for) investing activities from continuing operations | (90.0 | ) | | (324.6 | ) | |

| Net cash provided by (used for) investing activities | | (499.0 | ) | | (58.8 | ) |

| FINANCING ACTIVITIES | | | | | | |

| Borrowings under credit arrangements | 106.3 |

| | 20.6 |

| 983.2 |

| | 98.8 |

|

| Repayments under credit arrangements | (108.9 | ) | | (614.9 | ) | (541.8 | ) | | (61.5 | ) |

| Cash paid for debt financing costs | | (11.8 | ) | | (0.2 | ) |

| Cash paid for repurchases of common stock | (65.0 | ) | | (55.1 | ) | (49.8 | ) | | (30.0 | ) |

| Proceeds from exercise of stock options | 14.8 |

| | 13.3 |

| 6.4 |

| | 12.2 |

|

| Dividends paid | (43.0 | ) | | (24.1 | ) | |

| Distribution from GCP | — |

| | 750.0 |

| |

| Dividends paid to shareholders | | (32.4 | ) | | (28.7 | ) |

| Other financing activities | (3.8 | ) | | (2.4 | ) | (3.5 | ) | | (3.8 | ) |

| Net cash provided by (used for) financing activities from continuing operations | (99.6 | ) | | 87.4 |

| |

| Effect of currency exchange rate changes on cash and cash equivalents | 7.2 |

| | 2.7 |

| |

| Increase (decrease) in cash and cash equivalents from continuing operations | 85.1 |

| | (26.9 | ) | |

| Cash flows from discontinued operations | | | | |

| Net cash provided by (used for) operating activities | — |

| | 23.9 |

| |

| Net cash provided by (used for) investing activities | — |

| | (9.5 | ) | |

| Net cash provided by (used for) financing activities | — |

| | 31.4 |

| 350.3 |

| | (13.2 | ) |

| Effect of currency exchange rate changes on cash and cash equivalents | — |

| | (1.0 | ) | |

| Increase (decrease) in cash and cash equivalents from discontinued operations | — |

| | 44.8 |

| |

| Effect of currency exchange rate changes on cash, cash equivalents, and restricted cash | | (1.0 | ) | | 3.5 |

|

| Net increase (decrease) in cash and cash equivalents | 85.1 |

|

| 17.9 |

| (30.7 | ) |

| 72.0 |

|

| Less: cash and cash equivalents of discontinued operations | — |

| | (143.4 | ) | |

| Cash and cash equivalents, beginning of period | 90.6 |

| | 329.9 |

| |

| Cash and cash equivalents, end of period | $ | 175.7 |

| | $ | 204.4 |

| |

| Cash, cash equivalents, and restricted cash, beginning of period | | 163.5 |

| | 100.6 |

|

| Cash, cash equivalents, and restricted cash, end of period | | $ | 132.8 |

| | $ | 172.6 |

|

| | | | | | | |

| Supplemental disclosure of cash flow information | | | | | | |

| Capital expenditures in accounts payable | $ | 20.2 |

| | $ | 15.2 |

| $ | 38.7 |

| | $ | 17.8 |

|

| Net share settled stock option exercises | 1.2 |

| | 10.4 |

| |

The Notes to Consolidated Financial Statements are an integral part of these statements.

7

W. R. Grace & Co. and Subsidiaries

Consolidated Balance Sheets (unaudited)

| | | (In millions, except par value and shares) | September 30,

2017 | | December 31,

2016 | June 30,

2018 | | December 31,

2017 |

| ASSETS | | | | | | |

| Current Assets | | | | | | |

| Cash and cash equivalents | $ | 175.7 |

| | $ | 90.6 |

| $ | 131.5 |

| | $ | 152.8 |

|

| Restricted cash and cash equivalents | 10.8 |

| | 10.0 |

| 1.3 |

| | 10.7 |

|

| Trade accounts receivable, less allowance of $12.6 (2016—$2.2) | 253.1 |

| | 273.9 |

| |

| Trade accounts receivable, less allowance of $11.7 (2017—$11.7) | | 277.5 |

| | 285.2 |

|

| Inventories | 239.5 |

| | 228.0 |

| 307.4 |

| | 230.9 |

|

| Other current assets | 36.3 |

|

| 52.3 |

| 70.7 |

|

| 49.0 |

|

| Total Current Assets | 715.4 |

| | 654.8 |

| 788.4 |

| | 728.6 |

|

| Properties and equipment, net of accumulated depreciation and amortization of $1,438.2 (2016—$1,327.5) | 762.8 |

| | 729.6 |

| |

| Properties and equipment, net of accumulated depreciation and amortization of $1,482.4 (2017—$1,463.4) | | 955.9 |

| | 799.1 |

|

| Goodwill | 401.7 |

| | 394.2 |

| 541.2 |

| | 402.4 |

|

| Technology and other intangible assets, net | 259.2 |

| | 269.1 |

| 364.5 |

| | 255.4 |

|

| Deferred income taxes | 694.1 |

| | 709.4 |

| 535.4 |

| | 556.5 |

|

| Investment in unconsolidated affiliate | 118.0 |

| | 117.6 |

| 138.7 |

| | 125.9 |

|

| Other assets | 34.7 |

|

| 37.1 |

| 78.1 |

|

| 39.1 |

|

| Total Assets | $ | 2,985.9 |

| | $ | 2,911.8 |

| $ | 3,402.2 |

| | $ | 2,907.0 |

|

| LIABILITIES AND EQUITY | | | | | | |

| Current Liabilities | | | | | | |

| Debt payable within one year | $ | 46.5 |

| | $ | 76.5 |

| $ | 23.3 |

| | $ | 20.1 |

|

| Accounts payable | 195.2 |

| | 195.4 |

| 262.5 |

| | 210.3 |

|

| Other current liabilities | 207.9 |

| | 208.9 |

| 217.3 |

| | 217.8 |

|

| Total Current Liabilities | 449.6 |

| | 480.8 |

| 503.1 |

| | 448.2 |

|

| Debt payable after one year | 1,521.9 |

| | 1,507.6 |

| 1,963.3 |

| | 1,523.8 |

|

| Underfunded and unfunded defined benefit pension plans | 452.1 |

| | 424.3 |

| 452.2 |

| | 502.4 |

|

| Other liabilities | 165.3 |

| | 126.7 |

| 188.7 |

| | 169.3 |

|

| Total Liabilities | 2,588.9 |

| | 2,539.4 |

| 3,107.3 |

| | 2,643.7 |

|

| Commitments and Contingencies—Note 8 | | | |

| |

|

| Equity | | | | | | |

| Common stock issued, par value $0.01; 300,000,000 shares authorized; outstanding: 67,758,485 (2016—68,309,431) | 0.7 |

| | 0.7 |

| |

| Common stock issued, par value $0.01; 300,000,000 shares authorized; outstanding: 67,235,786 (2017—67,780,410) | | 0.7 |

| | 0.7 |

|

| Paid-in capital | 475.4 |

| | 487.3 |

| 472.1 |

| | 474.8 |

|

| Retained earnings | 710.3 |

| | 619.3 |

| 625.5 |

| | 573.1 |

|

| Treasury stock, at cost: shares: 9,698,142 (2016—9,147,196) | (837.2 | ) | | (804.9 | ) | |

| Treasury stock, at cost: shares: 10,220,841 (2017—9,676,217) | | (865.7 | ) | | (832.1 | ) |

| Accumulated other comprehensive income (loss) | 43.7 |

| | 66.4 |

| 55.8 |

| | 39.9 |

|

| Total W. R. Grace & Co. Shareholders' Equity | 392.9 |

| | 368.8 |

| |

| Total W. R. Grace & Co. Shareholders’ Equity | | 288.4 |

| | 256.4 |

|

| Noncontrolling interests | 4.1 |

| | 3.6 |

| 6.5 |

| | 6.9 |

|

| Total Equity | 397.0 |

| | 372.4 |

| 294.9 |

| | 263.3 |

|

| Total Liabilities and Equity | $ | 2,985.9 |

| | $ | 2,911.8 |

| $ | 3,402.2 |

| | $ | 2,907.0 |

|

The Notes to Consolidated Financial Statements are an integral part of these statements.

8

W. R. Grace & Co. and Subsidiaries

Consolidated Statements of Equity (unaudited)

| | | (In millions) | Common Stock and Paid-in Capital | | Retained Earnings | | Treasury Stock | | Accumulated Other Comprehensive Income (Loss) | | Noncontrolling Interests | | Total Equity | Common Stock and Paid-in Capital | | Retained Earnings | | Treasury Stock | | Accumulated Other Comprehensive Income (Loss) | | Noncontrolling Interests | | Total Equity |

| Balance, December 31, 2015 | $ | 496.7 |

| | $ | 436.3 |

| | $ | (658.4 | ) | | $ | (66.8 | ) | | $ | 4.7 |

| | $ | 212.5 |

| |

| Net income (loss) | — |

| | 78.8 |

| | — |

| | — |

| | (0.3 | ) | | 78.5 |

| |

| Repurchase of common stock | — |

| | — |

| | (55.1 | ) | | — |

| | — |

| | (55.1 | ) | |

| Stock-based compensation | 9.2 |

| | — |

| | — |

| | — |

| | — |

| | 9.2 |

| |

| Exercise of stock options | (16.2 | ) | | — |

| | 39.9 |

| | — |

| | — |

| | 23.7 |

| |

| Tax benefit related to stock plans | — |

| | 70.4 |

| | — |

| | — |

| | — |

| | 70.4 |

| |

| Shares issued | 0.7 |

| | — |

| | — |

| | — |

| | — |

| | 0.7 |

| |

| Other comprehensive (loss) income | — |

| | — |

| | — |

| | (10.1 | ) | | 2.6 |

| | (7.5 | ) | |

| Dividends declared | — |

| | (24.1 | ) | | — |

| | — |

| | — |

| | (24.1 | ) | |

| Distribution of GCP | — |

| | 54.7 |

| | — |

| | 135.3 |

| | (3.7 | ) | | 186.3 |

| |

| Balance, September 30, 2016 | $ | 490.4 |

| | $ | 616.1 |

| | $ | (673.6 | ) | | $ | 58.4 |

| | $ | 3.3 |

| | $ | 494.6 |

| |

| Balance, December 31, 2016 | $ | 488.0 |

| | $ | 619.3 |

| | $ | (804.9 | ) | | $ | 66.4 |

| | $ | 3.6 |

| | $ | 372.4 |

| $ | 488.0 |

| | $ | 619.3 |

| | $ | (804.9 | ) | | $ | 66.4 |

| | $ | 3.6 |

| | $ | 372.4 |

|

| Net income (loss) | — |

| | 134.2 |

| | — |

| | — |

| | (0.7 | ) | | 133.5 |

| — |

| | 86.8 |

| | — |

| | — |

| | (0.4 | ) | | 86.4 |

|

| Repurchase of common stock | — |

| | — |

| | (65.0 | ) | | — |

| | — |

| | (65.0 | ) | — |

| | — |

| | (30.0 | ) | | — |

| | — |

| | (30.0 | ) |

| Payments to taxing authorities in consideration of employee tax obligations relative to stock-based compensation arrangements | (2.5 | ) | | — |

| | — |

| | — |

| | — |

| | (2.5 | ) | |

| Payments to taxing authorities in consideration of employee tax obligations related to stock-based compensation arrangements | | (2.4 | ) | | — |

| | — |

| | — |

| | — |

| | (2.4 | ) |

| Stock-based compensation | 8.2 |

| | — |

| | — |

| | — |

| | — |

| | 8.2 |

| 5.4 |

| | — |

| | — |

| | — |

| | — |

| | 5.4 |

|

| Exercise of stock options | (18.3 | ) | | — |

| | 32.7 |

| | — |

| | — |

| | 14.4 |

| (17.0 | ) | | — |

| | 28.8 |

| | — |

| | — |

| | 11.8 |

|

| Shares issued | 0.7 |

| | — |

| | — |

| | — |

| | — |

| | 0.7 |

| 0.7 |

| | — |

| | — |

| | — |

| | — |

| | 0.7 |

|

| Other comprehensive (loss) income | — |

| | — |

| | — |

| | (22.7 | ) | | — |

| | (22.7 | ) | — |

| | — |

| | — |

| | (9.9 | ) | | — |

| | (9.9 | ) |

| Contribution to joint venture | — |

| | — |

| | — |

| | — |

| | 1.2 |

| | 1.2 |

| |

| Dividends declared | — |

| | (43.2 | ) | | — |

| | — |

| | — |

| | (43.2 | ) | — |

| | (28.8 | ) | | — |

| | — |

| | — |

| | (28.8 | ) |

| Balance, September 30, 2017 | $ | 476.1 |

| | $ | 710.3 |

| | $ | (837.2 | ) | | $ | 43.7 |

| | $ | 4.1 |

| | $ | 397.0 |

| |

| Balance, June 30, 2017 | | $ | 474.7 |

| | $ | 677.3 |

| | $ | (806.1 | ) | | $ | 56.5 |

| | $ | 3.2 |

| | $ | 405.6 |

|

| Balance, December 31, 2017 | | $ | 475.5 |

| | $ | 573.1 |

| | $ | (832.1 | ) | | $ | 39.9 |

| | $ | 6.9 |

| | $ | 263.3 |

|

| Net income (loss) | | — |

| | 82.4 |

| | — |

| | — |

| | (0.4 | ) | | 82.0 |

|

| Repurchase of common stock | | — |

| | — |

| | (49.8 | ) | | — |

| | — |

| | (49.8 | ) |

| Payments to taxing authorities in consideration of employee tax obligations related to stock-based compensation arrangements | | (3.0 | ) | | — |

| | — |

| | — |

| | — |

| | (3.0 | ) |

| Stock-based compensation | | 9.6 |

| | — |

| | — |

| | — |

| | — |

| | 9.6 |

|

| Exercise of stock options | | (4.1 | ) | | — |

| | 10.2 |

| | — |

| | — |

| | 6.1 |

|

| Shares issued | | (5.2 | ) | | — |

| | 6.0 |

| | — |

| | — |

| | 0.8 |

|

| Dividends declared | | — |

| | (32.5 | ) | | — |

| | — |

| | — |

| | (32.5 | ) |

| Other comprehensive (loss) income | | — |

| | — |

| | — |

| | 15.9 |

| | — |

| | 15.9 |

|

| Adjustment to retained earnings for adoption of ASC 606 | | — |

| | 2.5 |

| | — |

| | — |

| | — |

| | 2.5 |

|

| Balance, June 30, 2018 | | $ | 472.8 |

| | $ | 625.5 |

| | $ | (865.7 | ) | | $ | 55.8 |

| | $ | 6.5 |

| | $ | 294.9 |

|

The Notes to Consolidated Financial Statements are an integral part of these statements.

9

Notes to Consolidated Financial Statements

1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies

W. R. Grace & Co., through its subsidiaries, is engaged in specialty chemicals and specialty materials businesses on a global basis through two reportable segments: Grace Catalysts Technologies, which includes catalysts and related products and technologies used in refining, petrochemical and other chemical manufacturing applications; and Grace Materials Technologies, which includes specialty materials, including silica-based and silica-alumina-based materials, used in coatings, consumer, industrial, and pharmaceutical applications.

W. R. Grace & Co. conducts all of its business through a single wholly owned subsidiary, W. R. Grace & Co.–Conn. ("(“Grace–Conn."”). Grace–Conn. owns all of the assets, properties and rights of W. R. Grace & Co. on a consolidated basis, either directly or through subsidiaries.

As used in these notes, the term "Company"“Company” refers to W. R. Grace & Co. The term "Grace"“Grace” refers to the Company and/or one or more of its subsidiaries and, in certain cases, their respective predecessors.

Separation Transaction On January 27, 2016, Grace entered into a separation agreement with GCP Applied Technologies Inc., then a wholly-owned subsidiary of Grace ("GCP"), pursuant to which Grace agreed to transfer its Grace Construction Products operating segment and the packaging technologies business of its Grace Materials Technologies operating segment to GCP (the "Separation"). Grace and GCP completed the Separation on February 3, 2016 (the "Distribution Date"), by means of a pro rata distribution to the Company's stockholders of all of the outstanding shares of GCP common stock (the "Distribution"), with one share of GCP common stock distributed for each share of Company common stock held as of the close of business on January 27, 2016. As a result of the Distribution, GCP became an independent public company. GCP’s historical financial results through the Distribution Date are reflected in Grace’s Consolidated Financial Statements as discontinued operations.

Basis of Presentation The interim Consolidated Financial Statements presented herein are unaudited and should be read in conjunction with the Consolidated Financial Statements presented in the Company's 2016Company’s 2017 Annual Report on Form 10-K. Such interim Consolidated Financial Statements reflect all adjustments that, in the opinion of management, are necessary for a fair statement of the results of the interim periods presented; all such adjustments are of a normal recurring nature except for the impacts of adopting new accounting standards as discussed below. All significant intercompany accounts and transactions have been eliminated.

The results of operations for the nine-monthsix-month interim period ended SeptemberJune 30, 2017,2018, are not necessarily indicative of the results of operations to be attained for the year ending December 31, 2017.2018.

Use of Estimates The preparation of financial statements in conformity with U.S. generally accepted accounting principles ("(“U.S. GAAP"GAAP”) requires management to make estimates and assumptions that affect the reported amountamounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the Consolidated Financial Statements, and the reported amounts of revenues and expenses for the periods presented. Actual amounts could differ from those estimates, and the differences could be material. Changes in estimates are recorded in the period identified. Grace'sGrace’s accounting measurements that are most affected by management'smanagement’s estimates of future events are:

Realization values of net deferred tax assets, which depend on projections of future taxable income (see Note 5);income;

Pension and postretirement liabilities, which depend on assumptions regarding participant life spans, future inflation, discount rates and total returns on invested funds (see Note 6);

Carrying values of goodwill and other intangible assets, which depend on assumptions of future earnings and cash flows; and

Contingent liabilities, which depend on an assessment of the probability of loss and an estimate of ultimate obligation, such as litigation (see Note 8), income taxes (see Note 5), and environmental remediation (see Note 8).

Reclassifications Certain amounts in prior years'years’ Consolidated Financial Statements have been reclassified to conform to the current year presentation. Such reclassifications have not materially affected previously reported amounts in the Consolidated Financial Statements.

Long-Lived Assets During the 2018 first quarter, Grace, with the assistance of an outside accounting firm, completed a study to evaluate the useful lives of its operating machinery and equipment, including a review of historical asset retirement data as well as review and analysis of relevant industry practices. As a result of this study, effective January 1, 2018, Grace revised the accounting useful lives of certain machinery and equipment, which was determined to be a change in accounting estimate and is being applied prospectively. As a result of this change in accounting estimate, Grace’s depreciation expense with respect to such machinery and equipment was reduced by $6.2 million, resulting in an increase to net income of $4.8 million or $0.07 per diluted share, for the three months ended June 30, 2018. For the six months ended June 30, 2018, depreciation expense with respect to such machinery and equipment was reduced by $8.9 million, resulting in an increase to net income of $6.8 million or $0.10 per diluted share. Estimated useful lives for operating machinery and equipment, which previously ranged from 3 to 10 years, now range from 5 to 25 years.

Notes to Consolidated Financial Statements (Continued)

1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies (Continued)

Recently Issued Accounting StandardsIn May 2014, the FASB issued ASU 2014-09 "Revenue from Contracts with Customers." This update is intended to remove inconsistencies and weaknesses in revenue requirements; provide a more robust framework for addressing revenue issues; improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets; provide more useful information to users of financial statements through improved disclosure requirements; and simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer. The standard allows for two methods of adoption: (a) full retrospective adoption, meaning the standard is applied to all periods presented, or (b) modified retrospective adoption, meaning the cumulative effect of applying the new standard is recognized as an adjustment to the opening retained earnings balance. Grace has assessed specific areas of the standard and its impact on the Consolidated Financial Statements. Grace will adopt this standard in the 2018 first quarter under the modified retrospective approach and does not expect it to have a material effect on the Consolidated Financial Statements.

In February 2016, the FASB issued ASU 2016-02 "Leases“Leases (Topic 842)."” This update is intended to increase transparency and comparability among organizations by recognizing lease assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. The core principle of Topic 842 is that a lessee should recognize the assets and liabilities that arise from leases. A lessee should recognize in the statement of financial position a liability to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset for the lease term, including optional payments where they are reasonably certain to occur. Currently, as a lessee, Grace is a party to a number of leases which, under existing guidance, are classified as operating leases and not recorded on the balance sheet but are expensed as incurred. Under the new standard, many of these leases will be recorded on the Consolidated Balance Sheets. Grace will adopt the standard in the 2019 first quarter. Grace has begun its implementation of the new standard and at this time cannot reasonably estimate the effect of adoption.

In January 2017, the FASB issued ASU 2017-04 “Intangibles—Goodwill and Other (Topic 350).” This update modifies the concept of impairment from the condition that exists when the carrying amount of goodwill exceeds its implied fair value to the condition that exists when the carrying amount of a reporting unit exceeds its fair value. An entity no longer will determine goodwill impairment by calculating the implied fair value of goodwill by assigning the fair value of a reporting unit to all of its assets and liabilities as if that reporting unit had been acquired in a business combination (“Step 2”). Because these amendments eliminate Step 2 from the goodwill impairment test, they should reduce the cost and complexity of evaluating goodwill for impairment. Grace is required to adopt the amendments in this update on January 1, 2020. Early adoption is permitted. Grace is currently evaluating the timing of adoption and does not expect the update to have a material effect on the Consolidated Financial Statements.

In January 2018, the FASB issued ASU 2018-01 “Leases (Topic 842): Land Easement Practical Expedient for Transition to Topic 842.” This update provides an optional transition practical expedient that allows an entity to elect not to evaluate under Topic 842 existing or expired land easements not previously accounted for as leases. All land easements entered into or modified after the adoption of Topic 842 must be evaluated under Topic 842. Grace, which typically does not account for easements under current lease accounting, will use the transition practical expedient when adopting Topic 842 in the 2019 first quarter and at this time cannot reasonably estimate the effect of adoption.

In February 2018, the FASB issued ASU 2018-02 “Income Statement—Reporting Comprehensive Income (Topic 220).” This update addresses the revaluation of deferred tax assets and liabilities due to the Tax Cuts and Jobs Act of 2017 impacting income from continuing operations, even if the initial income tax effects were recognized in other comprehensive income. The update allows entities to reclassify the tax effects that were originally in other comprehensive income from accumulated other comprehensive income to retained earnings. The update requires entities to disclose whether the election was made and a description of the income tax effects. The update can be: (a) applied to the period of adoption, or (b) applied retrospectively to each period in which the Tax Cuts and Jobs Act of 2017 is in effect. Grace is required to adopt the amendments in this update on January 1, 2019, with early adoption permitted. Grace is currently evaluating the timing and effect of adoption.

Recently Adopted Accounting Standards In November 2016, the FASB issued ASU 2016-18 "Statement“Statement of Cash Flows (Topic 230): Restricted Cash,"” which requires that a statement of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. Therefore, amounts generally described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. The new requirements are effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years, with early adoption permitted. Grace is currently evaluating the timing of adoption and does not expectadopted the update to have a materialin the 2018 first quarter. The table below presents the effect of the adoption of ASU 2016-18 on thepreviously reported amounts.

Notes to Consolidated Financial Statements. AsStatements (Continued)

1. Basis of September 30, 2017,Presentation and December 31, 2016, restricted cash included in the Consolidated Balance Sheets was $10.8 millionSummary of Significant Accounting and $10.0 million, respectively.Financial Reporting Policies (Continued)

|

| | | | | | | | | | | |

| | Six Months Ended June 30, 2017 |

| (In millions) | Previously Reported | | Revised | | Effect of Change |

| Other investing activities | $ | (0.5 | ) | | $ | 0.3 |

| | $ | 0.8 |

|

| Net cash provided by (used for) investing activities | (59.6 | ) | | (58.8 | ) | | 0.8 |

|

| Cash, cash equivalents, and restricted cash, beginning of period | 90.6 |

| | 100.6 |

| | 10.0 |

|

| Cash, cash equivalents, and restricted cash, end of period | 161.8 |

| | 172.6 |

| | 10.8 |

|

In January 2017, the FASB issued ASU 2017-01 "Business“Business Combinations (Topic 805),"” which provides a screen to determine when an integrated set of assets and activities is not a business. The screen requires that when substantially all of the fair value of the gross assets acquired (or disposed of) is concentrated in a single identifiable asset or a group of similar identifiable assets, the set is not a business. This screen reduces the number of transactions that need to be further evaluated. If the screen is not met, the amendments in this update (1) require that to be considered a business, a set must include, at a minimum, an input and a substantive process that together significantly contribute to the ability to create output, and (2) remove the evaluation of whether a market participant could replace missing elements. The amendments in this update also narrow the definition of the term "output"“output” so that the term is consistent with how outputs are described in TopicASC 606. Public business entities are required to apply the amendments in this update to annual periods beginning after December 15, 2017, including interim periods within those periods. Early application is permitted. Grace will evaluate the effect ofadopted the update atin the time2018 first quarter and applied the new definition of any futurea business to the acquisition or disposal.completed during the 2018 second quarter.

In JanuaryMay 2017, the FASB issued ASU 2017-04 "Intangibles—Goodwill and Other2017-09 “Compensation—Stock Compensation (Topic 350)718)."” This update modifiesclarifies the conceptexisting definition of impairment from the condition that exists whenterm “modification,” which is currently defined as “a change in any of the carrying amountterms or conditions of goodwill exceeds its implieda share-based payment award.” The update requires entities to account for modifications of share-based payment awards unless the (1) fair value, (2) vesting conditions, and (3) classification as an equity instrument or a liability instrument of the modified award are the same as the original award before modification. Grace adopted the update in the 2018 first quarter, and it did not have an effect on the Consolidated Financial Statements.

Revenue Recognition

In May 2014, the FASB issued ASU 2014-09 “Revenue from Contracts with Customers (Topic 606)” (“ASC 606”). This update was intended to remove inconsistencies and weaknesses in revenue requirements; provide a more robust framework for addressing revenue issues; improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets; provide more useful information to users of financial statements through improved disclosure requirements; and simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer. Grace adopted ASC 606 with a date of initial application of January 1, 2018. Grace applied the standard to all customer contracts. As a result, Grace has changed its accounting policy for revenue recognition as detailed below.

Grace applied ASC 606 using the modified retrospective method, that is, by recognizing the cumulative effect of initially applying ASC 606 as an adjustment to “retained earnings” at the date of initial application. Results for periods beginning after December 31, 2017, are presented under ASC 606, while the comparative information has not been adjusted and continues to be reported in accordance with Grace’s historical accounting under ASC 605 “Revenue Recognition” (“ASC 605”).

Grace generates revenues predominantly from sales of manufactured products to customers and in part from licensing of technology. Under ASC 606, revenue from customer arrangements is recognized when control is transferred to the condition that exists whencustomer.

Product Sales Revenue Recognition

In its implementation of ASC 606, Grace assessed its customer arrangements at the carrying amountoperating segment level, and based on the similarity of a reporting unit exceeds its fair value. An entity no longer will determine goodwill impairment by calculatingarrangements, Grace elected to use the implied fair value of goodwill by assigning the fair value of a reporting unit to all of its assets and liabilities as if that reporting unit had beenportfolio method practical expedient.

Notes to Consolidated Financial Statements (Continued)

1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies (Continued)

acquiredBased on the promises made to customers in product sales arrangements, Grace determined that it has a performance obligation to manufacture and deliver products to its customers. Grace makes certain other promises in its customer arrangements that are immaterial in the context of the contracts. Revenue is recognized at amounts based on agreed upon prices in sales contracts and/or purchase orders. Grace offers various incentives to its product sales customers that result in variable consideration, including but not limited to volume discounts, which reward bulk purchases by lowering the price for future purchases, and volume rebates, which encourage customers to purchase volume levels that would reduce their current prices. These incentives are immaterial in the context of the contracts.

For product sales, control is transferred at the point in time at which risk of loss and title have transferred to the customer, which is determined based on shipping terms. Terms of delivery and terms of payment are generally included in customer contracts of sale, order confirmation documents, and invoices. Payment is generally due within 30 to 60 days of invoicing. Grace defers revenue recognition until no other significant Grace obligations remain. Grace’s customer arrangements do not contain significant acceptance provisions.

Taxes that Grace collects that are assessed by a governmental authority, and that are both imposed on and concurrent with any of its revenue-producing activities, are excluded from revenue. Grace considers shipping and handling activities that it performs as activities to fulfill the sales of its products. Amounts billed for shipping and handling are included in net sales, while costs incurred for shipping and handling are included in cost of sales, in accordance with the practical expedient provided by ASC 606.

Technology Licensing Revenue Recognition

For Grace’s technology licensing business, combination ("Step 2"). BecauseGrace determined that the customer arrangements contain multiple deliverables to enable licensees to realize the full benefit of the technology. These deliverables include licensing the technology itself; developing engineering design packages; and providing training, consulting, and technical services. Under these amendments eliminate Step 2arrangements, the license grant is not a distinct performance obligation, as the licensee only can benefit from the goodwill impairment test, they should reducelicense in conjunction with other integral services such as development of the costengineering design package, training, consulting, or technical services provided over the contract period. Therefore, Grace accounts for the license grant and complexityintegral services as a single performance obligation. Certain deliverables and services not included in the core bundled deliverables are accounted for as separate performance obligations.

The transaction price is specified in the technology licensing agreements and is substantially fixed. Some services are priced on a per-diem basis, but these are not material in the context of evaluating goodwillthe contracts. Grace invoices its technology licensing customers as certain project milestones are achieved. Payment terms are similar to those of Grace’s product sales.

Revenue for impairment.each performance obligation is recognized when control is transferred to the customer, which is generally over a period of time. As a result, Grace generally recognizes revenue for each performance obligation ratably over the period of the contract, which is requiredup to adoptseven years, depending on the amendments in this update for annual or any interim goodwill impairment tests in fiscal years beginning after December 15, 2019. Early adoption is permitted for interim or annual goodwill impairment tests performedscope of the licensee’s project. Based on testing dates after January 1, 2017. Grace is currently evaluating the timing of adoption and does not expectpayments, Grace records deferred revenue related to these agreements. See Note 13.

Impact of Adoption

Except for the updatechanges below, Grace has consistently applied its accounting policy for revenue recognition to have a material effect onall periods presented in the Consolidated Financial Statements.

Grace recorded a net increase to “retained earnings” of $2.5 million as of January 1, 2018, which represents the cumulative impact of adopting ASC 606, with a $3.2 million reduction to “other liabilities” and a $0.7 million reduction to “deferred income taxes.” The cumulative adjustment results from a change in accounting for contingent revenue related to technology licensing arrangements. Under ASC 605, certain revenue was not realized until a contractual contingency was resolved. Upon adoption of ASC 606, Grace estimates all forms of

Notes to Consolidated Financial Statements (Continued)

1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies (Continued)

variable consideration, including contingent amounts, at the inception of the arrangement and recognizes it over the period of performance.

The tables below present the effect of the adoption of ASC 606 on Grace’s Consolidated Statements of Operations and Consolidated Balance Sheets.

Consolidated Statements of Operations

|

| | | | | | | | | | | |

| | Three months ended June 30, 2018 |

| (In millions) | Under ASC 605 | | As Reported (ASC 606) | | Effect of Change |

| Net sales | $ | 485.4 |

| | $ | 485.7 |

| | $ | 0.3 |

|

| Gross profit | 198.4 |

| | 198.7 |

| | 0.3 |

|

| Income (loss) before income taxes | 63.3 |

| | 63.6 |

| | 0.3 |

|

| Provision for income taxes | (24.9 | ) | | (25.0 | ) | | (0.1 | ) |

| Net income (loss) | 38.4 |

| | 38.6 |

| | 0.2 |

|

| Net income (loss) attributable to W. R. Grace & Co. Shareholders | 38.6 |

| | 38.8 |

| | 0.2 |

|

|

| | | | | | | | | | | |

| | Six Months Ended June 30, 2018 |

| (In millions) | Under ASC 605 | | As Reported (ASC 606) | | Effect of Change |

| Net sales | $ | 916.8 |

| | $ | 917.2 |

| | $ | 0.4 |

|

| Gross profit | 367.8 |

| | 368.2 |

| | 0.4 |

|

| Income (loss) before income taxes | 131.4 |

| | 131.8 |

| | 0.4 |

|

| Provision for income taxes | (49.7 | ) | | (49.8 | ) | | (0.1 | ) |

| Net income (loss) | 81.7 |

| | 82.0 |

| | 0.3 |

|

| Net income (loss) attributable to W. R. Grace & Co. Shareholders | 82.1 |

| | 82.4 |

| | 0.3 |

|

Consolidated Balance Sheets

|

| | | | | | | | | | | |

| | June 30, 2018 |

| (In millions) | Under ASC 605 | | As Reported (ASC 606) | | Effect of Change |

| Deferred income taxes | $ | 536.2 |

| | $ | 535.4 |

| | $ | (0.8 | ) |

| Other liabilities | 192.3 |

| | 188.7 |

| | (3.6 | ) |

| Retained earnings | 622.7 |

| | 625.5 |

| | 2.8 |

|

ASU 2017-07 “Compensation—Retirement Benefits (Topic 715)”

In March 2017, the FASB issued ASU 2017-07 "Compensation—“Compensation—Retirement Benefits (Topic 715)."” This update requires that the service cost component of net benefit cost be presented with other compensation costs arising from services rendered. The remaining net benefit cost is either presented as a line item in the statement of operations outside of a subtotal for income from operations, if presented, or disclosed separately. OnlyIn addition, only the service cost component of net benefit expensecost can be capitalized. Grace is currently evaluating the update's effect on the Consolidated Financial Statements and will adoptadopted the update in the 2018 first quarter.

In May 2017,The changes in classification of net benefit costs within the FASB issued ASU 2017-09 "Compensation—Stock Compensation (Topic 718)." This update clarifies the existing definitionConsolidated Statements of the term "modification," which is currently defined as "aOperations have been retrospectively applied to all periods presented. The change in any of the terms or conditions of a share-based payment award." The update requires entities to account for modifications of share-based payment awards unless the (1) fair value, (2) vesting conditions, and (3) classification as an equity instrument or a liability instrument of the modified award are the same as of the original award before modification. Grace is required to adopt the amendments in this update for fiscal years and interim periods beginning after December 15, 2017, with early adoption permitted. Grace does not currently have any modifications of share-based awards and will adopt the update when it becomes effective.

In August 2017, the FASB issued ASU 2017-12 "Derivatives and Hedging (Topic 815)." This update improves the presentation of the results of hedges by requiring the earnings effect of the hedging instrument to be in the same income statement line item as the earnings of the hedged item. This update expands hedge accounting to include hedging relationships involving both financial and nonfinancial risks. Grace is required to adopt the amendments in this update for fiscal years and interim periods beginning after December 15, 2018, with early adoption permitted. Grace is currently evaluating the timing of adoption and does not expect the update to have a material effect on the Consolidated Financial Statements.

Recently Adopted Accounting StandardsIn July 2015, the FASB issued ASU 2015-11 "Simplifying the Measurement of Inventory." This update is part of the FASB's Simplification Initiative and is also intended to enhance convergence with the International Accounting Standards Board's ("IASB") measurement of inventory. The update requires thatcosts capitalizable into inventory be measured at the lower of cost or net realizable value for entities using FIFO (first-in, first-out) or average cost methods. Grace adopted this update in the first quarter of 2017, and it did not have a material effect on the Consolidated Financial Statements.was applied

In August 2016, the FASB issued ASU 2016-15 "Classification of Certain Cash Receipts and Cash Payments." This update is intended to reduce diversity in practice in how certain cash receipts and cash payments are presented and classified in the statement of cash flows. It addresses eight specific issues. Grace adopted this update in the 2017 second quarter, and it did not have a material effect on the Consolidated Financial Statements.

Notes to Consolidated Financial Statements (Continued)

2. Inventories1. Basis of Presentation and Summary of Significant Accounting and Financial Reporting Policies (Continued)

prospectively in accordance with the update. The tables below present the effect of the adoption of ASU 2017-07 on previously reported amounts.

Consolidated Statements of Operations

|

| | | | | | | | | | | |

| | Three Months Ended June 30, 2017 |

| (In millions) | Previously Reported | | Revised | | Effect of Change |

| Cost of goods sold | $ | 260.2 |

| | $ | 262.3 |

| | $ | 2.1 |

|

| Gross profit | 169.3 |

| | 167.2 |

| | (2.1 | ) |

| Selling, general and administrative expenses | 70.3 |

| | 70.8 |

| | 0.5 |

|

| Research and development expenses | 12.9 |

| | 13.6 |

| | 0.7 |

|

| Other (income) expense | (9.6 | ) | | (12.9 | ) | | (3.3 | ) |

|

| | | | | | | | | | | |

| | Six Months Ended June 30, 2017 |

| (In millions) | Previously Reported | | Revised | | Effect of Change |

| Cost of goods sold | $ | 505.0 |

| | $ | 507.1 |

| | $ | 2.1 |

|

| Gross profit | 322.5 |

| | 320.4 |

| | (2.1 | ) |

| Selling, general and administrative expenses | 136.8 |

| | 137.8 |

| | 1.0 |

|

| Research and development expenses | 26.1 |

| | 27.5 |

| | 1.4 |

|

| Other (income) expense | (11.8 | ) | | (16.3 | ) | | (4.5 | ) |

2. Inventories

Inventories are stated at the lower of cost or net realizable value, and cost is determined using FIFO. Inventories consisted of the following at SeptemberJune 30, 2017,2018, and December 31, 2016:2017:

| | | (In millions) | September 30,

2017 | | December 31,

2016 | June 30,

2018 | | December 31,

2017 |

| Raw materials | $ | 53.6 |

| | $ | 57.7 |

| $ | 60.3 |

| | $ | 48.8 |

|

| In process | 34.7 |

| | 33.4 |

| 56.8 |

| | 33.0 |

|

| Finished products | 128.2 |

| | 115.8 |

| 161.3 |

| | 124.7 |

|

| Other | 23.0 |

| | 21.1 |

| 29.0 |

| | 24.4 |

|

| Total inventory | $ | 239.5 |

| | $ | 228.0 |

| $ | 307.4 |

| | $ | 230.9 |

|

Notes to Consolidated Financial Statements (Continued)

3. Debt

Components of Debt

| | | (In millions) | September 30,

2017 | | December 31,

2016 | June 30,

2018 | | December 31,

2017 |

| 5.125% senior notes due 2021, net of unamortized debt issuance costs of $6.2 at September 30, 2017 (2016—$7.3) | $ | 693.8 |

| | $ | 692.7 |

| |

| U.S. dollar term loan, net of unamortized debt issuance costs and discounts of $4.7 at September 30, 2017 (2016—$5.7) | 403.7 |

| | 402.7 |

| |

| 5.625% senior notes due 2024, net of unamortized debt issuance costs of $3.6 at September 30, 2017 (2016—$4.0) | 296.4 |

| | 296.0 |

| |

| Euro term loan, net of unamortized debt issuance costs and discounts of $1.0 at September 30, 2017 (2016—$1.3) | 93.1 |

| | 82.5 |

| |

| 2018 U.S. dollar term loan, net of unamortized debt issuance costs of $9.7 | | $ | 940.3 |

| | $ | — |

|

| 5.125% senior notes due 2021, net of unamortized debt issuance costs of $5.0 (2017—$5.8) | | 695.0 |

| | 694.2 |

|

| 5.625% senior notes due 2024, net of unamortized debt issuance costs of $3.2 (2017—$3.5) | | 296.8 |

| | 296.5 |

|

| Debt payable to unconsolidated affiliate | 41.4 |

| | 39.5 |

| 46.3 |

| | 42.4 |

|

| Deferred payment obligation | — |

| | 30.0 |

| |

| 2014 U.S. dollar term loan, net of unamortized debt issuance costs and discounts (2017—$4.3) | | — |

| | 404.1 |

|

2014 Euro term loan, net of unamortized debt issuance costs and discounts (2017—$1.0) | | — |

| | 94.0 |

|

| Other borrowings(1) | 40.0 |

| | 40.7 |

| 8.2 |

| | 12.7 |

|

| Total debt | 1,568.4 |

| | 1,584.1 |

| 1,986.6 |

| | 1,543.9 |

|

| Less debt payable within one year | 46.5 |

| | 76.5 |

| 23.3 |

| | 20.1 |

|

| Debt payable after one year | $ | 1,521.9 |

| | $ | 1,507.6 |

| $ | 1,963.3 |

| | $ | 1,523.8 |

|

| Weighted average interest rates on total debt | 4.7 | % | | 4.6 | % | 3.8 | % | | 4.7 | % |

(1) Represents borrowings under various lines of credit and other borrowings, primarily by non-U.S. subsidiaries.

See Note 4On April 3, 2018, Grace entered into a Credit Agreement (the “Credit Agreement”), which provides for a discussionnew senior secured credit facilities, consisting of:

| |

| (a) | a $950 million term loan due in 2025, with interest at LIBOR +175 basis points, and |

| |

| (b) | a $400 million revolving credit facility due in 2023, with interest at LIBOR +175 basis points. |

The term loan will amortize in equal quarterly installments in aggregate annual amounts equal to 1.00% of the fair value of Grace's debt.original principal amount thereof, with the first payment due on December 31, 2018.

The Credit Agreement contains customary affirmative covenants, including, but not limited to: (i) maintenance of existence, and compliance with laws; (ii) delivery of consolidated financial statements and other information; (iii) payment of taxes; (iv) delivery of notices of defaults and certain other material events; and (v) maintenance of adequate insurance. The Credit Agreement also contains customary negative covenants, including but not limited to restrictions on: (i) dividends on, and redemptions of, equity interests and other restricted payments; (ii) liens; (iii) loans and investments; (iv) the sale, transfer or disposition of assets and businesses; (v) transactions with affiliates; and (vi) a maximum first lien leverage ratio.

Events of default under the Credit Agreement include, but are not limited to: (i) failure to pay principal, maturities of debt outstanding at September 30, 2017, were as follows:

|

| | | |

| | (In millions) |

| 2017 | $ | 40.4 |

|

| 2018 | 8.8 |

|

| 2019 | 8.3 |

|

| 2020 | 7.0 |

|

| 2021 | 1,196.1 |

|

| Thereafter | 307.8 |

|

| Total debt | $ | 1,568.4 |

|

On February 3, 2017, Grace fundedinterest, fees or other amounts under the PD trust with $30.0 millionCredit Agreement when due, taking into account any applicable grace period; (ii) any representation or warranty proving to have been incorrect in any material respect when made; (iii) failure to perform or observe covenants or other terms of the deferred payment obligation relatingCredit Agreement subject to ZAI PD Claims. (See Note 8.certain grace periods; (iv) a cross-default and cross-acceleration with certain other material debt; (v) bankruptcy events; (vi) certain defaults under ERISA; and (vii) the invalidity or impairment of security interests.

To secure its obligations under the Credit Agreement, Grace and certain of its U.S. subsidiaries have granted security interests in substantially all equity and debt interests in Grace–Conn. or any other Grace subsidiary owned by them and in substantially all their non-real estate assets and property.

The foregoing is a summary of the Credit Agreement. Grace has filed the full text of the Credit Agreement with the Securities and Exchange Commission (the “SEC”), which is readily available on the internet at www.sec.gov.

Notes to Consolidated Financial Statements (Continued)

3. Debt (Continued)

Grace also maintainsused a $300portion of the proceeds to repay in full the borrowings outstanding under its 2014 credit agreement, which was terminated, as well as to make a voluntary $50.0 million revolving credit facility. accelerated contribution to its U.S. qualified pension plans. In connection with the repayment of debt, Grace recorded a $4.8 million loss on early extinguishment of debt. As of SeptemberJune 30, 2017,2018, the available credit under thisthe revolving credit facility was reduced to $265.0$364.3 million by outstanding letters of credit.

DuringSee Note 4 for a discussion of the 2016 first quarter, in connection with the Separation, GCP distributed $750 million to Grace. Grace used $600 millionfair value of those funds to repay $526.9 million of its U.S. dollar term loan and €67.3 million of its euro term loan. As a result, Grace recorded a loss on early extinguishmentGrace’s debt.

The principal maturities of debt of $11.1 million, which is included in "other (income) expense, net" in the Consolidated Statements of Operations.outstanding at June 30, 2018, were as follows:

|

| | | |

| | (In millions) |

| 2018 | $ | 14.0 |

|

| 2019 | 19.1 |

|

| 2020 | 17.9 |

|

| 2021 | 711.4 |

|

| 2022 | 15.5 |

|

| Thereafter | 1,208.7 |

|

| Total debt | $ | 1,986.6 |

|

4. Fair Value Measurements and Risk

Certain of Grace'sGrace’s assets and liabilities are reported at fair value on a gross basis. ASC 820 "Fair“Fair Value Measurements and Disclosures"Disclosures” defines fair value as the value that would be received at the measurement date in the principal or "most advantageous"“most advantageous” market. Grace uses principal market data, whenever available, to value assets and liabilities that are required to be reported at fair value.

Grace has identified the following financial assets and liabilities that are subject to the fair value analysis required by ASC 820:

Fair Value of Debt and Other Financial InstrumentsDebt payable is recorded at carrying value. Fair value is determined based on Level 2 inputs, including expected future cash flows (discounted at market interest rates), estimated current market prices and quotes from financial institutions.

At SeptemberJune 30, 20172018, the carrying amounts and fair values of Grace'sGrace’s debt were as follows:

| | | | September 30, 2017 | | December 31, 2016 | June 30, 2018 | | December 31, 2017 |

| (In millions) | Carrying Amount | | Fair Value | | Carrying Amount | | Fair Value | Carrying Amount | | Fair Value | | Carrying Amount | | Fair Value |

| 5.125% senior notes due 2021(1) | $ | 693.8 |

| | $ | 752.8 |

| | $ | 692.7 |

| | $ | 721.3 |

| |

| U.S. dollar term loan(2) | 403.7 |

| | 405.7 |

| | 402.7 |

| | 408.2 |

| |

| 2018 U.S. dollar term loan(1) | | $ | 940.3 |

| | $ | 939.1 |

| | $ | — |

| | $ | — |

|

| 5.125% senior notes due 2021(2) | | 695.0 |

| | 709.2 |

| | 694.2 |

| | 728.7 |

|

5.625% senior notes due 2024(1)(2) | 296.4 |

| | 325.7 |

| | 296.0 |

| | 311.5 |

| 296.8 |

| | 311.3 |

| | 296.5 |

| | 321.3 |

|

| Euro term loan(2) | 93.1 |

| | 93.2 |

| | 82.5 |

| | 82.0 |

| |

| U.S. dollar term loan(3) | | — |

| | — |

| | 404.1 |

| | 409.7 |

|

| Euro term loan(3) | | — |

| | — |

| | 94.0 |

| | 93.7 |

|

| Other borrowings | 81.4 |

| | 81.4 |

| | 110.2 |

| | 110.2 |

| 54.5 |

| | 54.5 |

| | 55.1 |

| | 55.1 |

|

| Total debt | $ | 1,568.4 |

| | $ | 1,658.8 |

| | $ | 1,584.1 |

| | $ | 1,633.2 |

| $ | 1,986.6 |

| | $ | 2,014.1 |

| | $ | 1,543.9 |

| | $ | 1,608.5 |

|

| |

| (1) | Carrying amounts are net of unamortized debt issuance costs and discounts of $6.2 million and $3.6$9.7 million as of SeptemberJune 30, 2017, and $7.32018. |

| |

| (2) | Carrying amounts are net of unamortized debt issuance costs of $5.0 million and $4.0$3.2 million as of June 30, 2018, and $5.8 million and $3.5 million as of December 31, 2016,2017, related to the 5.125% senior notes due 2021 and 5.625% senior notes due 2024, respectively. |

| |

(2)(3) | Carrying amounts are net of unamortized debt issuance costs and discounts of $4.7$4.3 million and $1.0 million as of September 30, 2017, and $5.7 million and $1.3 million as of December 31, 2016,2017, related to the U.S. dollar term loan and euro term loan, respectively. |

Notes to Consolidated Financial Statements (Continued)

4. Fair Value Measurements and Risk (Continued)

At SeptemberJune 30, 20172018, the recorded values of other financial instruments such as cash equivalents and trade receivables and payables approximated their fair values, based on the short-term maturities and floating rate characteristics of these instruments.

Currency DerivativesBecause Grace operates and/or sells to customers in over 60 countries and in over 30 currencies, its results are exposed to fluctuations in currency exchange rates. Grace seeks to minimize exposure to these fluctuations by matching sales in volatile currencies with expenditures in the same currencies, but it is not always possible to do so. From time to time, Grace will useuses financial instruments such as currency forward contracts, options, swaps, or combinations thereof to reduce the risk of certain specific transactions. However, Grace does not have a policy of hedging all exposures, because management does not believe that such a level of hedging would be cost-effective. Forward contracts with maturities of not more than 1236 months are used and designated as cash flow hedges of forecasted repayments of intercompany loans. The effective portion of gains

Notes to Consolidated Financial Statements (Continued)

4. Fair Value Measurements and Risk (Continued)

and losses on these currency hedges is recorded in "accumulated“accumulated other comprehensive income (loss)"” and reclassified into "other“other (income) expense" whenexpense, net” to offset the remeasurement of the underlying hedged loans. Excluded components (forward points) on these derivatives mature. hedges are amortized to income on a systematic basis.

Grace also enters into foreign currency forward contracts to hedge a portion of its net outstanding monetary assets and liabilities. These forward contracts are not designated as hedging instruments under applicable accounting guidance, and therefore all changes in the fair value of the forward contracts are recorded in “other (income) expense, net,” in the Consolidated Statements of Operations. These forward contracts are intended to offset the foreign currency gains or losses associated with the underlying monetary assets and liabilities.

The valuation of Grace'sGrace’s currency exchange rate forward contracts and swaps is determined using both a market approach and an income approach. Inputs used to value currency exchange rate forward contracts consist of: (1) spot rates, which are quoted by various financial institutions; (2) forward points, which are primarily affected by changes in interest rates; and (3) discount rates used to present value future cash flows, which are based on the London Interbank Offered Rate (LIBOR) curve or overnight indexed swap rates. Total notional amounts for forward contracts outstanding as of June 30, 2018, were $67.1 million.

Cross-Currency Swap Agreements Grace uses cross-currency swaps designated as cash flow hedges to manage fluctuations in currency exchange rates and interest rates on variable rate debt. The effective portion of gains and losses on these cash flow hedges is recorded in “accumulated other comprehensive income (loss)” and reclassified into “other (income) expense, net” and “interest expense and related financing costs” during the hedged interest period.