On September 1, 2010, the Company entered into a Transaction Fee Agreement with a consultant for services related to soliciting offers from and in assisting in the negotiation with potential Company financiers, purchasers, acquisition targets and/or joint venture development partners (each such party being a “Potential Investor”). The initial term of the agreement was a period of 60 days and automatically renews monthly unless otherwise specifically renewed in writing by each party or terminated by the Company. Pursuant to the agreement, the Company agreed to pay the consultant a transaction fee for each completed property acquisition transaction in Tanzania (a “Completed Transaction”). The transaction fee is 12.5% of the shares issuable under each Completed Transaction, payable in restricted common shares at the lowest priced security issuable under each Completed Transaction. On September 30, 2010, the Company issued 16,666,667 restricted shares of common stock pursuant to the Transaction Fee Agreement in relation to the acquisition of the Handeni Properties.

The fair value of the 133,333,333 shares of the Company’s common stock issued to IPP Gold pursuant to the Acquisition Agreement and the 16,666,667 shares of the Company’s common stock issued pursuant to the Transaction Fee Agreement totaled $60,000,000.

On November 30, 2010, the capitalized acquisition costs of the Handeni Properties were tested for impairment by the Company’s management as required by ASC 360. Management determined that no positive cash flows from the Handeni Properties could be identified or supported and a full impairment loss was recognized in expenses for the $60,000,000 acquisition cost.

Under Tanzanian law, 50% of the area of PL’s need to be relinquished following a period of three years after allocation of the PLs to the Company (1998 Mining Act applicable to the Company’s PLs). On August 16, 2013, the Company applied for renewal of two of the licenses that expired in September 2013 and two of the licenses that expired in October 2013. The Company has received four renewal PLs of the renewal areas under PL6742/2010, PL6744/2010, PL6743/2010 and PL6779/2010 effective on October 5, 2013, September 13, 2013, October 13, 2013 and September 13, 2013, respectively. These four PLs are valid until October 4, 2016, September 12, 2016, October 12, 2016 and September 12, 2016, respectively. The total area occupied by the renewal licenses is approximately 359.80 km2 or 45% of the original area.

The Company is in the process of acquiring some portions of the relinquished areas deemed to be of interest to its continued exploration program. Offer HQ-P28045 has been granted as PL10000/2014 (33.62 km2) and offer HQ-P28108 has been granted as PL9853/2014 (12.32 km2). PL10000/2014 was granted on July 22, 2014 and PL9853/2014 was granted on July 2, 2014 and the licenses are valid till July 21, 2018 and July 1, 2018, respectively. On September 25, 2014, PL10262/2014 with an area of 6.97 km2 was granted. The acquisitions of the three additional PLs bring the total of land held by Handeni Gold in the Handeni district to 412.71 km2.

10

Handeni Gold Inc.(An Exploration Stage Company)Notes to the Interim Consolidated Financial Statements as of November 30, 2014(Expressed in U.S. dollars)(Unaudited)

|

| ||

| ||

On November 30, 2010, the capitalized acquisition costs of the Handeni Properties were tested for impairment by the Company’s management as required by ASC 360. Management determined that no positive cash flows from the Handeni Properties could be identified or supported and a full impairment loss was recognized in expenses for the $60,000,000 acquisition cost. | ||

The company now holds a total of approximately 423.03 km2 (53% of its previous license area). During October 2014, the Company fulfilled the requirements for its licenses to be uploaded on the Topo Cadastral system of the Ministry of Minerals and Energy of Tanzania. This enables rigorous control and transparency of all aspects of licensing, reporting and renewal of properties. | ||

During the |

Primary Mining Licenses (“PMLs”), | ||||

On August 5, 2011, the Company entered a Mineral Property Acquisition Agreement (the “2011 Acquisition Agreement”) with Handeni Resources Limited (“Handeni Resources”), a limited liability company registered under the laws of Tanzania. The Chairman of the Board of Directors of the Company has an existing ownership and/or beneficial interest(s) in Handeni Resources. Pursuant to the 2011 Acquisition Agreement, the Company had an exclusive option to acquire from Handeni Resources a 100% interest in mineral licenses covering an area of approximately 2.67 square kilometers to the east of Magambazi Hill, which is adjacent to the area covered by the Company’s four existing PLs in the Handeni District. | ||||

On November 30, 2011, the Company completed the 2011 Acquisition Agreement and issued 15,000,000 restricted common shares to Handeni Resources as payment. As at November 30, 2011, the fair market price of the Company’s common stock was $0.11 per share; accordingly, the Company recorded a total fair market value of $1,650,000 as the mineral licenses acquisition cost. | ||||

To comply with the laws and regulations of the Republic of Tanzania whereby foreign companies may not own PMLs, on July 19, 2012, the Company entered into an Addendum agreement to the 2011 Acquisition Agreement whereby Handeni Resources, on behalf of the Company, administers the 32 PMLs until such time as a mining license on the 32 PMLs (2.67 | ||||

| b) | Mkuvia Alluvial Gold Project, Tanzania, Africa | |||

The Mkuvia Alluvial Gold Project was comprised of four PLs covering a total area of 380 square kilometers located in the Nachingwea District, Lindi Region of the Republic of Tanzania. The Company is aware that the four PLs expired during May and June of 2012. | ||||

| ||||

| ||||

| ||||

| ||||

| ||||

| ||||

| ||||

| ||||

| ||||

| ||||

During fiscal 2010, the Company recognized $350,000 in other income for the receipt of option payments. On May 24, 2010, in a second agreement (fully executed on June 16, 2010) between RCR and the Company, RCR has to the right to earn a 70% interest in the remaining 255 square kilometers of the 380 square kilometer Mkuvia Alluvial Gold Project by making additional payments totaling $6,000,000 to the Company.

1110

Handeni Gold Inc.(An Exploration Stage Company)

Notes to the Interim Consolidated Financial Statements as of November 30, 2014February 28, 2015

(Expressed in U.S. dollars)

(Unaudited)

|

| ||

|

| ||

| ||

| ||

| ||

|

Thus, the combined payments under the November 7, 2009 and the May 24, 2010 agreements provided for a total commitment of $9,000,000 payable to the Company by RCR to purchase a 70% interest in the entire 380 square kilometer Mkuvia Alluvial Gold Project. The ownership structure of the interest in the Mkuvia Alluvial Gold Project shall be a 70% interest RCR, a 25% interest for the Company, and a 5% interest for Mr. Mkuvia Maita, the original owner of the underlying prospecting licenses. In addition, Mr. Maita retains a 3% net smelter royalty.

On June 3, 2010, the Company and RCR incorporated Ruby Creek Resources (Tanzania) Limited (“Ruby Creek Tanzania”) to manage the mining operations in the Mkuvia Gold Project in Tanzania. Ruby Creek Resources (Tanzania) Limited, a joint venture company (the “Joint Venture Company”), is owned by Ruby Creek Resources (70%), the Company (25%) and Mr. Mkuvia Maita (5%).

During fiscal 2011 the Company recognized a total of $3,110,000 in other income for the receipt of the shares at fair market value and the option payments (i) and (ii). The Company has not yet received the $450,000 option payment (iii) nor received the $1,000,000 option payment (iv) which are overdue and the agreement is in default. Prospecting licenses numbered 5664/2009 and 5669/2009, which form a part of the joint venture project, were allegedly registered to a third party without the Company’s approval.

RCR filed a lawsuit against the Company in the Supreme Court, State of New York, on February 8, 2012, alleging the Company’s involvement in a fraudulent transfer and breach of agreements. On May 21, 2012, in answering RCR’s claim in New York, the Company counter claimed against RCR. The Company is of the view that such allegations are without merit and intends to continue to vigorously contest the action in New York (see Note 13, below).

| 8. | Property and Equipment |

| November 30, 2014 | May 31, 2014 | ||||||||||||

| Accumulated | Net Book | Net Book | |||||||||||

| Cost | Depreciation | Value | Value | ||||||||||

| $ | $ | $ | $ | ||||||||||

| Automobiles | 290,014 | 290,014 | - | 4,583 | |||||||||

| Camp and equipment | 197,011 | 183,487 | 13,524 | 42,242 | |||||||||

| Office furniture and equipment | 100,222 | 97,338 | 2,884 | 6,635 | |||||||||

| Software | 7,930 | 7,205 | 725 | 1,986 | |||||||||

| 595,177 | 578,044 | 17,133 | 55,446 | ||||||||||

12

Handeni Gold Inc. February 28, 2015 May 31, 2014 Accumulated Net Book Net Book Cost Depreciation Value Value $ $ $ $ Automobiles 290,014 290,014 - 4,583 Camp and equipment 197,011 196,934 77 42,242 Office furniture and equipment 100,222 98,166 2,056 6,635 Software 7,930 7,487 443 1,986 595,177 592,601 2,576 55,446 (An Exploration Stage Company)Notes to the Interim Consolidated Financial Statements as of November 30, 2014(Expressed in U.S. dollars)(Unaudited)

| 9. | Related Party Transactions |

| a) | The Company has entered into the following facility agreements with related parties: |

| i) | On December 7, 2012, and as amended on September 4, 2013 and June 18, 2014, the Company entered into a facility agreement with IPP Ltd., a private company controlled by the Chairman of the Company. The funding is in the form of an interest free unsecured loan to the Company of up to $720,000 due June 30, 2015. As of | ||

| ii) | On October 9, 2013, and as amended on June 18, 2014, the Company entered into a facility agreement with Consultancy & Finance Company Associates Ltd. (“C&F”), a private company controlled by the Chairman of the Company. | ||

| iii) | On November 20, 2014, the Company entered into a facility agreement with C&F. The funding is in the form of an |

For the | |||

| b) | During the | ||

During the | |||

| c) | During the | ||

| d) | During the | ||

| e) | During the |

| 10. | Common Stock and Additional Paid-in Capital |

The authorized common stock of the Company consists of 500,000,000 shares, with $0.001 par value. During the | |

11

Handeni Gold Inc.

Notes to the Interim Consolidated Financial Statements as of February 28, 2015

(Expressed in U.S. dollars)

(Unaudited)

| 11. | Stock Options |

The Company adopted an Stock Option Plan, dated November 29, 2010 (the “November 2010 Stock Incentive Plan”), under which the Company is authorized to grant stock options to acquire up to a total of 40,000,000 shares of common shares. During the | |

There were no stock options exercised during the |

| Weighted | |||||||||||||

| Average | |||||||||||||

| Weighted | Remaining | Aggregate | |||||||||||

| Number of | Average | Contractual | Intrinsic | ||||||||||

| Options | Exercise Price | Term | Value | ||||||||||

| # | $ | (years) | $ | ||||||||||

| Outstanding, May 31, 2013 | 28,300,000 | 0.23 | 7.56 | - | |||||||||

| Outstanding, May 31, 2014 | 28,300,000 | 0.23 | 6.56 | - | |||||||||

| Outstanding and exercisable, November 30, 2014 | 28,300,000 | 0.23 | 6.06 | - |

13

Handeni Gold Inc. Weighted Average Weighted Remaining Aggregate Number of Average Contractual Intrinsic Options Exercise Price Term Value # $ (years) $ Outstanding, May 31, 2013 28,300,000 0.23 7.56 - Outstanding, May 31, 2014 28,300,000 0.23 6.56 - Outstanding and exercisable, February 28, 2015 28,300,000 0.23 5.82 - (An Exploration Stage Company)Notes to the Interim Consolidated Financial Statements as of November 30, 2014(Expressed in U.S. dollars)(Unaudited)

| |

The stock options outstanding are exercisable for cash or on a cashless exercise basis using a prorated formula whereby the number of shares issuable is equal to (a) the average closing price for the five days prior to exercise date (“ACP”) in excess of the exercise price, divided by (b) the exercise price multiplied by (c) the number of options exercised. During the | |

| 12. | Common Stock Purchase Warrants |

During the |

| Weighted | Weighted Average | |||||||||

| Average | Remaining Contractual | |||||||||

| Number of Warrants | Exercise Price | Life | ||||||||

| # | $ | (years) | ||||||||

| Balance, May 31, 2013 | 13,554,155 | 0.52 | 0.33 | |||||||

| Expired | (13,554,155 | ) | - | - | ||||||

| Balance, November 30 and May 31, 2014 | - | - | - |

| Weighted | Weighted Average | |||||||||

| Average | Remaining Contractual | |||||||||

| Number of Warrants | Exercise Price | Life | ||||||||

| # | $ | (years) | ||||||||

| Balance, May 31, 2013 | 13,554,155 | 0.52 | 0.33 | |||||||

| Expired | (13,554,155 | ) | - | - | ||||||

| Balance, February 28, 2015 and May 31, 2014 | - | - | - |

| 13. | Commitments and Contingencies |

On February 8, 2012, RCR filed a lawsuit against the Company in the Supreme Court, State of New York, in which RCR | |

On |

In addition to the British Columbia Action, on May 21, 2012, in answering RCR’s claim in New York, the Company counter claimed against RCR on the basis of the alleged breaches set out in the British Columbia Action (the “New York Counter Claim”). On November 19, 2012, the British Columbia Action was dismissed on the grounds that the Court in British Columbia did not have jurisdiction and further that the dismissal was without prejudice to either of the Company’s and RCR’s respective actions in New York against one another. This Order was granted by consent of both the Company and RCR.

The Company is of the view that RCR’s allegations are without merit and intends to continue to vigorously defend against the RCR lawsuit and to pursue its claims against RCR in New York. No future legal costs that may be incurred have been accrued as an expense and no loss or gain from the lawsuit and claim can be reasonably estimated or recorded at this time.

On September 23, 2014, RCR offered to dismiss its lawsuit and settle the case if the Company returned the 4,000,000 shares of RCR stock it previously received from RCR as payment under one of the purchase agreements. The Company accepted RCR’s offer. However, before a formal settlement agreement was signed, RCR reneged on the settlement and its counsel withdrew from the case. Accordingly, the Company has filed an application in New York Supreme Court to enforce the parties’ settlement agreement. While that application is pending, the Company will be conducting non-party depositions, which is likely the final phase of discovery.

| 14. | Fair Value Measurements |

ASC 820 requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. ASC 820 establishes a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used to measure fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. ASC 820 prioritizes the inputs into three levels that may be used to measure fair value: |

Level 1 applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2 applies to assets or liabilities for which there are inputs other than quoted prices that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data.

Level 3 applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

1412

Handeni Gold Inc.(An Exploration Stage Company)

Notes to the Interim Consolidated Financial Statements as of November 30, 2014February 28, 2015

(Expressed in U.S. dollars)

(Unaudited)

| 14. | Fair Value Measurements (continued) |

Pursuant to ASC 820, the fair value of cash, restricted cash equivalent and restricted marketable securities are determined based on “Level 1” inputs, which consist of quoted prices in active markets for identical assets. Management believes that the recorded values of all of the Company’s other financial instruments approximate their current fair values because of their nature and respective maturity dates or durations. | |

As at |

| Fair Value Measurements Using | |||||||||||||

| Quoted Prices in | Significant | ||||||||||||

| Active Markets | Other | Significant | |||||||||||

| For Identical | Observable | Unobservable | Balance as of | ||||||||||

| Instruments | Inputs | Inputs | November 30, | ||||||||||

| (Level 1 | ) | (Level 2 | ) | (Level 3 | ) | 2014 | |||||||

| Assets: | |||||||||||||

| Cash | $ | 135,317 | $ | – | $ | – | $ | 135,317 | |||||

| Restricted cash equivalent | 16,043 | – | – | 16,043 | |||||||||

| Restricted marketable securities | 40,000 | – | – | 40,000 | |||||||||

| Total assets measured at fair value | $ | 191,360 | $ | – | $ | – | $ | 191,360 | |||||

| Fair Value Measurements Using | |||||||||||||

| Quoted Prices in | Significant | ||||||||||||

| Active Markets | Other | Significant | |||||||||||

| For Identical | Observable | Unobservable | Balance as of | ||||||||||

| Instruments | Inputs | Inputs | February 28, | ||||||||||

| (Level 1 | ) | (Level 2 | ) | (Level 3 | ) | 2015 | |||||||

| Assets: | |||||||||||||

| Cash | $ | 82,801 | $ | – | $ | – | $ | 82,801 | |||||

| Restricted cash equivalent | 13,806 | – | – | 13,806 | |||||||||

| Total assets measured at fair value | $ | 96,607 | $ | – | $ | – | $ | 96,607 | |||||

As at May 31, 2014, there were no liabilities measured at fair value on a recurring basis presented on the Company’s consolidated balance sheet. Assets measured at fair value on a recurring basis were presented on the Company’s consolidated balance sheet as of May 31, 2014, as follows:

| Fair Value Measurements Using | |||||||||||||

| Quoted Prices in | Significant | ||||||||||||

| Active Markets | Other | Significant | |||||||||||

| For Identical | Observable | Unobservable | Balance as of | ||||||||||

| Instruments | Inputs | Inputs | May 31, | ||||||||||

| (Level 1 | ) | (Level 2 | ) | (Level 3 | ) | 2014 | |||||||

| Assets: | |||||||||||||

| Cash | $ | 532,694 | $ | – | $ | – | $ | 532,694 | |||||

| Restricted cash equivalent | 26,522 | – | – | 26,522 | |||||||||

| Restricted marketable securities | 73,600 | – | – | 73,600 | |||||||||

| Total assets measured at fair value | $ | 632,816 | $ | – | $ | – | $ | 632,816 | |||||

| 15. | Segment Disclosures |

The Company operates in one reportable segment, being the acquisition and exploration of mineral properties. Segmented information has been compiled based on the geographic regions that the Company and its subsidiary registered and performed exploration and administration activities. Assets by geographical segment are as follows: |

| Canada | Tanzania, Africa | Total | ||||||||

| Current assets | $ | 47,551 | $ | 139,661 | $ | 187,212 | ||||

| Restricted cash equivalent | 16,043 | - | 16,043 | |||||||

| Restricted marketable securities | 40,000 | - | 40,000 | |||||||

| Mineral licenses | - | 1,650,000 | 1,650,000 | |||||||

| Equipment, net | 1,528 | 15,605 | 17,133 | |||||||

| Total assets, at November 30, 2014 | $ | 105,122 | $ | 1,805,266 | $ | 1,910,388 |

| Canada | Tanzania, Africa | Total | ||||||||

| Current assets | $ | 147,957 | $ | 434,139 | $ | 582,096 | ||||

| Restricted cash equivalent | 26,522 | - | 26,522 | |||||||

| Restricted marketable securities | 73,600 | - | 73,600 | |||||||

| Mineral licenses | - | 1,650,000 | 1,650,000 | |||||||

| Property and equipment, net | 4,061 | 51,385 | 55,446 | |||||||

| Total assets, at May 31, 2014 | $ | 252,140 | $ | 2,135,524 | $ | 2,387,664 |

| Canada | Tanzania, Africa | Total | ||||||||

| Current assets | $ | 50,169 | $ | 73,610 | $ | 123,779 | ||||

| Restricted cash equivalent | 13,806 | - | 13,806 | |||||||

| Mineral licenses | - | 1,650,000 | 1,650,000 | |||||||

| Equipment, net | 895 | 1,681 | 2,576 | |||||||

| Total assets, at February 28, 2015 | $ | 64,870 | $ | 1,725,291 | $ | 1,790,161 | ||||

| Canada | Tanzania, Africa | Total | ||||||||

| Current assets | $ | 147,957 | $ | 434,139 | $ | 582,096 | ||||

| Restricted cash equivalent | 26,522 | - | 26,522 | |||||||

| Restricted marketable securities | 73,600 | - | 73,600 | |||||||

| Mineral licenses | - | 1,650,000 | 1,650,000 | |||||||

| Property and equipment, net | 4,061 | 51,385 | 55,446 | |||||||

| Total assets, at May 31, 2014 | $ | 252,140 | $ | 2,135,524 | $ | 2,387,664 |

1513

Handeni Gold Inc.(An Exploration Stage Company)Notes to the Interim Consolidated Financial Statements as of November 30, 2014(Expressed in U.S. dollars)(Unaudited)

| |

|

16

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion of our financial condition, changes in financial condition and results of operations for the three months and sixnine months ended November 30,February 28, 2015 and 2014 and 2013 should be read in conjunction with our unaudited interim financial statements and related notes for the three months and sixnine months ended November 30,February 28, 2015 and 2014 and 2013 included herewith and our audited consolidated financial statements as at May 31, 2014, May 31, 2013 and for the period from inception (January 5, 2004) to May 31, 2014 included in our Annual Report on Form 10-K for our fiscal year ended May 31, 2014 as filed with the SEC. All financial information in this Management’s Discussion and Analysis (“MD&A” or the “discussion”) is expressed and prepared in conformity with U.S. generally accepted accounting principles. All dollar references are to the U.S. dollar, the Company’s reporting currency, unless otherwise noted. Some numbers in this MD&A have been rounded to the nearest thousand for discussion purposes.

FORWARD-LOOKING STATEMENTS

This MD&A contains forward-looking statements that involve risks, uncertainties and assumptions with respect to the Company’s activities and future financial results, which are made based upon management’s current expectations and beliefs. These forward-looking statements involve risks and uncertainties, including statements regarding the Company’s capital needs, business plans and expectations. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of many factors, including, but not limited to, those set forth under “Risk Factors” and elsewhere in this annual report. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. Management disclaims any obligation to publicly update these statements, or disclose any difference between its actual results and those reflected in these statements. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

Overview

We are an exploration stage company engaged in the acquisition and exploration of mineral properties. Our principal area of focus is the Handeni Gold Project located in the Handeni district, within the Tanga region of the Republic of Tanzania in East Africa, in which we have interests in mineral claims through prospecting licenses (“PLs”) and/or primary mining licenses (“PMLs”) issued by the government of the Republic of Tanzania.

None of our mineral claims contain any substantiated mineral deposits, resources or reserves of minerals to date. Exploration has been carried out on these claims, in particular the 4eight PLs in the Handeni District. Accordingly, additional exploration of these mineral claims is required before any conclusion can be drawn as to whether any commercially viable mineral deposit may exist on any of our mineral claims. Our plan of operations is to continue exploration and drilling work when funds are available in order to ascertain whether our mineral claims warrant further advanced exploration to determine whether they possess commercially exploitable deposits of minerals. We will not be able to determine whether or not any of our mineral claims contain a commercially exploitable mineral deposit, resource or reserve, until appropriate exploratory work has been completed and an economic evaluation based on that work concludes economic viability.

We are considered an exploration or exploratory stage company, because we are involved in the examination and investigation of land that we believe may contain valuable minerals, for the purpose of discovering the presence of ore, if any, and its extent. There is no assurance that a commercially viable mineral deposit exists on the properties underlying our mineral claim interests, and considerable further exploration will be required before a final evaluation as to the economic and legal feasibility for our future exploration is determined.

Our Mineral Claims

Handeni District Gold Project

Location and Access

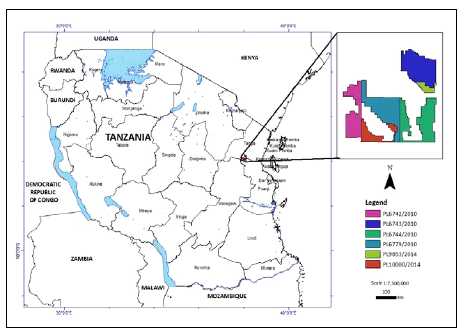

The Handeni Gold properties lie within the historic Handeni artisanal gold mining district, located in Tanga Province, roughly 175 km northwest of Tanzania’s largest city, Dar Es Salaam, and 100 km southwest of the more northerly coastal city of Tanga (Fig. 1). The road from Dar Es Salaam to Tanga is paved; the secondary road that heads northwest from this road to the town of Handeni, a distance of 65 km, has recently been paved. The Handeni property is located roughly 35 km south of the town of Handeni along a secondary gravel road. From this point, a number of dirt roads head south across various portions of the Handeni property and beyond. Driving time from Dar Es Salaam to the Handeni Gold properties is approximately five hours, depending on traffic and the weather.

20

Access during the dry season is not difficult and does not even require a 4X4 vehicle. Roads within the licenses are mostly tracks, some of which are not accessible during the rainy season. The area experiences two rainy seasons, namely a short wet period during November and December and the main rain season lasting from April to June. Exploration conditions during the rainy periods may be difficult, specifically during the April to June period. Fuel is available at a number of points along the north - south portion of the journey and in Handeni town itself.

The average elevation in the Company’s license area is 450 meters above sea level. The area is densely vegetated with tall trees and grass over undulating hills of gneiss that comprise the main topographic feature in the area. Muddy, slow moving rivers and creeks crisscross the valleys and plains; some of the larger streams may experience high flow during intense rainfalls.

The area is scarcely populated with occasional small villages where people are engaged in small scale mixed farming and artisanal gold mining. Handeni town is a community of several thousand inhabitants haphazardly spread over a series of small, rounded hills, where basic services and accommodation are available.

Fig. 1: Location Map: Handeni Property in Tanzania.

Prospecting Licenses (PLs)

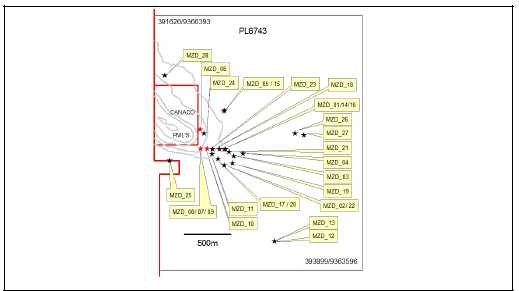

Currently, our primary focus is on the undivided 100% legal, beneficial and registerable interest in and to sixeight PLs, located in the Handeni District of Tanzania.

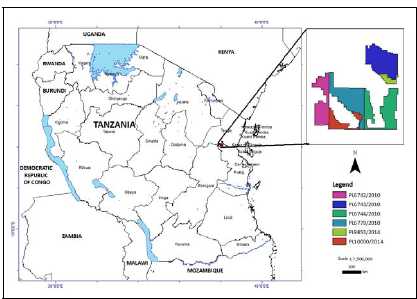

Under Tanzanian law, 50% of the original area of the four PLs of approximately 800 km2 obtained by HNDI according to the September 21, 2010 agreement were relinquished following a period of three years after allocation of the PLs to the Company (1998 Mining Act applicable to the Company’s PLs during their first period of allocation). The Company has received four renewal PLs of the renewal areas under PL6742/2010, PL6744/2010, PL6743/2010 and PL6779/2010 effective on October 5, 2013, September 13, 2013, October 13, 2013 and September 13, 2013, respectively. These four PLs are valid until October 4, 2016, September 12, 2016, October 12, 2016 and September 12, 2016, respectively. The total area occupied by the renewal licenses is approximately 359.80 km2 or 45% of the original area of 800 km2. The Company submitted applications for additional licenses on portions of the relinquished areas. To date four of the applications have been successfully granted on July 2, 2014 as PL9853/2014 (12.32 km2), July 22, 2014 as PL10000/2014 (33.62 km2), September 25, 2014 as PL10262/2014 (6.97 km2) and December 02, 2014 PL10409/2014 (10.32 km2) bringing the total area held by the Company in the Handeni district tois now 423.03 km2km2 (Fig. 2) (Table 1).

21

Fig. 2. Outline of Handeni Gold PLs in the Handeni district.

21

Table 1: List of Prospecting Licenses, Handeni Property (prior to the 2013 renewal of the licenses)

| PL No. | Area (Sq Km) | Issue Date | Original Recipient | Transfer Date (To IPP Gold) | Transfer Date (To Handeni Gold) | Expiry Date | Renewal Date |

| 6742/2010 | 197.98 | 05/10/10 | Diamonds Africa Ltd. | 18/11/10 | 12/12/10 | 04/10/13 | 05/10/13 |

| 6743/2010 | 195.48 | 13/10/10 | Gold Africa Ltd. | 18/11/10 | 12/12/10 | 12/10/13 | 13/10/13 |

| 6744/2010 | 198.70 | 13/09/10 | M-Mining Ltd. | 18/11/10 | 12/12/10 | 12/09/13 | 13/09/13 |

| 6779/2010 | 197.74 | 13/09/10 | Tanzania Gem Center Ltd. | 18/11/10 | 12/12/10 | 12/09/13 | 13/09/13 |

Following the 2013 renewal of the properties and acquisition of PLs in the current period, the Company now holds interests in PLs with details as described in Table 2.

Table 2: Handeni Gold Prospecting Licenses December 2, 2014.2014

| PL Number | Granted Date | Expiry Date | Area Size (km2) |

| 6742/2010 | 5/10/2013 | 4/10/2016 | 70.32 |

| 6743/2010 | 13/10/2013 | 12/10/2016 | 95.08 |

| 6744/2010 | 13/9/2013 | 12/9/2016 | 97.56 |

| 6779/2010 | 13/9/2013 | 12/9/2016 | 96.84 |

| 9853/2014 | 2/7/2014 | 1/7/2018 | 12.32 |

| 10000/2014 | 22/7/2014 | 21/7/2018 | 33.62 |

| 10262/2014 | 25/9/2014 | 24/9/2018 | 6.97 |

| 10409/2014 | 02/12/2014 | 01/12/2018 | 10.32 |

Primary Mining Licenses (PMLs)

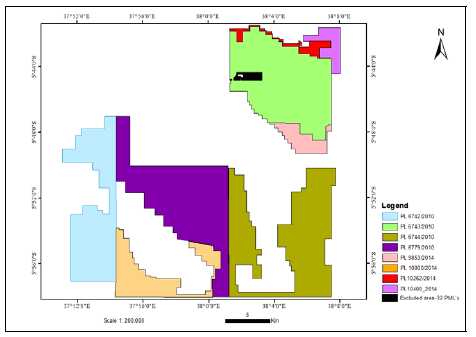

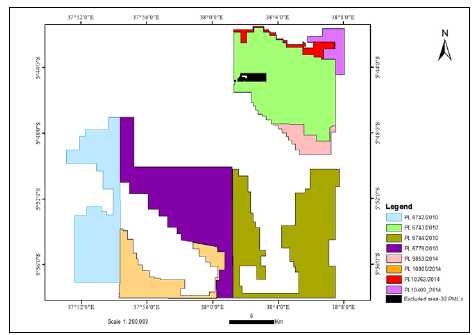

On November 30, 2011, the Company acquired from Handeni Resources a 100% interest in primary mining licenses covering an area of approximately 2.67 square kilometers to the east of Magambazi Hill (Figs. 2 and 3). To comply with the laws and regulations of the Republic of Tanzania whereby foreign companies may not own PMLs, on July 19, 2012, the Company:

22

| (1) | entered into an Addendum agreement to the 2011 Acquisition Agreement whereby Handeni Resources will administer the 32 PMLs until such time as a mining license (“ML”) on the 32 PMLs (2.67 | |

| (2) | during this period Handeni Resources will be conducting exploration and mining activities on the PMLs as directed by the Company. |

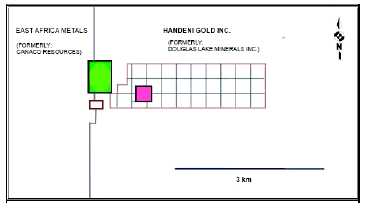

An enlargement of the “excluded area” as delineated on Fig. 1 is presented below (Fig. 3). Ownership of a single, isolated claim block, depicted in fuchsia, remains uncertain; and which is something that IPP Gold and the Company are attempting to ascertain. Ownership of the smaller, rectangular block that overlies the CRI-Company boundary also remains unknown; and which again is another matter that IPP Gold and the Company are currently pursuing. The remaining block of 32 PMLs, shown as a grid of blue lines below, belongs to the Company as described above.

![]()

Fig. 3: Exclusion areas within PL6743/2010.

22

West of the western border of PL 6743/2010 are several more PMLs that do not belong to the Company. The area colored in green (Fig. 3) is a unitized block of four PMLs that were acquired by Canaco Resources Inc. (“CRI”) (now East Africa Metals Inc.) from their owners.

Handeni District Project

We obtained a Technical Report on the Handeni Property (the “Handeni Report”), dated April 25, 2011, as prepared at our request by Avrom E. Howard, MSc, FGA, PGeol (Ontario), Principal Consultant at Nebu Consulting LLC. Mr. Howard is a Qualified Person in accordance with Canadian National Instrument 43-101 “Standards for Disclosure of Mineral Projects” and its Companion Policy (collectively, “NI 43-101”) and is a Practicing Professional Geologist registered with the Association of Professional Geoscientists of Ontario (registration number 0380). The Handeni Report follows on the heels of a detailed geological compilation and exploration report prepared in 2010 by Dr. Reyno Scheepers, a South African professional geologist who has been a director of our Company since 2010 and is our current Chief Executive Officer. Upon independent review by, and to the satisfaction of Mr. Howard, much of the content from Dr. Scheepers’ report has been referred to and referenced in the Handeni Report.

Subsequent to the publishing of the April 25, 2011 NI 43-101 report by Mr. Howard, the Company produced numerous in-house technical reports and is in the process of compiling an updated NI 43-101 report that will include the updated model for mineralization on our Handeni property. The drilling conducted by the Company was done implementing and following procedures recommended by SRK (Stephen, Roberstson and Kirsten).

Property Description

General.General

Mining in Tanzania in the modern era dates back over one hundred years, first under German colonial rule and then under British control under whose authority mining and other activities continued and expanded. Mining focused on gold, diamonds and a variety of colored gemstones, notably including the discovery and development of the world’s largest diamondiferous kimberlite pipe. Shortly after achieving independence from the British in 1961, Tanzania nationalized most private sector industries, in turn resulting in the exodus of foreign investment and private capital and the consequent decline in economic activity in all sectors, including mining. Finally, beginningBeginning in the 1990s, in line with many other developing countries around the world, the Tanzanian government instituted several reforms to move towards a free market economy, privatize the mining industry and encourage both domestic and foreign investment in all economic sectors. In the case of the mining industry, this was supplemented, in 1998, through the passage of a new, more industry-friendly mining code. This code has been streamlined under the Mining Act of 1998 (revised 2010) (the “Mining Act”) currently controlling exploration, mining and related activities in the country.

23

Tanzania is Africa’s thirdfourth leading gold producer, after Ghana and South Africa, with several major and junior companies producing and exploring for gold, mostly in northwestern Tanzania, south of Lake Victoria, in an area informally known as the Lake Victoria gold belt.

The Handeni Property

Gold has been known in the Handeni area for many years with some attributing its discovery to the Germans prior to World War One; however, it was the increase in gold prices and consequent increase in artisanal gold mining activity in the Handeni area that led to the discovery of larger deposits of placer gold, in turn leading in 2003 to a classic gold rush. The discovery and mining of lode deposits followed, soon after, along with the growth of a shanty mining town at the northern base of Magambazi Hill.

Between 2005 and 2010, IPP Gold carried out exploration over its PLR leading to the upgrading of its holdings from one PLR to four PLs of 800 km2,km2, in August 2010. Exploration work included airborne magnetic and radiometric surveys, ground magnetic surveys, reconnaissance geological mapping, soil sampling, pitting and trenching. It is these four PLs that were acquired by the Company from IPP Gold.

Geological Setting

Regional Geology

Regional geological mapping programs led to the recognition of several major litho-structural provinces from Archean to recent age in Tanzania. The Archean craton covers most of the western two thirds of the country, roughly bounded to the east by the East African Rift. Archean rocks host all of the country’s kimberlite pipes and contained lode diamond deposits, and most of its lode gold deposits. The Archean basement terrain is bounded to the east and west by a series of Proterozoic mobile belts; this area, particularly that to the east, hosts most of the country’s wide variety of colored gemstone deposits. Some recent research suggests that portions of this assumed Proterozoic terrane may actually consist of Archean crust that has undergone a later phase of higher grade metamorphism.

The Phanerozoic is represented by a series of sedimentary units of Paleozoic to Mesozoic age, in turn followed by a pre-rift period of kimberlitic and related, alkalic, mantle-derived intrusive and extrusive activity that presaged active rifting. Rocks related to this event intrude up to Upper Mesozoic and Lower Cenozoic sedimentary formations. Next came a period of rift-related intrusive and extrusive activity concentrated in the Arusha area – to the northeast and Mbeya area – to the southwest, which is responsible for volcanoes such as Mt. Meru and Mt. Kilimanjaro. Finally, a wide variety of recent and largely semi- to un-consolidated wind, water and weathering-derived recent formations are found across the country, a number of which host placer gold, diamond and colored gemstone deposits.

The Handeni district forms part of the Tanzanian Mozambique belt. The belt was subjected to four tectonothermal events at 830-800Ma, ~760Ma, 630-580Ma and 560-520Ma. All except the last attained upper amphibolites / granulite grade.

These rocks were initially deformed and metamorphosed during westward (cratonward) compression, folding and thrusting causing a near-horizontal fabric parallel to the sedimentary layering and the formation of paragneiss. This package was subsequently imbricated with allochtonous volcano sedimentary and ophiolitic packages from the east. Subsequent phases record further progressive shortening in the same direction ending in NNW (mainly sinistral) ductile shearing. The Handeni districts is located in an area where tectonic overprinting resulted in a number of refolding events with both NW- and NE-trending fold directions.

Property Geology

The Handeni area is situated in the Palaeoproterozoic Usugaran/Ubendian Metamorphic Terrane of Tanzania, along the northern extension of the north-trending Proterozoic Mozambique Mobile Belt. It is furthermore interpreted to comprise a metamorphosed/overprinted eastern extension/remnant of the Lake Victoria cratonic greenstone belt.

24

The geology of the Handeni area comprises amphibolite to granulite facies metamorphic rocks interpreted to originally have formed a sequence of ultramafic to felsic volcanic flows, black shales and quartz-bearing sedimentary rocks. It is furthermore interpreted to comprise a metamorphosed/overprinted eastern extension/remnant of the Lake Victoria cratonic greenstone belt. High grade metamorphism has converted these original lithologies to a variety of metamorphic equivalents, including biotite-hornblende-garnet-pyroxene gneiss, migmatitic augen garnet- hornblende-pyroxene gneiss, quartzo-feldspathic hornblende-biotite-pyroxene gneiss, pyroxene-hornblende-biotite-garnet granulite and others.

23

Recent research by geologists from the University of Western Australia suggests that much of what has previously been considered to be of Proterozic age (Usagaran System) may in fact be overprinted Archean crust. This hypothesis has been invoked to help interpret the geology within which gold in this area is found and as the basis for an analogy between this gold mineralization and that found in less metamorphosed, bona fide Archean rocks in the Lake Victoria gold district, a few hundred km to the northwest. However, this is a hypothesis, only, one that may be used for exploration modeling purposes but one that still requires more work.

Mineralization

The Handeni property is at an early stage of exploration. There are no known mineral resources or reserves on the Handeni property, nor are there any known deposits on the property. Gold is found within garnet-amphibolite zones within biotite-feldspar gneiss at three locations in the Company’s property, locations where historical lode gold occurrences have been documented. Gold occurs in quartz veins as well as within the garnet amphibolites adjacent to the quartz veins. Proof of this association is informally corroborated by the testimony of local, artisanal miners, who apparently recover gold both from quartz veins and gold-bearing gneiss that is not quartz vein bearing. Gold in the Company’s property has also been documented in soils and placers, at a variety of locations, as well.

Recent exploration increased the Company’s number of targets with known gold occurrences to six. Our drilling program conducted in 2012 supported the mineralization model.

Whereas gold was known in the Handeni area prior to the arrival in 2005 of the Company’s predecessor, IPP Gold, there is no history of any formal exploration in the area aside from limited work at Magambazi Hill itself.

The foundation for modern exploration activities on the Company’s properties were laid by the exploration work conducted by IPP. Their initial work consisted of soil sampling and a ground magnetic survey over an area of 200 square kilometers covering the area now located within PL6743/2010 immediately east of Magambazi Hill. Over the five years that ensued, this was followed by a series of exploration campaigns involving a variety of exploration methods, in turn followed by interpretation and further work in an iterative fashion. Notable programs during this period included an airborne Magnetic and Radiometric Survey, a ground magnetic survey, geological mapping and structural interpretation as well as several large soil sampling and geochemical surveys.

Handeni Gold’s intensive early exploration program following the September 2010 agreement achieved the following:

| • | It outlined a number of locations where intensive placer and artisanal gold mining took place within the Handeni property, notably the Kwandege and Mjembe areas. |

| • | Processed airborne magnetic and radiometric data have delineated linear features that have been interpreted to represent a variety of structures such as shears, thrust faults and cross faults. |

| • | Limited soil geochemical surveying, carried out across some of these interpreted northwest-southeast trending structural features, has revealed several locations hosting anomalous gold in soils. |

| • | Gold appeared to be further concentrated at the intersection between the northwest-southeast trending structural features and northeast-southwest trending structural features, interpreted to represent later cross faults. |

| • | These associations suggest a relationship between structures and gold, which provided a basis upon which to select additional areas within the Handeni property for more detailed gold exploration. |

The 2011 – 2012 exploration period used the foregoing as a basis and the following was conducted:

| • | A helicopter based TEM electromagnetic and radiometric aerial survey program was completed by FUGRO over the entire Company licence area (800 |

| • | The interpreted data clearly delineated subsurface geological features of importance to gold and base metal mineralization in this high grade metamorphic terrain. The data proved to be invaluable in the definition of structurally important sites and target definition. |

25

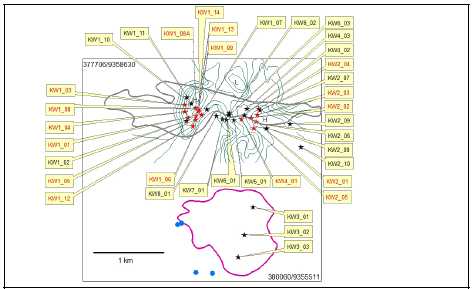

| • | An intensive ground based geophysical program on the Magambazi East as well as the Kwandege target zones was completed. This data (combined with geochemical results) were used to create drill targets on the two selected areas, the results of which are reported below. |

| • | A multi-element soil geochemical program was completed on the Kwandege target delineating the extent of the mineralization zone and assisting the interpretation of the geophysical data to locate drill positions. |

| • | A large soil sampling program of two targets in PL6743/2010 was initiated. |

| |

| • | Twenty-eight (28) diamond core holes (5,347 meters) were drilled on the Magambazi East and related targets |

delineated a gold enriched mineralization zone extending for a distance of approximately 500 meters to the south east of the Magambazi Hill mineralization as defined by CRI. The best intersection achieved on the main zone was 4.2 g/t over 5 meters. In addition a mineralization zone to the north of the main zone (the North eastern Zone) shows gold potential. The strike distance of this zone on the Handeni Gold property is approximately 330 meters. The most promising intersection on this zone was 3.75 g/t over 1 meter. A mineralization zone with a strike distance of approximately 450 m to the south of the main zone (the South western Zone) was also intersected. Four mineralized intersections were obtained in this zone of which 1.31 g/t over 1 meter was the best intersection obtained.24

Evaluation of the economic potential of the three mineralization zones will only be possible with closely spaced directional drilling to follow out the mineralization. We evaluated the Magambazi East project based on an interpretation of the available drill core and detailed mapping. Based on this information and our model of the mineralization at Magambazi East we are now convinced that the gold potential of this target may be proven with drilling of 5 directional drill holes.

| i) | KW2_01 with 4.40 g/t over 12 meters, including 29.5 g/t over 1 m as well as 3.54 g/t over 1 m; | |

| ii) | KW2_07 with 6.20 g/t over 5 m including 29.60 g/t over 1 m; | |

| iii) | KW1_08 with 1.1 g/t over 9 m including 5.67 g/t over 1 m; | |

| iv) | KW1_14 with 1.74 g/t over 6 m including 2.45 g/t over 2m and 3.51 g/t over 1m; | |

| v) | KW1_07 and KW4_03 each with 2.11 g/t over 1 m, and | |

| vi) | KW2_08 with 3.70 g/t over 1 m. |

An important feature of the Kwandege target is the fact that low level gold values (0.5 g/t to 1 g/t) were encountered in numerous intersections in the drill holes and also confirmed by the latest assay results. Anomalous gold with some potentially economic intersections have been encountered in an E - W (strike) direction of 1,501 meters (based on the results of the completed phase 1 drilling program). The open ended nature of the mineralization in an E-W direction was confirmed.

Exploration Activities.

The company’s exploration activities are mainly focused on delineating a hard-rock based economic deposit, but it also includes efforts to outline an economically viable alluvial (in broad terms) gold deposit/s.

| • | A confined alluvial mining evaluation program was initiated in 2012 and is still on going to investigate the potential to economically mine alluvial gold on the prospecting licenses. The results of this program are discussed below. |

| • | The results of the soil sampling program on Target 5 received to date are highly encouraging with gold in soil values of up to 200 ppb encountered. Au (gold) assay results received for 2331 samples |

27

During the 2013 – 2014 periodperiods up to date we achieved the following:

| • | collected a total of 5,050 soil samples (including blanks and standards) from targets in PL6743 that are currently being analyzed by XRF and prepared for submission to assay laboratories. |

| • | A soil sampling program on Target 6 (in collaboration with the Tanzania Geological Survey) was recently completed. A total of 2,756 soil samples collected on an area of approximately 16 |

| • | An area to the east of Magambazi hill was selected as a first target and pilot study area to test the gold distribution in various secondary geological regimes in the Handeni terrain. Bulk samples of approximately 3 500 kg each were treated (total mass of excavated samples just over 1 000 tons) by wet gravity separation. Oversize material was crushed in a ball mill prior to treatment. Gold was recovered from the final concentrate by panning. The method is prone to favour the evaluation of the presence of coarser grained gold and is at best an underestimation of the total gold content. Alluvial, fluvial and colluvial regimes were selected. Forty three pits to a maximum depth of 8.2 m, yielding a total of 145 samples, were investigated in the alluvial regime. Samples were taken every 1 m with an average mass of 3794 kg. The highest panned grade obtained for alluvial samples were 0.14 g/t. Fifteen pits on colluvial material dug to a maximum depth of 9 m yielded 87 samples with an average mass of 3,696 kg. The highest panned grade obtained for colluvial material was also 0.14 g/t. In the fluvial regime a total of 5 trenches to a depth of 9.2 m (31 samples) and 6 pits (28 samples) to a depth of 6.3 m provided samples with an average mass of 3,366 kg and 3,674 kg respectively. The highest panned grade obtained was 0.7 g/t from a stratigraphic horizon at a depth of 4.3 m to 5.3 m. |

25

The following conclusions were drawn from the alluvial program:

| a) | The fluvial environment has the largest potential for the extraction of coarse grained gold. | |

| b) | A large proportion of gold is contained as fine grained gold. This conclusion is based on the fact that geochemically analyzed samples of the same locations as the bulk sampled areas yielded significantly higher gold values. | |

| c) | Some specific horizons in the fluvial horizon yield higher values than others. | |

| d) | Allowing for a mere 50% efficiency of the applied processes, the overburden, the grade as well as consistency of gold on this target indicated that it is not economically mineable as an alluvial mining program. |

Preparations are now underway to investigate the alluvial potential of the area surrounding the Kwandege project anomaly as well as several other alluvial targets identified using airborne techniques. The Company will increase its ability to extract fine grained gold prior to commencing the next target evaluation phase by acquiring the appropriate equipment.

28

Preparations are now underway to investigate the alluvial potential of the area surrounding the Kwandege project anomaly as well as several other alluvial targets identified using airborne techniques. The Company will increase its ability to extract fine grained gold prior to commencing the next target evaluation phase by acquiring the appropriate equipment. | |

| • | completed the geophysical evaluation of our four PLs. |

| • | completed a detailed structural investigation into structural controls on gold mineralization on our 4 prospecting licenses. |

| • | completed a structural model on the |

| • | completed a ground geophysics investigation on the Mjembe target to the southeast of Magambazi. The Company completed a soil sampling program and the desk top XRF analyses of 5,028 samples and standards on the Mjembe project. Combined with the geophysics and the structural geology the geochemical signature of this mineralized area is highly encouraging. |

| • | Completed our evaluation process of the application of XRF to identify soil samples with a high likelihood to contain anomalous gold values. This process was completed with the submission of 232 of 5028 soil samples for gold assay of which 57% returned anomalous gold. |

| • | Following the success of the program described in above the Company is nearing completion of the evaluation of XRF applications to its Magambazi and Kwandege drillcore. The aim of the program is to: |

| i) | Identify more potential gold bearing intersections in the core than that was previously analyzed. | |

| ii) | Combine the results of the soil sample XRF results with the drillcore results to further refine our XRF applications to our exploration program. |

| • | Completed the XRF analyses of 5,672 soil samples, standards and blanks of target A. These samples are being treated statistically and those with a high likelihood of anomalous gold will be submitted for assays. |

| • | Completed a detailed structural interpretation of the Kwandege target with the aim of completion the final recommendations for the further drilling of this target. |

| • | Submitted 84 samples for gold assay as a pilot investigation on one of the targets on PL6743/2010. In combination with the large amount of XRF results conducted on this target the soil sampling method will be adapted to yield the best possible results in the Handeni district. |

| • | Completed mapping and lithogeochemical sampling on Target 5 and submitted samples for gold assays. This remains a target with high potential based on the results of the lithogeochemical gold assays and soil sample results combined with the geophysics. |

| • | Completed a detailed geological map, a preliminary structural interpretation, a ground magnetic survey as well as detailed soil sampling and XRF analyses on our Mjembe target. The results defined a significant potential gold mineralization zone with a high correlation between geochemical, structural and geophysical data. Mjembe will be the Company’s primary target during the 2014/2015 field season. |

| • | Initiated mapping programs on Target 8. |

| • | An extensive soil sampling program and ground magnetic survey on the Mjembe target |

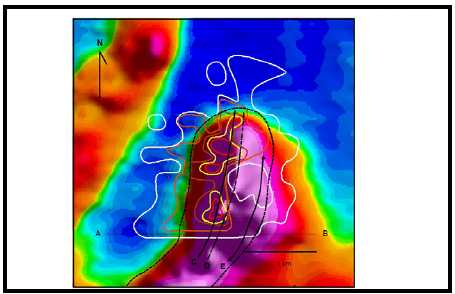

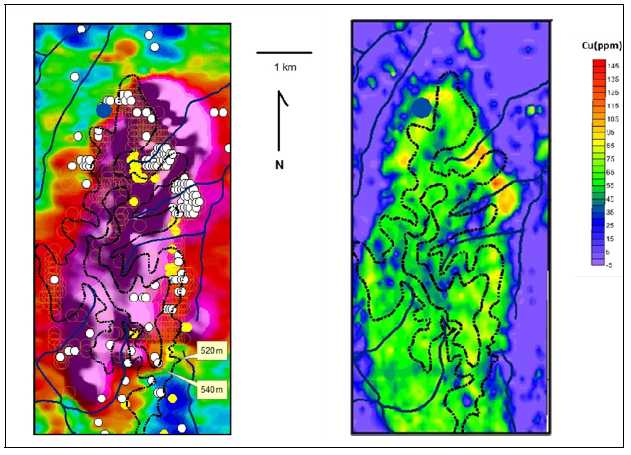

An EM (electromagnetic) anomaly of approximately 5.5 km (NNE strike distance) is particularly well defined and corroborated by enriched Fe and a depletion in Sr as determined in soil samples. Anomalously enriched As, Cu, Co and Zn values also coincide with the geophysical anomaly. The artisanal gold activity is on the north western fringe of the electromagnetic and geochemical anomaly. Ground magnetic data outlines a superimposed NW-SE structural trend seemingly coinciding with the geochemical anomalies and artisanal mining sites. Preliminary interpretation suggests that the Mjembe anomalous area represents a target within a plunging sheeth fold on a scale of 10 km by 3.5 km. The geophysics indicates the continuation of this structure in depth to the east of the surface geochemical anomaly. Exploration on each of the anomalies within this structure will now focus on more detailed ground geophysics and mapping to be able to prepare drill targets within the larger Mjembe target area. |

An EM (electromagnetic) anomaly of approximately 5.5 km (NNE strike distance) is particularly well defined and corroborated by enriched Fe and a depletion in Sr as determined in soil samples. Anomalously enriched As, Cu, Co and Zn values also coincide with the geophysical anomaly (Fig. 2). The artisanal gold activity is on the north western fringe of the electromagnetic and geochemical anomaly. Ground magnetic data outlines a superimposed NW-SE structural trend seemingly coinciding with the geochemical anomalies and artisanal mining sites. Preliminary interpretation suggests that the Mjembe anomalous area represents a target within a plunging sheeth fold on a scale of 10 km by 3.5 km. The geophysics indicates the continuation of this structure in depth to the east of the surface geochemical anomaly. Exploration on each of the anomalies within this structure will now focus on more detailed ground geophysics and mapping to be able to prepare drill targets within the larger Mjembe target area.

2926

| • | Completed mapping and soil sampling programs on target 15 along 47 km line traverses and collected 932 soil samples. XRF analyses on soil samples completed. Selected samples submitted for Au assays. |

| • | Initiated and completed mapping programs on Target 10 and completed a preliminary soil sampling program on this target (673 samples). XRF analyses completed and samples selected for Au assays. |

| • | Initiated and completed mapping programs on target 16 and planning of soil sampling program. |

Mkuvia Alluvial Gold Project

The Mkuvia Alluvial Gold Project is comprised of four PLs covering a total area of 380 square kilometers and is located in the Nachingwea District, Lindi Region of the Republic of Tanzania. The Company is aware that the four prospecting licenses expired during May and June of 2012. The Company is currently evaluating whether any viable interest remains in these PLs, but no final determination has been made as of yet.

Compliance with Government Regulation

We are subject to local laws and regulation governing the exploration, development, mining, production, importing and exporting of minerals; taxes; labor standards; occupational health; waste disposal; protection of the environment; mine safety; toxic substances; and other matters. We require licenses and permits to conduct exploration and mining operations. Amendments to current laws and regulations governing operations and activities of mining companies or more stringent implementation thereof could have a material adverse impact on our Company. Applicable laws and regulations will require us to make certain capital and operating expenditures to initiate new operations. Under certain circumstances, we may be required to close an operation once it is started until a particular problem is remedied or to undertake other remedial actions. This would have a material adverse effect on our results and financial condition.

30

Four of our mineral interests in Tanzania are currently held under PLs granted pursuant to the Mining Act for an initial period of three years and are renewable in two successive periods of two years only. Four of ourThe remaining four PL’s are being held under the 2010 Mining Act and are valid for an initial period of 4 years (the initial period expiring in 2018 (Table 2)). Following this the first renewal is for 3 years and the second renewal for 2 years, each renewal withaccompanied by a mandatory relinquishment of at least 50% of the license area. The application fees are US$300$300 on initial application and US$300$300 for each renewal. There is a preparation fee of US$500$500 applicable on each license. The annual rent for the licenses are US$100/km2$100/km2 (initial period), US$150/km2 (1st$150/km2 (1st renewal) and US$200/km2 (2nd$200/km2 (2nd renewal). Renewals of our PLs can take many months and even years to process by the regulatory authority in Tanzania.

All PLs in Tanzania require the holder to employ and train local residents, typically amounting to $5,000 per year, and make exploration expenditures, as set out in the Mining Act. At each renewal, at least 50% of our licensed area must be relinquished. If we wish to keep the relinquished one-half portion, we must file a new application for the relinquished portion.

The geographical area covered by a PL may contain one or more previously granted PML’s. A PML is a mining license granted only to a Tanzanian citizen consisting of an area of not to exceed 10 hectares. Once a PL is granted, no additional PMLs can be granted within the geographical area covered by the PL. The PL is subject to the rights of previously granted and existing PMLs. The holder of a PL will have to work around the geographical area of the PML unless the PL holder acquires the PML and any rights to the land covered by the PML.

We must hold a mining license to carry out mining activities, which are granted only to the holder of a PL covering a particular area. A mining license is granted for a period of 25 years or the life of the mine. It is renewable after 10 years for a period not exceeding 15 years. Other than the PMLs being held under Handeni Resources, we do not hold any mining licenses, only PL’s. An application for the 32 PMLs being held under agreement by Handeni Resources to be changed into a mining license (ML) is underway. Prospecting and mining license holders must submit regular reports in accordance with mining regulations. Upon commercial production, the government of Tanzania imposes a royalty on the gross value of all production at the rate of 3% of all gold produced. The applicable regulatory body in Tanzania is the Ministry of Energy and Minerals.

In July 1999, environmental management and protection regulations under the Mining Act came into force. An environmental impact statement and an environmental management plan must accompany special mining license, mining license and gemstone mining license applications for mineral rights. In addition to the establishment of environmental regulations, the Tanzanian government has improved management procedures for effective monitoring and enforcement of these regulations by strengthening the institutional capacity, especially in the field offices. The government has provided rules for the creation of reclamation funds to reinstate land to alternative uses after mining and it has developed guidelines for mining in restricted areas, such as forest reserves, national parks, near sources of water and other designated areas. These regulations have not had any material effect on our operations to date.

Competition

We operate in a highly competitive industry, competing with other mining and exploration companies, and institutional and individual investors, which are actively seeking minerals exploration properties throughout the world together with the equipment, labour and materials required to exploit such properties. Many of our competitors have financial resources, staff and facilities substantially greater than ours. The principal area of competition is encountered in the financial ability to cost effectively acquire prime minerals exploration prospects and then exploit such prospects. Competition for the acquisition of minerals exploration properties is intense, with many properties available in a competitive bidding process in which we may lack technological information or expertise available to other bidders. Therefore, we may not be successful in acquiring, exploring and developing profitable properties in the face of this competition. No assurance can be given that a sufficient number of suitable minerals exploration properties will be available for acquisition, exploration and development.

27

Employees

Other than our directors and executive officers, we had approximately five full-time equivalent employees and consultants as of November 30, 2014February 28, 2015, all located in Tanzania. We also retain independent geologists and consultants on a contract basis to conduct the work programs on our mineral properties in order to carry out our plan of operations.

31

Research and Development Expenditures

We have not incurred any research or development expenditures since our incorporation.

Subsidiaries

The Company has two subsidiaries, both of which are Tanzanian companies: (i) HG Limited (formerly DLM Tanzania Limited); and (ii) Douglas Lake Tanzania Limited, which is inactive.

Plan of Operations

Our plan of operations through our fiscal year ending May 31, 2015 is to continue to focus on the exploration of our Handeni mineral property in Tanzania, and the budget for this plan requires approximately $0.8 million for our plan of the exploration work and $0.9 million for our general and administration expenses, professional and consulting fees and other operating expenses. We anticipate that we will not generate any revenues for so long as we are an exploration stage company. Accordingly, we will be required to obtain additional financing in order to pursue our plan of operations.

Other explorationExploration related activities currently under way on the Company’s Handeni licenses include:

| a) | Identification of potential alluvial mining areas other than those currently known and being evaluated by utilizing remote sensing activities. | |

| b) | A detailed interpretation of already collected geophysical data, specifically aimed at Target 8 and the Mjembe target. | |

| c) | A petrological, geochemical and mineralogical investigation of the Kwandege drill core to understand the style of gold mineralization at this locality. | |

| d) | The planning and siting of drill holes as a follow up Reverse Circulation program to evaluate the near – surface potential of the Kwandege target. | |

| e) | Continued work on development of other targets to drill target status, specifically Mjembe and Target 5. | |

| f) | Detailed structural work on the Mjembe target as well as on targets on PL6743/2010. | |

| g) | Adapting our soil sampling technique to yield the best possible results under the conditions experienced in the Handeni district further increasing exploration activity at a reduced cost. Evaluate the ground relinquished but currently on offer to us to establish any potential interest of it to the Company’s exploration program. | |

| h) | Drastically reduce our land holding in our Handeni properties to remain with only targets with high potential. | |

| i) | A re-evaluation of some target areas by doing bulk leaching analyses for Au instead of standard assays. |

The estimated budget for the completion of these exploration programs is provided below:

| EXPLORATION WORK | BUDGET |

| Ground Geophysics | 50,000 |

| Mapping, trenching, sampling, etc. | 50,000 |

| Drilling | 250,000 |

| Geologists, field personnel and general exploration | 250,000 |

| Sundry & contingencies | 200,000 |

| TOTAL | $800,000 |

At November 30, 2014,February 28, 2015, we had cash of $135,000$83,000 but a working capital deficit of $1,360,000.$1,490,000. On November 20, 2014, the Company entered into a facility agreement with a related party. The funding is in the form of an interest free unsecured loan to the Company of up to $500,000 due May 31, 2017. As of the date of this report, the Company has received $125,000 pursuant to this facility agreement. In addition, the Company has $1.125 million in loans from related parties due June 30, 2015.

We assume such related parties’ loans to the Company from the Company’s major shareholder will not be demanded for repayment by the Company’s major shareholder at the due date on June 30, 2015.date. As such, we estimate that we will still need a minimum of $1.4$1.1 million additional funds in order to cover our planned operations over the fiscal year ending May 31, 2015. Our actual expenditures may exceed our estimations.

We anticipate that we will not generate any revenues for so long as we are an exploration stage company. Accordingly, we will be required to obtain additional financing in order to pursue our plan of operations.

3228

We believe that external debt financing will not be an alternative for funding our next fiscal year exploration, as we do not have significant tangible assets to secure any debt financing. Therefore, we anticipate that additional funding will be in the form of equity financing from the sale of our common stock and/or related parties debt financing. We cannot provide investors with any assurance that we will be able to obtain sufficient financing to fund our acquisition and exploration program going forward. In the absence of sufficient funding, we will not be able to continue acquisition and exploration of mineral claims and we will be forced to abandon our mineral claims and our plan of operations. Even if we are successful in obtaining financing to fund our acquisition and exploration program, there is no assurance that we will obtain the funding necessary to pursue any advanced exploration of any mineral claims.

Results of Operations

We have had no operating revenues and accumulated net loss of $117 million since our inception (January 5, 2004) to November 30, 2014.February 28, 2015. The following table sets out our losses from operations for the periods indicated:

| Accumulated from | |||||||||||||||||||||||||||

| For the Three Months Ended, | For the Six Months Ended, | January 5, 2004 | |||||||||||||||||||||||||

| (Date of Inception) to | |||||||||||||||||||||||||||

| November 30, 2014 | November 30, 2013 | November 30, 2014 | November 30, 2013 | November 30, 2014 | For the Three Months Ended, | For the Nine Months Ended, | |||||||||||||||||||||

| February 28, 2015 | February 28, 2014 | February 28, 2015 | February 28, 2014 | ||||||||||||||||||||||||

| Revenue | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | |||||||||

| Expenses | |||||||||||||||||||||||||||

| Consulting fees | 5,070 | 5,000 | 10,920 | 22,500 | 24,103,144 | 3,610 | - | 14,530 | 22,500 | ||||||||||||||||||

| Depreciation | 15,956 | 48,655 | 38,162 | 97,651 | 669,971 | 14,557 | 46,320 | 52,719 | 143,971 | ||||||||||||||||||

| Exploration expenses | 92,743 | 68,952 | 138,320 | 110,207 | 8,415,910 | 35,925 | 70,678 | 174,245 | 180,885 | ||||||||||||||||||

| Loss (Gain) on disposal or | |||||||||||||||||||||||||||

| write-down of equipment | 151 | (2,820 | ) | (20,058 | ) | (2,820 | ) | (1,528 | ) | ||||||||||||||||||

| Gain on disposal or write-down of equipment | - | - | (20,058 | ) | (2,820 | ) | |||||||||||||||||||||

| General and administrative | 104,445 | 118,329 | 230,205 | 244,028 | 3,912,439 | 110,450 | 138,281 | 340,655 | 382,309 | ||||||||||||||||||

| Impairment of mineral property | - | - | - | - | 77,492,074 | ||||||||||||||||||||||

| Interest expenses | 27,170 | 18,988 | 54,157 | 35,126 | 172,405 | ||||||||||||||||||||||

| Interest expense | 28,638 | 23,469 | 82,795 | 58,595 | |||||||||||||||||||||||

| Professional | 17,312 | 10,575 | 49,815 | 36,282 | 2,746,191 | 57,198 | 16,008 | 107,013 | 52,290 | ||||||||||||||||||

| Rent | 10,328 | 11,188 | 58,543 | 52,345 | 584,215 | 332 | 17,871 | 58,875 | 70,216 | ||||||||||||||||||

| Travel and investor relations | 26,032 | 2,857 | 27,166 | 5,187 | 2,039,673 | 4,871 | 9,508 | 32,037 | 14,695 | ||||||||||||||||||

| Total Expenses | 299,207 | 281,724 | 587,230 | 600,506 | 120,134,494 | 255,581 | 322,135 | 842,811 | 922,641 | ||||||||||||||||||

| Loss From Operations | (299,207 | ) | (281,724 | ) | (587,230 | ) | (600,506 | ) | (120,134,494 | ) | (255,581 | ) | (322,135 | ) | (842,811 | ) | (922,641 | ) | |||||||||

| Other Income (Expenses) | |||||||||||||||||||||||||||

| Gain on write-down of accrued liabilities | - | - | - | - | 458,058 | ||||||||||||||||||||||

| Impairment of marketable securities (Note 6) | (86,400 | ) | (420,000 | ) | (86,400 | ) | (1,000,000 | ) | (2,686,400 | ) | |||||||||||||||||

| Impairment of marketable securities | (53,600 | ) | - | (140,000 | ) | (1,000,000 | ) | ||||||||||||||||||||

| Loss on marketable securities | (20,000 | ) | - | (20,000 | ) | - | |||||||||||||||||||||

| Interest income | 31 | 64 | 95 | 155 | 1,839 | 28 | 61 | 123 | 216 | ||||||||||||||||||

| Loss on sale of investment securities | - | - | - | - | (57,071 | ) | |||||||||||||||||||||

| Loss on write-down of amounts receivable | - | - | - | - | (66,771 | ) | |||||||||||||||||||||

| Mineral property option payments received | - | - | - | - | 3,616,017 | ||||||||||||||||||||||

| Recovery of mineral property costs for stock not issuable | - | - | - | - | 2,253,000 | ||||||||||||||||||||||

| Total other (Expenses) / Income | (86,369 | ) | (419,936 | ) | (86,305 | ) | (999,845 | ) | 3,518,672 | (73,572 | ) | 61 | (159,877 | ) | (999,784 | ) | |||||||||||

| Net Loss | (385,576 | ) | (701,660 | ) | (673,535 | ) | (1,600,351 | ) | (116,615,822 | ) | (329,153 | ) | (322,074 | ) | (1,002,688 | ) | (1,922,425 | ) | |||||||||

Three Months Ended November 30, 2014February 28, 2015 Compared to Three Months Ended November 30, 2013February 28, 2014

Our net loss for the three months ended November 30, 2014February 28, 2015 was $386,000,$329,000, compared to $702,000$322,000 for the same period ended November 30, 2013,February 28, 2014, the difference is mainly due to $420,000$53,600 permanent impairment of marketable securities and loss on marketable securities of $20,000 recorded during the three months ended November 30, 2013February 28, 2015 and the following operation expenses changes.

Our operating expenses for the three months ended November 30, 2014 increased slightlyFebruary 28, 2015 decreased by $17,000$67,000 to $299,000$255,000 from $282,000$322,000 for the same period ended November 30, 2013,February 28, 2014, and the main changes are as follows:

our general and administrative fees decreased by

$14,000$28,000 to$104,000$110,000 during the period endedNovember 30, 2014 (2013February 28, 2015 (2014 -$118,000)$138,000), primarily due to continuing cost management; AtNovember 30, 2014,February 28, 2015, approximately$367,000$423,000 (May 31, 2014 - $278,000) of general and administrative fees remained as payables due to related parties;

33our exploration expenses decreased by $35,000 to $36,000 during the three months ended February 28, 2015 (2014 - $71,000) mainly due to our reduced exploration and drilling activities caused by our funding limitations;

depreciation fees decreased by $32,000 to $14,000 during the three months ended February 28, 2015 (2014 - $46,000) mainly because the majority of our equipment was fully depreciated;

29

| |||

| |||

| |||

| |||

| |||

| |||

interest expenses increased by $5,000 to $28,000 during the three months ended February 28, 2015 (2014 - $23,000), which represented deemed interest on an interest free unsecured loan from a related party. Such deemed interest was recorded as donated capital;

our professional fees increased by $41,000 to $57,000 during the three months ended February 28, 2015 (2014 - $16,000) primarily due to increased legal fees on the RC litigation;

our rent expenses decreased by $18,000 during the three months ended February 28, 2015 compared to the same period ended February 28, 2014 mainly because our Vancouver office lease expired and our Tanzania office has been moved to a smaller space; and

our travel and investor relations expenses decreased by $5,000 to $5,000 during the three months ended February 28, 2015 (2014 - $10,000) primarily due to less travel expenses incurred for investors relations.

SixNine Months Ended November 30, 2014February 28, 2015 Compared to SixNine Months Ended November 30, 2013February 28, 2014

Our net loss for the sixnine months ended November 30, 2014February 28, 2015 was $674,000,$1,003,000, compared to $1,600,000$1,922,000 for the same period ended November 30, 2013,February 28, 2014, the difference mainly due to $86,000$860,000 additional permanent impairment of marketable securities recorded during the sixnine months ended November 30, 2014 and $1 million permanent impairment of marketable securities recorded during the six months ended November 30, 2013.February 28, 2014.

Our operating expenses for the sixnine months ended November 30, 2014February 28, 2015 decreased slightly by $13,000$80,000 to $587,000$843,000 from $600,000$923,000 for the same period ended November 30, 2013,February 28, 2014, and the main changes are as follows:

34our consulting, general and administrative fees decreased by $50,000 to $355,000 during the nine months ended February 28, 2015 (2014 - $405,000), primarily due to continuing cost management; At February 28, 2015, approximately $423,000 (May 31, 2014 - $278,000) of general and administrative fees remained as payables due to related parties;•increased rent of $36,000 included in the six months ended November 30, 2014 (2013: $25,200) representing 60% of rental expense associated with renting our Chief Executive Officer’s family house in Tanzania pursuant to the Executive Services Agreement, offset by a significant decrease on the rent on our Tanzania office as a result of moving to a small office and Vancouver office lease expiry.•our travel and investor relations expenses increased by $22,000 to $27,000 during the three months ended November 30, 2014 (2013 - $5,000) primarily due to travel expenses incurred for an in-person Board of Directors meeting held in Dar er Salaam, Tanzania.our exploration expenses decreased slightly by $7,000 to $174,000 during the nine months ended February 28, 2015 (2014 - $181,000) mainly due to decreased exploration activities caused by our funding limitations;

depreciation fees decreased by $91,000 to $53,000 during the nine months ended February 28, 2015 (2014 - $144,000) mainly because the majority of our equipment was fully depreciated;

gain on disposal of equipment increased by $17,000 to $20,000 during the nine months ended February 28, 2015 (2014 - $3,000) mainly due to vehicle and office furniture disposal in our subsidiary in Tanzania.

interest expenses increased by $24,000 to $83,000 during the nine months ended February 28, 2015 (2014 - $59,000), which represented deemed interest on an interest free unsecured loan from a related party. Such deemed interest was recorded as donated capital;

our professional fees increased by $55,000 to $107,000 during the nine months ended February 28, 2015 (2014 - $52,000) primarily due to increased legal fees on the RC litigation and additional audit fees in Tanzania related to our subsidiary’s value added tax recovery;