UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period endedMarch 31,September 30, 2019

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________________to ________________ to ________________

Commission file number333-209143000-56024

SUSGLOBAL ENERGY CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 38-4039116 |

| (State or other jurisdiction of incorporation or organization) | (I. R. S. Employer Identification No.) |

| 200 Davenport Road | M5R 1J2 |

| Toronto, ON | |

| (Address of principal executive offices) | (Zip Code) |

416-223-8500

(Registrant’sRegistrant's telephone number, including area code)

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| N/A | N/A | N/A |

![]()

1

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large"large accelerated filer,” “accelerated filer”" "accelerated filer," "smaller reporting company" and “smaller reporting company” and “emerging"emerging growth company”company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [X] | Smaller reporting company | [X] |

| (Do not check if a smaller reporting company) | Emerging growth company | [X] | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. [X]

Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

Securities registered pursuant to Section 12(b) of the Act:

The number of shares of the registrant’sregistrant's common stock outstanding as of May 15,November 14, 2019 was 42,484,53147,833,401 shares.

![]()

2

| INDEX TO FORM 10-Q |

| For the Three and Nine-Month Periods Ended September 30, 2019 and 2018 |

SusGlobal Energy Corp.INDEX TO FORM 10-QFor the Three-Month Periods Ended March 31, 2019 and 2018

![]()

3

| INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| CONTENTS |

SUSGLOBAL ENERGY CORP.CONSOLIDATED FINANCIAL STATEMENTSMarch 31, 2019 and 2018

(Expressed in United States Dollars)

CONTENTS

![]()

4

| Interim Condensed Consolidated Balance Sheets |

| As at September 30, 2019 and December 31, 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

SusGlobal Energy Corp.Interim Condensed Consolidated Balance SheetsAs at March 31, 2019 and December 31, 2018(Expressed in United States Dollars)(unaudited)

| March 31, 2019 | December 31, 2018 | |||||

| ASSETS | ||||||

| Current Assets | ||||||

| Cash and cash equivalents | $ | - | $ | 42,711 | ||

| Trade receivables | 101,616 | 129,981 | ||||

| Inventory | 26,409 | 18,550 | ||||

| Prepaid expenses and deposits | 110,763 | 23,172 | ||||

| Total Current Assets | 238,788 | 214,414 | ||||

| Intangible Assets(note 6) | 148,655 | 135,189 | ||||

| Long-lived Assets, net(note 7) | 3,334,072 | 3,361,110 | ||||

| Operating Lease Right-Of-Use Asset(note 8) | 218,657 | - | ||||

| Long-Term Assets | 3,701,384 | 3,496,299 | ||||

| Total Assets | $ | 3,940,172 | $ | 3,710,713 | ||

| LIABILITIES AND STOCKHOLDERS’ DEFICIENCY | ||||||

| Current Liabilities | ||||||

| Bank indebtedness | $ | 3,933 | $ | - | ||

| Accounts payable (note 9) | 398,125 | 353,728 | ||||

| Government remittances payable | 5,904 | 35,169 | ||||

| Accrued liabilities (notes 9 and 14) | 630,322 | 646,003 | ||||

| Current portion of long-term debt (note 10) | 3,784,588 | 3,727,778 | ||||

| Current portion of obligations under capital lease (note 11) | 87,717 | 81,109 | ||||

| Convertible promissory notes (note 12) | 770,497 | - | ||||

| Current portion of operating lease liability (Note 13) | 11,430 | - | ||||

| Loans payable to related parties (note 14) | 112,245 | 201,575 | ||||

| Total Current Liabilities | 5,804,761 | 5,045,362 | ||||

| Long-Term Liabilities | ||||||

| Obligations under capital lease (note 11) | 190,438 | 207,599 | ||||

| Operating lease liability (note 13) | 209,770 | - | ||||

| Total Long-term Liabilities | 400,208 | 207,599 | ||||

| Total Liabilities | 6,204,969 | 5,252,961 | ||||

| Stockholders’ Deficiency | ||||||

| Preferred stock, $.0001 par value, 10,000,000 authorized, none issued and outstanding Common stock, $.0001 par value, 150,000,000 authorized, 41,404,531 (2018- 40,299,531) shares issued and outstanding (note 15) | 4,142 | 4,031 | ||||

| Additional paid-in capital | 6,811,749 | 5,754,260 | ||||

| Subscriptions payable | - | 4,600 | ||||

| Stock compensation reserve | 662,500 | 1,330,000 | ||||

| Accumulated deficit | (9,634,856 | ) | (8,554,312 | ) | ||

| Accumulated other comprehensive loss | (108,332 | ) | (80,827 | ) | ||

| Stockholders’ deficiency | (2,264,797 | ) | (1,542,248 | ) | ||

| Total Liabilities and Stockholders’ Deficiency | $ | 3,940,172 | $ | 3,710,713 | ||

| Going concern(note 2) | ||||||

| Commitments(note 16) |

| September 30, | December 31, | |||||

| 2019 | 2018 | |||||

| ASSETS | ||||||

| Current Assets | ||||||

| Cash and cash equivalents | $ | - | $ | 42,711 | ||

| Trade receivables (note 7) | 149,933 | 129,981 | ||||

| Inventory | 27,538 | 18,550 | ||||

| Prepaid expenses and deposits | 18,367 | 23,172 | ||||

| Total Current Assets | 195,838 | 214,414 | ||||

| Intangible Assets(note 8) | 232,796 | 135,189 | ||||

| Long-lived Assets, net(note 9) | 4,762,989 | 3,361,110 | ||||

| Long-Term Assets | 4,995,785 | 3,496,299 | ||||

| Total Assets | $ | 5,191,623 | $ | 3,710,713 | ||

| LIABILITIES AND STOCKHOLDERS' DEFICIENCY | ||||||

| Current Liabilities Bank indebtedness | $ | 7,350 | $ | - | ||

| Accounts payable (note 11) | 708,940 | 353,728 | ||||

| Government remittances payable | 23,529 | 35,169 | ||||

| Accrued liabilities (notes 11, 15 and 17) | 602,916 | 646,003 | ||||

| Advance (note 12) | 21,166 | - | ||||

| Current portion of long-term debt (note 13) | 3,785,210 | 3,727,778 | ||||

| Current portion of obligations under capital lease (note 14) | 235,222 | 81,109 | ||||

| Convertible promissory notes (note 15) | 1,370,683 | - | ||||

| Mortgage payable (note 16) | 1,306,407 | - | ||||

| Loans payable to related parties (note 17) | - | 201,575 | ||||

| Total Current Liabilities | 8,061,423 | 5,045,362 | ||||

| Long-Term Liabilities | ||||||

| Obligations under capital lease (note 14) | - | 207,599 | ||||

| Total Long-term Liabilities | - | 207,599 | ||||

| Total Liabilities | 8,061,423 | 5,252,961 | ||||

| Stockholders' Deficiency | ||||||

| Preferred stock, $.0001 par value, 10,000,000 authorized, none issued and outstanding Common stock, $.0001 par value, 150,000,000 authorized, 44,376,716 (2018- 40,299,531) shares issued and outstanding (note 18) | 4,439 | 4,031 | ||||

| Additional paid-in capital | 7,274,449 | 5,754,260 | ||||

| Subscriptions payable | - | 4,600 | ||||

| Stock compensation reserve | 750,000 | 1,330,000 | ||||

| Accumulated deficit | (10,766,212 | ) | (8,554,312 | ) | ||

| Accumulated other comprehensive loss | (132,476 | ) | (80,827 | ) | ||

| Stockholders' deficiency | (2,869,800 | ) | (1,542,248 | ) | ||

| Total Liabilities and Stockholders' Deficiency | $ | 5,191,623 | $ | 3,710,713 | ||

| Going concern(note 2) | ||||||

| Commitments(note 19) |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

![]()

5

| Interim Condensed Consolidated Statements of Operations and Comprehensive Loss |

| For the three and nine-month periods ended September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

SusGlobal Energy Corp.Interim Condensed Consolidated Statements of Operations and Comprehensive LossFor the three-month periods ended March 31, 2019 and 2018(Expressed in United States Dollars)(unaudited)

| For the three-month periods ended | For the nine-month periods ended | |||||||||||||||||

| For the three-month periods ended | September 30, | September 30, | September 30, | September 30, | ||||||||||||||

| March 31, 2019 | March 31, 2018 | 2019 | 2018 | 2019 | 2018 | |||||||||||||

| Revenue | $ | 253,138 | $ | 132,721 | $ | 390,723 | $ | 279,394 | $ | 1,025,695 | $ | 639,538 | ||||||

| Cost of Sales | ||||||||||||||||||

| Opening inventory | 18,550 | 53,964 | 24,738 | 115,733 | 18,550 | 53,964 | ||||||||||||

| Depreciation | 95,754 | 94,043 | 105,990 | 98,823 | 302,816 | 291,134 | ||||||||||||

| Direct wages and benefits | 49,365 | 40,059 | 71,347 | 41,526 | 180,379 | 125,634 | ||||||||||||

| Equipment rental, delivery, fuel and repairs and maintenance | 99,566 | 35,040 | ||||||||||||||||

| Equipment rental, delivery, fuel and repairs | ||||||||||||||||||

| and maintenance | 24,053 | 41,354 | 228,535 | 102,552 | ||||||||||||||

| Utilities | 27,531 | 22,200 | 19,309 | 22,755 | 79,535 | 54,643 | ||||||||||||

| Outside contractors | 105 | 3,844 | 17,824 | (27 | ) | 22,526 | 16,654 | |||||||||||

| 290,871 | 249,150 | 263,261 | 320,164 | 832,341 | 644,581 | |||||||||||||

| Less: closing inventory | (26,409 | ) | (67,210 | ) | (27,538 | ) | (73,795 | ) | (27,538 | ) | (73,795 | ) | ||||||

| Total cost of sales | 264,462 | 181,940 | 235,723 | 246,369 | 804,803 | 570,786 | ||||||||||||

| Gross loss | (11,324 | ) | (49,219 | ) | ||||||||||||||

| Gross profit | 155,000 | 33,025 | 220,892 | 68,752 | ||||||||||||||

| Operating expenses | ||||||||||||||||||

| Management compensation-stock- based | ||||||||||||||||||

| compensation (note 9) | 332,500 | 82,500 | ||||||||||||||||

| Management compensation-fees (note 9) | 81,238 | 90,174 | ||||||||||||||||

| compensation (note 11) | 85,000 | 332,500 | 750,000 | 1,997,500 | ||||||||||||||

| Management compensation-fees (note 11) | 81,800 | 82,619 | 243,778 | 256,377 | ||||||||||||||

| Marketing | 280,000 | - | 5,785 | - | 252,462 | - | ||||||||||||

| Professional fees | 134,702 | 60,822 | 63,357 | 246,245 | 270,328 | 383,287 | ||||||||||||

| Interest expense (notes 9, 10, 11, 12, 13 and 14) | 105,023 | 85,240 | ||||||||||||||||

| Office and administration | 67,564 | 51,084 | ||||||||||||||||

| Rent and occupancy (note 9) | 24,241 | 34,201 | ||||||||||||||||

| Interest expense (notes 10, 11, 13, 14, 15, 16 and 17) | 152,952 | 90,939 | 408,382 | 267,958 | ||||||||||||||

| Office and administration (note 11) | 62,906 | 39,182 | 176,850 | 102,767 | ||||||||||||||

| Rent and occupancy (note 11) | 33,024 | 54,925 | 92,085 | 123,842 | ||||||||||||||

| Insurance | 14,059 | 15,119 | 17,508 | 14,172 | 45,518 | 44,757 | ||||||||||||

| Filing fees | 12,683 | 6,458 | 2,546 | 1,479 | 31,643 | 11,518 | ||||||||||||

| Amortization of financing costs | 11,997 | - | 88,956 | - | 154,721 | - | ||||||||||||

| Directors’ compensation (note 9) | 2,952 | 791 | ||||||||||||||||

| Directors' compensation (note 11) | (14,648 | ) | 766 | (1,948 | ) | 2,331 | ||||||||||||

| Repairs and maintenance | 2,261 | 8,009 | 4,219 | 1,471 | 8,973 | 20,240 | ||||||||||||

| Total operating expenses | 1,069,220 | 434,398 | 583,405 | 864,298 | 2,432,792 | 3,210,577 | ||||||||||||

| Net loss | (1,080,544 | ) | (483,617 | ) | (428,405 | ) | (831,273 | ) | (2,211,900 | ) | (3,141,825 | ) | ||||||

| Other comprehensive (loss) income | ||||||||||||||||||

| Foreign exchange (loss) gain | (27,505 | ) | 28,314 | |||||||||||||||

| Other comprehensive income (loss) | ||||||||||||||||||

| income | ||||||||||||||||||

| Foreign exchange gain (loss) | 25,828 | (27,107 | ) | (51,649 | ) | (6,093 | ) | |||||||||||

| Comprehensive loss | $ | (1,108,049 | ) | $ | (455,303 | ) | $ | (402,577 | ) | $ | (858,380 | ) | $ | (2,263,549 | ) | $ | (3,147,918 | ) |

| Net loss per share-basic and diluted | $ | (0.03 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.02 | ) | $ | (0.05 | ) | $ | (0.08 | ) |

| Weighted average number of common sharesoutstanding- basic and diluted | 41,291,864 | 38,556,254 | 43,082,783 | 40,003,672 | 42,285,041 | 39,222,148 | ||||||||||||

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

![]()

6

| Interim Condensed Consolidated Statements of Changes in Stockholders' Deficiency |

| For the three and nine-month periods ended September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

| Number of Shares | Common Shares | Additional Paid- in Capital | Share Subscriptions Payable | Stock Compensation Reserve | Accumulated Deficit | Accumulated Other Comprehensive Loss | Stockholders' Deficiency | |||||||||||||||||

| Balance-December 31, 2018 | 40,299,531 | $ | 4,031 | $ | 5,754,260 | $ | 4,600 | $ | 1,330,000 | $ | (8,554,312 | ) | $ | (80,827 | ) | $ | (1,542,248 | ) | ||||||

| Shares issuedfor proceedspreviously received | 5,000 | 1 | 4599 | (4,600 | ) | - | - | - | ||||||||||||||||

| Shares issuedon vesting of 2018stock award | 1,000,000 | 100 | 999,900 | - | (1,000,000 | ) | - | - | - | |||||||||||||||

| Shares issuedfor professionalservices | 100,000 | 10 | 52,990 | - | - | - | - | 53,000 | ||||||||||||||||

| Stock compensationexpensed on vestingof stock awards | - | - | - | - | 332,500- | - | - | 332,500 | ||||||||||||||||

| Othercomprehensive loss | - | - | - | - | - | - | (27,505 | ) | (27,505 | ) | ||||||||||||||

| Net loss | - | - | - | - | - | (1,080,544 | ) | - | (1,080,544 | ) | ||||||||||||||

| Balance-March 31,2019 | 41,404,531 | $ | 4,142 | $ | 6,811,749 | $ | - | $ | 662,500 | $ | (9,634,856 | ) | $ | (108,332 | ) | $ | (2,264,797 | ) | ||||||

| Shares issued onvesting of 2018stock award | 1,000,000 | 100 | 329,900 | - | (330,000 | ) | - | - | - | |||||||||||||||

| Shares issuedto directors | 80,000 | 8 | 39,192 | - | - | - | - | 39,200 | ||||||||||||||||

| Stock compensationexpensed on vestingof stock awards | - | - | - | - | 332,500 | - | - | 332,500 | ||||||||||||||||

| Othercomprehensive loss | - | - | - | - | - | - | (49,972 | ) | (49,972 | ) | ||||||||||||||

| Net loss | - | - | - | - | - | (702,951 | ) | - | (702,951 | ) | ||||||||||||||

| Balance-June 30,2019 | 42,484,531 | $ | 4,250 | $ | 7,180,841 | $ | - | $ | 665,000 | $ | (10,337,807 | ) | $ | (158,304 | ) | $ | (2,646,020 | ) | ||||||

| Shares issued on conversion of debt to equity | 1,892,185 | 189 | 93,608 | - | - | - | - | 93,797 | ||||||||||||||||

| Stock compensationexpensed on vestingof stock awards | - | - | - | - | 85,000 | - | - | 85,000 | ||||||||||||||||

| Othercomprehensive income | - | - | - | - | - | - | 25,828 | 25,828 | ||||||||||||||||

| Net loss | - | - | - | - | - | (428,405 | ) | - | (428,405 | ) | ||||||||||||||

| Balance-September30, 2019 | 44,376,716 | $ | $ 4,439 | $ | 7,274,449 | $ | - | $ | 750,000 | $ | (10,766,212 | ) | $ | (132,476 | ) | $ | (2,869,800 | ) |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

![]()

7

SusGlobal Energy Corp.Interim Condensed Consolidated Statements of Changes in Stockholders’ Deficiency

| SusGlobal Energy Corp. |

| Interim Condensed Consolidated Statements of Changes in Stockholders' Deficiency |

| For the three and nine-month periods ended September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

| Additional | Accumulated | |||||||||||||||||||||||

| Number of | Common | Paid- | Share | Stock | Accumulated | Other | Stockholders’ | |||||||||||||||||

| Shares | Shares | in Capital | Subscriptions | Compensation | Deficit | Comprehensive | Deficiency | |||||||||||||||||

| Payable | Reserve | Loss | ||||||||||||||||||||||

| Balance – December31, 2017 | 37,393,031 | $ | 3,740 | $ | 3,576,111 | $ | 178,200 | $ | 330,000 | $ | (4,660,296 | ) | $ | (148,093 | ) | $ | (720,338 | ) | ||||||

Shares issued forproceeds previously received | 190,000 | 19 | 178,181 | (178,200 | ) | - | - | - | - | |||||||||||||||

| Shares issued onvesting of 2017 stockaward | 2,000,000 | 200 | 1,329,800 | - | (330,000 | ) | - | - | 1,000,000 | |||||||||||||||

| Shares issued forprivate placement, netof share issue costs | 696,500 | 70 | 650,170 | - | - | - | - | 650,240 | ||||||||||||||||

| Shares issued todirector | 20,000 | 2 | 19,998 | - | - | - | - | 20,000 | ||||||||||||||||

| Stockcompensation expensedon vesting of stockaward | - | - | - | - | 1,330,000 | - | - | 1,330,000 | ||||||||||||||||

| Proceeds received forshares yet to be issued | - | -- | 4,600 | - | - | - | 4,600 | |||||||||||||||||

| Other comprehensiveincome | - | - | - | - | - | - | 67,266 | 67,266 | ||||||||||||||||

| Net loss | - | - | - | - | - | (3,894,016 | ) | - | (3,894,016 | ) | ||||||||||||||

| Balance – December 31,2018 | 40,299,531 | 4,031 | 5,754,260 | 4,600 | 1,330,000 | (8,554,312 | ) | (80,827 | ) | (1,542,248 | ) | |||||||||||||

| Shares issued forproceeds previouslyreceived | 5,000 | 1 | 4599 | (4,600 | ) | - | - | - | - | |||||||||||||||

| Shares issued onvesting of 2018 stock award | 1,000,000 | 100 | 999,900 | - | (1,000,000 | ) | - | - | - | |||||||||||||||

| Shares issued forprofessional services | 100,000 | 10 | 52,990 | - | - | - | - | 53,000 | ||||||||||||||||

| Stockcompensation expensedon vesting of stockawards | - | - | - | - | 332,500 | - | - | 332,500 | ||||||||||||||||

| Other comprehensiveloss | - | - | - | - | - | - | (27,505 | ) | (27,505 | ) | ||||||||||||||

| Net loss March 31, 2019 | - | - | - | - | - | (1,080,544 | ) | - | (1,080,544 | ) | ||||||||||||||

| Balance-March 31, 2019 | 41,404,531 | $ | 4,142 | $ | 6,811,749 | $ | - | $ | 662,500 | $ | (9,634,856 | ) | $ | (108,332 | ) | $ | (2,264,797 | ) |

| Number of Shares | Common Shares | Additional Paid- in Capital | Share Subscriptions Payable | Stock Compensation Reserve | Accumulated Deficit | Accumulated Other Comprehensive Loss | Stockholders' Deficiency | ||||||||||||||||

| Balance – December 31, 2017 | 37,393,031 | $ | 3,740 | $ | 3,576,111 | $ | 178,200 | $ | 330,000 | $ | (4,660,296 | ) | $ | (148,093 | ) | $ | (720,338 | ) | |||||

| Shares issued for proceeds previously received | 190,000 | 19 | 178,181 | (178,200 | ) | - | - | - | - | ||||||||||||||

| Shares issued on vesting of stock award | 1,000,000 | 100 | 329,900 | - | (330,000 | ) | - | - | - | ||||||||||||||

| Shares issued for private placement, net of share issue costs | 50,000 | 5 | 44,995 | - | - | - | - | 45,000 | |||||||||||||||

| Stock compensation expensed on vesting of stock award | - | - | - | - | 82,500 | - | - | 82,500 | |||||||||||||||

| Other comprehensive income | - | - | - | - | - | - | 28,314 | 28,314 | |||||||||||||||

| Net loss | - | - | - | - | - | (483,617 | ) | - | (483,617 | ) | |||||||||||||

| Balance-March 31, 2018 | 38,633,031 | $ | 3,864 | $ | 4,129,187 | $ | - | $ | 82,500 | $ | (5,143,913 | ) | $ | (119,779 | ) | $ | (1,048,141 | ) | |||||

| Shares issued on vesting of 2017 stock award | 1,000,000 | 100 | 999,900 | - | - | - | - | 1,000,000 | |||||||||||||||

| Shares issued for private placement, net of share issue costs | 280,000 | 28 | 259,472 | - | - | - | - | 259,500 | |||||||||||||||

| Stock compensation expensed on vesting of stock award | - | - | - | - | 582,500 | - | - | 582,500 | |||||||||||||||

| Other comprehensive income | - | - | - | - | - | - | (7,300 | ) | (7,300 | ) | |||||||||||||

| Net loss | - | - | - | - | - | (1,826,935 | ) | - | (1,826,935 | ) | |||||||||||||

| Balance-June 30, 2018 | 39,913,031 | $ | 3,992 | $ | 5,388,559 | $ | - | $ | 665,000 | $ | (6,970,848 | ) | $ | (127,079 | ) | $ | (1,040,376 | ) | |||||

| Shares issued for private placement, net of share issue costs | 137,000 | 14 | 132,026 | - | - | - | - | 132,040 | |||||||||||||||

| Stock compensation expensed on vesting of stock award | - | - | - | - | 332,500 | - | - | 332,500 | |||||||||||||||

| Other comprehensive loss | - | - | - | - | - | - | (27,107 | ) | (27,107 | ) | |||||||||||||

| Net loss | - | - | - | - | - | (831,273 | ) | - | (831,273 | ) | |||||||||||||

| Balance-September 30, 2018 | 40,050,031 | $ | 4,006 | $ | 5,520,585 | $ | - | $ | 997,500 | $ | (7,802,121 | ) | $ | (154,186 | ) | $ | (1,434,216 | ) |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

![]()

8

| Interim Condensed Consolidated Statements of Cash Flows |

| For the three and nine-month periods ended September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

SusGlobal Energy Corp.Interim Condensed Consolidated Statements of Cash FlowsFor the three-month periods ended March 31, 2019 and 2018(Expressed in United States Dollars)(unaudited)

| For the three-month | For the three-month | |||||||||||

| period ended | period ended | For the nine-month period ended | For the nine-month period ended | |||||||||

| March 31, 2019 | March 31, 2018 | September 30, 2019 | September 30, 2018 | |||||||||

| Cash flows from operating activities | ||||||||||||

| Net loss | $ | (1,080,544 | ) | $ | (483,617 | ) | $ | (2,211,900 | ) | $ | (3,141,825 | ) |

| Adjustments for: | ||||||||||||

| Depreciation | 97,701 | 94,354 | 308,588 | 297,294 | ||||||||

| Amortization of intangible asset | 50 | 50 | 832 | 150 | ||||||||

| Amortization of operating right-of-use asset | 3,663 | - | 6,107 | - | ||||||||

| Amortization of financing fees | 11,997 | - | 154,721 | - | ||||||||

| Stock-based compensation | 332,500 | 82,500 | 750,000 | 1,997,500 | ||||||||

| Shares issued for professional services | 53,000 | - | 53,000 | - | ||||||||

| Shares issued to directors | 39,200 | - | ||||||||||

| Interest capitalized | - | 53,873 | ||||||||||

| Changes in non-cash working capital: | ||||||||||||

| Trade receivables | 31,239 | 124,296 | (10,279 | ) | 40,282 | |||||||

| Government remittances receivable | - | 3,578 | ||||||||||

| Inventory | (7,511 | ) | (14,994 | ) | (8,399 | ) | (21,620 | ) | ||||

| Prepaid expenses and deposits | (87,561 | ) | 45,156 | 5,484 | 36,829 | |||||||

| Accounts payable | 37,207 | 22,968 | 335,056 | 1,186 | ||||||||

| Government remittances payable | (30,156 | ) | - | (12,656 | ) | 22,470 | ||||||

| Accrued liabilities | (29,316 | ) | 45,499 | (62,340 | ) | 196,276 | ||||||

| Net cash used in operating activities | (667,731 | ) | (83,788 | ) | (652,586 | ) | (514,007 | ) | ||||

| Cash flows from investing activities | ||||||||||||

| Business acquisition | (1,468,226 | ) | - | |||||||||

| Purchase of intangible assets | (10,777 | ) | - | (11,149 | ) | - | ||||||

| Purchase of long-lived assets | - | - | (199,434 | ) | (1,553 | ) | ||||||

| Net cash used in investing activities | (10,777 | ) | - | (1,678,809 | ) | (1,553 | ) | |||||

| Cash flows from financing activities | ||||||||||||

| Bank indebtedness | 4,055 | 119 | 7,323 | 820 | ||||||||

| Advance | 30,096 | - | ||||||||||

| Repayments of advance | (9,006 | ) | - | |||||||||

| Repayment of long-term debt | (21,109 | ) | (40,441 | ) | (54,764 | ) | (138,303 | ) | ||||

| Repayments of obligations under capital lease | (16,665 | ) | (32,173 | ) | (61,967 | ) | (71,970 | ) | ||||

| Advances of convertible promissory notes | 758,500 | - | 1,328,975 | - | ||||||||

| Repayments of operating lease liability | (1,107 | ) | - | (1,864 | ) | - | ||||||

| Advance of mortgage payable | 1,272,993 | - | ||||||||||

| Repayments of loans payable to related parties | (94,025 | ) | (15,820 | ) | (206,910 | ) | (15,538 | ) | ||||

| Advances of loans payable to related parties | - | 213,648 | ||||||||||

| Private placement proceeds (net of share issue costs) | - | 45,000 | - | 436,540 | ||||||||

| Net cash provided by (used in) financingactivities | 629,649 | (43,315 | ) | |||||||||

| Net cash provided by financing activities | 2,304,876 | 425,197 | ||||||||||

| Effect of exchange rate on cash | 6,148 | 986 | (16,192 | ) | (35,754 | ) | ||||||

| Decrease in cash | (42,711 | ) | (126,117 | ) | (42,711 | ) | (126,117 | ) | ||||

| Cash and cash equivalents-beginning ofperiod | 42,711 | 126,117 | 42,711 | 126,117 | ||||||||

| Cash and cash equivalents-end of period | $ | - | $ | - | $ | - | $ | - | ||||

| Supplemental Cash Flow Disclosures: | ||||||||||||

| Interest paid | $ | 81,394 | $ | 62,932 | $ | 171,675 | $ | 279,320 | ||||

| Income taxes paid | - | - | - | - | ||||||||

| (i) | Refer to note |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

![]()

9

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| (Expressed in United States Dollars) |

| (unaudited) |

1. Nature of Business and Basis of Presentation

SusGlobal Energy Corp. (“SusGlobal”("SusGlobal") was formed by articles of amalgamation on December 3, 2014, in the Province of Ontario, Canada and its executive office is in Toronto, Ontario, Canada. SusGlobal, a company in the start-up stages and Commandcredit Corp. (“Commandcredit”("Commandcredit"), an inactive Canadian public company, amalgamated to continue business under the name of SusGlobal Energy Corp.

On May 23, 2017, SusGlobal filed an Application for Authorization to continue in another Jurisdiction with the Ministry of Government Services in Ontario and a certificate of corporate domestication and certificate of incorporation with the Secretary of State of the State of Delaware under which it changed its jurisdiction of incorporation from Ontario to the State of Delaware (the “Domestication”"Domestication"). In connection with the Domestication each of the currently issued and outstanding common shares were automatically converted on a one-for-one basis into common shares compliant with the laws of the state of Delaware (the “Shares”"Shares"). As a result of the Domestication, pursuant to Section 388 of the General Corporation Law of the State of Delaware (the “DGCL”"DGCL"), SusGlobal continued its existence under the DGCL as a corporation incorporated in the State of Delaware. The business, assets and liabilities of SusGlobal and its subsidiaries on a consolidated basis, as well as its principal location and fiscal year, were the same immediately after the Domestication as they were immediately prior to the Domestication. SusGlobal filed a Registration Statement on Form S-4 to register the Shares and this registration statement was declared effective by the Securities and Exchange Commission on May, 23, 2017.

On December 11, 2018, the Company began trading on the Over the Counter QB venture market exchange, under the ticker symbol SNRG.

SusGlobal is a renewable energy company focused on acquiring, developing and monetizing a global portfolio of proprietary technologies in the waste to energy and regenerative products application.

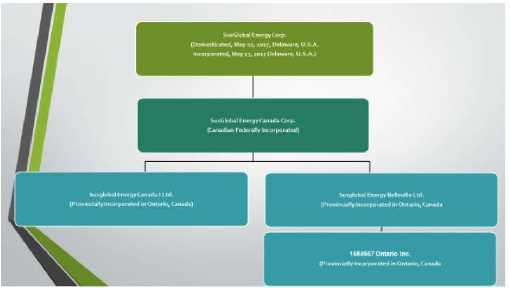

These interim condensed consolidated financial statements of SusGlobal and its wholly-owned subsidiaries, SusGlobal Energy Canada Corp., SusGlobal Energy Canada I Ltd. (“SGECI”("SGECI") and, SusGlobal Energy Belleville Ltd. ("SGEBL") and 1684567 Ontario Inc. ("1684567") (together, the “Company”"Company"), have been prepared following generally accepted accounting principles in the United States (“("US GAAP”GAAP") for interim financial information and the Securities Exchange Commission (“SEC”("SEC") instructions to Form 10-Q and Article 8 of SEC Regulation S-X, and are expressed in United States Dollars. The Company’sCompany's functional currency is the Canadian Dollar (“CAD”("CAD"). In the opinion of management, all adjustments necessary for a fair presentation have been included.

2. Going Concern

The interim condensed consolidated financial statements have been prepared in accordance with US GAAP, which assumes that the Company will be able to meet its obligations and continue its operations for the next twelve months.

As at March 31,September 30, 2019, the Company had a working capital deficit of $5,565,973$7,865,585 (December 31, 2018-$4,830,948), incurred a net loss of $1,080,544$2,211,900 (2018-$483,617)3,141,825) for the threenine months ended March 31,September 30, 2019 and had an accumulated deficit of $9,634,856$10,766,212 (December 31, 2018-$8,554,312) and expects to incur further losses in the development of its business.

![]()

10

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

2. Going Concern,(continued)

On August 28, 2019, Pace Savings & Credit Union Limited (“PACE”) informed the Company via letter that the credit facilities and corporate term loan (the “Debt”) was in default due to the Company’s going concern disclosure in the Company’s consolidated financial statements for the years ended December 31, 2018 and 2017 and as a result of the Company’s failure to respond to an e-mail request from PACE with respect to the Company’s efforts to arrange for a payout. As a result, PACE was not agreeable to continue with the Debt and had requested that the Company’s indebtedness to PACE be paid in full on or before December 31, 2019. PACE requested that their letter be fully executed by September 5, 2019. On September 3, 2019, PACE informed the Company via letter that the interest rates on the Debt be increased effective September 15, 2019, by 0.50%, and each month thereafter by a further 0.50%. On September 5, 2019, management arranged to meet with PACE to discuss their demands and to discuss the Company’s refinancing efforts. Management expressed their concerns over PACE’s actions in describing the details of the default and in increasing the interest rates as per their written communication. Management indicated to PACE that it was agreeable to a partial paydown of the Debt, as management was in discussions with obtaining a first mortgage over the Company’s property which included their organic composting facilities, from a chartered bank. PACE requested management to continue to update PACE on management’s refinancing plans. Management did not fully execute the September 5, 2019 letter from PACE nor any future letters from PACE. The Company “stopped payments” on the September and October instalments on the Debt with PACE. On September 11, 2019, PACE informed the Company that it failed to execute the new terms by September 5, 2019 and that it failed to make the required September payments on two of the three credit facilities that are part of the Debt, which were due on September 2, 2019. PACE also requested payments for the September monthly instalment payment on each of the two credit facilities, not sufficient fund fees and default and administrative fees totaling $1,978 ($2,620 CAD) and the letter of credit fee in the amount of $1,888 ($2,500 CAD). The letter of credit fee was paid and the letter of credit was extended to December 31, 2019. PACE also requested that the Company provide cash collateral to PACE for the letter of credit, in the amount of $209,035 ($276,831 CAD). PACE requested the consent of management to have PACE appoint a financial advisor to inspect and assess the assets and operations of the Company and requested that the letter be executed and returned to PACE by September 12, 2019. In a letter to PACE, management noted that the company’s financial report due by November 14, 2019, will be provided to PACE subsequent to the filing of the financial report and that no further payments will be made to PACE pending resolution of a paydown schedule to facilitate the principal reduction required by PACE on or before December 31, 2019. In a letter from PACE on September 13, 2019, they agreed to renew the letter of credit to December 31, 2019 but still consider the Debt in default. In a letter from PACE on October 9, 2019, PACE confirmed that the letter of credit was renewed to December 31, 2019 and noted further instalments payments returned stop payment, which were due on September 13, 2019 and October 2 and 4, 2019. PACE reiterated that they did not want to continue to be the Company’s banker and that it did not agree to any partial reduction of the Debt and requested that the Company provide a written repayment plan to have the credit facilities permanently retired. On November 1, 2019, the Company responded to PACE’s demands to repay all Debt by offering to repay two credit facilities totaling $460,413 ($609,738 CAD) on or before December 31, 2019, in return for a forbearance to December 31, 2020 and repayment of the remaining credit facility and corporate term loan no later than December 31, 2020 or upon the completion of the refinancing with the Canadian chartered bank. On November 12, 2019, PACE responded to the Company accepting the repayment of the two noted credit facilities, but, in addition, required that all the Debt be made current, that the Company provide written reports to PACE on its refinancing with the Canadian chartered bank on a monthly basis commencing December 15, 2019, that all remaining debt be repaid by June 30, 2020 and that PACE be permitted to appoint a financial advisor to inspect the assets and operations of the Company. In addition, the Company’s letter of credit with PACE is expected to be renewed to June 30, 2020. All terms are subject to credit approval.

As a result of the PACE default, the advance is also in default (refer to advance, note 12), the obligations under capital lease are also in default (refer to obligations under capital lease, note 14) and the convertible promissory notes are also in default (refer to convertible promissory notes, note 15).

![]()

11

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

2. Going Concern,(continued)

Further, on September 25, 2019, the Company’s chief executive officer (the “CEO”), resigned as a member of the Board of Directors (the “Board”) and ceased providing his services as CEO. On November 6, 2019, by resolution of the Board, the president of the Company (the “President”), was appointed CEO.

These factors cast substantial doubt as to the Company’sCompany's ability to continue as a going concern, which is dependent upon its ability to obtain the necessary financing to further the development of its business, satisfy its obligations to PACE Savings & Credit Union Limited (“PACE”)and its other creditors, whose debt is also in default and upon achieving profitable operations. There is no assurance of funding being available or available on acceptable terms. Realization values may be substantially different from carrying values as shown.

These interim condensed consolidated financial statements do not include any adjustments to reflect the future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result if the Company was unable to continue as a going concern.

3. Significant Accounting Policies

These interim condensed consolidated financial statements do not include all of the information and footnotes required by US GAAP for complete financial statements and should be read in conjunction with the consolidated financial statements of the Company for the years ended December 31, 2018 and 2017 and their accompanying notes.

Recently Adopted Accounting Pronouncements:

On January 1, 2019, the Company adopted Accounting Standards Update (“ASU”("ASU") No. 2016-02, Leases which is also known as Accounting Standard Codification (“ASC”("ASC") Topic 842, that requires lessees to recognize for all operating leases a right-of-use asset and a lease obligation in the interim condensed consolidated balance sheets. Expenses are recognized in the interim condensed consolidated statements of operations and comprehensive loss in a manner similar to previous accounting guidance. Lessor accounting under the new standard is substantially unchanged and is not relevant to the Company. The Company adopted the accounting standard using a prospective transition approach, which applies the provisions of the new guidance at the effective date without adjusting the comparative periods presented, with certain practical expedients available to ease the burden of adoption.

![]()

12

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

3. Significant Accounting Policies, (continued)

The Company elected the following practical expedients upon adoption: not to reassess whether any expired or existing contracts are or contain leases, not to reassess the lease classification for any expired or existing leases, not to reassess initial direct costs for any existing leases, not to separately identify lease and non-lease components (i.e. maintenance costs) except for fleet vehicles and real estate, and not to evaluate historical land easements under the new guidance. Additionally, the Company elected the short-term lease exemption policy, applying the requirements of ASC 842 to long-term leases (leases greater than 1 year) for which it only has one.

Adoption of the new standard resulted in $217,755 ($297,074 CAD) of additional right-of-use lease asset and lease liability as of January 1, 2019. The new standard did not have a significant impact on the interim condensed consolidated statements of operations and comprehensive loss. See note 8,9, operating lease right-of-use asset and operating lease liability, for additional information.

4. Recent Accounting Pronouncements

From time to time, new accounting pronouncements are issued by the financial accounting standards board (the “FASB”"FASB") or other standard setting bodies and adopted by the Company as of the specified effective date or possibly early adopted, where permitted. Unless otherwise discussed, the impact of recently issued standards that are not yet effective are not expected to have a material impact on the Company’sCompany's financial position, results of operations or cash flows.

In August 2018, the FASB issued an update, ASU No. 2018-13, “Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurements to ASC Topic 820, Fair Value Movement. ASU No. 2018-13 modifies the disclosure requirements for fair value measurements by removing, modifying, and/or adding certain disclosures. ASU No. 2018-13 is effective for interim and annual reporting periods in fiscal years beginning after December 15, 2019. The Company is currently evaluating the impact of adopting ASU No. 2018-13.

In January 2017, the FASB issued ASU No. 2017-04, “Intangibles-Goodwill"Intangibles-Goodwill and Other (Topic 350) - Simplifying the Test for GoodwillImpairment”GoodwillImpairment". The new standard simplifies the accounting for goodwill impairments by eliminating step 2 from the goodwill quantitative impairment test. Instead, if the carrying amount of a reporting unit exceeds its fair value, an impairment loss is to be recognized in an amount equal to that excess, limited to the total amount of goodwill allocated to that reporting unit. The standard is to be effective for interim and annual periods beginning after December 15, 2019 and early adoption is permitted. The Company is currently evaluating the impact of adopting ASU No. 2017-04.

![]()

13

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

4. Recent Accounting Pronouncements,(continued)

In June 2016, the FASB issued ASU 2016-13, Measurement of Credit Losses on Financial Instruments (Topic 326), which replaces the incurred-loss impairment methodology and requires immediate recognition of estimated credit losses expected to occur for most financial assets, including trade receivables. Credit losses on available-for-sale debt securities with unrealized losses will be recognized as allowances for credit losses limited to the amount by which fair value is below amortized cost. ASU 2016-13 is effective for the Company beginning January 1, 2020 and early adoption is permitted. The Company does not believe the potential impact of the new guidance and related codification improvements will be material to its financial position, results of operations and cash flows.

5. Financial Instruments

The carrying value of cash and cash equivalents, trade receivables, bank indebtedness, accounts payable, and accrued liabilities approximated their fair values as of March 31,September 30, 2019 due to their short-term nature. The carrying value of the advance, long-term debt, obligations under capital lease, convertible promissory notes, operating lease obligationmortgage payable and loans payable to related parties approximated their fair values due to their market interest rates.

Interest, Credit and Concentration Risk

In the opinion of management, the Company is exposed to significant interest rate risk on its long-term debt of $3,784,588$3,785,210 ($5,057,5815,012,859 CAD) (December 31, 2018-$3,727,778; $5,085,645 CAD). and on its convertible promissory notes, should the Company repay all or some of these convertible promissory notes within the stipulated time period.

With regards to credit risk with customers, the customers’ credit evaluation is reviewed by management and account monitoring procedures are used to minimize the risk of loss. The Company believes that no additional credit risk beyond amounts provided for by the allowance for doubtful accounts are inherent in accounts receivable. As at MarchSeptember 30, 2019, the allowance for doubtful accounts was $nil (December 31, 2018-$nil).

As at September 30, 2019, the Company is exposed to concentration risk as it had sixthree customers (2018-five(December 31, 2018-five customers) representing greater than 5% of total trade receivables and these sixthree customers (December 31, 2018-five customers) represented 93%73% (2018-90%) of trade receivables. The Company had certain customers whose revenue individually represented 10% or more of the Company’sCompany's total revenue. These customers accounted for 90% (42%71% (37%, 21%, and 13%) (September 30, 2018-67%; 31%, 26%, 11% and 11%) (March 31, 2018-69%; 24%, 23% and 22%10%) of total revenue.

Liquidity Risk

Liquidity risk is the risk that the Company is unable to meet its obligations as they fall due. The Company takes steps to ensure it has sufficient working capital and available sources of financing to meet future cash requirements for capital programs and operations. The Company is in discussions with a Canadian chartered bank to refinance its obligations to PACE and to another creditor. Refer also to going concern, note 2.

The Company actively monitors its liquidity to ensure that its cash flows and working capital are adequate to support its financial obligations and the Company’sCompany's capital programs. In order to continue operations, the Company will need to raise capital.capital, repay PACE for all or a portion of its credit facilities and complete the refinancing of its real property and organic composting facility. There is no assurance of funding being available or available on acceptable terms. Realization values may be substantially different from carrying values as shown. Refer also to going concern, note 2.

![]()

14

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

5. Financial Instruments,(continued)

Currency Risk

Although the Company’sCompany's functional currency is the CAD, the Company realizes a portion of its expenses in USD. Consequently, certain assets and liabilities are exposed to foreign currency fluctuations. As at March 31,September 30, 2019, $63,104$169,249 (December 31, 2018-$68,393) of the Company’sCompany's net monetary liabilities were denominated in USD. The Company has not entered into any hedging transactions to reduce the exposure to currency risk.

6. Business Acquisition

Effective May 24, 2019, the Company purchased all the issued and outstanding shares of 1684567. The acquisition was accounted for as a business combination using the acquisition method of accounting. The purchase price paid in the acquisition has been preliminarily allocated to record the assets acquired and liabilities assumed based on their estimated fair value. When determining the fair values of assets acquired and liabilities assumed, management made significant estimates. The transaction closed on May 28, 2019. The purchase consideration consisted of cash from working capital of $209,952 ($282,308 CAD) and cash from a third-party mortgage obtained in the amount of $1,258,273 ($1,691,910 CAD, net of financing fees of $80,387 ($108,090 CAD)). The total purchase price includes the original offer of $1,314,304 ($1,767,250 CAD) and acquisition costs of $153,922 ($206,968 CAD).

The allocation of the purchase price is as follows:

| May 24, 2019 | |||

| Purchase consideration | |||

| Cash ($1,974,218 CAD) | $ | 1,468,225 | |

| Assets acquired | |||

| Accounts receivable ($ 7,573 CAD) | 5,632 | ||

| Land ($1,850,892 CAD) | 1,376,508 | ||

| Automotive equipment and machinery ($16,525 CAD) | 12,290 | ||

| Customer list ($10,205 CAD) | 7,589 | ||

| Environmental compliance approval ($100,000 CAD) | 74,370 | ||

| Liabilities assumed | |||

| Accounts payable ($10,977 CAD) | 8,164 | ||

| Net assets acquired ($1,974,218 CAD) | $ | 1,468,225 |

![]()

15

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

7. Trade Receivables

On December 17, 2017, the Company filed a motion record in the Ontario Superior Court of Justice (the “Court”) against the Business Development Bank of Canada and Astoria Organic Matters Ltd. and Astoria Organic Matters Canada LP (“Astoria”), together, in the amount of $453,060 ($600,000 CAD), in connection with the Company’s purchase of certain assets from the court appointed receiver for Astoria, BDO Canada Limited. (“BDO”). The basis for the claim is for the Company’s costs to process biosolids stored onsite in an amount that was approximately ten times the amount permitted to be stored by conditions set in the Environmental Compliance Approval (the “ECA”) for the Company’s organic composting facility. The Court dismissed each of the Company’s motions, including on November 13, 2019, the Court dismissed the final motion and stayed the private prosecution. A further court date is set for November 4, 2019. As a result of this legal proceeding, BDO, through its legal representative, filed garnishment orders to collect on its outstanding fees, expenses and court costs, with three of the Company’s current customers. The garnishment orders, dated August 16, 2019, totaled $100,046 ($132,494 CAD) each. Since the garnishment orders were delivered to several customers, the payments of the Company’s accounts receivable to satisfy the garnishment orders, exceeded the amount of the garnishment orders. As at September 30, 2019, $114,284 ($151,350 CAD) had been collected, which represented an amount of $14,238 ($18,856 CAD) over and above the garnishment orders. The amounts collected as at September 30, 2019 have been applied against the outstanding accruals for legal fees, expenses and court costs, included in accrued liabilities, on this legal proceeding.

Refer also to subsequent events, note 21(c), for details on garnishment orders issued subsequent to September 30, 2019.

8. Intangible Assets

| March 31, 2019 | December 31, 2018 | |||||

| Technology license (net of accumulated amortization of $781 (2018- $731)) | $ | 1,220 | $ | 1,270 | ||

| Trademarks-indefinite life-$14,327 CAD | 10,721 | - | ||||

| Environmental compliance approvals-indefinite life- $182,700 CAD | 136,714 | 133,919 | ||||

| $ | 148,655 | $ | 135,189 |

| September 30, 2019 | December 31, 2018 | |||||

| Technology license (net of accumulated amortization of $881 (2018- $731)) | $ | 1,120 | $ | 1,270 | ||

| Customer list-limited life-$9,298 CAD (net of accumulated amortization of $907) | 7,021 | - | ||||

| Trademarks-indefinite life-$14,817 CAD | 11,188 | - | ||||

| Environmental compliance approvals-indefinite life- $282,700 CAD | 213,467 | 133,919 | ||||

| $ | 232,796 | $ | 135,189 |

On May 6, 2015, the Company acquired an exclusive license from Syngas SDN BHD (“Syngas”("Syngas"), a Malaysian company to use Syngas intellectual property within North America for a period of five years for $1 consideration, renewable every five years upon written request. Syngas manufactures equipment that produces liquid transportation fuel from plastic waste material. The Company issued 20,000 common shares of the Company to an introducing party, determined to be valued at $2,000.

On March 14, 2019, the Company incurred fees to register various trademarks in the United States and Canada.Canada, in the amount $11,188 ($14,817 CAD).

On September 15, 2017, the Company acquired the environmental compliance approvals on the purchase of certain assets of Astoria from BDO Canada Limited (‘BDO”(“BDO") under an asset purchase agreement (the “APA”"APA").

Effective May 24, 2019, the Company acquired an additional environmental compliance approval of $75,510 ($100,000 CAD) and a customer list $7,021 ($9,298 CAD), net of accumulated amortization of $685 ($907 CAD), relating to certain municipal contracts (forty-five-month life) on the purchase of the shares of 1684567.

![]()

16

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| (Expressed in United States Dollars) |

| (unaudited) |

79.Long-lived Assets, net

| March 31, 2019 | December 31, 2018 | September 30, | December 31, | |||||||||||||||||||||

| Cost | Accumulated | Net book value | Net book value | 2019 | 2018 | |||||||||||||||||||

| depreciation | Cost | Accumulated | Net book value | Net book value | ||||||||||||||||||||

| depreciation | ||||||||||||||||||||||||

| Land | $ | 1,397,609 | $ | - | $ | 1,397,609 | $ | - | ||||||||||||||||

| Composting buildings | $ | 2,200,566 | $ | 202,956 | $ | 1,997,610 | $ | 1,988,144 | 2,220,563 | 272,402 | 1,948,161 | 1,988,144 | ||||||||||||

| Gore cover system | 877,008 | 135,205 | 741,803 | 748,112 | 1,071,346 | 191,043 | 880,303 | 748,112 | ||||||||||||||||

| Driveway and paving | 346,837 | 42,777 | 304,060 | 304,639 | 349,989 | 57,165 | 292,824 | 304,639 | ||||||||||||||||

| Machinery and equipment | 58,502 | 26,777 | 31,725 | 27,661 | 62,806 | 36,252 | 26,554 | 27,661 | ||||||||||||||||

| Equipment under capital lease | 399,667 | 151,341 | 248,326 | 280,323 | 408,774 | 213,759 | 195,015 | 280,323 | ||||||||||||||||

| Office trailer | 6,361 | 2,942 | 3,419 | 3,817 | 9,061 | 4,195 | 4,866 | 3,817 | ||||||||||||||||

| Vacuum trailer | 5,663 | 425 | 5,238 | - | ||||||||||||||||||||

| Computer equipment | 6,614 | 3,722 | 2,892 | 3,186 | 6,673 | 4,483 | 2,190 | 3,186 | ||||||||||||||||

| Computer software | 6,884 | 5,307 | 1,577 | 2,389 | 6,947 | 6,947 | - | 2,389 | ||||||||||||||||

| Automotive equipment | 1,497 | 636 | 861 | 953 | 10,216 | 1,739 | 8,477 | 953 | ||||||||||||||||

| Signage | 2,540 | 741 | 1,799 | 1,886 | 2,564 | 812 | 1,752 | 1,886 | ||||||||||||||||

| $ | 3,906,476 | $ | 572,404 | $ | 3,334,072 | $ | 3,361,110 | $ | 5,552,211 | $ | 789,222 | $ | 4,762,989 | $ | 3,361,110 | |||||||||

Included above are certain assets of Astoria acquired from BDO under the APA, which closed on September 15, 2017. The purchase price for the purchased assets, described as an organic composting facility, including composting buildings, gore cover system, driveway and paving, certain machinery and equipment, an office trailer, certain computer equipment and computer software consisted of cash of $3,026,114 ($3,917,300 CAD) and 529,970 restricted common shares of the Company, determined to be valued at $529,970 ($700,000 CAD), based on recent private placement pricing. In addition, legal costs in connection with acquiring the assets of $22,598 ($29,253 CAD), are included in the cost of the composting buildings. The purchase price was allocated to thelong-lived assets acquired based on their estimated relative fair value as at the date the assets were acquired.business acquisition described under note 6.

8.10. Operating Lease Right-of-Use Asset and Operating Lease Liability

The Company hashad one operating lease right-of-use asset and related operating leasaelease liability and hashad recognized as such, effective January 1, 2019, based on the present value of lease payments over the lease term that expires on March 31, 2034, calculated to be $217,755 ($297,074 CAD) which were included in the interim condensed consolidated balance sheet.. The Company has used its estimated secured incremental borrowing rate based on the information available at the commencement date in determining the present value of lease payments. The operating lease right-of-use asset iswas being amortized on a straight-line basis over the lease term which expires March 31, 2034 and amortization expense is included under office and administration expense in the interim condensed consolidated statements of operations and comprehensive loss. The Company does not act as a lessor nor does it have any leases classified as financing leases.

The operating lease right-of-use asset iswas periodically reviewed for impairment losses. The Company usesused the long-lived assets impairment guidance in ASC Subtopic 360-10, Property, Plant and Equipment-Overall, to determine whether the operating lease right-of-use asset iswas impaired, and if so, the amount of the impairment loss to recognize.

The Company monitorsmonitored for events or changes in circumstances that requirerequired a reassessment of its operating lease right-of-use asset. When a reassessment results in the remeasurement of a lease liability, a corresponding adjustment is made to the carrying amount of the corresponding operating lease right-of-use asset.

Effective May 24, 2019, the Company acquired the shares of 1684567, the company that owned the land upon which the right-of-use asset was situated. As a result, the Company is both the tenant and the landlord and as such, no longer recognizes an operating right-of-use asset and related operating lease liability.

For the three-month periodthree and nine-month periods ended March 31,September 30, 2019, the Company recorded $3,663$nil ($4,870nil CAD) and $6,107 ($8,117 CAD (2018-$nil; $nil CAD and $nil; $nil CAD) respectively, for the amortization of the operating lease right-of-use asset.

The following summarizes quantitative information aboutFor the Company’sthree and nine-month periods ended September 30, 2019, the Company incurred interest of $2,437 ($3,239 CAD) (2018-$nil; $nil CAD and $nil and $nil CAD) respectively, on the operating lease:lease liability.

![]()

17

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| (Expressed in United States Dollars) |

| (unaudited) |

9.11. Related Party Transactions

During the three-month periodthree and nine-month periods ended March 31,September 30, 2019, the Company incurred $33,849$34,083 ($45,000 CAD) and $101,574 ($135,000 CAD) (2018-$35,595;34,425; $45,000 CAD and $104,881; $135,000 CAD) respectively, in management fees expense with Travellers International Inc. (“Travellers”("Travellers"), an Ontario company controlled by a director and president of the Company (the “President”); $33,849President; $34,083 ($45,000 CAD) and $101,574 ($135,000 CAD) (2018-$35,595;34,425; $45,000 CAD and $104,881; $135,000 CAD) respectively, in management fees expense with Landfill Gas Canada Ltd. (“LFGC”("LFGC"), an Ontario company controlled by a previous director and chief executive officer of the Company (the “CEO”); $13,540CEO; $13,634 ($18,000 CAD) and $40,630 ($54,000 CAD) (2018-$9,492; $12,00013,769; $18,000 CAD and $37,291; $48,000 CAD) respectively, in management fees expense with the Company’sCompany's chief financial officer (the “CFO”"CFO"); and $nil ($nil CAD) and $nil ($nil CAD) (2018-$9,492;nil; $nil CAD and $9,324; $12,000 CAD) respectively, in management fees expense with the Company’sCompany's vice-president of corporate development (the “VPCD”"VPCD"). As at March 31,September 30, 2019, unpaid remuneration and unpaid expenses in the amount of $80,759$72,062 ($107,92395,434 CAD) (December 31, 2018-$48,691; $66,426 CAD) is included in accounts payable and $177,347$242,387 ($237,000321,000 CAD) (December 31, 2018-$184,714; $251,997 CAD) is included in accrued liabilities.

On September 25, 2019, the CEO resigned from the Board and ceased providing his services as CEO.

In addition, during the three-month periodthree and nine-month periods ended March 31,September 30, 2019, the Company incurred interest expense of $3,802$150 ($5,055180 CAD) and $4,631 ($6,155 CAD) (2018-$293; $3714,664; $6,049 CAD and $9,482; $12,205 CAD) respectively, on the outstanding loansloan from Travellers and $1,669$364 ($2,219469 CAD) and $3,711 ($4,932 CAD) (2018-$nil; $nil1,751; $2,268 CAD and $3,295; $4,241 CAD) respectively, on the outstanding loans from the directors. As at March 31,September 30, 2019, interest of $23,698$nil ($31,669nil CAD) (December 31, 2018-$17,882; $24,395 CAD) on these loans is included in accrued liabilities.

During the three-month periodthree and nine-month periods ended March 31,September 30, 2019, the Company incurred $16,998$23,382 ($22,59830,934 CAD) and $55,678 ($74,001 CAD) (2018-$15,500; $19,59521,066; $27,426 CAD and $53,565; $68,947 CAD) respectively, in rent paid under a rental agreement to Haute Inc. (“Haute”("Haute"), an Ontario company controlled by the President.

The Company accrued directors’recorded directors' compensation for its five independent directors for services provided based on the share price at the end of each period and for the three-month periodthree and nine-month periods ended March 31,September 30, 2019, including the audit committee chairman's fees, in the amount of $2,952($14,648) and ($1,948) (2018-$791).766 and $2,331) respectively. As at MarchSeptember 30, 2019, $2,560 ($3,390 CAD) (December 31, 2019, $54,2002018-$nil) of outstanding fees to the directors is included in accounts payable and $7,133 (December 31, 2018-$52,000) of outstanding fees to the directors is included in accrued liabilities.

Furthermore, the Company granted the CEO 3,000,000 restricted stock units (“RSU”("RSU"), under a consulting agreement effective January 1, 2017, determined to be valued at $990,000 based on private placement pricing at the time. On each of February 25, 2018 and April 2, 2019, 1,000,000 RSUs were exchanged into 1,000,000 common stock of the Company. The RSUs for the remaining installment arewhich were expected to vest annually on January 1, 2020, subject to meeting certain performance objectives.objectives, have been forfeited by the CEO on his resignation in September 2019. On May 17, 2018, at a meeting of the board of directors (the “Board”"Board"), approved an amendment to the President’sPresident's consulting agreement, to include the granting of 3,000,000 RSUs to the President, determined to be valued at $3,000,000, based on private placement pricing at the time, on the same terms and conditions as those granted to the CEO. Immediately thereafter, 1,000,000 of the President’sPresident's RSUs were exchanged forinto 1,000,000 common stock of the Company. On January 9,8, 2019, 1,000,000 of the President’sPresident's RSUs were exchanged into 1,000,000 common stock of the Company. Based on private placement pricing at the time, the common stock issued to the President on each exchange of the RSUs, was determined to be valued at $1,000,000. The RSUs for the remaining installment are expected to vest annually on January 1, 2020, subject to meeting certain performance objectives.

For the three-month periodthree and nine-month periods ended March 31,September 30, 2019, the Company recognized management compensation expense of $332,500$85,000 and $750,000 (2018-$82,500332,500 and $1,997,500) respectively, on the awards to the President and the CEO) on the award to the CEO)President, representing one-quarter of the total value of the award of $3,000,000, based on private placement pricing at the time. In the three and nine-month periods ended September 30, 2018, the Company recognized management compensation expense of $332,500 and $1,997,500 on the awards to the President and the CEO, representing one-sixthone-quarter of the total value of the awards of $3,990,000 and the award granted to the President in the amount of $1,000,000, as noted above, based on private placement pricing at the time.

![]()

18

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| (Expressed in United States Dollars) |

| (unaudited) |

10.11. Related Party Transactions,(continued)

Refer also to subsequent events, note 21(g).

12. Advance

On July 29, 2019, the Company received an advance in the amount of $30,204 ($40,000 CAD) from a private lender. The advance is repayable at an amount of $368 ($488 CAD) every business day until repaid in full on January 13, 2020. Transaction related expenses in connection with this advance totaled $4,213 ($5,600 CAD) and included an interest expense in the interim condensed consolidated statements of operations and comprehensive loss. For the three and nine-month periods ended September 30, 2019, the Company incurred interest charges of $6,773 ($9,002 CAD) and $6,773 ($9,002 CAD) respectively. Total interest on the advance to January 13, 2020 is $11,737 ($15,600 CAD). The advance is guaranteed by the President. As a result of the PACE default, this advance is also in default. The lender may demand full repayment.

Refer also to going concern, note 2 and subsequent events, note 21(f).

13. Long-Term Debt

| March | December | |||||||||||||||||||||||||||||||||||

| Credit | Credit | Credit | Corporate | 31, 2019 | 31, 2018 | |||||||||||||||||||||||||||||||

| Facility | Facility | Facility | Term | Total | Total | Credit | Credit | Credit | Corporate | September 30, 2019 | December 31, 2018 | |||||||||||||||||||||||||

| Loan | Facility | Facility | Facility | TermLoan | Total | Total | ||||||||||||||||||||||||||||||

| (a) | (b) | (c) | (d) | |||||||||||||||||||||||||||||||||

| Long-Term Debt | $ | 757,258 | $ | 423,490 | $ | 36,898 | $ | 2,566,942 | $ | 3,784,588 | $ | 3,727,778 | $ | 757,406 | $ | 423,573 | $ | 36,840 | $ | 2,567,391 | $ | 3,785,210 | $ | 3,727,778 | ||||||||||||

| Current portion | (757,258 | ) | (423,490 | ) | (36,898 | ) | (2,566,942 | ) | (3,784,588 | ) | (3,727,778 | ) | (757,406 | ) | (423,573 | ) | (36,840 | ) | (2,567,391 | ) | (3,785,210 | ) | (3,727,778 | ) | ||||||||||||

| Long-term Debt | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||||||||||||||

| Long-term portion | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||||||||||||||||

The credit facilities and corporate term loan (the “Debt”) described below in paragraphs (a) to (d) are due on demand. On August 28, 2019, PACE demanded repayment on or before December 31, 2019. Management met with PACE on September 5, 2019, to resolve the matters and offered a paydown of the Debt. Management is also in discussions with a Canadian chartered bank to refinance the PACE Debt and the mortgage payable and formulate a paydown. The Company was informed on September 3, 2019, that effective September 15, 2019, the interest rate on the credit facilities and corporate term loan increased by 0.50% to the PACE base rate of 7.00% plus 1.75% per annum. Discussions are ongoing.

Refer also to going concern, note 2 and subsequent events note 21(f).

The Debt is otherwise payable as noted below.

(a) | The credit facility bears interest at the PACE base rate of 7.00% plus 1.25% per annum, currently 8.25% |

, | |

(b) | The credit facility advanced on June 15, 2017, in the amount of $448,980 ($600,000 CAD), bears interest at the PACE base of 7.00% plus 1.25% per annum, currently 8.25% |

(c) | The credit facility advanced on August 4, 2017, in the amount of $37,415 ($50,000 CAD), bears interest at the PACE base of 7.00% plus 1.25% per annum, currently 8.25% |

(d) | The corporate term loan advanced on September 13, 2017, in the amount of $2,786,779 ($3,724,147 CAD), bears interest at PACE base rate of 7.00% plus 1.25% per annum, currently 8.25% |

The shares of the wholly-owned subsidiaries and those shares held by the companies and the CFO noted under (a) above, represent security for the corporate term loan. |

Repayments are as follows:

For the three-month periodthree and nine-month periods ended March 31,September 30, 2019, $77,619$78,919 ($103,189104,202 CAD) and $234,441 ($311,592 CAD) (2018-$80,775; $102,11882,720; $107,984 CAD and $241,153; $310,403 CAD) respectively, in interest was charged.incurred.

![]()

19

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| (Expressed in United States Dollars) |

| (unaudited) |

11.14. Obligations under Capital Lease

| March 31, | December 31, | |||||||||||

| 2019 | 2018 | |||||||||||

| (a) | (b) | Total | Total | |||||||||

| Obligations under Capital Lease | $ | 143,493 | $ | 134,662 | $ | 278,155 | $ | 288,708 | ||||

| Less: current portion | (48,961 | ) | (38,756 | ) | (87,717 | ) | (81,109 | ) | ||||

| Obligations under Capital Lease-Long-term | $ | 94,532 | $ | 95,906 | $ | 190,438 | $ | 207,599 |

| September 30, | December 31, | ||||||||||||

| 2019 | 2018 | ||||||||||||

| (a) | (b) | Total | Total | ||||||||||

| Obligations under Capital Lease | $ | 118,591 | $ | 116,631 | $ | 235,222 | $ | 288,708 | |||||

| Less: current portion | (118,591 | ) | (116,631 | ) | (235,222 | ) | (81,109 | ) | |||||

| Long-term portion | $ | - | $ | - | $ | - | $ | 207,599 |

As a result of the PACE default, these leases are also in default. The lessor may demand full repayment of these obligations under capital lease. And, as a result, the obligations under capital lease have been presented as current liabilities. The original terms of the obligations under capital lease are noted below under paragraphs (a) and (b). Also refer to going concern, note 2 and subsequent events, note 21(f).

| (a) | The lease agreement for certain equipment for the | |

| (b) | The lease agreement for certain equipment for the |

The lease liabilities are secured by the equipment under capital lease as described in note 7.9.

Refer also to going concern, note 2 and subsequent events, note 21(f).

Minimum lease payments as per the original terms of the obligations under capital lease are as follows:

| In the | $ | | |

| In the year ending December 31, 2020 | |||

| In the year ending December 31, 2021 | |||

| In the year ending December 31, 2022 | |||

| Less: imputed interest | ( | ) | |

| Total | $ | |

For the three-month periodthree and nine-month periods ended March 31,September 30, 2019, $3,670$3,682 ($4,8794,856 CAD) and $12,237 ($16,264 CAD) (2018-$4,172; $5,2744,290; $5,615 CAD and $14,028; $18,056 CAD) respectively, in interest was charged.incurred.

12.![]()

20

| SusGlobal Energy Corp. |

| Notes to the Interim Condensed Consolidated Financial Statements |

| September 30, 2019 and 2018 |

| (Expressed in United States Dollars) |

| (unaudited) |

15. Convertible Promissory Notes

| March 31, | December 31, | ||||||

| 2019 | 2018 | ||||||

| (a) | Convertible promissory notes-January 28, 2019 (net of unamortized financing costs of $29,055 (2018- $nil)) | $ | 308,445 | $ | - | ||

| (b) | Convertible promissory notes-March 7 and March 8, 2019 (net of unamortized financing costs of $87,948) (2018- $nil)) | 462,052 | - | ||||

| $ | 770,497 | $ | - |

(a) On January 28, 2019, the Company entered into securities purchase agreements (the “January 2019 SPAs”) with three investors (the “January 2019 Investors”) pursuant to which the Company issued to the January 2019 Investors 12% unsecured convertible promissory notes (the “January 2019 Notes”) in the aggregate principal amount of $337,500, with such principal and the interest thereon convertible into shares of the Company’s common stock (the “Common Stock”) at the January 2019 Investors’ option. Although the January 2019 SPAs are dated January 28, 2019 (the “January 2019 Effective Date”

| September 30, 2019 | December 31, 2018 | ||||||

| (a) | Convertible promissory notes-January 28, 2019 (net of unamortizedfinancing costs of $11,507 (2018- $nil)) | $ | 261,723 | $ | - | ||

| (b) | Convertible promissory notes-March 7 and March 8, 2019 (net ofunamortized financing costs of $61,165) (2018- $nil)) | 743,835 | - | ||||

| (c) | Convertible promissory note-May 23, 2019 (net of unamortizedfinancing costs of $29,455 (2018-$nil)) | 220,545 | - | ||||

| (d) | Convertible promissory note-July 19, 2019 (net of unamortizedfinancing costs of $25,420 (2018-$nil)) | 144,580 | - | ||||

| $ | 1,370,683 | $ | - |

| (a) | On January 28, 2019, the Company entered into securities purchase agreements (the "January 2019 SPAs") with three investors (the "January 2019 Investors") pursuant to which the Company issued to the January 2019 Investors 12% unsecured convertible promissory notes (the "January 2019 Notes") in the aggregate principal amount of $337,500, with such principal and the interest thereon convertible into shares of the Company's common stock (the "Common Stock") at the January 2019 Investors' option. Although the January 2019 SPAs are dated January 28, 2019 (the "January 2019 Effective Date"), they became effective upon the receipt in cash of the issue price by the January 2019 Investors.

21

22

The

23

15. Convertible Promissory Notes, Pursuant to the terms of the

The

As a result of the PACE default, these convertible promissory notes are also in default. The investors may demand full repayment with accrued interest and further penalties that they are entitled to. Refer also to going concern, note 2 and subsequent events, note 21(f). 16. Mortgage Payable The Company obtained a mortgage provided by private lenders to finance the acquisition of the shares of 1684567, as noted under note 6, business acquisition. The mortgage has a principal amount of $1,359,180 ($1,800,000 CAD), is repayable interest only on a monthly basis at an annual rate of 10% per annum and is due May 24, 2020. The mortgage payable is secured by way of shares for 1684567, a first mortgage on the premises, a general assignment of rents, a fire insurance policy and is guaranteed by the Company. Financing fees on the mortgage totaled $81,619 ($108,090 CAD).

For the three and nine-month periods ended September 30, 2019, $34,162 ($45,343 CAD) and $47,845 ($63,590 CAD) (2018-$nil; $nil CAD and $nil; $nil CAD respectively, in interest was incurred.

24

Loan payable in the amount of Loans payable to directors in the amount of $nil ($nil CAD) (December 31, 2018-$54,975; $75,000 CAD), owing to three directors bear interest at the rate of 12% per annum, is due on demand and is unsecured. The loans and related accrued interest were repaid on July 19, 2019. As at

As at

In addition, during the prior year, the Company issued 190,000 common shares of the Company, in regard to the $178,200 proceeds received from a private placement prior to December 31, 2017, net of share issue costs of $11,800 and issued 20,000 common shares of the Company to a new director, determined to be valued at $20,000, based on private placement pricing at the time. All non-cash transactions were valued based on the proceeds of a recent private placement.

25

18. Capital Stock, (continued) The Company also granted the CEO 3,000,000 RSUs under a new consulting agreement effective January 1, 2017. The RSUs are expected to vest in three equal installments annually on each of January 1, 2018, 2019 and 2020. The CEO has forfeited his 2019 RSUs, as a result of his ceasing in providing his services as a CEO in September 2019. On February 25, 2018, the Company issued 1,000,000 common shares in exchange for 1,000,000 RSUs to the CEO. In addition, on May 17, 2018, at a meeting of the Board, the Board approved an amendment to the

The CFO is currently consulting on a month to month basis at $4,531 ($6,000 CAD) per month, on the same terms and conditions as his consulting agreement, which expired March 31, 2019. Refer also to subsequent events, note 21(g).

26

The Company generated

The

27

28 Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations. Certain statements in this Management's Discussion and Analysis ("MD&A"), other than purely historical information, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements generally can be identified by the use of forward-looking terminology such as "may," "would," "expect," "intend," "could," "estimate," "should," "anticipate," or "believe," and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise. Readers should carefully review the risk factors in our Annual Report on Form 10-K for the fiscal year ended December 31, 2018 filed with the Securities and Exchange Commission on April 1, 2019. The following MD&A is intended to help readers understand the results of our operation and financial condition, and is provided as a supplement to, and should be read in conjunction with, our Interim Unaudited Financial Statements and the accompanying Notes to Interim Unaudited Financial Statements under Part 1, Item 1 of this Quarterly Report on Form 10-Q. Growth and percentage comparisons made herein generally refer to the SPECIAL NOTICE ABOUT GOING CONCERN AUDIT OPINION OUR AUDITOR ISSUED AN OPINION EXPRESSING SUBSTANTIAL DOUBT AS TO OUR ABILITY TO CONTINUE IN BUSINESS AS A GOING CONCERN FOR THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2018 AND 2017. YOU SHOULD READ THIS QUARTERLY REPORT ON FORM 10-Q WITH THE This OVERVIEW The following organization chart sets forth our wholly-owned subsidiaries:

29