UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

| |

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended SeptemberJune 30, 20172019

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-14287

Centrus Energy Corp.

|

| |

| Delaware | 52-2107911 |

| (State of incorporation) | (I.R.S. Employer Identification No.) |

6901 Rockledge Drive, Suite 800, Bethesda, Maryland 20817

(301) 564-3200

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically, and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | |

| Large accelerated filer | o | | Smaller reporting company | ý |

| Accelerated filer | o | | Non-accelerated filer | ý |

| Smaller reporting company | ý | | Emerging growth company | o |

Non-accelerated filer | o | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ý No o

Securities registered pursuant to Section 12(b) of the Act: |

| | |

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered |

| Class A Common Stock, par value $0.10 per share | LEU | NYSE American |

| Rights to purchase Series A Participating Cumulative Preferred Stock, par value $1.00 per share | LEU* | Not applicable |

*The rights currently transfer with the shares of Common Stock

As of NovemberAugust 1, 2017,2019, there were 7,632,6698,051,307 shares of the registrant’s Class A Common Stock, par value $0.10 per share, and 1,406,082 shares of the registrant’s Class B Common Stock, par value $0.10 per share, outstanding.

TABLE OF CONTENTS

|

| | |

| | | Page |

| | PART I – FINANCIAL INFORMATION | |

| | |

| | |

| | | |

| | | |

| | |

| | | |

| | | |

| | | |

| | |

| | |

| | |

| | | |

| | PART II – OTHER INFORMATION | |

| | |

| | |

| | |

| |

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q, including Management’s Discussion and Analysis of Financial Condition and Results of Operations in Part I, Item 2, contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934 - that is, statements related to future events. In this context, forward-looking statements may address our expected future business and financial performance, and often contain words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “will”, “should”, “could”, “would” or “may” and other words of similar meaning. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For Centrus Energy Corp., particular risks and uncertainties that could cause our actual future results to differ materially from those expressed in our forward-looking statements includeinclude: risks related to our significant long-term liabilities, including material unfunded defined benefit pension plan obligations and postretirement health and life benefit obligations; risks relating to our outstanding 8.0% paid-in-kind (“PIK”) toggle notes (the “8% PIK Toggle Notes”) maturing in September 2019, our 8.25% notes (the “8.25% Notes”) maturing in February 2027 (the “8.25% Notes”) and our Series B Senior Preferred Stock, (the “Series B Preferred Stock”), including the potential termination of the guarantee by our principal subsidiary United States Enrichment Corporation (“Enrichment Corp.”) of the 8% PIK Toggle Notes; risks related to the limited trading markets in our securities; risks related to our ability to maintain the listing of our Class A Common Stock on the NYSE American LLC; risks related to decisions made by our Class B stockholders regarding their investment in the Company based upon factors that are unrelated to the Company’s performance; risks related to the use of our net operating lossesloss (“NOLs”) carryforwards and net unrealized built-in losses (“NUBILs”) to offset future taxable income and the use of the Rights Agreement (as defined herein) to prevent an “ownership change” as defined in Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”) and our ability to generate taxable income to utilize all or a portion of the NOLs and NUBILs prior to the expiration thereof; risks related to the limited trading markets in our securities; risks related to our ability to maintain the listing of our Class A Common Stock on the NYSE American LLC (the “NYSE American”); risks related to decisions made by our Class B stockholders regarding their investment in the Company based upon factors that are unrelated to the Company’s performance; risks related to the Company’s capital concentration; the continued impact of the March 2011 earthquake and tsunami in Japan on the nuclear industry and on our business, results of operations and prospects; the impact and potential extended duration of the current supply/demand imbalance in the market for low-enriched uranium (“LEU”);our dependence on others fordeliveries of LEU including deliveries from the Russian governmentgovernment-owned entity Joint Stock Company “TENEX” (“TENEX”) under a commercial supply agreement with

TENEX (the “Russian Supply Agreement”and deliveries under a long-term supply agreement with Orano Cycle (“Orano”); risks related to our ability to sell the LEU we procure pursuant to our purchase obligations under our supply agreements, including the Russian Supply Agreement;agreements; risks relating to our sales order book, including uncertainty concerning customer actions under current contracts and in future contracting due to market conditions and lack of current production capability; risks related to financial difficulties experienced by

customers, including possible bankruptcies, insolvencies or any other inability to pay for our products or services; pricing trends and demand in the uranium and enrichment markets and their impact on our profitability; movement and timing of customer orders; risks related to the value of our intangible assets related to the sales order book and customer relationships; risks associated with our reliance on third-party suppliers to provide essential products and services to us; pricing trends and demand in the uranium and enrichment markets and their impact on our profitability; movement and timing of customer orders; risks related to existing or new trade barriers and contract terms that limit our ability to deliver LEU to customers; risks related to actions, including government reviews, that may be taken by the U.S. government, the Russian government or other governments that could affect our ability to perform under our contract obligations or the ability of our sources of supply to perform under their contract obligations to us, including the imposition of sanctions, restrictions or other requirements; the impact of government regulation including by the U.S. Department of Energy (“DOE”) and the U.S. Nuclear Regulatory Commission; uncertainty regarding our ability to commercially deploy competitive enrichment technology; risks and uncertainties regarding funding for the American Centrifuge project and our ability to perform under our agreement with DOE to demonstrate the capability to produce high assay low enriched uranium (“HALEU”) and our ability to obtain and/or perform under our future agreements with the DOE, UT-Battelle, LLC (“UT-Battelle”), the management and operating contractor for Oak Ridge National Laboratory (“ORNL”), for continued research and development of the American Centrifuge technology; the potential for further demobilization or termination of the American Centrifuge project; risks related to our ability to perform and receive timely payment under agreements with the current demobilization of portionsDOE, including risk and uncertainties related to the ongoing funding of the American Centrifuge project,government and potential audits; the competitive bidding process associated with obtaining a federal contract; risks related to our ability to perform fixed-price contracts, including risksthe risk that the schedule could be delayed and costs could be higher than expected; risks that we will be unable to obtain new business opportunities, achieve market acceptance of our products and services or that products or services provided by others will render our goods or services obsolete or noncompetitive; risks that we will not be able to timely complete the work that we are obligated to perform; failures or security breaches of our information technology systems; potential strategic transactions, which could be difficult to implement, disrupt our business or change our business profile significantly; the outcome of legal proceedings and other contingencies (including lawsuits and government investigations or audits); thecompetitive environment for our products and services; changes in the nuclear energy industry; the impact of financial market conditions on our business, liquidity, prospects, pension assets and insurance facilities; risks related to the identification of a material weakness in our internal controls over financial reporting; the risks of revenue and operating results can fluctuatefluctuating significantly from quarter to quarter, and in some cases, year to year; and other risks and uncertainties discussed in this and our other filings with the Securities and Exchange Commission, including under Part 1. Item1A - “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2016.2018.

These factors may not constitute all factors that could cause actual results to differ from those discussed in any forward-looking statement. Accordingly, forward-looking statements should be not be relied upon as a predictor of actual results. Readers are urged to carefully review and consider the various disclosures made in this report and in our other filings with the Securities and Exchange Commission that attempt to advise interested parties of the risks and factors that may affect our business. We do not undertake to update our forward-looking statements to reflect events or circumstances that may arise after the date of this Quarterly Report on Form 10-Q, except as required by law.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

(Unaudited; in millions, except share and per share data)

| | | | September 30,

2017 | | December 31,

2016 | June 30,

2019 | | December 31,

2018 |

| ASSETS | | | | | | |

| Current assets | | | | |

| Current assets: | | | | |

| Cash and cash equivalents | $ | 135.9 |

| | $ | 260.7 |

| $ | 88.3 |

| | $ | 123.1 |

|

| Accounts receivable | 14.2 |

| | 19.9 |

| 30.2 |

| | 60.2 |

|

| Inventories | 124.1 |

| | 177.4 |

| 141.7 |

| | 129.7 |

|

| Deferred costs associated with deferred revenue | 94.5 |

| | 89.3 |

| 138.7 |

| | 134.9 |

|

| Deposits for financial assurance | | 18.0 |

| | 30.3 |

|

| Other current assets | 15.6 |

| | 13.3 |

| 7.4 |

| | 6.3 |

|

| Total current assets | 384.3 |

| | 560.6 |

| 424.3 |

| | 484.5 |

|

| Property, plant and equipment, net | 5.2 |

| | 6.0 |

| |

| Deposits for surety bonds | 29.6 |

| | 29.5 |

| |

| Property, plant and equipment, net of accumulated depreciation of $1.9 as of June 30, 2019 and $1.6 as of December 31, 2018 | | 3.9 |

| | 4.2 |

|

| Deposits for financial assurance | | 5.7 |

| | 6.3 |

|

| Intangible assets, net | 87.6 |

| | 93.3 |

| 73.7 |

| | 76.0 |

|

| Other long-term assets | 15.2 |

| | 24.1 |

| 7.7 |

| | 0.7 |

|

| Total assets | $ | 521.9 |

| | $ | 713.5 |

| $ | 515.3 |

| | $ | 571.7 |

|

| | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | |

| | |

| |

| | |

|

| Current liabilities | |

| | |

| |

| Current liabilities: | | |

| | |

|

| Accounts payable and accrued liabilities | $ | 50.7 |

| | $ | 46.4 |

| $ | 37.9 |

| | $ | 52.4 |

|

| Payables under SWU purchase agreements | 17.3 |

| | 59.6 |

| 14.9 |

| | 46.0 |

|

| Inventories owed to customers and suppliers | 22.1 |

| | 57.5 |

| 59.0 |

| | 103.0 |

|

| Deferred revenue | 131.7 |

| | 123.6 |

| |

| Decontamination and decommissioning obligations | 16.6 |

| | 38.6 |

| |

| Deferred revenue and advances from customers | | 267.2 |

| | 204.5 |

|

| Current debt | | 33.6 |

| | 32.8 |

|

| Total current liabilities | 238.4 |

| | 325.7 |

| 412.6 |

| | 438.7 |

|

| Long-term debt | 157.5 |

| | 234.1 |

| 117.1 |

| | 120.2 |

|

| Postretirement health and life benefit obligations | 170.0 |

| | 171.3 |

| 132.6 |

| | 136.2 |

|

| Pension benefit liabilities | 175.0 |

| | 179.9 |

| 161.5 |

| | 168.9 |

|

| Advances from customers | | 29.4 |

| | 15.0 |

|

| Other long-term liabilities | 35.6 |

| | 38.6 |

| 20.4 |

| | 14.6 |

|

| Total liabilities | 776.5 |

| | 949.6 |

| 873.6 |

| | 893.6 |

|

| Commitments and contingencies (Note 12) |

|

| |

|

|

|

| |

|

|

| Stockholders’ deficit | | | | |

| Stockholders’ deficit: | | | | |

| Preferred stock, par value $1.00 per share, 20,000,000 shares authorized | | | | | | |

| Series A Participating Cumulative Preferred Stock, none issued | — |

| | — |

| — |

| | — |

|

| Series B Senior Preferred Stock, 7.5% cumulative, 104,574 shares issued and outstanding and an aggregate liquidation preference of $109.6 million as of September 30, 2017 | 4.6 |

| | — |

| |

| Class A Common Stock, par value $0.10 per share, 70,000,000 shares authorized, 7,632,669 and 7,563,600 shares issued and outstanding as of September 30, 2017 and December 31, 2016 | 0.8 |

| | 0.8 |

| |

| Class B Common Stock, par value $0.10 per share, 30,000,000 shares authorized, 1,406,082 and 1,436,400 shares issued and outstanding as of September 30, 2017 and December 31, 2016 | 0.1 |

| | 0.1 |

| |

| Series B Senior Preferred Stock, 7.5% cumulative, 104,574 shares issued and outstanding and an aggregate liquidation preference of $123.2 as of June 30, 2019 and $119.3 as of December 31, 2018 | | 4.6 |

| | 4.6 |

|

| Class A Common Stock, par value $0.10 per share, 70,000,000 shares authorized, 8,051,307 shares issued and outstanding as of June 30, 2019 and 8,031,307 as of December 31, 2018 | | 0.8 |

| | 0.8 |

|

| Class B Common Stock, par value $0.10 per share, 30,000,000 shares authorized, 1,406,082 shares issued and outstanding as of June 30, 2019 and December 31, 2018 | | 0.1 |

| | 0.1 |

|

| Excess of capital over par value | 59.8 |

| | 59.5 |

| 61.3 |

| | 61.2 |

|

| Accumulated deficit | (320.0 | ) | | (296.7 | ) | (425.0 | ) | | (388.5 | ) |

| Accumulated other comprehensive income, net of tax | 0.1 |

| | 0.2 |

| (0.1 | ) | | (0.1 | ) |

| Total stockholders’ deficit | (254.6 | ) | | (236.1 | ) | (358.3 | ) | | (321.9 | ) |

| Total liabilities and stockholders’ deficit | $ | 521.9 |

| | $ | 713.5 |

| $ | 515.3 |

| | $ | 571.7 |

|

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(Unaudited; in millions, except share and per share data)

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | 2017 | | 2016 | | 2017 | | 2016 | 2019 | | 2018 | | 2019 | | 2018 |

| Revenue: | | | | | | | | | | | | | | |

| Separative work units | $ | 43.5 |

| | $ | 14.1 |

| | $ | 82.2 |

| | $ | 128.3 |

| $ | — |

| | $ | 32.9 |

| | $ | 12.4 |

| | $ | 50.6 |

|

| Uranium | — |

| | — |

| | — |

| | 14.3 |

| 2.6 |

| | — |

| | 25.3 |

| | 3.6 |

|

| Contract services | 6.8 |

| | 7.3 |

| | 19.3 |

| | 32.2 |

| 8.0 |

| | 6.5 |

| | 11.6 |

| | 20.9 |

|

| Total revenue | 50.3 |

| | 21.4 |

| | 101.5 |

| | 174.8 |

| 10.6 |

| | 39.4 |

| | 49.3 |

| | 75.1 |

|

| Cost of Sales: | | | | | | | | | | | | | | |

| Separative work units and uranium | 32.4 |

| | 15.9 |

| | 76.8 |

| | 130.7 |

| 7.7 |

| | 42.9 |

| | 46.0 |

| | 77.7 |

|

| Contract services | 6.3 |

| | 7.6 |

| | 19.9 |

| | 24.9 |

| 7.2 |

| | 7.2 |

| | 13.1 |

| | 13.4 |

|

| Total cost of sales | 38.7 |

| | 23.5 |

| | 96.7 |

| | 155.6 |

| 14.9 |

| | 50.1 |

| | 59.1 |

| | 91.1 |

|

| Gross profit (loss) | 11.6 |

| | (2.1 | ) | | 4.8 |

| | 19.2 |

| |

| Advanced technology license and decommissioning costs | 4.5 |

| | 21.9 |

| | 15.0 |

| | 38.6 |

| |

| Gross loss | | (4.3 | ) | | (10.7 | ) | | (9.8 | ) | | (16.0 | ) |

| Advanced technology costs | | 5.1 |

| | 5.4 |

| | 11.7 |

| | 13.4 |

|

| Selling, general and administrative | 11.0 |

| | 10.7 |

| | 33.1 |

| | 34.6 |

| 7.7 |

| | 9.7 |

| | 15.8 |

| | 20.9 |

|

| Amortization of intangible assets | 2.5 |

| | 1.7 |

| | 5.7 |

| | 7.6 |

| 1.2 |

| | 1.5 |

| | 2.3 |

| | 2.8 |

|

| Special charges for workforce reductions and advisory costs | 2.4 |

| | 0.6 |

| | 7.1 |

| | 1.2 |

| |

| Gains on sales of assets | (0.6 | ) | | (0.3 | ) | | (2.3 | ) | | (1.0 | ) | |

| Special charges (credits) for workforce reductions and advisory costs | | (2.9 | ) | | 0.3 |

| | (3.0 | ) | | 0.9 |

|

| Gain on sales of assets | | (0.1 | ) | | (0.2 | ) | | (0.5 | ) | | (0.3 | ) |

| Operating loss | (8.2 | ) | | (36.7 | ) | | (53.8 | ) | | (61.8 | ) | (15.3 | ) | | (27.4 | ) | | (36.1 | ) | | (53.7 | ) |

| Gain on early extinguishment of debt | — |

| | — |

| | (33.6 | ) | | (16.7 | ) | |

| Nonoperating components of net periodic benefit expense (income) | | — |

| | (1.7 | ) | | (0.1 | ) | | (3.3 | ) |

| Interest expense | 0.7 |

| | 4.7 |

| | 4.3 |

| | 14.8 |

| 1.0 |

| | 1.0 |

| | 2.0 |

| | 2.0 |

|

| Investment income | (0.4 | ) | | (0.1 | ) | | (1.0 | ) | | (0.5 | ) | (0.7 | ) | | (0.6 | ) | | (1.4 | ) | | (1.2 | ) |

| Loss before income taxes | (8.5 | ) | | (41.3 | ) | | (23.5 | ) | | (59.4 | ) | (15.6 | ) | | (26.1 | ) | | (36.6 | ) | | (51.2 | ) |

| Income tax benefit | — |

| | — |

| | (0.2 | ) | | (0.6 | ) | — |

| | — |

| | (0.1 | ) | | (0.1 | ) |

| Net loss | (8.5 | ) | | (41.3 | ) | | (23.3 | ) | | (58.8 | ) | |

| Net loss and comprehensive loss | | (15.6 | ) | | (26.1 | ) | | (36.5 | ) | | (51.1 | ) |

| Preferred stock dividends - undeclared and cumulative | 2.0 |

| | — |

| | 5.0 |

| | — |

| 2.0 |

| | 2.0 |

| | 4.0 |

| | 4.0 |

|

| Net loss allocable to common stockholders | $ | (10.5 | ) | | $ | (41.3 | ) | | $ | (28.3 | ) | | $ | (58.8 | ) | $ | (17.6 | ) | | $ | (28.1 | ) | | $ | (40.5 | ) | | $ | (55.1 | ) |

| | | | | | | | | | | | | | | |

| Net loss per common share – basic and diluted | $ | (1.15 | ) | | $ | (4.54 | ) | | $ | (3.12 | ) | | $ | (6.46 | ) | |

| Average number of common shares outstanding – basic and diluted (in thousands) | 9,103 |

| | 9,096 |

| | 9,081 |

| | 9,102 |

| |

| Net loss per common share - basic and diluted | | $ | (1.84 | ) | | $ | (3.08 | ) | | $ | (4.24 | ) | | $ | (6.05 | ) |

| Average number of common shares outstanding - basic and diluted (in thousands) | | 9,565 |

| | 9,118 |

| | 9,549 |

| | 9,111 |

|

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (Unaudited)CASH FLOWS

(Unaudited; in millions)

|

| | | | | | | |

| | Six Months Ended

June 30, |

| | 2019 | | 2018 |

| OPERATING | | | |

| Net loss | $ | (36.5 | ) | | $ | (51.1 | ) |

| Adjustments to reconcile net loss to cash used in operating activities: | | | |

| Depreciation and amortization | 2.6 |

| | 3.3 |

|

| PIK interest on paid-in-kind toggle notes | 0.7 |

| | 0.9 |

|

| Gain on sales of assets | (0.5 | ) | | (0.3 | ) |

| Inventory valuation adjustments | 2.3 |

| | — |

|

| Changes in operating assets and liabilities: | | | |

| Accounts receivable | 24.6 |

| | 32.1 |

|

| Inventories, net | (6.6 | ) | | 20.4 |

|

| Payables under SWU purchase agreements | (31.1 | ) | | (59.9 | ) |

| Deferred revenue and advances from customers, net of deferred costs | 27.0 |

| | 9.8 |

|

| Accounts payable and other liabilities | (15.8 | ) | | (12.5 | ) |

| Pension and postretirement liabilities | (11.1 | ) | | (9.0 | ) |

| Other, net | (0.7 | ) | | 0.6 |

|

| Cash used in operating activities | (45.1 | ) | | (65.7 | ) |

| | | | |

| INVESTING | | | |

| Capital expenditures | — |

| | (0.1 | ) |

| Proceeds from sales of assets | 0.5 |

| | 0.3 |

|

| Cash provided by investing activities | 0.5 |

| | 0.2 |

|

| | | | |

| FINANCING | | | |

| Payment of interest classified as debt | (3.1 | ) | | (3.0 | ) |

| Cash used in financing activities | (3.1 | ) | | (3.0 | ) |

| | | | |

| Decrease in cash, cash equivalents and restricted cash | (47.7 | ) | | (68.5 | ) |

Cash, cash equivalents and restricted cash, beginning of period (1) | 159.7 |

| | 244.8 |

|

Cash, cash equivalents and restricted cash, end of period (1) | $ | 112.0 |

| | $ | 176.3 |

|

| | | | |

| Supplemental cash flow information: | | | |

| Interest paid in cash | $ | 0.4 |

| | $ | 0.4 |

|

| Non-cash activities: | | | |

| Conversion of interest payable-in-kind to debt | $ | 0.7 |

| | $ | 0.9 |

|

_______________

(1)Refer to Note 4, Cash, Cash Equivalents and Restricted Cash.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ DEFICIT

(Unaudited; in millions, except per share data)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Net loss | $ | (8.5 | ) | | $ | (41.3 | ) | | $ | (23.3 | ) | | $ | (58.8 | ) |

| Other comprehensive loss, before tax (Note 13): | | | | | | | |

| Amortization of prior service credits, net | — |

| | (0.1 | ) | | (0.1 | ) | | (0.2 | ) |

| Other comprehensive loss, before tax | — |

| | (0.1 | ) | | (0.1 | ) | | (0.2 | ) |

| Income tax benefit related to items of other comprehensive income | — |

| | — |

| | — |

| | — |

|

| Other comprehensive loss, net of tax benefit | — |

| | (0.1 | ) | | (0.1 | ) | | (0.2 | ) |

| Comprehensive loss | $ | (8.5 | ) | | $ | (41.4 | ) | | $ | (23.4 | ) | | $ | (59.0 | ) |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Preferred Stock, Series B | | Common Stock, Class A, Par Value $.10 per Share | | Common Stock, Class B, Par Value $.10 per Share | | Excess of Capital Over Par Value | | Accumulated Deficit | | Accumulated Other Comprehensive Income | | Total |

| | | | | | | | | | | | | | |

| Balance at December 31, 2018 | $ | 4.6 |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 61.2 |

| | $ | (388.5 | ) | | $ | (0.1 | ) | | $ | (321.9 | ) |

| Net loss for the three months ended March 31, 2019 | — |

| | — |

| | — |

| | — |

| | (20.9 | ) | | — |

| | (20.9 | ) |

| Issuance and amortization of restricted stock units and stock options | — |

| | — |

| | — |

| | 0.1 |

| | — |

| | — |

| | 0.1 |

|

| Balance at March 31, 2019 | 4.6 |

| | 0.8 |

| | 0.1 |

| | 61.3 |

| | (409.4 | ) | | (0.1 | ) | | (342.7 | ) |

| | | | | | | | | | | | | | |

| Net loss for the three months ended June 30, 2019 | — |

| | — |

| | — |

| | — |

| | (15.6 | ) | | — |

| | (15.6 | ) |

| Balance at June 30, 2019 | $ | 4.6 |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 61.3 |

| | $ | (425.0 | ) | | $ | (0.1 | ) | | $ | (358.3 | ) |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Preferred Stock, Series B | | Common Stock, Class A, Par Value $.10 per Share | | Common Stock, Class B, Par Value $.10 per Share | | Excess of Capital Over Par Value | | Accumulated Deficit | | Accumulated Other Comprehensive Income | | Total |

| | | | | | | | | | | | | | |

| Balance at December 31, 2017 | $ | 4.6 |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 60.0 |

| | $ | (284.5 | ) | | $ | 0.1 |

| | $ | (218.9 | ) |

| Adoption of Accounting Standards Codification 606 as of January 1, 2018 | — |

| | — |

| | — |

| | — |

| | 0.1 |

| | — |

| | 0.1 |

|

| Net loss for the three months ended March 31, 2018 | — |

| | — |

| | — |

| | — |

| | (25.0 | ) | | — |

| | (25.0 | ) |

| Issuance and amortization of restricted stock units and stock options | — |

| | — |

| | — |

| | 0.1 |

| | — |

| | — |

| | 0.1 |

|

| Balance at March 31, 2018 | 4.6 |

| | 0.8 |

| | 0.1 |

| | 60.1 |

| | (309.4 | ) | | 0.1 |

| | (243.7 | ) |

| | | | | | | | | | | | | | |

| Net loss for the three months ended June 30, 2018 | — |

| | — |

| | — |

| | — |

| | (26.1 | ) | | — |

| | (26.1 | ) |

| Other comprehensive loss, net of tax benefit | — |

| | — |

| | — |

| | — |

| | — |

| | (0.1 | ) | | (0.1 | ) |

| Issuance and amortization of restricted stock units and stock options | — |

| | — |

| | — |

| | 0.1 |

| | — |

| | — |

| | 0.1 |

|

| Balance at June 30, 2018 | $ | 4.6 |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 60.2 |

| | $ | (335.5 | ) | | $ | — |

| | $ | (269.8 | ) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(in millions)

|

| | | | | | | |

| | Nine Months Ended

September 30, |

| | 2017 | | 2016 |

| Operating Activities | | | |

| Net loss | $ | (23.3 | ) | | $ | (58.8 | ) |

| Adjustments to reconcile net loss to cash used in operating activities: | | | |

| Depreciation and amortization | 6.6 |

| | 8.1 |

|

| PIK interest on paid-in-kind toggle notes | 1.2 |

| | 9.7 |

|

| Gain on early extinguishment of debt | (33.6 | ) | | (16.7 | ) |

| Gain on sales of assets | (2.3 | ) | | (1.0 | ) |

| Inventory valuation adjustments | — |

| | 3.0 |

|

| Changes in operating assets and liabilities: | | | |

| Accounts receivable | 14.5 |

| | 18.4 |

|

| Inventories, net | 17.9 |

| | 45.8 |

|

| Payables under SWU purchase agreements | (42.3 | ) | | (68.9 | ) |

| Deferred revenue, net of deferred costs | 2.9 |

| | 5.8 |

|

| Accounts payable and other liabilities | (35.3 | ) | | 2.2 |

|

| Other, net | (1.9 | ) | | 0.5 |

|

| Cash used in operating activities | (95.6 | ) | | (51.9 | ) |

| | | | |

| Investing Activities | | | |

| Capital expenditures | (0.3 | ) | | (3.0 | ) |

| Proceeds from sales of assets | 2.1 |

| | 1.2 |

|

| Deposits for surety bonds - net decrease | — |

| | 0.3 |

|

| Cash provided by (used in) investing activities | 1.8 |

| | (1.5 | ) |

| | | | |

| Financing Activities | | | |

| Payment of interest classified as debt | (3.4 | ) | | — |

|

| Repurchase of debt | (27.6 | ) | | (9.8 | ) |

| Cash used in financing activities | (31.0 | ) | | (9.8 | ) |

| | | | |

| Decrease in cash and cash equivalents | (124.8 | ) | | (63.2 | ) |

| Cash and cash equivalents at beginning of period | 260.7 |

| | 234.0 |

|

| Cash and cash equivalents at end of period | $ | 135.9 |

| | $ | 170.8 |

|

| | | | |

| Supplemental cash flow information: | | | |

| Interest paid in cash | $ | 4.2 |

| | $ | 6.5 |

|

| Non-cash activities: | | | |

| Conversion of interest payable-in-kind to long-term debt | $ | 0.4 |

| | $ | 3.4 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

CENTRUS ENERGY CORP.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ DEFICIT (Unaudited)

(in millions, except per share data)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Preferred Stock, Series B | | Common Stock, Class A, Par Value $.10 per Share | | Common Stock, Class B, Par Value $.10 per Share | | Excess of Capital Over Par Value | | Accumulated Deficit | | Accumulated Other Comprehensive Income | | Total |

| | | | | | | | | | | | | | |

| Balance at December 31, 2015 | $ | — |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 59.0 |

| | $ | (229.7 | ) | | $ | 4.1 |

| | $ | (165.7 | ) |

| Net loss | — |

| | — |

| | — |

| | — |

| | (58.8 | ) | | — |

| | (58.8 | ) |

| Other comprehensive loss, net of tax benefit (Note 13) | — |

| | — |

| | — |

| | — |

| | — |

| | (0.2 | ) | | (0.2 | ) |

| Restricted stock units and stock options issued, net of amortization | — |

| | — |

| | — |

| | 0.4 |

| | — |

| | — |

| | 0.4 |

|

| Balance at September 30, 2016 | $ | — |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 59.4 |

| | $ | (288.5 | ) | | $ | 3.9 |

| | $ | (224.3 | ) |

| | | | | | | | | | | | | | |

| Balance at December 31, 2016 | $ | — |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 59.5 |

| | $ | (296.7 | ) | | $ | 0.2 |

| | $ | (236.1 | ) |

| Net loss | — |

| | — |

| | — |

| | — |

| | (23.3 | ) | | — |

| | (23.3 | ) |

| Issuance of preferred stock | 4.6 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 4.6 |

|

| Other comprehensive loss, net of tax benefit (Note 13) | — |

| | — |

| | — |

| | — |

| | — |

| | (0.1 | ) | | (0.1 | ) |

| Restricted stock units and stock options issued, net of amortization | — |

| | — |

| | — |

| | 0.3 |

| | — |

| | — |

| | 0.3 |

|

| Balance at September 30, 2017 | $ | 4.6 |

| | $ | 0.8 |

| | $ | 0.1 |

| | $ | 59.8 |

| | $ | (320.0 | ) | | $ | 0.1 |

| | $ | (254.6 | ) |

The accompanying notes are an integral part of theseunaudited condensed consolidated financial statements.

CENTRUS ENERGY CORP.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

1. BASIS OF PRESENTATION

Basis of Presentation and Principles of Consolidation

The unaudited condensed consolidated financial statements of Centrus Energy Corp. (“Centrus” or the “Company”), which include the accounts of the Company, its principal subsidiary, United States Enrichment Corporation, (“Enrichment Corp.”) and its other subsidiaries, as of SeptemberJune 30, 2017,2019, and for the three and ninesix months ended SeptemberJune 30, 20172019 and 2016,2018, have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). The condensed consolidated balance sheet as of December 31, 2016,2018, was derived from audited consolidated financial statements, but does not include all disclosures required by generally accepted accounting principles in the United States (“GAAP”). TheIn the opinion of management, the unaudited condensed consolidated financial statements reflect all adjustments, that are, in the opinion of management,including normal recurring adjustments, necessary for a fair statement of the financial results for the interim period. Certain prior year amounts have been reclassified for consistency with the current year presentation. Certain information and notes normally included in financial statements prepared in accordance with GAAP have been omitted pursuant to such rules and regulations. All material intercompany transactions have been eliminated. The Company’s components of comprehensive income for the three and six months ended June 30, 2019 and 2018 are insignificant.

Operating results for the three and ninesix months ended SeptemberJune 30, 2017,2019, are not necessarily indicative of the results that may be expected for the year ending December 31, 2017.2019. The unaudited condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and related notes and Management's Discussion and Analysis of Financial Condition and Results of Operations included in the Annual Report on Form 10-K for the year ended December 31, 2016.2018.

New Accounting Standards

Recently Adopted Accounting Standards

In May 2014,February 2016, the Financial Accounting Standards Board (the “FASB”(“FASB”) issued Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers (Topic 606). ASU 2014-09 introduces a new five-step revenue recognition model in which an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. ASU 2014-09 also requires disclosures sufficient to enable users to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers, including qualitative and quantitative disclosures about contracts with customers, significant judgments and changes in judgments, and assets recognized from the costs to obtain or fulfill a contract. The FASB has since issued amendments that clarify a number of specific issues as well as require additional disclosures. The revenue recognition standard will become effective for the Company beginning with the first quarter of 2018. The Company has started an implementation process, including a review of customer contracts, to evaluate the effect this standard will have on its consolidated financial statements and related disclosures. The Company continues to assess the potential impacts of the new standard on its consolidated financial statements, including substantive new disclosures. The Company plans to select the modified retrospective transition method upon adoption effective January 1, 2018.

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842)(“Topic 842”), which requires lessees to recognize a right-of-use asset and lease liability on the balance sheet for all leases with termsa term longer than 12 months. Leases will be classifiedThe Company adopted this standard on January 1, 2019, using the modified transition method which provides for recognition of existing leases as either finance or operating, with classification affecting expense recognition inof the statement of operations. ASU 2016-02 will become effectiveadoption date without requiring comparable presentation for the Company beginning inprior period. Lease assets and liabilities are recognized based on the first quarterpresent value of 2019, with early adoption permitted, and is to be applied using a modified retrospective approach.lease payments over the lease term. The Company’s leases do not provide an implicit interest rate. The Company is evaluatinguses an estimated incremental borrowing rate based on the effect that the provisions of ASU 2016-02 will have on its consolidated financial statements.

In March 2016, the FASB issued ASU 2016-09, Stock Compensation - Improvements to Employee Share-Based Payment Accounting (Topic 718). ASU 2016-09 simplifies several aspectsterm of the accounting for share-based payment transactions,lease using information available at the adoption date or the lease commencement, if later, including income tax consequences, classification of awards as either equity or liabilities, and classificationthe yield on the statement of cash flows. ASU 2016-09 became effective for the Company in the first quarter of 2017. Under ASU 2016-09, entities are permitted to make an accounting policy election to either estimate forfeitures on share-based payment awards, as previously required, or to recognize forfeitures as they occur.Company’s collateralized debt. The Company has elected to recognize forfeitures as they occur.adopt the package of practical expedients provided under Topic 842, which allowed the Company to not apply a reassessment of whether any existing or expired contracts contain leases, reassessment of lease classification for existing or expired leases and reassessment of initial direct costs for leases. The adoption of ASU 2016-09 did not have a materialthis standard had no impact on the Company’s consolidated financial statements.statement of operations or statement of cash flows. Refer to Note 8, Leases, for additional information.

In February 2018, the FASB issued ASU 2018-02, Income Statement-Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income. The amendments in ASU 2018-02 allow a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the Tax Cut and Jobs Act of 2017 (the “Tax Act”). However, because the amendments only relate to the reclassification of the income tax effects of the Tax Act, the underlying guidance that requires that the effect of a change in tax laws or rates be included in income from continuing operations is not affected. The Company adopted the new standard effective January 1, 2019, and elected not to reclassify the stranded tax effect resulting from the 2017 Tax Act to retained earnings.

Accounting Standards Effective in Future Periods

In August 2016,2018, the FASB issued ASU 2016-15,2018-14, Statement of Cash Flows (Topic 230): Classification of Certain Cash ReceiptsCompensation - Retirement Benefits - Defined Benefit Plans - General (Subtopic 715-20), which modifies the disclosure requirements for employers that sponsor defined benefit pension plans and Cash Payments.other postretirement plans. ASU 2016-15 addresses the presentation and classification of certain cash receipts and cash payments in the statement of cash flows. It2018-14 is intended to reduce diversity in practice by providing guidance on eight specific cash flow issues. ASU 2016-15 will become effective for the Companypublic companies for fiscal years, and interim periods within those fiscal years, beginning in the first quarter of 2018, with early adoption permitted, andafter December 15, 2020. The standard is to be applied usingon a retrospective approach. The Company is evaluating the effect that the provisions of ASU 2016-15 will have on its consolidated financial statements.

In October 2016, the FASB issued ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory, requiring an entitybasis to recognize the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs. ASU 2016-16 will become effective for the Company beginning in the first quarter of 2018, withall periods presented and early adoption is permitted. The Company is evaluating the effect that the provisions of ASU 2016-162018-14 will have on its consolidated financial statements.

In November 2016, the FASB issued ASU 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash. ASU 2016-18 requires that the statement of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. ASU 2016-18 is to be applied retrospectively for each period presented, and will become effective for the Company beginning in the first quarter of 2018, with early adoption permitted. The Company is evaluating the effect that the provisions of ASU 2016-18 will have on its consolidated financial statements.Significant Accounting Policies

In March 2017,The accounting policies of the FASB issued ASU 2017-07, Compensation-Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost. ASU 2017-07 requires changesCompany are set forth in Note 1 to the presentationConsolidated Financial Statements contained in the Company’s Annual Report on Form 10-K for the year ended December 31, 2018. Updates to those policies as a result of the componentsadoption of net periodic benefit cost on the statement of operations by requiring service cost to be presented with other employee compensation costs and other components of net periodic benefit cost to be presented outside of any subtotal of operating income. ASU 2017-07 also stipulates that only the service cost component of net benefit cost is eligible for capitalizationASC 842 have been included in assets. The guidance will become effective for the Company beginning in the first quarter of 2018, with early adoption permitted. The Company is evaluating the effect that the provisions of ASU 2017-07 will have on its consolidated financial statements.Note 8, Leases.

2. REVENUE AND CONTRACTS WITH CUSTOMERS

Disaggregation of Revenue

The following table presents revenue from separative work units (“SWU”) and uranium sales disaggregated by geographical region based on the billing addresses of customers (in millions):

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | 2019 | | 2018 | | 2019 | | 2018 |

| United States | $ | 2.6 |

| | $ | 32.9 |

| | $ | 37.7 |

| | $ | 54.0 |

|

| Foreign | — |

| | — |

| | — |

| | 0.2 |

|

| Revenue - SWU and uranium | $ | 2.6 |

| | $ | 32.9 |

| | $ | 37.7 |

| | $ | 54.2 |

|

Refer to Note 13, Segment Information, for disaggregation of revenue by segment. Disaggregation by end-market is provided in Note 13 and the condensed consolidated statements of operations. SWU and uranium sales are made primarily to electric utility customers. Contract services revenue resulted primarily from services provided to government contractors and, in the first quarter of 2018, the settlement with DOE and the U.S. government. SWU and uranium revenue is recognized at point of sale and contract services revenue is generally recognized over time.

Contract Balances

The following table represents changes in contract assets and contract liabilities balances (in millions):

|

| | | | | | | | | | | | |

| | | June 30, 2019 | | December 31, 2018 | | Year-To-Date Change |

| Contract assets | | | | | | |

| Accounts receivable: | | | | | | |

| Billed | | $ | 20.1 |

| | $ | 50.4 |

| | $ | (30.3 | ) |

| Unbilled | | 5.6 |

| | — |

| | 5.6 |

|

| Uranium feed receivable | | 4.5 |

| | 9.8 |

| | (5.3 | ) |

| Accounts receivable | | $ | 30.2 |

| | $ | 60.2 |

| | $ | (30.0 | ) |

| | | | | | | |

| Deferred costs associated with deferred revenue | | $ | 138.7 |

| | $ | 134.9 |

| | $ | 3.8 |

|

| | | | | | | |

| Contract liabilities | | | | | | |

| Accounts payable and accrued liabilities | | $ | 0.5 |

| | $ | — |

| | $ | 0.5 |

|

| Deferred revenue - current | | $ | 220.5 |

| | $ | 204.5 |

| | $ | 16.0 |

|

| Advances from customers - current | | $ | 46.7 |

| | $ | — |

| | $ | 46.7 |

|

| Advances from customers - noncurrent | | $ | 29.4 |

| | $ | 15.0 |

| | $ | 14.4 |

|

Deferred cost and deferred revenue activity in the six months ended June 30, 2019, follows (in millions):

|

| | | | | | | | | | | |

| | Deferred Sales in the Period | | Previously Deferred Sales Recognized in the Period | | Year-To-Date Change |

| Deferred costs associated with deferred revenue | $ | 3.8 |

| | $ | — |

| | $ | 3.8 |

|

| Deferred revenue | 16.0 |

| | — |

| | 16.0 |

|

LEU Segment

Under the terms of certain contracts with customers in the low-enriched uranium (“LEU”) segment, the Company will accept payment in the form of uranium. Revenue from the sale of SWU under such contracts is recognized at the time LEU is delivered and is based on the fair value of the uranium at contract inception, or as the quantity of uranium is finalized, if variable.

In the three months ended June 30, 2019, the Company received uranium from customers valued at $61.1 million as advance payments for the future sales of SWU. The advance payments are included in either Advances from Customers, Current or Advances from Customers, Noncurrent, based on the anticipated SWU sales period.

In the three months ended June 30, 2018, the Company received uranium from customers valued at $14.5 million as advance payments for the future sales of SWU. The advance payments are included in Advances from Customers, Noncurrent, based on the anticipated SWU sales period.

In the three months ended December 2018, the Company borrowed SWU inventory valued at $7.3 million from a customer under terms that require repayment within 48 months. The Company recorded the SWU and the related liability for the borrowing using an average purchase price over the borrowing period. The liability to the customer is included in Other Liabilities, which is included in noncurrent liabilities.

Contract Services Segment

Revenue for the contract services segment, representing the Company’s technical, manufacturing, engineering and operations services offered to public and private sector customers, is recognized over the contractual period as services are rendered.

On May 31, 2019, the Company entered in a letter agreement with DOE (“the HALEU Letter Agreement”) for the Company to demonstrate the ability to produce high assay, low-enriched uranium (“HALEU”) with existing United States origin enrichment technology and provide DOE with HALEU for near term use in its research and development for the advancement of civilian nuclear energy and security, and other programmatic missions. HALEU is an advanced nuclear reactor fuel that is not commercially available today. The Company commenced work pursuant to the letter agreement on June 1, 2019, and will work with DOE to enter into a definitive contract by October 31, 2019. According to the letter agreement, the definitive contract is anticipated to be an incrementally funded, cost reimbursable contract with DOE reimbursing up to 80% of costs and the Company incurring 20% of costs. Allocable costs include project costs, classified as Cost of Sales, and an allocation of corporate costs classified as Selling, General and Administrative Expenses. It is anticipated that the definitive contract will run through May 31, 2022, and the total amount of DOE’s share will be capped at $115 million. However, the Company has no assurance that a definitive contract will be executed. Based upon the anticipated cost share described above, and the total amount of DOE’s share of $115 million, the Company’s cost share would be approximately $29 million. Any costs incurred above these amounts would be borne by the Company. The HALEU Letter Agreement obligates DOE for costs up to $18.6 million of the $115 million and currently authorizes up to $6.4 million in payments to the Company.

Services to be provided over the anticipated three-year contract involve constructing and assembling centrifuge machines and related infrastructure in a cascade formation. When estimates of total project costs to be incurred for such an integrated, construction-type contract exceed estimates of total revenue to be earned, a provision for the entire loss on the contract is recorded to Cost of Sales in the period the loss is determined, and is reflected in Current Liabilities. For the quarter ended June 30, 2019, the Company recorded a loss provision of $0.5 million which represents the anticipated gross loss for the remaining initial phase of contract work performed under the HALEU Letter Agreement as the parties work to enter into a definitive contract.

On January 11, 2018, the Company entered into a settlement agreement with DOE and the U.S. government regarding breach of contract claims brought by the Company relating to work performed by the Company under contracts with DOE and subcontracts with DOE contractors. In connection with the settlement, the Company (a) received $4.7 million from the U.S. government, (b) applied approximately $19.3 million of advances from the U.S. government received in prior years against the receivables balance, and (c) recorded additional revenue of $9.5 million.

Centrus and DOE have yet to fully settle the Company’s claims for reimbursements for certain pension and postretirement benefits costs related to past contract work performed for DOE. There is the potential for additional revenue to be recognized for this work pending the outcome of legal proceedings related to the Company’s claims for payment and the potential release of previously established valuation allowances on receivables. As a result of the application of fresh start accounting following the Company’s emergence from Chapter 11 bankruptcy on September 30, 2014, the receivables related to the Company’s claims for payment are carried at fair value as of September 30, 2014, which is net of the valuation allowances. Refer to Note 12, Commitments and Contingencies.

LEU Segment Order Book

The SWU component of LEU is typically bought and sold under long-term contracts with deliveries over several years. The Company’s agreements for natural uranium sales are generally shorter-term, fixed-commitment contracts. The Company’s order book sales under contract in the LEU segment (“order book”) extends to 2030. The order book represents the Company’s remaining performance obligations under these contracts and includes the Deferred Revenue and Advances from Customers amounts in the Contract Balances table above. As of June 30, 2019, the order book was $1.1 billion, compared to $1.0 billion at December 31, 2018, reflecting completed deliveries and new contracts signed in the six months ended June 30, 2019.

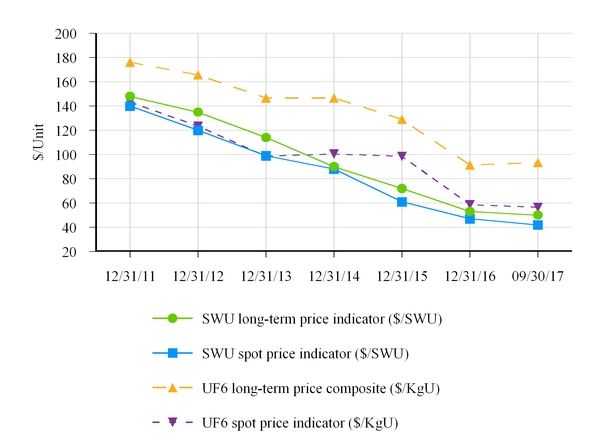

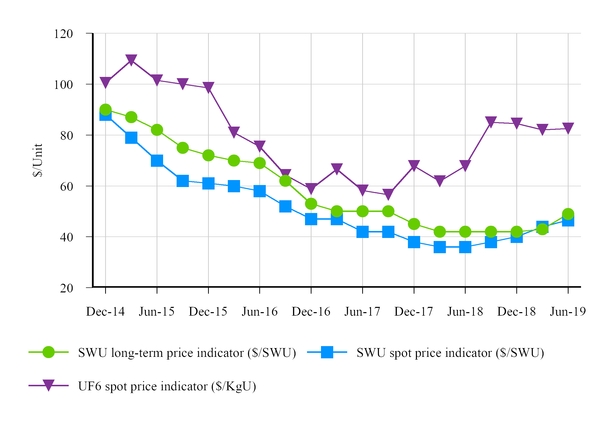

Most of the Company’s contracts provide for fixed purchases of SWU during a given year. The Company’s estimate of the aggregate dollar amount of future SWU and uranium sales is partially based on customers’ estimates of the timing and size of their fuel requirements and other assumptions that are subject to change. For example, depending on the terms of specific contracts, the customer may be able to increase or decrease the quantity delivered within an agreed range. The Company’s order book estimate is also based on the Company’s estimates of selling prices, which are subject to change. For example, depending on the terms of specific contracts, prices may be adjusted based on escalation using a general inflation index, published SWU price indicators prevailing at the time of delivery, and other factors, all of which are variable. The Company uses external composite forecasts of future market prices and inflation rates in its pricing estimates.

3. SPECIAL CHARGES

Evolving Business Needs

Evolving business needs have resultedAs a result of the HALEU Letter Agreement, special charges in workforce reductions since 2013. In the ninethree and six months ended SeptemberJune 30, 2017,2019, included a credit of $2.9 million for the reversal of accrued termination benefits for employees who were retained at the Company’s facility in Piketon, Ohio. For the six months ended June 30, 2018, special charges includedtotaled $0.9 million, consisting of estimated employee termination benefits of $2.2 million, including $0.7 million in the three months ended September 30, 2017. Centrus expects to make payments primarily in the fourth quarter of 2017 related to corporate functions of $0.8 million and advisory costs related to updating the $1.4 million balance payable at September 30, 2017.

In the second quarter of 2016, the Company commenced a project to align its corporate structure to the scale of its ongoing business operations and to update relatedCompany’s information technology systems. systems of $0.1 million. The Company incurred advisory costsremaining balance of $0.3termination benefits of $0.6 million is expected to be paid within twelve months and $0.8 million related to the reengineering project in the three and nine months ended September 30, 2016, respectively. The Company incurred advisory costs of $1.7 million and $5.0 million in the three and nine months ended September 30, 2017, respectively.

Piketon Demonstration Facility

In September 2015, Centrus completed a successful three-year demonstration of its American Centrifuge technology at its facility in Piketon, Ohio. The demonstration effort was primarily funded by the U.S. government. As a result of reduced program funding, Centrus incurred a special charge in the third quarter of 2015 for estimated employee termination benefits. Of the remaining $4.9 million liability as of September 30, 2017, $2.8 million is classified as current and included in Accounts Payable and Accrued Liabilitiesin the condensed consolidated balance sheet. The remaining $2.1 million is included in Other Long-Term Liabilities and is expected to be paid through 2019.

A summary of termination benefit activity and the accrued liability follows (in millions):

|

| | | | | | | | | | | | | | | | |

| | | Liability December 31, 2018 | | Six Months Ended

June 30, 2019 | | Liability

June 30, 2019 |

| | | | Charges (Credits) for Termination Benefits | | Paid/ Settled | |

| Workforce reductions: | | | | | | | | |

| Corporate functions | | $ | 0.9 |

| | $ | — |

| | $ | (0.7 | ) | | $ | 0.2 |

|

| Piketon facility | | 3.2 |

| | (2.9 | ) | | 0.1 |

| | 0.4 |

|

| Total | | $ | 4.1 |

| | $ | (2.9 | ) | | $ | (0.6 | ) | | $ | 0.6 |

|

4. CASH, CASH EQUIVALENTS AND RESTRICTED CASH

The following table summarizes the Company’s cash, cash equivalents and related liabilities followsrestricted cash as presented on the condensed consolidated balance sheet to amounts on the condensed consolidated statement of cash flows (in millions):

|

| | | | | | | | | | | | | | | | | |

| | | Liability December 31, 2016 | | Nine Months Ended

September 30, 2017 | | Liability

September 30,

2017 | |

| | | | Charges for Termination Benefits | | Paid/ Settled | | |

| Workforce reductions: | | | | | | | | | |

| Evolving business needs | | $ | 0.1 |

| | $ | 2.2 |

| | $ | (0.9 | ) | | $ | 1.4 |

| |

| Piketon demonstration facility | | 5.4 |

| | 0.1 |

| | (0.6 | ) | | 4.9 |

| |

| | | $ | 5.5 |

| | $ | 2.3 |

| | $ | (1.5 | ) | | $ | 6.3 |

| |

3. CONTRACT SERVICES AND ADVANCED TECHNOLOGY LICENSE AND DECOMMISSIONING COSTS

The contract services segment includes Revenue and Cost of Sales for engineering and testing work Centrus performs on the American Centrifuge technology under a government contract with UT-Battelle, LLC (“UT-Battelle”), the operator of Oak Ridge National Laboratory (“ORNL”). The recently completed fixed priced contract between Centrus and UT-Battelle (the “2017 ORNL Contract”) was for the period from October 1, 2016, through September 30, 2017 and generated revenue of approximately $25 million. On October 26, 2017, the parties executed a new fixed priced contract for the period from October 1, 2017, through September 30, 2018, that is expected to generate total revenue of approximately $16 million upon completion of defined milestones. The ORNL contracts have been funded incrementally. Funding for the program is provided to UT-Battelle by the U.S. government which is currently operating under a continuing resolution. |

| | | | | | | |

| | June 30, 2019 | | December 31, 2018 |

| | | | |

| Cash and cash equivalents | $ | 88.3 |

| | $ | 123.1 |

|

| Deposits for financial assurance - current | 18.0 |

| | 30.3 |

|

| Deposits for financial assurance - noncurrent | 5.7 |

| | 6.3 |

|

| Total cash, cash equivalents and restricted cash | $ | 112.0 |

| | $ | 159.7 |

|

The 2017 ORNL Contract providedfollowing table provides additional detail regarding the Company’s deposits for payments for monthly reports of deliverables of approximately $2.0 million per month and additional aggregate payments of $1.0 million based on completion of defined milestones.financial assurance (in millions):

|

| | | | | | | | | | | | | | | |

| | June 30, 2019 | | December 31, 2018 |

| | Current | | Long-Term | | Current | | Long-Term |

| NRC license | $ | 16.9 |

| | $ | — |

| | $ | 16.6 |

| | $ | — |

|

| DOE lease | — |

| | — |

| | 13.5 |

| | — |

|

| Workers compensation | 0.6 |

| | 5.4 |

| | — |

| | 6.0 |

|

| Other | 0.5 |

| | 0.3 |

| | 0.2 |

| | 0.3 |

|

| Total deposits for financial assurance | $ | 18.0 |

| | $ | 5.7 |

| | $ | 30.3 |

| | $ | 6.3 |

|

Piketon Facility Obligations and Surety Bonds

The Company’s contract with UT-BattelleCentrus leases gas centrifuge enrichment plant facilities and related personal property in Piketon, Ohio from DOE. Centrus previously provided financial assurance to DOE for lease turnover obligations in the form of surety bonds that ended September 30, 2016 (the “2016 ORNL Contract”), provided for payments for monthly reports of deliverables of approximately $2.7 million per month. The 2016 ORNL Contract,were fully cash collateralized. On May 31, 2019, DOE and Centrus amended the lease agreement, which was signed in March 2016, provided for payments for reportsscheduled to expire by its terms on June 30, 2019. In the second quarter of 2019, Centrus completed its lease turnover obligations related to work performed since October 1, 2015. Revenue in the nine monthsterm ended SeptemberJune 30, 2016, includes $24.2 million for reports on work performed in2019. DOE released the nine months ended September 30, 2016,bonds and $8.1 million for March 2016 reports on work performed inCentrus received the three months ended December 31, 2015. Expenses for contract work performed in the nine months ended September 30, 2016, are included in Costcash collateral of Sales. Expenses for work performed in the three months ended December 31, 2015, before entering into the 2016 ORNL Contract, were included in Advanced Technology License and Decommissioning Costs in 2015.

American Centrifuge expenses that are outside of the Company’s contracts with UT-Battelle are included in Advanced Technology License and Decommissioning Costs, including ongoing costs$13.5 million. In addition, Centrus has previously provided financial assurance to maintain the demobilized Piketon facility and our licenses from the U.S. Nuclear Regulatory Commission (“NRC”) at that location. In the second quarter of 2016, the Company commencedfor the decontamination and decommissioning (“D&D”) of the Piketon facility in the form of surety bonds that are fully cash collateralized by Centrus for $16.9 million. The Company has completed the D&D work required for elimination of financial assurance under NRC license requirements and is working with the NRC to have the surety bonds cancelled, which would permit the Company to receive the cash collateral.

Financial Assurance for Workers’ Compensation

The Company has provided financial assurance to states in which it was previously self-insured for workers’ compensation in accordance with each state’s requirements in the requirementsform of NRCa surety bond and a letter of credit that are fully cash collateralized by Centrus. When each state determines that Centrus is likely to have no further workers’ compensation obligations related to the period of self-insurance, the surety bond and letter of credit will be cancelled and the U.S. Department of Energy (“DOE”). ReferCompany expects to Note 12, Commitments and Contingencies, for additional details.

4. RECEIVABLES

|

| | | | | | | |

| | September 30,

2017 | | December 31,

2016 |

| | (in millions) |

| Utility customers and other | $ | 9.1 |

| | $ | 15.3 |

|

| Contract services, primarily DOE | 5.1 |

| | 4.6 |

|

| Accounts receivable | $ | 14.2 |

| | $ | 19.9 |

|

Centrus formerly performed site services work under contracts with DOE atreceive the former Portsmouth and Paducah gaseous diffusion plants. Overdue receivables from DOE of $14.2cash collateral. Of the $6.0 million in cash collateral as of SeptemberJune 30, 2017, and $22.82019, $0.6 million asrelates to a letter of December 31, 2016, are included in Other Long-Term Assets based on the extended timeframe expected to resolve the Company’s claims for payment.

Centrus has unapplied payments from DOEcredit that may be used, at DOE’s direction, (a) to pay for future services provided by the Company, or (b) to reduce outstanding receivables balances due from DOE. The balance of unapplied payments of $19.3 million as of September 30, 2017, and December 31, 2016, is included in Other Long-Term Liabilities pending resolution of the long-term receivables from DOE described above.cancelling within 12 months.

5. INVENTORIES

Centrus holds uranium at licensed locations in the form of natural uranium and as the uranium component of low enriched uranium (“LEU”).LEU. Centrus also holds separative work units (“SWU”)SWU as the SWU component of LEU at licensed locations (e.g., fabricators) to meet book transfer requests by customers. Fabricators process LEU into fuel for use in nuclear reactors. Components of inventories followare as follows (in millions):

| | | | September 30, 2017 | | December 31, 2016 | June 30, 2019 | | December 31, 2018 |

| | Current Assets | | Current Liabilities (a) | | Inventories, Net | | Current Assets | | Current Liabilities (a) | | Inventories, Net | Current Assets | | Current Liabilities (a) | | Inventories, Net | | Current Assets | | Current Liabilities (a) | | Inventories, Net |

| Separative work units | $ | 73.7 |

| | $ | 3.2 |

| | $ | 70.5 |

| | $ | 115.8 |

| | $ | 15.2 |

| | $ | 100.6 |

| $ | 18.4 |

| | $ | 0.5 |

| | $ | 17.9 |

| | $ | 20.1 |

| | $ | 3.6 |

| | $ | 16.5 |

|

| Uranium | 50.2 |

| | 18.9 |

| | 31.3 |

| | 61.4 |

| | 42.3 |

| | 19.1 |

| 123.3 |

| | 58.5 |

| | 64.8 |

| | 109.6 |

| | 99.4 |

| | 10.2 |

|

| Materials and supplies | 0.2 |

| | — |

| | 0.2 |

| | 0.2 |

| | — |

| | 0.2 |

| |

| | $ | 124.1 |

| | $ | 22.1 |

| | $ | 102.0 |

| | $ | 177.4 |

| | $ | 57.5 |

| | $ | 119.9 |

| |

| Total | | $ | 141.7 |

| | $ | 59.0 |

| | $ | 82.7 |

| | $ | 129.7 |

| | $ | 103.0 |

| | $ | 26.7 |

|

| |

| (a) | Inventories owed to customers and suppliers, included in current liabilities, include SWU and uranium inventories owed to fabricators. |

6. PROPERTY, PLANT AND EQUIPMENT

|

| | | | | | | |

| | September 30,

2017 | | December 31,

2016 |

| | (in millions) |

| Property, plant and equipment, gross | 6.9 |

| | 6.8 |

|

| Accumulated depreciation | (1.7 | ) | | (0.8 | ) |

| Property, plant and equipment, net | $ | 5.2 |

| | $ | 6.0 |

|

Inventories are valued at the lower of cost or net realizable value. Valuation adjustments for uranium inventory to reflect declines in uranium market price indicators totaled $2.3 million in the six months ended June 30, 2019, including $2.0 million in the second quarter of 2019.

7.6. INTANGIBLE ASSETS

Intangible assets originated from the Company’s reorganization and application of fresh start accounting as of the date the Company emerged from bankruptcy, September 30, 2014, and reflect the conditions at that time. The intangible asset related to the sales order book is amortized as the order book existing at emergence is reduced, principally as a result of deliveries to customers. The intangible asset related to customer relationships is amortized using the straight-line method over the estimated average useful life of 15 years. Amortization expense is presented below gross profit on the condensed consolidated statements of operations. Intangible asset balances are as follows (in millions):

| | | | September 30, 2017 | | December 31, 2016 | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | June 30, 2019 | | December 31, 2018 |

| | | | | | (in millions) | | | | | | | | | | | | | | | |

| | Gross Carrying Amount | | Accumulated Amortization | | Net Amount | | Gross Carrying Amount | | Accumulated Amortization | | Net Amount | Gross Carrying Amount | | Accumulated Amortization | | Net Amount | | Gross Carrying Amount | | Accumulated Amortization | | Net Amount |

| Sales order book | $ | 54.6 |

| | $ | 22.1 |

| | $ | 32.5 |

| | $ | 54.6 |

| | $ | 19.9 |

| | $ | 34.7 |

| $ | 54.6 |

| | $ | 28.0 |

| | $ | 26.6 |

| | $ | 54.6 |

| | $ | 28.0 |

| | $ | 26.6 |

|

| Customer relationships | 68.9 |

| | 13.8 |

| | 55.1 |

| | 68.9 |

| | 10.3 |

| | 58.6 |

| 68.9 |

| | 21.8 |

| | 47.1 |

| | 68.9 |

| | 19.5 |

| | 49.4 |

|

| Total | $ | 123.5 |

| | $ | 35.9 |

| | $ | 87.6 |

| | $ | 123.5 |

| | $ | 30.2 |

| | $ | 93.3 |

| $ | 123.5 |

| | $ | 49.8 |

| | $ | 73.7 |

| | $ | 123.5 |

| | $ | 47.5 |

| | $ | 76.0 |

|

8.7. DEBT

A summary of long-term debt is as follows (in millions):

| | | | | | | | | | | | | June 30, 2019 | | December 31, 2018 |

| | Maturity | | September 30, 2017 | | December 31, 2016 | Maturity | | Current | | Long-Term | | Current | | Long-Term |

| 8.25% Notes: | Feb. 2027 | | | | | Feb. 2027 | | | | | | | | |

| Principal | | $ | 74.3 |

| | $ | — |

| | $ | — |

| | $ | 74.3 |

| | $ | — |

| | $ | 74.3 |

|

| Interest | | 58.1 |

| | — |

| | 6.1 |

| | 42.8 |

| | 6.1 |

| | 45.9 |

|

| 8.25% Notes | | 132.4 |

| | — |

| | $ | 6.1 |

| | $ | 117.1 |

| | $ | 6.1 |

| | $ | 120.2 |

|

| | | | | | | | | | |

| 8% PIK Toggle Notes | Sep. 2019 (a) | | 31.3 |

| | 234.6 |

| Sep. 2019 (a) | | $ | 27.5 |

| | $ | — |

| | $ | 26.7 |

| | $ | — |

|

| Subtotal | | 163.7 |

| | 234.6 |

| |

| Less deferred issuance costs | | 0.1 |

| | 0.5 |

| | — |

| | — |

| | — |

| | — |

|

| Total debt | | 163.6 |

| | 234.1 |

| |

| Less current portion | | 6.1 |

| | — |

| |

| Long-term debt | | $ | 157.5 |

| | $ | 234.1 |

| |

| 8% PIK Toggle Notes | | | $ | 27.5 |

| | $ | — |

| | $ | 26.7 |

| | $ | — |

|

| | | | | | | | | | |

| Total | | | $ | 33.6 |

| | $ | 117.1 |

| | $ | 32.8 |

| | $ | 120.2 |

|

(a) Maturity can be extended to September 2024 upon the satisfaction of certain funding conditions described below.

Note Exchange

On February 14, 2017, pursuant to an exchange offer and consent solicitation, Centrus exchanged $204.9 million principal amount ofin the Company’s 8% paid-in-kind (“PIK”) toggle notes (the “8% PIK Toggle Notes”) for $74.3 million principal amount of 8.25% notes due February 2027 (the “8.25% Notes”), 104,574 shares of Series B Preferred Stock with a liquidation preference of $1,000 per share, and $27.6 million of cash. The exchange is accounted for as a troubled debt restructuring (a “TDR”) under Accounting Standards Codification Subtopic 470-60, Debt-Troubled Debt Restructurings by Debtors. For an exchange classified as a TDR, if the future undiscounted cash flows of the newly issued debt and other consideration are less than the net carrying value of the original debt, a gain is recorded for the difference and the carrying value of the newly issued debt is adjusted to the future undiscounted cash flow amount and no future interest expense is recorded. All future interest payments on the newly issued debt reduce the carrying value. Accordingly, the Company recognizes the 8.25% Notes on the condensed consolidated balance sheet as the sum of the principal balance and all future interest payments. The Company recognized a gain of $33.6 million related to the note exchange for the quarter ended March 31, 2017, which is net of transaction costs of $9.0 million and previously deferred issuance costs related to the 8% PIK Toggle Notes of $0.4 million. Refer to Note 13, Stockholders’ Equity for details related to the newly issued preferred stock.applicable indenture.

8.25% Notes

Interest on the 8.25% Notes is payable semi-annually in arrears as of February 28 and August 31 based on a 360-day year consisting of twelve 30-day months. The 8.25% Notes mature on February 28, 2027. As described above, all future interest payment obligations on the 8.25% Notes are included in the carrying value of the 8.25% Notes. As a result, the Company’s reported interest expense will be less than its contractual interest payments throughout the term of the 8.25% Notes. As of SeptemberJune 30, 2017,2019, and December 31, 2018, $6.1 million of interest is recorded as current and classified as Accounts Payable and Accrued LiabilitiesCurrent Debt in the condensed consolidated balance sheet.

The 8.25% Notes rank equally in right of payment with all of our existing and future unsubordinated indebtedness other than our Issuer Senior Debt and our Limited Secured Acquisition Debt (each as defined below). The 8.25% Notes rank senior in right of payment to all of our existing and future subordinated indebtedness and to certain limited secured acquisition indebtedness of the Company (the “Limited Secured Acquisition Debt”). The Limited Secured Acquisition Debt includes (i) any indebtedness, the proceeds of which are used to finance all or a portion of an acquisition or similar transaction if any lender’s lien is solely limited to the assets acquired in such a transaction and (ii) any indebtedness, the proceeds of which are used to finance all or a portion of the American Centrifuge project or another next generation enrichment technology if any lender’s lien is solely limited to such

assets, provided that a lien securing the 8.25% Notes that is junior with respect to the lien securing such indebtedness, will be effected for the 8.25% Notes, which will be limited to the assets acquired with such Limited Secured Acquisition Debt.

The 8.25% Notes are subordinated in right of payment to certain indebtedness and obligations of the Company, as described in the 8.25% Notes Indenture (the “Issuer Senior Debt”), including (i) any indebtedness of the Company (inclusive of any indebtedness of Enrichment Corp.) under a future credit facility up to $50 million with a maximum net borrowing of $40 million after taking into account any minimum cash balance (unless a higher amount is approved with the consent of the holders of a majority of the aggregate principal amount of the 8.25% Notes then outstanding), (ii) any revolving credit facility to finance inventory purchases and related working capital needs, and (iii) any indebtedness of the Company to Enrichment Corp. under the secured intercompany notes.

The 8.25% Notes are guaranteed on a subordinated and limited basis by, and secured by substantially all of the assets of, Enrichment Corp. The Enrichment Corp. guarantee is a secured obligation and ranks equally in right of payment with all existing and future unsubordinated indebtedness of Enrichment Corp. (other than Designated Senior Claims (as defined below) and Limited Secured Acquisition Debt) and senior in right of payment to all existing and future subordinated indebtedness of Enrichment Corp. and Limited Secured Acquisition Debt. The Enrichment Corp. guarantee is subordinated in right of payment to certain obligations of, and claims against, Enrichment Corp. described in the 8.25% Notes Indenture (collectively, the “Designated Senior Claims”), including obligations and claims:

under a future credit facility up to $50 million with a maximum net borrowing of $40 million after taking into account any minimum cash balance;

under any revolving credit facility to finance inventory purchases and related working capital needs;

held by or for the benefit of the Pension Benefit Guaranty Corporation (“PBGC”) pursuant to any settlement (including any required funding of pension plans); and

under surety bonds or similar obligations held by or on behalf of the U.S. government pursuant to regulatory requirements.

The liens securing the Enrichment Corp. guarantee of the 8% PIK Toggle Notes and the 8.25% Notes are pari passu with each other, and are junior in priority with respect to the lien securing Limited Secured Acquisition Debt, which is limited to the assets acquired with such Limited Secured Acquisition Debt.

8% PIK Toggle Notes

Interest on the 8% PIK Toggle Notes is payable semi-annually in arrears on March 31 and September 30 based on a 360-day year consisting of twelve 30-day months. The principal amount is increased by any payment of interest in the form of PIK payments. The Company has the option to pay up to 5.5% per annum of interest due on the 8% PIK Toggle Notes in the form of in-kind PIK payments. For the semi-annual interest periods ended March 31, 2017,in 2018 and September 30, 2017,2019, the Company elected to pay interest in the form of PIK payments at 5.5% per annum.

Financing costs for the issuance of the 8% PIK Toggle Notes were deferred and are being amortized on a straight-line basis, which approximates the effective interest method, over the life of the 8% PIK Toggle Notes.

The 8% PIK Toggle Notes mature on September 30, 2019. However, the maturity date can be extended to September 30, 2024, upon the satisfaction of certain funding conditions described in the Indenture relating to the funding, under binding agreements, of (i) the American Centrifuge project or (ii) the implementation and deployment of a National Security Train Program utilizing American Centrifuge technology.