0001069157us-gaap:FinancingReceivables60To89DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-31ExtendedMaturityAndInterestRateReductionMember2023-01-012023-06-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended SeptemberJune 30, 20222023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 000-24939

EAST WEST BANCORP, INC.

(Exact name of registrant as specified in its charter)

Delaware

(State or other jurisdiction of incorporation or organization)

95-4703316

(I.R.S. Employer Identification No.)

135 North Los Robles Ave., 7th Floor, Pasadena, California 91101

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code:

(626) 768-6000

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | | | | | | |

| Title of each class | | Trading

Symbol(s) | | Name of each exchange

on which registered | |

| Common Stock, par value $0.001 per share | | EWBC | | The Nasdaq Global Select Market | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

Number of shares outstanding of the issuer’s common stock on the latest practicable date: 140,946,569141,483,668 shares as of OctoberJuly 31, 20222023.

TABLE OF CONTENTS

Forward-Looking Statements

Certain matters discussed in this Quarterly Report on Form 10-Q (this “Form 10-Q”) contain forward-looking statements that are intended to be covered by the safe harbor provisions for such statements provided by the Private Securities Litigation Reform Act of 1995. In addition, East West Bancorp, Inc. (referred to herein on an unconsolidated basis as “East West” and on a consolidated basis as the “Company,” “we” or “EWBC”) may make forward-looking statements in other documents that it files with, or furnishes to, the United States (“U.S.”) Securities and Exchange Commission (“SEC”) and management may make forward-looking statements to analysts, investors, media members and others. Forward-looking statements are those that do not relate to historical facts, and that are based on current assumptions, beliefs, estimates, expectations and projections, many of which, by their nature, are inherently uncertain and beyond the Company’s control. Forward-looking statements may relate to various matters, including the Company’s financial condition, results of operations, plans, objectives, future performance, business or industry, and usually can be identified by the use of forward-looking words, such as “anticipates,” “assumes,” “believes,” “can,” “continues,” “could,” “estimates,” “expects,” “forecasts,” “goal,” “intends,” “likely,” “may,” “might,” “objective,” “plans,” “potential,” “projects,” “remains,” “should,” “target,” “trend,” “will,” “would,” or similar expressions or variations thereof, and the negative thereof, but these terms are not the exclusive means of identifying such statements. You should not place undue reliance on forward-looking statements, as they are subject to risks and uncertainties, including, but not limited to, those described below. When considering these forward-looking statements, you should keep in mind these risks and uncertainties, as well as any cautionary statements the Company may make.

There are various important factors that could cause future results to differ materially from historical performance and any forward-looking statements. Factors that might cause such differences, include, but are not limited to:

•changes in the global economy, including an economic slowdown, capital or financial market disruption, supply chain disruption, level of inflation, interest rate environment, housing prices, employment levels, rate of growth and general business conditions, which could result in, among other things, reduced demand for loans, reduced availability of funding or increased funding costs, declines in asset values and/or recognition of allowance for credit losses;

•changes in local, regional and global business, economic and political conditions and geopolitical events, such as Russia’s invasion of Ukraine;

•the soundness of other financial institutions and the impacts related to or resulting from recent bank failures and other economic and industry volatility, including potential increased regulatory requirements, Federal Deposit Insurance Corporation (“FDIC”) insurance premiums, losses in the value of our investment portfolio, deposit withdrawals, or other adverse consequences of negative market perceptions of the banking industry or the Company;

•changes in laws or the regulatory environment, including regulatory reform initiatives and policies of the U.S. Department of the Treasury, the Board of Governors of the Federal Reserve System (“Federal Reserve”), the FDIC, the SEC, the Consumer Financial Protection Bureau (“CFPB”), the California Department of Financial Protection and Innovation — Division of Financial Institutions, the National Administration of Financial Regulation, the Hong Kong Monetary Authority, the Hong Kong Securities and Futures Commission, and the Monetary Authority of Singapore;

•changes and effects thereof in trade, monetary and fiscal policies and laws, including the ongoing trade, economic and political disputes between the U.S. and the People’s Republic of China and the monetary policies of the Federal Reserve;

•changes in the commercial and consumer real estate markets;

•changes in consumer or commercial spending, savings and borrowing habits, and patterns and behaviors;

•the impact from potential changes to income tax laws and regulations, federal spending and economic stimulus programs;

•the impact of any future U.S. federal government shutdown and uncertainty regarding the U.S. federal government’s debt limit and credit rating;

•the Company’s ability to compete effectively against financial institutions and other entities, including as a result of emerging technologies;

•the success and timing of the Company’s business strategies;

•the Company’s ability to retain key officers and employees;

•the impact on the Company’s funding costs, net interest income and net interest margin from changes in key variable market interest rates, competition, regulatory requirements and the Company’s product mix;

•changes in the Company’s costs of operation, compliance and expansion;

•the Company’s ability to adopt and successfully integrate new technologies into its business in a strategic manner;

•the impact of communications or technology disruption, failure in, or breach of, the Company’s operational or security systems or infrastructure, or those of third party vendors with which the Company does business, including as a result of cyber-attacks; and other similar matters which could result in, among other things, confidential and/or proprietary information being disclosed or misused, and materially impact the Company’s ability to provide services to its clients;

•the adequacy of the Company’s risk management framework, disclosure controls and procedures and internal control over financial reporting;

•future credit quality and performance, including the Company’s expectations regarding future credit losses and allowance levels;

•the impact of adverse changes to the Company’s credit ratings from major credit rating agencies;

•the impact of adverse judgments or settlements in litigation;

•the impact of political developments, pandemics, wars, civil unrest, terrorism or other hostilities that may disrupt or increase volatility in securities or otherwise affect business and economic conditions on the Company and its customers;

•heightened regulatory and governmental oversight and scrutiny of the Company’s business practices, including dealings with consumers;

•the impact of reputational risk from negative publicity, fines, penalties and other negative consequences from regulatory violations, legal actions and the Company’s interactions with business partners, counterparties, service providers and other third parties;

•the impact of regulatory investigations and enforcement actions;

•changes in accounting standards as may be required by the Financial Accounting Standards Board (“FASB”) or other regulatory agencies and their impact on the Company’s critical accounting policies and assumptions;

•the Company’s capital requirements and its ability to generate capital internally or raise capital on favorable terms;

•the impact on the Company’s liquidity due to changes in the Company’s ability to receive dividends from its subsidiaries;

•any strategic acquisitions or divestitures;

•changes in the equity and debt securities markets;

•fluctuations in the Company’s stock price;

•fluctuations in foreign currency exchange rates;

•the impact of increased focus on social, environmental and sustainability matters, which may affect the operations of the Company and its customers and the economy more broadly; and

•the impact of climate change, natural or man-made disasters or calamities, such as wildfires, droughts, hurricanes, flooding and earthquakes or other events that may directly or indirectly result in a negative impact on the financial performance of the Company and its customers.

For a more detailed discussion of some of the factors that might cause such differences, see the Company’s Annual Report on Form 10-K for the year ended December 31, 2022, filed with the SEC on February 27, 2023 (the “Company’s 2022 Form 10-K”) under the heading Item 1A. Risk Factors, and Item 1A. Risk Factors of this Form 10-Q. You should treat forward-looking statements as speaking only as of the date they are made and based only on information then actually known to the Company. The Company does not undertake, and specifically disclaims, any obligation to update or revise any forward-looking statements to reflect the occurrence of events or circumstances after the date of such statements except as required by law.

PART I — FINANCIAL INFORMATION

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

($ in thousands, except shares)

(Unaudited)

| | | | September 30,

2022 | | December 31,

2021 | | June 30,

2023 | | December 31,

2022 |

| | (Unaudited) | | | |

| ASSETS | ASSETS | | ASSETS | | | | |

| Cash and due from banks | Cash and due from banks | | $ | 554,260 | | | $ | 527,317 | | Cash and due from banks | | $ | 614,053 | | | $ | 534,980 | |

| Interest-bearing cash with banks | Interest-bearing cash with banks | | 1,609,093 | | | 3,385,618 | | Interest-bearing cash with banks | | 5,763,834 | | | 2,946,804 | |

| Cash and cash equivalents | Cash and cash equivalents | | 2,163,353 | | | 3,912,935 | | Cash and cash equivalents | | 6,377,887 | | | 3,481,784 | |

| Interest-bearing deposits with banks | Interest-bearing deposits with banks | | 630,543 | | | 736,492 | | Interest-bearing deposits with banks | | 17,169 | | | 139,021 | |

| Assets purchased under resale agreements (“resale agreements”) | Assets purchased under resale agreements (“resale agreements”) | | 892,986 | | | 2,353,503 | | Assets purchased under resale agreements (“resale agreements”) | | 635,000 | | | 792,192 | |

| Securities: | Securities: | | Securities: | |

| Available-for-sale (“AFS”) debt securities, at fair value (amortized cost of $6,771,354 and $10,087,179) | | 5,906,090 | | | 9,965,353 | | |

| Held-to-maturity (“HTM”) debt securities, at amortized cost (fair value of $2,459,135) | | 3,012,667 | | | — | | |

| Available-for-sale (“AFS”) debt securities, at fair value (amortized cost of $6,820,569 and $6,879,225) | | Available-for-sale (“AFS”) debt securities, at fair value (amortized cost of $6,820,569 and $6,879,225) | | 5,987,258 | | | 6,034,993 | |

| Held-to-maturity (“HTM”) debt securities, at amortized cost (fair value of $2,440,484 and $2,455,171) | | Held-to-maturity (“HTM”) debt securities, at amortized cost (fair value of $2,440,484 and $2,455,171) | | 2,975,933 | | | 3,001,868 | |

| | Loans held-for-sale | Loans held-for-sale | | 14,500 | | | 635 | | Loans held-for-sale | | 2,830 | | | 25,644 | |

| Loans held-for-investment (net of allowance for loan losses of $582,517 and $541,579) | | 46,859,738 | | | 41,152,202 | | |

| Loans held-for-investment (net of allowance for loan losses of $635,400 and $595,645) | | Loans held-for-investment (net of allowance for loan losses of $635,400 and $595,645) | | 49,192,964 | | | 47,606,785 | |

| Investments in qualified affordable housing partnerships, tax credit and other investments, net | Investments in qualified affordable housing partnerships, tax credit and other investments, net | | 725,254 | | | 628,263 | | Investments in qualified affordable housing partnerships, tax credit and other investments, net | | 815,471 | | | 763,256 | |

| | Premises and equipment (net of accumulated depreciation of $146,073 and $139,358) | | 91,587 | | | 97,302 | | |

| Premises and equipment (net of accumulated depreciation of $153,079 and $148,126) | | Premises and equipment (net of accumulated depreciation of $153,079 and $148,126) | | 88,966 | | | 89,191 | |

| Goodwill | Goodwill | | 465,697 | | | 465,697 | | Goodwill | | 465,697 | | | 465,697 | |

| Operating lease right-of-use assets | Operating lease right-of-use assets | | 105,411 | | | 98,632 | | Operating lease right-of-use assets | | 100,500 | | | 103,681 | |

| Other assets | Other assets | | 1,708,235 | | | 1,459,687 | | Other assets | | 1,873,006 | | | 1,608,038 | |

| TOTAL | TOTAL | | $ | 62,576,061 | | | $ | 60,870,701 | | TOTAL | | $ | 68,532,681 | | | $ | 64,112,150 | |

| LIABILITIES | LIABILITIES | | | | | LIABILITIES | | | | |

| Deposits: | Deposits: | | Deposits: | |

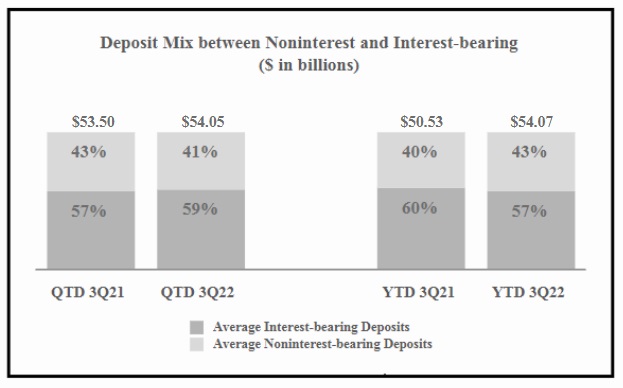

| Noninterest-bearing | Noninterest-bearing | | $ | 21,645,394 | | | $ | 22,845,464 | | Noninterest-bearing | | $ | 16,741,099 | | | $ | 21,051,090 | |

| Interest-bearing | Interest-bearing | | 32,211,968 | | | 30,505,068 | | Interest-bearing | | 38,917,687 | | | 34,916,759 | |

| Total deposits | Total deposits | | 53,857,362 | | | 53,350,532 | | Total deposits | | 55,658,786 | | | 55,967,849 | |

| Short-term borrowings | | Short-term borrowings | | 4,500,000 | | | — | |

| | Federal funds purchased | | 200,000 | | | — | | |

| Federal Home Loan Bank (“FHLB”) advances | | 324,920 | | | 249,331 | | |

| | Assets sold under repurchase agreements (“repurchase agreements”) | Assets sold under repurchase agreements (“repurchase agreements”) | | 611,785 | | | 300,000 | | Assets sold under repurchase agreements (“repurchase agreements”) | | — | | | 300,000 | |

| Long-term debt and finance lease liabilities | Long-term debt and finance lease liabilities | | 152,610 | | | 151,997 | | Long-term debt and finance lease liabilities | | 152,951 | | | 152,400 | |

| Operating lease liabilities | Operating lease liabilities | | 113,477 | | | 105,534 | | Operating lease liabilities | | 110,383 | | | 111,931 | |

| Accrued expenses and other liabilities | Accrued expenses and other liabilities | | 1,655,239 | | | 876,089 | | Accrued expenses and other liabilities | | 1,648,864 | | | 1,595,358 | |

| Total liabilities | Total liabilities | | 56,915,393 | | | 55,033,483 | | Total liabilities | | 62,070,984 | | | 58,127,538 | |

| COMMITMENTS AND CONTINGENCIES (Note 10) | | | | | |

| COMMITMENTS AND CONTINGENCIES (Note 11) | | COMMITMENTS AND CONTINGENCIES (Note 11) | | | | |

| STOCKHOLDERS’ EQUITY | STOCKHOLDERS’ EQUITY | | STOCKHOLDERS’ EQUITY | |

| Common stock, $0.001 par value, 200,000,000 shares authorized; 168,427,227 and 167,790,645 shares issued | | 168 | | | 168 | | |

| Common stock, $0.001 par value, 200,000,000 shares authorized; 169,310,864 and 168,459,045 shares issued | | Common stock, $0.001 par value, 200,000,000 shares authorized; 169,310,864 and 168,459,045 shares issued | | 169 | | | 168 | |

| Additional paid-in capital | Additional paid-in capital | | 1,926,393 | | | 1,893,557 | | Additional paid-in capital | | 1,959,615 | | | 1,936,389 | |

| Retained earnings | Retained earnings | | 5,302,897 | | | 4,683,659 | | Retained earnings | | 6,075,735 | | | 5,582,546 | |

| Treasury stock, at cost 27,509,715 and 25,882,691 shares | | (768,758) | | | (649,785) | | |

| Treasury stock, at cost 27,827,196 and 27,511,199 shares | | Treasury stock, at cost 27,827,196 and 27,511,199 shares | | (791,890) | | | (768,862) | |

| Accumulated other comprehensive loss (“AOCI”), net of tax | Accumulated other comprehensive loss (“AOCI”), net of tax | | (800,032) | | | (90,381) | | Accumulated other comprehensive loss (“AOCI”), net of tax | | (781,932) | | | (765,629) | |

| Total stockholders’ equity | Total stockholders’ equity | | 5,660,668 | | | 5,837,218 | | Total stockholders’ equity | | 6,461,697 | | | 5,984,612 | |

| TOTAL | TOTAL | | $ | 62,576,061 | | | $ | 60,870,701 | | TOTAL | | $ | 68,532,681 | | | $ | 64,112,150 | |

|

See accompanying Notes to Consolidated Financial Statements.

35

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF INCOME

($ and shares in thousands, except per share data)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, | | | | |

| | 2022 | | 2021 | | 2022 | | 2021 | | | | | | |

| INTEREST AND DIVIDEND INCOME | | | | | | | | | | | | | | |

| Loans receivable, including fees | | $ | 560,452 | | | $ | 363,503 | | | $ | 1,376,978 | | | $ | 1,057,964 | | | | | | | |

| Debt securities | | 51,092 | | | 37,826 | | | 139,935 | | | 101,616 | | | | | | | |

| | | | | | | | | | | | | | |

| Resale agreements | | 6,769 | | | 8,957 | | | 23,705 | | | 23,077 | | | | | | | |

| Restricted equity securities | | 843 | | | 500 | | | 2,274 | | | 1,588 | | | | | | | |

| Interest-bearing cash and deposits with banks | | 9,080 | | | 4,521 | | | 17,127 | | | 11,781 | | | | | | | |

| Total interest and dividend income | | 628,236 | | | 415,307 | | | 1,560,019 | | | 1,196,026 | | | | | | | |

| INTEREST EXPENSE | | | | | | | | | | | | | | |

| Deposits | | 68,894 | | | 15,970 | | | 104,371 | | | 55,790 | | | | | | | |

| Federal funds purchased and other short-term borrowings | | 1,177 | | | — | | | 1,427 | | | 42 | | | | | | | |

| FHLB advances | | 392 | | | 857 | | | 1,529 | | | 6,025 | | | | | | | |

| Repurchase agreements | | 4,421 | | | 2,012 | | | 8,855 | | | 5,981 | | | | | | | |

| Long-term debt and finance lease liabilities | | 1,543 | | | 762 | | | 3,463 | | | 2,314 | | | | | | | |

| Total interest expense | | 76,427 | | | 19,601 | | | 119,645 | | | 70,152 | | | | | | | |

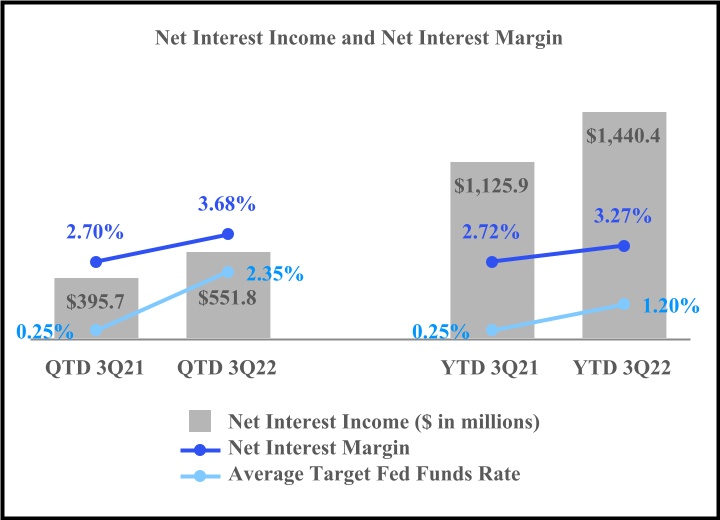

| Net interest income before provision for (reversal of) credit losses | | 551,809 | | | 395,706 | | | 1,440,374 | | | 1,125,874 | | | | | | | |

| Provision for (reversal of) credit losses | | 27,000 | | | (10,000) | | | 48,500 | | | (25,000) | | | | | | | |

| Net interest income after provision for (reversal of) credit losses | | 524,809 | | | 405,706 | | | 1,391,874 | | | 1,150,874 | | | | | | | |

| NONINTEREST INCOME | | | | | | | | | | | | | | |

| Lending fees | | 20,289 | | | 17,516 | | | 59,869 | | | 56,965 | | | | | | | |

| Deposit account fees | | 23,636 | | | 18,508 | | | 66,323 | | | 51,233 | | | | | | | |

| Interest rate contracts and other derivative income | | 8,761 | | | 7,156 | | | 29,695 | | | 20,981 | | | | | | | |

| Foreign exchange income | | 10,083 | | | 13,101 | | | 34,143 | | | 35,634 | | | | | | | |

| Wealth management fees | | 8,903 | | | 5,598 | | | 21,494 | | | 20,460 | | | | | | | |

| Net gains on sales of loans | | 2,129 | | | 3,329 | | | 5,968 | | | 6,601 | | | | | | | |

| Gains on sales of AFS debt securities | | — | | | 354 | | | 1,306 | | | 1,178 | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Other investment (loss) income | | (580) | | | 5,349 | | | 5,910 | | | 13,870 | | | | | | | |

| Other income | | 2,331 | | | 2,198 | | | 9,031 | | | 7,484 | | | | | | | |

| Total noninterest income | | 75,552 | | | 73,109 | | | 233,739 | | | 214,406 | | | | | | | |

| NONINTEREST EXPENSE | | | | | | | | | | | | | | |

| Compensation and employee benefits | | 127,580 | | | 105,751 | | | 357,213 | | | 318,985 | | | | | | | |

| Occupancy and equipment expense | | 15,920 | | | 15,851 | | | 46,853 | | | 47,150 | | | | | | | |

| Deposit insurance premiums and regulatory assessments | | 4,875 | | | 4,641 | | | 14,519 | | | 12,791 | | | | | | | |

| Deposit account expense | | 6,707 | | | 4,136 | | | 17,071 | | | 11,845 | | | | | | | |

| Data processing | | 3,725 | | | 3,575 | | | 10,876 | | | 12,088 | | | | | | | |

| Computer software expense | | 6,889 | | | 8,426 | | | 20,755 | | | 23,106 | | | | | | | |

| Consulting expense | | 1,620 | | | 1,635 | | | 5,474 | | | 4,978 | | | | | | | |

| Legal expense | | 689 | | | 2,363 | | | 2,454 | | | 5,840 | | | | | | | |

| Other operating expense | | 28,094 | | | 20,998 | | | 78,315 | | | 58,544 | | | | | | | |

| Amortization of tax credit and other investments | | 19,874 | | | 38,008 | | | 48,753 | | | 90,657 | | | | | | | |

| | | | | | | | | | | | | | |

| Total noninterest expense | | 215,973 | | | 205,384 | | | 602,283 | | | 585,984 | | | | | | | |

| INCOME BEFORE INCOME TAXES | | 384,388 | | | 273,431 | | | 1,023,330 | | | 779,296 | | | | | | | |

| INCOME TAX EXPENSE | | 89,049 | | | 47,982 | | | 232,010 | | | 124,111 | | | | | | | |

| NET INCOME | | $ | 295,339 | | | $ | 225,449 | | | $ | 791,320 | | | $ | 655,185 | | | | | | | |

| EARNINGS PER SHARE (“EPS”) | | | | | | | | | | | | | | |

| BASIC | | $ | 2.10 | | | $ | 1.59 | | | $ | 5.59 | | | $ | 4.62 | | | | | | | |

| DILUTED | | $ | 2.08 | | | $ | 1.57 | | | $ | 5.55 | | | $ | 4.58 | | | | | | | |

| WEIGHTED-AVERAGE NUMBER OF SHARES OUTSTANDING | | | | | | | | | | | | | | |

| BASIC | | 140,917 | | | 141,880 | | | 141,453 | | | 141,799 | | | | | | | |

| DILUTED | | 142,011 | | | 143,143 | | | 142,601 | | | 143,051 | | | | | | | |

|

See accompanying Notes to Consolidated Financial Statements.

4

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

($ in thousands)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, | | | | |

| | 2022 | | 2021 | | 2022 | | 2021 | | | | | | |

| Net income | | $ | 295,339 | | | $ | 225,449 | | | $ | 791,320 | | | $ | 655,185 | | | | | | | |

| Other comprehensive loss, net of tax: | | | | | | | | | | | | | | |

| Net changes in unrealized losses on AFS debt securities | | (161,445) | | | (41,178) | | | (523,593) | | | (101,577) | | | | | | | |

| Net changes in unrealized gains (losses) on securities transferred from AFS to HTM | | 3,256 | | | — | | | (103,674) | | | — | | | | | | | |

| Net changes in unrealized (losses) gains on cash flow hedges | | (33,269) | | | 51 | | | (64,372) | | | 551 | | | | | | | |

| Foreign currency translation adjustments | | (7,926) | | | (1,752) | | | (18,012) | | | (867) | | | | | | | |

| Other comprehensive loss | | (199,384) | | | (42,879) | | | (709,651) | | | (101,893) | | | | | | | |

| COMPREHENSIVE INCOME | | $ | 95,955 | | | $ | 182,570 | | | $ | 81,669 | | | $ | 553,292 | | | | | | | |

|

See accompanying Notes to Consolidated Financial Statements.

5

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

($ in thousands, except shares)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Common Stock and

Additional Paid-in Capital | | Retained Earnings | | Treasury Stock | | AOCI,

Net of Tax | | Total

Stockholders’ Equity |

| | Shares | | Amount | | | | |

| BALANCE, JULY 1, 2021 | | 141,877,505 | | | $ | 1,876,247 | | | $ | 4,335,327 | | | $ | (649,337) | | | $ | (14,689) | | | $ | 5,547,548 | |

| Net income | | — | | | — | | | 225,449 | | | — | | | — | | | 225,449 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (42,879) | | | (42,879) | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 9,643 | | | 7,792 | | | — | | | — | | | — | | | 7,792 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (3,417) | | | — | | | — | | | (254) | | | — | | | (254) | |

| Cash dividends on common stock ($0.33 per share) | | — | | | — | | | (47,455) | | | — | | | — | | | (47,455) | |

| BALANCE, SEPTEMBER 30, 2021 | | 141,883,731 | | | $ | 1,884,039 | | | $ | 4,513,321 | | | $ | (649,591) | | | $ | (57,568) | | | $ | 5,690,201 | |

| BALANCE, JULY 1, 2022 | | 140,917,389 | | | $ | 1,914,232 | | | $ | 5,064,650 | | | $ | (768,752) | | | $ | (600,648) | | | $ | 5,609,482 | |

| Net income | | — | | | — | | | 295,339 | | | — | | | — | | | 295,339 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (199,384) | | | (199,384) | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 206 | | | 12,329 | | | — | | | — | | | — | | | 12,329 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (83) | | | — | | | — | | | (6) | | | — | | | (6) | |

| | | | | | | | | | | | |

| Cash dividends on common stock ($0.40 per share) | | — | | | — | | | (57,092) | | | — | | | — | | | (57,092) | |

| BALANCE, SEPTEMBER 30, 2022 | | 140,917,512 | | | $ | 1,926,561 | | | $ | 5,302,897 | | | $ | (768,758) | | | $ | (800,032) | | | $ | 5,660,668 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Common Stock and

Additional Paid-in Capital | | Retained Earnings | | Treasury Stock | | AOCI,

Net of Tax | | Total

Stockholders’ Equity |

| | Shares | | Amount | | | | |

| BALANCE, JANUARY 1, 2021 | | 141,565,229 | | | $ | 1,858,519 | | | $ | 4,000,414 | | | $ | (634,083) | | | $ | 44,325 | | | $ | 5,269,175 | |

| | | | | | | | | | | | |

| Net income | | — | | | — | | | 655,185 | | | — | | | — | | | 655,185 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (101,893) | | | (101,893) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 523,449 | | | 25,520 | | | — | | | — | | | — | | | 25,520 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (204,947) | | | — | | | — | | | (15,508) | | | — | | | (15,508) | |

| | | | | | | | | | | | |

| Cash dividends on common stock ($0.99 per share) | | — | | | — | | | (142,278) | | | — | | | — | | | (142,278) | |

| BALANCE, SEPTEMBER 30, 2021 | | 141,883,731 | | | $ | 1,884,039 | | | $ | 4,513,321 | | | $ | (649,591) | | | $ | (57,568) | | | $ | 5,690,201 | |

| BALANCE, JANUARY 1, 2022 | | 141,907,954 | | | $ | 1,893,725 | | | $ | 4,683,659 | | | $ | (649,785) | | | $ | (90,381) | | | $ | 5,837,218 | |

| | | | | | | | | | | | |

| Net income | | — | | | — | | | 791,320 | | | — | | | — | | | 791,320 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (709,651) | | | (709,651) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 640,053 | | | 32,836 | | | — | | | — | | | — | | | 32,836 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (244,978) | | | — | | | — | | | (18,983) | | | — | | | (18,983) | |

| | | | | | | | | | | | |

| Repurchase of common stock pursuant to the Stock Repurchase Plan | | (1,385,517) | | | — | | | — | | | (99,990) | | | — | | | (99,990) | |

| Cash dividends on common stock ($1.20 per share) | | — | | | — | | | (172,082) | | | — | | | — | | | (172,082) | |

| BALANCE, SEPTEMBER 30, 2022 | | 140,917,512 | | | $ | 1,926,561 | | | $ | 5,302,897 | | | $ | (768,758) | | | $ | (800,032) | | | $ | 5,660,668 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Three Months Ended June 30, | | Six Months Ended June 30, | | |

| | 2023 | | 2022 | | 2023 | | 2022 | | | | |

| INTEREST AND DIVIDEND INCOME | | | | | | | | | | | | |

| Loans receivable, including fees | | $ | 771,264 | | | $ | 439,416 | | | $ | 1,499,650 | | | $ | 816,526 | | | | | |

| Debt securities | | 68,970 | | | 46,176 | | | 134,901 | | | 88,843 | | | | | |

| | | | | | | | | | | | |

| Resale agreements | | 3,969 | | | 8,553 | | | 8,472 | | | 16,936 | | | | | |

| Restricted equity securities | | 936 | | | 822 | | | 1,975 | | | 1,431 | | | | | |

| Interest-bearing cash and deposits with banks | | 60,995 | | | 4,787 | | | 96,642 | | | 8,047 | | | | | |

| Total interest and dividend income | | 906,134 | | | 499,754 | | | 1,741,640 | | | 931,783 | | | | | |

| INTEREST EXPENSE | | | | | | | | | | | | |

| Deposits | | 287,477 | | | 22,488 | | | 504,271 | | | 35,477 | | | | | |

| Federal funds purchased and other short-term borrowings | | 49,032 | | | 241 | | | 57,857 | | | 250 | | | | | |

| Federal Home Loan Bank (“FHLB”) advances | | — | | | 559 | | | 6,430 | | | 1,137 | | | | | |

| Repurchase agreements | | 211 | | | 2,418 | | | 1,263 | | | 4,434 | | | | | |

| Long-term debt and finance lease liabilities | | 2,668 | | | 1,096 | | | 5,212 | | | 1,920 | | | | | |

| Total interest expense | | 339,388 | | | 26,802 | | | 575,033 | | | 43,218 | | | | | |

| Net interest income before provision for credit losses | | 566,746 | | | 472,952 | | | 1,166,607 | | | 888,565 | | | | | |

| Provision for credit losses | | 26,000 | | | 13,500 | | | 46,000 | | | 21,500 | | | | | |

| Net interest income after provision for credit losses | | 540,746 | | | 459,452 | | | 1,120,607 | | | 867,065 | | | | | |

| NONINTEREST INCOME | | | | | | | | | | | | |

| Lending fees | | 20,901 | | | 20,142 | | | 41,487 | | | 39,580 | | | | | |

| Deposit account fees | | 22,285 | | | 22,372 | | | 43,988 | | | 42,687 | | | | | |

| Interest rate contracts and other derivative income | | 7,373 | | | 9,801 | | | 9,937 | | | 20,934 | | | | | |

| Foreign exchange income | | 13,251 | | | 11,361 | | | 25,911 | | | 24,060 | | | | | |

| Wealth management fees | | 6,889 | | | 6,539 | | | 13,193 | | | 12,591 | | | | | |

| Net (losses) gains on sales of loans | | (7) | | | 917 | | | (29) | | | 3,839 | | | | | |

| Net gains (losses) on AFS debt securities | | — | | | 28 | | | (10,000) | | | 1,306 | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Other investment income | | 4,003 | | | 4,863 | | | 5,924 | | | 6,490 | | | | | |

| Other income | | 3,936 | | | 2,421 | | | 8,198 | | | 6,700 | | | | | |

| Total noninterest income | | 78,631 | | | 78,444 | | | 138,609 | | | 158,187 | | | | | |

| NONINTEREST EXPENSE | | | | | | | | | | | | |

| Compensation and employee benefits | | 124,937 | | | 113,364 | | | 254,591 | | | 229,633 | | | | | |

| Occupancy and equipment expense | | 16,088 | | | 15,469 | | | 31,675 | | | 30,933 | | | | | |

| Deposit insurance premiums and regulatory assessments | | 8,262 | | | 4,927 | | | 16,172 | | | 9,644 | | | | | |

| Deposit account expense | | 10,559 | | | 5,671 | | | 20,168 | | | 10,364 | | | | | |

| Data processing | | 3,213 | | | 3,486 | | | 6,560 | | | 7,151 | | | | | |

| Computer software expense | | 7,479 | | | 6,572 | | | 14,839 | | | 13,866 | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Other operating expense | | 35,337 | | | 32,392 | | | 70,207 | | | 55,840 | | | | | |

| Amortization of tax credit and other investments | | 55,914 | | | 14,979 | | | 66,024 | | | 28,879 | | | | | |

| | | | | | | | | | | | |

| Total noninterest expense | | 261,789 | | | 196,860 | | | 480,236 | | | 386,310 | | | | | |

| INCOME BEFORE INCOME TAXES | | 357,588 | | | 341,036 | | | 778,980 | | | 638,942 | | | | | |

| INCOME TAX EXPENSE | | 45,557 | | | 82,707 | | | 144,510 | | | 142,961 | | | | | |

| NET INCOME | | $ | 312,031 | | | $ | 258,329 | | | $ | 634,470 | | | $ | 495,981 | | | | | |

| EARNINGS PER SHARE (“EPS”) | | | | | | | | | | | | |

| BASIC | | $ | 2.21 | | | $ | 1.83 | | | $ | 4.49 | | | $ | 3.50 | | | | | |

| DILUTED | | $ | 2.20 | | | $ | 1.81 | | | $ | 4.47 | | | $ | 3.47 | | | | | |

| WEIGHTED-AVERAGE NUMBER OF SHARES OUTSTANDING | | | | | | | | | | | | |

| BASIC | | 141,468 | | | 141,429 | | | 141,291 | | | 141,725 | | | | | |

| DILUTED | | 141,876 | | | 142,372 | | | 141,910 | | | 142,838 | | | | | |

|

See accompanying Notes to Consolidated Financial Statements.

6

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWSCOMPREHENSIVE INCOME (LOSS)

($ in thousands)

(Unaudited)

| | | | | | | | | | | | | | | | |

|

| | Nine Months Ended September 30, | | |

| | 2022 | | 2021 | | |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | |

| Net income | | $ | 791,320 | | | $ | 655,185 | | | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | |

| Depreciation and amortization | | 81,980 | | | 116,371 | | | |

| Amortization of premiums and accretion of discount, net | | 26,336 | | | 17,392 | | | |

| Stock compensation costs | | 29,338 | | | 24,047 | | | |

| Deferred income tax (benefit) expense | | (6,107) | | | 787 | | | |

| Provision for (reversal of) credit losses | | 48,500 | | | (25,000) | | | |

| Net gains on sales of loans | | (5,968) | | | (6,601) | | | |

| Gains on sales of AFS debt securities | | (1,306) | | | (1,178) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Loans held-for-sale: | | | | | | |

| Originations and purchases | | (447) | | | (9,323) | | | |

| Proceeds from sales and paydowns/payoffs of loans originally classified as held-for-sale | | 461 | | | 11,337 | | | |

| | | | | | |

| | | | | | |

| Proceeds from distributions received from equity method investees | | 5,642 | | | 7,624 | | | |

| Net change in accrued interest receivable and other assets | | 56,958 | | | (78,649) | | | |

| Net change in accrued expenses and other liabilities | | 584,655 | | | 30,179 | | | |

| Other operating activities, net | | 5,057 | | | 3,660 | | | |

| Total adjustments | | 825,099 | | | 90,646 | | | |

| Net cash provided by operating activities | | 1,616,419 | | | 745,831 | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | |

| Net change in: | | | | | | |

| Investments in qualified affordable housing partnerships, tax credit and other investments | | (91,710) | | | (141,882) | | | |

| Interest-bearing deposits with banks | | 105,479 | | | 4,576 | | | |

| Resale agreements: | | | | | | |

| Proceeds from paydowns and maturities | | 1,719,076 | | | 698,274 | | | |

| Purchases | | (258,559) | | | (1,834,416) | | | |

| AFS debt securities: | | | | | | |

| Proceeds from sales | | 129,181 | | | 236,967 | | | |

| Proceeds from repayments, maturities and redemptions | | 711,950 | | | 1,346,839 | | | |

| Purchases | | (769,007) | | | (5,884,389) | | | |

| HTM debt securities: | | | | | | |

| Proceeds from repayments, maturities and redemptions | | 60,140 | | | — | | | |

| Purchases | | (50,000) | | | — | | | |

| Loans held-for-investment: | | | | | | |

| Proceeds from sales of loans originally classified as held-for-investment | | 453,315 | | | 416,426 | | | |

| Purchases | | (599,660) | | | (746,395) | | | |

| Other changes in loans held-for-investment, net | | (5,675,012) | | | (1,798,011) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Proceeds from sales of OREO | | — | | | 28,560 | | | |

| Purchase of bank-owned life insurance | | — | | | (150,000) | | | |

| Proceeds from distributions received from equity method investees | | 13,557 | | | 5,626 | | | |

| | | | | | |

| Other investing activities, net | | 920 | | | (61) | | | |

| Net cash used in investing activities | | (4,250,330) | | | (7,817,886) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Three Months Ended June 30, | | Six Months Ended June 30, | | | | | | |

| | 2023 | | 2022 | | 2023 | | 2022 | | | | | | | | | | |

| Net income | | $ | 312,031 | | | $ | 258,329 | | | $ | 634,470 | | | $ | 495,981 | | | | | | | | | | | |

| Other comprehensive loss, net of tax: | | | | | | | | | | | | | | | | | | |

| Net changes in unrealized (losses) gains on AFS debt securities | | (43,618) | | | (192,878) | | | 7,701 | | | (362,148) | | | | | | | | | | | |

| Reclassification of unrealized losses on debt securities transferred from AFS to HTM | | — | | | — | | | — | | | (112,991) | | | | | | | | | | | |

| Amortization of unrealized losses on debt securities transferred from AFS to HTM | | 2,816 | | | 3,750 | | | 5,578 | | | 6,061 | | | | | | | | | | | |

| Net changes in unrealized losses on cash flow hedges | | (53,887) | | | (6,380) | | | (25,274) | | | (31,103) | | | | | | | | | | | |

| Foreign currency translation adjustments | | (7,249) | | | (10,215) | | | (4,308) | | | (10,086) | | | | | | | | | | | |

| Other comprehensive loss | | (101,938) | | | (205,723) | | | (16,303) | | | (510,267) | | | | | | | | | | | |

| COMPREHENSIVE INCOME (LOSS) | | $ | 210,093 | | | $ | 52,606 | | | $ | 618,167 | | | $ | (14,286) | | | | | | | | | | | |

|

See accompanying Notes to Consolidated Financial Statements.

7

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

($ in thousands, except shares and per share data)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Common Stock and Additional Paid-in Capital | | Retained Earnings | | Treasury Stock | | AOCI, Net of Tax | | Total Stockholders’ Equity |

| | Shares | | Amount | | | | |

| BALANCE, APRIL 1, 2022 | | 142,256,520 | | | $ | 1,903,042 | | | $ | 4,863,721 | | | $ | (668,382) | | | $ | (394,925) | | | $ | 5,703,456 | |

| Net income | | — | | | — | | | 258,329 | | | — | | | — | | | 258,329 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (205,723) | | | (205,723) | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 51,733 | | | 11,190 | | | — | | | — | | | — | | | 11,190 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (5,347) | | | — | | | — | | | (380) | | | — | | | (380) | |

| Repurchase of common stock pursuant to the Stock Repurchase Program | | (1,385,517) | | | — | | | — | | | (99,990) | | | — | | | (99,990) | |

| Cash dividends on common stock ($0.40 per share) | | — | | | — | | | (57,400) | | | — | | | — | | | (57,400) | |

| BALANCE, JUNE 30, 2022 | | 140,917,389 | | | $ | 1,914,232 | | | $ | 5,064,650 | | | $ | (768,752) | | | $ | (600,648) | | | $ | 5,609,482 | |

| BALANCE, APRIL 1, 2023 | | 141,395,800 | | | $ | 1,947,687 | | | $ | 5,832,291 | | | $ | (790,653) | | | $ | (679,994) | | | $ | 6,309,331 | |

| | | | | | | | | | | | |

| Net income | | — | | | — | | | 312,031 | | | — | | | — | | | 312,031 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (101,938) | | | (101,938) | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 111,097 | | | 12,097 | | | — | | | — | | | — | | | 12,097 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (23,229) | | | — | | | — | | | (1,237) | | | — | | | (1,237) | |

| | | | | | | | | | | | |

| Cash dividends on common stock ($0.48 per share) | | — | | | — | | | (68,587) | | | — | | | — | | | (68,587) | |

| BALANCE, JUNE 30, 2023 | | 141,483,668 | | | $ | 1,959,784 | | | $ | 6,075,735 | | | $ | (791,890) | | | $ | (781,932) | | | $ | 6,461,697 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Common Stock and Additional Paid-in Capital | | Retained Earnings | | Treasury Stock | | AOCI,

Net of Tax | | Total

Stockholders’ Equity |

| | Shares | | Amount | | | | |

| BALANCE, JANUARY 1, 2022 | | 141,907,954 | | | $ | 1,893,725 | | | $ | 4,683,659 | | | $ | (649,785) | | | $ | (90,381) | | | $ | 5,837,218 | |

| | | | | | | | | | | | |

| Net income | | — | | | — | | | 495,981 | | | — | | | — | | | 495,981 | |

| Other comprehensive loss | | — | | | — | | | — | | | | | (510,267) | | | (510,267) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 639,847 | | | 20,507 | | | — | | | — | | | — | | | 20,507 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (244,895) | | | — | | | — | | | (18,977) | | | — | | | (18,977) | |

| Repurchase of common stock pursuant to the Stock Repurchase Program | | (1,385,517) | | | — | | | — | | | (99,990) | | | — | | | (99,990) | |

| Cash dividends on common stock ($0.80 per share) | | — | | | — | | | (114,990) | | | — | | | — | | | (114,990) | |

| BALANCE, JUNE 30, 2022 | | 140,917,389 | | | $ | 1,914,232 | | | $ | 5,064,650 | | | $ | (768,752) | | | $ | (600,648) | | | $ | 5,609,482 | |

| BALANCE, JANUARY 1, 2023 | | 140,947,846 | | | $ | 1,936,557 | | | $ | 5,582,546 | | | $ | (768,862) | | | $ | (765,629) | | | $ | 5,984,612 | |

| | | | | | | | | | | | |

Cumulative-effect of a change in accounting principle (1) | | — | | | — | | | (4,262) | | | — | | | — | | | (4,262) | |

| Net income | | — | | | — | | | 634,470 | | | — | | | — | | | 634,470 | |

| Other comprehensive loss | | — | | | — | | | — | | | — | | | (16,303) | | | (16,303) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Issuance of common stock pursuant to various stock compensation plans and agreements | | 851,819 | | | 23,227 | | | — | | | — | | | — | | | 23,227 | |

| Repurchase of common stock pursuant to various stock compensation plans and agreements | | (315,997) | | | — | | | — | | | (23,028) | | | — | | | (23,028) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Cash dividends on common stock ($0.96 per share) | | — | | | — | | | (137,019) | | | — | | | — | | | (137,019) | |

| BALANCE, JUNE 30, 2023 | | 141,483,668 | | | $ | 1,959,784 | | | $ | 6,075,735 | | | $ | (791,890) | | | $ | (781,932) | | | $ | 6,461,697 | |

| | | | | | | | | | | | |

(1)Represents the change in the Company’s allowance for loan losses as a result of the adoption of Accounting Standards Update (“ASU”) 2022-02, Financial Instruments - Credit Losses (Topic 326): Troubled Debt Restructurings and the Vintage Disclosures on January 1, 2023. Refer to Note 2 — Current Accounting Developments and Summary of Significant Accounting Policies in this Form 10-Q for additional information.

See accompanying Notes to Consolidated Financial Statements.

8

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

($ in thousands)

(Unaudited)

| | | | | | | | | | | | | | | | |

|

| | Six Months Ended June 30, | | |

| | 2023 | | 2022 | | |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | |

| Net income | | $ | 634,470 | | | $ | 495,981 | | | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | |

| Depreciation and amortization | | 106,579 | | | 48,911 | | | |

| Amortization of premiums and accretion of discount, net | | (10,489) | | | 21,519 | | | |

| Stock compensation costs | | 20,439 | | | 17,009 | | | |

| Deferred income tax expense (benefit) | | 1,098 | | | (7,554) | | | |

| Provision for credit losses | | 46,000 | | | 21,500 | | | |

| Net losses (gains) on sales of loans | | 29 | | | (3,839) | | | |

| Net losses (gains) on AFS debt securities | | 10,000 | | | (1,306) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Loans held-for-sale: | | | | | | |

| Originations and purchases | | — | | | (447) | | | |

| Proceeds from sales and paydowns/payoffs of loans originally classified as held-for-sale | | — | | | 461 | | | |

| | | | | | |

| | | | | | |

| Proceeds from distributions received from equity method investees | | 2,696 | | | 4,412 | | | |

| Net change in accrued interest receivable and other assets | | (273,537) | | | (128,071) | | | |

| Net change in accrued expenses and other liabilities | | (55,634) | | | 457,296 | | | |

| Other operating activities, net | | (283) | | | 3,182 | | | |

| Total adjustments | | (153,102) | | | 433,073 | | | |

| Net cash provided by operating activities | | 481,368 | | | 929,054 | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | |

| Net change in: | | | | | | |

| Investments in qualified affordable housing partnerships, tax credit and other investments | | (69,946) | | | (49,545) | | | |

| Interest-bearing deposits with banks | | 121,774 | | | 23,442 | | | |

| Resale agreements: | | | | | | |

| Proceeds from paydowns and maturities | | 169,917 | | | 1,162,172 | | | |

| Purchases | | (12,725) | | | (231,463) | | | |

| AFS debt securities: | | | | | | |

| Proceeds from sales | | — | | | 129,181 | | | |

| Proceeds from repayments, maturities and redemptions | | 623,108 | | | 613,244 | | | |

| Purchases | | (594,214) | | | (767,015) | | | |

| HTM debt securities: | | | | | | |

| Proceeds from repayments, maturities and redemptions | | 33,882 | | | 40,072 | | | |

| Purchases | | — | | | (50,000) | | | |

| Loans held-for-investment: | | | | | | |

| Proceeds from sales of loans originally classified as held-for-investment | | 302,811 | | | 325,813 | | | |

| Purchases | | (272,637) | | | (541,997) | | | |

| Other changes in loans held-for-investment, net | | (1,649,160) | | | (4,639,384) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Proceeds from distributions received from equity method investees | | 13,113 | | | 8,717 | | | |

| | | | | | |

| Other investing activities, net | | (6,170) | | | 1,354 | | | |

| Net cash used in investing activities | | (1,340,247) | | | (3,975,409) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

See accompanying Notes to Consolidated Financial Statements.

9

EAST WEST BANCORP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

($ in thousands)

(Unaudited)

(Continued)

| | | | Nine Months Ended September 30, | | | Six Months Ended June 30, | |

| | 2022 | | 2021 | | | 2023 | | 2022 | |

| | CASH FLOWS FROM FINANCING ACTIVITIES | CASH FLOWS FROM FINANCING ACTIVITIES | | | | | | CASH FLOWS FROM FINANCING ACTIVITIES | | | | | |

| Net change in deposits | Net change in deposits | | 623,025 | | | 8,486,734 | | | Net change in deposits | | (262,287) | | | 1,046,046 | | |

| Net change in federal funds purchased and short-term borrowings | | 200,006 | | | (21,143) | | | |

| Net change in short-term borrowings | | Net change in short-term borrowings | | 4,500,017 | | | (49) | | |

| | FHLB advances: | FHLB advances: | | | FHLB advances: | | |

| Proceeds | Proceeds | | 4,600,200 | | | — | | | Proceeds | | 6,000,000 | | | 3,950,000 | | |

| Repayment | Repayment | | (4,525,200) | | | (405,000) | | | Repayment | | (6,000,000) | | | (4,025,000) | | |

| Repurchase agreements: | Repurchase agreements: | | | Repurchase agreements: | | |

| Proceeds from repurchase agreements | Proceeds from repurchase agreements | | 311,785 | | | — | | | Proceeds from repurchase agreements | | — | | | 311,785 | | |

| | Repayment of repurchase agreements | | Repayment of repurchase agreements | | (300,000) | | | — | | |

| Repurchase agreements’ extinguishment cost | | Repurchase agreements’ extinguishment cost | | (3,872) | | | — | | |

| Long-term debt and lease liabilities: | Long-term debt and lease liabilities: | | | Long-term debt and lease liabilities: | | |

| | Repayment of long-term debt and lease liabilities | Repayment of long-term debt and lease liabilities | | (710) | | | (909) | | | Repayment of long-term debt and lease liabilities | | (421) | | | (457) | | |

| Common stock: | Common stock: | | | Common stock: | | |

| Repurchase of common stocks pursuant to the Stock Repurchase Program | Repurchase of common stocks pursuant to the Stock Repurchase Program | | (99,990) | | | — | | | Repurchase of common stocks pursuant to the Stock Repurchase Program | | — | | | (99,990) | | |

| Proceeds from issuance pursuant to various stock compensation plans and agreements | Proceeds from issuance pursuant to various stock compensation plans and agreements | | 1,444 | | | 1,180 | | | Proceeds from issuance pursuant to various stock compensation plans and agreements | | — | | | 1,444 | | |

| Stocks tendered for payment of withholding taxes | | (18,983) | | | (15,508) | | | |

| Stock tendered for payment of withholding taxes | | Stock tendered for payment of withholding taxes | | (23,028) | | | (18,977) | | |

| Cash dividends paid | Cash dividends paid | | (171,991) | | | (141,911) | | | Cash dividends paid | | (138,914) | | | (115,623) | | |

| Net cash provided by financing activities | Net cash provided by financing activities | | 919,586 | | | 7,903,443 | | | Net cash provided by financing activities | | 3,771,495 | | | 1,049,179 | | |

| Effect of exchange rate changes on cash and cash equivalents | Effect of exchange rate changes on cash and cash equivalents | | (35,257) | | | 3,542 | | | Effect of exchange rate changes on cash and cash equivalents | | (16,513) | | | (13,706) | | |

| NET (DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS | | (1,749,582) | | | 834,930 | | | |

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | | NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | | 2,896,103 | | | (2,010,882) | | |

| CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | | 3,912,935 | | | 4,017,971 | | | CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | | 3,481,784 | | | 3,912,935 | | |

| CASH AND CASH EQUIVALENTS, END OF PERIOD | CASH AND CASH EQUIVALENTS, END OF PERIOD | | $ | 2,163,353 | | | $ | 4,852,901 | | | CASH AND CASH EQUIVALENTS, END OF PERIOD | | $ | 6,377,887 | | | $ | 1,902,053 | | |

| | SUPPLEMENTAL CASH FLOW INFORMATION | SUPPLEMENTAL CASH FLOW INFORMATION | | | SUPPLEMENTAL CASH FLOW INFORMATION | | |

| Cash paid during the period for: | Cash paid during the period for: | | | Cash paid during the period for: | | |

| Interest | Interest | | $ | 107,146 | | | $ | 70,833 | | | Interest | | $ | 504,774 | | | $ | 45,057 | | |

| Income taxes, net | Income taxes, net | | $ | 233,082 | | | $ | 137,452 | | | Income taxes, net | | $ | 255,432 | | | $ | 188,510 | | |

| Noncash investing and financing activities: | Noncash investing and financing activities: | | | | | | Noncash investing and financing activities: | | | | | |

| | Securities transferred from AFS to HTM debt securities | Securities transferred from AFS to HTM debt securities | | $ | 3,010,003 | | | $ | — | | | Securities transferred from AFS to HTM debt securities | | $ | — | | | $ | 3,010,003 | | |

| Loans transferred from held-for-investment to held-for-sale | Loans transferred from held-for-investment to held-for-sale | | $ | 463,769 | | | $ | 411,416 | | | Loans transferred from held-for-investment to held-for-sale | | $ | 280,026 | | | $ | 351,406 | | |

| Loans transferred from held-for-sale to held-for-investment | | Loans transferred from held-for-sale to held-for-investment | | $ | — | | | $ | 631 | | |

| | Loans transferred to other real estate owned (“OREO”) and other foreclosed assets | | $ | — | | | $ | 49,122 | | | |

|

See accompanying Notes to Consolidated Financial Statements.

810

EAST WEST BANCORP, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1 — Basis of Presentation

East West Bancorp, Inc. (referred to herein on an unconsolidated basis as “East West” and on a consolidated basis as the “Company”) is a registered bank holding company that offers a full range of banking services to individuals and businesses through its subsidiary bank, East West Bank and its subsidiaries (“East West Bank” or the “Bank”). The unaudited interim Consolidated Financial Statements in this Quarterly Report on Form 10-Q (“this Form 10-Q”) include the accounts of East West, East West Bank and East West’s subsidiaries. Intercompany transactions and accounts have been eliminated in consolidation. As of SeptemberJune 30, 2022,2023, East West also has six wholly-owned subsidiaries that are statutory business trusts (the “Trusts”). In accordance with Financial Accounting Standards BoardFASB Accounting Standards Codification (“ASC”) Topic 810, Consolidation, the Trusts are not included on the Consolidated Financial Statements.

The unaudited interim Consolidated Financial Statements are presented in accordance with United States (“U.S.”) Generally Accepted Accounting Principles (“GAAP”), applicable guidelines prescribed by regulatory authorities and general practices in the banking industry. While the unaudited interim Consolidated Financial Statements reflect all adjustments that, in the opinion of management, are necessary for fair presentation, they primarily serve to update the most recently filed annual report on Form 10-K, and may not include all the information and notes necessary to constitute a complete set of financial statements. Accordingly, they should be read in conjunction with the audited Consolidated Financial Statements and notes thereto included in the Company’s Annual Report on2022 Form 10-K for the year ended December 31, 2021, filed with the U.S. Securities and Exchange Commission on February 28, 2022 (the “Company’s 2021 Form 10-K”). In addition, certain items on the Consolidated Financial Statements and notes for the prior periods have been reclassified to conform to the current period presentation.10-K.

The preparation of the Consolidated Financial Statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the Consolidated Financial Statements, income and expenses during the reporting periods, and the related disclosures. Although our current estimates contemplate current conditions and how we expect them to change in the future, it is reasonably possible that actual results could be materially different from those estimates. Hence, the current period’s results of operations are not necessarily indicative of results that may be expected for any future interim period or for the year as a whole. Events subsequent to the Consolidated Balance Sheet date have been evaluated through the date the Consolidated Financial Statements are issued for inclusion in the accompanying Consolidated Financial Statements.

Risk and Uncertainties

The failures of Silicon Valley Bank, Signature Bank and First Republic Bank earlier in the year have resulted in significant disruption in the financial services industry, which has adversely impacted the volatility and market prices of the securities of financial institutions. In addition, these bank failures have caused concern and uncertainty regarding the liquidity of the banking sector as a whole and resulted in some regional bank customers choosing to maintain deposits with larger financial institutions. Further, competition for deposits has increased in recent periods, and the cost of funding has similarly increased, putting pressure on our net interest margin. These events have adversely impacted, and could continue to adversely affect, our business, results of operations, and financial condition, as well as the market price and volatility of our common stock.

Note 2 — Current Accounting Developments and Summary of Significant Accounting Policies

Accounting Pronouncements Adopted in 2023

| | | | | | | | | | | |

| Standard | Required Date of Adoption | Description | Effect on Financial Statements |

ASU 2022-02, Financial Instruments —Credit Losses (Topic 326): Troubled Debt Restructurings and the Vintage Disclosures | January 1, 2023

Early adoption is permitted | ASU 2022-02 eliminates the •accounting guidance for troubled debt restructurings (“TDR”), and requires the Company to apply the loan refinancing and restructuring guidance to determine whether a modification made to a loan results in a new loan or a continuation of an existing loan; and •requirement to use a discounted cash flow method to measure receivables.

The guidance also requires •enhanced disclosures for certain loan refinancings and restructurings by creditors when the borrower is experiencing financial difficulty; and •vintage disclosures of current period gross charge-offs (on a current year-to-date basis) by year of loan origination for financing receivables and net investments in leases within the scope of ASC 326-20: Financial Instruments — Credit Losses — Measured at Amortized Cost. | The Company adopted ASU 2022-02 on January 1, 2023 on a prospective basis, except for the guidance related to the elimination of TDR recognition and measurement, which was adopted on a modified retrospective approach.

This adoption increased the allowance for loan losses on TDRs as of December 31, 2022 by $6.0 million and decreased opening retained earnings on January 1, 2023 by $4.3 million after-tax. Disclosures as of June 30, 2023 are presented in accordance with this guidance while prior year amounts are reported in accordance with previously applicable GAAP. |

| | | |

Recent Accounting Pronouncements Yet to be Adopted

| | | | | | | | | | | |

| Standard | Required Date of Adoption | Description | Effect on Financial Statements |

| Standards Not Yet Adopted |

Accounting Standards Update (“ASU”) 2022-02,ASU 2023-01, Financial Instruments - Credit LossesLeases (Topic 842): (Topic 326): Troubled Debt Restructurings and the Vintage Disclosures

| January 1, 20232024

Early adoption is permitted | ASU 2022-02 eliminates2023-01 amends the troubled debt restructuring (“TDRs”) accounting model for creditors and insteadleasehold improvements for leases between entities under common control arrangements. The guidance requires leasehold improvements associated with leases between companies under common control to applybe amortized by a lessee over the loan refinancing and restructuring guidanceeconomic life of the leasehold improvements, regardless of the lease term or, until the lessee ceases to determine whether a modification made to a borrower results in a new loan or a continuation of an existing loan. In addition, companies are no longer required to use a discounted cash flow method to measure the allowance for credit losses for certain TDRs and instead allows forcontrol the use of the underlying asset through a lease, at which time the remaining value of the leasehold improvement would be accounted for as a transfer between companies under common control through an expected loss approach for all loans. The guidance also introduces new disclosure requirements relatedadjustment to restructuring of financing receivables made to borrowers experiencing financial difficulty, and amends vintage disclosures to require current-period gross write-off by year of origination. equity.

The amendments in this guidance shouldmay be applied retrospectively to the beginning of the period in which the entity first applied Topic 842 or prospectively (1) to all new leasehold improvements recognized on a prospective basis except foror after the date the entity first applies the amendments, relatedor (2) to recognitionall new and measurement of TDRs, where a modified retrospective transition method is optional. existing leasehold improvements recognized on or after the date the entity first applies the amendments. | The Company does not expect the adoption of this guidance to have a material impact on the Company’s Consolidated Financial Statements. The Company expects to adopt ASU 2022-022023-01 on January 1, 2023.

|

ASU 2022-03,2023-02, Fair Value MeasurementInvestments — Equity Method and Joint Ventures (Topic 820)(Topic 323): Fair Value Measurement of Equity Securities Subject to Contractual Sale RestrictionsAccounting for Investments in Tax Credit Structures Using the Proportional Amortization Method | January 1, 2024 | ASU 2022-03 clarifies that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring fair value. This ASU also requires the following disclosures for equity securities that are subject to contractual restrictions: the fair value of equity securities subject to contractual sale restrictions; nature and remaining duration of the restrictions; and circumstances that could cause a lapse in the restrictions.

Early adoption is permitted | ASU 2023-02 expands the scope of the proportional amortization method to equity tax credit investment programs if certain conditions are met. Previously, the proportional amortization method could only be used for investments in low-income housing tax credit structures. Under this guidance, companies are able to elect, on a tax credit program-by-tax credit program basis, to apply the proportional amortization method to all equity investments meeting the criteria in ASC 323-740-25-1.

The amendments in this guidance shouldmust be applied on a prospective basis with any adjustments from the adoption of the amendment recognized in earnings and disclosed on the date of adoption.modified retrospective or a retrospective basis. | The Company does not expectis currently evaluating the adoptionimpact of this guidance to have an impact on the Company’s Consolidated Financial Statements. The Company expects to adopt ASU 2022-03 on January 1, 2024. |

| | | |

| | | |

Significant Accounting Policies Update

DuringLoan Modifications — Certain loans are modified in the first quarternormal course of 2022,business for competitive reasons or in conjunction with the Company’s loss mitigation activities. Upon the adoption of ASU 2022-02, the Company transferred $3.01 billionapplies the general loan modification guidance provided in fair value of debt securities from AFSASC 310-20 to HTM.

Transfer between Categories of Debt Securities— Upon transfer ofall loan modifications, including modifications made to borrowers experiencing financial difficulty. Under the general loan modification guidance, a debt security frommodification is treated as a new loan only if the AFS to HTM category,following two conditions are met: (1) the security’s new amortized cost is reset to fair value, reduced by any previous write-offs but excluding any allowance for credit losses. Unrealized gains or losses at the date of transfer of these securities continue to be reported in AOCI and are amortized into interest income over the remaining lifeterms of the securitiesnew loan are at least as effective yield adjustments, in a manner consistentfavorable to the Company as the terms for comparable loans to other customers with similar collection risks; and (2) modifications to the amortization or accretionterms of the original purchase premiumloan are more than minor. If either condition is not met, the modification is accounted for as a continuation of the existing loan with any effect of the modification treated as a prospective adjustment to the loan’s effective interest rate. A modification made to borrowers experiencing financial difficulty may vary by program and by borrower-specific characteristics, and may include rate reductions, principal forgiveness, term extensions, and payment delays, and is intended to minimize the Company’s economic loss and to avoid foreclosure or discount onrepossession of collateral. The Company applies the associated security.same credit loss methodology it uses for similar loans that were not modified. For transfers of securities from the AFSCompany’s accounting policy related to HTM category, anythe loan modifications’ allowance for creditloan losses, that was previously recorded under the AFS model is reversedsee Note 7 — Loans Receivable and an allowance for credit losses is subsequently recorded under the HTM debt security model. The reversal and re-establishment of the allowance for credit losses are recorded in the provision for credit losses.

Held-to-Maturity Debt Securities— Debt securities that the Company has the intent and ability to hold until maturity are classified as HTM and are carried at amortized cost, net of allowance for credit losses. The criteria used to place HTM debt securities on nonaccrual are largely similar to those described for loans. The amortized cost of the Company’s HTM debt securities excludes accrued interest, which is included in Other assets on the Consolidated Balance Sheet. The Company has made an accounting policy election not to recognize an allowance for credit losses for accrued interest receivables on HTM debt securities, as the Company reverses any accrued interest against interest income if a debt security is placed on nonaccrual status. Any cash collected on nonaccrual HTM securities is applied to reduce the security’s amortized cost basis and not as interest income. Generally, the Company returns an HTM security to accrual status when all delinquent interest and principal become current under the contractual terms of the security, and the collectability of remaining principal and interest is no longer doubtful.

Allowance for Credit Losses on Held-to-Maturity Debt Securities— Allowance for Credit Losses —For each major HTM debt security type,to the allowance for credit losses is estimated collectively for groups of securities with similar risk characteristics. For securities that do not share similar risk characteristics, the losses are estimated individually. The Company applies a zero credit loss assumption to certain HTM debt securities, including debt securities that are either guaranteed or issued by the U.S. government or government-sponsored enterprises, are highly rated by nationally recognized statistical rating organizations (“NRSROs”), and have a long history of no credit losses. Any expected credit loss is recorded through the allowance for credit losses on HTM debt securities and deducted from the amortized cost basis of the security, reflecting the net amount the Company expects to collect.Consolidated Financial Statements in this Form 10-Q.

Note 3 — Fair Value Measurement and Fair Value of Financial Instruments

Fair Value Determination

Fair value is defined as the price that would be received to sell an asset or the price that would be paid to transfer a liability in an orderly transaction between market participants at the measurement date. In determining the fair value of financial instruments,Under applicable accounting standards, the Company uses various methods including market and income approaches. Based on these approaches, the Company utilizes certain assumptions that market participants would use in pricing an asset ormeasures a liability. These inputs can be readily observable, market corroborated or generally unobservable. The Company utilizes valuation techniques that maximize the useportion of observable inputs and minimize the use of unobservable inputs. The fair value hierarchy described below is based on the quality and reliability of the information used to determine fair value. The fair value hierarchy gives the highest priority to quoted prices available in active markets and the lowest priority to prices derived from data lacking transparency. The fair value of the Company’sits assets and liabilities is classified and disclosed in one of the following three categories:

•Level 1 — Valuation is based on quoted prices for identical instruments traded in active markets.

•Level 2 — Valuation is based on quoted prices for similar instruments traded in active markets; quoted prices for identical or similar instruments traded in markets that are not active; and model-derived valuations whose inputs are observable and can be corroborated by market data.

•Level 3 — Valuation is based on significant unobservable inputs for determining theat fair value of assets or liabilities.value. These significant unobservable inputs reflect assumptions that market participants may use in pricing the assets or liabilities.

The classification of assets and liabilities within the hierarchy is based on whether inputs to the valuation methodology used are observable or unobservable, and the significance of those inputs in the fair value measurement. The Company’s assets and liabilities are classified in their entiretypredominantly recorded at fair value on a recurring basis. From time to time, certain assets and liabilities are measured at fair value on a nonrecurring basis; that is, they are subject to fair value adjustments only as required through the application of an accounting method such as lower of cost or fair value or write-down of individual assets. The Company categorizes its assets and liabilities into three levels based on the lowest level of input that is significant to theirestablished fair value measurements.hierarchy and conducts a review of fair value hierarchy classifications on a quarterly basis. For more information regarding the fair value hierarchy and how the Company measures fair value, see Note 1 — Summary of Significant Accounting Policies — Significant Accounting Policies — Fair Value to the Consolidated Financial Statements in the Company’s 2022 Form 10-K for additional information.

Assets and Liabilities Measured at Fair Value on a Recurring Basis

The following section describes the valuation methodologies used by the Company to measure financial assets and liabilities on a recurring basis, as well as the general classification of these instruments pursuant towithin the fair value hierarchy.

Available-for-Sale Debt Securities — The fair value of AFS debt securities is generally determined by independent external pricing service providers who have experience in valuing these securities or by taking the average quoted market prices obtained from independent external brokers. The valuations provided by the third-party pricing service providers are based on observable market inputs, which include benchmark yields, reported trades, issuer spreads, benchmark securities, bids, offers, prepayment expectations and reference data obtained from market research publications. Inputs used by the third-party pricing service providers in valuing collateralized mortgage obligations and other securitization structures also include new issuenewly issued data, monthly payment information, whole loan collateral performance, tranche evaluation and “To Be Announced” prices. In valuing securities issued by state and political subdivisions, inputs used by third-party pricing service providers also include material event notices.

On a monthly basis, the Company validates the valuations provided by third-party pricing service providers to ensure that the fair value determination is consistent with the applicable accounting guidance and the financial instruments are properly classified in the fair value hierarchy. To perform this validation, the Company evaluates the fair values of securities by comparing the fair values provided by the third-party pricing service providers to prices from other available independent sources for the same securities. When significant variances in prices are identified, the Company further compares inputs used by different sources to ascertain the reliability of these sources. On a quarterly basis, the Company reviews the valuation inputs and methodology for each security category furnished by third-party pricing service providers.

When available,a quoted price in an active market exists for the Company uses quoted market pricesidentical security, this price is used to determine the fair value ofand the AFS debt securities that aresecurity is classified as Level 1. Level 1 AFS debt securities consist of U.S. Treasury securities. When pricing is unavailable from third-party pricing service providers for certain securities, the Company requests market quotes from various independent external brokers and utilizes the average quoted market prices. In addition, the Company obtains market quotes from other official published sources. As these valuations are based on observable inputs in the current marketplace, they are classified as Level 2. The Company periodically communicates with the independent external brokers to validate their pricing methodology. Information such as pricing sources, pricing assumptions, data inputs and valuation techniques are reviewed periodically.

Equity Securities — Equity securities consisted of mutual funds as of both SeptemberJune 30, 20222023 and December 31, 2021.2022. The Company invested in these mutual funds for Community Reinvestment Act (“CRA”) purposes. The Company uses net asset value (“NAV”) information to determine the fair value of these equity securities. When NAV is available periodically and the equity securities can be put back to the transfer agents at the publicly available NAV, the fair value of the equity securities is classified as Level 1. When NAV is available periodically, but the equity securities may not be readily marketable at its periodic NAV in the secondary market, the fair value of these equity securities is classified as Level 2.