Exploration and Development Costs

Exploration costs incurred in locating areas of potential mineralization or evaluating properties or working interests with specific areas of potential mineralization are expensed as incurred. Development costs of proven mining properties not yet producing are capitalized at cost and classified as capitalized exploration costs under property, plant and equipment. Property holding costs are charged to operations during the period if no significant exploration or development activities are being conducted on the related properties. Upon commencement of production, capitalized exploration and development costs would be amortized based on the estimated proven and probable reserves benefited. Properties determined to be impaired or that are abandoned are written-down to the estimated fair value. Carrying values do not necessarily reflect present or future values.

Mineral Property Rights

Costs of acquiring mining properties are capitalized upon acquisition. Mine development costs incurred either to develop new ore deposits, to expand the capacity of mines, or to develop mine areas substantially in advance of current production are also capitalized once proven and probable reserves exist and the property is a commercially mineable property. Costs incurred to maintain current production or to maintain assets on a standby basis are charged to operations. Costs of abandoned projects are charged to operations upon abandonment. The Company evaluates the carrying value of capitalized mining costs and related property and equipment costs, to determine if these costs are in excess of their recoverable amount whenever events or changes in circumstances indicate that their carrying amounts may not be recoverable. Evaluation of the carrying value of capitalized costs and any related property and equipment costs are based upon expected future cash flows and/or estimated salvage value in accordance with Accounting Standards Codification (ASC) 360-10-35-15,Impairment or Disposal of Long-Lived Assets.

Long-Lived Assets

In accordance with ASC 360, Property Plant and Equipment the Company tests long-lived assets or asset groups for recoverability when events or changes in circumstances indicate that their carrying amount may not be recoverable. Circumstances which could trigger a review include, but are not limited to: significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed significantly before the end of its estimated useful life. Recoverability is assessed based on the carrying amount of the asset and its fair value which is generally determined based on the sum of the undiscounted cash flows expected to result from the use and the eventual disposal of the asset, as well as specific appraisal in certain instances. An impairment loss is recognized when the carrying amount is not recoverable and exceeds fair value.

Fair Value of Financial Instruments

ASC Topic 820 defines fair value, establishes a framework for measuring fair value, and expands disclosures about fair value measurements.

8

Included in the ASC Topic 820 framework is a three level valuation inputs hierarchy with Level 1 being inputs and transactions that can be effectively fully observed by market participants spanning to Level 3 where estimates are unobservable by market participants outside of the Company and must be estimated using assumptions developed by the Company. The Company discloses the lowest level input significant to each category of asset or liability valued within the scope of ASC Topic 820 and the valuation method as exchange, income or use. The Company uses inputs which are as observable as possible and the methods most applicable to the specific situation of each company or valued item.

The Company's financial instruments consist of cash, accounts payable, accrued liabilities, advances, notes payable, and a promissory note payable. The carrying amount of these financial instruments approximate fair value due to either length of maturity or interest rates that approximate prevailing market rates unless otherwise disclosed in these financial statements.

Secured convertible promissory note derivative liability is measured at fair value on a recurring basis using Level 3 inputs.

6

Interest rate risk is the risk that the value of a financial instrument might be adversely affected by a change in the interest rates. The notes payable, loans payable and secured convertible promissory notes have fixed interest rates therefore the Company is exposed to interest rate risk in that they could not benefit from a decrease in market interest rates. In seeking to minimize the risks from interest rate fluctuations, the Company manages exposure through its normal operating and financing activities.

Derivative Instruments

Accounting standards require that an entity recognize all derivatives as either assets or liabilities in the statement of financial position and measure those instruments at fair value. A change in the market value of the financial instrument is recognized as a gain or loss in results of operations in the period of change.

Foreign Currency Translation

The Company’s functional and reporting currency is the United States dollar. Monetary assets and liabilities denominated in foreign currencies are translated to United States dollars in accordance with ASC 740, Foreign Currency Translation Matters, using the exchange rate prevailing at the balance sheet date. Gains and losses arising on translation or settlement of foreign currency denominated transactions or balances are included in the determination of income.

To the extent that the Company incurs transactions that are not denominated in its functional currency, they are undertaken in Mexican Pesos. The Company has not, as of the date of these financial statements, entered into derivative instruments to offset the impact of foreign currency fluctuations.

Comprehensive Loss

ASC 220, Comprehensive Income establishes standards for the reporting and display of comprehensive loss and its components in the consolidated financial statements. As at December 31, 2017For the three and 2016,six months ended September 30, 2021 and 2020, the Company had no items that represent a comprehensive loss, and therefore has not included a schedule of comprehensive loss in the consolidated financial statements.

Income Taxes

The Company accounts for income taxes using the asset and liability method in accordance with ASC 740, “Accounting for Income Tax”. The asset and liability method provides that deferred tax assets and liabilities are recognized for the expected future tax consequences of temporary differences between the financial reporting and tax bases of assets and liabilities, and for operating loss and tax credit carry forwards.carryforwards. Deferred tax assets and liabilities are measured using the currently enacted tax rates and laws that will be in effect when the differences are expected to reverse. The Company records a valuation allowance to reduce deferred tax assets to the amount that is believed more likely than not to be realized.

9

Asset Retirement Obligations

In accordance with accounting standards for asset retirement obligations (ASC 410), the Company records the fair value of a liability for an asset retirement obligation (ARO) when there is a legal obligation associated with the retirement of a tangible long-lived asset and the liability can be reasonably estimated. The associated asset retirement costs are supposed to be capitalized as part of the carrying amount of the related mineral properties. As of DecemberSeptember 30, 2021 and March 31, 2017 and 2016,2021, the Company has not recorded AROs associated with legal obligations to retire any of the Company’s mineral properties as the settlement dates are not presently determinable.

Revenue Recognition

In accordance with ASC 606, revenue is recognized when a customer obtains control of promised goods or services. The Company recognizes revenuesamount of revenue recognized reflects the consideration to which we expect to be entitled to receive in exchange for these goods or services. The provisions of ASC 606 include a five-step process by which we determine revenue recognition, depicting the transfer of goods or services to customers in amounts reflecting the payment to which we expect to be entitled in exchange for those goods or services. ASC 606 requires us to apply the following steps: (1) identify the contract with the customer; (2) identify the performance obligations in the contract; (3) determine the transaction price; (4) allocate the transaction price to the performance obligations in the contract; and (5) recognize revenue when, or as, we satisfy the related costs when persuasive evidence of an arrangement exists, delivery and acceptance has occurred or service has been rendered, the price is fixed or determinable, and collection of the resulting receivable is reasonably assured.performance obligation.

7

Stock-based Compensation

The Company records stock based compensation in accordance with the guidance in ASC Topic 718 which requires the Company to recognize expenses related to the fair value of its employee stock option awards. This eliminates accounting for share-based compensation transactions using the intrinsic value and requires instead that such transactions be accounted for using a fair-value-based method. The Company recognizes the cost of all share-based awards on a graded vesting basis over the vesting period of the award.

ASC 505, "Compensation-Stock Compensation", establishes standards for the accounting for transactions in which an entity exchanges its equity instruments to non-employees for goods or services. Under this transition method, stock compensation expense includes compensation expense for all stock-based compensation awards granted on or after January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of ASC 505.

Per Share Data

Net loss per common share is computed by dividing net loss by the weighted average common shares outstanding during the period as defined by Financial Accounting Standards, ASC Topic 260, "Earnings per Share". Basic earnings per common share (“EPS”) calculations are determined by dividing net income by the weighted average number of shares of common stock outstanding during the year. Diluted earnings per common share calculations are determined by dividing net income by the weighted average number of common shares and dilutive common share equivalents outstanding. During periods when common stock equivalents, if any, are anti-dilutive they are not considered in the computation.

On September 30, 2021 and March 31, 2021, we excluded the outstanding securities summarized below, which entitle the holders thereof to acquire shares of common stock as their effect would have been anti-dilutive:

September 30, 2021 |

| March 31, 2021 | |

Common stock issuable upon conversion of notes payable and convertible notes payable | 23,790,035 |

| 16,317,058 |

Common stock issuable upon conversion of warrants | 610,000 |

| 610,000 |

Common stock issuable to satisfy stock payable obligations | 12,100,547 |

| 4,970,315 |

Common stock issuable upon conversion of Series A Preferred Stock | 1,000,000 |

| 1,000,000 |

Total | 37,500,582 |

| 22,897,373 |

10

Recently Issued Accounting Pronouncements

In August 2020, the FASB issued ASU 2020-06, Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40). This update amends the guidance on convertible instruments and the derivatives scope exception for contracts in an entity's own equity and improves and amends the related EPS guidance for both Subtopics. This standard is effective for fiscal years and interim periods within those fiscal years beginning after December 15, 2023, which means it will be effective for our fiscal year beginning April 1, 2024. Early adoption is permitted but no earlier than fiscal years beginning after December 15, 2020, including interim periods within those fiscal years. We are currently evaluating the impact of ASU 2020-06 on our consolidated financial statements.

Other recent accounting pronouncements issued by the FASB, including its Emerging Issues Task Force, the American Institute of Certified Public Accountants, and the Securities and Exchange Commission did not or are not believed by management to have a material impact on the Company's present or future consolidated financial statements.

3.GOING CONCERN

The accompanying condensed consolidated financial statements have been prepared assuming the Company will continue as a going concern, which contemplates the realization of assets and satisfaction of liabilities in the normal course of business. During the ninesix months ended December 31, 2017,September 30, 2021, the Company incurred a net loss of $2,906,769$1,693,565 and used cash in operating activities of $793,668,$335,835, and at December 31, 2017,on September 30, 2021, had an accumulated deficit of $25,850,802.$37,371,363. On September 30, 2021, the Company is in the exploration stage. These factors, among others, raise substantial doubt about the Company’s ability to continue as a going concern within one year of the date that the financial statements are issued. The Company’s independent registered public accounting firm, in their report on the Company’s financial statements for the year ending March 31, 2017,2021, expressed substantial doubt about the Company’s ability to continue as a going concern.

The Company is dependent upon outside financing to continue operations. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. It is management’s plans to raise necessary funds through a private placement of its common stock to satisfy the capital requirements of the Company’s business plan. There is no assurance that the Company will be able to raise the necessary funds, or that if it is successful in raising the necessary funds, that the Company will successfully execute its business plan. The Company is unable to predict the effect, if any, that the coronavirus COVID-19 global pandemic may have on its access to the financing markets.

The condensed consolidated financial statements do not include any adjustments relating to the recoverability and classification of assets and/or liabilities that might be necessary should the Company be unable to continue as a going concern. The continuation as a going concern is dependent upon the ability of the Company to meet our obligations on a timely basis, and, ultimately to attain profitability.

8

4.RECENT ACCOUNTING PRONOUNCEMENTS AFFECTING THE COMPANYPROPERTY & EQUIPMENT

In May 2014, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2014-09,Revenue from Contracts with Customers. ASU 2014-09 is a comprehensive revenue recognition standard that will supersede nearly all existing revenue recognition guidance under current U.S. GAAP and replace it with a principle based approach for determining revenue recognition. ASU 2014-09 will require that companies recognize revenue based on the value of transferred goods or services as they occur in the contract. The ASU also will require additional disclosure about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts, including significant judgments and changes in judgments and assets recognized from costs incurred to obtain or fulfill a contract. In addition, during 2016 the FASB issued ASU 2016-08, ASU 2016-10 and ASU 2016-12, all of which clarify certain implementation guidance within ASU 2014-09, and ASU 2016-11, which rescinds certain SEC guidance effective upon an entity’s adoption of ASU 2014-09. ASU 2014-09 is effective for interim and annual periods beginning after December 15, 2017. Early adoption is permitted only in annual reporting periods beginning after December 15, 2016, including interim periods therein. The standard can be adopted either retrospectively to each prior reporting period presented or as a cumulative effect adjustment as of the date of adoption. The Company is currently in the process of evaluating the impact of ASU 2014-09 on the Company’s consolidated financial statements and disclosures.

Cost | Accumulated Depreciation | September 30, 2021 Net Book Value | March 31, 2021 Net Book Value | |

Mining tools and equipment | $ 1,867,746 | $ 1,613,323 | $ 254,423 | $ 286,860 |

Vehicles | 178,810 | 175,566 | 3,244 | 6,532 |

$ 2,046,556 | $ 1,788,889 | $ 257,667 | $ 293,392 |

In February 2016, the FASB issued ASU No. 2016-02,Leases.ASU 2016-02 requires a lessee to record a right of use assetDepreciation expense for three and a corresponding lease liability on the balance sheet for all leases with terms longer than 12 months. ASU 2016-02 is effective for all interimsix months ended September 30, 2021 and annual reporting periods beginning after December 15, 2018. Early adoption is permitted. A modified retrospective transition approach is required for lessees for capital2020 was $17,863 and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. The Company is currently evaluating the expected impact that the standard could have on its consolidated financial statements$35,725 and related disclosures.

Other recent accounting pronouncements issued by the FASB, including its Emerging Issues Task Force, the American Institute of Certified Public Accountants,$25,149 and the Securities and Exchange Commission did not or are not believed by management to have a material impact on the Company's present or future consolidated financial statements.$50,318, respectively.

11

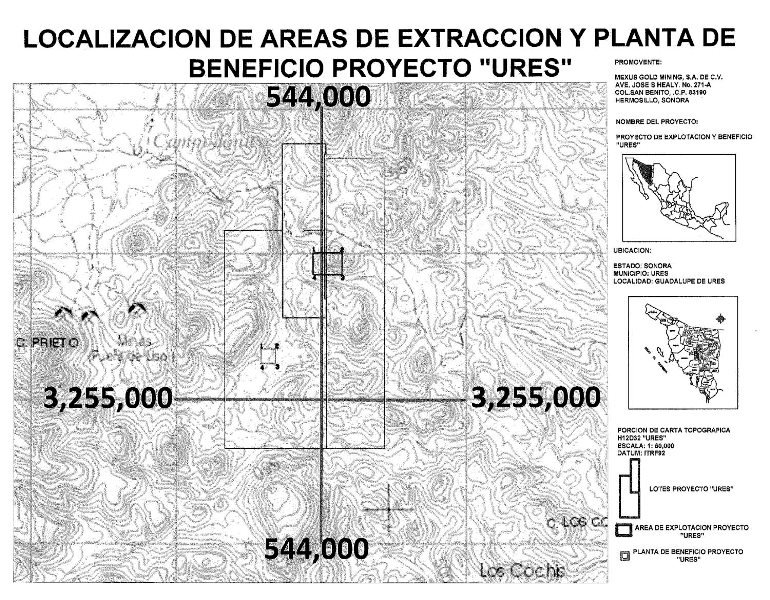

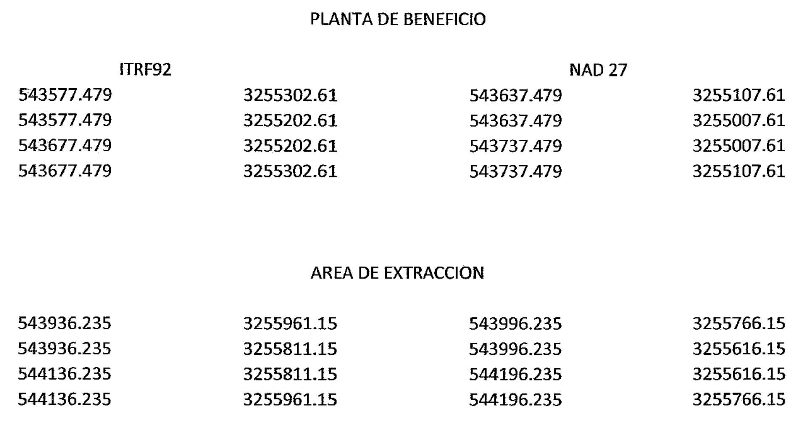

5.MINERAL PROPERTIES AND EXPLORATION COSTS

Impairment of San Felix Project

Effective January 13, 2017, Mexus Gold Mining, S.A. de C.V., a wholly owned Mexican subsidiary of the Company, entered into a purchase agreement with Jesus Leopoldo Felix Mazon, Leonardo Elias Jaime Perez, and Elia Lizardi Perez, wherein the Company purchased a 50% interest in the “San Felix” mining site located in the La Alameda area of Caborca, State of Sonora, Mexico. The remaining 50% of the site is owned jointly by Mar Holdings S.A. de C.V. and Marco Antonio Martinez Mora.

The San Felix mining site contains seven (7) concessions over an area of approximately 26,000 acres.

The total purchase price is US$2,000,000 of which the Company is 50% responsible. The required payment schedule is a follows: $150,000 by January 30, 2017, $500,000 by August 13, 2017, $500,000 by March 13, 2018, $500,000 by October 13, 2018, and $350,000 by May 13, 2019. On January 30, 2017, the Company paid $75,000 (50% of $150,000).

During the nine months ended December 31, 2017, the Company recorded an impairment of mineral property for the San Felix Project of $75,000 because the requirement payment of $500,000 due on August 13, 2017 was not paid in accordance with the purchase agreement.

6.EQUIPMENT

|

| Cost |

| Accumulated Depreciation |

| December 31, 2017 Net Book Value |

| March 31, 2017 Net Book Value |

Mining tools and equipment | $ | 1,505,387 | $ | 1,045,202 | $ | 460,185 | $ | 490,888 |

Vehicles |

| 153,639 |

| 129,481 |

| 24,158 |

| 14,695 |

| $ | 1,659,026 | $ | 1,174,683 | $ | 484,343 | $ | 505,583 |

Depreciation expense for the three and nine months ended December 31, 2017 and 2016 was $67,796 and $55,063 and $187,764 and $170,396, respectively.

9

7.ACCOUNTS PAYABLE – RELATED PARTYPARTIES

During the ninethree and six months ended December 31, 2017September 30, 2021 and 2016,2020, the Company incurred rent expense to Paul D. Thompson, the sole director and officer of the Company, of $34,200$11,400 and $34,200,$22,800 and $11,400 and $22,800, respectively. At December 31, 2017On September 30, 2021 and March 31, 2017, $90,7232021, $157,092 and $65,203$147,153 for this obligation is outstanding, respectively.

Compensation

On July 2, 2015,September 30, 2021, the Company entered into a compensation agreement with Paul D. Thompson Sr., the sole director and officer of the Company. Mr. Thompson is compensated $15,000 per month and has the option to take payment in Company stock, valued at an average of 5 days closing price, cash paymentspayment or deferred payment in stock or cash. In addition,addition. Mr. Thompson is due 2,000,000 shares of common stock at the end of each fiscal quarter. At December 31, 2017On September 30, 2021 and March 31, 2017, $210,8862021, $303,318 and $195,657$280,949 of compensation due is included in accounts payable – related party, respectively and $32,600$33,800 for 2,000,000 shares and $51,400 for 2,000,000 shares of common stock due is included in share subscriptions payable, respectively.

8.6.NOTES PAYABLE –AND NOTES PAYABLE - RELATED PARTY

Notes due to Taurus Gold, Inc. are unsecured, non-interest bearing and due on demand. These notes were accumulated through a series of cash advances to the Company. Taurus Gold, Inc. is controlled by Paul D. Thompson, the sole director and officer of the Company. As of December 31, 2017 and March 31, 2017, notes payable due to Taurus Gold Inc. totaled $4,514 and $67,224, respectively.

Notes due to North Pacific Gold were accumulated through a series of cash advances to the Company which are unsecured, non-interest bearing and due on demand. North Pacific Gold is controlled by Paul Thompson, Jr., an immediate family member of Paul D. Thompson, the sole director and officer of the Company. As of December 31, 2017 and March 31, 2017, notes payable due to North Pacific Gold totaled $9,227 and $19,531, respectively.

9.NOTES PAYABLE

During the year ended March 31, 2014, the Company received cash advances of $164,502 from three unrelated shareholders of the Company. These advances are non-interest bearing, unsecured and have no specific terms of repayment. On August 19, 2014, the Company issued 1,750,020 shares of common stock valued at $70,000. The shares were issued in settlement of the convertible promissory note ($0.04 per share) to settle $87,501 in advances. As a result, the Company recorded a gain on settlement of debt of $17,501. On February 28, 2015, the Company issued 2,272,727 shares of common stock valued at $48,636 ($0.0214 per share) to settle $25,000 in advances. As a result, the Company recorded a loss on settlement of debt of $23,636. On August 24, 2015, $37,001 of these advances were settled on issuance of the convertible promissory note. At December 31, 2017 and March 31, 2017, the balance of these advances totaled $15,000 and $15,000, respectively.

During the years ended March 31, 2017, 2016 and 2015, the Company received $0 in advances, various advances totaling $290,300 from nineteen investors and received various advances totaling $286,757 from twenty-two investors, respectively. These advances are unsecured and are due within 30 to 180 days of issue. Upon receipt of the cash advances, the Company paid a majority of the investors the value of their investment in shares of common stock of the Company as a finance fee. The investor has the option to be repaid when due by one of the following: (i) In cash (ii) One-half in cash and one—half in shares converted into common stock of the Company or (iii) The entire amount of the investment converted into shares of common stock of the Company. The conversion prices range from $0.0018 per share to $0.040 per share. For one promissory note with principal of $15,000 payments equal to 20% of cash proceeds received by the Company are due when equipment held for sale is sold.

During the ninesix months ended December 31, 2017September 30, 2021 and 2016, the Company received various advances for notes payable totaling $135,000 from eight investors and received $0 in advances, respectively. These notes are unsecured, due in three to six months of issue and earn a finance fee of 15% to 20% of principal. The investors have the option for principal and the finance fee to be repaid when due by one of the following: (i) In cash or (ii) Converted into shares of common stock of the Company $0.02 to $0.10 per share. These notes were initially recorded net of a debt discount of $80,000 for a beneficial conversion feature with a corresponding increase in additional paid-in capital of $80,000. In conjunction with issuance of these notes payable 300,000 shares of common stock of the Company valued at $9,568 were issued to the note holders and recorded as debt discount. At December 31, 2017 and March 31, 2017, a debt discount of $5,541 and $0, respectively has been recorded on the condensed consolidated balance sheet related to these notes.

During the nine months ended December 31, 2017 and 2016,2020, note principal and interest of $60,000$156,641 and $3,000 was paid through$2,000, respectively, the issuance ofCompany agreed to issue 8,416,395 shares and 50,000 shares of common stock, respectively,respectively. In addition, for six months ended September 30, 2021 and 2020, the Company paid $0 and $1,500$7,000 in cash, respectively.respectively, to settle debt.

10

At December 31, 2017On September 30, 2021 and March 31, 2017,2021, the balancecarrying value of these advancesthe notes payable totaled $118,600$1,153,147 (net of unamortized debt discount of $0) and $43,600,$1,232,576 (net of unamortized debt discount of $0), respectively. At December 31, 2017, $33,300

Notes payable – related party – On September 30, 2021 and 2020, notes payable – related party of these$141,169 and $141,169, respectively, are due to Paul Thompson Sr., the sole officer and director of the Company. These notes were in default. There are no default provisions stated inbear interest from 0% to 12% per annum.

Interest and amortization of debt discount was $77,211 and $136,185 for the notes. At December 31, 2017six months ended September 30, 2021 and 2020, respectively.

On September 30, 2021 and March 31, 20172021, accrued interest of $6,236$267,919 and $0,$214,744, respectively, is included in accounts payable and accrued liabilities.

On January 19, 2016, the Company issued a promissory note (“Note”) with a principalSeptember 30, 2021, $1,194,016 of amount of $77,150 bearing interest of 10% per annum to settle $77,150 in accountsnotes payable due for accounting fees. Payments equal to 15% of cash proceeds received by the Company are due when equipment held for sale is sold. Any unpaid principal and interest is due in full on July 19, 2016. At December 31, 2017 and March 31, 2017, the balance of this note was $74,297 and $74,297, respectively. At December 31, 2017, this note wasnotes payable – related party were in default. There are no default provisions stated in the Note.

Amortization of debt discount was $84,026 and $54,112 for the nine months ended December 31, 2017 and 2016, respectively, and $38,917 and $54,112 for the three months ended December 31, 2017 and 2016, respectively.these notes.

10.7.PROMISSORY NOTESNOTE

On April 18, 2013, the Company issuedSeptember 30, 2021 and March 31, 2021, outstanding Promissory Notes for $255,000 in cash.were $65,000 and $65,000, respectively. The NotesNote bear interest of 4% per annum and are due on December 31, 2013. The Notes areNote is secured by all of Mexus Gold US shares of stock in Mexus Resources S.A. de C.V. and a personal guarantee of Paul D. Thompson. In addition, a fee of 2,550,000 shares of common stock of the Company valued at $501,075 ($0.1965 per share) was paid to the Note holders on April 18, 2013. These financing fees were capitalized in the consolidated balance sheet as deferred finance expense and were being amortized on a straight-line basis, which approximates the effective interest rate method, as interest expense over the life of the Promissory Notes. On August 24, 2015, $100,000 of these Promissory Notes were settled on issuance of a convertible promissory note. On December 1, 2015, $60,000 of these Promissory Notes were settled on issuance of a convertible promissory note. On September 19, 2016, the Company issued 570,750 shares of common stock with a fair value $44,234 ($0.0775 per share) to settle a promissory note with principal of $20,000. On March 31, 2017, a promissory note with principal of $10,000 was settled for no consideration and recorded as a gain on the consolidated statement of operations. At December 31, 2017 and March 31, 2017, outstanding Promissory Notes were $65,000 and $65,000, respectively. As of December 31, 2017,September 30, 2021, the Company has not made the scheduled payments and is in default on thesethis promissory notes.note. The default rate on the notes is seven percent. At December 31, 2017On September 30, 2021 and March 31, 20172021, accrued interest of $23,151$50,193 and $25,399,$46,351, respectively, is included in accounts payable and accrued liabilities.

On August 24, 2015, the Company issued a convertible promissory note (“Note”) for a total amount of $343,973 due on February 24, 2017 to William H. Brinker (“Holder”). The total amount of the Note is due in three equal payments plus any accrued interest at 180 days, 360 days and 540 days from the issuance date. The Holder upon annual election may elect to be paid in cash or stock (but not both) as follows: (a) in cash, with interest at 4% per annum (b) in shares of common stock of the Company, with interest at 12% per annum (“Stock Payment”). For a Stock Payment, the number of shares is determined by multiplying the outstanding principal of the Note by 12% divided by 100% of the average of the closing price of the Stock for ten trading days immediately preceding the payment date. This Note has been accounted for in accordance with ASC 480Distinguishing Liabilities from Equity. In consideration of the Company issuing the Note, the Holder agreed to cancel all other notes, contracts or other agreements with a carrying value totaling $458,402 prior to the issuance of the Note comprising unsecured promissory note dated January 8, 2013 of $140,000, promissory note of $100,000 dated April 18, 2013, various notes payable of $41,001, interest payable of $9,372 and share subscriptions payable of $168,029. In conjunction with the Note, on September 2, 2015, the Company issued the Holder 8,732,880 shares of common stock with a fair value of $134,486 ($0.0154 per share) which was recorded as debt discount. The issuance of the Note resulted in gain on settlement of $114,429. On September 19, 2016, the Company issued 6,665,786 shares of common stock with a fair value $516,597 ($0.0775 per share) to fully settle the Note with principal of $343,973 and a note payable with principal of $30,000.

On December 1, 2015, the Company issued a convertible promissory note (“Note”) dated August 24, 2015 for a total amount of $41,189 due on February 24, 2017 to David Long (“Holder”). The total amount of the Note is due in three equal payments plus any accrued interest at 180 days, 360 days and 540 days from the date of the Note. The Holder upon annual election may elect to be paid in cash or stock (but not both) as follows: (a) in cash, with interest at 4% per annum (b) in shares of common stock of the Company, with interest at 12% per annum (“Stock Payment”). For a Stock Payment, the number of shares is determined by multiplying the outstanding principal of the Note by 12% divided by 100% of the average of the closing price of the Stock for ten trading days immediately preceding the payment date. This Note has been accounted for in accordance with ASC 480Distinguishing Liabilities from Equity. In consideration of the Company issuing the Note, the Holder agreed to cancel all other notes, contracts or other agreements with a carrying value totaling $60,000 prior to the issuance of the Note comprising a promissory note of $60,000 dated April 18, 2013. In conjunction with the Note, on September 2, 2015, the Company issued the Holder 686,475 shares of common stock with a fair value of $10,297 ($0.015 per share) which as recorded as debt discount. The issuance of the Note resulted in gain on settlement of $18,811. On September 19, 2016, the Company issued 800,000 shares of common stock with a fair value $62,000 ($0.0775 per share) to fully settle the promissory note with principal of $41,189.

11

Amortization of debt discount was $0 and $142,592 for the nine months ended December 31, 2017 and 2016, respectively, and $0 and $0 for the three months ended December 31, 2017 and 2016, respectively.

11.8.CONVERTIBLE PROMISSORY NOTENOTES

Power Up Lending Group Ltd.

On November 14, 2017,October 15, 2020, the Company issued a Convertible Promissory Note (“Note”) to JMJ FinancialPower Up Lending Group Ltd. (“Holder”), in the original principal amount of $52,500 less transaction costs of $2,500 bearing a 12% annual interest rate and maturing October 15, 2021 for a principal sum of $166,667 plus one-time 10% interest charge of $16,667 which matures on May 14, 2018 for $150,000$50,000 in cash. The Company may repayAfter 180 days after the Note and interest any time in cash before the maturityissue date, without a prepayment penalty. If the Company defaults on repayment, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s

12

option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $11,818 (accreted value of $80,769 less debt discount of $68,951). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On March 31, 2021, the Note is recorded at an accreted value of $47,801 ($85,205 less unamortized debt discount of $37,404). From April 22, 2021 to April 30, 2021, the Company issued 4,274,515 shares of common stock of the Company with the fair value $102,609 to the Holder to fully settle the Note resulting in a loss on settlement of $16,993. Interest and amortization of debt discount was $37,815 for the six months ended September 30, 2021.

On December 15, 2020, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $43,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing December 15, 2021 for $40,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as lesser of (a) $0.0375 or (b) 50% (40% if the conversion shares are not deliverable by DWAC)average of the lowest trade occurringtwo trading prices during the 25 consecutivefifteen (15) trading days immediately precedingday period ending on the latest complete trading day prior to the conversion date. On issuanceAt inception, the carrying value of the Note an embedded derivative with a fairwas $6,797 (accreted value of $66,205 was identified and recorded as$66,923 less debt discount (Seeof $60,126). The Company may repay the Note 12). In conjunction withif repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On March 31, 2021, the Note is recorded at an accreted value of $26,590 ($69,255 less unamortized debt discount of $42,665). From June 16, 2021 to June 18, 2021, the Company issued 3,591,9402,891,728 shares of common stock (“Origination Shares”) of the Company which was recorded as debt discount. The Origination Shares andwith the fair value $82,483 to the Holder to fully settle the Note were valued at $51,920resulting in a loss on settlement of $11,544. Interest and $31,875 upon issuance, respectively, usingamortization of debt discount was $44,348 for the relative fair value method. Additionalsix months ended September 30, 2021.

On January 20, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $43,500 less transaction costs of $3,500 bearing a 12% annual interest expense is accreted onrate and maturing January 20, 2022 for $40,000 in cash. After 180 days after the issue date, this Note between issuance and maturity datestogether with the expectation that principal andany unpaid accrued interest is likely to be settled inconvertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 40%65% of tradethe market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $0 (accreted value of $66,923 less debt discount of $66,923). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On March 31, 2021, the Note is recorded at an accreted value of $11,364 ($68,463 less unamortized debt discount of $57,099). From July 26, 2021 to August 9, 2021, the Company issued 3,137,298 shares of common stock of the Company. At December 31, 2017,Company with the principal and interest outstandingfair value $73,615 to the Holder to fully settle the Note resulting in a loss on settlement of $254,742 is recorded net of unamortized debt discount of $112,129.$2,677. Interest and amortization of debt discount was $110,738$59,574 for the three and ninesix months ended DecemberSeptember 30, 2021.

On March 1, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $38,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing March 1, 2022 for $35,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $1,453 (accreted value of $59,231 less debt discount of $57,778). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 2017.days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days

13

at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On March 31, 2021, the Note is recorded at an accreted value of $6,786 ($59,815 less unamortized debt discount of $53,029), respectively. From September 7, 2021 to September 14, 2021, the Company issued 4,877,232 shares of common stock of the Company with the fair value $82,985 to the Holder to fully settle the Note resulting in a loss on settlement of $20,201. Interest and amortization of debt discount was $55,999 for the six months ended September 30, 2021.

On April 5, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $40,000 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing April 5, 2022 for $36,500 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $13,462 (accreted value of $61,538 less debt discount of $48,076).The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $40,509 ($50,605 less unamortized debt discount of $10,096). Interest and amortization of debt discount was $27,047 for the six months ended September 30, 2021.

On April 29, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $38,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing April 29, 2022 for $35,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $12,600 (accreted value of $59,231 less debt discount of $46,631). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $35,273 ($46,745 less unamortized debt discount of $11,472). Interest and amortization of debt discount was $22,673 for the six months ended September 30, 2021.

On May 20, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $43,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing May 20, 2022 for $40,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $11,694 (accreted value of $66,923 less debt discount of $55,229). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $34,745 ($51,461 less unamortized debt discount of $16,716). Interest and amortization of debt discount was $23,051 for the six months ended September 30, 2021.

On June 14, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $43,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing June 14, 2022 for $40,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a

14

variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $10,341 (accreted value of $66,923 less debt discount of $56,582). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $29,459 ($49,307 less unamortized debt discount of $19,848). Interest and amortization of debt discount was $19,118 for the six months ended September 30, 2021.

On July 28, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $38,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing July 28, 2022 for $35,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $15,712 (accreted value of $59,231 less debt discount of $43,519). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $24,589 ($39,881 less unamortized debt discount of $15,292). Interest and amortization of debt discount was $8,877 for the six months ended September 30, 2021.

On August 17, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $45,000 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing August 17, 2022 for $41,500 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. At inception, the carrying value of the Note was $21,454 (accreted value of $69,231 less debt discount of $47,776). The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. On September 30, 2021, the Note is recorded at an accreted value of $28,881 ($45,422 less unamortized debt discount of $16,541). Interest and amortization of debt discount was $6,761 for the six months ended September 30, 2021.

Crown Bridge Partners, LLC

On August 11, 2020, the Company issued a Convertible Promissory Note (“Note”) to Crown Bridge Partners, LLC (“Holder”) in the original principal amount of $55,000 less transaction costs of $5,000 bearing a 12% annual interest rate and maturing August 10, 2021 for $50,000 in cash. This Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 60% of the market price defined as the lowest trading price during the twenty trading day period ending on the latest complete trading day prior to the conversion date. The Company determined that upon issuance of the Note, the initial fair value of the embedded conversion feature was $91,113 which was recorded as a debt discount. At inception, the carrying value of the Note was $0 (accreted value of $91,667 less debt discount of $91,667). The Company may repay the Note if repaid within 60 days of date of issue at 125% of the original principal amount plus interest, between 61 days and 120 days at 135% of the original principal amount plus interest and between 121 days and 180 days at 145% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment. The Company determined that upon issuance of the Note, the initial fair value of the embedded conversion feature was $91,113, of which $50,000 was recorded as debt discount and the remainder of $41,113 was recorded expensed and included in gain (loss) on derivative liability. On September 30, 2021 and March 31, 2021,

15

the Note is recorded at an accreted value of $104,174 ($104,174 less unamortized debt discount of $0) and $65,419 (98,659 less unamortized debt discount of $33,240), respectively). Interest and amortization of debt discount was $38,917 for the six months ended September 30, 2021.

12.9.CONVERTIBLE PROMISSORY NOTE DERIVATIVE LIABILITY

The Convertible Promissory Notes (“Notes”) with JMJ Financial with an issue date of November 14, 2017Power Up Lending Group Ltd. and Crown Bridge Partners, LLC was accounted for under ASC 815. The variable conversion price is not considered predominately based on a fixed monetary amount settleable with a variable number of shares due to the volatility and trading volume of the Company’s common stock. The Company’s convertible promissory notenotes derivative liabilities has been measured at fair value at November 14, 2017 and December 31, 2017 using the Black-Scholes model.

The inputs into the Black-Scholes models are as follows:

|

| November 14, 2017 |

| December 31, 2017 | September 30, 2021 | June 30, 2021 | March 31, 2021 |

Closing share price | $ | 0.038 | $ | 0.0547 | $0.0169 | $0.0285 | $0.0257 |

Conversion price | $ | 0.0348 | $ | 0.0375 | $0.013 - $0.0142 | $0.0256 | $0.0233 - $0.0234 |

Risk free rate |

| 0.050% |

| 0.050% | 0.05% - 0.07% | 0.05% | 0.04% |

Expected volatility |

| 109% |

| 134% | 103% - 117% | 94% - 153% | 136% - 161% |

Dividend yield |

| 0% |

| 0% | 0% | 0% | |

Expected life |

| 0.5 years |

| 0.37 years | |||

Expected life (years) | 0.50- 0.88 | 0.11- 0.96 | 0.36 – 0.81 | ||||

Continuity of the Fair value of the Conversion Option Derivative Liabilities | Three Months Ended September 30, 2021 | Six Months Ended September 30, 2021 | Three Months Ended September 30, 2020 | Six Months Ended September 30, 2020 |

Opening | $146,243 | $138,539 | $215,086 | $486,663 |

Initial value | 38,576 | 141,979 | 115,367 | 292,366 |

Decrease in fair value | (21,749) | (117,448) | (115,711) | (564,287) |

Closing | $163,070 | $163,070 | $214,742 | $214,742 |

10.WARRANT LIABILITY

In conjunction with the issuance of the Convertible Promissory Notes with Crown Bridge Partners, LLC on November 21, 2019 and August 11, 2020, the Company issued, with each Note, 1,100,000 warrants with an exercise price of $1.00 and a term of five years.

Also, in conjunction with the issuance of the Convertible Promissory Note with Auctus Fund, LLC (the “Note”) on December 19, 2019, the Company issued 10,000,000 warrants with an exercise price of $0.10 and a term of five years.

These warrants are subject to down round and other anti-dilution protections. These warrants are classified as a liability since there is a possibility during the life of these warrants the Company would not have enough authorized shares available if these warrants are exercised.

The fair value ofinputs into the conversion option derivative liability is $66,205 and $120,788 at November 14, 2017 and December 31, 2017, respectively. The increase in the fair value of the conversion option derivative liability of $54,583 is recordedBlack-Scholes models are as a loss in the unaudited condensed consolidated statements of operations for the three and nine months ended December 30, 2017.follows:

| September 30, 2021 | June 30, 2021 | March 31, 2021 |

Closing share price | $0.0169 | $0.0285 | $0.0257 |

Conversion price | $1.00 - $0.10 | $1.00 - $0.10 | $1.00 - $0.10 |

Risk free rate | 0.50 - 0.70% | 0.50 - 0.70% | 0.35% |

Expected volatility | 175 - 179% | 172 - 182% | 170 - 180% |

Dividend yield | 0% | 0% | 0% |

Expected life (years) | 3.15 – 3.86 | 3.40 - 4.12 | 3.65 – 4.36 |

16

Continuity of the Fair value of the Warrant Liabilities | Three Months Ended September 30, 2021 | Six Months Ended September 30, 2021 | Three Months Ended September 30, 2020 | Six Months Ended September 30, 2020 |

Opening, March 31 | $13,935 | $12,669 | $34,268 | $39,387 |

Increase (decrease) in fair value | (6,440) | (5,174) | (6,238) | (11,357) |

Closing, September 30 | $7,495 | $7,495 | $28,030 | $28,030 |

13.11.CONTINGENT LIABILITIES

An asset retirement obligation is a legal obligation associated with the disposal or retirement of a tangible long-lived asset that results from the acquisition, construction or development, or the normal operations of a long-lived asset, except for certain obligations of lessees. While the Company, as of December 31, 2017,September 30, 2021, does not have a legal obligation associated with the disposal of certain chemicals used in its leaching process, the Company estimates it will incur costs up to $50,000 to neutralize those chemicals at the close of the leaching pond.

14.12.STOCKHOLDERS’ EQUITYDEFICIT

The stockholders’ equity of the Company comprises the following classes of capital stock as of December 31, 2017September 30, 2021 and March 31, 2017:2021:

Preferred Stock, $0.001 par value per share; 9,000,000 shares authorized, 0 issued and outstanding at December 31, 2017on September 30, 2021 and March 31, 2017.2021.

Series A Convertible Preferred Stock (‘Series A Preferred Stock”), $0.001 par value share; 1,000,000 shares authorized: 1,000,000 shares issued and outstanding at December 31, 2017on September 30, 2021 and March 31, 2017.2021.

12

Holders of Series A Preferred Stock may convert one share of Series A Preferred Stock into one shareten shares of Common Stock. Holders of Series A Preferred Stock have the number of votes determined by multiplying (a) the number of Series A Preferred Stock held by such holder, (b) the number of issued and outstanding Series A Preferred Stock and Common Stock on a fully diluted basis, and (c) 0.000006.

Common Stock, par value of $0.001 per share; 850,000,0005,000,000,000 shares authorized: 740,543,789244,305,989 and 665,556,526177,714,055 shares issued and outstanding at December 31, 2017on September 30, 2021 and March 31, 2017,2021, respectively. Holders of Common Stock have one vote per share of Common Stock held.

Common Stock Issued

On April 11, 2017,7, 2021, the Company issued 1,097,8261,675,000 shares of common stock to satisfy obligations under share subscription agreements for $9,000 for settlement of equipment and $50,000 in cash receipts included in share subscriptions payable.

On April 17, 2017, the Company issued 621,954 shares of common stock to satisfy obligations under share subscription agreements for $15,000 for settlement of services and $25,000 in cash receipts included in share subscriptions payable.

On May 15, 2017, the Company issued 108,696 shares of common stock to satisfy obligations under share subscription agreements for $10,000$43,048 for settlement of services included in share subscriptions payable.

On June 2, 2017,April 20, 2021, the Company issued 4,593,3333,735,000 shares of common stock to satisfy obligations under share subscription agreements of $20,000 for $41,300cash and $54,870 for settlement of services and $36,500 in cash receiptsfor the settlement of interest included in share subscriptions payable.

On July 5, 2017,April 23, 2021, the Company issued 600,0002,307,692 shares of common stock to satisfy obligations under share subscription agreements for $5,760of $60,692 for settlement of services and $32,485 for settlement of stock payableconvertible notes included in share subscriptions payable.

On July 11 2017,April 28, 2021, the Company issued 2,949,25310,000,000 shares of common stock to satisfy obligations under share subscription agreements for $25,975 for settlement of services and $88,500 in cash receipts included in share subscriptions payable.

On August 1, 2017, the Company issued 3,693,333 shares of common stock to satisfy obligations under share subscription agreements for $38,000 for settlement of services and $76,500 in cash receipts included in share subscriptions payable.

On August 15, 2017, the Company issued 11,436,667 shares of common stock to satisfy obligations under share subscription agreements for $102,000 for settlement of accounts payable, $405,500 for settlement of services and $36,000 in cash receipts included in share subscriptions payable.

On September 12, 2017, the Company issued 4,500,000 shares of common stock to satisfy obligations under share subscription agreements for $85,400 for settlement of services and $71,600 in cash receipts included in share subscriptions payable.

On September 25, 2017, the Company issued 3,500,000 shares of common stock to satisfy obligations under share subscription agreements for $61,300 for settlement of services and $45,000 in cash receipts included in share subscriptions payable.

On September 28, 2017, the Company issued 2,275,000 shares of common stock to satisfy obligations under share subscription agreements for $23,500 for settlement of services and $35,500 in cash receipts included in share subscriptions payable.

On October 13, 2017, the Company issued 3,814,232 shares of common stock to satisfy obligations under share subscription agreements for $47,000 for settlement of services, $10,000 for settlement of notes payable, interest of $2,303 and $44,785 in cash receipts included in share subscriptions payable.

On November 6, 2017, the Company issued 5,430,030 shares of common stock to satisfy obligations under share subscription agreements for $57,575 for settlement of services, $4,000 for settlement of notes payable, interest of $2,395 and $16,040 in cash receipts included in share subscriptions payable.

On November 13, 2017, the Company issued 6,591,666 shares of common stock to satisfy obligations under share subscription agreements for $6,000 for settlement of services, $57,500 for settlement of notes payable, interest of $1,632 and $50,000 in cash receipts included in share subscriptions payable.

On November 30, 2017, the Company issued 3,591,940 shares of common stock to satisfy obligations under share subscription agreements for interest of $51,920 and included in share subscriptions payable.

13

On December 12, 2017, the Company issued 2,283,333 shares of common stock to satisfy obligations under share subscription agreements for $29,000 in cash receipts included in share subscriptions payable.

On December 14, 2017, the Company issued 3,600,000 shares of common stock to satisfy obligations under share subscription agreements for $136,800$212,000 for settlement of services included in share subscriptions payable.

On December 20, 2017,April 29, 2021, the Company issued 8,050,0001,153,846 shares of common stock to satisfy obligations under share subscription agreements for $106,400of $24,519 for settlement of services, $80,000 for equipment and $44,200 in cash receiptsconvertible notes included in share subscriptions payable.

On December 28, 2017,May 3, 2021, the Company issued 6,250,000812,977 shares of common stock to satisfy obligations under share subscription agreements of $17,398 for $250,000settlement of convertible notes included in share subscriptions payable.

17

On May 20, 2021, the Company issued 4,461,163 shares of common stock to satisfy obligations under share subscription agreements of $89,223 for settlement of notes payable included in share subscriptions payable.

Common Stock Payable

On June 26, 2017,May 28, 2021, the Company issued subscriptions payable for 500,000 shares in common stock valued at $32,485 ($0.06497 per share) to fully settle subscription payable and other liabilities totaling $137,004. The settlement resulted in an increase of additional paid-in capital of $104,519.

As at December 31, 2017, the Company had total subscriptions payable for 24,016,394 shares of common stock for $80,038 in cash, shares of common stock for equipment valued at $1,500, shares of common stock for interest valued at $8,237, shares of common stock for services valued at $369,976 and common stock for settlement of notes payable valued at $5,000.

15.SUBSEQUENT EVENTS

Common Stock

On January 5, 2018, the Company issued 7,666,666400,000 shares of common stock to satisfy obligations under share subscription agreements of $6,000 for $79,400 for settlement of services, $162,500 for settlement of accounts payable, $825 for interest and $39,000 in cash receipts included in share subscriptions payable.

On January 19, 2018,June 16, 2021, the Company issued 633,3321,419,753 shares of common stock to satisfy obligations under share subscription agreements of $42,593 for $10,000 in cash receiptssettlement of convertible notes included in share subscriptions payable.

On January 29, 2018,June 18, 2021, the Company issued 3,187,0001,471,975 shares of common stock to satisfy obligations under share subscription agreements for $8,448of $39,891 for settlement of services and $36,600 in cash receiptsconvertible notes included in share subscriptions payable.

On January 30, 2018,June 24, 2021, the Company issued 527,779800,000 shares of common stock to satisfy obligations under share subscription agreements of $10,000 for $20,650cash included in share subscriptions payable.

On July 2, 2021, the Company issued 5,600,000 shares of common stock to satisfy obligations under share subscription agreements of $159,600 for settlement of services included in share subscriptions payable.

On July 12, 2021, the Company issued 1,640,000 shares of common stock to satisfy obligations under share subscription agreements of $25,000 for cash, $3,800 for settlement of notes payable and $3,556$4,160 for settlement of services included in share subscriptions payable.

On July 14, 2021, the Company issued 4,900,000 shares of common stock to satisfy obligations under share subscription agreements of $138,670 for settlement of services included in share subscriptions payable.

On July 26, 2021, the Company issued 4,000,000 shares of common stock to satisfy obligations under share subscription agreements of $107,200 for settlement of services included in share subscriptions payable.

On July 27, 2021, the Company issued 1,634,616 shares of common stock to satisfy obligations under share subscription agreements of $11,125 for cash receiptsand $24,500 for settlement of services included in share subscriptions payable.

On July 27, 2021, the Company issued 1,324,503 shares of common stock to satisfy obligations under share subscription agreements of $31,258 for settlement of convertible notes included in share subscriptions payable.

On July 30, 2021, the Company issued 1,013,514 shares of common stock to satisfy obligations under share subscription agreements of $24,932 for settlement of convertible notes included in share subscriptions payable.

On July 30, 2021, the Company issued 1,800,000 shares of common stock to satisfy obligations under share subscription agreements of $10,000 for cash and $26,800 for settlement of services included in share subscriptions payable.

On August 3, 2021, the Company issued 1,000,000 shares of common stock to satisfy obligations under share subscription agreements of $12,500 for cash included in share subscriptions payable.

On August 10, 2021, the Company issued 799,281 shares of common stock to satisfy obligations under share subscription agreements of $17,424 for settlement of convertible notes included in share subscriptions payable.

On August 31 2021, the Company issued 3,280,000 shares of common stock to satisfy obligations under share subscription agreements of $36,000 for cash included in share subscriptions payable.

On September 7, 2021, the Company issued 1,914,894 shares of common stock to satisfy obligations under share subscription agreements of $30,255 for settlement of convertible notes included in share subscriptions payable.

On September 9, 2021, the Company issued 1,280,563 shares of common stock to satisfy obligations under share subscription agreements of $16,647 for settlement of notes payable included in share subscriptions payable.

18

On September 14, 2021, the Company issued 2,962,338 shares of common stock to satisfy obligations under share subscription agreements of $52,730 for settlement of convertible notes included in share subscriptions payable.

On September 16, 2021, the Company issued 4,000,000 shares of common stock to satisfy obligations under share subscription agreements of $20,000 for cash included in share subscriptions payable.

On September 20, 2021, the Company issued 1,204,819 shares of common stock to satisfy obligations under share subscription agreements of $10,000 for cash included in share subscriptions payable.

Common Stock Payable

From the period of January 1, 2018 to February 7, 2018,As at September 30, 2021, the Company issuedhad total subscriptions payable for 4,555,00012,100,547 shares of common stock ($0.0135 per share) for $61,600$34,366 in cash.

From the period of January 1, 2018 to February 7, 2018, the Company issued subscriptions payable for 6,482,000cash, shares of common stock ($0.0553 per share) for $15,975 in services.

From the period of January 1, 2018 to February 7, 2018, the Company issued subscriptions payable for 2,708,333interest valued at $27,911, shares of common stock ($0.0600 per share) for $162,500 inservices valued at $154,331 and shares of common stock for notes payable of $80,164.

13.RELATED PARTY TRANSACTIONS

During the six months ended September 30, 2021 and March 31, 2021, the Company entered into the following transactions with related parties:

Paul D. Thompson, sole director and officer of the Company

Taurus Gold, Inc., controlled by Paul D. Thompson

Accounts payable – related parties – Note 5

Notes payable and notes payable – relate party – Note 6

14.SUBSEQUENT EVENTS

Common Stock Issued

On October 6, 2021, the Company issued 1,900,000 shares of common stock to satisfy obligations under share subscription agreements of $46,740 for settlement of accountsservices included in share subscriptions payable.

14

On October 7, 2021, the Company issued 1,978,022 shares of common stock to satisfy obligations under share subscription agreements of $31,055 for settlement of convertible notes included in share subscriptions payable.

On October 20, 2021, the Company issued 4,400,000 shares of common stock to satisfy obligations under share subscription agreements of $74,360 for settlement of services included in share subscriptions payable.

On October 20, 2021, the Company issued 2,741,573 shares of common stock to satisfy obligations under share subscription agreements of $37,560 for settlement of convertible notes included in share subscriptions payable.

On October 22, 2021, the Company issued 1,250,000 shares of common stock to satisfy obligations under share subscription agreements of $8,500 for cash and $6,360 for settlement of services included in share subscriptions payable.

On October 26, 2021, the Company issued 3,965,232 shares of common stock to satisfy obligations under share subscription agreements of $5,020 for services and $59,491 for settlement of notes payable included in share subscriptions payable.

On November 2, 2021, the Company issued 1,000,000 shares of common stock to satisfy obligations under share subscription agreements of $10,000 for settlement of cash included in share subscriptions payable.

On November 4, 2021, the Company issued 3,731,343 shares of common stock to satisfy obligations under share subscription agreements of $37,313 for settlement of convertible notes included in share subscriptions payable.

19

Common Stock Payable

As at November 8, 2021, the Company had total subscriptions payable for 835,315 shares of common stock for $28,366 in cash, shares of common stock for interest valued at $27,911, shares of common stock for services valued at $21,850 and shares of common stock for notes payable of $20,673.

Power Up Lending Group Ltd.

On October 5, 2021, the Company issued a Convertible Promissory Note (“Note”) to Power Up Lending Group Ltd. (“Holder”) in the original principal amount of $38,500 less transaction costs of $3,500 bearing a 12% annual interest rate and maturing October 5, 2022 for $35,000 in cash. After 180 days after the issue date, this Note together with any unpaid accrued interest is convertible into shares of common stock of the Company at the Holder’s option at a variable conversion price calculated at 65% of the market price defined as the average of the lowest two trading prices during the fifteen (15) trading day period ending on the latest complete trading day prior to the conversion date. The Company may repay the Note if repaid in cash within 30 days of date of issue at 110% of the original principal amount plus interest, between 31 days and 60 days at 115% of the original principal amount plus interest, between 61 days and 90 days at 120% of the original principal amount plus interest, between 91 days and 120 days at 125% of the original principal amount plus interest and between 121 days and 180 days at 135% of the original principal amount plus interest. Thereafter, the Company does not have the right of prepayment.

ITEM 2.MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Cautionary Statement Concerning Forward-Looking Statements

The following discussion and analysis should be read in conjunction with our unaudited condensedaudited consolidated financial statements and related notes included in this report. This report contains “forward-looking statements.” The statements contained in this report that are not historic in nature, particularly those that utilize terminology such as “may,” “will,” “should,” “expects,” “anticipates,” “estimates,” “believes,” or “plans” or comparable terminology are forward-looking statements based on current expectations and assumptions.

Various risks and uncertainties could cause actual results to differ materially from those expressed in forward-looking statements. Factors that could cause actual results to differ from expectations include, but are not limited to, those set forth under the section “Risk Factors” set forth in this report.

The forward-looking events discussed in this report, the documents to which we refer you and other statements made from time to time by us or our representatives, may not occur, and actual events and results may differ materially and are subject to risks, uncertainties and assumptions about us. For these statements, we claim the protection of the “bespeaks caution” doctrine. All forward-looking statements in this document are based on information currently available to us as of the date of this report, and we assume no obligation to update any forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements.

COVID-19

The recent outbreak of the coronavirus COVID-19 has spread across the globe and is impacting worldwide economic activity. Conditions surrounding the coronavirus continue to rapidly evolve and government authorities have implemented emergency measures to mitigate the spread of the virus. The outbreak and the related mitigation measures have had and will continue to have a material adverse impact on global economic conditions as well as on the Company's business activities. The extent to which COVID-19 may impact the Company's business activities will depend on future developments, such as the ultimate geographic spread of the disease, the duration of the outbreak, travel restrictions, business disruptions, and the effectiveness of actions taken in the United States, Mexico and other

20

countries to contain and treat the disease. These events are highly uncertain and, as such, the Company cannot determine their financial impact at this time. No adjustments have been made to the amounts reported in the consolidated financial statements as a result of this matter.

The Company

Mexus Gold US is an exploration stage mining company engaged in the evaluation, acquisition, exploration and advancement of gold, silver and copper projects in the State of Sonora, Mexico. Mexus Gold US is dedicated to protect the environment and provide employment and education opportunities for the communities that it operates in.

Our President and CEO, Paul Thompson, brings over 45 years’ experience in mining and mining development to Mexus Gold US. Mr. Thompson is currently recruiting additional management personnel for its Mexico and Nevada mining operations.

Our executive offices are located at, 1805 N. Carson Street, #150, Carson City, Nevada 89701. Our telephone number is (916) 776 2166.

We were originally incorporated under the laws of the State of Colorado on June 22, 1990, as U.S.A. Connection, Inc. On September 18, 2009, we changed our domicile to Nevada and changed our name to Mexus Gold US to better reflect our new business operations. Our fiscal year end is March 31st.

Description of the Business of Mexus Gold US

Mexus Gold US is engaged in the evaluation, acquisition, exploration and advancement of gold exploration and development projects in the United Mexican States, as well as the salvage of precious metals from identifiable sources. Our main activities in the near future will be comprised of our mining operations in Mexico. Our mining opportunities located in the State of Sonora, Mexico will provide us with projects to recover gold, silver, copper and other precious metals.

In addition, our management will look for opportunities to improve the value of the gold projects that we own or may acquire knowledge of or may acquire control through exploration drilling, introduction of technological innovations or acquisition with the goal of developing those properties into operating mines. We expect that emphasis on gold project acquisition and development will continue in the future.

Business Strategy