UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2005March 31, 2006

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________to________ to _________

Commission file number: 333-77499

333-77499-01

Charter Communications Holdings, LLC

Charter Communications Holdings Capital Corporation *Corporation*

(Exact name of registrants as specified in their charters)

Delaware Delaware | | 43-1843179 |

Delaware

| | 43-1843177 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

12405 Powerscourt Drive

St. Louis, Missouri 63131

(Address of principal executive offices including zip code)

(314) 965-0555

(Registrants’ telephone number, including area code)

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrants are large accelerated filers, accelerated filers, or non-accelerated filers. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer oAccelerated filer oNon-accelerated filer þ

Indicate by check mark whether the registrants are shell companies (as defined in Rule 12b-2 of the Exchange Act). YES [ ] NO [X]Yes oNo þ

Number of shares of common stock of Charter Communications Holdings Capital Corporation outstanding as of November 5, 2005:May 11, 2006: 100

* Charter Communications Holdings Capital Corporation meets the conditions set forth in General Instruction H(1)(a) and (b) to Form 10-Q and is therefore filing with the reduced disclosure format.

Charter Communications Holdings, LLC

Charter Communications Holdings Capital Corporation

Quarterly Report on Form 10-Q for the Period ended September30, 2005March 31, 2006

PART I. FINANCIAL INFORMATION | Page |

| | |

| PART I. FINANCIAL INFORMATION | |

| |

Item 1.Report of Independent Registered Public Accounting Firm | 4 |

| | |

Financial Statements - Charter Communications Holdings, LLC and Subsidiaries | |

| March 31, 2006 | |

| 2005 | 5 |

| |

| 6 |

| |

| 7 |

| 8 |

| | |

Item 2.Management's Discussion and Analysis of Financial Condition and Results of Operations | 2826 |

| | |

Item 3.Quantitative and Qualitative Disclosures about Market Risk | 5235 |

| | |

| 5335 |

| | |

| PART II. OTHER INFORMATION | |

| | |

| 5437 |

| |

| Item 1A. Risk Factors | 37 |

| |

| Item 5. Other Information | 46 |

| | |

| 5647 |

| | |

| SIGNATURES | 5648 |

| | |

| 57 |

| |

| 5849 |

This quarterly report on Form 10-Q is for the three and nine months ended September 30, 2005.March 31, 2006. The Securities and Exchange Commission ("SEC") allows us to "incorporate by reference" information that we file with the SEC, which means that we can disclose important information to you by referring you directly to those documents. Information incorporated by reference is considered to be part of this quarterly report. In addition, information that we file with the SEC in the future will automatically update and supersede information contained in this quarterly report. In this quarterly report, "we," "us" and "our" refer to Charter Communications Holdings, LLC and its subsidiaries.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS:

This quarterly report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), regarding, among other things, our plans, strategies and prospects, both business and financial including, without limitation, the forward-looking statements set forth in the "Results of Operations" and "Liquidity and Capital Resources" sections under Part I, Item 2. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in this quarterly report. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions including, without limitation, the factors described under "Certain Trends and Uncertainties" under Part I, Item 2. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in this quarterly report. Many of the forward-looking statements contained in this quarterly report may be identified by the use of forward-looking words such as "believe," "expect," "anticipate," "should," "planned," "will," "may," "intend," "estimated" and "potential" among others. Important factors that could cause actual results to differ materially from the forward-looking statements we make in this quarterly report are set forth in this quarterly report and in other reports or documents that we file from time to time with the SEC, and include, but are not limited to:

| | · | the availability, in general, of funds to meet interest payment obligations under our and our parent company’scompanies’ debt and to fund our operations and necessary capital expenditures, either through cash flows from operating activities, further borrowings or other sources and, in particular, our ability to be able to provide under the applicable debt instruments such funds (by dividend, investment or otherwise) to the applicable obligor of such debt; |

| · | our and our parent companies’ ability to comply with all covenants in our and our parent companies’ indentures and credit facilities, any violation of which would result in a violation of the applicable facility or indenture and could trigger a default of other obligations under cross-default provisions; |

| · | our and our parent companies’ ability to pay or refinance debt prior to or when it becomes due and/or to take advantage of market opportunities and market windows to refinance that debt through new issuances, exchange offers or otherwise, including restructuring our and our parent companies’ balance sheet and leverage position; |

| | · | our ability to sustain and grow revenues and cash flows from operating activities by offering video, high-speed Internet, telephone and other services and to maintain and grow a stable customer base, particularly in the face of increasingly aggressive competition from other service providers; |

| · | our and our parent company’s ability to comply with all covenants in our and our parent company’s indentures, the Bridge Loan and credit facilities, any violation of which would result in a violation of the applicable facility or indenture and could trigger a default of other obligations under cross-default provisions; |

| · | our and our parent company’s ability to pay or refinance debt prior to or when it becomes due and/or to take advantage of market opportunities and market windows to refinance that debt in the capital markets through new issuances, exchange offers or otherwise, including restructuring our and our parent company’s balance sheet and leverage position; |

| | · | our ability to obtain programming at reasonable prices or to pass programming cost increases on to our customers; |

| | · | general business conditions, economic uncertainty or slowdown; and |

| | · | the effects of governmental regulation, including but not limited to local franchise authorities, on our business. |

All forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by this cautionary statement. We are under no duty or obligation to update any of the forward-looking statements after the date of this quarterly report.

PART I. FINANCIAL INFORMATION.

Item 1. Financial Statements.

The Board of Directors

Charter Communications Holdings, LLC:

We have reviewed the condensed consolidated balance sheet of Charter Communications Holdings, LLC and subsidiaries (the “Company”)Company) as of September 30, 2005,March 31, 2006, and the related condensed consolidated statements of operations for the three-month and nine-month periods ended September 30, 2005 and 2004, and the related condensed consolidated statements of cash flows for the nine-monththree-month periods ended September 30, 2005March 31, 2006 and 2004.2005. These condensed consolidated financial statements are the responsibility of the Company’s management.

We conducted our reviews in accordance with the standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States), the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our reviews, we are not aware of any material modifications that should be made to the condensed consolidated financial statements referred to above for them to be in conformity with U.S. generally accepted accounting principles.

We have previously audited, in accordance with standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of the Company as of December 31, 2004,2005, and the related consolidated statements of operations, changes in member’s equity (deficit), and cash flows for the year then ended (not presented herein);, and in our report dated MarchFebruary 27, 2006, which includes explanatory paragraphs regarding the adoption, effective September 30, 2004, of EITF Topic D-108, Use of the Residual Method to Value Acquired Assets Other than Goodwill, and effective January 1, 2005, 2003, of Statement of Financial Accounting Standards (SFAS) No. 123, Accounting for Stock-Based Compensation, as amended by SFAS No. 148, Accounting for Stock Based Compensation—Transition and Disclosure—an amendment of FASB Statement No. 123, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2004,2005, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

As discussed in Note 4 to the condensed consolidated financial statements, effective September 30, 2004, the Company adopted EITF Topic D-108, Use of the Residual Method to Value Acquired Assets Other than Goodwill.

/s/ KPMG LLP

St. Louis, Missouri

October 31, 2005April 28, 2006

CONDENSED CONSOLIDATED BALANCE SHEETS

(DOLLARS IN MILLIONS)

| | | September 30, | | December 31, | | | March 31, | | December 31, | |

| | | 2005 | | 2004 | | | 2006 | | 2005 | |

| | | (Unaudited) | | | | | (Unaudited) | | | |

ASSETS | | | | | | | | | | |

| CURRENT ASSETS: | | | | | | | | | | | | |

| Cash and cash equivalents | | $ | 20 | | $ | 546 | | | $ | 29 | | $ | 14 | |

| Accounts receivable, less allowance for doubtful accounts of | | | | | | | | | | | | | | |

| $15 and $15, respectively | | | 185 | | | 186 | | |

| $15 and $17, respectively | | | | 148 | | | 212 | |

| Prepaid expenses and other current assets | | | 23 | | | 20 | | | | 23 | | | 22 | |

| Assets held for sale | | | | 754 | | | -- | |

| Total current assets | | | 228 | | | 752 | | | | 954 | | | 248 | |

| | | | | | | | | | | | | | | |

| INVESTMENT IN CABLE PROPERTIES: | | | | | | | | | | | | | | |

| Property, plant and equipment, net of accumulated | | | | | | | | | | | | | | |

| depreciation of $6,357 and $5,142, respectively | | | 5,895 | | | 6,110 | | |

| depreciation of $6,679 and $6,712, respectively | | | | 5,402 | | | 5,800 | |

| Franchises, net | | | 9,830 | | | 9,878 | | | | 9,287 | | | 9,826 | |

| Total investment in cable properties, net | | | 15,725 | | | 15,988 | | | | 14,689 | | | 15,626 | |

| | | | | | | | | | | | | | | |

| OTHER NONCURRENT ASSETS | | | 323 | | | 344 | | | | 329 | | | 318 | |

| | | | | | | | | | | | | | | |

| Total assets | | $ | 16,276 | | $ | 17,084 | | | $ | 15,972 | | $ | 16,192 | |

| | | | | | | | | | | | | | | |

LIABILITIES AND MEMBER’S DEFICIT | | | | | | | | | | | | | | |

| CURRENT LIABILITIES: | | | | | | | | | | | | | | |

| Accounts payable and accrued expenses | | $ | 1,055 | | $ | 1,112 | | | $ | 1,184 | | $ | 1,096 | |

| Payables to related party | | | 105 | | | 19 | | | | 82 | | | 83 | |

| Liabilities held for sale | | | | 19 | | | -- | |

| Total current liabilities | | | 1,160 | | | 1,131 | | | | 1,285 | | | 1,179 | |

| | | | | | | | | | | | | | | |

| LONG-TERM DEBT | | | 18,254 | | | 18,474 | | | | 18,656 | | | 18,525 | |

| LOANS PAYABLE - RELATED PARTY | | | 57 | | | 29 | | | | 24 | | | 22 | |

| DEFERRED MANAGEMENT FEES - RELATED PARTY | | | 14 | | | 14 | | | | 14 | | | 14 | |

| OTHER LONG-TERM LIABILITIES | | | 418 | | | 493 | | | | 369 | | | 392 | |

| MINORITY INTEREST | | | 665 | | | 656 | | | | 626 | | | 622 | |

| | | | | | | | | | | | | | | |

| MEMBER’S DEFICIT: | | | | | | | | | | | | | | |

| Member’s deficit | | | (4,292 | ) | | (3,698 | ) | | | (5,003 | ) | | (4,564 | ) |

| Accumulated other comprehensive loss | | | -- | | | (15 | ) | |

| Accumulated other comprehensive income | | | | 1 | | | 2 | |

| | | | | | | | | | | | | | | |

| Total member’s deficit | | | (4,292 | ) | | (3,713 | ) | | | (5,002 | ) | | (4,562 | ) |

| | | | | | | | | | | | | | | |

| Total liabilities and member’s deficit | | $ | 16,276 | | $ | 17,084 | | | $ | 15,972 | | $ | 16,192 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(DOLLARS IN MILLIONS)

Unaudited

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | |

| | | 2005 | | 2004 | | 2005 | | 2004 | |

| | | | | | | | | | |

| REVENUES | | $ | 1,318 | | $ | 1,248 | | $ | 3,912 | | $ | 3,701 | |

| | | | | | | | | | | | | | |

| COSTS AND EXPENSES: | | | | | | | | | | | | | |

| Operating (excluding depreciation and amortization) | | | 586 | | | 525 | | | 1,714 | | | 1,552 | |

| Selling, general and administrative | | | 269 | | | 252 | | | 762 | | | 735 | |

| Depreciation and amortization | | | 375 | | | 371 | | | 1,134 | | | 1,105 | |

| Impairment of franchises | | | -- | | | 2,433 | | | -- | | | 2,433 | |

| Asset impairment charges | | | -- | | | -- | | | 39 | | | -- | |

| (Gain) loss on sale of assets, net | | | 1 | | | -- | | | 5 | | | (104 | ) |

| Option compensation expense, net | | | 3 | | | 8 | | | 11 | | | 34 | |

| Hurricane asset retirement loss | | | 19 | | | -- | | | 19 | | | -- | |

| Special charges, net | | | 2 | | | 3 | | | 4 | | | 100 | |

| | | | | | | | | | | | | | |

| | | | 1,255 | | | 3,592 | | | 3,688 | | | 5,855 | |

| | | | | | | | | | | | | | |

| Income (loss) from operations | | | 63 | | | (2,344 | ) | | 224 | | | (2,154 | ) |

| | | | | | | | | | | | | | |

| OTHER INCOME AND EXPENSES: | | | | | | | | | | | | | |

| Interest expense, net | | | (442 | ) | | (413 | ) | | (1,297 | ) | | (1,193 | ) |

| Gain (loss) on derivative instruments and hedging activities, net | | | 17 | | | (8 | ) | | 43 | | | 48 | |

| Gain (loss) on extinguishment of debt | | | 490 | | | -- | | | 494 | | | (21 | ) |

| Gain on investments | | | -- | | | -- | | | 21 | | | -- | |

| | | | | | | | | | | | | | |

| | | | 65 | | | (421 | ) | | (739 | ) | | (1,166 | ) |

| | | | | | | | | | | | | | |

| Income (loss) before minority interest, income taxes and cumulative effect of accounting change | | | 128 | | | (2,765 | ) | | (515 | ) | | (3,320 | ) |

| | | | | | | | | | | | | | |

| MINORITY INTEREST | | | (3 | ) | | 34 | | | (9 | ) | | 25 | |

| | | | | | | | | | | | | | |

| Income (loss) before income taxes and cumulative effect of accounting change | | | 125 | | | (2,731 | ) | | (524 | ) | | (3,295 | ) |

| | | | | | | | | | | | | | |

| INCOME TAX BENEFIT (EXPENSE) | | | (2 | ) | | 45 | | | (10 | ) | | 41 | |

| | | | | | | | | | | | | | |

| Income (loss) before cumulative effect of accounting change | | | 123 | | | (2,686 | ) | | (534 | ) | | (3,254 | ) |

| | | | | | | | | | | | | | |

| CUMULATIVE EFFECT OF ACCOUNTING CHANGE, NET OF TAX | | | -- | | | (840 | ) | | -- | | | (840 | ) |

| | | | | | | | | | | | | | |

| Net income (loss) | | $ | 123 | | $ | (3,526 | ) | $ | (534 | ) | $ | (4,094 | ) |

| | | Three Months Ended March 31, | |

| | | 2006 | | 2005 | |

| | | | | | |

| REVENUES | | $ | 1,374 | | $ | 1,271 | |

| | | | | | | | |

| COSTS AND EXPENSES: | | | | | | | |

| Operating (excluding depreciation and amortization) | | | 626 | | | 559 | |

| Selling, general and administrative | | | 281 | | | 241 | |

| Depreciation and amortization | | | 358 | | | 381 | |

| Asset impairment charges | | | 99 | | | 31 | |

| Other operating expenses, net | | | 3 | | | 8 | |

| | | | | | | | |

| | | | 1,367 | | | 1,220 | |

| | | | | | | | |

| Income from operations | | | 7 | | | 51 | |

| | | | | | | | |

| OTHER INCOME AND (EXPENSES): | | | | | | | |

| Interest expense, net | | | (450 | ) | | (424 | ) |

| Other income, net | | | 6 | | | 31 | |

| | | | | | | | |

| | | | (444 | ) | | (393 | ) |

| | | | | | | | |

| Loss before income taxes | | | (437 | ) | | (342 | ) |

| | | | | | | | |

| INCOME TAX EXPENSE | | | (2 | ) | | (6 | ) |

| | | | | | | | |

| Net loss | | $ | (439 | ) | $ | (348 | ) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(DOLLARS IN MILLIONS)

Unaudited

| | | Nine Months Ended September 30, | | |

| �� | | | Three Months Ended March 31, | |

| | | 2005 | | 2004 | | | 2006 | | 2005 | |

| | | | | | | | | | | | | |

| CASH FLOWS FROM OPERATING ACTIVITIES: | | | | | | | | | | | | |

| Net loss | | $ | (534 | ) | $ | (4,094 | ) | | $ | (439 | ) | $ | (348 | ) |

| Adjustments to reconcile net loss to net cash flows from operating activities: | | | | | | | | | | | | | | |

| Minority interest | | | 9 | | | (25 | ) | |

| Depreciation and amortization | | | 1,134 | | | 1,105 | | | | 358 | | | 381 | |

| Asset impairment charges | | | 39 | | | -- | | | | 99 | | | 31 | |

| Impairment of franchises | | | -- | | | 2,433 | | |

| Option compensation expense, net | | | 11 | | | 25 | | |

| Hurricane asset retirement loss | | | 19 | | | -- | | |

| Special charges, net | | | -- | | | 85 | | |

| Noncash interest expense | | | 195 | | | 232 | | | | 46 | | | 65 | |

| Gain on derivative instruments and hedging activities, net | | | (43 | ) | | (48 | ) | |

| (Gain) loss on sale of assets, net | | | 5 | | | (104 | ) | |

| (Gain) loss on extinguishment of debt | | | (501 | ) | | 18 | | |

| Gain on investments | | | (21 | ) | | -- | | |

| Deferred income taxes | | | 6 | | | (44 | ) | | | -- | | | 5 | |

| Cumulative effect of accounting change, net of tax | | | -- | | | 840 | | |

| Other, net | | | -- | | | (1 | ) | | | (2 | ) | | (28 | ) |

| Changes in operating assets and liabilities, net of effects from dispositions: | | | | | | | | |

| Changes in operating assets and liabilities, net of effects from acquisitions and dispositions: | | | | | | | | |

| Accounts receivable | | | (5 | ) | | 2 | | | | 60 | | | 42 | |

| Prepaid expenses and other assets | | | (7 | ) | | (3 | ) | | | (2 | ) | | (2 | ) |

| Accounts payable, accrued expenses and other | | | (121 | ) | | (15 | ) | | | 87 | | | 10 | |

| Receivables from and payables to related party, including deferred management fees | | | (65 | ) | | (53 | ) | |

| Receivables from and payables to related party, including management fees | | | | (2 | ) | | (14 | ) |

| | | | | | | | | |

| Net cash flows from operating activities | | | 121 | | | 353 | | | | 205 | | | 142 | |

| | | | | | | | | | | | | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES: | | | | | | | | | | | | | | |

| Purchases of property, plant and equipment | | | (815 | ) | | (616 | ) | | | (241 | ) | | (211 | ) |

| Change in accrued expenses related to capital expenditures | | | 39 | | | (11 | ) | | | (7 | ) | | 16 | |

| Proceeds from sale of assets | | | 38 | | | 727 | | | | 9 | | | 6 | |

| Purchase of cable system | | | | (42 | ) | | -- | |

| Purchases of investments | | | (1 | ) | | (14 | ) | | | -- | | | (1 | ) |

| Proceeds from investments | | | 16 | | | -- | | | | 5 | | | -- | |

| Other, net | | | (2 | ) | | (2 | ) | |

| | | | | | | | | |

| Net cash flows from investing activities | | | (725 | ) | | 84 | | | | (276 | ) | | (190 | ) |

| | | | | | | | | | | | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES: | | | | | | | | | | | | | | |

| Borrowings of long-term debt | | | 897 | | | 2,873 | | | | 415 | | | 200 | |

| Borrowings from related parties | | | 140 | | | -- | | | | -- | | | 139 | |

| Repayments of long-term debt | | | (1,014 | ) | | (4,707 | ) | | | (759 | ) | | (740 | ) |

| Repayments to related parties | | | (112 | ) | | -- | | | | -- | | | (7 | ) |

| Proceeds from issuance of debt | | | 294 | | | 1,500 | | | | 440 | | | -- | |

| Payments for debt issuance costs | | | (67 | ) | | (97 | ) | | | (10 | ) | | (3 | ) |

| Distributions | | | (60 | ) | | -- | | | | -- | | | (60 | ) |

| | | | | | | | | |

| Net cash flows from financing activities | | | 78 | | | (431 | ) | | | 86 | | | (471 | ) |

| | | | | | | | | | | | | | | |

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | | | (526 | ) | | 6 | | | | 15 | | | (519 | ) |

| CASH AND CASH EQUIVALENTS, beginning of period | | | 546 | | | 85 | | | | 14 | | | 546 | |

| | | | | | | | | |

| CASH AND CASH EQUIVALENTS, end of period | | $ | 20 | | $ | 91 | | | $ | 29 | | $ | 27 | |

| | | | | | | | | |

| CASH PAID FOR INTEREST | | $ | 1,139 | | $ | 809 | | | $ | 240 | | $ | 243 | |

| | | | | | | | | |

| NONCASH TRANSACTIONS: | | | | | | | | | | | | | | |

| Issuance of debt by CCH I Holdings, LLC | | $ | 2,423 | | $ | -- | | |

| Issuance of debt by CCH I, LLC | | $ | 3,686 | | $ | -- | | |

| Issuance of debt by Charter Communications Operating, LLC | | $ | 333 | | $ | -- | | | $ | 37 | | $ | 271 | |

| Retirement of Renaissance Media Group LLC debt | | | $ | (37 | ) | $ | -- | |

| Retirement of Charter Communications Holdings, LLC debt | | $ | (7,000 | ) | $ | -- | | | $ | -- | | $ | (284 | ) |

| Transfer of property, plant and equipment from parent company | | $ | 139 | | $ | -- | | | $ | -- | | $ | 139 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

| Organization and Basis of Presentation |

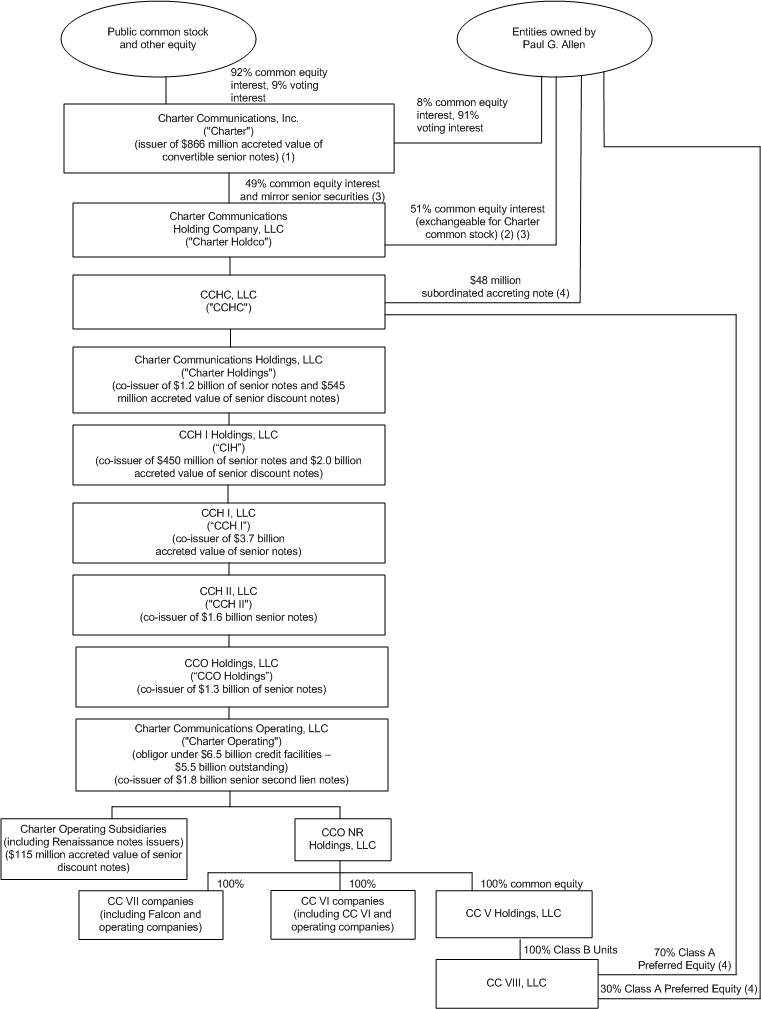

Charter Communications Holdings, LLC ("Charter Holdings") is a holding company whose principal assets at September 30, 2005March 31, 2006 are equity interests in its operating subsidiaries. Charter Holdings is a subsidiary of CCHC, LLC ("CCHC") which is a subsidiary of Charter Communications Holding Company, LLC ("Charter Holdco"), which is a subsidiary of Charter Communications, Inc. ("Charter"). The condensed consolidated financial statements include the accounts of Charter Holdings and all of its direct and indirect subsidiaries where the underlying operations reside, which are collectively referred to herein as the "Company." All significant intercompany accounts and transactions among consolidated entities have been eliminated. The Company is a broadband communications company operating in the United States. The Company offers its customers traditional cable video programming (analog and digital video) as well as high-speed Internet services and, in some areas, advanced broadband services such as high definition television, video on demand and telephone. The Company sells its cable video programming, high-speed Internet and advanced broadband services on a subscription basis. The Company also sells local advertising on satellite-delivered networks.

The accompanying condensed consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States for interim financial information and the rules and regulations of the Securities and Exchange Commission (the "SEC"). Accordingly, certain information and footnote disclosures typically included in Charter Holdings'Holdings’ Annual Report on Form 10-K have been condensed or omitted for this quarterly report. The accompanying condensed consolidated financial statements are unaudited and are subject to review by regulatory authorities. However, in the opinion of management, such financial statements include all adjustments, which consist of only normal recurring adjustments, necessary for a fair presentation of the results for the periods presented. Interim results are not necessarily indicative of results for a full year.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Areas involving significant judgments and estimates include capitalization of labor and overhead costs; depreciation and amortization costs; impairments of property, plant and equipment, franchises and goodwill; income taxes; and contingencies. Actual results could differ from those estimates.

Reclassifications

Certain 20042005 amounts have been reclassified to conform with the 20052006 presentation.

| Liquidity and Capital Resources |

The Company had net incomeloss of $123$439 million and $348 million for the three months ended September 30, 2005. The Company incurred net loss of $534 million for the nine months ended September 30,March 31, 2006 and 2005, and $3.5 billion and $4.1 billion for the three and nine months ended September 30, 2004, respectively. The Company’s net cash flows from operating activities were $121$205 million and $353$142 million for the ninethree months ended September 30,March 31, 2006 and 2005, and 2004, respectively.

The Company has a significant levelRecent Financing Transactions

On January 30, 2006, CCH II, LLC ("CCH II") and CCH II Capital Corp. issued $450 million in debt securities, the proceeds of debt. The Company's long-term financing as of September 30, 2005 consists of $5.5 billion of credit facility debt and $12.7 billion accreted value of high-yield notes. For the remainder of 2005, $7 million of the Company’s debt matures, and in 2006, an additional $30 million of the Company’s debt matures. In 2007 and beyond, significant additional amounts will become duewhich were provided, directly or indirectly, to Charter Communications Operating, LLC ("Charter Operating"), which used such funds to reduce borrowings, but not commitments, under the Company’s remaining long-term debt obligations.revolving portion of its credit facilities.

In September 2005,April 2006, Charter HoldingsOperating completed a $6.85 billion refinancing of its credit facilities including a new $350 million revolving/term facility (which converts to a term loan in one year), a $5.0 billion term loan due in 2013 and its wholly owned subsidiaries, CCH I, LLC (“CCH I”)certain amendments to the existing $1.5 billion revolving credit facility. In addition, the refinancing reduced margins on Eurodollar rate Term A & B loans to 2.625% from a weighted average of 3.15% previously and CCH Imargins on base rate term loans to 1.625% from a weighted average of 2.15% previously. Concurrent with this refinancing, the CCO Holdings, LLC (“CIH”("CCO Holdings"), completed the exchange of approximately $6.8 billion total principal amount of outstanding debt securities of Charter Holdings in a private placement for new debt securities. Holders of Charter Holdings notes due in 2009 and 2010 exchanged $3.4 billion principal amount of notes for $2.9 billion principal amount of new 11% CCH I senior secured notes due 2015. Holders of Charter Holdings notes due 2011 and 2012 exchanged $845 million bridge loan was terminated.

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

principal amountThe Company has a significant level of notesdebt. The Company's long-term financing as of March 31, 2006 consists of $5.4 billion of credit facility debt and $13.3 billion accreted value of high-yield notes. Pro forma for $662the completion of the credit facility refinancing discussed above, none of the Company’s debt matures in the remainder of 2006, and in 2007 and 2008, $130 million principal amount of 11% CCH I senior secured notesand $128 million mature, respectively. In 2009 and beyond, significant additional amounts will become due 2015. In addition, holders of Charter Holdings notes due 2011 and 2012 exchanged $2.5 billion principal amount of notes for $2.5 billion principal amount of various series of new CIH notes. Each series of new CIH notes hasunder the same stated interest rate and provisions for payment of cash interest as the series of old Charter Holdings notes for which such CIH notes were exchanged. In addition, the maturities for each series were extended three years. See Note 6 for discussion of transaction and related financial statement impact.Company’s remaining long-term debt obligations.

The Company has historically requiredrequires significant cash to fund debt service costs, capital expenditures and ongoing operations. Historically, theThe Company has historically funded these requirements through cash flows from operating activities, borrowings under its credit facilities, equity contributions from Charter Holdco, sales of assets, issuances of debt securities and from cash on hand. However, the mix of funding sources changes from period to period. For the ninethree months ended September 30, 2005,March 31, 2006, the Company generated $121$205 million of net cash flows from operating activities, after paying cash interest of $1.1 billion.$240 million. In addition, the Company used approximately $815$241 million for purchases of property, plant and equipment. Finally, the Company had net cash flows from financing activities of $78$86 million.

In October 2005, CCO Holdings, LLC (“CCO Holdings”) and CCO Holdings Capital Corp., as guarantor thereunder, entered into a senior bridge loan agreement (the "Bridge Loan") with JPMorgan Chase Bank, N.A., Credit Suisse, Cayman Islands Branch and Deutsche Bank AG Cayman Islands Branch (the "Lenders") whereby the Lenders have committed to make loans to CCO Holdings in an aggregate amount of $600 million. CCO Holdings may draw upon the facility between January 2, 2006 and September 29, 2006 and the loans will mature on the sixth anniversary of the first borrowing under the Bridge Loan.

The Company expects that cash on hand, cash flows from operating activities, proceeds from sales of assets and the amounts available under its credit facilities and Bridge Loan will be adequate to meet its and Charter’sits parent companies’ cash needs for the remainder of 2005 and 2006. Cash flows from operating activities and amounts available under the Company’s credit facilities and Bridge Loan may not be sufficient to fund the Company’s operations and satisfy its and Charter’s interest payment obligations in 2007. It is likely that Charter and the Company will require additional funding to satisfy their debt repayment obligations inthrough 2007. The Company believes that cash flows from operating activities and amounts available under itsthe Company’s credit facilities may not be sufficient to fund the Company’s operations and Bridge Loansatisfy its and its parent companies’ interest and debt repayment obligations in 2008 and will not be sufficient to fund its operationssuch needs in 2009 and satisfy its and Charter’s interest and principal repayment obligations thereafter.

beyond. The Company has been advised that Charter is workingcontinues to work with its financial advisors in its approach to address itsaddressing liquidity, debt maturities and the Company’s funding requirements. However, there can be no assurance that such funding will be available to the Company. Although Paul G. Allen, Charter’s Chairman and controlling shareholder, and his affiliates have purchased equity from Charter and Charter Holdco in the past, Mr. Allen and his affiliates are not obligated to purchase equity from, contribute to or loan funds to Charter, Charter Holdco or the Company in the future.overall balance sheet leverage.

Credit Facilities andDebt Covenants

The Company’s ability to operate depends upon, among other things, its continued access to capital, including credit under the Charter Communications Operating LLC ("Charter Operating") credit facilities. TheseThe Charter Operating credit facilities, along with the Company’s indentures, and Bridge Loan, contain certain restrictive covenants, some of which require the Company to maintain specified financial ratios and meet financial tests and to provide annual audited financial statements with an unqualified opinion from the Company’s independent auditors. As of September 30, 2005,March 31, 2006, the Company is in compliance with the covenants under its indentures and credit facilities, and the Company expects to remain in compliance with those covenants and the Bridge Loan covenants for the next twelve months. TheAs of March 31, 2006, the Company’s total potential borrowing availability under the currentits credit facilities totaled $786approximately $904 million, as of September 30, 2005, although the actual availability at that time was only $648$516 million because of limits imposed by covenant restrictions. In addition, effective January 2,However, pro forma for the completion of the credit facility refinancing discussed above, the Company’s potential availability under its credit facilities as of March 31, 2006 the Company willwould have additional borrowingbeen approximately $1.3 billion, although actual covenanted availability of $600$516 million as a result of the Bridge Loan.would remain unchanged. Continued access to the Company’s credit facilities and Bridge Loan is subject to the Company remaining in compliance with thethese covenants, of these credit facilities and Bridge Loan, including covenants tied to the Company’s operating performance. If the Company’s operating performance results in non-compliance with these covenants, or if any of certain other events of non-compliance under these credit facilities, Bridge Loan or

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

the indentures governing the Company’s debt occur, funding under the credit facilities and Bridge Loan may not be available and defaults on some or potentially all of the Company’s debt obligations could occur. An event of default under the covenants governing any of the Company’s debt instruments could result in the acceleration of its payment obligations under that debt and, under certain circumstances, in cross-defaults under its other debt obligations, which could have a material adverse effect on the Company’s consolidated financial condition orand results of operations.

Parent Company Debt Obligations

Any financial or liquidity problems of the Company’s parent companies could cause serious disruption to the Company's business and have a material adverse effect on the Company’s business and results of operations.

Specific Limitations

Charter’s ability to make interest payments on its convertible senior notes, and, in 2006 and 2009, to repay the outstanding principal of its convertible senior notes of $25$20 million and $863 million, respectively, will depend on its

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

ability to raise additional capital and/or on receipt of payments or distributions from Charter Holdco orand its subsidiaries, including Charter Holdings, CIH, CCH I, CCH II, LLC ("CCH II"), CCO Holdings and Charter Operating. During the nine months ended September 30, 2005, Charter Holdings distributed $60 million to Charter Holdco.subsidiaries. As of September 30, 2005,March 31, 2006, Charter Holdco was owed $57$24 million in intercompany loans from its subsidiaries, which amount waswere available to pay interest and principal on Charter's convertible senior notes. In addition, Charter has $123$99 million of governmental securities pledged as security for the next fivefour scheduled semi-annual interest payments on Charter’s 5.875% convertible senior notes.

Distributions by Charter Holdings’Charter’s subsidiaries to a parent company (including Charter, CCHC, Charter Holdco CCHC and Charter Holdings) for payment of principal on parent company notes are restricted by the Bridge Loan andunder the indentures governing the CIH notes, CCH I notes, CCH II notes, CCO Holdings notes and Charter Operating notes unless under their respective indentures there is no default, and a specifiedeach applicable subsidiary’s leverage ratio test is met at the time of such event.distribution and, in the case of Charter’s convertible senior notes, other specified tests are met. For the quarter ended September 30, 2005,March 31, 2006, there was no default under any of these indentures and the aforementioned indentures.other specified tests were met. However, CCO Holdingscertain of the Company’s subsidiaries did not meet itstheir respective leverage ratio test of 4.5 to 1.0.tests based on March 31, 2006 financial results. As a result, distributions from CCO Holdings to CCH II, CCH I, CIH, Charter Holdings, CCHC, Charter Holdco or Charter for payment of principalcertain of the respectiveCompany’s subsidiaries to their parent company’s debt are currentlycompanies have been restricted and will continue to be restricted until that testthose tests are met. Distributions by Charter Operating for payment of principal on parent company notes are further restricted by the covenants in the credit facilities.

Distributions by CIH, CCH I, CCH II, CCO Holdings and Charter Operating to a parent company for payment of parent company interest are permitted if there is met.no default under the aforementioned indentures. However, distributions for payment of interest on Charter’s convertible senior notes are further limited to when each applicable subsidiary’s leverage ratio test is met and other specified tests are met. There can be no assurance that they will satisfy these tests at the respective parent company’s interest are permitted.

Specific Limitationstime of such distribution.

The indentures governing the Charter Holdings notes permit Charter Holdings to make distributions to Charter Holdco for payment of interest or principal on theCharter’s convertible senior notes, only if, after giving effect to the distribution, Charter Holdings can incur additional debt under the leverage ratio of 8.75 to 1.0, there is no default under Charter Holdings'Holdings’ indentures and other specified tests are met. For the quarter ended September 30, 2005,March 31, 2006, there was no default under Charter Holdings'Holdings’ indentures and the other specified tests were met. However, Charter Holdings did not meet the leverage ratio test of 8.75 to 1.0 based on September 30, 2005March 31, 2006 financial results. As a result, distributions from Charter Holdings to Charter or Charter Holdco or CCHC for payment of interest or principal are currentlyhave been restricted and will continue to be restricted until that test is met. During this restriction period, the indentures governing the Charter Holdings notes permit Charter Holdings and its subsidiaries to make specified investments (that are not restricted payments) in Charter Holdco or Charter up to an amount determined by a formula, as long as there is no default under the indentures.

In July 2005,February 2006, the Company closed the sale ofsigned three separate definitive agreements to sell certain cable television systems in Texas and West Virginia and closed the sale of an additional cable system in Nebraska in October 2005, representingserving a total of approximately 33,000 customers. During the nine months ended September 30, 2005,360,000 analog video customers in West Virginia, Virginia, Illinois, Kentucky, Nevada, Colorado, New Mexico and Utah for a total of approximately $971 million. As of March 31, 2006, those cable systems met the criteria for assets held for sale under Statement of Financial Accounting Standards ("SFAS") No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets. As such, the assets were written down to fair value less estimated costs to sell resulting in asset impairment charges during the ninethree months ended September 30,March 31, 2006 of approximately $99 million. In addition, assets and liabilities to be sold were reclassified as held for sale. Assets held for sale on the Company's balance sheet as of March 31, 2006 included current assets of approximately $5 million, property, plant and equipment of approximately $312 million and franchises of approximately $437 million. Liabilities held for sale on the Company's balance sheet as of March 31, 2006 included current liabilities of approximately $6 million and other long-term liabilities of approximately $13 million.

In 2005, the Company closed the sale of certain cable systems in Texas, West Virginia and Nebraska representing a total of approximately 33,000 analog video customers. During the three months ended March 31, 2005, certain of those cable systems met the criteria for assets held for sale. As such, the assets were written down to fair value less estimated costs to sell resulting in asset impairment charges during the three months ended March 31, 2005 of approximately $39$31 million. At September 30, 2005 assets held for sale, included in investment in cable properties, are approximately $7 million.

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

In March 2004, the Company closed the sale of certain cable systems in Florida, Pennsylvania, Maryland, Delaware and West Virginia to Atlantic Broadband Finance, LLC. The Company closed the sale of an additional cable system in New York to Atlantic Broadband Finance, LLC in April 2004. These transactions resulted in a $106 million pretax gain recorded as a gain on sale of assets in the Company’s consolidated statements of operations. The total net proceeds from the sale of all of these systems were approximately $735 million. The proceeds were used to repay a portion of amounts outstanding under the Company’s revolving credit facility.

Gain on investments for the nine months ended September 30, 2005 primarily represents a gain realized on an exchange of the Company’s interest in an equity investee for an investment in a larger enterprise.

4. | Franchises and Goodwill |

Franchise rights represent the value attributed to agreements with local authorities that allow access to homes in cable service areas acquired through the purchase of cable systems. Management estimates the fair value of franchise rights at the date of acquisition and determines if the franchise has a finite life or an indefinite-life as defined by SFAS No. 142, Goodwill and Other Intangible Assets. Franchises that qualify for indefinite-life treatment under SFAS No. 142 are tested for impairment annually each October 1 based on valuations, or more frequently as warranted by events or changes in circumstances. Such test resulted in a total franchise impairment of approximately $3.3 billion during the third quarter of 2004. The October 1, 2005 annual impairment test will be finalized in the fourth quarter of 2005 and any impairment resulting from such test will be recorded in the fourth quarter. Franchises are aggregated into essentially inseparable asset groups to conduct the valuations. The asset groups generally represent geographic clustering of the Company’s cable systems into groups by which such systems are managed. Management believes such grouping represents the highest and best use of those assets.

The Company’s valuations, which are based on the present value of projected after tax cash flows, result in a value of property, plant and equipment, franchises, customer relationships and its total entity value. The value of goodwill is the difference between the total entity value and amounts assigned to the other assets.

Franchises, for valuation purposes, are defined as the future economic benefits of the right to solicit and service potential customers (customer marketing rights), and the right to deploy and market new services such as interactivity and telephone to the potential customers (service marketing rights). Fair value is determined based on estimated discounted future cash flows using assumptions consistent with internal forecasts. The franchise after-tax cash flow is calculated as the after-tax cash flow generated by the potential customers obtained and the new services added to those customers in future periods. The sum of the present value of the franchises’ after-tax cash flow in years 1 through 10 and the continuing value of the after-tax cash flow beyond year 10 yields the fair value of the franchise.

The Company follows the guidance of Emerging Issues Task Force (“EITF”) Issue 02-17, Recognition of Customer Relationship Intangible Assets Acquired in a Business Combination, in valuing customer relationships. Customer relationships, for valuation purposes, represent the value of the business relationship with existing customers and are calculated by projecting future after-tax cash flows from these customers including the right to deploy and market additional services such as interactivity and telephone to these customers. The present value of these after-tax cash flows yields the fair value of the customer relationships. Substantially all acquisitions occurred prior to January 1, 2002. The Company did not record any value associated with the customer relationship intangibles related to those acquisitions. For acquisitions subsequent to January 1, 2002 the Company did assign a value to the customer relationship intangible, which is amortized over its estimated useful life.

In September 2004, the SEC staff issued EITF Topic D-108 which requires the direct method of separately valuing all intangible assets and does not permit goodwill to be included in franchise assets. The Company adopted Topic D-108 in its impairment assessment as of September 30, 2004 that resulted in a total franchise impairment of approximately $3.3 billion. The Company recorded a cumulative effect of accounting change of $840 million (approximately $875 million before tax effects of $16 million and minority interest effects of $19 million) for the nine months ended September 30, 2004 representing the portion of the Company's total franchise impairment attributable to no longer

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

including goodwill with franchise assets. The remaining $2.4 billion of the total franchise impairment was attributable to the use of lower projected growth rates and the resulting revised estimates of future cash flows in the Company's valuation, and was recorded as impairment of franchises in the Company's accompanying consolidated statements of operations for the nine months ended September 30, 2004. Sustained analog video customer losses by the Company in the third quarter of 2004 primarily as a result of increased competition from direct broadcast satellite providers and decreased growth rates in the Company's high-speed Internet customers in the third quarter of 2004, in part, as a result of increased competition from digital subscriber line service providers led to the lower projected growth rates and the revised estimates of future cash flows from those used at October 1, 2003.

As of September 30, 2005March 31, 2006 and December 31, 2004,2005, indefinite-lived and finite-lived intangible assets are presented in the following table:

| | | September 30, 2005 | | December 31, 2004 | | | March 31, 2006 | | December 31, 2005 | |

| | | | Gross Carrying Amount | | | Accumulated Amortization | | | Net Carrying Amount | | | Gross Carrying Amount | | | Accumulated Amortization | | | Net Carrying Amount | | | Gross Carrying Amount | | Accumulated Amortization | | Net Carrying Amount | | Gross Carrying Amount | | Accumulated Amortization | | Net Carrying Amount | |

Indefinite-lived intangible assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Franchises with indefinite lives | | $ | 9,797 | | $ | -- | | $ | 9,797 | | $ | 9,845 | | $ | -- | | $ | 9,845 | | | $ | 9,270 | | $ | -- | | $ | 9,270 | | $ | 9,806 | | $ | -- | | $ | 9,806 | |

| Goodwill | | | 52 | | | -- | | | 52 | | | 52 | | | -- | | | 52 | | | | 52 | | | -- | | | 52 | | | 52 | | | -- | | | 52 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $ | 9,849 | | $ | -- | | $ | 9,849 | | $ | 9,897 | | $ | -- | | $ | 9,897 | | | $ | 9,322 | | $ | -- | | $ | 9,322 | | $ | 9,858 | | $ | -- | | $ | 9,858 | |

Finite-lived intangible assets: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Franchises with finite lives | | $ | 40 | | $ | 7 | | $ | 33 | | $ | 37 | | $ | 4 | | $ | 33 | | | $ | 23 | | $ | 6 | | $ | 17 | | $ | 27 | | $ | 7 | | $ | 20 | |

FranchisesFor the three months ended March 31, 2006, the net carrying amount of indefinite-lived and finite-lived franchises was reduced by $434 million and $3 million, respectively, related to franchises reclassified as assets held for sale. For the three months ended March 31, 2006, franchises with indefinite lives also decreased $39$3 million related to a cable asset sale completed in the first quarter of 2006 and $99 million as a result of the asset impairment charges recorded related to three cable asset sales and $9 million as a result of the closing of two of the cable asset sales in July 2005assets held for sale (see Note 3). Franchise amortization expense for the three and nine months ended September 30,March 31, 2006 and 2005 was approximately $0 and 2004 was $1 million and $3 million, respectively, which represents the amortization relating to franchises that did not qualify for indefinite-life treatment under SFAS No. 142, including costs associated with franchise renewals. The Company expects that amortization expense on franchise assets will be approximately $3$2 million annually for each of the next five years. Actual amortization expense in future periods could differ from these estimates as a result of new intangible asset acquisitions or divestitures, changes in useful lives and other relevant factors.

5.

| Accounts Payable and Accrued Expenses

|

Accounts payable and accrued expenses consist of the following as of September 30, 2005 and December 31, 2004:

| | | September 30, 2005 | | December 31, 2004 | |

| | | | | | | | |

| Accounts payable - trade | | $ | 67 | | $ | 140 | |

| Accrued capital expenditures | | | 99 | | | 60 | |

| Accrued expenses: | | | | | | | |

| Interest | | | 278 | | | 310 | |

| Programming costs | | | 287 | | | 278 | |

| Franchise-related fees | | | 56 | | | 67 | |

| Compensation | | | 57 | | | 47 | |

| Other | | | 211 | | | 210 | |

| | | | | | | | |

| | | $ | 1,055 | | $ | 1,112 | |

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

5. | Accounts Payable and Accrued Expenses |

Accounts payable and accrued expenses consist of the following as of March 31, 2006 and December 31, 2005:

| | | March 31, 2006 | | December 31, 2005 | |

| | | | | | |

| Accounts payable - trade | | $ | 82 | | $ | 102 | |

| Accrued capital expenditures | | | 66 | | | 73 | |

| Accrued expenses: | | | | | | | |

| Interest | | | 491 | | | 329 | |

| Programming costs | | | 288 | | | 272 | |

| Franchise-related fees | | | 44 | | | 67 | |

| Compensation | | | 54 | | | 60 | |

| Other | | | 159 | | | 193 | |

| | | | | | | | |

| | | $ | 1,184 | | $ | 1,096 | |

Long-term debt consists of the following as of September 30, 2005March 31, 2006 and December 31, 2004:2005:

| | | September 30, 2005 | | December 31, 2004 | |

| | | Principal Amount | | Accreted Value | | Principal Amount | | Accreted Value | |

Long-Term Debt | | | | | | | | | | | | | |

| Charter Communications Holdings, LLC: | | | | | | | | | | | | | |

| 8.250% senior notes due 2007 | | $ | 105 | | $ | 105 | | $ | 451 | | $ | 451 | |

| 8.625% senior notes due 2009 | | | 292 | | | 292 | | | 1,244 | | | 1,243 | |

| 9.920% senior discount notes due 2011 | | | 198 | | | 198 | | | 1,108 | | | 1,108 | |

| 10.000% senior notes due 2009 | | | 154 | | | 154 | | | 640 | | | 640 | |

| 10.250% senior notes due 2010 | | | 49 | | | 49 | | | 318 | | | 318 | |

| 11.750% senior discount notes due 2010 | | | 43 | | | 43 | | | 450 | | | 448 | |

| 10.750% senior notes due 2009 | | | 131 | | | 131 | | | 874 | | | 874 | |

| 11.125% senior notes due 2011 | | | 217 | | | 217 | | | 500 | | | 500 | |

| 13.500% senior discount notes due 2011 | | | 94 | | | 91 | | | 675 | | | 589 | |

| 9.625% senior notes due 2009 | | | 107 | | | 107 | | | 640 | | | 638 | |

| 10.000% senior notes due 2011 | | | 137 | | | 136 | | | 710 | | | 708 | |

| 11.750% senior discount notes due 2011 | | | 125 | | | 116 | | | 939 | | | 803 | |

| 12.125% senior discount notes due 2012 | | | 113 | | | 97 | | | 330 | | | 259 | |

| CCH I Holdings, LLC: | | | | | | | | | | | | | |

| 11.125% senior notes due 2014 | | | 151 | | | 151 | | | -- | | | -- | |

| 9.920% senior discount notes due 2014 | | | 471 | | | 471 | | | -- | | | -- | |

| 10.000% senior notes due 2014 | | | 299 | | | 299 | | | -- | | | -- | |

| 11.750% senior discount notes due 2014 | | | 815 | | | 759 | | | -- | | | -- | |

| 13.500% senior discount notes due 2014 | | | 581 | | | 559 | | | -- | | | -- | |

| 12.125% senior discount notes due 2015 | | | 217 | | | 187 | | | -- | | | -- | |

| CCH I, LLC: | | | | | | | | | | | | | |

| 11.00% senior notes due 2015 | | | 3,525 | | | 3,686 | | | -- | | | -- | |

| CCH II, LLC: | | | | | | | | | | | | | |

| 10.250% senior notes due 2010 | | | 1,601 | | | 1,601 | | | 1,601 | | | 1,601 | |

| CCO Holdings, LLC: | | | | | | | | | | | | | |

| 8¾% senior notes due 2013 | | | 800 | | | 794 | | | 500 | | | 500 | |

| Senior floating rate notes due 2010 | | | 550 | | | 550 | | | 550 | | | 550 | |

| Charter Communications Operating, LLC: | | | | | | | | | | | | | |

| 8% senior second lien notes due 2012 | | | 1,100 | | | 1,100 | | | 1,100 | | | 1,100 | |

| 8 3/8% senior second lien notes due 2014 | | | 733 | | | 733 | | | 400 | | | 400 | |

| Renaissance Media Group LLC: | | | | | | | | | | | | | |

| 10.000% senior discount notes due 2008 | | | 114 | | | 115 | | | 114 | | | 116 | |

| CC V Holdings, LLC: | | | | | | | | | | | | | |

| 11.875% senior discount notes due 2008 | | | -- | | | -- | | | 113 | | | 113 | |

Credit Facilities | | | | | | | | | | | | | |

| Charter Operating | | | 5,513 | | | 5,513 | | | 5,515 | | | 5,515 | |

| | | $ | 18,235 | | $ | 18,254 | | $ | 18,772 | | $ | 18,474 | |

The accreted values presented above represent the principal amount of the notes less the original issue discount at the time of sale plus the accretion to the balance sheet date. The accreted value of CIH notes and CCH I notes issued in exchange for Charter Holdings notes are recorded in accordance with generally accepted accounting principles (“GAAP”). GAAP requires that the CIH notes issued in exchange for Charter Holdings notes and the CCH I notes| | | March 31, 2006 | | December 31, 2005 | |

| | | Principal Amount | | Accreted Value | | Principal Amount | | Accreted Value | |

Long-Term Debt | | | | | | | | | |

| Charter Communications Holdings, LLC: | | | | | | | | | |

| 8.250% senior notes due 2007 | | $ | 105 | | $ | 105 | | $ | 105 | | $ | 105 | |

| 8.625% senior notes due 2009 | | | 292 | | | 292 | | | 292 | | | 292 | |

| 9.920% senior discount notes due 2011 | | | 198 | | | 198 | | | 198 | | | 198 | |

| 10.000% senior notes due 2009 | | | 154 | | | 154 | | | 154 | | | 154 | |

| 10.250% senior notes due 2010 | | | 49 | | | 49 | | | 49 | | | 49 | |

| 11.750% senior discount notes due 2010 | | | 43 | | | 43 | | | 43 | | | 43 | |

| 10.750% senior notes due 2009 | | | 131 | | | 131 | | | 131 | | | 131 | |

| 11.125% senior notes due 2011 | | | 217 | | | 217 | | | 217 | | | 217 | |

| 13.500% senior discount notes due 2011 | | | 94 | | | 94 | | | 94 | | | 94 | |

| 9.625% senior notes due 2009 | | | 107 | | | 107 | | | 107 | | | 107 | |

| 10.000% senior notes due 2011 | | | 137 | | | 136 | | | 137 | | | 136 | |

| 11.750% senior discount notes due 2011 | | | 125 | | | 123 | | | 125 | | | 120 | |

| 12.125% senior discount notes due 2012 | | | 113 | | | 103 | | | 113 | | | 100 | |

| CCH I Holdings, LLC: | | | | | | | | | | | | | |

| 11.125% senior notes due 2014 | | | 151 | | | 151 | | | 151 | | | 151 | |

| 9.920% senior discount notes due 2014 | | | 471 | | | 471 | | | 471 | | | 471 | |

| 10.000% senior notes due 2014 | | | 299 | | | 299 | | | 299 | | | 299 | |

| 11.750% senior discount notes due 2014 | | | 815 | | | 804 | | | 815 | | | 781 | |

| 13.500% senior discount notes due 2014 | | | 581 | | | 581 | | | 581 | | | 578 | |

| 12.125% senior discount notes due 2015 | | | 217 | | | 198 | | | 217 | | | 192 | |

| CCH I, LLC: | | | | | | | | | | | | | |

| 11.000% senior notes due 2015 | | | 3,525 | | | 3,680 | | | 3,525 | | | 3,683 | |

| CCH II, LLC: | | | | | | | | | | | | | |

| 10.250% senior notes due 2010 | | | 2,051 | | | 2,041 | | | 1,601 | | | 1,601 | |

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

| CCO Holdings, LLC: | | | | | | | | | | | | | |

| 8¾% senior notes due 2013 | | | 800 | | | 795 | | | 800 | | | 794 | |

| Senior floating notes due 2010 | | | 550 | | | 550 | | | 550 | | | 550 | |

| Charter Communications Operating, LLC: | | | | | | | | | | | | | |

| 8% senior second lien notes due 2012 | | | 1,100 | | | 1,100 | | | 1,100 | | | 1,100 | |

| 8 3/8% senior second lien notes due 2014 | | | 770 | | | 770 | | | 733 | | | 733 | |

| Renaissance Media Group LLC: | | | | | | | | | | | | | |

| 10.000% senior discount notes due 2008 | | | 77 | | | 78 | | | 114 | | | 115 | |

Credit Facilities | | | | | | | | | | | | | |

| Charter Operating | | | 5,386 | | | 5,386 | | | 5,731 | | | 5,731 | |

| | | $ | 18,558 | | $ | 18,656 | | $ | 18,453 | | $ | 18,525 | |

The accreted values presented above generally represent the principal amount of the notes less the original issue discount at the time of sale plus the accretion to the balance sheet date except as follows. The accreted value of the CIH notes issued in exchange for Charter Holdings notes and the portion of the CCH I notes issued in 2005 in exchange for the 8.625% Charter Holdings notes due 2009 beare recorded at the historical book values of the Charter Holdings notes for financial reporting purposes as opposed to the current accreted value for legal purposes and notes indenture purposes (the amount that is currently payable if the debt becomes immediately due). As of September 30, 2005,March 31, 2006, the accreted value of the Company’s debt for legal purposes and notes indenture purposes is $17.7approximately $18.2 billion.

In October 2005, CCO HoldingsOn January 30, 2006, CCH II and CCO HoldingsCCH II Capital Corp., as guarantor thereunder, entered into the Bridge Loan with the Lenders whereby the Lenders have committed to make loans to CCO Holdings in an aggregate amount of $600 million. CCO Holdings may draw upon the facility between January 2, 2006 and September 29, 2006 and the loans will mature on the sixth anniversary of the first borrowing under the Bridge Loan. Each loan will accrue interest at a rate equal to an adjusted LIBOR rate plus a spread. The spread will initially be 450 basis points and will increase (a) by an additional 25 basis points at the end of the six-month period following the date of the first borrowing, (b) by an additional 25 basis points at the end of each of the next two subsequent three month periods and (c) by 62.5 basis points at the end of each of the next two subsequent three-month periods. CCO Holdings will be required to prepay loans from the net proceeds from (i) the issuance of equity or incurrence of debt by Charter and its subsidiaries, with certain exceptions, and (ii) certain asset sales (to the extent not used for other purposes permitted under the Bridge Loan).

In August 2005, CCO Holdings issued $300$450 million in debt securities, the proceeds of which were provided, directly or indirectly, to Charter Operating, which used such funds to reduce borrowings, but not commitments, under the revolving portion of its credit facilities.

On March 13, 2006, the Company exchanged $37 million of Renaissance Media Group LLC 10% senior discount notes due 2008 for general corporate purposes, including$37 million principal amount of new Charter Operating 8 3/8% senior second-lien notes due 2014 issued in a private transaction under Rule 144A. The terms and conditions of the payment of distributionsnew Charter Operating 8 3/8% senior second-lien notes due 2014 are identical to its parent companies, including Charter Holdings, to pay interest expense.Operating’s currently outstanding 8 3/8% senior second-lien notes due 2014.

Gain (loss) on extinguishment of debt

In September 2005, Charter Holdings and its wholly owned subsidiaries, CCH I and CIH, completed the exchange of approximately $6.8 billion total principal amount of outstanding debt securities of Charter Holdings in a private placement for new debt securities. Holders of Charter Holdings notes due in 2009 and 2010 exchanged $3.4 billion principal amount of notes for $2.9 billion principal amount of new 11% CCH I senior secured notes due 2015. Holders of Charter Holdings notes due 2011 and 2012 exchanged $845 million principal amount of notes for $662 million principal amount of 11% CCH I senior secured notes due 2015. In addition, holders of Charter Holdings notes due 2011 and 2012 exchanged $2.5 billion principal amount of notes for $2.5 billion principal amount of various series of new CIH notes. Each series of new CIH notes has the same stated interest rate and provisions for payment of cash interest as the series of old Charter Holdings notes for which such CIH notes were exchanged. In addition, the maturities for each series were extended three years. The exchanges resulted in a net gain on extinguishment of debt of approximately $490 million for the three and nine months ended September 30, 2005.

In March and June 2005, Charter Operating consummated exchange transactions with a small number of institutional holders of Charter Holdings 8.25% senior notes due 2007 pursuant to which Charter Operating issued, in private placements, approximately $333$271 million principal amount of new notes with terms identical to Charter Operating's 8.375% senior second lien notes due 2014 in exchange for approximately $346$284 million of the Charter Holdings 8.25% senior notes due 2007. The exchanges resulted in a net gain on extinguishment of debt of approximately $10$11 million for the ninethree months ended September 30, 2005.March 31, 2005 included in other expense on the Company’s condensed consolidated statements of operations. The Charter Holdings notes received in the exchange were thereafter distributed to Charter Holdings and cancelled.canceled.

In March 2005, Charter Holdings’ subsidiary, CC V Holdings, LLC, redeemed all of its 11.875% notes due 2008, at 103.958% of principal amount, plus accrued and unpaid interest to the date of redemption. The total cost of redemption was approximately $122 million and was funded through borrowings under the Charter Operating credit facilities. The redemption resulted in a loss on extinguishment of debt for the ninethree months ended September 30,March 31, 2005 of approximately $5 million. Following such redemption, CC V Holdings, LLC and its subsidiaries (other than non-guarantor subsidiaries) guaranteedmillion included in other expense on the Charter Operating credit facilities and granted a lien on allCompany’s condensed consolidated statements of their assets as to which a lien can be perfected under the Uniform Commercial Code by the filing of a financing statement.operations.

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

Minority interest on the Company’s consolidated balance sheets as of September 30, 2005March 31, 2006 and December 31, 20042005 primarily represents preferred membership interests in CC VIII, LLC ("CC VIII"), an indirect subsidiary of Charter Holdco,Holdings, of $665$626 million and $656$622 million, respectively. As more fully described in Note 18, this preferred interest arises from the approximately $630 million of preferred membership units issuedis held by CC VIII in connection with an acquisition in February 2000 and was the subject of a dispute between CharterCCHC and Mr. Allen, Charter’s Chairman and controlling shareholder that was settled October 31, 2005. The Company is currently determiningshareholder. Minority interest in the impactaccompanying condensed consolidated statements of operations includes the 2% accretion of the settlement to be recorded in the fourth quarter of 2005. Due to the uncertainties that existed prior to October 31, 2005 related to the ultimate resolution of the dispute, effective January 1, 2005, the Company ceased recognizing minority interest in earnings or losses of CC VIII for financial reporting purposes until such time as the resolution of the matter was determinable or other events occurred. For the three and nine months ended September 30, 2005, the Company’s results include income of $8 million and $25 million, respectively, attributable to CC VIII. Subsequent to recording the impact of the settlement in the fourth quarter of 2005,preferred membership interests plus approximately 6%18.6% of CC VIII’s income, will be allocated to minority interest.net of accretion.

8. | Comprehensive Income (Loss)Loss |

Certain marketable equity securities are classified as available-for-sale and reported at market value with unrealized gains and losses recorded as accumulated other comprehensive income (loss)loss on the accompanying condensed consolidated balance sheets. Additionally, the Company reports changes in the fair value of interest rate agreements designated as hedging the variability of cash flows associated with floating-rate debt obligations, that meet the effectiveness criteria of SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities, in accumulated other comprehensive income (loss).loss. Comprehensive income for the three months ended September 30, 2005 was $128 million and comprehensive loss for the three months ended September 30, 2004March 31, 2006 and 2005 was $3.5 billion and was $519$440 million and $4.1 billion for the nine months ended September 30, 2005 and 2004,$339 million, respectively.

9. | Accounting for Derivative Instruments and Hedging Activities |

The Company uses interest rate risk management derivative instruments, such as interest rate swap agreements and interest rate collar agreements (collectively referred to herein as interest rate agreements) to manage its interest costs. The Company’s policy is to manage interest costs using a mix of fixed and variable rate debt. Using interest rate swap agreements, the Company has agreed to exchange, at specified intervals through 2007, the difference between fixed and variable interest amounts calculated by reference to an agreed-upon notional principal amount. Interest rate collar agreements are used to limit the Company’s exposure to and benefits from interest rate fluctuations on variable rate debt to within a certain range of rates.

The Company does not hold or issue derivative instruments for trading purposes. The Company does, however, have certain interest rate derivative instruments that have been designated as cash flow hedging instruments. Such instruments effectively convert variable interest payments on certain debt instruments into fixed payments. For qualifying hedges, SFAS No. 133 allows derivative gains and losses to offset related results on hedged items in the consolidated statement of operations. The Company has formally documented, designated and assessed the effectiveness of transactions that receive hedge accounting. For the three months ended September 30,March 31, 2006 and 2005, and 2004, net gain (loss) on derivative instruments and hedging activities includes gains of $1 million and $1 million, respectively, and for the nine months ended September 30, 2005 and 2004, net gain (loss) on derivative instruments and hedging activitiesother income includes gains of $2 million and $3$1 million, respectively, which represent cash flow hedge ineffectiveness on interest rate hedge agreements arising from differences between the critical terms of the agreements and the related hedged obligations. Changes in the fair value of interest rate agreements designated as hedging instruments of the variability of cash flows associated with floating-rate debt obligations that meet the effectiveness criteria of SFAS No. 133 are reported in accumulated other comprehensive loss. For the three months ended September 30,March 31, 2006 and 2005, a loss of $1 million and 2004, a gain of $5 million and $2 million, respectively, and for the nine months ended September 30, 2005 and 2004, a gain of $14 million and $31$9 million, respectively, related to derivative instruments designated as cash flow hedges, was recorded in accumulated other comprehensive income (loss).loss. The amounts are

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

subsequently reclassified into interest expense as a yield adjustment in the same period in which the related interest on the floating-rate debt obligations affects earnings (losses).

Certain interest rate derivative instruments are not designated as hedges as they do not meet the effectiveness criteria specified by SFAS No. 133. However, management believes such instruments are closely correlated with the respective debt, thus managing associated risk. Interest rate derivative instruments not designated as hedges are marked to fair value, with the impact recorded as gain (loss) on derivative instruments and hedging activitiesother income in the Company’s condensed consolidated statements of operations. For the three months ended September 30,March 31, 2006 and 2005, and 2004, net gain (loss) on derivative instruments and hedging activitiesother income includes gains of $16$6 million and losses of $9 million, respectively, and for the nine months ended September 30, 2005 and 2004, net gain (loss) on derivative instruments and hedging activities includes gains of $41 million and $45$26 million, respectively, for interest rate derivative instruments not designated as hedges.

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

As of September 30, 2005March 31, 2006 and December 31, 2004,2005, the Company had outstanding $2.1$1.8 billion and $2.7$1.8 billion and $20 million and $20 million, respectively, in notional amounts of interest rate swaps and collars, respectively. The notional amounts of interest rate instruments do not represent amounts exchanged by the parties and, thus, are not a measure of exposure to credit loss. The amounts exchanged are determined by reference to the notional amount and the other terms of the contracts.

Revenues consist of the following for the three and nine months ended September 30, 2005March 31, 2006 and 2004:2005:

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | | | Three Months Ended March 31, | |

| | | 2005 | | 2004 | | 2005 | | 2004 | | | 2006 | | 2005 | |

| | | | | | | | | | | | | | | |

| Video | | $ | 848 | | $ | 839 | | $ | 2,551 | | $ | 2,534 | | | $ | 869 | | $ | 842 | |

| High-speed Internet | | | 230 | | | 189 | | | 671 | | | 538 | | | | 254 | | | 215 | |

| Telephone | | | | 20 | | | 6 | |

| Advertising sales | | | 74 | | | 73 | | | 214 | | | 205 | | | | 70 | | | 64 | |

| Commercial | | | 71 | | | 61 | | | 205 | | | 175 | | | | 76 | | | 65 | |

| Other | | | 95 | | | 86 | | | 271 | | | 249 | | | | 85 | | | 79 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | $ | 1,318 | | $ | 1,248 | | $ | 3,912 | | $ | 3,701 | | | $ | 1,374 | | $ | 1,271 | |

Operating expenses consist of the following for the three and nine months ended September 30, 2005March 31, 2006 and 2004:2005:

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | |

| | | | 2005 | | | 2004 | | | 2005 | | | 2004 | |

| | | | | | | | | | | | | | |

| Programming | | $ | 357 | | $ | 328 | | $ | 1,066 | | $ | 991 | |

| Service | | | 203 | | | 173 | | | 572 | | | 489 | |

| Advertising sales | | | 26 | | | 24 | | | 76 | | | 72 | |

| | | | | | | | | | | | | | |

| | | $ | 586 | | $ | 525 | | $ | 1,714 | | $ | 1,552 | |

CHARTER COMMUNICATIONS HOLDINGS, LLC AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

(dollars in millions, except where indicated)

| | | Three Months Ended March 31, | |

| | | 2006 | | 2005 | |

| | | | | | |

| Programming | | $ | 391 | | $ | 358 | |

| Service | | | 209 | | | 176 | |

| Advertising sales | | | 26 | | | 25 | |

| | | | | | | | |

| | | $ | 626 | | $ | 559 | |

12. | Selling, General and Administrative Expenses |

Selling, general and administrative expenses consist of the following for the three and nine months ended September 30, 2005March 31, 2006 and 2004:2005:

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | | | Three Months Ended March 31, | |

| | | | 2005 | | | 2004 | | | 2005 | | | 2004 | | | 2006 | | 2005 | |

| | | | | | | | | | | | | | | | | | | |

| General and administrative | | $ | 231 | | $ | 220 | | $ | 658 | | $ | 636 | | | $ | 243 | | $ | 206 | |

| Marketing | | | 38 | | | 32 | | | 104 | | | 99 | | | | 38 | | | 35 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | $ | 269 | | $ | 252 | | $ | 762 | | $ | 735 | | | $ | 281 | | $ | 241 | |

Components of selling expense are included in general and administrative and marketing expense.

13. Hurricane Asset Retirement Loss

Certain of the Company’s cable systems in Louisiana suffered significant plant damage as a result of hurricanes Katrina and Rita. Based on preliminary evaluations, the Company wrote off $19 million of its plants’ net book value. Insignificant amounts of other expenses were recorded related to hurricanes Katrina and Rita.

The Company has insurance coverage for both property and business interruption. The Company has not recorded any potential insurance recoveries as it is still assessing the damage of its plant and the extent of insurance coverage.

The Company has recorded special charges as a result of reducing its workforce, consolidating administrative offices and management realignment in 2004 and 2005. The activity associated with this initiative is summarized in the table below.

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | |