25

We have also entered into other operating lease agreements, primarily for office and warehouse space, that expire at various times through July 2026. These facility leases have annual rental increases ranging from approximately 2.5% to 4%. The difference between the straight-line expense over the term of the lease and actual amounts paid are recorded as deferred rent.

Rental obligations, excluding real estate taxes, operating costs, and tenant improvement allowances, under all lease agreements as of September 30, 2017 were as follows (in millions): |

| | | |

| Fiscal Year Ending | |

| Remainder of 2017 | $ | 2.2 |

|

| 2018 | 10.1 |

|

| 2019 | 11.0 |

|

| 2020 | 11.4 |

|

| 2021 | 11.7 |

|

| Thereafter | 13.1 |

|

| Total | $ | 59.5 |

|

Total rent expense for the three and nine months ended September 30, 2017 was $2.7 million and $8.3 million, compared to $2.4 million and $6.6 million for the same periods in 2016.

Litigation

On March 28, 2016, AgaMatrix, Inc. filed a patent infringement lawsuit against us in the United States District Court for the District of Oregon, asserting that certain of our products infringe certain patents held by AgaMatrix. On June 6, 2016, AgaMatrix filed a First Amended Complaint asserting the same three patents. On August 25, 2016, we filed petitions for inter partes review with the Patent Trial and Appeal Board of the U.S. Patent and Trademark Office seeking a determination that two of the three asserted patents are invalid under the U.S. patent law and those petitions were granted on March 6, 2017. Based on those grants, most activity in the patent infringement lawsuit against us in the District of Oregon was stayed until the inter

partes review of the Patent Trial and Appeal Board is completed. On March 8, 2017, we filed a petition for inter partes review with the Patent Trial and Appeal Board seeking a determination that the third of the three asserted patents is invalid under U.S. patent law. This petition was granted on September 15, 2017. It is our position that AgaMatrix’s assertions of infringement have no merit.

On August 6, 2016, DexCom filed a patent infringement lawsuit in the United States Central District Court of California, asserting certain AgaMatrix products infringed a patent held by DexCom. On September 30, 2016 DexCom filed a First Amended Complaint asserting the same patent. DexCom believes certain AgaMatrix single-point blood glucose monitoring products infringe the asserted patent. On September 15, 2017, DexCom filed a patent infringement lawsuit against Agamatrix in the United States District Court for the District of Delaware, asserting certain single-point blood glucose monitoring products of Agamatrix infringe two patents held by DexCom. The patents asserted in the Delaware litigation are unrelated to the patent asserted in the Central District of California litigation. On September 18, 2017, we also filed a Complaint against Agamatrix in the International Trade Commission (“ITC”) requesting the ITC institute an investigation and issue an order excluding certain products of Agamatrix from importation into or sale in the United States based on Agamatrix’s infringement of the same two patents asserted in the Delaware litigation. The ITC granted DexCom’s request to institute the investigation on October 18, 2017.

Neither the outcome of these lawsuits nor the amount and range of potential fees associated with the lawsuits can be assessed at this time. As of September 30, 2017, no amounts have been accrued in respect of these suits.We are subject to various claims, complaints and legal actions that arise from time to time in the normal course of business, including commercial insurance, product liability, intellectual property and employment related matters. In addition, from time to time we may bring claims or initiate lawsuits against various third parties with respect to matters arising out of the ordinary course of our business, including commercial and employment related matters.

Between June 2021 through the three months ended March 31, 2024, we and certain Abbott Diabetes Care, Inc. (“Abbott”) entities have served patent infringement complaints against each other in multiple jurisdictions against certain continuous glucose monitoring products of each company.

Abbott’s patent infringement trial, “D1”, against Dexcom commenced in the U.S.D.C., District of Delaware in March 2024. In the lead up to trial, the U.S.D.C., District of Delaware invalidated one of Abbott’s patents on factory calibration and Abbott dropped four other patents from the litigation. The claims litigated were isolated to the inserter mechanism and the wearable seal and mount of Dexcom’s G6. On March 22, 2024, a jury returned a mixed verdict. The jury found that Dexcom infringes one patent, that Dexcom did not infringe a second patent, and that Dexcom also did not infringe a third patent, which the jury also found invalid. The jury found that any infringement was not willful. It could not reach unanimity as to a fourth patent. No determination of damages was made or awarded by the jury. Dexcom will challenge the sole finding of infringement and continue to defend itself vigorously. We analyzed the potential for a loss from this litigation in accordance with ASC 450, Contingencies. We believe it is not probable that we will have an unfavorable outcome and incur a material loss contingency due to our beliefs about our position in the case. In addition, the jury did not award damages for the one patent they believe we infringed nor can we reasonably estimate the amount of loss we would incur if we do not prevail. As a result, we have not recorded an accrual for a contingent liability.

Due to uncertainty surrounding the other patent litigation procedures initiated by Dexcom and Abbott throughout multiple jurisdictions, we are unable to reasonably estimate the ultimate outcome of any of the litigation matters at this time. We intend to protect our intellectual property and defend against Abbott’s claims vigorously in all of these actions.

We do not expect thatbelieve we are party to any other currently pending legal proceedings, the resolutionoutcome of these matters would, or will,which could have a material adverse effect or material impact on our consolidatedbusiness, financial position.condition, or results of operations. There can be no assurance that existing or future legal proceedings arising in the ordinary course of business or otherwise will not have a material adverse effect on our business, financial condition, or results of operations.

Purchase Commitments

We estimate our annual effective tax rate to be 23.8% for the full year 2024, which differs from the U.S. federal statutory rate due to state and foreign income taxes and nondeductible executive compensation, partially offset by federal tax credits generated. Our negative effective tax rate of10.5% for the three months ended March 31, 2024 was primarily due to income tax expense from normal, recurring operations, offset by tax benefits recognized for share-based compensation for employees, net of disallowed executive compensation, and the Verily milestone payment.

The Organization for Economic Co-operation and Development has a framework to implement a global minimum corporate tax of 15% for companies with global revenues and profits above certain thresholds (referred to as Pillar 2), with certain aspects of Pillar 2 effective January 1, 2024 and other aspects effective January 1, 2025. While it is uncertain whether the United States will enact legislation to adopt Pillar 2, certain countries in which we operate have adopted legislation, and other countries in which we operate are partyin the process of introducing legislation to various purchase arrangementsimplement Pillar 2. We have assessed the impact of Pillar 2 and the impact is immaterial.

In January 2024, the California Franchise Tax Board commenced an audit of our California income tax returns for the 2020 and 2021 years primarily related to our manufacturingresearch and development activities including materials usedtax credit carryforwards. We do not expect any significant adjustments as a result of the audit.

Share-Based Compensation

Our share-based compensation expense is associated with RSUs, PSUs, and our Employee Stock Purchase Plan, or ESPP. The following table summarizes our share-based compensation expense included in our CGM systems. consolidated statements of operations for the periods shown:

| | | | | | | | | | | | | | | |

| Three Months Ended

March 31, | | |

| (In millions) | 2024 | | 2023 | | | | |

| Cost of sales | $ | 3.7 | | | $ | 3.3 | | | | | |

| Research and development | 11.5 | | | 11.1 | | | | | |

| Selling, general and administrative | 23.8 | | | 20.8 | | | | | |

| Total share-based compensation expense | $ | 39.0 | | | $ | 35.2 | | | | | |

As of September 30, 2017,March 31, 2024, unrecognized estimated compensation costs related to RSUs and PSUs totaled $362.5 million and are expected to be recognized over a weighted-average period of approximately 2.2 years.

Treasury Shares

In the first quarter of 2024, we had purchase commitmentsissued 7.9 million treasury shares to settle a portion of the 2023 Warrants. See Note 5 “Debt—Senior Convertible Notes” to the consolidated financial statements for more information.

In the first quarter of 2024, we issued 1.5 million treasury shares in connection with vendors totaling $78.4 million due within one year. There are no material purchase commitments due beyond one year.

6. our achievement of the second sales-based milestone under the Restated Collaboration Agreement. See Note 2 “Development and Other Agreements

Agreements—Collaboration with Verily Life Sciences

On August 10, 2015, we entered into a Collaboration and License Agreement (the “Verily Collaboration Agreement”) with Google Life Sciences LLC, now renamed Verily Life Sciences (“Verily”). Pursuant” to the Verily Collaboration Agreement, we and Verily have agreed to jointly develop a series of next-generation CGM products. The Verily Collaboration Agreement provides us with an exclusive license to use certain intellectual property of Verily related to the development, manufacture and commercialization of the products contemplated under the Verily Collaboration Agreement. The Verily Collaboration Agreement providesconsolidated financial statements for the establishment of a joint steering committee, joint development committee and joint commercialization committee to oversee and coordinate the parties’ activities under the collaboration. We and Verily have agreed to make committee decisions by consensus. Certain aspects of this collaboration were clarified and amended on October 25, 2016.more information.

Under the terms of Verily Collaboration Agreement we paid an upfront fee of $35.0 million through the issuance of 404,591 shares of our common stock. We recorded $36.5 million in research and development expense in our consolidated statement of operations during 2015 related to the issuance of the 404,591Repurchased shares of our common stock based onare held as treasury shares until they are reissued or retired. We have not yet determined the ultimate disposition of repurchased shares and consequently we continue to hold them as treasury shares rather than retiring them. Authorization of future stock repurchase programs is subject to the final determination of our stock priceBoard of $90.29 per shareDirectors.

| | |

| 9. Business Segment and Geographic Information |

Reportable Segments

An operating segment is identified as a component of a business that has discrete financial information available and for which the CODM must decide the level of resource allocation. In addition, the guidance for segment reporting indicates certain quantitative materiality thresholds. None of the date of Verily Collaboration Agreement. In addition, we will pay Verily up to $65.0 million in additional milestones upon achievement of various development and regulatory objectives, which payments may be paid in cash or sharescomponents of our common stock atbusiness meet the definition of an operating segment.

We currently consider our sole election, calculatedoperations to be, and manage our business globally within, one reportable segment, which is consistent with how our President and Chief Executive Officer, who is our CODM, reviews our business, makes investment and resource allocation decisions, and assesses operating performance.

Disaggregation of Revenue

We disaggregate revenue by geographic region and by major sales channel. We have determined that disaggregating revenue into these categories achieves the ASC Topic 606 disclosure objectives of depicting how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

Revenue by geographic region

During the three months ended March 31, 2024 and March 31, 2023, no individual country outside the United States generated revenue that represented more than 10% of our total revenue. The following table sets forth revenue by our two primary geographical markets, the United States and International, based on the volume weighted average trading price during a period of twenty consecutive trading days ending ongeographic location to which we deliver the trading day prior to the date on which the applicable objective has been achieved.

In addition, Verily is eligible to receive tiered royalty payments associated with the commercialization of the products contemplated under the Verily Collaboration Agreement, which are subject to regulatory approval. Unless we attain annual product sales subject to the Verily Collaboration Agreement in excess of $750.0 million, there will be no royalty paid by us to

Verily. Above this range, and upon marketing approval of the initial product contemplated by the Verily Collaboration Agreement, or upon commercialization of any other DexCom product that incorporates Verily intellectual property, we will pay to Verily a royalty percentage starting in the high single digits and declining to the mid-single digits based on our annual aggregate product sales.

The Verily Collaboration Agreement shall be terminable by either party (a) upon uncured material breach of the Verily Collaboration Agreement by the other party, (b) if the second product contemplated by the Verily Collaboration Agreement has not been submitted to the FDA for approval by a specified date and (c) if the annual net salescomponents, for the products developed with Verily under the Verily Collaboration Agreement are less than a specified aggregate dollar amount. Additionally, we have the right to terminate the Verily Collaboration Agreement upon the expiration of the last to expire patent that covers a product developed under the Verily Collaboration Agreement.periods shown:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended

March 31, 2024 | | Three Months Ended

March 31, 2023 |

| (In millions) | Amount | | % of Total | | Amount | | % of Total |

| United States | $ | 653.2 | | | 71 | % | | $ | 526.0 | | | 71 | % |

| International | 267.8 | | | 29 | % | | 215.5 | | | 29 | % |

| Total revenue | $ | 921.0 | | | 100 | % | | $ | 741.5 | | | 100 | % |

| | | | | | | |

| | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

7. Fair Value MeasurementsRevenue by customer sales channel

We base the fair value ofsell our Level 1 financial instrumentsCGM systems through a direct sales organization and through distribution arrangements that are in active markets using quoted market prices for identical instruments.

We obtain the fair value ofallow distributors to sell our Level 2 financial instruments, which are not in active markets, from a primary professional pricing source using quoted market prices for identical or comparable instruments, rather than direct observations of quoted prices in active markets. Fair value obtained from this professional pricing source can also be based on pricing models whereby all significant observable inputs, including maturity dates, issue dates, settlement date, benchmark yields, reported trades, broker-dealer quotes, issue spreads, benchmark securities, bids, offers or other market related data, are observable or can be derived from, or corroborated by, observable market data for substantially the full term of the asset.

We validate the quoted market prices provided by our primary pricing service by comparing the fair values of our Level 2 marketable securities portfolio balance provided by our primary pricing service against the fair values of our Level 2 marketable securities portfolio balance provided by our investment managers.

products. The following table represents our fair value hierarchy for our financial assets (cash equivalents and marketable securities) measured at fair value on a recurring basis as of September 30, 2017 (in millions): |

| | | | | | | | | | | | | | | |

| | Fair Value Measurements Using |

| | Level 1 | | Level 2 | | Level 3 | | Total |

| Cash equivalents | $ | — |

| | $ | 327.0 |

| | $ | — |

| | $ | 327.0 |

|

| Marketable securities, available for sale | | | | | | | |

| U.S. government agencies | — |

| | 96.9 |

| | — |

| | 96.9 |

|

| Commercial paper | — |

| | 21.5 |

| | — |

| | 21.5 |

|

| Corporate debt | — |

| | 5.3 |

| | — |

| | 5.3 |

|

| Total marketable securities, available for sale | $ | — |

| | $ | 123.7 |

| | $ | — |

| | $ | 123.7 |

|

The following table represents our fair value hierarchy for our financial assets (cash equivalents and marketable securities) measured at fair value on a recurring basis as of December 31, 2016 (in millions): |

| | | | | | | | | | | | | | | |

| | Fair Value Measurements Using |

| | Level 1 | | Level 2 | | Level 3 | | Total |

| Cash equivalents | $ | — |

| | $ | 32.3 |

| | $ | — |

| | $ | 32.3 |

|

| Marketable securities, available for sale | | | | | | | |

| U.S. government agencies | — |

| | 22.2 |

| | — |

| | 22.2 |

|

| Corporate debt | — |

| | 3.8 |

| | — |

| | 3.8 |

|

| Commercial paper | — |

| | 3.2 |

| | — |

| | 3.2 |

|

| Total marketable securities, available for sale | $ | — |

| | $ | 29.2 |

| | $ | — |

| | $ | 29.2 |

|

There were no transfers between Level 1 and Level 2 securities during the three and nine months ended September 30, 2017 and 2016. There were no transfers into or out of Level 3 securities during the three and nine months ended September 30, 2017 and 2016.

The fair values of the Company’s outstanding 2022 Note was $357.2 million at September 30, 2017 and is a Level 2 measurement. See Note 4 to the Unaudited Consolidated Financial Statements for further discussion on the carrying value of the Company’s 2022 Notes.

8. Income Taxes

Our effective tax ratesets forth revenue by major sales channel for the three and nine months ended September 30, 2017 was 20% and 29% compared to a negative rate of 1% and 1% for the same periods of 2016. Our effective tax rate was impacted primarily by a $1.1 million and $18.2 million benefit related to the issuance of convertible debt, for the three and nine months ended September 30, 2017, respectively. Under intraperiod allocation, the deferred tax liability related to the equity component of convertible debt is a source of income that can be used to recognize the tax benefit of the current year loss through continuing operations. The estimated tax benefit for the year is recorded at each interim period through the annual effective tax rate and may change with updates to our earnings through the future quarters of 2017. The tax benefit related to the issuance of the convertible debt will not recur in future years. The income tax benefit was offset by current income tax expense in profitable jurisdictions, withholding taxes, and state taxes.shown:

We maintain a full valuation allowance against our net deferred tax assets as of September 30, 2017 based on our assessment that it is not more likely than not these future benefits will be realized before expiration. | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended

March 31, 2024 | | Three Months Ended

March 31, 2023 |

| (In millions) | Amount | | % of Total | | Amount | | % of Total |

| Distributor | $ | 778.8 | | | 85 | % | | $ | 618.9 | | | 83 | % |

| Direct | 142.2 | | | 15 | % | | 122.6 | | | 17 | % |

| Total revenue | $ | 921.0 | | | 100 | % | | $ | 741.5 | | | 100 | % |

| | | | | | | |

| | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | |

ITEM 2. | 2 - MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document,Quarterly Report on Form 10-Q, including the following Management’s Discussion and Analysis of Financial Condition and Results of Operations, contains forward-looking statements that are not purely historical regarding DexCom'sDexcom’s or its management'smanagement’s intentions, beliefs, expectations and strategies for the future. These forward-looking statements fall within the meaning of the federal securities laws that relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “intend,” “potential” or “continue” or the negative of these terms or other comparable terminology. Forward-looking statements are made as of the date of this report,Quarterly Report on Form 10-Q, deal with future events, are subject to various risks and uncertainties, and actual results could differ materially from those anticipated in thosethe forward looking statements. The risks and uncertainties that could cause actual results to differ materially are more fully described under “Risk Factors” andin our Annual Report on Form 10-K for the fiscal year ended December 31, 2023 filed with the SEC on February 8, 2024, together with any updates identified under “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2023 filed with the SEC on February 8, 2024, together with any updates identified under “Risk Factors” in Part II, Item 1A of this Quarterly Report on Form 10-Q, elsewhere in this reportQuarterly Report on Form 10-Q, and in our other reports filed with the SEC. We assume no obligation to update any of the forward-looking statements after the date of this report or to conform these forward-looking statements to actual results.

Overview

We are a medical device company primarily focused on You should read the design, developmentfollowing discussion and commercialization of continuous glucose monitoring (“CGM”) systems for use by people with diabetes and by healthcare providers for the treatment of people with diabetes. Unless the context requires otherwise, the terms “we,” “us,” “our,” the “company,” or “DexCom” refer to DexCom, Inc. and its subsidiaries.

From inception to 2006, we devoted substantially all of our resources to start-up activities, raising capital and research and development, including product design, testing, manufacturing and clinical trials. Since 2006, we have devoted considerable resources to the commercialization of our continuous glucose monitoring systems, including the G4 PLATINUM and G5 Mobile, as well as the continued research and clinical development of our technology platform.

From inception through September 30, 2017, we have generated $2.2 billion of product, development grant and other (non-product) revenue, and we have incurred operating losses in each year since our inception in May 1999. As of September 30, 2017, we had an accumulated deficit of $662.4 million.

We expect our losses to continue as we proceedanalysis together with our commercializationconsolidated financial statements and research and development activities. We have financed our operations primarily through offeringsrelated notes in Part I, Item 1 of equity securities and debt, and the sales of our products.

Financial Operations

Revenue

We sell our durable systems and disposable units through a direct sales force in the United States, Canada and portions of Europe, and through distribution arrangements in the United States, Australia, New Zealand, and in portions of Europe, Asia, Latin America, the Middle East and Africa. We have contracts with certain distributors, the majority of whom stock our products, and we refer to these distributors as Stocking Distributors, whereby the Stocking Distributors fulfill orders for our product from their inventory. We also have contracts with certain distributors that do not stock our products, but rather products are shipped directly to the customer by us on behalf of our distributor, and we refer to these distributors as Drop-Ship Distributors. We expect that revenues we generate from the sales of our products will fluctuate from quarter to quarter. We typically experience seasonality with lower sales in the first quarter of each year, compared to the previous fourth quarter, related to annual insurance deductible resets and unfunded flexible spending accounts.

Cost of Sales

Cost of sales includes direct labor and materials costs related to each product sold or produced, including assembly, test labor and scrap, as well as factory overhead supporting our manufacturing operations. Factory overhead includes facilities, material procurement and control, manufacturing engineering, quality assurance, supervision and management. These costs are primarily salary, fringe benefits, share-based compensation, facility expense, supplies and purchased services. A portion of our costs are currently fixed due to our moderate level of production volumes compared to our potential capacity. All of our manufacturing costs are included in cost of sales.

Research and Development

Our research and development expenses primarily consist of engineering and research expenses related to our continuous glucose monitoring technology, clinical trials, regulatory expenses, quality assurance programs, materials and products for clinical trials. Research and development expenses are primarily related to employee compensation, including salary, fringe benefits, share-based compensation, and temporary employee expenses. We also incur significant expenses to operate our clinical trials including clinical site reimbursement, clinical trial product and associated travel expenses. Our research and development expenses also include fees for design services, contractors and development materials.

Selling, General and Administrative

Our selling, general and administrative expenses primarily consist of salary, fringe benefits and share-based compensation for our executive, financial, sales, marketing, information technology and administrative functions. Other significant expenses include commissions, marketing and advertising, IT software license costs, insurance, professional fees for our outside legal counsel and independent auditors, litigation expenses, patent application expenses and consulting expenses.

Results of Operations

Quarter Ended September 30, 2017 Compared to September 30, 2016

Revenue, Cost of Sales and Gross Profit

Revenues increased $36.0 million to $184.6 million for the three months ended September 30, 2017 compared to $148.6 million for the three months ended September 30, 2016 based primarily on increased sales volume of our disposable sensors due to the continued growth of our installed base of customers using our G4 PLATINUM and G5 Mobile systems, and durable systems to both new and existing customers. Revenue attributable to our disposable sensors and durable systems was approximately 70% and 30%, respectively, of revenue, for each of the three months ended September 30, 2017 and September 30, 2016. Revenue from products shipped to our distributors, which are primarily Stocking Distributors, for the three months ended September 30, 2017 was approximately $137.0 million or 74% of our revenue compared to $104.9 million or 71% of our total revenue for the three months ended September 30, 2016.

Cost of sales increased $10.1 million to $57.6 million for the three months ended September 30, 2017 compared to $47.5 million for the three months ended September 30, 2016, primarily due to increased sales volume. The gross profit of $127.0 million, or 69% for the three months ended September 30, 2017 increased $25.9 million compared to $101.1 million, or 68%, for the same period in 2016, primarily due to increased revenue and a decrease in warranty costs.

Research and Development. Research and development expense decreased $0.6 million to $43.3 million for the three months ended September 30, 2017, compared to $43.9 million for the three months ended September 30, 2016. The decrease was primarily due to a decrease of $2.5 million in share-based compensation and a decrease of $2.1 million in consulting

expenses, offset by a $2.9 million increase of supply expenses, and $1.3 million of additional salaries, bonus and payroll related costs.

Selling, General and Administrative. Selling, general and administrative expense increased $8.5 million to $84.2 million for the three months ended September 30, 2017 compared to $75.7 million for the three months ended September 30, 2016. The increase was primarily due to higher sales related costs primarily due to increased headcount and higher marketing costs to support revenue growth and the continued commercialization of our products in both the United States and Europe. Significant elements of the increase in selling, general, and administrative expenses included $7.6 million in additional salaries, bonus, and payroll related costs and $1.3 million in additional marketing costs.

Interest Expense. Interest expense increased $4.3 million to $4.5 million for the three months ended September 30, 2017 compared to $0.2 million for the three months ended September 30, 2016. The increase was primarily due to an additional $4.3 million of interest expense related to the 2022 Notes.

Income Tax Benefit. Our income tax benefit was $0.5 million on a pre-tax loss of $2.5 million, resulting in an effective tax rate of 20% for the three months ended September 30, 2017, compared to income tax expense of $0.2 million on a pre-tax loss of $18.6 million and a negative effective tax rate of 1% for the three months ended September 30, 2016. The current period benefit is primarily attributable to an income tax benefit of $1.1 million for current year losses, as the deferred tax liability created by the issuance of convertible debt we issued during the second quarter of 2017 is considered a source of income to recognize the tax benefit of the current year loss. The tax benefit is offset by withholding and other income tax expense in profitable jurisdictions.

Nine Months Ended September 30, 2017 Compared to September 30, 2016

Revenue, Cost of Sales and Gross Profit

Revenues increased $95.4 million to $497.5 million for the nine months ended September 30, 2017 compared to $402.1 million for the nine months ended September 30, 2016 based primarily on increased sales volume of our disposable sensors due to the continued growth of our installed base of customers using our G4 PLATINUM and G5 Mobile systems and durable systems to both new and existing customers. Revenue attributable to our disposable sensors and durable systems was approximately 70% and 30%, respectively, of total revenue, for each of the nine months ended September 30, 2017 and 2016. Revenue from products shipped to our distributors, which are primarily Stocking Distributors, for the nine months ended September 30, 2017 was approximately $372.5 million or 75% of our revenue compared to $289.1 million or 72% of our total revenue for the nine months ended September 30, 2016.

Cost of sales increased $18.5 million to $158.9 million for the nine months ended September 30, 2017 compared to $140.4 million for the nine months ended September 30, 2016, primarily due to increased sales volume. The gross profit of $338.6 million, or 68% for the nine months ended September 30, 2017 increased $76.9 million compared to $261.7 million, or 65% for the same period in 2016, primarily due to increased revenue and a decrease in warranty costs.

Research and Development. Research and development expense increased $24.3 million to $136.7 million for the nine months ended September 30, 2017, compared to $112.4 million for the nine months ended September 30, 2016. The increase was primarily due to $14.2 million in additional salaries, bonus and payroll related costs, a $3.9 million increase of expensed equipment, $2.3 million of additional supply expenses, and $2.0 million of additional clinical trial costs related to development of our future products.

Selling, General and Administrative. Selling, general and administrative expense increased $49.3 million to $256.4 million for the nine months ended September 30, 2017, compared to $207.1 million for the nine months ended September 30, 2016. The increase was primarily due to higher headcount related selling, marketing and customer support costs to support revenue growth and the continued commercialization of our products. Significant elements of the increase in selling, general, and administrative expenses included $26.9 million in additional salaries, bonus, and payroll related costs, $10.3 million of additional marketing costs, $3.9 million of additional software license costs, $1.5 million in additional consulting fees and $1.3 million in additional share-based compensation.

Other Income. Other Income was $3.5 million for the nine months ended September 30, 2017 compared to $0.0 million for the nine months ended September 30, 2016 and is primarily related to foreign currency transaction gains and losses.

Interest Expense. Interest expense was $8.1 million for the nine months ended September 30, 2017 compared to $0.4 million for the nine months ended September 30, 2016 and is related to our 2022 Notes and Revolving Credit Agreement. The increase was primarily due to an additional $6.6 million of interest expense related to the 2022 Notes.

Income Tax Benefit. Income tax benefit was $16.4 million on a pre-tax loss of $57.2 million, resulting in an effective tax rate of 29% for the nine months ended September 30, 2017, compared to income tax expense of $0.3 million on a pre-ta

x loss of $57.9 million and a negative effective tax rate of 1% for the nine months ended September 30, 2016. The current period benefit is primarily attributable to an income tax benefit of $18.2 million for current year losses, as the deferred tax liability created by the issuance of convertible debt during the second quarter of 2017 is considered a source of income to recognize the tax benefit of the current year loss. The tax benefit is offset by withholding and other income tax expense in profitable jurisdictions.

Liquidity and Capital Resources

We have incurred losses since our inception in May 1999. As of September 30, 2017, we had an accumulated deficit of $662.4 million and had working capital of $574.7 million. To date, we have funded our operations primarily through offerings of equity securities and debt, and the sales of our products.

In June 2016, we entered into a $200.0 million Credit Agreement, including a subfacility of up to $10.0 million for letters of credit, of which $5.6 million is still available. The revolving loans under the Credit Agreement will be available for general corporate purposes, including working capital and capital expenditures. On March 3, 2017 we drew $75.0 million on the Credit Agreement under a six month term and we repaid the entire principal balance on May 19, 2017. As of September 30, 2017 we had no outstanding borrowings under the Credit Agreement, and $200.0 million under the Credit Agreement remains available.

In May 2017, we completed an offering of $350.0 million aggregate principal amount of 0.75% convertible senior notes due 2022 (the "2022 Notes") and, in June 2017 the initial purchasers exercised their option to purchase an additional $50.0 million aggregate principal amount. The 2022 Notes have a stated interest rate of 0.75% and a maturity date of May 15, 2022. Holders may elect to convert any time after February 15, 2022 for shares. The 2022 Notes may be settled in cash, stock, or a combination thereof, solely at our discretion. We used a portion of the net proceeds of the offering of the 2022 Notes to repay $75.0 million of borrowings under our existing credit facility. The remainder of the proceeds are available for general corporate purposes and capital expenditures, including working capital needs and buildout of our manufacturing facility in Arizona. We may also use the net proceeds to expand our current business through in-licensing or acquisitions of, or investments in, other businesses, products or technologies; however, we do not have any commitments with respect to any such acquisitions or investments at this time.

Our cash, cash equivalents and marketable securities totaled $525.8 million as of September 30, 2017. Our cash, cash equivalents, and marketable securities portfolio is primarily denominated in U.S. dollars and consists of investment grade, highly liquid securities of various holdings including obligations of U.S. government sponsored enterprises, commercial paper, corporate debt, and money market funds. The change in our cash, cash equivalents and marketable securities during the nine months ended September 30, 2017 was due to the factors described in the “Cash Flow Summary” below.

Cash Flow Summary

The following table sets forth a summary of our cash flows for the periods indicated (in millions): |

| | | | | | | | | | | |

| | Nine Months Ended

September 30, | | Change |

| | 2017 | | 2016 | | |

| Net cash provided by operating activities | $ | 50.8 |

| | $ | 42.9 |

| | $ | 7.9 |

|

| Net cash used in investing activities | $ | (143.3 | ) | | $ | (38.6 | ) | | $ | (104.7 | ) |

| Net cash provided by financing activities | $ | 399.0 |

| | $ | 7.6 |

| | $ | 391.4 |

|

As of September 30, 2017, we had $402.1 million of cash and cash equivalents compared to $94.5 million as of December 31, 2016, an increase of $307.6 million. The cash flows during the nine months ended September 30, 2017 were related primarily to the following items:

Cash inflows:

Net cash provided by operating activities of $50.8 million comprised of net loss of $40.8 million, offset by $83.9 million of net non-cash expenses and $7.7 million changes in working capital balances. Non-cash expenses of $102.1 million were primarily related to share-based compensation, depreciation and amortization, and non-cash interest expense related to our senior convertible notes, partially offset by $18.2 million of deferred tax benefits related to our senior convertible notes.

Proceeds from issuance of common stock of $10.0 million pursuant to the exercise of then-outstanding stock options.

Proceeds from short-term borrowings of $75.0 million.

Proceeds from issuance of senior convertible notes, net of issuance costs, of $389.0 million.

Cash outflows:

Capital expenditures of $48.4 million primarily related to purchase of facility related build-outs, office equipment and machinery and equipment.

Net cash outflow of $94.9 million as a result of marketable securities transactions.

Repayment of short-term borrowings of $75.0 million.

Net Cash Provided by Operating Activities. The increase in cash provided by operating activities was primarily due to a $17.4 million in lower net loss, partially offset by a decrease of $9.9 million in non-cash expenses. The decrease in non-cash expenses was due to $18.2 million deferred tax benefit for the nine months ended September 30, 2017 related to our senior convertible notes, partially offset by an increase in non-cash interest expense related to our senior convertible notes.

Net Cash Used in Investing Activities. The change in cash used in investing activities was primarily due to $94.0 million net cash used as a result of marketable securities transactions and an additional $10.3 million to purchase equipment to support facility related build-outs, manufacturing equipment and information technology infrastructure.

Net Cash Provided by Financing Activities. The increase in cash provided by financing activities was primarily due to $389.0 million proceeds from the issuance of senior convertible notes, net of issuance costs.

Operating Capital and Capital Expenditure Requirements

We anticipate that we will continue to incur operating losses as we incur expenses and expand the commercialization of our approved products domestically and internationally, develop additional continuous glucose monitoring products, and expand our marketing, manufacturing and corporate infrastructure.

We believe that our cash, cash equivalents, marketable securities balances, projected cash contributions from our commercial operations and $200.0 million available under our Credit Agreement, of which $200.0 million remains available, will be sufficient to meet our anticipated cash requirements with respect to the continued scale-up of our commercialization activities, research and development activities, including clinical trials, the expansion of our marketing, manufacturing and corporate infrastructure, and to meet our other anticipated cash needs through at least September 30, 2018. If our available cash, cash equivalents and marketable securities are insufficient to satisfy our liquidity requirements, or if we develop additional products or new markets for our existing products, we may seek to sell additional equity or debt securities or obtain an additional credit facility. The sale of additional equity and debt securities may result in additional dilution to our stockholders. If we raise additional funds through the issuance of debt securities or preferred stock, these securities could have rights senior to those of our common stock and could contain covenants that would restrict our operations. We may require additional capital beyond our currently forecasted amounts. Any such required additional capital may not be available on reasonable terms, if at all. Additionally, we cannot guarantee that we will be successful in obtaining additional cash contributions from future partnership arrangements. Our ability to transition to, and maintain profitable operations is dependent upon achieving a level of revenues adequate to support our cost structure. If events or circumstances occur such that we do not meet our operating plan as expected, or if we are unable to obtain additional financing, we may be required to reduce planned increases in compensation related expenses or other operating expenses related to research, development, and commercialization activities, which could have an adverse impact on our ability to achieve our intended business objectives.

Because of the numerous risks and uncertainties associated with the development of continuous glucose monitoring technologies, we are unable to estimate the exact amounts of capital outlays and operating expenditures associated with our current and anticipated clinical trials. Our future funding requirements will depend on many factors, including, but not limited to:

the revenue generated by sales of our approved products and other future products;

the expenses we incur in manufacturing, developing, selling and marketing our products;

the quality levels of our products and services;

the third-party reimbursement of our products for our customers;

our ability to efficiently scale our manufacturing operations to meet demand for our current and any future products;

the costs, timing and risks of delays of additional regulatory approvals;

the costs of filing, prosecuting, defending and enforcing any patent claims and other intellectual property rights;

the rate of progress and cost of our clinical trials and other development activities;

the success of our research and development efforts;

the emergence of competing or complementary technological developments;

the terms and timing of any collaborative, licensing and other arrangements that we may establish; and

the acquisition of businesses, products and technologies and our ability to integrate and manage any acquired businesses, products and technologies.

Contractual Obligations

We are party to various purchase arrangements related to components used in manufacturing and research and development activities. As of September 30, 2017, we had firm purchase commitments with certain vendors totaling approximately $78.4 million due within one year. There are no material purchase commitments due beyond one year.

We are party to various leasing arrangements as described in the Management’s Discussion and Analysis of Financial Condition and Results of Operations in Item 7 of our AnnualQuarterly Report on Form 10-K for the fiscal year ended December 31, 2016 and Note 4 to our Consolidated Financial Statements in this Form 10-Q. We have not entered into any significant new leasing arrangements during the three and nine months ended September 30, 2017.

The following table summarizes our outstanding contractual obligations as of September 30, 2017 and the effect those obligations are expected to have on our liquidity and cash flows in future periods (in millions):

|

| | | | | | | | | | | | | | | | | | | | |

| Contractual Obligations: | | Total | | Less than 1 Year | | 1-3 Years | | 3-5 Years | | More than 5 Years |

| Operating leases | | $ | 59.5 |

| | $ | 2.2 |

| | $ | 21.1 |

| | $ | 23.1 |

| | $ | 13.1 |

|

Senior convertible notes (1) | | 415.0 |

| | 3.0 |

| | 9.0 |

| | 403.0 |

| | — |

|

| Purchase commitments | | 78.4 |

| | 78.4 |

| | — |

| | — |

| | — |

|

| Total | | $ | 552.9 |

| | $ | 83.6 |

| | $ | 30.1 |

| | $ | 426.1 |

| | $ | 13.1 |

|

| | | | | |

| Who We Are |

| (1)Senior convertible notes were issuedWe are a medical device company primarily focused on the design, development and commercialization of continuous glucose monitoring, or CGM, systems for the management of diabetes by patients, caregivers, and clinicians around the world. We received approval from the Food and Drug Administration, or FDA, and commercialized our first product in May2006. We launched our latest generation system, the Dexcom G6® integrated Continuous Glucose Monitoring System, or G6, in 2018, and June 2017 whichwe launched the Dexcom G7®, or G7,in 2023. In March 2024, we received marketing clearance from the FDA on Stelo, our new 15-day sensor designed for people with Type 2 diabetes who do not use insulin, as the first glucose biosensor that does not require a prescription. Unless the context requires otherwise, the terms “we,” “us,” “our,” the “company,” or “Dexcom” refer to DexCom, Inc. and its subsidiaries. |

| | | | | |

| Global Presence |

| We have built a direct sales organization in North America and certain international markets to call on health care professionals, such as endocrinologists, physicians and diabetes educators, who can educate and influence patient adoption of continuous glucose monitoring. To complement our direct sales efforts, we have entered into distribution arrangements in North America and several international markets that allow distributors to sell our products. |

| |

| |

| Future Developments |

| Product Development:We plan to develop future generations of technologies that are due in May 2022, obligations include both principalfocused on improved performance and interest. Although these notes mature in 2022, they may be converted into cashconvenience and sharesthat will enable intelligent insulin administration. Over the longer term, we plan to continue to develop and improve networked platforms with open architecture, connectivity and transmitters capable of communicating with other devices. We also intend to expand our common stock priorefforts to maturity if certain conditionsaccumulate CGM patient data and metrics and apply predictive modeling and machine learning to generate interactive CGM insights that can inform patient behavior. |

| |

| |

| Partnerships: We also continue to pursue and support development partnerships with insulin pump companies and companies or institutions developing insulin delivery systems, including automated insulin delivery systems. |

| |

| |

| New Opportunities:We are met. Any conversion prioralso exploring how to maturity can result in repayment of the principal amounts sooner than scheduled repayment as indicatedextend our offerings to other opportunities, including for people with Type 2 diabetes that are non-insulin using, people with pre-diabetes, people who are obese, people who are pregnant, and people in the table. See Note 4hospital setting. Eventually, we may apply our technological expertise to our Consolidated Financial Statements for further discussion of the terms of the senior convertible notes.products beyond glucose monitoring. |

| |

| |

| | |

| Critical Accounting Estimates |

Off-Balance Sheet Arrangements

We have not engaged in any off-balance sheet activities.

Critical Accounting Policies and Estimates

The discussion and analysis of our financial condition and results of operations are based on our consolidated financial statements, which we have prepared in accordance with U.S. GAAP. The preparation of these consolidated financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements as well as the reported revenue and expenses during the reporting periods. On an ongoing basis, we evaluate our estimates and judgments. We base our estimates on historical experience and on various other factors that we believe are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

Our significantWe believe that the estimates, assumptions and judgments involved in the accounting policies are more fully described in Note 1 to our consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2016. Our accounting policies and estimates which are most critical to a full understanding and evaluation of our reported financial results are described in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of our Annual Report on Form 10-K for the fiscal year ended December 31, 2016.2023, have the greatest potential impact on our financial statements, so we consider them to be our critical accounting policies and estimates. There were no material changes to our critical accounting policiesestimates during the ninethree months ended September 30, 2017.March 31, 2024.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Overview of Financial Results |

| The most important financial indicators that we use to assess our business are revenue, gross profit, operating income, net income, and operating cash flow. |

| Key Highlights for the Three Months Ended March 31, 2024 include the following: |

|

| Revenue | | | Gross Profit | | | Operating Income | | | Net Income | | | Operating

Cash Flow |

| $921.0 million | | | $561.9 million | | | $101.1 million | | | $146.4 million | | | $209.2 million |

| up 24% from the same period 2023 | | | up 21% from the same period 2023 | | | up 114% from the same period 2023 | | | up 201% from the same period 2023 | | | up 35% from the same period 2023 |

| | | | | | | | | | | | |

|

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Recent Accounting Guidance

In May 2014,We ended the Financial Accounting Standards Board ("FASB") issued authoritative guidance for Revenue from Contracts with Customers, to supersede nearly all existing revenue recognition guidance under U.S. GAAP. The core principle of the guidance is to recognize revenues when promised goods or services are transferred to customers in an amount that reflects the consideration that is expected to be received for those goods or services. The guidance defines a five step process to achieve this core principle and it is possible when the five step process is applied, more judgment and estimates may be required within the revenue recognition process than required under existing U.S. GAAP, including identifying performance obligations in the contract, estimating the amount of variable consideration to include in the transaction price and allocating the transaction price to each separate performance obligation. The updated standard permits the use of either the retrospective or modified retrospective transition method and is effective for us in our first quarter of 2018. 2024 with cash, cash equivalents and short-term marketable securities totaling $2.90 billion.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2024 Compared to Three Months Ended March 31, 2023 |

| Three Months Ended March 31, | | 2024 - 2023 |

| (In millions, except per share amounts) | 2024 | | % of Revenue (1) | | 2023 | | % of Revenue (1) | | $ Change | | % Change |

| Revenue | $ | 921.0 | | | 100 | % | | $ | 741.5 | | | 100 | % | | $ | 179.5 | | | 24 | % |

| Cost of sales | 359.1 | | | 39 | % | | 278.9 | | | 38 | % | | 80.2 | | | 29 | % |

| Gross profit | 561.9 | | | 61.0 | % | | 462.6 | | | 62.4 | % | | 99.3 | | | 21 | % |

| Operating expenses: | | | | | | | | | | | |

| Research and development | 141.5 | | | 15 | % | | 119.0 | | | 16 | % | | 22.5 | | | 19 | % |

| | | | | | | | | | | |

| Selling, general and administrative | 319.3 | | | 35 | % | | 296.4 | | | 40 | % | | 22.9 | | | 8 | % |

| Total operating expenses | 460.8 | | | 50 | % | | 415.4 | | | 56 | % | | 45.4 | | | 11 | % |

| Operating income | 101.1 | | | 11 | % | | 47.2 | | | 6 | % | | 53.9 | | | 114 | % |

| Other income (expense), net | 31.4 | | | 3 | % | | 17.3 | | | 2 | % | | 14.1 | | | 82 | % |

| Income before income taxes | 132.5 | | | 14 | % | | 64.5 | | | 9 | % | | 68.0 | | | ** |

| Income tax expense (benefit) | (13.9) | | | (2) | % | | 15.9 | | | 2 | % | | (29.8) | | | ** |

| Net income | $ | 146.4 | | | 16 | % | | $ | 48.6 | | | 7 | % | | $ | 97.8 | | | 201 | % |

| | | | | | | | | | | |

| Basic net income per share | $ | 0.38 | | | ** | | $ | 0.13 | | | ** | | $ | 0.25 | | | ** |

| Diluted net income per share | $ | 0.36 | | | ** | | $ | 0.12 | | | ** | | $ | 0.24 | | | ** |

| | | | | | | | | | | |

(1) The sum of the individual percentages may not equal the total due to rounding. |

| ** Not meaningful |

Revenue

We currentlygenerate our revenue from the sale of disposable sensors and our reusable transmitter and receiver, collectively referred to as Reusable Hardware. We expect to usethat the modified retrospective method to adopt this standard. We are currently inrevenue we generate from the process of completing the initial assessment of the impact that this new revenue recognition standard will have on our consolidated financial statements. As part of the initial assessment, we are reviewing a representative sample of contracts across our various streams of revenue and geographies to identify potential differences that could result from applying the requirements of the new standard. The analysis includes identifying whether there may be differences in timing of revenue recognition under the new standard as well as assessing performance obligations, variable consideration and contract costs. We have not yet estimated the impact, if any, of the new standard on the timing and patternsales of our revenue recognition.products will fluctuate from quarter to quarter. We will continue to evaluate the future impact and method of adoption of ASU 2014 -09 and related amendments on the Consolidated Financial Statements and related disclosures throughout 2017.

In July 2015, the FASB issued guidance to change the subsequent measurement of inventory fromtypically experience seasonality, with lower of cost or market to lower of cost and net realizable value. The guidance requires that inventory accounted for under the first-in, first-out (FIFO) or average cost methods be measured at the lower of cost and net realizable value, where net realizable value represents the estimated selling price of inventory in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. The guidance was effective for ussales in the first quarter of fiscal 2017 with no material impact on our consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842) (“ASU 2016-02”), which require a lessee to recognize a lease payment liability and a corresponding right of use asset on their balance sheet for all lease terms longer than 12 months, lessor accounting remains largely unchanged. ASU 2016-02 is effective for fiscal years, and interim periods within those years, beginning on or after December 15, 2018 and early adoption is permitted. We are currently evaluating the effect this guidance will have on our consolidated financial statements.

In March 2016, the FASB issued ASU 2016-09, Compensation - Stock Compensation (Topic 718) (“ASU 2016-09”), which is intended to simplify several areas of accounting for share-based payment arrangements. The amendments in this update cover such areas as the recognition of excess tax benefits and deficiencies, the classification of those excess benefits on the statement of cash flows, an accounting policy election for forfeitures, the amount an employer can withhold to cover income taxes and still qualify for equity classification and the classification of those taxes paid on the statement of cash flows. ASU 2016-09 is effective for fiscal years beginning after December 15, 2016, and interim periods within those annual periods. We will prospectively adopt this standard beginning in the first quarter of 2017. We have excess tax benefits for which a benefit could not be previously recognized of approximately $161.0 million. Upon adoption the balance of the unrecognized excess tax benefits will be reversed with the impact recorded to (accumulated deficit) retained earnings, including any changeeach year compared to the valuation allowanceimmediately preceding fourth quarter. This seasonal sales pattern relates to U.S. annual insurance deductible resets and unfunded flexible spending accounts.

Cost of sales

Cost of sales includes direct labor and materials costs related to each product sold or produced, including assembly, test labor and scrap, as a resultwell as factory overhead supporting our manufacturing operations. Factory overhead includes facilities, material procurement and control, manufacturing engineering, quality assurance, supervision and management. These costs are primarily salary, fringe benefits, share-based compensation, facility expense, supplies and purchased services. All of the adoption. Due to the full valuation allowance on the U.S. deferred tax assets asour manufacturing costs are included in cost of December 31, 2016, we do not expect any impact to the financial statements as a result of this adoption in the first quarter of 2017.

We have excess tax benefits for which a benefit could not be previously recognized of approximately $161.0 million. Upon adoption, we recognized the previously unrecognized excess tax benefits of $161.0 million deferred tax assets with an offsetting increase in our valuation allowance using a modified retrospective method through a cumulative effect adjustment to the accumulated deficit, with no net impact on our financial statements. All excess tax benefits and all tax deficiencies generated in the current and future periods will be recognized prospectively and recorded as income tax benefit or expense in our Consolidated Statements of Operations in the reporting period in which they occur. Until such time that we release our valuation allowance against deferred tax assets, the tax impact of any excess tax benefits and deficiencies will be offset with the change in our valuation allowance.sales. In addition, we electedamortization of certain licensing related intangibles are also included in cost of sales.

Research and development

Our research and development expenses primarily consist of engineering and research expenses related to accountour sensing technology, clinical trials, regulatory expenses, quality assurance programs, employee compensation, and business process outsourcers.

Amortization of intangible assets

Our amortization expense primarily relates to acquired technology and intellectual property and other acquired intangible assets.

Selling, general and administrative

Our selling, general and administrative expenses primarily consist of employee compensation for forfeitures as they occur with the change applied on a modified retrospective basis with a cumulative effect adjustment to accumulated deficitour executive, financial, sales, marketing, information technology and administrative functions. Other significant expenses include commissions, marketing and advertising, IT software license costs, insurance, professional fees for our outside legal counsel and independent auditors, litigation expenses, patent application expenses and consulting expenses.

Income from equity investments

Income from equity investments is comprised of $0.6 million. Due to the full valuation allowance on the U.S. deferred tax assets, we have determined that none of the provisions of ASU 2016-09 will have a significant impact our 2017 consolidated financial statements.

In October 2016, the FASB issued ASU 2016-16, Accounting for Income Taxes - Intra-Entity Asset Transfer other than Inventory (Topic 740) ("ASU 2016-16), which would require the recognition of the tax expenserealized gains from the sale of an asset other than inventory when the transfer occurs, rather than when the asset is sold to a third party or otherwise recovered through use. The new guidance is effective for public business entities for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. Early adoption is permitted. The amendment should be applied on a modified retrospective basis through a cumulative-effect adjustment directly to retained earnings asequity investment.

Other income (expense), net

Other income (expense), net consists primarily of the beginning period of adoption. We are considering the impact the adoption of ASU 2016-16 may haveinterest and dividend income on our consolidated financial statements.

| |

ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

Interest Rate Risk

The primary objective of our investment activities is to preserve our capital for the purpose of funding operations while at the same time maximizing the income we receive from our investments without significantly increasing risk. To achieve these objectives, our investment policy allows us to maintain a portfolio ofcash, cash equivalents and short-term marketable securities portfolio, foreign currency transaction gains and losses due to the effects of foreign currency fluctuations, and interest expense related to our senior convertible notes.

| | | | | | | | | | | | | | |

| Three Months Ended March 31, 2024 Compared to Three Months Ended March 31, 2023 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended March 31, | | 2024 - 2023 |

| | 2024 | | 2023 | | Change in Revenues |

| (In millions) | | Revenue | | % of Total | | Revenue | | % of Total | | $ | | % |

| United States | | $ | 653.2 | | | 71% | | $ | 526.0 | | | 71% | | $ | 127.2 | | | 24% |

| International | | 267.8 | | | 29% | | 215.5 | | | 29% | | 52.3 | | | 24% |

| Total Revenue | | $ | 921.0 | | | 100% | | $ | 741.5 | | | 100% | | $ | 179.5 | | | 24% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

| | Three Months Ended March 31, 2024 Compared to Three Months Ended March 31, 2023 |

| | | | | | | | | | | | |

| Revenue | | The revenue increase was primarily driven by increased sales volume of our disposable sensors due to the continued growth of our worldwide customer base. We added approximately 600,000 users to our worldwide customer base in 2023.

Disposable sensor and other revenue comprised approximately 93% of total revenue and Reusable Hardware revenue comprised approximately 7% of total revenue for the three months ended March 31, 2024. Disposable sensor and other revenue comprised approximately 88% of total revenue and Reusable Hardware revenue comprised approximately 12% of total revenue for the three months ended March 31, 2023. |

| | |

| | |

| Cost of sales & Gross profit | | Cost of sales and gross profit increased primarily due to an increase in sales volume driven by the addition of approximately 600,000 users to our worldwide customer base in 2023.

The decrease in gross profit margin percentage in the first quarter of 2024 compared to the first quarter of 2023 was primarily driven by product and channel mix changes. |

| | | | | | | | |

|

| | Three Months Ended March 31, 2024 Compared to Three Months Ended March 31, 2023 |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Research and development expense | | Research and development expense increased primarily due to $6.8 million in compensation-related costs most notably due to higher headcount, $5.0 million in supplies and other support costs, and $3.2 million in clinical trials costs.

We continue to believe that focused investments in research and development are critical to our future growth and competitive position in the marketplace, and to the development of new and updated products and services that are central to our core business strategy. |

| | |

| | |

| | |

| | |

| | |

| Selling, general and administrative expense | | Selling, general and administrative expense increased primarily due to $16.0 million in compensation-related costs most notably due to higher headcount, $5.9 million of travel related expenses, and $2.5 million related to the divestiture of certain non-CGM assets, partially offset by $9.6 million in lower advertising and marketing costs. |

| | |

| | |

| | |

| | |

| | |

| Other income (expense), net | | Other income (expense), net, increased primarily due to $14.0 million in interest and dividend income on our cash, cash equivalents, and marketable securities portfolio. The increase in interest income was related to a change in market interest rates, as well as an increase in the average invested balances compared to the same period in 2023. |

| | |

| | |

| Income tax expense (benefit) | | The income tax benefit recorded for the three months ended March 31, 2024 was primarily attributable to income tax expense from normal, recurring operationsat an estimated annual effective tax rate of 23.8%, offset by discrete excess tax benefits recognized for share-based compensation for employees, net of disallowed executive compensation and the Verily milestone payment. The income tax expense recorded for the three months ended March 31, 2023 was primarily attributable to income tax expense from normal, recurring operations, partially offset by discrete excess tax benefits recognized for share-based compensation for employees, net of disallowed executive compensation. The decrease in our effective tax rate for the three months ended March 31, 2024 compared to the same period in 2023 is primarily attributable to impacts of the prior year tax restructuring and the Verily milestone payment. |

| | |

| Liquidity and Capital Resources |

| | |

| Overview, Capital Resources, and Capital Requirements |

Our principal sources of liquidity are our existing cash, cash equivalents and marketable securities, cash generated from operations, proceeds from our senior convertible notes issuances, and access to our Credit Facility. Our primary uses of cash have been for research and development programs, selling and marketing activities, capital expenditures, acquisitions of businesses, and debt service costs.

We expect that cash provided by our operations may fluctuate in future periods as a varietyresult of securities,a number of factors, including fluctuations in our operating results, working capital requirements and capital deployment decisions. We have historically invested our cash primarily in U.S. dollar-denominated, investment grade, highly liquid obligations of U.S. government agencies, commercial paper, corporate debt, and money market funds, U.S. Treasuryfunds. Certain of these investments are subject to general credit, liquidity and other market risks. The general condition of the financial markets and the economy may increase those risks and may affect the value and liquidity of investments and restrict our ability to access the capital markets.

Our future capital requirements will depend on many factors, including but not limited to:

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| The evolution of the international expansion of our business and the revenue generated by sales of our approved products and any future products; | | | Our ability to efficiently scale our operations to meet demand for our current and any future products; | | | The success of our research and development efforts; | |

| | | | | | | |

| | | | | | | |

| The expenses we incur in manufacturing, developing, selling and marketing our products; | | | The costs, timing and risks of delays of additional regulatory approvals; | | | The costs of filing, prosecuting, defending and enforcing any patent claims and other intellectual property rights; | |

| | | | | | | |

| | | | | | | |

| The quality levels of our products and services; | | | The emergence of competing or complementary technological developments; | | | The terms and timing of any collaborative, licensing and other arrangements that we may establish; and | |

| | | | | | | |

| | | | | | | |

| The third-party reimbursement of our products for our customers; | | | The rate of progress and cost of our clinical trials and other development activities; | | | The acquisition of businesses, products and technologies and our ability to integrate and manage any acquired businesses, products and technologies. | |

We expect that existing cash and short-term investments and cash flows from our future operations will generally be sufficient to fund our ongoing core business. As current borrowing sources become due, we may be required to access the capital markets for additional funding. As we assess inorganic growth strategies, we may need to supplement our internally generated cash flow with outside sources. In the event that we are required to access the debt and corporate debt securities. Due to the short-term nature of our investments,market, we believe that we have no material exposurewill be able to interest rate risk.secure reasonable borrowing rates. As part of our liquidity strategy, we will continue to monitor our current level of earnings and cash flow generation as well as our ability to access the market in light of those earning levels.

Foreign Currency Risk

A substantial portion of our operations are located in the United States, and the majority of our sales since inception have been made in United StatesU.S. dollars. Accordingly, we have assessed that we do not have any material net exposure to foreign currency exchange rate fluctuations at this time. However, as our business in markets outside of the United States continues to increase, weWe will be exposed to additional foreign currency exchange risk related to our foreign operations. Fluctuationsinternational operations as we expand our manufacturing internationally and as our business continues to increase in international markets. See “Foreign Currency Exchange Risk” in Part II, Item 7A of our Annual Report on Form 10-K for the fiscal year endedDecember 31, 2023, for more information.

Main Sources of Liquidity

Cash, cash equivalents and short-term marketable securities

Our cash, cash equivalents and short-term marketable securities totaled $2.90 billion as of March 31, 2024. None of those funds were restricted and $2.67 billion (approximately 92%) of those funds were located in the rateUnited States.

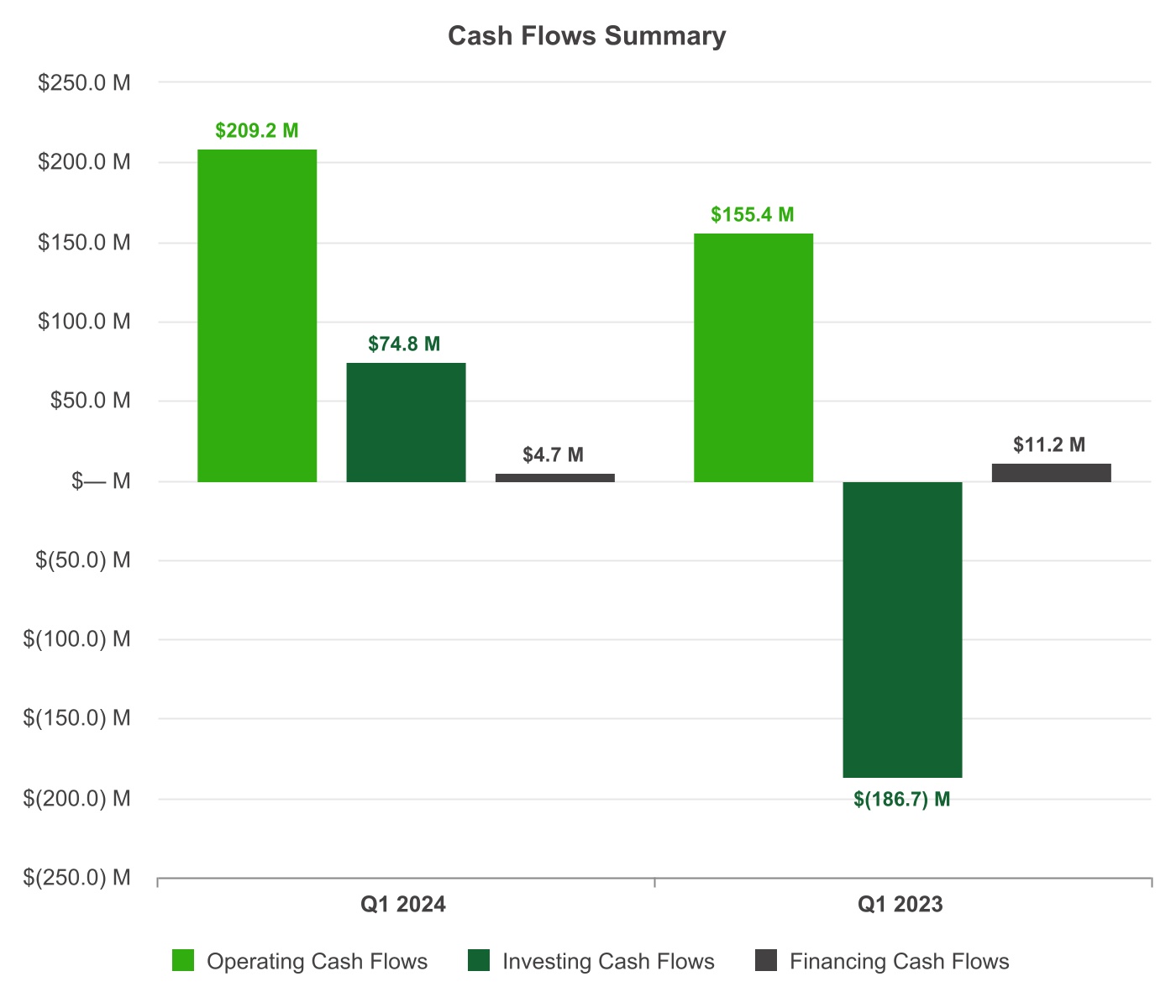

Cash flow from Operations

For the three months ended March 31, 2024, we had positive cash flows of exchange between the United States dollar and foreign currencies, primarily the British Pound, the Euro and the Swiss Franc, could adversely affect our financial results, including our revenues, revenue growth rates, gross margins, income and losses as well as assets and liabilities.

$209.2 million from operating activities. We do not currently engage in hedging or similar transactions to reduce our foreign currency risks. Weanticipate that we will continue to generate positive cash flows from operations for the foreseeable future.

Senior Convertible Notes

We received net proceeds of $1.19 billion in May 2020 from the 2025 Notes offering, and net proceeds of $1.23 billion in May 2023 from the 2028 Notes offering. We used $282.6 million of the net proceeds from the offering of the 2025 Notes to repurchase a portion of our senior convertible notes due in 2022. We used $289.9 million of the net proceeds from the offering of the 2028 Notes to purchase capped call transactions and repurchase shares of our common stock in May 2023. We intend to use the remainder of the net proceeds from the 2025 Notes offering and 2028 Notes offering for general corporate purposes and capital expenditures, including working capital needs. We may also use the net proceeds to expand our current business through in-licensing or acquisitions of, or investments in, other businesses, products or technologies; however, we do not have any significant commitments with respect to any such acquisitions or investments at this time.

In connection with the 2028 Notes offering, we purchased the 2028 Capped Calls. See Note 5 “Debt” to the consolidated financial statements in Part I, Item 1 of this Quarterly Report on Form 10-Q for more information about our senior convertible notes and the 2028 Capped Calls.

Revolving Credit Agreement

As of March 31, 2024, we had no outstanding borrowings, $7.6 million in outstanding letters of credit, and a total available balance of $192.4 million under the Amended Credit Agreement. We monitor counterparty risk associated with the institutional lenders that are providing the Credit Facility. We currently believe that the Credit Facility will be available to us should we choose to borrow under it. Revolving loans will be available for general corporate purposes, including working capital and evaluatecapital expenditures. See Note 5 “Debt” to the consolidated financial statements in Part I, Item 1 of this Quarterly Report on Form 10-Q for more information on the Revolving Credit Agreement.

Short-term Liquidity Requirements

Our short-term liquidity requirements primarily consist of regular operating costs, interest payments related to our internal processes relatingsenior convertible notes, capital expenditures for the development of our manufacturing facilities and office spaces, and short-term material cash requirements as described below. As of March 31, 2024, we had a working capital ratio of 2.90 and a quick ratio of 2.43, which indicates that our current assets are more than enough to foreign currencycover our short-term liabilities. We expect to have significant capital expenditures for the next year to scale-up capacity in Mesa, Arizona and drive our strategic initiatives of building out our manufacturing facilities and/or equipment in Malaysia and Ireland.

We believe that our cash, cash equivalents, and marketable securities balances, projected cash contributions from our commercial operations, and borrowings under our Credit Facility will be sufficient to meet our anticipated seasonal working capital needs, all capital expenditure requirements, material cash requirements as described below, and other liquidity requirements associated with our operations for at least the next 12 months. We may use cash to repurchase Dexcom shares or for other strategic initiatives that strengthen our foundation for long-term growth.

Long-term Liquidity Requirements