Washington, D.C. 20549

ALIGN TECHNOLOGY, INC.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging“emerging growth company"company” in Rule 12b-2 of the Exchange Act. (Check one):

ALIGN TECHNOLOGY, INC.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

ALIGN TECHNOLOGY, INC.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

ALIGN TECHNOLOGY, INC.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

ALIGN TECHNOLOGY, INC.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

ALIGN TECHNOLOGY, INC.

Note 1. Summary of Significant Accounting Policies

The accompanying unaudited Condensed Consolidated Financial Statements have been prepared by Align Technology, Inc. (“we”, “our”, "Company", or “Align”) on a consistent basis with the audited Consolidated Financial Statements for the year ended December 31, 2022, and contains all adjustments, including normal recurring adjustments, necessary to fairly state the information set forth herein. The unaudited Condensed Consolidated Financial Statements have been prepared in accordance with the rules and regulations of the Securities and Exchange Commission ("SEC"(“SEC”), and, contain all adjustments, including normal recurring adjustments,therefore, omit certain information and footnote disclosures necessary to state fairly our results of operations forpresent the three and nine months ended September 30, 2017 and 2016, our comprehensive income for the three and nine months ended September 30, 2017 and 2016, our financial position as of September 30, 2017 and our cash flows for the nine months ended September 30, 2017 and 2016. Theunaudited Condensed Consolidated Balance Sheet as of December 31, 2016 was derived from the December 31, 2016 audited financial statements but does not include all disclosures required byFinancial Statements in accordance with accounting principles generally accepted in the United States of America.America (“U.S.”).

The preparation of financial statements in conformity with generally accepted accounting principles ("GAAP"(“GAAP”) in the United States of America (“U.S.”) requires our management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ materially from those estimates. On an ongoing basis, we evaluate our estimates, including those related to the fair values of financial instruments, long-lived assets and goodwill, equity method investments,revenue recognition, useful lives of intangible assets and property and equipment, revenue recognition,long-lived assets and goodwill, income taxes, contingent liabilities, the fair values of financial instruments, stock-based compensation equity lossesand the valuation of investee, income taxes and contingent liabilities,investments in privately held companies among others. We base our estimates on historical experience and on various other assumptions that are believed to be reasonable, the results of which form the basis for making judgments about the carrying values of assets and liabilities.

The securities that we invest in are generally deemed to be low risk based on their credit ratings from the major rating agencies. The longer the duration of these securities, the more susceptible they are to changes in market interest rates and bond yields. As interest rates increase, those securities purchased at a lower yield show a mark-to-market unrealized loss. TheOur unrealized losses as of March 31, 2023 and December 31, 2022 are primarily due primarily to changes in interest rates and credit spreads and interest rates. We expect to realizespreads.

In the normal course of business to facilitate transactions in our services and products, we indemnify certain parties: customers, vendors, lessors, and other parties with respect to certain matters, including, but not limited to, services to be provided by us and intellectual property infringement claims made by third parties. In addition, we have entered into indemnification agreements with our directors and our executive officers that will require us, among other things, to indemnify them against certain liabilities that may arise by reason of their status or service as directors or officers. Several of these agreements limit the time within which an indemnification claim can be made and the amount of the claim.

It is not possible to make a reasonable estimate of the maximum potential amount under these indemnification agreements due to the unique facts and circumstances involved in each particular agreement. Additionally, we have a limited history of prior indemnification claims and the payments we have made under such agreements have not had a material adverse effect on our results of operations, cash flows or financial position. However, to the extent that valid indemnification claims arise in the future, future payments by us could be significant and could have a material adverse effect on our results of operations or cash flows in a particular period. As of September 30, 2017,March 31, 2023, we did not have any material indemnification claims that were probable or reasonably possible.

The fair value of the option component of the 2010 Purchase Plan shares was estimated at the grant date using the Black-Scholes option pricing model with the following weighted average assumptions:

We exercise significant judgment in regards to estimates of future market growth, forecasted earnings and projected taxable income in determining the provision for income taxes and for purposes of assessing our ability to utilize any future benefit from deferred tax assets. We continue to assess the realizability of the deferred tax assets as we take into account new information.

The following discussion and analysis of our financial condition and results of operations should be read together with our condensed consolidated financial statements and related notes included elsewhere in this Quarterly Report on Form 10-Q and with our audited consolidated financial statements included in our Annual Report on formForm 10-K for the year ended December 31, 2016,2022 as filed with the Securities and Exchange Commission.Commission (the “SEC”).

Stock Repurchases: April 2016 Repurchase Program. On April 28, 2016, we announced that our Board of Directors had authorized a plan to repurchase up to $300.0 million of our stock. On May 2, 2017, we entered into an accelerated share repurchase ("ASR") to repurchase $50.0 million of our common stock ("2017 ASR"). The 2017 ASR was completed on August 3, 2017. The final number of shares repurchased wasbudgets based on our volume-weighted average stock price duringexisting and new products. Our efforts to succeed with these innovative treatment options may result in larger and unpredictable variations in geographic and product mix and selling prices, causing uncertainty, including variations in products sold, changes in the termamount and timing of deferred revenues and other potential impacts on our financial statements and business operations.

We strive to manage the challenges from the macroeconomic conditions, the conflict in Ukraine, COVID-19 and the evolution of our target markets by focusing on improving our operations, building flexibility and efficiencies in our processes, adjusting our business models to changing circumstances and offering products that meet market demand. Specifically, we are managing cost impacts through pricing actions, cost saving measures that drive value and maintaining control of our employee headcount. We also continue to innovate, introducing new and enhanced products that augment our doctor customer and patient experiences.

Further discussion of the transaction, less an agreed upon discount. We received a totalimpact of approximately 0.4 million shares at a weighted average share pricethese challenges on our business may be found in Part II, Item 1A of $146.48this Quarterly Report on Form 10-Q under the 2017 ASR. All repurchased shares were retired. heading “Risk Factors.”

Key Financial and Operating Metrics

We measure our performance against these strategic priorities by the achievement of key financial and operating metrics.

For the three months ended March 31, 2023, our business operations reflect the following:

•Revenues of $943.1 million, a decrease of 3.1% year-over-year;

•Clear Aligner revenues of $789.8 million, a decrease of 2.5% year-over-year;

◦Americas Clear Aligner revenues of $361.3 million, a decrease of 4.0% year-over-year;

◦International Clear Aligner revenues of $354.2 million, a decrease of 4.5% year-over-year;

◦Clear Aligner case volume decrease of 3.9% year-over-year and Clear Aligner case volume increase for teenage patients of 3.8% year-over-year;

•Imaging Systems and CAD/CAM Services revenues of $153.3 million, a decrease of 6.2% year-over-year;

•Income from operations of $133.5 million and operating margin of 14.2%;

•Effective tax rate of 34.8%;

•Net income of $87.8 million with diluted net income per share of $1.14;

•Cash, cash equivalents and marketable securities of $921.4 million as of March 31, 2023;

•Operating cash flow of $199.9 million;

•Capital expenditures of $64.1 million, predominantly related to increases in our manufacturing capacity and facilities; and

•Number of employees was 23,035 as of March 31, 2023, a decrease of 2.5% year-over-year.

Other Statistical Data and Trends

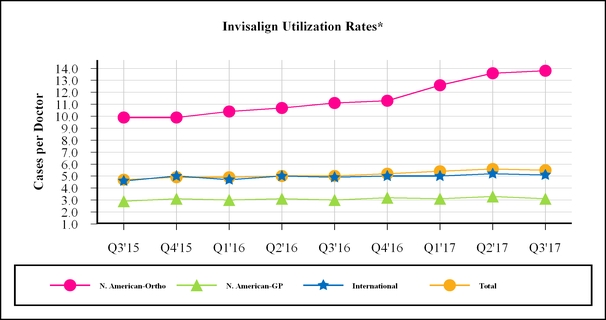

•As of September 30, 2017, weMarch 31, 2023, approximately 15.1 million people worldwide have $250.0 million remaining underbeen treated with our Invisalign system. Management measures these results by comparing to the April 2016 Repurchase Plan.millions of people who can benefit from straighter teeth and uses this data to target opportunities to expand the market for orthodontics by educating consumers about the benefits of straighter teeth using the Invisalign system.

•For the first quarter of 2023, total Invisalign cases submitted with a digital scanner in the Americas increased to 93.1%, up from 90.6% in the first quarter of 2022 and international scans increased to 87.0%, up from 82.8% in the first quarter of 2022. For the first quarter of 2023, 97.7% of Invisalign cases submitted by North American orthodontists were submitted digitally.

•The total utilization rate in the first quarter of 2023 decreased to 7.0 cases per doctor compared to 7.3 cases per doctor in the first quarter of 2022. Utilization rates in North America and our International locations were as follows:

▪North America: Theutilization rate among our North American orthodontist customers decreased to 26.2 cases per doctor in the first quarter of 2023 compared to 26.8 cases per doctor in the first quarter of 2022 and the utilization rate among our North American GP customers decreased to 4.9 cases per doctor in the first quarter of 2023 compared to 5.0 cases per doctor in the first quarter of 2022.

▪International: International doctor utilization rate was 6.2 cases per doctor in the first quarter of 2023 compared to 6.4 cases per doctor in the first quarter of 2022.

SmileDirectClub. On July 24, 2017, we increased* Invisalign utilization rates are calculated by the revolving linenumber of creditcases shipped divided by the number of doctors to SmileDirectClub, LLC ("SDC"whom cases were shipped. Our International region includes Europe, Middle East and Africa (“EMEA”) and Asia Pacific (“APAC”). Latin America (“LATAM”) is excluded from $15.0 millionthe International region based on its immateriality to $30.0 million. As of September 30, 2017, $17.0 million under the Loan Facility was outstanding. On July 24, 2017, we purchased an additional 2% equity interestquarter; however is included in SDC for $12.8 million. As a result of this purchase, we hold a 19% equity interest in SDC on a fully diluted basis (Refer to Note 4 "Equity Method Investments" of the Notes to Condensed Consolidated Financial Statements for details on accounting treatment). Additionally, we expect the supply agreement to be incremental to revenue growth in 2017.

Total utilization.

New Corporate Headquarters Office Purchase. We completed the purchase of our new headquarters on January 26, 2017 for the purchase price of $44.1 million. In addition, we incurred $29.7 million in building improvements during 2017 and moved into the facility in August 2017.

Results of Operations

Net revenuesRevenues by Reportable Segment

We group our operations into two reportable segments: Clear Aligner segment and ScannerSystems and Services segment.

•Our Clear Aligner segment consists of Comprehensive Products, Non-Comprehensive Products and Non-Case revenues as defined below:

| |

◦ | Comprehensive Products include our Invisalign Full, Teen and Assist products. |

| |

◦ | Non-Comprehensive Products include our Express/Lite products in addition to revenues from the sale of aligners to SmileDirectClub (“SDC”) under our supply agreement, which commenced in the fourth quarter of 2016. Revenue from SDC is recorded after eliminating outstanding intercompany transactions. |

| |

◦ | Non-Case includes our Vivera retainers along with our training and ancillary products for treating malocclusion. |

▪Comprehensive Products include, but are not limited to, Invisalign Comprehensive and Invisalign First.

▪Non-Comprehensive Products include, but are not limited to, Invisalign Moderate, Lite and Express packages and Invisalign Go and Invisalign Go Plus.

▪Non-Case products include, but are not limited to, retention products, Invisalign training, adjusting tools used by dental professionals during the course of treatment and Invisalign Accessory Products that are complementary to our doctor-prescribed principal products such as aligner cases (clamshells), teeth whitening products, cleaning solutions (crystals, foam and other material) and other oral health products available in certain commerce channels in select markets. We also offer in the U.S. and Canada, a Doctor Subscription Program which is a monthly subscription program based on the doctor’s monthly need for retention or limited treatment. The program allows doctors the flexibility to order both “touch-up” or retention aligners within their subscribed tier and is designed for a segment of experienced Invisalign trained doctors who are currently not regularly using our retainers or low-stage aligners.

•Our ScannerSystems and Services segment consists of our iTero intraoral scanning systems, which includes a single hardware platform and additionalrestorative or orthodontic software options. Our services available with the intraoral scannersinclude subscription software, disposables, rentals, leases, pay per scan services, as well as exocad’s CAD/CAM software solutions that provide digital alternativesintegrate workflows to the traditional cast models. This segment includes our iTero scannerdental labs and OrthoCAD services.dental practices.

Net revenues for our Clear Aligner and Scanner segmentSystems and Services segments by region for the three and nine months ended September 30, 2017March 31, 2023 and 2016 is2022 are as follows (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | | | | | |

| Net Revenues | | 2023 | | 2022 | | Change | | | | | | |

| Clear Aligner net revenues: | | | | | | | | | | | | | | | | |

| Americas | | $ | 361.3 | | | $ | 376.2 | | | $ | (15.0) | | | (4.0) | % | | | | | | | | |

| International | | 354.2 | | | 371.1 | | | (16.9) | | | (4.5) | % | | | | | | | | |

| Non-case | | 74.3 | | | 62.4 | | | 12.0 | | | 19.2 | % | | | | | | | | |

| Total Clear Aligner net revenues | | $ | 789.8 | | | $ | 809.7 | | | $ | (19.9) | | | (2.5) | % | | | | | | | | |

| Systems and Services net revenues | | 153.3 | | | 163.5 | | | (10.2) | | | (6.2) | % | | | | | | | | |

| Total net revenues | | $ | 943.1 | | | $ | 973.2 | | | $ | (30.1) | | | (3.1) | % | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| Net Revenues | 2017 | | 2016 | | Net Change | | % Change | | 2017 | | 2016 | | Net Change | | % Change |

| Clear Aligner revenues: | | | | | | | | | | | | | | | |

| North America | $ | 193.8 |

| | $ | 143.8 |

| | $ | 50.0 |

| | 34.8 | % | | $ | 545.1 |

| | $ | 423.4 |

| | $ | 121.7 |

| | 28.7 | % |

| International | 126.6 |

| | 84.3 |

| | 42.3 |

| | 50.2 | % | | 340.2 |

| | 237.9 |

| | 102.3 |

| | 43.0 | % |

| Non-case | 21.2 |

| | 15.6 |

| | 5.6 |

| | 35.9 | % | | 59.7 |

| | 45.5 |

| | 14.2 |

| | 31.2 | % |

| Total Clear Aligner net revenues | $ | 341.6 |

| | $ | 243.7 |

| | $ | 97.9 |

| | 40.2 | % | | $ | 945.0 |

| | $ | 706.8 |

| | $ | 238.2 |

| | 33.7 | % |

| Scanner net revenues | 43.7 |

| | 34.9 |

| | 8.8 |

| | 25.2 | % | | 107.0 |

| | 79.9 |

| | 27.1 |

| | 33.9 | % |

| Total net revenues | $ | 385.3 |

| | $ | 278.6 |

| | $ | 106.7 |

| | 38.3 | % | | $ | 1,052.1 |

| | $ | 786.7 |

| | $ | 265.4 |

| | 33.7 | % |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Clear Aligner Case Volume by Region

Case volume data which represents Clear Aligner case shipments by region for the three and nine months ended September 30, 2017March 31, 2023 and 20162022 is as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | | | | | | | |

| | 2023 | | 2022 | | Change | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Total case volume | | 575.3 | | | 598.8 | | | (23.6) | | | (3.9) | % | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| Region | 2017 | | 2016 | | Net Change | | % Change | | 2017 | | 2016 | | Net Change | | % Change |

| North America | 164.2 |

| | 115.9 |

| | 48.3 |

| | 41.7 | % | | 455.0 |

| | 341.3 |

| | 113.7 |

| | 33.3 | % |

| International | 91.2 |

| | 61.9 |

| | 29.3 |

| | 47.3 | % | | 251.8 |

| | 177.2 |

| | 74.6 |

| | 42.1 | % |

| Total case volume | 255.4 |

| | 177.8 |

| | 77.6 |

| | 43.6 | % | | 706.7 |

| | 518.5 |

| | 188.2 |

| | 36.3 | % |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

For the three and nine months ended September 30, 2017, total net revenues increased by $106.7 million and $265.4 million as compared to the same periods in 2016 primarily as a result of case volume growth across all regions and most products as well as increased non-case revenues.

Clear Aligner - North America

For the three months ended September 30, 2017, North AmericaMarch 31, 2023, total net revenues increased by $50.0decreased $30.1 million as compared to the same period in 20162022, primarily due to a decrease in both Clear Aligner case volume growth across all channelsvolumes and most products which increased netscanner volumes and unfavorable foreign exchange rates, partially offset by increases in service revenues by $59.8 million. This increase was offset in part by lower average selling prices (“ASP”) which decreased net revenues by $9.8 million. The ASP decline is a result of a shift in product mix towards Non-Comprehensive Products, primarily driven by increased SDC revenues which carry a lower ASP and higher promotional discounts, which collectively reduced revenues by $19.6 million. These factors contributing to the decline in ASP were offset in part by an increase in additional aligner revenue, which contributed $6.7 million to net revenues, as well as price increases on our Comprehensive Products effective April 1, 2017, which contributed $4.5 million to netClear Aligner non-case revenues.

Clear Aligner - Americas

For the ninethree months ended September 30, 2017, North AmericaMarch 31, 2023, Americas net revenues increaseddecreased by $121.7$15.0 million as compared to the same period in 2016 primarily2022 due to a 5.3% decrease in case volume growth across all channels and productsvolumes, which reduced net revenues by $20.0 million, partially offset by an increase in ASP which increased net revenues by $141.0$5.0 million. This increaseHigher ASP was mainly due to price increases on most products which increased revenues by $19.3 million along with higher additional aligners which increased net revenues by $5.0 million. The increases in ASP were partially offset in part by lower ASPunfavorable promotional discounts which decreased net revenues by $19.3 million. The ASP decline is$15.8 million and a result

of a shift in product mix towards Non-Comprehensive Products, primarily driven by increased SDC revenuesshift to lower priced products which carry a lower ASP and higher Invisalign promotional discounts, which collectively reduceddecreased net revenues by $34.1$2.6 million. These factors contributing to the decline in ASP were offset in part by an increase in additional aligner revenue, which contributed $10.0 million to net revenues, as well as price increases on our Comprehensive Products effective on April 1 of 2016 and 2017, which contributed $6.9 million to net revenues.

Clear Aligner - International

For the three months ended September 30, 2017,March 31, 2023, International net revenues increaseddecreased by $42.3$16.9 million as compared to the same period in 2016 primarily driven2022, due to a 2.3% decrease in case volumes, which decreased net revenues by case volume growth across all channels$8.4 million, and lower ASP which decreased net revenues by $8.5 million. Lower ASP was largely due to a product mix shift to lower priced products which decreased net revenues by $33.1 million, unfavorable foreign exchange rates which resulted in lower net revenues of $26.4 million, and unfavorable promotional discounts which decreased net revenues $6.0 million. The decrease in ASP was partially offset by higher additional aligners which increased net revenues by $30.9 million and price increases on most products which increased net revenues by $40.0$24.4 million. This increase resulted in higher ASP which increased net revenues by $2.3 million. The increase in ASP is primarily a result of price increases in our Comprehensive Products effective July 1, 2017, a favorable impact of foreign exchange rates and the impact from acquiring a distributor as we now recognize direct sales at full ASP rather than the discounted ASP, all of which collectively contributed $6.6 million to net revenues. These factors contributing to the increase in ASP were offset in part by $4.9 million related to higher promotional discounts and increased net deferrals.

Clear Aligner - Non-Case

For the ninethree months ended September 30, 2017, InternationalMarch 31, 2023, non-case net revenues increased by $102.3$12.0 million as compared to the same period in 20162022 mainly due to increased volumes from the Doctor Subscription program and retention products across all regions primarily driven by case volume growth across all channelsVivera retainers.

Systems and products which increased net revenues by $102.5 million. This increase was offset in part by slightly lower ASP. The ASP decline was primarily due to higher promotional discounts and the impact of foreign exchange rates, offset in part by price increases in our Comprehensive Products effective on July 1 of 2016 and 2017, the impact from acquiring certain distributors as we now recognize direct sales at full ASP rather than the discounted ASP, as well as an increase in additional aligner revenue.Services

Clear Aligner - Non-Case

For the three and nine months ended September 30, 2017, non-caseMarch 31, 2023, Systems and Services net revenues consisting of training fees and ancillary product revenues, increaseddecreased by $5.6 million and $14.2$10.2 million as compared to the same periodsperiod in 20162022 primarily due to increased Vivera volume in both North America and International.

Scanner

For the three and nine months ended September 30, 2017, scanner and services net revenues increased by $8.8 million and $27.1 million as compared to the same periods in 2016. Scanner and services net revenues increased for the three and nine months ended September 30, 2017 as compared to the same periods in 2016 primarily as a result of an increase in thelower number of scanners recognizedsold which decreased net revenues by $27.3 million.

The decrease in net revenue due to lower scanner volume was partially offset by higher service and other revenues which increased net revenues by $15.2 million mostly due to a larger scanner installed base and higher volume of CAD/CAM services resulting from a larger installed base of scanners, offset in part by a decrease in scanner ASP.ASP which increased net revenues $1.9 million.

Cost of net revenues and gross profit (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Clear Aligner | | | | | | | | | | | | |

| Cost of net revenues | | $ | 223.7 | | | $ | 204.0 | | | $ | 19.7 | | | | | | | |

| % of net segment revenues | | 28.3 | % | | 25.2 | % | | | | | | | | |

| Gross profit | | $ | 566.1 | | | $ | 605.7 | | | $ | (39.6) | | | | | | | |

| Gross margin % | | 71.7 | % | | 74.8 | % | | | | | | | | |

| Systems and Services | | | | | | | | | | | | |

| Cost of net revenues | | $ | 58.8 | | | $ | 59.9 | | | $ | (1.0) | | | | | | | |

| % of net segment revenues | | 38.4 | % | | 36.6 | % | | | | | | | | |

| Gross profit | | $ | 94.5 | | | $ | 103.7 | | | $ | (9.1) | | | | | | | |

| Gross margin % | | 61.6 | % | | 63.4 | % | | | | | | | | |

| Total cost of net revenues | | $ | 282.5 | | | $ | 263.9 | | | $ | 18.6 | | | | | | | |

| % of net revenues | | 30.0 | % | | 27.1 | % | | | | | | | | |

| Gross profit | | $ | 660.7 | | | $ | 709.3 | | | $ | (48.7) | | | | | | | |

| Gross margin % | | 70.0 | % | | 72.9 | % | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Clear Aligner | | | | | | | | | | | |

| Cost of net revenues | $ | 75.3 |

| | $ | 54.4 |

| | $ | 20.9 |

| | $ | 208.0 |

| | $ | 154.1 |

| | $ | 53.9 |

|

| % of net segment revenues | 22.1 | % | | 22.3 | % | | | | 22.0 | % | | 21.8 | % | | |

| Gross profit | $ | 266.3 |

| | $ | 189.3 |

| | $ | 77.0 |

| | $ | 737.0 |

| | $ | 552.6 |

| | $ | 184.4 |

|

| Gross margin % | 77.9 | % | | 77.7 | % | | | | 78.0 | % | | 78.2 | % | | |

| Scanner | | | | | | | | | | | |

| Cost of net revenues | $ | 17.5 |

| | $ | 15.0 |

| | $ | 2.5 |

| | $ | 45.1 |

| | $ | 37.5 |

| | $ | 7.6 |

|

| % of net segment revenues | 40.0 | % | | 42.9 | % | | | | 42.1 | % | | 46.9 | % | | |

| Gross profit | $ | 26.2 |

| | $ | 20.0 |

| | $ | 6.2 |

| | $ | 62.0 |

| | $ | 42.4 |

| | $ | 19.6 |

|

| Gross margin % | 60.0 | % | | 57.1 | % | | | | 57.9 | % | | 53.1 | % | | |

| Total cost of net revenues | $ | 92.8 |

| | $ | 69.4 |

| | $ | 23.4 |

| | $ | 253.1 |

| | $ | 191.6 |

| | $ | 61.5 |

|

| % of net revenues | 24.1 | % | | 24.9 | % | | | | 24.1 | % | | 24.4 | % | | |

| Gross profit | $ | 292.5 |

| | $ | 209.2 |

| | $ | 83.3 |

| | $ | 799.0 |

| | $ | 595.0 |

| | $ | 204.0 |

|

| Gross margin % | 75.9 | % | | 75.1 | % | | | | 75.9 | % | | 75.6 | % | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Cost of net revenues for our Clear Aligner and Scanner segments includes personnel-related costs including payroll and stock-based compensation for staff involved in the production process, the cost of materials, packaging, freight and shipping related costs, depreciation on capital equipment and facilities used in the production process, amortization of acquired intangible assets and training costs.

Clear Aligner

For the three months ended September 30, 2017, gross margin percentage increased as compared to the same period in 2016 primarily driven by lower costs per case.

For the nine months ended September 30, 2017, gross margin percentage declined as compared to the same period in 2016 primarily due to an increase in aligners per case driven by additional aligners and lower ASP.

Scanner

For the three ended September 30, 2017, gross margin increased compared to the same period in 2016 primarily driven by lower service costs. This was partially offset by a lower ASP.

For the nine months ended September 30, 2017, gross margin increased compared to the same period in 2016 primarily due to a favorable product mix shift to our lower cost iTero Element scanner.

Selling, general and administrative (in millions):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Selling, general and administrative | $ | 169.5 |

| | $ | 126.7 |

| | $ | 42.8 |

| | $ | 483.6 |

| | $ | 360.4 |

| | $ | 123.2 |

|

| % of net revenues | 44.0 | % | | 45.5 | % | | | | 46.0 | % | | 45.8 | % | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Selling, general and administrative expense includes personnel-related costs including payroll, commissions and stock-based compensation, marketing and administration in addition to media and advertising expenses, clinical education, trade shows and industry events, product marketing, outside consulting services, equipment and maintenance costs, depreciation and amortization expense and allocations of corporate overhead expenses including facilities and IT.

For the three months ended September 30, 2017, selling, general and administrative expense increased compared to the same period in 2016 primarily due to higher compensation related costs of $23.8 million mainly as a result of increased headcount. We also incurred higher expenses from equipment and maintenance costs of $6.6 million, advertising and marketing of $5.5 million, and outside services costs of $4.2 million.

For the nine months ended September 30, 2017, selling, general and administrative expense increased compared to the same period in 2016 primarily due to higher compensation related costs of $57.9 million mainly as a result of increased headcount. We also incurred higher expenses from advertising and marketing of $23.9 million, equipment and maintenance costs of $17.5 million, and outside services costs of $15.4 million.

Research and development (in millions):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Research and development | $ | 24.2 |

| | $ | 20.4 |

| | $ | 3.8 |

| | $ | 71.4 |

| | $ | 54.1 |

| | $ | 17.3 |

|

| % of net revenues | 6.3 | % | | 7.3 | % | | | | 6.8 | % | | 6.9 | % | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Research and development expense includes the personnel-related costs including payroll and stock-based compensation and outside consulting expenses associated with the research and development of new products and enhancements to existing products and allocations of corporate overhead expenses including facilities and IT.

For the three and nine months ended September 30, 2017, research and development expense increased compared to the same periods in 2016 primarily due to higher compensation costs as a result of increased headcount.

Income from operations (in millions):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Clear Aligner | | | | | | | | | | | |

| Income from operations | $ | 154.6 |

| | $ | 102.4 |

| | $ | 52.2 |

| | $ | 403.3 |

| | $ | 306.8 |

| | $ | 96.5 |

|

| Operating margin % | 45.3 | % | | 42.0 | % | | | | 42.7 | % | | 43.4 | % | | |

| Scanner | | | | | | | | | | | |

| Income from operations | $ | 13.5 |

| | $ | 12.0 |

| | $ | 1.5 |

| | $ | 28.3 |

| | $ | 20.3 |

| | $ | 8.0 |

|

| Operating margin % | 31.0 | % | | 34.3 | % | | | | 26.5 | % | | 25.5 | % | | |

Total income from operations (1) | $ | 98.8 |

| | $ | 62.1 |

| | $ | 36.7 |

| | $ | 244.0 |

| | $ | 180.5 |

| | $ | 63.5 |

|

| Operating margin % | 25.6 | % | | 22.3 | % | | | | 23.2 | % | | 23.0 | % | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

(1) Refer to Note 14 "Segments and Geographical Information" of the Notes to Condensed Consolidated Financial Statements for details on unallocated corporate expenses and the reconciliation to consolidated income from operations.

Clear Aligner

For the three months ended September 30, 2017, operatingMarch 31, 2023, our gross margin percentage increaseddecreased as compared to the same period in 20162022 primarily due to greater Invisalign revenuesincreased manufacturing spend as we continue to ramp our new manufacturing facility in Poland in addition to higher mix of additional aligners.

Systems and higher operating margin from sales to SDC, lower costs per case, partially offset by higher compensation related costs and marketing expenses.Services

For the ninethree months ended September 30, 2017, operatingMarch 31, 2023, our gross margin percentage declineddecreased as compared to the same period in 20162022 primarily due to manufacturing inefficiencies from lower production volumes and higher marketing spend and, to a lesser extent, lower ASP,inventory costs. These factors were partially offset by a higher operating margin from sales to SDC.service revenues and higher ASP.

Scanner

For the three ended September 30, 2017, operating margin percentage decreased compared to the same period in 2016 due to higher operating expenses along with a lower ASP. This was partially offset by lower service costs.

For the nine months ended September 30, 2017, operating margin percentage increased compared to the same period in 2016 due to a favorable product mix shift to our lower cost iTero Element scanner.

InterestSelling, general and other income (expenses), netadministrative (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Selling, general and administrative | | $ | 439.7 | | | $ | 439.5 | | | $ | 0.2 | | | | | | | |

| % of net revenues | | 46.6 | % | | 45.2 | % | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Interest and other income (expenses), net | $ | 3.8 |

| | $ | 1.5 |

| | $ | 2.3 |

| | $ | 8.6 |

| | $ | 1.2 |

| | $ | 7.4 |

|

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

InterestSelling, general and other income (expenses), net,administrative expense generally includes foreign currency revaluation gainspersonnel-related costs, including payroll, stock-based compensation and losses, interest income earned on cash, cash equivalentscommissions for our sales force, marketing and investment balances, gainsadvertising expenses including media, clinical education, marketing materials, trade shows and losses on foreign currency forward contractsindustry events, legal and other miscellaneous charges.outside service costs, equipment, software and maintenance costs, depreciation and amortization expense and allocations of corporate overhead expenses including facilities and Information Technology (“IT”).

For the three and nine months ended September 30, 2017, interestMarch 31, 2023, selling, general and other income (expenses), net increasedadministrative expense remained flat compared to the same periodsperiod in 2016 mainly2022 primarily due to higher foreign exchange gains as a result of the Euro strengthening to the U.S. dollar.salaries expense, fringe benefits and stock-based and incentive compensation, offset by lower advertising and marketing costs and outside service costs.

Equity in losses of investee, net of tax

Research and development (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Research and development | | $ | 87.4 | | | $ | 71.8 | | | $ | 15.6 | | | | | | | |

| % of net revenues | | 9.3 | % | | 7.4 | % | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Equity in losses of investee, net of tax | $ | 1.6 |

| | $ | 0.5 |

| | $ | 1.1 |

| | $ | 5.0 |

| | $ | 0.5 |

| | $ | 4.5 |

|

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Research and development expense generally includes personnel-related costs, including payroll and stock-based compensation, outside service costs associated with the research and development of new products and enhancements to existing products, software, equipment, material and maintenance costs, depreciation and amortization expense and allocations of corporate overhead expenses including facilities and IT.

For the three and nine months ended September 30, 2017, equity in losses of investee, net of taxMarch 31, 2023, research and development expense increased compared to the same periodsperiod in 20162022 primarily due to higher losses attributablesalaries expense, fringe benefits and stock-based and incentive compensation as we continue to equity methodfocus on our investments including a higher sharein innovation and research.

Income from operations (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Clear Aligner | | | | | | | | | | | | |

| Income from operations | | $ | 277.5 | | | $ | 312.7 | | | $ | (35.2) | | | | | | | |

| Operating margin % | | 35.1 | % | | 38.6 | % | | | | | | | | |

| Systems and Services | | | | | | | | | | | | |

| Income from operations | | $ | 35.6 | | | $ | 50.8 | | | $ | (15.2) | | | | | | | |

| Operating margin % | | 23.2 | % | | 31.1 | % | | | | | | | | |

Total income from operations 1 | | $ | 133.5 | | | $ | 198.1 | | | $ | (64.6) | | | | | | | |

| Operating margin % | | 14.2 | % | | 20.4 | % | | | | | | | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to an additional investment in the third quarter of 2017 (rounding.

1 Refer to Note 4 "Equity Method Investments"13 “Segments and Geographical Information” of the Notes to Condensed Consolidated Financial Statements for details on equity method investments).unallocated corporate expenses and the reconciliation to Condensed Consolidated Income from Operations.

Income tax (in millions):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2017 | | 2016 | | Change | | 2017 | | 2016 | | Change |

| Provision for income taxes | $ | 18.3 |

| | $ | 11.7 |

| | $ | 6.6 |

| | $ | 26.5 |

| | $ | 39.2 |

| | $ | (12.7 | ) |

| Effective tax rates | 17.9 | % | | 18.4 | % | | | | 10.5 | % | | 21.6 | % | | |

For the three months ended September 30, 2017March 31, 2023, our operating margin percentage decreased compared to the same period in 2022 primarily due to lower gross margin.

Systems and 2016, provisionServices

For the three months ended March 31, 2023, our operating margin percentage decreased compared to the same period in 2022 primarily due to higher operating expenses as a percentage of net revenues as well as lower gross margin.

Interest income (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Interest income | | $ | 2.3 | | | $ | 0.7 | | | $ | 1.7 | | | | | | | |

| % of net revenues | | 0.2 | % | | 0.1 | % | | | | | | | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Interest income generally includes interest earned on cash, cash equivalents and investment balances.

For the three months ended March 31, 2023, interest income increased compared to the same period in 2022 primarily due to higher interest rates in the first quarter of 2023.

Other income (expense), net (in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Other income (expense), net | | $ | (1.2) | | | $ | (11.3) | | | $ | 10.0 | | | | | | | |

| % of net revenues | | (0.1) | % | | (1.2) | % | | | | | | | | |

Changes and percentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Other income (expense), net, generally includes foreign exchange gains and losses, gains and losses on foreign currency forward contracts, interest expense, gains and losses on equity investments and other miscellaneous charges.

For the three months ended March 31, 2023, other income (expense), net increased compared to the same period in 2022 primarily due to the favorable impact of foreign exchange rates and higher interest rates.

Provision for income taxes was $18.3 million(in millions): | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, | | | | | | |

| | | 2023 | | 2022 | | Change | | | | | | |

| Provision for income taxes | | $ | 46.8 | | | $ | 53.2 | | | $ | (6.4) | | | | | | | |

| Effective tax rates | | 34.8 | % | | 28.4 | % | | | | | | | | |

Changes and $11.7 million, respectively, representingpercentages are based on actual values. Certain tables may not sum or recalculate due to rounding.

Our effective tax rate differs from the statutory federal income tax rate of 21% for both the three month periods ended March 31, 2023 and 2022 primarily due to the recognition of additional tax expense resulting from foreign income taxed at different rates, of 17.9% and 18.4%, respectively. Our provision forstate income taxes, was $26.5 million and $39.2 million fornon-deductible expenses in the nine months ended September 30, 2017 and 2016, respectively, representing effective tax rates of 10.5% and 21.6%, respectively. U.S.

The decreaseincrease in our effective tax rate for the three months ended September 30, 2017March 31, 2023 compared to the same period in 20162022 is primarily attributable to the adoptiondecrease and change in our jurisdictional mix of ASU 2016-09 in 2017 which requiresincome, foreign income taxed at different rates, and lower excess tax benefits related tofrom stock-based compensation to be recognized as a reduction of income tax expense, and certain one-time tax charges recognized as a result of the implementation of the international corporate restructure on July 1, 2016 that is no longer pertinent to the current period. The decrease in effective tax rate for the nine months ended September 30, 2017 compared to the same period in 2016 is primarily attributable to the adoption of ASU 2016-09 in the first quarter of fiscal year 2017, which requires excess tax benefits related to stock-based compensation to be recognized as a reduction of income tax expense. In addition, the effective tax rate for the prior period was increased due to certain one-time tax charges recognized as a result of the implementation of the international corporate restructure during the third quarter of fiscal year 2016. For the three and nine months ended September 30, 2017, we recognized excess tax benefits of $1.7 million and $24.1 million, respectively, in our provision for income taxes.compensation.

On July 1, 2016, we implemented a new international corporate structure. This changed the structure of our international procurement and sales operations, as well as realigned the ownership and use of intellectual property among our wholly-owned subsidiaries. We continue to anticipate that an increasing percentage of our consolidated pre-tax income will be derived from, and reinvested in our foreign operations. We believe that income taxed in certain foreign jurisdictions at a lower rate relative to the U.S. federal statutory rate will have a beneficial impact on our worldwide effective tax rate over time.

In June 2017, the Costa Rica Ministry of Foreign Trade, an agency of the Government of Costa Rica, granted an extension of certain income tax incentives for an additional twelve year period, which were originally granted in 2002 and was set to expire in June 2017. Under these incentives, all of the income in Costa Rica is subject to a reduced tax rate. In order to receive the benefit of these incentives, we must hire specified numbers of employees and maintain certain minimum levels of fixed asset investment in Costa Rica. If we do not fulfill these conditions for any reason, our incentive could lapse, and our income in Costa Rica would be subject to taxation at higher rates which could have a negative impact on our operating results. The Costa Rica corporate income tax rate that would apply, absent the incentives, is 30% for 2017 and 2016. For the three and nine months ended September 30, 2017, the reduction in income taxes was minimal primarily due to the new international corporate structure implemented on July 1, 2016. For the three and nine months ended September 30, 2016, income taxes were reduced by $0.3 million with minimal impact to diluted net income per share and $17.5 million representing a benefit to diluted net income per share of $0.21, respectively (Refer to Note 12 "Accounting for Income Taxes" for details on income taxes).

Liquidity and Capital Resources

We fund our operations primarily from product salesLiquidity and available cash and cash equivalents and marketable securities. Trends

As of September 30, 2017March 31, 2023 and December 31, 2016,2022, we had the following cash and cash equivalents and short-term and long-term marketable securities (in thousands):

|

| | | | | | | | |

| | | September 30, | | December 31, |

| | | 2017 | | 2016 |

| Cash and cash equivalents | | $ | 362,613 |

| | $ | 389,275 |

|

| Short-term marketable securities | | 316,454 |

| | 250,981 |

|

| Long-term marketable securities | | 58,842 |

| | 59,783 |

|

| Total | | $ | 737,909 |

| | $ | 700,039 |

|

| | | | | | | | | | | | | | |

| | March 31, 2023 | | December 31, 2022 |

| Cash and cash equivalents | | $ | 832,383 | | | $ | 942,050 | |

| Marketable securities, short-term | | 51,644 | | | 57,534 | |

| Marketable securities, long-term | | 37,379 | | | 41,978 | |

| Total | | $ | 921,406 | | | $ | 1,041,562 | |

Cash flows (in thousands):

|

| | | | | | | | |

| | | Nine Months Ended

September 30, |

| | | 2017 | | 2016 |

| Net cash flow provided by (used in): | | | | |

| Operating activities | | $ | 276,213 |

| | $ | 166,674 |

|

| Investing activities | | (228,620 | ) | | 142,859 |

|

| Financing activities | | (79,036 | ) | | (57,619 | ) |

| Effect of exchange rate changes on cash and cash equivalents | | 4,781 |

| | 320 |

|

| Net increase (decrease) in cash and cash equivalents | | $ | (26,662 | ) | | $ | 252,234 |

|

As of September 30, 2017, we had $737.9March 31, 2023 and December 31, 2022, approximately $610.9 million in cash, cash equivalents and short-term and long-term marketable securities. Cash equivalents and marketable securities are comprised of money market funds and highly liquid debt instruments which primarily include commercial paper, corporate bonds, U.S. government agency bonds, U.S. government treasury bonds and certificates of deposit.

As of September 30, 2017, approximately $501.6$653.7 million, respectively, of cash, cash equivalents and short-term and long-term marketable securities waswere held by our foreign subsidiaries. Amounts held by foreign subsidiaries are generally subjectWe intend to U.S. income taxation on repatriation to the U.S. The costs to repatriatecontinue reinvesting our foreign subsidiary earnings indefinitely and expect the additional costs upon repatriation of these foreign earnings not to the U.S. would likely be material; however, our intent is to permanently reinvest our earnings from foreign operations, and our current plans do not require us to repatriate them to fund our U.S. operations as wesignificant. We generate sufficient domestic operating cash flow and have access to external funding under our current$300.0 million revolving line of credit. We believe that our current cash balances and the borrowing capacity under our credit facility, if necessary, will be sufficient to fund our business for at least the next 12 months.

Stock RepurchasesThe sanctions against Russian banks or international bank messaging systems due to the military conflict between Ukraine and Russia could impact our ability to access our cash in Russia but would not materially impact our liquidity position. As of March 31, 2023, cash and cash equivalents domiciled in Russia, which is required to fund their current operating requirements, represent approximately 2.2% of our total cash, cash equivalents and marketable securities.

Our material cash requirements are as follows:

•For 2023, we expect our investments in capital expenditures to exceed $200.0 million. Capital expenditures primarily relate to building construction and improvements as well as additional manufacturing capacity to support our international expansion. This includes our investment in an aligner fabrication facility in Wroclaw, Poland which began serving doctors during the second quarter of 2022 as a part of our strategy to bring operational facilities closer to customers. As we continue growing, we intend to expand our investments in research and development, manufacturing, treatment planning, sales and marketing operations to meet actual and anticipated local and regional demands.

•During the three months ended March 31, 2023, we entered into or completed ASRs providing for the repurchase of our common stock based on the volume-weighted average price during the term of the agreement, less an agreed upon discount. As of March 31, 2023, the May 2021 Repurchase Program was completed. In January 2023, our Board of Directors authorized a plan to repurchase up to $1.0 billion of our common stock (“January 2023 Repurchase Program”), none of which had been utilized as of March 31, 2023. Refer to Note 11 "Common9 “Common Stock Repurchase Program"Program” of the Notes to Condensed Consolidated Financial Statements for details on our stock repurchase program.programs.

April 2016 Repurchase Program. On April 28, 2016, we announced that•There have been no material changes to our Boardpurchase commitments for goods and services and future operating lease payments during the periods covered by this 10-Q outside the normal course of Directors had authorized a planbusiness compared to repurchase up to $300.0 millionthe disclosures in Part II, Item 7 of our stock. On May 2, 2017, we entered into an accelerated share repurchase ("ASR") to repurchase $50.0 millionAnnual Report on Form 10-K for the year ended December 31, 2022.

Sources and Uses of Cash

The following table summarizes our common stock ("2017 ASR"). The 2017 ASR was completed on August 3, 2017. The final numbercondensed consolidated cash flows for the three months ended March 31, 2023 and 2022 (in thousands):

| | | | | | | | | | | | | | |

| | | Three Months Ended

March 31, |

| | | 2023 | | 2022 |

| Net cash flow provided by (used in): | | | | |

| Operating activities | | $ | 199,895 | | | $ | 30,498 | |

| Investing activities | | (52,829) | | | (90,198) | |

| Financing activities | | (258,961) | | | (111,742) | |

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | | 2,221 | | | (1,826) | |

| Net (decrease) increase in cash, cash equivalents, and restricted cash | | $ | (109,674) | | | $ | (173,268) | |

Operating Activities

For the ninethree months ended September 30, 2017,March 31, 2023, cash flows from operations of $276.2$199.9 million resulted primarily from our net income of approximately $221.2$87.8 million as well as the following:

Significant non-cash activitiesadjustments to net income

•Stock-based compensation was $44.0of $37.7 million related to equity incentive compensationawards granted to employees and directors,directors;

•Depreciation and amortization of $26.7$35.8 million related to our investments in property, plant and equipment and intangible assets, andassets;

Net change•Deferred taxes of $18.4 million related to increase in long term deferred tax assetsposition; and

•Non-cash operating lease costs of $5.5 million.$7.8 million related majority to amortization of deferred commissions.

Significant changes in working capital

•Increase of $84.4 million in accounts receivable which is primarily a result of the increase in net revenues,

Increase of $53.2 million in deferred revenues corresponding to the increases in case shipments, and

Increase of $19.0$37.4 million in accrued and other long-term liabilities primarily due to higher incentive accruals for 2023, as well as timing of payment of other activities;

•Decrease of $32.7 million in accounts receivable due to timing of paymentscollections and activities.offset by an increased sales volumes;

•Increase of $27.7 million in deferred revenues due to the deferral of revenue on shipments over the period as well as timing of revenue recognition; and

•Increase of $24.0 million in inventories primarily due our efforts to manage stock at appropriate levels as required.

Investing Activities

Net cash used in investing activities was $228.6$52.8 million for the ninethree months ended September 30, 2017March 31, 2023 which primarily consisted of purchases of marketable securities of $356.9 million, property, and plant and equipment purchases of $126.2$64.1 million of which $63.0 million is related to the purchase of our new headquarters along with building improvements, $23.0 million of loan advances to equity investee and $9.0 million paid for certain distributor acquisitions, net of cash received. These outflows were partially offset by maturities and salespurchases of marketable securities of $292.8$2.4 million, partially offset by sales and loan repayment from equity investeematurities of $6.0our marketable securities of $13.7 million.

For the remainder of 2017, we expect to invest an additional $55.0 million to $60.0 million on capital expenditures primarily related to additional manufacturing capacity to support our international expansion. Although we believe our current investment portfolio has little risk of impairment, we cannot predict future market conditions or market liquidity and can provide no assurance that our investment portfolio will remain unimpaired.

Financing Activities

Net cash used in financing activities was $79.0$259.0 million for the ninethree months ended September 30, 2017 primarily resulting fromMarch 31, 2023 which consisted of common stock repurchases of $53.8$252.4 million and payroll taxes paid for vesting of restricted stock unitsequity awards through share withholdings of $39.1 million. These outflows$20.9 million which were partially offset in part by $13.9$14.3 million fromof proceeds from the issuance of common stock.

Contractual Obligations

Our contractual obligations have not significantly changed since December 31, 2016 as disclosed in our Annual Report on Form 10-K, other than obligations described in the Form 10-Q herein. We believe that our current cash, cash equivalents and short-term marketable securities combined with our existing borrowing capacity will be sufficient to fund our operations for at least the next 12 months. If we are unable to generate adequate operating cash flows and need more funds beyond our available liquid investments and those availablestock under our credit facility, we may need to suspend ouremployee stock repurchase program or seek additional sources of capital through equity or debt financing, collaborative or other arrangements with other companies, bank financing and other sources in order to realize our objectives and to continue our operations. There can be no assurance that we will be able to obtain additional debt or equity financing on terms acceptable to us, or at all. If adequate funds are not available, we may need to make business decisions that could adversely affect our operating results such as modifications to our pricing policy, business structure or operations. Accordingly, the failure to obtain sufficient funds on acceptable terms when needed could have a material adverse effect on our business, results of operations and financial condition.purchase plan.

Off-Balance Sheet Arrangements

As of September 30, 2017, we had no off-balance sheet arrangements that have, or are reasonably likely to have, a current or future material effect on our consolidated financial condition, results of operations, liquidity, capital expenditures or capital resources.

Critical Accounting Policies and Estimates

Management’s discussion and analysis of our financial condition and results of operations is based upon our Condensed Consolidated Financial Statements which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of condensed consolidated financial statements requires management to make estimates and judgments that affect the reported amounts of assets and liabilities, revenues and expenses and disclosures at the date of the financial statements. We evaluate our estimates on an on-going basis, including those related to revenue recognition, stock-based compensation, goodwill and finite-lived acquired intangible assets, income taxes, legal proceedings and related impairment, and income taxes.litigations. We use authoritative pronouncements, historical experience and other assumptions as the basis for making the estimates. Actual results could differ from those estimates.

Revenue Recognition

Our revenues are derived primarily from the sale of aligners, scanners, and services from our Clear Aligner and Systems and Services segments. We enter into sales contracts that may consist of multiple distinct performance obligations where certain performance obligations of the sales contract are not delivered in one reporting period. We measure and allocate revenues according to ASC 606-10, “Revenues from Contracts with Customers.”

Determining the standalone selling price (“SSP”) in order to allocate consideration from the contract to the individual performance obligations is the result of various factors, such as changing trends and market conditions, historical prices, costs, and gross margins. While changes in the allocation of the SSP between performance obligations will not affect the amount of total revenues recognized for a particular contract, any material changes could impact the timing of revenue recognition, which would have a material effect on our financial position and result of operations. This is because the contract consideration is allocated to each performance obligation, delivered or undelivered, at the inception of the contract based on the SSP of each distinct performance obligation.

We believeallocate revenues for each clear aligner treatment plan based on each unit’s SSP. Management considers a variety of factors such as same or similar product historical sales, costs, and gross margin, which may vary over time depending upon the following critical accounting policiesunique facts and estimates affectcircumstances related to each performance obligation in making these estimates. In addition to historical data, we take into consideration changing trends and market conditions. For treatment plans with multiple options, we also consider usage rates, which is the number of times a customer is expected to order more aligners after the initial shipment. Our process for estimating usage rates requires significant judgment and evaluation of inputs, including historical usage data by region, country and channel.

We estimate the SSP of each element in a scanner system and services sale taking into consideration same or similar product historical prices as well as our more significant judgments used in the preparation of our consolidated financial statements. These critical accounting policies and related disclosures appear in our Annual Report on Form 10-K for the year ended December 31, 2016:discounting strategies.

Revenue Recognition;

Stock-Based Compensation Expense;

Goodwill and Finite-Lived Acquired Intangible Assets;

Impairment of Goodwill, Finite-Lived Acquired Intangible Assets and Long-Lived Assets; and

Accounting for Income Taxes.

Recent Accounting Pronouncements

See Note 1 “Summary“Summary of Significant Accounting Policies” Policies” of the Notes to Condensed Consolidated Financial Statements for a discussion of recent accounting pronouncements.

ITEMItem 3.QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK Quantitative and Qualitative Disclosures About Market Risk.

In the normal course of business, we are exposed to interest rate, foreign currency exchange rate and interest rateinflation risks that could impact our financial position and results of operations. In addition, we are subject to the broad market risk that is created by the global market disruptions and uncertainties resulting from macroeconomic challenges, the military conflict between Russia and Ukraine and the COVID-19 pandemic. Further discussion on these risks may be found in Item 1A of this is Quarterly Report on Form 10-Q under the heading “Risk Factors.”

Interest Rate Risk

Changes in interest rates could impact our anticipated interest income on our cash equivalents and investments in marketable securities. Our cash equivalents and investments are fixed-rate short-term and long-term securities. Fixed-rate securities may have their fair market value adversely impacted due to a rise in interest rates, and, as a result, our future investment income may fall short of expectations due to changes in interest rates or we may suffer losses in principal if forced to sell securities which have declined in market value due to changes in interest rates. As of September 30, 2017,March 31, 2023, we had approximately $566.1$89.0 million invested in available-for-sale marketable securities. An immediate 10% change in interest rates would not have a material adverse impact on our future operating results and cash flows.

We do not enter into investments for trading or speculative purposes and have not used any derivative financial instruments to manage our interest rate risk exposure. We do not have interest bearing liabilities asAs of September 30, 2017, and, therefore,March 31, 2023, we are not subject to risks from immediate interest rate increases.increases on our unsecured revolving line of credit facility.

Currency Rate Risk

As a result of our international business activities, our financial results could behave been affected by factors such as changes in foreign currency exchange rates oras well as economic conditions in foreign markets, and there is no assurance that exchange rate fluctuations will not harm our business in the future. We generally sell our products in the local currency of the respective countries. This provides some natural hedging because most of the subsidiaries’ operating expenses are generally denominated in their local currencies as discussed further below.currencies. Regardless of this natural hedging, our results of operations may be adversely impacted by exchange rate fluctuations.

We have in the past and may in the future enter into foreign currency hedging transactions in an effortforward contracts for currencies where we have exposures, primarily the Euro, Chinese Yuan, Polish Zloty, Canadian Dollar, to cover someminimize the short-term impact of our exposure to foreign currency exchange rate fluctuations on cash and certain trade and intercompany receivables and payables.These forward contracts are not designated as hedging instruments and do not subject us to material balance sheet risk due to fluctuations in foreign currency exchange rates. The gains and losses on these forward contracts are intended to offset the gains and losses in the underlying foreign currency denominated monetary assets and liabilities being economically hedged. These instruments are generally one month in original maturity and are marked to market through earnings every period and generally are one month in original maturity.period. We do not enter into foreign currency forward contracts for trading or speculative purposes. As our international operations grow, we will continue to reassess our approach to managing the risks relating to fluctuations in currency rates. It is difficult to predict the impact hedging activitiesforward contracts could have on our results of operations. As

Although we will continue to monitor our exposure to currency fluctuations, and, where appropriate, may use financial hedging techniques in the futureforward contracts to minimize the effect of these fluctuations, the impact of an aggregate change of 10% in foreign currency exchange rates relative to the U.S. dollar on our results of operations and financial position could be material.

Military Conflict in Ukraine ITEM

After beginning in 2022, the military conflict between Russia and Ukraine has continued to escalate and create challenges to already uncertain macroeconomic conditions. As of March 31, 2023, we do not expect these events to have any material impact on our operations. Our Russia net revenues as a percentage of our consolidated net revenues and our assets domiciled in Russia, including cash and cash equivalents, as a percentage of our total assets, are immaterial.

Inflation Risk

The economy has been impacted by certain macroeconomic challenges which have contributed to a rising inflationary trend that have impacted both our revenues and costs globally, and which we expect will continue into the foreseeable future. If our costs become subject to significant inflationary pressures, we may not be able to fully offset such higher costs through price increases. There can be no assurance that our results of operations and financial condition will not be materially impacted by inflation in the future.

Item 4.CONTROLS AND PROCEDURES Controls and Procedures.

Evaluation of disclosure controls and procedures.

Under the supervision and with the participation of our management, including our Chief Executive Officer and our Chief Financial Officer, we have evaluated the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) as of the end of the period covered by this Quarterly Report on Form 10-Q. Based upon that evaluation, our Chief Executive Officer and our Chief Financial Officer have concluded that our disclosure controls and procedures are effective as of September 30, 2017,March 31, 2023, to provide reasonable assurance that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is accumulated and communicated to our management, including our Chief Executive Officer and our Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure, and that such information is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange CommissionSEC rules and forms.

Changes in internal control over financial reporting.

There were no changes in our internal control over financial reporting during the quarter ended September 30, 2017March 31, 2023 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II—OTHER INFORMATION

ITEMItem 1. LEGAL PROCEEDINGSLegal Proceedings.

In the courseFor a discussion of Align's operations, Align is involved in a variety of claims, suits, investigations, and proceedings, including actions with respect to intellectual property claims, patent infringement claims, government investigations, labor and employment claims, breach of contract claims, tax, and other matters. Regardless of the outcome, these proceedings can have an adverse impact on us because of defense costs, diversion of management resources, and other factors. Although the results of complex legal proceedings, are difficultrefer to predict and Align's view of these matters may change in the future as litigation and events related thereto unfold; Align currently does not believe that these matters, individually or in the aggregate, will materially affect Align's financial position, results of operations or cash flows (Refer to Note 8 "Legal Proceedings"6 “Legal Proceedings” of the Notes to Condensed Consolidated Financial StatementsStatements in Part I, Item 1 of this Form 10-Q.

Item 1A. Risk Factors.

The following discusses some of the risks that may affect our business, results of operations, financial condition and the price of our stock. You should carefully review this section, as well as our condensed consolidated financial statements and notes thereto and other information appearing in this Quarterly Report on Form 10-Q, for detailsimportant information regarding these and other risks that may affect us. The order we have chosen to list the risks below or the sections in which we have identified them should not be interpreted to mean we deem any risks to be more or less important or likely to occur or, if any do occur, that their impact may be any less significant than others. These risk factors should be considered in connection with evaluating the forward-looking statements contained in this report because they could cause our actual results and conditions to differ materially from those statements. Before you invest in Align, you should know that investing involves risks, including those described below. The risks below are not the only ones we face. If any of the risks actually occur, our business, financial

condition and results of operations could be negatively affected, the trading price of our common stock could decline, and you may lose all or part of your investment.

Summary of Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows, and prospects. These risks are discussed more fully below and include, but are not limited to:

Macroeconomic and External Risks

•Global and regional economic conditions

•Major health crises

•Political events, international disputes, war and terrorism

•Natural disasters

Business and Industry Risks

•Changes in demand for our products

•Increased competition

•Failure of our new products, or changes to our existing products, to attract or retain consumers or generate revenue

•Our ability to successfully integrate our acquisitions

Operational Risks

•Business disruptions

•Predicting demand

•Availability of supplies

•Shipping delays

•Personnel development and retention

•Effectiveness of marketing and our ability to attract consumers

Legal, Regulatory and Compliance Risks

•Government investigations, enforcement actions, and settlements

•Our ability to comply with laws and regulatory and legislative mandates or guidance

•Privacy, cybersecurity and data protection

•Litigation, including class action lawsuits

Intellectual Property Risks

•Our ability to obtain, maintain, protect, and enforce our intellectual property rights

Financial, Tax and Accounting Risks

•Impairment of our goodwill

•Compliance with accounting, financial reporting, and tax laws

•Management of our stock plans

•Volatility of our stock

Macroeconomic and External Risks

Our operations and financial performance depend on legal proceedings).global and regional economic conditions. Inflation, fluctuations in currency exchange rates, changes in consumer confidence and demand, and general economic weakness and threats, or actual recessions, have and could in the future materially affect our business, results of operations, and financial condition.

Macroeconomic conditions impact consumer confidence and discretionary spending, which can adversely affect demand for our products. Consumer spending habits are affected by, among other things, inflation, fluctuations in currency exchange rates, general economic weakness, threats or actual recessions, pandemics, wars and military actions, employment levels, wages, debt obligations, discretionary income, interest rates, volatility in capital, and consumer confidence and perceptions of current and future economic conditions. Changes and uncertainty can, among other things, reduce or shift spending away from elective procedures, drive patients to purchase orthodontic treatments that cost less than our Invisalign treatment options, decrease the number of orthodontic and dental case starts, reduce patient traffic in dentists’ offices or reduce demand for dental services generally. Further, decreased demand for dental services can cause dentists and labs to postpone investments in capital equipment, such as intraoral scanners and CAD/CAM equipment and software. The recent declines in, or uncertain economic outlooks for, the U.S., Chinese, European and certain other international economies have and may continue to adversely affect consumer and dental practice spending. The increase in the cost of fuel and energy, food and other essential items along with higher interest rates could reduce consumers' disposable income, resulting in decreased discretionary spending for products like ours. Decreases in disposable income and discretionary spending or changes in consumer confidence and spending habits has and may continue to adversely affect our revenues and operating results.

ITEM 1A.RISK FACTORSInflation continues to adversely impact spending and trade activities, causing unpredictable impacts on global and regional economies. Higher inflation has also increased domestic and international shipping costs, raw material prices, and labor rates, which has adversely impacted the costs of producing, procuring and shipping our products. Our ability to recover these cost