UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended SeptemberJune 30, 2017 2020

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File Number:file number 333-201029

AMERICAN EDUCATION CENTER INC.

(Exact Name of Registrant as Specified in Its Charter)

AMERICAN EDUCATION CENTER, INC. |

| ( |

| Nevada | 38-3941544

| |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 10020 | |

| (Address of |

( |

(212) 825-0437(646) 722-2931

(Registrant’s Telephone Number, Including Area Code)number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| None | None | None |

Indicate by check mark whether the registrant:registrant (1) has filed all reports required to be filed by SectionsSection 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the pastlast 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” andfiler,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | Smaller reporting company | x | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☐¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date 41,350,000date: 57,497,113 shares of common stock, at$0.001 par value, of $0.001 as of November 9, 2017.August 14, 2020.

TABLE OF CONTENTS

Index to Form 10-Q

Throughout this Quarterly Report on Form 10-Q, the “Company”, “we,” “us,” and “our,” refer to (i) American Education Center, Inc., a Nevada corporation (“AEC Nevada”); (ii) American Education Center, Inc., a New York corporation ("AEC New York"); and (iii) AEC Southern Management Co., Ltd, a company formed pursuant to the laws of England and Wales (the “AEC Southern UK”) and the subsidiaries of AEC Southern UK unless otherwise indicated or the context otherwise requires.

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains certain forward-looking statements (as such term is defined in Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934). The statements herein which are not historical reflect our current expectations and projections about the Company’s future results, performance, liquidity, financial condition, prospects and opportunities and are based upon information currently available to us and our management and our interpretation of what we believe to be significant factors affecting our business, including many assumptions about future events. Such forward-looking statements include statements regarding, among other things:

| ● | our ability to deliver, market, and generate sales of our advisory services; | |

| ● | our ability to develop and/or introduce new advisory services; | |

| ● | our projected revenues, profitability, and other financial metrics; | |

| ● | our future financing plans; | |

| ● | our anticipated needs for working capital; | |

| ● | the anticipated trends in our industry; | |

| ● | our ability to expand our sales and marketing capability; | |

| ● | acquisitions of other companies or assets that we might undertake in the future; | |

| ● | competition existing today or that will likely arise in the future; | |

| ● | the impact of the COVID-19 pandemic on our operations and revenue; and | |

| ● | other factors discussed elsewhere herein. |

Forward-looking statements, which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words “may,” “should,” “will,” “plan,” “could,” “target,” “contemplate,” “predict,” “potential,” “continue,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “seek,” or “project” or the negative of these words or other variations on these or similar words. Actual results, performance, liquidity, financial condition and results of operations, prospects and opportunities could differ materially from those expressed in, or implied by, these forward-looking statements becauseas a result of various risks, uncertainties and other factors, including the ability to raise sufficient capital to continue the Company’s operations. These statements may be found under Part I, Item 2—“Management’s “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as elsewhere in this Quarterly Report on Form 10-Q generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, matters described in this Quarterly Report on Form 10-Q.

In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this Quarterly Report on Form 10-Q will in fact occur.

Potential investors should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, there is no undertaking to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason.

The forward-looking statements in this Quarterly Report on Form 10-Q represent our views as of the date of this Quarterly Report on Form 10-Q. Such statements are presented only as somea guide about future possibilities and do not represent assured events, and we anticipate that subsequent events and developments will cause our views to change. You should, therefore, not rely on these forward-looking statements as representing our views as of any date after the date of this Quarterly Report on Form 10-Q.

This Quarterly Report on Form 10-Q also contains estimates and other statistical data prepared by independent parties and by us relating to market size and growth and other data about our industry. These estimates and data involve a number of assumptions and limitations, and potential investors are cautioned not to give undue weight to these estimates and data. We have not independently verified the statistical and other industry data generated by independent parties and contained in this Quarterly Report on Form 10-Q. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of uncertainty and risk.

Potential investors should not make an investment decision based solely on our projections, estimates or expectations.

FINANCIAL INFORMATION

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

| June 30, | December 31, | |||||||

| ASSETS | 2020 | 2019 | ||||||

| Current assets: | ||||||||

| Cash | $ | 922,567 | $ | 1,035,395 | ||||

| Accounts receivable, net of allowance for doubtful accounts of $3,068,759 and 2,605,348 at June 30, 2020 and 2019, respectively | 1,733,435 | 2,874,125 | ||||||

| Prepaid expenses | 225,459 | 253,530 | ||||||

| Total current assets | 2,881,461 | 4,163,050 | ||||||

| Noncurrent assets: | ||||||||

| Fixed Asset, net | 5,037 | 6,226 | ||||||

| Deferred income taxes | 861,307 | 557,615 | ||||||

| Intangible asset, net | 198,136 | 272,226 | ||||||

| Operating lease right-of-use asset | 1,983,406 | 2,149,710 | ||||||

| Security deposits | 282,215 | 285,041 | ||||||

| Total noncurrent assets | 3,330,101 | 3,270,818 | ||||||

| Total assets of continuing operations | 6,211,562 | 7,433,868 | ||||||

| Assets of discontinued operations, net | - | - | ||||||

| TOTAL ASSETS | $ | 6,211,562 | $ | 7,433,868 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued expenses | $ | 2,586,596 | $ | 2,867,133 | ||||

| Taxes payable | - | 60,511 | ||||||

| Deferred revenue | 95,059 | 215,500 | ||||||

| Advances from clients | - | 60 | ||||||

| Short-term loan from related party | 849,245 | 574,564 | ||||||

| Short-term loan due within a year | - | 98,433 | ||||||

| Operating lease liability - current portion | 363,035 | 331,670 | ||||||

| Total current liabilities | 3,893,935 | 4,147,871 | ||||||

| Noncurrent liabilities: | ||||||||

| Operating lease liability | 1,876,381 | 2,067,504 | ||||||

| Long-term loan | 236,588 | - | ||||||

| Total liabilities of continuing operations | 6,006,904 | 6,215,375 | ||||||

| Liabilities of discontinued operations | - | - | ||||||

| Total liabilities | 6,006,904 | 6,215,375 | ||||||

| Stockholders’ equity: | ||||||||

| Series A Convertible Preferred stock, $0.001 par value; 20,000,000 shares authorized 0 shares issued and outstanding at June 30, 2020 and December 31, 2019, respectively | - | - | ||||||

| Series B Convertible Preferred stock, $0.001 par value; 25,000,000 shares authorized 25,000,000 and 0 shares issued and outstanding at June 30, 2020 and December 31, 2019, respectively | 25,000 | 25,000 | ||||||

| Common stock, $0.001 par value; | ||||||||

| 450,000,000 shares authorized; 56,497,113 shares and 55,797,113 shares outstanding at June 30, 2020 and December 31, 2019 respectively | 57,497 | 56,797 | ||||||

| Additional paid-in capital | 8,274,230 | 8,267,930 | ||||||

| Treasury stock at cost, 1,000,000 shares at 0.66 per share | (660,000 | ) | (660,000 | ) | ||||

| Subscription receivables | (592,305 | ) | (592,305 | ) | ||||

| Retained earnings | (6,947,911 | ) | (5,924,231 | ) | ||||

| Accumulated other comprehensive income | 1,120 | (4,678 | ) | |||||

| Total controlling interest | 157,631 | 1,168,513 | ||||||

| Noncontrolling Interest | 47,027 | 49,980 | ||||||

| Total stockholders' equity | 204,658 | 1,218,493 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 6,211,562 | $ | 7,433,868 | ||||

See accompanying notes to consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (UNAUDITED)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Revenues | $ | 161,984 | $ | 1,169,044 | $ | 276,182 | $ | 3,139,791 | ||||||||

| Cost of revenues | 55,717 | 686,290 | 166,054 | 1,768,687 | ||||||||||||

| Gross profit | 106,267 | 482,754 | 110,128 | 1,371,104 | ||||||||||||

| Operating expenses: | ||||||||||||||||

| Selling and marketing | 60,754 | 61,960 | 74,115 | 201,249 | ||||||||||||

| General and administrative | 777,991 | 1,059,041 | 1,425,116 | 1,451,878 | ||||||||||||

| Total operating expenses | 838,745 | 1,121,001 | 1,499,231 | 1,653,127 | ||||||||||||

| (Loss) from operations | (732,478 | ) | (638,247 | ) | (1,389,103 | ) | (282,023 | ) | ||||||||

| Other income | 3 | 95 | 317 | 1,297 | ||||||||||||

| (Loss) before provision for income taxes | (732,475 | ) | (638,152 | ) | (1,388,786 | ) | (280,726 | ) | ||||||||

| Provision for income taxes (benefit) | (199,530 | ) | 366,076 | (362,153 | ) | 366,076 | ||||||||||

| Net (loss) from continuing operations including noncontrolling interest | $ | (532,945 | ) | $ | (1,004,228 | ) | $ | (1,026,633 | ) | $ | (646,802 | ) | ||||

| Net income (loss) from discontinued operations, net of income taxes benefit | - | 836,807 | - | 561,807 | ||||||||||||

| Net (loss) including noncontrolling interest | (532,945 | ) | (167,421 | ) | (1,026,633 | ) | (84,995 | ) | ||||||||

| Less: Net (loss) attributable to noncontrolling interest | (1,470 | ) | (1,470 | ) | (2,953 | ) | (2,940 | ) | ||||||||

| Net(loss) attributable to American Education Center | $ | (531,475 | ) | $ | (165,951 | ) | $ | (1,026,680 | ) | $ | (82,055 | ) | ||||

| Net (loss) including noncontrolling interest | $ | (532,945 | ) | $ | (167,421 | ) | $ | (1,026,633 | ) | $ | (84,995) | |||||

| Other comprehensive (loss) | ||||||||||||||||

| Foreign currency translation income (loss) | (1,434 | ) | 6 | 5,798 | 1,171 | |||||||||||

| Comprehensive (loss) including noncontrolling interest | $ | (534,379 | ) | (167,415 | ) | $ | (1,026,835 | ) | (83,824 | ) | ||||||

| Less: Comprehensive (loss) attributable to noncontrolling interest | (1,470 | ) | (1,470 | ) | (2,953 | ) | (2,940 | ) | ||||||||

| Comprehensive (loss) attributable to American Education Center | $ | (532,909 | ) | $ | (165,945 | ) | $ | (1,017,882 | ) | $ | (80,884 | ) | ||||

| Income (loss) earnings per common share - basic and diluted | ||||||||||||||||

| Income (loss) from continuing operations | $ | (0.01 | ) | $ | (0.02 | ) | $ | (0.02 | ) | $ | (0.01 | ) | ||||

| (Loss) from discontinued operations | $ | - | $ | 0.01 | $ | - | $ | 0.02 | ||||||||

| Net income (loss) earnings per common share - basic and diluted | (0.01 | ) | (0.01 | ) | (0.02 | ) | 0.01 | |||||||||

| Weighted average shares | ||||||||||||||||

| Outstanding, basic and diluted | 55,957,769 | 56,058,483 | 55,957,769 | 56,058,483 | ||||||||||||

See accompanying notes to consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Six Months Ended June 30, | ||||||||

| 2020 | 2019 | |||||||

| Cash flows from operating activities: | ||||||||

| Net (loss) | $ | (1,026,633 | ) | $ | (84,995) | |||

| Loss from discontinued operation, net of income taxes | - | - | ||||||

| Adjustments to reconcile net (loss) including noncontrolling interest to net cash | ||||||||

| (Used in) operating activities: | ||||||||

| Deferred tax provision (benefit) | (303,692 | ) | 285,608 | |||||

| Stock-based compensation expense | 7,000 | 62,000 | ||||||

| Provision for doubtful accounts | 463,411 | 395,566 | ||||||

| Depreciation expense for fixed assets | 1,103 | - | ||||||

| Gain from disposal of the discontinued operation, net of income taxes | (561,807 | ) | ||||||

| Amortization expense for learning platform | 6,000 | 6,000 | ||||||

| Amortization expense | 68,090 | 68,090 | ||||||

| Change in operating assets and liabilities: | ||||||||

| in other assets and liabilities | 6,657 | 13,625 | ||||||

| in accounts receivable | 676,860 | (728,785 | ) | |||||

| in prepaid expenses | 26,517 | (124,186 | ) | |||||

| in security deposits | 2,548 | (18,249 | ) | |||||

| in accounts payable and accrued expenses | (278,483 | ) | (192,277 | ) | ||||

| in taxes payable | (62,368 | ) | 62,482 | |||||

| in deferred revenue | (120,500 | ) | 42,425 | |||||

| in advances from clients | - | (23,526 | ) | |||||

| Net cash (used in) continuing operating activities | (533,490 | ) | (798,029 | ) | ||||

| Net cash (used in) discontinued operating activities | - | - | ||||||

| Net cash (used in) operating activities | (533,490 | ) | (798,029 | ) | ||||

| Cash flows from financing activities: | ||||||||

| (Repayment) of short-term loan | (98,434 | ) | - | |||||

| Proceeds from SBA Loan | 236,588 | - | ||||||

| Loan from stockholder | 283,082 | 580,867 | ||||||

| Net cash provided by continuing financing activities | 421,236 | 580,867 | ||||||

| Net cash provided by discontinued financing activities | - | - | ||||||

| Net cash provided by financing activities | 421,236 | 580,867 | ||||||

| Effect of exchange rates changes on cash | (574 | ) | 1,171 | |||||

| Net change in cash | (112,828 | ) | (215,991 | ) | ||||

| Cash at beginning of period | 1,035,395 | 1,985,133 | ||||||

| Cash at end of period | $ | 922,567 | $ | 1,769,142 | ||||

| Less cash of discontinued operations - end of period | - | - | ||||||

| Cash of continuing operations - end of period | 922,567 | 1,769,142 | ||||||

| Supplemental disclosure of cash flow information | ||||||||

| Cash paid for income taxes | $ | 12,696 | $ | 30,162 | ||||

| Cash paid for interest | $ | 1,566 | $ | 10,918 | ||||

See accompanying notes to consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (UNAUDITED)

| FOR THE SIX MONTHS ENDED JUNE 30, 2020 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||||||||||||||||||

| Additional | other | |||||||||||||||||||||||||||||||||||||||||||||||

| Common stock | Series B Preferred Stock | paid-in | Treasury Stock | Subscription | Retained | comprehensive | Noncontrolling | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | capital | Shares | Amount | Receivables | earnings | income | Interest | Total | |||||||||||||||||||||||||||||||||||||

| January 1, 2020 | 55,797,113 | $ | 56,797 | 25,000,000 | $ | 25,000 | $ | 8,267,930 | 1,000,000 | $ | (660,000 | ) | $ | (592,305 | ) | $ | (5,924,231 | ) | $ | (4,678 | ) | $ | 49,980 | $ | 1,218,493 | |||||||||||||||||||||||

| Net loss | (492,205 | ) | (1,483 | ) | (493,688 | ) | ||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock for services | 700,000 | 700 | 6,300 | 7,000 | ||||||||||||||||||||||||||||||||||||||||||||

| Foreign currency translation income | 7,232 | 7,232 | ||||||||||||||||||||||||||||||||||||||||||||||

| March 31, 2020 | 56,497,113 | $ | 57,497 | 25,000,000 | $ | 25,000 | $ | 8,274,230 | 1,000,000 | $ | (660,000 | ) | $ | (592,305 | ) | $ | (6,416,436 | ) | $ | 2,554 | $ | 48,497 | $ | 739,037 | ||||||||||||||||||||||||

| Net loss | (531,475 | ) | (1,470 | ) | (532,945 | ) | ||||||||||||||||||||||||||||||||||||||||||

| Foreign currency translation income | (1,434 | ) | (1,434 | ) | ||||||||||||||||||||||||||||||||||||||||||||

| June 30, 2020 | 56,497,113 | $ | 57,497 | 25,000,000 | $ | 25,000 | $ | 8,274,230 | 1,000,000 | $ | (660,000 | ) | $ | (592,305 | ) | $ | (6,947,911 | ) | $ | 1,120 | $ | 47027 | $ | 204,658 | ||||||||||||||||||||||||

See accompanying notes to consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (UNAUDITED)

| FOR THE SIX MONTHS ENDED JUNE 30, 2019 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||||||||||||||||||

| Additional | other | |||||||||||||||||||||||||||||||||||||||||||||||

| Common stock | Series B Preferred Stock | paid-in | Treasury Stock | Subscription | Retained | comprehensive | Noncontrolling | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | capital | Shares | Amount | Receivables | earnings | income | Interest | Total | |||||||||||||||||||||||||||||||||||||

| January 1, 2019 | 56,597,113 | $ | 56,597 | 25,000,000 | $ | 25,000 | $ | 8,206,130 | $ | - | $ | (719,911 | ) | $ | (5,714,688 | ) | $ | (13,865 | ) | $ | 55,860 | $ | 1,895,123 | |||||||||||||||||||||||||

| Net income | 83,896 | (1,470 | ) | 82,426 | ||||||||||||||||||||||||||||||||||||||||||||

| Foreign currency translation income | 1165 | 1165 | ||||||||||||||||||||||||||||||||||||||||||||||

| March 31, 2019 | 56,597,113 | 56,597 | 25,000,000 | 25,000 | 8,206,130 | - | - | (719,911 | ) | (5,633,732 | ) | (12,700 | ) | 54,390 | 1,978,714 | |||||||||||||||||||||||||||||||||

| Realization upon disposal of subsidiary by reacquiring stock | (1,000,000 | ) | 1,000,000 | (660,000 | ) | 1,062,541 | 402,541 | |||||||||||||||||||||||||||||||||||||||||

| Net income | (165,951 | ) | (1,470 | ) | (167,421 | ) | ||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock for services | 200,000 | 200 | 61,800 | 62,000 | ||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock for cash | 143,982 | 143,982 | ||||||||||||||||||||||||||||||||||||||||||||||

| Foreign currency translation income | 6 | 6 | ||||||||||||||||||||||||||||||||||||||||||||||

| June 30, 2019 | 55,797,113 | 56,797 | 25,000,000 | $ | 25,000 | $ | 8,267,930 | 1,000,000 | $ | (660,000 | ) | $ | (575,929 | ) | $ | (4,734,202 | ) | $ | (12,694 | ) | $ | 52,920 | $ | 2,419,822 | ||||||||||||||||||||||||

See accompanying notes to consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| September 30, | December 31, | |||||||

| ASSETS | 2017 | 2016 | ||||||

| (Unaudited) | ||||||||

| Current assets: | ||||||||

| Cash | $ | 1,609,945 | $ | 2,290,429 | ||||

| Accounts receivable, net of allowance for doubtful accounts of $108,300 and $63,000 | 6,604,059 | 2,887,837 | ||||||

| at September 30, 2017 and December 31, 2016, respectively | ||||||||

| Prepaid expenses | 92,787 | 61,600 | ||||||

| Total current assets | 8,306,791 | 5,239,866 | ||||||

| Noncurrent assets: | ||||||||

| Deferred compensation | 2,437,501 | 3,315,001 | ||||||

| Deferred income taxes | 33,436 | 97,936 | ||||||

| Intangible asset, net | 476,633 | 578,769 | ||||||

| Security deposits | 266,021 | 266,021 | ||||||

| Total noncurrent assets | 3,213,591 | 4,257,727 | ||||||

| TOTAL ASSETS | $ | 11,520,382 | $ | 9,497,593 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued expenses | $ | 4,067,358 | $ | 3,452,231 | ||||

| Taxes payable | 826,370 | 511,355 | ||||||

| Deferred revenue | 100,000 | 177,132 | ||||||

| Loan from stockholders | 113,906 | 113,906 | ||||||

| Total current liabilities | 5,107,634 | 4,254,624 | ||||||

| Noncurrent liabilities: | ||||||||

| Deferred rent | 182,510 | 155,707 | ||||||

| Long-term loan | 295,579 | 295,579 | ||||||

| Total liabilities | 5,585,723 | 4,705,910 | ||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $0.001 par value; | ||||||||

| 20,000,000 shares authorized; none issued | - | - | ||||||

| Common stock, $0.001 par value; | ||||||||

| 180,000,000 shares authorized; 41,350,000 shares issued and outstanding | ||||||||

| at September 30, 2017 and December 31, 2016 | 41,350 | 41,350 | ||||||

| Additional paid-in capital | 4,021,626 | 4,021,626 | ||||||

| Retained earnings | 1,867,080 | 728,707 | ||||||

| Accumulated other comprehensive income | 4,603 | - | ||||||

| Total stockholders' equity | 5,934,659 | 4,791,683 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 11,520,382 | $ | 9,497,593 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (UNAUDITED)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Revenues | $ | 5,215,743 | $ | 969,959 | $ | 20,379,142 | $ | 4,880,614 | ||||||||

| Cost of revenues | 3,890,800 | 794,273 | 13,670,929 | 3,899,032 | ||||||||||||

| Gross profit | 1,324,943 | 175,686 | 6,708,213 | 981,582 | ||||||||||||

| Operating expenses: | ||||||||||||||||

| Selling and marketing | 750,565 | 48,465 | 3,320,568 | 180,612 | ||||||||||||

| General and administrative | 656,317 | 257,606 | 1,862,901 | 985,373 | ||||||||||||

| Total operating expenses | 1,406,882 | 306,071 | 5,183,469 | 1,165,985 | ||||||||||||

| Income (loss) from operations | (81,939 | ) | (130,385 | ) | 1,524,744 | (184,403 | ) | |||||||||

| Other income | 82 | 2,409 | 84 | 7,602 | ||||||||||||

| Income (loss) before provision for income taxes | (81,857 | ) | (127,976 | ) | 1,524,828 | (176,801 | ) | |||||||||

| Provision for (benefit from) income taxes | (78,803 | ) | (76,028 | ) | 386,455 | (92,770 | ) | |||||||||

| Net income (loss) | $ | (3,054 | ) | $ | (51,948 | ) | $ | 1,138,373 | $ | (84,031 | ) | |||||

| Other comprehensive income | ||||||||||||||||

| Foreign currency translation gain | 4,603 | - | 4,603 | - | ||||||||||||

| Comprehensive income | $ | 1,549 | $ | (51,948 | ) | $ | 1,142,976 | (84,031 | ) | |||||||

| Earnings per share - basic and diluted | $ | (0.00 | ) | $ | (0.00 | ) | $ | 0.03 | $ | (0.00 | ) | |||||

| Weighted average shares | ||||||||||||||||

| outstanding, basic and diluted | 41,350,000 | 31,558,889 | 41,350,000 | 30,584,000 | ||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Nine Months Ended September 30, | ||||||||

| 2017 | 2016 | |||||||

| Cash flows from operating activities: | ||||||||

| Net income (loss) | $ | 1,138,373 | $ | (84,031 | ) | |||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||

| Deferred tax provision (benefit) | 64,500 | (73,719 | ) | |||||

| Deferred rent expense | 26,803 | 36,877 | ||||||

| Deferred compensation | 877,500 | - | ||||||

| Provision for doubtful accounts | 45,300 | - | ||||||

| Stock issued for services | - | 95,500 | ||||||

| Amortization expense | 102,136 | - | ||||||

| Change in operating assets and liabilities: | ||||||||

| (Increase) decrease in accounts receivable | (3,761,522 | ) | 317,242 | |||||

| (Increase) decrease in prepaid expenses | (31,187 | ) | 79,830 | |||||

| Increase (decrease) in accounts payable and accrued expenses | 615,127 | (692,502 | ) | |||||

| Increase (decrease) in taxes payable | 315,015 | (31,574 | ) | |||||

| Decrease in deferred revenue | (77,132 | ) | (553,624 | ) | ||||

| Increase in advances from clients | - | 93,790 | ||||||

| Net cash used in operating activities | (685,087 | ) | (812,211 | ) | ||||

| Effect of exchange rates changes on cash | 4,603 | - | ||||||

| Net change in cash | (680,484 | ) | (812,211 | ) | ||||

| Cash at beginning of period | 2,290,429 | 1,093,755 | ||||||

| Cash at end of period | $ | 1,609,945 | $ | 281,544 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Cash paid for income taxes | $ | 6,940 | $ | - | ||||

| Cash paid for interest | $ | 14,778 | $ | 22,167 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

AMERICAN EDUCATION CENTER, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (UNAUDITED)

FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2017

| Accumulated | ||||||||||||||||||||||||

| Additional | other | |||||||||||||||||||||||

| Common stock | paid-in | Retained | comprehensive | |||||||||||||||||||||

| Shares | Amount | capital | earnings | income | Total | |||||||||||||||||||

| Balance as of December 31, 2016 | 41,350,000 | $ | 41,350 | $ | 4,021,626 | $ | 728,707 | $ | - | $ | 4,791,683 | |||||||||||||

| Net income | - | - | - | 1,138,373 | - | 1,138,373 | ||||||||||||||||||

| Foreign currency translation gain | - | - | - | - | 4,603 | 4,603 | ||||||||||||||||||

| Balance as of September 30, 2017 | 41,350,000 | $ | 41,350 | $ | 4,021,626 | $ | 1,867,080 | $ | 4,603 | $ | 5,934,659 | |||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARies

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 1. | ORGANIZATION AND BUSINESS |

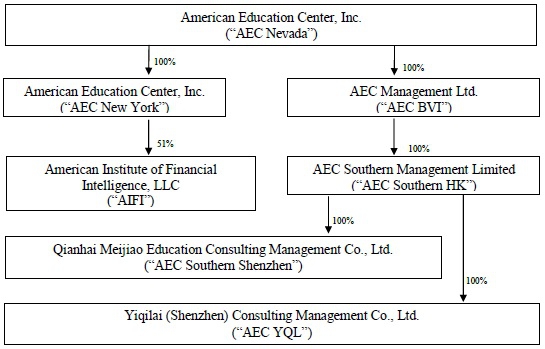

American Education Center, Inc. (“AEC New York”) is a New York Corporation organizedcorporation incorporated on November 8, 1999 and is licensed by the Education Department of the State of New York to engage in education related consulting services.

On May 7, 2014, the President and then sole shareholder of AEC New York formed a new company, (“AEC Nevada”)American Education Center, Inc. in the State of Nevada with the same name.(“AEC Nevada”). On May 31, 2014, the President and thenthe sole shareholder of AEC New York exchanged his 200 shares for 10,563,000 shares of AEC Nevada. The share exchange resulted in AEC New York becoming a wholly owned subsidiary of AEC Nevada (hereinafter the “Company”).

On October 31, 2016, the Company completed an acquisition transaction through a share exchange with two stockholders, Rongxia Wang and Ye Tian, of AEC Southern Management Co., Ltd. (“AEC Southern UK”), a company incorporatedformed in December 2015 with a registered capital of 10,000 British Pounds pursuant to the laws of England and Wales. The Company acquired 100% of the outstanding shares of AEC Southern UK in exchange for 1,500,000 shares of its common stock valued at $210,000. Prior to October 31, 2016, Ye Tian and Rongxia Wang held 51% and 49%, respectively, ownership interest in AEC$210,000 (the “AEC Southern UK.UK Share Exchange”). As a result of the acquisition,AEC Southern UK Share Exchange, AEC Southern UK became a wholly owned subsidiary of the Company.

AEC Southern UK holdsheld 100% of the equity interestinterests in AEC Southern Management Limited, a Hong Kong company (“AEC Southern HK”) incorporatedformed on December 29, 2015, with a registered capital of HK$10,000.2015. AEC Southern HK owns 100% equity interest inthen formed Qianhai Meijiao Education Consulting Management Co., Ltd., a foreign wholly owned subsidiary incorporated pursuant to the PRC laws (“AEC Southern Shenzhen”) on March 29, 2016 pursuant to PRC laws, with a registered capital of RMB 5,000,000.

Therefore, under PRC laws, AEC Southern Shenzhen was a foreign wholly owned subsidiary of AEC Southern UK.

The Company’s corporate structureOn July 13, 2018, pursuant to a Business Purchase Agreement (the “Purchase Agreement”), the Company acquired 51% of the issued and outstanding equity interests of American Institute of Financial Intelligence LLC (“AIFI”), a New Jersey limited liability company formed on May 10, 2017, in exchange for 100,000 shares of the Company common stock issued to the then sole shareholder of AIFI. As a result, AIFI became a 51% majority owned subsidiary of the Company.

On October 23, 2018, AEC Nevada incorporated a subsidiary, AEC Management Ltd. (“AEC BVI”) in the British Virgin Islands, pursuant to the laws of British Virgin Islands. AEC BVI is a wholly owned subsidiary of AEC Nevada, and as follows:of the date of this report, does not have significant business activities.

On April 22, 2019, AEC Southern UK sold 100% of the equity interests of AEC Southern HK to AEC BVI and AEC Southern HK and its subsidiary became wholly-owned subsidiaries of AEC BVI.

On May 1, 2019, the Company sold 100% of the equity interest in AEC Southern UK to three individuals who were Ye Tian, Rongxia Wang and Weishou Li, and received a consideration of 1,000,000 shares of outstanding shares of AEC Nevada.

On May 22, 2020, AEC Southern HK formed Yiqilai (Shenzhen) Consulting Management Co., Ltd. (“AEC YQL”) in Shenzhen, China on May 22, 2020 pursuant to PRC laws. AEC YQL is a wholly owned subsidiary of AEC Southern HK, and as of the date of this report, does not have significant business activities.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARies

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 1. | ORGANIZATION AND BUSINESS (continued) |

Headquartered in New York with operations in the PRC (People’sPeople’s Republic of China)China (“PRC”), the Company covers two market segments:segments through two subsidiaries:

| (1) | AEC New York capitalizes on the rising demand |

| (2) | AEC AEC Southern is all generated from AEC Southern Shenzhen. |

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARies

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Basis of Consolidation and Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”). These unaudited condensed consolidated financial statements include the accounts of the Company and its subsidiaries. All significant intercompany transactions and balances have been eliminated in consolidation. In the opinion of management, all adjustments considered necessary to give a fair presentation have been included.

Interim results are not necessarily indicative of full-year results. Certain prior year balances have been reclassified to conform to the current year'syear’s presentation; none of these reclassifications had an impact on reported financial position or cash flows for any of the periods presented. The information in this Form 10-Q should be read in conjunction with information included in the Company’s annual report on Form 10-K for the fiscal year ended December 31, 20162019 filed with the SEC on April 17, 2017.SEC.

Cash

Cash consists of all cash balances and liquid investments with an original maturity of three months or less to beare considered as cash equivalents.

Accounts Receivable

Accounts receivable are carried at net realizable value. The Company maintains an allowance for doubtful account,accounts, periodically evaluates its accounts receivable balances and makes general and/or specific allowances when there is doubt as to their collectability. In evaluating the collectability of individual receivable balances, the Company considers many factors, including the age of the balances, customers’ historical payment history, their current credit-worthiness and current economic trends. Accounts receivable are written off against the allowance only after exhaustive collection efforts. At September 30, 2017 and December 31, 2016, the allowance for doubtful accounts was $108,300 and $63,000, respectively.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 2016

2019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Foreign Currency Translation

The Company’s functional currency is US dollars. The companyCompany has onethree bank accountaccounts located in the PRC.PRC and one located in Hong Kong. Translation adjustments arising from the use of different exchange rates, in the circumstance any subsidiary’s functional currency is not US dollars, from period to period are included as a separate component of accumulated other comprehensive income included in statements of changes in stockholders’ equity. Gain and losses from foreign currency transactions are included in the condensed consolidated statements of operations and comprehensive income.

Revenue Recognition

RevenueThe Company adopted ASU No. 2014-09, Topic 606 on January 1, 2018, using the modified retrospective method. ASC 606 requires the use of a new five-step model to recognize revenue from customer contracts. The five-step model requires that the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is recorded pursuantprobable that a significant future reversal will not occur, (iv) allocate the transaction price to Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 605, “Revenue Recognition,”the respective performance obligations in the contract, and (v) recognize revenue when persuasive evidence of an arrangement exists, delivery of(or as) the services has occurred,Company satisfies the fee is fixed or determinable and collectability is reasonably assured.performance obligation.

AEC New York delivers customized high school and college placement, career advisory as well as student and family services. Fees related to such advisory services that are collected from individuals are generally paid to the Company in advance and they are recorded as deferred revenue. Revenues are recognized proportionally as services are rendered or upon completion. Fees related to our advisory services provided by AEC New York to corporate customers (such as staffing agencies and placement agencies) are generally collected after services are provided, and are recorded as accounts receivable.

AEC Shenzhen delivers customized high school and college placement and career advisory services. Fees related to such advisory services are generally paid to the Company in advance and they are recorded as deferred revenue. Revenues are recognized proportionally as services are rendered or upon completion.

AEC Southern UK delivers customized compliance trainingFor the six months ended June 30, 2020, approximately $104,000, or more than 38%, of the revenue was realized as accounts receivable and advisory services. It receives monthly non-refundable retainer paymentsapproximately $120,000 of the revenue was realized from services completed.

Property and recognizes revenue when servicesequipment, net

Property and equipment are rendered.stated at cost less accumulated depreciation. Depreciation is computed using the straight-line method over the estimated useful lives of the assets. The estimated useful lives are as follows:

| Estimated useful lives (years) | ||||

| Office furniture | 5 | |||

| Electronic equipment | 3 | |||

Intangible Asset

The Company’s finite-lived intangible asset consists of a customized online campus system that was acquired from a third party. The system is used to provide online training for career advisory services and compliancecorporate training and advisory services. The asset was recorded at cost on the acquisition date and is amortized on a straight-line basis over its economic useful life.

The Company reviews its finite-lived intangible asset for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of the asset to be held and used is measured by a comparison of the carrying amount of an asset to its undiscounted future net cash flows expected to be generated by the asset. If such asset is not recoverable, a potential impairment loss is recognized to the extent the carrying amount of the asset exceeds its fair value. Fair value is generally determined using a discounted cash flow approach.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Stock-Based Compensation

The Company uses the fair value-based method for stock issued for services rendered and therefore all awards to employees and non-employees will be recorded at the market price on the date of the grant and expensed over the required period of services to be rendered.

The fair value of stock options issued to third party consultants and to employees, officers and directors are recorded in accordance with the measurement and recognition criteria of FASB ASC 505-50, “Equity-Based“Equity-Based Payments to Non-Employees”Non-Employees” and FASB ASC 718, “Compensation“Compensation – Stock Based Compensation,,” respectively.

The options are valued using the Black-Scholes valuation model. This model is affected by the Company’s stock price as well as assumptions regarding a number of subjective variables. These subjective variables include but are not limited to the Company’s expected stock price volatility over the expected term of the awards, and actual and projected stock option and warrant exercise behaviors and forfeitures.

Income Taxes

The Company accounts for income taxes in accordance with FASB ASC 740, “Income“Income Taxes,” which requires the recognition of deferred income taxes for differences between the basis of assets and liabilities for financial statement and income tax purposes. Deferred tax assets and liabilities represent the future tax consequences for those differences, which will either be taxable or deductible when the assets and liabilities are recovered or settled. Deferred taxes are also recognized for operating losses that are available to offset future taxable income. A valuation allowance is established when necessary to reduce deferred tax assets to the amount expected to be realized.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Income Taxes (continued)

ASC 740 also addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements. Under ASC 740, the Company may recognize the tax benefit from an uncertain tax position only if it is “more likely than not” that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position would be measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement. ASC 740 also provides guidance on derecognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, and accounting for interest and penalties associated with tax positions. At SeptemberJune 30, 20172020 and December 31, 2016,2019, the Company does not have a liability for any unrecognized tax benefits.

The income tax laws of various jurisdictions in which the Company and its subsidiaries operate are summarized as follows:

United States (“US”)

On December 22, 2017, the U.S. Tax Cuts and Jobs Act (TCJA) was signed into law. The TCJA results in significant revisions to the U.S. corporate income tax system, including a reduction in the U.S. corporate income tax rate, implementation of a territorial system and a one-time deemed repatriation tax on untaxed foreign earnings. Generally, the impacts of the new legislation would be required to be recorded in the period of enactment.

The Company is subject to Federal corporate income tax in the US at 34%21%. Provisions for income taxes infor the United States have been made for taxable income the Company had in the US for the three and ninesix months ended SeptemberJune 30, 2017 and 2016.2020.

United KingdomBritish Virgin Island (“UK”BVI”)

According to BVI corporate taxation, there is a zero-rated income tax regime for all BVI-domiciled corporate entities, and there is no concept of residence applicable to BVI corporate taxation.

AEC Southern UKBVI was incorporated in the United KingdomBVI and is governed by the income tax laws of England and Wales. According to current England and Wales income tax law, the applicable income tax rate for AEC Southern UK is 20%.BVI.

Hong Kong

AEC Southern HK was formed in Hong Kong. Pursuant to the income tax laws of Hong Kong, the Company is not subject to tax on non-Hong Kong source income.

The People's Republic of China (“PRC”)

AEC Southern Shenzhen was incorporated in the PRC. Pursuant to the income tax laws of China, the Company is not subject to tax on non-China source income. The Company is subject to corporate tax in China at 25% for the net taxable income. AEC Southern Shenzhen has no income tax for the six months ended June 30, 2020 due to the net operating loss for the period.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

The provisions of ASC 740-10-25, “Accounting for Uncertainty in Income Taxes,” prescribe a more-likely-than-not threshold for consolidated financial statement recognition and measurement of a tax position taken (or expected to be taken) in a tax return. This ASC also provides guidance on the recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, and related disclosures.

Fair Value Measurements

FASB ASC 820, “Fair“Fair Value Measurement,,” specifies a hierarchy of valuation techniques based upon whether the inputs to those valuation techniques reflect assumptions other market participants would use based upon market data obtained from independent sources (observable inputs). In accordance with ASC 820, the following summarizes the fair value hierarchy:

Level 1 Inputs – Unadjusted quoted market prices for identical assets and liabilities in an active market that the Company has the ability to access.

Level 2 Inputs – Inputs other than the quoted prices in active markets that are observable either directly or indirectly.

Level 3 Inputs – Inputs based on prices or valuation techniques that are both unobservable and significant to the overall fair value measurements.

| Level 1 Inputs – | Unadjusted quoted market prices for identical assets and liabilities in an active market that the Company has the ability to access. | |

| Level 2 Inputs – | Inputs other than the quoted prices in active markets that are observable either directly or indirectly. | |

| Level 3 Inputs – | Inputs based on prices or valuation techniques that are both unobservable and significant to the overall fair value measurements. |

FASB ASC 820 requires the use of observable market data, when available, in making fair value measurements. When inputs used to measure fair value fall within different levels of the hierarchy, the level within which the fair value measurement is categorized is based on the lowest level input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs.

The Company did not identify any assets or liabilities that are required to be presented at fair value on a recurring basis. Non-derivative financial instruments include cash, accounts receivable, prepaid expenses, accounts payable and accrued expenses, taxes payable, and loan from stockholders. At SeptemberAs of June 30, 20172020 and December 31, 2016,2019, respectively, the carrying values of these financial instruments approximated their fair values due to their short-term nature.

COVID-19 Outbreak

In March 2020 the World Health Organization declared coronavirus COVID-19 a global pandemic. The COVID-19 pandemic has negatively impacted the global economy, workforces, customers, and created significant volatility and disruption of financial markets. It has also disrupted the normal operations of many businesses, including ours. This outbreak could decrease spending, adversely affect demand for our services and harm our business and results of operations. It is not possible for us to predict the duration or magnitude of the adverse results of the outbreak and its effects on our business or results of operations at this time.

Use of Estimates

The preparation of the unaudited condensed consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions that affect certain reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

Earnings (Loss) per Share

Earnings (loss) per share is calculated in accordance with FASB ASC 260, “Earnings“Earnings Per Share.Share.” Basic earnings (loss) per share is based upon the weighted average number of common shares outstanding during the period. Diluted earnings per share is based on the assumption that all dilutive convertible shares and stock options are converted or exercised. Dilution is computed by applying the treasury stock method. Under this method, options and warrants are assumed to be exercised at the beginning of the period (or at the time of issuance, if later), and as if funds obtained thereby were used to purchase common stock at the average market price during the period. Options and warrants are only dilutive when the average market price of the underlying common stock exceeds the exercise price of the options or warrants because it is unlikely that they would be exercised if the exercise price were higher than the market price.

Noncontrolling interest

According to Financial Accounting Standards Board (FASB) Statement No. 160, the noncontrolling interest shall be reported in the consolidated statement of financial position within equity, separately from the parent’s equity. That amount shall be clearly identified and labeled, for example, as noncontrolling interest in subsidiaries. An entity with noncontrolling interests in more than

one subsidiary may present those interests in aggregate in the consolidated financial statements。

Bargain Purchase

According to Financial Accounting Standards Board (FASB) Accounting Standards, a barging purchase is defined as a business combination in which the total acquisition-date fair value of the identifiable net assets acquired exceeds the fair value of the consideration transferred plus any noncontrolling interest in the acquiree, and it requires the acquirer to recognize that excess in earnings as a gain attributable to the acquire.

Contingent Consideration

The Company recognizes the fair value of any contingent consideration that is transferred to the seller in a business combination on the date at which control of the acquiree is obtained. This value is generally determined through a probability-weighted analysis of the expected cash flows.

Contingent consideration is classified as a liability or as equity on the basis of the definitions of an equity instrument and a financial liability. The contingent consideration is payable in cash and, accordingly, the Company classified its contingent consideration as a liability. It is not remeasured, and any gain or loss on settlement at an amount different from its carrying value will be recognized in net income in the period during which it is settled.

Leases

On January 1, 2019, the Company adopted Accounting Standards Update No. 2016-02, Leases (Topic 842) (ASU 2016-02), as amended, which supersedes the lease accounting guidance under Topic 840, and generally requires lessees to recognize operating and financing lease liabilities and corresponding right-of-use (ROU) assets on the balance sheet and to provide enhanced disclosures surrounding the amount, timing and uncertainty of cash flows arising from leasing arrangements.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) |

The Company adopted the new guidance using the modified retrospective transition approach by applying the new standard to all leases existing at the date of initial application and not restating comparative periods. The most significant impact was the recognition of ROU assets and lease liabilities for operating leases, while accounting for finance leases remained substantially unchanged.

The Company determined if an arrangement is a lease at inception. Operating leases are included in operating lease right-of-use (“ROU”) assets and short- and long-term lease liabilities in our consolidated balance sheets. Finance leases are included in property and equipment, other current liabilities, and other long-term liabilities in our consolidated balance sheets.

As of adoption of ASC 842 and as of January 1, 2019, the Company was not a party to finance lease arrangements.

ROU assets represent the Company’s right to use an underlying asset for the lease term and lease liabilities represent the Company’s obligation to make lease payments arising from the lease. Operating lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. As most of the leases do not provide an implicit rate, the Company use the industry incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company use the implicit rate when readily determinable. The operating lease ROU asset also includes any lease payments made and excludes lease incentives. The lease terms may include options to extend or terminate the lease when it is reasonably certain that we will exercise that option. Lease expense for lease payments is recognized on a straight-line basis over the lease term.

Under the available practical expedient, the Company account for the lease and non-lease components as a single lease component.

Adoption of the standard resulted in the recognition of $2,016,142 of ROU assets and $2,237,583 of lease liabilities for leases on our consolidated balance sheet at adoption on January 1, 2019 related to office space lease commitment on March 1, 2015. The difference between the ROU assets and lease liabilities was due to prepaid rent. For a new lease commitment on May 1, 2019, the company initially recognized $414,157 (RMB2,899,099) of ROU assets and lease liabilities of $399,048 (RMB2,793,341). The difference between the ROU assets and lease liabilities was due to prepaid rent and initial direct cost.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2020 AND 2019

| 3. | RECENTLY ISSUED ACCOUNTING STANDARDS |

In May 2014,January 2017, the FASB issued Accounting Standards Update (the “ASU”) No. 2014-09, "Revenue from Contracts with Customers (Topic 606).'' This guidance supersedes current guidance on revenue recognition in Topic 605, "Revenue Recognition.'' In addition, there are disclosure requirements related toaccounting standard update which simplifies the nature, amount, timing, and uncertainty of revenue recognition. In August 2015, the FASB issued ASU No.2015-14 to defer the effective date of ASU No. 2014-09test for all entities by one year. For public business entities that follow U.S. GAAP, the deferral results in the new revenue standard being effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017, with early adoption permitted for interim and annual periods beginning after December 15, 2016. In March 2016, the FASB issued ASU No. 2016-12, “Revenue from Contracts with Customers,” with respect to Principal versus Agent Considerations. In April 2016, the FASB issued ASU No. 2016-12, “Revenue from Contracts with Customers,” with respect to Identifying Performance Obligations and Licensing. In April 2016, the FASB additionally issued ASU No. 2016-12, “Revenue from Contracts with Customers,” with respect to Narrow-Scope Improvements and Practical Expedients. In December 2016, the FASB issued ASU No. 2016-20, “Revenue from Contracts with Customers,” with respect to Technical Corrections and Improvements. The Company does not believe the adoption will have a material impact on its consolidated financial statements.

In April 2016, FASB issued ASU No. 2016-10, Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing. The amendments clarify the following two aspects of Topic 606: (a) identifying performance obligations; and (b) the licensing implementation guidance. The amendments do not change the core principle of the guidance in Topic 606. The effective date and transition requirements for the amendments are the same as the effective date and transition requirements in Topic 606. Public entities should apply the amendments for annual reporting periods beginning after December 15, 2017, including interim reporting periods therein (i.e., January 1, 2018, for a calendar year entity). Early application for public entities is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period. The Company does not anticipate that this adoption will have a significant impact on its consolidated financial position, results of operations, or cash flows.

In May 2016, the FASB issued ASU No. 2016-11,Revenue Recognition (Topic 605) and Derivatives and Hedging (Topic 815): Rescission of SEC Guidance Because of Accounting Standards Updates 2014-09 and 2014-16 Pursuant to Staff Announcements at the March 3, 2016 EITF Meeting, which is rescinding certain SEC Staff Observer comments that are codified in Topic 605, Revenue Recognition. The Company does not anticipate that this adoption will have a significant impact on its consolidated financial position, results of operations, or cash flows.

In May 2016, FASB issued ASU No. 2016-12, Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients, which is intended to not change the core principle of the guidance in Topic 606, but rather affect only the narrow aspects of Topic 606 by reducing the potential for diversity in practice at initial application and by reducinggoodwill impairment. To address concerns over the cost and complexity of applying Topic 606 both at transitionthe two-step goodwill impairment test, the amendments in this update remove the second step of the test. An entity will apply a one-step quantitative test and on an ongoing basis.record the amount of goodwill impairment as the excess of a reporting unit's carrying amount over its fair value, not to exceed the total amount of goodwill allocated to the reporting unit. The Companynew guidance does not anticipate that this adoption will have a significant impact on its consolidated financial position, resultsamend the optional qualitative assessment of operations, or cash flows.

In February 2016, the FASB issued ASU 2016-02, “Leases.” The new standard establishes a right-of-use (“ROU”) model that requires a lessee to record a ROU asset and a lease liability on the balance sheet for all leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. The new standard is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. A modified retrospective transition approach is required for lessees for capital and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. The Company is currently evaluating the impact of pending adoption of the new standard on its consolidated financial statements.

In March 2016, the FASB issued ASU 2016-09, Compensation – Stock Compensation (ASC 718): Improvements to Employee Share-Based Payment Accounting. The objective is to identity, evaluate, and improve areas of generally accepted accounting principles (GAAP) for which cost and complexity can be reduced while maintaining or improving the usefulness of the information provided to users of financial statements. The areas for simplification include the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. Some of the areas apply only to nonpublic entities. For public business entities, the ASUgoodwill impairment. This update is effective for annual periods beginning after December 15, 2016, and interim periods within those annual periods. For all other entities, the ASU is effective for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018. Early adoption is permitted for any entity inor any interim or annual period. If an entity early adopts the amendmentsgoodwill impairment tests in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period. An entity that elects early adoption must adopt all of the amendments in the same period. The adoption of ASU 2016-09 did not impact our consolidated financial statements.

In May 2017, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2017-09, Scope of Modification Accounting, which amends the scope of modification accounting for share-based payment arrangements and provides guidance on the types of changes to the terms or conditions of share-based payment awards to which an entity would be required to apply modification accounting under ASC 718. For all entities, this ASU is effective for annual reporting periods, including interim periods within those annual reporting periods, beginning after December 15, 2017. Early adoption is permitted, including adoption in any interim period. The adoption of this ASU is not expected to have a material effect on its consolidated financial statements.

In August 2016, the FASB has issued ASU No. 2016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments, to address diversity in how certain cash receipts and cash payments are presented and classified in the statement of cash flows. The amendments provide guidance on the following eight specific cash flow issues: (1) Debt Prepayment or Debt Extinguishment Costs; (2) Settlement of Zero-Coupon Debt Instruments or Other Debt Instruments with Coupon Interest Rates That Are Insignificant in Relation to the Effective Interest Rate of the Borrowing; (3) Contingent Consideration Payments Made after a Business Combination; (4) Proceeds from the Settlement of Insurance Claims; (5) Proceeds from the Settlement of Corporate-Owned Life Insurance Policies, including Bank-Owned; (6) Life Insurance Policies; (7) Distributions Received from Equity Method Investees; (8) Beneficial Interests in Securitization Transactions; and Separately Identifiable Cash Flows and Application of the Predominance Principle. The amendments are effective for public business entities for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019. Early adoption is permitted includingfor interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. The Company adopted the update in the fourth quarter of 2018. The adoption of the new standard did not have an impact on our consolidated financial statements.

In October 2018, the FASB issued ASU 2018-17, Consolidation (Topic 810): Targeted Improvements to the Related Party Guidance for Variable Interest Entities. ASU 2018-17 changes how entities evaluate decision-making fees under the variable interest entity guidance. To determine whether decision-making fees represent a variable interest, an entity considers indirect interests held through related parties under common control on a proportional basis, rather than in an interim period. The amendments shouldtheir entirety. This guidance will be appliedadopted using a retrospective transition method to each period presented. If itapproach and is impracticable to applyeffective for the amendments retrospectively for some of the issues, the amendments for those issues would be applied prospectively as of the earliest date practicable.Company on January 1, 2020. The Company expects thathas evaluated the effect of the adoption of this ASU wouldand the standard did not have a materialan impact on the Company’sits consolidated financial statements.statements and related disclosures from the adoption of the new guidance.

In November 2016,December 2019, the FASB issued ASU No. 2016-18, Statement of Cash Flows: Restricted Cash. The amendments address diversity2019-12 - Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes. This ASU provides an exception to the general methodology for calculating income taxes in practicean interim period when a year-to-date loss exceeds the anticipated loss for the year. This update also (1) requires an entity to recognize a franchise tax (or similar tax) that existsis partially based on income as an income-based tax and account for any incremental amount incurred as a non-income-based tax, (2) requires an entity to evaluate when a step-up in the classificationtax basis of goodwill should be considered part of the business combination in which goodwill was originally recognized for accounting purposes and presentationwhen it should be considered a separate transaction, and (3) requires that an entity reflect the effect of changesan enacted change in restricted cash ontax laws or rates in the statement of cash flows.annual effective tax rate computation in the interim period that includes the enactment date. The amendmentstandard is effective for public companiesthe Company for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years.2020, with early adoption permitted. The Company does not anticipate that this adoption will have a significant impact on its consolidated financial position, resultsis currently in the process of operations, or cash flows.

In January 2017, the FASB issued ASU No. 2017-01, Business Combinations (Topic 805): Clarifying the definition of a business. The amendments in this ASU is to clarify the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The definition of a business affects many areas of accounting including acquisitions, disposals, goodwill, and consolidation. The amendments are effective for public business entities for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. For all other entities, the amendments in this ASU are effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019. The Company does not believe the adoption of this ASU would have a material effect on its consolidated financial statements.

In January 2017, the FASB issued ASU No. 2017-03, Accounting Changes and Error Corrections (Topic 250) and Investments—Equity Method and Joint Ventures (Topic 323). The amendments amended Accounting Changes and Error Corrections (Topic 250) to state that registrants should consider additional qualitative disclosures if the impact of an issued but not yet adopted ASU is unknown or cannot be reasonably estimated and to include a description of the effect of the accounting policies that the registrant expects to apply, if determined. Transition guidance included in certain issued but not yet adopted ASUs was also updated to reflect this amendment. The Company does not expect that the adoption of this guidance will have a material impact on its consolidated financial statements.

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 4. |

Activity in the allowance for doubtful accounts was as followings:

| June 30, | December 31, | |||||||

| 2020 | 2019 | |||||||

| Accounts receivable | $ | 4,802,194 | $ | 5,479,473 | ||||

| Allowance for bad debts | (3,068,759 | ) | (2,605,348 | ) | ||||

| Accounts receivable, net | $ | 1,733,435 | $ | 2,874,125 | ||||

| Balance, beginning of year | $ | 2,605,348 | $ | 1,189,147 | ||||

| Provision (net of recover) | 463,411 | 1,557,201 | ||||||

| Amounts written off, net of recoveries | - | (141,000 | ) | |||||

| Balance, end of year | $ | 3,068,759 | $ | 2,605,348 | ||||

| 5. | FIXED ASSET, NET |

As of June 30, 2020 and December 31, 2019, fixed asset, net as follows:

| June 30, | December 31, | |||||||

| 2020 | 2019 | |||||||

| Electronic equipment | $ | 6,103 | $ | 6194 | ||||

| Office furniture | 805 | 817 | ||||||

| Less: accumulated depreciation | (1,871 | ) | (785 | ) | ||||

| Fixed asset - net | $ | 5,037 | $ | 6,226 | ||||

For the three and six months ended June 30, 2020 and 2019, depreciation expense was $556 and $1,103, $0 and $0 respectively.

| 6. | INTANGIBLE ASSET, NET |

The gross carrying amount and accumulated amortization of this asset as of June 30, 2020 and December 31, 2019 are as follows:

June 30, | December 31, 2019 | |||||||

| Intangible asset: online campus system | $ | 612,814 | $ | 612,814 | ||||

| Intangible asset: learning platform | 120,000 | 120,000 | ||||||

| Less: accumulated amortization | (534,678 | ) | (460,588 | ) | ||||

| Intangible asset - net | $ | 198,136 | $ | 272,226 | ||||

The Company’s customized online campus system is being amortized on a straight-line basis over four and a half years. For the three and six months ended June 30, 2020 and 2019, amortization expense was $34,045, $74,090 and $37,045, $74,090, respectively.

The following table is the future amortization expense to be recognized:

| Year Ending December 31, | ||||

| 2020 | 74,091 | |||

| 2021 | 46,045 | |||

| 2022 | 12,000 | |||

| 2022 | 66,000 | |||

| 198,136 | ||||

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2020 AND 2019

| 7. | DEFERRED COMPENSATION |

On October 31, 2016, 1,500,000 shares of common stock of the Company were granted and issued to AEC Southern UK’s CEO who would provide service over a three-year period commencing November 1, 2016. The shares were valued using the market price of the Company’s common stock on the grant date of $0.14 per share. On the grant date, $210,000 was recognized as deferred compensation, which was expensed over the three-year period using the straight-line method. On December 31, 2017, the remaining balance of $198,333.33 deferred compensation was expensed due to the resignation of AEC Southern UK’s CEO.

On December 31, 2016, the Company granted and issued 6,000,000 shares of common stock to AEC Southern UK’s Chairman who would provide services over a three-year period commencing November 1, 2016. The shares were valued using the market price of the Company’s common stock on the grant date of $0.55 per share. On the grant date, $3,300,000 was recognized as deferred compensation, which was expensed over a three-year period using the straight-line method. The Company decided not to cancel or retrieve the shares issued to the CEO of AEC Southern UK as compensation and recognized the remaining of the compensation as part of the loss from disposal during 2019.

| 8. | SECURITY DEPOSITS |

The Company has security deposits with the landlord for its New York office and the office in Shenzhen, China of $282,215 and $285,041 as of June 30, 2020 and December 31, 2019 respectively. As of June 30, 2020, AEC New York has security deposits of $266,021 and AEC Shenzhen has security deposits of $16,194 (translation from RMB114,412).

| 9. | CONCENTRATION OF CREDIT AND BUSINESS RISK |

The Company maintains its cash accounts at two commercial banks in the US, three commercial banks in the USPRC and one commercial bank in the PRC and Hong Kong, respectively. The Federal Deposit Insurance Corporation covers fundsKong.

Funds held in US banks and it insuresinsured by Federal Deposit Insurance Corporation up to $250,000 per depositor, per insured bank, for each account ownership category.

Funds held in the PRC banks are covered by Deposit Insurance Ordinance (index: 000014349/2015-00031) that insures RMB500,000 for the total of all depository accounts. The

Funds held in HK banks are insured by Hong Kong Deposit Protection Board covers funds held in HK banks and it insuresup to HK$500,000 per bank for the total of all depository accounts. Fund held in the PRC bank is covered by Deposit Insurance Ordinance (index: 000014349/2015-00031) that insures CNY¥500,000 for the total of all depository accounts. At September 30, 2017, the Company’s US bank accounts had cash balances in excess of federally insured limits of approximately $409,000.

The Company performs ongoing evaluation of its financial institutions to limit its concentration of risk exposure. Management believes this risk is not significant due to the financial strength of the financial institutions utilized by the Company.

The following table represents major customers that individually accounted for more than 10% of the Company’s gross revenue for the ninesix months ended SeptemberJune 30, 20172020 and 2016:2019:

| 2017 | ||||||||||||||||

| Gross Revenue | Percentage | Accounts Receivable | Percentage | |||||||||||||

| Customer 1 | $ | 12,180,697 | 59.8 | % | $ | 3,376,689 | 51.1 | % | ||||||||

| Customer 2 | 2,826,640 | 13.9 | % | 2,244,716 | 34.0 | % | ||||||||||

| Customer 3 | 2,376,125 | 11.7 | % | 301,219 | 4.6 | % | ||||||||||

| June 30, 2020 | ||||||||||||||||

| Gross Revenue | Percentage | Accounts Receivable | Percentage | |||||||||||||

| Customer 1 | $ | 103,980 | 37.6 | % | $ | 1,582,433 | 33.6 | % | ||||||||

| 2016 | ||||||||||||||||

| Gross Revenue | Percentage | Accounts Receivable | Percentage | |||||||||||||

| Customer 1 | $ | 1,621,590 | 33.2 | % | $ | 468,650 | 58.8 | % | ||||||||

| Customer 2 | 814,000 | 16.7 | % | - | - | |||||||||||

| June 30, 2019 | ||||||||||||||||

| Gross Revenue | Percentage | Accounts Receivable | Percentage | |||||||||||||

| Customer 1 | $ | 1,611,820 | 51.3 | % | $ | 1,534,441 | 32.1 | % | ||||||||

| Customer 2 | 798,800 | 25.4 | % | 1,193,345 | 25.0 | % | ||||||||||

AMERICAN EDUCATION CENTER, Inc. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINESIX MONTHS ENDED SEPTEMBERJUNE 30, 20172020 AND 20162019

| 10. |

On May 1, 2019, AEC Nevada sold 100% of the equity interest in AEC Southern UK to three individuals, Ye Tian, Rongxia Wang and Weishou Li, and received a consideration of 1,000,000 shares of outstanding shares of AEC Nevada which was valued at $660,000 and the debt owed to AEC Southern UK in the amount of $268,475 was forgiven by AEC Southern UK. The Company has classified the results of AEC Southern UK as discontinued operations in the unaudited consolidated statement of income for all periods presented. The Company decided not to cancel or retrieve the shares issued to the CEO of AEC UK as compensation and recognized the remaining of the compensation as part of the loss from disposal. Additionally, the related assets and liabilities associated with the discontinued operations in the prior year consolidated balance sheet are classified as discontinued operations. The Company recognized a gain of $561,808 from the disposition.