Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Balance SheetsStatements of Operations

| March 31, 2019 | December 31, 2018 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Investment properties, net | $ | 45,837,106 | $ | 45,323,497 | ||||

| Cash | 1,269,765 | 1,327,424 | ||||||

| Restricted cash | 1,970,018 | 2,793,372 | ||||||

| Rent and other receivables, net of allowance of $4,191 and $15,194, as of March 31, 2019 and December 31, 2018, respectively | 96,604 | 108,478 | ||||||

| Unbilled rent | 344,542 | 259,216 | ||||||

| Advance deposits | 281,148 | 423,747 | ||||||

| Intangible assets, net | 2,368,067 | 2,585,834 | ||||||

| Interest rate cap, at fair value | 76,394 | 126,797 | ||||||

| Prepaid expenses | 153,595 | 158,687 | ||||||

| Total Assets | $ | 52,397,239 | $ | 53,107,052 | ||||

| LIABILITIES | ||||||||

| Accounts payable and accrued liabilities | $ | 1,125,045 | $ | 826,336 | ||||

| Intangible liabilities, net | 416,214 | 439,726 | ||||||

| Mortgages payable, net | 33,246,700 | 33,236,397 | ||||||

| Total Liabilities | $ | 34,787,959 | $ | 34,502,459 | ||||

| EQUITY | ||||||||

| Preferred stock, $.01 par value, 250,000,000 shares authorized, none issued and outstanding | $ | - | $ | - | ||||

| Common stock, $.01 par value, 750,000,000 shares authorized, 2,321,582 shares issued and outstanding at Common stock March 31, 2019 and December 31, 2018 | 23,216 | 23,216 | ||||||

| Additional paid-in capital | 22,077,827 | 22,077,827 | ||||||

| Offering costs | (1,974,118 | ) | (1,835,291 | ) | ||||

| Accumulated deficit | (5,916,399 | ) | (5,229,760 | ) | ||||

| Total Shareholders' Equity | 14,210,526 | 15,035,992 | ||||||

| Noncontrolling interests - Hampton Inn Property | 1,876,152 | 2,009,031 | ||||||

| Noncontrolling interests - Hanover Square Property | 588,238 | 608,943 | ||||||

| Noncontrolling interests - Operating Partnership | 934,364 | 950,627 | ||||||

| Total Equity | $ | 17,609,280 | $ | 18,604,593 | ||||

| Total Liabilities and Equity | $ | 52,397,239 | $ | 53,107,052 | ||||

(Unaudited)

| | | | | | | |

| | Three Months Ended | | ||||

| | March 31, | | ||||

|

| 2023 |

| 2022 |

| ||

| | | | | | | |

REVENUE |

| |

|

| |

| |

Retail center property revenues | | $ | 1,891,679 | | $ | 1,525,085 | |

Flex center property revenues | | | 569,297 | | | 613,390 | |

Hotel property room revenues | |

| — | |

| 762,200 | |

Hotel property other revenues | |

| — | |

| 3,289 | |

Total Revenue | | $ | 2,460,976 | | $ | 2,903,964 | |

| | | | | | | |

OPERATING EXPENSES | |

|

| |

|

| |

Retail center property operating expenses | | $ | 520,615 | | $ | 450,125 | |

Flex center property operating expenses | | | 176,737 | | | 161,381 | |

Hotel property operating expenses | |

| — | |

| 372,860 | |

Bad debt expense | | | 27,122 | | | 12,783 | |

Share based compensation expenses | |

| — | |

| 233,100 | |

Legal, accounting and other professional fees | |

| 767,078 | |

| 459,869 | |

Corporate general and administrative expenses | |

| 117,049 | |

| 80,706 | |

Loss on impairment | |

| 36,743 | |

| 36,670 | |

Impairment of assets held for sale | | | — | | | 175,671 | |

Depreciation and amortization | |

| 1,156,348 | | | 1,155,197 | |

Total Operating Expenses | |

| 2,801,692 | |

| 3,138,362 | |

Operating loss | |

| (340,716) | |

| (234,398) | |

Interest expense | |

| 864,052 | |

| 841,424 | |

Net Loss from Operations | |

| (1,204,768) | |

| (1,075,822) | |

Other (loss) income | |

| (29,038) | |

| 95,439 | |

Net Loss | |

| (1,233,806) | |

| (980,383) | |

Less: Net loss attributable to Hanover Square Property noncontrolling interests | | | (1,241) | | | (319) | |

Less: Net (loss) income attributable to Parkway Property noncontrolling interests | |

| (8,367) | |

| 10,193 | |

Less: Net loss attributable to Operating Partnership noncontrolling interests | |

| (2,903) | |

| (973) | |

Net Loss Attributable to Medalist Common Shareholders | | $ | (1,221,295) | | $ | (989,284) | |

| | | | | | | |

Loss per share from operations - basic and diluted | | $ | (0.07) | | $ | (0.06) | |

| | | | | | | |

Weighted-average number of shares - basic and diluted | |

| 17,758,421 | |

| 16,037,073 | |

| | | | | | | |

Dividends paid per common share | | $ | 0.01 | | $ | 0.02 | |

See notes to condensed consolidated financial statements.statements

4

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of OperationsStockholders’ Equity

(Unaudited)For the three months ended March 31, 2023 and 2022

| Three Months Ended | ||||||||

| March 31, | ||||||||

| 2019 | 2018 | |||||||

| REVENUE | ||||||||

| Retail center property revenues | $ | 750,820 | $ | 384,502 | ||||

| Retail center property tenant reimbursements | 143,174 | 72,369 | ||||||

| Hotel property room revenues | 630,035 | 733,566 | ||||||

| Hotel property other revenues | 14,453 | 12,413 | ||||||

| Total Revenue | $ | 1,538,482 | $ | 1,202,850 | ||||

| OPERATING EXPENSES | ||||||||

| Retail center property operating expenses | $ | 269,275 | $ | 192,681 | ||||

| Hotel property operating expenses | 581,975 | 563,054 | ||||||

| Legal, accounting and other professional fees | 353,747 | 212,179 | ||||||

| Corporate general and administrative expenses | 55,705 | 2,305 | ||||||

| Depreciation and amortization | 566,163 | 393,964 | ||||||

| Total Operating Expenses | 1,826,865 | 1,364,183 | ||||||

| Operating Loss | (288,383 | ) | (161,333 | ) | ||||

| Interest expense | 506,074 | 424,281 | ||||||

| Net Loss from Operations | (794,457 | ) | (585,614 | ) | ||||

| Other income | 4,374 | - | ||||||

| Decrease (increase) in fair value - interest rate cap | 50,403 | (74,289 | ) | |||||

| Net Loss | (840,486 | ) | (511,325 | ) | ||||

| Less: Net loss attributable to Hampton Inn Property noncontrolling interests | (132,879 | ) | (40,767 | ) | ||||

| Less: Net loss attributable to Hanover Square Property noncontrolling interests | (4,705 | ) | - | |||||

| Less: Net loss attributable to Operating Partnership noncontrolling interests | (16,263 | ) | (19,683 | ) | ||||

| Net Loss Attributable to Medalist Common Shareholders | $ | (686,639 | ) | $ | (450,875 | ) | ||

| Loss per share from operations - basic and diluted | $ | (0.30 | ) | $ | (0.27 | ) | ||

| Weighted-average number of shares - basic and diluted | 2,321,582 | 1,687,516 | ||||||

| Dividends declared per common share | $ | - | $ | - | ||||

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | For the three months ended March 31, 2023 | |||||||||||||||||||||||||||

|

| Common Stock | | | | | | | | | | | | | | Noncontrolling Interests | | | | ||||||||||

| | | | | | | Additional | | | Offering | | Accumulated | | | Shareholders’ | | | Hanover Square | | | Parkway | | | Operating | | |

| ||

| | Shares |

| Par Value |

| Paid in Capital |

|

| Costs |

| Deficit |

| | Equity |

| | Property |

| | Property |

| | Partnership |

| | Total Equity | |||

Balance, January 1, 2023 | | 17,758,421 | | $ | 177,584 | | $ | 51,363,812 | | $ | (3,350,946) | | $ | (30,939,020) | | $ | 17,251,430 | | $ | 127,426 | | $ | 470,685 | | $ | 842,898 | | $ | 18,692,439 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

Net loss |

| — | | $ | — | | $ | — | | $ | — | | $ | (1,221,295) | | $ | (1,221,295) | | $ | (1,241) | | $ | (8,367) | | $ | (2,903) | | $ | (1,233,806) |

Dividends and distributions |

| — | | | — | | | — | | | — | | | (176,810) | | | (176,810) | | | — | | | — | | | (2,135) | | | (178,945) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance, March 31, 2023 |

| 17,758,421 |

| $ | 177,584 |

| $ | 51,363,812 |

| $ | (3,350,946) |

| $ | (32,337,125) |

| $ | 15,853,325 |

| $ | 126,185 |

| $ | 462,318 |

| $ | 837,860 |

| $ | 17,279,688 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | For the three months ended March 31, 2022 | |||||||||||||||||||||||||||

|

| Common Stock | | | | | | | | | | | | | | Noncontrolling Interests | | | | ||||||||||

| | | | | | | Additional | | | Offering | | Accumulated | | | Shareholders’ | | | Hanover Square | | | Parkway | | | Operating | | | | ||

| | Shares |

| Par Value |

| Paid in Capital |

|

| Costs |

| Deficit |

| | Equity |

| | Property |

| | Property |

| | Partnership |

| | Total Equity | |||

Balance, January 1, 2022 | | 16,052,617 | | $ | 160,526 | | $ | 49,645,426 | | $ | (3,350,946) | | $ | (24,981,346) | | $ | 21,473,660 | | $ | 146,603 | | $ | 500,209 | | $ | 877,917 | | $ | 22,998,389 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

|

Common stock issuances | | 1,119,668 | | $ | 11,197 | | $ | 1,177,377 | | $ | — | | $ | — | | $ | 1,188,574 | | $ | — | | $ | — | | $ | — | | $ | 1,188,574 |

Common stock repurchases |

| (268,070) | | | (2,681) | | | (283,862) | | | — | | | — | | | (286,543) | | | — | | | — | | | — | | | (286,543) |

Share based compensation |

| 210,000 | | | 2,100 | | | 231,000 | | | — | | | — | | | 233,100 | | | — | | | — | | | — | | | 233,100 |

Net (loss) income |

| — | | | — | | | — | | | — | | | (989,284) | | | (989,284) | | | (319) | | | 10,193 | | | (973) | | | (980,383) |

Dividends and distributions |

| — | | | — | | | — | | | — | | | (316,450) | | | (316,450) | | | (10,000) | | | (10,800) | | | (4,271) | | | (341,521) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance, March 31, 2022 |

| 17,114,215 |

| $ | 171,142 |

| $ | 50,769,941 |

| $ | (3,350,946) |

| $ | (26,287,080) |

| $ | 21,303,057 |

| $ | 136,284 |

| $ | 499,602 |

| $ | 872,673 |

| $ | 22,811,616 |

See notes to condensed consolidated financial statements

5

Table of ContentsMEDALISTDIVERSIFIEDREIT,INC. ANDSUBSIDIARIES

CondensedCONSOLIDATEDSTATEMENTs OFEQUITY

(Unaudited)

| Common Stock | Noncontrolling Interests | |||||||||||||||||||||||||||||||||||||||

| Shares | Par Value | Additional Paid in Capital | Offering Costs | Accumulated Deficit | Total Shareholders' Equity | Hampton Inn Property | Hanover Square Property | Operating Partnership | Total Equity | |||||||||||||||||||||||||||||||

| Balance, January 1, 2018 | 1,148,002 | $ | 11,480 | $ | 11,086,897 | $ | (912,060 | ) | $ | (1,398,222 | ) | $ | 8,788,095 | $ | 2,211,345 | $ | - | $ | 1,082,591 | $ | 12,082,031 | |||||||||||||||||||

| Common stock issuances | 839,080 | $ | 8,391 | $ | 7,885,045 | $ | - | $ | - | $ | 7,893,436 | $ | - | $ | - | $ | - | $ | 7,893,436 | |||||||||||||||||||||

| Offering costs | - | - | - | (265,612 | ) | - | (265,612 | ) | - | - | - | (265,612 | ) | |||||||||||||||||||||||||||

| Net loss | - | - | - | - | (450,875 | ) | (450,875 | ) | (40,767 | ) | - | (19,683 | ) | (511,325 | ) | |||||||||||||||||||||||||

| Balance, March 31, 2018 | 1,987,082 | $ | 19,871 | $ | 18,971,942 | $ | (1,177,672 | ) | $ | (1,849,097 | ) | $ | 15,965,044 | $ | 2,170,578 | $ | - | $ | 1,062,908 | $ | 19,198,530 | |||||||||||||||||||

| Common Stock | Noncontrolling Interests | |||||||||||||||||||||||||||||||||||||||

| Shares | Par Value | Additional Paid in Capital | Offering Costs | Accumulated Deficit | Total Shareholders' Equity | Hampton Inn Property | Hanover Square Property | Operating Partnership | Total Equity | |||||||||||||||||||||||||||||||

| Balance, January 1, 2019 | 2,321,582 | $ | 23,216 | $ | 22,077,827 | $ | (1,835,291 | ) | $ | (5,229,760 | ) | $ | 15,035,992 | $ | 2,009,031 | $ | 608,943 | $ | 950,627 | $ | 18,604,593 | |||||||||||||||||||

| Offering costs | - | $ | - | $ | - | $ | (138,827 | ) | $ | - | $ | (138,827 | ) | $ | - | $ | - | $ | - | $ | (138,827 | ) | ||||||||||||||||||

| Net loss | - | - | - | - | (686,639 | ) | (686,639 | ) | (132,879 | ) | (4,705 | ) | (16,263 | ) | (840,486 | ) | ||||||||||||||||||||||||

| Dividends and distributions | - | - | - | - | - | - | - | (16,000 | ) | - | (16,000 | ) | ||||||||||||||||||||||||||||

| Balance, March 31, 2019 | 2,321,582 | $ | 23,216 | $ | 22,077,827 | $ | (1,974,118 | ) | $ | (5,916,399 | ) | $ | 14,210,526 | $ | 1,876,152 | $ | 588,238 | $ | 934,364 | $ | 17,609,280 | |||||||||||||||||||

See notes to consolidated financial statements

Medalist Diversified REIT, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| For the Three Months Ended | ||||||||

| March 31, | ||||||||

| 2019 | 2018 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

| Net Loss | $ | (840,486 | ) | $ | (511,325 | ) | ||

| Adjustments to reconcile consolidated net loss to net cash provided by (used in) operating activities | ||||||||

| Depreciation | 403,330 | 302,304 | ||||||

| Amortization | 162,833 | 91,660 | ||||||

| Loan cost amortization | 42,711 | 39,528 | ||||||

| Amortization of tenant inducements | 4,260 | - | ||||||

| Decrease (increase) in fair value - interest rate cap | 50,403 | (74,289 | ) | |||||

| Above (below) market lease amortization, net | 31,422 | 36,386 | ||||||

| Changes in assets and liabilities | ||||||||

| Rent and other receivables, net | 11,874 | 13,775 | ||||||

| Unbilled rent | (85,326 | ) | (18,575 | ) | ||||

| Prepaid expenses | 5,092 | 20,748 | ||||||

| Other assets | - | (50,000 | ) | |||||

| Accounts payable and accrued liabilities | 298,709 | (73,143 | ) | |||||

| Net cash provided by (used in) operating activities | 84,822 | (222,931 | ) | |||||

| CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||

| Capital expenditures | (405,769 | ) | (46,568 | ) | ||||

| Advance deposits | (372,831 | ) | - | |||||

| Net cash used in investing activities | (778,600 | ) | (46,568 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

| Dividends and distributions paid | (16,000 | ) | - | |||||

| Repayment of notes payable and related party notes payable | - | (2,177,538 | ) | |||||

| Repayment of mortgages payable | (32,408 | ) | - | |||||

| Proceeds from sales of common stock, net of offering costs | (138,827 | ) | 7,590,356 | |||||

| Net cash (used in) provided by investing activities | (187,235 | ) | 5,412,818 | |||||

| (DECREASE) INCREASE IN CASH, CASH EQUIVALENTS AND RESTRICTED CASH | (881,013 | ) | 5,143,319 | |||||

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH, beginning of period | 4,120,796 | 3,294,847 | ||||||

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period | $ | 3,239,783 | $ | 8,438,166 | ||||

| - | - | |||||||

| CASH AND CASH EQUIVALENTS, end of period shown in consolidated balance sheets | 1,269,765 | 5,290,371 | ||||||

| RESTRICTED CASH including assets restricted for capital and operating reserves and tenant deposits | 1,970,018 | 3,147,795 | ||||||

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period shown in the statement of cash flows | $ | 3,239,783 | $ | 8,438,166 | ||||

| Supplemental Disclosures and Non-Cash Activities: | ||||||||

| Interest paid, net of interest rate cap offsetting receipts | 427,674 | 409,702 | ||||||

| Transfer advance deposits to investment properties | 515,430 | - | ||||||

| Short term receivable in lieu of proceeds from sale of common stock | - | 37,468 | ||||||

| | | | | | |

| | Three months ended March 31, | ||||

|

| 2023 |

| 2022 | ||

CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | |

| | | | | | |

Net Loss | | $ | (1,233,806) | | $ | (980,383) |

| | | | | | |

Adjustments to reconcile consolidated net loss to net cash flows from operating activities | |

| | |

| |

Depreciation | |

| 911,481 | |

| 771,560 |

Amortization | |

| 244,867 | |

| 383,637 |

Loan cost amortization | |

| 26,990 | |

| 28,118 |

Mandatorily redeemable preferred stock issuance cost and discount amortization | | | 58,804 | | | 53,923 |

Above (below) market lease amortization, net | |

| (73,018) | |

| (26,034) |

Bad debt expense | | | 27,122 | | | 12,783 |

Share-based compensation | | | — | | | 233,100 |

Impairment of assets held for sale | |

| — | |

| 175,671 |

Loss on impairment | | | 36,743 | | | 36,670 |

| | | | | | |

Changes in assets and liabilities | |

| | |

| |

Rent and other receivables, net | |

| 84,476 | |

| 109,000 |

Unbilled rent | |

| (48,899) | |

| (14,846) |

Other assets | |

| 66,796 | |

| (128,599) |

Accounts payable and accrued liabilities | |

| 349,168 | |

| 38,263 |

Net cash flows from operating activities | |

| 450,724 | |

| 692,863 |

| | | | | | |

CASH FLOWS FROM INVESTING ACTIVITIES | |

| | |

| |

| | | | | | |

Capital expenditures | | | (647,690) | | | (366,059) |

Net cash flows from investing activities | |

| (647,690) | |

| (366,059) |

| | | | | | |

CASH FLOWS FROM FINANCING ACTIVITIES | |

|

| |

|

|

| | | | | | |

Dividends and distributions paid | |

| (178,945) | |

| (341,521) |

Repayment of mortgages payable | | | (301,577) | | | (192,257) |

Proceeds from sales of common stock, net of capitalized offering costs | | | — | | | 1,188,574 |

Repurchases of common stock, including costs and fees | |

| — | |

| (286,543) |

Net cash flows from financing activities | |

| (480,522) | |

| 368,253 |

| | | | | | |

(DECREASE) INCREASE IN CASH, CASH EQUIVALENTS AND RESTRICTED CASH | |

| (677,488) | |

| 695,057 |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, beginning of period | |

| 5,662,853 | |

| 7,383,977 |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period | | $ | 4,985,365 | | $ | 8,079,034 |

| | | | | | |

CASH AND CASH EQUIVALENTS, end of period, shown in condensed consolidated balance sheets | | | 3,048,100 | | | 4,629,945 |

RESTRICTED CASH including assets restricted for capital and operating reserves and tenant deposits, end of period, shown in condensed consolidated balance sheets | | | 1,937,265 | | | 3,449,089 |

CASH, CASH EQUIVALENTS AND RESTRICTED CASH, end of period shown in the condensed consolidated statements of cash flows | | $ | 4,985,365 | | $ | 8,079,034 |

| | | | | | |

Supplemental Disclosures and Non-Cash Activities: | |

| | |

| |

| | | | | | |

Other cash transactions: | |

|

| |

|

|

Interest paid | | $ | 796,268 | | $ | 682,456 |

| | | | | | |

See notes to condensed consolidated financial statements

6

Medalist Diversified REIT, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. Organization and Basis of Presentation and Consolidation |

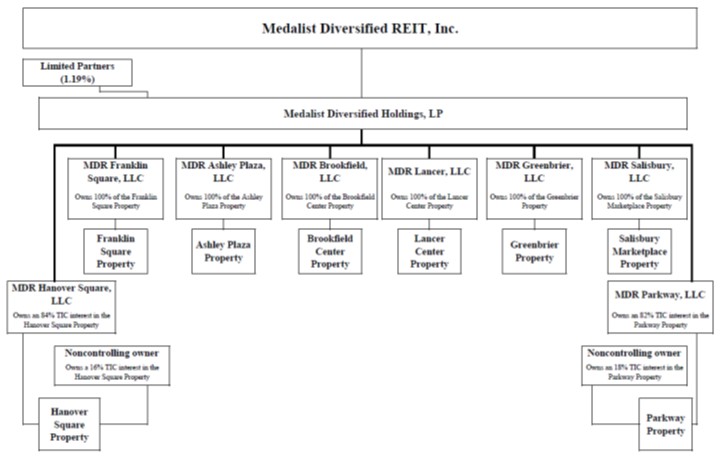

Medalist Diversified Real Estate Investment Trust, Inc. (the “REIT”) is a Maryland corporation formed on September 28, 2015. Beginning with the taxable year ended December 31, 2017, the REIT has elected to be taxed as a real estate investment trust for federal income tax purposes. The REIT serves as the general partner of Medalist Diversified Holdings, LP (the “Operating Partnership”) which was formed as a Delaware limited partnership on September 29, 2015. As of March 31, 2019,2023, the REIT, through the Operating Partnership, owned and operated threeeight properties, including the Shops at Franklin Square, a 134,239 square foot retail property located in Gastonia, North Carolina (the “Franklin Square Property”), the Greensboro Airport Hampton Inn, a hotel with 125 rooms on 2.162 acres in Greensboro, North Carolina (the “Hampton Inn Property”), and the Shops at Hanover Square North, (the “Hanover Square Property”), a 73,440 square foot retail property located in Mechanicsville, Virginia.Virginia (the “Hanover Square Property”), the Ashley Plaza Shopping Center, a 164,012 square foot retail property located in Goldsboro, North Carolina (the “Ashley Plaza Property”), Brookfield Center, a 64,880 square foot mixed-use industrial/office property located in Greenville, South Carolina (the “Brookfield Center Property”), the Lancer Center, a 181,590 square foot retail property located in Lancaster, South Carolina (the “Lancer Center Property”), the Greenbrier Business Center, an 89,280 square foot mixed-use industrial/office property located in Chesapeake, Virginia (the “Greenbrier Business Center Property "), the Parkway Property, a 64,109 square foot mixed-use industrial office property located in Virginia Beach, Virginia (the "Parkway Property") and the Salisbury Marketplace Shopping Center, a 79,732 square foot retail property located in Salisbury, North Carolina (the “Salisbury Marketplace Property”). The Company owns 64 percent of the Hampton Inn Property as a tenant in common with a noncontrolling owner which owns the remaining 36 percent interest. The Company owns 84 percent84% of the Hanover Square Property as a tenant in common with a noncontrolling owner which owns the remaining 16 percent16% interest and 82% of the Parkway Property as a tenant in common with a noncontrolling owner which owns the remaining 18% interest.

7

The use of the word “Company” refers to the REIT and its consolidated subsidiaries, except where the context otherwise requires. The Company includes the REIT, the Operating Partnership, wholly owned limited liability corporationscompanies which own or operate the properties and, for the periods presented prior to September 30, 2022, the taxable REIT subsidiary which operatesformerly operated the HamptonClemson Best Western University Inn, Property.a hotel with 148 rooms on 5.92 acres in Clemson, South Carolina (“the Clemson Best Western Property”), which the Company sold on September 29, 2022. As a REIT, certain tax laws limit the amount of “non-qualifying” income that Company can earn, including income derived directly from the operation of hotels. As a result, the Company and the tenant in common (“TIC”) noncontrolling owner, leaseleased its consolidated hotel property to a taxable REIT subsidiary (“TRS”) for federal income tax purposes. The Company’s TRS iswas subject to income tax and iswas not limited as to the amount of nonqualifying income it cancould generate, but it isthe Company’s TRS was limited in terms of its value as a percentage of the total value of the Company’s assets. The Company’s TRS entersentered into an agreement with a third party to manage the operations of the hotel. The Company prepared the accompanying condensed consolidated financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”). References to the condensed consolidated financial statements and references to individual financial statements included herein, reference the condensed consolidated financial statements or the respective individual financial statement. All material balances and transactions between the consolidated entities of the Company have been eliminated.

The Company was formed to acquire, reposition, renovate, lease and manage income-producing properties, with a primary focus on (i) commercial properties, including flex-industrial, limited servicelimited-service hotels, and retail properties, and (ii) multi-family residential properties in secondary and tertiary markets in the southeastern part of the United States, with an expected concentration in Virginia, North Carolina, South Carolina, Georgia, Florida and Alabama. The Company may also pursue, in an opportunistic manner, other real estate-related investments, including, among other things, equity or other ownership interests in entities that are the direct or indirect owners of real property, indirect investments in real property, such as those that may be obtained in a joint venture. While these types of investments are not intended to be a primary focus, the Company may make such investments in its Manager’s discretion.

the discretion of Medalist Fund Manager, Inc. (the “Manager”).

The Company is externally managed by Medalist Fund Manager, Inc. (the ‘‘Manager’’).the Manager. The Manager makes all investment decisions for the Company. The Manager and its affiliated companies specialize in acquiring, developing, owning and managing value-added commercial real estate in the Mid-Atlantic and Southeast regions. The Manager oversees the Company’s overall business and affairs and has broad discretion to make operating decisions on behalf of the Company and to make investment decisions. The Company’s stockholders are not involved in its day-todayday-to-day affairs.

2. Summary of Significant Accounting Policies

Investment Properties

As of January 1, 2017, theThe Company has adopted Accounting Standards Update (“ASU”) 2017-01,Business Combinations (Topic 805), which clarifies the framework for determining whether an integrated set of assets and activities meets the definition of a business. The revised framework establishes a screen for determining whether an integrated set of assets and activities is a business and narrows the definition of a business, which is expected to result in fewer transactions being accounted for as business combinations. Acquisitions of integrated sets of assets and activities that do not meet the definition of a business are accounted for as asset acquisitions. As a result, all of the Company’s acquisitions that occurred in 2017 and 2018to date qualified as asset acquisitions and most of the Company’sCompany expects future acquisitions of operating properties willto qualify as asset acquisitions. Accordingly, third-party transaction costs associated with these acquisitions have been and will be capitalized, while internal acquisition costs will continue to be expensed.

Accounting Standards Codification (“ASC”) 805 mandates that “an acquiring entity shall allocate the cost of an acquired entity to the assets acquired and liabilities assumed based on their estimated fair values at date of acquisition.” ASC 805 results in an allocation of acquisition costs to both the tangible and intangible assets associated with income producing real estate. Tangible assets include land, buildings, site improvements, tenant improvements and furniture, fixtures and fixtures,equipment, while intangible assets include the value of in-place leases, lease origination costs (leasing commissions and tenant improvements), legal and marketing costs and leasehold assets and liabilities (above or below market)market leases), among others.

The Company uses independent, third partythird-party consultants to assist management with its ASC 805 evaluations. The Company determines fair value based on accepted valuation methodologies including the cost, market, and income capitalization approaches. The purchase price is allocated to the tangible and intangible assets identified in the evaluation.

8

The Company records depreciation on buildings and improvements utilizing the straight-line method over the estimated useful life of the asset, generally 54 to 4042 years. The Company reviews depreciable lives of investment properties periodically and makes adjustments to reflect a shorter economic life, when necessary. Tenant allowances, tenant inducementsCapitalized leasing commissions and tenant improvements incurred and paid by the Company subsequent to the acquisition of the investment property are amortized utilizing the straight-line method over the term of the related lease. Amounts allocated to buildings are depreciated over the estimated remaining life of the acquired building or related improvements.

Acquisition and closing costs are capitalized as part of each tangible asset on a pro rata basis. Improvements and major repairs and maintenance are capitalized when the repair and maintenance substantially extend the useful life, increases capacity or improves the efficiency of the asset. All other repair and maintenance costs are expensed as incurred.

The Company reviews investment properties for impairment on a property-by-property basis whenever events or changes in circumstances indicate that the carrying value of investment properties may not be recoverable, but at least annually. These circumstances include, but are not limited to, declines in the property’s cash flows, occupancy and fair market value. The Company measures any impairment of investment property when the estimated undiscounted cash flows plus its residual value, is less than the carrying value of the property. To the extent impairment has occurred, the Company charges to income the excess of the carrying value of the property over its estimated fair value. The Company estimates fair value using unobservable data such as projected future operating income, estimated capitalization rates, or multiples, leasing prospects and local market information. The Company may decide to sell properties that are held for use and the sale prices of these properties may differ from their carrying values. The

Other than the tenant-specific losses on impairment and the impairment of assets held for sale described below, the Company did not record any impairment adjustments to its investment properties resulting from events or changes in circumstances during the three months ended March 31, 20192023 and 2022, that would result in the projected value being below the carrying value of the Company’s properties.

Assets Held for Sale

The Company may decide to sell properties that are held as investment properties. The accounting treatment for the disposal of long-lived assets is covered by ASC 360. Under this guidance, the Company records the assets associated with these properties, and any associated mortgages payable, as held for sale when management has committed to a plan to sell the assets, actively seeks a buyer for the assets, and the consummation of the sale is considered probable and is expected within one year. Delays in the time required to complete a sale do not preclude a long-lived asset from continuing to be classified as held for sale beyond the initial one-year period if the delay is caused by events or circumstances beyond an entity’s control and there is sufficient evidence that the entity remains committed to a qualifying plan to sell the long-lived asset.

Properties classified as held for sale are reported at the lower of their carrying value or their fair value, less estimated costs to sell. When the carrying value exceeds the fair value, less estimated costs to sell, an impairment charge is recognized. The Company determines fair value based on the three-level valuation hierarchy for fair value measurement. Level 1 inputs are quoted prices in active markets for identical assets or liabilities. Level 2 inputs are quoted prices for similar assets or liabilities in active markets; quoted prices for identical or similar assets in markets that are not active; and inputs other than quoted prices. Level 3 inputs are unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities.

During February 2021, the Company committed to a plan for the sale of an asset group associated with the Clemson Best Western Hotel Property that included the land, site improvements, building, building improvements and furniture, fixtures and equipment. As of March 31, 2018.2021, the Company recorded this asset group, and the associated mortgage payable, as held for sale. As of March 31, 2021, the date the Company originally recorded this asset group as held for sale, the Company determined that the fair value of the Clemson Best Western Property exceeded the carrying value of its asset group, and the Company did not record impairment of assets held for sale associated with this asset group.

During subsequent periods since the asset group associated with the Clemson Best Western Property was initially classified as held for sale, the Company continued to follow its disposal plan. Under ASC 360, during subsequent reporting periods after the asset group is classified as held for sale, it is necessary to evaluate the amounts previously used for the estimated fair value of the asset group. Up to and including the reporting periods ending December 31, 2021, the Company reviewed and reassessed the estimated fair value of the asset group and believed that the fair value, less estimated costs to sell, exceeds the Company’s carrying cost in the property.

9

Accordingly, the Company did not record impairment of assets held for sale related to the Clemson Best Western Property for the year ended December 31, 2021.

As of March 31, 2022, the Company determined that the carrying value of the asset group associated with the Clemson Best Western Hotel Property exceeded its fair value, less estimated costs to sell, and recorded impairment of assets held for sale of $175,671 on its condensed consolidated statement of operations for the three months ended March 31, 2022. No such impairment of assets held for sale was recorded during the three months ended March 31, 2023.

On September 29, 2022, the Company closed on the sale of the Clemson Best Western Hotel Property to an unaffiliated purchaser. See Note 3 for additional details.

Intangible Assets and Liabilities, net

The Company determines, through the ASC 805 evaluation, the above and below market lease intangibles upon acquiring a property. Intangible assets (or liabilities) such as above or below-market leases and in-place lease value are recorded at fair value and are amortized as an adjustment to rental revenue or amortization expense, as appropriate, over the remaining terms of the underlying leases. The Company amortizes amounts allocated to tenant improvements, in-place lease assets and other lease-related intangibles over the remaining life of the underlying leases. The analysis is conducted on a lease-by-lease basis.

The Company reviews its intangible assets for impairment whenever events or changes in circumstances indicate that the carrying value of its intangible assets may not be recoverable, but at least annually. During the three months ended March 31, 20192023, a tenant defaulted on its lease and 2018, respectively,abandoned its premises. The Company determined that the carrying value of the intangible assets and liabilities, net, associated with this lease of $35,551 that were recorded as part of the purchase of this property should be written off. This amount is included in the loss on impairment reported on the Company’s condensed consolidated statement of operations for the three months ended March 31, 2023. During the three months ended March 31, 2022, two tenants defaulted on their leases and abandoned their premises. The Company did not record anydetermined that the carrying value of the intangible assets and liabilities, net, associated with these leases of $36,670 that were recorded as part of the purchase of these properties should be written off. This amount is included in the loss on impairment adjustments to its intangible assets.

reported on the Company’s condensed consolidated statement of operations for the three months ended March 31, 2022.

Details of thesethe deferred costs, net of amortization, arising from the Company’s purchases of the Franklin Square Propertyits retail center properties and Hanover Square Propertyflex center properties are as follows:

| March 31, 2019 | December 31, 2018 | |||||||

| (unaudited) | ||||||||

| Intangible Assets | ||||||||

| Leasing commissions | $ | 282,409 | $ | 305,646 | ||||

| Legal and marketing costs | 87,440 | 95,950 | ||||||

| Above market leases | 593,475 | 648,409 | ||||||

| Leases in place | 1,404,743 | 1,535,829 | ||||||

| $ | 2,368,067 | $ | 2,585,834 | |||||

| Intangible Liabilities | ||||||||

| Below market leases, net | $ | (416,214 | ) | $ | (439,726 | ) | ||

| | | | | | | |

| | | March 31, 2023 | | | |

|

|

| (unaudited) |

| December 31, 2022 |

| ||

Intangible Assets, net | | | | | | | |

Leasing commissions | | $ | 1,074,551 | | $ | 1,135,421 | |

Legal and marketing costs | |

| 150,957 | |

| 169,437 | |

Above market leases | |

| 175,839 | |

| 209,860 | |

Net leasehold asset | |

| 2,048,253 | |

| 2,233,988 | |

| | $ | 3,449,600 | | $ | 3,748,706 | |

| | | | | | | |

Intangible Liabilities, net | |

| | |

| | |

Below market leases | | $ | (2,133,752) | | $ | (2,234,113) | |

Capitalized above-market lease values are amortized as a reduction of rental income over the remaining terms of the respective leases. Capitalized below-market lease values are amortized as an increase to rental income over the remaining terms of the respective leases. Adjustments to rental revenue related to the above and below market leases during the three months ended March 31, 20192023 and 2018,2022, respectively, were as follows:

| Three months ended March 31, | ||||||||

| 2019 | 2018 | |||||||

| (unaudited) | (unaudited) | |||||||

| Amortization of above market leases | $ | 54,934 | $ | 47,898 | ||||

| Amortization of below market leases | (23,512 | ) | (11,512 | ) | ||||

| $ | 31,422 | $ | 36,386 | |||||

10

| | | | | | | |

| | For the three months ended |

| ||||

| | March 31, | | ||||

| | | 2023 | | | 2022 | |

|

| (unaudited) |

| (unaudited) |

| ||

Amortization of above market leases | | $ | (27,343) | | $ | (69,583) | |

Amortization of below market leases | |

| 100,361 | |

| 95,617 | |

| | $ | 73,018 | | $ | 26,034 | |

Amortization of lease origination costs, leases in place and legal and marketing costs represent a component of depreciation and amortization expense. Amortization related to these intangible assets during the three months ended March 31, 20192023 and 2018,2022, respectively, were as follows:

| Three months ended March 31, | |||||||||||||||

| 2019 | 2018 | ||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||

| | | | | | | | ||||||||

| | For the three months ended |

| ||||||||||||

| | March 31, | | ||||||||||||

| | | 2023 | | | 2022 | | ||||||||

|

| (unaudited) |

| (unaudited) |

| ||||||||||

| Leasing commissions | $ | (23,237 | ) | $ | (15,602 | ) | | $ | (56,618) | | $ | (63,032) | | ||

| Legal and marketing costs | (8,510 | ) | (7,031 | ) | |

| (16,205) | |

| (14,559) | | ||||

| Leases in place | (131,086 | ) | (69,027 | ) | |||||||||||

| $ | (162,833 | ) | $ | (91,660 | ) | ||||||||||

Net leasehold asset | |

| (172,044) | |

| (306,046) | | ||||||||

| | $ | (244,867) | | $ | (383,637) | | ||||||||

As of March 31, 20192023 and December 31, 2018,2022, the Company’s accumulated amortization of lease origination costs, leases in place and legal and marketing costs totaled $983,847$2,148,257 and $821,014,$2,198,049, respectively.

During the three months ended March 31, 2023 and 2022, the Company wrote off $273,252 and $486,785, respectively, in accumulated amortization related to fully amortized intangible assets and $21,407 and $5,108, respectively, in accumulated amortization related to the write off of intangible assets related to the tenant defaults, discussed above.

Future amortization of above and below market leases, lease origination costs, leases in place, legal and marketing costs and tenant relationships is as follows:

| For the remaining nine months ending December 31, 2019 | 2020 | 2021 | 2022 | 2023 | 2024- 2027 | Total | |||||||||||||||||||||||||||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

|

| | For the | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

| | | remaining nine | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

| | | months ending | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

| | | December 31, | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

| | 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028-2042 |

| Total | |||||||||||||||||||||||||||||||||||

| Intangible Assets |

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

| ||||||||||||||||||||||||||||

| Leasing commissions | $ | 65,094 | $ | 75,332 | $ | 67,721 | $ | 36,661 | $ | 17,855 | $ | 19,746 | $ | 282,409 | | $ | 160,102 | | $ | 171,601 | | $ | 145,550 | | $ | 107,312 | | $ | 88,394 | | $ | 401,592 | | $ | 1,074,551 | ||||||||||||||

| Legal and marketing costs | 21,544 | 20,736 | 16,127 | 11,739 | 8,126 | 9,168 | 87,440 | |

| 43,963 | |

| 38,900 | |

| 24,004 | |

| 13,160 | |

| 7,917 | |

| 23,013 | |

| 150,957 | |||||||||||||||||||||

| Above market leases, net | 157,930 | 180,650 | 173,712 | 81,183 | - | - | 593,745 | ||||||||||||||||||||||||||||||||||||||||||

| Leases in place | 359,098 | 404,455 | 365,252 | 157,418 | 54,354 | 64,166 | 1,404,743 | ||||||||||||||||||||||||||||||||||||||||||

| $ | 603,666 | $ | 681,173 | $ | 622,812 | $ | 287,001 | $ | 80,335 | $ | 93,080 | $ | 2,368,067 | ||||||||||||||||||||||||||||||||||||

Above market leases | |

| 66,689 | |

| 42,858 | |

| 21,526 | |

| 15,629 | |

| 14,543 | |

| 14,594 | |

| 175,839 | ||||||||||||||||||||||||||||

Net leasehold asset | |

| 443,833 | |

| 394,874 | |

| 295,851 | |

| 199,466 | |

| 153,142 | |

| 561,087 | |

| 2,048,253 | ||||||||||||||||||||||||||||

| | $ | 714,587 | | $ | 648,233 | | $ | 486,931 | | $ | 335,567 | | $ | 263,996 | | $ | 1,000,286 | | $ | 3,449,600 | ||||||||||||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | ||||||||||||||||||||||||||||

| Intangible Liabilities | |

| | |

| | |

| | |

| | |

| | |

| | |

| | ||||||||||||||||||||||||||||

| Below market leases, net | $ | (70,533 | ) | $ | (88,558 | ) | $ | (85,321 | ) | $ | (63,749 | ) | $ | (48,840 | ) | $ | (59,213 | ) | $ | (416,214 | ) | | $ | (268,441) | | $ | (285,892) | | $ | (213,348) | | $ | (178,776) | | $ | (161,866) | | $ | (1,025,429) | | $ | (2,133,752) | |||||||

Conditional Asset Retirement Obligation

A conditional asset retirement obligation represents a legal obligation to perform an asset retirement activity in which the timing and/or method of settlement depends on a future event that may or may not be withwithin the Company’s control. Currently, the Company does not have any conditional asset retirement obligations. However, any such obligations identified in the future would result in the Company recording a liability if the fair value of the obligation can be reasonably estimated. Environmental studies conducted at the time the Company acquired its properties did not reveal any material environmental liabilities, and the Company is unaware of any subsequent environmental matters that would have created a material liability.

The Company believes that its properties are currently in material compliance with applicable environmental, as well as non-environmental, statutory and regulatory requirements. The Company did not record any conditional asset retirement obligation liabilities during the three months ended March 31, 20192023 and 2018,2022, respectively.

11

Cash and Cash Equivalents and Restricted Cash

The Company considers all highly liquid investments purchased with an original maturity of 90 days or less to be cash and cash equivalents. Cash equivalents are carried at cost, which approximates fair value. Cash equivalents consist primarily of bank operating accounts and money markets. Financial instruments that potentially subject the Company to concentrations of credit risk include its cash and cash equivalents and its trade accounts receivable.

Restricted cash represents (i) amounts held by the Company for tenant security deposits, (ii) escrow deposits held by lenders for real estate tax, insurance, and operating reserves and (iii) capital reserves held by lenders for investment property capital improvements.

The Company places its cash and cash equivalents and any restricted cash held by the Company on deposit with financial institutions in the United States which are insured by the Federal Deposit Insurance Company ("FDIC") up to $250,000. The Company's credit loss in the event of failure of these financial institutions is represented by the difference between the FDIC limit and the total amounts on deposit. Management monitors the financial institutions credit worthiness in conjunction with balances on deposit to minimize risk. As of March 31, 2019,2023, the Company held aone cash account at a financial institution with a balance that exceeded the FDIC limit by $255,042.$1,404,374. As of December 31, 2018,2022, the Company held two cash accounts at a cash accountsingle financial institution with a balancecombined balances that exceeded the FDIC limit by $650,699.$2,613,789.

Restricted cash represents (i) amounts held by the Company for tenant security deposits, (ii) escrow deposits held by lenders for real estate tax, insurance, and operating reserves, (iii) an escrow for the first year of dividends on the Company’s mandatorily redeemable preferred stock, and (iv) capital reserves held by lenders for investment property capital improvements.

Tenant security deposits are restricted cash balances held by the Company to offset potential damages, unpaid rent or other unmet conditions of its tenant leases. As of March 31, 20192023 and December 31, 2018,2022, the Company reported $77,351$283,646 and $71,022,$267,854, respectively, in security deposits.

deposits held as restricted cash.

Escrow deposits are restricted cash balances held by lenders for real estate taxes, insurance and other operating reserves. As of March 31, 20192023 and December 31, 2018,2022, the Company reported $456,663$736,865 and $719,588,$579,785, respectively, in escrow deposits.

Capital reserves are restricted cash balances held by lenders for capital improvements, leasing commissions furniture, fixtures and equipment, and tenant improvements. As of March 31, 20192023 and December 31, 2018,2022, the Company reported $1,436,004$916,754 and $2,002,762,$893,078, respectively, in capital property reserves. These funds are being held in reserve

| | | | | | | |

| | March 31, 2023 | | December 31, | | ||

Property and Purpose of Reserve |

| (unaudited) |

| 2022 | | ||

| | | | | | | |

Franklin Square Property - leasing costs | | $ | 858,509 | | $ | 845,765 | |

Brookfield Center Property - maintenance and leasing cost reserve | |

| 58,245 | |

| 47,313 | |

Total | | $ | 916,754 | | $ | 893,078 | |

Share Retirement

ASC 505-30-30-8 provides guidance on accounting for improvements to the Hampton Inn Property ($1,034,626share retirement and $1,601,809 as of March 31, 2019 and December 31, 2018 respectively) and tenant improvements and leasing commissionsestablishes two alternative methods for accounting for the Franklin Square Property ($401,378 and $400,953 asrepurchase price paid in excess of March 31, 2019 and December 31, 2018 respectively).

Revenue Recognition

par value. The Company adoptedASU No. 2014-09,Revenuefrom Contracts with Customers (Topic 606) effective on January 1, 2019 (see Recent Accounting Pronouncements, below). This adoption did not have a material impacthas elected the method by which the excess between par value and the repurchase price, including costs and fees, is recorded to additional paid in capital on the Company’s recognitioncondensed consolidated balance sheets. During the three months ended March 31, 2022, the Company repurchased 268,070 shares of revenues from either its retail properties or its hotel property.common stock at a total cost of $278,277 at an average price of $1.038 per common share. The Company incurred fees of $8,266 associated with these transactions. Of the total repurchase price, $2,681 was recorded to common stock and the difference, $283,862, was recorded to additional paid in capital on the Company’s condensed consolidated balance sheet. No such amounts were recorded during the three months ended March 31, 2023.

12

Revenue Recognition

Retail and Flex Center Property Revenues

The Company recognizes minimum rents from its retail center properties (the Franklin Square and Hanover Square properties)flex center properties on a straight-line basis over the terms of the respective leases which results in an unbilled rent asset or deferred rent liability being recorded on the condensed consolidated balance sheet. sheets. As of March 31, 2023 and December 31, 2022, the Company reported $1,069,860 and $1,022,153, respectively, in unbilled rent. During the three months ended March 31, 2023, the Company recorded a loss on impairment of $1,192 related to previously recognized straight-line rent related to a defaulting tenant’s lease. No such loss on impairment related to straight-line rent was recorded during the three months ended March 31, 2022.

The Company’s leases generally require the tenant to reimburse the Company for a substantial portion of its expenses incurred in operating, maintaining, repairing, insuring and managing the shopping center and common areas (collectively defined as Common Area Maintenance or “CAM” expenses). The Company includes these reimbursements, along with other revenue derived from late fees and seasonal events, underon the condensed consolidated statements of operations captionunder the captions "Retail center property tenant reimbursements."revenues” and “Flex center property revenues.” (See Recent Accounting Pronouncements, below.) This significantly reduces the Company’s exposure to increases in costs and operating expenses resulting from inflation or other outside factors. The Company accrues reimbursements from tenants for recoverable portions of all these expenses as revenue in the period the applicable expenditures are incurred. The Company calculates the tenant’s share of operating costs by multiplying the total amount of the operating costs by a fraction, the numerator of which is the total number of square feet being leased by the tenant, and the denominator of which is the average total square footage of all leasable buildings at the property. The Company also receives escrow payments for these reimbursements from substantially all its tenants on a monthly basis throughout the year.

The Company recognizes differences between previously estimated recoveries and the final billed amounts in the year in which the amounts become final. Since these differences are determined annually under the leases and accrued as of December 31 in the impact onyear earned, no such revenues were recognized forduring the three months ended March 31, 2019 is not known.

2023 and 2022.

The Company recognizes lease termination fees in the period that the lease is terminated and collection of the fees is reasonably assured. Upon early lease termination, the Company provides for losses related to unrecovered intangibles and other assets. During the three months ended March 31, 20192023 and 2018,2022, respectively, no such termination costs were recognized.

Hotel Property Revenues

Hotel revenues (fromfrom the Hampton Inn Property) areClemson Best Western Property were recognized as earned, which is generally defined as the date upon which a guest occupies a room or utilizes the hotel’s services. Revenues from the Company’s occupancy agreement with Clemson University were recognized as earned, which is as rooms are occupied or otherwise reserved for use by the University. The Clemson University occupancy agreement ended on May 15, 2022 and the Company sold the Clemson Best Western Property on September 29, 2022.

The Clemson Best Western Property was required to collect certain taxes and fees from customers on behalf of government agencies and remit them back to the applicable governmental agencies on a periodic basis. The Clemson Best Western Property had a legal obligation to act as a collection agent. The Clemson Best Western Property did not retain these taxes and fees; therefore, they were not included in revenues. The Clemson Best Western Property recorded a liability when the amounts were collected and relieved the liability when payments were made to the applicable taxing authority or other appropriate governmental agency.

TenantHotel Property Operating Expenses

All personnel of the Clemson Best Western Property were directly or indirectly employees of Marshall Hotels and Resorts, Inc. (“Marshall”), the Company’s hotel management firm. In addition to fees and services discussed above, the Clemson Best Western Property reimbursed Marshall for all employee related service costs, including payroll salaries and wages, payroll taxes and other employee benefits paid by Marshall on its behalf. The total amounts incurred for payroll salaries and wages, payroll taxes and other employee benefits for the three months ended March 31, 2023 and 2022 were $0 and $131,939, respectively.

13

Rent and other receivables

Rent and unbilled rent

Tenantother receivables include tenant receivables related to base rents and tenant reimbursementsreimbursements. Rent and other receivables do not include receivables attributable to recording rents on a straight-line basis.basis, which are included in unbilled rent, discussed above. The Company determines an allowance for the uncollectible portion of accrued rents and accounts receivable based upon customer credit-worthinesscredit worthiness (including expected recovery of a claim with respect to any tenants in bankruptcy), historical bad debt levels, and current economic trends. The Company considers a receivable past due once it becomes delinquent per the terms of the lease. A past due receivable triggers certain events such as notices, fees and other allowable and required actions per the lease. TheAs of March 31, 2023 and December 31, 2022, the Company’s allowance for uncollectible accountsrent totaled $62,960 and $47,109, respectively, which are comprised of amounts specifically identified based on management’s review of individual tenants’ outstanding receivables. Management determined that no additional general reserve is considered necessary as of March 31, 2023 and December 31, 2022, respectively.

Income Taxes

Beginning with the Company’s taxable year ended December 31, 2017, the REIT has elected to be taxed as a real estate investment trust for federal income tax purposes under Sections 856 through 860 of the Internal Revenue Code and applicable Treasury regulations relating to REIT qualification. In order to maintain this REIT status, the regulations require the Company to distribute at least 90% of its taxable income to shareholders and meet certain other asset and income tests, as well as other requirements. If the Company fails to qualify as a REIT, it will be subject to tax at regular corporate rates for the years in which it fails to qualify. If the Company loses its REIT status it could not elect to be taxed as a REIT for five years unless the Company’s failure to qualify was due to reasonable cause and certain other conditions were satisfied.

During the three months ended March 31, 2022, the Company's Clemson Best Western TRS entity generated taxable income. The Company believed that the net operating loss carry forward from prior years would offset the taxable income for the three months ended March 31, 2022, so no income tax expense was recorded. During the three months ended March 31, 2023, the Company no longer owned the Clemson Best Western Hotel Property.

Management has evaluated the effect of the guidance provided by GAAP on Accounting for Uncertainty of Income Taxes and has determined that the Company had no uncertain income tax positions.

During the three months ended March 31, 2019 and 2018, respectively, the Company’s Hampton Inn TRS entity generated a tax loss, so no income tax expense was recorded.

Use of Estimates

The Company has made estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements, and revenues and expenses during the reported period. The Company’s actual results could differ from these estimates.

Noncontrolling Interests

The ownership interests not held by the REIT are considered noncontrolling interests. There are three elements of noncontrolling interests in the capital structure of the Company. The ownership interests not held by the REIT are considered noncontrolling interests. Accordingly,These noncontrolling interests have been reported in equity on the condensed consolidated balance sheets but separate from the Company’s equity. On the condensed consolidated statements of operations, the subsidiaries are reported at the consolidated amount, including both the amount attributable to the Company and noncontrolling interests. ConsolidatedThe Company’s condensed consolidated statements of changes in stockholders’ equity includeincludes beginning balances, activity for the period and ending balances for shareholders’ equity, noncontrolling interests and total equity.

The first noncontrolling interest is in the Hampton Inn Property in which the Company owns a 64 percent tenancy in common interest through its subsidiaries and an outside party owns a 36 percent tenancy in common interest. In 2017, the noncontrolling owner of the Hampton Inn Property provided $2.3 million as part of the acquisition of the Hampton Inn Property. The Hampton Inn Property’s net loss is allocated to the noncontrolling ownership interest based on its 36 percent ownership. During the three months ended March 31, 2019, 36 percent of the Hampton Inn’s net loss of $369,109, or $132,879 was allocated to the noncontrolling partnership interest. During the three months ended March 31, 2018, 36 percent of the Hampton Inn’s net loss of $113,241, or $40,767, was allocated to the noncontrolling ownership interest.

The second noncontrolling interest is in the Hanover Square Property in which the Company owns an 84 percent84% tenancy in common interest through its subsidiary and an outside party owns a 16 percent16% tenancy in common interest. The Hanover Square Property’s net loss is allocated to the noncontrolling ownership interest based on its 16 percent16% ownership. During the three months ended March 31, 2019, 16 percent2023, 16% of the Hanover Square Property’s net loss of $29,409,$7,755, or $4,705, $1,241, was allocated to the noncontrolling ownership interest. The Company did not own the Hanover Square Property duringDuring the three months ended March 31, 2018.2022, 16% of the Hanover Square Property’s net loss of $1,992, or $319, was allocated to the noncontrolling ownership interest.

The second noncontrolling interest is in the Parkway Property in which the Company owns an 82% tenancy in common interest through its subsidiary and an outside party owns an 18% tenancy in common interest. The Parkway Property's net (loss) income is

14

allocated to the noncontrolling ownership interest based on its 18% ownership. During the three months ended March 31, 2023, 18% of the Parkway Property's net loss of $46,482, or $8,367, was allocated to the noncontrolling ownership interest. During the three months ended March 31, 2022, 18% of the Parkway Property’s net income of $56,624, or $10,193, was allocated to the noncontrolling ownership interest.

The third noncontrolling ownership interest are the units in the Operating Partnership that are not held by the REIT. In 2017, 125,000 Operating Partnership units were issued to members of the selling LLClimited liability company which owned the Hampton Inn Property who elected to participate in a 721 exchange, which allows the exchange of interests in real property for shares in a real estate investment trust. These members of the selling LLClimited liability company invested $1,175,000 in the Operating Partnership in exchange for 125,000 Operating Partnership units. Additionally, as discussed above, effective on January 1, 2020, 93,850 Operating Partnership units were issued in exchange for approximately 3.45% of the noncontrolling owner’s tenant in common interest in the Hampton Inn Property. On August 31, 2020, a unitholder converted 5,319 Operating Partnership units into shares of Common Stock. As of March 31, 2023 and December 31, 2022, there were 213,531 Operating Partnership units outstanding.

The Operating Partnership units not held by the REIT represent 5.11 percent1.19% of the outstanding Operating Partnership units as of March 31, 20192023 and December 31, 2018.2022. The noncontrolling interest percentage is calculated at any point in time by dividing the number of units not owned by the Company by the total number of units outstanding. The noncontrolling interest ownership percentage will change as additional common or preferred shares are issued by the REIT, or additional Operating Partnerships units are issued or as units are exchanged for the Company’s $0.01 par value per share Common Stock. During periods when the Operating Partnership’s noncontrolling interest changes, the noncontrolling ownership interest is calculated based on the weighted average Operating Partnership noncontrolling ownership interest during that period. The Operating Partnership’s net loss is allocated to the noncontrolling unit holders based on their ownership interest.

During the three months ended March 31, 2019,2023, a weighted average of 5.11 percent1.19% of the Operating Partnership’s net loss of $318,258, $243,989, or $16,263, $2,903,was allocated to the noncontrolling unit holders. During the three months ended March 31, 2018,2022, a weighted average of 7.25 percent1.28% of the Operating Partnership’s net loss of $271,478, $75,882, or $19,683, $973, was allocated to the noncontrolling unit holders.

Recent Accounting Pronouncements

For each of the accounting pronouncements that affect the Company,Since its initial public offering, the Company has elected or plans to elect to follow the rule that allows companies engaging in an initial public offeringbe classified as an Emerging Growth Companyemerging growth company in its periodic reporting to followthe U.S. Securities and Exchange Commission (the “SEC”), and accordingly has followed the private company implementation dates.dates for new accounting pronouncements. Effective for the three months ending March 31, 2023, the Company will no longer be classified as an emerging growth company, but will retain its classification as a smaller reporting company and therefore follow implementation dates applicable to smaller reporting companies with respect to new accounting pronouncements. In addition, the Company has elected to follow scaled disclosure requirements applicable to smaller reporting companies.

Recently Adopted Accounting Pronouncements

Revenue Recognition

Accounting for Leases

In May 2014,February 2016, the Financial Accounting Standards Board (FASB)(“FASB”) issued ASU 2014-09,Revenue from Contracts with Customers (Topic 606), which supersedes the revenue recognition requirements of Accounting Standards Codification (“ASC”) Topic 605,Revenue Recognition and most industry-specific guidance on revenue recognition throughout the ASC. The new standard is principles based and provides a five step model to determine when and how revenue is recognized. The core principle of the new standard is that revenue should be recognized when a company transfers promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. The new standard also requires disclosure of qualitative and quantitative information surrounding the amount, nature, timing and uncertainty of revenues and cash flows arising from contracts with customers. In March 2016, the FASB issued ASU No. 2016-08,Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net), which clarifies the implementation guidance on principal versus agent considerations. In June 2016, the FASB issued ASU 2016-12,Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients, which relates to assessing collectability, presentation of sales taxes, noncash consideration and completed contracts and contract modifications in transition. In December 2016, the FASB issued 2016-20,Technical Corrections and Improvements to Topic 606, Revenue from Contracts with Customers, which clarifies or corrects unintended application of the standard. Companies are permitted to adopt the ASUs as early as fiscal years beginning after December 15, 2016, but the adoption is required for private companies for fiscal years beginning after December 15, 2018. In September 2017, the FASB issued ASU 2017-13,Revenue Recognition (Topic 605)," "Revenue from Contracts with Customers (Topic 606),Leases (Topic 840)," and2016-02, Leases (Topic 842). These amendments provide additional clarification and implementation guidance on the previously issued ASU 2014-09,Revenue from Contracts with Customers (Topic 606). The Company adopted Topic 606 effective on January 1, 2019.

A majority of the Company’s tenant-related revenue from its Franklin Square Property and Hanover Square Property is recognized pursuant to lease agreements and will be governed by the leasing guidance discussed below. The Company has evaluated its hotel revenues and concluded that the adoption of this standard did not impact the amount or timing of revenue recognition in its consolidated financial statements. The Company completed its assessment of ASU No. 2014-09 and has concluded that the guidance does not have a material impact on the Company’s method of revenue recognition or on the consolidated financial statements.

Accounting for Leases

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842). The amendments in this update govern a number of areas including, but not limited to, accounting for leases, replacing the existing guidance in ASC No. 840, Leases. Under this standard, among other changes in practice, a lessee’s rights and obligations under most leases, including existing and new arrangements, wouldmust be recognized as assets and liabilities, respectively, on the balance sheet.sheets. Other significant provisions of this standard include (i) defining the “lease term” to include the non-cancelable period together with periods for which there is a significant economic incentive for the lessee to extend or not terminate the lease; (ii) defining the initial lease liability to be recorded on the balance sheetsheets to contemplate only those variable lease payments that depend on an index or that are in substance “fixed,” (iii) a dual approach for determining whether lease expense is recognized on a straight-line or accelerated basis, depending on whether the lessee is expected to consume more than an insignificant portion of the leased asset’s economic benefits and (iv) a requirement to bifurcate certain lease and non-lease components. The lease standard iswas effective for public companies for fiscal years beginning after December 15, 2018 (including interim periods within those fiscal years) and for private companies, fiscal years beginning after December 15, 2019, with early adoption permitted. The FASB subsequently deferred the effective date of ASU 2016-02 for private companies by one year, to fiscal years beginning after December 15, 2020, to provide those companies with additional time to address various implementation challenges and complexities. In June 2020, the FASB further deferred the effective date due to the effects on private companies from business and capital market disruptions caused by the novel coronavirus (“COVID-19”) pandemic. Following those deferrals, ASU 2016-02 became effective for private companies for fiscal years beginning after December 15, 2021, and for

15

interim periods within fiscal years beginning after December 15, 2022. The Company plans to adoptadopted the standard effective on January 1, 2020. Management does2022 using the modified retrospective approach within ASU 2018-11, which allows for the application date to be the beginning of the reporting period in which the entity first applies the new standard. The Company historically has not believebeen and is not currently a “lessee” under any lease agreements, and thus did not have any arrangements requiring the recognition of lease assets or liabilities on its balance sheet.

As a “lessor”, the Company has active lease agreements with over 100 tenants across its portfolio of investment properties. On a prospective and retrospective basis, the accounting for those leases under ASU 2016-02 (ASC No. 842) is substantially unchanged from the previous guidance in ASC No. 840. However, upon the adoption of ASC No. 842, the Company has elected the practical expedient permitting lessors to elect by class of underlying asset to not separate non-lease components (for example, maintenance services, including common area maintenance) from associated lease components (the “non-separation practical expedient”) if both of the following criteria are met: (1) the timing and pattern of transfer of the lease and non-lease component(s) are the same and (2) the lease component would be classified as an operating lease if it were accounted for separately. If both criteria are met, the combined component is accounted for in accordance with ASC No. 842 if the lease component is the predominant component of the combined component; otherwise, the combined component is accounted for in accordance with the revenue recognition standard. Prior to the adoption of ASC No. 842, the Company separated lease-related revenue from its retail center and flex center properties into two components. Fixed rental payments under its leases (recognized on a straight-line basis over the term of the underlying lease) were recorded as retail center property revenues and flex center property revenues. Variable payments under the leases made by tenants for real estate taxes, insurance and common area maintenance (“CAM”) expenses were recorded as retail center and flex center tenant reimbursements. With the adoption of ASC No. 842, the Company determined that its retail center and flex center operating leases qualify for the non-separation practical expedient based on the guidance. As a result, the Company has accounted for and presented the revenues from these leases, including tenant reimbursements, as a single line item on its condensed consolidated statements of operations.

Debt With Conversion Options

In August 2020, the FASB issued ASU 2020-06, Debt - Debt With Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging - Contracts in an Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity. The objective of ASU 2020-06 is to reduce the current complexity involved in accounting for convertible financial instruments by reducing the number of accounting models applicable to those instruments in the existing guidance. Following the adoption of ASU 2020-06, companies are expected to encounter fewer instances in which a convertible financial instrument must be separated into a debt or equity component and a derivative component for accounting purposes due to the embedded conversion feature. As a result of these revisions, debt instruments issued with a beneficial conversion feature will no longer require separation and thus will be accounted for as a single debt instrument under the updated guidance. In addition to those changes, ASU 2020-06 adds several incremental financial statement disclosures with respect to a company’s convertible financial instruments and makes certain refinements with respect to calculating the effect of those instruments on a company’s diluted earnings per share. ASU 2020-06 is effective for public companies for fiscal years beginning after December 15, 2021 (including interim periods within those fiscal years), and for private companies, fiscal years beginning after December 15, 2022. Early adoption of the guidance is permitted, but no earlier than fiscal years beginning after December 15, 2020. The updated guidance in ASU 2020-06 was adopted effective January 1, 2023, which did not have a material impact on the Company’s condensed consolidated financial statements.

Credit Losses on Financial Instruments

In June 2016, the FASB issued ASU 2016-13,Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. This update enhances the methodology of measuring expected credit losses to include the use of forward-looking information to better calculate credit loss estimates. The guidance will applyapplies to most financial assets measured at amortized cost and certain other instruments, such as accounts receivable and loans. The guidance will requireloans; however, it does not apply to receivables arising from operating leases accounted for in accordance with ASC Topic 842. ASU 2016-13 requires that the Company estimate the lifetime expected credit loss with respect to theseapplicable receivables and record allowances that, when deducted from the balance of the receivables, represent the net amounts expected to be collected. The Company willis also be required to disclose information about how it developed the allowances, including changes in the factors that influenced the Company’s estimate of expected credit losses and the reasons for those changes. For public companies,The Company’s credit losses primarily arise from tenant defaults on amounts due under operating leases. As noted, these losses are not subject to the guidance will be effective for interimin ASU 2016-13, and annual reporting periods beginning after December 15, 2019 and for private companies, periods after December 15, 2020.historically have not been significant. The Company is currently inadopted the processupdate on the required effective date of evaluatingJanuary 1, 2023, which did not have a material impact on the impact the adoption of the guidance will have on itsCompany’s condensed consolidated financial statements.

16

Cash FlowsUpcoming Accounting Pronouncements

Effects of Reference Rate Reform

In November 2016,March 2020, the FASB issued ASU 2016-18,Statement of Cash Flows2020-04, Reference Rate Reform (Topic 230)848): Restricted Cash (a consensusFacilitation of the FASB Emerging Issues Task Force)Effects ofReference Rate Reform on Financial Reporting. The London Interbank Offered Rate (LIBOR), which is widely used as a reference interest rate in debt agreements and other contracts, was effectively discontinued for new contracts as of December 31, 2021, and its publication for existing contracts is scheduled to be discontinued by June 30, 2023. Financial market regulators in certain jurisdictions throughout the world undertook reference rate reform initiatives to guide the transition and modification of debt agreements and other contracts that are based on LIBOR to the successor reference rate that will replace it. ASU provides2020-04 was issued to provide companies that are impacted by these changes with the opportunity to elect certain expedients and exceptions that are intended to ease the potential burden of accounting for or recognizing the effects of reference rate reform on financial reporting. Under ASU 2020-04, companies may generally elect to make use of the expedients and exceptions provided therein for any reference rate contract modifications that occur in reporting periods that encompass the timeline from March 12, 2020 to December 31, 2022. The FASB subsequently issued ASU 2022-06, Reference Rate Reform (Topic 848): Deferral of the Sunset of Topic 848, to extend that timeline from December 31, 2022 to December 31, 2024. The Company’s Parkway Property is financed by a mortgage loan with a corresponding interest rate protection agreement which both use USD LIBOR as the reference interest rate (see Note 5, below). The mortgage loan matures on November 1, 2031, and the interest rate protection agreement expires on December 1, 2026. The Company is continuing to review the guidance in ASU 2020-04 and anticipates that it will use the expedients and exceptions provided therein with respect to the replacement of USD LIBOR as the reference rate in the Parkway Property mortgage loan and corresponding interest rate protection agreement. However, the Company does not expect that any changes under ASU 2020-04 will have a material impact on its condensed consolidated financial statements.

Evaluation of the Company’s Ability to Continue as a Going Concern