UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended September 30, 2006March 31, 2007

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission File Number 1-3157

INTERNATIONAL PAPER COMPANY

(Exact name of registrant as specified in its charter)

| New York | 13-0872805 | |

(State or other jurisdiction of incorporation of organization) | (I.R.S. Employer Identification No.) | |

| 6400 Poplar Avenue, Memphis, TN | 38197 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (901) 419-7000

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes¨ No x

The number of shares outstanding of the registrant’s common stock as of October 31, 2006May 4, 2007 was 454,969,467.435,568,358.

| PAGE NO. | |||||

| PART I. | FINANCIAL INFORMATION | |||||

Item 1. | Financial Statements | |||||

| 1 | ||||||

Consolidated Balance Sheet - | 2 | |||||

| 3 | ||||||

| 4 | ||||||

| Condensed Notes to Consolidated Financial Statements | 5 | |||||

| Financial Information by Industry Segment | ||||||

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 41 | ||||

| Item 4. | Controls and Procedures | 42 | ||||

| OTHER INFORMATION | |||||

| Item 1. | 43 | |||||

| Risk Factors | 43 | ||||

Item | ||||||

| ||||||

| ||||||

Item 3. | Defaults | * | ||||

Item 4. | Submission of Matters to a Vote of Security Holders | * | ||||

Item 5. | Other Information | * | ||||

Item 6. | Exhibits | |||||

| * | Omitted since no answer is called for, answer is in the negative or inapplicable. |

Consolidated Statement of Operations

(Unaudited)

(In millions, except per share amounts)

| Three Months Ended September 30, | Nine Months Ended September 30, | Three Months Ended March 31, | ||||||||||||||||||||||

| 2006 | 2005 | 2006 | 2005 | 2007 | 2006 | |||||||||||||||||||

Net Sales | $ | 5,867 | $ | 5,925 | $ | 18,107 | $ | 17,650 | $ | 5,217 | $ | 5,526 | ||||||||||||

Costs and Expenses | ||||||||||||||||||||||||

Cost of products sold | 4,335 | 4,444 | 13,513 | 13,162 | 3,851 | 4,168 | ||||||||||||||||||

Selling and administrative expenses | 471 | 459 | 1,431 | 1,408 | 435 | 472 | ||||||||||||||||||

Depreciation, amortization and cost of timber harvested | 308 | 339 | 944 | 1,005 | 262 | 314 | ||||||||||||||||||

Distribution expenses | 291 | 261 | 905 | 776 | 256 | 285 | ||||||||||||||||||

Taxes other than payroll and income taxes | 55 | 58 | 171 | 174 | 42 | 53 | ||||||||||||||||||

Restructuring and other charges | 92 | 70 | 192 | 125 | 18 | 44 | ||||||||||||||||||

Insurance recoveries | — | (188 | ) | (19 | ) | (223 | ) | — | (19 | ) | ||||||||||||||

Net (gains) losses on sales and impairments of businesses | (110 | ) | 5 | 1,248 | 65 | (314 | ) | 1,283 | ||||||||||||||||

Reversal of reserves no longer required, net | — | (3 | ) | — | (3 | ) | ||||||||||||||||||

Interest expense, net | 144 | 121 | 441 | 444 | 61 | 149 | ||||||||||||||||||

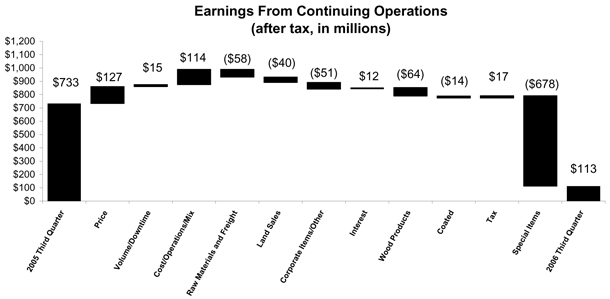

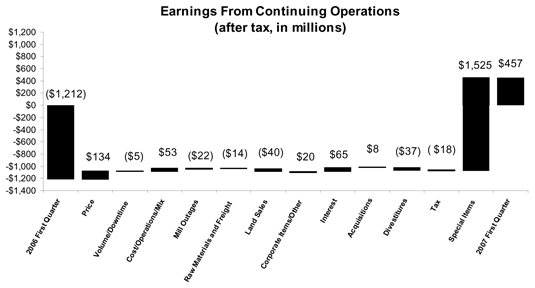

Earnings (Loss) From Continuing Operations Before Income Taxes and Minority Interest | 281 | 359 | (719 | ) | 717 | 606 | (1,223 | ) | ||||||||||||||||

Income tax provision | 163 | (377 | ) | 227 | (210 | ) | ||||||||||||||||||

Income tax provision (benefit) | 143 | (16 | ) | |||||||||||||||||||||

Minority interest expense, net of taxes | 5 | 3 | 14 | 8 | 6 | 5 | ||||||||||||||||||

Earnings (Loss) From Continuing Operations | 113 | 733 | (960 | ) | 919 | 457 | (1,212 | ) | ||||||||||||||||

Discontinued operations, net of taxes and minority interest | 88 | 290 | 39 | 258 | (23 | ) | (24 | ) | ||||||||||||||||

Net Earnings (Loss) | $ | 201 | $ | 1,023 | $ | (921 | ) | $ | 1,177 | $ | 434 | $ | (1,236 | ) | ||||||||||

Basic Earnings (Loss) Per Common Share | ||||||||||||||||||||||||

Earnings (loss) from continuing operations | $ | 0.23 | $ | 1.51 | $ | (1.98 | ) | $ | 1.89 | $ | 1.03 | $ | (2.49 | ) | ||||||||||

Discontinued operations | 0.19 | 0.59 | 0.08 | 0.53 | (0.05 | ) | (0.05 | ) | ||||||||||||||||

Net earnings (loss) | $ | 0.42 | $ | 2.10 | $ | (1.90 | ) | $ | 2.42 | $ | 0.98 | $ | (2.54 | ) | ||||||||||

Diluted Earnings (Loss) Per Common Share | ||||||||||||||||||||||||

Earnings (loss) from continuing operations | $ | 0.23 | $ | 1.46 | $ | (1.98 | ) | $ | 1.85 | $ | 1.02 | $ | (2.49 | ) | ||||||||||

Discontinued operations | 0.19 | 0.57 | 0.08 | 0.51 | (0.05 | ) | (0.05 | ) | ||||||||||||||||

Net earnings (loss) | $ | 0.42 | $ | 2.03 | $ | (1.90 | ) | $ | 2.36 | $ | 0.97 | $ | (2.54 | ) | ||||||||||

Average Shares of Common Stock Outstanding - assuming dilution | 484.9 | 507.1 | 485.2 | 507.5 | 448.4 | 486.3 | ||||||||||||||||||

Cash Dividends Per Common Share | $ | 0.25 | $ | 0.25 | $ | 0.75 | $ | 0.75 | $ | 0.25 | $ | 0.25 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Balance Sheet

(Unaudited)

(In millions)

| September 30, 2006 | December 31, 2005 | March 31, 2007 | December 31, 2006 | |||||||||||||

Assets | ||||||||||||||||

Current Assets | ||||||||||||||||

Cash and temporary investments | $ | 736 | $ | 1,641 | $ | 2,390 | $ | 1,624 | ||||||||

Accounts and notes receivable, net | 3,048 | 2,750 | 2,924 | 2,704 | ||||||||||||

Inventories | 2,306 | 2,287 | 2,009 | 1,909 | ||||||||||||

Assets of businesses held for sale | 270 | 3,321 | 100 | 1,778 | ||||||||||||

Deferred income tax assets | 288 | 279 | 491 | 490 | ||||||||||||

Other current assets | 136 | 110 | 163 | 132 | ||||||||||||

Total Current Assets | 6,784 | 10,388 | 8,077 | 8,637 | ||||||||||||

Plants, Properties and Equipment, net | 9,992 | 10,137 | 9,992 | 8,993 | ||||||||||||

Forestlands | 357 | 2,127 | 637 | 259 | ||||||||||||

Forestlands Held for Sale | 1,575 | — | ||||||||||||||

Investments | 648 | 625 | 631 | 641 | ||||||||||||

Goodwill | 3,661 | 3,838 | 3,251 | 2,929 | ||||||||||||

Assets Held for Exchange | — | 1,324 | ||||||||||||||

Deferred Charges and Other Assets | 1,672 | 1,656 | 1,278 | 1,251 | ||||||||||||

Total Assets | $ | 24,689 | $ | 28,771 | $ | 23,866 | $ | 24,034 | ||||||||

Liabilities and Common Shareholders’ Equity | ||||||||||||||||

Current Liabilities | ||||||||||||||||

Notes payable and current maturities of long-term debt | $ | 1,399 | $ | 1,181 | $ | 542 | $ | 692 | ||||||||

Accounts payable | 2,000 | 1,967 | 1,911 | 1,907 | ||||||||||||

Accrued payroll and benefits | 401 | 396 | 303 | 466 | ||||||||||||

Liabilities of businesses held for sale | 98 | 238 | 31 | 333 | ||||||||||||

Other accrued liabilities | 1,137 | 1,094 | 1,120 | 1,243 | ||||||||||||

Total Current Liabilities | 5,035 | 4,876 | 3,907 | 4,641 | ||||||||||||

Long-Term Debt | 9,051 | 11,023 | 6,358 | 6,531 | ||||||||||||

Deferred Income Taxes | 754 | 711 | 3,277 | 2,233 | ||||||||||||

Other Liabilities | 3,790 | 3,599 | 2,163 | 2,453 | ||||||||||||

Minority Interest | 185 | 211 | 236 | 213 | ||||||||||||

Common Shareholders’ Equity | ||||||||||||||||

Common stock, $1 par value, 493.3 shares in 2006 and 490.5 shares in 2005 | 494 | 491 | ||||||||||||||

Common stock, $1 par value, 493.3 shares in 2007 and 2006 | 493 | 493 | ||||||||||||||

Paid-in capital | 6,710 | 6,627 | 6,660 | 6,735 | ||||||||||||

Retained earnings | 1,879 | 3,172 | 3,963 | 3,737 | ||||||||||||

Accumulated other comprehensive loss | (1,817 | ) | (1,935 | ) | (1,452 | ) | (1,564 | ) | ||||||||

| 7,266 | 8,355 | 9,664 | 9,401 | |||||||||||||

Less: Common stock held in treasury, at cost, 2006 - 38.5 shares; 2005 - 0.1 shares | 1,392 | 4 | ||||||||||||||

Less: Common stock held in treasury, at cost, 48.4 shares in 2007 and 39.8 shares in 2006 | 1,739 | 1,438 | ||||||||||||||

Total Common Shareholders’ Equity | 5,874 | 8,351 | 7,925 | 7,963 | ||||||||||||

Total Liabilities and Common Shareholders’ Equity | $ | 24,689 | $ | 28,771 | $ | 23,866 | $ | 24,034 | ||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Statement of Cash Flows

(Unaudited)

(In millions)

| Nine Months Ended September 30, | Three Months Ended March 31, | |||||||||||||||

| 2006 | 2005 | 2007 | 2006 | |||||||||||||

| Operating Activities | ||||||||||||||||

Net (loss) earnings | $ | (921 | ) | $ | 1,177 | |||||||||||

Net earnings (loss) | $ | 434 | $ | (1,236 | ) | |||||||||||

Discontinued operations, net of taxes and minority interest | (39 | ) | (258 | ) | 23 | 24 | ||||||||||

Net (loss) earnings from continuing operations | (960 | ) | 919 | |||||||||||||

Earnings (loss) from continuing operations | 457 | (1,212 | ) | |||||||||||||

Depreciation and amortization | 944 | 1,005 | 262 | 314 | ||||||||||||

Deferred income tax expense | 132 | 139 | ||||||||||||||

Tax benefit - non-cash settlement of IRS audits | — | (553 | ) | |||||||||||||

Deferred income tax expense (benefit), net | 74 | (10 | ) | |||||||||||||

Restructuring and other charges | 192 | 125 | 18 | 44 | ||||||||||||

Payments related to restructuring and legal reserves | (65 | ) | (133 | ) | (22 | ) | (26 | ) | ||||||||

Insurance recoveries | (19 | ) | (223 | ) | — | (19 | ) | |||||||||

Reversal of reserves no longer required, net | — | (3 | ) | |||||||||||||

Net losses on sales and impairments of businesses held for sale | 1,248 | 65 | ||||||||||||||

Net (gains) losses on sales and impairments of businesses | (314 | ) | 1,283 | |||||||||||||

Periodic pension expense, net | 283 | 182 | 52 | 93 | ||||||||||||

Other, net | 145 | 167 | 51 | (11 | ) | |||||||||||

Changes in current assets and liabilities | ||||||||||||||||

Accounts and notes receivable | (164 | ) | (91 | ) | (81 | ) | (110 | ) | ||||||||

Inventories | (31 | ) | (25 | ) | (129 | ) | 9 | |||||||||

Accounts payable and accrued liabilities | 90 | (609 | ) | (61 | ) | (83 | ) | |||||||||

Other | (201 | ) | (56 | ) | (11 | ) | (87 | ) | ||||||||

Cash provided by operations - continuing operations | 1,594 | 909 | 296 | 185 | ||||||||||||

Cash provided by operations - discontinued operations | 44 | 47 | ||||||||||||||

Cash (used for) provided by operations - discontinued operations | (44 | ) | 61 | |||||||||||||

Cash Provided by Operations | 1,638 | 956 | 252 | 246 | ||||||||||||

Investment Activities | ||||||||||||||||

Invested in capital projects | (802 | ) | (756 | ) | (178 | ) | (168 | ) | ||||||||

Acquisitions, net of cash acquired | — | (39 | ) | |||||||||||||

Proceeds from divestitures | 2,163 | 1,440 | 1,633 | — | ||||||||||||

Other | (241 | ) | 63 | (118 | ) | (100 | ) | |||||||||

Cash provided by investment activities - continuing operations | 1,120 | 708 | ||||||||||||||

Cash provided by (used for) investment activities - continuing operations | 1,337 | (268 | ) | |||||||||||||

Cash used for investment activities - discontinued operations | (19 | ) | (219 | ) | (11 | ) | (31 | ) | ||||||||

Cash Provided by Investment Activities | 1,101 | 489 | ||||||||||||||

Cash Provided by (Used for) Investment Activities | 1,326 | (299 | ) | |||||||||||||

Financing Activities | ||||||||||||||||

Repurchases of common stock | (398 | ) | — | |||||||||||||

Issuance of common stock | 26 | 20 | 30 | 7 | ||||||||||||

Repurchase of common stock | (1,385 | ) | — | |||||||||||||

Issuance of debt | 1,259 | 278 | ||||||||||||||

Reduction of debt | (3,156 | ) | (2,543 | ) | (362 | ) | (743 | ) | ||||||||

Change in book overdrafts | (50 | ) | (30 | ) | 20 | (38 | ) | |||||||||

Dividends paid | (372 | ) | (368 | ) | (114 | ) | (123 | ) | ||||||||

Other | (3 | ) | (44 | ) | (3 | ) | 4 | |||||||||

Cash used for financing activities - continuing operations | (3,681 | ) | (2,687 | ) | (827 | ) | (893 | ) | ||||||||

Cash used for financing activities - discontinued operations | 22 | (172 | ) | |||||||||||||

Cash provided by financing activities - discontinued operations | — | 2 | ||||||||||||||

Cash Used for Financing Activities | (3,659 | ) | (2,859 | ) | (827 | ) | (891 | ) | ||||||||

Effect of Exchange Rate Changes on Cash - Continuing Operations | 14 | (85 | ) | |||||||||||||

Effect of Exchange Rate Changes on Cash - Discontinued Operations | 1 | (5 | ) | |||||||||||||

Effect of Exchange Rate Changes on Cash | 15 | 12 | ||||||||||||||

Change in Cash and Temporary Investments | (905 | ) | (1,504 | ) | 766 | (932 | ) | |||||||||

Cash and Temporary Investments | ||||||||||||||||

Beginning of the period | 1,641 | 2,596 | 1,624 | 1,641 | ||||||||||||

End of the period | 736 | 1,092 | $ | 2,390 | $ | 709 | ||||||||||

Less - Cash, End of Period - Discontinued Operations | — | — | ||||||||||||||

Cash, End of Period - Continuing Operations | $ | 736 | $ | 1,092 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Statement of Changes in Common Shareholders’ Equity

(Unaudited)

(In millions, except share amounts in thousands)

NineThree Months Ended September 30,March 31, 2007

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Income (Loss) | Treasury Stock | Total Common Shareholders’ Equity | |||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2006 | 493,340 | $ | 493 | $ | 6,735 | $ | 3,737 | $ | (1,564 | ) | 39,844 | $ | 1,438 | $ | 7,963 | |||||||||||||

Issuance of stock for various plans, net | 2 | — | (75 | ) | — | — | (2,681 | ) | (97 | ) | 22 | |||||||||||||||||

Repurchases of stock | — | — | — | — | — | 11,231 | 398 | (398 | ) | |||||||||||||||||||

Cash dividends - Common stock ($0.25 per share) | — | — | — | (114 | ) | — | — | — | (114 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net earnings | — | — | — | 434 | — | — | — | 434 | ||||||||||||||||||||

Amortization of pension and post retirement prior service costs and net loss (less tax of $10) | — | — | — | — | 18 | — | — | 18 | ||||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $0) | — | — | — | — | 88 | — | — | 88 | ||||||||||||||||||||

Net gains on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net gain arising during the period (less tax of $1) | — | — | — | — | 10 | — | — | 10 | ||||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $0) | — | — | — | — | (4 | ) | — | — | (4 | ) | ||||||||||||||||||

Total comprehensive income | 546 | |||||||||||||||||||||||||||

Adoption of FIN 48 (Note 8) | — | — | — | (94 | ) | — | — | — | (94 | ) | ||||||||||||||||||

Balance, March 31, 2007 | 493,342 | $ | 493 | $ | 6,660 | $ | 3,963 | $ | (1,452 | ) | 48,394 | $ | 1,739 | $ | 7,925 | |||||||||||||

Three Months Ended March 31, 2006

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Income (Loss) | Treasury Stock | Total Equity | ||||||||||||||||||||||

| Shares | Amount | Shares | Amount | ||||||||||||||||||||||||

Balance, December 31, 2005 | 490,501 | $ | 491 | $ | 6,627 | $ | 3,172 | $ | (1,935 | ) | 112 | $ | 4 | $ | 8,351 | ||||||||||||

Issuance of stock for various plans, net | 2,802 | 3 | 83 | — | — | (115 | ) | (4 | ) | 90 | |||||||||||||||||

Repurchase of stock | — | — | — | — | — | 38,465 | 1,392 | (1,392 | ) | ||||||||||||||||||

Cash dividends - Common stock ($0.75 per share) | — | — | — | (372 | ) | — | — | — | (372 | ) | |||||||||||||||||

Comprehensive income (loss): | |||||||||||||||||||||||||||

Net loss | — | — | — | (921 | ) | — | — | — | (921 | ) | |||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $8) | — | — | — | — | 135 | — | — | 135 | |||||||||||||||||||

Net gains (losses) on cash flow hedging derivatives: | |||||||||||||||||||||||||||

Net loss arising during the period (less tax of $6) | — | — | — | — | (9 | ) | — | — | (9 | ) | |||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $0) | — | — | — | — | (8 | ) | — | — | (8 | ) | |||||||||||||||||

Total comprehensive income | (803 | ) | |||||||||||||||||||||||||

Balance, September 30, 2006 | 493,303 | $ | 494 | $ | 6,710 | $ | 1,879 | $ | (1,817 | ) | 38,462 | $ | 1,392 | $ | 5,874 | ||||||||||||

Nine Months Ended September 30, 2005

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Income (Loss) | Treasury Stock | Total Equity | ||||||||||||||||||||

| Shares | Amount | Shares | Amount | ||||||||||||||||||||||

Balance, December 31, 2004 | 487,495 | $ | 487 | $ | 6,562 | $ | 2,562 | $ | (1,357 | ) | 16 | $ | — | $ | 8,254 | ||||||||||

Issuance of stock for various plans, net | 3,004 | 3 | 42 | — | — | 78 | 3 | 42 | |||||||||||||||||

Cash dividends - Common stock ($0.75 per share) | — | — | — | (368 | ) | — | — | — | (368 | ) | |||||||||||||||

Comprehensive income (loss): | |||||||||||||||||||||||||

Net earnings | — | — | — | 1,177 | — | — | — | 1,177 | |||||||||||||||||

Minimum pension liability adjustment (less tax of $1) | — | — | — | — | 3 | — | — | 3 | |||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $1) | — | — | — | — | (215 | ) | — | — | (215 | ) | |||||||||||||||

Net gains (losses) on cash flow hedging derivatives: | |||||||||||||||||||||||||

Net gain arising during the period (less tax of $13) | — | — | — | — | 38 | — | — | 38 | |||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $29) | — | — | — | — | (64 | ) | — | — | (64 | ) | |||||||||||||||

Total comprehensive income | 939 | ||||||||||||||||||||||||

Balance, September 30, 2005 | 490,499 | $ | 490 | $ | 6,604 | $ | 3,371 | $ | (1,595 | ) | 94 | $ | 3 | $ | 8,867 | ||||||||||

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Total Common Shareholders’ Equity | |||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2005 | 490,501 | $ | 491 | $ | 6,627 | $ | 3,172 | $ | (1,935 | ) | 112 | $ | 4 | $ | 8,351 | |||||||||||||

Issuance of stock for various plans, net | 2,216 | 2 | (28 | ) | — | — | (79 | ) | (3 | ) | (23 | ) | ||||||||||||||||

Cash dividends - Common stock ($0.25 per share) | — | — | — | (123 | ) | — | — | — | (123 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net earnings | — | — | — | (1,236 | ) | — | — | — | (1,236 | ) | ||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $2) | — | — | — | — | 81 | — | — | 81 | ||||||||||||||||||||

Net gains (losses) on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net gain arising during the period (less tax of $0) | — | — | — | — | — | — | — | — | ||||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $1) | — | — | — | — | (1 | ) | — | — | (1 | ) | ||||||||||||||||||

Total comprehensive income | (1,156 | ) | ||||||||||||||||||||||||||

Balance, March 31, 2006 | 492,717 | $ | 493 | $ | 6,599 | $ | 1,813 | $ | (1,855 | ) | 33 | $ | 1 | $ | 7,049 | |||||||||||||

The accompanying notes are an integral part of these financial statements.

Condensed Notes to Consolidated Financial Statements

(Unaudited)

NOTE 1 - BASIS OF PRESENTATION

The accompanying unaudited consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and, in the opinion of Management, include all adjustments that are necessary for the fair presentation of International Paper’s (the Company)the Company’s financial position, results of operations, and cash flows for the interim periods presented. Except as disclosed in these Condensedthe Notes to Consolidated Financial Statements, such adjustments are of a normal, recurring nature. Results for the first ninethree months of the year may not necessarily be indicative of full year results. It is suggested that these consolidated financial statements be read in conjunction with the audited financial statements and the notes thereto included in International Paper’s (the Company) Annual Report on Form 10-K for the year ended December 31, 2005, and in International Paper’s Current Report on Form 8-K filed on August 14, 2006, to update the historical financial statements included in the Company’s Form 10-K for the year ended December 31, 2005, as amended by Form 10-K/A, to reflect that the Company’s Kraft Papers business is treated as a discontinued operation (collectively the “2005 10-K”), both of which havehas previously been filed with the Securities and Exchange Commission.

Financial information by industry segment is presented on page 23.

See Note 10 for required pro forma21. In connection with sales of businesses under the Transformation Plan and additional disclosures related to stock-based compensation awards.

Prior-year amounts have been restated to presentthe resulting changes in the Company’s Kraftbusiness portfolio, a review of the Company’s operating business segments was conducted during the first quarter of 2007 under the provisions of Statement of Financial Accounting Standards No. 131. While this review resulted in no changes in the Company’s reportable segments, a decision was made to include the Company’s European coated paperboard operations, previously reported in the Printing Papers and Brazilian Coated Papers businesses as discontinuedsegment, with other similar operations (see Note 4).in the Consumer Packaging segment. Accordingly, prior period industry segment information has been revised to reflect this presentation.

NOTE 2 - EARNINGS PER COMMON SHARE

EarningsBasic earnings per common share from continuing operations are computed by dividing earnings from continuing operations by the weighted average number of common shares outstanding. EarningsDiluted earnings per common share from continuing operations assuming dilution, are computed assuming that all potentially dilutive securities, including “in-the-money” stock options, are converted into common shares at the beginning of each period. In addition, the computation of diluted earnings per share reflects the inclusion of contingently convertible securities in periods when dilutive. A reconciliation of the amounts included in the computation of earnings per common share from continuing operations, and diluted earnings per common share from continuing operations assuming dilution, is shown below:as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | Three Months Ended March 31, | ||||||||||||||||||

In millions, except per share amounts | 2006 | 2005 | 2006 | 2005 | 2007 | 2006 | ||||||||||||||

Earnings (loss) from continuing operations | $ | 113 | $ | 733 | $ | (960 | ) | $ | 919 | $ | 457 | $ | (1,212 | ) | ||||||

Effect of dilutive securities | — | 7 | — | 20 | — | — | ||||||||||||||

Earnings (loss) from continuing operations - assuming dilution | $ | 113 | $ | 740 | $ | (960 | ) | $ | 939 | $ | 457 | $ | (1,212 | ) | ||||||

Average common shares outstanding | 482.5 | 486.0 | 485.2 | 486.0 | 445.3 | 486.3 | ||||||||||||||

Effect of dilutive securities | ||||||||||||||||||||

Profit sharing plan | 2.1 | 1.0 | — | 1.2 | ||||||||||||||||

Restricted performance share plan | 2.7 | — | ||||||||||||||||||

Stock options | 0.3 | 0.1 | — | 0.3 | 0.4 | — | ||||||||||||||

Zero coupon convertible debentures | — | 20.0 | 20.0 | |||||||||||||||||

Average common shares outstanding - assuming dilution | 484.9 | 507.1 | 485.2 | 507.5 | 448.4 | 486.3 | ||||||||||||||

Earnings (loss) per common share from continuing operations | $ | 0.23 | $ | 1.51 | $ | (1.98 | ) | $ | 1.89 | $ | 1.03 | $ | (2.49 | ) | ||||||

Earnings (loss) per common share from continuing operations - assuming dilution | $ | 0.23 | $ | 1.46 | $ | (1.98 | ) | $ | 1.85 | |||||||||||

Diluted earnings (loss) per common share from continuing operations | $ | 1.02 | $ | (2.49 | ) | |||||||||||||||

| Note: |

In July 2006, in connection with the planned use of projected proceeds from the Company’s Transformation Plan, International Paper’s Board of Directors authorized a share repurchase program to acquire up to $3.0 billion of the Company’s stock. In a modified “Dutch Auction” tender offer completed in September 2006, International Paper purchased 38,465,260 shares of its common stock at a price of $36.00 per share, plus costs to acquire the shares, for a total cost of approximately $1.4 billion. Following the completion of this tender offer, International Paper had approximately 454.8 million shares of common stock outstanding.

NOTE 3 - RESTRUCTURING AND OTHER CHARGES

20062007::

During the thirdfirst quarter of 2006,2007, restructuring and other charges totaling $92$18 million before taxes ($5611 million after taxes) were recorded. These charges consisted of a pre-tax charge of $57 million ($35 million after taxes), including severance and other termination benefit costs of approximately $15 million, $25 million of lease termination costs and $17 million of other chargesrecorded for organizational restructuring programs associated with the Company’s Transformation Plan, andPlan. Additionally, a $35$2 million pre-tax chargecredit ($211 million after taxes) was recorded in Interest expense, net, for adjustments to legal reserves (see Note 7).interest received from the Canadian government on refunds of prior-year softwood lumber duties.

During the second quarter of 2006 restructuring and other charges totaling $54 million before taxes ($33 million after taxes) were recorded, consisting of a pre-tax charge of $50 million ($30 million after taxes), including severance and other termination benefit costs of approximately $31 million and $19 million of other charges associated with the Company’s Transformation Plan, and a $4 million pre-tax charge ($3 million after taxes) for legal settlements.:

During the first quarter of 2006, restructuring and other charges totaling $46$44 million before taxes ($2827 million after taxes) were recorded. Included in these charges were a pre-tax charge of $20$18 million ($1211 million after taxes) for organizational restructuring programs, principally severance costs associated with the Company’s Transformation Plan, a pre-tax charge of $8 million ($5 million after taxes) for losses on early extinguishment of debt, and a pre-tax charge of $18 million ($11 million after taxes) for adjustments to legal reserves. Also recorded was a pre-tax credit of $19 million ($12 million after taxes) for net insurance recoveries related to the hardboard siding and roofing litigation (see Note 7)9) and a charge of $6$3 million for tax adjustments.

2005:NOTE 4 – ACQUISITIONS

DuringOn February 1, 2007, the thirdCompany completed the non-cash exchange of certain pulp and paper assets in Brazil with Votorantim Celulose e Papel S.A. (VCP) that had been announced in the fourth quarter of 2005, restructuring2006. The Company exchanged its in-progress pulp mill project and other charges totaling $70certain forestland operations including approximately 100,000 hectares of surrounding forestlands in Tres Lagoas, Brazil, for VCP’s Luiz Antonio uncoated paper and pulp mill and approximately 55,000 hectares of forestlands in the state of Sao Paulo, Brazil. The exchange was accounted for based on the fair value of assets exchanged, resulting in the recognition in the 2007 first quarter of a pre-tax gain of $205 million before taxes ($48164 million after taxes) were recorded. Includedrepresenting the difference between the fair value and book value of the assets exchanged. This gain is included in this charge were a pre-tax chargeNet losses (gains) on sales and impairments of $44 million ($32 million after taxes) for organizational restructuring charges and a pre-tax charge of $26 million ($16 million after taxes) for losses on early extinguishment of debt. Also recordedbusinesses in the thirdaccompanying consolidated statement of operations. The net assets exchanged were included as Assets held for exchange in the accompanying consolidated balance sheet at December 31, 2006.

Based on preliminary estimates, expected to be finalized during the 2007 second quarter were a pre-tax creditupon the completion of $188 million ($109 million after taxes) for insurance recoveries relatedfinal asset appraisals and any post-closing adjustments, the following table summarizes the allocation of the fair value of the assets exchanged to the hardboard sidingassets and roofing litigation (see Note 7)liabilities acquired:

In millions | |||

Accounts receivable | $ | 55 | |

Inventory | 24 | ||

Other current assets | 40 | ||

Plants, properties and equipment, net | 1,000 | ||

Forestlands | 355 | ||

Goodwill | 304 | ||

Other intangible assets | 160 | ||

Other long-term assets | 7 | ||

Total assets acquired | 1,945 | ||

Other current liabilities | 20 | ||

Deferred taxes | 382 | ||

Other liabilities | 23 | ||

Total liabilities assumed | 425 | ||

Net assets acquired | $ | 1,520 | |

Net sales and a $3 million pre-tax credit ($2 million after taxes)earnings before income taxes for the net adjustment of previously provided reserves. In addition, a $517 million net reduction of the income tax provision was recorded, including a credit from an agreement reached with the U.S. Internal Revenue Service concerning the 1997 through 2000 U.S. federal income tax audits, a charge related to cash repatriations from non-U.S. subsidiaries, and a charge relating to a change in Ohio state tax laws. Interest expense, net, also includes a $43 million pre-tax credit ($26 million after taxes) relating to this agreement.

During the second quarter of 2005, a pre-tax charge of $31 million ($19 million after taxes)Luiz Antonio mill for organizational restructuring charges, and a pre-tax credit of $35 million ($21 million after taxes) for insurance recoveries related to the hardboard siding and roofing litigation were recorded. The organizational restructuring charges included $17 million before taxes ($11 million after taxes) recorded in the Printing Papers business segment for severance and other charges associated with the indefinite shutdown of three U.S. paper machines, and $14 million before taxes ($8 million after taxes) in the Forest Products business segment for costs associated with relocating the business headquarters to Memphis, Tennessee from Savannah, Georgia. Additionally, an $82 million increase in the income tax provision was recorded, including approximately $79 million for deferred taxes related to earnings repatriated during the quarter under the American Jobs Creation Act of 2004.

During the first quarter of 2005,2007, and pro-forma amounts as if this transaction has occurred as of the beginning of the period, are not material to consolidated results of operations.

In October and November 2006, International Paper paid approximately $82 million for a special charge50% interest in the International Paper & Sun Cartonboard Co., Ltd. joint venture that currently operates two coated paperboard machines in Yanzhou City, China. In December 2006, a 50% interest was acquired in a second joint venture, Shandong International Paper & Sun Coated Paperboard Co., Ltd., for approximately $28 million. The operating results of $24 million before taxes ($15 million after taxes) was recorded for lossesthese consolidated joint ventures did not have a material effect on early extinguishmentthe Company’s consolidated results of high-coupon-rate debt.operations in 2007 or 2006.

NOTE 45 - BUSINESSES HELD FOR SALE AND DIVESTITURES

Discontinued Operations:

2007:

During the first quarter of 2007, the Company recorded pre-tax credits of $21 million ($9 million after taxes) and $6 million ($4 million after taxes) relating to the sales of its Wood Products and Kraft Papers businesses, respectively. In addition, a $15 million pre-tax charge ($39 million after taxes) was recorded for adjustments to the loss on the completion of the sale of most of the Beverage Packaging business. Finally, a pre-tax credit of approximately $10 million ($6 million after taxes) was recorded for refunds received from the Canadian government of duties paid by the Company’s former Weldwood of Canada Limited business.

2006:

During the fourth quarter of 2006, the Company entered into an agreement to sell its Beverage Packaging business to Carter Holt Harvey Limited for approximately $500 million, subject to certain adjustments. The sale of the North American Beverage Packaging operations subsequently closed on January 31, 2007, with the sale of the remaining non-U.S. operations expected to close later in 2007.

Also during the fourth quarter of 2006, the Company entered into separate agreements for the sale of 13 lumber mills for approximately $325 million, and five wood products plants for approximately $237 million, both subject to various adjustments at closing. Both of the sales were completed in March 2007.

The Company determined that the accounting requirements for both businesses under Statement of Financial Accounting Standards (SFAS) No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets,” as discontinued operations were met. Accordingly, the operating results for these businesses are included in Discontinued operations for all periods presented.

Revenues, earnings and earnings per share related to the Beverage Packaging business were as follows:

In millions, except per share amounts | Three Months Ended March 31, 2007 | Three Months Ended March 31, 2006 | ||||||

Revenues | $ | 86 | $ | 211 | ||||

Earnings from discontinued operation | ||||||||

Earnings from operation | $ | 15 | $ | 11 | ||||

Income tax expense | (5 | ) | (4 | ) | ||||

Earnings from operation, net of taxes | 10 | 7 | ||||||

Loss on sales and impairments | (15 | ) | — | |||||

Income tax expense | (24 | ) | — | |||||

Loss on sales and impairments, net of taxes | (39 | ) | — | |||||

Earnings (loss) from discontinued operation, net of taxes | $ | (29 | ) | $ | 7 | |||

Earnings (loss) per common share from discontinued operation - assuming dilution | ||||||||

Earnings from operation | $ | 0.02 | $ | 0.01 | ||||

Loss on sales and impairments | (0.08 | ) | — | |||||

Earnings (loss) per common share from discontinued operation, net of taxes and minority interest - assuming dilution | $ | (0.06 | ) | $ | 0.01 | |||

Revenues, earnings and earnings per share related to the Wood Products business were as follows: |

| |||||||

In millions, except per share amounts | Three Months Ended March 31, 2007 | Three Months Ended March 31, 2006 | ||||||

Revenues | $ | 201 | $ | 394 | ||||

Earnings (loss) from discontinued operation | ||||||||

Earnings (loss) from operation | $ | (22 | ) | $ | 36 | |||

Income tax benefit (expense) | 9 | (14 | ) | |||||

Earnings (loss) from operation, net of taxes | (13 | ) | 22 | |||||

Gain on sales and impairments | 21 | — | ||||||

Income tax expense | (12 | ) | — | |||||

Gain on sales and impairments, net of taxes | 9 | — | ||||||

Earnings (loss) from discontinued operation, net of taxes | $ | (4 | ) | $ | 22 | |||

Earnings (loss) per common share from discontinued operation - assuming dilution | ||||||||

Earnings (loss) from operation | $ | (0.03 | ) | $ | 0.05 | |||

Gain on sales and impairments | 0.02 | — | ||||||

Earnings (loss) per common share from discontinued operation, net of taxes - assuming dilution | $ | (0.01 | ) | $ | 0.05 | |||

During the 2006 third quarter, International Paper completed the previously announced sale of its Brazilian Coated Papers business to Stora Enso Oyj for approximately $420 million, subject to certain post-closing adjustments. The business includes a coated paper mill and lumber mill in Arapoti, Parana State, Brazil, as well as 50,000 hectares (approximately 124,000 acres) of forestland in Parana.business. The operating results of this business for all periods presented are included in Discontinued operations infor all periods presented.

Revenues, earnings and earnings per share related to the accompanying consolidated statementBrazilian Coated Papers business were as follows:

In millions, except per share amounts | Three Months Ended March 31, 2006 | |||

Revenues | $ | 42 | ||

Earnings from discontinued operation | ||||

Earnings from operation | $ | 10 | ||

Income tax expense | (6 | ) | ||

Earnings from operation, net of taxes | 4 | |||

Gain on sale | — | |||

Income tax expense | — | |||

Gain on sale, net of taxes | — | |||

Earnings from discontinued operation, net of taxes | $ | 4 | ||

Earnings per common share from discontinued operation - assuming dilution | ||||

Earnings from operation | $ | 0.01 | ||

Gain on sale | — | |||

Earnings per common share from discontinued operation, net of taxes - assuming dilution | $ | 0.01 | ||

During the first quarter of operations, including2006, the Company determined that the accounting requirements under SFAS No. 144 for reporting the Kraft Papers business as a discontinued operation were met. Accordingly, a $100 million pre-tax gain of $101 millioncharge ($8061 million after taxes) was recorded in the 2006 third quarter as a result of the sale. Revenues associated with this business were $33 million and $127 million, respectively for the three-month and nine-month periods ended September 30, 2006. Revenues for the comparable 2005 periods were $57 million and $149 million, respectively.

During the 2006 second quarter, the Company signed a definitive agreement to sell its Kraft Papers business for approximately $155 million in cash, subject to certain closing and post-closing adjustments, and two additional payments totaling up to $60 million payable five years from the date of closing contingent upon business performance. The operating results of this business for all periods presented are included in Discontinued operations in the accompanying consolidated statement of operations, including a pre-tax charge of $101 million ($62 million after taxes) recorded in the 2006 first quarter to reduce the carrying value of the business’s net assets of this business to their estimated fair values. Additionally, a pre-tax chargevalue. The sale of $16 million ($10 million after taxes)this business was recordedcompleted in January 2007. The operating results of this business are included in Discontinued operations in the 2006 second quarter to further reduce the carrying value of the assets of this business based on the terms of the definitive agreement

discussed above. Revenues, associated with the Kraft Papers business were $62 millionearnings and $174 million, respectively for the three-month and nine-month periods ended September 30, 2006. Revenues for the comparable 2005 periods were $54 million and $165 million, respectively.

Earnings and diluted earnings per share related to the Kraft Papers and Brazilian Coated Papers operationsbusiness were as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

In millions, except per share amounts | 2006 | 2005 | 2006 | 2005 | ||||||||||||

Earnings (loss) from discontinued operations | ||||||||||||||||

Earnings from operations | $ | 14 | $ | 14 | $ | 49 | $ | 33 | ||||||||

Gain (loss) on sales or impairments | 101 | — | (16 | ) | — | |||||||||||

Income tax (expense) benefit | (27 | ) | (5 | ) | 6 | (11 | ) | |||||||||

Earnings from discontinued operations, net of taxes | $ | 88 | $ | 9 | $ | 39 | $ | 22 | ||||||||

Earnings (loss) per common share from discontinued operations - assuming dilution | ||||||||||||||||

Earnings from operations, net of taxes | $ | 0.02 | $ | 0.02 | $ | 0.06 | $ | 0.05 | ||||||||

Gain on sales or impairments, net of taxes | 0.17 | — | 0.02 | — | ||||||||||||

Earnings per common share from discontinued operations, net of taxes - assuming dilution | $ | 0.19 | $ | 0.02 | $ | 0.08 | $ | 0.05 | ||||||||

In millions, except per share amounts Three Months Ended March 31, 2007 Three Months Ended March 31, 2006 Revenues Earnings from discontinued operation Earnings from operation Income tax expense Earnings from operation, net of taxes Gain (loss) on sales and impairments Income tax (expense) benefit Gain (loss) on sales and impairments, net of taxes Earnings (loss) from discontinued operation, net of taxes Earnings (loss) per common share from discontinued operation - assuming dilution Earnings from operation Gain (loss) on sales and impairments Earnings (loss) per common share from discontinued operation, net of taxes - assuming dilutionAt September 30, 2006 and December 31, 2005, assets of businesses held for sale totaled $270 million and $3.3 billion, respectively, and liabilities of businesses held for sale totaled $98 million and $238 million, respectively, and included the Kraft Papers business, the Brazilian Coated Papers business, the Coated and Supercalendered Papers business and certain smaller businesses, as follows: $ — $ 55 $ — $ 7 — (3 ) — 4 6 (100 ) (2 ) 39 4 (61 ) $ 4 $ (57 ) $ — $ 0.01 0.01 (0.13 ) $ 0.01 $ (0.12 )

In millions | September 30, 2006 | December 31, 2005 | ||||

Accounts receivable, net | $ | 48 | $ | 176 | ||

Inventories | 52 | 161 | ||||

Plants, properties and equipment, net | 114 | 1,664 | ||||

Forestland | 38 | 63 | ||||

Goodwill | — | 1,205 | ||||

Other assets | 18 | 52 | ||||

Assets of businesses held for sale | $ | 270 | $ | 3,321 | ||

Accounts payable | $ | 35 | $ | 137 | ||

Accrued payroll and benefits | 14 | 37 | ||||

Other accrued liabilities | 23 | 29 | ||||

Other liabilities | 26 | 35 | ||||

Liabilities of businesses held for sale | $ | 98 | $ | 238 | ||

2005:

In the third quarter of 2005, International Paper completed the sale of its 50.5% interest in Carter Holt Harvey Limited (CHH) for approximately U.S. $1.1 billion. The pre-tax gain on the sale of $29 million ($361 million after taxes and minority interest), including a $186 million pre-tax credit from cumulative translation adjustments, was included in Discontinued operations, together with CHH’s operating results prior to the sale. Revenues associated with the discontinued operation were $541 million and $1.7 billion for the three-month and nine-month periods ended September 30, 2005. Earnings and diluted earnings per share related to these operations were as follows:

In millions, except per share amounts Earnings (loss) from discontinued operations Earnings (loss) from operations Gain on sale of business Income tax expense Minority interest, net of taxes Loss from discontinued operations, net of taxes and minority interest Earnings (loss) per common share from discontinue operation - assuming dilution Loss from operations, net of taxes Gain on sale, net of taxes and minority interest Earnings per common share from discontinued operations, net of taxes and minority interest - assuming dilution Three Months Ended

September 30, 2005 Nine Months Ended

September 30, 2005 $ (11 ) $ (43 ) 29 29 265 242 (2 ) 8 $ 281 $ 236 $ (0.16 ) $ (0.25 ) 0.71 0.71 $ 0.55 $ 0.46

Other Transactions:Divestitures and Impairments of Businesses:

20062007::

During the thirdfirst quarter of 2006,2007, a net$103 million pre-tax gain of $110 million (a loss of $13($96 million after taxes) was recorded for gains (losses) on sales and impairments of businesses. This net gain included pre-tax credits of $304 million ($185 million after taxes) for gains on sales of U.S. forestlands included in the Transformation Plan, the recognition of a previously deferred $110 million pre-tax gain ($68 million after taxes) related to a 2004 sale of forestlands in Maine, pre-tax losses of $165 million and $115 million ($165 million and $82 million after taxes) to adjust the carrying values of the Company’s Wood Products and Beverage Packaging businesses to estimated fair values based on preliminary bids received, a pre-tax charge of $38 million ($23 million after taxes) to reflectupon the completion of the sale of the Company’s Coated and Supercalendered Papers businessArizona Chemical business. As part of the transaction, International Paper acquired a minority interest of approximately 10% in the 2006 third quarter, and a net pre-tax gain of $14 million (a loss of $2 million after taxes) related to other smaller sales.

Also duringresulting new entity. Since the third quarter of 2006, International Paper Investments (Holland) B.V. (IPI), a wholly-owned subsidiary of International Paper, announced that it had entered into an agreement with Votorantim Celulose e Papel S.A. (VCP) to exchange IPI’s pulp mill project being developed in Tres Lagoas, state of Mato Grosso do Sul, Brazil (together with approximately 100,000 hectares of forestlands) for VCP’s Luiz Antonio pulp and uncoated paper mill and approximately 60,000 hectares of forestlands locatedinterest acquired represents significant continuing involvement in the stateoperations of Sao Paulo, Brazil. IPI will fund the Tres Lagoas pulp mill projectbusiness under U.S. Generally Accepted Accounting Principles, the operating results for Arizona Chemical are included in continuing operations in the amountaccompanying consolidated statement of U.S. $1.15 billion. This transaction isoperations. Final sale proceeds are subject to post-closing adjustments, expected to close by February 1, 2007.be finalized in the 2007 second quarter.

During the second quarter of 2006,In addition, a net$6 million pre-tax charge of $75 millioncredit ($514 million after taxes) was recorded including a pre-tax creditto adjust previously estimated gains/losses of $62 million ($39 million after taxes)businesses previously sold.

These gains are included, along with the gain on the exchange for gainsthe Luiz Antonio mill in Brazil (see Note 4), in Net losses (gains) on sales and impairments of U.S. forestlands includedbusinesses in the Transformation Plan, a pre-tax chargeaccompanying consolidated statement of $85 million ($53 million after taxes) recorded to adjust the carrying value of the assets of the Company’s Coated and Supercalendered Papers business to their estimated fair value based on the terms of the definitive sales agreement signed in the second quarter, and a pre-tax charge of $52 million ($37 million after taxes) recorded to write down the carrying value of certain assets in Brazil to their estimated fair value. The assets in Brazil were written down to estimated net realizable value upon sale since the sale of these assets was considered probable at June 30, 2006.operations.

2006:

During the first quarter, of 2006, a pre-tax special charge of $1.3 billion was recorded to write down the assets of the Company’s Coated and Supercalendered Papers business to their estimated fair value.value, as management had committed to a plan to sell this business. In addition, other pre-tax charges totaling $3 million ($2 million after taxes) were recorded to adjust estimated losses of certain smaller operations that are held for sale.

InAt December 31, 2006, assets and liabilities of businesses held for sale included the 2006 first quarter, the Company had reported its Coated and SupercalenderedKraft Papers business, as a discontinued operation based on a plan to sell the business. InBeverage Packaging business, the second quarterWood Products business, and the Arizona Chemical business, and consisted of:

In millions | December 31, 2006 | ||

Accounts receivable, net | $ | 298 | |

Inventories | 401 | ||

Plants, properties and equipment, net | 995 | ||

Goodwill | 10 | ||

Other assets | 74 | ||

Assets of businesses held for sale | $ | 1,778 | |

Accounts payable | $ | 184 | |

Accrued payroll and benefits | 50 | ||

Other accrued liabilities | 32 | ||

Other liabilities | 67 | ||

Liabilities of businesses held for sale | $ | 333 | |

Assets and liabilities of 2006, the Company signed a definitive agreement to sell this business for approximately $1.4 billion, subject to certain post-closing adjustments, and agreed to acquire a 10% limited partnership interest in CMP Investments L.P., the parent company that will own this business. Since this limited partnership interest will represent significant continuing involvement in the operations of this business under U.S. generally accepted accounting principles, the operating results for Coated and Supercalendered Papers are required to be included in continuing operations in the accompanying consolidated statement of operations. Accordingly, the operating results for this business, including a charge in the first quarter of $1.3 billion before and after taxes to write down the assets of the business to their estimated fair value, are now included in continuing operations for all periods presented. This sale was subsequently completed on August 1, 2006.

In March 2006, International Paper, The Nature Conservancy and The Conservation Fund reached an agreement to sell approximately 218,000 acres of forestlands across 10 U.S. states. The Nature Conservancy will acquire more than 173,000 acres in North Carolina, Virginia, Georgia, Florida, Alabama, Arkansas, Tennessee, Louisiana and Mississippi. The Conservation Fund will acquire more than 5,000 acres in Florida and 500 acres in North Carolina. The two groups will jointly purchase an additional 39,000 acres in South Carolina. Also in March 2006, International Paper announced an agreement to sell 69,000 acres of forestlands in Wisconsin to The Nature Conservancy for approximately $83 million.

On April 4, 2006 International Paper announced definitive agreements with two separate investor groups under which it will sell a total of approximately 5.1 million acres of forestlands for aggregate proceeds of approximately $6.1 billion. Under one of the agreements, International Paper will sell approximately 3.8 million acres of forestlands located in the southern U.S. and 440,000 acres in Michigan to an investor group led by Resource Management Service, LLC (RMS) for approximately $5 billion in cash and notes at closing. Under a separate agreement, International Paper will sell approximately 900,000 acres of forestlands in Louisiana, Texas and Arkansas to an investor group led by TimberStar for approximately $1.1 billion in cash and notes at closing.

On April 11, 2006, International Paper announced a definitive agreement with The Lyme Timber Company, for the benefit of the Lyme Forest Fund L.P., for the sale of approximately 275,000 acres of forestlands in New York’s Adirondack Park for approximately $137 million.

During the third quarter of 2006, the Company completed sales of approximately 477,000 acres of forestlands under the Nature Conservancy, Conservation Fund and Lyme Forest Fund L.P. agreements for approximately $401 million, including an installment note receivable of $136 million, resulting in a pre-tax gain of approximately $304 million ($185 million after taxes). During the second quarter of 2006, the Company completed the sales of approximately 75,000 acres of forestlands under the above agreements for approximately $97 million, resulting in a pre-tax gain of approximately $62 million ($39 million after taxes).

The remaining sales under the agreements discussed above are expected to be completed during the fourth quarter of 2006. This will substantially complete International Paper’s sales of U.S. forestlands identified as part of the Company’s Transformation Plan. Anticipated total proceeds from all of these sale agreements, covering about 5.7 million acres or over 85% of the Company’s U.S. forestland holdings, are approximately $6.6 billion. The carrying value of these forestlands is included in the accompanying consolidated balance sheet as of September 30, 2006 under the caption Forestlandsbusinesses held for sale. The amount of gain that will be recognizedsale by the Company upon the completion of these transactions will be dependent upon the final amount of proceeds received, costs incurred and transactions terms, and the portion, if any, of the gain that will be required to be deferred under applicable accounting standards. International Paper has retained approximately 660,000 acres of forestlands at September 30, 2006, some of which may be later sold in separate transactions to maximize the proceeds from the land.

2005:

In the third quarter of 2005, charges totaling $5 million before taxes ($3 million after taxes) were recorded for adjustments of losses on businesses previously sold.

In the second quarter of 2005, a $19 million pre-tax credit ($12 million after taxes) was recorded, including a $25 million credit before taxes ($15 million after taxes) from the collection of a note receivable from the 2001 sale of the Flexible Packaging business, final charges related to the sale of Fine Papers and Industrial Papers, as well as net adjustments of losses from businesses previously sold.

During the first quarter of 2005, International Paper announced an agreement to sell its Fine Papers business to Mohawk Paper Mills, Inc. of Cohoes, New York. A $24 million pre-tax loss ($13 million after taxes) was recorded in the first quarter to write down the net assets of the Fine Papers business to their estimated net realizable value. The sale of Fine Papers was completed in the second quarter of 2005.

Also during the first quarter of 2005, International Paper announced that it had signed an agreement to sell its Industrial Papers business to an affiliate of Kohlberg and Company, LLC. A $49 million pre-tax loss ($35 million after taxes) was recorded in the first quarter to write down the net assets of the Industrial Papers business and related corporate assets to their estimated net realizable value. The sale of Industrial Papers was completed in the second quarter of 2005.

Also in the first quarter of 2005, charges totaling $6 million before taxes ($4 million after taxes) were recorded for adjustments to estimated losses on sales of certain smaller operations.

In millions | December 31, 2006 | |||||

| Assets | Liabilities | |||||

Kraft | $ | 148 | $ | 16 | ||

Arizona Chemical | 496 | 159 | ||||

Beverage Packaging | 572 | 107 | ||||

Wood Products | 562 | 51 | ||||

Total | $ | 1,778 | $ | 333 | ||

NOTE 56 - SUPPLEMENTAL FINANCIAL STATEMENT INFORMATION

Inventories by major category were:

In millions | September 30, 2006 | December 31, 2005 | March 31, 2007 | December 31, 2006 | ||||||||

Raw materials | $ | 380 | $ | 376 | $ | 292 | $ | 265 | ||||

Finished pulp, paper and packaging products | 1,519 | 1,534 | 1,398 | 1,341 | ||||||||

Finished lumber and panel products | 17 | 31 | ||||||||||

Operating supplies | 319 | 276 | 288 | 271 | ||||||||

Other | 71 | 70 | 31 | 32 | ||||||||

Total | $ | 2,306 | $ | 2,287 | $ | 2,009 | $ | 1,909 | ||||

Temporary investments with an original maturity of three months or less are treated as cash equivalents and are stated at cost. Temporary investments totaled $473 million$1.8 billion and $1.4 billion at September 30, 2006March 31, 2007 and December 31, 2005,2006, respectively.

Interest payments made during the nine-monththree-month periods ended September 30,March 31, 2007 and 2006 and 2005 were $507$108 million and $630$159 million, respectively. The 2005 interest payments include a $52 million payment to the U.S. Internal Revenue Service related to the settlement of the 1997 – 2000 U.S. federal income tax audits. Capitalized net interest costs were $13$11 million and $8$3 million for the ninethree months ended September 30,March 31, 2007 and 2006, and 2005, respectively. Total interest expense was $498$114 million for the first ninethree months of 20062007 and $507$171 million for the first ninethree months of 2005, net of a $43 million credit related to the settlement of the tax audits described above.2006. Preferred Securities distributions paid by Southeast Timber, Inc., a consolidated subsidiary of International Paper, were $10 million and $7$3 million during the first ninethree months of 2006both 2007 and 2005, respectively.2006. The expense related to these preferred securities was included in minority interest expense in the consolidated statement of operations. Income tax payments of $114$33 million and $357$37 million were made during the first ninethree months of 2007 and 2006, and 2005, respectively.

Accumulated depreciation was $17.9$14.3 billion at September 30, 2006March 31, 2007 and $18.2$14.0 billion at December 31, 2005.2006. The allowance for doubtful accounts was $100$86 million at September 30, 2006March 31, 2007 and $98$85 million at December 31, 2005.2006.

The following tables present changes in the goodwill balances as allocated to each business segment for the nine-monththree-month periods ended September 30, 2006March 31, 2007 and 2005:

2006:

In millions | Balance December 31, 2005 | Reclassifications and Other (a) | Additions/ (Reductions) | Balance September 30, 2006 | Balance December 31, 2006 | Reclassifications Other (a) | Additions/ (Reductions) | Balance March 31, 2007 | |||||||||||||||||||

Printing Papers | $ | 1,674 | $ | 1 | $ | — | $ | 1,675 | $ | 1,500 | $ | (47 | ) | $ | 304 | (b) | $ | 1,757 | |||||||||

Industrial Packaging | 676 | 3 | 11 | (b) | 690 | 670 | — | (3 | )(c) | 667 | |||||||||||||||||

Consumer Packaging | 987 | 1 | (28 | )(c) | 960 | 451 | 60 | 8 | (d) | 519 | |||||||||||||||||

Distribution | 299 | — | — | 299 | 308 | — | — | 308 | |||||||||||||||||||

Forest Products | 191 | — | (165 | )(c) | 26 | ||||||||||||||||||||||

Corporate | 11 | — | — | 11 | |||||||||||||||||||||||

Total | $ | 3,838 | $ | 5 | $ | (182 | ) | $ | 3,661 | $ | 2,929 | $ | 13 | $ | 309 | $ | 3,251 | ||||||||||

| (a) | Represents the effects of foreign currency translations and |

| (b) | Reflects a |

| (c) | Reflects a |

| Reflects |

2005:

In millions | Balance December 31, 2004 | Reclassifications and Other (a) | Additions/ (Reductions) | Balance September 30, 2005 | Balance December 31, 2005 | Reclassifications Other (a) | Additions/ (Reductions) | Balance March 31, 2006 | |||||||||||||||||||

Printing Papers | $ | 1,671 | $ | 3 | $ | — | $ | 1,674 | $ | 1,674 | $ | — | $ | — | $ | 1,674 | |||||||||||

Industrial Packaging | 591 | (5 | ) | 16 | (b) | 602 | 677 | 1 | 1 | (b) | 679 | ||||||||||||||||

Consumer Packaging | 1,014 | (4 | ) | 51 | (c) | 1,061 | 960 | — | — | 960 | |||||||||||||||||

Distribution | 299 | — | — | 299 | 299 | — | — | 299 | |||||||||||||||||||

Forest Products | 190 | 1 | — | 191 | |||||||||||||||||||||||

Corporate | 24 | — | (13 | )(d) | 11 | 11 | — | — | 11 | ||||||||||||||||||

Total | $ | 3,789 | $ | (5 | ) | $ | 54 | $ | 3,838 | $ | 3,621 | $ | 1 | $ | 1 | $ | 3,623 | ||||||||||

| (a) | Represents the effects of foreign currency translations and reclassifications. |

| (b) | Reflects the completion of the accounting for the acquisition of |

Goodwill totaling approximately $1.2 billion at December 31, 2005 relating to the Company’s Coated and Supercalendered Papers business was written off in connection with the 2006 first-quarter $1.3 billion pre-tax charge to reduce the net assets of that business to estimated fair value (see Note 4).

The following table presents an analysis of activity related to the Company’s asset retirement obligations:

| Nine Months Ended September 30, | Three Months Ended March 31, | ||||||||||||||

In millions | 2006 | 2005 | 2007 | 2006 | |||||||||||

Asset retirement obligation, January 1 | $ | 33 | $ | 30 | $ | 29 | $ | 33 | |||||||

New liabilities | 1 | 6 | — | — | |||||||||||

Liabilities settled | (3 | ) | (4 | ) | — | (1 | ) | ||||||||

Net adjustments to existing liabilities | 1 | (4 | ) | — | — | ||||||||||

Accretion expense | 1 | 1 | — | 1 | |||||||||||

Asset retirement obligation, September 30 | $ | 33 | $ | 29 | |||||||||||

Asset retirement obligation, March 31 | $ | 29 | $ | 33 | |||||||||||

This obligation is included in Other liabilities in the accompanying consolidated balance sheet.

The components of the Company’s postretirement benefit expense were as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||

In millions | Three Months Ended March 31, | |||||||||||||||||||||||

| 2006 | 2005 | 2006 | 2005 | 2007 | 2006 | |||||||||||||||||||

Service cost | $ | 1 | $ | 1 | $ | 2 | $ | 2 | $ | — | $ | 1 | ||||||||||||

Interest cost | 8 | 10 | 24 | 29 | 9 | 9 | ||||||||||||||||||

Actuarial loss | 6 | 5 | 17 | 15 | 5 | 4 | ||||||||||||||||||

Amortization of prior service cost | (13 | ) | (10 | ) | (37 | ) | (30 | ) | (11 | ) | (9 | ) | ||||||||||||

Net postretirement benefit cost (a) | $ | 2 | $ | 6 | $ | 6 | $ | 16 | $ | 3 | $ | 5 | ||||||||||||

| (a) | Excludes a |

NOTE 67 – RECENT ACCOUNTING DEVELOPMENTS

Employers’ AccountingFair Value Option for Defined Benefit PensionFinancial Assets and Other Postretirement Plans:Financial Liabilities:

In September 2006,February 2007, the Financial Accounting Standards Board (FASB) issued SFAS No. 158, “Employers’ Accounting159, “The Fair Value Option for Defined Benefit PensionFinancial Assets and Other Postretirement PlansFinancial Liabilities – Including an Amendment of FASB StatementsStatement No. 87, 88, 106, and 132(R).115.” This Statement requires a calendar year-end companystatement permits an entity to measure certain financial assets and financial liabilities at fair value which would result in the reporting of unrealized gains and losses in earnings at each subsequent reporting date. The fair value option may be elected on an instrument-by-instrument basis, with publicly traded equity securities that sponsors a postretirement benefit planfew exceptions, as long as it is applied to fully recognize, as an asset or liability, the overfunded or underfunded status of its benefit plan(s)instrument in its 2006 year-end balance sheet. It also requires a companyentirety. The statement establishes presentation and disclosure requirements to measurehelp financial statement users understand the effect of an entity’s election on its plan assets and benefit obligationsearnings, but does not eliminate the disclosure requirements of other accounting standards. This statement will be effective as of its year-end balance sheet datethe beginning withof the first fiscal years endingyear that begins after DecemberNovember 15, 2008.2007, and is to be applied prospectively as of the beginning of the year in which it is initially applied. The Company is currently evaluating the provisions of this Statement.statement.

Fair Value Measurements:

In September 2006, the FASB also issued SFAS No. 157, “Fair Value Measurements,” which provides a single definition of fair value, together with a framework for measuring it, and requires additional disclosure about the use of fair value to measure assets and liabilities. It also emphasizes that fair value is a market-based measurement, not an entity-specific measurement, and sets out a fair value hierarchy with the highest priority being quoted prices in active markets. This Statement isstatement will be effective for financial statements issued for fiscal years beginning after November 15, 2007, and interim periods within those fiscal years, and is to be applied prospectively as of the beginning of the year in which it is initially applied. The Company is currently evaluating the provisions of this statement.

Accounting for Planned Major Maintenance Activities:

In September 2006, the FASB issued FSPFASB Staff Position (FSP) No. AUG AIR-1, “Accounting for Planned Major Maintenance Activities,” which prohibits the use of the accrue-in-advance method of accounting for planned major maintenance activities in annual and interim reporting periods. The FSP permits the application of three alternative methods of accounting for planned major maintenance activities: the direct expense, built-in-overhaul, and deferral methods. The FSP iswas effective for the first fiscal year beginning after December 15, 2006. International Paper is currently evaluatingadopted the direct expense method of accounting for these costs in the first quarter of 2007 with no impact on its annual consolidated financial statements. See Note 13 for a discussion of the effects of implementing the provisions of this FSP.accounting change on quarterly financial information.

Accounting for Uncertainty in Income Taxes:

In June 2006, the FASB issued FASB Interpretation No. 48 (FIN 48), “Accounting for Uncertainty in Income Taxes, an interpretationInterpretation of FASB Statement No. 109.” FIN 48 prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. This Interpretationinterpretation also provides guidance on classification, interest and penalties, accounting in interim periods and transition, and significantly expands income tax disclosure requirements. It applies to all tax positions accounted for in accordance with SFAS No. 109 and iswas effective for fiscal years beginning after December 15, 2006. The Company is currently evaluating the effects of implementingInternational Paper applied the provisions of this Interpretation.interpretation beginning January 1, 2007. See Note 8 for a discussion of the effects of this accounting change.

Accounting for Certain Hybrid Financial Instruments:

In February 2006, the FASB issued SFAS No. 155, “Accounting for Certain Hybrid Financial Instruments – an Amendment of FASB Statements No. 133 and 140,” which provides entities with relief from having to separately determine the fair value of an embedded derivative that would otherwise be required to be bifurcated from its host contract in accordance with SFAS No. 133. This Statementstatement allows an entity to make an irrevocable election to measure such a hybrid financial instrument at fair value in its entirety, with changes in fair value recognized in earnings. This Statement isstatement was effective for International Paper for all financial instruments acquired, issued, or subject to a remeasurement event occurring after the beginning of an entity’s first fiscal year that begins after September 15, 2006. International Paper believes that theJanuary 1, 2007. The adoption of SFAS No. 155 in 2007 willdid not have a material impact on itsthe Company’s consolidated financial statements.

Exchanges of Nonmonetary Assets:NOTE 8 – INCOME TAXES

In December 2004, theInternational Paper adopted FASB issued SFASInterpretation No. 153, “Exchanges of Nonmonetary Assets, an Amendment of APB Opinion No. 29,” that replaces the exception from fair value measurement in APB Opinion No. 29,48, “Accounting for Nonmonetary Transactions,Uncertainty in Income Taxes,” for nonmonetary exchangeson January 1, 2007. The adoption of similar productive assets withthis standard resulted in a general exception from fair value measurement for exchangescharge to the beginning balance of nonmonetary assetsretained earnings of $94 million at the date of adoption. Including this cumulative effect amount, total unrecognized tax benefits at the date of adoption were $919 million. Of this total, $562 million represents unrecognized tax benefits that, do not have commercial substance. A nonmonetary exchange has commercial substance if recognized, would reduce the future cash flows ofCompany’s effective tax rate.

The major jurisdictions where the entityCompany files income tax returns are expectedthe United States, Brazil, France, Poland and Russia. Generally, tax years 2001 through 2006 remain open and subject to change significantly asexamination by the relevant tax authorities. The Company is typically engaged in various tax examinations at any given time, both in the United States and overseas. As a result of tax audit closings, settlements, and the exchange. International Paper appliedexpiration of statutes to examine such returns in various jurisdictions over the provisionsnext 12 months, the Company estimates that the amount of SFAS No. 153 prospectively in the first quarterunrecognized tax benefits could be reduced by approximately $150 million.

The Company accrues interest on unrecognized tax benefits as a component of 2006, with no material effect on its consolidated financial statements.

Inventory Costs:

In November 2004, the FASB issued SFAS No. 151, “Inventory Costs, an Amendment of ARB No. 43, Chapter 4.” This Statement requires that abnormal amounts of idle facility expense, freight, handling costs and wasted materialinterest expense. Penalties, if incurred, would be recognized as current-period charges. This Statement also introduces the concepta component of “normal capacity” and requires the allocation of fixed production overhead to inventory based on the normal capacityincome tax expense. As of the production facilities. Unallocated overhead must be recognized as an expensedate of adoption of this standard, the Company had approximately $88 million of such accrued interest and penalties included in the period in which it is incurred. International Paper adopted SFAS No. 151 in the first quarter of 2006,Other accrued liabilities associated with no material effect on its consolidated financial statements.unrecognized tax benefits.

Share-Based Payment Transactions:

In December 2004, the FASB issued SFAS No. 123 (revised 2004), “Share-Based Payment,” that requires compensation costs related to share-based payment transactions to be recognized in the financial statements. The amount of the compensation cost is measured based on the grant-date fair value of the equity or liability instruments issued. In addition, liability awards are remeasured each reporting period. Compensation cost is recognized over the period that an employee provides service in exchange for the award. This Statement applies to all awards granted after the required effective date and to awards modified, repurchased, or cancelled after that date. International Paper adopted SFAS No. 123(R) in the first quarter 2006, with no material effect on its consolidated financial statements. See Note 10 for a further discussion of stock-based compensation plans.

NOTE 79 - COMMITMENTS AND CONTINGENCIES

Under the terms of the sale agreement for the Beverage Packaging business, the purchase price received by the Company is subject to a post-closing adjustment if adjusted annualized earnings of the Beverage Packaging business for the first six months of 2007 are less than a targeted amount. The adjustment, if any, would equal five times the shortfall from the targeted amount. Management does not currently believe that any such adjustment is probable based upon current operating results. However, such an adjustment could be required in 2007 if expected second-quarter results are not met.

Exterior Siding and Roofing Litigation:

International Paper has established reserves relating to the settlement, during 1998 and 1999, of three nationwide class action lawsuits against the Company and Masonite Corp., a former wholly-owned subsidiary of the Company. Those settlements relate to (1) exterior hardboard siding installed during the 1980’s (the “1980’s1980’s Hardboard Claims”)Claims) and during the 1990’s (the “1990’s1990’s Hardboard Claims,” and together with the 1980’s Hardboard Claims, the “Hardboard Claims”)Hardboard Claims); (2) Omniwood siding installed during the 1990’s (the “Omniwood Claims”)Omniwood Claims); and (3) Woodruf roofing installed during the 1980’s and 1990’s (the “Woodruf Claims”)Woodruf Claims). Each of these settlements is discussed in detail in Note 10, Commitments and Contingent Liabilities, to the Financial Statements included in International Paper’s Annual Report on Form 10-K for the year ended December 31, 2005 (the “2005 10-K”).2006.

Claims Data

1980’s Hardboard Claims

Since 2002,Throughout 2006, Omniwood and until 2005, the aggregateWoodruf claims activity with respect to the exterior siding and roofing settlements (the “Settlements”) had been in line with the projections prepared by the Company’s third-party consultant. As reported in the 2005 10-K, the number of valid 1980’s Hardboard Claims filed prior to the January 18, 2005 filing deadline significantly exceeded those projections. This increase, together with an increase in the average cost per claim, had resulted in payments by the Company in 2005 of approximately $119 million. These amounts exceeded projections by approximately $40 million.

Substantially all of the 1980’s Hardboard Claims were settled as of June 30, 2006, although settlement payments made in 2006 were approximately $8 million more than projected.

1990’s Hardboard Claims

In 2005, the number of 1990’s Hardboard Claims filed was in line with projections. However, as reportedactivity for Hardboard claims in the 2005 10-K,first three quarters of 2006 was in excess of projected amounts. Accordingly, additional pre-tax charges totaling $50 million were recorded in the average costfirst three quarters of those2006 to reflect this higher claims increased aboveactivity pending completion of an updated projection by the Company’s third-party consultant. In the fourth quarter of 2006, this updated projection was completed, resulting in an additional pre-tax charge of $40 million to increase the reserve to management’s best estimate of projected levels in 2005. As wasfuture claims and expense payments through the caseend of the Hardboard claims period (January 15, 2008). Claims activity for the 1980’s Hardboard Claims, the increased cost was due,first quarter of 2007 has been generally in part, to a 2005 increase in the Means Price Data (an inflation-adjusted compensation formula based on replacement and refinishing cost for a particular area that is used in the determination of claims payments) compared to prior years. For the nine months ended September 30, 2006, the number of 1990’s Hardboard Claims filed and the average cost per claim were both higher than projected,line with claims payments totaling approximately $8 million more than projected. The claims filing deadline for the 1990’s Hardboard Claims is January 15, 2008.these updated projections.

The following table presents the claims activity of the 1980’s and 1990’s Hardboard Claims for the nine-monththree-month period ended September 30, 2006:March 31, 2007:

In thousands | Single Family | Multi- Family | Total | Single Family | Multi- Family | Total | ||||||||||||

December 31, 2005 | 20.2 | 3.2 | 23.4 | |||||||||||||||

December 31, 2006 | 21.8 | 2.1 | 23.9 | |||||||||||||||

No. of Claims Filed | 14.1 | 0.4 | 14.5 | 4.9 | 0.2 | 5.1 | ||||||||||||

No. of Claims Paid | (9.9 | ) | (1.4 | ) | (11.3 | ) | (4.5 | ) | (0.3 | ) | (4.8 | ) | ||||||

No. of Claims Dismissed | (4.0 | ) | (0.1 | ) | (4.1 | ) | (1.3 | ) | — | (1.3 | ) | |||||||

September 30, 2006 | 20.4 | 2.1 | 22.5 | |||||||||||||||

March 31, 2007 | 20.9 | 2.0 | 22.9 | |||||||||||||||

The average settlement cost per claim for the nine-monththree-month period ended September 30, 2006March 31, 2007 for the Hardboard settlement was $2,369.$2,231.

Omniwood and Woodruf Claims

Throughout 2005, and through September 30, 2006, the Omniwood Claims activity and the Woodruf Claims activity have been in line with projections. The Company expects this trend to continue. The filing deadline for both the Omniwood and Woodruf Claims is January 6, 2009. The following table presents the claims activity of the Omniwood Claims and the Woodruf Claims for the nine-monththree-month period ended September 30, 2006:March 31, 2007:

| Omniwood | Woodruf | Total | Omniwood | Woodruf | Total | |||||||||||||||||||||||||||||||||

In thousands | Single Family | Multi- Family | Single Family | Multi- Family | Single Family | Multi- Family | Total | Single Family | Multi- Family | Single Family | Multi- Family | Single Family | Multi- Family | Total | ||||||||||||||||||||||||

December 31, 2005 | 2.4 | 0.5 | 0.8 | 0.3 | 3.2 | 0.8 | 4.0 | |||||||||||||||||||||||||||||||

December 31, 2006 | 2.7 | 0.6 | 0.8 | 0.3 | 3.5 | 0.9 | 4.4 | |||||||||||||||||||||||||||||||

No. of Claims Filed | 4.2 | 0.2 | 0.4 | — | 4.6 | 0.2 | 4.8 | 1.4 | 0.1 | — | — | 1.4 | 0.1 | 1.5 | ||||||||||||||||||||||||