UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended September 30, 2007March 31, 2008

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission File Number 1-3157

INTERNATIONAL PAPER COMPANY

(Exact name of registrant as specified in its charter)

| New York | 13-0872805 | |

(State or other jurisdiction of incorporation of organization) | (I.R.S. Employer Identification No.) | |

| 6400 Poplar Avenue, Memphis, TN | 38197 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (901) 419-7000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a non-accelerated filer.smaller reporting company. See definitiondefinitions of “accelerated filer,” “large accelerated filer” and large accelerated filer”“smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

| Large accelerated filer x | Accelerated filer ¨ | |

| Non-accelerated filer ¨ | Smaller company ¨ | |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

The number of shares outstanding of the registrant’s common stock as of November 6, 2007May 7, 2008 was 428,137,645.

427,625,220.

INTERNATIONAL PAPER COMPANYINDEX

INDEX

| PAGE NO. | ||||||

PART I. | FINANCIAL INFORMATION | |||||

Item 1. | ||||||

| 1 | ||||||

Consolidated Balance Sheet - | 2 | |||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

Item 3. | ||||||

Item 4. | ||||||

PART II. | OTHER INFORMATION | |||||

Item 1. | ||||||

Item 1A. | Risk Factors | |||||

Item 2. | ||||||

Item 3. | Defaults upon Senior Securities | * | ||||

Item 4. | Submission of Matters to a Vote of Security Holders | * | ||||

Item 5. |

| |||||

Item 6. | ||||||

| * | Omitted since no answer is called for, answer is in the negative or inapplicable. |

| ITEM 1. | FINANCIAL STATEMENTS |

Consolidated Statement of Operations

(Unaudited)

(In millions, except per share amounts)

Three Months Ended September 30, | Nine Months Ended September 30, | Three Months Ended March 31, | ||||||||||||||||||||||

| 2007 | 2006 | 2007 | 2006 | 2008 | 2007 | |||||||||||||||||||

Net Sales | $ | 5,541 | $ | 5,429 | $ | 16,049 | $ | 16,671 | $ | 5,668 | $ | 5,217 | ||||||||||||

Costs and Expenses | ||||||||||||||||||||||||

Cost of products sold | 4,086 | 3,906 | 11,818 | 12,345 | 4,261 | 3,851 | ||||||||||||||||||

Selling and administrative expenses | 455 | 465 | 1,331 | 1,394 | 472 | 435 | ||||||||||||||||||

Depreciation, amortization and cost of timber harvested | 277 | 287 | 808 | 883 | 286 | 262 | ||||||||||||||||||

Distribution expenses | 255 | 267 | 765 | 828 | 285 | 256 | ||||||||||||||||||

Taxes other than payroll and income taxes | 42 | 52 | 131 | 160 | 44 | 42 | ||||||||||||||||||

Restructuring and other charges | 42 | 92 | 86 | 189 | 42 | 18 | ||||||||||||||||||

Insurance recoveries | — | — | — | (19 | ) | |||||||||||||||||||

Forestland sales | (9 | ) | (304 | ) | (9 | ) | (366 | ) | ||||||||||||||||

Net losses (gains) on sales and impairments of businesses | 1 | (74 | ) | (314 | ) | 1,346 | ||||||||||||||||||

Net gains on sales and impairments of businesses | (1 | ) | (314 | ) | ||||||||||||||||||||

Interest expense, net | 77 | 144 | 218 | 441 | 81 | 61 | ||||||||||||||||||

Earnings (Loss) From Continuing Operations Before Income Taxes and Minority Interest | 315 | 594 | 1,215 | (530 | ) | |||||||||||||||||||

Earnings From Continuing Operations Before Income Taxes, Equity Earnings and Minority Interest | 198 | 606 | ||||||||||||||||||||||

Income tax provision | 89 | 204 | 321 | 221 | 59 | 143 | ||||||||||||||||||

Equity earnings, net of taxes | 16 | — | ||||||||||||||||||||||

Minority interest expense, net of taxes | 6 | 5 | 17 | 14 | 5 | 6 | ||||||||||||||||||

Earnings (Loss) From Continuing Operations | 220 | 385 | 877 | (765 | ) | |||||||||||||||||||

Earnings From Continuing Operations | 150 | 457 | ||||||||||||||||||||||

Discontinued operations, net of taxes and minority interest | (3 | ) | (161 | ) | (36 | ) | (164 | ) | (17 | ) | (23 | ) | ||||||||||||

Net Earnings (Loss) | $ | 217 | $ | 224 | $ | 841 | $ | (929 | ) | |||||||||||||||

Net Earnings | $ | 133 | $ | 434 | ||||||||||||||||||||

Basic Earnings (Loss) Per Common Share | ||||||||||||||||||||||||

Earnings (loss) from continuing operations | $ | 0.52 | $ | 0.81 | $ | 2.03 | $ | (1.57 | ) | |||||||||||||||

Basic Earnings Per Common Share | ||||||||||||||||||||||||

Earnings from continuing operations | $ | 0.36 | $ | 1.03 | ||||||||||||||||||||

Discontinued operations | (0.01 | ) | (0.34 | ) | (0.08 | ) | (0.34 | ) | (0.04 | ) | (0.05 | ) | ||||||||||||

Net earnings (loss) | $ | 0.51 | $ | 0.47 | $ | 1.95 | $ | (1.91 | ) | |||||||||||||||

Net earnings | $ | 0.32 | $ | 0.98 | ||||||||||||||||||||

Diluted Earnings (Loss) Per Common Share | ||||||||||||||||||||||||

Earnings (loss) from continuing operations | $ | 0.52 | $ | 0.80 | $ | 2.01 | $ | (1.57 | ) | |||||||||||||||

Diluted Earnings Per Common Share | ||||||||||||||||||||||||

Earnings from continuing operations | $ | 0.35 | $ | 1.02 | ||||||||||||||||||||

Discontinued operations | (0.01 | ) | (0.34 | ) | (0.08 | ) | (0.34 | ) | (0.04 | ) | (0.05 | ) | ||||||||||||

Net earnings (loss) | $ | 0.51 | $ | 0.46 | $ | 1.93 | $ | (1.91 | ) | |||||||||||||||

Net earnings | $ | 0.31 | $ | 0.97 | ||||||||||||||||||||

Average Shares of Common Stock Outstanding - assuming dilution | 425.6 | 484.9 | 435.7 | 485.2 | 423.3 | 448.4 | ||||||||||||||||||

Cash Dividends Per Common Share | $ | 0.25 | $ | 0.25 | $ | 0.75 | $ | 0.75 | $ | 0.25 | $ | 0.25 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Balance Sheet

(In millions)

| September 30, 2007 | December 31, 2006 | March 31, 2008 | December 31, 2007 | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

Assets | ||||||||||||||||

Current Assets | ||||||||||||||||

Cash and temporary investments | $ | 1,702 | $ | 1,624 | $ | 880 | $ | 905 | ||||||||

Accounts and notes receivable, net | 3,080 | 2,704 | 3,206 | 3,152 | ||||||||||||

Inventories | 2,030 | 1,909 | 2,147 | 2,071 | ||||||||||||

Assets of businesses held for sale | 21 | 1,778 | — | 24 | ||||||||||||

Deferred income tax assets | 516 | 490 | 206 | 213 | ||||||||||||

Other current assets | 156 | 132 | 273 | 370 | ||||||||||||

Total Current Assets | 7,505 | 8,637 | 6,712 | 6,735 | ||||||||||||

Plants, Properties and Equipment, net | 9,842 | 8,993 | 10,290 | 10,141 | ||||||||||||

Forestlands | 735 | 259 | 778 | 770 | ||||||||||||

Investments | 608 | 641 | 1,317 | 1,276 | ||||||||||||

Goodwill | 3,652 | 2,929 | 3,658 | 3,650 | ||||||||||||

Assets Held for Exchange | — | 1,324 | ||||||||||||||

Deferred Charges and Other Assets | 1,373 | 1,251 | 1,600 | 1,587 | ||||||||||||

Total Assets | $ | 23,715 | $ | 24,034 | $ | 24,355 | $ | 24,159 | ||||||||

Liabilities and Common Shareholders’ Equity | ||||||||||||||||

Current Liabilities | ||||||||||||||||

Notes payable and current maturities of long-term debt | $ | 586 | $ | 692 | $ | 727 | $ | 267 | ||||||||

Accounts payable | 2,070 | 1,907 | 2,184 | 2,145 | ||||||||||||

Accrued payroll and benefits | 347 | 466 | 279 | 400 | ||||||||||||

Liabilities of businesses held for sale | 5 | 333 | — | 4 | ||||||||||||

Other accrued liabilities | 1,021 | 1,243 | 955 | 1,026 | ||||||||||||

Total Current Liabilities | 4,029 | 4,641 | 4,145 | 3,842 | ||||||||||||

Long-Term Debt | 6,191 | 6,531 | 6,037 | 6,353 | ||||||||||||

Deferred Income Taxes | 2,751 | 2,233 | 3,117 | 2,919 | ||||||||||||

Other Liabilities | 2,567 | 2,453 | 1,823 | 2,145 | ||||||||||||

Minority Interest | 221 | 213 | 234 | 228 | ||||||||||||

Common Shareholders’ Equity | ||||||||||||||||

Common stock, $1 par value, 493.6 shares in 2007 and 493.3 shares in 2006 | 494 | 493 | ||||||||||||||

Common stock, $1 par value, 493.6 shares in 2008 and 2007 | 494 | 494 | ||||||||||||||

Paid-in capital | 6,718 | 6,735 | 6,671 | 6,755 | ||||||||||||

Retained earnings | 4,154 | 3,737 | 4,396 | 4,375 | ||||||||||||

Accumulated other comprehensive loss | (1,030 | ) | (1,564 | ) | (179 | ) | (471 | ) | ||||||||

| 10,336 | 9,401 | 11,382 | 11,153 | |||||||||||||

Less: Common stock held in treasury, at cost, 65.4 shares in 2007 and 39.8 shares in 2006 | 2,380 | 1,438 | ||||||||||||||

Less: Common stock held in treasury, at cost, 65.9 shares in 2008 and 68.4 shares in 2007 | 2,383 | 2,481 | ||||||||||||||

Total Common Shareholders’ Equity | 7,956 | 7,963 | 8,999 | 8,672 | ||||||||||||

Total Liabilities and Common Shareholders’ Equity | $ | 23,715 | $ | 24,034 | $ | 24,355 | $ | 24,159 | ||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Statement of Cash Flows

(Unaudited)

(In millions)

Nine Months Ended September 30, | Three Months Ended March 31, | |||||||||||||||

| 2007 | 2006 | 2008 | 2007 | |||||||||||||

Operating Activities | ||||||||||||||||

Net earnings (loss) | $ | 841 | $ | (929 | ) | |||||||||||

Net earnings | $ | 133 | $ | 434 | ||||||||||||

Discontinued operations, net of taxes and minority interest | 36 | 164 | 17 | 23 | ||||||||||||

Earnings (loss) from continuing operations | 877 | (765 | ) | |||||||||||||

Earnings from continuing operations | 150 | 457 | ||||||||||||||

Depreciation, amortization and cost of timber harvested | 808 | 883 | 286 | 262 | ||||||||||||

Deferred income tax expense, net | 125 | 133 | ||||||||||||||

Deferred income tax (benefit) expense, net | (130 | ) | 74 | |||||||||||||

Restructuring and other charges | 86 | 189 | 42 | 18 | ||||||||||||

Payments related to restructuring and legal reserves | (60 | ) | (65 | ) | (22 | ) | (22 | ) | ||||||||

Insurance recoveries | — | (19 | ) | |||||||||||||

Net (gains) losses on sales and impairments of businesses | (314 | ) | 1,346 | |||||||||||||

Gain on sales of forestlands | (9 | ) | (366 | ) | ||||||||||||

Net gains on sales and impairments of businesses | (1 | ) | (314 | ) | ||||||||||||

Equity earnings, net | (16 | ) | — | |||||||||||||

Periodic pension expense, net | 158 | 283 | 28 | 52 | ||||||||||||

Other, net | 145 | 184 | 81 | 51 | ||||||||||||

Changes in current assets and liabilities | ||||||||||||||||

Accounts and notes receivable | (6 | ) | (249 | ) | 5 | (81 | ) | |||||||||

Inventories | (91 | ) | (32 | ) | (32 | ) | (129 | ) | ||||||||

Accounts payable and accrued liabilities | (313 | ) | 152 | (75 | ) | (61 | ) | |||||||||

Other | 1 | (182 | ) | 118 | (11 | ) | ||||||||||

Cash provided by operations - continuing operations | 1,407 | 1,492 | 434 | 296 | ||||||||||||

Cash (used for) provided by operations - discontinued operations | (56 | ) | 146 | |||||||||||||

Cash used for operations - discontinued operations | — | (44 | ) | |||||||||||||

Cash Provided by Operations | 1,351 | 1,638 | 434 | 252 | ||||||||||||

Investment Activities | ||||||||||||||||

Invested in capital projects | (804 | ) | (764 | ) | (215 | ) | (178 | ) | ||||||||

Acquisitions, net of cash acquired | (227 | ) | — | |||||||||||||

Proceeds from divestititures | 1,675 | 2,163 | 14 | 1,633 | ||||||||||||

Other | (135 | ) | (241 | ) | (140 | ) | (118 | ) | ||||||||

Cash provided by investment activities - continuing operations | 509 | 1,158 | ||||||||||||||

Cash (used for) provided by investment activities - continuing operations | (341 | ) | 1,337 | |||||||||||||

Cash used for investment activities - discontinued operations | (12 | ) | (57 | ) | — | (11 | ) | |||||||||

Cash Provided by Investment Activities | 497 | 1,101 | ||||||||||||||

Cash (Used for) Provided by Investment Activities | (341 | ) | 1,326 | |||||||||||||

Financing Activities | ||||||||||||||||

Repurchases of common stock | (1,124 | ) | (1,385 | ) | ||||||||||||

Repurchases of common stock and payments of restricted stock tax withholding | (47 | ) | (398 | ) | ||||||||||||

Issuance of common stock | 122 | 26 | 1 | 30 | ||||||||||||

Issuance of debt | 15 | 1,258 | 83 | — | ||||||||||||

Reduction of debt | (528 | ) | (3,156 | ) | (26 | ) | (362 | ) | ||||||||

Change in book overdrafts | (3 | ) | (50 | ) | (39 | ) | 20 | |||||||||

Dividends paid | (330 | ) | (372 | ) | (112 | ) | (114 | ) | ||||||||

Other | — | (2 | ) | — | (3 | ) | ||||||||||

Cash used for financing activities - continuing operations | (1,848 | ) | (3,681 | ) | ||||||||||||

Cash provided by financing activities - discontinued operations | — | 22 | ||||||||||||||

Cash Used for Financing Activities | (1,848 | ) | (3,659 | ) | (140 | ) | (827 | ) | ||||||||

Effect of Exchange Rate Changes on Cash - Continuing operations | 78 | 14 | ||||||||||||||

Effect of Exchange Rate Changes on Cash - Discontinued operations | — | 1 | ||||||||||||||

Effect of Exchange Rate Changes on Cash | 22 | 15 | ||||||||||||||

Change in Cash and Temporary Investments | 78 | (905 | ) | (25 | ) | 766 | ||||||||||

Cash and Temporary Investments | ||||||||||||||||

Beginning of the period | 1,624 | 1,641 | 905 | 1,624 | ||||||||||||

End of the period | $ | 1,702 | $ | 736 | $ | 880 | $ | 2,390 | ||||||||

The accompanying notes are an integral part of these financial statements.

Consolidated Statement of Changes in Common Shareholders’ Equity

(Unaudited)

(In millions, except share amounts in thousands)

NineThree Months Ended September 30, 2007March 31, 2008

| Common Stock Issued | Paid-in | Retained | Accumulated Comprehensive | Treasury Stock | Total Shareholders’ | |||||||||||||||||||||||

| Shares | Amount | Capital | Earnings | (Loss) Income | Shares | Amount | Equity | |||||||||||||||||||||

Balance, December 31, 2006 | 493,340 | $ | 493 | $ | 6,735 | $ | 3,737 | $ | (1,564 | ) | 39,844 | $ | 1,438 | $ | 7,963 | |||||||||||||

Issuance of stock for various plans, net | 216 | 1 | (17 | ) | — | — | (5,031 | ) | (182 | ) | 166 | |||||||||||||||||

Repurchase of stock | — | — | — | — | — | 30,577 | 1,124 | (1,124 | ) | |||||||||||||||||||

Cash dividends - Common stock ($0.75 per share) | — | — | — | (330 | ) | — | — | — | (330 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net earnings | — | — | — | 841 | — | — | — | 841 | ||||||||||||||||||||

Pension and post retirement divestitures, amortization of prior service costs and net loss | — | — | — | — | 78 | — | — | 78 | ||||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $0) | — | — | — | — | 451 | — | — | 451 | ||||||||||||||||||||

Net gains on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net gain arising during the period (less tax of $0) | — | — | — | — | 17 | — | — | 17 | ||||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $1) | — | — | — | — | (12 | ) | — | — | (12 | ) | ||||||||||||||||||

Total comprehensive income | 1,375 | |||||||||||||||||||||||||||

Adoption of FIN 48 (Note 8) | — | — | — | (94 | ) | — | — | — | (94 | ) | ||||||||||||||||||

Balance, September 30, 2007 | 493,556 | $ | 494 | $ | 6,718 | $ | 4,154 | $ | (1,030 | ) | 65,390 | $ | 2,380 | $ | 7,956 | |||||||||||||

| Nine Months Ended September 30, 2006 | ||||||||||||||||||||||||||||

| Common Stock Issued | Paid-in | Retained | Accumulated Comprehensive | Treasury Stock | Total Shareholders’ | |||||||||||||||||||||||

| Shares | Amount | Capital | Earnings | (Loss) Income | Shares | Amount | Equity | |||||||||||||||||||||

Balance, December 31, 2005 | 490,501 | $ | 491 | $ | 6,627 | $ | 3,172 | $ | (1,935 | ) | 112 | $ | 4 | $ | 8,351 | |||||||||||||

Issuance of stock for various plans, net | 2,802 | 3 | 83 | — | — | (115 | ) | (4 | ) | 90 | ||||||||||||||||||

Repurchase of stock | — | — | — | — | — | 38,465 | 1,392 | (1,392 | ) | |||||||||||||||||||

Cash dividends - Common stock ($0.75 per share) | — | — | — | (372 | ) | — | — | — | (372 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net loss | — | — | — | (929 | ) | — | — | — | (929 | ) | ||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $8) | — | — | — | — | 135 | — | — | 135 | ||||||||||||||||||||

Net gains (losses) on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net loss arising during the period (less tax of $6) | — | — | — | — | (9 | ) | — | — | (9 | ) | ||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $0) | — | — | — | — | (8 | ) | — | — | (8 | ) | ||||||||||||||||||

Total comprehensive loss | (811 | ) | ||||||||||||||||||||||||||

Balance, September 30, 2006 | 493,303 | $ | 494 | $ | 6,710 | $ | 1,871 | $ | (1,817 | ) | 38,462 | $ | 1,392 | $ | 5,866 | |||||||||||||

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive (Loss) Income | Treasury Stock | Total Common Shareholders’ Equity | |||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2007 | 493,556 | $ | 494 | $ | 6,755 | $ | 4,375 | $ | (471 | ) | 68,436 | $ | 2,481 | $ | 8,672 | |||||||||||||

Issuance of stock for various plans, net | — | — | (84 | ) | — | — | (2,501 | ) | (98 | ) | 14 | |||||||||||||||||

Cash dividends - Common stock ($0.25 per share) | — | — | — | (112 | ) | — | — | — | (112 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net earnings | — | — | — | 133 | — | — | — | 133 | ||||||||||||||||||||

Amortization of pension and post retirement prior service costs and net loss: | ||||||||||||||||||||||||||||

U.S. plans (less tax of $15) | — | — | — | — | 20 | — | — | 20 | ||||||||||||||||||||

Non-U.S. plans (less tax of $0) | — | — | — | — | 3 | — | — | 3 | ||||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $0) | — | — | — | — | 246 | — | — | 246 | ||||||||||||||||||||

Net gains on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net gain arising during the period | ||||||||||||||||||||||||||||

(less tax of $17) | — | — | — | — | 36 | — | — | 36 | ||||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $4) | — | — | — | — | (13 | ) | — | — | (13 | ) | ||||||||||||||||||

Total comprehensive income | 425 | |||||||||||||||||||||||||||

Balance, March 31, 2008 | 493,556 | $ | 494 | $ | 6,671 | $ | 4,396 | $ | (179 | ) | 65,935 | $ | 2,383 | $ | 8,999 | |||||||||||||

| Three Months Ended March 31, 2007 | ||||||||||||||||||||||||||||

| Common Stock Issued | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive (Loss) Income | Treasury Stock | Total Common Shareholders’ Equity | |||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||

Balance, December 31, 2006 | 493,340 | $ | 493 | $ | 6,735 | $ | 3,737 | $ | (1,564 | ) | 39,844 | $ | 1,438 | $ | 7,963 | |||||||||||||

Issuance of stock for various plans, net | 2 | — | (75 | ) | — | — | (2,681 | ) | (97 | ) | 22 | |||||||||||||||||

Repurchase of stock | — | — | — | — | — | 11,231 | 398 | (398 | ) | |||||||||||||||||||

Cash dividends - Common stock ($0.25 per share) | — | — | — | (114 | ) | — | — | — | (114 | ) | ||||||||||||||||||

Comprehensive income (loss): | ||||||||||||||||||||||||||||

Net earnings | — | — | — | 434 | — | — | — | 434 | ||||||||||||||||||||

Amortization of pension and post-retirement prior service costs and net loss (less tax of $10) | — | — | — | — | 18 | — | — | 18 | ||||||||||||||||||||

Change in cumulative foreign currency translation adjustment (less tax of $0) | — | — | — | — | 88 | — | — | 88 | ||||||||||||||||||||

Net gains on cash flow hedging derivatives: | ||||||||||||||||||||||||||||

Net gain arising during the period (less tax of $1) | — | — | — | — | 10 | — | — | 10 | ||||||||||||||||||||

Less: Reclassification adjustment for gains included in net income (less tax of $0) | — | — | — | — | (4 | ) | — | — | (4 | ) | ||||||||||||||||||

Total comprehensive income | 546 | |||||||||||||||||||||||||||

Adoption of FIN 48 (Note 8) | — | — | — | (94 | ) | — | — | — | (94 | ) | ||||||||||||||||||

Balance, March 31, 2007 | 493,342 | $ | 493 | $ | 6,660 | $ | 3,963 | $ | (1,452 | ) | 48,394 | $ | 1,739 | $ | 7,925 | |||||||||||||

The accompanying notes are an intergralintegral part of these financial statements.

Condensed Notes to Consolidated Financial Statements

(Unaudited)

NOTE 1 - BASIS OF PRESENTATION

The accompanying unaudited consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and, in the opinion of Management, include all adjustments that are necessary for the fair presentation of the Company’s financial position, results of operations, and cash flows for the interim periods presented. Except as disclosed herein, such adjustments are of a normal, recurring nature. Results for the first ninethree months of the year may not necessarily be indicative of full year results. It is suggested that these consolidated financial statements be read in conjunction with the audited financial statements and the notes thereto included in International Paper’s (the Company) Annual Report on Form 10-K for the year ended December 31, 2006, and in International Paper’s Current Report on Form 8-K filed on August 14, 2007 to update the historical financial statements included in the Company’s Form 10-K for the year ended December 31, 2006, both of which havehas previously been filed with the Securities and Exchange Commission.

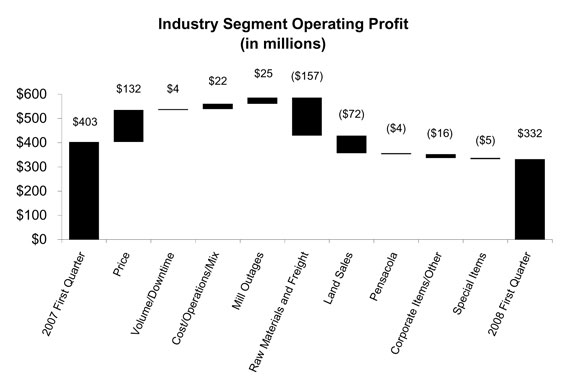

Financial information by industry segment is presented on page 24. In connection with sales19. Effective January 1, 2008, the Company changed its method of businesses underallocating corporate overhead to increase the Transformation Plan and the resulting changes in the Company’s business portfolio, a review of the Company’s operatingexpense amounts allocated to its business segments was conducted during the first quarter of 2007 under the provisions of Statement of Financial Accounting Standards No. 131. While this review resulted in no changes in the Company’s reportable segments, a decision was madereports reviewed by its chief executive officer to include the Company’s European coated paperboard operations, previously reported in the Printing Papers segment,facilitate performance comparisons with other similar operations incompanies. Accordingly, the Consumer Packaging segment. Accordingly, prior periodCompany has revised its presentation of industry segment information has been revisedoperating profit to reflect this presentation.change in allocation method, and has restated all comparative prior period information on this basis, reducing reported industry segment operating profits by $127 million and $145 million for the three months ended March 31, 2007 and December 31, 2007, respectively, with no effect on reported net income.

NOTE 2 - EARNINGS PER COMMON SHARE

Basic earnings per common share from continuing operations are computed by dividing earnings from continuing operations by the weighted average number of common shares outstanding. Diluted earnings per common share from continuing operations are computed assuming that all potentially dilutive securities, including “in-the-money” stock options, are converted into common shares at the beginning of each period. A reconciliation of the amounts included in the computation of earnings per common share from continuing operations, and diluted earnings per common share from continuing operations is as follows:

| Three Months Ended March 31, | ||||||||

In millions, except per share amounts | 2008 | 2007 | ||||||

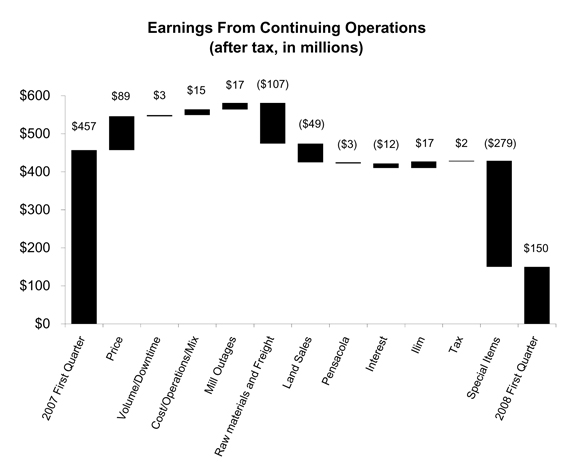

Earnings from continuing operations | $ | 150 | $ | 457 | ||||

Effect of dilutive securities | — | — | ||||||

Earnings from continuing operations - assuming dilution | $ | 150 | $ | 457 | ||||

Average common shares outstanding | 420.6 | 445.3 | ||||||

Effect of dilutive securities | ||||||||

Restricted stock performance share plan | 2.6 | 2.7 | ||||||

Stock options | (a) | 0.1 | 0.4 | |||||

Average common shares outstanding - assuming dilution | 423.3 | 448.4 | ||||||

Earnings per common share from continuing operations | $ | 0.36 | $ | 1.03 | ||||

Diluted earnings per common share from continuing operations | $ | 0.35 | $ | 1.02 | ||||

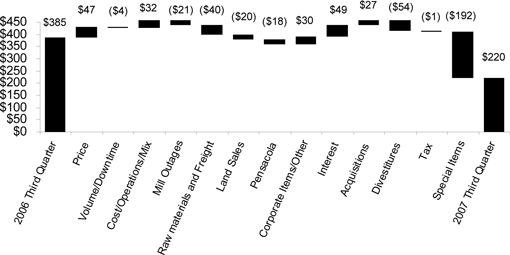

Three Months Ended September 30, Nine Months Ended September 30, In millions, except per share amounts Earnings (loss) from continuing operations Effect of dilutive securities Earnings (loss) from continuing operations - assuming dilution Average common shares outstanding Effect of dilutive securities Restricted stock performance share plan Stock options (a) Average common shares outstanding - assuming dilution Earnings (loss) per common share from continuing operations Diluted earnings (loss) per common share from continuing operations 2007 2006 2007 2006 $ 220 $ 385 $ 877 $ (765 ) — �� — — — $ 220 $ 385 $ 877 $ (765 ) 422.3 482.5 431.8 485.2 2.9 2.1 3.4 — 0.4 0.3 0.5 — 425.6 484.9 435.7 485.2 $ 0.52 $ 0.81 $ 2.03 $ (1.57 ) $ 0.52 $ 0.80 $ 2.01 $ (1.57 )

| (a) | Options to purchase |

NOTE 3 - RESTRUCTURING AND OTHER CHARGES

2007:2008:

During the thirdfirst quarter of 2007,2008, restructuring and other charges totaling $42 million before taxes ($26 million after taxes) were recorded. These charges consisted ofrecorded, including a pre-tax$40 million charge of $27 millionbefore taxes ($17 million after taxes) of accelerated depreciation charges for the Terre Haute mill, a pre-tax charge of $10 million ($625 million after taxes) for closureadjustments of legal reserves associated with the Terre Haute mill,(see Note 9), a pre-tax$5 million charge of $3 millionbefore taxes ($23 million after taxes) related to the restructuringreorganization of the Company’s BrazilShorewood operations in Canada and a pre-tax charge of $2$3 million credit before taxes ($12 million after taxes) for organizational restructuring programsadjustments to previously recorded reserves associated with the Company’s Transformation Plan. Additionally, a $3 million increase to the income tax provision was recorded related to the settlement of a prior year tax audit.

During the second quarter of 2007, restructuring and other charges totaling $26 million before taxes ($16 million after taxes) were recorded for organizational restructuring programs associated with the Company’s Transformation Plan, including $17 million ($11 million after taxes) of accelerated depreciation expense for long-lived assets being removed from service.programs.

2007:

During the first quarter of 2007, restructuring and other charges totaling $18 million before taxes ($11 million after taxes) were recorded for organizational restructuring programs associated with the Company’s Transformation Plan, including $12 million before taxes ($7 million after taxes) of accelerated depreciation charges for long-lived assets being removed from service. Additionally, a $2 million pre-tax credit ($1 million after taxes) was recorded in Interest expense, net, for interest received from the Canadian government on refunds of prior-year softwood lumber duties.

NOTE 4 - ACQUISITIONS, EXCHANGES AND JOINT VENTURES

Acquisitions:

20062008:

DuringOn March 17, 2008, International Paper announced that it had signed an agreement with Weyerhaeuser Company to purchase its Containerboard, Packaging and Recycling (CBPR) business for $6 billion in cash, subject to post-closing adjustments. International Paper expects to finance the purchase with debt financing. The business will become part of International Paper’s North American Packaging business. The transaction has been approved by United States regulators but additional pre-merger approvals are required in other jurisdictions. The acquisition is expected to close in the third quarter of 2006, restructuring2008, subject to customary closing conditions. The agreement provides that a termination fee of $100 million could become payable to Weyerhaeuser Company if International Paper were unable to obtain sufficient financing for the acquisition and certain other charges totaling $92 million before taxes ($56 million after taxes)conditions were recorded. These charges consisted of a pre-tax charge of $57 million ($35 million after taxes), including severance and other termination benefit costs of approximately $15 million, $25 million of lease termination costs and $17 million of other charges associated with the Company’s Transformation Plan, and a $35 million pre-tax charge ($21 million after taxes) for adjustments to legal reserves (see Note 9).met.

During the second quarter of 2006, restructuring and other charges totaling $53 million before taxes ($32 million after taxes) were recorded. Included in these charges were a pre-tax charge of $49 million ($29 million after taxes) for organizational restructuring programs, including severance and other termination benefits costs of approximately $31 million ($19 million after taxes) and other charges associated with the Company’s Transformation Plan, and a $4 million pre-tax charge ($3 million after taxes) for legal settlements.

During the first quarter of 2006, restructuring and other charges totaling $44 million before taxes ($27 million after taxes) were recorded. Included in these charges were a pre-tax charge of $18 million ($11 million after taxes) for organizational restructuring programs, principally severance costs associated with the Company’s Transformation Plan, a pre-tax charge of $8 million ($5 million after taxes) for losses on early extinguishment of debt, and a pre-tax charge of $18 million ($11 million after taxes) for adjustments to legal reserves. Also recorded was a pre-tax credit of $19 million ($12 million after taxes) for net insurance recoveries related to the hardboard siding and roofing litigation (see Note 9) and a charge of $3 million for tax adjustments.

NOTE 4 - ACQUISITIONS2007:

On August 24, 2007, International Paper completed the acquisition of Central Lewmar LLC, one of the largesta privately held paper and packaging distributorsdistributor in the United States, for $189 million. International Paper’s distribution business, xpedx, will operate Central Lewmar as a business unit within its multiple brand strategy.

The following table summarizesDuring the preliminaryfirst quarter of 2008, the Company finalized the allocation of the purchase price to the fair value of the assets and liabilities acquired. The final allocation is expected to be completed by March 31, 2008:acquired as follows:

In millions | ||||||

Accounts receivable | $ | 114 | $ | 116 | ||

Inventory | 31 | 31 | ||||

Other current assets | 7 | 7 | ||||

Plants, properties and equipment, net | 3 | 2 | ||||

Goodwill | 96 | 78 | ||||

Deferred tax asset | 5 | |||||

Other intangible assets | 15 | 33 | ||||

Other long-term assets | 3 | |||||

Total assets acquired | 269 | 272 | ||||

Other current liabilities | 79 | 79 | ||||

Other liabilities | 1 | 4 | ||||

Total liabilities assumed | 80 | 83 | ||||

Net assets acquired | $ | 189 | $ | 189 | ||

The identifiable intangible assets acquired in connection with the Central Lewmar acquisition included the following:

In millions | Estimated Fair Value | Average Useful Life | |||

Asset Class: | |||||

Customer lists | $ | 18 | 13 years | ||

Non-compete covenants | 7 | 5 years | |||

Trade names | 8 | 15 years | |||

Total | $ | 33 | |||

Central Lewmar’s financial position and results of operations have been included in International Paper’s consolidated financial statements since its acquisition on August 24, 2007.

In October 2005, International Paper acquired approximately 65% of Compagnie Marocaine des Cartons et des Papiers (CMCP) in Morocco. On July 31, 2007, the Company completed the purchase of the remaining shares of CMCP for approximately $40 million. The Moroccan packaging company is now wholly owned by International Paper and fully managed as part of the Company’s European Container business.Exchanges:

Total identifiable intangible assets acquired in connection with both of the CMCP acquisitions included the following:

In millions | Estimated Fair Value | Average Remaining Useful Life | |||

Asset Class: | |||||

Trademarks and trade names | $ | 2 | 3 years | ||

Customer portfolio | 22 | 23 years | |||

Total | $ | 24 | |||

On February 1, 2007, the Company completed the non-cash exchange of certain pulp and paper assets in Brazil with Votorantim Celulose e Papel S.A. (VCP) that had been announced in the fourth quarter of 2006. The Company exchanged its in-progress pulp mill project and certain forestland operations including approximately 100,000 hectares of surrounding forestlands in Tres Lagoas, Brazil, for VCP’s Luiz Antonio uncoated paper and pulp mill and approximately 55,000 hectares of forestlands in the state of Sao Paulo, Brazil. The exchange improved the Company’s competitive position by adding a globally cost-competitive paper mill, thereby expanding the Company’s uncoated freesheet capacity in Latin America and providing additional growth opportunities in the region. The exchange was accounted for based on the fair value of assets exchanged, resulting in the recognition in the 2007 first quarter of a pre-tax gain of $205 million ($164 million after taxes) representing the difference between the fair value and book value of the assets exchanged. This gain is included in Net losses (gains)gains on sales and impairments of businesses in the accompanying consolidated statement of operations. The net assets exchanged were included as Assets held for exchange in the accompanying consolidated balance sheet at December 31, 2006.

The following table summarizes the preliminaryfinal allocation of the fair value of the assets exchanged to the assets and liabilities acquired. The final allocation is expected to be completed by December 31, 2007:

In millions | |||

Accounts receivable | $ | 55 | |

Inventory | 24 | ||

Other current assets | 40 | ||

Plants, properties and equipment, net | 582 | ||

Forestlands | 414 | ||

Goodwill | 546 | ||

Other intangible assets | 154 | ||

Other long-term assets | 7 | ||

Total assets acquired | 1,822 | ||

Other current liabilities | 20 | ||

Deferred income taxes | 256 | ||

Other liabilities | 26 | ||

Total liabilities assumed | 302 | ||

Net assets acquired | $ | 1,520 | |

In millions Accounts receivable Inventory Other current assets Plants, properties and equipment, net Forestlands Goodwill Other intangible assets Other long-term assets Total assets acquired Other current liabilities Deferred income taxes Other liabilities Total liabilities assumed Net assets acquired $ 55 19 40 582 434 521 154 9 1,814 18 270 6 294 $ 1,520

Identifiable intangible assets included the following:

In millions | Estimated Fair Value | Average Remaining Useful Life | Estimated Fair Value | Average Useful Life | ||||||

Asset Class: | ||||||||||

Non-competition agreement | $ | 10 | 2 years | $ | 10 | 2 years | ||||

Customer relationships | 144 | 10-20 years | ||||||||

Customer lists | 144 | 10 - 20 years | ||||||||

Total | $ | 154 | $ | 154 | ||||||

The following unaudited pro forma information for the three and nine months ended September 30,March 31, 2007 and 2006 presents the results of operations of International Paper as if these acquisitionsthe Central Lewmar acquisition and the Luiz Antonio asset exchange had occurred on January 1, 2006.2007. This pro forma information does not purport to represent International Paper’s actual results of operations if the transactions described above would have occurred on January 1, 2006,2007, nor is it necessarily indicative of future results.

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||

In millions, except per share amounts | 2007 | 2006 | 2007 | 2006 | |||||||||

Net sales | $ | 5,669 | $ | 5,775 | $ | 16,627 | $ | 17,613 | |||||

Earnings (loss) from continuing operations | 225 | 414 | 886 | (707 | ) | ||||||||

Net earnings (loss) | 222 | 253 | 851 | (871 | ) | ||||||||

Earnings (loss) from continuing operations per common share | 0.53 | 0.85 | 2.03 | (1.46 | ) | ||||||||

Net earnings (loss) per common share | 0.52 | 0.52 | 1.95 | (1.80 | ) | ||||||||

In millions, except per share amounts | Three Months Ended March 31, 2007 | ||

Net sales | $ | 5,539 | |

Earnings from continuing operations | 483 | ||

Net earnings | 460 | ||

Earnings from continuing operations per common share | 1.08 | ||

Net earnings per common share | 1.03 | ||

InJoint Ventures:

On October and November 2006,5, 2007, International Paper paidand Ilim Holding S.A. announced the completion of the formation of a 50:50 joint venture to operate in Russia as Ilim Group. To form the joint venture, International Paper purchased 50% of Ilim Holding S.A. (Ilim) for approximately $82$620 million, including $545 million in cash and $75 million of notes payable. The Company’s investment in Ilim totaled $697 million at March 31, 2008, which is approximately $350 million higher than the Company’s share of the underlying net assets of Ilim. Based on initial estimates, approximately $150 million of this basis difference, principally related to the estimated fair value write-up of Ilim plant, property and equipment, is being amortized as a reduction of reported net income over the estimated remaining useful lives of the related assets. An estimated $200 million of the difference represents estimated goodwill.

International Paper is accounting for its investment in Ilim, a 50% interestseparate reportable industry segment, using the equity method of accounting. Due to the complex organization structure of Ilim’s operations, and the extended time required for Ilim to prepare consolidated financial information in accordance with accounting principles generally accepted in the International Paper & Sun Cartonboard Co., Ltd. joint venture that currently operates two coated paperboard machines in Yanzhou City, China. In December 2006, a 50% interest withUnited States, the same partner was acquired in a second joint venture, Shandong International Paper & Sun Coated Paperboard Co., Ltd., for approximately $28 million. The operating resultsCompany is reporting its share of these consolidated joint ventures did not have a material effect on the Company’s consolidatedIlim’s results of operations inon a one-quarter lag basis. Accordingly, the accompanying consolidated statement of operations for the three months ended March 31, 2008 includes the Company’s share of Ilim’s operating results for the three-month period ended December 31, 2007 or 2006.under the caption Equity earnings, net of taxes.

NOTE 5 - BUSINESSES HELD FOR SALE AND DIVESTITURES

Discontinued Operations:

2007:2008:

During the thirdfirst quarter of 2007,2008, the Company completedrecorded a pre-tax charge of $25 million ($16 million after taxes) related to the final settlement of a post-closing adjustment to the purchase price received by the Company for the sale of the remainder of its non-U.S. Beverage Packaging business.

During the second quarter of 2007, the Company recorded pre-tax charges of $7business (see Note 9), and a $2 million charge before taxes ($41 million after taxes) and $4 million ($3 million after taxes) relatingfor operating losses related to adjustments to estimated losses on the sales of its Wood Products and Beverage Packaging businesses, respectively.certain wood products facilities.

2007:

During the first quarter of 2007, the Company recorded pre-tax credits of $21 million ($9 million after taxes) and $6 million ($4 million after taxes) relating to the sales of its Wood Products and Kraft Papers businesses, respectively. In addition, a $15 million pre-tax charge ($39 million after taxes) was recorded for adjustments to the loss on the completion of the sale of most of the Beverage Packaging business. Finally, a pre-tax credit of approximately $10 million ($6 million after taxes) was recorded for refunds received from the Canadian government of duties paid by the Company’s former Weldwood of Canada Limited business.

2006:

During the fourth quarter of 2006, the Company entered into an agreement to sell its Beverage Packaging business to Carter Holt Harvey Limited for approximately $500 million, subject to certain adjustments (see Note 9). The sale of the North American Beverage Packaging operations subsequently closed on January 31, 2007, and the sale of the remaining non-U.S. operations closed in the third quarter of 2007.

Also during the fourth quarter of 2006, the Company entered into separate agreements for the sale of 13 lumber mills for approximately $325 million, and five wood products plants for approximately $237 million, both subject to various adjustments at closing. Both of the sales were completed in March 2007.

The Company determined that the accounting requirements for both businesses under Statement of Financial Accounting Standards (SFAS) No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets,” as discontinued operations were met. Accordingly, the operating results for these businesses are included in Discontinued operations for all periods presented.

Revenues, earnings(loss) and earnings(loss) per share related to the Beverage Packaging business were as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

In millions, except per share amounts | 2007 | 2006 | 2007 | 2006 | ||||||||||||

Revenues | $ | 1 | $ | 201 | $ | 91 | $ | 612 | ||||||||

Earnings from discontinued operation | ||||||||||||||||

Earnings from operation | $ | — | $ | 21 | $ | 15 | $ | 38 | ||||||||

Income tax expense | — | (7 | ) | (5 | ) | (12 | ) | |||||||||

Earnings from operation, net of taxes | — | 14 | 10 | 26 | ||||||||||||

Loss on sales and impairments | (2 | ) | (103 | ) | (21 | ) | (103 | ) | ||||||||

Income tax benefit (expense) | 1 | 24 | (22 | ) | 24 | |||||||||||

Loss on sales and impairments, net of taxes | (1 | ) | (79 | ) | (43 | ) | (79 | ) | ||||||||

Loss from discontinued operation, net of taxes | $ | (1 | ) | $ | (65 | ) | $ | (33 | ) | $ | (53 | ) | ||||

Earnings (loss) per common share from discontinued operation - assuming dilution | ||||||||||||||||

Earnings from operation | $ | — | $ | 0.03 | $ | 0.02 | $ | 0.05 | ||||||||

Loss on sales and impairments | — | (0.16 | ) | (0.09 | ) | (0.16 | ) | |||||||||

Loss per common share from discontinued operation, net of taxes and minority interest - assuming dilution | $ | — | $ | (0.13 | ) | $ | (0.07 | ) | $ | (0.11 | ) | |||||

Revenues, earnings(loss) and earnings(loss) per share related to the Wood Products business were as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

In millions, except per share amounts | 2007 | 2006 | 2007 | 2006 | ||||||||||||

Revenues | $ | 34 | $ | 240 | $ | 275 | $ | 825 | ||||||||

(Loss) earnings from discontinued operation | ||||||||||||||||

(Loss) earnings from operation | $ | (6 | ) | $ | (36 | ) | $ | (32 | ) | $ | 24 | |||||

Income tax benefit (expense) | 3 | 14 | 13 | (9 | ) | |||||||||||

(Loss) earnings from operation, net of taxes | (3 | ) | (22 | ) | (19 | ) | 15 | |||||||||

Gain (loss) on sales and impairments | 2 | (165 | ) | 16 | (165 | ) | ||||||||||

Income tax expense | (1 | ) | — | (10 | ) | — | ||||||||||

Gain (loss) on sales and impairments, net of taxes | 1 | (165 | ) | 6 | (165 | ) | ||||||||||

Loss from discontinued operation, net of taxes | $ | (2 | ) | $ | (187 | ) | $ | (13 | ) | $ | (150 | ) | ||||

(Loss) earnings per common share from discontinued operation - assuming dilution | ||||||||||||||||

(Loss) earnings from operation | $ | (0.01 | ) | $ | (0.05 | ) | $ | (0.04 | ) | $ | 0.03 | |||||

(Loss) gain on sales and impairments | — | (0.34 | ) | 0.01 | (0.34 | ) | ||||||||||

Loss per common share from discontinued operation, net of taxes - assuming dilution | $ | (0.01 | ) | $ | (0.39 | ) | $ | (0.03 | ) | $ | (0.31 | ) | ||||

During the 2006 third quarter, International Paper completed the sale of its Brazilian Coated Papers business. The operating results of this business are included in Discontinued operations for all applicable periods presented.

Revenues, earnings and earnings per share related to the Brazilian Coated Papers business were as follows:

In millions, except per share amounts | Three Months Ended September 30, 2006 | Nine Months Ended September 30, 2006 | ||||||

Revenues | $ | 33 | $ | 127 | ||||

Earnings from discontinued operation | ||||||||

Earnings from operation | $ | 2 | $ | 20 | ||||

Income tax expense | — | (9 | ) | |||||

Earnings from operation, net of taxes | 2 | 11 | ||||||

Gain on sale | 101 | 101 | ||||||

Income tax expense | (21 | ) | (21 | ) | ||||

Gain on sale, net of taxes | 80 | 80 | ||||||

Earnings from discontinued operation, net of taxes | $ | 82 | $ | 91 | ||||

Earnings per common share from discontinued operation - assuming dilution | ||||||||

Earnings from operation | $ | — | $ | 0.02 | ||||

Gain on sale | 0.16 | 0.16 | ||||||

Earnings per common share from discontinued operation, net of taxes - assuming dilution | $ | 0.16 | $ | 0.18 | ||||

During the first quarter of 2006, the Company determined that the accounting requirements under SFAS No. 144 for reporting the Kraft Papers business as a discontinued operation were met. Accordingly, a $100 million pre-tax charge ($61 million after taxes) was recorded to reduce the carrying value of the net assets of this business to their estimated fair value. The sale of this business was completed in January 2007. The operating results of this business are included in Discontinued operations for all applicable periods presented.

Revenues, earnings(loss) and earnings(loss) per share related to the Kraft Papers business were as follows:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||

In millions, except per share amounts | 2006 | 2007 | 2006 | |||||||||

Revenues | $ | 62 | $ | — | $ | 174 | ||||||

Earnings from discontinued operation | ||||||||||||

Earnings from operation | $ | 15 | $ | — | $ | 32 | ||||||

Income tax expense | (6 | ) | — | (12 | ) | |||||||

Earnings from operation, net of taxes | 9 | — | 20 | |||||||||

Gain (loss) on sales and impairments | — | 6 | (116 | ) | ||||||||

Income tax (expense) benefit | — | (2 | ) | 44 | ||||||||

Gain (loss) on sales and impairments, net of taxes | — | 4 | (72 | ) | ||||||||

Earnings (loss) from discontinued operation, net of taxes | $ | 9 | $ | 4 | $ | (52 | ) | |||||

Earnings (loss) per common share from discontinued operation - assuming dilution | ||||||||||||

Earnings from operation | $ | 0.02 | $ | — | $ | 0.04 | ||||||

Gain (loss) on sales and impairments | — | 0.01 | (0.15 | ) | ||||||||

Earnings (loss) per common share from discontinued operation, net of taxes - assuming dilution | $ | 0.02 | $ | 0.01 | $ | (0.11 | ) | |||||

Transformation Plan Forestland Sales:

During the third quarter of 2007, a pre-tax gain of $9 million ($5 million after taxes) was recorded to reduce estimated transaction costs accrued in connection with the 2006 Transformation Plan forestland sales.

During the third quarter of 2006, the Company completed the sales of approximately 476,000 acres of forestlands for approximately $401 million, including $265 million in cash and $136 million of installment notes, resulting in a pre-tax gain of $304 million ($185 million after taxes).

During the second quarter of 2006, the Company completed the sales of approximately 76,000 acres of forestlands for approximately $97 million, resulting in a pre-tax gain of approximately $62 million ($39 million after taxes).

Other Divestitures and Impairments:

2007:2008:

During the secondfirst quarter of 2007,2008, a $1 million net pre-tax credit (a $7($1 million charge after taxes, including a $5 million tax charge in Brazil)taxes) was recorded to adjust previously estimated gains/losses of businesses previously sold.

2007:

During the first quarter of 2007, a $103 million pre-tax gain ($96 million after taxes) was recorded upon the completion of the sale of the Company’s Arizona Chemical business. As part of the transaction, International Paper acquired a minority interest of approximately 10% in the resulting new entity. Since the interest acquired represents significant continuing involvement in the operations of the business under U.S. Generally Accepted Accounting Principles, the operating results for Arizona Chemical have been included in continuing operations in the accompanying consolidated statement of operations through the date of sale.

In addition, during the first quarter of 2007, a $6 million pre-tax credit ($4 million after taxes) was recorded to adjust previously estimated gains/losses of businesses previously sold.

These gains are included, along with the gain on the exchange for the Luiz Antonio mill in Brazil (see Note 4), in Net losses (gains)gains on sales and impairments of businesses in the accompanying consolidated statement of operations.

2006:

During the third quarter of 2006, a net pre-tax gain of $74 million ($44 million after taxes) was recorded for losses (gains) on sales and impairments of businesses. This net gain included the recognition of a previously deferred $110 million pre-tax gain ($68 million after taxes) related to a 2004 sale of forestlands in Maine, a pre-tax charge of $38 million ($23 million after taxes) to reflect the completion of the sale of the Company’s Coated and Supercalendered Papers business in the 2006 third quarter, and a net pre-tax gain of $2 million (a $1 million loss after taxes) related to other smaller sales.

During the 2006 second quarter, the Company recorded a pre-tax charge of $85 million ($53 million after taxes) to adjust the carrying value of the assets of the Company’s Coated and Supercalendered Papers business to their estimated fair value. This charge, together with a pre-tax charge of $52 million ($37 million after taxes) recorded to write down the carrying value of certain assets in Brazil to their estimated fair value, is included in Net losses (gains) on sales and impairments of businesses in the accompanying consolidated statement of operations.

During the first quarter, a pre-tax charge of $1.3 billion was recorded to write down the assets of the Company’s Coated and Supercalendered Papers business to their estimated fair value, as management had committed to a plan to sell this business. In addition, other pre-tax charges totaling $3 million ($2 million after taxes) were recorded to adjust estimated losses of certain smaller operations held for sale.

At December 31, 2006, assets and liabilities of businesses held for sale included the Kraft Papers business, the Beverage Packaging business, the Wood Products business, and the Arizona Chemical business, and consisted of:

In millions | December 31, 2006 | ||

Accounts receivable, net | $ | 298 | |

Inventories | 401 | ||

Plants, properties and equipment, net | 995 | ||

Goodwill | 10 | ||

Other assets | 74 | ||

Assets of businesses held for sale | $ | 1,778 | |

Accounts payable | $ | 184 | |

Accrued payroll and benefits | 50 | ||

Other accrued liabilities | 32 | ||

Other liabilities | 67 | ||

Liabilities of businesses held for sale | $ | 333 | |

Assets and liabilities of businesses held for sale by business were:

| December 31, 2006 | ||||||

In millions | Assets | Liabilities | ||||

Kraft | $ | 148 | $ | 16 | ||

Arizona Chemical | 496 | 159 | ||||

Beverage Packaging | 572 | 107 | ||||

Wood Products | 562 | 51 | ||||

Total | $ | 1,778 | $ | 333 | ||

NOTE 6 - SUPPLEMENTAL FINANCIAL STATEMENT INFORMATION

Temporary investments with an original maturity of three months or less are treated as cash equivalents and are stated at cost. Temporary investments totaled $961$598 million and $1.4 billion$578 million at September 30, 2007March 31, 2008 and December 31, 2006,2007, respectively.

Inventories by major category were:

In millions | September 30, 2007 | December 31, 2006 | March 31, 2008 | December 31, 2007 | ||||||||

Raw materials | $ | 315 | $ | 265 | $ | 409 | $ | 320 | ||||

Finished pulp, paper and packaging products | 1,372 | 1,341 | 1,380 | 1,413 | ||||||||

Operating supplies | 304 | 271 | 314 | 308 | ||||||||

Other | 39 | 32 | 44 | 30 | ||||||||

Total | $ | 2,030 | $ | 1,909 | $ | 2,147 | $ | 2,071 | ||||

Interest payments made during the nine-month periods ended September 30, 2007 and 2006 were $344 million and $507 million, respectively. Capitalized interest costs were $25 million and $13 million for the nine months ended September 30, 2007 and 2006, respectively. Total interest expenseAccumulated depreciation was $360 million for the first nine months of 2007 and $498 million for the first nine months of 2006. Distributions under preferred securities paid by Southeast Timber, Inc., a consolidated subsidiary of International Paper, were $10 million during the first nine months of both 2007 and 2006. The expense related to these preferred securities was included in minority interest expense in the consolidated statement of operations. Income tax payments of $243 million and $109 million were made during the first nine months of 2007 and 2006, respectively.

Accumulated depreciation was $14.7$15.3 billion at September 30, 2007March 31, 2008 and $14.0$14.9 billion at December 31, 2006.2007. Theallowance for doubtful accounts was $101$102 million at September 30, 2007March 31, 2008 and $85$95 million at December 31, 2006.2007.

The following tables present changes in the goodwill balances as allocated to each business segment for the nine-monththree-month periods ended September 30, 2007March 31, 2008 and 2006:2007:

In millions | Balance December 31, 2006 | Reclassifications and Other (a) | Additions/ (Reductions) | Balance September 30, 2007 | Balance December 31, 2007 | Reclassifications and Other (a) | Additions/ (Reductions) | Balance March 31, 2008 | ||||||||||||||||||

Printing Papers | $ | 1,441 | $ | 81 | $ | 531 | (b) | $ | 2,053 | $ | 2,043 | $ | 11 | $ | (7 | )(b) | $ | 2,047 | ||||||||

Industrial Packaging | 670 | 3 | (6 | )(c) | 667 | 683 | 3 | — | 686 | |||||||||||||||||

Consumer Packaging | 510 | 4 | 14 | (d) | 528 | 530 | 4 | — | 534 | |||||||||||||||||

Distribution | 308 | — | 96 | (e) | 404 | 394 | — | (3 | )(c) | 391 | ||||||||||||||||

Total | $ | 2,929 | $ | 88 | $ | 635 | $ | 3,652 | $ | 3,650 | $ | 18 | $ | (10 | ) | $ | 3,658 | |||||||||

| (a) | Represents the effects of foreign currency translations and reclassifications. |

| (b) |

| (c) | Reflects a |

In millions | Balance December 31, 2005 (a) | Reclassifications and Other (b) | Additions/ (Reductions) | Balance September 30, 2006 | |||||||||

Printing Papers | $ | 1,616 | $ | — | $ | — | $ | 1,616 | |||||

Industrial Packaging | 676 | 3 | 11 | (c) | 690 | ||||||||

Consumer Packaging | 1,019 | 1 | (1 | )(d) | 1,019 | ||||||||

Distribution | 299 | — | — | 299 | |||||||||

Corporate | 11 | — | — | 11 | |||||||||

Total | $ | 3,621 | $ | 4 | $ | 10 | $ | 3,635 | |||||

In millions | Balance December 31, 2006 | Reclassifications and Other (a) | Additions/ (Reductions) | Balance March 31, 2007 | |||||||||

Printing Papers | $ | 1,441 | $ | 12 | $ | 304 | (b) | $ | 1,757 | ||||

Industrial Packaging | 670 | — | (3 | )(c) | 667 | ||||||||

Consumer Packaging | 510 | 1 | 8 | (d) | 519 | ||||||||

Distribution | 308 | — | — | 308 | |||||||||

Total | $ | 2,929 | $ | 13 | $ | 309 | $ | 3,251 | |||||

| (a) |

| Represents the effects of foreign currency translations and reclassifications. |

| (b) | Reflects initial goodwill estimate from the Luiz Antonio mill transaction in February 2007. |

| (c) | Reflects a |

| (d) | Reflects |

The following table presents an analysis ofThere was no material activity related toasset retirement obligationsduring either the first quarter of 2008 or 2007.

Interest payments made during the three-month periods ended March 31, 2008 and 2007 were $86 million and $96 million, respectively. Capitalized interest costs were $4 million and $11 million for the three months ended March 31, 2008 and 2007, respectively.Total interest expense was $99 million for the first three months of 2008 and $112 million for the first three months of 2007.Interest income was $18 million and $51 million for the three months ended March 31, 2008 and 2007, respectively. Interest expense and interest income in 2008 and 2007 exclude approximately $74 million and $83 million, respectively, related to investments in and borrowings from variable interest entities for which the Company has a legal right of offset.Distributions under preferred securitiespaid by Southeast Timber, Inc., a consolidated subsidiary of International Paper, were $3 million during the first three months of both 2008 and 2007. The expense related to these preferred securities was included in Minority interest expense in the consolidated statement of operations.Income tax payments of $19 million and $33 million were made during the first three months of 2008 and 2007, respectively.

Equity earnings, net of taxes includes the Company’s asset retirement obligations:share of earnings from its investment in Ilim Holding S.A. ($17 million) and certain other smaller investments.

Nine Months Ended Septemebr 30, | ||||||||

In millions | 2007 | 2006 | ||||||

Asset retirement obligation, January 1 | $ | 29 | $ | 33 | ||||

New liabilities | — | 1 | ||||||

Liabilities settled | (3 | ) | (3 | ) | ||||

Net adjustments to existing liabilities | 1 | 1 | ||||||

Accretion expense | 1 | 1 | ||||||

Asset retirement obligation, September 30 | $ | 28 | $ | 33 | ||||

This obligation is included in Other liabilities in the accompanying consolidated balance sheet.

The components of the Company’spostretirement benefit cost were as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

In millions | 2007 | 2006 | 2007 | 2006 | ||||||||||||

Service cost | $ | — | $ | 1 | $ | 1 | $ | 2 | ||||||||

Interest cost | 9 | 8 | 26 | 24 | ||||||||||||

Actuarial loss | 6 | 6 | 17 | 17 | ||||||||||||

Amortization of prior service cost | (11 | ) | (13 | ) | (33 | ) | (37 | ) | ||||||||

Net postretirement benefit cost (a) | $ | 4 | $ | 2 | $ | 11 | $ | 6 | ||||||||

| Three Months Ended March 31, | ||||||||

In millions | 2008 | 2007 | ||||||

Service cost | $ | — | $ | — | ||||

Interest cost | 9 | 9 | ||||||

Actuarial loss | 7 | 5 | ||||||

Amortization of prior service cost | (9 | ) | (11 | ) | ||||

Net postretirement benefit cost (a) | $ | 7 | $ | 3 | ||||

| (a) | Excludes |

Fair Value Measurements

In accordance with the provisions of FASB Staff Position FAS 157-2 (see Note 7), the Company has partially applied the provisions of SFAS No. 157 only to its financial assets and liabilities recorded at fair value, which consist of derivative contracts, including interest rate swaps, foreign currency forward contracts, and other financial instruments that are used to hedge exposures to interest rate, commodity and currency risks. For these financial instruments, fair value is determined at each balance sheet date using an income approach, which consists of a discounted cash flow model that takes into account the present value of future cash flows under the terms of the contracts using current market information as of the reporting date, such as prevailing interest rates and foreign currency spot and forward rates. The following table provides a summary of the inputs used to develop these estimated fair values under the hierarchy defined in SFAS No. 157:

In millions Assets: Interest rate swaps (a) Commodity forward contracts (b) Foreign currency forward contracts (c) Total Liabilities: Foreign currency forward contracts (d) Total Fair Value Measurements at March 31, 2008 Using Total Quoted Prices in

Active Markets for

Identical Assets

(Level 1) Significant Other

Observable Inputs

(Level 2) Significant

Unobservable

Inputs

(Level 3) $ 69 $ — $ 69 $ — 32 — 32 — 126 — 126 — $ 227 $ — $ 227 $ — $ 6 $ — $ 6 $ — $ 6 $ — $ 6 $ —

| (a) | Includes $8 million recorded in Other current assets and |

| (b) | Includes $22 million recorded in Other current assets and $10 million recorded in Deferred charges and other assets in the accompanying consolidated balance sheet. |

| (c) | Includes $88 million recorded in Other current assets and $38 million recorded in Deferred charges and other assets in the accompanying consolidated balance sheet. |

| (d) | Includes $5 million recorded in Other accrued liabilities and $1 million recorded in Other liabilities in the accompanying consolidated balance sheet. |

NOTE 7 - RECENT ACCOUNTING DEVELOPMENTS

Intangible Assets:

In April 2008, the Financial Accounting Standards Board (FASB) issued FSP FAS 142-3, “Determination of the Useful Life of Intangible Assets,” which amends the factors that should be considered in developing renewal or extension assumptions used in determining the useful life of a recognized intangible asset. This FSP is effective for financial statements issued for fiscal years beginning after December 15, 2008 (calendar year 2009). The Company is currently evaluating the provisions of this FSP.

Derivative Instruments and Hedging Activities:

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities – An Amendment of FASB Statement No. 133.” This statement requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of, and gains and losses on, derivative instruments, and disclosures about credit-risk-related contingent features in derivative agreements. Statement No. 161 is effective for fiscal years and interim periods beginning after November 15, 2008 (calendar year 2009). The Company is currently evaluating the provisions of this statement.

Business Combinations:

In December 2007, the FASB issued SFAS No. 141(R), “Business Combinations.” Statement No. 141(R) establishes principles and requirements for how an acquiring entity in a business combination recognizes and measures the assets acquired and liabilities assumed in the transaction; establishes the acquisition-date fair value as the measurement objective for all assets acquired and liabilities assumed; and requires the acquirer to disclose to investors and other users all of the information needed to evaluate and understand the nature and financial effect of the business combination. This statement will be effective prospectively for business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2008 (calendar year 2009). The Company is currently evaluating the provisions of this statement.

Noncontrolling Interests in Consolidated Financial Statements:

In December 2007, the FASB also issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements, an amendment of ARB 51.” This statement clarifies that a noncontrolling (minority) interest in a subsidiary is an ownership interest in the entity that should be reported as equity in the consolidated financial statements. It also requires consolidated net income to include the amounts attributable to both the parent and noncontrolling interest, with disclosure on the face of the consolidated income statement of the amounts attributed to the parent and to the noncontrolling interest. This statement will be effective prospectively for fiscal years beginning after December 15, 2008 (calendar year 2009), with presentation and disclosure requirements applied retrospectively to comparative financial statements. The Company is currently evaluating the provisions of this statement.

Fair Value Option for Financial Assets and Financial Liabilities:

In February 2007, the Financial Accounting Standards Board (FASB)FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities – Including an Amendment of FASB Statement No. 115.” This statement permits an entity to measure certain financial assets and financial liabilities at fair value, which would result in the reporting of unrealized gains and losses in earnings at each subsequent reporting date. The fair value option may be elected on an instrument-by-instrument basis, with few exceptions, as long as it is applied to the instrument in its entirety. The statement establishes presentation and disclosure requirements to help financial statement users understand the effect of an entity’s election on its earnings, but does not eliminate the disclosure requirements of other accounting standards. This statement will be effective as of the beginning of the first fiscal year that begins after November 15, 2007 (calendar year 2008), and is to be applied prospectively as of the beginning of the year in which it is initially applied. The Company is currently evaluatingelected not to apply the provisionsfair value option to any of this statement.its financial assets or liabilities.

Fair Value Measurements:

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements,” which provides a single definition of fair value, together with a framework for measuring it, and requires additional disclosuredisclosures about the use of fair value to measure assets and liabilities. It also emphasizes that fair value is a market-based measurement, not an entity-specific measurement, and sets out a fair value hierarchy with the highest priority being quoted prices in active markets. This statement will beIn February 2008, the FASB issued FSP FAS 157-2 which delays the effective date of Statement No. 157 for financial statements issued forall nonrecurring fair value measurements of nonfinancial assets and liabilities until fiscal years beginning after November 15, 20072008 (calendar year 2008),2009). The Company partially adopted the provisions of SFAS No. 157 with respect to its financial assets and interim periods within those fiscal years, and is to be applied prospectively as of the beginning of the year in which it is initially applied.liabilities that are measured at fair value effective January 1, 2008 (see Note 6). The Company is currently evaluating the provisions of this statement.

Accounting for Planned Major Maintenance Activities:

In September 2006, the FASB issued FASB Staff Position (FSP) No. AUG AIR-1, “Accounting for Planned Major Maintenance Activities,” which permits the application of three alternative methods of accounting for planned major maintenance activities: the direct expense, built-in-overhaul, and deferral methods. The FSP was effective for the first fiscal year beginning after December 15, 2006. International Paper adopted the direct expense method of accounting for these costs in the first quarter of 2007 with no impact on its annual consolidated financial statements. See Note 13 for a discussioneffects of the effects of this accounting change on quarterly financial information.

Accounting for Uncertainty in Income Taxes:

In June 2006, the FASB issued FASB Interpretation No. 48 (FIN 48), “Accounting for Uncertainty in Income Taxes, an Interpretation of FASB Statement No. 109.” FIN 48 prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. This interpretation also provides guidance on classification, interest and penalties, accounting in interim periods and transition, and significantly expands income tax disclosure requirements. It applies to all tax positions accounted for in accordance with SFAS No. 109 and was effective for fiscal years beginning after December 15, 2006. International Paper applied theremaining provisions of this interpretation beginning January 1, 2007. See Note 8 for a discussion of the effects of this accounting change.

Accounting for Certain Hybrid Financial Instruments:

In February 2006, the FASB issued SFAS No. 155, “Accounting for Certain Hybrid Financial Instruments – an Amendment of FASB Statements No. 133 and 140,” which provides entities with relief from having to separately determine the fair value of an embedded derivative that would otherwise be required to be bifurcated from its host contract in accordance with SFAS No. 133. This statement allows an entity to make an irrevocable election to measure such a hybrid financial instrument at fair value in its entirety, with changes in fair value recognized in earnings. This statement was effective for International Paper for all financial instruments acquired, issued, or subject to a remeasurement event occurring after January 1, 2007. The adoption of SFAS No. 155 did not have a material impact on the Company’s consolidated financial statements.157.

NOTE 8 -– INCOME TAXES

International Paper adopted FINFASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes” (FIN 48), on January 1, 2007. The adoption of this standard resulted in a charge to the beginning balance of retained earnings of $94 million at the date of adoption. Total unrecognized tax benefits at the date of adoption including this cumulative effect charge were $919 million, including $562 million that would reducemillion. At December 31, 2007, unrecognized tax benefits totaled $794 million.

During the Company’s effective tax rate if recognized.

The major jurisdictions wherefirst quarter of 2008, the Company files income tax returns are the United States, Brazil, France, Poland and Russia. Generally, tax years 2001 through 2006 remain open and subjectsettled certain issues relating to examination by the relevant tax authorities. The Company is typically engaged in various tax examinations at any given time, both in the United States and in other countries. Currently, the Company is engaged in discussions with the U.S. Internal Revenue Service to conclude the examination of tax years 2001 –through 2003. As a result of these discussions, other pending audit settlements and the expirationother current period transactions, unrecognized tax benefits were reduced by $282 million to $512 million and accrued estimated interest and tax penalties were reduced by $19 million to $72 million at March 31, 2008 with no effect on net earnings. The Company currently estimates that, as a result of ongoing discussions, pending tax settlements and expirations of statutes of limitation, the Company currently estimates thatlimitations, the amount of unrecognized tax benefits could be reduced by up to $500$75 million during the next twelve months, with no significant impact on earnings or cash tax payments.12 months.

The Company accrues interest on unrecognized tax benefits as a component of interest expense. Penalties, if incurred, would be recognized as a component of income tax expense. As of the date of adoption of this standard, the Company had approximately $88 million of such accrued interest and penalties included in Other accrued liabilities associated with unrecognized tax benefits.

NOTE 9 - COMMITMENTS AND CONTINGENCIES

UnderAs previously disclosed, under the terms of the sale agreement for the Beverage Packaging business, the initial purchase price of approximately $500 million received by the Company iswas subject to a possible post-closing adjustment based on adjusted annualized earnings of the Beverage Packaging business for the first six months of 2007 and other

factors. In SeptemberAs of December 31, 2007, the purchaser of the business had proposed a reduction in the purchase price of $59totaling $48 million for this adjustment. While it is possible that such an adjustment could be required when this matter is finalized,and the Company believes, based on a preliminary review of the purchaser’s proposal,believed that no such adjustment iswas required under the sale agreement.

During the first quarter of 2008, representatives of the Company met with representatives of the purchaser of the business in an effort to resolve this matter. After considering many factors, including the prospect of protracted litigation, the complexity of this matter and other commercial relationships between the parties, the matter was settled for $25 million, and this amount was accrued on the balance sheet as of March 31, 2008. In April, a net payment of approximately $20 million was paid to the purchaser of the business for this adjustment, net of a separate post-closing adjustment amount owed by the purchaser to the Company.

Exterior Siding and Roofing Litigation:

International Paper has established reserves relating to the settlement, during 1998 and 1999, of three nationwide class action lawsuits against the Company and Masonite Corp., a former wholly-owned subsidiary of the Company. Those settlements relate to (1) exterior hardboard siding installed during the 1980’s (the 1980’s Hardboard Claims) and during the 1990’s (the 1990’s Hardboard Claims, and together with the 1980’s Hardboard Claims, the Hardboard Claims); (2) Omniwood siding installed during the 1990’s (the Omniwood Claims); and (3) Woodruf roofing installed during the 1980’s and 1990’s (the Woodruf Claims). Each of these settlements is discussed in detail in Note 10, Commitments and Contingent Liabilities, to the Financial Statements included in International Paper’s Annual Report on Form 10-K for the year ended December 31, 2006.2007. All Hardboard Claims mustwere required to be made by January 15, 2008, while all Omniwood and Woodruf Claims must be made by January 6, 2009.

Claims Data and Reserve Analysis

Throughout 2006 andClaims activity for the first nine months of 2007,Hardboard, Omniwood and Woodruf claims activity has beenduring 2007 was generally in line with projections. However, activity for Hardboard claimsupdated projections made in the first three quarters of 2006 was in excess of projected amounts. Accordingly, additional pre-tax charges totaling $50 million were recorded in the first three quarters of 2006 to reflect this higher claims activity pending completion of an updated projection by the Company’s third-party consultant. In the fourth quarter of 2006, this updated projection was completed, resultingalthough in connection with the January 15, 2008 filing deadline for Hardboard siding claims, the Company received a large number of claims at the end of 2007 and the beginning of 2008. During the first quarter of 2008, based on a current estimate of payments to be made for all claims received to date and projected future claim filings, an additional pre-tax charge of $40 million was recorded to increase the reserve to management’s best estimate of the amount required for future projected payments for claims and expenses that have been filed by the end of the claims period. Claims activity for Hardboard claims for the first three quarters of 2007 has been generally in line with these updated projections.payments.

The following table presents the claims activity of the Hardboard Claims for the nine-monththree-month period ended September 30, 2007:March 31, 2008:

In thousands | Single Family | Multi- Family | Total | Single Family | Multi- Family | Total | ||||||||||||

December 31, 2006 | 21.8 | 2.1 | 23.9 | |||||||||||||||

December 31, 2007 | 29.8 | 2.2 | 32.0 | |||||||||||||||

No. of Claims Filed | 18.9 | 1.0 | 19.9 | 8.7 | 1.5 | 10.2 | ||||||||||||

No. of Claims Paid | (12.8 | ) | (0.8 | ) | (13.6 | ) | (4.6 | ) | (0.2 | ) | (4.8 | ) | ||||||

No. of Claims Dismissed | (3.9 | ) | (0.2 | ) | (4.1 | ) | (2.0 | ) | (0.4 | ) | (2.4 | ) | ||||||

September 30, 2007 | 24.0 | 2.1 | 26.1 | |||||||||||||||

March 31, 2008 | 31.9 | 3.1 | 35.0 | |||||||||||||||