i

PART I — FINANCIAL INFORMATION

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEET

| September 30, 2019 | December 31, 2018 | |||||||

| (UNAUDITED) | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 14,338,637 | $ | 15,662,201 | ||||

| Restricted cash | 11,713,004 | 6,690,870 | ||||||

| Accounts receivable (net of allowance for doubtful accounts of $130,420 and $120,010 as of September 30, 2019 and December 31, 2018, respectively) | 54,859,801 | 34,274,728 | ||||||

| Inventories | 35,447,383 | 21,997,868 | ||||||

| Notes receivable | 41,549,888 | 72,712 | ||||||

| Notes receivable from the Affiliate Company and related party | - | 3,861,032 | ||||||

| Other receivables | 12,859,304 | 1,264,323 | ||||||

| Prepayments and prepaid expense | 9,497,459 | 11,136,408 | ||||||

| Due from employees | 5,499 | 1,001 | ||||||

| Advances to suppliers | 4,474,104 | 4,705,183 | ||||||

| Amount due from the Affiliate Company, net | 25,335,894 | 67,683,462 | ||||||

| Right - of - use asset | 42,974 | - | ||||||

| TOTAL CURRENT ASSETS | 210,123,947 | 167,349,788 | ||||||

| LONG-TERM ASSETS | ||||||||

| Property, plant and equipment, net | 74,491,204 | 82,045,923 | ||||||

| Land use rights, net | 11,084,717 | 11,749,728 | ||||||

| Construction in progress | 17,781 | - | ||||||

| Deferred taxes assets | - | 8,204 | ||||||

| Investment in the Affiliate Company | 53,837,011 | 128,929,893 | ||||||

| Goodwill | 27,762,120 | 28,552,215 | ||||||

| Intangible assets | 3,723,988 | 4,328,127 | ||||||

| Other long term assets | 4,803,349 | 5,865,386 | ||||||

| TOTAL Long-Term Assets | 175,720,170 | 261,479,476 | ||||||

| TOTAL ASSETS | $ | 385,844,117 | $ | 428,829,264 | ||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | 79,632,036 | $ | 112,309,683 | ||||

| Other payables and accrued expenses | 4,843,001 | 4,251,487 | ||||||

| Short-term loans | 30,969,731 | 30,539,236 | ||||||

| Customer deposits | 33,535 | 94,408 | ||||||

| Notes payable | 11,463,004 | 12,787,619 | ||||||

| Income tax payable | 1,519,699 | 3,471,366 | ||||||

| Due to employees | 7,105 | 28,473 | ||||||

| Deferred income | 1,237,556 | 1,340,605 | ||||||

| Lease liability | 44,121 | - | ||||||

| Total Current Liabilities | 129,749,788 | 164,822,877 | ||||||

| LONG-TERM LIABILITIES | ||||||||

| Long term bank loans | 27,606,502 | 28,794,136 | ||||||

| Deferred taxes liability | 1,758,643 | 1,711,343 | ||||||

| Contingent consideration liability | 6,562,000 | 7,256,000 | ||||||

| Other long-term liability | - | 622,034 | ||||||

| Total Long-Term Liabilities | 35,927,145 | 38,383,513 | ||||||

| TOTAL LIABILITIES | 165,676,933 | 203,206,390 | ||||||

| STOCKHOLDER’S EQUITY | ||||||||

| Common stock, $0.001 par value; 100,000,000 shares authorized; 56,263,102 and 55,992,002 shares issued and 52,839,441 and 51,484,444 outstanding at September 30, 2019 and December 31, 2018, respectively | 52,839 | 51,484 | ||||||

| Less: Treasury stock (487,155 shares with average price of $5.09 and 0 shares at September 30, 2019 and December 31, 2018, respectively ) | (2,477,965 | ) | - | |||||

| Additional paid-in capital | 259,691,370 | 254,989,657 | ||||||

| Accumulated deficit (the restricted portion is $4,422,033 and $4,422,033 at September 30, 2019 and December 31, 2018, respectively) | (9,135,198 | ) | (9,497,009 | ) | ||||

| Accumulated other comprehensive loss | (27,963,862 | ) | (19,921,258 | ) | ||||

| TOTAL STOCKHOLDERS’ EQUITY | 220,167,184 | 225,622,874 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 385,844,117 | $ | 428,829,264 | ||||

See accompanying notes to condensed consolidated financial statements

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS) AND

COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

| Three Months Ended | Nine Months Ended | |||||||||||||||

| September 30, 2019 | September 30, 2018 | September 30, 2019 | September 30, 2018 | |||||||||||||

| REVENUES FROM UNRELATED PARTY, NET | $ | 26,968,385 | $ | 14,860,034 | $ | 63,360,044 | $ | 32,211,352 | ||||||||

| REVENUES FROM THE AFFILIATE COMPANY AND RELATED PARTY, NET | 4,720,159 | 23,135,326 | 10,543,190 | 30,479,521 | ||||||||||||

| REVENUES, NET | 31,688,544 | 37,995,360 | 73,903,234 | 62,690,873 | ||||||||||||

| COST OF GOODS SOLD | (26,412,129 | ) | (31,753,311 | ) | (61,288,228 | ) | (53,044,861 | ) | ||||||||

| GROSS PROFIT | 5,276,415 | 6,242,049 | 12,615,006 | 9,646,012 | ||||||||||||

| OPERATING EXPENSES: | ||||||||||||||||

| Research and development | (596,187 | ) | (5,691,649 | ) | (1,766,210 | ) | (7,091,836 | ) | ||||||||

| Selling and marketing | (930,810 | ) | (898,896 | ) | (2,448,291 | ) | (1,875,294 | ) | ||||||||

| General and administrative | (3,432,920 | ) | (2,070,947 | ) | (11,096,246 | ) | (5,534,039 | ) | ||||||||

| Total Operating Expenses | (4,959,917 | ) | (8,661,492 | ) | (15,310,747 | ) | (14,501,169 | ) | ||||||||

| INCOME (LOSS) FROM OPERATIONS | 316,498 | (2,419,443 | ) | (2,695,741 | ) | (4,855,157 | ) | |||||||||

| OTHER INCOME (EXPENSE): | �� | |||||||||||||||

| Interest income | 209,736 | 52,745 | 559,954 | 1,452,522 | ||||||||||||

| Interest expense | (435,524 | ) | (483,376 | ) | (1,304,062 | ) | (1,505,409 | ) | ||||||||

| Change in fair value of contingent consideration | 57,000 | (1,552,686 | ) | 694,000 | 1,814,326 | |||||||||||

| Government grants | 502,146 | 607,008 | 725,189 | 717,821 | ||||||||||||

| Gain from equity dilution in the Affiliate Company | (49,285 | ) | - | 4,291,974 | - | |||||||||||

| Gain from equity sale in the Affiliate Company | 20,574,217 | - | 20,574,217 | - | ||||||||||||

| Share of loss after tax of the Affiliate Company | (8,433,767 | ) | (3,247,343 | ) | (22,883,126 | ) | (79,592 | ) | ||||||||

| Other income , net | 57,833 | 15,735 | 357,626 | 666,294 | ||||||||||||

| Total other income (expense), net | 12,482,356 | (4,607,917 | ) | 3,015,772 | 3,065,962 | |||||||||||

| INCOME (LOSS) BEFORE INCOME TAXES | 12,798,854 | (7,027,360 | ) | 320,031 | (1,789,195 | ) | ||||||||||

| INCOME TAX (EXPENSE) BENEFIT | (709,413 | ) | 505,961 | 41,780 | 370,316 | |||||||||||

| NET INCOME (LOSS) | 12,089,441 | (6,521,399 | ) | 361,811 | (1,418,879 | ) | ||||||||||

| OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||

| Foreign currency translation | (8,531,043 | ) | (8,108,270 | ) | (8,042,604 | ) | (13,230,652 | ) | ||||||||

| COMPREHENSIVE INCOME (LOSS) | $ | 3,558,398 | $ | (14,629,669 | ) | $ | (7,680,793 | ) | $ | (14,649,531 | ) | |||||

| WEIGHTED AVERAGE SHARES OUTSTANDING BASIC AND DILUTED | 52,613,642 | 51,474,048 | 52,332,260 | 51,089,047 | ||||||||||||

| NET INCOME (LOSS) PER SHARE, BASIC AND DILUTED | $ | 0.23 | $ | (0.13 | ) | $ | 0.01 | $ | (0.03 | ) | ||||||

See accompanying notes to condensed consolidated financial statements

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(UNAUDITED)

| September 30, 2018 | December 31, 2017 | |||||||

| (Unaudited) | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 1,342,085 | $ | 4,891,808 | ||||

| Restricted cash | 9,104,584 | 11,218,688 | ||||||

| Accounts receivable (net of allowance for doubtful accounts of $319,421 and $133,930 as of September 30, 2018 and December 31, 2017, respectively) | 40,111,173 | 34,397,858 | ||||||

| Inventories (net of provision for slow moving inventory of $662,769 and $620,919 as of September 30, 2018 and December 31, 2017, respectively) | 15,676,683 | 15,979,794 | ||||||

| Notes receivable | 72,817 | - | ||||||

| Notes receivable from JV Company and related party | 2,184,519 | 1,137,289 | ||||||

| Other receivables | 1,233,460 | 2,650,668 | ||||||

| Prepayments and prepaid expense | 6,662,684 | 6,536,839 | ||||||

| Due from employees | 6,668 | 7,070 | ||||||

| Advances to suppliers | 8,794,653 | 14,908,385 | ||||||

| Amount due from JV Company, net | 77,386,193 | 146,422,440 | ||||||

| Amount due from related party | - | 162,048 | ||||||

| TOTAL CURRENT ASSETS | 162,575,519 | 238,312,887 | ||||||

| LONG-TERM ASSETS | ||||||||

| Property, Plant and Equipment, net | 83,664,992 | 12,000,971 | ||||||

| Land use rights, net | 11,848,966 | 12,666,047 | ||||||

| Construction in progress | - | 53,083,925 | ||||||

| Deferred taxes assets | 3,294,885 | 4,383,425 | ||||||

| Long Term Investment | - | 1,460,034 | ||||||

| Investment in JV Company | 146,272,731 | 70,681,013 | ||||||

| Goodwill | 28,583,528 | 322,591 | ||||||

| Intangible assets | 4,491,080 | 331,116 | ||||||

| Advances to suppliers | - | 21,592,918 | ||||||

| Other long term assets | 6,168,533 | 7,590,734 | ||||||

| Amount due from JV Company, net | - | 15,907,183 | ||||||

| TOTAL Long-Term Assets | 284,324,715 | 200,019,957 | ||||||

| TOTAL ASSETS | $ | 446,900,234 | $ | 438,332,844 | ||||

| CURRENT LIABILITIES | ||||||||

| Accounts payables | $ | 111,376,786 | $ | 111,595,540 | ||||

| Other payables and accrued expenses | 6,065,379 | 6,556,209 | ||||||

| Short-term loans | 30,583,267 | 33,042,864 | ||||||

| Customer deposits | 214,079 | 205,544 | ||||||

| Notes payable | 24,663,846 | 28,075,945 | ||||||

| Income tax payable | 471,184 | 2,902,699 | ||||||

| Due to employees | 34,070 | 35,041 | ||||||

| Deferred income | 1,353,819 | 2,191,143 | ||||||

| Total Current Liabilities | 174,762,430 | 184,604,985 | ||||||

| LONG-TERM LIABILITIES | ||||||||

| Long term bank loans | 28,981,286 | 30,737,547 | ||||||

| Contingent liability | 12,204,964 | - | ||||||

| Other long-term liability | 681,768 | - | ||||||

| Total Long-Term Liabilities | 41,868,018 | 30,737,547 | ||||||

| TOTAL LIABILITIES | 216,630,448 | 215,342,532 | ||||||

| STOCKHOLDER’S EQUITY | ||||||||

| Common stock, $0.001 par value; 100,000,000 shares authorized; 55,989,502 and 48,036,538 shares issued and 51,481,944 and 48,036,538 outstanding at September 30, 2018 and December 31,2017, respectively | 51,482 | 48,037 | ||||||

| Additional paid-in capital | 254,980,909 | 233,055,348 | ||||||

| Retained earnings (the restricted portion is $4,422,033 and $4,422,033 at September 30,2018 and December 31,2017, respectively) | (5,221,190 | ) | (3,802,310 | ) | ||||

| Accumulated other comprehensive loss | (19,541,415 | ) | (6,310,763 | ) | ||||

| TOTAL STOCKHOLDERS’ EQUITY | 230,269,786 | 222,990,312 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 446,900,234 | $ | 438,332,844 | ||||

| Number of Outstanding Shares | Common Stock | Treasury Stock | Additional Paid-in Capital | Accumulated Deficit | Accumulated Other Comprehensive Income | Total | ||||||||||||||||||||||

| Balance, December 31, 2018 | 51,484,444 | 51,484 | - | 254,989,657 | (9,497,009 | ) | (19,921,258 | ) | 225,622,874 | |||||||||||||||||||

| Stock issuance and award | 1,096,397 | 1,097 | - | 3,387,379 | - | - | 3,388,476 | |||||||||||||||||||||

| Net income (loss) | - | - | - | - | (4,409,472 | ) | - | (4,409,472 | ) | |||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | 5,404,028 | 5,404,028 | |||||||||||||||||||||

| Balance, March 31, 2019 | 52,580,841 | 52,581 | - | 258,377,036 | (13,906,481 | ) | (14,517,230 | ) | 230,005,906 | |||||||||||||||||||

| Stock issuance and award | 238,600 | 238 | - | 1,259,569 | - | - | 1,259,807 | |||||||||||||||||||||

| Net income (loss) | - | - | - | - | (7,318,158 | ) | - | (7,318,158 | ) | |||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | (4,915,589 | ) | (4,915,589 | ) | |||||||||||||||||||

| Balance, June 30, 2019 | 52,819,441 | 52,819 | - | 259,636,605 | (21,224,639 | ) | (19,432,819 | ) | 219,031,966 | |||||||||||||||||||

| Stock issuance and award | 20,000 | 20 | - | 69,380 | - | - | 69,400 | |||||||||||||||||||||

| Stock buyback | - | - | (2,477,965 | ) | - | - | - | (2,477,965 | ) | |||||||||||||||||||

| Commission in stock buyback | - | - | - | (14,615 | ) | - | - | (14,615 | ) | |||||||||||||||||||

| Net income (loss) | - | - | - | - | 12,089,441 | - | 12,089,441 | |||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | (8,531,043 | ) | (8,531,043 | ) | |||||||||||||||||||

| Balance, September 30, 2019 | 52,839,441 | 52,839 | (2,477,965 | ) | 259,691,370 | (9,135,198 | ) | (27,963,862 | ) | 220,167,184 | ||||||||||||||||||

| Number of Outstanding Shares | Common Stock | Treasury Stock | Additional Paid-in Capital | Accumulated Deficit | Accumulated Other Comprehensive Income | Total | ||||||||||||||||||||||

| Balance, December 31, 2017 | 48,036,538 | 48,037 | - | 233,055,348 | (3,802,310 | ) | (6,310,763 | ) | 222,990,312 | |||||||||||||||||||

| Stock issuance and award | 2,972,337 | 2,972 | - | 19,099,556 | - | - | 19,102,528 | |||||||||||||||||||||

| Net income (loss) | - | - | - | - | 3,727,995 | - | 3,727,995 | |||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | 7,465,240 | 7,465,240 | |||||||||||||||||||||

| Balance, March 31, 2018 | 51,008,875 | 51,009 | - | 252,154,904 | (74,315 | ) | 1,154,477 | 253,286,075 | ||||||||||||||||||||

| Stock issuance and award | 288,600 | 289 | - | 2,038,476 | - | - | 2,038,765 | |||||||||||||||||||||

| Net income (loss) | - | - | - | - | 1,374,525 | - | 1,374,525 | |||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | (12,587,622 | ) | (12,587,622 | ) | |||||||||||||||||||

| Balance, June 30, 2018 | 51,297,475 | 51,298 | - | 254,193,380 | 1,300,210 | (11,433,145 | ) | 244,111,743 | ||||||||||||||||||||

| Stock issuance and award | 184,469 | 184 | - | 787,529 | - | - | 787,713 | |||||||||||||||||||||

| Net income (loss) | - | - | - | - | (6,521,399 | ) | - | (6,521,399 | ) | |||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | (8,108,271 | ) | (8,108,271 | ) | |||||||||||||||||||

| Balance, September 30, 2018 | 51,481,944 | 51,482 | - | 254,980,909 | (5,221,189 | ) | (19,541,416 | ) | 230,269,786 | |||||||||||||||||||

See accompanying notes to condensed consolidated financial statements

statements.

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS) ANDCASH FLOWSCOMPREHENSIVE INCOME (LOSS)(UNAUDITED)

(UNAUDITED)

| Three Months Ended | Nine Months Ended | |||||||||||||||

| September 30, 2018 | September 30, 2017 | September 30, 2018 | September 30, 2017 | |||||||||||||

| REVENUES FROM UNRELATED PARTY, NET | $ | 14,860,034 | $ | 6,604,109 | $ | 32,211,352 | $ | 10,720,595 | ||||||||

| REVENUES FROM JV COMPANY AND RELATED PARTY, NET | 23,135,326 | 21,749,790 | 30,479,521 | 49,233,156 | ||||||||||||

| REVENUES, NET | 37,995,360 | 28,353,899 | 62,690,873 | 59,953,751 | ||||||||||||

| COST OF GOODS SOLD | (31,753,311 | ) | (23,522,406 | ) | (53,044,861 | ) | (50,697,990 | ) | ||||||||

| GROSS PROFIT | 6,242,049 | 4,831,493 | 9,646,012 | 9,255,761 | ||||||||||||

| OPERATING EXPENSES: | ||||||||||||||||

| Research and development | (5,691,649 | ) | (657,851 | ) | (7,091,836 | ) | (26,569,624 | ) | ||||||||

| Selling and marketing | (898,896 | ) | (216,351 | ) | (1,875,294 | ) | (976,913 | ) | ||||||||

| General and administrative | (2,070,947 | ) | (2,196,201 | ) | (5,534,039 | ) | (12,074,147 | ) | ||||||||

| Total Operating Expenses | (8,661,492 | ) | (3,070,403 | ) | (14,501,169 | ) | (39,620,684 | ) | ||||||||

| (LOSS) INCOME FROM OPERATIONS | (2,419,443 | ) | 1,761,090 | (4,855,157 | ) | (30,364,923 | ) | |||||||||

| OTHER INCOME (EXPENSE): | ||||||||||||||||

| Interest income | 52,745 | 619,923 | 1,452,522 | 1,709,990 | ||||||||||||

| Interest expense | (483,376 | ) | (598,523 | ) | (1,505,409 | ) | (1,761,786 | ) | ||||||||

| Change in fair value of contingent consideration | (1,552,686 | ) | - | 1,814,326 | - | |||||||||||

| Government grants | 607,008 | 474,950 | 717,821 | 5,804,561 | ||||||||||||

| Share of (loss) income after tax of JV | (3,247,343 | ) | 444,181 | (79,592 | ) | (13,455,786 | ) | |||||||||

| Other income (expense), net | 15,735 | (6,560 | ) | 666,294 | 143,617 | |||||||||||

| Total other (expense) income, net | (4,607,917 | ) | 933,971 | 3,065,962 | (7,559,404 | ) | ||||||||||

| (LOSS) INCOME BEFORE INCOME TAXES | (7,027,360 | ) | 2,695,061 | (1,789,195 | ) | (37,924,327 | ) | |||||||||

| INCOME TAX BENEFIT (EXPENSE) | 505,961 | (776,985 | ) | 370,316 | 4,130,951 | |||||||||||

| NET (LOSS) INCOME | (6,521,399 | ) | 1,918,076 | (1,418,879 | ) | (33,793,376 | ) | |||||||||

| OTHER COMPREHENSIVE (LOSS) INCOME | ||||||||||||||||

| Foreign currency translation | (8,108,270 | ) | 4,032,652 | (13,230,652 | ) | 8,942,931 | ||||||||||

| COMPREHENSIVE (LOSS) INCOME | $ | (14,629,669 | ) | $ | 5,950,728 | $ | (14,649,531 | ) | $ | (24,850,445 | ) | |||||

| WEIGHTED AVERAGE SHARES OUTSTANDING BASIC | 51,474,048 | 48,028,467 | 51,089,047 | 47,913,028 | ||||||||||||

| WEIGHTED AVERAGE SHARES OUTSTANDING DILUTED | 51,474,048 | 48,028,467 | 51,089,047 | 47,913,028 | ||||||||||||

| NET (LOSS) INCOME PER SHARE, BASIC | $ | (0.13 | ) | $ | 0.04 | $ | (0.03 | ) | $ | (0.71 | ) | |||||

| NET (LOSS) INCOME PER SHARE, DILUTED | $ | (0.13 | ) | $ | 0.04 | $ | (0.03 | ) | $ | (0.71 | ) | |||||

| Nine Months Ended | ||||||||

| September 30, 2019 | September 30, 2018 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net income (loss) | $ | 361,811 | $ | (1,418,879 | ) | |||

| Adjustments to reconcile net income to net cash provided by operating activities | ||||||||

| Depreciation and amortization | 6,443,422 | 2,271,599 | ||||||

| Impairments | 44,544 | 24,854 | ||||||

| Allowance for doubtful accounts | 15,366 | (7,093 | ) | |||||

| Deferred taxes | 50,693 | - | ||||||

| Share of loss after tax of the Affiliate Company | 22,883,126 | 79,592 | ||||||

| Gain from equity dilution in the Affiliate Company | (4,291,974 | ) | - | |||||

| Gain from equity sale in the Affiliate Company | (20,574,217 | ) | - | |||||

| Change in fair value of contingent consideration | (694,000 | ) | (1,814,326 | ) | ||||

| Stock compensation cost | 1,337,333 | 253,934 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| (Increase) Decrease In: | ||||||||

| Accounts receivable | (36,822,184 | ) | (52,845,923 | ) | ||||

| Deferred taxes assets | - | (52,126 | ) | |||||

| Notes receivable | 174,881 | 491,272.00 | ||||||

| Notes receivable from the Affiliate Company and related party | 437,203 | 3,196,340 | ||||||

| Inventories | (14,813,147 | ) | 1,555,993 | |||||

| Other receivables and other assets | (17,275,954 | ) | 1,497,230 | |||||

| Due from employee | (25,861 | ) | 945 | |||||

| Advances to supplier and prepayments and prepaid expenses | 1,357,001 | (4,590,404 | ) | |||||

| Amount due from the Affiliate Company | 30,549,072 | (81,549,214 | ) | |||||

| Amount due from Affiliate Company-Long term | - | 15,907,183 | ||||||

| Due from related party | - | 161,874 | ||||||

| Increase (Decrease) In: | ||||||||

| Accounts payable | 11,383,411 | 101,684,965 | ||||||

| Other payables and accrued liabilities | 7,791,028 | 29,845,307 | ||||||

| Notes payable | (11,836,950 | ) | (12,434,813 | ) | ||||

| Customer deposits | (59,734 | ) | 20,350 | |||||

| Income tax payable | (1,803,574 | ) | (2,353,826 | ) | ||||

| Deferred income | (56,448 | ) | (761,643 | ) | ||||

| Net cash used in operating activities | $ | (25,425,152 | ) | $ | (836,809 | ) | ||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchases of property, plant and equipment, net | (955,670 | ) | (304,745 | ) | ||||

| Purchases of land use rights and other intangible assets | - | (105,480 | ) | |||||

| Acquisition of Jinhua An Kao (net of cash received) | - | (3,610,846 | ) | |||||

| Acquisition of SC Autosports | - | 486,954 | ||||||

| Purchases of construction in progress | (18,491 | ) | (425,241 | ) | ||||

| Reimbursement of capitalize interests for construction in progress | - | 1,818,390 | ||||||

| Cash received from equity sale in the Affiliate Company | 32,061,558 | - | ||||||

| Long Term Investment | - | 1,458,464 | ||||||

| Net cash provided by (used in) investing activities | $ | 31,087,397 | $ | (682,504 | ) | |||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from short-term bank loans | 27,864,409 | 25,515,452 | ||||||

| Repayments of short-term bank loans | (26,261,331 | ) | (26,283,065 | ) | ||||

| Repayments of long-term bank loans | (145,734 | ) | (153,523 | ) | ||||

| Proceeds from notes payable | - | 40,313,800 | ||||||

| Repayment of notes payable | - | (43,024,633 | ) | |||||

| Cash used for stock buyback | (2,492,579 | ) | - | |||||

| Net cash used in financing activities | $ | (1,035,235 | ) | $ | (3,631,969 | ) | ||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS AND RESTRICTED CASH | 4,627,010 | (5,151,282 | ) | |||||

| Effect of exchange rate changes on cash | (928,440 | ) | (512,545 | ) | ||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT BEGINNING OF YEAR | 22,353,071 | 16,110,496 | ||||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT END OF PERIOD | 26,051,641 | 10,446,669 | ||||||

| -CASH AND CASH EQUIVALENTS AT END OF PERIOD | 14,338,637 | 1,342,085 | ||||||

| -RESTRICTED CASH AT END OF PERIOD | 11,713,004 | 9,104,584 | ||||||

| SUPPLEMENTARY CASH FLOW INFORMATION | ||||||||

| Income taxes paid | 1,711,101 | 1,981,072 | ||||||

| Interest paid | 1,304,062 | 1,274,399 | ||||||

| SUPPLEMENTAL NON-CASH DISCLOSURES: | ||||||||

| Acquisition of Jinhua An Kao by stock | - | 20,718,859 | ||||||

| Acquisition of SC Autosports by stock | - | 756,664 | ||||||

| Amount due from the Affiliate Company converted to investment in the Affiliate Company | - | 83,669,804 | ||||||

| Notes receivable from unrelated parties for equity transfer payment | 43,137,369 | - | ||||||

See accompanying notes to condensed consolidated financial statements

KANDI TECHNOLOGIES GROUP, INC.AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Nine Months Ended | ||||||||

| September 30, 2018 | September 30, 2017 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net (loss) | $ | (1,418,879 | ) | $ | (33,793,376 | ) | ||

| Adjustments to reconcile net income to net cash provided by operating activities | ||||||||

| Depreciation and amortization | 2,271,599 | 3,556,661 | ||||||

| Assets impairments | 78,415 | 136,936 | ||||||

| Allowance for doubtful accounts | (7,093 | ) | - | |||||

| Deferred taxes | - | (5,596,103 | ) | |||||

| Share of income after tax of JV Company | 79,592 | 13,455,786 | ||||||

| Reserve for fixed assets | (53,561 | ) | - | |||||

| Change in fair value of contingent consideration | (1,814,326 | ) | - | |||||

| Stock compensation cost | 253,934 | 5,498,183 | ||||||

| Changes in operating assets and liabilities, net of effects of acquisition: | ||||||||

| (Increase) Decrease In: | ||||||||

| Accounts receivable | (52,845,923 | ) | (8,926,990 | ) | ||||

| Deferred taxes assets | (52,126 | ) | - | |||||

| Notes receivable | 491,272 | - | ||||||

| Notes receivable from JV Company and related party | 3,196,340 | 4,923,967 | ||||||

| Inventories | 1,555,993 | (2,814,129 | ) | |||||

| Other receivables and other assets | 1,497,230 | 754,661 | ||||||

| Due from employee | 945 | (10,766 | ) | |||||

| Advances to supplier and prepayments and prepaid expenses | (4,590,404 | ) | 23,878,150 | |||||

| Advances to suppliers-long term | - | (4,804,200 | ) | |||||

| Amount due from JV Company | (81,549,214 | ) | (33,071,177 | ) | ||||

| Amount due from JV Company-long-term | 15,907,183 | (15,907,183 | ) | |||||

| Due from related party | 161,874 | 4,406,105 | ||||||

| Increase (Decrease) In: | ||||||||

| Accounts payable | 101,684,965 | 53,102,716 | ||||||

| Other payables and accrued liabilities | 29,845,307 | 2,173,413 | ||||||

| Notes payable | (12,434,813 | ) | (3,933,839 | ) | ||||

| Customer deposits | 20,350 | 80,057 | ||||||

| Income tax payable | (2,353,826 | ) | 732,405 | |||||

| Deferred income | (761,643 | ) | (5,127,455 | ) | ||||

| Loss contingency-litigation | - | 587,579 | ||||||

| Net cash used in operating activities | $ | (836,809 | ) | $ | (698,599 | ) | ||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchases of property, plant and equipment, net | $ | (304,745 | ) | $ | (420,037 | ) | ||

| Purchases of land use rights and other intangible assets | (105,480 | ) | - | |||||

| Acquisition of Jinhua An Kao (net of cash received) | (3,610,846 | ) | - | |||||

| Acquisition of SC Autosports (net of cash received) | 486,954 | - | ||||||

| Purchases of construction in progress | (425,241 | ) | (1,565,244 | ) | ||||

| Reimbursement of capitalize interests for construction in progress | 1,818,390 | - | ||||||

| Long Term Investment | 1,458,464 | - | ||||||

| Short term investment | - | 4,553,734 | ||||||

| Net cash (used in) provided by investing activities | $ | (682,504 | ) | $ | 2,568,453 | |||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from short-term bank loans | $ | 25,515,452 | $ | 24,854,574 | ||||

| Repayments of short-term bank loans | (26,283,065 | ) | (27,939,362 | ) | ||||

| Repayments of long-term bank loans | (153,523 | ) | - | |||||

| Proceeds from notes payable | 40,313,800 | 13,367,413 | ||||||

| Repayment of notes payable | (43,024,633 | ) | (14,060,961 | ) | ||||

| Net cash used in financing activities | $ | (3,631,969 | ) | $ | (3,778,336 | ) | ||

| NET (DECREASE) IN CASH AND CASH EQUIVALENTS AND RESTRICTED CASH | $ | (5,151,282 | ) | $ | (1,908,482 | ) | ||

| Effect of exchange rate changes on cash | $ | (512,545 | ) | $ | 1,011,615 | |||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT BEGINNING OF YEAR | $ | 16,110,496 | $ | 25,193,298 | ||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT END OF PERIOD | $ | 10,446,669 | $ | 24,296,431 | ||||

| SUPPLEMENTARY CASH FLOW INFORMATION | ||||||||

| Income taxes paid | $ | 1,981,072 | $ | 1,072,082 | ||||

| Interest paid | $ | 1,274,399 | $ | 1,164,774 | ||||

| SUPPLEMENTAL NON-CASH DISCLOSURES: | ||||||||

| Construction in progress transferred to property, plant and equipment | $ | 75,266,352 | $ | - | ||||

| Long term and short term advances to suppliers transferred to construction in progress | $ | 31,786,196 | $ | 12,241,736 | ||||

| Settlement of due from JV Company and related parties with notes receivable | $ | 62,549,758 | $ | 39,197,964 | ||||

| Settlement of accounts receivables with notes receivable from unrelated parties | $ | 49,620,953 | $ | 1,150,038 | ||||

| Settlement of other receivables with notes receivable from unrelated parties | $ | 930,347 | $ | - | ||||

| Assignment of notes receivable from unrelated parties to supplier to settle accounts payable | $ | 20,126,196 | $ | 1,150,038 | ||||

| Assignment of notes receivable from JV Company and related parties to supplier to settle accounts payable | $ | 57,956,363 | $ | 33,175,103 | ||||

| Assignment of notes receivable from unrelated parties to supplier to settle other payable | $ | 29,857,070 | $ | - | ||||

| Assignment of notes receivable from JV Company and related parties to supplier to settle other payable | $ | 230,284 | $ | - | ||||

| Settlement of accounts payable with notes payables | $ | 23,846,161 | $ | 15,149,150 | ||||

| Acquisition of Jinhua An Kao by stock | $ | 20,718,859 | $ | - | ||||

| Acquisition of SC by stock | $ | 756,664 | $ | - | ||||

| Cancellation of notes payables | $ | 10,746,580 | $ | - | ||||

| Amount due from JV Company converted to investment in JV Company | $ | 83,669,804 | $ | - | ||||

| Adjustment of construction in progress with accounts payable | $ | 8,153,573 | $ | - | ||||

| Adjustment of advance to supplier with accounts payable | $ | 479,575 | $ | - | ||||

| Deferred tax changed to other comprehensive income | $ | - | $ | 52,266 | ||||

| Adjustment of Construction in progress | $ | - | $ | 1,057,152 | ||||

| Purchase of construction in progress in accounts payable | $ | - | $ | 6,244,120 | ||||

See accompanying notes to condensed consolidated financial statements

NOTE 1 - ORGANIZATION AND PRINCIPAL ACTIVITIES

Kandi Technologies Group, Inc. (“Kandi Technologies”) was incorporated under the laws of the State of Delaware on March 31, 2004 as Stone Mountain Resources, Inc. It changed its name to Kandi Technologies, Corp. on August 13, 2007, and on December 21, 2012, it further changed its name to its current name.2004. As used herein, the term theterms “Company” meansor “Kandi” refer to Kandi Technologies and its operating subsidiaries, as described below.

Headquartered in Jinhua City, Zhejiang Province, People’s Republic of China (“China”), the Company is one of the People’s Republic of China’s (“China”) leading producers and manufacturers of electric vehicle (“EV”) products (through the Affiliate Company, formerly defined as the JV Company), EV parts, and off-road vehicles for sale in ChinaChinese and global markets. The Company conducts its primary business operations through its wholly-owned subsidiaries, Zhejiang Kandi Vehicles Co., Ltd. (“Kandi Vehicles”), Kandi Vehicles’ wholly and Sportsman Country, LLC (“Sportsman Country”) which changed its name to SC Autosports LLC (“SC Autosports”) in August 2018,partially-owned subsidiaries, and the partially and wholly-owned subsidiaries of Kandi Vehicles.

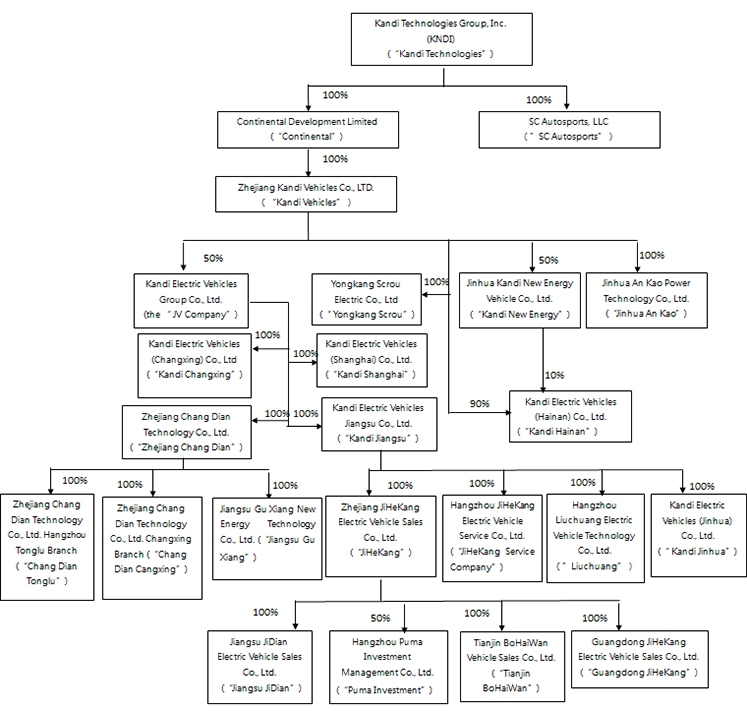

The Company’s organizational chart as of November 6, 2018 is as follows:

Operating Subsidiaries:

Pursuant to the agreements executed in January 2011, Kandi Vehicles is entitled to 100% of the economic benefits, voting rights and residual interests (100% of profits and losses) of Jinhua Kandi New Energy Vehicles Co., Ltd. (“Kandi New Energy”). Kandi New Energy currently holds battery pack production licensing rights and supplies battery packs to the JV Company (as such term is defined below).

In April 2012, pursuant to an agreement with the shareholders of YongkangScrou Electric Co, Ltd. (“YongkangScrou”), the Company acquired 100% of YongkangScrou, a manufacturer of automobile and EV parts. YongkangScrou currently manufactures and sells EV drive motors, EV controllers, air conditioners and other electric products to the JV Company.

In March 2013, pursuant to a joint venture agreement (the “JV Agreement”) entered into by Kandi Vehicles and Shanghai Maple Guorun Automobile Co., Ltd. (“Shanghai Guorun”), a 99%-owned subsidiary of Geely Automobile Holdings Ltd. (“Geely”), the parties established Zhejiang Kandi Electric Vehicles Co., Ltd. (the “JV Company”) to develop, manufacture and sell EV products and related auto parts. Each of Kandi Vehicles and Shanghai Guorun has 50% ownership interest in the JV Company. In March 2014, the JV Company changed its name to Kandi Electric Vehicles Group Co., Ltd. At present, the JV Company is a holding company and all products are manufactured by its subsidiaries. In an effort to improve the JV Company’s development, Zhejiang Geely Holding Group, the parent company of Geely, became a JV Company shareholder on October 26, 2016, through its purchase of the 50% equity of the JV Company held by Shanghai Guorun at a premium price (a price exceeding the cash amount of the aggregate of the original investment and the shared profits over the years). On May 19, 2017, due to business development, Zhejiang Geely Holding Group, Ltd. (Geely Holding) transferred its equity in the JV Company to Geely Group (Ningbo) Ltd., a company wholly owned by Mr. Li Shufu, Chairman of the Board of Geely Holding. On May 23, 2018, in order to obtain the manufacturing license, according to the recent notice (FGBCY[2018] No.547) from the National Development and Reform Commission in China, the JV Company increased its registered capital by RMB 1.09 billion (approximately $165 million), of which Kandi Vehicle increased its capital contribution to the JV Company by converting its RMB 545 million (approximately $79 million) loans to the JV Company to registered capital in the JV Company. Geely Group, Ltd. (“Geely Group”) became a new shareholder of the JV Company by investing RMB 545 million (approximately $79million). After this restructure, Kandi Vehicles, Geely Group and Geely Group (Ningbo) Ltd., each own 50%, 26.08%, and 23.92% of equity in the JV Company, respectively.

In March 2013, Kandi Vehicles formed Kandi Electric Vehicles (Changxing) Co., Ltd. (“KandiChangxing”) in the Changxing (National) Economic and Technological Development Zone. KandiChangxing is engaged in the production of EV products. In the fourth quarter of 2013, Kandi Vehicles entered into an ownership transfer agreement with the JV Company pursuant to which Kandi Vehicles transferred 100% of its ownership in KandiChangxing to the JV Company. The Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in KandiChangxing.

In July 2013, Zhejiang ZuoZhongYou Electric Vehicle Service Co., Ltd. (the “Service Company”) was formed. The Service Company is engaged in various pure EV leasing businesses, generally referred to as the Micro Public Transportation (“MPT”) and other EV share programs. Kandi Vehicle had a 9.5% ownership interest in the Service Company. After various tests and thorough assessments in the last five years, the Company determined that a large sum of capital still needs to be invested in order to increase the size of EV share programs. After considering Geely Group’s ability to grow the Service Company’s business to be stronger and more expansive and a successful growth of the Service Company would have positive impact on the development of the JV Company’s business, Kandi Vehicle transferred its 9.5% of ownership interest in the Service Company to Geely Group in June 2018.

In November 2013, Kandi Electric Vehicles Jinhua Co., Ltd. (“Kandi Jinhua”) was formed by the JV Company. The JV Company has a 100% ownership interest in Kandi Jinhua, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Kandi Jinhua. In April 2017, Kandi Jinhua was reorganized to be owned directly by Kandi Jiangsu, which is 100% directly owned by the JV Company.

In November 2013, Zhejiang Ji He Kang Electric Vehicle Sales Co., Ltd. (“Ji He Kang”) was formed by the JV Company. JiHeKang is engaged in the car sales business. The JV Company has a 100% ownership interest in JiHeKang, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in JiHeKang. In April 2017, JiHeKang was reorganized to be owned directly by Kandi Jiangsu, which is 100% directly owned by the JV Company.

In December 2013, the JV Company entered into an ownership transfer agreement with Shanghai Guorun, pursuant to which the JV Company acquired a 100% ownership interest in Kandi Electric Vehicles (Shanghai) Co., Ltd. (“Kandi Shanghai”). As a result, Kandi Shanghai is a wholly-owned subsidiary of the JV Company, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Kandi Shanghai.

In January 2014, KandiElectric Vehicles Jiangsu Co., Ltd. (“Kandi Jiangsu”) was formed by the JV Company. The JV Company has a 100% ownership interest in Kandi Jiangsu, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Kandi Jiangsu. Kandi Jiangsu is mainly engaged in EV research and development, manufacturing, and sales. As of the date of this report, Kandi Jiangsu directly owns 100% of JiHeKang, JiHeKang Service Company, Liuchuang and KandiJinhua.

In November 2015, Hangzhou Puma Investment Management Co., Ltd. (“Puma Investment”) was formed by the JV Company. Puma Investment provides investment and consulting services. The JV Company has a 50% ownership interest in Puma Investment (the other 50% is owned by Zuozhongyou Electric Vehicles Service (Hangzhou) Co., Ltd., a subsidiary of the Service Company), and the Company, indirectly through the JV Company, has a 25% economic interest in Puma Investment.

In November 2015, Hangzhou JiHeKang Electric Vehicle Service Co., Ltd. (the “JiHeKang Service Company”) was formed by the JV Company. The JiHeKang Service Company focuses on after-market services for EV products. In April 2017, JiHeKang Service Company was reorganized to be owned directly by Kandi Jiangsu, which is 100% directly owned by the JV Company. The JV Company has a 100% ownership interest in the JiHeKang Service Company, and the Company, indirectly through the JV Company, has a 50% economic interest in the JiHeKang Service Company.

In December 2015, Zhejiang JiHeKang Electric Vehicle Sales Co., Ltd. Tianjin Branch (“JiHeKang Tianjin”) was formed by JiHeKang. JiHeKang Tianjin was engaged in the car sales business. JiHeKang Tianjin was dissolved in September 2018.

In January 2016, Kandi Electric Vehicles (Wanning) Co., Ltd. was renamed Kandi Electric Vehicles (Hainan) Co., Ltd. (“Kandi Hainan”). Kandi Hainan was originally formed in Wanning City in Hainan Province by Kandi Vehicles and Kandi New Energy in April 2013, and was transferred to Haikou City in January 2016. Kandi Vehicles has a 90% ownership interest in Kandi Hainan, and Kandi New Energy has the remaining 10% ownership interest. In fact, Kandi Vehicles is, effectively, entitled to 100% of the economic benefits, voting rights and residual interests (100% of the profits and losses) of Kandi Hainan as Kandi Vehicles is entitled to 100% of the economic benefits, voting rights and residual interests of Kandi New Energy.

In August 2016, Jiangsu JiDian Electric Vehicle Sales Co., Ltd. (“Jiangsu JiDian”) was formed by JiHeKang. Jiangsu JiDian is engaged in the car sales business. Since JiHeKang is 100% owned by the JV Company, the JV Company has a 100% ownership interest in Jiangsu JiDian, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Jiangsu JiDian.

In October 2016, JiHeKang acquired Tianjin BoHaiWan Vehicle Sales Co., Ltd. (“Tianjin BoHaiWan”), which is engaged in the car sales business. Since JiHeKang is 100% owned by the JV Company, the JV Company has a 100% ownership interest in Tianjin BoHaiWan, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Tianjin BoHaiWan.

In November 2016, Changxing Kandi Vehicle Maintenance Co., Ltd. (“Changxing Maintenance”) was formed by Kandi Changxing. Changxing Maintenance is engaged in the car repair and maintenance business. In December 2017, the Service Company entered into an agreement with the JV Company to acquire 100% of Changxing Maintenance for RMB 1,089,887 or approximately $167,501. The transaction was completed in April 2018.

In November 2016, Guangdong JiHeKang Electric Vehicle Sales Co., Ltd. (“Guangdong JiHeKang”) was formed by JiHeKang. Guangdong JiHeKang is engaged in the car sales business. Since JiHeKang is 100% owned by the JV Company, the JV Company has a 100% ownership interest in Guangdong JiHeKang, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Guangdong JiHeKang.

In March 2017, Hangzhou Liuchuang Electric Vehicle Technology Co., Ltd. (“Liuchuang”) was formed by Kandi Jiangsu. Since Kandi Jiangsu is 100% owned by the JV Company, the JV Company has a 100% ownership interest in Liuchuang, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Liuchuang.

In April 2017, in order to promote business development, KandiJinhua, JiHeKang, and the JiHeKang Service Company were reorganized to become subsidiaries of Kandi Jiangsu. As the JV Company has a 100% ownership interest in Kandi Jiangsu, the JV Company has 100% ownership interests in KandiJinhua, JiHeKang, and the JiHeKang Service Company; the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Kandi Jinhua, JiHeKang, and the JiHeKang Service Company.

In December 2017, Zhejiang Chang Dian Technology Co., Ltd. (“Zhejiang Chang Dian”) was formed by the JV Company. Zhejiang Chang Dian is primarily engaged in the battery replacement business. Since Zhejiang Chang Dian is 100% owned by the JV Company, and the Company, indirectly through its 50% ownership interest in the JV Company, has a 50% economic interest in Zhejiang Chang Dian.

In December 2017, Kandi Vehicles and the sole shareholder of Jinhua An Kao Power Technology Co., Ltd. (“Jinhua An Kao”) entered into a Share Transfer Agreement and a Supplementary Agreement, pursuant to which Kandi Vehicles acquired Jinhua An Kao. The two agreements were signed on December 12, 2017 and the closing took place on January 3, 2018. Kandi Vehicles acquired 100% of the equity interests of Jinhua An Kao for a purchase price of approximately RMB 25.93 million (approximately $3.9 million) in cash. In addition, pursuant to the Supplementary Agreement, the Company issued a total of 2,959,837 shares of restrictive stock, or 6.2% of the Company’s total outstanding shares of the common stock to the shareholder of Jinhua An Kao. An additional 2,959,837 shares were placed as make good shares for the undertaking of Jinhua An Kao to achieve no less than a total of RMB 120,000,000 (approximately $18.1 million) net income over the course of the following three years. The Supplementary Agreement set forth the terms and conditions of the issuance of these shares, including that the Company will have the voting rights of the make good shares until conditions for vesting those shares are satisfied.

In March 2018, Jiangsu Gu Xiang New Energy Technology Co., Ltd. (“Jiangsu Gu Xiang”) was formed by Zhejiang Chang Dian. Jiangsu Gu Xiang is primarily engaged in technical research, development, services and consultation of new energy vehicles, battery replacement and maintenance, and other business.

In April 2018, Zhejiang Chang Dian Technology Co., Ltd. Hangzhou Tonglu Branch (“Chang Dian Tonglu”) was formed by Zhejiang Chang Dian. Chang Dian Tonglu is primarily engaged in the battery replacement business.

In April 2018, Zhejiang Chang Dian Technology Co., Ltd. Changxing Branch (“Chang Dian Changxing”) was formed by Zhejiang Chang Dian. Chang Dian Changxing is primarily engaged in the battery replacement business.

On May 31, 2018, the Company entered into a Membership Interests Transfer Agreement (the “Transfer Agreement”) with the two members of Sportsman Country, LLC (“Sportsman Country”) under which the Company acquired 100% of the ownership of Sportsman Country. Sportsman Country is a Dallas based sales company primarily engaged in the wholesale of off-road vehicle products, with a small percentage of business in off-road vehicle parts wholesale and retail. According to the terms of the Transfer Agreement, the Company transferred $10.0 million worth of restricted shares to acquire 100% membership interests in Sportsman Country, of which the Company was required to issue $1.0 million worth of corresponding restricted shares within 30 days from the signing date of the Transfer Agreement, and the remaining $9.0 million worth of corresponding restricted shares to be released from escrow based on Sportsman Country’s pre-tax profit performance over the course of the following three years. The transaction closed in July 2018.In August 2018, Sportsman Country changed its name to SC Autosports LLC (“SC Autosports”).

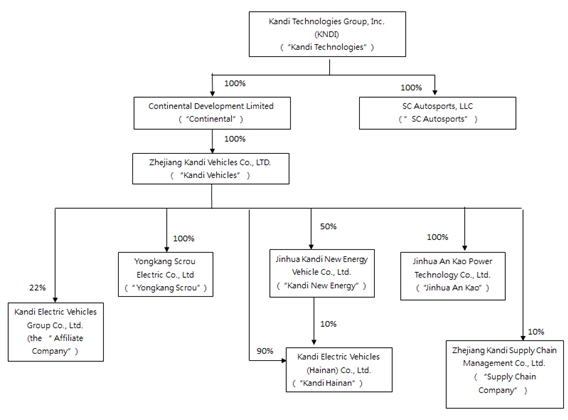

The Company’s organizational chart as of September 30, 2019 is as follows:

On March 21, 2019, Kandi Vehicle signed an Equity Transfer Agreement (the “Transfer Agreement”) with Geely Technologies Group Co., Ltd. (“Geely”) to transfer certain equity interests in the Kandi Electric Vehicles Group Co., Ltd. (the “Affiliate Company”, formerly defined as the “JV Company”) to Geely. Pursuant to the Transfer Agreement, the Affiliate Company converted a loan of RMB 314 million (approximately $46.7 million) from Geely last year to equity in order to increase its cash flow. As a result, the registered capital of the Affiliate Company became RMB 2.40 billion (approximately $336.3 million), of which Kandi Vehicles then owned 43.47% and Geely owned 56.53%, respectively, upon the conversion of the loan into equity in the Affiliate Company. After that, Kandi Vehicles further agreed to sell 21.47% of its equity interests in the Affiliate Company to Geely for a total amount of RMB 516 million (approximately $72.3 million). As of September 29, 2019, Kandi Vehicles has received payments in cash totaling RMB 220 million (approximately $30.9 million) and certain commercial acceptance notes of RMB 296 million (approximately $41.6 million), of which RMB 140 million (approximately $19.7 million) shall mature on January 20, 2020 and the remaining RMB 156 million (approximately $21.9 million) shall mature on March 29, 2020. As a result of the completion of the equity transfer on September 29, 2019, Kandi Vehicles now owns 22% and Geely and its affiliates own 78% of the equity interests of the Affiliate Company. As now the Company only owns 22% of the JV Company, it was redefined as the Affiliate Company.

The Company’s primary business operations areconsist of designing, developing, manufacturing and commercializing EV products (through Kandi Electric Vehicles (Hainan) Co., Ltd. and the Affiliate Company), EV parts and off-road vehicles. As part of its strategic objective of becoming a leading manufacturer of EV products (through the JVAffiliate Company) and related services, the Company has increased its focus on pure EV-related products, and is actively pursuing expansion in the China marketChinese and international markets, especially the U.S. market.

NOTE 2 - LIQUIDITY

The Company had a working capital deficit of $12,186,911$80,374,159 as of September 30, 2018, a decrease2019, an increase of $65,894,813$77,847,248 from a working capital surplus of $53,707,902$2,526,911 as of December 31, 2017.

2018. As of September 30, 2019 and December 31, 2018, the Company’s cash and cash equivalents was $14,338,637 and $ 15,662,201, respectively, the Company’s restricted cash was $11,713,004 and $6,690,870, respectively.

During the first quarter of 2019, the Company had credit lines availablesigned an agreement to sell 21.47% of its equity interests in the Affiliate Company to Geely for a total amount of RMB 516 million (approximately $72.3 million). As of September 29, 2019, the Company has received payments in cash totaling RMB 220 million (approximately $30.9 million) and certain commercial acceptance notes of RMB 296 million (approximately $41.6 million) from commercial banksGeely, of $30,583,267. which RMB 140 million (approximately $19.7 million) shall mature on January 20, 2020 and the remaining RMB 156 million (approximately $21.9 million) shall mature on March 29, 2020. The Company plans to apply the proceeds from the equity transfer to its ongoing operations. The cash flow and operating capacity of the Company will be greatly improved after receiving the above payments.

Although the Company expects that most of its outstanding trade receivables from customers will be collected in the next twelve months, there are uncertainties aboutwith respect to the timing in collecting these receivables, especially the receivables due from the JVAffiliate Company, because most of them are indirectly impacted by the progress of the receipt of government subsidies. Since the amount due from the JV Company accounts for the majority of the Company’s outstanding receivables, and since the Company cannot control the timing of the receipt of government subsidies, the Company believes that its internally-generated cash flows may not be sufficient to support the growth of future operations and to repay short-term bank loans for the next twelve months. However, the Company believes its access to existing financing sources and its good credit will enable it to meet its obligations and fund its ongoing operations for the next twelve months. The Company expects to approximately maintain the current debt level for the next twelve months given the Company’s current financial position and business development needs.

The Company’s primary need for liquidity isstems from its need to fund working capital requirements of the Company’s businesses, its capital expenditures and forits general operational purposes,operations, including debt repayment. The Company has incurred losses and experienced negative operating cash flows for the past two years, and accordingly, the Company has taken a number of actions to continue to support its operations and meet its obligations. The Company has historically financed its operations through short-term commercial bank loans from Chinese banks. The term of these loans is typically for one year, and upon the payment of all outstanding principal and interest on a particular loan, the banks, have typically rolled over the loan for an additional one-year term, with adjustments made to the interest rate to reflect prevailing market rates. This practice has been ongoing and the Company believes that short-term bank loans will remain available on normal trade terms if needed. For the remainder of 2018, the management will take measures to grow the business and further improve the Company’s liquidity. The Company acknowledges that it continues to face a challenging competitive environment and expects to take actions that will enhance the Company’s liquidity and financial flexibility to support the Company’s operation needs.

We finance ouras well as its ongoing operating activities by using funds from our operations, and external credit or financing arrangements. WeThe Company routinely monitormonitors current and expected operational requirements and financial market conditions to evaluate the use of available financing sources. Considering ourthe existing working capital position and ourthe ability to access debt funding sources, we believethe management believes that ourthe Company’s operations and borrowing resources are sufficient to provide for ourits current and foreseeable capital requirements to support ourits ongoing operations for the next twelve months.

NOTE 3 - BASIS OF PRESENTATION

The Company maintains its general ledger and journals using the accrual method of accounting for financial reporting purposes. The Company’saccompanying unaudited condensed consolidated financial statements and notes are the representations of the Company’s management. Accounting policies adopted by the Company conform tohave been prepared in accordance with accounting principles generally accepted accounting principles in the United States of America (“U.S. GAAP”) for interim information, and havewith the instructions to Form 10-Q and Rule 10-01 of Regulation S-X promulgated by the Securities and Exchange Commission (“SEC”). Accordingly, they do not include all of the information and notes required by U.S. GAAP for annual financial statements. In the management’s opinion, the interim financial statements reflect all normal adjustments that are necessary to provide a fair presentation of the financial results for the interim periods presented. Operating results for interim periods are not necessarily indicative of results that may be expected for an entire fiscal year. The condensed consolidated balance sheet as of December 31, 2018 has been consistently applied inderived from the audited consolidated financial statements as of such date. For a more complete understanding of the Company’s presentation ofbusiness, financial position, operating results, cash flows, risk factors and other matters, please refer to its financial statements.Annual Report on Form 10-K for the fiscal year ended December 31, 2018 (the “2018 Form 10-K”).

NOTE 4 - PRINCIPLES OF CONSOLIDATION

The Company’s consolidated financial statements reflect the accounts of the Company and its ownership interests in the following subsidiaries:

| (1) | Continental Development Limited (“Continental”), a wholly-owned subsidiary of the Company incorporated under the laws of Hong Kong; |

| (2) | Kandi Vehicles, a wholly-owned subsidiary of Continental; |

| (3) | Jinhua Kandi New Energy Vehicles Co., Ltd. (“Kandi New Energy”), a 50%-owned subsidiary of Kandi Vehicles (Mr. Hu Xiaoming owns the other 50%). Pursuant to agreements executed in January 2011, Mr. Hu Xiaoming contracted with Kandi Vehicles for the operation and management of Kandi New Energy and put his shares of Kandi New Energy into escrow. As a result, Kandi Vehicles is entitled to 100% of the economic benefits, voting rights and residual interests of Kandi New Energy; |

| (4) | YongkangScrou Electric Co, Ltd. (“YongkangScrou”), a wholly-owned subsidiary of Kandi |

| (5) | Kandi |

| (6) | Jinhua An Kao Power Technology Co., Ltd. (“Jinhua An Kao”), a wholly-owned subsidiary of Kandi |

| (7) | SC Autosports, a wholly-owned subsidiary of the |

Equity Method Investees

The Company’s consolidated net income also includes the Company’s proportionate share of the net income or loss of its equity method investees as follows:

The Affiliate Company, a 22% owned subsidiary of Kandi Vehicles and its subsidiaries

All intra-entity profits and losses with regard to the Company’s equity method investees have been eliminated.

NOTE 5 - USE OF ESTIMATES

The preparation of financial statements in conformity with generally accepted accounting principles in the United States requires the Company’s management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of revenue and expenses during the reporting period. Management makes these estimates using the best information available at the time the estimates are made; however actual results when ultimately realized could differ from those estimates.

NOTE 6 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Company’s operations are conducted in China. As a result, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environments in China, and by the general state of the Chinese economy. In addition, the Company’s earnings are subject to movements in foreign currency exchange rates when transactions are denominated in Renminbi (“RMB”), which is the Company’s functional currency. Accordingly, the Company’s operating results are affected by changes in the exchange rate between the U.S. dollar and the RMB.

The Company’s operationsOur significant accounting policies are detailed in China are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange restrictions. The Company’s performance may be adversely affected by changes in the political and social conditions in China, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods“Note 2 - Summary of taxation, among other things.

ASC 820 establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. The hierarchy prioritizes the inputs into three levels based on the extent to which inputs used in measuring fair value are observable in the market.

These tiers include:

Level 1—defined as observable inputs such as quoted prices in active markets;

Level 2—defined as inputs other than quoted prices in active markets that are either directly or indirectly observable; and

Level 3—defined as unobservable inputs for which little or no market data exists, therefore requiring an entity to develop its own assumptions.

The Company’s financial instruments primarily consist of cash and cash equivalents, restricted cash, accounts receivable, notes receivable, other receivables, accounts payable, other payables and accrued liabilities, short-term bank loans, notes payable, and warrants.

The carrying value of cash and cash equivalents, restricted cash, accounts receivable, notes receivable, other receivables, accounts payable, other payables and accrued liabilities, and notes payable approximate fair value because of the short-term nature of these items. The estimated fair values of short-term bank loans were not materially different from their carrying value as presented due to the brief maturities and because the interest rates on these borrowings approximate those that would have been available for loans of similar remaining maturities and risk profiles. As the carrying amounts are reasonable estimates of fair value, these financial instruments are classified within Level 1 of the fair value hierarchy. The Company identified notes payable as Level 2 instruments due to the fact that the inputs to valuation are primarily based upon readily observable pricing information. The balance of notes payable, which was measured and disclosed at fair value, was $24,663,846 and $28,075,945 at September 30, 2018 and December 31, 2017, respectively.

Contingent consideration related to the acquisitions of Jinhua An Kao and SC Autosports, which is accounted for as liabilities, are measured at each reporting date for their fair value using Level 3 inputs. The fair value of contingent consideration was $12,204,964 and $0 at September 30, 2018 and December 31, 2017, respectively. Also see Note 26.

The Company considers highly-liquid investments purchased with original maturities of three months or less to be cash equivalents.

As of September 30, 2018, and December 31, 2017, the Company’s restricted cash was $9,104,584 and $11,218,688, respectively.

Inventories are stated at the lower of cost or net realizable value (market value). The cost of raw materials is determined on the basis of weighted average. The cost of finished goods is determined on the basis of weighted average and comprises direct materials, direct labor and an appropriate proportion of overhead.

Net realizable value is based on estimated selling prices less selling expenses and any further costs expected to be incurred for completion. Adjustments to reduce the cost of inventory to net realizable value are made, if required, for estimated excess, obsolescence, or impaired balances.

Accounts receivable are recognized and carried at net realizable value. An allowance for doubtful accounts is recorded for periods in which the Company determines a loss is probable, based on its assessment of specific factors, such as troubled collections, historical experience, accounts aging, ongoing business relations and other factors. Accounts are written off after exhaustive collection efforts. If accounts receivable are to be provided for, or written off, they are recognized in the consolidated statement of operations within the operating expenses line item. If accounts receivable previously written off is recovered in a later period or when facts subsequently become available to indicate that the amount provided as an allowance for doubtful accounts was incorrect, an adjustment is made to restate allowance for doubtful accounts.

As of September 30, 2018 and December 31, 2017, credit terms with the Company’s customers were typically 180 to 360 days after delivery. As of September 30, 2018 and December 31, 2017, the Company had a $319,421and $133,930 allowance for doubtful accounts, as per the Company management’s judgment based on their best knowledge. The Company conducts quarterly assessments of the state of the Company’s outstanding receivables and reserves any allowance for doubtful accounts if it becomes necessary.

Notes receivable represent short-term loans to third parties with maximum terms of six months. Interest income is recognized according to each agreement between a borrower and the Company on an accrual basis. For notes receivable with banks, the interest rates are determined by banks. For notes receivable with other parties, the interest rates are based on agreements between the parties. If notes receivable are paid back, that transaction will be recognized in the relevant year. If notes receivable are not paid back, or are written off, that transaction will be recognized in the relevant year if default is probable, reasonably assured, and the loss can be reasonably estimated. The Company will recognize income if the written-off loan is recovered at a future date. In case of any foreclosure proceedings or legal actions, the Company provides an accrual for the related foreclosure and litigation expenses. The Company also receives notes receivable from the JV Company and other parties to settle accounts receivable. If the Company decides to discount notes receivable for the purpose of receiving immediate cash, the current discount rate is approximately in the range of 4.80% to 5.00% annually. As of September 30, 2018 and December 31, 2017, the Company had notes receivable from unrelated parties of $72,817 and $0, respectively, which notes receivable typically mature within six months. As of September 30, 2018 and December 31, 2017, the Company had notes receivable from JV Company and other related parties of $2,184,519 and $1,137,289, respectively, which notes receivable typically mature within six months.

Advances to suppliers represent cash paid in advance to suppliers, and include advances to raw material suppliers, mold manufacturers, and equipment suppliers.

As of September 30, 2018, the Company had made a total advance payments of RMB 756 million (approximately $110 million) to Nanjing Shangtong Auto Technologies Co., Ltd. (“Nanjing Shangtong”) as an advance to purchase a production line and develop a new EV model for Kandi Hainan. Nanjing Shangtong is a total solutions contractor for Kandi Hainan and provides all the equipment and EV product design and research services used by Kandi Hainan. After a portion of such advances were transferred to construction in progress and expensed for R&D purposes, the Company had $3,924,501 left in Advance to Suppliers in current assets related to the purchases from Nanjing Shangtong as of September 30, 2018.

Advances for raw material purchases are typically settled within two months of the Company’s receipt of the raw materials. Prepayment is offset against the purchase price after the equipment or materials are delivered.

Property, plants and equipment are carried at cost less accumulated depreciation. Depreciation is calculated over the asset’s estimated useful life using the straight-line method. Leasehold improvements are amortized over the life of the asset or the term of the lease, whichever is shorter. Estimated useful lives are as follows:

The costs and related accumulated depreciation of assets sold or otherwise retired are eliminated from the Company’s accounts and any gain or loss is included in the statements of income. The cost of maintenance and repairs is charged to expenses as incurred, whereas significant renewals and betterments are capitalized.

Construction in progress (“CIP”) represents the direct costs of construction, and the acquisition costs of buildings or machinery. Capitalization of these costs ceases, and construction in progress is transferred to plants and equipment, when substantially all the activities necessary to prepare the assets for their intended use are completed. No depreciation is provided for until the assets are completed and ready for their intended use. As of September 30, 2018, $2,854,673 of interest expenses previously capitalized for CIP have been reimbursed by the government.

Land in China is owned by the government and land ownership rights cannot be sold to an individual or to a private company. However, the Chinese government grants the user a “land use right” to use the land. The land use rights granted to the Company are amortized using the straight-line method over a term of fifty years.

The Company periodically evaluates the carrying value of long-lived assets to be held and used, including intangible assets subject to amortization, when events and circumstances warrant such a review, pursuant to the guidelines established in Statement of FinancialSignificant Accounting Standards (“SFAS”) No. 144 (now known as “ASC 360”). The carrying value of a long-lived asset is considered impaired when the anticipated undiscounted cash flow from such asset is separately identifiable and is less than its carrying value. In that event, a loss is recognized based on the amount by which the carrying value exceeds the fair market value of the long-lived asset. Fair market value is determined primarily using the anticipated cash flows discounted at a rate commensurate with the risk involved. Losses on long-lived assets to be disposed of are determined in a similar manner, except that fair market values are reduced for disposal costs.

The Company recognized no impairment loss during the reporting period.

The Company adopted ASC Topic 606 Revenue from Contracts with Customers with a date of the initial application of January 1, 2018 using the modified retrospective method. As a result, the Company has changed its accounting policy for revenue recognition. The impact of the adoption of ASC Topic 606 on the Company’s condensed consolidated financial statements is not material.

The Company recognizes revenue when goods or services are transferred to customers in an amount that reflects the consideration which it expects to receive in exchange for those goods or services. In determining when and how revenue is recognized from contracts with customers, the Company performs the following five-step analysis: (i) identification of contract with customer; (ii) determination of performance obligations; (iii) measurement of the transaction price; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue when (or as) the Company satisfies each performance obligation.

The Company generates revenue through the sale of EV products, EV parts and off-road vehicles. The revenue is recognized at a point in time once the Company has determined that the customer has obtained control over the product. Control is typically deemed to have been transferred to the customer when the performance obligation is fulfilled, usually at the time of delivery, at the net sales price (transaction price). Estimates of variable consideration, such as volume discounts and rebates, are determined, reviewed and revised periodically by management. Revenue is recognized net of any taxes collected from customers, which are subsequently remitted to governmental authorities. Shipping and handling costs for product shipments occur prior to the customer obtaining control of the goods are accounted for as fulfillment costs rather than separate performance obligations and recorded as sales and marketing expenses.

The Company’s contracts are predominantly short-term in nature with a contract term of one year or less. For those contracts, the Company has utilized the practical expedient in ASC Topic 606 exempting the Company from disclosure of the transaction price allocated to remaining performance obligations if the performance obligation is part of a contract that has an original expected duration of one year or less.

Receivables are recorded when the Company has an unconditional right to consideration.

See Note 24 “Segment Reporting” for disaggregation of revenue by reporting segments. The Company believes this disaggregation best depicts how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

Expenditures relating to the development of new products and processes, including improvements to existing products, are expensed as incurred. Research and development expenses were $5,691,649 and $657,851for the three months ended September 30, 2018, and September 30, 2017, respectively. Research and development expenses were $7,091,836 and $26,569,624 for the nine months ended September 30, 2018, and September 30, 2017, respectively.

Grants and subsidies received from the Chinese government are recognized when the proceeds are received or collectible and related milestones have been reached and all contingencies have been resolved.

For the three months ended September 30, 2018 and September 30, 2017, $607,008 and $474,950, respectively, were received by the Company’s subsidiaries from the Chinese government. For the nine months ended September 30, 2018 and September 30, 2017, $717,821 and $5,804,561, respectively, were received by the Company’s subsidiaries from the Chinese government.

The Company accounts for income tax using an asset and liability approach, which allows for the recognition of deferred tax benefits in future years. Under the asset and liability approach, deferred taxes are provided for the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. The accounting for deferred tax calculation represents the Company management’s best estimate of the most likely future tax consequences of events that have been recognized in our financial statements or tax returns and related future anticipation. A valuation allowance is provided for deferred tax assets if it is more likely than not these items will either expire before the Company is able to realize their benefits, or that future realization will be uncertain.

The accompanying consolidated financial statements are presented in United States dollars. The functional currencyPolicies” of the Company is the Renminbi (RMB). Capital accounts of the consolidated financial statements are translated into United States dollars from RMB at their historical exchange rates when the capital transactions occurred.

Assets and liabilities are translated at the exchange rates as of balance sheet date. Income and expenditures are translated at the average exchange rate of the reporting period, which rates are obtained from the website: http://www.oanda.com

| September 30, | December 31, | September 30, | ||||||||||

| 2018 | 2017 | 2017 | ||||||||||

| Period end RMB : USD exchange rate | 6.8665 | 6.5067 | 6.6536 | |||||||||

| Average RMB : USD exchange rate | 6.5137 | 6.7568 | 6.807608 | |||||||||

Comprehensive income is defined to include all changes in equity except those resulting from investments by owners and distributions to owners. Among other disclosures, all items that are required to be recognized under current accounting standards as components of comprehensive income are required to be reported in a financial statement that is presented with the same prominence as other financial statements. Comprehensive income includes net income and the foreign currency translation changes.

In accordance with ASC 280-10, Segment Reporting, the Company’s chief operating decision makers rely upon the consolidated results of operations when making decisions about allocating resources and assessing the performance of the Company. As a result of the assessment made by the Company’s chief operating decision makers, the Company has only one operating segment. The Company does not distinguish between markets or segments for the purpose of internal reporting.

The Company’s stock option expenses are recorded in accordance with ASC 718 and ASC 505.

The fair value of stock options is estimated using the Black-Scholes-Merton model. The Company’s expected volatility assumption is based on the historical volatility of the Company’s common stock. The expected life assumption is primarily based on the expiration date of the option. The risk-free interest rate for the expected term of the option is based on the U.S. Treasury yield curve in effect at the time of grant.

The recognition of stock option expenses is based on awards expected to vest. ASC standards require forfeitures to be estimated at the time of grant and revised in subsequent periods, if necessary, if actual forfeitures differ from those estimates.

The stock-based option expenses for the three months ended September 30, 2018 and September 30, 2017, were $0 and $997,496. The stock-based option expenses for the nine months ended September 30, 2018 and September 30, 2017, were $1,586,926 net of a reversal for forfeited stock option of $2,644,877 and $4,126,008, respectively. See Note 19. There were no forfeitures estimated during the reporting period.Form 10-K.

The Company allocates goodwill from business combinations to reporting units based on the expectation that the reporting unit is to benefit from the business combination. The Company evaluates its reporting units on an annual basis and, if necessary, reassigns goodwill using a relative fair value allocation approach. Goodwill is tested for impairment at the reporting unit level on an annual basis and between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying value. These events or circumstances could include a significant change in the business climate, legal factors, operating performance indicators, competition, or sale or disposition of a significant portion of a reporting unit.

Application of the goodwill impairment test requires judgments, including the identification of reporting units, assignment of assets and liabilities to reporting units, assignment of goodwill to reporting units, and the determination of the fair value of each reporting unit. The Company first assesses qualitative factors to determine whether it is more likely than not that goodwill is impaired. If the more likely than not threshold is met, the Company performs a quantitative impairment test.

As of September 30, 2018 and September 30, 2017, the Company determined that its goodwill was not impaired.

Intangible assets consist of patent, trade names and customer relations associated with the purchase price from the allocation of YongkangScrou and Jinhua An Kao. Such assets are being amortized over their estimated useful lives. Intangible assets are amortized as of September 30, 2018. The amortization expenses for intangible assets were $157,817 and $20,524 for the three months ended September 30, 2018 and September 30, 2017, respectively. The amortization expenses for intangible assets were $493,405 and $61,571 for the nine months ended September 30, 2018 and September 30, 2017, respectively.

Gross proceeds are first allocated according to the initial fair value of the freestanding derivative instruments (i.e. the warrants issued to the Company’s investors in its previous offerings, or the “Investor Warrants”). The remaining proceeds are allocated to common stock. The related issuance expenses, including the placement agent cash fees, legal fees, the initial fair value of the warrants issued to the placement agent and others were allocated between the common stock and the Investor Warrants based on how the proceeds are allocated to these instruments. Expenses related to the issuance of common stock were charged to paid-in capital. Expenses related to the issuance of derivative instruments were expensed upon issuance.

In accordance with accounting standards regarding consolidation of variable interest entities, or VIEs, VIEs are generally entities that lack sufficient equity to finance their activities without additional financial support from other parties or whose equity holders lack adequate decision making ability. All VIEs with which the Company is involved must be evaluated to determine the primary beneficiary of the risks and rewards of the VIE. The primary beneficiary is required to consolidate the VIE for financial reporting purposes.

The Company has concluded, based on the contractual arrangements, that Kandi New Energy is a VIE and that the Company’s wholly-owned subsidiary, Kandi Vehicles, absorbs a majority of the risk of loss from the activities of this company, thereby enabling the Company, through Kandi Vehicles, to receive a majority of its respective expected residual returns.

Additionally, because Kandi New Energy is under common control with other entities, the consolidated financial statements have been prepared as if the transactions had occurred retroactively as to the beginning of the reporting period of these consolidated financial statements.