☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended Securities registered pursuant to Section 12(b) of the Act: Indicate by check mark whether the Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes☒ No ☐ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the TABLE OF CONTENTS Class A Ordinary Shares Class B Ordinary Shares Additional Paid-in Accumulated Total The accompanying unaudited condensed consolidated financial statements Status: Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. The Company has elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, the Company, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of the Company’s financial statements with another public company which is neither an emerging growth company nor an emerging growth company which has opted out of using the extended transition period difficult or impossible because of the potential differences in accounting standards used. guidance in Topic 840. The •Liquor licenses:The Company records the fair value of brokered liquor licenses acquired in Business Combinations and Asset Acquisitions using the The Company The “fair market value” of the Class A September 30, Quoted Significant Significant The inputs). The key inputs into the Monte Carlo simulation as of March The following table sets forth a summary of designated, respectively, Class A related capital expenditures. We expect to As Off-Balance Sheet Arrangements As of Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under As required by Rules 13a-15 and 15d-15 under the Exchange Act, our Chief Executive Changes in Internal Control September 30, 2021March 27, 2022☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from toCommission File No. 001-40142ISOS ACQUISITION CORPORATION(Exact name of registrant as specified in its charter)Cayman IslandsDelaware 98-1632024 (State or other jurisdiction of

incorporation or organization) (I.R.S. Employer

Identification No.)55 Post Road West, Suite 200Westport, CT 06880(Address of Principal Executive Offices, including zip code)(203) 554-5641(Registrant’s telephone number, including area code)N/A(Former name, former address and former fiscal year, if changed since last report)Title of each class Trading Symbol(s) Name of each exchange on which registered Units, each consisting of one Class A Ordinary Share and one-third of one Redeemable WarrantISOS.UThe New York Stock ExchangeClass A Ordinary Shares,common stock, par value $0.0001 per share ISOSBOWL The New York Stock Exchange Redeemable Warrants, each whole warrant exercisable for one share of Class A Ordinary Sharecommon stock at an exercise price of $11.50ISOSBOWL WSThe New York Stock Exchange registrantregistrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),; and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”filer” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.☐ ☐ Large accelerated filer☐ Accelerated filer ☒ ☒ Non-accelerated filer☒ ☐Smaller reporting company ☒ ☒ Emerging growth companyAct.Act ☐Exchange Act):. Yes ☒☐ No ☐AsThe registrant had outstanding 111,184,028 shares of November 15, 2021, there were 25,483,700 Class A ordinarycommon stock (the “Class A common stock”), 55,911,203 shares par value $0.0001 per share, and 6,370,925of Class B ordinarycommon stock (“Class B common stock”), and 200,000 shares par value $0.0001 per share, of the registrantSeries A convertible preferred stock (the “Preferred Stock”), and 8,472,398 warrants issued and outstanding.ISOS ACQUISITION CORPORATIONFORM 10-Q FOR THE QUARTER ENDED September 30, 2021March 27,

2022June 27,

2021Assets Current assets: Cash and cash equivalents $ 172,977 $ 187,093 Accounts and notes receivable, net of allowance for doubtful accounts of $327 and $204, respectively 4,409 3,300 Inventories, net 10,056 8,310 Prepaid expenses and other current assets 11,668 8,056 Assets held-for-sale 14,506 686 Total current assets 213,616 207,445 Property and equipment, net 512,343 415,661 Internal use software, net 10,251 9,062 Property and equipment under capital leases, net 260,632 284,077 Intangible assets, net 93,192 96,057 Goodwill 738,787 726,156 Investment in joint venture 1,250 1,230 Other assets 41,491 42,550 Total assets $ 1,871,562 $ 1,782,238 Liabilities, Temporary Equity and Stockholders’ Deficit Current liabilities: Accounts payable $ 29,267 $ 29,489 Accrued expenses 80,113 63,650 Current maturities of long-term debt 4,944 5,058 Other current liabilities 6,876 9,176 Total current liabilities 121,200 107,373 Long-term debt, net 868,370 870,528 Long-term obligations under capital leases 394,708 374,598 Earnout liability 204,416 — Warrant liability 37,952 — Other long-term liabilities 56,991 87,749 Deferred income tax liabilities 14,346 11,867 Total liabilities 1,697,983 1,452,115 Temporary Equity Series A preferred stock - Old Bowlero — 141,162 ISOS ACQUISITION CORPORATIONSeries A preferred stock 200,489 — Redeemable Class A common stock - Old Bowlero — 464,827 Stockholders’ deficit: Class A common stock 11 10 Class B common stock 6 — Additional paid-in capital 296,790 — Treasury stock, at cost (1,026) — Accumulated deficit (319,794) (266,472) Accumulated other comprehensive loss (2,897) (9,404) Total stockholders’ deficit (26,910) (275,866) Total liabilities, temporary equity and stockholders’ deficit $ 1,871,562 $ 1,782,238 CONDENSED BALANCE SHEETS September 30,

2021 December 31,

2020 (unaudited) Assets Cash $ 1,215,849 $ — Prepaid expenses 205,477 — Deferred offering costs — 47,500 Total current assets 1,421,326 47,500 Marketable securities held in Trust Account 254,845,389 — Prepaid expenses, non-current 79,110 — Total Assets $ 256,345,825 $ 47,500 Liabilities and Shareholders’ (Deficit) Equity Current liabilities: Accrued offering costs and expenses $ 220,963 $ 5,000 Due to related party 1,000 — Promissory note - related party — 22,500 Total current liabilities 221,963 27,500 Forward Purchase Agreement liability 4,225,138 — Warrant liability 19,233,202 — Deferred underwriting fees 8,919,295 — Total liabilities 32,599,598 27,500 Commitments and Contingencies (Note 8) Class A ordinary shares subject to possible redemption, 25,483,700 shares and 0 shares at redemption value, at September 30, 2021 and December 31, 2020, respectively 254,844,389 — Shareholders’ (Deficit) Equity: Preference shares, $0.0001 par value; 1,000,000 shares authorized; none issued and outstanding — — Class A ordinary shares, $0.0001 par value; 300,000,000 shares authorized; 0 shares and 0 shares issued and outstanding (excluding 25,483,700 shares and 0 shares subject to possible redemption) at September 30, 2021 and December 31, 2020, respectively — — Class B ordinary shares, $0.0001 par value; 20,000,000 shares authorized; 6,370,925 shares and 6,468,750 shares issued and outstanding at September 30, 2021 and December 31, 2020, respectively 637 647 Additional paid-in capital — 24,353 Accumulated deficit (31,098,799 ) (5,000 ) Total shareholders’ (deficit) equity (31,098,162 ) 20,000 Total Liabilities and Shareholders’ (Deficit) Equity $ 256,345,825 $ 47,500 TheSee accompanying notes are an integral part of theseto unaudited condensed consolidated financial statements.Three Months Ended Nine Months Ended March 27,

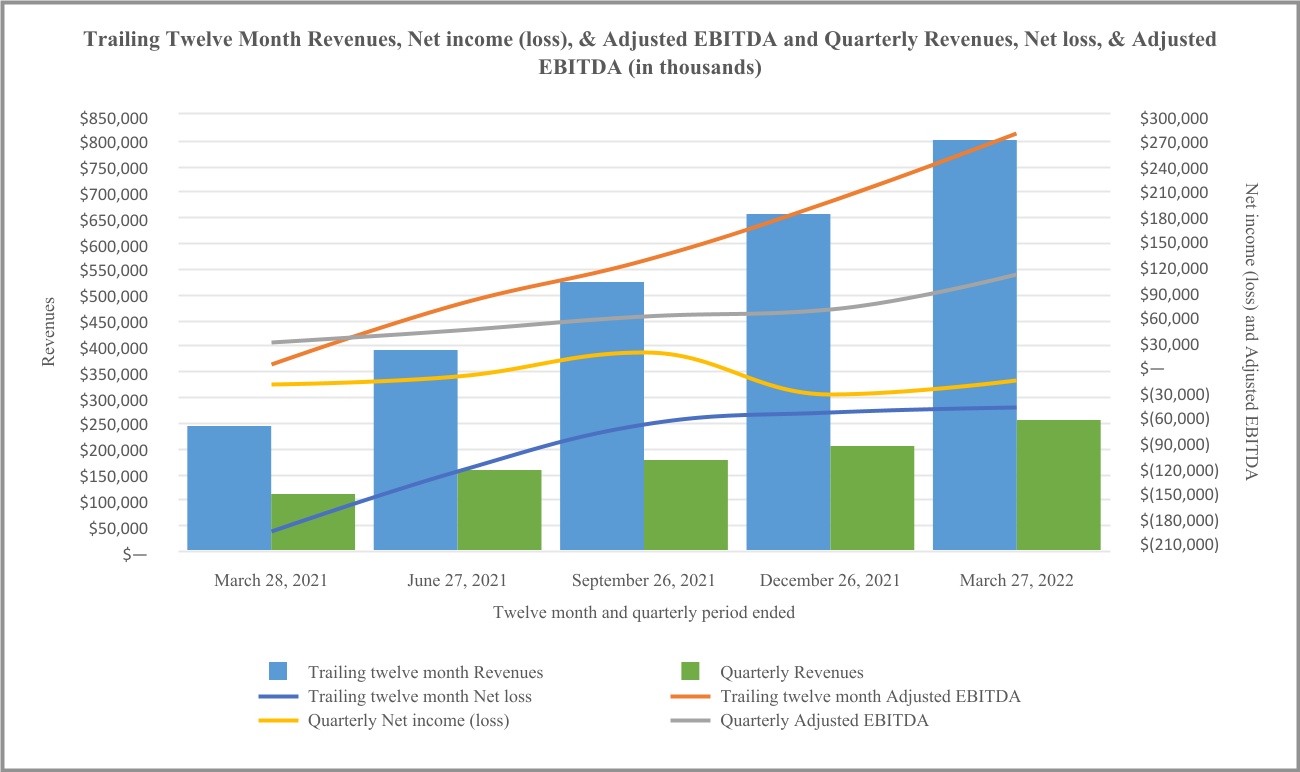

2022March 28,

2021March 27,

2022March 28,

2021Revenues $ 257,820 $ 112,212 $ 643,988 $ 236,131 Costs of revenues 156,491 94,113 424,742 253,654 Gross profit (loss) 101,329 18,099 219,246 (17,523) Operating (income) expenses: Selling, general and administrative expenses 30,315 17,695 145,013 49,217 (Gain) loss on sale or disposal of assets (1,601) 64 (1,755) (77) Income from joint venture (127) (69) (285) (126) Management fee income (307) (25) (564) (132) Other operating expense 2,333 1,119 6,557 721 Business interruption insurance recoveries — — — (20,188) Total operating expense, net 30,613 18,784 148,966 29,415 Operating profit (loss) 70,716 (685) 70,280 (46,938) Other expenses: Interest expense, net 22,293 22,303 69,101 65,729 Change in fair value of earnout shares 45,778 — 23,236 — Change in fair value of warrant liability 20,678 — 20,748 — Other expense 161 — 161 — Total other expense, net 88,910 22,303 113,246 65,729 Loss before income tax (benefit) expense (18,194) (22,988) (42,966) (112,667) Income tax (benefit) expense (207) 103 (6,089) 333 Net loss $ (17,987) $ (23,091) $ (36,877) $ (113,000) Series A preferred stock dividends (2,818) (2,012) (7,290) (5,998) Net loss attributable to common stockholders $ (20,805) $ (25,103) $ (44,167) $ (118,998) Net loss per share attributable to Class A and B common stockholders, basic and diluted $ (0.13) $ (0.17) $ (0.29) $ (0.81) Weighted-average shares used in computing net loss per share attributable to common stockholders, basic and diluted 162,590,921 146,848,329 152,731,385 146,848,329 Three Months Ended Nine Months Ended March 27,

2022March 28,

2021March 27,

2022March 28,

2021Net loss $ (17,987) $ (23,091) $ (36,877) $ (113,000) Other comprehensive income (loss), net of income tax: Unrealized gain (loss) on derivatives 97 (47) 55 (330) Reclassification to earnings 2,205 2,266 6,610 6,798 Foreign currency translation adjustment 214 78 (158) 789 Other comprehensive income 2,516 2,297 6,507 7,257 Total comprehensive loss $ (15,471) $ (20,794) $ (30,370) $ (105,743) Accumulated Total Redeemable Class A Series A Class A Class B Treasury Additional other stockholders’ common stock preferred stock Common stock Common stock Stock paid-in Accumulated comprehensive equity Shares Amount Shares Amount Shares Amount Shares Amount Shares Amount capital deficit loss (deficit) Balance, June 28, 2020 2,069,000 $ 160,601 106,378 $ 133,147 3,842,428 $ 1 — $ — — $ — $ 271,776 $ (102,701) $ (19,012) $ 150,064 Retroactive application of recapitalization 49,328,025 — 2,536,209 — 91,608,875 9 — — — — — (9) — — Adjusted balance, beginning of period 51,397,025 160,601 2,642,587 133,147 95,451,303 10 — — — — 271,776 (102,710) (19,012) 150,064 Net loss — — — — — — — — — — — (40,772) — (40,772) Foreign currency translation adjustment — — — — — — — — — — — — 216 216 Unrealized loss on derivatives — — — — — — — — — — — — (156) (156) Reclassification to earnings — — — — — — — — — — — — 2,266 2,266 Accrued dividends on pre-merger Series A preferred stock — — — 2,026 — — — — — — (2,026) — — (2,026) Stock based compensation — — — — — — — — — — 849 — — 849 Balance, September 27, 2020 51,397,025 160,601 2,642,587 135,173 95,451,303 10 — — — — 270,599 (143,482) (16,686) 110,441 Net loss — — — — — — — — — — — (49,137) — (49,137) Foreign currency translation adjustment — — — — — — — — — — — — 495 495 Unrealized loss on derivatives — — — — — — — — — — — — (127) (127) Reclassification to earnings — — — — — — — — — — — — 2,266 2,266 Accrued dividends on pre-merger Series A preferred stock — — — 1,960 — — — — — — (1,960) — — (1,960) Stock based compensation — — — — — — — — — — 696 — — 696 Balance, December 27, 2020 51,397,025 160,601 2,642,587 137,133 95,451,303 10 — — — — 269,335 (192,619) (14,052) 62,674 Net loss — — — — — — — — — — — (23,091) — (23,091) Foreign currency translation adjustment — — — — — — — — — — — — 78 78 Unrealized loss on derivatives — — — — — — — — — — — — (47) (47) Reclassification to earnings — — — — — — — — — — — — 2,266 2,266 Accrued dividends on pre-merger Series A preferred stock — — — 2,012 — — — — — — (2,012) — — (2,012) Stock based compensation — — — — — — — — 826 — — 826 Balance, March 28, 2021 51,397,025 $ 160,601 2,642,587 $ 139,145 95,451,303 $ 10 — $ — — $ — $ 268,149 $ (215,710) $ (11,755) $ 40,694 Balance, June 27, 2021 (retroactively stated for application of recapitalization) 51,397,025 $ 464,827 2,642,587 $ 141,162 95,451,303 $ 10 — $ — — $ — $ — $ (266,472) $ (9,404) $ (275,866) Net income — — — — — — — — — — — 15,564 — 15,564 Foreign currency translation adjustment — — — — — — — — — — — — (164) (164) Unrealized loss on derivatives — — — — — — — — — — — — (32) (32) Reclassification to earnings — — — — — — — — — — — — 2,202 2,202 Accrued dividends on pre-merger Series A preferred stock — — — 2,251 — — — — — — (2,251) — — (2,251) Change in fair value of redeemable Class A common stock of Old Bowlero — 14,995 — — — — — — — — (14,995) — — (14,995) Stock based compensation — — — — — — — — — — 801 — — 801 Reclass of negative APIC to accumulated deficit — — — — — — — — — — 16,445 (16,445) — — Balance, September 26, 2021 51,397,025 479,822 2,642,587 143,413 95,451,303 10 — — — — — (267,353) (7,398) (274,741) Net loss — — — — — — — — — — — (34,454) — (34,454) Foreign currency translation adjustment — — — — — — — — — — — — (208) (208) Unrealized loss on derivatives — — — — — — — — — — — — (10) (10) Reclassification to earnings — — — — — — — — — — — — 2,203 2,203 Accrued dividends on pre-merger Series A preferred stock — — — 1,885 — — — — — — (1,885) — — (1,885) Change in fair value of redeemable Class A common stock of Old Bowlero — 23,869 — — — — — — — — (23,869) — — (23,869) Merger induced stock based compensation — — — — 2,529,360 — 5,839,993 1 — — 42,555 — — 42,556 Issuance of common stock and preferred stock in connection with Merger Capitalization, net of Bowlero equity issuance costs and fair value of liability-classified warrants and earnout — — 95,000 95,000 42,185,233 4 1,074,185 — — — 120,805 — — 120,809 Settlement of pre-merger Series A preferred stock — — (2,642,587) (145,298) — — — — — — — — — — Conversion of Class A common stock of Old Bowlero to Series A preferred stock — — 105,000 105,000 (10,499,900) (1) — — — — (104,999) — — (105,000) Consideration to existing shareholders of Old Bowlero — — — — (22,599,800) (2) — — — — (225,998) — — (226,000) Consideration paid to Old Bowlero optionholders — — — — — — — — — — (15,467) — — (15,467) Exchange of redeemable Class A common stock of Old Bowlero for Class B common stock (51,397,025) (503,691) — — — — 51,397,025 5 — — 503,686 — — 503,691 Balance, December 26, 2021 — — 200,000 200,000 107,066,196 11 58,311,203 6 — — 294,828 (301,807) (5,413) (12,375) Net loss — — — — — — — — — — — (17,987) — (17,987) Foreign currency translation adjustment — — — — — — — — — — — — 214 214 Unrealized gain on derivatives — — — — — — — — — — — — 97 97 Reclassification to earnings — — — — — — — — — — — — 2,205 2,205 Accrual of paid-in-kind dividends on Series A preferred stock — — — 489 — — — — — — (489) — — (489) Repurchase of Class A common stock into Treasury stock — — — — (109,754) — — — 109,754 (1,026) — — — (1,026) Stock based compensation — — — — 69,086 — — — — — 2,451 — — 2,451 Balance, March 27, 2022 — $ — 200,000 $ 200,489 107,025,528 $ 11 58,311,203 $ 6 109,754 $ (1,026) $ 296,790 $ (319,794) $ (2,897) $ (26,910) Nine Months Ended March 27,

2022March 28,

2021Operating activities Net loss $ (36,877) $ (113,000) Adjustments to reconcile net loss to net cash provided by operating activities: Depreciation and amortization 78,487 67,979 Gain on sale or disposal of assets, net (1,755) (77) Income from joint venture (285) (126) Loss on refinance of debt 953 — Loss on repurchase of warrants 161 — Amortization of deferred financing costs 2,769 2,529 Amortization of deferred rent incentive (281) 1,338 Non-cash interest expense on capital lease obligation 4,514 4,603 Amortization of deferred sale lease-back gain (770) (770) Deferred income taxes (6,587) — Stock based compensation 46,376 2,371 Distributions from joint venture 265 122 Change in fair value of earnout liability 23,236 — Change in fair value of warrant liability 20,748 — Changes in assets and liabilities, net of business acquisitions: Accounts receivable and notes receivable, net 23 2,563 Inventories (1,708) 460 Prepaids, other current assets and other assets (5,723) 594 Accounts payable and accrued expenses 10,777 23,608 Other current liabilities 4,265 5,101 Other long-term liabilities 4,273 19,828 Net cash provided by operating activities 142,861 17,123 Investing activities Purchases of property, equipment, and internal use software (135,548) (26,598) Proceeds from sale of property and equipment 6,160 482 Proceeds from sale of intangibles — 60 Purchases of intangible assets (2,602) — Acquisitions, net of cash acquired (46,754) (2,132) Net cash used in investing activities (178,744) (28,188) Financing activities Repurchase of Series A preferred stock - Old Bowlero (145,298) — Proceeds from issuance of Series A preferred stock 95,000 — Proceeds from issuance of Class A common stock to Isos investors 94,413 — Transaction costs related to Merger recapitalization (20,670) — Proceeds from PIPE Investment 150,604 — Proceeds from Forward Investment 100,000 — Payment to existing shareholders of Old Bowlero (226,000) — Consideration paid to existing option holders of Old Bowlero (15,467) — Repurchase of treasury stock (1,026) — Repurchase of warrants (5,382) — Payment of long-term debt (6,158) (6,158) Payment of First Lien Credit Facility Revolver (39,853) — Proceeds from Incremental Liquidity Facility — 45,000 Payment of Incremental Liquidity Facility (45,000) — Proceeds from New Revolver 86,434 — Payment of deferred financing costs (977) (1,984) Construction allowance receipts 1,132 — Net cash provided by financing activities 21,752 36,858 Effect of exchange rates on cash 15 71 Net (decrease) increase in cash and equivalents (14,116) 25,864 Cash and cash equivalents at beginning of period 187,093 140,705 Cash and cash equivalents at end of period $ 172,977 $ 166,569 Note 1 Note 2 Note 3 Note 4 Note 5 Note 6 Note 7 Note 8 Note 9 Note 10 Note 11 Note 12 Note 13 Note 14 Note 15 Note 16 Note 17 Note 18 Note 19 Note 20 Note 21 ISOS ACQUISITION CORPORATION

CONDENSED STATEMENTS OF OPERATIONS(Unaudited) Three months

ended

September 30,

2021 Nine months

ended

September 30,

2021 General and administrative expenses $ 785,494 $ 1,260,847 Loss from Operations (785,494 ) (1,260,847 ) Other income (expense): Trust interest income 3,848 7,389 Warrant issuance costs - (638,847 ) Unrealized loss on change in fair value of FPA (2,208,594 ) (3,667,048 ) Unrealized loss on change in fair value of warrants (5,266,872 ) (811,507 ) Total other expense (7,471,618 ) (5,110,013 ) Net loss $ (8,257,112 ) $ (6,370,860 ) Basic and diluted weighted average shares outstanding, ordinary share subject to redemption 25,483,700 19,454,853 Basic and diluted net loss per ordinary share $ (0.26 ) $ (0.26 ) Basic and diluted weighted average shares outstanding, ordinary share 6,370,925 6,182,395 Basic and diluted net loss per ordinary share $ (0.25 ) $ (0.25 ) The accompanying notesBowlero Corp., a Delaware corporation, and its subsidiaries (Bowlero Corp. and subsidiaries are an integral partreferred to collectively as “we,” “our,” the “Company,” “Bowlero Corp.” or “Bowlero”) are the world’s largest operator of these unaudited condensed financial statements.ISOS ACQUISITION CORPORATIONCONDENSED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY (DEFICIT)(unaudited)

Shareholders’ Equity Shares Amount Shares Amount Capital Deficit (Deficit) Balance as of December 31, 2020 - $ - 6,468,750 $ 647 $ 24,353 $ (5,000 ) $ 20,000 Sale of 22,500,000 Units through initial public offering 22,500,000 2,250 - - 224,997,750 - 225,000,000 Sale of 2,983,700 Units through over-allotment 2,983,700 298 - - 29,836,702 - 29,837,000 Sale of 5,397,828 Private Placement Warrants to Sponsor in private placement - - - - 8,096,742 - 8,096,742 Underwriting fee - - - - (5,096,742 ) - (5,096,742 ) Deferred underwriting fee - - - - (8,919,295 ) - (8,919,295 ) Offering costs charged to the shareholders’ equity - - - - (479,680 ) - (479,680 ) Initial classification of warrant liability - - - - (18,421,695 ) - (18,421,695 ) Reclassification of offering costs related to warrants - - - - 638,847 - 638,847 Initial classification of FPA liability - - - - (53,954 ) - (53,954 ) Forfeiture of founder shares - - (97,825 ) (10 ) 10 - - Net loss - - - - - (916,888 ) (916,888 ) Change in Class A ordinary shares subject to possible redemption (25,483,700 ) (2,548 ) - - (230,623,038 ) (24,211,414 ) (254,837,000 ) Balance as of March 31, 2021 (restated) - $ - 6,370,925 $ 637 $ - $ (25,133,302 ) $ (25,132,665 ) Net income - - - - - 2,803,140 2,803,140 Change in Class A ordinary shares subject to possible redemption - - - - - (3,541 ) (3,541 ) Balance as of June 30, 2021 (restated) - $ - 6,370,925 $ 637 $ - $ (22,333,703 ) $ (22,333,066 ) Net loss - - - - - (8,257,112 ) (8,257,112 ) Initial classification of FPA liability - - - - (504,136 ) - (504,136 ) Change in Class A ordinary shares subject to possible redemption - - - - 504,136 (507,984 ) (3,848 ) Balance as of September 30, 2021 - $ - 6,370,925 $ 637 $ - $ (31,098,799 ) $ (31,098,162 ) The accompanying notes are an integral part of these unaudited condensed financial statements.ISOS ACQUISITION CORPORATIONCONDENSED STATEMENT OF CASH FLOWS For the

nine months ended

September 30,

2021 (unaudited) Cash flows from Operating Activities: Net loss $ (6,370,860 ) Adjustments to reconcile net loss to net cash used in operating activities: Trust interest income (7,389 ) Unrealized loss on change in fair value of FPA 3,667,048 Unrealized gain on change in fair value of warrants 811,507 Warrant issuance costs 638,847 Changes in current assets and current liabilities: Prepaid assets (284,587 ) Accrued offering cost and expenses 366,230 Due to related party 1,000 Net cash used in operating activities (1,178,204 ) Cash Flows from Investing Activities: Investment held in Trust Account (254,838,000 ) Net cash used in investing activities (254,838,000 ) Cash flows from Financing Activities: Proceeds from Initial Public Offering, net of underwriters’ fees 249,740,258 Proceeds from private placement 8,096,742 Repayment of promissory note to related party (125,267 ) Payments of offering costs (479,680 ) Net cash provided by financing activities 257,232,053 Net change in cash 1,215,849 Cash, beginning of the period - Cash, end of the period $ 1,215,849 Supplemental disclosure of noncash investing and financing activities: Deferred underwriting commissions charged to additional paid in capital $ 8,919,295 Initial value of Class A ordinary shares subject to possible redemption $ 254,837,000 Change in value of Class A ordinary shares subject to possible redemption $ 7,389 Forfeiture of founder shares $ 10 Deferred offering costs paid by Sponsor loan $ 102,767 Initial classification of warrant liability $ 18,421,695 Initial classification of FPA liability $ 558,090 The accompanying notes are an integral part of these unaudited condensed financial statements.ISOS ACQUISITION CORPORATIONNOTES TO CONDENSED FINANCIAL STATEMENTSNote 1 - Organization and Business OperationsOrganization and GeneralIsos Acquisition Corporation (the “Company”) was incorporated as a Cayman Islands exempted company on December 29, 2020. The Company was incorporatedoperates bowling centers under different brand names. The AMF branded centers are traditional bowling centers and the Bowlmor and Bowlero branded centers offer a more upscale entertainment concept with lounge seating, enhanced food and beverage offerings, and more robust customer service for individuals and group events. Additionally, within the purposebrands, there exists a spectrum where some AMF branded centers are more upscale and some Bowlero branded centers are more traditional. All of effectingour centers, regardless of branding, are managed in a merger, share exchange, asset acquisition, share purchase, reorganization or similarfully integrated and consistent basis since all of our centers are in the same business of operating bowling entertainment. The following summarizes the Company’s centers by country and major brand as of March 27, 2022 and June 27, 2021:March 27,

2022June 27,

2021AMF & other 147 136 Bowlmor 2 14 Bowlero 160 133 Total centers in the United States 309 283 Mexico (AMF) 6 6 Canada (AMF and Bowlero) 2 2 Total 317 291 with one or more businesses or entities (the “Business Combination”). On July 1, 2021, pursuant to the Company entered into a business combination agreement (the “BCA”) withdated as of July 1, 2021, by and among the Old Bowlero and Isos Acquisition Corporation (“Isos”). Old Bowlero refers to Bowlero Corp. (“Bowlero”) pursuant to which Bowlero will merge with and into the Company (as described below).The Company’s sponsor is Isos Acquisition Sponsor LLC, a Delaware limited liability company (the “Sponsor”).The Company has selected December 31 as its fiscal year end.As of September 30, 2021, the Company had not commenced any operations. All activity for the period from December 29, 2020 (inception) through September 30, 2021 relatesprior to the Company’s formation andClosing Date.Initial Public Offering (“IPO”) described below, and, since the closing of the IPO, the search for a prospective Business Combination and its negotiationlegal form of the Business Combination Agreement. The Company will not generate any operating revenues until afterpursuant to the completion of its initial Business Combination, at the earliest. The Company will generate non-operating income in the form of interest income on cash and cash equivalents from the proceeds derived from the IPO and will recognize changes in the fair value of warrant liability and FPA as other income (expense).On July 1, 2021, the Company (which shall transfer by way of continuation to and domesticate as a Delaware corporation) entered intoBCA, the Business Combination Agreement withis accounted for as a reverse recapitalization. Under this method of accounting, Isos is treated as the acquired company and Old Bowlero is treated as the world’s largest owneracquirer for accounting and operator of bowling centers as well as ownerfinancial statement reporting purposes.Professional Bowlers Association. Followingfollowing facts and circumstances:Company willpredecessor and legal successor to the Company. The historical operations of Old Bowlero are deemed to be renamed “Bowlero”those of the Company. Thus, the financial statements included in this report reflect (i) the historical operating results of Old Bowlero prior to the Business Combination, (ii) the combined results of the Old Bowlero and itsIsos following the Business Combination on December 15, 2021, (iii) the assets and liabilities of Old Bowlero at their historical cost and (iv) the Company’s post-merger equity structure for all periods presented. The recapitalization of the number of shares of common stock and warrants are expectedpreferred stock attributable to remainthe purchase of Bowlero Corp. in connection with the Business Combination is reflected retroactively to the earliest period presented and is utilized for calculating earnings per share in all prior periods presented. No step-up basis of intangible assets or goodwill was recorded in the Business Combination transaction consistent with the treatment of the transaction as a reverse recapitalization of Isos.new ticker symbol “BOWL”BOWL and “BOWL WS”,warrants to purchase the Class A common stock are listed on the NYSE under the symbol BOWL.WS in lieu of the Isos ordinary shares and Isos’s warrants, respectively. TheIsos’ units automatically separated into the Isos ordinary shares and Isos’ warrants and ceased trading separately on the NYSE following the Closing Date. Prior to the Business Combination, is structuredIsos neither engaged in any operations nor generated any revenue. Until the Business Combination, based on Isos’ business activities, it was a shell company as a mergerdefined under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).Bowlero,corresponding capital amounts and losses per share, prior to the reverse recapitalization, have been retroactively restated based on shares reflecting the exchange ratio of 24.841 established in the BCA.Bowlero merging withaccounting principles generally accepted in the United States ("GAAP") and intoapplicable rules and regulations of the Company,SEC regarding interim financial reporting. Certain information and note disclosures normally included in annual financial statements have been condensed or omitted pursuant to such rules and regulations. Therefore, these interim condensed consolidated financial statements should be read in conjunction with the Company surviving, following the Company domesticatingaudited consolidated financial statements and related notes of Bowlero Corp. as a Delaware corporation. Bowlero’s stockholders will receive, as consideration for the Business Combination, a mix of cash, shares of the Company’s common stockJune 27, 2021 and shares of the Company’s preferred stock.FinancingThe registration statement for the Company’s IPO was declared effective on March 2, 2021 (the “Effective Date”). On March 5, 2021, the Company consummated the IPO of 22,500,000 units (the “Units” and, with respect to the ordinary sharesJune 28, 2020 included in the Units being offered, the “Public Shares”), at $10.00 per Unit, generating gross proceeds of $225,000,000, which is discussed in Note 4, and incurred $4,500,000 in cash underwriting fees and $7,875,000 in deferred underwriting fees.Simultaneously with the closing of the IPO, the Company consummated the sale of 5,000,000 warrants (the “Private Placement Warrants”) at a price of $1.50 per Private Placement Warrant in a private placement to the Sponsor and LionTree Partners LLC, generating gross proceeds of $7,500,000, which is discussed in Note 5.The Company granted the underwriters in the IPO a 45-day option to purchase up to 3,375,000 additional Units to cover over-allotments, if any. On March 10, 2021, the underwriters partially exercised the over-allotment option to purchase 2,983,700 Units (the “Over-allotment Units”), generating an aggregate of gross proceeds of $29,837,000, and incurred $596,742 in cash underwriting fees and $1,044,295 in deferred underwriting fees.Transaction costs amounted to $14,495,717 consisting of $5,096,742 of underwriting fees, $8,919,295 of deferred underwriting fees, and $479,680 of other offering costs.Trust AccountFollowing the closing of the IPO on March 5, 2021 and the underwriters’ partial exercise of their over-allotment option on March 10, 2021, $254,837,000 ($10.00 per Unit) from the net proceeds of the sale of the Units in the IPO and the sale of the Private Placement Warrants and $1,000 overfunded by the Sponsor was placed in a Trust Account, which can only be invested in United States “government securities” within the meaning of Section 2(a)(16) of the Investment Company Act having a maturity of 185 days or less or in money market funds meeting certain conditions under Rule 2a-7 promulgated under the Investment Company Act which invest only in direct U.S. government treasury obligations. $1,000 was overfunded by the Sponsor. The Trust Account is intended as a holding place for funds pending the earliest to occur of either: (i) the completion of the initial Business Combination; (ii) the redemption of any public shares properly tendered in connection with a shareholder vote to amend the Company’s amended and restated memorandum and articles of association (A) to modify the substance or timing of the Company’s obligation to provide holders of the Class A ordinary shares the right to have their shares redeemed in connection with the initial Business Combination or to redeem 100% of the public shares if the Company does not complete the initial Business Combination within 24 months from the closing of the IPO (the “Combination Period”) or (B) with respect to any other provision relating to the rights of holders of the Class A ordinary shares or pre-initial Business Combination activity, and (iii) the redemption of the public shares if the Company has not consummated an initial Business Combination within the Combination Period, subject to applicable law. Initial Business CombinationThe Company must complete one or more initial Business Combinations having an aggregate fair market value of at least 80% of the value of the assets held in the Trust Account (excluding the deferred underwriting commissions and taxes payable on the interest earned on the Trust Account) at the time of the agreement to enter into the initial Business Combination. However, the Company will only complete a Business Combination if the post-transaction company owns or acquires 50% or more of the issued and outstanding voting securities of the target or otherwise acquires a controlling interest in the target sufficient for it not to be required to register as an investment company under the Investment Company Act 1940, as amended (the “Investment Company Act”). There is no assurance that the Company will be able to complete a Business Combination successfully.The Class A ordinary shares subject to redemption were recorded at a redemption value and classified as temporary equity upon the completion of the IPO, in accordance with Financial Accounting Standards Board’s (“FASB”) Accounting Standards Codification (“ASC”) Topic 480 “Distinguishing Liabilities from Equity.” In such case, the Company will proceed with a Business Combination if the Company seeks shareholder approval, a majority of the issued and outstanding shares voted are voted in favor of the Business Combination.If the Company is unable to complete the initial Business Combination within the Combination Period, the Company will (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible, but not more than ten business days thereafter, redeem the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company to pay income taxes, if any (less up to $100,000 of interest to pay dissolution expenses), divided by the number of then-outstanding public shares, which redemption will completely extinguish public shareholders’ rights as shareholders (including the right to receive further liquidating distributions, if any), and (3) as promptly as reasonably possible following such redemption, subject to the approval of the remaining shareholders and board of directors, liquidate and dissolve, subject in each case to the Company’s obligations under Cayman Islands law to provide for claims of creditors and the requirements of other applicable law.The Sponsor and the Company’s founding team have entered into a letter agreement with the Company,final prospectus filed pursuant to which they have agreed to waive their redemption rights with respect to their founder shares (as described in Note 6) and any public shares purchased during or after the IPO in connection with (i) the completion of the initial Business Combination and (ii) a shareholder vote to approve an amendment to the amended and restated memorandum and articles of association (A) that would modify the substance or timing of the Company’s obligation to provide holders of the Class A ordinary shares the right to have their shares redeemed in connection with the initial Business Combination or to redeem 100% of the Company’s public shares if the Company does not complete the initial Business Combination within the Combination Period or (B) with respect to any other provision relating to the rights of holders of the Class A ordinary shares or pre-initial Business Combination activity. Additionally, the Sponsor has agreed to waive its rights to liquidating distributions from the Trust Account with respect to its founder shares if the Company fails to complete the initial Business Combination within the Combination Period (although they will be entitled to liquidating distributions from the Trust Account with respect to any public shares they hold if the Company fails to complete the initial Business Combination within the Combination Period). If the Company submits the initial Business Combination to the public shareholders for a vote, the Sponsor and each member of the founding team have agreed to vote their founder shares and any public shares purchased during or after the IPO in favor of the initial Business Combination.The Sponsor has agreed that it will be liable to the Company if and to the extent any claims by a third party (excluding the Company’s independent registered public accounting firm) for services rendered or products sold to the Company, or a prospective partner business with which the Company has discussed entering into a transaction agreement, reduce the amounts in the Trust Account to below the lessor of (i) $10.00 per public share and (ii) the actual amount per share held in the Trust Account as of the date of the liquidation of the Trust Account if less than $10.00 per public share due to reductions in the value of the trust assets, in each case net of the interest that may be withdrawn to pay the Company’s tax obligations, provided that such liability will not apply to any claims by a third party or prospective partner business who executed a waiver of any and all rights to seek access to the Trust Account nor will it apply to any claims under the Company’s indemnity of the underwriters of the IPO against certain liabilities, including liabilitiesRule 424(b)(2) under the Securities Act of 1933, as amended (the “Securities Act”"Securities Act"). Moreover, in, with the event that an executed waiver is deemed to be unenforceable against a third party, the Sponsor will not be responsible to the extent of any liability for such third-party claims. SEC, on February 1, 2022.Company has not asked the Sponsor to reserve for such indemnification obligations, or has the Company independently verified whether the Sponsor has sufficient funds to satisfy its indemnity obligations and the Company believes that the Sponsor’s only assets are securities of the Company. The Sponsor may not be able to satisfy those obligations.Liquidity and Capital ResourcesAs of September 30, 2021, the Company had approximately $1.2 million in its operating bank account and working capital of approximately $1.2 million.Prior to the completion of the IPO, the Company’s liquidity needs had been satisfied through a capital contribution from the Sponsor of $25,000, to cover certain offering costs, for the purchase of founder shares (see Note 6), and a loan under an unsecured promissory note from the Sponsor of $125,267 (see Note 6). The promissory note from the Sponsor was paid in full on March 15, 2021. Subsequent to the consummation of the IPO and Private Placement, the Company’s liquidity needsunaudited interim condensed consolidated financial statements have been satisfied through the proceeds from the consummation of the Private Placement not held in the Trust Account.In addition, in order to finance transaction costs in connection with a Business Combination, the Company’s Sponsor or an affiliate of the Sponsor, or certain of the Company’s officers and directors may, but are not obligated to, provide the Company Working Capital Loans (see Note 6). To date, there were no amounts outstanding under any Working Capital Loans.Basedprepared on the foregoing, management believes thatsame basis as the Company will have sufficient working capital and borrowing capacity to meet its needs through the earlier of the consummation of a Business Combination or one year from this filing. Over this time period, the Company will be using these funds for paying existing accounts payable, paying for travel expenditures, and consummating the Business Combination with Bowlero.Risks and UncertaintiesManagement continues to evaluate the impact of the COVID-19 pandemic and has concluded that while it is reasonably possible that the virus could have a negative effect on the Company’s financial position, results of its operations, cash flows and/or consummation of Bowlero transaction, the specific impact is not readily determinable as of the date of the condensed financial statements. The condensedaudited consolidated financial statements, do notand in management’s opinion, include any adjustments that might result from the outcome of this uncertainty.Note 2 — Restatement of Previously Issued Financial StatementsIn connection with the preparation of the Company’s financial statements as of September 30, 2021, management determined it should restate its previously reported financial statements. The Company previously determined the Class A ordinary shares subject to possible redemption to be equal to the redemption value of $10.00 per Class A ordinary share while also taking into consideration the requirement of the Company’s memorandum and articles of association that a redemption cannot result in net tangible assets being less than $5,000,001. Upon review of its financial statements for the period ended September 30, 2021, the Company reevaluated the classification of the Class A ordinary shares and determined that the Class A ordinary shares issued during the IPO and pursuant to the exercise of the underwriters’ over-allotment can be redeemed or become redeemable subject to the occurrence of future events considered outside the Company’s control under ASC 480-10-S99. Therefore, management concluded that the carrying value should include all Class A ordinary shares subject to possible redemption, resulting in the Class A ordinary shares subject to possible redemption being classified as temporary equity in its entirety. As a result, management has recorded a reclassification adjustment related to temporary equity and permanent equity. This resulted in an adjustment to the initial carrying value of the Class A ordinary shares subject to possible redemption with the offset recorded to additional paid-in capital (to the extent available), accumulated deficit and Class A ordinary shares.In connection with the change in presentation for the Class A ordinary shares subject to redemption, the Company also restated its earnings per share calculation to allocate net income (loss) pro rata to Class A and Class B ordinary shares. This presentation contemplates a Business Combination as the most likely outcome, in which case, both classes of ordinary shares share pro rata in the income (loss) of the Company.Other than a change in amounts classified in temporary and permanent equity and adjustments to earnings per share, there has been no other changes in the Company’s total assets, liabilities or operating results as a result of this reclassification.The impact of the restatement on the Company’s financial statements is reflected in the following table. As Previously

Reported Adjustments As Restated Balance Sheet at March 5, 2021 (audited) Class A ordinary shares subject to possible redemption $ 198,014,150 $ 26,985,850 $ 225,000,000 Class A ordinary shares 270 (270 ) - Additional paid-in capital 5,591,050 (5,591,050 ) - Accumulated deficit $ (591,962 ) $ (21,394,530 ) $ (21,986,492 ) Balance Sheet at March 31, 2021 Class A ordinary shares subject to possible redemption $ 224,704,330 $ 30,132,670 $ 254,837,000 Class A ordinary shares 301 (301 ) - Additional paid-in capital 5,920,955 (5,920,955 ) - Accumulated deficit $ (921,888 ) $ (24,211,414 ) $ (25,133,302 ) Statement of Operations for the three months March 31, 2021 Basic and diluted weighted average shares outstanding, ordinary shares subject to redemption 5,720,409 1,475,788 7,196,197 Basic and diluted net income (loss) per share $ 0.00 $ (0.07 ) $ (0.07 ) Basic and diluted weighted average shares outstanding, ordinary shares 7,846,713 (2,047,664 ) 5,799,049 Basic and diluted net loss per share $ (0.12 ) $ 0.05 $ (0.07 ) Statement of Cash Flows for the three months March 31, 2021 Initial value of Class A ordinary shares subject to possible redemption $ 198,014,150 $ 56,822,850 $ 254,837,000 Change in value of Class A ordinary shares subject to possible redemption $ 26,690,180 $ (26,690,180 ) $ - Balance Sheet at June 30, 2021 Class A ordinary shares subject to possible redemption $ 227,507,470 $ 27,333,071 $ 254,840,541 Class A ordinary shares 273 (273 ) - Additional paid-in capital 3,117,843 (3,117,843 ) - Accumulated deficit $ 1,881,252 $ (24,214,955 ) $ (22,333,703 ) Statement of Operations for the three months ended June 30, 2021 Basic and diluted weighted average shares outstanding, ordinary shares subject to redemption 22,470,433 3,013,267 25,483,700 Basic and diluted net income per share $ 0.00 $ 0.09 $ 0.09 Basic and diluted weighted average shares outstanding, ordinary shares 9,384,192 (3,013,267 ) 6,370,925 Basic and diluted net income per share $ 0.30 $ (0.21 ) $ 0.09 Statement of Operations for the six months ended June 30, 2021 Basic and diluted weighted average shares outstanding, ordinary shares subject to redemption 14,141,692 2,248,774 16,390,466 Basic and diluted net income per share $ 0.00 $ 0.08 $ 0.08 Basic and diluted weighted average shares outstanding, ordinary shares 8,619,700 (2,533,133 ) 6,086,567 Basic and diluted net income per share $ 0.22 $ (0.14 ) $ 0.08 Statement of Cash Flows for the six months ended June 30, 2021 Initial value of Class A ordinary shares subject to possible redemption $ 224,704,330 $ 30,132,670 $ 254,837,000 Change in value of Class A ordinary shares subject to possible redemption $ 2,803,140 $ (2,799,599 ) $ 3,541 Note 3 - Significant Accounting PoliciesBasis of PresentationThe accompanying unaudited condensed financial statements are presented in U.S. dollars in conformity with accounting principles generally accepted in the United States of America (“GAAP”) for financial information and pursuant to the rules and regulations of the SEC. Accordingly, they do not include all of the information and footnotes required by GAAP. In the opinion of management, the unaudited condensed financial statements reflect all adjustments, which includeconsist of only normal recurring adjustments necessary for the fair statement of the balancesCompany’s condensed consolidated balance sheet as of March 27, 2022 and resultsthe related condensed statements of operations, comprehensive income (loss), temporary equity and stockholders' equity (deficit), and cash flows for the periods presented. Operatingthree and nine months ended March 27, 2022 and March 28, 2021. The results for the three and nine months ended September 30, 2021March 27, 2022 are not necessarily indicative of the results that may be expected through December 31, 2021.should be readinclude the accounts and operations of the Company. All intercompany accounts and transactions have been eliminated.conjunction withNote 7 - Property and Equipment to conform to current period presentation. Please refer to Note 8 – Internal Use Software for more information.statementsstatements. During the nine months ended March 27, 2022, there were no significant revisions to the Company’s significant accounting policies, other than those indicated herein.notes thereto includedimpacting production and sales across a wide range of industries. The full economic impact of this pandemic has not been determined, including the impact on the Company’s employees, suppliers, customers and credit markets. Due to the evolving and uncertain nature of COVID-19 pandemic, it is reasonably possible that it could materially impact the Company’s estimates, particularly those that require consideration of forecasted financial information, in the Form 8-Knear to medium term. The ultimate impact will depend on numerous evolving factors that the Company may not be able to accurately predict, including the duration and extent of the pandemic, the impact of federal, state, local and foreign governmental actions, and consumer behavior in response to the pandemic and other economic and operational conditions.final prospectus filedCompany’s statutory tax rate in the jurisdiction in which it will receive a deduction.SECexpected term of the option.March 12, 2021common stock. Since the Company has reported net losses for all periods presented, all potentially dilutive securities have been excluded from the calculation of the diluted net loss per share attributable to common stockholders as their effect is antidilutive and March 4, 2021, respectively.Status“JOBS Act”"JOBS Act"), and it may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act and reduced disclosure obligations regarding executive compensation in its periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved.Usepreparationmain objectives are to increase transparency and comparability among organizations by recognizing right-of-use assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. The right-of-use asset reflects the lessee’s right to direct the use of these unaudited condensed financial statements in conformity with US GAAP requires managementand obtain substantially all the economic benefits from that asset over the lease term, and it will be based on the lease liability subject to certain adjustments such as accrued rent, lease incentives, lease intangibles, initial direct costs and prepaid rent. The lease liability reflects the obligation to make payments for the right to use that asset. Operating leases will retain a straight-line lease expense, and finance leases will retain their front-loaded expense pattern, similar to current capital leases.and assumptions that affectthis standard will result in a material impact to our balance sheet from the reported amountsrecognition of right of use assets and liabilities, but not to our statement of operations or cash flows.Three Months Ended Nine Months Ended March 27,

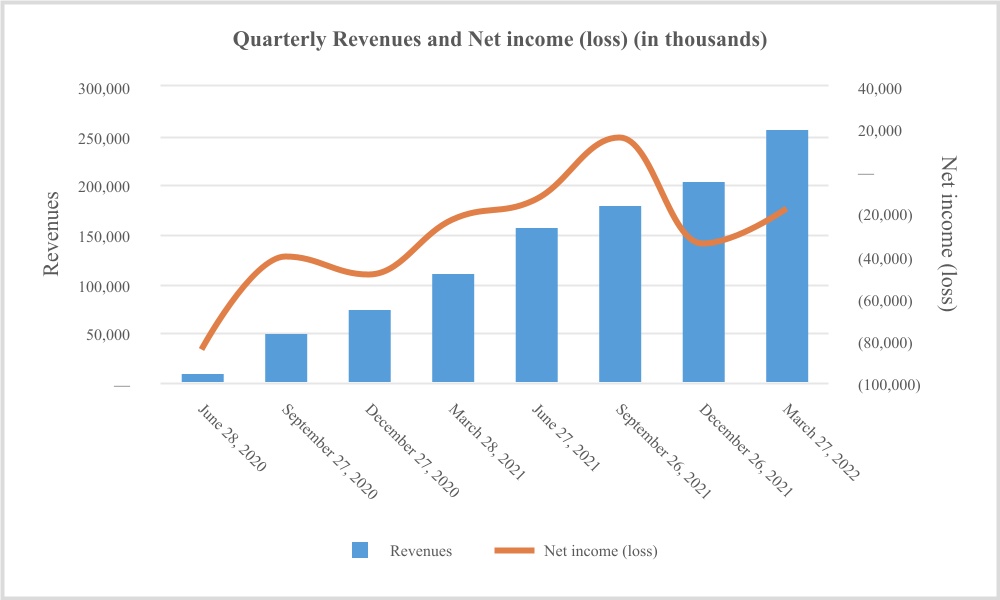

2022% March 28,

2021% March 27,

2022% March 28,

2021% Major revenue categories: Bowling $ 130,394 51 % $ 56,826 51 % $ 326,536 51 % $ 124,351 53 % Food and beverage 88,187 34 % 36,866 33 % 221,206 34 % 75,653 32 % Amusement 33,781 13 % 14,146 13 % 83,967 13 % 25,699 11 % Media 5,458 2 % 4,374 4 % 12,279 2 % 10,428 4 % Total revenues $ 257,820 100 % $ 112,212 100 % $ 643,988 100 % $ 236,131 100 % disclosurerecognized when earned.contingent assetsfood and liabilitiesbeverages at our bowling centers are recognized at a point-in-time.sheet. Actual results could differsheets as of March 27, 2022 and June 27, 2021, respectively.Three Months Ended Nine Months Ended March 27,

2022March 28,

2021March 27,

2022March 28,

2021Operating Leases Rent expense $ 8,041 $ 13,969 $ 39,979 $ 42,669 Capital Leases Interest expense 9,255 8,722 28,080 26,050 Amortization expense 3,003 3,049 9,313 9,300 Total Capital Lease Cost $ 12,258 $ 11,771 $ 37,393 $ 35,350 Operating

LeasesCapital

Leases Remainder of 2022 $ 16,003 $ 11,159 2023 46,450 40,879 2024 45,559 41,954 2025 47,031 42,146 2026 45,090 37,353 Thereafter 566,291 1,030,886 Total Rental Payments: $ 766,424 $ 1,204,377 Less imputed interest expense for capital leases: 809,526 Present value: $ 394,851 Recapitalization Cash-Isos Acquisition Corporation Trust $ 254,851 Less: Isos transaction costs paid from Trust (23,869) Less: Redemptions of existing shareholders of Isos (136,569) Net proceeds from SPAC shareholders 94,413 Cash-PIPE 150,604 Cash-PIPE preferred 95,000 Cash-Forward 100,000 Total Cash received 440,017 Less: Bowlero transaction costs (20,670) Total Cash received, net of Bowlero transaction costs 419,347 Earnout liability (181,113) Warrant liability (22,426) New equity, net 215,808 Less: Consideration payment to Bowlero shareholders (226,000) Less: Payoff of preferred stock and accumulated dividends (145,298) Less: Payments for stock options (15,467) Net distributions to existing shareholders (386,765) Net contribution from Business Combination and preferred financing $ (170,957) those estimates. Significantcertain current and former employees and the conversion of common shares to preferred shares, there were 165,378,145 shares of the Common Stock issued and outstanding as of the Closing Date, of which 107,066,302 shares were Class A common stock and 58,311,203 shares were Class B common stock. There were 17,225,692 warrants outstanding as of the Closing Date.estimatesintangibles, and property and equipment.forwardacquired assets and assumed liabilities. The Company obtains this information during due diligence and through other sources. The following table summarizes the purchase agreement liability andprice allocation for the warrant liability (see Note 7)Marketable securities held in Trust AccountAt September 30, 2021, the assets held in the Trust Account were substantially held in mutual funds comprised of U.S. Treasury Bills, classified as trading securities. Trading securities are presented on the balance sheet at fair value at the end of each reporting period. Gains and losses resulting from the change in fair value of these securities are included in Trust interest income in the statement of operations. The estimated fair values of investments heldthe identifiable assets acquired, components of consideration transferred and the transactional related expenses.Identifiable assets acquired and liabilities assumed Business Combination Totals Current assets $ 2,510 Property and equipment 29,027 Identifiable intangible assets 3,080 Goodwill 12,763 Total assets acquired $ 47,380 Current liabilities (415) Total assumed liabilities (415) Total consideration transferred, net of cash acquired of $25 $ 46,965 Components of consideration transferred Cash $ 44,027 Holdback 1,468 Contingent consideration 1,470 Total $ 46,965 Transaction expenses included in “other operating expense” in the condensed consolidated statement of operations for the nine months ended March 27, 2022 $ 759 Trust Account are determined using available market information.Fair Value MeasurementsFair value is defined asapplicable accounting standards. The cost accumulation model requires us to measure all the price that would be received for sale of an asset or paid for transfer of a liability, in an orderly transaction between market participantsacquired assets and assumed liabilities at the measurement date. GAAP establishes a three-tiertheir fair value hierarchy, which prioritizesand then adjust them based on the inputs used in measuring fair value.total consideration transferred. The hierarchy givesfollowing table summarizes the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). These tiers include:●Level 1, defined as observable inputs such as quoted prices (unadjusted) for identical instruments in active markets;●Level 2, defined as inputs other than quoted prices in active markets that are either directly or indirectly observable such as quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in markets that are not active; and●Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions, such as valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable.In some circumstances, the inputs used to measure fair value might be categorized within different levelsallocation of the fair value hierarchy. In those instances,amounts under a cost accumulation approach:Identifiable assets acquired and liabilities assumed Bowl

AmericaOther Asset Acquisition Total Current assets $ 2,949 $ 5 $ 2,954 Property and equipment 40,121 8,564 48,685 Identifiable intangible assets 1,099 1,136 2,235 Assets held for sale 10,985 — 10,985 Current liabilities (1,426) (81) (1,507) Deferred tax liability (9,107) — (9,107) Total consideration transferred $ 44,621 $ 9,624 $ 54,245 is categorizeddue to the use of unobservable inputs. Significant assumptions used in its entiretythe calculation include: revenue projections, a royalty rate based on qualitative factors and the market-derived royalty rates, discount rate based on the Company’s weighted average cost of capital ("WACC") adjusted for risks commonly inherent in trade names.hierarchycalculations for non-competition agreements include: potential competitor impact on revenue and expense projections, discount rate based on the lowest level input that is significant toCompany’s WACC adjusted for risks commonly inherent in intangible assets, specifically non-compete agreements.measurement.Company’s certain assets and liabilities, which qualify as financial instruments under ASC 820, “Fair Value Measurements and Disclosures,” approximates the carrying amounts representedmarket approach. Significant assumptions used in the balance sheet. The fair values of cash and cash equivalents, prepaid expenses, due to related party are estimated to approximate the carrying values as of September 30, 2021 due to the short maturities of such instruments.The Company’s Private Placement Warrants liability and forward purchase agreements (FPA) liability arecalculation include approximation based on a valuation model utilizing management judgmentrecent sales of liquor licenses in the respective jurisdictions and pricing inputs from observableassignment of an indefinite useful life as licenses do not expire and unobservable markets with less volume and transaction frequency than active markets. Significant deviations from these estimates and inputs could resultcan be sold to third parties.a material change in fair value.the event of certain decisions being made. The fairrange of contingent consideration is $0 - $1,470. We recorded the amount based on:warrant liability and FPA liability isnon-cash consideration.3. See Note 7 for additional information3 on assets and liabilities measured atthe fair value.Concentration of Credit RiskFinancial instruments that potentially subjectDeferred Tax Liability – Since the Bowl America acquisition was a non-taxable stock acquisition, the Company to concentrations of credit risk consist of a cash account in a financial institution, which, at times, may exceedrecorded deferred tax liabilities for the Federal Depository Insurance Coverage of $250,000. At September 30, 2021difference between the tax carryover basis and December 31, 2020, the Company has not experienced losses on this account and management believes the Company is not exposed to significant risks on such account.Ordinary Shares Subject to Possible RedemptionAllbook value of the 25,483,700 Class A ordinary shares sold as part of the Units in the IPO contain a redemption featureopening balances, which allows for the redemption of such public shares in connection with the Company’s liquidation or if there is a shareholder vote or tender offer in connection with the Business Combinationwere recorded and in connection with certain amendmentsallocated based on fair values to the Company’s amendedrespective assets acquired.restated memorandum and articles of association. In accordance with SEC and its staff’s guidance on redeemable equity instruments, which has been codified in ASC 480-10-S99, redemption provisions not solely within the control of the Company require ordinary shares subject to redemption to be classified outside of permanent equity. Therefore, all Class A ordinary shares have been classified outside of permanent equity.Company recognizes changes in redemption value immediately as they occur and adjusts the carrying value of redeemable ordinary shares to equal the redemption value at the end of each reporting period. Increases or decreases in the carrying amount of redeemable ordinary shares are affected by charges against additional paid in capital togoodwill for the extent available and accumulated deficit.Balance as of June 27, 2021 $ 726,156 Goodwill resulting from acquisitions 12,631 Balance as of March 27, 2022 $ 738,787

Intangible Assets:March 27, 2022 June 27, 2021 Weighted average life

(in years)Gross carrying amount Accumulated amortization Net carrying amount Weighted average life

(in years)Gross carrying amount Accumulated amortization Net carrying amount Finite-lived intangible assets: AMF trade name 2 $ 9,900 $ (8,415) $ 1,485 1 $ 9,900 $ (7,920) $ 1,980 Bowlmor trade name 0 6,500 (6,500) — 6 6,500 (2,600) 3,900 Other acquisition trade names 5 1,610 (507) 1,103 7 1,010 (173) 837 Customer relationships 2 20,652 (13,017) 7,635 3 18,370 (10,471) 7,899 Management contracts 2 1,800 (1,366) 434 2 1,800 (1,150) 650 Non-compete agreements 4 1,921 (769) 1,152 4 1,200 (514) 686 PBA member, sponsor & media relationships 8 1,400 (456) 944 8 1,400 (322) 1,078 Other intangible assets 4 921 (217) 704 — — — $ 44,704 $ (31,247) $ 13,457 $ 40,180 $ (23,150) $ 17,030 Indefinite-lived intangible assets: Liquor licenses 9,735 — 9,735 9,027 — 9,027 PBA trade name 3,100 — 3,100 3,100 — 3,100 Bowlero trade name 66,900 — 66,900 66,900 — 66,900 79,735 — 79,735 79,027 — 79,027 $ 124,439 $ (31,247) $ 93,192 $ 119,207 $ (23,150) $ 96,057 Net Loss Per Ordinary Sharehas two classesreviewed the estimated useful life of shares, which are referred toits Bowlmor tradename as Class A ordinary shares and Class B ordinary shares. Earnings and losses are shared pro rata between the two classespart of shares. The 13,892,395 ordinary shares issuable upon exercise of outstanding warrants to purchase the Company’s shares were excludedplans to rebrand its Bowlmor centers to Bowlero centers. Based on that review, the Company determined that the intangible asset associated with the Company’s Bowlmor tradename has a useful life shorter than initially estimated. During the fiscal quarter ended December 26, 2021, the Company adjusted the remaining useful life of the Bowlmor tradename from diluted earnings per share5.75 years to 6 months. The change in useful life was made as a prospective adjustment and resulted in an increase in amortization expense of $1,706 and $3,412 for the three and nine months ended September 30,March 27, 2022, respectively.becauseproperty and equipment consists of:March 27,

2022June 27,

2021Land $ 71,723 $ 19,879 Buildings and improvements 53,974 16,155 Leasehold improvements 342,524 313,441 Equipment, furniture, and fixtures 359,782 315,719 Construction in progress 15,707 27,028 $ 843,710 $ 692,222 Accumulated depreciation (331,367) (276,561) Property and equipment, net of accumulated depreciation $ 512,343 $ 415,661 warrants are contingently exercisable,three and nine months ended March 27, 2022, and March 28, 2021, respectively:Three Months Ended Nine Months Ended March 27,

2022March 28,

2021March 27,

2022March 28,

2021Depreciation expense $ 20,578 $ 17,036 $ 55,525 $ 50,408 Capitalized internal use software Balance at June 27, 2021 Additions Balance at March 27, 2022 Internal use software, gross $ 20,420 $ 3,534 $ 23,954 Accumulated amortization (11,358) (2,345) (13,703) Internal use software, net $ 9,062 $ 1,189 $ 10,251 Three Months Ended Nine Months Ended March 27,

2022March 28,

2021March 27,

2022March 28,

2021Amortization expense $ 1,016 $ 625 $ 2,345 $ 1,712 March 27,

2022June 27,

2021Customer deposits $ 24,258 $ 7,114 Compensation 12,347 13,577 Taxes and licenses 10,465 9,646 Insurance 6,238 8,285 Deferred revenue 4,814 5,885 Deferred rent 3,950 4,384 Utilities 3,844 3,399 Interest 3,839 4,693 Professional fees 1,752 4,473 Other 8,606 2,194 Total accrued expenses $ 80,113 $ 63,650 March 27,

2022June 27,

2021First Lien Credit Facility Revolver $ — $ 39,853 First Lien Credit Facility Term Loan (Maturing July 3, 2024 and bearing variable rate interest; 4.50%nd 4.55% at March 27, 2022 and June 27, 2021, respectively, excluding impact of hedging) 794,376 800,534 Incremental Liquidity Facility — 45,000 New Revolver (Maturing April 4, 2024) 86,434 — $ 880,810 $ 885,387 Less: Unamortized financing costs (7,496) (9,800) Current portion of unamortized financing costs 3,267 3,152 Current maturities of long-term debt (8,211) (8,211) Total long-term debt $ 868,370 $ 870,528 contingencies have not yet been met. Aslenders.result, diluted net loss per ordinary share$140,000 senior secured revolving credit facility (“New Revolver”), which has a maturity date of the earlier of December 15, 2026 or the date that is 90 days prior to the same as basic net loss per ordinary sharescheduled maturity date of any term loans outstanding under the First Lien Credit Agreement in an aggregate principal amount exceeding $175,000. Since the term loan under the First Lien Credit Agreement matures on July 3, 2024, the maturity date for the periods presented. The table below presentsNew Revolver is currently April 4, 2024. Interest on borrowings under the New Revolver is initially based on either the Adjusted Term Secured Overnight Financing Rate (“SOFR”) or the Alternate Base Rate, as further described in the First Lien Credit Agreement.reconciliationSeventh Amendment (“Seventh Amendment”) to the First Lien Credit Agreement pursuant to which the total revolving commitments under the New Revolver were increased by $25,000 to an aggregate amount of $165,000. No changes, other than increasing the aggregate principal amount of revolving commitments thereunder, were made to the terms of the numerator and denominator used to compute basic and diluted net loss per share for each class of ordinary shares: For the Three Months Ended

September 30, 2021 For the Nine Months Ended