UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended December 31, 20222023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________________ to __________________________

Commission File Number 001-31921

Compass Minerals International, Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 36-3972986 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer

Identification Number) |

9900 West 109th Street

Suite 100

Overland Park, KS 66210

(913) 344-9200

(Address of principal executive offices, zip code and telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common stock, $0.01 par value | | CMP | | The New York Stock Exchange |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such |

| reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes | ☑ | No | ☐ |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that |

| the registrant was required to submit such files). | Yes | ☑ | No | ☐ |

| | | | | | | | | | | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer | ☑ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | | | | | Emerging growth company | ☐ |

| | | | | | | | | | | | | | |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ |

| | | | |

| | | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | ☐ | No | ☑ |

The number of shares outstanding of the registrant’s common stock, $0.01 par value per share, as of February 3, 2023,2, 2024, was 41,098,58541,311,296 shares.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

TABLE OF CONTENTS

| | | | | | | | |

| PART I. FINANCIAL INFORMATION | Page |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II. OTHER INFORMATION | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

CONSOLIDATED BALANCE SHEETS

(in millions, except share data)

| | (Unaudited) | |

| | | (Unaudited) | |

| | | December 31,

2022 | | September 30,

2022 | December 31,

2023 | | September 30,

2023 |

| ASSETS | ASSETS | ASSETS |

| Current assets: | Current assets: | |

| Cash and cash equivalents | Cash and cash equivalents | $ | 146.1 | | | $ | 46.1 | |

| Receivables, less allowance for doubtful accounts of $3.8 at December 31, 2022 and $3.4 at September 30, 2022 | 202.2 | | | 167.2 | |

| Cash and cash equivalents | |

| Cash and cash equivalents | |

| Receivables, less allowance for doubtful accounts of $2.6 at December 31, 2023 and $2.3 at September 30, 2023 | |

| Inventories | Inventories | 301.0 | | | 304.4 | |

| | Other | |

| Other | |

| Other | Other | 35.4 | | | 44.3 | |

| Total current assets | Total current assets | 684.7 | | | 562.0 | |

| Property, plant and equipment, net | Property, plant and equipment, net | 774.8 | | | 776.6 | |

| Intangible assets, net | Intangible assets, net | 45.3 | | | 45.4 | |

| Goodwill | Goodwill | 56.8 | | | 56.4 | |

| Equity method investments | 45.7 | | | 46.6 | |

| | Other | |

| Other | |

| Other | Other | 157.4 | | | 156.5 | |

| Total assets | Total assets | $ | 1,764.7 | | | $ | 1,643.5 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| Current liabilities: | Current liabilities: | |

| Current portion of long-term debt | |

| Current portion of long-term debt | |

| Current portion of long-term debt | Current portion of long-term debt | $ | — | | | $ | — | |

| Accounts payable | Accounts payable | 113.4 | | | 114.7 | |

| Accrued salaries and wages | Accrued salaries and wages | 15.4 | | | 22.2 | |

| Income taxes payable | Income taxes payable | 6.6 | | | 1.0 | |

| Accrued interest | Accrued interest | 8.5 | | | 14.1 | |

| | Accrued expenses and other current liabilities | Accrued expenses and other current liabilities | 74.8 | | | 81.1 | |

| Accrued expenses and other current liabilities | |

| Accrued expenses and other current liabilities | |

| Total current liabilities | Total current liabilities | 218.7 | | | 233.1 | |

| Long-term debt, net of current portion | Long-term debt, net of current portion | 832.1 | | | 947.6 | |

| Deferred income taxes, net | Deferred income taxes, net | 59.2 | | | 63.4 | |

| Other noncurrent liabilities | Other noncurrent liabilities | 144.9 | | | 143.0 | |

Commitments and contingencies (Note 10) | |

Commitments and contingencies (Note 9) | | Commitments and contingencies (Note 9) | | | |

| Stockholders’ equity: | Stockholders’ equity: | |

| Common stock: $0.01 par value, 200,000,000 authorized shares; 42,197,964 issued shares at December 31, 2022 and 35,367,264 issued shares at September 30, 2022 | 0.4 | | | 0.4 | |

| Common stock: $0.01 par value, 200,000,000 authorized shares; 42,197,964 issued shares at December 31, 2023 and September 30, 2023 | |

| Common stock: $0.01 par value, 200,000,000 authorized shares; 42,197,964 issued shares at December 31, 2023 and September 30, 2023 | |

| Common stock: $0.01 par value, 200,000,000 authorized shares; 42,197,964 issued shares at December 31, 2023 and September 30, 2023 | |

| Additional paid-in capital | Additional paid-in capital | 403.4 | | | 152.1 | |

| Treasury stock, at cost — 1,174,077 shares at December 31, 2022 and 1,196,300 shares at September 30, 2022 | (7.6) | | | (7.3) | |

| Treasury stock, at cost — 976,106 shares at December 31, 2023 and 1,038,168 shares at September 30, 2023 | |

| Retained earnings | Retained earnings | 219.9 | | | 226.5 | |

| Accumulated other comprehensive loss | Accumulated other comprehensive loss | (106.3) | | | (115.3) | |

| Total stockholders’ equity | Total stockholders’ equity | 509.8 | | | 256.4 | |

| Total liabilities and stockholders’ equity | Total liabilities and stockholders’ equity | $ | 1,764.7 | | | $ | 1,643.5 | |

The accompanying notes are an integral part of the consolidated financial statements.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, in millions, except share and per share data)

| | | |

| | |

| | |

| | | | Three Months Ended

December 31, | |

| | | 2022 | | 2021 | |

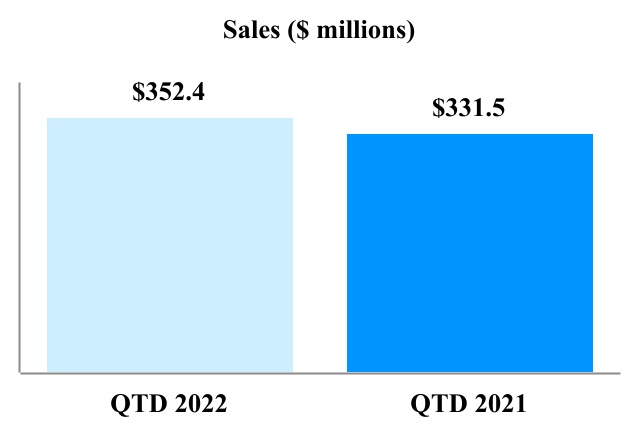

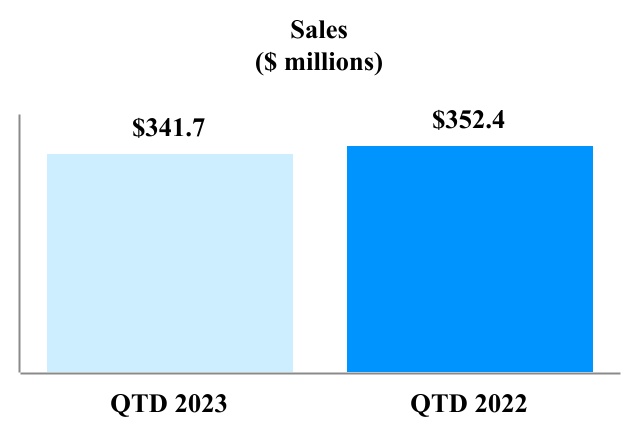

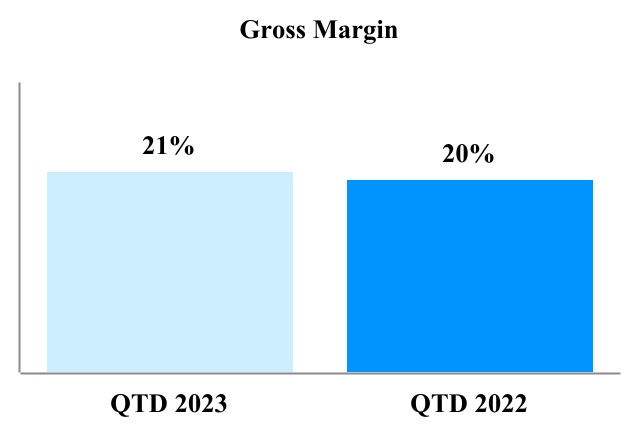

| Sales | Sales | $ | 352.4 | | | $ | 331.5 | | |

| Sales | |

| Sales | |

| Shipping and handling cost | |

| Shipping and handling cost | |

| Shipping and handling cost | Shipping and handling cost | 107.4 | | | 95.7 | | |

| Product cost | Product cost | 175.0 | | | 175.9 | | |

| Product cost | |

| Product cost | |

| Gross profit | |

| Gross profit | |

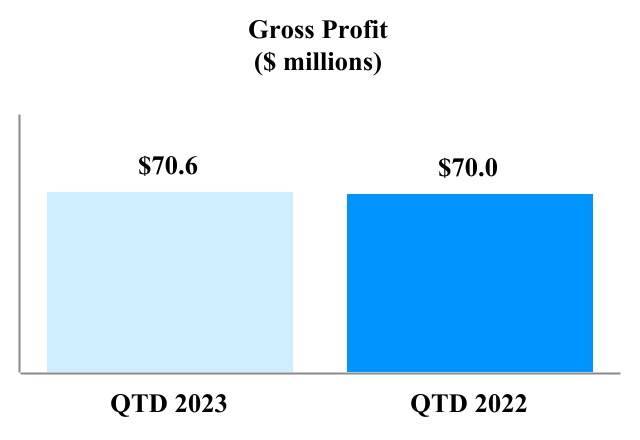

| Gross profit | Gross profit | 70.0 | | | 59.9 | | |

| Selling, general and administrative expenses | Selling, general and administrative expenses | 42.1 | | | 39.5 | | |

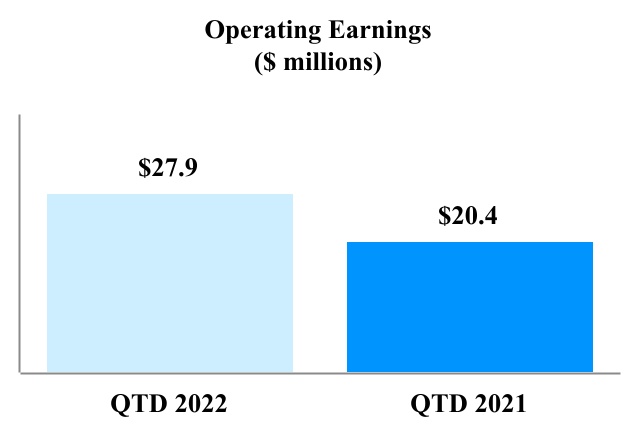

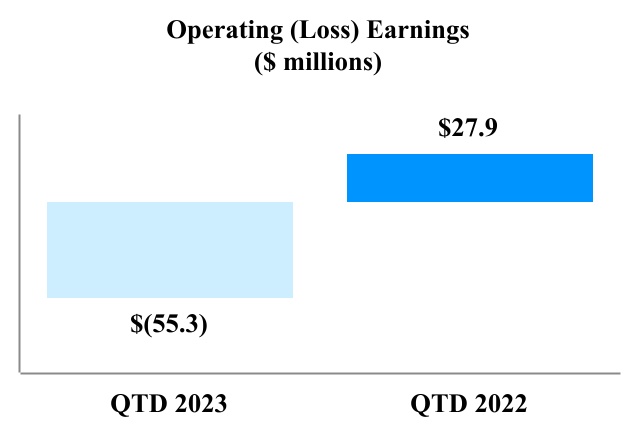

| Operating earnings | 27.9 | | | 20.4 | | |

| Selling, general and administrative expenses | |

| Selling, general and administrative expenses | |

| Loss on impairment of long-lived assets, net | |

| Loss on impairment of long-lived assets, net | |

| Loss on impairment of long-lived assets, net | |

| Other operating expense | |

| Other operating expense | |

| Other operating expense | |

| Operating (loss) earnings | |

| Operating (loss) earnings | |

| Operating (loss) earnings | |

| | Other (income) expense: | |

| | Other (income) expense: | |

| | Other (income) expense: | Other (income) expense: | | |

| Interest income | Interest income | (1.1) | | | (0.3) | | |

| Interest income | |

| Interest income | |

| Interest expense | Interest expense | 13.9 | | | 13.9 | | |

| Loss (gain) on foreign exchange | 2.5 | | | (0.4) | | |

| Interest expense | |

| Interest expense | |

| Loss on foreign exchange | |

| Loss on foreign exchange | |

| Loss on foreign exchange | |

| Net loss in equity investee | Net loss in equity investee | 0.9 | | | 0.4 | | |

| Net loss in equity investee | |

| Net loss in equity investee | |

| | Other expense, net | Other expense, net | 0.1 | | | 0.1 | | |

| Earnings from continuing operations before income taxes | 11.6 | | | 6.7 | | |

| Income tax expense (benefit) from continuing operations | 11.9 | | | (1.2) | | |

| Net (loss) earnings from continuing operations | (0.3) | | | 7.9 | | |

| Net loss from discontinued operations | — | | | (5.5) | | |

| Net (loss) earnings | $ | (0.3) | | | $ | 2.4 | | |

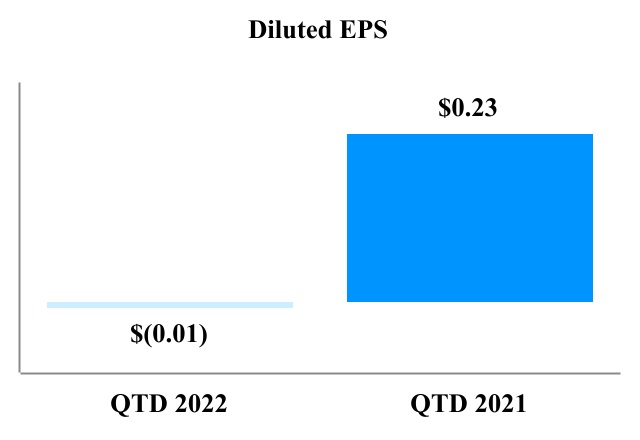

| | Basic net (loss) earnings from continuing operations per common share | $ | (0.01) | | | $ | 0.23 | | |

| Basic net loss from discontinued operations per common share | — | | | (0.16) | | |

| Basic net (loss) earnings per common share | $ | (0.01) | | | $ | 0.07 | | |

| Other expense, net | |

| | Diluted net (loss) earnings from continuing operations per common share | $ | (0.01) | | | $ | 0.23 | | |

| Diluted net loss from discontinued operations per common share | — | | | (0.16) | | |

| Diluted net (loss) earnings per common share | $ | (0.01) | | | $ | 0.07 | | |

| Other expense, net | |

| (Loss) earnings before income taxes | |

| (Loss) earnings before income taxes | |

| (Loss) earnings before income taxes | |

| Income tax expense | |

| Income tax expense | |

| Income tax expense | |

| Net loss | |

| Net loss | |

| Net loss | |

| | Basic net loss per common share | |

| | Basic net loss per common share | |

| | Basic net loss per common share | |

| | Diluted net loss per common share | |

| | Diluted net loss per common share | |

| | Diluted net loss per common share | |

| | Weighted-average common shares outstanding (in thousands): | |

| | Weighted-average common shares outstanding (in thousands): | |

| | Weighted-average common shares outstanding (in thousands): | Weighted-average common shares outstanding (in thousands): | | |

| Basic | Basic | 39,751 | | | 34,060 | | |

| Basic | |

| Basic | |

| Diluted | Diluted | 39,751 | | | 34,089 | | |

| Diluted | |

| Diluted | |

The accompanying notes are an integral part of the consolidated financial statements.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME (LOSS)

(Unaudited, in millions)

| | | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | | |

| | 2022 | | 2021 | | | | |

| Net (loss) earnings | $ | (0.3) | | | $ | 2.4 | | | | | |

| Other comprehensive income (loss): | | | | | | | |

| Unrealized gain from change in pension obligations, net of tax of $0.0 for the three months ended December 31, 2022 and 2021 | 0.1 | | | 0.1 | | | | | |

| Unrealized loss on cash flow hedges, net of tax of $0.4 and $0.7 for the three months ended December 31, 2022 and 2021, respectively | (2.8) | | | (2.0) | | | | | |

| Cumulative translation adjustment | 11.7 | | | (3.8) | | | | | |

| Comprehensive income (loss) | $ | 8.7 | | | $ | (3.3) | | | | | |

| | | | | | | | | | | | | | | |

| | Three Months Ended

December 31, | | |

| | 2023 | | 2022 | | | | |

| Net loss | $ | (75.1) | | | $ | (0.3) | | | | | |

| Other comprehensive income (loss): | | | | | | | |

| Unrealized gain from change in pension obligations, net of tax of $(0.1) and $0.0 for the three months ended December 31, 2023 and 2022, respectively | 0.2 | | | 0.1 | | | | | |

| Unrealized loss on cash flow hedges, net of tax of $0.0 and $0.4 for the three months ended December 31, 2023 and 2022, respectively | (1.8) | | | (2.8) | | | | | |

| Cumulative translation adjustment | 14.6 | | | 11.7 | | | | | |

| Comprehensive (loss) income | $ | (62.1) | | | $ | 8.7 | | | | | |

The accompanying notes are an integral part of the consolidated financial statements.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

For the three months ended December 31, 20222023 and 20212022

(Unaudited, in millions)

| | | | Common

Stock | | Additional

Paid-In

Capital | | Treasury

Stock | | Retained

Earnings | | Accumulated

Other

Comprehensive

(Loss) Income | | Total | | Common

Stock | | Additional

Paid-In

Capital | | Treasury

Stock | | Retained

Earnings | | Accumulated

Other

Comprehensive

Loss | | Total |

| Balance, September 30, 2022 | $ | 0.4 | | | $ | 152.1 | | | $ | (7.3) | | | $ | 226.5 | | | $ | (115.3) | | | $ | 256.4 | |

| Balance, September 30, 2023 | |

| Comprehensive (loss) income | Comprehensive (loss) income | — | | | — | | | — | | | (0.3) | | | 9.0 | | | 8.7 | |

| Dividends on common stock ($0.15 per share) | Dividends on common stock ($0.15 per share) | — | | | — | | | — | | | (6.3) | | | — | | | (6.3) | |

| Private placement of common stock | — | | | 240.7 | | | — | | | — | | | — | | | 240.7 | |

| Shares issued for stock units, net of shares withheld for taxes | Shares issued for stock units, net of shares withheld for taxes | — | | | — | | | (0.3) | | | — | | | — | | | (0.3) | |

| | Stock-based compensation | Stock-based compensation | — | | | 10.6 | | | — | | | — | | | — | | | 10.6 | |

| Balance, December 31, 2022 | $ | 0.4 | | | $ | 403.4 | | | $ | (7.6) | | | $ | 219.9 | | | $ | (106.3) | | | $ | 509.8 | |

| Stock-based compensation | |

| Stock-based compensation | |

| Balance, December 31, 2023 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | Additional

Paid-In

Capital | | Treasury

Stock | | Retained

Earnings | | Accumulated

Other

Comprehensive

Loss | | Total |

| Balance, September 30, 2021 | $ | 0.4 | | | $ | 136.3 | | | $ | (5.5) | | | $ | 272.4 | | | $ | (110.5) | | | $ | 293.1 | |

| Comprehensive income (loss) | — | | | — | | | — | | | 2.4 | | | (5.7) | | | (3.3) | |

| Dividends on common stock ($0.15 per share) | — | | | (0.1) | | | — | | | (5.2) | | | — | | | (5.3) | |

| | | | | | | | | | | |

| Stock options exercised, net of shares withheld for taxes | — | | | 0.2 | | | — | | | — | | | — | | | 0.2 | |

| Stock-based compensation | — | | | 3.3 | | | — | | | — | | | — | | | 3.3 | |

| Balance, December 31, 2021 | $ | 0.4 | | | $ | 139.7 | | | $ | (5.5) | | | $ | 269.6 | | | $ | (116.2) | | | $ | 288.0 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | Additional

Paid-In

Capital | | Treasury

Stock | | Retained

Earnings | | Accumulated

Other

Comprehensive

Loss | | Total |

| Balance, September 30, 2022 | $ | 0.4 | | | $ | 152.1 | | | $ | (7.3) | | | $ | 226.5 | | | $ | (115.3) | | | $ | 256.4 | |

| Comprehensive (loss) income | — | | | — | | | — | | | (0.3) | | | 9.0 | | | 8.7 | |

| Dividends on common stock ($0.15 per share) | — | | | — | | | — | | | (6.3) | | | — | | | (6.3) | |

| Private placement of common stock | — | | | 240.7 | | | — | | | — | | | — | | | 240.7 | |

| Shares issued for stock units, net of shares withheld for taxes | — | | | — | | | (0.3) | | | — | | | — | | | (0.3) | |

| Stock-based compensation | — | | | 10.6 | | | — | | | — | | | — | | | 10.6 | |

| Balance, December 31, 2022 | $ | 0.4 | | | $ | 403.4 | | | $ | (7.6) | | | $ | 219.9 | | | $ | (106.3) | | | $ | 509.8 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

The accompanying notes are an integral part of the consolidated financial statements.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in millions)

| | | | Three Months Ended

December 31, | | Three Months Ended

December 31, |

| | | 2022 | | 2021 | | 2023 | | 2022 |

| Cash flows from operating activities: | Cash flows from operating activities: | |

| Net (loss) earnings | $ | (0.3) | | | $ | 2.4 | |

| Adjustments to reconcile net (loss) earnings to net cash flows provided by operating activities: | |

| Net loss | |

| Net loss | |

| Net loss | |

| Adjustments to reconcile net loss to net cash flows provided by operating activities: | |

| Depreciation, depletion and amortization | |

| Depreciation, depletion and amortization | |

| Depreciation, depletion and amortization | Depreciation, depletion and amortization | 23.9 | | | 28.3 | |

| Amortization of deferred financing costs | Amortization of deferred financing costs | 0.7 | | | 0.7 | |

| | Stock-based compensation | Stock-based compensation | 10.6 | | | 3.3 | |

| Stock-based compensation | |

| Stock-based compensation | |

| Deferred income taxes | Deferred income taxes | (5.4) | | | (1.4) | |

| Unrealized foreign exchange loss | Unrealized foreign exchange loss | 2.0 | | | 2.2 | |

| Loss on impairment of long-lived assets | — | | | 8.4 | |

| Loss on impairment of long-lived assets, net | |

| Net loss in equity investees | Net loss in equity investees | 0.9 | | | 0.4 | |

| | Other, net | Other, net | 1.0 | | | 0.1 | |

| Other, net | |

| Other, net | |

| Changes in operating assets and liabilities: | Changes in operating assets and liabilities: | |

| Receivables | |

| Receivables | |

| Receivables | Receivables | (34.0) | | | (68.8) | |

| Inventories | Inventories | 5.1 | | | 12.6 | |

| Other assets | Other assets | 10.4 | | | (1.2) | |

| Accounts payable and accrued expenses and other current liabilities | Accounts payable and accrued expenses and other current liabilities | (13.1) | | | 2.7 | |

| Other liabilities | Other liabilities | 0.3 | | | (4.0) | |

| Net cash provided by (used in) operating activities | 2.1 | | | (14.3) | |

| Net cash (used in) provided by operating activities | |

| Cash flows from investing activities: | Cash flows from investing activities: | |

| Capital expenditures | Capital expenditures | (19.9) | | | (14.5) | |

| Capital expenditures | |

| Capital expenditures | |

| | Investments in equity method investees | — | | | (28.2) | |

| | Other, net | |

| | Other, net | |

| | Other, net | Other, net | (0.2) | | | 1.5 | |

| Net cash used in investing activities | Net cash used in investing activities | (20.1) | | | (41.2) | |

| Cash flows from financing activities: | Cash flows from financing activities: | |

| Proceeds from revolving credit facility borrowings | |

| Proceeds from revolving credit facility borrowings | |

| Proceeds from revolving credit facility borrowings | Proceeds from revolving credit facility borrowings | 16.7 | | | 162.4 | |

| Principal payments on revolving credit facility borrowings | Principal payments on revolving credit facility borrowings | (168.2) | | | (122.8) | |

| Proceeds from issuance of long-term debt | Proceeds from issuance of long-term debt | 35.4 | | | 32.5 | |

| Principal payments on long-term debt | Principal payments on long-term debt | — | | | (3.3) | |

| Net proceeds from private placement of common stock | Net proceeds from private placement of common stock | 240.7 | | | — | |

| Dividends paid | Dividends paid | (6.3) | | | (5.3) | |

| | Proceeds from stock options exercised | — | | | 0.2 | |

| | Shares withheld to satisfy employee tax obligations | |

| | Shares withheld to satisfy employee tax obligations | |

| | Shares withheld to satisfy employee tax obligations | Shares withheld to satisfy employee tax obligations | (0.3) | | | — | |

| Other, net | Other, net | (0.3) | | | (0.4) | |

| Net cash provided by financing activities | Net cash provided by financing activities | 117.7 | | | 63.3 | |

| Effect of exchange rate changes on cash and cash equivalents | Effect of exchange rate changes on cash and cash equivalents | 0.3 | | | 0.1 | |

| Net change in cash and cash equivalents | Net change in cash and cash equivalents | 100.0 | | | 7.9 | |

| Cash and cash equivalents, beginning of the year | Cash and cash equivalents, beginning of the year | 46.1 | | | 21.0 | |

| Cash and cash equivalents, end of period | Cash and cash equivalents, end of period | 146.1 | | | 28.9 | |

| Less: cash and cash equivalents included in current assets held for sale | — | | | (8.6) | |

| Cash and cash equivalents of continuing operations, end of period | $ | 146.1 | | | $ | 20.3 | |

| |

| | Supplemental cash flow information: | Supplemental cash flow information: | | | | Supplemental cash flow information: | | | |

| Interest paid, net of amounts capitalized | Interest paid, net of amounts capitalized | $ | 18.8 | | | $ | 18.6 | |

| Income taxes paid, net of refunds | Income taxes paid, net of refunds | $ | 2.0 | | | $ | 5.5 | |

The accompanying notes are an integral part of the consolidated financial statements.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Accounting Policies and Basis of Presentation:

Compass Minerals International, Inc. (“CMI”), through its subsidiaries (collectively, the “Company”), is a leading global provider of essential minerals focused on safely delivering where and when it matters to help solve nature’s challenges for customers and communities. The Company��sCompany’s salt products help keep roadways safe during winter weather and are used in numerous other consumer, industrial, chemical and agricultural applications. Its plant nutrition business is the leading North American producer of sulfate of potash (“SOP”), which is used in the production of specialty fertilizers for high-value crops and turf and helps improve the quality and yield of crops, while supporting sustainable agriculture. The Company’s principal products are salt, consisting of sodium chloride and magnesium chloride, and SOP. The Company’s next-generation fire retardants help to slow, stop and prevent wildfires through the use of high-performing and environmentally-friendly products. Additionally, the Company ishad been pursuing the development of a sustainable lithium brinesalt resource to support the North American battery market and is a minority ownermarket. However, as described in Note 5, the Company has terminated its pursuit of Fortress North America, LLC (“Fortress”), a next-generation fire retardant company.the lithium development. The Company’s production sites are located in the United States (“U.S.”), Canada and the United Kingdom (“U.K.”). The Company also provides records management services to businesses located in the U.K. Except where otherwise noted, references to North America include only the continental U.S. and Canada, and references to the U.K. include only England, Scotland and Wales. References to “Compass Minerals,” “our,” “us” and “we” refer to CMI and its consolidated subsidiaries.

CMI is a holding company with no significant operations other than those of its wholly-owned subsidiaries. The consolidated financial statements include the accounts of CMI and its wholly-owned domestic and foreign subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

The accompanying unaudited consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete consolidated financial statements. These unaudited consolidated financial statements should be read in conjunction with the consolidated financial statements of the Company for the annual period ended September 30, 2022,2023, as filed with the Securities and Exchange Commission (the “SEC”) in its Annual Report on Form 10-K on December 14, 2022.November 29, 2023 (“2023 Form 10-K”). In the opinion of management, all adjustments, consisting of normal recurring adjustments considered necessary for a fair presentation, have been included.

The Company experiences a substantial amount of seasonality in its sales, including its salt deicing salt product sales. As a result,Consequently, Salt segment sales and operating income are generally higher in the first and second fiscal quarters (ending December 31 and March 31) and lower during the third and fourth fiscal quarters (ending June 30 and September 30) of each year.. In particular, sales of highway and consumer deicing salt and magnesium chloride products vary based on the severity of the winter conditions in areas where the products are used. Following industry practice in North America and the U.K., the Company seeks to stockpile sufficient quantities of deicing salt throughout the first, third and fourth fiscal quarters (ending December 31, June 30 and September 30) to meet the estimated requirements for the winter season. Production of deicing salt can also vary based on the severity or mildness of the preceding winter season. Due to the seasonal nature of the deicing product lines, operating results for the interim periods are not necessarily indicative of the results that may be expected for the full fiscal year. The Company’s plant nutrition business is also seasonal. As a result, the Company and its customers generally build inventories during the plant nutrition business’ low demand periods of the year (which are typically winter and summer, but can vary due to weather and other factors) to ensure timely product availability during the peak sales seasons (which are typically spring and autumn, but can also vary due to weather and other factors). Lastly, the results of the Company’s fire retardant business are also seasonal with peak demand for fire retardant products and services occurring from June through September.

Significant Accounting Policies

The Company’s significant accounting policies are detailed in “Note 2 – Summary of Significant Accounting Policies” within Part II, Item 8 of its Annual Report on2023 Form 10-K for the annual period ended September 30, 2022. The Company reports its financial results10-K. There were no material changes in our significant accounting policies from discontinued operations and continuing operations separately to recognize the financial impact of disposal transactions apart from ongoing operations. Discontinued operations reporting occurs when a component or a group of components of an entity has been disposed or classified as held for sale and represents a strategic shift that has a major effect on the entity’s operations and financial results. In the Company’s Consolidated Statements of Cash Flows, the cash flows from discontinued operations are not separately classified. Unless otherwise indicated, amounts providedthose described in these Notes pertain to continuing operations. See Note 2 for information on discontinued operations and Note 11 for information on the Company’s reportable segments.our 2023 Form 10-K.

Recent Accounting Pronouncements

In November 2023, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures”, which updates reportable

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

Recent Accounting Pronouncementssegment disclosure requirements primarily to include enhanced disclosures about significant segment expenses. The amendments are effective for fiscal years beginning after December 15, 2023, and for interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. The amendments should be applied retrospectively to all prior periods presented in the financial statements. Management is currently evaluating this ASU to determine its impact on the Company's disclosures.

In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures”, which updates income tax disclosures by requiring consistent categories and additional disaggregation of information in the rate reconciliation and income taxes paid by jurisdiction. The Company has evaluated all of the recently issued, but not yetamendments are effective accounting standards that have been issued or proposed by the Financial Accounting Standards Board or other standards-setting bodies through the filing date of these unaudited consolidated financial statements and does not believe the futurefor fiscal years beginning after December 15, 2024. Early adoption of any such pronouncements will have a materialis permitted. The amendments should be applied prospectively; however, retrospective application is permitted. Management is currently evaluating this ASU to determine its impact on its consolidated financial statements.

Strategic Evaluation and Plan to Sell Businesses

Following an evaluation of the strategic fit of certain of the Company’s businesses and subsequent restructuring of its former South American Plant Nutrition segment to enable separate sales processes for its chemicals and specialty plant nutrition businesses and equity investment in Fermavi Eletroquímica Ltda. (“Fermavi”), in fiscal 2021 the Company’s Board of Directors approved the plan to sell each of these businesses and the North America micronutrient business (the “Specialty Businesses”) with a goal of reducing the Company’s leverage and enabling increased focus on optimizing the Company’s core businesses.

The Company concluded that the sale of the Specialty Businesses represented a strategic shift for the Company that would have a material effect on its operations and financial results. Consequently, the Specialty businesses were reclassified as discontinued operations on the Consolidated Statements of Operations. See Note 2 for further discussion of the sales of these businesses.

Unless otherwise indicated, amounts provided in these Notes pertain to continuing operations.disclosures.

2. Discontinued Operations:Business Acquisition:

During fiscal 2021Beginning in 2020, the Company sold its South America specialty plant nutrition business andbegan a series of equity investmentinvestments in Fermavi and itsFortress North America, micronutrient business. In connection with the saleLLC (“Fortress”), a next-generation fire retardant business dedicated to developing and producing a portfolio of its South America specialty plant nutrition businessmagnesium chloride-based fire retardant products to help combat wildfires. On May 5, 2023, the Company received netacquired the remaining 55% interest in Fortress not previously owned in exchange for an initial cash payment of approximately $318.4$18.9 million with an(net of cash held by Fortress of $6.5 million), and additional earnout paymentcontingent consideration of up to R$88$28 million Brazilian reais. On April 7, 2022,to be paid in cash and/or Compass Minerals common stock upon the achievement of certain performance measures over the next five years, and a cash earn-out based on volumes of certain Fortress fire retardant products sold over a 10-year period. Building upon the previous 45% minority ownership stake in Fortress, the transaction provided the Company received the maximum earnout possible under the termsfull ownership of the sale, or $18.5 million based on exchange rates at the time of receipt.

all Fortress assets, contracts, and intellectual property. See

Also in fiscal 2021, the Company completed the sale of its North America micronutrient business for approximately $56.7 million and its investment in Fermavi for R$45 million Brazilian reais (including R$30 million Brazilian reais of deferred purchase price). The Company received gross proceeds of approximately $2.9 million and recorded a discounted deferred proceeds receivable of approximately $4.8 million (based on exchange rates at the time of closing). As of December 31, 2022 approximately R$22.5 million Brazilian reais of deferred proceeds remains outstanding.

On April 20, 2022, the Company completed the sale of its South America chemicals business to a subsidiary of Cape Acquisitions LLC. Upon closing of the all-cash sale, the Company received gross proceeds of approximately $51.5 million based on exchange rates at the time of receipt, including a post-closing adjustment and compensation of $6.4 million for cash on hand that transferred to the buyer. The Company also paid fees of $2.4 million related to this sale. The Company recognized a loss recovery of $1.6 million during the three months ended June 30, 2022, an incremental loss from the sale of $23.1 million during the nine months ended June 30, 2022 and released $49.5 million from accumulated currency translation adjustment (“CTA”). The sale included all of the Company’s remaining operations in Brazil, concluding its previously announced plan to exit the South American market.

In measuring the assets and liabilities held for sale at fair value less estimated costs to sell, the Company completed an impairment analysis when its Board of Directors committed to a plan to sell the Specialty Businesses and the Company updated the analysis each quarter until each of the Specialty Businesses were sold.

The information below sets forth selected financial information related to the operating resultscontingent consideration as of the Specialty Businesses classified as discontinued operations. The Specialty Businesses’ revenue and expenses have been reclassified to net earnings from discontinued operations in prior periods. The Consolidated Statements of Operations present the revenue and expenses that were reclassified from the specified line items to discontinued operations.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

The following table represents summarized Consolidated Statements of Operations information of discontinued operations (in millions):

| | | | | | | | | | | |

| | | Three Months Ended

December 31, | | |

| | | 2021 | | | | |

Sales | | | $ | 22.4 | | | | | |

Shipping and handling cost | | | 1.2 | | | | | |

Product cost | | | 10.9 | | | | | |

Gross profit | | | 10.3 | | | | | |

Selling, general and administrative expenses | | | 1.6 | | | | | |

Operating earnings | | | 8.7 | | | | | |

| | | | | | | |

Loss on foreign exchange | | | 3.1 | | | | | |

Net loss on adjustment to fair value less estimated costs to sell | | | 8.4 | | | | | |

| | | | | | | |

Other income, net | | | (0.2) | | | | | |

Loss from discontinued operations before income taxes | | | (2.6) | | | | | |

Income tax expense | | | 2.9 | | | | | |

Net loss from discontinued operations | | | $ | (5.5) | | | | | |

The significant components included in the Company’s Consolidated Statements of Cash Flows for discontinued operations are as follows (in millions):

| | | | | | | |

| | | Three Months Ended

December 31, |

| | | 2021 |

| | | |

| | | |

| | | |

Loss on impairment of long-lived assets | | | $ | 8.4 | |

| | | |

Capital expenditures | | | (0.7) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

3. Revenues:

Nature of Products and ServicesDeferred Revenue

The Company’s Salt segment products include salt and magnesium chloride for use in road deicing and dust control, food processing, water softening, and agricultural and industrial applications. The Company’s Plant Nutrition segment produces and markets SOP in various grades worldwide to distributors and retailers of crop inputs, as well as growers and for industrial uses. In the U.K., the Company operates a records management business utilizing excavated areas of its Winsford salt mine with one other location in London, England.

Identifying the Contract

The Company accounts for a customer contract when there is approval and commitment from both parties, the rights of the parties and payment terms are identified, the contract has commercial substance and collectability of consideration is probable.

Identifying the Performance Obligations

At contract inception, the Company assesses the goods and services it has promised to its customers and identifies a performance obligation for each promise to transfer to the customer a distinct good or service (or bundle of goods or services). Determining whether products and services are considered distinct performance obligations that should be accounted for separately or aggregated together may require significant judgment.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

Identifying and Allocating the Transaction Price

The Company’s revenues are measured based on consideration specified in the customer contract, net of any sales incentives and amounts collected on behalf of third parties such as sales taxes. In certain cases, the Company’s customerDeferred revenue represents billings under non-cancellable contracts may include promises to transfer multiple products and services to a customer. For multiple-element arrangements, the Company generally allocates the transaction price to each performance obligation in proportion to its stand-alone selling price.

When Performance Obligations Are Satisfied

The vast majority of the Company’s revenues are recognized at a point in time when the performance obligations are satisfied based upon transfer of control of the product or service to a customer. To determine when the control of goods is transferred, the Company typically assesses, among other things, the shipping terms of the contract, as shipping is an indicator of transfer of control. Some of the Company’s products are sold when the control of the goods transfers to the customer at the time of shipment. There are also instances when the Company provides shipping services to deliver its products. Shipping and handling costs that occur before the customer obtains control of the goods are deemed to be fulfillment activities and are accounted for as fulfillment costs. The Company has made an accounting policy election to recognize any shipping and handling costs that are incurred after the customer obtains control of the goods as fulfillment costs which are accrued at the time of revenue recognition.

Significant Payment Terms

The customer contract states the final terms of the sale, including the description, quantity and price of eachrelated product or service purchased. Payment is typically due in full within 30 days of delivery. The Company does not adjust the consideration for the effects of a significant financing component if the Company expects, at contract inception, that the period between when the good or service is transferred to the customercustomer. The portion of deferred revenue that is anticipated to be recognized as revenue during the succeeding twelve-month period is recorded in accrued expenses and when the customer pays for that good or service will be one year or less.

Refunds, Returns and Warranties

The Company’s products are generally not sold with a right of returnother current liabilities and the Company does not generally provide credits or incentives, which may be required to be accounted forremaining portion is recorded in other non-current liabilities on the Consolidated Balance Sheets. Deferred revenue as variable consideration when estimating the amount of revenue to be recognized. The Company uses historical experience to estimate accruals for refunds due to manufacturing or other defects.December 31, 2023 and September 30, 2023 was approximately $3.5 million and $8.5 million, respectively.

See Note 1110 for disaggregation of sales by segment, type and geographical region.

4. Inventories:

Inventories consist of the following (in millions):

| | | | December 31,

2022 | | September 30,

2022 | | December 31,

2023 | | September 30,

2023 |

| Finished goods | Finished goods | $ | 242.3 | | | $ | 251.6 | |

| Raw materials and supplies | Raw materials and supplies | 58.7 | | | 52.8 | |

| Total inventories | Total inventories | $ | 301.0 | | | $ | 304.4 | |

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

5. Property, Plant and Equipment, Net:

Property, plant and equipment, net, consists of the following (in millions):

| | | | December 31,

2022 | | September 30,

2022 | | December 31,

2023 | | September 30,

2023 |

| Land, buildings and structures, and leasehold improvements | Land, buildings and structures, and leasehold improvements | $ | 543.0 | | | $ | 534.8 | |

| Machinery and equipment | Machinery and equipment | 1,058.2 | | | 1,026.3 | |

| Office furniture and equipment | Office furniture and equipment | 56.9 | | | 56.8 | |

| Mineral interests | Mineral interests | 168.7 | | | 167.1 | |

| Construction in progress | Construction in progress | 48.0 | | | 64.3 | |

| | | 1,874.8 | | | 1,849.3 | |

| Less: accumulated depreciation and depletion | Less: accumulated depreciation and depletion | (1,100.0) | | | (1,072.7) | |

| Property, plant and equipment, net | Property, plant and equipment, net | $ | 774.8 | | | $ | 776.6 | |

The Company had been pursuing the development of a sustainable lithium salt resource to support the North American battery market. The passage of Utah House Bill 513 in March 2023 and the subsequent rulemaking process altered certain aspects of the regulatory landscape that will govern the development of lithium at the Great Salt Lake, introducing uncertainty into how development would proceed. As previously disclosed in the Company’s 2023 Form 10-K, the Company indefinitely paused new investment in its lithium development project pending greater clarity on the evolving regulatory environment in Utah. In December of 2023, a revised draft of the aforementioned rulemaking was published that continued to be, in the Company's assessment, adverse to its lithium development project. In addition, in December of 2023, the Company further refined its engineering estimates that, taken together with the proposed rules and decline in market price for lithium products, would result in inadequate risk-adjusted returns on capital.

On January 23, 2024, the Company severed certain members of its lithium development team and terminated its pursuit of the lithium development. Consequently, the Company evaluated the capitalized assets, including site preparation, project engineering, equipment and materials and capitalized labor and interest. As a result, the Company recorded an impairment charge of $74.8 million, including $7.6 million associated with future commitments, as of December 31, 2023 to reflect the assets at their estimated fair value, considering equipment expected to be used by the on-going business and amounts estimated to be recoverable through returns or salvage value. Prior to recognizing an impairment, the Company had capitalized $72.7 million to its property, plant and equipment on its Consolidated Balance Sheet with approximately $5.5 million remaining as of December 31, 2023. The Company engaged a valuation specialist to assist in determining the appropriate fair value of the lithium assets and the resulting impairment charge. Given the assets are likely to either be used in other operations or liquidated at a later date, the Company utilized a market-based approach that relied on Level 3 inputs (see Note 13 for a discussion of the levels in the fair value hierarchy).

6. Goodwill and Intangible Assets, Net:Goodwill:

Amounts related toChanges in the Company’s amortizationcarrying amount of intangible assetsgoodwill are summarized as follows (in millions):

| | | | | | | | | | | | | | | |

| Three Months Ended

December 31, | | |

| 2022 | | 2021 | | | | |

| Aggregate amortization expense | $ | 0.4 | | | $ | 0.4 | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | Plant Nutrition | | Corporate & Other(a) | | Consolidated |

| Balance as of September 30, 2023 | | $ | 51.1 | | | $ | 45.7 | | | $ | 96.8 | |

| Foreign currency translation adjustment | | 0.2 | | | 0.2 | | | 0.4 | |

| Balance as of December 31, 2023 | | $ | 51.3 | | | $ | 45.9 | | | $ | 97.2 | |

Amounts(a)Includes approximately $40.0 million of goodwill related to the Company’s goodwill areacquisition of Fortress, as follows (in millions):

| | | | | | | | | | | |

| December 31,

2022 | | September 30,

2022 |

| Plant Nutrition | $ | 51.0 | | | $ | 50.9 | |

| Other | 5.8 | | | 5.5 | |

| Total | $ | 56.8 | | | $ | 56.4 | |

The change in goodwill between September 30, 2022,2023, and December 31, 20222023 was due to the impact from translating foreign-denominated amounts to U.S. dollars. As of December 31, 2022,2023, there were no indicators necessitating an interim impairment test of the Company’s reporting unitsgoodwill based on the Company’s review of operating performance, among other factors, for the relevant reporting units.

7. Equity Method Investments:

The Company uses the equity method of accounting for equity securities when it has significant influence or when it has more than a minor ownership interest or more than minor influence over an investee’s operations but does not have a controlling financial interest. Initial investments are recorded at cost (including certain transaction costs) and are adjusted by the Company’s share of the investees’ undistributed earnings and losses. The Company may recognize its share of an investee’s earnings on a lag, if an investee’s financial results are not available in a timely manner.

For certain of the Company's equity method investments, such as investments where the capital structure of the equity investment results in different liquidation rights and priorities than what is reflected by the underlying percentage ownership interests, the Company's proportionate share of net earnings is accounted for using the Hypothetical Liquidation at Book Value ("HLBV") methodology available under the equity method of accounting. When applying HLBV, the Company determines the amount that would be received if the investee were to liquidate all of its assets and distribute the resulting cash to the investors based on contractually defined liquidation priorities, assuming the net assets were liquidated at their net book value.

The Company evaluates its equity method investments for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

On November 2, 2021, the Company announced an investment in Fortress, a next-generation fire retardant business dedicated to developing and producing a portfolio of magnesium chloride-based fire retardant products to help combat wildfires. As of December 31, 2022, the Company has invested $50 million in Fortress in exchange for an ownership interest of approximately 45%. Under the HLBV methodology available under the equity method of accounting, the Company reflects its share of the income or loss of Fortress, net of tax, in its results each period on a one quarter reporting lag. The Company recorded $0.5 million and $0.1 million for its share of Fortress’ net losses in the three months ended December 31, 2022 and 2021, respectively.

The carrying value of the Company’s equity investment in Fortress is in excess of its share of Fortress’s net book value by approximately $27 million as of December 31, 2022. The basis difference primarily represents incremental value attributable to intangible assets and goodwill that has not been recognized in the financial statements of Fortress. The Company has liquidation preference under the terms of Fortress’ LLC agreement. Additionally, the Company has the right to purchase units from other Fortress unit holders and the right of first refusal to purchase all or any portion of any available Fortress units, both subject to certain conditions.

The balance of the Company’s net investment in Fortress of $45.3 million and $45.8 million as of December 31, 2022 and September 30, 2022, respectively is recorded in equity method investments in the Consolidated Balance Sheets. The Company also has other immaterial equity investments of $0.4 million and $0.8 million as of December 31, 2022 and September 30, 2022, respectively, for which it has recorded $0.4 million and $0.3 million for its share of losses in the three months ended December 31, 2022 and 2021, respectively.

8.7. Income Taxes:

The Company’s effective income tax rate differs from the U.S. statutory federal income tax rate primarily due to U.S. statutory depletion, state income taxes (net of federal tax benefit), nondeductible executive compensation over $1 million, foreign income, mining and withholding taxes, base erosion and anti-abuse tax, and for the period ended December 31, 2022, valuation allowances recorded on deferred tax assets. For the period ended December 31, 2021, there were also interest expense recognition differences for book and tax purposes.

Management assesses the available positive and negative evidence to estimate whether sufficient future taxable income will be generated to permit use of the existing deferred tax assets. A significant piece of objective negative evidence evaluated was the cumulative loss incurred in the U.S. over the three-year period ended December 31, 2022.2023. Such objective evidence limits the ability to consider other subjective evidence, such as the Company’s projections for future income. On the basis of this evaluation, during the three months ended December 31, 2022, a2023, an additional valuation allowance of $6.1$19.6 million has been recorded to recognize only the portion of the U.S. deferred tax assets that is more likely than not to be realized. The amount of the deferred tax assets considered realizable, however, could be adjusted if estimates of future taxable income during the carryforward period are increased or reduced or if objective negative evidence in the form of cumulative losses is no longer present and additional weight is given to subjective evidence such as the Company’s projections for income.

As of December 31, 2022,2023, and September 30, 2022,2023, the Company had $87.2 $63.1 million and $94.1$65.4 million, respectively of gross foreign federal NOL carryforwards that have no expiration date and $3.2$2.9 million at both December 31, 20222023 and September 30, 20222023 of net operating tax-effected state NOL carryforwards which expire beginning in 2035.

Canadian provincial tax authorities have challenged tax positions claimed by one of the Company’s Canadian subsidiaries and have issued tax reassessments for fiscal years 2002-2017.2002-2018. The reassessments are a result of ongoing audits and total $170.2total $189.8 million, including interest, through December 31, 2022.2023. The Company disputes these reassessments and will continue to work with thethe appropriate authorities in Canada to resolve the dispute. There is a reasonable possibility that the ultimate resolution of this dispute, and any related disputes for other open tax years, may be materially higher or lower than the amounts the Company has reserved for such disputes.disputes. In connection with this dispute, local regulations require the Company to post security with the tax authority until the dispute is resolved. The Company has posted collateral in the form of a $143.4$166.1 million performance bond and has paid $36.7$37.7 million to the Canadian tax authorities (most of which is recorded in other assets inin the Consolidated Balance Sheets at December 31, 2022,2023, and September 30, 2022)2023), which is necessary to proceed with future appeals or litigation.

The Company expects that it will be required by local regulations to provide security for additional interest on the above unresolved disputed amounts and for any future reassessments issued by these Canadian tax authorities in the form of cash, letters of credit, performance bonds, asset liens or other arrangements agreeable with the tax authorities until the disputes are resolved.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

The Company expects that the ultimate outcome of these matters will not have a material impact on its results of operations or financial condition. However, the Company can provide no assurance as to the ultimate outcome of these matters, and the impact could be material if they are not resolved in the Company’s favor. As of December 31, 2022,2023, the Company believes it has adequately reserved for these reassessments.

Additionally, the Company has other uncertain tax positions as well as assessments and disputed positions with taxing authorities in its various jurisdictions, which are consistent with those matters disclosed in the Company’s Annual Report on Form 10-K for the annual period ended September 30, 2022.2023 Form10-K.

9.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

8. Long-Term Debt:

Long-term debt consists of the following (in millions):

| | | | December 31,

2022 | | September 30,

2022 | | December 31,

2023 | | September 30,

2023 |

| 4.875% Senior Notes due July 2024 | $ | 250.0 | | | $ | 250.0 | |

| Term Loan due January 2025 | 16.9 | | | 16.9 | |

| Revolving Credit Facility due January 2025 | — | | | 151.5 | |

| 6.75% Senior Notes due December 2027 | 6.75% Senior Notes due December 2027 | 500.0 | | | 500.0 | |

| Term Loan due May 2028 | |

| Revolving Credit Facility due May 2028 | |

| AR Securitization Facility expires June 2025 | AR Securitization Facility expires June 2025 | 72.9 | | | 37.5 | |

| 839.8 | | | 955.9 | |

| 919.2 | |

| Less unamortized debt issuance costs | Less unamortized debt issuance costs | (7.7) | | | (8.3) | |

| Total debt | Total debt | 832.1 | | | 947.6 | |

| Less current portion | Less current portion | — | | | — | |

| Long-term debt | Long-term debt | $ | 832.1 | | | $ | 947.6 | |

|

As of December 31, 2022,2023, the term loan and revolving credit facility under the Company’s credit agreement entered into on November 26, 2019 (as amended, the “Credit Agreement”)2023 Credit Agreement were secured by substantially all existing and future U.S. assets of the Company, the Goderich mine in Ontario, Canada and capital stock of certain subsidiaries. As of December 31, 2022, the2023 and September 30, 2023, the weighted average interest rate on all borrowings outstanding under the term loan under the Credit Agreement was approximately 6.4%.7.9% and 7.8%, respectively. Depending on the type, borrowings under the 2023 Credit Agreement accrue interest at a rate per annum equal to the Adjusted Term SOFR Rate, the Adjusted EURIBO Rate, Prime Rate or the CDO Rate (as defined in the credit agreement), as applicable, plus Applicable Margins (as defined in the credit agreement) which resulted in interest rates between 7.7% and 9.8% as of both December 31, 2023 and September 30, 2023.

As of December 31, 2023, the Company had $207.5 million of availability under its $375 million revolving credit facility. The term loan requires the Company to maintain certain financial ratios, including a minimum interest coverage ratio and a maximum total net leverage ratio. The Company is in compliance as of December 31, 20222023 with its debt covenants under the 2023 Credit Agreement and its AR Securitization Facility. Pursuant to the terms of the second amendment to the2023 Credit Agreement, the maximum allowed consolidated total net leverage ratio (as defined and calculated under the terms of the Credit Agreement and discussed further below) was 5.0x for the quarter ended December 31, 2022,2023, which steps down to 4.75x in the quarter ending March 31, 2024, and to 4.5x for the fiscal quarter ended June 30, 2024 and thereafter. The consolidated total net leverage ratio represents the ratio of (a) consolidated total net debt to (b) consolidated adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”).amortization. Consolidated total net debt includes the aggregate principal amount of total debt, net of unrestricted cash not to exceed $50.0$75.0 million.

In November 2022, the Company entered into the third amendment to the 2019 Credit Agreement, principally to affect a transition from the London Inter-Bank Offered Rate to the Secured Overnight Financing Rate pricing benchmark provisions.

During the quarter ended December 31, 2022, the Company paid off the outstanding revolving credit facility balance utilizing proceeds from a private placement of common stock. Refer to Note 12 for additional details of the private placement transaction.

In January 2023, certain of the Company’s U.S. subsidiaries entered into the second amendment to the AR Securitization Facility with PNC Bank, which temporarily eases the restrictions of certain covenants contained in the agreement through March 2023. The amendment made certain adjustments to the financial tests including: (i) the default ratio and (ii) the delinquency ratio to make compliance with such tests more likely.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

10.9. Commitments and Contingencies:

As previously disclosed, the Company was the subject of an investigation by the Division of Enforcement of the SEC regarding the Company’s disclosures primarily concerning the operation of the Goderich mine, the former South American businesses, and related accounting and internal control matters including Salt interim inventory valuation methodology issues that were disclosed in the Company’s Form 10-K/A for the year ended December 31, 2020, and Form 10-Q/A for the quarter ended March 31, 2021, each filed with the SEC on September 3, 2021.

On September 23, 2022, the Company reached a settlement with the SEC, concluding and resolving the SEC investigation in its entirety. Under the terms of the settlement, the Company, without admitting or denying the findings in the administrative order issued by the SEC, agreed to pay a civil penalty of $12 million and to cease and desist from violations of specified provisions of the federal securities laws and rules promulgated thereunder, and to retain an independent compliance consultant for a period of approximately one year to review certain accounting practices and procedures. As set forth in the administrative order, the $12 million civil penalty is to bewas paid in installments: $2 million, which was paid on September 29, 2022, andinstallments with $10 million to be paid no later than September 30, 2023. The Company previously recorded an accrual for the full amount of the penalty in the third quarter of fiscal 2022, which is reflected in accrued expenses and other current liabilities on the Company’s Consolidated Balance Sheets.Sheets as of September 30, 2023 and subsequently paid in during the first quarter of fiscal 2024.

The Company is also involved in legal and administrative proceedings and claims of various types from the ordinary course of the Company’s business.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

Management cannot predict the outcome of legal claims and proceedings with certainty. Nevertheless, management believes that the outcome of legal proceedingproceedings and claims, which are pending or known to be threatened, even if determined adversely, will not, individually or in the aggregate, have a material adverse effect on the Company’s results of operations, cash flows or financial position, except as otherwise described in Note 87 and this Note 10.9.

11.10. Operating Segments:

The Company’s reportable segments are strategic business units that offer different products and services, and each business requires different technology and marketing strategies. In connection with the executed business disposals discussed in Note 1 and Note 2, the Company has identified two reportable segments. The Specialty Businesses that comprised the Company’s former Plant Nutrition South America reportable segment and the North America micronutrient product business previously reported within the former Plant Nutrition North America reportable segment were classified as discontinued operations for all periods presented in its consolidated financial statements in this Quarterly Report on Form 10-Q.

For the three months ended December 31,

20222023 and

2021,2022, the Company has presented two reportable segments in its Consolidated Financial Statements: Salt and Plant Nutrition. The Salt segment produces and markets salt, consisting of sodium chloride and magnesium chloride, for use in road deicing for winter roadway safety and for dust control, food processing, water softening and other consumer, agricultural and industrial applications. The Plant Nutrition segment produces and markets various grades of SOP.

The results of operations for the Company’s fire retardant and records management businesses are included in Corporate and Other in the tables below. Refer to Note 2 for a discussion of the acquisition of the fire retardant business.

Segment information is as follows (in millions):

| | Three Months Ended December 31, 2022 | | Salt | | Plant

Nutrition | | Corporate & Other(a)(b) | | Total |

| Three Months Ended December 31, 2023 | | Three Months Ended December 31, 2023 | | Salt | | Plant

Nutrition | | Corporate & Other(a) | | Total |

| Sales to external customers | Sales to external customers | | $ | 308.1 | | | $ | 41.6 | | | $ | 2.7 | | | $ | 352.4 | |

| Intersegment sales | Intersegment sales | | — | | | 2.9 | | | (2.9) | | | — | |

| Shipping and handling cost | Shipping and handling cost | | 102.7 | | | 4.7 | | | — | | | 107.4 | |

Operating earnings (loss)(b) | Operating earnings (loss)(b) | | 47.1 | | | 11.0 | | | (30.2) | | | 27.9 | |

| Depreciation, depletion and amortization | Depreciation, depletion and amortization | | 13.9 | | | 8.3 | | | 1.7 | | | 23.9 | |

| Total assets (as of end of period) | Total assets (as of end of period) | | 985.2 | | | 456.5 | | | 323.0 | | | 1,764.7 | |

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

| | Three Months Ended December 31, 2021 | | Salt | | Plant

Nutrition | | Corporate & Other(a)(b) | | Total |

| Three Months Ended December 31, 2022 | | Three Months Ended December 31, 2022 | | Salt | | Plant

Nutrition | | Corporate & Other(a) | | Total |

| Sales to external customers | Sales to external customers | | $ | 273.9 | | | $ | 54.6 | | | $ | 3.0 | | | $ | 331.5 | |

| Intersegment sales | Intersegment sales | | — | | | 2.4 | | | (2.4) | | | — | |

| Shipping and handling cost | Shipping and handling cost | | 88.4 | | | 7.3 | | | — | | | 95.7 | |

Operating earnings (loss)(b) | | 39.4 | | | 9.5 | | | (28.5) | | | 20.4 | |

Operating earnings (loss)(c) | |

| Depreciation, depletion and amortization | Depreciation, depletion and amortization | | 16.2 | | | 8.8 | | | 3.3 | | | 28.3 | |

| Total assets (as of end of period) | Total assets (as of end of period) | | 1,035.4 | | | 445.3 | | | 206.7 | | | 1,687.4 | |

Disaggregated revenue by product type is as follows (in millions):

| | Three Months Ended December 31, 2022 | | Salt | | Plant

Nutrition | | Corporate & Other(a)(b) | | Total |

| Three Months Ended December 31, 2023 | | Three Months Ended December 31, 2023 | | Salt | | Plant

Nutrition | | Corporate & Other(a) | | Total |

| Highway Deicing Salt | Highway Deicing Salt | | $ | 190.3 | | | $ | — | | | $ | — | | | $ | 190.3 | |

| Consumer & Industrial Salt | Consumer & Industrial Salt | | 117.8 | | | — | | | — | | | 117.8 | |

| | SOP | SOP | | — | | | 44.5 | | | — | | | 44.5 | |

| | SOP | |

| | SOP | |

| Fire Retardant | |

| Revenue from Services | |

| Eliminations & Other | Eliminations & Other | | — | | | (2.9) | | | 2.7 | | | (0.2) | |

| Sales to external customers | Sales to external customers | | $ | 308.1 | | | $ | 41.6 | | | $ | 2.7 | | | $ | 352.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, 2021 | | Salt | | Plant

Nutrition | | Corporate & Other(a)(b) | | Total |

| Highway Deicing Salt | | $ | 163.7 | | | $ | — | | | $ | — | | | $ | 163.7 | |

| Consumer & Industrial Salt | | 110.2 | | | — | | | — | | | 110.2 | |

| | | | | | | | |

| | | | | | | | |

| SOP | | — | | | 57.0 | | | — | | | 57.0 | |

| Eliminations & Other | | — | | | (2.4) | | | 3.0 | | | 0.6 | |

| Sales to external customers | | $ | 273.9 | | | $ | 54.6 | | | $ | 3.0 | | | $ | 331.5 | |

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, 2022 | | Salt | | Plant

Nutrition | | Corporate & Other(a) | | Total |

| Highway Deicing Salt | | $ | 190.3 | | | $ | — | | | $ | — | | | $ | 190.3 | |

| Consumer & Industrial Salt | | 117.8 | | | — | | | — | | | 117.8 | |

| | | | | | | | |

| | | | | | | | |

| SOP | | — | | | 44.5 | | | — | | | 44.5 | |

| Eliminations & Other | | — | | | (2.9) | | | 2.7 | | | (0.2) | |

| Sales to external customers | | $ | 308.1 | | | $ | 41.6 | | | $ | 2.7 | | | $ | 352.4 | |

(a)Corporate and Other includes corporate entities, records management operations, the Fortress fire retardant business, equity method investments, lithium development costs and other incidental operations and eliminations. Operating earnings (loss) for corporate and other includes indirect corporate overhead, including costs for general corporate governance and oversight, lithium-related expenses, as well as costs for the human resources, information technology, legal and finance functions.

(b)As a result of the Company’s decision to cease the pursuit of the lithium development, the Company recognized an impairment of long-lived assets of $74.8 million and severance of $2.5 million, which impacted operating results for the three months ended December 31, 2023. Refer to Note 5 for additional information about the impairment of lithium development assets. (c)Corporate operating results include costs related to the settled SEC investigation of $0.3 million for the three months ended December 31, 2022. Corporate operating results for the three months ended December 31, 2021 include executive transition costs of $3.3 million and costs, net of reimbursements, related to the settled SEC investigation of $3.1 million. Refer to Note 109 for more information regarding the SEC investigation.investigation and settlement.

The Company’s revenue by geographic area is as follows (in millions):

| | Three Months Ended

December 31, | |

| Three Months Ended

December 31, | |

| Three Months Ended

December 31, | |

| Three Months Ended

December 31, | |

| Revenue | |

| Revenue | |

| Revenue | Revenue | | 2022 | | 2021 | |

United States(a) | United States(a) | | $ | 248.2 | | | $ | 221.3 | | |

United States(a) | |

United States(a) | |

| Canada | |

| Canada | |

| Canada | Canada | | 87.6 | | | 89.4 | | |

| United Kingdom | United Kingdom | | 14.1 | | | 19.8 | | |

| United Kingdom | |

| United Kingdom | |

| Other | |

| Other | |

| Other | Other | | 2.5 | | | 1.0 | | |

| Total revenue | Total revenue | | $ | 352.4 | | | $ | 331.5 | | |

| Total revenue | |

| Total revenue | |

(a)United States sales exclude product sold to foreign customers at U.S. ports.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

12.11. Stockholders’ Equity and Equity Instruments:

Equity Compensation Awards

In May 2020, the Company’s stockholders approved the 2020 Incentive Award Plan (as amended, the “2020 Plan”), which authorized the issuance of 2,977,933 shares of Company common stock. In February 2022, the Company’s stockholders approved an amendment to the 2020 Plan authorizing an additional 750,000 shares of Company stock. Since the date the 2020 Plan was approved, the Company ceased issuing equity awards under the 2015 Incentive Award Plan (as amended, the “2015 Plan”). Since the approval of the 2015 Plan in May 2015, the Company ceased issuing equity awards under the 2005 Incentive Award Plan (as amended, the “2005 Plan”). The 2005 Plan, the 2015 Plan and the 2020 Plan allow for grants of equity awards to executive officers, other employees and directors, including restricted stock units (“RSUs”), performance stock units (“PSUs”), stock options and deferred stock units.

Koch For additional information regarding equity awards issued under the Company’s incentive plans refer to “Note 16 – Stockholder’s Equity Investment

On September 14, 2022, the Company entered into a Stock Purchase Agreement with Koch Minerals & Trading, LLC (“KM&T”), a subsidiary of Koch Industries, Inc. (“KII”), pursuant to which the Company agreed to issue and sell 6,830,700 sharesEquity Instruments” within Part II, Item 8 of its common stock at a purchase price of $36.87 for aggregate net proceeds of approximately $240.7 million, net of transaction costs. On October 18, 2022, the Company closed the direct private placement with KM&T, through its affiliate KM&T Investment Holdings, LLC, resulting in their ownership of approximately 17% of the Company’s outstanding common stock. The Company expects to use approximately $200 million of the proceeds from the private placement to advance the first development phase of its sustainable lithium development project at its Ogden site. The Company used the remaining approximately $40.7 million of proceeds to reduce debt.

Options

Substantially all of the stock options granted vest ratably, in tranches, over a four-year service period. Unexercised options expire after seven years. Options do not have dividend or voting rights. Upon vesting, each option can be exercised to purchase one share of the Company’s common stock. The exercise price of options is equal to the closing stock price on the grant date.

To estimate the fair value of options on the grant date, the Company uses the Black-Scholes option valuation model. Award recipients are grouped according to expected exercise behavior. Unless better information is available to estimate the expected term of the options, the estimate is based on historical exercise experience. The risk-free rate, using U.S. Treasury yield curves in effect at the time of grant, is selected based on the expected term of each group. The Company’s historical stock price is used to estimate expected volatility.

RSUs

Typically, the RSUs granted under the 2015 Plan and the 2020 Plan vest after one to three years of service. RSUs entitle the holders to one share of common stock for each vested RSU. Unvested RSUs do not have voting rights but are entitled to receive non-forfeitable dividends (generally after a performance hurdle has been satisfied for the year of the grant) or other distributions equal to those declared on the Company’s common stock for RSUs that are earned as a result of the satisfaction of the performance hurdle. The closing stock price on the grant date is used to determine the fair value of RSUs.

PSUs

Substantially all of the PSUs outstanding under the 2015 Plan and the 2020 Plan are either total stockholder return PSUs (“TSR PSUs”) or adjusted EBITDA growth PSUs (“EBITDA Growth PSUs”). The actual number of shares of the Company’s common stock that may be earned with respect to TSR PSUs is calculated by comparing the Company’s total stockholder return to the total stockholder return for each company comprising the Company’s peer group or a total return percentage target over a two- or three-year performance period and may range from 0% to 300% of the target number of shares based upon the attainment of these performance conditions. The actual number of shares of common stock that may be earned with respect to EBITDA Growth PSUs is calculated based on the attainment of adjusted EBITDA growth during the performance period and may range from 0% to 300% of the target number of shares based upon the attainment of these performance conditions.

PSUs represent a target number of shares of the Company’s common stock that may be earned before adjustment based upon the attainment of certain performance conditions. Holders of PSUs do not have voting rights but are entitled to receive non-forfeitable dividends or other distributions equal to those declared on the Company’s common stock for PSUs that are earned, which are paid when the shares underlying the PSUs are issued.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

To estimate the fair value of the TSR PSUs on the grant date for accounting purposes, the Company uses a Monte-Carlo simulation model, which simulates future stock prices of the Company as well as the Company’s peer group. This model uses historical stock prices to estimate expected volatility and the Company’s correlation to the peer group. The risk-free rate was determined using the same methodology as the option valuations as discussed above. The Company’s closing stock price on the grant date was used to estimate the fair value of the EBITDA Growth PSUs. The Company will adjust the expense of the EBITDA Growth PSUs based upon its estimate of the number of shares that will ultimately vest at each interim date during the vesting period.2023 Form 10-K.

During the three months ended December 31, 2022,2023, the Company reissued the following number of shares from treasury stock: 31,14086,597 shares related to the release of RSUs which vestedand 9365,556 shares related to stock payments. In fiscal 2022,2023, the Company issued 117,390158,132 net shares from treasury stock. The Company withheld a total of 9,85330,091 shares with a fair value of $0.4$0.8 million related to the vesting of RSUs PSUs, and stock payments during the three months ended December 31, 2022.2023. The fair value of the shares werewas valued at the closing price at the vesting date and represent the employee tax withholding for the employee’s compensation. The Company recognized tax expense of $0.1$0.4 million from its equity compensation awards as an increase to income tax expense during the three months ended December 31, 2022.2023. During the three months ended December 31, 20222023 and 2021,2022, the Company recorded $10.6$11.9 million and $4.7$10.6 million, (includes $1.4 million paid in cash), respectively, of compensation expense pursuant to its stock-based compensation plans. No amounts have been capitalized.

| | | | | | | | |

| | COMPASS MINERALS INTERNATIONAL, INC. |

PSUs