UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________

FORM 10-Q

________________________________________

(Mark One)

|

| |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018March 31, 2019

or

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-34475

________________________________________

OMEROS CORPORATION

(Exact name of registrant as specified in its charter)

|

| | |

| Washington | | 91-1663741 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| | | |

201 Elliott Avenue West Seattle, Washington | | 98119 |

| (Address of principal executive offices) | | (Zip Code) |

(206) 676-5000 (Registrant’s telephone number, including area code) |

(206) 676-5000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended, during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

| Large accelerated filer | | x | | Accelerated filer | | o |

| Non-accelerated filer | | o | | Smaller reporting company | | o |

| Emerging growth company | | o | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x |

| | |

| Securities Registered pursuant to Section 12(b) of the Securities Exchange Act of 1934: |

| Common Stock, $0.01 par value per share | OMER | The Nasdaq Stock Market LLC |

| (Title of each class) | (Trading symbol) | (Name of each exchange on which registered) |

As of November 6, 2018May 7, 2019, the number of outstanding shares of the registrant’s common stock, par value $0.01 per share, was 49,009,310.49,057,866.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, or the Exchange Act, which are subject to the “safe harbor” created by those sections for such statements. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to our management. All statements other than statements of historical fact are “forward-looking statements.” Terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “goal,” “intend,” “likely,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will,” “would,” “target,” and similar expressions and variations thereof are intended to identify forward-looking statements, but these terms are not the exclusive means of identifying such statements. Examples of these statements include, but are not limited to, statements regarding:

| |

| • | our expectations relating to demand for OMIDRIA® (phenylephrine and ketorolac intraocular solution) 1%/0.3% from wholesalers, ambulatory surgery centers, or ASCs, and hospitals, and our expectations regarding OMIDRIA product sales; |

our plans for the marketing and distribution of OMIDRIA and our estimates of OMIDRIA chargebacks and rebates, distribution fees and product returns;

our estimates regarding how long our existing cash, cash equivalents, short-term investments and revenues will be sufficient to fund our anticipated operating expenses, and capital expenditures as well as and debt service obligations;

our interest and principal payments on our outstanding notes under our Term Loan Agreement,expectations related to obtaining a permanent separate or similar reimbursement for OMIDRIA from the CRG Loan Agreement, with CRG Servicing LLC,Centers for Medicare & Medicaid Services, or CRG, and the lenders identified therein, and the satisfaction of covenants thereunder;CMS, particularly for periods after September 30, 2020;

our expectations regarding the clinical, therapeutic and competitive benefits and importance of OMIDRIA and our product candidates;

our expectations related to obtaining permanent separate or similar reimbursement for OMIDRIA from the Centers for Medicare & Medicaid Services, or CMS, and/or from Congress, particularly after September 30, 2020;

our ability to design, initiate and/or successfully complete clinical trials and other studies for our products and product candidates and our plans and expectations regarding our ongoing or planned clinical trials, including for our clinical trials for OMS721, for OMS906lead MASP-2 inhibitor, narsoplimab (also referred to as OMS721), and for OMS527;OMS527 and OMS906;

in our OMS721 program,narsoplimab clinical programs, our expectations regarding: whether enrollment in any or all ongoing and planned Phase 3 and Phase 2 clinical trials will proceed as expected; whether accelerated approval, fast track designation, breakthrough therapy designation and/or orphan drug designation may be granted by the U.S. Food and Drug Administration, or FDA, or conditional marketing authorization, orphan medicinal product designation may be granted by the European Commission, or EC, or the European Medicines Agency, or EMA, as applicable, for indications for which we are pursuing such approval or designation; and whether we can capitalize on the financial and regulatory incentives provided by orphan drug designations granted by the foregoing;U.S. Food and Drug Administration, or FDA, the European Commission, or EC, or the European Medicines Agency, or EMA; and whether we can capitalize on the regulatory incentives provided by fast-track and/or breakthrough therapy designations granted by the FDA;

our expectations regarding clinical plans and anticipated or potential paths to regulatory approval of narsoplimab by the FDA and/or EMA in our OMS721 program, hematopoietic stem cell transplant-associated thrombotic microangiopathy (HSCT-TMA), Immunoglobulin A (IgA) nephropathy, and/or atypical hemolytic uremic syndrome (aHUS);

whether and when a Biologics License Application, or BLA, for accelerated approval of OMS721 may be filed with the FDA for narsoplimab in any indication and whether the FDA will grant accelerated or fullregular (full) approval for OMS721; paths to acceleratednarsoplimab in any indication;

whether and fullwhen a marketing authorization application, or MAA, may be filed with the EMA for narsoplimab in any indication, and whether the EMA will grant approval of OMS721for narsoplimab in hematopoietic stem cell transplant-associated thrombotic microangiopathy, or HSCT-TMA, and atypicalhemolytic uremic syndrome, or aHUS ; and potential approval with respect to our Phase 3 clinical program for patients with Immunoglobulin A, or IgA, nephropathy;

any indication;our anticipationexpectation that we will rely on contract manufacturers to manufacture OMIDRIA for commercial sale and to manufacture our product candidates for purposes of clinical trial supply and if approved, for commercial sale;in anticipation of potential commercialization;

our ability to enter into acceptable arrangements with potential corporate partners or contract service providers, including with respect to OMIDRIA or our product candidates, and our ability and plans to effect any such arrangementsarrangement with respect to OMIDRIA in the European Union, or EU, or in other foreign countries;

our ability to raise additional capital through the capital markets or through one or more corporate partnerships, equity offerings, debt financings, collaborations, licensing arrangements or asset sales;

our expectations about the commercial competition that OMIDRIA and our product candidates, if commercialized, face or may face;

the expected course and costs of existing claims, legal proceedings and administrative actions, our involvement in potential claims, legal proceedings and administrative actions, and the merits, potential outcomes and effects of both existing and potential claims, legal proceedings and administrative actions, as well as regulatory determinations, on our business, prospects, financial condition and results of operations;

the extent of protection that our patents provide and that our pending patent applications will provide, if patents issueare issued from such applications, for our technologies, programs, products and product candidates;

the factors on which we base our estimates for accounting purposes and our expectations regarding the effect of changes in accounting guidance or standards on our operating results; and

our expected financial position, performance, revenues, growth, costs and expenses, magnitude of net losses and the availability of resources; and

the expected course and costs of potential claims, legal proceedings and administrative actions, and the merits, potential outcomes and effects of potential claims, legal proceedings and administrative actions, as well as regulatory determinations, on our business, prospects, financial condition and results of operations.resources.

Our actual results could differ materially from those anticipated in these forward-looking statements for many reasons, including the risks, uncertainties and other factors described in this Quarterly Report on Form 10-Q under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in our other filings with the U.S. Securities and Exchange Commission, or SEC. Given these risks, uncertainties and other factors, actual results or anticipated developments may not be realized or, even if substantially realized, may not have the expected consequences to or effects on our company, business or operations. Accordingly, you should not place undue reliance on these forward-looking statements, which represent our estimates and assumptions only as of the date of the filing of this Quarterly Report on Form 10-Q. You should read this Quarterly Report on Form 10-Q completely and with the understanding that our actual results in subsequent periods may materially differ from current expectations. Except as required by applicable law, we assume no obligation to update or revise any forward-looking statements contained herein, whether as a result of any new information, future events or otherwise.

OMEROS CORPORATION

FORM 10-Q FOR THE QUARTER ENDED September 30, 2018MARCH 31, 2019

INDEX

PART I — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

OMEROS CORPORATION

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except share and per share data)

(unaudited)

| | | | September 30,

2018 | | December 31,

2017 | March 31,

2019 | | December 31,

2018 |

| Assets | | | | | | |

| Current assets: | | | | | | |

| Cash and cash equivalents | $ | 2,787 |

| | $ | 3,394 |

| $ | 4,054 |

|

| $ | 5,861 |

|

| Short-term investments | 52,369 |

| | 80,355 |

| 43,168 |

|

| 54,637 |

|

| Receivables, net | 2,297 |

| | 17,144 |

| 24,718 |

|

| 22,818 |

|

| Inventory | 214 |

| | 443 |

| 736 |

|

| 88 |

|

| Prepaid expense | 8,334 |

| | 7,036 |

| |

| Prepaid expense and other assets | | 4,195 |

|

| 6,463 |

|

| Total current assets | 66,001 |

| | 108,372 |

| 76,871 |

|

| 89,867 |

|

| Property and equipment, net | 2,520 |

| | 2,121 |

| 4,479 |

|

| 3,845 |

|

| Right of use assets | | 17,514 |

|

| — |

|

| Restricted investments | 5,779 |

| | 5,835 |

| 1,154 |

|

| 1,154 |

|

| Advanced payments, non-current | 1,310 |

| | — |

| 1,228 |

|

| 1,070 |

|

| Total assets | $ | 75,610 |

| | $ | 116,328 |

| $ | 101,246 |

|

| $ | 95,936 |

|

| Liabilities and shareholders’ deficit | | | |

|

|

|

|

|

| Current liabilities: | | | |

|

|

|

|

|

| Accounts payable | $ | 8,847 |

| | $ | 6,691 |

| $ | 7,121 |

|

| $ | 6,281 |

|

| Accrued expenses | 15,180 |

| | 19,126 |

| 34,823 |

|

| 30,186 |

|

| Current portion of lease financing obligations | 560 |

| | 490 |

| |

| Current portion of lease liabilities | | 2,561 |

|

| 889 |

|

| Total current liabilities | 24,587 |

| | 26,307 |

| 44,505 |

|

| 37,356 |

|

| Notes payable and lease financing obligations, net | 131,695 |

| | 84,117 |

| |

| Lease liabilities, non-current | | 26,578 |

|

| 1,578 |

|

| Unsecured convertible senior notes, net | | 151,182 |

|

| 148,981 |

|

| Deferred rent | 8,325 |

| | 8,718 |

| — |

|

| 8,177 |

|

| Commitments and contingencies (Note 7) | — |

| | — |

| |

| Commitments and contingencies (Note 8) | |

|

|

|

|

| Shareholders’ deficit: |

| |

|

|

|

|

|

|

| Preferred stock, par value $0.01 per share, 20,000,000 shares authorized; none issued and outstanding at September 30, 2018 and December 31, 2017, respectively | — |

| | — |

| |

| Common stock, par value $0.01 per share, 150,000,000 shares authorized; 49,009,310 and 48,211,226 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively | 490 |

| | 482 |

| |

| Preferred stock, par value $0.01 per share, 20,000,000 shares authorized; none issued and outstanding at March 31, 2019 and December 31, 2018. | | — |

|

| — |

|

| Common stock, par value $0.01 per share, 150,000,000 shares authorized at March 31, 2019 and December 31, 2018; 49,022,428 and 49,011,684 shares issued and outstanding at March 31, 2019 and December 31, 2018, respectively. | | 490 |

|

| 490 |

|

| Additional paid-in capital | 537,104 |

| | 520,072 |

| 552,961 |

|

| 549,479 |

|

| Accumulated deficit | (626,591 | ) | | (523,368 | ) | (674,470 | ) |

| (650,125 | ) |

| Total shareholders’ deficit | (88,997 | ) | | (2,814 | ) | (121,019 | ) |

| (100,156 | ) |

| Total liabilities and shareholders’ deficit | $ | 75,610 |

| | $ | 116,328 |

| $ | 101,246 |

|

| $ | 95,936 |

|

See accompanying Notes to Condensed Consolidated Financial Statements

OMEROS CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(In thousands, except share and per share data)

(unaudited)

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

March 31, |

| | 2018 | | 2017 | | 2018 | | 2017 | 2019 | | 2018 |

| Revenue: |

|

|

| |

|

|

|

|

|

|

| Product sales, net | $ | 4,608 |

|

| $ | 21,658 |

| | $ | 7,852 |

|

| $ | 51,067 |

| $ | 21,779 |

|

| $ | 1,588 |

|

|

|

|

| |

|

|

|

|

|

|

| Costs and expenses: |

|

|

| |

|

|

|

|

|

|

| Cost of product sales | 36 |

|

| 184 |

| | 355 |

|

| 613 |

| 131 |

|

| 203 |

|

| Research and development | 26,862 |

|

| 14,835 |

| | 64,414 |

|

| 40,212 |

| 26,255 |

|

| 18,140 |

|

| Selling, general and administrative | 13,152 |

|

| 11,749 |

| | 36,830 |

|

| 40,016 |

| 14,632 |

|

| 10,934 |

|

| Total costs and expenses | 40,050 |

|

| 26,768 |

| | 101,599 |

|

| 80,841 |

| 41,018 |

|

| 29,277 |

|

| Loss from operations | (35,442 | ) |

| (5,110 | ) | | (93,747 | ) |

| (29,774 | ) | (19,239 | ) |

| (27,689 | ) |

| Interest expense | (4,602 | ) |

| (2,780 | ) | | (11,104 | ) |

| (8,166 | ) | (5,600 | ) |

| (2,825 | ) |

| Other income | 572 |

|

| 408 |

| | 1,628 |

|

| 1,010 |

| 494 |

|

| 460 |

|

| Net loss | $ | (39,472 | ) |

| $ | (7,482 | ) | | $ | (103,223 | ) |

| $ | (36,930 | ) | $ | (24,345 | ) |

| $ | (30,054 | ) |

| Comprehensive loss | $ | (39,472 | ) |

| $ | (7,482 | ) | | $ | (103,223 | ) |

| $ | (36,930 | ) | $ | (24,345 | ) |

| $ | (30,054 | ) |

| Basic and diluted net loss per share | $ | (0.81 | ) |

| $ | (0.16 | ) | | $ | (2.13 | ) |

| $ | (0.83 | ) | $ | (0.50 | ) |

| $ | (0.62 | ) |

| Weighted-average shares used to compute basic and diluted net loss per share | 48,647,416 |

|

| 46,262,211 |

| | 48,437,870 |

|

| 44,709,418 |

| 49,014,009 |

|

| 48,284,019 |

|

See accompanying Notes to Condensed Consolidated Financial Statements

OMEROS CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(unaudited)

| | | | Nine Months Ended

September 30, | Three Months Ended

March 31, |

| | 2018 |

| 2017 | 2019 |

| 2018 |

| Operating activities: | | | | | | |

| Net loss | $ | (103,223 | ) | | $ | (36,930 | ) | $ | (24,345 | ) |

| $ | (30,054 | ) |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | |

|

|

|

| Stock-based compensation expense | 8,896 |

| | 9,449 |

| 3,374 |

|

| 2,966 |

|

| Non-cash interest expense | 4,308 |

| | 3,056 |

| 2,201 |

|

| 1,086 |

|

| Depreciation and amortization | 654 |

| | 378 |

| 377 |

|

| 223 |

|

| Changes in operating assets and liabilities: | | | |

|

|

|

| Receivables | 14,847 |

| | (12,534 | ) | (1,900 | ) |

| 16,962 |

|

| Inventory | 229 |

| | 306 |

| (648 | ) |

| 196 |

|

| Prepaid expenses and other assets | (2,608 | ) | | (3,925 | ) | 2,110 |

|

| (840 | ) |

| Accounts payable, accrued expenses and other | (2,183 | ) | | 8,145 |

| |

| Accounts payable and accrued expenses | | 5,883 |

|

| (1,835 | ) |

| Net cash used in operating activities | (79,080 | ) | | (32,055 | ) | (12,948 | ) |

| (11,296 | ) |

| Investing activities: | | | |

|

|

|

| Purchases of property and equipment | (474 | ) | | (350 | ) | (182 | ) |

| (183 | ) |

| Purchases of investments | (45,514 | ) | | (65,109 | ) | (281 | ) |

| (270 | ) |

| Proceeds from the sale and maturities of investments | 73,500 |

| | 22,429 |

| 11,750 |

|

| 9,000 |

|

| Net cash provided by (used in) investing activities | 27,512 |

| | (43,030 | ) | |

| Net cash provided by investing activities | | 11,287 |

|

| 8,547 |

|

| Financing activities: | | | |

|

|

|

| Proceeds from issuance of common stock | — |

|

| 63,627 |

| |

| Proceeds from borrowings under notes payable | 44,550 |

|

| — |

| |

| Proceeds upon exercise of stock options and warrants | 6,720 |

| | 10,512 |

| 108 |

|

| 687 |

|

| Release of restricted investments | 56 |

|

| — |

| |

| Payments on lease financing obligations | (365 | ) | | (252 | ) | |

| Net cash provided by financing activities | 50,961 |

| | 73,887 |

| |

| Payments on finance lease liabilities | | (254 | ) |

| (143 | ) |

| Net cash provided by (used in) financing activities | | (146 | ) |

| 544 |

|

| Net decrease in cash and cash equivalents | (607 | ) | | (1,198 | ) | (1,807 | ) |

| (2,205 | ) |

| Cash and cash equivalents at beginning of period | 3,394 |

| | 2,224 |

| 5,861 |

|

| 3,394 |

|

| Cash and cash equivalents at end of period | $ | 2,787 |

| | $ | 1,026 |

| $ | 4,054 |

|

| $ | 1,189 |

|

| | | | | |

| Supplemental cash flow information | | | |

|

|

|

| Cash paid for interest | $ | 6,796 |

|

| $ | 5,110 |

| $ | 82 |

|

| $ | 1,739 |

|

| Conversion of accrued interest to notes payable | $ | 3,246 |

|

| $ | 2,467 |

| $ | — |

|

| $ | 838 |

|

| Fair value of warrants issued in connection with notes payable amendment | $ | 1,424 |

|

| $ | — |

| |

| Property acquired under capital lease | $ | 579 |

|

| $ | 632 |

| |

See accompanying Notes to Condensed Consolidated Financial Statements

OMEROS CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Note 1—Organization and Significant Accounting Policies

Organization

We are a commercial-stage biopharmaceutical company committed to discovering, developing and commercializing small-molecule and protein therapeutics for large-market as well as orphan indications targeting inflammation, complement-mediated diseases, and disorders of the central nervous system.system, and immune-related diseases, including cancers. Our first drug product, OMIDRIA, is marketed in the United States (U.S.) for use during cataract surgery or intraocular lens replacement.

Basis of Presentation

Our condensed consolidated financial statements include the financial position and results of operations of Omeros Corporation (Omeros) and our wholly owned subsidiaries. All inter-company transactions have been eliminated and we have determined we operate in one segment. The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (GAAP) for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. The information as of September 30, 2018March 31, 2019 and for the three and nine months ended September 30, 2018March 31, 2019 and 20172018 includes all adjustments, which include normal recurring adjustments, necessary to present fairly our interim financial information. The Condensed Consolidated Balance Sheet at December 31, 20172018 has been derived from our audited financial statements but does not include all of the information and footnotes required by GAAP for audited annual financial information.

The accompanying unaudited condensed consolidated financial statements and related notes thereto should be read in conjunction with the audited consolidated financial statements and related notes thereto that are included in our Annual Report on Form 10-K for the year ended December 31, 2017,2018, which was filed with the U.S. Securities and Exchange Commission (SEC) on March 1, 2018.2019.

Going Concern

We continue to advance a series of clinical and preclinical programs (including three programs currently in Phase 3). CMS granted transitional pass-through reimbursement status for OMIDRIA from January 1, 2015 through December 31, 2017 for patients covered by Medicare Part B. On an interimOctober 1, 2018, OMIDRIA pass-through reimbursement was reinstated for a two-year period and annual basisquarterly OMIDRIA net sales returned to historical levels. We believe OMIDRIA sales will continue to grow in 2019; however, due to the recent re-introduction of OMIDRIA, we cannot predict with precision the extent of growth in OMIDRIA revenues in 2019. As a result, despite our significant historical growth in OMIDRIA sales, meaningful growth in OMIDRIA sales in 2019 and beyond are required to assessnot included in the determination regarding our ability to continueprospects as a going concern for one year after the date the financial statements are issued using rules defined by Accounting Standards Codification (ASC) No. 205-40 - Going Concern (the Standard). As required by the Standard, management’s evaluation shall initially not take into consideration the potential mitigating effects of management’s plans that have not been fully implemented as of the date the financial statements are issued. In the second step of this evaluation, management’s assumptions and plans are derived according to restrictions and definitions in the Standard. As such, for purposes of this exercise, the following assumptions (which are discussed in further detail following this summary) were made:

Limited cash receipts from sales of OMIDRIA. Even though we have received an extension of transitional pass-through reimbursement for OMIDRIA for a period of two years effective October 1, 2018,concern. Similarly, we are unable at this time to predict accurately revenueinclude in the determination any proceeds from sales of OMIDRIA given that transitional pass-through reimbursement for the product has just recently been reinstated. In addition, sales of OMIDRIA are generally made with 90-day collection terms and, therefore, minimal OMIDRIA cash receipts were included for this exercise prior to January 2019; and

No public or private equitydebt transactions or partnering revenues can be considered for purposes of this exerciseother financing instruments despite our successful track record in accessing capital through these avenues. We also have not included any potential partnerships related to our products or product candidates. The conditions described above, when evaluated within the absence of any existing or committed arrangements to raise additional capital or of any existing or consummated partnerships.

In performing the first stepconstraints of the assessment, we concluded that the following conditionsaccounting literature, raise substantial doubt about our abilitywith respect to meet our financial obligations as they become due. As of September 30, 2018, we had $55.2 million in cash, cash equivalents and short-term investments, $2.3 million of accounts receivable and $24.6 million in current liabilities. We have a history of net losses ($103.2 million for the nine months ended September 30, 2018) and use of cash for operations ($79.1 million for the nine months ended September 30, 2018).

In performing the second step of this assessment, we are required to evaluate whether our plans to mitigate the conditions above alleviate the substantial doubt about our ability to meet our obligations as they become due within one year after the date the financial statements are issued. In performing this second step of the assessment, we are limited to those assumptions listed above, including nominal revenues from OMIDRIA despite the reinstatement of the product’s pass-through status effective October 1, 2018 pursuant to the Consolidated Appropriations Act of 2018 (Appropriations Act),through May 9, 2020 and, the restrictions and definitions in the Standard. Consequently, based on this assessment performed using the associated limitations required by the

Standard, we have concluded there is substantial doubt about our abilitytherefore, to continue as a going concernconcern.

We plan to continue to fund our operations through November 8, 2019.

Given our inability to assumeproceeds from sales of OMIDRIA and, if necessary, through other revenue sources and financial instruments as noted above. If these capital sources, for any meaningful OMIDRIA sales revenues for the purpose of this exercise due to only recently reinstated pass-through, if wereason, are unable to raise additional equity, debt or partnering capital when needed or upon acceptable terms, such failurebut inaccessible, it would have a significantsignificantly negative impact oneffect our financial condition. Should it be necessary to manage our operating expenses, we would reduce our projected cash requirements through reduction of our expenses by delaying clinical trials, reducing selected research and development efforts, and/or implementing other restructuring activities.

The accompanying consolidated financial statements have been prepared on a going-concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The accompanying consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from uncertainty related to our ability to continue as a going concern.

Revenue Recognition

In May 2014, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2014-09- Revenue from Contracts with Customers (Topic 606), which requires entities to recognize revenue when control of the promised goods or services is transferred to customers at an amount that reflects the consideration to which the entity expects to be entitled to in exchange for those goods or services. We adopted Topic 606 on January 1, 2018 using the modified retrospective transition method.

Once we determine that an arrangement is within the scope of Topic 606 and we believe it is probable that we will collect the consideration, we perform the following five steps: (i) identify the contract with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when (or as) we satisfy a performance obligation.

Upon adoption, we evaluated our contracts with customers and determined the adoption of the standard did not change the timing or the amounts of our previously recognized revenues.

Product Sales, Net

We generally record revenue from product sales when the product is delivered to our wholesalers. Product sales are recorded net of wholesaler distribution fees and estimated chargebacks, rebates and purchase volume discounts. Accruals or allowances are established for these deductions in the same period when revenue is recognized, and actual amounts incurred are offset against the applicable accruals or allowances. We reflect each of these accruals or allowances as either a reduction in the related account receivable or as an accrued liability, depending on how the amount is expected to be settled.

The Centers for Medicare & Medicaid Services (CMS) initially granted transitional pass-through reimbursement status for OMIDRIA from January 1, 2015 through December 31, 2017. Pass-through status for OMIDRIA allowed for reimbursement payment to Ambulatory Surgery Centers (ASCs) and hospitals using OMIDRIA in procedures involving patients covered by Medicare Part B. In March 2018, the Appropriations Act was signed into law, which among other things extended pass-through reimbursement status for certain drugs, including OMIDRIA, for a two-year period beginning October 1, 2018. For the period January 1, 2018 through September 30, 2018, OMIDRIA was not yet subject to separate reimbursement for procedures involving patients covered by Medicare Part B.

Advanced Payments

We have various agreements with third parties that require us to pay part of the contractually due amounts in advance of receiving goods and services. These agreements relate primarily to clinical and manufacturing activities. Amounts paid in advance of services to be delivered to us beyond 12 months of the balance sheet date are recorded as non-current assets.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Significant items subject to such estimates include revenue recognition, stock-based compensation expense and accruals for clinical trials, manufacturing of drug product and clinical drug supply and contingencies. We base our estimates on historical experience and on various other factors that we believe are reasonable under the circumstances; however, actual results could differ from these estimates.

Recently Adopted PronouncementsRevenue Recognition

When we enter into a customer contract, we perform the following five steps: (i) identify the contract with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when (or as) we satisfy a performance obligation.

Product Sales, Net

We generally record revenue from product sales when the product is delivered to our wholesalers. Product sales are recorded net of wholesaler distribution fees and estimated chargebacks, rebates, returns and purchase-volume discounts. Accruals or allowances are established for these deductions in the same period when revenue is recognized, and actual amounts incurred are offset against the applicable accruals or allowances. We reflect each of these accruals or allowances as either a reduction in the related accounts receivable or as an accrued liability depending on how the amount is expected to be settled.

Right-of-Use Assets and Related Lease Liabilities

On January 1, 2019, we adopted Accounting Standards Update (ASU) 2016-02, Leases, (Topic 842) using a modified retrospective approach. We elected the package of practical expedients permitted under the transition guidance, which allowed us to carryforward our historical assessment of whether 1) contracts contain leases, 2) lease classifications and 3) initial direct costs. Upon adoption we recognized right-of-use assets and lease liabilities of $17.7 million and $26.4 million, respectively, in our Consolidated Balance Sheet. The balance of the net right-of-use asset resulted from the reversal of the outstanding balance of deferred rent of $8.7 million.

We record operating leases on our Consolidated Balance Sheet as right-of-use assets and recognize the related lease liabilities equal to the fair value of the lease payments using our incremental borrowing rate when the implicit rate in the lease agreement is not readily available. We recognize variable lease payments, when incurred. Costs associated with operating lease assets are recognized on a straight-line basis within operating expenses over the term of the lease.

We record finance leases on our Consolidated Balance Sheet as a component of property and equipment and amortize these assets within operating expenses on a straight-line basis to their residual values over the shorter of the term of the underlying lease or the estimated useful life of the equipment. The interest component of a finance lease is included in interest expense and recognized using the effective interest method over the lease term.

We account for leases with initial terms of 12 months or less as operating expenses on a straight-line basis over the lease term.

Advance Payments

Advance payments for goods or services that will be used or rendered for future research and development activities are deferred and then recognized as an expense as the related goods are delivered or the services are performed, or when the goods or services are no longer expected to be provided.

Stock-Based Compensation

On January 1, 2019, we adopted ASU 2018-05 issued by the FASB in March 2018 related to the Tax Cuts and Jobs Act (Tax Act) that was enacted in December 2017. We remeasured certain deferred tax assets and liabilities based on the rates at which they are expected to reverse in the future, which is generally 21.0%. The standard requires that we record and disclose any provisional amounts related to the Tax Act. We recorded and disclosed the provisional impact to our deferred tax balance in our Annual Report on Form 10-K for the year ended December 31, 2017 that was filed with the SEC on March 1, 2018.

In May 2016, the FASB issued ASU 2017-09 related to stock-based compensation, which provides guidance on the accounting for changes to the terms and conditions of stock-based payment arrangement, or modifications. We adopted the guidance January 1, 2018 and the adoption did not have a material impact on our stock-based compensation expense.

Recent Accounting Pronouncements

In August 2018, the FASB issued ASU 2018-15 related to the accounting for cloud computing arrangements and to follow the internal-use software guidance in determining which implementation costs to defer and recognize as an asset. The guidance is effective for annual periods, and interim periods beginning after December 15, 2019. Early adoption is permitted, including adoption in any interim period. We do not expect the adoption of this accounting guidance to have a material impact on our condensed consolidated financial statements.

In June 2018, the FASB issued ASU 2018-07,Compensation— Stock Compensation, (Topic 958) which simplifies the accounting for share-based payments granted to non-employees for services by aligning it with the accounting for share-based payments to employees, with certain exceptions. The guidanceadoption was immaterial to our consolidated financial statements.

Stock-based compensation expense is recognized for all share-based payments made to employees, directors and non-employees based on estimated fair values as of the date of grant. The fair value of our stock options is calculated using the Black-Scholes option-pricing model which requires judgmental assumptions including volatility, forfeiture rates and expected option life. We use the straight-line method to allocate stock-based compensation cost to reporting periods over each optionee’s requisite service period, which is generally the vesting period.

Recent Accounting Pronouncement Not Yet Adopted

In June 2016, the Financial Accounting Standards Board (FASB) issued ASU 2016-13, Financial Instruments — Credit Losses, (Topic 326) which changes how entities account for credit losses on most financial assets and certain other instruments, and expands disclosures. The standard is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. We do not expect the adoption of this accounting guidance to have a material impact on our condensed consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02 related to lease accounting. The new standard requires lessees to recognize a right-of-use asset and a lease liability for most leases. This standard must be applied using a modified retrospective transition method and is effective for all annual and interim periods beginning after December 15, 2018.2019 with early adoption permitted. We expect to adopt the standard on January 1, 20192020 and are still in the process of evaluating the effect of adoption on our consolidated financial statements and are currently assessing our leases.

Note 2—Net Loss Per Share

Basic net loss per share is calculated by dividing the net loss by the weighted-average number of common shares outstanding for the period. Diluted net loss per share is computed by dividing the net loss by the weighted-average number of common shares and dilutive common share equivalents outstanding for the period, determined using the treasury-stock method. Common share equivalents are excluded from the diluted net loss per share computation if their effect is anti-dilutive.

The basic and diluted net loss per share amounts for the ninethree months ended September 30,March 31, 2019 and 2018 and 2017 were computed based on the shares of common stock outstanding during the respective periods. Potentially dilutive securities excluded from the diluted loss per share calculation are as follows:

| | | | September 30, | March 31, |

| | 2018 | | 2017 | 2019 | | 2018 |

| Outstanding options to purchase common stock | 10,123,530 |

| | 9,813,462 |

| 11,840,521 |

| | 9,640,452 |

|

| Outstanding warrants to purchase common stock | 243,115 |

| | 100,602 |

| 243,115 |

| | 100,602 |

|

| Total | 10,366,645 |

| | 9,914,064 |

| |

| Total potentially dilutive shares excluded from loss per share | | 12,083,636 |

| | 9,741,054 |

|

Note 3—Certain Balance Sheet Accounts

Accounts Receivable, Netnet

Accounts receivable, net consist of the following:

| | | | September 30,

2018 | | December 31,

2017 | March 31,

2019 | | December 31,

2018 |

| | (In thousands) | (In thousands) |

| Trade receivables, net | $ | 2,165 |

| | $ | 17,079 |

| $ | 24,580 |

| | $ | 22,654 |

|

| Sublease and other receivables | 132 |

| | 65 |

| 138 |

| | 164 |

|

| Total accounts receivables net | $ | 2,297 |

| | $ | 17,144 |

| |

| Total accounts receivables, net | | $ | 24,718 |

| | $ | 22,818 |

|

Trade receivables are shown net of $0.4 million and $0.4 million of chargeback and product return allowances as of March 31, 2019 and December 31, 2018, respectively.

Inventory

Inventory consists of the following:

|

| | | | | | | |

| | March 31,

2019 | | December 31,

2018 |

| | (In thousands) |

| Raw materials | $ | 43 |

|

| $ | 83 |

|

| Work-in-progress | 392 |

|

| — |

|

| Finished goods | 301 |

|

| 5 |

|

| Total inventory | $ | 736 |

| | $ | 88 |

|

Property and Equipment, Net

Property and equipment, net consists of the following:

|

| | | | | | | |

| | March 31,

2019 | | December 31,

2018 |

| | (In thousands) |

| Finance leases | $ | 4,863 |

|

| $ | 4,034 |

|

| Laboratory equipment | 2,717 |

|

| 2,569 |

|

| Computer equipment | 896 |

|

| 862 |

|

| Office equipment and furniture | 625 |

|

| 625 |

|

| Total cost | 9,101 |

|

| 8,090 |

|

| Less accumulated depreciation and amortization | (4,622 | ) |

| (4,245 | ) |

| Total property and equipment, net | $ | 4,479 |

|

| $ | 3,845 |

|

For the three months ended March 31, 2019 and 2018, depreciation and amortization expenses were $0.4 million and $0.2 million, respectively.

Accrued Expenses

Accrued expenses consist of the following:

|

| | | | | | | |

| | March 31,

2019 | | December 31,

2018 |

| | (In thousands) |

| Contract research and development | $ | 14,460 |

|

| $ | 12,012 |

|

| Sales rebates, fees and discounts | 8,161 |

|

| 8,075 |

|

| Employee compensation | 2,233 |

|

| 2,714 |

|

| Consulting and professional fees | 3,344 |

|

| 3,669 |

|

| Interest payable | 4,995 |

|

| 1,677 |

|

| Clinical trials | 913 |

|

| 820 |

|

| Other accrued expenses | 717 |

|

| 1,219 |

|

| Total accrued expenses | $ | 34,823 |

|

| $ | 30,186 |

|

Note 4—Fair-Value Measurements

As of September 30, 2018,March 31, 2019, and December 31, 2017,2018, all investments were classified as short-term and available-for-sale on the accompanying Condensed Consolidated Balance Sheets. Investment income, which was included as a component of other income, consists of interest earned.

On a recurring basis, we measure certain financial assets at fair value. Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability, an exit price, in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. The accounting standard establishes a fair value hierarchy that requires an entity to maximize the use of observable inputs, where available. The following summarizes the three levels of inputs required:

Level 1—Observable inputs for identical assets or liabilities, such as quoted prices in active markets;

Level 2—Inputs other than quoted prices in active markets that are either directly or indirectly observable; and

Level 3—Unobservable inputs in which little or no market data exists, therefore they are developed using estimates and assumptions developed by us, which reflect those that a market participant would use.

Our fair value hierarchy for our financial assets and liabilities measured at fair value on a recurring basis are as follows:

| | | | September 30, 2018 | March 31, 2019 |

| | Level 1 | | Level 2 | | Level 3 | | Total | Level 1 | | Level 2 | | Level 3 | | Total |

| | (In thousands) | (In thousands) |

| Assets: | | | | | | | | | | | | | | |

| Money-market funds classified as non-current restricted cash and investments | $ | 5,779 |

| | $ | — |

| | $ | — |

| | $ | 5,779 |

| $ | 1,154 |

| | $ | — |

| | $ | — |

| | $ | 1,154 |

|

| Money-market funds classified as short-term investments | 52,369 |

| | — |

| | — |

| | 52,369 |

| 43,168 |

| | — |

| | — |

| | 43,168 |

|

| Total | $ | 58,148 |

| | $ | — |

| | $ | — |

| | $ | 58,148 |

| $ | 44,322 |

| | $ | — |

| | $ | — |

| | $ | 44,322 |

|

| | | | December 31, 2017 | December 31, 2018 |

| | Level 1 | | Level 2 | | Level 3 | | Total | Level 1 | | Level 2 | | Level 3 | | Total |

| | (In thousands) | (In thousands) |

| Assets: | | | | | | | | | | | | | | |

| Money-market funds classified as non-current restricted cash and investments | $ | 5,835 |

| | $ | — |

| | $ | — |

| | $ | 5,835 |

| $ | 1,154 |

| | $ | — |

| | $ | — |

| | $ | 1,154 |

|

| Money-market funds classified as short-term investments | 80,355 |

| | — |

| | — |

| | 80,355 |

| 54,637 |

| | — |

| | — |

| | 54,637 |

|

| Total | $ | 86,190 |

| | $ | — |

| | $ | — |

| | $ | 86,190 |

| $ | 55,791 |

| | $ | — |

| | $ | — |

| | $ | 55,791 |

|

Cash held in demand deposit accounts of $2.8$4.1 million and $3.4$5.9 million is excluded from our fair-value hierarchy disclosure as of September 30, 2018March 31, 2019 and December 31, 20172018, respectively. There were no unrealized gains or losses associated with our short-term investments as of September 30, 2018March 31, 2019 or December 31, 20172018. The carrying amounts reported in the accompanying Condensed Consolidated Balance Sheets for receivables, accounts payable, other current monetary assets and liabilities and notes payable and lease financing obligations approximate fair value.

Note 5—Accrued Liabilities

Accrued liabilities consist of the following:

|

| | | | | | | |

| | September 30,

2018 | | December 31,

2017 |

| | (In thousands) |

| Contract research and development | $ | 6,760 |

|

| $ | 4,251 |

|

| Employee compensation | 2,993 |

|

| 2,178 |

|

| Sales rebates, fees and discounts | 2,250 |

|

| 6,561 |

|

| Consulting and professional fees | 1,570 |

|

| 1,758 |

|

| Clinical trials | 453 |

|

| 1,026 |

|

| ASC/hospital product return liability | — |

|

| 2,350 |

|

| Other accruals | 1,154 |

|

| 1,002 |

|

| Total accrued liabilities | $ | 15,180 |

|

| $ | 19,126 |

|

Note 6—5—Notes Payable and Lease Financing Obligations

Notes payable and lease financing obligations consist of the following:

|

| | | | | | | |

| | September 30,

2018 | | December 31,

2017 |

| | (In thousands) |

| Notes payable | $ | 132,077 |

| | $ | 83,831 |

|

| Lender facility fee payable upon maturity | 6,604 |

| | 4,192 |

|

| Lease financing obligations | 1,513 |

| | 1,300 |

|

| Notes payable, facility fee and lease financing obligations | 140,194 |

| | 89,323 |

|

| Unamortized debt discount | (6,510 | ) | | (3,527 | ) |

| Unamortized debt issuance costs | (1,429 | ) | | (1,189 | ) |

| Current portion of lease financing obligations | (560 | ) | | (490 | ) |

| Non-current portion of notes payable and lease financing obligations, net | $ | 131,695 |

| | $ | 84,117 |

|

In October 2016, we entered into thea term loan agreement with CRG Loan Agreement which permits interest-only payments through December 31, 2020. Subject to the achievement of certain milestones, this interest-only period potentially could be extended through the maturity date of September 30, 2022. InServicing LLC (the CRG Loan) and, in November 2016, we borrowed $80.0 million under the CRG Loan Agreement and, inmillion. In May 2018, we borrowed the remaining $45.0 million available to us under the CRG Loan Agreement.and issued warrants to purchase up to 200,000 shares of our common stock with an exercise price of $23.00 per share. The warrants have a five-year term and remained outstanding as of March 31, 2019.

In November 2018, we issued unsecured convertible senior notes (see Note 6 - “Convertible Senior Notes”) and repaid the CRG Loan. Upon repayment, we incurred a loss on early extinguishment of debt of $13.0 million. As of March 31, 2019 and December 31, 2018 we did not have any notes payable outstanding.

Note 6—Convertible Senior Notes

On November 15, 2018, we issued at face value $210.0 million aggregate principal amount of our 6.25% Convertible Senior Notes due 2023 (the Convertible Notes). The CRG Loan Agreement accruesConvertible Notes are unsecured and accrue interest at an annual rate of 12.25% (4.00%6.25% per annum, payable semi-annually in arrears on May 15 and November 15 of which caneach year, beginning on May 15, 2019.

The Convertible Notes will be deferredconvertible into cash, shares of our common stock or a combination thereof, as we elect at our option throughsole discretion. The initial conversion rate is 52.0183 shares of our common stock per $1,000 of note principal (equivalent to an initial conversion price of approximately $19.22 per share of common stock), subject to adjustment in certain circumstances. As of March 31, 2019, all Convertible Notes remain outstanding.

The balance of our Convertible Notes at March 31, 2019 and December 31, 2020 by adding such amount to the aggregate principal amount). As of September 30, 2018, is as allowed under the CRG Loan Agreement, we have deferred $7.1 million ($3.2 million for the nine months ended September 30, 2018) of accrued interest by increasing the principal amount outstanding. The CRG Loan Agreement requires us to maintain cash and cash equivalents of $5.0 million during the term of the agreement which is recorded as restricted investments in our Condensed Consolidated Balance Sheet.follows:

We are also required to pay a facility fee equal to 5.00% of the aggregate principal amount borrowed (including principal additions related to deferred interest) on repayment of the CRG Loan Agreement. The facility fee is being accreted to notes payable using the effective interest method over the term of the CRG Loan Agreement.We may prepay all or a portion of the outstanding principal under the CRG Loan Agreement at any time upon prior notice subject to a 4.00% prepayment fee through September 30, 2019, and with no prepayment fee being owed thereafter. In certain circumstances, including a change of control and certain asset sales or licensing transactions, we are required to prepay all or a portion of the loan, including the applicable prepayment premium on the outstanding principal to be prepaid. |

| | | | | | | |

| | March 31,

2019 | | December 31,

2018 |

| | (In thousands) |

| Principal amount | $ | 210,000 |

| | $ | 210,000 |

|

| Unamortized discount | (54,130 | ) | | (56,156 | ) |

| Unamortized issuance costs attributable to principal amount | (4,688 | ) | | (4,863 | ) |

| Total Convertible Notes, net | $ | 151,182 |

| | $ | 148,981 |

|

For calendar year 2019 and beyond, the CRG Loan Agreement requires us to achieve either (a) certain minimum net revenue amounts through the end of 2021, which is $75.0 million for the 2019 calendar year, or (b) a minimum market capitalization threshold equal to the product of 3.0 multiplied by the aggregate principal amount of loans outstanding under the CRG Loan Agreement determined as of the fifth business day following announcement of earnings results for the applicable year (i.e., $375.0 million). In the event we do not achieve either the minimum revenue amount or the minimum market capitalization threshold for a year, we can satisfy the requirement by raising additional funds through an equity or subordinated debt issuance and using the proceeds to pay down the loan balance by an amount equal to the difference between the minimum revenue amount for such year and the actual revenue amount for such year.

The CRG Loan Agreement includes customary events of default (seemore details on our Convertible Notes see Part II, Item 8, Note 7 of the “Notes to Consolidated Financial Statements” included8 - “Convertible Senior Notes” in our Annual Report on Form 10-K for the year ended December 31, 2017). If there is an event of default the lenders may have the right to accelerate all our repayment obligations under the CRG Loan Agreement and to take control of our pledged assets, which consists of substantially all of our assets including our intellectual property. Under certain circumstances, a default interest rate of an additional 4.00% per annum will apply to all outstanding obligations during the existence of an event of default.2018.

Note 7—Lease Liabilities

We have operating leases related to our office and laboratory space in The Omeros Building. The initial term of the leases is through November 2027 and we have two options to extend the lease term, each by five years. We have finance leases for certain laboratory and office equipment that have lease terms expiring through December 2021.

The lease-related assets and liabilities recorded on the balance sheet are as follows. Prior year interim financial statements were not recast under the new standard and, therefore, those amounts are not presented below.

|

| | | | | | |

| | | | | |

| | | Classification on the Balance Sheet | | March 31, 2019 |

| Assets | | | | (In thousands) |

| Operating lease assets | | Right of use assets | | $ | 17,514 |

|

| Finance lease assets | | Property and equipment, net | | 3,413 |

|

| Total lease assets | | | | $ | 20,927 |

|

| | | | | |

| Liabilities | | | | |

| Current: | | | | |

| Operating Leases | | Current portion of lease liabilities | | $ | 1,415 |

|

| Finance Lease | | Current portion of lease liabilities | | 1,146 |

|

| Non-current: | | | |

|

| Operating | | Lease liability, non-current | | 24,683 |

|

| Finance | | Lease liability, non-current | | 1,895 |

|

| Total lease liabilities | | | | $ | 29,139 |

|

| | | | | |

| Weighted-average remaining lease term | | | | |

| Operating leases | | | | 8.6 years |

|

| Finance leases | | | | 2.9 years |

|

| Weighted-average discount rate | | | | |

| Operating leases (1) | | | | 12.85 | % |

| Finance leases | | | | 12.31 | % |

(1) Upon adoption of the new lease standard, Topic 842, the discount rate used for existing operating leases was established at January 1, 2019 and represents our incremental borrowing rate.

The components of total lease costs are as follows:

|

| | | |

| | Three Months Ended

March 31, 2019 |

| | (In thousands) |

| Lease cost | |

| Operating lease cost | $ | 1,031 |

|

| Finance lease cost: | |

| Amortization | 290 |

|

| Interest | 82 |

|

| Short-term lease cost | 138 |

|

| Variable lease costs | 486 |

|

| Sublease income | (224 | ) |

| Total lease cost | $ | 1,803 |

|

The supplemental cash flow information related to leases during 2019 is as follows:

|

| | | |

| Cash paid for amounts included in the measurement of lease liabilities: | |

| Operating cash flows from operating leases | $ | 1,647 |

|

| Operating cash flows from finance leases | $ | 82 |

|

| Financing cash flows from finance leases | $ | 254 |

|

The future maturities of our lease liabilities as of March 31, 2019 are as follows:

|

| | | | | | | |

| | Operating Leases | | Finance Leases |

| | (In thousands) |

| 2019 | $ | 3,499 |

|

| $ | 1,060 |

|

| 2020 | 4,770 |

|

| 1,224 |

|

| 2021 | 4,880 |

|

| 866 |

|

| 2022 | 4,995 |

|

| 290 |

|

| 2023 | 5,112 |

|

| 95 |

|

| Thereafter | 20,728 |

|

| — |

|

| Total undiscounted lease payments | $ | 43,984 |

|

| $ | 3,535 |

|

| Less interest | (17,886 | ) |

| (494 | ) |

| Lease liabilities | $ | 26,098 |

|

| $ | 3,041 |

|

As of March 31, 2019, we have a lease for additional space in The Omeros Building that will commence in late 2019. The expected lease term is seven years and the monthly lease payments are approximately $0.1 million over the expected term lease.

Note 7—8—Commitments and Contingencies

Contracts

We have various agreements with third parties that collectively require payment of termination fees totaling $13.7 million as of March 31, 2019 if we cancel the work within specific time frames, either prior to commencing or during performance of the contracted services.

Development Milestones and Product Royalties

We have licensed a variety of intellectual property from third parties that we are currently developing or may develop in the future. These licenses may require milestone payments during the clinical development processes as well as low single to low double-digit royalties on the net income or net sales of the product.

Contracts

We have various agreements with third parties that collectively require payment of termination fees totaling $11.5 million as of September 30, 2018 if we cancel work within specific time frames, either prior to commencing or during performance of For the contracted services. This is in addition to fees associated with the CRG Loan Agreement (see Note 6).

Litigation

In May 2017, we received Notice Letters from Sandoz Inc. (Sandoz) and Lupin Ltd. and Lupin Pharmaceuticals, Inc. (collectively, Lupin), respectively, that Sandoz and Lupin had each filed an Abbreviated New Drug Application (ANDA) seeking approval from the U.S. Food and Drug Administration (FDA) to market a generic version of OMIDRIA prior to the expiration our patents covering OMIDRIA. In June 2017, we filed patent infringement lawsuits against Sandoz and Lupin. In May 2018, we entered into a settlement agreement and consent judgment with Lupin resolving our patent litigation against Lupin and, in July 2018, our patent infringement lawsuit against Sandoz was dismissed by stipulation of the parties based on Sandoz’s revision of its Patent and Exclusivity Certification to a Paragraph III certification with respect to the patents-in-suit. As a result of an earlier settlement in October 2017 involving substantially similar assertions with Par Pharmaceutical, Inc. and its subsidiary, Par Sterile Products, LLC (collectively, Par), the Lupin settlement agreement and consent judgmentthree months ended March 31, 2019 and the Sandoz dismissal, all of our litigation with ANDA filers has been concluded. Based on the Paryear ended December 31, 2018, development milestones incurred were immaterial and Lupin settlement agreements and Sandoz’s conversion to a Paragraph III certification, the earliest ANDA entry date forwe did not owe any of the three generic manufacturers is April 2032 unless otherwise subsequently authorized pursuant to the settlement agreements.royalties.

Note 8—9—Shareholders’ EquityDeficit

Common Stock

For the ninethree months ended September 30, 2018,March 31, 2019, we received proceeds of $6.7$0.1 million upon the exercise of stock options which resulted in the issuance of 763,57510,744 shares of common stock. For the ninethree months ended September 30, 2017,March 31, 2018, we received proceeds of $10.5$0.7 million upon the exercise of stock options and warrants which resulted in the issuance of 628,47075,616 shares of common stock.

Warrants

In connection with the April 2018 amendment to the CRG Loan Agreement,and the May 2018 borrowing under the CRG Loan, we issued warrants to purchase up to 200,000 shares of our common stock with an exercise price of $23.00 per share and total fair value of $1.4 million. The warrants have a five-year term.term and remain outstanding as of March 31, 2019.

In September 2018, other warrant holders with a right to purchase 57,487 sharesInterim Condensed Consolidated Statements of Shareholders’ Deficit

The changes in interim balances of the components of our common stock exercised their warrants. In conjunction with this cashless exercise, we issued 34,509 shares of our common stock.shareholders’ deficit are as follows:

|

| | | | | | | |

| | Three Months Ended

March 31, |

| | 2019 | | 2018 |

| | (In thousands) |

| | | | |

| Beginning and ending common stock | $ | 490 |

|

| $ | 483 |

|

|

|

|

|

| Beginning additional paid-in capital | $ | 549,479 |

|

| $ | 520,071 |

|

| Exercise of stock options | 108 |

|

| 687 |

|

| Stock-based compensation expense | 3,374 |

|

| 2,966 |

|

| Ending additional paid-in capital | $ | 552,961 |

|

| $ | 523,724 |

|

|

|

|

|

| Beginning accumulated deficit | $ | (650,125 | ) |

| $ | (523,368 | ) |

| Net loss | (24,345 | ) |

| (30,054 | ) |

| Ending accumulated deficit | $ | (674,470 | ) |

| $ | (553,422 | ) |

Note 9—10—Stock-Based Compensation

Stock-based compensation expense includes the amortization of stock options granted to employees and non-employees and has been reported in our Condensed Consolidated Statements of Operations and Comprehensive Loss as follows:

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

March 31, |

| | 2018 | | 2017 | | 2018 | | 2017 | 2019 | | 2018 |

| | (In thousands) | | (In thousands) | (In thousands) |

| Research and development | $ | 1,334 |

| | $ | 1,297 |

| | $ | 3,720 |

| | $ | 4,034 |

| $ | 1,494 |

| | $ | 1,200 |

|

| Selling, general and administrative | 1,595 |

|

| 1,744 |

|

| 5,176 |

|

| 5,415 |

| 1,880 |

|

| 1,766 |

|

| Total | $ | 2,929 |

| | $ | 3,041 |

| | $ | 8,896 |

| | $ | 9,449 |

| $ | 3,374 |

| | $ | 2,966 |

|

The fair value of each option grant to employees, directors and directorsnon-employees is estimated on the date of grant using the Black-Scholes option-pricing model. The following assumptions were applied to employee and directorall stock option grants as follows:grants:

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

March 31, |

| | 2018 | | 2017 | | 2018 | | 2017 | 2019 | | 2018 |

| Estimated weighted-average fair value | $ | 16.30 |

|

| $ | 13.66 |

|

| $ | 10.22 |

|

| $ | 8.38 |

| $ | 9.47 |

|

| $ | 9.79 |

|

| Weighted-average assumptions | |

|

|

|

|

|

| |

|

|

| Expected volatility | 78 | % |

| 74 | % |

| 77 | % |

| 74 | % | 81 | % |

| 76 | % |

| Expected term, in years | 6.1 |

|

| 6.1 |

|

| 6.0 |

|

| 6.0 |

| 6.0 |

|

| 6.1 |

|

| Risk-free interest rate | 2.77 | % |

| 1.95 | % |

| 2.66 | % |

| 1.99 | % | 2.48 | % |

| 2.54 | % |

| Expected dividend yield | — | % |

| — | % |

| — | % |

| — | % | — | % |

| — | % |

Stock option activity for all stock plans and related information is as follows:

|

| | | | | | | | | | | | |

| | Options Outstanding | | Weighted- Average Exercise Price per Share | | Remaining Contractual Life (In years) | | Aggregate Intrinsic Value (In thousands) |

| Balance at December 31, 2017 | 9,657,259 |

| | $ | 10.39 |

| | | | |

| Granted | 1,692,207 |

| | 14.91 |

| | | | |

| Exercised | (763,575 | ) | | 8.80 |

| | | | |

| Forfeited | (462,361 | ) | | 13.39 |

| | | | |

| Balance at September 30, 2018 | 10,123,530 |

| | $ | 11.13 |

| | 6.6044 | | $ | 134,484 |

|

| Vested and expected to vest at September 30, 2018 | 9,818,340 |

| | $ | 11.06 |

| | 6.5344 | | $ | 131,102 |

|

| Exercisable at September 30, 2018 | 7,155,818 |

| | $ | 10.13 |

| | 5.6582 | | $ | 102,201 |

|

|

| | | | | | | | | | | | |

| | Options Outstanding | | Weighted- Average Exercise Price per Share | | Remaining Contractual Life (In years) | | Aggregate Intrinsic Value (In thousands) |

| Balance at December 31, 2018 | 10,313,138 |

| | $ | 11.22 |

| | | | |

| Granted | 1,606,500 |

| | 13.49 |

| | | | |

| Exercised | (10,744 | ) | | 10.01 |

| | | | |

| Forfeited | (68,373 | ) | | 14.67 |

| | | | |

| Balance at March 31, 2019 | 11,840,521 |

| | $ | 11.51 |

| | 6.62 | | $ | 71,857 |

|

| Vested and expected to vest at March 31, 2019 | 11,402,367 |

| | $ | 11.41 |

| | 6.53 | | $ | 70,182 |

|

| Exercisable at March 31, 2019 | 7,815,290 |

| | $ | 10.31 |

| | 5.35 | | $ | 56,232 |

|

At September 30, 2018,March 31, 2019, there were 2,967,7124,025,230 unvested options outstanding that will vest over a weighted-average period of 2.89.1 years and 2,210,945554,083 shares were available to grant. Excluding non-employee stock options, theThe total estimated compensation expense to be recognized on our unvested options is $32.3$15.6 million.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read in conjunction with the unaudited condensed consolidated financial statements and notes thereto included elsewhere in this Quarterly Report on Form 10-Q.

Overview

We are a commercial-stage biopharmaceutical company committed to discovering, developing and commercializing small-molecule and protein therapeutics for large-market as well as orphan indications targeting inflammation, complement-mediated diseases, and disorders of the central nervous system.system, and immune-related diseases, including cancers.

Our drug product OMIDRIA® is marketed in the United States or U.S., for use during cataract surgery or intraocular lens, or IOL, replacement to maintain pupil size by preventing intraoperative miosis (pupil constriction) and to reduce postoperative pain. In our pipeline we have clinical-stage development programs focused on: complement-associated thrombotic microangiopathies; complement-mediated glomerulonephropathies; cognitive impairment; and addictive and compulsive disorders. In addition, we have a diverse group of preclinical programs and two platforms: one capable of unlocking new G protein-coupled receptor, or GPCR, drug targets and the other used to generate antibodies. For OMIDRIA and each of our product candidates and our programs, we have retained control of all commercial rights.

Commercial Products, Product Candidates, Development Programs and Platforms

- OMIDRIA. ® (phenylephrine and ketorolac intraocular solution) 1%/0.3%

OMIDRIA is approved inby the U.S.by the U.S. Food and Drug Administration, or FDA for use during cataract surgery or IOL replacement to maintain pupil size by preventing intraoperative miosis (pupil constriction) and to reduce postoperative ocular pain. InOutside of the U.S., we have received approval from the European Commission, or EC, to market OMIDRIA in the European Economic Area, or EEA, for use during cataract surgery and other IOL replacement procedures for maintenance of intraoperative mydriasis (pupil dilation), prevention of intraoperative miosis and reduction of acute postoperative ocular pain. OMIDRIA is solda proprietary drug product containing two active pharmaceutical ingredients, or APIs: ketorolac, an anti-inflammatory agent, and phenylephrine, a mydriatic, or pupil dilating, agent. Cataract and other lens replacement surgery involves replacement of the original lens of the eye with an artificial intraocular lens. These procedures are typically performed to replace a lens opacified by a cataract and/or to correct a refractive error. OMIDRIA is added to standard irrigation solution used during cataract and lens replacement surgery and is delivered intracamerally, or within the anterior chamber of the eye, to the site of the surgical trauma throughout the procedure. Preventing pupil constriction is essential for these procedures and, if miosis occurs, the risk of damaging structures within the eye and other complications increases, as does the operating time required to perform the procedure.

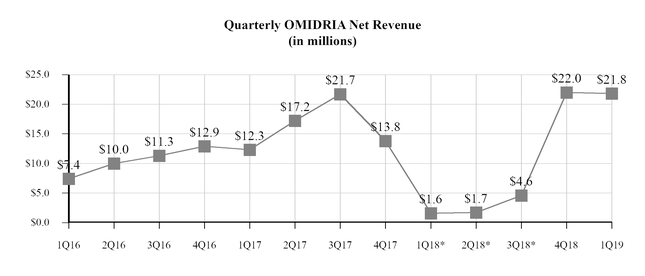

We launched OMIDRIA in the U.S. in the second quarter of 2015 and sell OMIDRIA primarily through wholesalers which, in turn, sell to ASCs and hospitals. The Centers for Medicare & Medicaid Services, or CMS, the federal agency responsible for administering the Medicare program, granted transitional pass-through reimbursement status for OMIDRIA in 2014, effective from January 1, 2015 through December 31, 2017. Pass-through status allows for separate payment (i.e.(i.e., outside the procedural packaged payment rate)rate for the surgical procedure) under Medicare Part B. In March 2018, the Consolidated Appropriations Act of 2018, or the Appropriations Act, was signed into law. The Appropriations Act includes a provision that extendsby which Congress extended pass-through reimbursement status for a small number of drugs, including OMIDRIA, used during procedures performed on Medicare Part B fee-for-service patients for an additional two years, running from October 1, 2018 until October 1, 2020. As a result of this extension, each of these drugs, including OMIDRIA, receives separate payment for the two-year period that began on October 1, 2018. We also continue to pursue permanent separate reimbursement for OMIDRIA. In the recently released 2019 final rule for CMS’ outpatient prospective payment system, or OPPS, CMS indicated that, in the ASC setting, it will separately pay in the ASC setting for certain non-opioid drugs used during surgery that have an FDA-approved indication for postoperative pain relief and are currently packaged with the procedure in calendar year 2019. Although OMIDRIA is not specifically named because it currently is paid separately, we believe that OMIDRIA meets this definition. The preamble todefinition and would qualify for separate payment under this section of the OPPS Final Rule indicates that CMS will apply the exclusion from packaged payment to other drugsprovision if it is continued in the future if they meet the criteria.subsequent years. The OPPS Final Rule also states that CMS will consider in future rule-making a policy that pays separately for drugs used during cataract surgery that have an FDA-approved indication to address postoperative issues. We believe that OMIDRIA also meets this definition. We are continuing to confirm these beliefs and to pursue other avenues of permanent separate payment or similar reimbursement for OMIDRIA beyond September 30, 2020 but we cannot provide assurance that these efforts will be successful. We also continue to pursue expansion of reimbursement for OMIDRIA by Medicare Advantage and other third-party payers. OMIDRIA revenues in the first three quarters of 2018 were significantly reduced due to the expiration of pass-through reimbursement status on January 1, 2018. Since pass-through reimbursement was reinstated on October 1 of this year, weekly sales of OMIDRIA have increased substantially from levels seen during the first nine months of the year. For more information regarding OMIDRIA reimbursement, see “Results of Operations” and “Financial Condition - Liquidity and Capital Resources” below.

In October 2017 and May 2018, we entered into a settlement agreement and consent judgment with Par Pharmaceutical, Inc. and its subsidiary, Par Sterile Products, LLC, or collectively Par, and with Lupin Ltd. and Lupin Pharmaceuticals, Inc., or collectively Lupin, respectively, resolving our patent infringement lawsuits against these companies that resulted from each having filed with the FDA an Abbreviated New Drug Application, or ANDA, containing a Paragraph IV Certification under the Hatch-Waxman Act seeking approval to market a generic version of OMIDRIA prior to the expiration of our Orange Book Patents for OMIDRIA. In addition, in July 2018 we announced that our patent infringement lawsuit against Sandoz, Inc., or Sandoz, which had also filed an ANDA containing a Paragraph IV Certification seeking approval to market a generic version of OMIDRIA, had been dismissed by stipulation of the parties based on Sandoz’s conversion to Paragraph III certifications with respect to the patents covering OMIDRIA. As a result, all of our litigation with ANDA filers has been concluded. Based on the Par and Lupin settlement agreements and Sandoz’s conversion to a Paragraph III certification, the earliest ANDA entry date for any of the three generic manufacturers is April 2032 unless otherwise subsequently authorized pursuant to the settlement agreements. For more information regarding these matters, see Part II, Item 1, “Legal Proceedings.”

Outside of the U.S., we have received approval from the European Commission, or EC, to market OMIDRIA in the European Economic Area, or EEA, for use during cataract surgery and other IOL replacement procedures to maintain mydriasis (pupil dilation), to prevent miosis (pupil constriction), and to reduce postoperative eye pain. In July 2018, we reported that OMIDRIA had been placed on the market in the European Union, or EU, on a limited basis, which maintained the ongoing validity of the European marketing authorization for OMIDRIA. Decisions about price and reimbursement for OMIDRIA are made on a country-by-country basis and may be required before marketing may occur in a particular country. Timing of any partnerships or independent launch depends on numerous factors, including domestic sales of OMIDRIA, completion of mutual diligence exercises and/or entry into suitable agreements with contract service vendors. In addition, we have an exclusive supply and distribution agreement for the sale of OMIDRIA in certain countries in the Middle East, including the Kingdom of Saudi Arabia and the United Arab Emirates, under which sales began on a limited basis in the Kingdom of Saudi Arabia in 2016. At this time we do not expect to see significant sales of OMIDRIA in any countries within the EEA or

other international territories if we are unable to enter into partnershipsterritories. We have an exclusive supply and distribution agreement with ITROM Trading Drug Store, or ITROM, for the marketing and distributionsale of OMIDRIA or complete an independent broad launch in any such country.the Kingdom of Saudi Arabia, the United Arab Emirates and certain other countries in the Middle East. Under our agreement, ITROM is responsible for obtaining marketing authorizations for OMIDRIA on our behalf and for promoting, marketing, selling and distributing product supplied by us within the licensed territory. ITROM began selling OMIDRIA in December 2016 on a limited basis in the Kingdom of Saudi Arabia. Revenues to date under our agreement with ITROM have not been material.