UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

For the Quarterly Period Ended June 30, 2012March 31, 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

ARMOUR RESIDENTIAL REIT, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 001-34766 | 26-1908763 |

| (State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

3001 Ocean Drive, Suite 201, Vero Beach, FL 32963

(Address of principal executive offices)(zip code)

(772) 617-4340

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES ý NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding twelve12 months (or for such shorter period that the registrant was required to submit and post such files). YES ý NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See definitionthe definitions of "larger"large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer oý Accelerated filer ýo Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES o NO ý

The number of outstanding shares of the Registrant’s common stock as of July 30, 2012May 1, 2013 was 234,226,342.374,119,857.

ARMOUR Residential REIT, Inc.

TABLE OF CONTENTS

| PART I. FINANCIAL INFORMATION | 3 |

| Item 1. Financial Statements | 3 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 2125 |

Item 3. Quantitative and Qualitative Disclosures Aboutabout Market Risk | 3240 |

| Item 4. Controls and Procedures | 3442 |

| PART II. OTHER INFORMATION | 3542 |

| Item 1. Legal Proceedings | 3542 |

| Item 1A. Risk Factors | 3542 |

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | 3542 |

| Item 3. Defaults Upon Senior Securities | 3542 |

| Item 4. Mine Safety Disclosures | 3542 |

| Item 5. Other Information | 3542 |

| Item 6. Exhibits | 3542 |

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except per share amounts)

(Unaudited)

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED BALANCE SHEETS

(dollars in thousands, except share and per share amounts)

(Unaudited)| | | March 31, 2013 | | | December 31, 2012 | |

| Assets | | | | | | | | |

| Cash and cash equivalents | | $ | 836,501 | | | $ | 771,282 | |

| Cash collateral posted | | | 230,451 | | | | 265,552 | |

| Agency Securities, available for sale, at fair value (including pledged assets of $23,810,215 and $18,578,690) | | | 24,339,169 | | | | 19,096,562 | |

| Receivable for unsettled securities | | | 2,226,168 | | | | 668,244 | |

| Derivatives, at fair value | | | 38,923 | | | | 5,367 | |

| Principal payments receivable | | | 9,381 | | | | 16,037 | |

| Accrued interest receivable | | | 71,664 | | | | 55,430 | |

| Prepaid and other assets | | | 559 | | | | 404 | |

| Total Assets | | $ | 27,752,816 | | | $ | 20,878,878 | |

| | | | | | | | | |

| Liabilities and Stockholders’ Equity | | | | | | | | |

| Liabilities: | | | | | | | | |

| Repurchase agreements | | $ | 24,828,614 | | | $ | 18,366,095 | |

| Derivatives, at fair value | | | 191,514 | | | | 190,540 | |

| Accrued interest payable | | | 10,302 | | | | 10,064 | |

| Cash collateral held | | | 10,155 | | | | - | |

| Accounts payable and accrued expenses | | | 3,425 | | | | 4,395 | |

| Dividends payable | | | 8 | | | | 9 | |

| Total Liabilities | | | 25,044,018 | | | | 18,571,103 | |

| | | | | | | | | |

| Stockholders’ Equity: | | | | | | | | |

| Preferred stock, $0.001 par value, 50,000 shares authorized; | | | | | | | | |

8.250% Series A Cumulative Preferred Stock; 2,181 and 2,006 issued and outstanding at March 31, 2013 and December 31, 2012 | | | 2 | | | | 2 | |

| 7.875% Series B Cumulative Preferred Stock; 5,650 and none issued and outstanding at March 31, 2013 and December 31, 2012 | | | 6 | | | | - | |

| Common stock, $0.001 par value, 1,000,000 shares authorized, 374,053 and 309,013 shares issued and outstanding at March 31, 2013 and December 31, 2012 | | | 374 | | | | 309 | |

| Additional paid-in capital | | | 2,805,755 | | | | 2,226,198 | |

| Accumulated deficit | | | (129,334 | ) | | | (149,298 | ) |

| Accumulated other comprehensive income | | | 31,995 | | | | 230,564 | |

| Total Stockholders’ Equity | | | 2,708,798 | | | | 2,307,775 | |

| Total Liabilities and Stockholders’ Equity | | $ | 27,752,816 | | | $ | 20,878,878 | |

| Assets | | June 30, 2012 | | | December 31, 2011 | |

| Cash | | $ | 326,736 | | | $ | 252,372 | |

| Restricted cash | | | 193,086 | | | | 147,199 | |

| Agency securities, available for sale, at fair value (including pledged assets of $12,758,125 and $5,225,234) | | | 13,328,514 | | | | 5,393,675 | |

| Receivable for unsettled securities | | | - | | | | 382,931 | |

| Derivatives, at fair value | | | 9,600 | | | | - | |

| Principal payments receivable | | | 9,190 | | | | 12,493 | |

| Accrued interest receivable | | | 38,544 | | | | 18,637 | |

| Prepaid and other assets | | | 823 | | | | 440 | |

| Total Assets | | $ | 13,906,493 | | | $ | 6,207,747 | |

| | | | | | | | | |

| Liabilities and Stockholders’ Equity | | | | | | | | |

| Liabilities: | | | | | | | | |

| Repurchase agreements | | $ | 12,112,586 | | | $ | 5,335,962 | |

| Payable for unsettled securities | | | 272,863 | | | | 117,885 | |

| Derivatives, at fair value | | | 156,515 | | | | 121,727 | |

| Accrued interest payable | | | 3,373 | | | | 2,154 | |

| Accounts payable and accrued expenses | | | 2,790 | | | | 2,663 | |

| Dividends payable | | | 276 | | | | 750 | |

| Total Liabilities | | | 12,548,403 | | | | 5,581,141 | |

| | | | | | | | | |

| Stockholders’ Equity: | | | | | | | | |

| Preferred stock, $0.001 par value, 25,000,000 shares authorized, 1,400,000 8.250% Series A Cumulative Preferred Stock issued and outstanding at June 30, 2012 and none issued and outstanding at December 31, 2011 | | | 1 | | | | - | |

| Common stock, $0.001 par value, 500,000,000 shares authorized, 188,185,880 and 95,436,949 shares issued and outstanding at June 30, 2012 and December 31, 2011, respectively | | | 188 | | | | 95 | |

| Additional paid-in capital | | | 1,340,403 | | | | 678,641 | |

| Accumulated deficit | | | (150,152 | ) | | | (100,878 | ) |

| Accumulated other comprehensive income | | | 167,650 | | | | 48,748 | |

| Total Stockholders’ Equity | | | 1,358,090 | | | | 626,606 | |

| Total Liabilities and Stockholders’ Equity | | $ | 13,906,493 | | | $ | 6,207,747 | |

See notes to condensed consolidated financial statements.

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(dollars in thousands, except per share amounts)

(Unaudited)

| | For the Quarters Ended | | For the Six Months Ended | | For the Quarters Ended | |

| | June 30, 2012 | | June 30, 2011 | | | June 30, 2012 | | June 30, 2011 | | | March 31, 2013 | | March 31, 2012 | |

| Interest Income: | | | | | | | | | | | | | | |

| Interest income, net of amortization of premium | $ | 86,204 | | $ | 29,105 | | | $ | 148,967 | | | $ | 42,629 | | | $ | 130,637 | | | $ | 62,763 | |

| Interest expense: | | | | | | | | | | | | | | | | |

| Repurchase agreements | | (11,106 | ) | | (2,351 | ) | | | (18,036 | ) | | | (3,707 | ) | | | (25,475 | ) | | | (6,929 | ) |

| Net interest income | | 75,098 | | | 26,754 | | | | 130,931 | | | | 38,922 | | | | 105,162 | | | | 55,834 | |

| Other (Loss) Income: | | | | | | | | | | | |

| Realized (loss) gain on sale of agency securities | | (1,268 | ) | | - | | | | 5,048 | | | | - | | |

| Other income | | 1,043 | | | - | | | 1,043 | | | - | | |

| Other Income: | | | | | | | |

Realized gain on sale of Agency Securities (reclassified from Other comprehensive (loss) income) | | | | 18,514 | | | | 6,316 | |

Realized loss on derivatives (Note 8) | | | | (29,053 | ) | | | (9,741 | ) |

| Unrealized gain on derivatives | | | | 16,301 | | | | 17,614 | |

| Subtotal | | (225 | ) | | - | | | | 6,091 | | | | - | | | | (12,752 | ) | | | 7,873 | |

| Realized loss on derivatives (1) | | (12,400 | ) | | (6,078 | ) | | | (22,140 | ) | | | (8,004 | ) | |

| Unrealized loss on derivatives | | (70,394 | ) | | (25,817 | ) | | | (52,780 | ) | | | (26,083 | ) | |

| Subtotal | | (82,794 | ) | | (31,895 | ) | | | (74,920 | ) | | | (34,087 | ) | |

| Total other (loss) | | (83,019 | ) | | (31,895 | ) | | | (68,829 | ) | | | (34,087 | ) | |

| Total other income | | | | 5,762 | | | | 14,189 | |

| Expenses: | | | | | | | | | | | | | | | | |

| Management fee | | 4,298 | | 1,495 | | | | 7,811 | | | | 2,251 | | | | 6,633 | | 3,512 | |

| Professional fees | | 425 | | 242 | | | | 936 | | | | 613 | | | | 1,004 | | | | 511 | |

| Insurance | | 55 | | 51 | | | | 104 | | | | 103 | | | | 78 | | | | 49 | |

| Compensation | | 498 | | 140 | | | | 992 | | | | 272 | | | | 257 | | | | 493 | |

| Other | | 407 | | | 200 | | | | 672 | | | | 260 | | | | 662 | | | | 266 | |

| Total expenses | | 5,683 | | | 2,128 | | | | 10,515 | | | | 3,499 | | | | 8,634 | | | | 4,831 | |

| Net (loss) income before taxes | | (13,604 | ) | | (7,269 | ) | | | 51,587 | | | | 1,336 | | |

| Income tax (expense) benefit | | (3 | ) | | (3 | ) | | | 29 | | | | (12 | ) | |

| Net (Loss) Income | $ | (13,607 | ) | $ | (7,272 | ) | | $ | 51,616 | | | $ | 1,324 | | |

| Dividends on preferred stock | | (160 | ) | | - | | | (160 | ) | | | - | | |

| Net (Loss) Income (related) available to common stockholders | $ | (13,767 | ) | $ | (7,272 | ) | | $ | 51,456 | | $ | 1,324 | | |

| Net (loss) income (related) available per share to common stockholders: | | | | | | | | | | | |

| Net income before taxes | | | | 102,290 | | | | 65,192 | |

| Income tax benefit | | | | - | | | | 32 | |

| Net Income | | | | 102,290 | | | | 65,224 | |

| Dividends declared on preferred stock | | | | (2,497 | ) | | | - | |

| Net Income available to common stockholders | | | $ | 99,793 | | | $ | 65,224 | |

| Net income available per share to common stockholders: | | | | | | | |

| Basic | $ | (0.08 | ) | $ | (0.14 | ) | | $ | 0.33 | | | $ | 0.03 | | | $ | 0.30 | | | | 0.48 | |

| Diluted | $ | (0.08 | ) | $ | (0.14 | ) | | $ | 0.32 | | $ | 0.03 | | | $ | 0.29 | | | $ | 0.48 | |

| Dividends per common share | $ | 0.30 | | $ | 0.36 | | | $ | 0.62 | | | $ | 0.70 | | |

| Dividends declared per common share | | | $ | 0.24 | | | $ | 0.32 | |

| Weighted average common shares outstanding: | | | | | | | | | | | | | | | | |

| Basic | | 180,773 | | | 53,259 | | | | 157,838 | | | | 39,903 | | | | 337,935 | | | 134,903 | |

| Diluted | | 180,773 | | | 53,259 | | | 158,553 | | | 40,062 | | | | 339,722 | | | | 134,903 | |

(1) | Interest expense related to our interest rate swap contracts is recorded in realized loss on derivatives on the condensed consolidated statements of operations. For additional information, see Note 8 to the condensed consolidated financial statements. |

See notes to condensed consolidated financial statements.

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(dollars (in thousands)

(Unaudited)

| | | For the Quarters Ended |

| | | March 31, 2013 | | | March 31, 2012 | |

| Net Income | | $ | 102,290 | | | $ | 65,224 | |

| Other comprehensive (loss) income : | | | | | | | | |

| Reclassification adjustment for realized gain on sale of Agency Securities | | | (18,514 | ) | | | (6,316 | ) |

| Net unrealized (loss) gain on Agency Securities | | | (180,055 | ) | | | 11,622 | |

| Other comprehensive (loss) income | | | (198,569 | ) | | | 5,306 | |

| Comprehensive (Loss) Income | | $ | (96,279 | ) | | $ | 70,530 | |

| | | For the Quarters Ended | | For the Six Months Ended |

| | | June 30, 2012 | | | June 30, 2011 | | | June 30, 2012 | | | June 30, 2011 | |

| Net (Loss) Income | | $ | (13,607 | ) | | $ | (7,272 | ) | | $ | 51,616 | | | $ | 1,324 | |

| Other comprehensive income : | | | | | | | | | | | | | | | | |

| Reclassification adjustment for realized loss (gain) on sale of Agency Securities | | | 1,268 | | | | - | | | | (5,048 | ) | | | - | |

| Net unrealized gain on available for sale securities | | | 112,328 | | | | 36,787 | | | | 123,950 | | | | 36,542 | |

| Other comprehensive income | | | 113,596 | | | | 36,787 | | | | 118,902 | | | | 36,542 | |

| Comprehensive Income | | $ | 99,989 | | | $ | 29,515 | | | $ | 170,518 | | | $ | 37,866 | |

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(in thousands, except per share amounts)

(Unaudited)

| | Preferred Stock | | Common Stock | | | | | | | | | |

| | 8.250% Series A | | 7.875% Series B | | | | | | | | | | | | | | | |

| | Shares | | Par Amount | | Additional Paid in Capital | | Shares | | Par Amount | | Additional Paid in Capital | | Shares | | Par Amount | | Additional Paid in Capital | | Total Additional Paid in Capital | | Accumulated Deficit | | Accumulated Other Comprehensive Income | | Total | |

| Balance, December 31, 2012 | 2,006 | | $ | 2 | | $ | 48,792 | | - | | $ | - | | $ | - | | 309,013 | | $ | 309 | | $ | 2,177,406 | | $ | 2,226,198 | | $ | (149,298 | ) | $ | 230,564 | | $ | 2,307,775 | |

| Series A Preferred dividends declared | - | | | - | | | - | | - | | | - | | | - | | - | | | - | | | - | | | - | | | (1,107 | ) | | - | | | (1,107 | ) |

| Series B Preferred dividends declared | - | | | - | | | - | | - | | | - | | | - | | - | | | - | | | - | | | - | | | (1,390 | ) | | - | | | (1,390 | ) |

| Common dividends declared | - | | | - | | | - | | - | | | - | | | - | | - | | | - | | | - | | | - | | | (79,829 | ) | | - | | | (79,829 | ) |

| Issuance of Series A Preferred stock, net | 175 | | | - | | | 4,381 | | - | | | - | | | - | | - | | | - | | | - | | | 4,381 | | | - | | | - | | | 4,381 | |

| Issuance of Series B Preferred stock | - | | | - | | | - | | 5,650 | | | 6 | | | 136,565 | | - | | | - | | | - | | | 136,565 | | | - | | | | | | 136,571 | |

| Issuance of common stock, net | - | | | - | | | - | | - | | | - | | | - | | 65,010 | | | 65 | | | 438,421 | | | 438,421 | | | - | | | - | | | 438,486 | |

| Stock based compensation, net of withholding requirements | - | | | - | | | - | | - | | | - | | | - | | 30 | | | - | | | 190 | | | 190 | | | - | | | - | | | 190 | |

| Net income | - | | | - | | | - | | - | | | - | | | - | | - | | | - | | | - | | | - | | | 102,290 | | | - | | | 102,290 | |

| Other comprehensive loss | - | | | - | | | - | | - | | | - | | | - | | - | | | - | | | - | | | - | | | - | | | (198,569 | ) | | (198,569 | ) |

| Balance, March 31, 2013 | 2,181 | | $ | 2 | | $ | 53,173 | | 5,650 | | $ | 6 | | $ | 136,565 | | 374,053 | | $ | 374 | | $ | 2,616,017 | | $ | 2,805,755 | | $ | (129,334 | ) | $ | 31,995 | | $ | 2,708,798 | |

See notes to condensed consolidated financial statements.

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED STATEMENTS of STOCKHOLDERS’ EQUITYOF CASH FLOWS

(dollars in thousands)

(Unaudited)

| | | Preferred Stock | | Common Stock | | | | | | | | | | | | |

| | | Shares | | | Par Amount | | | Additional Paid in Capital | | | Shares | | | Par Amount | | | Additional Paid in Capital | | Total Additional Paid in Capital | | Accumulated Deficit | | | Accumulated Other Comprehensive Income | | | Total | |

| Balance, December 31, 2011 | | | - | | | $ | - | | | | - | | | | 95,437 | | | $ | 95 | | | $ | 678,641 | | $ | 678,641 | | $ | (100,878 | ) | | $ | 48,748 | | | $ | 626,606 | |

| Preferred dividends declared | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | - | | | (160 | ) | | | - | | | | (160 | ) |

| Common dividends declared | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | - | | | (100,730 | ) | | | - | | | | (100,730 | ) |

| Issuance of Preferred stock, net | | | 1,400 | | | | 1 | | | | 33,778 | | | | - | | | | - | | | | - | | | 33,778 | | | - | | | | - | | | | 33,779 | |

| Issuance of common stock, net | | | - | | | | - | | | | - | | | | 92,705 | | | | 92 | | | | 627,724 | | | 627,724 | | | - | | | | - | | | | 627,816 | |

| Stock based compensation, net of withholding requirements | | | - | | | | - | | | | - | | | | 44 | | | | 1 | | | | 260 | | | 260 | | | - | | | | - | | | | 261 | |

| Net income | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | - | | | 51,616 | | | | - | | | | 51,616 | |

| Other comprehensive income | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | - | | | - | | | | 118,902 | | | | 118,902 | |

| Balance, June 30, 2012 | | | 1,400 | | | $ | 1 | | | $ | 33,778 | | | | 188,186 | | | $ | 188 | | | $ | 1,306,625 | | $ | 1,340,403 | | $ | (150,152 | ) | | $ | 167,650 | | | $ | 1,358,090 | |

| | | For the Quarters Ended | |

| | | March 31, 2013 | | | March 31, 2012 | |

| Cash Flows From Operating Activities: | | | | | | |

| Net income | | $ | 102,290 | | | $ | 65,224 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | |

| Net amortization of premium on Agency Securities | | | 60,698 | | | | 13,943 | |

| Realized gain on sale of Agency Securities | | | (18,514 | ) | | | (6,316 | ) |

| Stock based compensation | | | 190 | | | | 61 | |

| Changes in operating assets and liabilities: | | | | | | | | |

| Increase in accrued interest receivable | | | (16,234 | ) | | | (17,366 | ) |

| Increase in prepaid and other assets | | | (150 | ) | | | (213 | ) |

| Increase in derivatives, at fair value | | | (32,582 | ) | | | (20,938 | ) |

| Increase (decrease) in accrued interest payable | | | 238 | | | | (41 | ) |

| (Decrease) increase in accounts payable and accrued expenses | | | (970 | ) | | | 1,247 | |

| Net cash provided by operating activities | | | 94,966 | | | | 35,601 | |

| Cash Flows From Investing Activities: | | | | | | | | |

| Purchases of Agency Securities | | | (8,944,656 | ) | | | (7,086,954 | ) |

| Principal repayments of Agency Securities | | | 1,208,551 | | | | 331,955 | |

| Proceeds from sales of Agency Securities | | | 701,476 | | | | 452,171 | |

| Decrease in cash collateral | | | 45,256 | | | | 8,550 | |

| Net cash used in investing activities | | | (6,989,373 | ) | | | (6,294,278 | ) |

| Cash Flows From Financing Activities: | | | | | | | | |

| Issuance of Series A Preferred stock, net of expenses | | | 4,381 | | | | - | |

| Issuance of Series B Preferred stock, net of expenses | | | 136,571 | | | | - | |

| Issuance of common stock, net of expenses | | | 438,481 | | | | 555,911 | |

| Proceeds from repurchase agreements | | | 42,366,300 | | | | 25,719,289 | |

| Principal repayments on repurchase agreements | | | (35,903,781 | ) | | | (19,957,390 | ) |

| Series A Preferred dividends paid | | | (1,107 | ) | | | - | |

| Series B Preferred dividends paid | | | (1,390 | ) | | | - | |

| Common dividends paid | | | (79,829 | ) | | | (46,755 | ) |

| Net cash provided by financing activities | | | 6,959,626 | | | | 6,271,055 | |

| Net increase in cash | | | 65,219 | | | | 12,378 | |

| Cash - beginning of period | | | 771,282 | | | | 252,372 | |

| Cash - end of period | | $ | 836,501 | | | $ | 264,750 | |

| Supplemental Disclosure: | | | | | | | | |

| Cash paid during the period for interest | | $ | 55,254 | | | $ | 20,478 | |

| Non-Cash Investing and Financing Activities: | | | | | | | | |

| Receivable for unsettled security sales | | $ | 2,226,168 | | | $ | 218,873 | |

| Payable for unsettled security purchases | | $ | - | | | $ | 391,678 | |

| Unrealized (loss) gain on investment on Agency Securities | | $ | (180,055 | ) | | $ | 11,622 | |

| Amounts receivable for issuance of common stock | | $ | 5 | | | $ | 2 | |

| Common dividends declared, to be paid in subsequent period | | $ | - | | | $ | 91 | |

See notes to condensed consolidated financial statements.

ARMOUR Residential REIT, Inc. and Subsidiary

CONDENSED CONSOLIDATED STATEMENTS of CASH FLOWS

(dollars in thousands)

(Unaudited)

| | | For the Six Months Ended June 30, 2012 | | | For the Six Months Ended June 30, 2011 | |

| Cash Flows From Operating Activities: | | | | | | |

| Net income | | $ | 51,616 | | | $ | 1,324 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | |

| Net amortization of premium on Agency Securities | | | 33,737 | | | | 7,933 | |

| Unrealized loss on derivatives | | | 25,188 | | | | 33,478 | |

| Realized gain on sale of Agency Securities | | | (5,048 | ) | | | - | |

| Stock based compensation | | | 261 | | | | 145 | |

| Changes in operating assets and liabilities: | | | | | | | | |

| Increase in accrued interest receivable | | | (19,919 | ) | | | (12,064 | ) |

| (Increase) decrease in prepaid income taxes and other assets | | | (678 | ) | | | 430 | |

| Increase in accrued interest payable | | | 1,218 | | | | 428 | |

| Increase in accounts payable and accrued expenses | | | 1,498 | | | | 993 | |

| Net cash provided by operating activities | | | 87,873 | | | | 32,667 | |

| Cash Flows From Investing Activities: | | | | | | | | |

| Purchases of Agency Securities | | | (8,745,763 | ) | | | (4,074,907 | ) |

| Principal repayments of Agency Securities | | | 777,772 | | | | 183,355 | |

| Proceeds from sales of Agency Securities | | | 664,588 | | | | - | |

| Decrease in restricted cash | | | (45,887 | ) | | | (50,631 | ) |

| Net cash used in investing activities | | | (7,349,290 | ) | | | (3,942,183 | ) |

| Cash Flows From Financing Activities: | | | | | | | | |

| Issuance of preferred stock, net of expenses | | | 33,779 | | | | - | |

| Issuance of common stock, net of expenses | | | 627,813 | | | | 408,837 | |

| Proceeds from repurchase agreements | | | 57,438,695 | | | | 13,771,873 | |

| Principal repayments on repurchase agreements | | | (50,663,141 | ) | | | (10,088,322 | ) |

| Common dividends paid | | | (101,365 | ) | | | (29,982 | ) |

| Net cash provided by financing activities | | | 7,335,781 | | | | 4,062,406 | |

| Net increase in cash | | | 74,364 | | | | 152,890 | |

| Cash - beginning of period | | | 252,372 | | | | 35,344 | |

| Cash - end of period | | $ | 326,736 | | | $ | 188,234 | |

| Supplemental Disclosure: | | | | | | | | |

| Cash paid for income taxes (not including tax refunds received) | | $ | 12 | | | $ | 15 | |

| Cash paid during the period for interest | | $ | 46,012 | | | $ | 2,970 | |

| Non-Cash Investing and Financing Activities: | | | | | | | | |

| Payable for unsettled security purchases | | $ | 272,863 | | | $ | 302,680 | |

| Unrealized gain on investment in available for sale securities | | $ | 123,950 | | | $ | 36,542 | |

| Amounts receivable for issuance of common stock | | $ | 3 | | | $ | 8,225 | |

| Common dividends declared, to be paid in subsequent period | | $ | 8 | | | $ | 9 | |

| Preferred dividends declared, to be paid in subsequent period | | $ | 160 | | | $ | - | |

See notes to condensed consolidated financial statements

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1 – Basis of Presentation

The accompanying unaudited financial statements have been prepared in accordance with U.S. generally accepted accounting principles in the U.S. (“GAAP”) for interim financial information and with the instructions to Form 10-Q and Rule 10-011001 of Regulation S-X promulgated by the Securities and Exchange Commission (the “SEC”). Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the quarter and six months ended June 30, 2012March 31, 2013 are not necessarily indicative of the results that may be expected for the calendar year ending December 31, 2012.2013. These unaudited financial statements should be read in conjunction with the audited financial statements and notes thereto included in the Company’sour annual report on Form 10-K for the year ended December 31, 2011.2012.

Our financial statements are presented in accordance with GAAP. The condensed consolidated financial statements include the accounts of ARMOUR Residential REIT, Inc. and its subsidiary, allsubsidiary. All intercompany accounts and transactions have been eliminated. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates affecting the accompanying condensed consolidated financial statements include the valuation of Agency Securities (as defined below) and derivative instruments.

Note 2 -– Organization and Nature of Business Operations

Business

References to “we”, “us”, “our”,“we,” “us,” “our,” "ARMOUR" or the “Company” are to ARMOUR Residential REIT, Inc. References to "ARRM" are to ARMOUR Residential Management LLC, a Delaware limited liability company. References to “Enterprise” are to Enterprise Acquisition Corp., which is a wholly-owned subsidiary of ARMOUR.

We are an externally managed Maryland corporation organized in 2008, managed by ARRM.ARRM (see Note 14, “Related Party Transactions” for additional discussion). We invest primarily in hybrid adjustable rate, adjustable rate and fixed rate residential mortgage backed securities. These securities are issued or guaranteed by a U.S. Government-sponsored entity (“GSE”), such as the Federal National Mortgage Association ( Fannie(Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac) or guaranteed by the Government National Mortgage Administration (Ginnie Mae) (collectively, "Agency Securities"). As of March 31, 2013, Agency Securities account for 100% of our portfolio. It is expected that the percentage will continue to be 100% or close thereto. Our portfolio consists primarily of securities backed by fixed rate, hybrid adjustable rate, and adjustable rate home loans. From time to time, a portion of our portfolio may be invested in unsecured notes and bonds issued by U.S. Government-charteredGovernment-sponsored entities (collectively, “Agency Debt”), U.S. Treasuries and money market instruments, subject to certain income tests we must satisfy for our qualification as a real estate investment trust (“REIT”). On December 1, 2011, our stockholders approved an amendment to our charter to alter our investment asset class restriction in response to potential changes in Agency Securities to include non-AgencyNon-Agency as well as Agency Securities in our investment asset class restriction. While we remain committed to investing in Agency Securities for so long as an adequate supply and pricing exists, we believe it is prudent for us to have the flexibility to invest in non-AgencyNon-Agency Securities and respond to changes in GSE policy.

We intend to qualify and have elected to be taxed as a REIT under the Internal Revenue Code (“the Code”). Our qualification as a REIT depends on our ability to meet, on a continuing basis, various complex requirements under the Code relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the concentration of ownership of our capital stock. We believe that we are organized in conformity with the requirements for qualification as a REIT under the Code and our manner of operations enables us to meet the requirements for taxation as a REIT for federal income tax purposes.

As a REIT, we will generally not be subject to federal income tax on the REIT taxable income that we currently distribute to our stockholders. If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we will be subject to federal income tax at regular corporate rates. Even if we qualify as a REIT for federal income tax purposes, we may still be subject to some federal, state and local taxes on our income.

Note 3 -– Summary of Significant Accounting Policies

Reclassification

We reclassified previously presented financial information to conform to the presentation in our condensed consolidated financial statements for the quarterCash and six months ended June 30, 2012 and for the year ended December 31, 2011. Certain commissions with respect to Eurodollar Futures Contracts (“Futures Contracts”) which were previously included in interest expense have been reclassified into realized gain or loss on those contracts. The unrealized gains and losses on our derivatives previously classified on our condensed consolidated statement of operations as an adjustment to arrive at “net interest income after change in fair value of interest rate contracts” is no longer presented as an adjustment to interest income and has been reclassified into “other income” as part of the unrealized gain or loss on derivatives. This reclassification had no effect on previously reported net income or comprehensive income. This reclassification caused interest income to decrease by $0.4 million and $0.6 million, respectively and interest expense to decrease by $6.1 million and $8.1 million, respectively for the quarter and six months ended June 30, 2011. Realized loss on derivatives increased by the net amount of $5.7 million and $7.5 million, respectively for the quarter and six months ended June 30, 2011.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Cashcash equivalents

Cash and cash equivalents includes cash on deposit with financial institutions and investments in high quality overnight money market funds, all of which have original maturities of three months or less, at the time of purchase. We may maintain deposits in federally insured financial institutions in excess of federally insured limits. However, management believes we are not exposed to significant credit risk due to the financial position and creditworthiness of the depository institutions in which those deposits are held.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

RestrictedCash Collateral

The following table presents information related to margin collateral posted (held) for interest rate swap contracts, interest rate swaptions and Eurodollar Futures Contracts (“Futures Contracts”) which are included in cash at June 30, 2012collateral on the accompanying condensed consolidated balance sheets as of March 31, 2013 and December 31, 2011 represents approximately $193.1 million and $147.2 million, respectively, held by counterparties as collateral.2012.

| | | March 31, 2013 | | | December 31, 2012 | |

| | | (in thousands) | |

| | | Fair Value (1) | | | Fair Value (1) | |

| Interest rate swap contracts | | $ | 227,008 | | | $ | 261,364 | |

| Interest rate swaptions | | | (10,155 | ) | | | - | |

| Futures Contracts | | | 3,443 | | | | 4,188 | |

| Totals | | $ | 220,296 | | | $ | 265,552 | |

| (1) | See Note 6, “Fair Value of Financial Instruments” for additional discussion. |

Agency Securities, at Fair Value

We invest primarily in Agency Securities. A portion of our portfolio may be invested in Agency Debt, U.S. Treasuries and money market instruments, subject to certain income tests we must satisfy for our qualification as a REIT. As of June 30,March 31, 2013 and December 31, 2012, all of our financial instrument investments consist of Agency Securities Agency Debt, U.S. Treasuries, money market instruments (including reverse repurchase agreements),and hedging and other derivative instruments related to the foregoing investments.

We generally intend to hold most of our Agency Securities for long-term periods.long periods of time. We may, from time to time, sell any of our Agency Securities as part of ourthe overall management of our portfolio. Management determines the appropriate classifications of the securities at the time they are acquired and evaluates the appropriateness of such classifications at each balance sheet date. As of June 30,March 31, 2013 and December 31, 2012, all of our Agency Securities were classified as available for sale. Agency securitiesSecurities classified as available for sale are reported at their estimated fair values, based on fair values obtained from third-party sources, with unrealized gains and losses excluded from earnings and reported as part of the separate condensed consolidated statements of comprehensive income. Agency securities transactions are recorded on the trade date and are valued using third-party pricing services and dealer quotes.

We evaluate securities for other than temporary impairment at least on a quarterly basis and more frequently when economic or market concerns warrant such evaluation. We determine if we (1) have the intent to sell the Agency Securities, (2) believe it is more likely than not that we will be required to sell the securities before recovery or (3) do not expect to recover the entire amortized cost basis of the Agency Securities. There was no other than temporary impairment for the quarters ended March 31, 2013 and six months ended June 30, 2012 and June 30, 2011.March 31, 2012.

Repurchase Agreements

We finance the acquisition of our Agency Securities through the use of repurchase agreements. Our repurchase agreements are secured by our Agency Securities and bear interest rates that have historically moved in close relationship to the Federal Funds Rate and the London Interbank Offered Rate (“LIBOR”). Under these agreements, we sell securities to a lender and agree to repurchase the same securities in the future for a price that is higher than the original sales price. The difference between the sales price that we receive and the repurchase price that we pay represents interest paid to the lender. A repurchase agreement operates as financing under which we pledge our securities as collateral to secure a loan which is equal in value to a specified percentage of the estimated fair value of the pledged collateral. We retain beneficial ownership of the pledged collateral. At the maturity of a repurchase agreement, we are required to repay the loan and concurrently receive back our pledged collateral from the lender or, with the consent of the lender, we may renew such agreement at the then prevailing interest rate. The repurchase agreements may require us to pledge additional assets to the lender in the event the estimated fair value of the existing pledged collateral declines.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Derivatives

We recognize all derivative instrumentsderivatives as either assets or liabilities at fair value on our condensed consolidated balance sheets. We do not designate our derivative activitiesderivatives as cash flow hedges, which, among other factors, would require us to match the pricing dates of both derivative transactionsderivatives and repurchase agreements. Operational issues and credit market volatility make such matching impractical for us. Since we have not elected cash flow hedge accounting treatment as allowed by GAAP, all changes in the fair values of our derivatives are reflected in our condensed consolidated statements of operations. Accordingly, our operating results may reflect greater volatility than otherwise would be the case, because gains or losses on derivatives may not be offset by changes in the fair value or cash flows of the transaction within the same accounting period or ever. Consequently, any declines in the fair value of our derivatives result in a charge to earnings. We will continue to designate derivative activitiesderivatives as hedges for tax purposes and any unrealized derivative gains or losses would not affect our distributable net taxable income.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Accrued Interest Receivable and Payable

Accrued interest receivable includes interest accrued between payment dates on Agency Securities. Accrued interest payable includes interest payable on our repurchase agreements.

Credit Risk

We have limited our exposure to credit losses on our portfolio of Agency Securities by only purchasing securities issued by Freddie Mac, Fannie Mae or Ginnie Mae.Securities. The payment of principal and interest on the Freddie Mac and Fannie Mae Agency Securities are guaranteed by those respective agencies and the payment of principal and interest on the Ginnie Mae Agency Securities are backed by the full faith and credit of the U.S. Government.

In September 2008, both Freddie Mac and Fannie Mae were placed in the conservatorship of the U.S. Government. While it is hoped that the conservatorship will help stabilize Freddie Mac's and Fannie Mae's losses and overall financial position, there can be no assurance that it will succeed or that, if necessary, Freddie Mac or Fannie Mae will be able to satisfy their guarantees of Agency Securities. On August 5, 2011, Standard & Poor’s Corporation downgraded the U.S.’s Government’s credit rating from AAA to AA+ and on August 8, 2011, Fannie Mae and Freddie Mac’s credit ratings were downgraded from AAA to AA+. Because Fannie Mae and Freddie Mac areremain in conservatorship of the U.S. Government,Government. There can be no assurances how or when the U.S.'s credit rating downgrade and Government will end these conservatorships or how the future profitability of Fannie Mae and Freddie Mac’sMac and any future credit rating downgrades willactions may impact the credit risk associated with Agency Securities and, therefore, may decrease the value of the Agency Securities in our portfolio.

Market Risk

Weakness in the mortgage market may adversely affect the performance and market value of our investments. This could negatively impact our net book value. Furthermore, if our lenders are unwilling or unable to provide additional financing, we could be forced to sell our Agency Securities at an inopportune time when prices are depressed.

Preferred Stock

At June 30, 2012,March 31, 2013, we were authorized to issue up to 25,000,00050,000,000 shares of preferred stock, par value $0.001 per share with such designations, voting and other rights and preferences as may be determined from time to time by our Board of Directors (“Board”) or a committee thereof.

Series A Cumulative Preferred Shares (”Series A Preferred Stock”)

On June 6, 2012, we filed with the Maryland State Department of Assessments and Taxation of the State of Maryland to designate 1,610,000 shares of the 25,000,00050,000,000 authorized preferred stock as 8.250% Series A Cumulative Preferred Shares (“Series A Preferred Stock”)Stock with the powers, designations, preferences and other rights as set forth therein. On July 13, 2012, we entered into an At June 30,Market Issuance Sales Agreement with MLV & Co. LLC, as our agent, to offer and sell, from time to time, up to 6,000,000 shares of Series A Preferred Stock. On July 27, 2012, we entered into an Equity Distribution Agreement with Citadel Securities LLC, as our agent, to offer and sell, from time to time, up to 2,000,000 shares of Series A Preferred Stock. At March 31, 2013, there were 9,610,000 shares designated as Series A Preferred Stock.

At March 31, 2013, we had issued and outstanding 1,400,0002,180,572 shares of Series A Preferred Stock, with a par value of $0.001 per share and a liquidation preference of $25.00 per share plus accrued and unpaid dividends. The Series A Preferred Stock is entitled to a dividend at a rate of 8.250% per year based on the $25.00 liquidation preference before the common stock is entitled to receive any dividends. The Series A Preferred Stock is redeemable at $25.00 per share plus accrued and unpaid dividends exclusively at our option commencing on June 7, 2017 (subject to our right under limited circumstances to redeem the Series A Preferred Stock earlier in order to preserve our qualification as a REIT). The Series A Preferred Stock is senior to the our common stock and therefore in the event of liquidation, dissolution or winding up, the Series A Preferred Stock will receive a liquidation preference of $25.00 per share plus accumulated and unpaid dividends before distributions are paid to holders of our common stock, with no right or claim to any of our remaining assets thereafter. The Series A Preferred Stock generally does not have voting rights except if we fail to pay dividends on the Series A Preferred Stock for eighteen months, whether or not consecutive. Under such circumstances, the Series A Preferred Stock will be entitled to vote to elect two additional directors to the Board, until all unpaid dividends have been paid or declared and restrictedset aside for payment. The Series A Preferred Stock has no stated maturity, is not subject to any sinking fund or mandatory redemption and will remain outstanding indefinitely unless repurchased or redeemed by us or converted into our common stock in connection with a change of control by the holders of Series A Preferred Stock.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Series B Cumulative Preferred Shares (”Series B Preferred Stock”)

On February 11, 2013, we filed with the Maryland State Department of Assessments and Taxation to designate 6,210,000 shares of the 50,000,000 authorized preferred stock as 7.875% Series B Preferred Stock with the powers, designations, preferences and other rights as set forth therein.

At March 31, 2013, we had issued and outstanding 5,650,000 shares of Series B Preferred Stock, with a par value of $0.001 per share and a liquidation preference of $25.00 per share plus accrued and unpaid dividends. The Series B Preferred Stock is entitled to a dividend at a rate of 7.875% per year based on the $25.00 liquidation preference before the common stock is entitled to receive any dividends. The Series B Preferred Stock is redeemable at $25.00 per share plus accrued and unpaid dividends exclusively at our option commencing on February 12, 2018 (subject to our right under limited circumstances to redeem the Series A Preferred Stock earlier in order to preserve our qualification as a REIT). The Series B Preferred Stock is senior to our common stock and rank on parity with the Series A Preferred Stock. In the event of liquidation, dissolution or winding up, the Series B Preferred Stock will receive a liquidation preference of $25.00 per share plus accumulated and unpaid dividends before distributions are paid to holders of our common stock, with no right or claim to any of our remaining assets thereafter. The Series B Preferred Stock generally does not have voting rights except if we fail to pay dividends on the Series B Preferred Stock for eighteen months, whether or not consecutive. Under such circumstances, the Series B Preferred Stock will be entitled to vote to elect two additional directors to the Board, until all unpaid dividends have been paid or declared and set aside for payment. The Series B Preferred Stock has no stated maturity, is not subject to any sinking fund or mandatory redemption and will remain outstanding indefinitely unless repurchased or redeemed by us or converted into our common stock in connection with a change of control by the holders of Series B Preferred Stock.

Common Stock and Warrants

At June 30, 2012,March 31, 2013, we were authorized to issue up to 500,000,0001,000,000,000 shares of common stock, par value $0.001 per share, with such designations, voting and other rights and preferences as may be determined from time to time by our Board. We had 188,185,880374,053,198 shares of common stock issued and outstanding at June 30, 2012.March 31, 2013. At June 30, 2012,March 31, 2013, we had outstanding warrants to purchase 32,500,000 shares of common stock, which are exercisable at $11.00 per share and expire in November 2013.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Income per Common Share

The following table presents a reconciliation of the net (loss) income and the shares used in calculating basic and diluted earnings per share for the quarters and six months ended June 30, 2012 and June 30, 2011.

| | | For the Quarters Ended | | For the Six Months Ended |

| | | June 30, 2012 | | | June 30, 2011 | | | June 30, 2012 | | | June 30, 2011 | |

| Net (Loss) Income (related) available to common stockholders | | $ | (13,767 | ) | | $ | (7,272 | ) | | $ | 51,456 | | | $ | 1,324 | |

| | | | | | | | | | | | | | | | | |

| Weighted average common shares outstanding - basic | | | 180,773 | | | | 53,259 | | | | 157,838 | | | | 39,903 | |

| Add: Effect of dilutive non-vested restricted stock awards, assumed vested | | | - | | | | - | | | | 715 | | | | 159 | |

| Weighted average common shares outstanding- diluted | | | 180,773 | | | | 53,259 | | | | 158,553 | | | | 40,062 | |

32,500,000 warrants were outstanding and considered anti-dilutive as their exercise price exceeded the average stock price for the quarters and six months ended June 30, 2012 and June 30, 2011.

Comprehensive Income

Comprehensive income refers to changechanges in equity during a period from transactions and other events and circumstances from non-owner sources. It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners.

Revenue Recognition

Interest income is earned and recognized based on the unpaid principal amount of the Agency Securities and their contractual terms. Premiums and discounts associated with the purchase of Agency Securities are amortized or accreted into interest income over the actual lives of the securities using the effective interest method.

Income Taxes

We intend to qualify and have elected to be taxed as a REIT under the Code. We will generally not be subject to federal income tax to the extent that we distribute our taxable income to our stockholders and as long as we satisfy the ongoing REIT requirements under the Code including meeting certain asset, income and stock ownership tests.securities.

Our management is responsible for determining whether a tax position taken by us is more likely than not to be sustained on its merits. We have no material unrecognized tax benefits and have not recognized in these financial statements any interest or penalties related to income taxes. Should any such interest and penalties be recognized, they will be included in interest expense and other expenses, respectively. None of our income tax returns have been examined by federal, state or local authorities; therefore our 2009, 2010 and 2011 federal and state tax returns remain open for examination.

Note 4 -– Recent Accounting Pronouncements

Accounting Standards Adopted in 2012

We adopted recent amendmentsIn January 2013, the FASB issued ASU 2013-01, Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities, Balance Sheet (Topic 210). This update to authoritative guidance issued by the Financial Accounting Standards Board (“FASB”)ASU 2011-11 addressed implementation issues and applied to derivatives accounted for in April 2011 related to the accounting foraccordance with Topic 815, Derivatives and Hedging, including bifurcated embedded derivatives, repurchase agreements and otherreverse repurchase agreements, and securities borrowing and securities lending transactions that entitleare either offset in accordance with ASC 210-20-45 or ASC 815-10-45 or subject to an enforceable master netting arrangement or similar agreement. The guidance was effective January 1, 2013 and obligate a transferor to repurchase or redeem financial assets before their maturity.

We adopted recent amendments to authoritativewas applied retrospectively. This guidance issued by FASB in May 2011 to establish commondid not affect the presentation of Derivatives, at fair value measurementon our condensed consolidated balance sheets and disclosure requirements in GAAP and International Financial Reporting Standards.

We adopted recent amendments to authoritative guidance issued by FASB in June and December 2011 providing for the option to present the total of comprehensive income, the components of net income, and the components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutivetherefore, did not affect our financial statements.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Accounting Standards to be Adopted in Future Periods

In December 2011,February 2013, the FASB issued amendmentsASU 2013-02, Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income, Comprehensive Income (Topic 220). This update to authoritative guidanceASU 2011-12 addressed improving the reporting of reclassifications out of accumulated other comprehensive income by requiring entities that have financial instruments and derivative instrumentsreporting of the effect of significant reclassifications out of accumulated net income if the amount being reclassified is required under GAAP to disclose information about offsetting and related arrangements. Thebe classified in its entirety to net income. For amounts not required to be reclassified in their entirety to net income in the same reporting period, an entity is required to cross-reference other disclosures required under this amendedGAAP that provide additional detail about these amounts. The update did not change the current requirements for reporting net income or other comprehensive income and resulted in additional disclosure but had no significant effect on our condensed consolidated financial statements. The guidance are intended to enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements on an entity’s financial position, including the effect or potential effect of rights of offset associated with certain financial instruments and derivative instruments. The provisions of these amendments arewas effective for annualreporting periods beginning after January 1, 2013. We anticipate the adoption of these amendments may change the presentation of our financial statementsDecember 15, 2012 and related disclosures.was applied prospectively.

Note 5 -– Agency Securities, Available for Sale

All of our Agency Securities are classified as available for sale and, as such, are reported at their estimated fair value.value and reported as part of the condensed consolidated statements of comprehensive income. As of March 31, 2013 and December 31, 2012, investments in Agency Securities accounted for 100% of our portfolio.

As of June 30, 2012,March 31, 2013, we had the following securities in an unrealized gain or loss position as presented below. The components of the carrying value of our Agency Securities as of June 30, 2012March 31, 2013 are also presented below.

| June 30, 2012 | | Fannie Mae | | Freddie Mac | | Ginnie Mae | | Total Agency Securities | | |

| March 31, 2013 | | | Fannie Mae | | Freddie Mac | | Ginnie Mae | | Total Agency Securities | |

| | | (dollars in thousands) | | | (in thousands) | |

| Principal Amount | | $ | 8,253,755 | | | $ | 3,963,691 | | | $ | 344,154 | | | $ | 12,561,600 | | | $ | 16,460,012 | | | $ | 6,471,944 | | $ | 265,852 | | | $ | 23,197,808 | |

| Net unamortized premium | | | 393,551 | | | | 189,778 | | | | 15,935 | | | | 599,264 | | | | 794,430 | | | | 302,778 | | | 12,158 | | | | 1,109,366 | |

| Amortized cost | | | 8,647,306 | | | | 4,153,469 | | | | 360,089 | | | | 13,160,864 | | | | 17,254,442 | | | | 6,774,722 | | 278,010 | | | | 24,307,174 | |

| | | | | | | | | | | | | | | | | | | |

| Unrealized gains | | | 111,484 | | | | 53,084 | | | | 5,488 | | | | 170,056 | | | | 79,035 | | | | 31,278 | | 5,894 | | | | 116,207 | |

| Unrealized losses | | | (1,912 | ) | | | (491 | ) | | | (3 | ) | | | (2,406 | ) | | | (65,242 | ) | | | (18,962 | ) | | | (8 | ) | | | (84,212 | ) |

| Fair value | | $ | 8,756,878 | | | $ | 4,206,062 | | | $ | 365,574 | | | $ | 13,328,514 | | | $ | 17,268,235 | | | $ | 6,787,038 | | $ | 283,896 | | | $ | 24,339,169 | |

| June 30, 2012 | | Adjustable Rate | | Fixed Rate | | Total Agency Securities | | |

| March 31, 2013 | | | Adjustable Rate | | | Fixed Rate | | | Total Agency Securities | |

| | | (dollars in thousands) | | | (in thousands) | |

| Principal Amount | | $ | 2,685,281 | | | $ | 9,876,319 | | | $ | 12,561,600 | | | $ | 1,812,295 | | | $ | 21,385,513 | | | $ | 23,197,808 | |

| Net unamortized premium | | | 113,379 | | | | 485,885 | | | | 599,264 | | | | 75,239 | | | | 1,034,127 | | | | 1,109,366 | |

| Amortized cost | | | 2,798,660 | | | | 10,362,204 | | | | 13,160,864 | | | | 1,887,534 | | | | 22,419,640 | | | | 24,307,174 | |

| | | | | | | | | | | | | | | | | | | | |

| Unrealized gains | | | 39,755 | | | | 130,301 | | | | 170,056 | | | | 34,425 | | | | 81,782 | | | | 116,207 | |

| Unrealized losses | | | (687 | ) | | | (1,719 | ) | | | (2,406 | ) | | | (112 | ) | | | (84,100 | ) | | | (84,212 | ) |

| Fair value | | $ | 2,837,728 | | | $ | 10,490,786 | | | $ | 13,328,514 | | | $ | 1,921,847 | | | $ | 22,417,322 | | | $ | 24,339,169 | |

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

As of December 31, 2011,2012, we had the following securities in an unrealized gain or loss position as presented below. The components of the carrying value of our Agency Securities as of December 31, 20112012 are also presented below.

| December 31, 2011 | | Fannie Mae | | Freddie Mac | | Ginnie Mae | | Total Agency Securities | | |

| December 31, 2012 | | | Fannie Mae | | Freddie Mac | | Ginnie Mae | | Total Agency Securities | |

| | | (dollars in thousands) | | | (in thousands) | |

| Principal Amount | | $ | 3,451,906 | | | $ | 1,283,848 | | | $ | 392,476 | | | $ | 5,128,230 | | | $ | 12,328,493 | | | $ | 5,305,071 | | $ | 292,434 | | | $ | 17,925,998 | |

| Net unamortized premium | | | 144,337 | | | | 54,059 | | | | 18,301 | | | | 216,697 | | | | 641,833 | | | | 284,739 | | | 13,428 | | | | 940,000 | |

| Amortized cost | | | 3,596,243 | | | | 1,337,907 | | | | 410,777 | | | | 5,344,927 | | | | 12,970,326 | | | | 5,589,810 | | 305,862 | | | | 18,865,998 | |

| | | | | | | | | | | | | | | | | | | |

| Unrealized gains | | | 33,558 | | | | 13,657 | | | | 5,439 | | | | 52,654 | | | | 169,227 | | | | 66,904 | | 6,466 | | | | 242,597 | |

| Unrealized losses | | | (3,269 | ) | | | (613 | ) | | | (24 | ) | | | (3,906 | ) | | | (9,815 | ) | | | (2,170 | ) | | | (48 | ) | | | (12,033 | ) |

| Fair value | | $ | 3,626,532 | | | $ | 1,350,951 | | | $ | 416,192 | | | $ | 5,393,675 | | | $ | 13,129,738 | | | $ | 5,654,544 | | $ | 312,280 | | | $ | 19,096,562 | |

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

| December 31, 2011 | | Adjustable Rate | | Fixed Rate | | Total Agency Securities | | |

| December 31, 2012 | | | Adjustable Rate | | Fixed Rate | | Total Agency Securities | |

| | | (dollars in thousands) | | | (in thousands) | |

| Principal Amount | | $ | 2,681,911 | | | $ | 2,446,319 | | | $ | 5,128,230 | | | $ | 2,037,778 | | $ | 15,888,220 | | | $ | 17,925,998 | |

| Net unamortized premium | | | 107,641 | | | | 109,056 | | | | 216,697 | | | | 84,255 | | | 855,745 | | | | 940,000 | |

| Amortized cost | | | 2,789,552 | | | | 2,555,375 | | | | 5,344,927 | | | | 2,122,033 | | 16,743,965 | | | | 18,865,998 | |

| | | | | | | | | | | | | | | |

| Unrealized gains | | | 26,157 | | | | 26,497 | | | | 52,654 | | | | 36,758 | | 205,839 | | | | 242,597 | |

| Unrealized losses | | | (2,534 | ) | | | (1,372 | ) | | | (3,906 | ) | | | (222 | ) | | | (11,811 | ) | | | (12,033 | ) |

| Fair value | | $ | 2,813,175 | | | $ | 2,580,500 | | | $ | 5,393,675 | | | $ | 2,158,569 | | $ | 16,937,993 | | | $ | 19,096,562 | |

Actual maturities of Agency Securities are generally shorter than stated contractual maturities because actual maturities of Agency Securities are affected by the contractual lives of the underlying mortgages, periodic payments of principal and prepayments of principal.

The following table summarizes the weighted average lives of our Agency Securities as of June 30, 2012March 31, 2013 and December 31, 2011.2012.

| | | June 30, 2012 | | December 31, 2011 | | | March 31, 2013 | | December 31, 2012 | |

| | | (dollars in thousands) | | | (in thousands) | |

| Weighted Average Life of all Agency Securities | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost | | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost | |

| Less than one year | | $ | 2,682 | | | $ | 2,637 | | | $ | 179 | | | $ | 179 | | | $ | 10 | | | $ | 10 | | | $ | 2,647 | | | $ | 2,593 | |

| Greater than one year and less than five years | | | 13,309,810 | | | | 13,142,241 | | | | 5,274,072 | | | | 5,226,255 | | |

| Greater than one year and less than three years | | | 2,603,053 | | 2,554,020 | | 8,618,862 | | 8,476,157 | |

| Greater than three years and less than five years | | | 10,926,786 | | 10,882,077 | | 9,681,538 | | 9,592,001 | |

| Greater than or equal to five years | | | 16,022 | | | | 15,986 | | | | 119,424 | | | | 118,493 | | | | 10,809,320 | | | | 10,871,067 | | | | 793,515 | | | | 795,247 | |

| Total Agency Securities | | $ | 13,328,514 | | | $ | 13,160,864 | | | $ | 5,393,675 | | | $ | 5,344,927 | | | $ | 24,339,169 | | | $ | 24,307,174 | | | $ | 19,096,562 | | | $ | 18,865,998 | |

We use a third-party model to calculate the weighted average life of Agency Securities. Weighted average life is calculated based on expectations for estimated prepayments for the underlying mortgage loans of our Agency Securities. These estimated prepayments are based on assumptions such as interest rates, current and future home prices, housing policy and borrower incentives. The weighted average lives of theour Agency Securities as of June 30, 2012March 31, 2013 and December 31, 20112012 in the table above are based upon market factors, assumptions, models and estimates from the third partythird-party model and also incorporate ARRM’smanagement’s judgment and experience. The actual weighted average lives of the Agency Securities could be longer or shorter than estimated.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table presents the unrealized losses and estimated fair value of our Agency Securities by length of time that such securities have been in a continuous unrealized loss position as of June 30, 2012March 31, 2013 and December 31, 2011.2012.

| | | Unrealized Loss Position For: (dollars in thousands) | |

| | | Less than 12 months | | | 12 Months or More | | | Total | |

| | | | | | | | | | | | | | | | | | | |

| As of | | Fair Value | | | Unrealized Losses | | | Fair Value | | | Unrealized Losses | | | Fair Value | | | Unrealized Losses | |

| June 30, 2012 | | $ | 804,479 | | | $ | (2,390 | ) | | $ | 1,653 | | | $ | (16 | ) | | $ | 806,132 | | | $ | (2,406 | ) |

| December 31, 2011 | | | 1,173,098 | | | | (3,560 | ) | | | 96,684 | | | | (346 | ) | | | 1,269,782 | | | | (3,906 | ) |

| | | Unrealized Loss Position For: (in thousands) | |

| | | Less than 12 months | | | 12 Months or More | | | Total | |

| As of | | Fair Value | | | Unrealized Losses | | | Fair Value | | | Unrealized Losses | | | Fair Value | | | Unrealized Losses | |

| March 31, 2013 | | $ | 13,004,337 | | | $ | (84,210 | ) | | $ | 65 | | | $ | (2 | ) | | $ | 13,044,402 | | | $ | (84,212 | ) |

| December 31, 2012 | | | 1,521,052 | | | | (12,030 | ) | | | 836 | | | | (3 | ) | | | 1,521,888 | | | | (12,033 | ) |

The decline in value of these securities is solely due to market conditions and not the credit quality of the assets. All of our Agency Securities are issued by the GSEs. The GSEs have a rating of AA+. The investments are not considered other than temporarily impaired because we currently have the ability and intent to hold the investments to maturity or for a period of time sufficient for a forecasted market price recovery up to or beyond the cost of the investments and we are not required to sell for regulatory or other reasons. Also, we are guaranteed payment of the principal amount of the securities by the GSEs that created them.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

During the quarterquarters ended June 30,March 31, 2013 and March 31, 2012, we did not sell any Agency Securities. However, we realized a loss on sale of Agency Securities of $1.3 million. $1.1 million of this amount is due to the bankruptcy of a counterparty to a repurchase agreementsold $2.3 billion and the remaining $0.2 million is a reduction of the first quarter realized gains due to factor updates. In addition, due to the bankruptcy we also recorded $1.0 million of other income resulting from the non-performance of the counterparty on the related repurchase agreement. During the six months ended June 30, 2012 we sold $0.2 billion of Agency Securities resulting in a realized gain of $5.0 million. We did not sell any Agency Securities during the quarter$18.5 million and six months ended June 30, 2011.$6.3 million, respectively.

Note 6 -– Fair Value of Financial Instruments

Our valuation techniques for financial instruments are based on observable and unobservable inputs. Observable inputs reflect readily obtainable data from third-party sources, while unobservable inputs reflect management’s market assumptions. The ASCAccounting Standards Codification Topic No. 820 “Fair Value Measurement” classifies these inputs into the following hierarchy:

Level 1 Inputs- Quoted prices for identical instruments in active markets.

Level 2 Inputs- Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable.

Level 3 Inputs- Instruments with primarily unobservable value drivers.

The following describes the valuation methodologies used for our assets and liabilities measured at fair value, as well as the general classification of such instruments pursuant to the valuation hierarchy.

Cash - Cash and restricted cash - Cashequivalents includes cash on deposit with financial institutions and investments in high quality overnight money market funds, all of which have maturities of three months or less, at the time of purchase. The carrying amount of cash is deemed to be its fair value. RestrictedOur cash includes cashbalances are classified as Level 1. Cash balances posted or held by counterparties as collateral.collateral are classified as Level 2.

Agency Securities Available for Sale - Fair value for the Agency Securities in our portfolio is based on obtaining a valuation for each Agency Security from third-party pricing services and dealer quotes. The third-party pricing services use common market pricing methods that may include pricing models that may incorporate such factors as coupons, prepayment speeds, spread to the Treasury curves and interest rate swap curves, duration, periodic and life caps and credit enhancement. If the fair value of a security is not available from the third-party pricing serviceservices or such data appears unreliable, we obtain valuations from up to three dealers who make markets in similar financial instruments. In general, the dealers incorporate common market pricing methods, including a spread measurement to the Treasury curve or interest rate swap curve as well as underlying characteristics of the particular security including coupon, periodic and life caps, collateral type, rate reset period and seasoning or age of the security. Management reviews pricing used to ensure that current market conditions are properly represented. This review includes, but is not limited to, comparisons of similar market transactions or alternative third-party pricing services, dealer quotes and comparisons to a pricing model. Values obtained from the third-party pricing serviceservices for similar instruments are classified as Level 2 securities if the pricing methods used are consistent with the Level 2 definition. If quoted prices for a security are not reasonably available from the pricing service, but dealer quotes are, the security will be classified as a Level 2 security. If neither is available, management will determine the fair value based on characteristics of the security that we receive from the issuer and based on available market information received from dealers and classify it as a Level 3 security. At June 30, 2012March 31, 2013 and December 31, 2011,2012, all of our Agency Security values were based solely on third-party sources.sources and therefore were classified as Level 2.

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Repurchase Agreements -The fair value of repurchase agreements reflects the present value of the contractual cash flows discounted at the estimated LIBOR based market interest rates at the valuation date for repurchase agreements with a term equivalent to the remaining term to interest rate repricing, which may be at maturity, of our repurchase agreements. The fair value of the repurchase agreements approximates their carrying amount due to the short-term nature of these financial instruments. Our repurchase agreements are classified as Level 2.

Derivative Transactions - The fair values of our– Our Futures Contracts are based on closing pricestraded on the Chicago Mercantile Exchange (“CME”). and are classified as Level 1. The fair values of our interest rate swap contracts and options to enter into interest rate swaps (“interest rate swaptions”)swaptions are valued using a third-party pricing serviceservices that incorporates common market pricing methods that may include current interest rate curves, forward interest rate curves and market spreads to interest rate curves. Management compares pricing used to dealer quotes to ensure that the current market conditions are properly represented. Our Futures Contracts are classified as Level 1 and theThe fair values of our interest rate swap contracts and our interest rate swaptions are classified as Level 2.

Excluded from the tables below are financial instruments carried on the accompanying condensed consolidated balance sheets at cost basis, which is deemed to approximate fair value, primarily due to the short-term nature of these instruments, including cash, restricted cash, receivables for unsettled securities, principal payments receivables, accrued interest receivables, payables for unsettled securities, payables and borrowings under repurchase arrangements. The fair values of these instruments are determined using Level 1 inputs. The following tables provide a summary of our assets and liabilities that are measured at fair value on a recurring basis as of June 30, 2012March 31, 2013 and December 31, 2011.2012.

| | | Quoted Prices in Active Markets for Identical Assets (Level 1) | | | Significant Observable Inputs (Level 2) | | | Significant Unobservable Inputs (Level 3) | | | Balance at March 31, 2013 | |

| | | (in thousands) | |

| Assets at Fair Value: | | | | | | | | | | | | | |

| Agency Securities, available for sale | | $ | - | | | $ | 24,339,169 | | | $ | - | | | $ | 24,339,169 | |

| Derivatives | | $ | - | | | $ | 38,923 | | | $ | - | | | $ | 38,923 | |

| Liabilities at Fair Value: | | | | | | | | | | | | | | | | |

| Derivatives | | $ | 3,262 | | | $ | 188,252 | | | $ | - | | | $ | 191,514 | |

| | | Quoted Prices in Active Markets for Identical Assets (Level 1) | | | Significant Observable Inputs (Level 2) | | | Significant Unobservable Inputs (Level 3) | | | Balance at December 31, 2012 | |

| | | (in thousands) | |

| Assets at Fair Value: | | | | | | | | | | | | | |

| Agency Securities, available for sale | | $ | - | | | $ | 19,096,562 | | | $ | - | | | $ | 19,096,562 | |

| Derivatives | | $ | - | | | $ | 5,367 | | | $ | - | | | $ | 5,367 | |

| Liabilities at Fair Value: | | | | | | | | | | | | | | | | |

| Derivatives | | $ | 3,919 | | | $ | 186,621 | | | $ | - | | | $ | 190,540 | |

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

| June 30, 2012 | | Level 1 | | | Level 2 | | | Level 3 | | | Totals | |

| | | (dollars in thousands) | |

| Assets: | | | | | | | | | | | | |

| Agency Securities, available for sale | | $ | - | | | $ | 13,328,514 | | | $ | - | | | $ | 13,328,514 | |

| Derivatives, at fair value | | $ | - | | | $ | 9,600 | | | | - | | | $ | 9,600 | |

| Liabilities: | | | | | | | | | | | | | | | | |

| Derivatives, at fair value | | $ | (4,916 | ) | | $ | (151,599 | ) | | | - | | | $ | (156,515 | ) |

| December 31, 2011 | | Level 1 | | | Level 2 | | | Level 3 | | | Totals | |

| | | (dollars in thousands) | |

| Assets: | | | | | | | | | | | | |

| Agency Securities, available for sale | | $ | - | | | $ | 5,393,675 | | | $ | - | | | $ | 5,393,675 | |

| Liabilities: | | | | | | | | | | | | | | | | |

| Derivatives, at fair value | | $ | (5,292 | ) | | $ | (116,435 | ) | | | - | | | $ | (121,727 | ) |

| | | At March 31, 2013 | | | Fair Value Measurements using: | |

| | | Carrying Value | | | Fair Value | | | Quoted Prices in Active Markets for Identical Assets (Level 1) | | | Significant Observable Inputs (Level 2) | | | Significant Unobservable Inputs (Level 3) | |

| | | (in thousands) | |

| Financial Assets: | | | | | | | | | | | | | | | | | | | | |

| Cash | | $ | 836,501 | | | $ | 836,501 | | | $ | 836,501 | | | $ | | | | $ | - | |

| Cash collateral posted | | | 230,451 | | | | 230,451 | | | | - | | | | 230,451 | | | | - | |

| Receivable for unsettled securities | | | 2,226,168 | | | | 2,226,168 | | | | - | | | | 2,226,168 | | | | - | |

| Principal payments receivable | | | 9,381 | | | | 9,381 | | | | - | | | | 9,381 | | | | - | |

| Accrued interest receivable | | | 71,664 | | | | 71,664 | | | | - | | | | 71,664 | | | | - | |

| Financial Liabilities: | | | | | | | | | | | | | | | | | | | | |

| Repurchase agreements | | $ | 24,828,614 | | | $ | 24,828,614 | | | $ | - | | | $ | 24,828,614 | | | $ | - | |

| Accrued interest payable | | | 10,302 | | | | 10,302 | | | | - | | | | 10,302 | | | | - | |

| Cash collateral held | | | 10,155 | | | | 10,155 | | | | - | | | | 10,155 | | | | - | |

| | | At December 31, 2012 | | | Fair Value Measurements using: | |

| | | Carrying Value | | | Fair Value | | | Quoted Prices in Active Markets for Identical Assets (Level 1) | | | Significant Observable Inputs (Level 2) | | | Significant Unobservable Inputs (Level 3) | |

| | | (in thousands) | |

| Financial Assets: | | | | | | | | | | | | | | | | | | | | |

| Cash and cash equivalents | | $ | 771,282 | | | $ | 771,282 | | | $ | 771,282 | | | $ | - | | | $ | - | |

| Cash collateral posted | | | 265,552 | | | | 265,552 | | | | - | | | | 265,552 | | | | - | |

| Receivable for unsettled securities | | | 668,244 | | | | 668,244 | | | | - | | | | 668,244 | | | | - | |

| Principal payments receivable | | | 16,037 | | | | 16,037 | | | | - | | | | 16,037 | | | | - | |

| Accrued interest receivable | | | 55,430 | | | | 55,430 | | | | - | | | | 55,430 | | | | - | |

| Financial Liabilities: | | | | | | | | | | | | | | | | | | | | |

| Repurchase agreements | | $ | 18,366,095 | | | $ | 18,366,095 | | | $ | - | | | $ | 18,366,095 | | | $ | - | |

| Accrued interest payable | | | 10,064 | | | | 10,064 | | | | - | | | | 10,064 | | | | - | |

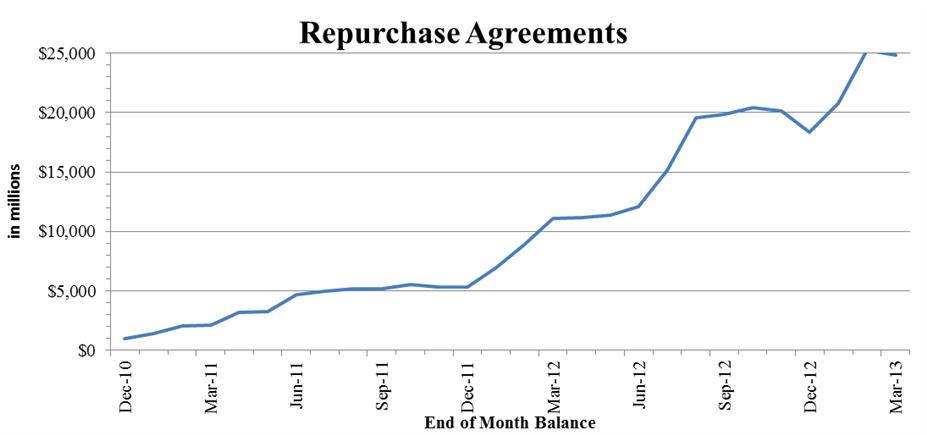

Note 7 -– Repurchase Agreements

As of June 30, 2012 and December 31, 2011, we had repurchase agreements in place in the amount of $12.1 billion and $5.3 billion, respectively, to finance Agency Security purchases. At June 30, 2012 and December 31, 2011, the weighted average interest rate or cost of funds was 0.40% and 0.37%, respectively. At June 30, 2012 and December 31, 2011, we had repurchase agreements outstanding with 26 and 23 counterparties, respectively, with a weighted average maturity of 32 days and 18 days, respectively.

The following table represents the contractual repricing regarding our repurchase agreements to finance Agency Security purchases as of March 31, 2013 and December 31, 2012.

| | | March 31, 2013 | | | December 31, 2012 | |

| | | (in thousands) | |

| Within 30 days | | $ | 11,626,612 | | | $ | 7,771,444 | |

| 31 days to 60 days | | | 11,540,240 | | | | 7,840,268 | |

| 61 days to 90 days | | | 562,762 | | | | 2,699,706 | |

| Greater than 90 days | | | 1,099,000 | | | | 54,677 | |

| Total | | $ | 24,828,614 | | | $ | 18,366,095 | |

ARMOUR Residential REIT, Inc. and Subsidiary

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

The following table represents the Master Repurchase Agreements (“MRAs”) and other information regarding our repurchase agreements to finance Agency Security purchases as of June 30, 2012March 31, 2013 and December 31, 2011.

| | | June 30, 2012 | | | December 31, 2011 | |

| | | (dollars in thousands) | |

| Within 30 days | | $ | 7,823,536 | | | $ | 4,068,197 | |

| 31 days to 60 days | | | 2,038,459 | | | | 1,111,480 | |

| 61 days to 90 days | | | 1,707,767 | | | | 156,285 | |

| Greater than 90 days | | | 542,824 | | | | - | |

| Total | | $ | 12,112,586 | | | $ | 5,335,962 | |

As of June 30, 2012 and December 31, 2011,| | | March 31, 2013 | | | December 31, 2012 | |

| Number of MRA’s | | | 33 | | | | 33 | |

| Number of counterparties with repurchase agreements outstanding | | | 28 | | | | 26 | |

| Weighted average maturity in days | | | 36 | | | | 34 | |

| Weighted average contractual rate | | | 0.43 | % | | | 0.49 | % |

Haircut for repurchase agreements (1) | | | 4.8 | % | | | 4.8 | % |

(1) The Haircut represents the weighted average margin requirement, or the percentage amount by which the collateral value must exceed the loan amount, which we also refer to as the haircut, under all our repurchase agreements was approximately 4.8% and 5.0%, respectively.amount.

Note 8 -– Derivatives