| Three Months Ended June 30, 2018 | |||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Non- controlling Interests | Total Equity | ||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||

| Balance at March 31, 2018 | 128.8 | $ | 1 | $ | 5,179 | $ | (2,711 | ) | $ | (44 | ) | $ | 3 | $ | 2,428 | ||||||||||||

| Net Income | — | — | — | 123 | — | 1 | 124 | ||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | (3 | ) | — | (3 | ) | ||||||||||||||||||

| Repurchase of common stock | (4.3 | ) | — | (106 | ) | — | — | — | (106 | ) | |||||||||||||||||

| Stock-based compensation | — | — | 12 | — | — | — | 12 | ||||||||||||||||||||

| Issuance of shares for vesting of equity awards | 0.2 | — | — | — | — | — | — | ||||||||||||||||||||

| Shares withheld for taxes on equity awards | (0.1 | ) | — | (1 | ) | — | — | — | (1 | ) | |||||||||||||||||

| Dividends declared ($0.09 per share) | — | — | (11 | ) | — | — | (1 | ) | (12 | ) | |||||||||||||||||

| Balance at June 30, 2018 | 124.6 | $ | 1 | $ | 5,073 | $ | (2,588 | ) | $ | (47 | ) | $ | 3 | $ | 2,442 | ||||||||||||

| Six Months Ended June 30, 2019 | |||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Non- controlling Interests | Total Equity | ||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||

| Balance at December 31, 2018 | 114.6 | $ | 1 | $ | 4,869 | $ | (2,507 | ) | $ | (52 | ) | $ | 4 | $ | 2,315 | ||||||||||||

| Net Loss | — | — | — | (30 | ) | — | 1 | (29 | ) | ||||||||||||||||||

| Other comprehensive income | — | — | — | — | 1 | — | 1 | ||||||||||||||||||||

| Repurchase of common stock | (1.2 | ) | — | (20 | ) | — | — | — | (20 | ) | |||||||||||||||||

| Stock-based compensation | — | — | 15 | — | — | — | 15 | ||||||||||||||||||||

| Issuance of shares for vesting of equity awards | 1.3 | — | — | — | — | — | — | ||||||||||||||||||||

| Shares withheld for taxes on equity awards | (0.4 | ) | — | (6 | ) | — | — | — | (6 | ) | |||||||||||||||||

| Dividends declared ($0.18 per share) | — | — | (21 | ) | — | — | (2 | ) | (23 | ) | |||||||||||||||||

| Balance at June 30, 2019 | 114.3 | $ | 1 | $ | 4,837 | $ | (2,537 | ) | $ | (51 | ) | $ | 3 | $ | 2,253 | ||||||||||||

| Six Months Ended June 30, 2018 | |||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Non- controlling Interests | Total Equity | ||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||

| Balance at December 31, 2017 | 131.6 | $ | 1 | $ | 5,285 | $ | (2,631 | ) | $ | (37 | ) | $ | 4 | $ | 2,622 | ||||||||||||

| Cumulative effect of adoption of new accounting pronouncements | — | — | — | (13 | ) | (9 | ) | — | (22 | ) | |||||||||||||||||

| Net Income | — | — | — | 56 | — | 1 | 57 | ||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | (1 | ) | — | (1 | ) | ||||||||||||||||||

| Repurchase of common stock | (7.8 | ) | — | (200 | ) | — | — | — | (200 | ) | |||||||||||||||||

| Stock-based compensation | — | — | 21 | — | — | — | 21 | ||||||||||||||||||||

| Issuance of shares for vesting of equity awards | 1.2 | — | — | — | — | — | — | ||||||||||||||||||||

| Shares withheld for taxes on equity awards | (0.4 | ) | — | (10 | ) | — | — | — | (10 | ) | |||||||||||||||||

| Dividends declared ($0.18 per share) | — | — | (23 | ) | — | — | (2 | ) | (25 | ) | |||||||||||||||||

| Balance at June 30, 2018 | 124.6 | $ | 1 | $ | 5,073 | $ | (2,588 | ) | $ | (47 | ) | $ | 3 | $ | 2,442 | ||||||||||||

| Three Months Ended March 31, 2019 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Non- controlling Interests | Total Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2018 | 114.6 | $ | 1 | $ | 4,869 | $ | (2,507) | $ | (52) | $ | 4 | $ | 2,315 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | (99) | — | — | (99) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | 2 | — | 2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | (1.2) | — | (20) | — | — | — | (20) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | 8 | — | — | — | 8 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares for vesting of equity awards | 1.2 | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares withheld for taxes on equity awards | (0.4) | — | (6) | — | — | — | (6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends declared ($0.09 per share) | — | — | (10) | — | — | (1) | (11) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2019 | 114.2 | $ | 1 | $ | 4,841 | $ | (2,606) | $ | (50) | $ | 3 | $ | 2,189 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Condensed Consolidated Statement of Changes in Equity for Realogy Group

The Company has not included a statement of changes in equity for Realogy Group as the operating results of Group are consistent with the operating results of Realogy Holdings as all revenue and expenses of Realogy Group flow up to Realogy Holdings and there are no incremental activities at the Realogy Holdings level. The only difference between Realogy Group and Realogy Holdings is that the $1 million in par value of common stock in Realogy Holdings' equity is included in additional paid inpaid-in capital in Realogy Group's equity.

Stock Repurchases

The Company may repurchase shares of its common stock under authorizations from its Board of Directors. Shares repurchased are retired and not displayed separately as treasury stock on the consolidated financial statements. The par value of the shares repurchased and retired is deducted from common stock and the excess of the purchase price over par value is first charged against any available additional paid-in capital with the balance charged to retained earnings. Direct costs incurred to repurchase the shares are included in the total cost of the shares.

The Company's Board of Directors authorized a share repurchase program of up to $275 million, $300 million, $350 million and $175 million of the Company's common stock in February 2016, 2017, 2018 and 2019, respectively.

In the first quarter of 2019, the Company repurchased and retired 1.2 million shares of common stock for $20 million at a weighted average market price of $17.21 per share. The Company didhas not repurchaserepurchased any shares under the share repurchase programs during the second quarter ofsince 2019. As of June 30, 2019, the Company had repurchased and retired 35.5 million shares of common stock for an aggregate of $896 million at a total weighted average market price of $25.22 per share. As of June 30, 2019,March 31, 2020, $204 million remained available for repurchase under the share repurchase programs. In May 2020, the Company's Board of Directors terminated its outstanding share repurchase programs.

The restrictive covenants in the indenture governing the 9.375% Senior Notes restrict the Company's ability to repurchase shares. See "Note 5. Short and Long-Term Debt—Unsecured Notes."

Stock-Based Compensation

During the first quarter of 2019,2020, the Company granted 0.9 million shares of non-qualified stock options with a weighted average exercise price of $13.45, restricted stock units related to 2.50.7 million shares with a weighted average grant date fair value of $13.53$9.70 and performance stock units related to 1.20.9 million shares with a weighted average grant date fair value of $11.08.$9.23. The Company shifted away from the use of options and granted all time-based equity awards in the form of restricted stock units which are subject to ratable vesting over a three-year period. Therefore, the Company did not grant shares of non-qualified stock options during the first quarter of 2020.

26

Earnings (loss) per share attributable to Realogy Holdings

Basic earnings (loss) per share is computed based on net income (loss) attributable to Realogy Holdings stockholders divided by the basic weighted-average shares outstanding during the period. Dilutive earnings per share is computed consistently with the basic computation while giving effect to all dilutive potential common shares and common share equivalents that were outstanding during the period. Realogy Holdings uses the treasury stock method to reflect the potential dilutive effect of unvested stock awards and unexercised options.

The Company was in a net loss position for the three months ended March 31, 2020 and 2019 and therefore the impact of incentive equity awards were excluded from the computation of dilutive loss per share as the inclusion of such amounts would be anti-dilutive.

9. COMMITMENTS AND CONTINGENCIES

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

| (in millions, except per share data) | 2019 | 2018 | 2019 | 2018 | |||||||||||

| Net income (loss) attributable to Realogy Holdings stockholders | $ | 69 | $ | 123 | $ | (30 | ) | $ | 56 | ||||||

| Basic weighted average shares | 114.3 | 126.5 | 114.1 | 128.4 | |||||||||||

| Stock options, restricted stock units and performance share units (a)(b) | 0.6 | 1.1 | — | 1.3 | |||||||||||

| Weighted average diluted shares | 114.9 | 127.6 | 114.1 | 129.7 | |||||||||||

| Earnings (Loss) Per Share: | |||||||||||||||

| Basic | $ | 0.60 | $ | 0.97 | $ | (0.26 | ) | $ | 0.44 | ||||||

| Diluted | $ | 0.60 | $ | 0.96 | $ | (0.26 | ) | $ | 0.43 | ||||||

Litigation

The Company is involved in claims, legal proceedings, alternative dispute resolution and governmental inquiries related to alleged contract disputes, business practices, intellectual property and other commercial, employment, regulatory and tax matters. Examples of such matters include but are not limited to allegations:

•that independent residential real estate sales agents engaged by NRTRealogy Brokerage Group or by affiliated franchisees—under certain state or federal laws—are potentially employees instead of independent contractors, and they or regulators therefore may bring claims against NRTRealogy Brokerage Group for breach of contract, wage and hour classification claims, wrongful discharge, unemployment and workers' compensation and could seek benefits, back wages, overtime, indemnification, penalties related to classification practices and expense reimbursement available to employees or similar claims against our franchise operationsRealogy Franchise Group as an alleged joint employer of an affiliated franchisee’s independent sales agents;

•concerning other employment law matters, including other types of worker classification claims as well as wage and hour claims and retaliation claims;

•concerning anti-trust and anti-competition matters;

•that the Company is vicariously liable for the acts of franchisees under theories of actual or apparent agency;

•by current or former franchisees that franchise agreements were breached including improper terminations;

•concerning alleged RESPA or state real estate law violations;

•concerning claims related to the Telephone Consumer Protection Act, including autodialer claims;

•concerning claims generally against the company owned brokerage operations for negligence, misrepresentation or breach of fiduciary duty in connection with the performance of real estate brokerage or other professional services as well as other brokerage claims associated with listing information and property history;

related to copyright law, including infringement actions alleging improper use of copyrighted photographs on websites or in marketing materials without consent of the copyright holder;

•concerning breach of obligations to make websites and other services accessible for consumers with disabilities;

•concerning claims generally against the title companyagent contending that as the escrow company, the companyagent knew or should have known that a transaction was fraudulent or concerning otherthat the agent was negligent in addressing title defects or settlement errors;conducting the settlement;

•concerning information security and cyber-crime, including claims under new and emerging data privacy laws related to the protection of customer, employee or third-party information, as well as those related to the diversion of homesale transaction closing funds; and

•those related to general fraud claims.

Worker Classification Litigation

Whitlach v. Premier Valley, Inc. d/b/a Century 21 M&M and Century 21 Real Estate LLC (Superior Court of California, AlamedaStanislaus County). This was filed as a putative class action complaint on December 20, 2018 by plaintiff James Whitlach against Premier Valley Inc., a Century 21 Real Estate independently-owned franchisee doing business as Century 21 M&M (“Century 21 M&M”). The complaint also names Century 21 Real Estate LLC, a wholly-owned subsidiary of the Company and the franchisor of Century 21 Real Estate (“Century 21”), as an alleged joint employer of the franchisee’s independent

27

sales agents and seeks to certify a class that could potentially include all agents of both Century 21 M&M and Century 21 in California. The plaintiff alleges that Century 21 M&M misclassified all of its independent real estate agents, salespeople, sales professionals, broker associates and other similar positions as independent contractors, failed to pay minimum wages, failed to provide meal and rest breaks, failed to pay timely wages, failed to keep proper records, failed to provide appropriate wage statements, made unlawful deductions from wages, and failed to reimburse plaintiff and the putative class for business related expenses, resulting in violations of the California Labor Code. The complaint also asserts an unfair business practice claim based on the alleged violations described above.

On February 15, 2019, the plaintiff amended his complaint to assert claims pursuant to the California Private Attorneys General Act (“PAGA”). The PAGA claims included in the amended complaint are substantively similar to those asserted in the original complaint. Under California law, PAGA claims are generally not subject to arbitration and may result in exposure in the form of additional penalties. In April 2019, the defendants filed motions to compel arbitration of the non-PAGA claims and to stay the PAGA claims pending resolution of the arbitrable claims and to change venue.claims. On June 5, 2019, the courtCourt dismissed the plaintiff’s non-PAGA claims without prejudice and withdrew the defendants’ motion to compel arbitration by stipulation of the parties. The plaintiff continues to pursue his PAGA claims as a representative of purported "aggrieved employees" as defined by PAGA. The plaintiff currently seeks, as the representative of all purported aggrieved employees, all non-individualized relief available to the purported aggrieved employees under PAGA, as well as attorneys’ fees. On November 15, 2019, Century 21 M&M filed a demurrer to the complaint, seeking to dismiss the remaining claim in the action, to which Century 21 filed a joinder, and on February 12, 2020 a brief in opposition was filed by the plaintiff. The hearing on the demurrer has been deferred and will not be heard until the courts reopen in California and resume addressing non-emergent civil motions.

Fenley v. Realogy Franchise Group LLC, Sotheby’s International Realty, Inc., Wish Properties, Inc. and DOES 1-100 (Superior Court of California, Kern County). This is a putative class action complaint filed on April 25, 2019 by plaintiff Elizabeth Fenley against Wish Properties, Inc, a Sotheby’s International Realty independently-owned franchisee doing business as Wish Sotheby’s International Realty (“Wish SIR”). The complaint also names Realogy Franchise Group LLC and Sotheby’s International Realty, Inc., wholly-owned subsidiaries of the Company, as alleged joint employers of the franchisee’s independent sales agents and seeks to certify a class that could potentially include all agents in California affiliated with any Realogy Franchise Group brand. The plaintiff alleges that all defendants are jointly responsible for misclassifying Wish SIR’s agents as independent contractors and failed to reimburse for business expenses, provide accurate wage statements and pay wages timely, all in violation of the California Labor Code. The complaint also asserts an unfair business practice claim based on the violations previously described. The plaintiff seeks reimbursement of allegedly necessary expenses, liquidated damages, waiting time penalties, civil penalties, pre- and post-judgment interest, restitution, injunctive relief, and attorneys’ fees and costs. On July 26,September 17, 2019, Wish SIR filed a motionthe Court denied the defendants’ motions to compel arbitration and stay all legal proceedings pending conclusion ofarbitration. In February 2020, the arbitration. On the same day, Realogy Franchise Group LLC and Sotheby’s International Realty, Inc. filed their own motion to compel arbitration and a joinder in Wish SIR’s motion.matter was settled on an individual basis.

These cases raise various previously unlitigated claims and the PAGA claims in the Whitlach matter add additional litigation, financial and operating uncertainties. There are similar classification cases pending against several other brokerages in the state of California and developments in one or more of those cases could impact progress in these cases.

Real Estate Industry Litigation

Moehrl, Cole, Darnell, Nager, Ramey, Sawbill Strategic, Inc., Umpa and Ruh v. The National Association of Realtors, Realogy Holdings Corp., Homeservices of America, Inc., BHH Affiliates, LLC, The Long & Foster Companies, Inc., RE/MAX LLC, and Keller Williams Realty, Inc. (U.S. District Court for the Northern District of Illinois). This amended putative class action complaint (the "amended MoehlerMoehrl complaint"), filed on June 14, 2019, (i) consolidates the Moehrl and Sawbill litigation reported in our Form 10-Q for the period ended March 31, 2019, (ii) adds certain plaintiffs and defendants, and (iii) serves as a response to the separate motions to dismiss filed on May 17, 2019 in the prior Moehrl litigation by each of NAR and the Company (along with the other defendants named in the prior Moehrl complaint).

In the amended Moehrl complaint, the plaintiffs allege that the defendants engaged in a continuing contract, combination, or conspiracy to unreasonably restrain trade and commerce in violation of Section 1 of the Sherman Act because defendant NAR allegedly established mandatory anticompetitive policies for the multiple listing services and its member brokers that require brokers to make an offer of buyer broker compensation when listing a property. The plaintiffs further allege that commission sharing, which provides for the broker representing the seller sharing or paying a portion of its commission to the broker representing the buyer, is anticompetitive and violates the Sherman Act, and that the defendant franchisors conspired with NAR by requiring their respective franchisees to comply with NAR’s policies and Code of Ethics. The plaintiffs seek a permanent injunction enjoining the defendants from requiring home sellers to pay buyer broker

28

commissions or to otherwise restrict competition among buyer brokers, an award of damages and/or restitution, attorneys fees and costs of suit. Plaintiffs' counsel has filed a motion to appoint lead counsel in the case, which has yet to be decided by the court.Court. On August 9, 2019, NAR and the Company (together with the other defendants named in the amended Moehrl complaint) each filed separate motions to dismiss this litigation. The plaintiffs filed their opposition to the motions to dismiss on September 13, 2019, and the defendants filed their replies in support of the motions on October 18, 2019. Discovery between the parties is stayed pending rulings on the outstanding motions to dismiss this litigation.

Sitzer and Winger v. The National Association of Realtors, Realogy Holdings Corp., Homeservices of America, Inc., RE/MAX Holdings, Inc., and Keller Williams Realty, Inc. (U.S. District Court for the Western District of Missouri). This is a putative class action complaint filed on April 29, 2019 and amended on June 21, 2019 by plaintiffs Joshua Sitzer and Amy Winger against NAR, the Company, Homeservices of America, Inc., RE/MAX Holdings, Inc., and Keller Williams Realty, Inc. The complaint contains substantially similar allegations, and seeks the same relief under the Sherman Act, as the Sawbill and Moehrl litigations.litigation. The Sitzer litigation is limited both in allegations and relief sought to the State of Missouri and includes an additional cause of action for alleged violation of the Missouri Merchandising Practices Act, or MMPA. On July 10,August 22, 2019, defendants filedthe Court denied defendants' motions to transfer the Sitzermatter to the U.S. District Court for the Northern District of Illinois. On August 5,Illinois and on October 16, 2019, denied the motions to dismiss this litigation filed respectively by NAR and the Company (together with the other defendants named inbrokerage/franchisor defendants). Discovery between the Sitzer complaint) each filed separate motions to dismiss this litigation.parties is ongoing.

Securities Litigation

Tanaskovic v. Realogy Holdings Corp., et. al. (U.S. District Court for the District of New Jersey). This is a putative class action complaint filed on July 11, 2019 by plaintiff Sasa Tanaskovic against the Company and certain of its current and former executive officers. The lawsuit alleges violations of Sections 10(b), 20(a) and Rule 10b-5 of the Exchange Act in connection with allegedly false and misleading statements made by the Company about its business, operations, and prospects. The plaintiffs seek, among other things, compensatory damages for purchasers of the Company’s common stock between February 24, 2017 through May 22, 2019, as well as attorneys’ fees and costs. Locals 302 and 612 of the International Union of Operating Engineers-Employers Construction Industry Retirement Trust (the “Retirement Trust”), was appointed lead plaintiff on November 7, 2019. Lead plaintiff filed its amended complaint on March 6, 2020 and the Company has until August 3, 2020 to file its response per the stipulation of the parties entered by the Court on March 25, 2020.

Fried v. Realogy Holdings Corp., et al. (U.S. District Court for the District of New Jersey). This is a putative derivative action filed on October 23, 2019 by plaintiff Adam Fried against the Company (as nominal defendant) and certain of its current and former executive officers and members of its Board of Directors (as defendants). The lawsuit alleges violations of Section 14(a) of the Exchange Act and breach of fiduciary duties for, among other things, allegedly false and misleading statements made by the Company about its business, operations and prospects as well as unjust enrichment claims. The plaintiff seeks, among other things, compensatory damages, disgorgement of improper compensation, certain reforms to the Company’s corporate governance and internal procedures and attorneys’ fees and costs. On December 23, 2019, the Court approved a motion staying this case pending further action in the Tanaskovic matter.

The Company disputes the allegations in each of the captioned matters described above and will vigorously defend these actions. Given the early stages of each of these cases, we cannot estimate a range of reasonably possible losses for this litigation.

The Company believes that it has adequately accrued for legal matters as appropriate. The Company records litigation accruals for legal matters which are both probable and estimable.

Litigation and other disputes are inherently unpredictable and subject to substantial uncertainties and unfavorable resolutions could occur. In addition, class action lawsuits can be costly to defend and, depending on the class size and claims, could be costly to settle. As such, the Company could incur judgments or enter into settlements of claims with liability that are materially in excess of amounts accrued and these settlements could have a material adverse effect on the Company’s financial condition, results of operations or cash flows in any particular period.

* * *

Company-Initiated Litigation

Realogy Holdings Corp. v. SIRVA Worldwide, Inc., North American Van Lines, Inc., Madison Dearborn Capital Partners VII-A, L.P., Madison Dearborn Capital Partners VII-C, L.P., and Madison Dearborn Capital Partners VII

29

Executive-A, L.P. (Court of Chancery of the State of Delaware). On April 27, 2020, the Company filed a complaint against affiliates of MDP and SIRVA to enforce SIRVA’s obligations under the Purchase Agreement for the sale of the Company’s employee relocation services business. The Company alleges breach of contract and seeks specific performance by SIRVA to perform its obligations under the Purchase Agreement, or in the alternative, ordering the defendants to specifically perform their contractual obligations to pay the Company a $30 million termination fee, as well as costs and expenses, including reasonable attorney’s fees. On April 30, 2020, the Company filed a motion to the expedite proceedings and the Court has scheduled a telephonic hearing for such motion on May 8, 2020.

Realogy Holdings Corp., NRT New York LLC (d/b/a The Corcoran Group), Sotheby’s International Realty, Inc., Coldwell Banker Residential Brokerage Company, Coldwell Banker Residential Real Estate LLC, NRT West, Inc., Martha Turner Properties, L.P. And Better Homes and Gardens Real Estate LLC v. Urban Compass, Inc., and Compass, Inc.

* * *

The Company is involved in certain other claims and legal actions arising in the ordinary course of our business. Such litigation, regulatory actions and other proceedings may include, but are not limited to, actions relating to intellectual property, commercial arrangements, franchising arrangements, the fiduciary duties of brokers, standard brokerage disputes like the failure to disclose accurate square footage or hidden defects in the property such as mold, vicarious liability based upon conduct of individuals or entities outside of our control, including franchisees and independent sales agents, antitrust and anti-competition claims, general fraud claims (including wire fraud associated with third-party diversion of funds from a brokerage transaction), employment law claims, including claims challenging the classification of our sales agents as independent contractors, wage and hour classificationrelated claims, and claims related to business actions responsive to the COVID-19 outbreak and governmental and regulatory directives thereto, and claims alleging violations of RESPA, state consumer fraud statutes or federal consumer protection statutes. While the results of such claims and legal actions cannot be predicted with certainty, we do not believe based on information currently available to us that the final outcome of current proceedings against the Company will have a material adverse effect on our consolidated financial position, results of operations or cash flows. In addition, with the increasing requirements resulting from government laws and regulations concerning data breach notifications and data privacy and protection obligations, claims associated with these laws may become more common. While most litigation involves claims against the Company, from time to time the Company commences litigation, including litigation against former employees, franchisees and competitors when it alleges that such persons or entities have breached agreements or engaged in other wrongful conduct.

* * *

Cendant Corporate Liabilities and Guarantees to Cendant and Affiliates

Realogy Group (then Realogy Corporation) separated from Cendant on July 31, 2006 (the "Separation"), pursuant to a plan by Cendant (now known as Avis Budget Group, Inc.) to separate into four4 independent companies—one1 for each of Cendant's business units—real estate services (Realogy Group), travel distribution services ("Travelport"), hospitality services, including timeshare resorts ("Wyndham Worldwide"), and vehicle rental ("Avis Budget Group"). Pursuant to the Separation and Distribution Agreement dated as of July 27, 2006 among Cendant, Realogy Group, Wyndham Worldwide and Travelport (the "Separation and Distribution Agreement"), each of Realogy Group, Wyndham Worldwide and

30

Travelport have assumed certain contingent and other corporate liabilities (and related costs and expenses), which are primarily related to each of their respective businesses. In addition, Realogy Group has assumed 62.5% and Wyndham Worldwide has assumed 37.5% of certain contingent and other corporate liabilities (and related costs and expenses) of Cendant.

The due to former parent balance was $18 million at June 30, 2019both March 31, 2020 and $21 million at December 31, 2018, respectively.2019. The due to former parent balance was comprised of the Company’s portion of the following: (i) Cendant’s remaining contingent tax liabilities, (ii) accrued interest on contingent tax liabilities, (iii) potential liabilities related to Cendant’s terminated or divested businesses, and (iv) potential liabilities related to the residual portion of accruals for Cendant operations.

Tax Matters

The Company is subject to income taxes in the United States and several foreign jurisdictions. Significant judgment is required in determining the worldwide provision for income taxes and recording related assets and liabilities. In the ordinary course of business, there are many transactions and calculations where the ultimate tax determination is uncertain. The Company is regularly under audit by tax authorities whereby the outcome of the audits is uncertain. The Company believes there is appropriate support for positions taken on its tax returns. The liabilities that have been recorded represent the best estimates of the probable loss on certain positions and are adequate for all open years based on an assessment of many factors including past experience and interpretations of tax law applied to the facts of each matter. However, the outcomes of tax audits are inherently uncertain.

Escrow and Trust Deposits

As a service to its customers, the Company administers escrow and trust deposits which represent undisbursed amounts received for the settlement of real estate transactions. Deposits at FDIC-insured institutions are insured up to $250 thousand.$250 thousand. These escrow and trust deposits totaled $685$556 million at June 30, 2019March 31, 2020 and $426$475 million at December 31, 2018.2019. These escrow and trust deposits are not assets of the Company and, therefore, are excluded from the accompanying Condensed Consolidated Balance Sheets. However, the Company remains contingently liable for the disposition of these deposits.

10. SEGMENT INFORMATION

The reportable segments presented below represent the Company’s operating segments for which separate financial information is available and which is utilized on a regular basis by its chief operating decision maker to assess performance and to allocate resources. In identifying its reportable segments, the Company also considers the nature of services provided by its operating segments. During the first quarter of 2020, Realogy Leads Group was consolidated into Realogy Franchise Group and the segment change is reflected for all periods presented. Realogy Leads Group, which previously was part of Cartus, consists of the Company's affinity and broker-to-broker business, as well as the broker network made up of agents and brokers from Realogy’s residential real estate brands and certain independent real estate brokers (which is referred to as the Realogy Advantage Broker Network). The Company initiated litigation against MDP and SIRVA to enforce SIRVA’s obligations under the Purchase Agreement as described in Note 11. "Subsequent Events". Based upon developments in this litigation, the Company may reassess segment classification in future periods.

Management evaluates the operating results of each of its reportable segments based upon revenue and Operating EBITDA. Operating EBITDA is defined by us as net income (loss) before depreciation and amortization, interest expense, net, (other than relocation services interest for securitization assets and securitization obligations), income taxes, and other items that are not core to the operating activities of the Company such as restructuring charges, former parent legacy items, gains or losses on the early extinguishment of debt, asset impairments, gains or losses on discontinued operations and gains or losses on the sale of investments or other assets. The Company’s presentation of Operating EBITDA may not be comparable to similar measures used by other companies.

| Revenues (a) (b) | |||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||

| 2020 | 2019 | ||||||||||||||||

| Realogy Franchise Group | $ | 168 | $ | 179 | |||||||||||||

| Realogy Brokerage Group | 869 | 816 | |||||||||||||||

| Realogy Title Group | 137 | 114 | |||||||||||||||

| Corporate and Other (c) | (58) | (55) | |||||||||||||||

| Total Company | $ | 1,116 | $ | 1,054 | |||||||||||||

31

| Revenues (a) (b) | |||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||||

| Real Estate Franchise Services | $ | 234 | $ | 237 | $ | 397 | $ | 413 | |||||||

| Company Owned Real Estate Brokerage Services | 1,331 | 1,408 | 2,147 | 2,325 | |||||||||||

| Relocation Services | 97 | 105 | 173 | 184 | |||||||||||

| Title and Settlement Services | 160 | 162 | 274 | 282 | |||||||||||

| Corporate and Other (c) | (87 | ) | (92 | ) | (142 | ) | (155 | ) | |||||||

| Total Company | $ | 1,735 | $ | 1,820 | $ | 2,849 | $ | 3,049 | |||||||

_______________

| Operating EBITDA | |||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||||

| Real Estate Franchise Services | $ | 163 | $ | 173 | $ | 253 | $ | 278 | |||||||

| Company Owned Real Estate Brokerage Services | 47 | 61 | (15 | ) | 16 | ||||||||||

| Relocation Services | 27 | 34 | 29 | 33 | |||||||||||

| Title and Settlement Services | 32 | 31 | 23 | 25 | |||||||||||

| Corporate and Other (a) | (24 | ) | (23 | ) | (49 | ) | (42 | ) | |||||||

| Less: Depreciation and amortization (b) | 50 | 49 | 99 | 99 | |||||||||||

| Interest expense, net | 81 | 46 | 144 | 79 | |||||||||||

| Income tax expense (benefit) | 34 | 52 | (1 | ) | 33 | ||||||||||

| Restructuring costs, net (c) | 9 | 6 | 21 | 36 | |||||||||||

| Impairment | 2 | — | 3 | — | |||||||||||

| Loss on the early extinguishment of debt (d) | — | — | 5 | 7 | |||||||||||

| Net income (loss) attributable to Realogy Holdings and Realogy Group | $ | 69 | $ | 123 | $ | (30 | ) | $ | 56 | ||||||

| Operating EBITDA | |||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||

| 2020 | 2019 | ||||||||||||||||

| Realogy Franchise Group | $ | 101 | $ | 98 | |||||||||||||

| Realogy Brokerage Group | (51) | (62) | |||||||||||||||

| Realogy Title Group | 12 | (9) | |||||||||||||||

| Corporate and Other (a) | (25) | (25) | |||||||||||||||

| Total continuing operations | 37 | 2 | |||||||||||||||

| Less: Depreciation and amortization | 45 | 41 | |||||||||||||||

| Interest expense, net | 101 | 63 | |||||||||||||||

| Income tax benefit | (132) | (32) | |||||||||||||||

| Restructuring costs, net (b) | 11 | 9 | |||||||||||||||

| Impairments (c) | 447 | 1 | |||||||||||||||

| Loss on the early extinguishment of debt (d) | — | 5 | |||||||||||||||

| Net loss from continuing operations | (435) | (85) | |||||||||||||||

| Net loss from discontinued operations | (27) | (14) | |||||||||||||||

| Net loss attributable to Realogy Holdings and Realogy Group | $ | (462) | $ | (99) | |||||||||||||

_______________

(a)Includes the elimination of transactions between segments.

(b)The three months ended March 31, 2020 includes restructuring charges of $1 million at Realogy Franchise Group, $9 million at Realogy Brokerage Group and $1 million at Realogy Title Group.

The three months ended June 30, 2018March 31, 2019 includes restructuring charges of $4 million in the Company Owned Real Estateat Realogy Brokerage Services segment,Group, $1 million inat Realogy Title Group and $4 million at Corporate and Other.

(c)Impairments for the Relocation Services segmentthree months ended March 31, 2020 include a goodwill impairment charge of $413 million which reduced the net carrying value of Realogy Brokerage Group by $314 million after accounting for the related income tax benefit of $99 million, an impairment charge of $30 million which reduced the carrying value of trademarks at Realogy Franchise Group and $4 million related to lease asset impairments. Impairments for the three months ended March 31, 2019 include $1 million inof impairment charges related to lease asset impairments.

(d)Loss on the Title and Settlement Services segment.

32

11. SUBSEQUENT EVENTS

Update to Planned Sale of Cartus Relocation Services

The Company entered into a Purchase and Sale Agreement on November 6, 2019 (the "Purchase Agreement"), for the acquisition of Cartus Relocation Services, the Company's global employee relocation business, by North American Van Lines, Inc. (as assignee of SIRVA) for $375 million in cash at closing, subject to certain adjustments set forth in the Purchase Agreement, and a $25 million deferred payment after the closing of the transaction. SIRVA is a portfolio company of Madison Dearborn Partners, LLC ("MDP").

The Company strongly believes that all conditions to SIRVA’s obligations to effect the closing have been and continue to be satisfied. On April 24, 2020, the Company delivered notice to SIRVA that it had satisfied all such conditions under the Purchase Agreement and was committed to closing the transaction on April 29, 2020. On April 25, 2020, SIRVA notified the Company that it did not believe that all conditions to closing have been or will be satisfied by the April 30, 2020 termination date under the Purchase Agreement.

On April 27, 2020, the Company filed a lawsuit against affiliates of MDP and SIRVA to enforce SIRVA’s obligations under the Purchase Agreement. SIRVA has since delivered notices to the Company purportedly terminating the Purchase Agreement, the validity of which the Company disputes. The Company strongly disagrees with SIRVA’s position and will pursue all legal remedies to enforce SIRVA’s obligations under the Purchase Agreement.

As of March 31, 2020, the assets and liabilities of Cartus Relocation Services are classified as held for sale in the Condensed Consolidated Balance Sheets and the results are reported in this Quarterly Report as discontinued operations. "Net loss from discontinued operations" is reflected on the Condensed Consolidated Statements of Operations for all periods presented. Based upon developments in this litigation, the Company will reassess held for sale and discontinued operations accounting treatment in future periods.

33

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis should be read in conjunction with our Condensed Consolidated Financial Statements and accompanying notes thereto included elsewhere herein and with our Consolidated Financial Statements and accompanying notes included in the 20182019 Form 10-K. Unless otherwise noted, all dollar amounts in tables are in millions. Neither Realogy Holdings, the indirect parent of Realogy Group, nor Realogy Intermediate, the direct parent company of Realogy Group, conducts any operations other than with respect to its respective direct or indirect ownership of Realogy Group. As a result, the condensed consolidated financial positions, results of operations and cash flows of Realogy Holdings, Realogy Intermediate and Realogy Group are the same. This Management's Discussion and Analysis of Financial Condition and Results of Operations, or MD&A, contains forward-looking statements. See "Forward-Looking Statements" in this report and "Forward-Looking Statements" and "Risk Factors" in this Quarterly Report as well as our 20182019 Form 10-K for a discussion of the uncertainties, risks and assumptions associated with these statements. Actual results may differ materially from those contained in any forward-looking statements.

OVERVIEW

We are a global provider of real estate and relocation services and report our operations in the following fourthree business segments:

•Realogy Brokerage Group—operates a full-service real estate brokerage business with approximately 700 owned and operated brokerage offices with approximately 52,200 independent sales agents principally under the Coldwell Banker®, Corcoran® and Sotheby’s International Realty® brand names in many of the largest metropolitan areas in the U.S.

•Realogy Title Group—provides full-service title and settlement services to real estate companies, affinity groups, corporations and financial institutions with many of these services provided in connection with the Company's real estate brokerage business. This segment also includes the Company's share of equity earnings and losses for our Guaranteed Rate Affinity mortgage origination joint venture.

Our technology and data group pursues technology-enabled solutions to support our business segments and franchisees as well as independent sales agents affiliated with Realogy Brokerage and Franchise Groups and their customers.

RECENT DEVELOPMENTS

COVID-19

The COVID-19 pandemic is having a profound effect on the global economy and financial markets. This unprecedented situation has created considerable risks and uncertainties for almost all sectors, including the U.S. real estate services industry, as well as for the Company and its affiliated franchisees, including those arising from the adverse effects on the economy as well as risks related to employees, independent sales agents, franchisees, and consumers.

In the United States, federal, state and local governments continue to react to this evolving public health crisis by, among other actions, recommending or requiring the avoidance of gatherings of people or significantly or entirely curtailing activities categorized as non-essential. The first statewide "shelter in place" order in the U.S. was issued by the State of California on March 19, 2020 and as of April 30, 2020, the vast majority of all Americans were subject to restrictions on their activities due to the public health crisis, although the level and duration of such restrictions vary by state and local mandates. Our near-term priority has been, and continues to be, the protection of the health and safety of our employees,

34

affiliated agents and franchisees and customers. Substantially all of our employees have been working remotely since mid-March 2020 and in early March 2020, we moved quickly to transform several near-term brand events to a virtual-only format.

Federal guidance from the U.S. Department of Homeland Security issued on March 28, 2020 included residential real estate services (including settlement services) on the list of essential services that are deemed critical to public health and safety as well as economic and national security. However, the definition of real estate services and whether the provision of real estate services is deemed to constitute an essential business varies by state and can also differ between counties and cities. Furthermore, even if such services are categorized as essential in any particular geography, local or state regulations may preclude or strictly limit traditional methods of marketing homes, such as open houses or in-person showings of property and may not include all aspects of home selling, such as home inspections and home repairs.

The ability of company owned and franchised brokerages to provide such services may also be limited by brokerage policies and procedures designed to protect the health and safety of independent sales agents and consumers. Residential real estate transactions may be additionally restricted due to each consumer's preferences, including with respect to health, financial and other matters, including, but not limited to, whether the home buyer or seller is affected by the heightened economic uncertainties resulting from the pandemic, including significant declines in the value of stock (and stock market volatility), declining wages and increasing unemployment.

We are taking actions to leverage technology for virtual showings, alternative processes for contract negotiation and execution, and recent legislative and procedural changes related to items such as remote appraisals and remote notarization. However, it is currently not clear whether, and how quickly and widespread, these alternatives may be adopted by independent sales agents and consumers. In addition, remote notarization and other closing procedures are not legally permitted in all states.

We experienced positive growth in closed homesale sides and strong year-over-year increases in homesale transaction volume and homesale transaction price during January and February. Homesale transaction volume was up 13% in January and 11% in February compared to the prior year. However, commencing around mid-March 2020, we began to see declines in new contracts to buy or sell a home (commonly referred to as "open homesale contracts"), which steepened during the last week of the quarter, when we also began to see declines in closed homesale transactions. As a result, homesale transaction volume was up 3% in March compared to March 2019. Declines in open homesale contracts and closed transactions during March 2020 were particularly pronounced in densely populated areas, such as California and the New York metropolitan area (geographies which also have an average sales price much higher than the U.S. average). This trend is continuing, with sustained declines in open homesale contracts and closed transactions in April 2020, as well as declines in average sale price due to geography mix and lower inventory in the high-end markets. In addition, these trends may continue or may worsen for so long as the COVID-19 crisis continues to have a material impact on the industry, consumers and the overall economy.

Accordingly, we anticipate that our revenue for the second quarter of 2020 will be materially lower than during the comparable period in 2019, primarily due to lower homesale transaction volume.

In mid-March 2020, we began taking a series of proactive measures intended to increase liquidity to support our operations, identify and implement cost-saving measures, and to work to provide liquidity to affiliated franchisees in light of the emerging COVID-19 crisis. These measures are assessed by management on an ongoing basis and may be extended and/or expanded as the situation evolves. Specifically:

•To supplement available cash on hand, we borrowed an additional $400 million under our Revolving Credit Facility in March 2020 resulting in $755 million of outstanding borrowings under our Revolving Credit Facility at March 31, 2020 and $628 million of cash and cash equivalents as of March 31, 2020.

•To preserve capital, we implemented a series of cost saving initiatives, which we expect to result in cost savings of $80 to $100 million for each full quarter for so long as such measures remain in place. Depending on management’s ongoing assessments, we may expand or contract the mix and scope of these cost saving initiatives (which may have an impact on quarterly savings). Current initiatives include:

◦employee-related cost-savings actions covering the vast majority of our employee base, which we expect will result in cost-savings of approximately $60 million for each full quarter for so long as such measures remain in place, including:

▪temporary salary reductions for all of our exempt employees, including our executive leadership, and temporary work-week reductions for certain non-exempt employees, each effective April 4, 2020;

▪temporary employment furloughs of certain employees, although we have continued to cover the

35

employee-portion of health insurance premiums for such employees;

▪reductions in workforce of certain non-exempt employees;

▪freezing new hires; and

▪elimination of our employee 401(k) match effective April 4, 2020;

◦other cost saving actions including reductions in marketing expense, incremental office optimization activities, delaying events and conferences as well as other actions focused on reducing operating expenses and delaying investments in certain initiatives.

•To provide enhanced liquidity to affiliated franchisees we took the following actions, which we believe are meaningful to franchisees, but are not expected to have a material impact on our financial results for the second quarter of 2020:

◦accelerated April payment of franchisee rebates by two weeks;

◦waived all domestic U.S. brand marketing fund fees (which we generally apply on a dollar-for-dollar basis to marketing expenses), including monthly minimums, if applicable, for all homesale transactions closing in the second quarter of 2020;

◦waived applicable domestic U.S. monthly minimum royalty fees due in the second quarter of 2020; and

◦agreed to retain franchisee rebate tiers at 2019 levels for the duration of 2020.

In addition, we have proactively shared information with affiliated franchisees and independent sales agents regarding the potential benefits which are available to sole proprietors and independent contractors under the "Coronavirus Aid, Relief, and Economic Security Act," or CARES Act, provision aimed at assisting small businesses during the crisis.

Material revenue declines relating to this crisis, including in the second quarter of 2020, are expected to have a material negative impact on our earnings and may also adversely impact our liquidity, notwithstanding the mitigation actions we have initiated and expect to continue during this crisis and, given the significant uncertainties created by the COVID-19 crisis and related economic downturn, may continue to have such an effect in future periods.

We are currently in compliance with our senior secured leverage ratio; however, a material decline in our franchise systemability to generate EBITDA calculated on a Pro Forma Basis, as defined in the Senior Secured Credit Agreement governing the Senior Secured Credit Facility and Term Loan A Facility, could result in our failure to comply with the senior secured leverage ratio covenant in future periods. In addition, prior to making new borrowings under the Revolving Credit Facility, we are required to certify that the representations and warranties in the Senior Secured Credit Agreement remain true and correct in all material respects as of the date of any borrowing (except to the extent such representations and warranties relate to an earlier date), including the absence of any material adverse effect on our business, property, operations or condition.

See Financial Condition, Liquidity and Capital Resources in this Item 2. for additional information on our near-term liquidity. See Note 5, "Short and Long-Term Debt", to the Condensed Consolidated Financial Statements for additional information on our short- and long-term debt. For important risks regarding our indebtedness, see Part II, Item 1A, "Risk Factors", of this Form 10-Q as well as their customers, including through ZapLabsthe risk factors that appear under the header Risks Related to Our Indebtedness in Part I, Item 1A, "Risk Factors" of the 2019 Form 10-K.

Update to the Planned Sale of Cartus Relocation Services

As previously disclosed, the Company entered into a Purchase and Sale Agreement on November 6, 2019 (the "Purchase Agreement"), for the acquisition of Cartus Relocation Services, the Company's global employee relocation business, by North American Van Lines, Inc. (as assignee of SIRVA Worldwide, Inc., or "SIRVA") for $375 million in cash at closing, subject to certain adjustments set forth in the Purchase Agreement, and a $25 million deferred payment after the closing of the transaction. SIRVA is a portfolio company of affiliates of Madison Dearborn Partners, LLC our wholly-owned subsidiary.("MDP").

On April 27, 2020, the Company filed a lawsuit against affiliates of MDP and SIRVA to enforce SIRVA’s obligations under the Purchase Agreement. SIRVA has since delivered notices to the Company purportedly terminating the Purchase

As of March 31, 2020, the assets and liabilities of Cartus Relocation Services are classified as held for sale in the Condensed Consolidated Balance Sheets and the results are reported in this Quarterly Report as discontinued operations. "Net loss from discontinued operations" is reflected on the Condensed Consolidated Statements of Operations for all periods presented.

Impairment of Goodwill and Other Indefinite-lived Intangible Assets

During the first quarter of 2020, we determined that the impact on future earnings related to the COVID-19 pandemic qualified as a triggering event for all of our reporting units and accordingly, we performed an impairment assessment of goodwill and indefinite-lived intangible assets as of March 31, 2020. This assessment resulted in the recognition of an impairment of Realogy Franchise Group trademarks of $30 million and a goodwill impairment of $413 million for Realogy Brokerage Group offset by an income tax benefit of $99 million resulting in a net reduction to Realogy Brokerage Group's carrying value of $314 million. The primary drivers to the impairments were a significant increase in the weighted average cost of capital due to the volatility in the capital and debt markets due to COVID-19 and the related lower projected financial results for 2020. The impairment charges are recorded on a separate line in the accompanying Condensed Consolidated Statements of Operations and are non-cash in nature.

Impairment analyses are highly complex and involve many subjective assumptions, estimates and judgments made by management.Suchassumptions, estimates and judgments may change in the near term due to multiple factors, including continued business and economic disruptions related to the ongoing COVID-19 crisis. If business conditions deteriorate further than we have modeled or if changes in key assumptions and estimates differ significantly from management’s expectations, it may be necessary to record additional impairment charges in the future, which may be material. See Note 3, "Goodwill and Intangible Assets", to the Condensed Consolidated Financial Statements for additional information related to impairment.

CURRENT BUSINESS AND INDUSTRY TRENDS

According to the National Association of Realtors ("NAR"), during the first halfquarter of 2019,2020, homesale transaction volume decreased 1%volume increased 13% due to a 4% decrease6% increase in the average homesale price and a 7% increase in the number of homesale transactions, partially offset bytransactions.

Homesale transaction volume on a combined basis for Realogy Franchise and Brokerage Groups increased 8% during the three months ended March 31, 2020 compared to the three months ended March 31, 2019. Homesale transaction volume at Realogy Brokerage Group increased 8%, primarily as a result of a 4% increase in average homesale price and a 3% increase in theexisting homesale transactions and homesale transaction volume at Realogy Franchise Group increased 8%, as a result of an 8% increase in average homesale price.price while existing homesale transactions remained flat.

2020. We believe that whileour first quarter 2020 results reflect these general market conditions; however, in addition to the industry fundamentals in late 2018 described above drove a significant portion of our decline in homesale transaction volume in the first half of 2019, our results for the second quarter of 2019 reflect someimpact of the modest improvements in market conditions also described above. However, during both the three- and six-month periods ended June 30, 2019,COVID-19 crisis which began around mid-March 2020, we were also negatively impacted during the first quarter of 2020 by the intensehighly competitive environment in 2019 which is reflected in our year over year comparison of the first quarter, as well as our geographic concentration.

Inventory. Although inventory levels have shown some signs of improvement during 2019,We expect that for so long as the COVID-19 crisis continues, affected geographies will experience dramatic declines in inventory. Even before the COVID-19 crisis, low housing inventory levels continue to behad been an industry-wide concern, in particular in certain highly sought-after geographies and at lower price points. According to NAR, the inventory of existing homes for sale in the U.S. increaseddecreased from 1.531.67 million as of December 2018March 2019 to 1.931.50 million as of June 2019 which is consistent with June 2018.March 2020. As a result, inventory has increased from 3.7decreased from 3.8 months of supply in December 2018March 2019 to 4.43.4 months as of June 2019. However, theseMarch 2020. These levels continue to be significantly below the 10-year average of 5.85.4 months, the 15-year average of 6.1 months and the 25-year average of 5.85.7 months.

Unemployment. More than 30 million Americans have applied for unemployment benefits since March 15, 2020 through April 25, 2020 and since the onset of the pandemic, many companies have announced reductions in work weeks and salaries. If the COVID-19 pandemic continues to curtail employment levels and economic activity for a substantial period,

37

it is likely to lead to an increase in loan defaults and foreclosure activity and make it more difficult for potential home buyers to arrange financing.

Mortgage Rates. A wide variety of factors can contribute to mortgage rates, including federal interest rates, demand, consumer income, unemployment levels and foreclosure rates. In response to the growing economic effects of the COVID-19 crisis, the Federal Reserve Board has cut the interest rate two times, dropping its benchmark interest rate to a range of 0% to 0.25% on March 15, 2020. According to Freddie Mac, mortgage rates on commitments for a 30-year, conventional, fixed-rate first mortgage averaged 4.00%3.51% for the secondfirst quarter of 20192020 compared to 4.54%4.37% for the secondfirst quarter of 2018. While2019. On March 31, 2020, mortgage rates reached as high as 4.87% in November 2018, rates have recently moderated, and on June 30, 2019 were 3.80%3.45%, according to Freddie Mac. A decline in mortgage rates generally drives increased refinancing activity, however, the demand for mortgages to purchase homes will generally decrease with declining homesale transaction activity. Due to the economic effects of the COVID-19 crisis, mortgage standards may tighten, even as rates declines, which could limit the availability of mortgage financing. Increases in mortgage rates adversely impact housing affordability and we have been and could continue toagain be negatively impacted by a rising interest rate environment. For example, a rise in mortgage rates could result in decreased homesale transaction volume if potential home sellers choose to stay with their lower mortgage rate rather than sell their home and pay a higher mortgage rate with the purchase of another home or, similarly, if potential home buyers choose to rent rather than pay higher mortgage rates.

Affordability. The fixed housing affordability index, as reported by NAR, increasedincreased from 142158 for May 2018February 2019 to 150170 for May 2019. As noted above,February 2020, which we believe that a decelerated rise in home prices contributedhas been primarily attributable to the increase in affordability.lower mortgage rates. A housing affordability index above 100 signifies that a family earning the median income has sufficient income to purchase a median-priced home, assuming a 20 percent down payment and ability to qualify for a mortgage. We expect housing affordability to be significantly impacted by the unprecedented rise in unemployment as a result of the COVID-19 crisis, but are unable to estimate the extent or duration of such decrease due to the uncertainties regarding the duration and severity of the COVID-19 crisis and its related impact on the global economy.

Recruitment and Retention of Independent Sales Agents; Commission Income. Recruitment and retention of independent sales agents and independent sales agent teams are critical to the business and financial results of a brokerage, including our company owned brokerages and those operated by our affiliated franchisees. CompetitionAggressive competition for the affiliation of independent sales agents in our industry, including within our franchise system, is high,has negatively impacted recruitment and retention efforts at both Realogy Franchise and Brokerage Groups, in particular with respect to more productive sales agents. agents, and drove a loss in our market share for 2019 compared to 2018. This loss of market share contributed to the decline in homesale transaction volume at both Realogy Franchise and Brokerage Groups and is expected to continue to adversely impact results.

We believe that a variety of factors in recent years have negatively impacted thedriven intensifying recruitment and retention oftactics for independent sales agents in the industry and has increasingly impacted theour recruitment and retention of top producing agents. Such factors include increasing competition, (which has particularly intensified in the last several quarters), increasing levels of commissions paid to agents possibly including up front(including up-front payments and equity,equity), changes in the spending

patterns of independent sales agents (as more independent sales agents purchase services from third-parties outside of their affiliated broker) and the growth in independent sales agent teams. The

In addition, industry competition for independent sales agents has been and is expected to continue to be further complicated by competitive models that do not prioritize traditional business objectives. For example, we believe that certain owned-brokerage competitors have investors that have historically allowed the pursuit of increases in market share over profitability, which not only exacerbates competition for independent sales agents, but places additional pressure on the share of commission income received by the agent.

This competitive environment has continued competitiondespite general business disruption due to the COVID-19 crisis. Competition for productive agents couldis expected to continue to have a negative impact on our homesale transaction volume and market share and could continue to put upward pressure on the average share of commissions earned by independent sales agents. These competitive market factors also impact our franchisees and such franchisees have and may continue to seek reduced royalty fee arrangements or other incentives from us to offset the continued business pressures on such franchisees, which would result in a reduction in royalty fees paid to us.

A growing number of companies are competing in non-traditional ways for a portion of the gross commission income generated by homesale transactions. For example, although most iBuying models paused home-buying activity in late March due to the COVID-19 pandemic (including our own version of such model), these models could restart as conditions

38

improve. Many iBuying business models seek to disintermediate real estate brokers and independent sales agents from buyers and sellers of homes by reducing brokerage commissions that may be earned on addressingthose transactions. In addition, the concentration and market power of the top listing aggregators allow them to monetize their platforms by a variety of actions, including expanding into the brokerage business, charging significant referral fees, charging listing and display fees, diluting the relationship between agents and brokers (and between agents and the consumer), tying referrals to use of their products, consolidating and leveraging data, and engaging in preferential or exclusionary practices to favor or disfavor other industry participants. These actions divert and reduce the earnings of other industry participants, including our company owned and franchised brokerages. Aggregators could intensify their current market dynamics by expandingbusiness tactics or introduce new programs that could be materially disadvantageous to our basebusiness and other brokerage participants in the industry and such tactics could further increase pressures on the profitability of our company owned and franchised brokerages and affiliated independent sales agents, reduce our franchisor service revenue and dilute our relationships with our franchisees and our and our franchisees' relationships with affiliated independent sales agents and affiliated franchisees, providing them with compelling databuyers and technology productssellers of homes.

As previously disclosed, we currently receive meaningful listing fees for our provision of real estate listings under agreements scheduled to expire in March 2022. Due to disputes between the parties, which heightened during the COVID-19 crisis, there is an increased risk that performance and services, generating high quality leads,payments under these agreements may be suspended or terminated. The suspension or termination of these agreements would have a negative impact on our revenues and enhancing the consumer experienceearnings but would eliminate various obligations and could result in certain reduced spend. We will continue to movefocus efforts on lead generation and other programs designed to benefit affiliated agents closerand franchisees.

New Development. Realogy Brokerage Group has relationships with developers, primarily in major cities, in particular New York City, to provide marketing and brokerage services in new developments. New development closings can vary significantly from year to year due to timing matters that are outside of our control, including long cycle times and irregular project completion timing. In addition, the new development industry has also experienced significant disruption related to the customer.

| Total amount expected to be incurred | Amount incurred to date | Total amount remaining to be incurred | |||||||||

| Real Estate Franchise Services | $ | — | $ | — | $ | — | |||||

| Company Owned Real Estate Brokerage Services | 44 | 10 | 34 | ||||||||

| Relocation Services | 4 | 4 | — | ||||||||

| Title and Settlement Services | 1 | 1 | — | ||||||||

| Corporate and Other | 5 | 3 | 2 | ||||||||

| Total | $ | 54 | $ | 18 | $ | 36 | |||||

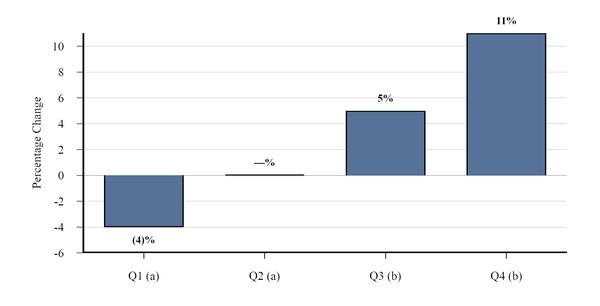

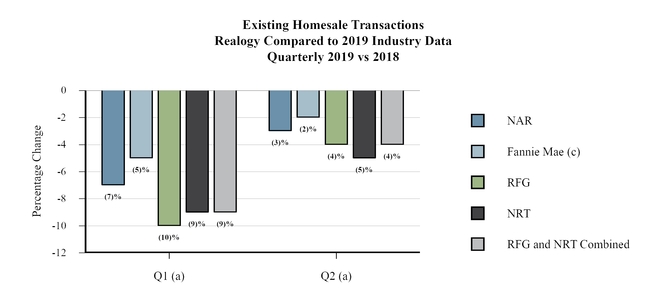

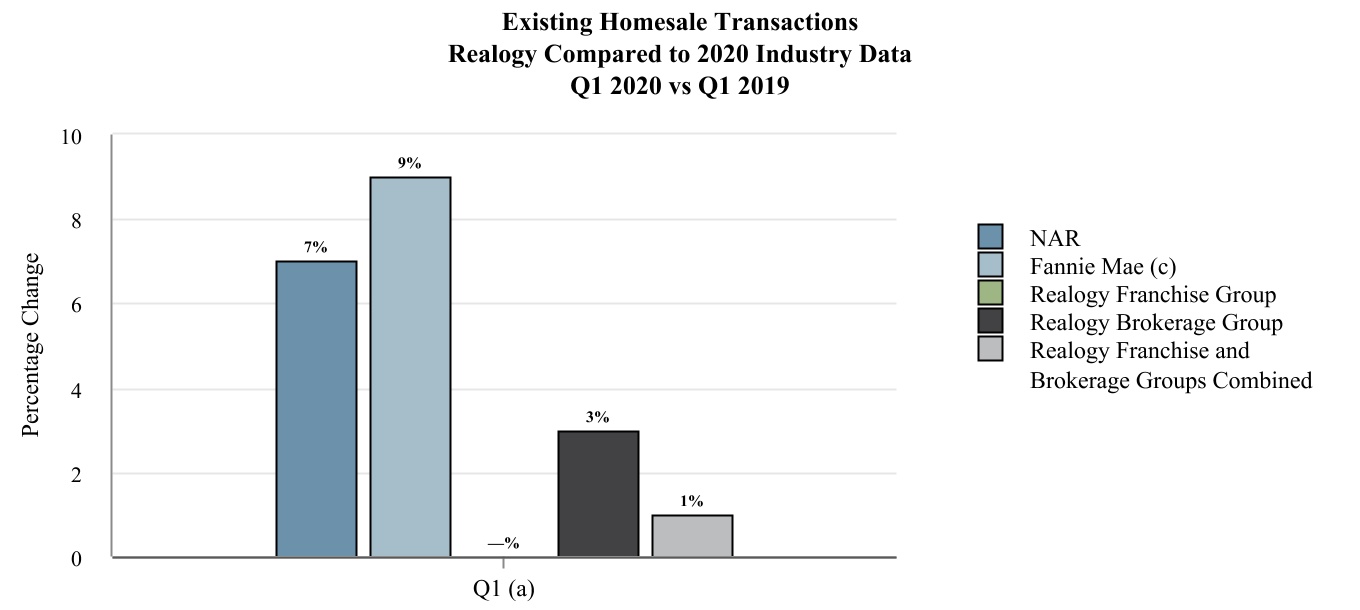

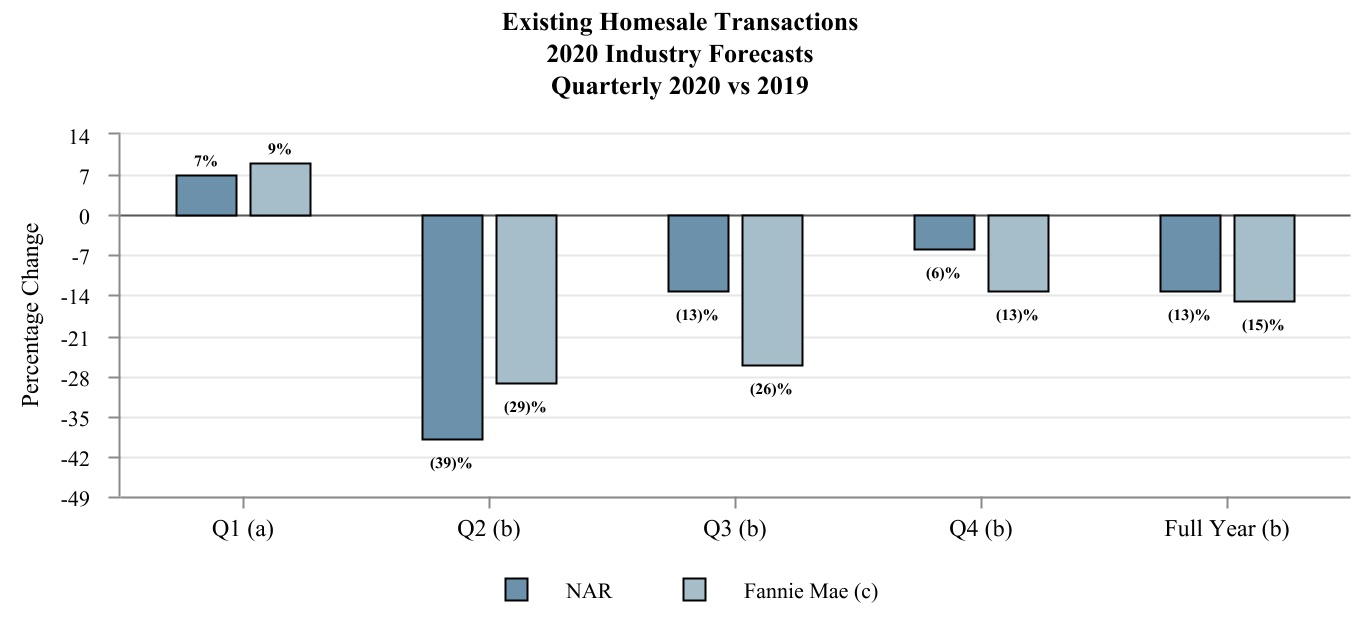

Existing Homesales

For the six monthsquarter ended June 30, 2019March 31, 2020 compared to the same period in 2018,2019, NAR existing homesale transactions decreasedtransactions increased to 2.5 million1.1 homes or down 4%up 7%. For the six monthsquarter ended June 30, 2019, RFG and NRTMarch 31, 2020, homesale transactions on a combined basis decreased 6%for Realogy Franchise and Brokerage Groups increased 1% compared to the same period in 20182019 due primarily to challenging market fundamentals,the impact, starting around mid-March 2020, of the COVID-19 crisis, the impact of competition (including on our market share), the loss of certain franchisees and the geographic concentration (in particular at NRT in California).of Realogy Brokerage Group. The quarterly and annual year-over-year trends in homesale transactions are as follows:

39

_______________

(a)Q1 existing homesale data is as of the most recent NAR press release, which is subject to sampling error.

(b)Forecasted existing homesale data, on a seasonally adjusted basis, is as of the most recent NAR forecast.

(c)Forecasted existing homesale data, on a seasonally adjusted basis, is as of the most recent Fannie Mae press release.

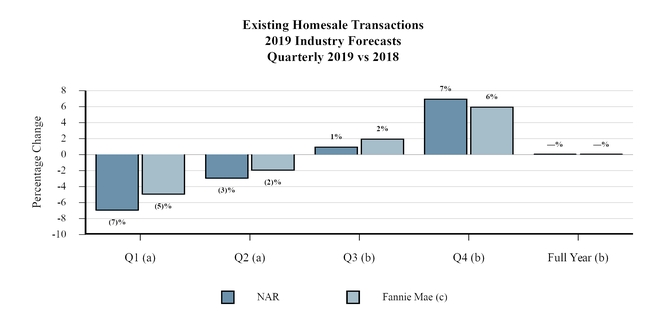

As of their most recent releases, NAR isand Fannie Mae are both forecasting existing homesale transactions to increase 5%15% in 2020 while Fannie Mae is forecasting existing homesale transactions to increase 1% for the same period.

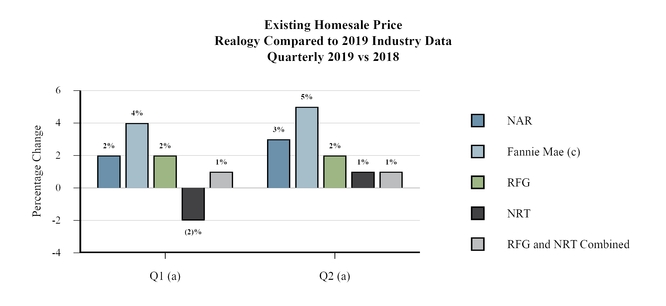

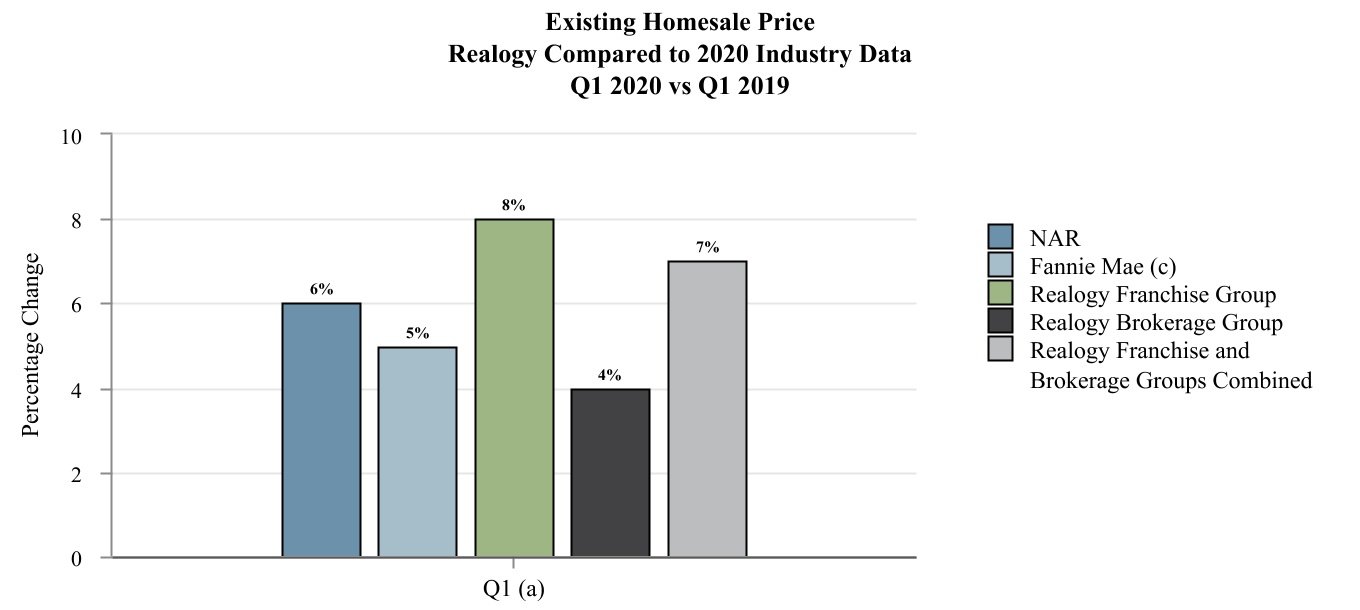

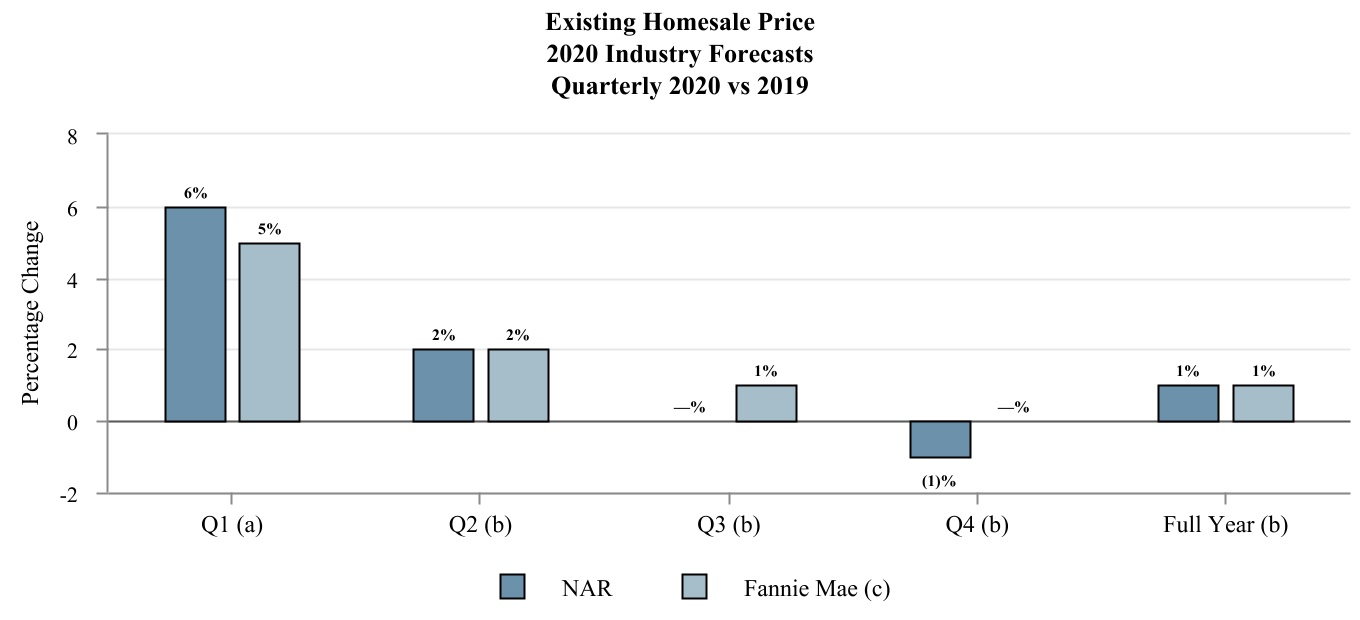

Existing Homesale Price

For the six monthsquarter ended June 30, 2019March 31, 2020 compared to the same period in 2018,2019, NAR existing homesale average price increased 3%6%. For the six monthsquarter ended June 30, 2019, RFG and NRT'sMarch 31, 2020, average homesale price on a combined basis for Realogy Franchise and Brokerage Groups increased 1%7% compared to the same period in 20182019. However, as noted above, beginning in April 2020, our company owned brokerages have experienced declines in average sale price due to geography mix and consisted of RFG's average homesale price increase of 2%, partially offset by NRT's average homesale price decrease of 1%. NRT'slower inventory in the high-end markets. Realogy Brokerage Group's geographic concentration in California and exposure to the high-end of the market plus the associated competitive pressures drove the year-over-year decline in homesale price compared to the overall industry. The quarterly and annual year-over-year trends in the price of homes are as follows:

40

_______________

(a)Q1 homesale price data is for existing homesale average price and is as of the most recent NAR press release.

(b)Forecasted homesale price data is for median price and is as of the most recent NAR forecast.

(c)Existing homesale price data is for median price and is as of the most recent Fannie Mae press release.

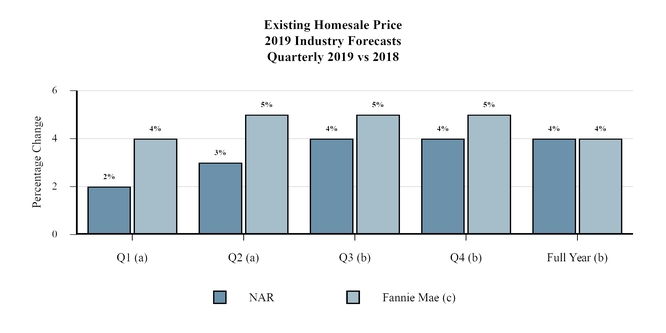

As of their most recent releases, NAR is forecasting median existing homesale price to increase 3% in 20202% while Fannie Mae is forecasting median existing homesale price to increase 4%1% in 2020.

* * *

We believe that long-term demand for housing and the growth of our industry are primarily driven by the affordability of housing, the economic health of the U.S. economy, demographic trends such as generational transitions, increases in U.S. household formation, mortgage rate levels and mortgage availability, certain tax benefits, job growth, increases in renters that qualify as homebuyers, the inherent attributes of homeownership versus renting and the influence of local housing dynamicsavailability of inventory supply versus demand.in the consumer's desired location and within the consumer's price range. At this time, certain of these factors are trending favorably, such as mortgage rate levels and household formation, although the COVID-19 pandemic continues to materially impact the entire industry and job growth.the global economy. Factors that may negatively affect growth in the housing industry include:

•the severity, length and spread of the COVID-19 pandemic and the speed of the U.S. and global economic recoveries;

•increased levels of unemployment and/or stagnant wage growth in the U.S.;

•economic stagnation or contraction in the U.S. economy;

•decreasing consumer confidence in the economy and/or the residential real estate market;

•an increase in potential homebuyers with low credit ratings or inability to afford down payments;

•reduced availability of mortgage financing or increasing down payment requirements or other mortgage challenges due to disrupted earnings;

•weak credit markets and/or instability of financial institutions;

•renewed high levels of foreclosure activity;

•a reduction in the affordability of homes;

•continued insufficient inventory levels or stagnant and/or declining home prices;

•certain provisions of the 2017 Tax Act that directly impact traditional incentives associated with home ownership and may reduce the financial distinction between renting and owning a home, including those that reduce the

41

amount that certain taxpayers would be allowed to deduct for home mortgage interest or state, local and property taxes;taxes as well as certain state or local tax reform, such as the "mansion tax" in New York City;

•decelerated or lack of building of new housing for homesales, increased building of new rental properties, or irregular timing of new development closings leading to lower unit sales at NRT,Realogy Brokerage Group, which has relationships with developers, primarily in major cities, to provide marketing and brokerage services in new developments;

•homeowners retaining their homes for longer periods of time;

•changing attitudes towards home ownership, particularly among potential first-time homebuyers who may delay, or decide not to, purchase a home, as well as changing preferences to rent versus purchase a home;

•the impact of limited or negative equity of current homeowners, as well as the lack of available inventory may limit their proclivity to purchase an alternative home;

•a decline in home ownership levels in the U.S.;

•natural disasters, such as hurricanes, earthquakes, wildfires, mudslides and other events that disrupt local or regional real estate markets, including public health crises, such as pandemics and epidemics;

•higher mortgage rates due to increases in long-term interest rates; and

•other legislative or regulatory reforms, including but not limited to reform that adversely impacts the financing of the U.S. housing market, changes relating to RESPA, potential reform of Fannie Mae and Freddie Mac, immigration reform, and further potential federal, state or local tax code reform;reform (including, for example, the proposed "pied-a-terre tax" in New York City).

* * *

While data provided by NAR and Fannie Mae are two indicators of the direction of the residential housing market, we believe that homesale statistics will continue to vary between us and NAR and Fannie Mae because:

•they use survey data and estimates in their historical reports and forecasting models, which are subject to sampling error, whereas we use data based on actual reported results;

there are geographical differences and concentrations in the markets in which we operate versus the national market. For example, many of our company owned brokerage offices are geographically located where average homesale prices are generally higher than the national average and therefore NAR survey data will not correlate with NRT'sRealogy Brokerage Group's results;

•comparability is also diminished due to NAR’s utilization of seasonally adjusted annualized rates whereas we report actual period-over-period changes and their use of median price for their forecasts compared to our average price;

•NAR historical data is subject to periodic review and revision and these revisions have been material in the past, and could be material in the future; and

•NAR and Fannie Mae generally update their forecasts on a monthly basis and a subsequent forecast may change materially from a forecast that was previously issued.

While we believe that the industry data presented herein is derived from the most widely recognized sources for reporting U.S. residential housing market statistical data, we do not endorse or suggest reliance on this data alone. We also note that forecasts are inherently uncertain or speculative in nature and actual results for any period could materially differ.

KEY DRIVERS OF OUR BUSINESSES

Within RFGRealogy Franchise and NRT,Brokerage Groups, we measure operating performance using the following key operating metrics: (i) closed homesale sides, which represents either the "buy" side or the "sell" side of a homesale transaction, (ii) average homesale price, which represents the average selling price of closed homesale transactions, and (iii) average homesale broker commission rate, which represents the average commission rate earned on either the "buy" side or "sell" side of a homesale transaction.

42

For RFG,Realogy Franchise Group, we also use net royalty per side, which represents the royalty payment to RFGRealogy Franchise Group for each homesale transaction side taking into account royalty rates, average broker commission rates, volume incentives achieved and other incentives. We utilize net royalty per side as it includes the impact of changes in average homesale price as well as all incentives and represents the royalty revenue impact of each incremental side.

For NRT,Realogy Brokerage Group, we also use gross commission income per side, which represents gross commission income divided by closed homesale sides. Gross commission income includes commissions earned in homesale transactions and certain other activities, primarily leasing and property management transactions. NRT,Realogy Brokerage Group, as a franchisee of RFG,Realogy Franchise Group, pays a royalty fee of approximately 6% per transaction to RFGRealogy Franchise Group from the commission earned on a real estate transaction. The remainder of gross commission income is split between the broker (NRT)(Realogy Brokerage Group) and the independent sales agent.