UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_______________________

FORM 10-Q

_______________________

☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2023March 31, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission File Number 001-35761

____________________

American Coastal Insurance Corporation

(Exact Name of Registrant as Specified in its Charter)

| | | | | | | | | | | | | | |

| Delaware | | 75-3241967 | |

| (State or Other Jurisdiction of

Incorporation or Organization) | | (IRS Employer Identification Number) | |

| | | | | | | | | | | | | | | | | |

| 800 2nd Avenue S. | | 33701 | |

| St. Petersburg, | Florida | | |

| (Address of Principle Executive Offices) | | (Zip Code) | |

727-895-7737727-633-0851

(Registrant's telephone number, including area code)

United Insurance Holdings Corp.

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| Common Stock, $0.0001 par value per share | ACIC | Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | Accelerated filer | ☐☑ | Emerging growth company | ☐ |

| Non-accelerated filer | ☑☐ | Smaller reporting company | ☑ | | |

If an emerging growth company, indicate by check mark if the registrant has elected to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. £

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No R

As of August 9, 2023, 43,406,486May 3, 2024, 47,828,491 shares of common stock, par value $0.0001 per share, were outstanding.

AMERICAN COASTAL INSURANCE CORPORATION

| | | | | | | | |

PART I. FINANCIAL INFORMATION | |

| Item 1. Financial Statements | |

| Condensed Consolidated Balance Sheets (Unaudited) | |

| Condensed Consolidated Statements of Comprehensive Income (Loss) (Unaudited) | |

| Condensed Consolidated Statements of Stockholders' Equity (Deficit) (Unaudited) | |

| Condensed Consolidated Statements of Cash Flows (Unaudited) | |

| Notes to Unaudited Condensed Consolidated Financial Statements | |

| Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 3. Quantitative and Qualitative Disclosures About Market Risk | |

| Item 4. Controls and Procedures | |

| PART II. OTHER INFORMATION | |

| Item 1. Legal Proceedings | |

| Item 1A. Risk Factors | |

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | |

| Item 3. Defaults Upon Senior Securities | |

| Item 4. Mine Safety Disclosures | |

| Item 5. Other Information | |

| Item 6. Exhibits | |

| Signatures | |

Throughout this Quarterly Report on Form 10-Q (Form 10-Q), we present amounts in all tables in thousands, except for share amounts, per share amounts, policy counts or where more specific language or context indicates a different presentation. In the narrative sections of this Form 10-Q, we show full values rounded to the nearest thousand.

AMERICAN COASTAL INSURANCE CORPORATION

FORWARD-LOOKING STATEMENTS

This Form 10-Q contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements include statements about anticipated growth in revenues, gross written premium, earnings per share, estimated unpaid losses on insurance policies, investment returns, and diversification and expectations about our liquidity, our ability to meet our investment objectives, our ability to manage and mitigate market risk with respect to our investments and our ability to continue as a going concern. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “endeavor,” “project,” “believe,” “plan,” “anticipate,” “intend,” “could,” “would,” “estimate,” or “continue” or the negative variations thereof or comparable terminology are intended to identify forward-looking statements. These statements are based on current expectations, estimates and projections about the industry and market in which we operate, and management's beliefs and assumptions. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. The risks and uncertainties include, without limitation:

•our exposure to catastrophic events and severe weather conditions;

•the regulatory, economic and weather conditions present in Florida and New York the states in which we write business as of March 1, 2023;business;

•our ability to cultivate and maintain agent relationships, particularly our relationship with AmRisc, LLC;LLC (AmRisc);

•the possibility that actual claims incurred may exceed our loss reserves for claims;

•assessments charged by various governmental agencies;

•our ability to implement and maintain adequate internal controls over financial reporting;reporting, including our ability to remediate any existing material weakness in our internal controls over financial reporting and the timing of any such remediation, as well as our ability to reestablish effective internal controls over financial reporting and disclosure controls and procedures;

•our ability to maintain information technology and data security systems, and to outsource relationships;

•our reliance on key vendor relationships, and the ability of our vendors to protect the personally identifiable information of our customers, claimants or employees;

•our ability to attract and retain the services of senior management;

•risks and uncertainties relating to our acquisitions, mergers, dispositions and other strategic transactions;

•risks associated with investments in which we share ownership or management with third parties;

•our ability to generate sufficient cash to service all of our indebtedness and comply with covenants and other requirements related to our indebtedness;

•our ability to maintain our market share;

•changes in the regulatory environment present in the states in which we operate;

•the impact of new federal or state regulations that affect the insurance industry;

•the cost, viability and availability of reinsurance;

•our ability to collect from our reinsurers or others on our reinsurance claims;

•dependence on investment income and the composition of our investment portfolio and related market risks;

•the possibility of the pricing and terms for our products to decline due to the historically cyclical nature of the property and casualty insurance and reinsurance industry;

•the outcome of litigation pending against us, including the terms of any settlements;

•downgrades in our financial strength or stability ratings;

•the impact of future transactions of substantial amounts of our common stock by us or our significant stockholders on our stock price;

•our ability to meet the standards for continued listing on Nasdaq;

•our ability to pay dividends in the future, which may be constrained by our holding company structure;

•the ability of our subsidiaries to pay dividends in the future, which may affect our liquidity and our ability to meet our obligations;

•the ability of R. Daniel Peed and his affiliates to exert significant control over us due to substantial ownership of our common stock, subject to certain restrictive covenants that may restrict our ability to pursue certain opportunities;

•the impact of transactions by R. Daniel Peed and his affiliates on the price of our common stock;

•provisions in our charter documents that may make it harder for others to obtain control of us; and

•other risks and uncertainties described in the section entitled "Risk Factors" in Part I, Item 1A in our Annual Report on Form 10-K for the year ended December 31, 20222023 and in Part II, Item 1A of this Form 10-Q.

We caution you not to rely on these forward-looking statements, which are valid only as of the date they were made. Except as may be required by applicable law, we undertake no obligation to update or revise any forward-looking statements to reflect new information, the occurrence of unanticipated events or otherwise.

AMERICAN COASTAL INSURANCE CORPORATION

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

Condensed Consolidated Balance Sheets (Unaudited)

| | June 30,

2023 | | December 31, 2022 |

| | March 31,

2024 | | | | March 31,

2024 | | December 31, 2023 |

| ASSETS | ASSETS | | | | | ASSETS | | | | |

| Investments, at fair value: | Investments, at fair value: | | | | | Investments, at fair value: | | |

| Fixed maturities, available-for-sale (amortized cost of $185,046 and $237,735, respectively) | | $ | 160,863 | | | $ | 204,682 | |

| Fixed maturities, available-for-sale (amortized cost of $198,750 and $200,951, respectively) | |

| Equity securities | Equity securities | | — | | | 15,657 | |

| Other investments (amortized cost of $3,403 and $3,072, respectively) | | 3,583 | | | 3,675 | |

| Other investments (amortized cost of $14,121 and $16,118, respectively) | |

| | Total investments | |

| Total investments | |

| Total investments | Total investments | | $ | 164,446 | | | $ | 224,014 | |

| Cash and cash equivalents | Cash and cash equivalents | | 27,767 | | | 70,903 | |

| Restricted cash | Restricted cash | | 49,501 | | | 45,988 | |

| Total cash, cash equivalents and restricted cash | Total cash, cash equivalents and restricted cash | | $ | 77,268 | | | $ | 116,891 | |

| Accrued investment income | Accrued investment income | | 1,632 | | | 1,605 | |

| Property and equipment, net | Property and equipment, net | | 4,474 | | | 5,293 | |

| Premiums receivable, net (credit allowance of $28 and $32, respectively) | | 55,651 | | | 39,301 | |

| Reinsurance recoverable on paid and unpaid losses, net (credit allowance of $169 and $333, respectively) | | 658,814 | | | 796,546 | |

| Premiums receivable, net (credit allowance of $53 and $51, respectively) | |

| Reinsurance recoverable on paid and unpaid losses, net (credit allowance of $65 and $97, respectively) | |

| Ceded unearned premiums | Ceded unearned premiums | | 329,676 | | | 90,496 | |

| Goodwill | Goodwill | | 59,476 | | | 59,476 | |

| Deferred policy acquisition costs, net | Deferred policy acquisition costs, net | | 34,821 | | | 52,369 | |

| Intangible assets, net | Intangible assets, net | | 10,946 | | | 12,770 | |

| Other assets | Other assets | | 35,546 | | | 3,920 | |

| Assets held for disposal | Assets held for disposal | | 12,105 | | | 1,434,815 | |

| Total Assets | Total Assets | | $ | 1,444,855 | | | $ | 2,837,496 | |

| LIABILITIES AND STOCKHOLDERS' EQUITY | LIABILITIES AND STOCKHOLDERS' EQUITY | | | | |

| Liabilities: | Liabilities: | |

| Liabilities: | |

| Liabilities: | |

| Unpaid losses and loss adjustment expenses | |

| Unpaid losses and loss adjustment expenses | |

| Unpaid losses and loss adjustment expenses | Unpaid losses and loss adjustment expenses | | $ | 534,676 | | | $ | 842,958 | |

| Unearned premiums | Unearned premiums | | 387,311 | | | 258,978 | |

| Reinsurance payable on premiums | Reinsurance payable on premiums | | 140,662 | | | 30,503 | |

| Payments outstanding | Payments outstanding | | 17,532 | | | 2,000 | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | | 93,184 | | | 74,386 | |

| Operating lease liability | Operating lease liability | | 1,172 | | | 1,689 | |

| Other liabilities | Other liabilities | | 7,606 | | | 5,849 | |

| Notes payable, net | Notes payable, net | | 148,521 | | | 148,355 | |

| Liabilities held for disposal | Liabilities held for disposal | | 1,795 | | | 1,654,817 | |

| Total Liabilities | Total Liabilities | | $ | 1,332,459 | | | $ | 3,019,535 | |

| Commitments and contingencies (Note 12) | | | | |

| Commitments and Contingencies (Note 12) | | Commitments and Contingencies (Note 12) | | |

| Stockholders' Equity: | Stockholders' Equity: | |

| Preferred stock, $0.0001 par value; 1,000,000 shares authorized; none issued or outstanding | Preferred stock, $0.0001 par value; 1,000,000 shares authorized; none issued or outstanding | | $ | — | | | $ | — | |

| Common stock, $0.0001 par value; 100,000,000 shares authorized; 43,618,569 and 43,492,256 issued, respectively; 43,406,486 and 43,280,173 outstanding, respectively | | 4 | | | 4 | |

| Preferred stock, $0.0001 par value; 1,000,000 shares authorized; none issued or outstanding | |

| Preferred stock, $0.0001 par value; 1,000,000 shares authorized; none issued or outstanding | |

| Common stock, $0.0001 par value; 100,000,000 shares authorized; 48,011,548 and 46,989,089 issued, respectively; 47,799,465 and 46,777,006 outstanding, respectively | |

| Additional paid-in capital | Additional paid-in capital | | 396,136 | | | 395,631 | |

| Treasury shares, at cost: 212,083 shares | Treasury shares, at cost: 212,083 shares | | (431) | | | (431) | |

| Accumulated other comprehensive loss | Accumulated other comprehensive loss | | (21,072) | | | (30,947) | |

| Retained earnings (deficit) | Retained earnings (deficit) | | (262,241) | | | (546,296) | |

| | Total Stockholders' Equity (Deficit) | | $ | 112,396 | | | $ | (182,039) | |

| Total Stockholders' Equity | |

| | Total Stockholders' Equity | |

| | Total Stockholders' Equity | |

| Total Liabilities and Stockholders' Equity | Total Liabilities and Stockholders' Equity | | $ | 1,444,855 | | | $ | 2,837,496 | |

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

AMERICAN COASTAL INSURANCE CORPORATION

Condensed Consolidated Statements of Comprehensive Income (Loss) (Unaudited)

| | Three Months Ended | | Six Months Ended |

| June 30, | | June 30, |

| 2023 | | 2022 | | 2023 | | 2022 |

| | | | Three Months Ended | |

| | | | Three Months Ended | |

| | | | Three Months Ended | |

| | | | March 31, | | | | | | March 31, |

| | | | | | 2024 | | | | | | | | 2024 | | 2023 |

| REVENUE: | REVENUE: | | | | | | | | |

| Gross premiums written | |

| Gross premiums written | |

| Gross premiums written | Gross premiums written | | $ | 243,885 | | | $ | 207,632 | | | $ | 431,008 | | | $ | 350,046 | |

| Change in gross unearned premiums | Change in gross unearned premiums | | (85,686) | | | (78,149) | | | (128,333) | | | (97,830) | |

| Gross premiums earned | Gross premiums earned | | 158,199 | | | 129,483 | | | 302,675 | | | 252,216 | |

| Ceded premiums earned | Ceded premiums earned | | (75,030) | | | (64,951) | | | (132,182) | | | (129,938) | |

| Net premiums earned | Net premiums earned | | 83,169 | | | 64,532 | | | 170,493 | | | 122,278 | |

| Net investment income | Net investment income | | 2,692 | | | 1,839 | | | 5,281 | | | 3,243 | |

| Net realized investment losses | Net realized investment losses | | (6,725) | | | (77) | | | (6,808) | | | (40) | |

| Net unrealized gains (losses) on equity securities | Net unrealized gains (losses) on equity securities | | 141 | | | (2,391) | | | 615 | | | (3,161) | |

| | Other revenue | Other revenue | | 18 | | | 7 | | | 34 | | | 22 | |

| Other revenue | |

| Other revenue | |

| Total revenue | Total revenue | | 79,295 | | | 63,910 | | | 169,615 | | | 122,342 | |

| EXPENSES: | EXPENSES: | |

| Losses and loss adjustment expenses | |

| Losses and loss adjustment expenses | |

| Losses and loss adjustment expenses | Losses and loss adjustment expenses | | 20,915 | | | 14,032 | | | 37,327 | | | 40,347 | |

| Policy acquisition costs | Policy acquisition costs | | 25,545 | | | 23,570 | | | 52,517 | | | 43,878 | |

| Operating expenses | Operating expenses | | 3,274 | | | 3,820 | | | 5,442 | | | 7,527 | |

| General and administrative expenses | General and administrative expenses | | 6,583 | | | 8,208 | | | 15,376 | | | 16,272 | |

| Interest expense | Interest expense | | 2,719 | | | 2,363 | | | 5,438 | | | 4,722 | |

| Total expenses | Total expenses | | 59,036 | | | 51,993 | | | 116,100 | | | 112,746 | |

| Income before other income | Income before other income | | 20,259 | | | 11,917 | | | 53,515 | | | 9,596 | |

| Other income | Other income | | 806 | | | 258 | | | 1,394 | | | 1,591 | |

| Income before income taxes | Income before income taxes | | 21,065 | | | 12,175 | | | 54,909 | | | 11,187 | |

| Provision for income taxes | Provision for income taxes | | 713 | | | 25,486 | | | 4,190 | | | 24,771 | |

| Income from continuing operations, net of tax | Income from continuing operations, net of tax | | $ | 20,352 | | | $ | (13,311) | | | $ | 50,719 | | | $ | (13,584) | |

| Income (loss) from discontinued operations, net of tax | | (2,573) | | | (55,744) | | | 234,340 | | | (88,728) | |

| Net income (loss) | | 17,779 | | | (69,055) | | | $ | 285,059 | | | $ | (102,312) | |

| Less: Net loss attributable to NCI | | — | | | (26) | | | — | | | (111) | |

| Net income (loss) attributable to ACIC | | $ | 17,779 | | | $ | (69,029) | | | $ | 285,059 | | | $ | (102,201) | |

| Income from discontinued operations, net of tax | |

| Net income | |

| | OTHER COMPREHENSIVE INCOME (LOSS): | OTHER COMPREHENSIVE INCOME (LOSS): | | | | | | | | |

| | OTHER COMPREHENSIVE INCOME (LOSS): | |

| | OTHER COMPREHENSIVE INCOME (LOSS): | |

| Change in net unrealized gains (losses) on investments | |

| Change in net unrealized gains (losses) on investments | |

| Change in net unrealized gains (losses) on investments | Change in net unrealized gains (losses) on investments | | (2,168) | | | (16,590) | | | 2,063 | | | (44,279) | |

| Reclassification adjustment for net realized investment losses | Reclassification adjustment for net realized investment losses | | 6,725 | | | 78 | | | 6,808 | | | 1,847 | |

| | Income tax benefit (expense) related to items of other comprehensive income (loss) | | — | | | (6,187) | | | — | | | 49 | |

| Total comprehensive income (loss) | | $ | 22,336 | | | $ | (91,754) | | | $ | 293,930 | | | $ | (144,695) | |

| Less: Comprehensive income (loss) attributable to NCI | | — | | | 479 | | | — | | | (164) | |

| Comprehensive income (loss) attributable to ACIC | | $ | 22,336 | | | $ | (92,233) | | | $ | 293,930 | | | $ | (144,531) | |

| Income tax benefit related to items of other comprehensive income (loss) | |

| Income tax benefit related to items of other comprehensive income (loss) | |

| Income tax benefit related to items of other comprehensive income (loss) | |

| Total comprehensive income | |

| | | Weighted average shares outstanding | Weighted average shares outstanding | |

| | Weighted average shares outstanding | |

| | Weighted average shares outstanding | |

| Basic | |

| Basic | |

| Basic | Basic | | 43,229,416 | | | 43,049,227 | | | 43,178,758 | | | 43,015,114 | |

| Diluted | Diluted | | 43,805,217 | | | 43,049,227 | | | 43,690,435 | | | 43,015,114 | |

| | Earnings available to ACIC common stockholders per share | Earnings available to ACIC common stockholders per share | |

| Earnings available to ACIC common stockholders per share | |

| Earnings available to ACIC common stockholders per share | |

| Basic | Basic | |

| Basic | |

| Basic | |

| Continuing operations | |

| Continuing operations | |

| Continuing operations | Continuing operations | | $ | 0.48 | | | $ | (0.31) | | | $ | 1.16 | | | $ | (0.31) | |

| Discontinued operations | Discontinued operations | | (0.06) | | | (1.29) | | | 5.43 | | | (2.06) | |

| Total | Total | | $ | 0.42 | | | $ | (1.60) | | | $ | 6.59 | | | $ | (2.37) | |

| Diluted | Diluted | | | | | | | | |

| Continuing operations | Continuing operations | | $ | 0.47 | | | $ | (0.31) | | | $ | 1.16 | | | $ | (0.31) | |

| Continuing operations | |

| Continuing operations | |

| Discontinued operations | Discontinued operations | | (0.06) | | | (1.29) | | | 5.36 | | | (2.06) | |

| Total | Total | | $ | 0.41 | | | $ | (1.60) | | | $ | 6.52 | | | $ | (2.37) | |

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

AMERICAN COASTAL INSURANCE CORPORATION

Condensed Consolidated Statements of Stockholders’ Equity for the Three Months Ended

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Stockholders' Equity Attributable to ACIC | | NCI | | Total Stockholders’ Equity |

| Number of Shares | | Dollars | | | | | | |

| | | | | | |

| March 31, 2022 | 43,257,595 | | | $ | 4 | | | $ | 394,720 | | | $ | (431) | | | $ | (25,657) | | | $ | (110,665) | | | $ | 257,971 | | | $ | 18,908 | | | $ | 276,879 | |

| Net loss | — | | | — | | | — | | | — | | | — | | | (69,029) | | | (69,029) | | | (26) | | | (69,055) | |

| Other comprehensive income (loss), net | — | | | — | | | — | | | — | | | (23,204) | | | — | | | (23,204) | | | 505 | | | (22,699) | |

| Return of Capital to NCI | — | | | — | | | — | | | — | | | — | | | 1,052 | | | 1,052 | | | (19,387) | | | (18,335) | |

| Stock Compensation | 55,571 | | | — | | | 182 | | | — | | | — | | | — | | | 182 | | | — | | | 182 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| June 30, 2022 | 43,313,166 | | | $ | 4 | | | $ | 394,902 | | | $ | (431) | | | $ | (48,861) | | | $ | (178,642) | | | $ | 166,972 | | | $ | — | | | $ | 166,972 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Stockholders' Equity Attributable to ACIC | | NCI | | Total Stockholders’ Equity |

| Number of Shares | | Dollars | | | | | | | |

| | | | | | | |

| March 31, 2023 | 43,274,359 | | | $ | 4 | | | $ | 395,966 | | | $ | (431) | | | $ | (25,629) | | | $ | (280,020) | | | $ | 89,890 | | | $ | — | | | $ | 89,890 | |

| Net Income | — | | | — | | | — | | | — | | | — | | | 17,779 | | | 17,779 | | | — | | | 17,779 | |

| Other comprehensive income, net | — | | | — | | | — | | | — | | | 4,557 | | | — | | | 4,557 | | | — | | | 4,557 | |

| | | | | | | | | | | | | | | | | |

| Stock Compensation | 132,127 | | | — | | | 170 | | | — | | | — | | | — | | | 170 | | | — | | | 170 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| June 30, 2023 | 43,406,486 | | | $ | 4 | | | $ | 396,136 | | | $ | (431) | | | $ | (21,072) | | | $ | (262,241) | | | $ | 112,396 | | | $ | — | | | $ | 112,396 | |

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements. | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Total

Stockholders' Equity (Deficit) | | | | |

| Number of Shares | | Dollars | | | | | | |

| | | | | | |

| December 31, 2022 | 43,280,173 | | | $ | 4 | | | $ | 395,631 | | | $ | (431) | | | $ | (30,947) | | | $ | (546,296) | | | $ | (182,039) | | | | | |

| Net income | — | | | — | | | — | | | — | | | — | | | 267,280 | | | 267,280 | | | | | |

| Other comprehensive income, net | — | | | — | | | — | | | — | | | 4,314 | | | — | | | 4,314 | | | | | |

| Impact of Deconsolidation of Discontinued Operations | — | | | — | | | — | | | — | | | 1,004 | | | (1,004) | | | — | | | | | |

| Stock Compensation | (5,814) | | | — | | | 335 | | | — | | | — | | | — | | | 335 | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| March 31, 2023 | 43,274,359 | | | $ | 4 | | | $ | 395,966 | | | $ | (431) | | | $ | (25,629) | | | $ | (280,020) | | | $ | 89,890 | | | | | |

AMERICAN COASTAL INSURANCE CORPORATION

Condensed Consolidated Statements of Stockholders’ Equity for the Six Months Ended

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Stockholders' Equity Attributable to ACIC | | NCI | | Total Stockholders’ Equity |

| Number of Shares | | Dollars | | | | | | |

| | | | | | |

| December 31, 2021 | 43,370,442 | | | $ | 4 | | | $ | 394,268 | | | $ | (431) | | | $ | (6,531) | | | $ | (74,904) | | | $ | 312,406 | | | $ | 19,551 | | | $ | 331,957 | |

| Net loss | — | | | — | | | — | | | — | | | — | | | (102,201) | | | (102,201) | | | (111) | | | (102,312) | |

| Other comprehensive loss, net | — | | | — | | | — | | | — | | | (42,330) | | | — | | | (42,330) | | | (53) | | | (42,383) | |

| Return of Capital to NCI | — | | | — | | | — | | | — | | | — | | | 1,052 | | | 1,052 | | | (19,387) | | | (18,335) | |

| Stock Compensation | (57,276) | | | — | | | 634 | | | — | | | — | | | — | | | 634 | | | — | | | 634 | |

| | | | | | | | | | | | | | | | | |

| Cash dividends on common stock ($0.06 per common share) | — | | | — | | | — | | | — | | | — | | | (2,589) | | | (2,589) | | | — | | | (2,589) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| June 30, 2022 | 43,313,166 | | | $ | 4 | | | $ | 394,902 | | | $ | (431) | | | $ | (48,861) | | | $ | (178,642) | | | $ | 166,972 | | | $ | — | | | $ | 166,972 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Stockholders' Equity (Deficit)

Attributable to ACIC | | NCI | | Total Stockholders’ Equity (Deficit) |

| Number of Shares | | Dollars | | | | | | | |

| | | | | | | |

| December 31, 2022 | 43,280,173 | | | $ | 4 | | | $ | 395,631 | | | $ | (431) | | | $ | (30,947) | | | $ | (546,296) | | | $ | (182,039) | | | $ | — | | | $ | (182,039) | |

| Net Income | — | | | — | | | — | | | — | | | — | | | 285,059 | | | 285,059 | | | — | | | 285,059 | |

| Other comprehensive income, net | — | | | — | | | — | | | — | | | 8,871 | | | — | | | 8,871 | | | — | | | 8,871 | |

| Impact of Deconsolidation of Discontinued Operations | — | | | — | | | — | | | — | | | 1,004 | | | (1,004) | | | — | | | — | | | — | |

| Stock Compensation | 126,313 | | | — | | | 505 | | | — | | | — | | | — | | | 505 | | | — | | | 505 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| June 30, 2023 | 43,406,486 | | | $ | 4 | | | $ | 396,136 | | | $ | (431) | | | $ | (21,072) | | | $ | (262,241) | | | $ | 112,396 | | | $ | — | | | $ | 112,396 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Treasury Stock | | Accumulated Other Comprehensive Loss | | Retained Earnings (Deficit) | | Total

Stockholders' Equity | | | | |

| Number of Shares | | Dollars | | | | | | | |

| | | | | | | |

| December 31, 2023 | 46,777,006 | | | $ | 5 | | | $ | 423,717 | | | $ | (431) | | | $ | (17,137) | | | $ | (237,389) | | | $ | 168,765 | | | | | |

| Net Income | — | | | — | | | — | | | — | | | — | | | 23,599 | | | 23,599 | | | | | |

| Other comprehensive loss, net | — | | | — | | | — | | | — | | | (198) | | | — | | | (198) | | | | | |

| | | | | | | | | | | | | | | | | |

| Stock Compensation | 22,459 | | | — | | | 428 | | | — | | | — | | | — | | | 428 | | | | | |

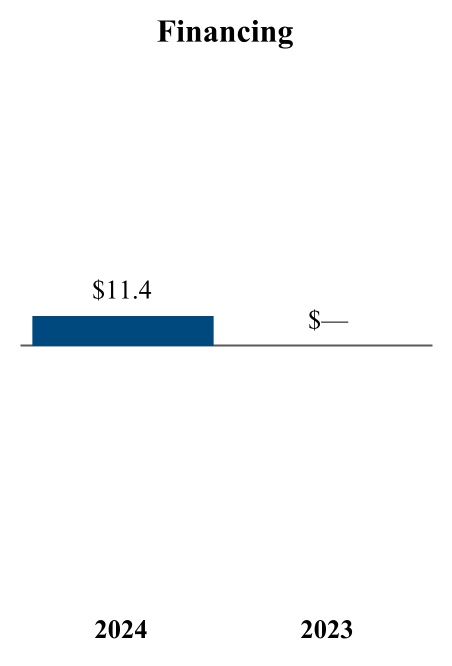

| Issuance of common stock | 1,000,000 | | | — | | | 11,398 | | | — | | | — | | | — | | | 11,398 | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| March 31, 2024 | 47,799,465 | | | $ | 5 | | | $ | 435,543 | | | $ | (431) | | | $ | (17,335) | | | $ | (213,790) | | | $ | 203,992 | | | | | |

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

AMERICAN COASTAL INSURANCE CORPORATION

Condensed Consolidated Statements of Cash Flows (Unaudited) | | Six Months Ended June 30, |

| 2023 | | 2022 |

| | Three Months Ended March 31, | | | | Three Months Ended March 31, |

| | 2024 | | | | 2024 | | 2023 |

| OPERATING ACTIVITIES | OPERATING ACTIVITIES | | | | |

| Net income (loss) | | $ | 285,059 | | | $ | (102,312) | |

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | |

| Net income | |

| Net income | |

| Net income | |

| Adjustments to reconcile net loss to net cash used in operating activities: | |

| Depreciation and amortization | |

| Depreciation and amortization | |

| Depreciation and amortization | Depreciation and amortization | | 4,281 | | | 5,042 | |

| Bond amortization and accretion | Bond amortization and accretion | | 499 | | | 3,041 | |

| Net realized losses on investments | | 5,464 | | | 1,847 | |

| Net realized gains on investments | |

| Net unrealized losses (gains) on equity securities | Net unrealized losses (gains) on equity securities | | (2,694) | | | 7,352 | |

| Provision for uncollectable premiums | Provision for uncollectable premiums | | 4 | | | 6 | |

| Provision for uncollectable reinsurance recoverables | Provision for uncollectable reinsurance recoverables | | 164 | | | 223 | |

| | Deferred income taxes, net | Deferred income taxes, net | | 3,310 | | | 24,764 | |

| Deferred income taxes, net | |

| Deferred income taxes, net | |

| Stock based compensation | Stock based compensation | | 505 | | | 634 | |

| | Settlement of receivable owed by HCI in connection with purchase agreement | | — | | | 3,800 | |

| Gain on sale of property and equipment | Gain on sale of property and equipment | | (559) | | | (1,528) | |

| Fixed asset disposal | Fixed asset disposal | | 953 | | | 343 | |

| Gain on disposition of former subsidiary | Gain on disposition of former subsidiary | | (238,440) | | | — | |

| Changes in operating assets and liabilities: | Changes in operating assets and liabilities: | |

| Accrued investment income | |

| Accrued investment income | |

| Accrued investment income | Accrued investment income | | 555 | | | 200 | |

| Premiums receivable | Premiums receivable | | 7,648 | | | (22,386) | |

| Reinsurance recoverable on paid and unpaid losses | Reinsurance recoverable on paid and unpaid losses | | 423,501 | | | 239,386 | |

| Ceded unearned premiums | Ceded unearned premiums | | (191,910) | | | (72,033) | |

| Deferred policy acquisition costs, net | Deferred policy acquisition costs, net | | 24,201 | | | (38,671) | |

| Other assets | Other assets | | (49,699) | | | (1,728) | |

| | Unpaid losses and loss adjustment expenses | |

| Unpaid losses and loss adjustment expenses | |

| Unpaid losses and loss adjustment expenses | Unpaid losses and loss adjustment expenses | | (491,831) | | | (234,456) | |

| Unearned premiums | Unearned premiums | | (59,854) | | | 14,657 | |

| Reinsurance payable on premiums | Reinsurance payable on premiums | | 93,378 | | | 189,059 | |

| Payments outstanding | Payments outstanding | | (53,287) | | | (5,561) | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | | 21,837 | | | (7,693) | |

| Operating lease liability | Operating lease liability | | (517) | | | (334) | |

| Other liabilities | Other liabilities | | (15,391) | | | 4,634 | |

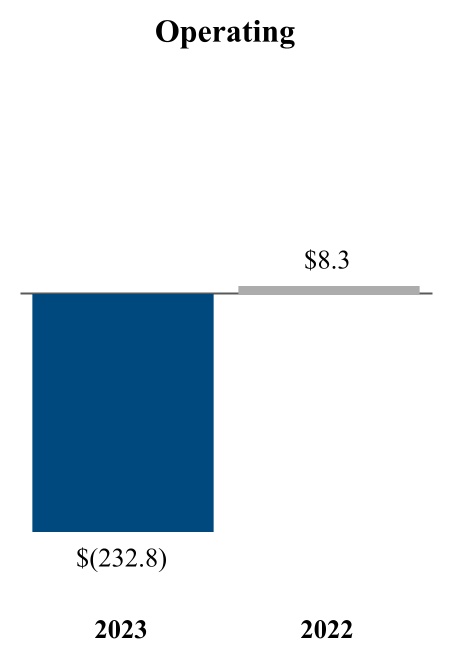

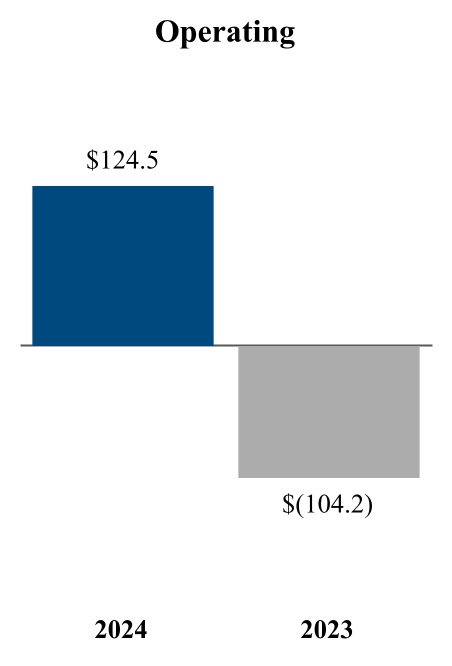

| Net cash provided by (used in) operating activities | Net cash provided by (used in) operating activities | | $ | (232,823) | | | $ | 8,286 | |

| INVESTING ACTIVITIES | INVESTING ACTIVITIES | | | | |

| Proceeds from sales, maturities and repayments of: | Proceeds from sales, maturities and repayments of: | |

| Proceeds from sales, maturities and repayments of: | |

| Proceeds from sales, maturities and repayments of: | |

| Fixed maturities | |

| Fixed maturities | |

| Fixed maturities | Fixed maturities | | 230,424 | | | 107,536 | |

| Equity securities | Equity securities | | 40,322 | | | 88 | |

| Other investments | Other investments | | 500 | | | 1,464 | |

| | Purchases of: | Purchases of: | |

| Fixed maturities | Fixed maturities | | (11,786) | | | (18,334) | |

| Fixed maturities | |

| Fixed maturities | |

| Equity securities | Equity securities | | 35 | | | (6,253) | |

| Other investments | | (759) | | | (840) | |

| | Proceeds from sale of property and equipment | |

| Proceeds from sale of property and equipment | |

| Proceeds from sale of property and equipment | Proceeds from sale of property and equipment | | 599 | | | 3,966 | |

| Cost of property, equipment and capitalized software acquired | Cost of property, equipment and capitalized software acquired | | (273) | | | (2,360) | |

| Disposition of cash on divestiture of subsidiary | Disposition of cash on divestiture of subsidiary | | (232,582) | | | — | |

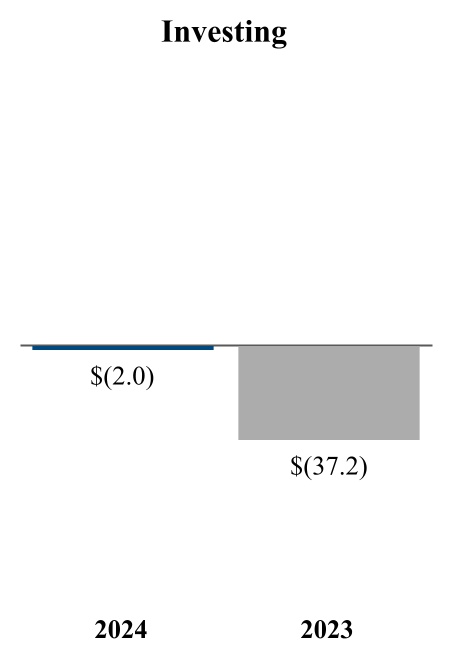

| Net cash provided by investing activities | | $ | 26,480 | | | $ | 85,267 | |

| Net cash used in investing activities | |

| FINANCING ACTIVITIES | FINANCING ACTIVITIES | |

| Repayments of borrowings | | — | | | (761) | |

| Dividends | | — | | | (2,589) | |

| | Return of capital in connection with termination of noncontrolling interest | | — | | | (18,335) | |

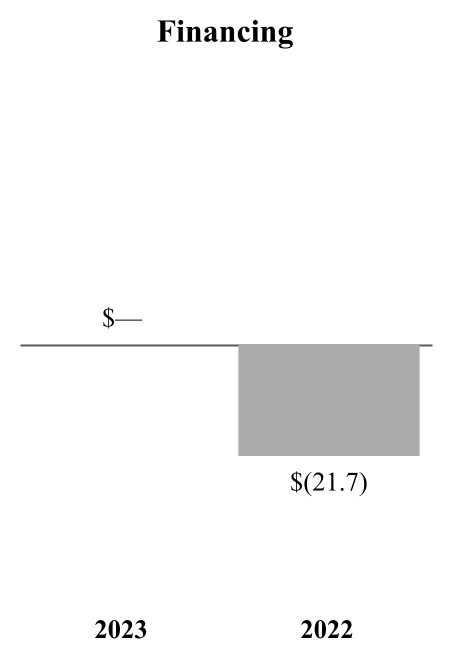

| Net cash used in financing activities | | $ | — | | | $ | (21,685) | |

| Increase in cash, cash equivalents and restricted cash, including cash classified as assets held for disposal | | (206,343) | | | 71,868 | |

| Cash, cash equivalents and restricted cash at beginning of period | | 283,611 | | | 245,278 | |

| | | Proceeds from issuance of common stock | |

| | Proceeds from issuance of common stock | |

| | Proceeds from issuance of common stock | |

| Net cash provided by financing activities | |

| Increase (decrease) in cash, cash equivalents and restricted cash, including cash classified as assets held for disposal | |

| Cash, cash equivalents and restricted cash at beginning of period | |

| Cash, cash equivalents and restricted at end of period | Cash, cash equivalents and restricted at end of period | | $ | 77,268 | | | $ | 317,146 | |

| Supplemental Cash Flows Information | Supplemental Cash Flows Information | | | | |

| Interest paid | Interest paid | | $ | 5,438 | | | $ | 4,771 | |

| Income taxes paid | | $ | 614 | | | $ | 644 | |

| | Interest paid | |

| Interest paid | |

| Income taxes paid (refunded) | |

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023March 31, 2024

1) ORGANIZATION, CONSOLIDATION AND PRESENTATION

(a)Business

American Coastal Insurance Corporation (referred to in this document as we, our, us, the Company or ACIC) is a property and casualty insurance holding company that sources, writes and services residential commercial and personal property and casualty insurance policies using a network of agents and two wholly-owned insurance subsidiaries. On July 10, 2023, we changed our corporate name from United Insurance Holdings Corp. to American Coastal Insurance Corporation. Our two insurance subsidiaries are Interboro Insurance Company (IIC), acquired via mergeracquisition on April 29, 2016; and American Coastal Insurance Company (AmCoastal), acquired via merger on April 3, 2017.

Our other subsidiaries include United Insurance Management, L.C. (UIM), a managing general agent; Skyway Claims Services, LLC (SCS), which provides claims adjusting services to AmCoastal;our insurance companies; AmCo Holding Company, LLC (AmCo) which is a holding company subsidiary that consolidates its respective insurance company; BlueLine Cayman Holdings (BlueLine), which reinsures portfolios of excess and surplus policies; UPC Re, which provides a portion of the reinsurance protection purchased by our insurance subsidiaries when needed; Skyway Reinsurance Services, LLC, which provides reinsurance brokerage services for our insurance companies; Skyway Legal Services, LLC (SLS), which provides claims litigation services to our insurance companies; and Skyway Technologies,Underwriters, LLC, (SCS), a managing general agent that provides technological and distribution services to our insurance companies.

Our primary products are commercial and homeowners' residential property insurance. We currently offer commercial residential insurance in Florida. During 2022, we also wrote commercial residential insurance in South CarolinaFlorida and Texas, however, effective May 1, 2022, we no longer write in these states. In addition, we write personal residential insurance in New York. During 2022, we wroteWe conduct our operations under two reportable segments, commercial residential property and casualty insurance policies (commercial lines) and personal residential business in six other states; however onproperty and casualty insurance policies (personal lines). Our chief operating decision maker is our President, who makes decisions to allocate resources and assesses performance at both segment levels, as well as at the corporate level.

On February 27, 2023, our former insurance subsidiary, United Property & Casualty Insurance Company (UPC) was placed into receivership with the Florida Department of Financial Services (DFS), which divested our ownership of UPC. The events leading to receivership and results of this subsidiary, now included within discontinued operations, are discussed in Note 3 below.

On August 25, 2022, we announced that our former subsidiary UPC had filed plans for withdrawal in the states of Florida, Louisiana, and Texas and intended to file a plan for withdrawal in the state of New York. All filed plans entail non-renewing personal lines policies in these states. Additionally, we announced that Demotech, Inc. (Demotech), an insurance rating agency, notified UPC of its intent to withdraw UPC's Financial Stability Rating. On December 5, 2022, the Florida Office of Insurance Regulation ("FLOIR") issued Consent Order No. 303643-22- CO that provided for the administrative supervision and approval of the plan of run-off for UPC (the "Consent Order"). The Consent Order provided formal approval of UPC's Plan of Run-Off (the "Plan") to facilitate a solvent wind down of its affairs in an orderly fashion. Additionally, in connection with the Plan, IIC agreed to not pay ordinary dividends without the prior approval of the New York Department of Financial Services until January 1, 2025. On February 10, 2023, we announced that a solvent run-off of UPC was unlikely and on February 27, 2023, UPC was placed into receivership with the Florida Department of Financial Services (the "DFS") which divested our ownership of UPC.

Effective June 1, 2022, we merged our majority-owned insurance subsidiary, Journey Insurance Company (JIC) into AmCoastal, with AmCoastal being the surviving entity. JIC was formed in strategic partnership with a subsidiary of Tokio Marine Kiln Group Limited (Kiln) on August 30, 2018 and operated independently from AmCoastal prior to the merging of the entities. The Kiln subsidiary held a noncontrolling interest in JIC, which was terminated prior to the merger.

Effective June 1, 2022, we entered into a quota share reinsurance agreement with TypTap Insurance Company (Typtap). Under the terms of this agreement, we ceded 100% of our former subsidiary UPC's in-force, new, and renewal policies in the states of Georgia, North Carolina and South Carolina. Effective June 1, 2022, we began the transition of South Carolina policies to Homeowners Choice Property and Casualty Insurance Company, Inc. (HCPCI) in connection with our renewal rights agreement. Effective October 1, 2022, we transitioned Georgia policies to HCPCI in connection with our renewal rights agreement. Effective December 1, 2022, we began the transition of North Carolina policies to HCPCI in connection with our renewal rights agreement. As a result, these policies will no longer be covered under this agreement upon their renewal. This agreement replaces the 85% quota share agreement with HCPCI effective December 31, 2021.

Effective May 31, 2022, we merged Family Security Insurance Company, Inc. (FSIC) into our former subsidiary UPC, with UPC being the surviving entity. FSIC was acquired via merger on February 3, 2015, and operated independently from

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023

UPC prior to the merging of the entities. In conjunction with the merger, we dissolved Family Security Holdings (FSH), a holding company subsidiary that consolidated its respective insurance company, FSIC.

Effective June 1, 2021, we entered into a quota share reinsurance agreement with HCPCI and TypTap. Under the terms of this agreement, we ceded 100% of our former subsidiary UPC's in-force, new, and renewal policies in the states of Connecticut, New Jersey, Massachusetts, and Rhode Island. The cession of these policies was 50% to HCPCI and 50% to TypTap. HCPCI is responsible for processing all claims as a part of this agreement. As of April 1, 2022, we completed the transition of all policies in these four states to HCPCI in connection with our renewal rights agreement (Northeast Renewal Agreement) to sell UPC's personal lines homeowners business in these states.

We conduct our operations under two reportable segments, commercial residential property and casualty insurance policies (commercial lines) and personal residential property and casualty insurance policies (personal lines). Our chief operating decision maker is our President, who makes decisions to allocate resources and assesses performance at both segment levels, as well as at the corporate level.

(b)Consolidation and Presentation

We prepare our unaudited condensed consolidated interim financial statements in conformity with U.S. generally accepted accounting principles (GAAP). We have condensed or omitted certain information and footnote disclosures normally included in the annual consolidated financial statements presented in accordance with GAAP. In management's opinion, the accompanying unaudited condensed consolidated financial statements reflect all adjustments, including normal recurring items, considered necessary for a fair presentation of interim periods. We include all of our subsidiaries in our consolidated financial statements, eliminating intercompany balances and transactions during consolidation. As described in Note 23, our former subsidiary, UPC, and activities related directly to supporting the business conducted by UPC qualifyqualified as discontinued operations. Our unaudited condensed consolidated interim financial statements and footnotes should be read in conjunction with our consolidated financial statements and footnotes in our Annual Report on Form 10-K for the year ended December 31, 2022.2023.

While preparing our unaudited condensed consolidated financial statements, we make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the unaudited condensed consolidated financial statements, as well as reported amounts of revenues and expenses during the reporting period. Accordingly, actual results could differ from those estimates. Reported amounts that require us to make extensive use of estimates include our reserves for unpaid losses and loss adjustment expenses, investments and goodwill. Except for the captions on our Unaudited Condensed Consolidated Balance Sheets and Unaudited Condensed Consolidated Statements of Comprehensive Loss,Income, we generally use the term loss(es) to collectively refer to both loss and loss adjustment expenses.

Our results of operations and our cash flows as of the end of the interim periods reported herein do not necessarily indicate our results for the remainder of the year or for any other future period.

(c) Going Concern

Our unaudited condensed consolidated interim financial statements have been prepared in accordance with GAAP assuming the Company will continue as a going concern. As disclosed in our Annual Report on Form 10-K for the year ended December 31, 2022, our subsidiary AmCoastal is a part of a combined reinsurance program with our former subsidiary, UPC.

To properly allocate the reinsurance recoverables under the shared catastrophe treaties, UPC and AmCoastal entered into a reinsurance allocation agreement that became effective on June 1, 2022 (the "Allocation Agreement"). The Allocation Agreement was filed with and approved by the FLOIR on December 5, 2022. On February 10, 2023, we announced that a solvent run-off of UPC was unlikely, driven by Hurricane Ian losses which exhausted UPC's reinsurance coverage. On February 27, 2023, UPC was placed into receivership with the DFS which divested our ownership of UPC. As of the date of filing our Annual Report, the DFS had not recognized the Allocation Agreement, leaving uncertainty regarding the timing of both recoveries currently held by UPC that are allocated to AmCoastal and future recoverables. Management also believed that the ability for AmCoastal to obtain adequate reinsurance to meet its needs for the June 1, 2023 to May 31, 2024 catastrophe cover could only be accomplished assuming that recoveries due to AmCoastal pursuant to the Allocation Agreement could be resolved in short order.

However, on April 19, 2023, AmCoastal entered into a Memorandum of Understanding with the DFS. Under the terms of the Memorandum, AmCoastal and the DFS as receiver of UPC have reached the following agreement:

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023

1.The DFS adopts, ratifies and affirms the Allocation Agreement.

2.All future reinsurance recoverable under reinsurance agreements applicable to the Allocation Agreement for Hurricane Ian losses shall be paid, either directly from the reinsurers or directly from the reinsurance intermediary responsible therefor, to AmCoastal. If a true up adjustment demonstrates that any future reinsurance recoveries were over-collected by AmCoastal, AmCoastal will remit any over-payment to UPC.

On May 15, 2023, the Company, together with it's subsidiary, AmCoastal, entered into a Tax Memorandum of Understanding (the "Tax Memorandum") with the DFS as receiver of the Company's former subsidiary, UPC. On February 27, 2023, UPC entered into receivership with the DFS as receiver. As of March 31, 2023, in accordance with the various reinsurance allocation agreements including the Allocation Agreement described above, the Company is due approximately $38,352,000 of net reinsurance recoveries received by UPC on behalf of the Company but not settled prior to receivership. In addition, in April ACIC paid reinsurance premiums on behalf of UPC totaling $12,929,000. The Company and the DFS believe that an opportunity exists to settle these balances via the realization of certain deferred tax assets of the Company's consolidated Federal and Florida tax returns to which ACIC and UPC belong. UPC holds certain deferred tax assets that are believed to be on no value to UPC on a stand-alone basis. However, AmCoastal and the Company have the opportunity, subject to certain conditions such as continuing and adequate profitability, to realize these assets. Under the terms of the Tax Memorandum, the Company, AmCoastal and the DFS as receiver of UPC have reached the following agreement:2024

1.The parties agree to cooperate with one another to achieve realization of the deferred tax assets;

2.The parties agree to deposit the funds that are or may be due to UPC pursuant to the Tax Allocation Agreement into a segregated account (the "DTA Account") held by AmCoastal that will serve as collateral for any amount payable from or to UPC;

3.The parties agree that the Federal Income Tax Allocation Agreement entered into prior to UPC’s receivership is ratified and accepted by all parties;

4.The parties agree to an annual “true up” of the allocation of the disputed recoveries to the extent that such recoveries were not allocated correctly according to the Reinsurance Allocation Agreement;

5.In the event that AmCoastal, ACIC, or any of their affiliates make a claim or file a proof of claim in the UPC estate, the reviewed, approved, and/or adjudicated claim shall be reduced by the amount of (a) any tax benefit collectively received by AmCoastal, ACIC, or any of their affiliates as well as (b) any money withdrawn from the DTA Account for the benefit of any entity other than UPC; and

6.In the event that the benefit received by the Company is greater than the disputed recoveries, the difference shall be paid to DFS as receiver of UPC.

The Tax Memorandum allows the Company to secure amounts due from UPC to AmCoastal provided the Internal Revenue Service does not object to the Company utilizing UPC's net operating loss carry-forward against its future taxable income. We believe probability of the Internal Revenue Service (IRS) allowing the Company to utilize UPC's net operating losses is more likely than not based on other entities having successfully accomplished this and prior permission or approval from the IRS not being required.

The execution of these MOUs prior to June 30, 2023 alleviate the uncertainty regarding future recoverables, and recoveries currently held by UPC. In addition, as of March 31, 2023, the Company had not finalized its catastrophe cover for June 1, 2023 to May 31, 2024. However, as of June 30, 2023, the Company has finalized this cover, alleviating the uncertainty of this placement. As a result, the Company has concluded substantial doubt no longer exists regarding its ability to continue as a going concern.

2) SIGNIFICANT ACCOUNTING POLICIES

(a) Income Taxes

In June 2022, we assessed our deferred tax position and believed it was more likely than not that the benefit from certain net operating loss (NOL) carryforwards, net capital operating loss carryforwards and other net deferred tax assets would not be realized. In recognition of this risk, we recorded a valuation allowance against these deferred tax assets as of June 30, 2022. During the second quarter of 2023, we evaluated our position based on the results of our continuing operations and determined that it is more likely than not that we will be able to realize the benefit from these NOL carryforwards and other net deferred tax assets. Accordingly, we have reversed the valuation allowance on these deferred tax assets, totaling $2,223,000.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023

On May 15, we entered into the Tax Memorandum with DFS, as described in Note 1 above. As a result of this Memorandum, any benefit received from the use of UPC's net operating losses are due to to the DFS as receiver of UPC. The expense related to this remittance is presented within our provision for income taxes on our Unaudited Condensed Consolidated Statements of Comprehensive Income (Loss), offsetting the tax benefit recognized.

(b) Changes to Significant Accounting Policies

During the three months ended March 31, 2023, our former subsidiary, UPC, was placed into receivership with the DFS. As described in Note 1, effective February 27, 2023, this receivership divested our ownership of UPC. This disposal, as well as the activities related directly to supporting the business conducted by UPC were evaluated for qualification as discontinued operations. The results of operations of business are reported as discontinued operations when the disposal represents a strategic shift that will have a major effect on the entity's operations and financial results. When a business is identified for discontinued operations reporting:

•Results for prior periods are retroactively reclassified as discontinued operations;

•Results of operations are reported in a single line, net of tax, in the Unaudited Condensed Consolidated Statements of Comprehensive Income (Loss); and

•Assets and liabilities are reported as held for disposal in the Unaudited Condensed Consolidated Balance Sheets

Additional details by major classification of operating results and financial position are included in Note 3.

There have been no other changes to our significant accounting policies as reported in our Annual Report on Form 10-K for the year ended December 31, 2022.2023.

(c)(b) Pending Accounting Pronouncements

In November 2023, the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280) Improvements to Reportable Segments Disclosures. This update requires the disclosure of significant segment expenses that are part of an entity’s segment measure of profit or loss and regularly provided to the chief operating decision maker. In addition, it adds or makes clarifications to other segment-related disclosures, such as clarifying that the disclosure requirements in ASC 280 are required for entities with a single reportable segment and that an entity may disclose multiple measures of segment profit and loss. ASU 2023-07 is effective for fiscal years beginning after December 15, 2023 and interim periods beginning after December 15, 2024, with early adoption permitted. We have evaluated pending accounting pronouncements and do not believe any would haveintend to elect to early adopt and are assessing the impact of adopting this new accounting standard on our consolidated financial statements and related disclosures.

In December 2023, the FASB issued ASU No. 2023-09, Income Taxes (Topic 740) Improvements to Income Tax Disclosures. This update amends the Codification to enhance the transparency and decision usefulness of income tax disclosures. This ASU requires additional disaggregation of the reconciliation between the statutory and effective tax rate for an entity and of income taxes paid, both of which are disclosures required by current GAAP. The amendments improve the transparency of income tax disclosures by requiring (1) consistent categories and greater disaggregation of information in the rate reconciliation and (2) income taxes paid disaggregated by jurisdiction. ASU 2023-09 is effective for annual periods beginning after December 15, 2024, with early adoption permitted. We do not intend to elect to early adopt and are assessing the impact of adopting this new accounting standard on the operations orour consolidated financial reporting of our company.statements and related disclosures.

3) DISCONTINUED OPERATIONS

On August 25, 2022, we announced that our former subsidiary UPC had filed plans for withdrawal in the states of Florida, Louisiana, and Texas and intended to file a plan for withdrawal in the state of New York. All filed plans entailed non-renewing personal lines policies in these states. Additionally, we announced that Demotech, an insurance rating agency, notified UPC of its intent to withdraw UPC's Financial Stability Rating. On December 5, 2022, the FLOIR issued Consent Order No. 303643-22- CO that provided for the administrative supervision and approval of the plan of run-off for UPC (the "Consent Order"). The Consent Order provided formal approval of UPC's Plan of Run-Off (the "Plan") to facilitate a solvent wind down of its affairs in an orderly fashion. On February 10, 2023, we announced that a solvent run-off of UPC was unlikely, driven by Hurricane Ian losses which exhausted UPC's reinsurance coverage. On February 27, 2023, UPC was placed into receivership with the DFS which divested our ownership of UPC.

In the first quarter of 2023, the assets and liabilities of UPC were divested. In addition, activities provided by our entities, SCS, SLS and UIM, related directly to supporting the business conducted by UPC have been included. The remaining assets and liabilities for the balance sheet as of December 31, 20222023 are reclassifiedpresented as held for disposal, retrospectively, and the results of UPC and activities related directly to supporting the business conducted by UPC are presented as discontinued operations for all periods presented.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023March 31, 2024

The results from discontinued operations for the three and six months ended June 30,March 31, 2024 and 2023 and 2022 are presented below.

| | Results From Discontinued Operations | Results From Discontinued Operations | |

| Three Months Ended

June 30, | | Six Months Ended

June 30, |

| 2023 | | 2022 | | 2023 | | 2022 |

| Results From Discontinued Operations | |

| Results From Discontinued Operations | |

| | | | Three Months Ended March 31, | |

| | | | Three Months Ended March 31, | |

| | | | Three Months Ended March 31, | |

| | | | | | 2024 | | | | | | | | 2024 | | 2023 |

| REVENUE: | REVENUE: | | | | | | | | |

| Gross premiums written | |

| Gross premiums written | |

| Gross premiums written | Gross premiums written | | $ | — | | | $ | 174,094 | | | $ | (120,608) | | | $ | 320,922 | |

| Change in gross unearned premiums | Change in gross unearned premiums | | — | | | 13,243 | | | 198,154 | | | 72,969 | |

| Gross premiums earned | Gross premiums earned | | — | | | 187,337 | | | 77,546 | | | 393,891 | |

| Ceded premiums earned | Ceded premiums earned | | — | | | (140,463) | | | (48,203) | | | (303,906) | |

| Net premiums earned | Net premiums earned | | — | | | 46,874 | | | 29,343 | | | 89,985 | |

| Net investment income | Net investment income | | — | | | 1,301 | | | 2,182 | | | 2,375 | |

| Net realized investment gains (losses) | | — | | | (1) | | | 1,343 | | | (1,807) | |

| Net unrealized gains (losses) on equity securities | | — | | | (2,693) | | | 2,080 | | | (4,191) | |

| Net realized investment gains | |

| Net unrealized gains on equity securities | |

| Other revenue | Other revenue | | — | | | 6,411 | | | 2,717 | | | 9,474 | |

| Total revenue | Total revenue | | — | | | 51,892 | | | 37,665 | | | 95,836 | |

| EXPENSES: | EXPENSES: | |

| Losses and loss adjustment expenses | |

| Losses and loss adjustment expenses | |

| Losses and loss adjustment expenses | Losses and loss adjustment expenses | | 1,191 | | | 76,051 | | | 36,417 | | | 141,115 | |

| Policy acquisition costs | Policy acquisition costs | | (170) | | | 5,418 | | | (1,522) | | | 11,126 | |

| Operating expenses | Operating expenses | | 507 | | | 9,199 | | | 4,503 | | | 17,740 | |

| General and administrative expenses | General and administrative expenses | | 1,275 | | | 6,286 | | | 2,559 | | | 14,227 | |

| Interest expense | Interest expense | | — | | | 31 | | | 22 | | | 50 | |

| Total expenses | Total expenses | | 2,803 | | | 96,985 | | | 41,979 | | | 184,258 | |

| Loss before other income | Loss before other income | | (2,803) | | | (45,093) | | | (4,314) | | | (88,422) | |

| Other income (loss) | | — | | | 13 | | | — | | | 23 | |

| Other income | |

| Loss before income taxes | Loss before income taxes | | (2,803) | | | (45,080) | | | (4,314) | | | (88,399) | |

| Provision (benefit) for income taxes | Provision (benefit) for income taxes | | (230) | | | 10,664 | | | (214) | | | 329 | |

| Income (loss) from discontinued operations, net of tax | | $ | (2,573) | | | $ | (55,744) | | | $ | (4,100) | | | $ | (88,728) | |

| Loss from discontinued operations, net of tax | |

As of February 28, 2023, the Company completed the disposal of its former subsidiary, UPC. This divestiture resulted in a gain of $238,440,000 for the three months ended March 31, 2023. This gain was driven by the negative equity position of UPC.

AMERICAN COASTAL INSURANCE CORPORATION

NotesUPC prior to Unaudited Condensed Consolidated Financial Statements

June 30, 2023

the divestiture.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

March 31, 2024

The major classes of assets and liabilities transferred as a result of the transaction as of the date of transfer and December 31, 2022 are presented below.

| | | | | | | | | | | | | | |

| Major Classes of Assets and Liabilities Disposed | | | | |

| | Closing (1) | | December 31, 2022 |

| ASSETS | | | | |

| Fixed maturities, available-for-sale | | $ | 1,380 | | | $ | 171,781 | |

| Equity securities | | 272 | | | 23,363 | |

| Other investments | | 12,882 | | | 12,952 | |

| Cash and cash equivalents | | 224,824 | | | 158,990 | |

| Restricted cash | | 7,758 | | | 7,730 | |

| Accrued investment income | | 875 | | | 1,457 | |

| Premiums receivable, net | | 22,733 | | | 46,736 | |

| Reinsurance recoverable on paid and unpaid losses, net | | 548,929 | | | 834,863 | |

| Ceded unearned premiums | | 75,262 | | | 122,533 | |

| Deferred policy acquisition costs, net | | (89) | | | (2,046) | |

| Other assets | | 53,675 | | | 33,548 | |

| Total assets | | $ | 948,501 | | | $ | 1,411,907 | |

| | | | |

| LIABILITIES | | | | |

| Unpaid losses and loss adjustment expenses | | 920,431 | | | 1,103,980 | |

| Unearned premiums | | 98,655 | | | 286,842 | |

| Reinsurance payable on premiums | | 12,612 | | | 29,394 | |

| Payments outstanding | | 144,238 | | | 213,058 | |

| Accounts payable and accrued expenses | | 1,361 | | | (872) | |

| Other liabilities | | 3,476 | | | 14,658 | |

| Notes payable, net | | 4,118 | | | 4,118 | |

| Total Liabilities | | $ | 1,184,891 | | | $ | 1,651,178 | |

| | | | | | | | | | |

| Major Classes of Assets and Liabilities Disposed | | | | |

| | Closing (1) | | |

| ASSETS | | | | |

| Fixed maturities, available-for-sale | | $ | 1,380 | | | |

| Equity securities | | 272 | | | |

| Other investments | | 12,882 | | | |

| Cash and cash equivalents | | 224,824 | | | |

| Restricted cash | | 7,758 | | | |

| Accrued investment income | | 875 | | | |

| Premiums receivable, net | | 22,733 | | | |

| Reinsurance recoverable on paid and unpaid losses, net | | 548,929 | | | |

| Ceded unearned premiums | | 75,262 | | | |

| Deferred policy acquisition costs, net | | (89) | | | |

| Other assets | | 51,625 | | | |

| Total assets | | $ | 946,451 | | | |

| | | | |

| LIABILITIES | | | | |

| Unpaid losses and loss adjustment expenses | | $ | 920,431 | | | |

| Unearned premiums | | 98,655 | | | |

| Reinsurance payable on premiums | | 12,612 | | | |

| Payments outstanding | | 144,238 | | | |

| Accounts payable and accrued expenses | | 1,361 | | | |

| Other liabilities | | 3,476 | | | |

| Notes payable, net | | 4,118 | | | |

| Total Liabilities | | $ | 1,184,891 | | | |

(1) The Company divested its ownership on February 27, 2023, the date the DFS was appointed as receiver of the entity.

In addition,During the major classesfirst quarter of assets2024, due to a change in circumstances, the Company evaluated its capitalized software, previously classified as held for disposal at December 31, 2023. As a result of this evaluation, it was determined that the use case of the software by the Company has shifted. The Company has reclassified this asset and liabilities remaining related to activities directly supporting the business conducted by UPC are outlinedassociated amortization expense in the table below ascurrent period presented within this footnote in accordance with GAAP guidance, resulting in amortization expense for the capitalized software being captured in continuing operations prospectively. Property & equipment of June 30, 2023 and$8,095,000 at December 31, 2022.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023

| | | | | | | | | | | | | | |

| Major Classes of Assets and Liabilities Held for Disposal | | | | |

| | June 30, 2023 | | December 31, 2022 |

| ASSETS | | | | |

| Property and equipment, net | | 12,105 | | | 14,299 | |

| Deferred policy acquisition costs | | — | | | 8,609 | |

| Total assets | | $ | 12,105 | | | $ | 22,908 | |

| | | | |

| LIABILITIES | | | | |

| Commissions Payable | | 1,795 | | | 987 | |

| Unearned Policy Fees | | — | | | 2,652 | |

| Total Liabilities | | $ | 1,795 | | | $ | 3,639 | |

The discontinued operationsAs a result of the reclassification in the first quarter of 2024, described above, the Company incurred $488,000 and $748,000held no assets or liabilities for disposal at March 31, 2024. At December 31, 2023, assets held for disposal consisted of amortization expense during the six months ended June 30, 2023 and 2022, respectively.property & equipment totaling $8,095,000. There were no liabilities held for disposal at December 31, 2023. In addition, other noncashthan the item related to capitalized software noted above, there were no non-cash transactions for either period.during the three months ended March 31, 2024. During the three months ended March 31, 2023, amortization attributed to discontinued operations totaled $252,000.

4) SEGMENT REPORTING

Personal Lines Business

Our personal lines business provides structure, content and liability coverage for standard single-family homeowners, renters and condominium unit owners, through our subsidiary IIC. Personal residential products are offered in New York. We include coverage to policyholders for loss or damage to dwellings, detached structures or equipment caused by covered causes of loss such as fire, wind, hail, water, theft and vandalism.

We have developed a unique and proprietary homeowners’ product. This product uses a granular approach to pricing for catastrophe perils. We have focused on using independent agencies as a channel of distribution for our personal lines business. All of our personal lines business is managed internally.

Commercial Lines Business

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

March 31, 2024

Our commercial lines business primarily provides commercial multi-peril property insurance for residential condominium associations and apartments in Florida, through our subsidiary AmCoastal. We include coverage to policyholders for loss or damage to buildings, inventory or equipment caused by covered causes of loss such as fire, wind, hail, water, theft and vandalism. We also wrote commercial residential coverage through our subsidiary JIC, in South Carolina and Texas. Effective June 1, 2022, JIC was merged into AmCoastal, with AmCoastal being the surviving entity. As a result, the commercial residential policies originally written by JIC were not renewed effective May 31, 2022.

All of our commercial lines business is administered by an outside managing general underwriter, AmRisc, LLC (AmRisc).AmRisc. This includes handling the underwriting, claims processing and premium collection related to our commercial business. In return, AmRisc is reimbursed through monthly management fees. International Catastrophe Insurance Managers (ICAT) handled the underwriting

Personal Lines Business

Our personal lines business provides structure, content and premium collectionliability coverage for JIC’s commercial business writtenstandard single-family homeowners, renters and condominium unit owners, through our subsidiary IIC. Personal residential products are offered in South CarolinaNew York. We include coverage to policyholders for loss or damage to dwellings, detached structures or equipment caused by covered causes of loss such as fire, wind, hail, water, theft and Texas and was also reimbursed through monthly management fees. Effective May 31, 2022, the Company terminated its agreement with ICAT.vandalism.

Please note the following similarities pertaining to the accounting and transactions of our operating segments for the three and six months ended June 30, 2023March 31, 2024 and 2022:2023:

•Both operating segments follow the accounting policies as reported in our Annual Report on Form 10-K for the year ended December 31, 2022;2023;

•Neither operating segment experienced significant noncashnon-cash transactions outside of depreciation and amortization for the three and six months ended June 30, 2023March 31, 2024 and 2022.2023.

The tables below present the information for each of the reportable segment's profit or loss for the three months ended March 31, 2024 and 2023.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023March 31, 2024

The tables below present the information for each of the reportable segment's profit or loss, as well as segment assets for the three and six months ended June 30, 2023 and 2022. We have restated our segments to reflect the discontinued operations disclosed in Note 3, excluding the result of the entity for all periods presented.

| | Three Months Ended June 30, 2023 |

| Commercial | | Personal (1) | | Adjustments | | Consolidated |

| | Three Months Ended March 31, 2024 | | | | Three Months Ended March 31, 2024 |

| | Commercial | | | | Commercial | | Personal (1) | | Adjustments | | Consolidated |

| REVENUE: | REVENUE: | | | | | | | | |

| Gross premiums written | |

| Gross premiums written | |

| Gross premiums written | Gross premiums written | | $ | 236,822 | | | $ | 7,063 | | | $ | — | | | $ | 243,885 | |

| Change in gross unearned premiums | Change in gross unearned premiums | | (91,011) | | | 5,325 | | | — | | | (85,686) | |

| Gross premiums earned | Gross premiums earned | | 145,811 | | | 12,388 | | | — | | | 158,199 | |

| Ceded premiums earned | Ceded premiums earned | | (71,825) | | | (3,205) | | | — | | | (75,030) | |

| Net premiums earned | Net premiums earned | | 73,986 | | | 9,183 | | | — | | | 83,169 | |

| Net investment income | Net investment income | | 1,866 | | | 804 | | | 22 | | | 2,692 | |

| Net realized gains (losses) | | (6,708) | | | (17) | | | — | | | (6,725) | |

| Net realized investment losses | |

| Net unrealized losses on equity securities | Net unrealized losses on equity securities | | 140 | | | — | | | 1 | | | 141 | |

| | Other revenue | |

| Other revenue | |

| Other revenue | Other revenue | | — | | | 18 | | | — | | | 18 | |

| Total revenues | Total revenues | | 69,284 | | | 9,988 | | | 23 | | | 79,295 | |

| EXPENSES: | EXPENSES: | |

| Losses and loss adjustment expenses | Losses and loss adjustment expenses | | 16,245 | | | 4,670 | | | — | | | 20,915 | |

| Losses and loss adjustment expenses | |

| Losses and loss adjustment expenses | |

| Policy acquisition costs | Policy acquisition costs | | 23,526 | | | 2,019 | | | — | | | 25,545 | |

| Operating expenses | Operating expenses | | 1,501 | | | 1,669 | | | 104 | | | 3,274 | |

General and administrative expenses (2) | | 2,631 | | | 3,772 | | | 180 | | | 6,583 | |

| General and administrative expenses | |

| Interest expense | Interest expense | | — | | | — | | | 2,719 | | | 2,719 | |

| Total expenses | Total expenses | | 43,903 | | | 12,130 | | | 3,003 | | | 59,036 | |

| Income (loss) before other income | Income (loss) before other income | | 25,381 | | | (2,142) | | | (2,980) | | | 20,259 | |

| Other income (loss) | Other income (loss) | | — | | | 806 | | | — | | | 806 | |

| Income (loss) before income taxes | Income (loss) before income taxes | | $ | 25,381 | | | $ | (1,336) | | | (2,980) | | | 21,065 | |

| Provision for income taxes | Provision for income taxes | | | | | | 713 | | | 713 | |

| Net income (loss) | Net income (loss) | | $ | (3,693) | | | $ | 20,352 | |

| Less: Net loss attributable to noncontrolling interests | | — | | | — | |

| Net income (loss) attributable to ACIC | | $ | (3,693) | | | $ | 20,352 | |

| Loss ratio, net (3) (4) | | 22.0 | % | | 50.9 | % | | 25.1 | % |

Expense ratio (3) (5) | | 37.4 | % | | 81.2 | % | | 42.6 | % |

Combined ratio (3) (6) | | 59.4 | % | | 132.1 | % | | 67.7 | % |

| | Total segment assets | | $ | 1,612,469 | | | $ | (233,324) | | | $ | 53,605 | | | $ | 1,432,750 | |

| Loss ratio, net (2) (3) | |

| Loss ratio, net (2) (3) | |

| Loss ratio, net (2) (3) | | | 18.4 | % | | 71.4 | % | | | | 23.1 | % |

Expense ratio (2) (4) | | Expense ratio (2) (4) | | 34.6 | % | | 36.7 | % | | | | 35.2 | % |

Combined ratio (2) (5) | | Combined ratio (2) (5) | | 53.0 | % | | 108.1 | % | | | | 58.3 | % |

(1) Our personal lines income statement also includes amounts related to subsidiaries outside of our insurance companies. We have included these items as these subsidiaries directly support our personal lines operations.

(2) Included in our General and Administrative expenses is $996,000 and $811,000 of depreciation and amortization expense related to our personal and commercial lines assets, respectively.

(3) As these are calculated ratios, the addition of the ratios will not result in the same value as the consolidated ratio. To calculate the consolidated ratio please see the corresponding footnote below.

(4)(3) Loss ratio, net is calculated as losses and LAE net of losses ceded to reinsurers, relative to net premiums earned. Management uses this operating metric to analyze our loss trends and believes it is useful for investors to evaluate this component separately from our other operating expenses.

(5)(4) Expense ratio is calculated as the sum of all operating expenses less interest expense relative to net premiums earned. Management uses this operating metric to analyze our expense trends and believes it is useful for investors to evaluate these components separately from our loss expenses.

(6)(5) Combined ratio is the sum of the loss ratio, net and expense ratio. Management uses this operating metric to analyze our total expense trends and believes it is a key indicator for investors when evaluating the overall profitability of our business.

AMERICAN COASTAL INSURANCE CORPORATION

Notes to Unaudited Condensed Consolidated Financial Statements

June 30, 2023March 31, 2024

| | Three Months Ended June 30, 2022 |

| Commercial | | Personal (1) | | Adjustments | | Consolidated |

| | Three Months Ended March 31, 2023 | | | | Three Months Ended March 31, 2023 |

| | Commercial | | | | Commercial | | Personal (1) | | Adjustments | | Consolidated |

| REVENUE: | REVENUE: | | | | | | | | |

| Gross premiums written | |

| Gross premiums written | |

| Gross premiums written | Gross premiums written | | $ | 181,067 | | | $ | 26,565 | | | $ | — | | | $ | 207,632 | |

| Change in gross unearned premiums | Change in gross unearned premiums | | (67,849) | | | (10,300) | | | — | | | (78,149) | |

| Gross premiums earned | Gross premiums earned | | 113,218 | | | 16,265 | | | — | | | 129,483 | |