UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-Q

(Mark One)

|

| |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20182019

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-35281

Forbes Energy Services Ltd.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 98-0581100 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | |

3000 South Business Highway 281 Alice, Texas | | 78332 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code:

(361) 664-0549

Securities registered pursuant to Section 12(b) of the Act: |

| | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common stock, $0.01 par value | | FLSS | | OTCQX Best Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | |

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| | | | |

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company)

x | Smaller reporting company | x |

| | | | |

| | | Emerging growth company | ¨ |

| | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). ¨ Yes x No

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court (as defined in Exchange Act Rule 12b-2). x Yes ¨ No

The number ofwere 5,522,822 shares of the registrant's common stock par value $0.01 per share, of Forbes Energy Services Ltd. outstanding as of November 14, 2018 was 5,421,967.11, 2019.

FORBES ENERGY SERVICES LTD.

TABLE OF CONTENTS

|

| | |

| | | Page |

| |

| Item 1. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| Item 5. | Other Information | |

| Item 6. | Exhibits | |

| | Signatures | |

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q and any oral statements made in connection with it include certain forward-looking statements within the meaning of the federal securities laws. You can generally identify forward-looking statements by the appearance in such a statement of words like “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project” or “should” or other comparable words or the negative of these words. When you consider our forward-looking statements, you should keep in mind the risk factors we describe and other cautionary statements we make in this Quarterly Report on Form 10-Q. Our forward-looking statements are only predictions based on expectations that we believe are reasonable. Our actual results could differ materially from those anticipated in, or implied by, these forward-looking statements as a result of known risks and uncertainties set forth below and elsewhere in this Quarterly Report on Form 10-Q. These factors include or relate to the following:

the effect of the continuing industry-wide downturn in and the cyclical nature of, energy exploration and development activities;

continuing incurrence of operating losses due to such downturn;

oil and natural gas commodity prices;

market response to global demands to curtail use of oil and natural gas;

capital budgets and spending by the oil and natural gas industry;

the ability or willingness of the Organization of Petroleum Exporting Countries, or OPEC, to set and maintain production levels for oil;

oil and natural gas production levels by non-OPEC countries;

supply and demand for oilfield services and industry activity levels;

our ability to maintain stable pricing;

possible impairment of our long-lived assets;

potential for excess capacity;

competition;

substantial capital requirements;

significant operating and financial restrictions under our loan and security agreement which provides for a term loan, of $50.0 million, or the NewTerm Loan Agreement;Agreement, excluding paid in kind interest;

technological obsolescence of operating equipment;

dependence on certain key employees;

concentration of customers;

substantial additional costs of compliance with reporting obligations, the Sarbanes-Oxley Act, and NewTerm Loan Agreement, Revolving Loan Agreement and the PIK Notes covenants;

seasonality of oilfield services activity;

collection of accounts receivable;

environmental and other governmental regulation;

the potential disruption of business activities caused by the physical effects, if any, of climate change;

risks inherent in our operations;

ability to fully integrate future acquisitions;

variation from projected operating and financial data;

variation from budgeted and projected capital expenditures;

volatility of global financial markets; and

the other factors discussed under “Risk Factors” beginning on page 10 of the Annual Report on Form 10-K for the year ended December 31, 2017.2018.

We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. To the extent these risks, uncertainties and assumptions give rise to events that vary from our

expectations, the forward-looking events discussed in this Quarterly Report on Form 10-Q may not occur. All forward-looking statements attributable to us are qualified in their entirety by this cautionary statement.

PART I—FINANCIAL INFORMATION

Item 1. Unaudited Condensed Consolidated Financial Statements

Forbes Energy Services Ltd.

Condensed Consolidated Balance Sheets (unaudited)(unaudited)

(in thousands, except par value amounts)

| |

| Successor | | | | | |

| September 30,

2018 |

| December 31,

2017 | September 30, 2019 |

| December 31, 2018 |

| Assets |

|

|

|

|

|

|

| Current assets |

|

|

|

|

|

|

| Cash and cash equivalents | $ | 6,617 |

|

| $ | 5,465 |

| $ | 6,268 |

| | $ | 8,083 |

|

| Cash - restricted | 14,701 |

|

| 30,015 |

| 73 |

| | 73 |

|

| Accounts receivable - trade, net | 34,717 |

|

| 24,341 |

| 30,060 |

| | 45,950 |

|

| Accounts receivable - other | 908 |

|

| 496 |

| 2,337 |

| | 2,228 |

|

| Prepaid expenses and other current assets | 5,030 |

|

| 11,212 |

| 7,631 |

| | 14,691 |

|

| Total current assets | 61,973 |

|

| 71,529 |

| 46,369 |

|

| 71,025 |

|

| Property and equipment, net | 113,103 |

|

| 117,191 |

| 131,209 |

| | 148,608 |

|

| Operating lease right-of-use assets | | 6,701 |

| | — |

|

| Intangible assets, net | 11,012 |

|

| 11,852 |

| 12,797 |

| | 13,980 |

|

| Goodwill | | — |

| | 19,700 |

|

| Other assets | 883 |

|

| 1,185 |

| 1,476 |

| | 3,072 |

|

| Total assets | $ | 186,971 |

|

| $ | 201,757 |

| $ | 198,552 |

|

| $ | 256,385 |

|

| | | | | |

| Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

| Current liabilities |

|

|

|

|

|

|

| Current portions of long-term debt | $ | 2,054 |

|

| $ | 7,566 |

| |

| Accounts payable - trade | 15,769 |

|

| 7,497 |

| $ | 7,962 |

| | $ | 17,841 |

|

| Accounts payable - related parties | — |

|

| 11 |

| |

| Accrued interest payable | 1,304 |

|

| 998 |

| 2,421 |

| | 1,993 |

|

| Accrued expenses | 12,035 |

|

| 11,084 |

| 15,040 |

| | 14,348 |

|

| Current portion of operating lease liabilities | | 1,865 |

| | — |

|

| Current portion of long-term debt | | 61,679 |

| | 59,321 |

|

| Total current liabilities | 31,162 |

|

| 27,156 |

| 88,967 |

|

| 93,503 |

|

| Long-term debt, net of current portion | 55,486 |

|

| 51,288 |

| |

| Long-term operating lease liabilities, net of current portion | | 4,836 |

| | — |

|

| Long-term debt, net of current portion and debt discount | | 65,662 |

| | 71,095 |

|

| Deferred tax liability | 362 |

|

| 379 |

| 365 |

| | 357 |

|

| Total liabilities | 87,010 |

|

| 78,823 |

| 159,830 |

|

| 164,955 |

|

|

|

|

|

| |

| Commitments and contingencies (Note 8) |

| |

| |

|

|

|

| |

| Common stock, $0.01 par value, 40,000 shares authorized, 5,422 and 5,336 shares issued and outstanding at September 30, 2018 and December 31, 2017, respectively | 54 |

| | 53 |

| |

| Commitments and contingencies (Note 7) | |

| |

|

| Stockholders’ equity | |

|

|

|

| Common stock, $0.01 par value, 40,000 shares authorized, 5,523 and 5,439 shares issued and outstanding at September 30, 2019 and December 31, 2018, respectively | | 55 |

| | 54 |

|

| Additional paid-in capital | 149,620 |

| | 148,866 |

| 150,716 |

| | 149,968 |

|

| Accumulated deficit | (49,713 | ) |

| (25,985 | ) | (112,049 | ) | | (58,592 | ) |

| Total stockholders’ equity | 99,961 |

|

| 122,934 |

| 38,722 |

|

| 91,430 |

|

| Total liabilities and stockholders’ equity | $ | 186,971 |

|

| $ | 201,757 |

| $ | 198,552 |

|

| $ | 256,385 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

Forbes Energy Services Ltd.

Condensed Consolidated Statements of Operations (unaudited)

(in thousands, except per share amounts)

| | | | Successor | | | | | |

| | Three Months Ended September 30, | Three Months Ended September 30, |

| | 2018 | | 2017 | 2019 | | 2018 |

| Revenues | | | | | | |

| Well servicing | $ | 32,175 |

| | $ | 23,513 |

| $ | 23,141 |

| | $ | 22,551 |

|

| Coiled tubing | | 10,398 |

| | 9,624 |

|

| Fluid logistics | 15,437 |

| | 10,782 |

| 10,655 |

| | 15,437 |

|

| Total revenues | 47,612 |

| | 34,295 |

| 44,194 |

| | 47,612 |

|

| | | | | |

| Expenses | | | |

| | |

| Well servicing | 25,350 |

| | 16,883 |

| 19,246 |

| | 18,135 |

|

| Coiled tubing | | 11,865 |

| | 7,215 |

|

| Fluid logistics | 12,079 |

| | 10,371 |

| 7,499 |

| | 12,079 |

|

| Impairment of goodwill | | 19,222 |

| | — |

|

| General and administrative | 6,545 |

| | 6,458 |

| 5,242 |

| | 6,545 |

|

| Depreciation and amortization | 7,566 |

| | 7,134 |

| 6,483 |

| | 7,566 |

|

| Total expenses | 51,540 |

| | 40,846 |

| 69,557 |

| | 51,540 |

|

| Operating loss | (3,928 | ) | | (6,551 | ) | (25,363 | ) | | (3,928 | ) |

| | | | | |

| Other income (expense) | | | |

| | |

| Interest income | 1 |

| | 5 |

| 16 |

| | 1 |

|

| Interest expense | (2,474 | ) | | (2,170 | ) | (5,704 | ) | | (2,474 | ) |

| Pre-tax loss | (6,401 | ) | | (8,716 | ) | (31,051 | ) | | (6,401 | ) |

| Income tax expense | 32 |

| | 260 |

| 23 |

| | 32 |

|

| Net loss | $ | (6,433 | ) | | $ | (8,976 | ) | $ | (31,074 | ) | | $ | (6,433 | ) |

| | |

|

| | |

| Loss per share of common stock | | | | | | |

| Basic and diluted loss per share | $ | (1.20 | ) | | $ | (1.70 | ) | |

| Weighted average number of shares outstanding | | | | |

| Basic and diluted | 5,368 |

| | 5,279 |

| $ | (5.68 | ) | | $ | (1.20 | ) |

| | | | | |

| Weighted average number of shares of common stock outstanding: | | | | |

| Basic and diluted | | 5,471 |

| | 5,368 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

Forbes Energy Services Ltd.

Condensed Consolidated Statements of Operations (unaudited)

(in thousands, except per share amounts)

| | | | Successor | | | Predecessor | | | | | |

| | Nine months ended September 30, 2018 | | April 13 through September 30, 2017 | | | January 1 through April 12, 2017 | Nine Months Ended September 30, |

| | | | | 2019 | | 2018 |

| Revenues | | | | | | | | | |

| Well servicing | $ | 82,406 |

| | $ | 41,652 |

| | | $ | 19,554 |

| $ | 73,653 |

| | $ | 60,620 |

|

| Coiled tubing | | 43,700 |

| | 21,786 |

|

| Fluid logistics | 42,038 |

| | 20,493 |

| | | 11,211 |

| 36,294 |

| | 42,038 |

|

| Total revenues | 124,444 |

| | 62,145 |

| | | 30,765 |

| 153,647 |

| | 124,444 |

|

| | | | | |

| Expenses | | | | | | | | | |

| Well servicing | 67,689 |

| | 30,698 |

| | | 15,952 |

| 57,766 |

| | 50,099 |

|

| Coiled tubing | | 43,657 |

| | 17,590 |

|

| Fluid logistics | 33,919 |

| | 19,425 |

| | | 11,207 |

| 26,974 |

| | 33,919 |

|

| Impairment of goodwill | | 19,222 |

| | — |

|

| General and administrative | 17,341 |

| | 9,588 |

| | | 5,012 |

| 17,486 |

| | 17,341 |

|

| Depreciation and amortization | 22,381 |

| | 12,815 |

| | | 13,601 |

| 22,935 |

| | 22,381 |

|

| Total expenses | 141,330 |

| | 72,526 |

| | | 45,772 |

| 188,040 |

| | 141,330 |

|

| Operating loss | (16,886 | ) | | (10,381 | ) | | | (15,007 | ) | (34,393 | ) | | (16,886 | ) |

| | | | | |

| Other income (expense) | | | | | | | | | |

| Interest income | 3 |

| | 11 |

| | | 13 |

| 20 |

| | 3 |

|

| Interest expense | (7,267 | ) | | (4,067 | ) | | | (2,254 | ) | (19,113 | ) | | (7,267 | ) |

| Gain (loss) on reorganization items, net | — |

| | (1,299 | ) | | | 44,503 |

| |

| Pre-tax income (loss) | (24,150 | ) | | (15,736 | ) | | | 27,255 |

| |

| Income tax (benefit) expense | (422 | ) | | 243 |

| | | 27 |

| |

| Net income (loss) | (23,728 | ) | | (15,979 | ) | | | 27,228 |

| |

| Preferred stock dividends | — |

| | — |

| | | (46 | ) | |

| Net income (loss) attributable to common stockholders | $ | (23,728 | ) | | $ | (15,979 | ) | | | $ | 27,182 |

| |

| Income (loss) per share of common stock | | | | | | | |

| Basic and diluted income (loss) per share | $ | (4.44 | ) | | $ | (3.04 | ) | | | $ | 0.99 |

| |

| Weighted average number of shares outstanding | | | | | | | |

| Pre-tax loss | | (53,486 | ) | | (24,150 | ) |

| Income tax benefit | | (27 | ) | | (422 | ) |

| Net loss | | $ | (53,459 | ) | | $ | (23,728 | ) |

| | | | | |

| Loss per share of common stock | | | | |

| Basic and diluted | 5,347 |

| | 5,262 |

| | | 27,508 |

| $ | (9.80 | ) | | $ | (4.44 | ) |

| | | | | |

| Weighted average number of shares of common stock outstanding: | | | | |

| Basic and diluted | | 5,453 |

| | 5,347 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

Forbes Energy Services Ltd.

Condensed Consolidated Statements of Cash Flows (unaudited)

(in thousands)

| | | | Successor | | | Predecessor | | | | | |

| | Nine months ended September 30, 2018 | | April 13 through September 30, 2017 | | | January 1 through April 12, 2017 | Nine Months Ended September 30, |

| | | | | | | | 2019 | | 2018 |

| Cash flows from operating activities: | | | | | | | | | |

| Net income (loss) | $ | (23,728 | ) | | $ | (15,979 | ) | | | $ | 27,228 |

| |

| Adjustments to reconcile net income (loss) to net cash used in operating activities: | | | | | | | |

| Net loss | | $ | (53,459 | ) | | $ | (23,728 | ) |

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | | | | |

| Depreciation and amortization | 22,381 |

| | 12,815 |

| | | 13,601 |

| 22,935 |

| | 22,381 |

|

| Share-based compensation | 755 |

| | 1,034 |

| | | — |

| 749 |

| | 755 |

|

| Reorganization items (non-cash) | — |

| | — |

| | | (51,166 | ) | |

| Deferred tax (benefit) expense | (17 | ) | | 15 |

| | | (47 | ) | |

| Deferred tax benefit | | 8 |

| | (17 | ) |

| Impairment of goodwill | | 19,222 |

| | — |

|

| Gain on disposal of assets | (427 | ) | | (338 | ) | | | (950 | ) | (4,565 | ) | | (427 | ) |

| Bad debt expense | 89 |

| | 145 |

| | | 1 |

| 3,242 |

| | 89 |

|

| Amortization of debt discount | 653 |

| | 968 |

| | | 234 |

| |

| Amortization of debt discount/deferred financing costs/premium conversion | | 6,550 |

| | 653 |

|

| Interest paid in kind | 3,027 |

| | 1,676 |

| | | — |

| 7,372 |

| | 3,027 |

|

| Changes in operating assets and liabilities: | | | | | | | | | |

| Accounts receivable | (10,877 | ) | | (8,069 | ) | | | (916 | ) | 12,539 |

| | (10,877 | ) |

| Prepaid expenses and other assets | 602 |

| | 2,985 |

| | | (748 | ) | 2,450 |

| | 602 |

|

| Accounts payable - trade | 4,349 |

| | (4,457 | ) | | | 6,608 |

| (9,879 | ) | | 4,349 |

|

| Accounts payable - related parties | (11 | ) | | (8 | ) | | | 2 |

| — |

| | (11 | ) |

| Accrued expenses | 913 |

| | 549 |

| | | 324 |

| 654 |

| | 913 |

|

| Accrued interest payable | 306 |

| | (6 | ) | | | 1,575 |

| 428 |

| | 306 |

|

| Net cash used in operating activities | (1,985 | ) | | (8,670 | ) | | | (4,254 | ) | |

| Net cash provided by (used in) operating activities | | 8,246 |

| | (1,985 | ) |

| Cash flows from investing activities: | | | | | | |

| |

|

| Purchases of property and equipment | | (11,640 | ) | | (12,769 | ) |

| Purchase of Cretic, net of cash acquired | | 285 |

| | — |

|

| Proceeds from sale of property and equipment | 2,086 |

| | 1,086 |

| | | 937 |

| 13,715 |

| | 2,086 |

|

| Purchases of property and equipment | (12,769 | ) | | (4,044 | ) | | | (400 | ) | |

| Net cash provided by (used in) investing activities | (10,683 | ) | | (2,958 | ) | | | 537 |

| 2,360 |

| | (10,683 | ) |

| Cash flows from financing activities: | | | | | | |

| |

|

| Payments for capital leases | (1,494 | ) | | (664 | ) | | | (444 | ) | |

| Payments for debt issuance costs | — |

| | — |

| | | (5,000 | ) | |

| Payment of Prior Senior Notes | — |

| | — |

| | | (20,000 | ) | |

| Repayment of Prior Loan Agreement | — |

| | — |

| | | (15,000 | ) | |

| Proceeds from New Loan Agreement | — |

| | — |

| | | 50,000 |

| |

| Net cash provided by (used in) financing activities | (1,494 | ) | | (664 | ) | | | 9,556 |

| |

| Net increase (decrease) in cash, cash equivalents, and cash - restricted | (14,162 | ) | | (12,292 | ) | | | 5,839 |

| |

| Cash, cash equivalents, and cash - restricted: | | | | | | | |

| Payments for finance leases | | (3,823 | ) | | (1,494 | ) |

| Proceeds from Revolving Loan Agreement | | 4,000 |

| | — |

|

| Payments on Term Loan Agreement | | (12,598 | ) | | — |

|

| Payments for Bridge Loan | | (4,422 | ) | | — |

|

| Proceeds from PIK Notes | | 4,422 |

| | — |

|

| Net cash used in financing activities | | (12,421 | ) | | (1,494 | ) |

| Net decrease in cash, cash equivalents and cash - restricted | | (1,815 | ) | | (14,162 | ) |

| Cash, cash equivalents and cash - restricted: | |

| | |

| Beginning of period | 35,480 |

| | 53,839 |

| | | 48,000 |

| 8,156 |

| | 35,480 |

|

| End of period | $ | 21,318 |

| | $ | 41,547 |

| | | $ | 53,839 |

| $ | 6,341 |

| | $ | 21,318 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

Forbes Energy Services Ltd.

Condensed Consolidated Statement of Changes in Stockholders’ Equity (unaudited)

(in thousands)

For the three and nine months ended September 30, 2019

|

| | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional

Paid-In

Capital | | Accumulated

Deficit | | Total

Stockholders’ Equity |

| | Shares | | Amount | | | |

| Balance at December 31, 2018 | 5,439 |

| | $ | 54 |

| | $ | 149,968 |

| | $ | (58,592 | ) | | $ | 91,430 |

|

| Share-based compensation | 7 |

| | — |

| | 253 |

| | — |

| | 253 |

|

| Net loss | — |

| | — |

| | — |

| | (11,634 | ) | | (11,634 | ) |

| Balance at March 31, 2019 | 5,446 |

| | 54 |

| | 150,221 |

| | (70,226 | ) | | 80,049 |

|

| Share-based compensation | — |

| | — |

| | 256 |

| | — |

| | 256 |

|

| Net loss | — |

| | — |

| | — |

| | (10,749 | ) | | (10,749 | ) |

| Balance at June 30, 2019 | 5,446 |

| | $ | 54 |

| | $ | 150,477 |

| | $ | (80,975 | ) | | $ | 69,556 |

|

| Share-based compensation | 77 |

| | 1 |

| | 239 |

| | — |

| | 240 |

|

| Net loss | — |

| | — |

| | — |

| | (31,074 | ) | | (31,074 | ) |

| Balance at September 30, 2019 | 5,523 |

| | $ | 55 |

| | $ | 150,716 |

| | $ | (112,049 | ) | | $ | 38,722 |

|

For the three and nine months ended September 30, 2018

|

| | | | | | | | | | | | | | | | | | |

| | Common Stock | | Additional

Paid-In

Capital | | Accumulated

Deficit | | Total

Stockholders’ Equity |

| | Shares | | Amount | | | |

| Balance at December 31, 2017 | 5,336 |

| | $ | 53 |

| | $ | 148,866 |

| | $ | (25,985 | ) | | $ | 122,934 |

|

| Share-based compensation | — |

| | — |

| | 251 |

| | — |

| | 251 |

|

| Net loss | — |

| | — |

| | — |

| | (8,529 | ) | | (8,529 | ) |

| Balance at March 31, 2018 | 5,336 |

| | 53 |

| | 149,117 |

| | (34,514 | ) | | 114,656 |

|

| Share-based compensation | — |

| | — |

| | 247 |

| | — |

| | 247 |

|

| Net loss | — |

| | — |

| | — |

| | (8,766 | ) | | (8,766 | ) |

| Balance at June 30, 2018 | 5,336 |

| | $ | 53 |

| | $ | 149,364 |

| | $ | (43,280 | ) | | $ | 106,137 |

|

| Share-based compensation | 86 |

| | 1 |

| | 256 |

| | — |

| | 257 |

|

| Net loss | — |

| | — |

| | — |

| | (6,433 | ) | | (6,433 | ) |

| Balance at September 30, 2018 | 5,422 |

| | $ | 54 |

| | $ | 149,620 |

| | $ | (49,713 | ) | | $ | 99,961 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

Forbes Energy Services Ltd.

Notes to Condensed Consolidated Financial Statements

(unaudited)

1. Organization and Nature of Operations

Nature of BusinessOperations

Forbes Energy Services Ltd., or FES Ltd., is an independent oilfield services contractor that provides a wide range of well site services to oil and natural gas drilling and producing companies to help develop and enhance the production of oil and natural gas. These services include fluid hauling, fluid disposal, well maintenance, completion services, workovers and re-completions,recompletions, plugging and abandonment, and tubing testing. The Company's operations are concentrated in the major onshore oil and natural gas producing regions of Texas, with an additional location in Pennsylvania. The Company believes that its broad range of services, which extends from initial drilling, through production, to eventual abandonment, is fundamental to establishing and maintaining the flow of oil and natural gas throughout the life cycle of its customers'our customers’ wells.

As used in these Consolidated Financial Statements,condensed consolidated financial statements, the “Company,” “we,”“Company”, “we” and “our” mean FES Ltd. and its direct and indirect subsidiaries, except as otherwise indicated.

2. Basis of Presentation

Fresh Start Accounting

On January 22, 2017, FES Ltd. and its domestic subsidiaries, or collectively, the Debtors, filed voluntary petitions for reorganization under chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the Southern District of Texas-Corpus Christi Division, or the Bankruptcy Court, pursuant to the terms of a restructuring support agreement that contemplated the reorganization of the Debtors pursuant to a prepackaged plan of reorganization, as amended and supplemented, the Plan. On March 29, 2017, the Bankruptcy Court entered an order confirming the Plan. On April 13, 2017, or the Effective Date, the Plan became effective pursuant to its terms and the Debtors emerged from their chapter 11 cases.

Upon emergence from bankruptcy on the Effective Date, the Company qualified for and adopted fresh start accounting in accordance with the provisions of ASC 852 as (i) the holders of FES Ltd.’s prior common stock, par value $0.04 per share, or the Old Common Stock, received none of the new class of common stock, par value $0.01 per share, or the New Common Stock, issued upon the Debtors' emergence from bankruptcy and (ii) the reorganization value of the Company's assets immediately prior to confirmation of the Plan was less than the post-petition liabilities and allowed claims. The effects of the Plan and the application of fresh start accounting are reflected in the Company's condensed consolidated financial statements from and after April 13, 2017. References to the "Successor" pertain to the Company from and after the Effective Date. References to "Predecessor" pertain to the Company prior to the Effective Date.

The Company applied fresh start accounting from and after the Effective Date. Fresh start accounting required the Company to present its assets, liabilities and equity as if it were a new entity upon emergence from bankruptcy, with no beginning retained earnings or deficit as of the fresh start reporting date. As a result of the adoption of fresh start accounting, the Company’s unaudited condensed consolidated financial statements from and after the Effective Date will not be comparable to its financial statements prior to such date.

Reorganization Items

Reorganization items represent amounts incurred subsequent to the filing of the Bankruptcy Petitions as a direct result of the filing of the Plan and are comprised of the following (in thousands):

|

| | | | | | | | | |

| | | Successor | | | Predecessor |

| | | April 13 through September 30, 2017 | | | January 1 through April 12, 2017 |

| Reorganization legal and professional fees | | $ | (1,299 | ) | | | $ | (6,729 | ) |

| Deferred loan costs expensed | | — |

| | | (2,104 | ) |

| Gain on settlement of liabilities subject to compromise | | — |

| | | 140,441 |

|

| Fresh start adjustments | | — |

| | | (87,105 | ) |

| Gain (loss) on reorganization items, net | | $ | (1,299 | ) | | | $ | 44,503 |

|

Interim Financial Information

The unaudited condensed consolidated financial statements of the Company are prepared in conformity with accounting principles generally accepted in the United States of America, or GAAP, for interim financial reporting. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to the rules and regulations of the Securities and Exchange Commission. Therefore, these condensed consolidated financial statements should be read along with the annual audited consolidated financial statements and notes thereto included in the Company's Annual Report on Form 10-K for the year ended December 31, 2017. All significant intercompany accounts and transactions have been eliminated in consolidation. In the opinion of management, all adjustments which are of normal recurring natures considered necessary for a fair representation have been made in the accompanying unaudited financial statements.

Use of Estimates,

The preparation of condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated balance sheets and the reported amounts of revenues and expenses during the reporting period. Actual results could materially differ from those estimates.

Cash - Restricted

Restricted cash at September 30, 2018 (Successor) and December 31, 2017 (Successor) was $14.7 million and $30.0 million, respectively. The components of restricted cash at September 30, 2018 (Successor) included $6.0 million related to the loan and security agreement which provides for a term loan of $50.0 million, or the New Loan Agreement, which is subject to satisfaction of certain release restrictions and $8.7 million in a cash collateral account related to letters of credit and the Company's corporate credit card program under a new letter of credit facility entered into with Regions, or the New Regions Letter of Credit Facility. The release conditions set forth in the New Loan Agreement include, among other things, (i) no default or event of default under the New Loan Agreement having occurred or being continuing as of the date of the requested release of proceeds of the New Loan Agreement, or that would exist after giving effect to the release requested to be made on such date, and (ii) the Company’s unrestricted cash and cash equivalents being less than $7.0 million after giving pro forma effect to the requested release.

Revenue Recognition

In May 2014, the FASB issued ASU No. 2014-09, "Revenue from Contracts with Customers (Topic 606)," or ASU 2014-09, which provides guidance for revenue recognition and which supersedes nearly all existing revenue recognition guidance under ASU 2014-09 and created ASC 606. This ASU provides guidance that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods and services. On January 1, 2018, the Company adopted ASC 606 on a modified retrospective basis for all contracts. As a result of the Company's adoption, there were no changes to the timing of the revenue recognition or measurement of revenue, and there was no cumulative effect of adoption as of January 1, 2018. Therefore, the only changes to the financial statements related to the adoption are in the footnote disclosures as included here-in.

Revenue is measured as consideration specified in a contract with a customer and excludes any sales incentives and amounts collected on behalf of third parties. The Company recognizes revenue when it satisfies a performance obligation by providing service to a customer. Amounts are billed upon completion of service and are generally due within 30 days.

The Company has its principal revenue generating activities organized into two service lines, well servicing and fluid logistics. The Company's well servicing line consists primarily of maintenance, workover, completion, plugging and

abandonment, and tubing testing services. The Company's fluid logistics line provides supporting services to the well servicing line as well as direct sales to customers for fluid management and movement. The Company generally establishes a master services agreement with each customer and provides associated services on a work order basis in increments of days, by the hour for services performed or on occasion, bid/turnkey pricing. Services provided under the well servicing and the fluid logistics segments are short in duration and generally completed within 30 days.

The majority of the Company’s contracts with customers in both the well servicing and fluid logistics segments are short-term in nature and are recognized as “over-time” performance obligations as the services are performed. The Company applies the “as-invoiced” practical expedient as the amount of consideration the Company has a right to invoice corresponds directly with the value of the Company’s performance to date. Because of the short-term nature of the Company’s services, which generally last a few hours to multiple days, the Company does not have any contracts with a duration longer than one year that require disclosure. The Company has no material contract assets or liabilities.

The Company does not have any revenue expected to be recognized in the future related to remaining performance obligations or contracts with variable consideration related to undelivered performance obligations. There was no revenue recognized in the current period from performance obligations satisfied in previous periods. The Company's significant judgments made in connection with the adoption of ASC 606 included the determination of when the Company satisfies its performance obligation to customers and the applicability of the as invoiced practical expedient.

The following tables show revenue disaggregated by primary geographical markets and major service lines for the three months ended September 30, 2018 (Successor) and the three months ended September 30, 2017 (Successor).

|

| | | | | | | | | | | |

| Successor | | | Three months ended September 30, 2018 |

| | | Well Servicing | Fluid Logistics | Total |

| Primary Geographical Markets | | (in thousands) |

| South Texas | | | $ | 20,260 |

| $ | 7,580 |

| $ | 27,840 |

|

East Texas (1) | | | 1,630 |

| 835 |

| 2,465 |

|

| Central Texas | | | — |

| 3,728 |

| 3,728 |

|

| West Texas | | | 10,285 |

| 3,294 |

| 13,579 |

|

| Total | | | $ | 32,175 |

| $ | 15,437 |

| $ | 47,612 |

|

| | | | | | |

| Successor | | | Three months ended September 30, 2017 |

| | | Well Servicing | Fluid Logistics | Total |

| Primary Geographical Markets | | (in thousands) |

| South Texas | | | $ | 18,397 |

| $ | 5,681 |

| $ | 24,078 |

|

East Texas (1) | | | 1,378 |

| 810 |

| 2,188 |

|

| Central Texas | | | — |

| 1,511 |

| 1,511 |

|

| West Texas | | | 3,738 |

| 2,780 |

| 6,518 |

|

| Total | | | $ | 23,513 |

| $ | 10,782 |

| $ | 34,295 |

|

| | | | | | |

| (1) Includes revenues from the Company's operations in Pennsylvania. | | |

The following tables show revenue disaggregated by primary geographical markets and major service lines for the nine months ended September 30, 2018 (Successor) and the periods of April 13 through September 30, 2017 (Successor) and January 1 through April 12, 2017 (Predecessor).

|

| | | | | | | | | | | |

| Successor | | | Nine months ended September 30, 2018 |

| | | Well Servicing | Fluid Logistics | Total |

| Primary Geographical Markets | | (in thousands) |

| South Texas | | | $ | 54,955 |

| $ | 20,879 |

| $ | 75,834 |

|

East Texas (1) | | | 3,382 |

| 1,987 |

| 5,369 |

|

| Central Texas | | | — |

| 10,193 |

| 10,193 |

|

| West Texas | | | 24,069 |

| 8,979 |

| 33,048 |

|

| Total | | | $ | 82,406 |

| $ | 42,038 |

| $ | 124,444 |

|

|

| | | | | | | | | | | |

| Successor | | | April 13 through September 30, 2017 |

| | | Well Servicing | Fluid Logistics | Total |

| Primary Geographical Markets | | (in thousands) |

| South Texas | | | $ | 32,867 |

| $ | 10,942 |

| $ | 43,809 |

|

East Texas (1) | | | 5,047 |

| 1,436 |

| 6,483 |

|

| Central Texas | | | — |

| 2,850 |

| 2,850 |

|

| West Texas | | | 3,738 |

| 5,265 |

| 9,003 |

|

| Total | | | $ | 41,652 |

| $ | 20,493 |

| $ | 62,145 |

|

|

| | | | | | | | | | | |

| Predecessor | | | January 1 through April 12, 2017 |

| | | Well Servicing | Fluid Logistics | Total |

| Primary Geographical Markets | | (in thousands) |

| South Texas | | | $ | 14,691 |

| $ | 5,872 |

| $ | 20,563 |

|

East Texas (1) | | | 868 |

| 945 |

| 1,813 |

|

| Central Texas | | | — |

| 1,593 |

| 1,593 |

|

| West Texas | | | 3,995 |

| 2,801 |

| 6,796 |

|

| Total | | | $ | 19,554 |

| $ | 11,211 |

| $ | 30,765 |

|

| | | | | | |

| (1) Includes revenues from the Company's operations in Pennsylvania. | | |

3. Risk Risks and Uncertainties

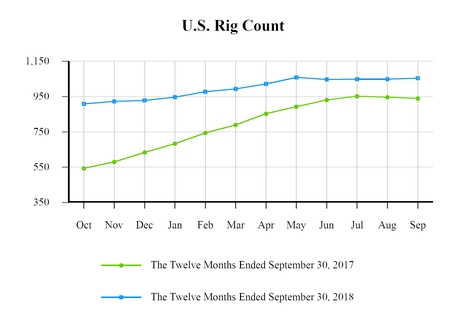

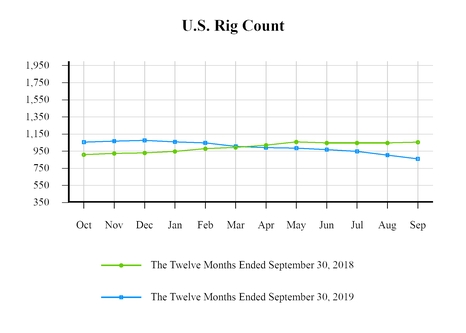

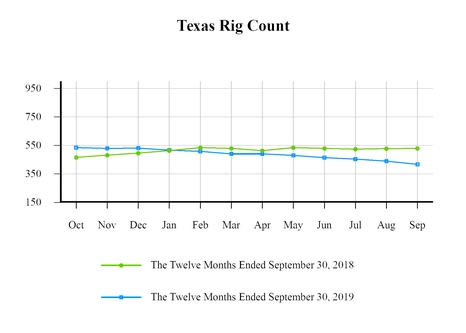

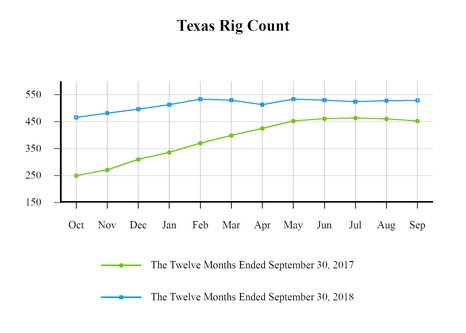

As an independent oilfield services contractor that provides a broad range of drilling-related and production-related services to oil and natural gas companies, primarily onshore in Texas, the Company's revenue, profitability, cash flows and future rate of growth are substantially dependent on its ability to (1) maintain adequate equipment utilization, (2) maintain adequate pricing for the services it provides, and (3) maintain a trained workforce. Failure to do so could adversely affect the Company's financial position, results of operations, and cash flows.

Because the Company's revenues are generated primarily from customers who are subject to the same factors as the Company, the Company's operations are also susceptible to market volatility resulting from economic, cyclical, weather, or other factors related to such industry. The Company is subject to changes in the level of operating and capital spending in the industry, decreases in oil and natural gas prices, and/or industry perception about future oil and natural gas prices that may materially decrease demand for the Company's services, or may have an adverse effect on our financial position, results of operations and cash flows.

2. Basis of Presentation

Interim Financial Information

The unaudited condensed consolidated financial statements of the Company are prepared in conformity with accounting principles generally accepted in the United States of America, or GAAP, for interim financial reporting. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to the rules and regulations of the Securities and Exchange Commission. Therefore, these condensed consolidated financial statements should be read along with the annual audited consolidated financial statements and notes thereto included in the Company's Annual Report on Form 10-K for the year ended December 31, 2018. All significant intercompany accounts and transactions have been eliminated in consolidation. In the opinion of management, all adjustments which are of normal recurring natures considered necessary for a fair representation have been made in the accompanying unaudited financial statements.

Use of Estimates

The preparation of condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated balance sheets and the reported amounts of revenues and expenses during the reporting period. Actual results could materially differ from those estimates.

Reclassification

Certain prior year amounts have been reclassified to conform to the current year presentation with no material effect on the unaudited condensed consolidated financial statements.

Fair Values of Financial Instruments

Fair value is the price that would be received to sell an asset, or the amount paid to transfer a liability in an orderly transaction between market participants (an exit price) at the measurement date.

There is a fair value hierarchy that prioritizes the inputs used to measure fair value. The hierarchy gives the highest priority to quoted prices in active markets for identical assets or liabilities (Level 1 measurement) and the lowest priority to unobservable inputs (Level 3 measurement). The Company classifies fair value balances based on the observability of those inputs. The three levels of the fair value hierarchy are as follows:

Level 1 - Quoted prices in active markets for identical assets or liabilities that the Company has the ability to access. Active markets are those in which transactions for the asset or liability occur in sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2 - Inputs are other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable. These inputs are either directly observable in the marketplace or indirectly observable through corroboration with market data for substantially the full contractual term of the asset or liability being measured.

Level 3 - Inputs reflect management’s best estimate of what market participants would use in pricing the asset or liability at the measurement date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model.

In valuing certain assets and liabilities, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. For disclosure purposes, assets and liabilities are classified in their entirety in the fair value hierarchy level based on the lowest level of input that is significant to the overall fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment and may affect the placement within the fair value hierarchy levels.

The carrying amounts of cash and cash equivalents, accounts receivable-trade, accounts receivable-other, accounts payable-trade and insurance notes approximate fair value because of the short maturity of these instruments. The fair values of finance leases approximate their carrying values, based on current market rates at which the Company could borrow funds with similar maturities (Level 2 in the fair value hierarchy). The fair value of the Term Loan is based on quoted prices provided by a third party broker (Level 2 in the fair value hierarchy). The fair values of the Term Loan Agreement and Bridge Loan as of the respective dates are set forth below (in thousands):

|

| | | | | | | | | | | | | | | |

| | September 30, 2019 | | December 31, 2018 |

| | Carrying Amount | | Fair Value | | Carrying Amount | | Fair Value |

| Term Loan Agreement | $ | 55,397 |

| | $ | 55,674 |

| | $ | 62,335 |

| | $ | 65,794 |

|

| Bridge Loan | $ | — |

| | $ | — |

| | $ | 49,568 |

| | $ | 50,000 |

|

Cash, Cash Equivalents and Cash - Restricted

The following table provides a reconciliation of cash, cash equivalents and cash - restricted reported within the consolidated balance sheets to the same such amounts shown in the consolidated statements of cash flows (in thousands).

|

| | | | | | | | |

| | | September 30, |

| | | 2019 | | 2018 |

| Cash and cash equivalents | | $ | 6,268 |

| | $ | 6,617 |

|

| Cash - restricted | | 73 |

| | 14,701 |

|

| Cash and cash equivalents and cash - restricted as shown in the consolidated statement of cash flows | | $ | 6,341 |

| | $ | 21,318 |

|

The Company's restricted cash at September 30, 2018 included $6.0 million related to a prior restriction under the Term Loan Agreement and $8.7 million as collateral for certain outstanding letters of credit and the Company's corporate credit card program under a prior credit facility with Regions.

Revenue Recognition

Revenue is measured as consideration specified in a contract with a customer and excludes any sales incentives and amounts collected on behalf of third parties. The Company recognizes revenue when it satisfies a performance obligation by providing service to a customer. Amounts are billed upon completion of service and are generally due within 30 days.

The Company has its principal revenue generating activities organized into three service lines, well servicing, coiled tubing and fluid logistics. The Company's well servicing line consists primarily of maintenance, workover, completion, plugging and abandonment, and tubing testing services. The Company's coiled tubing line consists of maintenance, workover and completion services. The Company's fluid logistics line provides supporting services to the well servicing line as well as direct sales to customers for fluid management and movement. The Company generally establishes a master services agreement with each customer and provides associated services on a work order basis in increments of days, by the hour for services performed or on occasion, bid/turnkey pricing. Services provided under the well servicing, coiled tubing and the fluid logistics segments are short in duration and generally completed within 30 days.

The majority of the Company’s contracts with customers in the well servicing, coiled tubing and fluid logistics segments are short-term in nature and are recognized as “over-time” performance obligations as the services are performed. The Company applies the “as-invoiced” practical expedient as the amount of consideration the Company has a right to invoice corresponds directly with the value of the Company’s performance to date. Because of the short-term nature of the Company’s services, which generally last a few hours to multiple days, the Company does not have any contracts with a duration longer than one year that require disclosure. The Company has no material contract assets or liabilities.

The Company does not have any revenue expected to be recognized in the future related to remaining performance obligations or contracts with variable consideration related to undelivered performance obligations. There was no revenue recognized in the current period from performance obligations satisfied in previous periods. The Company's significant judgments made in connection with the adoption of ASC 606 included the determination of when the Company satisfies its performance obligation to customers and the applicability of the as invoiced practical expedient.

Leases

Effective January 1, 2019, the Company adopted an accounting standard update issued by the Financial Accounting Standards Board (FASB) related to accounting for leases, which requires lessees to record assets and liabilities that arise for all leases on their balance sheet and expanded financial statement disclosures for both lessees and lessors. Previously, only capital leases were recorded on the balance sheet. This update requires lessees to recognize a lease liability equal to the present value of its lease payments and a right-of-use asset representing its right to use the underlying asset for the lease term for all leases longer than 12 months. For leases with a term of 12 months or less, a lessee is permitted to make an accounting policy election by class of underlying asset not to recognize lease assets and liabilities and instead recognize lease expense for such leases generally on a straight-line basis over the lease term. Leases with a term of longer than 12 months will be classified as finance or operating, with classification affecting the pattern and classification of expense recognition in the income statement.

The Company adopted this standard on a prospective basis using the optional modified retrospective transition method. As such, the comparative financial information has not been restated and continues to be reported under the lease standard in effect during those periods. The Company also elected other practical expedients provided by the new standard, including the package of practical expedients, the hindsight practical expedient and the short-term lease recognition practical expedient in which leases with a term of 12 months or less are not recognized on the balance sheet. The adoption of this standard resulted in the recognition of approximately $6.2 million of operating lease right-of-use assets and operating lease liabilities on the balance sheet as of January 1, 2019. The adoption of this standard did not materially impact the condensed consolidated statements of operations for the three and nine months ended September 30, 2019. See Note 8 for the expanded lease disclosures required by the new standard.

3. Acquisition of Cretic Energy Services, LLC

On November 16, 2018, the Company acquired 100% of the outstanding units of Cretic Energy Services, LLC (Cretic). The acquisition of Cretic was accounted for as a business combination using the acquisition method of accounting. The aggregate purchase price was $69.1 million in cash (net of $2.2 million cash acquired).

The purchase price paid in the acquisition has been allocated to record the acquired assets and assumed liabilities based on their fair value. When determining the fair values of assets acquired and liabilities assumed, management made significant estimates, judgments and assumptions. Management estimated that consideration paid exceeded the fair value of the net assets acquired. The goodwill recorded was primarily attributable to synergies related to the Company’s coiled tubing business strategy that are expected to arise from the Cretic acquisition and was attributable to the Company’s coiled tubing segment.

Proforma Results from the Cretic Acquisition (unaudited)

The following unaudited consolidated pro forma information is presented as if the Cretic acquisition had occurred on January 1, 2018 (in thousands):

|

| | | | | | | | |

| | | Pro Forma |

| | | Three Months Ended September 30, 2018 | | Nine Months Ended September 30, 2018 |

| Revenue | | $ | 68,408 |

| | $ | 175,474 |

|

| | | | | |

| Net loss | | $ | (5,267 | ) | | $ | (24,865 | ) |

The unaudited pro forma amounts above have been calculated after applying the Company’s accounting policies and adjusting the Cretic acquisition results to reflect the increase to interest expense and depreciation and amortization that would have been charged assuming the fair value adjustments to property and equipment and intangible assets had been applied from January 1, 2018 and other related pro forma adjustments. The pro forma amounts do not include any potential synergies, cost savings or other expected benefits of the Cretic acquisition, and are presented for illustrative purposes only and are not necessarily indicative of results that would have been achieved if the Cretic acquisition had occurred as of January 1, 2018 or of future operating performance.

4. Property and Equipment

Property and equipment consisted of the following:following (in thousands):

| | | | | Successor | |

| | Estimated Life in Years | | September 30, 2018 | | December 31, 2017 | | | | | | |

| | | | (in thousands) | Estimated Life in Years | | September 30, 2019 | | December 31, 2018 |

| Well servicing equipment | 9-15 years | | $ | 93,329 |

| | $ | 80,899 |

| 9-15 years | | $ | 132,630 |

| | $ | 128,647 |

|

| Autos and trucks | 5-10 years | | 46,146 |

| | 42,831 |

| 5-10 years | | 21,428 |

| | 32,132 |

|

| Autos and trucks - finance lease | | 5-10 years | | 22,487 |

| | 20,416 |

|

| Disposal wells | 5-15 years | | 3,977 |

| | 3,977 |

| 5-15 years | | 3,862 |

| | 3,977 |

|

| Building and improvements | 5-30 years | | 5,614 |

| | 5,474 |

| 5-30 years | | 5,906 |

| | 5,705 |

|

| Furniture and fixtures | 3-15 years | | 2,246 |

| | 1,950 |

| 3-15 years | | 3,097 |

| | 2,797 |

|

| Land | | 868 |

| | 868 |

| | 868 |

| | 868 |

|

| | | 152,180 |

| | 135,999 |

| | 190,278 |

| | 194,542 |

|

| Accumulated depreciation | | (39,077 | ) | | (18,808 | ) | |

Accumulated depreciation (1) | | | (59,069 | ) | | (45,934 | ) |

| | | $ | 113,103 |

| | $ | 117,191 |

| | $ | 131,209 |

| | $ | 148,608 |

|

(1) Includes accumulated depreciation of finance lease assets of $7.0 million and $4.5 million at September 30, 2019 and December 31, 2018, respectively.

Depreciation expense was $7.3$6.0 million and $6.8$7.3 million for the three months ended September 30, 2019 and 2018, (Successor)respectively, and 2017 (Successor), respectively. Depreciation expense was $21.5 million, $12.3$21.7 million and $13.4$21.5 million for the nine months ended September 30, 2019 and 2018, (Successor), the periodrespectively. Depreciation of April 13 through September 30, 2017 (Successor)assets held under finance leases was $1.1 million and January 1 through April 12, 2017 (Predecessor), respectively.

5. Intangible Assets

The Company's major class of intangible assets subject to amortization consists of customer relationships, trade names and covenants not to compete. The Company expenses costs associated with extensions or renewals of intangible assets. There were no such extensions or renewals in each of the three and nine months ended September 30, 2018 (Successor), the period of April 13 through September 30, 2017 (Successor) and the period of January 1 through April 12, 2017 (Predecessor). Amortization expense is calculated using the straight-line method over the period indicated. Amortization expense$0.7 million for the three months ended September 30, 2019 and 2018, (Successor)respectively, and 2017 (Successor) was $0.3 million. Amortization expense$3.4 million and $2.1 million for the nine months ended September 30, 2019 and 2018, (Successor),respectively, and is included in depreciation and amortization expense in the periodaccompanying condensed consolidated statements of April 13 throughoperations. Gain/(loss) that resulted from the sale of property and equipment was $2.1 million and $0.3 million for the three months ended September 30, 2017 (Successor)2019 and 2018, respectively, and $4.6 million and $0.4 million for the nine months ended September 30, 2019 and 2018, respectively, which are included as direct operating costs.

5. Goodwill and Other Intangible Assets

Goodwill

Goodwill totaled $0.0 million at September 30, 2019 and $19.7 million at December 31, 2018 related to the acquisition of

Cretic, which is attributable to the Company's coiled tubing reporting unit, and is deductible for tax purposes. During the third quarter of 2019, the company recognized a measurement period adjustment of January 1 through April 12, 2017 (Predecessor) was$0.5 million related to the acquisition of Cretic. The measurement period adjustment related to certain finance leases of $1.0 million being assigned back to the seller along with property and equipment of $0.8 million $0.5and a cash payment received from the seller of $0.3 million. The measurement period adjustment settled a dispute with the seller over the amount of debt assumed in the purchase of Cretic as of the acquisition date.

During the third quarter ended September 30, 2019, the Company adopted the guidance contained in ASU No. 2017-04, “Intangibles-Goodwill and Other ASC Topic 350: Simplifying the Test for Goodwill Impairment,” which removes the step 2 requirement to perform a hypothetical purchase price allocation to measure goodwill impairment. Goodwill impairment is the amount by which the Company’s reporting unit carrying value exceeds its fair value, not to exceed the recorded amount of goodwill. To estimate the fair value of the Company’s invested capital, the Company used both a market approach based on the guideline companies’ method (“Market Comparable Approach”), and an income approach based on a discounted cash flow analysis.

The Market Comparable Approach estimates fair value using market multiples calculated from a set of comparable public companies. In performing the valuations, significant assumptions utilized include unobservable Level 3 inputs including cash flows, long-term growth rates reflective of management’s forecasted outlook, and discount rates inclusive of risk adjustments consistent with current market conditions. Discount rates are based on the development of a weighted average cost of capital using guideline public company data, factoring in current market data and any Company specific risk factors. The value indicated by both methods was weighted to arrive at a concluded value.

The Company completed a goodwill impairment test as of September 30, 2019. The Company’s forecasted future cash flow declined from prior estimates because the Company experienced challenging sales trends and a downturn in the coiled tubing segment. These declining cash flows in our coiled tubing segment during 2019 and lower than previously forecasted cash flows, resulted in the Company recognizing a goodwill impairment charge of $19.2 million and $0.2 million, respectively.at September 30, 2019.

The following table sets forth the changes in goodwill (in thousands):

|

| | | | |

| | | Goodwill |

| |

| | Balance at December 31, 2018 | $ | 19,700 |

|

| | Measurement period adjustment | (478 | ) |

| | Impairment | (19,222 | ) |

| | Balance at September 30, 2019 | $ | — |

|

Other Intangible Assets

The following table sets forth the identified other intangible assets by major asset class:class (in thousands):

| | | | Useful Life (years) | | Gross Carrying Value | | Accumulated Amortization | | Net Book Value | Useful Life (years) | | Gross Carrying Value | | Accumulated Amortization | | Net Book Value |

| | | | (in thousands) | |

| As of September 30, 2018 (Successor) | | | | | | | |

| September 30, 2019 | | | | | | | |

| Customer relationships | 15 | | $ | 8,678 |

| | $ | (849 | ) | | $ | 7,829 |

| 6-15 | | $ | 11,378 |

| | $ | (1,566 | ) | | $ | 9,812 |

|

| Trade names | 15 | | 2,472 |

| | (242 | ) | | 2,230 |

| 10-15 | | 3,072 |

| | (664 | ) | | 2,408 |

|

| Covenants not to compete | 4 | | 1,505 |

| | (552 | ) | | 953 |

| 4 | | 1,505 |

| | (928 | ) | | 577 |

|

| | | $ | 12,655 |

| | $ | (1,643 | ) | | $ | 11,012 |

| | $ | 15,955 |

| | $ | (3,158 | ) | | $ | 12,797 |

|

| | | | | | | | |

| | Useful Life

(years) | | Gross Carrying Value | | Accumulated Amortization | | Net Book Value | |

| | | | (in thousands) | |

| As of December 31, 2017 (Successor) | | | | | | | |

| December 31, 2018 | | | | | | | |

| Customer relationships | 15 | | $ | 8,678 |

| | $ | (415 | ) | | $ | 8,263 |

| 6-15 | | $ | 11,378 |

| | $ | (832 | ) | | $ | 10,546 |

|

| Trade names | 15 | | 2,472 |

| | (118 | ) | | 2,354 |

| 10-15 | | 3,072 |

| | (496 | ) | | 2,576 |

|

| Covenants not to compete | 4 | | 1,505 |

| | (270 | ) | | 1,235 |

| 4 | | 1,505 |

| | (647 | ) | | 858 |

|

| | | $ | 12,655 |

| | $ | (803 | ) | | $ | 11,852 |

| | $ | 15,955 |

| | $ | (1,975 | ) | | $ | 13,980 |

|

Amortization expense was $0.4 million and $0.3 million for the three months ended September 30, 2019 and 2018, respectively, and $1.2 million and $0.8 million for the nine months ended September 30, 2019 and 2018, respectively.

Future amortization of these intangibles will be as follows:

|

| | | |

| 2019 | $ | 421 |

|

| 2020 | 1,637 |

|

| 2021 | 1,367 |

|

| 2022 | 1,261 |

|

| 2023 | 1,261 |

|

| Thereafter | 6,850 |

|

| | $ | 12,797 |

|

6. Long-Term Debt

Long-term debt at September 30, 2018 and December 31, 2017 consisted of the following (in thousands):

| | | | Successor | September 30, 2019 | | December 31, 2018 |

| | September 30, 2018 | | | December 31, 2017 | |

| | (in thousands) | |

| Third party equipment capital leases | $ | 6,711 |

| | $ | 5,822 |

| |

| Term Loan Agreement of $47.4 million and $60.0 million, plus $10.7 million and $6.0 million of accrued interest paid in kind and net of debt discount of $2.7 million and $3.6 million as of September 30, 2019 and December 31, 2018, respectively | | $ | 55,397 |

| | $ | 62,335 |

|

| PIK Notes, plus $0.9 million of accrued interest paid in kind, and including $4.2 million accretion of interest and conversion premium | | 56,818 |

| | — |

|

| Bridge Loan of $50.0 million, net of debt discount of $0.4 million as of December 31, 2018 | | — |

| | 49,568 |

|

| Revolving Loan Agreement | | 4,000 |

| | — |

|

| Finance leases | | 11,126 |

| | 13,319 |

|

| Insurance notes | — |

| | 5,882 |

| — |

| | 5,194 |

|

| New Loan Agreement, including $4.7 million and $1.7 million of accrued interest paid in kind and net of debt discount of $3.9 million and $4.5 million as of September 30, 2018 and December 31, 2017, respectively | 50,829 |

| | 47,150 |

| |

| Total debt | 57,540 |

| | 58,854 |

| 127,341 |

| | 130,416 |

|

| Less: Current portion | (2,054 | ) | | (7,566 | ) | (61,679 | ) | | (59,321 | ) |

| Total long-term debt | $ | 55,486 |

| | $ | 51,288 |

| $ | 65,662 |

| | $ | 71,095 |

|

NewTerm Loan Agreement

On the Effective Date,April 13, 2017, the Company entered into the NewTerm Loan Agreement. Forbes Energy ServicesFES LLC is the borrower, or the Borrower, is the borrower under the NewTerm Loan Agreement. The Borrower’s obligations have been guaranteed by FES Ltd. and by Texas Energy Services, LLC, C.C. Forbes, LLCTES, CCF and Forbes Energy International, LLC,FEI, each direct subsidiaries of the Borrower and indirect subsidiaries of FES Ltd. The NewTerm Loan Agreement, providesas amended, provided for a term loan of $50.0$60.0 million, which was fully funded on the Effective Date.excluding paid in kind interest. Subject to certain exceptions and permitted encumbrances, the obligations under this loanthe Term Loan Agreement are secured by a first priority security interest in substantially all the assets of the Company other than accounts receivable, cash collateralizingand related assets, which constitute priority collateral under the New Regions Letters of Credit Facility. Such term loanRevolving Loan Agreement (described below). The Term Loan Agreement has a stated maturity date of April 13, 2021. The proceeds of such term loan are only permitted to be used for (i) the payment on account of the Prior Senior Notes in an amount equal to $20.0 million; (ii) the payment of costs, expenses and fees incurred on or prior to the Effective Date in connection with the preparation, negotiation, execution and delivery of the New Loan Agreement and documents related thereto; and (iii) subject to satisfaction of certain release conditions set forth in the New Loan Agreement, for general operating, working capital and other general corporate purposes of the Borrower not otherwise prohibited by the terms of the New Loan Agreement. The release conditions set forth in the New Loan Agreement include, among other things, (i) no default or event of default under the New Loan Agreement having occurred or being continuing as of the date of the requested release of proceeds of the New Loan Agreement, or that would exist after giving effect to the release requested to be made on such date, and (ii) the Company’s unrestricted cash and cash equivalents being less than $7.0 million after giving pro forma effect to the requested release. At September 30, 2018, $6.0 million included in restricted cash was subject to these release restrictions.

Borrowings under this term loanthe Term Loan Agreement bear interest at a rate equal to five percent (5%) per annum payable quarterly in cash, or the Cash Interest Rate, plus (ii) an initial rate for paid in kind interest rate of seven percent (7%) commencing April 13, 2017 to be capitalized and added to the principal amount of the term loan on the first day of each quarter or, at the election of the Borrower, paid in cash. The paid in kind interest increases by two percent (2%) twelve months after the Effective DateApril 13, 2017 and every twelve months thereafter until maturity. Upon and after the occurrence of an event of default, the Cash Interest Rate will increase by two percentage points per annum. During the nine months ended September 30, 2019, $4.7 million of interest was paid in kind. At September 30, 2018,2019, the applicablepaid in kind interest rate was 14% per annum.

11%.

The NewTerm Loan Agreement includes customary negative covenants for an asset-based term loan, including covenants limiting the ability of the Company to, among other things, (i) effect mergers and consolidations, (ii) sell assets, (iii) create or suffer to exist any lien, (iv) make certain investments, (v) incur debt and (vi) transact with affiliates. In addition, the NewTerm Loan Agreement includes customary affirmative covenants for an asset-based term loan, including covenants regarding the delivery of financial statements, reports and notices to the Agent. The NewTerm Loan Agreement also contains customary representations and warranties and event of default provisions for a secured term loan.

Amendment to Term Loan Agreement and Joinder

In connection with the Cretic acquisition, on November 16, 2018, the Company, as a guarantor, FES LLC, as borrower, and certain of their subsidiaries, as guarantors, entered into Amendment No. 1 to Loan and Security Agreement and Pledge and Security Agreement (the “Term Loan Amendment”) with the lenders party thereto and Wilmington Trust, National Association, as agent (the “Term Loan Agent”), pursuant to which the Term Loan Agreement was amended to, among other things, permit (i) debt under the Revolving Loan Agreement (described below) and the liens securing the obligations thereunder, (ii) the incurrence of add-on term loans under the Term Loan Agreement in an aggregate principal amount of $10.0 million and (iii) the incurrence of one-year “last-out” bridge loans under the Term Loan Agreement in an aggregate principal amount of $50.0 million (the “Bridge Loan”).

In addition, on November 16, 2018, Cretic entered into joinder documentation pursuant to which it became a guarantor under the Term Loan Agreement and a pledgor under the Pledge and Security Agreement referred to in the Term Loan Agreement.

Revolving Loan Agreement

In connection with the Cretic Acquisition, on November 16, 2018, the Company and certain of its subsidiaries, as borrowers, entered into a Credit Agreement (the “Revolving Loan Agreement”) with the lenders party thereto and Regions Bank, as administrative agent and collateral agent (the “Revolver Agent”). The Revolving Loan Agreement provides for $35 million of revolving loan commitments, subject to a borrowing base comprised of 85% of eligible accounts receivable, 90% of eligible investment grade accounts receivable and 100% of eligible cash, less reserves. The loans under the Revolving Loan Agreement are due in January 2021, accrue interest at a floating rate of LIBOR plus 2.50% - 3.25%, or a base rate plus 1.50% - 2.25%, with the margin based on the fixed charge coverage ratio from time to time.

The Revolving Loan Agreement is secured on a first lien basis by substantially all assets of the Company and its subsidiaries, subject to an intercreditor agreement between the Revolver Agent and the Term Loan Agent which provides that the priority collateral for the Revolving Loan Agreement consists of accounts receivable, cash and related assets, and that the other assets of the Company and its subsidiaries constitute priority collateral for the Term Loan Agreement. At September 30, 2018,2019 we arehad $4.0 million borrowings outstanding, $6.1 million in compliance with our New Loan Agreement.

New Regions Letters of Credit Facility

On the Effective Date the Company entered into the New Regions Letters of Credit Facility pursuant to which Regions may issue, upon request by the Company, letters of credit outstanding and continue to provide charge cards for use byavailability of $6.9 million.

5% Subordinated Convertible PIK Notes

On March 4, 2019, the Company. Amounts available underCompany issued $51.8 million aggregate original principal amount of 5.00% Subordinated Convertible PIK Notes due June 30, 2020 (the “PIK Notes”). On March 4, 2019, the New Regions Letters of Credit Facility are subject to customary feesCompany, as Issuer, and are secured by a first-priority lien on, and security interest in, a cash collateral account with Regions containing cash equal to at least (i) 105%Wilmington Trust, National Association, as Trustee, entered into an Indenture governing the terms of the sumPIK Notes.

The PIK Notes bear interest at a rate of (a) all amounts owing for any drawings under letters5.00% per annum. Interest on the PIK Notes will be capitalized to principal semi-annually in arrears on July 1 and January 1 of credit, including any reimbursement obligations, (b)each year, commencing on July 1, 2019.

The PIK Notes are the aggregate undrawn amount of all outstanding letters of credit, (c) all sums owing to Regions or any affiliate pursuant to any letter of credit document and (d) allunsecured general subordinated obligations of the Company arising thereunder, includingand are subordinated in right of payment to any indemnitiesexisting and obligations for reimbursementfuture secured or unsecured senior debt of expenses and (ii) 120% of the aggregate line of credit for charge cards issued by Regions to the Company. The feespayment of the principal of, premium, if any, and interest on the PIK Notes will be subordinated to the prior payment in full of all of the Company’s existing and future senior indebtedness. In the event of a liquidation, dissolution, reorganization or any similar proceeding, obligations on the PIK Notes will be paid only after senior indebtedness has been paid in full. Pursuant to the Indenture, the Company is not permitted to (1) make cash payments to pay principal of, premium, if any, and interest on or any other amounts owing in respect of the PIK Notes, or (2) purchase, redeem or otherwise retire the PIK Notes for each lettercash, if any senior indebtedness is not paid when due or any other default on senior indebtedness occurs and the maturity of credit forsuch indebtedness is accelerated in accordance with its terms unless, in any case, the period fromdefault has been cured or waived, and excludingthe acceleration has been rescinded or the senior indebtedness has been repaid in full.

The Indenture also provides that upon a default by the Company in the payment when due of principal of, or premium, if any, or interest on, indebtedness in the aggregate principal amount then outstanding of $5.0 million or more, or acceleration of the Company’s indebtedness so that it becomes due and payable before the date on which it would otherwise have become due and payable, and if such default is not cured or waived within 30 days after notice to the Company by the Trustee or by holders of issuance of such letter of credit to and including the date of expiration or termination, are equal to (x) the average daily faceat least 25% in aggregate principal amount of eachthe PIK Notes then outstanding, letterthe principal of, credit multiplied by (y) a per annum rate determined by Regions(and premium, if any) and accrued and unpaid interest on, the PIK Notes may be declared immediately due and payable.

The PIK Notes are redeemable in whole or from time to time in its discretion based upon such factors as Regions shall determine, including, without limitation,part at the credit quality and financial performanceCompany’s option at a redemption price equal to the sum of (i) 100.0% of the Company.principal amount of the PIK Notes to be redeemed and (ii) accrued and unpaid interest thereon to, but excluding, the redemption date, which amounts may be payable in cash or in shares of the Company’s common stock, (subject to limitations, if any, in the documentation governing the Company’s senior indebtedness). If redeemed for the Company’s common stock the holder will receive a number of shares of the Company’s common stock calculated based on the Fair Market Value of a share of the Company’s common stock at such time, in each case less a 15% discount per share. The 15% discount represents an implied conversion premium at issuance which will be settled in common stock at the date of conversion. As such, the face value of Septemberthe PIK Notes will be accreted to the settlement amount at June 30, 2018, such rate was 3.00%. In the event the Company is unable to repay amounts due under the New Regions Letters of Credit Facility, Regions could proceed against such cash collateral account. Regions has no commitment under the New Regions Letters of Credit Facility to issue letters of credit. At September 30, 2018, the facility had $8.6 million in letters of credit outstanding.

Capital Leases

The Company financed the purchase of certain vehicles and equipment through commercial loans and capital leases with aggregate principal amounts outstanding as of September 30, 2018 (Successor) and December 31, 2017 (Successor) of approximately $6.7 million and $5.8 million, respectively. These loans are repayable in a range of 42 to 48 monthly installments with the maturity dates to September 2022. Interest accrues at rates ranging from 3.4% to 4.9% and is payable monthly. The loans are collateralized by equipment purchased with the proceeds of such loans. The Company paid total principal payments of approximately $0.5 million during2020. For the three and nine months ended September 30, 2018 (Successor)

2019, the Company recorded $1.8 million and $0.3$4.2 million, duringrespectively in interest expense related to the three months ended September 30, 2017. accretion of the conversion premium.

The Indenture contains provisions permitting the Company and the trustee in certain circumstances, without the consent of the holders of the PIK Notes, and in certain other circumstances, with the consent of the holders of not less than a majority in aggregate principal amount of the PIK Notes at the time outstanding to execute supplemental indentures modifying the terms of the Indenture and the PIK Notes as described It also provided in the Indenture that, subject to certain exceptions, the holders of a majority in aggregate principal amount of the PIK Notes at the time outstanding may on behalf of the holders of all the PIK Notes waive any past default or event of default under the Indenture and its consequences.