UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2020March 31, 2021

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

Commission file number 001-39028

CROSSFIRST BANKSHARES, INC.

(Exact Name of Registrant as Specified in its Charter)

| | | | | | | | | | | | | | |

| Kansas | | | | 26-3212879 |

| (State or other jurisdiction of incorporation or organization) | | | | (I.R.S. Employer Identification No.) |

| | | | |

| 11440 Tomahawk Creek Parkway | | | | |

| Leawood, | | KS | | 66211 |

| (Address of principal executive offices) | | | | (Zip Code) |

| | | | |

| | | |

|

| | | | |

| | | | |

| | | | |

| | | | |

(913) 312-6822

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | CFB | | The Nasdaq Stock Market LLC |

| | | | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | ☐ | | Accelerated filer | | ☐☒ |

| Non-accelerated filer | | ☒☐ | | Smaller reporting company | | ☐ |

| Emerging growth company | | ☒ | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 10, 2020,May 5, 2021, the registrant had 52,188,70851,580,761 shares of common stock, par value $0.01, outstanding.

CrossFirst Bankshares, Inc.

Form 10-Q

for the Quarter Ended June 30, 2020March 31, 2021

Index

| | | | | |

| Part I. Financial Information | |

| Item 1. Financial Statements | |

| |

| |

| |

| |

| |

| |

| |

| Notes to Consolidated Financial Statements (unaudited) | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | | | | |

| |

| |

| |

| |

| |

| |

| |

| |

| Part II. Other Information | |

| |

| |

| |

| |

| |

| |

| |

| |

| Signatures | |

Forward-Looking Information

This report may contain forward-looking statements that reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “might,” “should,” “could,” “predict,” “potential,” “believe,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “strive,” “projection,” “goal,” “target,” “outlook,” “aim,” “would,” “annualized” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature.

These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions, estimates and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements. Such possible events or factors include: risks associated with the current outbreak of the novel coronavirus, or the COVID-19 pandemic, changes in economic conditions in the Company’s market area, changes in policies by regulatory agencies, governmental legislation and regulation, fluctuations in interest rates, changes in liquidity requirements, demand for loans in the Company’s market area, changes in accounting and tax principles, estimates made on income taxes, competition with other entities that offer financial services, cybersecurity threats, and such other factors as discussed in our Annual Report on Form 10-K for the fiscal year ended December 31, 2019,2020, filed with the Securities and Exchange Commission (“SEC”) on March 10, 2020, in our Quarterly ReportFebruary 26, 2021, any subsequent quarterly report on Form 10-Q for the quarter ended March 31, 2020 filed with the SEC on May 14, 2020, andas well as in our other filings with the SEC.

We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED BALANCE SHEETS

| | | June 30, 2020 | | December 31, 2019 | | March 31, 2021 | | December 31, 2020 |

| | | (Unaudited) | | | | (Unaudited) | | |

| | (Dollars in thousands) | | | (Dollars in thousands) |

| Assets | Assets | | Assets | |

| | Cash and cash equivalents | Cash and cash equivalents | $ | 194,371 | | | $ | 187,320 | | Cash and cash equivalents | $ | 630,787 | | | $ | 408,810 | |

| Available-for-sale securities - taxable | Available-for-sale securities - taxable | 256,121 | | | 298,208 | | Available-for-sale securities - taxable | 192,031 | | | 177,238 | |

| Available-for-sale securities - tax-exempt | Available-for-sale securities - tax-exempt | 443,962 | | | 443,426 | | Available-for-sale securities - tax-exempt | 493,423 | | | 477,350 | |

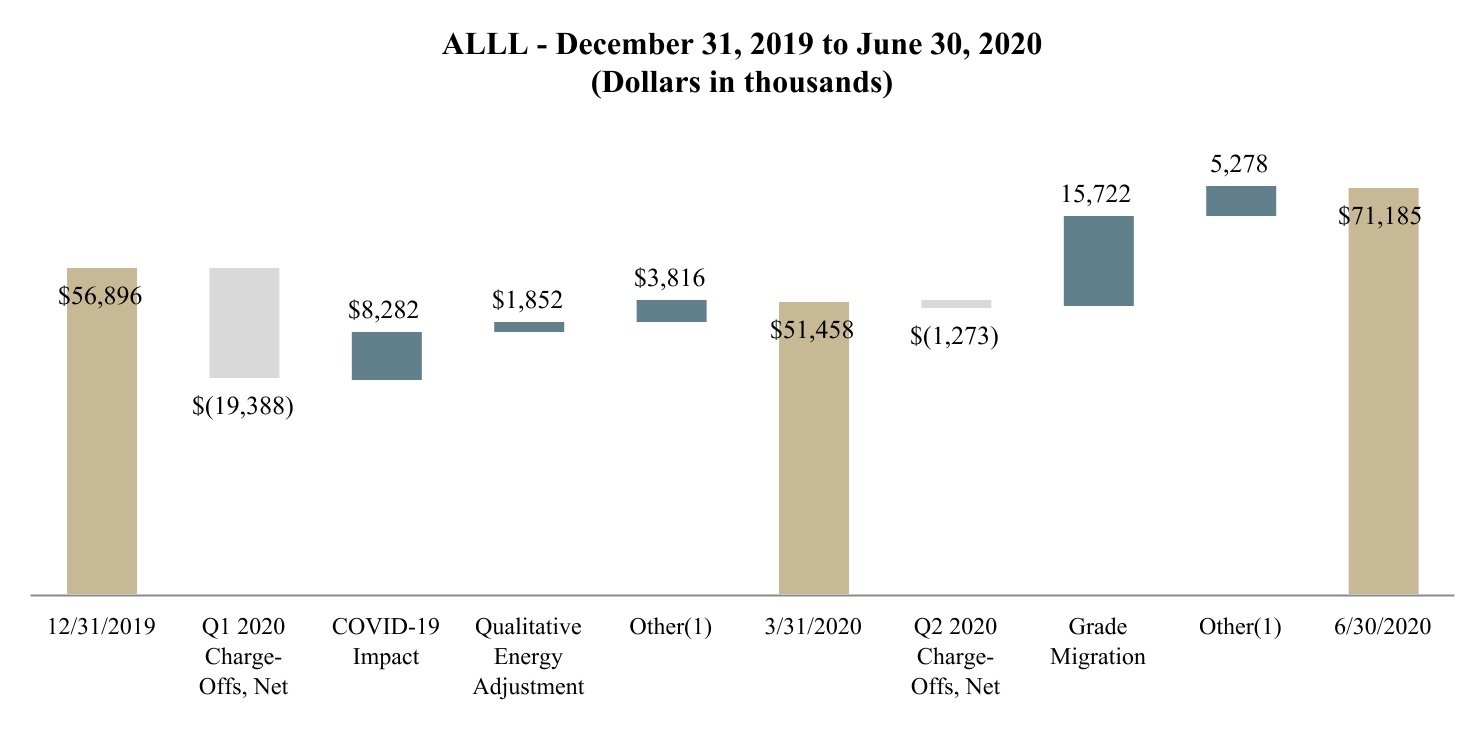

| | Loans, net of allowance for loan losses of $71,185 and $56,896 at June 30, 2020 and December 31, 2019, respectively | 4,342,039 | | | 3,795,348 | | |

| Loans, net of allowance for loan losses of $74,551 and $75,295 at March 31, 2021 and December 31, 2020, respectively | | Loans, net of allowance for loan losses of $74,551 and $75,295 at March 31, 2021 and December 31, 2020, respectively | 4,434,049 | | | 4,366,602 | |

| Premises and equipment, net | Premises and equipment, net | 68,889 | | | 70,210 | | Premises and equipment, net | 69,270 | | | 70,509 | |

| Restricted equity securities | Restricted equity securities | 20,675 | | | 17,278 | | Restricted equity securities | 14,080 | | | 15,543 | |

| Interest receivable | Interest receivable | 19,399 | | | 15,716 | | Interest receivable | 17,987 | | | 17,236 | |

| Foreclosed assets held for sale | Foreclosed assets held for sale | 2,502 | | | 3,619 | | Foreclosed assets held for sale | 2,347 | | | 2,347 | |

| Deferred tax asset | 14,841 | | | 13,782 | | |

| Goodwill and other intangible assets, net | 247 | | | 7,694 | | |

| | Bank-owned life insurance | Bank-owned life insurance | 66,598 | | | 65,689 | | Bank-owned life insurance | 67,914 | | | 67,498 | |

| Other | Other | 32,610 | | | 12,943 | | Other | 76,186 | | | 56,170 | |

| Total assets | Total assets | $ | 5,462,254 | | | $ | 4,931,233 | | Total assets | $ | 5,998,074 | | | $ | 5,659,303 | |

| Liabilities and stockholders’ equity | Liabilities and stockholders’ equity | | | | Liabilities and stockholders’ equity | | | |

| Deposits | Deposits | | Deposits | |

| Non-interest bearing | $ | 750,333 | | | $ | 521,826 | | |

| Noninterest-bearing | | Noninterest-bearing | $ | 794,559 | | | $ | 718,459 | |

| Savings, NOW and money market | Savings, NOW and money market | 2,393,269 | | | 2,162,187 | | Savings, NOW and money market | 3,325,220 | | | 2,932,799 | |

| Time | Time | 1,160,541 | | | 1,239,746 | | Time | 931,791 | | | 1,043,482 | |

| Total deposits | Total deposits | 4,304,143 | | | 3,923,759 | | Total deposits | 5,051,570 | | | 4,694,740 | |

| Federal funds purchased and repurchase agreements | Federal funds purchased and repurchase agreements | 49,881 | | | 14,921 | | Federal funds purchased and repurchase agreements | 3,294 | | | 2,306 | |

| Federal Home Loan Bank advances | Federal Home Loan Bank advances | 450,617 | | | 358,743 | | Federal Home Loan Bank advances | 283,100 | | | 293,100 | |

| | Other borrowings | Other borrowings | 942 | | | 921 | | Other borrowings | 974 | | | 963 | |

| Interest payable and other liabilities | Interest payable and other liabilities | 48,579 | | | 31,245 | | Interest payable and other liabilities | 30,302 | | | 43,766 | |

| Total liabilities | Total liabilities | 4,854,162 | | | 4,329,589 | | Total liabilities | 5,369,240 | | | 5,034,875 | |

| Stockholders’ equity | Stockholders’ equity | | | | Stockholders’ equity | | | |

| Redeemable preferred stock, $0.01 par value, $25.00 liquidation value: | | |

| | authorized - 5,000,000 shares, issued - 0 shares at June 30, 2020 and December 31, 2019, respectively | — | | | — | | |

| | Common stock, $0.01 par value: | Common stock, $0.01 par value: | | Common stock, $0.01 par value: | |

| | authorized - 200,000,000 shares, issued - 52,167,573 and 51,969,203 shares at June 30, 2020 and December 31, 2019, respectively | 521 | | | 520 | | |

| authorized - 200,000,000 shares, issued - 52,376,779 and 52,289,129 shares at March 31, 2021 and December 31, 2020, respectively | | authorized - 200,000,000 shares, issued - 52,376,779 and 52,289,129 shares at March 31, 2021 and December 31, 2020, respectively | 523 | | | 523 | |

| Treasury stock, at cost: | | Treasury stock, at cost: | |

| 698,110 and 609,613 shares held at March 31, 2021 and December 31, 2020, respectively | | 698,110 and 609,613 shares held at March 31, 2021 and December 31, 2020, respectively | (7,113) | | | (6,061) | |

| Additional paid-in capital | Additional paid-in capital | 521,133 | | | 519,870 | | Additional paid-in capital | 523,156 | | | 522,911 | |

| Retained earnings | Retained earnings | 61,344 | | | 64,803 | | Retained earnings | 89,722 | | | 77,652 | |

| | Accumulated other comprehensive income | Accumulated other comprehensive income | 25,094 | | | 16,451 | | Accumulated other comprehensive income | 22,546 | | | 29,403 | |

| Total stockholders’ equity | Total stockholders’ equity | 608,092 | | | 601,644 | | Total stockholders’ equity | 628,834 | | | 624,428 | |

| Total liabilities and stockholders’ equity | Total liabilities and stockholders’ equity | $ | 5,462,254 | | | $ | 4,931,233 | | Total liabilities and stockholders’ equity | $ | 5,998,074 | | | $ | 5,659,303 | |

See Notes to Consolidated Financial Statements (unaudited)

4

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED STATEMENTS OF INCOME - UNAUDITED

| | | | | | | | | | | | | | | |

| Three Months Ended | | |

| March 31, | | |

| 2021 | | 2020 | | | | |

| (Dollars in thousands except per share data) |

| Interest Income | | | | | | | |

| Loans, including fees | $ | 43,758 | | | $ | 48,339 | | | | | |

| | | | | | | |

| Available-for-sale securities - taxable | 751 | | | 1,774 | | | | | |

| Available-for-sale securities - tax-exempt | 3,351 | | | 3,312 | | | | | |

| Deposits with financial institutions | 128 | | | 491 | | | | | |

| Dividends on bank stocks | 165 | | | 292 | | | | | |

| | | | | | | |

| Total interest income | 48,153 | | | 54,208 | | | | | |

| Interest Expense | | | | | | | |

| Deposits | 5,728 | | | 14,272 | | | | | |

| Fed funds purchased and repurchase agreements | 1 | | | 62 | | | | | |

| Federal Home Loan Bank Advances | 1,283 | | | 1,611 | | | | | |

| Other borrowings | 24 | | | 35 | | | | | |

| Total interest expense | 7,036 | | | 15,980 | | | | | |

| Net Interest Income | 41,117 | | | 38,228 | | | | | |

| Provision for Loan Losses | 7,500 | | | 13,950 | | | | | |

| Net Interest Income after Provision for Loan Losses | 33,617 | | | 24,278 | | | | | |

| Non-Interest Income | | | | | | | |

| Service charges and fees on customer accounts | 957 | | | 508 | | | | | |

| Realized gains on available-for-sale securities | 10 | | | 393 | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| Income from bank-owned life insurance | 416 | | | 456 | | | | | |

| Swap fees and credit valuation adjustments, net | 155 | | | (9) | | | | | |

| ATM and credit card interchange income | 2,328 | | | 485 | | | | | |

| Other non-interest income | 278 | | | 254 | | | | | |

| Total non-interest income | 4,144 | | | 2,087 | | | | | |

| Non-Interest Expense | | | | | | | |

| Salaries and employee benefits | 13,553 | | | 14,390 | | | | | |

| Occupancy | 2,494 | | | 2,085 | | | | | |

| Professional fees | 782 | | | 671 | | | | | |

| Deposit insurance premiums | 1,151 | | | 1,016 | | | | | |

| Data processing | 716 | | | 692 | | | | | |

| Advertising | 303 | | | 500 | | | | | |

| Software and communication | 1,065 | | | 876 | | | | | |

| | | | | | | |

| Foreclosed assets, net | 50 | | | 10 | | | | | |

| | | | | | | |

| Other non-interest expense | 2,704 | | | 1,975 | | | | | |

| Total non-interest expense | 22,818 | | | 22,215 | | | | | |

| Net Income Before Taxes | 14,943 | | | 4,150 | | | | | |

| Income tax expense | 2,908 | | | 293 | | | | | |

| Net Income | $ | 12,035 | | | $ | 3,857 | | | | | |

| Basic Earnings Per Share | $ | 0.23 | | | $ | 0.07 | | | | | |

| Diluted Earnings Per Share | $ | 0.23 | | | $ | 0.07 | | | | | |

See Notes to Consolidated Financial Statements (unaudited)

5

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED STATEMENTS OF OPERATIONSCOMPREHENSIVE INCOME - UNAUDITED

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | | | Six Months Ended | | |

| June 30, | | | | June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (Dollars in thousands except per share data) | | | | | | |

| Interest Income | | | | | | | |

| Loans, including fees | $ | 46,323 | | | $ | 47,989 | | | $ | 94,662 | | | $ | 92,992 | |

| | | | | | | |

| Available-for-sale securities - taxable | 1,358 | | | 2,335 | | | 3,132 | | | 4,655 | |

| Available-for-sale securities - tax-exempt | 3,260 | | | 2,916 | | | 6,572 | | | 5,851 | |

| Deposits with financial institutions | 45 | | | 676 | | | 536 | | | 1,482 | |

| Dividends on bank stocks | 268 | | | 276 | | | 560 | | | 529 | |

| | | | | | | |

| Total interest income | 51,254 | | | 54,192 | | | 105,462 | | | 105,509 | |

| Interest Expense | | | | | | | |

| Deposits | 8,405 | | | 17,497 | | | 22,677 | | | 33,418 | |

| Fed funds purchased and repurchase agreements | 46 | | | 133 | | | 108 | | | 427 | |

| Federal Home Loan Bank Advances | 1,620 | | | 1,651 | | | 3,231 | | | 3,110 | |

| Other borrowings | 26 | | | 37 | | | 61 | | | 75 | |

| Total interest expense | 10,097 | | | 19,318 | | | 26,077 | | | 37,030 | |

| Net Interest Income | 41,157 | | | 34,874 | | | 79,385 | | | 68,479 | |

| Provision for Loan Losses | 21,000 | | | 2,850 | | | 34,950 | | | 5,700 | |

| Net Interest Income after Provision for Loan Losses | 20,157 | | | 32,024 | | | 44,435 | | | 62,779 | |

| Non-Interest Income | | | | | | | |

| Service charges and fees on customer accounts | 647 | | | 211 | | | 1,155 | | | 369 | |

| Gain on sale of available-for-sale debt securities | 320 | | | 406 | | | 713 | | | 433 | |

| | | | | | | |

| Impairment of premises and equipment held for sale | — | | | (424) | | | — | | | (424) | |

| Gain on sale of loans | — | | | 79 | | | — | | | 158 | |

| Income from bank-owned life insurance | 453 | | | 473 | | | 909 | | | 940 | |

| Swap fee income (loss), net | (32) | | | 159 | | | (41) | | | 536 | |

| ATM and credit card interchange income | 896 | | | 459 | | | 1,381 | | | 836 | |

| Other non-interest income | 350 | | | 309 | | | 612 | | | 469 | |

| Total non-interest income | 2,634 | | | 1,672 | | | 4,729 | | | 3,317 | |

| Non-Interest Expense | | | | | | | |

| Salaries and employee benefits | 14,004 | | | 14,450 | | | 28,394 | | | 29,040 | |

| Occupancy | 2,045 | | | 2,062 | | | 4,130 | | | 4,221 | |

| Professional fees | 1,295 | | | 714 | | | 1,966 | | | 1,496 | |

| Deposit insurance premiums | 1,039 | | | 881 | | | 2,055 | | | 1,718 | |

| Data processing | 721 | | | 625 | | | 1,413 | | | 1,219 | |

| Advertising | 223 | | | 477 | | | 723 | | | 1,190 | |

| Software and communication | 937 | | | 828 | | | 1,813 | | | 1,507 | |

| | | | | | | |

| Foreclosed assets, net | 1,135 | | | 19 | | | 1,154 | | | 25 | |

| Goodwill impairment | 7,397 | | | — | | | 7,397 | | | — | |

| Other non-interest expense | 2,214 | | | 1,904 | | | 4,188 | | | 4,175 | |

| Total non-interest expense | 31,010 | | | 21,960 | | | 53,233 | | | 44,591 | |

| Net Income (Loss) Before Taxes | (8,219) | | | 11,736 | | | (4,069) | | | 21,505 | |

| Income tax expense (benefit) | (863) | | | 2,297 | | | (570) | | | 2,716 | |

| Net Income (Loss) | $ | (7,356) | | | $ | 9,439 | | | $ | (3,499) | | | $ | 18,789 | |

| Basic Earnings (Loss) Per Share | $ | (0.14) | | | $ | 0.21 | | | $ | (0.07) | | | $ | 0.41 | |

| Diluted Earnings (Loss) Per Share | $ | (0.14) | | | $ | 0.20 | | | $ | (0.07) | | | $ | 0.40 | |

| | | | | | | | | | | | | | | |

| Three Months Ended | | |

| March 31, | | |

| 2021 | | 2020 | | | | |

| (Dollars in thousands) |

| Net Income | $ | 12,035 | | | $ | 3,857 | | | | | |

| Other Comprehensive Income (Loss) | | | | | | | |

| Unrealized gain (loss) on available-for-sale securities | (9,070) | | | 8,532 | | | | | |

| Less: income tax expense (benefit) | (2,221) | | | 2,084 | | | | | |

| Unrealized gain (loss) on available-for-sale securities, net of income tax | (6,849) | | | 6,448 | | | | | |

| Reclassification adjustment for realized gains included in income | 10 | | | 393 | | | | | |

| Less: income tax | 2 | | | 96 | | | | | |

| Less: reclassification adjustment for realized gains included in income, net of income tax | 8 | | | 297 | | | | | |

| Other comprehensive income (loss) | (6,857) | | | 6,151 | | | | | |

| Comprehensive Income | $ | 5,178 | | | $ | 10,008 | | | | | |

See Notes to Consolidated Financial Statements (unaudited)

6

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED STATEMENTS OF OTHER COMPREHENSIVE INCOME (LOSS)STOCKHOLDERS’ EQUITY - UNAUDITED

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | | | Six Months Ended | | |

| June 30, | | | | June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (Dollars in thousands) | | | | | | |

| Net Income (Loss) | $ | (7,356) | | | $ | 9,439 | | | $ | (3,499) | | | $ | 18,789 | |

| Other Comprehensive Income | | | | | | | |

| Unrealized gain on available-for-sale debt securities | 3,618 | | | 9,977 | | | 12,150 | | | 22,327 | |

| Less: income tax | 884 | | | 2,449 | | | 2,968 | | | 5,480 | |

| Unrealized gain on available-for-sale debt securities, net of income tax | 2,734 | | | 7,528 | | | 9,182 | | | 16,847 | |

| Reclassification adjustment for realized gains included in income | 320 | | | 406 | | | 713 | | | 433 | |

| Less: income tax | 78 | | | 100 | | | 174 | | | 107 | |

| Less: reclassification adjustment for realized gains included in income, net of income tax | 242 | | | 306 | | | 539 | | | 326 | |

| Other comprehensive income | 2,492 | | | 7,222 | | | 8,643 | | | 16,521 | |

| Comprehensive Income (Loss) | $ | (4,864) | | | $ | 16,661 | | | $ | 5,144 | | | $ | 35,310 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | Additional Paid-in Capital | | Retained Earnings | | | | Accumulated Other Comprehensive Income | | Treasury Stock | | Total |

| | | | | Shares | | Amount | | | | | | | |

| | | | | (Dollars in thousands) |

| Balance at December 31, 2019 | | | | | 51,969,203 | | | $ | 520 | | | $ | 519,870 | | | $ | 64,803 | | | | | $ | 16,451 | | | $ | 0 | | | $ | 601,644 | |

| Net income | | | | | — | | | — | | | — | | | 3,857 | | | | | — | | | — | | | 3,857 | |

| Change in unrealized appreciation on available-for-sale securities | | | | | — | | | — | | | — | | | — | | | | | 6,151 | | | — | | | 6,151 | |

| | | | | | | | | | | | | | | | | | | |

| Issuance of shares from equity-based awards | | | | | 128,859 | | | 1 | | | (671) | | | — | | | | | — | | | — | | | (670) | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Employee receivables from sale of stock | | | | | — | | | — | | | 1 | | | 29 | | | | | — | | | — | | | 30 | |

| Stock-based compensation | | | | | — | | | — | | | 934 | | | — | | | | | — | | | — | | | 934 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Balance at March 31, 2020 | | | | | 52,098,062 | | | $ | 521 | | | $ | 520,134 | | | $ | 68,689 | | | | | $ | 22,602 | | | $ | 0 | | | $ | 611,946 | |

| | | | | | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | Additional Paid-in Capital | | Retained Earnings | | | | Accumulated Other Comprehensive Income | | Treasury Stock | | Total |

| | | | | Shares | | Amount | | | | | | | |

| | | | | (Dollars in thousands) |

| Balance at December 31, 2020 | | | | | 51,679,516 | | | $ | 523 | | | $ | 522,911 | | | $ | 77,652 | | | | | $ | 29,403 | | | $ | (6,061) | | | $ | 624,428 | |

| Net income | | | | | — | | | — | | | — | | | 12,035 | | | | | — | | | — | | | 12,035 | |

| | | | | | | | | | | | | | | | | | | |

| Change in unrealized depreciation on available-for-sale securities | | | | | — | | | — | | | — | | | — | | | | | (6,857) | | | — | | | (6,857) | |

| | | | | | | | | | | | | | | | | | | |

| Issuance of shares from equity-based awards | | | | | 87,650 | | | — | | | (404) | | | — | | | | | — | | | — | | | (404) | |

| Open market common share repurchases | | | | | (88,497) | | | — | | | — | | | — | | | | | — | | | (1,052) | | | (1,052) | |

| | | | | | | | | | | | | | | | | | | |

| Employee receivables from sale of stock | | | | | — | | | — | | | — | | | 35 | | | | | — | | | — | | | 35 | |

| Stock-based compensation | | | | | — | | | — | | | 649 | | | — | | | | | — | | | — | | | 649 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| Balance at March 31, 2021 | | | | | 51,678,669 | | | $ | 523 | | | $ | 523,156 | | | $ | 89,722 | | | | | $ | 22,546 | | | $ | (7,113) | | | $ | 628,834 | |

| | | | | | | | | | | | | | | | | | | |

See Notes to Consolidated Financial Statements (unaudited)

7

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITYCASH FLOWS - UNAUDITED

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Accumulated | | |

| | | | | | | | | Additional | | | | | | Other | | |

| Preferred Stock | | | | Common Stock | | | | Paid in | | Retained | | | | Comprehensive | | |

| Shares | | Amount | | Shares | | Amount | | Capital | | Earnings | | | | Income | | Total |

| (Dollars in thousands) | | | | | | | | | | | | | | | | |

| Balance at March 31, 2019 | — | | | $ | — | | | 45,202,370 | | | $ | 452 | | | $ | 428,412 | | | $ | 45,293 | | | | | $ | 6,357 | | | $ | 480,514 | |

| Net income | — | | | — | | | — | | | — | | | — | | | 9,439 | | | | | — | | | 9,439 | |

| Change in unrealized appreciation on available-for-sale securities | — | | | — | | | — | | | — | | | — | | | — | | | | | 7,222 | | | 7,222 | |

| Issuance of shares | — | | | — | | | 149,765 | | | 1 | | | 889 | | | — | | | | | — | | | 890 | |

| Issuance of shares from equity-based awards | — | | | — | | | 15,506 | | | — | | | (102) | | | — | | | | | — | | | (102) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Employee receivables from sale of stock | — | | | — | | | — | | | — | | | 2 | | | 84 | | | | | — | | | 86 | |

| Stock-based compensation | — | | | — | | | — | | | — | | | 1,147 | | | — | | | | | — | | | 1,147 | |

| Employee stock purchase plan additions | — | | | — | | | — | | | — | | | (1) | | | — | | | | | — | | | (1) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Balance at June 30, 2019 | — | | | $ | — | | | 45,367,641 | | | $ | 453 | | | $ | 430,347 | | | $ | 54,816 | | | | | $ | 13,579 | | | $ | 499,195 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Accumulated | | |

| | | | | | | | | Additional | | | | | | Other | | |

| Preferred Stock | | | | Common Stock | | | | Paid in | | Retained | | | | Comprehensive | | |

| Shares | | Amount | | Shares | | Amount | | Capital | | Earnings | | | | Income | | Total |

| (Dollars in thousands) | | | | | | | | | | | | | | | | |

| Balance at March 31, 2020 | — | | | $ | — | | | 52,098,062 | | | $ | 521 | | | $ | 520,134 | | | $ | 68,689 | | | | | $ | 22,602 | | | $ | 611,946 | |

| Net loss | — | | | — | | | — | | | — | | | — | | | (7,356) | | | | | — | | | (7,356) | |

| | | | | | | | | | | | | | | | | |

| Change in unrealized appreciation on available-for-sale securities | — | | | — | | | — | | | — | | | — | | | — | | | | | 2,492 | | | 2,492 | |

| | | | | | | | | | | | | | | | | |

| Issuance of shares from equity-based awards | — | | | — | | | 69,511 | | | — | | | (83) | | | — | | | | | — | | | (83) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Employee receivables from sale of stock | — | | | — | | | — | | | — | | | — | | | 11 | | | | | — | | | 11 | |

| Stock-based compensation | — | | | — | | | — | | | — | | | 1,082 | | | — | | | | | — | | | 1,082 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Balance at June 30, 2020 | — | | | $ | — | | | 52,167,573 | | | $ | 521 | | | $ | 521,133 | | | $ | 61,344 | | | | | $ | 25,094 | | | $ | 608,092 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

| Three Months Ended |

| March 31, |

| 2021 | | 2020 |

| (Dollars in thousands) |

| Operating Activities | | | |

| Net income | $ | 12,035 | | | $ | 3,857 | |

| Items not requiring (providing) cash | | | |

| Depreciation and amortization | 1,375 | | | 1,295 | |

| Provision for loan losses | 7,500 | | | 13,950 | |

| | | |

| Accretion of discounts and amortization of premiums on securities | 1,310 | | | 1,473 | |

| Equity based compensation | 649 | | | 934 | |

| | | |

| | | |

| | | |

| Deferred income taxes | 1,824 | | | 2,881 | |

| | | |

| | | |

| Net realized gains on available-for-sale securities | (10) | | | (393) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Changes in | | | |

| | | |

| | | |

| Interest receivable | (751) | | | (1,242) | |

| Other assets | (28,730) | | | (717) | |

| Other liabilities | (4,937) | | | (9,368) | |

| Net cash provided by (used in) operating activities | (9,735) | | | 12,670 | |

| Investing Activities | | | |

| Net change in loans | (74,947) | | | (169,595) | |

| Purchases of available-for-sale securities | (74,575) | | | (11,861) | |

| Proceeds from maturities of available-for-sale securities | 33,329 | | | 21,528 | |

| Proceeds from sale of available-for-sale securities | 0 | | | 3,841 | |

| | | |

| Purchase of premises and equipment | (118) | | | (331) | |

| | | |

| Purchase of restricted equity securities | 0 | | | (970) | |

| | | |

| Proceeds from sale of restricted equity securities | 1,626 | | | 0 | |

| | | |

| Net cash used in investing activities | (114,685) | | | (157,388) | |

| | | |

| |

| | | |

| | | |

| Financing Activities | | | |

| | | |

| Net increase in demand deposits, savings, NOW and money market accounts | 468,521 | | | 185,747 | |

| Net decrease in time deposits | (111,691) | | | (136,684) | |

| | | |

| Net increase in fed funds purchased and repurchase agreements | 988 | | | 24,025 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Proceeds from Federal Home Loan Bank advances | 0 | | | 70,000 | |

| Repayment of Federal Home Loan Bank advances | (10,000) | | | (26,063) | |

| | | |

| | | |

| | | |

| | | |

| Issuance of common shares, net of issuance cost | 0 | | | 1 | |

| | | |

| | | |

| Repurchase of common stock | (1,052) | | | 0 | |

| Acquisition of common stock for tax withholding obligations | (404) | | | (671) | |

| Net decrease in employee receivables | 35 | | | 30 | |

| | | |

| Net cash provided by financing activities | 346,397 | | | 116,385 | |

| Increase (Decrease) in Cash and Cash Equivalents | 221,977 | | | (28,333) | |

| Cash and Cash Equivalents, Beginning of Period | 408,810 | | | 187,320 | |

| Cash and Cash Equivalents, End of Period | $ | 630,787 | | | $ | 158,987 | |

| | | |

| Supplemental Cash Flows Information | | | |

| Interest paid | $ | 7,287 | | | $ | 17,199 | |

| Income taxes paid | $ | 130 | | | $ | 0 | |

| | | |

| | | |

| | | |

See Notes to Consolidated Financial Statements (unaudited)

8

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | Accumulated | | |

| | | | | | | | | Additional | | | | Other | | |

| Preferred Stock | | | | Common Stock | | | | Paid in | | Retained | | Comprehensive | | |

| Shares | | Amount | | Shares | | Amount | | Capital | | Earnings | | Income (Loss) | | Total |

| (Dollars in thousands) | | | | | | | | | | | | | | |

| Balance at December 31, 2018 | 1,200,000 | | | $ | 12 | | | 45,074,322 | | | $ | 451 | | | $ | 454,512 | | | $ | 38,371 | | | $ | (3,010) | | | $ | 490,336 | |

| Net income | — | | | — | | | — | | | — | | | — | | | 18,789 | | | — | | | 18,789 | |

| Change in unrealized appreciation on available-for-sale securities | — | | | — | | | — | | | — | | | — | | | — | | | 16,521 | | | 16,521 | |

| Issuance of shares | — | | | — | | | 250,968 | | | 2 | | | 1,715 | | | — | | | — | | | 1,717 | |

| Issuance of shares from equity-based awards | — | | | — | | | 52,351 | | | — | | | (236) | | | — | | | — | | | (236) | |

| Retired shares | (1,200,000) | | | (12) | | | (10,000) | | | — | | | (30,088) | | | (55) | | | — | | | (30,155) | |

| Preferred dividends declared | — | | | — | | | — | | | — | | | — | | | (175) | | | — | | | (175) | |

| Employee receivables from sale of stock | — | | | — | | | — | | | — | | | 4 | | | 113 | | | — | | | 117 | |

| Stock-based compensation | — | | | — | | | — | | | — | | | 2,245 | | | — | | | — | | | 2,245 | |

| Employee stock purchase plan additions | — | | | — | | | — | | | — | | | 36 | | | — | | | — | | | 36 | |

| Adoption of ASU 2016-01 | — | | | — | | | — | | | — | | | — | | | (68) | | | 68 | | | — | |

| Adoption of ASU 2018-07 | — | | | — | | | — | | | — | | | 2,159 | | | (2,159) | | | — | | | — | |

| Balance at June 30, 2019 | — | | | $ | — | | | 45,367,641 | | | $ | 453 | | | $ | 430,347 | | | $ | 54,816 | | | $ | 13,579 | | | $ | 499,195 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Accumulated | | |

| | | | | | | | | Additional | | | | | | Other | | |

| Preferred Stock | | | | Common Stock | | | | Paid in | | Retained | | | | Comprehensive | | |

| Shares | | Amount | | Shares | | Amount | | Capital | | Earnings | | | | Income | | Total |

| (Dollars in thousands) | | | | | | | | | | | | | | | | |

| Balance at December 31, 2019 | — | | | $ | — | | | 51,969,203 | | | $ | 520 | | | $ | 519,870 | | | $ | 64,803 | | | | | $ | 16,451 | | | $ | 601,644 | |

| Net loss | — | | | — | | | — | | | — | | | — | | | (3,499) | | | | | — | | | (3,499) | |

| | | | | | | | | | | | | | | | | |

| Change in unrealized appreciation on available-for-sale securities | — | | | — | | | — | | | — | | | — | | | — | | | | | 8,643 | | | 8,643 | |

| | | | | | | | | | | | | | | | | |

| Issuance of shares from equity-based awards | — | | | — | | | 198,370 | | | 1 | | | (754) | | | — | | | | | — | | | (753) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Employee receivables from sale of stock | — | | | — | | | — | | | — | | | 1 | | | 40 | | | | | — | | | 41 | |

| Stock-based compensation | — | | | — | | | — | | | — | | | 2,016 | | | — | | | | | — | | | 2,016 | |

| | | | | | | | | | | | | | | | | |

| Balance at June 30, 2020 | — | | | $ | — | | | 52,167,573 | | | $ | 521 | | | $ | 521,133 | | | $ | 61,344 | | | | | $ | 25,094 | | | $ | 608,092 | |

| | | | | | | | | | | | | | | | | |

See Notes to Consolidated Financial Statements (unaudited)

9

CROSSFIRST BANKSHARES, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS - UNAUDITED

| | | | | | | | | | | |

| Six Months Ended | | |

| June 30, | | |

| 2020 | | 2019 |

| (Dollars in thousands) | | |

| Operating Activities | | | |

| Net income (loss) | $ | (3,499) | | | $ | 18,789 | |

| Items not requiring (providing) cash | | | |

| Depreciation and amortization | 2,587 | | | 2,703 | |

| Provision for loan losses | 34,950 | | | 5,700 | |

| | | |

| Accretion of discounts and amortization of premiums on securities | 3,063 | | | 2,535 | |

| Equity based compensation | 2,016 | | | 2,281 | |

| | | |

| Foreclosed asset impairment | 1,117 | | | — | |

| | | |

| Deferred income taxes | (3,853) | | | 2,056 | |

| | | |

| | | |

| Net realized gains on available-for-sale debt securities | (713) | | | (433) | |

| Goodwill impairment | 7,397 | | | — | |

| | | |

| | | |

| | | |

| | | |

| Changes in | | | |

| | | |

| | | |

| Interest receivable | (3,683) | | | (2,611) | |

| Other assets | (1,284) | | | (6,172) | |

| Other liabilities | (2,130) | | | 5,195 | |

| Net cash provided by operating activities | 35,968 | | | 30,043 | |

| Investing Activities | | | |

| Net change in loans | (581,641) | | | (409,602) | |

| Purchases of available-for-sale securities | (27,312) | | | (107,948) | |

| Proceeds from maturities of available-for-sale securities | 58,974 | | | 26,468 | |

| Proceeds from sale of available-for-sale securities | 19,052 | | | 60,254 | |

| | | |

| Proceeds (purchase) of premises and equipment, net | (1,658) | | | 3,014 | |

| Purchase of restricted equity securities, net | (2,839) | | | (558) | |

| | | |

| | | |

| | | |

| Net cash used in investing activities | (535,424) | | | (428,372) | |

| | | |

| | | |

| | | |

| Financing Activities | | | |

| | | |

| Net increase in demand deposits, savings, NOW and money market accounts | 459,589 | | | 84,269 | |

| Net increase (decrease) in time deposits | (79,205) | | | 291,770 | |

| | | |

| Net increase (decrease) in repurchase agreements and federal funds purchased | 34,960 | | | (49,025) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Proceeds from Federal Home Loan Bank advances | 118,000 | | | 45,000 | |

| Repayment of Federal Home Loan Bank advances | (26,126) | | | (20,120) | |

| | | |

| | | |

| | | |

| Retirement of preferred stock | — | | | (30,000) | |

| Issuance of common shares, net and change in employee receivables | 43 | | | 1,677 | |

| | | |

| | | |

| Acquisition of common stock for tax withholding obligations | (754) | | | (235) | |

| | | |

| Dividends paid on preferred stock | — | | | (175) | |

| Net cash provided by financing activities | 506,507 | | | 323,161 | |

| Increase (Decrease) in Cash and Cash Equivalents | 7,051 | | | (75,168) | |

| Cash and Cash Equivalents, Beginning of Period | 187,320 | | | 216,541 | |

| Cash and Cash Equivalents, End of Period | $ | 194,371 | | | $ | 141,373 | |

| | | |

| Supplemental Cash Flows Information | | | |

| Interest paid | $ | 27,818 | | | $ | 35,366 | |

| Income taxes paid | — | | | 775 | |

| Foreclosed assets in settlement of loans | $ | — | | | $ | 2,471 | |

| | | |

| | | |

See Notes to Consolidated Financial Statements (unaudited)

10

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

Note 1:Nature of Operations and Summary of Significant Accounting Policies

Organization and Nature of Operations

CrossFirst Bankshares, Inc. (the “Company”), a Kansas corporation, was incorporated in December 2017. Prior to incorporation, the Company was registered as a limited liability company under the name CrossFirst Holdings, LLC. The Company is a bank holding company whose principal activities are the ownership and management of its wholly-owned subsidiaries,subsidiary, CrossFirst Bank (the “Bank”) and CFSA, LLC (“CFSA”), which holds cash.. In addition, the Bank has three subsidiaries including CrossFirst Investments, Inc. (“CFI”) is a wholly-owned subsidiary of the Bank, whichthat holds investments in marketable securities.securities, CFBSA I, LLC that holds foreclosed assets and CFBSA II, LLC that holds foreclosed assets.

Basis of Presentation

The Company’s accounting and reporting policies conform to accounting principles generally accepted in the United States (“GAAP”). The consolidated financial statements include the accounts of the Company, the Bank, CFI, CFBSA I, LLC and CFSA.CFBSA II, LLC. All significant intercompany accounts and transactions have been eliminated in consolidation.

The consolidated interim financial statements are unaudited and certain information and footnote disclosures presented in accordance with GAAP have been condensed or omitted and should be read in conjunction with the Company’s consolidated financial statements and notesfootnotes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 20192020 (the “2019“2020 Form 10-K”), filed with the Securities and Exchange Commission (the “SEC”) on March 10, 2020.February 26, 2021.

In the opinion of management, the interim financial statements include all adjustments which are of a normal, recurring nature necessary for the fair presentation of the financial position, results of operations, and cash flows of the Company and the disclosures made are adequate to make the interim financial information not misleading. The consolidated financial statements have been prepared in accordance with GAAP for interim financial information and the instructions to Form 10-Q adopted by the SEC.

Except for the accounting changes mentioned under “Coronavirus Aid, Relief, and Economic Security Act” and “Change in Accounting Principle” section below, no otherNo significant changes in the accounting policies of the Company occurred since December 31, 2019,2020, the most recent date financial statements were provided within the Company’s 20192020 Form 10-K. The information contained in the financial statements and footnotes for the period ended December 31, 2019 included in the Company’s 2019 Form 10-K should be referred to in connection with these unaudited interim consolidated financial statements.

Operating results for the interim periods disclosed herein are not necessarily indicative of the results that may be expected for a full year or any future period.

Use of Estimates

The Company has identified accounting policies and estimates that, due to the difficult, subjective or complex judgments and assumptions inherent in those policies and estimates and the potential sensitivity of the Company’s financial statements to those judgments and assumptions, are critical to an understanding of the Company’s financial condition and results of operations. Actual results could differ from those estimates. In particular, the novel coronavirus (“COVID-19”) pandemic and resulting impacts to economic conditions, as well as adverse impacts to the Company’s operations, may impact future estimates. The Allowanceallowance for Loanloan losses, deferred tax asset, and Lease Losses, Deferred Tax Asset, and Fair Valuefair value of Financial Instrumentsfinancial instruments are particularly susceptible to significant change.

Cash Equivalents

The Company had $126$541 million of cash and cash equivalents at the Federal Reserve Bank of Kansas City as of June 30, 2020.March 31, 2021. The reserve required at June 30, 2020March 31, 2021 was $0. In addition, the Company is at times required to place cash collateral with a third party as part of its back-to-back swap agreements. At June 30, 2020, approximately $31 million was required as cash collateral.

Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”)

The CARES Act allowsgave financial institutions the right to elect not to consider whethersuspend GAAP principles and regulatory determinations for loan modifications relating to the COVID-19 pandemic that they make betweenwould otherwise be categorized as TDRs from March 1, 2020, and the earlier ofthrough December 31, 2020. On December 27, 2020, the Consolidated Appropriations Act, 2021 was signed into law, which extended the period during which the Company may suspend GAAP principles and regulatory determinations for loan modifications relating to COVID-19 that would otherwise be categorized as TDRs through January 1, 2022 or 60 days after the date when the national emergency related to theconcerning COVID-19 pandemic ends are troubled debt restructurings (“TDRs”), which require additional disclosures. The relief can be applied to modifications of loans to borrowers that were not more than 30 days past due as of December 31, 2019.

terminates. The Company elected to apply the guidance duringstarting in the first quarter of 2020.

Changes Affecting Comparability

Beginning with the quarter ended March 31, 2021, the Company consolidated the “Goodwill and other intangible assets, net” into “other assets” within the Consolidated Balance Sheets. The review of loans that meetconsolidation was due to the criteria is overseen by the Officeimmateriality of the Chief Credit Officer and his team.remaining intangible assets. The change had no impact on net income.

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

Loans Individually Evaluated for Impairment

Prior to the quarter ended June 30, 2020, loans risk rated substandard or lower were considered impaired and evaluated on an individual basis. As of June 30, 2020, loans risk rated substandard and on accrual were evaluated collectively. The new approach provided a better estimate of potential losses inherent in the substandard portfolio.

A loan is considered impaired when, based on current information and events, it is probable that the Company will be unable to collect the scheduled payments of principal and interest when due according to the contractual terms of the loan agreement. The Company’s definition of a substandard credit was unchanged. Substandard loans exhibit a well-defined weakness or weaknesses that jeopardize repayment. A distinct possibility exists that the Company will sustain some loss if deficiencies are not corrected.

Loss potential, while existing in the aggregate amount of substandard loans, does not have to exist in individual loans classified substandard. As a result, the Company revised its allowance methodology to evaluate substandard, performing loans collectively for impairment as opposed to evaluating these loans individually for impairment. As of June 30, 2020, the change in methodology impacted $200 million of performing, substandard loans that were reviewed on a collective basis.

Change in Accounting Principle

On January 1, 2020, the Company adopted the Financial Accounting Standards Board (“FASB”) Accounting Standard Update (“ASU”) 2017-04, Intangibles—Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment, which was applied on a prospective basis. A description of the nature and reason for the change in accounting principle is provided below in the recent accounting pronouncements section.

On January 1, 2020, the Company adopted FASB ASU 2019-12, Simplifying the Accounting for Income Taxes, which was applied as of the adoption date. A description of the nature and reason for the change in accounting principle is provided below in the recent accounting pronouncements section.

Changes Affecting Comparability

During the quarter ended June 30, 2020, the Company changed loans individually evaluated for impairment. A discussion regarding this change is provided above under “Loans Individually Evaluated for Impairment” and in Note 4: Loans and Allowance for Loan Losses within the Notes to the Unaudited Consolidated Financial Statements. The Company separated substandard loans into performing and nonperforming categories that were previously consolidated within the loan footnote disclosures. The change in disclosure did not impact the Company's net income during the three or six-months ended June 30, 2019, Balance Sheet at December 31, 2019, Statement of Stockholders’ Equity at December 31, 2019, or the impaired loan information at December 31, 2019 as presented in Note 4: Loans and Allowance for Loan Losses within the Notes to the Unaudited Consolidated Financial Statements.

Beginning withFor the quarter ended March 31, 2020,2021, the Company consolidated the “Other” line item previously included in stockholders’ equity“equipment costs, other asset depreciation and amortization” into retained earnings“other noninterest expense” within the Consolidated Balance Sheets and the Consolidated Statements of Stockholders’ Equity. The consolidationIncome. In addition, the Company broke out “foreclosed assets, net” that was previously consolidated. As a result, changes within the Consolidated Statements of Income in the prior periods were made dueto conform to the immateriality ofcurrent period presentation. The changes: (i) consolidate lower balance line items or (ii) provide additional detail about the “Other” line item.Company’s operations. The changechanges had no impact on net income or total stockholders’ equity.income.

Initial Public OfferingEmerging Growth Company (“EGC”)

On August 19, 2019, the Company completed its initial public offering (“IPO”) of common stock. The Company issued and sold 5,750,000 shares of common stock at a public offering price of $14.50 per share. After deducting the underwriting discounts and offering expenses, the Company received total net proceeds of $76 million from the IPO. Certain selling stockholders participated in the offering and soldis currently an aggregate of 1,261,589 shares of common stock at a public offering price of $14.50 per share. The Company did not receive any proceeds from the sales of shares by the selling stockholders.

On September 17, 2019, the underwriters partially exercised their option to purchase additional shares. The Company issued and sold 844,362 shares of common stock at a public offering price of $14.50 per share of common stock. After deducting the underwriting discounts and offering expenses, the Company received total net proceeds of $11 million.

As of June 30, 2020, the Company qualified as an emerging growth company (“EGC”) under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”).EGC. An EGC may take advantage of reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. Among the reductions and reliefs, the Company elected to extend the transition period for complying with new or revised accounting standards affecting public companies. This means that the financial statements the Company files or furnishes, will not be subject to all new or revised accounting standards generally applicable to public companies for the transition period for so long as the Company remains an EGC or until the Company affirmatively and irrevocably opts out of the extended transition period under the JOBS Act.

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

Recent Accounting Pronouncements

The following table provides information about Accounting Standard Updates (“ASUs”) the Company has implemented the following ASUs during 2020:

| | | | | | | | | | | | | | | | | | | | |

Standard | | Date of Adoption | | Description | | Effect on Financial Statements or Other Significant Matters |

| | | | | | |

ASU 2020-04:

Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting

| | June 30, 2020 | | The ASU provides optional expedients and exceptions to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met.

The ASU only applies to transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. The expedients and exceptions provided by the amendments do not apply to contract modifications made and hedging relationships entered into or evaluated after December 31, 2022, except for hedging relationships existing as of December 31, 2022, that an entity has elected certain optional expedients for and that are retained through the end of the hedging relationship. The amendments include:

(1) Optional expedients to contract modifications that allow the Company to adjust the effective interest rate of receivables and debt, account for lease modifications as a continuation of the existing lease, and remove the requirement to reassess its original conclusions for contract modifications about whether that contract contains an embedded derivative that is clearly and closely related to the economic characteristics and risks of the host contract under Subtopic 815-15, Derivatives and Hedging—Embedded Derivatives;

(2) Exceptions to the guidance in Topic 815 related to changes in the critical terms of a hedging relationship due to reference rate reform; and

(3) Optional expedients for cash flow and fair value hedges. | | The Company had more than $1 billion in loans tied to LIBOR as of June 30, 2020.

The Company does not believe the adoption will have a material accounting impact on the Company’s consolidated financial position or results of operations. Additionally, LIBOR fallback language has been included in key loan provisions of new and renewed loans in preparation for transition from LIBOR to the new benchmark rate when such transition occurs. This standard is expected to ease the administrative burden in accounting for the future effects of reference rate reform.

The ASU allows the Company to recognize the modification related to LIBOR as a continuation of the old contract, rather than a cancellation of the old contract resulting in a write off of unamortized fees and creation of a new contract.

|

ASU 2019-12:

Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes

| | January 1, 2020

(Early Adoption) | | The ASU simplifies the accounting for income taxes. Among other changes, the ASU:

(1) Removes the exception to the incremental approach for intraperiod tax allocation when there is a loss from continuing operations and income or a gain from other items;

(2) Removes the exception to the general methodology for calculating income taxes in an interim period when a year-to-date loss exceeds the anticipated loss for the year;

(3) Requires an entity to recognize a franchise tax that is partially based on income as an income-based tax and account for any incremental amount incurred as a nonincome based tax; and

(4) Requires an entity reflect the effect of an enacted change in tax laws or rates in the annual effective tax rate computation in the interim period that includes the enactment date. | | The amendments in the ASU did not have a material impact on the Company’s tax methodology, processes, or the Company’s financial statements. |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

| | | | | | | | | | | | | | | | | | | | |

Standard | | Date of Adoption | | Description | | Effect on Financial Statements or Other Significant Matters |

ASU 2018-13:

Fair Value Measurement (Topic 820): Disclosure Framework

| | January 1, 2020 | | Improves the effectiveness of disclosures in the notes to financial statements by facilitating clear communication of the information. The amendments modify certain disclosure requirements of fair value measurements in Topic 820, Fair Value Measurement.

Entities are no longer required to disclose transfers between Level 1 and Level 2 of the fair value hierarchy or qualitatively disclose the valuation process for Level 3 fair value measurements. The updated guidance requires disclosure of the changes in unrealized gains and losses for the period included in Other Comprehensive Income for recurring Level 3 fair value measurements. Entities are required to disclose the range and weighted average used to develop significant unobservable inputs for Level 3 fair value measurements.

The additional provisions of the guidance should be adopted prospectively. The eliminated requirements should be adopted retrospectively. | | The adoption did not have a material impact to the financial statements.

No transfers between Level 1 and Level 2 occurred in 2019 or 2020 and the Company did not have any recurring Level 3 fair value measurements that created an unrealized gain or loss in Other Comprehensive Income. In addition, the Company previously disclosed the range and weighted average used to develop significant unobservable inputs for Level 3 fair value measurements. |

| | | | | | |

ASU 2017-04:

Intangibles—Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment

| | January 1, 2020

(Early Adoption) | | Eliminates Step 2 from the goodwill impairment test which required entities to compute the implied fair value of goodwill. An entity should perform an annual, or interim, goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity should recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. | | On the date of adoption there was no impact to the financial statements.

The Company’s process for evaluating goodwill impairment was modified to align with the elimination of Step 2. In the second quarter of 2020, the Company performed a Step 0 analysis then a Step 1 analysis and determined that goodwill was fully impaired. |

| | | | | | |

| | | | | | |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

The Company has provided updatesanticipates to the following ASUs that have not yet been adopted. A complete list of recent, applicable accounting pronouncements was providedadopt in the Company’s 2019 Form 10-K:future:

| | | | | | | | | | | | | | | | | | | | |

| Standard | | Anticipated Date of Adoption | | Description | | Effect on Financial Statements or Other Significant Matters |

ASU 2016-13

Financial Instruments-Credit Losses | | If we maintain ourthe Company maintains its EGC status, the Company is not required to implement this standard until January 2023. The Company will continue to monitor its progress and the requirements related to adoption.anticipates an adoption date of January 2022. | | Requires an entity to utilize a new impairment model known as the current expected credit loss (“CECL”) model to estimate its lifetime expected credit loss and record an allowance that, when deducted from the amortized cost basis of the financial asset, presents the net amount expected to be collected on the financial asset. | | The Company established a committee of individuals from applicable departments to oversee the implementation process.

implemented a third-party software solution and completed the third-party software implementation phase of the transition. The software implementation phasethat included data capture and portfolio segmentation amongst other items.

The Company completed an initial parallel run using 2019 data and completed a second parallel run during the fourth quarter ofruns in 2019. During the first half ofperiod ended December 31, 2020, the Company continued to perform parallel runs using 2020 data and continuescontinued to recalibrate inputs as necessary.

platform.platform and third-party testing is anticipated later in 2021.

At this time, an estimate of the impact cannot be established as the Company continues to evaluate the inputs into the model. The actual impact could be significantly affected by the composition, characteristics, and quality of the underlying loan portfolio at the time of adoption. |

ASU 2016-02

Leases (Topic 842) | | The Company expects to implement this standard in 2021 if EGC status is maintained. Ifon January 1, 2022, unless the Company loses its EGC status in 2020,during 2021. If EGC status changes, the Company would therefore be required to implement the ASU as of the beginning of 2020.

On April 8, 2020, the FASB proposed a one-year deferral on the ASU. If EGC status is maintained and the FASB issues the final amendment, the Company would be able to defer implementation until January 1, 2022.2021. | | Requires lessees and lessors to recognize lease assets and lease liabilities on the balance sheet and disclose key information about leasing arrangements.

The update requires lessees and lessors to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach with the option to elect certain practical expedients.

The update will also increase disclosures around leases, including qualitative and specific quantitative measures. | | The Company expects to apply the update as of the beginning of the period of adoption and the Company does not plan to restate comparative periods. The Company expects to elect certain optional practical expedients.

The Company gathered all potential lease and embedded lease agreements during 2019 and 2020 and is evaluating the applicability and impact to the financial statements.

The Company’s current operating leases relate primarily to four branch locations, as well as one future lease obligation.locations. Based on the current leases, the Company anticipates recognizing a lease liability and related right-to-use asset on its balance sheet, with an immaterial impact to its income statement compared to the current lease accounting model. However, the ultimate impact of the standard will depend on the Company's lease portfolio as of the adoption date. |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

Note 2:Earnings (Loss) Per Share

The following table presents the computation of basic and diluted earnings (loss) per share:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | | | Six Months Ended | | |

| June 30, | | | | June 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (Dollars in thousands except per share data) | | | | | | |

| Earnings (Loss) per Share | | | | | | | |

| Net income (loss) | $ | (7,356) | | | $ | 9,439 | | | $ | (3,499) | | | $ | 18,789 | |

| Less: preferred stock dividends | — | | | — | | | — | | | 175 | |

| Net income (loss) available to common stockholders | $ | (7,356) | | | $ | 9,439 | | | $ | (3,499) | | | $ | 18,614 | |

| Weighted average common shares | 52,104,994 | | | 45,236,264 | | | 52,088,239 | | | 45,165,248 | |

| Earnings (loss) per share | $ | (0.14) | | | $ | 0.21 | | | $ | (0.07) | | | $ | 0.41 | |

| Dilutive Earnings (Loss) Per Share | | | | | | | |

| | | | | | | |

| | | | | | | |

| Net income (loss) available to common stockholders | $ | (7,356) | | | $ | 9,439 | | | $ | (3,499) | | | $ | 18,614 | |

| Weighted average common shares | 52,104,994 | | | 45,236,264 | | | 52,088,239 | | | 45,165,248 | |

| Effect of dilutive shares | — | | | 975,516 | | | — | | | 994,577 | |

| Weighted average dilutive common shares | 52,104,994 | | | 46,211,780 | | | 52,088,239 | | | 46,159,825 | |

| Diluted earnings (loss) per share | $ | (0.14) | | | $ | 0.20 | | | $ | (0.07) | | | $ | 0.40 | |

| | | | | | | |

| Stock-based awards not included because to do so would be antidilutive | 2,417,205 | | | 403,722 | | | 2,417,205 | | | 424,972 | |

| | | | | | | | | | | | | | | |

| Three Months Ended | | |

| March 31, | | |

| 2021 | | 2020 | | | | |

| (Dollars in thousands except per share data) |

| Earnings per Share | | | | | | | |

| | | | | | | |

| | | | | | | |

| Net income available to common stockholders | $ | 12,035 | | | $ | 3,857 | | | | | |

| Weighted average common shares | 51,657,204 | | | 52,071,484 | | | | | |

| Earnings per share | $ | 0.23 | | | $ | 0.07 | | | | | |

| Dilutive Earnings Per Share | | | | | | | |

| | | | | | | |

| | | | | | | |

| Net income available to common stockholders | $ | 12,035 | | | $ | 3,857 | | | | | |

| Weighted average common shares | 51,657,204 | | | 52,071,484 | | | | | |

| Effect of dilutive shares | 724,270 | | | 588,786 | | | | | |

| Weighted average dilutive common shares | 52,381,474 | | | 52,660,270 | | | | | |

| Diluted earnings per share | $ | 0.23 | | | $ | 0.07 | | | | | |

| | | | | | | |

| Stock-based awards not included because to do so would be antidilutive | 669,112 | | | 905,406 | | | | | |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

Note 3:Securities

Available-for-Sale Debt and Equity Securities

The amortized cost and approximate fair values, together with gross unrealized gains and losses, of period end available-for-sale debt and equity securities consisted of the following:

| | | June 30, 2020 | | | March 31, 2021 |

| | Amortized Cost | | Gross Unrealized Gains | | Gross Unrealized Losses | | Approximate Fair Value | | Amortized Cost | | Gross Unrealized Gains | | Gross Unrealized Losses | | Approximate Fair Value |

| | (Dollars in thousands) | | | (Dollars in thousands) |

| Available-for-sale debt securities | | |

| Available-for-sale securities | | Available-for-sale securities | |

| Mortgage-backed - GSE residential | Mortgage-backed - GSE residential | $ | 139,615 | | | $ | 4,983 | | | $ | — | | | $ | 144,598 | | Mortgage-backed - GSE residential | $ | 138,231 | | | $ | 2,912 | | | $ | 1,464 | | | $ | 139,679 | |

| Collateralized mortgage obligations - GSE residential | Collateralized mortgage obligations - GSE residential | 94,189 | | | 1,472 | | | 20 | | | 95,641 | | Collateralized mortgage obligations - GSE residential | 38,206 | | | 785 | | | 26 | | | 38,965 | |

| State and political subdivisions | State and political subdivisions | 429,603 | | | 26,966 | | | 255 | | | 456,314 | | State and political subdivisions | 474,912 | | | 28,517 | | | 862 | | | 502,567 | |

| Corporate bonds | Corporate bonds | 1,212 | | | 86 | | | 4 | | | 1,294 | | Corporate bonds | 4,251 | | | 74 | | | 82 | | | 4,243 | |

| Total available-for-sale debt securities | 664,619 | | | 33,507 | | | 279 | | | 697,847 | | |

| Equity securities | | |

| Mutual funds | 2,183 | | | 53 | | | — | | | 2,236 | | |

| Total equity securities | 2,183 | | | 53 | | | — | | | 2,236 | | |

| Total available-for-sale securities | Total available-for-sale securities | $ | 666,802 | | | $ | 33,560 | | | $ | 279 | | | $ | 700,083 | | Total available-for-sale securities | $ | 655,600 | | | $ | 32,288 | | | $ | 2,434 | | | $ | 685,454 | |

| |

| | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2020 |

| Amortized Cost | | Gross Unrealized Gains | | Gross Unrealized Losses | | Approximate Fair Value |

| (Dollars in thousands) |

| Available-for-sale securities | | | | | | | |

| Mortgage-backed - GSE residential | $ | 104,839 | | | $ | 4,277 | | | $ | 0 | | | $ | 109,116 | |

| Collateralized mortgage obligations - GSE residential | 52,070 | | | 984 | | | 42 | | | 53,012 | |

| State and political subdivisions | 454,486 | | | 33,642 | | | 31 | | | 488,097 | |

| Corporate bonds | 4,259 | | | 104 | | | 0 | | | 4,363 | |

| Total available-for-sale securities | $ | 615,654 | | | $ | 39,007 | | | $ | 73 | | | $ | 654,588 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

| | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2019 | | | | | | |

| Amortized Cost | | Gross Unrealized Gains | | Gross Unrealized Losses | | Approximate Fair Value |

| (Dollars in thousands) | | | | | | |

| Available-for-sale debt securities | | | | | | | |

| Mortgage-backed - GSE residential | $ | 151,037 | | | $ | 1,668 | | | $ | 193 | | | $ | 152,512 | |

| Collateralized mortgage obligations - GSE residential | 128,876 | | | 625 | | | 289 | | | 129,212 | |

| State and political subdivisions | 436,448 | | | 19,996 | | | 104 | | | 456,340 | |

| Corporate bonds | 1,321 | | | 88 | | | — | | | 1,409 | |

| Total available-for-sale debt securities | 717,682 | | | 22,377 | | | 586 | | | 739,473 | |

| Equity securities | | | | | | | |

| Mutual funds | 2,190 | | | — | | | 29 | | | 2,161 | |

| Total equity securities | 2,190 | | | — | | | 29 | | | 2,161 | |

| Total available-for-sale securities | $ | 719,872 | | | $ | 22,377 | | | $ | 615 | | | $ | 741,634 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

The carrying value of securities pledged as collateral was $56 million and $41 million at June 30, 2020 and December 31, 2019, respectively.

The amortized cost and fair value of available-for-sale debt securities at June 30, 2020,March 31, 2021, by contractual maturity, are shown below:

| | | June 30, 2020 | | | March 31, 2021 | |

| | Within | | After One to | | After Five to | | After | | | | Within | | After One to | | After Five to | | After | | |

| | One Year | | Five Years | | Ten Years | | Ten Years | | Total | | | One Year | | Five Years | | Ten Years | | Ten Years | | Total | |

| | (Dollars in thousands) | | | (Dollars in thousands) | |

| Available-for-sale debt securities | | | |

| Available-for-sale securities | | Available-for-sale securities | | |

Mortgage-backed - GSE residential(1) | Mortgage-backed - GSE residential(1) | | | Mortgage-backed - GSE residential(1) | | |

| Amortized cost | Amortized cost | $ | — | | | $ | 56 | | | $ | 220 | | | $ | 139,339 | | | $ | 139,615 | | | Amortized cost | $ | 0 | | | $ | 48 | | | $ | 181 | | | $ | 138,002 | | | $ | 138,231 | | |

| Estimated fair value | Estimated fair value | $ | — | | | $ | 57 | | | $ | 236 | | | $ | 144,305 | | | $ | 144,598 | | | Estimated fair value | $ | 0 | | | $ | 50 | | | $ | 193 | | | $ | 139,436 | | | $ | 139,679 | | |

Weighted average yield(2) | Weighted average yield(2) | — | % | | 4.55 | % | | 3.91 | % | | 2.04 | % | | 2.04 | % | | Weighted average yield(2) | 0 | % | | 4.60 | % | | 3.91 | % | | 1.72 | % | | 1.72 | % | |

Collateralized mortgage obligations - GSE residential(1) | Collateralized mortgage obligations - GSE residential(1) | | | Collateralized mortgage obligations - GSE residential(1) | | |

| Amortized cost | Amortized cost | $ | — | | | $ | — | | | $ | 2,507 | | | $ | 91,682 | | | $ | 94,189 | | | Amortized cost | $ | 0 | | | $ | 0 | | | $ | 2,469 | | | $ | 35,737 | | | $ | 38,206 | | |

| Estimated fair value | Estimated fair value | $ | — | | | $ | — | | | $ | 2,755 | | | $ | 92,886 | | | $ | 95,641 | | | Estimated fair value | $ | 0 | | | $ | 0 | | | $ | 2,645 | | | $ | 36,320 | | | $ | 38,965 | | |

Weighted average yield(2) | Weighted average yield(2) | — | % | | — | % | | 2.77 | % | | 1.62 | % | | 1.65 | % | | Weighted average yield(2) | 0 | % | | 0 | % | | 2.75 | % | | 1.59 | % | | 1.66 | % | |

| State and political subdivisions | State and political subdivisions | | | State and political subdivisions | | |

| Amortized cost | Amortized cost | $ | 653 | | | $ | 7,234 | | | $ | 61,170 | | | $ | 360,546 | | | $ | 429,603 | | | Amortized cost | $ | 652 | | | $ | 5,947 | | | $ | 65,518 | | | $ | 402,795 | | | $ | 474,912 | | |

| Estimated fair value | Estimated fair value | $ | 656 | | | $ | 7,419 | | | $ | 66,034 | | | $ | 382,205 | | | $ | 456,314 | | | Estimated fair value | $ | 654 | | | $ | 6,024 | | | $ | 70,889 | | | $ | 425,000 | | | $ | 502,567 | | |

Weighted average yield(2) | Weighted average yield(2) | 8.24 | % | | 5.33 | % | | 3.58 | % | | 3.10 | % | | 3.22 | % | | Weighted average yield(2) | 3.54 | % | | 3.86 | % | | 3.32 | % | | 2.82 | % | | 2.90 | % | |

| Corporate bonds | Corporate bonds | | | Corporate bonds | | |

| Amortized cost | Amortized cost | $ | — | | | $ | 345 | | | $ | 867 | | | $ | — | | | $ | 1,212 | | | Amortized cost | $ | 0 | | | $ | 357 | | | $ | 3,894 | | | $ | 0 | | | $ | 4,251 | | |

| Estimated fair value | Estimated fair value | $ | — | | | $ | 358 | | | $ | 936 | | | $ | — | | | $ | 1,294 | | | Estimated fair value | $ | 0 | | | $ | 366 | | | $ | 3,877 | | | $ | 0 | | | $ | 4,243 | | |

Weighted average yield(2) | Weighted average yield(2) | — | % | | 5.89 | % | | 5.68 | % | | — | % | | 5.74 | % | | Weighted average yield(2) | 0 | % | | 4.10 | % | | 4.54 | % | | 0 | % | | 4.51 | % | |

| Total available-for-sale debt securities | | | |

| Total available-for-sale securities | | Total available-for-sale securities | | |

| Amortized cost | Amortized cost | $ | 653 | | | $ | 7,635 | | | $ | 64,764 | | | $ | 591,567 | | | $ | 664,619 | | | Amortized cost | $ | 652 | | | $ | 6,352 | | | $ | 72,062 | | | $ | 576,534 | | | $ | 655,600 | | |

| Estimated fair value | Estimated fair value | $ | 656 | | | $ | 7,834 | | | $ | 69,961 | | | $ | 619,396 | | | $ | 697,847 | | | Estimated fair value | $ | 654 | | | $ | 6,440 | | | $ | 77,604 | | | $ | 600,756 | | | $ | 685,454 | | |

Weighted average yield(2) | Weighted average yield(2) | 8.24 | % | | 5.34 | % | | 3.53 | % | | 2.63 | % | | 2.75 | % | | Weighted average yield(2) | 3.54 | % | | 3.88 | % | | 3.37 | % | | 2.48 | % | | 2.59 | % | |

(1) Actual maturities may differ from contractual maturities because issuers may have the rights to call or prepay obligations with or without prepayment penalties. | (1) Actual maturities may differ from contractual maturities because issuers may have the rights to call or prepay obligations with or without prepayment penalties. | | (1) Actual maturities may differ from contractual maturities because issuers may have the rights to call or prepay obligations with or without prepayment penalties. | |

(2) Yields are calculated based on amortized cost. | (2) Yields are calculated based on amortized cost. | | (2) Yields are calculated based on amortized cost. | |

| | | | | | | | |

| Notes to Consolidated Financial Statements (unaudited) | |

The following tables show gross unrealized losses, the number of securities, that are in an unrealized loss, position, and fair value of the Company’s investments with unrealized losses that are not deemed to be other-than-temporarily impaired (“OTTI”), aggregated by investment class and length of time that individual securities have been in a continuous unrealized loss position at June 30, 2020March 31, 2021 and December 31, 2019:2020:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2021 |

| Less than 12 Months | | 12 Months or More | | Total |

| Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities |

| (Dollars in thousands) |

| Available-for-sale securities | | | | | | | | | | | | |

| Mortgage-backed - GSE residential | $ | 55,185 | | | $ | 1,464 | | | 8 | | $ | 0 | | | $ | 0 | | | 0 | | $ | 55,185 | | | $ | 1,464 | | | 8 |

| Collateralized mortgage obligations - GSE residential | 7,591 | | | 26 | | | 6 | | 0 | | | 0 | | | 0 | | 7,591 | | | 26 | | | 6 |

| State and political subdivisions | 44,008 | | | 861 | | | 32 | | 24 | | | 1 | | | 1 | | 44,032 | | | 862 | | | 33 |

| Corporate bonds | 3,418 | | | 82 | | | 1 | | 0 | | | 0 | | | 0 | | 3,418 | | | 82 | | | 1 |

| Total temporarily impaired securities | $ | 110,202 | | | $ | 2,433 | | | 47 | | $ | 24 | | | $ | 1 | | | 1 | | $ | 110,226 | | | $ | 2,434 | | | 48 |

| | | June 30, 2020 | | | December 31, 2020 |

| | Less than 12 Months | | | 12 Months or More | | | Total | | | Less than 12 Months | | 12 Months or More | | Total |

| | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities | | Fair Value | | Unrealized Losses | | Number of Securities |

| | (Dollars in thousands) | | | (Dollars in thousands) |

| Available-for-Sale Debt Securities | | | |

| Available-for-sale securities | | Available-for-sale securities | |

| Mortgage-backed - GSE residential | Mortgage-backed - GSE residential | $ | — | | | $ | — | | | — | | $ | — | | | $ | — | | | — | | $ | — | | | $ | — | | | — | Mortgage-backed - GSE residential | $ | 0 | | | $ | 0 | | | 0 | | $ | 0 | | | $ | 0 | | | 0 | | $ | 0 | | | $ | 0 | | | 0 |

| Collateralized mortgage obligations - GSE residential | Collateralized mortgage obligations - GSE residential | 12,050 | | | 20 | | | 4 | | — | | | — | | | — | | 12,050 | | | 20 | | | 4 | Collateralized mortgage obligations - GSE residential | 9,933 | | | 42 | | | 5 | | 0 | | | 0 | | | 0 | | 9,933 | | | 42 | | | 5 |

| State and political subdivisions | State and political subdivisions | 11,471 | | | 255 | | | 11 | | 27 | | | — | | | 1 | | 11,498 | | | 255 | | | 12 | State and political subdivisions | 8,525 | | | 31 | | | 8 | | 25 | | | 0 | | | 1 | | 8,550 | | | 31 | | | 9 |

| Corporate bonds | Corporate bonds | 456 | | | 4 | | | 1 | | — | | | — | | | — | | 456 | | | 4 | | | 1 | Corporate bonds | 0 | | | 0 | | | 0 | | 0 | | | 0 | | | 0 | | 0 | | | 0 | | | 0 |

| Total temporarily impaired debt securities | $ | 23,977 | | | $ | 279 | | | 16 | | $ | 27 | | | $ | — | | | 1 | | $ | 24,004 | | | $ | 279 | | | 17 | |