UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

x Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended DecemberMarch 31, 20152017

¨ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from __________ to __________.

Commission File Number: 000-54277

BANJO & MATILDA, INC. |

(Exact name of registrant as specified in its charter) |

Nevada |

| 27-1519178 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. employer identification number) |

1221 2nd Street #300

Santa Monica CA 90401

(Address of principal executive offices and zip code)

(855) 245-1613 724 769 3091

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ox No xo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer | o | Accelerated filer | o |

Non-accelerated filer | o | Smaller reporting company | x |

(Do not check if a smaller reporting company) | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of December 31, 2016,May 22, 2017, the Registrant had outstanding 58,823,116 shares of common stock.

BANJO & MATILDA, INC.

FORM 10-Q

| Page | ||||

| |||||

| 3 | ||||

| |||||

| |||||

| 4 |

| |||

| F-1 |

| |||

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS |

| F-2 |

| ||

| F-3 |

| |||

| F-4 | ||||

| |||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| 5 |

| ||

|

|

| |||

|

| ||||

| |||||

| |||||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

| ||||

| |||||

|

| ||||

| 2 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains certain statements of a forward-looking nature. Such forward-looking statements, including but not limited to statements regarding projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond the control of the Company. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of risks and uncertainties that could cause actual results to differ materially from those projected or anticipated, including but not limited to those set forth herein and in our Annual Report on Form 10-K.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Except as required by the federal securities laws, we undertake no obligation to update forward-looking information. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Report. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

| 3 |

| Table of Contents |

PART I – FINANCIAL INFORMATION

BANJO & MATILDA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

DECEMBERMARCH 31, 20152017

(UNAUDITED)

INDEX TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

| F-1 | |||

| ||||

Condensed Consolidated Statements of Operations and Comprehensive Loss |

| F-2 | ||

| ||||

| F-3 | |||

| ||||

| F-4 |

| 4 |

BANJO & MATILDA INC. AND SUBSIDIARIES

March 31, June 30, 2017 2016 (Unaudited) ASSETS LIABILITIES AND STOCKHOLDERS' DEFICIT Preferred stock, $0.00001 par value, 100,000,000 shares authorized and 1,000,000 shares issued and outstanding, respectively Common stock, $0.00001 par value, 100,000,000 shares authorized and 58,823,116 and 58,823,116 shares issued and outstanding, respectively CURRENT ASSETS Cash and cash equivalents $ 6,828 $ 11,056 Trade receivables, net - 2,870 Inventory, net 51,718 102,427 Deposit on purchases 1,153 1,153 Other assets 11,000 - TOTAL CURRENT ASSETS 70,698 117,506 NON-CURRENT ASSETS Intangible assets, net 31,528 38,269 Deferred financing costs, net 19,630 31,407 Property, plant and equipment, net 8,069 11,976 TOTAL NON-CURRENT ASSETS 59,227 81,652 TOTAL ASSETS $ 129,925 $ 199,157 CURRENT LIABILITIES Trade and other payables $ 1,118,137 $ 1,008,772 Deposit payable 4,621 4,621 Trade financing 256,191 249,720 Accrued interest 423,624 236,398 Loans payable (net of related discoumt) 538,265 306,092 Loan from related parties 181,737 183,269 Convertible loan from related parties (net of related discount) 381,583 370,008 TOTAL CURRENT LIABILITIES 2,904,158 2,358,880 NON-CURRENT LIABILITIES Loans payable (net of related discount) (net of current portion) 318,966 325,137 TOTAL LIABILITIES 3,223,124 2,684,017 STOCKHOLDERS' DEFICIT 10 10 588 588 Additional paid in capital 1,632,517 1,632,517 Other accumulated comprehensive gain 100,007 100,007 Accumulated deficit (4,826,321 ) (4,217,982 ) TOTAL STOCKHOLDERS' DEFICIT (3,093,199 ) (2,484,860 ) TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT $ 129,925 $ 199,157

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

| F-1 |

| Table of Contents |

BANJO & MATILDA INC. AND SUBSIDIARIES December 31, June 30, 2015 2015 (Unaudited) ASSETS CURRENT ASSETS Cash and cash equivalents Trade receivables, net Inventory, net Deposit on purchases Other assets TOTAL CURRENT ASSETS NON-CURRENT ASSETS Intangible assets, net Deferred financing costs, net Other receivable Property, plant and equipment, net TOTAL NON-CURRENT ASSETS TOTAL ASSETS LIABILITIES AND STOCKHOLDERS' DEFICIT CURRENT LIABILITIES Trade and other payables Deposit payable Trade financing Accrued interest Loans payable Loan from related parties Convertible loan from related party (net of discount) TOTAL CURRENT LIABILITIES NON-CURRENT LIABILITIES Loans payable (net of related discount) (net of current portion) Convertible loan from related party (net of discount) (net of current portion) TOTAL NON-CURRENT LIABILITIES TOTAL LIABILITIES STOCKHOLDERS' DEFICIT Preferred stock, $0.00001 par value, 100,000,000 shares authorized and 1,000,000 shares issued and outstanding, respectively Common stock, $0.00001 par value, 100,000,000 shares authorized and 58,823,116 and 58,323,116 shares issued and outstanding, respectively Additional paid in capital Other accumulated comprehensive gain Accumulated deficit TOTAL STOCKHOLDERS' DEFICIT TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT $ 114,285 $ 362,668 162,609 180,289 133,830 174,792 171,370 357,804 70,983 5,550 653,077 1,081,103 41,640 45,011 39,257 47,107 - 66,952 13,288 12,139 94,185 171,208 $ 747,262 $ 1,252,311 $ 611,474 $ 633,394 1,159 1,159 649,502 779,653 128,174 69,824 239,369 229,288 143,422 217,855 257,835 - 2,030,934 1,931,172 407,645 563,357 121,756 - 529,401 563,357 2,560,335 2,494,529 10 10 588 583 1,591,051 1,759,187 100,007 100,007 (3,504,729 ) (3,102,005 ) (1,813,073 ) (1,242,219 ) $ 747,262 $ 1,252,311

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME

FOR THE THREE AND NINE MONTH PERIODS ENDED MARCH 31, 2017 AND 2016

(UNAUDITED)

Three month periods ended Nine month periods ended March 31, 2017 March 31. 2016 March 31, 2017 March 31. 2016 $ Foreign currency translation Revenue 133,408 $ 446,509 $ 493,450 $ 2,058,876 Cost of sales 41,772 321,087 185,519 1,410,046 Gross profit 91,636 125,422 307,931 648,830 Payroll and employee related expenses 129,149 124,085 375,511 517,738 Operating expense 82,054 22,731 122,976 128,176 Marketing expense 491 15,666 35,408 107,587 Samples & design expense 718 335 8,479 44,404 Occupancy expenses 7,014 16,701 33,072 53,416 Depreciation and amortization expense 5,324 2,341 10,648 6,897 Finance Charges 31,370 17,206 58,628 36,488 Corporate and public company expense 24,411 30,260 38,958 103,545 280,532 229,326 683,681 998,252 Loss from operations (188,896 ) (103,904 ) (375,750 ) (349,422 ) Other Income (Expense) Other income 6,389 9,567 10,466 12,399 Amortization of debt discount (16,392 ) (17,079 ) (49,177 ) (53,266 ) Interest expense (57,074 ) (48,677 ) (193,878 ) (172,527 ) Total Other Expense (67,077 ) (56,189 ) (232,589 ) (213,394 ) Loss before income tax (255,973 ) (160,093 ) (608,339 ) (562,816 ) Provision for income taxes - - - - Net loss (255,973 ) (160,093 ) (608,339 ) (562,816 ) Other comprehensive income - - - - Comprehensive loss $ (255,973 ) $ (160,093 ) $ (608,339 ) $ (562,816 ) Net loss per share Basic $ (0.00 ) $ (0.00 ) $ (0.01 ) $ (0.01 ) Diluted $ (0.00 ) $ (0.00 ) $ (0.01 ) $ (0.01 ) Weighted average number of shares outstanding: Basic 58,823,116 58,823,116 58,823,116 58,755,598 Diluted 58,823,116 58,823,116 58,823,116 58,755,598

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

| F-2 |

| Table of Contents |

BANJO & MATILDA, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE NINE MONTH PERIODS ENDED MARCH 31, 2017 AND 2016

(UNAUDITED)

2017 2016 Adjustments to reconcile net loss to net cash provided by (used in) operating activities: Trade receivables Inventory Deposit on Purchases Other assets Other receivable Deferred financing costs Trade payables and other liabilities Accrued interest Income tax payments Interest paymentsNet loss $ (608,339 ) $ (562,816 ) Depreciation 3,905 1,841 Amortization 6,743 5,057 AR allowance (5,725 ) 873 Debt discount amortization 49,177 53,266 Amortization of deferred finance fee 58,628 11,777 (Increase) / decrease in assets: 8,595 157,926 50,709 69,613 - 356,651 (11,000 ) (150,542 ) - 66,952 (46,851 ) - Increase/ (decrease) in current liabilities: 109,365 118,759 187,226 99,848 Net cash provided by (used in) operating activities (197,567 ) 229,203 CASH FLOWS FROM INVESTING ACTIVITIES Purchase of property and equipment - (2,334 ) CASH FLOWS FROM FINANCING ACTIVITIES Net proceeds (net payments) on related party loan (1,532 ) 225,603 Net proceeds (net payments) on loan payables 188,401 (327,624 ) Net trade financing 6,471 (366,689 ) Net cash provided by (used in) financing activities 193,340 (468,710 ) Net increase (decrease) in cash and cash equivalents (4,228 ) (241,841 ) Cash and cash equivalents at the beginning of the period $ 11,056 $ 362,668 Cash and cash equivalents at the end of the period $ 6,828 $ 120,827 SUPPLEMENTAL DISCLOSURES: Cash paid during the year for: $ - $ - $ 36,286 $ 84,456 SUPPLEMENTAL DISCLOSURES FOR NON CASH: FINANCING AND INVESTING ACTIVITIES Debt converted to equity $ - $ 27,123

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

BANJO & MATILDA, INC. AND SUBSIDIARIES CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME FOR THE THREE AND SIX MONTH PERIODS ENDED DECEMBER 31, 2015 AND 2014 (UNAUDITED) Three month periods ended Six month periods ended December 31, 2015 December 31, 2014 December 31, 2015 December 31, 2014 Revenue Cost of sales Gross profit Payroll and employee related expenses Operating expense Marketing expense Samples & design expense Occupancy expenses Depreciation and amortization expense Finance Charges Corporate and public company expense Loss from operations Other Income (Expense) Other income Amortization of debt discount Interest expense Total Other Expense Loss before income tax Provision for income taxes Net loss Other comprehensive income Foreign currency translation Comprehensive loss Net loss per share Basic Diluted Weighted average number of shares outstanding: Basic Diluted $ 732,063 $ 1,038,418 $ 1,612,367 $ 1,785,181 517,152 581,999 1,088,959 993,732 214,911 456,419 523,408 791,449 131,688 193,226 393,653 365,630 42,725 123,110 105,445 177,658 23,501 41,454 91,921 147,246 7,466 - 44,069 - 23,350 11,398 36,715 24,637 2,291 3,020 4,556 6,289 12,299 52,872 27,680 93,623 40,898 61,333 73,285 97,872 284,219 486,413 777,325 912,955 (69,307 ) (29,994 ) (253,916 ) (121,506 ) (9,846 ) - 2,832 - (18,093 ) - (36,187 ) - (52,120 ) (48,638 ) (115,453 ) (94,817 ) (80,059 ) (48,638 ) (148,808 ) (94,817 ) (149,366 ) (78,632 ) (402,724 ) (216,323 ) - - - - (149,366 ) (78,632 ) (402,724 ) (216,323 ) - 18,548 - 13,124 $ (149,366 ) $ (60,084 ) $ (402,724 ) $ (203,199 ) $ (0.00 ) $ (0.00 ) $ (0.01 ) $ (0.01 ) $ (0.00 ) $ (0.00 ) $ (0.01 ) $ (0.01 ) 58,823,116 31,790,918 58,722,023 29,493,137 58,823,116 31,790,918 58,722,023 29,493,137

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

BANJO & MATILDA, INC. AND SUBSIDIARIES FOR THE SIX MONTH PERIODS ENDED DECEMBER 31, 2015 AND 2014 (UNAUDITED) December 31, 2015 December 31, 2014 Net loss Adjustments to reconcile net loss to net cash provided by (used in) operating activities: Depreciation Amortization Effect of exchange rate changes on cash and cash equivalents AR allowance Shares issued in exchange for services Debt discount amortization Amortization of deferred finance fee (Increase) / decrease in assets: Trade receivables Inventory Deposit on Purchases Other assets Other receivable Increase/ (decrease) in current liabilities: Trade payables and other liabilities Accrued interest Deposits payable Net cash provided by (used in) operating activities CASH FLOWS FROM INVESTING ACTIVITIES Purchase of property and equipment CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from issuance of stock Net proceeds (payments) on related party loan Net loan proceeds Net trade financing Net cash provided by (used in) financing activities Net increase (decrease) in cash and cash equivalents Cash and cash equivalents at the beginning of the period Cash and cash equivalents at the end of the period SUPPLEMENTAL DISCLOSURES: Cash paid during the year for: Income tax payments Interest payments SUPPLEMENTAL DISCLOSURES FOR NON CASH: FINANCING AND INVESTING ACTIVITIES Debt converted to equity $ (402,724 ) $ (216,323 ) 1,185 2,003 3,371 4,286 - 23,619 873 - - 14,878 36,187 - 7,851 - 16,808 (296,032 ) 40,962 (151,707 ) 186,434 - (65,433 ) 6,429 66,952 23,529 5,203 247,716 58,350 81,265 - (2,408 ) (43,982 ) (262,745 ) (2,334 ) (2,764 ) - 44,770 268,970 (120,385 ) (340,886 ) (38,205 ) (130,151 ) 357,094 (202,067 ) 243,274 (248,383 ) (22,235 ) $ 11,132 $ 33,367 $ (237,251 ) $ 11,132 $ - $ - $ 64,953 $ 229,033 $ 27,123 $ 97,800

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements

| F-3 |

| Table of Contents |

BANJO & MATILDA, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 – BASIS OF PRESENTATION AND ORGANIZATION

All currencies represented in the notes to the condensed consolidated financial statements are in United States Dollars (USD) unless specified as AUD (Australian Dollars).

Banjo and Matilda, Inc. was incorporated in Nevada on December 18, 2009 under the name Eastern World Group, Inc. On September 24, 2013, its name was changed to Banjo & Matilda, Inc.

On November 14, 2013, Banjo & Matilda, Inc., entered into a Share Exchange Agreement (the "Exchange Agreement") with Banjo & Matilda, Pty Ltd., a corporation formed under the laws of Australia (the "Company") and the shareholders of the Company. Pursuant to the Exchange Agreement, at the closing of the transaction contemplated thereunder (the "Transaction"), the Company became a wholly-owned subsidiary of Banjo & Matilda, Inc.

Banjo & Matilda Pty Ltd. was incorporated under the laws of Australia on May 27, 2009 and manufactures and sells cashmere fashion. Headquartered at Bondi Beach, the Aussie lifestyle of sun, sand and surf resonates innately with this label and its philosophy of low maintenance, style and comfort.

Banjo & Matilda USA, Inc. was incorporated in the State of Delaware on October 14, 2013 and is owned 100% by Banjo & Matilda, Inc.

The ultra-soft cashmere staples, pairing simplicity with cool sophistication has rapidly gained loyal customers worldwide positioning the label as the 'go-to' for contemporary cashmere products.

Under accounting principles generally accepted in the United States, the share exchange is considered to be a capital transaction in substance, rather than a business combination. That is, the share exchange is equivalent to the issuance of stock by Banjo & Matilda Pty Ltd. for the net monetary assets of the Banjo & Matilda, Inc. accompanied by a recapitalization, and is accounted for as a change in capital structure. Accordingly, the accounting for the share exchange will be identical to that resulting from a reverse acquisition, except no goodwill will be recorded. Under share reverse takeover accounting, the post reverse acquisition comparative historical financial statements of the legal acquirer, Banjo & Matilda, Inc. are those of the legal acquiree, Banjo & Matilda Pty Ltd., which is considered to be the accounting acquirer. Share and per share amounts stated have been retroactively adjusted to reflect the merger.

As a result of the exchange agreement, the reorganization was treated as an acquisition by the accounting acquiree that is being accounted for as a recapitalization and as a reverse merger by the legal acquirer for accounting purposes. Pursuant to the recapitalization, all capital stock shares and amounts and per share data have been retroactively restated. Accordingly, the financial statements include the following:

(1) | The balance sheet consists of the net assets of the accounting acquirer at historical cost and the net assets of the legal acquirer at fair value. | |

(2) | The statements of operations include the operations of the accounting acquirer for the period presented and the operations of the legal acquirer from the date of the merger. |

Note 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying financial statements were prepared in conformity with generally accepted accounting principles in the United States of America ("US GAAP").

Principles of Consolidation

The consolidated financial statements include the accounts of Banjo & Matilda, Inc. ("Banjo" or "the Company") and its wholly owned subsidiaries Banjo & Matilda Pty Ltd. and Banjo & Matilda USA, Inc., collectively referred to as the Company. All material intercompany accounts, transactions and profits were eliminated in consolidation.

Exchange Gain (Loss)

During the six-month periodnine month periods ended DecemberMarch 31, 2015,2017 and 2016, the transactions of the Company were denominated in US Dollars. Some transactions were denominated in AUD and British pounds for the sales made outside US and for rent paid for the Australian store. Such transactions were converted to US$ on the date of transaction and the exchange gains or losses were recorded in the statement of operations. During the six-month period ended December 31, 2014, the transactions of the Company were denominated in foreign currency and were recorded in Australian dollar (AUD) at the rates of exchange in effect when the transactions occurred. Exchange gains and losses are recognized for the different foreign exchange rates applied when the foreign currency assets and liabilities are settled.

| F-4 |

| Table of Contents |

Foreign Currency Translation and Comprehensive Income (Loss)

During the six-month periodnine month periods ended DecemberMarch 31, 2015,2017 and 2016, the transactions of the Company were denominated in US Dollars. All the transactions which were denominated in other currencies were converted to US$ on the date of settlement and the exchange gains and losses were recorded in the statement of operations. No change was recorded in the comprehensive income (loss). During the three-month period ended September 30, 2014, the accounts of the Company were maintained, and its financial statements were expressed, in AUD. Such financial statements were translated into USD with the AUD as the functional currency. All assets and liabilities were translated at the exchange rate at the balance sheet date, stockholder's equity is translated at the historical rates and income statement items are translated at the average exchange rate for the period. Transactions in foreign currencies are initially recorded at the functional currency rate ruling at the date of transaction. Any differences between the initially recorded amount and the settlement amount are recorded as a gain or loss on foreign currency transaction in the statements of operations. The resulting translation adjustments are reported under other comprehensive income as a component of shareholders' equity. There were no significant fluctuations in the exchange rate for the conversion of AUD to USD after the balance sheet date.

Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates include collectability of accounts receivable, accounts payable, sales returns and recoverability of long-term assets.

Reportable Segment

The Company has one reportable segment. The Company's activities are interrelated and each activity is dependent upon and supportive of the other. Accordingly, all significant operating decisions are based on analysis of financial products provided as a single global business.

Revenue Recognition

Revenue is recognized when persuasive evidence of an arrangement exists, delivery has occurred, the fee is fixed or determinable, and collectability is probable. Revenue generally is recognized net of allowances for returns and any taxes collected from customers and subsequently remitted to governmental authorities.

Cost of Sales

Cost of sales consists primarily of inventory costs, as well as warehousing costs (including the cost of warehouse labor), shipping, importation duties and charges, third party royalties, and product sampling.

Operating Overhead Expense

Operating overhead expense consists primarily of payroll and benefit related costs, rent, depreciation and amortization, professional services, and meetings and travel.

Income Taxes

The Company utilizes FASB Accounting Standards Codification (ASC) Topic 740, Income Taxes, which requires recognition of deferred tax assets and liabilities for the expected future tax consequences of events that were included in the financial statements or tax returns. Under this method, deferred income taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each period end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established, when necessary, to reduce deferred tax assets to the amount expected to be realized.

The Company follows FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes, (codified in FASB ASC Topic 740). When tax returns are filed, it is likely that some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. The benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above is reflected as a liability for unrecognized tax benefits in the accompanying balance sheets along with any associated interest and penalties that would be payable to the taxing authorities upon examination. Interest associated with unrecognized tax benefits is classified as interest expense and penalties are classified in selling, general and administrative expenses in the statements of income.

| F-5 |

| Table of Contents |

At DecemberMarch 31, 20152017 and 2014,2016, the Company had not taken any significant uncertain tax positions on its tax returns for periods ended DecemberMarch 31, 20152017 and prior years or in computing its tax provision for 2015.2016. Management has considered its tax positions and believes that all of the positions taken by the Company in its Federal and State tax returns are more likely than not to be sustained upon examination. The Company is subject to examination by U.S. Federal and State tax authorities from the period ended June 30, 20122013 to the present, generally for three years after they are filed.

The Company has been behind in filing its payroll tax returns and sales tax returns. The Company has recorded $1,580 as penalties for the late payment of taxes in the accompanying financials.

Concentration of Credit Risk

Financial instruments that potentially subject the Company to concentrations of credit risk are cash, accounts receivable and other receivables arising from its normal business activities. The Company places its cash in what it believes to be credit-worthy financial institutions. The Company has a diversified customer base across many markets, predominantly Australia, United States of America, United Kingdom, Europe and the Middle East. The Company controls credit risk related to accounts receivable through credit approvals, credit limits and monitoring procedures. The Company routinely assesses the financial strength of its customers and, based upon factors surrounding the credit risk, establishes an allowance, if required, for uncollectible accounts and, as a consequence, believes that its accounts receivable credit risk exposure beyond such allowance is limited. In addition, Receivables that are factored through the Company's Receivable finance facility are guaranteed by the finance company that further mitigates Credit Risk.

Risks and Uncertainties

The Company is subject to risks from, among other things, competition associated with the industry in general, other risks associated with financing, liquidity requirements, rapidly changing customer requirements, limited operating history, foreign currency exchange rates and the volatility of public markets.

Contingencies

Certain conditions may exist as of the date the financial statements are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company's management and legal counsel assess such contingent liabilities, and such assessment inherently involves judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or unasserted claims that may result in such proceedings, the Company's legal counsel evaluates the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought.

If the assessment of a contingency indicates it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in the Company's financial statements. If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material would be disclosed. Loss contingencies considered to be remote by management are generally not disclosed unless they involve guarantees, in which case the guarantee would be disclosed.

Cash and Equivalents

Cash and equivalents include cash in hand and cash in demand deposits, certificates of deposit and all highly liquid debt instruments with original maturities of three months or less. At DecemberMarch 31, 20152017 and June 30, 2015,2016, the Company had $114,285$6,828 and $362,668$11,056 in cash in Australia and in the United States. The Company has not experienced any losses in such accounts and believes it is not exposed to any risks on its cash in bank accounts.

Allowance for Doubtful Accounts

The Company maintains reserves for potential credit losses on accounts receivable. Management reviews the composition of accounts receivable and analyzes historical bad debts, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate the adequacy of these reserves. The allowances for doubtful accounts as of DecemberMarch 31, 20152017 and June 30, 20152016 are $147,870$142,145 and $140,870$147,870 respectively.

Inventory

Inventories are valued at the lower of cost (determined on a weighted average basis) or market. Management compares the cost of inventories with the market value and allowance is made to write down inventories to market value, if lower. As of DecemberMarch 31, 20152017 and June 30, 2015,2016, the Company had outstanding balances of Finished Goods Inventory of $133,830$58,770 and $174,792$102,427 respectively.

| F-6 |

| Table of Contents |

As of March 31, 2017 and June 30, 2016, a reserve for Estimated Inventory Charges in the amount of $7,052 was established.

Property, Plant & Equipment

Property and equipment is stated at cost and depreciated using the straight-line method over the shorter of the estimated useful life of the asset or the lease term. The estimated useful lives of our property and equipment are generally as follows: computer software developed or acquired for internal use, three to 10 years; computer equipment, two to three years; buildings and improvements, five to 15 years; leasehold improvements, two to 10 years; and furniture and equipment, one to five years.

As of DecemberMarch 31, 20152017 and June 30, 2015,2016, Plant and Equipment consisted of the following:

|

| March 31 |

| June 30 |

| |||||||||||

|

| December 31, 2015 |

| June 30, 2015 |

|

| 2017 |

| 2016 |

| ||||||

Property, plant & equipment |

| $ | 31,378 |

| $ | 29,044 |

|

| $ | 31,378 |

| $ | 31,378 |

| ||

Accumulated depreciation |

| $ | (18,090 | ) |

| $ | (16,905 | ) |

| $ | (23,308 | ) |

| $ | (19,402 | ) |

|

| $ | 13,288 |

|

| $ | 12,139 |

|

| $ | 8,069 |

| $ | 11,976 |

| |

Depreciation was $1,185$3,905 and $2,003$1,841 for the three-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively. Depreciation was $605$1,952 and $1,311$656 for the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively.

Fair Value of Financial Instruments

For certain of the Company's financial instruments, including cash and equivalents, restricted cash, accounts receivable, accounts payable, accrued liabilities and short-term debt, the carrying amounts approximate their fair values due to their short maturities. ASC Topic 820, "Fair Value Measurements and Disclosures," requires disclosure of the fair value of financial instruments held by the Company. ASC Topic 825, "Financial Instruments," defines fair value, and establishes a three-level valuation hierarchy for disclosures of fair value measurement that enhances disclosure requirements for fair value measures. The carrying amounts reported in the balance sheets for receivables and current liabilities each qualify as financial instruments and are a reasonable estimate of their fair values because of the short period of time between the origination of such instruments and their expected realization and their current market rate of interest. The three levels of valuation hierarchy are defined as follows:

Level 1 inputs to the valuation methodology are quoted prices for identical assets or liabilities in active markets.

Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument.

Level 3 inputs to the valuation methodology are unobservable and significant to the fair value measurement.

The Company analyzes all financial instruments with features of both liabilities and equity under ASC 480, "Distinguishing Liabilities from Equity," and ASC 815.

As of DecemberMarch 31, 20152017 and June 30, 2015,2016, the Company did not identify any assets and liabilities that are required to be presented on the balance sheet at fair value.

Earnings Per Share (EPS)

Basic EPS is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for the period. Diluted EPS is computed similar to basic net income per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if all the potential common shares, warrants and stock options had been issued and if the additional common shares were dilutive. Diluted EPS is based on the assumption that all dilutive convertible shares and stock options were converted or exercised. Dilution is computed by applying the treasury stock method for the outstanding options and the if-converted method for the outstanding convertible preferred shares. Under the treasury stock method, options and warrants are assumed to be exercised at the beginning of the period (or at the time of issuance, if later), and as if funds obtained thereby were used to purchase common stock at the average market price during the period. Under the if-converted method, convertible outstanding instruments are assumed to be converted into common stock at the beginning of the period (or at the time of issuance, if later).

| Table of Contents |

The following table sets for the computation of basic and diluted earnings per share for three and sixnine month periods ended DecemberMarch 31, 20152017 and 2014:2016:

|

| Three month periods ended |

| Six month periods ended |

|

| Three month periods ended |

| Nine month periods ended |

| ||||||||||||||||||||||

|

| December 31, 2015 |

|

| December 31, 2014 |

|

| December 31, 2015 |

|

| December 31, 2014 |

|

| March 31, 2017 |

| March 31, 2016 |

| March 31, 2017 |

| March 31, 2016 |

| |||||||||||

Basic and diluted |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Net loss |

| $ | (149,366 | ) |

| $ | (78,632 | ) |

| $ | (402,724 | ) |

| $ | (216,323 | ) |

| $ | (255,973 | ) |

| $ | (160,093 | ) |

| $ | (608,339 | ) |

| $ | (562,816 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Net loss per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Basic |

| $ | (0.00 | ) |

| $ | (0.00 | ) |

| $ | (0.01 | ) |

| $ | (0.01 | ) |

| $ | (0.00 | ) |

| $ | (0.00 | ) |

| $ | (0.01 | ) |

| $ | (0.01 | ) |

Diluted |

| $ | (0.00 | ) |

| $ | (0.00 | ) |

| $ | (0.01 | ) |

| $ | (0.01 | ) |

| $ | (0.00 | ) |

| $ | (0.00 | ) |

| $ | (0.01 | ) |

| $ | (0.01 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Weighted average number of shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Basic & diluted |

|

| 58,823,116 |

|

|

| 31,790,918 |

|

|

| 58,722,023 |

|

|

| 29,493,137 |

|

|

| 58,823,116 |

|

| 58,823,116 |

|

| 58,823,116 |

|

| 58,722,023 |

| |||

Intangible Assets

The Company records identifiable intangible assets at fair value on the date of acquisition and evaluates the useful life of each asset.

Finite-lived intangible assets primarily consist of software development capitalized. Finite-lived intangible assets are amortized on a straight-line basis and are tested for recoverability if events or changes in circumstances indicate that their carrying amounts may not be recoverable. These intangibles have useful lives ranging from 1 to 10 years. No events or changes in circumstances indicate that impairment existed as of DecemberMarch 31, 2015.

Going Concern

The accompanying financial statements have been prepared in conformity with generally accepted accounting principles, which contemplate the continuation of the Company as a going concern. The Company reported accumulated deficit of $3,504,729 as of December 31, 2015. The Company also incurred net losses of $402,724 and $216,323 for the six-month periods ended December 31, 2015 and 2014, respectively and had negative working capital for the six-month periods ended December 31, 2015 and 2014. To date, these losses and deficiencies have been financed principally through the loans from related parties and from third parties.

In view of the matters described, there is substantial doubt as to the Company's ability to continue as a going concern without a significant infusion of capital. We anticipate that we will have to raise additional capital to fund operations over the next 12 months. To the extent that we are required to raise additional funds to acquire properties, and to cover costs of operations, we intend to do so through additional offerings of debt or equity securities. There are no commitments or arrangements for other offerings in place, no guaranties that any such financings would be forthcoming, or as to the terms of any such financings. Any future financing will involve substantial dilution to existing investors.

Subsequent to the period ended December 31, 2015, the Company entered into an equity line funding agreement with Spider Investments, LLC to sell up to $1,500,000 of our common stock, subject to certain terms and conditions some of which are out of our control, including the (i) filing and obtaining effectiveness of a registration statement registering the issuance of our shares of common stock under the Act to be issued pursuant to the equity line and (ii) certain volume and other trading conditions of our common stock. The Company plans to file the registration statement and to obtain effectiveness thereof as soon as practicable.

Recently Issued Accounting Pronouncements

In August 2014, the FASB issued Accounting Standards Update No. 2014-15, Presentation of Financial Statements – Going Concern (Subtopic 205-40), Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern (ASU 2014-15). The guidance in ASU 2014-15 sets forth management’s responsibility to evaluate whether there is substantial doubt about an entity’s ability to continue as a going concern as well as required disclosures. ASU 2014-15 indicates that, when preparing financial statements for interim and annual financial statements, management should evaluate whether conditions or events, in the aggregate, raise substantial doubt about the entity’s ability to continue as a going concern for one year from the date the financial statements are issued or are available to be issued. This evaluation should include consideration of conditions and events that are either known or are reasonably knowable at the date the financial statements are issued or are available to be issued, as well as whether it is probable that management’s plans to address the substantial doubt will be implemented and, if so, whether it is probable that the plans will alleviate the substantial doubt. ASU 2014-15 is effective for annual periods ending after December 15, 2016, and interim periods and annual periods thereafter. Early application is permitted. The Company is currently evaluating the impact of the adoption of this standard on its consolidated financial statements.

In November 2015, the Financial Accounting Standards Board (FASB) issued ASU 2015-17, “Balance Sheet Classification of Deferred Taxes” (ASU 2015-17), which changes how deferred taxes are classified on the balance sheet and is effective for financial statements issued for annual periods beginning after December 15, 2016, with early adoption permitted. ASU 2015-17 requires all deferred tax assets and liabilities to be classified as non-current. The Company is currently evaluating the impact of the adoption of this standard on its consolidated financial statements.

In January 2016, the FASB issued ASU 2016-01, “Recognition and Measurement of Financial Assets and Financial Liabilities” (ASU 2016-01), which requires equity investments that are not accounted for under the equity method of accounting to be measured at fair value with changes recognized in net income and updates certain presentation and disclosure requirements. ASU 2016-01 is effective beginning after December 15, 2017. The adoption of this guidance is not expected to have a material impact on the Company’s results of operations, financial position or disclosures.

In February 2016, the FASB issued ASU No. 2016-02, “Leases,” which requires lessees to recognize right-of-use assets and lease liabilities, for all leases, with the exception of short-term leases, at the commencement date of each lease. This ASU requires lessees to apply a dual approach, classifying leases as either finance or operating leases based on the principle of whether or not the lease is effectively a financed purchase by the lessee. This classification will determine whether lease expense is recognized based on an effective interest method or on a straight-line basis over the term of the lease. This ASU is effective for annual periods beginning after December 15, 2018 and interim periods within those annual periods. Early adoption is permitted. The amendments of this update should be applied using a modified retrospective approach, which requires lessees and lessors to recognize and measure leases at the beginning of the earliest period presented. The adoption of this guidance is not expected to have a material impact on the Company’s results of operations, financial position or disclosures.

| F-8 |

| Table of Contents |

In March 2016, the FASB issued ASU 2016-09, “Improvements to Employee Share-Based Payment Accounting.” The guidance simplifies accounting for share-based payments, most notably by requiring all excess tax benefits and tax deficiencies to be recorded as income tax benefits or expense in the income statement and by allowing entities to recognize forfeitures of awards when they occur. This new guidance is effective for annual reporting periods beginning after December 15, 2016 and may be adopted prospectively or retroactively. The Company is currently evaluating the impact the adoption of this standard would have on its financial condition, results of operations and cash flows.

In May 2016, the FASB issued ASU 2016-12, “Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients” (“ASU 2016-12”), which amends the guidance in the new revenue standard on collectability, noncash consideration, presentation of sales tax, and transition. The amendments are intended to address implementation issues and provide additional practical expedients to reduce the cost and complexity of applying the new revenue standard. The new guidance is effective for annual periods beginning after December 15, 2017, including interim periods within those annual periods, which will be our interim period beginning January 1, 2018. Early adoption is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods with that reporting period. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In August 2016, the FASB issued ASU 2016-15, regarding ASC Topic 230 “Statement“Statement of Cash Flows.” This update addresses eight specific cash flow issues with the objective of reducing the existing diversity in practice. The new guidance is effective for annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period. Early adoption is permitted. The Company does not expect the adoption of this standard to have a significant effect on its consolidated financial statements.

There were no other new accounting pronouncements during the six-monththree month period ended December 31,September 30, 2015 that we believe would have a material impact on our financial position or results of operations.

Reclassification

Certain prior year amounts have been reclassified for consistency with the current period presentation. These reclassifications had no effect on the reported results of operations or cash flow.

Going Concern

The accompanying financial statements have been prepared in conformity with generally accepted accounting principles, which contemplate the continuation of the company as a going concern. The Company reported accumulated deficit of $4,826,321 as of March 31, 2017. The Company also incurred net losses of $608,339 and $562,816 for the nine-month periods ended March 31, 2017 and 2016, respectively and had negative working capital for the nine-month periods ended December 31, 2016 and 2015. To date, these losses and deficiencies have been financed principally through the loans from related parties and from third parties. In view of the matters described, there is substantial doubt as to the Company's ability to continue as a going concern without a significant infusion of capital. We anticipate that we will have to raise additional capital to fund operations over the next 12 months. To the extent that we are required to raise additional funds to acquire properties, and to cover costs of operations, we intend to do so through additional offerings of debt or equity securities. There are no commitments or arrangements for other offerings in place, no guaranties that any such financings would be forthcoming, or as to the terms of any such financings. Any future financing will involve substantial dilution to existing investors.

Note 3 – TRADE RECEIVABLES

Trade receivables consist principally of accounts receivable from sales to small to medium sized businesses, principally in Australia, Europe and the United States. Trade receivables are recorded at the invoiced amount and net of allowances for doubtful accounts. The allowance for doubtful accounts represents management's estimate of the amount of probable credit losses in existing accounts receivable, as determined from a review of past due balances and other specific account data. The assessment includes actually incurred historical data as well as current economic conditions. Account balances are written off against the allowance when management determines the receivable is uncollectible.

Collectability of trade receivables is reviewed on an ongoing basis. Debts which are known to be uncollectable are written off by reducing the carrying amount directly. A provision for impairment of trade receivables is raised when there is objective evidence that the consolidated entity or parent entity will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganization and default or delinquency in payments (more than 60 days overdue) are considered indicators that the trade receivable may be impaired. The amount of the impairment allowance is the difference between the asset's carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. Cash flows relating to short-term receivables are not discounted if the effect of discounting is immaterial.

Trade receivables that are past their normal payment terms are overdue and once 60 days past due are considered delinquent. Minimum payment terms vary by product. The maximum payment term for all products is 90 days. All trade receivables that are overdue are individually assessed for impairment.

The allowances for doubtful accounts as of DecemberMarch 31, 20152017 and June 30, 20152016 are $142,145 and $147,870 and $140,870 respectively.

Note 4 – INTANGIBLE ASSETS

Intangible assets consist of the following as of DecemberMarch 31, 20152017 and June 30, 2015:2016:

|

| December 31, |

| June 30, |

|

| March 31 |

| June 30 |

| ||||||

|

| 2015 |

| 2015 |

|

| 2017 |

| 2016 |

| ||||||

Website |

| $ | 60,781 |

| $ | 60,781 |

|

| $ | 60,781 |

| $ | 60,781 |

| ||

Accumulated amortization |

| $ | (19,141 | ) |

| $ | (15,770 | ) |

| $ | (29,253 | ) |

| $ | (22,512 | ) |

|

| $ | 41,640 |

|

| $ | 45,011 |

|

| $ | 31,528 |

| $ | 38,269 |

| |

| F-9 |

| Table of Contents |

The intangible assets are amortized over 1 to 10 years. Amortization expense was $3,371$6,743 and $4,286$5,057 for the six-monthnine month periods ended DecemberMarch 31, 20152017 and 20142016 respectively Amortization expense was $1,685$3,372 and $1,709$1,685 for the three-monththree month periods ended DecemberMarch 31, 20152017 and 20142016 respectively.

Note 5 – TRADE AND OTHER PAYABLES

As of DecemberMarch 31, 20152017 and June 30, 2015,2016, trade and other payable are comprised of the following:

|

| December 31, 2015 |

| June 30, 2015 |

|

| March 31 |

| June 30 |

| ||||||

|

|

|

|

| 2017 |

| 2016 |

| ||||||||

Trade payable |

| $ | 371,575 |

| $ | 463,107 |

|

| $ | 567,225 |

| $ | 593,009 |

| ||

| Officer compensation |

| $ | 122,778 |

| $ | 83,739 |

| |||||||||

Payroll payable |

| $ | 13,561 |

| $ | 91,018 |

|

| $ | 104,725 |

| $ | 29,616 |

| ||

Payroll taxes |

| $ | 109,017 |

| $ | - |

|

| $ | 160,662 |

| $ | 158,518 |

| ||

Employee benefits |

| $ | 82,671 |

| $ | 82,671 |

|

| $ | 92,626 |

| $ | 88,097 |

| ||

Other liabilities |

| $ | 34,650 |

| $ | (3,402 | ) |

| $ | 70,122 |

|

| $ | 55,793 |

| |

|

| $ | 611,474 |

|

| $ | 633,394 |

|

| $ | 1,118,137 |

| $ | 1,008,772 |

| |

Note 6 – TRADE FINANCING

The Company entered into a Note Purchase Agreement for $65,000 dated January 4, 2017 with a third party. The amount is due on July 4, 2017 and bears interest at the rate of 18%. The agreement is for the purchase of inventory and is repaid in line with sales of inventory units with repayments beginning in the March quarter as the inventory is received and sold.

The Company has a trade financing agreement with a financial institution in Australia with a maximum limit of AUD $150,000 at an interest rate of 20.95% per annum. The Company reached a settlement with its obligation with the entity in the amount of AUD $165,523. The amount is to be paid through application of its EMDG grant and up to 25% of the Company's store sales in Australia. All of the amounts referenced are in Australian dollars. As of DecemberMarch 31, 20152017 and June 30, 2015,2016, the Company had outstanding balances of USD $89,950$57,841 and $112,436,$72,936, respectively.

On August 14, 2014 the Company entered into a trade finance agreement with an entity in the United States with a total maximum facility of $1,500,000 based on $1,000,000 towards sales invoiced and $500,000 towards purchase order financing. As of DecemberMarch 31, 20152017 and June 30, 2015,2016, the Company had an outstanding balance of $559,552$133,592 and $646,078,$176,783, respectively.

On November 20, 2014,2, 2016, the Company entered into a new retail trade financemerchant agreement with an entitya capital funding group for a purchase price of $35,000 and purchased amount of $47,250. The Company is amortizing the excess of purchase amount over the purchase price, over the term of the financing of 21 months. Pursuant to the agreement, the Company cannot obtain future financing by selling receivables without consent from the lender. The Merchant holds a security interest in Australiaall accounts and proceeds. During the nine-month period ended March 31, 2017, the Company amortized interest of $2,197. As of March 31, 2017, the balance owed to the lender amounted to $15,324.

On November 3, 2016, the Company entered into a payments rights purchase and sale agreement for AUD $75,000$72,500. The financing has a purchase price of $50,000 with 100 equalthe purchased amount of $72,500. The Company is amortizing the excess of purchased amount over purchase price, over the term of the financing of six months. The Company has to make daily payments of AUD $871.80 daily.$575.40 to the lender. During the nine-month period ended March 31, 2017, the Company amortized $18,750 of the excess purchased amount, as interest expense, in the accompanying financials. As of September 30, 2015 and June 30, 2015,March 31, 2017, the balance owed to the lender amounted to $27,190.

On November 29, 2016, the Company had outstanding balancesentered into a consignment agreement. It is a platform for funding advance inventory production. This facility allowed the Company to fund manufacturing with a consignment facility which pegs repayment to the sales of USD $0 and USD $21,139 (AUD $27,500), respectively.inventory. During the period ended March 31, 2017, the Company initially raised $21,928 for a purchase price of $26,313. This amount was paid off as of March 31, 2017. The difference of $4,385 was amortized over the period of financing. The Company again raised $114,888 for a purchase price of $133,342. The difference of $18,454 is being amortized over the period of financing. During the nine-month period ended March 31, 2017, the Company recorded an interest expense of $10,537.

| F-10 |

| Table of Contents |

Note 7 – LOANS–LOANS

In December 2013, the Companycompany entered into a short-termshort term loan arrangement in the amount of $100,000 with an individual. Terms of the note require interest payment of $5,000 on the repayment date, 30 days after the note date. If not repaid at that time, interest will accrue at the rate of $166 per day until the note is repaid. The outstanding balance as of DecemberMarch 31, 20152017 and as of June 30, 20152016 was $100,000 and $100,000 respectively. During the six-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, the Company recorded an interest of $30,046$45,318 and $7,386,$45,318, respectively, on the note. During the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, the Company recorded an interest of $14,940$15,272 and $14,772,$15,272, respectively, on the note.

In May 2014 and July 2014, the Company entered into two convertible loan agreements in the amount of $72,800 each. Interest accrued at the rate of 8% per annum. Loan and accrued interest were due in February 2015 and April 2015. The loans may be converted into common stock of the Company at any time by the election of the lender at a predetermined conversion price. During the quarter ended March 31, 2015, $72,800 was converted into 2,402,141 shares and $20,000 was converted into 943,396 shares. The remaining loan balance plus accrued interest was repaid during the quarter ended March 31, 2015. The outstanding balance as of December 31, 2015 and as of June 30, 2015 was $0.

From May 2014 to September 2015,March 2017, the Company entered into several convertible loan agreements with a lender aggregating in the amount of $121,500.$162,500. The notes bear interest at 6% per annummonth and are due and payable six months from the date of each note. The loans may be converted into common stock at any time by the election of the lender after a period of six months at a predetermined conversion price. The outstanding balance as of DecemberMarch 31, 20152017 and as of June 30, 20152016 was $131,500$162,500 and $121,500$131,500 respectively. The Company accrued interest of $3,945$7,313 and $0$5,918 during the three-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively. The Company accrued interest of $2,122$2,438 and $0$1,973 during the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively.

In December 2014, the Company entered into a loan agreement in the amount of $10,000 AUD with an individual in Australia. The note was repaid in full in July 2015.

In June 2015, the Company entered into a secured promissory note in the amount of $500,000 with a Delaware statutory trust. The note bears interest at the rate of 18% per annum and iswas due or before July 1, 2017. The note has various covenants attached including one in which all credit card receipts are to be swept into an account which will fund payments on the note that are not in excess of the minimum quarterly payments required. As a condition of the note, an affiliate of the lender was granted a warrant to purchase 6,000,000 shares of the common stock of Banjo & Matilda, Inc.the Company at a price of $.08 in whole or in part. The outstanding balance as of December 31, 2015, net of related discount,June 30, 2016 was $415,208.$500,000.

On February 5, 2016, The Company signed an amendment to the secured promissory note extending the maturity date by one year to July 17, 2018. The amendment changed the terms of the credit card receipts used to fund payments required by the note. The amendment also cancelled the warrants to purchase 6,000,000 shares at a price of $0.08. New warrants were granted to purchase 6,000,000 shares at $0.05 per share and to purchase 2,000,000 shares at $0.02 per share. The Company determined that the fair value of the warrants using the Black – Scholes model withand recorded the variableadditional value of $41,467 for the modified warrants. The variables used for the Black –Scholes model are as listed below:

| · | Volatility: | |

| · | Risk free rate of return: | |

| · | Expected term: |

In connection with the issuance of the above notes, the Company recorded a note discount of $115,274. The Company amortized $28,470$37,601 and $0,$41,732, of the note discount during the six-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively. The Company amortized $14,235$12,534 and $0,$13,262, of the note discount during the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively. The Company recorded an interest of $36,721$67,500 and $0,$51,847, on the note during the six-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively. The Company recorded an interest of $14,622$22,500 and $0,$15,125, on the note during the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, respectively.

Subsequent to the period, on February 5, 2016, the Company signed an amendment to the secured promissory note extending the maturity date by one year to July 17, 2018.

Related Party Payable

The Company had several outstanding convertible note agreements with a shareholder aggregating to AUD $370,000 plus interest.$370,000. The notes had interest rates varying from 6% to 15% per annum. In March 2015, the outstanding balance and accrued interest was refinanced by a AUD526,272$526,272 convertible note. The Convertible Note bears interest at the rate of 18% per annum and is due on or before April 30, 2017. The interest portion of the note shall be paid weekly starting in April 2015. Principle payments of $9,929 AUD weekly arewere to commence in April 2016. All or any portion of the principal amount of the Convertible Note and all accrued interest is convertible at the option of the holder into common stock of the Company at a conversion price of five cents ($0.05) per share, subject to various standard provisions. The outstanding balance as of DecemberMarch 31, 20152017 and June 30, 2015,2016, net of related discount, was USD $379,591$381,523 and $217,855,$370,008, respectively. The Company determined the fair value of the convertible note of $80,909 using the intrinsic value method. The Company recorded an amortization of the debt discount of $7,717$11,575 and $0,$11,533, during the six-monthnine month period ended DecemberMarch 31, 20152017 and 2014,2016, respectively. The Company recorded an amortization of the debt discount of $3,858 and $0,$3,858, during the three-monththree month period ended DecemberMarch 31, 20152017 and 2014,2016, respectively. During the six-monthnine month periods ended DecemberMarch 31, 20152017 and 2014,2016, the Company recorded an interest of $34,227$63,909 and $0,$51,326, respectively, on the note. During the three-monththree month periods ended DecemberMarch 31, 20152017 and 2014,2016, the Company recorded an interest of $17,049$21,303 and $0,$17,099, respectively, on the note.

| Table of Contents |

The Company has liabilities payable in the amount of $143,422$181,737 and $217,855$183,269 to shareholders and officers of the Company as of DecemberMarch 31, 20152017 and June 30, 2015,2016, respectively. The note bears interest at the rate of 3% per annum and was due on or before June 30, 2014. The outstanding balance, including accrued interest, may be converted into common shares of Banjo & Matilda, Inc. at a pre-determined rate. The Company has granted the Lenders a security interest in the intellectual property of the Borrower.

Scheduled principal payments on loans are as follow;

Year ending December 31, Loan 1 Loan 2 Loan 3 Loan 4 Loan 5 Total 2016 2017 $ 100,000 $ 131,806 $ 9,107 $ 274,786 $ 143,422 $ 659,121 $ - $ - $ 490,893 $ 129,759 $ - $ 620,652 $ 100,000 $ 131,806 $ 500,000 $ 404,545 $ 143,422 $ 1,279,773 Year ending March 31, Loan 1 Loan 2 Loan 3 Loan 4 Loan 5 Total 2018 $ 100,000 $ 162,500 $ 331,500 $ 387,328 $ 181,737 $ 1,163,065 2019 $ - $ - $ 168,500 $ - $ - $ 168,500 $ 100,000 $ 162,500 $ 500,000 $ 387,328 $ 181,737 $ 1,331,565

Note 8 – COMMITMENTS

The Company leases commercial space in Sydney, Australia that serves as its flagship as well as a retail store. We lease approximately 2,500 square feet of space pursuant to a three-yearthree year lease agreement which expired in October 2014. After expiration, the lease converted to a month-to-month basis. The annual rent for the premises is AUD $57,200.

The Company also leases space on an as needed basis in Santa Monica, California that serves as its corporate headquarters. We utilize approximately 1,000 square feet of space pursuant to a month-to-month basis.

For the six-monthnine month periods ended DecemberMarch 31 20152017 and 20142016 the aggregate rental expense was $36,715$33,072 and $24,637,$53,416, respectively. For the three-monththree month periods ended DecemberMarch 31 20152017 and 20142016 the aggregate rental expense was $23,350$7,014 and $11,398,$16,701, respectively.

Note 9 – INCOME TAXES

Based on the available information and other factors, management believes it is more likely than not that the net deferred tax assets at, DecemberMarch 31 20152017 and June 30, 20152016 will not be fully realizable. Accordingly, management has recorded a full valuation allowance against its net deferred tax assets at, DecemberMarch 31 20152017 and June 30, 2015.2016. At DecemberMarch 31 20152017 and June 30, 2015,2016, the Company had federal net operating loss carry-forwards of approximately $3,340,000$4,229,000 and $2,555,000,$3,664,000, respectively, expiring beginning in 2032.

Deferred tax assets consist of the following components:

|

| December 31, |

| June 30, |

|

| 31 Mar, |

| June 30, |

| ||||||

|

| 2015 |

| 2015 |

|

| 2017 |

| 2016 |

| ||||||

Net loss carryforward |

| $ | 1,030,000 |

| $ | 767,000 |

|

| $ | 1,264,500 |

| $ | 1,095,000 |

| ||

Valuation allowance |

| $ | (1,030,000 | ) |

| $ | (767,000 | ) |

| $ | (1,264,500 | ) |

| $ | (1,095,000 | ) |

Total deferred tax assets |

| $ | - |

| $ | - |

|

| $ | - |

| $ | - |

| ||

| Table of Contents |

Note 10 – STOCKHOLDERS' EQUITY

CommonPreferred Stock

On July 24, 2014,Pursuant to an Employment Agreement (the "Agreement") with the Chief Executive Officer on November 15, 2013, The Company agreed to issue 55,200issued 1,000,000 undesignated shares of Preferred Stock each having a par value of $0.00001. The preferred shares shall be entitled to 100 votes to every one share of common stock. The Preferred Shares shall only valid during the Company stock for $13,800 or $0.25 per shareterm of this Agreement. The Agreement was renewed on November 15, 2016. At the end of the Agreement, November 15, 2019, the shares shall be cancelled and returned to an individual investor. Treasury and the Executive shall have no preferential voting rights. If this Agreement is renewed the preferred shares remain the Executives.

On October 28, 2014, the Company agreed to issue 5,833,333 shares of the Company stock to the original shareholders of Banjo & Matilda Pty Ltd related to the merger and reorganization based on the original agreement.

On October 28, 2014, the Company agreed to issue 92,593 shares of common stock to an individual for compensation from Banjo Australia. The shares were valued at $15,339 or approximately $0.17 per share.

On November 3, 2014, the Company issued 25,000 shares of common stock to an individual in exchange for interest expense. The shares were valued at $5,000 or $.25 per share.Common Stock

During the quarternine month period ended March 31, 2015, the Company agreed to convert $92,800 of convertible debt for 3,345,537 shares of common stock at prices from $0.02 to $0.0901 per share to a corporate investor.

During the quarter ended March 31, 2015, the Company agreed to issue 400,000 shares of the Company stock for $60,000 or $0.15 per share to a company for consulting services. The terms of the service agreement is from January 1, 2015 to June 1, 2015. As of June 30, 2015, the Company recognized consulting expense of $60,000.

During the first and second quarter of 2015, the Company agreed to issue 21,039,970 shares of the Company stock for $450,799 or approximately $0.02 per share to five investors.

During the fiscal year ended June 30, 2015, the Company voided 475,000 shares of the Company stock for the value of $95,000. The shares were originally considered converted from debt when they were in fact not converted. The debt is still outstanding.

During the six-month period ended December 31, 2015,2016, the Company issued 500,000 shares of the Company’s common stock for settlement of an outstanding vendor balance amounting to USD $27,123.

No shares were issued during the nine month period ended March 31, 2017.

Note 11 – RELATED PARTY TRANSACTIONS

During the six-monthnine month period ended DecemberMarch 31, 2015,2017, the Company paid $14,076$0 and $0 as compensation, respectively, to the sister and mother of the CEO. During the six-monthnine month period ended DecemberMarch 31, 2015,2016, the Company paid $20,113 and $1,005 as compensation, respectively, to the sister and mother of the CEO. During the nine month period ended March 31, 2017 and 2016, the Company accrued interest of $14,149$1,532 and $29,653, respectively, on a loan owed to the CEO of the Company.

Note 12 – SUBSEQUENT EVENTS

Subsequent to the March period, ended December 31, 2015, on November 2, 2016,Banjo & Matilda filed a form S-8 authorizing the issuance of 20,000,000 shares to fulfill its obligations under various employee and consulting agreements. On April 4th, 2017 the Company entered into a merchant agreement with a capital funding group for $47,250. Pursuantissued 5,400,000 shares of common stock pursuant to the agreement,registration statement. On May 1, 2017 Banjo & Matilda filed a form S-8 POS amending the Company cannot obtain future financing by selling receivables without consent from the lender. The Merchant holds a security interest in all accounts and proceeds.registration statement to deregister 13,600,000 shares of common stock.

| Table of Contents |

Subsequent to the period ended December 31, 2015, on November 3, 2016, the Company entered into a payments rights purchase and sale agreement for $72,500.

Subsequent to the period, on February 5, 2016, The Company signed an amendment to the secured promissory note of $500,000, extending the maturity date by one year to July 17, 2018. The amendment changed the terms of the credit card receipts used to fund payments required by the note. The amendment also cancelled the warrants to purchase 6,000,000 shares at a price of $0.08. New warrants were granted to purchase 6,000,000 shares at $0.05 per share and to purchase 2,000,000 shares at $0.02 per share. The Company determined the fair value of the warrants using the Black – Scholes model and recorded the additional value of $87,553 for the modified warrants. The variables used for the Black –Scholes model are as listed below:

Subsequent to the period, on October 27, 2015, the Company entered into a convertible loan agreement in the amount of $41,000 with a lender with whom they have several other loans. The note bears interest at 6% per annum and is due and payable in six months. The loan may be converted into common stock at any time by the election of the lender after a period of six months at a predetermined conversion price.

Subsequent to the period, on November 29, 2016, the Company entered into a consignment agreement. It is a platform for funding advance inventory production. This facility allowed the Company to fund manufacturing with a consignment facility which pegs repayment to the sales of inventory.

Subsequent to the period ended December 31, 2015, the Company entered into an equity line funding agreement with Spider Investments, LLC to sell up to $1,500,000 of our common stock, subject to certain terms and conditions some of which are out of our control, including the (i) filing and obtaining effectiveness of a registration statement registering the issuance of our shares of common stock under the Act to be issued pursuant to the equity line and (ii) certain volume and other trading conditions of our common stock. The Company plans to file the registration statement within 30 days from the date hereof and to obtain effectiveness thereof as soon as practicable.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our Company’s financial condition and results of operations should be read in conjunction with our unaudited financial statements and the related notes included elsewhere in this report and with the financial statements and notes thereto included in the Company’s most recent Annual Report on Form 10-K. This discussion contains forward-looking statements that involve risks and uncertainties. Actual results and the timing of selected events could differ materially from those anticipated in these forward-looking statements.

Results of Operations

The following discussion of the results of operations constitutes management’s view of the factors that affected the financial and operating performance for the sixnine months ended DecemberMarch 31, 2015 and 2014.2017. This discussion should be read in conjunction with the financial statements and notes thereto contained elsewhere in this report. The Company has a June 30 fiscal year end.

During the six-monthnine-month period ended DecemberMarch 31, 2015,2017, the transactions of the Company were denominated in US Dollars. All the transactions which were denominated in other currencies were converted to US$ on the date of settlement and the exchange gains and losses were recorded in the statement of operations. No change was recorded in the comprehensive income (loss). During the three-month period ended September 30, 2014, the accounts of the Company were maintained, and its financial statements were expressed, in AUD. Such financial statements were translated into USD with the AUD as the functional currency. All assets and liabilities were translated at the exchange rate at the balance sheet date, stockholder's equity is translated at the historical rates and income statement items are translated at the average exchange rate for the period. Transactions in foreign currencies are initially recorded at the functional currency rate ruling at the date of transaction. Any differences between the initially recorded amount and the settlement amount are recorded as a gain or loss on foreign currency transaction in the statements of operations. The resulting translation adjustments are reported under other comprehensive income as a component of shareholders' equity. There were no significant fluctuations in the exchange rate for the conversion of AUD to USD after the balance sheet date.

Summary

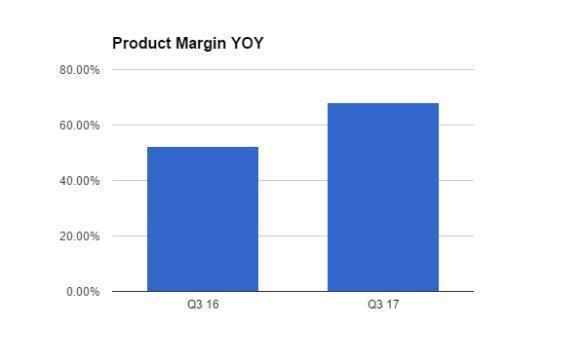

Management is pleased with the continued operating improvements after implementing our new digital vertical strategy as outlined in March 2017. See a summary of the revised strategy at the end of the Management’s Discussion and Analysis. Unit economics and operating metrics continued to improve in the March 2017 quarter, demonstrating the potential of the business model.

The March Q3-17 operating results reflect the revised strategy and demonstrates underlying unit economics which position the company to leverage its new operating platform to efficiently drive profitability.

Revenue

Sales

The Company generated revenue of $133,408 during the three-months ended March 31, 2017 compared to $446,509 for the same period during the prior fiscal year, and $493,450 during the 9 months to March 31 compared to $2,058,876 for the same period during the prior fiscal year. The reduction in sales from is a result of eliminating our low margin wholesale sales channel per our new operating strategy adopted in 2016. While sales were down significantly in the Q3-17 vs Q3-16, the underlying online sales trend strengthened in the current quarter. The March quarter is traditionally the weakest period and online sales were down only marginally compared to the December 2016 quarter, which is traditionally the strongest quarter

Inventory

Management is highly focused on inventory efficiency. The March quarter revenue of $133,408 was generated utilizing an ending inventory value of $51,718 for the period compared to $129,272 ending inventory value in the December 2016 quarter, resulting in a significant (>200%) increase in inventory efficiency, stock turn and sell through. This represents a significant reduction in working capital requirements, and therefore meaningful improvement working capital leverage as the company scales.

Our inventory level remains low, and additional inventory in this quarter would have resulted in meaningfully higher sales (5). Requests by customers to be notified when out-of-stock items come back in-stock reached a peak in this period compared to all prior periods. Based on web site usage data, out of stock notification requests, and historical sales data, management believes sales could have been more than 50% higher during this period.