UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2023March 31, 2024

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 000-55190

NORTHSTAR HEALTHCARE INCOME, INC.

(Exact Name of Registrant as Specified in its Charter)

| | | | | |

| Maryland | 27-3663988 |

| (State or Other Jurisdiction of | (IRS Employer |

| Incorporation or Organization) | Identification No.) |

16 East 34th Street, 18th575 Lexington Avenue, 14th Floor, New York, NY 1001610022

(Address of Principal Executive Offices, Including Zip Code)

(929) 777-3135

(Registrant’s Telephone Number, Including Area Code)

16 East 34th Street, 18th Floor,

New York, NY 10016

(Former name or former address, if changed since last report.)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common stock, par value $0.01 per share | None | None |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ¨ | Accelerated filer | ¨ | Non-accelerated filer | ý | Smaller reporting company | ☐ |

| | | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ý

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

The Company has one class of common stock, $0.01 par value per share, 185,712,103 shares outstanding as of November 13, 2023.May 7, 2024.

NORTHSTAR HEALTHCARE INCOME, INC.

FORM 10-Q

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, or Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “seek,” “anticipate,” “estimate,” “believe,” “could,” “project,” “predict,” “continue,” “future” or other similar words or expressions. Forward-looking statements are not guarantees of performance and are based on certain assumptions, discuss future expectations, describe plans and strategies, contain projections of results of operations or of financial condition or state other forward-looking information. Such statements include, but are not limited to, those relating to our ability to make distributions to our stockholders; our ability to retain our senior executives and other sufficient personnel to manage our business; our ability to realize substantial efficiencies as well as anticipated strategic and financial benefits of the internalization of our management function as operating costs and business disruption may be greater than expected;function; the operating performance of our investments,investments; our financing needs,needs; the effects of our current strategies and investment activitiesactivities; and our ability to effectively deploy capital. Our ability to predict results or the actual effect of plans or strategies is inherently uncertain. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements and you should not unduly rely on these statements. These forward-looking statements involve risks, uncertainties and other factors that may cause our actual results in future periods to differ materially from those forward-looking statements.

All forward-looking statements included in this Quarterly Report on Form 10-Q are based on information available to us on the date hereof and we are under no duty to update any of the forward-looking statements after the date of this report to conform these statements to actual results.

Factors that could have a material adverse effect on our operations and future prospects are set forth in our filings with the U.S. Securities and Exchange Commission, or the SEC, including Part I, Item 1A of our Annual Report on Form 10-K for the fiscal year ended December 31, 20222023 and in Part II, Item 1A of this Quarterly Report on Form 10-Q under the heading “Risk Factors.” The risk factors set forth in our filings with the SEC could cause our actual results to differ significantly from those contained in any forward-looking statement contained in this report.

PART I—Financial Information

Item 1. Financial Statements

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Dollars in Thousands, Except Per Share Data)

| | September 30, 2023 (Unaudited) | | December 31, 2022 |

| March 31, 2024 (Unaudited) | | | March 31, 2024 (Unaudited) | | December 31, 2023 |

| Assets | Assets | | | | Assets | | | |

| Cash and cash equivalents | Cash and cash equivalents | $ | 87,581 | | | $ | 103,926 | |

| Restricted cash | Restricted cash | 11,386 | | | 11,734 | |

| Operating real estate, net | Operating real estate, net | 894,245 | | | 933,002 | |

| Investments in unconsolidated ventures ($3,075 held at fair value as of September 30, 2023) | 128,026 | | | 176,502 | |

| | Investments in unconsolidated ventures ($142 held at fair value as of March 31, 2024 and December 31, 2023) | |

| Assets held for sale | |

| Receivables, net | Receivables, net | 2,253 | | | 2,815 | |

| Intangible assets, net | Intangible assets, net | 2,000 | | | 2,253 | |

| Other assets | Other assets | 10,425 | | | 7,603 | |

Total assets(1) | Total assets(1) | $ | 1,135,916 | | | $ | 1,237,835 | |

| | Liabilities | Liabilities | |

| Liabilities | |

| Liabilities | |

| Mortgage notes payable, net | Mortgage notes payable, net | $ | 901,610 | | | $ | 912,248 | |

| | Mortgage notes payable, net | |

| Mortgage notes payable, net | |

| Due to related party | Due to related party | 292 | | | 469 | |

| Escrow deposits payable | Escrow deposits payable | 1,023 | | | 993 | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | 23,967 | | | 21,034 | |

| Other liabilities | Other liabilities | 1,592 | | | 2,019 | |

Total liabilities(1) | Total liabilities(1) | 928,484 | | | 936,763 | |

| Commitments and contingencies (Note 12) | Commitments and contingencies (Note 12) | | | | Commitments and contingencies (Note 12) | | | |

| Equity | Equity | |

| NorthStar Healthcare Income, Inc. Stockholders’ Equity | NorthStar Healthcare Income, Inc. Stockholders’ Equity | |

| Preferred stock, $0.01 par value, 50,000,000 shares authorized, no shares issued and outstanding as of September 30, 2023 and December 31, 2022 | — | | | — | |

| Common stock, $0.01 par value, 400,000,000 shares authorized, 185,712,103 and 195,421,656 shares issued and outstanding as of September 30, 2023 and December 31, 2022, respectively | 1,857 | | | 1,954 | |

| NorthStar Healthcare Income, Inc. Stockholders’ Equity | |

| NorthStar Healthcare Income, Inc. Stockholders’ Equity | |

| Preferred stock, $0.01 par value, 50,000,000 shares authorized, no shares issued and outstanding as of March 31, 2024 and December 31, 2023 | |

| Preferred stock, $0.01 par value, 50,000,000 shares authorized, no shares issued and outstanding as of March 31, 2024 and December 31, 2023 | |

| Preferred stock, $0.01 par value, 50,000,000 shares authorized, no shares issued and outstanding as of March 31, 2024 and December 31, 2023 | |

| Common stock, $0.01 par value, 400,000,000 shares authorized, 185,712,103 shares issued and outstanding as of March 31, 2024 and December 31, 2023 | |

| Additional paid-in capital | Additional paid-in capital | 1,716,701 | | | 1,729,589 | |

| Retained earnings (accumulated deficit) | Retained earnings (accumulated deficit) | (1,511,765) | | | (1,428,840) | |

| Accumulated other comprehensive income (loss) | — | | | (3,679) | |

| | Total NorthStar Healthcare Income, Inc. stockholders’ equity | |

| Total NorthStar Healthcare Income, Inc. stockholders’ equity | |

| Total NorthStar Healthcare Income, Inc. stockholders’ equity | Total NorthStar Healthcare Income, Inc. stockholders’ equity | 206,793 | | | 299,024 | |

| Non-controlling interests | Non-controlling interests | 639 | | | 2,048 | |

| Total equity | Total equity | 207,432 | | | 301,072 | |

| Total liabilities and equity | Total liabilities and equity | $ | 1,135,916 | | | $ | 1,237,835 | |

(1)Includes $174.4$107.6 million and $180.2$174.9 million of assets and liabilities, respectively, of certain VIEs that are consolidated by the Operating Partnership.Partnership as of March 31, 2024. Refer to Note 2, “Summary of Significant Accounting Policies.”

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in Thousands, Except Per Share Data)

(Unaudited)

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| 2023 | | 2022 | | 2023 | | 2022 |

| Three Months Ended March 31, | |

| Three Months Ended March 31, | |

| Three Months Ended March 31, | |

| 2024 | |

| 2024 | |

| 2024 | |

| Property and other revenues | |

| Property and other revenues | |

| Property and other revenues | Property and other revenues | | | | | | | |

| Resident fee income | Resident fee income | $ | 11,966 | | | $ | 11,274 | | | $ | 35,655 | | | $ | 32,987 | |

| Resident fee income | |

| Resident fee income | |

| Rental income | |

| Rental income | |

| Rental income | Rental income | 40,330 | | | 36,165 | | | 115,897 | | | 103,001 | |

| Other revenue | Other revenue | 1,078 | | | 300 | | | 2,893 | | | 457 | |

| Other revenue | |

| Other revenue | |

| Total property and other revenues | |

| Total property and other revenues | |

| Total property and other revenues | Total property and other revenues | 53,374 | | | 47,739 | | | 154,445 | | | 136,445 | |

| | Expenses | Expenses | |

| | Expenses | |

| | Expenses | |

| Property operating expenses | |

| Property operating expenses | |

| Property operating expenses | Property operating expenses | 36,890 | | | 35,134 | | | 106,993 | | | 101,258 | |

| Interest expense | Interest expense | 14,250 | | | 11,014 | | | 37,143 | | | 31,877 | |

| Interest expense | |

| Interest expense | |

| Transaction costs | Transaction costs | 358 | | | 857 | | | 455 | | | 857 | |

| Asset management fees - related party | — | | | 2,428 | | | — | | | 7,532 | |

| Transaction costs | |

| Transaction costs | |

| General and administrative expenses | |

| General and administrative expenses | |

| General and administrative expenses | General and administrative expenses | 2,921 | | | 2,859 | | | 10,424 | | | 10,300 | |

| Depreciation and amortization | Depreciation and amortization | 9,848 | | | 9,642 | | | 29,305 | | | 29,105 | |

| Depreciation and amortization | |

| Depreciation and amortization | |

| Impairment loss | |

| Impairment loss | |

| Impairment loss | Impairment loss | — | | | 18,500 | | | 43,422 | | | 31,502 | |

| Total expenses | Total expenses | 64,267 | | | 80,434 | | | 227,742 | | | 212,431 | |

| Total expenses | |

| Total expenses | |

| Other income (loss) | |

| Other income (loss) | |

| Other income (loss) | Other income (loss) | |

| Other income, net | Other income, net | — | | | — | | | 202 | | | 77 | |

| Other income, net | |

| Other income, net | |

| Gain (loss) on investments and other | |

| Gain (loss) on investments and other | |

| Gain (loss) on investments and other | Gain (loss) on investments and other | (347) | | | 325 | | | (4,662) | | | 660 | |

| Income (loss) before equity in earnings (losses) of unconsolidated ventures and income tax expense | Income (loss) before equity in earnings (losses) of unconsolidated ventures and income tax expense | (11,240) | | | (32,370) | | | (77,757) | | | (75,249) | |

| Income (loss) before equity in earnings (losses) of unconsolidated ventures and income tax expense | |

| Income (loss) before equity in earnings (losses) of unconsolidated ventures and income tax expense | |

| Equity in earnings (losses) of unconsolidated ventures | |

| Equity in earnings (losses) of unconsolidated ventures | |

| Equity in earnings (losses) of unconsolidated ventures | Equity in earnings (losses) of unconsolidated ventures | (127) | | | 2,872 | | | (6,595) | | | 39,427 | |

| Income tax expense | Income tax expense | (17) | | | (15) | | | (43) | | | (45) | |

| Income tax expense | |

| Income tax expense | |

| Net income (loss) | |

| Net income (loss) | |

| Net income (loss) | Net income (loss) | (11,384) | | | (29,513) | | | (84,395) | | | (35,867) | |

| Net (income) loss attributable to non-controlling interests | Net (income) loss attributable to non-controlling interests | 166 | | | 73 | | | 1,470 | | | 298 | |

| Net (income) loss attributable to non-controlling interests | |

| Net (income) loss attributable to non-controlling interests | |

| Net income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | |

| Net income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | |

| Net income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | Net income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | $ | (11,218) | | | $ | (29,440) | | | $ | (82,925) | | | $ | (35,569) | |

Net income (loss) per share of common stock, basic/diluted(1) | Net income (loss) per share of common stock, basic/diluted(1) | $ | (0.06) | | | $ | (0.15) | | | $ | (0.43) | | | $ | (0.18) | |

Net income (loss) per share of common stock, basic/diluted(1) | |

Net income (loss) per share of common stock, basic/diluted(1) | |

Weighted average number of shares of common stock outstanding, basic/diluted(1) | |

Weighted average number of shares of common stock outstanding, basic/diluted(1) | |

Weighted average number of shares of common stock outstanding, basic/diluted(1) | Weighted average number of shares of common stock outstanding, basic/diluted(1) | 185,712,103 | | | 194,670,948 | | | 191,367,117 | | | 194,032,819 | |

| Distributions declared per share of common stock | Distributions declared per share of common stock | $ | — | | | $ | — | | | $ | — | | | $ | 0.50 | |

| Distributions declared per share of common stock | |

| Distributions declared per share of common stock | |

(1) The Company had issued 203,742 and 116,712 restricted stock units as of September 30,March 31, 2024 and 2023, and September 30, 2022, respectively. The restricted stock units have been excluded from the diluted earnings per share calculation as their impact is anti-dilutive due to the net loss generated during the three and nine months ended September 30, 2023March 31, 2024 and 2022.2023.

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Dollars in Thousands)

(Unaudited)

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| 2023 | | 2022 | | 2023 | | 2022 |

| | Three Months Ended March 31, | |

| | Three Months Ended March 31, | |

| | Three Months Ended March 31, | |

| | 2024 | |

| | 2024 | |

| | 2024 | |

| Net income (loss) | |

| Net income (loss) | |

| Net income (loss) | Net income (loss) | | $ | (11,384) | | | $ | (29,513) | | | $ | (84,395) | | | $ | (35,867) | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | |

| Other comprehensive income (loss) | |

| Other comprehensive income (loss) | |

| Foreign currency translation adjustments related to investment in unconsolidated venture | |

| Foreign currency translation adjustments related to investment in unconsolidated venture | |

| Foreign currency translation adjustments related to investment in unconsolidated venture | Foreign currency translation adjustments related to investment in unconsolidated venture | | — | | | (1,664) | | | 3,679 | | | (4,602) | |

| Total other comprehensive income (loss) | Total other comprehensive income (loss) | | — | | | (1,664) | | | 3,679 | | | (4,602) | |

| Total other comprehensive income (loss) | |

| Total other comprehensive income (loss) | |

| Comprehensive income (loss) | |

| Comprehensive income (loss) | |

| Comprehensive income (loss) | Comprehensive income (loss) | | (11,384) | | | (31,177) | | | (80,716) | | | (40,469) | |

| Comprehensive (income) loss attributable to non-controlling interests | Comprehensive (income) loss attributable to non-controlling interests | | 166 | | | 73 | | | 1,470 | | | 298 | |

| Comprehensive (income) loss attributable to non-controlling interests | |

| Comprehensive (income) loss attributable to non-controlling interests | |

| Comprehensive income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | Comprehensive income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | | $ | (11,218) | | | $ | (31,104) | | | $ | (79,246) | | | $ | (40,171) | |

| Comprehensive income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | |

| Comprehensive income (loss) attributable to NorthStar Healthcare Income, Inc. common stockholders | |

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF EQUITY

(Dollars and Shares in Thousands)

| | Common Stock | | Additional Paid-in Capital | | Retained Earnings (Accumulated Deficit) | | Accumulated Other Comprehensive Income (Loss) | | Total Company’s Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| Shares | | Amount | |

| Balance as of December 31, 2021 | 193,121 | | | $ | 1,930 | | | $ | 1,720,719 | | | $ | (1,277,688) | | | $ | (486) | | | $ | 444,475 | | | $ | 2,343 | | | $ | 446,818 | |

| Share-based payment of advisor asset management fees | 698 | | | 7 | | | 2,722 | | | — | | | — | | | 2,729 | | | — | | | 2,729 | |

| Amortization of equity-based compensation | — | | | — | | | 15 | | | — | | | — | | | 15 | | | — | | | 15 | |

| Common Stock | | | Common Stock | | Additional Paid-in Capital | | Retained Earnings (Accumulated Deficit) | | Accumulated Other Comprehensive Income (Loss) | | Total Company’s Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| Shares | |

| Balance as of December 31, 2022 | |

| Balance as of December 31, 2022 | |

| Balance as of December 31, 2022 | |

| Non-controlling interests - contributions | Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 64 | | | 64 | |

| Non-controlling interests - distributions | Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (53) | | | (53) | |

| Other comprehensive income (loss) | Other comprehensive income (loss) | — | | | — | | | — | | | — | | | (568) | | | (568) | | | — | | | (568) | |

| Net income (loss) | Net income (loss) | — | | | — | | | — | | | (12,936) | | | — | | | (12,936) | | | (45) | | | (12,981) | |

| Balance as of March 31, 2022 (Unaudited) | 193,819 | | | $ | 1,937 | | | $ | 1,723,456 | | | $ | (1,290,624) | | | $ | (1,054) | | | $ | 433,715 | | | $ | 2,309 | | | $ | 436,024 | |

| Share-based payment of advisor asset management fees | 637 | | | 8 | | | 2,507 | | | — | | | — | | | 2,515 | | | — | | | 2,515 | |

| Balance as of March 31, 2023 (Unaudited) | |

| | Balance as of December 31, 2023 | |

| Balance as of December 31, 2023 | |

| Balance as of December 31, 2023 | |

| Amortization of equity-based compensation | Amortization of equity-based compensation | — | | | — | | | 13 | | | — | | | — | | | 13 | | | — | | | 13 | |

| Non-controlling interests - contributions | Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 113 | | | 113 | |

| Non-controlling interests - distributions | Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (61) | | | (61) | |

| Distributions declared | — | | | — | | | — | | | (97,052) | | | — | | | (97,052) | | | — | | | (97,052) | |

| Other comprehensive income (loss) | — | | | — | | | — | | | — | | | (2,370) | | | (2,370) | | | — | | | (2,370) | |

| Net income (loss) | Net income (loss) | — | | | — | | | — | | | 6,807 | | | — | | | 6,807 | | | (180) | | | 6,627 | |

| Balance as of June 30, 2022 (Unaudited) | 194,456 | | | $ | 1,945 | | | $ | 1,725,976 | | | $ | (1,380,869) | | | $ | (3,424) | | | $ | 343,628 | | | $ | 2,181 | | | $ | 345,809 | |

| Share-based payment of advisor asset management fees | 623 | | | 6 | | | 2,407 | | | — | | | — | | | 2,413 | | | — | | | 2,413 | |

| | Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 86 | | | 86 | |

| Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (74) | | | (74) | |

| | Other comprehensive income (loss) | — | | | — | | | — | | | — | | | (1,664) | | | (1,664) | | | — | | | (1,664) | |

| Net income (loss) | — | | | — | | | — | | | (29,440) | | | — | | | (29,440) | | | (73) | | | (29,513) | |

| Balance as of September 30, 2022 (Unaudited) | 195,079 | | | $ | 1,951 | | | $ | 1,728,383 | | | $ | (1,410,309) | | | $ | (5,088) | | | $ | 314,937 | | | $ | 2,120 | | | $ | 317,057 | |

| Balance as of March 31, 2024 (Unaudited) | |

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF EQUITYCASH FLOWS

(Dollars and Shares in Thousands)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Retained Earnings (Accumulated Deficit) | | Accumulated Other Comprehensive Income (Loss) | | Total Company’s Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| Shares | | Amount | | | | | | |

| Balance as of December 31, 2022 | 195,422 | | | $ | 1,954 | | | $ | 1,729,589 | | | $ | (1,428,840) | | | $ | (3,679) | | | $ | 299,024 | | | $ | 2,048 | | | $ | 301,072 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 45 | | | 45 | |

| Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (22) | | | (22) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Other comprehensive income (loss) | — | | | — | | | — | | | — | | | 1,248 | | | 1,248 | | | — | | | 1,248 | |

| Net income (loss) | — | | | — | | | — | | | (13,926) | | | — | | | (13,926) | | | (71) | | | (13,997) | |

| Balance as of March 31, 2023 (Unaudited) | 195,422 | | | $ | 1,954 | | | $ | 1,729,589 | | | $ | (1,442,766) | | | $ | (2,431) | | | $ | 286,346 | | | $ | 2,000 | | | $ | 288,346 | |

| Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 55 | | | 55 | |

| Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (33) | | | (33) | |

| Retirement of common stock (Note 8) | (9,710) | | | (97) | | | (13,302) | | | — | | | — | | | (13,399) | | | — | | | (13,399) | |

| Other comprehensive income (loss) | — | | | — | | | — | | | — | | | (844) | | | (844) | | | — | | | (844) | |

Reclassification of accumulated other comprehensive loss(1) | — | | | — | | | — | | | — | | | 3,275 | | | 3,275 | | | — | | | 3,275 | |

| Net income (loss) | — | | | — | | | — | | | (57,781) | | | — | | | (57,781) | | | (1,233) | | | (59,014) | |

| Balance as of June 30, 2023 (Unaudited) | 185,712 | | | $ | 1,857 | | | $ | 1,716,287 | | | $ | (1,500,547) | | | $ | — | | | $ | 217,597 | | | $ | 789 | | | $ | 218,386 | |

| Amortization of equity-based compensation | — | | | — | | | 414 | | | — | | | — | | | 414 | | | — | | | 414 | |

| Non-controlling interests - contributions | — | | | — | | | — | | | — | | | — | | | — | | | 44 | | | 44 | |

| Non-controlling interests - distributions | — | | | — | | | — | | | — | | | — | | | — | | | (28) | | | (28) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Net income (loss) | — | | | — | | | — | | | (11,218) | | | — | | | (11,218) | | | (166) | | | (11,384) | |

| Balance as of September 30, 2023 (Unaudited) | 185,712 | | | $ | 1,857 | | | $ | 1,716,701 | | | $ | (1,511,765) | | | $ | — | | | $ | 206,793 | | | $ | 639 | | | $ | 207,432 | |

| | | | | | | | | | | |

| Three Months Ended March 31, |

| 2024 | | 2023 |

| Cash flows from operating activities: | | | |

| Net income (loss) | $ | (8,047) | | | $ | (13,997) | |

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | | | |

| Equity in (earnings) losses of unconsolidated ventures | (1,014) | | | 3,922 | |

| Depreciation and amortization | 8,901 | | | 9,649 | |

| Impairment loss | 456 | | | — | |

| | | |

| Amortization of below market debt | 844 | | | 824 | |

| | | |

| | | |

| Amortization of deferred financing costs | 140 | | | 155 | |

| Amortization of equity-based compensation | 56 | | | 57 | |

| | | |

| (Gain) loss on investments and other | 178 | | | (332) | |

| Change in allowance for uncollectible accounts | 139 | | | 167 | |

| | | |

| | | |

| Changes in assets and liabilities: | | | |

| Receivables | (438) | | | 587 | |

| Other assets | 628 | | | (374) | |

| Due to related party | (121) | | | (208) | |

| Escrow deposits payable | 367 | | | 330 | |

| Accounts payable and accrued expenses | (1,203) | | | (4,445) | |

| Other liabilities | 41 | | | 129 | |

| Net cash provided by (used in) operating activities | 927 | | | (3,536) | |

| Cash flows from investing activities: | | | |

| Capital expenditures for operating real estate | (2,926) | | | (3,810) | |

| Sales of real estate | 11,573 | | | 135 | |

| | | |

| | | |

| | | |

| Distributions from unconsolidated ventures | — | | | 2,334 | |

| | | |

| Sales of other assets | — | | | 523 | |

| Net cash provided by (used in) investing activities | 8,647 | | | (818) | |

| Cash flows from financing activities: | | | |

| | | |

| Repayments of mortgage notes | (15,299) | | | (4,819) | |

| | | |

| | | |

| | | |

| Payments on financing and other obligations | (13) | | | (32) | |

| | | |

| | | |

| | | |

| Contributions from non-controlling interests | 13 | | | 45 | |

| Distributions to non-controlling interests | (38) | | | (22) | |

| Net cash provided by (used in) financing activities | (15,337) | | | (4,828) | |

| Net increase (decrease) in cash, cash equivalents and restricted cash | (5,763) | | | (9,182) | |

| Cash, cash equivalents and restricted cash-beginning of period | 92,943 | | | 115,660 | |

| Cash, cash equivalents and restricted cash-end of period | $ | 87,180 | | | $ | 106,478 | |

(1)

The Company reclassified the accumulated other comprehensive loss related to foreign currency adjustments for an unconsolidated venture ownership interest that was sold during the three months ended June 30, 2023. The accumulated balance was reclassified to gain (loss) on investments and other on the consolidated statements of operations.

| | | | | | | | | | | |

| Three Months Ended March 31, |

| 2024 | | 2023 |

| Supplemental disclosure of cash flow information: | | | |

| Cash paid for interest | $ | 8,673 | | | $ | 10,434 | |

| | | |

| Supplemental disclosure of non-cash investing and financing activities: | | | |

| Accrued capital expenditures | $ | 972 | | | $ | 1,071 | |

| | | |

| | | |

| Reclassification of assets held for sale | 534 | | | — | |

| | | |

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Dollars in Thousands)

(Unaudited)

| | | | | | | | | | | |

| Nine Months Ended September 30, |

| 2023 | | 2022 |

| Cash flows from operating activities: | | | |

| Net income (loss) | $ | (84,395) | | | $ | (35,867) | |

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | | | |

| Equity in (earnings) losses of unconsolidated ventures | 6,595 | | | (39,427) | |

| Depreciation and amortization | 29,305 | | | 29,105 | |

| Impairment loss | 43,422 | | | 31,502 | |

| | | |

| Amortization of below market debt | 2,487 | | | 2,428 | |

| | | |

| | | |

| Amortization of deferred financing costs | 988 | | | 475 | |

| Amortization of equity-based compensation | 170 | | | 150 | |

| | | |

| (Gain) loss on investments and other | 4,662 | | | (660) | |

| Change in allowance for uncollectible accounts | 360 | | | 326 | |

| Issuance of common stock as payment for asset management fees | — | | | 7,532 | |

| Distributions from unconsolidated ventures | 10,640 | | | — | |

| Changes in assets and liabilities: | | | |

| Receivables | 203 | | | (114) | |

| Other assets | (3,786) | | | 3,583 | |

| Due to related party | (177) | | | (3,868) | |

| Escrow deposits payable | 30 | | | 256 | |

| Accounts payable and accrued expenses | 2,640 | | | (8,727) | |

| Other liabilities | (78) | | | (298) | |

| Net cash provided by (used in) operating activities | 13,066 | | | (13,604) | |

| Cash flows from investing activities: | | | |

| Capital expenditures for operating real estate | (28,425) | | | (17,924) | |

| Sales of real estate | 135 | | | — | |

| | | |

| | | |

| Distributions from unconsolidated ventures | 13,472 | | | 42,173 | |

| | | |

| Sales of other assets | 523 | | | — | |

| Net cash provided by (used in) investing activities | (14,295) | | | 24,249 | |

| Cash flows from financing activities: | | | |

| | | |

| Repayments of mortgage notes | (14,066) | | | (16,514) | |

| Payment of deferred financing costs | (48) | | | — | |

| | | |

| Payments under finance leases | (96) | | | (36) | |

| Acquisition and retirement of common stock | (1,315) | | | (408) | |

| Distributions paid on common stock | — | | | (97,018) | |

| | | |

| Contributions from non-controlling interests | 144 | | | 263 | |

| Distributions to non-controlling interests | (83) | | | (188) | |

| Net cash provided by (used in) financing activities | (15,464) | | | (113,901) | |

| Net increase (decrease) in cash, cash equivalents and restricted cash | (16,693) | | | (103,256) | |

| Cash, cash equivalents and restricted cash-beginning of period | 115,660 | | | 210,938 | |

| Cash, cash equivalents and restricted cash-end of period | $ | 98,967 | | | $ | 107,682 | |

| | | | | | | | | | | |

| Nine Months Ended September 30, |

| 2023 | | 2022 |

| Supplemental disclosure of cash flow information: | | | |

| Cash paid for interest | $ | 29,666 | | | $ | 28,625 | |

| Cash paid for income taxes | 61 | | | 41 | |

| Supplemental disclosure of non-cash investing and financing activities: | | | |

| Accrued capital expenditures | $ | 540 | | | $ | 2,561 | |

| | | |

| Exchange of ownership interests in unconsolidated ventures for common stock | 13,399 | | | — | |

| Assets acquired under capital lease obligations | 25 | | | — | |

Refer to accompanying notes to consolidated financial statements (unaudited).

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Business and Organization

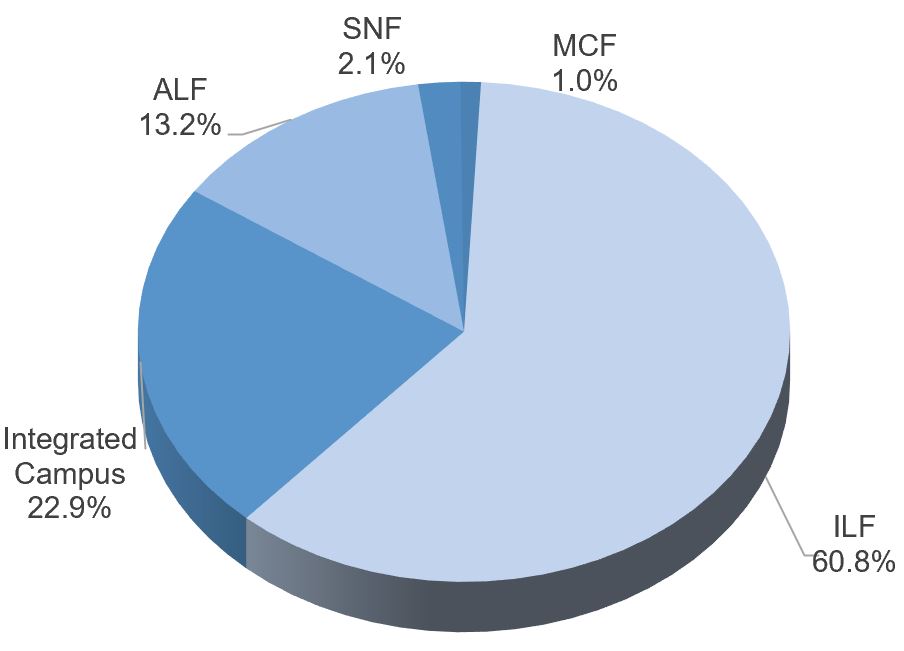

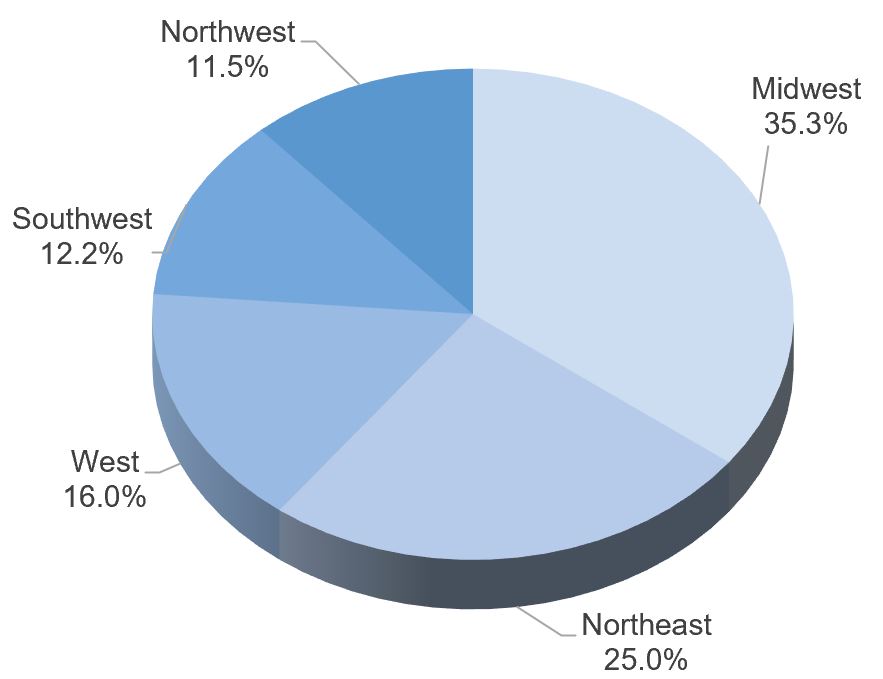

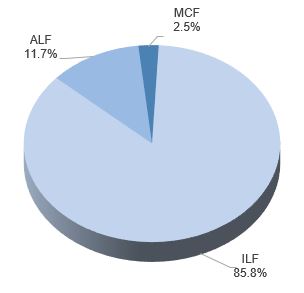

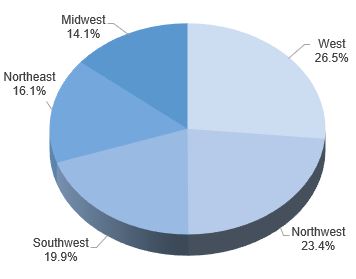

NorthStar Healthcare Income, Inc., together with its consolidated subsidiaries (the “Company”), owns a diversified portfolio of seniors housing properties, including independent living facilities (“ILF”), assisted living facilities (“ALF”) and memory care facilities (“MCF”) located throughout the United States. In addition, the Company also has investmentsan investment through a non-controlling interests in joint venturesinterest in a broader spectrum of healthcare real estate, including seniors housing properties, as well asjoint venture that invests in integrated senior health campuses, which provide services associated with ILFs, ALFs, MCFs and skilled nursing facilities (“SNF”) and ancillary services businesses, located throughout, across the Midwest region of the United States.

The Company was formed in October 2010 as a Maryland corporation and commenced operations in February 2013. The Company elected to be taxed as a real estate investment trust (“REIT”) under the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), commencing with the taxable year ended December 31, 2013. The Company has conducted its operations, and intends to do so in the future, so as to continue to qualify as a REIT for U.S. federal income tax purposes.

Substantially all of the Company’s business is conducted through NorthStar Healthcare Income Operating Partnership, LP (the “Operating Partnership”). The Company is the sole general partner of the Operating Partnership. The limited partners of the Operating Partnership are NorthStar Healthcare Income Advisor, LLC and NorthStar Healthcare Income OP Holdings, LLC (the “Special Unit Holder”), which became indirect subsidiaries of the Company on June 9, 2023. NorthStar Healthcare Income Advisor, LLC invested $1,000 in the Operating Partnership in exchange for common units and the Special Unit Holder invested $1,000 in the Operating Partnership and was issued a separate class of limited partnership units (the “Special Units”), which were collectively recorded as non-controlling interests on the accompanying consolidated balance sheets prior to June 9, 2023. As the Company issued shares, it contributed substantially all of the proceeds from its continuous, public offerings to the Operating Partnership as a capital contribution. As of September 30, 2023,March 31, 2024, the Company’s limited partnership interest in the Operating Partnership, directly or indirectly, was 100.0%100%.

The Company’s charter authorizes the issuance of up to 400.0 million shares of common stock with a par value of $0.01 per share and up to 50.0 million shares of preferred stock with a par value of $0.01 per share. The board of directors of the Company is authorized to amend its charter, without the approval of the stockholders, to increase the aggregate number of authorized shares of capital stock or the number of shares of any class or series that the Company has authority to issue.

The Company raised $2.0 billion in total gross proceeds from the sale of shares of common stock in its continuous, public offerings (the “Offering”), including $232.6 million pursuant to its distribution reinvestment plan (the “DRP”).

The Internalization

From inception through October 21, 2022, the Company was externally managed by CNI NSHC Advisors, LLC or its predecessor (the “Former Advisor”), an affiliate of NRF Holdco, LLC (the “Former Sponsor”). The Former Advisor was responsible for managing the Company’s operations, subject to the supervision of the Company’s board of directors, pursuant to an advisory agreement. On October 21, 2022, the Company completed the internalization of the Company’s management function (the “Internalization”). In connection with the Internalization, the Company agreed with the Former Advisor to terminate the advisory agreement and arranged for the Former Advisor to continue to provide certain services for a transition period.

2. Summary of Significant Accounting Policies

Basis of Accounting

The accompanying consolidated financial statements and related notes of the Company have been prepared in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”) for interim financial reporting and the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, certain information and note disclosures normally included in the consolidated financial statements prepared under U.S. GAAP have been condensed or omitted. In the opinion of management, all adjustments considered necessary for a fair presentation of the Company’s financial position, results of operations and cash flows have been included and are of a normal and recurring nature. The operating results presented for interim periods are not necessarily indicative of the results that may be expected for any other interim period or for the entire year. These consolidated financial statements should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022,2023, which was filed with the U.S. Securities and Exchange Commission on March 27, 2023.22, 2024.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Principles of Consolidation

The consolidated financial statements include the accounts of the Company, the Operating Partnership and their consolidated subsidiaries. The Company consolidates entities in which it has a controlling financial interest by first considering if an entity meets the definition of a variable interest entity (“VIE”) for which the Company is deemed to be the primary beneficiary or if the Company has the power to control an entity through majority voting interest or other arrangements. All significant intercompany balances are eliminated in consolidation.

Variable Interest Entities

A VIE is an entity that lacks one or more of the characteristics of a voting interest entity. A VIE is defined as an entity in which equity investors do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. The determination of whether an entity is a VIE includes both a qualitative and quantitative analysis. The Company bases its qualitative analysis on its review of the design of the entity, its organizational structure including decision-making ability and relevant financial agreements and the quantitative analysis on the forecasted cash flow of the entity. The Company reassesses its initial evaluation of an entity as a VIE upon the occurrence of certain reconsideration events.

A VIE must be consolidated only by its primary beneficiary, which is defined as the party who, along with its affiliates and agents, has both the: (i) power to direct the activities that most significantly impact the VIE’s economic performance; and (ii) obligation to absorb the losses of the VIE or the right to receive the benefits from the VIE, which could be significant to the VIE. The Company determines whether it is the primary beneficiary of a VIE by considering qualitative and quantitative factors, including, but not limited to: which activities most significantly impact the VIE’s economic performance and which party controls such activities; the amount and characteristics of its investment; the obligation or likelihood for the Company or other interests to provide financial support; consideration of the VIE’s purpose and design, including the risks the VIE was designed to create and pass through to its variable interest holders and the similarity with and significance to the business activities of the Company and the other interests. The Company reassesses its determination of whether it is the primary beneficiary of a VIE each reporting period. Judgments related to these determinations include estimates about the current and future fair value and performance of investments held by these VIEs and general market conditions.

The Company evaluates its investments and financings, including investments in unconsolidated ventures and securitization financing transactions to determine whether each investment or financing is a VIE. The Company analyzes new investments and financings, as well as reconsideration events for existing investments and financings, which vary depending on type of investment or financing.

As of September 30, 2023,March 31, 2024, the Company has identified certain consolidated and unconsolidated VIEs. Assets of each of the VIEs may only be used to settle obligations of the respective VIE. Creditors of each of the VIEs have no recourse to the general credit of the Company.

Consolidated VIEs

The most significant VIEs of the Company are certain entities that are consolidated by the Operating Partnership. These entities are VIEs because of non-controlling interests owned by third parties, which do not have substantive kick-out or participating rights. Included in operating real estate, net and mortgage notes payable, net on the Company’s consolidated balance sheet as of September 30, 2023March 31, 2024 is $170.1$100.3 million and $172.0$160.8 million, respectively, related to such consolidated VIEs.

Unconsolidated VIEs

As of September 30, 2023,March 31, 2024, the Company identified unconsolidated VIEs related to its investments in unconsolidated ventures with a carrying value of $128.0$124.0 million. The Company’s maximum exposure to loss as of September 30, 2023March 31, 2024 would not exceed the carrying value of its investment in the VIEs. The Company determined that it is not the primary beneficiary of these VIEs and, accordingly, they are not consolidated in the Company’s financial statements as of September 30, 2023.March 31, 2024. The Company did not provide financial support to its unconsolidated VIEs during the ninethree months ended September 30, 2023.March 31, 2024. As of September 30, 2023,March 31, 2024, there were no explicit arrangements or implicit variable interests that could require the Company to provide financial support to its unconsolidated VIEs.

Voting Interest Entities

A voting interest entity is an entity in which the total equity investment at risk is sufficient to enable it to finance its activities independently and the equity holders have the power to direct the activities of the entity that most significantly impact its

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

economic performance, the obligation to absorb the losses of the entity and the right to receive the residual returns of the entity. The usual condition for a controlling financial interest in a voting interest entity is ownership of a majority voting interest. If the Company has a majority voting interest in a voting interest entity, the entity will generally be consolidated. The Company does

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

not consolidate a voting interest entity if there are substantive participating rights by other parties and/or kick-out rights by a single party or through a simple majority vote.

The Company performs on-going reassessments of whether entities previously evaluated under the voting interest framework have become VIEs, based on certain events, and therefore subject to the VIE consolidation framework.

Investments in Unconsolidated Ventures

A non-controlling, unconsolidated ownership interest in an entity may be accounted for using the equity method or the Company may elect the fair value option.

The Company will account for an investment under the equity method of accounting if it has the ability to exercise significant influence over the operating and financial policies of an entity, but does not have a controlling financial interest. Under the equity method, the investment is adjusted each period for capital contributions and distributions and its share of the entity’s net income (loss). Capital contributions, distributions and net income (loss) of such entities are recorded in accordance with the terms of the governing documents. An allocation of net income (loss) may differ from the stated ownership percentage interest in such entity as a result of preferred returns and allocation formulas, if any, as described in such governing documents. Equity method investments are recognized using a cost accumulation model, in which the investment is recognized based on the cost to the investor, which includes acquisition fees. The Company records as an expense certain acquisition costs and fees associated with consolidated investments deemed to be business combinations and capitalizes these costs for investments deemed to be acquisitions of an asset, including an equity method investment.

The Company may elect the fair value option of accounting for an investment that would otherwise be accounted for under the equity method. The fair value option election allows an entity to make an irrevocable election of fair value for certain financial assets and liabilities on an instrument-by-instrument basis at the initial or subsequent measurement. The decision to elect the fair value option must be applied to an entire instrument and is irrevocable once elected. Under the fair value option, the Company records its share of the changes to fair value of the investment and any unrealized gains and losses.

On June 30, 2023, the Company elected the fair value option method to account for its investment in the Espresso joint venture, which is included in investments in unconsolidated ventures on the consolidated balance sheets. The fair value election was made based on the Company’s assessment that the expected return of investment was lower than the Company’s carrying value of its investment in the Espresso joint venture, which resulted in an impairment of $4.7 million and reduced the carrying value of its investment to recoverable fair value of $3.1 million as of June 30, 2023. The Company’s assessment for the recoverability of its investment took into consideration the joint venture’s remaining assets and estimated future cash distributions, less transaction and wind down costs. The Company will record any changes to its investment’s fair value in gain (loss) on investments and other in the consolidated statements of operations. DuringFrom the three months ended September 30, 2023,date of the election of fair value through March 31, 2024, the Company did not record any changes to the fair value of its investment in the Espresso joint venture. Refer to Note 4 “Investment in Unconsolidated Ventures” and Note 10 “Fair Value” for further discussion.

Non-controlling Interests

A non-controlling interest in a consolidated subsidiary is defined as the portion of the equity (net assets) in a subsidiary not attributable, directly or indirectly, to the Company. A non-controlling interest is required to be presented as a separate component of equity on the consolidated balance sheets and presented separately as net income (loss) and comprehensive income (loss) attributable to controlling and non-controlling interests. An allocation to a non-controlling interest may differ from the stated ownership percentage interest in such entity as a result of a preferred return and allocation formula, if any, as described in suchthe relevant governing documents.

Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that could affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could materially differ from those estimates and assumptions. Any estimates of the effects of the COVID-19 pandemic, inflation, rising interest rates, risk of recession and other economic conditions as reflected and/or discussed in these financial statements are based upon the Company's best estimates using information known to the Company as of the date of this Quarterly Report on Form 10-Q. Such estimates may change and the impact of which could be material.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Cash, Cash Equivalents and Restricted Cash

The Company considers all highly-liquid investments with an original maturity date of three months or less to be cash equivalents. Cash, including amounts restricted, may at times exceed the Federal Deposit Insurance Corporation deposit insurance limit of $250,000 per institution. The Company mitigates credit risk by placing cash and cash equivalents with major

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

financial institutions and money market funds invested in short-term U.S. government securities. To date, the Company has not experienced any losses on cash and cash equivalents.

Restricted cash consists of amounts related to operating real estate (escrows for taxes, insurance, capital expenditures, security deposits received from residents and payments required under certain lease agreements) and other escrows required by lenders of the Company’s borrowings.

The following table provides a reconciliation of cash, cash equivalents and restricted cash as reported on the consolidated balance sheets to the total of such amounts as reported on the consolidated statements of cash flows (dollars in thousands):

| | September 30, 2023 (Unaudited) | | December 31, 2022 |

| | March 31, 2024 (Unaudited) | | | | March 31, 2024 (Unaudited) | | December 31, 2023 |

| Cash and cash equivalents | Cash and cash equivalents | | $ | 87,581 | | | $ | 103,926 | |

| Restricted cash | Restricted cash | | 11,386 | | | 11,734 | |

| Total cash, cash equivalents and restricted cash | Total cash, cash equivalents and restricted cash | | $ | 98,967 | | | $ | 115,660 | |

Operating Real Estate

Operating real estate is carried at historical cost less accumulated depreciation. Major replacements and betterments which improve or extend the life of the asset are capitalized and depreciated over their useful life. Ordinary repairs and maintenance are expensed as incurred. Operating real estate is depreciated using the straight-line method over the estimated useful life of the assets, summarized as follows:

| | | | | | | | |

| Category: | | Term: |

| Building | | 3039 to 5049 years |

| Building improvements | | Lesser of the useful life or remaining life of the building |

| Land improvements | | 9 to 15 years |

| Tenant improvements | | Lesser of the useful life or remaining term of the lease |

| Furniture, fixtures and equipment | | 5 to 14 years |

Construction costs incurred in connection with the Company’s investments are capitalized and included in operating real estate, net on the consolidated balance sheets. Construction in progress is not depreciated until the asset is available for its intended use.

Lessee Accounting

A leasing arrangement, a right to control the use of an identified asset for a period of time in exchange for consideration, is classified by the lessee either as a finance lease, which represents a financed purchase of the leased asset, or as an operating lease. For leases with terms greater than 12 months, a lease asset and a lease liability are recognized on the balance sheet at commencement date based on the present value of lease payments over the lease term.

Lease renewal or termination options are included in the lease asset and lease liability only if it is reasonably certain that the option to extend would be exercised or the option to terminate would not be exercised. As the implicit rate in most leases are not readily determinable, the Company’s incremental borrowing rate for each lease at commencement date is used to determine the present value of lease payments. Consideration is given to the Company’s recent debt financing transactions, as well as publicly available data for instruments with similar characteristics, adjusted for the respective lease term, when estimating incremental borrowing rates.

Lease expense is recognized over the lease term based on an effective interest method for finance leases and on a straight-line basis for operating leases.

Right of Use (“ROU”) - Finance Assets

The Company has entered into finance leases for equipment which are included in operating real estate, net on the Company’s consolidated balance sheets. As of March 31, 2024, furniture, fixtures and equipment under finance leases totaled $0.2 million. The leased equipment is amortized on a straight-line basis. Payments for finance leases totaled $9,399 and $29,070 for the three months ended March 31, 2024 and 2023, respectively.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Right of Use (“ROU”) - Finance Assets

The Company has entered into finance leases for equipment which are included in operating real estate, net on the Company’s consolidated balance sheets. As of September 30, 2023, furniture, fixtures and equipment under finance leases totaled $0.3 million. The leased equipment is amortized on a straight-line basis. Payments for finance leases totaled $0.1 million and $0.4 million for the nine months ended September 30, 2023 and 2022, respectively.

The following table presents the future minimum lease payments under finance leases and the present value of the minimum lease payments, which are included in other liabilities on the Company’s consolidated balance sheets (dollars in thousands):

| | October 1 through December 31, 2023 | | $ | 18 | |

| April 1 through December 31, 2024 | |

| Years Ending December 31: | Years Ending December 31: | |

| 2024 | | 69 | |

| 2025 | |

| 2025 | |

| 2025 | 2025 | | 38 | |

| 2026 | 2026 | | 33 | |

| 2027 | 2027 | | 18 | |

| Thereafter | | 10 | |

| 2028 | |

| | Total minimum lease payments | |

| Total minimum lease payments | |

| Total minimum lease payments | Total minimum lease payments | | $ | 186 | |

| Less: Amount representing interest | Less: Amount representing interest | | (27) | |

| Present value of minimum lease payments | Present value of minimum lease payments | | $ | 159 | |

The weighted average interest rate related to the finance lease obligations is 6.8%6.6% with a weighted average lease term of 3.43.6 years.

As of September 30, 2023,March 31, 2024, there were no leases that had yet to commence which would create significant rights and obligations to the Company as lessee.

Assets Held For Sale

The Company classifies certain long-lived assets as held for sale once the criteria, as defined by U.S. GAAP, have been met and are expected to sell within one year. Long-lived assets to be disposed of are reported at the lower of their carrying amount or fair value minus cost to sell, with any write-down recorded to impairment loss on the consolidated statements of operations. Depreciation and amortization is not recorded for assets classified as held for sale.

In March 2024, the Company entered into an agreement to sell a land parcel within the Rochester portfolio for $0.5 million, and as of March 31, 2024, has classified the property as held for sale on its consolidated balance sheets. At the time of the reclassification to held for sale, the Company recorded an impairment loss of $39,000. As of December 31, 2023, the Company had one property within the Rochester portfolio classified as held for sale, which was sold in February 2024.

Intangible Assets and Deferred Costs

Deferred Costs

Deferred costs consist of deferred financing costs. Deferred financing costs represent commitment fees, legal and other third-party costs associated with obtaining financing. These costs are recorded against the carrying value of such financing and are amortized to interest expense over the term of the financing using the effective interest method. Unamortized deferred financing costs are expensed to gain (loss) on investments and other, when the associated borrowing is repaid before maturity. Costs incurred in seeking financing transactions which do not close are expensed in the period in which it is determined that the financing will not occur.

Identified Intangibles

The Company records acquired identified intangibles, such as the value of in-place leases and other intangibles, based on estimated fair value at the acquisition date. The value allocated to the identified intangibles is amortized over the remaining lease term. In-place leases are amortized into depreciation and amortization expense.

Impairment analysis for identified intangible assets is performed in connection with the impairment assessment of the related operating real estate. An impairment establishes a new basis for the identified intangible asset and any impairment loss recognized is not subject to subsequent reversal. Refer to “—Impairment on Operating Real Estate and Investments in Unconsolidated Ventures” for additional information.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Identified intangibleIntangible assets, are recorded in intangible assets, net, as presented on the consolidated balance sheets. Intangible assetssheets relate to the Company’s in-place lease values for the Company’s four net lease properties. The following table presents intangible assets, net (dollars in thousands):

| | September 30, 2023 (Unaudited) | | December 31, 2022 |

| | March 31, 2024 (Unaudited) | | | | March 31, 2024 (Unaudited) | | December 31, 2023 |

| In-place lease value | In-place lease value | | $ | 120,149 | | | $ | 120,149 | |

| Less: Accumulated amortization | Less: Accumulated amortization | | (118,149) | | | (117,896) | |

| Intangible assets, net | Intangible assets, net | | $ | 2,000 | | | $ | 2,253 | |

The Company recorded $0.1 million and $0.3 million of amortization expense for in-place leases for the three and nine months ended September 30, 2023March 31, 2024 and 2022, respectively.2023.

The following table presents future amortization of in-place lease value (dollars in thousands):

| | October 1 through December 31, 2023 | | $ | 84 | | |

| April 1 through December 31, 2024 | |

| April 1 through December 31, 2024 | |

| April 1 through December 31, 2024 | |

| Years Ending December 31: | Years Ending December 31: | | |

| 2024 | | 337 | | |

| Years Ending December 31: | |

| Years Ending December 31: | |

| 2025 | |

| 2025 | |

| 2025 | 2025 | | 337 | | |

| 2026 | 2026 | | 337 | | |

| 2026 | |

| 2026 | |

| 2027 | 2027 | | 337 | | |

| 2027 | |

| 2027 | |

| 2028 | |

| 2028 | |

| 2028 | |

| Thereafter | |

| Thereafter | |

| Thereafter | Thereafter | | 568 | | |

| Total | Total | | $ | 2,000 | | |

| Total | |

| Total | |

Derivative Instruments

The Company uses derivative instruments to manage its interest rate risk. The Company’s derivative instruments are recorded at fair value. The accounting for changes in fair value of derivatives depends upon whether or not the Company has elected to designate the derivative in a hedging relationship and the derivative qualifies for hedge accounting. Under hedge accounting, changes in fair value for derivatives are recorded through other comprehensive income. When hedge accounting is not elected, changes in fair value for derivatives are recorded through the income statement.

The Company has interest rate caps that have not been designated for hedge accounting. The fair value of the Company's interest rate caps totaled $0.8$0.2 million and $0.7$0.4 million as of September 30, 2023March 31, 2024 and December 31, 2022,2023, respectively, and are included in other assets on the consolidated balance sheets. Changes in fair value of derivatives have been recorded in gain (loss) on investments and other in the consolidated statements of operations. The Company recognized losses totaling $0.3$0.1 million and $0.5$0.2 million for the three and nine months ended September 30,March 31, 2024 and 2023, respectively, and gains totaling $0.3 million and $0.6 million for the three and nine months ended September 30, 2022, respectively.

Revenue Recognition

Operating Real Estate

Rental income from operating real estate is derived from leasing of space to operators and residents, including rent received from the Company’s net lease properties and rent, ancillary service fees and other related revenue earned from ILF residents. Rental income recognition commences when the operator takes legal possession of the leased space and the leased space is substantially ready for its intended use. The leases are for fixed terms of varying length and generally provide for rentals and expense reimbursements to be paid in monthly installments. Rental income from leases, which includes community and move-in fees, is recognized over the term of the respective leases. ILF resident agreements are generally short-term in nature and may allow for termination with 30 days’ notice.

The Company also generates revenue from operating healthcare properties. Revenue related to operating healthcare properties includes resident room and care charges, ancillary fees and other resident service charges. Rent is charged and revenue is recognized when such services are provided, generally defined per the resident agreement as of the date upon which a resident occupies a room or uses the services. Resident agreements are generally short-term in nature and may allow for termination with 30 days’ notice. Revenue derived from our ALFs and MCFs is recorded in resident fee income in the consolidated statements of operations.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Revenue from operators and residents is recognized at lease commencement only to the extent collection is expected to be probable. This assessment is based on several qualitative and quantitative factors, including and as appropriate, the payment

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

history, ability to satisfy its lease obligations, the value of the underlying collateral or deposit, if any, and current economic conditions. If collection is assessed to not be probable, thereafter lease income recognized is limited to amounts collected, with the reversal of any revenue recognized to date in excess of amounts received. If collection is subsequently reassessed to be probable, revenue is adjusted to reflect the amount that would have been recognized had collection always been assessed as probable.

TheBeginning in February 2021, the operator of the Company’s four net lease properties failed to remit contractual monthly rent obligations and the Company deemed it not probable that these obligations will be satisfied in the foreseeable future. On March 27, 2023, the Company entered into a lease forbearance and modification agreement (the “Forbearance Agreement”) with the existing operator, pursuant to which, among other things, the Company will be entitled to receive all cash flow in excess of permitted expenses, and be required to fund any operating deficits, through 2025, subject to the terms and conditions thereof. For the three and nine months ended September 30,March 31, 2024 and 2023, the Company receiveddid not receive any excess cash flow of $0.8 millionor fund any operating deficits and, $1.2 million, respectively, which was recorded as such, did not record any rental income.income related to its net lease properties.

For the three months ended September 30,March 31, 2024 and 2023, and 2022, total property and other revenues includes variable lease revenue of $3.6 million and $2.1 million, respectively. For the nine months ended September 30, 2023 and 2022, total property and other revenue includes variable lease revenue of $10.7$3.5 million and $9.2$3.4 million, respectively. Variable lease revenue includes ancillary services provided to operator/residents, as well as non-recurring services and fees at the Company’s operating facilities.

Impairment on Operating Real Estate and Investments in Unconsolidated Ventures

At this time, it is difficult for the Company to assess and estimate the lasting effects of the COVID-19 pandemic, inflation, rising interest rates, risk of recession and other economic conditions. The future economic effects will depend on many factors beyond the Company’s control and knowledge. The resulting effect on impairment of the Company's real estate held for investment and held for sale and investments in unconsolidated ventures may materially differ from the Company's current expectations and further impairment charges may be recorded in future periods.

Operating Real Estate and Assets Held for Sale

The Company’s real estate portfolio is reviewed on a quarterly basis, or more frequently as necessary, to assess whether there are any indicators that the value of its operating real estate may be impaired or that its carrying value may not be recoverable. A property’s value is considered impaired if the Company’s estimate of the aggregate expected future undiscounted cash flow generated by the property is less than the carrying value. In conducting this review, the Company considers U.S. macroeconomic factors, real estate and healthcare sector conditions, together with asset specific and other factors. To the extent an impairment has occurred, the loss is measured as the excess of the carrying value of the property over the estimated fair value and recorded in impairment loss in the consolidated statements of operations.

Real estate held for sale is stated at the lower of its carrying amount or estimated fair value less disposal cost, with any write-down to disposal cost recorded as an impairment loss. For any increase in fair value less disposal cost subsequent to classification as held for sale, the impairment may be reversed, but only up to the amount of cumulative loss previously recognized.

The Company considered the potential impact of the lasting effects of the COVID-19 pandemic, inflation, rising interest rates, risk of recession and other economic conditions on the future net operating income of its healthcare real estate held for investment as an indicator of impairment. Fair values were estimated based upon the income capitalization approach, using net operating income for each property and applying indicative capitalization rates.

During the ninethree months ended September 30, 2023,March 31, 2024, the Company recorded impairment losses on its operating real estate totaling $38.7$0.5 million including impairment lossesto reflect the market value of $38.6 million for five facilities within the Rochester portfolio as a result of revised holding period assumptions. Additionally, the Company recorded impairment losses totaling $0.1 million for a land parcel within the Rochester portfolio designated as a result of lower estimated market value.held for sale and for property damage sustained by facilities within the Winterfell and Aqua portfolios.

During the ninethree months ended September 30, 2022,March 31, 2023, the Company recordeddid not record any impairment losses on its operating real estate totaling $31.5 million. The Company recorded impairment losses of $18.5 million, $8.5 million, and $3.9 million for facilities in its Arbors, Winterfell and Rochester portfolios, respectively, as a result of declining operating margins and lower projected future cash flows. In addition, the Company recorded impairment losses totaling $0.6 million for property damage sustained by facilities in its Winterfell portfolio.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

estate.Investments in Unconsolidated Ventures

The Company reviews its investments in unconsolidated ventures on a quarterly basis, or more frequently as necessary, to assess whether there are any indicators that the value may be impaired or that its carrying value may not be recoverable. An investment is considered impaired if the projected net recoverable amount over the expected holding period is less than the carrying value. In conducting this review, the Company considers global macroeconomic factors, including real estate sector conditions, together with investment specific and other factors. To the extent an impairment has occurred on the Company’s investment in unconsolidated ventures, and is considered to be other than temporary, the loss is measured as the excess of the carrying value of the investment over the estimated fair value and recorded in impairment loss in the consolidated statements of operations.

During the ninethree months ended September 30,March 31, 2024 and 2023, the Company recorded an impairment on its investment in the Espresso joint venture totaling $4.7 million, which reduced the carrying valuedid not impair any of its investment to $3.1 million. The Company’s assessment for the recoverability of its investment took into consideration the joint venture’s remaining assets and estimated future cash distributions, less transaction and wind down costs. Upon impairing its investment, the Company elected the fair value option method to account for its investment in the Espresso joint venture on June 30, 2023. During the nine months ended September 30, 2022, there was no impairment recorded on any of the Company’s investments in unconsolidated ventures.

The joint ventures, underlying the Company’s unconsolidated ventures assess and record impairment and reserves on their respective real estate portfolios, goodwill, and other assets, and the Company recognizes its proportionate share through equity in earnings (losses). In May 2023, prior to the Sale of Minority Interests (as defined in Note 4, “Investments in Unconsolidated Ventures”), the Diversified US/UK joint venture recorded impairment losses on its remaining properties, 48 care homes located in the United Kingdom (the “UK Portfolio”), due to, among other things, the extended period contemplated for the UK Portfolio to reach stabilization. The Company’s proportionate share of the impairment losses recorded by the Diversified US/UK portfolio totaled $11.4 million. The Company’s proportionate share of impairment and reserves recognized bynor did the underlying joint ventures record any impairments or reserves on properties in their respective portfolios.

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

Credit Losses on Receivables

The current expected credit loss model, in estimating expected credit losses over the life of a financial instrument at the time of origination or acquisition, considers historical loss experiences, current conditions and the effects of reasonable and supportable expectations of changes in future macroeconomic conditions. The Company assesses the estimate of expected credit losses on a quarterly basis or more frequently as necessary. The Company considers historical credit loss information that is adjusted for current conditions and reasonable and supportable forecasts.

The Company measures expected credit losses of receivables on a collective basis when similar risk characteristics exist. If the Company determines that a particular receivable does not share risk characteristics with its other receivables, the Company evaluates the receivable for expected credit losses on an individual basis.

When developing an estimate of expected credit losses on receivables, the Company considers available information relevant to assessing the collectability of cash flows. This information may include internal information, external information, or a combination of both relating to past events, current conditions, and reasonable and supportable forecasts. The Company considers relevant qualitative and quantitative factors that relate to the environment in which the Company operates and are specific to the borrower.

Further, the fair value of the collateral, less estimated costs to sell, may be used when determining the allowance for credit losses for a receivable for which the repayment is expected to be provided substantially through the sale of the collateral when the borrower is experiencing financial difficulty.

As of September 30, 2023,March 31, 2024, the Company has not recorded an allowance for credit losses on its receivables.

Acquisition Fees and Expenses

The Company recorded an expense for certain acquisition costs and fees associated with transactions deemed to be business combinations in which it consolidated the asset and capitalized these costs for transactions deemed to be acquisitions of an asset, including an equity investment.

Equity-Based Compensation

The Company accounts for equity-based compensation awards using the fair value method, which requires an estimate of fair value of the award at the time of grant. All fixed equity-based awards to directors, which have no vesting conditions other than

NORTHSTAR HEALTHCARE INCOME, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Unaudited)

time of service, are amortized to compensation expense over the awards’ vesting period on a straight-line basis. Equity-based compensation is classified within general and administrative expenses in the consolidated statements of operations.

Income Taxes

The Company elected to be taxed as a REIT and to comply with the related provisions of the Internal Revenue Code beginning in its taxable year ended December 31, 2013. Accordingly, the Company will generally not be subject to U.S. federal income tax to the extent of its distributions to stockholders as long as certain asset, gross income and share ownership tests are met. To maintain its qualification as a REIT, the Company must annually distribute dividends equal to at least 90.0% of its REIT taxable income (with certain adjustments) to its stockholders and meet certain other requirements. The Company believes that all of the criteria to maintain the Company’s REIT qualification have been met for the applicable periods, but there canperiods.

For the taxable year ended December 31, 2023, the Company anticipates that its REIT taxable income, if any, will be no assurance that these criteriaoffset by its net operating loss carry-forward and as such, the Company will continuenot be subject to be met in subsequent periods. the distribution requirements. The Company’s most recently filed tax return is for the year ended December 31, 2022 and includes a net operating loss carry-forward of $248.5 million.