WASHINGTON,

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| ☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission file number: 001-38175

Aspen Group, Inc.

(Exact name of registrant as specified in its charter)

|

| ||||

| For the transition period from ___________ to ___________ | |||||

| Delaware | 27-1933597 | |||||||||||||

| State or |

| I.R.S. Employer Identification No. | ||||||||||||

| 276 Fifth Avenue, Suite

|

| 10001 | |||||||||||

| Address of |

| Zip | |||||||||||

Registrants

number, including area code)

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common Stock, par value $0.001 | ASPU | The Nasdaq Stock Market (The Nasdaq Global Market) | ||||||

Large accelerated filer ¨ | Accelerated filer | ||||||||

| Non-accelerated filer |

| Smaller reporting company | |||||||

| Emerging growth company | ||||||||

☐

Class | Outstanding as of March | |||||||

Common Stock, $0.001 par value per share |

| |||||||

INDEX

| Page Number | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

January 31, April 30, 2018 2017 (Unaudited) Assets Current assets: Cash and cash equivalents $ 3,803,080 $ 2,756,217 Restricted cash 190,506 — Accounts receivable, net of allowance of $544,492 and $328,864, respectively 8,592,958 4,434,862 Prepaid expenses 288,640 133,531 Promissory note receivable — 900,000 Other receivables 233,862 81,464 Accrued interest receivable — 8,000 Total current assets 13,109,046 8,314,074 Property and equipment: Call center equipment 96,305 53,748 Computer and office equipment 130,137 103,649 Furniture and fixtures 712,209 255,984 Software 2,590,297 2,131,344 3,528,948 2,544,725 Less accumulated depreciation and amortization (1,161,030 ) (1,090,010 ) Total property and equipment, net 2,367,918 1,454,715 Goodwill 5,011,432 — Intangible assets, net 9,916,667 — Courseware, net 137,557 145,477 Accounts receivable, secured - related party, net of allowance of $625,963, and $625,963, respectively 45,329 45,329 Long term contractual receivable 935,878 657,542 Other assets 585,206 56,417 Total assets $ 32,109,033 $ 10,673,554 January 31, April 30, 2018 2017 (Unaudited) Liabilities and Stockholders’ Equity Current liabilities: Accounts payable $ 1,273,990 $ 756,701 Accrued expenses 596,633 262,911 Deferred revenue 4,156,550 1,354,989 Refunds due students 730,722 310,576 Deferred rent, current portion 7,429 11,200 Convertible notes payable- related party, current portion 1,000,000 — Convertible notes payable, current portion 50,000 50,000 Other current liabilities 186,134 — Total current liabilities 8,001,458 2,746,377 Convertible note payable - related party 1,000,000 — Senior secured term loan, net of discount 6,769,932 — Warrant Liability — 52,500 Deferred rent 60,295 34,437 Total liabilities 15,831,685 2,833,314 Commitments and contingencies - See Note 7 — — Stockholders’ equity: Common stock, $0.001 par value; 250,000,000 shares authorized, 15,072,332 issued and 15,055,665 outstanding at January 31, 2018 13,504,012 issued and 13,487,345 outstanding at April 30, 2017 15,072 13,504 Additional paid-in capital 45,439,538 33,607,423 Treasury stock (16,667 shares) (70,000 ) (70,000 ) Accumulated deficit (29,107,262 ) (25,710,687 ) Total stockholders’ equity 16,277,348 7,840,240 Total liabilities and stockholders’ equity $ 32,109,033 $ 10,673,554 For the For the Three Months Ended Nine Months Ended January 31, January 31, 2018 2017 2018 2017 Revenues $ 5,701,958 $ 3,735,626 $ 14,796,483 $ 9,957,467 Operating expenses Cost of revenues (exclusive of depreciation and amortization shown separately below) 2,665,664 1,359,131 6,282,814 3,490,046 General and administrative 4,677,359 2,133,074 10,975,085 6,228,554 Program review settlement expense — 25,000 — 25,000 Depreciation and amortization 347,894 132,727 631,969 422,782 Total operating expenses 7,690,917 3,649,932 17,889,868 10,166,382 Operating (loss) income (1,988,959 ) 85,694 (3,093,385 ) (208,915 ) Other income (expense): Other income 46,179 1,684 88,067 3,047 Gain on extinguishment of warrant liability 52,500 — 52,500 — Interest expense (257,665 ) (80,001 ) (443,757 ) (175,662 ) Total other expense, net (158,986 ) (78,317 ) (303,190 ) (172,615 ) (Loss) income before income taxes (2,147,945 ) 7,377 (3,396,575 ) (381,530 ) Income tax expense (benefit) — — — — Net (loss) income $ (2,147,945 ) $ 7,377 $ (3,396,575 ) $ (381,530 ) Net (loss) income per share allocable to common stockholders - basic $ (0.15 ) $ 0.00 $ (0.25 ) $ (0.03 ) Net (loss) income per share allocable to common stockholders - diluted $ (0.15 ) $ 0.00 $ (0.25 ) $ (0.03 ) Weighted average number of common shares outstanding: basic 14,491,634 11,467,345 13,862,992 11,419,270 Weighted average number of common shares outstanding: diluted 14,491,634 13,040,970 13,862,992 11,419,270 2022 and 2021 Additional Total Common Stock Paid-In Treasury Accumulated Stockholders' Shares Amount Capital Stock Deficit Equity Balance at April 30, 2017 13,504,012 $ 13,504 $ 33,607,423 $ (70,000 ) $ (25,710,687 ) $ 7,840,240 Fees associated with equity raise — — (14,033 ) — — (14,033 ) Restricted stock issued for services 10,000 10 88,690 — — 88,700 Stock-based compensation — — 466,468 — — 466,468 Common stock issued for acquisition 1,203,209 1,203 10,214,041 — — 10,215,244 Common stock issued for cashless warrant exercises 162,072 162 (162 ) — — — Common stock issued for warrants exercised for cash 79,442 79 143,410 — — 143,489 Common stock issued for stock options exercised 113,597 114 455,273 — — 455,387 Warrants issued with senior secured term loan — — 478,428 — — 478,428 Net loss, for the Nine months ended January 31, 2018 — — — — (3,396,575 ) (3,396,575 ) Balance at January 31, 2018 15,072,332 $ 15,072 $ 45,439,538 $ (70,000 ) $ (29,107,262 ) $ 16,277,348 CHANGES IN STOCKHOLDERS’ EQUITY (CONTINUED) For the Nine months ended January 31, 2018 2017 Cash flows from operating activities: Net loss $ (3,396,575 ) $ (381,530 ) Adjustments to reconcile net loss to net cash used in operating activities: Bad debt expense (recovery) 298,144 (25,680 ) Gain on extinguishment of warrant liability (52,500 ) — Depreciation and amortization 631,969 422,782 Loss on asset disposal 27,590 — Stock-based compensation 466,468 253,833 Amortization of debt discounts 99,726 15,625 Amortization of prepaid shares for services 37,039 52,500 Warrant buyback expense — 206,000 Changes in operating assets and liabilities: Accounts receivable (4,534,118 ) (2,331,140 ) Prepaid expenses (59,451 ) 28,715 Accrued interest receivable (45,400 ) — Other receivables (152,398 ) — Other assets (528,789 ) (25,241 ) Accounts payable 366,044 875,110 Accrued expenses 218,476 105,111 Deferred rent 22,087 17,318 Refunds due students 420,146 124,912 Deferred revenue 2,340,461 562,643 Other liabilities 186,134 — Net cash used in operating activities (3,654,947 ) (99,042 ) Cash flows from investing activities: Cash paid in asset acquisition (2,589,719 ) — Proceeds from promissory note interest receivable 53,400 — Increase in restricted cash (190,506 ) — Purchases of courseware (33,369 ) (6,550 ) Purchases of property and equipment (1,171,473 ) (565,306 ) Proceeds from promissory note receivable 900,000 — Net cash used in investing activities (3,031,667 ) (571,856 ) Cash flows from financing activities: Warrant Buyback — (400,000 ) Borrowing of bank line of credit — 247,000 Payments for bank line of credit — (248,783 ) Borrowing of third party line of credit — 1,250,000 Third party line of credit financing costs — (60,000 ) Proceeds of warrant and stock options exercised 598,876 — Offering costs paid on debt financing (351,366 ) — Disbursements for equity offering costs (14,033 ) (4,017 ) Proceeds from senior secured term loan 7,500,000 — Net cash provided by financing activities 7,733,477 784,200 Net increase in cash 1,046,863 113,302 Cash at beginning of period 2,756,217 783,796 Cash at end of period $ 3,803,080 $ 897,098 CONSOLIDATED BALANCE SHEETSJanuary 31, 2022 April 30, 2021 (Unaudited) Assets Current assets: Cash and cash equivalents $ 5,969,286 $ 12,472,082 Restricted cash 1,433,397 1,193,997 Accounts receivable, net of allowance of $3,381,204 and $3,289,816, respectively 19,635,715 16,724,744 Prepaid expenses 1,375,628 1,077,831 Other current assets 31,032 68,529 Total current assets 28,445,058 31,537,183 Property and equipment: Computer equipment and hardware 1,486,201 956,463 Furniture and fixtures 2,153,124 1,705,101 Leasehold improvements 7,179,896 5,729,324 Instructional equipment 656,409 421,039 Software 9,829,329 8,488,635 Construction in progress 900 247,767 21,305,859 17,548,329 Less: accumulated depreciation and amortization (7,533,571) (4,892,987) Total property and equipment, net 13,772,288 12,655,342 Goodwill 5,011,432 5,011,432 Intangible assets, net 7,907,075 7,908,360 Courseware, net 289,680 187,296 Accounts receivable, net of allowance of $— and $625,963, respectively — 45,329 Long-term contractual accounts receivable 12,701,452 10,249,833 Deferred financing costs 88,393 18,056 Operating lease right of use assets, net 13,090,470 12,714,863 Deposits and other assets 523,898 479,212 Total assets $ 81,829,746 $ 80,806,906 (Continued)The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.1ASPEN GROUP, INC. AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS (CONTINUED)January 31, 2022 April 30, 2021 (Unaudited) Liabilities and Stockholders’ Equity Liabilities: Current liabilities: Accounts payable $ 1,806,656 $ 1,466,488 Accrued expenses 2,079,249 2,040,896 Deferred revenue 6,182,781 6,825,014 Due to students 3,229,516 2,747,484 Operating lease obligations, current portion 2,106,981 2,029,821 Credit Facility 5,000,000 — Other current liabilities 136,027 307,921 Total current liabilities 20,541,210 15,417,624 Operating lease obligations, less current portion 17,317,396 16,298,808 Total liabilities 37,858,606 31,716,432 Commitments and contingencies – see Note 11 0 0 Stockholders’ equity: Preferred stock, $0.001 par value; 1,000,000 shares authorized, 0 issued and 0 outstanding at January 31, 2022 and April 30, 2021 — — Common stock, $0.001 par value; 40,000,000 shares authorized, 25,228,580 issued and 25,073,094 outstanding at January 31, 2022 25,066,297 issued and 24,910,811 outstanding at April 30, 2021 25,229 25,067 Additional paid-in capital 111,378,471 109,040,824 Treasury stock (155,486 at both January 31, 2022 and April 30, 2021) (1,817,414) (1,817,414) Accumulated deficit (65,615,146) (58,158,003) Total stockholders’ equity 43,971,140 49,090,474 Total liabilities and stockholders’ equity $ 81,829,746 $ 80,806,906 The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.2CONSOLIDATED STATEMENTS OF OPERATIONS(Unaudited)Three Months Ended January 31, Nine Months Ended January 31, 2022 2021 2022 2021 Revenue $ 18,944,798 $ 16,624,837 $ 57,316,004 $ 48,761,444 Operating expenses: Cost of revenue (exclusive of depreciation and amortization shown separately below) 9,275,419 7,559,951 26,658,188 20,732,254 General and administrative 11,771,487 10,644,438 34,359,276 30,723,349 Bad debt expense 350,000 670,000 1,050,000 1,702,000 Depreciation and amortization 883,536 535,273 2,480,179 1,552,254 Total operating expenses 22,280,442 19,409,662 64,547,643 54,709,857 Operating loss (3,335,644) (2,784,825) (7,231,639) (5,948,413) Other income (expense): Interest expense (180,697) (33,539) (353,738) (2,018,664) Other income (expense), net 13,954 13,558 516,754 (116,820) Total other (expense) income, net (166,743) (19,981) 163,016 (2,135,484) Loss before income taxes (3,502,387) (2,804,806) (7,068,623) (8,083,897) Income tax expense 231,610 10,460 388,520 45,090 Net loss $ (3,733,997) $ (2,815,266) $ (7,457,143) $ (8,128,987) Net loss per share - basic and diluted $ (0.15) $ (0.11) $ (0.30) $ (0.35) Weighted average number of common stock outstanding - basic and diluted 25,041,733 24,544,334 24,971,056 23,354,036 The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.3CONSOLIDATED STATEMENTSTATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITYFOR THE NINE MONTHS ENDED JANUARYThree Months Ended January 31, 2018(Unaudited)Common Stock Additional

Paid-In

CapitalTreasury

StockAccumulated

DeficitTotal

Stockholders’

EquityShares Amount Balance at October 31, 2021 25,148,194 $ 25,149 $ 110,526,729 $ (1,817,414) $ (61,881,149) $ 46,853,315 Stock-based compensation — — 700,697 — — 700,697 Common stock issued for stock options exercised for cash 41,667 41 134,959 — — 135,000 Common stock issued for vested restricted stock units 38,719 39 (39) — — — Amortization of warrant based cost — — 16,125 — — 16,125 Net loss — — — — (3,733,997) (3,733,997) Balance at January 31, 2022 25,228,580 $ 25,229 $ 111,378,471 $ (1,817,414) $ (65,615,146) $ 43,971,140 Common Stock Additional

Paid-In

CapitalTreasury

StockAccumulated

DeficitTotal

Stockholders’

EquityShares Amount Balance at October 31, 2020 24,416,539 $ 24,417 $ 105,092,551 $ — $ (53,022,751) $ 52,094,217 Stock-based compensation — — 701,170 — — 701,170 Common stock issued for stock options exercised for cash 447,134 447 2,180,352 (1,817,414) — 363,385 Common stock issued for vested restricted stock units 74,000 74 (74) — — — Common stock issued for services 2,000 2 19,898 — — 19,900 Amortization of warrant based cost — — 9,125 — — 9,125 Net loss — — — — (2,815,266) (2,815,266) Balance at January 31, 2021 24,939,673 $ 24,940 $ 108,003,022 $ (1,817,414) $ (55,838,017) $ 50,372,531 The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.4CONSOLIDATED STATEMENTS OF CASH FLOWSNine Months Ended January 31, 2022 and 2021(Unaudited)(Continued)Common Stock Additional

Paid-In

CapitalTreasury

StockAccumulated

DeficitTotal

Stockholders’

EquityShares Amount Balance at April 30, 2021 25,066,297 $ 25,067 $ 109,040,824 $ (1,817,414) $ (58,158,003) $ 49,090,474 Stock-based compensation — — 1,965,567 — — 1,965,567 Common stock issued for stock options exercised for cash 58,419 58 190,976 — — 191,034 Common stock issued for cashless stock options exercised 30,156 30 (30) — — — Common stock issued for vested restricted stock units 73,708 74 (74) — — — Amortization of warrant based cost — — 43,708 — — 43,708 Warrants issued for deferred financing costs related to Credit Facility — — 137,500 — — 137,500 Net loss — — — — (7,457,143) (7,457,143) Balance at January 31, 2022 25,228,580 $ 25,229 $ 111,378,471 $ (1,817,414) $ (65,615,146) $ 43,971,140 Common Stock Additional

Paid-In

CapitalTreasury

StockAccumulated

DeficitTotal

Stockholders’

EquityShares Amount Balance at April 30, 2020 21,770,520 $ 21,771 $ 89,505,216 $ (70,000) $ (47,709,030) $ 41,747,957 Stock-based compensation — — 3,019,828 — — 3,019,828 Common stock issued for stock options exercised for cash 1,364,721 1,365 4,394,749 (1,817,414) — 2,578,700 Common stock issued for cashless stock options exercised 22,339 22 (22) — — — Common stock issued for conversion of Convertible Notes 1,398,602 1,399 9,998,601 — — 10,000,000 Common stock issued for vested restricted stock units 206,109 206 (206) — — — Common stock issued for warrants exercised for cash 192,049 192 1,081,600 — — 1,081,792 Common stock issued for services 2,000 2 19,898 — — 19,900 Modification charge for warrants exercised — — 25,966 — — 25,966 Amortization of warrant based cost — — 27,375 — — 27,375 Cancellation of Treasury Stock (16,667) (17) (69,983) 70,000 — — Net loss — — — — (8,128,987) (8,128,987) Balance at January 31, 2021 24,939,673 $ 24,940 $ 108,003,022 $ (1,817,414) $ (55,838,017) $ 50,372,531 The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

|

| For the |

| |||||

|

| Nine months ended |

| |||||

|

| January 31, |

| |||||

|

| 2018 |

|

| 2017 |

| ||

Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

Cash paid for interest |

| $ | 316,781 |

|

| $ | 145,105 |

|

Cash paid for income taxes |

| $ | — |

|

| $ | — |

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of non-cash investing and financing activities |

|

|

|

|

|

|

|

|

Warrants issued as part of senior secured loan |

| $ | 478,428 |

|

| $ | — |

|

Assets acquired net of liabilities assumed for non-cash consideration |

| $ | 12,215,244 |

|

| $ | — |

|

Common stock issued for services |

| $ | — |

|

| $ | 62,002 |

|

Warrant derivative liability |

| $ | — |

|

| $ | 52,500 |

|

| Nine Months Ended January 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net loss | $ | (7,457,143) | $ | (8,128,987) | |||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | |||||||||||

| Bad debt expense | 1,050,000 | 1,702,000 | |||||||||

| Depreciation and amortization | 2,480,179 | 1,552,254 | |||||||||

| Stock-based compensation | 1,965,567 | 3,019,828 | |||||||||

| Amortization of warrant based cost | 43,708 | 27,375 | |||||||||

| Amortization of debt discounts | — | 1,550,854 | |||||||||

| Amortization of debt issue costs | 18,056 | 156,029 | |||||||||

| Amortization of deferred financing costs | 49,107 | — | |||||||||

| Modification charge for warrants exercised | — | 25,966 | |||||||||

| Loss on asset disposition | 36,445 | — | |||||||||

| Lease benefit | (96,450) | — | |||||||||

| Tenant improvement allowances received from landlords | 816,591 | — | |||||||||

| Common stock issued for services | — | 19,900 | |||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | (6,412,590) | (6,493,238) | |||||||||

| Prepaid expenses | (297,797) | (267,526) | |||||||||

| Other receivables | — | 23,097 | |||||||||

| Other current assets | 37,498 | (1,205,083) | |||||||||

| Accounts receivable, other | 45,329 | — | |||||||||

| Deposits and other assets | (44,686) | (185,599) | |||||||||

| Accounts payable | 340,168 | (349,882) | |||||||||

| Accrued expenses | 38,353 | 1,756,102 | |||||||||

| Due to students | 482,032 | (128,154) | |||||||||

| Deferred revenue | (642,233) | 1,887,377 | |||||||||

| Other current liabilities | (171,894) | (238,032) | |||||||||

| Net cash used in operating activities | (7,719,760) | (5,275,719) | |||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of courseware and accreditation | (161,262) | (31,330) | |||||||||

| Purchases of property and equipment | (3,573,408) | (2,877,758) | |||||||||

| Net cash used in investing activities | (3,734,670) | (2,909,088) | |||||||||

| Cash flows from financing activities: | |||||||||||

| Borrowings under the Credit Facility | 5,000,000 | — | |||||||||

| Proceeds from stock options exercised | 191,034 | 2,578,700 | |||||||||

| Proceeds from warrants exercised | — | 1,081,792 | |||||||||

| Net cash provided by financing activities | 5,191,034 | 3,660,492 | |||||||||

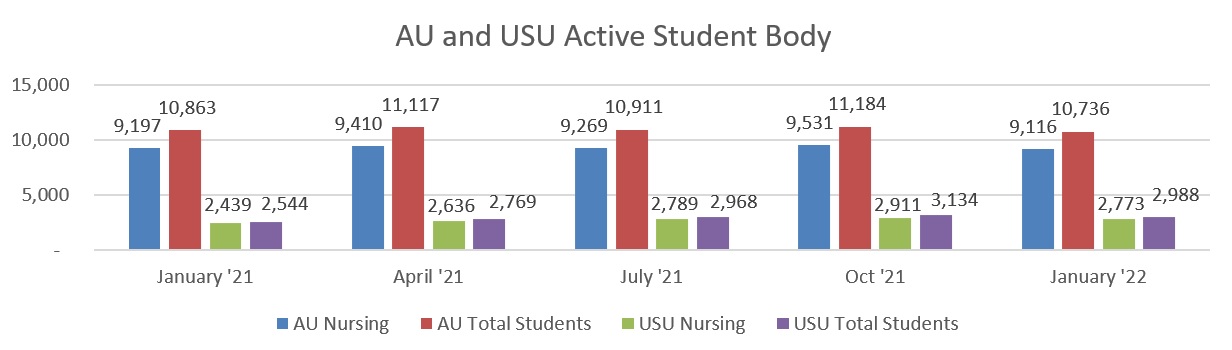

2022 profession. 2024. certification resulting from the ownership change of control in connection with the acquisition by AGI on December 1, 2017.6ASPEN GROUP, INC. AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CASH FLOWS (CONTINUED)(Unaudited)Nine Months Ended January 31, 2022 2021 Net decrease in cash, cash equivalents and restricted cash $ (6,263,396) $ (4,524,315) Cash, cash equivalents and restricted cash at beginning of period 13,666,079 17,906,765 Cash, cash equivalents and restricted cash at end of period $ 7,402,683 $ 13,382,450 Supplemental disclosure cash flow information: Cash paid for interest $ 258,630 $ 310,958 Cash paid for income taxes $ 13,520 $ 49,008 Supplemental disclosure of non-cash investing and financing activities: Common stock issued for conversion of Convertible Notes $ — $ 10,000,000 Warrants issued as part of Credit Facility $ 137,500 $ — The following table provides a reconciliation of cash and cash equivalents and restricted cash reported within the accompanying consolidated balance sheet to the total amounts shown in the accompanying unaudited consolidated statements of cash flows:January 31, 2022 April 30, 2021 Cash and cash equivalents $ 5,969,286 $ 12,472,082 Restricted cash 1,433,397 1,193,997 Total cash, cash equivalents and restricted cash $ 7,402,683 $ 13,666,079 The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.7ASPEN GROUP, INC. AND SUBSIDIARIESCONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTSJANUARYJanuary 31, 2018(Unaudited)Note 1. Nature of Operations and LiquidityOverviewAspen Group, Inc. (together with its subsidiaries, the “Company” or “AGI”("AGI") is aan education technology holding company, whichcompany. AGI has two subsidiaries.2 subsidiaries, Aspen University Inc. (“("Aspen University”University") was, organized in 1987, and United States University Inc. (“USU”("United States University" or "USU") was formed May 2017.All references to the “Company”, “AGI”, “Aspen Group”, “we”, “our” and certain assets were acquired“us” refer to Aspen Group, Inc., unless the context otherwise indicates.AGI leverages its education technology infrastructure and liabilities assumedexpertise to allow its two universities, Aspen University and United States University, to deliver on December 1, 2017. (See Note 10)Aspen Group’sthe vision is to makeof making college affordable again in America.again. Because we believe higher education should be a catalyst to our students’ long-term economic success, we exert financial prudence by offering affordable tuition that is one of the greatest values in online higher education. In March 2014, Aspen University unveiled a monthly payment plan aimed at reversingAGI’s primary focus relative to future growth is to target the college-debt sentence plaguing working-class Americans. The monthly payment plan offers bachelor students (except RN to BSN) the opportunity to pay their tuition at $250/month for 72 months ($18,000),high growth nursing bachelor students (RN to BSN) $250/month for 39 months ($9,750), master students $325/month for 36 months ($11,700) and doctoral students $375/month for 72 months ($27,000), interest free, thereby giving students a monthly payment tuition payment option versus taking out a federal financial aid loan.United States University (USU) began offering monthly payment plans in the summer of 2017. Today, monthly payment plans are available for the RN to BSN program ($250/month), MBA/M.A.Ed/MSN programs ($325/month), and the MSN-FNP program ($375/month).Since 1993, Aspen University has been nationally accredited by the Distance Education and Accrediting Council (“DEAC”), a nationalan institutional accrediting agency recognized by the U.S.United States Department of Education (the “DOE”). On February 25, 2015, the DEAC informed Aspen University that it had renewed its accreditation for five years to, through January 2019.Since 2009, USU has been regionallyinstitutionally accredited by WASC Senior College and University Commission. (“WSCUC”).Both universities are qualified to participate under the Higher Education Act of 1965, as amended (HEA) and the Federal student financial assistance programs (Title IV, HEA programs). USU has a provisional certification.COVID-19 UpdateNursing students represented 87% or 11,889 of the Company’s total student body of 13,724 students at the end of the third quarter of fiscal 2022. Of the 11,889 nursing students, 2,277 are BSN Pre-Licensure students located across our 4 metro locations (Phoenix, Austin, Tampa and Nashville). The remaining 9,612 nursing students are licensed registered nurses (RNs) studying to earn an advanced degree (RN to BSN, MSN, MSN-FNP or DNP degree programs). Therefore, these 9,612 post-licensure nursing students represent 70% of the Company’s total student body at the end of the third quarter and are the AGI students primarily affected by the COVID-19 pandemic.Starting in the second half of June 2021 and continuing through January 2022, the Company saw lower course starts than seasonally expected among our RN student body. For example, at Aspen University, course starts among RNs from June through January 2022 increased by approximately 3% year-over-year.By comparison, over the previous two full fiscal years (Fiscal Year 2021 and Fiscal Year 2020), course starts among RNs at Aspen University increased by an average of approximately 10% year-over-year.We cannot be certain what impact future COVID-19 variants will have on the Company’s results as we progress through the remainder of fiscal 2022.Basis of PresentationA. Interim Financial StatementsThe interim consolidated financial statements included herein have been prepared by the Company, without audit, pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”). In the opinion of the Company’s management, all adjustments (consisting of normal recurring adjustments and reclassifications and non-recurring adjustments) necessary to present fairly our results of operations for the three and nine months ended January 31, 20182022 and 2017,2021, our cash flows for the nine months ended January 31, 20182022 and 2017,2021, and our financial position as of January 31, 20182022 have been made.8ASPEN GROUP, INC. AND SUBSIDIARIESCONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTSJanuary 31, 2022(Unaudited)The results of operations for such interim periods are not necessarily indicative of the operating results to be expected for the full year.Certain information and disclosures normally included in the notes to the annual consolidated financial statements have been condensed or omitted from these interim consolidated financial statements. Accordingly, these interim consolidated financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the periodfiscal year ended April 30, 20172021 as filed with the SEC on July 25, 2017.13, 2021. The April 30, 20172021 consolidated balance sheet is derived from those statements.7ASPEN GROUP, INC. AND SUBSIDIARIESCONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTSJANUARY 31, 2018(Unaudited)B. LiquidityAt January 31, 2018, the Company had a cash balance of $3,803,080 plus $190,506 in restricted cash.On July 25, 2017, the Company signed a $10 million senior secured term loan with Runway Growth Capital Fund (formerly known as GSV Growth Capital Fund). The Company drew $5 million under the facility at closing, with an additional $2.5 million drawn following the closing of the Company’s acquisition of substantially all the assets of United States University, including receipt of all required regulatory approvals, among other conditions to funding. Terms of the 4-year senior loan include a 10% over 3-month LIBOR per annum interest rate. (See Notes 5 and 10).

Principles

Use

The

and Restricted Cash

Goodwill and Intangibles

Goodwill represents the excess of purchase price over the fair market value of assets acquired and liabilities assumed from Educacion Significativa, LLC. Goodwill has an indefinite life and is not amortized. Goodwill is tested annually for impairment.

Intangibles represent both indefinite lived and definite lived assets. Accreditation and regulatory approvals and Trade name and trademarks are deemed to have indefinite useful lives and accordingly are not amortized but are tested annually for impairment. Student relationships and curriculums are deemed to have definite lives and are amortized accordingly.

8

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

Fair Value Measurements

Fair value is the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants. The Company classifies assets and liabilities recorded at fair value under the fair value hierarchy based upon the observability of inputs used in valuation techniques. Observable inputs (highest level) reflect market data obtained from independent sources, while unobservable inputs (lowest level) reflect internally developed market assumptions. The fair value measurements are classified under the following hierarchy:

Level 1—Observable inputs that reflect quoted market prices (unadjusted) for identical assets and liabilities in active markets;

Level 2—Observable inputs, other than quoted market prices, that are either directly or indirectly observable in the marketplace for identical or similar assets and liabilities, quoted prices in markets that are not active, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets and liabilities; and

Level 3—Unobservable inputs that are supported by little or no market activity that are significant to the fair value of assets or liabilities.

The estimated fair value of certain financial instruments, including cash and cash equivalents, accounts receivable, accounts payable and accrued expenses are carried at historical cost basis, which approximates their fair values because of the short-term nature of these instruments.

Refunds Due Students

The Company receives Title IV funds from the Department of Education to cover tuition and living expenses. After deducting tuition and fees, the Company sends checks for the remaining balances to the students.

institutions.

Revenues consist

The Company has revenues from students outside the United States representing 2.1% of the revenues for the quarter ended January 31, 2018.

Accounting for Derivatives

The Company evaluates its convertible instruments, options, warrants or other contracts to determine if those contracts or embedded components of those contracts qualify as derivatives to be separately accounted for under ASC Topic 815, “Derivatives and Hedging”. The result of this accounting treatment is that the fair value of the derivative is marked-to-market each balance sheet date and recorded as a liability. In the event that the fair value is recorded as a liability, the change in fair value is recorded in the statement of operations as other income (expense). Upon conversion, exercise, or other extinguishment (transaction) of a derivative instrument, the instrument is marked to fair value at the transaction date and then that fair value is recognized as an extinguishment gain or loss. Equity instruments that are initially classified as equity that become subject to reclassification under ASC Topic 815 are reclassified to liability at the fair value of the instrument on the reclassification date.

9

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

Business Combinations

We include the results of operations of businesses we acquire from the date of the respective acquisition. We allocate the purchase price of acquisitions to the assets acquired and liabilities assumed at fair value. The excess of the purchase price of an acquired business over the amount assigned to the assets acquired and liabilities assumed is recorded as goodwill. We expense transaction costs associated with business combinations as incurred.

As required to be disclosed for quarters with net income, basiccurriculum and diluted income per share foreducational delivery needs of its online and campus students regardless of geography. The Company's chief operating decision makers, its Chief Executive Officer, Chief Operating Officer and Chief Academic Officer, manage the three months ended January 31, 2017, were calculatedCompany's operations as follows:

|

| Basic |

|

| Diluted |

| ||

Numerator |

|

|

|

|

|

| ||

Net income applicable to common stock |

| $ | 7,377 |

|

| $ | 7,377 |

|

Convertible debt interest |

|

| — |

|

|

| 4,010 |

|

|

| $ | 7,377 |

|

| $ | 11,387 |

|

|

|

|

|

|

|

|

|

|

Denominator |

|

|

|

|

|

|

|

|

Weighted average common shares outstanding |

|

| 11,467,345 |

|

|

| 11,467,345 |

|

Convertible debt |

|

| — |

|

|

| 75,596 |

|

Warrants and options |

|

| — |

|

|

| 1,498,029 |

|

|

|

| 11,467,345 |

|

|

| 13,040,970 |

|

|

|

|

|

|

|

|

|

|

Net income per share |

| $ | 0.00 |

|

| $ | 0.00 |

|

a whole.

Pronouncement Not Yet Adopted

ASU 2017-04 - In January 2017,2022 for SEC filers that are eligible to be smaller reporting companies under the Financial Accounting Standards Board issued Accounting Standards Update No. 2017-04: "Intangibles - GoodwillSEC’s definition, as well as private companies and Other (Topic 350)” - to simplify how an entity is required to test goodwill for impairment by eliminating Step 2 from the goodwill impairment test. Step 2 measures a goodwill impairment loss by comparing the implied fair value of a reporting unit’s goodwill with the carrying amount of that goodwill. This guidance is effective for interim and annual reporting periods beginning after December 15, 2019.not-for-profit entities. The Company is currently evaluating the effects of this standard on its consolidated financial statements.

ASU 2016-02- In February 2016, the Financial Accounting Standards Board issued Accounting Standards Update No. 2016-02: “Leases (Topic 842)”whereby lessees will need to recognize almost all leases on their balance sheet as a right of use assetnew guidance and a lease liability. This guidance is effective for interim and annual reporting periods beginning after December 15, 2018. The Company expects this ASU will increase its assets and liabilities, but have no net material impact on its consolidated financial statements.

10

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

ASU 2014-09 - In May 2014, the Financial Accounting Standards Board issued Update No. 2014-09: “Revenue from Contracts with Customers (Topic 606)” which requires that an entity recognize revenue to depict the transfer of promised goods and services to customers in an amount that reflects the consideration to which the Company expects to be entitled in exchange for those goods or services. Since the issuance of the original standard, the FASB has issued several updates to the standard which i) clarify the application of the principal versus agent guidance; ii) clarify the guidance relating to performance obligations and licensing; iii) clarify assessment of the collectability criterion, presentation of sales taxes, measurement date for non-cash consideration and completed contracts at transaction; and iv) clarify narrow aspects of ASC 606 or corrects unintended application of the guidance. The new revenue recognition standard, amended by the updates, becomes effective in the first quarter of fiscal 2019 and is to be applied retrospectively using one of two prescribed methods. Early adoption is permitted. The Company currently plans to adopt the new standard effective May 1, 2018 and does not believeyet determined whether the adoption of thisthe new standard will have a material impact on its consolidated financial statements or the amount or timingmethod of its revenues.

|

| January 31, |

|

| April 30, |

| ||

|

| 2018 |

|

| 2017 |

| ||

Call center hardware |

| $ | 96,305 |

|

| $ | 53,748 |

|

Computer and office equipment |

|

| 130,137 |

|

|

| 103,649 |

|

Furniture and fixtures |

|

| 712,209 |

|

|

| 255,984 |

|

Software |

|

| 2,590,297 |

|

|

| 2,131,344 |

|

|

|

| 3,528,948 |

|

|

| 2,544,725 |

|

Accumulated depreciation and amortization |

|

| (1,161,030 | ) |

|

| (1,090,010 | ) |

Property and equipment, net |

| $ | 2,367,918 |

|

| $ | 1,454,715 |

|

the corresponding amount of accumulated depreciation is reversed. Any remaining difference between the two is recognized as either other income or expense.

|

| January 31, |

|

| April 30, |

| ||

|

| 2018 |

|

| 2017 |

| ||

Software |

| $ | 2,590,297 |

|

| $ | 2,131,344 |

|

Accumulated amortization |

|

| (1,012,655 | ) |

|

| (994,017 | ) |

Software, net |

| $ | 1,577,642 |

|

| $ | 1,137,327 |

|

following:

| January 31, 2022 | April 30, 2021 | ||||||||||

| Software | $ | 9,829,329 | $ | 8,488,635 | |||||||

| Accumulated amortization | (4,727,413) | (3,444,325) | |||||||||

| Software, net | $ | 5,101,916 | $ | 5,044,310 | |||||||

|

| For the |

|

| For the |

| ||||||||||

|

| Three Months Ended January 31, |

|

| Nine Months Ended January 31, |

| ||||||||||

|

| 2018 |

|

| 2017 |

|

| 2018 |

|

| 2017 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Depreciation and amortization Expense |

| $ | 150,596 |

|

| $ | 119,064 |

|

| $ | 407,346 |

|

| $ | 378,118 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Software amortization Expense |

| $ | 121,695 |

|

| $ | 105,914 |

|

| $ | 341,825 |

|

| $ | 342,938 |

|

The following is a schedule of estimated future amortization expense of software at January 31, 2018:

Year Ending April 30, |

|

|

| |

2018 |

| $ | 127,811 |

|

2019 |

|

| 456,038 |

|

2020 |

|

| 386,196 |

|

2021 |

|

| 313,749 |

|

2022 |

|

| 293,848 |

|

Total |

| $ | 1,577,642 |

|

11

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

summarized below:

| Three Months Ended January 31, | Nine Months Ended January 31, | ||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||

| Depreciation and amortization expense: | |||||||||||||||||||||||

| Property and equipment, excluding software | $ | 418,081 | $ | 158,110 | $ | 1,136,929 | $ | 490,868 | |||||||||||||||

| Software | $ | 443,284 | $ | 366,908 | $ | 1,283,088 | $ | 1,028,668 | |||||||||||||||

Courseware costs capitalized were $33,369 for and Accreditation

Courseware consisted of the following at January 31, 2018 and April 30, 2017:

|

| January 31, |

|

| April 30, |

| ||

|

| 2018 |

|

| 2017 |

| ||

Courseware |

| $ | 283,046 |

|

| $ | 271,777 |

|

Accumulated amortization |

|

| (145,489 | ) |

|

| (126,300 | ) |

Courseware, net |

| $ | 137,557 |

|

| $ | 145,477 |

|

Amortization expense of coursewarewrite-offs for the three and nine months ended January 31, 20182022 and 2017:

|

| For the |

|

| For the |

| ||||||||||

|

| Three Months Ended January 31, |

|

| Nine Months Ended January 31, |

| ||||||||||

|

| 2018 |

|

| 2017 |

|

| 2018 |

|

| 2017 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Amortization expense |

| $ | 13,966 |

|

| $ | 13,663 |

|

| $ | 41,289 |

|

| $ | 44,664 |

|

The following2021.

| January 31, 2022 | April 30, 2021 | ||||||||||

| Courseware | $ | 569,483 | $ | 408,222 | |||||||

| Accreditation | 59,350 | 59,350 | |||||||||

| 628,833 | 467,572 | ||||||||||

| Accumulated amortization | (339,153) | (280,276) | |||||||||

| Courseware and accreditation, net | $ | 289,680 | $ | 187,296 | |||||||

| Three Months Ended January 31, | Nine Months Ended January 31, | ||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||

| Amortization expense | $ | 21,744 | $ | 10,255 | $ | 58,877 | $ | 32,718 | |||||||||||||||

Year Ending April 30, |

|

|

| |

2018 |

| $ | 14,152 |

|

2019 |

|

| 56,143 |

|

2020 |

|

| 42,301 |

|

2021 |

|

| 15,336 |

|

2022 |

|

| 9,625 |

|

Total |

| $ | 137,557 |

|

2022

Note and Accounts Receivable

The Company will be required to begin making principal repayments upon the 24-month anniversary of the initial closing (July 24, 2019), and each month thereafter will repay 1/24th of the total loan amount outstanding. Should the Company achieve both annualized revenue growth of at least 30% and operating margin of at least 7.5% for any 12-month trailing period, thenissuance at the quarter-end of that 12-month trailing period, the Company may elect to extend the interest only period for the quarter immediately following the 12-month trailing period throughout the duration of the loan.

Additionally, the Company paid a 0.25% origination fee on the initial $5 million draw and paid another 0.25% origination fee upon the second $2.5 million draw, will be subject to a final payment fee of 3.25% of the principal lent, and issued 224,174 5-year warrants at an exercise price of $6.87.$5.85 per share. The relative fair value of the warrants was $478,428 and was recorded as debt discount along with other direct costs of the term loanis $137,500 and is being amortized to interest expense over the 14-month line of credit period. The fair value of the warrants are treated as deferred financing costs in the accompanying consolidated balance sheets at January 31, 2022 to be amortized over the term of the loan.

12

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARYCredit Facility. Total unamortized costs at January 31, 2018

(Unaudited)

2022 were $88,393. See Note 6. Convertible Notes – Related Party

On December 1, 2017,7. Stockholders’ Equity for additional information related to these warrants.

Note 7. Commitments and Contingencies

Employment Agreements

From time to time, the Company enters into employment agreements with certain of its employees. These agreements typically include bonuses, some of which are performance-based in nature. As of January 31, 2018, no performance bonuses have been earned.

Legal Matters

From time to time, we may be involved in litigation relating to claims arising out of our operations in the normal course of business. As of January 31, 2018, there were no pending or threatened lawsuits that could reasonably be expecteddeemed to have a material effectrelative fair value of $255,071 (the "2018 Cooperman Warrants"). These warrants were exercised on the results of our operations.

Regulatory Matters

June 8, 2020. The Company’s subsidiaries, Aspen University and United States University, are subject to extensive regulation by Federal and State governmental agencies and accrediting bodies. In particular, the Higher Education Act (the “HEA”) and the regulations promulgated thereunder by the DOE subject the subsidiaries to significant regulatory scrutiny on the basis of numerous standards that schools must satisfy to participate in the various types of federal student financial assistance programs authorized under Title IVfair value of the HEA.

On August 22, 2017,warrants along with the DOE informed Aspen Universityupfront Facility fee were treated as debt issue cost assets to be amortized over the term of its determination that the institution has qualified to participate underloan. As a result of the HEA andaforementioned note extension, the Federal student financial assistance programs (Title IV, HEA programs), and set a subsequent program participation agreement reapplication dateremainder of Marchthe unamortized costs of $9,722 were written off during the quarter ended October 31, 2021.

USU currently has provisional certification to participate in the Title IV Programs due to the business combination. The provisional certification allows the school to continue to receive Title IV funding as it did prior to the change Total unamortized costs at January 31, 2022 and April 30, 2021 were $0 and $18,056, respectively.

JANUARY

(Unaudited)

Return Equity Incentive Plan (the “2018 Plan”) that provide for the grant of Title IV Funds

An institution participatingshares in Title IV Programs must correctly calculatethe form of incentive stock options, non-qualified stock options, restricted shares, stock appreciation rights and RSUs to employees, consultants, officers and directors. The 2012 Plan expired March 15, 2022 and remains in effect for outstanding grants only, and is no longer available for new grants. On March 8, 2022 we transferred the 129,009 unused shares under the 2012 Plan to the 2018 Plan.

| Restricted Stock Units | Number of Shares | Weighted Average Grant Price | ||||||||||||

| Unvested balance outstanding, April 30, 2021 | 549,972 | $ | 6.58 | |||||||||||

| Granted | 514,142 | 5.62 | ||||||||||||

| Forfeits | (36,353) | 9.67 | ||||||||||||

| Vested | (75,124) | (1) | 4.54 | |||||||||||

| Expired | — | — | ||||||||||||

| Unvested balance outstanding, January 31, 2022 | 952,637 | $ | 4.84 | |||||||||||

| Warrants | Number of Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term | Aggregate Intrinsic Value | ||||||||||||||||||||||

| Balance Outstanding, April 30, 2021 | 374,174 | $ | 6.37 | 1.90 | $ | — | ||||||||||||||||||||

| Granted | 75,000 | $ | 6.23 | 4.55 | — | |||||||||||||||||||||

| Exercised | — | $ | — | — | — | |||||||||||||||||||||

| Surrendered | — | $ | — | — | — | |||||||||||||||||||||

| Expired | — | $ | — | — | — | |||||||||||||||||||||

| Balance Outstanding, January 31, 2022 | 449,174 | $ | 6.35 | 1.71 | $ | — | ||||||||||||||||||||

| Exercisable, January 31, 2022 | 424,174 | $ | 6.31 | 1.55 | $ | — | ||||||||||||||||||||

| OUTSTANDING WARRANTS | EXERCISABLE WARRANTS | |||||||||||||||||||||||||||||||

| Exercise Price | Weighted Average Exercise Price | Outstanding No. of Warrants | Weighted Average Exercise Price | Weighted Average Remaining Life In Years | Exercisable No. of Warrants | |||||||||||||||||||||||||||

| $ | 4.89 | $ | 4.89 | 50,000 | $ | 4.89 | 2.19 | 50,000 | ||||||||||||||||||||||||

| $ | 5.85 | $ | 5.85 | 50,000 | $ | 5.85 | 4.58 | 50,000 | ||||||||||||||||||||||||

| $ | 6.00 | $ | 6.00 | 100,000 | $ | 6.00 | 2.09 | 100,000 | ||||||||||||||||||||||||

| $ | 6.87 | $ | 6.87 | 224,174 | $ | 6.87 | 0.48 | 224,174 | ||||||||||||||||||||||||

| $ | 6.99 | $ | 6.99 | 25,000 | ||||||||||||||||||||||||||||

| 449,174 | 424,174 | |||||||||||||||||||||||||||||||

| Options | Number of Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term | Aggregate Intrinsic Value | ||||||||||||||||||||||

| Balance Outstanding, April 30, 2021 | 1,214,473 | $ | 6.24 | 1.88 | $ | 204,719 | ||||||||||||||||||||

| Granted | — | — | — | — | ||||||||||||||||||||||

| Exercised | (258,419) | 5.60 | — | — | ||||||||||||||||||||||

| Forfeited | (4,586) | 4.59 | — | — | ||||||||||||||||||||||

| Expired | (22,793) | 3.21 | — | — | ||||||||||||||||||||||

| Balance Outstanding, January 31, 2022 | 928,675 | $ | 6.84 | 1.41 | $ | — | ||||||||||||||||||||

| Exercisable, January 31, 2022 | 891,264 | $ | 6.92 | 1.38 | $ | — | ||||||||||||||||||||

| OUTSTANDING OPTIONS | EXERCISABLE OPTIONS | |||||||||||||||||||||||||||||||

| Exercise Price | Weighted Average Exercise Price | Outstanding Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Life In Years | Exercisable Number of Options | |||||||||||||||||||||||||||

| $3.24 to $4.38 | $ | 4.14 | 115,890 | $ | 4.15 | 0.94 | 103,389 | |||||||||||||||||||||||||

| $4.50 to $5.20 | $ | 4.99 | 153,944 | $ | 5.03 | 1.77 | 137,394 | |||||||||||||||||||||||||

| $5.95 to $6.28 | $ | 5.95 | 28,000 | $ | 5.95 | 0.55 | 28,000 | |||||||||||||||||||||||||

| $7.17 to $7.55 | $ | 7.45 | 473,092 | $ | 7.46 | 1.57 | 465,092 | |||||||||||||||||||||||||

| $8.57 to $9.07 | $ | 8.98 | 157,749 | $ | 8.98 | 0.93 | 157,749 | |||||||||||||||||||||||||

| 928,675 | 891,624 | |||||||||||||||||||||||||||||||

| Three Months Ended January 31, | Nine Months Ended January 31, | ||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||

Tuition - recognized over period of instruction | $ | 16,550,586 | $ | 14,580,439 | $ | 50,304,380 | $ | 42,922,429 | |||||||||||||||

Course fees - recognized over period of instruction | 1,981,470 | 1,834,251 | 5,967,581 | 5,220,308 | |||||||||||||||||||

Book fees - recognized at a point in time | — | 44,468 | 42,777 | 129,643 | |||||||||||||||||||

Exam fees - recognized at a point in time | 199,924 | 69,500 | 590,337 | 219,055 | |||||||||||||||||||

Service fees - recognized at a point in time | 212,818 | 96,179 | 410,929 | 270,009 | |||||||||||||||||||

| $ | 18,944,798 | $ | 16,624,837 | $ | 57,316,004 | $ | 48,761,444 | ||||||||||||||||

Subsequent to a compliance audit, USU recognized that it had not fully complied with all requirements for calculating and making timely returns of Title IV funds (R2T4). In 2016, USU had a material findingsummarized below:

| January 31, 2022 | April 30, 2021 | |||||||||||||

| ROU assets - Operating facility leases | $ | 15,958,721 | $ | 14,308,296 | ||||||||||

| Less: accumulated amortization | (2,868,251) | (1,593,433) | ||||||||||||

| Total ROU assets | $ | 13,090,470 | $ | 12,714,863 | ||||||||||

| January 31, 2022 | April 30, 2021 | |||||||||||||

| Total lease liabilities | $ | 22,509,568 | $ | 19,946,229 | ||||||||||

| Reduction of lease liabilities | (3,085,191) | (1,617,600) | ||||||||||||

| Total operating lease obligations | $ | 19,424,377 | $ | 18,328,629 | ||||||||||

Delaware Approval to Confer Degrees

Aspen Universityfollowing is a Delaware corporation. Delaware law requires an institutionschedule by fiscal years of future minimum lease payments required under operating leases that have initial or remaining non-cancelable lease terms in excess of one year as of January 31, 2022

| Maturity of Lease Obligations | Lease Payments | |||||||

| 2022 (remaining) | $ | 1,139,587 | ||||||

| 2023 | 4,142,637 | |||||||

| 2024 | 4,018,977 | |||||||

| 2025 | 3,802,960 | |||||||

| 2026 | 3,908,722 | |||||||

| Thereafter | 11,963,226 | |||||||

| Total future minimum lease payments | 28,976,109 | |||||||

| Less: imputed interest | (9,551,732) | |||||||

| Present value of operating lease liabilities | $ | 19,424,377 | ||||||

| Balance Sheet Classification | January 31, 2022 | April 30, 2021 | ||||||||||||

| Operating lease obligations, current portion | $ | 2,106,981 | $ | 2,029,821 | ||||||||||

| Operating lease obligations, less current portion | 17,317,396 | 16,298,808 | ||||||||||||

| Total operating lease liabilities | $ | 19,424,377 | $ | 18,328,629 | ||||||||||

| Other Information | January 31, 2022 | |||||||

| Weighted average remaining lease term (in years) | 6.97 | |||||||

| Weighted average discount rate | 12 | % | ||||||

USU is alsoreserve of approximately $300,000 for the estimate of the 2013 through 2021 tax year foreign income tax liability. Additionally, for the 2022 tax year, the Company recorded a Delaware corporation and is inreserve of approximately $75,000 for the process of obtaining Delaware approval.

Common Stock

Effective May 24, 2017,11. Commitments and Contingencies

JANUARY 31, 2018

(Unaudited)

Warrants

A summary of the Company’s warrant activity during the nine months ended

|

|

|

|

|

|

|

| Weighted |

|

|

|

| ||||

|

|

|

|

| Weighted |

|

| Average |

|

|

|

| ||||

|

|

|

|

| Average |

|

| Remaining |

|

| Aggregate |

| ||||

|

| Number of |

|

| Exercise |

|

| Contractual |

|

| Intrinsic |

| ||||

Warrants |

| Shares |

|

| Price |

|

| Term |

|

| Value |

| ||||

Balance outstanding, April 30, 2017 |

|

| 914,123 |

|

| $ | 2.82 |

|

|

| 1.6 |

|

| $ | 1,100,203 |

|

Granted |

|

| 224,174 |

|

|

| 6.87 |

|

|

| 5.0 |

|

|

| 307,118 |

|

Exercised |

|

| (356,267 | ) |

|

| 0.55 |

|

|

| — |

|

|

| — |

|

Forfeited |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Expired |

|

| (38,257 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

Balance outstanding, January 31, 2018 |

|

| 743,773 |

|

| $ | 4.08 |

|

|

| 2.1 |

|

| $ | 3,095,502 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Exercisable, January 31, 2018 |

|

| 743,773 |

|

| $ | 4.08 |

|

|

| 2.1 |

|

| $ | 3,095,502 |

|

In connection with the Senior Secured Term Loan that was finalized on July 25, 2017, the Company issued 224,174 5-year warrants at an exercise price2022

The Company issued 241,514 shares of Common Stock in conjunction with the cash and cashless exercise of 356,267 warrants. The Company received $143,489 in conjunction with the cash exercises.

Stock Incentive Plan and Stock Option Grants to Employees and Directors

On March 13, 2012, the Company adopted the 2012 Equity Incentive Plan (the “Plan”) that provides for the grant of 1,691,667 shares effective November 2015, 2,108,333 shares effective June 2016 and 3,500,000 shares effective July 2017,our operations in the formnormal course of incentive stock options, non-qualified stock options, restricted shares, stock appreciation rights and restricted stock units to employees, consultants, officers and directors.business. As of January 31, 2018,2022, except as discussed below, there were 622,454no other pending or threatened lawsuits that could reasonably be expected to have a material effect on the results of our consolidated operations and there are no proceedings in which any of our directors, officers or affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to our interest.

| ||||||||

| ||||||||

|

| |||||||

|

|

| ||||||

|

|

| ||||||

|

| |||||||

The Company utilized the simplified method to estimate the expected life for stock options granted to employees. The simplified method was used as the Company does not have sufficient historical data regarding stock option exercises. The expected volatility is basedsignificant regulatory scrutiny on the averagebasis of numerous standards that schools must satisfy to participate in the various types of federal student financial assistance programs authorized under Title IV of the expected volatilities fromHEA.

15

JANUARY 31, 2018

(Unaudited)

A summary of the Company’s stock option activity for employees and directors during the nine months ended

|

|

|

|

| Weighted |

|

| Average |

|

|

|

| ||||

|

|

|

|

| Average |

|

| Remaining |

|

| Aggregate |

| ||||

|

| Number of |

|

| Exercise |

|

| Contractual |

|

| Intrinsic |

| ||||

Options |

| Shares |

|

| Price |

|

| Term |

|

| Value |

| ||||

Balance outstanding, April 30, 2017 |

|

| 2,097,384 |

|

| $ | 1.86 |

|

|

| 2.7 |

|

| $ | 12,489,871 |

|

Granted |

|

| 844,000 |

|

| $ | 3.53 |

|

|

| 3.4 |

|

|

| 1,867,740 |

|

Exercised |

|

| (63,838 | ) |

| $ | 3.13 |

|

|

| — |

|

|

| — |

|

Forfeited |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Expired |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Balance outstanding, January 31, 2018 |

|

| 2,877,546 |

|

| $ | 3.52 |

|

|

| 3.24 |

|

| $ | 17,658,268 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Exercisable, January 31, 2018 |

|

| 1,083,484 |

|

| $ | 2.22 |

|

|

| 2.07 |

|

| $ | 8,727,757 |

|

On May 13, 2017,also subject to regulation by self-regulatory bodies such as accreditors and by state regulators in certain states including states where the Company granted its executive officershas a total of 500,000 five-year options to purchase shares of the Company’s common stock under the Plan. The options vest annually over three years, subject to continued employment at each applicable vesting date,physical presence. For certain recent information, see Note 12. Subsequent Events.

In May 2017, the Company issued 5,500 stock options to various employees at exercise prices ranging from $4.95 to $5.10 per share.

Effective June 11, 2017, the Company granted the Chief Academic Officer 30,000 five-year options. The options vest quarterly over a three-year period in 12 equal quarterly increments with the first vesting date being September 11, 2017, subject to continued employment on each applicable vesting date. The options are exercisable at $6.28 per share and the fair value is $54,000.

On August 21, 2017, 53,000 options were issued to 26 employees with an exercise price of $5.95 per share and a fair value of $90,630.

On January 4, 2018, 180,000 options were issued to the board of directors with an exercise price of $9.07 per share and a fair value of $421,200.

On January 14, 2018, 75,500 options were issued to employees with an exercise price of $8.57 per share and a fair value of $152,510.

During the nine months ended January 31, 2018, the company issued 113,597 shares of common stock in conjunction with the exercise of 63,838 stock options. The company received $455,387 related to these exercises.

As of January 31, 2018, there was $1,474,855 of unrecognized compensation costs related to nonvested share-based compensation arrangements. That cost is expected to be recognized over a weighted-average period of 2.0 years.

The Company recorded compensation expense of $466,468 and $253,833 for the nine months ended January 31, 2018 and 2017, respectively, in connection with stock options.

Note 9. Related Party Transactions

See Note 6 for discussion of convertible notes payable to a related party.

16

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

Note 10 – Acquisition of USU

On December 1, 2017 certain assets were acquired and certain liabilities assumed from Educacion Significativa, LLC (dba United States University) by United States University Inc. United States University, Inc. isderive a wholly owned subsidiaryportion of Aspen Group Inc. (“AGI”) and was set up for purposes of finalizing the asset purchase transaction. For purposes of purchase accounting, Aspen Group, Inc. is referred to as the acquirer. Aspen Group, Inc. acquired the assets and assumed the liabilities of Educacion Significativa, LLC (dba United States University) for a purchase price of approximately $14.8 million. The purchase consideration consisted of a cash payment of $2,500,000 less an adjustment for working capital of approximately $110,000 plus approximately $200,000 of additional costs paid to/on behalf of and for the benefittheir revenue from financial aid received by its students under programs authorized by Title IV of the seller, a convertible noteHEA, which are administered by the US Department of $2,000,000Education. When students seek funding from the federal government, they receive loans and 1,203,209 shares of AGI stock valued at the quoted closing price of $8.49 per share as of November 30, 2017. The stock consideration represents $10,215,244 of the purchase consideration.

The acquisition was accounted for by AGI in accordance with the acquisition method of accounting pursuantgrants to ASC 805 “Business Combinations” and pushdown accounting was applied to record the fair value of the assets acquired and liabilities assumed on United States University, Inc. Under this method, the purchase price is allocated to the identifiable assets acquired and liabilities assumed based onfund their estimated fair values at the date of acquisition. The excess of the amount paid over the estimated fair values of the identifiable net assets was $5,011,432 which has been reflected in the balance sheet as goodwill.

The following is a summary of the estimated fair value of the assets acquired and liabilities assumed at the date of acquisition:

|

| Purchase Price Allocation |

|

| Useful Life |

| ||

Cash and cash equivalents |

| $ | — |

|

|

|

| |

Current assets acquired |

|

| 244,465 |

|

|

|

|

|

Other assets acquired |

|

| 176,667 |

|

|

|

|

|

Intangible assets |

|

|

|

|

|

|

|

|

Accreditation and regulatory approvals |

|

| 6,200,000 |

|

|

|

|

|

Trade name and trademarks |

|

| 1,700,000 |

|

|

|

|

|

Student relationships |

|

| 2,000,000 |

|

| 2 years |

| |

Curriculum |

|

| 200,000 |

|

| 1 year |

| |

Goodwill |

|

| 5,011,432 |

|

|

|

|

|

Less: Current liabilities assumed |

|

| (727,601 | ) |

|

|

|

|

Total purchase price |

| $ | 14,804,963 |

|

|

|

|

|

We determined the fair value of assets acquired and liabilities assumed based on assumptions that reasonable market participants would use while employing the concept of highest and best use of the respective items. We usededucation under the following assumptions,Title IV Programs: (1) the majority of which include significant unobservable inputs (Level 3),Federal Direct Loan program, or Direct Loan; (2) the Federal Pell Grant program, or Pell; (3) Federal Work Study and valuation methodologies to determine fair value:

·

Intangibles - We used the multiple period excess earnings method to value the Accreditation and regulatory approvals. The Trade name and trademarks were valued using the relief-from-royalty method, which represents the benefit of owning these intangible assets rather than paying royalties for their use. The Student relationships were valued using the excess earnings method. The curriculum was valued using the replacement cost approach.

·

Other assets and liabilities - The carrying value of all other assets and liabilities approximated fair value at the time of acquisition.

The goodwill resulting from the acquisition may become deductible for tax purposes in the future. The goodwill resulting from the acquisition is principally attributable to the future earnings potential associated with enrollment growth and other intangibles that do not qualify for separate recognition such as the assembled workforce.

We have selected an April 30th annual goodwill impairment test date.

17

ASPEN GROUP, INC. AND SUBSIDIARIES

CONDENSED NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

JANUARY 31, 2018

(Unaudited)

We assigned an indefinite useful life to the accreditation and regulatory approvals and the trade name and trademarks as we believe they have the ability to generate cash flows indefinitely. In addition, there are no legal, regulatory, contractual, economic or other factors to limit the intangibles’ useful life and we intend to renew the intangibles, as applicable, and renewal can be accomplished at little cost. We determined all other acquired intangibles are finite-lived and we are amortizing them on either a straight-line basis or using an accelerated method to reflect the pattern in which the economic benefits of the assets are expected to be consumed. Amortization for the period of inception through January 31, 2018 was $183,333.

The expected benefits from the business acquisition will allow USU, Inc. to achieve its vision of making college affordable again on a much broader scale along with providing various accreditations.

The Company is in the process of completing its accounting and valuations of USU, Inc. and accordingly, the estimated fair values and allocation of purchase price noted above is provisional pending the final valuation of the assets acquired and liabilities assumed which will not exceed one-year in accordance with ASC 805.

The total acquisition costs that AGI incurred was approximately $1,050,000, of which approximately $200,000 was incurred in(4) Federal Supplemental Opportunity Grants. For the fiscal year ended April 30, 20172021, 44.72% of Aspen University’s and $850,000 was incurred33.81% for United States University's cash-basis revenue for eligible tuition and fees were derived from Title IV Programs.

The resultsamount of operationsunearned Title IV Program funds that have been disbursed to students who withdraw from their educational programs before completion and must return those unearned funds in a timely manner, no later than 45 days of USU are included in the Company’s consolidated statement of operations from the date of acquisition of December 1, 2017. The following supplemental unaudited pro forma combined information assumesthe school determines that the acquisitions had occurred asstudent has withdrawn. Under the DOE regulations, failure to make timely returns of the beginningTitle IV Program funds for 5% or more of each period present:

|

| For the Year Ended |

|

| For the Nine Months Ended |

| ||

|

| (unaudited) |

|

| (unaudited) |

| ||

Revenue |

| $ | 18,038,474 |

|

| $ | 10,719,546 |

|

Net Loss |

| $ | (5,444,205 | ) |

| $ | (3,521,086 | ) |

Loss per common share- basic and diluted |

| $ | (0.47 | ) |

|

| $(0.26 | ) |

The pro forma financial information is not necessarily indicative of the results that would have occurred if these acquisitions had occurredstudents sampled on the dates indicated or thatinstitution's annual compliance audit in either of its two most recently completed fiscal years can result in the future.

Aspen’s pre-licensure BSN program is offered asArizona Board of Nursing regarding our future status, and until we have a full-time, three-year (nine semester) program that is specifically designed for students who do not currently hold a state nursing license and have no prior nursing experience. Aspen will admit students into three tracks; 1) High school graduates with no prior college credits, 2) students that have less than 48 general education prerequisites completed, and 3) students that have completed all 48 general education prerequisite credits and are ready to enterformal agreement in place we won’t be publicly commenting on the core Nursing courses and clinical experiences.

Related to that announcement, matter.