UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| |

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20172019

OR

| |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________ to _________

DASEKE, INC.

(Exact name of registrant as specified in its charter)

| | | | |

Delaware

(State or Other Jurisdictionother jurisdiction of Incorporation)incorporation or organization) | | 001-37509

(Commission

File Number) | | 47-3913221

(IRS Employer

Identification No.) |

| | | | |

15455 Dallas Parkway, Suite 440

550

Addison, Texas | | 75001 |

(Address of Principal Executive Offices) | | (Zip Code) |

| | | | |

Registrant’s Telephone Number, Including Area Code: (972) 248-0412 Not applicable (Former name, former address and former fiscal year, if changed since last report) |

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | |

☐ Large accelerated filer | | | | ☒ Accelerated filer |

☐ Non-accelerated filer (Do not check if a smaller | | | | ☐ Smaller reporting company)company |

| | | |

☐ Smaller reporting company | | | | ☒ Emerging growth company

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

| | |

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, par value $0.0001 per share | DSKE | The NASDAQ Capital Market |

Common shares of the registrant outstanding at November 6, 20178, 2019 were 44,392,349.64,589,075.

DASEKE, INC.

FORM 10-Q

For the Quarterly Period Ended September 30, 20172019

INDEX

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q (this Report) of Daseke, Inc. (Daseke or the Company) contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Except as otherwise indicated by the context, references in this Report to “we,” “us” and “our” are to the consolidated business of the Company. All statements in this Report, including those made by the management of the Company, other than statements of historical fact, are forward-looking statements. These forward-looking statements are based on management’s estimates, projections and assumptions as of the date hereof. Forward-looking statements may contain words such as “may,” “will,” “expect,” “anticipate,” “continue,” “estimate,” “project,” “believe,” “plan,” “should,” “could,” “would,” “expect,” “plan,” “estimate,” “project,” “forecast,” “seek,” “target,” “anticipate,” “believe,” “estimate,” “predict,” “potential” and “continue,“potential,” the negative of these terms, or other comparable terminology. Examples of forward-lookingForward-looking statements may include statements regardingabout the Company’s goals; the Company’s financial strategy, liquidity and capital required for its business strategy and plans; the Company’s competition and government regulations; general economic conditions; and the Company’s future financial results, operating results, business strategies, projected costs, management’s plans and objectives for future acquisitions, and industry trends.results.

These forward-looking statements are based on information available as of the date of this Report (or, in the case of forward-looking statements incorporated herein by reference, as of the date of the applicable filed document), and current expectations, forecasts and assumptions. While management believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments affecting us will be those that we anticipate.the Company anticipates. Accordingly, forward-looking statements should not be relied upon as representing the Company’s views as of any subsequent date, and the Company does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. Accordingly, readers are cautioned not to place undue reliance on the forward-looking statements.

Forward-looking statements are subject to risks and uncertainties (many of which are beyond ourthe Company’s control) that could cause actual results to differ materially from ourthe Company’s historical experience and our present expectations or projections. Important factors that could cause actual results to differ materially from those in the forward-looking statements include, but are not limited to, general economic risks (such as downturns in customers’and business cycles and disruptions in capital and credit markets),risks, driver shortages and increases in driver compensation or owner-operator contracted rates, loss of senior management or key operating personnel, our ability to identify and execute future acquisitions successfully, seasonality and the impact of weather and other catastrophic events, fluctuations in the price or availability of diesel fuel, increased prices for, or decreases in the availability of, new revenue equipment and decreases in the value of used revenue equipment, ourthe failure of any restructuring actions and cost reduction initiatives that the Company undertakes to meet the expected results, the Company’s ability to generate sufficient cash to service all of ourthe Company’s indebtedness, restrictions in ourits existing and future debt agreements, increases in interest rates, changes in existing laws or regulations, including environmental and worker health safety laws and regulations and those relating to tax rates or taxes in general, the impact of governmental regulations and other governmental actions related to the Company and its operations, litigation and governmental proceedings, and insurance and claims expenses. For additional information regarding known material factors that could cause ourthe Company’s actual results to differ from ourits projected results, please see the Company’s filings with the Securities and Exchange Commission (the SEC), particularly the section titled “Risk“Item 1A. Risk Factors” in the Company’s CurrentAnnual Report on Form 8-K,10-K, filed with the SEC on March 3, 2017, as amended8, 2019, and the Company’s Quarterly Report on March 16, 2017 and May 4, 2017.Form 10-Q, filed with the SEC on August 5, 2019.

All forward-looking statements, expressed or implied, attributed to the Company or persons acting on its behalf are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that the Company or persons acting on its behalf may issue.

Part I – FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Unaudited)

(In thousands,millions, except share and per share data)

| | | | | | | | | | | | |

| | September 30, | | December 31, | | September 30, | | December 31, |

| | 2017 | | 2016 | | 2019 | | 2018 |

ASSETS | | | | | | | | | | | | |

Current assets: | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 112,510 | | $ | 3,695 | | $ | 79.6 | | $ | 46.0 |

Accounts receivable, net of allowance of $382 and $321 at September 30, 2017 and December 31, 2016, respectively | | | 106,081 | | | 54,177 | |

Accounts receivable, net of allowance of $2.6 at September 30, 2019 and $1.2 at December 31, 2018 | | | | 230.3 | | | 209.2 |

Drivers’ advances and other receivables | | | 2,809 | | | 2,632 | | | 8.0 | | | 5.5 |

Current portion of net investment in sales-type leases | | | 6,022 | | | 3,516 | | | — | | | 16.2 |

Parts supplies | | | 4,365 | | | 1,467 | | | 3.9 | | | 4.9 |

Income tax receivable | | | 111 | | | 719 | |

Prepaid and other current assets | | | 20,321 | | | 13,504 | | | 21.9 | | | 26.3 |

Total current assets | | | 252,219 | | | 79,710 | | | 343.7 | | | 308.1 |

| | | | | | | | | | | | |

Property and equipment, net | | | 369,199 | | | 318,747 | | | 463.1 | | | 572.7 |

Intangible assets, net | | | 77,541 | | | 71,653 | | | 111.0 | | | 208.8 |

Goodwill | | | 139,889 | | | 89,035 | | | 145.7 | | | 258.4 |

Right-of-use assets | | | | 97.0 | | | — |

Other long-term assets | | | 18,573 | | | 11,090 | | | 29.6 | | | 42.9 |

Total assets | | | 857,421 | | | 570,235 | | $ | 1,190.1 | | $ | 1,390.9 |

| | | | | | | | | | | | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | | | | | |

Current liabilities: | | | | | | | | | | | | |

Checks outstanding in excess of bank balances | | | 1,479 | | | 1,166 | |

Accounts payable | | | 12,493 | | | 4,788 | | $ | 24.0 | | $ | 22.2 |

Accrued expenses and other liabilities | | | 24,660 | | | 16,104 | | | 54.2 | | | 46.5 |

Accrued payroll, benefits and related taxes | | | 12,027 | | | 7,835 | | | 39.6 | | | 21.7 |

Accrued insurance and claims | | | 10,248 | | | 9,840 | | | 18.6 | | | 18.1 |

Current portion of long-term debt | | | 26,514 | | | 52,665 | | | 61.6 | | | 63.5 |

Other current liabilities | | | | 49.9 | | | 21.9 |

Total current liabilities | | | 87,421 | | | 92,398 | | | 247.9 | | | 193.9 |

| | | | | | | | | | | | |

Line of credit | | | — | | | 6,858 | |

Long-term debt, net of current portion | | | 395,841 | | | 208,372 | | | 639.1 | | | 622.7 |

Deferred tax liabilities | | | 114,900 | | | 92,815 | | | 66.2 | | | 126.8 |

Other long-term liabilities | | | 1,342 | | | 286 | | | 79.6 | | | 0.5 |

Subordinated debt | | | — | | | 66,443 | |

Total liabilities | | | 599,504 | | | 467,172 | | | 1,032.8 | | | 943.9 |

| | | | | | | | | | | | |

Commitments and contingencies (Note 15) | | | | | | | |

Commitments and contingencies (Note 14) | | | | | | | |

| | | | | | | | | | | | |

Stockholders’ equity: | | | | | | | | | | | | |

Series A convertible preferred stock, $0.0001 par value; 10,000,000 shares authorized; 650,000 shares issued with liquidation preference of $65,000 | | | 65,000 | | | — | |

Series B convertible preferred stock, $0.01 par value; 75,000 shares authorized; zero and 64,500 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively | | | — | | | 1 | |

Common stock, par value $0.0001 per share; 250,000,000 shares authorized, 44,480,232 and 20,980,961 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively | | | 4 | | | 1 | |

Series A convertible preferred stock, $0.0001 par value; 10,000,000 shares authorized; 650,000

shares issued with liquidation preference of $65.0 at September 30, 2019 and December 31, 2018 | | | | 65.0 | | | 65.0 |

Common stock, par value $0.0001 per share; 250,000,000 shares authorized, 64,583,275 and

64,455,174 shares issued and outstanding at September 30, 2019 and December 31, 2018, respectively | | | | — | | | — |

Additional paid-in-capital | | | 222,102 | | | 117,807 | | | 436.6 | | | 433.9 |

Accumulated deficit | | | (30,221) | | | (14,694) | | | (343.7) | | | (51.0) |

Accumulated other comprehensive income (loss) | | | 1,032 | | | (52) | |

Accumulated other comprehensive loss | | | | (0.6) | | | (0.9) |

Total stockholders’ equity | | | 257,917 | | | 103,063 | | | 157.3 | | | 447.0 |

Total liabilities and stockholders’ equity | | $ | 857,421 | | $ | 570,235 | | $ | 1,190.1 | | $ | 1,390.9 |

The accompanying notes are an integral part of the consolidated financial statements.

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

(Unaudited)

(In thousands,millions, except share and per share data)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended | | Three Months Ended | | Nine Months Ended |

| | September 30, | | September 30, | | September 30, | | September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 | | 2019 | | 2018 | | 2019 | | 2018 |

Revenues: | | | | | | | | | | | | | | | | | | | | | | | | |

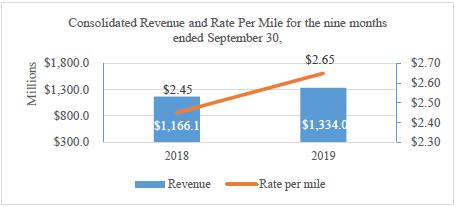

Freight | | $ | 171,245 | | $ | 135,415 | | $ | 446,454 | | $ | 398,466 | |

Company freight | | | $ | 205.2 | | $ | 206.9 | | $ | 618.2 | | $ | 511.4 |

Owner operator freight | | | | 118.3 | | | 122.6 | | | 351.1 | | | 330.7 |

Brokerage | | | 34,198 | | | 25,977 | | | 83,723 | | | 68,358 | | | 78.6 | | | 82.2 | | | 222.8 | | | 188.4 |

Logistics | | | 7,871 | | | — | | | 10,571 | | | — | | | 13.5 | | | 11.6 | | | 39.0 | | | 31.3 |

Fuel surcharge | | | 18,008 | | | 12,756 | | | 48,331 | | | 34,562 | | | 34.8 | | | 38.3 | | | 102.9 | | | 104.3 |

Total revenue | | | 231,322 | | | 174,148 | | | 589,079 | | | 501,386 | | | 450.4 | | | 461.6 | | | 1,334.0 | | | 1,166.1 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | | | | | |

Salaries, wages and employee benefits | | | 64,955 | | | 49,298 | | | 174,253 | | | 149,861 | | | 127.7 | | | 114.8 | | | 371.1 | | | 287.7 |

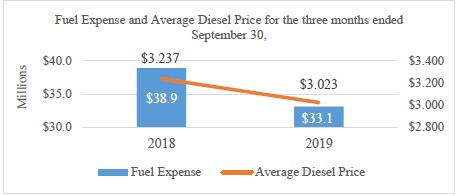

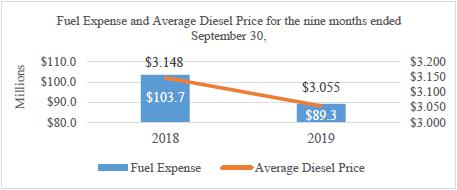

Fuel | | | 24,734 | | | 17,296 | | | 64,423 | | | 49,076 | | | 34.1 | | | 38.9 | | | 105.3 | | | 103.7 |

Operations and maintenance | | | 35,132 | | | 27,874 | | | 86,332 | | | 72,933 | | | 56.8 | | | 51.5 | | | 164.7 | | | 126.4 |

Communications | | | 539 | | | 370 | | | 1,491 | | | 1,208 | | | 1.0 | | | 0.9 | | | 3.2 | | | 2.4 |

Purchased freight | | | 61,598 | | | 42,541 | | | 148,945 | | | 120,501 | | | 155.5 | | | 170.6 | | | 458.5 | | | 429.9 |

Administrative expenses | | | 8,619 | | | 5,221 | | | 24,019 | | | 17,711 | | | 21.4 | | | 16.1 | | | 54.7 | | | 41.3 |

Sales and marketing | | | 488 | | | 435 | | | 1,425 | | | 1,280 | | | 1.3 | | | 1.0 | | | 3.8 | | | 2.3 |

Taxes and licenses | | | 2,963 | | | 2,268 | | | 7,855 | | | 6,946 | | | 4.8 | | | 4.7 | | | 14.7 | | | 12.3 |

Insurance and claims | | | 6,351 | | | 5,065 | | | 15,516 | | | 13,648 | | | 13.4 | | | 12.7 | | | 38.1 | | | 32.4 |

Acquisition-related transaction expenses | | | 773 | | | — | | | 2,255 | | | 18 | | | — | | | 0.6 | | | — | | | 2.4 |

Depreciation and amortization | | | 19,805 | | | 16,998 | | | 53,758 | | | 50,515 | | | 38.3 | | | 36.8 | | | 119.5 | | | 93.8 |

(Gain) loss on disposition of revenue property and equipment | | | (339) | | | (495) | | | (513) | | | 158 | |

Impairment of revenue property and equipment | | | — | | | 1,195 | | | — | | | 1,195 | |

Gain on disposition of property and equipment | | | | (1.0) | | | (0.9) | | | (2.1) | | | (1.5) |

Impairment | | | | 306.8 | | | — | | | 306.8 | | | 2.8 |

Restructuring charges | | | | 6.9 | | | — | | | 6.9 | | | — |

Total operating expenses | | | 225,618 | | | 168,066 | | | 579,759 | | | 485,050 | | | 767.0 | | | 447.7 | | | 1,645.2 | | | 1,135.9 |

Income from operations | | | 5,704 | | | 6,082 | | | 9,320 | | | 16,336 | |

Income (loss) from operations | | | | (316.6) | | | 13.9 | | | (311.2) | | | 30.2 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Other (income) expense: | | | | | | | | | | | | | |

Other expense (income): | | | | | | | | | | | | | |

Interest income | | | (76) | | | (4) | | | (130) | | | (40) | | | (0.3) | | | (0.2) | | | (0.7) | | | (1.2) |

Interest expense | | | 8,624 | | | 6,724 | | | 21,064 | | | 17,521 | | | 12.8 | | | 11.9 | | | 38.2 | | | 33.2 |

Write-off of unamortized deferred financing fees | | | — | | | — | | | 3,883 | | | — | |

Write-off of deferred financing fees | | | | 2.0 | | | — | | | 2.0 | | | — |

Other | | | (32) | | | (64) | | | (247) | | | (266) | | | — | | | (0.7) | | | (1.3) | | | (2.5) |

Total other expense | | | 8,516 | | | 6,656 | | | 24,570 | | | 17,215 | | | 14.5 | | | 11.0 | | | 38.2 | | | 29.5 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Loss before provision (benefit) for income taxes | | | (2,812) | | | (574) | | | (15,250) | | | (879) | |

Income (loss) before benefit for income taxes | | | | (331.1) | | | 2.9 | | | (349.4) | | | 0.7 |

Provision (benefit) for income taxes | | | (2,862) | | | 683 | | | (3,448) | | | 607 | | | (57.8) | | | 0.7 | | | (60.4) | | | (14.2) |

Net income (loss) | | | 50 | | | (1,257) | | | (11,802) | | | (1,486) | | | (273.3) | | | 2.2 | | | (289.0) | | | 14.9 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Other comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | |

Unrealized income (loss) on interest rate swaps | | | — | | | 61 | | | 52 | | | (1) | |

Foreign currency translation adjustments | | | 526 | | | — | | | 1,032 | | | — | |

Foreign currency translation adjustments, net of tax of $0.1, $0.1, $(0.2) and $(0.1), respectively | | | | (0.2) | | | 0.3 | | | 0.3 | | | (0.6) |

Comprehensive income (loss) | | | 576 | | | (1,196) | | | (10,718) | | | (1,487) | | | (273.5) | | | 2.5 | | | (288.7) | | | 14.3 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | | 50 | | | (1,257) | | | (11,802) | | | (1,486) | | | (273.3) | | | 2.2 | | | (289.0) | | | 14.9 |

Less dividends to Series A convertible preferred stockholders | | | (1,225) | | | — | | | (2,919) | | | — | | | (1.2) | | | (1.2) | | | (3.7) | | | (3.7) |

Less dividends to Series B convertible preferred stockholders | | | — | | | (1,243) | | | (806) | | | (3,729) | |

Net loss attributable to common stockholders | | $ | (1,175) | | $ | (2,500) | | $ | (15,527) | | $ | (5,215) | |

Net income (loss) attributable to common stockholders | | | $ | (274.5) | | $ | 1.0 | | $ | (292.7) | | $ | 11.2 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net loss per common share: | | | | | | | | | | | | | |

Net income (loss) per common share: | | | | | | | | | | | | | |

Basic and Diluted | | $ | (0.03) | | $ | (0.12) | | $ | (0.45) | | $ | (0.25) | | $ | (4.25) | | $ | 0.01 | | $ | (4.54) | | $ | 0.18 |

Weighted-average common shares outstanding: | | | | | | | | | | | | | | | | | | | | | | | | |

Basic and Diluted | | | 39,359,523 | | | 20,980,961 | | | 34,790,861 | | | 20,980,961 | | | 64,583,275 | | | 65,289,320 | | | 64,525,777 | | | 60,413,694 |

| | | | | | | | | | | | | | | | | | | | | | | | |

Dividends declared per Series A convertible preferred share | | $ | 1.91 | | $ | — | | $ | 2.59 | | $ | — | | $ | 1.91 | | $ | 1.91 | | $ | 5.72 | | $ | 5.72 |

Dividends declared per Series B convertible preferred share | | $ | — | | $ | 18.75 | | $ | 12.50 | | $ | 18.75 | |

The accompanying notes are an integral part of the consolidated financial statements.

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

Nine Months Ended September 30, 20172019

(Unaudited)

(In thousands,millions, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Series A Convertible | | Series B Convertible | | | | | | | | | | | | Accumulated | | | |

| | Preferred Stock | | Preferred Stock | | Common Stock | | | | | | | Other | | | |

| | | | | | | | Par | | | | Par | | Additional | | Accumulated | | Comprehensive | | | |

| | Shares | | Amount | | Shares | | Value | | Shares | | Value | | Paid- In Capital | | Deficit | | Income (Loss) | | Total |

Balance, January 1, 2017 as previously reported | | — | | $ | — | | 64,500 | | $ | 1 | | 145,495 | | $ | 1 | | $ | 117,807 | | $ | (14,694) | | $ | (52) | | $ | 103,063 |

Effect of reverse acquisition | | — | | | — | | — | | | — | | 20,835,466 | | | 1 | | | — | | | — | | | — | | | 1 |

Balance at January 1, 2017 | | — | | | — | | 64,500 | | | 1 | | 20,980,961 | | | 2 | | | 117,807 | | | (14,694) | | | (52) | | | 103,064 |

Income on interest rate swaps | | — | | | — | | — | | | — | | — | | | — | | | — | | | — | | | 52 | | | 52 |

Series B convertible preferred stock dividend | | — | | | — | | — | | | — | | — | | | — | | | — | | | (806) | | | — | | | (806) |

Repurchase of common shares | | — | | | — | | — | | | — | | (3,616,781) | | | (1) | | | (36,167) | | | — | | | — | | | (36,168) |

Conversion of Series B convertible preferred stock to common shares | | — | | | — | | (64,500) | | | (1) | | 9,301,150 | | | 1 | | | — | | | — | | | — | | | — |

Shares assumed by legal acquirer | | — | | | — | | — | | | — | | 11,050,630 | | | 1 | | | 83,639 | | | — | | | — | | | 83,640 |

Settlement of legal acquirer transaction costs | | — | | | — | | — | | | — | | — | | | — | | | (19,063) | | | — | | | — | | | (19,063) |

Issuance of Series A convertible preferred stock | | 650,000 | | | 65,000 | | — | | | — | | — | | | — | | | — | | | — | | | — | | | 65,000 |

Issuance of common stock | | — | | | — | | — | | | — | | 6,764,272 | | | 1 | | | 74,685 | | | — | | | — | | | 74,686 |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | — | | | — | | | — | | | (2,919) | | | — | | | (2,919) |

Stock-based compensation expense | | — | | | — | | — | | | — | | — | | | — | | | 1,201 | | | — | | | — | | | 1,201 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | — | | | — | | | — | | | — | | | 1,032 | | | 1,032 |

Net loss | | — | | | — | | — | | | — | | — | | | — | | | — | | | (11,802) | | | — | | | (11,802) |

Balance at September 30, 2017 | | 650,000 | | $ | 65,000 | | — | | $ | — | | 44,480,232 | | $ | 4 | | $ | 222,102 | | $ | (30,221) | | $ | 1,032 | | $ | 257,917 |

| | | | | | | | | | | | | | | | | | | | | | |

| | Series A Convertible | | | | | | | | | | | | Accumulated | | | |

| | Preferred Stock | | Common Stock | | | | | | | Other | | | |

| | | | | | | | Par | | Additional | | Accumulated | | Comprehensive | | | |

| | Shares | | Amount | | Shares | | Value | | Paid- In Capital | | Deficit | | Income (Loss) | | Total |

Balance at January 1, 2019 | | 650,000 | | $ | 65.0 | | 64,455,174 | | $ | — | | $ | 433.9 | | $ | (51.0) | | $ | (0.9) | | $ | 447.0 |

Vesting of restricted stock units | | — | | | — | | 14,498 | | | — | | | — | | | — | | | — | | | — |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.2) | | | — | | | (1.2) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 1.0 | | | — | | | — | | | 1.0 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | 0.1 | | | 0.1 |

Net loss | | — | | | — | | — | | | — | | | — | | | (9.3) | | | — | | | (9.3) |

Balance at March 31, 2019 | | 650,000 | | $ | 65.0 | | 64,469,672 | | $ | — | | $ | 434.9 | | $ | (61.5) | | $ | (0.8) | | $ | 437.6 |

Vesting of restricted stock units | | — | | | — | | 110,321 | | | — | | | (0.2) | | | — | | | — | | | (0.2) |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.3) | | | — | | | (1.3) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 0.9 | | | — | | | — | | | 0.9 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | 0.4 | | | 0.4 |

Net loss | | — | | | — | | — | | | — | | | — | | | (6.4) | | | — | | | (6.4) |

Balance at June 30, 2019 | | 650,000 | | $ | 65.0 | | 64,579,993 | | $ | — | | $ | 435.6 | | $ | (69.2) | | $ | (0.4) | | $ | 431.0 |

Vesting of restricted stock units | | — | | | — | | 3,282 | | | — | | | — | | | — | | | — | | | — |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.2) | | | — | | | (1.2) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 1.0 | | | — | | | — | | | 1.0 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | (0.2) | | | (0.2) |

Net loss | | — | | | — | | — | | | — | | | — | | | (273.3) | | | — | | | (273.3) |

Balance at September 30, 2019 | | 650,000 | | $ | 65.0 | | 64,583,275 | | $ | — | | $ | 436.6 | | $ | (343.7) | | $ | (0.6) | | $ | 157.3 |

The accompanying notes are an integral part of the consolidated financial statements.

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

Nine Months Ended September 30, 2018

(Unaudited)

(In millions, except share data)

| | | | | | | | | | | | | | | | | | | | | | |

| | Series A Convertible | | | | | | | | | | | | Accumulated | | | |

| | Preferred Stock | | Common Stock | | | | | | | Other | | | |

| | | | | | | | Par | | Additional | | Retained | | Comprehensive | | | |

| | Shares | | Amount | | Shares | | Value | | Paid- In Capital | | Earnings | | Income (Loss) | | Total |

Balance at January 1, 2018 | | 650,000 | | $ | 65.0 | | 48,712,288 | | $ | — | | $ | 277.9 | | $ | 7.3 | | $ | 1.0 | | $ | 351.2 |

Exercise of stock options | | — | | | — | | 5,000 | | | — | | | 0.1 | | | — | | | — | | | 0.1 |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.2) | | | — | | | (1.2) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 0.9 | | | — | | | — | | | 0.9 |

Issuance of common stock | | — | | | — | | 8,545,000 | | | — | | | 84.5 | | | — | | | — | | | 84.5 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | (0.3) | | | (0.3) |

Net loss | | — | | | — | | — | | | — | | | — | | | (0.8) | | | — | | | (0.8) |

Balance at March 31, 2018 | | 650,000 | | $ | 65.0 | | 57,262,288 | | $ | — | | $ | 363.4 | | $ | 5.3 | | $ | 0.7 | | $ | 434.4 |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.3) | | | — | | | (1.3) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 0.9 | | | — | | | — | | | 0.9 |

Issuance of common stock | | — | | | — | | 1,612,979 | | | — | | | 15.4 | | | — | | | — | | | 15.4 |

Issuance of earnout shares | | — | | | — | | 5,000,000 | | | — | | | 48.2 | | | (48.2) | | | — | | | — |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | (0.6) | | | (0.6) |

Net income | | — | | | — | | — | | | — | | | — | | | 13.5 | | | — | | | 13.5 |

Balance at June 30, 2018 | | 650,000 | | $ | 65.0 | | 63,875,267 | | $ | — | | $ | 427.9 | | $ | (30.7) | | $ | 0.1 | | $ | 462.3 |

Exercise of warrants | | — | | | — | | 2 | | | — | | | — | | | — | | | — | | | — |

Vesting of restricted stock units | | — | | | — | | 74,713 | | | — | | | (0.4) | | | — | | | — | | | (0.4) |

Series A convertible preferred stock dividend | | — | | | — | | — | | | — | | | — | | | (1.2) | | | — | | | (1.2) |

Stock-based compensation expense | | — | | | — | | — | | | — | | | 0.9 | | | — | | | — | | | 0.9 |

Issuance of common stock | | — | | | — | | 495,389 | | | — | | | 4.4 | | | — | | | — | | | 4.4 |

Foreign currency translation adjustments | | — | | | — | | — | | | — | | | — | | | — | | | 0.3 | | | 0.3 |

Net income | | — | | | — | | — | | | — | | | — | | | 2.2 | | | — | | | 2.2 |

Balance at September 30, 2018 | | 650,000 | | $ | 65.0 | | 64,445,371 | | $ | — | | $ | 432.8 | | $ | (29.7) | | $ | 0.4 | | $ | 468.5 |

The accompanying notes are an integral part of the consolidated financial statements.

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(in thousands)millions)

| | | | | | | | | | | | |

| | Nine months ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2017 | | 2016 | | 2019 | | 2018 |

Cash flows from operating activities | | | | | | | | | | | | |

Net loss | | $ | (11,802) | | $ | (1,486) | |

Adjustments to reconcile net loss to net cash provided by operating activities | | | | | | | |

Net income (loss) | | | $ | (289.0) | | $ | 14.9 |

Adjustments to reconcile net income (loss) to net cash provided by operating activities | | | | | | | |

Depreciation | | | 49,109 | | | 45,973 | | | 107.1 | | | 81.6 |

Amortization of intangible assets | | | 4,649 | | | 4,542 | | | 12.4 | | | 12.2 |

Amortization of deferred financing fees | | | 1,330 | | | 934 | | | 2.4 | | | 2.2 |

Non-cash operating lease expense | | | | 19.7 | | | — |

Write-off of deferred financing fees | | | 3,883 | | | — | | | 2.0 | | | — |

Stock-based compensation expense | | | 1,201 | | | — | | | 2.9 | | | 2.7 |

Deferred taxes | | | (4,849) | | | (245) | | | (60.4) | | | (16.1) |

Bad debt expense | | | 347 | | | 176 | | | 2.7 | | | 0.6 |

Non-cash interest expense | | | 92 | | | 805 | |

(Gain) loss on disposition of property and equipment | | | (513) | | | 158 | |

Gain on disposition of property and equipment | | | | (2.1) | | | (1.5) |

Gain on disposition of building | | | | — | | | (0.8) |

Deferred gain recognized on sales-type leases | | | (793) | | | (532) | | | — | | | (2.0) |

Impairment of revenue equipment | | | — | | | 1,195 | |

Impairment | | | | 306.8 | | | 2.8 |

Restructuring charges | | | | 6.9 | | | — |

Changes in operating assets and liabilities | | | | | | | | | | | | |

Accounts receivable | | | (28,567) | | | (7,156) | | | (23.5) | | | (57.5) |

Drivers’ advances and other receivables | | | 547 | | | (274) | | | (2.4) | | | (0.6) |

Payments received on sales-type leases | | | 3,774 | | | 2,776 | | | — | | | 10.5 |

Other current assets | | | (339) | | | 3,524 | |

Prepaid and other current assets | | | | (2.3) | | | (9.5) |

Accounts payable | | | 2,911 | | | 894 | | | 1.8 | | | (5.6) |

Accrued expenses and other liabilities | | | 5,478 | | | (2,176) | | | 4.4 | | | 12.9 |

Net cash provided by operating activities | | | 26,458 | | | 49,108 | | | 89.4 | | | 46.8 |

| | | | | | | | | | | | |

Cash flows from investing activities | | | | | | | | | | | | |

Purchase of property and equipment | | | (15,565) | | | (3,143) | |

Purchases of property and equipment | | | | (17.4) | | | (58.8) |

Proceeds from sale of property and equipment | | | 5,252 | | | 4,424 | | | 23.8 | | | 15.5 |

Cash paid in acquisitions, net of cash acquired | | | (91,133) | | | — | |

Cash paid for acquisitions, net of cash received | | | | — | | | (131.8) |

Net cash provided by (used in) investing activities | | | (101,446) | | | 1,281 | | | 6.4 | | | (175.1) |

| | | | | | | | | | | | |

Cash flows from financing activities: | | | | | | | | | | | | |

Checks outstanding in excess of bank balances | | | 313 | | | 317 | |

Advances on line of credit | | | 543,404 | | | 528,664 | | | 980.8 | | | 775.0 |

Repayments on line of credit | | | (550,261) | | | (528,603) | | | (980.8) | | | (763.9) |

Principal payments on and payoff of long-term debt | | | (231,817) | | | (59,656) | |

Proceeds from Term Loan Facility | | | 350,000 | | | 14,188 | |

Advances on long-term debt | | | | — | | | 6.1 |

Principal payments on long-term debt | | | | (57.8) | | | (41.0) |

Deferred financing fees | | | (14,411) | | | (1,788) | | | (0.4) | | | (1.0) |

Pay off of subordinated debt | | | (66,715) | | | — | |

Issuance of common stock | | | 128,184 | | | — | |

Repurchase of common stock | | | (36,168) | | | — | |

Issuance of Series A convertible preferred stock | | | 65,000 | | | — | |

Proceeds from issuance of common stock | | | | — | | | 84.2 |

Series A convertible preferred stock dividends | | | (1,680) | | | — | | | (3.7) | | | (3.7) |

Series B convertible preferred stock dividends | | | (2,016) | | | (3,628) | |

Net cash provided by (used in) financing activities | | | 183,833 | | | (50,506) | | | (61.9) | | | 55.7 |

| | | | | | | | | | | | |

Effect of exchange rates on cash and cash equivalents | | | (30) | | | — | | | (0.3) | | | — |

| | | | | | | | | | | | |

Net increase (decrease) in cash and cash equivalents | | | 108,815 | | | (117) | | | 33.6 | | | (72.6) |

Cash and cash equivalents – beginning of period | | | 3,695 | | | 4,886 | | | 46.0 | | | 90.7 |

Cash and cash equivalents – end of period | | $ | 112,510 | | $ | 4,769 | | $ | 79.6 | | $ | 18.1 |

The accompanying notes are an integral part of the consolidated financial statements.

DASEKE, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS – (Continued)

(Unaudited)

(in thousands)millions)

| | | | | | | | | | | | |

| | Nine months ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2017 | | 2016 | | 2019 | | 2018 |

Supplemental disclosure of cash flow information | | | | | | | | | | | | |

Cash paid for interest | | $ | 20,916 | | $ | 15,637 | | $ | 35.6 | | $ | 31.0 |

Cash paid for income taxes | | $ | 629 | | $ | 942 | | | 1.6 | | | 1.8 |

| | | | | | | | | | | | |

Noncash investing and financing activities | | | | | | | | | | | | |

Property and equipment acquired with debt or capital lease obligations | | $ | 13,609 | | $ | 32,517 | |

Property and equipment acquired with debt or finance lease obligations | | | | 65.6 | | | 36.1 |

Accrued capital expenditures | | | | — | | | 5.9 |

Property and equipment sold for notes receivable | | $ | 412 | | $ | 408 | | | 0.4 | | | 0.4 |

Property and equipment transferred to sales-type lease | | $ | 7,042 | | $ | 6,193 | | | — | | | 8.4 |

Assets held for sale returned to property and equipment | | $ | — | | $ | 351 | |

Sales-type lease returns to property and equipment | | $ | 724 | | $ | 1,188 | | | — | | | 0.5 |

Sales-type lease assets acquired with debt or capital lease obligations | | | | — | | | 9.9 |

Sales-type lease assets sold for notes receivable | | $ | 21,488 | | $ | 18,609 | | | — | | | 46.2 |

Sales-type lease returns to sales-type lease assets | | $ | 13,795 | | $ | 12,026 | | | — | | | 24.0 |

Common stock issued in acquisitions | | $ | 11,079 | | $ | — | | | — | | | 19.7 |

Accrued Series A convertible preferred dividends | | $ | 1,239 | | $ | — | |

Accrued Series B convertible preferred dividends | | $ | — | | $ | 1,378 | |

Issuance of earnout shares | | | | — | | | 48.2 |

Right-of-use assets acquired | | | $ | 33.5 | | $ | — |

The accompanying notes are an integral part of the consolidated financial statements.

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Operations

The registrant was originally formed in April 2015 as a special purpose acquisition company (SPAC) under the name Hennessy Capital Acquisition Corp. II (Hennessy). As a SPAC, Hennessy had no operations and its purpose was to go public with the intention of merging withDaseke, Inc.’s (the Company or acquiring an operating company with the proceeds of the SPAC’s initial public offering (the IPO).

On February 27, 2017, Hennessy consummated the Business Combination (as defined and described in Note 2) with Daseke, Inc. Upon consummation of the Business Combination, Daseke, Inc. changed its name toDaseke) wholly-owned subsidiary Daseke Companies, Inc. and Hennessy changed its name to Daseke, Inc.

Daseke, Inc., was formedincorporated in December 2008 and began operations on January 1, 2009. Daseke is engaged in full service open-deck trucking that specializes primarily in flatbed truckload and heavy haul transportation of specialized items throughout the United States, and Canada and into Mexico with trailers.Mexico. The Company also provides logistical planning and warehousing services to customers. The Company is subject to regulation by the Department of Transportation, the Department of Defense, the Department of Energy, and various state regulatory authorities. Additionally, due toauthorities in the recent acquisition of R&R Trucking Holdings, LLC (see Note 3), theUnited States. The Company is also subject to regulationsregulation by the DepartmentMinistries of DefenseTransportation and the Department of Energy.

Unless expressly stated otherwise, references to the Company or Daseke refers to Daseke, Inc.Communications and its wholly owned subsidiaries, Hennessy refers to the registrant prior to the closing of the Business Combination, and Private Daseke refers to Daseke, Inc. and its subsidiaries prior to the closing of the Business Combination.various provincial regulatory authorities in Canada.

Basis of Presentation

These interim consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (GAAP) for interim financial information and with the instructions for Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the three and nine month periodsmonths ended September 30, 20172019 are not necessarily indicative of the results that may be expected for the year ended December 31, 2017.2019.

The consolidated balance sheet as of December 31, 20162018 has been derived from the audited consolidated financial statements at that date. For additional information, including the Company’s significant accounting policies, refer to the consolidated financial statements and related footnotes for the year ended December 31, 20162018 as set forth in the Company’s CurrentAnnual Report on Form 8-K/A,10-K, filed with the SEC on March 16, 2017.8, 2019.

Certain items have been reclassified for presentation purposes to conform to the accounting policies of the consolidated entity. These reclassifications had no material impact on income from operations, net loss and comprehensive loss, the balance sheets or statements of cash flows.

Principles of Consolidation

The consolidated financial statements include the accounts of Daseke, Inc. and its wholly ownedwholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

Use of Estimates

The preparation of the consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

Deferred Financing Fees

In conjunction with obtaining long-term debt, the Company incurred financing costs which are being amortized using the straight-line method, which approximates the effective interest rate method, over the terms of the obligations. As of September 30, 20172019 and December 31, 2016,2018, the balance of deferred financing feesfinance charges was $13.3$12.5 million and $4.1$16.2 million, respectively, which is included as a reduction of long-term debt, net of current portion in the consolidated balance sheets. Amortization expense was $0.5$0.9 million and $0.3$0.7 million for the three months ended September 30, 20172019 and 2016, respectively,2018, and $1.3$2.4 million and $0.9$2.2 million for the nine months ended September 30, 20172019 and 2016, respectively, which2018, respectively. Amortization expense is included in interest expense. In February 2017,expense in conjunction with new term loan financing discussed in Note 9,the consolidated statements of operations and comprehensive income (loss). During the third quarter of 2019, the Company incurred deferred financing costs of $14.2expensed $2.0 million and expensed unamortizedto write-off certain deferred financing fees totaling $3.9 million.due to unsuccessful efforts to restructure the debt facilities.

Impairment of Long-Lived Assets

Long-lived assets are reviewed for impairment at the asset group level whenever events or changes in circumstances indicate that the carrying value may not be recoverable. If the sum of the expected future undiscounted cash flow is less than the carrying amount of the asset, an impairment is indicated. A loss is then recognized for the difference, if any, between the fair value of the asset (as estimated by management using its best judgment) and the carrying value of the asset. If actual market value is less favorable than that estimated by management, additional write-downs may be required. In the three months ended September 30, 2019, the Company recognized asset impairments, which

are more fully described in Notes 2, 5 and 7.

Fair Value Measurements

The Company follows the accounting guidance for fair value measurements of financial assets and financial liabilities and for fair value measurements of nonfinancial items that are recognized or disclosed at fair value in the financial statements on a recurring basis. Fair value guidance defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. It also establishes a framework for measuring fair value and expands disclosures about fair value measurements. The three levels of the fair value framework are as follows:

Level 1 - Quoted market prices in active markets for identical assets or liabilities.

Level 2 - Observable market-based inputs or unobservable inputs that are corroborated by market data.

Level 3 - Unobservable inputs reflecting the reporting entity’s own assumptions or external inputs from inactive markets.

A financial asset or liability’s classification within the framework is determined based on the lowest level of input that is significant to the fair value measurement.

Contingent Consideration

The contingent consideration liabilities, included in other current liabilities on the consolidated balance sheet, represent future payment obligations for certain EBITDA thresholds related to the Company’s acquisitions over a defined period of time. See Note 3 for additional details on the future payment obligations connected to the Company’s acquisitions. The fair value of the Company’s interest rate swaps iscontingent consideration liabilities are determined using cash flow computer models with unobservable inputs,estimates based on discount rates that reflect the risk involved and the projected EBITDA of the acquired businesses, therefore the liability for interest rate swaps isliabilities are classified within Level 3 of the fair value framework. In conjunction with the Business Combination discussed in Note 2, the Company’s lone interest rate swap was terminated. AtThe balance of contingent consideration as of September 30, 2019 and December 31, 2016, the fair value of this liability2018 was $51,871$21.5 million and is classified in accrued expenses and other liabilities on the consolidated balance sheets. $21.9 million, respectively. The tablestable below areis a summary of the changes in the fair value of this liability for the three and nine months ended September 30, 20172019 and 20162018 (in thousands)millions):

| | | |

| | 2016

|

Balance at January 1, 2016

| | $

| (124)

|

Change in fair value

| | | (63)

|

| | | |

Balance at June 30, 2016

| | | (187)

|

Change in fair value

| | | 72

|

Balance at September 30, 2016

| | $

| (115)

|

| | | | | | |

| | Nine Months Ended |

| | September 30, |

| | 2019 | | 2018 |

Balance at beginning of period | | $ | 21.9 | | $ | 0.8 |

Fair value of earn-out liability for acquisition | | | — | | | 20.3 |

Change in fair value | | | (0.4) | | | (0.7) |

Balance at end of period | | $ | 21.5 | | $ | 20.4 |

| | | |

| | 2017

|

Balance at January 1, 2017

| | $

| (52)

|

Change in fair value

| | | 52

|

| | | |

Balance at June 30, 2017

| | | —

|

Change in fair value

| | | —

|

Balance at September 30, 2017

| | $

| —

|

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

Stock-Based Compensation

Awards of equity instruments issued to employees and directors are accounted for under the fair value method of accounting and recognized in the consolidated statements of operations.operations and comprehensive income (loss). Compensation cost is measured for all stock-based awards at fair value on the date of grant and recognized using the straight-line method over the service period over which the awards are expected to vest.

Fair value of all time-vested options as of the date of grant is estimated using the Black-Scholes option valuation model, which was developed for use in estimating the fair value of traded options that have no vesting restrictions and are fully transferable. Option valuation models require the input of highly subjective assumptions, including the expected stock price volatility. Since the Company does not have a sufficient history of exercise behavior, expected term is calculated using the assumption that the options will be exercised ratably from the date of vesting to the end of the contractual term for each vesting tranche of awards. The risk-free interest rate is based on the U.S. Treasury yield curve for the period of the expected term of the stock option. Expected volatility is calculated using an index of publicly traded peer companies.

Fair values of nonvestednon-vested stock awards (restricted stock units) are equal to the market value of the common stock on the date of the award with compensation costs amortized over the vesting period of the award.

Segment Reporting

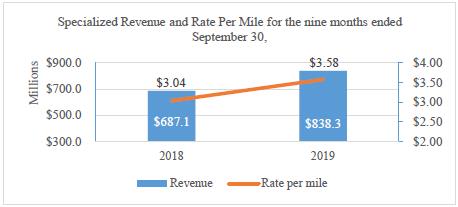

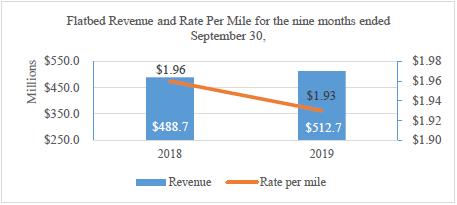

The Company determines its operating segments based on the information utilized by the chief operating decision maker to allocate resources and assess performance. Based on this information, the Company has determined it has twelvehad 16 operating segments as of September 30, 20172019 and eight operating segments as of September 30, 20162018 that are aggregated into two reportable segments: Flatbed Solutions, which delivers its services using primarily flatbed transportation equipment to meet the needs of high-volume, time-sensitive shippers, and Specialized Solutions, which delivers transportation and logistics solutions for super heavy haul, high-value customized and over-dimensional loads, many of which require engineering and customized equipment.

Earnings (Loss) Per Share

Basic earnings (loss) per common share is calculated by dividing net income (loss) attributable to common stockholders by the weighted average number of shares of common stock outstanding during the period. Diluted earnings (loss) per share reflect the potential dilution of earnings per share that could occur if securities or other contracts to issue common stock were exercised or converted into common stock or resulted in the issuance of common stock that then shared in the Company’s earnings (loss).

For the three and nine months ended September 30, 2017,2019 and 2018, shares of the Company’s 7.625% Series A Convertible Cumulative Preferred Stock (Series A Preferred Stock) were not included in the computation of diluted loss per share as their effects were anti-dilutive. For the three and nine months ended September 30, 2017 and 2016, shares of Private Daseke’s Series B Convertible Preferred Stock (Series B Preferred Stock)outstanding stock options were not included in the computation of diluted earnings (loss) per share as their effects were anti-dilutive. ForAdditionally, for the three and nine months ended September 30, 2017,2019 and 2018, there was no dilutive effect from the Merger Agreement earn-out provision (see Note 2)found in the Agreement and Plan of Merger, dated December 22, 2016, in which a wholly-owned subsidiary of Hennessy Capital Acquisition Corp. II (Hennessy) merged with and into Daseke, with Daseke surviving as a direct wholly-owned subsidiary of Hennessy, (the Merger Agreement) or the outstanding warrants to purchase shares of the Company’s common stock (the common stock purchase warrants).See Note 16 for the effects of non-vested restricted stock units on basic and diluted earnings per share under the two-class method.

Common Stock Purchase Warrants

The Company accounts for the issuance of common stock purchase warrants in connection with equity offerings in accordance with the provisions of the Accounting Standards Codification (ASC) 815, Derivatives and Hedging (ASC(Topic 815). The Company classifies as equity any contractscontract that (i) requirerequires physical settlement or net-share settlement or (ii) gives the Company a choice of net-cash settlement or settlement in its own shares (physical settlement or net-share settlement). The Company classifies as assets or liabilities any contractscontract that (i) requirerequires net-cash settlement (including a requirement to net-cash settle the contract if an event occurs and if that event is outside the control of the Company) or (ii) gives the counterparty a choice of net-cash settlement or settlement in shares (physical settlement or net-share settlement). See Note 11 for additional details on the common stock purchase warrants.

The Company assessed the classification of its common stock purchase warrants and determined that such instruments meet the criteria for equity classification at the time of issuance.

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

Foreign Currency Gains and Losses

The functional currency for all operations except Canada is the U.S. dollar. The local currency is the functional currency for the Company’s operations in Canada. For these operations, assets and liabilities are translated at the rates of exchange on the consolidated balance sheet date, while income and expense items are translated at average rates of exchange during the period. The resulting gains or losses arising from the translation of accounts from the functional currency into U.S. dollars are included as a separate component of stockholders’ equity in accumulated other comprehensive income (loss) until a partial or complete liquidation of the Company’s net investment in the foreign operation.

From time to time, the Company’s foreign operations may enter into transactions that are denominated in a currency other than their functional currency (U.S. dollars).currency. These transactions are initially recorded in the functional currency of the operating company based on the applicable exchange rate in effect on the date of the transaction. Monthly, these transactions are remeasured to an equivalent amount of the functional currency based on the applicable exchange rate in effect on the remeasurement date. Any adjustment required to remeasure a transaction to the equivalent amount of functional currency is recorded in the consolidated statements of operations and comprehensive income (loss) of the foreign operating company as a component of foreign exchange gain or loss.

Assets Held for Sale

AssetsThrough December 31, 2018, assets held for sale iswere primarily comprised of revenue equipment in ourthe Company’s lease purchase program and is recorded as a component of prepaid and other current assets on the consolidated balance sheets. Assets held for sale at September 30, 2017 and December 31, 2016, totaled $7.1 million and $2.8 million, respectively. Assets held for sale arewere not subject to depreciation, and arewere recorded at the lower of depreciated carrying value or fair market value less selling costs. The Company expects to sell these assetsAssets held for sale as of December 31, 2018, totaled $3.6 million, consisting of $2.7 million for the Flatbed Solutions segment and $0.9 million for the Specialized Solutions.

Following the adoption of Accounting Standards Update (ASU) No. 2016-02, Leases (Topic 842), the revenue equipment in itsthe Company’s lease purchase program within twelve months of being classified asno longer meets the criteria for assets held for sale. See Note 2 for additional information on the adoption of ASU No. 2016-02.

Revenue and Expense Recognition

The Company’s revenue and related costs are recognized when the Company satisfies its performance obligation(s) transferring goods or services to the customer and the customer obtains control of such goods and services. With respect to freight, brokerage, logistics and fuel surcharge revenue, these conditions are met, and the Company recognizes company freight, owner operator freight, brokerage and fuel surcharge revenue, over time, and logistics revenue, as the services are provided. While the Company may enter into master service agreements with its customers, a contract is not established until the customer specifically requests the Company’s services and the Company accepts.

The Company evaluates each contract for distinct performance obligations. In the Company’s business, a typical performance obligation is the transportation of a load including any highly interrelated ancillary services.

The Company predominantly estimates the standalone selling price of its services based upon observable evidence, market conditions and other relevant inputs. The Company allocates the total transaction price to each distinct performance obligation based upon the relative standalone selling prices.

The Company’s customers simultaneously receive and consume the benefits of the Company’s contracts; therefore, revenue is recognized over time. This is a faithful depiction of the satisfaction of the performance obligation, as the customer does not need to re-perform the transportation services the Company has provided to date.

Generally, the Company’s customers are billed upon delivery of the freight or monthly and remit payment according to the approved payment terms.

Freight Revenue

Freight revenue is generated by hauling customer freight using company owned equipment (company freight) and owner-operator equipment (owner-operator freight). Freight revenue is the product of the number of revenue-generating miles driven and the rate per mile received from customers plus accessorial charges, such as loading and unloading freight, cargo protection, fees for detained equipment or fees for route planning and supervision.

Brokerage Revenue

The Company regularly engages third-party capacity providers to haul loads. The Company is primarily responsible for fulfilling the promise to provide load transportation services, and has discretion in setting prices, along with the risk to fulfill the contract to the customer. Based upon this evaluation, the Company has determined that it is the principal and therefore, records gross revenues and expenses for brokerage services.

Logistics Revenue

Logistics revenue is generated from a range of services, including value-added warehousing, loading and unloading, vehicle maintenance and repair, preparation and packaging, fuel management, and other fleet management solutions. The Company recognizes logistics revenue as services are completed.

Fuel Surcharge

Fuel surcharge revenue compensates the Company for fuel costs above a certain cost per gallon base. Generally, the Company receives fuel surcharges on the miles for which it is compensated by customers.

The Company has designated the following preference and practical expedients:

| · | | To not disclose remaining performance obligations when the expected performance obligation duration is one year or less. The vast majority of the Company’s services transfer control within a month of the inception of the contract with select specialized loads taking several months to allow for increased planning and permitting. |

| · | | Recognize the incremental costs of obtaining or fulfilling a contract as an expense when incurred, as the amortization period of a potential asset would be recognized in one year or less. |

| · | | Exclude taxes collected on behalf of government authorities from the Company’s measurement of transaction prices. Tax amounts are not included within net income or cost of sales. |

New Accounting Pronouncements

In July 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU)ASU 2017-11, Earnings per Share (Topic 260),; Distinguishing Liabilities from Equity (Topic 480); and Derivatives and Hedging (Topic 815). ASU 2017-11 provides guidance on accounting for financial instruments with down round features and clarifyclarifies the deferral of certain provisions in Topic 480. ASU 2017-11 will become effective for annual periods beginning after December 15, 2018 and interim periods within those periods. The Company is currently evaluating the impact of adoptingadopted this guidance.

In May 2017, the FASB issued ASU 2017-09, Compensation – Stock Compensation (Topic 718). ASU 2017-09 provides guidance about which changes to the terms or conditions of a share-based payment award requires the application of modification accounting. Modification accounting will apply unless the fair value of the modified award is the same as the original award, the vesting conditions of the modified award are the same as the original award and the classification of the modified award as an equity instrument or liability instrument is the same as the original award. ASU 2017-09 will become effective for annual periods beginning after December 15, 2017 and interim periods within those periods. Early adoption is permitted. The Company does not expect ASU 2017-09 to have a material impactpronouncement on its consolidated results of operations, financial condition, cash flows, or financial statement disclosures.

In January 2017, the FASB issued ASU 2017-04, Intangibles – Goodwill and Other (Topic 350). ASU 2017-04 removes the requirement to perform a hypothetical purchase price allocation to measure goodwill impairment. A goodwill impairment will now be the amount by which a reporting unit’s carrying value exceeds its fair value, not to exceed the carrying amount of goodwill. ASU 2017-04 is effective for fiscal years beginning December 15, 2019, with early adoption permitted for interim and annual goodwill impairment tests performed on testing dates after January 1, 2017, and applied prospectively. The Company does2019, which did not expect ASU 2017-04 to have a material impact on itsthe consolidated results of operations, financial condition, cash flows, or financial statement disclosures.statements.

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued)

In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230). ASU 2016-15 provides new guidance intended to reduce diversity in practice in how certain cash receipts and payments are classified in the statement of cash flows, including debt prepayment or extinguishment costs, the settlement of contingent liabilities arising from a business combination, proceeds from insurance settlements, and distributions from certain equity method investees. ASU 2016-05 will become effective for fiscal years beginning after December 15, 2018 and interim periods within fiscal years beginning after December 31, 2019. Early adoption is permitted. ASU 2016-15 requires application using a retrospective transition method. The Company is currently evaluating the impact of adopting this guidance.

In June 2016, the FASB issued ASU No. 2016-13, Accounting for Credit Losses (Topic 326). ASU 2016-13 requires the use of an “expected loss” model on certain types of financial instruments. ASU 2016-13 is effective for fiscal years, and interim periods within those years, beginning after December 15, 2019, with early adoption permitted. The Company is currently evaluating the impact of adopting this guidance.guidance and does not believe it will have a material impact on the consolidated financial statements.

NOTE 2 – LEASES

Change in Accounting Principle

In MarchFebruary 2016, the FASB issued ASU 2016-09, Stock CompensationNo. 2016-02, Leases (Topic 718). ASU 2016-09842), which amends the FASB ASC and creates Topic 842 (ASC 842), Leases. On January 1, 2019, the Company adopted ASC 842, which is effective for interim and annual reporting periods beginning on or after December 15, 2018. This Topic requires thebalance sheet recognition of lease assets and lease liabilities for leases classified as operating leases under GAAP. Under the income tax effectsstandard, disclosures are required to meet the objective of awards inenabling users of financial statements to assess the income statement whenamount, timing, and uncertainty of cash flows arising from leases.

The Company has completed its evaluation of the awards vest or are settled, thus eliminating additional paid in capital pools. ASU 2016-09 also allows for the Company to repurchase morerequirements of ASC 842 and related amendments. As part of the Company’s sharesevaluation, management compiled and analyzed contracts, identified the full lease population, implemented and populated leasing software and implemented new controls associated with adopting and adhering to the standard, and reviewed its accounting practices for tax withholding purposes without triggering liability accounting. In addition, ASU 2016-09 allows for a policy electionrevenue equipment that it leased to account for forfeitures as they occur rather than on an estimated basis. ASU 2016-13 is effective for fiscal years, and interim periods within those years, beginning after December 15, 2016, with early adoption permitted. certain of its owner-operators.

The Company adopted this pronouncementguidance as of January 1, 2019, using the optional transition method and elected the option to not apply ASC 842 to comparative periods, which continue to be presented under the accounting standards in effect for those periods.

Lessee

The adoption of this standard had a material impact on Aprilthe Company’s financial position. Adoption of the new standard resulted in the recording of right-of-use assets and lease liabilities on the Company’s consolidated balance sheets of approximately $96.9 million and $96.9 million, respectively, as of January 1, 20172019. The right-of-use assets recorded on the balance sheet include primarily trucking facilities and election to account for forfeitures as they occurterminals and revenue equipment leases. The standard did not have a material impact on the Company’s consolidated resultsstatements of operations and comprehensive income (loss), however, there have been additions and modifications to its existing financial condition, cash flows or financial statement disclosures.

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842). ASU 2016-02 amends various aspects of existing guidance for leases. ASU 2016-02 requires an entity to recognize assets and liabilities arising from a lease for both financing and operating leases, along with additional qualitative and quantitative disclosures. The main difference between previous GAAP and the amended standard is the recognition of lease assets and lease liabilities of lessees on the balance sheet for those leases classified as operating leases under previous GAAP. ASU 2016-02 is effective for fiscal years beginning after December 15, 2018, with early adoption permitted. The Company is currently evaluating the effect this ASU will have on its consolidated financial position and results of operations.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606). The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. In August 2015, the FASB issued updated guidance with ASU 2015-14 and deferred the effective date of ASU 2014-09 by one year. The guidance in ASU 2014-09 is effective for annual periods beginning after December 15, 2017, and interim periods within those annual periods.

In March 2016, the FASB issued an ASU that further clarifies guidance under ASU 2014-09 with respect to principal versus agent considerations in revenue from contracts with customers. In the second quarter of 2016, the FASB issued two ASUs that provide additional guidance when identifying performance obligations and licenses as well as allowing for certain narrow scope improvements and practical expedients. In May 2017, the FASB issued an ASU that provides guidance on the identification of the customer in a service concession arrangement. The guidance permits two methods of adoption: retrospectively to each prior reporting period presented (full retrospective), or retrospectively with the cumulative effect of initially applying the guidance recognized at the date of initial application (modified retrospective). The Company plans to adopt this new guidance in the first quarter of 2018 and would apply the modified retrospective method, which may result in a cumulative-effect adjustment to opening retained earnings with an insignificant change to revenue on a go-forward basis. The Company has completed its review of a sample of revenue contracts for all revenue sourcesdesignated the following preferences and has concluded that the new guidance will not have a material impact on its revenue recognition practices, business processes, systems and controls. The new guidance will result in changes to the timing of recognition for certain revenue streams, namely freight revenue, where a contract has not been completed by the end of a reporting period. Based on a review of our customer shipping arrangements, we currently believe the implementation of this standard will change our revenue recognition policy from recognizing revenue upon shipment completion to recognizing revenue over time based on the progress toward completion of shipments in transit at each period end.practical expedients:

| · | | To not reassess whether any expired or existing contracts contain a lease; |

| · | | Carryforward previous conclusions related to prior lease classification under the prior lease accounting standard to lease classification for existing leases under ASC 842; |

| · | | To not reassess initial indirect costs; |

Table of Contents

DASEKE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)

| · | | Elect the hindsight practical expedient related to lease term and impairment; |

| · | | Adopt the land easement practical expedient; |

NOTE 2 – BUSINESS COMBINATION

On February 27, 2017, Hennessy consummated the merger of Hennessy’s wholly-owned subsidiary with and into Daseke, Inc., with Daseke, Inc. surviving as a direct wholly-owned subsidiary of Hennessy (the Business Combination) pursuant to the Agreement and Plan of Merger, dated December 22, 2016 (the Merger Agreement). The aggregate consideration received by Private Daseke stockholders upon closing was $266.7 million, consisting of newly issued shares of common stock at a value of $10.00 per share. The Merger Agreement contains an earn-out provision through which Private Daseke stockholders could receive up to 15 million additional shares of common stock (with up to 5 million shares payable annually with respect to 2017, 2018 and 2019 performance). The full 15 million shares are only payable if (i) the annualized Adjusted EBITDA (giving effect to acquisitions and as defined in the Merger Agreement) for 2017, 2018 and 2019 is at least $140.0 million, $170.0 million and $200.0 million, respectively, and (ii) the closing share price of the Company’s common stock is at least $12.00, $14.00 and $16.00 for any 20 trading days in a consecutive 30 trading day period in 2017, 2018 and 2019, respectively. For each year, the 5 million earn-out shares will be prorated to the extent the annualized Adjusted EBITDA (giving effect to acquisitions and as defined in the Merger Agreement) exceeds 90% but represents less than 100%, of the applicable earn-out target.

Following the consummation of the Business Combination on February 27, 2017 (the Closing), there were 37,715,960 shares of common stock issued and outstanding, consisting of (i) 26,665,330 shares issued to Private Daseke stockholders pursuant to the Merger Agreement, (ii) 419,669 shares issued in a private placement that closed in conjunction with the Business Combination, (iii) 2,288,043 shares originally issued to Hennessy Capital Partners II LLC (the Sponsor) in a private placement that closed simultaneously with the consummation of the IPO, and (iv) 8,342,918 shares, following redemptions, which shares were originally issued in the IPO. In connection with the Business Combination, $65.0 million of Series A Preferred Stock (650,000 shares) were issued in a private placement.

In conjunction with the Closing, the Company entered into (i) a $350.0 million term loan credit facility (the Term Loan Facility), which consists of a $250.0 million term loan funded on the closing date of the Term Loan Facility and up to $100.0 million of term loans to be funded from time to time under a delayed draw term loan facility, and (ii) an asset-based revolving credit facility (the ABL Facility), in an aggregate maximum credit amount equal to $70.0 million (subject to availability under a borrowing base). See Note 9 for more information regarding the Term Loan Facility and the ABL Facility. Prior to the Closing, the Company had a credit facility consisting of a term loan (Senior Term Loan) and a revolving line of credit (Line of Credit).

DASEKE, INC. AND SUBSIDIARIES

| · | | To not separate the non-lease components of a contract from the lease component for its office equipment asset class; |

| · | | To not apply the recognition requirements to leases with terms of twelve months or less; and |

| · | | To apply the portfolio approach in determination of the incremental borrowing rate. |

The Company has capitalized operating and finance leases for various real estate including corporate offices, trucking facilities and terminals, warehouses, and tractor parking as well as various types of equipment including tractors, trailers, forklifts, and office equipment. New real estate lease agreements will typically have initial terms between 3 to 15 years and new equipment lease agreements will typically have initial terms of 3 to 9 years. Leases with an initial term of 12 months or less (short term leases) across all asset classes are not recorded on the balance sheet; the Company recognizes lease expense for these leases on a straight-line basis over the lease term.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

(Unaudited)Some of the Company’s leases include one or more options to renew, with renewals that can extend the lease term from 1 to 5 years. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that the Company will exercise that option. The exercise of lease renewal options is at the Company’s sole discretion. Certain leases also include options to purchase the leased property. The depreciable life of assets and leasehold improvements are limited by the expected lease term, unless there is a transfer of title or purchase option reasonably certain of exercise. Rights and obligations related to lease agreements the Company has signed but that have not yet commenced are not material. The Company has certain lease agreements related to its revenue equipment that contain residual value guarantees. These residual value guarantees require the Company to return the revenue equipment at the end of the lease term in a certain condition as specified by the lessor in the lease agreement.

The Company determines whether an arrangement is classified as a lease at inception. The right-of-use assets and lease liabilities relating to operating leases are included in right-of-use assets, other current liabilities, and other long-term liabilities on the Company's consolidated balance sheets. The right-of-use assets and lease liabilities relating to finance leases are included in other long-term assets, current portion of long-term debt, and long-term debt, net of current portion on the Company's consolidated balance sheets. The Company's right-of-use assets represent its right to use the underlying assets for the lease term and the Company's right-of-use liabilities represent its obligation to make lease payments arising from the leases. Operating lease right-of-use assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. The Company's capitalized operating lease agreements generally do not provide an implicit rate. The Company developed an incremental borrowing rate based on the information available at the commencement date regarding the interest rate applicable to collateralized borrowings for a period similar to the original lease period. The incremental borrowing rates were used in determining the present value of lease payments which is reflected as the lease liability.

The Company follows ASC 360, “Impairment or Disposal of Long-Lived Assets” guidance to determine whether right-of-use assets relating to operating and finance leases are impaired. The Company recorded impairment charges of $10.0 million to right-of-use assets relating to operating leases and $0.7 million to right-of-use assets relating to finance leases for the three and nine months ended September 30, 2019. See Note 5 for discussion on impairment charges.

The following table reflects the Company’s components of lease expenses for the three and nine months ended September 30, 2019 (in millions):

| | | | | | | | |

| | | | Three Months Ended | | Nine Months Ended |

| | Classification | | September 30, 2019 |

Operating lease cost | | | | | | | | |

Revenue equipment | | Operations and maintenance | | $ | 2.8 | | $ | 16.3 |

Real estate | | Administrative expense | | | 1.1 | | | 10.2 |

Total operating lease cost | | | | $ | 3.9 | | $ | 26.5 |

| | | | | | | | |

Finance lease cost | | | | | | | | |

Amortization of right-of-use assets | | Depreciation and amortization | | $ | 1.5 | | $ | 3.9 |

Interest on lease liabilities | | Interest expense | | | 0.2 | | | 0.7 |

Total finance lease cost | | | | $ | 1.7 | | $ | 4.6 |

| | | | | | | | |

Total lease cost(a) | | | | $ | 5.6 | | $ | 31.1 |

| (a) | | Short-term lease expense and variable lease expense are immaterial. |

NOTE 2 – BUSINESS COMBINATION – (Continued)The components of assets and liabilities for operating and finance leases are as follows as of September 30, 2019 (in millions):

| | | | | |

| | | | September 30, |

| | Classification | | 2019 |

Assets | | | | | |

Capitalized operating lease right-of-use assets | | Right-of-use assets | | $ | 97.0 |

Finance lease right-of-use assets | | Other long-term assets | | | 25.0 |

Total lease assets | | | | $ | 122.0 |

| | | | | |

Liabilities | | | | | |

Capitalized operating lease liabilities: | | | | | |

Current | | Other current liabilities | | $ | 28.4 |

Non-current | | Other long-term liabilities | | | 78.6 |

Total capitalized operating lease liabilities | | | | $ | 107.0 |

| | | | | |

Finance lease liabilities: | | | | | |

Current | | Current portion of long-term debt | | $ | 6.0 |

Non-current | | Long-term debt, net of current portion | | | 20.0 |

Total finance lease liabilities | | | | $ | 26.0 |

| | | | | |

Total lease liabilities | | | | $ | 133.0 |

The following table is a summary of supplemental cash proceeds and utilization of proceeds inflows related to leases for the Business Combinationnine months ended September 30, 2019 (in thousands)millions):

| | | |

Proceeds | | | |

| | | |