SECURITIES AND EXCHANGE COMMISSION

Quarterly report pursuant to Section 13 or 15(d) of

the Securities Exchange Act of 1934

☒xQUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30,

20212022

☐oTRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

|

|

| | | | | | |

For the quarterly period ended |

| Commission file |

June 30, 2021 2022 |

| number 001-39215 |

Professional Holding Corp.

(Exact name of Registrant as specified in its charter) | | | | | | | | | | | | | |

|---|

Florida

|

| | FL | | 46-5144312 |

| 46-5144312

|

|---|

| (State or other jurisdiction of |

|

|

| (I.R.S. Employer

|

|---|

incorporation or organization)

| | | |

|

| (I.R.S. Employer

Identification Number) |

|---|

396 Alhambra Circle, Suite 255,

Coral Gables,

, FL33134 (786) 483-1757(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

Title of each class: |

| Trading Symbol |

| Name of each exchange on which registered: |

Class A Common Stock | | PFHD | | NASDAQ Global Select Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒Yes☐x Yes oNo

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒x Yes☐o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

| | | | | | | | |

Large accelerated filer | ☐

o | Accelerated filer | ☐

o |

|

|

|

|

Non-accelerated filer | ☒

x | Smaller reporting company | ☒

x |

|

|

|

|

|

| Emerging growth company | ☒

|

|

|

|

x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐Yes ☒o Yes xNo

Number of shares of common stock outstanding as of August

13, 2021: 13,419,01010, 2022: 13,773,115

PART I—FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements (unaudited).

PROFESSIONAL HOLDING CORP.

CONSOLIDATED BALANCE SHEETS (Unaudited)

(Dollar amounts in thousands, except share data)

| | | | | | |

| | June 30, | | December 31, |

| | 2021 | | 2020 |

ASSETS | | | | | | |

Cash and due from banks | | $ | 29,803 | | $ | 62,305 |

Interest-bearing deposits | | | 586,377 | | | 129,291 |

Federal funds sold | | | 36,156 | | | 25,376 |

Cash and cash equivalents | | | 652,336 | | | 216,972 |

Securities available for sale, at fair value - taxable | | | 100,735 | | | 65,110 |

Securities available for sale, at fair value - tax exempt | | | 19,761 | | | 22,398 |

Securities held to maturity (fair value June 30, 2021 – $1,296, December 31, 2020 – $1,561) | | | 1,285 | | | 1,547 |

Equity securities | | | 5,942 | | | 6,005 |

Loans, net of allowance of $10,418 and $16,259 as of June 30, 2021 and December 31, 2020, respectively | | | 1,680,168 | | | 1,643,373 |

Loans held for sale | | | 2,039 | | | 1,270 |

Federal Home Loan Bank stock, at cost | | | 2,341 | | | 3,229 |

Federal Reserve Bank stock, at cost | | | 4,954 | | | 4,762 |

Accrued interest receivable | | | 5,449 | | | 6,666 |

Premises and equipment, net | | | 4,000 | | | 4,370 |

Bank owned life insurance | | | 37,923 | | | 37,360 |

Deferred tax asset | | | 9,446 | | | 10,525 |

Goodwill | | | 24,621 | | | 24,621 |

Core deposit intangibles | | | 1,280 | | | 1,422 |

Other assets | | | 8,738 | | | 7,640 |

Total assets | | $ | 2,561,018 | | $ | 2,057,270 |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | |

Deposits | | | | | | |

Demand – non-interest bearing | | $ | 854,673 | | $ | 475,598 |

Demand – interest bearing | | | 286,173 | | | 232,367 |

Money market and savings | | | 874,637 | | | 715,003 |

Time deposits | | | 261,680 | | | 236,575 |

Total deposits | | | 2,277,163 | | | 1,659,543 |

Official checks | | | 3,289 | | | 4,447 |

Federal Home Loan Bank advances | | | 35,000 | | | 40,000 |

Other borrowings | | | — | | | 114,573 |

Subordinated debt | | | 10,062 | | | 10,153 |

Accrued interest and other liabilities | | | 12,476 | | | 12,989 |

Total liabilities | | | 2,337,990 | | | 1,841,705 |

Stockholders’ equity | | | | | | |

Preferred stock, 10,000,000 shares authorized, NaN issued | | | — | | | — |

Class A Voting Common stock, $0.01 par value; authorized 50,000,000 shares, issued 14,289,480 and outstanding 13,475,781 shares as of June 30, 2021, and authorized 50,000,000 shares, issued 14,100,760 and outstanding 13,534,829 shares at December 31, 2020 | | | 143 | | | 141 |

Class B Non-Voting Common stock, $0.01 par value; 10,000,000 shares authorized, NaN issued and outstanding at June 30, 2021 and December 31, 2020 | | | — | | | — |

Treasury stock, at cost | | | (13,544) | | | (9,209) |

Additional paid-in capital | | | 210,274 | | | 208,995 |

Retained earnings | | | 25,872 | | | 14,756 |

Accumulated other comprehensive income (loss) | | | 283 | | | 882 |

Total stockholders’ equity | | | 223,028 | | | 215,565 |

Total liabilities and stockholders' equity | | $ | 2,561,018 | | $ | 2,057,270 |

| | | | | | | | | | | | | | |

| | June 30,

2022 | | December 31,

2021 |

| ASSETS | | | | |

| Cash and due from banks | | $ | 41,202 | | | $ | 38,469 | |

| Interest earning deposits | | 299,834 | | | 545,521 | |

| Federal funds sold | | 27,043 | | | 13,477 | |

| Cash and cash equivalents | | 368,079 | | | 597,467 | |

| Securities available for sale, at fair value - taxable | | 164,354 | | | 175,536 | |

| Securities available for sale, at fair value - tax-exempt | | 27,453 | | | 18,765 | |

| Securities held to maturity (fair value June 30, 2022 – $197, December 31, 2021 – $242) | | 204 | | | 236 | |

| Equity securities | | 6,359 | | | 6,638 | |

| Loans, net of allowance of $15,142 and $12,704 as of June 30, 2022 and December 31, 2021, respectively | | 1,972,091 | | | 1,764,460 | |

| Loans held for sale | | — | | | 165 | |

| Premises and equipment, net | | 8,570 | | | 9,020 | |

| Bank owned life insurance | | 54,134 | | | 38,485 | |

| Goodwill and intangibles | | 25,639 | | | 25,766 | |

| Other assets | | 34,631 | | | 27,573 | |

| Total assets | | $ | 2,661,514 | | | $ | 2,664,111 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | |

| Deposits | | | | |

| Demand – noninterest bearing | | $ | 777,501 | | | $ | 674,003 | |

| Demand – interest bearing | | 339,942 | | | 310,362 | |

| Money market and savings | | 1,055,813 | | | 1,121,330 | |

| Time deposits | | 208,479 | | | 265,693 | |

| Total deposits | | 2,381,735 | | | 2,371,388 | |

| Federal Home Loan Bank advances | | — | | | 35,000 | |

| Official checks | | 5,815 | | | 4,125 | |

| Other borrowings | | — | | | 10,000 | |

| Subordinated debt | | 24,436 | | | — | |

| Accrued interest and other liabilities | | 15,930 | | | 12,074 | |

| Total liabilities | | 2,427,916 | | | 2,432,587 | |

| Stockholders’ equity | | | | |

| Preferred stock, 10,000,000 shares authorized, none issued | | — | | | — | |

| Class A Voting Common stock, $0.01 par value; authorized 50,000,000 shares, issued 14,699,975 and outstanding 13,742,381 shares as of June 30, 2022, and authorized 50,000,000 shares, issued 14,393,750 and outstanding 13,446,400 shares at December 31, 2021 | | 147 | | | 144 | |

| Class B Non-Voting Common stock, $0.01par value; 10,000,000 shares authorized, none issued and outstanding on June 30, 2022 and December 31, 2021 | | — | | | — | |

| Treasury stock, at cost | | (16,201) | | | (16,003) | |

| Additional paid-in capital | | 215,541 | | | 212,012 | |

| Retained earnings | | 45,533 | | | 36,120 | |

| Accumulated other comprehensive income (loss) | | (11,422) | | | (749) | |

| Total stockholders’ equity | | 233,598 | | | 231,524 | |

| Total liabilities and stockholders' equity | | $ | 2,661,514 | | | $ | 2,664,111 | |

See accompanying notes to consolidated financial statements.

PROFESSIONAL HOLDING CORP.

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(LOSS) (Unaudited)

(Dollar amounts in thousands, except share data)

| | | | | | | | | | | | | |

| | Three Months Ended June 30, | | | Six Months Ended June 30, |

| | 2021 | | 2020 | | | 2021 | | 2020 |

Interest income | | | | | | | | | | | | | |

Loans, including fees | | $ | 18,311 | | $ | 17,897 | | | $ | 37,544 | | $ | 27,912 |

Investment securities - taxable | | | 161 | | | 232 | | | | 340 | | | 434 |

Investment securities - tax exempt | | | 189 | | | 206 | | | | 392 | | | 226 |

Dividend income on restricted stock | | | 99 | | | 131 | | | | 194 | | | 210 |

Other | | | 202 | | | 56 | | | | 264 | | | 760 |

Total interest income | | | 18,962 | | | 18,522 | | | | 38,734 | | | 29,542 |

| | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | |

Deposits | | | 1,430 | | | 1,617 | | | | 2,747 | | | 4,243 |

Federal Home Loan Bank advances | | | 190 | | | 287 | | | | 386 | | | 565 |

Subordinated debt | | | 77 | | | 59 | | | | 207 | | | 189 |

Other borrowings | | | 63 | | | 268 | | | | 313 | | | 193 |

Total interest expense | | | 1,760 | | | 2,231 | | | | 3,653 | | | 5,190 |

| | | | | | | | | | | | | |

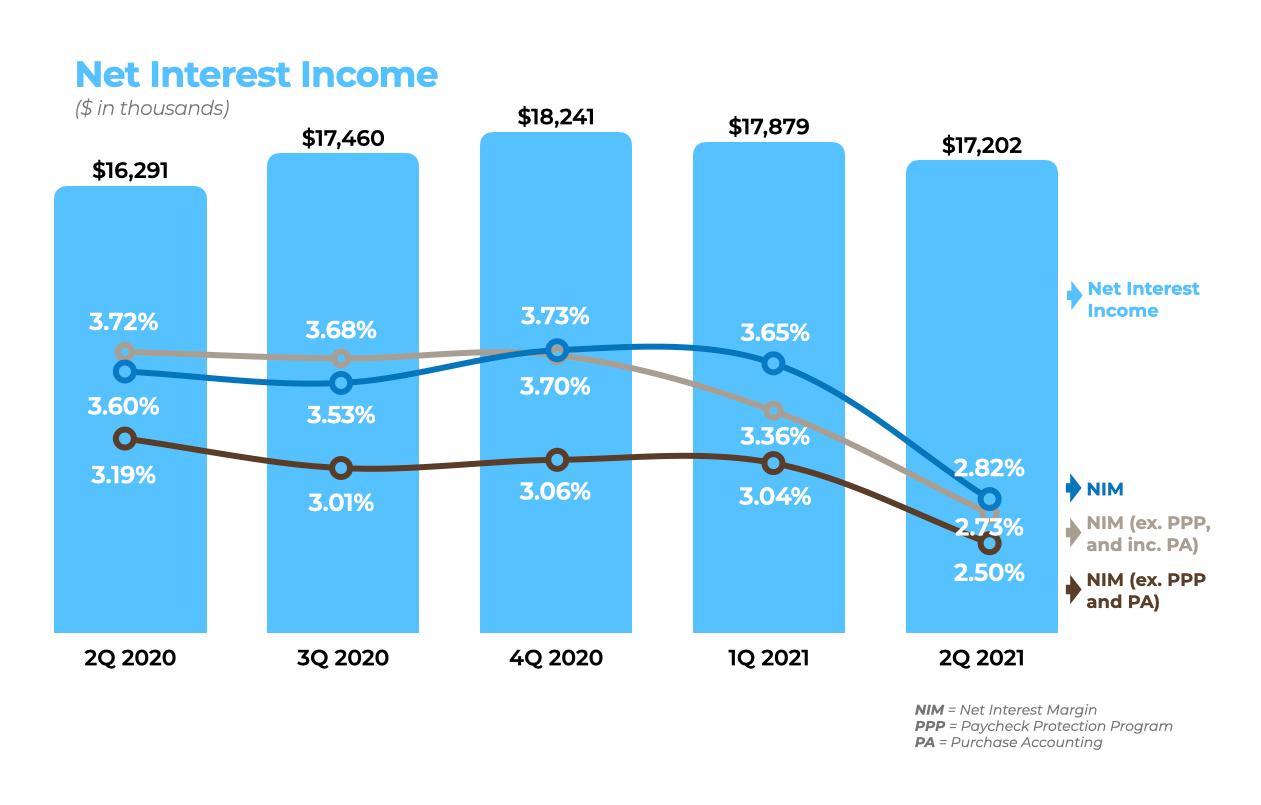

Net interest income | | | 17,202 | | | 16,291 | | | | 35,081 | | | 24,352 |

Provision for loan losses | | | 762 | | | 1,750 | | | | 1,800 | | | 2,595 |

Net interest income after provision for loan losses | | | 16,440 | | | 14,541 | | | | 33,281 | | | 21,757 |

| | | | | | | | | | | | | |

Non-interest income | | | | | | | | | | | | | |

Service charges on deposit accounts | | | 1,199 | | | 307 | | | | 1,594 | | | 529 |

Income from Bank owned life insurance | | | 281 | | | 126 | | | | 563 | | | 255 |

SBA origination fees | | | — | | | 84 | | | | 145 | | | 114 |

SWAP fees | | | 364 | | | 210 | | | | 573 | | | 473 |

Third party loan sales | | | 226 | | | 157 | | | | 301 | | | 267 |

Gain on sale and call of securities | | | 21 | | | 11 | | | | 22 | | | 15 |

Other | | | 211 | | | 73 | | | | 223 | | | 171 |

Total non-interest income | | | 2,302 | | | 968 | | | | 3,421 | | | 1,824 |

| | | | | | | | | | | | | |

Non-interest expense | | | | | | | | | | | | | |

Salaries and employee benefits | | | 7,099 | | | 6,912 | | | | 13,883 | | | 12,175 |

Occupancy and equipment | | | 905 | | | 1,081 | | | | 2,007 | | | 1,855 |

Data processing | | | 276 | | | 421 | | | | 566 | | | 597 |

Marketing | | | 165 | | | 151 | | | | 318 | | | 288 |

Professional fees | | | 770 | | | 806 | | | | 1,398 | | | 1,161 |

Acquisition expenses | | | — | | | 560 | | | | 684 | | | 2,223 |

Regulatory assessments | | | 418 | | | 300 | | | | 767 | | | 514 |

Other | | | 1,321 | | | 1,317 | | | | 3,119 | | | 2,221 |

Total non-interest expense | | | 10,954 | | | 11,548 | | | | 22,742 | | | 21,034 |

| | | | | | | | | | | | | |

Income before income taxes | | | 7,788 | | | 3,961 | | | | 13,960 | | | 2,547 |

Income tax provision | | | 1,457 | | | 830 | | | | 2,844 | | | 733 |

Net income | | | 6,331 | | | 3,131 | | | | 11,116 | | | 1,814 |

| | | | | | | | | | | | | |

Earnings per share: | | | | | | | | | | | | | |

Basic | | $ | 0.47 | | $ | 0.23 | | | $ | 0.83 | | $ | 0.16 |

Diluted | | $ | 0.45 | | $ | 0.22 | | | $ | 0.80 | | $ | 0.15 |

| | | | | | | | | | | | | |

Other comprehensive income: | | | | | | | | | | | | | |

Unrealized holding gain (loss) on securities available for sale | | | (505) | | | 743 | | | | (794) | | | 1,068 |

Tax effect | | | 124 | | | (188) | | | | 195 | | | (271) |

Other comprehensive gain (loss), net of tax | | | (381) | | | 555 | | | | (599) | | | 797 |

Comprehensive income | | $ | 5,950 | | $ | 3,686 | | | $ | 10,517 | | $ | 2,611 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | | Six Months Ended June 30, |

| | 2022 | | 2021 | | | 2022 | | 2021 |

| Interest income | | | | | | | | | |

| Loans, including fees | | $ | 21,600 | | | $ | 18,311 | | | | $ | 41,380 | | | $ | 37,544 | |

| Investment securities - taxable | | 704 | | | 161 | | | | 1,342 | | | 340 | |

| Investment securities - tax-exempt | | 232 | | | 189 | | | | 445 | | | 392 | |

| Dividend income on restricted stock | | 105 | | | 99 | | | | 202 | | | 194 | |

| Other | | 1,029 | | | 202 | | | | 1,323 | | | 264 | |

| Total interest income | | 23,670 | | | 18,962 | | | | 44,692 | | | 38,734 | |

| | | | | | | | | |

| Interest expense | | | | | | | | | |

| Deposits | | 1,491 | | | 1,430 | | | | 3,077 | | | 2,747 | |

| Federal Home Loan Bank advances | | 3 | | | 190 | | | | 137 | | | 386 | |

| Subordinated debt | | 266 | | | 77 | | | | 498 | | | 207 | |

| Other borrowings | | 1 | | | 63 | | | | 24 | | | 313 | |

| Total interest expense | | 1,761 | | | 1,760 | | | | 3,736 | | | 3,653 | |

| | | | | | | | | |

| Net interest income | | 21,909 | | | 17,202 | | | | 40,956 | | | 35,081 | |

| Provision for loan losses | | 2,240 | | | 762 | | | | 3,091 | | | 1,800 | |

| Net interest income after provision for loan losses | | 19,669 | | | 16,440 | | | | 37,865 | | | 33,281 | |

| | | | | | | | | |

| Noninterest income | | | | | | | | | |

| Service charges on deposit accounts | | 577 | | | 1,199 | | | | 1,094 | | | 1,594 | |

| Income from bank owned life insurance | | 376 | | | 281 | | | | 649 | | | 563 | |

| SBA origination fees | | 48 | | | — | | | | 48 | | | 145 | |

| Swap fee income | | — | | | 364 | | | | 112 | | | 573 | |

| Loans held for sale income | | 45 | | | 226 | | | | 116 | | | 301 | |

| Gain on sale and call of securities | | 13 | | | 21 | | | | 13 | | | 22 | |

| Other | | 722 | | | 211 | | | | 1,022 | | | 223 | |

| Total noninterest income | | 1,781 | | | 2,302 | | | | 3,054 | | | 3,421 | |

| | | | | | | | | |

| Noninterest expense | | | | | | | | | |

| Salaries and employee benefits | | 7,473 | | | 7,099 | | | | 18,693 | | | 13,883 | |

| Occupancy and equipment | | 1,010 | | | 905 | | | | 2,012 | | | 2,007 | |

| Data processing | | 304 | | | 276 | | | | 618 | | | 566 | |

| Marketing | | 125 | | | 165 | | | | 321 | | | 318 | |

| Professional fees | | 886 | | | 770 | | | | 1,805 | | | 1,398 | |

| Acquisition expenses | | — | | | — | | | | — | | | 684 | |

| Regulatory assessments | | 473 | | | 418 | | | | 1,022 | | | 767 | |

| Other | | 2,333 | | | 1,321 | | | | 4,628 | | | 3,119 | |

| Total noninterest expense | | 12,604 | | | 10,954 | | | | 29,099 | | | 22,742 | |

| | | | | | | | | |

| Income before income taxes | | 8,846 | | | 7,788 | | | | 11,820 | | | 13,960 | |

| Income tax provision | | 1,852 | | | 1,457 | | | | 2,407 | | | 2,844 | |

| Net income | | $ | 6,994 | | | $ | 6,331 | | | | $ | 9,413 | | | $ | 11,116 | |

| | | | | | | | | |

| Earnings per share: | | | | | | | | | |

| Basic | | $ | 0.52 | | | $ | 0.47 | | | | $ | 0.70 | | | $ | 0.83 | |

| Diluted | | $ | 0.50 | | | $ | 0.45 | | | | $ | 0.67 | | | $ | 0.80 | |

| | | | | | | | | |

| Other comprehensive income: | | | | | | | | | |

| Unrealized holding gain (loss) on securities available for sale | | (5,841) | | | (505) | | | | (14,308) | | | (794) | |

| Tax effect | | 1,481 | | | 124 | | | | 3,635 | | | 195 | |

| Other comprehensive gain (loss), net of tax | | (4,360) | | | (381) | | | | (10,673) | | | (599) | |

| Comprehensive income (loss) | | $ | 2,634 | | | $ | 5,950 | | | | $ | (1,260) | | | $ | 10,517 | |

See accompanying notes to consolidated financial statements.

PROFESSIONAL HOLDING CORP.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (Unaudited)

(Dollar amounts in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | Accumulated | | | |

| | | | | | | | | | Additional | | | | | Other | | | |

| | Common Stock | | Treasury | | Paid-in | | Retained | | Comprehensive | | | |

| | Shares | | Amount | | Stock | | Capital | | Earnings | | Income (Loss) | | Total |

Balance at April 1, 2020 | | 13,537,565 | | $ | 138 | | $ | (6,257) | | $ | 201,670 | | $ | 5,134 | | $ | 169 | | $ | 200,854 |

Issuance of common stock, net of issuance cost | | 89,167 | | | 1 | | | — | | | 450 | | | — | | | — | | | 451 |

Employee stock purchase plan | | — | | | — | | | — | | | 27 | | | — | | | — | | | 27 |

Stock based compensation | | — | | | — | | | — | | | 296 | | | — | | | — | | | 296 |

Treasury stock | | (182,097) | | | — | | | (2,875) | | | (5) | | | — | | | — | | | (2,880) |

Net loss | | — | | | — | | | — | | | — | | | 3,131 | | | — | | | 3,131 |

Other comprehensive income | | — | | | — | | | — | | | — | | | — | | | 555 | | | 555 |

Balance at June 30, 2020 | | 13,444,635 | | $ | 139 | | $ | (9,132) | | $ | 202,438 | | $ | 8,265 | | $ | 724 | | $ | 202,434 |

| | | | | | | | | | | | | | | | | | | | |

Balance at April 1, 2021 | | 13,661,567 | | $ | 143 | | $ | (10,087) | | $ | 209,770 | | $ | 19,541 | | $ | 664 | | $ | 220,031 |

Issuance of common stock, net of issuance cost | | 8,359 | | | — | | | — | | | 107 | | | — | | | — | | | 107 |

Employee stock purchase plan | | 978 | | | — | | | — | | | 18 | | | — | | | — | | | 18 |

Stock based compensation | | (1,834) | | | — | | | — | | | 385 | | | — | | | — | | | 385 |

Treasury stock | | (193,289) | | | — | | | (3,457) | | | (6) | | | — | | | — | | | (3,463) |

Net income | | — | | | — | | | — | | | — | | | 6,331 | | | — | | | 6,331 |

Other comprehensive income | | — | | | — | | | — | | | — | | | — | | | (381) | | | (381) |

Balance at June 30, 2021 | | 13,475,781 | | $ | 143 | | $ | (13,544) | | $ | 210,274 | | $ | 25,872 | | $ | 283 | | $ | 223,028 |

| | | | | | | | | | | | | | | | | | | | |

Balance at January 1, 2020 | | 5,867,446 | | $ | 60 | | $ | (4,155) | | $ | 77,019 | | $ | 6,451 | | $ | (73) | | $ | 79,302 |

Issuance of common stock, net of issuance cost | | 3,664,667 | | | 37 | | | — | | | 60,221 | | | — | | | — | | | 60,258 |

Marquis Bancorp (MBI) acquisition | | 4,227,816 | | | 42 | | | — | | | 64,657 | | | — | | | — | | | 64,699 |

Employee stock purchase plan | | — | | | — | | | — | | | 58 | | | — | | | — | | | 58 |

Stock based compensation | | — | | | — | | | — | | | 492 | | | — | | | — | | | 492 |

Treasury stock | | (315,294) | | | — | | | (4,977) | | | (9) | | | — | | | — | | | (4,986) |

Net loss | | — | | | — | | | — | | | — | | | 1,814 | | | — | | | 1,814 |

Other comprehensive income | | — | | | — | | | — | | | — | | | — | | | 797 | | | 797 |

Balance at June 30, 2020 | | 13,444,635 | | $ | 139 | | $ | (9,132) | | $ | 202,438 | | $ | 8,265 | | $ | 724 | | $ | 202,434 |

| | | | | | | | | | | | | | | | | | | | |

Balance at January 1, 2021 | | 13,534,829 | | $ | 141 | | $ | (9,209) | | $ | 208,995 | | $ | 14,756 | | $ | 882 | | $ | 215,565 |

Issuance of common stock, net of issuance cost | | 61,204 | | | 1 | | | — | | | 543 | | | — | | | — | | | 544 |

Employee stock purchase plan | | 1,851 | | | — | | | — | | | 34 | | | — | | | — | | | 34 |

Stock based compensation | | 125,665 | | | 1 | | | — | | | 709 | | | — | | | — | | | 710 |

Treasury stock | | (247,768) | | | — | | | (4,335) | | | (7) | | | — | | | — | | | (4,342) |

Net income | | — | | | — | | | — | | | — | | | 11,116 | | | — | | | 11,116 |

Other comprehensive income | | — | | | — | | | — | | | — | | | — | | | (599) | | | (599) |

Balance at June 30, 2021 | | 13,475,781 | | $ | 143 | | $ | (13,544) | | $ | 210,274 | | $ | 25,872 | | $ | 283 | | $ | 223,028 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock | | Treasury

Stock | | Additional

Paid-in

Capital | | Retained

Earnings | | Accumulated

Other

Comprehensive

Income (Loss) | | Total |

| | Shares | | Amount | | | | | |

| Balance on December 31, 2020 | | 13,534,829 | | | $ | 141 | | | $ | (9,209) | | | $ | 208,995 | | | $ | 14,756 | | | $ | 882 | | | $ | 215,565 | |

| | | | | | | | | | | | | | |

| Employee stock purchase plan | | 1,851 | | | — | | | — | | | 34 | | | — | | | — | | | 34 | |

| Stock based compensation | | — | | | 1 | | | — | | | 709 | | | — | | | — | | | 710 | |

| Exercise of stock options | | 64,414 | | | — | | | — | | | — | | | — | | | — | | | — | |

| Restricted stock issued | | 122,455 | | | 1 | | | — | | | 543 | | | — | | | — | | | 544 | |

| Treasury stock | | (247,768) | | | — | | | (4,335) | | | (7) | | | — | | | — | | | (4,342) | |

| Net income | | — | | | — | | | — | | | — | | | 11,116 | | | — | | | 11,116 | |

| Other comprehensive income (loss) | | — | | | — | | | — | | | — | | | — | | | (599) | | | (599) | |

| Balance on June 30, 2021 | | 13,475,781 | | | $ | 143 | | | $ | (13,544) | | | $ | 210,274 | | | $ | 25,872 | | | $ | 283 | | | $ | 223,028 | |

| | | | | | | | | | | | | | |

| Balance on December 31, 2021 | | 13,446,400 | | | $ | 144 | | | $ | (16,003) | | | $ | 212,012 | | | $ | 36,120 | | | $ | (749) | | | $ | 231,524 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Stock based compensation | | — | | | — | | | — | | | 2,230 | | | — | | | — | | | 2,230 | |

| Exercise of stock options | | 115,472 | | | 1 | | | — | | | 1,301 | | | — | | | — | | | 1,302 | |

| Restricted stock issued | | 190,753 | | | 2 | | | — | | | (2) | | | — | | | — | | | — | |

| Treasury stock | | (10,244) | | | — | | | (198) | | | — | | | — | | | — | | | (198) | |

| Net income | | — | | | — | | | — | | | — | | | 9,413 | | | — | | | 9,413 | |

| Other comprehensive income (loss) | | — | | | — | | | — | | | — | | | — | | | (10,673) | | | (10,673) | |

| June 30, 2022 | | 13,742,381 | | | $ | 147 | | | $ | (16,201) | | | $ | 215,541 | | | $ | 45,533 | | | $ | (11,422) | | | $ | 233,598 | |

| | | | | | | | | | | | | | |

| Balance on March 31, 2021 | | 13,661,567 | | | $ | 143 | | | $ | (10,087) | | | $ | 209,770 | | | $ | 19,541 | | | $ | 664 | | | $ | 220,031 | |

| | | | | | | | | | | | | | |

| Employee stock purchase plan | | 978 | | | — | | | — | | | 18 | | | — | | | — | | | 18 | |

| Stock based compensation expense | | — | | | — | | | — | | | 385 | | | — | | | — | | | 385 | |

| Exercise of stock options | | 8,359 | | | — | | | — | | | — | | | — | | | — | | | — | |

| Restricted stock issued | | (1,834) | | | — | | | — | | | 107 | | | — | | | — | | | 107 | |

| Treasury stock | | (193,289) | | | — | | | (3,457) | | | (6) | | | — | | | — | | | (3,463) | |

| Net income | | — | | | — | | | — | | | — | | | 6,331 | | | — | | | 6,331 | |

| Other comprehensive income (loss) | | — | | | — | | | — | | | — | | | — | | | (381) | | | (381) | |

| Balance on June 30, 2021 | | 13,475,781 | | | $ | 143 | | | $ | (13,544) | | | $ | 210,274 | | | $ | 25,872 | | | $ | 283 | | | $ | 223,028 | |

| | | | | | | | | | | | | | |

| Balance on March 31, 2022 | | 13,665,801 | | | $ | 146 | | | $ | (16,201) | | | $ | 214,351 | | | $ | 38,539 | | | $ | (7,062) | | | $ | 229,773 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| Stock based compensation expense | | — | | | — | | | — | | | 505 | | | — | | | — | | | 505 | |

| Exercise of stock options | | 55,807 | | | 1 | | | — | | | 685 | | | — | | | — | | | 686 | |

| Restricted stock issued | | 20,773 | | | — | | | — | | | — | | | — | | | — | | | — | |

| | | | | | | | | | | | | | |

| Net income | | — | | | — | | | — | | | — | | | 6,994 | | | — | | | 6,994 | |

| Other comprehensive income (loss) | | — | | | — | | | — | | | — | | | — | | | (4,360) | | | (4,360) | |

| Balance on June 30, 2022 | | 13,742,381 | | | $ | 147 | | | $ | (16,201) | | | $ | 215,541 | | | $ | 45,533 | | | $ | (11,422) | | | $ | 233,598 | |

See accompanying notes to consolidated financial statements

PROFESSIONAL HOLDING CORP.

CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(Dollar amounts in thousands, except share data)

| | | | | | |

| | Six Months Ended June 30, |

| | 2021 | | 2020 |

Cash flows from operating activities | | | | | | |

Net income (loss) | | $ | 11,116 | | $ | 1,814 |

Adjustments to reconcile net income to net cash from operating activities | | | | | | |

Provision for loan losses | | | 1,800 | | | 2,595 |

Deferred income tax benefit (expense) | | | 988 | | | (499) |

Depreciation and amortization | | | 739 | | | 739 |

Gain on sale of securities | | | — | | | (4) |

Gain on call of securities | | | (22) | | | (11) |

Equity unrealized change in market value | | | 63 | | | (24) |

Net amortization of securities | | | 1,396 | | | (906) |

Net amortization of deferred loan fees | | | (4,400) | | | 1,118 |

Loans held for sale | | | (769) | | | (1,070) |

Proceeds from sale of loans | | | — | | | 110 |

Income from bank owned life insurance | | | (563) | | | (255) |

Loss on disposal of premises and equipment | | | 137 | | | — |

Employee stock purchase plan | | | 34 | | | 58 |

Stock compensation | | | 710 | | | 492 |

Changes in operating assets and liabilities: | | | | | | |

Accrued interest receivable | | | 1,217 | | | (1,472) |

Other assets | | | (1,098) | | | 1,887 |

Official checks, accrued interest, interest payable and other liabilities | | | (1,385) | | | (3,395) |

Net cash provided by operating activities | | | 9,963 | | | 1,177 |

| | | | | | |

Cash flows from investing activities | | | | | | |

Proceeds from maturities and paydowns of securities available for sale | | | 11,123 | | | 6,256 |

Proceeds from calls of securities available for sale | | | 4,648 | | | 4,835 |

Proceeds from maturities and paydowns of securities held to maturity | | | 257 | | | 44 |

Purchase of securities available for sale | | | (50,922) | | | (60,693) |

Proceeds from sale of securities available for sale | | | — | | | 1,739 |

Loans originations, net of principal repayments | | | (47,410) | | | (256,731) |

Purchase of Federal Reserve Bank stock | | | (192) | | | (2,671) |

Proceeds from maturities of Federal Home Loan Bank Stock | | | 888 | | | — |

Purchase of Federal Home Loan Bank Stock | | | — | | | (1,297) |

Purchases of premises and equipment | | | (455) | | | (741) |

Proceeds from acquisition | | | — | | | 26,860 |

Net cash used in investing activities | | | (82,063) | | | (282,399) |

| | | | | | |

Cash flows from financing activities | | | | | | |

Net increase (decrease) in deposits | | | 617,620 | | | 126,404 |

Proceeds from issuance of stock, net of issuance costs | | | 544 | | | 60,258 |

Purchase of treasury stock | | | (4,342) | | | (4,986) |

Proceeds from Federal Home Loan Bank advances | | | — | | | 10,000 |

Repayments of Federal Home Loan advances | | | (5,000) | | | (25,000) |

Repayment of line of credit | | | — | | | (9,999) |

Proceeds from PPPLF advances | | | — | | | 218,080 |

Repayments of PPPLF advances | | | (101,358) | | | — |

Net cash provided by financing activities | | | 507,464 | | | 374,757 |

| | | | | | |

Increase in cash and cash equivalents | | | 435,364 | | | 93,535 |

| | | | | | |

Cash and cash equivalents at beginning of period | | | 216,972 | | | 198,950 |

| | | | | | |

Cash and cash equivalents at end of period | | $ | 652,336 | | $ | 292,485 |

| | | | | | |

Supplemental cash flow information: | | | | | | |

Cash paid during the period for interest | | $ | 4,425 | | $ | 4,907 |

Cash paid during the period for taxes | | | 3,000 | | | 20 |

| | | | | | |

Supplemental noncash disclosures: | | | | | | |

Lease liabilities arising from obtaining right of use assets | | $ | — | | $ | 1,620 |

Total assets acquired | | | — | | | 589,374 |

Total liabilities assumed | | | — | | | 539,403 |

| | | | | | | | | | | | | | |

| | Six Months Ended June 30, |

| | 2022 | | 2021 |

| Cash flows from operating activities | | | | |

| Net income | | $ | 9,413 | | $ | 11,116 |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | |

| Provision for loan losses | | 3,091 | | | 1,800 | |

| Amortization of purchase accounting adjustments | | (3,262) | | | (2,581) | |

| | | | |

| Depreciation and amortization | | 89 | | | 702 | |

| | | | |

| Gain on call of securities | | (13) | | | (22) | |

| Gain on loans held for sale | | (116) | | | (301) | |

| Equity unrealized change in market value | | 336 | | | 63 | |

| Net amortization of securities | | 726 | | | 1,396 | |

| Net amortization of deferred loan fees | | (2,865) | | | (4,400) | |

| Originations of loans held for sale | | (7,713) | | | (15,728) | |

| Proceeds from sales of loans held for sale | | 7,994 | | | 15,260 | |

| Income from bank-owned life insurance | | (649) | | | (563) | |

| Loss (gain) on disposal of premises and equipment | | (1) | | | 137 | |

| Employee stock purchase plan | | — | | | 34 | |

| Stock compensation | | 2,230 | | | 710 | |

| Changes in operating assets and liabilities: | | | | |

| Accrued interest receivable | | 8 | | | 1,217 | |

| Other assets | | (3,823) | | | 811 | |

| Official checks, accrued interest, interest payable and other liabilities | | 5,630 | | | (1,227) | |

| Net cash provided by (used in) operating activities | | 11,075 | | | 8,424 | |

| | | | |

| Cash flows from investing activities | | | | |

| Proceeds from maturities and paydowns of securities available for sale | | 14,036 | | | 11,123 | |

| Proceeds from calls of securities available for sale | | 4,175 | | | 4,648 | |

| Proceeds from paydowns of securities held to maturity | | 31 | | | 257 | |

| Purchase of securities available for sale | | (30,737) | | | (50,922) | |

| | | | |

| Purchase of equity securities | | (57) | | | — | |

| Loans originations, net of principal repayments | | (204,791) | | | (45,437) | |

| | | | |

| Redemption of Federal Reserve Bank stock | | (589) | | | — | |

| Purchase of Federal Home Loan Bank Stock | | — | | | (192) | |

| Net redemption of Federal Home Loan Bank Stock | | 981 | | | 888 | |

| Purchase of bank-owned life insurance | | (15,000) | | | — | |

| Purchases of premises and equipment, net | | (206) | | | (1,376) | |

| | | | |

| Net cash used in investing activities | | (232,157) | | | (81,011) | |

| | | | |

| Cash flows from financing activities | | | | |

| Net increase in deposits | | 10,590 | | | 618,107 | |

| Proceeds from issuance of stock, net of issuance costs | | 1,302 | | | 544 | |

| | | | |

| Purchase of treasury stock | | (198) | | | (4,342) | |

| | | | |

| Repayments of Federal Home Loan advances | | (35,000) | | | (5,000) | |

| Net proceeds from issuance of subordinated notes payable | | 25,000 | | | — | |

| | | | |

| | | | |

| Repayment of line of credit | | (10,000) | | | — | |

| | | | |

| Repayments of PPPLF advances | | — | | | (101,358) | |

| Net cash provided by (used in) financing activities | | (8,306) | | 507,951 |

| | | | |

| | | | | | | | | | | | | | |

| Increase (decrease) in cash and cash equivalents | | (229,388) | | 435,364 |

| Cash and cash equivalents at beginning of period | | 597,467 | | 216,972 |

| Cash and cash equivalents at end of period | | $ | 368,079 | | $ | 652,336 |

| | | | |

| Supplemental cash flow information: | | | | |

| Cash paid during the period for interest | | $ | 3,872 | | $ | 4,425 |

| Cash paid during the period for taxes | | 3,956 | | 3,000 |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

See accompanying notes to consolidated financial statements

PROFESSIONAL HOLDING CORP.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

(Tables in thousands, except share data)

NOTE 1 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited consolidated financial statements of Professional Holding Corp. and its subsidiary, Professional Bank (the “Bank” and collectively with Professional Holding Corp., the “Company”), have been prepared in accordance with U.S. generally accepted accounting principles for interim financial information. Accordingly, they do not include all of the information and footnotes required by U.S. generally accepted accounting principles for complete financial statements. In the opinion of management,

all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Certain prior period amounts have been reclassified to conform to the current period presentation.

Operating results for the six months ended June 30,

2021,2022, are not necessarily indicative of the results that may be expected for the year ending December 31,

2021,2022, or any other period. For further information, refer to the consolidated financial statements and footnotes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31,

2020.2021.

The preparation of these financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Adoption of new accounting standards:

ASU 2019-12, Income Taxes (Topic 740)

In December 2019, FASB issued guidance which simplifies the accounting for income taxes by removing multiple exceptions to the general principals in Topic 740. The standard is effective for public business entities for fiscal years, and for interim periods within those fiscal years, beginning after December 15, 2020. The new guidance did not materially impact the Company’s Consolidated Financial Statements or disclosures.

ASU 2020-04, Reference Rate Reform (Topic 848)

In March 2020, FASB issued guidance which provides optional guidance to ease the accounting burden in accounting for, or recognizing the effects from, reference rate reform on financial reporting. The new standard is a result of the London Interbank Offered Rate ("LIBOR") likely being discontinued as an available benchmark rate. The standard is elective and provides optional expedients and exceptions for applying U.S. Generally Accepted Accounting Principles (“GAAP”) to contracts, hedging relationships, or other transactions that reference LIBOR, or another reference rate expected to be discontinued. The amendments in the update are effective for all entities between March 12, 2020 and December 31, 2022. The Company has established a cross-functional working group to guide the Company’s transition from LIBOR and has begun efforts to transition to alternative rates consistent with industry timelines. The Company has identified its products that utilize LIBOR and has implemented enhanced fallback language to facilitate the transition to alternative reference rates. The Company is evaluating existing platforms and systems and preparing to offer new rates. The new guidance did not materially impact the Company’s Consolidated Financial Statements or disclosures.

New accounting standards that have not yet been adopted:

The following provides a brief description of accounting standards that have been issued but are not yet adopted that could have a material effect on the Company’s financial statements:

| | | | | |

ASU 2016-13, 2022-02, Financial Instruments – Credit Losses (Topic 326) |

Description | In June 2016,March 2022, FASB issued ASU 2022-02 which eliminates the guidance on troubled debt restructurings and requires entities to replaceevaluate all loan modifications to determine if they result in a new loan or a continuation of the incurred loss model with an expected loss model, which is referred to as the current expected credit loss (CECL) model. The CECL model is applicable to the measurementexisting loan. ASU 2022-02 also requires that entities disclose current-period gross charge-offs by year of credit losses on financial assets measured at amortized cost, including loan receivablesorigination for loans and held to maturity debt securities. It also applies to off-balance sheet credit exposures not accounted for as insurance (i.e. loan commitments, standby letters of credit, financial guarantees and other similar instruments). leases. |

Date of Adoption | For PBEs that are non-SEC filers and for SEC filers that are considered small reporting companies, itASU 2022-02 is effective for January 1, 2023. Early adoption is still permitted.

|

Effect on the Consolidated Financial Statements | The Company's management is in the process of evaluating credit loss estimation models. Updates to business processes and the documentation of accounting policy decisions are ongoing. The company may recognizeThis ASU will have an increase in the allowance for credit losses upon adoption, recorded as a one-time cumulative adjustment to retained earnings. However, the magnitude of the impact on the Company's consolidatedour financial statements hasstatement disclosures but not yet been determined. The Company will adopt this accounting standarda material impact on our financial statements.

|

| | | | | |

| ASU 2022-03, Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions |

| Description | In June 2022, FASB issued ASU 2022-03 which clarifies that a contractual sale restriction should not be considered in measuring fair value. ASU 2022-03 also requires that entities disclose certain qualitative and quantitative information about securities with contractual sale restrictions. |

| Date of Adoption | ASU 2022-03 is effective January 1, 2023. |

| Effect on the Consolidated Financial Statements | We are evaluating the impact of this ASU, however it is not believed to be material. |

NOTE 2 — EARNINGS PER SHARE

Basic earnings per common share is computed by dividing net income available to common stockholders by the weighted average number of shares of common stock outstanding during the year. Diluted earnings per common share is computed by

dividing net income available to common stockholders by the weighted average number of shares of common stock outstanding plus the effect of employee stock

optionsawards during the year.

| | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| | 2021 | | 2020 | | 2021 | | 2020 |

Basic earnings per share: | | | | | | | | | | | | |

Net income | | $ | 6,331 | | $ | 3,131 | | $ | 11,116 | | $ | 1,814 |

Total weighted average common stock outstanding | | | 13,397,747 | | | 13,415,525 | | | 13,419,929 | | | 11,516,756 |

Net income per share | | $ | 0.47 | | $ | 0.23 | | $ | 0.83 | | $ | 0.16 |

Diluted earnings per share: | | | | | | | | | | | | |

Net income | | $ | 6,331 | | $ | 3,131 | | $ | 11,116 | | $ | 1,814 |

Total weighted average common stock outstanding | | | 13,397,747 | | | 13,415,525 | | | 13,419,929 | | | 11,516,756 |

Add: Dilutive effect of employee stock options | | | 564,822 | | | 518,435 | | | 521,900 | | | 526,503 |

Total weighted average diluted stock outstanding | | | 13,962,569 | | | 13,933,960 | | | 13,941,829 | | | 12,043,259 |

Net income per share | | $ | 0.45 | | $ | 0.22 | | $ | 0.80 | | $ | 0.15 |

For the three months ended June 30, 2021, there were 270,850 thousand stock options that were anti-dilutive and for the three months ended June 30, 2020, there were 29,350 thousand stock options that were anti-dilutive. For the six months ended June 30, 2021, there were 270,850 thousand stock options that were anti-dilutive and for the six months ended June 30, 2020, there were 29,350 thousand stock options that were anti-dilutive.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | Six Months Ended June 30, |

| (Dollar amounts in thousands, except per share data) | | 2022 | | 2021 | | 2022 | | | | 2021 |

| Basic earnings per share: | | | | | | | | | | |

| Net income | | $ | 6,994 | | | $ | 6,331 | | | $ | 9,413 | | | | | $ | 11,116 | |

| Total weighted average common stock outstanding | | 13,446,335 | | | 13,397,747 | | | 13,396,240 | | | | | 13,419,929 | |

| Net income per share | | $ | 0.52 | | | $ | 0.47 | | | $ | 0.70 | | | | | $ | 0.83 | |

| Diluted earnings per share: | | | | | | | | | | |

| Net income | | $ | 6,994 | | | $ | 6,331 | | | $ | 9,413 | | | | | $ | 11,116 | |

| Total weighted average common stock outstanding | | 13,446,335 | | | 13,397,747 | | | 13,396,240 | | | | | 13,419,929 | |

| Add: dilutive effect of employee restricted stock and options | | 628,550 | | | 564,822 | | | 614,006 | | | | | 521,900 | |

| Total weighted average diluted stock outstanding | | 14,074,885 | | | 13,962,569 | | | 14,010,246 | | | | | 13,941,829 | |

| Net income per share | | $ | 0.50 | | | $ | 0.45 | | | $ | 0.67 | | | | | $ | 0.80 | |

| | | | | | | | | | |

| Anti-dilutive restricted stock and options | | 29,250 | | | 270,850 | | | 65,672 | | | | | 270,850 | |

The following table summarizes the amortized cost and fair value of securities

available-for-saleavailable for sale and securities

held-to-maturity atheld to maturity on June 30,

20212022, and December 31,

2020,2021, and the corresponding amounts of gross unrealized gains and losses recognized in accumulated other comprehensive loss and gross unrecognized gains and losses:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair Value |

| June 30, 2022 | | | | | | | | |

| Available for sale - taxable | | | | | | | | |

| Small Business Administration loan pools | | $ | 35,355 | | | $ | 33 | | | $ | (442) | | | $ | 34,946 | |

Mortgage-backed securities (1) | | 138,666 | | | — | | | (13,529) | | | 125,137 | |

| United States agency obligations | | 2,945 | | | — | | | (178) | | | 2,767 | |

| Corporate bonds | | 1,500 | | | 4 | | | — | | | 1,504 | |

| Total available for sale - taxable | | $ | 178,466 | | | $ | 37 | | | $ | (14,149) | | | $ | 164,354 | |

| Available for sale - tax-exempt | | | | | | | | |

| Community Development District bonds | | $ | 25,488 | | | $ | 13 | | | $ | (1,069) | | | $ | 24,432 | |

| Municipals | | 3,155 | | | — | | | (134) | | | 3,021 | |

| Total available for sale - tax-exempt | | $ | 28,643 | | | $ | 13 | | | $ | (1,203) | | | $ | 27,453 | |

| | | | | | | | |

| | Amortized

Cost | | Gross

Unrecognized

Gains | | Gross

Unrecognized

Losses | | Fair Value |

| Held to Maturity | | | | | | | | |

| Residential mortgage-backed securities | | $ | 204 | | | $ | — | | | $ | (7) | | | $ | 197 | |

| | | | | | | | |

| | | | | | | | |

| Total Held to Maturity | | $ | 204 | | | $ | — | | | $ | (7) | | | $ | 197 | |

(1) | | | | | | | | | | | | |

| | | | | Gross | | Gross | | | |

| | Amortized | | Unrealized | | Unrealized | | | |

June 30, 2021 | | Cost | | Gains | | Losses | | Fair Value |

Available-for-sale - taxable | | | | | | | | | | | | |

Small Business Administration loan pools | | $ | 43,091 | | $ | 78 | | $ | (573) | | $ | 42,596 |

Mortgage-backed securities | | | 54,517 | | | 205 | | | (182) | | | 54,540 |

United States agency obligations | | | 2,001 | | | 88 | | | - | | | 2,089 |

Corporate bonds | | | 1,500 | | | 10 | | | - | | | 1,510 |

Total available-for-sale - taxable | | $ | 101,109 | | $ | 381 | | $ | (755) | | $ | 100,735 |

Available-for-sale - tax exempt | | | | | | | | | | | | |

Community Development District bonds | | $ | 17,954 | | $ | 704 | | $ | - | | $ | 18,658 |

Municipals | | | 1,057 | | | 46 | | | - | | | 1,103 |

Total available-for-sale - tax exempt | | $ | 19,011 | | $ | 750 | | $ | - | | $ | 19,761 |

| | | | | | | | | | | | |

| | | | | Gross | | Gross | | | |

| | Amortized | | Unrecognized | | Unrecognized | | | |

| | Cost | | Gains | | Losses | | Fair Value |

Held-to-Maturity | | | | | | | | | | | | |

Mortgage-backed securities | | $ | 285 | | $ | 11 | | $ | — | | $ | 296 |

Foreign Bonds | | | 1,000 | | | — | | | — | | | 1,000 |

Total Held-to-Maturity | | $ | 1,285 | | $ | 11 | | $ | — | | $ | 1,296 |

$100.0 million is residential mortgage-backed and $25.2 million is commercial mortgage-backed.

| | | | | | | | | | | | |

| | | | | Gross | | Gross | | | |

| | Amortized | | Unrealized | | Unrealized | | Fair |

December 31, 2020 | | Cost | | Gains | | Losses | | Value |

Available-for-sale - taxable | | | | | | | | | | | | |

Small Business Administration loan pools | | $ | 30,678 | | $ | 77 | | $ | (199) | | $ | 30,556 |

Mortgage-backed securities | | | 28,514 | | | 438 | | | (30) | | | 28,922 |

United States agency obligations | | | 3,000 | | | 122 | | | - | | | 3,122 |

Corporate bonds | | | 2,501 | | | 9 | | | - | | | 2,510 |

Total available-for-sale - taxable | | $ | 64,693 | | $ | 646 | | $ | (229) | | $ | 65,110 |

Available-for-sale - tax exempt | | | | | | | | | | | | |

Community Development District bonds | | $ | 20,582 | | $ | 717 | | $ | - | | $ | 21,299 |

Municipals | | | 1,064 | | | 35 | | | - | | | 1,099 |

Total available-for-sale - tax exempt | | $ | 21,646 | | $ | 752 | | $ | - | | $ | 22,398 |

| | | | | | | | | | | | |

| | | | | Gross | | Gross | | | |

| | Amortized | | Unrecognized | | Unrecognized | | Fair |

| | Cost | | Gains | | Losses | | Value |

Held-to-Maturity | | | | | | | | | | | | |

Mortgage-backed securities | | $ | 345 | | $ | 14 | | $ | — | | $ | 359 |

United States Treasury | | | 202 | | | — | | | — | | | 202 |

Foreign Bonds | | | 1,000 | | | — | | | — | | | 1,000 |

Total Held-to-Maturity | | $ | 1,547 | | $ | 14 | | $ | — | | $ | 1,561 |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Amortized

Cost | | Gross

Unrecognized

Gains | | Gross

Unrecognized

Losses | | Fair Value |

| Equity | | | | | | | | |

| Mutual Funds | | $ | 5,502 | | | $ | — | | | $ | — | | | $ | 5,502 | |

| Other equity securities | | 857 | | | — | | | — | | | 857 | |

| Total Equity | | $ | 6,359 | | | $ | — | | | $ | — | | | $ | 6,359 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

(Dollars in thousands) | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| December 31, 2021 | | | | | | | | |

| Available for sale - taxable | | | | | | | | |

| Small Business Administration loan pools | | $ | 40,368 | | $ | 38 | | $ | (472) | | | $ | 39,934 |

Mortgage-backed securities (1) | | 131,273 | | 70 | | (1,240) | | | 130,103 |

| United States agency obligations | | 3,939 | | 54 | | (7) | | 3,986 |

| Corporate bonds | | 1,500 | | 13 | | — | | 1,513 |

| Total available for sale - taxable | | $ | 177,080 | | $ | 175 | | $ | (1,719) | | $ | 175,536 |

| Available for sale - tax-exempt | | | | | | | | |

| Community development district bonds | | $ | 17,163 | | $ | 512 | | $ | (1) | | $ | 17,674 |

| | | | | | | | |

| Municipals | | 1,051 | | 40 | | — | | 1,091 |

| Total available for sale - tax-exempt | | $ | 18,214 | | $ | 552 | | $ | (1) | | $ | 18,765 |

| | | | | | | | |

| | Amortized

Cost | | Gross

Unrecognized

Gains | | Gross

Unrecognized

Losses | | Fair

Value |

| Held to Maturity | | | | | | | | |

| Residential mortgage-backed securities | | $ | 236 | | $ | 6 | | $ | — | | $ | 242 |

| | | | | | | | |

| | | | | | | | |

| Total held to maturity | | $ | 236 | | $ | 6 | | $ | — | | $ | 242 |

(1)$104.0 million is residential mortgage-backed and $26.1 million is commercial mortgage-backed.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Amortized

Cost | | Gross

Unrecognized

Gains | | Gross

Unrecognized

Losses | | Fair Value |

| Equity | | | | | | | | |

| Mutual funds | | $ | 5,838 | | | $ | — | | | $ | — | | | $ | 5,838 | |

| Other equity securities | | 800 | | | — | | | — | | | 800 | |

| Total equity | | $ | 6,638 | | | $ | — | | | $ | — | | | $ | 6,638 | |

As of June 30, 20212022, and December 31, 2020, Corporate2021, corporate bonds were comprised of investments in the financial services industry. During the six months ended June 30, 2021,2022, the net investment portfolio increaseddecreased by $32.6$2.8 million as a result of increases from purchases of $50.9primarily due to $18.2 million in SBAinvestment calls, redemptions and MBS securities combinedpaydowns, coupled with decreasesunrealized losses of $17.4$14.3 million from paydowns, maturities and calls, as well asduring the unrealized holding loss on securities available for sale of $0.7 millionyear with a related tax effect of $0.2 million. Proceeds from the maturity$3.6 million, partially offset by purchases of approximately $30.7 million in mortgage-backed securities ("MBS") community development district bonds ("CDD"), and redemption of securities during the three and six months ended June 30, 2021, were $3.2 million and $4.7 million, with gross realized gains of $21 thousand and $22 thousand, respectively. Proceeds from the sales of securities during the year ended December 31, 2020,municipal bonds.

were $1.7 million, with gross realized gains of $4 thousand. Proceeds from redemption of securities for the year ended December 31, 2020, were $9.1 million, with gross realized gains of $33 thousand. Total securities pledged as of June 30, 20212022, and December 31, 2020,2021, were $13.3$1.9 million and $12.5$2.4 million, respectively. Securitiesrespectively, which included securities pledged for derivative SWAPswap transactions as of June 30, 2021, were $1.1 million which were included in the total securities pledged, such securities were generallyand pledged for public funds. There were no securities pledged for derivate SWAP transactions at December 31, 2020.

The amortized cost and fair value of debt securities are shown by contractual maturity. Expected maturities may differ from contractual maturities if borrowers have the right to call or prepay obligations with or without call or prepayment penalties.

Securities not due at a single maturity date are shown separately. The scheduled maturities of securities as of June 30,

2021,2022, are as follows:

| | | | | | |

| | June 30, 2021 |

| | Amortized | | Fair |

| | Cost | | Value |

Available-for-sale | | | | | | |

Due in one year or less | | $ | 1,038 | | $ | 1,056 |

Due after one year through five years | | | 21,159 | | | 21,975 |

Due after five years through ten years | | | 315 | | | 329 |

Due after ten years | | | — | | | — |

Subtotal | | $ | 22,512 | | $ | 23,360 |

| | | | | | |

Small Business Administration loan pools | | $ | 43,091 | | $ | 42,596 |

Mortgage-backed securities | | | 54,517 | | | 54,540 |

Total available-for-sale | | $ | 120,120 | | $ | 120,496 |

| | | | | | |

Held-to-maturity | | | | | | |

Due in one year or less | | $ | 1,000 | | $ | 1,000 |

Due after one year through five years | | | — | | | — |

Subtotal | | $ | 1,000 | | $ | 1,000 |

| | | | | | |

Mortgage-backed securities | | $ | 285 | | $ | 296 |

Total held-to-maturity | | $ | 1,285 | | $ | 1,296 |

At

| | | | | | | | | | | | | | |

| | June 30, 2022 |

| (Dollars in thousands) | | Amortized

Cost | | Fair

Value |

| Available for sale | | | | |

| Due in one year or less | | $ | 5,440 | | | $ | 5,426 | |

| Due after one year through five years | | 22,955 | | | 21,971 | |

| Due after five years through ten years | | 4,693 | | | 4,327 | |

| Due after ten years | | — | | | — | |

| Subtotal | | 33,088 | | | 31,724 | |

| | | | |

| Small Business Administration loan pools | | 35,355 | | | 34,946 | |

| Mortgage-backed securities | | 138,666 | | | 125,137 | |

| Total available for sale | | $ | 207,109 | | | $ | 191,807 | |

| | | | |

| Held to maturity | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| Mortgage-backed securities | | $ | 204 | | | $ | 197 | |

| Total held to maturity | | $ | 204 | | | $ | 197 | |

On June 30,

20212022, and December 31,

2020,2021, there were

0no holdings of securities of any one issuer, other than the U.S. Government and its agencies, in an amount greater than 10% of stockholders’ equity.

At On June 30, 20212022, and December 31, 2020,2021, the number of investment positions that are in an unrealized loss position were 48198 and 36,92, respectively.

The tables below indicate the fair value of debt securities with unrealized losses and for the period of time of which these

losses were outstanding aton June 30, 20212022, and December 31, 2020,2021, respectively, aggregated by major security type and length of time in a continuous unrealized loss position:

| | | | | | | | | | | | | | | | | | |

| | Less Than 12 Months | | 12 Months or Longer | | Total |

| | Fair | | Unrealized | | Fair | | Unrealized | | Fair | | Unrealized |

| | Value | | Losses | | Value | | Losses | | Value | | Losses |

June 30, 2021 | | | | | | | | | | | | | | | | | | |

Available-for-sale - taxable | | | | | | | | | | | | | | | | | | |

Small Business Administration loan pools | | $ | 15,273 | | $ | (427) | | $ | 17,777 | | $ | (146) | | $ | 33,050 | | $ | (573) |

Mortgage-backed securities | | | 14,648 | | | (181) | | | 1,286 | | | (1) | | | 15,934 | | | (182) |

United States agency obligations | | | — | | | — | | | — | | | — | | | — | | | — |

Corporate bonds | | | — | | | — | | | — | | | — | | | — | | | — |

Total available-for-sale - taxable | | $ | 29,921 | | $ | (608) | | $ | 19,063 | | $ | (147) | | $ | 48,984 | | $ | (755) |

Available-for-sale - tax exempt | | | | | | | | | | | | | | | | | | |

Community Development District bonds | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — |

Municipals | | | — | | | — | | | — | | | — | | | — | | | — |

Total available-for-sale - tax exempt | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — |

| | | | | | | | | | | | | | | | | | |

December 31, 2020 | | | | | | | | | | | | | | | | | | |

Available-for-sale - taxable | | | | | | | | | | | | | | | | | | |

Small Business Administration loan pools | | $ | 18,849 | | $ | (133) | | $ | 8,945 | | $ | (66) | | $ | 27,794 | | $ | (199) |

Mortgage-backed securities | | | 5,839 | | | — | | | 2,510 | | | (30) | | | 8,349 | | | (30) |

United States agency obligations | | | 227 | | | — | | | — | | | — | | | 227 | | | — |

Corporate bonds | | | — | | | — | | | — | | | — | | | — | | | — |

Total available-for-sale - taxable | | $ | 24,915 | | $ | (133) | | $ | 11,455 | | $ | (96) | | $ | 36,370 | | $ | (229) |

Available-for-sale - tax exempt | | | | | | | | | | | | | | | | | | |

Community Development District bonds | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — |

Municipals | | | — | | | — | | | — | | | — | | | — | | | — |

Total available-for-sale - tax exempt | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Less Than 12 Months | | 12 Months or Longer | | Total |

| (Dollars in thousands) | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses |

| June 30, 2022 | | | | | | | | | | | | |

| Available for sale - taxable | | | | | | | | | | | | |

| Small Business Administration loan pools | | $ | 4,145 | | | $ | (79) | | | $ | 24,445 | | | $ | (363) | | | $ | 28,590 | | | $ | (442) | |

| Mortgage-backed securities | | 114,856 | | | (12,206) | | | 10,375 | | | (1,323) | | | 125,231 | | | (13,529) | |

| United States agency obligations | | 2,767 | | | (178) | | | — | | | — | | | 2,767 | | | (178) | |

| | | | | | | | | | | | |

| Total available for sale - taxable | | $ | 121,768 | | | $ | (12,463) | | | $ | 34,820 | | | $ | (1,686) | | | $ | 156,588 | | | $ | (14,149) | |

| Available for sale - tax-exempt | | | | | | | | | | | | |

| Community Development District bonds | | $ | 20,627 | | | $ | (1,069) | | | $ | — | | | $ | — | | | $ | 20,627 | | | $ | (1,069) | |

| Municipals | | 3,020 | | | (134) | | | — | | | — | | | 3,020 | | | (134) | |

| Total available for sale - tax-exempt | | $ | 23,647 | | | $ | (1,203) | | | $ | — | | | $ | — | | | $ | 23,647 | | | $ | (1,203) | |

| | | | | | | | | | | | |

| December 31, 2021 | | | | | | | | | | | | |

| Available for sale - taxable | | | | | | | | | | | | |

| Small Business Administration loan pools | | $ | 17,428 | | | $ | (335) | | | $ | 14,872 | | | $ | (136) | | | $ | 32,300 | | | $ | (471) | |

| Mortgage-backed securities | | 109,621 | | | (1,168) | | | 1,710 | | | (73) | | | 111,331 | | | (1,241) | |

| United States agency obligations | | 1,930 | | | (7) | | | — | | | — | | | 1,930 | | | (7) | |

| | | | | | | | | | | | |

| Total available for sale - taxable | | $ | 128,979 | | | $ | (1,510) | | | $ | 16,582 | | | $ | (209) | | | $ | 145,561 | | | $ | (1,719) | |

| Available for sale - tax-exempt | | | | | | | | | | | | |

| Community Development District bonds | | $ | 809 | | | $ | (1) | | | $ | — | | | $ | — | | | $ | 809 | | | $ | (1) | |

| | | | | | | | | | | | |

| Total available for sale - tax-exempt | | $ | 809 | | | $ | (1) | | | $ | — | | | $ | — | | | $ | 809 | | | $ | (1) | |

The unrealized holding losses within the investment portfolio are considered to be temporary and are mainly due to changes in the interest rate cycle. The unrealized loss positions may fluctuate positively or negatively with changes in interest rates or spreads. Since SBA loan pools and mortgage-backed securities are government sponsored entities that are highly rated, the decline in fair value is attributable to changes in interest rates and not credit quality. The Company does not have any securities in an Other Than Temporary Impairment (“OTTI”) position. The Company does not intend to sell these securities and it is likely that it will not be required to sell the securities before their anticipated recovery.

The Company does not consider these securities to be other-than-temporarily impaired at June 30, 2021. NaNNo credit losses were recognized

in operations during the six months ended June 30,

2021,2022, or during the year ended December 31,

2020.

2021.

Loans

aton June 30,

20212022, and December 31,

2020,2021, were as follows:

| | | | | | |

| | June 30, 2021 | | December 31, 2020 |

Commercial real estate | | $ | 875,453 | | $ | 777,776 |

Residential real estate | | | 361,946 | | | 380,491 |

Commercial | | | 373,333 | | | 396,642 |

Construction and land development | | | 74,175 | | | 99,883 |

Consumer and other | | | 14,575 | | | 11,688 |

Total loans | | | 1,699,482 | | | 1,666,480 |

Unearned loan origination (fees) costs, net | | | (1,984) | | | (1,323) |

Unearned PPP loan origination (fees) costs, net | | | (4,855) | | | (4,255) |

Allowance for loan loss | | | (10,418) | | | (16,259) |

Loans held for sale | | | (2,039) | | | (1,270) |

Other | | | (18) | | | — |

Loans, net | | $ | 1,680,168 | | $ | 1,643,373 |

| | | | | | | | | | | | | | |

| (Dollars in thousands) | | June 30, 2022 | | December 31, 2021 |

| Loans held for investment: | | | | |

| Commercial real estate | | $ | 1,034,487 | | $ | 902,654 |

| Residential real estate | | 422,239 | | 377,511 |

| Commercial (non-PPP) | | 387,317 | | 325,415 |

| Commercial (PPP) | | 8,176 | | 58,615 |

| Construction and land development | | 114,938 | | 91,520 |

| Consumer and other | | 20,076 | | 21,449 |

| Total loans held for investment, gross | | 1,987,233 | | 1,777,164 |

| Allowance for loan losses | | (15,142) | | | (12,704) | |

| Loans held for investment, net | | $ | 1,972,091 | | $ | 1,764,460 |

| | | | |

| Loans held for sale: | | | | |

| Loans held for sale | | $ | — | | $ | 165 |

| Total loans held for sale | | $ | — | | $ | 165 |

The recorded investment in loans excludes accrued interest receivable due to immateriality.

At

On June 30,

20212022, and December 31,

2020,2021, there were

$209.9$245.4 million and

$227.8$235.3 million, respectively in total loans pledged to the Federal Home Loan Bank (“FHLB”)

for liquidity..

Loan premiums for loans purchased are amortized over the life of the loan with acceleration upon the increase in principal paydowns or payoffs.

AtOn June 30,

20212022, and December 31,

2020,2021, loan premiums for purchased loans were

$0.5$0.3 million and

$0.6$0.4 million, respectively.

Net discounts for loans acquired through business acquisitions totaled $9.9 million and $13.0 million, as of June 30, 2022, and December 31, 2021, respectively.

There are 0no loans over 90 days past due and accruing as of June 30, 2021,2022, or December 31, 2020. 2021.

The following table presents the aging of the recorded investment in past due loans as of June 30,

20212022, and December 31,

2020,2021, by class of loans:

| | | | | | | | | | | | | | | | | | | | | |

| | 30 – 59 | | 60 – 89 | | Greater than | | | | | | | | | | | | |

| | Days | | Days | | 89 Days | | | | | Total | | Loans Not | | | |

| | Past Due | | Past Due | | Past Due | | Nonaccrual | | Past Due | | Past Due | | Total |

June 30, 2021 | | | | | | | | | | | | | | | | | | | | | |

Commercial real estate | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 875,453 | | $ | 875,453 |

Residential real estate | | | — | | | — | | | — | | | — | | | — | | | 361,946 | | | 361,946 |

Commercial | | | — | | | — | | | — | | | 1,468 | | | 1,468 | | | 371,865 | | | 373,333 |

Construction and land development | | | — | | | — | | | — | | | — | | | — | | | 74,175 | | | 74,175 |

Consumer and other | | | — | | | 94 | | | — | | | 1,307 | | | 1,401 | | | 13,174 | | | 14,575 |

Total | | $ | — | | $ | 94 | | $ | — | | $ | 2,775 | | $ | 2,869 | | $ | 1,696,613 | | $ | 1,699,482 |

| | | | | | | | | | | | | | | | | | | | | |

| | 30 – 59 | | 60 – 89 | | Greater than | | | | | | | | | | | | |

| | Days | | Days | | 89 Days | | | | | Total | | Loans Not | | | |

| | Past Due | | Past Due | | Past Due | | Nonaccrual | | Past Due | | Past Due | | Total |

December 31, 2020 | | | | | | | | | | | | | | | | | | | | | |

Commercial real estate | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 777,776 | | $ | 777,776 |

Residential real estate | | | 1,303 | | | — | | | — | | | — | | | 1,303 | | | 379,188 | | | 380,491 |

Commercial | | | 278 | | | — | | | — | | | 9,127 | | | 9,405 | | | 387,237 | | | 396,642 |

Construction and land development | | | — | | | — | | | — | | | — | | | — | | | 99,883 | | | 99,883 |

Consumer and other | | | — | | | — | | | — | | | 1,307 | | | 1,307 | | | 10,381 | | | 11,688 |

Total | | $ | 1,581 | | $ | — | | $ | — | | $ | 10,434 | | $ | 12,015 | | $ | 1,654,465 | | $ | 1,666,480 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | 30 – 59

Days

Past Due | | 60 – 89

Days

Past Due | | Greater than

90 Days

Past Due | | Nonaccrual | | Total

Past Due | | Loans Not

Past Due | | Total |

| June 30, 2022 | | | | | | | | | | | | | | |

| Commercial real estate | | $ | — | | $ | 284 | | $ | — | | $ | — | | $ | 284 | | $ | 1,034,203 | | $ | 1,034,487 |

| Residential real estate | | — | | — | | — | | — | | — | | 422,239 | | 422,239 |

| Commercial (non-PPP) | | 326 | | 88 | | — | | 1,468 | | 1,882 | | 385,435 | | 387,317 |

| Commercial (PPP) | | 178 | | 7 | | — | | — | | 185 | | 7,991 | | 8,176 |

| Construction and land development | | — | | — | | — | | — | | — | | 114,938 | | 114,938 |

| Consumer and other | | — | | — | | — | | — | | — | | 20,076 | | 20,076 |

| Total | | $ | 504 | | $ | 379 | | $ | — | | $ | 1,468 | | $ | 2,351 | | $ | 1,984,882 | | $ | 1,987,233 |

At June 30, 2021, there were 6 impaired loans (consisting of nonaccrual loans, troubled debt restructured loans, loans past due 90 days or more and still accruing interest and other loans based on management’s judgment) with both unpaid principal balance and recorded investments totaling $5.4 million. NaN of these loans were impaired loans with a recorded investment of $2.8 million with an allowance of $0.7 million and 1 substandard accruing loan with a recorded investment of $2.3 million with no allowance. The average net investment on the impaired residential real estate and commercial loans during the three months ended June 30, 2021, were $0.9 million. Residential real estate loans had $2.4 thousand and $5.0 thousand interest income recognized for the three and six months ended June 30, 2021 and 2020, respectively, which was equal to the cash basis interest income. At December 31, 2020, there were 6 impaired loans with recorded investments totaling $13.1 million, of which there were 3 impaired loans with a recorded investment of $10.4 million on nonaccrual with an allowance of $8.3 million and 1 substandard accruing loan with a recorded investment of $2.4 million with no allowance. The average net investment on the impaired residential real estate and commercial loans during the year ended December 31, 2020, was $2.2 million. The residential real estate loans had $12.7 thousand of interest income recognized during the year ended December 31, 2020, which was equal to the cash basis interest income.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | 30 – 59

Days

Past Due | | 60 – 89

Days

Past Due | | Greater than

90 Days

Past Due | | Nonaccrual | | Total

Past Due | | Loans Not

Past Due | | Total |

| December 31, 2021 | | | | | | | | | | | | | | |

| Commercial real estate | | $ | 292 | | $ | — | | $ | — | | $ | — | | $ | 292 | | $ | 902,362 | | $ | 902,654 |

| Residential real estate | | — | | — | | — | | — | | — | | 377,511 | | 377,511 |

| Commercial (non-PPP) | | 449 | | — | | — | | 1,468 | | 1,917 | | 323,498 | | 325,415 |

| Commercial (PPP) | | 7 | | — | | — | | — | | 7 | | 58,608 | | 58,615 |

| Construction and land development | | — | | — | | — | | — | | — | | 91,520 | | 91,520 |

| Consumer and other | | — | | — | | — | | 654 | | 654 | | 20,795 | | 21,449 |

| Total | | $ | 748 | | $ | — | | $ | — | | $ | 2,122 | | $ | 2,870 | | $ | 1,774,294 | | $ | 1,777,164 |

Troubled Debt Restructurings:

The principal carrying balances of loans that met the criteria for consideration as troubled debt restructurings (“TDR”) were

$252 thousand$1.0 million and

$298$55 thousand as of June 30,

20212022, and December 31,

2020,2021, respectively. The Company has allocated

0no specific reserves to customers whose loan terms have been modified in troubled debt restructurings as of June 30,

20212022, and December 31,

2020.2021. The Company has not committed any additional amounts to customers whose loans are classified as a troubled debt restructuring.

Credit Quality Indicators:

The Company categorizes loans into risk categories based on relevant information about the ability of borrowers to service their debt including: current financial information, historical payment experience, credit documentation, public information, and current economic trends, among other factors. Generally, all credits greater than $1.0 million are reviewed at least annually to monitor and adjust, if necessary, the credit risk profile. Loans classified as substandard or special mention are reviewed quarterly by the Company for further evaluation to determine if they are appropriately classified and whether there is any impairment. Beyond the annual review, all loans are graded upon initial issuance. In addition, during the renewal process of any loan, as well as if a loan becomes past due, the Company will determine the appropriate loan grade.

Loans excluded from the review process above are generally classified as pass credits until: (a) they become past due; (b) management becomes aware of deterioration in the creditworthiness of the borrower; or (c) the customer contacts the Company for a modification. In these circumstances, the loan is specifically evaluated for potential classification as to special mention, substandard, doubtful, or even charged-off. The Company uses the following definitions for risk ratings:

Pass: A Pass loan’s primary source of loan repayment is satisfactory, with secondary sources very likely to be realized if necessary. The pass category includes the following:Riskless:

•Riskless:Loans that are fully secured by liquid, properly margined collateral (listed stock, bonds, or other securities; savings accounts; certificates of deposit; loans or that portion thereof which are guaranteed by the U.S. Government or agencies backed by the “full faith and credit” thereof; loans secured by properly executed letters of credit from prime financial institutions).

•High Quality Risk:Loans to recognized national companies and well-seasoned companies that enjoy ready access to major capital markets or to a range of financing alternatives. Borrower’s public debt offerings are accorded highest ratings by recognized rating agencies, e.g., Moody’s or Standard & Poor’s. Companies display sound financial conditions and consistent superior income performance. The borrower’s trends and those of the industry to which it belongs are positive.

•Satisfactory Risk:Loans to borrowers, reasonably well established, that display satisfactory financial conditions, operating results, and excellent future potential. Capacity to service debt is amply demonstrated. Current financial strength, while financially adequate, may be deficient in a number of respects. Normal comfort levels are achieved through a closely monitored collateral position and/or the strength of outside guarantors.

•Moderate Risk:Loans to borrowers who are in non-compliance with periodic reporting requirements of the loan agreement, and any other credit file documentation deficiencies, which do not otherwise affect the borrower’s credit

risk profile. This may include borrowers who fail to supply updated financial information that supports the adequacy of the primary source of repayment to service the Bank’s debt and prevents bank management to evaluate the borrower’s current debt service capacity. Existing loans will include those with consistent

track record of timely loan payments, no material adverse changes to underlying collateral, and no material adverse change to guarantor(s) financial capacity, evidenced by public record searches.

Special mention: A Special Mention loan has potential weaknesses that deserve management’s close attention. If left uncorrected, these potential weaknesses may result in the deterioration of the repayment prospects for the asset or the Company’s credit position at some future date. Special Mention loans are not adversely classified and do not expose an institution to sufficient risk to warrant adverse classification.

Substandard: A Substandard loan is inadequately protected by the current sound worth and paying capacity of the obligor or of the collateral pledged, if any. Loans so classified must have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt. They are characterized by the distinct possibility that the Company will sustain some loss if the deficiencies are not corrected.

Doubtful: A loan classified Doubtful has all the weaknesses inherent in one classified Substandard with the added characteristics that the weaknesses make collection or liquidation in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable.

Loss: A loan classified Loss is considered uncollectible and of such little value that continuance as a bankable asset is not warranted. This classification does not mean that the asset has absolutely no recovery or salvage value, but rather it is not practical or desirable to defer writing off this basically worthless asset even though partial recovery may be affected in the future. Based on the most recent analysis performed, the risk category of loans by class of loans is as follows:

| | | | | | | | | | | | | | | |

| | | | | Special | | | | | | | | | |

(Dollars in thousands) | | Pass | | Mention | | Substandard | | Doubtful | | Total |

June 30, 2021 | | | | | | | | | | | | | | | |

Commercial real estate | | $ | 873,127 | | $ | — | | $ | 2,326 | | $ | — | | $ | 875,453 |

Residential real estate | | | 361,946 | | | — | | | — | | | — | | | 361,946 |

Commercial | | | 371,400 | | | 465 | | | 1,468 | | | — | | | 373,333 |

Construction and land development | | | 74,175 | | | — | | | — | | | — | | | 74,175 |

Consumer | | | 13,174 | | | 94 | | | 1,307 | | | — | | | 14,575 |

Total | | $ | 1,693,822 | | $ | 559 | | $ | 5,101 | | $ | — | | $ | 1,699,482 |

| | | | | | | | | | | | | | | |

December 31, 2020 | | | | | | | | | | | | | | | |

Commercial real estate | | $ | 775,420 | | $ | — | | $ | 2,356 | | $ | — | | $ | 777,776 |

Residential real estate | | | 380,062 | | | 429 | | | — | | | — | | | 380,491 |

Commercial | | | 387,403 | | | 112 | | | 9,127 | | | — | | | 396,642 |

Construction and land development | | | 99,883 | | | — | | | — | | | — | | | 99,883 |

Consumer | | | 10,381 | | | — | | | 1,307 | | | — | | | 11,688 |

Total | | $ | 1,653,149 | | $ | 541 | | $ | 12,790 | | $ | — | | $ | 1,666,480 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | Pass | | Special

Mention | | Substandard | | Doubtful | | Total |

| June 30, 2022 | | | | | | | | | | |

| Commercial real estate | | $ | 1,031,944 | | $ | 285 | | $ | 2,258 | | $ | — | | $ | 1,034,487 |

| Residential real estate | | 421,199 | | 1,040 | | — | | — | | 422,239 |

| Commercial (non-PPP) | | 385,435 | | 414 | | 1,468 | | — | | 387,317 |

| Commercial (PPP) | | 8,176 | | — | | — | | — | | 8,176 |

| Construction and land development | | 114,938 | | — | | — | | — | | 114,938 |

| Consumer | | 20,004 | | 72 | | — | | — | | 20,076 |

| Total | | $ | 1,981,696 | | $ | 1,811 | | $ | 3,726 | | $ | — | | $ | 1,987,233 |

| | | | | | | | | | |

| December 31, 2021 | | | | | | | | | | |

| Commercial real estate | | $ | 900,364 | | $ | — | | $ | 2,290 | | $ | — | | $ | 902,654 |

| Residential real estate | | 377,511 | | — | | — | | — | | 377,511 |

| Commercial (non-PPP) | | 323,657 | | 290 | | 1,468 | | — | | 325,415 |

| Commercial (PPP) | | 58,615 | | — | | — | | — | | 58,615 |