The Company’s available-for-sale securities as of September 30, 2017 can be summarized as follows:

|

| At September 30, 2017 |

| |||||||||||||

|

| Cost |

|

| Gross Unrealized Gains |

|

| Gross Unrealized Losses |

|

| Fair Value |

| ||||

|

| (In millions) |

| |||||||||||||

Common stock |

| $ | 0.2 |

|

| $ | — |

|

| $ | (0.1 | ) |

| $ | 0.1 |

|

The Company’s available-for-sale securities as of December 31, 2016 can be summarized as follows:

|

| At December 31, 2016 |

| |||||||||||||

|

| Cost |

|

| Gross Unrealized Gains |

|

| Gross Unrealized Losses |

|

| Fair Value |

| ||||

|

| (In millions) |

| |||||||||||||

Common stock |

| $ | 0.4 |

|

| $ | — |

|

| $ | — |

|

| $ | 0.4 |

|

There is no maturity date for these investments and there have been no sales during the nine months ended September 30, 2017.

NOTE 10:13: STOCKHOLDERS’ EQUITY, (DEFICIT), ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS), AND REDEEMABLE NONCONTROLLING INTEREST

On May 13, 2022, Platinum closed on an underwritten secondary offering of 3,500,000 shares of its common stock. Concurrently, Ryerson Holding completed a share repurchase from Platinum of 1,613,022 shares of common stock for $47.7 million. Ryerson did 0t offer any shares of its common stock in the transaction and did 0t receive any of the proceeds from the sale of the shares offered by Platinum. The Company funded the share repurchase with cash on hand. Following the closing of these transactions, Platinum's ownership of our common stock decreased from approximately 54% to approximately 43% and Ryerson Holding is no longer a “controlled company” within the meaning of the corporate governance standards of The New York Stock Exchange.

The following table details changes in these accounts:Ryerson Holding Corporation Stockholders’ Equity accounts for the three and six month periods ended June 30, 2022:

|

| Ryerson Holding Corporation Stockholders' Equity (Deficit) |

| |||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated Other Comprehensive Income (Loss) |

|

|

|

|

|

|

| |||||||||||

|

| Common Stock |

|

| Treasury Stock |

|

| Capital in Excess of Par Value |

|

| Accumulated Deficit |

|

| Foreign Currency Translation |

|

| Benefit Plan Liabilities |

|

| Unrealized Gain (Loss) on Available- For-Sale Investments |

|

| Non-controlling Interest |

|

| Total Equity |

| |||||||||||||||||

|

| Shares |

|

| Dollars |

|

| Shares |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

| |||||||||||

|

| (In millions, except shares in thousands) |

| |||||||||||||||||||||||||||||||||||||||||

Balance at January 1, 2017 |

|

| 37,345 |

|

| $ | 0.4 |

|

|

| 213 |

|

| $ | (6.6 | ) |

| $ | 375.4 |

|

| $ | (112.2 | ) |

| $ | (50.2 | ) |

| $ | (258.7 | ) |

| $ | 1.1 |

|

| $ | 1.5 |

|

| $ | (49.3 | ) |

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 17.1 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.6 |

|

|

| 17.7 |

|

Foreign currency translation |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 5.5 |

|

|

| — |

|

|

| — |

|

|

| 0.3 |

|

|

| 5.8 |

|

Gain on intra-entity foreign currency transactions |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 3.6 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 3.6 |

|

Changes in defined benefit pension and other post-retirement benefit plans, net of tax of $3.9 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 6.4 |

|

|

| — |

|

|

| — |

|

|

| 6.4 |

|

Unrealized loss on available-for-sale investment, net of tax of $0.1 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (0.2 | ) |

|

| — |

|

|

| (0.2 | ) |

Other than temporary impairment, net of tax of $0.1 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.1 |

|

|

| — |

|

|

| 0.1 |

|

Stock-based compensation expense |

|

| 76 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

Balance at September 30, 2017 |

|

| 37,421 |

|

| $ | 0.4 |

|

|

| 213 |

|

| $ | (6.6 | ) |

| $ | 376.9 |

|

| $ | (95.1 | ) |

| $ | (41.1 | ) |

| $ | (252.3 | ) |

| $ | 1.0 |

|

| $ | 2.4 |

|

| $ | (14.4 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated Other |

|

|

|

|

|

|

| |||||||||||||||||

|

| Common |

|

| Treasury |

|

| Capital in |

|

| Retained Earnings |

|

| Foreign |

|

| Benefit Plan |

|

| Interest Rate Swap |

|

| Non-controlling |

|

| Total |

| |||||||||||||||||

|

| Shares |

|

| Dollars |

|

| Shares |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

| |||||||||||

|

| (In millions, except shares in thousands) |

| |||||||||||||||||||||||||||||||||||||||||

Balance at January 1, 2022 |

|

| 38,687 |

|

| $ | 0.4 |

|

|

| (293 | ) |

| $ | (8.4 | ) |

| $ | 388.6 |

|

| $ | 321.7 |

|

| $ | (49.1 | ) |

| $ | (114.5 | ) |

| $ | (1.5 | ) |

| $ | 7.4 |

|

| $ | 544.6 |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 163.6 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.2 |

|

|

| 163.8 |

|

Foreign currency translation |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

Changes in defined benefit pension and other post-retirement benefit plans, net of tax of $0.1 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.7 |

|

|

| — |

|

|

| — |

|

|

| 0.7 |

|

Share repurchases |

|

| — |

|

|

| — |

|

|

| (20 | ) |

|

| (0.5 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (0.5 | ) |

Stock-based compensation expense, net |

|

| 371 |

|

|

| — |

|

|

| (77 | ) |

|

| (2.7 | ) |

|

| 1.3 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (1.4 | ) |

Cash dividends and dividend equivalents |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (3.9 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (3.9 | ) |

Interest rate swap, net of tax of 0 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.7 |

|

|

| — |

|

|

| 0.7 |

|

Balance at March 31, 2022 |

|

| 39,058 |

|

| $ | 0.4 |

|

|

| (390 | ) |

| $ | (11.6 | ) |

| $ | 389.9 |

|

| $ | 481.4 |

|

| $ | (47.6 | ) |

| $ | (113.8 | ) |

| $ | (0.8 | ) |

| $ | 7.6 |

|

| $ | 705.5 |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 196.4 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 196.4 |

|

Foreign currency translation |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (2.2 | ) |

|

| — |

|

|

| — |

|

|

| (0.1 | ) |

|

| (2.3 | ) |

Changes in defined benefit pension and other post-retirement benefit plans, net of tax of $0.4 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| — |

|

|

| 0.2 |

|

Share repurchases |

|

| — |

|

|

| — |

|

|

| (1,613 | ) |

|

| (47.7 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (47.7 | ) |

Stock-based compensation expense, net |

|

| 1 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.6 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.6 |

|

Cash dividends and dividend equivalents |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (4.7 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (4.7 | ) |

Interest rate swap, net of tax of $0.2 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.5 |

|

|

| — |

|

|

| 0.5 |

|

Balance at June 30, 2022 |

|

| 39,059 |

|

| $ | 0.4 |

|

|

| (2,003 | ) |

| $ | (59.3 | ) |

| $ | 392.5 |

|

| $ | 673.1 |

|

| $ | (49.8 | ) |

| $ | (113.6 | ) |

| $ | (0.3 | ) |

| $ | 7.5 |

|

| $ | 850.5 |

|

16

The following table details changes in Ryerson Holding Corporation Stockholders’ Equity accounts for the three and six month periods ended June 30, 2021:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated Other |

|

|

|

|

|

|

| |||||||||||||||||

|

| Common |

|

| Treasury |

|

| Capital in |

|

| Retained Earnings |

|

| Foreign |

|

| Benefit Plan |

|

| Interest Rate Swap |

|

| Non-controlling |

|

| Total |

| |||||||||||||||||

|

| Shares |

|

| Dollars |

|

| Shares |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

|

| Dollars |

| |||||||||||

|

| (In millions, except shares in thousands) |

| |||||||||||||||||||||||||||||||||||||||||

Balance at January 1, 2021 |

|

| 38,330 |

|

| $ | 0.4 |

|

|

| (213 | ) |

| $ | (6.6 | ) |

| $ | 383.1 |

|

| $ | 33.8 |

|

| $ | (47.0 | ) |

| $ | (221.8 | ) |

| $ | (3.1 | ) |

| $ | 6.3 |

|

| $ | 145.1 |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 25.3 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.3 |

|

|

| 25.6 |

|

Foreign currency translation |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.1 |

|

|

| — |

|

|

| — |

|

|

| (0.1 | ) |

|

| — |

|

Changes in defined benefit pension and other post-retirement benefit plans, net of tax of $0.5 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

Stock-based compensation expense |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.6 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.6 |

|

Interest rate swap, net of tax of $0.1 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.4 |

|

|

| — |

|

|

| 0.4 |

|

Balance at March 31, 2021 |

|

| 38,330 |

|

| $ | 0.4 |

|

|

| (213 | ) |

| $ | (6.6 | ) |

| $ | 384.7 |

|

| $ | 59.1 |

|

| $ | (46.9 | ) |

| $ | (219.8 | ) |

| $ | (2.7 | ) |

| $ | 6.5 |

|

| $ | 174.7 |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 112.9 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.4 |

|

|

| 113.3 |

|

Foreign currency translation |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

|

| — |

|

|

| — |

|

|

| 0.1 |

|

|

| 1.6 |

|

Changes in defined benefit pension and other post-retirement benefit plans, net of tax of $0.6 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

Stock-based compensation expense |

|

| 357 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.5 |

|

Interest rate swap, net of tax of $0.2 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.4 |

|

|

| — |

|

|

| 0.4 |

|

Balance at June 30, 2021 |

|

| 38,687 |

|

| $ | 0.4 |

|

|

| (213 | ) |

| $ | (6.6 | ) |

| $ | 386.2 |

|

| $ | 172.0 |

|

| $ | (45.4 | ) |

| $ | (217.8 | ) |

| $ | (2.3 | ) |

| $ | 7.0 |

|

| $ | 293.5 |

|

The following table details changes in accumulated other comprehensive income (loss), net of tax, for the ninesix months ended SeptemberJune 30, 2017:2022:

|

| Changes in Accumulated Other Comprehensive Income (Loss) by Component |

| |||||||||||||

|

| Foreign Currency Translation |

|

| Benefit Plan Liabilities |

|

| Available- For-Sale Investments |

|

| Cash Flow Hedge - Interest Rate Swap |

| ||||

|

| (In millions) |

| |||||||||||||

Balance at January 1, 2017 |

| $ | (50.2 | ) |

| $ | (258.7 | ) |

| $ | 1.1 |

|

| $ | — |

|

Other comprehensive income (loss) before reclassifications |

|

| 9.1 |

|

|

| 7.8 |

|

|

| (0.2 | ) |

|

| (0.3 | ) |

Amounts reclassified from accumulated other comprehensive income (loss) |

|

| — |

|

|

| (1.4 | ) |

|

| 0.1 |

|

|

| 0.3 |

|

Net current-period other comprehensive income (loss) |

|

| 9.1 |

|

|

| 6.4 |

|

|

| (0.1 | ) |

|

| — |

|

Balance at September 30, 2017 |

| $ | (41.1 | ) |

| $ | (252.3 | ) |

| $ | 1.0 |

|

| $ | — |

|

|

| Changes in Accumulated Other Comprehensive |

| |||||||||

|

| Foreign |

|

| Benefit |

|

| Interest Rate Swap |

| |||

|

| (In millions) |

| |||||||||

Balance at January 1, 2022 |

| $ | (49.1 | ) |

| $ | (114.5 | ) |

| $ | (1.5 | ) |

Other comprehensive loss before reclassifications |

|

| (0.7 | ) |

|

| — |

|

|

| — |

|

Amounts reclassified from accumulated other comprehensive income into net income |

|

| — |

|

|

| 0.9 |

|

|

| 1.2 |

|

Net current-period other comprehensive income (loss) |

|

| (0.7 | ) |

|

| 0.9 |

|

|

| 1.2 |

|

Balance at June 30, 2022 |

| $ | (49.8 | ) |

| $ | (113.6 | ) |

| $ | (0.3 | ) |

17

The following table details the reclassifications out of accumulated other comprehensive income (loss) for the three and ninesix month periods ended SeptemberJune 30, 2017:2022:

|

| Reclassifications Out of Accumulated Other Comprehensive Income (Loss) |

| Reclassifications Out of Accumulated Other Comprehensive Income (Loss) | ||||||||||||||||

|

| Amount reclassified from Accumulated |

|

|

|

| Amount reclassified from Accumulated |

| ||||||||||||

|

| Other Comprehensive Income (Loss) |

|

|

|

| Other Comprehensive Income (Loss) |

|

| |||||||||||

|

| Three Months Ended |

|

| Nine Months Ended |

|

| Affected line item in the Condensed |

| Three Months Ended |

|

| Six Months Ended |

|

| Affected line item in the Condensed | ||||

Details about Accumulated Other |

| September 30, 2017 |

|

| Consolidated Statements of |

| June 30, 2022 |

|

| Consolidated Statements of | ||||||||||

Comprehensive Income (Loss) Components |

| (In millions) |

|

| Comprehensive Income |

| (In millions) |

| Comprehensive Income | |||||||||||

Other-than-temporary impairment |

|

|

|

|

|

|

|

|

|

| ||||||||||

Other-than-temporary impairment charge |

| $ | — |

|

| $ | 0.2 |

|

| Other income and (expense), net | ||||||||||

Amortization of defined benefit pension and other post-retirement benefit plan items |

|

|

|

|

|

|

| |||||||||||||

Actuarial loss |

| $ | 0.7 |

|

| $ | 1.2 |

|

| Other income and (expense), net | ||||||||||

Pension settlement |

|

| — |

|

|

| 0.1 |

|

| Other income and (expense), net | ||||||||||

Prior service credits |

|

| (0.1 | ) |

|

| (0.1 | ) |

| Other income and (expense), net | ||||||||||

Total before tax |

|

| 0.6 |

|

|

| 1.2 |

|

| |||||||||||

Tax benefit |

|

| — |

|

|

| (0.1 | ) |

|

|

|

| (0.4 | ) |

|

| (0.3 | ) |

| |

Net of tax |

| $ | — |

|

| $ | 0.1 |

|

|

|

| $ | 0.2 |

|

| $ | 0.9 |

|

| |

Cash flow hedge - interest rate swap |

|

|

|

|

|

|

|

|

|

| ||||||||||

Realized swap interest loss |

| $ | 0.1 |

|

| $ | 0.5 |

|

| Interest and other expense on debt | ||||||||||

Interest rate swap |

|

|

|

|

|

|

| |||||||||||||

Realized swap interest |

| $ | 0.7 |

|

| $ | 1.4 |

|

| Interest and other expense on debt | ||||||||||

Tax benefit |

|

| (0.1 | ) |

|

| (0.2 | ) |

|

|

|

| (0.2 | ) |

|

| (0.2 | ) |

|

|

Net of tax |

| $ | — |

|

| $ | 0.3 |

|

|

|

| $ | 0.5 |

|

| $ | 1.2 |

|

|

|

Amortization of defined benefit pension and other post- retirement benefit plan items |

|

|

|

|

|

|

|

|

|

| ||||||||||

Actuarial (gain) loss |

| $ | 1.9 |

|

| $ | (0.2 | ) |

| Warehousing, delivery, selling, general and administrative | ||||||||||

Prior service credits |

|

| (0.8 | ) |

|

| (2.3 | ) |

| Warehousing, delivery, selling, general and administrative | ||||||||||

Total before tax |

|

| 1.1 |

|

|

| (2.5 | ) |

|

| ||||||||||

Tax provision (benefit) |

|

| (0.3 | ) |

|

| 1.1 |

|

|

| ||||||||||

Net of tax |

| $ | 0.8 |

|

| $ | (1.4 | ) |

|

| ||||||||||

|

| Reclassifications Out of Accumulated Other Comprehensive Income (Loss) | ||||||||

|

| Amount reclassified from Accumulated |

|

|

| |||||

|

| Other Comprehensive Income (Loss) |

|

|

| |||||

|

| Three Months Ended |

|

| Six Months Ended |

|

| Affected line item in the Condensed | ||

Details about Accumulated Other |

| June 30, 2021 |

|

| Consolidated Statements of | |||||

Comprehensive Income (Loss) Components |

| (In millions) |

|

| Comprehensive Income | |||||

Amortization of defined benefit pension and other post-retirement benefit plan items |

|

|

|

|

|

|

|

| ||

Actuarial loss |

| $ | 2.5 |

|

| $ | 4.9 |

|

| Other income and (expense), net |

Pension settlement |

|

| 0.2 |

|

|

| 0.4 |

|

| Other income and (expense), net |

Prior service credits |

|

| (0.1 | ) |

|

| (0.2 | ) |

| Other income and (expense), net |

Total before tax |

|

| 2.6 |

|

|

| 5.1 |

|

|

|

Tax benefit |

|

| (0.6 | ) |

|

| (1.1 | ) |

|

|

Net of tax |

| $ | 2.0 |

|

| $ | 4.0 |

|

|

|

Interest rate swap |

|

|

|

|

|

|

|

| ||

Realized swap interest |

| $ | 0.6 |

|

| $ | 1.1 |

|

| Interest and other expense on debt |

Tax benefit |

|

| (0.2 | ) |

|

| (0.3 | ) |

|

|

Net of tax |

| $ | 0.4 |

|

| $ | 0.8 |

|

|

|

18

NOTE 14: REVENUE RECOGNITION

We are a leading value-added processor and distributor of industrial metals with operations in the United States, Canada, Mexico, and China. We purchase large quantities of metal products from primary producers and sell these materials in smaller quantities to a wide variety of metals-consuming industries. Nearly 80% of the metals products sold are processed by us to a specified thickness, length, width, shape, and surface quality pursuant to specific customer orders.

Disaggregated Revenue

We have 1 operating and reportable segment, metals service centers.

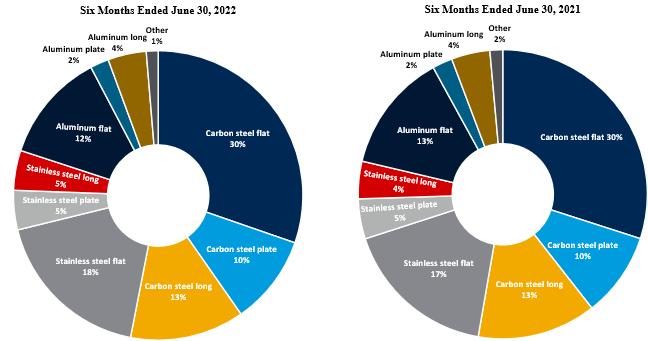

The Company derives substantially all of its sales from the distribution of metals. The following table detailsshows the reclassifications outCompany’s percentage of accumulatedsales by major product line:

|

| Three Months Ended |

|

| Six Months Ended |

| ||||||||||

|

| June 30, |

|

| June 30, |

| ||||||||||

Product Line |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Carbon Steel Flat |

|

| 29 | % |

|

| 31 | % |

|

| 30 | % |

|

| 30 | % |

Carbon Steel Plate |

|

| 10 |

|

|

| 10 |

|

|

| 10 |

|

|

| 10 |

|

Carbon Steel Long |

|

| 13 |

|

|

| 13 |

|

|

| 13 |

|

|

| 13 |

|

Stainless Steel Flat |

|

| 18 |

|

|

| 17 |

|

|

| 18 |

|

|

| 17 |

|

Stainless Steel Plate |

|

| 4 |

|

|

| 5 |

|

|

| 5 |

|

|

| 5 |

|

Stainless Steel Long |

|

| 5 |

|

|

| 4 |

|

|

| 5 |

|

|

| 4 |

|

Aluminum Flat |

|

| 13 |

|

|

| 13 |

|

|

| 12 |

|

|

| 13 |

|

Aluminum Plate |

|

| 2 |

|

|

| 2 |

|

|

| 2 |

|

|

| 2 |

|

Aluminum Long |

|

| 4 |

|

|

| 4 |

|

|

| 4 |

|

|

| 4 |

|

Other |

|

| 2 |

|

|

| 1 |

|

|

| 1 |

|

|

| 2 |

|

Total |

|

| 100 | % |

|

| 100 | % |

|

| 100 | % |

|

| 100 | % |

A significant majority of the Company’s sales are attributable to its U.S. operations. The only operations attributed to foreign countries relate to the Company’s subsidiaries in Canada, China, and Mexico. The following table summarizes consolidated financial information of our operations by geographic location based on where sales originated:

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Net Sales | (In millions) |

| |||||||||||||

United States |

| 1,589.9 |

|

| $ | 1,276.8 |

|

| $ | 3,193.2 |

|

| $ | 2,302.5 |

|

Foreign countries |

| 153.6 |

|

|

| 142.2 |

|

| $ | 299.1 |

|

|

| 263.8 |

|

Total | $ | 1,743.5 |

|

| $ | 1,419.0 |

|

| $ | 3,492.3 |

|

| $ | 2,566.3 |

|

Revenue is recognized either at a point in time or over time based on if the contract has an enforceable right to payment and the type of product that is being sold to the customer, with products that are determined to have no alternative use being recognized over time. The following table summarizes revenues by the type of item sold:

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

Timing of Revenue Recognition |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Revenue on products with an alternative use |

|

| 90 | % |

|

| 90 | % |

|

| 90 | % |

|

| 90 | % |

Revenue on products with no alternative use |

|

| 10 |

|

|

| 10 |

|

|

| 10 |

|

|

| 10 |

|

Total |

|

| 100 | % |

|

| 100 | % |

|

| 100 | % |

|

| 100 | % |

Contract Balances

A receivable is recognized in the period in which an invoice is issued, which is generally when the product is delivered to the customer. Payment terms on invoiced amounts are typically 30 days from the invoice date. We do not have any contracts with significant financing components.

Receivables, which are included in accounts receivables within the Condensed Consolidated Balance Sheet, from contracts with customers were $759.5 million and $633.0 million as of June 30, 2022 and December 31, 2021, respectively.

19

Contract assets, which consist primarily of revenues recognized over time that have not yet been invoiced and estimates of the value of inventory that will be received in conjunction with product returns, are reported in prepaid expenses and other comprehensive income (loss)current assets within the Condensed Consolidated Balance Sheets. Contract liabilities, which consist primarily of accruals associated with amounts that will be paid to customers for volume rebates, cash discounts, sales returns and allowances, estimates of shipping and handling costs associated with performance obligations recorded over time, and bill and hold transactions are reported in other accrued liabilities within the threeCondensed Consolidated Balance Sheets. Significant changes in the contract assets and nine month periods ended Septemberthe contract liabilities balances during the period are as follows:

|

| Contract Assets |

|

| Contract Liabilities |

| ||

|

| (In millions) |

| |||||

Beginning Balance at January 1, 2022 |

| $ | 21.3 |

|

| $ | 15.1 |

|

Contract liability satisfied during the period |

|

| — |

|

|

| (11.9 | ) |

Contract liability incurred during the period |

|

| — |

|

|

| 15.3 |

|

Net change in contract assets and liabilities for products with no alternative use during the period |

|

| (4.5 | ) |

|

| — |

|

Changes to reserves |

|

| 0.5 |

|

|

| 1.0 |

|

Ending Balance at June 30, 2022 |

| $ | 17.3 |

|

| $ | 19.5 |

|

The Company’s performance obligations are typically short-term in nature. As a result, the Company has elected the practical expedient that provides an exemption of the disclosure requirements regarding information about remaining performance obligations on contracts that have original expected durations of one year or less.

NOTE 15: PROVISION FOR CREDIT LOSSES

Provisions for allowances and claims on accounts receivables and contract assets are based upon historical rates, expected trends, and estimates of potential returns, allowances, customer discounts, and incentives. The Company considers all available information when assessing the adequacy of the provision for allowances, claims, and doubtful accounts.

The Company performs ongoing credit evaluations of customers and sets credit limits based upon review of the customers’ current credit information, payment history, and the current economic and industry environments. The Company’s credit loss reserve consists of two parts: a) a provision for estimated credit losses based on historical experience and b) a reserve for specific customer collection issues that the Company has identified. Estimation of credit losses requires adjusting historical loss experience for current economic conditions and judgments about the probable effects of economic conditions on certain customers.

The following table provides a reconciliation of the provision for credit losses reported within the Condensed Consolidated Balance Sheets as of June 30, 2016:2022:

|

| Reclassifications Out of Accumulated Other Comprehensive Income (Loss) | ||||||||

|

| Amount reclassified from Accumulated |

|

|

| |||||

|

| Other Comprehensive Income (Loss) |

|

|

| |||||

|

| Three Months Ended |

|

| Nine Months Ended |

|

| Affected line item in the Condensed | ||

Details about Accumulated Other |

| September 30, 2016 |

|

| Consolidated Statements of | |||||

Comprehensive Income (Loss) Components |

| (In millions) |

|

| Comprehensive Income | |||||

Other-than-temporary impairment |

|

|

|

|

|

|

|

|

|

|

Other-than-temporary impairment charge |

| $ | — |

|

| $ | 2.8 |

|

| Other income and (expense), net |

Tax benefit |

|

| — |

|

|

| (1.1 | ) |

|

|

Net of tax |

| $ | — |

|

| $ | 1.7 |

|

|

|

Amortization of defined benefit pension and other post- retirement benefit plan items |

|

|

|

|

|

|

|

|

|

|

Actuarial loss |

| $ | 1.1 |

|

| $ | 3.4 |

|

| Warehousing, delivery, selling, general and administrative |

Prior service credits |

|

| (0.7 | ) |

|

| (2.2 | ) |

| Warehousing, delivery, selling, general and administrative |

Total before tax |

|

| 0.4 |

|

|

| 1.2 |

|

|

|

Tax benefit |

|

| (0.1 | ) |

|

| (0.4 | ) |

|

|

Net of tax |

| $ | 0.3 |

|

| $ | 0.8 |

|

|

|

| Changes in Provision for Expected Credit Losses |

| |

| (In millions) |

| |

Balance at January 1, 2022 | $ | 2.2 |

|

Current period provision |

| 0.7 |

|

Write-offs charged against allowance |

| (0.3 | ) |

Recoveries |

| 0.3 |

|

Translation |

| 0.1 |

|

Balance at June 30, 2022 | $ | 3.0 |

|

For the three months ended SeptemberJune 30, 2017,2022, the Company recorded an income tax benefitexpense of $0.7$66.8 million compared to income tax expense of $1.6$38.5 million in the prior year. The $0.7 millionincome tax benefitexpense for the three months ended SeptemberJune 30, 20172022 and 2021 primarily represents the reversal of previous uncertain tax provisions due to the lapse of the statute of limitations andrepresent taxes at federal and local statutory rates where the Company operates, but generally excludesexclude any tax benefit for losses in jurisdictions with historical losses.

For the ninesix months ended SeptemberJune 30, 2017,2022, the Company recorded income tax expense of $5.3$121.8 million compared to $14.0$46.1 million in the prior year. The $5.3 millionincome tax expense for the ninesix months ended SeptemberJune 30, 20172022 and 2021 primarily representsrepresent taxes at federal and local statutory rates where the Company operates, but generally excludesexclude any tax benefit for losses in jurisdictions with historical losses.losses. The increase in the income tax provision in the first six months of 2022 compared to the first six months of 2021 is primarily a result of the increase in actual and forecasted earnings between the two periods as conditions have improved year-over-year.

In accordance with

20

As required by ASC 740, “Income Taxes,” the Company assesses the realizability of its deferred tax assets. The Company records a valuation allowance when, based upon the evaluation of all available evidence, it is more-likely-than-not that all or a portion of the deferred tax assets will not be realized. In making this determination, we analyze, among other things, our recent history of earnings, the nature and timing of reversing book-tax temporary differences, tax planning strategies, and future income. The Company maintains a valuation allowance on certain foreign and U.S. federal and state deferred tax assets until such time as in management’s judgment, considering all available positive and negative evidence, the Company determines that these deferred tax assets are more likely than not realizable. The valuation allowance is reviewed quarterly and will be maintained until sufficient positive evidence exists to support the reversal of some or all of the valuation allowance. The valuation allowance was $19.5 million and $20.0$5.0 million at Septemberboth June 30, 20172022 and December 31, 2016, respectively.2021.

The Company accounts for uncertain income tax positions in accordance with ASC 740. We anticipate that certain statutes of limitation will close within the next twelve months resulting in the immaterial reduction of the reserve for uncertain tax benefits related to various intercompany transactions. No changes were recorded in the first six months of 2022, therefore, the balance of $0.8 million at December 31, 2021 remains unchanged.

NOTE 12:17: EARNINGS PER SHARE

Basic earnings per share attributable to Ryerson Holding’s common stock is determined based on earnings for the period divided by the weighted average number of common shares outstanding during the period. Diluted earnings per share attributable to Ryerson Holding’s common stock considers the effect of potential common shares, unless inclusion of the potential common shares would have an antidilutive effect. Stock-based awards with a grant price greater than the average market price of our common stock are excluded from the calculation of diluted earnings per share because the impact would have been antidilutive. The weighted average number of shares excluded as they would have had an antidilutive effect were 145,833199,045 and 96,80899,522 for the three and nine-monthsix-month periods ended SeptemberJune 30, 2017,2022, respectively, and 81,877 and 40,939 for the three and six-month periods ended June 30, 2021, respectively.

The following table sets forth the calculation of basic and diluted earnings per share:

|

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||||||||||||

Basic and diluted earnings per share |

|

| 2017 |

|

|

| 2016 |

|

|

| 2017 |

|

|

| 2016 |

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

|

| (In millions, except share and per share data) |

|

| (In millions, except number of shares which are reflected in thousands and per share data) |

| ||||||||||||||||||||||||||

Numerator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Net income attributable to Ryerson Holding Corporation |

| $ | 1.7 |

|

| $ | 8.2 |

|

| $ | 17.1 |

|

| $ | 27.3 |

|

| $ | 196.4 |

|

| $ | 112.9 |

|

| $ | 360.0 |

|

| $ | 138.2 |

|

Denominator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Weighted average shares outstanding |

|

| 37,190,927 |

|

|

| 35,804,069 |

|

|

| 37,165,552 |

|

|

| 33,343,503 |

|

|

| 37,799 |

|

|

| 38,459 |

|

|

| 38,093 |

|

|

| 38,289 |

|

Dilutive effect of stock-based awards |

|

| 103,781 |

|

|

| 161,615 |

|

|

| 125,041 |

|

|

| 92,009 |

|

|

| 725 |

|

|

| 271 |

|

|

| 779 |

|

|

| 397 |

|

Weighted average shares outstanding adjusted for dilutive securities |

|

| 37,294,708 |

|

|

| 35,965,684 |

|

|

| 37,290,593 |

|

|

| 33,435,512 |

|

|

| 38,524 |

|

|

| 38,730 |

|

|

| 38,872 |

|

|

| 38,686 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Earnings per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Basic and diluted |

| $ | 0.05 |

|

| $ | 0.23 |

|

| $ | 0.46 |

|

| $ | 0.82 |

| ||||||||||||||||

Basic |

| $ | 5.20 |

|

| $ | 2.94 |

|

| $ | 9.45 |

|

| $ | 3.61 |

| ||||||||||||||||

Diluted |

| $ | 5.10 |

|

| $ | 2.91 |

|

| $ | 9.26 |

|

| $ | 3.57 |

| ||||||||||||||||

NOTE 18: SUBSEQUENT EVENTS

Bond Repurchase. On July 23, 2022, the Company redeemed $50.0 million in aggregate principal amount of the 2028 Notes for $51.5 million, which was at a redemption price of 103.0% of the principal amount, resulting in the recognition of a $1.5 million loss within other income and (expense), net in the third quarter Condensed Consolidated Statement of Comprehensive Income. The Company funded the transaction with cash on hand. As a result of this redemption, 0 2028 Notes remain outstanding. The Company will write-off the remaining balance of the 2028 Notes issuance costs and will record a charge of $0.7 million within other interest and other expense on debt in the third quarter Condensed Consolidated Statement of Comprehensive Income.

Share Repurchase Authorization. On August 3, 2022, the Board of Directors approved a $75.0 million share repurchase authorization after the exhaustion of the previous share repurchase authorization during the second quarter of 2022. Under the authorization, which is effective through August 3, 2024, management has discretion in determining the conditions under which shares may be purchased from time to time.

Dividends. On August 3, 2022 , the Board of Directors declared a quarterly cash dividend in the amount of $0.15 per share of common stock, payable on September 15, 2022 to stockholders of record as of September 1, 2022. Future quarterly dividends, if any, will be subject to Board approval.

21

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

This Quarterly Report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements can be identified by the use of forward-looking terminology such as “objectives,” “goals,” “preliminary,” “range,” “believes,” “expects,” “may,” “estimates,” “will,” “should,” “plans”“plans,” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and may involve significant risks and uncertainties, and that actual results may vary materially from those anticipated or implied in the forward-looking statements as a result of various factors. These forward-looking statements involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. Forward-looking statements should, therefore, be considered in light of various factors, including those set forth under “Special Note Regarding Forward-Looking Statements” and “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 20162021 filed on March 13, 2017February 23, 2022 and the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Industry and Operating Trends” and elsewhere in this Quarterly Report on Form 10-Q. Moreover, we caution you not to place undue reliance on these forward-looking statements, which speak only as of the date they were made. We do not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this Quarterly Report or to reflect the occurrence of unanticipated events.

The contents herein are provided for general information purposes only and do not constitute an offer to sell or buy, or a solicitation of an offer to buy, any security (“Security”) of Ryerson Holding or its affiliates in any jurisdiction. Ryerson does not intend to solicit and is not soliciting, any action with respect to any Security or any other contractual relationship with Ryerson. Nothing in this Form 10-Q, individually or taken in the aggregate, constitutes an offer of securities for sale or buy, or a solicitation of an offer to buy, any Security in the United States, or to US persons, or in any other jurisdiction in which such an offer or solicitation is unlawful.

The following discussion should be read in conjunction with our Condensed Consolidated Financial Statements and related Notes thereto in Item 1, “Financial Statements” in this Quarterly Report on Form 10-Q and our Consolidated Financial Statements and related Notes thereto for the year ended December 31, 20162021 in our Annual Report on Form 10-Kfiled on March 13, 2017.February 23, 2022.

Industry and Operating Trends

We are a leading metals service center that distributesproviding value-added processing and provides value-added processingdistribution of industrial metals with operations in the United States, Canada, Mexico, and China. We purchase large quantities of metal products from primary producers and sell these materials in smaller quantities to a wide variety of metals-consuming industries. More than 75%We carry a full line of nearly 75,000 products in stainless steel, aluminum, carbon steel, and alloy steels and a limited line of nickel and red metals in various shapes and forms. In addition to our metals products, we offer numerous value-added processing and fabrication services, and nearly 80% of the metals products soldwe sell are processed by us by bending, beveling, blanking, blasting, burning, cutting-to-length, drilling, embossing, flattening, forming, grinding, laser cutting, machining, notching, painting, perforating, polishing, punching, rolling, sawing, scribing, shearing, slitting, blanking, cutting to lengthstamping, tapping, threading, welding, or other techniques. techniques to process materials to a specified thickness, length, width, shape, and surface quality pursuant to specific customer orders.

Similar to other metals service centers, we maintain substantial inventories of metals to accommodate the short lead times and just-in-time delivery requirements of our customers. Accordingly, we purchase metals in an effort to maintain our inventory at levels that we believe to be appropriate to satisfy the anticipated needs of our customers based upon customer forecasts, historic buying practices, supply agreements with customers, mill lead times, and market conditions. Our commitments to purchase metals are generally at prevailing market prices in effect at the time we place our orders. At the request of our customers, we have entered into swaps in order to mitigate our customers’ risk of volatility in the price of metals and we have entered into metals hedges to mitigate our own risk of volatility in the price of metals. We have no long-term, fixed-price metals purchase contracts. When metals prices decline, customer demands for lower prices and our competitors’ responses to those demands could result in lower sale prices and, consequently, lower gross profits and earnings as we usesell existing metals inventory. When metals prices increase, competitive conditions will influence how much of the price increase we may pass on to our customers.

The metals service center industry is cyclical and volatile in terms of both pricing and demand, and pricing, as such, industrial metals prices are volatile and remain difficult to predict. In the thirdfirst half of 2022, Ryerson experienced stronger pricing compared to the first half of 2021, with average selling prices 42.6% higher, reflective of the strong commodity pricing environment caused by global demand outpacing supply availability, trade disruption due to the Russian war on Ukraine, and customers building inventory in preparation for continued supply chain issues. Changes in average selling prices are primarily driven by commodity metals prices, which impact Ryerson’s selling prices.

Key industry indicators showed slowing growth in the second quarter of 2017, we continue to see improved demand when viewed against2022. This is evidenced by the Institute for Supply Management’s Purchasing Managers’ Index (“PMI”), which reported sequential declines in April, May, and June. Additionally, U.S. Industrial Production decreased year-over year ago period. for the month of June, signifying slowing conditions.

According to the Metal Service Center Institute, U.S.North American service center volumes per day have increaseddeclined by more than three percent4.4% in the first half of 2022 compared to the second quarterfirst half of 2017. In2021. On a North American basis, Ryerson performed better than the third quarterindustry with volumes

22

declining 2.7% over the same period. However, on a quarterly sequential basis, industry volume growth of 2017, we experienced0.3% was greater than Ryerson’s volume decrease of 0.7%. On a quarterly year-over-yearsequential basis, Ryerson end-market demand decreased in the HVAC and food processing and agricultural equipment sectors, but was partially offset by demand growth in shipment volumes to nearly all of our end markets, most notably inthe oil & gas, metal fabrication and machine shops, as well as commercial ground transportation oil & gas, and construction equipment sectors. However, we saw quarterly year-over-year shipment declines in consumer durables.

Overall, a weaker U.S. dollar and improved global pricing conditions narrowed spreads between foreign and domestic steel pricingFirst Six Months 2022 vs. First Six Months 2021 performance highlights

$3.5B |

|

|

| 25.1% |

|

|

| $360M |

| |

Total Revenues |

|

| Gross Margin |

| Net Income Attributable to Ryerson |

| ||||

| 36% increase |

|

| 740 bps increase |

|

| $222M increase | |||

$9.26 |

|

|

| $9.56 |

|

|

| $168M |

| |

Diluted EPS |

|

| Adj. Diluted EPS* |

| Cash from Operating Activities | |||||

| $5.69 increase |

|

| $8.06 increase |

|

| $219M increase | |||

*A reconciliation of the non-GAAP financial measure to the comparable GAAP measure is included in the third quartersubsequent table.

Ryerson generated revenues of 2017. Commodity prices on balance trended higher sequentially from$3.5 billion in the second quarter throughfirst six months of 2022, an increase of 36.1% compared to $2.6 billion for the third quarterfirst six months of 2017 despite continuing volatility in industrial base metal markets. However, elevated import levels and well supplied metals markets muted service center pricing power,2021, with our average selling prices down one percent42.6% higher and tons shipped 4.5% lower. In the first six months of 2022, gross margin expanded to 25.1% compared to 17.7% for the first six months of 2021. Included in the third quarterfirst six months of 20172022 cost of materials sold was LIFO income of $71.6 million, compared to LIFO expense of $188.6 million in the first six months of 2021. Net income attributable to Ryerson Holding Corporation was $360.0 million, or earnings of $9.26 per diluted share, in the first six months of 2022 compared to net income attributable to Ryerson Holding Corporation of $138.2 million, or income of $3.57 per diluted share, for the first six months of 2021.

To provide greater insight into the Company’s operating trends for the first six months of 2022 apart from the period’s one-time transactions, Ryerson provides adjusted net income and adjusted diluted earnings per share figures, which are not U.S. generally accepted accounting principles (“GAAP”) financial measures, to compliment the reported GAAP net income and diluted earnings per share figures. Management uses these metrics to assess year-over-year performance excluding non-recurring transactions. Adjusted net income and adjusted diluted earnings per share do not represent, and should not be used as a substitute for, net income or diluted earnings per share determined in accordance with GAAP. Illustrated in the below table, the first six months of 2022 net income attributable to Ryerson of $360.0 million includes a loss on retirement of debt of $19.8 million and a gain on sale of assets of $3.8 million. After adjusting for these non-core business transactions and the related income tax provision, the adjusted net income attributable to Ryerson for the first six months of 2022 is $371.9 million, an increase of $313.8 million compared to the prior quarter.year-ago adjusted net income attributable to Ryerson of $58.1 million which adjusted a gain on the sale of assets of $107.7 million and related income taxes.

(Dollars and shares in millions, except per share data) |

| First Half 2022 |

|

| First Half 2021 |

| ||

Net income attributable to Ryerson Holding Corporation |

| $ | 360.0 |

|

| $ | 138.2 |

|

Gain on sale of assets |

|

| (3.8 | ) |

|

| (107.7 | ) |

Loss on retirement of debt |

|

| 19.8 |

|

|

| — |

|

Provision (benefit) for income taxes on above items |

|

| (4.1 | ) |

|

| 27.6 |

|

Adjusted net income attributable to Ryerson Holding Corporation |

| $ | 371.9 |

|

| $ | 58.1 |

|

Diluted earnings per share |

| $ | 9.26 |

|

| $ | 3.57 |

|

Adjusted diluted earnings per share |

| $ | 9.56 |

|

| $ | 1.50 |

|

Shares outstanding – diluted |

|

| 38.9 |

|

|

| 38.7 |

|

Recent Developments

After the Russian forces invaded Ukraine on February 24, 2022, the Biden administration issued executive orders prohibiting the importation of goods from covered regions related to Ukraine and Russia. Ryerson takes this very seriously and has reviewed our direct and indirect material purchases to ensure compliance. On April 8, 2022, President Biden signed into law the Suspending Normal Trade Relations with Russia and Belarus Act, which denies "most-favored nation" tariff treatment to products of Russia and Belarus

23

and extends the President’s authority to impose sanctions under the Global Magnitsky Human Rights Accountability Act. Beginning April 9, 2022, the Act imposes a 10.5% import duty on unalloyed primary aluminum and 11.0% on value-add aluminum products. The muted pricing together with higher procuredimport duties are not expected to have a meaningful impact on the availability of aluminum for Ryerson. In 2022, the Company has not purchased material from Russia or the named Ukrainian regions and has no open purchases orders issued to Russian suppliers as of June 30, 2022.

On August 10, 2021, the Senate passed the Infrastructure Investment and Jobs Act, a $1.2 trillion bill which features $550 billion in new federal spending over 5 years. Included in this spending is investment in roads, bridges, and major projects, passenger and freight rail, electrical grid improvements, expansion of broadband access, transit systems, infrastructure for electric vehicles, and improvements to water systems. This bill was signed into law on November 15, 2021. The Company believes that the additional government spending on infrastructure projects under the Infrastructure Investment and Jobs Act may generate additional demand for our products especially within the industrial equipment, construction, green energy, and transportation industries. Accordingly, we anticipate that the Infrastructure Investment and Jobs Act will be beneficial to the Company, but ultimately the impact on the Company’s operations is unclear.

On April 22, 2021, the U.S. International Trade Commission (“USITC”) confirmed the Department of Commerce’s affirmative antidumping duty determinations and injury determinations regarding US imports of common alloy aluminum sheet. As a result, the USITC has issued final antidumping duty orders on U.S. imports of common alloy aluminum sheet from the following sixteen countries: Bahrain, Brazil, Croatia, Egypt, Germany, India, Indonesia, Italy, Oman, Romania, Serbia, Slovenia, South Africa, Spain, Taiwan, and Turkey. Antidumping rates differ greatly depending on country of origin and producing mill and range from the low single digits to as high as 243%. Ryerson anticipates that the actions of the USITC will support the prices of domestically produced aluminum sheet and therefore benefit the Company’s average selling prices.

On March 1, 2018, the White House announced a 25% tariff on all imported steel products and 10% tariff on all imported aluminum products for an indefinite amount of time under Section 232 of the Trade Expansion Act (“Section 232”). These tariffs, while in effect, have discouraged metal costs resultedimports from non-exempt countries and have had a favorable impact on the prices of the products we sell and our results of operations. In October 2021, the US and European Union agreed to revise Section 232 tariffs applied to the import of European steel and aluminum, allowing for the duty-free import of European steel and aluminum into the US, subject to tariff rate quotas. Specifically, the tariff rate quota includes the duty-free import of 3.3 million metric tons of steel melted and poured in margin compression through the third quarterEuropean Union, 18 thousand metric tons of 2017.unwrought aluminum, and 366 thousand metric tons of semi-finished aluminum. The revision is to be applied on January 1, 2022. Tariff rate quotas have since been implemented for Japan and the United Kingdom at 1.25 million metric tons and 0.5 million metric tons, respectively. Effective dates for the revisions are April 1, 2022 for Japan and June 1, 2022 for the United Kingdom.

On January 9, 2017, we acquired The Laserflex Corporation (“Laserflex”), a privately-owned metal fabricator with locations in Columbus, Ohio and Wellford, South Carolina. Laserflex specializes in laser fabrication metal processing and welding and further enhances our existing fabrication and metals processing capabilities.

On February 15, 2017, we acquired Guy Metals, Inc. (“Guy Metals”), a privately-owned metal service center company located in Hammond, Wisconsin. Guy Metals processes stainless and nickel alloy products including its trademarked “Pit Free Dairy” and “Super4” finishes used in food, dairy, pharmaceutical, and beverage applications. Consistent with the Laserflex acquisition, Guy Metals bolsters our value-added processing capabilities to provide additional services to our customers.

Components of Results of Operations

We generate substantially all of our revenue from sales of our metals products. RevenueThe majority of revenue is recognized upon delivery of product to customers. The timing of shipment is substantially the same as the timing of delivery to customers given the proximity of our distribution sites to our customers. Revenues associated with products which we believe have no alternative use, and where the Company has an enforceable right to payment, are recognized on an over-time basis. Over-time revenues are recorded in proportion with the progress made toward completing the performance obligation.

Sales, cost of materials sold, gross profit, and operating expense control are the principal factors that impact our profitability.

Net sales. Our sales volume and pricing isare driven by market demand, which is largely determined by overall industrial production and conditions in the specific industries in which our customers operate. Sales prices are also primarily driven by market factors such as overall demand and availability of product. Our net sales include revenue from product sales, net of returns, allowances, customer discounts, and incentives.

Cost of materials sold. Cost of materials sold includes metal purchase and in-bound freight costs, third-party processing costs, and direct and indirect internal processing costs. The cost of materials sold fluctuates with our sales volume and our ability to purchase metals at competitive prices. Increases in sales volume generally enable us both to improve purchasing leverage with suppliers, as we buy larger quantities of metals inventories, and to reduce operating expenses per ton sold.inventories.

Gross profit. Gross profit is the difference between net sales and the cost of materials sold. Our sales prices to our customers are subject to market competition. Achieving acceptable levels of gross profit is dependent on our acquiring metals at competitive prices, our ability to manage the impact of changing prices, and efficiently managing our internal and external processing costs.

Operating expenses. Optimizing business processes and asset utilization to lower fixed expenses such as employee, facility, and truck fleet costs, which cannot be rapidly reduced in times of declining volume, and maintaining a low fixed cost structure in times of increasing sales volume, have a significant impact on our profitability. Operating expenses include costs related to warehousing and distributing our products as well as selling, general, and administrative expenses.

24

Results of Operations—Operations — Comparison of Three and NineSix Months Ended SeptemberJune 30, 20172022 to Three and NineSix Months Ended SeptemberJune 30, 20162021

The following table sets forth our condensed consolidated statements of income data for the three-month and nine-monthsix-month periods ended SeptemberJune 30, 20172022 and 2016:2021 (certain percentages may not calculate due to rounding):

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||||||||||||||||||

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||||||||||||||||||

|

| $ |

|

| % of Net |

|

| $ |

|

| % of Net |

|

| $ |

|

| % of Net |

|

| $ |

|

| % of Net |

| ||||||||

|

| ($ in millions) |

|

| ($ in millions) |

| ||||||||||||||||||||||||||

Net sales |

| $ | 1,743.5 |

|

|

| 100.0 | % |

| $ | 1,419.0 |

|

|

| 100.0 | % |

| $ | 3,492.3 |

|

|

| 100.0 | % |

| $ | 2,566.3 |

|

|

| 100.0 | % |

Cost of materials sold |

|

| 1,277.6 |

|

|

| 73.3 |

|

|

| 1,162.0 |

|

|

| 81.9 |

|

|

| 2,616.3 |

|

|

| 74.9 |

|

|

| 2,111.4 |

|

|

| 82.3 |

|

Gross profit |

|

| 465.9 |

|

|

| 26.7 |

|

|

| 257.0 |

|

|

| 18.1 |

|

|

| 876.0 |

|

|

| 25.1 |

|

|

| 454.9 |

|

|

| 17.7 |

|

Warehousing, delivery, selling, general, and administrative expenses |

|

| 182.9 |

|

|

| 10.5 |

|

|

| 178.3 |

|

|

| 12.6 |

|

|

| 358.2 |

|

|

| 10.3 |

|

|

| 350.1 |

|

|

| 13.6 |

|

Gain on sale of assets |

|

| (3.8 | ) |

|

| (0.2 | ) |

|

| (87.4 | ) |

|

| (6.2 | ) |

|

| (3.8 | ) |

|

| (0.1 | ) |

|

| (107.7 | ) |

|

| (4.2 | ) |

Operating profit |

|

| 286.8 |

|

|

| 16.4 |

|

|

| 166.1 |

|

|

| 11.7 |

|

|

| 521.6 |

|

|

| 14.9 |

|

|

| 212.5 |

|

|

| 8.3 |

|

Other (expenses) and income |

|

| (23.6 | ) |

|

| (1.4 | ) |

|

| (14.3 | ) |

|

| (1.0 | ) |

|

| (39.6 | ) |

|

| (1.1 | ) |

|

| (27.5 | ) |

|

| (1.1 | ) |

Income before income taxes |

|

| 263.2 |

|

|

| 15.1 |

|

|

| 151.8 |

|

|

| 10.7 |

|

|

| 482.0 |

|

|

| 13.8 |

|

|

| 185.0 |

|

|

| 7.2 |

|

Provision for income taxes |

|

| 66.8 |

|

|

| 3.8 |

|

|

| 38.5 |

|

|

| 2.7 |

|

|

| 121.8 |

|

|

| 3.5 |

|

|

| 46.1 |

|

|

| 1.8 |

|

Net income |

|

| 196.4 |

|

|

| 11.3 |

|

|

| 113.3 |

|

|

| 8.0 |

|

|

| 360.2 |

|

|

| 10.3 |

|

|

| 138.9 |

|

|

| 5.4 |

|

Less: Net income attributable to noncontrolling interest |

|

| — |

|

|

| — |

|

|

| 0.4 |

|

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| 0.7 |

|

|

| — |

|

Net income attributable to Ryerson Holding Corporation |

| $ | 196.4 |

|

|

| 11.3 | % |

| $ | 112.9 |

|

|

| 8.0 | % |

| $ | 360.0 |

|

|

| 10.3 | % |

| $ | 138.2 |

|

|

| 5.4 | % |

Basic earnings per share |

| $ | 5.20 |

|

|

|

|

| $ | 2.94 |

|

|

|

|

| $ | 9.45 |

|

|

|

|

| $ | 3.61 |

|

|

|

| ||||

Diluted earnings per share |

| $ | 5.10 |

|

|

|

|

| $ | 2.91 |

|

|

|

|

| $ | 9.26 |

|

|

|

|

| $ | 3.57 |

|

|

|

| ||||

|

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

| ||||||||||||||||||||||||||

|

| 2017 |

|

| 2016 |

|

| 2017 |

|

| 2016 |

| ||||||||||||||||||||

|

| $ |

|

| % of Net Sales |

|

| $ |

|

| % of Net Sales |

|

| $ |

|

| % of Net Sales |

|

| $ |

|

| % of Net Sales |

| ||||||||

|

| ($ in millions) |

|

| ($ in millions) |

| ||||||||||||||||||||||||||

Net sales |

| $ | 864.2 |

|

|

| 100.0 | % |

| $ | 735.1 |

|

|

| 100.0 | % |

| $ | 2,554.1 |

|

|

| 100.0 | % |

| $ | 2,177.5 |

|

|

| 100.0 | % |

Cost of materials sold |

|

| 719.2 |

|

|

| 83.2 |

|

|

| 589.7 |

|

|

| 80.2 |

|

|

| 2,108.1 |

|

|

| 82.5 |

|

|

| 1,721.5 |

|

|

| 79.1 |

|

Gross profit |

|

| 145.0 |

|

|

| 16.8 |

|

|

| 145.4 |

|

|

| 19.8 |

|

|

| 446.0 |

|

|

| 17.5 |

|

|

| 456.0 |

|

|

| 20.9 |

|

Warehousing, delivery, selling, general and administrative expenses |

|

| 119.2 |

|

|

| 13.8 |

|

|

| 109.1 |

|

|

| 14.8 |

|

|

| 353.2 |

|

|

| 13.9 |

|

|

| 331.5 |

|

|

| 15.2 |

|

Restructuring and other charges |

|

| — |

|

|

| — |

|

|

| 2.5 |

|

|

| 0.4 |

|

|

| — |

|

|

| — |

|

|

| 2.5 |

|

|

| 0.1 |

|

Operating profit |

|

| 25.8 |

|

|

| 3.0 |

|

|

| 33.8 |

|

|

| 4.6 |

|

|

| 92.8 |

|

|

| 3.6 |

|

|

| 122.0 |

|

|

| 5.6 |

|

Other expenses |

|

| (24.6 | ) |

|

| (2.9 | ) |

|

| (23.8 | ) |

|

| (3.2 | ) |

|

| (69.8 | ) |

|

| (2.7 | ) |

|

| (80.7 | ) |

|

| (3.7 | ) |

Income before income taxes |

|

| 1.2 |

|

|

| 0.1 |

|

|

| 10.0 |

|

|

| 1.4 |

|

|

| 23.0 |

|

|

| 0.9 |

|

|

| 41.3 |

|

|

| 1.9 |

|

Provision (benefit) for income taxes |

|

| (0.7 | ) |

|

| (0.1 | ) |

|

| 1.6 |

|

|

| 0.3 |

|

|

| 5.3 |

|

|

| 0.2 |

|

|

| 14.0 |

|

|

| 0.6 |

|

Net income |

|

| 1.9 |

|

|

| 0.2 |

|

|

| 8.4 |

|

|

| 1.1 |

|

|

| 17.7 |

|

|

| 0.7 |

|

|

| 27.3 |

|

|

| 1.3 |

|

Less: Net income attributable to noncontrolling interest |

|

| 0.2 |

|

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| 0.6 |

|

|

| — |

|

|

| — |

|

|

| — |

|

Net income attributable to Ryerson Holding Corporation |

| $ | 1.7 |

|

|

| 0.2 | % |

| $ | 8.2 |

|

|

| 1.1 | % |

| $ | 17.1 |

|

|

| 0.7 | % |

| $ | 27.3 |

|

|

| 1.3 | % |

Basic and diluted earnings per share |

| $ | 0.05 |

|

|

|

|

|

| $ | 0.23 |

|

|

|

|

|

| $ | 0.46 |

|

|

|

|

|

| $ | 0.82 |

|

|

|

|

|

25

The following table shows ourcharts show the Company’s percentage of sales revenue by major product lines for the threesix months ended June 30, 2022 and nine month periods ended September 30, 2017 and 2016:2021:

|

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

| ||||||||||

Product Line |

| 2017 |

|

| 2016 |

|

| 2017 |

|

| 2016 |

| ||||

Carbon Steel Flat |

|

| 29 | % |

|

| 29 | % |

|

| 28 | % |

|

| 27 | % |

Carbon Steel Plate |

|

| 10 |

|

|

| 9 |

|

|

| 10 |

|

|

| 9 |

|

Carbon Steel Long |

|

| 12 |

|

|

| 13 |

|

|

| 12 |

|

|

| 14 |

|

Stainless Steel Flat |

|

| 17 |

|

|

| 17 |

|

|

| 18 |

|

|

| 16 |

|

Stainless Steel Plate |

|

| 4 |

|

|

| 4 |

|

|

| 4 |

|

|

| 4 |

|

Stainless Steel Long |

|

| 4 |

|

|

| 3 |

|

|

| 4 |

|

|

| 4 |

|

Aluminum Flat |

|

| 16 |

|

|

| 16 |

|

|

| 15 |

|

|

| 16 |

|

Aluminum Plate |

|

| 3 |

|

|

| 3 |

|

|

| 3 |

|

|

| 3 |

|

Aluminum Long |

|

| 4 |

|

|

| 4 |

|

|