| |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

March 31, 2020

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

WMIH Corp.

|

| |||

| Delaware | 91-1653725 | |||

| (State or other jurisdiction of | ( Identification No.) | |||

|

| |||

8950 Cypress Waters Blvd, Coppell, TX | 75019 | |||

| (Address of principal executive offices) | (Zip Code) | |||

| (469) 549-2000 | ||||

| Registrant’s telephone number, including area code | ||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, $0.01 par value per share | COOP | The Nasdaq Stock Market |

(206) 922-2957

(Registrant’s telephone number, including area code)

|

|

|

| |||||||

| ¨ |

| x | |||||||

| Non-Accelerated Filer | ¨ | Smaller reporting company |

| |||||||

| Emerging growth company |

| ¨ | ||||||||

Indicate the number

|

| |||

|

| |||

Forward-Looking Statements

Certain information included in this Quarterly Report on Form 10-Q and the documents incorporated herein by reference contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical fact included in this Quarterly Report on Form 10-Q that address activities, events, conditions or developments that we expect, believe or anticipate will or may occur in the future are forward-looking statements. Forward-looking statements give our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business and these statements are not guarantees of future performance. These statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements may include the words “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “strategy,” “future,” “opportunity,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result” and similar expressions. Such forward-looking statements involve risks and uncertainties that may cause actual events, results or performance to differ materially from those indicated by such statements. Some of these risks are identified and discussed under Risk Factors in Part I, Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2016. These risk factors will be important to consider in determining future results and should be reviewed in their entirety. These forward-looking statements are expressed in good faith and we believe there is a reasonable basis for them. However, there can be no assurance that the events, results or trends identified in these forward-looking statements will occur or be achieved. Forward-looking statements speak only as of the date they are made, and we do not undertake to update any forward-looking statement, except as required by law.

* * * * *

As used in this Quarterly Report on Form 10-Q, unless the context requires otherwise, (i) the terms “Company,” “we,” “us,” or “our” refer to WMIH Corp. (formerly WMI Holdings Corp.) and its subsidiaries on a consolidated basis; (ii) “WMIH” refers only to WMIH Corp., without regard to its subsidiaries; (iii) “WMIHC” refers only to WMI Holdings Corp., without regard to its subsidiaries; (iv) “WMMRC” means WM Mortgage Reinsurance Company, Inc. (a wholly-owned subsidiary of WMIH); and (v) “WMIIC” means WMI Investment Corp. (a wholly-owned subsidiary of WMIH).

1

FORM 10-Q

INDEX

| |||

| Page | |||

| PART I | |||

| Item 1. | |||

Consolidated Balance Sheets as of March 31, 2020 (unaudited) and December 31, 2019 | |||

Consolidated Statements of Operations (unaudited) for the Three Months Ended March 31, 2020 and Three Months Ended March 31, 2019 | |||

Consolidated Statements of Stockholders’ Equity (unaudited) for the Three Months Ended March 31, 2020 and Three Months Ended March 31, 2019 | |||

Consolidated Statements of Cash Flows (unaudited) for the Three Months Ended March 31, 2020 and Three Months Ended March 31, 2019 | |||

| |||

| Item 2. |

| ||

| Item 3. |

| ||

| Item 4. |

| ||

| PART II | |||

| Item 1. |

| ||

| Item 1A. |

| ||

| |||

| Item 2. |

| ||

| Item 3. | |||

| Item 4. | |||

| Item 5. | |||

| Item 6. | |||

2

FINANCIAL INFORMATION

WMIH CORP. AND SUBSIDIARIES

CONDENSED

(Unaudited)

| September 30, 2017 |

|

| December 31, 2016 (1) |

| ||

ASSETS: |

|

|

|

|

|

|

|

Investments held in trust: |

|

|

|

|

|

|

|

Fixed-maturity securities | $ | 9,022 |

|

| $ | 29,206 |

|

Cash equivalents held in trust |

| 6,804 |

|

|

| 2,176 |

|

Total investments held in trust |

| 15,826 |

|

|

| 31,382 |

|

Cash and cash equivalents |

| 25,542 |

|

|

| 2,491 |

|

Fixed-maturity securities |

| 1,400 |

|

|

| 47,625 |

|

Restricted cash |

| 577,220 |

|

|

| 573,347 |

|

Derivative asset - embedded conversion feature |

| 111,877 |

|

|

| 80,651 |

|

Accrued investment income |

| 109 |

|

|

| 187 |

|

Other assets |

| 764 |

|

|

| 507 |

|

Total assets | $ | 732,738 |

|

| $ | 736,190 |

|

LIABILITIES, REDEEMABLE CONVERTIBLE PREFERRED STOCK AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

|

Notes payable - principal | $ | — |

|

| $ | 18,774 |

|

Notes payable - interest |

| — |

|

|

| 203 |

|

Losses and loss adjustment reserves |

| 705 |

|

|

| 811 |

|

Losses payable |

| 29 |

|

|

| 53 |

|

Unearned premiums |

| 33 |

|

|

| 270 |

|

Accrued ceding commissions |

| 57 |

|

|

| 22 |

|

Loss contract reserve |

| — |

|

|

| 5,645 |

|

Other liabilities |

| 13,774 |

|

|

| 14,063 |

|

Total liabilities |

| 14,598 |

|

|

| 39,841 |

|

Commitments and contingencies |

|

|

|

|

|

|

|

Redeemable convertible series B preferred stock, $0.00001 par value; 600,000 shares issued and outstanding as of September 30, 2017 and December 31, 2016; aggregate liquidation preference of $600,000,000 as of September 30, 2017 and December 31, 2016 |

| 502,213 |

|

|

| 502,213 |

|

Stockholders’ equity: |

|

|

|

|

|

|

|

Convertible series A preferred stock, $0.00001 par value; 1,000,000 shares issued and outstanding as of September 30, 2017 and December 31, 2016; aggregate liquidation preference of $10 as of September 30, 2017 and December 31, 2016 |

| — |

|

|

| — |

|

Common stock, $0.00001 par value; 3,500,000,000 authorized; 206,714,132 and 206,380,800 shares issued and outstanding as of September 30, 2017 and December 31, 2016, respectively |

| 2 |

|

|

| 2 |

|

Additional paid-in capital |

| 108,830 |

|

|

| 108,415 |

|

Retained earnings |

| 107,095 |

|

|

| 85,719 |

|

Total stockholders’ equity |

| 215,927 |

|

|

| 194,136 |

|

Total liabilities, redeemable convertible preferred stock and stockholders’ equity | $ | 732,738 |

|

| $ | 736,190 |

|

The

| March 31, 2020 | December 31, 2019 | ||||||

| (unaudited) | |||||||

| Assets | |||||||

| Cash and cash equivalents | $ | 579 | $ | 329 | |||

| Restricted cash | 266 | 283 | |||||

| Mortgage servicing rights, $3,109 and $3,496 at fair value, respectively | 3,115 | 3,502 | |||||

| Advances and other receivables, net of reserves of $193 and $175, respectively | 685 | 988 | |||||

| Reverse mortgage interests, net of reserves of $3 and $3, respectively | 5,955 | 6,279 | |||||

| Mortgage loans held for sale at fair value | 3,922 | 4,077 | |||||

| Property and equipment, net of accumulated depreciation of $65 and $55, respectively | 111 | 112 | |||||

| Deferred tax assets, net | 1,411 | 1,345 | |||||

| Other assets | 1,569 | 1,390 | |||||

| Total assets | $ | 17,613 | $ | 18,305 | |||

| Liabilities and Stockholders’ Equity | |||||||

| Unsecured senior notes, net | $ | 2,259 | $ | 2,366 | |||

| Advance facilities, net | 489 | 422 | |||||

| Warehouse facilities, net | 4,551 | 4,575 | |||||

| Payables and other liabilities | 1,965 | 2,016 | |||||

| MSR related liabilities - nonrecourse at fair value | 1,285 | 1,348 | |||||

| Mortgage servicing liabilities | 53 | 61 | |||||

| Other nonrecourse debt, net | 4,945 | 5,286 | |||||

| Total liabilities | 15,547 | 16,074 | |||||

| Commitments and contingencies (Note 18) | |||||||

| Preferred stock at $0.00001 - 10 million shares authorized, 1 million shares issued and outstanding, respectively; aggregate liquidation preference of ten dollars, respectively | — | — | |||||

| Common stock at $0.01 par value - 300 million shares authorized, 92.0 million and 91.1 million shares issued, respectively | 1 | 1 | |||||

| Additional paid-in-capital | 1,108 | 1,109 | |||||

| Retained earnings | 961 | 1,122 | |||||

| Total Mr. Cooper stockholders’ equity | 2,070 | 2,232 | |||||

| Non-controlling interests | (4 | ) | (1 | ) | |||

| Total stockholders’ equity | 2,066 | 2,231 | |||||

| Total liabilities and stockholders’ equity | $ | 17,613 | $ | 18,305 | |||

(1)Balances derived from audited financial statements as of December 31, 2016.(unaudited).

3

CONDENSED

(Unaudited)

| Three months ended September 30, 2017 |

|

| Three months ended September 30, 2016 |

|

| Nine months ended September 30, 2017 |

|

| Nine months ended September 30, 2016 |

| ||||

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Premiums earned | $ | 344 |

|

| $ | 786 |

|

| $ | 1,103 |

|

| $ | 2,426 |

|

Net investment income |

| 1,943 |

|

|

| 498 |

|

|

| 4,826 |

|

|

| 1,747 |

|

Total revenues |

| 2,287 |

|

|

| 1,284 |

|

|

| 5,929 |

|

|

| 4,173 |

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Losses and loss adjustment expense |

| 48 |

|

|

| 183 |

|

|

| 207 |

|

|

| 702 |

|

Ceding commission expense |

| 44 |

|

|

| 75 |

|

|

| 137 |

|

|

| 234 |

|

General and administrative expense |

| 2,117 |

|

|

| 1,357 |

|

|

| 5,915 |

|

|

| 4,878 |

|

Loss contract reserve reduction |

| (210 | ) |

|

| (565 | ) |

|

| (5,645 | ) |

|

| (2,362 | ) |

Interest expense |

| 579 |

|

|

| 636 |

|

|

| 1,788 |

|

|

| 1,994 |

|

Total operating expenses |

| 2,578 |

|

|

| 1,686 |

|

|

| 2,402 |

|

|

| 5,446 |

|

Net operating (loss) income |

| (291 | ) |

|

| (402 | ) |

|

| 3,527 |

|

|

| (1,273 | ) |

Other (income) expense: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other (income) |

| (123 | ) |

|

| — |

|

|

| (123 | ) |

|

| — |

|

Unrealized (gain) loss on change in fair value of derivative embedded conversion feature |

| (38,579 | ) |

|

| 16,243 |

|

|

| (31,226 | ) |

|

| (62,587 | ) |

Total other (income) expense |

| (38,702 | ) |

|

| 16,243 |

|

|

| (31,349 | ) |

|

| (62,587 | ) |

Income (loss) before income taxes |

| 38,411 |

|

|

| (16,645 | ) |

|

| 34,876 |

|

|

| 61,314 |

|

Income tax expense (benefit) |

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Net income (loss) |

| 38,411 |

|

|

| (16,645 | ) |

|

| 34,876 |

|

|

| 61,314 |

|

Redeemable convertible series B preferred stock dividends |

| (4,500 | ) |

|

| (4,500 | ) |

|

| (13,500 | ) |

|

| (13,500 | ) |

Net income (loss) attributable to common and participating stockholders | $ | 33,911 |

|

| $ | (21,145 | ) |

| $ | 21,376 |

|

| $ | 47,814 |

|

Basic net income (loss) per share attributable to common stockholders (Note 12) | $ | 0.06 |

|

| $ | (0.10 | ) |

| $ | 0.04 |

|

| $ | 0.10 |

|

Shares used in computing basic net income (loss) per share |

| 202,660,492 |

|

|

| 202,341,209 |

|

|

| 202,573,315 |

|

|

| 202,247,275 |

|

Diluted net income (loss) per share attributable to common stockholders (Note 12) | $ | 0.06 |

|

| $ | (0.10 | ) |

| $ | 0.04 |

|

| $ | 0.09 |

|

Shares used in computing diluted net income (loss) per share |

| 212,726,121 |

|

|

| 202,341,209 |

|

|

| 212,638,944 |

|

|

| 237,575,014 |

|

The

| Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | ||||||

| Revenues: | |||||||

| Service related, net | $ | (53 | ) | $ | 84 | ||

| Net gain on mortgage loans held for sale | 331 | 166 | |||||

| Total revenues | 278 | 250 | |||||

| Expenses: | |||||||

| Salaries, wages and benefits | 246 | 215 | |||||

| General and administrative | 198 | 228 | |||||

| Total expenses | 444 | 443 | |||||

| Other income (expenses), net: | |||||||

| Interest income | 118 | 134 | |||||

| Interest expense | (192 | ) | (189 | ) | |||

| Other income, net | 1 | 15 | |||||

| Total other income (expenses), net | (73 | ) | (40 | ) | |||

| Loss before income tax benefit | (239 | ) | (233 | ) | |||

| Less: Income tax benefit | (68 | ) | (47 | ) | |||

| Net loss | (171 | ) | (186 | ) | |||

| Less: Net loss attributable to non-controlling interests | (3 | ) | — | ||||

| Net loss attributable to Mr. Cooper | (168 | ) | (186 | ) | |||

| Less: Undistributed earnings attributable to participating stockholders | — | — | |||||

| Net loss attributable to common stockholders | $ | (168 | ) | $ | (186 | ) | |

| Net loss per common share attributable to Mr. Cooper: | |||||||

| Basic | $ | (1.84 | ) | $ | (2.05 | ) | |

| Diluted | $ | (1.84 | ) | $ | (2.05 | ) | |

4

statements (unaudited).

CONDENSED

PREFERRED STOCK AND STOCKHOLDERS’ EQUITY

(Unaudited)

| Series B Redeemable Convertible Preferred Stock |

|

|

| Series A Convertible Preferred Stock |

|

|

| Common Stock |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| Shares |

|

| Amount |

|

|

| Shares |

|

| Amount |

|

|

| Shares |

|

| Amount |

|

| Additional paid-in capital |

|

| (Accumulated deficit) retained earnings |

|

| Total stockholders’ equity |

| |||||||||

Balance at January 1, 2016 |

| 600,000 |

|

|

| 502,213 |

|

|

|

| 1,000,000 |

|

|

| — |

|

|

|

| 206,168,035 |

|

|

| 2 |

|

|

| 107,757 |

|

|

| (97,981 | ) |

|

| 9,778 |

|

Net income |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 201,700 |

|

|

| 201,700 |

|

Redeemable convertible series B preferred stock dividends |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (18,000 | ) |

|

| (18,000 | ) |

Issuance of common stock under restricted stock compensation arrangement |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| 212,765 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Equity-based compensation |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| 658 |

|

|

| — |

|

|

| 658 |

|

Balance at December 31, 2016 |

| 600,000 |

|

|

| 502,213 |

|

|

|

| 1,000,000 |

|

|

| — |

|

|

|

| 206,380,800 |

|

|

| 2 |

|

|

| 108,415 |

|

|

| 85,719 |

|

|

| 194,136 |

|

Net income |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 34,876 |

|

|

| 34,876 |

|

Redeemable convertible series B preferred stock dividends |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (13,500 | ) |

|

| (13,500 | ) |

Issuance of common stock under restricted stock compensation arrangement |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| 333,332 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Equity-based compensation |

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| — |

|

|

| 415 |

|

|

| — |

|

|

| 415 |

|

Balance at September 30, 2017 |

| 600,000 |

|

| $ | 502,213 |

|

|

|

| 1,000,000 |

|

| $ | — |

|

|

|

| 206,714,132 |

|

| $ | 2 |

|

| $ | 108,830 |

|

| $ | 107,095 |

|

| $ | 215,927 |

|

The

| Preferred Stock | Common Stock | |||||||||||||||||||||||||||||||||

| Shares (in thousands) | Amount | Shares (in thousands) | Amount | Additional Paid-in Capital | Retained Earnings | Total Mr. Cooper Stockholders’ Equity | Non-controlling Interests | Total Equity | ||||||||||||||||||||||||||

| Balance at January 1, 2019 | 1,000 | $ | — | 90,821 | $ | 1 | $ | 1,093 | $ | 848 | $ | 1,942 | $ | 3 | $ | 1,945 | ||||||||||||||||||

| Shares issued / (surrendered) under incentive compensation plan | — | — | 221 | — | (2 | ) | — | (2 | ) | — | (2 | ) | ||||||||||||||||||||||

| Share-based compensation | — | — | — | — | 4 | — | 4 | — | 4 | |||||||||||||||||||||||||

| Net loss | — | — | — | — | — | (186 | ) | (186 | ) | — | (186 | ) | ||||||||||||||||||||||

| Balance at March 31, 2019 | 1,000 | $ | — | 91,042 | $ | 1 | $ | 1,095 | $ | 662 | $ | 1,758 | $ | 3 | $ | 1,761 | ||||||||||||||||||

| Balance at January 1, 2020 | 1,000 | $ | — | 91,118 | $ | 1 | $ | 1,109 | $ | 1,122 | $ | 2,232 | $ | (1 | ) | $ | 2,231 | |||||||||||||||||

| Shares issued / (surrendered) under incentive compensation plan | — | — | 852 | — | (5 | ) | — | (5 | ) | — | (5 | ) | ||||||||||||||||||||||

| Share-based compensation | — | — | — | — | 4 | — | 4 | — | 4 | |||||||||||||||||||||||||

| Cumulative effect adjustments pursuant to the adoption of ASU 2016-13 | — | — | — | — | — | 7 | 7 | — | 7 | |||||||||||||||||||||||||

| Net loss | — | — | — | — | — | (168 | ) | (168 | ) | (3 | ) | (171 | ) | |||||||||||||||||||||

| Balance at March 31, 2020 | 1,000 | $ | — | 91,970 | $ | 1 | $ | 1,108 | $ | 961 | $ | 2,070 | $ | (4 | ) | $ | 2,066 | |||||||||||||||||

5

statements (unaudited).

CONDENSED

(Unaudited)

| Nine months ended September 30, 2017 |

| Nine months ended September 30, 2016 |

| ||

Cash flows from operating activities: |

|

|

|

|

|

|

Net income | $ | 34,876 |

| $ | 61,314 |

|

Adjustments to reconcile net income to net cash (used in) operating activities: |

|

|

|

|

|

|

Amortization of premium or discount on fixed maturity securities |

| 108 |

|

| 247 |

|

Net realized loss (gain) on sale of investments |

| 63 |

|

| (19 | ) |

Unrealized (gain) on trading securities |

| (67 | ) |

| (83 | ) |

Unrealized (gain) on derivative embedded conversion feature |

| (31,226 | ) |

| (62,587 | ) |

Equity-based compensation |

| 415 |

|

| 484 |

|

Changes in assets and liabilities: |

|

|

|

|

|

|

Accrued investment income |

| 78 |

|

| (18 | ) |

Other assets |

| (257 | ) |

| (270 | ) |

Cash equivalents held in trust |

| (4,628 | ) |

| 1,358 |

|

Restricted cash |

| (3,873 | ) |

| (1,476 | ) |

Losses and loss adjustment reserves |

| (106 | ) |

| (2,733 | ) |

Losses payable |

| (24 | ) |

| (395 | ) |

Unearned premiums |

| (237 | ) |

| (463 | ) |

Accrued ceding commission expense |

| 35 |

|

| (8 | ) |

Accrued interest on notes payable |

| (203 | ) |

| (24 | ) |

Loss contract reserve |

| (5,645 | ) |

| (2,362 | ) |

Other liabilities |

| (289 | ) |

| (626 | ) |

Total adjustments |

| (45,856 | ) |

| (68,975 | ) |

Net cash used in operating activities |

| (10,980 | ) |

| (7,661 | ) |

Cash flows from investing activities: |

|

|

|

|

|

|

Purchase of investments |

| (19,973 | ) |

| (130,469 | ) |

Proceeds from sales and maturities of investments |

| 86,278 |

|

| 146,920 |

|

Net cash provided by investing activities |

| 66,305 |

|

| 16,451 |

|

Cash flows from financing activities: |

|

|

|

|

|

|

Redeemable convertible series B preferred stock dividends |

| (13,500 | ) |

| (13,500 | ) |

Notes payable – principal repayments |

| (18,774 | ) |

| (2,185 | ) |

Net cash used in financing activities |

| (32,274 | ) |

| (15,685 | ) |

Increase (decrease) in cash and cash equivalents |

| 23,051 |

|

| (6,895 | ) |

Cash and cash equivalents, beginning of period |

| 2,491 |

|

| 9,924 |

|

Cash and cash equivalents, end of period | $ | 25,542 |

| $ | 3,029 |

|

Supplementary disclosure of cash flow information: |

|

|

|

|

|

|

Cash paid during the period: |

|

|

|

|

|

|

Interest | $ | 1,991 |

| $ | 2,008 |

|

The

| Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | ||||||

| Operating Activities | |||||||

| Net loss | $ | (171 | ) | $ | (186 | ) | |

| Adjustments to reconcile net loss to net cash attributable to operating activities: | |||||||

| Deferred tax benefit | (68 | ) | (47 | ) | |||

| Net gain on mortgage loans held for sale | (331 | ) | (166 | ) | |||

| Interest income on reverse mortgage loans | (62 | ) | (82 | ) | |||

| Provision for reserves | 8 | 11 | |||||

| Fair value changes and amortization/accretion of mortgage servicing rights/liabilities | 526 | 379 | |||||

| Fair value changes in excess spread financing | (35 | ) | (69 | ) | |||

| Fair value changes in mortgage servicing rights financing liability | 6 | 2 | |||||

| Fair value changes in mortgage loans held for investment | — | (1 | ) | ||||

| Amortization of premiums, net of discount accretion | 23 | 2 | |||||

| Depreciation and amortization for property and equipment and intangible assets | 19 | 21 | |||||

| Share-based compensation | 4 | 4 | |||||

| Other loss | 7 | — | |||||

| Repurchases of forward loan assets out of Ginnie Mae securitizations | (919 | ) | (364 | ) | |||

| Mortgage loans originated and purchased for sale, net of fees | (12,375 | ) | (5,717 | ) | |||

| Sales proceeds and loan payment proceeds for mortgage loans held for sale and held for investment | 13,724 | 6,197 | |||||

| Changes in assets and liabilities: | |||||||

| Advances and other receivables | 300 | 120 | |||||

| Reverse mortgage interests | 400 | 614 | |||||

| Other assets | (91 | ) | (216 | ) | |||

| Payables and other liabilities | (255 | ) | (217 | ) | |||

| Net cash attributable to operating activities | 710 | 285 | |||||

| Investing Activities | |||||||

| Acquisitions, net of cash acquired | — | (85 | ) | ||||

| Property and equipment additions, net of disposals | (12 | ) | (10 | ) | |||

| Purchase of forward mortgage servicing rights, net of liabilities incurred | (27 | ) | (130 | ) | |||

| Proceeds on sale of forward and reverse mortgage servicing rights | 43 | 243 | |||||

| Net cash attributable to investing activities | 4 | 18 | |||||

| Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | ||||||

| Financing Activities | |||||||

| (Decrease) increase in warehouse facilities | (25 | ) | 307 | ||||

| Increase (decrease) in advance facilities | 68 | (30 | ) | ||||

| Repayment of notes payable | — | (294 | ) | ||||

| Proceeds from sale of HECM securitizations | — | 20 | |||||

| Repayment of HECM securitizations | (99 | ) | (127 | ) | |||

| Proceeds from issuance of participating interest financing in reverse mortgage interests | 55 | 86 | |||||

| Repayment of participating interest financing in reverse mortgage interests | (330 | ) | (494 | ) | |||

| Proceeds from the issuance of excess spread financing | 24 | 245 | |||||

| Settlements and repayments of excess spread financing | (58 | ) | (50 | ) | |||

| Issuance of unsecured senior debt | 600 | — | |||||

| Repayment of nonrecourse debt – legacy assets | — | (3 | ) | ||||

| Redemption and repayment of unsecured senior notes | (698 | ) | — | ||||

| Repayment of finance lease liability | (1 | ) | (1 | ) | |||

| Surrender of shares relating to stock vesting | (5 | ) | (2 | ) | |||

| Debt financing costs | (12 | ) | (1 | ) | |||

| Net cash attributable to financing activities | (481 | ) | (344 | ) | |||

| Net increase (decrease) in cash, cash equivalents, and restricted cash | 233 | (41 | ) | ||||

| Cash, cash equivalents, and restricted cash - beginning of period | 612 | 561 | |||||

Cash, cash equivalents, and restricted cash - end of period(1) | $ | 845 | $ | 520 | |||

| Supplemental Disclosures of Cash Activities | |||||||

| Cash paid for interest expense | $ | 89 | $ | 74 | |||

(1) | The following table provides a reconciliation of cash, cash equivalents and restricted cash to amount reported within the consolidated balance sheets. |

| March 31, 2020 | March 31, 2019 | ||||||

| Cash and cash equivalents | $ | 579 | $ | 181 | |||

| Restricted cash | 266 | 339 | |||||

| Total cash, cash equivalents, and restricted cash | $ | 845 | $ | 520 | |||

6

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Unless otherwise indicated, financial information, including dollar values statedlargest home loan originators and servicers in the textcountry focused on delivering a variety of the notesservicing and lending products, services and technologies. Xome provides real estate data as well as a range of services including real estate brokerage, title, closing, valuation and field services to financial statements,lenders, investors and consumers. The Company’s corporate website is expressed in thousands.

References herein, unless the context requires otherwise, to (i) the terms “Company,” “we,” “us” or “our” generally are intended to refer to WMIH Corp. (formerly WMI Holdings Corp.) and its subsidiaries on a consolidated basis; (ii) “WMIH” refers only to WMIH Corp. without regard to its subsidiaries; (iii) “WMIHC” refers only to WMI Holdings Corp. without regard to its subsidiaries; (iv) “WMMRC” means WM Mortgage Reinsurance Company, Inc. (a wholly-owned subsidiary of WMIH); and (v) “WMIIC” means WMI Investment Corp. (a wholly-owned subsidiary of WMIH)located at

Note 1: The Company has provided a glossary of terms, which defines certain industry-specific and its Subsidiaries

WMIH Corp.

other terms that are used herein, in the MD&A section of this Form 10-Q.

WMIH, formerly known as WMIHC and Washington Mutual, Inc. (“WMI”), is the direct parent of WM Mortgage Reinsurance Company, Inc., a Hawaii corporation (“WMMRC”), and WMI Investment Corp., a Delaware corporation (“WMIIC”). Since the emergence from bankruptcy on March 19, 2012, our business activities consist of operating WMMRC’s legacy reinsurance business in runoff mode. In addition, we are actively seeking acquisition opportunities across a broad array of industries with a specific focus in the financial services industry, including targets with consumer finance, specialty finance, leasing and insurance operations.

As of September 30, 2017, WMIH was authorized to issue up to 3,500,000,000 shares of common stock, and up to 10,000,000 shares of preferred stock (in one or more series), in each case with a par value of $0.00001 per share. As of September 30, 2017 and December 31, 2016, 206,714,132 and 206,380,800 shares, respectively, of WMIH’s common stock were issued and outstanding. As of September 30, 2017 and December 31, 2016, 1,000,000 shares of WMIH’s Series A Convertible Preferred Stock (the “Series A Preferred Stock”) were issued and outstanding. As of September 30, 2017 and December 31, 2016, 600,000 shares of WMIH’s 3% Series B Convertible Preferred Stock (the “Series B Preferred Stock”) were issued and outstanding.

While we remain committed to consummating an acquisition, we also are mindful that the Company’s Series B Preferred Stock is redeemable on January 5, 2018 if we have not consummated a Qualified Acquisition, as more fully described in Note 6: Service Agreements and Related Party Transactions, or executed a definitive agreement to consummate an Acquisition (as such term is defined in Article VI of WMIH’s Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”)), prior to that date. Accordingly, as previously disclosed, we formed the Finance Committee of the Company’s Board of Directors (the “Finance Committee”), comprised solely of independent directors, to explore potential financing and refinancing alternatives, including the potential restructuring or refinancing of the Series B Preferred Stock. The Finance Committee has retained financial advisors to provide certain financial advisory services in connection with the Finance Committee’s mandate to review the Company’s capital structure and potential financing alternatives. There can be no assurance that any transaction, including a refinancing of the Series B Preferred Stock, will occur or if so on what terms.

WMMRC

WMMRC is a wholly-owned subsidiary of WMIH. Prior to August 2008 (at which time WMMRC became a direct subsidiary of WMI)WMIH merged with and into Nationstar Mortgage Holdings Inc. (“Nationstar”), WMMRC waswith Nationstar continuing as a wholly-owned subsidiary of FA Out-of-State Holdings, Inc., a second-tier subsidiary of Washington Mutual Bank (“WMB”) and third-tier subsidiary of WMI. WMMRC is a pure captive insurance company domiciled in the State of Hawaii. WMMRC was incorporated on February 25, 2000, and received a Certificate of Authority, dated March 2, 2000, from the Insurance Division of the State of Hawaii.

WMMRC was originally organized to reinsure private mortgage insurance risk for seven primary mortgage insurers then offering private mortgage insurance on loans originated or purchased by former subsidiaries of WMI. The seven primary mortgage insurers are United Guaranty Residential Insurance Company (“UGRIC”), Genworth Mortgage Insurance Corporation (“GMIC”), Mortgage Guaranty Insurance Corporation (“MGIC”), PMI Mortgage Insurance Company (“PMI”), Radian Guaranty Incorporated (“Radian”), Republic Mortgage Insurance Company (“RMIC”) and Triad Guaranty Insurance Company (“Triad”WMIH (the “Merger”).

7

Due Prior to the then deteriorating performanceMerger, WMIH had limited operations other than its reinsurance business that operated in the mortgage guarantee markets and the closure and receivership of WMB, the reinsurance agreements with each of the primary mortgage insurers were terminated or placed into runoff during 2008. The agreements with UGRIC and Triad were placed into runoff effective May 31, 2008. The agreements with all other primary mortgage insurers were placed into runoff effective September 26, 2008.mode. As a result effective September 26, 2008, WMMRC’s continuing operations consisted solely of the runoffMerger, shares of coverage associatedNationstar common stock were delisted from the New York Stock Exchange. Following the Merger closing, the combined company traded on NASDAQ under the ticker symbol “WMIH” until October 10, 2018, when WMIH changed its name to “Mr. Cooper Group Inc.” and its ticker symbol to “COOP”.

WMIIC

WMIIC does not currently have any operations and is fully eliminated upon consolidation.

Note 2: Significant Accounting Policies

Basis of Presentation

WMIH resumed timely filing of all periodic reports for a reporting company under the Exchange Act for all periods after emergence from bankruptcy on March 19, 2012 (the “Effective Date”).

The accompanying unaudited condensed consolidated financial statements have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”) for quarterly reporting. Certain information and footnote disclosures normally included inSEC. Accordingly, the financial statements do not include all of the information and prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”) have been condensed or omitted pursuant to such rules and regulations; however, the Company believes that the disclosures included are appropriate. The condensed consolidated balance sheet as of December 31, 2016, included herein, was derived from the audited consolidatedfootnotes required by GAAP for complete financial statements as of that date.

These interim unaudited condensed consolidated financial statements and notes thereto should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto filedincluded in the Company’s Annual ReportReports on Form 10-K filed withfor the SEC on March 14, 2017. Interim information presented in the unaudited condensedyear ended December 31, 2019.

All significant intercompanyas cost method investments. Intercompany balances and transactions and balanceson consolidated entities have been eliminatedeliminated. Business combinations are included in preparing the condensed consolidated financial statements.

statements from their respective dates of acquisition.

| Final Estimated Fair Value of Net Assets Acquired: | |||

| Cash and cash equivalents | $ | 37 | |

| Restricted cash | 2 | ||

| Mortgage servicing rights | 271 | ||

| Advances and other receivables | 84 | ||

| Mortgage loans held for sale | 536 | ||

| Mortgage loans held for investment | 1 | ||

| Property and equipment | 8 | ||

| Other assets | 483 | ||

| Fair value of assets acquired | 1,422 | ||

Notes payable(1) | 294 | ||

| Advance facilities | 13 | ||

| Warehouse facilities | 393 | ||

| Payables and other liabilities | 530 | ||

| Other nonrecourse debt | 129 | ||

| Fair value of liabilities assumed | 1,359 | ||

| Total fair value of net tangible assets acquired | 63 | ||

| Intangible assets: | |||

Customer relationships(2) | 13 | ||

| Goodwill | 40 | ||

| Final purchase price | $ | 116 | |

(1) | Notes payable was subsequently paid off in February 2019 after the consummation of the acquisition. |

(2) | The estimated fair values for customer relationships were measured using the excess earnings method and were determined to have a remaining useful life of 10 years. |

| Three Months Ended March 31, 2019 | |||

| Pro forma financial information | (unaudited) | ||

| Pro forma total revenues | $ | 269 | |

| Pro forma net loss | $ | (184 | ) |

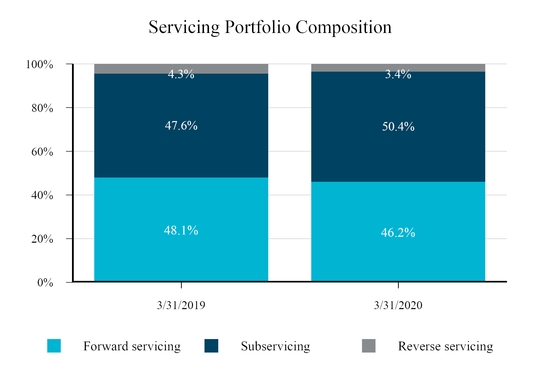

| MSRs and Related Liabilities | March 31, 2020 | December 31, 2019 | |||||

| Forward MSRs - fair value | $ | 3,109 | $ | 3,496 | |||

| Reverse MSRs - amortized cost | 6 | 6 | |||||

| Mortgage servicing rights | $ | 3,115 | $ | 3,502 | |||

| Mortgage servicing liabilities - amortized cost | $ | 53 | $ | 61 | |||

| Excess spread financing - fair value | $ | 1,242 | $ | 1,311 | |||

| Mortgage servicing rights financing - fair value | 43 | 37 | |||||

| MSR related liabilities - nonrecourse at fair value | $ | 1,285 | $ | 1,348 | |||

| Forward MSRs - Fair Value | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Fair value - beginning of period | $ | 3,496 | $ | 3,665 | |||

| Additions: | |||||||

| Servicing retained from mortgage loans sold | 123 | 66 | |||||

Purchases of servicing rights(1) | 24 | 409 | |||||

| Dispositions: | |||||||

| Sales of servicing assets | — | (260 | ) | ||||

| Changes in fair value: | |||||||

| Changes in valuation inputs or assumptions used in the valuation model | (401 | ) | (332 | ) | |||

| Other changes in fair value | (133 | ) | (67 | ) | |||

| Fair value - end of period | $ | 3,109 | $ | 3,481 | |||

(1) | Purchases of servicing rights during the three months ended March 31, 2019 includes $271 of mortgage servicing rights that were acquired from Pacific Union. See Note 2, Acquisitions, for further discussion. |

8

Fair Valuetherefore, behave more like the interest sensitive portfolio. Interest sensitive portfolios generally consist of Certain Financial Instruments

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Generally,lower delinquency, single-family conforming residential forward mortgage loans for assets that are reportedagency investors.

| March 31, 2020 | December 31, 2019 | ||||||||||||||

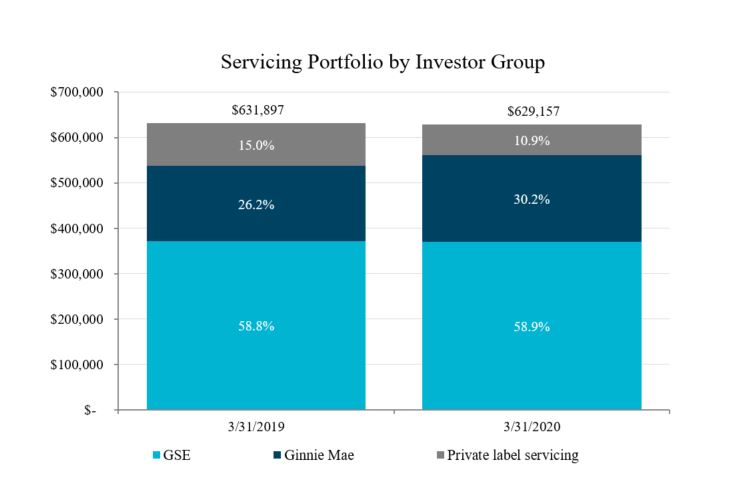

| Forward MSRs - UPB and fair value breakdown | UPB | Fair Value | UPB | Fair Value | |||||||||||

| Acquisition Pools | |||||||||||||||

| Credit sensitive | $ | 138,726 | $ | 1,386 | $ | 147,895 | $ | 1,613 | |||||||

| Interest sensitive | 151,908 | 1,723 | 148,887 | 1,883 | |||||||||||

| Total | $ | 290,634 | $ | 3,109 | $ | 296,782 | $ | 3,496 | |||||||

| Investors Pools | |||||||||||||||

Agency(1) | $ | 238,956 | $ | 2,618 | $ | 240,688 | $ | 2,944 | |||||||

Non-agency(2) | 51,678 | 491 | 56,094 | 552 | |||||||||||

| Total | $ | 290,634 | $ | 3,109 | $ | 296,782 | $ | 3,496 | |||||||

(1) | Agency investors primarily consist of government sponsored enterprises (“GSE”), such as the Federal National Mortgage Association (“Fannie Mae” or “FNMA”) and the Federal Home Loan Mortgage Corp (“Freddie Mac” or “FHLMC”), and the Government National Mortgage Association (“Ginnie Mae” or “GNMA”). |

(2) | Non-agency investors consist of investors in private-label securitizations. |

| Forward MSRs - Key inputs and assumptions | March 31, 2020 | December 31, 2019 | |||

| Total MSR Portfolio | |||||

| Discount rate | 9.7 | % | 9.7 | % | |

| Prepayment speeds | 13.4 | % | 13.1 | % | |

| Average life | 5.7 years | 5.8 years | |||

| Acquisition Pools: | |||||

| Credit Sensitive | |||||

| Discount rate | 10.2 | % | 10.4 | % | |

| Prepayment speeds | 13.0 | % | 12.7 | % | |

| Average life | 5.9 years | 6.0 years | |||

| Interest Sensitive | |||||

| Discount rate | 9.1 | % | 9.1 | % | |

| Prepayment speeds | 13.8 | % | 13.5 | % | |

| Average life | 5.5 years | 5.7 years | |||

| Investor Pools: | |||||

| Agency | |||||

| Discount rate | 9.0 | % | 9.0 | % | |

| Prepayment speeds | 13.2 | % | 13.0 | % | |

| Average life | 5.6 years | 5.8 years | |||

| Non-agency | |||||

| Discount rate | 12.6 | % | 12.6 | % | |

| Prepayment speeds | 14.3 | % | 13.8 | % | |

| Average life | 6.1 years | 6.2 years | |||

| Discount Rate | Total Prepayment Speeds | ||||||||||||||

| Forward MSRs - Hypothetical Sensitivities | 100 bps Adverse Change | 200 bps Adverse Change | 10% Adverse Change | 20% Adverse Change | |||||||||||

| March 31, 2020 | |||||||||||||||

| Mortgage servicing rights | $ | (111 | ) | $ | (214 | ) | $ | (158 | ) | $ | (305 | ) | |||

| December 31, 2019 | |||||||||||||||

| Mortgage servicing rights | $ | (127 | ) | $ | (245 | ) | $ | (165 | ) | $ | (317 | ) | |||

one factor may lead to changes in other factors, which could impact the above hypothetical effects.

| Three Months Ended March 31, | |||||||||||||||

| 2020 | 2019 | ||||||||||||||

| Reverse MSRs and Liabilities - Amortized Cost | Assets | Liabilities | Assets | Liabilities | |||||||||||

| Balance - beginning of period | $ | 6 | $ | 61 | $ | 11 | $ | 71 | |||||||

| Amortization/accretion | — | (8 | ) | — | (18 | ) | |||||||||

Adjustments(1) | — | — | (4 | ) | 37 | ||||||||||

| Balance - end of the period | $ | 6 | $ | 53 | $ | 7 | $ | 90 | |||||||

| Fair value - end of period | $ | 6 | $ | 27 | $ | 7 | $ | 75 | |||||||

(1) | Reverse MSR and MSL net adjustments recorded by the Company during the three months ended March 31, 2019 primarily relate to the fair value adjustments for reverse MSR and MSL assumed from the Merger resulting from the revised cost to service assumption used in the valuation of reverse MSR and MSL during the measurement period. |

| Excess Spread Financing Assumptions | March 31, 2020 | December 31, 2019 | |||

| Discount rate | 11.6 | % | 11.6 | % | |

| Prepayment speeds | 12.8 | % | 12.6 | % | |

| Recapture rate | 18.6 | % | 20.1 | % | |

| Average life | 5.7 years | 5.8 years | |||

excess spread financing fair value when applying certain unfavorable variations of key assumptions to these liabilities for the dates indicated:

| Discount Rate | Prepayment Speeds | ||||||||||||||

| Excess Spread Financing - Hypothetical Sensitivities | 100 bps Adverse Change | 200 bps Adverse Change | 10% Adverse Change | 20% Adverse Change | |||||||||||

| March 31, 2020 | |||||||||||||||

| Excess spread financing | $ | 43 | $ | 89 | $ | 48 | $ | 98 | |||||||

| December 31, 2019 | |||||||||||||||

| Excess spread financing | $ | 46 | $ | 95 | $ | 46 | $ | 96 | |||||||

The carrying valuethe relationship of the loss contract reserve approximates itschange in assumptions to the fair value andmay not be linear. Additionally, the impact of a variation in a particular assumption on the fair value is based on valuation methodologies using discounted cash flows at interest ratescalculated while holding other assumptions constant. In reality, changes in one factor may lead to changes in other factors, which approximatecould impact the Company’s weighted-average cost of capital.

Theabove hypothetical effects. Also, a positive change in the above assumptions would not necessarily correlate with the corresponding decrease in the net carrying valueamount of the derivative embedded conversion feature of the Series B Preferred Stock is adjusted to itsexcess spread financing. Excess Spread financing’s cash flow assumptions that are utilized in determining fair value as determined using Level 3 inputs described below under fair value measurement.

The carrying value of notes payable approximates fair value based on time to maturity, underlying collateral, and prevailing interest rates.

Fair Value Measurement

The Company’s estimates of fair value for financial assets and financial liabilities are based on the framework establishedrelated cash flow assumptions used in the Financial Accounting Standards Boardfinanced MSRs. Any fair value change recognized in the financed MSRs attributable to related cash flows assumptions would inherently have an inverse impact on the carrying amount of the related excess spread financing.

| Mortgage Servicing Rights Financing Assumptions | March 31, 2020 | December 31, 2019 | |||

| Advance financing rates | 1.7 | % | 3.5 | % | |

| Annual advance recovery rates | 18.4 | % | 18.8 | % | |

| Total Revenues - Servicing | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

Contractually specified servicing fees(1) | $ | 297 | $ | 281 | |||

Other service-related income(1) | 49 | 50 | |||||

Incentive and modification income(1) | 10 | 7 | |||||

Late fees(1) | 27 | 25 | |||||

| Reverse servicing fees | 6 | 9 | |||||

Mark-to-market adjustments(2) | (383 | ) | (293 | ) | |||

Counterparty revenue share(3) | (76 | ) | (48 | ) | |||

Amortization, net of accretion(4) | (76 | ) | (23 | ) | |||

| Total revenues - Servicing | $ | (146 | ) | $ | 8 | ||

(1) | The Company recognizes revenue on an earned basis for services performed. Amounts include subservicing related revenues. |

(2) | Mark-to-market (“MTM”) adjustments include fair value adjustments on MSR, excess spread financing and MSR financing liabilities. The amount of MSR MTM includes the impact of negative modeled cash flows which have been transferred to reserves on advances and other receivables. The negative modeled cash flows relate to advances and other receivables associated with inactive and liquidated loans that are no longer part of the MSR portfolio. The impact of negative modeled cash flows for the Company was $10 and $11 for the three months ended March 31, 2020 and 2019, respectively. |

(3) | Counterparty revenue share represents the excess servicing fee that the Company pays to the counterparties under the excess spread financing arrangements and the payments made associated with MSR financing arrangements. |

(4) | Amortization for the Company is net of excess spread accretion of $68 and $36 and MSL accretion of $8 and $18 for the three months ended March 31, 2020 and 2019, respectively. |

| Advances and Other Receivables, Net | March 31, 2020 | December 31, 2019 | |||||

| Servicing advances, net of $125 and $131 discount, respectively | $ | 688 | $ | 970 | |||

| Receivables from agencies, investors and prior servicers, net of $21 and $21 discount, respectively | 190 | 193 | |||||

| Reserves | (193 | ) | (175 | ) | |||

| Total advances and other receivables, net | $ | 685 | $ | 988 | |||

| Reserves for Advances and Other Receivables | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Balance - beginning of period | $ | 168 | $ | 47 | |||

Provision and other additions(1) | 30 | 30 | |||||

| Write-offs | (5 | ) | (6 | ) | |||

| Balance - end of period | $ | 193 | $ | 71 | |||

(1) | The Company recorded a provision of $10 and $11 through the MTM adjustments in revenues - service related, net, in the consolidated statements of operations for the three months ended March 31, 2020 and 2019, respectively, for inactive and liquidated loans that are no longer part of the MSR portfolio. Other additions represent reclassifications of required reserves provisioned within other balance sheet accounts as associated serviced loans become inactive or liquidate. |

| Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | ||||||||||||||

| Purchase Discounts | Servicing Advances | Receivables from Agencies, Investors and Prior Servicers | Servicing Advances | Receivables from Agencies, Investors and Prior Servicers | |||||||||||

| Balance - beginning of period | $ | 131 | $ | 21 | $ | 205 | $ | 48 | |||||||

| Addition from acquisition | — | — | 19 | — | |||||||||||

| Utilization of purchase discounts | (6 | ) | — | (55 | ) | — | |||||||||

| Balance - end of period | $ | 125 | $ | 21 | $ | 169 | $ | 48 | |||||||

| Reverse Mortgage Interests, Net | March 31, 2020 | December 31, 2019 | |||||

| Participating interests in HECM mortgage-backed securities (“HMBS”), net of $16 and $10 purchase discount and premium, respectively | $ | 4,027 | $ | 4,292 | |||

| Other interests securitized, net of $44 and $56 purchase discount, respectively | 851 | 938 | |||||

| Unsecuritized interests, net of $69 and $68 purchase discount, respectively | 1,080 | 1,052 | |||||

| Reserves | (3 | ) | (3 | ) | |||

| Total reverse mortgage interests, net | $ | 5,955 | $ | 6,279 | |||

| Unsecuritized interests | March 31, 2020 | December 31, 2019 | |||||

| Repurchased HECM loans (exceeds 98% MCA) | $ | 782 | $ | 789 | |||

HECM related receivables(1) | 257 | 250 | |||||

| Funded borrower draws not yet securitized | 64 | 67 | |||||

| Real estate owned (“REO”) related receivables | 46 | 14 | |||||

| Purchase discount, net | (69 | ) | (68 | ) | |||

| Total unsecuritized interests | $ | 1,080 | $ | 1,052 | |||

(1) | HECM related receivables consist primarily of receivables from FNMA for corporate advances and service fees and claims receivables from the U.S. Department of Housing and Urban Development (“HUD”) on reverse mortgage interests. |

| Reserves for reverse mortgage interests | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Balance - beginning of period | $ | 3 | $ | 13 | |||

| Provision (release), net | — | — | |||||

| Write-offs | — | (5 | ) | ||||

| Balance - end of period | $ | 3 | $ | 8 | |||

| Three Months Ended March 31, 2020 | |||||||||||

| Purchase premiums and discounts for reverse mortgage interests | Net Discount for Participating Interests in HMBS(1) | Net Discount for Other Interest Securitized(1) | Net Discount for Unsecuritized Interests(1) | ||||||||

| Balance - beginning of period | $ | 10 | $ | (56 | ) | $ | (68 | ) | |||

Utilization of purchase discounts(2) | — | 5 | 5 | ||||||||

| (Amortization)/Accretion | (44 | ) | 17 | 2 | |||||||

Transfers(3) | 18 | (10 | ) | (8 | ) | ||||||

| Balance - end of period | $ | (16 | ) | $ | (44 | ) | $ | (69 | ) | ||

| Three Months Ended March 31, 2019 | |||||||||||

| Purchase premiums and discounts for reverse mortgage interests | Net Premium for Participating Interests in HMBS(1) | Net Discount for Other Interest Securitized(1) | Net Discount for Unsecuritized Interests(1) | ||||||||

| Balance - beginning of period | $ | 58 | $ | (100 | ) | $ | (122 | ) | |||

Adjustments(4) | (16 | ) | (2 | ) | (6 | ) | |||||

Utilization of purchase discounts(2) | — | 6 | 22 | ||||||||

| (Amortization)/Accretion | (14 | ) | (15 | ) | 18 | ||||||

Transfers(3) | 8 | (1 | ) | (7 | ) | ||||||

| Balance - end of period | $ | 36 | $ | (112 | ) | $ | (95 | ) | |||

(1) | Net position as certain items are in a premium/(discount) position, based on the characteristics of underlying tranches of loans. |

(2) | Utilization of purchase discounts on liquidated loans, for which the remaining receivable was written-off. |

(3) | Transfer of premium/(discount) based on the transfer of associated loans between categories consistent with the underlying loan characteristics. |

(4) | Adjustments to premium/(discount) due to revised cost to service assumption utilized in the valuation of reverse mortgage assets and liabilities acquired from the Merger during the measurement period. |

| Mortgage Loans Held for Sale | March 31, 2020 | December 31, 2019 | |||||

| Mortgage loans held for sale – UPB | $ | 3,735 | $ | 3,949 | |||

Mark-to-market adjustment(1) | 187 | 128 | |||||

| Total mortgage loans held for sale | $ | 3,922 | $ | 4,077 | |||

(1) | The mark-to-market adjustment is recorded in net gain on mortgage loans held for sale in the consolidated statements of operations. |

| March 31, 2020 | December 31, 2019 | ||||||||||||||

| Mortgage Loans Held for Sale | UPB | Fair Value | UPB | Fair Value | |||||||||||

Non-accrual(1) | $ | 33 | $ | 23 | $ | 29 | $ | 22 | |||||||

(1) | Non-accrual - UPB includes $28 and $25 of UPB related to Ginnie Mae repurchased loans as of March 31, 2020 and December 31, 2019, respectively. |

| Mortgage Loans Held for Sale | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Balance - beginning of period | $ | 4,077 | $ | 1,631 | |||

| Loans sold | (13,510 | ) | (6,088 | ) | |||

Mortgage loans originated and purchased, net of fees(1) | 12,375 | 6,253 | |||||

| Repurchase of loans out of Ginnie Mae securitizations | 919 | 364 | |||||

| Changes in fair value | 61 | 10 | |||||

Net transfers of mortgage loans held for sale(2) | — | — | |||||

| Balance - end of period | $ | 3,922 | $ | 2,170 | |||

(1) | Mortgage loans originated and purchased during the three months ended March 31, 2019 includes $536 of loans held for sale that were acquired from Pacific Union. See Note 2, Acquisitions, for further discussion. |

(2) | Amount reflects transfers to other assets for loans transitioning into REO status and transfers to advances and other receivables, net for claims made on certain government insurance mortgage loans. Transfers out are net of transfers in upon receipt of proceeds from an REO sale or claim filing. |

| Net lease cost | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Operating lease cost | $ | 10 | $ | 8 | |||

| Short-term lease cost | — | 1 | |||||

| Sublease income | (1 | ) | — | ||||

| Net lease cost | $ | 9 | $ | 9 | |||

| Operating leases | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Cash paid for amounts included in the measurement of lease liabilities: | |||||||

| Operating cash flows from operating leases | $ | 10 | $ | 6 | |||

| Leased assets obtained in exchange for new operating lease liabilities | $ | — | $ | 127 | |||

| Weighted average remaining lease term | 5.6 years | 5.5 years | |||||

| Weighted average discount rate | 5.0 | % | 5.0 | % | |||

| Year Ending December 31, | Operating Leases | |||

2020(1) | $ | 37 | ||

| 2021 | 29 | |||

| 2022 | 20 | |||

| 2023 | 16 | |||

| 2024 | 11 | |||

| 2025 and thereafter | 30 | |||

| Total future minimum lease payments | 143 | |||

| Less: imputed interest | 18 | |||

| Total operating lease liabilities | $ | 125 | ||

(1) | Excluding the three months ended March 31, 2020. |

| Other assets | March 31, 2020 | December 31, 2019 | |||||

| Loans subject to repurchase right from Ginnie Mae | $ | 468 | $ | 560 | |||

| Derivative financial instruments | 294 | 153 | |||||

| Trade receivables and accrued revenues | 143 | 126 | |||||

| Goodwill | 120 | 120 | |||||

| Right-of-use assets | 111 | 121 | |||||

| Intangible assets | 61 | 74 | |||||

| Other | 372 | 236 | |||||

| Total other assets | $ | 1,569 | $ | 1,390 | |||

| March 31, 2020 | Three Months Ended March 31, 2020 | ||||||||||||

| Derivative Financial Instruments | Expiration Dates | Outstanding Notional | Fair Value | Recorded Gains/(Losses) | |||||||||

| Assets | |||||||||||||

| Mortgage loans held for sale | |||||||||||||

| Loan sale commitments | 2020 | $ | 2,598 | $ | 111 | $ | 79 | ||||||

| Derivative financial instruments | |||||||||||||

| IRLCs | 2020 | 6,923 | 263 | 128 | |||||||||

| LPCs | 2020 | 834 | 25 | 13 | |||||||||

| Forward MBS trades | 2020 | 886 | 6 | — | |||||||||

| Eurodollar futures | 2020-2021 | 6 | — | — | |||||||||

| Total derivative financial instruments - assets | $ | 8,649 | $ | 294 | $ | 141 | |||||||

| Liabilities | |||||||||||||

| Derivative financial instruments | |||||||||||||

| IRLCs | 2020 | $ | 22 | $ | — | $ | — | ||||||

| LPCs | 2020 | 10 | — | (3 | ) | ||||||||

| Forward MBS trades | 2020 | 10,229 | 223 | 211 | |||||||||

| Eurodollar futures | 2020-2021 | 6 | — | — | |||||||||

| Total derivative financial instruments - liabilities | $ | 10,267 | $ | 223 | $ | 208 | |||||||

| March 31, 2019 | Three Months Ended March 31, 2019 | ||||||||||||

| Derivative Financial Instruments | Expiration Dates | Outstanding Notional | Fair Value | Recorded Gains/(Losses) | |||||||||

| Assets | |||||||||||||

| Mortgage loans held for sale | |||||||||||||

| Loan sale commitments | 2019 | $ | 365 | $ | 17 | $ | (9 | ) | |||||

| Derivative financial instruments | |||||||||||||

| IRLCs | 2019 | 2,557 | 69 | 9 | |||||||||

| LPCs | 2019 | 216 | 2 | 1 | |||||||||

| Forward MBS trades | 2019 | 410 | 1 | (1 | ) | ||||||||

| Eurodollar futures | 2019-2021 | 7 | — | — | |||||||||

| Total derivative financial instruments - assets | $ | 3,190 | $ | 72 | $ | 9 | |||||||

| Liabilities | |||||||||||||

| Derivative financial instruments | |||||||||||||

| LPCs | 2019 | $ | 52 | $ | — | $ | — | ||||||

| Forward MBS trades | 2019 | 3,804 | 22 | (3 | ) | ||||||||

| Eurodollar futures | 2019-2021 | 13 | — | — | |||||||||

| Total derivative financial instruments - liabilities | $ | 3,869 | $ | 22 | $ | (3 | ) | ||||||

| March 31, 2020 | December 31, 2019 | |||||||||||||||||||||||||

| Advance Facilities | Interest Rate | Maturity Date | Collateral | Capacity Amount | Outstanding | Collateral Pledged | Outstanding | Collateral pledged | ||||||||||||||||||

$325 advance facility(1) | LIBOR+1.5% to 6.5% | August 2021 | Servicing advance receivables | $ | 325 | $ | 223 | $ | 283 | $ | 224 | $ | 285 | |||||||||||||

$250 advance facility(2) | LIBOR+1.5% to 2.6% | December 2020 | Servicing advance receivables | 250 | 118 | 138 | 98 | 167 | ||||||||||||||||||

| $200 advance facility | LIBOR+2.5% | January 2021 | Servicing advance receivables | 200 | 83 | 117 | 63 | 125 | ||||||||||||||||||

$125 advance facility(3) | LIBOR+1.5% to 7.4% | July 2020 | Servicing advance receivables | 125 | 66 | 76 | 37 | 88 | ||||||||||||||||||

| Advance facilities principal amount | 490 | $ | 614 | 422 | $ | 665 | ||||||||||||||||||||

| Unamortized debt issuance costs | (1 | ) | — | |||||||||||||||||||||||

| Advance facilities, net | $ | 489 | $ | 422 | ||||||||||||||||||||||

(1) | The capacity amount was subsequently increased to $425 in April 2020 with a maturity date of October 2021. |

(2) | This advance facility was subsequently terminated and transferred to another advance facility in April 2020. |

(3) | The capacity amount was subsequently increased to $875 in April 2020 with a maturity date of April 2021. |

| March 31, 2020 | December 31, 2019 | |||||||||||||||||||||||||

| Warehouse Facilities | Interest Rate | Maturity Date | Collateral | Capacity Amount | Outstanding | Collateral pledged | Outstanding | Collateral pledged | ||||||||||||||||||

| $1,500 warehouse facility | LIBOR+1.0% | June 2020 | Mortgage loans or MBS | $ | 1,500 | $ | 1,214 | $ | 1,160 | $ | 759 | $ | 733 | |||||||||||||

| $1,200 warehouse facility | LIBOR+1.5% to 3.0% | November 2020 | Mortgage loans or MBS | 1,200 | 566 | 602 | 683 | 724 | ||||||||||||||||||

| $1,000 warehouse facility | LIBOR+1.4% to 2.3% | September 2020 | Mortgage loans or MBS | 1,000 | 593 | 608 | 762 | 783 | ||||||||||||||||||

$800 warehouse facility(1) | LIBOR+2.1% to 3.8% | April 2021 | Mortgage loans or MBS | 800 | 528 | 639 | 589 | 656 | ||||||||||||||||||

| $750 warehouse facility | LIBOR+1.4% to 2.8% | September 2020 | Mortgage loans or MBS | 750 | 347 | 355 | 411 | 425 | ||||||||||||||||||

| $700 warehouse facility | LIBOR+1.3% to 2.2% | November 2020 | Mortgage loans or MBS | 700 | 628 | 649 | 469 | 488 | ||||||||||||||||||

| $600 warehouse facility | LIBOR+2.0% | February 2021 | Mortgage loans or MBS | 600 | 169 | 203 | 174 | 202 | ||||||||||||||||||

| $500 warehouse facility | LIBOR+2.0% to 4.0% | May 2020 | Mortgage loans or MBS | 500 | 22 | 23 | 336 | 349 | ||||||||||||||||||

| $200 warehouse facility | LIBOR+1.4% | January 2021 | Mortgage loans or MBS | 200 | 100 | 101 | 136 | 136 | ||||||||||||||||||

| $200 warehouse facility | LIBOR+1.2% | April 2021 | Mortgage loans or MBS | 200 | 21 | 21 | 27 | 27 | ||||||||||||||||||

| $200 warehouse facility | LIBOR+2.0% | May 2020 | Mortgage loans or MBS | 200 | 59 | 83 | 54 | 78 | ||||||||||||||||||

| $200 warehouse facility | LIBOR+1.3% | October 2020 | Mortgage loans or MBS | 200 | — | — | — | — | ||||||||||||||||||

| $50 warehouse facility | LIBOR+2.0% to 6.0% | June 2020 | Mortgage loans or MBS | 50 | 4 | 6 | 11 | 15 | ||||||||||||||||||

| $40 warehouse facility | LIBOR+3.3% | September 2020 | Mortgage loans or MBS | 40 | 6 | 7 | 5 | 6 | ||||||||||||||||||

| Warehouse facilities principal amount | 4,257 | 4,457 | 4,416 | 4,622 | ||||||||||||||||||||||

| MSR Facility | ||||||||||||||||||||||||||

| $400 warehouse facility | LIBOR+3.5% or 6.1% | January 2023 | Mortgage loans or MBS | 400 | 150 | 836 | 150 | 945 | ||||||||||||||||||

| $400 warehouse facility | LIBOR+2.3% | December 2020 | Mortgage loans or MBS | 400 | 75 | 190 | — | 200 | ||||||||||||||||||

$150 warehouse facility(1) | LIBOR+2.8% | April 2021 | Mortgage loans or MBS | 150 | 40 | 119 | — | 130 | ||||||||||||||||||

| $50 warehouse facility | LIBOR+2.8% | August 2020 | Mortgage loans or MBS | 50 | 30 | 71 | 10 | 84 | ||||||||||||||||||

| MSR facilities principal amount | 295 | 1,216 | 160 | 1,359 | ||||||||||||||||||||||

| Warehouse and MSR facilities principal amount | 4,552 | $ | 5,673 | 4,576 | $ | 5,981 | ||||||||||||||||||||

| Unamortized debt issuance costs | (1 | ) | (1 | ) | ||||||||||||||||||||||

| Warehouse facilities, net | $ | 4,551 | $ | 4,575 | ||||||||||||||||||||||

| Pledged Collateral: | ||||||||||||||||||||||||||

| Mortgage loans held for sale | $ | 3,659 | $ | 3,748 | $ | 3,826 | $ | 3,931 | ||||||||||||||||||

| Reverse mortgage interests | 598 | 709 | 590 | 691 | ||||||||||||||||||||||

| MSR | 295 | 1,216 | 160 | 1,359 | ||||||||||||||||||||||

(1) | Total capacity amount for this facility is $800 of which $150 is a sublimit for MSR financing. |

| Unsecured senior notes | March 31, 2020 | December 31, 2019 | |||||

| $950 face value, 8.125% interest rate payable semi-annually, due July 2023 | $ | 950 | $ | 950 | |||

| $750 face value, 9.125% interest rate payable semi-annually, due July 2026 | 750 | 750 | |||||

$600 face value, 6.000% interest rate payable semi-annually, due January 2027(1) | 600 | — | |||||

$600 face value, 6.500% interest rate payable semi-annually, due July 2021(2) | — | 492 | |||||

$300 face value, 6.500% interest rate payable semi-annually, due June 2022(2) | — | 206 | |||||

| Unsecured senior notes principal amount | 2,300 | 2,398 | |||||

| Unamortized debt issuance costs, premium and discount | (41 | ) | (32 | ) | |||

| Unsecured senior notes, net | $ | 2,259 | $ | 2,366 | |||

(1) | On January 16, 2020, the Company completed an offering of $600 aggregate principal amount of 6.000% Senior Notes due 2027 (the “2027 notes”). |

(2) | This note was redeemed in full on February 15, 2020 using the net proceeds of the 2027 notes offering, together with cash on hand. |

| Year Ending December 31, | Amount | |||

| 2020 | $ | — | ||

| 2021 | — | |||

| 2022 | — | |||

| 2023 | 950 | |||

| 2024 | — | |||

| Thereafter | 1,350 | |||

| Total unsecured senior notes principal amount | $ | 2,300 | ||

| March 31, 2020 | December 31, 2019 | ||||||||||||||||

| Other nonrecourse debt | Issue Date | Maturity Date | Class of Note | Collateral Amount | Outstanding | Outstanding | |||||||||||

Participating interest financing(1) | — | — | — | $ | — | $ | 4,045 | $ | 4,284 | ||||||||

| Securitization of nonperforming HECM loans | |||||||||||||||||

| Trust 2019-2 | November 2019 | November 2029 | A, M1, M2, M3, M4, M5 | 306 | 297 | 333 | |||||||||||

| Trust 2019-1 | June 2019 | June 2029 | A, M1, M2, M3, M4, M5 | 286 | 269 | 302 | |||||||||||

| Trust 2018-3 | November 2018 | November 2028 | A, M1, M2, M3, M4, M5 | 209 | 190 | 209 | |||||||||||

| Trust 2018-2 | July 2018 | July 2028 | A, M1, M2, M3, M4, M5 | 157 | 137 | 148 | |||||||||||

| Other nonrecourse debt principal amount | 4,938 | 5,276 | |||||||||||||||

| Unamortized debt issuance costs, premium and discount | 7 | 10 | |||||||||||||||

| Other nonrecourse debt, net | $ | 4,945 | $ | 5,286 | |||||||||||||

(1) | Amounts represent the Company’s participating interest in GNMA HMBS securitized portfolios. |

| Payables and other liabilities | March 31, 2020 | December 31, 2019 | |||||

| Loans subject to repurchase right from Ginnie Mae | $ | 468 | $ | 560 | |||

| Payables to servicing and subservicing investors | 407 | 423 | |||||

| Derivative financial instruments | 223 | 15 | |||||

| Payable to GSEs and securitized trusts | 148 | 182 | |||||

| Operating lease liabilities | 125 | 135 | |||||

| Other liabilities | 594 | 701 | |||||

| Total payables and other liabilities | $ | 1,965 | $ | 2,016 | |||

| Repurchase Reserves | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Balance - beginning of period | $ | 25 | $ | 8 | |||

| Provisions | 5 | 8 | |||||

| Releases | (1 | ) | — | ||||

| Balance - end of period | $ | 29 | $ | 16 | |||

| March 31, 2020 | December 31, 2019 | ||||||||||||||

| Consolidated transactions with VIEs | Transfers Accounted for as Secured Borrowings | Reverse Secured Borrowings | Transfers Accounted for as Secured Borrowings | Reverse Secured Borrowings | |||||||||||

| Assets | |||||||||||||||

| Restricted cash | $ | 53 | $ | 43 | $ | 66 | $ | 42 | |||||||

Reverse mortgage interests, net(1) | — | 4,878 | — | 5,230 | |||||||||||

| Advances and other receivables, net | 498 | — | 540 | — | |||||||||||

| Total assets | $ | 551 | $ | 4,921 | $ | 606 | $ | 5,272 | |||||||

| Liabilities | |||||||||||||||

Advance facilities(2) | $ | 407 | $ | — | $ | 359 | $ | — | |||||||

| Payables and other liabilities | — | 1 | 1 | 1 | |||||||||||

| Participating interest financing | — | 4,045 | — | 4,284 | |||||||||||

| HECM Securitizations (HMBS) | |||||||||||||||

| Trust 2019-2 | — | 297 | — | 333 | |||||||||||

| Trust 2019-1 | — | 269 | — | 302 | |||||||||||

| Trust 2018-3 | — | 190 | — | 209 | |||||||||||

| Trust 2018-2 | — | 137 | — | 148 | |||||||||||

| Total liabilities | $ | 407 | $ | 4,939 | $ | 360 | $ | 5,277 | |||||||

(1) | Amounts include net purchase discount of $60 and $46 as of March 31, 2020 and December 31, 2019, respectively. |

(2) | Amounts include the Nationstar agency advance financing facility and notes payable recorded by the Nationstar Mortgage Advance Receivable Trust, and the Nationstar Agency Advance Receivables Trust. Refer to Notes Payable in Note 10, Indebtedness, for additional information. |

| Unconsolidated securitization trusts | March 31, 2020 | December 31, 2019 | |||||

| Total collateral balances - UPB | $ | 1,460 | $ | 1,503 | |||

| Total certificate balances | $ | 1,467 | $ | 1,512 | |||

| Principal Amount of Transferred Loans 60 Days or More Past Due | March 31, 2020 | December 31, 2019 | |||||

| Unconsolidated securitization trusts | $ | 184 | $ | 193 | |||

| Computation of earnings per share | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Net loss attributable to Mr. Cooper | $ | (168 | ) | $ | (186 | ) | |

| Less: Undistributed earnings attributable to participating stockholders | — | — | |||||

| Net loss attributable to common stockholders | $ | (168 | ) | $ | (186 | ) | |

| Net loss per common share attributable to Mr. Cooper: | |||||||

| Basic | $ | (1.84 | ) | $ | (2.05 | ) | |

| Diluted | $ | (1.84 | ) | $ | (2.05 | ) | |

| Weighted average shares of common stock outstanding (in thousands): | |||||||

| Basic | 91,385 | 90,828 | |||||

Dilutive effect of stock awards(1) | — | — | |||||

Dilutive effect of participating securities(1) | — | — | |||||

| Diluted | 91,385 | 90,828 | |||||

(1) | Due to year-to-date loss, the Company excluded potential common shares from the computation of diluted EPS because inclusion would be antidilutive. |

| Income taxes | Three Months Ended March 31, 2020 | Three Months Ended March 31, 2019 | |||||

| Loss before income tax benefit | $ | (239 | ) | $ | (233 | ) | |

| Income tax benefit | $ | (68 | ) | $ | (47 | ) | |

Effective tax rate(1) | 28.4 | % | 20.3 | % | |||

(1) | Effective tax rate is calculated using whole numbers. |

The three levels of the hierarchy are as follows:

(e.g., Level 1–Inputs to the valuation methodology are1 representing quoted prices for identical assets or liabilities traded in an active markets.

market; Level 2–Inputs to the valuation methodology include quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active,2 representing values using observable inputs other than quoted prices that are observable for the asset or liabilityincluded within Level 1; and market corroborated inputs.

Level 3–Valuations3 representing estimated values based on models where significant inputs are not observable. unobservable inputs).

Fair values are based on quoted pricesCompany in active markets when availableestimating fair values:

9

Fixed-maturity securities consistportfolio, and estimated participating income. Discounted cash flows are applied based on collateral stratifications and include loan rate type, loan status (active vs. inactive), and securitization. Prices are also influenced from both internal models and other observable inputs. The Company determined fair value for all loans based on the applicable tranches established during the Merger valuation. Tranches are segregated based on participation percentages, original loan status as of U.S. Treasury securities, obligationsthe Merger date, and interest rate types, and loan status (active vs inactive). Prices are also influenced from both internal models and other observable inputs, including applicable forward interest rate curves. Additionally, historical loss factors are considered within the overall valuation. Because of U.S. government sponsored agenciesthe unobservable nature of the valuation inputs, the Company classifies these valuations as Level 3 in the fair value disclosures. See

Investments Held in Trust

Investments held in trust consist of cash equivalents, which include highly liquid overnight money market instruments, and fixed-maturity securitiesunderlying mortgage loans which are held in trust forbased on observable market data. The Company adjusts the benefit of the primary insurers, as more fully described in Note 3: Insurance Activity and Note 4: Investment Securities, and are subject to the restrictionsoutstanding IRLCs with prospective borrowers based on distribution of net assets of subsidiaries as described below.

Third Party Restrictions on Distribution of Net Assets of Wholly-Owned Subsidiaries

The net assets of WMMRC are subject to restrictions on distribution from multiple sources, including the primary insurers who have approval control of distributions from the trust,an expectation that it will be exercised, and the Insurance Division of the State of Hawaii who has approval authority over distributions or intercompany advances. As more fully described in Note 14: Subsequent Events, a distribution from WMMRC to WMIH of up to $10.7 million was approved by the Insurance Division of the State of Hawaii on September 13, 2017.

Premium Recognition

Premiums assumed are earned on a daily pro-rata basis over the underlying policy terms. Premiums assumed relating to the unexpired portion of policies in force at the balance sheet dateloan will be funded. IRLCs and LPCs are recorded in derivative financial instruments in the consolidated balance sheets. These commitments are classified as unearned premiums. Unearned premiums also include a reserve for post default premium reserves. Post default premium reserves occur when a loan isLevel 2 in a default position and the servicer continues to advancefair value disclosures, as the premiums. If the loan ultimately goes to claim, the premiums advanced during the period of defaultvaluations are subject to recapture. The Company records a default premium reserve based on information provided by the underlying mortgage insurers when they provide information on the default premium reserve separately from other reserves. The change in the post default premium reserve is reflected as a reduction or increase, as the case may be, in premiums assumed.market observable inputs. The Company has entered into Eurodollar futures contracts as part of its hedging strategy. The futures contracts are measured at fair value on a recurring basis and classified as Level 2 in the fair value disclosures as the valuation is based on market observable data. Derivative financial instruments are recorded unearned premiums totaling $33 thousandin other assets and $0.3 million aspayables and other liabilities within the consolidated balance sheets. See

is considered Level 1 from the market observable inputs used to determine fair value. See

Note 10, Indebtedness, for more information.| March 31, 2020 | |||||||||||||||

| Recurring Fair Value Measurements | |||||||||||||||

| Fair value - Recurring basis | Total Fair Value | Level 1 | Level 2 | Level 3 | |||||||||||

| Assets | |||||||||||||||

| Mortgage loans held for sale | $ | 3,922 | $ | — | $ | 3,922 | $ | — | |||||||

| Forward mortgage servicing rights | 3,109 | — | — | 3,109 | |||||||||||

| Derivative financial instruments | |||||||||||||||

| IRLCs | 263 | — | 263 | — | |||||||||||

| Forward MBS trades | 6 | — | 6 | — | |||||||||||

| LPCs | 25 | — | 25 | — | |||||||||||

| Total assets | $ | 7,325 | $ | — | $ | 4,216 | $ | 3,109 | |||||||

| Liabilities | |||||||||||||||

| Derivative financial instruments | |||||||||||||||

| Forward MBS trades | $ | 223 | $ | — | $ | 223 | $ | — | |||||||

| Mortgage servicing rights financing | 43 | — | — | 43 | |||||||||||

| Excess spread financing | 1,242 | — | — | 1,242 | |||||||||||

| Total liabilities | $ | 1,508 | $ | — | $ | 223 | $ | 1,285 | |||||||

| December 31, 2019 | |||||||||||||||