UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20182019

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-33303

TARGA RESOURCES PARTNERS LP

(Exact name of registrant as specified in its charter)

Delaware |

| 65-1295427 | ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) | ||

|

|

| ||

811 Louisiana St, Suite 2100, Houston, Texas |

| 77002 | ||

(Address of principal executive offices) |

| (Zip Code) |

(713) 584-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of exchange on which registered | ||

9.0% Series A Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | NGLS/PA | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ |

| Accelerated filer | ☐ | |

Non-accelerated filer | ☑ |

| Smaller reporting company | ☐ | |

|

|

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes☐ No☑.

As of November 5, 2018,1, 2019, there were 5,000,000 9.0% Series A Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units outstanding.

1

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING STATEMENTS

Targa Resources Partners LP’s (together with its subsidiaries, “we,” “us,” “our,” “TRP” or “the Partnership”the “Partnership”) reports, filings and other public announcements may from time to time contain statements that do not directly or exclusively relate to historical facts. Such statements are “forward-looking statements.” You can typically identify forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, by the use of forward-looking statements, such as “may,” “could,” “project,” “believe,” “anticipate,” “expect,” “estimate,” “potential,” “plan,” “forecast” and other similar words.

All statements that are not statements of historical facts, including statements regarding our future financial position, business strategy, budgets, projected costs and plans and objectives of management for future operations, are forward-looking statements.

These forward-looking statements reflect our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors, many of which are outside our control. Important factors that could cause actual results to differ materially from the expectations expressed or implied in the forward-looking statements include known and unknown risks. Known risks and uncertainties include, but are not limited to, the following risks and uncertainties:

the timing and extent of changes in natural gas, natural gas liquids, crude oil and other commodity prices, interest rates and demand for our services;

• | the timing and extent of changes in natural gas, natural gas liquids, crude oil and other commodity prices, interest rates and demand for our services; |

the level and success of crude oil and natural gas drilling around our assets, our success in connecting natural gas supplies to our gathering and processing systems, oil supplies to our gathering systems and natural gas liquid supplies to our logistics and marketing facilities and our success in connecting our facilities to transportation services and markets;

• | the level and success of crude oil and natural gas drilling around our assets, our success in connecting natural gas supplies to our gathering and processing systems, oil supplies to our gathering systems and natural gas liquid supplies to our transportation and logistics and marketing facilities and our success in connecting our facilities to transportation services and markets; |

our ability to access the capital markets, which will depend on general market conditions and the credit ratings for our debt obligations;

• | our ability to access the capital markets, which will depend on general market conditions and the credit ratings for our debt obligations; |

the amount of collateral required to be posted from time to time in our transactions;

• | the amount of collateral required to be posted from time to time in our transactions; |

our success in risk management activities, including the use of derivative instruments to hedge commodity price risks;

• | our success in risk management activities, including the use of derivative instruments to hedge commodity price risks; |

the level of creditworthiness of counterparties to various transactions with us;

• | the level of creditworthiness of counterparties to various transactions with us; |

changes in laws and regulations, particularly with regard to taxes, safety and protection of the environment;

• | changes in laws and regulations, particularly with regard to taxes, safety and protection of the environment; |

weather and other natural phenomena;

• | weather and other natural phenomena; |

industry changes, including the impact of consolidations and changes in competition;

• | industry changes, including the impact of consolidations and changes in competition; |

our ability to obtain necessary licenses, permits and other approvals;

• | our ability to obtain necessary licenses, permits and other approvals; |

our ability to grow through acquisitions or internal growth projects and the successful integration and future performance of such assets;

• | our ability to grow through acquisitions or internal growth projects and the successful integration and future performance of such assets; |

general economic, market and business conditions; and

• | general economic, market and business conditions; and |

the risks described in our Annual Report on Form 10-K for the year ended December 31, 2017 (“Annual Report”) and our reports and registration statements filed from time to time with the United States Securities and Exchange Commission (“SEC”).

• | the risks described in our Annual Report on Form 10-K for the year ended December 31, 2018 (“Annual Report”) and our reports and registration statements filed from time to time with the United States Securities and Exchange Commission (“SEC”). |

Although we believe that the assumptions underlying our forward-looking statements are reasonable, any of the assumptions could be inaccurate, and, therefore, we cannot assure you that the forward-looking statements included in this Quarterly Report on Form 10-Q for the quarter ended September 30, 20182019 (“Quarterly Report”) will prove to be accurate. Some of these and other risks and uncertainties that could cause actual results to differ materially from such forward-looking statements are more fully described in our Annual Report. Except as may be required by applicable law, we undertake no obligation to publicly update or advise of any change in any forward-looking statement, whether as a result of new information, future events or otherwise.

2

As generally used in the energy industry and in this Quarterly Report, the identified terms have the following meanings:

Bbl | Barrels (equal to 42 U.S. gallons) | |

BBtu | Billion British thermal units | |

Bcf | Billion cubic feet | |

Btu | British thermal units, a measure of heating value | |

/d | Per day | |

GAAP | Accounting principles generally accepted in the United States of America | |

gal | U.S. gallons | |

|

| |

|

| |

LIBOR | London Interbank Offered Rate | |

LPG | Liquefied petroleum gas | |

MBbl | Thousand barrels | |

MMBbl | Million barrels | |

MMBtu | Million British thermal units | |

MMcf | Million cubic feet | |

MMgal | Million U.S. gallons | |

NGL(s) | Natural gas liquid(s) | |

NYMEX | New York Mercantile Exchange | |

NYSE | New York Stock Exchange | |

SCOOP | South Central Oklahoma Oil Province | |

STACK | Sooner Trend, Anadarko, Canadian and Kingfisher | |

|

|

PART I – FINANCIALFINANCIAL INFORMATION

TARGA RESOURCES PARTNERS LP

|

|

| September 30, 2018 |

|

| December 31, 2017 |

|

|

| September 30, 2019 |

|

| December 31, 2018 |

| ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

| (Unaudited) |

| |||||||||||||||||

|

|

| (In millions) |

|

|

| (In millions) |

| ||||||||||||||||||||||||||

ASSETS | ASSETS |

|

|

|

|

|

|

|

| ASSETS |

| |||||||||||||||||||||||

Current assets: | Current assets: |

|

|

|

|

|

|

|

| Current assets: |

|

|

|

|

|

|

|

| ||||||||||||||||

Cash and cash equivalents | Cash and cash equivalents |

| $ | 187.5 |

|

| $ | 124.7 |

| Cash and cash equivalents |

| $ | 294.9 |

|

| $ | 203.3 |

| ||||||||||||||||

Trade receivables, net of allowances of $0.1 and $0.1 million at September 30, 2018 and December 31, 2017 |

|

| 1,036.0 |

|

|

| 825.7 |

| ||||||||||||||||||||||||||

Trade receivables, net of allowances of $0.0 and $0.1 million at September 30, 2019 and December 31, 2018 | Trade receivables, net of allowances of $0.0 and $0.1 million at September 30, 2019 and December 31, 2018 |

|

| 742.9 |

|

|

| 864.4 |

| |||||||||||||||||||||||||

Inventories | Inventories |

|

| 177.9 |

|

|

| 204.5 |

| Inventories |

|

| 210.9 |

|

|

| 164.7 |

| ||||||||||||||||

Assets from risk management activities | Assets from risk management activities |

|

| 59.6 |

|

|

| 37.9 |

| Assets from risk management activities |

|

| 140.1 |

|

|

| 115.3 |

| ||||||||||||||||

Other current assets | Other current assets |

|

| 66.4 |

|

|

| 55.8 |

| Other current assets |

|

| 43.4 |

|

|

| 32.2 |

| ||||||||||||||||

Held for sale assets (see Note 4) |

|

| 165.7 |

|

|

| — |

| ||||||||||||||||||||||||||

Total current assets | Total current assets |

|

| 1,693.1 |

|

|

| 1,248.6 |

| Total current assets |

|

| 1,432.2 |

|

|

| 1,379.9 |

| ||||||||||||||||

Property, plant and equipment | Property, plant and equipment |

|

| 16,214.6 |

|

|

| 14,198.6 |

| Property, plant and equipment |

|

| 19,589.1 |

|

|

| 17,213.8 |

| ||||||||||||||||

Accumulated depreciation |

|

| (4,133.8 | ) |

|

| (3,768.7 | ) | ||||||||||||||||||||||||||

Accumulated depreciation and amortization | Accumulated depreciation and amortization |

|

| (4,892.4 | ) |

|

| (4,285.5 | ) | |||||||||||||||||||||||||

Property, plant and equipment, net | Property, plant and equipment, net |

|

| 12,080.8 |

|

|

| 10,429.9 |

| Property, plant and equipment, net |

|

| 14,696.7 |

|

|

| 12,928.3 |

| ||||||||||||||||

Intangible assets, net | Intangible assets, net |

|

| 2,029.6 |

|

|

| 2,165.8 |

| Intangible assets, net |

|

| 1,854.4 |

|

|

| 1,983.2 |

| ||||||||||||||||

Goodwill, net | Goodwill, net |

|

| 256.6 |

|

|

| 256.6 |

| Goodwill, net |

|

| 46.6 |

|

|

| 46.6 |

| ||||||||||||||||

Long-term assets from risk management activities | Long-term assets from risk management activities |

|

| 8.4 |

|

|

| 23.2 |

| Long-term assets from risk management activities |

|

| 60.0 |

|

|

| 34.1 |

| ||||||||||||||||

Investments in unconsolidated affiliates | Investments in unconsolidated affiliates |

|

| 441.5 |

|

|

| 221.6 |

| Investments in unconsolidated affiliates |

|

| 718.5 |

|

|

| 490.5 |

| ||||||||||||||||

Other long-term assets | Other long-term assets |

|

| 16.5 |

|

|

| 13.3 |

| Other long-term assets |

|

| 49.9 |

|

|

| 27.5 |

| ||||||||||||||||

Total assets | Total assets |

| $ | 16,526.5 |

|

| $ | 14,359.0 |

| Total assets |

| $ | 18,858.3 |

|

| $ | 16,890.1 |

| ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

LIABILITIES AND OWNERS' EQUITY | LIABILITIES AND OWNERS' EQUITY |

|

|

|

|

|

|

|

| LIABILITIES AND OWNERS' EQUITY |

| |||||||||||||||||||||||

Current liabilities: | Current liabilities: |

|

|

|

|

|

|

|

| Current liabilities: |

|

|

|

|

|

|

|

| ||||||||||||||||

Accounts payable and accrued liabilities | Accounts payable and accrued liabilities |

| $ | 1,984.1 |

|

| $ | 1,106.6 |

| Accounts payable and accrued liabilities |

| $ | 1,234.8 |

|

| $ | 1,636.9 |

| ||||||||||||||||

Accounts payable to Targa Resources Corp. | Accounts payable to Targa Resources Corp. |

|

| 136.5 |

|

|

| 76.9 |

| Accounts payable to Targa Resources Corp. |

|

| 194.0 |

|

|

| 187.4 |

| ||||||||||||||||

Liabilities from risk management activities | Liabilities from risk management activities |

|

| 176.3 |

|

|

| 79.7 |

| Liabilities from risk management activities |

|

| 83.5 |

|

|

| 33.6 |

| ||||||||||||||||

Current debt obligations | Current debt obligations |

|

| 290.0 |

|

|

| 350.0 |

| Current debt obligations |

|

| 258.0 |

|

|

| 1,027.9 |

| ||||||||||||||||

Held for sale liabilities (see Note 4) |

|

| 1.7 |

|

|

| — |

| ||||||||||||||||||||||||||

Total current liabilities | Total current liabilities |

|

| 2,588.6 |

|

|

| 1,613.2 |

| Total current liabilities |

|

| 1,770.3 |

|

|

| 2,885.8 |

| ||||||||||||||||

Long-term debt | Long-term debt |

|

| 5,243.9 |

|

|

| 4,268.0 |

| Long-term debt |

|

| 6,844.7 |

|

|

| 5,197.4 |

| ||||||||||||||||

Long-term liabilities from risk management activities | Long-term liabilities from risk management activities |

|

| 67.5 |

|

|

| 19.6 |

| Long-term liabilities from risk management activities |

|

| 46.1 |

|

|

| 3.1 |

| ||||||||||||||||

Deferred income taxes, net | Deferred income taxes, net |

|

| 24.0 |

|

|

| 24.0 |

| Deferred income taxes, net |

|

| 23.9 |

|

|

| 23.9 |

| ||||||||||||||||

Other long-term liabilities | Other long-term liabilities |

|

| 245.2 |

|

|

| 576.0 |

| Other long-term liabilities |

|

| 261.7 |

|

|

| 233.8 |

| ||||||||||||||||

Contingencies (see Note 15) |

|

|

|

|

|

|

|

| ||||||||||||||||||||||||||

Contingencies (see Note 16) | Contingencies (see Note 16) |

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Owners' equity: | Owners' equity: |

|

|

|

|

|

|

|

| Owners' equity: |

|

|

|

|

|

|

|

| ||||||||||||||||

Series A preferred limited partners | Series A preferred limited partners | Issued |

|

| Outstanding |

|

|

|

| 120.6 |

|

|

| 120.6 |

| Issued |

|

| Outstanding |

|

|

|

| 120.6 |

|

|

| 120.6 |

| |||||

September 30, 2018 |

| 5,000,000 |

|

|

| 5,000,000 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2017 |

| 5,000,000 |

|

|

| 5,000,000 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

September 30, 2019 |

| 5,000,000 |

|

|

| 5,000,000 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2018 |

| 5,000,000 |

|

|

| 5,000,000 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Common limited partners | Common limited partners | Issued |

|

| Outstanding |

|

|

|

| 6,525.5 |

|

|

| 6,500.3 |

| Issued |

|

| Outstanding |

|

|

|

| 5,437.1 |

|

|

| 6,227.2 |

| |||||

September 30, 2018 |

| 275,168,410 |

|

|

| 275,168,410 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2017 |

| 275,168,410 |

|

|

| 275,168,410 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

September 30, 2019 |

| 275,168,410 |

|

|

| 275,168,410 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2018 |

| 275,168,410 |

|

|

| 275,168,410 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

General partner | General partner | Issued |

|

| Outstanding |

|

|

|

| 808.7 |

|

|

| 808.2 |

| Issued |

|

| Outstanding |

|

|

|

| 786.4 |

|

|

| 802.6 |

| |||||

September 30, 2018 |

| 5,629,136 |

|

|

| 5,629,136 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2017 |

| 5,629,136 |

|

|

| 5,629,136 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

September 30, 2019 |

| 5,629,136 |

|

|

| 5,629,136 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2018 |

| 5,629,136 |

|

|

| 5,629,136 |

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Accumulated other comprehensive income (loss) | Accumulated other comprehensive income (loss) |

|

|

|

|

| (165.7 | ) |

|

| (46.0 | ) |

|

|

|

|

| 186.6 |

|

|

| 124.9 |

| |||||||||||

|

|

|

| 7,289.1 |

|

|

| 7,383.1 |

|

|

|

| 6,530.7 |

|

|

| 7,275.3 |

| ||||||||||||||||

Noncontrolling interests in subsidiaries |

|

|

|

|

| 1,068.2 |

|

|

| 475.1 |

| |||||||||||||||||||||||

Noncontrolling interests |

|

|

|

|

| 3,380.9 |

|

|

| 1,270.8 |

| |||||||||||||||||||||||

Total owners' equity | Total owners' equity |

|

| 8,357.3 |

|

|

| 7,858.2 |

| Total owners' equity |

|

| 9,911.6 |

|

|

| 8,546.1 |

| ||||||||||||||||

Total liabilities and owners' equity | Total liabilities and owners' equity |

| $ | 16,526.5 |

|

| $ | 14,359.0 |

| Total liabilities and owners' equity |

| $ | 18,858.3 |

|

| $ | 16,890.1 |

| ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

See notes to consolidated financial statements. | See notes to consolidated financial statements. |

| See notes to consolidated financial statements. |

| ||||||||||||||||||||||||||||||

CONSOLIDATED STATEMENTS OF OPERATIONS

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

| ||||||||||||||||||||

| 2018 |

|

| 2017 |

|

| 2018 |

|

| 2017 |

| 2019 |

|

| 2018 |

|

| 2019 |

|

| 2018 |

| ||||||||

| (Unaudited) |

| (Unaudited) |

| ||||||||||||||||||||||||||

| (In millions) |

| (In millions) |

| ||||||||||||||||||||||||||

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales of commodities (see Note 3) | $ | 2,654.1 |

|

| $ | 1,871.5 |

|

| $ | 6,981.4 |

|

| $ | 5,353.1 |

| |||||||||||||||

Fees from midstream services (see Note 3) |

| 332.3 |

|

|

| 260.3 |

|

|

| 904.9 |

|

|

| 759.0 |

| |||||||||||||||

Sales of commodities | $ | 1,594.2 |

|

| $ | 2,654.1 |

|

| $ | 5,254.8 |

|

| $ | 6,981.4 |

| |||||||||||||||

Fees from midstream services |

| 308.3 |

|

|

| 332.3 |

|

|

| 942.4 |

|

|

| 904.9 |

| |||||||||||||||

Total revenues |

| 2,986.4 |

|

|

| 2,131.8 |

|

|

| 7,886.3 |

|

|

| 6,112.1 |

|

| 1,902.5 |

|

|

| 2,986.4 |

|

|

| 6,197.2 |

|

|

| 7,886.3 |

|

Costs and expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Product purchases (see Note 3) |

| 2,383.5 |

|

|

| 1,663.1 |

|

|

| 6,229.7 |

|

|

| 4,737.8 |

| |||||||||||||||

Product purchases |

| 1,328.1 |

|

|

| 2,383.5 |

|

|

| 4,415.7 |

|

|

| 6,229.7 |

| |||||||||||||||

Operating expenses |

| 194.9 |

|

|

| 155.5 |

|

|

| 538.7 |

|

|

| 462.6 |

|

| 200.2 |

|

|

| 194.9 |

|

|

| 600.7 |

|

|

| 538.7 |

|

Depreciation and amortization expense |

| 206.3 |

|

|

| 208.3 |

|

|

| 607.1 |

|

|

| 602.8 |

|

| 244.3 |

|

|

| 206.3 |

|

|

| 718.9 |

|

|

| 607.1 |

|

General and administrative expense |

| 59.3 |

|

|

| 46.6 |

|

|

| 165.0 |

|

|

| 139.4 |

|

| 65.6 |

|

|

| 59.3 |

|

|

| 212.3 |

|

|

| 165.0 |

|

Impairment of property, plant and equipment |

| — |

|

|

| 378.0 |

|

|

| — |

|

|

| 378.0 |

| |||||||||||||||

Other operating (income) expense |

| 61.8 |

|

|

| 0.6 |

|

|

| 15.7 |

|

|

| 17.2 |

|

| 18.4 |

|

|

| 61.8 |

|

|

| 21.7 |

|

|

| 15.7 |

|

Income (loss) from operations |

| 80.6 |

|

|

| (320.3 | ) |

|

| 330.1 |

|

|

| (225.7 | ) |

| 45.9 |

|

|

| 80.6 |

|

|

| 227.9 |

|

|

| 330.1 |

|

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense, net |

| (75.7 | ) |

|

| (51.9 | ) |

|

| (113.3 | ) |

|

| (169.5 | ) |

| (84.2 | ) |

|

| (75.7 | ) |

|

| (229.2 | ) |

|

| (113.3 | ) |

Equity earnings (loss) |

| 3.0 |

|

|

| 0.2 |

|

|

| 6.4 |

|

|

| (16.6 | ) |

| 10.0 |

|

|

| 3.0 |

|

|

| 15.9 |

|

|

| 6.4 |

|

Gain (loss) from financing activities |

| — |

|

|

| — |

|

|

| (1.3 | ) |

|

| (10.7 | ) |

| — |

|

|

| — |

|

|

| (1.4 | ) |

|

| (1.3 | ) |

Gain (loss) from sale of equity-method investment |

| 65.8 |

|

|

| — |

|

|

| 65.8 |

|

|

| — |

| |||||||||||||||

Change in contingent considerations |

| (16.6 | ) |

|

| 126.8 |

|

|

| (12.1 | ) |

|

| 125.6 |

|

| — |

|

|

| (16.6 | ) |

|

| (8.8 | ) |

|

| (12.1 | ) |

Other, net |

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| (2.7 | ) | |||||||||||||||

Income (loss) before income taxes |

| (8.7 | ) |

|

| (245.0 | ) |

|

| 209.8 |

|

|

| (299.6 | ) |

| 37.5 |

|

|

| (8.7 | ) |

|

| 70.2 |

|

|

| 209.8 |

|

Income tax (expense) benefit |

| — |

|

|

| — |

|

|

| — |

|

|

| 4.2 |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Net income (loss) |

| (8.7 | ) |

|

| (245.0 | ) |

|

| 209.8 |

|

|

| (295.4 | ) |

| 37.5 |

|

|

| (8.7 | ) |

|

| 70.2 |

|

|

| 209.8 |

|

Less: Net income (loss) attributable to noncontrolling interests |

| 9.7 |

|

|

| 9.7 |

|

|

| 32.0 |

|

|

| 25.9 |

|

| 76.6 |

|

|

| 9.7 |

|

|

| 144.3 |

|

|

| 32.0 |

|

Net income (loss) attributable to Targa Resources Partners LP | $ | (18.4 | ) |

| $ | (254.7 | ) |

| $ | 177.8 |

|

| $ | (321.3 | ) | $ | (39.1 | ) |

| $ | (18.4 | ) |

| $ | (74.1 | ) |

| $ | 177.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income attributable to preferred limited partners | $ | 2.8 |

|

| $ | 2.8 |

|

| $ | 8.4 |

|

| $ | 8.4 |

| $ | 2.8 |

|

| $ | 2.8 |

|

| $ | 8.4 |

|

| $ | 8.4 |

|

Net income (loss) attributable to general partner |

| (0.4 | ) |

|

| (5.2 | ) |

|

| 3.4 |

|

|

| (6.6 | ) |

| (0.9 | ) |

|

| (0.4 | ) |

|

| (1.7 | ) |

|

| 3.4 |

|

Net income (loss) attributable to common limited partners |

| (20.8 | ) |

|

| (252.3 | ) |

|

| 166.0 |

|

|

| (323.1 | ) |

| (41.0 | ) |

|

| (20.8 | ) |

|

| (80.8 | ) |

|

| 166.0 |

|

Net income (loss) attributable to Targa Resources Partners LP | $ | (18.4 | ) |

| $ | (254.7 | ) |

| $ | 177.8 |

|

| $ | (321.3 | ) | $ | (39.1 | ) |

| $ | (18.4 | ) |

| $ | (74.1 | ) |

| $ | 177.8 |

|

See notes to consolidated financial statements.

TARGA RESOURCESRESOURCES PARTNERS LP

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

|

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

|

| Three Months Ended September 30, |

|

| Nine Months Ended September 30, |

| ||||||||||||||||||||

|

| 2018 |

|

| 2017 |

|

| 2018 |

|

| 2017 |

|

| 2019 |

|

| 2018 |

|

| 2019 |

|

| 2018 |

| ||||||||

|

| (Unaudited) |

|

| (Unaudited) |

| ||||||||||||||||||||||||||

|

| (In millions) |

|

| (In millions) |

| ||||||||||||||||||||||||||

Net income (loss) |

| $ | (8.7 | ) |

| $ | (245.0 | ) |

| $ | 209.8 |

|

| $ | (295.4 | ) |

| $ | 37.5 |

|

| $ | (8.7 | ) |

| $ | 70.2 |

|

| $ | 209.8 |

|

Other comprehensive income (loss): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commodity hedging contracts: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in fair value |

|

| (139.6 | ) |

|

| (106.8 | ) |

|

| (178.0 | ) |

|

| (10.5 | ) |

|

| 118.2 |

|

|

| (139.6 | ) |

|

| 167.8 |

|

|

| (178.0 | ) |

Settlements reclassified to revenues |

|

| 23.9 |

|

|

| 2.1 |

|

|

| 58.3 |

|

|

| 2.2 |

|

|

| (41.5 | ) |

|

| 23.9 |

|

|

| (106.1 | ) |

|

| 58.3 |

|

Other comprehensive income (loss) |

|

| (115.7 | ) |

|

| (104.7 | ) |

|

| (119.7 | ) |

|

| (8.3 | ) |

|

| 76.7 |

|

|

| (115.7 | ) |

|

| 61.7 |

|

|

| (119.7 | ) |

Comprehensive income (loss) |

|

| (124.4 | ) |

|

| (349.7 | ) |

|

| 90.1 |

|

|

| (303.7 | ) |

|

| 114.2 |

|

|

| (124.4 | ) |

|

| 131.9 |

|

|

| 90.1 |

|

Less: Comprehensive income (loss) attributable to noncontrolling interests |

|

| 9.7 |

|

|

| 9.7 |

|

|

| 32.0 |

|

|

| 25.9 |

|

|

| 76.6 |

|

|

| 9.7 |

|

|

| 144.3 |

|

|

| 32.0 |

|

Comprehensive income (loss) attributable to Targa Resources Partners LP |

| $ | (134.1 | ) |

| $ | (359.4 | ) |

| $ | 58.1 |

|

| $ | (329.6 | ) |

| $ | 37.6 |

|

| $ | (134.1 | ) |

| $ | (12.4 | ) |

| $ | 58.1 |

|

See notes to consolidated financial statements.

CONSOLIDATED STATEMENTS OF CHANGES IN OWNERS' EQUITY

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| ||||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| ||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2017 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,500.3 |

|

|

| 5,629 |

|

| $ | 808.2 |

|

|

| $ | (46.0 | ) |

| $ | 475.1 |

|

| $ | 7,858.2 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 529.2 |

|

|

| — |

|

|

| 10.8 |

|

|

|

| — |

|

|

| — |

|

|

| 540.0 |

|

Acquisition of related party (see Note 14) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| 1.1 |

|

|

| 1.1 |

|

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| (51.5 | ) |

|

| (51.5 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| 611.6 |

|

|

| 611.6 |

|

Purchase of noncontrolling interests in subsidiary |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

|

| — |

|

|

| (0.1 | ) |

|

| (0.1 | ) |

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

|

| (119.7 | ) |

|

| — |

|

|

| (119.7 | ) |

Net income (loss) |

|

| — |

|

| 8.4 |

|

|

| — |

|

|

| 166.0 |

|

|

| — |

|

|

| 3.4 |

|

|

|

| — |

|

|

| 32.0 |

|

|

| 209.8 |

| |

Distributions |

|

| — |

|

|

| (8.4 | ) |

|

| — |

|

|

| (670.0 | ) |

|

| — |

|

|

| (13.7 | ) |

|

|

| — |

|

|

| — |

|

|

| (692.1 | ) |

Balance, September 30, 2018 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,525.5 |

|

|

| 5,629 |

|

| $ | 808.7 |

|

|

| $ | (165.7 | ) |

| $ | 1,068.2 |

|

| $ | 8,357.3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| |||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2019 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 5,703.1 |

|

|

| 5,629 |

|

| $ | 791.9 |

|

| $ | 109.9 |

|

| $ | 3,276.2 |

|

| $ | 10,001.7 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 9.8 |

|

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| — |

|

|

| 10.0 |

|

Sale of ownership interests in subsidiaries |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (87.2 | ) |

|

| (87.2 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 115.3 |

|

|

| 115.3 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 76.7 |

|

|

| — |

|

|

| 76.7 |

|

Net income (loss) |

|

| — |

|

|

| 2.8 |

|

|

| — |

|

|

| (41.0 | ) |

|

| — |

|

|

| (0.9 | ) |

|

| — |

|

|

| 76.6 |

|

|

| 37.5 |

|

Distributions |

|

| — |

|

|

| (2.8 | ) |

|

| — |

|

|

| (234.8 | ) |

|

| — |

|

|

| (4.8 | ) |

|

| — |

|

|

| — |

|

|

| (242.4 | ) |

Balance, September 30, 2019 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 5,437.1 |

|

|

| 5,629 |

|

| $ | 786.4 |

|

| $ | 186.6 |

|

| $ | 3,380.9 |

|

| $ | 9,911.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| |||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2018 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,322.2 |

|

|

| 5,629 |

|

| $ | 804.5 |

|

| $ | (49.9 | ) |

| $ | 911.8 |

|

| $ | 8,109.2 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 450.6 |

|

|

| — |

|

|

| 9.2 |

|

|

| — |

|

|

| — |

|

|

| 459.8 |

|

Acquisition of related party |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Purchase of noncontrolling interests in subsidiaries, net |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (17.7 | ) |

|

| (17.7 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 164.4 |

|

|

| 164.4 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (115.8 | ) |

|

| — |

|

|

| (115.8 | ) |

Net income (loss) |

|

| — |

|

|

| 2.8 |

|

|

| — |

|

|

| (20.8 | ) |

|

| — |

|

|

| (0.4 | ) |

|

| — |

|

|

| 9.7 |

|

|

| (8.7 | ) |

Distributions |

|

| — |

|

|

| (2.8 | ) |

|

| — |

|

|

| (226.5 | ) |

|

| — |

|

|

| (4.6 | ) |

|

| — |

|

|

| — |

|

|

| (233.9 | ) |

Balance, September 30, 2018 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,525.5 |

|

|

| 5,629 |

|

| $ | 808.7 |

|

| $ | (165.7 | ) |

| $ | 1,068.2 |

|

| $ | 8,357.3 |

|

See notes to consolidated financial statements.

TARGA RESOURCES PARTNERS LP

CONSOLIDATED STATEMENTS OF CHANGES IN OWNERS' EQUITY

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| |||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2018 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,227.2 |

|

|

| 5,629 |

|

| $ | 802.6 |

|

| $ | 124.9 |

|

| $ | 1,270.8 |

|

| $ | 8,546.1 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 196.0 |

|

|

| — |

|

|

| 4.0 |

|

|

| — |

|

|

| — |

|

|

| 200.0 |

|

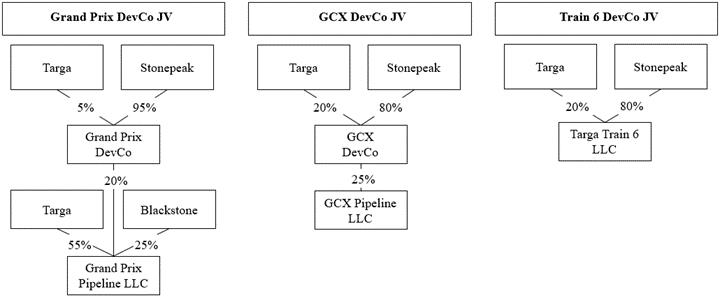

Sale of ownership interests in subsidiaries |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (10.5 | ) |

|

| — |

|

|

| (0.2 | ) |

|

| — |

|

|

| 1,619.7 |

|

|

| 1,609.0 |

|

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (172.6 | ) |

|

| (172.6 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 518.7 |

|

|

| 518.7 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 61.7 |

|

|

| — |

|

|

| 61.7 |

|

Net income (loss) |

|

| — |

|

| 8.4 |

|

|

| — |

|

|

| (80.8 | ) |

|

| — |

|

|

| (1.7 | ) |

|

| — |

|

|

| 144.3 |

|

|

| 70.2 |

| |

Distributions |

|

| — |

|

|

| (8.4 | ) |

|

| — |

|

|

| (894.8 | ) |

|

| — |

|

|

| (18.3 | ) |

|

| — |

|

|

| — |

|

|

| (921.5 | ) |

Balance, September 30, 2019 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 5,437.1 |

|

|

| 5,629 |

|

| $ | 786.4 |

|

| $ | 186.6 |

|

| $ | 3,380.9 |

|

| $ | 9,911.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| |||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| |||||||||||||||||||||||||||||||||

Balance, December 31, 2016 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 5,939.9 |

|

|

| 5,629 |

|

| $ | 796.7 |

|

| $ | (61.8 | ) |

| $ | 355.2 |

|

| $ | 7,150.6 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1,587.5 |

|

|

| — |

|

|

| 32.5 |

|

|

| — |

|

|

| — |

|

|

| 1,620.0 |

|

Purchase of noncontrolling interests in subsidiary |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (12.5 | ) |

|

| (12.5 | ) |

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (33.4 | ) |

|

| (33.4 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 93.8 |

|

|

| 93.8 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (8.3 | ) |

|

| — |

|

|

| (8.3 | ) |

Net income (loss) |

|

| — |

|

|

| 8.4 |

|

|

| — |

|

|

| (323.1 | ) |

|

| — |

|

|

| (6.6 | ) |

|

| — |

|

|

| 25.9 |

|

|

| (295.4 | ) |

Distributions |

|

| — |

|

|

| (8.4 | ) |

|

| — |

|

|

| (612.2 | ) |

|

| — |

|

|

| (12.5 | ) |

|

| — |

|

|

| — |

|

|

| (633.1 | ) |

Balance, September 30, 2017 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,592.1 |

|

|

| 5,629 |

|

| $ | 810.1 |

|

| $ | (70.1 | ) |

| $ | 429.0 |

|

| $ | 7,881.7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

| Limited |

|

| Limited |

|

| General |

|

| Other |

|

| Non- |

|

|

|

|

| |||||||||||||||||

|

| Partner |

|

| Partner |

|

| Partner |

|

| Comprehensive |

|

| controlling |

|

|

|

|

| |||||||||||||||||

|

| Preferred |

|

| Amount |

|

| Common |

|

| Amount |

|

| Units |

|

| Amount |

|

| Income (Loss) |

|

| Interests |

|

| Total |

| |||||||||

|

| (Unaudited) |

| |||||||||||||||||||||||||||||||||

|

| (In millions, except units in thousands) |

| |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2017 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,500.3 |

|

|

| 5,629 |

|

| $ | 808.2 |

|

| $ | (46.0 | ) |

| $ | 475.1 |

|

| $ | 7,858.2 |

|

Contributions from Targa Resources Corp. |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 529.2 |

|

|

| — |

|

|

| 10.8 |

|

|

| — |

|

|

| — |

|

|

| 540.0 |

|

Acquisition of related party |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.1 |

|

|

| 1.1 |

|

Purchase of noncontrolling interests in subsidiaries, net |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (0.1 | ) |

|

| (0.1 | ) |

Distributions to noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (51.5 | ) |

|

| (51.5 | ) |

Contributions from noncontrolling interests |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 611.6 |

|

|

| 611.6 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (119.7 | ) |

|

| — |

|

|

| (119.7 | ) |

Net income (loss) |

|

| — |

|

|

| 8.4 |

|

|

| — |

|

|

| 166.0 |

|

|

| — |

|

|

| 3.4 |

|

|

| — |

|

|

| 32.0 |

|

|

| 209.8 |

|

Distributions |

|

| — |

|

|

| (8.4 | ) |

|

| — |

|

|

| (670.0 | ) |

|

| — |

|

|

| (13.7 | ) |

|

| — |

|

|

| — |

|

|

| (692.1 | ) |

Balance, September 30, 2018 |

|

| 5,000 |

|

| $ | 120.6 |

|

|

| 275,168 |

|

| $ | 6,525.5 |

|

|

| 5,629 |

|

| $ | 808.7 |

|

| $ | (165.7 | ) |

| $ | 1,068.2 |

|

| $ | 8,357.3 |

|

See notes to consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

| Nine Months Ended September 30, |

| |||||||||||||||||

|

|

| 2018 |

|

| 2017 |

|

| Nine Months Ended September 30, |

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

| 2019 |

|

|

| 2018 |

| |||

|

| (Unaudited) |

| (Unaudited) |

| |||||||||||||||

|

| (In millions) |

| (In millions) |

| |||||||||||||||

Cash flows from operating activities | Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Net income (loss) | Net income (loss) |

| $ | 209.8 |

|

| $ | (295.4 | ) |

| $ | 70.2 |

|

|

| $ | 209.8 |

| ||

Adjustments to reconcile net income (loss) to net cash provided by operating activities: | Adjustments to reconcile net income (loss) to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Amortization in interest expense | Amortization in interest expense |

|

| 6.8 |

|

|

| 7.1 |

|

|

| 6.8 |

|

|

|

| 6.8 |

| ||

Depreciation and amortization expense | Depreciation and amortization expense |

|

| 607.1 |

|

|

| 602.8 |

|

|

| 718.9 |

|

|

|

| 607.1 |

| ||

Impairment of property, plant and equipment |

|

| — |

|

|

| 378.0 |

| ||||||||||||

Accretion of asset retirement obligations | Accretion of asset retirement obligations |

|

| 2.8 |

|

|

| 3.0 |

|

|

| 3.7 |

|

|

|

| 2.8 |

| ||

Increase (decrease) in redemption value of mandatorily redeemable preferred interests | Increase (decrease) in redemption value of mandatorily redeemable preferred interests |

|

| (66.3 | ) |

|

| 8.5 |

|

|

| — |

|

|

|

| (66.3 | ) | ||

Equity (earnings) loss of unconsolidated affiliates | Equity (earnings) loss of unconsolidated affiliates |

|

| (6.4 | ) |

|

| 16.6 |

|

|

| (15.9 | ) |

|

|

| (6.4 | ) | ||

Distributions of earnings received from unconsolidated affiliates | Distributions of earnings received from unconsolidated affiliates |

|

| 16.0 |

|

|

| 8.4 |

|

|

| 26.0 |

|

|

|

| 16.0 |

| ||

Risk management activities | Risk management activities |

|

| 9.6 |

|

|

| 7.3 |

|

|

| 100.8 |

|

|

|

| 9.6 |

| ||

(Gain) loss on sale or disposition of assets | (Gain) loss on sale or disposition of assets |

|

| 14.3 |

|

|

| 16.6 |

|

|

| 3.6 |

|

|

|

| 14.3 |

| ||

Write-down of assets |

|

| 17.9 |

|

|

|

| — |

| |||||||||||

(Gain) loss from financing activities | (Gain) loss from financing activities |

|

| 1.3 |

|

|

| 10.7 |

|

|

| 1.4 |

|

|

|

| 1.3 |

| ||

Change in contingent considerations included in Other expense (income) |

|

| 12.1 |

|

|

| (125.6 | ) | ||||||||||||

(Gain) loss from sale of equity-method investment |

|

| (65.8 | ) |

|

|

| — |

| |||||||||||

Change in contingent considerations |

|

| 8.8 |

|

|

|

| 12.1 |

| |||||||||||

Changes in operating assets and liabilities, net of business acquisitions: | Changes in operating assets and liabilities, net of business acquisitions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Receivables and other assets | Receivables and other assets |

|

| (221.7 | ) |

|

| (91.5 | ) |

|

| 108.0 |

|

|

|

| (221.7 | ) | ||

Inventories | Inventories |

|

| (16.6 | ) |

|

| (136.4 | ) |

|

| (89.7 | ) |

|

|

| (16.6 | ) | ||

Accounts payable and other liabilities | Accounts payable and other liabilities |

|

| 374.7 |

|

|

| 53.1 |

|

|

| 2.7 |

|

|

|

| 374.7 |

| ||

Net cash provided by operating activities | Net cash provided by operating activities |

|

| 943.5 |

|

|

| 463.2 |

|

|

| 897.4 |

|

|

|

| 943.5 |

| ||

Cash flows from investing activities | Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Outlays for property, plant and equipment | Outlays for property, plant and equipment |

|

| (2,033.6 | ) |

|

| (866.6 | ) |

|

| (2,433.8 | ) |

|

|

| (2,033.6 | ) | ||

Outlays for business acquisition, net of cash acquired |

|

| — |

|

|

| (570.8 | ) | ||||||||||||

Proceeds from sale of assets | Proceeds from sale of assets |

|

| 71.5 |

|

|

| — |

|

|

| 2.7 |

|

|

|

| 71.5 |

| ||

Investments in unconsolidated affiliates | Investments in unconsolidated affiliates |

|

| (223.7 | ) |

|

| (7.5 | ) |

|

| (243.7 | ) |

|

|

| (223.7 | ) | ||

Proceeds from sale of equity-method investment |

|

| 70.3 |

|

|

|

| — |

| |||||||||||

Return of capital from unconsolidated affiliates | Return of capital from unconsolidated affiliates |

|

| 2.2 |

|

|

| 2.2 |

|

|

| 1.1 |

|

|

|

| 2.2 |

| ||

Other, net | Other, net |

|

| (9.2 | ) |

|

| (14.8 | ) |

|

| (16.3 | ) |

|

|

| (9.2 | ) | ||

Net cash used in investing activities | Net cash used in investing activities |

|

| (2,192.8 | ) |

|

| (1,457.5 | ) |

|

| (2,619.7 | ) |

|

|

| (2,192.8 | ) | ||

Cash flows from financing activities | Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Debt obligations: | Debt obligations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

Proceeds from borrowings under credit facility | Proceeds from borrowings under credit facility |

|

| 950.0 |

|

|

| 1,496.0 |

|

|

| 2,180.0 |

|

|

|

| 950.0 |

| ||

Repayments of credit facility | Repayments of credit facility |

|

| (970.0 | ) |

|

| (1,216.0 | ) |

|

| (2,050.0 | ) |

|

|

| (970.0 | ) | ||

Proceeds from borrowings under accounts receivable securitization facility | Proceeds from borrowings under accounts receivable securitization facility |

|

| 440.0 |

|

|

| 281.6 |

|

|

| 770.0 |

|

|

|

| 440.0 |

| ||

Repayments of accounts receivable securitization facility | Repayments of accounts receivable securitization facility |

|

| (500.0 | ) |

|

| (278.5 | ) |

|

| (804.0 | ) |

|

|

| (500.0 | ) | ||

Proceeds from issuance of senior notes | Proceeds from issuance of senior notes |

|

| 1,000.0 |

|

|

| — |

|

|

| 1,500.0 |

|

|

|

| 1,000.0 |

| ||

Redemption of senior notes | Redemption of senior notes |

|

| — |

|

|

| (287.6 | ) |

|

| (749.4 | ) |

|

|

| — |

| ||

Principal payments of finance leases |

|

| (8.5 | ) |

|

|

| — |

| |||||||||||

Costs incurred in connection with financing arrangements | Costs incurred in connection with financing arrangements |

|

| (15.8 | ) |

|

| (0.1 | ) |

|

| (25.1 | ) |

|

|

| (15.8 | ) | ||

Purchase of noncontrolling interests in subsidiary |

|

| (0.1 | ) |

|

| (12.5 | ) | ||||||||||||

Payment of contingent consideration |

|

| (317.1 | ) |

|

|

| — |

| |||||||||||

Sale of ownership interests in subsidiaries |

|

| 1,619.7 |

|

|

|

| (0.1 | ) | |||||||||||

Contributions from general partner | Contributions from general partner |

|

| 10.8 |

|

|

| 32.5 |

|

|

| 4.0 |

|

|

|

| 10.8 |

| ||

Contributions from TRC | Contributions from TRC |

|

| 529.2 |

|

|

| 1,587.5 |

|

|

| 196.0 |

|

|

|

| 529.2 |

| ||

Contributions from noncontrolling interests | Contributions from noncontrolling interests |

|

| 611.6 |

|

|

| 93.8 |

|

|

| 518.7 |

|

|

|

| 611.6 |

| ||

Distributions to noncontrolling interests | Distributions to noncontrolling interests |

|

| (51.5 | ) |

|

| (33.4 | ) |

|

| (98.9 | ) |

|

|

| (51.5 | ) | ||

Distributions to unitholders | Distributions to unitholders |

|

| (692.1 | ) |

|

| (633.1 | ) |

|

| (921.5 | ) |

|

|

| (692.1 | ) | ||

Net cash provided by (used in) financing activities |

|

| 1,312.1 |

|

|

| 1,030.2 |

| ||||||||||||

Net cash provided by financing activities |

|

| 1,813.9 |

|

|

|

| 1,312.1 |

| |||||||||||

Net change in cash and cash equivalents | Net change in cash and cash equivalents |

|

| 62.8 |

|

|

| 35.9 |

|

|

| 91.6 |

|

|

|

| 62.8 |

| ||

Cash and cash equivalents, beginning of period | Cash and cash equivalents, beginning of period |

|

| 124.7 |

|

|

| 68.0 |

|

|

| 203.3 |

|

|

|

| 124.7 |

| ||

Cash and cash equivalents, end of period | Cash and cash equivalents, end of period |

| $ | 187.5 |

|

| $ | 103.9 |

|

| $ | 294.9 |

|

|

| $ | 187.5 |

| ||

See notes to consolidated financial statements.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Except as noted within the context of each footnote disclosure, the dollar amounts presented in the tabular data within these footnote disclosures are stated in millions of dollars.

Note 1 — Organization and Operations

Our Organization

Targa Resources Partners LP is a Delaware limited partnership formed in October 2006 by our parent, Targa Resources Corp. (“Targa” or “TRC” or the “Company” or “Parent”). In this Quarterly Report, unless the context requires otherwise, references to “we,” “us,” “our,” “TRP,” or the “Partnership” are intended to mean the business and operations of Targa Resources Partners LP and its consolidated subsidiaries.

Our common units are wholly owned by TRC and no longer publicly traded as a result of TRC’s acquisition of our outstanding common units that it and its subsidiaries did not already own in 2016.

The 5,000,000 9.00% Series A Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units (the “Preferred Units”) that were issued in October 2015 remain outstanding as limited partner interests in us and continue to trade on the NYSE under the symbol “NGLS PRA.“NGLS/PA.”

Our Operations

We are primarily engaged in the business of:

gathering, compressing, treating, processing and selling natural gas;

• | gathering, compressing, treating, processing, transporting and selling natural gas; |

storing, fractionating, treating, transporting and selling NGLs and NGL products, including services to LPG exporters;

• | transporting, storing, fractionating, treating and selling NGLs and NGL products, including services to LPG exporters; and |

gathering, storing, terminaling and selling crude oil; and

storing, terminaling and selling refined petroleum products.

• | gathering, storing, terminaling and selling crude oil. |

See Note 1920 – Segment Information for certain financial information regarding our business segments.

The employees supporting our operations are employed by Targa. Our consolidated financial statements include the direct costs of Targa employees deployed to our operating segments, as well as an allocation of costs associated with our usage of Targa’s centralized general and administrative services.

Note 2 — Basis of Presentation

We have prepared theseThe accompanying unaudited consolidated financial statements have been prepared in accordance with GAAP for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. While we derived the year-end balance sheet data from audited financial statements, this interim report does not include all disclosures required by GAAP for annual periods. These unaudited consolidated financial statements and otherGAAP. Therefore, this information included in this Quarterly Report should be read in conjunction with our consolidated financial statements and notes thereto includedcontained in our Annual Report.

The unaudited consolidated financial statements for the three and nine months ended September 30, 2018 includeinformation furnished herein reflects all adjustments that we believe are, in the opinion of management, necessary for a fair statement of the results forof the interim periods.periods reported. All significant intercompany balances and transactions have been eliminated in consolidation. Certain amounts in prior periods may have been reclassified to conform to the current year presentation.