UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

|

|

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 20192024

OR

|

|

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-07782

Parsons Corporation

(Exact Name of Registrant as Specified in its Charter)

Delaware | 95-3232481 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

|

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (703) (703) 988-8500

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Common Stock, $1 par value | PSN | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☐☒ No ☒☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

| Accelerated filer | ☐ | |

Non-accelerated filer |

| Smaller reporting company | ☐ | |

Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Securities registered pursuant to Section 12(b) of the Act:

|

|

| ||

|

|

|

As of June 6, 2019,April 23, 2024, the registrant had 99,434,877146,747,745 shares of common stock, $1.00 par value per share, outstanding.

Table of Contents

Page | |||

PART I. | 1 | ||

Item 1. | 1 | ||

1 | |||

2 | |||

3 | |||

4 | |||

Consolidated Statements of | 5 | ||

6 | |||

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| |

Item 3. |

| ||

Item 4. |

| ||

PART II. |

| ||

Item 1. |

| ||

Item 1A. |

| ||

Item 2. |

| ||

Item 3. |

| ||

Item 4. |

| ||

Item 5. |

| ||

Item 6. |

| ||

|

i

i

PART I—FINANCIALFINANCIAL INFORMATION

PARSONS CORPORATION AND SUBSIDIARIES

(in thousands, except share information)

(Unaudited)

|

|

| March 31, 2024 |

|

| December 31, 2023 |

| ||

|

|

| (Unaudited) |

|

|

|

| ||

Assets |

|

|

|

|

|

| |||

Current assets: |

|

|

|

|

|

| |||

| Cash and cash equivalents (including $84,810 and $128,761 Cash of consolidated joint ventures) |

| $ | 423,120 |

|

| $ | 272,943 |

|

| Accounts receivable, net (including $332,308 and $274,846 Accounts receivable of consolidated joint ventures, net) |

|

| 1,023,463 |

|

|

| 915,638 |

|

| Contract assets (including $8,521 and $11,096 Contract assets of consolidated joint ventures) |

|

| 768,007 |

|

|

| 757,515 |

|

| Prepaid expenses and other current assets (including $15,808 and $11,929 Prepaid expenses and other current assets of consolidated joint ventures) |

|

| 212,664 |

|

|

| 191,430 |

|

| Total current assets |

|

| 2,427,254 |

|

|

| 2,137,526 |

|

|

|

|

|

|

|

|

| ||

| Property and equipment, net (including $3,565 and $3,274 Property and equipment of consolidated joint ventures, net) |

|

| 98,499 |

|

|

| 98,957 |

|

| Right of use assets, operating leases (including $8,656 and $9,885 Right of use assets, operating leases of consolidated joint ventures) |

|

| 145,803 |

|

|

| 159,211 |

|

| Goodwill |

|

| 1,791,443 |

|

|

| 1,792,665 |

|

| Investments in and advances to unconsolidated joint ventures |

|

| 145,043 |

|

|

| 128,204 |

|

| Intangible assets, net |

|

| 261,856 |

|

|

| 275,566 |

|

| Deferred tax assets |

|

| 157,547 |

|

|

| 140,162 |

|

| Other noncurrent assets |

|

| 70,998 |

|

|

| 71,770 |

|

| Total assets |

| $ | 5,098,443 |

|

| $ | 4,804,061 |

|

|

|

|

|

|

|

|

| ||

Liabilities and Shareholders' Equity |

|

|

|

|

|

| |||

Current liabilities: |

|

|

|

|

|

| |||

| Accounts payable (including $33,339 and $49,234 Accounts payable of consolidated joint ventures) |

| $ | 274,140 |

|

| $ | 242,821 |

|

| Accrued expenses and other current liabilities (including $165,434 and $145,040 Accrued expenses and other current liabilities of consolidated joint ventures) |

|

| 739,211 |

|

|

| 801,423 |

|

| Contract liabilities (including $60,374 and $61,234 Contract liabilities of consolidated joint ventures) |

|

| 282,962 |

|

|

| 301,107 |

|

| Short-term lease liabilities, operating leases (including $4,445 and $4,753 Short-term lease liabilities, operating leases of consolidated joint ventures) |

|

| 55,024 |

|

|

| 58,556 |

|

| Income taxes payable |

|

| 2,366 |

|

|

| 6,977 |

|

| Total current liabilities |

|

| 1,353,703 |

|

|

| 1,410,884 |

|

|

|

|

|

|

|

|

| ||

| Long-term employee incentives |

|

| 24,447 |

|

|

| 22,924 |

|

| Long-term debt |

|

| 1,246,443 |

|

|

| 745,963 |

|

| Long-term lease liabilities, operating leases (including $4,211 and $5,132 Long-term lease liabilities, operating leases of consolidated joint ventures) |

|

| 106,692 |

|

|

| 117,505 |

|

| Deferred tax liabilities |

|

| 9,763 |

|

|

| 9,775 |

|

| Other long-term liabilities |

|

| 114,238 |

|

|

| 120,295 |

|

| Total liabilities |

|

| 2,855,286 |

|

|

| 2,427,346 |

|

Contingencies (Note 12) |

|

|

|

|

|

| |||

Shareholders' equity: |

|

|

|

|

|

| |||

| Common stock, $1 par value; authorized 1,000,000,000 shares; 146,717,387 and 146,341,363 shares issued; 48,205,185 and 45,960,122 public shares outstanding; 57,998,295 and 59,879,857 ESOP shares outstanding |

|

| 146,717 |

|

|

| 146,341 |

|

| Treasury stock, 40,501,385 shares at cost |

|

| (827,311 | ) |

|

| (827,311 | ) |

Additional paid-in capital |

|

| 2,759,867 |

|

|

| 2,779,365 |

| |

Retained earnings |

|

| 87,261 |

|

|

| 203,724 |

| |

Accumulated other comprehensive loss |

|

| (16,866 | ) |

|

| (14,908 | ) | |

Total Parsons Corporation shareholders' equity |

|

| 2,149,668 |

|

|

| 2,287,211 |

| |

Noncontrolling interests |

|

| 93,489 |

|

|

| 89,504 |

| |

Total shareholders' equity |

|

| 2,243,157 |

|

|

| 2,376,715 |

| |

| Total liabilities and shareholders' equity |

|

| 5,098,443 |

|

|

| 4,804,061 |

|

|

|

| December 31, 2018 |

|

| March 31, 2019 |

| ||

Assets |

|

|

|

|

|

|

|

| |

Current assets: |

|

|

|

|

|

|

|

| |

| Cash and cash equivalents (including $73,794 and $42,872 Cash of consolidated joint ventures) |

| $ | 280,221 |

|

| $ | 121,408 |

|

| Restricted cash and investments |

|

| 974 |

|

|

| 9,061 |

|

| Accounts receivable, net (including $180,325 and $193,597 Accounts receivable of consolidated joint ventures, net) |

|

| 623,286 |

|

|

| 651,924 |

|

| Contract assets (including $21,270 and $23,964 Contract assets of consolidated joint ventures) |

|

| 515,319 |

|

|

| 571,755 |

|

| Prepaid expenses and other current assets (including $11,837 and $9,423 Prepaid expenses and other current assets of consolidated joint ventures) |

|

| 69,007 |

|

|

| 77,013 |

|

| Total current assets |

|

| 1,488,807 |

|

|

| 1,431,161 |

|

|

|

|

|

|

|

|

|

|

|

| Property and equipment, net (including $2,561 and $2,507 Property and equipment of consolidated joint ventures, net) |

|

| 91,849 |

|

|

| 97,298 |

|

| Right of use assets, operating leases |

|

| - |

|

|

| 216,484 |

|

| Goodwill |

|

| 736,938 |

|

|

| 921,097 |

|

| Investments in and advances to unconsolidated joint ventures |

|

| 63,560 |

|

|

| 67,202 |

|

| Intangible assets, net |

|

| 179,519 |

|

|

| 250,948 |

|

| Deferred tax assets |

|

| 5,680 |

|

|

| 4,891 |

|

| Other noncurrent assets |

|

| 46,225 |

|

|

| 43,917 |

|

| Total assets |

| $ | 2,612,578 |

|

| $ | 3,032,998 |

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Shareholder’s Equity |

|

|

|

|

|

|

|

| |

Current liabilities: |

|

|

|

|

|

|

|

| |

| Accounts payable (including $87,914 and $91,505 Accounts payable of consolidated joint ventures) |

| $ | 226,345 |

|

| $ | 203,684 |

|

| Accrued expenses and other current liabilities (including $73,209 and $71,593 Accrued expenses and other current liabilities of consolidated joint ventures) |

|

| 559,700 |

|

|

| 547,954 |

|

| Contract liabilities (including $38,706 and $46,754 Contract liabilities of consolidated joint ventures) |

|

| 208,576 |

|

|

| 225,017 |

|

| Short-term lease liabilities, operating leases |

|

| - |

|

|

| 53,029 |

|

| Income taxes payable |

|

| 11,540 |

|

|

| 9,415 |

|

| Short-term notes payable |

|

| - |

|

|

| 149,786 |

|

| Total current liabilities |

|

| 1,006,161 |

|

|

| 1,188,885 |

|

| Long-term employee incentives |

|

| 41,913 |

|

|

| 29,991 |

|

| Deferred gain resulting from sale-leaseback transactions |

|

| 46,004 |

|

|

| - |

|

| Long-term debt |

|

| 429,164 |

|

|

| 509,211 |

|

| Long-term lease liabilities, operating leases |

|

| - |

|

|

| 181,274 |

|

| Deferred tax liabilities |

|

| 6,240 |

|

|

| 7,922 |

|

| Other long-term liabilities |

|

| 127,863 |

|

|

| 111,023 |

|

| Total liabilities |

|

| 1,657,345 |

|

|

| 2,028,306 |

|

Commitments and contingencies (Note 14) |

|

|

|

|

|

|

|

| |

| Redeemable common stock held by Employee Stock Ownership Plan (ESOP) ,$1 par value; authorized 150,000,000 shares; 125,097,684 shares issued; 78,172,809 and 78,138,831 shares outstanding, recorded at redemption value |

|

| 1,876,309 |

|

|

| 1,875,332 |

|

|

|

|

|

|

|

|

|

|

|

Shareholder's equity (deficit): |

|

|

|

|

|

|

|

| |

| Treasury Stock, 46,918,140 and 46,958,853 shares at cost |

|

| (957,025 | ) |

|

| (957,838 | ) |

| Retained earnings |

|

| 12,445 |

|

|

| 75,771 |

|

| Accumulated other comprehensive loss |

|

| (22,957 | ) |

|

| (20,401 | ) |

| Total Parsons Corporation shareholder's equity (deficit) |

|

| (967,537 | ) |

|

| (902,468 | ) |

| Noncontrolling interests |

|

| 46,461 |

|

|

| 31,828 |

|

| Total shareholder's equity (deficit) |

|

| (921,076 | ) |

|

| (870,640 | ) |

| Total liabilities, redeemable common stock and shareholder's equity (deficit) |

| $ | 2,612,578 |

|

| $ | 3,032,998 |

|

The accompanying notes are an integral part of these consolidated financial statements.

1

PARSONS CORPORATION AND SUBSIDIARIES

Consolidated Statements of Income (Loss)

(In thousands, except per share information)

(Unaudited)

|

| For the Three Months Ended |

| |||||

|

| March 30, 2018 |

|

| March 31, 2019 |

| ||

Revenues |

| $ | 754,679 |

|

| $ | 904,405 |

|

Direct costs of contracts |

|

| 602,972 |

|

|

| 714,237 |

|

Equity in earnings of unconsolidated joint ventures |

|

| 11,031 |

|

|

| 10,397 |

|

Indirect, general and administrative expenses |

|

| 123,847 |

|

|

| 177,519 |

|

Operating income |

|

| 38,891 |

|

|

| 23,046 |

|

Interest income |

|

| 741 |

|

|

| 477 |

|

Interest expense |

|

| (3,999 | ) |

|

| (8,292 | ) |

Other income, net |

|

| 1,152 |

|

|

| 41 |

|

(Interest and other expense) gain associated with claim on long-term contract |

|

| (2,330 | ) |

|

| - |

|

Total other expense |

|

| (4,436 | ) |

|

| (7,774 | ) |

Income before income tax provision |

|

| 34,455 |

|

|

| 15,272 |

|

Income tax provision |

|

| (5,353 | ) |

|

| (1,886 | ) |

Net income including noncontrolling interests |

|

| 29,102 |

|

|

| 13,386 |

|

Net income attributable to noncontrolling interests |

|

| (3,815 | ) |

|

| (3,645 | ) |

Net income attributable to Parsons Corporation |

| $ | 25,287 |

|

| $ | 9,741 |

|

Earnings per share: |

|

|

|

|

|

|

|

|

Basic and diluted |

| $ | 0.31 |

|

| $ | 0.12 |

|

|

| Three Months Ended |

| |||||

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||

Revenue |

| $ | 1,535,676 |

|

| $ | 1,173,466 |

|

Direct cost of contracts |

|

| 1,210,827 |

|

|

| 917,188 |

|

Equity in losses of unconsolidated joint ventures |

|

| (2,060 | ) |

|

| (5,840 | ) |

Selling, general and administrative expenses |

|

| 220,945 |

|

|

| 199,308 |

|

Operating income |

|

| 101,844 |

|

|

| 51,130 |

|

Interest income |

|

| 1,152 |

|

|

| 793 |

|

Interest expense |

|

| (12,998 | ) |

|

| (6,458 | ) |

Loss on extinguishment of debt |

|

| (211,018 | ) |

|

| - |

|

Other income (expense), net |

|

| (3,326 | ) |

|

| 1,314 |

|

Total other income (expense) |

|

| (226,190 | ) |

|

| (4,351 | ) |

(Loss) income before income tax expense |

|

| (124,346 | ) |

|

| 46,779 |

|

Income tax benefit (expense) |

|

| 32,234 |

|

|

| (11,503 | ) |

Net (loss) income including noncontrolling interests |

|

| (92,112 | ) |

|

| 35,276 |

|

Net income attributable to noncontrolling interests |

|

| (15,243 | ) |

|

| (9,723 | ) |

Net (loss) income attributable to Parsons Corporation |

| $ | (107,355 | ) |

| $ | 25,553 |

|

(Loss) earnings per share: |

|

|

|

|

|

| ||

Basic |

| $ | (1.01 | ) |

| $ | 0.24 |

|

Diluted |

| $ | (1.01 | ) |

| $ | 0.23 |

|

The accompanying notes are an integral part of these consolidated financial statements.

2

PARSONS CORPORATION AND SUBSIDIARIES

Consolidated Statements of Comprehensive Income (Loss)

(In thousands)

(Unaudited)

|

| For the Three Months Ended |

| |||||

|

| March 30, 2018 |

|

| March 31, 2019 |

| ||

Net income including noncontrolling interests |

| $ | 29,102 |

|

| $ | 13,386 |

|

Other comprehensive (loss) income, net of tax |

|

|

|

|

|

|

|

|

Foreign currency translation adjustment, net of tax |

|

| (2,784 | ) |

|

| 2,549 |

|

Pension adjustments, net of tax |

|

| (19 | ) |

|

| 9 |

|

Comprehensive income including noncontrolling interests, net of tax |

|

| 26,299 |

|

|

| 15,944 |

|

Comprehensive income attributable to noncontrolling interests, net of tax |

|

| (3,815 | ) |

|

| (3,645 | ) |

Comprehensive income attributable to Parsons Corporation, net of tax |

| $ | 22,484 |

|

| $ | 12,299 |

|

|

| Three Months Ended |

| |||||

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||

Net (loss) income including noncontrolling interests |

| $ | (92,112 | ) |

| $ | 35,276 |

|

Other comprehensive income, net of tax |

|

|

|

|

|

| ||

Foreign currency translation adjustment, net of tax |

|

| (1,927 | ) |

|

| (177 | ) |

Pension adjustments, net of tax |

|

| (31 | ) |

|

| 1 |

|

Comprehensive (loss) income including noncontrolling interests, net of tax |

|

| (94,070 | ) |

|

| 35,100 |

|

Comprehensive income attributable to noncontrolling interests, net of tax |

|

| (15,243 | ) |

|

| (9,723 | ) |

Comprehensive (loss) income attributable to Parsons Corporation, net of tax |

| $ | (109,313 | ) |

| $ | 25,377 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

PARSONS CORPORATION AND SUBSIDIARIES

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

|

|

| For the Three Months Ended |

|

| For the Three Months Ended |

| |||||||||||

|

|

| March 30, 2018 |

|

| March 31, 2019 |

|

| March 31, 2024 |

|

| March 31, 2023 |

| |||||

Cash flows from operating activities: | Cash flows from operating activities: |

|

|

|

|

|

|

|

| Cash flows from operating activities: |

|

|

|

|

| |||

| Net income including noncontrolling interests |

| $ | 29,102 |

|

| $ | 13,386 |

| |||||||||

| Adjustments to reconcile net income to net cash used in operating activities |

|

|

|

|

|

|

|

| |||||||||

| Depreciation and amortization |

|

| 9,009 |

|

|

| 30,591 |

| Net (loss) income including noncontrolling interests |

| $ | (92,112 | ) |

| $ | 35,276 |

|

| Amortization of deferred gain |

|

| (1,813 | ) |

|

| - |

| Adjustments to reconcile net (loss) income to net cash used in operating activities |

|

|

|

|

| |||

| Amortization of debt issue costs |

|

| 149 |

|

|

| 244 |

| Depreciation and amortization |

|

| 24,531 |

|

|

| 28,359 |

|

| (Gain) loss on disposal of property and equipment |

|

| 18 |

|

|

| (27 | ) | Amortization of debt issue costs |

|

| 4,099 |

|

|

| 657 |

|

| Provision for doubtful accounts |

|

| 2,426 |

|

|

| (279 | ) | Loss (gain) on disposal of property and equipment |

|

| 198 |

|

|

| (3 | ) |

| Deferred taxes |

|

| (138 | ) |

|

| 1,486 |

| Loss on extinguishment of debt |

|

| 211,018 |

|

|

| - |

|

| Foreign currency transaction gains and losses |

|

| (457 | ) |

|

| 618 |

| Deferred taxes |

|

| 4,796 |

|

|

| (2,586 | ) |

| Equity in earnings of unconsolidated joint ventures |

|

| (11,031 | ) |

|

| (10,397 | ) | Foreign currency transaction gains and losses |

|

| 2,311 |

|

|

| (290 | ) |

| Return on investments in unconsolidated joint ventures |

|

| 15,406 |

|

|

| 10,794 |

| Equity in losses of unconsolidated joint ventures |

|

| 2,060 |

|

|

| 5,840 |

|

| Contributions of treasury stock |

|

| 11,357 |

|

|

| 12,250 |

| Return on investments in unconsolidated joint ventures |

|

| 16,106 |

|

|

| 7,793 |

|

| Changes in assets and liabilities, net of acquisitions and newly consolidated joint ventures: |

|

|

|

|

|

|

|

| Stock-based compensation |

|

| 10,523 |

|

|

| 6,992 |

|

| Accounts receivable |

|

| 469,720 |

|

|

| (17,135 | ) | Contributions of treasury stock |

|

| 15,030 |

|

|

| 14,435 |

|

| Contract assets |

|

| (531,157 | ) |

|

| (46,984 | ) | Changes in assets and liabilities, net of acquisitions and consolidated |

|

|

|

|

| |||

| Prepaid expenses and current assets |

|

| (27,138 | ) |

|

| (1,424 | ) | Accounts receivable |

|

| (110,066 | ) |

|

| (47,482 | ) |

| Accounts payable |

|

| (723 | ) |

|

| (28,182 | ) | Contract assets |

|

| (11,715 | ) |

|

| (49,098 | ) |

| Accrued expenses and other current liabilities |

|

| (44,016 | ) |

|

| (24,023 | ) | Prepaid expenses and other assets |

|

| (21,602 | ) |

|

| (27,948 | ) |

| Billings in excess of costs |

|

| (152,147 | ) |

|

| - |

| Accounts payable |

|

| 31,685 |

|

|

| 8,009 |

|

| Contract liabilities |

|

| 299,639 |

|

|

| 14,884 |

| Accrued expenses and other current liabilities |

|

| (77,591 | ) |

|

| (10,898 | ) |

| Provision for contract losses |

|

| (143,666 | ) |

|

| - |

| Contract liabilities |

|

| (17,090 | ) |

|

| 16,113 |

|

| Income taxes |

|

| (597 | ) |

|

| (3,645 | ) | Income taxes |

|

| (51,080 | ) |

|

| 6,408 |

|

| Other long-term liabilities |

|

| 10,624 |

|

|

| (12,265 | ) | Other long-term liabilities |

|

| (4,521 | ) |

|

| (567 | ) |

| Net cash used in operating activities |

|

| (65,433 | ) |

|

| (60,108 | ) | Net cash used in operating activities |

|

| (63,420 | ) |

|

| (8,990 | ) |

Cash flows from investing activities: | Cash flows from investing activities: |

|

|

|

|

|

|

|

| Cash flows from investing activities: |

|

|

|

|

| |||

| Capital expenditures |

|

| (5,152 | ) |

|

| (11,041 | ) | Capital expenditures |

|

| (9,436 | ) |

|

| (8,146 | ) |

| Proceeds from sale of property and equipment |

|

| 29 |

|

|

| 135 |

| Proceeds from sale of property and equipment |

|

| 2 |

|

|

| 19 |

|

| Payments for acquisitions, net of cash acquired |

|

| - |

|

|

| (287,482 | ) | Investments in unconsolidated joint ventures |

|

| (36,076 | ) |

|

| (13,016 | ) |

| Investments in unconsolidated joint ventures |

|

| (3,058 | ) |

|

| (4,905 | ) | Proceeds from sales of investments in unconsolidated joint ventures |

|

| - |

|

|

| 381 |

|

| Return of investments in unconsolidated joint ventures |

|

| - |

|

|

| 2,234 |

| Net cash used in investing activities |

|

| (45,510 | ) |

|

| (20,762 | ) |

| Net cash used in investing activities |

|

| (8,181 | ) |

|

| (301,059 | ) | |||||||||

Cash flows from financing activities: | Cash flows from financing activities: |

|

|

|

|

|

|

|

| Cash flows from financing activities: |

|

|

|

|

| |||

| Proceeds from borrowings under credit agreement |

|

| - |

|

|

| 290,000 |

| Proceeds from borrowings under credit agreement |

|

| 153,200 |

|

|

| 5,700 |

|

| Repayments of borrowings under credit agreement |

|

| - |

|

|

| (60,000 | ) | Repayments of borrowings under credit agreement |

|

| (153,200 | ) |

|

| (5,700 | ) |

| Payments for debt costs and credit agreement |

|

| - |

|

|

| (286 | ) | Proceeds from issuance of convertible notes due 2029 |

|

| 800,000 |

|

|

| - |

|

| Contributions by (distributions to) noncontrolling interests, net |

|

| 6,497 |

|

|

| (18,278 | ) | Repurchases of convertible notes due 2025 |

|

| (495,575 | ) |

|

| - |

|

| Purchase of treasury stock |

|

| (366 | ) |

|

| (813 | ) | Payments for debt issuance costs |

|

| (18,941 | ) |

|

| - |

|

| Net cash provided by financing activities |

|

| 6,131 |

|

|

| 210,623 |

| Contributions by noncontrolling interests |

|

| - |

|

|

| 200 |

|

| Effect of exchange rate changes |

|

| (825 | ) |

|

| (182 | ) | Distributions to noncontrolling interests |

|

| (11,258 | ) |

|

| (638 | ) |

| Net increase (decrease) in cash, cash equivalents, and restricted cash |

|

| (68,308 | ) |

|

| (150,726 | ) | Repurchases of common stock |

|

| - |

|

|

| (6,000 | ) |

| Cash, cash equivalents and restricted cash |

|

|

|

|

|

|

|

| Taxes paid on vested stock |

|

| (16,914 | ) |

|

| (6,064 | ) |

| Beginning of year |

|

| 446,144 |

|

|

| 281,195 |

| Capped call transactions |

|

| (88,400 | ) |

|

| - |

|

| End of period |

| $ | 377,836 |

|

| $ | 130,469 |

| Bond hedge termination |

|

| 195,549 |

|

|

| - |

|

| Redemption of warrants |

|

| (104,952 | ) |

|

| - |

| |||||||||

Net cash (used in) provided by financing activities |

|

| 259,509 |

|

|

| (12,502 | ) | ||||||||||

Effect of exchange rate changes |

|

| (402 | ) |

|

| 154 |

| ||||||||||

Net increase (decrease) in cash, cash equivalents, and restricted cash |

|

| 150,177 |

|

|

| (42,100 | ) | ||||||||||

Cash, cash equivalents and restricted cash: |

|

|

|

|

| |||||||||||||

Beginning of year |

|

| 272,943 |

|

|

| 262,539 |

| ||||||||||

| End of period |

| $ | 423,120 |

|

| $ | 220,439 |

| |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

PARSONS CORPORATION AND SUBSIDIARIES

For the Three Months Ended March 31, 2024 and March 31, 2023

(In thousands)

(Unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| Redeemable |

|

|

|

|

|

|

|

|

|

| Other |

|

| Total |

|

|

|

|

|

|

|

|

| |||

|

| Common |

|

| Treasury |

|

| Retained |

|

| Comprehensive |

|

| Parsons |

|

| Noncontrolling |

|

|

|

|

| ||||||

|

| Stock |

|

| Stock |

|

| Earnings |

|

| Income (Loss) |

|

| Deficit |

|

| Interests |

|

| Total |

| |||||||

Balance at December 31, 2018 |

| $ | 1,876,309 |

|

| $ | (957,025 | ) |

| $ | 12,445 |

|

| $ | (22,957 | ) |

| $ | (967,537 | ) |

| $ | 46,461 |

|

| $ | (921,076 | ) |

Comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

|

|

|

|

|

|

|

|

|

| 9,741 |

|

|

|

|

|

|

| 9,741 |

|

|

| 3,645 |

|

|

| 13,386 |

|

Foreign currency translation gain |

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2,547 |

|

|

| 2,547 |

|

|

|

|

|

|

| 2,547 |

|

Pension adjustments |

|

|

|

|

|

|

|

|

|

|

|

|

|

| 9 |

|

|

| 9 |

|

|

|

|

|

|

| 9 |

|

ASC 842 transition adjustment |

|

|

|

|

|

|

|

|

|

| 52,608 |

|

|

|

|

|

|

| 52,608 |

|

|

|

|

|

|

| 52,608 |

|

Purchase of treasury stock |

|

| (813 | ) |

|

| (813 | ) |

|

| 813 |

|

|

|

|

|

|

| - |

|

|

|

|

|

|

| - |

|

Distributions, net of contributions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| - |

|

|

| (18,278 | ) |

|

| (18,278 | ) |

ESOP shares at redemption value |

|

| (164 | ) |

|

|

|

|

|

| 164 |

|

|

|

|

|

|

| 164 |

|

|

|

|

|

|

| 164 |

|

Balance at March 31, 2019 |

| $ | 1,875,332 |

|

| $ | (957,838 | ) |

| $ | 75,771 |

|

| $ | (20,401 | ) |

| $ | (902,468 | ) |

| $ | 31,828 |

|

| $ | (870,640 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at December 29, 2017 |

| $ | 1,855,305 |

|

| $ | (876,372 | ) |

| $ | (186,035 | ) |

| $ | (15,003 | ) |

| $ | (1,077,410 | ) |

| $ | 27,494 |

|

| $ | (1,049,916 | ) |

Comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

|

|

|

|

|

|

|

|

|

| 25,287 |

|

|

|

|

|

|

| 25,287 |

|

|

| 3,815 |

|

|

| 29,102 |

|

Foreign currency translation gain (loss) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| (2,781 | ) |

|

| (2,781 | ) |

|

| (3 | ) |

|

| (2,784 | ) |

Pension adjustments |

|

|

|

|

|

|

|

|

|

|

|

|

|

| (19 | ) |

|

| (19 | ) |

|

|

|

|

|

| (19 | ) |

Adoption of ASC 606 |

|

|

|

|

|

|

|

|

|

| (4,735 | ) |

|

|

|

|

|

| (4,735 | ) |

|

| 103 |

|

|

| (4,632 | ) |

Purchase of treasury stock |

|

| (367 | ) |

|

| (367 | ) |

|

| 367 |

|

|

|

|

|

|

| - |

|

|

|

|

|

|

| - |

|

Contributions, net of distributions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| - |

|

|

| 6,497 |

|

|

| 6,497 |

|

Balance at March 30, 2018 |

| $ | 1,854,938 |

|

| $ | (876,738 | ) |

| $ | (165,116 | ) |

| $ | (17,803 | ) |

| $ | (1,059,658 | ) |

| $ | 37,906 |

|

| $ | (1,021,752 | ) |

|

| Common |

|

| Treasury |

|

| Additional |

|

| Retained |

|

| Accumulated |

|

| Total |

|

| Noncontrolling |

|

| Total |

| ||||||||

Balance at December 31, 2023 |

| $ | 146,341 |

|

| $ | (827,311 | ) |

| $ | 2,779,365 |

|

| $ | 203,724 |

|

| $ | (14,908 | ) |

| $ | 2,287,211 |

|

| $ | 89,504 |

|

| $ | 2,376,715 |

|

Comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Net income |

|

| - |

|

|

| - |

|

|

| - |

|

|

| (107,355 | ) |

|

| - |

|

|

| (107,355 | ) |

|

| 15,243 |

|

|

| (92,112 | ) |

Foreign currency translation |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (1,927 | ) |

|

| (1,927 | ) |

|

| - |

|

|

| (1,927 | ) |

Pension adjustments, net |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (31 | ) |

|

| (31 | ) |

|

| - |

|

|

| (31 | ) |

Distributions |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (11,258 | ) |

|

| (11,258 | ) |

Capped call transactions |

|

| - |

|

|

| - |

|

|

| (66,121 | ) |

|

| - |

|

|

| - |

|

|

| (66,121 | ) |

|

| - |

|

|

| (66,121 | ) |

Repurchase of warrants |

|

| - |

|

|

| - |

|

|

| (104,952 | ) |

|

| - |

|

|

| - |

|

|

| (104,952 | ) |

|

| - |

|

|

| (104,952 | ) |

Bond hedge termination |

|

| - |

|

|

| - |

|

|

| 149,308 |

|

|

| - |

|

|

| - |

|

|

| 149,308 |

|

|

| - |

|

|

| 149,308 |

|

Issuance of equity securities, |

|

| 376 |

|

|

| - |

|

|

| (8,256 | ) |

|

| (9,108 | ) |

|

| - |

|

|

| (16,988 | ) |

|

| - |

|

|

| (16,988 | ) |

Stock-based compensation |

|

| - |

|

|

| - |

|

|

| 10,523 |

|

|

| - |

|

|

| - |

|

|

| 10,523 |

|

|

| - |

|

|

| 10,523 |

|

Balance at March 31, 2024 |

| $ | 146,717 |

|

| $ | (827,311 | ) |

| $ | 2,759,867 |

|

| $ | 87,261 |

|

| $ | (16,866 | ) |

| $ | 2,149,668 |

|

| $ | 93,489 |

|

| $ | 2,243,157 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Balance at December 31, 2022 |

| $ | 146,132 |

|

| $ | (844,936 | ) |

| $ | 2,717,134 |

|

| $ | 43,089 |

|

| $ | (17,849 | ) |

| $ | 2,043,570 |

|

| $ | 52,365 |

|

| $ | 2,095,935 |

|

Comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Net income |

|

| - |

|

|

| - |

|

|

| - |

|

|

| 25,553 |

|

|

| - |

|

|

| 25,553 |

|

|

| 9,723 |

|

|

| 35,276 |

|

Foreign currency translation |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (177 | ) |

|

| (177 | ) |

|

| - |

|

|

| (177 | ) |

Pension adjustments, net |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 1 |

|

|

| 1 |

|

|

| - |

|

|

| 1 |

|

Contributions |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 201 |

|

|

| 201 |

|

Distributions |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (638 | ) |

|

| (638 | ) |

Issuance of equity securities, |

|

| 251 |

|

|

| - |

|

|

| (6,098 | ) |

|

| (213 | ) |

|

| - |

|

|

| (6,060 | ) |

|

| - |

|

|

| (6,060 | ) |

Repurchases of common stock |

|

| (139 | ) |

|

| - |

|

|

| (5,861 | ) |

|

| - |

|

|

| - |

|

|

| (6,000 | ) |

|

| - |

|

|

| (6,000 | ) |

Stock-based compensation |

|

| - |

|

|

| - |

|

|

| 6,992 |

|

|

| - |

|

|

| - |

|

|

| 6,992 |

|

|

| - |

|

|

| 6,992 |

|

Balance at March 31, 2023 |

| $ | 146,244 |

|

| $ | (844,936 | ) |

| $ | 2,712,167 |

|

| $ | 68,429 |

|

| $ | (18,025 | ) |

| $ | 2,063,879 |

|

| $ | 61,651 |

|

| $ | 2,125,530 |

|

The accompanying notes are an integral part of these consolidated financial statements.

5

Parsons Corporation and Subsidiaries

Notes to Consolidated Financial Statements (unaudited)

|

|

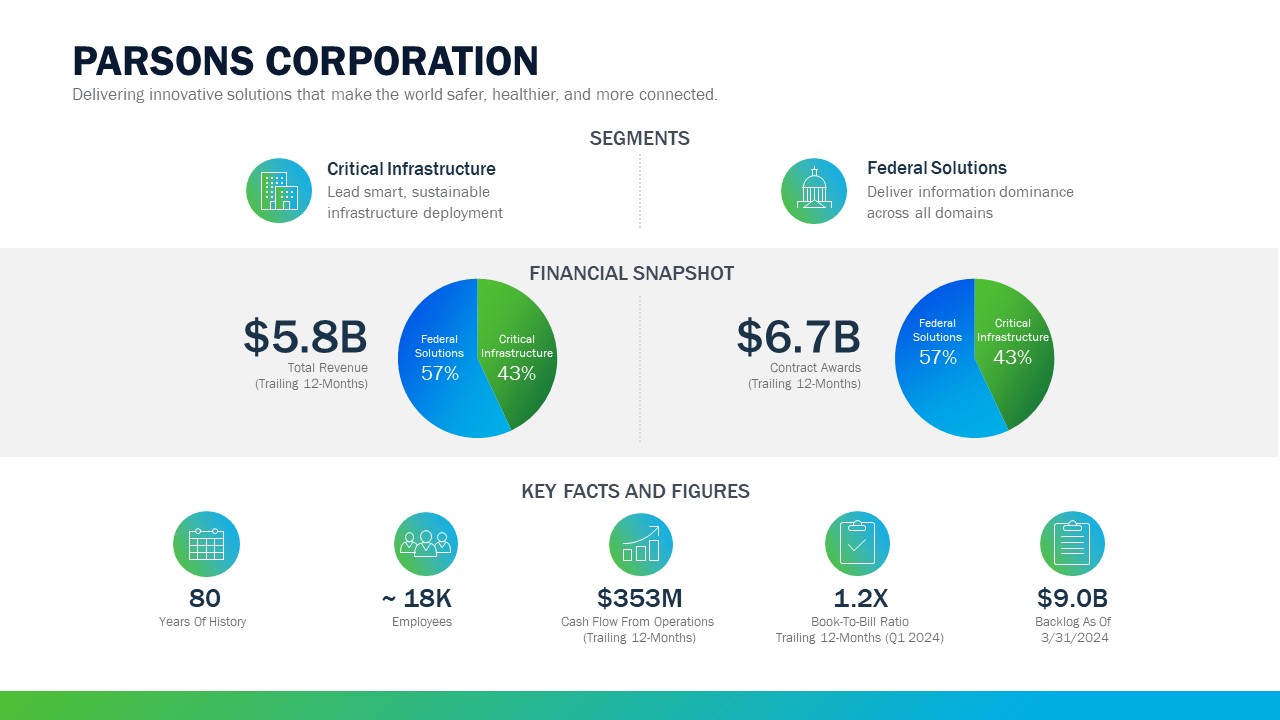

Organization

Parsons Corporation, a Delaware corporation, and its subsidiaries (collectively, the “Company”) provide sophisticated design, engineering and technical services, and smart and agile software to the United States federal government and Critical Infrastructure customers worldwide. The Company performs work in various foreign countries through local subsidiaries, joint ventures and foreign offices maintained to carry out specific projects. Parsons Employee Stock Ownership Plan (“ESOP”) is the sole shareholder

Initial Public Offering

Effective May 8, 2019, the Company consummated its initial public offering (“IPO”) whereby the Company sold 18,518,500 sharesPresentation and Principles of common stock for $27.00 per share. The underwriters exercised their share option effective May 14, 2019 to purchase an additional 2,777,775 shares at the share price of $25.515 which is the initial public offering share price of $27.00 less the underwriting discount of $1.485 per share. The net proceeds of the initial public offering and the underwriters’ share option was approximately $533.8 million, after deducting underwriting discounts and other fees, were used to fund an IPO dividend of $52.1 million, repay the outstanding balance of $150.0 million under our Term Loan, and repay outstanding indebtedness under our Revolving Credit Facility.

Stock Dividend

On April 15, 2019, the board of directors of the Company declared a common stock dividend in a ratio of two shares of common stock for every one share of common stock presently held by the Company’s stockholder (the “Stock Dividend”). The record date of this common Stock Dividend, which the Company refers to as the Stock Dividend was May 7, 2019, the day immediately prior to the consummation of the Company’s initial public offering on May 8, 2019, and the payment date of the Stock Dividend was May 8, 2019. Purchasers of the Company’s common stock in the Company’s public offering were not entitled to receive any portion of the Stock Dividend. The Company’s consolidated financial statements include the effects of this Stock Dividend.

The accompanying unaudited consolidated financial statements and related notes of the Company have been prepared in accordance with generally accepted accounting principles in the United States of America ("GAAP") and pursuant to the interim period reporting requirements of Form 10-Q. They do not include all of the information and footnotes required by GAAP for complete financial statements and, therefore, should be read in conjunction with our consolidated financial statements and the notes thereto included in the Company’s Annual Report on Form S-1/A filed on April 29, 2019.10-K for the year ended December 31, 2023.

In the opinion of management, the consolidated financial statements reflect all normal recurring adjustments necessary for a fair statement of the financial position, results of operations and cash flows for the interim periods presented. The results of operations and cash flows for any interim period are not necessarily indicative of results for the full year or for future years.

This Quarterly Report on Form 10-Q includes the accounts of our wholly-ownedParsons Corporation and its subsidiaries and affiliates which it controls. Interests in joint ventures ofthat are controlled by the Company, or for which we arethe Company is otherwise deemed to be the primary beneficiary. The equity method of accounting is applied for thebeneficiary, are consolidated. For joint ventures in which the Company does not have a controlling interest, but exerts a significant influence, the Company applies the equity method of accounting (see “Note 1614 –Investments in and Advances to Joint Ventures" for further discussion).

In the first quarter of 2019 the Company adopted Accounting Standards Update (‘ASU”) 2016-02, “Leases” (“Topic 842”), using the modified retrospective method. The new guidance was applied Intercompany accounts and transactions are eliminated in consolidation. Certain amounts may not foot due to leases that existed or were entered into on or after January 1. 2019. The Company’s results for the reporting period beginning January 1, 2019 have been presented under Topic 842, while prior period amounts have not been adjusted and continue to be reported in accordancerounding.

with previous guidance. See “Note 6 – Leases” for further discussion of the adoption and the impact on the Company’s financial statements.

Fiscal Periods

In October 2018, our board of directors approved a change in our annual and quarterly fiscal period ends from the last Friday on or before the calendar year or quarterly month-end to the last day of the calendar year or quarterly month-end. Accordingly, the period end for the first quarters of fiscal 2018 and fiscal 2019 are March 30, 2018 and March 31, 2019, respectively. The number of days in the quarters ended March 30, 2018 and March 31, 2019 were 91 and 90, respectively.

Use of Estimates

The preparation of the consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual amounts could differ from those estimates. The Company’s most significant estimates and judgments involve revenue recognition with respect to the determination of the costs to complete contracts and transaction price; determination of self-insurance reserves; valuation of the Company’s fair value of common stock; useful lives of property and equipment and intangible assets; calculation of allowance for doubtful accounts; valuation of deferred income tax assets and uncertain tax positions, among others. Please refer toSee “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates” and “Note 2 – 2—Summary of Significant Accounting Policies” of Notesin the notes to Consolidated Financial Statementsour consolidated financial statements included in the Company’s Form S-1/A filed April 29, 2019,10-K for the year ended December 31, 2023, for a discussion of the significant estimates and assumptions affecting our consolidated financial statements. Estimates of costs to complete contracts are continually evaluated as work progresses and are revised when necessary. When a change in estimate is determined to have an impact on contract profit, the Company records a positive or negative adjustment to the consolidated statement of income.

|

3. New Accounting Pronouncements |

In the firstfourth quarter of 2019, the Company adopted Topic 842. See “Note 6 – Leases” for further discussion of the adoption and the impact on the Company’s financial statements.

In the first quarter of 2019, the Company adopted ASU 2018-02, “Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income” under which the Company did not elect to reclassify the income tax effects stranded in accumulated other comprehensive income to retained earnings as a result of the enactment of comprehensive tax legislation, commonly referred to as the Tax Cuts and Jobs Act. As a result, there was no impact on the Company’s financial position, results of operations or cash flows.

On December 30, 2017, the Company adopted ASC 606, “Revenue from Contracts with Customers”, using the modified retrospective method, which provides for a cumulative effect adjustment to retained earnings beginning in fiscal 2018 for those uncompleted contracts impacted by the adoption of the new standard.2023, The difference between the recognition criteria under ASC 606 and our previous recognition practices under ASC 605-35 was recognized through a cumulative adjustment of $4.7 million that was made to the opening balance of accumulated deficit as of December 30, 2017.

In January 2017, the Financial Accounting Standards Board (“FASB”("FASB") issued Issued Accounting Standards Update (“ASU”) 2023-09, "Income Taxes (Topic 740)" ("ASU 2017-04, Simplifying2023-09"). ASU 2023-09 enhances the Testtransparency and decision usefulness of income tax disclosures. The amendments in ASU 2023-09 addresses investor requests for Goodwill Impairment.more transparency about income tax information through improvements to income tax disclosures primarily related to the rate reconciliation and income taxes paid information. ASU 2017-04 simplifies2023-09 also includes certain other amendments to improve the test for goodwill impairment by removing the second stepeffectiveness of the goodwill impairment test, which requires a hypothetical purchase price allocation. A goodwill impairment will now be the amount by which a reporting unit’s carrying value exceeds its fair value, not to exceed the carrying amount of goodwill. The guidanceincome tax disclosures. ASU 2023-09 is effective for interim and annual reporting periodsfiscal years beginning after December 15, 2024.

6

Early adoption is permitted. The adoption of this ASU will not have a material impact on the Company's consolidated financial statements.

In the fourth quarter of 2023, the FASB Issued ASU 2023-07, "Segment Reporting (Topic 280)". ASU 2023-07 introduces enhanced disclosures about significant segment expenses along with other enhanced segment disclosures. ASU 2023-07 is effective for fiscal years beginning after December 15, 20192023, and should be applied prospectively with earlyinterim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. The Company early adoptedadoption of this ASU will not have a material impact on the new standard asCompany's consolidated financial statements.

During July 2023, the FASB Issued ASU 2023-03. ASU 2023-03 incorporates, into certain accounting standards, amendments to SEC paragraphs pursuant to SEC Staff Accounting Bulletin No. 120, SEC Staff Announcement at the March 24, 2022 EITF meeting, and Staff Accounting Bulletin Topic 6.B, Accounting Series Release 280—General Revisions of the beginningRegulation S-X: Income or Loss Applicable to Common Stock. These rules are effective immediately. The adoption of fiscal 2018 and its adoptionthis ASU did not have a material impact on the Company's consolidated financial statements.

|

|

Polaris AlphaI.S. Engineers, LLC

On MayOctober 31, 2018,2023, the Company entered into a Membership Interest Purchase Agreement to acquired a 100%100% ownership interest in Polaris Alpha,I.S. Engineers, LLC (“I.S. Engineers”), a privately owned, advanced technology-focused provider of innovative mission solutionsprivately-owned company, for complex defense, intelligence, and security customers, as well as other U.S. federal government customers, for $489.1$12.2 million paid in cash. Headquartered in Texas, I.S. Engineers provides full service consulting specializing in transportation engineering, including roads and highways, and program management. The Company borrowed $260 million under the credit agreement, as described in “Note 12 – Debt and Credit Facilities,” to partially fund the acquisition.acquisition was entirely funded by cash on-hand. In

connection with this acquisition, the Company recognized $6.2$0.3 million of acquisition-related expenses in “Indirect,acquisition related “Selling, general and administrative expense” in the consolidated statements of income for the fiscal year ended December 31, 2018,2023, including legal fees, consulting fees, and other miscellaneous direct expenses associated with the acquisition. Polaris AlphaThe Company allocated the purchase price to the appropriate classes of tangible assets and liabilities and assigned the excess of $11.9 million entirely to goodwill. The entire value of goodwill was assigned to the Critical Infrastructure reporting unit and represents synergies expected to be realized from this business combination. No goodwill is deductible for income tax purposes.

Sealing Technologies, Inc.

On August 23, 2023, the Company acquired a 100% ownership interest in Sealing Technologies, Inc (“SealingTech”), a privately-owned company, for $179.3 million in cash and up to an additional $25 million in the event an earn out revenue target is exceeded. The Company borrowed $175 million under the Credit Agreement to fund the acquisition. Headquartered in Maryland, SealingTech expands Parsons’ customer base across the Department of Defense and Intelligence Community, and further enhances the Company’scompany’s capabilities in defensive cyber operations; integrated mission-solutions powered by artificial intelligence (AI) and machine learning (ML); edge computing and edge access modernization; critical infrastructure protection; and secure data analytics expertisemanagement. In connection with new technologiesthis acquisition, the Company recognized $3.3 million of acquisition-related expenses in “Selling, general and solutions. Customersadministrative expense” in the consolidated statements of income for the year ended December 31, 2023, including legal fees, consulting fees, and other miscellaneous direct expenses associated with the acquisition.

The Company has agreed to pay the selling shareholders up to an additional $25 million in the event an earn out revenue target of $110 million is exceeded during the fiscal year ended December 31, 2024. The earn out payment due and payable by the Company to the selling shareholders shall be equal to (i) five-tenths (0.5), multiplied by (ii) the difference of (A) the actual earn out revenue minus (B) the earn out revenue target; provided, however, that in no event shall the earn out payment exceed $25 million. In the event that the earn out revenue is less than or equal to the earn out revenue target, the earn out payment shall be zero. The earn out payment, if any, shall be paid by the Company to the selling shareholders within 15 days following the date the earn out statement becomes final and binding on both companies will benefitparties. The fair value of the earn out (contingent consideration in the table below) was calculated using a Black-Scholes model. See “Note 2—Summary of Significant Accounting Policies” in the notes to our consolidated financial statements included in the Company’s Form 10-K for the year ended December 31, 2023 for further information on how the fair value of contingent consideration is determined.

7

The following table summarizes the acquisition date fair value of the purchase consideration transferred (in thousands):

|

| Amount |

| |

Cash paid at closing |

| $ | 179,259 |

|

Fair value of contingent consideration to be achieved |

|

| 3,231 |

|

Total purchase price |

| $ | 182,490 |

|

The estimated fair value of the SealingTech contingent consideration as of March 31, 2024 was $4.1 million, a $1.8 million increase from existing, complementary technologies and increased scale, enabling end-to-end solutions under the shared visionestimated fair value as of rapid prototyping and agile development.December 31, 2023. The change in the estimated fair value was recorded to "other income (expense), net" in the consolidated financial statements.

The following table summarizes the estimated fair values of the assets acquired and liabilities assumed based on the preliminary purchase price allocation as of the date of acquisition (in thousands):

|

| Amount |

| |

Cash and cash equivalents |

| $ | 8,133 |

|

Accounts receivable |

|

| 17,889 |

|

Contract assets |

|

| 2,946 |

|

Prepaid expenses and other current assets |

|

| 1,379 |

|

Property and equipment |

|

| 2,025 |

|

Right of use assets, operating leases |

|

| 1,836 |

|

Deferred tax assets |

|

| 357 |

|

Goodwill |

|

| 90,593 |

|

Intangible assets |

|

| 75,000 |

|

Accounts payable |

|

| (15,987 | ) |

Accrued expenses and other current liabilities |

|

| (2,408 | ) |

Contract liabilities |

|

| (668 | ) |

Short-term lease liabilities, operating leases |

|

| (418 | ) |

Long-term lease liabilities, operating leases |

|

| (1,418 | ) |

Net assets acquired |

| $ | 179,259 |

|

|

| Amount |

| |

Cash and cash equivalents |

| $ | 7,914 |

|

Accounts receivable |

|

| 29,688 |

|

Contract assets |

|

| 35,229 |

|

Prepaid expenses and other current assets |

|

| 9,295 |

|

Property and equipment |

|

| 9,024 |

|

Goodwill |

|

| 243,471 |

|

Intangible assets |

|

| 199,520 |

|

Other noncurrent assets |

|

| 2,203 |

|

Accounts payable |

|

| (13,942 | ) |

Accrued expenses and other current liabilities |

|

| (26,419 | ) |

Contract liabilities |

|

| (3,529 | ) |

Deferred tax liabilities |

|

| (2,231 | ) |

Other long-term liabilities |

|

| (1,146 | ) |

Net assets acquired |

| $ | 489,077 |

|

Of the total purchase price, the following values were assigned to intangible assets (in thousands, except for years):

|

| Gross Carrying Amount |

|

| Amortization Period | |

|

|

|

|

|

| (in years) |

Developed technology |

| $ | 84,900 |

|

| 4 |

Customer relationships |

|

| 76,000 |

|

| 8 |

Backlog |

|

| 34,900 |

|

| 2 |

Trade name |

|

| 3,600 |

|

| 1 |

Leases |

| $ | 120 |

|

| 6 |

|

| Gross |

|

| Amortization | |

|

|

|

|

| (in years) | |

Customer relationships |

| $ | 40,000 |

|

| 14 |

Backlog |

|

| 26,000 |

|

| 3 |

Developed technologies |

|

| 8,000 |

|

| 3 |

Other |

| $ | 1,000 |

|

| 1 |

Amortization expense of $13.7$3.3 million related to these intangible assets was recorded for the three months ended March 31, 2019.2024. The entire value of goodwill of $243.5 million was assigned to the Parsons Federal Solutions reporting unit and represents synergies expected to be realized from this business combination. A portionThe entire value of goodwill is deductible for tax purposes. The Company is in the process of finalizing the amount.

The amount of revenue generated by Polaris AlphaSealingTech and included within consolidated revenuesrevenue is $16.9 million for the three months ended March 31, 2019 is $93.4 million.2024. The Company has determined that the presentation of net income from the date of acquisition is impracticable due to the integration of general corporate functions upon acquisition.

Supplemental Pro Forma Information (Unaudited)

Supplemental information on anof unaudited pro forma operating results assuming the Polaris AlphaSealingTech acquisition had been consummated as of the beginning of fiscal year 2018 (December 31, 2017)2022 (in thousands) is as follows:

|

| Three Months Ended |

| |

|

| March 30, 2018 |

| |

Pro forma revenue |

| $ | 840,487 |

|

Pro forma net income |

| $ | 10,532 |

|

8

|

| Three Months Ended |

| |||||

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||

Pro forma Revenue |

| $ | 1,535,676 |

|

| $ | 1,190,481 |

|

Pro forma Net Income including noncontrolling interests |

|

| (90,779 | ) |

|

| 34,195 |

|

IPKeys Power Partners

The unaudited pro forma supplemental information is based on estimates and assumptions whichOn April 13, 2023, the Company believes are reasonable and reflects the pro forma impact of additional amortization relatedentered into a merger agreement to the fair value of acquired intangible assets, pro forma impact of reflecting acquisition costs, which consisted of legal, advisory and due diligence fees and expenses and the additional pro forma interest expense related to the borrowings under the credit agreement as of the assumed acquisition date. This supplemental pro forma information has been prepared for comparative purposes and does not purport to be indicative of what would have occurred had the acquisition been consummated during the periods for which pro forma information is presented.

OGSystems

On January 7, 2019, the Company acquiredacquire a 100%100% ownership interest in OGSystems,IPKeys Power Partners (“IPKeys”), a privately owned, advanced technology-focused provider of innovative mission solutionsprivately-owned company, for complex defense, intelligence, and security customers, as well as other U.S. federal government customers, for $292.4$43.0 million paid in cash. The Company borrowed $110 million under the credit agreementmerger brings IPKeys' established customer base, expanding Parsons' presence in two rapidly growing end markets: grid modernization and $150 million oncyber resiliency for critical infrastructure. Headquartered in Tinton Falls, New Jersey, IPKeys is a short-term loan, as described in “Note 12 – Debttrusted provider of enterprise software platform solutions that is actively delivering cyber and Credit Facilities,”operational security to partially fund the acquisition.hundreds of electric, water, and gas utilities across North America. The acquisition was entirely funded by cash on-hand. In connection with this acquisition, the Company recognized $4.1$0.6 million of acquisition-related expenses in “Indirect,“Selling, general and administrative expense” in the consolidated statements of income for the periodyear ended MarchDecember 31, 2019,2023, respectively, including legal fees, consulting fees, and other miscellaneous direct expenses associated with the acquisition. OGSystems enhances the Company’s artificial intelligence and data analytics expertise with new technologies and solutions. Customers of both companies will benefit from existing, complementary technologies and increased scale, enabling end-to-end solutions under the shared vision of rapid prototyping and agile development.

The following table summarizes the estimated fair values of the assets acquired and liabilities assumed based on the preliminary purchase price allocation as of the date of acquisition (in thousands):

|

| Amount |

| |

Cash and cash equivalents |

| $ | 126 |

|

Accounts receivable |

|

| 3,937 |

|

Contract assets |

|

| 834 |

|

Prepaid expenses and other current assets |

|

| 455 |

|

Property and equipment |

|

| 86 |

|

Right of use assets, operating leases |

|

| 1,105 |

|

Other noncurrent assets |

|

| 152 |

|

Goodwill |

|

| 22,407 |

|

Intangible assets |

|

| 23,000 |

|

Accounts payable |

|

| (541 | ) |

Accrued expenses and other current liabilities |

|

| (1,768 | ) |

Contract liabilities |

|

| (1,936 | ) |

Short-term lease liabilities, operating leases |

|

| (343 | ) |

Deferred tax liabilities |

|

| (3,713 | ) |

Long-term lease liabilities, operating leases |

|

| (762 | ) |

Net assets acquired |

| $ | 43,039 |

|

|

| Amount |

| |

Cash and cash equivalents |

| $ | 5,772 |

|

Accounts receivable |

|

| 9,904 |

|

Contract assets |

|

| 9,747 |

|

Prepaid expenses and other current assets |

|

| 4,307 |

|

Property and equipment |

|

| 4,085 |

|

Right of use assets, operating leases |

|

| 8,826 |

|

Goodwill |

|

| 183,567 |

|

Intangible assets |

|

| 92,300 |

|

Other noncurrent assets |

|

| 10 |

|

Accounts payable |

|

| (5,450 | ) |

Accrued expenses and other current liabilities |

|

| (7,147 | ) |

Contract liabilities |

|

| (1,300 | ) |

Short-term lease liabilities, operating leases |

|

| (805 | ) |

Income tax payable |

|

| (1,469 | ) |

Deferred tax liabilities |

|

| (931 | ) |

Long-term lease liabilities, operating leases |

|

| (8,021 | ) |

Other long-term liabilities |

|

| (1,015 | ) |

Net assets acquired |

| $ | 292,380 |

|

Of the total purchase price, the following values were assigned to intangible assets (in thousands, except for years):

|

| Gross Carrying Amount |

|

| Amortization Period | |

|

|

|

|

|

| (in years) |

Customer relationships |

| $ | 57,100 |

|

| 5 |

Backlog |

|

| 27,700 |

|

| 3 |

Trade name |

|

| 3,800 |

|

| 2 |

Non compete agreements |

|

| 2,400 |

|

| 3 |

Developed technologies |

| $ | 1,300 |

|

| 3 |

|

| Gross |

|

| Amortization | |

|

|

|

|

| (in years) | |

Customer relationships (1) |

| $ | 15,900 |

|

| 16 |

Developed technologies |

|

| 7,000 |

|

| 11 |

Other |

| $ | 100 |

|

| 1 |

(1) The acquired business is a SaaS commercial business. Backlog for this type of business is included as customer relationships.

The Company is still in the process of finalizing its valuation of developed technology acquired.

Amortization expense of $5.9$0.4 million related to these intangible assets was recorded for the three months ended March 31, 2019.2024. The entire value of goodwill of $183.6 million was assigned to the Parsons FederalCritical Infrastructure reporting unit and represents synergies expected to be realized from this business combination. Goodwill$0.9 million of $16.0 milliongoodwill is deductible for tax purposes.

The amount of revenue generated by OGSystems since the acquisitionIPKeys and included within consolidated revenuesrevenue is $3.5 million for the three months ended March 31, 2019 is $29.0 million.2024. The Company has determined that the presentation of net income from the date of acquisition is impracticable due to the integration of general corporate functions upon acquisition.

9

Supplemental Pro Forma Information (Unaudited)

Supplemental information on anof unaudited pro forma operating results assuming the OGSystemsIPKeys acquisition had been consummated as of the beginning of fiscal year 2018 (December 31, 2017)2022 (in thousands) is as follows:

|

| Three Months Ended |

| |||||

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||

Pro forma Revenue |

| $ | 1,535,676 |

|

| $ | 1,176,321 |

|

Pro forma Net Income including noncontrolling interests |

|

| (91,953 | ) |

|

| 35,362 |

|

|

| Three Months Ended |

| |||||

|

| March 30, 2018 |

|

| March 31, 2019 |

| ||

Pro forma revenue |

| $ | 782,218 |

|

| $ | 906,360 |

|

Pro forma net income |

| $ | 15,739 |

|

| $ | 17,458 |

|

The unaudited pro forma supplemental information is based on estimates and assumptions which the Company believes are reasonable and reflects the pro forma impact of additional amortization related to the fair value of acquired intangible assets, pro forma impact of reflecting acquisition costs, which consisted of legal, advisory and due diligence fees and expenses and the additional pro forma interest expense related to the borrowings under the credit agreement as of the assumed acquisition date. This supplemental pro forma information has been prepared for comparative purposes and does not purport to be indicative of what would have occurred had the acquisition been consummated during the periods for which pro forma information is presented.

|

|

Disaggregation of Revenue

The Company’s contracts contain both fixed-price and cost reimbursable components. Contract types are based on the component that represents the majority of the contract. The following table presents revenue disaggregated by contract type (in thousands):

|

| Three Months Ended |

| |||||||||||||

|

| March 30, 2018 |

|

| March 31, 2019 |

|

| Three Months Ended |

| |||||||

Fixed-Price |

| $ | 265,408 |

|

| $ | 257,695 |

| ||||||||

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||||||||||

Fixed-price |

| $ | 631,219 |

|

| $ | 341,012 |

| ||||||||

Time-and-Materials |

|

| 227,741 |

|

|

| 255,706 |

|

|

| 350,651 |

|

|

| 318,315 |

|

Cost-Plus |

|

| 261,530 |

|

|

| 391,004 |

| ||||||||

Cost-plus |

|

| 553,806 |

|

|

| 514,139 |

| ||||||||

Total |

| $ | 754,679 |

|

| $ | 904,405 |

|

| $ | 1,535,676 |

|

| $ | 1,173,466 |

|

Refer toSee “Note 2018 – Segments Information” for the Company’s revenues by business lines.

Contract Assets and Contract Liabilities

Contract assets and contract liabilities balances at March 31, 2024 and December 31, 2018 and March 31, 20192023 were as follows (in thousands):

|

| March 31, 2024 |

|

| December 31, 2023 |

| ||

Contract assets |

| $ | 768,007 |

|

| $ | 757,515 |

|

Contract liabilities |

|

| 282,962 |

|

|

| 301,107 |

|

Net contract assets (liabilities) (1) |

| $ | 485,045 |

|

| $ | 456,408 |

|

|

| December 31, 2018 |

|

| March 31, 2019 |

|

| $ change |

|

| % change |

| ||||

Contract assets |

| $ | 515,319 |

|

| $ | 571,755 |

|

| $ | 56,436 |

|

|

| 11.0 | % |

Contract liabilities |

|

| 208,576 |

|

|

| 225,017 |

|

|

| 16,441 |

|

|

| 7.9 | % |

Net contract assets (liabilities) (1) |

| $ | 306,743 |

|

| $ | 346,738 |

|

| $ | 39,995 |

|

|

| 13.0 | % |

During the three months ended March 30, 201831, 2024 and March 31, 2019,2023, the Company recognized revenue of approximately $26.3$138.3 million and $85.7$78.1 million, respectively,that was included in the corresponding contract liability balancebalances at December 30, 201731, 2023 and December 31, 2018,2022, respectively. The change in contract assets and contract liabilities was the result of normal business activity and not significantly impacted by other factors, except as follows:

|

| December 31, 2018 |

|

| March 31, 2019 |

| ||

Acquired contract assets |

| $ | 35,229 |

|

| $ | 9,747 |

|

Acquired contract liabilities |

|

| 3,529 |

|

|

| 1,300 |

|

Reversal of provision for contract losses (1) |

| $ | 133,180 |

|

| $ | - |

|

|

|

There was no significant impairment of contract assets recognized during the three months ended March 30, 201831, 2024 and March 31, 2019.2023.

DuringThere have been no revisions in estimates, such as changes in estimated claims or incentives, related to performance obligations partially satisfied in previous periods that individually had an impact of $5 million or more on revenue.

10

Accounts Receivable, net

Accounts receivable, net consisted of the three months ended March 30, 2018 andfollowing as of March 31, 2019,2024 and December 31, 2023 (in thousands):

|

| 2024 |

|

| 2023 |

| ||

Billed |

| $ | 674,861 |

|

| $ | 646,375 |

|

Unbilled |

|

| 352,542 |

|

|

| 273,215 |