UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period endedMarch 31, 20202021

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period fromto

Commission file number: 1-36313

TIMKENSTEEL CORPORATION

(Exact name of registrant as specified in its charter)

Ohio |

| 46-4024951 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

1835 Dueber Avenue SW, Canton, OH |

| 44706 |

(Address of principal executive offices) |

| (Zip Code) |

330.471.7000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

Title of each class |

| Trading symbol |

| Name of exchange in which registered |

Common shares |

| TMST |

| New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).�� Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

Large accelerated filer |

| ☐ |

|

| Accelerated filer | ☒ |

|

|

|

|

|

|

|

Non-accelerated filer |

| ☐ |

|

| Smaller reporting company | ☐ |

|

|

|

|

|

|

|

|

|

|

|

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial reporting accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class |

| Outstanding at April 30, |

Common Shares, without par value |

|

|

TimkenSteel Corporation

|

|

|

| ||

| Consolidated Statements of Comprehensive Income (Loss) (Unaudited) | |

| ||

| ||

| ||

| ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||

| ||

2

Part I. FINANCIAL INFORMATIONFinancial Information

ITEMItem 1. FINANCIAL STATEMENTSFinancial Statements

TimkenSteel Corporation

Consolidated Statements of Operations (Unaudited)

|

|

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||||

|

|

|

|

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

(Dollars in millions, except per share data) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

|

|

|

|

| $ | 259.7 |

|

| $ | 371.0 |

|

| $ | 273.6 |

|

| $ | 259.7 |

|

Cost of products sold |

|

|

|

|

|

| 251.9 |

|

|

| 342.6 |

|

|

| 242.9 |

|

|

| 251.9 |

|

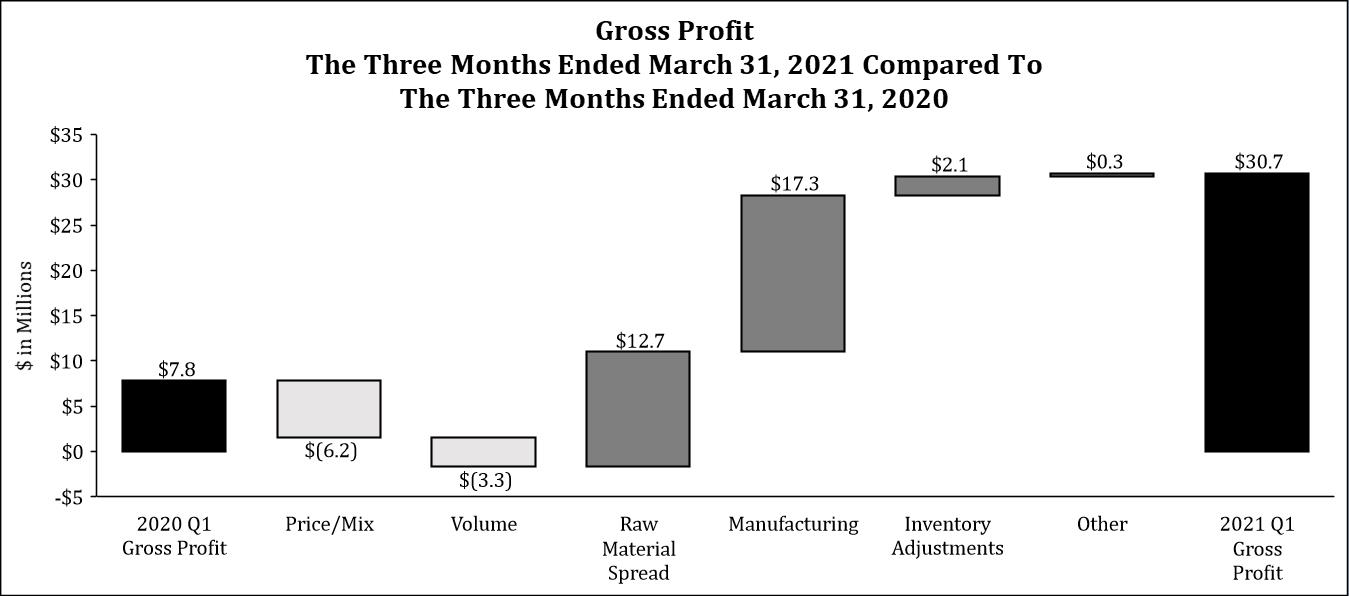

Gross Profit |

|

|

|

|

|

| 7.8 |

|

|

| 28.4 |

|

|

| 30.7 |

|

|

| 7.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

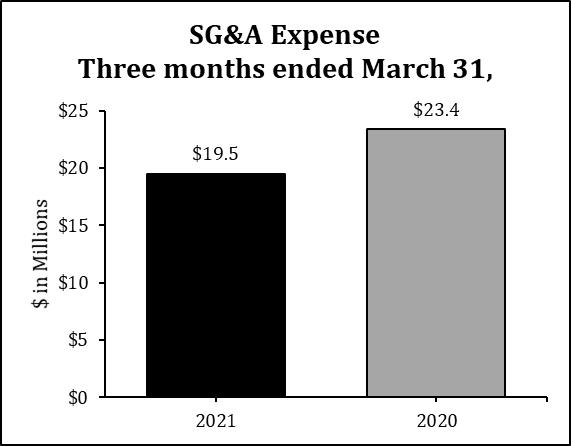

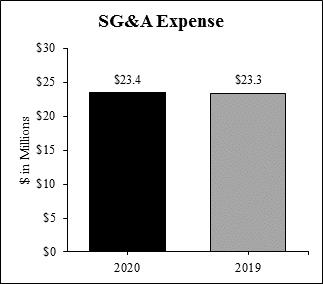

Selling, general and administrative expenses |

|

|

|

|

|

| 23.4 |

|

|

| 23.3 |

|

|

| 19.5 |

|

|

| 23.4 |

|

Restructuring charges |

|

|

|

|

|

| 0.6 |

|

|

| — |

|

|

| 0.5 |

|

|

| 0.6 |

|

Loss (gain) on sale or asset disposals |

|

|

|

|

|

| (2.3 | ) |

|

| — |

| ||||||||

Loss (gain) on sale or disposal of assets, net |

|

| — |

|

|

| (2.3 | ) | ||||||||||||

Impairment charges |

|

| 8.2 |

|

|

| — |

| ||||||||||||

Interest expense |

|

|

|

|

|

| 3.2 |

|

|

| 4.2 |

|

|

| 1.9 |

|

|

| 3.2 |

|

Other expense (income), net |

|

|

|

|

|

| 2.7 |

|

|

| (2.7 | ) | ||||||||

Other (income) expense, net |

|

| (9.4 | ) |

|

| 2.7 |

| ||||||||||||

Income (Loss) Before Income Taxes |

|

|

|

|

|

| (19.8 | ) |

|

| 3.6 |

|

|

| 10.0 |

|

|

| (19.8 | ) |

Provision (benefit) for income taxes |

|

|

|

|

|

| 0.1 |

|

|

| 0.1 |

|

|

| 0.2 |

|

|

| 0.1 |

|

Net Income (Loss) |

|

|

|

|

| $ | (19.9 | ) |

| $ | 3.5 |

|

| $ | 9.8 |

|

| $ | (19.9 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic earnings (loss) per share |

|

|

|

|

| $ | (0.44 | ) |

| $ | 0.08 |

|

| $ | 0.22 |

|

| $ | (0.44 | ) |

Diluted earnings (loss) per share |

|

|

|

|

| $ | (0.44 | ) |

| $ | 0.08 |

|

| $ | 0.20 |

|

| $ | (0.44 | ) |

See accompanying Notes to the unaudited Consolidated Financial Statements.

3

TimkenSteel Corporation

Consolidated Statement of Comprehensive Income (Loss) (Unaudited)

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

| $ | (19.9 | ) |

| $ | 3.5 |

|

| $ | 9.8 |

|

| $ | (19.9 | ) |

Other comprehensive income (loss), net of tax: |

|

|

|

|

|

|

|

| ||||||||

Other comprehensive income (loss) |

|

|

|

|

|

|

|

| ||||||||

Foreign currency translation adjustments |

|

| (1.8 | ) |

|

| 0.4 |

|

|

| 0.1 |

|

|

| (1.8 | ) |

Pension and postretirement liability adjustments |

|

| (1.1 | ) |

|

| 0.1 |

|

|

| (1.5 | ) |

|

| (1.1 | ) |

Other comprehensive income (loss), net of tax |

|

| (2.9 | ) |

|

| 0.5 |

|

|

| (1.4 | ) |

|

| (2.9 | ) |

Comprehensive Income (Loss), net of tax |

| $ | (22.8 | ) |

| $ | 4.0 |

|

| $ | 8.4 |

|

| $ | (22.8 | ) |

See accompanying Notes to the unaudited Consolidated Financial Statements.

4

TimkenSteel Corporation

Consolidated Balance Sheets (Unaudited)

|

| March 31, 2020 |

|

| December 31, 2019 |

|

| March 31, 2021 |

|

| December 31, 2020 |

| ||||

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

| $ | 65.6 |

|

| $ | 27.1 |

|

| $ | 115.7 |

|

| $ | 102.8 |

|

Accounts receivable, net of allowances (2020 - $2.8 million; 2019 - $1.5 million) |

|

| 94.9 |

|

|

| 77.5 |

| ||||||||

Accounts receivable, net of allowances (2021 - $1.6 million; 2020 - $1.3 million) |

|

| 96.3 |

|

|

| 63.3 |

| ||||||||

Inventories, net |

|

| 240.5 |

|

|

| 281.9 |

|

|

| 202.7 |

|

|

| 178.4 |

|

Deferred charges and prepaid expenses |

|

| 3.6 |

|

|

| 3.3 |

|

|

| 3.7 |

|

|

| 4.0 |

|

Assets held for sale |

|

| 2.2 |

|

|

| 4.1 |

|

|

| — |

|

|

| 0.3 |

|

Other current assets |

|

| 5.3 |

|

|

| 7.8 |

|

|

| 12.0 |

|

|

| 8.8 |

|

Total Current Assets |

|

| 412.1 |

|

|

| 401.7 |

|

|

| 430.4 |

|

|

| 357.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Property, plant and equipment, net |

|

| 608.7 |

|

|

| 626.4 |

|

|

| 550.0 |

|

|

| 569.8 |

|

Operating lease right-of-use assets |

|

| 16.3 |

|

|

| 14.3 |

|

|

| 19.3 |

|

|

| 21.0 |

|

Pension assets |

|

| 17.2 |

|

|

| 25.2 |

|

|

| 37.3 |

|

|

| 33.5 |

|

Intangible assets, net |

|

| 12.4 |

|

|

| 14.3 |

|

|

| 8.5 |

|

|

| 9.3 |

|

Other non-current assets |

|

| 3.3 |

|

|

| 3.3 |

|

|

| 2.6 |

|

|

| 2.8 |

|

Total Assets |

| $ | 1,070.0 |

|

| $ | 1,085.2 |

|

| $ | 1,048.1 |

|

| $ | 994.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 96.0 |

|

| $ | 69.3 |

|

| $ | 136.4 |

|

| $ | 89.5 |

|

Salaries, wages and benefits |

|

| 21.3 |

|

|

| 13.9 |

|

|

| 28.7 |

|

|

| 29.4 |

|

Accrued pension and postretirement costs |

|

| 3.0 |

|

|

| 3.0 |

|

|

| 2.3 |

|

|

| 2.3 |

|

Current operating lease liabilities |

|

| 6.6 |

|

|

| 6.2 |

|

|

| 7.0 |

|

|

| 7.5 |

|

Current convertible notes, net |

|

| 40.2 |

|

|

| 38.9 |

| ||||||||

Other current liabilities |

|

| 16.5 |

|

|

| 19.9 |

|

|

| 12.5 |

|

|

| 13.4 |

|

Total Current Liabilities |

|

| 143.4 |

|

|

| 112.3 |

|

|

| 227.1 |

|

|

| 181.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Convertible notes, net |

|

| 79.8 |

|

|

| 78.6 |

| ||||||||

Non-current convertible notes, net |

|

| 44.7 |

|

|

| 39.3 |

| ||||||||

Credit Agreement |

|

| 60.0 |

|

|

| 90.0 |

|

|

| — |

|

|

| — |

|

Non-current operating lease liabilities |

|

| 9.7 |

|

|

| 8.2 |

|

|

| 12.3 |

|

|

| 13.5 |

|

Accrued pension and postretirement costs |

|

| 222.3 |

|

|

| 222.1 |

|

|

| 239.4 |

|

|

| 240.7 |

|

Deferred income taxes |

|

| 0.9 |

|

|

| 0.9 |

|

|

| 1.0 |

|

|

| 1.0 |

|

Other non-current liabilities |

|

| 11.8 |

|

|

| 10.0 |

|

|

| 10.3 |

|

|

| 11.0 |

|

Total Liabilities |

|

| 527.9 |

|

|

| 522.1 |

|

|

| 534.8 |

|

|

| 486.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred shares, without par value; authorized 10.0 million shares, none issued |

|

| — |

|

|

| — |

| ||||||||

Common shares, without par value; authorized 200.0 million shares; issued 2020 and 2019 - 45.7 million shares |

|

| — |

|

|

| — |

| ||||||||

Preferred shares, without par value; authorized 10.0 million shares, NaN issued |

|

| 0 |

|

|

| 0 |

| ||||||||

Common shares, without par value; authorized 200.0 million shares; issued 2021 and 2020 - 45.7 million shares |

|

| 0 |

|

|

| 0 |

| ||||||||

Additional paid-in capital |

|

| 841.1 |

|

|

| 844.8 |

|

|

| 824.7 |

|

|

| 843.4 |

|

Retained deficit |

|

| (321.4 | ) |

|

| (301.5 | ) |

|

| (349.4 | ) |

|

| (363.4 | ) |

Treasury shares - 2020 - 0.8 million; 2019 - 0.9 million |

|

| (19.4 | ) |

|

| (24.9 | ) | ||||||||

Treasury shares - 2021 - 0.1 million; 2020 - 0.6 million |

|

| (1.0 | ) |

|

| (12.9 | ) | ||||||||

Accumulated other comprehensive income (loss) |

|

| 41.8 |

|

|

| 44.7 |

|

|

| 39.0 |

|

|

| 40.4 |

|

Total Shareholders’ Equity |

|

| 542.1 |

|

|

| 563.1 |

|

|

| 513.3 |

|

|

| 507.5 |

|

Total Liabilities and Shareholders’ Equity |

| $ | 1,070.0 |

|

| $ | 1,085.2 |

|

| $ | 1,048.1 |

|

| $ | 994.0 |

|

See accompanying Notes to the unaudited Consolidated Financial Statements.

5

TimkenSteel Corporation

Consolidated Statements of Shareholders’ Equity (Unaudited)

(Dollars in millions) |

| Common Shares Outstanding |

|

| Additional Paid-in Capital |

|

| Retained Deficit |

|

| Treasury Shares |

|

| Accumulated Other Comprehensive Income (Loss) |

|

| Total |

|

| Common Shares Outstanding |

|

| Additional Paid-in Capital |

|

| Retained Deficit |

|

| Treasury Shares |

|

| Accumulated Other Comprehensive Income (Loss) |

|

| Total |

| ||||||||||||

Balance at December 31, 2019 |

|

| 44,820,153 |

|

| $ | 844.8 |

|

| $ | (301.5 | ) |

| $ | (24.9 | ) |

| $ | 44.7 |

|

| $ | 563.1 |

| ||||||||||||||||||||||||

Balance at December 31, 2020 |

|

| 45,164,308 |

|

| $ | 843.4 |

|

| $ | (363.4 | ) |

| $ | (12.9 | ) |

| $ | 40.4 |

|

| $ | 507.5 |

| ||||||||||||||||||||||||

Net income (loss) |

|

| — |

|

|

| — |

|

|

| (19.9 | ) |

|

| — |

|

|

| — |

|

|

| (19.9 | ) |

|

| — |

|

|

| — |

|

|

| 9.8 |

|

|

| — |

|

|

| — |

|

|

| 9.8 |

|

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (2.9 | ) |

|

| (2.9 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (1.4 | ) |

|

| (1.4 | ) |

Adoption of new accounting standard |

|

| — |

|

|

| (10.6 | ) |

|

| 4.2 |

|

|

| — |

|

|

| — |

|

|

| (6.4 | ) | ||||||||||||||||||||||||

Stock-based compensation expense |

|

| — |

|

|

| 2.0 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

|

| — |

|

|

| 1.8 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1.8 |

|

Stock option activity |

|

| — |

|

|

| 2.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.5 |

| ||||||||||||||||||||||||

Issuance of treasury shares |

|

| 215,708 |

|

|

| (5.7 | ) |

|

| — |

|

|

| 5.7 |

|

|

| — |

|

|

| — |

|

|

| 580,248 |

|

|

| (12.4 | ) |

|

| — |

|

|

| 12.4 |

|

|

| — |

|

|

| — |

|

Shares surrendered for taxes |

|

| (70,033 | ) |

|

| — |

|

|

| — |

|

|

| (0.2 | ) |

|

| — |

|

|

| (0.2 | ) |

|

| (72,174 | ) |

|

| — |

|

|

| — |

|

|

| (0.5 | ) |

|

| — |

|

|

| (0.5 | ) |

Balance at March 31, 2020 |

|

| 44,965,828 |

|

| $ | 841.1 |

|

| $ | (321.4 | ) |

| $ | (19.4 | ) |

| $ | 41.8 |

|

| $ | 542.1 |

| ||||||||||||||||||||||||

Balance at March 31, 2021 |

|

| 45,672,382 |

|

| $ | 824.7 |

|

| $ | (349.4 | ) |

| $ | (1.0 | ) |

| $ | 39.0 |

|

| $ | 513.3 |

| ||||||||||||||||||||||||

|

| Common Shares Outstanding |

|

| Additional Paid-in Capital |

|

| Retained Deficit |

|

| Treasury Shares |

|

| Accumulated Other Comprehensive Income (Loss) |

|

| Total |

|

| Common Shares Outstanding |

|

| Additional Paid-in Capital |

|

| Retained Deficit |

|

| Treasury Shares |

|

| Accumulated Other Comprehensive Income (Loss) |

|

| Total |

| ||||||||||||

Balance at December 31, 2018 |

|

| 44,584,668 |

|

| $ | 846.3 |

|

| $ | (191.5 | ) |

| $ | (33.0 | ) |

| $ | (8.9 | ) |

| $ | 612.9 |

| ||||||||||||||||||||||||

Balance at December 31, 2019 |

|

| 44,820,153 |

|

| $ | 844.8 |

|

| $ | (301.5 | ) |

| $ | (24.9 | ) |

| $ | 44.7 |

|

| $ | 563.1 |

| ||||||||||||||||||||||||

Net income (loss) |

|

| — |

|

|

| — |

|

|

| 3.5 |

|

|

| — |

|

|

| — |

|

|

| 3.5 |

|

|

| — |

|

|

| — |

|

|

| (19.9 | ) |

|

| — |

|

|

| — |

|

|

| (19.9 | ) |

Other comprehensive income (loss) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.5 |

|

|

| 0.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (2.9 | ) |

|

| (2.9 | ) |

Stock-based compensation expense |

|

| — |

|

|

| 2.2 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.2 |

|

|

| — |

|

|

| 2.0 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2.0 |

|

Stock option activity |

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.2 |

| ||||||||||||||||||||||||

Issuance of treasury shares |

|

| 261,130 |

|

|

| (7.5 | ) |

|

| — |

|

|

| 7.5 |

|

|

| — |

|

|

| — |

|

|

| 215,708 |

|

|

| (5.7 | ) |

|

| — |

|

|

| 5.7 |

|

|

| — |

|

|

| — |

|

Shares surrendered for taxes |

|

| (79,889 | ) |

|

| — |

|

|

| — |

|

|

| (1.0 | ) |

|

| — |

|

|

| (1.0 | ) |

|

| (70,033 | ) |

|

| — |

|

|

| — |

|

|

| (0.2 | ) |

|

| — |

|

|

| (0.2 | ) |

Balance at March 31, 2019 |

|

| 44,765,909 |

|

| $ | 841.2 |

|

| $ | (188.0 | ) |

| $ | (26.5 | ) |

| $ | (8.4 | ) |

| $ | 618.3 |

| ||||||||||||||||||||||||

Balance at March 31, 2020 |

|

| 44,965,828 |

|

| $ | 841.1 |

|

| $ | (321.4 | ) |

| $ | (19.4 | ) |

| $ | 41.8 |

|

| $ | 542.1 |

| ||||||||||||||||||||||||

See accompanying Notes to the unaudited Consolidated Financial Statements.

6

TimkenSteel Corporation

Consolidated Statements of Cash Flows (Unaudited)

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CASH PROVIDED (USED) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

| $ | (19.9 | ) |

| $ | 3.5 |

|

| $ | 9.8 |

|

| $ | (19.9 | ) |

Adjustments to reconcile net income (loss) to net cash provided (used) by operating activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

| 18.6 |

|

|

| 17.8 |

|

|

| 17.6 |

|

|

| 18.6 |

|

Amortization of deferred financing fees and debt discount |

|

| 1.3 |

|

|

| 1.3 |

|

|

| 0.3 |

|

|

| 1.3 |

|

Loss (gain) on sale or disposal of assets |

|

| (2.3 | ) |

|

| — |

|

|

| — |

|

|

| (2.3 | ) |

Impairment charges |

|

| 8.2 |

|

|

| — |

| ||||||||

Deferred income taxes |

|

| 0.2 |

|

|

| (0.2 | ) |

|

| — |

|

|

| 0.2 |

|

Stock-based compensation expense |

|

| 2.0 |

|

|

| 2.2 |

|

|

| 1.8 |

|

|

| 2.0 |

|

Pension and postretirement expense (benefit), net |

|

| 8.1 |

|

|

| 1.8 |

| ||||||||

Pension and postretirement contributions and payments |

|

| (2.5 | ) |

|

| (2.4 | ) | ||||||||

Pension and postretirement (benefit) expense, net |

|

| (4.7 | ) |

|

| 8.1 |

| ||||||||

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts receivable, net |

|

| (16.3 | ) |

|

| 12.1 |

|

|

| (33.0 | ) |

|

| (16.3 | ) |

Inventories, net |

|

| 41.2 |

|

|

| (26.8 | ) |

|

| (28.2 | ) |

|

| 41.2 |

|

Accounts payable |

|

| 26.7 |

|

|

| (30.7 | ) |

|

| 48.1 |

|

|

| 26.7 |

|

Other accrued expenses |

|

| 5.7 |

|

|

| (11.4 | ) |

|

| (2.4 | ) |

|

| 5.7 |

|

Pension and postretirement contributions and payments |

|

| (1.6 | ) |

|

| (2.5 | ) | ||||||||

Deferred charges and prepaid expenses |

|

| (0.3 | ) |

|

| 0.1 |

|

|

| 0.3 |

|

|

| (0.3 | ) |

Other, net |

|

| 1.3 |

|

|

| (0.9 | ) |

|

| (3.0 | ) |

|

| 1.3 |

|

Net Cash Provided (Used) by Operating Activities |

|

| 63.8 |

|

|

| (33.6 | ) |

|

| 13.2 |

|

|

| 63.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investing Activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital expenditures |

|

| (2.9 | ) |

|

| (4.4 | ) |

|

| (2.3 | ) |

|

| (2.9 | ) |

Proceeds from disposals of property, plant and equipment |

|

| 7.8 |

|

|

| — |

|

|

| — |

|

|

| 7.8 |

|

Net Cash Provided (Used) by Investing Activities |

|

| 4.9 |

|

|

| (4.4 | ) |

|

| (2.3 | ) |

|

| 4.9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financing Activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proceeds from exercise of stock options |

|

| — |

|

|

| 0.2 |

|

|

| 2.5 |

|

|

| — |

|

Shares surrendered for employee taxes on stock compensation |

|

| (0.2 | ) |

|

| (1.0 | ) |

|

| (0.5 | ) |

|

| (0.2 | ) |

Repayments on credit agreements |

|

| (30.0 | ) |

|

| (5.0 | ) |

|

| — |

|

|

| (30.0 | ) |

Borrowings on credit agreements |

|

| — |

|

|

| 30.0 |

| ||||||||

Net Cash Provided (Used) by Financing Activities |

|

| (30.2 | ) |

|

| 24.2 |

|

|

| 2.0 |

|

|

| (30.2 | ) |

Increase (Decrease) in Cash and Cash Equivalents |

|

| 38.5 |

|

|

| (13.8 | ) |

|

| 12.9 |

|

|

| 38.5 |

|

Cash and cash equivalents at beginning of period |

|

| 27.1 |

|

|

| 21.6 |

|

|

| 102.8 |

|

|

| 27.1 |

|

Cash and Cash Equivalents at End of Period |

| $ | 65.6 |

|

| $ | 7.8 |

|

| $ | 115.7 |

|

| $ | 65.6 |

|

See accompanying Notes to the unaudited Consolidated Financial Statements.

7

TimkenSteel Corporation

Notes to Unaudited Consolidated Financial Statements

(dollars in millions, except per share data)

Note1-Basis of Presentation

The accompanying unaudited Consolidated Financial Statements have been prepared by TimkenSteel Corporation (the Company“Company” or TimkenSteel)“TimkenSteel”) in accordance with generally accepted accounting principles in the United States (U.S. GAAP)(“U.S. GAAP”) for interim financial information. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) and disclosures considered necessary for a fair presentation have been included. For further information, refer to TimkenSteel’s audited Consolidated Financial Statements and Notes included in its Annual Report on Form 10-K for the year ended December 31, 2019.2020.

Certain items previously reported in specific financial statement captions have been reclassified to conform with the current year presentation.

Customer Receivables

The Company’s accounts receivables arise from sales to customers across all end markets. Historically, TimkenSteel’s allowance for doubtful accounts write-offs have been immaterial. The allowance for doubtful account reserve has been established using qualitative and quantitative methods. In general, account balances greater than one year of age or sent to third party collection are fully reserved. Account balances for customers that are viewed as higher risk are also analyzed for a reserve. In addition to these methods, for the first quarter of 2020 the allowance for doubtful accounts was adjusted for forward looking uncollectible balances, primarily in the energy and automotive end markets. The amount recorded was based on the Company’s assessment of the risk presented to customers in these end markets as a result of the COVID-19 pandemic as well as geo-political factors facing the energy end market. At this time, the full impact of COVID-19 is difficult to predict with the current uncertainty surrounding the pandemic and the timeline for economic activities to recover.

Change in Accounting Principle

During the fourth quarter of 2019, TimkenSteel elected to change its method for valuing its inventories that previously used the last-in, first-out (LIFO) method to the first-in, first-out (FIFO) method. The Company believes that the FIFO method is preferable as it improves comparability with our peers, more closely resembles the physical flow of our inventory and aligns with how the Company internally manages the business. The effects of the change in accounting principle from LIFO to FIFO were retrospectively applied. As a result of the retrospective application of the change in accounting principle, certain financial statement line items in the Company’s consolidated balance sheets as of March 31, 2019 and the consolidated statements of operations, comprehensive income (loss), shareholders’ equity and cash flows for the three months ended March 31, 2019 were adjusted as necessary. For further information, refer to TimkenSteel’s audited Consolidated Financial Statements and Notes included in its Annual Report on Form 10-K for the year ended December 31, 2019.

The following tables reflect the impact to the financial statement line items as a result of the change in accounting principle for the prior periods presented in the accompanying financial statements (dollars in millions, except per share data):

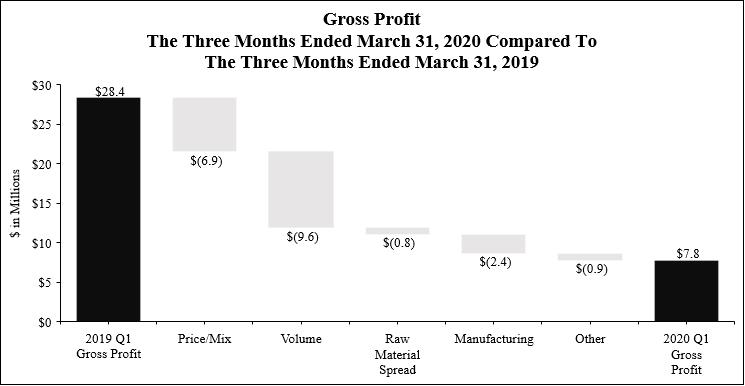

Consolidated Statement of Operations |

| Three Months Ended March 31, 2019 |

| |||||||||

|

| As Reported |

|

| Adjustments |

|

| As Adjusted |

| |||

Cost of products sold |

| $ | 341.9 |

|

| $ | 0.7 |

|

| $ | 342.6 |

|

Gross profit |

|

| 29.1 |

|

|

| (0.7 | ) |

|

| 28.4 |

|

Income (loss) before income taxes |

|

| 4.3 |

|

|

| (0.7 | ) |

|

| 3.6 |

|

Net income (loss) |

|

| 4.2 |

|

|

| (0.7 | ) |

|

| 3.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Data: |

|

|

|

|

|

|

|

|

|

|

|

|

Basic earnings (loss) per share |

|

| 0.09 |

|

|

| (0.01 | ) |

|

| 0.08 |

|

Diluted earnings (loss) per share |

|

| 0.09 |

|

|

| (0.01 | ) |

|

| 0.08 |

|

Consolidated Statement of Comprehensive Income (Loss) |

| Three Months Ended March 31, 2019 |

| |||||||||

|

| As Reported |

|

| Adjustments |

|

| As Adjusted |

| |||

Net income (loss) |

| $ | 4.2 |

|

| $ | (0.7 | ) |

| $ | 3.5 |

|

Comprehensive income (loss), net of tax |

|

| 4.7 |

|

|

| (0.7 | ) |

|

| 4.0 |

|

8

Consolidated Statement of Cash Flows |

| Three Months Ended March 31, 2019 |

| |||||||||

|

| As Reported |

|

| Adjustments |

|

| As Adjusted |

| |||

Net income (loss) |

| $ | 4.2 |

|

| $ | (0.7 | ) |

| $ | 3.5 |

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

Inventories, net |

|

| (27.5 | ) |

|

| 0.7 |

|

|

| (26.8 | ) |

Note2-Recent Accounting Pronouncements

Adoption of New Accounting Standards

The Company adopted the following Accounting Standard Updates (ASU)(“ASU”) in the first quarter of 2020, all of which were effective as of January 1, 2020, except ASU 2020-04, which became effective upon issuance on March 12, 2020. The adoption of these standards did not have a material impact on the unaudited Consolidated Financial Statements or the related Notes to the unaudited Consolidated Financial Statements.

|

|

|

|

|

|

|

|

|

|

Accounting Standards Issued But Not Yet Adopted

The Company has considered the recent ASUs issued by the Financial Accounting Standards Board summarized below:2021.

Standard | Description |

Date of Adoption |

|

ASU 2019-12, Income Taxes (Topic 740) | The standard simplifies the accounting for income taxes by removing various exceptions. | January 1, 2021 | The |

ASU | The standard | January 1, 2021 | The Company |

|

| January 1, 2021 | using the modified retrospective method of transition. The |

Upon adoption of ASU 2020-06 prospectively as of January 1, 2021, all outstanding Convertible Notes are now fully classified as a liability, there is no longer a separate equity component and the Convertible Notes will no longer have a debt discount that is amortized. This resulted in a decrease of $10.6 million to additional paid-in capital and an increase of $1.1 million and $5.3 million to current convertible notes, net and non-current convertible notes, net, respectively, on the Consolidated Balance Sheets as of January 1, 2021. Additionally, retained deficit was reduced by $4.2 million in the Consolidated Balance Sheets as of January 1, 2021 to remove amortization expense recognized in prior periods. The adoption of this standard did not have an effect on the Company’s cash flows, liquidity, and the methodology used for the earnings per share calculation. Refer to “Note 10 – Financing Arrangements” for additional information on the Company’s Convertible Notes.

9There are no current ASUs issued, but not adopted, that will have an impact on the Company.

Legislation related to the COVID-19 Pandemic

Coronavirus Aid, Relief, and Economic Security ("CARES") Act

On March 27, 2020, the President of the United States signed the Coronavirus Aid, Relief, and Economic Security ("CARES") Act, an economic stimulus package intended to provide support, principally in the form of tax benefits, to companies and individuals negatively impacted by the COVID-19 pandemic. Although the majority of the provisions included in the CARES Act did not immediately benefit the Company from a cash tax perspective due to its significant net operating losses, the Company took advantage of the deferral of the employer share (6.2% of employee wages) of Social Security payroll taxes that would otherwise have been owed from the date of enactment of the legislation through December 31, 2020, as afforded by the CARES Act. At December 31, 2020, the Company had deferred $6.4 million in cash payments and recorded reserves for such deferred payroll taxes in salaries, wages and benefits on the Consolidated Balance Sheets. The deferred amount of payments is to be paid in 2 equal installments at December 31, 2021 and December 31, 2022.

The CARES Act also provided for an employee retention credit (“Employee Retention Credit”), which is a refundable tax credit against certain employment taxes of up to $5,000 per employee for eligible employers. The tax credit is equal to 50% of qualified wages paid to

8

employees during a quarter, capped at $10,000 of qualified wages per employee throughout the year. The Company qualified for the tax credit in the second and third quarters of 2020 and accrued a benefit of $2.3 million in the fourth quarter of 2020 related to the Employee Retention Credit in other (income) expense, net on the Company’s Consolidated Statements of Operations. The Company is currently in the process of filing for this credit.

Consolidated Appropriations Act, 2021 (“CAA”)

On December 27, 2020, the President of the United States signed the Consolidated Appropriation Act, 2021 (“CAA”). The CAA includes additional COVID-19 relief that expands upon the relief provided in the CARES Act, including, but not limited to, the extension of tax deductions, credits, and incentives. The Company has evaluated the CAA for any potential impact. While it was determined that the CAA revised and extended the Employee Retention Credit into 2021, the CAA is not expected to have an impact on the Company as furloughs related to the COVID-19 pandemic ceased in 2020. Furthermore, the Company does not expect any of the other provisions within the CAA to provide a benefit.

American Rescue Plan Act of 2021 (“ARPA”)

On March 11, 2021, the President of the United States signed the American Rescue Plan Act of 2021 (“ARPA”). APRA strengthens and extends certain programs enacted through the CARES Act and establishes new relief programs aimed at mitigating the financial impact of the COVID-19 pandemic. The Company is evaluating the provisions within the ARPA. At this time, 2 provisions are anticipated to impact the Company.

The first applicable provision imposes new requirements related to health coverage provided by the Consolidated Omnibus Budget Reconciliation Act (“COBRA”). Under the ARPA, employers are required to provide a 100% premium subsidy for COBRA health care continuation coverage for certain employees for the period of April 1, 2021 through September 30, 2021. The Company will be reimbursed for this additional coverage through fully refundable payroll tax credits.

The second applicable provision offers funding relief for single-employer defined benefit pension plans. Specifically, the ARPA provides enhanced interest rate stabilization, as well as extended amortization of funding shortfalls. The Company is currently evaluating the impact and timing of election options permitted by the ARPA on required contributions to our domestic defined benefit pension plans. At this time based on current assumptions and expected asset returns, pending further IRS guidance, we believe that the ARPA provisions are likely to result in a delay in the timing of required Company contributions until 2028. However, these estimates are subject to significant uncertainty.

Note3-Revenue Recognition

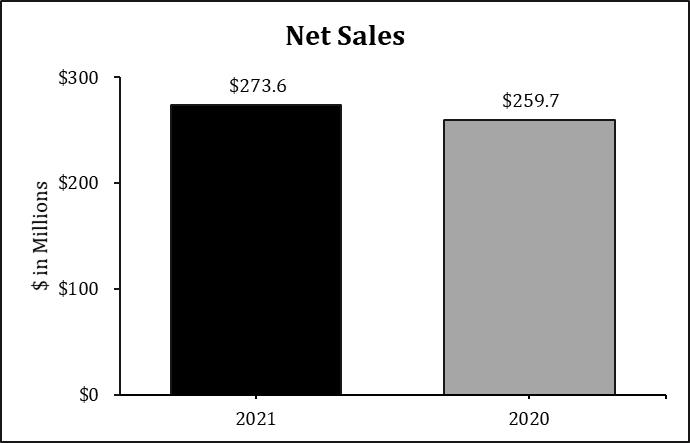

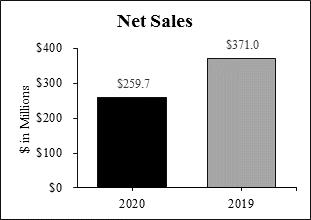

The following table provides the major sources of revenue by end-market sector for the three months ended March 31, 20202021 and 2019:2020:

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

Mobile |

| $ | 97.7 |

|

| $ | 144.2 |

|

| $ | 133.6 |

|

| $ | 97.7 |

|

Industrial |

|

| 113.3 |

|

|

| 147.0 |

|

|

| 124.7 |

|

|

| 113.3 |

|

Energy |

|

| 25.2 |

|

|

| 60.8 |

|

|

| 7.7 |

|

|

| 25.2 |

|

Other(1) |

|

| 23.5 |

|

|

| 19.0 |

|

|

| 7.6 |

|

|

| 23.5 |

|

Total Net Sales |

| $ | 259.7 |

|

| $ | 371.0 |

|

| $ | 273.6 |

|

| $ | 259.7 |

|

(1) “Other” for sales by end-market sector includes the Company’s scrap and oil country tubular goods (OCTG)(“OCTG”) billet sales.

The following table provides the major sources of revenue by product type for the three months ended March 31, 20202021 and 2019:2020:

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

Bar |

| $ | 168.1 |

|

| $ | 239.9 |

|

| $ | 173.2 |

|

| $ | 168.1 |

|

Tube |

|

| 30.4 |

|

|

| 49.6 |

|

|

| 36.1 |

|

|

| 30.4 |

|

Value-add |

|

| 55.5 |

|

|

| 73.7 |

|

|

| 56.7 |

|

|

| 55.5 |

|

Other(2) |

|

| 5.7 |

|

|

| 7.8 |

|

|

| 7.6 |

|

|

| 5.7 |

|

Total Net Sales |

| $ | 259.7 |

|

| $ | 371.0 |

|

| $ | 273.6 |

|

| $ | 259.7 |

|

(2) “Other” for sales by product type includes the Company’s scrap sales.

9

Note4-Restructuring Charges

DuringBeginning in 2019, and into the first quarter of 2020, TimkenSteel made organizational changes to enhance profitable and sustainable growth. These company-wide actions included the restructuring of its business support functions, the reduction of management layers throughout the organization, the closure of the TimkenSteel Material Services (TMS)(“TMS”) facility in Houston, Texas and other domestic and international actions to further improve the Company’s overall cost structure. Through these restructuring efforts, to date the Company has eliminated approximately 160230 salaried positions and recognized restructuring charges of $9.1$12.2 million.

Restructuring charges in the first quarter of 2021 amounted to $0.5 million,, consisting of $0.3 million related to the transition of customers to other TimkenSteel manufacturing equipment due to the discontinuation of specific small-diameter seamless mechanical tube manufacturing and the indefinite idling of our Harrison melt and casting activities (refer to “Note 5 – Disposition of Non-Core Assets” for additional information). The remaining $0.2 million related to severance and employee-related benefits.benefits as a result of continued organizational changes. Approximately 10 of these15 salaried positions were eliminated in the first quarter of 2020. 2021. TimkenSteel recorded reserves for such restructuring charges as other current liabilities on the Consolidated Balance Sheets. The reserve balance at March 31, 20202021 is expected to be substantially used in the next twelve months.

The following is a summary of the restructuring reserve for the three months ended March 31, 2020:2021 and 2020.

|

|

|

|

|

Balance at December 31, 2020 |

| $ | 1.5 |

|

Expenses |

|

| 0.5 |

|

Payments |

|

| (1.4 | ) |

Balance at March 31, 2021 |

| $ | 0.6 |

|

Balance at December 31, 2019 |

| $ | 6.0 |

|

Expenses |

|

| 0.6 |

|

Payments |

|

| (4.0 | ) |

Balance at March 31, 2020 |

| $ | 2.6 |

|

There was no reserve for restructuring at March 31, 2019.

Note 5 - Disposition of Non-Core Assets

During the fourth quarter of 2019, management entered into an agreement to dispose of the Company’s scrap processing facility in Akron, Ohio for cash consideration of approximately $4.0 million. An impairment charge of $7.3 million was recognized in the fourth quarter of 2019 in connection with the sale. The sale was completed, and the Company received all cash consideration in the first quarter of 2020. An additional loss on disposal of $0.2 million was recognized in the first quarter as the sale was completed.TimkenSteel Material Services Facility

Additionally, duringDuring the first quarter of 2020, management completed its previously announced plan to close the Company’s TMS facility in Houston and initiated a plan to market and sellbegan selling the assets at the facility. Accelerated depreciation and amortization on TMS assets of $1.6 million was recorded in the first quarter of 2020 to reduce the net book value of the machinery and equipment to its expected fair value. Subsequent to the closure, certain assets were sold and a gain on sale of $3.2 million was recognized. recognized for the three months ended March 31, 2020.

At March 31, 2020,2021, the remaining associated machinery and equipment that was classified as held for sale with a net book value of $2.2$0.3 million as of December 31, 2020, was fully impaired as there is no longer an expected market value for these assets. This is classified as held for saleimpairment charges on the Consolidated Balance Sheet. Statements of Operations.

The land and buildings associated with TMS were notare classified as heldproperty, plant and equipment, net on the Consolidated Balance Sheets, as it is not probable that these assets will be sold within the next 12 months.

Small-Diameter Seamless Mechanical Tubing Machinery and Equipment

In the third quarter of 2020, TimkenSteel informed customers that as of December 31, 2020 the Company will discontinue the commercial offering of specific small-diameter seamless mechanical tubing products. As a result, the Company recognized accelerated depreciation of $1.5 million for sale, as they were not considered available for immediate salethe three months ended March 31, 2021 in their present condition. The Company began sellingalignment with the inventory associated with TMSramp down of the machinery and equipment used in the manufacturing of these specific products, which was completed in the first quarter of 2020 at prices that were2021. Spare parts related to this machinery and equipment of $0.5 million was also written down in line with the net realizable valuefirst quarter of 2021, as management determined there was no alternative use.

Harrison Melt and Casting Assets

On February 16, 2021, management announced a plan to indefinitely idle its Harrison melt and casting assets, which was completed in the first quarter of 2021. Going forward, all of the inventory that was established inCompany’s melt and casting activities will take place at the fourth quarterFaircrest location. The Company worked collaboratively with employees, suppliers and a number of 2019. customers to ensure a well-organized and efficient transition. The Company’s rolling and finishing operations at Harrison were not impacted by this action.

10

10

The Company recognized non-cash charges of $9.5 million related to the write-down of the associated Harrison melt and casting assets in the first quarter of 2021. These charges include $7.9 million related to the impairment of the associated machinery and equipment, which is classified as impairment charges on the Consolidated Statements of Operations, as well as a write-down of spare parts of $1.6 million, as management determined there was no alternative use. The Company did not incur any cash expenditures related to these charges.

TimkenSteel (Shanghai) Corporation Limited

On March 31, 2021, the Company entered into an agreement pursuant to which Daido Steel (Shanghai) Co., Ltd. has agreed to acquire all of the Company’s ownership interest in TimkenSteel (Shanghai) Corporation Limited in an all-cash transaction for approximately $7 million, subject to certain regulatory approvals and other closing conditions. As of March 31, 2021, the Company does not expect a material impact to our Consolidated Statements of Operations. The transaction is expected to close during the third quarter of 2021.

Note6–Other (Income) Expense, (Income), net

The following table provides the components of other (income) expense, (income), net for the three months ended March 31, 20202021 and 2019:2020:

|

| Three Months Ended March 31, |

| |||||

|

| 2020 |

|

| 2019 |

| ||

Pension and postretirement non-service benefit loss (income) |

| $ | (6.6 | ) |

| $ | (2.8 | ) |

Loss from remeasurement of benefit plan |

|

| 9.5 |

|

|

| — |

|

Foreign currency exchange loss (gain) |

|

| — |

|

|

| 0.1 |

|

Miscellaneous expense (income) |

|

| (0.2 | ) |

|

| — |

|

Total other expense (income), net |

| $ | 2.7 |

|

| $ | (2.7 | ) |

|

| Three Months Ended March 31, |

| |||||

|

| 2021 |

|

| 2020 |

| ||

Pension and postretirement non-service benefit (income) loss |

| $ | (9.6 | ) |

| $ | (6.6 | ) |

Loss (gain) from remeasurement of benefit plans |

|

| 0.2 |

|

|

| 9.5 |

|

Miscellaneous (income) expense |

|

| — |

|

|

| (0.2 | ) |

Total other (income) expense, net |

| $ | (9.4 | ) |

| $ | 2.7 |

|

Non-service benefit income is derived from the Company’srelated pension and other postretirement plans. The Company’sbenefit income, for all years, consists of the interest cost, expected return on plan assets has exceeded the interest cost component, resulting in income for the three months ended March 31, 2020 and 2019.amortization components of net periodic cost.

The TimkenSteel Corporation Retirement Plan (Salaried Plan)(“Salaried Plan”) has a provision that permits employees to elect to receive their pension benefits in a lump sum. In the first quarter of 2020,2021, the cumulative cost of all lump sum payments was projected to exceedexceeded the sum of the service cost and interest cost components of net periodic pension cost for the Salaried Plan. TheAs a result, the Company completed a full remeasurement of its pension obligations and plan assets associated with the Salaried Plan asduring the first quarter of March 31, 2020,2021, which resulted in a non-cash loss from remeasurement of $0.2 million. A full remeasurement of the pension obligations and plan assets associated with the Salaried Plan was also required in the first quarter of 2020 resulting in a non-cash loss from remeasurement of $9.5 million.million for the three months ended March 31, 2020. For more details on the remeasurement, refer to “Note 11 - Retirement and Postretirement Plans.”

Plans”.

Note7-Income Tax Provision

TimkenSteel’s provision for income taxes in interim periods is computed by applying the appropriate estimated annual effective tax rates to income or loss before income taxes for the period. In addition, non-recurring or discrete items, including interest on prior-year tax liabilities, are recorded during the periods in which they occur.

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

Provision (benefit) for incomes taxes |

| $ | 0.1 |

|

| $ | 0.1 |

|

| $ | 0.2 |

|

| $ | 0.1 |

|

Effective tax rate |

|

| (0.5 | )% |

|

| 1.3 | % |

|

| 2.0 | % |

|

| (0.5 | )% |

In light ofDue to TimkenSteel’s recenthistorical operating performance in the U.S. and current industry conditions,, the Company assessed its U.S. deferred tax assets and concluded, based upon all available evidence, that it was more likely than not that it would not realize the assets. As a result, the Company maintains a full valuation allowance against its deferred tax assets in the U.S. and applicable foreign countries until sufficient positive evidence exists to conclude that a valuation allowance is not necessary. Going forward, the need to maintain valuation allowances against deferred tax assets in the U.S. and other affected countries will cause variability in the Company’s effective tax rate. The majority of TimkenSteel’s income taxes are derived from foreign operations.

On March 27, 2020, the President

11

Note 8 - Earnings (Loss) Per Share

Basic earnings (loss) per share is computed based upon the weighted average number of common shares outstanding. Diluted earnings (loss) per share is computed based upon the weighted average number of common shares outstanding plus the dilutive effect of common share equivalents calculated using the treasury stock method or if-converted method. For the Convertible Notes, the Company utilizes the if-converted method to calculate diluted earnings (loss) per share. Under the if-converted method, the Company adjusts net earnings to add back interest expense (including amortization of debt discount)issuance costs) recognized on the Convertible Notes and includes the number of shares potentially issuable related to the Convertible Notes in the weighted average shares outstanding. Treasury stock is excluded from the denominator in calculating both basic and diluted earnings (loss) per share.

11

CommonMarch 31, 2021 and March 31, 2020, respectively. As of March 31, 2021, 2.3 million shares primarily related to options with exercise prices more than the average market price of our common shares (i.e., “underwater” options) were excluded from the computation of diluted earnings (loss) per share because the effect of their inclusion would have been anti-dilutive. The difference between the remaining 2.8 million shares assumed issued and the 1.6 million shares assumed purchased with potential proceeds were included in the denominator of the diluted earnings (loss) per share calculation. All common share equivalents for shares issuable for equity-based awards were excluded from the computation of diluted earnings (loss) per share for the three months ended March 31, 2020 because the effect of their inclusion would have been anti-dilutive.

Common share equivalents for shares issuable upon the conversion of outstanding convertible notes were included in the computation of diluted earnings (loss) per share for the three months ended March 31, 2021 as these shares would be dilutive. Common share equivalents for shares issuable upon the conversion of outstanding convertible notes were excluded from the computation of diluted earnings (loss) per share for the three months ended March 31, 2020 and 2019 because the effect of their inclusion would have been anti-dilutive.

The following table sets forth the reconciliation of the numerator and the denominator of basic and diluted earnings (loss) per share for the three months ended March 31, 20202021 and 2019:2020:

|

| Three Months Ended March 31, |

|

| Three Months Ended March 31, |

| ||||||||||

|

| 2020 |

|

| 2019 |

|

| 2021 |

|

| 2020 |

| ||||

Numerator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

| $ | (19.9 | ) |

| $ | 3.5 |

| ||||||||

Net income (loss), basic |

| $ | 9.8 |

|

| $ | (19.9 | ) | ||||||||

Add convertible notes interest |

|

| 1.3 |

|

|

| — |

| ||||||||

Net income (loss), diluted |

| $ | 11.1 |

|

| $ | (19.9 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Denominator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average shares outstanding, basic |

|

| 44.9 |

|

|

| 44.7 |

|

|

| 45.4 |

|

|

| 44.9 |

|

Dilutive effect of stock-based awards |

|

| — |

|

|

| 0.5 |

|

|

| 1.2 |

|

|

| — |

|

Dilutive effect of convertible notes |

|

| 9.1 |

|

|

| — |

| ||||||||

Weighted average shares outstanding, diluted |

|

| 44.9 |

|

|

| 45.2 |

|

|

| 55.7 |

|

|

| 44.9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic earnings (loss) per share |

| $ | (0.44 | ) |

| $ | 0.08 |

|

| $ | 0.22 |

|

| $ | (0.44 | ) |

Diluted earnings (loss) per share |

| $ | (0.44 | ) |

| $ | 0.08 |

|

| $ | 0.20 |

|

| $ | (0.44 | ) |

Note9-Inventories

The components of inventories, net of reserves as of March 31, 20202021 and December 31, 20192020 were as follows:

|

| March 31, 2020 |

|

| December 31, 2019 |

|

| March 31, 2021 |

|

| December 31, 2020 |

| ||||

Manufacturing supplies |

| $ | 43.5 |

|

| $ | 49.8 |

|

| $ | 28.5 |

|

| $ | 37.6 |

|

Raw materials |

|

| 16.2 |

|

|

| 26.0 |

|

|

| 25.1 |

|

|

| 20.0 |

|

Work in process |

|

| 111.6 |

|

|

| 123.7 |

|

|

| 99.5 |

|

|

| 79.1 |

|

Finished products |

|

| 79.5 |

|

|

| 93.1 |

|

|

| 58.2 |

|

|

| 55.6 |

|

Gross inventory |

|

| 250.8 |

|

|

| 292.6 |

|

|

| 211.3 |

|

|

| 192.3 |

|

Allowance for inventory reserves |

|

| (10.3 | ) |

|

| (10.7 | ) |

|

| (8.6 | ) |

|

| (13.9 | ) |

Total Inventories, net |

| $ | 240.5 |

|

| $ | 281.9 |

| ||||||||

Total inventories, net |

| $ | 202.7 |

|

| $ | 178.4 |

| ||||||||

12

Note10-Financing Arrangements

For a detailed discussion of the Company's long-term debt and credit arrangements, refer to “Note 14 - Financing Arrangements” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019.

Convertible Notes2020.

The components offollowing table summarizes the Convertible Notescurrent and non-current debt as of March 31, 20202021 and December 31, 2019 were as follows:

|

| March 31, 2020 |

|

| December 31, 2019 |

| ||

Principal |

| $ | 86.3 |

|

| $ | 86.3 |

|

Less: Debt issuance costs, net of amortization |

|

| (0.6 | ) |

|

| (0.7 | ) |

Less: Debt discount, net of amortization |

|

| (5.9 | ) |

|

| (7.0 | ) |

Convertible notes, net |

| $ | 79.8 |

|

| $ | 78.6 |

|

The initial value of the principal amount recorded as a liability at the date of issuance was $66.9 million, using an effective interest rate of 12.0%. The remaining $19.4 million of principal amount was allocated to the conversion feature and recorded as a component of shareholders’ equity at the date of issuance. This amount represents a discount to the debt to be amortized through interest expense using the effective interest method through the maturity of the Convertible Notes. Transaction costs were allocated to the liability and equity components based on their relative values. Transaction costs attributable to the liability component of $2.4 million are amortized to interest expense over the term of the Convertible Notes, and transaction costs attributable to the equity component of $0.7 million are included in shareholders’ equity.

12

Table of Contents2020.

The following table sets forth total interest expense recognized related to the Convertible Notes:

|

| Three Months Ended March 31, |

| |||||

|

| 2020 |

|

| 2019 |

| ||

Contractual interest expense |

| $ | 1.3 |

|

| $ | 1.3 |

|

Amortization of debt issuance costs |

|

| 0.1 |

|

|

| 0.1 |

|

Amortization of debt discount |

|

| 1.1 |

|

|

| 1.0 |

|

Total |

| $ | 2.5 |

|

| $ | 2.4 |

|

|

| March 31, 2021 |

|

| December 31, 2020 |

| ||

Credit Agreement |

| $ | — |

|

| $ | — |

|

Convertible Senior Notes due 2021 |

|

| 40.2 |

|

|

| 38.9 |

|

Convertible Senior Notes due 2025 |

|

| 44.7 |

|

|

| 39.3 |

|

Total debt |

| $ | 84.9 |

|

| $ | 78.2 |

|

Less current portion of debt |

|

| 40.2 |

|

|

| 38.9 |

|

Total non-current portion of debt |

| $ | 44.7 |

|

| $ | 39.3 |

|

Amended Credit Agreement

On October 15, 2019, the Company, as borrower, and certain domestic subsidiaries of the Company, as subsidiary guarantors, entered into a Third Amended and Restated Credit Agreement (the Amended“Amended Credit Agreement)Agreement”), with JP Morgan Chase Bank, N.A., as administrative agent (the Administrative Agent)“Administrative Agent”), Bank of America, N.A., as syndication agent, and the other lenders party thereto (collectively, the Lenders)“Lenders”), which further amended and restated the Company’s Second Amended and Restated Credit Agreement dated as of January 26, 2018. The interest rateAs of March 31, 2021, the amount available under the Amended Credit Agreement was 2.2%$241.8 million, reflective of the Company’s asset borrowing base with 0 outstanding borrowings. Additionally, the Company is in compliance with all covenants outlined in the Amended Credit Agreement.

Convertible Senior Notes due 2021

The components of the Convertible Senior Notes due 2021 as of March 31, 2020. 2021 and December 31, 2020 were as follows:

|

| March 31, 2021 |

|

| December 31, 2020 |

| ||

Principal |

| $ | 40.2 |

|

| $ | 40.2 |

|

Less: Debt issuance costs, net of amortization |

|

| — |

|

|

| (0.1 | ) |

Less: Debt discount, net of amortization |

|

| — |

|

|

| (1.2 | ) |

Convertible Senior Notes due 2021, net |

| $ | 40.2 |

|

| $ | 38.9 |

|

The principal amount available for borrowings underof the credit agreementoutstanding Convertible Senior Notes due 2021 as of March 31, 2020 was $224.42021 is $40.2 million. AsTransaction costs related to the outstanding Convertible Senior Notes due 2021 were $1.4 million. These costs are amortized to interest expense over the term of the notes. The Convertible Senior Notes due 2021 mature on June 1, 2021. The Convertible Senior Notes due 2021 are currently convertible at the option of holders into a combination of the Company’s common shares and cash, up until the close of business on the business day immediately preceding the maturity date; upon maturity, the Convertible Senior Notes due 2021 remaining outstanding will be settled in cash. For details regarding conversion mechanics and method of settlement, refer to the Indenture for the Convertible Senior Notes due 2021 filed as an exhibit to a Form 8-K on May 31, 2016 and incorporated by reference in our most recent 10-K filing. The Convertible Senior Notes due 2021 are classified as a current liability in the Consolidated Balance Sheets as of March 31, 2021.

Convertible Senior Notes due 2025

The components of the Convertible Senior Notes due 2025 as of March 31, 2021 and December 31, 2020 were as follows:

|

| March 31, 2021 |

|

| December 31, 2020 |

| ||

Principal |

| $ | 46.0 |

|

| $ | 46.0 |

|

Less: Debt issuance costs, net of amortization |

|

| (1.3 | ) |

|

| (1.3 | ) |

Less: Debt discount, net of amortization |

|

| — |

|

|

| (5.4 | ) |

Convertible Senior Notes due 2025, net |

| $ | 44.7 |

|

| $ | 39.3 |

|

The principal amount of the Company wasConvertible Senior Notes due 2025 as of March 31, 2021 is $46.0 million. Transaction costs related to the Convertible Senior Notes due 2025 were $1.5 million. These costs are amortized to interest expense over the term of the notes. The Convertible Senior Notes due 2025 mature on December 1, 2025. The Convertible Senior Notes due 2025 are convertible at the option of holders in compliance with all covenants.certain circumstances and during certain periods into the Company’s common shares, cash, or a combination thereof, at the Company’s election. For details regarding conversion mechanics and method of settlement, refer to the Indenture for the Convertible Senior Notes due 2025 filed as an exhibit to a Form 8-K on December 15, 2020 and incorporated by reference in our most recent 10-K filing. The Convertible Senior Notes due 2025 are classified as a non-current liability in the Consolidated Balance Sheets as of March 31, 2021.

13

Convertible Notes Interest Expense

The following table sets forth total interest expense recognized related to the Convertible Notes:

|

| Three Months Ended March 31, |

| |||||

|

| 2021 |

|

| 2020 |

| ||

Contractual interest expense |

| $ | 1.2 |

|

| $ | 1.3 |

|

Amortization of debt issuance costs |

|

| 0.1 |

|

|

| 0.1 |

|

Amortization of debt discount |

|

| — |

|

|

| 1.1 |

|

Total |

| $ | 1.3 |

|

| $ | 2.5 |

|

Fair Value Measurement

The fair value of the Convertible Senior Notes due 2021 was approximately $69.0$40.8 million as of March 31, 2020.2021. The fair value of the Convertible Senior Notes due 2021, which falls within Level 1 of the fair value hierarchy as defined by Accounting Standards Codification (ASC) 820, Fair Value Measurements,applicable accounting guidance, is based on the price traded closest to March 31, 2021.

The fair value of the Convertible Senior Notes due 2025 was approximately $77.2 million as of March 31, 2021. The fair value of the Convertible Senior Notes due 2025, which falls within Level 1 of the fair value hierarchy as defined by applicable accounting guidance, is based on the last price traded in March 2020.2021.

TimkenSteel’s Credit AgreementFacility is variable-rate debt. As such, theany outstanding carrying value is a reasonable estimate of fair value as interest rates on these borrowings approximate current market rates. This valuation falls within Level 2 of the fair value hierarchy and is based on quoted prices for similar assets and liabilities in active markets that are observable either directly or indirectly. There were 0 outstanding borrowings on the Credit Facility as of March 31, 2021.

Cash Interest Paid

The total cash interest paid for the three months ended March 31, 2021 and 2020 and 2019 was $0.8$0.3 million and $1.5$0.8 million, respectively.

Note11-Retirement and Postretirement Plans

The components of net periodic benefit cost (income) for the three months ended March 31, 20202021 and 20192020 were as follows:

|

| Three Months Ended March 31, 2020 |

|

| Three Months Ended March 31, 2019 |

|

| Three Months Ended March 31, 2021 |

|

| Three Months Ended March 31, 2020 |

| ||||||||||||||||||||

|

| Pension |

|

| Postretirement |

|

| Pension |

|

| Postretirement |

|

| Pension |

|

| Postretirement |

|

| Pension |

|

| Postretirement |

| ||||||||

Service cost |

| $ | 4.9 |

|

| $ | 0.3 |

|

| $ | 4.3 |

|

| $ | 0.3 |

|

| $ | 4.4 |

|

| $ | 0.3 |

|

| $ | 4.9 |

|

| $ | 0.3 |

|

Interest cost |

|

| 10.9 |

|

|

| 1.0 |

|

|

| 12.2 |

|

|

| 2.0 |

|

|

| 9.1 |

|

|

| 0.8 |

|

|

| 10.9 |

|

|

| 1.0 |

|

Expected return on plan assets |

|

| (16.2 | ) |

|

| (0.9 | ) |

|

| (16.2 | ) |

|

| (0.9 | ) |

|

| (17.2 | ) |

|

| (0.9 | ) |

|

| (16.2 | ) |

|

| (0.9 | ) |

Amortization of prior service cost |

|

| 0.1 |

|

|

| (1.5 | ) |

|

| 0.1 |

|

|

| — |

|

|

| 0.1 |

|

|

| (1.5 | ) |

|

| 0.1 |

|

|

| (1.5 | ) |

Net remeasurement losses |

|

| 9.5 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 0.2 |

|

|

| — |

|

|

| 9.5 |

|

|

| — |

|

Net Periodic Benefit Cost (Income) |

| $ | 9.2 |

|

| $ | (1.1 | ) |

| $ | 0.4 |

|

| $ | 1.4 |

|

| $ | (3.4 | ) |

| $ | (1.3 | ) |

| $ | 9.2 |

|

| $ | (1.1 | ) |

The Salaried Plan has a provision that permits employees to elect to receive their pension benefits in a lump sum. In the first quarter of 2020,2021, the cumulative cost of all lump sum payments was projected to exceedexceeded the sum of the service cost and interest cost components of net periodic pension cost for the Salaried Plan. TheAs a result, the Company completed a full remeasurement of its pension obligations and plan assets associated with the Salaried Plan asduring the first quarter of March 31, 2020,2021, which resulted in a non-cash loss from remeasurement of $0.2 million. A full remeasurement of the pension obligations and plan assets associated with the Salaried Plan was also required in the first quarter of 2020, resulting in a non-cash loss from remeasurement of $9.5 million included in other expense (income), net onfor the Unaudited Consolidated Statements of Operation. As ofthree months ended March 31, 2019, the cumulative cost2020.

14

Note 12 – Stock-Based Compensation

During the first quarter of 20202021, the Board of Directors granted 598,919 time-vested restricted stock units, 143,280 performance-vested797,320 time-based restricted stock units and 511,020651,240 performance-based restricted stock options.units, which includes the annual grant to our employees, as well as the inducement grant made to our newly hired CEO in January 2021. There were 0 stock option grants in the first quarter of 2021.

13

Time-vestedTime-based restricted stock units are issued with the fair value equal to the closing market price of TimkenSteel common shares on the date of grant. These restricted stock units do not have any performance conditions for vesting. Expense is recognized over the service period, adjusted for any forfeitures that should occur during the vesting period. The weighted average fair value of the restricted stock units granted during the three months ended March 31, 20202021 was $5.26$6.79 per share.

Performance-vestedPerformance-based restricted stock units issued in the first quarter of 20202021 vest based on achievement of a total shareholder return (TSR)(“TSR”) metric. The TSR metric is considered a market condition, which requires TimkenSteel to reflect it in the fair value on grant date using an advanced option-pricing model. The fair value of each performance share was therefore determined using a Monte Carlo valuation model, a generally accepted lattice pricing model under ASC 718 – Stock-based Compensation. The Monte Carlo valuation model, among other factors, uses commonly-accepted economic theory underlying all valuation models, estimates fair value using simulations of future share prices based on stock price behavior and considers the correlation of peer company returns in determining fair value. The weighted average fair value of the performance-vestedperformance-based restricted stock units granted during the three months ended March 31, 20202021 was $5.23$7.57 per share.

Stock options are issued with an exercise price equal to the closing market price of TimkenSteel common shares on the date of grant. The fair value of stock options is determined using a Black-Scholes option pricing model, which incorporates assumptions regarding the expected volatility, the expected option life, the risk-free interest rate and the expected dividend yield. The weighted average exercise price and weighted average fair value of the stock option grants during the three months ended March 31, 2020 were $5.26 per share and $2.23 per share, respectively.