UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20202021

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number: 1-6615

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 95-2594729 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

|

|

26600 Telegraph Road, Suite 400 |

|

Southfield, Michigan | 48033 |

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: (248) 352-7300

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of Each Class |

| Trading Symbol |

| Name of Each Exchange on Which Registered |

Common Stock, $0.01 par value |

| SUP |

| New York Stock Exchange |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer | ☐ | Accelerated Filer |

|

Non-Accelerated Filer |

| Smaller Reporting Company | ☒ |

|

| Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of shares of common stock outstanding as of October 26, 2020: 25,591,930��28, 2021: 26,163,077

TABLE OF CONTENTS

|

|

|

|

| Page |

PART I | - |

| |||

|

|

|

|

|

|

|

| Item 1 |

|

| |

|

|

|

|

|

|

|

|

|

| 1 | |

|

|

|

|

|

|

|

|

|

| Condensed Consolidated Statements of Comprehensive Income (Loss) | 2 |

|

|

|

|

|

|

|

|

|

| 3 | |

|

|

|

|

|

|

|

|

|

| 4 | |

|

|

|

|

|

|

|

|

|

| Condensed Consolidated Statements of Shareholders’ Equity (Deficit) | 5 |

|

|

|

|

|

|

|

|

|

| 7 | |

|

|

|

|

|

|

|

| Item 2 | - | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

|

|

|

|

|

|

|

| Item 3 | - |

| |

|

|

|

|

|

|

|

| Item 4 | - |

| |

|

|

|

| ||

PART II | - |

| |||

|

|

|

|

|

|

|

| Item 1 | - |

| |

|

|

|

|

|

|

|

| Item 1A | - |

| |

|

|

|

|

|

|

|

| Item 2 | - |

| |

|

|

|

|

|

|

|

| Item 5 | - |

| |

|

|

|

|

|

|

|

| Item 6 | - |

| |

|

|

|

| ||

|

|

| |||

PART I

FINANCIAL INFORMATION

Item 1. Financial Statements

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS)

(Dollars in thousands, except per share data)amounts)

(Unaudited)

|

| Three Months Ended |

|

| Nine Months Ended |

|

| Three Months Ended |

|

| Nine Months Ended |

| ||||||||||||||||||||

|

| September 30, 2020 |

|

| September 30, 2019 |

|

| September 30, 2020 |

|

| September 30, 2019 |

|

| September 30, 2021 |

|

| September 30, 2020 |

|

| September 30, 2021 |

|

| September 30, 2020 |

| ||||||||

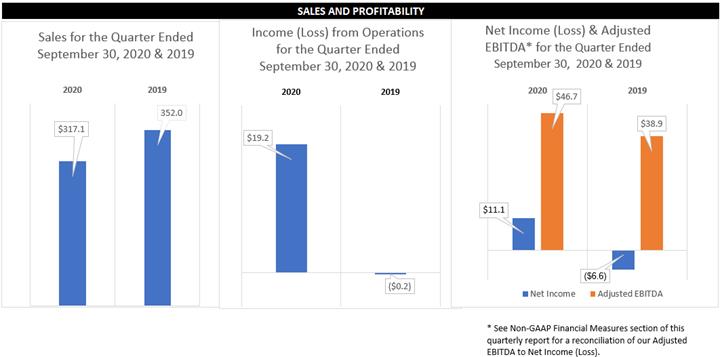

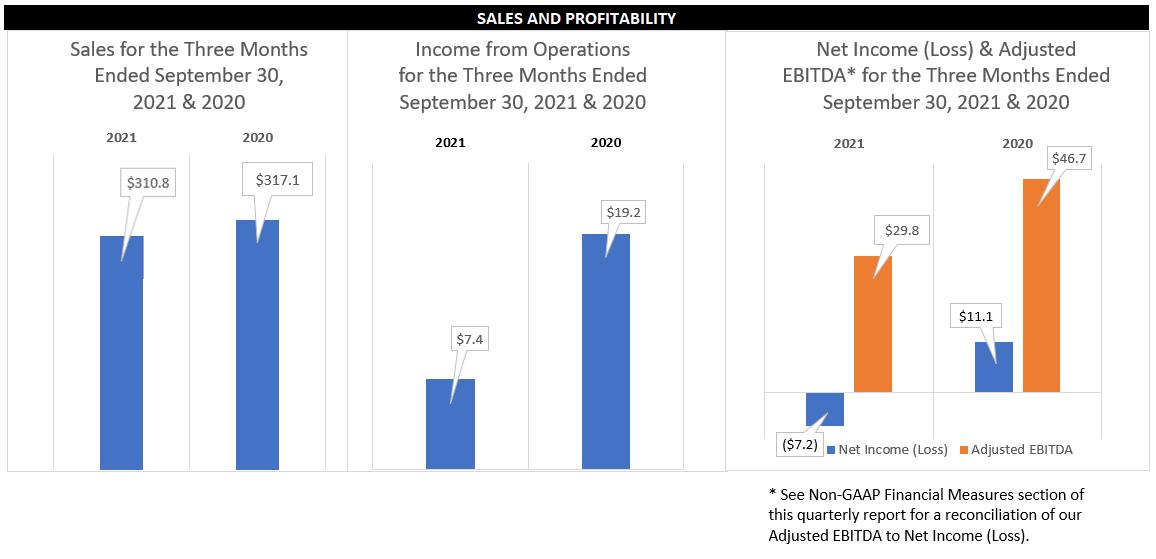

NET SALES |

| $ | 317,103 |

|

| $ | 352,014 |

|

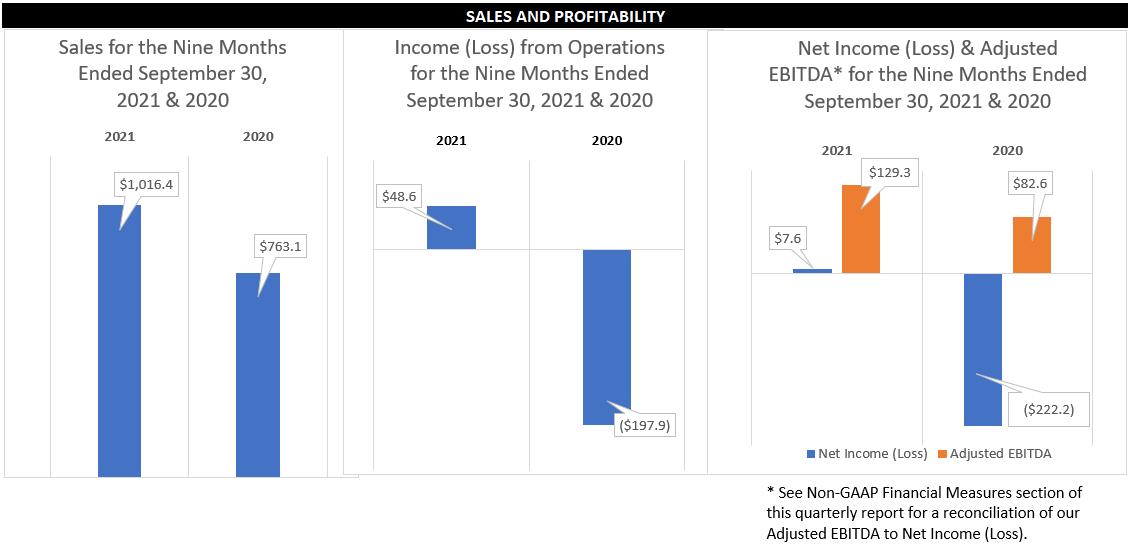

| $ | 763,050 |

|

| $ | 1,062,206 |

|

| $ | 310,780 |

|

| $ | 317,103 |

|

| $ | 1,016,440 |

|

| $ | 763,050 |

|

Cost of sales |

|

| 285,135 |

|

|

| 335,967 |

|

|

| 730,762 |

|

|

| 973,042 |

|

|

| 292,637 |

|

|

| 285,135 |

|

|

| 922,637 |

|

|

| 730,762 |

|

GROSS PROFIT |

|

| 31,968 |

|

|

| 16,047 |

|

|

| 32,288 |

|

|

| 89,164 |

|

|

| 18,143 |

|

|

| 31,968 |

|

|

| 93,803 |

|

|

| 32,288 |

|

Selling, general and administrative expenses |

|

| 12,730 |

|

|

| 16,290 |

|

|

| 36,541 |

|

|

| 46,737 |

|

|

| 10,769 |

|

|

| 12,730 |

|

|

| 45,190 |

|

|

| 36,541 |

|

Impairment of goodwill and indefinite-lived intangibles |

|

| — |

|

|

| — |

|

|

| 193,641 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 193,641 |

|

INCOME (LOSS) FROM OPERATIONS |

|

| 19,238 |

|

|

| (243 | ) |

|

| (197,894 | ) |

|

| 42,427 |

|

|

| 7,374 |

|

|

| 19,238 |

|

|

| 48,613 |

|

|

| (197,894 | ) |

Interest expense, net |

|

| (10,414 | ) |

|

| (11,807 | ) |

|

| (34,448 | ) |

|

| (35,532 | ) |

|

| (10,619 | ) |

|

| (10,414 | ) |

|

| (31,378 | ) |

|

| (34,448 | ) |

Other (expense) income, net |

|

| (1,576 | ) |

|

| 634 |

|

|

| (923 | ) |

|

| 3,393 |

| ||||||||||||||||

INCOME (LOSS) BEFORE INCOME TAXES |

|

| 7,248 |

|

|

| (11,416 | ) |

|

| (233,265 | ) |

|

| 10,288 |

| ||||||||||||||||

Income tax benefit (provision) |

|

| 3,898 |

|

|

| 4,785 |

|

|

| 11,111 |

|

|

| (7,699 | ) | ||||||||||||||||

NET INCOME (LOSS) |

| $ | 11,146 |

|

| $ | (6,631 | ) |

| $ | (222,154 | ) |

| $ | 2,589 |

| ||||||||||||||||

EARNINGS (LOSS) PER SHARE – BASIC |

| $ | 0.12 |

|

| $ | (0.57 | ) |

| $ | (9.66 | ) |

| $ | (0.84 | ) | ||||||||||||||||

EARNINGS (LOSS) PER SHARE – DILUTED |

| $ | 0.12 |

|

| $ | (0.57 | ) |

| $ | (9.66 | ) |

| $ | (0.84 | ) | ||||||||||||||||

Other expense, net |

|

| (2,094 | ) |

|

| (1,576 | ) |

|

| (6,028 | ) |

|

| (923 | ) | ||||||||||||||||

(LOSS) INCOME BEFORE INCOME TAXES |

|

| (5,339 | ) |

|

| 7,248 |

|

|

| 11,207 |

|

|

| (233,265 | ) | ||||||||||||||||

Income tax (provision) benefit |

|

| (1,841 | ) |

|

| 3,898 |

|

|

| (3,570 | ) |

|

| 11,111 |

| ||||||||||||||||

NET (LOSS) INCOME |

| $ | (7,180 | ) |

| $ | 11,146 |

|

| $ | 7,637 |

|

| $ | (222,154 | ) | ||||||||||||||||

(LOSS) EARNINGS PER SHARE – BASIC |

| $ | (0.61 | ) |

| $ | 0.12 |

|

| $ | (0.69 | ) |

| $ | (9.66 | ) | ||||||||||||||||

(LOSS) EARNINGS PER SHARE – DILUTED |

| $ | (0.61 | ) |

| $ | 0.12 |

|

| $ | (0.69 | ) |

| $ | (9.66 | ) | ||||||||||||||||

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Dollars in thousands)

(Unaudited)

|

| Three Months Ended |

|

| Nine Months Ended |

| ||||||||||

|

| September 30, 2020 |

|

| September 30, 2019 |

|

| September 30, 2020 |

|

| September 30, 2019 |

| ||||

Net income (loss) |

| $ | 11,146 |

|

| $ | (6,631 | ) |

| $ | (222,154 | ) |

| $ | 2,589 |

|

Other comprehensive income (loss), net of tax: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign currency translation gain (loss) |

|

| 16,384 |

|

|

| (22,143 | ) |

|

| (9,706 | ) |

|

| (21,459 | ) |

Change in unrecognized gains (losses) on derivative instruments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in fair value of derivatives |

|

| 5,818 |

|

|

| (10,406 | ) |

|

| (32,934 | ) |

|

| (1,862 | ) |

Tax (provision) benefit |

|

| (1,135 | ) |

|

| 2,104 |

|

|

| 7,618 |

|

|

| 342 |

|

Change in unrecognized gains (losses) on derivative instruments, net of tax |

|

| 4,683 |

|

|

| (8,302 | ) |

|

| (25,316 | ) |

|

| (1,520 | ) |

Defined benefit pension plan: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amortization of actuarial losses on pension obligations |

|

| 72 |

|

|

| 50 |

|

|

| 216 |

|

|

| 155 |

|

Tax (provision) |

|

| (15 | ) |

|

| (11 | ) |

|

| (45 | ) |

|

| (33 | ) |

Pension changes, net of tax |

|

| 57 |

|

|

| 39 |

|

|

| 171 |

|

|

| 122 |

|

Other comprehensive income (loss), net of tax |

|

| 21,124 |

|

|

| (30,406 | ) |

|

| (34,851 | ) |

|

| (22,857 | ) |

Comprehensive income (loss) |

| $ | 32,270 |

|

| $ | (37,037 | ) |

| $ | (257,005 | ) |

| $ | (20,268 | ) |

|

| Three Months Ended |

|

| Nine Months Ended |

| ||||||||||

|

| September 30, 2021 |

|

| September 30, 2020 |

|

| September 30, 2021 |

|

| September 30, 2020 |

| ||||

Net (loss) income |

| $ | (7,180 | ) |

| $ | 11,146 |

|

| $ | 7,637 |

|

| $ | (222,154 | ) |

Other comprehensive (loss) income, net of tax: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign currency translation (loss) gain |

|

| (9,068 | ) |

|

| 16,384 |

|

|

| (16,336 | ) |

|

| (9,706 | ) |

Change in unrecognized (losses) gains on derivative instruments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in fair value of derivatives |

|

| (7,735 | ) |

|

| 5,818 |

|

|

| 290 |

|

|

| (32,934 | ) |

Tax benefit (provision) |

|

| 851 |

|

|

| (1,135 | ) |

|

| (189 | ) |

|

| 7,618 |

|

Change in unrecognized (losses) gains on derivative instruments, net of tax |

|

| (6,884 | ) |

|

| 4,683 |

|

|

| 101 |

|

|

| (25,316 | ) |

Defined benefit pension plan: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amortization of actuarial losses on pension obligations |

|

| 96 |

|

|

| 72 |

|

|

| 290 |

|

|

| 216 |

|

Tax provision |

|

| — |

|

|

| (15 | ) |

|

| — |

|

|

| (45 | ) |

Pension changes, net of tax |

|

| 96 |

|

|

| 57 |

|

|

| 290 |

|

|

| 171 |

|

Other comprehensive (loss) income, net of tax |

|

| (15,856 | ) |

|

| 21,124 |

|

|

| (15,945 | ) |

|

| (34,851 | ) |

Comprehensive (loss) income |

| $ | (23,036 | ) |

| $ | 32,270 |

|

| $ | (8,308 | ) |

| $ | (257,005 | ) |

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Dollars in thousands)

(Unaudited)

|

| September 30, 2020 |

|

| December 31, 2019 |

|

| September 30, 2021 |

|

| December 31, 2020 |

| ||||

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

| $ | 111,131 |

|

| $ | 77,927 |

|

| $ | 76,117 |

|

| $ | 152,423 |

|

Accounts receivable, net |

|

| 77,675 |

|

|

| 76,786 |

|

|

| 94,167 |

|

|

| 48,995 |

|

Inventories, net |

|

| 141,287 |

|

|

| 168,470 |

|

|

| 214,972 |

|

|

| 154,980 |

|

Income taxes receivable |

|

| 4,067 |

|

|

| 4,630 |

|

|

| 4,689 |

|

|

| 4,957 |

|

Other current assets |

|

| 16,329 |

|

|

| 26,375 |

|

|

| 32,520 |

|

|

| 22,301 |

|

Total current assets |

|

| 350,489 |

|

|

| 354,188 |

|

|

| 422,465 |

|

|

| 383,656 |

|

Property, plant and equipment, net |

|

| 507,037 |

|

|

| 529,282 |

|

|

| 501,772 |

|

|

| 522,124 |

|

Deferred income tax assets, net |

|

| 53,307 |

|

|

| 38,607 |

|

|

| 28,020 |

|

|

| 30,860 |

|

Goodwill |

|

| — |

|

|

| 184,832 |

|

|

| — |

|

|

| — |

|

Intangibles, net |

|

| 112,341 |

|

|

| 137,078 |

|

|

| 85,177 |

|

|

| 110,796 |

|

Other non-current assets |

|

| 55,837 |

|

|

| 67,880 |

|

|

| 54,834 |

|

|

| 61,889 |

|

Total assets |

| $ | 1,079,011 |

|

| $ | 1,311,867 |

|

| $ | 1,092,268 |

|

| $ | 1,109,325 |

|

LIABILITIES, MEZZANINE EQUITY AND SHAREHOLDERS’ EQUITY (DEFICIT) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 149,808 |

|

| $ | 123,112 |

|

| $ | 162,936 |

|

| $ | 151,839 |

|

Short-term debt |

|

| 6,034 |

|

|

| 4,010 |

|

|

| 6,297 |

|

|

| 6,112 |

|

Accrued expenses |

|

| 72,857 |

|

|

| 60,845 |

|

|

| 76,573 |

|

|

| 71,079 |

|

Income taxes payable |

|

| 2,208 |

|

|

| 3,148 |

|

|

| 1,380 |

|

|

| 2,107 |

|

Total current liabilities |

|

| 230,907 |

|

|

| 191,115 |

|

|

| 247,186 |

|

|

| 231,137 |

|

Long-term debt (less current portion) |

|

| 611,706 |

|

|

| 611,025 |

|

|

| 609,445 |

|

|

| 625,492 |

|

Non-current income tax liabilities |

|

| 7,451 |

|

|

| 6,523 |

|

|

| 7,928 |

|

|

| 7,635 |

|

Deferred income tax liabilities, net |

|

| — |

|

|

| 12,369 |

|

|

| 3,243 |

|

|

| 9,104 |

|

Other non-current liabilities |

|

| 81,321 |

|

|

| 71,640 |

|

|

| 78,257 |

|

|

| 76,426 |

|

Commitments and contingent liabilities (Note 17) |

|

| — |

|

|

| — |

|

|

|

|

|

|

|

|

|

Mezzanine equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred stock, $0.01 par value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Authorized - 1,000,000 shares |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Issued and outstanding – 150,000 shares outstanding at September 30, 2020 and December 31, 2019 |

|

| 174,597 |

|

|

| 160,980 |

| ||||||||

Issued and outstanding – 150,000 shares outstanding at September 30, 2021 and December 31, 2020 |

|

| 194,560 |

|

|

| 179,387 |

| ||||||||

European non-controlling redeemable equity |

|

| 1,580 |

|

|

| 6,525 |

|

|

| 1,552 |

|

|

| 1,666 |

|

Shareholders’ equity (deficit): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock, $0.01 par value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Authorized - 100,000,000 shares |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Issued and outstanding – 25,591,930 and 25,128,158 shares at September 30, 2020 and December 31, 2019 |

|

| 94,058 |

|

|

| 93,331 |

| ||||||||

Issued and outstanding – 26,148,797 and 25,591,930 shares at September 30, 2021 and December 31, 2020 |

|

| 100,618 |

|

|

| 95,247 |

| ||||||||

Accumulated other comprehensive loss |

|

| (134,929 | ) |

|

| (100,078 | ) |

|

| (115,391 | ) |

|

| (99,446 | ) |

Retained earnings |

|

| 12,320 |

|

|

| 258,437 |

|

|

| (35,130 | ) |

|

| (17,323 | ) |

Total shareholders’ equity (deficit) |

|

| (28,551 | ) |

|

| 251,690 |

|

|

| (49,903 | ) |

|

| (21,522 | ) |

Total liabilities, mezzanine equity and shareholders’ equity (deficit) |

| $ | 1,079,011 |

|

| $ | 1,311,867 |

|

| $ | 1,092,268 |

|

| $ | 1,109,325 |

|

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Dollars in thousands)

(Unaudited)

|

| Nine Months Ended |

|

| Nine Months Ended |

| ||||||||||

|

| September 30, 2020 |

|

| September 30, 2019 |

|

| September 30, 2021 |

|

| September 30, 2020 |

| ||||

CASH FLOWS FROM OPERATING ACTIVITIES: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net (loss) income |

| $ | (222,154 | ) |

| $ | 2,589 |

| ||||||||

Adjustments to reconcile net (loss) income to net cash provided by operating activities: |

|

|

|

|

|

|

|

| ||||||||

Net income (loss) |

|

| 7,637 |

|

| $ | (222,154 | ) | ||||||||

Adjustments to reconcile net loss to net cash provided by operating activities: |

|

|

|

|

|

|

|

| ||||||||

Depreciation and amortization |

|

| 73,134 |

|

|

| 77,500 |

|

|

| 75,446 |

|

|

| 73,134 |

|

Income tax, non-cash changes |

|

| (19,389 | ) |

|

| (3,472 | ) |

|

| (4,198 | ) |

|

| (19,389 | ) |

Impairment of goodwill and indefinite-lived intangibles |

|

| 193,641 |

|

|

| — |

|

|

| - |

|

|

| 193,641 |

|

Stock-based compensation |

|

| 727 |

|

|

| 3,695 |

|

|

| 6,844 |

|

|

| 727 |

|

Amortization of debt issuance costs |

|

| 3,140 |

|

|

| 3,681 |

|

|

| 3,195 |

|

|

| 3,140 |

|

Other non-cash items |

|

| (1,493 | ) |

|

| 444 |

|

|

| (10,710 | ) |

|

| (1,493 | ) |

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts receivable |

|

| (4,062 | ) |

|

| (30,464 | ) |

|

| (47,899 | ) |

|

| (4,062 | ) |

Inventories |

|

| 29,292 |

|

|

| 9,028 |

|

|

| (66,513 | ) |

|

| 29,292 |

|

Other assets and liabilities |

|

| 11,520 |

|

|

| 20,313 |

|

|

| 14,538 |

|

|

| 11,520 |

|

Accounts payable |

|

| 27,438 |

|

|

| 11,176 |

|

|

| 7,181 |

|

|

| 27,438 |

|

Income taxes |

|

| 717 |

|

|

| 7,861 |

|

|

| (99 | ) |

|

| 717 |

|

NET CASH PROVIDED BY OPERATING ACTIVITIES |

|

| 92,511 |

|

|

| 102,351 |

| ||||||||

NET CASH (USED IN) PROVIDED BY OPERATING ACTIVITIES |

|

| (14,578 | ) |

|

| 92,511 |

| ||||||||

CASH FLOWS FROM INVESTING ACTIVITIES: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additions to property, plant and equipment |

|

| (33,592 | ) |

|

| (47,584 | ) | ||||||||

Additions to property, plant, and equipment |

|

| (47,571 | ) |

|

| (33,592 | ) | ||||||||

Proceeds from sale of fixed assets |

|

| 859 |

|

|

| — |

|

|

| 6,589 |

|

|

| 859 |

|

Other investing activities |

|

| — |

|

|

| 9,631 |

| ||||||||

NET CASH USED IN INVESTING ACTIVITIES |

|

| (32,733 | ) |

|

| (37,953 | ) |

|

| (40,982 | ) |

|

| (32,733 | ) |

CASH FLOWS FROM FINANCING ACTIVITIES: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proceeds from issuance of long-term debt |

|

| 11,690 |

|

|

| — |

|

|

| 1,658 |

|

|

| 11,690 |

|

Repayments of debt |

|

| (24,851 | ) |

|

| (35,015 | ) |

|

| (3,569 | ) |

|

| (24,851 | ) |

Cash dividends paid |

|

| (10,161 | ) |

|

| (19,171 | ) | ||||||||

Purchase of non-controlling redeemable shares |

|

| (4,981 | ) |

|

| (3,888 | ) | ||||||||

Payments related to tax withholdings for stock-based compensation |

|

| — |

|

|

| (108 | ) | ||||||||

Proceeds from borrowings on revolving credit facility |

|

| 313,825 |

|

|

| 69,600 |

|

|

| - |

|

|

| 313,825 |

|

Repayments of borrowings on revolving credit facility |

|

| (316,910 | ) |

|

| (69,600 | ) |

|

| - |

|

|

| (316,910 | ) |

Other financing activities |

|

| (723 | ) |

|

| (1,035 | ) | ||||||||

Cash dividends paid |

|

| (10,140 | ) |

|

| (10,161 | ) | ||||||||

Financing costs paid and other |

|

| (4,339 | ) |

|

| (4,981 | ) | ||||||||

Payments related to tax withholdings for stock-based compensation |

|

| (1,473 | ) |

|

| — |

| ||||||||

Finance lease payments |

|

| (1,012 | ) |

|

| (723 | ) | ||||||||

NET CASH USED IN FINANCING ACTIVITIES |

|

| (32,111 | ) |

|

| (59,217 | ) |

|

| (18,875 | ) |

|

| (32,111 | ) |

Effect of exchange rate changes on cash |

|

| 5,537 |

|

|

| (3,337 | ) |

|

| (1,871 | ) |

|

| 5,537 |

|

Net increase in cash and cash equivalents |

|

| 33,204 |

|

|

| 1,844 |

| ||||||||

Net (decrease) increase in cash and cash equivalents |

|

| (76,306 | ) |

|

| 33,204 |

| ||||||||

Cash and cash equivalents at the beginning of the period |

|

| 77,927 |

|

|

| 47,464 |

|

|

| 152,423 |

|

|

| 77,927 |

|

Cash and cash equivalents at the end of the period |

| $ | 111,131 |

|

| $ | 49,308 |

|

|

| 76,117 |

|

| $ | 111,131 |

|

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

SUPERIOR INDUSTRIES INTERNATIONAL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY (DEFICIT)

(Dollars in thousands)

For the nine months ended September 30, 2019(Unaudited)

(Unaudited) |

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT DECEMBER 31, 2018 |

|

| 25,019,237 |

|

| $ | 87,723 |

|

| $ | (3,205 | ) |

| $ | (3,000 | ) |

| $ | (99,290 | ) |

| $ | 391,037 |

|

| $ | 373,265 |

|

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2,589 |

|

|

| 2,589 |

|

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| (1,520 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (1,520 | ) |

|

Change in employee benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 122 |

|

|

| — |

|

|

| — |

|

|

| 122 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (21,459 | ) |

|

| — |

|

|

| (21,459 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 108,921 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 3,587 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 3,587 |

|

|

Cash dividend declared ($0.09 per common share) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (4,597 | ) |

|

| (4,597 | ) |

|

Redeemable preferred 9% dividend, participating dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (23,275 | ) |

|

| (23,275 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (496 | ) |

|

| (496 | ) |

|

BALANCE AT SEPTEMBER 30, 2019 |

|

| 25,128,158 |

|

| $ | 91,310 |

|

| $ | (4,725 | ) |

| $ | (2,878 | ) |

| $ | (120,749 | ) |

| $ | 365,258 |

|

| $ | 328,216 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the three months ended September 30, 2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Unaudited) |

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT JUNE 30, 2019 |

|

| 25,114,598 |

|

| $ | 89,532 |

|

| $ | 3,577 |

|

| $ | (2,917 | ) |

| $ | (98,606 | ) |

| $ | 379,604 |

|

| $ | 371,190 |

|

|

Net loss |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (6,631 | ) |

|

| (6,631 | ) |

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| (8,302 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (8,302 | ) |

|

Change in employee benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 39 |

|

|

| — |

|

|

| — |

|

|

| 39 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (22,143 | ) |

|

| — |

|

|

| (22,143 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 13,560 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 1,778 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 1,778 |

|

|

Cash dividend declared ($0.09 per common share) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (15 | ) |

|

| (15 | ) |

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (7,587 | ) |

|

| (7,587 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (113 | ) |

|

| (113 | ) |

|

BALANCE AT SEPTEMBER 30, 2019 |

|

| 25,128,158 |

|

| $ | 91,310 |

|

| $ | (4,725 | ) |

| $ | (2,878 | ) |

| $ | (120,749 | ) |

| $ | 365,258 |

|

| $ | 328,216 |

|

|

For the nine months ended September 30, 2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT DECEMBER 31, 2019 |

|

| 25,128,158 |

|

| $ | 93,331 |

|

| $ | 9,951 |

|

| $ | (5,571 | ) |

| $ | (104,458 | ) |

| $ | 258,437 |

|

| $ | 251,690 |

|

|

Net loss |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (222,154 | ) |

|

| (222,154 | ) |

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| (25,316 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (25,316 | ) |

|

Change in defined benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 171 |

|

|

| — |

|

|

| — |

|

|

| 171 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (9,706 | ) |

|

| — |

|

|

| (9,706 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 463,772 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 727 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 727 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (23,811 | ) |

|

| (23,811 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (152 | ) |

|

| (152 | ) |

|

BALANCE AT SEPTEMBER 30, 2020 |

|

| 25,591,930 |

|

| $ | 94,058 |

|

| $ | (15,365 | ) |

| $ | (5,400 | ) |

| $ | (114,164 | ) |

| $ | 12,320 |

|

| $ | (28,551 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the three months ended September 30, 2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT JUNE 30, 2020 |

|

| 25,591,930 |

|

| $ | 93,541 |

|

| $ | (20,048 | ) |

| $ | (5,457 | ) |

| $ | (130,548 | ) |

| $ | 9,336 |

|

| $ | (53,176 | ) |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 11,146 |

|

|

| 11,146 |

|

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| 4,683 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 4,683 |

|

|

Change in defined benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 57 |

|

|

| — |

|

|

| — |

|

|

| 57 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 16,384 |

|

|

| — |

|

|

| 16,384 |

|

|

Common stock issued, net of shares withheld for employee taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 517 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 517 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (8,056 | ) |

|

| (8,056 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (106 | ) |

|

| (106 | ) |

|

BALANCE AT SEPTEMBER 30, 2020 |

|

| 25,591,930 |

|

| $ | 94,058 |

|

| $ | (15,365 | ) |

| $ | (5,400 | ) |

| $ | (114,164 | ) |

| $ | 12,320 |

|

| $ | (28,551 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the nine months ended September 30, 2020

(Unaudited) |

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT DECEMBER 31, 2019 |

|

| 25,128,158 |

|

| $ | 93,331 |

|

| $ | 9,951 |

|

| $ | (5,571 | ) |

| $ | (104,458 | ) |

| $ | 258,437 |

|

| $ | 251,690 |

|

|

Net loss |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (222,154 | ) |

|

| (222,154 | ) |

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| (25,316 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (25,316 | ) |

|

Change in employee benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 171 |

|

|

| — |

|

|

| — |

|

|

| 171 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (9,706 | ) |

|

| — |

|

|

| (9,706 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 463,772 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 727 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 727 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (23,811 | ) |

|

| (23,811 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (152 | ) |

|

| (152 | ) |

|

BALANCE AT SEPTEMBER 30, 2020 |

|

| 25,591,930 |

|

| $ | 94,058 |

|

| $ | (15,365 | ) |

| $ | (5,400 | ) |

| $ | (114,164 | ) |

| $ | 12,320 |

|

| $ | (28,551 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the three months ended September 30, 2020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Unaudited) |

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT JUNE 30, 2020 |

|

| 25,591,930 |

|

| $ | 93,541 |

|

| $ | (20,048 | ) |

| $ | (5,457 | ) |

| $ | (130,548 | ) |

| $ | 9,336 |

|

| $ | (53,176 | ) |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 11,146 |

|

|

| 11,146 |

|

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| 4,683 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 4,683 |

|

|

Change in employee benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 57 |

|

|

| — |

|

|

| — |

|

|

| 57 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 16,384 |

|

|

| — |

|

|

| 16,384 |

|

|

Common stock issued, net of shares withheld for employee taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 517 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 517 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (8,056 | ) |

|

| (8,056 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (106 | ) |

|

| (106 | ) |

|

BALANCE AT SEPTEMBER 30, 2020 |

|

| 25,591,930 |

|

| $ | 94,058 |

|

| $ | (15,365 | ) |

| $ | (5,400 | ) |

| $ | (114,164 | ) |

| $ | 12,320 |

|

| $ | (28,551 | ) |

|

For the nine months ended September 30, 2021 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT DECEMBER 31, 2020 |

|

| 25,591,930 |

|

| $ | 95,247 |

|

| $ | (1,738 | ) |

| $ | (7,447 | ) |

| $ | (90,261 | ) |

| $ | (17,323 | ) |

| $ | (21,522 | ) |

|

Net income |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 7,637 |

|

|

| 7,637 |

|

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| 101 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 101 |

|

|

Change in defined benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 290 |

|

|

| — |

|

|

| — |

|

|

| 290 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (16,336 | ) |

|

| — |

|

|

| (16,336 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 556,867 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 5,371 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 5,371 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (25,310 | ) |

|

| (25,310 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (134 | ) |

|

| (134 | ) |

|

BALANCE AT SEPTEMBER 30, 2021 |

|

| 26,148,797 |

|

| $ | 100,618 |

|

| $ | (1,637 | ) |

| $ | (7,157 | ) |

| $ | (106,597 | ) |

| $ | (35,130 | ) |

| $ | (49,903 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the three months ended September 30, 2021 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Stock |

|

| Accumulated Other Comprehensive (Loss) Income |

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

| Number of Shares |

|

| Amount |

|

| Unrecognized Gains (Losses) on Derivative Instruments |

|

| Pension Obligations |

|

| Cumulative Translation Adjustment |

|

| Retained Earnings |

|

| Total |

|

| |||||||

BALANCE AT JUNE 30, 2021 |

|

| 26,107,462 |

|

| $ | 98,236 |

|

| $ | 5,247 |

|

| $ | (7,253 | ) |

| $ | (97,529 | ) |

| $ | (19,256 | ) |

| $ | (20,555 | ) |

|

Net loss |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (7,180 | ) |

|

| (7,180 | ) |

|

Change in unrecognized gains/losses on derivative instruments, net of tax |

|

| — |

|

|

| — |

|

|

| (6,884 | ) |

|

| — |

|

|

| — |

|

|

| — |

|

|

| (6,884 | ) |

|

Change in defined benefit plans, net of taxes |

|

| — |

|

|

| — |

|

|

| — |

|

|

| 96 |

|

|

| — |

|

|

| — |

|

|

| 96 |

|

|

Net foreign currency translation adjustment |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (9,068 | ) |

|

| — |

|

|

| (9,068 | ) |

|

Common stock issued, net of shares withheld for employee taxes |

|

| 41,335 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

Stock-based compensation |

|

| — |

|

|

| 2,382 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 2,382 |

|

|

Redeemable preferred 9% dividend and accretion |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (8,598 | ) |

|

| (8,598 | ) |

|

European non-controlling redeemable equity dividend |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| (96 | ) |

|

| (96 | ) |

|

BALANCE AT SEPTEMBER 30, 2021 |

|

| 26,148,797 |

|

| $ | 100,618 |

|

| $ | (1,637 | ) |

| $ | (7,157 | ) |

| $ | (106,597 | ) |

| $ | (35,130 | ) |

| $ | (49,903 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The accompanying unaudited notes are an integral part of these condensed consolidated financial statements.

Superior Industries International, Inc.

Notes to Condensed Consolidated Financial Statements

September 30, 20202021

(Unaudited)

NOTE 1 – NATURE OF OPERATIONS AND PRESENTATION OF CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Nature of Operations

Superior Industries International, Inc.’s (referred herein as the “Company,” “Superior,” or “we” and “our”) principal business is the design and manufacture of aluminum wheels for sale to original equipment manufacturers (OEMs)(“OEMs”) in North America and Europe and to the aftermarket distributors in Europe. We employ approximately 7,5008,000 full-time employees, operating in 8 manufacturing facilities in North America and Europe with a combined annual manufacturing capacity of approximately 20 million wheels.Europe. We are one of the largest aluminum wheel suppliers to global OEMs and we believe we are the #1 European aluminum wheel aftermarket manufacturer and supplier. Our OEM aluminum wheels accounted for approximately 92 percent of our sales in the first nine months of 20202021 and are primarily sold for factory installation on vehicle models manufactured by BMW (including Mini), Daimler AG Company (Mercedes-Benz, AMG, Smart), FCA, Ford, GM, Honda, Jaguar-Land Rover, Lucid Motors, Mazda, Mitsubishi, Nissan, PSA, Renault, Stellantis, Subaru, Suzuki, Toyota, VW Group (Volkswagen, Audi, SEAT, Skoda, Porsche, Bentley) and Volvo. We also sell aluminum wheels to the European aftermarket under the brands ATS, RIAL, ALUTEC and ANZIO. North America and Europe represent the principal markets for our products, but we have a diversified global presence and diversified customer base consisting of North American, European and Asian OEMs. We have determined that our North American and European operations should be treated as separate reportable segments as further described in Note 5, “Business Segments.”

Presentation of Condensed Consolidated Financial Statements

The accompanying unaudited condensed consolidated financial statements have been prepared in accordanceconformity with the Security and Exchange Commission’s (“SEC’s”) requirements for quarterly reports on Form 10-Q and U.S. Generally Accepted Accounting Principles (“GAAP”) pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”) for interim financial information. Accordingly, they do not include all the information and notes required by U.S. GAAP for complete financial statements. These unaudited condensed consolidated financial statements, in our opinion, containinclude all adjustments, of a normal and recurring nature, which are necessary for fair presentation of (i) the condensed consolidated statements of income (loss) for the three and nine-month periods ended September 30, 20202021 and September 30, 2019,2020, (ii) the condensed consolidated statements of comprehensive income (loss) for the three and nine-month periods ended September 30, 20202021 and September 30, 2019,2020, (iii) the condensed consolidated balance sheets at September 30, 20202021 and December 31, 2019,2020, (iv) the condensed consolidated statements of cash flows for the nine-month periods ended September 30, 20202021 and September 30, 2019,2020, and (v) the condensed consolidated statements of shareholders’ equity (deficit) for the three and nine-month periods ended September 30, 20202021 and September 30, 2019.2020. This Quarterly Report on Form 10-Q should be read in conjunction with our consolidated financial statements and notes thereto filed with the SEC in our 20192020 Annual Report on Form 10-K.

Interim financial reporting standards require us to make estimates that are based on assumptions regarding the outcome of future events and circumstances not known at that time, including the use of estimated effective tax rates.time. Inevitably, some assumptions will not materialize, unanticipated events or circumstances may occur which vary from those estimates and such variations may significantly affect our future results. Additionally, interim results may not be indicative of our results for future interim periods or our annual results.

Reclassifications

Certain prior year amounts have been reclassified to conform with the current year presentation.

Cash Paid for Interest and Taxes and Non-Cash Investing Activities

Cash paid for interest was $27.1$23.5 million and $28.2$27.1 million for the nine months ended September 30, 20202021 and September 30, 2019,2020, respectively. Net cash paid for income taxes paid was $7.6$8.3 million and $6.5$7.6 million for the nine months ended September 30, 20202021 and September 30, 2019,2020, respectively. As of September 30, 20202021 and September 30, 2019, $0.22020, $10.8 million and $15.8$0.2 million, respectively, of equipment had been purchased but not yet paid and was included in accounts payable in our condensed consolidated balance sheets.

New Accounting Standards

Accounting Standards Update (“ASU”) 2018-13, “Fair Value Measurement.” Effective January 1, 2020, the Company adopted ASU 2018-13 which allows companies to remove, modify and add certain disclosures related to fair value measurements. The adoption of this standard did not have a significant impact on the Company’s condensed consolidated financial statement disclosures.

Accounting Standards Issued but Not Yet Adopted

ASUAccounting Standards Update (ASU) 2016-13, “Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments.” In June 2016, the Financial Accounting Standards Board (“FASB”) issued ASU 2016-13, "Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments", which requires entities to use a new impairment

model based on current expected credit losses (“CECL”) rather than incurred losses. Under CECL, estimated credit losses would incorporate relevant information about past events, current conditions and reasonable and supportable forecasts and any expected credit losses would be recognized at the time of sale. As a smaller reporting company (as defined under SEC regulations), theThe Company is not required to adopt the standard until fiscal years beginning after December 31, 2022.January 1, 2023. We are evaluating the impact this standard will have on our financial statements and disclosures.

ASU 2018-14, “Compensation - Retirement Benefits - Defined Benefit Plans.” In August 2018, the FASB issued an ASU entitled “Compensation - Retirement Benefits - Defined Benefit Plans - General Subtopic 715-20 - Disclosure Framework - Changes to the Disclosure Requirements for Defined Benefit Plans” (ASU 2018-14), which is designed to improve the effectiveness of disclosures by removing and adding disclosures related to defined benefit plans. ASU 2018-14 is effective for fiscal years ending after December 15, 2020. We are evaluating the impact this new standard will have on our financial statement disclosures.

ASU 2020-04, “Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting.” In March 2020, the FASB issued ASU 2020-04 entitled “Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting,” which provides temporary optional guidance to ease the potential burden in accounting for (or recognizing the effects of) reference rate reform on financial reporting. The relief provided by this guidance is elective and applies to all entities, subject to meeting certain criteria, that have contracts, hedging relationships, and other transactions that reference the London Interbank Offered Rate (“LIBOR”) or another reference rate expected to be discontinued because of reference rate reform initiatives being undertaken in an effort to identify alternative reference rates that are more observable or transaction based and less susceptible to manipulation. The optional amendments of this guidance are effective for all entities upon adoption. We are currently assessing the impact of this new standard on our financial statements and disclosures.

NOTE 2 – REVENUE

In accordance with Accounting Standards Codification (“ASC”) 606, “Revenue from Contracts with Customers,” theThe Company disaggregates revenue from contracts with customers into our reportable segments, North America and Europe. Revenues by segment for the three and nine-month periods ended September 30, 2021 and September 30, 2020, and 2019respectively, are summarized in Note 5, “Business Segments.”

The opening and closing balances of the Company’s customer receivables and current and long-term contract liabilities balances as of September 30, 2020 and December 31, 2019 are as follows (in thousands):follows:

|

| September 30, 2020 |

|

| December 31, 2019 |

|

| Change |

| |||||||||||||||

(Dollars in thousands) |

| September 30, 2021 |

|

| December 31, 2020 |

|

| Change |

| |||||||||||||||

Customer receivables |

| $ | 72,272 |

|

| $ | 68,283 |

|

| $ | 3,989 |

|

| $ | 82,717 |

|

| $ | 40,785 |

|

| $ | 41,932 |

|

Contract liabilities—current |

|

| 8,105 |

|

|

| 5,880 |

|

|

| 2,225 |

|

|

| 7,193 |

|

|

| 8,249 |

|

|

| (1,056 | ) |

Contract liabilities—noncurrent |

|

| 12,465 |

|

|

| 13,577 |

|

|

| (1,112 | ) |

|

| 11,026 |

|

|

| 13,106 |

|

|

| (2,080 | ) |

NOTE 3 – FAIR VALUE MEASUREMENTS

The Company applies fair value accounting for all financial assets and liabilities and non-financial assets and liabilities that are recognized or disclosed at fair value in the financial statements on a recurring basis, while other assets and liabilities are measured at fair value on a nonrecurring basis, such as an asset impairment. Fair value is estimated by applying the following hierarchy, which prioritizes the inputs used to measure fair value into three levels and bases the categorization within the hierarchy upon the lowest level of input that is available and significant to the fair value measurement:

Level 1 - Quoted prices in active markets for identical assets or liabilities.

Level 2 - Observable inputs other than quoted prices in active markets for identical assets and liabilities, quoted prices for identical or similar assets or liabilities in inactive markets, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities.

Level 3 - Inputs that are generally unobservable and typically reflect management’s estimate of assumptions that market participants would use in pricing the asset or liability.

The carrying amounts for cash and cash equivalents, accounts receivable, accounts payable and accrued expenses approximate their fair values due to the short period of time until maturity.

Cash and Cash Equivalents

Cash and cash equivalents generally consist of cash, certificates of deposit and fixed deposits and money market funds with original maturities of three months or less.

Derivative Financial Instruments

Our derivatives are over-the-counter customized derivative transactions and are not exchange traded. We estimate the fair value of these instruments using industry-standard valuation models such as discounted cash flow. These models project future cash flows and discount the future amounts to a present value using market-based expectations for interest rates, foreign exchange rates, commodity prices and the contractual terms of the derivative instruments. The discount rate used is the relevant interbank deposit rate (e.g., LIBOR) plus an adjustment for non-performance risk.

The following tables categorize items measured at fair value as of September 30, 20202021 and December 31, 2019:2020:

|

|

|

|

|

| Fair Value Measurement at Reporting Date Using |

|

|

|

|

|

| Fair Value Measurement at Reporting Date Using |

| ||||||||||||||||||

September 30, 2020 |

|

|

|

|

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

| |||||||||||||||||||

September 30, 2021 |

|

|

|

|

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

| |||||||||||||||||||

(Dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Derivative contracts |

| $ | 3,016 |

|

| $ | — |

|

| $ | 3,016 |

|

| $ | — |

|

| $ | 13,884 |

|

| $ | — |

|

| $ | 13,884 |

|

| $ | — |

|

Total |

| $ | 3,016 |

|

| $ | — |

|

| $ | 3,016 |

|

| $ | — |

|

| $ | 13,884 |

|

| $ | — |

|

| $ | 13,884 |

|

| $ | — |

|

Liabilities |

|

|

|

|

|

|

|

|

| . |

|

|

|

|

|

|

|

|

|

|

|

|

|

| . |

|

|

|

|

| ||

Derivative contracts |

| $ | 28,984 |

|

| $ | — |

|

| $ | 28,984 |

|

| $ | — |

|

| $ | 17,213 |

|

| $ | — |

|

| $ | 17,213 |

|

| $ | — |

|

Total |

| $ | 28,984 |

|

| $ | — |

|

| $ | 28,984 |

|

| $ | — |

|

| $ | 17,213 |

|

| $ | — |

|

| $ | 17,213 |

|

| $ | — |

|

|

|

|

|

|

| Fair Value Measurement at Reporting Date Using |

|

|

|

|

|

| Fair Value Measurement at Reporting Date Using |

| ||||||||||||||||||

December 31, 2019 |

|

|

|

|

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

| |||||||||||||||||||

December 31, 2020 |

|

|

|

|

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

| |||||||||||||||||||

(Dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Derivative contracts |

| $ | 21,973 |

|

| $ | — |

|

| $ | 21,973 |

|

| $ | — |

|

| $ | 10,218 |

|

| $ | — |

|

| $ | 10,218 |

|

| $ | — |

|

Total |

| $ | 21,973 |

|

| $ | — |

|

| $ | 21,973 |

|

| $ | — |

|

| $ | 10,218 |

|

| $ | — |

|

| $ | 10,218 |

|

| $ | — |

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Derivative contracts |

| $ | 8,709 |

|

| $ | — |

|

| $ | 8,709 |

|

| $ | — |

|

| $ | 15,259 |

|

| $ | — |

|

| $ | 15,259 |

|

| $ | — |

|

Total |

| $ | 8,709 |

|

| $ | — |

|

| $ | 8,709 |

|

| $ | — |

|

| $ | 15,259 |

|

| $ | — |

|

| $ | 15,259 |

|

| $ | — |

|

Debt Instruments

The carrying values of the Company’s debt instruments vary from their fair values. The fair values were determined by reference to transacted prices ofand quotes for these instruments (Level 2 input based on the U.S. GAAP fair value hierarchy)2). The estimated fair value, as well as the carrying value, of the Company’s debt instruments are shown below:

|

| September 30, 2020 |

|

| December 31, 2019 |

|

| September 30, 2021 |

|

| December 31, 2020 |

| ||||

(Dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimated aggregate fair value |

| $ | 563,568 |

|

| $ | 606,093 |

|

| $ | 624,713 |

|

| $ | 624,207 |

|

Aggregate carrying value (1) |

|

| 630,200 |

|

|

| 630,635 |

|

|

| 624,223 |

|

|

| 643,184 |

|

(1) |

|