UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

☑ |

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 20222023

or

☐ |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-36228

Navient Corporation

(Exact name of registrant as specified in its charter)

Delaware | 46-4054283 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

|

(Address of principal executive offices) | ( |

(302) 283-8000(703)810-3000

(Registrant’s telephone number, including area code)

123 Justison Street, Wilmington, Delaware19801

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☑ No ☐☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§(§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☑ No ☐☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company”company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer |

| ☒ |

| Accelerated filer | ☐ | ||

Non-accelerated filer |

| ☐ | Smaller reporting company | ☐ | |||

Emerging growth company | ☐ | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

SecuSecurities registered pursuant to Section 12(b) of the Act.rities

registeredpursuanttoSection12(b)oftheAct.

Title of each class | Trading Symbol(s) |

| ||

Common stock, par value $.01 per share | NAVI | The NASDAQ Global Select Market | ||

6% Senior Notes due December 15, 2043 | JSM | The NASDAQ Global Select Market | ||

Preferred Stock Purchase Rights | None | The NASDAQ Global Select Market |

As of June 30, 2022,2023, there were 141,878,703121,601,864 shares of common stock outstanding.

TABLE OF CONTENTS

Organization ofOur Form 10-Q

The order and presentation of content in our Form 10-Q differsdiffers from the traditional Securities and Exchange Commission (SEC) Form 10-Q format. Our format is designed to improve readability and to betterpresent how we organize and manage our business. See Appendix A, "Form 10-Q Cross-Reference Index" for a cross-reference index to the traditional SEC Form 10-Q format.

Page Number | |||||

| |||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| ||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

FORWARD-LOOKING AND CAUTIONARY STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking” statements and other information that is based on management’s current expectations as of the date of this report. Statements that are not historical facts, including statements about our beliefs, opinions, or expectations and statements that assume or are dependent upon future events, are forward-looking statements and often contain words such as “expect,” “anticipate,”��� “intend,” “plan,” “believe,” “seek,” “see,” “will,” “would,” “may,” “could,” “should,” “goals,” or “target.” Such statements are based on management's expectations as of the date of this filing and involve many risks and uncertainties that could cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Such risks and uncertainties are discussed more fully under the section titled “Risk Factors” and include, but are not limited to the following:

• the continuing impacts of the COVID-19 pandemic and related risks; • general economic conditions, including the potential impact of persistent inflation and increasing interest rates on Navient and its clients and customers and on the creditworthiness of third parties; • increased defaults on education loans held by us; • the cost and availability of funding in the capital markets; • changes in the general interest rate environment, including the availability of any relevant money-market index rate, including LIBOR or SOFR, or the relationship between the relevant money-market index rate and the rate at which our assets are priced; • unanticipated repayment trends on education loans including prepayments or deferrals resulting from new interpretations of current laws, rules or regulations or future laws, executive orders or other policy initiatives that operate to encourage or require consolidation, abolish existing or create additional income-based repayment or debt forgiveness programs or establish other policies and programs which may increase the prepayment rates on education loans and accelerate repayment of the bonds in our securitization trusts; • our unhedged Floor Income is dependent on the future interest rate environment and therefore is variable; • a reduction in our credit ratings; • adverse market conditions or an inability to effectively manage our liquidity risk or access liquidity could negatively impact us; • the interest rate characteristics of our assets do not always match those of our funding arrangements; • our use of derivatives exposes us to credit and market risk; • our ability to continually and effectively align our cost structure with our business operations; • a failure or breach of our operating systems, infrastructure or information technology systems; • failure by any third party providing us material services or products or a breach or violation of law by one of these third parties; • changes to applicable laws, rules, regulations and government policies and expanded regulatory and governmental oversight; • our work with government clients exposes us to additional risks inherent in the government contracting environment; • shareholder activism; • shareholders’ percentage ownership in Navient may be diluted in the future; • reputational risk and social factors; • obligations owed to parties under various transaction agreements that were executed as part of the spin-off of Navient from SLM Corporation (the Spin-Off); and • acquisitions or strategic investments that we pursue. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Readers are urged to carefully review and consider the various disclosures made in this Form 10-Q and in other documents we file from time to time with the SEC that disclose risks and uncertainties that may affect our business.

The preparation of our consolidated financial statements also requires management to make certain estimates and assumptions including estimates and assumptions about future events. These estimates or assumptions may prove to be incorrect and actual results could differ materially. All forward-looking statements contained in this report are qualified by these cautionary statements and are made only as of the date of this report. We do not undertake any obligation to update or revise these forward-looking statements except as required by law.

Through this discussion and analysis, we intend to provide the reader with some narrative context for how our management views our consolidated financial statements, additional context within which to assess our operating results, and information on the quality and variability of our earnings, liquidity and cash flows.

1

USE OF NON-GAAP FINANCIAL MEASURES

We prepare financial statements and present financial results in accordance with GAAP. However, we also evaluate our business segments and present our financial results on a basis that differs from GAAP. We refer to this different basis of presentation as Core Earnings, which is a non-GAAP financial measure. We provide this Core Earnings basis of presentation on a consolidated basis and for each business segment because this is what we review internally when making management decisions regarding our performance and how we allocate resources. We also include this information in our presentations with credit rating agencies, lenders and investors. Because our Core Earnings basis of presentation corresponds tois our segment financial presentations,measure of profit or loss for our segments, we are required by GAAP to provide Core Earnings disclosures in the notes to our consolidated financial statements for our business segments.

In addition to Core Earnings, we present the following other non-GAAP financial measures: Adjusted Core Earnings, Tangible Equity, Adjusted Tangible Equity Ratio, Pro forma Adjusted Tangible Equity Ratio, and Earnings before Interest, Taxes, Depreciation and Amortization Expense (EBITDA) (for the Business Processing segment)., and Allowance for Loan Losses Excluding Expected Future Recoveries on Previously Fully Charged-off Loans. Definitions for the non-GAAP financial measures and reconciliations are provided below, except that reconciliations of forward-looking non-GAAP financial measures are not provided because the company is unable to provide such reconciliations without unreasonable effort due to the uncertainty and inherent difficulty of predicting the occurrence and financial impact of certain items, including, but not limited to, the impact of any mark-to-market gains/losses resulting from our use of derivative instruments to hedge our economic risks. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Non-GAAP Financial Measures” for a further discussion and a complete reconciliation between GAAP net income and Core Earnings.

2

OverviewOverview and Fundamentals of Our Business

Navient (Nasdaq: NAVI) provides technology-enabled education finance and business processing solutions that simplify complex programs and help millions of people achieve success. Our customer-focused, data-driven services deliver exceptional results for clients in education, health care and government. Learn more at navient.com.

With a focus on data-driven insights, service, compliance and innovative support, Navient’s business consists of:

| • Federal Education Loans

|

|

We own a portfolio of $49.2$40.9 billion of federally guaranteed Federal Family Education Loan Program (FFELP) Loans. We service and provide asset recovery servicesAs a servicer on thisour own portfolio and for third parties, deployingwe deploy data-driven approaches to support the success of our customers. Our flexible and scalable infrastructure manages large volumes of complex transactions, simplifying the customer experience and continually improving efficiency.

|

|

We own, servicehelp students and originatefamilies succeed through the college journey with innovative planning tools, student loans and refinancing products. Our $17.7 billion Private Education Loans that enable people to pursue higher education and improve their economic opportunities. Our $19.7 billion private loanLoan portfolio demonstrates high customer success rates. We help people simplify their finances through student loan refinancing, and we help families finance their higher education through transparent, affordable Private Education Loans. In the second quarter of 2022,2023, we originated $420$197 million inof Private Education Loans.

|

|

We leverage our loan servicing expertise to provide business processing solutions for more than 600approximately 500 public sector and healthcare organizations, and their tens of millions of clients, patients, and constituents. Our suite of solutions andomnichannel customer experience, expertise enabledigital processing and revenue cycle solutions enables our clients to focus on their missions, optimize their cash flow and deliver essential services, while helping thosebetter results for the people they serve successfully navigate complex programs, transactions and decisions. For each client, we customize a blend of technologies to deliver personalized, omnichannel communication experiences; machine learning automation; root-cause business analytics; secure cloud computing; and intelligent customer relationship platforms.serve.

Superior Operational Performance with a Strong Customer Service and Compliance Commitment

We help our customers — both individuals and institutions — navigate the path to financial success through proactive, data-driven, simplified service and innovative solutions.

| • Delivering superior performance. Whether supporting student loan borrowers in successfully managing their loans, designing and implementing omnichannel contact center solutions for public sector agencies, generating additional revenue for hospitals and medical systems, or helping a state manage communications or recover revenue that funds essential services, Navient delivers value for our clients and customers.

|

|

We leverage our omnichannel communication platform, predictive analytics, and decades of insight to stay in touch with people and address challenges that may arise.

Using technology-enabled solutions, we have rapidly staffed, trained, and activated several call centers with thousands of remote staff for clients needing urgent support, such as during the COVID-19 pandemic.

Across all our businesses, we use real-time dashboards and data visualization tools to monitor performance metrics and identify, track, and address trends and opportunities.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We leverage our experience,customer service expertise, data-driven insights, customer service skills, technology platforms, and scale to maximize value for our clients.

3

| • Simplify complex processes. On our clients’ behalf, we help individuals successfully navigate a broad spectrum of complex transactions. Our people and platforms simplify complex programs to help customers and constituents achieve their goals. • Improving customer experience and success. We continually make enhancements to improve the customer experience, drawing from a variety of inputs including customer surveys, research panels, analysis of customer inquiries and activities, complaint data, and regulator commentary. Across our businesses, our customer-facing representatives are trained to provide empathetic, accurate support. • Commitment to compliance. We maintain a robust, multi-layered compliance management system and thoroughly understand and comply with applicable federal, state, and local laws. We use a “Three Lines of Defense” compliance framework, considered best practice by the U.S. Federal Financial Institutions Examination Council (FFIEC). This framework and other compliance protocols ensure we adhere to key industry laws and regulations including: Fair and Accurate Credit Transactions Act (FACTA); Fair Credit Reporting Act (FCRA); Fair Debt Collection Practices Act (FDCPA); Electronic Funds Transfer Act (EFTA); Equal Credit Opportunity Act (ECOA); Federal Information Security Management Act (FISMA); Gramm-Leach-Bliley Act (GLBA); Health Insurance Portability and Accountability Act (HIPAA); IRS Publication 1075; Servicemembers Civil Relief Act (SCRA); Military Lending Act (MLA); Telephone Consumer Protection Act (TCPA); Truth in Lending Act (TILA); Unfair, Deceptive, or Abusive Acts and Practices (UDAAP); state laws; and state and city licensing. • Corporate social responsibility. We are committed to contributing to the social and economic wellbeing of our communities; fostering the success of our customers; supporting a culture of integrity, inclusion and equality in our workforce; and embracing sustainable business practices. Navient has earned recognition from the Forum of Executive Women, Human Rights Campaign Foundation, and military publisher VIQTORY, among other organizations, for our continued commitment to fostering diversity. Our employees are active in our communities, through local and national organizations, including a national partnership with Boys & Girls Clubs of America.

|

|

Navient is committed to a sustainable future. Our work is largely services based; as a result, our day-to-day operations require relatively small amounts of natural resource and energy inputs. We leverage technology that minimizes energy usageuse in our office buildings and promote widespread adoption of “paperless” digital customer communications. Navient prioritizes adding or updating insulation and otherthe usage of power-saving features to our buildings to further reduce energy usage. Energy efficiency and reducing CO2 and CO2 equivalents are among the many factors considered in our growth and real estate decisions.

Strong Financial Performance Resulting in a Strong Capital Return

Our second-quarter 20222023 results continue to build upon our previous year’s results demonstratingdemonstrate the strength of our business model and our ability to deliver predictable and meaningful cash flow and earnings in all types of economic environments.

Our significant earnings generate significant capital, which results inallows for a strong capital return to our investors. Navient expects to continue to return excess capital to shareholders through dividends and share repurchases in accordance with our capital allocation policy.

By optimizing capital adequacy and allocating capital to highly accretive opportunities, including organic growth and acquisitions, we remain well positioned to pay dividends and repurchase stock, while maintaining appropriate leverage that supports our credit ratings and ensures ongoing access to capital markets.

In December 2021, our Board approved a share repurchase program authorizing the purchase of up to $1 billion of the Company’s outstanding common stock. At June 30, 2022, $78030,2023, $435 million remained in share repurchase authorization.

To inform our capital allocation decisions, we use the Adjusted Tangible Equity Ratio(1) in addition to other metrics. Our Adjusted Tangible Equity Ratio(1) was 7.5%8.4% as of June 30, 2022.2023.

(Dollars and shares in millions) |

| Q2-23 |

|

| Q2-22 |

| ||

Shares repurchased |

|

| 4.9 |

|

|

| 6.9 |

|

Reduction in shares outstanding |

|

| 4 | % |

|

| 5 | % |

Total repurchases in dollars |

| $ | 80 |

|

| $ | 105 |

|

Dividends paid |

| $ | 20 |

|

| $ | 23 |

|

Total Capital Returned(2) |

| $ | 100 |

|

| $ | 128 |

|

Adjusted Tangible Equity Ratio(1) |

|

| 8.4 | % |

|

| 7.5 | % |

(Dollars and shares in millions) |

| Q2-22 |

|

| Q2-21 |

| ||

Shares repurchased |

|

| 6.9 |

|

|

| 11.8 |

|

Reduction in shares outstanding |

|

| 5 | % |

|

| 7 | % |

Total repurchases in dollars |

| $ | 105 |

|

| $ | 200 |

|

Dividends paid |

| $ | 23 |

|

| $ | 27 |

|

Total Capital Returned(2) |

| $ | 128 |

|

| $ | 227 |

|

Adjusted Tangible Equity Ratio(1) |

|

| 7.5 | % |

|

| 6.3 | % |

4

|

|

|

|

How We Organize Our Business

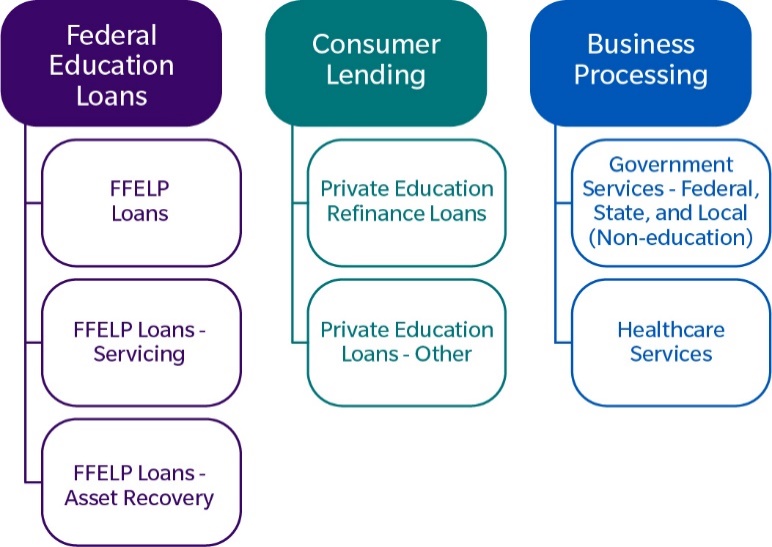

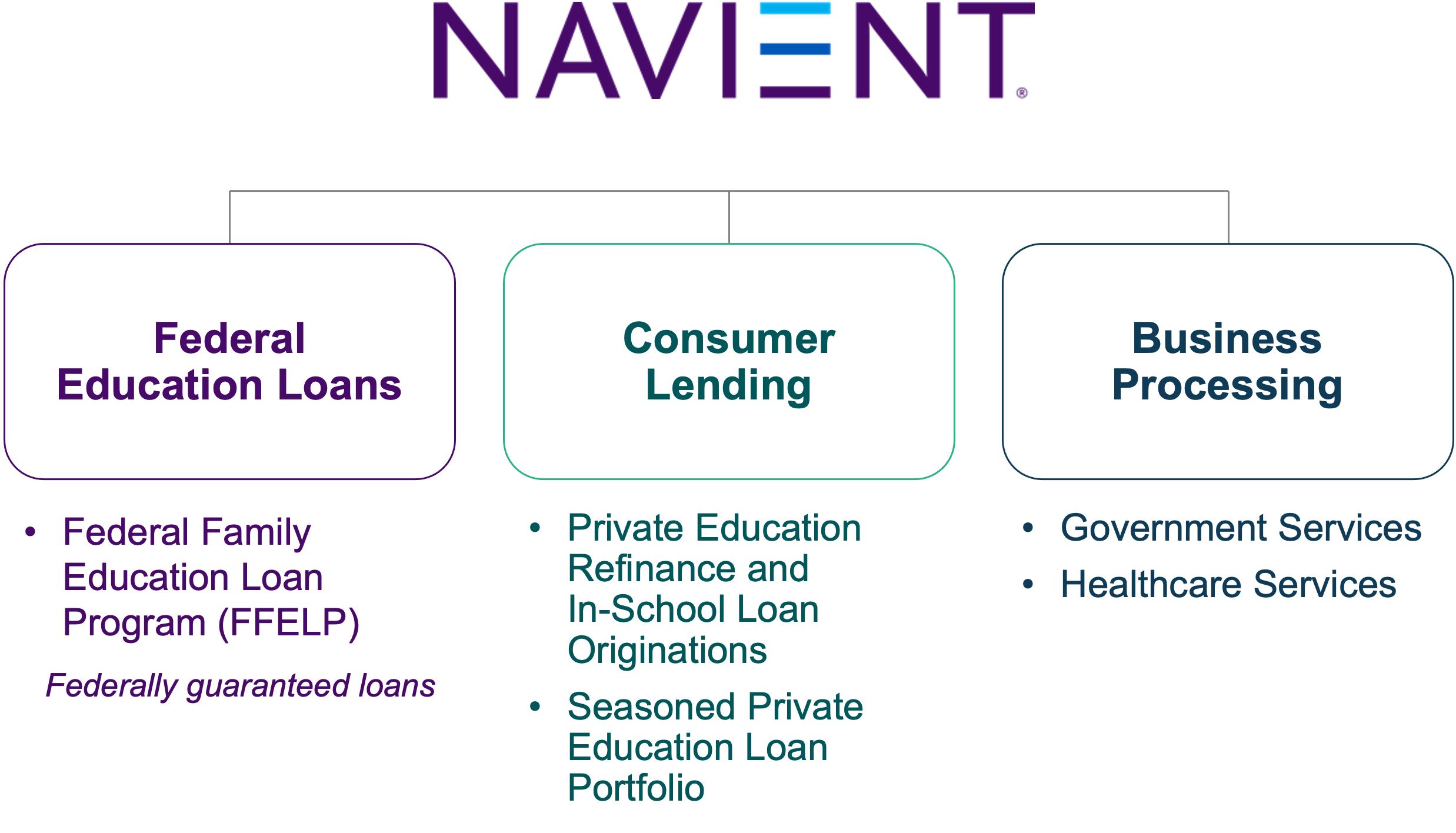

We operate our business in three primary segments: Federal Education Loans, Consumer Lending and Business Processing.

Federal Education Loans Segment

In this segment, Navient owns FFELP Loans and performs servicing and asset recovery services on this portfolio. We also service and perform asset recovery services on FFELP Loans owned by other institutions. Our servicing quality, data-driven strategies and omnichannel education about federal repayment options translate into positive results for the millions of borrowers we serve. We generate revenue primarily through net interest income on our FFELP Loans and servicing-related fee income.

Consumer Lending Segment

In this segment, Navient owns, originates acquires and services high-qualityin-school and refinance and in-school Private Education Loans. "In-school" Private Education Loans are loans originally made to borrowers while they are attending school whereas "Refinance" Private Education Loans are loans where a borrower has refinanced their education loans. We generate revenue primarily through net interest income on our Private Education Loan portfolio.

Navient helps students and families through the going-to and paying-for-college journey. Our digital tools empower people to find grants and scholarships, compare financial aid offers and complete the FAFSA. Our Private Education Loans offer easy-to-understand payment options. After graduation, we offer student loan refinancing to help people simplify their repayment and earn a better rate. We believe our more than 4550 years of experience, product design, digital marketing strategies, and origination and servicing platform provide a unique competitive advantage. We see meaningful growth opportunities in originating Private Education Loans, to financially responsible consumers, generating attractive long-term, risk-adjusted returns. We generate revenue primarily through net interest income on our Private Education Loan portfolio.

Business Processing Segment

In this segment, Navient performsprovides business processing solutions such as omnichannel contact center services, workflow processing, and revenue cycle optimization. We leverage the same expertise and intelligent tools we use to deliver successful results for over 600 governmentportfolios we own. Our support enables our clients to ensure better constituent outcomes, meet rapidly changing needs, improve technology, reduce operating expenses, manage risk and optimize revenue opportunities. Our clients include:

| providers and public health departments.

|

|

|

|

Other Segment

This segment consists of our corporate liquidity portfolio, gains and losses incurred on the repurchase of debt, unallocated expenses of shared services (which includes regulatory expenses) and restructuring/other reorganization expenses.

5

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Selected Historical Financial Information and Ratios

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

(In millions, except per share data) |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

GAAP Basis |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income |

| $ | 180 |

|

| $ | 185 |

|

| $ | 435 |

|

| $ | 555 |

|

Diluted earnings per common share |

| $ | 1.22 |

|

| $ | 1.05 |

|

| $ | 2.90 |

|

| $ | 3.08 |

|

Weighted average shares used to compute diluted earnings per share |

| $ | 147 |

|

|

| 176 |

|

|

| 150 |

|

|

| 180 |

|

Return on assets |

|

| .96 | % |

|

| .91 | % |

|

| 1.15 | % |

|

| 1.35 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Core Earnings Basis(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income(1) |

| $ | 134 |

|

| $ | 165 |

|

| $ | 269 |

|

| $ | 469 |

|

Diluted earnings per common share(1) |

| $ | .91 |

|

| $ | .94 |

|

| $ | 1.79 |

|

| $ | 2.61 |

|

Adjusted diluted earnings per common share(1) |

| $ | .92 |

|

| $ | .98 |

|

| $ | 1.82 |

|

| $ | 2.71 |

|

Weighted average shares used to compute diluted earnings per share |

|

| 147 |

|

|

| 176 |

|

|

| 150 |

|

|

| 180 |

|

Net interest margin, Federal Education Loans segment |

|

| 1.11 | % |

|

| .97 | % |

|

| 1.08 | % |

|

| .97 | % |

Net interest margin, Consumer Lending segment |

|

| 2.66 | % |

|

| 2.95 | % |

|

| 2.73 | % |

|

| 2.97 | % |

Return on assets |

|

| .72 | % |

|

| .81 | % |

|

| .71 | % |

|

| 1.14 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Education Loan Portfolios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ending FFELP Loans, net |

| $ | 49,214 |

|

| $ | 55,550 |

|

| $ | 49,214 |

|

| $ | 55,550 |

|

Ending Private Education Loans, net |

|

| 19,668 |

|

|

| 19,725 |

|

|

| 19,668 |

|

|

| 19,725 |

|

Ending total education loans, net |

| $ | 68,882 |

|

| $ | 75,275 |

|

| $ | 68,882 |

|

| $ | 75,275 |

|

Average FFELP Loans |

| $ | 50,534 |

|

| $ | 56,649 |

|

| $ | 51,391 |

|

| $ | 57,360 |

|

Average Private Education Loans |

|

| 20,856 |

|

|

| 20,730 |

|

|

| 21,006 |

|

|

| 21,433 |

|

Average total education loans |

| $ | 71,390 |

|

| $ | 77,379 |

|

| $ | 72,397 |

|

| $ | 78,793 |

|

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

(In millions, except per share data) |

| 2023 |

|

| 2022 |

|

| 2023 |

|

| 2022 |

| ||||

GAAP Basis |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Net income |

| $ | 66 |

|

| $ | 180 |

|

| $ | 177 |

|

| $ | 435 |

|

Diluted earnings per common share |

| $ | .52 |

|

| $ | 1.22 |

|

| $ | 1.39 |

|

| $ | 2.90 |

|

Weighted average shares used to compute diluted |

|

| 125 |

|

|

| 147 |

|

|

| 128 |

|

|

| 150 |

|

Return on assets |

|

| .41 | % |

|

| .96 | % |

|

| .55 | % |

|

| 1.15 | % |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Core Earnings Basis(1) |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Net income(1) |

| $ | 88 |

|

| $ | 134 |

|

| $ | 221 |

|

| $ | 269 |

|

Diluted earnings per common share(1) |

| $ | .70 |

|

| $ | .91 |

|

| $ | 1.73 |

|

| $ | 1.79 |

|

Weighted average shares used to compute diluted |

|

| 125 |

|

|

| 147 |

|

|

| 128 |

|

|

| 150 |

|

Net interest margin, Federal Education Loans segment |

|

| .97 | % |

|

| 1.11 | % |

|

| 1.05 | % |

|

| 1.08 | % |

Net interest margin, Consumer Lending segment |

|

| 2.97 | % |

|

| 2.66 | % |

|

| 3.05 | % |

|

| 2.73 | % |

Return on assets |

|

| .55 | % |

|

| .72 | % |

|

| .69 | % |

|

| .71 | % |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Education Loan Portfolios |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Ending FFELP Loans, net |

| $ | 40,851 |

|

| $ | 49,214 |

|

| $ | 40,851 |

|

| $ | 49,214 |

|

Ending Private Education Loans, net |

|

| 17,732 |

|

|

| 19,668 |

|

|

| 17,732 |

|

|

| 19,668 |

|

Ending total education loans, net |

| $ | 58,583 |

|

| $ | 68,882 |

|

| $ | 58,583 |

|

| $ | 68,882 |

|

Average FFELP Loans |

| $ | 41,869 |

|

| $ | 50,534 |

|

| $ | 42,562 |

|

| $ | 51,391 |

|

Average Private Education Loans |

|

| 18,690 |

|

|

| 20,856 |

|

|

| 18,988 |

|

|

| 21,006 |

|

Average total education loans |

| $ | 60,559 |

|

| $ | 71,390 |

|

| $ | 61,550 |

|

| $ | 72,397 |

|

76

The Quarter inin Review

We prepare financial statements and present financial results in accordance with GAAP. However, we also evaluate our business segments and present financial results on a basis that differs from GAAP. We refer to this different basis of presentation as Core Earnings. We provide this Core Earnings basis of presentation on a consolidated basis and for each business segment because this is what we review internally when making management decisions regarding our performance and how we allocate resources. We also include this information in our presentations with credit rating agencies, lenders and investors. Because our Core Earnings basis of presentation corresponds to our segment financial presentations, we are required by GAAP to provide certain Core Earnings disclosures in the notes to our consolidated financial statements for our business segments. See “Non-GAAP Financial Measures — Core Earnings” for a further discussion and a complete reconciliation between GAAP net income and Core Earnings.

Second-quarter 20222023 GAAP net income was $180$66 million ($1.220.52 diluted earnings per share), compared with $185$180 million ($1.051.22 diluted Core Earnings per share) for the year-ago quarter. See “Results of Operations – GAAP Comparison of Second-Quarter 20222023 Results with Second-Quarter 2021”2022" for a discussion of the primary contributors to the change in GAAP earnings between periods.

Second-quarter 20222023 Core Earnings net income was $88 million ($0.70 diluted Core Earnings per share), compared with $134 million ($0.91 diluted Core Earnings per share), compared with $165 million ($0.94 diluted Core Earnings per share) for the year-ago quarter. Second-quarter 2022 and 2021 adjusted diluted Core Earnings(1) per share were $0.92 and $0.98, respectively. See “Segment Results” for a discussion of the primary contributors to the change in Core Earnings between periods.

Financial highlights of second-quarter 20222023 include:

Federal Education Loans segment:

| • Net income of $76 million. • Net interest margin of 0.97%.

|

|

|

|

Consumer Lending segment:

| • Net income of $75 million. • Net interest margin of 2.97%. • Originated $197 million of Private Education Loans.

|

|

|

|

|

|

Business Processing segment:

| • Revenue of $83 million. • Net income of $6 million and EBITDA(1) of $8 million.

|

|

|

|

Capital, funding and liquidity:

|

|

|

|

|

|

|

|

Operating Expenses:

|

|

Restructuring Expenses:

|

|

Navient’s Response to COVID-19

Since its emergence in early 2020, the COVID-19 pandemic has been dynamic and unpredictable. Variants continue to emerge while efforts to mitigate and contain the impactRestructuring expenses of the pandemic continue to evolve. In response to the COVID-19 pandemic, we have prioritized the safety of our employees and business partners, while continually striving to support the needs of our customers and communities during this unprecedented period. During 2021 and the first half of 2022, the COVID-19 pandemic has continued to affect our business operations. The future direct and indirect impact of the pandemic on our businesses, results of operations and financial condition remains uncertain. Should current economic conditions deteriorate or if the pandemic worsens$15 million primarily due to various factors, including throughseverance costs in connection with the spread of more easily communicable variants of COVID-19, such conditions could have an adverse effect on our businessesCEO transition.

7

Results of Operations – Navient’s Response to COVID-19” in our 2021 Form 10-K.

Results of Operations

GAAP Income Statements (Unaudited)

|

| Three Months Ended June 30, |

|

| Increase (Decrease) |

|

| Six Months Ended June 30, |

|

| Increase (Decrease) |

|

| Three Months Ended June 30, |

|

| Increase |

|

| Six Months Ended June 30, |

|

| Increase |

| ||||||||||||||||||||||||||||||||||||||||

(In millions, except per share data) |

| 2022 |

|

| 2021 |

|

| $ |

|

| % |

|

| 2022 |

|

| 2021 |

|

| $ |

|

| % |

|

| 2023 |

|

| 2022 |

|

| $ |

|

| % |

|

| 2023 |

|

| 2022 |

|

| $ |

|

| % |

| ||||||||||||||||

Interest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

FFELP Loans |

| $ | 410 |

|

| $ | 365 |

|

| $ | 45 |

|

|

| 12 | % |

| $ | 759 |

|

| $ | 737 |

|

| $ | 22 |

|

|

| 3 | % |

| $ | 720 |

|

| $ | 410 |

|

| $ | 310 |

|

|

| 76 | % |

| $ | 1,413 |

|

| $ | 759 |

|

| $ | 654 |

|

|

| 86 | % |

Private Education Loans |

|

| 277 |

|

|

| 295 |

|

|

| (18 | ) |

|

| (6 | ) |

|

| 553 |

|

|

| 614 |

|

|

| (61 | ) |

|

| (10 | ) |

|

| 341 |

|

|

| 277 |

|

|

| 64 |

|

|

| 23 |

|

|

| 686 |

|

|

| 553 |

|

|

| 133 |

|

|

| 24 |

|

Cash and investments |

|

| 5 |

|

|

| 1 |

|

|

| 4 |

|

|

| 400 |

|

|

| 6 |

|

|

| 1 |

|

|

| 5 |

|

|

| 500 |

|

|

| 36 |

|

|

| 5 |

|

|

| 31 |

|

|

| 620 |

|

|

| 70 |

|

|

| 6 |

|

|

| 64 |

|

|

| 1,067 |

|

Total interest income |

|

| 692 |

|

|

| 661 |

|

|

| 31 |

|

|

| 5 |

|

|

| 1,318 |

|

|

| 1,352 |

|

|

| (34 | ) |

|

| (3 | ) |

|

| 1,097 |

|

|

| 692 |

|

|

| 405 |

|

|

| 59 |

|

|

| 2,169 |

|

|

| 1,318 |

|

|

| 851 |

|

|

| 65 |

|

Total interest expense |

|

| 371 |

|

|

| 339 |

|

|

| 32 |

|

|

| 9 |

|

|

| 660 |

|

|

| 667 |

|

|

| (7 | ) |

|

| (1 | ) |

|

| 919 |

|

|

| 371 |

|

|

| 548 |

|

|

| 148 |

|

|

| 1,756 |

|

|

| 660 |

|

|

| 1,096 |

|

|

| 166 |

|

Net interest income |

|

| 321 |

|

|

| 322 |

|

|

| (1 | ) |

|

| — |

|

|

| 658 |

|

|

| 685 |

|

|

| (27 | ) |

|

| (4 | ) |

|

| 178 |

|

|

| 321 |

|

|

| (143 | ) |

|

| (45 | ) |

|

| 413 |

|

|

| 658 |

|

|

| (245 | ) |

|

| (37 | ) |

Less: provisions for loan losses |

|

| 18 |

|

|

| (1 | ) |

|

| 19 |

|

|

| 1,900 |

|

|

| 34 |

|

|

| (88 | ) |

|

| 122 |

|

|

| 139 |

|

|

| 11 |

|

|

| 18 |

|

|

| (7 | ) |

|

| (39 | ) |

|

| (3 | ) |

|

| 34 |

|

|

| (37 | ) |

|

| (109 | ) |

Net interest income after provisions for loan losses |

|

| 303 |

|

|

| 323 |

|

|

| (20 | ) |

|

| (6 | ) |

|

| 624 |

|

|

| 773 |

|

|

| (149 | ) |

|

| (19 | ) |

|

| 167 |

|

|

| 303 |

|

|

| (136 | ) |

|

| (45 | ) |

|

| 416 |

|

|

| 624 |

|

|

| (208 | ) |

|

| (33 | ) |

Other income (loss): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Servicing revenue |

|

| 17 |

|

|

| 50 |

|

|

| (33 | ) |

|

| (66 | ) |

|

| 36 |

|

|

| 102 |

|

|

| (66 | ) |

|

| (65 | ) |

|

| 16 |

|

|

| 17 |

|

|

| (1 | ) |

|

| (6 | ) |

|

| 33 |

|

|

| 36 |

|

|

| (3 | ) |

|

| (8 | ) |

Asset recovery and business processing revenue |

|

| 88 |

|

|

| 142 |

|

|

| (54 | ) |

|

| (38 | ) |

|

| 185 |

|

|

| 281 |

|

|

| (96 | ) |

|

| (34 | ) |

|

| 83 |

|

|

| 88 |

|

|

| (5 | ) |

|

| (6 | ) |

|

| 155 |

|

|

| 185 |

|

|

| (30 | ) |

|

| (16 | ) |

Other income |

|

| 7 |

|

|

| 4 |

|

|

| 3 |

|

|

| 75 |

|

|

| 16 |

|

|

| 5 |

|

|

| 11 |

|

|

| 220 |

| ||||||||||||||||||||||||||||||||

Gains on sales of loans |

|

| — |

|

|

| 2 |

|

|

| (2 | ) |

|

| (100 | ) |

|

| — |

|

|

| 78 |

|

|

| (78 | ) |

|

| (100 | ) | ||||||||||||||||||||||||||||||||

Gains (losses) on debt repurchases |

|

| — |

|

|

| (12 | ) |

|

| 12 |

|

|

| (100 | ) |

|

| — |

|

|

| (12 | ) |

|

| 12 |

|

|

| (100 | ) | ||||||||||||||||||||||||||||||||

Other revenue |

|

| 4 |

|

|

| 7 |

|

|

| (3 | ) |

|

| (43 | ) |

|

| 11 |

|

|

| 16 |

|

|

| (5 | ) |

|

| (31 | ) | ||||||||||||||||||||||||||||||||

Gains (losses) on derivative and hedging activities, net |

|

| 22 |

|

|

| (10 | ) |

|

| 32 |

|

|

| 320 |

|

|

| 120 |

|

|

| 26 |

|

|

| 94 |

|

|

| 362 |

|

|

| 26 |

|

|

| 22 |

|

|

| 4 |

|

|

| 18 |

|

|

| 17 |

|

|

| 120 |

|

|

| (103 | ) |

|

| (86 | ) |

Total other income |

|

| 134 |

|

|

| 176 |

|

|

| (42 | ) |

|

| (24 | ) |

|

| 357 |

|

|

| 480 |

|

|

| (123 | ) |

|

| (26 | ) |

|

| 129 |

|

|

| 134 |

|

|

| (5 | ) |

|

| (4 | ) |

|

| 216 |

|

|

| 357 |

|

|

| (141 | ) |

|

| (39 | ) |

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Operating expenses |

|

| 190 |

|

|

| 252 |

|

|

| (62 | ) |

|

| (25 | ) |

|

| 395 |

|

|

| 510 |

|

|

| (115 | ) |

|

| (23 | ) |

|

| 182 |

|

|

| 190 |

|

|

| (8 | ) |

|

| (4 | ) |

|

| 368 |

|

|

| 395 |

|

|

| (27 | ) |

|

| (7 | ) |

Goodwill and acquired intangible assets impairment and amortization expense |

|

| 3 |

|

|

| 5 |

|

|

| (2 | ) |

|

| (40 | ) |

|

| 7 |

|

|

| 10 |

|

|

| (3 | ) |

|

| (30 | ) |

|

| 3 |

|

|

| 3 |

|

|

| — |

|

|

| — |

|

|

| 5 |

|

|

| 7 |

|

|

| (2 | ) |

|

| (29 | ) |

Restructuring/other reorganization expenses |

|

| — |

|

|

| 2 |

|

|

| (2 | ) |

|

| (100 | ) |

|

| 3 |

|

|

| 8 |

|

|

| (5 | ) |

|

| (63 | ) |

|

| 15 |

|

|

| — |

|

|

| 15 |

|

|

| 100 |

|

|

| 19 |

|

|

| 3 |

|

|

| 16 |

|

|

| 533 |

|

Total expenses |

|

| 193 |

|

|

| 259 |

|

|

| (66 | ) |

|

| (25 | ) |

|

| 405 |

|

|

| 528 |

|

|

| (123 | ) |

|

| (23 | ) |

|

| 200 |

|

|

| 193 |

|

|

| 7 |

|

|

| 4 |

|

|

| 392 |

|

|

| 405 |

|

|

| (13 | ) |

|

| (3 | ) |

Income before income tax expense |

|

| 244 |

|

|

| 240 |

|

|

| 4 |

|

|

| 2 |

|

|

| 576 |

|

|

| 725 |

|

|

| (149 | ) |

|

| (21 | ) |

|

| 96 |

|

|

| 244 |

|

|

| (148 | ) |

|

| (61 | ) |

|

| 240 |

|

|

| 576 |

|

|

| (336 | ) |

|

| (58 | ) |

Income tax expense |

|

| 64 |

|

|

| 55 |

|

|

| 9 |

|

|

| 16 |

|

|

| 141 |

|

|

| 170 |

|

|

| (29 | ) |

|

| (17 | ) |

|

| 30 |

|

|

| 64 |

|

|

| (34 | ) |

|

| (53 | ) |

|

| 63 |

|

|

| 141 |

|

|

| (78 | ) |

|

| (55 | ) |

Net income |

| $ | 180 |

|

| $ | 185 |

|

| $ | (5 | ) |

|

| (3 | )% |

| $ | 435 |

|

| $ | 555 |

|

| $ | (120 | ) |

|

| (22 | )% |

| $ | 66 |

|

| $ | 180 |

|

| $ | (114 | ) |

|

| (63 | )% |

| $ | 177 |

|

| $ | 435 |

|

| $ | (258 | ) |

|

| (59 | )% |

Basic earnings per common share |

| $ | 1.23 |

|

| $ | 1.07 |

|

| $ | .16 |

|

|

| 15 | % |

| $ | 2.93 |

|

| $ | 3.12 |

|

| $ | (.19 | ) |

|

| (6 | )% |

| $ | .53 |

|

| $ | 1.23 |

|

| $ | (.70 | ) |

|

| (57 | )% |

| $ | 1.40 |

|

| $ | 2.93 |

|

| $ | (1.53 | ) |

|

| (52 | )% |

Diluted earnings per common share |

| $ | 1.22 |

|

| $ | 1.05 |

|

| $ | .17 |

|

|

| 16 | % |

| $ | 2.90 |

|

| $ | 3.08 |

|

| $ | (.18 | ) |

|

| (6 | )% |

| $ | .52 |

|

| $ | 1.22 |

|

| $ | (.70 | ) |

|

| (57 | )% |

| $ | 1.39 |

|

| $ | 2.90 |

|

| $ | (1.51 | ) |

|

| (52 | )% |

Dividends per common share |

| $ | .16 |

|

| $ | .16 |

|

| $ | — |

|

|

| — |

|

| $ | .32 |

|

| $ | .32 |

|

| $ | — |

|

|

| — |

|

| $ | .16 |

|

| $ | .16 |

|

| $ | — |

|

|

| — |

|

| $ | .32 |

|

| $ | .32 |

|

| $ | — |

|

|

| — |

|

8

GAAP Comparison of Second-Quarter 20222023 Results with Second-Quarter 20212022

For the three months ended June 30, 2022,2023, net income was $180$66 million, or $1.22$0.52 diluted earnings per common share, compared with net income of $185$180 million, or $1.05$1.22 diluted earnings per common share, for the year-ago period.

The primary contributors to the change in net income are as follows:

|

Net interest income decreased by $143 million primarily as a result of an $87 million decrease in mark-to-market gains on fair value hedges recorded in interest expense, the • Provisions for loan losses decreased $7 million from $18 million to $11 million: o The provision for FFELP Loan losses increased $5 million from $0 to $5 million. o The provision for Private Education Loan losses decreased $12 million from $18 million to $6 million. The FFELP Loan |

|

|

|

|

|

|

The provision for loan losses of $18$5 million in the current period was primarily a result of the extension of the portfolio and the resulting increase in expected future defaults.

The Private Education Loan provision for loan losses of $6 million in the current period included $4 million in connection with loan originations, $10 million related to a reserve build and $(8) million in connection with the adoption of a new accounting standard (ASU 2022-02). The provision of $18 million in the year-ago quarter included $7 million of provision in connection with loan originations and $11 million related to ana reserve build.

|

|

|

|

|

|

|

|

|

|

We repurchased 6.94.9 million and 11.86.9 million shares of our common stock during the second quarters of 20222023 and 2021,2022, respectively. As a result of repurchases, our average outstanding diluted shares decreased by 2922 million common shares (or 16%15%) from the year-ago period.

9

GAAP Comparison of Six Months Ended June 30, 20222023 Results with Six Months Ended June 30, 20212022

For the six months ended June 30, 2022,2023, net income was $435$177 million, or $2.90$1.39 diluted earnings per common share, compared with net income of $555$435 million, or $3.08$2.90 diluted earnings per common share, for the year-ago period.

The primary contributors to the change in net income are as follows:

|

Net interest income decreased by $245 million primarily as a result of a $133 million decrease in mark-to-market gains on fair value hedges recorded in interest expense, the • Provisions for loan losses decreased $37 million from $34 million to $(3) million: o The provision for FFELP Loan losses increased $15 million from $0 to $15 million. o The provision for Private Education Loan losses decreased $52 million from $34 million to $(18) million. The FFELP Loan |

|

|

|

|

|

|

The provision for loan losses of $34$15 million in the current period was primarily a result of the extension of the portfolio and the resulting increase in expected future defaults.

The Private Education Loan provision for loan losses of $(18) million in the current period included $(60) million in connection with the adoption of a new accounting standard (ASU 2022-02), $9 million in connection with loan originations, $10 million related to a reserve build and $23 million in connection with the resolution of certain private legacy loans in bankruptcy in the first quarter of 2023. The provision of $34 million in the year-ago period included $18 million of provision in connection with loan originations and $16 million related to ana reserve build.

We adopted ASU No. 2022-02, “Financial Instruments – Credit Losses: Troubled Debt Restructurings and Vintage Disclosures” on January 1, 2023. This new ASU eliminates the troubled debt restructurings (TDRs) recognition and measurement guidance. Prior to adopting this new guidance, as it relates to interest rate concessions granted as part of our Private Education Loan modification program, a discounted cash flow model was used to calculate the amount of interest forgiven for loans that were in the program and the present value of that interest rate concession was included as a part of the allowance for loan loss. This new guidance no longer allows the measurement and recognition of this element of our allowance for loan loss for new modifications that occur subsequent to January 1, 2023. As of December 31, 2022, the allowance for loan loss included $77 million related to this interest rate concession component of the allowance for loan loss. We elected to adopt this amendment using a prospective transition method which results in the $77 million releasing in 2023 and 2024 as the borrowers exit their current modification programs. $60 million of the $77 million was released in the period.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We repurchased 13.19.8 million and 19.913.1 million shares of our common stock during the six months ended June 30, 20222023 and 2021,2022, respectively. As a result of repurchases, our average outstanding diluted shares decreased by 3022 million common shares (or 17%15%) from the year-ago period.

10

Segment Results

Federal Education Loans Segment

The following table presents Core Earnings results for our Federal Education Loans segment.

|

| Three Months Ended June 30, |

|

| % Increase (Decrease) |

|

| Six Months Ended June 30, |

|

| % Increase (Decrease) |

|

| Three Months Ended June 30, |

|

| % Increase |

|

| Six Months Ended June 30, |

|

| % Increase |

| ||||||||||||||||||||||||

(Dollars in millions) |

| 2022 |

|

| 2021 |

|

| 2022 vs. 2021 |

|

| 2022 |

|

| 2021 |

|

| 2021 vs. 2021 |

|

| 2023 |

|

| 2022 |

|

| 2023 vs. 2022 |

|

| 2023 |

|

| 2022 |

|

| 2023 vs. 2022 |

| ||||||||||||

Interest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

FFELP Loans |

| $ | 409 |

|

| $ | 351 |

|

|

| 17 | % |

| $ | 743 |

|

| $ | 709 |

|

|

| 5 | % |

| $ | 721 |

|

| $ | 409 |

|

|

| 76 | % |

| $ | 1,416 |

|

| $ | 743 |

|

|

| 91 | % |

Cash and investments |

|

| 3 |

|

|

| — |

|

|

| 100 |

|

|

| 3 |

|

|

| — |

|

|

| 100 |

|

|

| 18 |

|

|

| 3 |

|

|

| 500 |

|

|

| 38 |

|

|

| 3 |

|

|

| 1,167 |

|

Total interest income |

|

| 412 |

|

|

| 351 |

|

|

| 17 |

|

|

| 746 |

|

|

| 709 |

|

|

| 5 |

|

|

| 739 |

|

|

| 412 |

|

|

| 79 |

|

|

| 1,454 |

|

|

| 746 |

|

|

| 95 |

|

Total interest expense |

|

| 266 |

|

|

| 210 |

|

|

| 27 |

|

|

| 461 |

|

|

| 424 |

|

|

| 9 |

|

|

| 633 |

|

|

| 266 |

|

|

| 138 |

|

|

| 1,223 |

|

|

| 461 |

|

|

| 165 |

|

Net interest income |

|

| 146 |

|

|

| 141 |

|

|

| 4 |

|

|

| 285 |

|

|

| 285 |

|

|

| — |

|

|

| 106 |

|

|

| 146 |

|

|

| (27 | ) |

|

| 231 |

|

|

| 285 |

|

|

| (19 | ) |

Less: provision for loan losses |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 5 |

|

|

| — |

|

|

| 100 |

|

|

| 15 |

|

|

| — |

|

|

| 100 |

|

Net interest income after provision for loan losses |

|

| 146 |

|

|

| 141 |

|

|

| 4 |

|

|

| 285 |

|

|

| 285 |

|

|

| — |

|

|

| 101 |

|

|

| 146 |

|

|

| (31 | ) |

|

| 216 |

|

|

| 285 |

|

|

| (24 | ) |

Other income (loss): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Servicing revenue |

|

| 14 |

|

|

| 47 |

|

|

| (70 | ) |

|

| 30 |

|

|

| 99 |

|

|

| (70 | ) |

|

| 13 |

|

|

| 14 |

|

|

| (7 | ) |

|

| 27 |

|

|

| 30 |

|

|

| (10 | ) |

Asset recovery and business processing revenue |

|

| 1 |

|

|

| 12 |

|

|

| (92 | ) |

|

| 4 |

|

|

| 26 |

|

|

| (85 | ) |

|

| — |

|

|

| 1 |

|

|

| (100 | ) |

|

| — |

|

|

| 4 |

|

|

| (100 | ) |

Other income |

|

| 8 |

|

|

| 2 |

|

|

| 300 |

|

|

| 18 |

|

|

| 2 |

|

|

| 800 |

| ||||||||||||||||||||||||

Other revenue |

|

| 2 |

|

|

| 8 |

|

|

| (75 | ) |

|

| 7 |

|

|

| 18 |

|

|

| (61 | ) | ||||||||||||||||||||||||

Total other income |

|

| 23 |

|

|

| 61 |

|

|

| (62 | ) |

|

| 52 |

|

|

| 127 |

|

|

| (59 | ) |

|

| 15 |

|

|

| 23 |

|

|

| (35 | ) |

|

| 34 |

|

|

| 52 |

|

|

| (35 | ) |

Direct operating expenses |

|

| 25 |

|

|

| 55 |

|

|

| (55 | ) |

|

| 54 |

|

|

| 117 |

|

|

| (54 | ) |

|

| 18 |

|

|

| 25 |

|

|

| (28 | ) |

|

| 38 |

|

|

| 54 |

|

|

| (30 | ) |

Income before income tax expense |

|

| 144 |

|

|

| 147 |

|

|

| (2 | ) |

|

| 283 |

|

|

| 295 |

|

|

| (4 | ) |

|

| 98 |

|

|

| 144 |

|

|

| (32 | ) |

|

| 212 |

|

|

| 283 |

|

|

| (25 | ) |

Income tax expense |

|

| 34 |

|

|

| 34 |

|

|

| — |

|

|

| 67 |

|

|

| 70 |

|

|

| (4 | ) |

|

| 22 |

|

|

| 34 |

|

|

| (35 | ) |

|

| 50 |

|

|

| 67 |

|

|

| (25 | ) |

Net income |

| $ | 110 |

|

| $ | 113 |

|

|

| (3 | )% |

| $ | 216 |

|

| $ | 225 |

|

|

| (4 | )% |

| $ | 76 |

|

| $ | 110 |

|

|

| (31 | )% |

| $ | 162 |

|

| $ | 216 |

|

|

| (25 | )% |

Comparison of Second-Quarter 20222023 Results with Second-Quarter 20212022

| • Net income was $76 million compared to $110 million. • Net interest income decreased $40 million primarily due to the paydown of the loan portfolio as well as a reduction of floor income earned. • Provision for loan losses increased $5 million. The $5 million of provision for loan losses in the current period primarily was a result of the extension of the portfolio and the resulting increase in expected future defaults. o Net charge-offs were $19 million compared to $10 million. o Delinquencies greater than 90 days were $2.7 billion compared to $3.1 billion. o Forbearances were $6.3 billion compared to $6.2 billion. • Other income decreased $8 million primarily due to lower contract-exit transition services and the paydown of the loan portfolio. • Expenses were $7 million lower as a result of the paydown of the loan portfolio and the decrease in other revenue discussed above. 11

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Key performance metrics are as follows:

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

(Dollars in millions) |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

Segment net interest margin |

|

| 1.11 | % |

|

| .97 | % |

|

| 1.08 | % |

|

| .97 | % |

FFELP Loans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FFELP Loan spread |

|

| 1.19 | % |

|

| 1.03 | % |

|

| 1.15 | % |

|

| 1.03 | % |

Provision for loan losses |

| $ | — |

|

| $ | — |

|

| $ | — |

|

| $ | — |

|

Charge-offs |

| $ | 10 |

|

| $ | 5 |

|

| $ | 17 |

|

| $ | 11 |

|

Charge-off rate |

|

| .09 | % |

|

| .04 | % |

|

| .08 | % |

|

| .05 | % |

Greater than 30-days delinquency rate |

|

| 15.9 | % |

|

| 8.3 | % |

|

| 15.9 | % |

|

| 8.3 | % |

Greater than 90-days delinquency rate |

|

| 7.4 | % |

|

| 3.8 | % |

|

| 7.4 | % |

|

| 3.8 | % |

Forbearance rate |

|

| 13.1 | % |

|

| 13.9 | % |

|

| 13.1 | % |

|

| 13.9 | % |

Average FFELP Loans |

| $ | 50,534 |

|

| $ | 56,649 |

|

| $ | 51,391 |

|

| $ | 57,360 |

|

Ending FFELP Loans, net |

| $ | 49,214 |

|

| $ | 55,550 |

|

| $ | 49,214 |

|

| $ | 55,550 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in billions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total federal loans serviced(1) |

| $ | 57 |

|

| $ | 283 |

|

| $ | 57 |

|

| $ | 283 |

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net Interest Margin

The following table details the net interest margin.

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

|

| 2023 |

|

| 2022 |

|

| 2023 |

|

| 2022 |

| ||||

FFELP Loan yield |

|

| 6.46 | % |

|

| 2.80 | % |

|

| 6.27 | % |

|

| 2.44 | % |

Floor Income |

|

| .45 |

|

|

| .44 |

|

|

| .44 |

|

|

| .47 |

|

FFELP Loan net yield |

|

| 6.91 |

|

|

| 3.24 |

|

|

| 6.71 |

|

|

| 2.91 |

|

FFELP Loan cost of funds |

|

| (5.84 | ) |

|

| (2.05 | ) |

|

| (5.55 | ) |

|

| (1.76 | ) |

FFELP Loan spread |

|

| 1.07 |

|

|

| 1.19 |

|

|

| 1.16 |

|

|

| 1.15 |

|

Other interest-earning asset spread impact |

|

| (.10 | ) |

|

| (.08 | ) |

|

| (.11 | ) |

|

| (.07 | ) |

Net interest margin(1) |

|

| .97 | % |

|

| 1.11 | % |

|

| 1.05 | % |

|

| 1.08 | % |

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

|

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

FFELP Loan yield |

|

| 2.80 | % |

|

| 1.89 | % |

|

| 2.44 | % |

|

| 1.90 | % |

Hedged Floor Income |

|

| .34 |

|

|

| .41 |

|

|

| .35 |

|

|

| .41 |

|

Unhedged Floor Income |

|

| .10 |

|

|

| .18 |

|

|

| .12 |

|

|

| .18 |

|

FFELP Loan net yield |

|

| 3.24 |

|

|

| 2.48 |

|

|

| 2.91 |

|

|

| 2.49 |

|

FFELP Loan cost of funds |

|

| (2.05 | ) |

|

| (1.45 | ) |

|

| (1.76 | ) |

|

| (1.46 | ) |

FFELP Loan spread |

|

| 1.19 |

|

|

| 1.03 |

|

|

| 1.15 |

|

|

| 1.03 |

|

Other interest-earning asset spread impact |

|

| (.08 | ) |

|

| (.06 | ) |

|

| (.07 | ) |

|

| (.06 | ) |

Net interest margin(1) |

|

| 1.11 | % |

|

| .97 | % |

|

| 1.08 | % |

|

| .97 | % |

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| Three Months Ended June 30, |

|

| Six Months Ended June 30, |

| ||||||||||

(Dollars in millions) |

| 2022 |

|

| 2021 |

|

| 2022 |

|

| 2021 |

| ||||

FFELP Loans |

| $ | 50,534 |

|

| $ | 56,649 |

|

| $ | 51,391 |

|

| $ | 57,360 |

|

Other interest-earning assets |

|

| 1,917 |

|

|

| 1,832 |

|

|

| 1,924 |

|

|

| 1,813 |

|

Total FFELP Loan interest-earning assets |

| $ | 52,451 |

|

| $ | 58,481 |

|

| $ | 53,315 |

|

| $ | 59,173 |

|

As of June 30, 2022,2023, our FFELP Loan portfolio totaled $49.2$40.9 billion, comprised of $17.3$14.7 billion of FFELP Stafford Loans and $31.9$26.2 billion of FFELP Consolidation Loans. The weighted-average life of these portfolios as of June 30, 20222023 was 67 years and 78 years, respectively, assuming a Constant Prepayment Rate (CPR) of 9%8% and 5%, respectively.

12

Floor Income

The following table analyzes on a Core Earnings basis the ability of the FFELP Loans in our portfolio to earn Floor Income after June 30, 20222023 and 2021,2022, based on interest rates as of those dates.

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

(Dollars in billions) |

| June 30, 2022 |

|

| June 30, 2021 |

|

| June 30, 2023 |

|

| June 30, 2022 |

| ||||

Education loans eligible to earn Floor Income |

| $ | 49.0 |

|

| $ | 55.1 |

|

| $ | 40.5 |

|

| $ | 49.0 |

|

Less: post-March 31, 2006 disbursed loans required to rebate Floor Income |

|

| (22.9 | ) |

|

| (25.4 | ) |

|

| (19.3 | ) |

|

| (22.9 | ) |

Less: economically hedged Floor Income |

|

| (12.3 | ) |

|

| (13.8 | ) |

|

| (5.9 | ) |

|

| (12.3 | ) |

Education loans eligible to earn Floor Income after rebates and economically hedged |

| $ | 13.8 |

|

| $ | 15.9 |

|

| $ | 15.3 |

|

| $ | 13.8 |

|

Education loans earning Floor Income |

| $ | .8 |

|

| $ | 11.0 |

|

| $ | — |

|

| $ | .8 |

|

The following table presents a projection of the average balance of FFELP Consolidation Loans for which Fixed Rate Floor Income has been economically hedged with derivatives for the period July 1, 20222023 to December 31, 2026.2027.

(Dollars in billions) |

| July 1, 2022 to December 31, 2022 |

|

| 2023 |

|

| 2024 |

|

| 2025 |

|

| 2026 |

|

| July 1, 2023 |

|

| 2024 |

|

| 2025 |

|

| 2026 |

|

| 2027 |

| ||||||||||

Average balance of FFELP Consolidation Loans whose Floor Income is economically hedged |

| $ | 12.4 |

|

| $ | 7.8 |

|

| $ | 2.0 |

|

| $ | 1.0 |

|

| $ | 1.0 |

|

| $ | 5.2 |

|

| $ | 2.0 |

|

| $ | 1.0 |

|

| $ | 1.0 |

|

| $ | .3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Servicing Revenue

Servicing revenue decreased $33 million primarily related to the transfer of the servicing contract for 5.6 million ED owned student loan accounts from Navient to a third party in October 2021. As a result, Navient no longer is a party to the ED servicing contract. To aid in the transition, Navient will provide certain services into 2022 to the third party through a transition services agreement (see discussion below related to “Other income”). As part of the transaction, approximately 700 Navient employees were transferred to the third party.This transaction provided a seamless transition for millions of borrowers ensuring the ongoing servicing capacity for the Department of ED through the knowledge transfer and ongoing employment of 700 employees. Additional benefits to Navient of this transaction are the simplification of our business, reducing our overall risk profile and avoiding significant severance expense.

Third-party loan servicing fees in the three months ended June 30, 2022 and 2021 included $0 and $34 million, respectively, of servicing revenue related to the ED servicing contract.

Asset Recovery and Business Processing Revenue

Asset recovery and business processing revenue decreased $11$1 million primarily as a result of exiting the impactFFELP asset recovery business in the fourth quarter of COVID-19 on certain collection and processing activities (temporary stoppage or other restrictions on certain activities).2022.

Other IncomeRevenue

Other income increasedrevenue decreased $6 million primarily related to thelower contract-exit transition services being performed in connection with the transfer of the ED Servicing contract to a third party as discussed above. services.

Operating Expenses

Operating expenses for the Federal Education Loans segment primarily include costs incurred to perform servicing and asset recovery activities on our FFELP Loan portfolio and federal education loans held by other institutions. Expenses were $30$7 million lower primarily as a result of the paydown of the loan portfolio and the decrease in servicing and asset recoveryother revenue discussed above.

13

Federal Loan Forgiveness

On August 24, 2022, the Biden-Harris Administration announced its Student Debt Relief (SDR) Plan. The SDR Plan provided up to $20,000 in one-time debt relief to income-qualified recipients with ED held student loans and a repayment pause on ED held loans. Privately held FFELP Loans, like ours, were not eligible for debt forgiveness under the SDR Plan

Following publication of the SDR Plan, a number of states and private organizations initiated legal challenges to the SDR Plan in various courts throughout the country, which ultimately resulted in the implementation of the SDR Plan being disallowed. The Biden-Harris Administration and ED subsequently appealed both cases to the Supreme Court of the United States. On June 30, 2023, the Supreme Court ruled that ED was prohibited from implementing the SDR Plan; thus, payments are expected to resume in October 2023. While the current version of the SDR Plan has been invalidated, ED recently announced that it has begun a new rulemaking process to consider other ways to provide debt relief to borrowers, which could include borrowers with privately held FFELP Loans.

Further, on July 10, 2023, ED issued final regulations on income-driven repayment plans for Direct loans, which are student loans held by ED. Eligible FFELP borrowers can access the new changes by consolidating their loans into the Direct Loan Program. The new regulations are effective July 1, 2024; however, ED has elected early implementation for some features starting July 30, 2023. The regulations provide a lower monthly loan payment on a Direct loan by decreasing discretionary income (i.e., taxable income over 225% of the federal poverty guideline), decreasing the percentage of discretionary income that must be paid toward a Direct loan to 5% (for undergraduates), and providing the option for married borrowers to exclude their spouse’s income from being factored by filing a separate tax return. Other changes provide for the elimination of accrued interest that is not covered by the monthly payment amount, provide credit towards loan forgiveness that counts certain periods of deferment and forbearance, a shorter loan forgiveness period (10-years) for borrowers with an original principal balance less than or equal to $12,000, and credit toward loan forgiveness for eligible payments on a Direct or FFELP loan that is repaid by a Direct Consolidation loan. This new income-driven repayment plan may increase consolidation activity in the future as FFELP borrowers consolidate their loans into the Direct Loan Program in order to be eligible for the new income-driven repayment plan. This could have a material impact on the Company’s results in future periods.

14

Consumer Lending Segment

The following table presents Core Earnings results for our Consumer Lending segment.

|

| Three Months Ended June 30, |

|

| % Increase (Decrease) |

|

| Six Months Ended June 30, |

|

| % Increase (Decrease) |

|

| Three Months Ended June 30, |

|

| % Increase |

|

| Six Months Ended June 30, |

|

| % Increase |

| ||||||||||||||||||||||||

(Dollars in millions) |

| 2022 |

|

| 2021 |

|

| 2022 vs. 2021 |

|

| 2022 |

|

| 2021 |

|

| 2022 vs. 2021 |

|

| 2023 |

|

| 2022 |

|

| 2023 vs. 2022 |

|

| 2023 |

|

| 2022 |

|

| 2023 vs. 2022 |

| ||||||||||||

Interest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|