UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended SeptemberJune 30, 20202021

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 1-7665

LYDALL INC /DE/Lydall, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | | | | | | | |

| Delaware | | | | | | 06-0865505 |

| (State or Other Jurisdiction of Incorporation or Organization) | | | | | | (I.R.S. Employer Identification No.) |

| | | | | | |

| One Colonial Road | , | Manchester | , | Connecticut | | 06042 |

| (Address of principal executive offices) | | | | | | (zip code) |

(860) 646-1233

(Registrant’s telephone number, including area code)

None

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 par value | LDL | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐Accelerated filer ☒Non-accelerated filer ☐ Smaller reporting company ☐Emerging growth company☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| | | | | |

Total Shares outstanding OctoberJuly 15, 20202021 | 17,733,42918,033,012 | |

LYDALL, INC.

INDEXTABLE OF CONTENTS

| | | | | | | | | | | |

| | | | Page

Number |

| | | |

| | | |

| | | |

Part I. | Financial Information | | I |

| | | |

| Item 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 2. | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

| | | Part II |

Part II. | Other Information | | |

| | | |

| Item 1. | | |

| | | |

| Item 1A. | | |

| | | |

| Item 2. | | |

| | |

| Item 5. | | |

| | | |

| | | |

| Item 6. | | |

| | | |

| Signature | | | |

|

| | |

Lydall, Inc. and its subsidiaries are hereafter collectively referred to as “Lydall,” the “Company” or the “Registrant.” Lydall and its subsidiaries’ names, abbreviations thereof, logos, and product and service designators are all either the registered or unregistered trademarks or trade names of Lydall, Inc. and its subsidiaries.

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Any statements contained in this Quarterly Report on Form 10-Q that are not statements of historical fact may be deemed to be forward-looking statements. All such forward-looking statements are intended to provide management’s current expectations for the future operating and financial performance of the Company based on current assumptions relating to the Company’s business, the economy and future conditions. Forward-looking statements generally can be identified through the use of words such as “believes,” “anticipates,” “may,” “should,” “will,” “plans,” “projects,” “expects,” “expectations,” “estimates,” “forecasts,” “predicts,” “targets,” “prospects,” “strategy,” “signs” and other words of similar meaning in connection with the discussion of future operating or financial performance. Forward-looking statements may include, among other things, statements relating to future sales, earnings, cash flow, results of operations, uses of cash and other measures of financial performance. Because forward-looking statements relate to the future, they are subject to inherent risks, uncertainties and changes in circumstances that are difficult to predict. Accordingly, the Company’s actual results may differ materially from those contemplated by the forward-looking statements. Investors, therefore, are cautioned against relying on any of these forward-looking statements. They are neither statements of historical fact nor guarantees or assurances of future performance. Forward-looking statements in this Quarterly Report on Form 10-Q include, among others, statements relating to:

•The impact of the coronavirus pandemic ("COVID-19") on the Company's businesses;

•Overall economic and business conditions and the effects on the Company’s markets;

•Ability to meet financial covenants in the Company's credit agreement;

•Outlook for the fourth quarter and full year 2020;

•Ability to improve operational effectiveness;

•Expected vehicle production in the North American, European or Asian markets;

•Growth opportunities in markets served by the Company;

•Expected costs and future savings associated with restructuring, reduction-in-force, or other cost savings programs;

•Expected gross margin, operating margin and working capital improvements from cost control and other improvement programs;

•Future impact of raw material commodity costs;

•Product development and new business opportunities;

•Future strategic transactions, including but not limited to: acquisitions, joint ventures, alliances, licensing agreements and divestitures;

•Pension plan funding;

•Future cash flow and uses of cash;

•Future amounts of stock-based compensation expense;

•Future earnings and other measurements of financial performance;

•Ability to meet cash operating requirements;

•Future levels of indebtedness and capital spending;

•Future impact of the variability of interest rates and foreign currency exchange rates and impacts of hedging instruments;

•Expected future impact of recently issued accounting pronouncements upon adoption;

•Future effective income tax rates and realization of deferred tax assets;

•Estimates of fair values of reporting units and long-lived assets used in assessing goodwill and long-lived assets for possible impairment; and

•The expected outcomes of legal proceedings and other contingencies, including environmental matters.

All forward-looking statements are inherently subject to a number of risks and uncertainties that could cause the actual results of the Company to differ materially from those reflected in forward-looking statements made in this Quarterly Report on Form 10-Q, as well as in press releases and other statements made from time to time by the Company’s authorized officers. Such risks and uncertainties include, among others, the duration, severity, and impact of COVID-19 or other new pandemics and the measures taken in response thereto, in particular the impact the virus has on the Company's operations and ability to meet customer demands; worldwide economic cycles and political changes and uncertainties that affect the markets which the Company’s businesses serve, which could have an effect on demand for the Company’s products and impact the Company’s profitability; challenges encountered by the Company in the execution of restructuring programs; disruptions in the global credit and financial markets, including diminished liquidity and credit availability; changes in international trade agreements and policies, including tariff regulation and trade restrictions; swings in consumer confidence and spending; unstable economic growth; volatility in foreign currency exchange rates; raw material pricing and supply issues; fluctuations in unemployment rates; retention of key employees; increases in fuel prices; and outcomes of legal proceedings, claims and investigations, as well as other risks and uncertainties identified in Part II, Item 1A - Risk Factors of this Quarterly Report on Form 10-Q, and Part I, Item 1A - Risk Factors of the Company's Annual Report on Form 10-K for the year ended December 31, 2019. The Company does not assume any obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

PART I. FINANCIAL INFORMATION

Item 1. Financial StatementsFINANCIAL STATEMENTS

LYDALL, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In Thousands Except Per Share Amounts)thousands, except per share amounts) (Unaudited)

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | | | | | | | | | | | | | | | | | | | | | |

| | 2020 | | 2019 | | 2020 | | 2019 | | For the Three Months Ended | | For the Six Months Ended |

| | (Unaudited) | | | (Unaudited) | | | June 30, 2021 | | June 30, 2020 | | June 30, 2021 | | June 30, 2020 |

| Net sales | Net sales | $ | 207,085 | | | $ | 205,274 | | | $ | 553,772 | | | $ | 644,110 | | Net sales | $ | 221,744 | | | $ | 146,160 | | | $ | 448,843 | | | $ | 346,687 | |

| Cost of sales | Cost of sales | 169,155 | | | 168,918 | | | 448,856 | | | 520,423 | | Cost of sales | 173,958 | | | 117,742 | | | 352,508 | | | 279,701 | |

| Gross profit | Gross profit | 37,930 | | | 36,356 | | | 104,916 | | | 123,687 | | Gross profit | 47,786 | | | 28,418 | | | 96,335 | | | 66,986 | |

| Selling, product development and administrative expenses | Selling, product development and administrative expenses | 32,227 | | | 28,909 | | | 95,418 | | | 94,011 | | Selling, product development and administrative expenses | 38,182 | | | 30,164 | | | 73,815 | | | 63,191 | |

| Impairment of goodwill and other long-lived assets | Impairment of goodwill and other long-lived assets | 0 | | | 0 | | | 61,109 | | | 0 | | Impairment of goodwill and other long-lived assets | 0 | | | 0 | | | 0 | | | 61,109 | |

| Restructuring expenses | Restructuring expenses | 14,984 | | | 0 | | | 14,984 | | | 0 | | Restructuring expenses | 190 | | | 0 | | | 967 | | | 0 | |

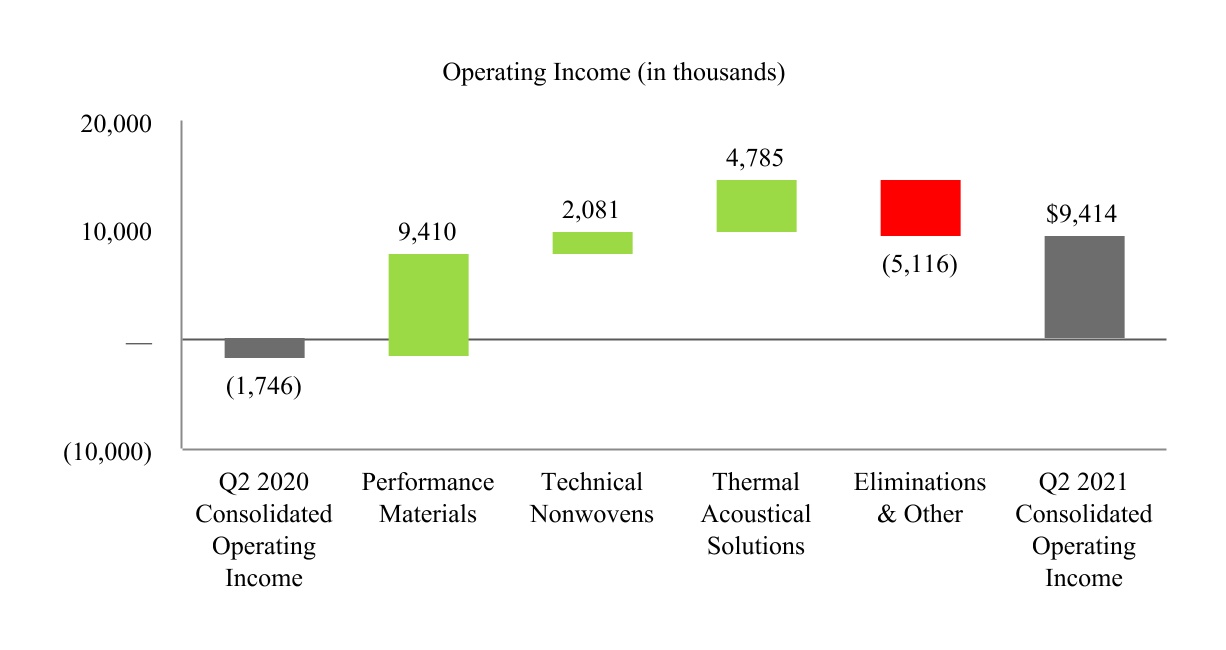

| Operating (loss) income | (9,281) | | | 7,447 | | | (66,595) | | | 29,676 | | |

| | Operating income (loss) | | Operating income (loss) | 9,414 | | | (1,746) | | | 21,553 | | | (57,314) | |

| (Gain) loss on the sale of a business | | (Gain) loss on the sale of a business | 266 | | | 0 | | | 964 | | | 0 | |

| Employee benefit plans settlement expenses | Employee benefit plans settlement expenses | 0 | | | 186 | | | 385 | | | 25,701 | | Employee benefit plans settlement expenses | 0 | | | 0 | | | 0 | | | 385 | |

| Interest expense | Interest expense | 4,537 | | | 3,666 | | | 11,870 | | | 11,025 | | Interest expense | 2,414 | | | 4,476 | | | 5,862 | | | 7,333 | |

| Other expense (income), net | 276 | | | (885) | | | 106 | | | (1,359) | | |

| (Loss) income before income taxes | (14,094) | | | 4,480 | | | (78,956) | | | (5,691) | | |

| Income tax (benefit) expense | (2,334) | | | 1,574 | | | (4,944) | | | (5,519) | | |

| Income from equity method investment | (50) | | | (98) | | | (24) | | | (120) | | |

| Net (loss) income | $ | (11,710) | | | $ | 3,004 | | | $ | (73,988) | | | $ | (52) | | |

| (Loss) earnings per share: | | | | | | | | |

| Other (income) expense, net | | Other (income) expense, net | 206 | | | 248 | | | 292 | | | (170) | |

| Income (loss) before income taxes | | Income (loss) before income taxes | 6,528 | | | (6,470) | | | 14,435 | | | (64,862) | |

| Income tax expense (benefit) | | Income tax expense (benefit) | 905 | | | (595) | | | 3,726 | | | (2,610) | |

| (Income) loss from equity method investment | | (Income) loss from equity method investment | (157) | | | (18) | | | (165) | | | 26 | |

| Net income (loss) | | Net income (loss) | $ | 5,780 | | | $ | (5,857) | | | $ | 10,874 | | | $ | (62,278) | |

| Earnings (loss) per share: | | Earnings (loss) per share: | | | | | | | |

| Basic | Basic | $ | (0.67) | | | $ | 0.17 | | | $ | (4.26) | | | $ | 0.00 | | Basic | $ | 0.33 | | | $ | (0.34) | | | $ | 0.62 | | | $ | (3.59) | |

| Diluted | Diluted | $ | (0.67) | | | $ | 0.17 | | | $ | (4.26) | | | $ | 0.00 | | Diluted | $ | 0.32 | | | $ | (0.34) | | | $ | 0.61 | | | $ | (3.59) | |

| Weighted average number of common shares outstanding: | Weighted average number of common shares outstanding: | | Weighted average number of common shares outstanding: | |

| Basic | Basic | 17,384 | | | 17,270 | | | 17,364 | | | 17,264 | | Basic | 17,575 | | | 17,372 | | | 17,560 | | | 17,354 | |

| Diluted | Diluted | 17,384 | | | 17,330 | | | 17,364 | | | 17,264 | | Diluted | 17,977 | | | 17,372 | | | 17,923 | | | 17,354 | |

See accompanying Notesnotes to Condensed Consolidated Financial Statements.condensed consolidated financial statements.

LYDALL, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(In thousands) (Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| For the Three Months Ended | | For the Six Months Ended |

| June 30, 2021 | | June 30, 2020 | | June 30, 2021 | | June 30, 2020 |

| Net income (loss) | $ | 5,780 | | | $ | (5,857) | | | $ | 10,874 | | | $ | (62,278) | |

| Other comprehensive income (loss), net of tax: | | | | | | | |

| Foreign currency translation adjustments | 3,060 | | | 5,146 | | | 46 | | | (4,811) | |

| Pension liability adjustment, net of taxes of less than $0.1 million, $0.0 million, $0.1 million and $0.1 million, respectively | 22 | | | 0 | | | 387 | | | 331 | |

| Unrealized gain (loss) on hedging activities, net of taxes of $0.4 million, $0.2 million, $0.9 million, and $0.1 million, respectively | (125) | | | (685) | | | 2,893 | | | (239) | |

| Other comprehensive income (loss) | 2,957 | | | 4,461 | | | 3,326 | | | (4,719) | |

| Total comprehensive income (loss) | $ | 8,737 | | | $ | (1,396) | | | $ | 14,200 | | | $ | (66,997) | |

See accompanying notes to condensed consolidated financial statements.

LYDALL, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except per share amounts) (Unaudited)

| | | | | | | | | | | |

| Assets | June 30, 2021 | | December 31, 2020 |

| | | |

| Current assets: | | | |

| Cash and cash equivalents | $ | 102,544 | | | $ | 102,176 | |

| Accounts receivable, net of allowance for doubtful accounts of $2,188 and $2,402, respectively | 128,407 | | | 116,947 | |

| Contract assets | 22,756 | | | 32,403 | |

| Inventories | 88,226 | | | 78,996 | |

| Taxes receivable | 12,687 | | | 6,652 | |

| Prepaid expenses | 5,066 | | | 4,870 | |

| Other current assets | 7,986 | | | 7,348 | |

| Assets of a business held-for-sale | 1,233 | | | 0 | |

| Total current assets | 368,905 | | | 349,392 | |

| Property, plant and equipment, at cost | 515,393 | | | 506,509 | |

| Accumulated depreciation | (303,908) | | | (291,996) | |

| Property, plant and equipment, net | 211,485 | | | 214,513 | |

| Operating lease right-of-use assets | 25,798 | | | 22,243 | |

| Goodwill | 87,842 | | | 87,595 | |

| Other intangible assets, net | 86,922 | | | 95,121 | |

| Other assets, net | 6,948 | | | 6,598 | |

| Total assets | $ | 787,900 | | | $ | 775,462 | |

| Liabilities and Stockholders' Equity | | | |

| Current liabilities: | | | |

| Current portion of long-term debt | $ | 8,609 | | | $ | 9,789 | |

| | | |

| Accounts payable | 116,631 | | | 101,905 | |

| Accrued payroll and other compensation | 23,177 | | | 24,589 | |

| Accrued taxes | 6,555 | | | 8,214 | |

| | | |

| Derivative liabilities | 8,147 | | | 11,996 | |

| Restructuring liabilities | 36 | | | 9,431 | |

| Other accrued liabilities | 24,442 | | | 21,705 | |

| Liabilities of a business held-for-sale | 1,933 | | | 0 | |

| Total current liabilities | 189,530 | | | 187,629 | |

| Long-term debt | 251,477 | | | 260,649 | |

| Long-term operating lease liabilities | 20,973 | | | 17,947 | |

| Deferred tax liabilities | 30,913 | | | 27,174 | |

| Benefit plan liabilities | 17,554 | | | 21,691 | |

| Other long-term liabilities | 2,254 | | | 2,676 | |

| | | |

| Commitments and Contingencies (Note 16) | 0 | | 0 |

| Stockholders' equity: | | | |

| Preferred stock, $0.01 per share par value, 500 shares authorized (NaN issued or outstanding) | 0 | | | 0 | |

| Common stock, $0.01 per share par value, 30,000 shares authorized (25,755 and 25,555 shares issued, respectively) | 258 | | | 256 | |

| Capital in excess of par value | 103,272 | | | 99,770 | |

| Retained earnings | 277,778 | | | 266,904 | |

| Accumulated other comprehensive income (loss) | (15,016) | | | (18,342) | |

| Less treasury stock, 7,722 and 7,717 shares of common stock, respectively, at cost | (91,093) | | | (90,892) | |

| Total stockholders' equity | 275,199 | | | 257,696 | |

| Total liabilities and stockholders’ equity | $ | 787,900 | | | $ | 775,462 | |

See accompanying notes to condensed consolidated financial statements.

LYDALL, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOMECASH FLOWS

(In Thousands)thousands) (Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended

September 30, | | | | Nine Months Ended

September 30, | | |

| 2020 | | 2019 | | 2020 | | 2019 |

| (Unaudited) | | | | (Unaudited) | | |

| Net (loss) income | $ | (11,710) | | | $ | 3,004 | | | $ | (73,988) | | | $ | (52) | |

| Other comprehensive income (loss): | | | | | | | |

| Foreign currency translation | 8,245 | | | (8,726) | | | 3,434 | | | (6,396) | |

| Pension and other postretirement benefit plans, net of tax | (49) | | | 21 | | | 282 | | | 19,395 | |

| Unrealized gain/(loss) on derivative instruments, net of tax | (1,963) | | | (148) | | | (2,202) | | | (2,174) | |

| | | | | | | |

| Comprehensive (loss) income | $ | (5,477) | | | $ | (5,849) | | | $ | (72,474) | | | $ | 10,773 | |

| | | | | | | | | | | |

| For the Six Months Ended |

| | June 30, 2021 | | June 30, 2020 |

| Cash flows from operating activities: | | | |

| Net income (loss) | $ | 10,874 | | | $ | (62,278) | |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | |

| | | |

| Depreciation and amortization | 22,794 | | | 24,035 | |

| Amortization of debt issuance costs | 252 | | | 807 | |

| Impairment of goodwill and long-lived assets | 0 | | | 61,109 | |

| Deferred income taxes | 3,094 | | | (6,048) | |

| (Gain) loss on the sale of a business | 964 | | | 0 | |

| Employee benefit plans settlement expenses | 0 | | | 385 | |

| Stock-based compensation | 2,695 | | | 1,799 | |

| | | |

| (Gain) loss on disposition of property, plant and equipment | 7 | | | 25 | |

| (Gain) loss from equity method investment | (165) | | | 26 | |

| Other, net | (88) | | | 53 | |

| Changes in operating assets and liabilities: | | | |

| Accounts receivable | (16,690) | | | 3,063 | |

| Contract assets | 9,594 | | | 222 | |

| Inventories | (9,508) | | | (353) | |

| Income taxes (receivable) payable | (6,753) | | | 886 | |

| Prepaid expenses and other assets | (648) | | | (953) | |

| Accounts payable | 11,415 | | | 8,342 | |

| Accrued payroll and other compensation | (2,378) | | | 2,974 | |

| | | |

| Deferred revenue | (768) | | | 1,850 | |

| Accrued taxes payable | (105) | | | 5,833 | |

| | | |

| Benefit plan liabilities | (3,899) | | | (434) | |

| Other, net | (2,190) | | | (928) | |

| Net cash provided by (used for) operating activities | 18,497 | | | 40,415 | |

| Cash flows from investing activities: | | | |

| Capital expenditures | (13,265) | | | (15,472) | |

| Collections of finance receivables | 3,111 | | | 3,390 | |

| Payments from divestitures | (2,715) | | | 0 | |

| Proceeds from the sale of property, plant and equipment | 19 | | | 2 | |

| | | |

| Net cash provided by (used for) investing activities | (12,850) | | | (12,080) | |

| Cash flows from financing activities: | | | |

| Proceeds from borrowings | 263,210 | | | 20,000 | |

| Debt repayments | (274,910) | | | (7,001) | |

| Proceeds from servicing receivables | 4,787 | | | 458 | |

| Common stock issued | 793 | | | 33 | |

| Common stock repurchased | (201) | | | (8) | |

| Net cash provided by (used for) financing activities | (6,321) | | | 13,482 | |

| Effect of exchange rate changes on cash | 1,042 | | | (602) | |

| Increase (decrease) in cash and cash equivalents | 368 | | | 41,215 | |

| Cash and cash equivalents at beginning of period | 102,176 | | | 51,331 | |

| Cash and cash equivalents at end of period | $ | 102,544 | | | $ | 92,546 | |

See accompanying Notesnotes to Condensed Consolidated Financial Statements.

condensed consolidated financial statements.

LYDALL, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In Thousands)

| | | | | | | | | | | |

| September 30,

2020 | | December 31,

2019 |

| (Unaudited) | | |

| ASSETS | | | |

| Current assets: | | | |

| Cash and cash equivalents | $ | 122,043 | | | $ | 51,331 | |

| Accounts receivable, net of allowance for doubtful accounts of $2,465 and $1,842, respectively | 113,258 | | | 107,786 | |

| Contract assets | 27,186 | | | 28,245 | |

| Inventories | 71,167 | | | 80,544 | |

| Taxes receivable | 6,636 | | | 3,427 | |

| Prepaid expenses | 6,117 | | | 3,814 | |

| Other current assets | 8,516 | | | 8,450 | |

| Total current assets | 354,923 | | | 283,597 | |

| Property, plant and equipment, at cost | 491,291 | | | 487,371 | |

| Accumulated depreciation | (286,713) | | | (265,729) | |

| Property, plant and equipment, net | 204,578 | | | 221,642 | |

| Operating lease right-of-use assets | 21,522 | | | 23,116 | |

| Goodwill | 85,385 | | | 133,912 | |

| Other intangible assets, net | 99,445 | | | 115,577 | |

| Other assets, net | 7,785 | | | 8,093 | |

| Total assets | $ | 773,638 | | | $ | 785,937 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

| Current liabilities: | | | |

| Current portion of long-term debt | $ | 9,844 | | | $ | 9,928 | |

| | | |

| Accounts payable | 101,785 | | | 73,426 | |

| Accrued payroll and other compensation | 24,806 | | | 17,198 | |

| Accrued taxes | 10,125 | | | 5,638 | |

| | | |

| Other accrued liabilities | 39,214 | | | 23,668 | |

| Total current liabilities | 185,774 | | | 129,858 | |

| Long-term debt | 273,195 | | | 262,713 | |

| Long-term operating lease liabilities | 17,369 | | | 18,424 | |

| Deferred tax liabilities | 27,016 | | | 34,561 | |

| Benefit plan liabilities | 18,770 | | | 18,957 | |

| Other long-term liabilities | 3,201 | | | 3,004 | |

| | | |

| Commitments and Contingencies (Note 16) | | | |

| Stockholders' equity: | | | |

| Preferred stock | 0 | | | 0 | |

| Common stock | 255 | | | 253 | |

| Capital in excess of par value | 96,536 | | | 94,140 | |

| Retained earnings | 266,641 | | | 340,629 | |

| Accumulated other comprehensive loss | (24,465) | | | (25,979) | |

| Treasury stock, at cost | (90,654) | | | (90,623) | |

| Total stockholders’ equity | 248,313 | | | 318,420 | |

| Total liabilities and stockholders’ equity | $ | 773,638 | | | $ | 785,937 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

LYDALL, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In Thousands)

| | | | | | | | | | | |

| For the Nine Months Ended September 30, | | |

| | 2020 | | 2019 |

| | (Unaudited) | | |

| Cash flows from operating activities: | | | |

| Net loss | $ | (73,988) | | | $ | (52) | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

| Gain on divestiture | 0 | | | (1,459) | |

| Depreciation and amortization | 42,349 | | | 36,682 | |

| Impairment of goodwill and long-lived assets | 61,109 | | | 0 | |

| Deferred income taxes | (6,911) | | | (12,849) | |

| | | |

| Employee benefit plans settlement expenses | 385 | | | 25,701 | |

| Stock-based compensation | 2,508 | | | 2,073 | |

| Other, net | 47 | | | 0 | |

| Loss (gain) on disposition of property, plant and equipment | 164 | | | (43) | |

| Income from equity method investment | (24) | | | (120) | |

| Changes in operating assets and liabilities: | | | |

| Accounts receivable | (8,288) | | | 10,528 | |

| Contract assets | 1,269 | | | (4,330) | |

| Inventories | 10,117 | | | (6,206) | |

| Accounts payable | 28,391 | | | 13,427 | |

| Accrued payroll and other compensation | 7,192 | | | 4,935 | |

| | | |

| Accrued taxes | 4,558 | | | 1,810 | |

| | | |

| Other, net | 5,735 | | | (7,133) | |

| Net cash provided by operating activities | 74,613 | | | 62,964 | |

| Cash flows from investing activities: | | | |

| Capital expenditures | (20,540) | | | (27,236) | |

| Collections of finance receivables | 4,257 | | | 0 | |

| Proceeds from divestiture | 0 | | | 2,298 | |

| Proceeds from the sale of property, plant and equipment | 14 | | | 297 | |

| Business acquisitions, net of cash acquired | 0 | | | 869 | |

| Net cash used for investing activities | (16,269) | | | (23,772) | |

| Cash flows from financing activities: | | | |

| Proceeds from borrowings | 20,000 | | | 0 | |

| Debt repayments | (9,500) | | | (38,185) | |

| Proceeds from servicing receivables | 207 | | | 0 | |

| Common stock issued | 32 | | | 5 | |

| Common stock repurchased | (31) | | | (50) | |

| Net cash provided by (used for) financing activities | 10,708 | | | (38,230) | |

| Effect of exchange rate changes on cash | 1,660 | | | (1,280) | |

| Increase (decrease) in cash and cash equivalents | 70,712 | | | (318) | |

| Cash and cash equivalents at beginning of period | 51,331 | | | 49,237 | |

| Cash and cash equivalents at end of period | $ | 122,043 | | | $ | 48,919 | |

Non-cash capital expenditures of $4.8 million and $3.8 million were included in accounts payable at September 30, 2020 and 2019, respectively.

See accompanying Notes to Condensed Consolidated Financial Statements.

LYDALL, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Basis of Financial Statement Presentation

Description of Business

Lydall, Inc. and its subsidiaries (collectively, the “Company” or “Lydall”) design and manufacture specialty engineered nonwoven filtration media, industrial thermal insulating solutions, and thermal and acoustical barriers for filtration/separation and heat abatement and sound dampening applications.

Recent Developments: COVID-19

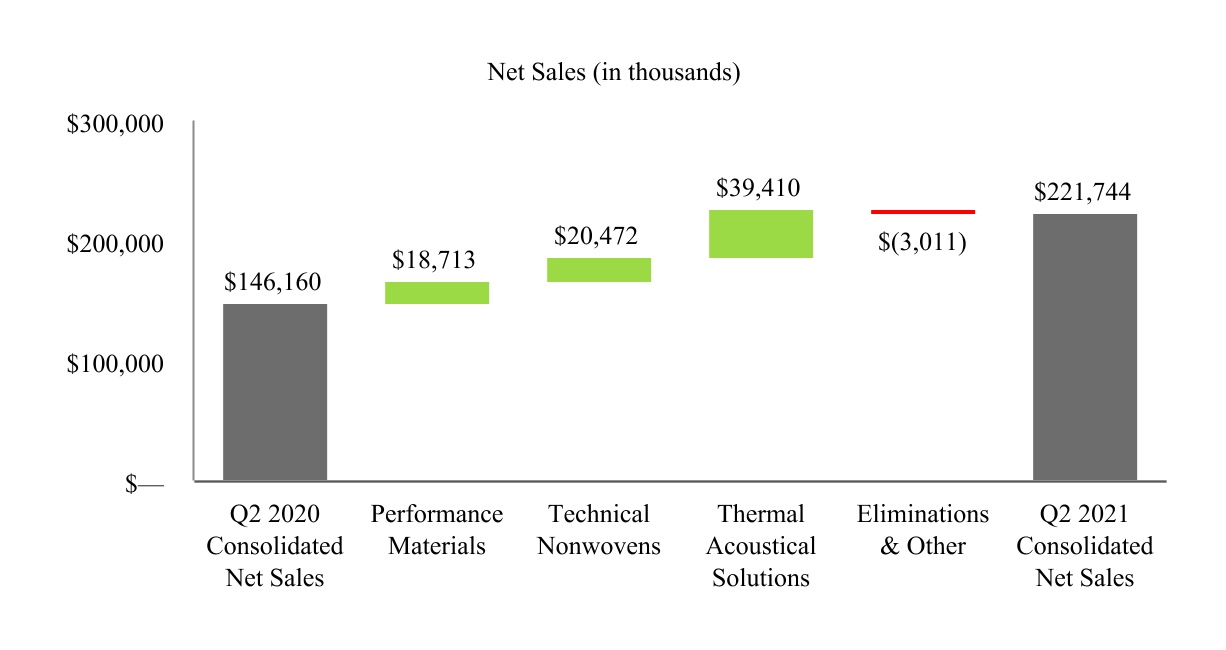

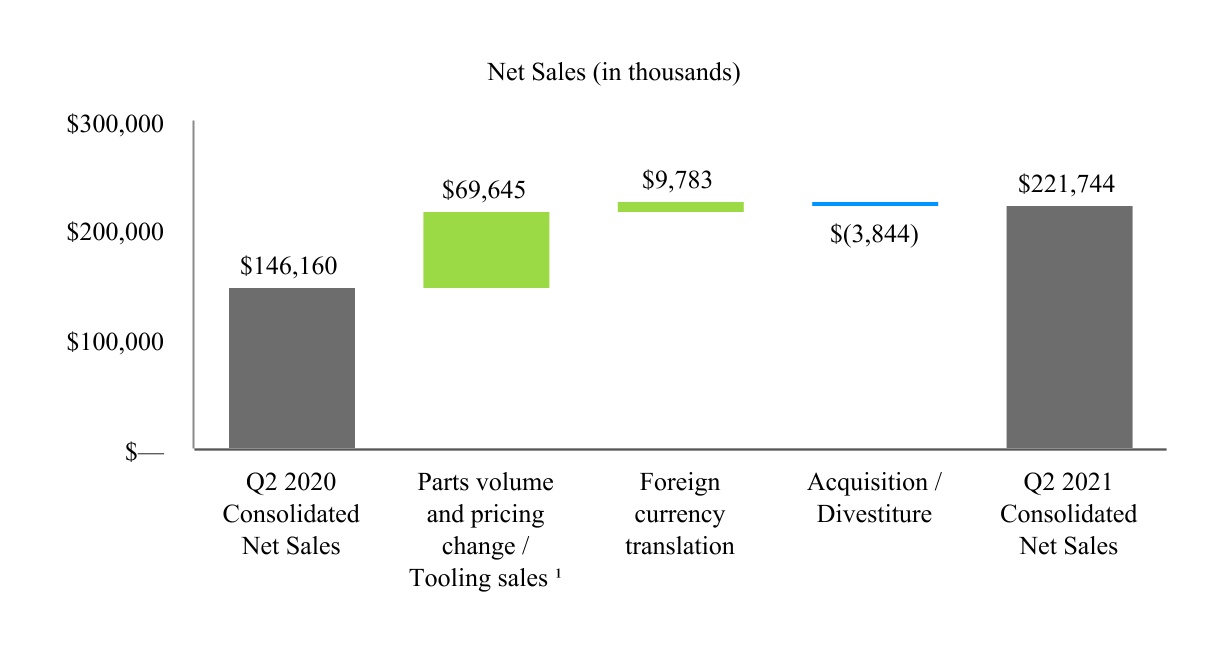

The impact of the novel strain of the coronavirus (“COVID-19”) has grown throughout the world, including in all global and regional markets served by the Company. During 2020, governmental authorities implemented numerous measures attempting to contain and mitigate the effects of COVID-19, including travel bans and restrictions, quarantines, social distancing orders, shelter in place orders, and shutdowns of non-essential activities. The Company’s manufacturing facilities are located in areas that have been affected by the pandemic and shutdowns. Certain Company facilities in the United States, Europe, and Asia carried out shutdowns as a result of government-imposed restrictions or in conjunction with customer plant closures during the first quarter. The Company’s Asia facilities resumed operations in late February and other facilities ramped back up moderately, in line with customer demand, during the second quarter. In the third quarter, the Company has seen a stronger recovery in the Performance Materials segment, specifically in the Filtration business, and in the Thermal Acoustical Solutions and Technical Nonwovens segments as discussed below.

Performance Materials (“PM”) Developments

Performance Materials sales were down 4.6% in the first half of 2020 from the comparative period in 2019 with incremental demand for specialty filtration media products more than offset by softer demand in the Sealing and Advanced Solutions business.PM’s Filtration sales continued to be very strong in the third quarter, up approximately 37.8% from the comparative period in the prior year, led by continued demand for fine fiber meltblown media used in personal protective equipment such as N95 respirators and surgical and medical masks. This demand is expected to moderate into the fourth quarter and expected to be down slightly on a sequential basis due to normal seasonality. Weaker demand in automotive, agricultural, and construction equipment markets resulted in a sales decline of approximately 1.7% in the Sealing and Advanced Solutions business in the third quarter of 2020 from the comparative period in 2019.

As a result of continued strong demand for filtration products, the Company approved investments to add 2 production lines in Performance Materials’ Rochester facility for the production of fine fiber meltblown filtration media used in the N95 respirator and surgical and medical masks.In addition, the Company has an agreement with the U.S. Government that provides partial funding of the investments in the production lines and funding for other technical resources.

In the third quarter of 2020, the Company announced an investment in a new fine fiber meltblown production line in its French facility to support the European Union face mask production and air filter production in the fight against COVID-19. The Company has a tentative agreement with the French Government to partially fund a portion of this investment.

In the third quarter, the Company initiated actions to close underperforming operating locations in Europe and discontinue production of a lower efficiency air filtration media product and, in turn, fully depreciated the supporting machinery and equipment in North America. These actions are part of the Company's ongoing assessment of underperforming assets and focus of resources on the significant investments to expand fine fiber meltblown production.These actions are expected to be completed in 2021 and projected to improve overall segment margin performance beginning in 2021. For additional information, see Note 12, "Restructuring".

Technical Nonwovens (“TNW”) Developments

During the first half of 2020, TNW experienced slowdowns in all geographic locations; predominantly in its facilities in South Carolina, the United Kingdom, and China. TNW’s Texel business in Canada, however, is a leading supplier of nonwoven products used in the production of healthcare applications including medical wipes, pads, and gowns. In response to the COVID-19 pandemic, the Company re-prioritized its manufacturing capabilities in North America and Europe to focus on serving customers for these products.

TNW’s sales in the first half of 2020 declined 18.8% from the comparable period in 2019 on generally slower demand in industrial end markets globally. In the third quarter of 2020, sales increased 12.5% on a sequential basis from the previous quarter but decreased 8.5% compared to the prior year quarter. Softer industrial end markets and lower sales into automotive applications resulted in the year-over-year sales declines in the quarter. Third quarter 2020 sales were down 10.0% in Industrial Filtration and 6.8% in Advanced Materials businesses from the same period in the previous year.

Thermal Acoustical Solutions (“TAS”) Developments

As previously disclosed, the Company ramped-down its TAS operations in North Carolina in the United States, as well as in France and Germany, coinciding with the shutdown of its major automotive customers' facilities in those regions beginning in late March 2020. During the first half of 2020, TAS sales decreased 35.4% from prior year, heavily impacted by customer shutdowns during March, April, and May. TAS began to ramp-up production in mid-second quarter of 2020 in North America and Europe as customers began to re-open their plants in these regions. During the third quarter 2020, part sales were down 0.8% from the previous year as TAS continued to see stronger demand in North America and Europe with sales increasing significantly compared to second quarter 2020.

As customer demand increased in North America, the Company began to experience an increase of COVID-19 cases, particularly at its North American operation, resulting in workforce shortages and other operational inefficiencies causing higher overtime, outsourcing costs, and logistics costs. In addition, recent recoveries in the manufacturing industries are causing higher commodity pricing in North America. In late third quarter 2020, as a result of labor shortages and operational inefficiencies directly related to COVID-19, TAS was unable to manufacture parts timely, resulting in customer production line stoppages. In early October 2020, due to the unforeseen and unforeseeable nature of the COVID-19 pandemic, which is out of the Company’s control, the Company invoked force majeure or commercial impracticability as legal excuse for delayed performance of contracts and defense to any claim that may be asserted by customers.A recent resurgence of cases in that same facility has caused the Company to expand its declaration of force majeure or commercial impracticability to other impacted customers. The Company has taken various actions to resolve these issues and expects TAS to continue to incur incremental costs in the fourth quarter of 2020.

Liquidity and Cash Preservation

The Company continued to experience working capital cash flow improvements through September 30, 2020, generating $74.6 million in cash from operating activities. As the Company continues to ramp-up production and invest in new fine fiber meltblown production equipment to meet customer demand, the Company expects cash outflows to support working capital requirements and capital projects.

During the first nine months of 2020, the Company took significant measures to reduce its overall cash expenditures, including the furlough or lay-off of hourly/salary plant workers and select furloughs of corporate and other salaried employees, deferred company contributions to its pension plans and matching contributions under the Company's 401(k) defined contribution plan, reduction of purchase obligations for raw materials, and reduction/delay of non-critical capital spending. As a result, the Company reduced its monthly cash expenditures. The Company may elect to continue certain actions if the COVID-19 pandemic continues.

In addition, the Company has taken advantage of specific benefits, including wage recovery provided by social programs in Europe and China and deferred domestic employer tax in the U.S. through the Coronavirus Aid, Relief and Economic Security (“CARES”) Act. Through September 30, 2020, the Company benefited from $2.0 million in social cost reimbursements predominately in Europe and China. The Company may pursue, wherever it qualifies, governmental assistance and take advantage of governmental programs. The Company cannot guarantee, however, that it will qualify for, or receive, any additional assistance that it pursues.

As noted above, the Company reached an agreement with the U.S. Government in June 2020 that provides funding to cover a portion of the cost to install 2 new production lines for the production of meltblown material for N95 respirators, surgical and medical masks, and for other technical resources. The Company will receive monthly payments in accordance with the agreement to fund up to $13.5 million. Additionally, the Company has a tentative agreement with the French Government to fund up to 30% of the Company’s investment in its facility in France supporting the European Union face mask production and air filter production.

In addition to the significant measures taken to reduce and contain costs, the Company took actions in March 2020 to provide additional liquidity, primarily including a $20.0 million draw down on its amended credit facility.On May 11, 2020, the Company entered into an amended credit agreement (see Note 6, "Long-term Debt and Financing Arrangements" for the key amended terms and conditions) to modify certain financial maintenance covenants, at least one of which the Company expected to fail during the second quarter of 2020 as a result of the impact of COVID-19.On October 14, 2020, the Company amended

its 2018 Credit Agreement to allow certain restructuring and other charges, as defined by the amendment, to be excluded from EBITDA in the calculation of the Company's financial covenants. The Company was in compliance with those modified financial covenants as of and for the three-month period ended September 30, 2020, and management does not anticipate noncompliance in the foreseeable future.

Through September of 2020, the Company generated $74.6 million of net cash provided by operations and had cash on hand of $122.0 million as of September 30, 2020. The Company continues to maintain the necessary capital to meet its debt obligations and interest payments. As previously disclosed in late 2019, the Company entered into arrangements with a banking institution to sell trade accounts receivable balances for selected customers. The Company continues to sell trade accounts receivable balances under these arrangements. See Transfer of Financial Assets in this Note 1, “Basis of Financial Statement Presentation” for more information.

The spread of COVID-19 and the measures taken to constrain the spread of the virus have had, and will continue to have, a material negative impact on the Company’s financial results, and such negative impact may continue well beyond the containment of such outbreak. There is inherent uncertainty in the assumptions the Company uses to estimate its future liquidity due to the impact of the COVID-19 outbreak. In addition, the magnitude, duration, and speed of the global pandemic is uncertain. Consequently, the impact on the Company's business, financial condition or longer-term financial or operational results is uncertain. However, management believes, based on the actions taken to reduce cash expenditures and the Company’s financial position, that net cash provided by operations combined with its cash and cash equivalents and borrowing availability under its Credit Facility will be sufficient to fund its current obligations, capital spending, debt service requirements, and working capital needs over at least the next twelve months.

Steps Taken to Protect Employees

The Company continues to monitor the global outbreak and spread of COVID-19 and take steps to mitigate the potential risks to the Company and its employees posed by the spread, related circumstances, and economic impacts of COVID-19. As the Company brings employees back to work, it has implemented changes to help ensure the safety and health of all its employees and continues to assess and update its business continuity plans in the context of this pandemic. The Company established the Lydall Emergency Preparedness Team (“LEPT”), implementing strict travel restrictions, enforcing rigorous hygiene protocols, increasing sanitization efforts at all facilities and implementing remote working arrangements for the majority of its employees who work outside the plants. The Company will continue its work to ensure it maintains a safe and healthy work environment and continue to allow remote working arrangements as long as necessary, where appropriate.BASIS OF FINANCIAL STATEMENT PRESENTATION

Basis of Presentation

The accompanying Condensed Consolidated Financial Statements include the accounts of Lydall, Inc. and its subsidiaries.subsidiaries (collectively, “Lydall”, “the Company”, “we”, and “our”). All financial information is unaudited for the interim periods reported. All significant intercompany transactions have been eliminated in the Condensed Consolidated Financial Statements. The Company's Condensed Consolidated Financial Statements have been prepared in accordance with accounting principlesU.S. generally accepted in the United States of Americaaccounting principles (“U.S. GAAP”). The year-end Condensed Consolidated Balance Sheet wasamounts have been derived from the audited financial statements for the year ended December 31, 2019,2020 but does not include all disclosures required by U.S. GAAP. In the opinion of management, the condensed consolidated financial information reflects all adjustments necessary for a fair statement of the Company’s consolidated financial position, results of operations, and cash flows for the interim periods reported, but do not include all the disclosures required by U.S. GAAP. All such adjustments are of a normal recurring nature, unless otherwise disclosed in this report. Certain amounts in prior year financial statements and notes thereto have been reclassified to conform to current year presentation. The statements should be read in conjunction with the consolidated financial statements and accompanying notes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019.2020.

Use of EstimatesMerger Agreement

The preparationAs previously announced, on June 21, 2021, the Company entered into an Agreement and Plan of condensed consolidated financial statements in conformityMerger (the “Merger Agreement”) by and among the Company, Unifrax Holding Co. (“Parent”), Outback Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of Parent (“Merger Sub”), and solely with U.S. GAAP requires managementrespect to make estimatescertain payment obligations of Parent thereunder, Unifrax I LLC (“Unifrax”). Subject to the terms and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the dateconditions of the condensed consolidated financial statementsMerger Agreement, Merger Sub will be merged with and into the reported amountsCompany (the “Merger”), with the Company surviving the Merger as a wholly owned subsidiary of revenuesParent. Unifrax is a global provider of specialty materials focused on thermal management, specialty filtration, battery materials, emission control, and expenses duringfire protection applications and is backed by Clearlake Capital Group, L.P.

Subject to the reporting period. The full extentterms and conditions of the Merger Agreement, each share of common stock, par value $0.01 per share, of the Company (the “common stock”) (other than shares of common stock held by the Company as treasury stock) issued and outstanding immediately prior to which the COVID-19 pandemiceffective time of the Merger (the “Effective Time”) (other than dissenting shares) will directly or indirectly impactbe converted into the right to receive $62.10 per share in cash, without interest. If the Merger is consummated, the Company’s business, resultssecurities will be de-listed from the New York Stock Exchange (the “NYSE”) and de-registered under the Securities Exchange Act of operations, and financial condition, including sales, expenses, reserves and allowances, manufacturing, research and development costs and employee-related amounts, will depend on future developments that are highly uncertain, including1934, as amended (the “Exchange Act”) as soon as practicable following the result of new information that may emerge concerning COVID-19 and the actions taken to contain or treat it. The Company has made estimates of the impact of COVID-19 within its financial statements and there may be changes to those estimates in future periods. Actual results could differ from those estimates.Effective Time.

The completion of the Merger is subject to customary closing conditions, including, among others, (i) the approval of the Company’s stockholders holding a majority of the outstanding shares of common stock and (ii) the expiration or termination of any waiting period applicable to the consummation of the Merger under the Hart-Scott Rodino Antitrust Improvements Act of 1976, and the expiration of applicable waiting periods or clearances of the Merger, as applicable, under the antitrust and foreign investment laws of certain other jurisdictions. Subject to the satisfaction or (to the extent permissible) waiver of such conditions, the Merger is currently expected to close in the second half of 2021. However, the Company cannot assure completion of the Merger by any particular date, if at all or that, if completed, it will be completed on the terms set forth in the Merger Agreement. The Company’s Condensed Consolidated Financial Statements and related disclosures for the three and six-month periods ended June 30, 2021 and 2020 do not reflect any potential impacts or effects the Merger may have on the Company’s financial statements if the Merger is finalized.

Additional Cash Flow Information

Non-cash investing activities include non-cash capital expenditures of $4.2 million and $2.7 million that were included in Accounts payable at June 30, 2021 and 2020, respectively.

Risks and Uncertainties

Worldwide economic cycles, political changes, and the COVID-19 pandemic affect the markets that the Company’s businesses serve, affect demand for the Company's products, and could impact profitability. Among other factors, disruptions in the global credit and financial markets, including diminished liquidity and credit availability, changes in international trade agreements,

Recent Accounting Pronouncements Adopted

Effective January 1, 2020, the Company adopted the Financial Accounting Standards Board ("FASB") Accounting Standards Update ("ASU") 2016-13, "Financial Instruments - Credit Losses (Topic 326)." The new standard amends guidance on reporting credit losses for assets held at amortized cost basis. The Company has determined the only financial assets subjectswings in consumer confidence and spending, and unstable economic growth, disruptions to the new standard are its trade receivablesglobal automotive supply chain, and contract assets. The adoption of this ASU did notfluctuations in unemployment rates have anycaused economic instability and can have a negative impact on the Company’s consolidatedresults of operations, financial statementscondition, and disclosures.liquidity.

Effective January 1, 2020, the Company adopted the FASB issued ASU 2018-13, "Fair Value Measurement (Topic 820): Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurement," which adds, amends, and removes certain disclosure requirements related to fair value measurements. Among other changes, this standard requires certain additional disclosure surrounding Level 3 assets, including changes in unrealized gains or losses in other comprehensive income and certain inputs in those measurements. Please refer to Note 5, “ImpairmentsTransfers of Goodwill and Other Long-Lived Assets”, for discussion of the inputs used in the quantitative impairment assessments for the three-month period ended March 31, 2020.Financial Assets

Effective January 1, 2020, theThe Company adopted FASB issued ASU2018-15, "Intangibles - Goodwill and Other - Internal-Use Software (Subtopic 350-40); Customer’s Accountingaccounts for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract."The amendments in this update require implementation costs incurred by customers in cloud computing arrangements (i.e., hosting arrangements) to be capitalized under the same premisestransfers of authoritative guidance for internal-use software, and deferredfinancial assets as sold when it has surrendered control over the noncancellable termrelated assets. Whether control has been relinquished requires, among other things, an evaluation of relevant legal considerations and an assessment of the cloud computing arrangement plusnature and extent of the Company's continuing involvement with the assets transferred. Gains or losses and any option renewal periods thatexpenditures stemming from the transfers are reasonably certain to be exercised by the customer or for which the exercise is controlled by the service provider. The adoption of this ASU did not have a material impactincluded in Other (income) expense, net on the Company’s consolidated financial statementsCompany's Condensed Consolidated Statements of Operations. Assets obtained and disclosures.liabilities incurred in connection with transfers reported as sold are initially recognized on the Company's Condensed Consolidated Balance Sheets at fair value.

In March 2020,The Company maintains arrangements with banking institutions to sell trade accounts receivable balances for select customers. Under the FASB issued ASU 2020-04, "Reference Rate Reform (Topic 848); Facilitationprograms, the Company has no risk of loss due to credit default and is charged a fee based on the nominal value of receivables sold between the time of the Effectssale of Reference Rate Reform on Financial Reporting." The amendments in this update are elective,the trade accounts receivables to banking institutions and provide optional expedients and exceptions in accounting for contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued becausecollection of reference rate reform. The guidance in this update is effective for transactions entered into between March 12, 2020 and December 31, 2022. Thethe trade accounts receivables from the customer. Under one of the programs, the Company adopted this ASU upon issuance and notes no impactservices the trade receivables after the sale to the bank and receives 90.0% of the trade receivables in cash at the time of sale and the remaining 10.0% in cash, net of fees, when the customer pays. Total activity under both arrangements was as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| For the Three Months Ended | | For the Six Months Ended |

| In thousands | June 30, 2021 | | June 30, 2020 | | June 30, 2021 | | June 30, 2020 |

| Total trade accounts receivable balances sold | $ | 30,961 | | | $ | 10,288 | | | $ | 65,107 | | | $ | 42,974 | |

| Total cash received | $ | 29,268 | | | $ | 9,374 | | | $ | 60,507 | | | $ | 39,533 | |

| Total fees incurred | $ | 173 | | | $ | 76 | | | $ | 308 | | | $ | 142 | |

The Company's consolidated financial statementssenior secured revolving credit agreement permits the Company to sell trade accounts receivable balances to approved third parties in connection with Receivable Purchases Agreements, or other similar agreements. At any given time, outstanding trade accounts receivable balances sold cannot exceed $10.0 million for a certain approved customer and disclosures as$50.0 million in aggregate for any other approved group of September 30, 2020.customers.

2. RECENT ACCOUNTING STANDARDS

Recent Accounting Pronouncements Not YetStandards Adopted

In August 2020, the FASB issued ASU 2020-06, "Debt-Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40)." The amendments in this update are intended to simplify the accounting for convertible debt instruments and convertible preferred stock. This ASU is effective for fiscal years and interim periods beginning after December 15, 2021 with early adoption permitted. The Company does not expect the adoption of this update to have a material impact on its consolidated financial statements and related disclosures.

In January 2020, the FASB issued ASU 2020-01, "Investments—Equity Securities (Topic 321), Investments—Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815)." The amendments in this update are intended to reduce diversity in practice and increase comparability of the accounting for interaction of equity securities, investments accounted for under the equity method of accounting, and the accounting for certain forward contracts and purchased options accounted for under Topic 815. This ASU is effective for fiscal years and interim periods beginning after December 15, 2020 with early adoption permitted. The Company is currently evaluating the impact of this update on its consolidated financial statements and related disclosures.

In December 2019, the FASB issued ASU 2019-12, "Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes". The new standard is intended to simplify accounting for income taxes by removing certain exceptions to the general principles in Topic 740, and by clarifying and amending existing guidance in other areas of the same topic. This ASU iswas effective for fiscal years and interim periods beginning after December 15, 2020 with early adoption permitted. The Company is currently evaluatingadopted this ASU upon issuance and there was no material impact to the impact of this update on its consolidated financial statementsCompany's Condensed Consolidated Financial Statements and related disclosures.

In August 2018,January 2020, the FASB issued ASU No. 2018-14, "Compensation2020-01, "Investments - Retirement BenefitsEquity Securities (Topic 321), Investments - Defined Benefit Plans - General (Subtopic 715-20): Disclosure Framework - ChangesEquity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815)". The amendments in this update were intended to reduce diversity in practice and increase comparability of the Disclosure Requirementsaccounting for Defined Benefit Plans."interaction of equity securities, investments accounted for under the equity method of accounting, and the accounting for certain forward contracts and purchased options accounted for under Topic 815. This ASU requires entities to disclose the weighted-average interest crediting rates for cash balance plans and other plans with promised interest crediting rates. This ASU also requires entities to disclose an explanation for significant gains and losses related to changes in the benefit obligation for the period. This ASU iswas effective for fiscal years and interim periods beginning after December 15, 2020, with early adoption permitted. The Company adopted this ASU upon issuance and there was no material impact to the Company's Condensed Consolidated Financial Statements and disclosures.

In March 2020, the FASB issued ASU 2020-04, "Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting". The amendments in this update are elective, and provide optional expedients and exceptions in accounting for contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. In January 2021, the FASB issued ASU 2021-01 to provide additional clarity around Topic 848. Specifically, certain provisions of Topic 848, if elected by an entity, apply to derivative instruments that use an interest rate for margining, discounting, or contract price alignment that is modified as a result of reference rate reform. The ASUs can be adopted no later than December 1, 2022 with early adoption permitted. The Company has reviewed the guidance and elected to adopt the use of the expedients permitted, however there have been no modifications

or other changes to the Company’s contracts, hedging relationships or other transactions due to reference rate reform as of June 30, 2021.

In October 2020, the FASB issued ASU 2020-10, "Codification Improvements". The amendments in this update were intended to clarify the location of certain disclosure guidance within the ASC, as well as clarify certain guidance in cases where the original guidance may have been unclear. These amendments do not change U.S. GAAP. This ASU was effective for fiscal years and interim periods beginning after December 15, 2020. The Company adopted this ASU upon issuance and notes no impact to the Company's Condensed Consolidated Financial Statements and disclosures.

Recent Accounting Standards Not Yet Adopted

In August 2020, the FASB issued ASU 2020-06, "Debt-Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40)". The amendments in this update were intended to simplify the accounting for convertible debt instruments and convertible preferred stock. This ASU is effective for fiscal years and interim periods beginning after December 15, 2021 with early adoption permitted. The Company is currently evaluating the impactdoes not expect the adoption of this ASU willupdate to have a material impact on its consolidated financial statementsthe Company's Condensed Consolidated Financial Statements and disclosures.

Significant Accounting Policies

3. DIVESTITURE ACTIVITIES

The Company’s significant accounting policies are detailed in Note 1, “Significant Accounting Policies” within Part IV, Item 15During the third quarter of 2020, the Company undertook actions to consolidate global production facilities for sealing & advanced solutions products, a part of the Company’s Annual Report on Form 10-K forCompany's Performance Materials segment. In the year ended December 31, 2019.

Risks and Uncertainties

Worldwide economic cycles, political changes, and the COVID-19 pandemic affect the markets that the Company’s businesses serve and affect demand for the Company's products and could impact profitability. Among other factors, disruptions in the global credit and financial markets, including diminished liquidity and credit availability, changes in international trade agreements, swings in consumer confidence and spending, and unstable economic growth and fluctuations in unemployment rates has caused economic instability and can have a negative impact on the Company’s resultsfirst quarter of operations, financial condition, and liquidity.

Transfers of Financial Assets

In December 2019,2021, the Company entered into 2 arrangements with a banking institutionan agreement to sell trade accounts receivable balances for select customers. Undera German facility, which closed on March 11, 2021. The Company agreed to pay $1.8 million (€1.5 million) to the programs, the Company has no riskbuyer and provide $2.3 million (€1.9 million) in additional funding, net of loss duecash and certain net working capital adjustments, to credit defaultcover pension and is chargedrestructuring liabilities recorded in 2020. As a fee based on the nominal valueresult of receivables sold and the time between the sale of the trade accounts receivables to banking institutions and collection from the customer. Under one of the programs,facility, the Company services the trade receivables after sale and receives 90.0%recorded a pre-tax loss of the trade receivables in cash at the time of sale and the remaining 10.0% in cash, net of fees, at the earlier of customer payment or 150 days. In the three-month and nine-month periods ended September 30, 2020, under both programs, the Company sold $21.3$0.3 million and $64.3$1.0 million respectively, in trade receivable balances, received $59.1 million in total cash under the programs, and incurred $0.2 million in fees. The Company expects to receive the remainder, net of fees, in the fourth quarter of 2020.

Condensed Consolidated Statements of Comprehensive Income

In connection with the preparation of its 2019 audited financial statements, the Company identified that in its previously filed unaudited interim financial statements for the three-monththree and six-month periods ended June 30, 20192021, respectively. The final consideration and loss are subject to a working capital adjustment expected to be settled in 2022.

In the nine-month period ended September 30, 2019,second quarter of 2021, the Company had incorrectly excluded, from its Condensed Consolidated Statementsreached an agreement to sell an operating facility located in the Netherlands, which is a component of Comprehensive Income, the impact to comprehensive income resulting from the settlement of its U.S. Lydall Pension Plan (see Note 11, "Employer Sponsored Benefit Plans"). As a result, unaudited comprehensive income for such periods was understated by approximately $19.0 million. This error did not have any impact on the Company’s corresponding previously filed Condensed Consolidated Balance Sheets, Condensed Consolidated Statements of Operations or Condensed Consolidated Statements of Cash Flows. Management has concluded that such errors did not resultPerformance Materials segment. The transaction was completed on July 9, 2021. The assets and liabilities sold in the previously issued unaudited financial statements being materially misstated. In connection with the filingtransaction met the criteria for held-for-sale reporting as of this Quarterly ReportJune 30, 2021. The Company did not report the transaction as discontinued operations as it was not considered a strategic shift in the Company’s business. The Company expects to record a gain on Form 10-Q, the Company has revisedsale in the Condensed Consolidated Statementsthird quarter of Comprehensive Income2021. The results of the operating facility are reflected in continuing operations for the nine-month periodthree and six-month periods ended SeptemberJune 30, 20192021. The assets and liabilities of the operating facility are reported as current “Assets of a business held-for-sale” and current “Liabilities of a business held-for-sale” as of June 30, 2021. The held-for-sale assets and liabilities of the operating facility were as follows:

| | | | | | | | | | | | | | | | |

| | | | Nine Months Ended September 30, 2019 | | |

| In thousands | | | | As reported | | As revised |

| Pension liability adjustment, net of tax | | | | $ | 379 | | | $ | 19,395 | |

| Comprehensive (loss) income | | | | $ | (8,243) | | | $ | 10,773 | |

| | | | | |

| In thousands | At June 30, 2021 |

| Accounts receivable, net | $ | 912 | |

| Inventories | 18 | |

| Taxes receivable | 35 | |

| Prepaid expenses | 22 | |

| Deferred tax assets | 246 | |

| Total assets held-for-sale | $ | 1,233 | |

| |

| Accounts payable | $ | 161 | |

| Accrued taxes | 58 | |

| Accrued payroll & other compensation | 300 | |

| Restructuring liabilities | 1,414 | |

| Total liabilities held-for-sale | $ | 1,933 | |

2. Revenue from Contracts with Customers4. REVENUE FROM CONTRACTS WITH CUSTOMERS

The Company accounts for revenue in accordance with ASC 606, "Revenue from Contracts with Customers". Revenues are generated from the design and manufacture of specialty engineered filtration media, industrial thermal insulating solutions, automotive thermal and acoustical barriers for filtration/separation and thermal/acoustical applications. The Company’s revenue

recognition policies require the Company to make significant judgments and estimates. In applying the Company’s revenue recognition policy, determinations must be made as to when the control of products passes to the Company’s customers which can be either at a point in time or over time. Revenue is generally recognized at a point in time when control passes to customers upon shipment of the Company’s products and revenue is generally recognized over time when control of the Company’s products transfers to customers during the manufacturing process. The Company analyzes several factors, including, but not limited to, the nature of the products being sold and contractual terms and conditions in contracts with customers to help the

Company make such judgments about revenue recognition. Unfulfilled performance obligations are generally expected to be satisfied within one year.

Contract Assets and Liabilities

The Company’s contract assets primarily include unbilled amounts typically resulting from sales under contracts when the over timeovertime method of revenue recognition is utilized and revenue recognized exceeds the amount billed to the customer. These unbilled accounts receivable in contract assets are transferred to accounts receivable upon invoicing, typically when the right to payment becomes unconditional, in which case payment is due based only upon the passage of time.

The Company’s contract liabilities primarily relate to billings and advance payments received from customers and deferred revenue. These contract liabilities represent the Company’s obligationobligations to transfer its products to its customers for which the Company has received, or is owed, consideration from its customers. Contract liabilities are included in Other long-termaccrued liabilities onin the Company’sCompany's Condensed Consolidated Balance Sheets.

Contract assets and liabilities consisted of the following:

| | | | | | | | | | | | | | | | | | | | | |

| In thousands | | | September 30, 2020 | | December 31, 2019 | | Dollar Change |

| Contract assets | | | $ | 27,186 | | | $ | 28,245 | | | $ | (1,059) | |

| Contract liabilities | | | $ | 3,414 | | | $ | 1,441 | | | $ | 1,973 | |

| | | | | | | | | | | | | | | | | | | | | |

| In thousands | | | At June 30, 2021 | | At December 31, 2020 | | Dollar Change |

| Contract assets | | | $ | 22,756 | | | $ | 32,403 | | | $ | (9,647) | |

| Contract liabilities | | | $ | 3,251 | | | $ | 3,686 | | | $ | (435) | |

The $1.1$9.6 million decrease in contactcontract assets from December 31, 20192020 to SeptemberJune 30, 20202021 was primarily due to timing of tooling billings to customers.customers and, to a lesser extent, the billings on last-time sales of membrane-based filtration media initiated in December 2020 in the Company's Netherlands facility.

The $2.0$0.4 million increasedecrease in contract liabilities from December 31, 20192020 to SeptemberJune 30, 20202021 was primarily due to an increase in customer deposits, offset by $1.1$2.7 million of revenue recognized in the first ninesix months of 20202021 related to contract liabilities at December 31, 2019.2020, offset by an increase in customer deposits.

Disaggregated Revenue

The Company disaggregates revenue from customers by geographic region, as it believes this disclosure best depicts how the nature, amount, timing, and uncertainty of the Company's revenues and cash flows are affected by economic factors. Disaggregated revenue by geographical region for the three-monththree and nine-monthsix-month periods ended SeptemberJune 30, 20202021 and 20192020 were as follows:

| | | For the Three Months Ended September 30, 2020 | | | For the Three Months Ended September 30, 2019 | | | For the Three Months Ended June 30, 2021 | | For the Three Months Ended June 30, 2020 |

| In thousands | In thousands | | North America | | Europe | | Asia | | Total Net Sales | | North America | | Europe | | Asia | | Total Net Sales | In thousands | | North America | | Europe | | Asia | | Total Net Sales | | North America | | Europe | | Asia | | Total Net Sales |

| | Performance Materials | Performance Materials | | $ | 45,759 | | | $ | 18,776 | | | $ | 3,282 | | | $ | 67,817 | | | $ | 42,693 | | | $ | 15,203 | | | $ | 2,104 | | | $ | 60,000 | | Performance Materials | | $ | 58,195 | | | $ | 15,272 | | | $ | 3,719 | | | $ | 77,186 | | | $ | 40,190 | | | $ | 16,501 | | | $ | 1,782 | | | $ | 58,473 | |

| Technical Nonwovens | Technical Nonwovens | | 34,727 | | | 17,318 | | | 6,464 | | | 58,509 | | | 42,128 | | | 16,544 | | | 5,240 | | | 63,912 | | Technical Nonwovens | | 46,443 | | | 18,077 | | | 7,959 | | | 72,479 | | | 31,236 | | | 15,418 | | | 5,353 | | | 52,007 | |

| Thermal Acoustical Solutions | Thermal Acoustical Solutions | | 57,841 | | | 22,861 | | | 4,821 | | | 85,523 | | | 61,315 | | | 22,208 | | | 4,403 | | | 87,926 | | Thermal Acoustical Solutions | | 50,709 | | | 22,673 | | | 3,476 | | | 76,858 | | | 22,575 | | | 11,424 | | | 3,449 | | | 37,448 | |

| Eliminations and Other | Eliminations and Other | | (4,569) | | | (195) | | | 0 | | | (4,764) | | | (6,405) | | | (159) | | | 0 | | | (6,564) | | Eliminations and Other | | (4,475) | | | (304) | | | 0 | | | (4,779) | | | (1,668) | | | (100) | | | 0 | | | (1,768) | |

| Total Net Sales | | $ | 133,758 | | | $ | 58,760 | | | $ | 14,567 | | | $ | 207,085 | | | $ | 139,731 | | | $ | 53,796 | | | $ | 11,747 | | | $ | 205,274 | | |

| Total net sales | | Total net sales | | $ | 150,872 | | | $ | 55,718 | | | $ | 15,154 | | | $ | 221,744 | | | $ | 92,333 | | | $ | 43,243 | | | $ | 10,584 | | | $ | 146,160 | |

| | | For the Nine Months Ended September 30, 2020 | | | For the Nine Months Ended September 30, 2019 | | | For the Six Months Ended June 30, 2021 | | For the Six Months Ended June 30, 2020 |

| In thousands | In thousands | | North America | | Europe | | Asia | | Total Net Sales | | North America | | Europe | | Asia | | Total Net Sales | In thousands | | North America | | Europe | | Asia | | Total Net Sales | | North America | | Europe | | Asia | | Total Net Sales |

| | Performance Materials | Performance Materials | | $ | 131,866 | | | $ | 52,552 | | | $ | 7,092 | | | $ | 191,510 | | | $ | 136,892 | | | $ | 47,589 | | | $ | 5,201 | | | $ | 189,682 | | Performance Materials | | $ | 117,069 | | | $ | 32,196 | | | $ | 7,254 | | | $ | 156,519 | | | $ | 86,107 | | | $ | 33,776 | | | $ | 3,810 | | | $ | 123,693 | |

| Technical Nonwovens | Technical Nonwovens | | 101,694 | | | 49,674 | | | 16,551 | | | 167,919 | | | 121,984 | | | 53,384 | | | 23,228 | | | 198,596 | | Technical Nonwovens | | 82,281 | | | 34,976 | | | 16,897 | | | 134,154 | | | 66,967 | | | 32,356 | | | 10,087 | | | 109,410 | |

| Thermal Acoustical Solutions | Thermal Acoustical Solutions | | 137,517 | | | 57,825 | | | 11,390 | | | 206,732 | | | 189,152 | | | 73,853 | | | 12,506 | | | 275,511 | | Thermal Acoustical Solutions | | 111,362 | | | 48,786 | | | 7,754 | | | 167,902 | | | 79,676 | | | 34,964 | | | 6,569 | | | 121,209 | |

| Eliminations and Other | Eliminations and Other | | (11,914) | | | (475) | | | 0 | | | (12,389) | | | (19,139) | | | (540) | | | 0 | | | (19,679) | | Eliminations and Other | | (9,153) | | | (579) | | | 0 | | | (9,732) | | | (7,345) | | | (280) | | | 0 | | | (7,625) | |

| Total Net Sales | | $ | 359,163 | | | $ | 159,576 | | | $ | 35,033 | | | $ | 553,772 | | | $ | 428,889 | | | $ | 174,286 | | | $ | 40,935 | | | $ | 644,110 | | |

| Total net sales | | Total net sales | | $ | 301,559 | | | $ | 115,379 | | | $ | 31,905 | | | $ | 448,843 | | | $ | 225,405 | | | $ | 100,816 | | | $ | 20,466 | | | $ | 346,687 | |

3. Inventories5. INVENTORIES

Inventories as of SeptemberJune 30, 20202021 and December 31, 20192020 were as follows:

| | | | | | | | | | | | | | |

| In thousands | | September 30,

2020 | | December 31,

2019 |

| Raw materials | | $ | 31,442 | | | $ | 36,322 | |

| Work in process | | 14,228 | | | 14,873 | |

| Finished goods | | 25,497 | | | 29,349 | |

| | | | |

| | | | |

| Total inventories | | $ | 71,167 | | | $ | 80,544 | |

Included | | | | | | | | | | | | | | |

| In thousands | | At June 30, 2021 (1) | | At December 31, 2020 |

| Raw materials | | $ | 40,805 | | | $ | 32,258 | |

Work in process (2) | | 16,093 | | | 17,087 | |

| Finished goods | | 31,328 | | | 29,651 | |

| | | | |

| | | | |

| Total inventories | | $ | 88,226 | | | $ | 78,996 | |

(1)Excludes inventories at the Netherlands operating facility that is classified as held-for-sale. See Note 3, "Divestiture Activities," in workthese Notes to Condensed Consolidated Financial Statements for additional information.

(2) Work in process isincludes net tooling inventory of $2.0$1.4 million and $1.8$2.8 million at SeptemberJune 30, 20202021 and December 31, 2019,2020, respectively.

4. Goodwill and Other Intangible Assets6. GOODWILL AND OTHER INTANGIBLE ASSETS

Goodwill

The Company performs an assessment of its goodwill for impairment at least annually, in the fourth quarter, and whenever events or changes in circumstances indicate that the carrying value may exceed its fair value. There were no such events or changes in circumstances during the three-monthsix-month period ended SeptemberJune 30, 2020. See Note 5, "Impairments of Goodwill and Other Long-Lived Assets", for discussion of the goodwill impairment recorded during the three-month period ended March 31, 2020.2021.

The changesfollowing table sets forth the change in the carrying amountvalue of goodwill byfor each reportable segment as of and for the nine-month period ended SeptemberCompany at June 30, 2020 were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| In thousands | | December 31,

2019 | | Currency translation adjustments | | Impairment | | September 30,

2020 |

| | | | | | | | |

| Performance Materials | | $ | 80,658 | | | $ | (22) | | | $ | (48,671) | | | $ | 31,965 | |

| Technical Nonwovens | | 53,254 | | | 166 | | | 0 | | | 53,420 | |

| Total goodwill | | $ | 133,912 | | | $ | 144 | | | $ | (48,671) | | | $ | 85,385 | |

Goodwill Impairment

During the three-month period ended March 31, 2020, the Company performed a goodwill impairment analysis in the Performance Materials and Technical Nonwovens reporting units and recorded a goodwill impairment charge of $48.7 million in the Performance Materials reporting unit. See Note 5, "Impairments of Goodwill and Other Long-Lived Assets", for further discussion of the goodwill impairment.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| In thousands | | Performance Materials | | Technical Nonwovens | | Thermal Acoustical Solutions | | Total |

| Gross balance at December 31, 2020 | | $ | 143,659 | | | $ | 55,607 | | | $ | 12,160 | | | $ | 211,426 | |

| Accumulated impairment | | (111,671) | | | 0 | | | (12,160) | | | (123,831) | |

| Net balance at December 31, 2020 | | 31,988 | | | 55,607 | | | 0 | | | 87,595 | |

| | | | | | | | |

| Foreign currency translation | | (17) | | | 264 | | | 0 | | | 247 | |

| Net balance at June 30, 2021 | | $ | 31,971 | | | $ | 55,871 | | | $ | 0 | | | $ | 87,842 | |

Other Intangible Assets

The table below presents the gross carrying amount and, as applicable, the accumulated amortization of the Company’s acquired intangible assets, other than goodwill, at June 30, 2021 and December 31, 2020. These amounts are included in “OtherOther intangible assets, net” innet on the Company's Condensed Consolidated Balance Sheets asSheets.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | At June 30, 2021 | | At December 31, 2020 |

| In thousands | | Amortization Period | | Gross Carrying Amount | | Accumulated Amortization | | Gross Carrying Amount | | Accumulated Amortization |

| Amortized intangible assets | | | | | | | | | | |

| Customer Relationships | | 10 - 14 years | | $ | 143,650 | | | $ | (58,187) | | | $ | 143,479 | | | $ | (50,076) | |

| Patents | | 28 years | | 650 | | | (623) | | | 650 | | | (616) | |

| Technology | | 15 years | | 2,500 | | | (1,227) | | | 2,500 | | | (1,144) | |

| Trade Names | | 5 years | | 7,495 | | | (7,336) | | | 7,495 | | | (7,167) | |

| License Agreements | | 10 years | | 0 | | | 0 | | | 185 | | | (185) | |

| Other | | 7 - 15 years | | 464 | | | (464) | | | 467 | | | (467) | |

| Total other intangible assets | | | | $ | 154,759 | | | $ | (67,837) | | | $ | 154,776 | | | $ | (59,655) | |

Estimated amortization expense for total intangible assets is expected to be $16.5 million, $14.5 million, $12.8 million, $11.4 million, $9.8 million, and $30.1 million, for each of September 30, 2020 andthe years ending December 31, 2019:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | September 30, 2020 | | | | December 31, 2019 | | |

| In thousands | | Gross Carrying Amount | | Accumulated Amortization | | Gross Carrying Amount | | Accumulated Amortization |

| Amortized intangible assets | | | | | | | | |

| Customer Relationships | | $ | 141,784 | | | $ | (44,636) | | | $ | 142,400 | | | $ | (30,648) | |

| Patents | | 791 | | | (670) | | | 759 | | | (607) | |

| Technology | | 2,500 | | | (1,102) | | | 2,500 | | | (977) | |

| Trade Names | | 7,322 | | | (6,544) | | | 7,293 | | | (5,143) | |

| License Agreements | | 629 | | | (629) | | | 610 | | | (610) | |

| Other | | 570 | | | (570) | | | 551 | | | (551) | |

| Total other intangible assets | | $ | 153,596 | | | $ | (54,151) | | | $ | 154,113 | | | $ | (38,536) | |

5. Impairments of Goodwill and Other Long-Lived Assets