0001465885wmc:CommercialMortgagePassThroughCertificateClassA1BMemberus-gaap:SecuredDebtMemberwmc:ArroyoMortgageTrust2020Member2022-01-012022-06-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One) | | | | | |

| ☒ | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended SeptemberJune 30, 20212022

| | | | | |

| ☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number: 001-35543

Western Asset Mortgage Capital Corporation

(Exact name of Registrant as specified in its charter) | | | | | | | | |

| Delaware | | 27-0298092 |

(State or other jurisdiction of

incorporation or organization) | | (IRS Employer

Identification Number) |

Western Asset Mortgage Capital Corporation

385 East Colorado Boulevard47 W 200 South, Suite 200

Pasadena, California 91101Salt Lake City, Utah 84101

(Address of Registrant’s principal executive offices)

(626) 844-9400(801) 952-3390

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | o | | Accelerated filer | x |

| Non-accelerated filer | o | | Smaller reporting company | x |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 under the Securities Exchange Act of 1934). Yes ☐ No ý

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of Each Class | | Trading Symbol(s) | | Name of Each Exchange on Which Registered |

| Common Stock, $0.01 par value | | WMC | | New York Stock Exchange |

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practical date.

As of November 3, 2021August 9, 2022 there were 60,859,9136,038,010 shares, par value $0.01, of the registrant’s common stock outstanding.

TABLE OF CONTENTS

Part I

ITEM I. Financial Statements

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Balance Sheets

(in thousands—except share and per share data)

(Unaudited) | | | | September 30,

2021 | | December 31, 2020 | | June 30,

2022 | | December 31, 2021 |

| Assets: | Assets: | | | | Assets: | | | |

| Cash and cash equivalents | Cash and cash equivalents | $ | 63,916 | | | $ | 31,613 | | Cash and cash equivalents | $ | 15,878 | | | $ | 40,193 | |

| Restricted cash | Restricted cash | 260 | | | 76,132 | | Restricted cash | 257 | | | 260 | |

| Agency mortgage-backed securities, at fair value ($1,342 and $1,708 pledged as collateral, at fair value, respectively) | 1,342 | | | 1,708 | | |

| Non-Agency mortgage-backed securities, at fair value ($153,460 and $167,970 pledged as collateral, at fair value, respectively) | 162,661 | | | 189,462 | | |

| Other securities, at fair value ($52,093 and $48,754 pledged as collateral, at fair value, respectively) | 52,093 | | | 48,754 | | |

| Residential Whole Loans, at fair value ($949,417 and $1,008,782 pledged as collateral, at fair value, respectively) | 949,417 | | | 1,008,782 | | |

| Residential Bridge Loans ($5,960 and $12,813 at fair value and $5,960 and $12,960 pledged as collateral, respectively) | 5,960 | | | 13,916 | | |

| Agency mortgage-backed securities, at fair value ($264 and $1,172 pledged as collateral, at fair value, respectively) | | Agency mortgage-backed securities, at fair value ($264 and $1,172 pledged as collateral, at fair value, respectively) | 785 | | | 1,172 | |

| Non-Agency mortgage-backed securities, at fair value ($116,331 and $123,947 pledged as collateral, at fair value, respectively) | | Non-Agency mortgage-backed securities, at fair value ($116,331 and $123,947 pledged as collateral, at fair value, respectively) | 125,294 | | | 133,127 | |

| Other securities, at fair value ($40,534 and $51,648 pledged as collateral, at fair value, respectively) | | Other securities, at fair value ($40,534 and $51,648 pledged as collateral, at fair value, respectively) | 40,534 | | | 51,648 | |

| Residential whole loans, at fair value ($1,195,853 and $1,023,502 pledged as collateral, at fair value, respectively) | | Residential whole loans, at fair value ($1,195,853 and $1,023,502 pledged as collateral, at fair value, respectively) | 1,195,853 | | | 1,023,502 | |

| Residential bridge loans, at fair value ($5,095 and $5,207 pledged as collateral, at fair value, respectively) | | Residential bridge loans, at fair value ($5,095 and $5,207 pledged as collateral, at fair value, respectively) | 5,095 | | | 5,428 | |

| Securitized commercial loans, at fair value | Securitized commercial loans, at fair value | 1,377,005 | | | 1,605,335 | | Securitized commercial loans, at fair value | 1,243,371 | | | 1,355,808 | |

| Commercial Loans, at fair value ($101,271 and $310,523 pledged as collateral, at fair value, respectively) | 128,766 | | | 310,523 | | |

| Commercial loans, at fair value ($101,487 and $101,459 pledged as collateral, at fair value, respectively) | | Commercial loans, at fair value ($101,487 and $101,459 pledged as collateral, at fair value, respectively) | 128,421 | | | 130,572 | |

| | Investment related receivable | Investment related receivable | 27,586 | | | 30,576 | | Investment related receivable | 11,952 | | | 22,133 | |

| Interest receivable | Interest receivable | 10,726 | | | 13,568 | | Interest receivable | 12,538 | | | 11,823 | |

| Due from counterparties | Due from counterparties | 2,842 | | | 2,327 | | Due from counterparties | 5,789 | | | 4,565 | |

| Derivative assets, at fair value | Derivative assets, at fair value | 94 | | | 161 | | Derivative assets, at fair value | 1,748 | | | 105 | |

| Other assets | Other assets | 46,676 | | | 3,152 | | Other assets | 3,734 | | | 45,364 | |

Total Assets (1) | Total Assets (1) | $ | 2,829,344 | | | $ | 3,336,009 | | Total Assets (1) | $ | 2,791,249 | | | $ | 2,825,700 | |

| | Liabilities and Equity: | Liabilities and Equity: | | | | Liabilities and Equity: | | | |

| Liabilities: | Liabilities: | | | | Liabilities: | | | |

| Repurchase agreements, net | Repurchase agreements, net | $ | 483,268 | | | $ | 356,923 | | Repurchase agreements, net | $ | 555,076 | | | $ | 617,189 | |

| Convertible senior unsecured notes, net | Convertible senior unsecured notes, net | 126,632 | | | 170,797 | | Convertible senior unsecured notes, net | 109,661 | | | 119,168 | |

| Securitized debt, net ($1,365,494 and $1,553,722 at fair value and $185,666 and $215,753 held by affiliates, respectively) | 1,970,513 | | | 2,446,012 | | |

| Interest payable (includes $712 and $784 on securitized debt held by affiliates, respectively) | 7,763 | | | 12,006 | | |

| Securitized debt, net ($1,574,468 and $1,344,370 at fair value and $164,264 and $180,116 held by affiliates, respectively) | | Securitized debt, net ($1,574,468 and $1,344,370 at fair value and $164,264 and $180,116 held by affiliates, respectively) | 1,962,787 | | | 1,863,488 | |

| Interest payable (includes $699 and $699 on securitized debt held by affiliates, respectively) | | Interest payable (includes $699 and $699 on securitized debt held by affiliates, respectively) | 10,740 | | | 10,272 | |

| | Due to counterparties | Due to counterparties | — | | | 321 | | Due to counterparties | 360 | | | — | |

| Derivative liability, at fair value | Derivative liability, at fair value | 562 | | | 656 | | Derivative liability, at fair value | 1,872 | | | 602 | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | 2,965 | | | 2,686 | | Accounts payable and accrued expenses | 3,585 | | | 4,842 | |

| Payable to affiliate | Payable to affiliate | 3,133 | | | 3,171 | | Payable to affiliate | 3,978 | | | 1,925 | |

| Dividend payable | Dividend payable | 3,651 | | | 3,649 | | Dividend payable | 2,415 | | | 3,623 | |

| Other liabilities | Other liabilities | 8,804 | | | 84,674 | | Other liabilities | 437 | | | 262 | |

Total Liabilities (2) | Total Liabilities (2) | 2,607,291 | | | 3,080,895 | | Total Liabilities(2) | 2,650,911 | | | 2,621,371 | |

| | Commitments and contingencies | 0 | | 0 | |

| Commitments and contingencies (Note 15) | | Commitments and contingencies (Note 15) | 0 | | 0 |

| | Stockholders’ Equity: | Stockholders’ Equity: | | | | Stockholders’ Equity: | | | |

| Common stock: $0.01 par value, 500,000,000 shares authorized, 60,859,913 and 60,812,701 outstanding, respectively | 609 | | | 609 | | |

Common stock: $0.01 par value, 50,000,000 shares authorized, 6,038,010 and 6,038,010 outstanding, respectively(3) | | Common stock: $0.01 par value, 50,000,000 shares authorized, 6,038,010 and 6,038,010 outstanding, respectively(3) | 60 | | | 60 | |

| Preferred stock, $0.01 par value, 100,000,000 shares authorized and no shares outstanding | Preferred stock, $0.01 par value, 100,000,000 shares authorized and no shares outstanding | — | | | — | | Preferred stock, $0.01 par value, 100,000,000 shares authorized and no shares outstanding | — | | | — | |

| Treasury stock, at cost, 100,000 and 100,000 shares held, respectively | (578) | | | (578) | | |

| Treasury stock, at cost, 57,981 and 57,981 shares held, respectively | | Treasury stock, at cost, 57,981 and 57,981 shares held, respectively | (1,665) | | | (1,665) | |

Additional paid-in capital | Additional paid-in capital | 917,963 | | | 915,458 | | Additional paid-in capital | 918,974 | | | 918,695 | |

| Retained earnings (accumulated deficit) | Retained earnings (accumulated deficit) | (707,808) | | | (660,377) | | Retained earnings (accumulated deficit) | (777,095) | | | (723,981) | |

| Total Stockholders’ Equity | Total Stockholders’ Equity | 210,186 | | | 255,112 | | Total Stockholders’ Equity | 140,274 | | | 193,109 | |

| Non-controlling interest | Non-controlling interest | 11,867 | | | 2 | | Non-controlling interest | 64 | | | 11,220 | |

| Total Equity | Total Equity | 222,053 | | | 255,114 | | Total Equity | 140,338 | | | 204,329 | |

| Total Liabilities and Equity | Total Liabilities and Equity | $ | 2,829,344 | | | $ | 3,336,009 | | Total Liabilities and Equity | $ | 2,791,249 | | | $ | 2,825,700 | |

See notes to unaudited consolidated financial statements.

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Balance Sheets (Continued)

(in thousands — except share and per share data)

(Unaudited) | | | September 30,

2021 | | December 31, 2020 | | June 30,

2022 | | December 31, 2021 |

(1) Assets of consolidated VIEs included in the total assets above: | (1) Assets of consolidated VIEs included in the total assets above: | | | | (1) Assets of consolidated VIEs included in the total assets above: | | | |

| Cash and cash equivalents | Cash and cash equivalents | $ | 9,245 | | | $ | — | | Cash and cash equivalents | $ | — | | | $ | 266 | |

| Restricted cash | Restricted cash | 260 | | | 76,132 | | Restricted cash | 257 | | | 260 | |

| Residential Whole Loans, at fair value ($949,417 and $1,008,782 pledged as collateral, at fair value, respectively) | 949,417 | | | 1,008,782 | | |

| Residential Bridge Loans ($5,960 and $11,858 at fair value and $5,960 and $12,960 pledged as collateral, respectively) | 5,960 | | | 12,960 | | |

| Residential whole loans, at fair value ($1,195,853 and $1,023,502 pledged as collateral, at fair value, respectively) | | Residential whole loans, at fair value ($1,195,853 and $1,023,502 pledged as collateral, at fair value, respectively) | 1,195,853 | | | 1,023,502 | |

| Residential bridge loans, at fair value ($5,095 and $5,207 pledged as collateral, at fair value, respectively) | | Residential bridge loans, at fair value ($5,095 and $5,207 pledged as collateral, at fair value, respectively) | 5,095 | | | 5,207 | |

| Securitized commercial loans, at fair value | Securitized commercial loans, at fair value | 1,377,005 | | | 1,605,335 | | Securitized commercial loans, at fair value | 1,243,371 | | | 1,355,808 | |

| Commercial Loans, at fair value ($14,362 and $68,466 pledged as collateral, at fair value, respectively) | 14,362 | | | 68,466 | | |

| Commercial loans, at fair value ($14,398 and $14,362 pledged as collateral, at fair value, respectively) | | Commercial loans, at fair value ($14,398 and $14,362 pledged as collateral, at fair value, respectively) | 14,398 | | | 14,362 | |

| Investment related receivable | Investment related receivable | 24,224 | | | 27,987 | | Investment related receivable | 11,906 | | | 22,087 | |

| Interest receivable | Interest receivable | 9,433 | | | 10,936 | | Interest receivable | 11,506 | | | 10,572 | |

| Other assets | 80 | | | 80 | | |

| | Total assets of consolidated VIEs | Total assets of consolidated VIEs | $ | 2,389,986 | | | $ | 2,810,678 | | Total assets of consolidated VIEs | $ | 2,482,386 | | | $ | 2,432,064 | |

| (2) Liabilities of consolidated VIEs included in the total liabilities above: | (2) Liabilities of consolidated VIEs included in the total liabilities above: | | | | (2) Liabilities of consolidated VIEs included in the total liabilities above: | | | |

| Securitized debt, net ($1,365,494 and $1,553,722 at fair value and $185,666 and $215,753 held by affiliates, respectively) | $ | 1,970,513 | | | $ | 2,446,012 | | |

| Interest payable (includes $712 and $784 on securitized debt held by affiliates, respectively) | 6,519 | | | 7,882 | | |

| Securitized debt, net ($1,574,468 and $1,344,370 at fair value and $164,264 and $180,116 held by affiliates, respectively) | | Securitized debt, net ($1,574,468 and $1,344,370 at fair value and $164,264 and $180,116 held by affiliates, respectively) | $ | 1,962,787 | | | $ | 1,863,488 | |

| Interest payable (includes $699 and $699 on securitized debt held by affiliates, respectively) | | Interest payable (includes $699 and $699 on securitized debt held by affiliates, respectively) | 6,901 | | | 6,480 | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | 49 | | | 89 | | Accounts payable and accrued expenses | 70 | | | 78 | |

| Other liabilities | Other liabilities | 260 | | | 76,132 | | Other liabilities | 257 | | | 260 | |

| Total liabilities of consolidated VIEs | Total liabilities of consolidated VIEs | $ | 1,977,341 | | | $ | 2,530,115 | | Total liabilities of consolidated VIEs | $ | 1,970,015 | | | $ | 1,870,306 | |

(3) Amounts have been adjusted to reflect the one-for-ten reverse stock split effected July 11, 2022. See Note 2 and Note 12 for additional details.

See notes to unaudited consolidated financial statements.

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Statements of Operations

(in thousands—except share and per share data)

(Unaudited)

| | | | For the three months ended September 30, 2021 | | For the three months ended September 30, 2020 | | For the nine months ended September 30, 2021 | | For the nine months ended September 30, 2020 | | For the three months ended June 30, 2022 | | For the three months ended June 30, 2021 | | For the six months ended June 30, 2022 | | For the six months ended June 30, 2021 |

| Net Interest Income | Net Interest Income | | | | | | | | Net Interest Income | | | | | | | |

| Interest income | Interest income | $ | 40,141 | | | $ | 43,970 | | | $ | 127,353 | | | $ | 130,310 | | Interest income | $ | 39,577 | | | $ | 41,195 | | | $ | 75,219 | | | $ | 87,212 | |

| Interest expense (includes $3,564, $2,647, $10,919 and $5,203 on securitized debt held by affiliates, respectively) | 32,978 | | | 33,853 | | | 104,352 | | | 94,376 | | |

| Interest expense (includes $3,476, $3,662, $6,919 and $7,355 on securitized debt held by affiliates, respectively) | | Interest expense (includes $3,476, $3,662, $6,919 and $7,355 on securitized debt held by affiliates, respectively) | 33,342 | | | 34,605 | | | 64,701 | | | 71,374 | |

| Net Interest Income | Net Interest Income | 7,163 | | | 10,117 | | | 23,001 | | | 35,934 | | Net Interest Income | 6,235 | | | 6,590 | | | 10,518 | | | 15,838 | |

| | Other Income (Loss) | Other Income (Loss) | | | | | | | | Other Income (Loss) | | | | | | | |

| Realized gain (loss), net | (1,526) | | | 718 | | | (7,367) | | | 82,944 | | |

| Realized loss, net | | Realized loss, net | (45,661) | | | (116) | | | (33,516) | | | (5,841) | |

| | Unrealized gain (loss), net | Unrealized gain (loss), net | (6,003) | | | 54,690 | | | (39,271) | | | (225,381) | | Unrealized gain (loss), net | 16,185 | | | (42,318) | | | (22,718) | | | (33,268) | |

| Gain (loss) on derivative instruments, net | 515 | | | (88) | | | 716 | | | (197,922) | | |

| Gain on derivative instruments, net | | Gain on derivative instruments, net | 4,781 | | | 175 | | | 11,717 | | | 201 | |

| Other, net | Other, net | 277 | | | (31) | | | 449 | | | 385 | | Other, net | (46) | | | 200 | | | (191) | | | 172 | |

| Other Income (Loss) | Other Income (Loss) | (6,737) | | | 55,289 | | | (45,473) | | | (339,974) | | Other Income (Loss) | (24,741) | | | (42,059) | | | (44,708) | | | (38,736) | |

| | Expenses | Expenses | | | | | | | | Expenses | | | | | | | |

| Management fee to affiliate | Management fee to affiliate | 1,502 | | | 1,513 | | | 4,469 | | | 3,016 | | Management fee to affiliate | 1,002 | | | 1,490 | | | 2,102 | | | 2,967 | |

| Financing fee | — | | | — | | | — | | | 20,540 | | |

| | Other operating expenses | Other operating expenses | 1,306 | | | 1,198 | | | 2,126 | | | 2,994 | | Other operating expenses | 262 | | | 428 | | | 558 | | | 820 | |

| Transaction costs | | Transaction costs | 344 | | | — | | | 2,955 | | | — | |

| General and administrative expenses: | General and administrative expenses: | | | | General and administrative expenses: | | | |

| Compensation expense | Compensation expense | 626 | | | 716 | | | 1,985 | | | 2,070 | | Compensation expense | 130 | | | 651 | | | 628 | | | 1,359 | |

| Professional fees | Professional fees | 947 | | | 827 | | | 2,864 | | | 3,848 | | Professional fees | 1,552 | | | 1,038 | | | 2,808 | | | 1,917 | |

| Other general and administrative expenses | Other general and administrative expenses | 747 | | | 1,138 | | | 2,793 | | | 2,263 | | Other general and administrative expenses | 637 | | | 984 | | | 1,373 | | | 2,046 | |

| Total general and administrative expenses | Total general and administrative expenses | 2,320 | | | 2,681 | | | 7,642 | | | 8,181 | | Total general and administrative expenses | 2,319 | | | 2,673 | | | 4,809 | | | 5,322 | |

| Total Expenses | Total Expenses | 5,128 | | | 5,392 | | | 14,237 | | | 34,731 | | Total Expenses | 3,927 | | | 4,591 | | | 10,424 | | | 9,109 | |

| | Income (loss) before income taxes | (4,702) | | | 60,014 | | | (36,709) | | | (338,771) | | |

| Loss before income taxes | | Loss before income taxes | (22,433) | | | (40,060) | | | (44,614) | | | (32,007) | |

| Income tax provision (benefit) | Income tax provision (benefit) | (218) | | | 205 | | | (19) | | | 367 | | Income tax provision (benefit) | (46) | | | 101 | | | 10 | | | 199 | |

| Net income (loss) | (4,484) | | | 59,809 | | | (36,690) | | | (339,138) | | |

| Net income (loss) attributable to non-controlling interest | (271) | | | 2 | | | (267) | | | 6 | | |

| Net income (loss) attributable to common stockholders and participating securities | $ | (4,213) | | | $ | 59,807 | | | $ | (36,423) | | | $ | (339,144) | | |

| Net loss | | Net loss | (22,387) | | | (40,161) | | | (44,624) | | | (32,206) | |

| Net income attributable to non-controlling interest | | Net income attributable to non-controlling interest | — | | | 2 | | | 3,616 | | | 4 | |

| Net loss attributable to common stockholders and participating securities | | Net loss attributable to common stockholders and participating securities | $ | (22,387) | | | $ | (40,163) | | | $ | (48,240) | | | $ | (32,210) | |

| | Net income (loss) per Common Share — Basic | $ | (0.07) | | | $ | 0.98 | | | $ | (0.60) | | | $ | (6.02) | | |

| Net income (loss) per Common Share — Diluted | $ | (0.07) | | | $ | 0.98 | | | $ | (0.60) | | | $ | (6.02) | | |

Net loss per Common Share — Basic(1) | | Net loss per Common Share — Basic(1) | $ | (3.71) | | | $ | (6.61) | | | $ | (8.00) | | | $ | (5.31) | |

Net loss per Common Share — Diluted(1) | | Net loss per Common Share — Diluted(1) | $ | (3.71) | | | $ | (6.61) | | | $ | (8.00) | | | $ | (5.31) | |

(1) Amounts have been adjusted to reflect the one-for-ten reverse stock split effected July 11, 2022. See Note 2 and Note 12 for additional details.

.

See notes to unaudited consolidated financial statements.

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Statements of Changes in Equity

(in thousands—except shares and share data)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended September 30, 2021 |

| | Common Stock Outstanding | | Additional

Paid-In Capital | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | Total Equity |

| Shares | | Par | | | | | | |

| Balance at June 30, 2021 | 60,812,701 | | | $ | 609 | | | $ | 915,782 | | | $ | (699,920) | | | $ | (578) | | | $ | 215,893 | | | $ | 2 | | | $ | 215,895 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Equity contributions | — | | | — | | | — | | | — | | | — | | | — | | | 12,138 | | | 12,138 | |

| Equity component of convertible senior unsecured notes | — | | | — | | | 2,060 | | | — | | | — | | | 2,060 | | | — | | | 2,060 | |

| Exchange of phantom stock to common stock | 47,212 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| | | | | | | | | | | | | | | |

| Offering costs | — | | | — | | | (68) | | | — | | | — | | | (68) | | | — | | | (68) | |

| Vesting of restricted stock | — | | | — | | | 165 | | | — | | | — | | | 165 | | | — | | | 165 | |

| | | | | | | | | | | | | | | |

| Net loss | — | | | — | | | — | | | (4,213) | | | — | | | (4,213) | | | (271) | | | (4,484) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (2) | | | (2) | |

| Dividends declared on common stock | — | | | — | | | 24 | | | (3,675) | | | — | | | (3,651) | | | — | | | (3,651) | |

| Balance at September 30, 2021 | 60,859,913 | | | $ | 609 | | | $ | 917,963 | | | $ | (707,808) | | | $ | (578) | | | $ | 210,186 | | | $ | 11,867 | | | $ | 222,053 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, 2022 |

| | Common Stock Outstanding | | Additional Paid-In Capital(1) | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | Total Equity |

| Shares(1) | | Par | | | | | | |

| Balance at March 31, 2022 | 6,038,010 | | | $ | 60 | | | $ | 918,874 | | | $ | (752,263) | | | $ | (1,665) | | | $ | 165,006 | | | $ | 144 | | | $ | 165,150 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Equity distribution | — | | | — | | | — | | | — | | | — | | | — | | | (78) | | | (78) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 70 | | | — | | | — | | | 70 | | | — | | | 70 | |

| | | | | | | | | | | | | | | |

| Net loss | — | | | — | | | — | | | (22,387) | | | — | | | (22,387) | | | — | | | (22,387) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (2) | | | (2) | |

| Dividends declared on common stock | — | | | — | | | 30 | | | (2,445) | | | — | | | (2,415) | | | — | | | (2,415) | |

| Balance at June 30, 2022 | 6,038,010 | | | $ | 60 | | | $ | 918,974 | | | $ | (777,095) | | | $ | (1,665) | | | $ | 140,274 | | | $ | 64 | | | $ | 140,338 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended September 30, 2020 |

| | Common Stock Outstanding | | Additional

Paid-In Capital | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | Total Equity |

| Shares | | Par | | | | | | |

| Balance at June 30, 2020 | 59,458,617 | | | $ | 595 | | | $ | 911,488 | | | $ | (724,252) | | | $ | (578) | | | $ | 187,253 | | | $ | 2 | | | $ | 187,255 | |

| Exchange of convertible senior unsecured notes | 1,354,084 | | | 14 | | | 3,574 | | | — | | | — | | | 3,588 | | | — | | | 3,588 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 182 | | | — | | | — | | | 182 | | | — | | | 182 | |

| | | | | | | | | | | | | | | |

| Net income | — | | | — | | | — | | | 59,807 | | | — | | | 59,807 | | | 2 | | | 59,809 | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (2) | | | (2) | |

| Dividends declared on common stock | — | | | — | | | 14 | | | (3,055) | | | — | | | (3,041) | | | | | (3,041) | |

| Balance at September 30, 2020 | 60,812,701 | | | $ | 609 | | | $ | 915,258 | | | $ | (667,500) | | | $ | (578) | | | $ | 247,789 | | | $ | 2 | | | $ | 247,791 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, 2021 |

| | Common Stock Outstanding | | Additional Paid-In Capital(1) | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | Total Equity |

| Shares(1) | | Par | | | | | | |

| Balance at March 31, 2021 | 6,081,270 | | | $ | 60 | | | $ | 916,208 | | | $ | (656,091) | | | $ | (578) | | | $ | 259,599 | | | $ | 2 | | | $ | 259,601 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 106 | | | — | | | — | | | 106 | | | — | | | 106 | |

| | | | | | | | | | | | | | | |

| Net income (loss) | — | | | — | | | — | | | (40,163) | | | — | | | (40,163) | | | 2 | | | (40,161) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (2) | | | (2) | |

| Dividends declared on common stock | — | | | — | | | 17 | | | (3,666) | | | — | | | (3,649) | | | — | | | (3,649) | |

| Balance at June 30, 2021 | 6,081,270 | | | $ | 60 | | | $ | 916,331 | | | $ | (699,920) | | | $ | (578) | | | $ | 215,893 | | | $ | 2 | | | $ | 215,895 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Nine Months Ended September 30, 2021 |

| | Common Stock Outstanding | | Additional

Paid-In Capital | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | |

| Shares | | Par | | | | | | | Total |

| Balance at December 31, 2020 | 60,812,701 | | | $ | 609 | | | $ | 915,458 | | | $ | (660,377) | | | $ | (578) | | | $ | 255,112 | | | $ | 2 | | | $ | 255,114 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Equity contributions | — | | | — | | | — | | | — | | | — | | | — | | | 12,138 | | | 12,138 | |

| Equity component of convertible senior unsecured notes | — | | | — | | | 2,060 | | | — | | | — | | | 2,060 | | | — | | | 2,060 | |

| Exchange of phantom stock to common stock | 47,212 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| Offering costs | — | | | — | | | (68) | | | — | | | — | | | (68) | | | — | | | (68) | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 454 | | | — | | | — | | | 454 | | | — | | | 454 | |

| | | | | | | | | | | | | | | |

| Net loss | — | | | — | | | — | | | (36,423) | | | — | | | (36,423) | | | (267) | | | (36,690) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (6) | | | (6) | |

| Dividends declared on common stock | — | | | — | | | 59 | | | (11,008) | | | — | | | (10,949) | | | — | | | (10,949) | |

| Balance at September 30, 2021 | 60,859,913 | | | $ | 609 | | | $ | 917,963 | | | $ | (707,808) | | | $ | (578) | | | $ | 210,186 | | | $ | 11,867 | | | $ | 222,053 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Six Months Ended June 30, 2022 |

| | Common Stock Outstanding | | Additional Paid-In Capital(1) | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | |

| Shares(1) | | Par | | | | | | | Total Equity |

| Balance at December 31, 2021 | 6,038,010 | | | $ | 60 | | | $ | 918,695 | | | $ | (723,981) | | | $ | (1,665) | | | $ | 193,109 | | | $ | 11,220 | | | $ | 204,329 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Equity distribution | — | | | — | | | — | | | — | | | — | | | — | | | (14,768) | | | (14,768) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 235 | | | — | | | — | | | 235 | | | — | | | 235 | |

| | | | | | | | | | | | | | | |

| Net income (loss) | — | | | — | | | — | | | (48,240) | | | — | | | (48,240) | | | 3,616 | | | (44,624) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (4) | | | (4) | |

| Dividends declared on common stock | — | | | — | | | 44 | | | (4,874) | | | — | | | (4,830) | | | — | | | (4,830) | |

| Balance at June 30, 2022 | 6,038,010 | | | $ | 60 | | | $ | 918,974 | | | $ | (777,095) | | | $ | (1,665) | | | $ | 140,274 | | | $ | 64 | | | $ | 140,338 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Nine Months Ended September 30, 2020 |

| | Common Stock Outstanding | | Additional

Paid-In Capital | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | |

| Shares | | Par | | | | | | | Total |

| Balance at December 31, 2019 | 53,523,876 | | | $ | 535 | | | $ | 889,227 | | | $ | (325,301) | | | $ | — | | | $ | 564,461 | | | $ | — | | | $ | 564,461 | |

| Proceeds from public offerings of common stock | 6,034,741 | | | 60 | | | 22,297 | | | — | | | — | | | 22,357 | | | — | | | 22,357 | |

| Offering costs | — | | | — | | | (371) | | | — | | | — | | | (371) | | | — | | | (371) | |

| Proceeds from non-controlling interest, net of offering costs | — | | | — | | | — | | | — | | | — | | | — | | | 2 | | | 2 | |

| | | | | | | | | | | | | | | |

| Exchange of convertible senior notes | 1,354,084 | | | 14 | | | 3,574 | | | — | | | — | | | 3,588 | | | — | | | 3,588 | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 517 | | | — | | | — | | | 517 | | | — | | | 517 | |

| Treasury stock | (100,000) | | | — | | | — | | | — | | | (578) | | | (578) | | | — | | | (578) | |

| Net loss | — | | | — | | | — | | | (339,144) | | | — | | | (339,144) | | | 6 | | | (339,138) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (6) | | | (6) | |

| Dividends declared on common stock | — | | | — | | | 14 | | | (3,055) | | | — | | | (3,041) | | | — | | | (3,041) | |

| Balance at September 30, 2020 | 60,812,701 | | | $ | 609 | | | $ | 915,258 | | | $ | (667,500) | | | $ | (578) | | | $ | 247,789 | | | $ | 2 | | | $ | 247,791 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Six Months Ended June 30, 2021 |

| | Common Stock Outstanding | | Additional Paid-In Capital(1) | | Retained

Earnings

(Accumulated Deficit) | | Treasury Stock | | Total Stockholders' Equity | | Non-Controlling Interest | | |

| Shares(1) | | Par | | | | | | | Total Equity |

| Balance at December 31, 2020 | 6,081,270 | | | $ | 60 | | | $ | 916,007 | | | $ | (660,377) | | | $ | (578) | | | $ | 255,112 | | | $ | 2 | | | $ | 255,114 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Vesting of restricted stock | — | | | — | | | 289 | | | — | | | — | | | 289 | | | — | | | 289 | |

| | | | | | | | | | | | | | | |

| Net income (loss) | — | | | — | | | — | | | (32,210) | | | — | | | (32,210) | | | 4 | | | (32,206) | |

| Dividends declared on non-controlling interest | — | | | — | | | — | | | — | | | — | | | — | | | (4) | | | (4) | |

| Dividends declared on common stock | — | | | — | | | 35 | | | (7,333) | | | — | | | (7,298) | | | — | | | (7,298) | |

| Balance at June 30, 2021 | 6,081,270 | | | $ | 60 | | | $ | 916,331 | | | $ | (699,920) | | | $ | (578) | | | $ | 215,893 | | | $ | 2 | | | $ | 215,895 | |

| | | | | | | | | | | | | | | |

(1) Amounts have been adjusted to reflect the one-for-ten reverse stock split effected July 11, 2022. See Note 2 and Note 12 for additional details.

See notes to unaudited consolidated financial statements.

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Statements of Cash Flows (in thousands)

(Unaudited)

| | | | For the nine months ended September 30, 2021 | | For the nine months ended September 30, 2020 | | For the six months ended June 30, 2022 | | For the six months ended June 30, 2021 |

| Cash flows from operating activities: | Cash flows from operating activities: | | | | Cash flows from operating activities: | | | |

| Net loss | Net loss | $ | (36,690) | | | $ | (339,138) | | Net loss | $ | (44,624) | | | $ | (32,206) | |

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | | | | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

| Premium amortization and (discount accretion), net | Premium amortization and (discount accretion), net | 145 | | | 5,291 | | Premium amortization and (discount accretion), net | 2,599 | | | 204 | |

| Interest income earned added to principal of investments | Interest income earned added to principal of investments | (310) | | | (647) | | Interest income earned added to principal of investments | (75) | | | (278) | |

| Amortization of deferred financing costs | Amortization of deferred financing costs | 3,935 | | | 2,165 | | Amortization of deferred financing costs | 1,298 | | | 2,660 | |

| Amortization of discount on convertible senior unsecured notes | Amortization of discount on convertible senior unsecured notes | 712 | | | 830 | | Amortization of discount on convertible senior unsecured notes | 439 | | | 484 | |

| Restricted stock amortization | Restricted stock amortization | 453 | | | 517 | | Restricted stock amortization | 235 | | | 288 | |

| | Interest payments and basis recovered on MAC interest rate swaps | — | | | 202 | | |

| Premium on purchase of Residential Whole Loans | (10,281) | | | (3,858) | | |

| | Premium on purchase of residential whole loans | | Premium on purchase of residential whole loans | (6,619) | | | (274) | |

| | Unrealized loss, net | Unrealized loss, net | 39,271 | | | 225,381 | | Unrealized loss, net | 22,718 | | | 33,268 | |

| Realized (gain) loss on extinguishment of convertible senior notes | Realized (gain) loss on extinguishment of convertible senior notes | 1,337 | | | (1,258) | | Realized (gain) loss on extinguishment of convertible senior notes | 132 | | | (240) | |

| Realized (gain) loss on sale of real estate owned ("REO") | (54) | | | 680 | | |

| Unrealized loss on derivative instruments, net | 97 | | | 4,122 | | |

| Realized gain on sale of real estate owned ("REO") | | Realized gain on sale of real estate owned ("REO") | (12,198) | | | — | |

| Unrealized gain on derivative instruments, net | | Unrealized gain on derivative instruments, net | (157) | | | (8) | |

| | Realized (gain) loss on investments, net | 6,084 | | | (82,366) | | |

| Loss on derivatives, net | — | | | 13,133 | | |

| Realized loss on investments, net | | Realized loss on investments, net | 45,582 | | | 6,081 | |

| Gain on derivatives, net | | Gain on derivatives, net | (732) | | | — | |

| | Changes in operating assets and liabilities: | Changes in operating assets and liabilities: | | | | Changes in operating assets and liabilities: | | | |

| Interest receivable | Interest receivable | 2,496 | | | 5,312 | | Interest receivable | (715) | | | 2,022 | |

| Investment related receivable | Investment related receivable | (704) | | | — | | Investment related receivable | — | | | 269 | |

| Other assets | Other assets | (973) | | | (1,933) | | Other assets | (853) | | | (787) | |

| Interest payable | Interest payable | (4,243) | | | (6,161) | | Interest payable | 468 | | | (1,358) | |

| Accounts payable and accrued expenses | Accounts payable and accrued expenses | 60 | | | 804 | | Accounts payable and accrued expenses | (1,255) | | | (799) | |

| Payable to affiliate | Payable to affiliate | (38) | | | 1,107 | | Payable to affiliate | 2,053 | | | (1,599) | |

| Other liabilities | Other liabilities | 1 | | | 20,540 | | Other liabilities | 179 | | | 145 | |

| Net cash provided by (used in ) in operating activities | 1,298 | | | (155,277) | | |

| Net cash provided by operating activities | | Net cash provided by operating activities | 8,475 | | | 7,872 | |

| | Cash flows from investing activities: | Cash flows from investing activities: | | | | Cash flows from investing activities: | | | |

| Purchase of securities | Purchase of securities | — | | | (320,996) | | Purchase of securities | (39,952) | | | — | |

| Proceeds from sale of securities | Proceeds from sale of securities | — | | | 2,216,830 | | Proceeds from sale of securities | 42,287 | | | — | |

| Proceeds from sale of REO | Proceeds from sale of REO | 738 | | | 2,491 | | Proceeds from sale of REO | 54,681 | | | — | |

| Principal repayments and basis recovered on securities | Principal repayments and basis recovered on securities | 14,685 | | | 32,401 | | Principal repayments and basis recovered on securities | 2,543 | | | 2,667 | |

| Purchase of Residential Whole Loans | (233,041) | | | (109,480) | | |

| Proceeds from sale of Residential Whole Loans | — | | | 144,258 | | |

| Principal repayments on Residential Whole Loans | 313,661 | | | 210,097 | | |

| Purchase of residential whole loans | | Purchase of residential whole loans | (405,298) | | | (9,799) | |

| | Principal repayments on residential whole loans | | Principal repayments on residential whole loans | 165,236 | | | 226,734 | |

| | Principal repayments on commercial loans | Principal repayments on commercial loans | 103,272 | | | 37,728 | | Principal repayments on commercial loans | 4 | | | 303 | |

| | Principal repayments on securitized commercial loans | Principal repayments on securitized commercial loans | 354,202 | | | 211,205 | | Principal repayments on securitized commercial loans | — | | | 139,657 | |

| | Principal repayments on Residential Bridge Loans | 7,052 | | | 16,759 | | |

| Principal repayments on residential bridge loans | | Principal repayments on residential bridge loans | 366 | | | 6,192 | |

| | Premium for credit default swaps, net | — | | | (14,028) | | |

| | Net settlements of TBAs | Net settlements of TBAs | — | | | (2,430) | | Net settlements of TBAs | 732 | | | — | |

| | Interest payments and basis recovered on MAC interest rate swaps | — | | | (202) | | |

| | Due from counterparties | Due from counterparties | 50 | | | 2,160 | | Due from counterparties | 150 | | | — | |

| | Premium for interest rate swaptions, net | — | | | 80 | | |

| Net cash provided by investing activities | 560,619 | | | 2,426,873 | | |

| | Net cash (used in) provided by investing activities | | Net cash (used in) provided by investing activities | (179,251) | | | 365,754 | |

| | Cash flows from financing activities: | Cash flows from financing activities: | | | | Cash flows from financing activities: | | | |

| Proceeds from issuance of common stock | — | | | 22,357 | | |

| | Payment of offering costs | Payment of offering costs | (86) | | | (374) | | Payment of offering costs | (2) | | | (24) | |

| Repurchase of common stock | — | | | (578) | | |

| | Proceeds from issuance of convertible senior unsecured notes | 86,250 | | | — | | |

| | Payments on extinguishment of convertible senior unsecured notes | Payments on extinguishment of convertible senior unsecured notes | (128,645) | | | — | | Payments on extinguishment of convertible senior unsecured notes | (10,690) | | | (6,315) | |

| | Proceeds from repurchase agreement borrowings | | Proceeds from repurchase agreement borrowings | 2,838,689 | | | 1,482,074 | |

| Repayments of repurchase agreement borrowings | | Repayments of repurchase agreement borrowings | (2,900,802) | | | (1,475,438) | |

| | Proceeds from securitized debt | | Proceeds from securitized debt | 397,934 | | | — | |

| Repayments of securitized debt | | Repayments of securitized debt | (156,843) | | | (351,428) | |

| | Payments made for deferred financing costs | | Payments made for deferred financing costs | — | | | (10) | |

| Due from counterparties, net | | Due from counterparties, net | (1,374) | | | (1,121) | |

| Due to counterparties, net | | Due to counterparties, net | 360 | | | 100 | |

| Decrease in other liabilities | | Decrease in other liabilities | (4) | | | (53,157) | |

Western Asset Mortgage Capital Corporation and Subsidiaries

Consolidated Statements of Cash Flows (Continued) (in thousands)

(Unaudited)

| | | | | | | | | | | |

| | For the nine months ended September 30, 2021 | | For the nine months ended September 30, 2020 |

| Proceeds from offering to non-controlling interest, net of offering costs | — | | | 2 | |

| Proceeds from repurchase agreement borrowings | 2,527,530 | | | 9,149,204 | |

| Repayments of repurchase agreement borrowings | (2,403,068) | | | (11,615,203) | |

| | | |

| Proceeds from securitized debt | — | | | 460,787 | |

| Repayments of securitized debt | (597,221) | | | (366,828) | |

| | | |

| | | |

| Payments made for deferred financing costs | (2,536) | | | (3,145) | |

| Due from counterparties, net | (565) | | | 95,595 | |

| Due to counterparties, net | (321) | | | (692) | |

| Increase (decrease) in other liabilities | (75,873) | | | 42,634 | |

| Dividends paid on common stock | (10,947) | | | (16,592) | |

| Dividends paid to non-controlling interest | (4) | | | (4) | |

| Net cash used in financing activities | (605,486) | | | (2,232,837) | |

| | | |

| | | |

| | | |

| Net (decrease) increase in cash, cash equivalents and restricted cash | (43,569) | | | 38,759 | |

| Cash, cash equivalents and restricted cash, beginning of period | 107,745 | | | 84,279 | |

| Cash, cash equivalents and restricted cash, end of period | $ | 64,176 | | | $ | 123,038 | |

| | | |

| Supplemental disclosure of operating cash flow information: | | | |

| Interest paid | $ | 87,658 | | | $ | 90,885 | |

| Income taxes paid | $ | 192 | | | $ | 810 | |

| Supplemental disclosure of non-cash financing/investing activities: | | | |

| Underwriting and offering costs payable | $ | 6 | | | $ | — | |

| Principal payments of securities, not settled | $ | — | | | $ | 44 | |

| | | |

| | | |

| Assets of deconsolidated VIE | $ | — | | | $ | (150,804) | |

| Liabilities of deconsolidated VIE | $ | — | | | $ | 143,952 | |

| Mortgage-backed securities recorded upon deconsolidation | $ | — | | | $ | 6,852 | |

| | | |

| Assets of consolidated VIE | $ | — | | | $ | 1,245,287 | |

| Liabilities of consolidated VIE | $ | — | | | $ | (1,231,549) | |

| Mortgage-backed securities derecognized upon VIE consolidation | $ | — | | | $ | (13,737) | |

| Dividends and distributions declared, not paid | $ | 3,651 | | | $ | 3,041 | |

| Dividends to non-controlling interest, not paid | $ | 2 | | | $ | 2 | |

| Principal payments of Residential Whole Loans, not settled | $ | 22,621 | | | $ | 16,097 | |

| Principal payments of Residential Bridge Loans, not settled | $ | 1,715 | | | $ | 2,720 | |

| | | |

| Other assets - Transfer of Bridge Loans to REO | $ | 752 | | | $ | 419 | |

| Other assets - Transfer of Commercial Loans to REO | $ | 30,345 | | | $ | — | |

| Other assets - Contribution of REO from non-controlling interest | $ | 12,138 | | | $ | — | |

| Financing fee payable | $ | — | | | $ | (20,540) | |

| Exchange of convertible senior notes for common stock | $ | — | | | $ | 3,588 | |

| | | |

| Reconciliation of cash, cash equivalents and restricted cash reported in the Consolidated Balance Sheets: | | | |

| Cash and cash equivalents | $ | 63,916 | | | $ | 27,459 | |

| Restricted cash | 260 | | | 95,579 | |

| Total cash, cash equivalents and restricted cash shown in the Consolidated Statements of Cash Flows | $ | 64,176 | | | $ | 123,038 | |

| | | | | | | | | | | |

| | For the six months ended June 30, 2022 | | For the six months ended June 30, 2021 |

| Equity distributions to non-controlling interest | (14,768) | | | — | |

| Dividends paid on common stock | (6,038) | | | (7,298) | |

| Dividends paid to non-controlling interest | (4) | | | (4) | |

| Net cash provided by (used in) financing activities | 146,458 | | | (412,621) | |

| | | |

| | | |

| | | |

| Net decrease in cash, cash equivalents and restricted cash | (24,318) | | | (38,995) | |

| Cash, cash equivalents and restricted cash, beginning of period | 40,453 | | | 107,745 | |

| Cash, cash equivalents and restricted cash, end of period | $ | 16,135 | | | $ | 68,750 | |

| | | |

| Supplemental disclosure of operating cash flow information: | | | |

| Interest paid | $ | 50,791 | | | $ | 58,531 | |

| Income taxes paid | $ | — | | | $ | 173 | |

| Supplemental disclosure of non-cash financing/investing activities: | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Dividends and distributions declared, not paid | $ | 2,415 | | | $ | 3,649 | |

| | | |

| Principal payments of residential whole loans, not settled | $ | 11,906 | | | $ | 28,695 | |

| Principal payments of residential bridge loans, not settled | $ | 46 | | | $ | — | |

| | | |

| Other assets - transfer of bridge loans to REO | $ | — | | | $ | 684 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Reconciliation of cash, cash equivalents and restricted cash reported in the Consolidated Balance Sheets: | | | |

| Cash and cash equivalents | $ | 15,878 | | | $ | 45,775 | |

| Restricted cash | 257 | | | 22,975 | |

| Total cash, cash equivalents and restricted cash shown in the Consolidated Statements of Cash Flows | $ | 16,135 | | | $ | 68,750 | |

See notes to unaudited consolidated financial statements.

Western Asset Mortgage Capital Corporation and Subsidiaries

Notes to Consolidated Financial Statements (Unaudited)

(in thousands- except share and per share data)

The following defines certain of the commonly used terms in these Notes to Consolidated Financial Statements: “Agency” or “Agencies” refer to a federally chartered corporation, such as the Federal National Mortgage Association (“Fannie Mae” or “FNMA”) or the Federal Home Loan Mortgage Corporation (“Freddie Mac” or “FHLMC”), or an agency of the U.S. Government, such as the Government National Mortgage Association (“Ginnie Mae” or “GNMA”); references to “MBS” refer to mortgage backed securities, including residential mortgage-backed securities or “RMBS,” commercial mortgage-backed securities or “CMBS,” and “Interest-Only Strips” (as defined herein); “Agency MBS” refer to RMBS, CMBS and Interest-Only Strips issued or guaranteed by the Agencies while “Non-Agency MBS” refer to RMBS, CMBS and Interest-Only Strips that are not issued or guaranteed by the Agencies; references to “ARMs” refers to adjustable rate mortgages; references to “Interest-Only Strips” refer to interest-only (“IO”) and inverse interest-only (“IIO”) securities issued as part of or collateralized with MBS; references to “TBA” refer to To-Be-Announced Securities; and references to “Residential Whole Loans,” “Residential Bridge Loans” and “Commercial Loans” (collectively “Whole Loans”) refer to individual mortgage loans secured by single family, multifamily and commercial properties.

Note 1 — Organization

Western Asset Mortgage Capital Corporation, a Delaware corporation, and its subsidiaries (the “Company”), commenced operations in May 2012. The Company invests in, finances and manages a diversified portfolio of real estate related securities, Whole Loans and other financial assets. The Company’s current portfolio is comprised of Non-Qualified ("Non-QM") Residential Whole Loans, ("Non-QM"),Non-Agency RMBS, Commercial Loans, Non-Agency CMBS and to a lesser extent Agency RMBS, Non-Agency RMBS, Residential Bridge Loans, GSE Risk Transfer Securities, Residential Bridge Loans, and asset-backed securities (“ABS”) secured by a portfolio of private student loans. The Company’s investment strategy is based on Western Asset Management Company, LLC’s (the “Manager”) perspective of which mix of portfolio assets it believes provides the Company with the best risk-reward opportunities at any given time. The Company's current investment strategy will focus on residential real estate related investments, including but not limited to non-qualified mortgage loans, Non-Agency RMBS, and other related investments. The Manager will vary the allocation among variousthese asset classes subject to maintaining the Company’s qualification as a REIT and maintaining its exemption from the Investment Company Act of 1940, as amended (the “1940 Act”). These restrictions limit the Company’s ability to invest in non-qualifyingnon-qualified MBS, non-real estate assets and/or assets which are not secured by real estate. Accordingly, the Company’s portfolio will continue to be principally invested in qualifying MBS, Whole Loans, and other real estate related assets.

The Company is externally managed by the Manager, an investment advisor registered with the Securities and Exchange Commission (“SEC”). The Manager is a wholly-owned subsidiary of Franklin Resources, Inc. (“Franklin”), which on July 31, 2020 acquired the Manager's previous parent Legg Mason Inc.. The Company operates and has elected to be taxed as a real estate investment trust or “REIT” commencing with its taxable year ended December 31, 2012.

Note 2 — Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation and Consolidation

The accompanying unaudited consolidated financial statements and related notes have been prepared on the accrual basis of accounting in conformityaccordance with accounting principles generally accepted accounting principles in the United States of America (“GAAP”("GAAP") for interim financial reporting in accordance with Article 10 of Regulation S-X and the instructions to Form 10-Q. In the opinion10-Q and Rule 10-01 of management,Regulation S-X. For all adjustments (which include only normal recurring adjustments) necessaryperiods presented, all per share amounts and common shares outstanding have been madeadjusted on a retroactive basis to state fairlyreflect the Company’s financial position, results of operations and cash flows.Company's one-for-ten reverse stock split, which was effected on July 11, 2022. The results of operations for the period ended SeptemberJune 30, 2021,2022, are not necessarily indicative of the results to be expected for the full year or any future period. These consolidated financial statements should be read in conjunction with the Company’s Annual Report on Form 10-K for the year ended December 31, 2020,2021, filed with the SEC on March 5, 2021.

8, 2022.

The consolidated financial statements include the accounts of the Company, its wholly-owned and majority-owned subsidiaries, and variable interest entities (“VIEs”) in which it is considered the primary beneficiary. All intercompany amounts between the Company and its subsidiaries and consolidated VIEs have been eliminated in consolidation.

Reverse Stock Split

Our amended and restated certificate of incorporation as of June 30, 2022, authorizes the Company to issue a total of 600,000,000 shares of capital stock, consisting of 500,000,000 shares of common stock, par value $0.01 per share, and 100,000,000 shares of preferred stock, par value $0.01 per share.

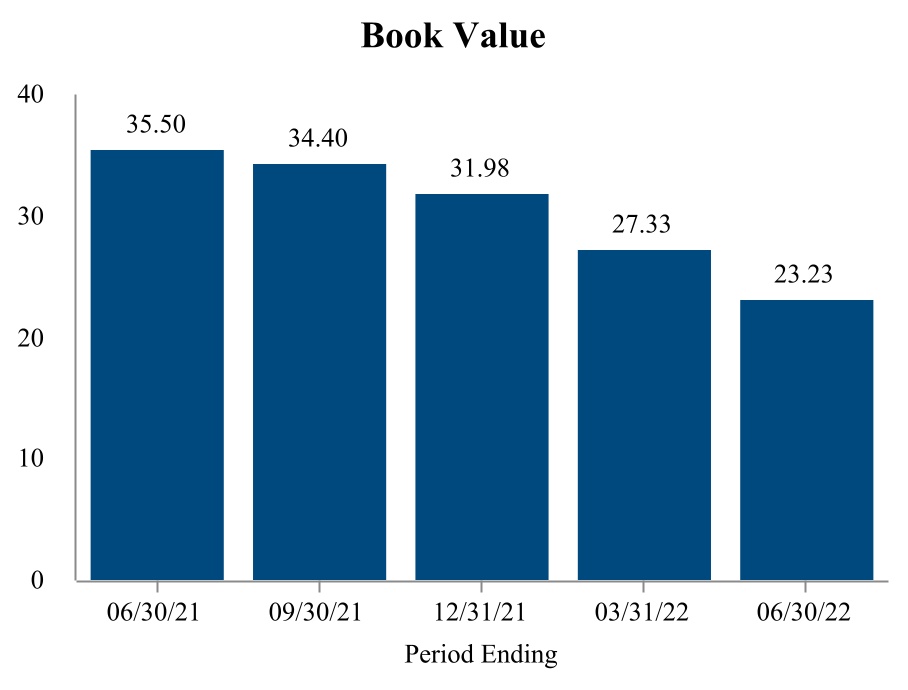

Following approval by the Company’s stockholders of a reverse stock split between a range of 1-for-5 and 1-for-10 of currently outstanding shares of the Company’s common stock, on June 30, 2022, the Company's board of directors selected a one-for-ten reverse stock split ratio. The one-for-ten reverse stock split was effected on July 11, 2022, which reduced the total number of authorized shares of common stock from 500,000,000 to 50,000,000 and the total number of issued and outstanding shares from 60,380,105 to 6,038,010. The par value per share of our common stock remained unchanged at $0.01. All per share amounts and common shares outstanding have been adjusted on a retroactive basis to reflect the Company's one-for-ten reverse stock split.

Our stockholders' equity, in the aggregate, will remain unchanged. Per share net income or loss will be increased because there will be fewer shares of common stock outstanding. The common stock held in treasury will be reduced in proportion to the Reverse Stock Split Ratio. The Company does not anticipate that any other accounting consequences, including changes to the amount of stock-based compensation expense to be recognized in any period, will arise as a result of the Reverse Stock Split. No fractional shares were issued in connection with the reverse stock split. Instead, each stockholder holding fractional shares was entitled to receive, in lieu of such fractional shares, cash in an amount determined based on the closing price of the Company's common stock the business day prior to the Effective Date. The reverse stock split applied to all of the Company's outstanding shares of common stock and did not affect any stockholder’s ownership percentage of shares of the Company's common stock, except for immaterial changes resulting from the payment of cash for fractional shares.

Variable Interest Entities

VIEs are defined as entities, that by design, either lack sufficient equity for the entity to finance its activities without additional subordinated financial support, or are unable to direct the entity’s activities, or are not exposed to the entity’s losses or entitled to its residual returns. The Company evaluates all of its interests in VIEs for consolidation. When the interests are determined to be variable interests, the Company assesses whether it is deemed the primary beneficiary. The primary beneficiary of a VIE is determined to be the party that has both the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance, and the obligation to absorb losses or the right to receive benefits of the VIE that could potentially be significant to the VIE.

To assess whether the Company has the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance, it considers all facts and circumstances, including its role in establishing the VIE and its ongoing rights and responsibilities. This assessment includes: first, identifying the activities that most significantly impact the VIE’s economic performance; and second, identifying which party, if any, has power over those activities. In general, the parties that make the most significant decisions affecting the VIE or have the right to unilaterally remove those decision makers are deemed to have the power to direct the activities of a VIE.

To assess whether the Company has the obligation to absorb losses of the VIE or the right to receive benefits from the VIE that could potentially be significant to the VIE, it considers all of its economic interests. This assessment requires the Company to apply judgment in determining whether these interests, in the aggregate, are considered potentially significant to the VIE. Factors considered in assessing significance include:include; the design of the VIE, including its capitalization structure;structure, subordination of interests;interests, payment priority;priority, relative share of interests held across various classes within the VIE’s capital structure;structure, and the reasons why the interests are held by the Company.

In instances where the Company and its related parties have variable interests in a VIE, the Company considers whether there is a single party in the related party group that meets both the power and losses or benefits criteria on its own as though no related party relationship existed. If one party within the related party group meets both these criteria, such reporting entity is the primary beneficiary of the VIE and no further analysis is needed. If no party within the related party group on its own meets both the power and losses or benefits criteria, but the related party group as a whole meets these two criteria, the determination of primary beneficiary within the related party group requires significant judgment. The analysis is based upon qualitative as well as quantitative factors, such as the relationship of the VIE to each of the members of the related-party group, as well as the significance of the VIE's activities to those members, with the objective of determining which party is most closely associated with the VIE.

Ongoing assessments of whether an enterprise is the primary beneficiary of a VIE are required.

Use of Estimates

The preparation of the consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Impact of the COVID-19 Pandemic

Beginning with the quarter ended March 31, 2020, the COVID-19 pandemic, created extensive disruptions to the global economy and the lives of individuals throughout the world. Governments and businesses have taken and are continuing to take unprecedented actions to contain the spread of COVID-19 and to mitigate its effects, including vaccination efforts, face covering mandates, quarantines, travel bans, shelter-in-place orders, closures of businesses and schools, fiscal stimulus, and legislation designed to deliver monetary aid and other relief. The pandemic and related efforts to contain the spread of COVID-19 have disrupted global economic activity, impacted interest rates, increased economic and market uncertainty, disrupted trade and supply chains, and created unprecedented financial market conditions and disruptions. This rapid disruption in the fixed income markets in early 2020 specifically in mortgage markets had an adverse impact on our book value, liquidity, results of operations, and financial position. Although market conditions have improved since the first quarter of 2020, the full

impact of COVID-19 on the mortgage REIT industry, credit markets, and consequently, on the Company's financial condition and results of operations for future periods remain uncertain.

While the roll out of vaccines and booster vaccines offer a prospective timeline for recovery, our Manager's view is that it will take some time, if ever, for economic and social conditions to fully rebound. Our Manager's outlook is that (i) the near-term, ii) COVID-19 continues to impact global populations, but the worst of the delta variant is behind us, iii) U.S. and global grow is decelerating from high levels, iv) monetary accommodation will be reduced from crisis levels, v) the bar for the Federal Reserve tightening remains high and is unlikely to be met in 2022, vi) global fiscal stimulus will be sharply reduced, vii) inflation remains challenging but will ease meaningfully during 2022, and viii)rates should remain range-bound in an estimated band of 1.25%-1.75% for 10-year U.S. treasuries.

Significant Accounting Policies

There have been no significant changes to our accounting policies included in Note 2 to the consolidated financial statements of our Annual Report on Form 10-K for the year ended December 31, 2020, other than the significant accounting policy disclosed below.

Real Estate Owned

REO represents real estate property acquired by the Company through foreclosure and it is classified as held for sale. Upon completion of the foreclosure, the Company initially records the REO at fair value less estimated costs to sell the property. In subsequent periods, REO is reported at the lower of the current carrying amount or fair value less estimated selling costs and it is classified in "Other assets" in the Consolidated Balance Sheets. Gains/losses recognized on foreclosure as well as realized gains/losses on the disposition of REO are reported by the Company in "Realized gain (loss), net" in the Consolidated Statements of Operations.

Recently adopted accounting pronouncements

| | | | | | | | | | | | | | |

| Description | | Adoption Date | | Effect on Financial Statements |

| | | | |

In January 2020, the FASB issued ASU 2020-01, “Investments-Equity Securities (Topic 321), Investment-Equity Method and Joint Ventures (Topic 323, and Derivatives and Hedging (Topic 815).” The amendments in this update clarified the interaction of the accounting for equity securities under Topic 321 and investments accounted for under the equity method of accounting in Topic 323 and the accounting for certain forward contracts and purchase options accounted for under Topic 815. | | January 1, 2021 | | The adoption of this standard did not have a material impact on the consolidated financial statements. |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Recently issued accounting pronouncements | | | | | | | | | | | | | | |

Description | | Effective Date | | Effect on Financial Statements |

| | | | |

| In August 2020, the FASB issued ASU 2020-06, “Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging— Contracts in Entity’s Own Equity (Subtopic 815-40).” The amendments in this Update affect entities that issue convertible instruments and/or contracts in an entity’s own equity. For convertible instruments, the instruments primarily affected are those issued with beneficial conversion features or cash conversion features because the accounting models for those specific features are removed. | | January 1, 2022.2022 | | The Company evaluated the impactadoption of this standard may have on its consolidated financial statements and doesdid not believe it will have a material impact on itsthe Company's consolidated financial statements due to the limited nature of such transactions. |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Recently issued accounting pronouncements | | | | | | | | | | | | | | |

| Description | | Effective Date | | Effect on Financial Statements |

| | | | |

| In March 2020, the FASB issued ASU 2020-04, “Reference Rate Reform (Topic 848), Facilitation of the Effects of Reference Rate Reform on Financial Reporting.” The amendments in this update provided optional expedients and exceptions for applying generally accepted accounting principles (GAAP) to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The amendments in this Update apply only to contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. In January 2021, the FASB issued ASU 2021-01, "Reference Rate Reform (Topic 848)." The amendments in this Update clarify that certain optional expedients and exceptions in Topic 848 for contract modifications and hedge accounting apply to derivatives that are affected by the discounting transition. | | March 12, 2020 through December 31, 2022 | | The Company may elect to adopt the amendments in ASU 2020-04 and ASU 2021-1 at any time after March 12, 2020 but not later than December 31, 2022. Currently, the Company's contracts that are referenced to LIBOR have not been affected by the amendments in these updates. The Company is in the process of evaluating the guidance and the other optional expedients, and the effect on the company'sCompany's financial statements has not yet been determineddetermined. |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Note 3 — Fair Value of Financial Instruments

The following tables present the Company’s financial instruments carried at fair value as of SeptemberJune 30, 20212022 and December 31, 2020,2021, based upon the valuation hierarchy (dollars in thousands):

| | | | September 30, 2021 | | June 30, 2022 |

| | | Fair Value | | Fair Value |

| | | Level I | | Level II | | Level III | | Total | | Level I | | Level II | | Level III | | Total |

| Assets | Assets | | | | | | | | Assets | | | | | | | |

| | Agency RMBS Interest-Only Strips | Agency RMBS Interest-Only Strips | $ | — | | | $ | — | | | $ | 134 | | | $ | 134 | | Agency RMBS Interest-Only Strips | $ | — | | | $ | — | | | $ | 57 | | | $ | 57 | |

| Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | — | | | — | | | 1,208 | | | 1,208 | | Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | — | | | — | | | 728 | | | 728 | |

| Subtotal Agency MBS | Subtotal Agency MBS | — | | | — | | | 1,342 | | | 1,342 | | Subtotal Agency MBS | — | | | — | | | 785 | | | 785 | |

| | Non-Agency CMBS | Non-Agency CMBS | — | | | 119,861 | | | 14,789 | | | 134,650 | | Non-Agency CMBS | — | | | 93,096 | | | — | | | 93,096 | |

| Non-Agency RMBS | Non-Agency RMBS | — | | | 25,731 | | | — | | | 25,731 | | Non-Agency RMBS | — | | | 31,017 | | | — | | | 31,017 | |

| Non-Agency RMBS Interest-Only Strips | Non-Agency RMBS Interest-Only Strips | — | | | — | | | 2,280 | | | 2,280 | | Non-Agency RMBS Interest-Only Strips | — | | | — | | | 1,181 | | | 1,181 | |

| | Subtotal Non-Agency MBS | Subtotal Non-Agency MBS | — | | | 145,592 | | | 17,069 | | | 162,661 | | Subtotal Non-Agency MBS | — | | | 124,113 | | | 1,181 | | | 125,294 | |

| | Other securities | Other securities | — | | | 52,093 | | | — | | | 52,093 | | Other securities | — | | | 40,534 | | | — | | | 40,534 | |

| Total mortgage-backed securities and other securities | Total mortgage-backed securities and other securities | — | | | 197,685 | | | 18,411 | | | 216,096 | | Total mortgage-backed securities and other securities | — | | | 164,647 | | | 1,966 | | | 166,613 | |

| | Residential Whole Loans | Residential Whole Loans | — | | | — | | | 949,417 | | | 949,417 | | Residential Whole Loans | — | | | — | | | 1,195,853 | | | 1,195,853 | |

| Residential Bridge Loans | Residential Bridge Loans | — | | | — | | | 5,960 | | | 5,960 | | Residential Bridge Loans | — | | | — | | | 5,095 | | | 5,095 | |

| Securitized commercial loans | Securitized commercial loans | — | | | — | | | 1,377,005 | | | 1,377,005 | | Securitized commercial loans | — | | | — | | | 1,243,371 | | | 1,243,371 | |

| Commercial Loans | Commercial Loans | — | | | — | | | 128,766 | | | 128,766 | | Commercial Loans | — | | | — | | | 128,421 | | | 128,421 | |

| Derivative assets | Derivative assets | — | | | 94 | | | — | | | 94 | | Derivative assets | — | | | 1,748 | | | — | | | 1,748 | |

| Total Assets | Total Assets | $ | — | | | $ | 197,779 | | | $ | 2,479,559 | | | $ | 2,677,338 | | Total Assets | $ | — | | | $ | 166,395 | | | $ | 2,574,706 | | | $ | 2,741,101 | |

| | Liabilities | Liabilities | | | | | | | | Liabilities | | | | | | | |

| Derivative liabilities | Derivative liabilities | $ | — | | | $ | 562 | | | $ | — | | | $ | 562 | | Derivative liabilities | $ | — | | | $ | 1,872 | | | $ | — | | | $ | 1,872 | |

| Securitized debt | Securitized debt | — | | | 1,350,574 | | | 14,920 | | | 1,365,494 | | Securitized debt | — | | | 1,559,549 | | | 14,919 | | | 1,574,468 | |

| | Total Liabilities | Total Liabilities | $ | — | | | $ | 1,351,136 | | | $ | 14,920 | | | $ | 1,366,056 | | Total Liabilities | $ | — | | | $ | 1,561,421 | | | $ | 14,919 | | | $ | 1,576,340 | |

| | | | December 31, 2020 | | December 31, 2021 |

| | | Fair Value | | Fair Value |

| | | Level I | | Level II | | Level III | | Total | | Level I | | Level II | | Level III | | Total |

| Assets | Assets | | | | | | | | Assets | | | | | | | |

| | Agency RMBS Interest-Only Strips | Agency RMBS Interest-Only Strips | $ | — | | | $ | — | | | $ | 143 | | | $ | 143 | | Agency RMBS Interest-Only Strips | $ | — | | | $ | — | | | $ | 114 | | | $ | 114 | |

| Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | — | | | — | | | 1,565 | | | 1,565 | | Agency RMBS Interest-Only Strips accounted for as derivatives, included in MBS | — | | | — | | | 1,058 | | | 1,058 | |

| Subtotal Agency MBS | Subtotal Agency MBS | — | | | — | | | 1,708 | | | 1,708 | | Subtotal Agency MBS | — | | | — | | | 1,172 | | | 1,172 | |

| | Non-Agency CMBS | Non-Agency CMBS | — | | | 155,093 | | | 8,988 | | | 164,081 | | Non-Agency CMBS | — | | | 99,630 | | | 5,728 | | | 105,358 | |

| Non-Agency RMBS | Non-Agency RMBS | — | | | — | | | 21,416 | | | 21,416 | | Non-Agency RMBS | — | | | 25,652 | | | — | | | 25,652 | |

| Non-Agency RMBS Interest-Only Strips | Non-Agency RMBS Interest-Only Strips | — | | | — | | | 3,965 | | | 3,965 | | Non-Agency RMBS Interest-Only Strips | — | | | — | | | 2,117 | | | 2,117 | |

| | Subtotal Non-Agency MBS | Subtotal Non-Agency MBS | — | | | 155,093 | | | 34,369 | | | 189,462 | | Subtotal Non-Agency MBS | — | | | 125,282 | | | 7,845 | | | 133,127 | |

| | Other securities | Other securities | — | | | 40,161 | | | 8,593 | | | 48,754 | | Other securities | — | | | 51,648 | | | — | | | 51,648 | |

| Total mortgage-backed securities and other securities | Total mortgage-backed securities and other securities | — | | | 195,254 | | | 44,670 | | | 239,924 | | Total mortgage-backed securities and other securities | — | | | 176,930 | | | 9,017 | | | 185,947 | |

| | Residential Whole Loans | Residential Whole Loans | — | | | — | | | 1,008,782 | | | 1,008,782 | | Residential Whole Loans | — | | | — | | | 1,023,502 | | | 1,023,502 | |

| Residential Bridge Loans | Residential Bridge Loans | — | | | — | | | 12,813 | | | 12,813 | | Residential Bridge Loans | — | | | — | | | 5,428 | | | 5,428 | |

| Securitized commercial loan | Securitized commercial loan | — | | | — | | | 1,605,335 | | | 1,605,335 | | Securitized commercial loan | — | | | — | | | 1,355,808 | | | 1,355,808 | |

| Commercial Loans | Commercial Loans | — | | | — | | | 310,523 | | | 310,523 | | Commercial Loans | — | | | — | | | 130,572 | | | 130,572 | |

| Derivative assets | Derivative assets | — | | | 161 | | | — | | | 161 | | Derivative assets | — | | | 105 | | | — | | | 105 | |

| Total Assets | Total Assets | $ | — | | | $ | 195,415 | | | $ | 2,982,123 | | | $ | 3,177,538 | | Total Assets | $ | — | | | $ | 177,035 | | | $ | 2,524,327 | | | $ | 2,701,362 | |

| | Liabilities | Liabilities | | | | | | | | Liabilities | | | | | | | |

| Derivative liabilities | Derivative liabilities | $ | — | | | $ | 656 | | | $ | — | | | $ | 656 | | Derivative liabilities | $ | — | | | $ | 602 | | | $ | — | | | $ | 602 | |

| Securitized debt | Securitized debt | — | | | 1,538,304 | | | 15,418 | | | 1,553,722 | | Securitized debt | — | | | 1,329,451 | | | 14,919 | | | 1,344,370 | |

| Total Liabilities | Total Liabilities | $ | — | | | $ | 1,538,960 | | | $ | 15,418 | | | $ | 1,554,378 | | Total Liabilities | $ | — | | | $ | 1,330,053 | | | $ | 14,919 | | | $ | 1,344,972 | |

When available, the Company uses quoted market prices to determineAs described in Note 2, the fair value of an asset or liability. Iffinancial instruments that are recorded at fair value is determined by the Manager in accordance with ASC 820, "Fair Value Measurements and Disclosures." When possible, the Company determines fair value using independent data sources. ASC 820 establishes a hierarchy that prioritizes the inputs to valuation techniques giving the highest priority to readily available unadjusted quoted prices in active markets for identical assets (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements) when market prices are not readily available the Company will use independent pricing services, and if the independent pricing service cannot price a particular asset or liability, the Company will obtain third party broker quotes. The Manager’s pricing group, which functions independently from its portfolio management personnel, reviews the third party broker quotes by comparing the broker quotes for reasonableness to alternate sources when available. If independent pricing services or third party broker quotes, are not available, the Company determines the fair value of the securities using valuation techniques that use, when possible, current market-based or independently sourced market parameters, such as interest rates and when applicable, estimates of prepayments and credit losses.reliable.

In instances when the Company is required to consolidate a VIE that is determined to be a qualifying collateralized financing entity ("CFE"), under GAAP, and if the Company has elected the fair value option for the securitized debt, the Company will measure both the financial assets and financial liabilities of the VIE using the fair value of either the VIE’s financial assets or financial liabilities, whichever is more observable.

Residential whole loans and residential bridge loans

In determining the fair value of the Company's residential whole loans and residential bridge loans, the Company considers data such as; loan origination information, borrower credit information, loan servicing data (as available), forward interest rates, general economic conditions, home price index forecasts, and monthly valuations of the underlying properties. The assumptions considered most significant to the determination of the fair value of the Company's mortgage loans include market-implied discount rates, projections of default rates, delinquency rates, prepayment rates and loss severity. Projections of default and prepayment rates are impacted by other variables such as re-performance rates and timeline to liquidation. The