TABLE OF CONTENTS

Index

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Quarterly Report on Form 10-Q of NRG YieldClearway Energy LLC, together with its consolidated subsidiaries, or the Company, includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. The words "believes," "projects," "anticipates," "plans," "expects," "intends," "estimates"“believes,” “projects,” “anticipates,” “plans,” “expects,” “intends,” “estimates” and similar expressions are intended to identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company'sCompany’s actual results, performance and achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These factors, risks and uncertainties include the factors described under Item 1A — Risk Factors in Part I of the Company'sCompany’s Annual Report on Form 10-K for the year ended December 31, 2016, and under Item 1A - Risk Factors in Part II on the Company's Quarterly Report on Form 10-Q for the quarter ended June 30, 2017,2022, as well as the following:

•The Company'sCompany’s ability to maintain and grow its quarterly distributions;

•Potential risks related to the Company as a result of the NRG Transformation Plan;Company's relationships with GIP, TotalEnergies and CEG;

•The Company'sCompany’s ability to successfully identify, evaluate and consummate acquisitions from, and dispositions to, third parties;

•The Company'sCompany’s ability to acquire assets from NRG;CEG;

•The Company'sCompany’s ability to raiseborrow additional funds and access capital due to itsmarkets, as well as the Company’s substantial indebtedness corporate structure, market conditions or otherwise;and the possibility that the Company may incur additional indebtedness going forward;

•Changes in law, including judicial decisions;

•Hazards customary to the power production industry and power generation operations such as fuel and electricity price volatility, unusual weather conditions (including wind and solar conditions), catastrophic weather-related or other damage to facilities, unscheduled generation outages, maintenance or repairs, unanticipated changes to fuel supply costs or availability due to higher demand, shortages, transportation problems or other developments, environmental incidents, or electric transmission or gas pipeline system constraints and the possibility that the Company may not have adequate insurance to cover losses as a result of such hazards;

•The Company'sCompany’s ability to operate its businesses efficiently, manage maintenance capital expenditures and costs effectively, and generate earnings and cash flows from its asset-based businesses in relation to its debt and other obligations;

•The willingness and ability of counterparties to the Company'sCompany’s offtake agreements to fulfill their obligations under such agreements;

•The Company'sCompany’s ability to enter into contracts to sell power and procure fuel on acceptable terms and prices as current offtake agreements expire;

•Government regulation, including compliance with regulatory requirements and changes in market rules, rates, tariffs and environmental laws;

•Operating and financial restrictions placed on the Company that are contained in the project-level debt facilities and other agreements of certain subsidiaries and project-level subsidiaries generally, in the NRG YieldClearway Energy Operating LLC amended and restated revolving credit facility and in the indentures governing the Senior Notes; and

•Cyber terrorism and inadequate cybersecurity, or the occurrence of a catastrophic loss and the possibility that the Company may not have adequate insurance to cover losses resulting from such hazards or the inability of the Company'sCompany’s insurers to provide coverage;

Forward-looking statements speak only as of the date they were made, and the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The foregoing review of factors that could cause the Company'sCompany’s actual results to differ materially from those contemplated in any forward-looking statements included in this Quarterly Report on Form 10-Q should not be construed as exhaustive.

3

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

| 2028 Senior Notes | $850 million aggregate principal amount of 4.75% unsecured senior notes due 2028, issued by Clearway Energy Operating LLC | ||||||||

| 2031 Senior Notes | $925 million aggregate principal amount of 3.75% unsecured senior notes due 2031, issued by Clearway Energy Operating LLC | ||||||||

| 2032 Senior Notes | $350 million aggregate principal amount of 3.75% unsecured senior notes due 2032, issued by Clearway Energy Operating LLC | ||||||||

| Adjusted EBITDA | A non-GAAP measure, represents earnings before interest (including loss on debt extinguishment), tax, depreciation and amortization adjusted for mark-to-market gains or losses, asset write offs and impairments; and factors which the Company does not consider indicative of future operating performance | ||||||||

The FASB Accounting Standards Codification, which the FASB established as the source of authoritative GAAP | |||||||||

| ASU | Accounting Standards Updates - updates to the ASC | ||||||||

| ATM Program | At-The-Market Equity Offering Program | ||||||||

| Senior secured bridge credit agreement entered into by Clearway Energy Operating LLC that provided a term loan facility in an aggregate principal amount of $335 million that was repaid on May 3, 2022 | |||||||||

| Battery energy storage system | |||||||||

| The capability of a generating asset to restore the grid in the event of a blackout without relying on the external electric power transmission network | |||||||||

| CAFD | A non-GAAP measure, Cash Available | ||||||||

| Five wind projects representing 413 MW of capacity, which includes Broken Bow and Crofton Bluffs located in Nebraska, Cedro Hill located in Texas and Mountain Wind Power I and II located in Wyoming | |||||||||

| CEG | Clearway Energy Group LLC (formerly Zephyr Renewables LLC) | ||||||||

| CEG Master Services Agreements | Master Services Agreements entered into as of August 31, 2018 and amended on February 2, 2023 between the Company, Clearway, Inc., Clearway Energy Operating LLC and CEG | ||||||||

| Clearway, Inc. | Clearway Energy, Inc., the holder of the Company’s Class A and Class C units | ||||||||

| Clearway Energy Group LLC | The holder of all of Clearway, Inc.’s Class B and Class D common stock, the Company’s Class B and Class D units and, from time to time, possibly shares of Clearway, Inc.’s Class A and/or Class C common stock | ||||||||

| Clearway Energy Operating LLC | The holder of the project assets that are owned by the Company | ||||||||

| Clearway Renew | Clearway Renew LLC, a subsidiary of CEG | ||||||||

| Company | Clearway Energy LLC, together with its consolidated subsidiaries | ||||||||

| CVSR | California Valley Solar Ranch | ||||||||

| CVSR Holdco LLC, the indirect owner of CVSR | |||||||||

| Distributed Solar | Solar power projects, typically less than 20 MW in size (on an alternating current, or AC, basis), that primarily sell power produced to customers for usage on site, or are interconnected to sell power into the local distribution grid | ||||||||

| Drop Down Assets | Assets under common control acquired by the Company from CEG | ||||||||

| Exchange Act | The Securities Exchange Act of 1934, as amended | ||||||||

| FASB | Financial Accounting Standards Board | ||||||||

| Accounting principles generally accepted in the U.S. | |||||||||

| GenConn | GenConn Energy LLC | ||||||||

4

| Global Infrastructure Partners | ||||||||

| HLBV | Hypothetical Liquidation at Book Value | |||||||

| KKR Thor Bidco, LLC, an affiliate of Kohlberg Kravis Roberts & Co. L.P. | |||||||||

| London Inter-Bank Offered Rate | |||||||||

| Mesquite Star Special LLC | |||||||||

| Mt. Storm | NedPower Mount Storm LLC | ||||||||

| MW | Megawatt | ||||||||

| MWh | Saleable megawatt hours, net of internal/parasitic load megawatt-hours | ||||||||

| MWt | Megawatts Thermal Equivalent | ||||||||

| Net Exposure | Counterparty credit exposure to | ||||||||

| Normal Purchases and Normal Sales | |||||||||

| Other comprehensive income/loss | |||||||||

| O&M | |||||||||

| Pacific Gas and Electric Company | |||||||||

| PPA | Power Purchase Agreement | ||||||||

| Resource adequacy | |||||||||

| Clearway Renewable Operation & Maintenance LLC | |||||||||

| Rosie BESS Devco LLC | |||||||||

| SCE | Southern California Edison | ||||||||

| SEC | U.S. Securities and Exchange Commission | ||||||||

| Senior Notes | Collectively, the | ||||||||

| Secured Overnight Financing Rate | |||||||||

| SPP | Solar Power Partners | ||||||||

| Solar Renewable Energy Credit | |||||||||

| Thermal Business | The | ||||||||

TotalEnergies | TotalEnergies SE | ||||||||

| U.S. | United States of America | ||||||||

| Utah Solar Portfolio | Seven utility-scale solar farms located in Utah, representing 530 MW of capacity | ||||||||

| Utility Scale Solar | Solar power projects, typically 20 MW or greater in size (on an alternating current, or AC, basis), that are interconnected into the transmission or distribution grid to sell power at a wholesale level | ||||||||

| Variable Interest Entity | |||||||||

5

PART I -— FINANCIAL INFORMATION

ITEM 1 — FINANCIAL STATEMENTS

CONSOLIDATED STATEMENTS OF OPERATIONSINCOME

(Unaudited)

| Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 (a) | 2017 | 2016 (a) | |||||||||||

| Operating Revenues | |||||||||||||||

| Total operating revenues | $ | 265 | $ | 272 | $ | 767 | $ | 789 | |||||||

| Operating Costs and Expenses | |||||||||||||||

| Cost of operations | 78 | 76 | 239 | 238 | |||||||||||

| Depreciation and amortization | 88 | 75 | 241 | 224 | |||||||||||

| General and administrative | 4 | 3 | 14 | 8 | |||||||||||

| Acquisition-related transaction and integration costs | — | — | 2 | — | |||||||||||

| Total operating costs and expenses | 170 | 154 | 496 | 470 | |||||||||||

| Operating Income | 95 | 118 | 271 | 319 | |||||||||||

| Other Income (Expense) | |||||||||||||||

| Equity in earnings of unconsolidated affiliates | 28 | 16 | 63 | 34 | |||||||||||

| Other income, net | 1 | 1 | 3 | 3 | |||||||||||

| Interest expense | (72 | ) | (68 | ) | (227 | ) | (204 | ) | |||||||

| Total other expense, net | (43 | ) | (51 | ) | (161 | ) | (167 | ) | |||||||

| Net Income | 52 | 67 | 110 | 152 | |||||||||||

| Less: Net loss attributable to noncontrolling interests | (23 | ) | (38 | ) | (56 | ) | (67 | ) | |||||||

| Net Income Attributable to NRG Yield LLC | $ | 75 | $ | 105 | $ | 166 | $ | 219 | |||||||

| Three months ended June 30, | Six months ended June 30, | ||||||||||||||||||||||

| (In millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Operating Revenues | |||||||||||||||||||||||

| Total operating revenues | $ | 406 | $ | 368 | $ | 694 | $ | 582 | |||||||||||||||

| Operating Costs and Expenses | |||||||||||||||||||||||

| Cost of operations, exclusive of depreciation, amortization and accretion shown separately below | 118 | 112 | 226 | 240 | |||||||||||||||||||

| Depreciation, amortization and accretion | 128 | 126 | 256 | 250 | |||||||||||||||||||

| General and administrative | 9 | 9 | 19 | 21 | |||||||||||||||||||

| Transaction and integration costs | 2 | 3 | 2 | 5 | |||||||||||||||||||

| Development costs | — | 1 | — | 2 | |||||||||||||||||||

| Total operating costs and expenses | 257 | 251 | 503 | 518 | |||||||||||||||||||

| Gain on sale of business | — | 1,291 | — | 1,291 | |||||||||||||||||||

| Operating Income | 149 | 1,408 | 191 | 1,355 | |||||||||||||||||||

| Other Income (Expense) | |||||||||||||||||||||||

| Equity in earnings of unconsolidated affiliates | 3 | 10 | — | 14 | |||||||||||||||||||

| Other income, net | 9 | 5 | 17 | 5 | |||||||||||||||||||

| Loss on debt extinguishment | — | — | — | (2) | |||||||||||||||||||

| Interest expense | (55) | (47) | (154) | (94) | |||||||||||||||||||

| Total other expense, net | (43) | (32) | (137) | (77) | |||||||||||||||||||

| Net Income | 106 | 1,376 | 54 | 1,278 | |||||||||||||||||||

| Less: Net loss attributable to noncontrolling interests and redeemable noncontrolling interests | — | (6) | (30) | (46) | |||||||||||||||||||

| Net Income Attributable to Clearway Energy LLC | $ | 106 | $ | 1,382 | $ | 84 | $ | 1,324 | |||||||||||||||

See accompanying notes to consolidated financial statements.

6

CLEARWAY ENERGY LLC

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

| Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 (a) | 2017 | 2016 (a) | |||||||||||

| Net Income | $ | 52 | $ | 67 | $ | 110 | $ | 152 | |||||||

| Other Comprehensive Gain (Loss) | |||||||||||||||

| Unrealized gain (loss) on derivatives | 7 | 20 | 7 | (49 | ) | ||||||||||

| Other comprehensive gain (loss) | 7 | 20 | 7 | (49 | ) | ||||||||||

| Comprehensive Income | 59 | 87 | 117 | 103 | |||||||||||

| Less: Comprehensive loss attributable to noncontrolling interests | (23 | ) | (30 | ) | (56 | ) | (67 | ) | |||||||

| Comprehensive Income Attributable to NRG Yield LLC | $ | 82 | $ | 117 | $ | 173 | $ | 170 | |||||||

| (In millions) | September 30, 2017 | December 31, 2016 (a) | |||||

| ASSETS | (unaudited) | ||||||

| Current Assets | |||||||

| Cash and cash equivalents | $ | 178 | $ | 321 | |||

| Restricted cash | 140 | 165 | |||||

| Accounts receivable — trade | 126 | 92 | |||||

| Accounts receivable — affiliate | 1 | 1 | |||||

| Inventory | 38 | 39 | |||||

| Derivative instruments | — | 2 | |||||

| Notes receivable | 15 | 16 | |||||

| Prepayments and other current assets | 22 | 20 | |||||

| Total current assets | 520 | 656 | |||||

| Property, plant and equipment, net | 5,247 | 5,460 | |||||

| Other Assets | |||||||

| Equity investments in affiliates | 1,183 | 1,152 | |||||

| Intangible assets, net | 1,234 | 1,286 | |||||

| Derivative instruments | — | 1 | |||||

| Other non-current assets | 56 | 65 | |||||

| Total other assets | 2,473 | 2,504 | |||||

| Total Assets | $ | 8,240 | $ | 8,620 | |||

| LIABILITIES AND MEMBERS' EQUITY | |||||||

| Current Liabilities | |||||||

| Current portion of long-term debt — external | $ | 300 | $ | 291 | |||

| Accounts payable — trade | 27 | 23 | |||||

| Accounts payable — affiliate | 45 | 40 | |||||

| Derivative instruments | 23 | 32 | |||||

| Accrued expenses and other current liabilities | 94 | 85 | |||||

| Total current liabilities | 489 | 471 | |||||

| Other Liabilities | |||||||

| Long-term debt — external | 4,914 | 5,098 | |||||

| Long-term debt — affiliate | 618 | 618 | |||||

| Accounts payable — affiliate | 3 | 9 | |||||

| Derivative instruments | 43 | 44 | |||||

| Other non-current liabilities | 87 | 76 | |||||

| Total non-current liabilities | 5,665 | 5,845 | |||||

| Total Liabilities | 6,154 | 6,316 | |||||

| Commitments and Contingencies | |||||||

| Members' Equity | |||||||

| Contributed capital | 1,897 | 2,127 | |||||

| Retained earnings | 86 | 36 | |||||

| Accumulated other comprehensive loss | (78 | ) | (85 | ) | |||

| Noncontrolling interest | 181 | 226 | |||||

| Total Members' Equity | 2,086 | 2,304 | |||||

| Total Liabilities and Members’ Equity | $ | 8,240 | $ | 8,620 | |||

| Three months ended June 30, | Six months ended June 30, | ||||||||||||||||||||||

| (In millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Net Income | $ | 106 | $ | 1,376 | $ | 54 | $ | 1,278 | |||||||||||||||

| Other Comprehensive Income | |||||||||||||||||||||||

| Unrealized gain on derivatives and changes in accumulated OCI/OCL | 4 | 7 | — | 23 | |||||||||||||||||||

| Other comprehensive income | 4 | 7 | — | 23 | |||||||||||||||||||

| Comprehensive Income | 110 | 1,383 | 54 | 1,301 | |||||||||||||||||||

| Less: Comprehensive income (loss) attributable to noncontrolling interests and redeemable noncontrolling interests | 1 | (5) | (30) | (42) | |||||||||||||||||||

| Comprehensive Income Attributable to Clearway Energy LLC | $ | 109 | $ | 1,388 | $ | 84 | $ | 1,343 | |||||||||||||||

See accompanying notes to consolidated financial statements.

CLEARWAY ENERGY LLC

CONSOLIDATED BALANCE SHEETS

| (In millions) | June 30, 2023 | December 31, 2022 | |||||||||

| ASSETS | (Unaudited) | ||||||||||

| Current Assets | |||||||||||

| Cash and cash equivalents | $ | 547 | $ | 657 | |||||||

| Restricted cash | 371 | 339 | |||||||||

| Accounts receivable — trade | 215 | 153 | |||||||||

| Accounts receivable — affiliates | 1 | — | |||||||||

| Inventory | 51 | 47 | |||||||||

| Derivative instruments | 34 | 26 | |||||||||

| Prepayments and other current assets | 64 | 54 | |||||||||

| Total current assets | 1,283 | 1,276 | |||||||||

| Property, plant and equipment, net | 7,748 | 7,421 | |||||||||

| Other Assets | |||||||||||

| Equity investments in affiliates | 352 | 364 | |||||||||

| Intangible assets for power purchase agreements, net | 2,397 | 2,488 | |||||||||

| Other intangible assets, net | 74 | 77 | |||||||||

| Derivative instruments | 83 | 63 | |||||||||

| Right-of-use assets, net | 550 | 527 | |||||||||

| Other non-current assets | 131 | 96 | |||||||||

| Total other assets | 3,587 | 3,615 | |||||||||

| Total Assets | $ | 12,618 | $ | 12,312 | |||||||

| LIABILITIES AND MEMBERS’ EQUITY | |||||||||||

| Current Liabilities | |||||||||||

| Current portion of long-term debt — external | $ | 330 | $ | 322 | |||||||

| Current portion of long-term debt — affiliate | 2 | 2 | |||||||||

| Accounts payable — trade | 63 | 55 | |||||||||

| Accounts payable — affiliates | 62 | 24 | |||||||||

| Derivative instruments | 44 | 50 | |||||||||

| Accrued interest expense | 54 | 54 | |||||||||

| Accrued expenses and other current liabilities | 54 | 95 | |||||||||

| Total current liabilities | 609 | 602 | |||||||||

| Other Liabilities | |||||||||||

| Long-term debt — external | 6,708 | 6,491 | |||||||||

| Deferred income taxes | 4 | 4 | |||||||||

| Derivative instruments | 259 | 303 | |||||||||

| Long-term lease liabilities | 578 | 548 | |||||||||

| Other non-current liabilities | 208 | 197 | |||||||||

| Total other liabilities | 7,757 | 7,543 | |||||||||

| Total Liabilities | 8,366 | 8,145 | |||||||||

| Redeemable noncontrolling interest in subsidiaries | 15 | 7 | |||||||||

| Commitments and Contingencies | |||||||||||

| Members’ Equity | |||||||||||

| Contributed capital | 1,275 | 1,308 | |||||||||

| Retained earnings | 1,126 | 1,240 | |||||||||

| Accumulated other comprehensive income | 21 | 21 | |||||||||

| Noncontrolling interest | 1,815 | 1,591 | |||||||||

| Total Members’ Equity | 4,237 | 4,160 | |||||||||

| Total Liabilities and Members’ Equity | $ | 12,618 | $ | 12,312 | |||||||

See accompanying notes to consolidated financial statements.

8

CLEARWAY ENERGY LLC

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

| Nine months ended September 30, | |||||||

| 2017 | 2016(a) | ||||||

| (In millions) | |||||||

| Cash Flows from Operating Activities | |||||||

| Net income | $ | 110 | $ | 152 | |||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

| Equity in earnings of unconsolidated affiliates | (63 | ) | (34 | ) | |||

| Distributions from unconsolidated affiliates | 52 | 43 | |||||

| Depreciation and amortization | 241 | 224 | |||||

| Amortization of financing costs | 7 | 6 | |||||

| Amortization of intangibles and out-of-market contracts | 52 | 57 | |||||

| Changes in derivative instruments | (2 | ) | (5 | ) | |||

| Loss on disposal of asset components | 8 | 5 | |||||

| Changes in prepaid and accrued liabilities for tolling agreements | 5 | 2 | |||||

| Changes in other working capital | (35 | ) | (6 | ) | |||

| Net Cash Provided by Operating Activities | 375 | 444 | |||||

| Cash Flows from Investing Activities | |||||||

| Payments for the Drop Down Assets | (176 | ) | (77 | ) | |||

| Capital expenditures | (23 | ) | (16 | ) | |||

| Cash receipts from notes receivable | 11 | 11 | |||||

| Return of investment from unconsolidated affiliates | 32 | 16 | |||||

| Investments in unconsolidated affiliates | (48 | ) | (69 | ) | |||

| Net Cash Used in Investing Activities | (204 | ) | (135 | ) | |||

| Cash Flows from Financing Activities | |||||||

| Net contributions from noncontrolling interests | 13 | 7 | |||||

| Net distributions and return of capital to NRG prior to the acquisition of Drop Down Assets | (49 | ) | (126 | ) | |||

| Proceeds from the issuance of Class C units | 33 | — | |||||

| Payments of distributions | (149 | ) | (127 | ) | |||

| Payments of debt issuance costs | (4 | ) | (6 | ) | |||

| Proceeds from the revolving credit facility | — | 60 | |||||

| Payments for the revolving credit facility | — | (366 | ) | ||||

| Proceeds from the issuance of long-term debt — external | 41 | 550 | |||||

| Payments for long-term debt | (224 | ) | (204 | ) | |||

| Net Cash Used in Financing Activities | (339 | ) | (212 | ) | |||

| Net Decrease in Cash, Cash Equivalents and Restricted Cash | (168 | ) | 97 | ||||

| Cash, Cash Equivalents and Restricted Cash at Beginning of Period | 486 | 241 | |||||

| Cash, Cash Equivalents and Restricted Cash at End of Period | $ | 318 | $ | 338 | |||

| Six months ended June 30, | |||||||||||

| (In millions) | 2023 | 2022 | |||||||||

| Cash Flows from Operating Activities | |||||||||||

| Net Income | $ | 54 | $ | 1,278 | |||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Equity in earnings of unconsolidated affiliates | — | (14) | |||||||||

| Distributions from unconsolidated affiliates | 11 | 17 | |||||||||

| Depreciation, amortization and accretion | 256 | 250 | |||||||||

| Amortization of financing costs and debt discounts | 6 | 7 | |||||||||

| Amortization of intangibles | 94 | 82 | |||||||||

| Loss on debt extinguishment | — | 2 | |||||||||

| Gain on sale of business | — | (1,291) | |||||||||

| Reduction in carrying amount of right-of-use assets | 8 | 7 | |||||||||

| Changes in derivative instruments and amortization of accumulated OCI/OCL | (51) | 92 | |||||||||

| Cash used in changes in other working capital: | |||||||||||

| Changes in prepaid and accrued liabilities for tolling agreements | (56) | (74) | |||||||||

| Changes in other working capital | (87) | (76) | |||||||||

| Net Cash Provided by Operating Activities | 235 | 280 | |||||||||

| Cash Flows from Investing Activities | |||||||||||

| Acquisition of Drop Down Assets, net of cash acquired | (7) | (51) | |||||||||

| Capital expenditures | (109) | (81) | |||||||||

| Return of investment from unconsolidated affiliates | 10 | 6 | |||||||||

| Investments in unconsolidated affiliates | (10) | — | |||||||||

| Proceeds from sale of business | — | 1,457 | |||||||||

| Net Cash (Used in) Provided by Investing Activities | (116) | 1,331 | |||||||||

| Cash Flows from Financing Activities | |||||||||||

| Contributions from noncontrolling interests, net of distributions | 209 | 16 | |||||||||

| Contributions from (distributions to) CEG, net | 66 | (23) | |||||||||

| Payments of distributions | (153) | (141) | |||||||||

| Tax-related distributions | (45) | — | |||||||||

| Distributions to CEG of escrowed amounts | — | (64) | |||||||||

| Proceeds from the revolving credit facility | — | 80 | |||||||||

| Payments for the revolving credit facility | — | (325) | |||||||||

| Proceeds from the issuance of long-term debt — external | 42 | 214 | |||||||||

| Payments of debt issuance costs | (8) | (4) | |||||||||

| Payments for long-term debt — external | (306) | (722) | |||||||||

| Payments for long-term debt — affiliate | — | (1) | |||||||||

| Other | (2) | (7) | |||||||||

| Net Cash Used in Financing Activities | (197) | (977) | |||||||||

| Net (Decrease) Increase in Cash, Cash Equivalents and Restricted Cash | (78) | 634 | |||||||||

| Cash, Cash Equivalents and Restricted Cash at Beginning of Period | 996 | 654 | |||||||||

| Cash, Cash Equivalents and Restricted Cash at End of Period | $ | 918 | $ | 1,288 | |||||||

See accompanying notes to consolidated financial statements.

9

CLEARWAY ENERGY LLC

CONSOLIDATED STATEMENTS OF MEMBERS’ EQUITY

For the Six Months Ended June 30, 2023

(Unaudited)

| (In millions) | Contributed Capital | Retained Earnings | Accumulated Other Comprehensive Income | Noncontrolling Interest | Total Members’ Equity | ||||||||||||||||||||||||

| Balances at December 31, 2022 | $ | 1,308 | $ | 1,240 | $ | 21 | $ | 1,591 | $ | 4,160 | |||||||||||||||||||

| Net loss | — | (22) | — | (33) | (55) | ||||||||||||||||||||||||

| Unrealized loss on derivatives and changes in accumulated OCI | — | — | (3) | (1) | (4) | ||||||||||||||||||||||||

| Contributions from CEG, net of distributions, cash | 30 | — | — | 30 | |||||||||||||||||||||||||

| Contributions from noncontrolling interests, net of distributions, cash | — | — | — | 215 | 215 | ||||||||||||||||||||||||

| Transfers of assets under common control | (59) | — | — | 53 | (6) | ||||||||||||||||||||||||

| Distributions paid to Clearway, Inc. | — | (44) | — | — | (44) | ||||||||||||||||||||||||

| Distributions paid to CEG Class B and Class D unit holders | — | (32) | — | — | (32) | ||||||||||||||||||||||||

| Balances at March 31, 2023 | 1,279 | 1,142 | 18 | 1,825 | 4,264 | ||||||||||||||||||||||||

| Net income (loss) | — | 106 | — | (6) | 100 | ||||||||||||||||||||||||

| Unrealized gain on derivatives | — | — | 3 | 1 | 4 | ||||||||||||||||||||||||

| Distributions to CEG, cash | (4) | — | — | — | (4) | ||||||||||||||||||||||||

| Distributions to noncontrolling interests, net of contributions, cash | — | — | — | (5) | (5) | ||||||||||||||||||||||||

| Tax-related distributions | — | (45) | — | — | (45) | ||||||||||||||||||||||||

| Distributions paid to Clearway, Inc. | — | (45) | — | — | (45) | ||||||||||||||||||||||||

| Distributions paid to CEG Class B and Class D unit holders | — | (32) | — | — | (32) | ||||||||||||||||||||||||

| Balances at June 30, 2023 | $ | 1,275 | $ | 1,126 | $ | 21 | $ | 1,815 | $ | 4,237 | |||||||||||||||||||

See accompanying notes to consolidated financial statements.

10

CLEARWAY ENERGY LLC

CONSOLIDATED STATEMENTS OF MEMBERS' EQUITY

For the Six Months Ended June 30, 2022

(Unaudited)

| (In millions) | Contributed Capital | Retained Earnings (Accumulated Deficit) | Accumulated Other Comprehensive(Loss) Income | Noncontrolling Interest | Total Members’ Equity | ||||||||||||||||||||||||

| Balances at December 31, 2021 | $ | 1,495 | $ | 43 | $ | (13) | $ | 1,692 | $ | 3,217 | |||||||||||||||||||

| Net loss | — | (58) | — | (42) | (100) | ||||||||||||||||||||||||

| Unrealized gain on derivatives | — | — | 13 | 3 | 16 | ||||||||||||||||||||||||

| Distributions to CEG, net of contributions, cash | (3) | — | — | — | (3) | ||||||||||||||||||||||||

| Contributions from noncontrolling interests, net of distributions, cash | — | — | — | 28 | 28 | ||||||||||||||||||||||||

| Transfers of assets under common control | (46) | — | — | 9 | (37) | ||||||||||||||||||||||||

| Distributions paid to Clearway, Inc. | (40) | — | — | — | (40) | ||||||||||||||||||||||||

| Distributions paid to CEG Class B and Class D unit holders | (5) | (25) | — | — | (30) | ||||||||||||||||||||||||

| Balances at March 31, 2022 | 1,401 | (40) | — | 1,690 | 3,051 | ||||||||||||||||||||||||

| Net income (loss) | — | 1,382 | — | (10) | 1,372 | ||||||||||||||||||||||||

| Unrealized gain on derivatives | — | — | 6 | 1 | 7 | ||||||||||||||||||||||||

| Contributions from (distributions to) CEG, cash | 11 | — | — | (31) | (20) | ||||||||||||||||||||||||

| Distributions to noncontrolling interests, net of contributions, cash | — | — | — | (10) | (10) | ||||||||||||||||||||||||

| Distributions paid to Clearway, Inc. | (41) | — | — | — | (41) | ||||||||||||||||||||||||

| Distributions paid to CEG Class B and Class D unit holders | (30) | — | — | — | (30) | ||||||||||||||||||||||||

| Balances at June 30, 2022 | $ | 1,341 | $ | 1,342 | $ | 6 | $ | 1,640 | $ | 4,329 | |||||||||||||||||||

See accompanying notes to consolidated financial statements.

11

CLEARWAY ENERGY LLC

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1 — Nature of Business

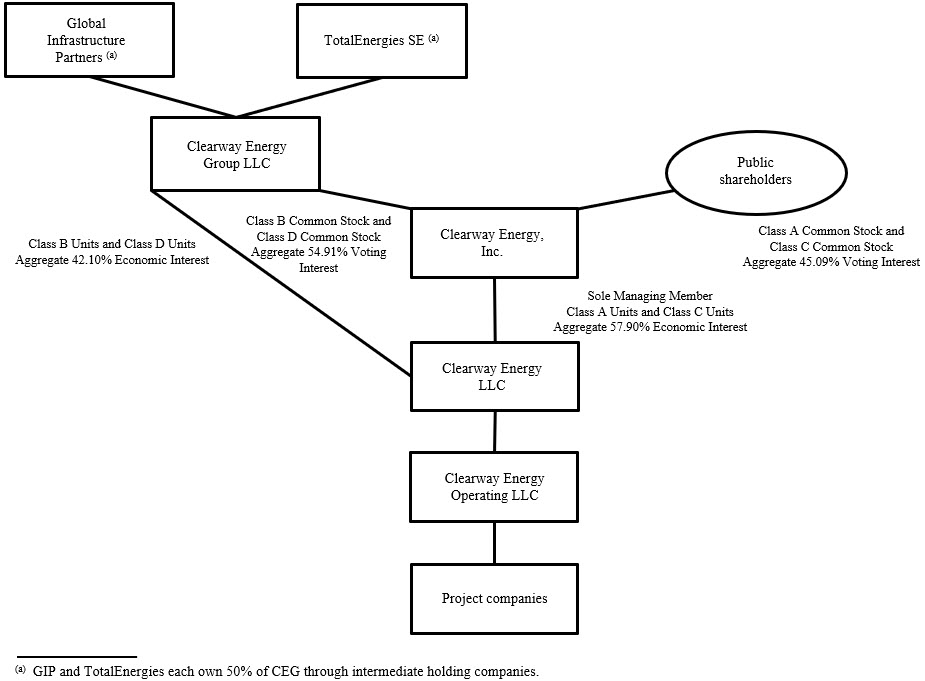

assets across North America. The Company ownsis sponsored by GIP and TotalEnergies through the portfolio company, Clearway Energy Group LLC, or CEG, which is equally owned by GIP and TotalEnergies. GIP is an independent infrastructure fund manager that makes equity and debt investments in infrastructure assets and businesses. TotalEnergies is a diversified portfolioglobal multi-energy company.

The Company is one of contractedthe largest renewable and conventional generation and thermal infrastructure assetsenergy owners in the U.S. with over 5,500 net MW of installed wind and solar generation projects. The Company’s contracted generation portfolio collectively represents 5,080over 8,000 net MW as of September 30, 2017. Eachassets also includes approximately 2,500 net MW of these assets sells substantially all ofenvironmentally-sound, highly efficient natural gas-fired generation facilities. Through this environmentally-sound, diversified and primarily contracted portfolio, the Company endeavors to increase distributions to its output pursuant to long-term offtake agreements with creditworthy counterparties.unit holders. The weighted average remaining contract duration of these offtake agreements was approximately 16 years as of September 30, 2017 based on CAFD. The Company also owns thermal infrastructure assets with an aggregate steam and chilled water capacity of 1,319 net MWt and electric generation capacity of 123 net MW. These thermal infrastructure assets provide steam, hot and/or chilled water, and, in some instances, electricity to commercial businesses, universities, hospitals and governmental units in multiple locations, principally through long-term contracts or pursuant to rates regulated by state utility commissions.

| Projects | Percentage Ownership | Net Capacity (MW)(a) | Offtake Counterparty | Expiration | ||||||

| Conventional | ||||||||||

| El Segundo | 100 | % | 550 | Southern California Edison | 2023 | |||||

| GenConn Devon | 50 | % | 95 | Connecticut Light & Power | 2040 | |||||

| GenConn Middletown | 50 | % | 95 | Connecticut Light & Power | 2041 | |||||

| Marsh Landing | 100 | % | 720 | Pacific Gas and Electric | 2023 | |||||

| Walnut Creek | 100 | % | 485 | Southern California Edison | 2023 | |||||

| 1,945 | ||||||||||

| Utility Scale Solar | ||||||||||

| Agua Caliente | 16 | % | 46 | Pacific Gas and Electric | 2039 | |||||

| Alpine | 100 | % | 66 | Pacific Gas and Electric | 2033 | |||||

| Avenal | 50 | % | 23 | Pacific Gas and Electric | 2031 | |||||

| Avra Valley | 100 | % | 26 | Tucson Electric Power | 2032 | |||||

| Blythe | 100 | % | 21 | Southern California Edison | 2029 | |||||

| Borrego | 100 | % | 26 | San Diego Gas and Electric | 2038 | |||||

| CVSR | 100 | % | 250 | Pacific Gas and Electric | 2038 | |||||

| Desert Sunlight 250 | 25 | % | 63 | Southern California Edison | 2035 | |||||

| Desert Sunlight 300 | 25 | % | 75 | Pacific Gas and Electric | 2040 | |||||

| Kansas South | 100 | % | 20 | Pacific Gas and Electric | 2033 | |||||

| Roadrunner | 100 | % | 20 | El Paso Electric | 2031 | |||||

| TA High Desert | 100 | % | 20 | Southern California Edison | 2033 | |||||

Utah Solar Portfolio (b) (e) | 50 | % | 265 | PacifiCorp | 2036 | |||||

| 921 | ||||||||||

| Distributed Solar | ||||||||||

| Apple I LLC Projects | 100 | % | 9 | Various | 2032 | |||||

| AZ DG Solar Projects | 100 | % | 5 | Various | 2025 - 2033 | |||||

| 14 | ||||||||||

| Wind | ||||||||||

| Alta I | 100 | % | 150 | Southern California Edison | 2035 | |||||

| Alta II | 100 | % | 150 | Southern California Edison | 2035 | |||||

| Alta III | 100 | % | 150 | Southern California Edison | 2035 | |||||

| Alta IV | 100 | % | 102 | Southern California Edison | 2035 | |||||

| Alta V | 100 | % | 168 | Southern California Edison | 2035 | |||||

Alta X (b) | 100 | % | 137 | Southern California Edison | 2038 | |||||

Alta XI (b) | 100 | % | 90 | Southern California Edison | 2038 | |||||

| Buffalo Bear | 100 | % | 19 | Western Farmers Electric Co-operative | 2033 | |||||

Crosswinds (b) (f) | 99 | % | 21 | Corn Belt Power Cooperative | 2027 | |||||

Elbow Creek (b) (f) | 100 | % | 122 | NRG Power Marketing LLC | 2022 | |||||

Elkhorn Ridge (b) (f) | 66.7 | % | 54 | Nebraska Public Power District | 2029 | |||||

Forward (b) (f) | 100 | % | 29 | Constellation NewEnergy, Inc. | 2017 | |||||

Goat Wind (b) (f) | 100 | % | 150 | Dow Pipeline Company | 2025 | |||||

Hardin (b) (f) | 99 | % | 15 | Interstate Power and Light Company | 2027 | |||||

| Laredo Ridge | 100 | % | 80 | Nebraska Public Power District | 2031 | |||||

Lookout (b) (f) | 100 | % | 38 | Southern Maryland Electric Cooperative | 2030 | |||||

| Projects | Percentage Ownership | Net Capacity (MW)(a) | Offtake Counterparty | Expiration | ||||||

Odin (b) (f) | 99.9 | % | 20 | Missouri River Energy Services | 2028 | |||||

| Pinnacle | 100 | % | 55 | Maryland Department of General Services and University System of Maryland | 2031 | |||||

San Juan Mesa (b) (f) | 75 | % | 90 | Southwestern Public Service Company | 2025 | |||||

Sleeping Bear (b) (f) | 100 | % | 95 | Public Service Company of Oklahoma | 2032 | |||||

| South Trent | 100 | % | 101 | AEP Energy Partners | 2029 | |||||

Spanish Fork (b) (f) | 100 | % | 19 | PacifiCorp | 2028 | |||||

Spring Canyon II (b) | 90.1 | % | 29 | Platte River Power Authority | 2039 | |||||

Spring Canyon III (b) | 90.1 | % | 25 | Platte River Power Authority | 2039 | |||||

| Taloga | 100 | % | 130 | Oklahoma Gas & Electric | 2031 | |||||

Wildorado (b) (f) | 100 | % | 161 | Southwestern Public Service Company | 2027 | |||||

| 2,200 | ||||||||||

| Thermal | ||||||||||

| NRG Dover Energy Center LLC | 100 | % | 103 | NRG Power Marketing LLC | 2018 | |||||

| Thermal generation | 100 | % | 20 | Various | Various | |||||

| 123 | ||||||||||

Total net generation capacity(c) | 5,203 | |||||||||

Thermal equivalent MWt (d) | 100 | % | 1,319 | Various | Various | |||||

Clearway Energy, Inc., or Clearway, Inc., consolidates the results of district energy systems and combined heat and power plants that produce steam, hot water and/or chilled water and, in some instances, electricity at a central plant. Certain district energy systems are subject to rate regulation by state public utility commissions (although they may negotiate certain rates) while the other district energy systems have rates determined by negotiated bilateral contracts.

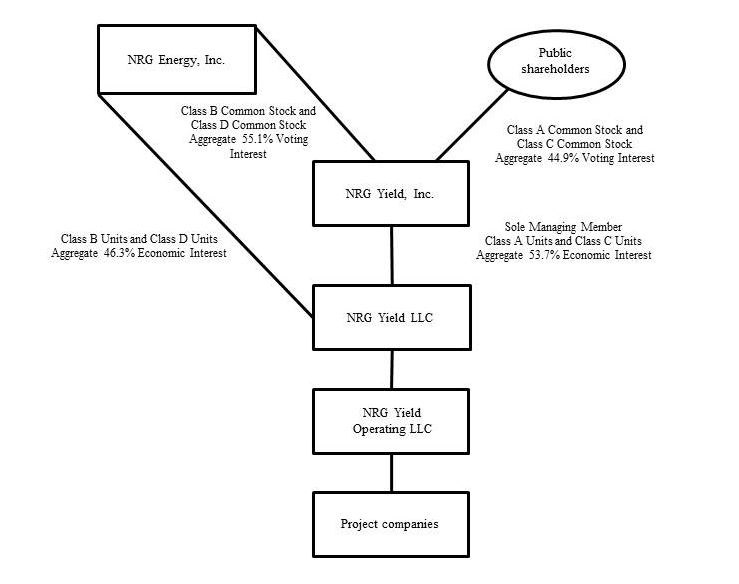

As of June 30, 2023, Clearway, Inc. owned 57.90% of the economic interests of the Company, with CEG owning 42.10% of the economic interests of the Company.

12

The following table represents a summarized structure of the Company as of SeptemberJune 30, 2017. On March 27, 2017, the Company acquired the following interests from NRG, referred to as the March 2017 Drop Down Assets: (i) Agua Caliente Borrower 2 LLC, which owns a 16% interest in the Agua Caliente solar farm, one2023:

Basis of the ROFO assets and (ii) NRG's interests in seven utility-scale solar farms located in Utah that were part of NRG's November 2, 2016 acquisition of projects from SunEdison, or the Utah Solar Portfolio. The Company paid total cash consideration of $130 million, plus a $2 million working capital adjustment, and assumed non-recourse debt of $328 million, which is consolidated, as well as its pro-rata share of non-recourse project-level debt of $135 million. The acquisition was funded with cash on hand.

The accompanying unaudited interim consolidated financial statements have been prepared in accordance with the SEC’s regulations for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. The following notes should be read in conjunction with the accounting policies and other disclosures as set forth in the notes to the consolidated financial statements for the year ended December 31, 2016 included in the Company's May 9, 2017Company’s 2022 Form 8-K.10-K. Interim results are not necessarily indicative of results for a full year.

In the opinion of management, the accompanying unaudited interim consolidated financial statements contain all material adjustments consisting of normal and recurring accruals necessary to present fairly the Company'sCompany’s consolidated financial position as of SeptemberJune 30, 2017,2023, and the results of operations, comprehensive income (loss) and cash flows for the three and ninesix months ended SeptemberJune 30, 20172023 and 2016.2022.

Note 2 — Summary of Significant Accounting Policies

Use of Estimates

The preparation of consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions. These estimates and assumptions impact the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities as of the date of the consolidated financial statements, andstatements. They also impact the reported amounts of revenues and expensesnet earnings during the reporting period.periods. Actual results could be different from these estimates.

13

Cash, Cash Equivalents and Restricted Cash

Cash and cash equivalents include highly liquid investments with an original maturity of three months or less at the time of purchase. Cash and cash equivalents held at project subsidiaries was $134 million and $121 million as of June 30, 2023 and December 31, 2022, respectively.

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within the consolidated balance sheets that sum to the total of the same such amounts shown in the consolidated statements of cash flows:

| June 30, 2023 | December 31, 2022 | ||||||||||

| (In millions) | |||||||||||

| Cash and cash equivalents | $ | 547 | $ | 657 | |||||||

| Restricted cash | 371 | 339 | |||||||||

| Cash, cash equivalents and restricted cash shown in the consolidated statements of cash flows | $ | 918 | $ | 996 | |||||||

Restricted cash consists primarily of funds held to satisfy the requirements of certain debt agreements and funds held within the Company’s projects that are restricted in their use. As of June 30, 2023, these restricted funds were comprised of $104 million designated to fund operating expenses, $168 million designated for current debt service payments and $85 million restricted for reserves including debt service, performance obligations and other reserves as well as capital expenditures. The remaining $14 million is held in distributions reserve accounts.

Accumulated Depreciation and Accumulated Amortization

The following table presents the accumulated depreciation included in the property, plant and equipment, net, and accumulated amortization included in intangible assets, net, respectively, as of September 30, 2017 and December 31, 2016:net:

| September 30, 2017 | December 31, 2016 | ||||||

| (In millions) | |||||||

| Property, Plant and Equipment Accumulated Depreciation | $ | 1,189 | $ | 951 | |||

| Intangible Assets Accumulated Amortization | 216 | 163 | |||||

| (In millions) | |||

| Balance as of December 31, 2016 as reported | $ | 313 | |

| Less: Adjustment for August 2017 Drop Down Assets | (87 | ) | |

| Balance as of December 31, 2016 as recast | 226 | ||

| Capital contributions from tax equity investors, net of distributions | 11 | ||

| Comprehensive loss | (56 | ) | |

| Balance as of September 30, 2017 | $ | 181 | |

| June 30, 2023 | December 31, 2022 | ||||||||||

| (In millions) | |||||||||||

| Property, Plant and Equipment Accumulated Depreciation | $ | 3,232 | $ | 3,024 | |||||||

| Intangible Assets Accumulated Amortization | 972 | 877 | |||||||||

Distributions

The following table lists the distributions paid on NRG Yield LLC'sthe Company's Class A, B, C and D units during the ninesix months ended SeptemberJune 30, 2017:2023:

| Third Quarter 2017 | Second Quarter 2017 | First Quarter 2017 | |||||||||

| Distributions per Class A, B, C and D unit | $ | 0.28 | $ | 0.27 | $ | 0.26 | |||||

| Second Quarter 2023 | First Quarter 2023 | |||||||||||||||||||||||||

| Distributions per Class A, B, C and D unit | $ | 0.3818 | $ | 0.3745 | ||||||||||||||||||||||

On October 31, 2017,August 7, 2023, the Company declared a distribution on its Class A, Class B, Class C and Class D units of $0.288$0.3891 per unit payable on DecemberSeptember 15, 20172023 to unit holders of record as of DecemberSeptember 1, 2017.2023.

Redeemable Noncontrolling Interests

To the extent that a third party has the right to redeem their interests for cash or other assets, the Company has included the noncontrolling interest attributable to the third party as a component of temporary equity distribution agreement, NRG Yield, Inc. may offer and sell shares of its Class C common stock par value $0.01 per share, from time to time throughin the sales agents up to an aggregate sales price of $150 million through an at-the-market equity offering program, or the ATM Program. NRG Yield, Inc. may also sell shares of its Class C common stock to anymezzanine section of the sales agents, as principalsconsolidated balance sheet. The following table reflects the changes in the Company’s redeemable noncontrolling interest balance:

| (In millions) | ||||||||

| Balance at December 31, 2022 | $ | 7 | ||||||

| Cash distributions to redeemable noncontrolling interests | (1) | |||||||

| Comprehensive income attributable to redeemable noncontrolling interests | 9 | |||||||

| Balance at June 30, 2023 | $ | 15 | ||||||

14

Revenue Recognition

Disaggregated Revenues

The following tables represent the Company’s disaggregation of revenue from contracts with customers along with the reportable segment for its own account, ateach category:

| Three months ended June 30, 2023 | |||||||||||||||||||||||||||||

| (In millions) | Conventional Generation | Renewables | Total | ||||||||||||||||||||||||||

Energy revenue (a) | $ | 3 | $ | 275 | $ | 278 | |||||||||||||||||||||||

Capacity revenue (a) | 96 | 5 | 101 | ||||||||||||||||||||||||||

Other revenue (a) | 21 | 27 | 48 | ||||||||||||||||||||||||||

| Contract amortization | (5) | (42) | (47) | ||||||||||||||||||||||||||

| Mark-to-market for economic hedges | — | 26 | 26 | ||||||||||||||||||||||||||

| Total operating revenues | 115 | 291 | 406 | ||||||||||||||||||||||||||

| Less: Mark-to-market for economic hedges | — | (26) | (26) | ||||||||||||||||||||||||||

| Less: Lease revenue | (104) | (237) | (341) | ||||||||||||||||||||||||||

| Less: Contract amortization | 5 | 42 | 47 | ||||||||||||||||||||||||||

| Total revenue from contracts with customers | $ | 16 | $ | 70 | $ | 86 | |||||||||||||||||||||||

(a) The following amounts of energy, capacity and other revenue relate to leases and are accounted for under ASC 842:

| (In millions) | Conventional Generation | Renewables | Total | ||||||||||||||

| Energy revenue | $ | 1 | $ | 233 | $ | 234 | |||||||||||

| Capacity revenue | 82 | 4 | 86 | ||||||||||||||

Other revenue (b) | 21 | — | 21 | ||||||||||||||

| Total | $ | 104 | $ | 237 | $ | 341 | |||||||||||

(b) On May 31, 2023, the Marsh Landing Black Start addition reached commercial operations and the Company will receive an annual fixed fee over a price agreed upon at the time of sale. During the first nine months of 2017, Yield, Inc. issued 1,921,866 shares of Class C common stockfive-year term under the ATM Programrelated agreement. The agreement was determined to be a sales-type lease resulting in the Company recording a lease receivable of $21 million included in total operating revenues, offset by net investment costs of $13 million included in cost of operations, resulting in a net pre-tax profit of $8 million.

15

| Three months ended June 30, 2022 | |||||||||||||||||||||||||||||||||||

| (In millions) | Conventional Generation | Renewables | Thermal | Total | |||||||||||||||||||||||||||||||

Energy revenue (a) | $ | 3 | $ | 306 | $ | 11 | $ | 320 | |||||||||||||||||||||||||||

Capacity revenue (a) | 106 | 1 | 4 | 111 | |||||||||||||||||||||||||||||||

| Other revenue | — | 27 | 3 | 30 | |||||||||||||||||||||||||||||||

| Contract amortization | (6) | (35) | — | (41) | |||||||||||||||||||||||||||||||

| Mark-to-market for economic hedges | — | (52) | — | (52) | |||||||||||||||||||||||||||||||

| Total operating revenues | 103 | 247 | 18 | 368 | |||||||||||||||||||||||||||||||

| Less: Mark-to-market for economic hedges | — | 52 | — | 52 | |||||||||||||||||||||||||||||||

| Less: Lease revenue | (109) | (268) | — | (377) | |||||||||||||||||||||||||||||||

| Less: Contract amortization | 6 | 35 | — | 41 | |||||||||||||||||||||||||||||||

| Total revenue from contracts with customers | $ | — | $ | 66 | $ | 18 | $ | 84 | |||||||||||||||||||||||||||

(a) The following amounts of energy and capacity revenue relate to leases and are accounted for gross proceedsunder ASC 842:

| (In millions) | Conventional Generation | Renewables | Total | ||||||||||||||||||||

| Energy revenue | $ | 3 | $ | 268 | $ | 271 | |||||||||||||||||

| Capacity revenue | 106 | — | 106 | ||||||||||||||||||||

| Total | $ | 109 | $ | 268 | $ | 377 | |||||||||||||||||

| Six months ended June 30, 2023 | |||||||||||||||||||||||||||||

| (In millions) | Conventional Generation | Renewables | Total | ||||||||||||||||||||||||||

Energy revenue (a) | $ | 4 | $ | 473 | $ | 477 | |||||||||||||||||||||||

Capacity revenue (a) | 196 | 10 | 206 | ||||||||||||||||||||||||||

Other revenue (a) | 21 | 39 | 60 | ||||||||||||||||||||||||||

| Contract amortization | (11) | (83) | (94) | ||||||||||||||||||||||||||

| Mark-to-market for economic hedges | — | 45 | 45 | ||||||||||||||||||||||||||

| Total operating revenues | 210 | 484 | 694 | ||||||||||||||||||||||||||

| Less: Mark-to-market for economic hedges | — | (45) | (45) | ||||||||||||||||||||||||||

| Less: Lease revenue | (205) | (393) | (598) | ||||||||||||||||||||||||||

| Less: Contract amortization | 11 | 83 | 94 | ||||||||||||||||||||||||||

| Total revenue from contracts with customers | $ | 16 | $ | 129 | $ | 145 | |||||||||||||||||||||||

(a) The following amounts of $35 million, with commission feesenergy, capacity and other revenue relate to leases and are accounted for under ASC 842:

| (In millions) | Conventional Generation | Renewables | Total | ||||||||||||||

| Energy revenue | $ | 2 | $ | 385 | $ | 387 | |||||||||||

| Capacity revenue | 182 | 8 | 190 | ||||||||||||||

Other revenue (b) | 21 | $ | — | 21 | |||||||||||||

| Total | $ | 205 | $ | 393 | $ | 598 | |||||||||||

(b) Includes revenue recognized for the Marsh Landing Black Start addition that reached commercial operations on May 31, 2023, as described above.

16

| Six months ended June 30, 2022 | |||||||||||||||||||||||||||||||||||

| (In millions) | Conventional Generation | Renewables | Thermal | Total | |||||||||||||||||||||||||||||||

Energy revenue (a) | $ | 3 | $ | 501 | $ | 48 | $ | 552 | |||||||||||||||||||||||||||

Capacity revenue (a) | 220 | 1 | 18 | 239 | |||||||||||||||||||||||||||||||

| Other revenue | — | 41 | 11 | 52 | |||||||||||||||||||||||||||||||

| Contract amortization | (12) | (71) | — | (83) | |||||||||||||||||||||||||||||||

| Mark-to-market for economic hedges | — | (178) | — | (178) | |||||||||||||||||||||||||||||||

| Total operating revenues | 211 | 294 | 77 | 582 | |||||||||||||||||||||||||||||||

| Less: Mark-to-market for economic hedges | — | 178 | — | 178 | |||||||||||||||||||||||||||||||

| Less: Lease revenue | (223) | (430) | (1) | (654) | |||||||||||||||||||||||||||||||

| Less: Contract amortization | 12 | 71 | — | 83 | |||||||||||||||||||||||||||||||

| Total revenue from contracts with customers | $ | — | $ | 113 | $ | 76 | $ | 189 | |||||||||||||||||||||||||||

(a) The following amounts of $346 thousand. Yield, Inc. usedenergy and capacity revenue relate to leases and are accounted for under ASC 842:

| (In millions) | Conventional Generation | Renewables | Thermal | Total | |||||||||||||||||||

| Energy revenue | $ | 3 | $ | 430 | $ | 1 | $ | 434 | |||||||||||||||

| Capacity revenue | 220 | — | — | 220 | |||||||||||||||||||

| Total | $ | 223 | $ | 430 | $ | 1 | $ | 654 | |||||||||||||||

Contract Balances

The following table reflects the net proceeds to acquire 1,921,866 Class C units fromcontract assets and liabilities included on the Company. At September 30, 2017, approximately $115 million remains available for issuance under the ATM Program.Company’s consolidated balance sheets:

| June 30, 2023 | December 31, 2022 | ||||||||||

| (In millions) | |||||||||||

| Accounts receivable, net - Contracts with customers | $ | 62 | $ | 37 | |||||||

| Accounts receivable, net - Leases | 153 | 116 | |||||||||

| Total accounts receivable, net | $ | 215 | $ | 153 | |||||||

17

Note 3 — Business Acquisitions and Dispositions

distributions in the consolidated statements of members’ equity.

The following is a summary of assets and liabilities transferred in connection with the acquisition of the November 2017 Drop Down Assets as of September 30, 2017:

| (In millions) | |||

| Assets: | |||

| Current assets | $ | 11 | |

| Property, plant and equipment | 84 | ||

| Non-current assets | 32 | ||

| Total assets | 127 | ||

| Liabilities: | |||

Debt (Current and non-current) (a) | 31 | ||

| Other current and non-current liabilities | 3 | ||

| Total liabilities assumed | 34 | ||

| Net assets acquired | $ | 93 | |

February 17, 2023:

| (In millions) | Daggett 3 | |||||||

| Restricted cash | $ | 14 | ||||||

| Property, plant and equipment | 534 | |||||||

| Right-of-use-assets, net | 31 | |||||||

| Derivative assets | 27 | |||||||

| Total assets acquired | 606 | |||||||

Long-term debt (a) | 480 | |||||||

| Long-term lease liabilities | 33 | |||||||

Other current and non-current liabilities (b) | 78 | |||||||

| Total liabilities assumed | 591 | |||||||

| Net assets acquired | $ | 15 | ||||||

(a)NetIncludes a $181 million construction loan, $75 million sponsor equity bridge loan and $229 million tax equity bridge loan, offset by $5 million in unamortized debt issuance costs. See Note 7, Long-term Debt, for further discussion of $2the long-term debt assumed in the acquisition.

(b) Includes $32 million of net debt issuanceproject costs that were subsequently funded by CEG. Subsequent to the acquisition date, CEG funded an additional $11 million in project costs.

| For the three months ended | For the nine months ended | ||||||||||||||

| September 30, 2017 | September 30, 2016 | September 30, 2017 | September 30, 2016 | ||||||||||||

| Total operating revenues | $ | 269 | $ | 275 | $ | 777 | $ | 798 | |||||||

| Net income | 30 | 69 | 90 | 155 | |||||||||||

Entities that are not Consolidated

The assets and liabilities transferred to the Company relate to interests under common control by NRG and were recorded at historical cost in accordance with ASC 805-50, Business Combination - Related Issues. The difference between the cash paid and the historical value of the entities' equity of $8 million was recorded ashas an adjustment to contributed capital. Since the transaction constituted a transfer of entities under common control, the accounting guidance requires retrospective combination of the entities for all periods presented as if the combination has been in effect from the beginning of the financial statement period or from the date the entities were under common control (if later than the beginning of the financial statement period). Accordingly, in connection with the retrospective adjustment of prior periods, the Company adjusted its financial statements to reflect its results of operations, financial position and cash flows as if it recorded its interests in the Agua Caliente Borrower 2 LLC on January 1, 2016, and its interests in the Utah Solar Portfolio on November 2, 2016.

| (In millions) | |||

| Assets: | |||

| Cash | $ | 6 | |

| Equity investment in projects | 456 | ||

| Total assets acquired | 462 | ||

| Liabilities: | |||

Debt (Current and non-current) (a) | 320 | ||

| Other current and non-current liabilities | 3 | ||

| Total liabilities assumed | 323 | ||

| Net assets acquired | $ | 139 | |

| Three months ended September 30, 2016 | Nine months ended September 30, 2016 | ||||||||||||||||||||||||||||||

| As Previously Reported | March 2017 Drop Down Assets | August 2017 Drop Down Assets | As Currently Reported | As Previously Reported | March 2017 Drop Down Assets | August 2017 Drop Down Assets | As Currently Reported | ||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||

| Total operating revenues | $ | 272 | $ | — | $ | — | $ | 272 | $ | 789 | $ | — | $ | — | $ | 789 | |||||||||||||||

| Operating income | 118 | — | — | 118 | 319 | — | — | 319 | |||||||||||||||||||||||

| Net income | 64 | 3 | — | 67 | 147 | 5 | — | 152 | |||||||||||||||||||||||

| Net income attributable to Yield LLC | 100 | 3 | 2 | 105 | 209 | 5 | 5 | 219 | |||||||||||||||||||||||

to the consolidated financial statements included in the Company’s 2022 Form 10-K.

18

Rosie Central BESS — On June 30, 2023, the Company, through its indirect subsidiary, Rosie Class B LLC, the indirect owner of the Rosamond Central solar project, became the owner of the Class B membership interests of Rosie BESS Devco LLC, or Rosie Central BESS, in order to facilitate and fund the construction of a 147 MW battery energy storage system, or BESS, that will be co-located at the Rosamond Central solar facility. Clearway Renew indirectly owns the Class A membership interests. The Company accounts for its investment in Rosie Central BESS as an equity method investment. The Company’s investment consists of $10 million contributed into Rosie Central BESS, funded through contributions from the Company and its cash equity investor in Rosie TargetCo LLC, which consolidates Rosie Class B LLC. On July 3, 2023, Rosie Class B LLC contributed an additional $20 million into Rosie Central BESS, as further described in Note 7, Long-term Debt.

Additionally, on June 30, 2023, Rosamond Central entered into an asset purchase agreement with Clearway Renew to acquire the BESS project assets at mechanical completion for a purchase price of $360 million, of which $72 million is payable at mechanical completion with the remaining $288 million payable at substantial completion. The Company will fund $17 million of the purchase price at mechanical completion and $67 million of the purchase price at substantial completion with the remaining purchase price funded through contributions from the cash equity investor in Rosie TargetCo LLC and the tax equity investor in Rosie TE Holdco LLC. The BESS project is anticipated to reach mechanical completion in the second half of 2023 and to reach substantial completion in the first half of 2024.

The Company’s maximum exposure to loss as of June 30, 2023 is limited to its equity investment in the unconsolidated entities, as further summarized in the table below:

| Name | Economic Interest | Investment Balance | ||||||

| (In millions) | ||||||||

| Avenal | 50% | $ | 5 | |||||

| Desert Sunlight | 25% | 227 | ||||||

| Elkhorn Ridge | 67% | 18 | ||||||

GenConn (a) | 50% | 80 | ||||||

| Rosie Central BESS | 50% | 10 | ||||||

| San Juan Mesa | 75% | 12 | ||||||

| $ | 352 | |||||||

(a)GenConn is a variable interest entity.

Entities that are Consolidated

The discussion below describes material changes to VIEs during the six months ended June 30, 2023.

Daggett Renewable Holdco LLC — As described in Note 5, Investments Accounted for by3, Acquisitions and Dispositions, on February 17, 2023, Daggett Solar Investment LLC, an indirect subsidiary of the Equity MethodCompany, acquired the Class A membership interests in Daggett TargetCo LLC while a cash equity investor acquired the Class B membership interests. The Company and Variable Interest Entities, the cash equity investor then contributed their Class A and B membership interests, respectively, into Daggett Renewable Holdco LLC, a partnership between the Company and the cash equity investor, and concurrently, Daggett TargetCo LLC became a wholly-owned subsidiary of Daggett Renewable Holdco LLC. The Company consolidates Daggett Renewable Holdco LLC as a VIE as the Company is the primary beneficiary, through its role as managing member. The Company recorded the noncontrolling interest of the cash equity investor in Daggett Renewable Holdco LLC at historical carrying amount, with the offset to contributed capital. Daggett TargetCo LLC consolidates, as the consolidated financial statements forindirect owner of the year ended December 31, 2016 included inprimary beneficiary, a tax equity fund, Daggett TE Holdco LLC, which owns the Company's May 9, 2017 Form 8-K.Daggett 3 solar project. The tax equity investor’s interest is shown as noncontrolling interest and the HLBV method is utilized to allocate the income or losses of Daggett TE Holdco LLC.

19

Summarized financial information for the Company'sCompany’s consolidated VIEs consisted of the following as of SeptemberJune 30, 2017:2023:

| (In millions) | Alta TE Holdco LLC | Buckthorn Holdings, LLC | DGPV Funds (a) | Daggett Renewable Holdco LLC (b) | Langford TE Partnership LLC | Lighthouse Renewable Holdco LLC (c) | |||||||||||||||||||||||||||||

| Other current and non-current assets | $ | 59 | $ | 6 | $ | 88 | $ | 142 | $ | 12 | $ | 123 | |||||||||||||||||||||||

| Property, plant and equipment | 290 | 189 | 510 | 570 | 119 | 819 | |||||||||||||||||||||||||||||

| Intangible assets | 193 | — | 13 | — | 2 | — | |||||||||||||||||||||||||||||

| Total assets | 542 | 195 | 611 | 712 | 133 | 942 | |||||||||||||||||||||||||||||

| Current and non-current liabilities | 37 | 11 | 66 | 492 | 53 | 299 | |||||||||||||||||||||||||||||

| Total liabilities | 37 | 11 | 66 | 492 | 53 | 299 | |||||||||||||||||||||||||||||

| Noncontrolling interest | 39 | 22 | 27 | 234 | 62 | 511 | |||||||||||||||||||||||||||||

| Net assets less noncontrolling interest | $ | 466 | $ | 162 | $ | 518 | $ | (14) | $ | 18 | $ | 132 | |||||||||||||||||||||||

| (In millions) | NRG Wind TE Holdco | Alta Wind TE Holdco | Spring Canyon | ||||||||

| Other current and non-current assets | $ | 175 | $ | 17 | $ | 4 | |||||

| Property, plant and equipment | 417 | 443 | 96 | ||||||||

| Intangible assets | 2 | 265 | — | ||||||||

| Total assets | 594 | 725 | 100 | ||||||||

| Current and non-current liabilities | 206 | 9 | 6 | ||||||||

| Total liabilities | 206 | 9 | 6 | ||||||||

| Noncontrolling interest | 22 | 96 | 63 | ||||||||

| Net assets less noncontrolling interests | $ | 366 | $ | 620 | $ | 31 | |||||

(c) Lighthouse Renewable Holdco LLC consolidates Mesquite Star Tax Equity Holdco LLC, Black Rock TE Holdco LLC, Mililani TE Holdco LLC and Waiawa TE Holdco LLC, which are considered VIEs under ASC 810, but for which it is not considered the primary beneficiary. The Company accounts for its interests in these entities under the equity method of accounting, as further described in Note 5, Investments Accounted for by the Equity Method and Variable Interest Entities, to the consolidated financial statements for the year ended December 31, 2016 included in the Company's May 9, 2017 Form 8-K.VIEs.

| (In millions) | Lighthouse Renewable Holdco 2 LLC(a) | Oahu Solar LLC | Pinnacle Repowering TE Holdco LLC | Rattlesnake TE Holdco LLC | Rosie TargetCo LLC | Wildorado TE Holdco LLC | Other (b) | ||||||||||||||||||||||||||||||||||

| Other current and non-current assets | $ | 42 | $ | 39 | $ | 6 | $ | 14 | $ | 45 | $ | 20 | $ | 14 | |||||||||||||||||||||||||||

| Property, plant and equipment | 353 | 160 | 100 | 180 | 234 | 202 | 148 | ||||||||||||||||||||||||||||||||||

| Intangible assets | — | — | 15 | — | — | — | 1 | ||||||||||||||||||||||||||||||||||

| Total assets | 395 | 199 | 121 | 194 | 279 | 222 | 163 | ||||||||||||||||||||||||||||||||||

| Current and non-current liabilities | 130 | 22 | 5 | 17 | 97 | 19 | 71 | ||||||||||||||||||||||||||||||||||

| Total liabilities | 130 | 22 | 5 | 17 | 97 | 19 | 71 | ||||||||||||||||||||||||||||||||||

| Noncontrolling interest | 232 | 24 | 42 | 83 | 128 | 105 | 67 | ||||||||||||||||||||||||||||||||||

| Net assets less noncontrolling interest | $ | 33 | $ | 153 | $ | 74 | $ | 94 | $ | 54 | $ | 98 | $ | 25 | |||||||||||||||||||||||||||

| (In millions) | Maximum exposure to loss | ||

| Four Brothers Solar, LLC | $ | 221 | |

| Granite Mountain Holdings, LLC | 81 | ||

| Iron Springs Holdings, LLC | 56 | ||

| GenConn Energy LLC | 102 | ||

| NRG DGPV Holdco 1 LLC | 71 | ||

| NRG RPV Holdco 1 LLC | 65 | ||

| NRG DGPV Holdco 2 LLC | 54 | ||

| NRG DGPV Holdco 3 LLC | 20 | ||

| Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Income Statement Data: | ||||||||||||||||

| Utah Solar Portfolio | ||||||||||||||||

| Operating revenues | $ | 23 | $ | — | $ | 60 | $ | — | ||||||||

| Operating income | 9 | — | 17 | — | ||||||||||||

| Net income | 9 | — | 17 | — | ||||||||||||

| September 30, 2017 | December 31, 2016 | |||||||||||||||

| Balance Sheet Data: | (In millions) | |||||||||||||||

| Utah Solar Portfolio | ||||||||||||||||

| Current assets | $ | 25 | $ | 20 | ||||||||||||

| Non-current assets | 1,091 | 1,105 | ||||||||||||||

| Current liabilities | 9 | 14 | ||||||||||||||

| Non-current liabilities | 21 | 38 | ||||||||||||||

Note 5 — Fair Value of Financial Instruments

Fair Value Accounting under ASC 820

ASC 820 establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value into three levels as follows:

•Level 1—quoted prices (unadjusted) in active markets for identical assets or liabilities that the Company has the ability to access as of the measurement date.

•Level 2—inputs other than quoted prices included within Level 1 that are directly observable for the asset or liability or indirectly observable through corroboration with observable market data.

•Level 3—unobservable inputs for the asset or liability only used when there is little, if any, market activity for the asset or liability at the measurement date.

In accordance with ASC 820, the Company determines the level in the fair value hierarchy within which each fair value measurement in its entirety falls, based on the lowest level input that is significant to the fair value measurement.

20

For cash and cash equivalents, restricted cash, accounts receivable — trade, accounts receivable — affiliate,affiliates, accounts payable current portion of the— trade, accounts payable — affiliates and accrued expenses and other current liabilities, the carrying amounts approximate fair value because of the short-term maturity of those instruments and are classified as Level 1 within the fair value hierarchy.

The estimated carrying amounts and estimated fair values of the Company’s recorded financial instruments not carried at fair market value or that do not approximate fair value are as follows:

| As of September 30, 2017 | As of December 31, 2016 | ||||||||||||||

| Carrying Amount | Fair Value | Carrying Amount | Fair Value | ||||||||||||

| (In millions) | |||||||||||||||

| Assets: | |||||||||||||||

Notes receivable (a) | $ | 18 | $ | 18 | $ | 30 | $ | 30 | |||||||

| Liabilities: | |||||||||||||||

| Long-term debt — affiliate | 618 | 626 | 618 | 608 | |||||||||||

Long-term debt — external, including current portion (b) | $ | 5,268 | $ | 5,301 | $ | 5,451 | $ | 5,435 | |||||||

| As of June 30, 2023 | As of December 31, 2022 | ||||||||||||||||||||||

| Carrying Amount | Fair Value | Carrying Amount | Fair Value | ||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Long-term debt, including current portion — affiliate | $ | 2 | $ | 2 | $ | 2 | $ | 2 | |||||||||||||||

Long-term debt, including current portion — external (a) | 7,097 | 6,516 | 6,874 | 6,288 | |||||||||||||||||||

(a) Includes the long-term portion of notes receivable, which is recorded in other noncurrent assets on the Company's consolidated balance sheets.

The fair value of the Company'sCompany’s publicly-traded long-term debt is based on quoted market prices and is classified as Level 2 within the fair value hierarchy. The fair value of debt securities, non-publicly traded long-term debt and certain notes receivable of the Company are based on expected future cash flows discounted at market interest rates, or current interest rates for similar instruments with equivalent credit quality and are classified as Level 3 within the fair value hierarchy. The following table presents the level within the fair value hierarchy for long-term debt, including current portion as of September 30, 2017 and December 31, 2016:portion:

| As of September 30, 2017 | As of December 31, 2016 | ||||||||||||||

| Level 2 | Level 3 | Level 2 | Level 3 | ||||||||||||

| (In millions) | |||||||||||||||

| Long-term debt, including current portion | $ | 884 | $ | 5,043 | $ | 833 | $ | 5,210 | |||||||

| As of June 30, 2023 | As of December 31, 2022 | ||||||||||||||||||||||

| Level 2 | Level 3 | Level 2 | Level 3 | ||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Long-term debt, including current portion | $ | 1,841 | $ | 4,677 | $ | 1,836 | $ | 4,454 | |||||||||||||||

Recurring Fair Value Measurements

The Company records its derivative assets and liabilities at fair market value on its consolidated balance sheet. The following table presents assets and liabilities measured and recorded at fair value on the Company'sCompany’s consolidated balance sheets on a recurring basis and their level within the fair value hierarchy:

| As of September 30, 2017 | As of December 31, 2016 | ||||||||||

Fair Value (a) | Fair Value (a) | Fair Value (a) | |||||||||

| (In millions) | Level 2 | Level 1 | Level 2 | ||||||||

| Derivative assets: | |||||||||||

| Commodity contracts | $ | — | $ | 1 | $ | 1 | |||||

| Interest rate contracts | — | — | 1 | ||||||||

| Total assets | — | 1 | 2 | ||||||||

| Derivative liabilities: | |||||||||||

| Commodity contracts | 2 | — | 1 | ||||||||

| Interest rate contracts | 64 | — | 75 | ||||||||

| Total liabilities | $ | 66 | $ | — | $ | 76 | |||||

| As of June 30, 2023 | As of December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||

Fair Value (a) | Fair Value (a) | ||||||||||||||||||||||||||||||||||||||||

| (In millions) | Level 2 | Level 3 | Level 2 | Level 3 | |||||||||||||||||||||||||||||||||||||

| Derivative assets: | |||||||||||||||||||||||||||||||||||||||||

| Interest rate contracts | $ | 117 | $ | — | $ | 89 | $ | — | |||||||||||||||||||||||||||||||||

Other financial instruments (b) | — | 12 | — | 17 | |||||||||||||||||||||||||||||||||||||

| Total assets | $ | 117 | $ | 12 | $ | 89 | $ | 17 | |||||||||||||||||||||||||||||||||

| Derivative liabilities: | |||||||||||||||||||||||||||||||||||||||||

| Commodity contracts | $ | — | $ | 303 | $ | — | $ | 353 | |||||||||||||||||||||||||||||||||

| Total liabilities | $ | — | $ | 303 | $ | — | $ | 353 | |||||||||||||||||||||||||||||||||

(a)There were no derivative assets classified as Level 1 or Level 3 and no liabilities classified as Level 1 as of SeptemberJune 30, 2017. There were no derivative assets or liabilities classified as Level 3 as of September 30, 20172023 and December 31, 2016.2022.

(b)Includes SREC contract.

21

The following table reconciles the beginning and ending balances for instruments that are recognized at fair value in the consolidated financial statements using significant unobservable inputs:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| (In millions) | Fair Value Measurement Using Significant Unobservable Inputs (Level 3) | Fair Value Measurement Using Significant Unobservable Inputs (Level 3) | ||||||||||||||||||||||||

| Beginning balance | $ | (316) | $ | (280) | $ | (336) | $ | (154) | ||||||||||||||||||

| Settlements | 5 | 22 | 9 | 28 | ||||||||||||||||||||||

| Additions due to loss of NPNS exception | — | — | — | (22) | ||||||||||||||||||||||

| Total gains (losses) for the period included in earnings | 20 | (74) | 36 | (184) | ||||||||||||||||||||||

| Ending balance | $ | (291) | $ | (332) | $ | (291) | $ | (332) | ||||||||||||||||||

| Change in unrealized gains included in earnings for derivatives and other financial instruments held as of June 30, 2023 | $ | 20 | $ | 36 | ||||||||||||||||||||||

Derivative and Financial Instruments Fair Value Measurements

The Company's contracts are non-exchange-traded and valued using prices provided by external sources. For the Company’s energy markets, management receives quotes from multiple sources.The Company uses quoted observable forward prices to value its commodity contracts. To the extent that multiple quotesobservable forward prices are received,not available, the quoted prices reflect the average of the bid-ask mid-pointforward prices obtained from all sources believedthe prior year, adjusted for inflation. As of June 30, 2023, contracts valued with prices provided by models and other valuation techniques make up 100% of derivative liabilities and other financial instruments.

The Company’s significant positions classified as Level 3 include physical commodity contracts executed in illiquid markets. The significant unobservable inputs used in developing fair value include illiquid power tenors and location pricing, which is derived by extrapolating pricing as a basis to provideliquid locations. The tenor pricing and basis spread are based on observable market data when available or derived from historic prices and forward market prices from similar observable markets when not available.

The following table quantifies the most liquid market forsignificant unobservable inputs used in developing the commodity.fair value of the Company’s Level 3 positions:

| June 30, 2023 | |||||||||||||||||||||||

| Fair Value | Input/Range | ||||||||||||||||||||||

| Assets | Liabilities | Valuation Technique | Significant Unobservable Input | Low | High | Weighted Average | |||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Commodity Contracts | $ | — | $ | (303) | Discounted Cash Flow | Forward Market Price (per MWh) | $ | 21.02 | $ | 71.74 | $ | 38.17 | |||||||||||

| Other Financial Instruments | 12 | — | Discounted Cash Flow | Forecast annual generation levels of certain DG solar facilities | 60,801 MWh | 121,602 MWh | 115,622 MWh | ||||||||||||||||

The following table provides the impact on the fair value measurements to increases/(decreases) in significant unobservable inputs as of June 30, 2023:

| Significant Unobservable Input | Position | Change In Input | Impact on Fair Value Measurement | ||||||||

| Forward Market Price Power | Sell | Increase/(Decrease) | Lower/(Higher) | ||||||||

| Forecast Generation Levels | Sell | Increase/(Decrease) | Higher/(Lower) | ||||||||

22

The fair value of each contract is discounted using a risk freerisk-free interest rate. In addition, a credit reserve is applied to reflect credit risk, which is, for interest rate swaps, calculated based on credit default swaps using the bilateral method. For commodities, to the extent that the net exposureNet Exposure under a specific master agreement is an asset, the Company uses the counterparty’s default swap rate. If the net exposureNet Exposure under a specific master agreement is a liability, the Company uses NRG'sa proxy of its own default swap rate. For interest rate swaps and commodities, the credit reserve is added to the discounted fair value to reflect the exit price that a market participant would be willing to receive to assume the liabilities or that a market participant would be willing to pay for the assets. As of SeptemberJune 30, 2017,2023, the creditnon-performance reserve resultedwas a $26 million gain recorded primarily to total operating revenues in a $1 million increase in fair value in interest expense.the consolidated statements of income. It is possible that future market prices could vary from those used in recording assets and liabilities and such variations could be material.

Concentration of Credit Risk

In addition to the credit risk discussion inas disclosed under Item 15 — Note 2, Summary of Significant Accounting Policies, to the consolidated financial statements for the year ended December 31, 2016 included in the Company's May 9, 2017Company’s 2022 Form 8-K,10-K, the following item is a discussion of the concentration of credit risk for the Company'sCompany’s financial instruments. Credit risk relates to the risk of loss resulting from non-performance or non-payment by counterparties pursuant to the terms of their contractual obligations. The Company monitors and manages credit risk through credit policies that include: (i) an established credit approval process; (ii) daily monitoring of counterparties' credit limits;limits on an as needed basis; (iii) as applicable, the use of credit mitigation measures such as margin, collateral, prepayment arrangements, or volumetric limits; (iv) the use of payment netting agreements; and (v) the use of master netting agreements that allow for the netting of positive and negative exposures of various contracts associated with a single counterparty. Risks surrounding counterparty performance and credit could ultimately impact the amount and timing of expected cash flows. The Company seeks to mitigate counterparty risk by having a diversified portfolio of counterparties.