UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10–Q10-Q

(Mark One)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended DecemberMarch 31, 20172023

or

¨TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ________________

Commission file number: 000-55276

Verde Resources, Inc. |

(Exact name of registrant as specified in its charter) |

Nevada |

| 32-0457838 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

(Address of principal executive offices) |

|

|

( |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x ☒ No ¨☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x ☒ No ¨☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large“large accelerated filer," "accelerated filer"” “accelerated filer” and "smaller“smaller reporting company"company” in Rule 12b-2 of the Exchange Act (Check one).

Large accelerated filer |

| Accelerated filer |

|

Non-accelerated |

| Smaller reporting company |

|

(Do not check if a smaller reporting company) |

| ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ ☐ No x☒

As of FebruaryMay 12, 20182023 there were 96,038,9091,176,200,278 shares of the issuer's common stock,issuer’s Common Stock, par value $0.001, outstanding.

FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED DECEMBERMARCH 31, 20172023

TABLE OF CONTENTS

|

| PAGE |

| ||

|

| ||||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

|

| ||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

Unregistered Sales of Equity Securities and Use of Proceeds. |

|

|

| ||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

| |||

|

|

|

| 2 |

| Table of Contents |

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, that are not historical facts, and involve risks and uncertainties that could cause actual results to differ materially from those expected and projected. All statements, other than statements of historical facts, included in this Form 10-Q including, without limitation, statements in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s financial position, business strategy and the plans and objectives of management for future operations, events or developments which the Company expects or anticipates will or may occur in the future, including such things as future capital expenditures (including the amount and nature thereof); expansion and growth of the Company’s business and operations; and other such matters are forward-looking statements. These statements are based on certain assumptions and analyses made by the Company in light of its experience and its perception of historical trends, current conditions and expected future developments, as well as other factors it believes are appropriate under the circumstances. However, whether actual results or developments will conform with the Company’s expectations and predictions is subject to a number of risks and uncertainties, including general economic, market and business conditions; the business opportunities (or lack thereof) that may be presented to and pursued by the Company; changes in laws or regulation; and other factors, most of which are beyond the control of the Company.

These forward-looking statements can be identified by the use of predictive, future-tense or forward-looking terminology, such as “believes,” “anticipates,” “expects,” “estimates,” “plans,” “may,” “will,” or similar terms. These statements appear in a number of places in this filing and include statements regarding the intent, belief or current expectations of the Company, and its directors or its officers with respect to, among other things: (i) trends affecting the Company’s financial condition or results of operations for its limited history; (ii) the Company’s business and growth strategies; and, (iii) the Company’s financing plans. Investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve significant risks and uncertainties, and that actual results may differ materially from those projected in the forward-looking statements as a result of various factors. Such factors that could adversely affect actual results and performance include, but are not limited to, the Company’s limited operating history, potential fluctuations in quarterly operating results and expenses, government regulation, technological change and competition. For information identifying important factors that could cause actual results to differ materially from those anticipated in the forward-looking statements, please refer to our filings with the SEC under the Exchange Act and the Securities Act of 1933, as amended, including our Current Report on Form 10-K filed with the Securities and Exchange Commission on November 4, 2022.

Consequently, all of the forward-looking statements made in this Form 10-Q are qualified by these cautionary statements and there can be no assurance that the actual results or developments anticipated by the Company will be realized or, even if substantially realized, that they will have the expected consequence to or effects on the Company or its business or operations. The Company assumes no obligations to update any such forward-looking statements.

| 3 |

| Table of Contents |

PART I - FINANCIAL INFORMATION

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and Item Regulation S-X, Rule 10-01(c) Interim Financial Statements, and, therefore, do not include all information and footnotes necessary for a complete presentation of financial position, results of operations, cash flows, and stockholders’ equity in conformity with generally accepted accounting principles. In the opinion of management, all adjustments considered necessary for a fair presentation of the results of operations and financial position have been included and all such adjustments are of a normal recurring nature. Operating results for the nine months ended March 31, 2023 are not necessarily indicative of the results that can be expected for the year ended June 30, 2023.

VERDE RESOURCES, INC.

INDEX TO INTERIMUNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE PERIOD OF ENDED DECEMBERMARCH 31, 20172023

|

| Page |

|

|

|

| |

Condensed Consolidated Balance Sheets as at March 31, 2023 (Unaudited) and June 30, 2022 |

|

|

|

|

|

| |

|

|

| |

|

|

| |

|

|

| |

F-4 | |||

|

|

| |

Notes to Condensed Consolidated Financial Statements (Unaudited) |

|

|

|

| Table of Contents |

VERDE RESOURCES, INC.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(Currency expressed in United States Dollars (“US$”), except for number of shares)

Condensed Consolidated Balance Sheets

|

| As at December 31, |

|

| As at June 30, |

| ||

|

| 2017 |

|

| 2017 |

| ||

ASSETS |

| (Unaudited) |

|

| (Audited) |

| ||

Current Assets |

|

|

|

|

|

| ||

Cash and cash equivalents |

| $ | 11,225 |

|

| $ | 38,616 |

|

Amount due from related parties |

|

| 4,614 |

|

|

| 4,088 |

|

Inventories |

|

| 13,278 |

|

|

| 8,832 |

|

Deposit & prepayment |

|

| 2,945 |

|

|

| 2,352 |

|

Total Current Assets |

| $ | 32,062 |

|

| $ | 53,888 |

|

Long Term Assets |

|

|

|

|

|

|

|

|

Property, plant and equipment |

| $ | 11,900 |

|

| $ | 23,388 |

|

Total Long Term Assets |

| $ | 11,900 |

|

| $ | 23,388 |

|

|

|

|

|

|

|

|

|

|

TOTAL ASSETS |

| $ | 43,962 |

|

| $ | 77,276 |

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' DEFICIT |

|

|

|

|

|

|

|

|

Current Liabilities |

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 1,644,145 |

|

| $ | 1,560,749 |

|

Advanced from related parties |

|

| 766,798 |

|

|

| 728,634 |

|

Accrual |

|

| 63,550 |

|

|

| 101,979 |

|

Taxation payable |

|

| (34 | ) |

|

| 3,758 |

|

Loans from banks |

|

| 2,397 |

|

|

| 4,645 |

|

Total Current Liabilities |

| $ | 2,476,856 |

|

| $ | 2,399,765 |

|

Long term Liabilities |

|

|

|

|

|

|

|

|

Loans from banks (non-current) |

| $ | 1,441 |

|

| $ | 2,466 |

|

Total Long Term Liabilities |

| $ | 1,441 |

|

| $ | 2,466 |

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES |

| $ | 2,478,297 |

|

| $ | 2,402,231 |

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS' DEFICIT |

|

|

|

|

|

|

|

|

Preferred stock, par value $0.001, 50,000,000 shares authorized, none issued and outstanding |

|

| - |

|

|

| - |

|

Common stock, par value $0.001, 250,000,000 shares authorized, 96,038,909 shares issued and outstanding as of December 31, 2017 & June 30, 2017 respectively |

| $ | 96,039 |

|

| $ | 96,039 |

|

Additional paid-in capital |

|

| 2,055,243 |

|

|

| 2,055,243 |

|

Accumulated deficit |

|

| (4,568,446 | ) |

|

| (4,628,182 | ) |

Accumulated other comprehensive income (loss) |

|

| 554,494 |

|

|

| 731,182 |

|

Non-controlled interest |

|

| (571,665 | ) |

|

| (579,237 | ) |

Total Stockholders' Deficit |

| $ | (2,434,335 | ) |

| $ | (2,324,955 | ) |

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT |

| $ | 43,962 |

|

| $ | 77,276 |

|

|

| March 31, 2023 |

|

| June 30, 2022 |

| ||

ASSETS |

|

|

|

|

|

| ||

Current assets: |

|

|

|

|

|

| ||

Cash and cash equivalents |

| $ | 241,371 |

|

| $ | 418,917 |

|

Accounts receivable |

|

| 13,760 |

|

|

| 21,028 |

|

Inventories |

|

| 97,336 |

|

|

| 87,035 |

|

Amount due from related party |

|

| 100 |

|

|

| - |

|

Prepayments |

|

| 450,470 |

|

|

| 722 |

|

Other receivables and deposits |

|

| 192,127 |

|

|

| 118,516 |

|

|

|

|

|

|

|

|

|

|

Total current assets |

|

| 995,164 |

|

|

| 646,218 |

|

|

|

|

|

|

|

|

|

|

Non-current assets: |

|

|

|

|

|

|

|

|

Property, plant and equipment, net |

|

| 7,272,555 |

|

|

| 1,048,893 |

|

Right of use assets, net |

|

| 663,455 |

|

|

| 685,714 |

|

Mining rights |

|

| - |

|

|

| 27,088 |

|

Intangible asset |

|

| 30,192,771 |

|

|

| - |

|

Security deposit |

|

| 80,000 |

|

|

| 320,000 |

|

Deposit paid for acquisition of subsidiaries |

|

| 22,609 |

|

|

| 25,935,550 |

|

Deposit paid for acquisition of property, plant and equipment |

|

| - |

|

|

| 5,000,000 |

|

|

|

|

|

|

|

|

|

|

Total non-current assets |

|

| 38,231,390 |

|

|

| 33,017,245 |

|

|

|

|

|

|

|

|

|

|

Assets of disposal group held for sale |

|

| 19,570 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

TOTAL ASSETS |

| $ | 39,246,124 |

|

| $ | 33,663,463 |

|

|

|

|

|

|

|

|

|

|

LIABILTIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 29,360 |

|

| $ | 18,211 |

|

Accrued liabilities and other payables |

|

| 579,374 |

|

|

| 283,656 |

|

Finance lease liabilities |

|

| 171,538 |

|

|

| 75,224 |

|

Operating lease liability |

|

| 19,851 |

|

|

| - |

|

Bank loan |

|

| 100,000 |

|

|

| - |

|

Promissory notes |

|

| - |

|

|

| 18,484,028 |

|

Amount due to director |

|

| 16,776 |

|

|

| - |

|

Amounts due to related parties |

|

| 178,492 |

|

|

| 555,527 |

|

|

|

|

|

|

|

|

|

|

Total current liabilities |

|

| 1,095,391 |

|

|

| 19,416,646 |

|

|

|

|

|

|

|

|

|

|

Non-current liabilities: |

|

|

|

|

|

|

|

|

Finance lease liabilities |

|

| 654,979 |

|

|

| 97,900 |

|

Operating lease liability |

|

| 35,032 |

|

|

| - |

|

Promissory notes |

|

| 481,023 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

Total non-current liabilities |

|

| 1,171,034 |

|

|

| 97,900 |

|

|

|

|

| �� |

|

|

|

|

Liabilities of disposal group held for sale |

|

| 40,007 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES |

|

| 2,306,432 |

|

|

| 19,514,546 |

|

|

|

|

|

|

|

|

|

|

Commitments and contingencies |

|

| - |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

Preferred stock, $0.001 par value, 50,000,000 shares authorized, none issued and outstanding |

|

| - |

|

|

| - |

|

Common stock, $0.001 par value; 10,000,000,000 shares authorized; 1,174,290,939 and 819,188,055 shares issued and outstanding as of March 31, 2023 and June 30, 2022 |

|

| 1,174,291 |

|

|

| 819,188 |

|

Common stock, $0.001 par value; 1,717,032 and 0 shares to be issued as of March 31, 2023 and June 30, 2022 |

|

| 1,717 |

|

|

| - |

|

Additional paid-in capital |

|

| 45,396,150 |

|

|

| 22,945,190 |

|

Accumulated other comprehensive income |

|

| 886,003 |

|

|

| 742,459 |

|

Accumulated deficit |

|

| (10,518,469 | ) |

|

| (10,357,920 | ) |

Stockholders’ equity |

|

| 36,939,692 |

|

|

| 14,148,917 |

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

| $ | 39,246,124 |

|

| $ | 33,663,463 |

|

TheSee accompanying notes are an integral part of theseto unaudited condensed consolidated financial statements.

| Table of Contents |

VERDE RESOURCES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME

(Currency expressed in United States Dollars (“US$”), except for number of shares)

Condensed Consolidated Statements of Operations

|

| Three Months Ended December 31, |

|

| Six Months Ended December 31, |

| ||||||||||

|

| 2017 |

|

| 2016 |

|

| 2017 |

|

| 2016 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

REVENUES |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Revenue |

|

| 22,802 |

|

|

| 186,767 |

|

| $ | 43,523 |

|

| $ | 557,003 |

|

Cost of revenue |

|

| (35,046 | ) |

|

| (131,028 | ) |

|

| (46,079 | ) |

|

| (636,050 | ) |

Gross profit (loss) |

|

| (12,244 | ) |

|

| 55,739 |

|

|

| (2,556 | ) |

|

| (79,047 | ) |

OPERATING EXPENSES: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selling, general & administrative expenses |

|

| 25,325 |

|

|

| (102,371 | ) |

|

| 11,300 |

|

|

| (196,039 | ) |

PROFIT (LOSS) FROM OPERATIONS |

|

| 13,081 |

|

|

| (46,632 | ) |

| $ | 8,744 |

|

| $ | (275,086 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OTHER INCOME(EXPENSES) |

|

| 16,557 |

|

|

| 35,450 |

|

|

| 58,564 |

|

|

| 47,744 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NET PROFIT (LOSS) BEFORE INCOME TAX |

|

| 29,638 |

|

|

| (11,182 | ) |

| $ | 67,308 |

|

| $ | (227,342 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Provision of Income Tax |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

NET PROFIT (LOSS) |

|

| 29,638 |

|

|

| (11,182 | ) |

| $ | 67,308 |

|

| $ | (227,342 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-controlled interest |

|

| (185 | ) |

|

| (10,045 | ) |

|

| (7,572 | ) |

|

| 11,625 |

|

Net profit (loss) contributed to the group |

|

| 29,453 |

|

|

| (21,227 | ) |

|

| 59,736 |

|

|

| (215,717 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other comprehensive income(loss) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign currency translation income(loss) |

|

| (128,578 | ) |

|

| 72,179 |

|

| $ | (176,688 | ) |

| $ | 158,538 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Comprehensive income(loss) |

| $ | (99,125 | ) |

| $ | 50,952 |

|

| $ | (116,952 | ) |

| $ | (57,179 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and Diluted Profit (Loss) per Common Share |

| $ | 0.0003 |

|

| $ | (0.0001 | ) |

| $ | 0.0007 |

|

| $ | (0.0024 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Common Shares Outstanding |

|

| 96,038,909 |

|

|

| 93,715,539 |

|

|

| 96,038,909 |

|

|

| 93,715,539 |

|

|

| Three Months ended March 31, |

|

| Nine Months ended March 31, |

| ||||||||||

|

| 2023 |

|

| 2022 |

|

| 2023 |

|

| 2022 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Revenue, net |

| $ | 26,586 |

|

| $ | 16,712 |

|

| $ | 134,038 |

|

| $ | 16,712 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost of revenue |

|

| (44,308 | ) |

|

| (86,701 | ) |

|

| (123,903 | ) |

|

| (86,701 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross (loss)/profit |

|

| (17,722 | ) |

|

| (69,989 | ) |

|

| 10,135 |

|

|

| (69,989 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative |

|

| (816,089 | ) |

|

| (498,774 | ) |

|

| (2,381,155 | ) |

|

| (1,221,875 | ) |

Total operating expenses |

|

| (816,089 | ) |

|

| (498,774 | ) |

|

| (2,381,155 | ) |

|

| (1,221,875 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOSS FROM OPERATION |

|

| (833,811 | ) |

|

| (568,763 | ) |

|

| (2,371,020 | ) |

|

| (1,291,864 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other (expense) income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense |

|

| (13,549 | ) |

|

| (486,977 | ) |

|

| (1,893,209 | ) |

|

| (1,441,911 | ) |

Other income |

|

| 194,917 |

|

|

| 99 |

|

|

| 196,514 |

|

|

| 12,214 |

|

Total other income (expense), net |

|

| 181,368 |

|

|

| (486,878 | ) |

|

| (1,696,695 | ) |

|

| (1,429,697 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOSS BEFORE INCOME TAXES |

|

| (652,443 | ) |

|

| (1,055,641 | ) |

|

| (4,067,715 | ) |

|

| (2,721,561 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income tax expense |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss from continuing operation |

|

| (652,443 | ) |

|

| (1,055,641 | ) |

|

| (4,067,715 | ) |

|

| (2,721,561 | ) |

Loss from discontinued operation |

|

| (55,884 | ) |

|

| - |

|

|

| (157,284 | ) |

|

| - |

|

NET LOSS |

|

| (708,327 | ) |

|

| (1,055,641 | ) |

|

| (4,224,999 | ) |

|

| (2,721,561 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Comprising: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net profit attributable to noncontrolling interest |

|

| - |

|

|

| 23,914 |

|

|

| - |

|

|

| 6,979 |

|

Net loss attributable to Verde Resources Inc., shareholders |

|

| (708,327 | ) |

|

| (1,079,555 | ) |

|

| (4,224,999 | ) |

|

| (2,728,540 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| $ | (708,327 | ) |

| $ | (1,055,641 | ) |

| $ | (4,224,999 | ) |

| $ | (2,721,561 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other comprehensive income (loss) : |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

– Foreign currency adjustment income (loss) |

|

| 154,912 |

|

|

| 11,600 |

|

|

| 143,544 |

|

|

| 15,171 |

|

Less: other comprehensive (loss) attributable to non-controlling interest |

|

| - |

|

|

| (13,285 | ) |

|

| - |

|

|

| (12,750 | ) |

Add: other comprehensive income attributable to Verde Resources Inc., shareholders |

|

| 154,912 |

|

|

| 24,885 |

|

|

| 143,544 |

|

|

| 27,921 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPREHENSIVE LOSS |

| $ | (553,415 | ) |

| $ | (1,044,041 | ) |

| $ | (4,081,455 | ) |

| $ | (2,706,390 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

– Basic |

| $ | 0.00 |

|

| $ | 0.00 |

|

| $ | 0.00 |

|

| $ | 0.00 |

|

– Diluted |

| $ | 0.00 |

|

| $ | 0.00 |

|

| $ | 0.00 |

|

| $ | 0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average Common Shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

– Basic |

|

| 967,932,561 |

|

|

| 810,742,109 |

|

|

| 967,932,561 |

|

|

| 810,742,109 |

|

– Diluted |

|

| 979,305,136 |

|

|

| 819,188,055 |

|

|

| 979,305,136 |

|

|

| 819,188,055 |

|

TheSee accompanying notes are an integral part of theseto unaudited condensed consolidated financial statements.

| Table of Contents |

VERDE RESOURCES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Currency expressed in United States Dollars (“US$”))

|

| Nine Months ended March 31, |

| |||||

|

| 2023 |

|

| 2022 |

| ||

|

|

|

|

|

|

| ||

Cash flows from operating activities: |

|

|

|

|

|

| ||

Net loss |

| $ | (4,224,999 | ) |

| $ | (2,721,561 | ) |

|

|

|

|

|

|

|

|

|

Adjustments to reconcile net loss to net cash (used in) provided by operating activities |

|

|

|

|

|

|

|

|

Depreciation of property, plant and equipment |

|

| 177,074 |

|

|

| 9,831 |

|

Amortization |

|

| 98,954 |

|

|

| 29,434 |

|

Stock-based compensation |

|

| 448,123 |

|

|

| 284,249 |

|

Finance cost interest element of promissory notes (non-cash) |

|

| 1,870,972 |

|

|

| 1,441,911 |

|

Lease interest expense |

|

| 22,237 |

|

|

| - |

|

Fair value adjustment on convertible promissory note |

|

| (194,865 | ) |

|

|

|

|

Gain on disposal of property, plant and equipment |

|

| (600 | ) |

|

| - |

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

Accounts receivable |

|

| 7,196 |

|

|

| (14,818 | ) |

Other receivables, deposits and prepayments |

|

| (96,124 | ) |

|

| (85,132 | ) |

Inventories |

|

| (10,600 | ) |

|

| (81,492 | ) |

Accounts payables |

|

| 25,970 |

|

|

| (719 | ) |

Accrued liabilities and other payables |

|

| 183,312 |

|

|

| 24,774 |

|

Advanced from director |

|

| (5,761 | ) |

|

| - |

|

Mining rights |

|

| - |

|

|

| 16,142 |

|

Advanced from related parties |

|

| 165,792 |

|

|

| - |

|

Net cash used in operating activities |

|

| (1,533,319 | ) |

|

| (1,097,381 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

Proceeds from disposal of property, plant and equipment |

|

| 23,000 |

|

|

| - |

|

Payments of deposit for property, plant and equipment |

|

| - |

|

|

| (240,000 | ) |

Advanced to related parties |

|

| - |

|

|

| 690 |

|

Proceed from disposal of discontinued operation, net |

|

| 107,824 |

|

|

| - |

|

Payments of deposit for acquisition of subsidiary company |

|

| (22,609 | ) |

|

| - |

|

Net cash flows on acquisition of subsidiary company |

|

| 1,140 |

|

|

| - |

|

Purchase of property, plant and equipment |

|

| (473,895 | ) |

|

| (70,332 | ) |

Net cash used in investing activities |

|

| (364,540 | ) |

|

| (309,642 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Repayments to lease liabilities |

|

| (56,356 | ) |

|

| (5,220 | ) |

Drawdown of bank loan |

|

| 150,000 |

|

|

| - |

|

Repayment of bank loan |

|

| (50,000 | ) |

|

| - |

|

Lease interest paid |

|

| (22,237 | ) |

|

| - |

|

Advanced from related parties |

|

| - |

|

|

| 9,417 |

|

Proceeds from issuance of Common Stock |

|

| 1,556,280 |

|

|

| 1,000,000 |

|

Net cash provided by financing activities |

|

| 1,577,687 |

|

|

| 1,004,197 |

|

|

|

|

|

|

|

|

|

|

Net change in cash and cash equivalent |

|

| (320,172 | ) |

|

| (402,826 | ) |

|

|

|

|

|

|

|

|

|

Foreign currency translation adjustment |

|

| 142,626 |

|

|

| 7,787 |

|

|

|

|

|

|

|

|

|

|

Net change in cash and cash equivalents |

|

| (177,546 | ) |

|

| (395,039 | ) |

|

|

|

|

|

|

|

|

|

BEGINNING OF PERIOD |

|

| 418,917 |

|

|

| 2,117,622 |

|

|

|

|

|

|

|

|

|

|

END OF PERIOD |

| $ | 241,371 |

|

| $ | 1,722,583 |

|

|

|

|

|

|

|

|

|

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: |

|

|

|

|

|

|

|

|

Cash paid for income taxes |

| $ | - |

|

| $ | - |

|

Cash paid for interest |

| $ | - |

|

| $ | - |

|

See accompanying notes to unaudited condensed consolidated financial statements.

| F-3 |

| Table of Contents |

VERDE RESOURCES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

FOR THE NINE MONTHS ENDED MARCH 31, 2023 AND 2022

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

| No. of shares |

|

| Common Shares Stock |

|

| Shares to be issued Amount |

|

| Additional paid-in capital |

|

| Accumulated other comprehensive income |

|

| Accumulated losses |

|

| Accumulated other comprehensive income of disposal group held for sale |

|

| Total stockholders’ equity |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Balance as of July 1, 2022 |

|

| 819,188,055 |

|

| $ | 819,188 |

|

| $ | - |

|

| $ | 22,945,190 |

|

| $ | 742,459 |

|

| $ | (10,357,920 | ) |

| $ | - |

|

| $ | 14,148,917 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share issued to service provider |

|

| 5,315,000 |

|

|

| 5,315 |

|

|

| - |

|

|

| 870,185 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 875,500 |

|

Shares issued for private placement |

|

| 15,931,210 |

|

|

| 15,931 |

|

|

| - |

|

|

| 1,381,349 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 1,397,280 |

|

Shares issued for conversion of promissory note (“PN”) |

|

| 333,142,389 |

|

|

| 333,142 |

|

|

| - |

|

|

| 20,021,858 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 20,355,000 |

|

Fair value adjustment on conversion of PN |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 4,064,450 |

|

|

| - |

|

|

| 4,064,450 |

|

Net loss for the period |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (3,516,672 | ) |

|

| - |

|

|

| (3,516,672 | ) |

Foreign currency translation adjustment |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (11,368 | ) |

|

| - |

|

|

| - |

|

|

| (11,368 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance as of December 31,2022 |

|

| 1,173,576,654 |

|

| $ | 1,173,576 |

|

| $ | - |

|

| $ | 45,218,582 |

|

| $ | 731,091 |

|

| $ | (9,810,142 | ) |

| $ | - |

|

| $ | 37,313,107 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares issued to service provider |

|

| 714,285 |

|

|

| 715 |

|

|

| - |

|

|

| 49,285 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 50,000 |

|

Shares to be issued for private placement |

|

| 1,717,032 |

|

|

| - |

|

| 1,717 |

|

|

| 128,283 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 130,000 |

| |

Net loss for the period |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (708,327 | ) |

|

| - |

|

|

| (708,327 | ) |

Foreign currency translation adjustment |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 154,912 |

|

|

| - |

|

|

| - |

|

|

| 154,912 |

|

Reclassification arising from disposal group held for sale |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (811,346 | ) |

|

| - |

|

|

| 811,346 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance as of March 31, 2023 |

|

| 1,176,007,971 |

|

| $ | 1,174,291 |

|

| $ | 1,717 |

|

| $ | 45,396,150 |

|

| $ | 74,657 |

|

| $ | (10,518,469 | ) |

| $ | 811,346 |

|

| $ | 36,939,692 |

|

| F-4 |

| Table of Contents |

Condensed Consolidated StatementsVERDE RESOURCES, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

FOR THE NINE MONTHS ENDED MARCH 31, 2023 AND 2022

(Currency expressed in United States Dollars (“US$”), except for number of Cash Flows

(Unaudited)shares)

|

| December 31, 2017 |

|

| December 31, 2016 |

| ||

Cash flows from operating activities: |

|

|

|

|

|

| ||

Net profit (loss) |

| $ | 67,308 |

|

| $ | (227,342 | ) |

Adjustments to reconcile loss to net cash used in operation |

|

|

|

|

|

|

|

|

Depreciation |

|

| 12,475 |

|

|

| 83,475 |

|

Waiver of consultancy service fee |

|

| (17,006 | ) |

|

| - |

|

Changes in operating assets and liabilities |

|

|

|

|

|

|

|

|

(Increase) decrease in: |

|

|

|

|

|

|

|

|

Accounts receivable from related parties |

|

| (267 | ) |

|

| (214 | ) |

Deposits and prepayment |

|

| - |

|

|

| (2,086 | ) |

Inventory |

|

| (3,773 | ) |

|

| 72,000 |

|

Increase (decrease) in: |

|

|

|

|

|

|

|

|

Accounts payable |

|

| 6,489 |

|

|

| 47,470 |

|

Accrued liabilities |

|

| (39,394 | ) |

|

| (52,385 | ) |

GST payable |

|

| (4,904 | ) |

|

| 687 |

|

Advanced from sub-contractor & related parties |

|

| (8,758 | ) |

|

| 11,382 |

|

Deposit received from customer |

|

| - |

|

|

| - |

|

Net cash (used in) operating activities |

|

| 12,170 |

|

|

| (67,013 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Repayments of bank loans |

|

| (3,581 | ) |

|

| (5,217 | ) |

Proceeds from issuance of common stock |

|

| - |

|

|

| 190,000 |

|

Net cash provided by (used in) financing activities |

|

| (3,581 | ) |

|

| 184,783 |

|

|

|

|

|

|

|

|

|

|

Net increase (decrease) in cash and cash equivalent |

|

| 8,589 |

|

|

| 117,770 |

|

|

|

|

|

|

|

|

|

|

Effect of exchange rate changes on cash |

|

| (35,980 | ) |

|

| (43,275 | ) |

|

|

|

|

|

|

|

|

|

Net increase (decrease) in cash and cash equivalents |

|

| (27,391 | ) |

|

| 74,495 |

|

Cash and cash equivalents at beginning of year |

|

| 38,616 |

|

|

| 16,113 |

|

Cash and cash equivalents at end of year |

| $ | 11,225 |

|

| $ | 90,608 |

|

|

|

|

|

|

|

|

|

|

Supplementary cash flow information |

|

|

|

|

|

|

|

|

Income taxes paid |

| $ | - |

|

| $ | - |

|

Interest paid |

| $ | 119 |

|

| $ | 280 |

|

Supplementary non-cash information |

|

|

|

|

|

|

|

|

Reorganization |

|

| - |

|

|

| - |

|

Issuance of common stock |

|

| - |

|

|

| - |

|

|

| No. of shares |

|

| Common Shares Amount |

|

| Shares to be issued Amount |

|

| Additional paid-in capital |

|

| Accumulated other comprehensive income |

|

| Accumulated losses |

|

| Non- controlling interest |

|

| Total stockholders’ equity |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Balance as of July 1, 2021 |

|

| 779,742,109 |

|

| $ | 779,742 |

|

|

| - |

|

| $ | 20,699,067 |

|

| $ | 646,205 |

|

| $ | (5,913,255 | ) |

| $ | (441,834 | ) |

| $ | 15,769,925 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares issued for acquisition |

|

| 31,000,000 |

|

|

| 31,000 |

|

|

| - |

|

|

| 899,000 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 930,000 |

|

Stock based compensation |

|

| - |

|

|

| - |

|

|

| - |

|

|

| 191,222 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 191,222 |

|

Net loss for the period |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (1,648,985 | ) |

|

| (16,935 | ) |

|

| (1,665,920 | ) |

Foreign currency translation adjustment |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 3,036 |

|

|

| - |

|

|

| 535 |

|

|

| 3,571 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance as of December 31, 2021 |

|

| 810,742,109 |

|

| $ | 810,742 |

|

| $ | - |

|

| $ | 21,789,289 |

|

| $ | 649,241 |

|

| $ | (7,562,240 | ) |

| $ | (458,234 | ) |

| $ | 15,228,798 |

|

|

|

|

|

|

|

|

|

|

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares to be issued for private placement |

|

| 8,445,946 |

|

|

| - |

|

|

| 8,446 |

|

|

| 991,554 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 1,000,000 |

|

Stock based compensation |

|

| - |

|

|

| - |

|

|

| - |

|

|

| 93,027 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 93,027 |

|

Net loss for the period |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| (1,079,555 | ) |

|

| 23,914 |

|

|

| (1,055,641 | ) |

Foreign currency translation adjustment |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 24,885 |

|

|

| - |

|

|

| (13,285 | ) |

| 11,600 |

| |

Accretion of interest |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| 202,628 |

|

|

| (685,852 | ) |

|

| 447,605 |

|

|

| (35,619 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance as of March 31, 2022 |

|

| 819,188,055 |

|

| $ | 810,742 |

|

| $ | 8,446 |

|

| $ | 22,873,870 |

|

| $ | 876,754 |

|

| $ | (9,327,647 | ) |

| $ | - |

|

| $ | 15,242,165 |

|

TheSee accompanying notes are an integral part of theseto unaudited condensed consolidated financial statements.

| Table of Contents |

VERDE RESOURCES, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE AND NINE MONTHS ENDED MARCH 31, 2023 AND 2022

(Currency expressed in United States Dollars (“US$”), except for number of shares)

Notes to Condensed Consolidated Financial Statements

December 31, 2017

(Unaudited)

NOTE 1 - ORGANIZATION AND DESCRIPTION OF BUSINESS BACKGROUND

Verde Resources, Inc. (the "Company"“We” or "VRDR"“Company” or “VRDR”) was incorporated on April 22, 2010, in the State of Nevada, U.S.A. U.S.A..

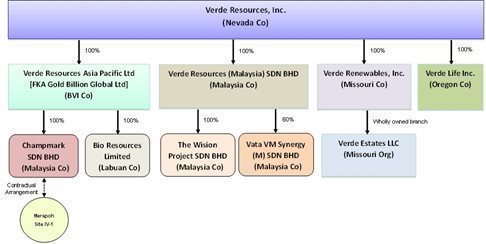

The accountingCompany currently is engaged in the distribution of THC-free cannabinoid (CBD) products, production and reporting policiesdistribution of renewable commodities and real property holding. However, the Company has been undergoing a restructuring exercise to shift its focus towards renewable energy and sustainability development with the world faced with challenges of climate change and environmental dehydration. The Company has initiated the disposition of the mining business via the sale of the entire issued and paid-up share capital of CSB to focus on renewable energy and sustainability.

As of March 31, 2023, the Company conformhas the following subsidiaries:-

Company name | Place of incorporation | Principal activities and place of operation | Effective interest held | |||

Verde Resources Asia Pacific Limited (“VRAP”) (fka Gold Billion Global Limited) | British Virgin Islands | Investment holding | 100% | |||

Verde Resources (Malaysia) Sdn Bhd (“VRSB”) | Malaysia | Provision of consultation service and distribution of renewable agricultural commodities | 100% | |||

Verde Renewables, Inc. (“VRI”) | State of Missouri, U.S.A. | Management of a processing and packaging facility | 100% | |||

Verde Life Inc. (“VLI”) | State of Oregon, U.S.A. | Distribution of THC-free cannabinoid (CBD) products | 100% | |||

Champmark Sdn Bhd (“Champmark”) | Malaysia | Mining of minerals | 100%* | |||

The Wision Project Sdn Bhd (“Wision”) | Malaysia | Digital innovation, marketing & consulting service, PR, branding, influencer marketing, event management and media relations services | 100% | |||

Verde Estates LLC (“VEL”) | State of Missouri, U.S.A. | Holding real property | 100% | |||

Bio Resources Limited (“BRL”) | Labuan, Malaysia | Provision of proprietary pyrolysis technology and investment holding | 100%** |

* The disposition of Champmark was initiated on March 13, 2023 and subsequently completed on April 20, 2023.

** The acquisition of BRL was completed on October 12, 2022.

The Company and its subsidiaries are hereinafter referred to as (the “Company”).

On March 23, 2023, the Company initiated the acquisition of 60% equity interest in Vata VM Synergy (M) Sdn Bhd (“VATA”), a company incorporated in Malaysia and engaged in the provision of green technology and creating high quality compost using agricultural waste and biomass products. The initial deposit has been paid and the transaction is yet to be completed as of today.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited condensed consolidated financial statements reflect the application of certain significant accounting policies as described in this note and elsewhere in the accompanying unaudited condensed consolidated financial statements and notes.

· | Basis of Presentation |

The accompanying unaudited condensed consolidated financial statements have been prepared by management in accordance with both accounting principles generally accepted in the United States of America,(“GAAP”), and the Company's fiscal year end is June 30.

Gold Billion Global Limited ("Gold Billion" or "GBL") was incorporated in British Virgin Islands on February 7, 2013. GBL was setup by the Boardinstructions to Form 10-Q and Rule 10-01 of Directors of Federal Mining Resources Limited ("FMR"). The major operation of GBL is to manage and monitor the mineral exploration and mining projects of FMR.

On July 1, 2013, FMR has assigned its rights and obligation on Champmark Sdn Bhd ("CSB") to GBL. Four of the five members of CSB Board of Directors were appointed by FMR, with two of the GBL Board of Directors currently sitting on the CSB Board. According to ASC 810-05-08 A, CSB is a deemed subsidiary of GBL where it has controlled the CSB Board of Directors, has assigned rights to receive future benefits and residual value, and obligation to absorb loss and finance for CSB by GBL. GBL has the power to direct the activities of CSB that most significantly impact CSB's economic performance and the obligation to absorb losses of CSB that could potentially be significant to the CSB or the right to receive benefits from CSB that could potentially be significant to CSB. GBL is the primary beneficiary of CSB because it has been assigned with all relevant rights and obligation and can direct the activities of CSB through the common directors and the 85% shareholder, FMR. Under 810-23-42, 43, it is determined that CSB is de-facto agent of GBL and GBL is the de-facto principal of CSB. GBL started to consolidate CSB from July 1, 2013 and the Company consolidated GBL and CSB from October 25, 2013 onwards.

On February 17, 2014, the Company entered into a Supplementary Agreement to the Assignment Agreement and completed an acquisition of GBL pursuant to the Supplementary Agreement. The acquisition was a reverse acquisition in accordance with ASC 805-40 "Reverse Acquisitions". The legal parent was VRDR which was the accounting acquiree while GBL was the accounting acquirer. There was a 15% non-controlling interest of Champmark SDN BHD ("CSB") after the acquisition. This transaction was accounted for as a recapitalization effected by a share exchange, wherein GBL with its 85% deemed subsidiary CSB was considered the acquirer for accounting and financial reporting purposes. The assets and liabilities of the acquired entity have been brought forward at their book value and no goodwill has been recognized.

As a result of the acquisition, the Company holds 100% equity interest in GBL and 85% variable interest in CSB. Our consolidated subsidiaries include GBL being our wholly-owned subsidiary and 85% of CSB being a variable interest entity (VIE) and deemed subsidiary of GBL.

On March 17, 2014, the Company through GBL and its deemed subsidiary CSB entered into a Sub-Contract Agreement with Borneo Oil & Gas Corporation Sdn Bhd ("BOG") for the engagement of its sub-contractor services to carry out exploration and exploitation works on alluvial and lode gold resources at Site IV-1 of the Merapoh Mine. The Sub-Contract Agreement is for a period of 5 years with a renewal for another 5 years subject to review by both parties. BOG is a wholly-owned subsidiary of Borneo Oil Berhad (BOB) which is listed on the main market of Kuala Lumpur Stock Exchange. BOG being a local company in Malaysia provides the Company with the advantage of local knowledge and well-established connection in dealing with the relevant local authorities in our mining operations.

On April 1, 2014, GBL purchased 85% equity interest of CSB, and CSB became indirect subsidiary of the Company.

Effective August 27, 2014, the Company's Articles of Incorporation were amended to increase the authorized shares of the Company from 100,000,000 shares of common stock to 250,000,000 shares of common stock. A copy of the Certificate of Amendment was filed with the Nevada Secretary of State. The Form 8K announcing the increase of the authorized shares of the Company was filed with SEC on September 15, 2014.

Effective February 20, 2016, Mr. Wu Ming Ding resigned all of his positions as President and Director of the Company with Mr. Balakrishnan B S Muthu being appointed President to fill the vacancy created. Effective February 20, 2016, Mr. Chen Ching was appointed Director of the Company and the entire Board of Directors now consists of Mr. Balakrishnan B S Muthu and Mr. Chen Ching. The SC 14F1 and Form 8-K announcing the change in officers and directors were filed with SEC on February 10, 2016 and February 22, 2016 respectively.

Effective February 2, 2018, the Company's Articles of Incorporation were amended to increase the authorized shares of the Company from 250,000,000 shares of common stock to 10,000,000,000 shares of common stock. A copy of the Certificate of Amendment was filed with the Nevada Secretary of State. The Form 8K announcing the increase of the authorized shares of the Company was filed with SEC on February 6, 2018.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Condensed Consolidated Financial Statements

Regulation S-X. Certain information and footnotenote disclosures normally included in audited financial statements prepared in accordance with accounting principles generally accepted in the United States of Americaaccounting principles have been condensed or omitted. Theomitted pursuant to those rules and regulations, although the Company believes that the disclosures made are adequate to make the information not misleading.

| F-6 |

| Table of Contents |

In the opinion of management, the condensed consolidated balance sheet as of June 30, 2022 which has been derived from audited financial statements and these unaudited condensed consolidated financial statements reflect all normal and recurring adjustments considered necessary to state fairly the results of operations for the periods presented. The results for the period ended DecemberMarch 31, 20172023 are not necessarily indicative of the operating results to be expected for the full years.entire fiscal year ending June 30, 2023 or for any future period.

Basis of Presentation

The accounting and reporting policies of the Company conform to accounting principles generally accepted in the United States of America (GAAP). These unaudited condensed consolidated financial statements are expressedand notes thereto should be read in United States dollars ($). Financial statements prepared in accordanceconjunction with GAAP contemplate the realization of assetsManagement’s Discussion and the satisfaction of liabilities in the normal course of business. These condensed consolidated audited financial statements include all adjustments that, in the opinion of management, are necessary in order to make the financial statements not misleading.

Basis of Consolidation

The condensed consolidated financial statements include the financial statements of Verde Resources, Inc., its wholly owned subsidiary Gold Billion Global Limited ("GBL") and the 85% of the deemed subsidiary variable interest of Champmark SDN BHD ("CSB"). All inter-company balances and transactions between the Company and its subsidiary and variable interest entity (VIE) have been eliminated upon consolidation.

The Company has adopted ASC Topic 810-10-5-8, "Variable Interest Entities", which requires a variable interest entity or VIE to be consolidated by a company if that company is subject to a majority of the risk of loss for the VIE or is entitled to receive a majority of the VIE's residual returns.

Variable Interest Entity

On July 1, 2013, the Company's subsidiary, GBL entered into a series of agreements ("VIE agreements") with FMR and details of the VIE agreements are as follows :

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

With the above agreements, GBL demonstrates its ability to control CSB as the primary beneficiary and the operating results of the VIE wasnotes thereto included in the condensed consolidated financial statementsAnnual Report on Form 10-K for the year ended June 30, 2014.2022, filed with the SEC on November 4, 2022.

On April 1, 2014, the Board of Director of GBL notified FMR upon the decision to exercise the right of option to purchase 85% equity interest of CSB under Management Agreement Section 3.2.4 dated July 1, 2013 between GBL and FMR. This acquisition was completed on April 1, 2014 with consideration of US$1. GBL then became 85% shareholder of CSB and is required to consolidate CSB as a subsidiary.

· | Use of Estimates and Assumptions |

Use of Estimates

The preparation of unaudited condensed consolidated financial statements in conformity with accounting principles generally accepted in the United States of AmericaGAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amount of revenues and expenses during the reporting period. Actual results could differ from those estimates. The Company'sCompany’s periodic filings with the Securities and Exchange Commission include, where applicable, disclosures of estimates, assumptions, uncertainties and markets that could affect the financial statements and future operations of the Company.

CashIn preparing these unaudited condensed consolidated financial statements, management makes estimates and Cash Equivalentsassumptions that affect the reported amounts of assets and liabilities in the balance sheet and revenues and expenses during the periods reported. Actual results may differ from these estimates.

Cash and cash equivalents include cash in banks, money market funds, and certificates of term deposits with maturities of less than three months, which are readily convertible to known amounts of cash and which, in the opinion of management, are subject to an insignificant risk of loss in value. The Company had $11,225 and $38,616 in cash and cash equivalents at December 31, 2017 and June 30, 2017, respectively.

Concentrations of Credit Risk

· | Basis of Consolidation |

The Company'sunaudited condensed consolidated financial statements include the financial statements of Verde Resources, Inc. and its subsidiaries. All significant inter-company balances and transactions within the Company and its subsidiaries have been eliminated upon consolidation. The Company accounts for acquisitions in accordance with guidance found in ASC 805, Business Combinations. The guidance requires consideration given, including contingent consideration, assets acquired, and liabilities assumed to be valued at their fair market values at the acquisition date.

· | Segment Reporting |

Accounting Standard Codification (“ASC”) Topic 280, Segment Reporting establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organization structure as well as information about geographical areas, business segments and major customers in consolidated financial statements. Currently, the Company operates in four reportable operating segments.

· | Concentrations of Credit Risk |

The Company’s financial instruments that are exposed to concentrations of credit risk primarily consist of its cash and cash equivalents and related party payables it will likely incur in the near future. The Company places its cash and cash equivalents with financial institutions of high credit worthiness. At times, its cash and cash equivalents with a particular financial institution may exceed any applicable government insurance limits. The Company'sCompany’s management plans to assess the financial strength and credit worthiness of any parties to which it extends funds, and as such, it believes that any associated credit risk exposures are limited.

· | Risks and Uncertainties |

The Company operates in the resource exploration industry and the production and distribution of renewable commodities that isare subject to significant risks and uncertainties, including financial, operational, technological, and other risks associated with operating a resource exploration business and a production operation for renewable commodities, including the potential risk of business failure.

· | Cash and Cash Equivalents |

Cash and cash equivalents are carried at cost and represent cash in banks, money market funds, and certificates of term deposits with maturities of less than three months, which are readily convertible to known amounts of cash and which, in the opinion of management, are subject to an insignificant risk of loss in value. The Company had $241,371 and $418,917 in cash and cash equivalents at March 31, 2023 and June 30, 2022.

At March 31, 2023 and June 30, 2022, cash and cash equivalents consisted of bank deposits and petty cash on hands.

· | Accounts Receivable |

Accounts receivable are recognized and carried at net realizable value. An allowance for doubtful accounts will be recorded in the period when a loss is probable based on an assessment of specific evidence indicating troubled collection, historical experience, accounts aging, ongoing business relation and other factors. Accounts are written off after exhaustive efforts at collection. If accounts receivable are to be provided for, or written off, they would be recognized in the consolidated statement of operations within operating expenses. At March 31, 2023 and June 30, 2022, the Company has no allowance for doubtful accounts, as per management'smanagement’s judgment based on their best knowledge. As of DecemberMarch 31, 20172023 and June 30, 2017,2022, the longest credit term for certain customers are 60 days.

| F-7 |

| Table of Contents |

Provision

· | Inventories |

Inventories are stated at the lower of cost or market value (net realizable value), cost being determined on a first-in-first-out method. Costs include material, labor and overhead costs. The Company provides inventory allowances based on excess and obsolete inventories determined principally by customer demand.

As of March 31, 2023 and June 30, 2022, the Company did not record an allowance for Doubtful Accountsobsolete inventories, nor have there been any write-offs.

· | Property, Plant and Equipment |

Property, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Depreciation is calculated on the straight-line basis over the following expected useful lives from the date on which they become fully operational and after taking into account their estimated residual values:

Expected useful life | |||

Land and buildings | 3-27.5 years | ||

Plant and machinery | 5-10 years | ||

Office equipment | 3 years | ||

Project equipment | 5 years | ||

Computer | 5 years | ||

Motor vehicle | 5 years | ||

Furniture & fittings | 5 years |

Expenditures for maintenance and repairs, which do not materially extend the useful lives of the assets, are charged to expense as incurred. Expenditures for major renewals and betterment which substantially extend the useful life of assets are capitalized. The cost and related accumulated depreciation of assets retired or sold are removed from the respective accounts, and any gain or loss is recognized in the unaudited condensed consolidated statements of income and other comprehensive income in other income or expenses.

· | Intangible assets |

Intangible assets acquired from third parties are measured initially at fair value, and have a finite lives of 10 years, which are reviewed for indicators of impairment at least annually. These intangible assets are to be amortized over these estimated useful lives on a straight-line basis, upon the success of its commercial operation.

· | Disposal group held for sale |

Disposal group comprising assets and liabilities, that are expected to be recovered primarily through sale rather than through continuing use, are classified as held for sale. Immediately before classification as held for sale, the assets or components of a disposal group, are remeasured at the lower of their carrying amount and fair value less costs of disposal. Mining rights and property, plant and equipment once classified as held for sale are not amortised or depreciated.

· | Impairment of Long-lived Assets |

In accordance with the provisions of ASC Topic 360, Impairment or Disposal of Long-Lived Assets, all long-lived assets such as property and equipment and intangible assets owned and held by the Company are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is evaluated by a comparison of the carrying amount of an asset to its estimated future undiscounted cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amounts of the assets exceed the fair value of the assets.

· | Revenue Recognition |

ASC Topic 606, Revenue from Contracts with Customers (“ASC Topic 606”), establishes principles for reporting information about the nature, amount, timing and uncertainty of revenue and cash flows arising from the entity’s contracts to provide goods or services to customers.

The Company maintains an allowanceapplies the following five steps in order to determine the appropriate amount of revenue to be recognized as it fulfills its obligations under each of its agreements:

· | identify the contract with a customer; |

· | identify the performance obligations in the contract; |

· | determine the transaction price; |

· | allocate the transaction price to performance obligations in the contract; and |

· | recognize revenue as the performance obligation is satisfied. |

| F-8 |

| Table of Contents |

Revenue is recognized when the Company satisfies its performance obligation under the contract by transferring the promised product to its customer that obtains control of the product and collection is reasonably assured. A performance obligation is a promise in a contract to transfer a distinct product or service to a customer. Most of the Company’s contracts have a single performance obligation, as the promise to transfer products or services is not separately identifiable from other promises in the contract and, therefore, not distinct.

Product sales

Revenues from product sales are recognized when the customer obtains control of the Company’s product, which occurs at a point in time, typically upon delivery to the customer. The Company expenses incremental costs of obtaining a contract as and when incurred if the expected amortization period of the asset that it would have recognized is one year or less or the amount is immaterial.

Revenues from product sales are recorded net of reserves established for doubtful accountsapplicable discounts and allowances that are offered within contracts with the Company’s customers.

Product revenue reserves, which are classified as a reduction in product revenues, are generally characterized in the following categories: discounts, returns and rebates. These reserves are based on estimates of the amounts earned or to reserve for potentially uncollectible receivablesbe claimed on the related sales and reviewsare classified as reductions of accounts receivable as the amount is payable to the Company’s customer.

Gold mining

Revenue from the sales of gold mineral or other minerals to registered gold trading companies or other customers in Malaysia is recognized as revenue in accordance with the following core principles: at the time of gold or minerals sales, the contract with customers and the performance obligations are identified. The transaction and selling price is determined by amounts duethe prevailing market value of gold bullion quoted by the leading registered gold trading company in Malaysia or at an agreed price. Sales invoice will be prepared to reflect the proper transaction price based on the performance obligation allocation. After delivery is completed and the performance obligation is satisfied, sales invoice will be presented to the customers whichand so revenue is then recognized accordingly.

· | Leases |