Washington, D.C. 20549

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Delek US Holdings, Inc.

Delek US Holdings, Inc.

Delek US Holdings, Inc.

Delek US Holdings, Inc.

Delek US Holdings, Inc.

Delek US Holdings, Inc. is the sole shareholder or owner of membership interests,operates through its wholly-owned subsidiaryconsolidated subsidiaries, which include Delek US Energy, Inc., of Delek Refining, Inc. ("Refining"), Delek Finance, Inc., Delek Marketing & Supply, LLC, Lion Oil Company ("Lion Oil"), Delek Renewables, LLC, Delek Rail Logistics, Inc., Delek Logistics Services Company, Delek Helena, LLC, Delek Land Holdings, LLC, (and its subsidiaries) and is also the sole shareholder of Alon USA Energy, Inc. ("Alon") (and in Alon's wholly-owned subsidiaries by virtue of Delek's ownership of Alon)its subsidiaries).

Effective July 1, 2017 (the "Effective Time"), we acquired the outstanding common stock of Alon (previously listed under NYSE: ALJ) (the "Delek/Alon Merger", as further discussed in Note 2), resulting in a new post-combination consolidated registrant renamed as Delek US Holdings, Inc. (“New Delek”), with Alon and the previous Delek US Holdings, Inc. (“Old Delek”) surviving as wholly-owned subsidiaries. New Delek is the successor issuer to Old Delek and Alon pursuant to Rule 12g-3(c) under the Securities Exchange Act of 1934, as amended (the "Exchange Act"). In addition, as a result of the Delek/Alon Merger, the shares of common stock of Old Delek and Alon were delisted from the New York Stock Exchange ("NYSE") in July 2017, and their respective reporting obligations under the Exchange Act were terminated.

Our condensed consolidated financial statements include the accounts of Delek and its consolidated subsidiaries. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with U.S. Generally Accepted Accounting Principles ("GAAP") have been condensed or omitted, although management believes that the disclosures herein are adequate to make the financial information presented not misleading. Our unaudited condensed consolidated financial statements have been prepared in conformity with GAAP applied on a consistent basis with those of the annual audited consolidated financial statements included in our Annual Report on Form 10-K filed with the Securities and Exchange Commission ("SEC") on February 28, 2017March 1, 2019 (the "Annual Report on Form 10-K") and in accordance with the rules and regulations of the SEC. These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and the notes thereto for the year ended December 31, 20162018 included in our Annual Report on Form 10-K.

Our condensed consolidated financial statements include Delek Logistics Partners, LP ("Delek Logistics"), Alon USA Partners, LP (the "Alon Partnership") and AltAir Paramount LLC ("AltAir"), allwhich is a variable interest entities.entity. As the indirect owner of the general partnerspartner of Delek Logistics, and the Alon Partnership and the managing member of AltAir, we have the ability to direct the activities of these entitiesthis entity that most significantly impact theirits economic performance. We are also considered to be the primary beneficiary for accounting purposes for all of these

In the opinion of management, all adjustments necessary for a fair presentation of the financial condition and the results of operations for the interim periods have been included. All significant intercompany transactions and account balances have been eliminated in consolidation. All adjustments are of a normal, recurring nature. Operating results for the interim period should not be viewed as representative of results that may be expected for any future interim period or for the full year.

Certain prior period amounts have been reclassified in order to conform to the current yearperiod presentation.

In June 2016, the FASB issued guidance requiring the measurement of all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. Financial institutions and other organizations will now use forward-looking information to better inform their credit loss estimates. This guidance is effective for interim and annual periods beginning after December 15, 2019. We expect to adopt this guidance on or before the effective date and are currently evaluating the impact that adopting this new guidance will have on our business, financial condition and results of operations.

In January 2017, we announced that Old Delek (and various related entities) entered into the Merger Agreementa merger agreement with Alon, as subsequently amended on February 27 and April 21, 2017.(the "Merger Agreement"). The related Merger (the "Merger" or(as previously defined, the "Delek/Alon Merger") was effective July 1, 2017 (as previously defined, the “Effective Time”), resulting in a new post-combination consolidated registrant renamed as Delek US Holdings, Inc. (as previously defined, “New Delek”), with Alon and Old Delek surviving as wholly-owned subsidiaries of New Delek. New Delek is the successor issuer to Old Delek and Alon pursuant to Rule 12g-3(c) under the Exchange Act, as amended. In addition, as a result of the Delek/Alon Merger, the shares of common stock of Old Delek and Alon were delisted from the New York Stock ExchangeNYSE in July 2017, and their respective reporting obligations under the Exchange Act were terminated. Prior to the Merger, Old Delek owned a non-controlling equity interest of approximately 47% of the outstanding shares of Alon , which was accounted for under the equity method of accounting (See Note 4).

Delek Logistics is a publicly traded limited partnership that was formed by Delek in 2012 to own, operate, acquire and construct crude oil and refined products logistics and marketing assets. A substantial majority of Delek Logistics' assets are integral to Delek’s refining and marketing operations. As of September 30, 2017,March 31, 2019, we owned a 61.5%61.4% limited partner interest in Delek Logistics, consisting of 15,294,046 common units, and a 94.6% interest in Delek Logistics GP, LLC, which owns the entire 2.0% general partner interest, consisting of 497,172498,110 general partner units, in Delek Logistics and all of the incentive distribution rights.

The limited partner interests in Delek Logistics not owned by us are reflected in net income attributable to non-controlling interest in the accompanying condensed consolidated statements of income and in non-controlling interest in subsidiaries in the accompanying condensed consolidated balance sheets.

We have agreements with Delek Logistics that, among other things, establish fees for certain administrative and operational services provided by us and our subsidiaries to Delek Logistics, provide certain indemnification obligations and establish terms for fee-based commercial logistics and marketing services provided by Delek Logistics and its subsidiaries to us.us, including new agreements related to the Big Spring Logistic Assets Acquisition. The revenues and expenses associated with these agreements are eliminated in consolidation.

Delek Logistics is a variable interest entity, as defined under GAAP, and is consolidated into our condensed consolidated financial statements.statements, representing our logistics segment. With the exception of intercompany balances and the marketing agreement intangible asset and Delek's related deferred revenue which are eliminated in consolidation, the Delek Logistics condensed consolidated balance sheets as of September 30, 2017March 31, 2019 and December 31, 2016,2018, as presented below, are included in the consolidated balance sheets of Delek (unaudited, in millions).

|

| | | | | | | | |

| | | September 30,

2017 | | December 31,

2016 |

| | | |

| ASSETS | | | | |

| Cash and cash equivalents | | $ | 5.3 |

| | $ | 0.1 |

|

| Accounts receivable | | 20.3 |

| | 19.2 |

|

| Accounts receivable from related parties | | 0.7 |

| | 2.8 |

|

| Inventory | | 7.9 |

| | 8.9 |

|

| Other current assets | | — |

| | 1.1 |

|

| Property, plant and equipment, net | | 250.7 |

| | 251.0 |

|

| Equity method investments | | 106.1 |

| | 101.1 |

|

| Goodwill | | 12.2 |

| | 12.2 |

|

| Intangible assets, net | | 16.2 |

| | 14.4 |

|

| Other non-current assets | | 3.5 |

| | 4.7 |

|

| Total assets | | $ | 422.9 |

| | $ | 415.5 |

|

| LIABILITIES AND DEFICIT | | | | |

| Accounts payable | | $ | 14.5 |

| | $ | 10.9 |

|

| Accrued expenses and other current liabilities | | 14.2 |

| | 9.8 |

|

| Long-term debt | | 401.3 |

| | 392.6 |

|

| Asset retirement obligations | | 4.0 |

| | 3.8 |

|

| Other non-current liabilities | | 14.7 |

| | 11.7 |

|

| Deficit | | (25.8 | ) | | (13.3 | ) |

| Total liabilities and equity | | $ | 422.9 |

| | $ | 415.5 |

|

Notes to Condensed Consolidated Financial Statements (Unaudited)

Alon Partnership

TheAs part of the Delek/Alon Merger, we acquired a majority interest in the Alon Partnership, is a publicly-traded limited partnership thatwhich owns the assets and conducts the operations of the Big Spring refinery and the associated integrated wholesale marketing operations. TheOn February 7, 2018 (the "Merger Date"), Delek acquired from the Alon Partnership all of the outstanding limited partner interestsunits that Delek did not already own in an all-equity transaction (the "Alon Partnership Merger"). Delek owned approximately 51.0 million limited partner units of the Alon Partnership, are represented as common units outstanding. As of September 30, 2017, the 11,492,800 common units held by the public represent 18.4% of the Alon Partnership’s common units outstanding. We own the remainingor approximately 81.6% of the Alon Partnership’s commonoutstanding units, and Alon USA Partners GP, LLC (the “Alon General Partner”), our wholly-owned subsidiary, owns 100%immediately prior to the Merger Date. Under terms of the general partner interestmerger agreement, the owners of the remaining outstanding units in the Alon Partnership which isthat Delek did not own immediately prior to the Merger Date received a non-economic interest.

Thefixed exchange ratio of 0.49 shares of New Delek common stock for each limited partner interests inunit of the Alon Partnership, notresulting in the issuance of approximately 5.6 million shares of New Delek common stock to the public unitholders of the Alon Partnership. Because the transaction represented a combination of ownership interests under common control, the transfer of equity from non-controlling interest to owned interest (additional paid-in capital) was recorded at carrying value and no gain or loss was recognized in connection with the transaction. Additionally, book-tax basis difference was created as a result of the transaction that resulted in a deferred tax asset of approximately $13.5 million, net of a valuation allowance on certain state income tax components, that also increased additional paid-in capital. Transaction costs incurred by us are reflectedthe Company in net income attributable to non-controlling interestconnection with the Alon Partnership Merger totaled approximately $3.3 million for the three months ended March 31, 2018. Such costs were included in general and administrative expenses in the accompanying condensed consolidated statements of income and in non-controlling interest in subsidiaries inincome.

Prior to the accompanying condensed consolidated balance sheets.

We have agreements withMerger Date, the Alon Partnership under which the Alon Partnership has agreed to reimburse us for certain administrative and operational services provided by us and our subsidiaries to the Alon Partnership, indemnify us with respect to certain matters and establish terms for the supply of products by the Alon Partnership to us.

The Alon Partnership iswas a variable interest entity as defined under GAAPfor which Delek was the primary beneficiary. As of March 31, 2019 and is consolidated into our condensed consolidated financial statements as part of the refining segment. We have elected to push down purchase accounting toDecember 31, 2018, the Alon Partnership which resultedis included in the push-down of the preliminary fair value of equity as purchase price consideration, and the preliminary fair valuing of assets and liabilities as of the Merger date. Such push-down purchase accounting also resulted in a preliminary determination of the fair value of our non-controlling interest in the Alon Partnership, which is estimated to be $120.6 million. With the exception of intercompany balances which are eliminated in consolidation, the Alon PartnershipDelek's condensed consolidated balance sheet as of September 30, 2017, as presented below, is included in the consolidated balance sheets of Delek (unaudited, in millions).a wholly-owned subsidiary.

|

| | | | |

| | | September 30,

2017 |

| | |

| ASSETS | | |

| Cash and cash equivalents | | $ | 268.6 |

|

| Accounts receivable | | 83.8 |

|

| Accounts receivable from related parties | | — |

|

| Inventories | | 99.8 |

|

| Prepaid expenses and other current assets | | 4.9 |

|

| Property, plant and equipment, net | | 418.1 |

|

| Goodwill | | 568.5 |

|

| Other non-current assets | | 54.0 |

|

| Total assets | | $ | 1,497.7 |

|

| LIABILITIES AND EQUITY | | |

| Accounts payable | | $ | 101.6 |

|

| Accounts payable to related parties, net of related receivables | | 84.6 |

|

| Accrued expenses and other current liabilities | | 181.8 |

|

| Current portion of long-term debt | | 2.5 |

|

Obligation under Supply and Offtake Agreement

| | 99.1 |

|

| Long-term debt, net of current portion | | 335.6 |

|

| Deferred income tax liability | | 2.4 |

|

| Other non-current liabilities | | 27.4 |

|

| Equity | | 662.7 |

|

| Total liabilities and equity | | $ | 1,497.7 |

|

4.Note 6 - Equity Method Investments

On May 14, 2015, Delek acquired from Alon Israel Oil Company, Ltd. ("Alon Israel") approximately 33.7 million shares of common stock (the "ALJ Shares") of Alon pursuant to the terms of a stock purchase agreement with Alon Israel dated April 14, 2015 (the "Alon Acquisition"). The ALJ Shares represented an equity interest in Alon of approximately 48% at the time of acquisition. We acquired the ALJ Shares with a combination of cash, Delek stock and seller-financed debt. Effective July 1, 2017, Alon became a wholly-owned subsidiary of New Delek in connection with the Delek/Alon Merger. See Note 2 for further discussion.

Below is summarized financial information of the financial condition and results of operations of Alon (in millions) for the previous periods when Alon was considered an equity method investment:

|

| | | |

| Balance Sheet Information | December 31, 2016 |

| Current assets | $ | 471.3 |

|

| Non-current assets | 1,624.0 |

|

| Current liabilities | 445.5 |

|

| Non-current liabilities | 1,067.4 |

|

| Non-controlling interests | 61.3 |

|

|

| | | | | | | |

| Income Statement Information | Three Months Ended September 30, 2016 | | Nine Months Ended September 30, 2016 |

| Revenue | $ | 1,043.7 |

| | $ | 2,902.1 |

|

| Gross profit | 147.8 |

| | 399.6 |

|

| Pre-tax loss | (13.0 | ) | | (99.4 | ) |

| Net loss | (7.3 | ) | | (64.0 | ) |

| Net loss attributable to Alon | (8.8 | ) | | (64.7 | ) |

In March 2015, Delek Logistics entered intohas two joint ventures that have constructedown and operate logistics assets, and which serve third parties and subsidiaries of Delek. As of March 31, 2019 and December 31, 2018, Delek Logistics' investment balances in these joint ventures was financed through a combination of cash from operations and borrowings under the DKL Revolver (as defined in Note 8). As of September 30, 2017, Delek Logistics' investment balance in these joint ventures was $106.1totaled $107.8 million and was$104.8 million, respectively, and were accounted for using the equity method. One of the joint venture projects was completed and began operations in September 2016. The other was completed and began operations in January 2017.

In July 2017, Delek Renewables, LLC, invested ina wholly-owned subsidiary of Delek, has a joint venture with an unrelated third party, that was formed to plan, develop, construct, own, operateowns, operates and maintainmaintains a terminal consisting of an ethanol unit train facility with an ethanol tank in North Little Rock, Arkansas. This investment was financed through cash from operations. As of September 30, 2017,March 31, 2019 and December 31, 2018, Delek Renewables, LLC's investment balance in this joint venture was $1.3$3.9 million and $2.4 million respectively, and was accounted for using the equity method. The investment in this joint venture is reflected in the refining segment.

Effective with the Delek/Alon Merger, we ownacquired a 50% interest in two joint ventures that own asphalt terminals located in Fernley, Nevada, and Brownwood, Texas. On May 21, 2018, Delek sold its 50% interest in the asphalt terminal located in Fernley, Nevada. See Note 7 for further discussion. As of September 30, 2017,March 31, 2019 and December 31, 2018, Delek's investment balance in thesethe Brownwood, Texas joint venturesventure was $34.0$23.3 million and $23.1 million, respectively. This investment is accounted for using the equity method. These investments aremethod and is included as part of total assets in the corporate, other and eliminations segment.

5.

Note 7 - Discontinued Operations and Assets Held for Sale

Retail EntitiesAsphalt Terminals Held for Sale

In August 2016,On February 12, 2018, Delek entered intoannounced it had reached a Purchase Agreementdefinitive agreement to sell certain assets and operations of four asphalt terminals (included in Delek's corporate, other and eliminations segment), as well as an equity method investment in an additional asphalt terminal located in Femley, Nevada, to an affiliate of Andeavor. On May 21, 2018, Delek completed the Retail Entities to COPEC. As a resulttransaction and received net proceeds of approximately $110.8 million, inclusive of the Purchase Agreement, we$75.0 million base proceeds as well as certain working capital adjustments. The assets associated with the owned terminals met the requirementsdefinition of ASC 205-20andheld for sale pursuant to ASC 360 to reportas of February 1, 2018, but did not meet the resultsdefinition of the Retail Entities as discontinued operations pursuant to ASC 205-20, Presentation of Financial Statements - Discontinued Operations ("ASC 205-20"), as the sale of these asphalt assets did not represent a strategic shift that would have a major effect on the entity's operations and financial results. Accordingly, depreciation ceased as of February 1, 2018, and the assets to classify the Retail Entities as a group ofbe sold were reclassified to assets held for sale. Thesale as of that date and were written down to the estimated fair value assessmentless costs to sell, resulting in an impairment loss on assets held for sale of $27.5 million for the three months ended March 31, 2018. All goodwill associated with the asphalt operations sold was written off in connection with the impairment charge discussed above. In connection with the completion of the Retail Entitiessale transaction in the second quarter of 2018, we recognized a gain of approximately $13.3 million, resulting primarily from the recognition of certain additional proceeds at closing associated with the asphalt terminals which were not previously determinable/probable and the recognition of the gain on the sale of the joint venture which was not previously recognized as of August 27, 2016held for sale (as it did not resultmeet the criteria).

Notes to Condensed Consolidated Financial Statements (Unaudited)

California Discontinued Entities

During the third quarter 2017, we committed to a plan to sell certain assets associated with our Paramount and Long Beach, California refineries and our California renewable fuels facility (as previously defined, the "California Discontinued Entities"). Such operations were designated and reported as discontinued operations. On March 16, 2018, Delek sold to World Energy, LLC (i) all of Delek’s membership interests in an impairment. We ceased depreciationthe California renewable fuels facility ("AltAir") (ii) certain refining assets and other related assets located in Paramount, California and (iii) certain associated tank farm and pipeline assets and other related assets located in California. Upon final settlement (excluding contingent components), Delek expects to receive net cash proceeds of theseapproximately $85.2 million, which includes a post-closing working capital settlement, Delek’s portion of the expected biodiesel tax credit for 2017 and certain customary adjustments. The sale resulted in a loss on sale of discontinued operations totaling approximately $41.4 million of which $41.2 million was recorded during the three months ended March 31, 2018. Of the total expected proceeds, $54.6 million was received during the three months ended March 31, 2018 ($14.9 million of which were included in net cash flows from investing activities in discontinued operations). As of March 31, 2019, we have received a total of $70.4 million of the total expected proceeds. Additionally, Delek will be entitled to its pro rata portion of any tax credits relating to AltAir activities in 2018 earned through the sale date if the 2018 biodiesel tax credit is re-enacted. A receivable for such additional contingent proceeds will be recorded when the criteria for recognition are met, which is predicated upon reenactment of the tax credit and determination of the amounts earned by AltAir.

The transaction to dispose of certain assets asand liabilities associated with our Long Beach, California refinery to Bridge Point Long Beach, LLC closed July 17, 2018 resulting in initial cash proceeds of August 27, 2016. The Retail Transaction closed in November 2016 and we received cash consideration of $378.9approximately $14.5 million, net of debt repaymentsexpenses, and transaction costs, and retained approximately $62.8 million of net liabilities from the Retail Entities. The Retail Transaction resultedresulting in a gain on sale of discontinued operations of approximately $1.4 million during the Retail Entities, before income tax,third quarter of $134.1 million in the three months ended December 31, 2016.2018.

Under the terms of the Purchase Agreement, Lion Oil and MAPCO Express entered into a supply agreement at the closing of the Retail Transaction pursuant to which Lion Oil will supply fuel to retail locations owned by MAPCO Express for a period of 18 months following the closing of the Retail Transaction (the "Fuel Supply Agreement"). We recorded net revenues of $97.7 million and $306.3 million and net cash inflows of $101.4 million and $337.5 million for the three and nine months ended September 30, 2017, respectively, associated with the Fuel Supply Agreement.

Once the Retail Entities were identified as assets held for sale, the operations associated with these properties qualified for reporting as discontinued operations. Accordingly, theThe operating results, net of tax, from discontinued operations associated with the California Discontinued Entities are presented separately in Delek’s condensed consolidated statements of income and the notes to the condensed consolidated financial statements have been adjusted to exclude the discontinued operations. Components of amounts reflected in income from discontinued operations are as follows (in millions):

|

| | | | |

| | Three Months Ended |

| | | March 31, 2018 |

| Net revenues | | 32.5 |

|

| Cost of sales: | | |

| Cost of materials and other | | 3.8 |

|

| Operating expenses (excluding depreciation and amortization) | | (7.8 | ) |

| Total cost of sales | | (4.0 | ) |

| General and administrative expenses | | (1.1 | ) |

| Interest income | | 0.3 |

|

| Other income, net | | 3.0 |

|

| Loss on sale of California Discontinued Entities | | (41.2 | ) |

| Loss from discontinued operations before taxes | | (10.5 | ) |

| Income tax benefit | | (2.3 | ) |

| Loss from discontinued operations, net of tax | | $ | (8.2 | ) |

|

| | | | | | | | |

| | | Three Months Ended | | Nine Months Ended |

| | | September 30, 2016 | | September 30, 2016 |

| Revenue | | $ | 361.7 |

| | $ | 1,034.7 |

|

| Cost of goods sold | | (306.6 | ) | | (884.5 | ) |

| Operating expenses | | (34.2 | ) | | (99.7 | ) |

| General and administrative expenses | | (5.4 | ) | | (16.7 | ) |

| Depreciation and amortization | | (4.5 | ) | | (20.3 | ) |

| Interest expense | | (1.8 | ) | | (5.4 | ) |

| Income from discontinued operations before taxes | | 9.2 |

| | 8.1 |

|

| Income tax expense | | 3.2 |

| | 2.6 |

|

| Income from discontinued operations, net of tax | | $ | 6.0 |

| | $ | 5.5 |

|

California Discontinued Entities

During the third quarter 2017, we committed to a plan to sell 100% of our equity interestsIncluded in (or substantially all of the assets of) our subsidiaries associated with our Paramount and Long Beach, California refineries and our California renewable fuels facility (AltAir Paramount, LLC), which were acquired as part of the Delek/Alon Merger. As a result of this decision and commitment to a plan, and because it was made within three months of the Delek/Alon Merger, we met the requirements under ASC 205-20 and ASC 360 to report the results of the California Discontinued Entities as discontinued operations and to classify the California Discontinued Entities as a group of assets held for sale as of July 1, 2017. The sale of the California Discontinued Entities is currently anticipated to occur within the next 12 months. The property, plant and equipment of the California Discontinued Entities were recorded at fair value as part of the Delek/Alon Merger, and we did not record any depreciation of these assets since the Delek/Alon Merger.

The carrying amount of the major classes of assets and liabilities of the California Discontinued Entities included in assets held for sale and liabilities associated with assets held for sale are as follows (in millions):

|

| | | | |

| | | September 30, 2017 |

| Assets held for sale: | | |

| Cash and cash equivalents | | $ | 6.4 |

|

| Accounts receivable | | 7.4 |

|

| Inventory | | 1.2 |

|

| Other current assets | | 1.7 |

|

| Property, plant & equipment, net | | 147.3 |

|

| Other intangibles, net | | 1.0 |

|

| Other non-current assets | | 2.2 |

|

| Assets held for sale | | $ | 167.2 |

|

| Liabilities associated with assets held for sale: | | |

| Accounts payable | | $ | 12.7 |

|

| Accrued expenses and other current liabilities | | 25.7 |

|

| Deferred tax liabilities | | 3.7 |

|

| Other non-current liabilities | | 61.0 |

|

| Liabilities associated with assets held for sale | | $ | 103.1 |

|

Once the operating assets of the California Discontinued Entities met the criteria to be classified as assets held for sale, the operations associated with these properties qualified for reporting as discontinued operations. Accordingly, the operating results, net of tax,loss from discontinued operations are presented separately in Delek’s condensed consolidated statements ofis net income and the notesattributable to the condensed consolidated financial statements have been adjusted to exclude the discontinued operations. Classification as discontinued operations requires retrospective reclassification of the associated assets, liabilities and results of operations for all periods presented, beginning (in this case) as of the date of acquisition, which was July 1, 2017. Components of amounts reflected in income from discontinued operations are as follows (in millions):

|

| | | | |

| | | Three and Nine Months Ended |

| | | September 30, 2017 |

| Revenue | | $ | 38.3 |

|

| Cost of goods sold | | (32.4 | ) |

| Operating expenses | | (8.4 | ) |

| General and administrative expenses | | (2.9 | ) |

| Interest expense | | (1.0 | ) |

| Loss from discontinued operations before taxes | | (6.4 | ) |

| Income tax benefit | | (2.3 | ) |

| Loss from discontinued operations, net of tax | | $ | (4.1 | ) |

The net assets of the California Discontinued Entities include a non-controlling interest totaling $2.6$8.1 million as of September 30, 2017, and the net loss attributablerelated to the California Discontinued Entities includes a net loss attributable to the non-controlling interest totaling $0.2 millionAltAir for the three months ended September 30, 2017.March 31, 2018.

6.

Note 8 - Inventory

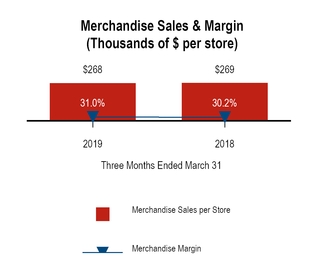

Crude oil, work-in-process,work in process, refined products, blendstocks and asphalt inventory for all of our operations, excluding the Tyler refinery and merchandisefuel inventory in our Retailretail segment, are stated at the lower of cost determined using the FIFOfirst-in, first-out (“FIFO”) basis or net realizable value. Cost of all inventory at the Tyler refinery is determined using the LIFOlast-in, first-out ("LIFO") inventory valuation method and inventory is stated at the lower of cost or market. Retail merchandise inventory consists of cigarettes, beer, convenience merchandise and food service merchandise and is stated at estimated cost as determined by the retail inventory method.

Notes to Condensed Consolidated Financial Statements (Unaudited)

Carrying value of inventories consisted of the following (in millions):

|

| | | | | | | | |

| | | March 31,

2019 | | December 31,

2018 |

| Refinery raw materials and supplies | | $ | 436.6 |

| | $ | 289.0 |

|

| Refinery work in process | | 69.7 |

| | 58.9 |

|

| Refinery finished goods | | 358.0 |

| | 304.1 |

|

| Retail fuel | | 10.2 |

| | 8.0 |

|

| Retail merchandise | | 24.6 |

| | 25.4 |

|

| Logistics refined products | | 6.7 |

| | 5.5 |

|

| Total inventories | | $ | 905.8 |

| | $ | 690.9 |

|

|

| | | | | | | | |

| | | September 30,

2017 | | December 31,

2016 |

| Refinery raw materials and supplies | | $ | 314.5 |

| | $ | 145.6 |

|

| Refinery work in process | | 64.5 |

| | 37.6 |

|

| Refinery finished goods | | 270.7 |

| | 200.3 |

|

| Retail fuel | | 9.3 |

| | — |

|

| Retail merchandise | | 26.6 |

| | — |

|

| Logistics refined products | | 7.9 |

| | 8.9 |

|

| Total inventories | | $ | 693.5 |

| | $ | 392.4 |

|

Due to a lower crude oil and refined product pricing environment experienced since the end of 2014, market prices have declined to a level below the average cost of our inventories. At September 30, 2017,March 31, 2019, we recorded a pre-tax inventory valuation reserve of $17.5$1.9 million, $16.4$1.3 million of which related to LIFO inventory which is subjectdue to reversal in subsequent periods, not to exceed LIFOa market price decline below our cost should market prices recover.of certain inventory products. At December 31, 2016,2018, we recorded a pre-tax inventory valuation reserve of $16.0$54.0 million, all$39.4 million of which related to LIFO inventory, which reversed in the first quarter of 2017, as2019 due to the inventories associated withsale of inventory quantities that gave rise to the valuation adjustment at the end of 2016 were sold or used.December 31, 2018 reserve. We recognized a net reduction in cost of materials and other in the accompanying condensed consolidated statements of income related to the change in pre-tax inventory valuation gains (losses) of $11.6$52.1 million and $(1.5)$0.9 million for the three and nine months ended September 30, 2017, respectively,March 31, 2019 and $7.8 million and $26.0 million for the three and nine months ended September 30, 2016,2018, respectively. These gains (losses) were recorded as a component of cost of goods sold in the consolidated statements of income.

At September 30, 2017 and December 31, 2016, the excess of replacement cost (FIFO) over the carrying value (LIFO) of the Tyler refinery inventories was $5.6 million and $3.5 million, respectively.

Permanent Liquidations

We incurred a permanent reduction in a LIFO layer resulting in liquidation gain (loss) in our refinery inventory of $0.4 million and $0.2 million during the three and nine months ended September 30, 2017, respectively, and $(2.4) million during the nine months ended September 30, 2016. These liquidation gains (losses) were recognized as a component of cost of goods sold.

7.

Note 9 - Crude Oil Supply and Inventory Purchase Agreements

Delek has Master Supply and Offtake Agreements (the "Supply and Offtake Agreements") with J. Aron & Company ("J. Aron").

El Dorado refinery operationsSupply and Offtake Agreement

Throughout the term of theThe El Dorado refinery's Supply and Offtake Agreement that supports the operations of our El Dorado refineryas amended and restated on February 27, 2017 and in effect through December 2018 (the "El Dorado Supply and Offtake Agreement"), which was amended on February 27, 2017 to change, among other things, certain terms related to pricing and an extension provided for Lion Oil Company ("Lion Oil") (as the primary legal entity associated with the El Dorado refinery for purposes of the maturity date to April 30, 2020, Lion Oilthis Agreement) and J. Aron willto identify mutually acceptable contracts for the purchase of crude oil from third parties and J. Aron willto supply up to 100,000 barrels per day ("bpd")bpd of crude oil to the El Dorado refinery. Crude oil supplied to the El Dorado refinery by J. Aron will beis purchased daily at an estimated average monthly market price by Lion Oil. J. Aron will also purchase all refined products from the El Dorado refinery at an estimated daily market price, as they are produced. These daily purchases and sales are trued-up on a monthly basis in order to reflect actual average monthly prices. We have recorded a (payable) receivable related to this monthly settlement of $1.5$15.8 million and $6.9$7.8 million as of September 30, 2017March 31, 2019 and December 31, 2016,2018, respectively. Also pursuant to the El Dorado Supply and Offtake Agreement and other related agreements, Lion Oil will endeavor to arrangearranges potential sales by either Lion Oil or J. Aron to third parties of the products produced at the El Dorado refinery or purchased from third parties. In instances where Lion Oil is the seller to such third parties, J. Aron will first transfer title to the applicable products to Lion Oil. The El Dorado Supply and Offtake Agreement has a maturity date of April 30, 2020. Based upon terms in effect as of December 31, 2018, upon the expiration or upon any earlier termination, Delek would be required to repurchase the consigned crude oil and refined products from J. Aron at then prevailing market prices.

Effective January 3, 2019, we amended the El Dorado Supply and Offtake Agreement with J. Aron that supports the operations of our El Dorado refinery so that the repurchase of baseline volumes at the end of the El Dorado Supply and Offtake Agreement term (representing the El Dorado "Baseline Step-Out Liability") will be based upon a fixed price instead of a market-indexed price. The modified arrangement results in a Baseline Step-Out Liability that is no longer subject to commodity volatility, but for which its fair value is now subject to interest rate risk. As a result, we recorded a gain on the change in fair value resulting from the modification of the instruments from commodities-based risk to interest rate risk in cost of materials and other totaling approximately $4.1 million in the first quarter of 2019, and we incurred $3.2 million in fees paid to J. Aron which were charged to interest expense. Such Baseline Step-Out Liability will continue to be recorded at fair value, where the fair value will reflect changes in interest rate risk rather than commodity price risk under the fair value election provided by ASC 815 Derivatives and Hedging ("ASC 815") and ASC 825, Financial Instruments ("ASC 825"). The change in fair value recorded during the three months ended March 31, 2019 related to the new instrument totaled $(2.5) million and is reflected as a reduction in interest expense.

At March 31, 2019 and December 31, 2018, Delek had 3.5 million barrels and 2.8 million barrels, respectively, of inventory consigned from J. Aron under the El Dorado Supply and Offtake Agreement, and we have recorded total liabilities associated with this consigned inventory of $190.9 million and $152.6 million, respectively, on the condensed consolidated balance sheets. As a result of the amendment to the El Dorado Supply and Offtake Agreement, as of March 31, 2019, the fair value of the Baseline Step-Out Liability totaling $103.6 million is reflected as a non-current obligation on our condensed consolidated balance sheet, and represents 2.0 million barrels of baseline consigned inventory.

We maintained letters of credit with respect to the El Dorado Supply and Offtake Agreement totaling $150.0 million and $120.0 million at March 31, 2019 and December 31, 2018, respectively.

This arrangement is accounted for as a product financing arrangement.financing. Delek incurred recurring fees payable to J. Aron under the El Dorado Supply and Offtake Agreement of $2.5$2.4 million and $7.3$2.7 million during the three and nine months ended September 30, 2017, respectively,March 31, 2019 and $2.6 million and $7.4 million during the three and nine months ended September 30, 2016,March 31, 2018, respectively. These amounts are included as a component of interest expense in the condensed consolidated statements of income. Upon any termination of the El Dorado Supply and Offtake Agreement, including in connection with a force majeure event, the parties are required to negotiate with third parties for the assignment to us of certain contracts, commitments and arrangements, including procurement contracts, commitments for the sale of product, and pipeline, terminalling, storage and shipping arrangements.

Upon the expiration of the El DoradoAlon Supply and Offtake Agreement on April 30, 2020, or upon any earlier termination, Delek will be required to repurchase the consigned crude oil and refined products from J. Aron at then prevailing market prices. At September 30, 2017, Delek had 2.9 million barrels of inventory consigned from J. Aron, and we have recorded liabilities associated with this consigned inventory of $157.3 million in the condensed consolidated balance sheet.

Alon refinery operationsAgreements

Effective with the Delek/Alon Merger, we assumed Alon's existing Supply and Offtake Agreements and other associated agreements with J. Aron to support the operations of our Big Spring and Krotz Springs and California refineries (as further defined in Note 14) and certain of our asphalt terminals (together, the “Alon Supply and Offtake Agreements”). Pursuant to the Alon Supply and Offtake Agreements, (i) J. Aron agreed to sell to us, and we agreed to buy from J. Aron, at market prices, crude oil for processing at these refineries and (ii) we agreed to sell, and J. Aron agreed to buy, at market prices, certain refined products produced at these refineries. The Alon Supply and Offtake Agreements also provide for the sale, at market prices, of our crude oil and certain refined product inventories to J. Aron, the lease to J. Aron of crude oil and refined product storage facilities and the identification of prospective purchasers of refined products on J. Aron’s behalf. The Alon Supply and Offtake Agreements for the Big Spring and Krotz Springs refineries have initial terms that expire in May 2021, and the Supply and Offtake Agreement for the California refineries has initial terms that expire in May 2019.2021. J. Aron or Delek may elect to terminate the Supply and Offtake Agreements for the Big Spring and Krotz Springs refineries prior to the expiration of the initial term beginning in May 2018 and upon each anniversary thereof, on six months' prior notice. We may elect to terminateagreements at the Big Spring and Krotz Springs refineries in May 2020 on six months' prior notice. J. Aron may elect to terminate the Supply and Offtake Agreement for the California refineries prior to the expiration of the initial term beginning in May 2017 and upon each anniversary thereof, on six months prior notice. We may elect to terminate at the California refineries in May 2018 on six months' prior notice.

TheseThe daily purchases and sales are trued-up on a monthly basis in order to reflect actual average monthly prices. We have recorded a net receivable (payable) related to this monthly settlement of $6.6$17.2 million and $(1.0) million as of September 30, 2017.March 31, 2019 and December 31, 2018, respectively. Based upon terms in effect prior to the December 2018 and January 2019 amendments discussed below, upon the expiration or upon any earlier termination, Delek would be required to repurchase the consigned crude oil and refined products from J. Aron at then prevailing market prices.

These arrangementsEffective December 21, 2018, we amended our Supply and Offtake Agreement related to the Big Spring refinery (the "Big Spring Supply and Offtake Agreement") so that the repurchase of baseline volumes at the end of the Supply and Offtake Agreement term (representing the Big Spring "Baseline Step-Out Liability") will be based upon a fixed price instead of a market-indexed price. The modified arrangement results in a Baseline Step-Out Liability that is no longer subject to commodity volatility, but for which its fair value is now subject to interest rate risk. As a result for the Big Spring Supply and Offtake Agreement, we recorded a gain on the change in fair value resulting from the modification of the instruments from commodities-based risk to interest rate risk in cost of materials and other in the fourth quarter of 2018. Such Baseline Step-Out Liability will continue to be recorded at fair value, where the fair value will reflect changes in interest rate risk rather than commodity price risk under the fair value election provided by ASC 815 and ASC 825. Fees paid to J Aron as a result of this transaction were recorded as interest expense. As of March 31, 2019 and December 31, 2018 , the fair value of the Baseline Step-Out Liability for the Big Spring refinery was $48.1 million and $49.6 million, respectively, each based on 0.8 million barrels of baseline consigned inventory. As a result of the amendment, as of both March 31, 2019 and December 31, 2018, this baseline consigned inventory for the Big Spring refinery is reflected as a non-current obligation on our condensed consolidated balance sheet. The change in fair value recorded during the three months ended March 31, 2019 related to the new instrument totaled $(1.5) million and is reflected as a reduction in interest expense. There were no changes in our credit spread during the period that would require recognition in accumulated other comprehensive income pursuant to ASC 825.

At March 31, 2019 and December 31, 2018, Delek had 1.5 million barrels and 1.7 million barrels, respectively, of inventory consigned from J. Aron under the Big Spring Supply and Offtake Agreement, and we have recorded total liabilities associated with this consigned inventory of $91.5 million and $96.5 million, respectively, on the condensed consolidated balance sheets.

Effective January 2, 2019, we amended our Supply and Offtake Agreement related to the Krotz Springs refinery (the "Krotz Springs Supply and Offtake Agreement") so that the repurchase of baseline volumes at the end of the Supply and Offtake Agreement term (representing the Krotz Springs "Baseline Step-Out Liability") will also be based upon a fixed price instead of a market-indexed price. Like the Big Spring amendment, this modified arrangement results in a Baseline Step-Out Liability that is no longer subject to commodity volatility, but for which its fair value is now subject to interest rate risk. As a result for the Krotz Springs Supply and Offtake Agreement, we recorded a gain on the change in fair value resulting from the modification of the instruments from commodities-based risk to interest rate risk in cost of materials and other of $3.5 million in the first quarter of 2019, and we incurred $1.8 million in fees paid to J Aron which were charged to interest expense. Such Baseline Step-Out Liability will continue to be recorded at fair value, where the fair value will reflect changes in interest rate risk rather than commodity price risk under the fair value election provided by ASC 815 and ASC 825.

At March 31, 2019, Delek had 1.4 million barrels of inventory consigned from J. Aron under the Krotz Springs Supply and Offtake Agreement, inclusive of both the baseline volumes and over, short and excess target quantities, and we have total recorded liabilities associated with this consigned inventory of $102.4 million in the condensed consolidated balance sheets. As a result of the amendment, as of March 31, 2019, the fair value of the Baseline Step-Out Liability totaling $74.2 million for the Krotz Springs refinery is reflected as a non-current obligation on our condensed consolidated balance sheet, and represents 1.3 million barrels of baseline consigned inventory. The change in fair value

recorded during the three months ended March 31, 2019 related to the new instrument totaled $(1.1) million and is reflected as a reduction in interest expense. There were no changes in our credit spread during the period that would require recognition in accumulated other comprehensive income pursuant to ASC 825.

Based upon terms in effect as of December 31, 2018 for the Krotz Springs Supply and Offtake Agreement, as of December 31, 2018, we had 1.8 million barrels of inventory consigned from J. Aron under the Krotz Springs Supply and Offtake Agreement, inclusive of both the baseline volumes and over, short and excess target quantities, and recorded a current liability associated with this consigned inventory of $113.1 million in the consolidated balance sheets, measured using the fair value election pursuant to ASC 825 (based on prevailing market-indexed pricing).

Both the Big Spring Supply and Offtake Agreement and the Krotz Springs Supply and Offtake Agreement are accounted for as product financing arrangements. Delek incurred recurring fees payable to J. Aron of $2.3$3.7 million and $3.4 million during the three months ended September 30, 2017.March 31, 2019 and 2018, respectively. These amounts are included as a component of interest expense in the condensed consolidated statements of income. Upon any termination of the Alon Supply and Offtake Agreement,Agreements, including in connection with a force majeure event, the parties are required to negotiate with third parties for the assignment to us of certain contracts, commitments and arrangements, including procurement contracts, commitments for the sale of product, and pipeline, terminalling, storage and shipping arrangements.

Upon the expirationWe maintain letters of credit totaling $44.0 million and $24.0 million, as of March 31, 2019 and December 31, 2018, respectively with respect to the Alon Supply and Offtake Agreements, or upon any earlier termination, Delek will be required to repurchase the consigned crude oil and refined products from J. Aron at then prevailing market prices. At September 30, 2017, Delek had 3.4 million barrels of inventory consigned from J. Aron, and we have recorded liabilities associated with this consigned inventory of $229.4 million in the condensed consolidated balance sheet.

Agreements. In connection with the AlonKrotz Springs Supply and Offtake Agreement, for our Krotz Springs refinery, we have granted a security interest to J. Aron in certain assets (including all of its accounts receivable and inventoryinventory) to secure its obligations to J. Aron. In addition, we have granted a security interest in all of the Krotz Springs refinery's real property and equipment to J. Aron to secure our obligations under a commodity hedge and sale agreement in lieu of posting cash collateral and being subject to cash margin calls.

8.Note 10 - Long-Term Obligations and Notes Payable

Outstanding borrowings, net of unamortized debt discounts and certain deferred financing costs, under Delek’s existing debt instruments are as follows (in millions):

|

| | | | | | | | |

| | | September 30,

2017 | | December 31,

2016 |

| DKL Revolver | | $ | 158.8 |

| | $ | 392.6 |

|

DKL Notes (1) | | 242.5 |

| | — |

|

Wells Term Loan(2) | | 46.3 |

| | 63.6 |

|

| Wells Revolving Loan | | 45.0 |

| | — |

|

| Reliant Bank Revolver | | 17.0 |

| | 17.0 |

|

| Promissory Notes | | 95.2 |

| | 130.0 |

|

Lion Term Loan Facility(3) | | 210.0 |

| | 229.7 |

|

| Alon Partnership Credit Facility | | 100.0 |

| | — |

|

| Alon Partnership Term Loan | | 238.1 |

| | — |

|

Alon Convertible Senior Notes (4) | | 144.7 |

| | — |

|

Alon Term Loan Credit Facilities (5) | | 42.0 |

| | ��� |

|

Alon Retail Credit Facilities (6) | | 88.2 |

| | — |

|

| | | 1,427.8 |

| | 832.9 |

|

| Less: Current portion of long-term debt and notes payable | | 351.0 |

| | 84.4 |

|

| | | $ | 1,076.8 |

| | $ | 748.5 |

|

|

| | | | | | | | |

| | | March 31,

2019 | | December 31,

2018 |

| Revolving Credit Facility | | $ | 300.0 |

| | $ | 300.0 |

|

Term Loan Credit Facility (1) | | 680.9 |

| | 682.9 |

|

| Delek Logistics Credit Facility | | 461.2 |

| | 456.7 |

|

Delek Logistics Notes (2) | | 244.0 |

| | 243.7 |

|

| Reliant Bank Revolver | | 30.0 |

| | 30.0 |

|

| Promissory Notes | | 45.0 |

| | 70.0 |

|

| | | 1,761.1 |

| | 1,783.3 |

|

| Less: Current portion of long-term debt and notes payable | | 32.0 |

| | 32.0 |

|

| | | $ | 1,729.1 |

| | $ | 1,751.3 |

|

| |

(1) | The DKLTerm Loan Credit Facility is net of deferred financing costs of $4.2 million and $3.5 million, respectively, and debt discount of $7.9 million and $8.4 million at March 31, 2019 and December 31, 2018. |

| |

(2) | The Delek Logistics Notes are net of deferred financing costs of $5.7$4.6 million and debt discount of $1.8 million at September 30, 2017. |

| |

(2)

| The Wells Term Loan is net of deferred financing costs of a nominal amount and $0.1$4.8 million, respectively, and debt discount of $0.4$1.4 million and $0.5$1.5 million, respectively, at September 30, 2017March 31, 2019 and December 31, 2016.2018. |

Outstanding Obligations/Facilities as of the Balance Sheet Dates

Delek Revolver and Term Loan

On March 30, 2018, (the "Closing Date"), Delek entered into (i) a new term loan credit agreement with Wells Fargo Bank, National Association, as administrative agent (the "Term Administrative Agent"), Delek, as borrower, certain subsidiaries of Delek, as guarantors, and the lenders from time to time party thereto, providing for a senior secured term loan facility in an amount of $700.0 million (the "Term Loan Credit Facility") and (ii) a second amended and restated credit agreement with Wells Fargo Bank, National Association, as administrative agent (the "Revolver Administrative Agent"), Delek, as borrower, certain subsidiaries of Delek, as guarantors, and the other lenders party thereto, providing for a senior secured asset-based revolving credit facility with commitments of $1.0 billion (the "Revolving Credit Facility" and, together with the Term Loan Credit Facility, the "New Credit Facilities").

|

| |

(3)

21 | | The Lion Term Loan Facility is net of deferred financing costs of $2.3 million and $3.0 million, respectively, and debt discount of $0.8 million and $1.1 million, respectively, at September 30, 2017 and December 31, 2016. |

(4)

Notes to Condensed Consolidated Financial Statements (Unaudited)

The Alon Convertible Senior Notes are netRevolving Credit Facility permits borrowings in Canadian dollars of debt discountup to $50.0 million. The Revolving Credit Facility also permits the issuance of $5.3letters of credit of up to $300.0 million, at September 30, 2017.including letters of credit denominated in Canadian dollars of up to $10.0 million. Delek may designate restricted subsidiaries as additional borrowers under the Revolving Credit Facility.

(5) The Alon Term Loan Credit Facility was drawn in full for $700.0 million on the Closing Date at an original issue discount of 0.50%. Proceeds under the Term Loan Credit Facility, as well as proceeds of approximately $300.0 million in borrowings under the Revolving Credit Facility on the Closing Date, were used to repay certain indebtedness of Delek and its subsidiaries (the “Refinancing”), as well as certain fees, costs and expenses in connection with the closing of the New Credit Facilities, are netwith any remaining proceeds held in cash. Proceeds of future borrowings under the Revolving Credit Facility will be used for working capital and general corporate purposes of Delek and its subsidiaries.

We recorded a loss on extinguishment of debt discounttotaling approximately $9.0 million during the three months ended March 31, 2018 in connection with the Refinancing.

Interest and Unused Line Fees

The interest rates applicable to borrowings under the Term Loan Credit Facility and the Revolving Credit Facility are based on a fluctuating rate of $0.7 millioninterest measured by reference to either, at Delek’s option, (i) a base rate, plus an applicable margin, or (ii) a reserve-adjusted London Interbank Offered Rate ("LIBOR"), plus an applicable margin (or, in the case of Revolving Credit Facility borrowings denominated in Canadian dollars, the Canadian dollar bankers' acceptances rate ("CDOR")). The initial applicable margin for all Term Loan Credit Facility borrowings was 1.50% per annum with respect to base rate borrowings and 2.50% per annum with respect to LIBOR borrowings.

On October 26, 2018, Delek entered into an amendment to the Term Loan Credit Facility (the “First Amendment”) to reduce the margin on certain borrowings under the Term Loan Credit Facility and incorporate certain other changes. The First Amendment prospectively decreases the applicable margins for borrowings under (i) Base Rate Loans from 1.50% to 1.25% and (ii) LIBOR Rate Loans from 2.50% to 2.25%, as such terms are defined in the Term Loan Credit Facility. The decreases to the applicable margins became effective upon execution of the First Amendment.

The initial applicable margin for Revolving Credit Facility borrowings was 0.25% per annum with respect to base rate borrowings and 1.25% per annum with respect to LIBOR and CDOR borrowings, and the applicable margin for such borrowings after September 30, 2017.2018 is based on Delek’s excess availability as determined by reference to a borrowing base, ranging from 0.25% to 0.75% per annum with respect to base rate borrowings and from 1.25% to 1.75% per annum with respect to LIBOR and CDOR borrowings.

In addition, the Revolving Credit Facility requires Delek to pay an unused line fee on the average amount of unused commitments thereunder in each quarter, which fee will be at a rate of 0.25% or 0.375% per annum, depending on average commitment usage for such quarter. As of March 31, 2019, the unused line fee was 0.375% per annum.

(6) Maturity and Repayments

The Alon RetailRevolving Credit Facility will mature and the commitments thereunder will terminate on March 30, 2023. The Term Loan Credit Facility requires scheduled quarterly principal payments of $1.75 million, with the balance of the principal due on March 30, 2025. Additionally, the Term Loan Credit Facility requires prepayments by Delek with the net cash proceeds from certain debt incurrences, asset dispositions and insurance or condemnation events with respect to Delek’s assets, subject to certain exceptions, thresholds and reinvestment rights. The Term Loan Credit Facility also requires prepayments with a variable percentage of Delek’s excess cash flow, ranging from 50.0% to 0% depending on Delek’s consolidated secured net leverage ratio from time to time. Delek may also make voluntarily prepayments under the Term Loan Credit Facility at any time, subject to a prepayment premium of 1.0% in connection with certain customary repricing events that may occur within six months after the Closing Date, with no premium applied after six months.

Guarantee and Security

The obligations of the borrowers under the New Credit Facilities are netguaranteed by Delek and each of debt discountits direct and indirect, existing and future, wholly-owned domestic subsidiaries, subject to customary exceptions and limitations, and excluding Delek Logistics Partners, LP, Delek Logistics GP, LLC, and each subsidiary of $2.8the foregoing (collectively, the "MLP Subsidiaries"). Borrowings under the New Credit Facilities are also guaranteed by DK Canada Energy ULC, a British Columbia unlimited liability company and a wholly-owned restricted subsidiary of Delek.

The Revolving Credit Facility is secured by a first priority lien over substantially all of Delek’s and each guarantor's receivables, inventory, renewable identification numbers, instruments, intercompany loan receivables, deposit and securities accounts and related books and records and certain other personal property, subject to certain customary exceptions (the "Revolving Priority Collateral"), and a second priority lien over substantially all of Delek's and each guarantor's other assets, including all of the equity interests of any subsidiary held by Delek or any guarantor (other than equity interests in certain MLP Subsidiaries) subject to certain customary exceptions, but excluding real property (such real property and equity interests, the "Term Priority Collateral").

Notes to Condensed Consolidated Financial Statements (Unaudited)

The Term Loan Credit Facility is secured by a first priority lien on the Term Priority Collateral and a second priority lien on the Revolving Priority Collateral, all in accordance with an intercreditor agreement between the Term Administrative Agent and the Revolver Administrative Agent and acknowledged by Delek and the subsidiary guarantors. Certain excluded assets are not included in the Term Priority Collateral and the Revolving Priority Collateral.

Additional Information

At March 31, 2019, the weighted average borrowing rate under the Revolving Credit Facility was 5.75% and was comprised entirely of a base rate borrowing, and the principal amount outstanding thereunder was $300.0 million. Additionally, there were letters of credit issued of approximately $226.4 million at September 30, 2017.as of March 31, 2019 under the Revolving Credit Facility. Unused credit commitments under the Revolving Credit Facility, as of March 31, 2019, were approximately $473.6 million

DKL RevolverAt March 31, 2019, the weighted average borrowing rate under the Term Loan Credit Facility was approximately 4.75% comprised entirely of a LIBOR borrowing and the principal amount outstanding thereunder was $693.0 million.

Delek Logistics hasCredit Facility

Prior to its amendment and restatement on September 28, 2018, Delek Logistics had a $700.0 million senior secured revolving credit agreement with Fifth Third Bank ("Fifth Third"), as administrative agent, and a syndicate of lenders (the "DKL Revolver""2014 Facility") with a $100.0 million accordion feature, bearing interest at (i) either a U.S. prime dollar rate or a LIBOR Rate for borrowings denominated in U.S. Dollars, or (ii) either a Canadian dollar prime rate, or a Canadian Dealer Offered Rate, for borrowing denominated in Canadian dollars (in each case plus applicable margins, at the election of the borrowers and as a function of draw down currency). On September 28, 2018, Delek Logistics and all of its existing wholly-owned subsidiaries are borrowers underentered into a third amended and restated senior secured revolving credit agreement, with Fifth Third, as administrative agent, and a syndicate of lenders (hereafter, the DKL Revolver, except"Delek Logistics Credit Facility"). Under the terms of the Delek Logistics Finance Corp., a Delaware corporation and a wholly-owned subsidiary ofCredit Facility, among other things, the lender commitments were increased from $700.0 million to $850.0 million. The Delek Logistics ("Finance Corp."). The DKL RevolverCredit Facility also contains a dual currency borrowing tranche that permits draw downs in U.S. or Canadian dollars and an accordion feature whereby Delek Logistics can increase the size of the credit facility to an aggregate of $800.0 million,$1.0 billion, subject to receiving increased or new commitments from lenders and the satisfaction of certain other conditions precedent.

The obligations under the DKL Revolver areDelek Logistics Credit Facility remain secured by a first priority lienliens on substantially all of Delek Logistics' tangible and intangible assets. Additionally, a subsidiary of Delek providescontinues to provide a limited guaranty of Delek Logistics' obligations under the DKL Revolver.Delek Logistics Credit Facility. The guaranty is (i) limited to an amount equal to the principal amount, plus unpaid and accrued interest, of a promissory note made by Delek in favor of the subsidiary guarantor (the "Holdings Note") and (ii) secured by the subsidiary guarantor's pledge of the Holdings Note to the DKL RevolverDelek Logistics Credit Facility lenders. As of September 30, 2017,both March 31, 2019 and December 31, 2018, the principal amount of the Holdings Note was $102.0 million.

The DKL Revolver will mature on December 30, 2019.Delek Logistics Credit Facility has a maturity date of September 28, 2023. Borrowings under the DKL RevolverDelek Logistics Credit Facility bear interest at either a U.S. basedollar prime rate, Canadian prime rate, LIBOR, or a Canadian Dealer Offered Rate,CDOR rate, in each case plus applicable margins, at the election of the borrowers and as a function of draw down currency. The applicable margin in each case variesand the fee payable for the unused revolving commitments vary based upon Delek Logistics' most recent total leverage ratio which iscalculation delivered to the lenders, as called for and defined asunder the ratioterms of total funded debt to EBITDA for the most recently ended four fiscal quarters.Delek Logistics Credit Facility. At September 30, 2017,March 31, 2019, the weighted average borrowing rate

was approximately 4.0%5.1%. Additionally, the DKL RevolverDelek Logistics Credit Facility requires Delek Logistics to pay a leverage ratio dependent quarterly fee on the average unused revolving commitment. As of September 30, 2017,March 31, 2019, this fee was 0.50%0.40% per year.

As of September 30, 2017,March 31, 2019, Delek Logistics had $158.8$461.2 million of outstanding borrowings under the credit facility, as well asDelek Logistics Credit Facility, with no letters of credit issued of $8.5 million.in place. Unused credit commitments under the DKL Revolver,Delek Logistics Credit Facility, as of September 30, 2017,March 31, 2019, were $532.7$388.8 million.

DKLDelek Logistics Notes

On May 23, 2017, Delek Logistics and Delek Logistics Finance Corp. (collectively, the “Issuers”), issued $250.0 million in aggregate principal amount of 6.750%6.75% senior notes due 2025 (the “DKL“Delek Logistics Notes”) at a discount. The DKLDelek Logistics Notes are general unsecured senior obligations of the Issuers. The DKLDelek Logistics Notes are unconditionally guaranteed jointly and severally on a senior unsecured basis by Delek Logistic'sLogistics' existing subsidiaries (other than Delek Logistics Finance Corp., the "Guarantors") and will be unconditionally guaranteed on the same basis by certain of Delek Logistic’sLogistics' future subsidiaries. The DKLDelek Logistics Notes rank equal in right of payment with all existing and future senior indebtedness of the Issuers, and senior in right of payment to any future subordinated indebtedness of the Issuers. Interest on the DKL Delek Logistics Notes is payable semi-annually in arrears on each May 15 and November 15, commencing November 15, 2017.

At any time prior to May 15, 2020, the Issuers may redeem up to 35% of the aggregate principal amount of the DKLDelek Logistics Notes with the net cash proceeds of one or more equity offerings by Delek Logistics at a redemption price of 106.750% of the redeemed principal amount, plus accrued and unpaid interest, if any, subject to certain conditions and limitations. Prior to May 15, 2020, the Issuers may redeem all or part of the DKLDelek Logistics Notes at a redemption price of the principal amount plus accrued and unpaid interest, if any, plus a "make whole" premium, subject to certain conditions and limitations. In addition, beginning on May 15, 2020, the Issuers may, subject to certain conditions and limitations, redeem all or part of the DKLDelek Logistics Notes, at a redemption price of 105.063% of the redeemed principal for

Notes to Condensed Consolidated Financial Statements (Unaudited)

the twelve-month period beginning on May 15, 2020, 103.375% for the twelve-month period beginning on May 15, 2021, 101.688% for the twelve-month period beginning on May 15, 2022 and 100.00% beginning on May 15, 2023 and thereafter, plus accrued and unpaid interest, if any. There are also certain redemption provisions in

In the event of a change of control, accompanied or followed by a ratings downgrade within a certain period of time, subject to certain conditions and limitations.

limitations, the Issuers will be obligated to make an offer for the purchase of the Delek Logistics Notes from holders at a price equal to 101.00% of the principal amount thereof, plus accrued and unpaid interest.

In connection withMay 2018, the issuance of the 2025Delek Logistics Notes the Issuers and the Guarantors entered into a registration rights agreement, whereby the Issuers and the Guarantors are required to exchange the 2025 Noteswere exchanged for new notes with terms substantially identical in all material respects with the 2025 Notes (exceptexcept the new notes willdo not contain terms with respect to transfer restrictions). The Issuers and the Guarantors will use their commercially reasonable efforts to cause the exchange offer to be consummated not later than 365 days after May 23, 2017.restrictions.

As of September 30, 2017,March 31, 2019, we had $250.0 million in outstanding principal amount under the 2025Delek Logistics Notes.

Wells ABL

Our subsidiary, Delek Refining, Ltd., has an asset-based loan credit facility with Wells Fargo Bank, National Association, as administrative agent, and a syndicate of lenders, which was amended and restated on September 29, 2016 (the "Wells ABL") and was most recently amended on May 17, 2017 to incorporate technical modifications related to the Delek/Alon Merger. The Wells ABL consists of (i) a $450.0 million revolving loan (the "Wells Revolving Loan"), which includes a $45.0 million swing line loan sub-limit and a $200.0 million letter of credit sub-limit, (ii) a $70.0 million term loan (the "Wells Term Loan"), and (iii) an accordion feature that permits an increase in the size of the revolving credit facility to an aggregate of $725.0 million, subject to additional lender commitments and the satisfaction of certain other conditions precedent. The Wells Revolving Loan matures on September 29, 2021 and the Wells Term Loan matures on September 29, 2019. The Wells Term Loan is subject to repayment in level principal installments of approximately $5.8 million per quarter, with the final installment due on September 29, 2019. As of September 30, 2017, under the Wells ABL, we had letters of credit issued totaling approximately $96.5 million, $45.0 million in borrowings outstanding under the Wells Revolving Loan and $46.7 million outstanding under the Wells Term Loan. The obligations under the Wells ABL are secured by (i) substantially all the assets of Refining and its subsidiaries, with certain limitations, (ii) guaranties provided by the general partner of Delek Refining, Ltd., as well as by the parent of Delek Refining, Ltd., Delek Refining, Inc. (iii) a limited guarantee provided jointly and severally by Old and New Delek in an amount up to $15.0 million in the aggregate and (iv) a limited guarantee provided by Lion Oil in an amount equal to the sum of the face amount of all letters of credit issued on behalf of Lion Oil under the Wells ABL and any loans made by Refining or its subsidiaries to Lion Oil. Under the facility, revolving loans and letters of credit are provided subject to availability requirements which are determined pursuant to a borrowing base calculation as defined in the credit agreement. The borrowing base as calculated is primarily supported by cash, certain accounts receivable and certain inventory. Borrowings under the Wells Revolving Loan and Wells Term Loan bear interest based on separate predetermined pricing grids that allow us to choose between base rate loans or LIBOR loans. At September 30, 2017, the weighted average borrowing rate was approximately 5.0% under the Wells Term Loan and 4.8% under the Wells Revolving Loan. Additionally, the Wells ABL requires us to pay a quarterly unused credit commitment fee. As of September 30, 2017, this fee was approximately 0.38% per year. Unused borrowing base availability, as calculated and reported under the terms of the Wells ABL credit facility, as of September 30, 2017, was approximately $229.9 million.

Reliant Bank Revolver

We have aDelek has an unsecured revolving credit agreement with Reliant Bank which was amended on May 26, 2016 (the "Reliant Bank Revolver") and was most recently amended on May 23, 2017 to incorporate technical modifications related to the Delek/Alon Merger. The Reliant Bank Revolverthat provides for unsecured loans of up to $17.0$30.0 million. As of September 30, 2017, we had $17.0 million outstanding under this facility. The Reliant Bank Revolver matures on June 28, 2018, and2020, bears interest at a fixed rate of 5.25%4.75% per annum. The Reliant Bank Revolverannum and requires us to pay a quarterly fee of 0.50% per year on the average available revolving commitment. As of September 30, 2017,March 31, 2019, we had $30.0 million outstanding and had no unused credit commitments under the Reliant Bank Revolver.Revolver

Promissory Notes

On April 29, 2011, Delek entered into a $50.0 million promissory note (the "Ergon Note") with Ergon, Inc. ("Ergon") in connection with the closing of our acquisition of Lion Oil. The Ergon Note required Delek to make annual amortization payments of $10.0 million each, commencing April 29, 2013. The Ergon Note matured on April 29, 2017 and was paid in full. Interest under the Ergon Note was computed at a fixed rate equal to 4.0% per annum.

On May 14, 2015, in connection with the the Company’s closing of the acquisition of an equity method investment in Alon Acquisition,(the "Alon Acquisition"), the Company issued the Alona promissory note (the "Alon Israel NoteNote") in the amount of $145.0 million, which was payable to Alon Israel.Israel Oil Company, Ltd. ("Alon Israel"). The Alon Israel Note bears interest at a fixed rate of 5.5%5.50% per annum and requires five annual principal amortization payments of $25.0 million beginning in January 2016 followed by a final principal amortization payment of $20.0 million at maturity on January 4, 2021. In October 2015, we prepaid the first annual principal amortization payment in the amount of $25.0 million, along with all interest due on the prepaid amount. On December 22, 2015, Alon Israel assigned the remaining $120.0 million of principal and all accrued interest due under the Alon Israel Note to assignees under four new notes in substantially the same form and on the same terms as the Alon Israel Note (collectively, the "Alon Successor Notes"). The $120.0 million in total principal of the four Alon Successor Notes collectively require the same principal amortization payments and schedule as under the Alon Israel Note, with payments due under each Alon Successor Note commensurate to such note's pro rata share of $120.0 million in assigned principal. As of September 30, 2017,March 31, 2019, a total principal amount of $95.0$45.0 million was outstanding under the Alon Successor Notes.

At September 30, 2017, one of our retail companies had a loan that matures in 2019 with an outstanding balance of $0.2 million and the weighted average borrowing rate was approximately 9.7%.

Lion Term Loan

Our subsidiary, Lion Oil, has a term loan credit facility with Fifth Third Bank, as administrative agent, and a syndicate of lenders, which was amended and restated on May 14, 2015 in connection with the Company’s closing of the Alon Acquisition to, among other things, increase the total loan size from $99.0 million to $275.0 million (the "Lion Term Loan"), and was most recently amended on April 13, 2017 to incorporate technical modifications related to the Delek/Alon Merger. The Lion Term Loan requires Lion Oil to make quarterly principal amortization payments of approximately $6.9 million each, commencing on September 30, 2015, with a final balloon payment due at maturity on May 14, 2020. The Lion Term Loan is secured by, among other things, (i) substantially all the assets of Lion Oil and its subsidiaries (excluding inventory and accounts receivable), (ii) all shares in Lion Oil, (iii) any subordinated and common units of Delek Logistics held by Lion Oil, and (iv) the ALJ Shares. Additionally, the Lion Term Loan is guaranteed by Old and New Delek and the subsidiaries of Lion Oil. Interest on the unpaid balance of the Lion Term Loan is computed at a rate per annum equal to LIBOR or a base rate, at our election, plus the applicable margins, subject in each case to an all-in interest rate floor of 5.50% per annum. As of September 30, 2017, approximately $213.1 million was outstanding under the Lion Term Loan and the weighted average borrowing rate was 5.8%.

Alon Partnership

Revolving Credit Facility

The Alon Partnership has a $240.0 million revolving credit facility (the “Alon Partnership Credit Facility”) that will mature on May 26, 2018. The Alon Partnership Credit Facility can be used both for borrowings and the issuance of letters of credit subject to a limit of the lesser of the facility amount or the borrowing base amount under the facility. Borrowings under the Alon Partnership Credit Facility bear interest at LIBOR or base rate, at our election, plus the applicable margins.

The Alon Partnership Credit Facility is secured by a first priority lien on the Alon Partnership’s cash, accounts receivables, inventories and related assets and a second priority lien on the Alon Partnership’s fixed assets and other specified property.

At September 30, 2017, the weighted average borrowing rate was approximately 5.3%. Additionally, the Alon Partnership Credit Facility requires the payment of a quarterly fee on the average unused revolving commitment. As of September 30, 2017, this fee was 0.65% per year. As of September 30, 2017, the Alon Partnership had $100.0 million of outstanding borrowings under the credit facility, as well as letters of credit issued of $14.4 million. Unused credit commitments under the Alon Partnership Credit Facility, as of September 30, 2017, were $125.6 million.

Partnership Term Loan Credit Facility

The Alon Partnership has a $250.0 million term loan (the “Alon Partnership Term Loan”). The Alon Partnership Term Loan requires principal payments of $2.5 million per annum paid in equal quarterly installments until maturity in November 2018. The Alon Partnership Term Loan bears interest at a rate equal to the sum of (i) the Eurodollar rate (with a floor of 1.25% per annum) plus (ii) a margin of 8.0% per annum. At September 30, 2017, the weighted average borrowing rate was approximately 9.3% under the Alon Partnership Term Loan. As of September 30, 2017, the Alon Partnership Term Loan had an outstanding principal balance of $238.1 million,

The Alon Partnership Term Loan is secured by a first priority lien on all of the Alon Partnership’s fixed assets and other specified property, as well as on the general partner interest in the Alon Partnership held by the Alon General Partner, and a second priority lien on the Alon Partnership’s cash, accounts receivables, inventories and related assets.

Alon Convertible Senior Notes(share values in dollars)