UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended SeptemberJune 30, 20212022

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-38124

GRANITE POINT MORTGAGE TRUST INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | | 61-1843143 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | | | | | | | | | | |

| 3 Bryant Park, Suite 2400A | | |

| New York, | New York | | 10036 |

| (Address of principal executive offices) | | (Zip Code) |

(212) 364-5500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | GPMT | | New YorkNYSE |

7.00% Series A Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock, Exchangepar value $0.01 per share | | GPMTPrA | | NYSE |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☐☒ | | Accelerated filer | ☒☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of NovemberAugust 4, 2021,2022, there were 53,789,46552,350,989 shares of outstanding common stock, par value $0.01 per share, issued and outstanding.

GRANITE POINT MORTGAGE TRUST INC.

INDEX

| | | | | | | | |

| | Page |

| PART I - FINANCIAL INFORMATION | |

| Item 1. | Financial Statements (unaudited) | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II - OTHER INFORMATION | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| |

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements (unaudited)

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

| | | September 30,

2021 | | December 31,

2020 | | June 30,

2022 | | December 31,

2021 |

| ASSETS | ASSETS | | | | ASSETS | | | |

| Loans held-for-investment | Loans held-for-investment | $ | 3,659,691 | | | $ | 3,914,469 | | Loans held-for-investment | $ | 3,877,294 | | | $ | 3,782,205 | |

| Allowance for credit losses | Allowance for credit losses | (45,480) | | | (66,666) | | Allowance for credit losses | (47,280) | | | (40,897) | |

| Loans held-for-investment, net | Loans held-for-investment, net | 3,614,211 | | | 3,847,803 | | Loans held-for-investment, net | 3,830,014 | | | 3,741,308 | |

| | Cash and cash equivalents | Cash and cash equivalents | 154,916 | | | 261,419 | | Cash and cash equivalents | 150,192 | | | 191,931 | |

| Restricted cash | Restricted cash | 20,602 | | | 67,774 | | Restricted cash | 69,492 | | | 12,362 | |

| Accrued interest receivable | Accrued interest receivable | 9,898 | | | 12,388 | | Accrued interest receivable | 11,455 | | | 10,716 | |

| | Other assets | Other assets | 99,563 | | | 30,264 | | Other assets | 35,893 | | | 32,201 | |

Total Assets (1) | Total Assets (1) | $ | 3,899,190 | | | $ | 4,219,648 | | Total Assets (1) | $ | 4,097,046 | | | $ | 3,988,518 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

| Liabilities | Liabilities | | Liabilities | |

| Repurchase facilities | Repurchase facilities | $ | 916,758 | | | $ | 1,708,875 | | Repurchase facilities | $ | 1,271,659 | | | $ | 677,285 | |

| Securitized debt obligations | Securitized debt obligations | 1,356,429 | | | 927,128 | | Securitized debt obligations | 1,425,556 | | | 1,677,619 | |

| Asset-specific financings | Asset-specific financings | 44,752 | | | 123,091 | | Asset-specific financings | 43,622 | | | 43,622 | |

| Term financing facility | Term financing facility | 127,867 | | | — | | Term financing facility | — | | | 127,145 | |

| Convertible senior notes | Convertible senior notes | 272,512 | | | 271,250 | | Convertible senior notes | 273,822 | | | 272,942 | |

| | Senior secured term loan facilities | Senior secured term loan facilities | 208,785 | | | 206,448 | | Senior secured term loan facilities | — | | | 139,880 | |

| | Dividends payable | Dividends payable | 13,713 | | | 25,049 | | Dividends payable | 17,008 | | | 14,406 | |

| | Other liabilities | Other liabilities | 25,140 | | | 22,961 | | Other liabilities | 20,545 | | | 21,436 | |

Total Liabilities (1) | Total Liabilities (1) | 2,965,956 | | | 3,284,802 | | Total Liabilities (1) | 3,052,212 | | | 2,974,335 | |

| Commitments and Contingencies (see Note 10) | Commitments and Contingencies (see Note 10) | 0 | | 0 | Commitments and Contingencies (see Note 10) | 0 | | 0 |

| 10% cumulative redeemable preferred stock, par value $0.01 per share; 50,000,000 shares authorized and 1,000 shares issued and outstanding ($1,000,000 liquidation preference) | 1,000 | | | 1,000 | | |

| 10.00% cumulative redeemable preferred stock, par value $0.01 per share; 50,000,000 shares authorized, and 1,000 shares issued and outstanding ($1,000,000 liquidation preference) | | 10.00% cumulative redeemable preferred stock, par value $0.01 per share; 50,000,000 shares authorized, and 1,000 shares issued and outstanding ($1,000,000 liquidation preference) | 1,000 | | | 1,000 | |

| Stockholders’ Equity | Stockholders’ Equity | | Stockholders’ Equity | |

| Common stock, par value $0.01 per share; 450,000,000 shares authorized and 53,789,465 and 55,205,082 shares issued and outstanding, respectively | 538 | | | 552 | | |

| 7.00% Series A cumulative redeemable preferred stock, par value $0.01 per share; 8,280,000 shares authorized, and 8,229,500 and 4,596,500 shares issued and outstanding, respectively; liquidation preference $25.00 per share | | 7.00% Series A cumulative redeemable preferred stock, par value $0.01 per share; 8,280,000 shares authorized, and 8,229,500 and 4,596,500 shares issued and outstanding, respectively; liquidation preference $25.00 per share | 82 | | | 46 | |

| Common stock, par value $0.01 per share; 450,000,000 shares authorized, and 52,350,989 and 53,789,465 shares issued and outstanding, respectively | | Common stock, par value $0.01 per share; 450,000,000 shares authorized, and 52,350,989 and 53,789,465 shares issued and outstanding, respectively | 524 | | | 538 | |

| Additional paid-in capital | Additional paid-in capital | 1,037,395 | | | 1,058,298 | | Additional paid-in capital | 1,199,367 | | | 1,125,241 | |

| Cumulative earnings | Cumulative earnings | 164,055 | | | 103,165 | | Cumulative earnings | 162,423 | | | 171,518 | |

| Cumulative distributions to stockholders | Cumulative distributions to stockholders | (269,879) | | | (228,169) | | Cumulative distributions to stockholders | (318,687) | | | (284,285) | |

| Total Granite Point Mortgage Trust, Inc. Stockholders’ Equity | 932,109 | | | 933,846 | | |

| Total Granite Point Mortgage Trust Inc. Stockholders’ Equity | | Total Granite Point Mortgage Trust Inc. Stockholders’ Equity | 1,043,709 | | | 1,013,058 | |

| Non-controlling interests | Non-controlling interests | 125 | | | — | | Non-controlling interests | 125 | | | 125 | |

| Total Equity | Total Equity | $ | 932,234 | | | $ | 933,846 | | Total Equity | $ | 1,043,834 | | | $ | 1,013,183 | |

| Total Liabilities and Stockholders’ Equity | Total Liabilities and Stockholders’ Equity | $ | 3,899,190 | | | $ | 4,219,648 | | Total Liabilities and Stockholders’ Equity | $ | 4,097,046 | | | $ | 3,988,518 | |

____________________

(1)The condensed consolidated balance sheets include assets of consolidated variable interest entities, or VIEs, that can only be used to settle obligations of these VIEs, and liabilities of the consolidated VIEs for which creditors do not have recourse to Granite Point Mortgage Trust Inc. At SeptemberJune 30, 20212022, and December 31, 2020,2021, assets of the VIEs totaled $1,824,173$1,851,063 and $1,255,932,$2,266,044, respectively, and liabilities of the VIEs totaled $1,357,675$1,426,954 and $928,220,$1,679,435, respectively. See Note 4 - Variable Interest Entities and Securitized Debt Obligations for additional information.

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME (LOSS)

(in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2021 | | 2020 | | 2021 | | 2020 | | |

| Interest income: | | | | |

| Loans held-for-investment | | $ | 48,312 | | | $ | 56,783 | | | $ | 151,701 | | | $ | 180,341 | | | |

| Loans held-for-sale | | — | | | 774 | | | — | | | 895 | | | |

| Available-for-sale securities | | — | | | 119 | | | — | | | 646 | | | |

| Held-to-maturity securities | | — | | | 113 | | | — | | | 659 | | | |

| Cash and cash equivalents | | 95 | | | 57 | | | 298 | | | 424 | | | |

| Total interest income | | 48,407 | | | 57,846 | | | 151,999 | | | 182,965 | | | |

| Interest expense: | | | | | | | | | | |

| Repurchase facilities | | 5,451 | | | 12,791 | | | 20,449 | | | 46,742 | | | |

| Securitized debt obligations | | 8,777 | | | 5,431 | | | 20,523 | | | 21,367 | | | |

| Convertible senior notes | | 4,556 | | | 4,529 | | | 13,618 | | | 13,570 | | | |

| Term financing facility | | 1,453 | | | — | | | 6,208 | | | — | | | |

| Asset-specific financings | | 414 | | | 901 | | | 1,959 | | | 2,962 | | | |

| Revolving credit facilities | | — | | | 217 | | | — | | | 779 | | | |

| Senior secured term loan facilities | | 5,654 | | | 145 | | | 16,587 | | | 145 | | | |

| Total interest expense | | 26,305 | | | 24,014 | | | 79,344 | | | 85,565 | | | |

| Net interest income | | 22,102 | | | 33,832 | | | 72,655 | | | 97,400 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Other income (loss): | | | | | | | | | | |

| Benefit from (provision for) credit losses | | 5,760 | | | 5,300 | | | 15,072 | | | (62,241) | | | |

| | | | | | | | | | |

| Realized losses on sales of loans held-for-sale | | — | | | (10,019) | | | — | | | (16,913) | | | |

| Fee income | | — | | | 595 | | | — | | | 1,117 | | | |

| | | | | | | | | | |

| Total other income (loss) | | 5,760 | | | (4,124) | | | 15,072 | | | (78,037) | | | |

| Expenses: | | | | | | | | | | |

| Base management fees | | — | | | 3,974 | | | — | | | 11,840 | | | |

| Compensation and benefits | | 5,634 | | | — | | | 16,111 | | | — | | | |

| Servicing expenses | | 1,323 | | | 914 | | | 3,763 | | | 3,025 | | | |

| Other operating expenses | | 2,276 | | | 5,808 | | | 6,967 | | | 24,421 | | | |

| Restructuring charges | | — | | | 43,682 | | | — | | | 43,682 | | | |

| Total expenses | | 9,233 | | | 54,378 | | | 26,841 | | | 82,968 | | | |

| Income (loss) before income taxes | | 18,629 | | | (24,670) | | | 60,886 | | | (63,605) | | | |

| Benefit from income taxes | | (1) | | | (4) | | | (4) | | | (15) | | | |

| Net income (loss) | | 18,630 | | | (24,666) | | | 60,890 | | | (63,590) | | | |

| Dividends on preferred stock | | 25 | | | 25 | | | 75 | | | 75 | | | |

| Net income (loss) attributable to common stockholders | | $ | 18,605 | | | $ | (24,691) | | | $ | 60,815 | | | $ | (63,665) | | | |

| Basic earnings (loss) per weighted average common share | | $ | 0.34 | | | $ | (0.45) | | | $ | 1.11 | | | $ | (1.15) | | | |

| Diluted earnings (loss) per weighted average common share | | $ | 0.33 | | | $ | (0.45) | | | $ | 1.05 | | | $ | (1.15) | | | |

| Dividends declared per common share | | $ | 0.25 | | | $ | 0.20 | | | $ | 0.75 | | | $ | 0.20 | | | |

| Weighted average number of shares of common stock outstanding: | | | | | | | | | | |

| Basic | | 54,453,546 | | | 55,205,082 | | | 54,864,456 | | | 55,140,163 | | | |

| Diluted | | 56,735,278 | | | 55,205,082 | | | 70,902,745 | | | 55,140,163 | | | |

| Comprehensive income (loss): | | | | | | | | | | |

| Net income (loss) attributable to common stockholders | | $ | 18,605 | | | $ | (24,691) | | | $ | 60,815 | | | $ | (63,665) | | | |

| Other comprehensive income (loss), net of tax: | | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Comprehensive income (loss) | | $ | 18,605 | | | $ | (24,691) | | | $ | 60,815 | | | $ | (63,665) | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Six Months Ended |

| | June 30, | | June 30, |

| | 2022 | | 2021 | | 2022 | | 2021 | | |

| Interest income: | | | |

| Loans held-for-investment | $ | 49,056 | | | $ | 49,350 | | | $ | 96,354 | | | $ | 103,389 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Cash and cash equivalents | 223 | | | 103 | | | 246 | | | 203 | | | |

| Total interest income | 49,279 | | | 49,453 | | | 96,600 | | | 103,592 | | | |

| Interest expense: | | | | | | | | | |

| Repurchase facilities | 10,380 | | | 6,047 | | | 15,388 | | | 14,998 | | | |

| Securitized debt obligations | 10,844 | | | 7,129 | | | 20,576 | | | 11,746 | | | |

| Convertible senior notes | 4,572 | | | 4,544 | | | 9,118 | | | 9,062 | | | |

| Term financing facility | 340 | | | 2,633 | | | 1,713 | | | 4,755 | | | |

| Asset-specific financings | 322 | | | 668 | | | 604 | | | 1,545 | | | |

| | | | | | | | | | |

| Senior secured term loan facilities | 886 | | | 5,653 | | | 3,754 | | | 10,933 | | | |

| Total interest expense | 27,344 | | | 26,674 | | | 51,153 | | | 53,039 | | | |

| Net interest income | 21,935 | | | 22,779 | | | 45,447 | | | 50,553 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Other (loss) income: | | | | | | | | | |

| (Provision for) benefit from credit losses | (13,627) | | | 193 | | | (17,315) | | | 9,312 | | | |

| Loss on extinguishment of debt | (13,032) | | | — | | | (18,823) | | | — | | | |

| | | | | | | | | | |

| Fee income | 461 | | | — | | | 954 | | | — | | | |

| | | | | | | | | | |

| Total other (loss) income | (26,198) | | | 193 | | | (35,184) | | | 9,312 | | | |

| Expenses: | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Compensation and benefits | 5,770 | | | 5,017 | | | 11,586 | | | 10,477 | | | |

| Servicing expenses | 1,500 | | | 1,124 | | | 2,961 | | | 2,440 | | | |

| Other operating expenses | 2,185 | | | 2,564 | | | 4,799 | | | 4,691 | | | |

| | | | | | | | | | |

| Total expenses | 9,455 | | | 8,705 | | | 19,346 | | | 17,608 | | | |

| (Loss) income before income taxes | (13,718) | | | 14,267 | | | (9,083) | | | 42,257 | | | |

| Provision for (benefit from) income taxes | 13 | | | (2) | | | 12 | | | (3) | | | |

| Net (loss) income | (13,731) | | | 14,269 | | | (9,095) | | | 42,260 | | | |

| Dividends on preferred stock | 3,625 | | | 25 | | | 7,250 | | | 50 | | | |

| Net (loss) income attributable to common stockholders | $ | (17,356) | | | $ | 14,244 | | | $ | (16,345) | | | $ | 42,210 | | | |

| Basic (loss) earnings per weighted average common share | $ | (0.32) | | | $ | 0.26 | | | $ | (0.30) | | | $ | 0.77 | | | |

| Diluted (loss) earnings per weighted average common share | $ | (0.32) | | | $ | 0.24 | | | $ | (0.30) | | | $ | 0.71 | | | |

| | | | | | | | | | |

| Weighted average number of shares of common stock outstanding: | | | | | | | | | |

| Basic | 53,512,005 | | | 55,009,732 | | | 53,683,575 | | | 55,073,317 | | | |

| Diluted | 53,512,005 | | | 58,526,985 | | | 53,683,575 | | | 72,564,914 | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Comprehensive (loss) income | $ | (17,356) | | | $ | 14,244 | | | $ | (16,345) | | | $ | 42,210 | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | | | | | | | | | | | | | |

| Shares | | Amount | | Additional Paid-in Capital | | Accumulated Other Comprehensive Income (Loss) | | Cumulative Earnings | | Cumulative Distributions to Stockholders | | Total Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Balance, December 31, 2019 | 54,853,205 | | | 549 | | | 1,048,484 | | | 32 | | | 162,076 | | | (192,005) | | | 1,019,136 | | | — | | | 1,019,136 | |

| Cumulative effect of adoption of new accounting principle | — | | | — | | | — | | | — | | | (18,472) | | | — | | | (18,472) | | | — | | | (18,472) | |

| Adjusted balance, January 1, 2020 | 54,853,205 | | | 549 | | | 1,048,484 | | | 32 | | | 143,604 | | | (192,005) | | | 1,000,664 | | | — | | | 1,000,664 | |

| Net loss | — | | | — | | | — | | | — | | | (37,191) | | | — | | | (37,191) | | | — | | | (37,191) | |

| Other comprehensive loss before reclassifications | — | | | — | | | — | | | (4,511) | | | — | | | — | | | (4,511) | | | — | | | (4,511) | |

| Amounts reclassified from accumulated other comprehensive income | — | | | — | | | — | | | 767 | | | — | | | — | | | 767 | | | — | | | 767 | |

| Net other comprehensive loss | — | | | — | | | — | | | (3,744) | | | — | | | — | | | (3,744) | | | — | | | (3,744) | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| | | | | | | | | | | | | | | | | |

| Non-cash equity award compensation | 283,680 | | | 3 | | | 1,352 | | | — | | | — | | | — | | | 1,355 | | | — | | | 1,355 | |

| Balance, March 31, 2020 | 55,136,885 | | | 552 | | | 1,049,836 | | | (3,712) | | | 106,413 | | | (192,030) | | | 961,059 | | | — | | | 961,059 | |

| Net loss | — | | | — | | | — | | | — | | | (1,733) | | | — | | | (1,733) | | | — | | | (1,733) | |

| Other comprehensive income before reclassifications | — | | | — | | | — | | | 4,223 | | | — | | | — | | | 4,223 | | | — | | | 4,223 | |

| Amounts reclassified from accumulated other comprehensive income | — | | | — | | | — | | | (511) | | | — | | | — | | | (511) | | | — | | | (511) | |

| Net other comprehensive income | — | | | — | | | — | | | 3,712 | | | — | | | — | | | 3,712 | | | — | | | 3,712 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| | | | | | | | | | | | | | | | | |

| Non-cash equity award compensation | 68,197 | | | — | | | 1,323 | | | — | | | — | | | — | | | 1,323 | | | — | | | 1,323 | |

| Balance, June 30, 2020 | 55,205,082 | | | 552 | | | 1,051,159 | | | — | | | 104,680 | | | (192,055) | | | 964,336 | | | — | | | 964,336 | |

| Net loss | — | | | — | | | — | | | — | | | (24,666) | | | — | | | (24,666) | | | — | | | (24,666) | |

| Issuance of warrants to purchase common stock | — | | | — | | | 4,541 | | | — | | | — | | | — | | | 4,541 | | | — | | | 4,541 | |

| Common dividends declared, $0.20 per share | — | | | $ | — | | | — | | | — | | | — | | | (11,040) | | | (11,040) | | | — | | | (11,040) | |

| Preferred dividends declared, $25.00 per share | — | | | $ | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| Non-cash equity award compensation | — | | | $ | — | | | 1,316 | | | — | | | — | | | — | | | 1,316 | | | — | | | 1,316 | |

| Balance, September 30, 2020 | 55,205,082 | | | $ | 552 | | | $ | 1,057,016 | | | $ | — | | | $ | 80,014 | | | $ | (203,120) | | | $ | 934,462 | | | — | | | $ | 934,462 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Preferred Stock | | | | | | | | | | | | | | |

| Shares | | Amount | | Shares | | Amount | | Additional Paid-in Capital | | | | Cumulative Earnings | | Cumulative Distributions to Stockholders | | Total Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2020 | 55,205,082 | | | 552 | | | — | | | — | | | 1,058,298 | | | | | 103,165 | | | (228,169) | | | 933,846 | | | — | | | 933,846 | |

| Net income | — | | | — | | | — | | | — | | | — | | | | | 27,991 | | | — | | | 27,991 | | | — | | | 27,991 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Restricted stock forfeiture | (97,425) | | | (1) | | | — | | | — | | | (918) | | | | | — | | | — | | | (919) | | | — | | | (919) | |

| | | | | | | | | | | | | | | | | | | | | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| | | | | | | | | | | | | | | | | | | | | |

| Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | | | — | | | (14,008) | | | (14,008) | | | — | | | (14,008) | |

| | | | | | | | | | | | | | | | | | | | | |

| Contributions from non-controlling interests | — | | | — | | | — | | | — | | | — | | | | | — | | | — | | | — | | | 125 | | | 125 | |

| Non-cash equity award compensation | — | | | — | | | — | | | — | | | 1,887 | | | | | — | | | — | | | 1,887 | | | — | | | 1,887 | |

| Balance, March 31, 2021 | 55,107,657 | | | 551 | | | — | | | — | | | 1,059,267 | | | | | 131,156 | | | (242,202) | | | 948,772 | | | 125 | | | 948,897 | |

| Net income | — | | | — | | | — | | | — | | | — | | | | | 14,269 | | | — | | | 14,269 | | | — | | | 14,269 | |

| Restricted stock forfeiture | (17,628) | | | — | | | — | | | — | | | (275) | | | | | — | | | — | | | (275) | | | — | | | (275) | |

| Repurchase of common stock | (300,891) | | | (3) | | | — | | | — | | | (4,267) | | | | | — | | | — | | | (4,270) | | | — | | | (4,270) | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | | | — | | | (13,939) | | | (13,939) | | | — | | | (13,939) | |

| | | | | | | | | | | | | | | | | | | | | |

| Non-cash equity award compensation | 1,048 | | | — | | | — | | | — | | | 1,639 | | | | | — | | | — | | | 1,639 | | | — | | | 1,639 | |

| Balance, June 30, 2021 | 54,790,186 | | | 548 | | | — | | | — | | | 1,056,364 | | | | | 145,425 | | | (256,166) | | | 946,171 | | | 125 | | | 946,296 | |

| | | | | | | | | | | | | | | | | | | | | |

GRANITE POINT MORTGAGE TRUST INC

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(in thousands, except share data) (Continued)

| | Common Stock | | | |

| Shares | | Amount | | Additional Paid-in Capital | | Accumulated Other Comprehensive Income (Loss) | | Cumulative Earnings | | Cumulative Distributions to Stockholders | | Total Stockholders’ Equity | | Non-controlling Interests | | Total Equity | |

| Balance, December 31, 2020 | 55,205,082 | | | 552 | | | 1,058,298 | | | — | | | 103,165 | | | (228,169) | | | 933,846 | | | — | | | 933,846 | | |

| | Net income | — | | | — | | | — | | | — | | | 27,991 | | | — | | | 27,991 | | | — | | | |

| | Restricted stock forfeiture | (97,425) | | | (1) | | | (918) | | | — | | | — | | | — | | | (919) | | | — | | | (919) | | |

| Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | (14,008) | | | (14,008) | | | — | | | (14,008) | | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | | |

| Non-cash equity award compensation | — | | | — | | | 1,887 | | | — | | | — | | | — | | | 1,887 | | | — | | | 1,887 | | |

| Contributions from non-controlling interests | — | | | — | | | — | | | — | | | — | | | — | | | — | | | 125 | | | 125 | | |

| Balance, March 31, 2021 | 55,107,657 | | | 551 | | | 1,059,267 | | | — | | | 131,156 | | | (242,202) | | | 948,772 | | | 125 | | | 948,897 | | |

| Net income | — | | | — | | | — | | | — | | | 14,269 | | | — | | | 14,269 | | | — | | | 14,269 | | |

| | | | Common Stock | | Preferred Stock | | | |

| | | Shares | | Amount | | Shares | | Amount | | Additional Paid-in Capital | | | Cumulative Earnings | | Cumulative Distributions to Stockholders | | Total Stockholders’ Equity | | Non-controlling Interests | | Total Equity |

| | Balance, December 31, 2021 | | Balance, December 31, 2021 | 53,789,465 | | | 538 | | | 4,596,500 | | | 46 | | | 1,125,241 | | | | 171,518 | | | (284,285) | | | 1,013,058 | | | 125 | | | 1,013,183 | |

| Net income | | Net income | — | | | — | | | — | | | — | | | — | | | | 4,636 | | | — | | | 4,636 | | | — | | | 4,636 | |

| | Issuance of preferred stock, net of offering costs | | Issuance of preferred stock, net of offering costs | — | | | 3,633,000 | | | 36 | | | 87,485 | | | | — | | | — | | | 87,521 | | | — | | | 87,521 | |

| Restricted stock forfeiture | Restricted stock forfeiture | (17,628) | | | (275) | | | — | | | — | | | — | | | (275) | | | — | | | (275) | | Restricted stock forfeiture | (69,039) | | | — | | | — | | | — | | | (824) | | | | — | | | — | | | (824) | | | — | | | (824) | |

| Repurchase of common stock | (300,891) | | | (3) | | | (4,267) | | | — | | | — | | | — | | | (4,270) | | | — | | | (4,270) | | |

| Restricted Stock Unit (RSU) forfeiture | | Restricted Stock Unit (RSU) forfeiture | — | | | — | | | — | | | — | | | (798) | | | | — | | | — | | | (798) | | | — | | | (798) | |

| Preferred dividends declared, $25.00 per share | | Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| Preferred dividends declared, $0.4375 per share | | Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

| Common dividends declared, $0.25 per share | Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | (13,939) | | | (13,939) | | | — | | | (13,939) | | Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (13,770) | | | (13,770) | | | — | | | (13,770) | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | | |

| | | Non-cash equity award compensation | Non-cash equity award compensation | 1,048 | | | — | | | 1,639 | | | — | | | — | | | — | | | 1,639 | | | — | | | 1,639 | | Non-cash equity award compensation | 135,151 | | | 1 | | | — | | | — | | | 2,170 | | | | — | | | — | | | 2,171 | | | — | | | 2,171 | |

| Balance, June 30, 2021 | 54,790,186 | | | 548 | | | 1,056,364 | | | — | | | 145,425 | | | (256,166) | | | 946,171 | | | 125 | | | 946,296 | | |

| Net income | — | | | — | | | — | | | — | | | 18,630 | | | — | | | 18,630 | | | — | | | 18,630 | | |

| Settlement of warrants to purchase common stock | — | | | — | | | (7,478) | | | — | | | — | | | — | | | (7,478) | | | — | | | (7,478) | | |

| Balance, March 31, 2022 | | Balance, March 31, 2022 | 53,855,577 | | | 539 | | | 8,229,500 | | | 82 | | | 1,213,274 | | | | 176,154 | | | (301,680) | | | 1,088,369 | | | 125 | | | 1,088,494 | |

| Net (loss) income | | Net (loss) income | — | | | — | | | — | | | — | | | — | | | | (13,731) | | | — | | | (13,731) | | | — | | | (13,731) | |

| | Repurchase of common stock | Repurchase of common stock | (1,000,721) | | | (10) | | | (13,523) | | | — | | | — | | | — | | | (13,533) | | | — | | | (13,533) | | Repurchase of common stock | (1,539,134) | | | (15) | | | — | | | — | | | (15,699) | | | | — | | | — | | | (15,714) | | | — | | | (15,714) | |

| Restricted Stock Unit (RSU) forfeiture | | Restricted Stock Unit (RSU) forfeiture | — | | | — | | | — | | | — | | | (114) | | | | — | | | — | | | (114) | | | — | | | (114) | |

| Preferred dividends declared, $25.00 per share | | Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (25) | | | (25) | | | — | | | (25) | |

| Preferred dividends declared, $0.4375 per share | | Preferred dividends declared, $0.4375 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (3,600) | | | (3,600) | | | — | | | (3,600) | |

| Common dividends declared, $0.25 per share | Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | (13,688) | | | (13,688) | | | — | | | (13,688) | | Common dividends declared, $0.25 per share | — | | | — | | | — | | | — | | | — | | | | — | | | (13,382) | | | (13,382) | | | — | | | (13,382) | |

| Preferred dividends declared, $25.00 per share | — | | | — | | | — | | | — | | | — | | | (25) | | | (25) | | | — | | | (25) | | |

| Non-cash equity award compensation | Non-cash equity award compensation | — | | | — | | | 2,032 | | | — | | | — | | | — | | | 2,032 | | | — | | | 2,032 | | Non-cash equity award compensation | 34,546 | | | — | | | — | | | — | | | 1,906 | | | | — | | | — | | | 1,906 | | | — | | | 1,906 | |

| Balance, September 30, 2021 | 53,789,465 | | | $ | 538 | | | $ | 1,037,395 | | | $ | — | | | $ | 164,055 | | | $ | (269,879) | | | $ | 932,109 | | | $ | 125 | | | $ | 932,234 | | |

| Balance, June 30, 2022 | | Balance, June 30, 2022 | 52,350,989 | | | 524 | | | 8,229,500 | | | 82 | | | 1,199,367 | | | | 162,423 | | | (318,687) | | | 1,043,709 | | | 125 | | | 1,043,834 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (in thousands) | | | | | | | | | | | | | | |

| | Nine Months Ended |

| | September 30, |

| | 2021 | | 2020 | | |

| Cash Flows From Operating Activities: | | | | |

| Net income (loss) | | $ | 60,890 | | | $ | (63,590) | | | |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | | | | |

| Accretion of discounts and net deferred fees on loans held-for-investment and deferred interest capitalized to loans held-for-investment | | (20,310) | | | (12,557) | | | |

| Amortization of deferred debt issuance costs on repurchase facilities, asset-specific financings, convertible senior notes, securitized debt obligations, senior secured term loan facilities and term financing facilities | | 9,692 | | | 4,646 | | | |

| (Benefit from) provision for credit losses | | (15,072) | | | 62,241 | | | |

| | | | | | |

| | | | | | |

| Realized losses on sales of loans held-for-sale | | — | | | 16,913 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Amortization of equity-based compensation | | 5,558 | | | 3,994 | | | |

| Depreciation of fixed assets | | — | | | — | | | |

| Net change in assets and liabilities: | | | | | | |

| Decrease (increase) in accrued interest receivable | | 2,490 | | | (610) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase in other assets | | (4,069) | | | (19,899) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase in other liabilities | | 5,846 | | | 44,911 | | | |

| | | | | | |

| Net cash provided by operating activities | | 45,025 | | | 36,049 | | | |

| Cash Flows From Investing Activities: | | | | | | |

| Originations, acquisitions and additional fundings of loans held-for-investment, net of deferred fees | | (549,705) | | | (314,722) | | | |

| | | | | | |

| Proceeds from repayment of loans held-for-investment | | 815,054 | | | 290,838 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase in other assets, due from servicer/trustee on repayments of loans held-for-investment | | (66,944) | | | — | | | |

| Principal payments on available-for-sale securities | | — | | | 12,798 | | | |

| | | | | | |

| | | | | | |

| Principal payments on held-to-maturity securities | | — | | | 18,076 | | | |

| | | | | | |

| Proceeds from sales of loans held-for-sale | | — | | | 193,538 | | | |

| | | | | | |

| | | | | | |

| Net cash provided by investing activities | | 198,405 | | | 200,528 | | | |

| | | | | | |

| Cash Flows From Financing Activities: | | | | | | |

| Proceeds from repurchase facilities | | 347,261 | | | 397,004 | | | |

| Principal payments on repurchase facilities | | (1,139,378) | | | (470,180) | | | |

| Proceeds from issuance of securitized debt obligations | | 685,766 | | | — | | | |

| Principal payments on securitized debt obligations | | (254,647) | | | (115,853) | | | |

| Proceeds from senior secured term loan facilities | | — | | | 205,647 | | | |

| Proceeds from asset-specific financings | | 2,785 | | | 6,626 | | | |

| Repayment of asset-specific financings | | (81,123) | | | — | | | |

| Proceeds from revolving credit facilities | | — | | | 38,361 | | | |

| Repayment of revolving credit facilities | | — | | | (80,369) | | | |

| Proceeds from term financing facility | | 349,291 | | | — | | | |

| Repayment of term financing facility | | (219,311) | | | — | | | |

| Payment of debt issuance costs | | (8,353) | | | — | | | |

| Proceeds from issuance of warrants to purchase common stock | | — | | | 4,541 | | | |

| Settlement of warrants to purchase common stock | | (7,478) | | | 0 | | |

| Contributions from non-controlling interests | | 125 | | | — | | | |

| Tax withholding on restricted stock | | (1,194) | | | — | | | |

| Repurchase of common stock | | (17,804) | | | — | | | |

| Dividends paid on preferred stock | | (75) | | | (75) | | | |

| Dividends paid on common stock | | (52,970) | | | (23,038) | | | |

| Net cash used in financing activities | | (397,105) | | | (37,336) | | | |

| Net (decrease) increase in cash, cash equivalents and restricted cash | | (153,675) | | | 199,241 | | | |

| Cash, cash equivalents and restricted cash at beginning of period | | 329,193 | | | 159,764 | | | |

| Cash, cash equivalents and restricted cash at end of period | | $ | 175,518 | | | $ | 359,005 | | | |

| Supplemental Disclosure of Cash Flow Information: | | | | | | |

| Cash paid for interest | | $ | 75,818 | | | $ | 83,366 | | | |

| Cash paid for taxes | | $ | 607 | | | $ | — | | | |

| Noncash Activities: | | | | | | |

| | | | | | |

| Transfers of loans held-for-investment to loans held-for-sale | | $ | — | | | $ | 210,452 | | | |

| Dividends declared but not paid at end of period | | $ | 13,713 | | | $ | 11,065 | | | |

| | | | | | | | | | | | | | |

| | Six Months Ended |

| | June 30, |

| | 2022 | | 2021 | | |

| Cash Flows From Operating Activities: | | | |

| Net (loss) income | $ | (9,095) | | | $ | 42,260 | | | |

| Adjustments to reconcile net (loss) income to net cash provided by operating activities: | | | | | |

| Accretion of discounts and net deferred fees on loans held-for-investment and deferred interest capitalized to loans held-for-investment | (7,907) | | | (16,652) | | | |

| Amortization of deferred debt issuance costs | 7,520 | | | 5,636 | | | |

| Provision for (benefit from) credit losses | 17,315 | | | (9,312) | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Loss on extinguishment of debt | 11,307 | | | — | | | |

| Amortization of equity-based compensation | 4,077 | | | 3,526 | | | |

| Proceeds received from deferred interest capitalized to loans held-for-investment | 2,407 | | | — | | | |

| Net change in assets and liabilities: | | | | | |

| (Increase) decrease in accrued interest receivable | (739) | | | 2,239 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Decrease in other assets | 121 | | | 1,355 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase (decrease) in other liabilities | (2,226) | | | 1,670 | | | |

| | | | | | |

| Net cash provided by operating activities | 22,780 | | | 30,722 | | | |

| Cash Flows From Investing Activities: | | | | | |

| Originations, acquisitions and additional fundings of loans held-for-investment, net of deferred fees | (379,493) | | | (228,750) | | | |

| Proceeds from loan sales | 43,714 | | | — | | | |

| Proceeds from repayment of loans held-for-investment | 236,594 | | | 524,557 | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Increase in other assets, due from servicer on repayments of loans held-for-investment | (689) | | | — | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Net cash (used in) provided by investing activities | (99,874) | | | 295,807 | | | |

| | | | | | |

| Cash Flows From Financing Activities: | | | | | |

| Proceeds from repurchase facilities | 677,175 | | | 82,931 | | | |

| Principal payments on repurchase facilities | (82,801) | | | (1,074,611) | | | |

| Proceeds from issuance of securitized debt obligations | — | | | 685,766 | | | |

| Principal payments on securitized debt obligations | (255,117) | | | (162,366) | | | |

| | | | | | |

| Repayment of senior secured term loan facilities | (150,000) | | | — | | | |

| | | | | | |

| Repayment of asset-specific financings | — | | | (40,323) | | | |

| | | | | | |

| | | | | | |

| Proceeds from term financing facility | — | | | 349,291 | | | |

| Repayment of term financing facility | (129,099) | | | (204,606) | | | |

| | | | | | |

| | | | | | |

| Payment of debt issuance costs | (5,943) | | | (8,353) | | | |

| | | | | | |

| Contributions from non-controlling interests | — | | | 125 | | | |

| | | | | | |

| Proceeds from issuance of preferred stock, net of offering costs | 87,521 | | | — | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Tax withholding on restricted stock and RSUs | (1,736) | | | (1,194) | | | |

| Repurchase of common stock | (15,714) | | | (4,270) | | | |

| Dividends paid on preferred stock | (4,343) | | | (50) | | | |

| Dividends paid on common stock | (27,458) | | | (39,032) | | | |

| Net cash provided by (used in) financing activities | 92,485 | | | (416,692) | | | |

| Net increase (decrease) in cash, cash equivalents and restricted cash | 15,391 | | | (90,163) | | | |

| Cash, cash equivalents, and restricted cash at beginning of period | 204,293 | | | 329,193 | | | |

| Cash, cash equivalents, and restricted cash at end of period | $ | 219,684 | | | $ | 239,030 | | | |

| Supplemental Disclosure of Cash Flow Information: | | | | | |

| Cash paid for interest | $ | 49,938 | | | $ | 53,505 | | | |

| Cash paid for taxes | $ | 420 | | | $ | 611 | | | |

| Noncash Activities: | | | | | |

| | | | | | |

| Dividends declared but not paid at end of period | $ | 17,007 | | | $ | 13,964 | | | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements (unaudited)

Note 1. Organization and Operations

Granite Point Mortgage Trust Inc., or the Company, is an internally managed real estate finance company that focuses primarily on directly originating, investing in and managing senior floating-rate commercial mortgage loans and other debt and debt-like commercial real estate investments. These investments are capitalized by accessing a variety of funding options,sources, including borrowing under ourthe Company’s bank credit facilities or other asset-specific financings, issuing commercial real estate collateralized loan obligations, or CRE CLOs, entering into term financing agreements, and issuing other forms of secured and unsecured debt and equity securities, depending on market conditions and ourthe Company’s view of the most appropriate funding option available for ourthe Company’s investments. OurThe Company is not in the business of buying or trading securities, and the only securities it owns are the retained interests from its CRE CLOs. The Company’s investment objective is to preserve ourthe Company’s stockholders’ capital while generating attractive risk-adjusted returns over the long term, primarily through dividends derived from current income produced by ourthe Company’s investment portfolio. OurThe Company’s common stock is listed on the New York Stock Exchange, or NYSE, under the symbol “GPMT”. The Company operates its business in a manner that is intended to permit it to maintain its exclusion from registration under the Investment Company Act of 1940, as amended, or the Investment Company Act. The Company operates its business as 1 segment. The Company was incorporated in Maryland on April 7, 2017, and commenced operations as a publicly traded company on June 28, 2017.

The Company has elected to be treated as a real estate investment trust, or REIT, as defined under the Internal Revenue Code of 1986, as amended, or the Code, for U.S. federal income tax purposes. As long as the Company continues to comply with a number of requirements under federal tax law and maintains its qualification as a REIT, the Company generally will not be subject to U.S. federal income taxes to the extent that the Company distributes its taxable income to its stockholders on an annual basis and does not engage in prohibited transactions. However, certain activities that the Company may perform may cause it to earn income which will not be qualifying income for REIT purposes. The Company has designated one of its subsidiaries as a taxable REIT subsidiary, or TRS, as defined in the Code, to engage in such activities.

The Company was externally managed by Pine River Capital Management L.P., or the Former Manager, through December 31, 2020, at which time the Company internalized its management function, or the Internalization.

Note 2. Basis of Presentation and Significant Accounting Policies

Consolidation and Basis of Presentation

The interim unaudited condensed consolidated financial statements of the Company have been prepared in accordance with the rules and regulations of the Securities and Exchange Commission, or the SEC. Certain information and note disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles, or GAAP, have been condensed or omitted according to such SEC rules and regulations. However, management believes that the disclosures included in these interim condensed consolidated financial statements are adequate to make the information presented not misleading. The accompanying unaudited condensed consolidated financial statements should be read in conjunction with the financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2020.2021. In the opinion of management, all normal and recurring adjustments necessary to present fairly the financial condition of the Company at SeptemberJune 30, 20212022, and results of operations for all periods presented, have been made. The results of operations for the three and ninesix months ended SeptemberJune 30, 20212022, should not be construed as indicative of the results to be expected for future periods or the full year.

The unaudited condensed consolidated financial statements of the Company include the accounts of all subsidiaries; inter-company accounts and transactions have been eliminated. Certain prior period amounts have been reclassified to conform to the current period presentation.

All entities in which the Company holds investments that are considered VIEs for financial reporting purposes were reviewed for consolidation under the applicable consolidation guidance. Whenever the Company has both the power to direct the activities of an entity that most significantly impact the entity’s performance, and the obligation to absorb losses or the right to receive benefits of the entity that could be significant, the Company consolidates the entity.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make a number of significant estimates. These include estimates of amount and timing of allowances for credit losses, fair value of certain assets and liabilities, and other estimates that affect the reported amounts of certain assets and liabilities as of the date of the condensed consolidated financial statements and the reported amounts of certain revenues and expenses during the reported period. It is likely that changes in these estimates (e.g., valuation changes to the underlying collateral of loans due to changes in market interest and capitalization rates, leasing, credit worthiness of major tenants, occupancy rates, availability of financing, exit plan, loan sponsorship, actions of other lenders, overall economic and capital markets conditions, the broader commercial real estate market, local geographic sub-markets or other factors) will occur in the near term. As of September 30, 2021, the COVID-19

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements (unaudited)

pandemic remains ongoing. SinceAs the beginning of 2020, thenovel coronavirus, or COVID-19, pandemic has significantly impacted theevolved from its emergence in early 2020, so has its global economy, created disruptionsimpact, including contributing to significant volatility in the global supply chain, increased rates of unemployment and adversely impactedfinancial markets. The longer-term macroeconomic effects continue to impact many industries, including those related to the real estate collateral underlying certain of ourthe Company’s loans. So farMoreover, with the potential for new strains of COVID-19 to emerge, governments and businesses may re-impose aggressive measures to help slow its spread in 2021, the global and U.S. economic activity has, to varying degrees, begun to improve,future. For this reason, among others, as wider distribution of the COVID-19 vaccinespandemic continues, the potential global impacts are uncertain and difficult to assess. In addition, the pandemic continues to disrupt global supply chains and cause labor shortages and has continued. As a result, macroeconomic forecasts have improved overadded to broad inflationary pressures, all of which could negatively impact the last few quarters, including expectations for unemploymentCompany’s borrowers’ ability to execute on the business plans on their properties and potentially affect their ability to perform under the terms of their loan agreements. In response to the inflationary pressures, the Federal Reserve has begun raising interest rates and overall economic output. Nonetheless, the ongoing pandemichas indicated it anticipates further interest rate increases. Such increases in interest rates may continue to adversely impact the macroeconomic recovery, particularly with respect to the emergence of new variants of the COVID-19 virus, the continued distribution and acceptance of vaccines and the effectiveness of such vaccines against new variants of the COVID-19 virus. Accordingly, given the ongoing nature of the outbreak, at this time the Company cannot reasonably estimate the magnitude of the long-term impact that COVID-19 may have on the economic activity and real estate market conditions, as well asincrease the Company’s business, financial performanceinterest expense, which may not be fully offset by any increases in interest income, and operating results. may also slow the pace of loan repayments and increase the number of borrowers who seek extension of term on their loans.

The Company believes the estimates and assumptions underlying its condensed consolidated financial statements are reasonable and supportable based on the information available as of SeptemberJune 30, 2021.2022. However, uncertainty over the ultimate impact the COVID-19, pandemicFederal Reserve actions and geopolitical uncertainty will have on the global economyand U.S. economies generally, and the Company’s business in particular, makes any estimates and assumptions as of SeptemberJune 30, 20212022, inherently less certain than they would be absent the current and potential impacts of the COVID-19 pandemic.these factors. The Company’s actual results could ultimately differ from its estimates and such differences may be material.

Significant Accounting Policies

Included in Note 2 to the Consolidated Financial Statements of the Company’s Annual Report on Form 10-K for the year ended December 31, 20202021, is a summary of the Company’s significant accounting policies. Provided below is a summary of additional accounting policies that are significant to the Company’s condensed consolidated financial condition and results of operations for the three and ninesix months ended SeptemberJune 30, 2021.

Term Financing Facility

The Company finances certain of its loans held-for-investment through the use of a term financing facility. Borrowings under the term financing facility bear an interest rate of a specified margin over the one-month London Interbank Offered Rate, or LIBOR. The term financing facility financings are treated as collateralized financing transactions and are carried at their contractual amounts, as specified in the respective agreements.2022.

Recently Issued and/or Adopted Accounting Standards

Financial Instruments-Credit Losses (Topic 326): Troubled Debt Restructurings and Vintage Disclosures

In March 2022, the Financial Accounting Standards Board, or FASB, issued ASU 2022-02, Financial Instruments – Credit Losses (Topic 326): Troubled Debt Restructurings and Vintage Disclosures, or ASU 2022-02. The intention of ASU 2022-02 is to simplify the guidance surrounding loan modifications and restructurings and to eliminate the accounting guidance related to troubled debt restructurings, or TDR. The new guidance deviates from TDR guidance as disclosures are now based on whether a modification or restructuring with a borrower experiencing financial difficulty results in principal forgiveness, an interest rate reduction, a significant payment delay or term extension as opposed to simply a concession. The new guidance requires disclosure by class of financing receivables, of the types of modifications, the financial effects of those modifications and the performance of those modified receivables in the last twelve months. As it relates to ASC 326-20 the Company is now allowed to use any acceptable method to determine credit losses as a result of modification or restructuring with a borrower experiencing financial difficulty. ASU 2022-02 also requires disclosure of gross write-offs recorded in the current period, on a year-to-date basis, by year of origination in the vintage disclosures. ASU 2022-02 is effective for fiscal years beginning after December 15, 2022. Entities are able to early adopt these amendments and have the ability to early adopt the TDR enhancements separately from the vintage disclosures. The Company has not yet adopted this ASU and will continue to evaluate the effects of adoption.

Facilitation of the Effects of Reference Rate Reform on Financial Reporting

In March 2020, the Financial Accounting Standards Board, or FASB issued ASU No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting, or ASU No. 2020-04, which provides optional expedients and exceptions for applying GAAP to debt instruments, derivatives, and other contracts that reference the London Interbank Offered Rate, or LIBOR, or other reference rates expected to be discontinued as a result of reference rate reform. This guidance is optional and may be elected through December 31, 2022, using a prospective application on all eligible contract modifications. The Company has loan agreements and debt agreements that incorporate LIBOR as a referenced interest rate. It is difficult to predict what effect, if any, the phase-out of LIBOR and the use of alternative benchmarks may have on the Company’s business or on the overall financial markets. The Company has not adopted any of the optional expedients or exceptions through SeptemberJune 30, 2021,2022, but will continue to evaluate the possible adoption of any such expedients or exceptions.

Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity7

In August 2020, FASB issued ASU No. 2020-06,

Debt – Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging – Contracts in an Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity,

or ASU No. 2020-06. The intention of ASU No. 2020-06 is

GRANITE POINT MORTGAGE TRUST INC.

Notes to address the complexities in accounting for certain financial instruments with a debt and equity component. Under ASU No. 2020-06, the number of accounting models for convertible notes will be reduced and entities that issue convertible debt will be required to use the if-converted method for the computation of diluted "Earnings per share" under ASC 260. ASC 2020-06 is effective for fiscal years beginning after December 15, 2021 and may be adopted through either a modified retrospective method of transition or a fully retrospective method of transition. The Company is currently assessing the impact this guidance will have on its condensed consolidated financial statements.Condensed Consolidated Financial Statements

Note 3. Loans Held-for-Investment, Net of Allowance for Credit Losses

The Company originates and acquires commercial real estate debt and related instruments generally to be held as long-term investments. These assets are classified as “loans held-for-investment” on the condensed consolidated balance sheets. Loans held-for-investment are reported at cost, net of any unamortized acquisition premiums or discounts, loan fees, origination costs and allowance for credit losses, as applicable.

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements (unaudited)

The following tables summarize the Company’s loans held-for-investment by asset type, property type and geographic location as of SeptemberJune 30, 20212022, and December 31, 2020:2021:

| | | September 30,

2021 | | June 30,

2022 |

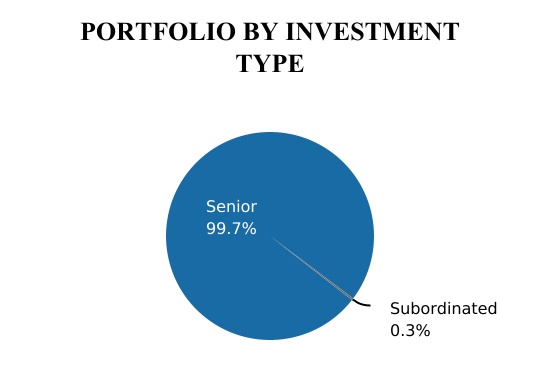

| (dollars in thousands) | (dollars in thousands) | Senior Loans (1) | | Mezzanine Loans | | B-Notes | | Total | (dollars in thousands) | Senior Loans (1) | | Mezzanine Loans | | B-Notes | | Total |

| Unpaid principal balance | Unpaid principal balance | $ | 3,657,401 | | | $ | 1,387 | | | $ | 14,065 | | | $ | 3,672,853 | | Unpaid principal balance | $ | 3,875,237 | | | $ | 356 | | | $ | 13,886 | | | $ | 3,889,479 | |

| Unamortized (discount) premium | Unamortized (discount) premium | (67) | | | — | | | — | | | (67) | | Unamortized (discount) premium | (55) | | | — | | | — | | | (55) | |

| Unamortized net deferred origination fees | Unamortized net deferred origination fees | (13,095) | | | — | | | — | | | (13,095) | | Unamortized net deferred origination fees | (12,130) | | | — | | | — | | | (12,130) | |

| Allowance for credit losses | Allowance for credit losses | (40,897) | | | (1,387) | | | (3,196) | | | (45,480) | | Allowance for credit losses | (46,188) | | | (356) | | | (736) | | | (47,280) | |

| Carrying value | Carrying value | $ | 3,603,342 | | | $ | — | | | $ | 10,869 | | | $ | 3,614,211 | | Carrying value | $ | 3,816,864 | | | $ | — | | | $ | 13,150 | | | $ | 3,830,014 | |

| Unfunded commitments | Unfunded commitments | $ | 430,105 | | | $ | — | | | $ | — | | | $ | 430,105 | | Unfunded commitments | $ | 358,705 | | | $ | — | | | $ | — | | | $ | 358,705 | |

| Number of loans | Number of loans | 98 | | | 1 | | | 1 | | | 100 | | Number of loans | 102 | | | 1 | | | 1 | | | 104 | |

| Weighted average coupon | Weighted average coupon | 4.6 | % | | 13.0 | % | | 8.0 | % | | 4.6 | % | Weighted average coupon | 4.6 | % | | 13.0 | % | | 8.0 | % | | 4.6 | % |

Weighted average years to maturity (2) | Weighted average years to maturity (2) | 1.0 | | 4.1 | | 5.3 | | 1.0 | Weighted average years to maturity (2) | 1.0 | | 3.4 | | 4.6 | | 1.0 |

| | | December 31,

2020 | | December 31,

2021 |

| (dollars in thousands) | (dollars in thousands) | Senior Loans (1) | | Mezzanine Loans | | B-Notes | | Total | (dollars in thousands) | Senior Loans (1) | | Mezzanine Loans | | B-Notes | | Total |

| Unpaid principal balance | Unpaid principal balance | $ | 3,915,833 | | | $ | 2,366 | | | $ | 14,235 | | | $ | 3,932,434 | | Unpaid principal balance | $ | 3,781,771 | | | $ | 1,048 | | | $ | 14,006 | | | $ | 3,796,825 | |

| Unamortized (discount) premium | Unamortized (discount) premium | (75) | | | — | | | — | | | (75) | | Unamortized (discount) premium | (70) | | | — | | | — | | | (70) | |

| Unamortized net deferred origination fees | Unamortized net deferred origination fees | (17,890) | | | — | | | — | | | (17,890) | | Unamortized net deferred origination fees | (14,550) | | | — | | | — | | | (14,550) | |

| Allowance for credit losses | Allowance for credit losses | (60,130) | | | (2,366) | | | (4,170) | | | (66,666) | | Allowance for credit losses | (38,719) | | | (1,048) | | | (1,130) | | | (40,897) | |

| Carrying value | Carrying value | $ | 3,837,738 | | | $ | — | | | $ | 10,065 | | | $ | 3,847,803 | | Carrying value | $ | 3,728,432 | | | $ | — | | | $ | 12,876 | | | $ | 3,741,308 | |

| Unfunded commitments | Unfunded commitments | $ | 503,726 | | | $ | — | | | $ | — | | | $ | 503,726 | | Unfunded commitments | $ | 403,584 | | | $ | — | | | $ | — | | | $ | 403,584 | |

| Number of loans | Number of loans | 101 | | | 1 | | | 1 | | | 103 | | Number of loans | 103 | | | 1 | | | 1 | | | 105 | |

| Weighted average coupon | Weighted average coupon | 5.1 | % | | 13.0 | % | | 8.0 | % | | 5.1 | % | Weighted average coupon | 4.5 | % | | 13.0 | % | | 8.0 | % | | 4.5 | % |

Weighted average years to maturity (2) | Weighted average years to maturity (2) | 1.1 | | 4.9 | | 6.1 | | 1.1 | Weighted average years to maturity (2) | 1.1 | | 3.9 | | 5.1 | | 1.1 |

____________________

(1)Loans primarily secured by a first priority lien on commercial real property and related personal property and also includes, when applicable, any companion subordinate loans.

(2)Based on contractual maturity date. Certain loans are subject to contractual extension options with such conditions stipulated in the applicable loan documents. Actual maturities may differ from contractual maturities stated herein as certain borrowers may have the right to prepay with or without paying a prepayment fee. The Company may also extend contractual maturities in connection with certain loan modifications.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | | September 30,

2021 | | December 31,

2020 |

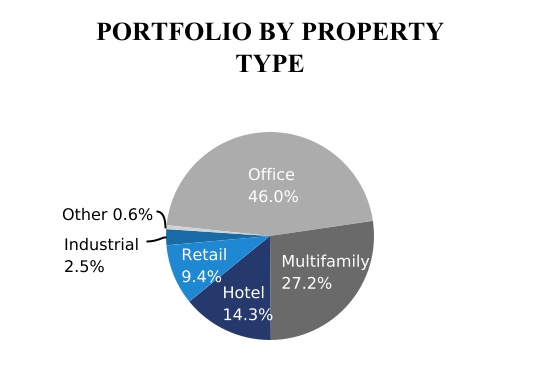

| Property Type | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Office | | $ | 1,663,478 | | | 46.0 | % | | $ | 1,720,705 | | | 44.7 | % |

| Multifamily | | 982,624 | | | 27.2 | % | | 910,557 | | | 23.7 | % |

| Hotel | | 517,028 | | | 14.3 | % | | 646,869 | | | 16.8 | % |

| Retail | | 340,265 | | | 9.4 | % | | 332,218�� | | | 8.6 | % |

| Industrial | | 89,456 | | | 2.5 | % | | 196,677 | | | 5.1 | % |

| Other | | 21,360 | | | 0.6 | % | | 40,777 | | | 1.1 | % |

| Total | | $ | 3,614,211 | | | 100.0 | % | | $ | 3,847,803 | | | 100.0 | % |

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | | September 30,

2021 | | December 31,

2020 |

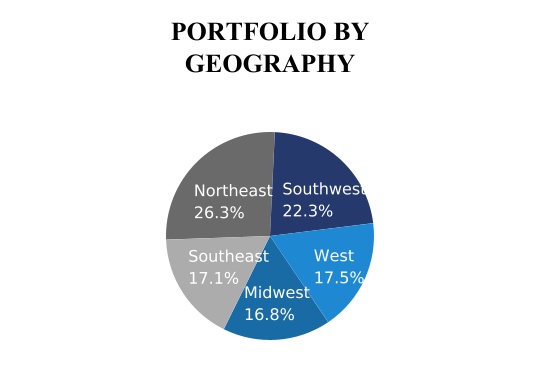

| Geographic Location | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Northeast | | $ | 950,447 | | | 26.3 | % | | $ | 1,028,584 | | | 26.8 | % |

| Southwest | | 807,483 | | | 22.3 | % | | 802,233 | | | 20.8 | % |

| West | | 630,826 | | | 17.5 | % | | 682,236 | | | 17.7 | % |

| Midwest | | 608,102 | | | 16.8 | % | | 712,675 | | | 18.5 | % |

| Southeast | | 617,353 | | | 17.1 | % | | 622,075 | | | 16.2 | % |

| | | | | | | | |

| Total | | $ | 3,614,211 | | | 100.0 | % | | $ | 3,847,803 | | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

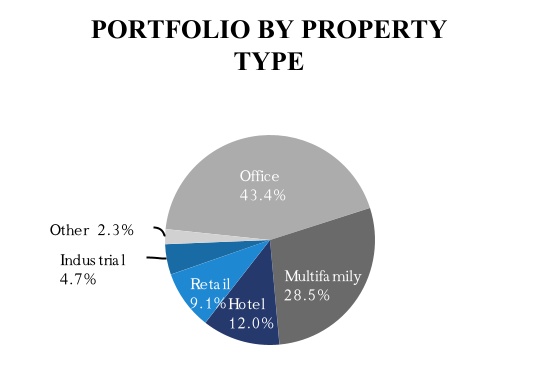

| (dollars in thousands) | | June 30,

2022 | | December 31,

2021 |

| Property Type | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Office | | $ | 1,663,577 | | | 43.4 | % | | $ | 1,703,951 | | | 45.5 | % |

| Multifamily | | 1,090,106 | | | 28.5 | % | | 1,061,434 | | | 28.4 | % |

| Hotel | | 460,432 | | | 12.0 | % | | 464,816 | | | 12.4 | % |

| Retail | | 347,287 | | | 9.1 | % | | 341,834 | | | 9.1 | % |

| Industrial | | 181,871 | | | 4.7 | % | | 118,564 | | | 3.2 | % |

| Other | | 86,741 | | | 2.3 | % | | 50,709 | | | 1.4 | % |

| Total | | $ | 3,830,014 | | | 100.0 | % | | $ | 3,741,308 | | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

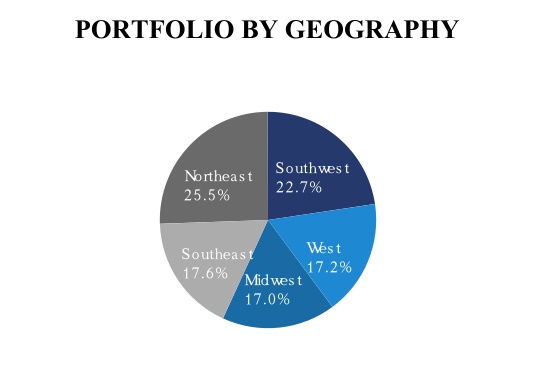

| (dollars in thousands) | | June 30,

2022 | | December 31,

2021 |

| Geographic Location | | Carrying Value | | % of Loan Portfolio | | Carrying Value | | % of Loan Portfolio |

| Northeast | | $ | 976,965 | | | 25.5 | % | | $ | 917,029 | | | 24.5 | % |

| Southwest | | 869,316 | | | 22.7 | % | | 836,955 | | | 22.4 | % |

| West | | 660,173 | | | 17.2 | % | | 658,429 | | | 17.6 | % |

| Midwest | | 649,233 | | | 17.0 | % | | 637,784 | | | 17.0 | % |

| Southeast | | 674,327 | | | 17.6 | % | | 691,111 | | | 18.5 | % |

| | | | | | | | |

| Total | | $ | 3,830,014 | | | 100.0 | % | | $ | 3,741,308 | | | 100.0 | % |

At SeptemberJune 30, 20212022, and December 31, 2020,2021, the Company pledged loans held-for-investment with a carrying value, net of allowance for credit losses, of $3.5$3.6 billion and $3.8$3.7 billion, respectively, as collateral under repurchase facilities, an asset-specifica term financing facility, a terman asset-specific financing facility and securitized debt obligations. See Note 4 - Variable Interest Entities and Securitized Debt Obligations and Note 5 - Secured Financing Agreements.

The following table summarizes activity related to loans held-for-investment, net of allowance for credit losses, for the three and ninesix months ended SeptemberJune 30, 20212022, and 2020:2021:

| | | Three Months Ended September 30, | | Nine Months Ended September 30, | | Three Months Ended June 30, | | Six Months Ended June 30, |

| (in thousands) | (in thousands) | 2021 | | 2020 | | 2021 | | 2020 | | (in thousands) | 2022 | | 2021 | | 2022 | | 2021 | |

| Balance at beginning of period | Balance at beginning of period | $ | 3,577,644 | | | $ | 4,290,047 | | | $ | 3,847,803 | | | $ | 4,226,212 | | | Balance at beginning of period | $ | 3,750,470 | | | $ | 3,799,836 | | | $ | 3,741,308 | | | $ | 3,847,803 | | |

| Originations, additional fundings and capitalized deferred interest | 325,597 | | | 57,617 | | | 565,212 | | | 317,630 | | | |

| Originations, additional fundings, upsizing of loans and capitalized deferred interest | | Originations, additional fundings, upsizing of loans and capitalized deferred interest | 212,245 | | | 197,838 | | | 385,110 | | | 239,615 | | |

| | Repayments | Repayments | (290,497) | | | (184,723) | | | (815,054) | | | (290,838) | | | Repayments | (120,107) | | | (422,969) | | | (238,490) | | | (524,557) | | |

| Transfers to loans held-for-sale | — | | | (190,787) | | | — | | | (210,452) | | | |

| Loan sales | | Loan sales | — | | | — | | | (43,714) | | | — | | |

| Net discount accretion (premium amortization) | Net discount accretion (premium amortization) | (2) | | | — | | | 9 | | | 16 | | | Net discount accretion (premium amortization) | 7 | | | 4 | | | 16 | | | 11 | | |

| (Increase) decrease in net deferred origination fees | (3,566) | | | 101 | | | (5,905) | | | (2,908) | | | |

| Increase in net deferred origination fees | | Increase in net deferred origination fees | (2,318) | | | (2,305) | | | (4,558) | | | (2,339) | | |

| Amortization of net deferred origination fees | Amortization of net deferred origination fees | 2,584 | | | 3,236 | | | 10,700 | | | 12,541 | | | Amortization of net deferred origination fees | 2,843 | | | 3,478 | | | 6,832 | | | 8,116 | | |

| | Benefit from (provision for) credit losses | 2,451 | | | 3,371 | | | 11,446 | | | (73,339) | | | |

| (Provision for) benefit from credit losses | | (Provision for) benefit from credit losses | (13,126) | | | 1,762 | | | (16,490) | | | 8,995 | | |

| Balance at end of period | Balance at end of period | $ | 3,614,211 | | | $ | 3,978,862 | | | $ | 3,614,211 | | | $ | 3,978,862 | | | Balance at end of period | $ | 3,830,014 | | | $ | 3,577,644 | | | $ | 3,830,014 | | | $ | 3,577,644 | | |

Allowance for Credit Losses

Subsequent to the adoption of ASU 2016-13 on January 1, 2020, to estimate and recognize an allowance for credit losses on loans held-for-investment and theirthe related unfunded commitments, the Company continues to use a third-party licensed probability-weighted analytical model. The Company employs quarterly updated macroeconomic forecasts, which reflect expectations for overall economic output, interest rates, values of real estate properties and other factors, including the ongoing impactimpacts of the COVID-19 pandemic, geopolitical instability and the Federal Reserve monetary policy on the overall U.S. economy and commercial real estate markets generally. Driven by the general progress around the development and distribution of the COVID-19 vaccines over the last few quarters, those macroeconomic forecasts have been improving, including expectations for unemployment rates, overall economic output and values of real estate properties. Significant inputs to the Company’s estimate of the allowance for credit

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements

losses include loan specific factors such as debt service coverage ratio, or DSCR, loan to value ratio, or LTV, remaining contractual loan term, property type and others. As part of the quarterly review of the portfolio, the Company assesses the expected repayment date of each loan, which is used to determine the contractual term for purposes of computing the current expected credit loss, or CECL, reserve. In certain instances, for loans with unique risk and credit characteristics, the Company may instead elect to employ different methods to estimate an allowance for credit losses that also conform to ASU 2016-13 and related guidance.

As of SeptemberJune 30, 2021,2022, the Company recognized an allowance for credit losses related to its loans held-for-investment of $45.5$47.3 million, which reflectedreflects a write-off of $9.7 million on a loan held-for-investment and a benefit fromtotal increase in the provision for credit losses of $2.5$13.1 million for the three months ended SeptemberJune 30, 2021.2022. The benefit fromincrease of $13.1 million includes a $4.0 million increase in the allowance for credit losses related to an office loan with an unpaid balance of $93.8 million that was individually assessed in accordance with ASU 2016-13 during the three months ended June 30, 2022, as further discussed below. The other loan that was individually assessed during the three months ended June 30, 2022, had been previously reserved for and there was no change in the reserve during the three months ended June 30, 2022. The remaining increase in the Company’s provision for credit losses reflects the continued general improvementwas related to changes in the overall performanceportfolio mix and implementing in its analysis a more conservative macroeconomic forecast driven by an elevated uncertainty for the macroeconomic outlook due to inflationary pressures, continuing supply chain disruptions, interest rate volatility and other factors, moderately offset by a recovery of the investment portfolio and current expectations for further improvement in macroeconomic conditions.$0.5 million on amounts previously written off.

The allowance for credit losses related to the Company’s loans held-for-investment is deducted from the amortized cost basis of related loans, while the allowance for credit losses related to off-balance sheet unfunded commitments on existing loans is recorded as a component of other liabilities on the Company’s condensed consolidated balance sheets. As of SeptemberJune 30, 2021,2022, the Company recognized $1.9$2.8 million in other liabilities related to the allowance for credit losses on unfunded

GRANITE POINT MORTGAGE TRUST INC.

Notes to the Condensed Consolidated Financial Statements (unaudited)

commitments. During the three months ended September 30, 2021, the Company recognized commitments and recorded a benefit from provision for credit losses of $3.3$1.0 million mainly related tofor the release of a $3.2 million allowance for credit losses related to unfunded commitments on the office loan that had previously been deemed to be collateral-dependent and for which the unfunded commitments were deemed to be unlikely to be funded, given the loan’s delinquent status as of Septemberthree months ended June 30, 2021.2022. Changes in the provision for credit losses for both loans held-for-investment and their related unfunded commitments are recognized through net (loss) income (loss) on the Company’s condensed consolidated statements of comprehensive income (loss).income.

The following table presents the changes for the three and ninesix months ended SeptemberJune 30, 20212022, and 20202021 in the allowance for credit losses on loans held-for-investment: