UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended JuneSeptember 30, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________to__________

Commission File Number 1-38315

CURO GROUP HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 90-0934597 |

(State or other jurisdiction Of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | |

| 3527 North Ridge Road, Wichita, KS | | 67205 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (316) 772-3801

Former name, former address and former fiscal year, if changed since last report: No Changes

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, $0.001 par value per share | CURO | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ | | | |

| Smaller reporting company | ☒ | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

At August 2,November 1, 2019 there were 45,267,76241,486,965 shares of the registrant’s Common Stock, $0.001 par value per share, outstanding.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

FORM 10-Q

SECONDTHIRD QUARTER ENDED JUNESEPTEMBER 30, 2019

INDEX

|

| | | | | | | |

| | | | | | | | Page |

|

| |

| Item 1. | Financial Statements (unaudited) |

| | | |

| | JuneSeptember 30, 2019 and December 31, 2018 | |

| | | |

| | Three and sixnine months ended JuneSeptember 30, 2019 and 2018 | |

| | | |

| | Three and sixnine months ended JuneSeptember 30, 2019 and 2018 | |

| | | |

| | SixNine months ended JuneSeptember 30, 2019 and 2018 | |

| | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | | | | | |

| |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| Item 5. | | |

| Item 6. | | |

| | | | | | | |

| | | | | | |

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

| | | | June 30, 2019 | | December 31,

2018 | September 30, 2019 | | December 31,

2018 |

| | (unaudited) | | (unaudited) | |

ASSETS | | Cash | $ | 92,297 |

| | $ | 61,175 |

| $ | 62,207 |

| | $ | 61,175 |

|

| Restricted cash (includes restricted cash of consolidated VIEs of $14,819 and $12,840 as of June 30, 2019 and December 31, 2018, respectively) | 33,712 |

| | 25,439 |

| |

| Gross loans receivable (includes loans of consolidated VIEs of $215,309 and $148,876 as of June 30, 2019 and December 31, 2018, respectively) | 609,593 |

| | 571,531 |

| |

| Less: allowance for loan losses (includes allowance for losses of consolidated VIEs of $25,188 and $12,688 as of June 30, 2019 and December 31, 2018, respectively) | (101,877 | ) | | (73,997 | ) | |

| Restricted cash (includes restricted cash of consolidated VIEs of $21,897 and $12,840 as of September 30, 2019 and December 31, 2018, respectively) | | 38,754 |

| | 25,439 |

|

| Gross loans receivable (includes loans of consolidated VIEs of $231,533 and $148,876 as of September 30, 2019 and December 31, 2018, respectively) | | 657,615 |

| | 571,531 |

|

| Less: allowance for loan losses (includes allowance for losses of consolidated VIEs of $25,375 and $12,688 as of September 30, 2019 and December 31, 2018, respectively) | | (108,385 | ) | | (73,997 | ) |

| Loans receivable, net | 507,716 |

| | 497,534 |

| 549,230 |

| | 497,534 |

|

| Right of use asset - operating leases (Note 1) | 140,982 |

| | — |

| 118,260 |

| | — |

|

| Deferred income taxes | 2,637 |

| | 1,534 |

| 1,846 |

| | 1,534 |

|

| Income taxes receivable | 37,579 |

| | 16,741 |

| 23,966 |

| | 16,741 |

|

| Prepaid expenses and other | 30,241 |

| | 43,588 |

| 32,228 |

| | 43,588 |

|

| Property and equipment, net | 72,993 |

| | 76,750 |

| 70,381 |

| | 76,750 |

|

| Goodwill | 120,450 |

| | 119,281 |

| 120,110 |

| | 119,281 |

|

| Other intangibles, net of accumulated amortization | 30,657 |

| | 29,784 |

| 32,666 |

| | 29,784 |

|

| Other | 16,091 |

| | 12,930 |

| 18,484 |

| | 12,930 |

|

| Assets from discontinued operations (Note 15) | — |

| | 34,861 |

| — |

| | 34,861 |

|

| Total Assets | $ | 1,085,355 |

| | $ | 919,617 |

| $ | 1,068,132 |

| | $ | 919,617 |

|

LIABILITIES AND STOCKHOLDERS' EQUITY | | Accounts payable and accrued liabilities | $ | 59,274 |

| | $ | 49,146 |

| |

| Accounts payable and accrued liabilities (includes accounts payable and accrued liabilities of consolidated VIEs of $7,259 and $4,980 as of September 30, 2019 and December 31, 2018, respectively) | | $ | 63,685 |

| | $ | 49,146 |

|

| Deferred revenue | 8,712 |

| | 9,483 |

| 9,052 |

| | 9,483 |

|

| Lease liability - operating leases (Note 1) | 148,843 |

| | — |

| 126,048 |

| | — |

|

| Income taxes payable | — |

| | 1,579 |

| — |

| | 1,579 |

|

| Accrued interest (includes accrued interest of consolidated VIEs of $713 and $831 as of June 30, 2019 and December 31, 2018, respectively) | 19,690 |

| | 20,904 |

| |

| Accrued interest (includes accrued interest of consolidated VIEs of $777 and $831 as of September 30, 2019 and December 31, 2018, respectively) | | 5,625 |

| | 20,904 |

|

| Liability for losses on CSO lender-owned consumer loans | 9,504 |

| | 12,007 |

| 10,249 |

| | 12,007 |

|

| Deferred rent | — |

| | 10,851 |

| — |

| | 10,851 |

|

| Long-term debt (includes long-term debt and issuance costs of consolidated VIEs of $94,565 and $3,588 as of June 30, 2019 and $111,335 and $3,856 as of December 31, 2018, respectively) | 768,512 |

| | 804,140 |

| |

| Debt (includes debt and issuance costs of consolidated VIEs of $105,742 and $3,259 as of September 30, 2019 and $111,335 and $3,856 as of December 31, 2018, respectively) | | 805,407 |

| | 804,140 |

|

| Subordinated stockholder debt | — |

| | 2,196 |

| — |

| | 2,196 |

|

| Other long-term liabilities | 8,594 |

| | 5,800 |

| 8,594 |

| | 5,800 |

|

| Deferred tax liabilities | 4,848 |

| | 13,730 |

| 4,427 |

| | 13,730 |

|

| Liabilities from discontinued operations (Note 15) | — |

| | 8,882 |

| — |

| | 8,882 |

|

| Total Liabilities | 1,027,977 |

| | 938,718 |

| 1,033,087 |

| | 938,718 |

|

| Commitments and contingencies (Note 13) |

|

| |

|

|

|

| |

|

|

| Stockholders' Equity |

|

| |

|

|

|

| |

|

|

| Preferred stock - $0.001 par value, 25,000,000 shares authorized; no shares were issued at either period end | — |

| | — |

| — |

| | — |

|

| Common stock - $0.001 par value; 225,000,000 shares authorized; 46,499,482 and 46,412,231 shares issued as of June 30, 2019 and December 31, 2018, respectively; and 46,255,282 and 46,412,231 shares outstanding as of June 30, 2019 and December 31, 2018, respectively | 9 |

| | 9 |

| |

| Treasury stock, at cost - 244,200 shares as of June 30, 2019 | (2,507 | ) | | — |

| |

| Common stock - $0.001 par value; 225,000,000 shares authorized; 46,503,406 and 46,412,231 shares issued as of September 30, 2019 and December 31, 2018, respectively; and 42,347,165 and 46,412,231 shares outstanding as of September 30, 2019 and December 31, 2018, respectively | | 9 |

| | 9 |

|

| Treasury stock, at cost - 4,156,241 as of September 30, 2019 | | (53,064 | ) | | — |

|

| Paid-in capital | 64,790 |

| | 60,015 |

| 67,579 |

| | 60,015 |

|

| Retained earnings (accumulated deficit) | 35,816 |

| | (18,065 | ) | 63,205 |

| | (18,065 | ) |

| Accumulated other comprehensive loss | (40,730 | ) | | (61,060 | ) | (42,684 | ) | | (61,060 | ) |

| Total Stockholders' Equity | 57,378 |

| | (19,101 | ) | 35,045 |

| | (19,101 | ) |

| Total Liabilities and Stockholders' Equity | $ | 1,085,355 |

| | $ | 919,617 |

| $ | 1,068,132 |

| | $ | 919,617 |

|

See accompanying Notes to Unauditedunaudited Condensed Consolidated Financial Statements.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

| | | | Three Months Ended

June 30, | | Six Months Ended

June 30, | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2019 | | 2018 | | 2019 | | 2018 | 2019 | | 2018 | | 2019 | | 2018 |

| Revenue | $ | 264,300 |

| | $ | 237,169 |

| | $ | 542,239 |

| | $ | 488,012 |

| $ | 297,264 |

| | $ | 269,482 |

| | $ | 839,503 |

| | $ | 757,494 |

|

| Provision for losses | 112,010 |

| | 86,347 |

| | 214,395 |

| | 163,230 |

| 123,867 |

| | 127,692 |

| | 338,262 |

| | 290,922 |

|

| Net revenue | 152,290 |

| | 150,822 |

| | 327,844 |

| | 324,782 |

| 173,397 |

| | 141,790 |

| | 501,241 |

| | 466,572 |

|

| | | | | | | | | | | | | | | |

| Cost of providing services | | | | | | | | | | | | | | |

| Salaries and benefits | 26,086 |

| | 26,908 |

| | 54,787 |

| | 53,826 |

| 27,462 |

| | 26,515 |

| | 82,249 |

| | 80,341 |

|

| Occupancy | 13,932 |

| | 13,320 |

| | 28,169 |

| | 26,747 |

| 14,036 |

| | 13,522 |

| | 42,205 |

| | 40,269 |

|

| Office | 5,457 |

| | 5,532 |

| | 10,570 |

| | 11,985 |

| 5,993 |

| | 7,326 |

| | 16,563 |

| | 19,311 |

|

| Other costs of providing services | 12,854 |

| | 12,601 |

| | 27,074 |

| | 26,032 |

| 12,843 |

| | 12,484 |

| | 39,917 |

| | 38,516 |

|

| Advertising | 12,780 |

| | 15,113 |

| | 20,566 |

| | 22,998 |

| 16,424 |

| | 21,349 |

| | 36,990 |

| | 44,347 |

|

| Total cost of providing services | 71,109 |

| | 73,474 |

| | 141,166 |

| | 141,588 |

| 76,758 |

| | 81,196 |

| | 217,924 |

| | 222,784 |

|

| Gross margin | 81,181 |

| | 77,348 |

| | 186,678 |

| | 183,194 |

| 96,639 |

| | 60,594 |

| | 283,317 |

| | 243,788 |

|

| | | | | | | | | | | | | | | |

| Operating expense | | | | | | | | | | | | | | |

| Corporate, district and other expenses | 39,038 |

| | 32,980 |

| | 88,126 |

| | 68,409 |

| 38,665 |

| | 27,495 |

| | 123,043 |

| | 95,904 |

|

| Interest expense | 17,023 |

| | 20,472 |

| | 34,713 |

| | 42,826 |

| 17,364 |

| | 23,403 |

| | 52,077 |

| | 66,229 |

|

| Loss on extinguishment of debt | — |

| | — |

| | — |

| | 11,683 |

| — |

| | 69,200 |

| | — |

| | 80,883 |

|

| Loss from equity method investment | | 1,384 |

| | — |

| | 5,132 |

| | — |

|

| Total operating expense | 56,061 |

| | 53,452 |

| | 122,839 |

| | 122,918 |

| 57,413 |

| | 120,098 |

| | 180,252 |

| | 243,016 |

|

| Income from continuing operations before income taxes | 25,120 |

| | 23,896 |

| | 63,839 |

| | 60,276 |

| |

| Provision for income taxes | 7,453 |

| | 5,178 |

| | 17,499 |

| | 16,645 |

| |

| Net income from continuing operations | 17,667 |

|

| 18,718 |

| | 46,340 |

| | 43,631 |

| |

| Net (loss) income from discontinued operations, net of tax | (834 | ) | | (2,743 | ) | | 7,541 |

| | (4,364 | ) | |

| Net income | $ | 16,833 |

|

| $ | 15,975 |

| | $ | 53,881 |

| | $ | 39,267 |

| |

| Income (loss) from continuing operations before income taxes | | 39,226 |

| | (59,504 | ) | | 103,065 |

| | 772 |

|

| Provision (benefit) for income taxes | | 11,239 |

| | (16,914 | ) | | 28,738 |

| | (269 | ) |

| Net income (loss) from continuing operations | | 27,987 |

|

| (42,590 | ) | | 74,327 |

| | 1,041 |

|

| Net loss from discontinued operations, before income tax | | — |

| | (4,293 | ) | | (39,048 | ) | | (8,518 | ) |

Income tax expense (benefit) related to disposition

| | $ | 598 |

| | $ | 139 |

| | $ | (45,991 | ) | | $ | 278 |

|

| Net (loss) income from discontinued operations | | $ | (598 | ) | | $ | (4,432 | ) | | $ | 6,943 |

| | $ | (8,796 | ) |

| Net income (loss) | | $ | 27,389 |

|

| $ | (47,022 | ) | | $ | 81,270 |

| | $ | (7,755 | ) |

| | | | | | | | | |

| Basic earnings (loss) per share: | | | | | | | | |

| Continuing operations | | $ | 0.63 |

| | $ | (0.93 | ) | | $ | 1.63 |

| | $ | 0.02 |

|

| Discontinued operations | | (0.01 | ) | | (0.10 | ) | | 0.15 |

| | (0.19 | ) |

| Basic earnings per share | | $ | 0.62 |

| | $ | (1.03 | ) | | $ | 1.78 |

| | $ | (0.17 | ) |

| | | | | | | | | |

| Diluted earnings (loss) per share: | | | | | | | | |

| Continuing operations | | $ | 0.61 |

| | $ | (0.93 | ) | | $ | 1.59 |

| | $ | 0.03 |

|

| Discontinued operations | | (0.01 | ) | | (0.10 | ) | | 0.15 |

| | (0.19 | ) |

Diluted earnings per share (1) | | $ | 0.60 |

| | $ | (1.03 | ) | | $ | 1.74 |

| | $ | (0.16 | ) |

| | | | | | | | | | | | | | | |

| Weighted average common shares outstanding: | | | | | | | | | | | | | | |

| Basic | 46,451 |

| | 45,650 |

| | 46,438 |

| | 45,578 |

| 44,422 |

| | 45,853 |

| | 45,759 |

| | 45,674 |

|

| Diluted | 47,107 |

| | 47,996 |

| | 47,335 |

| | 47,757 |

| |

| | | | | | | | | |

| Basic income (loss) per share: | | | | | | | | |

| Continuing operations | $ | 0.38 |

| | $ | 0.41 |

| | $ | 1.00 |

| | $ | 0.96 |

| |

| Discontinued operations | (0.02 | ) | | (0.06 | ) | | 0.16 |

| | (0.10 | ) | |

| Basic income per share | $ | 0.36 |

| | $ | 0.35 |

| | $ | 1.16 |

| | $ | 0.86 |

| |

| | | | | | | | | |

| Diluted income (loss) per share: | | | | | | | | |

| Continuing operations | $ | 0.38 |

| | $ | 0.39 |

| | $ | 0.98 |

| | $ | 0.92 |

| |

| Discontinued operations | (0.02 | ) | | (0.06 | ) | | 0.16 |

| | (0.10 | ) | |

| Diluted income per share | $ | 0.36 |

| | $ | 0.33 |

| | $ | 1.14 |

| | $ | 0.82 |

| |

Diluted (1) | | 46,010 |

| | 45,853 |

| | 46,887 |

| | 48,061 |

|

| (1) As of December 31, 2018, the Company made certain insignificant adjustments to previously-reported Earnings Per Share ("EPS") to correctly reflect the effect of anti-dilutive shares on diluted EPS calculations in accordance with ASC 260. These changes were immaterial to the overall EPS calculation. Diluted loss per share for the three months ended September 30, 2018 of $0.97 was corrected to $1.03. | | (1) As of December 31, 2018, the Company made certain insignificant adjustments to previously-reported Earnings Per Share ("EPS") to correctly reflect the effect of anti-dilutive shares on diluted EPS calculations in accordance with ASC 260. These changes were immaterial to the overall EPS calculation. Diluted loss per share for the three months ended September 30, 2018 of $0.97 was corrected to $1.03. |

See accompanying Notes to Unauditedunaudited Condensed Consolidated Financial Statements.

Statements.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(in thousands)

(unaudited)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | 2019 | | 2018 | | 2019 | | 2018 |

| Net income | $ | 16,833 |

| | $ | 15,975 |

| | $ | 53,881 |

| | $ | 39,267 |

|

| Other comprehensive income (loss): |

| |

| |

| |

|

| Cash flow hedges, net of $0 tax in both periods | — |

| | (439 | ) | | — |

| | (385 | ) |

| Foreign currency translation adjustment, net of $0 tax in both periods | 3,635 |

| | (6,752 | ) | | 20,330 |

| | (9,663 | ) |

| Other comprehensive income (loss) | 3,635 |

| | (7,191 | ) | | 20,330 |

| | (10,048 | ) |

| Comprehensive income | $ | 20,468 |

| | $ | 8,784 |

| | $ | 74,211 |

| | $ | 29,219 |

|

|

| | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, | | Nine Months Ended

September 30, |

| | 2019 | | 2018 | | 2019 | | 2018 |

| Net income (loss) | $ | 27,389 |

| | $ | (47,022 | ) | | $ | 81,270 |

| | $ | (7,755 | ) |

| Other comprehensive (loss) income: |

| |

| |

| |

|

| Cash flow hedges, net of $0 tax in both periods | — |

| | (187 | ) | | — |

| | (572 | ) |

| Foreign currency translation adjustment, net of $0 tax in both periods | (1,954 | ) | | 2,649 |

| | 18,376 |

| | (7,015 | ) |

| Other comprehensive (loss) income | (1,954 | ) | | 2,462 |

| | 18,376 |

| | (7,587 | ) |

| Comprehensive income (loss) | $ | 25,435 |

| | $ | (44,560 | ) | | $ | 99,646 |

| | $ | (15,342 | ) |

See accompanying Notes to Unauditedunaudited Condensed Consolidated Financial Statements.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(dollars in thousands, unaudited)

| | | | Six Months Ended June 30, | Nine Months Ended September 30, |

| | 2019 | | 2018 | 2019 | | 2018 |

| Cash flows from operating activities | | | | | | |

| Net income from continuing operations | $ | 46,340 |

| | $ | 43,631 |

| $ | 74,327 |

| | $ | 1,041 |

|

| Adjustments to reconcile net income to net cash provided by continuing operating activities: | | | | | | |

| Depreciation and amortization | 9,571 |

| | 9,005 |

| 14,180 |

| | 13,628 |

|

| Provision for loan losses | 214,395 |

| | 163,230 |

| 338,262 |

| | 290,922 |

|

| Amortization of debt issuance costs and bond (premium)/discount | 1,568 |

| | 2,117 |

| |

| Amortization of debt issuance costs and bond discount | | 2,273 |

| | 2,923 |

|

| Deferred income tax (benefit) expense | (3,596 | ) | | 3,199 |

| (3,147 | ) | | 3,005 |

|

| Loss on disposal of property and equipment | 1,834 |

| | 517 |

| 47 |

| | 640 |

|

| Loss on extinguishment of debt | — |

| | 11,683 |

| — |

| | 80,883 |

|

| Increase in cash surrender value of life insurance | (991 | ) | | (2,223 | ) | |

| Share-based compensation expense | 4,816 |

| | 4,023 |

| |

| Loss from equity method investment | | 5,132 |

| | — |

|

| Share-based compensation | | 7,587 |

| | 6,112 |

|

| Changes in operating assets and liabilities: | | | | | | |

| Accrued fees and service charges on loans receivable | (1,171 | ) | | 2,928 |

| |

| Accrued interest on loans receivable | | (11,446 | ) | | (5,986 | ) |

| Prepaid expenses and other assets | 16,344 |

| | 5,853 |

| 14,275 |

| | 2,695 |

|

| Other assets | (3,790 | ) | | — |

| (8,439 | ) | | (2,458 | ) |

| Accounts payable and accrued liabilities | 9,527 |

| | (2,080 | ) | 13,596 |

| | (4,862 | ) |

| Deferred revenue | (915 | ) | | (1,193 | ) | (533 | ) | | (1,984 | ) |

| Income taxes payable | 25,123 |

| | 26,727 |

| 25,117 |

| | 326 |

|

| Income taxes receivable | (8,253 | ) | | (18,436 | ) | 5,598 |

| | (12,908 | ) |

| Deferred rent | — |

| | 127 |

| |

| Accrued Interest | (1,247 | ) | | (3,284 | ) | |

| Accrued interest | | (15,303 | ) | | (18,060 | ) |

| Other liabilities | 2,764 |

| | 909 |

| 2,767 |

| | 1,162 |

|

| Net cash provided by continuing operating activities | 312,319 |

| | 246,733 |

| 464,293 |

| | 357,079 |

|

| Net cash (used in) provided by discontinued operating activities | (504 | ) | | 5,458 |

| (504 | ) | | 5,562 |

|

| Net cash provided by operating activities | 311,815 |

| | 252,191 |

| 463,789 |

| | 362,641 |

|

| Cash flows from investing activities | | | | | | |

| Purchase of property, equipment and software | (6,164 | ) | | (2,957 | ) | (8,667 | ) | | (8,030 | ) |

| Loans receivable originated or acquired | (879,081 | ) | | (1,063,072 | ) | (1,369,644 | ) | | (1,624,881 | ) |

| Loans receivable repaid | 661,882 |

| | 868,436 |

| 995,291 |

| | 1,212,446 |

|

| Investments in Cognical Holdings | (4,368 | ) | | (958 | ) | |

| Investments in Cognical Holdings, Inc. ("Zibby") | | (8,168 | ) | | (958 | ) |

| Net cash used in continuing investing activities | (227,731 | ) | | (198,551 | ) | (391,188 | ) | | (421,423 | ) |

| Net cash used in discontinued investing activities | (14,213 | ) | | (14,349 | ) | (14,213 | ) | | (24,481 | ) |

| Net cash used in investing activities | (241,944 | ) | | (212,900 | ) | (405,401 | ) | | (445,904 | ) |

| Cash flows from financing activities | | | | | | |

| Net proceeds from issuance of common stock | — |

| | 12,431 |

| — |

| | 11,549 |

|

| Proceeds from Non-Recourse U.S. SPV facility | — |

| | 13,000 |

| — |

| | 17,000 |

|

| Payments on Non-Recourse U.S. SPV facility | — |

| | (19,163 | ) | — |

| | (61,590 | ) |

| Proceeds from Non-Recourse Canada SPV facility | 3,750 |

| | — |

| 15,992 |

| | 89,949 |

|

| Payments on Non-Recourse Canada SPV facility | (24,752 | ) | | — |

| (24,835 | ) | | — |

|

| Payments on 12.00% Senior Secured Notes | — |

| | (77,500 | ) | — |

| | (605,000 | ) |

| Proceeds from 8.25% Senior Secured Notes | | — |

| | 690,000 |

|

| Debt issuance costs paid | (198 | ) | | (168 | ) | (198 | ) | | (17,517 | ) |

| Proceeds from credit facilities | 68,002 |

| | 18,798 |

| 179,811 |

| | 65,169 |

|

| Payments on credit facilities | (88,002 | ) | | (18,798 | ) | (174,811 | ) | | (36,169 | ) |

| Payments on subordinated stockholder debt | (2,245 | ) | | — |

| (2,252 | ) | | — |

|

| Payments of call premiums from early debt extinguishments | — |

| | (9,300 | ) | — |

| | (63,350 | ) |

| Proceeds from exercise of stock options | 27 |

| | 39 |

| 87 |

| | 408 |

|

| Payments to net share settle restricted stock units vesting | | (110 | ) | | — |

|

| Repurchase of common stock | (1,762 | ) | | — |

| (52,172 | ) | | — |

|

Net cash used in financing activities (1) | (45,180 | ) | | (80,661 | ) | |

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(dollars in thousands, unaudited)

|

| | | | | | | |

| Effect of exchange rate changes on cash and restricted cash | 1,461 |

| | (4,189 | ) |

| Net increase (decrease) in cash and restricted cash | 26,152 |

| | (45,559 | ) |

| Cash and restricted cash at beginning of period | 99,857 |

| | 174,491 |

|

| Cash and restricted cash at end of period | 126,009 |

| | 128,932 |

|

| Less: Cash and restricted cash of discontinued operations at end of period | — |

| | 12,460 |

|

| Cash and restricted cash of continuing operations at end of period | $ | 126,009 |

| | $ | 116,472 |

|

| (1) Financing activities include continuing operations only, and were not impacted by discontinued operations |

|

| | | | | | | |

Net cash (used in) provided by financing activities (1) | (58,488 | ) | | 90,449 |

|

| Effect of exchange rate changes on cash and restricted cash | 1,204 |

| | (4,080 | ) |

| Net increase in cash and restricted cash | 1,104 |

| | 3,106 |

|

| Cash and restricted cash at beginning of period | 99,857 |

| | 174,491 |

|

| Cash and restricted cash at end of period | 100,961 |

| | 177,597 |

|

| Less: Cash and restricted cash of discontinued operations at end of period | — |

| | 11,303 |

|

| Cash and restricted cash of continuing operations at end of period | $ | 100,961 |

| | $ | 166,294 |

|

| (1) Financing activities include continuing operations only, and were not impacted by discontinued operations |

See accompanying Notes to Unauditedunaudited Condensed Consolidated Financial Statements.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND NATURE OF OPERATIONS

Basis of Presentation

The terms “CURO" and the “Company” refer to CURO Group Holdings Corp. and its directly and indirectly owned subsidiaries as a combined entity, except where otherwise stated. The term "CFTC" refers to CURO Financial Technologies Corp., a wholly-owned subsidiary, and its directly and indirectly owned subsidiaries as a consolidated entity, except where otherwise stated.

The Company has prepared the accompanying unaudited Condensed Consolidated Financial Statements ("Condensed Consolidated Financial Statements") in accordance with accounting principles generally accepted in the United States of America (“US GAAP”), and with the accounting policies described in its Annual Report on Form 10-K for the year ended December 31, 2018 filed with the Securities and Exchange Commission (the "SEC") on March 18, 2019 ("2018 Form 10-K"). Certain information and note disclosures normally included in annual financial statements prepared in accordance with US GAAP have been condensed or omitted, although the Company believes that the disclosures are adequate to enable a reasonable understanding of the information presented. Additionally, in September 2018, and subsequently expanded in June 2019, the SEC changed the definition of a smaller reporting company ("SRC"). The change in definition of an SRC would allow more registrants to qualify to report under scaled disclosure requirements. Under these rules, CURO meets the definition of an SRC as of June 30, 2019.

The Condensed Consolidated Financial Statements and the accompanying notes reflect all adjustments, which are, in the opinion of management, necessary to present fairly the Company's results of operations, financial position and cash flows for the periods presented. On February 25, 2019, the Company's United Kingdom ("U.K.") operations were placed into administration, which resulted in treatment of the segment as discontinued operations for all periods presented. Throughout this Quarterly Report on Form 10-Q ("Form 10-Q"), current and prior period financial information is presented as if the U.K. segment was excluded from continuing operations. For further information about the placement of the segment into administration, refer to "--Nature of Operations" below.

The Condensed Consolidated Financial Statements should be read in conjunction with the Consolidated Financial Statements and related Notes included in the 2018 Form 10-K. Interim results of operations are not necessarily indicative of results that may be expected for future interim periods or for the year ending December 31, 2019.

Principles of Consolidation

The Condensed Consolidated Financial Statements include the accounts of CURO and its wholly-owned subsidiaries. Intercompany transactions and balances have been eliminated in consolidation.

Equity Investment in Unconsolidated Entity

In April 2019, as part of a broader capital structure reorganization by the investee company, the Company made an additional $2.8 million cash investment in Cognical Holdings, which operates under the Zibby brand. See Note 8 - "Financial Instruments" for additional detail on the adjustment to fair value for the quarter ended June 30, 2019.

Use of Estimates

The preparation of Condensed Consolidated Financial Statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenses during the periods reported. Some of the significant estimates that the Company made in the accompanying Condensed Consolidated Financial Statements include allowances for loan losses, certain assumptions related to goodwill and intangibles, accruals related to self-insurance, credit services organization ("CSO") liability for losses and estimated tax liabilities. Actual results may differ from those estimates.

Nature of Operations

CURO is a growth-oriented, technology-enabled, highly-diversified consumer finance company serving a wide range of underbanked consumers in the United States ("U.S."), Canada and, through February 25, 2019, the U.K.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

U.K. Segment Placed into Administration

On February 25, 2019, the Company announced that a proposed Scheme of Arrangement ("SOA"), as described in the Company's Current Report on Form 8-K filed January 31, 2019, would not be implemented. In accordance with the provisions of the U.K. Insolvency Act 1986 and as approved by the boards of directors of the Company’s U.K. subsidiaries, Curo Transatlantic Limited and SRC Transatlantic Limited (collectively, “the U.K. Subsidiaries”), insolvency practitioners from KPMG were appointed as administrators (“Administrators”) for the U.K. Subsidiaries. The effect of the U.K. Subsidiaries’ entry into administration was to place their management, affairs, business and property under the direct control of the Administrators. Accordingly, the Company deconsolidated the U.K. Subsidiaries as of February 25, 2019 and presented the U.K. Subsidiaries as Discontinued Operations for all periods presented in this Form 10-Q.

Basis of Presentation

The terms “CURO" and the “Company” refer to CURO Group Holdings Corp. and its directly and indirectly owned subsidiaries as a consolidated entity, except where otherwise stated. The term "CFTC" refers to CURO Financial Technologies Corp., a wholly-owned subsidiary of the Company, and its directly and indirectly owned subsidiaries as a consolidated entity, except where otherwise stated.

The Company has prepared the accompanying unaudited Condensed Consolidated Financial Statements ("Condensed Consolidated Financial Statements") in accordance with accounting principles generally accepted in the United States of America (“US GAAP”), and with the accounting policies described in its Annual Report on Form 10-K for the year ended December 31, 2018 filed with the Securities and Exchange Commission (the "SEC") on March 18, 2019 ("2018 Form 10-K"). Operating results for the three and nine month periods ended September 30, 2019 are not necessarily indicative of the results that might be expected for any other interim period or the fiscal year ending December 31, 2019.

Certain information and note disclosures normally included in annual financial statements prepared in accordance with US GAAP have been condensed or omitted, although the Company believes that the disclosures are adequate to enable a reasonable understanding of the information presented. Additionally, in September 2018, and subsequently expanded in June 2019, the SEC changed the definition of a smaller reporting company ("SRC"). The change in definition of an SRC allows more registrants to qualify to report under scaled disclosure requirements. Under these rules, CURO met the definition of an SRC as of June 30, 2019. Refer to "--FASB Definition of an SRC as related to the CECL standard and evaluation of the impact of the CECL standard" for information regarding the impact on the Company of meeting the definition of an SRC.

The Condensed Consolidated Financial Statements and the accompanying notes reflect all adjustments (consisting only of adjustments of a normal and recurring nature) which are, in the opinion of management, necessary to present fairly the Company's results of operations, financial position and cash flows for the periods presented. On February 25, 2019, the Company's United Kingdom ("U.K.") segment, as defined by ASC 280, was placed into administration, resulting in the treatment of it as discontinued operations per ASC 205-20. Throughout this Quarterly Report on Form 10-Q ("Form 10-Q"), current and prior-period financial information presents the U.K. segment as discontinued operations as required. For further information about the placement of the segment into administration, refer to "--Nature of Operations" below.

The Condensed Consolidated Financial Statements should be read in conjunction with the Consolidated Financial Statements and related Notes included in the 2018 Form 10-K. Interim results of operations are not necessarily indicative of results that may be expected for future interim periods or for the year ending December 31, 2019.

Principles of Consolidation

The Condensed Consolidated Financial Statements include the accounts of CURO and its wholly-owned subsidiaries. Intercompany transactions and balances have been eliminated in consolidation.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

Equity Investment in Unconsolidated Entity

During the nine months ended September 30, 2019, the Company invested an additional $6.6 million in Cognical Holdings, Inc. ("Zibby"), offset by a $3.7 million carrying value adjustment as a result of the additional investment. As of September 30, 2019, the Company owned 42.3% of Zibby. See Note 8 - "Fair Value Measurements" for additional detail on Zibby's fair value considerations for the nine months ended September 30, 2019.

Use of Estimates

The preparation of Condensed Consolidated Financial Statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenses during the periods reported. Some of the significant estimates that the Company made in the accompanying Condensed Consolidated Financial Statements include allowances for loan losses, certain assumptions related to equity investments, goodwill and intangibles, accruals related to self-insurance, credit services organization ("CSO") liability for losses, and estimated tax liabilities. Actual results may differ from those estimates.

Open-End Loss Recognition

Effective January 1, 2019, the Company modified the timeframe for which it charges-off Open-End loans and made related refinements to its loss provisioning methodology. Prior to January 1, 2019, the Company deemed Open-End loans uncollectible and charged-off when a customer missed a scheduled payment and the loan was considered past due.past-due. Because of the continuingcontinued shift to Open-End loans in Canada and analysis of payment patterns on early-stage versus late-stage delinquencies, the Company revised its estimates and now considers Open-End loans uncollectible when the loan has been contractually past-due for 90 consecutive days. Consequently, past duepast-due Open-End loans and related accrued interest now remain in loans receivable for 90 days before being charged-off against the allowance for loan losses. All recoveries on charged-off loans are credited to the allowance for loan losses. TheQuarterly, the Company evaluates the adequacy of the allowance for loan losses compared to the related gross loans receivable balances that include accrued interest.

The aforementioned change was treated as a change in accounting estimate for accounting purposes and applied prospectively effective January 1, 2019.

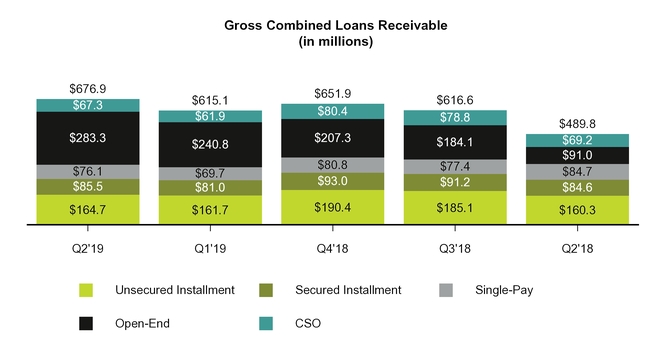

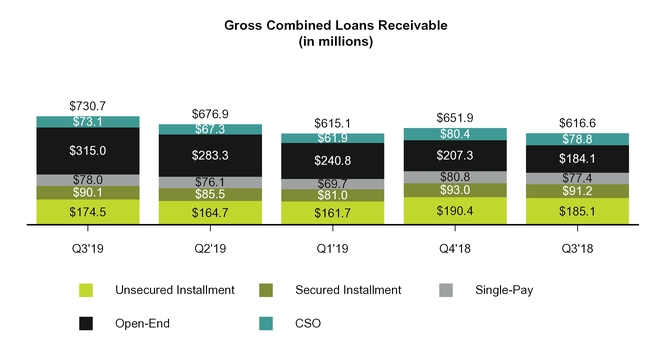

The change affects comparability towith prior periods as follows:

Gross combined loans receivable: balances as of JuneSeptember 30, 2019 include $35.4$46.1 million of Open-End loans that are up to 90 days past-due with related accrued interest, while such balances for periods prior to March 31, 2019 do not include any past duepast-due loans.

Revenues: for the three and sixnine months ended JuneSeptember 30, 2019, gross revenues include interest earned on past-due loan balances of approximately $12$15 million and $21$35 million, respectively, while revenues in prior-year periods do not include comparable amounts.

Provision for Losses: prospectively, from January 1, 2019, past-due, unpaid balances plus related accrued interest charge-off on day 91. Provision expense is affected by total charge-offs less total recoveries ("NCOs") plus changes to the Allowance for loan losses. Because NCOs prospectively include unpaid principal and up to 90 days of related accrued interest, NCO amounts and rates are higher and the Open-End Allowance for loan losses as a percentage of Open-End gross loans receivable is higher. The Open-End Allowance for loan losses as a percentage of Open-End gross loans receivable increased to 18.3%17.2% at JuneSeptember 30, 2019, compared to 10.7%9.8% in the samecomparable prior-year period.

Correction of Immaterial Errors in Previously-Issued Financial Statements

During the year ended December 31, 2018, the Company corrected immaterial errors toin its prior presentation of cash flows for loan originations and collections on principal. The Company determined that the historical presentation was in error by not conforming to US GAAP because it included outflows for loan originations and receipts on collections in Cash provided by operating activities rather than in Cash used in investing activities. Accordingly, the Company corrected previously filed financial statements by reclassifying cash outflows for loan originations and receipts on collections of principal of $48.2$412.4 million from net Cash provided by operating activities to net Cash used in investing activities for the sixnine months ended JuneSeptember 30, 2018. Total cash flows for each period presented did not change. The Company concluded that the errors were immaterial to the unaudited Condensed Consolidated Financial Statements included in the Company’s Quarterly Report on Form 10-Q for the three and sixnine months ended June 30, 2018. The Company has revised its Condensed Consolidated Financial Statements for the six months ended June 30, 2018 presented in this Form 10-Q. A summary of the correction follows:

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

ended September 30, 2018. The Company has revised its Condensed Consolidated Financial Statements for the nine months ended September 30, 2018 presented in this Form 10-Q. A summary of the correction follows (in thousands):

| | | (dollars in thousands) | | Six Months Ended June 30, 2018 | |

| | | | Nine Months Ended September 30, 2018 |

As Reported:(1) | | | | |

| Net cash provided by continuing operating activities | | $ | 52,097 |

| |

| Net cash used in continuing operating activities | | | $ | (55,356 | ) |

| Net cash used in continuing investing activities | | (3,915 | ) | | (8,988 | ) |

| | | | | |

| As Corrected: | | | | |

| Net cash provided by continuing operating activities | | 246,733 |

| | 357,079 |

|

| Net cash used in continuing investing activities | | (198,551 | ) | | (421,423 | ) |

(1) "As reported" balances include amounts from continuing operations historically presented within these captions. |

Recently Adopted Accounting Pronouncements

ASU 2016-02

In February 2016, the Financial Accounting Standards Board ("FASB") issuedestablished Topic 842, Leases, by issuing ASU No. 2016-02, which requires lessees to recognize leases on the balance sheet and disclose key information about leasing arrangements. The Company adopted ASU 2016-02the standard as of January 1, 2019 using the alternative modified retrospective approach,method, also known as the transition relief method, permitted under ASU 2018-11, which provides a method for recording existing leases at adoption and inallows companies to not recast comparative periods that approximatesin the resultsperiod of a full retrospective approach.adoption. The Company elected the package of practical expedients permitted under the transition guidance which, among other things, permits companies to not reassess prior conclusions on lease identification, lease classification and initial direct costs. The Company also elected to combine lease and non-lease components and to exclude short-term leases, defined as having an initial term of 12 months or less, from the Condensed Consolidated Balance Sheets. The Company did not elect the hindsight practical expedient.

Due to

As of September 30, 2019, the adoption of the new standard, theCompany held right of use assets ("ROU assets") and additional operating lease liabilities ("lease liabilities") as of June 30, 2019 were $141.0$118.3 million and $148.8$126.0 million, respectively. Prepaid rent of $2.7 million and deferred liabilityliabilities of $10.9 million were included in ROU assets and lease liabilities, respectively.respectively, at the time of adoption. During the three months ended September 30, 2019, the Company reduced initial opening balances for ROU assets and lease liabilities recorded on January 1, 2019 by $18.0 million as a result of a previous misapplication of certain provisions of Topic 842. The standard did not materially impact of this misapplication on the Company's consolidated net earnings. financial position, results of operations, and cash flows was not material.

ASU 2018-122018-02

In February 2018, the FASB issued ASU 2018-02, Income Statement - Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive income ("ASU 2018-02"), which permits the reclassification to retained earnings of disproportionate tax effects in accumulated other comprehensive income (loss) caused by the Tax Cuts and Jobs Act of 2017 ("2017 Tax Act"). The Company adopted ASU 2018-02 as of January 1, 2019, which did not have a material impact on the Condensed Consolidated Financial Statements.

Recently Issued Accounting Pronouncements Not Yet Adopted

Accounting Pronouncements Related to the Current Expected Credit Loss ("CECL") Standard

ASU 2016-13

In June 2016, the FASB issued ASU 2016-13, “Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,” and subsequent amendments to the guidance: ASU 2018-19 in November 2018, ASU 2019-04 in April 2019 and ASU 2019-05 in May 2019. The standard, as amended, changes how entities will measure credit losses for most financial assets and certain other instruments that are not measured at fair value through net income. The standard will replace the current “incurred loss” approach with an “expected loss” model for instruments measured at amortized cost. For available-for-sale debt securities, entities will be required to record allowances rather than reduce the carrying amount, as they currently do under the

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

other-than-temporary impairment model. The standard also simplifies the accounting model for purchased credit-impaired debt securities and loans. The amendment will affect loans, debt securities, trade receivables, net investments in leases, off-balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. ASU 2019-04 clarifies that equity instruments without readily determinable fair values for which an entity has elected the measurement alternative should be remeasured to fair value as of the date that an observable transaction occurred. ASU 2019-05 provides an option to irrevocably elect to measure certain individual financial assets at fair value instead of amortized cost. The amendments should be applied on either a prospective transition or modified-retrospective approach depending on the subtopic. As issued, this ASU 2016-13 is effective for annual periods beginning after December 15, 2019, and interim periods therein. Early adoption is permitted for annual periods beginning after December 15, 2018, and interim periods therein. The Company is evaluating its alternatives with respect to the available accounting methods under ASU 2016‑13, including the fair value option. If the fair value option is not utilized, adoption of ASU 2016-13 will increase the allowance for credit losses with a resulting negative adjustment to retained earnings on the date of adoption. Additionally, as disclosed below in "--FASB Definition of an SRC as related to the Company is evaluatingCECL standard and evaluation of the impact of the FASB's definition of a SRCCECL standard", the Company expects to defer the adoption of ASU 2016-13.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

2016-13 until at least January 1, 2021.

ASU 2019-05

In May 2019, the FASB issued ASU 2019-05,Financial Instruments - Credit Losses (Topic 326), which amends ASU 2016-13 to allow companies to irrevocably elect, upon adoption of ASU 2016-13, the fair value option on financial instruments that (i) were previously recorded at amortized cost and (ii) are within the scope of ASC 326-203326-20 if the instruments are eligible for the fair value option under ASC 825-10. The fair value option election does not apply to held-to-maturity debt securities. Entities are required to make this election on an instrument-by-instrument basis. ASU 2019-05’s amendments should be applied on a modified-retrospective basis by means of a cumulative-effect adjustment to the opening balance of retained earnings in the statement of financial position as of the date that an entity adopted the amendments in ASU 2016-13. For entities that have adopted ASU 2016-13, the amendments in ASU 2019-05 are effective for fiscal years beginning after December 15, 2019, including interim periods therein. An entity may early adopt the ASU in any interim period after its issuance if the entity has adopted ASU 2016-13. For all other entities, the effective date will be the same as the effective date for ASU 2016-13. We areThe Company expects to elect the option to defer adoption to a later effective date, as further described below in "--FASB Definition of an SRC as related to the CECL standard and evaluation of the impact of the CECL standard." The Company is currently evaluating the methods and impact of adopting this new standard on the Condensed Consolidated Financial Statements.

ASU 2019-04

In May 2019, the FASB issued ASU 2019-04,Codification Improvements to Topic 326, Financial Instruments - Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments, which clarifies certain aspects of accounting for credit losses, hedging activities, and financial instruments. The ASU’s amendments apply to all entities within the scope of the affected guidance. Accrued interest - Amortized cost basis is defined in ASU 2016-13 as "the amount at which a financing receivable or investment is originated or acquired, adjusted for applicable accrued interest, accretion or amortization of premium, discount, and net deferred fees or costs, collection of cash, write-offs, foreign exchange, and fair value hedge accounting adjustments".adjustments." To address stakeholders’ concerns that the inclusion of accrued interest in the definition of amortized cost basis could make application of the credit loss guidance operationally burdensome, ASU 2019-04 provides certain alternatives for the measurement of the allowance for credit losses (ALL)("ALL") on accrued interest receivable (AIR)("AIR"). These measurement alternatives include (1)(i) measuring an ALL on AIR separately, (2)(ii) electing to provide separate disclosure of the AIR component of amortized cost as a practical expedient, and (3)(iii) making accounting policy elections to simplify certain aspects of the presentation and measurement of such AIR. As issued, for entities that have adopted ASU 2016-13, the amendments in ASU 2019-04 related to ASU 2016-13 are effective for fiscal years beginning after December 15, 2019, and interim periods therein. ASU 2019-04’s amendments should be applied "on a modified-retrospective basis by means of a cumulative-effect adjustment to the opening retained earnings balance in the statement of financial position as of the date an entity adopted the amendments in ASU 2016-13." Certain disclosures are also required. For all other entities,Due to the effective date will beFASB's decision to allow a deferment option for SRCs applying ASU 2016-13, the same as the effective date inCompany expects to defer adoption of both ASU 2016-13.2016-13 and ASU 2019-04.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

FASB Definition of a Smaller Reporting Company ("SRC")an SRC as related to the CECL standard and evaluation of the impact of the CECL standard

On July 17,October 16, 2019, the FASB issued forapproved a 30-day comment period a draft proposal that would reconsider its philosophy for establishing effective dates for major projects for certain classes of companies, including SRCs. Under current SEC definitions, CURO meets the definition of an SRC as of June 30, 2019. The proposed standard wouldto defer required adoption of the CECL standard for SRCs until fiscal periods beginning after December 15, 2022. Under current SEC definitions, CURO met the definition of an SRC as of June 30, 2019. The FASB further confirmed that for CECL, a company makes an evaluation of SRC status in accordance with SEC rules at the time of standard effectiveness (i.e., as of June 30, 2019) and that status is effective for purposes of adopting the CECL standard regardless of future changes in SRC status. The FASB is expected to codify the approved proposal with issuance of a new ASU during the fourth quarter of 2019. The Company will continue to monitor the standard settingstandard-setting activities of the FASB and evaluate their potential impact on theexpects to elect to defer adoption of accounting standards such as ASU 2016-13 and ASU 2019-04. We arethe CECL standard. The Company is currently evaluating the methods and impact of adopting the CECL standard on the Condensed Consolidated Financial Statements.

SEC Disclosure Update

In August 2018, the SEC adopted final rules under SEC Release No. 33-10532, Disclosure Update and Simplification, amending certain disclosure requirements that had become redundant, duplicative, overlapping, outdated or superseded. Other than the amendment's expanded disclosure requirement for interim financial statements to disclose both current and comparative quarter and year-to-date reconciliations of changes in stockholders' equity, it did not have a material impact on the Company's Condensed Consolidated Financial Statements or Notes thereto for the three and sixnine months ended JuneSeptember 30, 2019, nor is it expected to have a material impact on the Company's annual disclosuresConsolidated Financial Statements or financial statements.Notes thereto.

NOTE 2 - VARIABLE INTEREST ENTITIES

In August 2018, the Company closed the Non-Recourse Canada SPV facility, whereby certain loan receivables were sold to wholly-owned, bankruptcy-remote special purpose subsidiaries ("VIEs") to collateralize debt incurred under the facility.

As the Company is the primary beneficiary of the VIEs, it includes the assets and liabilities related to the VIEs in its Condensed Consolidated Financial Statements. As required, the Company parenthetically discloses on the Condensed Consolidated Balance Sheets the

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

VIEs’ assets that can only be used to settle the VIEs' obligations and liabilities if the VIEs’ creditors have no recourse against the Company's general credit.

The carrying amounts of consolidated VIEs' assets and liabilities associated with the VIE subsidiaries were as follows:follows (in thousands):

| | | (in thousands) | June 30, 2019 | | December 31, 2018 | |

| | | | September 30, 2019 | | December 31, 2018 |

| Assets | | | | | | | |

| Restricted cash | $ | 14,819 |

| | $ | 12,840 |

| | $ | 21,897 |

| | $ | 12,840 |

|

| Gross loans receivable less allowance for loan losses | 190,121 |

| | 136,187 |

| | 206,158 |

| | 136,187 |

|

| Total Assets | $ | 204,940 |

| | $ | 149,027 |

| | $ | 228,055 |

| | $ | 149,027 |

|

| Liabilities | | | | | | | |

| Accounts payable and accrued liabilities | $ | 15,020 |

| | $ | 4,980 |

| | $ | 7,259 |

| | $ | 4,980 |

|

| Deferred revenue | 45 |

| | 40 |

| | 44 |

| | 40 |

|

| Accrued interest | 713 |

| | 831 |

| | 777 |

| | 831 |

|

| Intercompany payable | | | 93,671 |

| | 44,330 |

|

| Long-term debt | 90,977 |

| | 107,479 |

| | 102,483 |

| | 107,479 |

|

| Total Liabilities | $ | 106,755 |

| | $ | 113,330 |

| | $ | 204,234 |

| | $ | 157,660 |

|

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

NOTE 3 – LOANS RECEIVABLE AND REVENUE

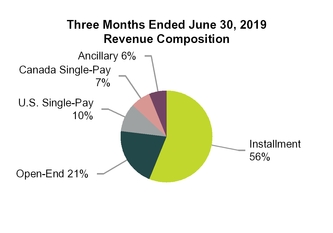

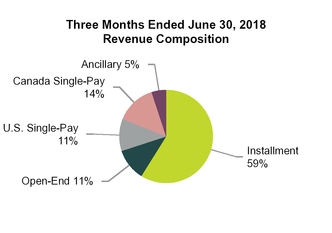

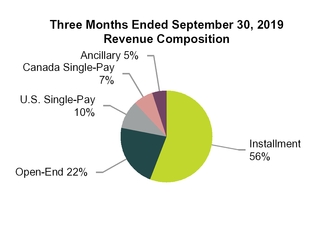

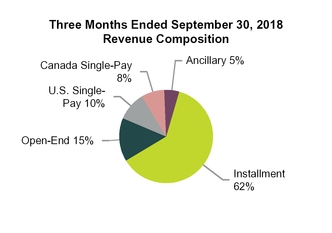

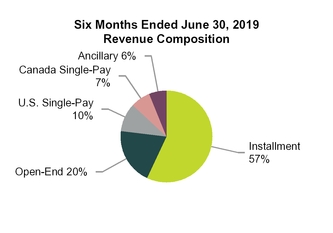

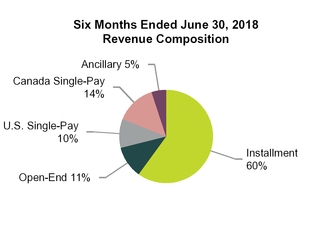

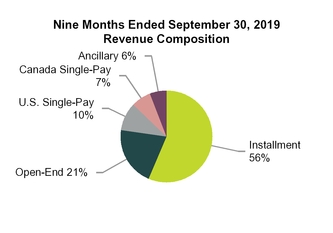

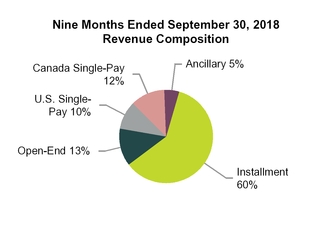

The following table summarizes revenue by product for the periods indicated:indicated (in thousands):

| | | | Three Months Ended June 30, | | Six Months Ended June 30, | | Three Months Ended September 30, | | Nine Months Ended September 30, |

| (in thousands) | 2019 | 2018 | | 2019 | | 2018 | |

| | | | 2019 | | 2018 | | 2019 | | 2018 |

| Unsecured Installment | $ | 122,112 |

| $ | 114,936 |

| | $ | 257,890 |

| | $ | 240,315 |

| | $ | 137,233 |

| | $ | 137,660 |

| | $ | 395,119 |

| | $ | 377,976 |

|

| Secured Installment | 26,076 |

| 25,777 |

| | 53,553 |

| | 52,633 |

| | 28,270 |

| | 28,562 |

| | 81,823 |

| | 81,195 |

|

| Open-End | 54,972 |

| 27,222 |

| | 107,841 |

| | 54,445 |

| | 66,120 |

| | 40,290 |

| | 173,961 |

| | 94,735 |

|

| Single-Pay | 45,528 |

| 58,325 |

| | 92,289 |

| | 118,682 |

| | 49,312 |

| | 50,614 |

| | 141,605 |

| | 169,296 |

|

| Ancillary | 15,612 |

| 10,909 |

| | 30,666 |

| | 21,937 |

| | 16,329 |

| | 12,356 |

| | 46,995 |

| | 34,292 |

|

| Total revenue | $ | 264,300 |

| $ | 237,169 |

| | $ | 542,239 |

| | $ | 488,012 |

| | $ | 297,264 |

| | $ | 269,482 |

| | $ | 839,503 |

| | $ | 757,494 |

|

The following tables summarize Loans receivable by product and the related delinquent loans receivable at JuneSeptember 30, 2019:2019 (in thousands):

| | | | | June 30, 2019 | | September 30, 2019 |

| (in thousands) | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total | |

| | | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total |

| Current loans receivable | | $ | 76,126 |

| $ | 126,685 |

| $ | 71,218 |

| $ | 247,915 |

| $ | 521,944 |

| | $ | 78,039 |

| $ | 127,952 |

| $ | 72,866 |

| $ | 268,918 |

| $ | 547,775 |

|

| Delinquent loans receivable | | — |

| 38,037 |

| 14,216 |

| 35,396 |

| 87,649 |

| | — |

| 46,537 |

| 17,250 |

| 46,053 |

| 109,840 |

|

| Total loans receivable | | 76,126 |

| 164,722 |

| 85,434 |

| 283,311 |

| 609,593 |

| | 78,039 |

| 174,489 |

| 90,116 |

| 314,971 |

| 657,615 |

|

| Less: allowance for losses | | (4,941 | ) | (35,223 | ) | (9,996 | ) | (51,717 | ) | (101,877 | ) | | (5,662 | ) | (38,127 | ) | (10,363 | ) | (54,233 | ) | (108,385 | ) |

| Loans receivable, net | | $ | 71,185 |

| $ | 129,499 |

| $ | 75,438 |

| $ | 231,594 |

| $ | 507,716 |

| | $ | 72,377 |

| $ | 136,362 |

| $ | 79,753 |

| $ | 260,738 |

| $ | 549,230 |

|

| | | | | June 30, 2019 | | September 30, 2019 |

| (in thousands) | | Unsecured Installment | Secured Installment | Open-End | Total | |

| | | | Unsecured Installment | Secured Installment | Open-End | Total |

| Delinquent loans receivable | | | | | | |

| 0-30 days past due | | $ | 14,995 |

| $ | 7,096 |

| $ | 14,997 |

| $ | 37,088 |

| | $ | 17,187 |

| $ | 7,456 |

| $ | 18,734 |

| $ | 43,377 |

|

| 31-60 days past due | | 11,176 |

| 3,358 |

| 9,455 |

| 23,989 |

| | 13,890 |

| 4,711 |

| 13,283 |

| 31,884 |

|

| 61-90 days past due | | 11,866 |

| 3,762 |

| 10,944 |

| 26,572 |

| |

| 61 + days past due | | | 15,460 |

| 5,083 |

| 14,036 |

| 34,579 |

|

| Total delinquent loans receivable | | $ | 38,037 |

| $ | 14,216 |

| $ | 35,396 |

| $ | 87,649 |

| | $ | 46,537 |

| $ | 17,250 |

| $ | 46,053 |

| $ | 109,840 |

|

The following tables summarize Loans receivable by product and the related delinquent loans receivable at December 31, 2018 (in thousands):

|

| | | | | | | | | | | | | | | | |

| | | December 31, 2018 |

| | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total |

| Current loans receivable | | $ | 80,823 |

| $ | 141,316 |

| $ | 75,583 |

| $ | 207,333 |

| $ | 505,055 |

|

| Delinquent loans receivable | | — |

| 49,087 |

| 17,389 |

| — |

| 66,476 |

|

| Total loans receivable | | 80,823 |

| 190,403 |

| 92,972 |

| 207,333 |

| 571,531 |

|

| Less: allowance for losses | | (4,189 | ) | (37,716 | ) | (12,191 | ) | (19,901 | ) | (73,997 | ) |

| Loans receivable, net | | $ | 76,634 |

| $ | 152,687 |

| $ | 80,781 |

| $ | 187,432 |

| $ | 497,534 |

|

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following tables summarize Loans receivable by product and the related delinquent loans receivable at December 31, 2018:

|

| | | | | | | | | | | | | | | | |

| | | December 31, 2018 |

| (in thousands) | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Total |

| Current loans receivable | | $ | 80,823 |

| $ | 141,316 |

| $ | 75,583 |

| $ | 207,333 |

| $ | 505,055 |

|

| Delinquent loans receivable | | — |

| 49,087 |

| 17,389 |

| — |

| 66,476 |

|

| Total loans receivable | | 80,823 |

| 190,403 |

| 92,972 |

| 207,333 |

| 571,531 |

|

| Less: allowance for losses | | (4,189 | ) | (37,716 | ) | (12,191 | ) | (19,901 | ) | (73,997 | ) |

| Loans receivable, net | | $ | 76,634 |

| $ | 152,687 |

| $ | 80,781 |

| $ | 187,432 |

| $ | 497,534 |

|

| | | | | December 31, 2018 | | December 31, 2018 |

| (in thousands) | | Unsecured Installment | Secured Installment | Total | |

| | | | Unsecured Installment | Secured Installment | Total |

| Delinquent loans receivable | | |

|

| | |

|

|

| 0-30 days past due | | $ | 17,850 |

| $ | 7,870 |

| $ | 25,720 |

| | $ | 17,850 |

| $ | 7,870 |

| $ | 25,720 |

|

| 31-60 days past due | | 14,705 |

| 4,725 |

| 19,430 |

| | 14,705 |

| 4,725 |

| 19,430 |

|

| 61-90 days past due | | 16,532 |

| 4,794 |

| 21,326 |

| |

| 61 + days past due | | | 16,532 |

| 4,794 |

| 21,326 |

|

| Total delinquent loans receivable | | $ | 49,087 |

| $ | 17,389 |

| $ | 66,476 |

| | $ | 49,087 |

| $ | 17,389 |

| $ | 66,476 |

|

The following tables summarize loans guaranteed by the Company under CSO programs and the related delinquent receivables at JuneSeptember 30, 2019:2019 (in thousands):

| | | | | June 30, 2019 | | September 30, 2019 |

| (in thousands) | | Unsecured Installment | Secured Installment | Total | |

| | | | Unsecured Installment | Secured Installment | Total |

| Current loans receivable guaranteed by the Company | | $ | 54,968 |

| $ | 1,930 |

| $ | 56,898 |

| | $ | 58,862 |

| $ | 1,966 |

| $ | 60,828 |

|

| Delinquent loans receivable guaranteed by the Company | | 10,087 |

| 354 |

| 10,441 |

| | 11,842 |

| 396 |

| 12,238 |

|

| Total loans receivable guaranteed by the Company | | 65,055 |

| 2,284 |

| 67,339 |

| | 70,704 |

| 2,362 |

| 73,066 |

|

| Less: Liability for losses on CSO lender-owned consumer loans | | (9,433 | ) | (71 | ) | (9,504 | ) | | (10,181 | ) | (68 | ) | (10,249 | ) |

| Loans receivable guaranteed by the Company, net | | $ | 55,622 |

| $ | 2,213 |

| $ | 57,835 |

| | $ | 60,523 |

| $ | 2,294 |

| $ | 62,817 |

|

| | | | | June 30, 2019 | | September 30, 2019 |

| (in thousands) | | Unsecured Installment | Secured Installment | Total | |

| | | | Unsecured Installment | Secured Installment | Total |

| Delinquent loans receivable | | |

|

| | |

|

|

| 0-30 days past due | | $ | 8,511 |

| $ | 299 |

| $ | 8,810 |

| | $ | 9,859 |

| $ | 330 |

| $ | 10,189 |

|

| 31-60 days past due | | 1,052 |

| 37 |

| 1,089 |

| | 1,229 |

| 41 |

| 1,270 |

|

| 61-90 days past due | | 524 |

| 18 |

| 542 |

| |

| 61+ days past due | | | 754 |

| 25 |

| 779 |

|

| Total delinquent loans receivable | | $ | 10,087 |

| $ | 354 |

| $ | 10,441 |

| | $ | 11,842 |

| $ | 396 |

| $ | 12,238 |

|

The following tables summarize loans guaranteed by the Company under CSO programs and the related delinquent receivables at December 31, 2018 (in thousands):

|

| | | | | | | | | | |

| | | December 31, 2018 |

| | | Unsecured Installment | Secured Installment | Total |

| Current loans receivable guaranteed by the Company | | $ | 65,743 |

| $ | 2,504 |

| $ | 68,247 |

|

| Delinquent loans receivable guaranteed by the Company | | 11,708 |

| 446 |

| 12,154 |

|

| Total loans receivable guaranteed by the Company | | 77,451 |

| 2,950 |

| 80,401 |

|

| Less: Liability for losses on CSO lender-owned consumer loans | | (11,582 | ) | (425 | ) | (12,007 | ) |

| Loans receivable guaranteed by the Company, net | | $ | 65,869 |

| $ | 2,525 |

| $ | 68,394 |

|

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following tables summarize loans guaranteed by the Company under CSO programs and the related delinquent receivables at December 31, 2018:

|

| | | | | | | | | | |

| | | December 31, 2018 |

| (in thousands) | | Unsecured Installment | Secured Installment | Total |

| Current loans receivable guaranteed by the Company | | $ | 65,743 |

| $ | 2,504 |

| $ | 68,247 |

|

| Delinquent loans receivable guaranteed by the Company | | 11,708 |

| 446 |

| 12,154 |

|

| Total loans receivable guaranteed by the Company | | 77,451 |

| 2,950 |

| 80,401 |

|

| Less: Liability for losses on CSO lender-owned consumer loans | | (11,582 | ) | (425 | ) | (12,007 | ) |

| Loans receivable guaranteed by the Company, net | | $ | 65,869 |

| $ | 2,525 |

| $ | 68,394 |

|

|

| | | | | | | | | | |

| | | December 31, 2018 |

| | | Unsecured Installment | Secured Installment | Total |

| Delinquent loans receivable | | | | |

| 0-30 days past due | | $ | 9,684 |

| $ | 369 |

| $ | 10,053 |

|

| 31-60 days past due | | 1,255 |

| 48 |

| 1,303 |

|

| 61 + days past due | | 769 |

| 29 |

| 798 |

|

| Total delinquent loans receivable | | $ | 11,708 |

| $ | 446 |

| $ | 12,154 |

|

|

| | | | | | | | | | |

| | | December 31, 2018 |

| (in thousands) | | Unsecured Installment | Secured Installment | Total |

| Delinquent loans receivable | | | | |

| 0-30 days past due | | $ | 9,684 |

| $ | 369 |

| $ | 10,053 |

|

| 31-60 days past due | | 1,255 |

| 48 |

| 1,303 |

|

| 61-90 days past due | | 769 |

| 29 |

| 798 |

|

| Total delinquent loans receivable | | $ | 11,708 |

| $ | 446 |

| $ | 12,154 |

|

The following table summarizes activity in the allowance for loan losses during the three months ended JuneSeptember 30, 2019:2019 (in thousands):

| | | | Three Months Ended June 30, 2019 | Three Months Ended September 30, 2019 |

| (in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | |

| | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total |

| Balance, beginning of period | $ | 3,897 |

| $ | 33,666 |

| $ | 9,796 |

| $ | 46,963 |

| $ | — |

| $ | 94,322 |

| $ | 4,941 |

| $ | 35,223 |

| $ | 9,996 |

| $ | 51,717 |

| $ | — |

| $ | 101,877 |

|

| Charge-offs | (35,759 | ) | (37,336 | ) | (10,295 | ) | (30,688 | ) | (1,342 | ) | (115,420 | ) | (40,512 | ) | (34,252 | ) | (10,592 | ) | (31,993 | ) | (1,382 | ) | (118,731 | ) |

| Recoveries | 24,301 |

| 5,366 |

| 2,693 |

| 5,537 |

| 822 |

| 38,719 |

| 26,599 |

| 5,279 |

| 2,445 |

| 3,791 |

| 845 |

| 38,959 |

|

| Net charge-offs | (11,458 | ) | (31,970 | ) | (7,602 | ) | (25,151 | ) | (520 | ) | (76,701 | ) | (13,913 | ) | (28,973 | ) | (8,147 | ) | (28,202 | ) | (537 | ) | (79,772 | ) |

| Provision for losses | 12,446 |

| 33,514 |

| 7,802 |

| 29,373 |

| 520 |

| 83,655 |

| 14,736 |

| 31,891 |

| 8,514 |

| 31,220 |

| 537 |

| 86,898 |

|

| Effect of foreign currency translation | 56 |

| 13 |

| — |

| 532 |

| — |

| 601 |

| (102 | ) | (14 | ) | — |

| (502 | ) | — |

| (618 | ) |

| Balance, end of period | $ | 4,941 |

| $ | 35,223 |

| $ | 9,996 |

| $ | 51,717 |

| $ | — |

| $ | 101,877 |

| $ | 5,662 |

| $ | 38,127 |

| $ | 10,363 |

| $ | 54,233 |

| $ | — |

| $ | 108,385 |

|

| Allowance for loan losses as a percentage of gross loan receivables | 6.5 | % | 21.4 | % | 11.7 | % | 18.3 | % | N/A |

| 16.7 | % | 7.3 | % | 21.9 | % | 11.5 | % | 17.2 | % | N/A |

| 16.5 | % |

The following table summarizes activity in the liability for losses on CSO lender-owned consumer loans during the three months ended JuneSeptember 30, 2019:2019 (in thousands):

| | | | Three Months Ended

June 30, 2019 | Three Months Ended September 30, 2019 |

| (in thousands) | Unsecured Installment | Secured Installment | Total | |

| | | Unsecured Installment | Secured Installment | Total |

| Balance, beginning of period | $ | 8,583 |

| $ | 78 |

| $ | 8,661 |

| $ | 9,433 |

| $ | 71 |

| $ | 9,504 |

|

| Charge-offs | (34,564 | ) | (683 | ) | (35,247 | ) | (43,072 | ) | (888 | ) | (43,960 | ) |

| Recoveries | 7,078 |

| 657 |

| 7,735 |

| 7,156 |

| 580 |

| 7,736 |

|

| Net charge-offs | (27,486 | ) | (26 | ) | (27,512 | ) | (35,916 | ) | (308 | ) | (36,224 | ) |

| Provision for losses | 28,336 |

| 19 |

| 28,355 |

| 36,664 |

| 305 |

| 36,969 |

|

| Balance, end of period | $ | 9,433 |

| $ | 71 |

| $ | 9,504 |

| $ | 10,181 |

| $ | 68 |

| $ | 10,249 |

|

The following table summarizes activity in the allowance for loan losses and the liability for losses on CSO lender-owned consumer loans, in total, during the three months ended September 30, 2019 (in thousands):

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

|

| | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, 2019 |

| | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total |

| Balance, beginning of period | $ | 4,941 |

| $ | 44,656 |

| $ | 10,067 |

| $ | 51,717 |

| $ | — |

| $ | 111,381 |

|

| Charge-offs | (40,512 | ) | (77,324 | ) | (11,480 | ) | (31,993 | ) | (1,382 | ) | (162,691 | ) |

| Recoveries | 26,599 |

| 12,435 |

| 3,025 |

| 3,791 |

| 845 |

| 46,695 |

|

| Net charge-offs | (13,913 | ) | (64,889 | ) | (8,455 | ) | (28,202 | ) | (537 | ) | (115,996 | ) |

| Provision for losses | 14,736 |

| 68,555 |

| 8,819 |

| 31,220 |

| 537 |

| 123,867 |

|

| Effect of foreign currency translation | (102 | ) | (14 | ) | — |

| (502 | ) | — |

| (618 | ) |

| Balance, end of period | $ | 5,662 |

| $ | 48,308 |

| $ | 10,431 |

| $ | 54,233 |

| $ | — |

| $ | 118,634 |

|

The following table summarizes activity in the allowance for loan losses during the three months ended September 30, 2018 (in thousands):

|

| | | | | | | | | | | | | | | | | | |

| | Three Months Ended September 30, 2018 |

| | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total |

| Balance, beginning of period | $ | 3,604 |

| $ | 30,291 |

| $ | 10,386 |

| $ | 9,717 |

| $ | — |

| $ | 53,998 |

|

| Charge-offs | (40,753 | ) | (32,115 | ) | (11,188 | ) | (32,770 | ) | (1,494 | ) | (118,320 | ) |

| Recoveries | 27,861 |

| 4,807 |

| 2,325 |

| 9,191 |

| 931 |

| 45,115 |

|

| Net charge-offs | (12,892 | ) | (27,308 | ) | (8,863 | ) | (23,579 | ) | (563 | ) | (73,205 | ) |

| Provision for losses | 12,757 |

| 32,946 |

| 9,698 |

| 31,686 |

| 563 |

| 87,650 |

|

| Effect of foreign currency translation | (179 | ) | 231 |

| — |

| 189 |

| — |

| 241 |

|

| Balance, end of period | $ | 3,290 |

| $ | 36,160 |

| $ | 11,221 |

| $ | 18,013 |

| $ | — |

| $ | 68,684 |

|

| Allowance for loan losses as a percentage of gross loan receivables | 4.3 | % | 19.5 | % | 12.3 | % | 9.8 | % | N/A |

| 12.8 | % |

The following table summarizes activity in the liability for losses on CSO lender-owned consumer loans during the three months ended September 30, 2018 (in thousands):

|

| | | | | | | | | |

| | Three Months Ended September 30, 2018 |

| | Unsecured Installment | Secured Installment | Total |

| Balance, beginning of period | $ | 11,193 |

| $ | 426 |

| $ | 11,619 |

|

| Charge-offs | (44,896 | ) | (1,088 | ) | (45,984 | ) |

| Recoveries | 6,901 |

| 665 |

| 7,566 |

|

| Net charge-offs | (37,995 | ) | (423 | ) | (38,418 | ) |

| Provision for losses | 39,552 |

| 490 |

| 40,042 |

|

| Balance, end of period | $ | 12,750 |

| $ | 493 |

| $ | 13,243 |

|

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(unaudited)

The following table summarizes activity in the allowance for loan losses and the liability for losses on CSO lender-owned consumer loans, in total, during the three months ended JuneSeptember 30, 2019:2018 (in thousands):

| | | | Three Months Ended June 30, 2019 | Three Months Ended September 30, 2018 |

| (in thousands) | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total | |

| | | Single-Pay | Unsecured Installment | Secured Installment | Open-End | Other | Total |

| Balance, beginning of period | $ | 3,897 |

| $ | 42,249 |

| $ | 9,874 |

| $ | 46,963 |

| $ | — |

| $ | 102,983 |

| $ | 3,604 |

| $ | 41,484 |

| $ | 10,812 |

| $ | 9,717 |

| $ | — |

| $ | 65,617 |

|

| Charge-offs | (35,759 | ) | (71,900 | ) | (10,978 | ) | (30,688 | ) | (1,342 | ) | (150,667 | ) | (40,753 | ) | (77,011 | ) | (12,276 | ) | (32,770 | ) | (1,494 | ) | (164,304 | ) |

| Recoveries | 24,301 |

| 12,444 |

| 3,350 |

| 5,537 |

| 822 |

| 46,454 |

| 27,861 |

| 11,708 |

| 2,990 |

| 9,191 |

| 931 |

| 52,681 |

|

| Net charge-offs | (11,458 | ) | (59,456 | ) | (7,628 | ) | (25,151 | ) | (520 | ) | (104,213 | ) | (12,892 | ) | (65,303 | ) | (9,286 | ) | (23,579 | ) | (563 | ) | (111,623 | ) |

| Provision for losses | 12,446 |

| 61,850 |

| 7,821 |

| 29,373 |

| 520 |

| 112,010 |

| 12,757 |

| 72,498 |

| 10,188 |

| 31,686 |

| 563 |

| 127,692 |

|

| Effect of foreign currency translation | 56 |

| 13 |

| — |

| 532 |

| — |

| 601 |

| (179 | ) | 231 |