UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON,Washington, D.C. 20549

FORM 20-F

(Mark One)oREGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

OR

|

|

|

|

|

For fiscal year ended December 31, 2009

OR

��oTRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

o

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934For the transition period from

_______________________ to__________________________OR

o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

o

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934Date of

theevent requiring this shell companyreportreport:

________________________Commission file number: 0-31062

|

ONCOLYTICS BIOTECH INC.

(Exact name of Registrant as specified in its charter)

Province of Alberta, Canada

(Jurisdiction of incorporation or organization)

Suite 210, 1167 Kensington Crescent, N. W.N.W. Calgary, Alberta, T2N 1X7 (403) 670-7377

(Address of principal executive offices)

Doug Ball

info@oncolytics.ca, Suite 210, 1167 Kensington Crescent, N. W.N.W. Calgary, Alberta, T2N 1X7

Tel: (403) 670-7377

E-mail: info@oncolytics.ca

(Name, telephone, email,Telephone, E-mail and/or Facsimile number and addressAddress of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

| Title of Each Class | Name of each exchange on which registered |

Common Shares, no par value |

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

None

(Title of Class)1

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Not Applicable

Indicate the number of outstanding shares of each of the Registrant’s classes of capital ofor common stock as of the close of the period covered by the annual report: 61,549,969 common shares as at December 31, 2008: 200943,830,748 Common Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

| Yes o No x |

If this report is an annual report or transition report, indicate by check mark if the registrantRegistrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

|

| Yes o No x |

Indicate by check mark whether the registrantRegistrant (1) has filed all reports required to be filed by Section 13 or 15 (d)15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesx No o |

|

|

Indicate by check mark whether the registrantRegistrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer”filer and “largelarge accelerated filer” in Rule 12b-2 of the Exchange ActAct. (Check one)

Large accelerated filer oAccelerated filer xNon-accelerated filer o |

|

|

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP o Other | x | International Reporting Standards as issued by the International Accounting Standards Board | o |

|

|

|

If “Other” has been checked in response to the previous questions,question, indicate by check mark which financial statement item the registrant has elected to follow.follow:

o Item 17 xo Item 18x

If this is an annual report, indicate by check mark whether the registrantRegistrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

|

|

|

2

ONCOLYTICS BIOTECH INC.

FORM 20-F

TABLE OF CONTENTS

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

|

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE |

|

ITEM 3. KEY INFORMATION |

|

ITEM 4. INFORMATION ON THE COMPANY |

|

|

|

ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS |

|

ITEM 6. DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES |

|

ITEM 7. MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS |

|

ITEM 8. FINANCIAL INFORMATION |

|

ITEM 9. THE OFFER AND LISTING |

|

ITEM 10. ADDITIONAL INFORMATION |

|

ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

|

ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES |

|

ITEM 13. DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES |

|

ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

|

ITEM 15. CONTROLS AND PROCEDURES |

|

ITEM 16A. AUDIT COMMITTEE FINANCIAL EXPERT |

|

ITEM 16B. CODE OF ETHICS |

|

ITEM 16C. PRINCIPAL ACCOUNTANT FEES AND |

|

ITEM 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES |

|

ITEM 16E. PURCHASE OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASES |

|

ITEM 16F. CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANTS |

|

ITEM 16.G. CORPORATE GOVERNANCE |

|

ITEM 17. FINANCIAL STATEMENTS |

|

ITEM |

|

ITEM 19. |

|

3

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this annual report and the documents attached as exhibits to this annual report constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Oncolytics Biotech Inc., or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements are statements that are not historical facts, and include, but are not limited to, estimates and their underlying assumptions; statements regarding plans, objectives and expectations with respect to the efficacy of our technologies; the timing and results of clinical studies related to our technologies; future operations, products and services; the impact of regulatory initiatives on our operations; the size of and opportunities related to the markets for our technologies; general industry and macroeconomic growth rates; expectations related to possible joint and/or strategic ventures and statements regarding future performance. Forward-looking statements generally, but not always, are identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates,” “projects”, “potential”, “possible” and similar expressions, or that events or conditions “will,” “may,” “could” or “should” occur.

The forward-looking statements in this annual report are subject to various risks and uncertainties, most of which are difficult to predict and generally beyond our control, including without limitation:

• | risks related all of our products, including REOLYSIN®, being in the research and development stage and requiring further development and testing before they can be marketed commercially; |

risks inherent in pharmaceutical research and development;

risks related to our pharmaceutical products being subject to intense regulatory approval processes;

risks related to the extremely competitive biotechnology industry and our competition with larger companies with greater resources;

risks related to our reliance on patents and proprietary rights to protect our technology;

risks related to potential products liability claims;

risks related to our limited manufacturing experience and reliance on third parties to commerically manufacture our products, if and when developed;

risks related to our new products not being accepted by the medical community or consumers;

risks related to our technologies becoming obsolete;

risks related to our dependence on third party relationships for research and clinical trials;

risks related to our lack of operating revenues and history of losses;

uncertainty asregarding our ability to obtain third-party reimbursement for the costs of our product;

risks related to our ability to achieve the goals and satisfy assumptions of management;

the uncertainties related to the outcome of clinical studies and the long process related to such studies;

|

|

our need forobtain additional financing which may not be available on acceptable terms or at all;

uncertainty as to whether we will be able to complete any licensing, partnering or marketing arrangements for our technologies;

uncertainty as to the market acceptancefund future research and development of our products and to meet ongoing capital requirements;

risks related to potential increases in the cost of director and officer liability insurance;

risks related to our abilitydependence on key employees and collaborators;

risks related to generate sufficient revenuesBarbados law;

risks related to makethe effect of changes in the law on our productscorporate structure;

risks related to expenses in foreign currencies and technologies commercially viable;our exposure to foreign currency exchange rate fluctuations;

risk related to possible “passive foreign investment company” status;

4

the intense competition

risks related to fluctuations in the biotechnology industryinterest rates; and risks related to changing technologyour common shares.

This list is not exhaustive of the factors that may render our technology obsolete;affect any of the Company’s forward-looking statements. Some of the important risks and

other factors identified uncertainties that could affect forward-looking statements are described further under the section heading “Risk“Item 3. Key Information – D. Risk Factors” in this annual report , and those that are discussed or identified in our other public filings with the SEC.

below. If one or more of these risks or uncertainties materializes, or if underlying assumptions prove incorrect, our actual results may vary materially from those expected, estimated or projected. Forward-looking statements in this document are not a prediction of future events or circumstances, and those future events or circumstances may not occur. Given these uncertainties, users of the information included herein, including investors and prospective investors are cautioned not to place undue reliance on such forward-looking statements. Investors should consult our quarterly and annual filings with Canadian and U.S. securities commissions for additional information on risks and uncertainties relating to forward-looking statements. We do not assume responsibility for the accuracy and completeness of these statements.

Forward-looking statements are based on our beliefs, opinions and expectations at the time they are made, and we do not assume any obligation to update our forward-looking statements if those beliefs, opinions, or expectations, or other circumstances, should change, except as required by applicable law.

All references in this annual report on Form 20-F to the terms “we”, “our”, “us”, “the Company” and “Oncolytics” refer to Oncolytics Biotech Inc.

1

CURRENCY AND EXCHANGE RATES

Canadian Dollars Per U.S. Dollar

The following table sets out the exchange rates for one United States dollar (“US$”) expressed in terms of one Canadian dollar (“Cdn$”) in effect at the end of the following periods, and the average exchange rates (based on the average of the exchange rates on the last day of each month in such periods) and the range of high and low exchange rates for such periods.

| Canadian Dollars Per U.S. Dollars | Canadian Dollars Per U.S. Dollars | |||||||||

| 2008 | 2007 | 2006 | 2005 | 2004 | 2009 | 2008 | 2007 | 2006 | 2005 | 2004 |

Average for the period | 0.9441 | 0.9348 | 0.8820 | 0.8259 | 0.7697 | 0.8760 | 0.9441 | 0.9348 | 0.8820 | 0.8259 | 0.7697 |

Low for the period | 1.0289 | 1.0905 | 0.9099 | 0.8690 | 0.8493 | 0.9755 | 1.0289 | 1.0905 | 0.9099 | 0.8690 | 0.8493 |

|

|

| |||||||||

For the Month of | For the Month of | For the Month of | ||||||||||

| February | January | December | November | October | September | February 2010 | January 2010 | December 2009 | November 2009 | October 2009 | September 2009 |

High for the period | 0.7758 | 0.7849 | 0.7711 | 0.7779 | 0.7726 | 0.9263 | 0.9283 | 0.9350 | 0.9304 | 0.9234 | 0.9123 | 0.9007 |

Low for the period | 0.8202 | 0.8458 | 0.8358 | 0.8696 | 0.9426 | 0.9673 | 0.9642 | 0.9780 | 0.9647 | 0.9590 | 0.9755 | 0.9442 |

Exchange rates are based on the Bank of Canada nominal noon exchange rates. The nominal noon exchange rate on March 6, 200911, 2010 as reported by the Bank of Canada for the conversion of United States dollars into Canadian dollars was US$1.00 = Cdn$1.2863.1.0265. Unless otherwise indicated, in this annual report on Form 20-F, all references herein are to Canadian Dollars.

2

5

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable

ITEM 3. KEY INFORMATION

| A. | Selected Financial Data |

The following table of selected financial data has been derived from financial statements prepared in accordance with Canadian generally accepted accounting principles (“GAAP”) which have been reconciled with U.S. GAAP in accordance with Item 18 (see note 2223 of the audited financial statements). The data is qualified by reference to, and should be read in conjunction with, the audited financial statements, and related notes thereto, prepared in accordance with Canadian GAAP (See Item 18, "Financial Statements"). All dollar amounts are expressed in Canadian dollars. For exchange rate data please see the section heading “Currency and Exchange Rates” above.

| 2008 | 2007 | 2006 | 2005 | 2004 |

Revenues | — | — | — | — | — |

Net loss, Canadian GAAP(2) | 17,550,204 | 15,950,426 | 14,628,291 | 13,256,271 | 13,640,338 |

Net loss, U.S. GAAP(2) | 17,188,704 | 15,588,926 | 14,266,791 | 12,894,771 | 13,278,838 |

Basic and diluted loss per share, Canadian GAAP(2), (3), (4) | 0.42 | 0.39 | 0.40 | 0.40 | 0.47 |

Basic and diluted loss per share, U.S. GAAP(2), (3), (4) | 0.42 | 0.39 | 0.39 | 0.39 | 0.46 |

Total assets, Canadian GAAP (1), (3), (4) | 13,987,195 | 26,297,567 | 29,389,636 | 42,449,038 | 36,117,793 |

Total assets, U.S. GAAP(1), (3), (4) | 13,806,445 | 25,755,317 | 28,485,886 | 41,183,788 | 34,491,043 |

Shareholders’ equity, Canadian GAAP (4) | 9,453,084 | 23,476,340 | 26,773,217 | 40,756,556 | 35,168,536 |

Shareholders’ equity, U.S. GAAP(4) | 9,272,334 | 22,934,090 | 25,869,467 | 39,491,306 | 33,541,786 |

Cash dividends declared per share(5) | Nil | Nil | Nil | Nil | Nil |

Weighted average number of common shares outstanding | 41,369,515 | 40,428,825 | 36,346,266 | 32,804,540 | 29,028,391 |

2009 | 2008 | 2007 | 2006 | 2005 | |

Revenues | — | — | — | — | — |

Net loss, Canadian GAAP(2) | 16,231,249 | 17,550,204 | 15,950,426 | 14,628,291 | 13,256,271 |

Net loss, U.S. GAAP(2) | 14,999,569 | 17,188,704 | 15,588,926 | 14,266,791 | 12,894,771 |

Basic and diluted loss per share, Canadian GAAP(2), (3) | 0.33 | 0.42 | 0.39 | 0.40 | 0.40 |

Basic and diluted loss per share, U.S. GAAP(2), (3) | 0.30 | 0.42 | 0.39 | 0.39 | 0.39 |

Total assets, Canadian GAAP (1), (3) | 35,593,391 | 13,987,195 | 26,297,567 | 29,389,636 | 42,449,038 |

Total assets, U.S. GAAP(1), (3) | 35,593,391 | 13,806,445 | 25,755,317 | 28,485,886 | 41,183,788 |

Shareholders’ equity, Canadian GAAP(3) | 31,366,458 | 9,453,084 | 23,476,340 | 26,773,217 | 40,756,556 |

Shareholders’ equity, U.S. GAAP(3) | 30,343,407 | 9,272,334 | 22,934,090 | 25,869,467 | 39,491,306 |

Cash dividends declared per share(4) | Nil | Nil | Nil | Nil | Nil |

Weighted average number of common shares outstanding | 49,370,175 | 41,369,515 | 40,428,825 | 36,346,266 | 32,804,540 |

Notes:

| 1) | Subsequent to the acquisition of Oncolytics Biotech Inc. by SYNSORB in April 1999, we applied push down accounting. See note 2 to the audited financial statements for 2008. |

| 2) | Included in net loss and net loss per share is stock based compensation expense of |

| 3) | We issued 17,524,211 common shares for net cash proceeds of $37,052,900 and 200,000 common shares for a $684,000 investment in British Canadian Biosciences Corp. (2008 – 2,650,000 commons shares for net cash proceeds of |

3

6

| 4) |

|

| We have not declared or paid any dividends since incorporation. |

| B. | Capitalization and Indebtedness |

Not Applicable

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable

| D. | Risk Factors |

Investment in shares of our common stock ("Common Shares") involves a degree of risk. These risks should be carefully considered before any investment decision is made. The following are some of the key risk factors generally associated with our business. However, the risks described below are not the only ones that we face. Additional risks not currently known to us, or that we currently deem immaterial, may also impair our business operations.

All of our potential products, including REOLYSIN®, are in the research and development stage and will require further development and testing before they can be marketed commercially.

Prospects for companies in the biotechnology industry generally may be regarded as uncertain given the nature of the industry and, accordingly, investments in biotechnology companies should be regarded as speculative. We are currently in the research and development stage on one product, REOLYSIN®, for human application, the riskiest stage for a company in the biotechnology industry. It is not possible to predict, based upon studies in animals and early stage human clinical trials, whether REOLYSIN® will prove to be safe and effective in humans. REOLYSIN® will require additional research and development, including extensive additional clinical testing, before we will be able to obtain the approvals of the relevant regulatory authorities in applicable countries to market REOLYSIN® commercially. There can be no assurance that the research and development programs we conducted will result in REOLYSIN® or any other products becoming commercially viable products, and in the event that any product or products result from the research and development program, it is unlikely they will be commercially available for a number of years.

To achieve profitable operations we, alone or with others, must successfully develop, introduce and market our products. To obtain regulatory approvals for products being developed for human use, and to achieve commercial success, human clinical trials must demonstrate that the product is safe for human use and that the product shows efficacy. Unsatisfactory results obtained from a particular study relating to a program may cause us to abandon our commitment to that program or the product being tested. No assurances can be provided that any current or future animal or human test, if undertaken, will yield favourable results. If we are unable to establish that REOLYSIN® is a safe, effective treatment for cancer, we may be required to abandon further development of the product and develop a new business strategy.

4

7

There are inherent risks in pharmaceutical research and development.

Pharmaceutical research and development is highly speculative and involves a high and significant degree of risk. The marketability of any product we develop will be affected by numerous factors beyond our control, including but not limited to:

the discovery of unexpected toxicities or lack of sufficient efficacy of products which make them unattractive or unsuitable for human use;

preliminary results as seen in animal and/or limited human testing may not be substantiated in larger, controlled clinical trials;

manufacturing costs or other production factors may make manufacturing of products ineffective, impractical and non-competitive;

proprietary rights of third parties or competing products or technologies may preclude commercialization;

requisite regulatory approvals for the commercial distribution of products may not be obtained; and

other factors may become apparent during the course of research, up-scaling or manufacturing which may result in the discontinuation of research and other critical projects.

Our products under development have never been manufactured on a commercial scale, and there can be no assurance that such products can be manufactured at a cost or in a quantity to render such products commercially viable. Production and utilization of our products may require the development of new manufacturing technologies and expertise. The impact on our business in the event that new manufacturing technologies and expertise are required to be developed is uncertain. There can be no assurance that we will successfully meet any of these technological challenges or others that may arise in the course of development.

Pharmaceutical products are subject to intense regulatory approval processes.

The regulatory process for pharmaceuticals, which includes preclinical studies and clinical trials of each compound to establish its safety and efficacy, takes many years and requires the expenditure of substantial resources. Moreover, if regulatory approval of a drug is granted, such approval may entail limitations on the indicated uses for which it may be marketed. Failure to comply with applicable regulatory requirements can, among other things, result in suspension of regulatory approvals, product recalls, seizure of products, operating restrictions and criminal prosecution. Further, government policy may change, and additional government regulations may be established that could prevent or delay regulatory approvals for our products. In addition, a marketed drug and its manufacturer are subject to continual review. Later discovery of previously unknown problems with the product or manufacturer may result in restrictions on such product or manufacturer, including withdrawal of the product from the market.

The U.S. FDA and similar regulatory authorities in other countries may deny approval of a new drug application if required regulatory criteria are not satisfied, or may require additional testing. Product approvals may be withdrawn if compliance with regulatory standards is not maintained or if problems occur after the product reaches the market. The FDA and similar regulatory authorities in other countries may require further testing and surveillance programs to monitor the pharmaceutical product that has been commercialized. Non-compliance with applicable requirements can result in fines and other judicially imposed sanctions, including product withdrawals, product seizures, injunction actions and criminal prosecutions.

In addition to our own pharmaceuticals, we may supply active pharmaceutical ingredients and advanced pharmaceutical intermediates for use in our customers’ drug products. The final drug products in which the pharmaceutical ingredients and advanced pharmaceutical intermediates are used, however, are subject to regulation for safety and efficacy by the FDA and possibly other regulatory authorities in other jurisdictions. Such products must be approved by such agencies before they can be commercially marketed. The process of obtaining regulatory clearance for marketing is uncertain, costly and time consuming. We cannot predict how long the necessary regulatory approvals will take or whether our customers will ever obtain such approval for their products. To the extent that our customers do not obtain the necessary regulatory approvals for marketing new products, our product sales could be adversely affected.

5

8

The FDA and other governmental regulators have increased requirements for drug purity and have increased environmental burdens upon the pharmaceutical industry. Because pharmaceutical drug manufacturing is a highly regulated industry, requiring significant documentation and validation of manufacturing processes and quality control assurance prior to approval of the facility to manufacture a specific drug, there can be considerable transition time between the initiation of a contract to manufacture a product and the actual initiation of manufacture of that product. Any lag time in the initiation of a contract to manufacture product and the actual initiation of manufacture could cause us to lose profits or incur liabilities.

The pharmaceutical regulatory regime in Europe and other countries is generally similar to that of the United States. We could face similar risks in these other jurisdictions as the risks described above.

Our operations and products may be subject to other government manufacturing and testing regulations.

Securing regulatory approval for the marketing of therapeutics by the FDA in the United States and similar regulatory agencies in other countries is a long and expensive process, which can delay or prevent product development and marketing. Approval to market products may be for limited applications or may not be received at all.

The products we anticipate manufacturing will have to comply with the FDA’s current Good Manufacturing Practices (“cGMP”) and other FDA and local government guidelines and regulations, including other international regulatory requirements and guidelines. Additionally, certain of our customers may require the manufacturing facilities contracted by us to adhere to additional manufacturing standards, even if not required by the FDA. Compliance with cGMP regulations requires manufacturers to expend time, money and effort in production and to maintain precise records and quality control to ensure that the product meets applicable specifications and other requirements. The FDA and other regulatory bodies periodically inspect drug-manufacturing facilities to ensure compliance with applicable cGMP requirements. If the manufacturing facilities contracted by us fail to comply with the cGMP requirements, the facilities may become subject to possible FDA or other regulatory action and manufacturing at the facility could consequently be suspended. We may not be able to contract suitable alternative or back-up manufacturing facilities on terms acceptable to us or at all.

The FDA or other regulatory agencies may also require the submission of any lot of a particular product for inspection. If the lot product fails to meet the FDA requirements, then the FDA could take any of the following actions: (i) restrict the release of the product; (ii) suspend manufacturing of the specific lot of the product; (iii) order a recall of the lot of the product; or (iv) order a seizure of the lot of the product.

We are subject to regulation by governments in many jurisdictions. If we do not comply with healthcare, drug, manufacturing and environmental regulations, among others, our existing and future operations may be curtailed, and we could be subject to liability.

In addition to the regulatory approval process, we may be subject to regulations under local, provincial, state, federal and foreign law, including, but not limited to, requirements regarding occupational health, safety, laboratory practices, environmental protection and hazardous substance control, and may be subject to other present and future local, provincial, state, federal and foreign regulations.

The biotechnology industry is extremely competitive and we must successfully compete with larger companies with substantially greater resources.

Technological competition in the pharmaceutical industry is intense and we expect competition to increase. Other companies are conducting research on therapeutics involving the Ras pathway as well as other novel treatments or therapeutics for the treatment of cancer which may compete with our product. Many of these competitors are more established, benefit from greater name recognition and have substantially greater financial, technical and marketing resources than us. In addition, many of these competitors have significantly greater experience in undertaking research, preclinical studies and human clinical trials of new pharmaceutical products, obtaining regulatory approvals and manufacturing and marketing such products. In addition, there are several other companies and products with which we may compete from time to time, and which may have significantly better and larger resources than we do. Accordingly, our competitors may succeed in manufacturing and/or commercializing products

6

9

more rapidly or effectively, which could have a material adverse effect on our business, financial condition or results of operations.

We anticipate that we will face increased competition in the future as new products enter the market and advanced technologies become available. There can be no assurance that existing products or new products developed by our competitors will not be more effective, or be more effectively manufactured, marketed and sold, than any that may be developed or sold by us. Competitive products may render our products obsolete and uncompetitive prior to recovering research, development or commercialization expenses incurred with respect to any such products.

We rely on patents and proprietary rights to protect our technology.

Our success will depend, in part, on our ability to obtain patents, maintain trade secret protection and operate without infringing the rights of third parties. We have received Granted Patents in countries throughout the world, including the United States, Canada, Europe, and Japan. We file our Applications for Patent in the United States and under the PCT, allowing us to subsequently file in other jurisdictions. See “Narrative Description—Patent and Patent Application Summary”. Our success will depend, in part, on our ability to obtain, enforce and maintain patent protection for our technology in Canada, the United States and other countries. We cannot be assured that patents will issue from any pending applications or that claims now or in the future, if any, allowed under issued patents will be sufficiently broad to protect our technology. In addition, no assurance can be given that any patents issued to, or licensed by us, will not be challenged, invalidated, infringed or circumvented, or that the rights granted thereunder will provide continuing competitive advantages to us.

The patent positions of pharmaceutical and biotechnology firms, including us, are generally uncertain and involve complex legal and factual questions. In addition, it is not known whether any of our current research endeavours will result in the issuance of patents in Canada, the United States, or elsewhere, or if any patents already issued will provide significant proprietary protection or will be circumvented or invalidated. Since patent applications in the United States and Canada may be maintained in secrecy until at least 18 months after filing of the original priority application, and since publication of discoveries in the scientific or patent literature tends to lag behind actual discoveries by several months, we cannot be certain that we or any licensor were the first to create inventions claimed by pending patent applications or that we or the licensor were the first to file patent applications for such inventions. Loss of patent protection could lead to generic competition for these products, and others in the future, which would materially and adversely affect our financial prospects for these products.

Similarly, since patent applications filed before November 29, 2000 in the United States may be maintained in secrecy until the patents issue or foreign counterparts, if any, publish, we cannot be certain that we or any licensor were the first creator of inventions covered by pending patent applications or that we or such licensor were the first to file patent applications for such inventions. There is no assurance that our patents, if issued, would be held valid or enforceable by a court or that a competitor’s technology or product would be found to infringe such patents.

Accordingly, we may not be able to obtain and enforce effective patents to protect our proprietary rights from use by competitors. If other such parties obtain patents for certain information relied on by us in conducting our business, then we may be required to stop using, or pay to use, certain intellectual property, and as such, our competitive position and profitability could suffer as a result.

In addition, we may be required to obtain licenses under patents or other proprietary rights of third parties. No assurance can be given that any licenses required under such patents or proprietary rights will be available on terms acceptable to us. If we do not obtain such licenses, we could encounter delays in introducing one or more of our products to the market while we attempt to design around such patents, or we could find that the development, manufacture or sale of products requiring such licenses could be foreclosed. In addition, we could incur substantial costs in defending ourselves in suits brought against us on such patents or in suits in which our attempts to enforce our own patents against other parties.

Our products may fail or cause harm, subjecting us to product liability claims.

Use of our product during current clinical trials may entail risk of product liability. We maintain clinical trial liability insurance; however, it is possible this coverage may not provide full protection against all risks. Given the

7

10

scope and complexity of the clinical development process, the uncertainty of product liability litigation, and the shrinking capacity of insurance underwriters, it is not possible at this time to assess the adequacy of current clinical trial coverage, nor the ability to secure continuing coverage at the same level and at reasonable cost in the foreseeable future. While we carry, and intend to continue carrying amounts believed to be appropriate under the circumstances, it is not possible at this time to determine the adequacy of such coverage.

In addition, the sale and commercial use of our product entails risk of product liability. We currently do not carry any product liability insurance for this purpose. There can be no assurance that we will be able to obtain appropriate levels of product liability insurance prior to any sale of our pharmaceutical products. An inability to obtain insurance on economically feasible terms or to otherwise protect against potential product liability claims could inhibit or prevent the commercialization of products developed by us. The obligation to pay any product liability claim or a recall of a product could have a material adverse effect on our business, financial condition and future prospects.

We have limited manufacturing experience and intend to rely on third parties to commercially manufacture our products, if and when developed.

To date, we have relied upon a contract manufacturer to manufacture small quantities of REOLYSIN®. The manufacturer may encounter difficulties in scaling up production, including production yields, quality control and quality assurance. Only a limited number of manufacturers can supply therapeutic viruses and failure by the manufacturer to deliver the required quantities of REOLYSIN® on a timely basis at a commercially reasonable price may have a material adverse effect on us. We have completed a program for the development of a commercial process for manufacturing REOLYSIN® and have filed a number of patent applications related to the process. There can be no assurance that we will successfully obtain sufficient patent protection related to our manufacturing process.

New products may not be accepted by the medical community or consumers.

Our primary activity to date has been research and development and we have no experience in marketing or commercializing products. We will likely rely on third parties to market our products, assuming that they receive regulatory approvals. If we rely on third parties to market our products, the commercial success of such product may be outside of our control. Moreover, there can be no assurance that physicians, patients or the medical community will accept our product, even if it proves to be safe and effective and is approved for marketing by Health Canada, the FDA and other regulatory authorities. A failure to successfully market our product would have a material adverse effect on our revenue.

Our technologies may become obsolete.

The pharmaceutical industry is characterized by rapidly changing markets, technology, emerging industry standards and frequent introduction of new products. The introduction of new products embodying new technologies, including new manufacturing processes and the emergence of new industry standards may render our products obsolete, less competitive or less marketable. The process of developing our products is extremely complex and requires significant continuing development efforts and third party commitments. Our failure to develop new technologies and products and the obsolescence of existing technologies could adversely affect our business.

We may be unable to anticipate changes in our potential customer requirements that could make our existing technology obsolete. Our success will depend, in part, on our ability to continue to enhance our existing technologies, develop new technology that addresses the increasing sophistication and varied needs of the market, and respond to technological advances and emerging industry standards and practices on a timely and cost-effective basis. The development of our proprietary technology entails significant technical and business risks. We may not be successful in using our new technologies or exploiting our niche markets effectively or adapting our businesses to evolving customer or medical requirements or preferences or emerging industry standards.

We are highly dependent on third-party relationships for research and clinical trials.

We rely upon third party relationships for assistance in the conduct of research efforts, pre-clinical development and clinical trials, and manufacturing. In addition, we expect to rely on third parties to seek regulatory approvals for and

8

11

to market our product. Although we believe that our collaborative partners will have an economic motivation to commercialize our product included in any collaborative agreement, the amount and timing of resources diverted to these activities generally is expected to be controlled by the third party. Furthermore, if we cannot maintain these relationships, our business may suffer.

We have no operating revenues and a history of losses.

To date, we have not generated sufficient revenues to offset our research and development costs and, accordingly, have not generated positive cash flow or made an operating profit. As of December 31, 2008,2009, we had an accumulated deficit of $102.6$118.8 million and we incurred net losses of $16.2 million, $17.6 million, $16.0 million, and $14.6$16.0 million, for the years ended December 31, 2009, 2008, 2007, and 2006,2007, respectively. We anticipate that we will continue to incur significant losses during 2009 and in the foreseeable future. We do not expect to reach profitability at least until after successful and profitable commercialization of one or more of our products. Even if one or more of our products are profitably commercialized, the initial losses incurred by us may never be recovered.

We may not be able to obtain third-party reimbursement for the cost of our product.

Uncertainty exists regarding the reimbursement status of newly-approved pharmaceutical products and reimbursement may not be available for REOLYSIN®. Any reimbursements granted may not be maintained or limits on reimbursements available from third-party payors may reduce the demand for, or negatively affect the price of, these products. If REOLYSIN® does not qualify for reimbursement, if reimbursement levels diminish, or if reimbursement is denied, our sales and profitability would be adversely affected.

Third-Party Risk

In the normal course of our business, we have entered into contractual arrangements with third parties which subject us to the risk that such parties may default on their obligations. Oncolytics may be exposed to third party credit risk through our contractual arrangements with our current contract manufacturer, the institutions which operate our clinical trials, or our contract research organizations and other parties. In the event such entities fail to meet their contractual obligations to Oncolytics, such failures could have a material adverse effect on Oncolytics and our operations.

We may need additional financing in the future to fund the research and development of our products and to meet our ongoing capital requirements.

As of December 31, 2008,2009, we had cash and cash equivalents (including short-term investments) of $13.3$34.1 million and working capital of approximately $9.0$30.5 million. We anticipate that we will need additional financing in the future to fund research and development and to meet our ongoing capital requirements. The amount of future capital requirements will depend on many factors, including continued scientific progress in our drug discovery and development programs, progress in our pre-clinical and clinical evaluation of drug candidates, time and expense associated with filing, prosecuting and enforcing our patent claims and costs associated with obtaining regulatory approvals. In order to meet such capital requirements, we will consider contract fees, collaborative research and development arrangements, and additional public or private financings (including the incurrence of debt and the issuance of additional equity securities) to fund all or a part of particular programs as well as potential partnering or licensing opportunities.

As a result of the weakened global economic situation, Oncolytics, along with all other pharmaceutical research and development entities, may have restricted access to capital, bank debt and equity, and is likely to face increased borrowing costs. Although our business and asset base have not changed, the lending capacity of all financial institutions has diminished and risk premiums have increased. As future operations will be financed out of funds generated from financing activities, our ability to do so is dependent on, among other factors, the overall state of capital markets and investor appetite for investments in the pharmaceutical industry and our securities in particular.

Should we elect to satisfy our cash commitments through the issuance of securities, by way of either private placement or public offering or otherwise, there can be no assurance that our efforts to raise such funding will be successful, or achieved on terms favourable to us or our existing shareholders. If adequate funds are not available on terms

12

9

on terms favorable to us, we may have to reduce substantially or eliminate expenditures for research and development, testing, production and marketing of our proposed product, or obtain funds through arrangements with corporate partners that require us to relinquish rights to certain of our technologies or product. There can be no assurance that we will be able to raise additional capital if our current capital resources are exhausted.

The cost of director and officer liability insurance may increase substantially and may affect our ability to retain quality directors and officers.

We carry liability insurance on behalf of our directors and officers. Given a number of large director and officer liability insurance claims in the U.S. equity markets, director and officer liability insurance has become increasingly more expensive with increased restrictions. Consequently, there is no assurance that we will continue to be offered this insurance or be able to obtain adequate coverage. The inability to acquire the appropriate insurance coverage may limit our ability to attract and maintain directors and officers as required to conduct our business.

We are dependent on our key employees and collaborators.

Our ability to develop the product will depend, to a great extent, on our ability to attract and retain highly qualified scientific personnel and to develop and maintain relationships with leading research institutions. Competition for such personnel and relationships is intense. We are highly dependent on the principal members of our management staff as well as our advisors and collaborators, the loss of whose services might impede the achievement of development objectives. The persons working with us are affected by a number of influences outside of our control. The loss of key employees and/or key collaborators may affect the speed and success of product development.

Our share priceBarbados law differs from the laws in effect in Canada and may be highly volatile.afford less protection to holders of our securities.

Market prices forCertain of our assets and intellectual property are held by our wholly-owned subsidiary, Oncolytics Barbados, which is organized under the laws of Barbados. It may not be possible to enforce court judgments obtained in Canada against Oncolytics Barbados in Barbados based on the civil liabilities provisions of applicable securities laws. In addition, there is some doubt as to whether the courts of biotechnology companies generally are volatile. This increases the riskBarbados would recognize or enforce judgments of securities litigation. Factors such as announcements (publicly made or at scientific conferences) of technological innovations, new commercial products, patents, the development of proprietary rights, results of clinical trials, regulatory actions, publications, quarterly financial results, our financial position, public concern over the safety of biotechnology, future sales of shares byCanadian courts obtained against us or our current shareholdersdirectors or officers based on the civil liabilities provisions of Canadian securities laws or hear actions against us or those persons based on such laws.

Changes in law could adversely affect our business and corporate structure.

There can be no assurances that there will not occur changes in corporate, tax, property and other factors could have a significant effect onlaws in Canada and/or Barbados (or the market priceinterpretation thereof by regulatory or tax authorities) which may materially and volatility of the common shares.adversely affect our businesses and corporate structure.

We incur some of our expenses in foreign currencies and therefore we are exposed to foreign currency exchange rate fluctuations.

We incur some of our manufacturing, clinical, collaborative and consulting expenses in foreign currencies, primarily the U.S. dollar and the British pound (“GBP”). We are therefore exposed to foreign currency rate fluctuations. Also, as we expand to other foreign jurisdictions there may be an increase in our foreign exchange exposure.

We earn interest income on our excess cash reserves and are exposed to changes in interest rates.

We invest our excess cash reserves in investment vehicles that provide a rate of return with little risk to principal. As interest rates change the amount of interest income we earn will be directly impacted.

The Corporation may fail to achieve and maintain adequate internal control over financial reporting pursuant to the requirements of the Sarbanes-Oxley Act and equivalent Canadian legislation.

13

The Corporation documented and tested during its most recent fiscal year its internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act (“SOX”) and equivalent Canadian legislation. SOX requires an annual assessment by management of the effectiveness of the Corporation’s internal controls over financial reporting and an attestation report by the Corporation’s independent auditors addressing this assessment. The Corporation may fail to achieve and maintain the adequacy of its internal controls over financial reporting as such standards are modified, supplemented, or amended from time to time, and the Corporation may not be able to ensure that it can conclude, on an ongoing basis, that it has effective internal controls over financial reporting in accordance with Section 404 of SOX. The Corporation’s failure to satisfy the requirements of Section 404 of SOX on an ongoing, timely basis could result in the loss of investor confidence in the reliability of its financial statements, which in turn could harm the Corporation’s business and negatively impact the trading price of the common shares or the market value of its other securities. In addition, any failure to implement required new or improved controls, or difficulties encountered in their implementation, could harm the Corporation’s operating results or cause it to fail to meet its reporting obligations. Future acquisitions of companies, if any, may provide the Corporation with challenges in implementing the required processes, procedures and controls in its acquired operations. No evaluation can provide complete assurance that the Corporation’s internal controls over financial reporting will detect or uncover all failures of persons within the Corporation to disclose material information otherwise required to be reported. The effectiveness of the Corporation’s processes, procedures and controls could also be limited by simple errors or faulty judgments. In addition, if the Corporation expands, the challenges involved in implementing appropriate internal controls over financial reporting will increase and will require that the Corporation continue to improve its internal controls over financial reporting.

Because the Corporation is a Canadian corporation and the majority of its directors and officers are resident in Canada, it may be difficult for investors in the United States to enforce civil liabilities against the Corporation based solely upon the federal securities laws of the United States.

The Corporation is a Canadian corporation, with its principal place of business in Canada. A majority of the Corporation’s directors and officers and some or all of the experts named in the registration statement to which this prospectus supplement relates are residents of Canada and a significant portion of the Corporation’s assets and the assets of a majority of the Corporation’s directors and officers and the experts named in this prospectus supplement are located outside the United States. Consequently, it may be difficult for U.S. investors to effect service of process within the United States upon the Corporation or its directors or officers or such experts who are not residents of the United States, or to realize in the United States upon judgments of courts of the United States predicated upon civil liabilities under the U.S. Securities Act of 1933, as amended. Investors should not assume that Canadian courts (1) would enforce judgments of U.S. courts obtained in actions against the Corporation or such directors, officers or experts predicated upon the civil liability provisions of the U.S. federal securities laws or the securities or “blue sky” laws of any state within the United States or (2) would enforce, in original actions, liabilities against the Corporation or such directors, officers or experts predicated upon the U.S. federal securities laws or any such state securities or “blue sky” laws. In addition, the protections afforded by Canadian securities laws may not be available to investors in the United States.

Possible “passive foreign investment company” status

Potential investors that are U.S. taxpayers should be aware that the Corporation believes that it qualified as a PFIC for the tax year ended December 31, 2009, and based on current business plans and financial projections, the Corporation anticipates that it may qualify as a PFIC for the subsequent taxable years. If the Corporation is or becomes a PFIC, any gain recognized on the sale of the Unit Shares, Warrants or Warrant Shares and any “excess distributions” (as specifically defined) paid on Unit Shares or Warrant Shares must be rateably allocated to each day in a U.S. taxpayer’s holding period for the Unit Shares, Warrants or Warrant Shares. The amount of any such gain or excess distribution allocated to prior years of such U.S. taxpayer’s holding period for the Unit Shares, Warrants or Warrant Shares generally will be subject to U.S. federal income tax at the highest tax rate applicable to ordinary income in each such prior year, and the U.S. taxpayer will be required to pay interest on the resulting tax liability for each such prior year, calculated as if such tax liability had been due in each such prior year.

The determination of whether the Corporation will be a PFIC for a taxable year depends, in part, on the application of complex U.S. federal income tax rules, which are subject to differing interpretations. In addition, whether the Corporation will be a PFIC for any taxable year generally depends on its assets and income over the course of each

14

such taxable year and, as a result, cannot be predicted with certainty as of the date of this prospectus supplement. Accordingly, there can be no assurance that the IRS will not challenge the determination made by the Corporation concerning its PFIC status or that the Corporation will not be a PFIC for any taxable year. For a more detailed discussion see “Certain United States Federal Income Tax Considerations” below.

Our share price may be highly volatile.

Market prices for securities of biotechnology companies generally are volatile. This increases the risk of securities litigation. Factors such as announcements (publicly made or at scientific conferences) of technological innovations, new commercial products, patents, the development of proprietary rights, results of clinical trials, regulatory actions, publications, quarterly financial results, our financial position, public concern over the safety of biotechnology, future sales of shares by us or our current shareholders and other factors could have a significant effect on the market price and volatility of the common shares.

Potential dilution of present and prospective shareholdings.

In order to finance future operations and development efforts, the Company may raise funds through the issue of common shares or the issue of securities convertible into common shares. The Company cannot predict the size of future issues of common shares or the issue of securities convertible into common shares or the effect, if any, that future issues and sales of the Company’s common shares will have on the market price of its common shares. Any transaction involving the issue of previously authorized but unissued shares, or securities convertible into shares, would result in dilution, possibly substantial, to present and prospective holders of shares.

The Company does not intend to pay cash dividends in the foreseeable future.

The Company has not declared or paid any dividends since its incorporation. The Company intends to retain earnings, if any, to finance the growth and development of its business and does not intend to pay cash dividends on the common shares in the foreseeable future. Any return on an investment in the common shares will come from the appreciation, if any, in the value of the common shares. The payment of future cash dividends, if any, will be reviewed periodically by the board of directors and will depend upon, among other things, conditions then existing including earnings, financial condition and capital requirements, restrictions in financing agreements, business opportunities and conditions and other factors.

ITEM 4. INFORMATION ON THE COMPANY

| A. | History and Development of the Company |

Oncolytics Biotech Inc. was formed under the Business Corporations Act (Alberta) on April 2, 1998 as 779738 Alberta Ltd. On April 8, 1998, we changed our name to Oncolytics Biotech Inc.

Our principal executive office is located at 210, 1167 Kensington Cres. NW, Calgary, Alberta, Canada, T2N 1X7, telephone (403) 670-7377. Our agent for service in the U.S. is DL Service, Inc. located at 1420 Fifth Avenue, Suite 3400, Seattle, Washington, 98101, telephone (206) 903-8800.

10

On July 1, 2008, we completed an internal reorganization to provide additional international flexibility and promote broadened opportunities for Oncolytics. Pursuant to the internal reorganization we transferred certain assets to our wholly-owned subsidiary, Oncolytics Biotech (Barbados) Inc. (“Oncolytics Barbados”OBB”), in consideration for additional shares in the capital of Oncolytics Barbados.OBB. The transferred assets consisted of: (a) the rights to certain regulatory submissions; (b) certain non-Canadian patents and patent applications; and (c) certain agreements to which we were a party, including, clinical research management agreements, clinical trial agreements, research agreements and manufacturing agreements. We also granted Oncolytics BarbadosOBB permission to use certain other intellectual property rights not transferred by us to Oncolytics Barbados.OBB. Concurrently with the asset transfer, the Corporation and Oncolytics BarbadosOBB entered into a trust agreement pursuant to which we agreed to hold legal title to the transferred assets with beneficial title remaining with Oncolytics Barbados.OBB.

15

As part of the internal reorganization, the Corporation and Oncolytics BarbadosOBB also entered into a research and development agreement on July 1, 2008 pursuant to which we agreed to provide certain services to Oncolytics Barbados,OBB, including: conducting research and development related to the transferred assets; coordinating clinical trials and the handling of data generated by such trials; pursuing regulatory approvals as required; coordinating the filing, prosecution and maintenance of patent applications and patents; and coordinating the development and implementation of manufacturing processes.

In December 2009,2008, we incorporated a Delaware company, Oncolytics Biotech (U.S.) Inc. As at December 31, 2008, there was no ongoing activity in this subsidiary.(“OBUS”) which is wholly owned by OBB. OBUS provides certain services to OBB including conducting research and development related to the transferred assets; coordinating clinical trials and the handling of data generated by such trials.

On March 2, 2009 we entered into an agreement to acquire an inactive private company ("PrivateCo"), pursuant to a plan of arrangement under the Business Corporations Act (Alberta) (the "Arrangement"). PrivateCo does not actively carry on any business operations, has accumulated tax losses from its previous development business, and is expected to have approximately $2.3 million in net cash available at the closing of the transaction.

Under the terms of the Arrangement, we will issueissued common shares of Oncolytics at an exchange ratio calculated based upon an agreed premium to PrivateCo's net cash per share at closing and using an ascribed price per common share of Oncolytics of $1.69 (which is based on the 20 day volume weighted average trading price of Oncolytics shares on the Toronto Stock Exchange up to and including March 2, 2009). Completion of this transaction is subject to a number of conditions including receipt of all necessary shareholder, court and regulatory approvals. The acquisition is expected to closeclosed in April 2009.

A description of our principal capital expenditures and divestitures and a description of acquisitions of material assets iscan be found in our MD&A and in the notes to our financial statements included elsewhere in this annual report.

| B. | Business Overview |

Since our inception in April of 1998, Oncolytics Biotech Inc. has been a development stage company and we have focused our research and development efforts on the development of REOLYSIN®, our potential cancer therapeutic. We have not been profitable since our inception and expect to continue to incur substantial losses as we continue research and development efforts. We do not expect to generate significant revenues until, if and when, our cancer product becomes commercially viable.

Our Business

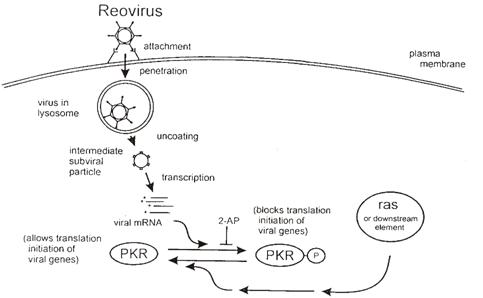

Our potential product for human use, REOLYSIN®, is developed from the reovirus. This virus has been demonstrated to replicate specifically in tumour cells bearing an activated Ras pathway. Activating mutations of Ras occur in approximately 30% of all human tumours directly, but considering its central role in signal transduction, activation of the Ras pathway has been shown to play a role in approximately two-thirds of all tumours.

The functionality of the product is based upon the finding that tumours bearing an activated Ras pathway are deficient in their ability to activate the anti-viral response mediated by the host cellular protein, PKR. Since PKR is responsible for preventing reovirus replication, tumour cells lacking the activity of PKR are susceptible to reovirus infections. As normal cells do not possess Ras activations, these cells are able to thwart reovirus infections by the activity of PKR. In a tumour cell with an activated Ras pathway, reovirus is able to freely replicate and hence kill the host tumour cell. The result of this replication is progeny viruses that are then free to infect surrounding cancer

11

cells. This cycle of infection, replication and cell death is believed to be repeated until there are no longer any tumour cells carrying an activated Ras pathway available.

The following schematic illustrates the molecular basis of how the reovirus kills cancer cells.

16

Scientific Background

The Ras protein is a key regulator of cell growth and differentiation. It transmits signals from the cell's surface, via growth factor receptors, to downstream elements, which are in turn relayed to the nucleus. This transmission of signals from the cell surface to the cell's nucleus is collectively referred to as "signal transduction." The transmission of these signals results in cell growth, division, and in some instances cellular differentiation. In normal cells, cell growth occurs only in the presence of factors stimulating the cells to grow. Mutations in Ras itself, or any of the elements along the Ras pathway, often lead to activation of the pathway in the absence of the appropriate growth stimuli, leading to the uncontrolled growth of these cells and ultimately to the development of a cancerous state. In fact, approximately 30% of all cancers are known to be due to mutations in Ras itself. The frequency of these Ras mutations, as well as their etiology in a given tumour is, however, tissue specific. Activating mutations in Ras are found in many types of human malignancies but are highly represented in pancreatic (90%), sporadic colorectal (50%), lung carcinomas (40%), and myeloid leukemia (30%). Because Ras is a regulator of key mitogenic signals, aberrant function of upstream elements such as receptor tyrosine kinases (RTKs) can also result in Ras activation in the absence of mutations in Ras itself. Indeed, over-expression of these RTKs such as HER2/neu/ErbB2 or the epidermal growth factor receptor is common in breast cancer (25-30%), and over-expression of the platelet-derived growth factor receptor (“PDGFR”) is common in glioblastomas and gliomas, all of which are tumour types in which Ras mutations are relatively rare. Although activating mutations of Ras itself are thought to occur in only about 30% of all tumours, it is expected that approximately two-thirds of all tumours have activated Ras signaling pathways as a result of mutations in genes that lie upstream of Ras. With this in mind, Ras becomes a significant therapeutic target in oncology.

All available scientific evidence developed or reviewed by us to date supports the premise that the reovirus only actively infects and replicates in cells with an activated Ras pathway. This naturally occurring virus is believed to cause only mild infections of the respiratory and gastrointestinal tract and in general, reovirus infections in humans are asymptomatic and usually sub-clinical. Research has indicated this virus replicates in, and therefore kills, only cancer cells (i.e. cancer cells with an activated Ras pathway), but does not replicate in normal cells. It has been demonstrated that reovirus replication is restricted in "normal" cells due to the activation of the double stranded RNA-activated protein kinase (“PKR”). PKR is a crucial element in protecting cells from reovirus infection and is

12

capable of blocking viral protein translation. Activated Ras (or an activated element of the Ras pathway) prevents PKR activation, and thus allows viral replication to ensue only in this subset of cancer cells. To prove that reovirus could be used as a potential cancer therapeutic, a number of animal models were developed. Experiments using this virus to treat mouse tumours, expanded animal models as well as human brain, breast, and prostate tumours implanted in immuno-compromised mice have yielded promising results. In animals where tumour regression was

17

noted, a single injection of reovirus is often enough to cause complete tumour regression. More importantly, it was demonstrated that this treatment is effective in causing tumour regression in immune competent animals. We believe that the nature of this virus, combined with its selective replication makes it an attractive candidate as a cancer therapy.

We also believe that this research may have broad utility in the treatment of tumours with an activated Ras pathway as well as a potential use as an adjuvant therapy following surgical tumour resection or as an adjuvant therapy to conventional chemotherapeutic or radiation therapies.

The Potential Cancer Product

Cancer is a group of related diseases characterized by the aberrant or uncontrolled growth of cells and the spread of these cells to other sites in the body. These cancer cells eventually accumulate and form tumours that can disrupt and impinge on normal tissue and organ function. In many instances, cells from these tumours can break away from the original tumour and travel through the body to form new tumours through a process referred to as metastasis.

Our cancer product is a potential therapeutic for tumours possessing an activated Ras pathway. In tumour cells with this type of activation, the virus is cytotoxic but may have no effect on the surrounding normal tissue. Activating mutations of Ras are believed to account for approximately 30% of all human tumours directly. It is also possible to activate Ras through mutation of proteins that control its activity rather than through direct mutations of Ras itself. This suggests that approximately two thirds of tumours may respond to this treatment.

Clinical Trial Program

We are directing a broad clinical trial program with the objective of developing REOLYSIN® as a human cancer therapeutic. The clinical program includes clinical trials which we sponsor directly along with clinical trials that are being sponsored by the U.S. National Cancer Institute (“NCI”), the University of Leeds and the Cancer Therapy & Research Center at the University of Texas Health Center in San Antonio (“CTRC”). Our clinical trial program includes human trials using REOLYSIN® alone, and in combination with radiation and chemotherapy, and delivered via local administration and/or intravenous administration.

Clinical Trial Chart

The following chart shows theour clinical trials that we have sponsored:trials:

Trial number | Delivery Method | Trial Program and Cancer Indication | Location | Status |

REO 020 | Intravenous administration in combination with paclitaxel and carboplatin (sponsored by the CTRC) | Phase II metastatic melanoma | United States | Ongoing |

REO 016 | Intravenous administration in combination with paclitaxel and carboplatin | Phase II non-small cell lung with K-RAS or EGFR-activated tumours | United States |

|

REO 015 | Intravenous administration in combination with paclitaxel and carboplatin | Phase II head and neck | United States | Ongoing |

|

|

|

|

|

13

18

Trial number | Delivery Method | Trial Program and Cancer Indication | Location | Status |

REO | Intravenous administration | Phase II | United States |

|

REO 013 | Intravenous administration monotherapy (sponsored by University of Leeds) | Translational metastatic colorectal | United Kingdom | Ongoing |

NCI Trial | Intravenous administration monotherapy (NCI) | Phase II melanoma | United States | Ongoing |

NCI Trial | Intravenous and intraperitoneal administration monotherapy (NCI) | Phase I/II ovarian | United States | Ongoing |

REO 012 | Intravenous administration in combination with cyclophosphamide | Phase I/II pancreatic, lung, ovarian | United Kingdom | Ongoing |

REO 011 | Intravenous administration in combination with paclitaxel and carboplatin | Phase I/II melanoma, lung, ovarian | United Kingdom |

|

REO 010 | Intravenous administration in combination with docetaxel | Phase I/II bladder, prostate, lung, upper gastro-intestinal | United Kingdom |

|

REO 009 | Intravenous administration in combination with gemcitabine | Phase I/II pancreatic, lung, ovarian | United Kingdom |

|

REO 008 | Local therapy in combination with radiation | Phase II various metastatic tumours, including head & neck | United Kingdom |

|

REO 007 | Infusion monotherapy | Phase I/II recurrent malignant gliomas | United States | Ongoing |

REO 006 | Local therapy in combination with radiation | Phase I various metastatic tumours | United Kingdom | Complete |

REO 005 | Intravenous administration | Phase I various metastatic tumours | United Kingdom | Complete |

19

Trial number | Delivery Method | Trial Program and Cancer Indication | Location | Status |

| monotherapy | ||||

REO 004 | Intravenous administration monotherapy | Phase I various metastatic tumours | United States | Complete |

REO 003 | Local monotherapy | Phase I recurrent malignant gliomas | Canada | Complete |

REO 002 | Local monotherapy | T2 prostate cancer | Canada | Complete |

REO 001 | Local monotherapy | Phase I trial for various subcutaneous tumours | Canada | Complete |

Patents and Trade Secrets

The patent positions and proprietary rights of pharmaceutical and biotechnology firms, including us, are generally uncertain and involve complex legal and factual questions. We believe there will continue to be significant litigation in the industry regarding patent and other intellectual property rights.

Currently, we have over 200 issued patents including 3133 issued U.S. patents. We hadalso have over 190180 patent applications filed in the U.S., Canada, and other jurisdictions, but we cannot be certain whether any given patent

14

application filed by us will result in the issuance of a patent or if any given patent issued to us will later be challenged and invalidated. Nor can we be certain whether any given patent that may be issued to us will provide any significant proprietary protection to our product and business.

Litigation or other proceedings may also be necessary to enforce or defend our proprietary rights and patents. To determine who was first to make an invention claimed in a United States patent application or patent and thus be entitled to a patent, the United States Patent and Trademark Office, or USPTO, can declare an interference proceeding. In Europe, patents can be revoked through opposition or nullity proceedings. In the United States patents may be revoked or invalidated in court actions or in re-examination proceedings in the USPTO. Such litigation or proceedings could result in substantial cost or distraction to us, or result in an adverse decision as to our or our licensors’ patent applications and patents. We are not currently involved in any interference proceedings, re-examination proceedings, opposition or nullity proceedings or any court actions concerning our patent applications and patents. We may be involved in such proceedings in the future.

Our commercial success depends, in part, on not infringing the patents or proprietary rights of others and not breaching licenses granted that may be granted to us. Competitors may have filed patent applications and obtained patents and may in the future file patent applications and obtain patents relevant to our product and technologies. We are not aware of competing intellectual property relating to our REOLYSIN® project. While we currently believe that we have the necessary freedom to operate in these areas, there can be no assurance that others will not challenge our position in the future. Litigation to defend our position could be costly and time consuming. We also cannot be certain that we will be successful. We may be required to obtain a license from the prevailing party in order to continue the portion of our business that relates to the proceeding. We may also be required to obtain licenses to other third-party technologies necessary in order to market our products. Such licenses may not be available to us on acceptable terms or on any terms and we may have to discontinue that portion of our business. Any failure to license any technologies required to commercialize our technologies or products at reasonable cost may have a material adverse effect on our business, results of operations, financial condition, cash flow and future prospects. We are not currently involved in any litigation concerning our competitors’ patent applications and patents. We may be involved in such litigation in the future.

We also rely on unpatented trade secrets and improvements, unpatented know-how and continuing technological innovation to develop and maintain our competitive position. No assurance can be given that others will not independently develop substantially equivalent proprietary information and techniques, or otherwise gain access to

20

our trade secrets or disclose such technology, or that we can meaningfully protect our rights to our unpatented trade secrets.

We require our employees and consultants to execute confidentiality agreements upon the commencement of employment and consulting relationships with us. These agreements provide that all confidential information developed by or made known to an individual during the course of the employment or consulting relationship generally must be kept confidential. In the case of employees, the agreements provide that all inventions conceived by the individual, while employed by us, relating to our business are our exclusive property. While we have implemented reasonable business measurements to protect confidential information, these agreements may not provide meaningful protection for our trade secrets in the event of unauthorized use or disclosure of such information.

Business Strategy

Our business strategy is to develop and market REOLYSIN® in an effective and timely manner, and access additional technologies at a time and in a manner that we believe is best for our development. We intend to achieve our business strategy by focusing on these key areas:

| • | Develop REOLYSIN® by continuing to progress the product through our clinical trial program assessing the safety and efficacy in human subjects; |

Establish collaborations with experts to assist us with scientific and clinical developments of this new potential pharmaceutical product;

15

Implement strategic alliances with selected pharmaceutical and biotechnology companies and selected laboratories, at a time and in a manner where such alliances may complement and expand our research and development efforts on the product and provide sales and marketing capabilities;

Utilize our broadening patent base and collaborator network as a mechanism to meet our strategic objectives; and

Develop relationships with companies that could be instrumental in assisting us to access other innovative therapeutics.

Our business strategy is based on attaining a number of commercial objectives, which, in turn, are supported by a number of product development goals. Our new product development presently being conducted is primarily of a research and development nature. In the context of this Annual Information Form,Report, statements of our "belief" are based primarily upon our results derived to date from our research and development program with animals, and early stage human trials, and upon which we believe that we have a reasonable scientific basis to expect the particular results to occur. It is not possible to predict, based upon studies in animals, or early stage human trials, whether a new therapeutic will ultimately prove to be safe and effective in humans. There are no assurances that the particular result expected by us will occur.